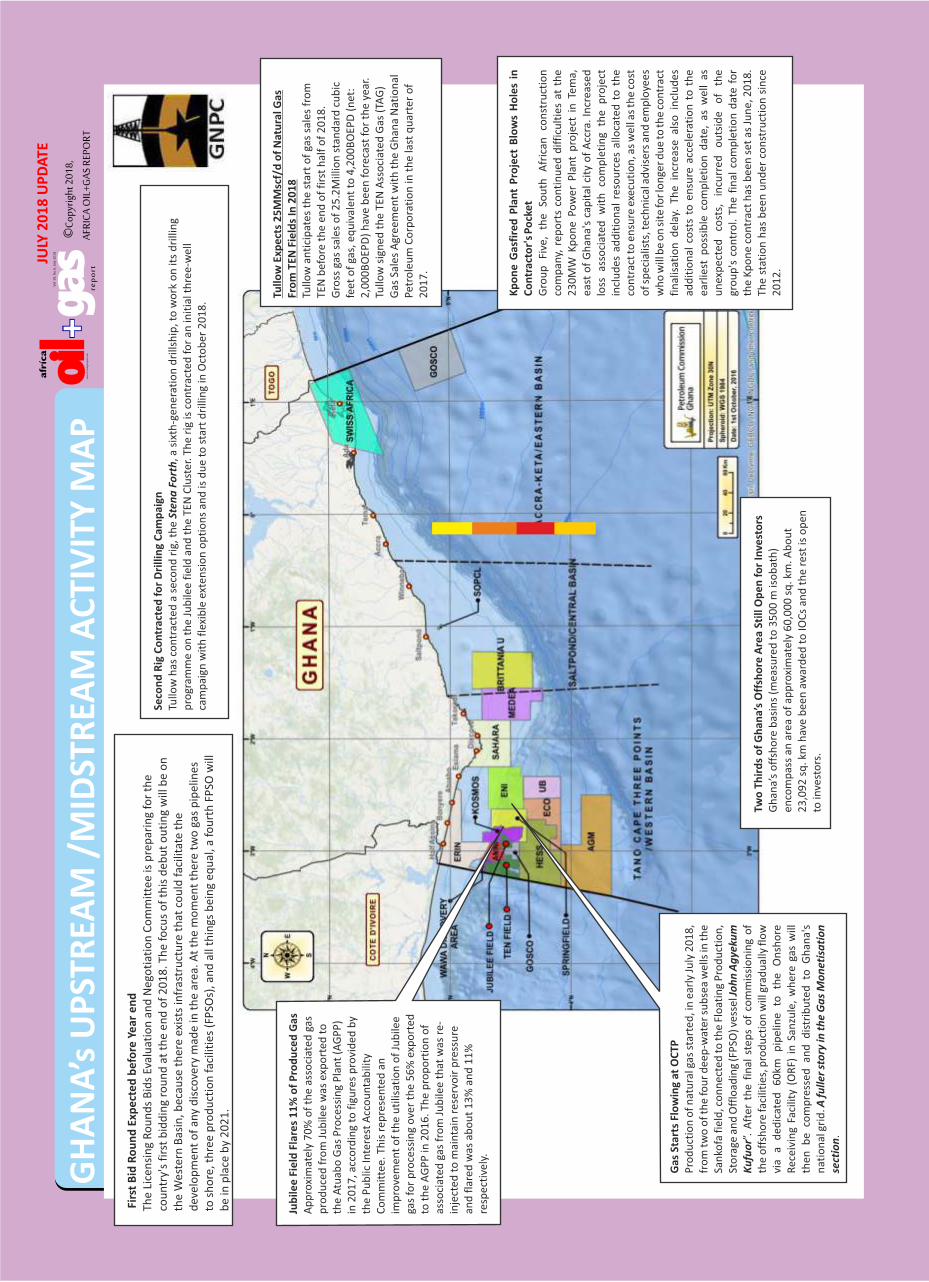

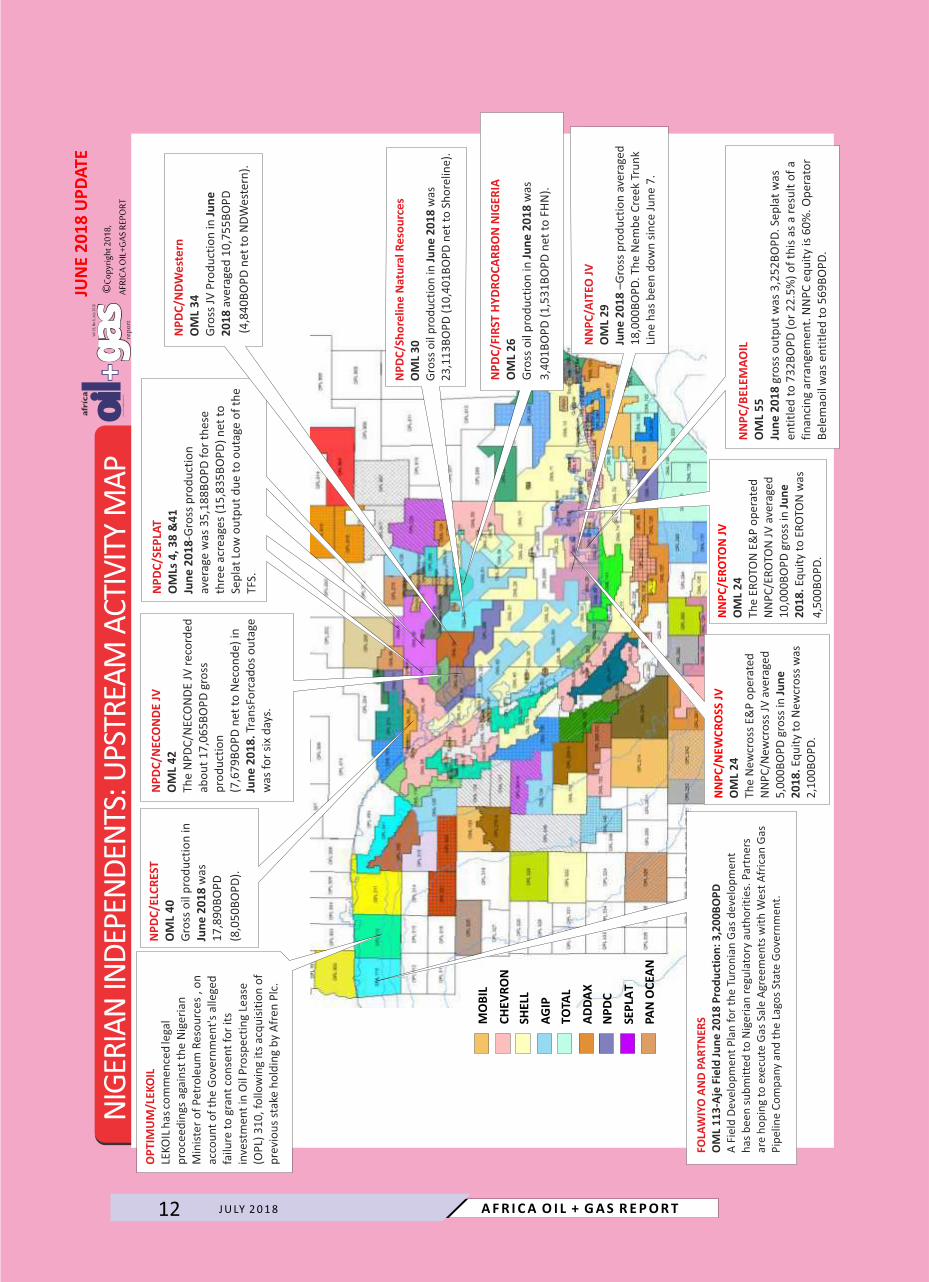

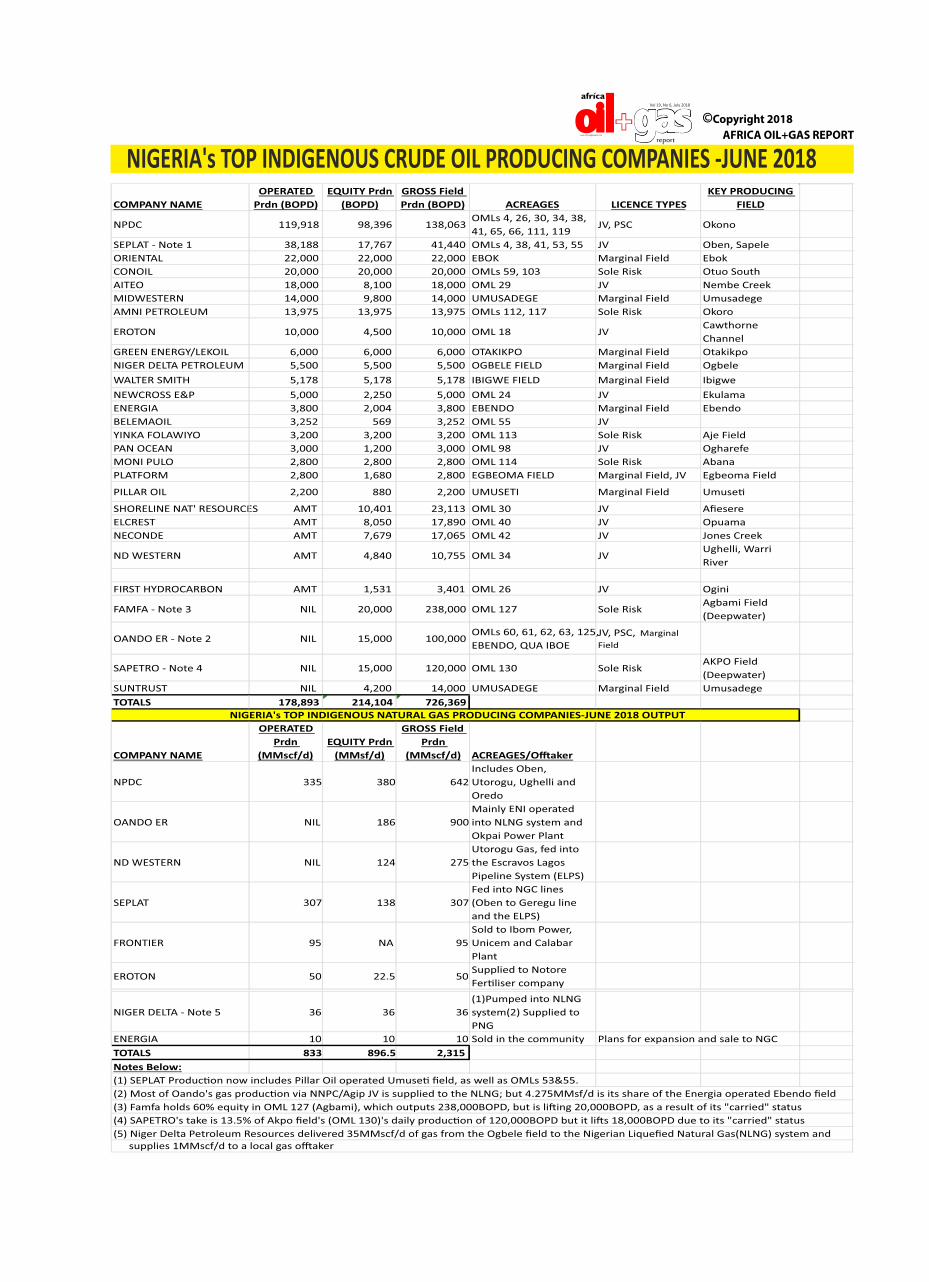

Oil+Gas_126th Edition_June 2018+NEW.cdr - CrudemixAfrica

44

www.africaoilgasreport.com

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Oil+Gas_126th Edition_June 2018+NEW.cdr - CrudemixAfrica

www.africaoilgasreport.com

FR

OM

TH

E E

DIT

OR

Vol 19, No 6, July 2018

report

Reporter: SEUN ALABIOWO

Business Development: PAUL KELECHI

REGIONAL REPRESENTATIVES

West Africa: DELALI OTCHI/Accra, Ghana

South Africa: ROBERT BAKRE/Cape Town, SA

North Africa: OYELADE ABASS/Cairo, Egypt

HQ(North): Abuja, KISH ONWUNALI

HQ(South): NOAH AJIBISE/Warri

AMY AVIA /Port Harcourt

Publisher: TOYIN AKINOSHO

Editor-In-Chief: FRED AKANNI

Editor: MOSES AKIN AREMU

Consultant: FIDELIS AKPOM

Editorial Assistant: AHMED GAFAR

Published by: FESTAC NEWS PRESS LTD.

OFFICE ADDRESS

12A, Animashaun Street,

FOLUSO OGUNSAN (Lagos)

Off Bode Thomas Street, Surulere, Lagos.

EDITORIAL EMAIL: [email protected]

WEBSITE: www.africaoilgasreport.com

TEL: 234-8036-525-979

DISPATCHER: Kayode Akinyele

LEGAL CONSULTANTS

OMISORE AND OMISORE

6th Floor, Western House, Broad Street, Lagos

REGIONAL CONTACTS

CAPE TOWN: ROBERT BAKRE

Western Cape Postnet Suite 226

Post Bag X16 Hermanus, 7200 South Africa

Phone: +277-96971531.

Email: [email protected]

ACCRA: DELALI OTCHI

Email: [email protected]

Phone: 233-2405-69650.

DANIEL BUDU

Phone: +233-243349209.

RIDGE CHURCH,

Tudu Branch, Accra. Phone: +234-243349209

CAIRO: AL-AHRAM NEWSPAPERS LTD.

Al Galaa Street, -11511, Cairo.

Phone: 5796997, Mobile: 012/2180706

OYELADE ABASS

SUBSCRIPTION/ADVERT PLACEMENT

SERVICES

Phone: +234-806-0095809, +234-8127483663,

+234-809-9903294, 234-8036-525-979

Email: [email protected]

REGIONAL CORRESPONDENTS

SA'AD BASHIR (Dar es Salaam)

JOHN ANKROMAH (Accra)

SULLY MANOPE (Windhoek)

MOHAMMED JETUTU (Cairo)

DEV George Houston

TAKO KONING Calgary

DESIGN & EDITORIAL CONSULTANTS

KAZMA CONCEPTS LAGOS

[email protected], 234-805-621-2178

Cover Design: OBAYANJU WALESEUN

INTERNATIONAL ADVISORY BOARD

MAKOJI ADUKU Abuja

AKIN ADESOKAN Indiana

AUSTIN AVURU Lagos

JAHMAN ANIKULAPO Lagos

ISSN: 1597-5274

Copyright 2018

FESTAC NEWS PRESS LTD.

AFRICA OIL + GAS REPORT J U LY 2 0 1 8 3

In Angola, this species has lost its lustre, for now. In Nigeria, foreign companies don't want to deal with the complications of Nigeria's regulatory agencies and so called state partners and the Nigerian independent, working in between, helps to perfume the process. In Algeria and Gabon and Egypt, the states are stronger than the cronies.

frican governments all over the continent are hoping that local businessmen could get Amore involved in operations of acreages. But African businessmen, as a rule, just want to collect the licence and rent to well-heeled tenants to do the hard work.

Is it true to say that whoever is coming into Africa to access E&P opportunities has to increasingly deal with the African independent.

This fourth annual edition of The African Independent allows us to view access to Africa's exploratory and producing acreage through the prism of the local player. Perhaps it helps fit some of the jigsaws?

Okay, the issue isn't as neat as that. There are African born operators who want to put in sweat equity develop the asset and, in the process, build capacity. There are those whose major competencies are their access to government officials. In between, it has emerged, there are those who have cravings for developed E&P assets and can leverage access to raise capital, but have no notion of capacity building. Asset stripping is more like what they do.

The Africa Oil+GasReport is the primer of the hydrocarbon industry on the continent. It is the market leader in local contextualizing of global developments and policy issues and is the go-to medium for decision makers, whether they be international corporations or local entrepreneurs, technical enterprises or financing institutions. It has been published by the Festac News Press Limited since November 2001, AOGR is a paid subscription based monthly, hardcopy and pdf publication delivered around the world. Its website remains www.africaoilgasreport.com m and the contact email address is . [email protected] telephone numbers in our West African regional headquarters in Lagos are +2348130733523,+2347062420127, +2348036525979 and +2348023902519.

You are not to think that anyone cares about you.

You are not to think you are as good as we are.

Sandemose's ten commandments referred to the mentality of a fictional town called Jante, but the values were immediately understood to capture the larger disposition of Scandinavians in general. The commandments are:

You are not to think you can teach us anything.

The actual commandments are less known in Finland, but Finns certainly recognise the sentiment. It's not that Nordics are proud of their Law of Jante, mind you. More than anything, the commandments are meant as a critique of a rather sad aspect of the Nordic character that is often taken too far. Efforts to stand apart from the crowd, or even to display self- confidence, can strike people steeped in the Nordic tradition as egotism or narcissism.

You are not to laugh at us.

The phrase is “the Law of Jante,” and it is shorthand for a list of ten commandments created by the Danish-Norwegian writer Aksel Sandermose in his 1933 novel A Fugutive Crosses His Tracks.

You are not to think you are smarter than we are.

You are not to think you know more than we do.

You are not to convince yourself that you are better than we are.

The Nordic tendency to downplay the unique talents of each person, as well as his or her unique pursuit of happiness and success can be petty and disheartening. Downplaying specialness

is so deeply ingrained and pervasive that the Scandinavians-that is, the Swedes, Danes and Norwegians-even have a literary phrase to describe this tendency.

You are not to think you are anything special.

You are not to think you are more important than we are.You are not to think you are good at anything.

-Editor

Excerpted from The Nordic Theory of Everything: In Search of a Better Life, by Anu Partanen, published by HarperCollins, 2016.

Licences, the Local Businessman and African Oil

BOOK EXCERPTThe Struggle Against Specialness

By Anu Partanen

FR

OM

TH

E E

DIT

OR

Vol 19, No 6, July 2018

report

Reporter: SEUN ALABIOWO

Business Development: PAUL KELECHI

REGIONAL REPRESENTATIVES

West Africa: DELALI OTCHI/Accra, Ghana

South Africa: ROBERT BAKRE/Cape Town, SA

North Africa: OYELADE ABASS/Cairo, Egypt

HQ(North): Abuja, KISH ONWUNALI

HQ(South): NOAH AJIBISE/Warri

AMY AVIA /Port Harcourt

Publisher: TOYIN AKINOSHO

Editor-In-Chief: FRED AKANNI

Editor: MOSES AKIN AREMU

Consultant: FIDELIS AKPOM

Editorial Assistant: AHMED GAFAR

Published by: FESTAC NEWS PRESS LTD.

OFFICE ADDRESS

12A, Animashaun Street,

FOLUSO OGUNSAN (Lagos)

Off Bode Thomas Street, Surulere, Lagos.

EDITORIAL EMAIL: [email protected]

WEBSITE: www.africaoilgasreport.com

TEL: 234-8036-525-979

DISPATCHER: Kayode Akinyele

LEGAL CONSULTANTS

OMISORE AND OMISORE

6th Floor, Western House, Broad Street, Lagos

REGIONAL CONTACTS

CAPE TOWN: ROBERT BAKRE

Western Cape Postnet Suite 226

Post Bag X16 Hermanus, 7200 South Africa

Phone: +277-96971531.

Email: [email protected]

ACCRA: DELALI OTCHI

Email: [email protected]

Phone: 233-2405-69650.

DANIEL BUDU

Phone: +233-243349209.

RIDGE CHURCH,

Tudu Branch, Accra. Phone: +234-243349209

CAIRO: AL-AHRAM NEWSPAPERS LTD.

Al Galaa Street, -11511, Cairo.

Phone: 5796997, Mobile: 012/2180706

OYELADE ABASS

SUBSCRIPTION/ADVERT PLACEMENT

SERVICES

Phone: +234-806-0095809, +234-8127483663,

+234-809-9903294, 234-8036-525-979

Email: [email protected]

REGIONAL CORRESPONDENTS

SA'AD BASHIR (Dar es Salaam)

JOHN ANKROMAH (Accra)

SULLY MANOPE (Windhoek)

MOHAMMED JETUTU (Cairo)

DEV George Houston

TAKO KONING Calgary

DESIGN & EDITORIAL CONSULTANTS

KAZMA CONCEPTS LAGOS

[email protected], 234-805-621-2178

Cover Design: OBAYANJU WALESEUN

INTERNATIONAL ADVISORY BOARD

MAKOJI ADUKU Abuja

AKIN ADESOKAN Indiana

AUSTIN AVURU Lagos

JAHMAN ANIKULAPO Lagos

ISSN: 1597-5274

Copyright 2018

FESTAC NEWS PRESS LTD.

AFRICA OIL + GAS REPORT J U LY 2 0 1 8 3

In Angola, this species has lost its lustre, for now. In Nigeria, foreign companies don't want to deal with the complications of Nigeria's regulatory agencies and so called state partners and the Nigerian independent, working in between, helps to perfume the process. In Algeria and Gabon and Egypt, the states are stronger than the cronies.

frican governments all over the continent are hoping that local businessmen could get Amore involved in operations of acreages. But African businessmen, as a rule, just want to collect the licence and rent to well-heeled tenants to do the hard work.

Is it true to say that whoever is coming into Africa to access E&P opportunities has to increasingly deal with the African independent.

This fourth annual edition of The African Independent allows us to view access to Africa's exploratory and producing acreage through the prism of the local player. Perhaps it helps fit some of the jigsaws?

Okay, the issue isn't as neat as that. There are African born operators who want to put in sweat equity develop the asset and, in the process, build capacity. There are those whose major competencies are their access to government officials. In between, it has emerged, there are those who have cravings for developed E&P assets and can leverage access to raise capital, but have no notion of capacity building. Asset stripping is more like what they do.

The Africa Oil+GasReport is the primer of the hydrocarbon industry on the continent. It is the market leader in local contextualizing of global developments and policy issues and is the go-to medium for decision makers, whether they be international corporations or local entrepreneurs, technical enterprises or financing institutions. It has been published by the Festac News Press Limited since November 2001, AOGR is a paid subscription based monthly, hardcopy and pdf publication delivered around the world. Its website remains www.africaoilgasreport.com m and the contact email address is . [email protected] telephone numbers in our West African regional headquarters in Lagos are +2348130733523,+2347062420127, +2348036525979 and +2348023902519.

You are not to think that anyone cares about you.

You are not to think you are as good as we are.

Sandemose's ten commandments referred to the mentality of a fictional town called Jante, but the values were immediately understood to capture the larger disposition of Scandinavians in general. The commandments are:

You are not to think you can teach us anything.

The actual commandments are less known in Finland, but Finns certainly recognise the sentiment. It's not that Nordics are proud of their Law of Jante, mind you. More than anything, the commandments are meant as a critique of a rather sad aspect of the Nordic character that is often taken too far. Efforts to stand apart from the crowd, or even to display self- confidence, can strike people steeped in the Nordic tradition as egotism or narcissism.

You are not to laugh at us.

The phrase is “the Law of Jante,” and it is shorthand for a list of ten commandments created by the Danish-Norwegian writer Aksel Sandermose in his 1933 novel A Fugutive Crosses His Tracks.

You are not to think you are smarter than we are.

You are not to think you know more than we do.

You are not to convince yourself that you are better than we are.

The Nordic tendency to downplay the unique talents of each person, as well as his or her unique pursuit of happiness and success can be petty and disheartening. Downplaying specialness

is so deeply ingrained and pervasive that the Scandinavians-that is, the Swedes, Danes and Norwegians-even have a literary phrase to describe this tendency.

You are not to think you are anything special.

You are not to think you are more important than we are.You are not to think you are good at anything.

-Editor

Excerpted from The Nordic Theory of Everything: In Search of a Better Life, by Anu Partanen, published by HarperCollins, 2016.

Licences, the Local Businessman and African Oil

BOOK EXCERPTThe Struggle Against Specialness

By Anu Partanen

KI

CK

ST

AR

TE

R

AFRICA OIL + GAS REPORT J U LY 2 0 1 8 5

“What do you know about them?”, the inquiries always state.

The geography is very specific and so is the nationality of the preferred licensee: Nigeria and Nigerian.

So a semi-official secondary market has grown to fill the gap.

Between 2013 and 2015, ConocoPhillips, the world's largest independent, received close to $1.5Billion for its sale of, mainly, 20% equity in four leases in the country, a transaction that marked its exit from Nigeria.

FAR LESS EXPENSIVE HAVE BEEN the deals involving farm ins into and operatorships of marginal fields and exploratory tracts.

The follow up statement to that query hardly varies; “I have people who have money to invest”. Indeed, the largest producing Nigerian independents: AITEO

~80,000BOPD, Seplat ~65,000BOPD, Shoreline ~50,000BOPD, Neconde ~50,000BOPD, Eroton ~40,000BOPD, came in to being through the secondary market.

The state itself has not exactly benefited from these sales. When the Department of Petroleum Resources staked a claim, for the first time, to 10% of the transaction money, in the last Shell-led bid round, which grossed $4.6Billion, it discovered a clause that said that any payment to government from the transactions had to be made by the buyers of the assets. And you know what? And since the buyers are “poor” Nigerian companies, the DOR found itself on the back foot.

Outside of the marginal fields league are a number of Oil Prospecting Licenced acreages that would appear on the surface, available. There are over 15 of them, mostly onshore Niger Delta, some in shallow water. But holders of these assets are not in a hurry to do deals. The fact that they escape even paying signature bonus after being awarded these assets, in cases for over 20 years, says something about state/regulatory capture in the Nigerian petroleum industry.

But these are the big ticket items, in which the cost of buying stakes in each acreage has ranged from $50 Million to $2.5Billion, because most of the assets involved are producing properties.

So Afren had taken advantage of Nigeria's informal secondary lease market. In spite of the access of some of the company's principals to the upper reaches of Nigerian political power structure, Afren never won an acreage from the Nigerian government, either in an open lease sale or a discretionary award.

Shell started the contemporary round of divestments of Nigerian

assets in 2008 when it sold 15% of the total equity in Oil Mining Leases (OMLs) 125 and 134 to Oando. It upped the game in 2010, when it began what has now become its frequent “bid round” of sale of onshore assets, leading its co-venturers TOTAL and ENI to collectively divest their 45% in eight acreages for a sum of around $7Billion.

One company that excelled in this area was Afren. Between its founding

in 2004 and its demise in 2015, the London headquartered independent signed MoUs with seven Nigerian marginal field acreage holders. In the end it consummated a deal with one; Oriental Resources, on the Ebok field, which it brought into production. It also farmed into Amni Petroleum's Okoro field, which it took to first oil. At the height of its powers, Afren was producing over 52,000BOPD gross from these two fields. It was convenient for the company not to quote the gross figures, since its equity volume from these two assets, at over 30,000BOPD, was also high.

THE ONLY LICENCING ROUND focused on marginal fields was conducted in 2001-2002. Out of the 24 such fields awarded to 31 Nigerian independents in 2003, 10 fields have not reached sustained production. Several of them are candidates for anyone who is interested in having a pie of the Nigerian marginal field basket. They are Bicta Energy's Ogedeh field, which has never really had an operationalized work programme; Sogenal's Akepo field, which has faced serious operational challenges in the journey to development; Goland's Oriri field has experienced failed re-entries; Movido's Ekeh field has had

intermittent production, with expensive, short term production facilities and the field has been shut in for over three years now; Dansaki/Associated's Tom Shot Bank field has not had the benefit of a robust development partner. Finally, Del Sigma's Ke Field needs a working up.

The big challenge of Nigeria's petroleum licencing operation is not in the frequency of bid rounds. It is in the management of licences. Companies hold on to asset, especially if it is awarded by the state, without payment of the most rudimentary charges and unwilling to embark on a work programme. And when would be partners come, the first thing on the table is to pay the signature bonus; the second thing is the sign on fee and the third is the regular, quarterly fee paid to “owners” of the licence.

Nigeria has not conducted a bid r o u n d s i n c e 2 0 0 7 . A n d discretionary awards by the government have been few and far between.

Chevron has, quietly earned over $800Million from the sale of its stakes in six acreages (three onshore and three shallow offshore) since 2014.

Meanwhile, in Guarantee/Owena owned Ororo marginal field, the partners have tied up with Sirius Petroleum, which acts as both technical operator and financier. There is ongoing work on Eurafric's Dawes Island field, by partners Petralon and Tako E&P. Sahara's Tsekelewu Field is clearly a no go area, less because there is anything going on than the fact that Sahara Energy is a well-heeled company which doesn't need a partner; it's just not keen on doing anything with this particular field. It should be at risk of losing the licence, but then, Sahara has a way with the Nigerian government.

“Do you know a Nigerian holder of petroleum acreage who is interested in funding partnership for field development?”It's a question I have been asked, quite routinely, in the last 10 years.

These enquiries are always about the marginal fields, awarded 15 years ago, that haven't been developed, as well as over 20 oil prospecting leases; exploratory tracts which have been granted to Nigerian companies, as far back as 25 years ago, but never experienced an active work programme.

By Toyin AkinoshoPublisher

The big challenge of Nigeria's petroleum licencing operation is not in the frequency of bid rounds. It is in

the management of licences.

Some Insight Into Nigeria's “Secondary Licencing” Market

KI

CK

ST

AR

TE

R

AFRICA OIL + GAS REPORT J U LY 2 0 1 8 5

“What do you know about them?”, the inquiries always state.

The geography is very specific and so is the nationality of the preferred licensee: Nigeria and Nigerian.

So a semi-official secondary market has grown to fill the gap.

Between 2013 and 2015, ConocoPhillips, the world's largest independent, received close to $1.5Billion for its sale of, mainly, 20% equity in four leases in the country, a transaction that marked its exit from Nigeria.

FAR LESS EXPENSIVE HAVE BEEN the deals involving farm ins into and operatorships of marginal fields and exploratory tracts.

The follow up statement to that query hardly varies; “I have people who have money to invest”. Indeed, the largest producing Nigerian independents: AITEO

~80,000BOPD, Seplat ~65,000BOPD, Shoreline ~50,000BOPD, Neconde ~50,000BOPD, Eroton ~40,000BOPD, came in to being through the secondary market.

The state itself has not exactly benefited from these sales. When the Department of Petroleum Resources staked a claim, for the first time, to 10% of the transaction money, in the last Shell-led bid round, which grossed $4.6Billion, it discovered a clause that said that any payment to government from the transactions had to be made by the buyers of the assets. And you know what? And since the buyers are “poor” Nigerian companies, the DOR found itself on the back foot.

Outside of the marginal fields league are a number of Oil Prospecting Licenced acreages that would appear on the surface, available. There are over 15 of them, mostly onshore Niger Delta, some in shallow water. But holders of these assets are not in a hurry to do deals. The fact that they escape even paying signature bonus after being awarded these assets, in cases for over 20 years, says something about state/regulatory capture in the Nigerian petroleum industry.

But these are the big ticket items, in which the cost of buying stakes in each acreage has ranged from $50 Million to $2.5Billion, because most of the assets involved are producing properties.

So Afren had taken advantage of Nigeria's informal secondary lease market. In spite of the access of some of the company's principals to the upper reaches of Nigerian political power structure, Afren never won an acreage from the Nigerian government, either in an open lease sale or a discretionary award.

Shell started the contemporary round of divestments of Nigerian

assets in 2008 when it sold 15% of the total equity in Oil Mining Leases (OMLs) 125 and 134 to Oando. It upped the game in 2010, when it began what has now become its frequent “bid round” of sale of onshore assets, leading its co-venturers TOTAL and ENI to collectively divest their 45% in eight acreages for a sum of around $7Billion.

One company that excelled in this area was Afren. Between its founding

in 2004 and its demise in 2015, the London headquartered independent signed MoUs with seven Nigerian marginal field acreage holders. In the end it consummated a deal with one; Oriental Resources, on the Ebok field, which it brought into production. It also farmed into Amni Petroleum's Okoro field, which it took to first oil. At the height of its powers, Afren was producing over 52,000BOPD gross from these two fields. It was convenient for the company not to quote the gross figures, since its equity volume from these two assets, at over 30,000BOPD, was also high.

THE ONLY LICENCING ROUND focused on marginal fields was conducted in 2001-2002. Out of the 24 such fields awarded to 31 Nigerian independents in 2003, 10 fields have not reached sustained production. Several of them are candidates for anyone who is interested in having a pie of the Nigerian marginal field basket. They are Bicta Energy's Ogedeh field, which has never really had an operationalized work programme; Sogenal's Akepo field, which has faced serious operational challenges in the journey to development; Goland's Oriri field has experienced failed re-entries; Movido's Ekeh field has had

intermittent production, with expensive, short term production facilities and the field has been shut in for over three years now; Dansaki/Associated's Tom Shot Bank field has not had the benefit of a robust development partner. Finally, Del Sigma's Ke Field needs a working up.

The big challenge of Nigeria's petroleum licencing operation is not in the frequency of bid rounds. It is in the management of licences. Companies hold on to asset, especially if it is awarded by the state, without payment of the most rudimentary charges and unwilling to embark on a work programme. And when would be partners come, the first thing on the table is to pay the signature bonus; the second thing is the sign on fee and the third is the regular, quarterly fee paid to “owners” of the licence.

Nigeria has not conducted a bid r o u n d s i n c e 2 0 0 7 . A n d discretionary awards by the government have been few and far between.

Chevron has, quietly earned over $800Million from the sale of its stakes in six acreages (three onshore and three shallow offshore) since 2014.

Meanwhile, in Guarantee/Owena owned Ororo marginal field, the partners have tied up with Sirius Petroleum, which acts as both technical operator and financier. There is ongoing work on Eurafric's Dawes Island field, by partners Petralon and Tako E&P. Sahara's Tsekelewu Field is clearly a no go area, less because there is anything going on than the fact that Sahara Energy is a well-heeled company which doesn't need a partner; it's just not keen on doing anything with this particular field. It should be at risk of losing the licence, but then, Sahara has a way with the Nigerian government.

“Do you know a Nigerian holder of petroleum acreage who is interested in funding partnership for field development?”It's a question I have been asked, quite routinely, in the last 10 years.

These enquiries are always about the marginal fields, awarded 15 years ago, that haven't been developed, as well as over 20 oil prospecting leases; exploratory tracts which have been granted to Nigerian companies, as far back as 25 years ago, but never experienced an active work programme.

By Toyin AkinoshoPublisher

The big challenge of Nigeria's petroleum licencing operation is not in the frequency of bid rounds. It is in

the management of licences.

Some Insight Into Nigeria's “Secondary Licencing” Market

IN

T

HE

NE

WS

AFRICA OIL + GAS REPORT J U LY 2 0 1 8 7

“Operational activity are continuing as planned”, the partners say.

OTAL, CNOOC and Tullow Oil continue Tto work towards reaching Final Investment Decision (FID) for the Albert

Basin development project in Uganda, around the end of 2018, according to the three companies.

The upstream Environmental and Social Impact Assessment (ESIA) was completed around May 2018 and has been submitted to the National Environmental Management Authority for review.

The milestones for the several conditions precedent before FID have shifted much farther towards year end 2018 than originally scheduled, such that none of the partners could refer to first or second quarter 2018 anymore-as they did as recently as late 2017,-for FID.

This is farther down the road than earlier announced and it makes first oil far less likely before 2022.

The upstream FEED was completed around

May 2018 and initial technical and commercial reviews of this work have begun, which will ultimately result in the award of the Engineering, Procurement and Construction contracts.

Discussions on the pipeline project continue between the Joint Venture Partners and both the Ugandan and Tanzanian Governments regarding the key commercia l and transportation agreements, Tullow Oil reports.

Tullow forecasts full year gross production from the Jubilee field to average around 78,100BOPD, up from 75,800BOPD gross previously guided.

The shut down of FPSO Kwame Nkrumah for two periods of maintenance was primarily responsible for the output decline, but the production was lower than the operator's expectations of at least 75,800BOPD.What has happened was that, apart from repairs on the FPSO, there has also been maintenance work on the gas compression system.

In the first half of the year, two new Jubilee production wells were drilled as part of the current drilling campaign. These wells will be completed and brought on stream during the third and fourth quarter of 2018 and a previously drilled Jubilee water injection well will also be tied-in.

ross production from the Jubilee field Go f f s h o r e G h a n a a v e r a g e d 67,500BOPD in the just concluded

first half of 2018. This is far lower than 89,700BOPD it averaged throughout 2017.

While this maintenance work briefly affected

production, it has resulted in increased gas compression capacity and as new wells are brought on stream this will positively impact oil production capacity. “The Jubilee FPSO has been regularly producing at around 100,000BOPD gross from existing wells since these works were carried out”, Tullow says in an operational update.

The repair work on Kwame Nkrumah was a turret remediation work to stabilise the turret bearing. “The maintenance work has successfully prepared the FPSO for long-term operations as a permanently spread moored vessel”, Tullow explains. A final planned shutdown is expected around the end of 2018 to rotate the FPSO to its permanent heading and install the final spread mooring anchoring system with minimal impact to production.

NCTL was heavily under repairs as of the time of going to press

Jubilee's Production Dips For Now, But…

FID Shifts Farther Down For Uganda's Albert Basin Oil Development Award of the Engineering, Procurement and Construction contracts moves towards 2019.

Nigerian companies pumping crude oil into the Nembe Creek Trunk Line (NCTL) have advanced so much in progressing alternative routes that several sources are “so sure” that there

will be hardly a drop of crude pumped into that line by June 2020.

The facility starts from the Nembe Creek field in Oil Mining Lease (OML) 29, and ends at a manifold at the Cawthorne Channel field on OML 18. From here, crude is evacuated the short distance to the Bonny oil terminal.

Shell doesn't pump its own crude into NCTL, but sends the liquid into the short line between Cawthorne Channel and the Bonny Terminal.

Up to 600,000 BOPD of liquids can be evacuated from the end point at Cawthorne Channel.

“The famous Bonny Terminal looks like is about to lose its relevance after several decades”, sources tell Africa Oil+Gas Report. NCTL was heavily under repairs as of the time of going to press in early July 2018, having been shut in since June 7, 2018.

AITEO, Eroton and Newcross, three Nigerian independents which evacuate their crude through the NCTL, lose as much as 40% of the crude routinely to oil theft, sources tell Africa Oil+Gas Report. They have each been working assiduously on alternatives, with Eroton reportedly being ahead of others, to install alternative pipelines that

evacuate their crude to FPSOs on the Atlantic.

The 97kilometre pipeline, with capacity to pump 150,000Barrels Per Day, is a favourite of oil thieves, who routinely hack into the line,

creating as many a s 2 4 i l l e g a l bunkering points t h a t r e q u i r e constant plugging.

In 24 Months, Nembe Creek Trunk Line Will Be Running Empty

www.africaoilgasreport.com

Vol 19, No 6, July 2018

report

State Capture NigeriaThere are over 15 Oil Prospecting Licenced acreages, mostly onshore Niger Delta, some in shallow water. But holders of these assets are not in a hurry to do deals. The fact that they escape even paying signature bonus after being awarded these assets, says a lot about the state capture in the Nigerian Petroleum system. Go to page 5

IN THIS ISSUEIN THIS ISSUEIN THIS ISSUECOVER STORIES

CONFERENCES, MEETINGS, EVENTS

Tel: 09092143198, 01-3429082

October 22-October 24, 2018

https://www.clocate.com/conference/4th-Oil-and-Gas-Tanzania-2018/48067/

November 18 - 22 , 2018

Oil &Gas TanzaniaDar es Salaam, Tanzania

MSGBC Basin Summit & ExhibitionDakar, Senegal

November 05-09, 2018Africa Oil Week 2018

Marrakech, Moroccowww.gasoptions-nwafrica.com

36th Annual International Conference and Exhibitions 2018

October 10-October 13, 2018

Venue: Eko Hotel and Suites, Victoria Island, Lagos.

oilandgascouncil.com/event-events/msgbc-basin-summit/

Gas Options North & West Africa

Cape Town, South [email protected]+44 (0) 207 384 8384

November 13-15, 2018

Cape Town International Convention Centre

Regional Energy Cooperation Summit: West

South Africa

www.futureenergyafrica.com

September 12-14, 2018

aricaoilandpower.com

at Eko Hotels & Suites, Victoria Island, Lagos, Nigeria.

September 26-28, 2018

Future Energy Africa Exhibition and Conference

Accra, Ghanawww.recs-west.com

Africa Oil & Power 2018

Oct 01-03, 2018

August 6-8, 2018

+971 4 248 3221

Cape town international convention centre, south africa

(SPE) Nigeria Annual International Conference and Exhibition (NAICE)

December 10-12, 2018 International Gas Cooperation SummitCape Town, South Africawww.igcs-sa.com

January 23-24, 2019

Eko Convention Centre, Lagos

07069117347

The West African International Petroleum

Exhibition and Conference (WAIPEC)

Feb 11-13, 2019

Egypt Petroleum Show 2019 (EGYPS)

North Africa Petroleum Exhibition and

Conference

March 10-13, 2019

www.egyps.com/cfp

Le Meridien Oran Hotel & Convention Center,

Oran, Algeria

+971 2 6970 508

http://www.napec-dz.com/

Cairo, Egypt

+213 (0) 770 70 94 85

+213 (0) 550 46 88 98

COVER PHOTO: ABC Orjiako, Chairman and co-founder of SEPLAT

Pages: 34-36Pages: 34-36Pages: 34-36

FROM THE EDITOR

KICKSTARTER

IN THE NEWS

PETROLEUM PEOPLE

OIL PATCH SAHARA

OIL PATCH SUBSAHARA

FARM IN FARM OUT

GAS MONETISATION

THE AFRICAN INDEPENDENT

MARITIME ISSUES

COMPANY UPDATE

23

25

30

34

38

41

03

05

07

17

20

CO

NT

EN

TS

A F R I C A O I L + G A S R E P O R T J U LY 2 0 1 86

IN

T

HE

NE

WS

AFRICA OIL + GAS REPORT J U LY 2 0 1 8 7

“Operational activity are continuing as planned”, the partners say.

OTAL, CNOOC and Tullow Oil continue Tto work towards reaching Final Investment Decision (FID) for the Albert

Basin development project in Uganda, around the end of 2018, according to the three companies.

The upstream Environmental and Social Impact Assessment (ESIA) was completed around May 2018 and has been submitted to the National Environmental Management Authority for review.

The milestones for the several conditions precedent before FID have shifted much farther towards year end 2018 than originally scheduled, such that none of the partners could refer to first or second quarter 2018 anymore-as they did as recently as late 2017,-for FID.

This is farther down the road than earlier announced and it makes first oil far less likely before 2022.

The upstream FEED was completed around

May 2018 and initial technical and commercial reviews of this work have begun, which will ultimately result in the award of the Engineering, Procurement and Construction contracts.

Discussions on the pipeline project continue between the Joint Venture Partners and both the Ugandan and Tanzanian Governments regarding the key commercia l and transportation agreements, Tullow Oil reports.

Tullow forecasts full year gross production from the Jubilee field to average around 78,100BOPD, up from 75,800BOPD gross previously guided.

The shut down of FPSO Kwame Nkrumah for two periods of maintenance was primarily responsible for the output decline, but the production was lower than the operator's expectations of at least 75,800BOPD.What has happened was that, apart from repairs on the FPSO, there has also been maintenance work on the gas compression system.

In the first half of the year, two new Jubilee production wells were drilled as part of the current drilling campaign. These wells will be completed and brought on stream during the third and fourth quarter of 2018 and a previously drilled Jubilee water injection well will also be tied-in.

ross production from the Jubilee field Go f f s h o r e G h a n a a v e r a g e d 67,500BOPD in the just concluded

first half of 2018. This is far lower than 89,700BOPD it averaged throughout 2017.

While this maintenance work briefly affected

production, it has resulted in increased gas compression capacity and as new wells are brought on stream this will positively impact oil production capacity. “The Jubilee FPSO has been regularly producing at around 100,000BOPD gross from existing wells since these works were carried out”, Tullow says in an operational update.

The repair work on Kwame Nkrumah was a turret remediation work to stabilise the turret bearing. “The maintenance work has successfully prepared the FPSO for long-term operations as a permanently spread moored vessel”, Tullow explains. A final planned shutdown is expected around the end of 2018 to rotate the FPSO to its permanent heading and install the final spread mooring anchoring system with minimal impact to production.

NCTL was heavily under repairs as of the time of going to press

Jubilee's Production Dips For Now, But…

FID Shifts Farther Down For Uganda's Albert Basin Oil Development Award of the Engineering, Procurement and Construction contracts moves towards 2019.

Nigerian companies pumping crude oil into the Nembe Creek Trunk Line (NCTL) have advanced so much in progressing alternative routes that several sources are “so sure” that there

will be hardly a drop of crude pumped into that line by June 2020.

The facility starts from the Nembe Creek field in Oil Mining Lease (OML) 29, and ends at a manifold at the Cawthorne Channel field on OML 18. From here, crude is evacuated the short distance to the Bonny oil terminal.

Shell doesn't pump its own crude into NCTL, but sends the liquid into the short line between Cawthorne Channel and the Bonny Terminal.

Up to 600,000 BOPD of liquids can be evacuated from the end point at Cawthorne Channel.

“The famous Bonny Terminal looks like is about to lose its relevance after several decades”, sources tell Africa Oil+Gas Report. NCTL was heavily under repairs as of the time of going to press in early July 2018, having been shut in since June 7, 2018.

AITEO, Eroton and Newcross, three Nigerian independents which evacuate their crude through the NCTL, lose as much as 40% of the crude routinely to oil theft, sources tell Africa Oil+Gas Report. They have each been working assiduously on alternatives, with Eroton reportedly being ahead of others, to install alternative pipelines that

evacuate their crude to FPSOs on the Atlantic.

The 97kilometre pipeline, with capacity to pump 150,000Barrels Per Day, is a favourite of oil thieves, who routinely hack into the line,

creating as many a s 2 4 i l l e g a l bunkering points t h a t r e q u i r e constant plugging.

In 24 Months, Nembe Creek Trunk Line Will Be Running Empty

www.africaoilgasreport.com

Vol 19, No 6, July 2018

report

State Capture NigeriaThere are over 15 Oil Prospecting Licenced acreages, mostly onshore Niger Delta, some in shallow water. But holders of these assets are not in a hurry to do deals. The fact that they escape even paying signature bonus after being awarded these assets, says a lot about the state capture in the Nigerian Petroleum system. Go to page 5

IN THIS ISSUEIN THIS ISSUEIN THIS ISSUECOVER STORIES

CONFERENCES, MEETINGS, EVENTS

Tel: 09092143198, 01-3429082

October 22-October 24, 2018

https://www.clocate.com/conference/4th-Oil-and-Gas-Tanzania-2018/48067/

November 18 - 22 , 2018

Oil &Gas TanzaniaDar es Salaam, Tanzania

MSGBC Basin Summit & ExhibitionDakar, Senegal

November 05-09, 2018Africa Oil Week 2018

Marrakech, Moroccowww.gasoptions-nwafrica.com

36th Annual International Conference and Exhibitions 2018

October 10-October 13, 2018

Venue: Eko Hotel and Suites, Victoria Island, Lagos.

oilandgascouncil.com/event-events/msgbc-basin-summit/

Gas Options North & West Africa

Cape Town, South [email protected]+44 (0) 207 384 8384

November 13-15, 2018

Cape Town International Convention Centre

Regional Energy Cooperation Summit: West

South Africa

www.futureenergyafrica.com

September 12-14, 2018

aricaoilandpower.com

at Eko Hotels & Suites, Victoria Island, Lagos, Nigeria.

September 26-28, 2018

Future Energy Africa Exhibition and Conference

Accra, Ghanawww.recs-west.com

Africa Oil & Power 2018

Oct 01-03, 2018

August 6-8, 2018

+971 4 248 3221

Cape town international convention centre, south africa

(SPE) Nigeria Annual International Conference and Exhibition (NAICE)

December 10-12, 2018 International Gas Cooperation SummitCape Town, South Africawww.igcs-sa.com

January 23-24, 2019

Eko Convention Centre, Lagos

07069117347

The West African International Petroleum

Exhibition and Conference (WAIPEC)

Feb 11-13, 2019

Egypt Petroleum Show 2019 (EGYPS)

North Africa Petroleum Exhibition and

Conference

March 10-13, 2019

www.egyps.com/cfp

Le Meridien Oran Hotel & Convention Center,

Oran, Algeria

+971 2 6970 508

http://www.napec-dz.com/

Cairo, Egypt

+213 (0) 770 70 94 85

+213 (0) 550 46 88 98

COVER PHOTO: ABC Orjiako, Chairman and co-founder of SEPLAT

Pages: 34-36Pages: 34-36Pages: 34-36

FROM THE EDITOR

KICKSTARTER

IN THE NEWS

PETROLEUM PEOPLE

OIL PATCH SAHARA

OIL PATCH SUBSAHARA

FARM IN FARM OUT

GAS MONETISATION

THE AFRICAN INDEPENDENT

MARITIME ISSUES

COMPANY UPDATE

23

25

30

34

38

41

03

05

07

17

20

CO

NT

EN

TS

A F R I C A O I L + G A S R E P O R T J U LY 2 0 1 86

A F R I C A O I L + G A S R E P O R T J U LY 2 0 1 88

IN

T

HE

NE

WS

Anadarko's release of a shift in the timelines for the project calendar came at about the same time that Tullow Oil announced in an update that the Ugandan Albert Basin oilfield development project was less likely to get Final Investment Decision before the end of 2018.

nadarko has formally admitted it cannot Atake the final investment decision on the Mozambican Liquefied Natural Gas LNG

project anytime in 2018.

Indeed, the Nigerian government only last June gave the nod to International Tenders for the

Shell operated Bonga South West in the country's deepwater, signalling Final Investment Decision was now more likely in early 2019. This is, in anyway, a more optimistic turn of events for the project than was anticipated just a few months earlier.

The 12Million Tonnes Per Annum LNG project was to have its first phase of 6MMTPA sanctioned in the year, but after several months of upbeat messages about converting MoUs to binding agreements for offtake, the American independent has admitted that it was unlikely to get enough buyers of the molecules to encourage it to bring the project to a financial close.

These announcements simply mean that contract awards, which usually happen as FIDs are announced, will slip.

The $20Billion Ugandan Albert Basin project, (200,0000BOPD at peak), was expected to be the most certain of the big ticket projects take FID in 2018. It was billed to take FID in late 2017 and then that shifted to early 2018, but as of July of the same year, there were still has a number of conditions precedent to reach the financing close. The upstream Environmental and Social Impact Assessment (ESIA), submitted to the National Environmental Management Authority, still has to be approved. And discussions on the pipeline project were still continuing, as of late July 2018, between the Joint Venture Partners and both the Ugandan and Tanzanian Governments, r e g a r d i n g t h e ke y c o m m e r c i a l a n d transportation agreements. The sanction for this project may happen in 2018, but we now know

that commissioning date will slip beyond 2021. This project has been on the drawing board for nine years.

Two smaller but no less significant projects that are unlikely to meet the earlier promise of FID in 2018 are Seplat Petroleum's Assa North-Ohaji South (ANOH) gas project onshore Nigeria and Ophir Energy operated Fortuna FLNG offshore Equatorial Guinea. ANOH's sanction depends on certain conditions, including the incorporation and operationalisaton of a midstream gas company and the completion of the 67km OB3, a crucial gas transmission line. In Fortuna's case, Ophir Energy just hasn't been able to raise the money to construct the facility, a situation complicated by the fact that its licence on the Block R, which hosts the gas, expires at the end of 2018.

It is now also certain that an FID in 2018 cannot work for the SNE field, offshore Senegal, located in 1,100metre Water Depth in the Rufisque, Sangomar and Sangomar Deep Blocks.

AITEO had, in the June 6 2018 statement declared; “any attempt by the embattled Admiral Suleiman to suggest AITEO's involvement in the activities of those who undertook the protest or indeed any other related activity is a distraction designed to fail. It does not, in any way, detract from the weight of allegations with which Admiral Suleiman has been publicly confronted”.

· “Third party interference with the line has often resulted in oil leaks which ultimately culminate in shutting down the NCTL to undertake emergency repairs. This in itself has resulted in the NCTL being shut down for about 145 days and an approximate deferment of 50.386 million barrels of Crude Oil (Net) for the 6 injectors into the NCTL since Aiteo took over the operatorship of the Trunk line in September 2015”.

ITEO's response to allegations that it Ahad masterminded protests by oil community groups against the Joint

Task Force in the Niger Delta, is one of the rare instances in which a high profile E&P company has called out the Nigerian security forces for likely complicity in the scourge.

Insinuations about complicity of security forces in the theft of crude oil in the region has always been made, in media reports, in the work of

researchers, and in declamations of civil society organisations. But as the work of journalism around this issue has hardly resulted in smoking gun evidence, and the other agencies are very much external actors, the default mode had been to dismiss their recurring finger pointing. On the contrary, AITEO is a significant participant in Nigeria's crude oil production, with nameplate output capacity (90,000BOPD), which is over 4% of the country's total export, so its statement about the security forces is hard to ignore. · Due to the continued vandalism of the

NCTL and resulting oil theft, AITEO has written to the Federal Government, through the Chief of Army Staff, General TY Buratai on two occasions (April 17 and 23, 2018), requesting the involvement of the Armed Forces in reinforcing existing security arrangements to the pipeline as the incessant security breaches were resulting in losses amounting to billions of Naira for the country.

And then it follows up: “How it is that vessel movement of the oil thieves occurs unnoticed in the region despite heightened activity in large scale illegal bunkering?”

In a 1,000 word statement, defending itself against charges by the JTF commander, Rear Admiral Apochi Suleiman, the Nigerian indigenous operator pointedly asks whether it was “correct that the security forces are now offering protection/escort services to those allegedly responsible for oil thefts?”

When Africa Oil+Gas Report reached the JTF for comments on AITEO's statement, we were referred to the Defence Headquarters, which did not even respond to our inquiry.The JTF is comprised of personnel from the Nigerian Navy, Army, Police, Nigeria Security and Civil Defence Corps and Custom Service. The JTF commander had accused AITEO of masterminding the protests against the task force in an interview with ThisDay, an influential local daily. A group named Niger Delta Oil Monitoring Group also, in a statement, accused AITEO of sponsoring the June 1 Abuja protest “to frustrate Rear Admiral Suleiman from consolidating on his successful curbing of oil theft in the Niger Delta”.

“We are one of the biggest victims of oil theft in the country”, the company laments.

AITEO operates the Nembe Creek Trunk Line NCTL, a crude export pipeline with capacity to pump 200,000Barrels of Oil Per Day throughout its 97km length; clearly one of the four largest crude oil to export pipelines in Nigeria. The company's statement revisits the key challenges faced by operators in the Niger Delta and reiterates the facts of huge losses of revenue that otherwise would have accrued to the Nigerian Government, which is struggling with a large debt burden and borrowing more billions of dollars to finance its budget.

· In December 2016 alone, the company explains, 45.46% of AITEO's total net crude injected into the NCTL was lost on the basis of crude oil theft “resulting in significant pressure reductions on the trunk line, theft points identification as well as illegal refineries, and corroborated by several Joint Investigative visits constituted by various regulatory bodies and the applicable host community”.

But the sting in the tail is the drawing out of the head of the security forces tasked with ensuring the safety of lives and property in the Niger-Delta.

Contract Awards Slip For Africa's Major O&G ProjectsBy McJohn Otutu

Nigerian Operator Highlights Possible Involvement of Security Forces in Crude Oil TheftIndigenous producer emphasises the “weight of allegations with which Admiral Suleiman has been publicly confronted”.

AFRICA OIL + GAS REPORT J U N E 2 0 1 8 9

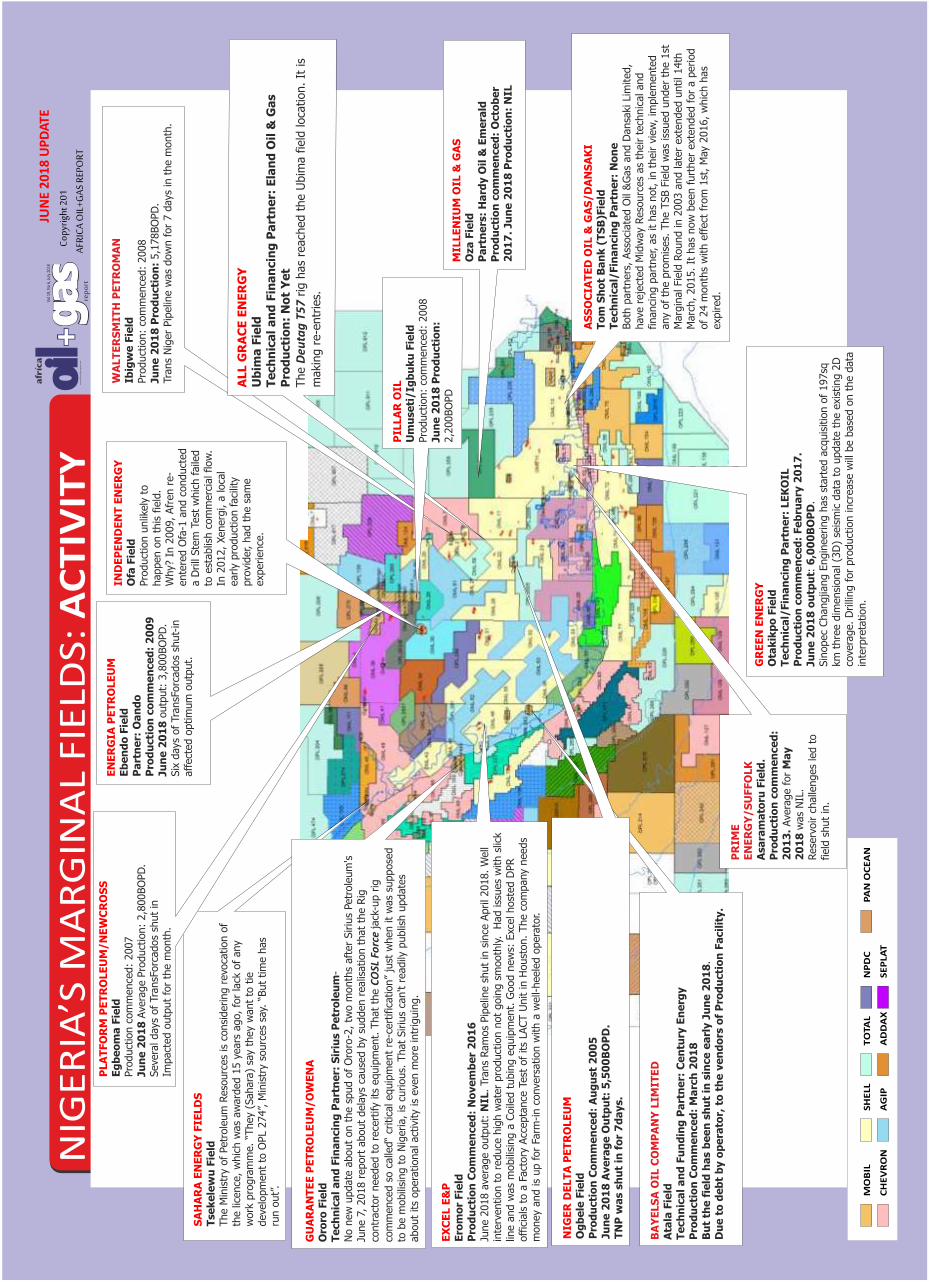

NIG

ER

IA’S

MA

RG

INA

L F

IELD

S:

AC

TIV

ITY

JUN

E 2

01

8 U

PD

ATE

Vol 1

9, N

o 6,

July

201

8

repo

rtw

ww

.afric

aoilg

asre

port.

com

�Co

pyrig

ht 2

01�

AFRI

CA O

IL+G

AS R

EPO

RT

Tr

ans

Nig

er

Pip

elin

e w

as

dow

n for

7 d

ays

in t

he m

onth

.

WA

LT

ER

SM

ITH

PE

TR

OM

AN

Ibig

we

Fie

ld

Ju

ne

20

18

Pro

du

cti

on

: 5,1

78BO

PD

.Pro

duct

ion:

com

mence

d:

2008

Six

days

of

TransF

orc

ados

shut-

in

Pa

rtn

er:

Oa

nd

oE

be

nd

o F

ield

affect

ed o

ptim

um

outp

ut.

Ju

ne

20

18

outp

ut:

3,8

00BO

PD

.P

rod

ucti

on

co

mm

en

ce

d:

20

09

EN

ER

GIA

PE

TR

OLE

UM O

tak

ikp

o F

ield

Ju

ne

20

18

ou

tpu

t: 6

,00

0B

OP

D.

GR

EE

N E

NE

RG

Y

Pro

du

cti

on

co

mm

en

ce

d:

Fe

bru

ary

20

17

.

Sin

opec

Changjiang E

ngin

eering h

as

start

ed a

cquis

itio

n o

f 197sq

km

thre

e d

imensi

onal (3

D)

seis

mic

data

to u

pdate

the e

xist

ing 2

D

cove

rage. D

rilli

ng for

pro

duct

ion incr

ease

will

be b

ase

d o

n t

he d

ata

in

terp

reta

tion.

Te

ch

nic

al/

Fin

an

cin

g P

art

ne

r: L

EK

OIL

To

m S

ho

t B

an

k (

TS

B)F

ield

Te

ch

nic

al/

Fin

an

cin

g P

art

ne

r: N

on

e

Marc

h, 2015. It

has

now

been furt

her

ext

ended for

a p

eriod

of

24 m

onth

s w

ith e

ffect

fro

m 1

st, M

ay

2016, w

hic

h h

as

exp

ired.

AS

SO

CIA

TE

D O

IL &

GA

S/D

AN

SA

KI

Both

part

ners

, Ass

oci

ate

d O

il &

Gas

and D

ansa

ki L

imited,

have

reje

cted M

idw

ay

Reso

urc

es

as

their t

ech

nic

al and

financi

ng p

art

ner, a

s it h

as

not,

in t

heir v

iew

, im

ple

mente

d

any

of

the p

rom

ises.

The T

SB F

ield

was

issu

ed u

nder

the 1

st

Marg

inal Fie

ld R

ound in 2

003 a

nd late

r ext

ended u

ntil 14th

SA

HA

RA

EN

ER

GY

FIE

LD

S

The M

inis

try

of

Petr

ole

um

Reso

urc

es

is c

onsi

dering r

evo

cation o

f th

e lic

ence

, w

hic

h w

as

aw

ard

ed 1

5 y

ears

ago, fo

r la

ck o

f any

work

pro

gra

mm

e. “T

hey

(Sahara

) sa

y th

ey

want

to t

ie

deve

lopm

ent

to O

PL

274”, M

inis

try

sourc

es

say.

“But

tim

e h

as

run o

ut”

.

Tse

ke

lew

u F

ield

MIL

LE

NIU

M O

IL &

GA

SO

za

Fie

ld

Pro

du

cti

on

co

mm

en

ce

d:

Octo

be

rP

art

ne

rs:

Ha

rdy O

il &

Em

era

ld

20

17

. Ju

ne

20

18

Pro

du

cti

on

: N

IL

IND

EP

EN

DE

NT

EN

ER

GY

Ofa

Fie

ldPro

duct

ion u

nlik

ely

to

happen o

n t

his

fie

ld.

Why?

In 2

009, Afr

en r

e-

ente

red O

fa-1

and c

onduct

ed

a D

rill

Ste

m T

est

whic

h faile

d

to e

stablis

h c

om

merc

ial flow

. In

2012, Xenerg

i, a

loca

l early

pro

duct

ion faci

lity

pro

vider, h

ad t

he s

am

e

exp

erience

.

ALL G

RA

CE

EN

ER

GY

Ub

ima

Fie

ldT

ech

nic

al

an

d F

ina

ncin

g P

art

ne

r: E

lan

d O

il &

Ga

s

The D

euta

g T

57 r

ig h

as

reach

ed t

he U

bim

a f

ield

loca

tion. It

is

maki

ng r

e-e

ntr

ies.

Pro

du

cti

on

: N

ot

Ye

t

Um

use

ti/Ig

bu

ku

Fie

ld

Ju

ne

20

18

Pro

du

cti

on

: 2,2

00BO

PD

Pro

duct

ion:

com

mence

d:

2008

PIL

LA

R O

IL

June 2

018 a

vera

ge o

utp

ut:

NIL

. Tr

ans

Ram

os

Pip

elin

e s

hut

in s

ince

April 2018. W

ell

inte

rvention t

o r

educe

hig

h w

ate

r pro

duct

ion n

ot

goin

g s

mooth

ly. H

ad iss

ues

with s

lick

line a

nd w

as

mobili

sing a

Coile

d t

ubin

g e

quip

ment.

Good n

ew

s: E

xcel host

ed D

PR

off

icia

ls t

o a

Fact

ory

Acc

epta

nce

Test

of

its

LACT U

nit in H

oust

on. The c

om

pany

needs

EX

CE

L E

&P

money

and is

up for

Farm

-in c

onve

rsation w

ith a

well-

heele

d o

pera

tor.

Ero

mo

r Fie

ldP

rod

ucti

on

Co

mm

en

ce

d:

No

ve

mb

er

20

16

Te

ch

nic

al

an

d F

ina

ncin

g P

art

ne

r: S

iriu

s P

etr

ole

um

-

GU

AR

AN

TE

E P

ET

RO

LE

UM

/O

WE

NA

Oro

ro F

ield

No n

ew

update

about

on t

he s

pud o

f O

roro

-2, tw

o m

onth

s aft

er

Siriu

s Petr

ole

um

's

June 7

, 2018 r

eport

about

dela

ys c

ause

d b

y su

dden r

ealis

ation t

hat

the R

ig

contr

act

or

needed t

o r

ece

rtify

its

equip

ment.

That

the C

OSL

Fo

rce

jack

-up r

ig

com

mence

d s

o c

alle

d“

critic

al equip

ment

re-c

ert

ific

ation”

just

when it

was

suppose

d

to b

e m

obili

sing t

o N

igeria, is

curious.

That

Siriu

s ca

n't r

eadily

publis

h u

pdate

s about

its

opera

tional act

ivity

is e

ven m

ore

intr

iguin

g.

Pro

du

cti

on

Co

mm

en

ce

d:

Ma

rch

20

18

Te

ch

nic

al

an

d F

un

din

g P

art

ne

r: C

en

tury

En

erg

yA

tala

Fie

ld

Du

e t

o d

eb

t b

y o

pe

rato

r, t

o t

he

ve

nd

ors

of

Pro

du

cti

on

Fa

cil

ity.

BA

YE

LS

A O

IL C

OM

PA

NY

LIM

ITE

D

Bu

t th

e f

ield

ha

s b

ee

n s

hu

t in

sin

ce

ea

rly J

un

e 2

01

8.

MO

BIL

CH

EV

RO

N

S

HE

LL

AG

IP

T

OTA

L

AD

DA

X

NP

DC

SE

PLA

T

PA

N O

CE

AN

NIG

ER

DE

LT

A P

ET

RO

LE

UM

O

gb

ele

Fie

ldP

rod

ucti

on

Co

mm

en

ce

d:

Au

gu

st

20

05

TN

P w

as s

hu

t in

fo

r 7

da

ys.

Ju

ne

20

18

Ave

rag

e O

utp

ut:

5,5

00

BO

PD

.

PR

IME

E

NE

RG

Y/S

UFFO

LK

A

sa

ram

ato

ru F

ield

. P

rod

ucti

on

co

mm

en

ce

d:

20

13

. Ave

rage for

Ma

y

Rese

rvoir c

halle

nges

led t

o

field

shut

in.

20

18

was

NIL

.

Impact

ed o

utp

ut

for

the m

onth

.Seve

ral days

of

TransF

orc

ados

shut

in

Eg

be

om

a F

ield

PLA

TFO

RM

PE

TR

OLE

UM

/N

EW

CR

OS

S

Pro

duct

ion c

om

mence

d:

2007

Ju

ne

20

18

Ave

rage P

roduct

ion:

2,8

00BO

PD

.

A F R I C A O I L + G A S R E P O R T J U LY 2 0 1 88

IN

T

HE

NE

WS

Anadarko's release of a shift in the timelines for the project calendar came at about the same time that Tullow Oil announced in an update that the Ugandan Albert Basin oilfield development project was less likely to get Final Investment Decision before the end of 2018.

nadarko has formally admitted it cannot Atake the final investment decision on the Mozambican Liquefied Natural Gas LNG

project anytime in 2018.

Indeed, the Nigerian government only last June gave the nod to International Tenders for the

Shell operated Bonga South West in the country's deepwater, signalling Final Investment Decision was now more likely in early 2019. This is, in anyway, a more optimistic turn of events for the project than was anticipated just a few months earlier.

The 12Million Tonnes Per Annum LNG project was to have its first phase of 6MMTPA sanctioned in the year, but after several months of upbeat messages about converting MoUs to binding agreements for offtake, the American independent has admitted that it was unlikely to get enough buyers of the molecules to encourage it to bring the project to a financial close.

These announcements simply mean that contract awards, which usually happen as FIDs are announced, will slip.

The $20Billion Ugandan Albert Basin project, (200,0000BOPD at peak), was expected to be the most certain of the big ticket projects take FID in 2018. It was billed to take FID in late 2017 and then that shifted to early 2018, but as of July of the same year, there were still has a number of conditions precedent to reach the financing close. The upstream Environmental and Social Impact Assessment (ESIA), submitted to the National Environmental Management Authority, still has to be approved. And discussions on the pipeline project were still continuing, as of late July 2018, between the Joint Venture Partners and both the Ugandan and Tanzanian Governments, r e g a r d i n g t h e ke y c o m m e r c i a l a n d transportation agreements. The sanction for this project may happen in 2018, but we now know

that commissioning date will slip beyond 2021. This project has been on the drawing board for nine years.

Two smaller but no less significant projects that are unlikely to meet the earlier promise of FID in 2018 are Seplat Petroleum's Assa North-Ohaji South (ANOH) gas project onshore Nigeria and Ophir Energy operated Fortuna FLNG offshore Equatorial Guinea. ANOH's sanction depends on certain conditions, including the incorporation and operationalisaton of a midstream gas company and the completion of the 67km OB3, a crucial gas transmission line. In Fortuna's case, Ophir Energy just hasn't been able to raise the money to construct the facility, a situation complicated by the fact that its licence on the Block R, which hosts the gas, expires at the end of 2018.

It is now also certain that an FID in 2018 cannot work for the SNE field, offshore Senegal, located in 1,100metre Water Depth in the Rufisque, Sangomar and Sangomar Deep Blocks.

AITEO had, in the June 6 2018 statement declared; “any attempt by the embattled Admiral Suleiman to suggest AITEO's involvement in the activities of those who undertook the protest or indeed any other related activity is a distraction designed to fail. It does not, in any way, detract from the weight of allegations with which Admiral Suleiman has been publicly confronted”.

· “Third party interference with the line has often resulted in oil leaks which ultimately culminate in shutting down the NCTL to undertake emergency repairs. This in itself has resulted in the NCTL being shut down for about 145 days and an approximate deferment of 50.386 million barrels of Crude Oil (Net) for the 6 injectors into the NCTL since Aiteo took over the operatorship of the Trunk line in September 2015”.

ITEO's response to allegations that it Ahad masterminded protests by oil community groups against the Joint

Task Force in the Niger Delta, is one of the rare instances in which a high profile E&P company has called out the Nigerian security forces for likely complicity in the scourge.

Insinuations about complicity of security forces in the theft of crude oil in the region has always been made, in media reports, in the work of

researchers, and in declamations of civil society organisations. But as the work of journalism around this issue has hardly resulted in smoking gun evidence, and the other agencies are very much external actors, the default mode had been to dismiss their recurring finger pointing. On the contrary, AITEO is a significant participant in Nigeria's crude oil production, with nameplate output capacity (90,000BOPD), which is over 4% of the country's total export, so its statement about the security forces is hard to ignore. · Due to the continued vandalism of the

NCTL and resulting oil theft, AITEO has written to the Federal Government, through the Chief of Army Staff, General TY Buratai on two occasions (April 17 and 23, 2018), requesting the involvement of the Armed Forces in reinforcing existing security arrangements to the pipeline as the incessant security breaches were resulting in losses amounting to billions of Naira for the country.

And then it follows up: “How it is that vessel movement of the oil thieves occurs unnoticed in the region despite heightened activity in large scale illegal bunkering?”

In a 1,000 word statement, defending itself against charges by the JTF commander, Rear Admiral Apochi Suleiman, the Nigerian indigenous operator pointedly asks whether it was “correct that the security forces are now offering protection/escort services to those allegedly responsible for oil thefts?”

When Africa Oil+Gas Report reached the JTF for comments on AITEO's statement, we were referred to the Defence Headquarters, which did not even respond to our inquiry.The JTF is comprised of personnel from the Nigerian Navy, Army, Police, Nigeria Security and Civil Defence Corps and Custom Service. The JTF commander had accused AITEO of masterminding the protests against the task force in an interview with ThisDay, an influential local daily. A group named Niger Delta Oil Monitoring Group also, in a statement, accused AITEO of sponsoring the June 1 Abuja protest “to frustrate Rear Admiral Suleiman from consolidating on his successful curbing of oil theft in the Niger Delta”.

“We are one of the biggest victims of oil theft in the country”, the company laments.

AITEO operates the Nembe Creek Trunk Line NCTL, a crude export pipeline with capacity to pump 200,000Barrels of Oil Per Day throughout its 97km length; clearly one of the four largest crude oil to export pipelines in Nigeria. The company's statement revisits the key challenges faced by operators in the Niger Delta and reiterates the facts of huge losses of revenue that otherwise would have accrued to the Nigerian Government, which is struggling with a large debt burden and borrowing more billions of dollars to finance its budget.

· In December 2016 alone, the company explains, 45.46% of AITEO's total net crude injected into the NCTL was lost on the basis of crude oil theft “resulting in significant pressure reductions on the trunk line, theft points identification as well as illegal refineries, and corroborated by several Joint Investigative visits constituted by various regulatory bodies and the applicable host community”.

But the sting in the tail is the drawing out of the head of the security forces tasked with ensuring the safety of lives and property in the Niger-Delta.

Contract Awards Slip For Africa's Major O&G ProjectsBy McJohn Otutu

Nigerian Operator Highlights Possible Involvement of Security Forces in Crude Oil TheftIndigenous producer emphasises the “weight of allegations with which Admiral Suleiman has been publicly confronted”.

AFRICA OIL + GAS REPORT J U N E 2 0 1 8 9

NIG

ER

IA’S

MA

RG

INA

L F

IELD

S:

AC

TIV

ITY

JUN

E 2

01

8 U

PD

ATE

Vol 1

9, N

o 6,

July

201

8

repo

rtw

ww

.afric

aoilg

asre

port.

com

�Co

pyrig

ht 2

01�

AFRI

CA O

IL+G

AS R

EPO

RT

Tr

ans

Nig

er

Pip

elin

e w

as

dow

n for

7 d

ays

in t

he m

onth

.

WA

LT

ER

SM

ITH

PE

TR

OM

AN

Ibig

we

Fie

ld

Ju

ne

20

18

Pro

du

cti

on

: 5,1

78BO

PD

.Pro

duct

ion:

com

mence

d:

2008

Six

days

of

TransF

orc

ados

shut-

in

Pa

rtn

er:

Oa

nd

oE

be

nd

o F

ield

affect

ed o

ptim

um

outp

ut.

Ju

ne

20

18

outp

ut:

3,8

00BO

PD

.P

rod

ucti

on

co

mm

en

ce

d:

20

09

EN

ER

GIA

PE

TR

OLE

UM O

tak

ikp

o F

ield

Ju

ne

20

18

ou

tpu

t: 6

,00

0B

OP

D.

GR

EE

N E

NE

RG

Y

Pro

du

cti

on

co

mm

en

ce

d:

Fe

bru

ary

20

17

.

Sin

opec

Changjiang E

ngin

eering h

as

start

ed a

cquis

itio

n o

f 197sq

km

thre

e d

imensi

onal (3

D)

seis

mic

data

to u

pdate

the e

xist

ing 2

D

cove

rage. D

rilli

ng for

pro

duct

ion incr

ease

will

be b

ase

d o

n t

he d

ata

in

terp

reta

tion.

Te

ch

nic

al/

Fin

an

cin

g P

art

ne

r: L

EK

OIL

To

m S

ho

t B

an

k (

TS

B)F

ield

Te

ch

nic

al/

Fin

an

cin

g P

art

ne

r: N

on

e

Marc

h, 2015. It

has

now

been furt

her

ext

ended for

a p

eriod

of

24 m

onth

s w

ith e

ffect

fro

m 1

st, M

ay

2016, w

hic

h h

as

exp

ired.

AS

SO

CIA

TE

D O

IL &

GA

S/D

AN

SA

KI

Both

part

ners

, Ass

oci

ate

d O

il &

Gas

and D

ansa

ki L

imited,

have

reje

cted M

idw

ay

Reso

urc

es

as

their t

ech

nic

al and

financi

ng p

art

ner, a

s it h

as

not,

in t

heir v

iew

, im

ple

mente

d

any

of

the p

rom

ises.

The T

SB F

ield

was

issu

ed u

nder

the 1

st

Marg

inal Fie

ld R

ound in 2

003 a

nd late

r ext

ended u

ntil 14th

SA

HA

RA

EN

ER

GY

FIE

LD

S

The M

inis

try

of

Petr

ole

um

Reso

urc

es

is c

onsi

dering r

evo

cation o

f th

e lic

ence

, w

hic

h w

as

aw

ard

ed 1

5 y

ears

ago, fo

r la

ck o

f any

work

pro

gra

mm

e. “T

hey

(Sahara

) sa

y th

ey

want

to t

ie

deve

lopm

ent

to O

PL

274”, M

inis

try

sourc

es

say.

“But

tim

e h

as

run o

ut”

.

Tse

ke

lew

u F

ield

MIL

LE

NIU

M O

IL &

GA

SO

za

Fie

ld

Pro

du

cti

on

co

mm

en

ce

d:

Octo

be

rP

art

ne

rs:

Ha

rdy O

il &

Em

era

ld

20

17

. Ju

ne

20

18

Pro

du

cti

on

: N

IL

IND

EP

EN

DE

NT

EN

ER

GY

Ofa

Fie

ldPro

duct

ion u

nlik

ely

to

happen o

n t

his

fie

ld.

Why?

In 2

009, Afr

en r

e-

ente

red O

fa-1

and c

onduct

ed

a D

rill

Ste

m T

est

whic

h faile

d

to e

stablis

h c

om

merc

ial flow

. In

2012, Xenerg

i, a

loca

l early

pro

duct

ion faci

lity

pro

vider, h

ad t

he s

am

e

exp

erience

.

ALL G

RA

CE

EN

ER

GY

Ub

ima

Fie

ldT

ech

nic

al

an

d F

ina

ncin

g P

art

ne

r: E

lan

d O

il &

Ga

s

The D

euta

g T

57 r

ig h

as

reach

ed t

he U

bim

a f

ield

loca

tion. It

is

maki

ng r

e-e

ntr

ies.

Pro

du

cti

on

: N

ot

Ye

t

Um

use

ti/Ig

bu

ku

Fie

ld

Ju

ne

20

18

Pro

du

cti

on

: 2,2

00BO

PD

Pro

duct

ion:

com

mence

d:

2008

PIL

LA

R O

IL

June 2

018 a

vera

ge o

utp

ut:

NIL

. Tr

ans

Ram

os

Pip

elin

e s

hut

in s

ince

April 2018. W

ell

inte

rvention t

o r

educe

hig

h w

ate

r pro

duct

ion n

ot

goin

g s

mooth

ly. H

ad iss

ues

with s

lick

line a

nd w

as

mobili

sing a

Coile

d t

ubin

g e

quip

ment.

Good n

ew

s: E

xcel host

ed D

PR

off

icia

ls t

o a

Fact

ory

Acc

epta

nce

Test

of

its

LACT U

nit in H

oust

on. The c

om

pany

needs

EX

CE

L E

&P

money

and is

up for

Farm

-in c

onve

rsation w

ith a

well-

heele

d o

pera

tor.

Ero

mo

r Fie

ldP

rod

ucti

on

Co

mm

en

ce

d:

No

ve

mb

er

20

16

Te

ch

nic

al

an

d F

ina

ncin

g P

art

ne

r: S

iriu

s P

etr

ole

um

-

GU

AR

AN

TE

E P

ET

RO

LE

UM

/O

WE

NA