Performance Evaluation of the Portuguese Seaports Evaluation in the European Context

97

INSTITUTO SUPERIOR TÉCNICO Universidade Técnica de Lisboa Performance Evaluation of the Portuguese Seaports Evaluation in the European Context Manuel Luz Nunes Cantarino de Carvalho Dissertação para obtenção do Grau de Mestre em Engenharia Civil Júri Presidente: Prof. Joaquim Jorge da Costa Paulino Pereira Orientador: Prof. Rui Domingos Ribeiro da Cunha Marques Vogal: Prof. Carlos Alberto Pestana Barros Outubro 2007

Transcript of Performance Evaluation of the Portuguese Seaports Evaluation in the European Context

INSTITUTO SUPERIOR TÉCNICO Universidade Técnica de Lisboa

Performance Evaluation of the Portuguese Seaports

Evaluation in the European Context

Manuel Luz Nunes Cantarino de Carvalho

Dissertação para obtenção do Grau de Mestre em

Engenharia Civil

Júri

Presidente: Prof. Joaquim Jorge da Costa Paulino Pereira

Orientador: Prof. Rui Domingos Ribeiro da Cunha Marques

Vogal: Prof. Carlos Alberto Pestana Barros

Outubro 2007

ii

iii

Abstract

A global reform of the Portuguese port sector favoured the involvement of private operators in

the provision of port services. The port system comprises five major ports, each managed by an

independent Port Authority. These were set up as limited liability companies with all their shares

held by the State. Port services are gradually being passed on to private operators through

concession contracts. The Portuguese and three other countries port sectors were analysed in

terms of regulatory policy, governance model, institutional setting and scale and type of

operations. The analysed countries were Spain, because it is our main competitor, and the

Netherlands and the UK, whose ports had the top scores in the performance measurement

procedure carried out. In this procedure reliability and coherence were stressed in order to

achieve realistic and useful results. All the options in the performance analysis were thoroughly

discussed and justified. Forty one ports from eleven European countries were included in the

sample. The study relied on input oriented Data Envelopment Analysis (DEA) models, using as

inputs Operational Expenses (OPEX) and Capital Expenses (CAPEX); and as outputs

conventional general cargo, containerized cargo, roll on-roll off cargo, dry bulk cargo, liquid bulk

cargo and passengers. All the Portuguese ports had very low efficiency scores except Lisbon

which was deemed as efficient due to a very high volume of passenger traffic. The possible cost

reduction if the Portuguese seaports had performed efficiently was estimated about 64 million

euros in 2005.

Keywords:

Seaports; Regulation; DEA; Performance; Portugal.

iv

Resumo

A reforma do sector portuário promoveu uma maior participação dos operadores privados. Os

cinco maiores portos portugueses, a saber, Leixões, Aveiro, Lisboa, Setúbal e Sines são

geridos por Autoridades Portuárias independentes, constituídas como sociedades anónimas

em que todas a acções são propriedade do Estado. Além do português, os sectores portuários

de três outros países são analisados segundo diversas perspectivas, entre as quais, os

modelos de gestão portuária, a estrutura institucional, as políticas regulatórias e a escala e o

tipo de operações. Os países analisados foram a Holanda e o Reino Unido, que obtiveram os

melhores resultados em termos de desempenho, e a Espanha, o nosso competidor directo na

prestação de serviços portuários. Na avaliação de desempenho utilizaram-se modelos Data

Envelopment Analysis (DEA) com orientação para os inputs. A fiabilidade e a coerência foram

tomadas como aspectos cruciais pelo que todas as decisões tomadas na implementação do

algoritmo foram amplamente discutidas e justificadas. Os custos de operação e de capital

foram tomados como inputs e os volumes de carga geral convencional, contentorizada, roll on-

roll off, de granéis líquidos e sólidos e de passageiros como outputs. Quarenta e um portos de

onze países europeus foram incluídos na amostra. Os níveis de desempenho dos portos

portugueses são baixos excepto o do porto de Lisboa que foi tido como eficiente devido ao

volume muito elevado de passageiros. A redução de custos potencial, caso os portos nacionais

operassem de forma eficiente, foi estimada em 64 milhões de euros para 2005.

Palavras-chave:

Portos; Regulação; DEA; Desempenho; Portugal.

v

Acknowledgements

This study would not have been possible without the extraordinary commitment, drive and

knowledge of Professor Rui Cunha Marques. I would like to gratefully acknowledge the

enthusiastic supervision. His comments and suggestions were always outstanding. The best

advisor and teacher I could have wished for, he is actively involved in the work of all his

students, and clearly always has their best interest in mind. His efforts managed to make of this

journey a rewarding one both in the academic and personal fields.

To CESUR, for the opportunity to write this study. I am grateful to my office colleagues Ana

Brochado, Clara Landeiro, Isabel Ramos and Marta Gomes for the interesting and stimulating

environment. Patrícia, Carina and Vanessa Sobral deserve a special thank you for their

technical help, support and good humour that greatly contributed to make my stay at CESUR a

pleasant one. The support, good will and technical help of Alexandra, Ana, Pedro, Rita and

Rute with the most annoying copy machine in the world was greatly appreciated. Last but not

the least I am thankful to the almost permanently underperforming copy machine for constantly

reminding me why performance matters so much in the everyday life.

I thank the help in the very early stages of this study of Dr. Bruno Miguel da Cunha Marcelo of

the Lisbon Port Authority.

The informed insights provided by Dr. Duarte Lynce de Faria and Eng. Eduardo Bandeira, of the

Sines Port Authority, greatly influenced the final result of this study.

The interest and knowledge of someone who is in the port business for so long was very

important. I thank Eng. Carlos Figueiredo of LISCONT.

To Professor Carlos Pestana Barros, from ISEG, for his availability during the early stages of

this research, for the continuous flow of interesting papers and for his interest in my research.

To Professor Jose Tongzon for sharing his highly praised opinions about seaport performance

measurement.

This study benefited from conversations with several persons: Professor Ana Paixão Casaca,

Professor Teng-Fei Wang, Dr. Sheila Farrel, Professor Michiel Nijdam, Professor Larissa van

der Lugt and Professor Adolf NG.

vi

To Fundação para a Ciência e Tecnologia (FCT) for the grant of a scholarship that helped to

financially support part of my research and for the endowment of a travel grant for the

presentation of a paper in Athens.

To the Portuguese journalists Luís Filipe Duarte of the “Cargo” magazine , Rui Neves of “Jornal

de Negócios” newspaper and Luís Abrunhosa Branco of the “Camião” magazine for helping me

in an unconventional manner with a towed car.

I wish to thank my friends for helping me get through the difficult times, and for all the emotional

support, camaraderie, entertainment, and caring they provided.

Finally, and most importantly, I wish to thank my whole family. Especially to my parents, my

brother, my grandfather and grandmother. They bore me, raised me, supported me, taught me,

and loved me. To them I dedicate this dissertation.

Printed on 100% recycled paper

vii

INDEX

1. INTRODUCTION....................................................................................................................... 1

1.1 Maritime transport and the port sector ................................................................................ 1

1.2 Objectives ........................................................................................................................... 3

1.3 Methodology........................................................................................................................ 4

1.4 Structure.............................................................................................................................. 5

2. SEAPORT SECTOR ANALYSIS............................................................................................... 6

2.1 Introduction ......................................................................................................................... 6

2.2 Portugal............................................................................................................................... 6

2.2.1 General context ........................................................................................................... 6

2.2.2 Institutional framework and the structural reform ........................................................ 7

2.2.3 Governance model ...................................................................................................... 8

2.2.4 Concessions ................................................................................................................ 9

2.2.5 Tariffs......................................................................................................................... 12

2.2.6 Market structure......................................................................................................... 13

2.2.7 Market share.............................................................................................................. 14

2.2.8 Calling vessels........................................................................................................... 15

2.2.9 Financial context........................................................................................................ 15

2.2.10 Future ...................................................................................................................... 17

2.3 United Kingdom................................................................................................................. 18

2.3.1 General context ......................................................................................................... 18

2.3.2 Privatization process.................................................................................................. 19

2.3.3 Private ports............................................................................................................... 19

2.3.4 Trust ports.................................................................................................................. 20

2.3.5 Municipal ports........................................................................................................... 21

2.3.6 Policies and legislation .............................................................................................. 21

2.4 Netherlands....................................................................................................................... 23

2.4.1 General context ......................................................................................................... 23

2.4.2 Legislation and policies ............................................................................................. 24

2.4.3 Institutional setting ..................................................................................................... 25

2.4.5 Governance models................................................................................................... 26

2.4.6 Private ports............................................................................................................... 27

2.5 Spain ................................................................................................................................. 28

2.5.1 General context ......................................................................................................... 28

2.5.2 Institutional setting ..................................................................................................... 28

2.5.3 Service provision ....................................................................................................... 29

2.5.4 Financing model, tariffs and charges......................................................................... 29

viii

2.6 European Union ................................................................................................................ 31

2.6.1 General context ......................................................................................................... 31

2.6.2 Legislation and regulatory policies ............................................................................ 32

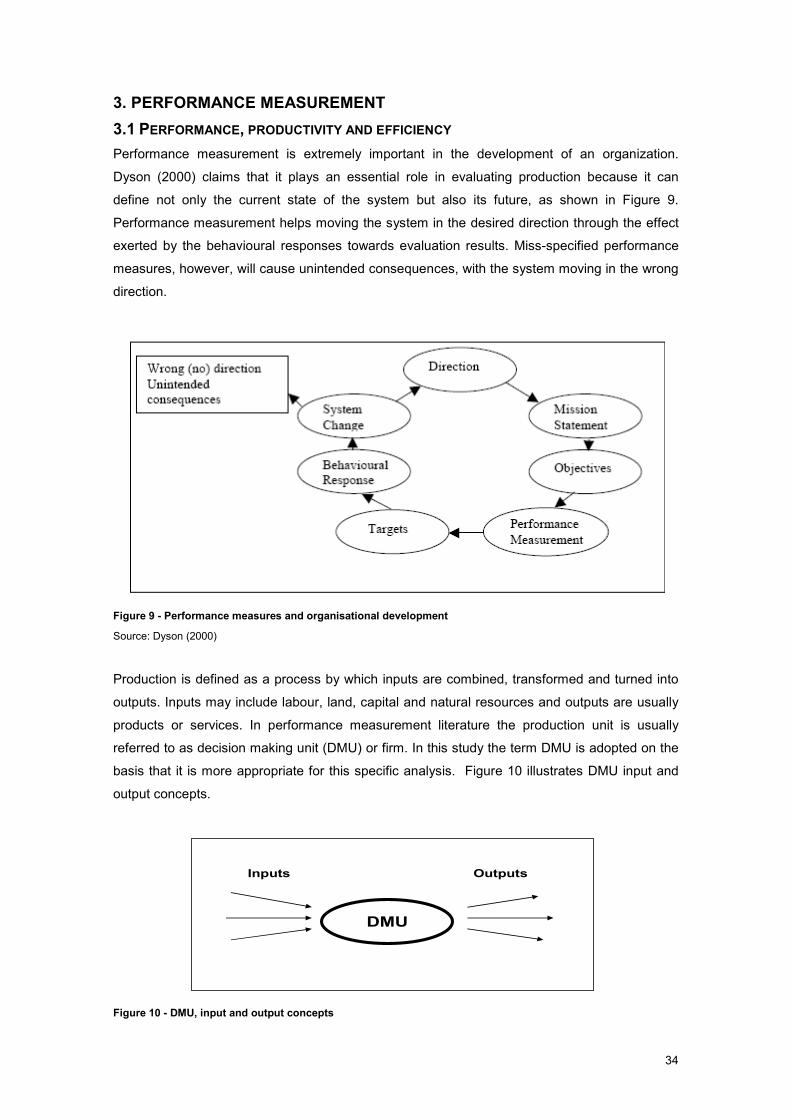

3. PERFORMANCE MEASUREMENT ....................................................................................... 34

3.1 Performance, productivity and efficiency .......................................................................... 34

3.2 Data Envelopment Analysis .............................................................................................. 38

3.3 State of the art................................................................................................................... 42

3.4 Model specification ........................................................................................................... 50

3.4.1 Outputs ...................................................................................................................... 51

3.4.2 Inputs ......................................................................................................................... 55

3.4.3 Models, Orientation and Data.................................................................................... 58

3.5 Results .............................................................................................................................. 60

3.5.1 Model results ............................................................................................................. 60

3.5.2 Aveiro......................................................................................................................... 63

3.5.3 Leixões ...................................................................................................................... 64

3.5.4 Setúbal....................................................................................................................... 64

3.5.5 Sines.......................................................................................................................... 66

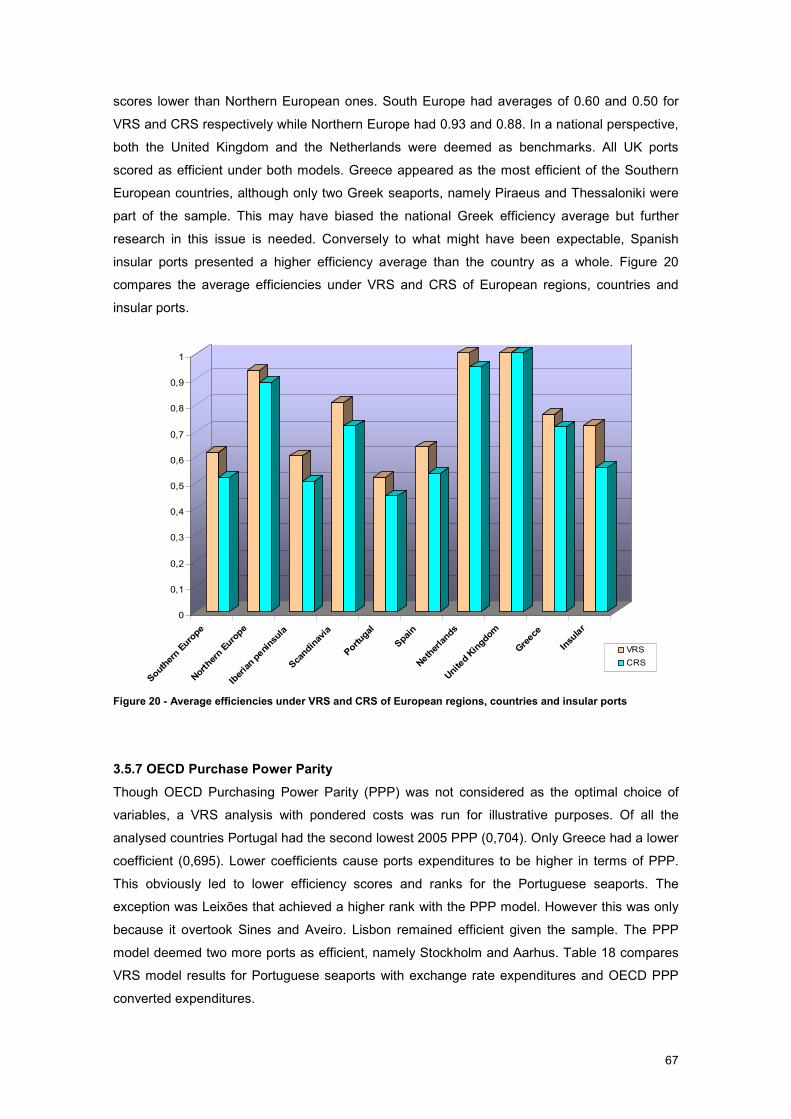

3.5.6 Geographical analysis ............................................................................................... 66

3.5.7 OECD Purchase Power Parity................................................................................... 67

3.5.8 Aggregated general cargo ......................................................................................... 68

3.5.9 Variable sensitivity of efficient DMUs ........................................................................ 69

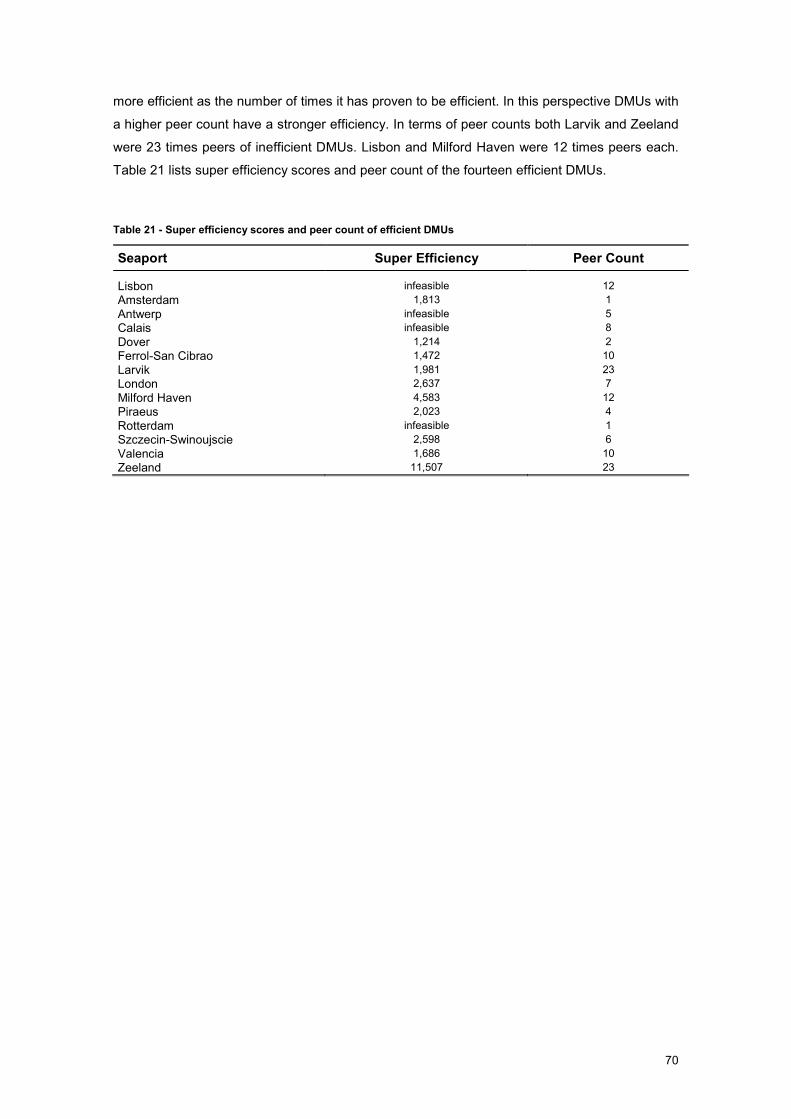

3.5.10 Super-Efficiency and peer count ............................................................................. 69

3.5.11 Is GDP related to port efficiency?............................................................................ 71

4 CONCLUSIONS ....................................................................................................................... 73

4.1 Concluding remarks .......................................................................................................... 73

4.2 Further research................................................................................................................ 77

5 REFERENCES......................................................................................................................... 78

ANNEX 1 – Portuguese Seaports throughputs and entered ships (2003-2005) ........................ 83

ANNEX 2 – Ranks and scores in the VRS and CRS models; scale efficiency........................... 84

ANNEX 3 – Efficient targets ........................................................................................................ 85

ANNEX 4 – Comparative VRS input oriented models: OECD PPP converted expenditures;

aggregated general cargo; Super Efficiency.................................................................. 86

ANNEX 5 – Scores of VRS input oriented models lacking each one of the variables ................ 87

ix

TABLE INDEX

Table 1 - Service provision in Portuguese ports ......................................................................... 11

Table 2 - Public service concessions in the Portuguese ports.................................................... 12

Table 3 - TPU-ship ...................................................................................................................... 13

Table 4 - Throughputs by cargo type of the Portuguese seaports in 2002-2005........................ 14

Table 5 - Throughputs by cargo type of the Portuguese main seaports in 2005 ........................ 15

Table 6 – Vessels calling in at Portuguese seaports (2002-2005).............................................. 15

Table 7 - Financial data of Portuguese main ports (year 2005).................................................. 17

Table 8 - Dutch seaports ............................................................................................................. 23

Table 9 - Investment and maintenance costs division in the Spanish port system..................... 30

Table 10 - Previous studies applying DEA to the port sector (1/2) ............................................. 44

Table 11 - Inputs and outputs used on previous studies ............................................................ 51

Table 12 - Input definition............................................................................................................ 56

Table 13 - Input and output Pearson’s correlation coefficients ................................................... 58

Table 14 – Variable statistics ...................................................................................................... 59

Table 15 - Descriptive statistics of the efficiency scores............................................................. 60

Table 16 - Efficient input and output targets under the VRS model............................................ 63

Table 17 – Peers and respective weights of the Portuguese seaports....................................... 66

Table 18 - VRS model results for Portuguese seaports (with exchange rate and OECD PPP

expenditures) ...................................................................................................................... 68

Table 19 - Target differences between the standard model and the aggregated general cargo

model .................................................................................................................................. 68

Table 20 - Variable sensitivity of efficient seaports ..................................................................... 69

Table 21 - Super efficiency scores and peer count of efficient DMUs ........................................ 70

Table 22- Sample statistics ......................................................................................................... 71

Table 23 – Mann-Whitney U and Kolmogorov-Smirnov tests ..................................................... 72

x

FIGURE INDEX

Figure 1 - Institutional framework of the Portuguese seaport sector ............................................ 8

Figure 2 - Financial evolution of the Portuguese port system (2002 - 2005) .............................. 16

Figure 3 - Cargo throughputs of the UK port system in 2005 ..................................................... 19

Figure 4 - Cargo throughputs of the Dutch port system in 2005 ................................................. 23

Figure 5 - Rotterdam and Amsterdam governance models ........................................................ 26

Figure 6 - Cargo throughputs of the Spanish port system in 2005 ............................................. 28

Figure 7 - Cargo volumes handled in European seaports by type in 2006................................. 31

Figure 8 - Chronogram of the regulation implementation in the maritime sector........................ 32

Figure 9 - Performance measures and organisational development .......................................... 34

Figure 10 - DMU, input and output concepts .............................................................................. 34

Figure 11 - Productivity frontier and inefficiency ......................................................................... 35

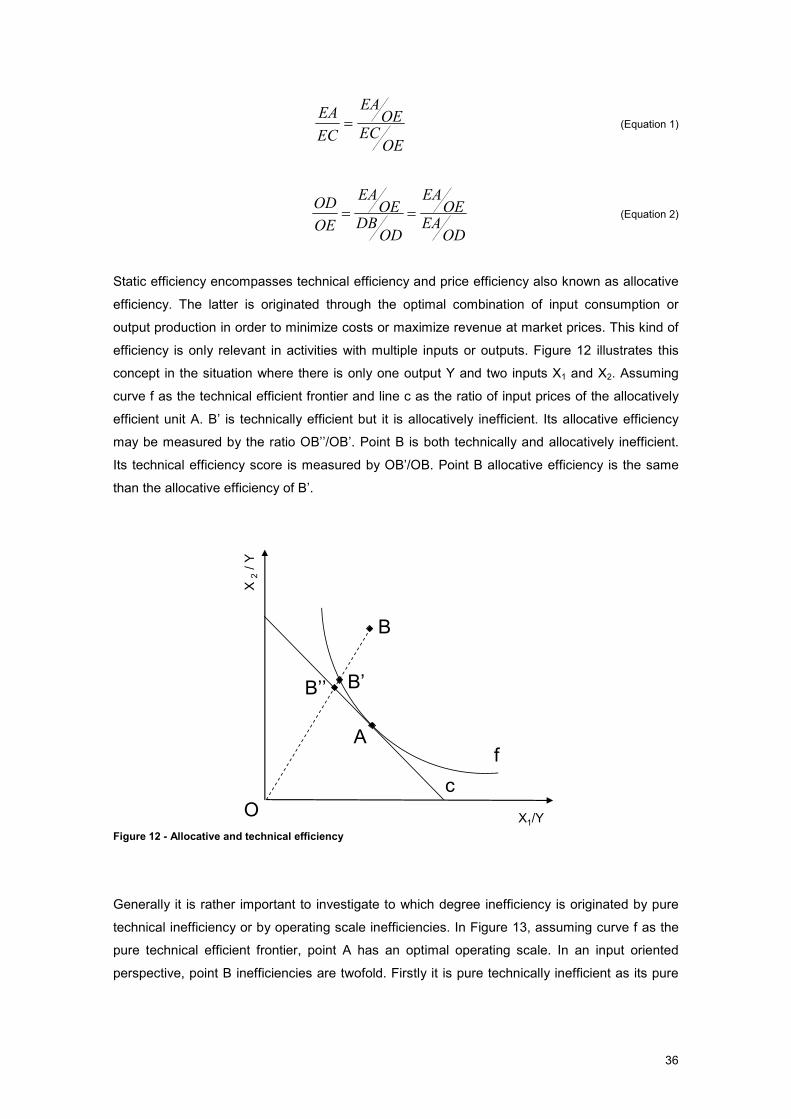

Figure 12 - Allocative and technical efficiency ............................................................................ 36

Figure 13 - Scale and pure technical efficiency .......................................................................... 37

Figure 14 - Efficiency decomposition .......................................................................................... 37

Figure 15 - Constant returns to scale efficiency frontier ............................................................. 39

Figure 16 - Variable returns to scale efficiency frontier............................................................... 39

Figure 17 - Slack and peer concepts .......................................................................................... 41

Figure 18 - Seaports with the highest passenger traffic.............................................................. 61

Figure 19 - CRS, VRS and SE scores ........................................................................................ 62

Figure 20 - Average efficiencies under VRS and CRS of European regions, countries and

insular ports ........................................................................................................................ 67

Figure 21 - Linear regression of the base model scores............................................................. 71

Figure 22 - Linear regression of the Super Efficiency scores .................................................... 72

1

1. INTRODUCTION 1.1 MARITIME TRANSPORT AND THE PORT SECTOR

The importance of maritime transportation for the global economy is paramount. In terms of

weight, about 96% of the world trade is carried by sea according to Rodrigue et al. (2006).

Maritime transportation is the only viable transport mode between a large number of the world’s

destinations. Even when alternative modes are available maritime is the one with the lowest

cost per ton km. Nowadays, sustainable development is seen as one of the main challenges of

our society and it is important to point out that sea shipping emits less CO2 than any other

transport mode.

Shipping was the first globalized industry in the world. This is proved by the fact that this activity

was the raison d’etre of the first international laws and conventions implemented in a global

scale. Moreover shipping constitutes the main pillar of globalization by daily transporting millions

of tons of all kinds of products between the five continents. A specialized world fleet is able to

cope with a wide variety of very different products and cargo types. In this fleet one can find

either giant bulk vessels carrying raw materials all around the world with significant economies

of scale or relatively small ultra-specialized reefer vessels transporting bananas and other

perishable products in a controlled atmosphere. The maturation process of certain fruits and

vegetables may be controlled by precisely adjusting temperature while at sea, allowing for these

to be delivered in perfect consumption conditions thousands of miles away from their plantation

sites.

Adam Smith, who is regarded as the father of modern economics, stated the access to water

transportation as an important catalyser of economic growth. In The Wealth of Nations1, his

most renowned work, he explains it in the following way:

“A broad-wheeled waggon, attended by two men, and drawn by eight horses, in about six weeks' time carries and brings back between London and Edinburgh near four ton weight of goods. In about the same time a ship navigated by six or eight men, and sailing between the ports of London and Leith, frequently carries and brings back two hundred ton weight of goods. Six or eight men, therefore, by the help of water-carriage, can carry and bring back in the same time the same quantity of goods between London and Edinburgh, as fifty broad-wheeled waggons, attended by a hundred men, and drawn by four hundred horses.[…] Since such, therefore, are the advantages of water-carriage, it is natural that the first improvements of art and industry should be made where this conveniency opens the whole world for a market to the produce of every sort of labour, and that they should always be much later in extending themselves into the inland parts of the country.”

Although written in the XVIII century these words remain valid as shipping continues to handle

the major stake of the world trade.

1 Smith (1776), Book I, Chapter 3, page 9.

2

The quality of the world’s ports and their performance is everything but uniform. There are vast

performance gaps between areas such as Northern Europe, where thousands of containers are

moved everyday, and some African ports where it is not uncommon for vessels to wait for

months before being allowed to moor. These differences are very significant in terms of

economic development as stated by the World Bank2:

“Excessive port costs or delays can prompt investors to locate production facilities in other countries or regions […] In many countries excessive port costs function like an additional import duty on all goods entering the country and a tax on exports.”

The relevance of global integrated transport chains has grown exponentially. Ports are one of

the fundamental elements in these chains, though the continuous escalation of cargo volumes

has greatly increased the pressure on them. More and more shippers are demanding not only a

swift cargo passage through seaports but also the lowest possible costs. Balancing between

these two aspects has led to an increasing interest of the scientific community in the

performance measurement of seaports. This research area focuses on finding the best

practices among seaports in order to spread them and allow for inefficient seaports to close the

gap that separates them from the top performing ones.

Performance measurement is seen as an essential tool towards the modernization and

competitiveness of all kinds of industries and organizations. By systematically comparing

organizations that provide the same type of services and measuring their performance one may

identify the best practices available and determine which role models the least performing

organizations should choose in order to improve. Measuring seaports performance is a complex

task because they provide a wide range of services and operate in significantly diverse contexts

however, Tongzon (1995) claims that the benchmarking of European seaports should be a

priority on the research agenda since, despite the clearly non-homogeneous nature of

European ports, they perform the same task and thus, may be compared for benchmarking

purposes.

An efficient and quality transport system is essential to provide the quality of life desired by most

of the developed countries. Nowadays the European Union suffers of chronic congestion in

some of its main road axis such as the Alps and the Pyrenees crossings. Besides, a significant

traffic growth is expectable according to forecasts. Congestion, environmental damages and

accidents are expected to increase appreciably if nothing is to be done, severely harming both

the users and the economy. Projections of 2010 congestion costs point to 1% of the European

Union GDP, according to the white paper for transport policy EU (2001). A modal shift was the

designated solution towards alleviating traffic pressure over the road infrastructures. The

promotion of Short Sea Shipping is seen as a way of achieving this modal shift. The sea is not

2 WB(2006); Port Reform Toolkit; page 273.

3

congested and it allows for the transportation of high volumes of goods in an environmentally

sustainable way at a relatively low cost.

Most of the analysed countries were reformed or under a reform processes aiming to increase

the participation of the private sector. Nevertheless, the form and the extent of private sector

participation varies widely from country to country. The European Union common policy

influence on the national policies towards the maritime sector has been gradually growing. In

the early days of the EU even a special derogation to the Rome Treaty was made in order to

exempt conference shipping from the competition rules. More and more these exemptions and

special differentiated treatment of the maritime sector are being phased out. European

environmental legislation has had a large impact on new port developments as most of the ports

are situated in estuarine areas which are especially sensitive areas. In addition the EU

significantly influences the development of new port projects since many of these, especially in

Southern Europe, are subject to European funding. Changes in the attribution criteria of

European funds may radically change investment patterns in port infrastructure.

The future enlargement of the Panama Canal will allow for the last generation of post-panamax

vessels to cross between the Pacific and the Atlantic Oceans. This will reinforce the importance

of the Trans-Atlantic route. Portugal, by means of its privileged geographical position, may take

advantage of this situation to greatly increase its cargo throughputs in the medium term.

Seaport infrastructures require lump investments and have a long life cycle, therefore it would

be advisable to establish, well in advance, a strategic planning and structural policy in order to

prepare our seaports to the predictable upcoming opportunities.

1.2 OBJECTIVES

This study has two major objectives. The first is to carry out a comparative analysis of the port

sectors of four European countries (Portugal, Spain, United Kingdom and the Netherlands). This

analysis intends to identify and understand the best practices available in order to improve

seaport performance and competitiveness. Several perspectives were considered and the

gathered facts and information should provide policy makers, port executives, researchers and

other readers with a solid background on aspects such as the regulatory policies, governance

models, legislation and cargo throughputs of each country and the European Union common

policies regarding this sector.

The second objective is to carry out a reliable performance evaluation of the Portuguese

seaports. Besides the evaluation results this study aims to establish a robust performance

measurement methodology standard. The ultimate achievement would be the use of the

developed methodology to perform periodical standardized analysis by Port Authorities or

regulators. In a more modest perspective, it would also be considered a success if this line of

4

research is continued in the academic field and more evaluations of this kind are produced with

comparable results.

1.3 METHODOLOGY

An holistic approach was undertaken in the implementation of the performance measurement

procedure. It is important to keep in mind the specific reality of the seaport’s activity and the

several relevant perspectives involved. It is often found that the operational aspects are not the

only causes of inefficiency or underperformance and that other factors do have a large

influence. Non-operational issues such as the legislatory framework and regulatory practices

may significantly affect the performance level of seaports. The consideration of the public

institutional setting and of the governance model is also relevant, since in most of the European

countries the State or the regional administrations have a high level of involvement in the port

sector. All these perspectives were considered in this study in order to provide an analysis as

relevant and realistic as possible.

A performance evaluation may be carried out through several alternative techniques. None is

clearly superior to the others but each one has its own particular advantages and

disadvantages. The choice of technique should be based on the objectives of the study and the

characteristics of the analysed activity. In previous studies of the seaport sector, the most

frequently used techniques were performance indicators and frontier models such as Stochastic

Frontier Analysis (SFA) and Data Envelopment Analysis (DEA). Performance indicators are

partial measures of productivity. Frontier models establish an efficient frontier and measure the

difference between what was actually produced and what could possibly have been produced if

performing efficiently or what was consumed and how much was effectively needed to be

consumed to produce the same of quantity goods or services. The difference between these

values constitutes the inefficiency. The most relevant characteristic of DEA in comparison with

other frontier methodologies is that it is a non-parametric deterministic model. The efficiency

frontier is determined through mathematical programming based solely on the analysed sample.

Thus, there is no the need to previously make any assumptions on the form of the efficiency

frontier which could bias the results. Stolp (1990) states that a non-parametric frontier model

lets the data ‘speak for itself’. In this study the emphasis is put on analysing data in a way as

reliable as possible avoiding any unnecessary hypothesis, assumptions and preconceived ideas

that may distort the final results. Following this rationale the DEA methodology was adopted on

the basis that it is able to cope with multiple outputs and inputs in an integrated way and that it

requires less subjective assumptions than the alternative methodologies.

In the implementation of the methodology the selection of variables is a critical issue. In this

study view, this specification is even more important than the choice of methodology or model

orientation since alternative variables may yield completely different results. If inconsistent

5

choices are made, and variables do not measure what they are supposed to, conclusions will be

unreliable and therefore useless. The adopted outputs and inputs were only defined after each

specific variable significance was thoroughly discussed and scrutinized in order to provide the

most realistic and useful results.

The analysed sample consisted of forty one seaports of Portugal and other ten European

countries. These countries were Spain, France, Belgium, United Kingdom, the Netherlands,

Denmark, Poland, Greece, Sweden and Norway, which is the only non-EU country included in

the group. In order to guarantee the maximum reliability, a great care was taken in collecting

data. Most of the data used in this study was collected directly from the annual reports and

statistical publications of the respective Port Authorities. However, in some, very few, cases, it

was necessary to withdraw figures from the EUROSTAT website when these where not found in

the Port Authorities publications.

The DEA results not only resulted in withdrawing efficiency scores, but also in matching each

Portuguese port with a ports that can serve as role models. These were determined based on

the peer concept. The potential cost reductions were computed, and it was investigated if scale

had significantly affected their performance.

1.4 STRUCTURE

This study is organized in the following way. Section 2 presents a general analysis of the

seaport sector focusing on important issues that may affect performance such as the

operational scale, public policies, regulatory practices and institutional settings in Portugal,

United Kingdom, the Netherlands and Spain. Finally the influence of the European Union

common policies affecting seaports and maritime transportation is analysed. Section 3 includes

the description of performance measurement concepts; an explanation of the DEA technique;

an analysis of the state of the art in terms of performance measurement of seaports; the

discussion of the implementation of the analysis in terms of variables, models and data and the

results presentation and discussion. In Section 4 conclusions from the present study are

withdrawn and further lines of research are established.

This study may be read in two different ways depending on one’s background and interests. If

the reader does not know the seaport sector or has a special interest in issues such as

regulation, privatization, legislation or governance models it is advisable to read this study in the

usual section order as Section 2 will help to understand the port concepts discussed in the next

section. On the other hand, if one has a good knowledge of the port sector, it is suitable to

proceed directly to Section 3, and then go back to read Section 2 case studies, already bearing

in mind the performance results of the analysed countries.

6

2. SEAPORT SECTOR ANALYSIS

2.1 INTRODUCTION

A performance analysis should never be carried out in a decontextualized way. It is crucial to

investigate and understand not only if certain context factors are influencing the analysis results

but also to which extent is their influence significant. This exercise requires a good knowledge

about the analysed organizations and their operating environment.

In this section the Portuguese seaport sector is thoroughly analysed and described in order to

favour an informed view of the analysis results. Several perspectives are integrated in the

analysis including regulatory policies, scale and type of operations, market structure,

institutional setting and investment policy among others which were found to be the most

relevant. Three other countries are analysed, the Netherlands, United Kingdom and Spain. The

first two were found to be the best overall performing countries in the performance evaluation

while Spain is Portugal’s main competitor in terms of port services. The European Union has

been gradually imposing important restrictions and policy orientations at a supra national level.

Therefore relevant common policies, directly or indirectly concerning the port sector, are also

analysed in this section.

2.2 PORTUGAL

2.2.1 General context

Portugal has a rich naval and maritime history and a favorable strategic geographic location,

close to the main sea trade routes. The continental port system comprises five major ports

namely, from North to South, Leixões, Aveiro, Lisbon, Setúbal and Sines; and four secondary

ports. The archipelagos of Azores and Madeira have their own autonomous port systems.

With the end of trade barriers in the European single market, Portuguese seaports have been

subject to higher levels of competition. Nowadays, it is indifferent to load or unload cargo in any

of the seaports inside the European Union. Besides, the external trade share with other

countries inside the EU has been growing, mainly with Spain, at the cost of extra-EU countries

trade share as evidenced by Afonso and Aguiar (2004). Trading more with closer countries

means that seaports now face fierce competition from other transport modes, mainly road

haulage.

Aiming at a higher competitiveness in a globalized market, a port sector reform was initiated

and has been gradually implemented. Monteiro (2003) establishes that the rationale behind this

reform was the belief that a competitive environment, with greater participation of private capital

in investment and in port related services provision, would decisively contribute to the

improvement of the seaports efficiency and competitiveness. Price reductions and significant

improvements of the service quality would contribute to a greater satisfaction of port users.

7

2.2.2 Institutional framework and the structural reform

In 1998, a governmental white paper entitled “Maritime and Port Policy towards the XXI century”

was published. The landlord port model was referred as the best method to induce private

sector participation. In this model a Port Authority owns the port infrastructure and fulfils

regulatory functions, while port services are provided by private operators who own assets

conforming to the port superstructure and the equipment required for service provision.

Port Authorities were set up as limited liability companies with all their shares held by the State,

allowing for a more business minded management. The five major seaports are now operating

with their own independent Port Authorities. These entities are in charge of promoting port

activities, attributing licenses or concessions in the areas under their jurisdiction and of

guaranteeing the public use of port services. It is their responsibility to ensure the regular

functioning of the port, with regard to its economic, financial and operational aspects. Security

and environmental protection, accident and pollution prevention at sea or inside the seaport fit

their attributions as well. Maintenance and development operations of access channels and

landside accessibilities inside the Port Authority’s jurisdiction area are under their direct

management. In a public utility basis they may expropriate and occupy lands needed for the

expansion or development of the port or related activities.

Port Authorities charge dues to the port users and receive rents from concessionaires.

Occasionally they also gather funds by renting assets under their jurisdiction for other purposes

rather than their core port business. For example, Lisbon Port Authority rents obsolete

warehouses to restaurants and bars on areas that are not deep enough to modern vessel

operations.

There are several public bodies with jurisdiction over the seaport areas besides Port Authorities.

Captainships ‘capitanias’ are delegations of the Portuguese Navy in each seaport with

attributions related to sovereignty, maritime and port security. The customs entity collects duties

related to goods shipped from outside the EU. The Borders and Immigration Service has

responsibilities related to migrants and asylum seekers. All animal origin products have to be

inspected by the Sanitary Authority. Finally, two police bodies, the Duty Brigade and the

Maritime Police have enforcement responsibilities in the port area as well.

The Port and Maritime Transport Institute (IPTM) was created by Decree-Law no. 257/2002. It

has juridical personality, administrative and financial autonomy and has its own patrimony. Its

functions include nationwide supervision, coordination and planning, strategic development,

standardization, regulation and fiscalization within maritime and port areas. Currently it works

under the government Secretary of State for Transportation supervision, which belongs to the

Ministry of Public Works, Transports and Communications. Administration of the secondary

continental ports and the navigability of the Douro River have also been delegated to the IPTM.

8

The National Council for Ports and Maritime Transport was created by Decree-Law no. 12/2003

of January 18th. It is a consultation body for the maritime and shipping affairs with

representatives of all the stakeholders (Port Authorities, government, worker’s unions and

industry). It was intended to provide technical and informed decision support in areas such as

the Port Authorities tariffs, the maritime sector policies, the articulation between ports and other

transport modes, the promotion of the Portuguese seaports and of the maritime transportation.

However, this council only effectively met during one year and it is now inactive.

As shown in Figure 1, this sector is currently supervised by the Ministry of Public Works,

Transportation and Communications (MOPTC) through the Secretary of State for Transportation

(SET). Both the Port Authorities and the IPTM are supervised at an arms length by the

Secretary of State for Transportation. Secondary ports are managed by the IPTM.

Ministry of Public

Works, Transportation

and Communications

(MOPTC)

Secretary of State for

Transportation

(SET)

Port and Maritime

Transport Institute

(IPTM)

Secondary Ports

Port Authorities:

Leixões, Aveiro, Lisbon,

Setúbal and Sines

Council for Ports

and Maritime

Transport

(inactive)

Figure 1 - Institutional framework of the Portuguese seaport sector

2.2.3 Governance model

Until the reform, Portuguese seaports roughly fitted in the tool port model, where the Port

Authority owned the infrastructure, the superstructure and the equipment as explained by

Bamford (2001). Private companies were limited to provide stevedoring labor.

Since those days several steps have been taken in order to increase private operators

participation in the Portuguese port sector. This has been carried out at various levels, including

operation, legislation and government policies. Nowadays the major share of cargo throughput

is handled by private operators on a concession basis. Legislation states that only in

exceptional situations may cargo handling services be provided in any other way than a

9

concession. However, some Port Authorities are still directly providing some of the cargo

handling services. In addition a port provides many other services besides cargo handling.

Several other activities are needed for a port to operate effectively (e.g. towage, mooring or

ancillary services) that account for a large share in the port overall performance. Most of these

other services are still directly provided by the Port Authorities instead of private operators.

Private sector participation is not an end by itself, but simply the way Portugal has chosen in its

search for more efficient and therefore more competitive seaports. Additionally, the State

divestiture in this public service creates higher requirements as far as regulation and

supervision efforts are concerned. Failure to provide a suitable economic regulatory framework

can be very costly in terms of inefficiency. In many countries, excessive port costs work as an

additional import duty on all goods entering the country and as a tax on exports.

Disproportionate port costs reduce the competitiveness of a nation’s products in world markets

and can stifle economic growth and development as stated by the World Bank (2006). In

Portugal, it is still rather unclear to know who detains regulatory functions due to a proliferation

of different organizations and entities with diverse attributions and sometimes conflicting or

overlapping responsibilities. Dias (2005) claims this has led to some disorientation by some of

the players in the seaport sector.

Nowadays service provision in ports is threefold: directly through Port Authority operational

resources, by private companies under short term license agreements or through concession

contracts where private operators perform under long term agreements.

2.2.4 Concessions

Private sector participation has been accomplished mainly through BOT (build, operate and

transfer) contracts. In this type of contract the operator compromises to invest in the

superstructure and sometimes in the infrastructure as well. In return it grants the right to operate

the service during a certain period. This period should be proportional to the required

investment. Usually, as the port industry has become a capital intensive one, contracts have

long time-spans of 20 or more years. At the end of the contract period both the infrastructure

and the superstructure should be transferred back to the Port Authority in perfect operating and

security conditions.

Already in 1993, with Decree-Law no. 298, the Portuguese legislation stated that concessions

should be the preferred way for the provision of cargo-handling services. Decree-Law 324/94

established the legal bases of public service cargo handling concessions in port areas.

Licensing is only allowed in cases where there is a serious probability that the tendering

process will have no participants or there is strategic national interest in the maintenance of this

situation. The former requires a ministerial official communication based on a previous

10

consultation to the stevedoring companies and the latter requires a specific resolution by the

Cabinet. Port Authorities are allowed to provide directly cargo handling in situations where the

service delivered by private companies has proved to be insufficient or to assure a minimum

level of intra-port competition. A concession contract maximum duration is thirty years and it

should be proportional to the operator’s investment. Port Authorities were endowed with the

responsibility of tendering, negotiating and supervising concession contracts procedures.

Cargo handling services in port areas are considered as a public service, therefore everyone

who requires them benefits from equal access conditions. Mooring priority is given to the first

vessel to present the documental request through its shipping agent. Dedicated terminals, i.e.,

terminal for the exclusive use of a liner service are not allowed. However, a private entity may

entail the exclusive use of a terminal for a specific industrial facility, under a private concession

use, if public interest is recognized by the Cabinet as stated by Dias (2005).

Awarding of a public service concession requires a public tendering process. A transitory

regime was established before the end of July 1995. It allowed for short term licenses to be

changed into concession of public service through direct negotiation between Port Authorities

and the incumbent.

Concession contracts establish both fixed and variable incomes due by the concessionaire to

the Port Authority. The fixed income refers to the infrastructures allocated to the concession,

calculated in terms of linear meter of quay, square meter of built and non built area. The

variable income is defined with regard to the volume of cargo handled. If the volume reaches

certain agreed levels, charges per extra handled unit are smaller. This scheme implies risk

sharing between both parts and is intended to promote efficiency. The annual rent setting

should obey the principle of indifference, i.e., the concession rent should be equivalent to the

operational result the Port Authority obtained prior to the concession as stated by Monteiro

(2003).

Further legislation, though not specific to the seaport sector, has introduced important new

regulation. Decree-Law no. 59/99 of March 2nd

, enlarges public work contracts juridical regime

to public service concessions. Thus a standardized public work tender process must be adopted

for public service concessions. In spite of the “Maritime and Port Policy towards the XXI century”

recommendation, a new base law specifically regulating port concessions has not yet been

produced. This way, the principal legislation concerning port concessions continues to be the

1994 Decree-Law. Port of Sines has had an exceptional treatment, as tailor made Decree-Laws

have been produced for each of its concessions.

Concerning other services besides cargo handling, only in 2001 was the possibility of licensing

or concession for other port services legally set through Decree-Law no. 75/2001 establishing

11

the juridical regime of tug services. These may be provided either through concession, licensing

or directly by the Port Authorities. Decree-Law no. 48/2002 does the same for the piloting

activity although it disregards licensing as a way of providing it.

Table 1 describes the way of provision of each type of port services.

Table 1 - Service provision in Portuguese ports

Service Provider

Cargo handling Private concessionaires and licensed operators or the Port Authority in exceptional situations

Pilotage Port Authority albeit concessions or licenses are established under legislation in force

Towage Port Authorities or concessionaires depending on the port

Mooring and Unmooring Port Authorities or concessionaires depending on the port

Fuel supply Concessionaires in general

Warehousing Concessionaires, licensed private enterprises and Port Authorities

Concessions of cargo handling, although being legally established for a long time, were not

common practice previously to the 1998 sector reform. Exceptional situations occurred where

previous operators claimed for public service concessions, under the transitory regime

mentioned above, which dismissed the public tender obligation. Table 2 lists public service

concessions in the Portuguese ports.

12

Table 2 - Public service concessions in the Portuguese ports

Port Terminal Cargo type Incumbent Timeframe

TCL (North and South container terminals)

Containers TCL, S.A. 25 year contract, eventually postponable for an extra 5 years period. Initiated in 2000.

Leixões

TCGL General cargo and dry bulk

TCGL, S.A. 25 year contract postponable for an extra 5 years period. Initiated in 2001.

Aveiro South Terminal General cargo SOCARPOR, S.A. 25 year contract postponable for an extra 5 years period. Initiated in 2001.

Alcântara Container Terminal

Containers LISCONT, S.A. 1985-2015

Santos Container Terminal

Containers TRANSINSULAR, S.A. 1995-2010

Santa Apolónia Container Terminal

Containers SOTAGUS, S.A. 2001-2021

Poço do Bispo Multipurpose

General cargo ETE, S.A. 2000-2020

Beato Multipurpose Terminal

General Cargo TMB, S.A. (consortium between Multiterminal, SPC and Sodiap)

2000-2020

Beato 1995-2025

Trafaria

Agribulk SILOPOR, S.A.

1995-2025

Palença Liquid bulk TAGOL, S.A. 1995-2025

Liquid bulk Barreiro

Liquid bulk LBC-Tanquipor, Ld.ª 1995-2025

Barreiro Conventional general cargo, liquid and dry bulk

ATLANPORT, S.A. 1995-2025

Lisbon

Seixal Dry bulk and general cargo

SNESGES, S.A. 1995-2025

Multipurpose-zone I

Dry bulk and general cargo

TERSADO, S.A. Initiated in 2004

Multipurpose Zone II

Dry bulk and general cargo

SADOPORT, S.A. Initiated in 2004

Setúbal

SAPEC Liquid bulk SAPEC

Multipurpose Terminal

General Cargo PORTSINES 25 years (initiated in 1992) Sines

Terminal XXI Containers PSA 30 years (initiated in 2004)

2.2.5 Tariffs

Port tariffs are established under the Decree-Law no. 273/2000 that sets out the Continental

Ports Tariff System. It stipulates the formulas for each and every tariff a Port Authority may

charge to cargo shippers and/or vessel owners. Based on these legally set formulas Port

Authorities annually define coefficients in order to calculate each tariff. These coefficients may

change depending on the cargo type (containers, conventional cargo, roll on-roll off, dry or liquid

bulk) and the ship type (tanker, containers, bulk ship, conventional cargo or roll on-roll off). The

13

legislation also defines the rebates that may be awarded to transshipment services, national

cabotage, regular lines, frequent users and oil tankers with green certification.

The tariff for port use is charged for the availability of access infra-structure and for the safety

and environmental protection measures. It encompasses two components. One applies to the

ships and vessels (henceforth referred to as TPU-Ship) while the other applies to cargo

(hereafter called TPU-Cargo).

According to the decree law referred above, TPU-Ship may be calculated in one of two ways as

shown in Table 3. The first relates to the gross tonnage of the ship and the ratio between the

weight of unloaded and loaded cargo. The second way refers to gross tonnage of the ship and

the length of stay. This tariff is charged to the ship owner.

Table 3 - TPU-ship

Tariff defined in ship gross tonnage and unloading to loading ratio

U1 × GT if R ≥ K U2 × GT + U3 × QT if R < K

GT - ship gross tonnage U1 - maximum rate per GT unit U2 - minimum rate per GT unit QT- handled cargo in tons U3 - rate per handled cargo R - ratio between unloaded and loaded cargo in tons K - set limit for R

Tariff defined in vessel gross tonnage and length of staying

GT × T

GT - vessel gross tonnage T - duration of vessel stay in port

TPU-cargo is computed on the basis of the amount of moved cargo measured in tons or units

depending on the type of cargo. Different tariffs may be set for loading and unloading

operations. This tariff is charged to the cargo shipper/receiver.

Other tariffs are defined for other services such as pilotage, tugs, mooring, storage and

supplies. Nevertheless, they only apply in the cases where the Port Authority directly supplies

those services. Concessionaires subject to public service contracts must submit tariffs to Port

Authority’s approval. However, they may freely offer rebates solely based on their commercial

policy.

2.2.6 Market structure

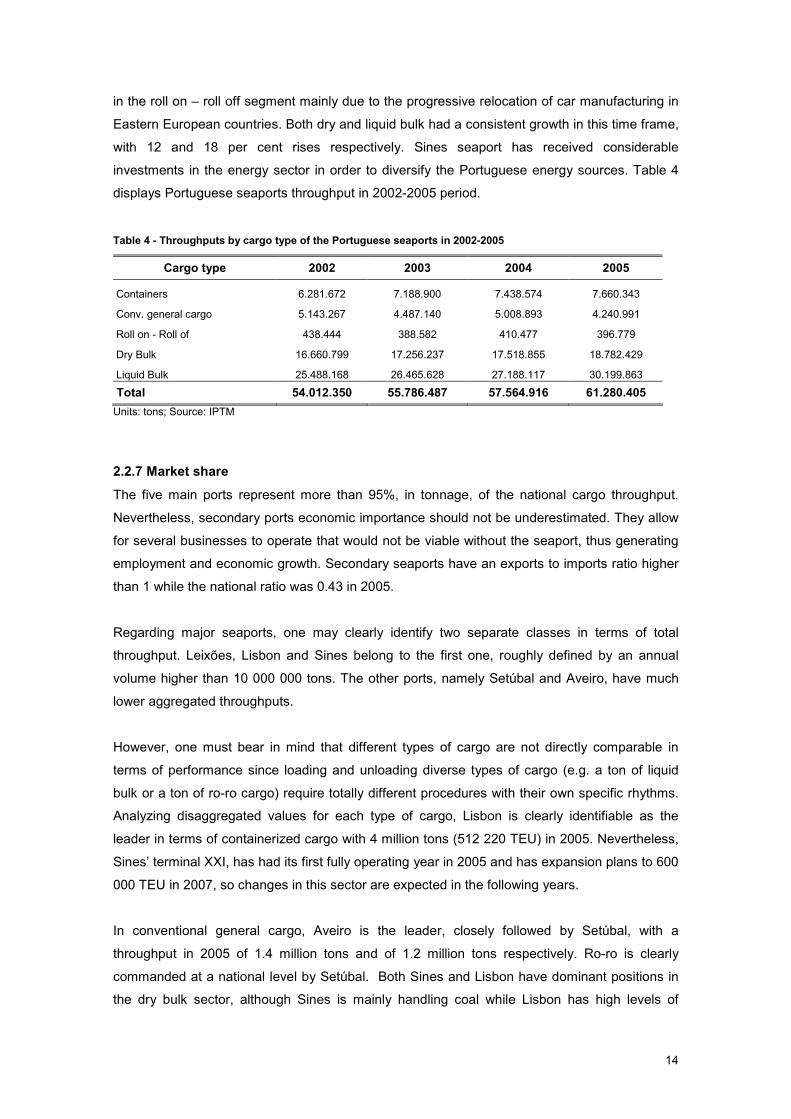

Portugal total throughput crossed the 60 million tons barrier in 2005 with a total throughput of

61 280 405 tons. Total throughput increased around 13 % between 2002 an 2005. The fastest

growing sector was containerized cargo, with an increase of 22%, while other unitized cargo

decreased, following the global shift towards containerization. There was a significant decrease

14

in the roll on – roll off segment mainly due to the progressive relocation of car manufacturing in

Eastern European countries. Both dry and liquid bulk had a consistent growth in this time frame,

with 12 and 18 per cent rises respectively. Sines seaport has received considerable

investments in the energy sector in order to diversify the Portuguese energy sources. Table 4

displays Portuguese seaports throughput in 2002-2005 period.

Table 4 - Throughputs by cargo type of the Portuguese seaports in 2002-2005

Cargo type 2002 2003 2004 2005

Containers 6.281.672 7.188.900 7.438.574 7.660.343

Conv. general cargo 5.143.267 4.487.140 5.008.893 4.240.991

Roll on - Roll of 438.444 388.582 410.477 396.779

Dry Bulk 16.660.799 17.256.237 17.518.855 18.782.429

Liquid Bulk 25.488.168 26.465.628 27.188.117 30.199.863

Total 54.012.350 55.786.487 57.564.916 61.280.405

Units: tons; Source: IPTM

2.2.7 Market share

The five main ports represent more than 95%, in tonnage, of the national cargo throughput.

Nevertheless, secondary ports economic importance should not be underestimated. They allow

for several businesses to operate that would not be viable without the seaport, thus generating

employment and economic growth. Secondary seaports have an exports to imports ratio higher

than 1 while the national ratio was 0.43 in 2005.

Regarding major seaports, one may clearly identify two separate classes in terms of total

throughput. Leixões, Lisbon and Sines belong to the first one, roughly defined by an annual

volume higher than 10 000 000 tons. The other ports, namely Setúbal and Aveiro, have much

lower aggregated throughputs.

However, one must bear in mind that different types of cargo are not directly comparable in

terms of performance since loading and unloading diverse types of cargo (e.g. a ton of liquid

bulk or a ton of ro-ro cargo) require totally different procedures with their own specific rhythms.

Analyzing disaggregated values for each type of cargo, Lisbon is clearly identifiable as the

leader in terms of containerized cargo with 4 million tons (512 220 TEU) in 2005. Nevertheless,

Sines’ terminal XXI, has had its first fully operating year in 2005 and has expansion plans to 600

000 TEU in 2007, so changes in this sector are expected in the following years.

In conventional general cargo, Aveiro is the leader, closely followed by Setúbal, with a

throughput in 2005 of 1.4 million tons and of 1.2 million tons respectively. Ro-ro is clearly

commanded at a national level by Setúbal. Both Sines and Lisbon have dominant positions in

the dry bulk sector, although Sines is mainly handling coal while Lisbon has high levels of

15

agribulk transshipment. Sines is the main energetic port, thus it has an overwhelming

advantage both regarding liquid bulk and total throughput. Disaggregated throughputs for the

main Portuguese seaports in 2005 are shown in Table 5.

Table 5 - Throughputs by cargo type of the Portuguese main seaports in 2005

Cargo type Leixões Aveiro Lisbon Setúbal Sines

Containerized 2.819.198

(352.001)*

4.040.127 (512.220)*

113.149 (13.145)*

546.287 (50.994)*

Other unitized cargo 487.152 1.376.328 438.812 1.212.426 28.771

Roll on - Roll off 9.108

(6.254)**

11.915 (6.686)**

375.756 (245.625)**

Dry Bulk 2.302.441 1.416.231 5.202.884 3.224.267 5.801.572

Liquid Bulk 7.713.004 536.257 1.608.827 1.716.538 18.552.681

TOTAL 13.330.903 3.328.816 11.302.565 6.642.136 24.929.311

Units: tons, *TEU, **vehicles; Source: 1 - IPTM, 2 - Port Authority of Setúbal

2.2.8 Calling vessels

There has been growth in the number, the total gross tonnage (GT) and the average gross

tonnage of the vessels calling in Portuguese seaports between 2002 and 2005. In 2003 and

2004 the number of vessels has decreased compared with the previous years, while the gross

tonnage has increased. This meant that fewer, but larger vessels were calling in. In 2005 both

the number of vessels and the average GT per ship increased. This illustrates the global trend

of shipping lines to deploy larger ships in order to exploit economies of scale, consequently

forcing seaports to invest in better (deeper) maritime accessibilities to remain competitive. The

evolution of vessel traffic in the period 2002-2005 is shown in Table 6.

Table 6 – Vessels calling in at Portuguese seaports (2002-2005)

Figures 2002 2003 2004 2005

Number of vessels 9.744 9.582 9.506 9.847

GT 90.913.324 93.330.458 94.010.931 101.266.904

Average vessel GT 9.330 9.740 9.890 10.284

Source: IPTM

2.2.9 Financial context

Facilities in the major seaports have been financed with public resources, including EU aids and

Port Authorities owned capitals and public resources, mainly EU funds. In some cases some

bank credit was also used, both from commercial banks and the European Investment Bank. In

the case of secondary ports, the investment was assigned to the extinct General Directorate for

Ports, Navigation and Maritime Transport, so they have benefited almost exclusively from public

16

financing (State budget and EU funds). Maintenance interventions in the main ports are

generally supported by the respective Port Authorities own capital. Exceptionally, sizeable

maintenance works in infrastructures necessary for the maritime accessibilities may be partially

funded by the State. Regarding secondary ports, when it involves substantial investments, the

government budget assures them through IPTM. Port Authorities have the competence to

approve their annual and pluriannual investment plans for port facilities as well as their

operational and annual investment budgets. Monteiro (2003) argues that, in practice, since

these companies are exclusively owned by public capitals, the State, through its representative

in the annual general meeting of each Port Authority, has the competence to approve the

proposed investments.

Nowadays, the main Port Authorities revenue sources are twofold: the tariffs directly charged to

the port users and the contractual rents with the concessionaires. However, some Port

Authorities have other revenue sources. Such is the case of the Port of Lisbon, where obsolete

warehouses have been rented to restaurants and bars. In Sines, a stone quarry situated inside

the port premises, originally intended to provide raw materials for the breakwater construction,

is now commercially exploited. Figure 2 portrays the financial evolution of the five main

continental ports in the 2002-2005 period.

-40

-20

0

20

40

60

80

100

120

140

160

180

2002 2003 2004 2005

(10

6 €

)

Costs before taxes Net Profit Investment

Figure 2 - Financial evolution of the Portuguese port system (2002 - 2005) (Unit: Euros; Sources: Leixões, Aveiro and Sines Port Authorities, Court of Auditors and National Statistic Institute)

As far as national performance is concerned, costs have been consistently decreasing.

Considering that throughput has been rising, it is acceptable to state that the reform has had a

positive overall effect in terms of performance improvement.

Large investments took place in 2002 with more than 90 million euros. The investment level by

Port Authorities has been largely reduced. In 2005 it was less than 25 % of the 2002 value. A

large share of port investment is now assured by private companies. This has had the positive

effect of allowing the State to use scarce public funds for other ends.

17

Results were negative during 2002 and 2003 and crossed the break even point in 2004.

Obtaining positive results is important in order to assure self-sustainability in the long term. It is

a prerequisite to ensure the user payer principle. European and national policies idealize about

achieving financial performance levels that generate enough revenue to sustain not only

running costs but also future investment needs. Even so, Portuguese ports are still far from

being able to support full investment costs without public funds aid.

All major ports achieved positive results in 2005 as shown in

Table 7. Lisbon and Leixões, the ones with higher container throughput obtained the highest

results. Investment levels were higher in Leixões, which invested heavily in improvements of its

maritime accessibilities. Setúbal and Aveiro have smaller private involvement in their ports,

which obliges their Port Authorities to allocate higher investment values.

Table 7 - Financial data of Portuguese main ports (year 2005)

Seaport Costs Results Investment

Leixões 37.449.718 4.179.000 7.376.000

Aveiro 12.004.449 1.401.000 6.500.000

Lisbon 46.865.553 5.833.000 4.267.000

Setúbal 20.581.747 762.000 6.930.000

Sines 34.806.114 1.311.000 3.658.000

Unit: Euros; Sources: Leixões, Aveiro and Sines Port Authorities, Court of Auditors and National Statistic Institute

2.2.10 Future

A governmental white paper was recently published under the title “Strategic Orientations for

the Maritime and Ports Sector”. The maintenance of port areas as public domain is

recommended in association with further implementation of the landlord port model. It

establishes the IPTM as the sole economic regulator at various levels: Port Authority tariffs and

operators’ tariffs. A gradual harmonization between ports tariffs will take place. Two secondary

ports with substantial commercial activity will have their own Port Authority, although all their

shares will be held by the closest major Port Authority. IPTM will also be responsible for the

maritime and seaport technical regulation and will assume an advisory role in strategic public

planning.

18

2.3 UNITED KINGDOM

2.3.1 General context

The United Kingdom is in the most advanced stage of port sector privatization worldwide. In

terms of economic regulation a laissez fair3 policy is pursued. Currently three models of port

governance coexist in the United Kingdom. Ports may be under private ownership, municipal

control, or managed by a trust. All of them are open to market forces, and are run independently

as stand-alone self-financing enterprises, free from Government support or subsidy, hence

relying solely on the dues charged to the port users. Commercial strategy and charging policies

are free from any governmental or regulatory interference though users may appeal against

them as stated in Modern Ports: A UK policy4:

“Government does not run the shipping industry or the ports industry. Government does

not decide the ports industry’s commercial strategy, or direct or fund its investment; nor

does it manage port operations. These are maters which Parliament has entrusted to local

statutory authorities, who fund their investment and operations from levies on users. In

general, port infrastructure can and should be commercially financed. Commercial funding

for development is unlikely to be a problem where a ports business is growing.

The Government and the devolved administrations retain powers to set dues when port

users appeal against them. This is because the public right to use a harbour depends

upon payment of dues. If they are not paid, the use is not by right. On the other hand, the

right could be practically extinguished if dues were unfair or unreasonable […] dues must

be fair and equitable. It is wrong for some users to have special treatment, and even to be

exempt from dues altogether, when their competitors are paying the going rate. […]

Harbour facilities cannot be maintained unless the user pays the going rate.”

Port charges should be set to cover not only the operational costs but also the lump costs

required for investments and maintenance. In contrast to the policies followed in other EU

countries the UK Government does not grant subsidies to ports.

In 2005 UK ports handled 426 million tons of external traffic and 127 million tons of cabotage.

Thus total throughput reached about 550 million tons. Total throughput has grown slowly in

recent years reflecting the economic trend towards lighter goods with higher added values.

Passenger traffic amounted to 31 million passengers in 2005 according to the Department for

Transport statistics. Figure 3 illustrates 2005 cargo throughputs in the UK.

3 Deregulation, non interference. 4 DfT (2000a); Modern Ports: A UK policy; 2.1.11 an 2.1.12

19

0

50

100

150

200

250

Liquid bulk Dry bulk Containerized Ro-ro Conventional

(million tonnes)

Figure 3 - Cargo throughputs of the UK port system in 2005

Source: Eurostat

2.3.2 Privatization process

During the last few decades, United Kingdom went through a generalized process of port

privatizations. Approximately 25% of the UK market, in tonnage, was publicly owned by the

British Transport Docks Board (BTDB) before 1983. In that year BTDB was converted into a

commercial company quoted on the London Stock Exchange with no Government shareholding.

The National Ports Council (NPC), an autonomous body that monitored the industry and had an

advisory role in applications to sizeable new port developments, was extinct.

In 1989 the ‘National Labour Dock Scheme’ (NLDS) was abolished. It compelled all dock

workers to have a permanent contract and to be subject to specific labour regulation. This was

leading to growing inefficiencies as new cargo types less demanding in terms of labour, namely

containerized cargo, were emerging. The UKMPG (2005) states that the NLDS abolishment led

to a dramatic improvement of port’s financial situation.

In 1990, legislation was enacted allowing for the privatization of trust ports. Seven former trust

ports were privatized, Clydeport, Dundee, Forth, Ipswich, Sherness, Teesport and Tilbury. Most

of them handle significant volumes of cargo. The government has the possibility to privatize a

trust Port Authority compulsorily, but it only exerted this prerogative on Ipswich in 1997. The

municipal port sector remains substantially unchanged except that Bristol was sold to a private

company.

2.3.3 Private ports

Private ports are owned by companies subject to private commercial law. The majority of

commercial ports are private comprising fourteen of the twenty largest UK ports in terms of

tonnage. Private ports with largest throughput are, according to official statistics of the DfT

20

(2006c), Grimsby & Immingham, Tees & Hartlepool and Southampton. Some of the more

relevant port companies are:

� ABP (Associated British Ports Holdings Ltd.), that withholds the former port assets of

the British Transport Dock Board (BTDB), is UK's leading ports group. ABP owns and

operates 21 ports all around the UK and handles approximately a quarter of the national

seaborne trade. Its ports are: Ayr, Barrow, Barry, Cardiff, Fleetwood, Garston, Goole,

Grimsby, Hull, Immingham, Ipswich, King's Lynn, Lowestoft, Newport, Plymouth, Port

Talbot, Silloth, Southampton, Swansea, Teignmouth and Troon. ABP is currently owned

by Admiral Acquisitions UK Ltd. quoted on the stock market of London;

� Hutchison Ports UK Ltd. which is a subsidiary company of Hutchison Whampoa Limited

quoted in the Hong Kong stock exchange. It operates Felixtowe, Harwich and

Thamesport;

� Forth Ports PLC is an independent company quoted in the London stock exchange. It

manages eight ports - Dundee on the Tay Estuary, Tilbury on the Thames and six on

the Forth Estuary - Leith, Grangemouth, Granton, Methil, Burntisland, Kirkcaldy and the

new Port of Rosyth.

This market structure reflects the advanced degree of liberalization of the British port sector,

with a dynamic market where mergers and acquisitions of port of companies or assets are

common.

As explained by the DfT (2000a) private ports are subject to the full freedoms and disciplines of

the commercial marketplace. Port companies may seek commercial funding borrowing on their

assets. As any other commercial company they are expected to generate dividends and to

increase share’s value over time. They are obliged to account to shareholders for their failures

as well as their successes. It is important to emphasize the fact that these private operators may

use their port assets as a guarantee for credit unlike in the rest of Europe.

2.3.4 Trust ports

Trust ports are unique to the UK as they have no shareholders or owners. Albeit not regarding

themselves as primarily profit driven, they nevertheless have to make a sufficient return on

capital to invest in new facilities and to compete with other ports. They are independent

statutory bodies, each governed by an independent board of trustees charged with acting in the

interest of all the stakeholders. As stated by the DfT (2000b) the stakeholders are all those

using the port, employees of the port, its users and all those individuals, organisations and

groups having an interest, not necessarily pecuniary, in the operation of the port.

21

Trust ports are very diverse, a few have significant commercial activities while others are only

dedicated to tourism and recreational purposes. Some trusts have a partial or total government

appointed board of trustees while others have their own selection procedures. London Port

Authority albeit having a trust status has all its terminals privatized while other trusts usually

provide their services directly. Under current legislation a trust has always the option to privatize

itself voluntarily.

The majority of UK commercial ports are trusts, though their total throughput is lower than the

one of private ports. Only a small number may be regarded as of national importance. A few are

important in specific markets. Dover handles almost 60 per cent of international sea borne