Piper Jaffray Technology, Media and Telecommunications ...

73

Piper Jaffray Technology, Media and Telecommunications Conference MARCH 12–13, 2013 IN NEW YORK CITY

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Piper Jaffray Technology, Media and Telecommunications ...

Piper Jaffray Technology, Media and Telecommunications Conference

M A R C H 1 2 – 1 3 , 2 0 1 3 I N N E W Y O R K C I T Y

Piper Jaffray does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decisions. This report should be read in conjunction with important disclosure information, including an attestation under Regulation Analyst Certification, found at the end of this report or at the following site: http://www.piperjaffray.com/researchdisclosures.

Piper Jaffray Technology, Media and Telecommunications Conference

M A R C H 12 – 13 , 2 0 13 I N N E W YO R K C I T Y

2

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

CONTENTS

Technology, Media and Telecommunications Conference

• Event Map . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

• Keynote Speakers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

• Panels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

• Participating Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

• Company Overviews . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

• Piper Jaffray Investment Research Team . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .41

• Technical Research . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

• Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

• Important Research Disclosures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

3

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

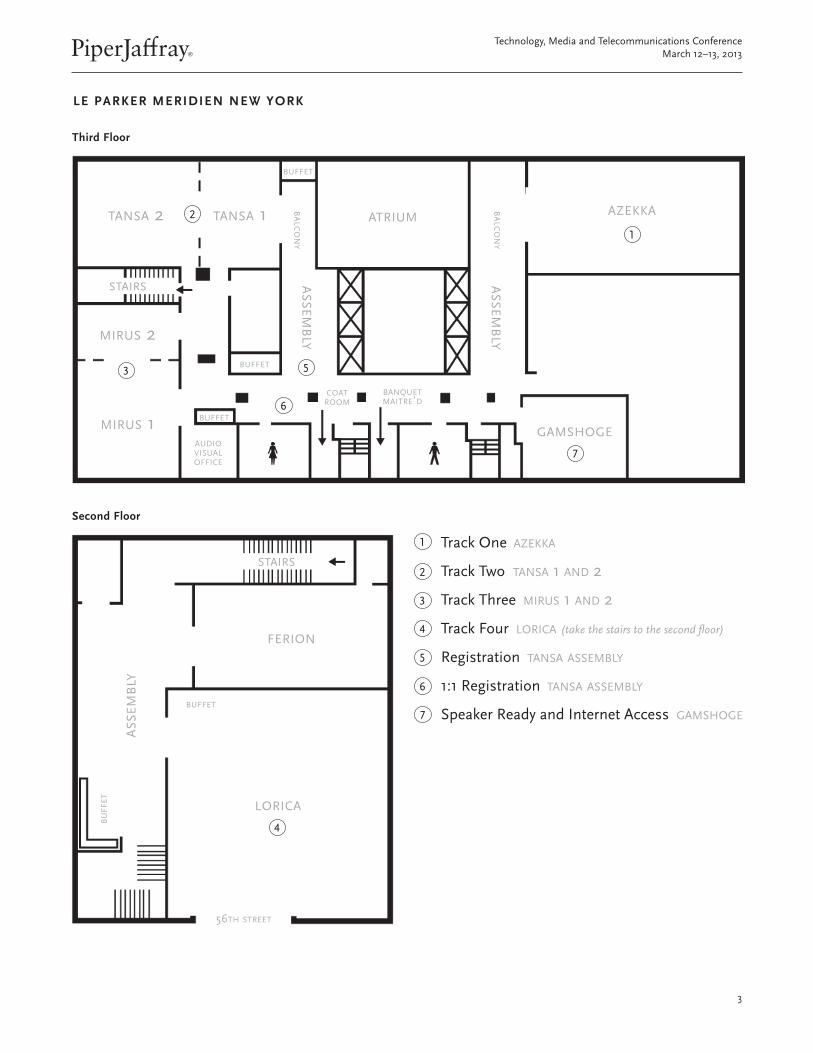

LE PARKER MERIDIEN NEW YORK

as

se

mb

ly

53

azekkaatrium

mirus 1 gamshoge

as

se

mb

lyb

alc

on

y

ba

lco

ny

buffet

buffet

buffet

audiovisualoffice

coat room

banquetmaitre’d6

tansa 2 tansa 1

mirus 2

2

1

7

Third Floor

stairs

Track One azekka

Track Two tansa 1 and 2

Track Three mirus 1 and 2

Track Four lorica (take the stairs to the second floor)

Registration tansa assembly

1:1 Registration tansa assembly

Speaker Ready and Internet Access gamshoge

4

3

2

5

1

6

7

bu

ffe

t

as

se

mb

ly

buffet

lorica

ferion

56th street

4

Second Floor

stairs

4

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

Steve CanianoVice President, Hosting, Managed Applications and Cloud SolutionsAT&T Business Solutions

Steve Caniano is responsible for developing the strategy and execution plan to scale AT&T’s cloud solutions business. This includes defining and establishing alignment with key industry players to ensure AT&T’s services are embedded in their cloud platforms, providing the broadest enablement of cloud solutions for our customers. Caniano previously led AT&T’s global hosting, application and cloud services business, where he directed product and investment strategy, marketing and communications, and held accountability for customer satisfaction, and the financial health of the business.

Caniano developed AT&T’s network enabled cloud strategy and led the transformation of the company’s hosting business into scalable, on-demand solutions. He has been instrumental in forging key partner alliances to support the business, while scaling services globally. Caniano regularly collaborates with customers to ensure AT&T is meeting customer expectations and requirements, but more importantly, incorporating customer insights into AT&T’s cloud solutions strategy and portfolio. He frequently represents AT&T in key industry events and analyst forums to position cloud solutions and to shape marketplace perceptions of AT&T’s role in the “cloud”.

During his career at AT&T, Caniano has held positions in sales, operations, program management, product management, strategic planning, supplier management and systems development. Caniano designed and launched the original Global Solution Center in support of business customers, and led the team having responsibility for engagement management, solution strategy and technical solution design for AT&T’s largest enterprise and global customers. He has worked with and managed leading-edge technologies throughout his career, while always maintaining focus on the customer solution.

David KirkpatrickInternet and Technology ExpertAuthor of The Facebook Effect

For more than 20 years, David Kirkpatrick was a writer for Fortune, most recently as senior editor of Internet and technology. He is regularly ranked one of the world’s top technology journalists.

Kirkpatrick created Fortune’s Brainstorm brand, which ran for five years. Now, with a group of former Fortune colleagues, Kirkpatrick has a media company called Techonomy, focusing on the centrality of technology to business and social progress and the urgency of embracing the rapid pace of change brought by technology.

Kirkpatrick’s expertise on technology subjects led him to pen the definitive book on Facebook, The Facebook Effect: The Inside Story of the Company That is Connecting the World. The Facebook Effect uncovers how in little more than half a decade, Facebook has gone from a dorm-room novelty to a company with over 900 million users. It is one of the fastest growing companies in history, an essential part of the social life not only of teenagers but hundreds of millions of adults worldwide. Kirkpatrick had the full cooperation of Facebook’s key executives in researching this fascinating history of the company and its impact on our lives.

K E Y N O T E S P E A K E R S

5

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

Zach NelsonPresident and Chief Executive OfficerNetSuite Inc.

Zach Nelson has more than 25 years of leadership experience in the high-tech industry, where he has held a variety of executive positions spanning marketing, sales, product development and business strategy with leading companies including Oracle, Sun Microsystems and McAfee/Network Associates.

Nelson has been CEO of NetSuite since 2002. He led NetSuite’s successful IPO in 2007 and its rise from start-up to the industry’s cloud ERP leader. Under his leadership, NetSuite has become the leading provider of cloud computing business management software suites in the world.

Nelson holds bachelor’s and master’s degrees from Stanford University.

Fred WilsonManaging PartnerUnion Square Ventures

Fred Wilson is a managing partner of Union Square Ventures (“USV”), a New York-based firm that manages $450 million and has been one of the top performing venture funds over the past decade. USV was the initial investor in companies including Twitter, Zynga, Foursquare, Etsy, Covestar, Tumblr, Disqus and Indeed. Wilson writes a widely followed blog called AVC. He has sold portfolio companies to Google, Yahoo, AOL and other prominent Internet consolidators.

At the conference, we will hear Wilsons’s view of the technology landscape, trends in the Internet and social media spaces, and his investment philosophy. We will also be exploring the growth of Silicon Alley and the opportunities it has provided. Finally, we will be discussing the differences between the Internet marketplace today and that of the late 90s.

Wilson has been a venture capitalist since 1987 and founded Flatiron Partners (JP Morgan) before founding USV.

Wilson holds a bachelor’s degree in mechanical engineering from MIT and a Master of Business Administration degree from The Wharton School of Business.

K E Y N O T E S P E A K E R S

6

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

P A N E L S

Accelerating Design Cycles and Direct Digital Manufacturing ApplicationsAs companies continue to search for ways to accelerate revenue growth and better compete in the global marketplace, design cycles are constantly being reworked in hopes of improving time to market for new product introductions. 3D printing manufacturers and service bureaus have experienced significant growth with product development teams, discovering how 3D printer and services can help accelerate design cycles. In addition to shortening design cycles, additive manufacturing technologies have had significant technological improvements and 3D printers are now being used for direct digital manufacturing (AKA rapid prototyping or rapid manufacturing) to produce end user parts. This panel will include service provider Proto Labs, investment firm Lux Capital Management, and system manufacturers 3D Systems, Arcam and Stratasys.

All-Flash StorageThe “I/O bottleneck” problem has quickly become the top threat to the data storage industry, driven by the accelerating improvements in CPU performance vs. the lagging performance of disk drives. This performance gap creates an I/O bottleneck, which severely hinders the performance of applications and the overall efficiency and productivity of the data center. In order to address this problem, storage vendors are turning toward NAND flash to provide extremely fast access to the data. This panel will focus on the I/O bottleneck problem, its implications to data center productivity and how each vendor is specifically addressing the problem. We will hear from Whiptail and Nimbus Data, both of which have incorporated NAND flash memory into their respective storage arrays.

Back-End Test Teradyne and LTX-Credence will join us in a panel on the back-end test market where we hope to get clarity on how the mobility and connectivity segments could evolve in 2013 and some of the key drivers. We hope to hear about the timing of the recovery in the microcontroller segments along with the competitive landscape in the RF testing segment. We expect an update on the overall wireless test segment and the medium-term and long-term prospects. We also expect to hear about traction of new product rollout. Use of cash is a key question given that both the companies have accumulated a pile of cash. Finally, we anticipate an update on OSAT’s spending outlook for 2013 along with a view on upcoming inflection points that would increase test intensity.

Big Data and Analytics The increase of large and complex data sets, driven by things like social networks, smart meters, RFID, and national defense or scientific research, is creating new opportunities for software vendors to tackle the difficult tasks associated with aggregating, storing, analyzing and searching data. Datawatch and Jaspersoft will join us for a discussion on big data and how new technologies are solving the problems presented by big data, and what technologies and methodologies will be most suitable for capturing big data spending in the future.

Cloud-Based Human ResourcesIT organizations are beginning to funnel greater amounts of money into HR and talent management solutions as more organizations are recognizing employees as assets to their business rather than simply resources. “Strategic HR” is becoming the talk of the table and next-generation HR processes are gaining importance. The emergence of cloud-based systems, which deliver a remarkable user experience and value proposition that eclipses that of pre-Internet solutions, is further catapulting this trend into an acceleration mode. With a panel of executives from Cornerstone OnDemand and Ultimate Software, we will discuss the impact of cloud-based software on the HR industry and the contribution of these two companies toward this trend.

Communicating with Customers in the CloudThe way companies interact with both business and consumers has changed dramatically over the last decade with the introduction of SaaS-based software and the explosion of open-source software. With a panel of executives from ON24, SugarCRM and LivePerson, we will discuss the impact of cloud-based and open-source software on customer interaction and which technologies will ultimately win or lose.

Consumer Applications in 3D PrintingThe additive manufacturing (3D printing) market has taken a step in a completely new direction, aimed at the consumer market. This market, which was relatively nonexistent a few years ago, has grown substantially as new technology and more user-friendly systems have hit the market. We believe several obstacles still remain before consumer 3D printers can go mainstream and this panel will address how the industry is addressing some of these hurdles. Our consumer 3D printing panel will include service and content providers (Shapeways), system manufacturers (MakerBot, 3D Systems) and venture capitalist firm Lux Capital.

Cross Media Convergence and Ad EffectivenessMobile is shifting media consumption from a single screen (TV or PC) to multi-screen (TV, PC, smartphone, tablet, radio) simultaneous usage, creating an increasingly challenging environment for advertisers to reach audiences. Key panel topics include: 1) Despite “big data” captured everywhere, capturing ROI across a multitude of mediums remains a distant hope. How close are we to a scalable cross-screen solution that can demonstrate ROI and ultimately answer the age-old question: “I know half of my ad dollars are wasted, I just don’t know which half”? 2) Are gross rating points (GRP: the standard unit of currency for TV reach and ad buying) an acceptable measure in the digital world? Do vast amounts of new digital media data argue for more advanced measurement beyond GRP? 3) How important is the ability to measure viewable impressions and how effective is measurement today?

7

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

Data Privacy/Do-Not-Track DebateMicrosoft’s decision to enable “Do Not Track” (DNT) as default setting in upcoming Internet Explorer 10 browser has brought online data privacy back to the front and center. Key panel topics include: 1) Can industry self-regulation come to a consensus on DNT, third-party cookie data collection and behavioral ad targeting standards before the FTC steps in and forces action? 2) How does European privacy regulation compare to the U.S. and why may/not the U.S. develop similar policy? 3) What impact would a DNT default setting on Internet Explorer 10 and/or other browsers have on the ad ecosystem? And on the consumer Web experience?

Emerging Laser TechnologyNewport and Raydiance join us to discuss current and emerging trends in laser technologies and applications. We expect to gain insight into growing markets and applications for lasers such as UV lasers and green lasers. Newport’s broad laser product offering should help in terms of understanding some of the key applications that are being actively targeted including microelectronic, semiconductor and industrial manufacturing markets. Raydiance’s fascinating femtosecond-based laser approach should help investors gain a perspective into some of the new applications that are being pursued.

FiberIf you have metro fiber, there’s someone out there who may want to buy it. If history is any indicator, Zayo, who will be on this panel, may be interested or has at least looked at it. While public investors were looking the other way, Zayo has quietly built one of the largest networks of metro fiber. Why are private market multiples so much higher? What is it that the public markets are missing? Cogent carries an estimated 15% of the world’s Internet traffic connecting more than 30,000 customers in nearly 2,000 buildings. Management will be on-hand to help discuss industry pricing and demand dynamics. RedIT, another private company that operates in the southwestern U.S. and Latin America, will address the importance of fiber and connectivity in a cloud and data center-centric IT world.

Future of RadioThe sector is in such a state of flux, it’s sometimes difficult to define ‘radio.’ We have assembled a panel (Slacker, CMLS and HD Radio (iBiquity)) to discuss the evolving radio landscape and explore competitive strengths and weaknesses, shifts in listenership growth, advertising trends, shift to mobile and how changes to music licensing could alter the landscape.

Green Power Power consumption is a critical consideration in designing any electronic system. In order to minimize power consumption in any system from a mainframe to a handheld, the power delivery needs to be optimized across a broad range of operating conditions. This creates opportunity for power semiconductor companies that solve these issues.

Healthcare in the CloudWith the increasing adoption of cloud-based technology solutions in healthcare, we are stepping into a new avenue of growth for healthcare technology companies. Our panel consists of the companies that are at the forefront of this SaaS-based cloud solution revolution. Athenahealth has built a strong reputation and foothold in physician-based cloud solutions and is considered the market leader in the segment, while CareCloud is the newcomer. Medidata has disrupted the clinical trials market with their revolutionary cloud-based EDC (Rave®) platform and is ramping up analytical capabilities. We will be discussing why healthcare is the ideal use case for the cloud, and how new technologies can truly reform the nation’s largest industry.

Local Local advertising remains the next frontier for online advertising dollars. As customers seek local information more rapidly on mobile devices, the opportunity has become much more important to local businesses. Our panel will include platform and technology providers Marchex and ReachLocal to discuss how local businesses are navigating the available ad products.

Next-Gen Content ConsumptionThe biggest story in consumer electronics over the last several years has been the explosive growth in the Internet-connected device ecosystem and the improving ways users can access and interact with content. Whether via iOS devices, game consoles, peripheral Internet set-top boxes or other, the average household now has multiple ways to access Internet-delivered content on both the living room TV and mobile devices. Panelists will discuss the future direction of content consumption devices and changes in how we will all interface with video content in the coming years.

Next Leg of Online TravelWhile traditional online travel agents (OTAs) have multiple avenues for continued growth, we believe peripheral online travel services that go beyond the traditional OTA will continue to emerge. Online travel offerings including reviews and recommendations, travel inspiration, last-minute bookings, vacation rentals, metasearch and others will be discussed in this panel. Additionally, we will focus on the panelists’ view of the leading OTAs in the current environment and how they will partner or be competitive with the major OTAs.

Online Ad The emergence of mobile, social and video has reshaped both the performance and branded online advertising spaces over the past two years. These three sectors will continue to increase in terms of advertising budget allocation, but we are only at the beginning of companies developing unique technologies to take advantage of each unique medium. Our panel will explore the overall state of the online ad industry and how each participant utilizes their technology platforms to serve advertisers.

P A N E L S

8

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

OpticalThe optical industry has been in a six-quarter funk with demand from telco service providers at a three-year low, but datacom optics have remained strong given the growing demand for 100G technologies and data center investments. Given the cyclical nature of the optical industry, we believe spending on these technologies will improve with bandwidth-thirsty devices and video applications consuming more data than ever before. This panel will focus on telco spending intentions in 2013 and emerging products and technologies such as iTLAs, ROADMs, Tunable-XFPs and 100G coherent. We will be hosting two optical panels, including component suppliers Ciena, EMCORE and Oclaro (day one) followed by FNSR, Fabrinet and Neophotonics (day two).

Rapid Growth in Real-Time Bidding (RTB) and Impacts on Display Ad MarketRTB has taken the online display market by storm the past two years (now 25%+ of online impression volumes) causing average premium pricing contractions of 40% in LTM (PJC estimate). Key panel topics include: 1) What prevents online/mobile/video display transactions moving to 100% RTB and how will ad networks, agencies, publishers and private exchanges be impacted? 2) How will Facebook’s exchange (FBX) impact supply and demand dynamics in the exchange marketplace? How much demand can Facebook ultimately capture and can it be a needle-mover for the stock? 3) How can Nielsen and comScore’s viewable impression solutions add support to display pricing and benefit publishers in an increasingly high-volume RTB world?

Semiconductor Opportunities in Communication InfrastructureWe anticipate a broad upgrade cycle in communications driven by deferred capital investments, increasing speeds and feeds in access, government targets for broadband coverage, IPv6 upgrades, the ongoing transition from SONET to Ethernet and the explosion of wireless data to name a few. We believe the communication infrastructure IC companies that address these issues best will outperform the chip market in the years to come.

Social Media, Video and Mobile Advertising 2.0We will debate the effectiveness of social, mobile and online video advertising beyond clicks to tangible sales and engagement. Key panel topics include: 1) What are the latest learnings of these next-gen ad mediums from an effectiveness standpoint? What is/is not working? 2) Are we closer to finding a holy grail (versus a year ago) to achieving high engagement and loyalty from an “always-on” and “on-the-go” consumer? 3) How have smartphones and tablets closed the gap between commerce and marketing? How effective are smartphone ads today? Will tablet ad platforms ultimately trump smartphones from an effectiveness standpoint?

Software-Defined NetworkingIn its most basic form, software-defined networking (SDN) aims to replace traditional networking architecture, creating a more flexible and scalable network environment. We believe the continued adoption and deployment of SDN will have a substantial effect on the core networking landscape, posing numerous challenges for traditional networking vendors. As such, a handful of these vendors have further explored the implications of SDN and are attempting to position themselves ahead of the curve. Our panel (consisting of Arista Networks, Brocade Communications and Silver Peak Systems) will provide incremental insight into current SDN trends and how they believe the market landscape will look as this revolutionary technology continues to penetrate the networking space.

What’s Next in Mobile and Social GamesExcitement in the social gaming arena has given way to disappointment in recent months as leaders in the space (Zynga, etc.) have faced challenges in replicating successful game launches and improving monetization. Mobile gaming continues to be an area of growth due to increasing footprint of mobile devices, but could potentially face similar challenges. Our panelists will provide insight on the changing dynamics of social gaming, the potential implications for mobile gaming and the impact that growth in these categories is having on console gaming.

P A N E L S

9

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

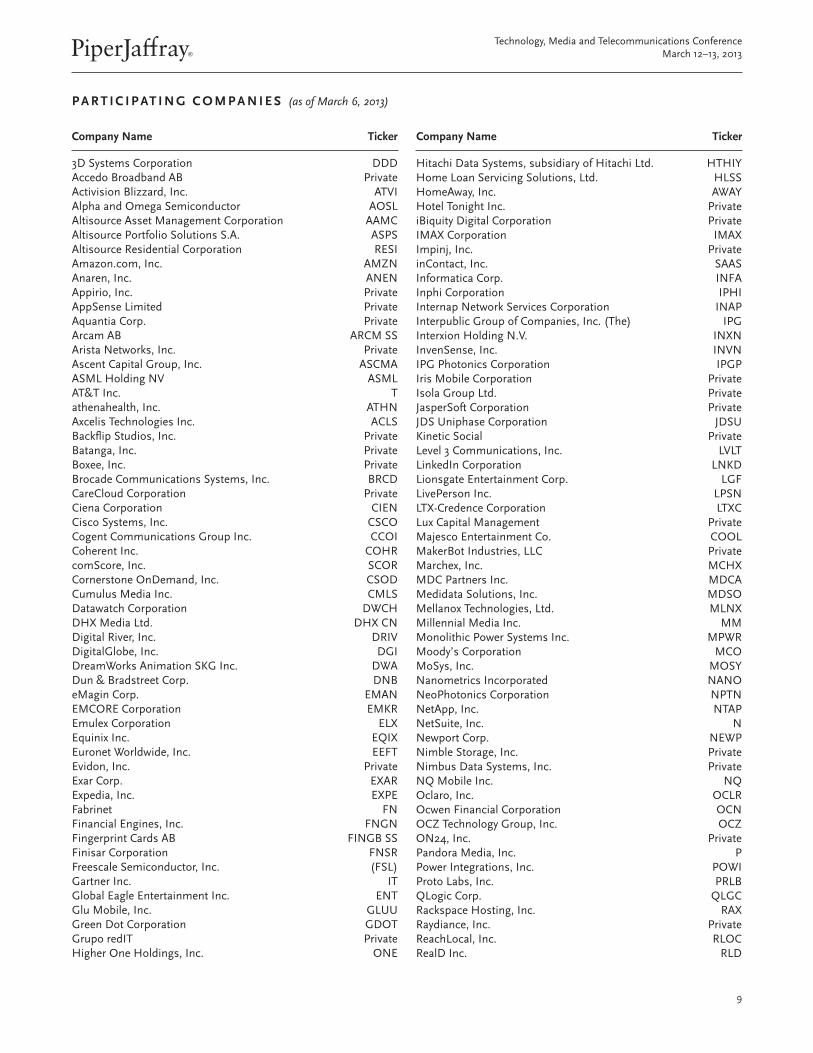

P A R T I C I P AT I N G C O M P A N I E S (as of March 6, 2013)

3D Systems Corporation DDDAccedo Broadband AB PrivateActivision Blizzard, Inc. ATVIAlpha and Omega Semiconductor AOSLAltisource Asset Management Corporation AAMCAltisource Portfolio Solutions S.A. ASPSAltisource Residential Corporation RESIAmazon.com, Inc. AMZNAnaren, Inc. ANENAppirio, Inc. PrivateAppSense Limited PrivateAquantia Corp. PrivateArcam AB ARCM SSArista Networks, Inc. PrivateAscent Capital Group, Inc. ASCMAASML Holding NV ASMLAT&T Inc. Tathenahealth, Inc. ATHNAxcelis Technologies Inc. ACLSBackflip Studios, Inc. PrivateBatanga, Inc. PrivateBoxee, Inc. PrivateBrocade Communications Systems, Inc. BRCDCareCloud Corporation PrivateCiena Corporation CIENCisco Systems, Inc. CSCOCogent Communications Group Inc. CCOICoherent Inc. COHRcomScore, Inc. SCOR Cornerstone OnDemand, Inc. CSODCumulus Media Inc. CMLSDatawatch Corporation DWCHDHX Media Ltd. DHX CNDigital River, Inc. DRIVDigitalGlobe, Inc. DGIDreamWorks Animation SKG Inc. DWADun & Bradstreet Corp. DNBeMagin Corp. EMANEMCORE Corporation EMKREmulex Corporation ELXEquinix Inc. EQIX Euronet Worldwide, Inc. EEFTEvidon, Inc. PrivateExar Corp. EXARExpedia, Inc. EXPEFabrinet FNFinancial Engines, Inc. FNGNFingerprint Cards AB FINGB SSFinisar Corporation FNSRFreescale Semiconductor, Inc. (FSL) Gartner Inc. ITGlobal Eagle Entertainment Inc. ENTGlu Mobile, Inc. GLUUGreen Dot Corporation GDOTGrupo redIT PrivateHigher One Holdings, Inc. ONE

Hitachi Data Systems, subsidiary of Hitachi Ltd. HTHIYHome Loan Servicing Solutions, Ltd. HLSSHomeAway, Inc. AWAYHotel Tonight Inc. PrivateiBiquity Digital Corporation PrivateIMAX Corporation IMAXImpinj, Inc. PrivateinContact, Inc. SAASInformatica Corp. INFAInphi Corporation IPHIInternap Network Services Corporation INAPInterpublic Group of Companies, Inc. (The) IPGInterxion Holding N.V. INXNInvenSense, Inc. INVNIPG Photonics Corporation IPGPIris Mobile Corporation PrivateIsola Group Ltd. PrivateJasperSoft Corporation PrivateJDS Uniphase Corporation JDSUKinetic Social PrivateLevel 3 Communications, Inc. LVLTLinkedIn Corporation LNKDLionsgate Entertainment Corp. LGFLivePerson Inc. LPSNLTX-Credence Corporation LTXCLux Capital Management PrivateMajesco Entertainment Co. COOLMakerBot Industries, LLC PrivateMarchex, Inc. MCHXMDC Partners Inc. MDCAMedidata Solutions, Inc. MDSOMellanox Technologies, Ltd. MLNXMillennial Media Inc. MMMonolithic Power Systems Inc. MPWRMoody’s Corporation MCOMoSys, Inc. MOSYNanometrics Incorporated NANONeoPhotonics Corporation NPTNNetApp, Inc. NTAPNetSuite, Inc. NNewport Corp. NEWPNimble Storage, Inc. PrivateNimbus Data Systems, Inc. PrivateNQ Mobile Inc. NQOclaro, Inc. OCLROcwen Financial Corporation OCNOCZ Technology Group, Inc. OCZON24, Inc. PrivatePandora Media, Inc. PPower Integrations, Inc. POWIProto Labs, Inc. PRLBQLogic Corp. QLGCRackspace Hosting, Inc. RAXRaydiance, Inc. PrivateReachLocal, Inc. RLOCRealD Inc. RLD

Company Name Ticker Company Name Ticker

10

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

Rentrak Corporation RENTRetail Solutions, Inc. PrivateRimini Street, Inc. PrivateRofin-Sinar Technologies Inc. RSTIRovi Corporation ROVIsalesforce.com, inc. CRMServiceSource International, Inc. SREVShapeways, Inc. PrivateSilver Peak Systems, Inc. PrivateSIRIUS XM Radio Inc. SIRISlacker, Inc. PrivateSolera Holdings Inc. SLHSTEC, Inc. STECStratasys, Inc. SSYSSugarCRM, Inc. PrivateTeradyne, Inc. TERTessera Technologies Inc. TSRAThe McGraw-Hill Companies, Inc. MHPThe Trade Desk, Inc. PrivateTiVo Inc. TIVOTripAdvisor, Inc. TRIPTurn Inc. PrivateUltimate Software Group, Inc. (The) ULTIUltra Clean Holdings, Inc. UCTTUnion Square Ventures PrivateValueVision Media, Inc. VVTVVeriFone Systems, Inc. PAYVerizon Communications Inc. VZVolterra Semiconductor Corporation VLTRWalter Investment Management Corp. WACWeb.com, Inc. WWWWWEX Inc. WXSWhipTail Technologies, Inc. PrivateWildTangent, Inc. PrivateWisdomTree Investments, Inc. WETFYelp, Inc. YELPZayo Group Inc. Private

P A R T I C I P AT I N G C O M P A N I E S (as of March 6, 2013)

Company Name Ticker

11

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

C O M P A N Y O V E R V I E W S (Highlighted companies are followed by Piper Jaffray investment research)

3D Systems (DDD) – $36.96 Market Cap: $2.14B Rating: Overweight 12-mo. Price Target: $42 (30x CY14E op income + cash)Thesis: We believe the market for 3D printers is in a secular growth phase and the growing adoption of 3D CAD usage coupled with price elasticity and increased awareness will continue to drive im-pressive 3D printer unit growth for the industry. This ultimately will create a growing annuity of high-margin consumable sales into this captive audience of 3D printing users. 3D Systems has also done an impressive job of rolling up the 3D printing service bureau industry, which has been one of the biggest factors in the company’s earnings accretion and operating margin expansion. We believe 3D Systems will continue to selectively acquire given the success it has had with this strategy and anticipate the ac-quisition focus will be more on international expansion. Given our belief in strong secular growth trends for the industry, and continued market penetration for 3D Systems, we reiterate our Overweight rating and $42 price target.Key Questions:• When do you believe the consumer 3D printing market will

start to drive meaningful revenue growth?• Can you discuss how 3D Systems is helping to grow the con-

sumer market by developing libraries of 3D content?• How have you been able to acquire so many different busi-

nesses without any channel/customer conflicts or integra-tion issues?

• Any estimate regarding how much of your system sales are going into direct digital manufacturing applications?

• How is 3D Systems protecting the material sales from third-party suppliers?

Description: 3D Systems is a leading provider of rapid prototyping services and 3D printers.Troy Jensen, CFA, Sr. Research Analyst, 612 303-6291

Accedo Broadband AB – PrivateDescription: Accedo is an enabler of TV application solutions to media companies, CE manufacturers and TV operators glob-ally. The company’s cloud-based platform provides applications, tools and services that allow customers to deliver IPTV solutions. Accedo’s platform enables companies to cost-efficiently develop, roll out, and manage IPTV applications and stores on multiple devices globally. Currently, CE device manufacturers and network operators are developing “TV Everywhere” solutions and are look-ing to roll these solutions out over the very near-term.Key Questions:• Will TV manufacturers attempt to build app ecosystems

themselves or increasingly look to third parties to enable this functionality?

• How does Apple’s rumored entry into the TV space change the landscape for devices app ecosystems in the living room? Will it be no more impactful than the existing Apple TV STB?

• Are TV operators supportive of enabling more content deliv-ery to the TV that is outside of the scope of their subscription offerings?

• Consumers are purchasing TVs that connect to the Internet, but in many cases not connecting them. What is the hurdle to increased usage of this functionality?

Activision Blizzard, Inc. (ATVI) – $14.30 Market Cap: $15.88B Rating: Overweight 12-mo. Price Target: $17 (19x CY13E EPS)Thesis: Activision holds a leading position among video game publishers due to the company’s ability to create engaging new content in existing titles, while also consistently generating new IP that adds layers to the story beyond to the core franchises. In 2013, Activision faces tough comps due to the massive success of Diablo 3 in 2012. The company has now factored this impact into CY13 guidance and, we believe, this outlook could prove conservative given the introduction of other new titles during the year, most notably Destiny (a Bungie title), and management’s consistent pattern of guiding initial full-year EPS well below ac-tual results. Additionally, with the catalyst of a new hardware cycle coming, there is potential for an improved trajectory of growth for video game publishers in 2014/15.Key Questions:• Will the company’s new game Destiny, a potentially material

title, ship in late 2013 or sometime in 2014? This could mate-rially impact EPS for the year.

• Is Activision gearing up to purchase a portion of the 61% stake in the company that Vivendi currently owns?

• How will video game software sales be impacted near-term by the announcement that new consoles are coming later this year and are likely not backward compatible?

• Can continued growth of Skylanders, shipment of Starcraft II and potential launch of Destiny lead to a revenue decline that is less material than the 14% year-over-year decline implied in Street consensus for CY13?

Michael Olson, Sr. Research Analyst, 612 303-6419

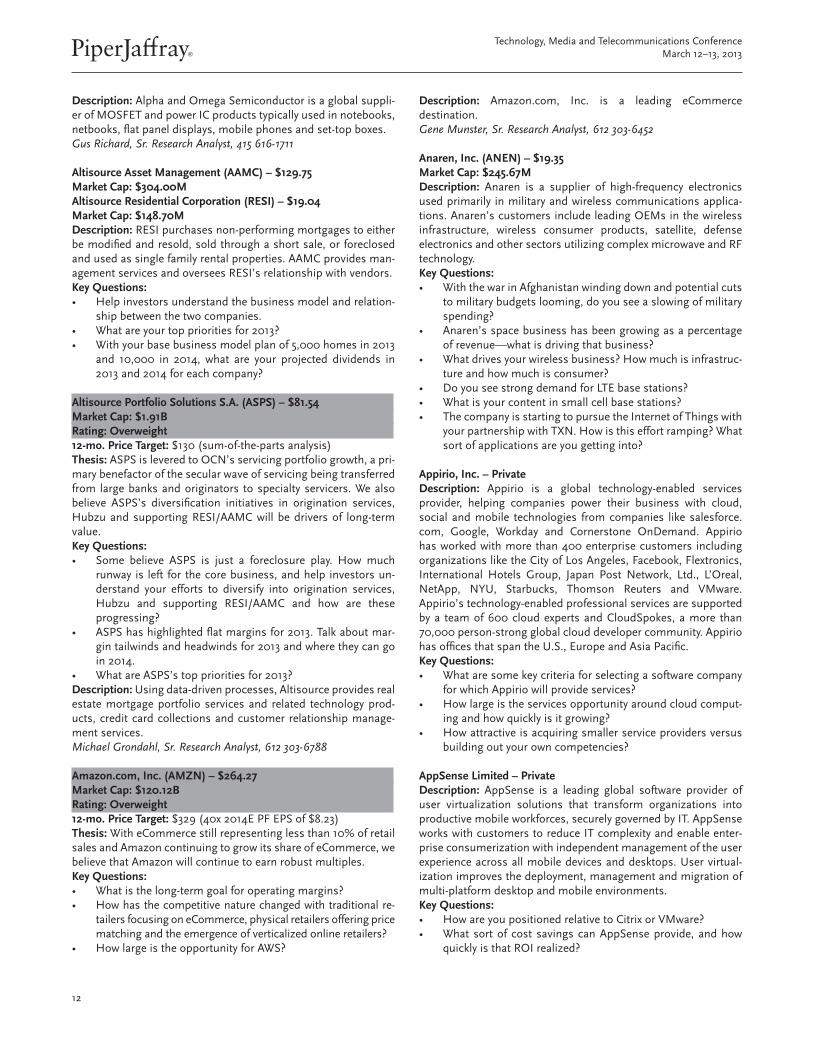

Alpha and Omega Semiconductor (AOSL) – $8.06; Market Cap: $204.96M Rating: Neutral 12-mo. Price Target: $8 (8x CY14E EPS)Thesis: Alpha and Omega is undergoing a unique transition from a fabless to a fab-lite business model, hoping to achieve margin expansion through accelerated new product introduction. We be-lieve this is still somewhat of a show-me story. We expect muted revenue growth as personal computer (PC) sales (56% of rev-enue) are likely to be weak. Moreover, we expect AOSL’s content per PC to decline. Gross margin expansion is also likely to slow as the company approaches its prior peak and tailwinds from its Oregon fab transition diminish. We remain Neutral due to high PC exposure and risks associated with a transition from a fabless to fab-lite business model.Key Questions:• The pace of new product introduction is important for the

company’s future; how will new products impact the com-pany’s mix and/or margin?

• How has owning a fab changed the way you run the company? • What is the current inventory situation in the distributor

channel?• How are your diversification efforts going? In what markets

are you gaining traction?• With increasing content in PCs, can that part of your busi-

ness be flat year-over-year?

12

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

Description: Alpha and Omega Semiconductor is a global suppli-er of MOSFET and power IC products typically used in notebooks, netbooks, flat panel displays, mobile phones and set-top boxes.Gus Richard, Sr. Research Analyst, 415 616-1711

Altisource Asset Management (AAMC) – $129.75 Market Cap: $304.00MAltisource Residential Corporation (RESI) – $19.04Market Cap: $148.70MDescription: RESI purchases non-performing mortgages to either be modified and resold, sold through a short sale, or foreclosed and used as single family rental properties. AAMC provides man-agement services and oversees RESI’s relationship with vendors.Key Questions:• Help investors understand the business model and relation-

ship between the two companies.• What are your top priorities for 2013?• With your base business model plan of 5,000 homes in 2013

and 10,000 in 2014, what are your projected dividends in 2013 and 2014 for each company?

Altisource Portfolio Solutions S.A. (ASPS) – $81.54 Market Cap: $1.91B Rating: Overweight 12-mo. Price Target: $130 (sum-of-the-parts analysis)Thesis: ASPS is levered to OCN’s servicing portfolio growth, a pri-mary benefactor of the secular wave of servicing being transferred from large banks and originators to specialty servicers. We also believe ASPS’s diversification initiatives in origination services, Hubzu and supporting RESI/AAMC will be drivers of long-term value.Key Questions:• Some believe ASPS is just a foreclosure play. How much

runway is left for the core business, and help investors un-derstand your efforts to diversify into origination services, Hubzu and supporting RESI/AAMC and how are these progressing?

• ASPS has highlighted flat margins for 2013. Talk about mar-gin tailwinds and headwinds for 2013 and where they can go in 2014.

• What are ASPS’s top priorities for 2013?Description: Using data-driven processes, Altisource provides real estate mortgage portfolio services and related technology prod-ucts, credit card collections and customer relationship manage-ment services.Michael Grondahl, Sr. Research Analyst, 612 303-6788

Amazon.com, Inc. (AMZN) – $264.27 Market Cap: $120.12B Rating: Overweight 12-mo. Price Target: $329 (40x 2014E PF EPS of $8.23)Thesis: With eCommerce still representing less than 10% of retail sales and Amazon continuing to grow its share of eCommerce, we believe that Amazon will continue to earn robust multiples. Key Questions:• What is the long-term goal for operating margins?• How has the competitive nature changed with traditional re-

tailers focusing on eCommerce, physical retailers offering price matching and the emergence of verticalized online retailers?

• How large is the opportunity for AWS?

Description: Amazon.com, Inc. is a leading eCommerce destination.Gene Munster, Sr. Research Analyst, 612 303-6452

Anaren, Inc. (ANEN) – $19.35Market Cap: $245.67MDescription: Anaren is a supplier of high-frequency electronics used primarily in military and wireless communications applica-tions. Anaren’s customers include leading OEMs in the wireless infrastructure, wireless consumer products, satellite, defense electronics and other sectors utilizing complex microwave and RF technology. Key Questions:• With the war in Afghanistan winding down and potential cuts

to military budgets looming, do you see a slowing of military spending?

• Anaren’s space business has been growing as a percentage of revenue—what is driving that business?

• What drives your wireless business? How much is infrastruc-ture and how much is consumer?

• Do you see strong demand for LTE base stations?• What is your content in small cell base stations?• The company is starting to pursue the Internet of Things with

your partnership with TXN. How is this effort ramping? What sort of applications are you getting into?

Appirio, Inc. – PrivateDescription: Appirio is a global technology-enabled services provider, helping companies power their business with cloud, social and mobile technologies from companies like salesforce.com, Google, Workday and Cornerstone OnDemand. Appirio has worked with more than 400 enterprise customers including organizations like the City of Los Angeles, Facebook, Flextronics, International Hotels Group, Japan Post Network, Ltd., L’Oreal, NetApp, NYU, Starbucks, Thomson Reuters and VMware. Appirio’s technology-enabled professional services are supported by a team of 600 cloud experts and CloudSpokes, a more than 70,000 person-strong global cloud developer community. Appirio has offices that span the U.S., Europe and Asia Pacific.Key Questions:• What are some key criteria for selecting a software company

for which Appirio will provide services?• How large is the services opportunity around cloud comput-

ing and how quickly is it growing?• How attractive is acquiring smaller service providers versus

building out your own competencies?

AppSense Limited – PrivateDescription: AppSense is a leading global software provider of user virtualization solutions that transform organizations into productive mobile workforces, securely governed by IT. AppSense works with customers to reduce IT complexity and enable enter-prise consumerization with independent management of the user experience across all mobile devices and desktops. User virtual-ization improves the deployment, management and migration of multi-platform desktop and mobile environments.Key Questions:• How are you positioned relative to Citrix or VMware?• What sort of cost savings can AppSense provide, and how

quickly is that ROI realized?

13

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

• Have we already reached the tipping point in BYOD (bring your own device) to the workplace? What sort of opportuni-ties does this open for AppSense?

Aquantia Corp. – Private Description: Aquantia provides high-speed Ethernet connectivity solutions for cloud computing and large-scale data center deploy-ments. The company recently acquired 10GBASE-T assets and patent portfolios from PLX Technologies. The acquisition added marquee customers such as Intel and Cisco to an already large OEM customer base. Key Questions:• Describe the role of connectivity solutions within the data

center and cloud environment.• What are the biggest trends in cloud computing in terms of

connectivity?• 10GBASE-T is seeing an uptick in adoption with Intel’s

Romley server launch. How big could that market be?• Describe the competitive landscape.

Arcam AB (ARCM SS) – 285.500 SEKMarket Cap: 1.02B SEKDescription: Arcam is an additive manufacturing company lo-cated in Gothenberg, Sweden. The company was founded in 1997 and is listed on the NASDAQ OMX Stockholm exchange. As of mid-2012, Arcam had 40 employees and more than 100 system installations worldwide. The company designs and manufactures additive manufacturing systems that utilize electron beam melt-ing (EBM) technology. The EBM process is carried out in a vac-uum at elevated temperatures, and involves melting electrically conductive powders layer by layer using electron beams. Arcam currently offers two printers in their product portfolio (Arcam A1 and A2), which are primarily sold into the aerospace, automotive and medical industries. Key Questions:• What are the major applications that your systems are cur-

rently being utilized for?• 3D metal printing has received a lot of attention as of late,

how has the technology changed over the last few years and where do you anticipate it going?

• What materials are you currently developing for use on the Arcam A1 and A2?

• What percent of your sales do you believe go to direct digital manufacturing applications?

• What do you believe will drive the majority of growth for the industry over the next few years?

Arista Networks, Inc. – PrivateDescription: Arista is a leading supplier of high-speed data center switching solutions. The company delivers software-defined cloud networking solutions for large data centers, high performance computing environments and specializes in low latency and high speeds. Arista’s portfolio includes 1, 10 and 40 GbE switches that redefine network architectures and dramatically change the price performance of these large-scale data centers. Key Questions:• Can you discuss the rollout of software-defined networks

with legacy switching and routing architectures?• Can you discuss the timeline for when software-defined net-

works will start getting deployed more broadly and is this a

significant risk to the established hardware suppliers?• Arista has had great success penetrating the financial ser-

vices vertical. Has the company been able to duplicate this success in non-financial verticals?

• Arista has historically been thought of as the leader in one-tier data center switching architectures, but the company’s positioning now appears to be more of an SDN supplier. How were you able to make this transition so quickly?

Ascent Capital Group, Inc. (ASCMA) – $68.59Market Cap: $968.90MDescription: Ascent Capital Group, through its subsidiary, Monitronics International, Inc., provides security alarm monitor-ing and related services to residential and business subscribers in the United States and Canada.Key Questions:• Late last year, you completed a sizable acquisition of custom-

er accounts. What’s the decision process you use in evaluat-ing the economics of such a deal?

• How scalable is your business to digest an influx of customer accounts?

• When you look at future acquisitions, are you primarily looking to add subscribers to the existing Monitronics busi-ness or are there other businesses in which you might be interested?

• We’ve been hearing a lot about the connected home from AT&T lately, and we know that cable MSOs like Comcast are getting into the smart home area as well. How active is Monitronics in this space and how big of an opportunity is it? What is the competitive threat of cable and phone?

ASML Holding NV (ASML) – €54.52 Market Cap: €24.83B Rating: Overweight 12-mo. Price Target: €57 (19x CY14E EPS)Thesis: As the leading lithography equipment supplier, ASML remains a key beneficiary of increasing litho spending from one node to another. The company is on the cusp of the next new product momentum—extreme ultraviolet (EUV) lithography tool where it has virtually no competition. By acquiring its critical sup-plier Cymer, we believe ASML de-risks itself on EUV given that Cymer is a mission-critical path in terms of adoption. By minimiz-ing duplication efforts and focusing on technology development, we think ASML could potentially accelerate EUV even further for greater adoption and into production. With overall gross margins >50% for Cymer, we see that in year two after the acquisition clos-es and assuming a nominal 10% savings in SG&A and 5% in R&D, ASML’s earnings could be accretive by $0.10.Key Questions:• What are the key areas of savings from Cymer acquisition?

Will Cymer help in accelerating any EUV shipments to cus-tomers next year?

• How should one think of Litho re-use amongst foundry/logic customers in 2013?

• Progress in terms of EUV at existing customers? What are the roadblocks and where do you expect you will be by YE13?

Description: ASML Holding is the leading provider of lithography solutions to the semi industry.Jagadish Iyer, Sr. Research Analyst, 212 284-5038

14

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

AT&T Inc. (T) – $35.91 Market Cap: $197.20B Rating: Overweight 12-mo. Price Target: $40 (DCF to 2017, 9.7% NT WACC, 7.9% ter-minal WACC, 2% terminal growth rate)Thesis: AT&T is a leading integrated telecom provider in the United States. AT&T’s wireless business, of which the company owns 100%, is one of the top two wireless providers. AT&T also operates a substantial wireline network that services residential voice, data and television needs, as well as provides business connectivity and services. While AT&T’s cloud and data center operation is relatively small compared to these two businesses, it is a formidable competitor in the data center, cloud and hosting industry.Key Questions: • Investors are familiar with AT&T overall—its wireline and

wireless operations—but probably not with its hosting and cloud efforts. Can you size up how big that business is, say in comparison to AT&T overall or in relation to other public players?

• How does AT&T look at cloud and hosting? Is this a loss leader/necessary offering to bring in more wireline business contracts, an add-on to existing customers to bring in extra revenue, a separate side business or something else?

• A few years ago, AT&T had a ‘measured’ approach to invest-ing in data centers while every other data center player could not pour enough money into the space. How would you characterize the availability of capital and the desired pace of growth from Dallas?

• How does AT&T overcome the fact that its data centers are not network neutral?

• What types of customers are coming to your cloud? Are they using a hybrid approach, where your cloud is for peak use, or are they fully running in your cloud?

Description: AT&T Inc. is the leading telecommunications com-pany in the U.S. with 35 million access lines, the second largest wireless network by subscribers, and one of the world’s most ad-vanced and powerful global backbone networks.Christopher Larsen, Sr. Research Analyst, 212 284-9339

athenahealth, Inc. (ATHN) – $93.79 Market Cap: $3.41B Rating: Overweight 12-mo. Price Target: $100 (5x EV/2014E revenue; net cash of $180M and 37M shares out)Thesis: athenahealth entered the physician market with disruptive cloud-based solutions and continues to out-innovate the tradi-tional players. While the company is strengthening its position in the revenue cycle management (RCM) and EHR market, it is also looking at new solutions that will expand its offerings. The com-pany’s announced acquisition of EPOC will add pharma diversi-fication and, more importantly, access to a large physician base to cross-sell its solutions. We expect the new physician additions to accelerate into 2013 and 2014 along with new solutions. Piper Jaffray is advising EPOC on this transaction. Key Questions:• Why is the cloud a better delivery platform for software in

healthcare?• What is the technology stack you use to deploy athenanet?• What are the greatest challenges to using the cloud in

healthcare?

• What are your plans to employ big data algorithms, and how do you thing about that opportunity?

• How does the cloud improve your ability to promote interoperability?

Description: athenahealth, Inc. is a leading provider of revenue cycle automation and EHR solutions to physician market in the United States.Sean W. Wieland, Sr. Research Analyst, 415 616-1710

Axcelis Technologies Inc. (ACLS) – $1.14Market Cap: $123.02MDescription: Axcelis Technologies provides ion implantation equipment to the semiconductor industry and also supplies tools to the MEMS, LED and chip packaging companies.Key Questions:• Discuss your roadmap in terms of profitability? • Discuss the traction of your high dose ion implanters with

customers. How are you able to compete with AMAT?• What are your growth paths?

Backflip Studios, Inc. – PrivateDescription: Backflip Studios is a mobile game studio, based in Boulder, Colo., that develops mobile games for a multitude of mobile app platforms including the Apple App Store and Android Marketplace. The company’s games have been downloaded more than 200 million times. Top games include DragonVale, Gizmonauts, Paper Toss, NinJump, Strike Knight, Army of Darkness Defense and ShapeShift. In total, the company’s games are played by more than 4 million users per day and over 30 mil-lion users per month.Key Questions:• What have been the monetization trends in the free-to-play

mobile game industry over the past 12 months and how do you expect this to change over the coming 12 months to two years?

• There is a lot of talk about Google Play growth outpacing that of Apple’s App Store. What are the dynamics at play for you between the two platforms currently and how do you expect this to change?

• How do you look to keep players engaged in your games as the mobile games market becomes increasingly competitive with new games releasing each day from a growing range of developers from relatively small studios to multibillion tradi-tional console focused studios?

• What kind of adoption of mobile games have you seen in the tablet market and do you see this as an incremental growth opportunity going forward or more of a cannibalizing effect from the smartphone market?

• Would you expect successful players in the market to focus on a strategy of gaining a substantial download/user base or rather looking to monetize a relatively smaller user base at higher rates in the future?

Batanga, Inc. – Private Description: Batanga operates two businesses: the leading Hispanic ad network, which reaches more than 15 million U.S. Hispanics, according to comScore, and an online music portal that offers content on Latin music and entertainment, includ-ing an online streaming radio service with more than 50,000 user-generated stations. Batanga is positioned to benefit from the growing Latin population both in the United States and globally.

15

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

Key Questions:• What types of strategies are advertisers using to reach

Hispanic customers that are unique to the demographic?• How can Batanga continue to expand its reach of Latin

American Internet users?• What important trends are you noticing about the usership of

the Internet around Latin American users?• How are mobile and video specifically impacting how adver-

tisers are reaching consumers online?

Boxee, Inc. – PrivateDescription: Boxee provides an Internet-connected set-top box (STB) that connects to a user’s TV and allows users to search, find and watch TV shows and movies available on the Internet. The STB is sold for a flat fee and does not require a monthly fee. The box also allows users to download their favorite apps includ-ing many of the most popular video, music and photo services and utilize them on their TV. Boxee is poised to benefit from the growing trend of “TV Everywhere,” which makes content available on every screen that is connected to the Internet.Key Questions:• How are devices enabling easier consumption of Internet-

delivered content impacting potential for cable cutting?• Is there a long-term market for peripheral hardware that

enables consumption of Internet-delivered content through the TV or will this shift to acquiring content directly through Internet-enabled TVs?

• Will Apple’s rumored entry into the TV space change the landscape for connected devices in the living room or will it be no more impactful than the existing Apple TV STB?

Brocade Communications Systems, Inc. (BRCD) – $5.61 Market Cap: $2.56B Rating: Neutral 12-mo. Price Target: $6 (8.5x FY14E EPS)Thesis: Brocade’s storage networking demand continues to largely outpace overall storage market growth due to its first-to-market advantage for 16Gb Fibre Channel, though we believe the industry is slowly migrating toward a converged network based on Ethernet. If this trend plays out, the Fibre Channel storage mar-ket will remain in a slow and steady decline over the next two to three years. As such, Brocade’s longer-term growth will be depen-dent on traction within the Ethernet market, particularly from the campus LAN and Fabric market segments. Despite the improving growth trends of the Ethernet segment, we see minimal oppor-tunities for operating margin expansion over the next two years and therefore little room for earnings growth. As such, we remain Neutral on BRCD shares.Key Questions:• Brocade is participating in the Software Defined Networking

panel, so most questions will be focused on this topic.• How does the trend toward software-defined networks im-

pact Brocade?• Which vendors do you typically compete against in the SDN

market?• What are the competitive advantages of Vyatta and how is it

different than the others?Description: Brocade is a leading provider of data center network-ing solutions.Andrew Nowinski, Sr. Research Analyst, 612 303-6933

CareCloud Corporation – PrivateDescription: CareCloud is a provider of cloud-based practice man-agement, electronic health record and medical billing software and services. The company’s products are connecting physicians in more than 45 states to their patients and each other through a fully integrated digital healthcare ecosystem that can be accessed on any browser or device.Key Questions:• Why is the cloud a better delivery platform for software in

healthcare?• What is the technology stack you use to deploy athenanet?• What are the greatest challenges to using the cloud in

healthcare?• What are your plans to employ big data algorithms, and how

do you think about that opportunity?• How does the cloud improve your ability to promote

interoperability?

Ciena Corporation (CIEN) – $15.24Market Cap: $1.53BDescription: Ciena Corporation is a leading supplier of optical transport equipment to service providers around the globe. The company leverages deep expertise in packet and optical network-ing along with advanced software functionality and is the founda-tion to some of the leading next-generation networks at numerous tier one service providers. Ciena is viewed by many in the industry as the leader in 100G coherent optical systems and is well-posi-tioned to benefit from the upcoming 100G coherent upgrade cycleKey Questions:• Expand on your pipeline of 100G coherent wins and when do

you expect to see a more material inflection in service pro-vider deployments?

• Can you discuss the process for carriers releasing capex budgets and when during the year does this typically start to happen?

• Can you size the market for optical equipment for core net-works, metro networks, wireless backhaul and FTTX?

• Can you discuss your supplier relationships—specifically with respect to dual sourcing, concerns regarding the finan-cial strength of some of your suppliers and your recent imple-mentation of vendor-managed inventory?

Cisco Corporation (CSCO) – $20.86 Market Cap: $111.20B Rating: Overweight 12-mo. Price Target: $25 (9x fully taxed FY14E op income + cash)Thesis: Cisco is our top pick for 2013. Despite lagging demand for core networking gear (switching and routing), Cisco has ef-fectively ramped up product offerings across additional areas of the network, which we believe will help reaccelerate product growth throughout the year. Through various acquisitions and internal development, the company continues to expand its prod-uct footprint to adapt to cloud, SDN and BYOB industry trends, which we anticipate will help Cisco remain on top of the IT sec-tor. Moreover, as the company begins to shift to a more software and service centric model, we believe better revenue visibility will likely occur, driving sustainable bottom-line growth over the next several years. Key Questions:• Can you discuss why the collaboration space has declined so

much in 2012?

16

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

• Is the video conferencing market moving more toward soft-ware and services? What does this mean for the hardware vendors?

• Is the set-top box, EMTA and WLAN likely to evolve into one platform? Or is the set-top functionality likely going to be a feature delivered from a cloud?

• How does the NDS acquisition fit with everything going on in the video delivery market?

• Will you discuss your VCE joint partnership with EMC and where you see the partnership headed?

Troy Jensen, CFA, Sr. Research Analyst, 612 303-6291

Cogent Communications Group Inc. (CCOI) – $25.14Market Cap: $1.14BDescription: Cogent is one of the lowest cost IP service providers in North America, Europe and Asia. The company’s longhaul and fiber networks extend to over 180 markets in 34 countries. Key Questions:• Describe the competitive environment and strategies to

compete effectively.• Where is demand coming from? How long is this level of

demand or growth in demand sustainable?• Is metro viable without long-haul? Vice versa?• What are the challenges of entering a new market? Is it typi-

cal to acquire an anchor tenant(s) before a new deployment?

Coherent (COHR) – $57.76Market Cap: $1.40BDescription: Coherent is a key provider of lasers and laser-based solutions for scientific, commercial and industrial customers.Key Questions:• What is the expected timing of recovery in the display

segment? • How is Coherent positioned in terms of OLEDs?• What progress has been made in fiber lasers? What is the

value proposition against IPGP? Where do you think your contribution from fiber lasers would be by YE13?

comScore, Inc. (SCOR) – $15.94 Market Cap: $537.32M Rating: Suspended Description: ComScore is a leading third-party digital marketing intelligence and measurement platform, providing proprietary measurement of digital activity (i.e., online digital usage and buy-ing patterns). The comScore solution is differentiated through its proprietary panel of 2M opt-in users, which combined with tag-ging data can provide customers with insight necessary to drive appropriate business model and strategy decisions, as well as help drive advertising effectiveness. comScore has evolved into the recognized independent industry leader, with its data often quoted as the standard for digital marketing success.Key Questions:• Following multiple delays in converting the ancillary product

pipeline, what gives you confidence in driving meaningful revenue growth from these channels?

• Do you subscribe to the prophecy of an ultimate “death of Web sites?” How does comScore evolve if less interaction is taking place on Web sites and more interaction moves to mobile, apps, social media platforms, etc.?

• comScore operates a margin structure well below its syndi-

cated measurement peers. What is the long-run margin po-tential for the business and how does it develop over the next couple years?

Cornerstone OnDemand, Inc. (CSOD) – $33.86 Market Cap: $1.71b Rating: Overweight 12-mo. Price Target: $36 (8.6x EV/2014E revenue + net cash)Thesis: Cornerstone OnDemand is a leading global provider of a comprehensive learning and talent management solutions delivered as software-as-a-service (SaaS). Cornerstone leverages its pure cloud architecture and also enjoys strong differentiation versus its peers because thus far, its enterprise suite is 100% homegrown and fully integrated. Competitors are racing to de-velop a broader suite of offerings, but struggling to integrate dis-parate, acquired piece-parts that can’t interoperate smoothly. We believe Cornerstone’s organically developed product set makes it extremely attractive to customers, and its industry-leading growth sets it apart as one of the highest-quality SaaS names.Key Questions:• How has the acquisition of several of your competitors by leg-

acy software companies given you a competitive advantage?• What are your biggest growth constraints?• How do you balance growth versus your timeline to

profitability?Description: Cornerstone OnDemand is a leading SaaS based Learning and Talent Management solution vendor.Mark Murphy, Sr. Research Analyst, 415 616-1705

Cumulus Media Inc. (CMLS) – $3.27 Market Cap: $570.26M Rating: Overweight 12-mo. Price Target: $4.50 (5-Yr DCF using 10.2% WACC and 6.5x terminal EBITDA multiple)Thesis: Despite the obvious growth challenges of the broadcast radio industry, we believe Cumulus can generate attractive equity returns driven by double-digit FCF growth. We think this growth can be achieved even if revenue growth is modest as costs are managed and the balance sheet is optimally levered. The story is more compelling if CMLS is successful in redeploying FCF and leveraging its substantial scale to conjure up some growth from new initiatives. We recommend the shares based on potential eq-uity returns of the core business alone, but a call option also exists to create even more value.Key Questions:• Network: We expect the recently announced partnership with

CBS Sports to help Cumulus capture a significant share of the $150M sports market through their new revenue share model. Discuss the opportunity in the network business and next milestones.

• SweetJack: Management expects daily deal site SweetJack to have some 300 dedicated employees and to operate in 200 markets by year-end. We expect CMLS to use their unsold in-ventory on-air talent to efficiently promote the service which could generate ~$30M in revenue and $10-12M in EBITDA by 2014. Update us on current tracking of this business segment.

• iHeartRadio: Cumulus has joined Clear Channel to push ra-dio streaming and playlist site iHeart.com, providing its own 525 radio stations. The iHeartRadio platform adds 30 mil-

17

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

lion ad units to Cumulus’ advertising inventory, and has no revenue share agreement with Clear Channel. Management highlighted on the call that they have already seen ‘meaning-ful’ increases in their streaming traffic in just a few weeks and expects over time to expand its digital ad revenue from 1% to 5%. Discuss current market share and expectations for this business given new entrants (Microsoft, Apple, etc)?

Description: Cumulus Media is the No. 3 radio broadcaster in the United States by revenue.James Marsh, CFA, Sr. Research Analyst, 212 284-9304

Datawatch Corporation (DWCH) – $10.88Market Cap: $69.77MDescription: Datawatch is a leader in providing information op-timization products and solutions that allow organizations to deliver the greatest data variety possible into their big data and analytic applications. Datawatch provides organizations the abil-ity to integrate structured, unstructured and semi-structured sources such as reports, PDF files and EDI streams into these applications to provide a 360 degree perspective of the issues and opportunities that exist in their businesses. More than 40,000 organizations worldwide use Datawatch’s products and services, including 99 of the Fortune 100. Datawatch is headquartered in Chelmsford, Mass. with offices in London, Munich, Singapore, Sydney and Manila.Key Questions:• How is Datawatch leveraged to the big data trend?• Which industries or markets are most suited to Datawatch’s

products?• Who else does what you do, and how does Datawatch do it

better?

DHX Media Ltd. (DHX CN) – C$2.65Market Cap: C$140.64MDescription: DHX Media produces, distributes and licenses television and film programming in Canada and internationally. It focuses primarily on children, family and youth programming. The company has approximately 15 children’s series including Yo Gabba Gabba. It also maintains a content library of approximately 2,550 half-hours of programming and approximately 60 individual titles.

Digital River, Inc. (DRIV) – $14.25 Market Cap: $466.70M Rating: Overweight 12-mo. Price Target: $18 (10x 2014E PF EPS + $9cash/sh)Thesis: Digital River is a leader in providing eCommerce solu-tions. One of its specialties is helping eCommerce sellers global-ize operations as it operates in more than 160 countries and has call center support in over 15 languages. Overall, it helps to man-age more than $10B in global online sales. One of Digital River’s recent pushes has been into payments. Currently, it can display sites in over 150 currencies and more than 30 languages, and it re-cently acquired LML Payment Systems, which provides electronic payment processing.Key Questions:• How big can the payments business become and how will

the LML acquisition be integrated into the existing Digital River payments business?

• Much of the concern regarding DRIV shares is the transition

away from the traditional software download business. How is Digital River transitioning to the SaaS and app world?

• What revenue opportunities are presented from the release of Windows 8, outside of the Windows store?

• What is the timeline for the rollout of standalone modules?Description: Digital River, Inc. provides technology and infrastruc-ture that enables software publishers and consumer electronics manufacturers to sell online.Gene Munster, Sr. Research Analyst, 612 303-6452

DigitalGlobe, Inc. (DGI) – $26.08 Market Cap: $1.23B Rating: Overweight 12-mo. Price Target: $32 (8.9x 2014 EBITDA)Thesis: We view the just completed acquisition of competitor GeoEye as a “game-changer” for DGI, with the potential to drive meaningful improvement in key financial metrics. Equally impor-tant, this transaction is another step in the transformation of DGI from a satellite/defense business into a higher-growth, higher-margin information services firm. We believe this transaction can drive meaningful valuation upside in the shares over the next several years.Key Questions:• Provide updated thoughts on cost and capital synergies as-

sociated with the acquisition.• What are the drivers of growth in the commercial business?• Discuss risks around further cuts in federal funding for sat-

ellite imagery; successes in reducing government exposure.Description: DigitalGlobe operates a collection of satellites used to provide commercial high resolution earth imagery.Peter Appert, Sr. Research Analyst, 415 616-1709

DreamWorks Animation SKG Inc. (DWA) – $16.60 Market Cap: $982.75M Rating: Neutral 12-mo. Price Target: $18 (5 yr DCF, 6.5% WACC, 7.0x terminal EBITDA multiple)Thesis: DWA shares lack catalysts for 2013 so we see little reason for investors to jump into the shares. Fundamentals look shaky, valuation is not compelling and upcoming films could present some headline risk. Accordingly, we suggest investors re-evaluate the shares as we approach 2014 when the slate improves (and moves to three releases per year), film production costs decline (from the current $145M to $120M), and ancillary revenue streams from Netflix and others start to hit the income statement.Key Questions:Discuss the upcoming slate and what actions are you taking to prevent Guardians-like results?Discuss the merchandizing opportunity and what are you doing differently to drive higher sales?What are you expectations for the DVD and digital sales trends over the next few years?Description: DreamWorks develops and produces computer-gen-erated animated feature films.James Marsh, CFA, Sr. Research Analyst, 212 284-9304

18

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

Dun & Bradstreet Corp. (DNB) – $80.60 Market Cap: $3.59B Rating: Neutral 12-mo. Price Target: $80 (11x 2013E EPS)Thesis: An attractive, sector-dominant franchise plus an appeal-ing business model add to DNB’s long-term investment appeal. However, near-term results have been constrained by soft revenue trends in the core risk business and heavy investment spending designed to accelerate revenue growth. Until the returns on this investment become visible, which we do not anticipate before mid-to-late 2013, the stock will likely be range-bound.Key Questions:• What are the catalysts to improved revenue growth in the

core risk business and when might we expect to see im-proved revenue trends?

• Comment on progress in the “MaxCV” technology invest-ment program. Can you quantify the potential returns?

• Discuss competitive dynamics in the risk business.Description: Dun & Bradstreet is a leading provider of commercial credit data and marketing information.Peter Appert, Sr. Research Analyst, 415 616-1709

eMagin Corp. (EMAN) – $3.18 Market Cap: $74.81M Rating: Overweight 12-mo. Price Target: $6.00 (12x CY14E diluted proforma EPS0.50)Thesis: We expect eMagin to grow its revenues at least 20% YOY for the next two years given the secular industry growth for mi-crodisplays. We see the company benefiting from share gains against LCD microdisplays. In addition, we hope to see leverage in the company’s operating model that is likely to unfold on ris-ing revenues, which translates into 1500 bps of operating margin improvement by 2014. Emerging applications in military and con-sumer devices as well as disruptive technologies such as Google Glass position eMagin for revenue and earnings upside over the next 12-24 months.Key Questions:• Provide an update on the new deposition tool, and any color

on yield or yield targets.• Any new military contracts, and discuss your view of how

CY13 is shaping up given potential cuts to defense spending?• Discuss any wins on the consumer side for electronic view

finders, gaming applications, etc. When can we see this in the numbers? Give the activity in Google Glasses, where do you expect the next action in terms of OLED microdisplays?

Description: eMagin is the leading supplier of OLED-based microdisplays.Jagadish Iyer, Sr. Research Analyst, 212 284-5038

EMCORE Corporation (EMKR) – $5.83Market Cap: $154.08MDescription: EMCORE offers a broad portfolio of compound semiconductor-based products for the fiber optics and solar pow-er markets. EMCORE’s fiber optics business segment provides optical components, subsystems and systems for high-speed telecommunications, cable television (CATV) and fiber-to-the-premises (FTTP) networks, as well as products for satellite com-munications, video transport and specialty photonics technolo-gies for defense and homeland security applications. EMCORE’s solar photovoltaics business segment provides products for

space power applications including high-efficiency multi-junction solar cells, covered interconnect cells (CICs) and complete satel-lite solar panels. Key Questions:• Are service provider capital expenditure plans shifting more

toward optical equipment in 2013?• Is vertical integration by system manufacturers going to con-

tinue to eat into the optical component market?• How much of a lead do you have before more competitors

introduce ITLAs?• After reaching profitability, what do you think is a reasonable

near-midterm operating margin target? • What is the next catalyst for the optical component industry?

Emulex Corporation (ELX) – $6.45 Market Cap: $584.35M Rating: Neutral 12-mo. Price Target: $8 (10x FY14E EPS)Thesis: Emulex’s core market (Fibre Channel HBA) has been in a secular decline for the last few years, which has prompted management to search for new growth opportunities in the Ethernet market. While we are confident Emulex can succeed in the Ethernet market, the ongoing patent litigation, coupled with the pending closure of the Endace acquisition, keeps us on the sidelines. If revenue and cost synergies from this acquisition start to play out sooner than expected, we would be inclined to re-eval-uate our overall thesis on shares of ELX. We are maintaining our Neutral rating.Key Questions:• What drives 10GB Ethernet adoption? • Does Ethernet switch pricing have to fall before we see a

ramp in 10GB Ethernet products?• What are the next catalysts for your 16Gb Fibre Channel

products?• Update us on the Endace acquisition.Description: Emulex is a global provider of Fibre Channel and Ethernet interconnect products that facilitate the transmission of data between servers, switches and storage systems.Andrew Nowinski, Sr. Research Analyst, 612 303-6933

Equinix Inc. (EQIX) – $211.55 Market Cap: $10.30B Rating: Overweight 12-mo. Price Target: $245 (DCF to 2017; 10.4% NT WACC, 8.7% Terminal WACC and 3% terminal growth)Thesis: We’ve highlighted Equinix as a top pick for 2013. While the stock appreciated materially in 2012 and into 2013, we believe there are a number of positive fundamental reasons the business will continue to perform. The secular trend to outsourced IT is not changing, enhanced by the cyclical trend to asset-light, and supply/demand trends are favorable. Equinix’s conversion to REIT process could act as a catalyst, and we believe the company is set up for continued positive estimate revisions.Key Questions:• How have “ecosystems” enabled you to grow? What new

ecosystems are you targeting today?• Europe has been an area of concern for some investors.

What are you seeing in Europe today and how do you feel about the next 12 months?

• Equinix just reported near-record bookings in the fourth

19

Technology, Media and Telecommunications ConferenceMarch 12–13, 2013

quarter. Can you talk about the conversion of bookings to revenues, the length of the sales cycle and how adding new sales representatives impacts your growth?

• What types of supply and demand trends are out there (pric-ing, booking pipeline, changes in RFPs)?

• Can you walk us through the REIT conversion process, where you stand today and the benefits of converting to a REIT?

• How can Equinix benefit from the shift to cloud computing as a colocation services provider?

Description: Equinix is a global provider of network-neutral data centers and Internet exchange services for enterprises, content companies and network services providers.Christopher Larsen, Sr. Research Analyst, 212 284-9339

Euronet Worldwide, Inc. (EEFT) – $24.14 Market Cap: $1.21B Rating: Overweight 12-mo. Price Target: $27 (9x 2013E EV/EBITDA, assuming $110M net debt and 52.5M shares out)Thesis: We believe robust ATM unit growth over the past 12 months is set to continue as EEFT benefits from growing out-source trends in Europe, and expansion opportunities in India. Money transfer transaction volume has been strong, and FX has recently turned into a tailwind after being a headwind for three consecutive quarters. epay is also set to show year-over-year im-provement after 1Q13.Key Questions:• What are you most excited about for 2013? What are your top

priorities for 2013?• What can you do to jump start growth or improve margins

at epay?• What is new in Europe?• Is your end customer/consumer feeling better or worse in

2013? Your leverage is extremely low—any plans to deploy more capital?

Description: Euronet owns and operates the largest independent ATM network in Europe, and offers prepaid wireless top up and money transfer services.Michael Grondahl, Sr. Research Analyst, 612 303-6788

Evidon, Inc. – PrivateDescription: Evidon, headquartered in New York, is a technology solutions provider providing businesses and consumers unique insight into the collection, control and usage of online data. Its technology solutions include the Ghostery browser extension, enabling businesses and consumers to identify data collection (cookies) and tracking activity on accessed Web sites, helping to protect sensitive personal data, improve Web performance, and maintain transparency in the control/use of online information. Evidon’s solutions also enable businesses to remain compliant with privacy laws and self-regulation across North America and Europe. Evidon was founded in 2009 by Scott Meyer (CEO).Key Questions:• How would Do Not Track (DNT) of third-party cookie block-

ing default setting on Web browsers impact both the adver-tising ecosystem as well as consumers’ Web experience?