OSBORNE BOOKS TUTOR ZONE Chapter activities

24

OSBORNE BOOKS TUTOR ZONE Personal taxation 2011/2012 Finance Act 2011 Chapter activities © Osborne Books Limited, 2011

-

Upload

independent -

Category

Documents

-

view

5 -

download

0

Transcript of OSBORNE BOOKS TUTOR ZONE Chapter activities

OSBORNE BOOKS TUTOR ZONE

Personal taxation 2011/2012

Finance Act 2011

Chapter activities

© Osborne Books Limited, 2011

2 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

1.1 State whether each of the following statements is true or false.

True False

(a) All an individual’s tax records need to be kept until at least fiveyears after the end of the tax year, unless an investigation isbeing carried out.

(b) It is the taxpayer’s responsibility to inform HMRC of any taxableincome or gains on which tax has not been paid, even if theydon’t normally have to complete a tax return.

(c) If the tax return relating to a client omits certain information,then there is nothing that the accountant can or should doabout it.

(d) If HMRC wish to carry out a compliance check on anaccountant’s premises, then the accountant can normallyrefuse access.

(e) Accountants should never warn clients if they suspect moneylaundering as this would give the client a chance to cease theactivity.

(f) When an accountant is advising a client the greatest duty ofcare is to the accountant’s professional body.

1.2 Match the following examples of income with the correct income category.

Sample Income Income Category

Interest from bank accounts Property Income

Income from buy to let Savings and Investment Incomeaccommodation

Income from a company Trading Incomepension scheme

Earnings from self employment Employment, Pension and Social Security Income

Chapter activities

Introduction to income tax1

�

c h a p t e r a c t i v i t i e s 3

1.3 Which one of the following phrases describes the elements of the law governing UK tax?

(a) Statute law only

(b) HMRC guides and case law

(c) Statute law and HMRC statements of practice

(d) Statute law and case law

(e) Statute law and HMRC extra-statutory concessions

�

1.4 Analyse the income shown in the following table into those that are taxable and those that areexempt from income tax, by ticking the appropriate column.

Income Category Taxable Exempt

(a) Income from self-employment

(b) Prize from charity raffle

(c) Interest from an individual savings account (ISA)

(d) Rental income

(e) Income from a private pension

(f) Prize from national lottery

(g) Interest from a bank deposit account

(h) Partnership income

�

2.1 Charlie has two properties in addition to his home, details of which are as follows:

Two bedroom house:

(1) This unfurnished house is rented out for £775 per month. The property was occupied thistax year until 1 December when the tenants suddenly moved out, owing the rent forNovember. Charlie knows that he will not recover this rent. The property was let again from1 January to another family at the same rent.

(2) Charlie had to pay £600 for redecoration in December following the poor condition of theproperty at that time.

(3) Charlie paid buildings insurance of £200 for the year.

One bedroom flat:

(1) This furnished flat is rented out for £450 per month. The property was rented all tax year.

(2) Charlie paid council tax and water rates on the flat, totalling £1,000 for the year. He also paidinsurance of £150 for the building plus £90 for the contents for the year.

Calculate the taxable profit or loss made on each property, using the following table.

Two bedroom house One bedroom flat

£ £

Income

Expenses:

4 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

Chapter activities

Income from property2

c h a p t e r a c t i v i t i e s 5

2.2 Mary rents a furnished room in her own house to a lodger for £160 per week, including breakfasteach day. Heating the room costs Mary £130 for the year, and food for the lodger’s meals costs £12per week.

(i) Calculate the assessable amount for the tax year, based on

(a) claiming rent a room relief, and

(b) preparing a normal rental income computation

using the following table.

Claiming rent a Normal rental income room relief computation

£ £

Income

Allowable deductions

(ii) Complete the following sentence:

To pay the minimum income tax, Mary should claim / not claim rent a room relief.

6 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

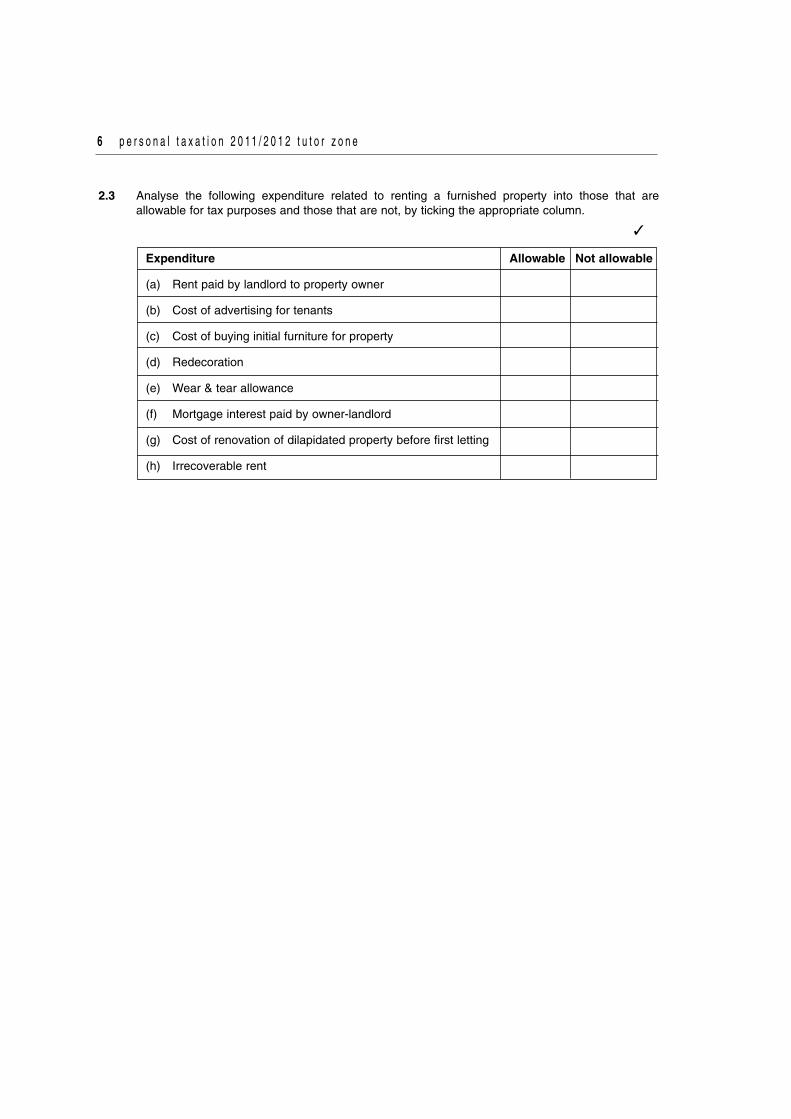

2.3 Analyse the following expenditure related to renting a furnished property into those that areallowable for tax purposes and those that are not, by ticking the appropriate column.

Expenditure Allowable Not allowable

(a) Rent paid by landlord to property owner

(b) Cost of advertising for tenants

(c) Cost of buying initial furniture for property

(d) Redecoration

(e) Wear & tear allowance

(f) Mortgage interest paid by owner-landlord

(g) Cost of renovation of dilapidated property before first letting

(h) Irrecoverable rent

�

2.4 George rents out one furnished property. He claims wear and tear allowance for furniture. Thefollowing is a statement compiled from his accounting records relating to the tax year.

£ £

Rental Income Receivable 10,000

less expenditure:

Council Tax 800

Water Rates 350

Mortgage Interest 1,500

Insurance 320

Cost of Replacement Furniture 3,200

Depreciation of Furniture 900

Managing Agent’s Charges 1,000

8,070

Profit 1,930

Required

(a) Calculate the assessable property income for George, using the following table.

£ £

Income

Expenditure:

Assessable Income

(b) Complete page UKP2 of the UK Property supplementary pages, (2010/11 versionreproduced on the next page) for George.

c h a p t e r a c t i v i t i e s 7

8 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

c h a p t e r a c t i v i t i e s 9

3.1 Some savings and investment income is received net (after basic rate tax has been deducted)while other income is received gross, yet is still taxable. A third group is exempt from tax (tax free).Analyse the following examples of income by ticking the appropriate column.

Received Received Exemptnet of tax gross (but from tax

taxable)

Premium bond prizes

Bank deposit account interest

NS&I investment account interest

NS&I fixed interest savings certificates

Dividends from UK companies

Government securities (‘Gilts’)

Interest from cash ISA account

Building society account interest

3.2 During the tax year, William received UK dividends of £1,350 and £530 income from his NS&Iindex-linked savings certificates.

(i) What is the total amount of tax that is treated as already paid?

(a) None

(b) £470

(c) £282

(d) £150

(ii) What is the total assessable income from these sources for the tax year?

(a) £1,500

(b) £2,350

(c) £2,030

(d) £530

Chapter activities

Income from savings and investments3

�

�

�

3.4 In what circumstances will the starting rate of 10% tax for savings income apply to an individual?(select one phrase)

(a) In all circumstances

(b) Only when their total savings income is below £2,560

(c) Only when their total savings income is above £2,560

(d) Only when their taxable general income is below £2,560

(e) Only when their taxable dividend income is below £2,560

3.3 Kate has received the amounts shown in the following table from various investments. Completethe table to show the assessable amounts and the amounts of tax that are treated as having beenpaid.

Investment Amount Received Assessable Amount Tax treated as paid

£ £ £

Building Society Account 1,120

UK Dividends 225

Government Security (Gilt) 400

NS&I Easy Access 16Savings Account

Local Authority Loan 1,440

Totals 3,201

1 0 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

�

4.1 Sophie has been offered a company car as part of a salary and benefits review. She can eitherchoose:

� A petrol engine Ford with a list price of £15,000 and emissions of 155 g/km, or

� A diesel engine Vauxhall with a list price of £14,500 and emissions of 149 g/km.

In each case she would also be entitled to all business fuel, and private fuel up to a maximum of£50 per month paid for by the company.

(a) Use the following table to calculate the total taxable benefit in each situation.

Ford Vauxhall

List Price £

Car Benefit Percentage

Car Benefit £

Fuel Benefit £

Total Benefit £

(b) Complete the following sentence:

The option with the lowest assessable benefit is the Ford / Vauxhall.

c h a p t e r a c t i v i t i e s 1 1

Chapter activities

Income from employment4

1 2 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

4.2 Analyse the benefits shown in the following table into those that are taxable and those that areexempt from tax, by ticking the appropriate column.

Income Category Taxable Tax Exempt

(a) Use of pool car for business purposes

(b) Significant private use of company van

(c) Interest free loan of £10,000

(d) Use of a workplace creche

(e) Free workplace parking

(f) Private use of company asset

(g) Living in job-related accommodation

(h) £2,000 award under a staff suggestion scheme

�

4.3 Gemma’s employer pays her 35p per mile for all her business travel using her own car. During thetax year Gemma drove 12,000 business miles and claimed the agreed amount. If Gemma is a basicrate taxpayer, what impact will this have on the total amount of tax that she must pay?

(a) No impact

(b) It increases her tax by £160

(c) It reduces her tax by £160

(d) It reduces her tax by £240

(e) It increases her tax by £800

(f) It reduces her tax by £800

�

c h a p t e r a c t i v i t i e s 1 3

4.4 John has the following employment data:

� His salary is £30,000 per year

� He has use of a petrol engine company car with a list price of £14,000 and emissions of 115 g/km, and all fuel

� He had an interest free loan of £6,000 throughout the tax year

� He paid his own subscription to an approved professional body of £200

Assume that the HMRC interest rate is 4.00% for 2011/12.

(a) Calculate the total assessable employment income for John, using the following table.

Benefit / (Deduction) £

Salary

Company car benefit

Company car fuel benefit

Interest free loan benefit

Professional subscription

Total assessable employment income

(b) Complete page E1 of John’s tax return (as far as possible). The form (2010/11 version) isreproduced on the following page.

1 4 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

c h a p t e r a c t i v i t i e s 1 5

5.1 Teresa, who is 78 years old, had pension income of £25,300 and received dividends of £1,305.

She paid £360 (net) to charities under the gift aid scheme.

Calculate her total income tax liability (ie before deduction of tax paid) for the tax year, using thetable given below.

£

Pension income

Gross dividends

Personal allowance

Taxable income

Chapter activities

Preparing income tax computations5

1 6 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

5.2 Select from the following statements, those which are correct.

True False

(a) Payments on account relating to a tax year are paid on 31January following the tax year, and on the 31 July after that.

(b) The final payment of income tax relating to a tax year is paidon 31 January following the end of the tax year.

(c) If a taxpayer is 3 months late paying income tax then he willbe subject to both a penalty and interest.

(d) If an online tax return is submitted on 31 December followingthe end of the tax year, the taxpayer would not be subject toany penalty.

(e) If a tax return is submitted on 31 March (approximately 12months after the end of the tax year), the taxpayer would besubject to a penalty of £200.

(f) If there is an error or omission on a tax return then the size ofthe penalty will depend on whether the error was due to lackof reasonable care, or was deliberate, or was deliberate andconcealed.

�

c h a p t e r a c t i v i t i e s 1 7

5.3 John is a higher rate taxpayer. He did not declare the income from his NS&I Fixed Interest SavingsCertificates on his tax return.

Select the correct statement from the following.

True False

(a) John did nothing wrong as the higher rate tax on this incomehas already been deducted at source.

(b) John did nothing wrong as the income is exempt from incometax.

(c) John will be subject to a penalty of between 0% and 100% ofthis income that he has not declared.

(d) John will not be subject to a penalty because every taxpayer isallowed to make one omission on their tax return.

(e) John cannot be charged a penalty if it is his first offence.

5.4 William earns £145,000 per year from his job as a manager, and is entitled to a diesel company carand all fuel (business and private). The car has a list price of £28,000, but was purchased secondhand for £16,500. It has emissions of 163 g/km.

William makes gift aid cash contributions of £2,400 per year.

Calculate William’s tax liability (to the nearest £), using the following table.

Workings

£

Salary

Car benefit

Fuel benefit

Personal allowance

Taxable income

Tax at 20%

Tax at 40%

Tax at 50%

Total tax liability

�

6.1 (i) Andrew bought an asset in January 2005 for £23,000, selling it in the tax year for £20,000.He paid auctioneers commission of 4% when he bought the asset and 5% when he sold theasset.

The loss on this asset is:

(a) £nil

(b) £3,000

(c) £2,920

(d) £4,920

(e) £4,950

(ii) Advertising costs incurred to sell an asset are not an allowable deduction as they are arevenue item.

Chapter activities

Capital gains tax – the main principles6

1 8 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

6.2 State which of the following statements are true:

True False

(a) The annual exemption is always applied before capital lossesare deducted.

(b) The setting off of capital losses brought forward will not wastethe annual exemption.

(c) Capital gains are taxed at 20% for all basic rate tax payers.

(d) Capital losses cannot be set against gains of the previous taxyear.

(e) Capital losses of the current year cannot safeguard the annual exemption when offset against current year gains.

�

�

True / False

c h a p t e r a c t i v i t i e s 1 9

6.3 Joanne has a capital loss brought forward of £2,400.

She sold an asset during the tax year for £17,900. She had been left the asset by her grandfatherin his will when it was worth £6,300. Her grandfather originally paid £2,500 for the asset.

Joanne is a higher rate income tax payer.

Complete the following sentences:

(a) The gain on the asset is

(b) The amount of loss that will be relieved is

(c) The capital gains tax payable is

(d) The loss to be carried forwards to the next tax year is

6.4 Complete the following table to show which assets are exempt from capital gains tax and which arechargeable.

Asset Exempt Chargeable

(a) Antique painting

(b) Holiday home

(c) Caravan

(d) Shares

(e) Pet cat

(f) Government securities

(g) Classic car

(h) Field

£

£

£

£

7.1 David bought a house in Bristol on 1 January 1999 for £121,000. He lived in the house until 31December 2002 when he moved to work elsewhere in the UK for two years. He returned on 31December 2004, and lived in his house until 31 December 2006. On 1 January 2007 he purchasedanother house in Brighton and moved there, putting the house in Bristol on the market. The housein Bristol was eventually sold on 1 January 2012 for £205,000.

(a) Which periods are treated as occupied and which are not?

Occupation / Deemed Occupation Non-occupation

(b) The chargeable gain on the property is to the nearest £.

2 0 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

Chapter activities

Capital gains tax – some special rules7

£

c h a p t e r a c t i v i t i e s 2 1

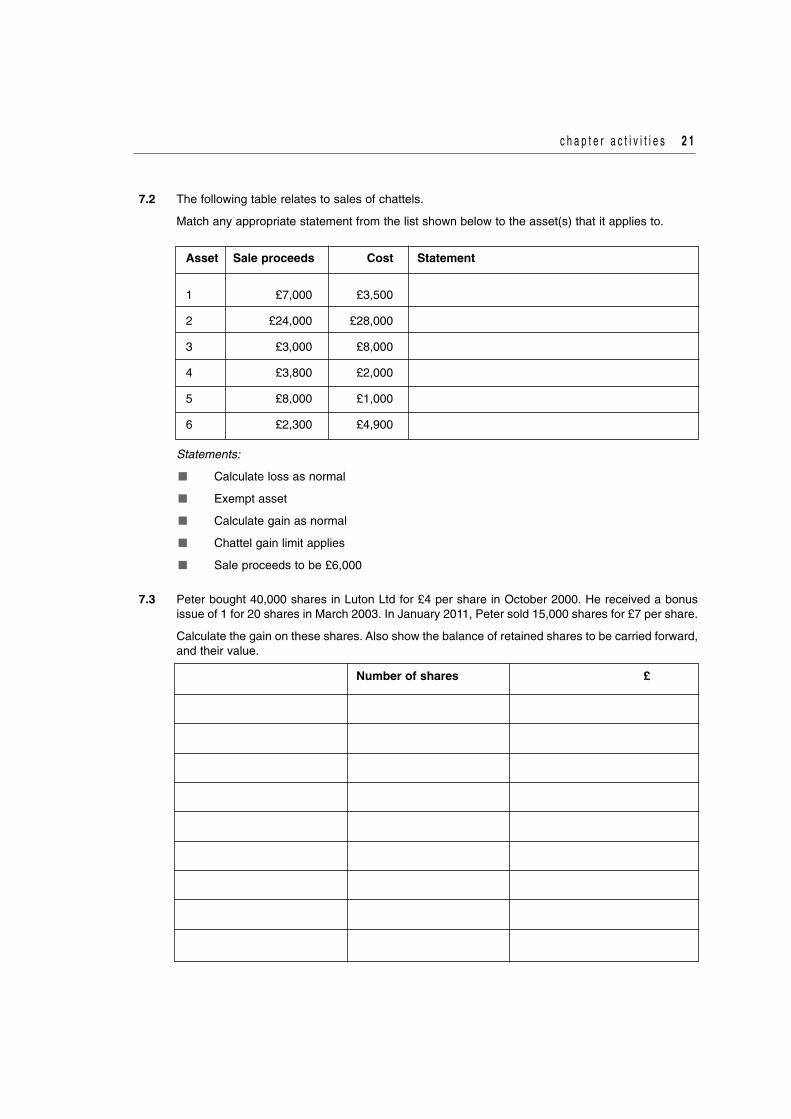

7.2 The following table relates to sales of chattels.

Match any appropriate statement from the list shown below to the asset(s) that it applies to.

Asset Sale proceeds Cost Statement

1 £7,000 £3,500

2 £24,000 £28,000

3 £3,000 £8,000

4 £3,800 £2,000

5 £8,000 £1,000

6 £2,300 £4,900

Statements:

� Calculate loss as normal

� Exempt asset

� Calculate gain as normal

� Chattel gain limit applies

� Sale proceeds to be £6,000

7.3 Peter bought 40,000 shares in Luton Ltd for £4 per share in October 2000. He received a bonusissue of 1 for 20 shares in March 2003. In January 2011, Peter sold 15,000 shares for £7 per share.

Calculate the gain on these shares. Also show the balance of retained shares to be carried forward,and their value.

Number of shares £

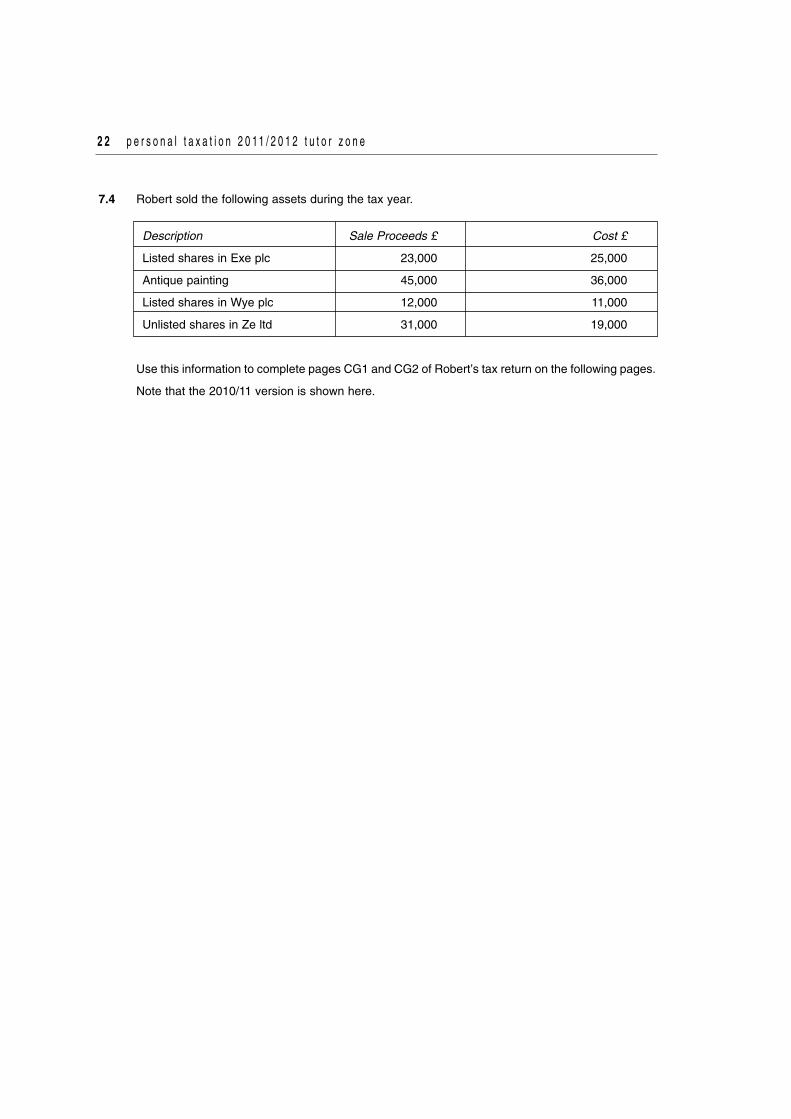

7.4 Robert sold the following assets during the tax year.

Description Sale Proceeds £ Cost £

Listed shares in Exe plc 23,000 25,000

Antique painting 45,000 36,000

Listed shares in Wye plc 12,000 11,000

Unlisted shares in Ze ltd 31,000 19,000

Use this information to complete pages CG1 and CG2 of Robert’s tax return on the following pages.

Note that the 2010/11 version is shown here.

2 2 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e

c h a p t e r a c t i v i t i e s 2 3

2 4 p e r s o n a l t a x a t i o n 2 0 1 1 / 2 0 1 2 t u t o r z o n e