Petition No. 156/TT/2015

48

Page 1 of 48 Order in Petition No. 156/TT/2015 CENTRAL ELECTRICITY REGULATORY COMMISSION NEW DELHI Petition No. 156/TT/2015 Coram: Shri Gireesh B. Pradhan, Chairperson Shri A.K. Singhal, Member Shri A.S. Bakshi, Member Dr. M.K. Iyer, Member Date of Order : 29.12.2016 In the matter of: Approval of transmission tariff for Asset-1: 400 kV (Quad) 2xS/C Parbati- Koldam transmission line portion starting from Parbati-II HEP to LILO point of Parbati(Banala) Pooling Station to Koldam HEP (Ckt.-I) and Asset-2: Portion starting from Parbati-II HEP LILO point of Parbati-III HEP (Ckt.-II) in Northern Region for 2014-19 period under Regulation 86 of Central Electricity Regulatory Commission (Conduct of business) Regulations, 1999 and Central Electricity Regulatory Commission (Terms and Conditions of Tariff) Regulations, 2014. And in the matter of: Parbati Koldam Transmission Company Limited, B-9, Qutab Institutional Area, Katwaria Sarai, New Delhi-110 016 ….Petitioner Vs 1. Rajasthan Rajya Vidyut Prasaran Nigam Limited, Vidyut Bhawan, Vidyut Marg, Jaipur- 302 005 2. Ajmer Vidyut Vitran Nigam Limited, 400 kV GSS Building (Ground Floor), Ajmer Road, Heerapura, Jaipur 3. Jaipur Vidyut Vitran Nigam Limited, 400 kV GSS Building (Ground Floor), Ajmer Road, Heerapura, Jaipur 4. Jodhpur Vidyut Vitran Nigam Limited, 400 kV GSS Building (Ground Floor), Ajmer Road, Heerapura, Jaipur 5. Himachal Pradesh State Electricity Board, Vidyut Bhawan, Kumar House Complex Building II, Shimla-171 004

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Petition No. 156/TT/2015

Page 1 of 48

Order in Petition No. 156/TT/2015

CENTRAL ELECTRICITY REGULATORY COMMISSION

NEW DELHI

Petition No. 156/TT/2015

Coram:

Shri Gireesh B. Pradhan, Chairperson Shri A.K. Singhal, Member

Shri A.S. Bakshi, Member

Dr. M.K. Iyer, Member

Date of Order : 29.12.2016

In the matter of:

Approval of transmission tariff for Asset-1: 400 kV (Quad) 2xS/C Parbati-

Koldam transmission line portion starting from Parbati-II HEP to LILO point of Parbati(Banala) Pooling Station to Koldam HEP (Ckt.-I) and Asset-2: Portion

starting from Parbati-II HEP LILO point of Parbati-III HEP (Ckt.-II) in Northern Region for 2014-19 period under Regulation 86 of Central Electricity Regulatory Commission (Conduct of business) Regulations, 1999 and Central Electricity

Regulatory Commission (Terms and Conditions of Tariff) Regulations, 2014.

And in the matter of:

Parbati Koldam Transmission Company Limited, B-9, Qutab Institutional Area, Katwaria Sarai, New Delhi-110 016 ….Petitioner

Vs

1. Rajasthan Rajya Vidyut Prasaran Nigam Limited, Vidyut Bhawan, Vidyut Marg,

Jaipur- 302 005

2. Ajmer Vidyut Vitran Nigam Limited, 400 kV GSS Building (Ground Floor), Ajmer Road, Heerapura, Jaipur

3. Jaipur Vidyut Vitran Nigam Limited,

400 kV GSS Building (Ground Floor), Ajmer Road, Heerapura, Jaipur

4. Jodhpur Vidyut Vitran Nigam Limited, 400 kV GSS Building (Ground Floor),

Ajmer Road, Heerapura, Jaipur 5. Himachal Pradesh State Electricity Board,

Vidyut Bhawan, Kumar House Complex Building II, Shimla-171 004

Page 2 of 48

Order in Petition No. 156/TT/2015

6. Punjab State Power Corporation Limited, Thermal Shed TIA, Near 22 Phatak,

Patiala-147 001

7. Haryana Power Purchase Centre, Shakti Bhawan, Sector-6,

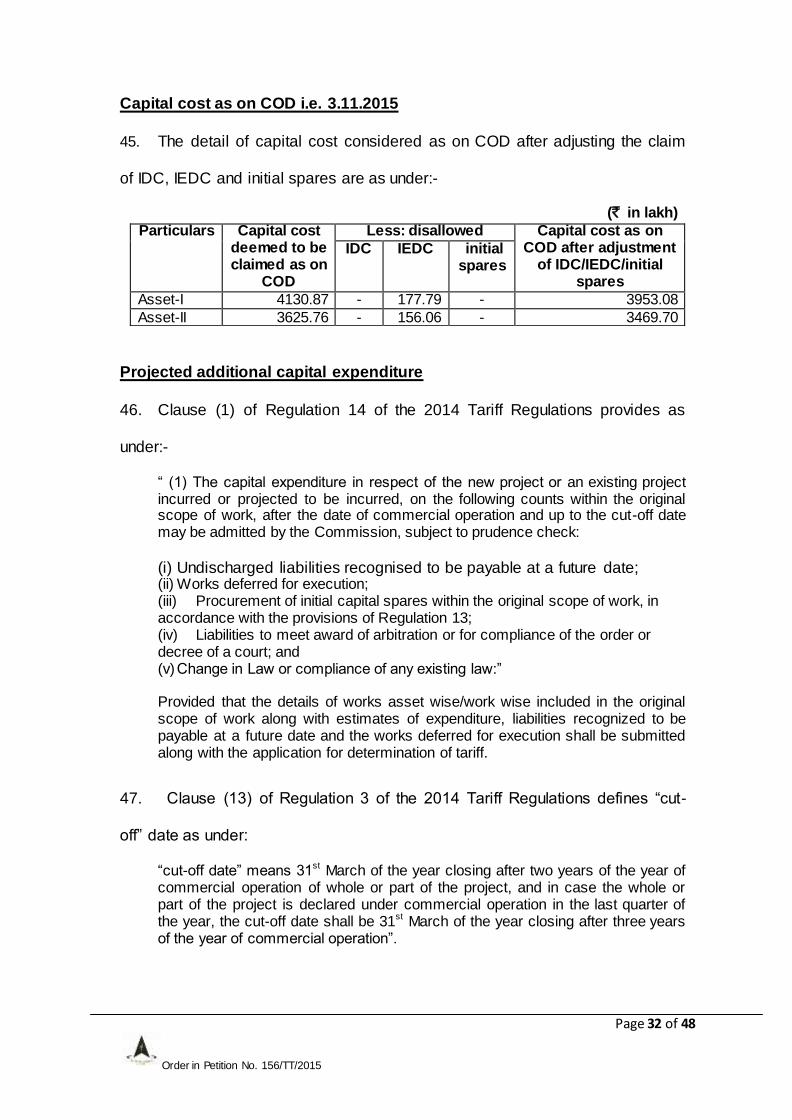

Panchkula (Haryana)-134 109

8. Power Development Department,

Government of Jammu & Kashmir, Mini Secretariat, Jammu

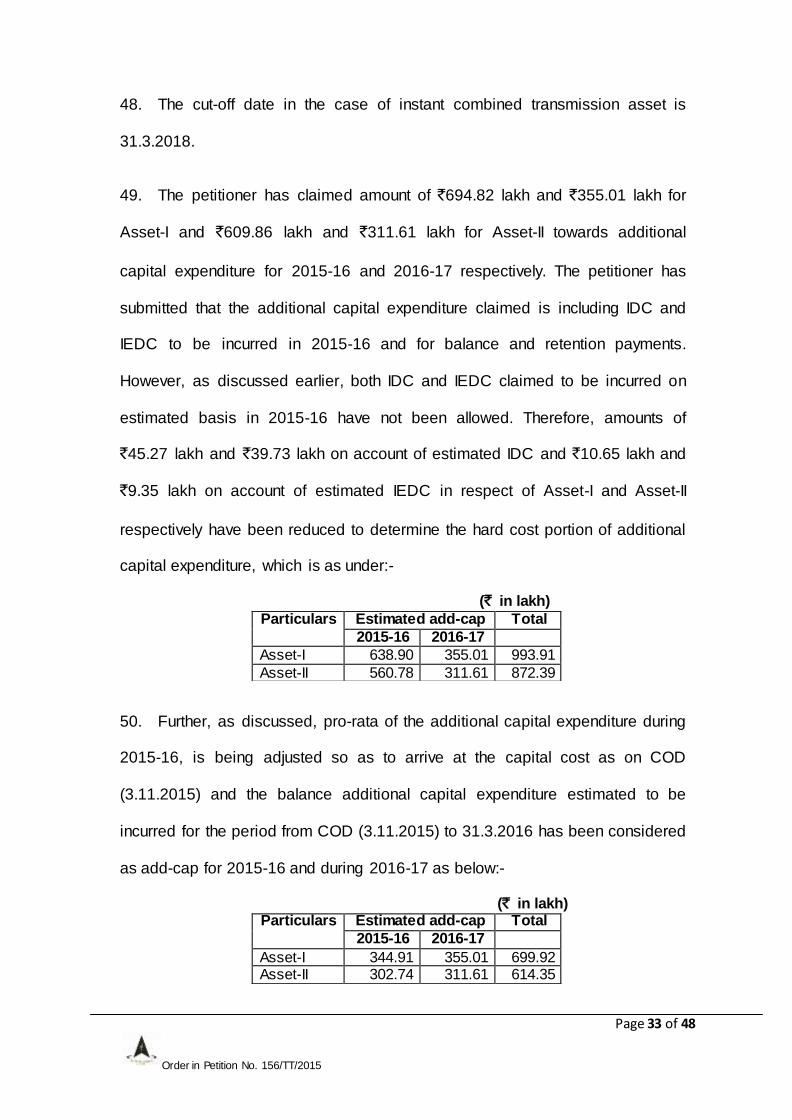

9. Uttar Pradesh Power Corporation Limited, (Formerly Uttar Pradesh State Electricity Board),

Shakti Bhawan, 14, Ashok Marg, Lucknow-226 001

10. Delhi Transco Limited,

Shakti Sadan, Kotla Road, New Delhi-110 002

11. BSES Yamuna Power Limited,

BSES Bhawan, Nehru Place,

New Delhi

12. BSES Rajdhani Power Limited, BSES Bhawan, Nehru Place,

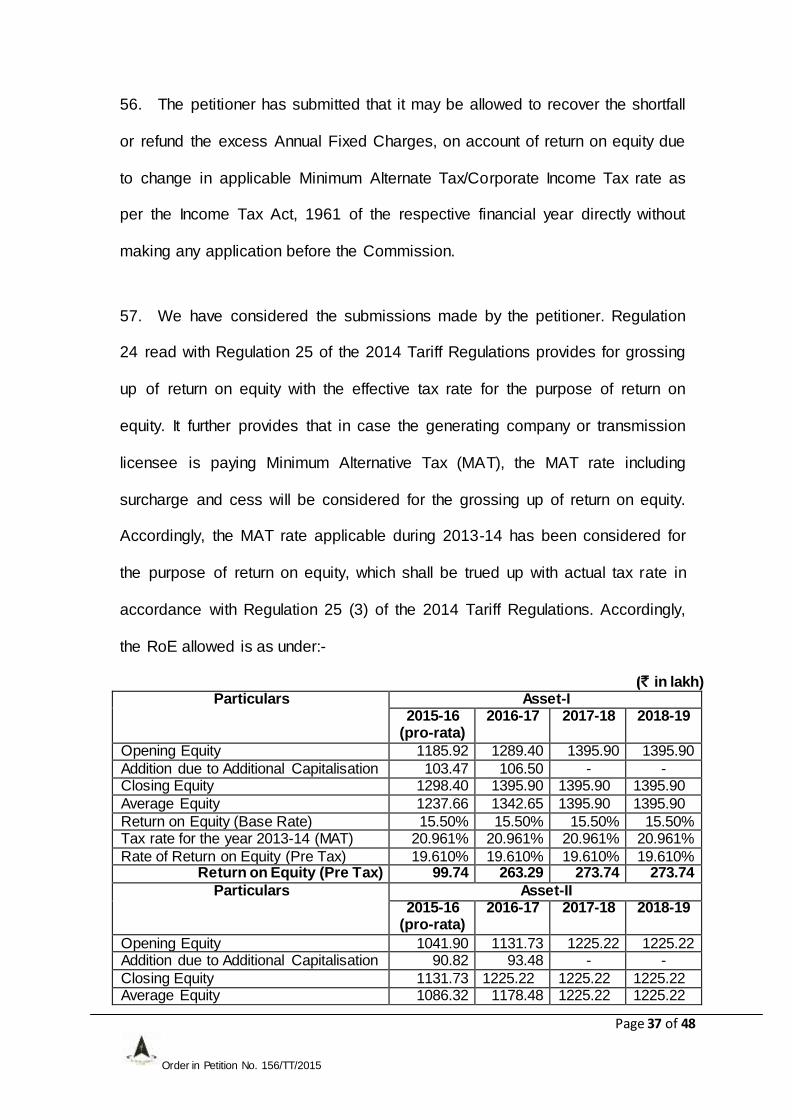

New Delhi

13. Tata Power Delhi Distribution Limited,

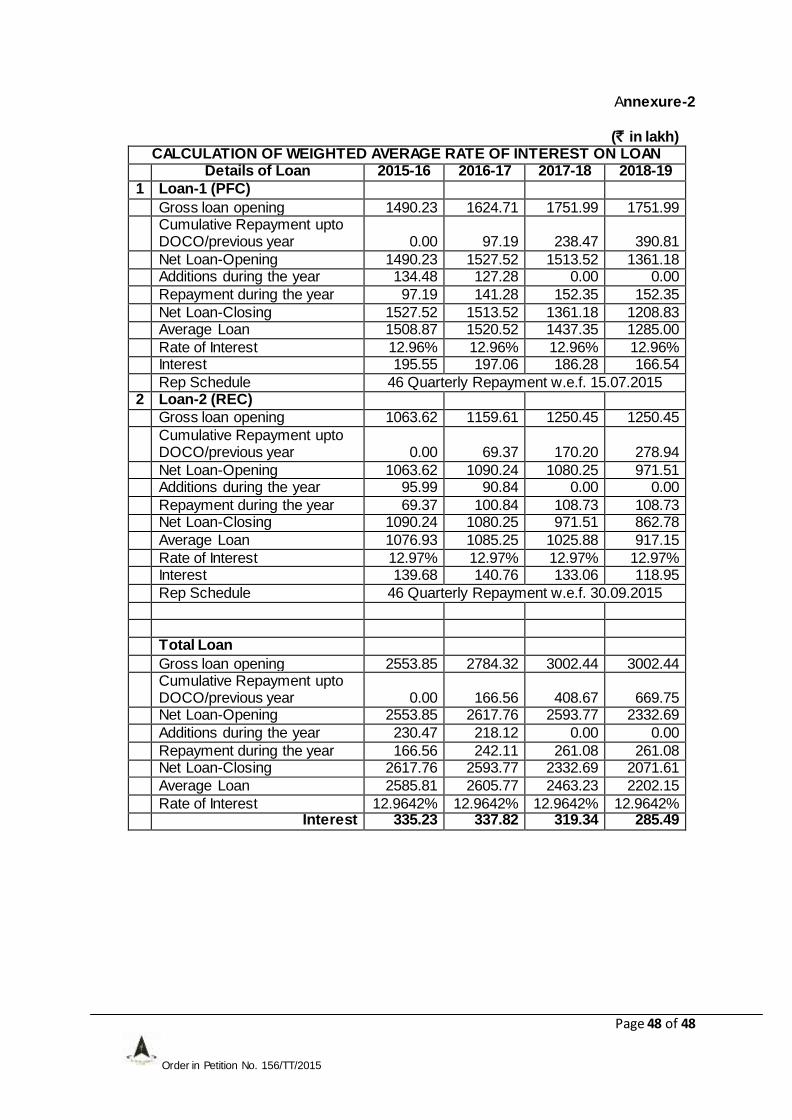

Cennet Building, Adjacent to 66/11kV Pitampura-3Grid Building, Near PP Jewellers, Pitampura, New Delhi-110 034

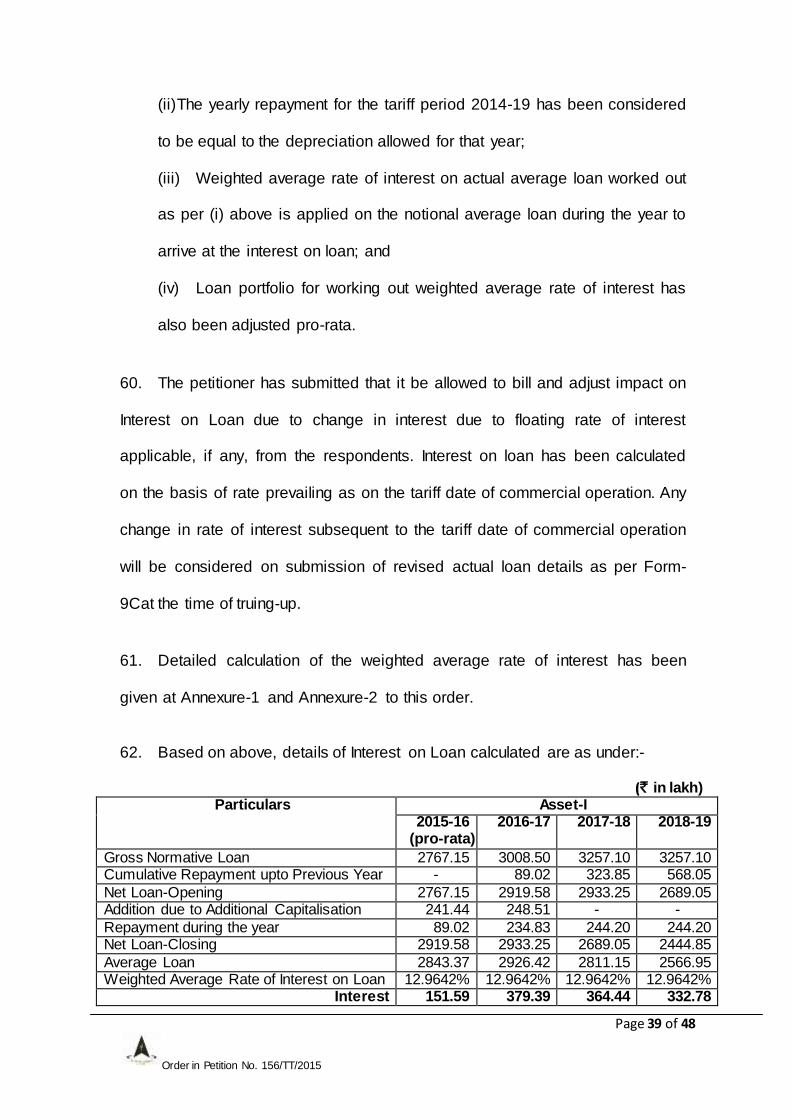

14. Chandigarh Administration, Sector-9, Chandigarh

15. Uttarakhand Power Corporation Limited,

Urja Bhawan, Kanwali Road, Dehradun

16. North Central Railway,

Allahabad

17. New Delhi Municipal Council,

Palika Kendra, Sansad Marg, New Delhi-110 002

18. Northern Region Electricity Board,

18-A, Shaheed Jeet Singh Marg, Katwaria Sarai, New Delhi-110016

Page 3 of 48

Order in Petition No. 156/TT/2015

19. Power Grid Corporation of India Limited, Saudamini, Plot No.-2, Sector-29

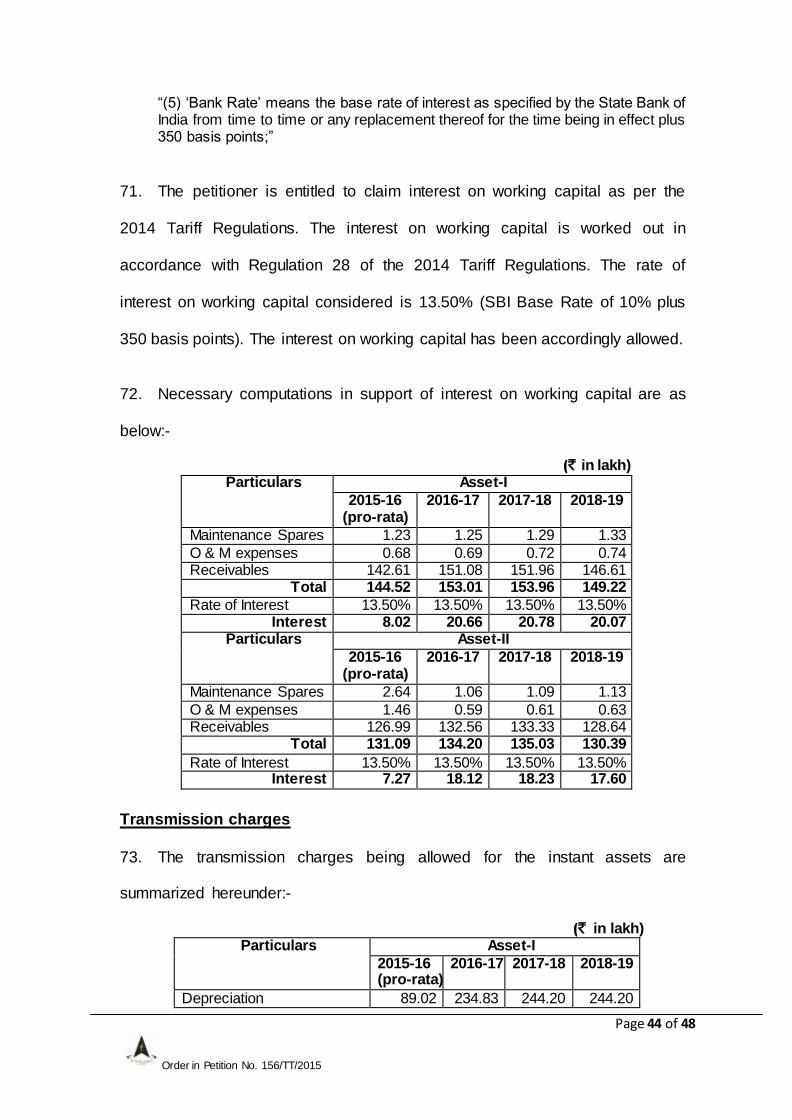

Gurgaon-122001 (Haryana)

20. National Hydro Power Corporation Limited, NHPC Office Complex, Sector-33, Faridabad, Haryana-121 003

21. NTPC Limited, Scope Complex, Institutional Area,

Lodhi Road, Pragati Vihar, New Delhi-110 016

22. Himachal Pradesh Power Corporation Limited,

Sainj (HEP), Himfed Bhawan, Below Old MLA Quarters,

Bypass Road, Tutikandi, Shimla-171 005, Himachal Pradesh ….Respondents

For Petitioner : Shri Anil Rawal, PKTCL

For Respondents: None

ORDER

The instant petition has been filed by Parbati Koldam Transmission

Company Limited (PKTCL), a joint venture company of Reliance Infrastructure

Limited (RIL) (74%) and Power Grid Corporation of India Limited (PGCIL)

(26%), incorporated under the Companies Act, 1956, seeking approval of

transmission tariff for Asset-1: 400 kV (Quad) 2xS/C Parbati-Koldam

transmission line, portion starting from Parbati-II HEP to LILO point of

Parbati(Banala) Pooling Station to Koldam HEP (Ckt.-I) and Asset-2: Portion

starting from Parbati-II HEP LILO point of Parbati-III HEP (Ckt.-II) (hereinafter

referred to as “transmission asset”) in Northern Region for Tariff block 2014-19

under Central Electricity Regulation Commission (Terms and Conditions of

Tariff) Regulations, 2014 (hereinafter referred to as “the 2014 Tariff

Regulations”).

Page 4 of 48

Order in Petition No. 156/TT/2015

Background

2. The petitioner was entrusted with implementation of inter-State transmission

system comprising the 400 kV (Quad) transmission lines for evacuation of

power from the 4x200 MW Parbati-II Hydroelectric Power Project (“Parbati-II

HEP”) and 4x200 MW Koldam Hydroelectric Power Project (“Koldam HEP”) in

the state of Himachal Pradesh for its onward transmission to the beneficiary

states in the Northern Region. The Standing Committee on Transmission

System Planning of Northern Region, in its 14th and 15th meetings held on

30.12.2002 and 30.5.2003 respectively, approved the construction of the

Project i.e., the Associated Transmission System for Koldam HEP implemented

by NTPC and Parbati-II HEP implemented by NHPC Ltd. In a meeting held on

19.12.2011, it was reiterated that as agreed in earlier meetings, the petitioner‟s

lines shall continue to be part of a composite transmission scheme for Parbati II,

Parbati III and Koldam Hydro Electric Power Project (“Koldam HEP”). A tender

for selection of Joint Venture Partner (JVP) was floated by PGCIL on 2.2.2004

and Reliance Infrastructure Ltd. was selected as JVP for implementation of the

project on 26.12.2005. In the meantime, PGCIL prepared the Feasibility Report

on the basis of the Ministry of Power order dated 7.9.2005, granting Investment

Approval for the transmission system associated with Koldam HEP. Ministry of

Power decided to get the project executed on Build, Own and Operate (BOO)

basis instead of initial approval for execution on Build, Own, Operate and

Transfer (BOOT) basis. The petitioner company was formed on 23.11.2007 by

executing Share Holders Agreement between Reliance Energy Ltd. and PGCIL

and an Implementation Agreement was entered into between Reliance Energy

Ltd. and PGCIL on 23.11.2007. As per para 2.0 of Schedule 5 of the

Page 5 of 48

Order in Petition No. 156/TT/2015

Implementation Agreement, the project consists of following transmission lines:-

Transmission line Route length

(i) Parbati-Koldam 400 kV (Quad) a) S/C line-I b) S/C line-II c) D/C line d) S/C line (Realignment at Koldam)

61 km 68 km 20 km 3 km

(ii) Koldam-Ludhiana 400 kV D/C (Triple ACSR) 153 km

3. Thereafter, the petitioner applied for grant of transmission licence on

17.3.2008 and was granted transmission licence by the Commission on

15.9.2008 to construct, maintain and operate for a period of 25 years the

following transmission assets-(a) 400 kV S/C Parbati-Koldam transmission line-I

(Quad Moose conductor) (b) 400 kV S/C Parbati-Koldam transmission line-II

(Quad Moose conductor) (c) 400 kV D/C Parbati-Koldam transmission line

(Quad Moose conductor) and (d) 400 kV D/C Koldam-Ludhiana transmission

line (Triple Snowbird conductor).

4. Thereafter, Bulk Power Transmission Agreements (BPTA) were executed

between PKTCL and Northern Region beneficiaries for supply of power from

Parbati-II HEP, as the transmission system for evacuation of power of Parbati-II

HEP was entrusted to PKTCL and that of Parbati-III HEP was entrusted to

PGCIL.

5. Subsequently, in the 30th meeting of Standing Committee of Northern

Region held on 19.12.2011, it was reiterated that as agreed in the 14 th, 15th and

16th meetings of Standing Committee of Northern Region, the transmission lines

as a composite transmission scheme for Parbati II, Parbati III and Koldam

Hydro Electric Projects (HEPs) to be executed by the petitioner, were still

required, but some changes in priorities were envisaged, due to commissioning

Page 6 of 48

Order in Petition No. 156/TT/2015

of Parbat-III-HEP and on account of delay in Parbati II-HEP. As such, the tariff

for one element i.e. (3.518 km) section of 400 kV (Quad) S/C Parbati-II Koldam

Transmission Line (Ckt-II) starting from LILO point of Parbati-III HEP to LILO

point of Parbati Pooling Station, was claimed by the petitioner and allowed vide

order dated 15.1.2016 in Petition No. 297/TT/2013. Thereafter, the petitioner

has filed Petition No. 312/TT/2014 for final tariff of both circuits of 400 kV D/C

Koldam-Ludhiana transmission line (Triple Snowbird Conductor)and Petition

No. 384/TT/2014 for final tariff of both circuits comprising of 129.02 ckt. km

section starting from LILO point of Parbati (Banala) Pooling Point to Koldam

HEP, 2x400 kV (Quad) S/C Parbati-II to Koldam.

6. The administrative approval to the transmission system of 2xS/C 400 kV

Parbati-Koldam transmission lines, to be executed by PKTCL, was given by the

Board of Directors of PGCIL on 20.12.2005 at an estimated cost of the project

of `35842 lakh including IDC of `2905 lakh (based on 2nd Quarter, 2005 price

level). In addition, the administrative approval and expenditure sanction to the

transmission project of Koldam-Ludhiana 400 kV D/C transmission line (Triple

Aluminum Conductor Steel Reinforced) (also to be executed by PKTCL) was

also accorded by the Ministry of Power (MoP) vide order No. 12/19/2003-PG

dated 7.9.2005 for `30195 lakh including IDC of `2048 lakh (based on

2ndQuarter, 2005 price level). The project was scheduled to be completed in

time frame of 36 months from the date of Investment Approval (IA) to match the

commissioning of generation project.

7. Thereafter, a cost estimate of the combined transmission project was

submitted for financing purpose and approved by the lenders and also admitted

Page 7 of 48

Order in Petition No. 156/TT/2015

by the Board of Directors of PKTCL in meeting held on 23.8.2010 for `110169

lakh including an IDC of `17267 lakh. Subsequently, the Revised Cost Estimate

of the combined transmission project was approved by the Board of Directors of

PKTCL vide meeting held on 19.5.2014 for `100653 lakh including IDC of

`14340 lakh (based on November, 2013 price level). The details of the project

costs are as follows:-

a. Transmission system associated with Parbati-Koldam transmission

lines-`50897 lakh, including IDC of `7438 lakh.

b. Transmission system associated with Koldam-Ludhiana

transmission line-`49756 lakh, including IDC of `6901 lakh.

8. The scope of work covered under the combined project is as follows:-

Transmission Lines

(i) 400 kV S/C Parbati-Koldam transmission line-I (Quad Moose Conductor);

(ii) 400 kV S/C Parbati-Koldam transmission line-II (Quad Moose Conductor);

(iii) 400 kV D/C Parbati-Koldam transmission line (Quad Moose

Conductor); and

(iv) 400 kV D/C Koldam-Ludhiana transmission line (Triple Snowbird

Conductor).

9. However, based on the proceedings of 26th, 29th and 32nd meetings of

Standing Committee Meeting of Power System Planning of Northern Region

held on 13.10.2008, 29.12.2010 and 31.8.2013 respectively and the 26th TCC

and 29th NRPC meetings held on 12.9.2013 and 13.9.2013 respectively, it was

decided to apportion the complete 2XS/C line of Parbati-Koldam (Ckt-I and Ckt-

II of Quad Moose conductor) traversing the total length of about 157 ckt. km to

three distinct sections for the commissioning purposes as follows:-

Page 8 of 48

Order in Petition No. 156/TT/2015

(i) Section-I: 3.518 ckt. km section of the Ckt.-II of the 2x400 kV S/C

Parbati-Koldam TL starting from LILO point of Parbati III HEP to LILO point

of Parbati (Banala) Pooling Station (COD August, 2013)-(Tariff claimed in

Petition No. 297/TT/2013).

(ii) Section-II: 129.02 ckt. km section starting from LILO point of Parbati

(Banala) Pooling Point to Koldam HEP, 2x400 kV (Quad) S/C Parbati-II to

Koldam-(Tariff claimed in Petition No. 384/TT/2014).

(iii) Section-III: 24 ckt. km section starting from LILO point of Parbati-III

to Parbati-II having a line length of 8.25 km of S/C and from Parbati

(Banala) Pooling point to Parbati-II with a line length of 12.838 km of S/C

along with a stretch of 1.511 km of Double Circuit.

10. This order is issued after considering PKTCL‟s affidavits dated 21.7.2015

(filed before the bench), 4.9.2015, 18.12.2015, 22.12.2015, 11.2.2016, and

31.8.2016.

11. The petitioner, as per the original petition, claimed tariff for Section of 400

kV (Quad) 2xS/C Parbati-Koldam Transmission line, starting from Parbati-II

HEP to LILO point of Parbati (Banala) Pooling Station for Circuit-I and from

Parbati-II HEP to LILO point of Parbati-III HEP for Circuit-II, which was included

in the original scope of work of Parbati HEP transmission system entrusted to

PKTCL as per implementation agreement entered into between PGCIL and

PKTCL as well as transmission licence granted by the Commission to PKTCL.

12. Annual Fixed Charges (AFC) for the transmission assets were allowed

vide order dated 30.12.2015 under Regulation 7(7) of the 2014 Tariff

Page 9 of 48

Order in Petition No. 156/TT/2015

Regulations, subject to adjustment as per the said Regulation and final decision

on COD of the instant assets after hearing NHPC and Sainj HEP.

13. The petition was heard on 21.7.2015 and the petitioner was directed to file

certain information. The petitioner in reply vide affidavit dated 4.9.2015, has

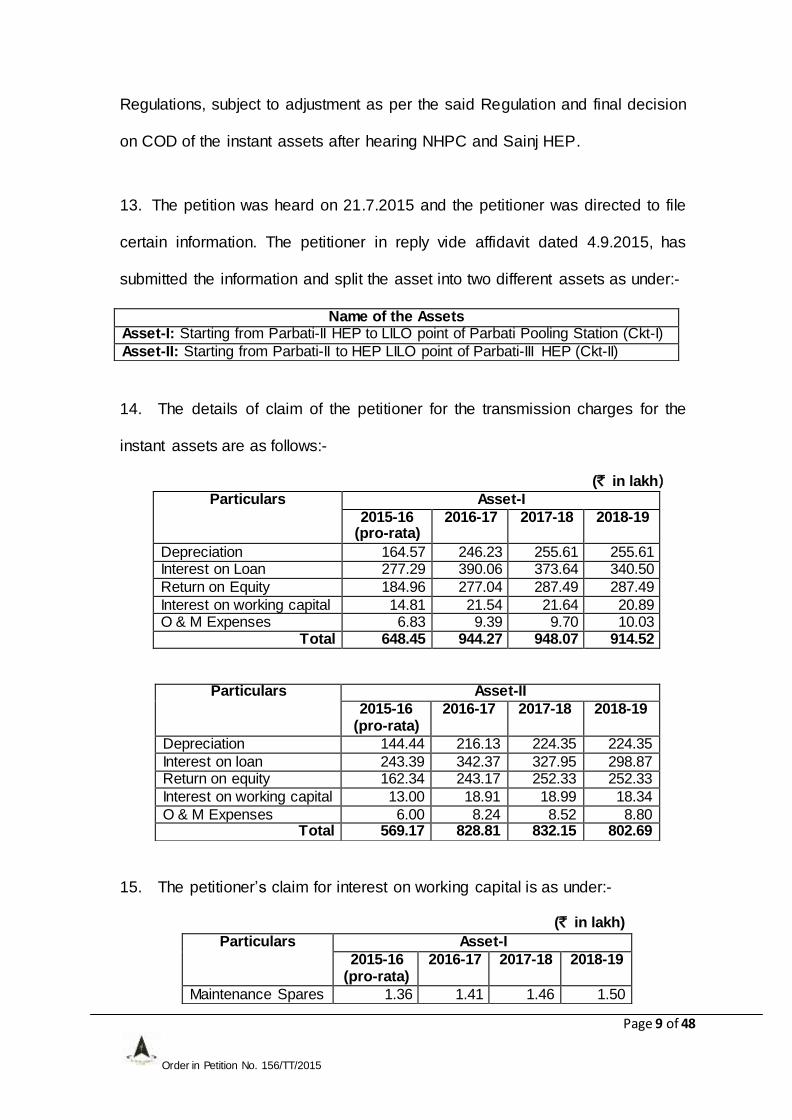

submitted the information and split the asset into two different assets as under:-

14. The details of claim of the petitioner for the transmission charges for the

instant assets are as follows:-

(` in lakh)

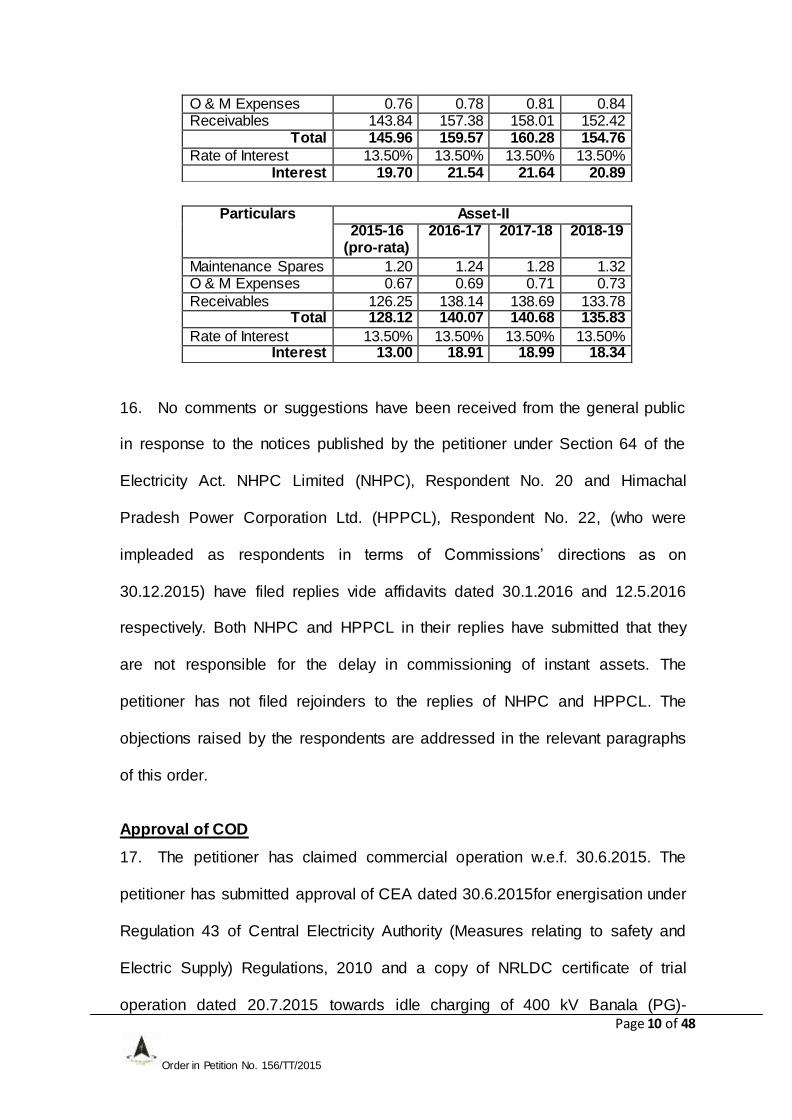

15. The petitioner‟s claim for interest on working capital is as under:-

(` in lakh)

Name of the Assets Asset-I: Starting from Parbati-II HEP to LILO point of Parbati Pooling Station (Ckt-I)

Asset-II: Starting from Parbati-II to HEP LILO point of Parbati-III HEP (Ckt-II)

Particulars Asset-I

2015-16 (pro-rata)

2016-17 2017-18 2018-19

Depreciation 164.57 246.23 255.61 255.61 Interest on Loan 277.29 390.06 373.64 340.50

Return on Equity 184.96 277.04 287.49 287.49

Interest on working capital 14.81 21.54 21.64 20.89 O & M Expenses 6.83 9.39 9.70 10.03

Total 648.45 944.27 948.07 914.52

Particulars Asset-II

2015-16 (pro-rata)

2016-17 2017-18 2018-19

Depreciation 144.44 216.13 224.35 224.35

Interest on loan 243.39 342.37 327.95 298.87 Return on equity 162.34 243.17 252.33 252.33

Interest on working capital 13.00 18.91 18.99 18.34

O & M Expenses 6.00 8.24 8.52 8.80 Total 569.17 828.81 832.15 802.69

Particulars Asset-I

2015-16 (pro-rata)

2016-17 2017-18 2018-19

Maintenance Spares 1.36 1.41 1.46 1.50

Page 10 of 48

Order in Petition No. 156/TT/2015

16. No comments or suggestions have been received from the general public

in response to the notices published by the petitioner under Section 64 of the

Electricity Act. NHPC Limited (NHPC), Respondent No. 20 and Himachal

Pradesh Power Corporation Ltd. (HPPCL), Respondent No. 22, (who were

impleaded as respondents in terms of Commissions‟ directions as on

30.12.2015) have filed replies vide affidavits dated 30.1.2016 and 12.5.2016

respectively. Both NHPC and HPPCL in their replies have submitted that they

are not responsible for the delay in commissioning of instant assets. The

petitioner has not filed rejoinders to the replies of NHPC and HPPCL. The

objections raised by the respondents are addressed in the relevant paragraphs

of this order.

Approval of COD

17. The petitioner has claimed commercial operation w.e.f. 30.6.2015. The

petitioner has submitted approval of CEA dated 30.6.2015for energisation under

Regulation 43 of Central Electricity Authority (Measures relating to safety and

Electric Supply) Regulations, 2010 and a copy of NRLDC certificate of trial

operation dated 20.7.2015 towards idle charging of 400 kV Banala (PG)-

O & M Expenses 0.76 0.78 0.81 0.84 Receivables 143.84 157.38 158.01 152.42

Total 145.96 159.57 160.28 154.76

Rate of Interest 13.50% 13.50% 13.50% 13.50% Interest 19.70 21.54 21.64 20.89

Particulars Asset-II 2015-16

(pro-rata) 2016-17 2017-18 2018-19

Maintenance Spares 1.20 1.24 1.28 1.32 O & M Expenses 0.67 0.69 0.71 0.73

Receivables 126.25 138.14 138.69 133.78 Total 128.12 140.07 140.68 135.83

Rate of Interest 13.50% 13.50% 13.50% 13.50% Interest 13.00 18.91 18.99 18.34

Page 11 of 48

Order in Petition No. 156/TT/2015

Parbati-II (NHPC) transmission line. Further, the petitioner vide affidavit dated

22.12.2015 has submitted the NRLDC certificate of trial operation dated

30.11.2015 for starting of power flow through its portion of 400 kV Banala (PG)-

Parbati-II (NHPC) transmission line and successful trial run operation of Circuit-I

Parbati-II to LILO point of Banala Pooling Station and Circuit-II Parbati-II to LILO

point of Parbati-III HEP on 3.11.2015.

18. The petitioner has further submitted that inspite of finishing construction on

both the circuits and obtaining the energisation certificate, it was not able to

charge the said line, as the bay to which the Circuit-II of the Parbati-III-Koldam

lines connects at Parbati-III, was not charged by NHPC, as is evident from

NHPC‟s email dated 2.7.2015 and therefore the petitioner was prevented from

charging and putting the Parbati-III-Koldam lines to regular use and that the

construction and commissioning of the said bay is the responsibility of NHPC.

Therefore, the petitioner, on account of delay of NHPC in charging the bays,

has been prevented from charging and putting the Parbati-III-Koldam lines to

regular use. The petitioner has also submitted that at the 114th OCC meeting

held on 17.8.2015, in NRPC, NHPC‟s representative has admitted that the

charging of the bay is delayed further by one month. Therefore, the petitioner

has prayed that the case accordingly qualifies for approval of the date of

commercial operation (COD) as 30.6.2015 for instant assets prior to the

element coming into regular service and grant of consequential tariff to it.

19. The dates of commercial operation of Asset-I and Asset-II were not

approved by the Commission in order dated 30.12.2015, while allowing AFC

under Regulation 7(7) of the 2014 Tariff Regulations which was left to be

Page 12 of 48

Order in Petition No. 156/TT/2015

decided at the time of final tariff after hearing NHPC and Sainj HEP. The

relevant portion of the order is as under:-

“8. None of the respondents, including NHPC and Sainj HEP, made submissions during the hearing on 22.12.2015. As observed earlier, we would like to hear NHPC and Sainj HEP before approving the date of COD as claimed by the petitioner. As the instant assets were charged by the petitioner on 3.11.2015 and the power is flowing, we allow recovery of transmission tariff from 3.11.2015. The claim of the petitioner with regard to COD and sharing of transmission charges from COD to 2.11.2015 shall be decided at the time of final tariff after hearing NHPC and Sainj HEP.”

20. NHPC, in response, vide affidavit dated 30.1.2016 has submitted that the

claim made by the petitioner on non-commissioning/commissioning of

switchyard/Gantry of Parbati-II HEP is not correct, as erection at GIS & Pot

Head Yard of Parbati-II is under progress and is scheduled to be commissioned

in September, 2018. However, 2nd evacuation line of Parbati-III has been

charged by passing Parbati-II GIS on 2.11.2015 and power flow started on

3.11.2015. Further, commissioning of bay at Parbati-II was in no way required

for immediate charging of this line and NHPC also suggested exploring

possibility of power flow in second evacuation circuit of Parbati-III power station

by by-passing Parbati-II HEP Project vide letter dated 18.8.2015. Therefore,

NHPC has requested to allow the AFC to the petitioner for the subject line

segment w.e.f. 3.11.2015, and not from 30.6.2015.

21. As per proviso (ii) of Regulation 4 (3) of the 2014 Tariff Regulations, in

case of non-readiness of downstream/upstream system, the transmission

licensee shall approach the Commission for approval of the COD of such

transmission system. Regulation 4(3) of the 2014 Tariff Regulations, provides

as under:-

Page 13 of 48

Order in Petition No. 156/TT/2015

"4. Date of Commercial Operation: The date of commercial operation of a

generating station or unit or block thereof or a transmission system or element thereof shall be determined as under: xxxxx] (3) Date of commercial operation in relation to a transmission system shall mean

the date declared by the transmission licensee from 0000 hour of which an element of the transmission system is in regular service after successful trial operation for transmitting electricity and communication signal from sending end to receiving end: Provided that: i) Where the transmission line or substation is dedicated for evacuation of power from a particular generating station, the generating company and transmission licensee shall endeavour to commission the generating station and the transmission system simultaneously as far as practicable and shall ensure the same through appropriate Implementation Agreement in accordance with Regulation 12(2) of these Regulations: ii) in case a transmission system or an element thereof is prevented from regular service for reasons not attributable to the transmission licensee or its supplier or its contractors but is on account of the delay in commissioning of the concerned generating station or in commissioning of the upstream or downstream transmission system, the transmission licensee shall approach the Commission through an appropriate application for approval of the date of commercial operation of such transmission system or an element thereof.”

22. Thus, an element of the transmission system can be in regular service

after successful trial operation for transmitting electricity and communication

signal from sending end to receiving end. Regulation 5(2) of the 2014 Tariff

Regulations specifies as follows:-

“5. Trial Run and Trial Operation.- (2) Trial operation in relation to a transmission system or an element thereof shall mean successful charging of the transmission system or an element thereof for 24 hours at continuous flow of power, and communication signal from sending end to receiving end and with requisite metering system, telemetry and protection system in service enclosing certificate to that effect from concerned Regional Load Dispatch Centre.”

23. In the light of the above statutory provisions, we have considered the

submissions of the petitioner and NHPC and the documents available on

Page 14 of 48

Order in Petition No. 156/TT/2015

record. It is observed that the petitioner was ready with the circuit-I and circuit-II

of Parbati-III-Koldam line for charging after receiving the „Approval for

Energization‟ certificate from CEA under Regulation 43 of CEA (Measures

relating to safety and Electric Supply) Regulations, 2010 on 30.6.2015. The

upstream 400 kV bays for the Parbati-III-Koldam line were within the scope of

NHPC and were required to be matched with the commissioning of Parbati-III-

Koldam line for regular service of the transmission line. These upstream 400 kV

bays for the Parbati-III-Koldam line at Parbati-II pot head yard of NHPC was not

ready on 30.6.2015, but ckt.-I and ckt.-II of Parbati-III-Koldam line were

commissioned on 30.6.2015. However, actual power flow started on Parbati-III-

Koldam line on 3.11.2015 and Parbati-III-Koldam line is being put to use only

with effect from 3.11.2015. Since Parbati-III-Koldam line did not fulfill the

condition of successful trial operation on 30.6.2015, the said line could not be

said to be ready for declaration of commercial operation. Accordingly, we are

not inclined to approve the petitioner‟s prayer for approval of COD of the ckt.-I

and ckt.-II of Parbati-III-Koldam line as 30.6.2015 under Regulation 4(3)(ii) of

the 2014 Tariff Regulations. The COD of both Ckt.-I and Ckt.-II of Parbati-III-

Koldam line shall be reckoned as 3.11.2015.

24. It is observed that Ckt.-I and Ckt.-II of Parbati-III-Koldam line were

originally envisaged to be commissioned with the 400 kV bays in Parbati-II

switchyard of NHPC. On account of delay in commissioning of 400 kV bays in

Parbati-II switchyard of NHPC, the Ckt.-I and Ckt.-II of Parbati-III-Koldam line

were put into use only on 3.11.2015 through an alternate arrangement. Since

the delay is attributable to the non-commissioning of 400 kV bays by NHPC, we

Page 15 of 48

Order in Petition No. 156/TT/2015

are of the view that the IDC and IEDC from 30.6.2015 for instant assets till

2.11.2015 shall be borne by NHPC. With effect from 3.11.2015, the

transmission charges for the instant assets shall be serviced in accordance with

Sharing Regulations. The IDC and IEDC borne by NHPC shall not be

capitalized by NHPC in its book of accounts for the purpose of claiming tariff for

its generation from Parbati HEPs as well as for transmission services by the

petitioner.

Capital cost

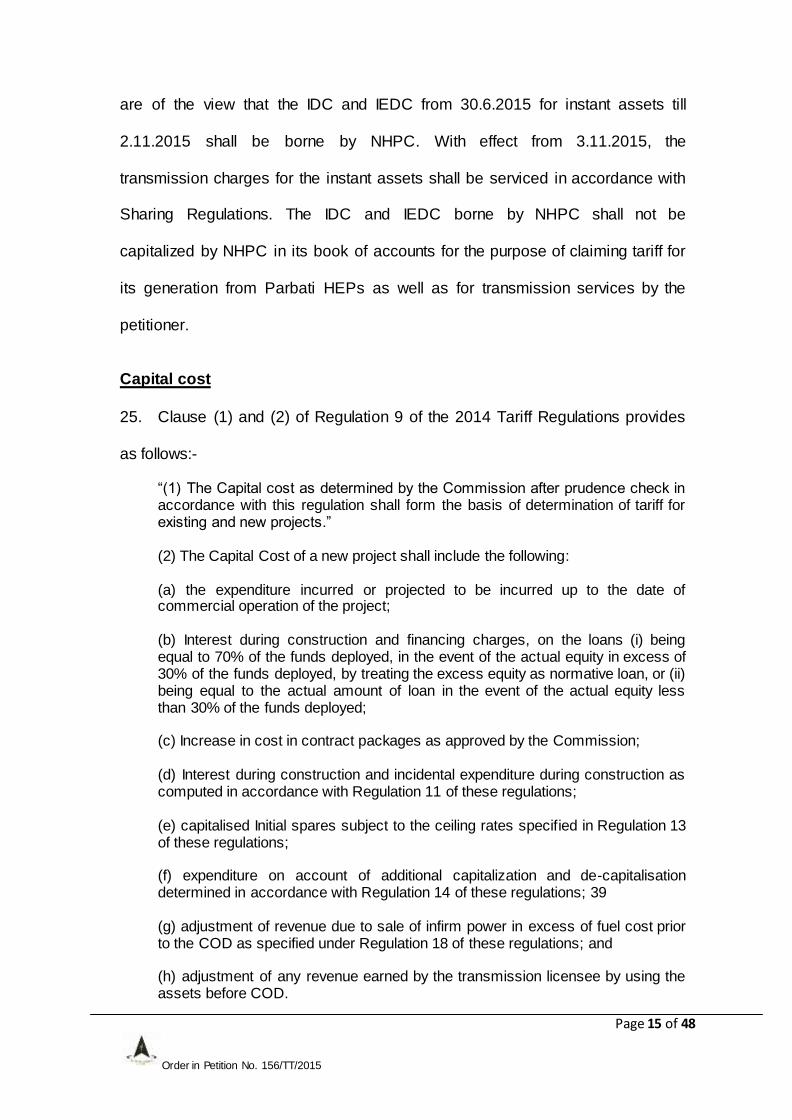

25. Clause (1) and (2) of Regulation 9 of the 2014 Tariff Regulations provides

as follows:-

“(1) The Capital cost as determined by the Commission after prudence check in accordance with this regulation shall form the basis of determination of tariff for existing and new projects.” (2) The Capital Cost of a new project shall include the following: (a) the expenditure incurred or projected to be incurred up to the date of commercial operation of the project; (b) Interest during construction and financing charges, on the loans (i) being equal to 70% of the funds deployed, in the event of the actual equity in excess of 30% of the funds deployed, by treating the excess equity as normative loan, or (ii) being equal to the actual amount of loan in the event of the actual equity less than 30% of the funds deployed; (c) Increase in cost in contract packages as approved by the Commission; (d) Interest during construction and incidental expenditure during construction as computed in accordance with Regulation 11 of these regulations; (e) capitalised Initial spares subject to the ceiling rates specified in Regulation 13 of these regulations; (f) expenditure on account of additional capitalization and de-capitalisation determined in accordance with Regulation 14 of these regulations; 39 (g) adjustment of revenue due to sale of infirm power in excess of fuel cost prior to the COD as specified under Regulation 18 of these regulations; and (h) adjustment of any revenue earned by the transmission licensee by using the assets before COD.

Page 16 of 48

Order in Petition No. 156/TT/2015

26. The petitioner has submitted Management Certificates for expenditure

incurred/projected to be incurred along with revised tariff forms and other

information as sought for the expenditure incurred against the instant assets.

The details of apportioned approved cost, expenditure incurred/projected to be

incurred as on COD claimed vide reply dated 4.9.2015 and details of additional

capitalization incurred/ projected to be incurred for the period from claimed COD

to 31.3.2019 for the assets covered in the petition are as under:-

(` in lakh) Particulars Apportioned

/approved cost

Expenditure up to claimed

COD (30.6.2015)

Estimated add-cap Total estimated completion cost up

to 31.3.2017 2015-16 2016-17

Asset-I 4943.01 3836.88 694.82 355.01 4886.71 Asset-II 4338.60 3367.72 609.86 311.61 4289.19

27. Further, the petitioner has also submitted the details of IEDC and IDC

estimated to be paid after claimed COD of 30.6.2015 to 31.3.2016, which are as

below:-

(` in lakh) Particulars IEDC IDC Total

Asset-I 10.65 45.27 55.92

Asset-II 9.35 39.73 49.08

28. The petitioner has further submitted vide affidavits dated 22.12.2015 and

31.8.2016 that the instant assets have been put under commercial operation on

3.11.2015 but the petitioner has neither submitted any revised Management

certificates/Auditors‟ Certificates nor any revised tariff forms. Therefore, on the

basis of available information, the IDC and IEDC claimed on estimated basis

and included in the add-cap of 2015-16 have not been allowed. Further, we

have considered pro-rata add-cap claimed during the 2015-16 as a part of

capital cost as on tariff COD i.e. 3.11.2015 and considered the details of

Page 17 of 48

Order in Petition No. 156/TT/2015

additional capitalization incurred/projected to be incurred for the period from

Tariff COD of 3.11.2015 to 31.3.2019 for the purpose of working out tariff for

instant assets as under:-

(` in lakh) Particulars Apportioned

/approved cost

Expenditure up to tariff

COD (3.11.2015)

2015-16 2016-17 Total estimated completion cost up to 31.3.2017

Asset-I 4943.01 4130.87 344.91 355.01 4830.79

Asset-II 4338.60 3625.76 302.74 311.61 4240.11

Cost Over-run

29. The total estimated completion cost of instant assets is within the RCE.

Hence, there is no cost over-run in the case of instant assets.

Time Over-run:

30. As per the Investment Approval, the instant assets were scheduled to be

commissioned within 36 months as per the Investment Approval dated

26.12.2005, matching with the commissioning of generation project. Thus, the

scheduled COD of the instant assets was 25.12.2008, say 1.1.2009 whereas

the COD accepted in this order is 3.11.2015. Excluding the period for which

NHPC has been held liable to pay IDC and IEDC, there is a time over-run of

approximately 78 months. The petitioner has attributed the time over-run to

events as shifting of COD due to delay in the commissioning of HEPs, delay in

obtaining forest clearance, ROW issues and adverse weather conditions. The

submissions made by the petitioner are as under:-

A. Shifting of COD

i. COD shifted from 25.12.2008 to 31.12.2011: In the 26th Meeting of the

Standing Committee on Power System Planning of Northern Region held

Page 18 of 48

Order in Petition No. 156/TT/2015

on 13.10.2008, it was agreed that NHPC would inform the possible date of

commissioning of Parbati-II HEP to work out the Revised Commercial

Operation Date (RCOD) of the Parbati-II-Koldam. The petitioner signed an

Indemnification Agreement with NHPC. As per the said agreement, the

COD of first unit of Parbati-II HEP was scheduled on 31.12.2011 (Zero

Date) which was subject to review on account of the change in

commissioning schedule of Parbati-II HEP. On account of delay in COD of

Parbati-II HEP, the petitioner, vide letters dated 13.2.2009 and 5.3.2009

requested PGCIL to amend the Implementation Agreement and suitably

revise the RCOD. PGCIL (CTU) amended the Implementation Agreement

on 22.4.2009 revising the RCOD as 31.12.2011

ii. COD shifted from 31.12.2011 to 30.6.2012 : NHPC vide its letter

dated 26.3.2009, informed that the zero date was further required to be

revised to December, 2012 on account of delay in COD of Parbati II HEP.

A supplementary agreement was signed with NHPC on 15.6.2009 revising

the zero date to 31.12.2012. Accordingly, on 27.8.2009, the CTU and the

petitioner amended the Implementation Agreement revising the RCOD to

30.6.2012

iii. COD Shifted From 30.6.2012 to 31.3.2013: NHPC on 16.3.2011

informed the petitioner that the revised COD of Parbati-II is July, 2014.

Thereafter, CEA sent a letter dated 18.5.2011 to the petitioner intimating

that the commissioning schedules of the transmission lines associated

with Koldam HEP and Parbati-II HEP were as under:-

(a) Koldam HEP-March 2013 onwards;

(b) Parbati-II HEP-2014-15

Page 19 of 48

Order in Petition No. 156/TT/2015

In view of the periodic shifting of the COD of the Koldam HEP and Parbati-

II HEP, the commissioning of the Parbati-II-Koldam Transmission Line was

revised. Further, in the 30th Meeting of the Standing Committee on Power

System Planning of Northern Region held on 19.12.2011, the petitioner

confirmed that though it was putting in its best efforts for completion of

these lines, the pace of execution is hampered on account of non-receipt

of the Stage-II forest clearance. Accordingly, CTU amended the

Implementation Agreement on 12.9.2012revising the RCOD to 31.3.2013.

B.Delay due to Forest Clearance

The Parbati-Koldam line 2xS/C 400 kV (Quad) traverses through 231.347

ha. of forest area in Banjar, Mandi, Nachan, Suket and Bilaspur forest

divisions of the state of Himachal Pradesh and out of this, about 76 ha. are

of Parbati-III-Koldam line. Thus, forest clearance was required for total

231.347 ha. of forest area. The portion of the Parbati-III-Koldam line falling

in forest areas is approximately 61.28 km, although construction is

affected to the extent of approximately 13.30 km. PGCIL submitted

proposals for diversion of forest land in Himachal Pradesh during the

period of 2005 to 2006, before the formation of the joint venture company,

Parbati-Koldam Transmission Company Limited, to the concerned

Divisional Forest Officers in the aforesaid forest divisions in Himachal

Pradesh. The Petitioner has submitted about the reasons for delay in

obtaining forest clearance as under:

i. Forest Clearance for Himachal Pradesh Portion: Stage-I (in-

principle) Forest Clearance in respect of the State of Himachal Pradesh

Page 20 of 48

Order in Petition No. 156/TT/2015

was granted on 5.12.2007 by MoEF. Stage-II (final) Forest Clearance was

granted on 30.11.2012 in the name of PGCIL. It took 89 months and 30

days to obtain the forest approval. However, as the clearance was issued

in the name of PGCIL, the petitioner requested MoEF on 12.11.2011 for

change in the name of user agency. Thereafter, it sent a letter to PGCIL

on 19.3.2013 intimating receipt of Stage-II Forest Clearance, wherein it

was stated that, considering the work involved in the forest stretches, it

would be able to complete the line by the last quarter 2013 or the first

quarter of 2014. This letter dated 19.3.2013 was also deliberated upon, in

the 25th Meeting of Technical Coordination Sub-committee held on

25.4.2013 and the 28th Meeting of Northern Region Power Committee held

on 26.4.2013.Further, upon receipt of Stage-II Forest Clearance in

Himachal Pradesh, the petitioner came to know that a separate tree

cutting approval was required from the State authorities for felling of trees

in forest stretches en-route the transmission line. The tree cutting was a

very lengthy and tedious exercise which was to be exclusively carried out

by the State Forest Authorities and included recounting/enumeration as

per the locations and approval by divisional forest tender economics/cost

estimate prepared and approved by Director, HPSFDC. Thereafter, bids

were invited and scrutinized to determine the lowest bidder. The

consolidated report, after discounted price of lowest bidder, was sent to

Director for approval and placement of award. Thereafter, all the tree

cutting approvals were obtained by late September, 2013. The actual site

was available for work only in the month of October, 2013 after cutting of

trees in the forest area and the construction could be started thereafter.

Page 21 of 48

Order in Petition No. 156/TT/2015

The Board of Directors of the petitioner company, it its 59th meeting held

on 16.8.2013, deliberated in detail, on the developments and approved the

revision of COD to 30.6.2014. CTU on 24.1.2014 amended the

Implementation Agreement to further revise the RCOD to 31.12.2014.

C. Delay due to ROW issues

The Petitioner has submitted that in addition to usual challenges faced

while undertaking construction of transmission lines in hilly areas, severe

right of way challenges were faced, while implementing the Parbati-III-

Koldam Line despite having secured authorization under Section 164 of

the Electricity Act, 2003. The local panchayats and local administration

were involved to persuade the landowners to settle out of court by holding

meetings with all stakeholders. The land owners, local administration and

local leaders were impressed upon about the national importance of

project and authorization under Section 164 of the Electricity Act, 2003

granted to the Petitioner to develop the project. However, many

landowners/occupiers moved the courts. 35 court cases were filed

affecting a large stretch of the Parbati-III-Koldam Line. Landowners

demanded unreasonable amounts in terms of crop compensation defying

the rates prescribed by the State authorities and the prevailing rates in the

area. Therefore, time taken for disposal and final settlement of the court

cases prevented construction of work on the affected portions of the line

route for varying periods of time ranging from one month to one year. By

December, 2014, 64% of the foundation work, 50% of erection and 20% of

stringing work were completed for Ckt.-I and 83% of foundation work, 75%

Page 22 of 48

Order in Petition No. 156/TT/2015

of erection work and 40% of stringing work were completed for Ckt.-II.

Significant portion of balance work got delayed on account of the shifting

in construction schedule. It was the last stretch of the Parbati-Koldam

Transmission line and the locals were aware of the fact. As there was

delay in disposal of the court cases, out-of-court settlements were reached

with the land owners with the help of local administration. Wherever, the

cases could not be settled out of court, the cases were pursued in court,

police protection was sought and under situations of extreme resistance

and distress, the work was completed. While the final orders from various

courts on any additional compensation required to be paid were awaited,

the transmission line was expected to be commissioned by 31.5.2015. In

some of the cases, odds were too high and the executives and workers on

site were mistreated, manhandled and threatened by land owners. Thus,

court cases regarding right of way on some of the locations were taking

long periods of time to resolve leading to inordinate delays in completion

of the line.

The RoW problems started on 19.3.2013. PKTCL intimated Deputy

Collector, Kullu that the obstruction was being faced at Location No. 17

and requested for issuance of orders under Section 16 of Indian Telegraph

Act, 1885 and pursued the matter with SDM/DM/Police officers and

meeting with MLA of the area. Thereafter, the issue of RoW could be

resolved on 26.11.2014, thus the RoW issue took about more than 20

months (19.3.2013 to 26.11.2014). The sequence of events is as follows:-

Page 23 of 48

Order in Petition No. 156/TT/2015

Srl. No.

Date Events

1 19.3.2013

PKTCL intimated the obstruction being faced at Loc. No. 17 to DC, Kullu and requested for issuance of orders u/s 16 of Indian Telegraph Act, 1885. Letter was forwarded by DC, Kullu to SDM, Banjar to look into the matter and resolve the issue.

2 23.3.2013 One of the land owners Sh. Narain Chand filed a civil suit in the court of Civil Judge (Sr. Division), Lauhal and Spiti at Kullu for permanent injunction

3 27.7.2013 Application of injunction was dismissed in the civil Court

4 27.7.2013 PKTCL filed application for issuance of orders under Section 16 of Indian Telegraph Act, 1885 to remove the obstruction

5 3.8.2013 Interim order was passed by Distt. Magistate, Kullu with the direction to SDM, Banjar to hear both the parties on 16.9.2013 for consideration of compensation

6 7.9.2013 SDM, Banjar fixed the hearing for 19.9.2013 and directed the Horticulture, Agriculture and Forest officials to assets the compensation

7 10.9.2013 PKTCL requested Naib-Tehsildar, Sainj to depute the concerned Patwari to accompany the team for assessment of compensation on 12.9.2014

8 11.9.2013 PKTCL requested SP, Kullu for police assistance

9 12.9.2013 Officials of Horticulture, Forest, Agriculture and Revenue along with police visited the site but the land owners did not allow to enter into the land. Joint inspection Report submitted by them to SDM, Banjar

10 19.9.2013

SDM heard both the parties. Sh. Narain Chand stated that the installation of the tower would lead to damage to his house, crops and fruit bearing trees and requested for site inspection. SDM, Banjar constituted a committee under the chairmanship of Naib Tehsildar, Sainj

11 28.9.2013 Committee alongwith police personnel visited the site but the land owners did not allow to enter the team in their land. Neither the compensation could be assessed nor work was allowed to be started.

12 29.10.2013 Sh. Ludar Chand and other villagers filed another suit in the court of civil Judge (Sr. Division), Kullu for permanent prohibitory injunction

13 10.1.2014 Suit for permanent Prohibitory injunction was dismissed

14 3.2.2014 SDM, Banjar hold a meeting with the land owners but they refused to allow the start of work

15 4.2.2014 SDM, Banjar submitted his report to DC, Kullu

16 11.2.2014 PKTCL requested DC, Kullu for police assistance for implementation of order dated 3.8.2013

17 12.2.2014 Distt. Magistrate passed order for providing assistance to PKTCL for start of work

18 21.2.2014 PKTCL requested SP, Kullu for providing police assistance as per order dt. 12.2.2014

19 21.2.2014 PKTCL requested SDM, Banjar for deputation of officials of Revenue, Agriculture, forest and Horticulture Deptt. For assessment of compensation

20 25.2.2014 The officials of revenue, agriculture, forest and horticulture deptts. alongwith police personnel visited the spot. The land owners did not allow to enter into the land

Page 24 of 48

Order in Petition No. 156/TT/2015

21 27.2.2014 SHO, Bhunter along with police personnel visited the spot and tried to get the work start but there was some political pressure due to which SHO had to withdraw the action and work could not be started

22 5.3.2014

Land owners along with other villagers met DC, Kullu and requested for shifting of line. Accordingly a meeting was held in the office of ADM, Kullu which was attended by MLA, Kullu, SDM, Banjar, Land owner Sh. Narain Chand and rep. of PKTCL. Land owner alleged that the line is passing over the houses and requested for site inspection. ADM, Kullu directed SDM, Banjar to inspect the site and report

23 1.4.2014 SDM, Banjar fixed the site inspection for 5.4.2014

24 5.4.2014 Site inspection was carried out by SDM in the presence of land owners and villagers.

25 11.4.2014 PKTCL Submitted the measurement details taken at site

26 17.4.2014 SDM, Banjar asked PKTCL to explore alternative alignment to avoid the present location of towers.

27 28.4.2014 PKTCL submitted the letter regarding inability to shift the alignment

28 17.6.2014 SDM, Banjar submitted his report to DC, Kullu depicting the constraints for shifting of alignment

29 25.6.2014 PKTCL requested DC, Kullu to remove the obstruction for start of work

30 15.7.2014 Based on the report of SDM, Banjar, Distt. Magistrate, Kullu passed order for police assistance and directed Executive Magistrate to ensure that work is not obstructed by any one

31 1.8.2014 PKTCL intimated SP, Kullu, SDM, Banjar and executive Magistrate regarding deployment of manpower on 5.8.2014

32 21.8.2014 SDM, Banjar requested the officials and police to be present on the spot on 25.8.2014 to start the work

33 25.8.2014

Tehsildar, officials of revenue, horticulture, agriculture and forest along with police visited the site. Again the land owners did not allow to start the work. Tehsildar intimated the situation to SDM who directed him to record the statements of both the parties and keep the matter pending till he discusses the matter with DC, Kullu

34 28.8.2014

Met with SDM, Banjar who talked to DC, Kullu and suggested him that before taking police action, they must verify the record regarding proper public notification/information as the villagers alleged that they were not given any opportunity to submit their objections during the preparation of scheme. SDM asked us to show the record regarding publication of the scheme.

35 3.9.2014 All the record was placed before SDM who was satisfied and intimated the DC, Kullu in this regard. DC called petitioner and SDM, Banjar to meet in his office

36 5.9.2014

Met with DC,Kullu along with SDM, Banjar. SDM, Banjar intimated that the people had represented to MLA, Banjar, however, he has appraised the MLA and asked him to persuade the villagers let the work start. SDM intimated that MLA has asked him to wait for two weeks to let him talk with villagers

37 24.9.2014 Director (Projects) met with DC, Kullu. SDM was also present during this meeting. DC and SDM suggested PKTCL to have a meeting with MLA, Banjar to sort out the issue

Page 25 of 48

Order in Petition No. 156/TT/2015

38 24.9.2014

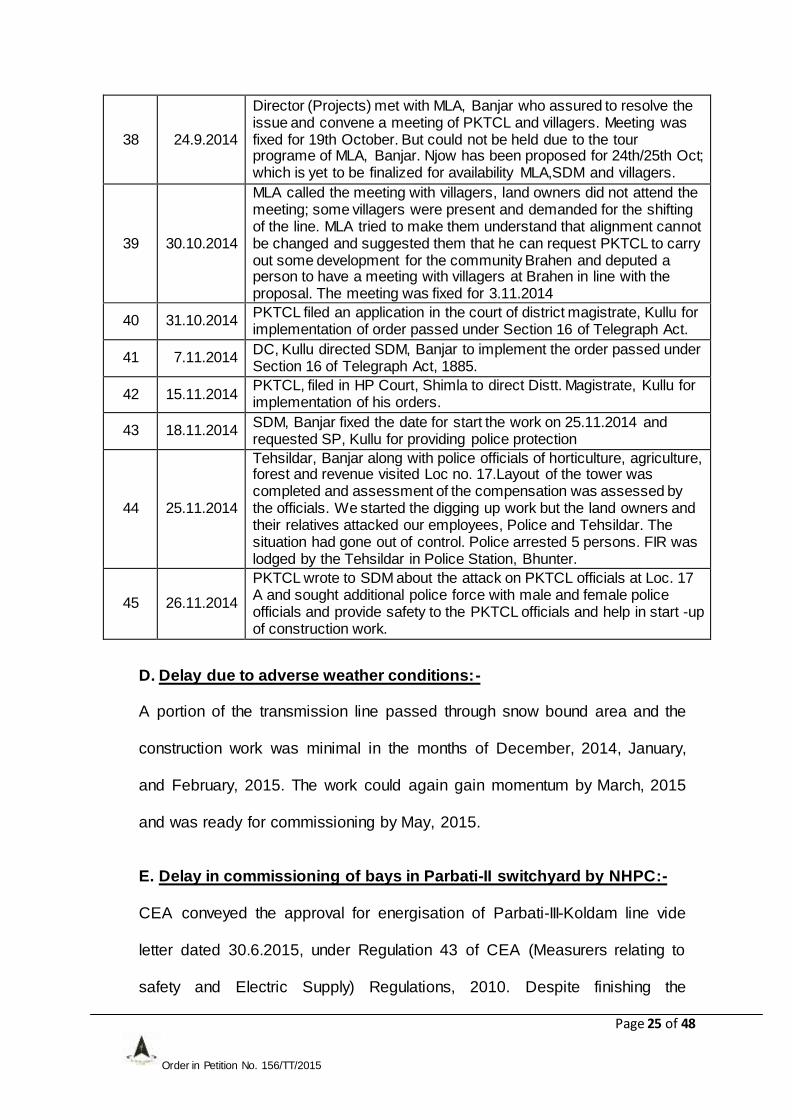

Director (Projects) met with MLA, Banjar who assured to resolve the issue and convene a meeting of PKTCL and villagers. Meeting was fixed for 19th October. But could not be held due to the tour programe of MLA, Banjar. Njow has been proposed for 24th/25th Oct; which is yet to be finalized for availability MLA,SDM and villagers.

39 30.10.2014

MLA called the meeting with villagers, land owners did not attend the meeting; some villagers were present and demanded for the shifting of the line. MLA tried to make them understand that alignment cannot be changed and suggested them that he can request PKTCL to carry out some development for the community Brahen and deputed a person to have a meeting with villagers at Brahen in line with the proposal. The meeting was fixed for 3.11.2014

40 31.10.2014 PKTCL filed an application in the court of district magistrate, Kullu for implementation of order passed under Section 16 of Telegraph Act.

41 7.11.2014 DC, Kullu directed SDM, Banjar to implement the order passed under Section 16 of Telegraph Act, 1885.

42 15.11.2014 PKTCL, filed in HP Court, Shimla to direct Distt. Magistrate, Kullu for implementation of his orders.

43 18.11.2014 SDM, Banjar fixed the date for start the work on 25.11.2014 and requested SP, Kullu for providing police protection

44 25.11.2014

Tehsildar, Banjar along with police officials of horticulture, agriculture, forest and revenue visited Loc no. 17.Layout of the tower was completed and assessment of the compensation was assessed by the officials. We started the digging up work but the land owners and their relatives attacked our employees, Police and Tehsildar. The situation had gone out of control. Police arrested 5 persons. FIR was lodged by the Tehsildar in Police Station, Bhunter.

45 26.11.2014

PKTCL wrote to SDM about the attack on PKTCL officials at Loc. 17 A and sought additional police force with male and female police officials and provide safety to the PKTCL officials and help in start -up of construction work.

D. Delay due to adverse weather conditions:-

A portion of the transmission line passed through snow bound area and the

construction work was minimal in the months of December, 2014, January,

and February, 2015. The work could again gain momentum by March, 2015

and was ready for commissioning by May, 2015.

E. Delay in commissioning of bays in Parbati-II switchyard by NHPC:-

CEA conveyed the approval for energisation of Parbati-III-Koldam line vide

letter dated 30.6.2015, under Regulation 43 of CEA (Measurers relating to

safety and Electric Supply) Regulations, 2010. Despite finishing the

Page 26 of 48

Order in Petition No. 156/TT/2015

construction of both the circuits and obtaining the energisation certificate, the

petitioner was not able to charge the Parbati-III-Koldam Line as the bay to

which the Ckt.-II of the line had to be connected was not charged by NHPC.

The Parbati-III-Koldam Line was finally charged on 3.11.2015.

31. We have considered the submissions of the petitioner. Thus, there was

time over-run of 78 months in execution of the instant assets. The petitioner has

attributed the time over-run to delay in commissioning of generation project,

forest clearance, RoW issues and adverse weather conditions. The details of

the period of time over-run due to these reasons is under:-

S. No.

Reason for time over-run Duration Period

1. Rescheduling of COD due to delay in commissioning of generation

25.12.2008 to 31.3.2013 51 months

2. Forest clearance 31.5.2005 to 30.11.2012 90 months 3. Row Issues 19.3.2013 to 26.11.2013 20 months

4. Adverse weather conditions December, 2014 to

March, 2015 3 months

32. It is observed that the commissioning of the instant assets was initially

revised from 25.12.208 to 31.3.2013 to match with the commissioning of

Koldam HEP and Parbati-II HEP. We are of the view that time over-run due to

the delay in commissioning of the instant assets on account of rescheduling of

Koldam HEP and Parbati-II HEP cannot be attributed to the petitioner.

33. As regards the delay in obtaining forest clearance approval, it is observed

that PGCIL approached the DFO, Himachal Pradesh for obtaining forest

clearance approvalfor Parbati-III-Koldam line on 31.5.2005 i.e. 6 months 25

days before the Investment Approval dated 26.12.2005. As per the Forest

(Conservation) Amendment Rules, 2004 notified by MoEF dated 3.2.2004, the

Page 27 of 48

Order in Petition No. 156/TT/2015

timeline for forest approval after submission of proposal is 210 days by State

Government and 90 days by Forest Advisory Committee of Central Government

i.e. total 300 days. Accordingly, the petitioner should have obtained the forest

clearance in 300 days of application. However, the stage-II clearance for

Parbati-III-Koldam line was granted on 30.11.2012. It took 90 months for the

petitioner to obtain all the forest clearance. Considering a normal period of 10

months required for forest clearance, we are of the view that the delay of 80

months in getting forest approval was also beyond the control of the petitioner.

34. It is observed that there were RoW issues leading to filing of court cases

by land owners. The petitioner has submitted that on 19.3.2013 it intimated the

obstruction being faced at Location 17 to Deputy Collector, Kullu and requested

for issuance of orders under Section 16 of Indian Telegraph Act, 1885 and only

after pursuing the matter with SDM/DM/Police officers and meeting with MLA of

the area, the issue was resolved on 26.11.2014. Thus, it took about 20 months

to settle the RoW issues. The RoW issues and court cases hindered the

progress of work. In our view, the delay due to RoW issues and court case was

beyond the control of the petitioner.

35. The petitioner has also submitted that it was able to carry out only minimal

work during the peak winter months of December, 2014, January and February,

2015 which led to delay in commissioning of the instant assets. The momentum

of work picked up March, 2015 and the remaining work was completed and the

line was ready for commissioning by May, 2015. It is observed that the

petitioner approached CEA on 28.5.2015 for inspection and CEA issued the

Inspection Report on 30.6.2015. As stated earlier, due to non-availability of 400

Page 28 of 48

Order in Petition No. 156/TT/2015

kV bays at Parbati-III HEP of NHPC, the actual power flow took place on

3.11.2015. We are of the view that the petitioner should have been aware of

heavy snow during the winter months and be prepared to meet such

eventualities. However, taking into consideration that the work did not

completely come to standstill and the work was under progress during

December, 2014 to March, 2015, the time over-run of three months due to

adverse weather conditions is condoned.

36. We are of the view that time over-runs due to delay in commissioning of

Koldam HEP, Parbati III HEP, forest clearance, RoW issues and adverse

weather conditions were beyond the control of petitioner. Accordingly, the time

over-run of 78 months in commissioning of the instant assets is condoned.

Treatment of IDC and IEDC

37. The petitioner has claimed Interest During Construction (IDC) of `923.33

lakh and `810.43 lakh for Asset-I and Asset-II respectively. However, out of the

IDC claimed, `45.27 lakh and `39.73 lakh for Asset-I and Asset-II respectively

are not allowed, as it is the estimated IDC payment beyond 30.6.2015. Further,

the petitioner has not submitted the documents in support of dates of drawl of

loans, repayment schedule of loans, interest rate, interest payment dates of the

loans and undischarged liability of IDC. Accordingly, IDC of `878.06 lakh and

`770.70 lakh for Asset-I and Asset-II respectively, has been considered for

computation of capital cost and tariff. Further, the IDC from 30.6.2015 for Ckt.-I

and Ckt.-II of Parbati-III-Koldam line respectively, till the date of usage of the

Parbati-III-Koldam Line i.e. 3.11.2015, would be borne by NHPC. The details of

IDC allowed and disallowed are as follows:-

Page 29 of 48

Order in Petition No. 156/TT/2015

(` in lakh)

38. The petitioner is directed to submit documents in support of date of drawl

of loans, repayment schedule, dates of interest payments, documentary proof of

interest rate of the loans and details of undischarged liability of IDC for the

instant assets covered in the instant petition, as well as information related to

the discharge of IDC on cash basis (3.11.2015) i.e. IDC discharged from

30.6.2015 upto COD on cash basis and IDC discharged after tariff COD during

the years 2015-16 and 2016-17, if any. The IDC allowed shall be subject to

prudence check and review at the time of the true-up petition.

39. The petitioner has submitted vide affidavit dated 4.9.2015, Management

Certificate for its claim of IEDC of `334.87 lakh and `293.93 lakh for Asset-I and

Asset-II respectively and is also indicated in Form-12A for instant assets.

However, IEDC of `10.65 lakh and `9.35 lakh in case of Assets-I and Asset-II

respectively claimed as estimated expenses and included in add-cap for 2015-

16 is not allowed. Further, the IEDC from 30.6.2015 both for Ckt.-I and Ckt.-II of

Parbati-III-Koldam line, till the date of usage of the Parbati-III-Koldam line i.e.

3.11.2015, would be borne by NHPC.

40. Further, the petitioner has submitted “RCE abstract cost estimate” which

indicates the limit of IEDC as 5.00% of the estimated Hard Cost. Therefore,

IEDC limit of 5.00% on Hard Cost is the allowable limit and it works out to

`163.68 lakh and `143.66 lakh for Assets-I and Asset-II respectively. Thus, the

Particulars IDC claimed

IDC disallowed due to estimation beyond 30.6.2015

(to be borne by NHPC)

IDC allowed

Asset-I 923.33 45.27 878.06

Asset-II 810.43 39.73 770.70

Page 30 of 48

Order in Petition No. 156/TT/2015

additional excess amount of `160.55 lakh and `140.92 lakh, claimed on account

of IEDC for Asset-I and Asset-II respectively, is disallowed. Accordingly, the

details of IEDC allowed and disallowed are as under:-

(` in lakh)

41. However, the petitioner is directed to submitdetails of expenditure, duly

audited statement of IEDC and separate information related to the discharge of

IEDC i.e. IEDC discharged upto COD and IEDC discharged after tariff COD in

2015-16 and 2016-17, if any. The IEDC allowed shall be subject to prudence

check and review at the time of the true-up petition.

42. As discussed, IDC and IEDC incurred by the petitioner from 30.6.2015

upto 2.11.2015 would be borne by NHPC. However, the petitioner has neither

submitted any calculations regarding IDC and IDC for the period 30.6.2015 upto

2.11.2015 nor has submitted the relevant information required for working out

the IDC and IEDC incurred for this period. Therefore, we direct the petitioner

and NHPC to settle the billing and payment of IDC and IEDC for period

30.6.2015 upto 2.11.2015 mutually amongst themselves. In case of any

difference, both PKTCL and NHPC or one of them may file an appropriate

petition before the Commission.

Particulars IEDC claimed

IEDC disallowed IEDC allowed due to

estimation beyond

30.6.2015

Due to excess over allowable

limit

Asset-I 334.87 10.65 177.79 146.43 Asset-II 293.93 9.35 156.56 128.52

Page 31 of 48

Order in Petition No. 156/TT/2015

Treatment of Initial Spares

43. Regulation 13 of the 2014 Tariff Regulations specifies ceiling norms for

capitalization of initial spares in respect of transmission system as under:-

“13. Initial Spares

Initial spares shall be capitalised as a percentage of the Plant and Machinery cost upto cut-off date, subject to following ceiling norms: (d) Transmission system

(i) Transmission line - 1.00% (ii) Transmission Sub-station (Green Field)-4.00% (iii) Transmission Sub-station (Brown Field)-6.00% (iv) Series Compensation devices and HVDC Station-4.00% (v) Gas Insulated Sub-station (GIS)-5.00% (vi) Communication system-3.5%

Provided that: (i) where the benchmark norms for initial spares have been published as part of the benchmark norms for capital cost by the Commission, such norms shall apply to the exclusion of the norms specified above: (ii) where the generating station has any transmission equipment forming part of the generation project, the ceiling norms for initial spares for such equipments shall be as per the ceiling norms specified for transmission system under these regulations; (iii) once the transmission project is commissioned, the cost of initial spares shall be restricted on the basis of plant and machinery cost corresponding to the transmission project at the time of truing up: (iv) for the purpose of computing the cost of initial spares, plant and machinery cost shall be considered as project cost as on cut-off date excluding IDC, IEDC, Land Cost and cost of civil works. The transmission licensee shall submit the breakup of head wise IDC & IEDC in its tariff application.”

44. The petitioner has claimed initial spares of `34.74 lakh and `30.49 lakh for

Assets-I and Asset-II respectively, pertaining to the transmission line, which are

within the ceiling limit and are allowed as per Regulation 13 of the 2014 Tariff

Regulations.

Page 32 of 48

Order in Petition No. 156/TT/2015

Capital cost as on COD i.e. 3.11.2015

45. The detail of capital cost considered as on COD after adjusting the claim

of IDC, IEDC and initial spares are as under:-

(` in lakh)

Projected additional capital expenditure

46. Clause (1) of Regulation 14 of the 2014 Tariff Regulations provides as

under:-

“ (1) The capital expenditure in respect of the new project or an existing project incurred or projected to be incurred, on the following counts within the original scope of work, after the date of commercial operation and up to the cut-off date may be admitted by the Commission, subject to prudence check:

(i) Undischarged liabilities recognised to be payable at a future date; (ii) Works deferred for execution; (iii) Procurement of initial capital spares within the original scope of work, in accordance with the provisions of Regulation 13; (iv) Liabilities to meet award of arbitration or for compliance of the order or decree of a court; and (v) Change in Law or compliance of any existing law:” Provided that the details of works asset wise/work wise included in the original scope of work along with estimates of expenditure, liabilities recognized to be payable at a future date and the works deferred for execution shall be submitted along with the application for determination of tariff.

47. Clause (13) of Regulation 3 of the 2014 Tariff Regulations defines “cut-

off” date as under:

“cut-off date” means 31st March of the year closing after two years of the year of commercial operation of whole or part of the project, and in case the whole or part of the project is declared under commercial operation in the last quarter of the year, the cut-off date shall be 31st March of the year closing after three years of the year of commercial operation”.

Particulars Capital cost deemed to be claimed as on

COD

Less: disallowed Capital cost as on COD after adjustment

of IDC/IEDC/initial spares

IDC IEDC initial spares

Asset-I 4130.87 - 177.79 - 3953.08

Asset-II 3625.76 - 156.06 - 3469.70

Page 33 of 48

Order in Petition No. 156/TT/2015

48. The cut-off date in the case of instant combined transmission asset is

31.3.2018.

49. The petitioner has claimed amount of `694.82 lakh and `355.01 lakh for

Asset-I and `609.86 lakh and `311.61 lakh for Asset-II towards additional

capital expenditure for 2015-16 and 2016-17 respectively. The petitioner has

submitted that the additional capital expenditure claimed is including IDC and

IEDC to be incurred in 2015-16 and for balance and retention payments.

However, as discussed earlier, both IDC and IEDC claimed to be incurred on

estimated basis in 2015-16 have not been allowed. Therefore, amounts of

`45.27 lakh and `39.73 lakh on account of estimated IDC and `10.65 lakh and

`9.35 lakh on account of estimated IEDC in respect of Asset-I and Asset-II

respectively have been reduced to determine the hard cost portion of additional

capital expenditure, which is as under:-

(` in lakh)

50. Further, as discussed, pro-rata of the additional capital expenditure during

2015-16, is being adjusted so as to arrive at the capital cost as on COD

(3.11.2015) and the balance additional capital expenditure estimated to be

incurred for the period from COD (3.11.2015) to 31.3.2016 has been considered

as add-cap for 2015-16 and during 2016-17 as below:-

(` in lakh)

Particulars Estimated add-cap Total

2015-16 2016-17

Asset-I 638.90 355.01 993.91

Asset-II 560.78 311.61 872.39

Particulars Estimated add-cap Total

2015-16 2016-17

Asset-I 344.91 355.01 699.92 Asset-II 302.74 311.61 614.35

Page 34 of 48

Order in Petition No. 156/TT/2015

51. In view of above, the total estimated cost allowed from COD to 31.3.2017

for the purpose of working out tariff is summarized as under:-

(` in lakh)

*This expenditure has been claimed as a part of add-cap during 2015-16.

Debt-Equity Ratio

52. Clause 1 and 5 of Regulation 19 of the 2014 Tariff Regulations specifies

as follows:-

“(1) For a project declared under commercial operation on or after 1.4.2014, the debt-equity ratio would be considered as 70:30 as on COD. If the equity actually deployed is more than 30% of the capital cost, equity in excess of 30%shall be treated as normative loan: Provided that: i. where equity actually deployed is less than 30% of the capital cost, actual equity shall be considered for determination of tariff: ii. the equity invested in foreign currency shall be designated in Indian rupees on the date of each investment: iii. any grant obtained for the execution of the project shall not be considered as a part of capital structure for the purpose of debt : equity ratio. Explanation.-The premium, if any, raised by the generating company or the transmission licensee, as the case may be, while issuing share capital and investment of internal resources created out of its free reserve, for the funding of the project, shall be reckoned as paid up capital for the purpose of computing return on equity, only if such premium amount and internal resources are actually utilised for meeting the capital expenditure of the generating station or the transmission system.”

Particulars Asset-I Asset-II

Total Capital Cost claimed up to 31.3.2017 4886.71 4289.19

(-) Add Cap during 2016-17 355.01 311.61 Capital Cost claimed up to 31.3.2016 4531.70 3977.58

*(-) IEDC and IDC not considered being claimed on estimated basis for payment beyond 30.6.2015 55.92 49.08

(-) Pro-rata Add Cap (Hard Cost) claimed for the period from Tariff-COD (3.11.2015 to 31.3.2016) 344.91 302.74 Capital Cost deemed to be claimed up to COD (3.11.2015) 4130.87 3625.76

(-) IEDC/IDC disallowed as on COD due to Time over-run - - (-) IEDC disallowed as on COD due to Excess Limit 177.79 156.06

(-) Excess Initial Spares disallowed as on COD - - Total Capital Cost allowable as on COD (3.11.2015) 3953.08 3469.70

Page 35 of 48

Order in Petition No. 156/TT/2015

“(5) Any expenditure incurred or projected to be incurred on or after 1.4.2014 as maybe admitted by the Commission as additional capital expenditure for determination of tariff, and renovation and modernisation expenditure for life extension shall be serviced in the manner specified in clause (1) of this regulation.”

53. The petitioner has claimed debt: equity ratio of 70:30 as on the tariff date

of commercial operation of the instant assets. The details of debt: equity in

respect of the instant assets covered in the instant petition as on tariff date of

commercial operation and as on 31.3.2019 respectively are as under:-

Particulars Asset-I

Capital cost as on COD (3.11.2015)

Capital cost as on 31.3.2019

Amount

(` in lakh) % Amount

(` in lakh) %

Debt 2767.15 70.00 3257.10 70.00 Equity 1185.92 30.00 1395.90 30.00

Total 3953.08 100.00 4653.00 100.00

Particulars Asset-II Capital cost as on COD (3.11.2015)

Capital cost as on 31.3.2019

Amount

(` in lakh) %

Amount

(` in lakh) %

Debt 2428.79 70.00 2858.84 70.00

Equity 1040.91 30.00 1225.22 30.00 Total 3469.70 100.00 4084.05 100.00

54. The above stated debt-equity ratio has been applied for the purpose of

tariff calculation in this order.

Return on Equity

55. Clause (1) and (2) of Regulation 24 and Clause (1) and (2) of Regulation

25 of the 2014 Tariff Regulations specify as under:-

“24. Return on Equity: (1) Return on equity shall be computed in rupee terms,

on the equity base determined in accordance with regulation 19. (2) Return on equity shall be computed at the base rate of 15.50% for thermal generating stations, transmission system including communication system and run of the river hydro generating station, and at the base rate of 16.50% for the

Page 36 of 48

Order in Petition No. 156/TT/2015

storage type hydro generating stations including pumped storage hydro generating stations and run of river generating station with pondage: Provided that: (i) in case of projects commissioned on or after 1st April, 2014, an additional return of 0.50 % shall be allowed, if such projects are completed within the timeline specified in Appendix-I:

(ii) the additional return of 0.5% shall not be admissible if the project is not completed within the timeline specified above for reasons whatsoever: (iii) additional RoE of 0.50% may be allowed if any element of the transmission project is completed within the specified timeline and it is certified by the Regional Power Committee/National Power Committee that commissioning of the particular element will benefit the system operation in the regional/national grid:

(iv) the rate of return of a new project shall be reduced by 1% for such period as may be decided by the Commission, if the generating station or transmission system is found to be declared under commercial operation without commissioning of any of the Restricted Governor Mode Operation (RGMO)/ Free Governor Mode Operation (FGMO), data telemetry, communication system up to load dispatch centre or protection system: (v) as and when any of the above requirements are found lacking in a generating station based on the report submitted by the respective RLDC, RoE shall be reduced by 1% for the period for which the deficiency continues:

(vi) additional RoE shall not be admissible for transmission line having length of less than 50 kilometers. “25. Tax on Return on Equity:

(1) The base rate of return on equity as allowed by the Commission under Regulation 24 shall be grossed up with the effective tax rate of the respective financial year. For this purpose, the effective tax rate shall be considered on the basis of actual tax paid in the respect of the financial year in line with the provisions of the relevant Finance Acts by the concerned generating company or the transmission licensee, as the case may be. The actual tax income on other income stream (i.e., income of non generation or non transmission business, as the case may be) shall not be considered for the calculation of “effective tax rate”. (2) Rate of return on equity shall be rounded off to three decimal places and shall be computed as per the formula given below: Rate of pre-tax return on equity = Base rate / (1-t) Where “t” is the effective tax rate in accordance with Clause (1) of this regulation and shall be calculated at the beginning of every financial year based on the estimated profit and tax to be paid estimated in line with the provisions of the relevant Finance Act applicable for that financial year to the company on pro-rata basis by excluding the income of non-generation or non-transmission business, as the case may be, and the corresponding tax thereon. In case of generating company or transmission licensee paying Minimum Alternate Tax (MAT), “t” shall be considered as MAT rate including surcharge and cess.”

Page 37 of 48

Order in Petition No. 156/TT/2015

56. The petitioner has submitted that it may be allowed to recover the shortfall

or refund the excess Annual Fixed Charges, on account of return on equity due

to change in applicable Minimum Alternate Tax/Corporate Income Tax rate as

per the Income Tax Act, 1961 of the respective financial year directly without

making any application before the Commission.

57. We have considered the submissions made by the petitioner. Regulation

24 read with Regulation 25 of the 2014 Tariff Regulations provides for grossing

up of return on equity with the effective tax rate for the purpose of return on

equity. It further provides that in case the generating company or transmission

licensee is paying Minimum Alternative Tax (MAT), the MAT rate including

surcharge and cess will be considered for the grossing up of return on equity.

Accordingly, the MAT rate applicable during 2013-14 has been considered for

the purpose of return on equity, which shall be trued up with actual tax rate in

accordance with Regulation 25 (3) of the 2014 Tariff Regulations. Accordingly,

the RoE allowed is as under:-

(` in lakh) Particulars Asset-I

2015-16 (pro-rata)

2016-17 2017-18 2018-19

Opening Equity 1185.92 1289.40 1395.90 1395.90

Addition due to Additional Capitalisation 103.47 106.50 - - Closing Equity 1298.40 1395.90 1395.90 1395.90 Average Equity 1237.66 1342.65 1395.90 1395.90 Return on Equity (Base Rate) 15.50% 15.50% 15.50% 15.50% Tax rate for the year 2013-14 (MAT) 20.961% 20.961% 20.961% 20.961%

Rate of Return on Equity (Pre Tax) 19.610% 19.610% 19.610% 19.610% Return on Equity (Pre Tax) 99.74 263.29 273.74 273.74

Particulars Asset-II 2015-16

(pro-rata) 2016-17 2017-18 2018-19

Opening Equity 1041.90 1131.73 1225.22 1225.22 Addition due to Additional Capitalisation 90.82 93.48 - -

Closing Equity 1131.73 1225.22 1225.22 1225.22 Average Equity 1086.32 1178.48 1225.22 1225.22

Page 38 of 48

Order in Petition No. 156/TT/2015

Return on Equity (Base Rate) 15.50% 15.50% 15.50% 15.50% Tax rate for the year 2013-14 (MAT) 20.961% 20.961% 20.961% 20.961%

Rate of Return on Equity (Pre Tax) 19.610% 19.610% 19.610% 19.610% Return on Equity (Pre Tax) 87.55 231.10 240.27 240.27

Interest on loan

58. Regulation 26 of the 2014 Tariff Regulations are provides as under:-

“(1) The loans arrived at in the manner indicated in regulation 19 shall be considered as gross normative loan for calculation of interest on loan (2) The normative loan outstanding as on 1.4.2014 shall be worked out by deducting the cumulative repayment as admitted by the Commission up to 31.3.2014 from the gross normative loan. (3) The repayment for each of the year of the tariff period 2014-19 shall be deemed to be equal to the depreciation allowed for the corresponding year/period. In case of decapitalization of assets, the repayment shall be adjusted by taking into account cumulative repayment on a pro rata basis and the adjustment should not exceed cumulative depreciation recovered upto the date of decapitalisation of such asset. (4) Notwithstanding any moratorium period availed by the generating company or the transmission licensee, as the case may be, the repayment of loan shall be considered from the first year of commercial operation of the project and shall be equal to the depreciation allowed for the year or part of the year. (5) The rate of interest shall be the weighted average rate of interest calculated on the basis of the actual loan portfolio after providing appropriate accounting adjustment for interest capitalized: Provided that if there is no actual loan for a particular year but normative loan is still outstanding, the last available weighted average rate of interest shall be considered: Provided further that if the generating station or the transmission system, as the case may be, does not have actual loan, then the weighted average rate of interest of the generating company or the transmission licensee as a whole shall be considered. (6) The interest on loan shall be calculated on the normative average loan of the year by applying the weighted average rate of interest.”

59. In these calculations, interest on loan has been worked out as hereinafter:-

(i) Gross amount of loan, repayment of instalments and rate of interest on

actual average loan have been considered as per the petition;

Page 39 of 48

Order in Petition No. 156/TT/2015

(ii) The yearly repayment for the tariff period 2014-19 has been considered

to be equal to the depreciation allowed for that year;

(iii) Weighted average rate of interest on actual average loan worked out

as per (i) above is applied on the notional average loan during the year to

arrive at the interest on loan; and

(iv) Loan portfolio for working out weighted average rate of interest has

also been adjusted pro-rata.

60. The petitioner has submitted that it be allowed to bill and adjust impact on

Interest on Loan due to change in interest due to floating rate of interest

applicable, if any, from the respondents. Interest on loan has been calculated