office of the principal commissioner of cgst, ahmedabad south

70

\ OFFICE OF THE PRINCIPAL COMMISSIONER OF C. G. S. T., AHMEDABAD SOUTH •t G. S. T. BHAVAN, AMBAWADI, AHMEDABAD - 380 015 F. No.STC/04-46/GIDC/0&A/2019-20 DIN no. 20201164WS0000818936 3it&r#<rTftW: Date of Order: 13.11.2020 Date of Issue : 13.11.2020 SHT vrfcf/Passed by: Shri MohitAgrawal, ADDITIONAL COMMISSIONER ******************************************************************************* W&r W/Order-In-Original No.24/CGST/Ahmd-South/ADC/MA/2020 ******************************************************************************* (^ff) ^ 3tr%9T ^rrft Rv4i trt ^h41<i % f%tr This copy is granted free of charge for private use of the person(s) to whom it is sent. 3n^tF(3pfttT), -15 # 7TW?.TT.-1 t spfler | | SpftrT WTTT TT 3H^«r cmftTT ftfr odTp w 3ti%?r ^ ?«nr ^1 ^>rtri 'jflt(+tfl VWH, dtiaiqijfl, SRt^T apiT^T ^ SKRTfT ^1 mfly ^ % 4htT 'Jit’fl I 2.00/- epnr^hrr^rf^tr i Any person deeming himself aggrieved by this Order may appeal against this order in Form E.A.I to Commissioner (Appeals), Central GST, Central GST Bhavan, Near Government Polytechnic, Ambawadi, Ahmedabad -15 within sixty days from date of its communication. The appeal should bear a court fee stamp of Rs.2.00/-only. ' apfhr vi(cl4) viicH 'Jii4l I d«H<, ^JcTT? ^<t+(3i41<H) Pi<1*11=141, 2001 % R'-trs%%sr^mrsrfhr^crf^f^Rrrarf%tr«rr^rrf^tTi RviRtPaci ti<i« f^rr'Jim: The Appeal should be filed in form No. E.A.-l in duplicate. It should be filed by the appellants in accordance with provisions of Rule 3 of the Central Excise (Appeals) Rules, 2001. It shall be accompanied with the following: apftcT # I Copy of the aforesaid appeal. trsp sn%9T vl^iRld yRRlR Rpa% SEfNl cPl<ii t) arq'gT 3tr^?T^ 2.00/-4fT R+e al^OT.ennui'll I Copies of the Decision (one of which at least shall be certified copy of the order appealed against) or copy of the said Order bearing a court feestamp of Rs.2.00/-. W sntw % atrjcKiapflw) # % 7.5% srft trt^nRr ^r | ami % qft ^+dH spOr qr cHcfl f 1 R=li<i f 'Stl+l An appeal against this order shall lie before the Commissioner (Appeal) on payment of 7.5% of the duty demanded where duty or duty and penalty are in dispute, or penalty, where penalty alone is in dispute." tTT^/Reference TT-tt. F.No. VI/l(b)/CTA/Tech-42/SCN/GIDC/18-19 dated 14.10.2019 issued to M/s. Gujarat Industrial Development Corporation, Fadia Chambers, 3rd Floor, Ashram Road, Ahmedabad

-

Upload

khangminh22 -

Category

Documents

-

view

7 -

download

0

Transcript of office of the principal commissioner of cgst, ahmedabad south

\

OFFICE OF THE PRINCIPAL COMMISSIONER OF C. G. S. T.,AHMEDABAD SOUTH

•t

G. S. T. BHAVAN, AMBAWADI, AHMEDABAD - 380 015

F. No.STC/04-46/GIDC/0&A/2019-20 DIN no. 20201164WS0000818936

3it&r#<rTftW: Date of Order: 13.11.2020 Date of Issue : 13.11.2020

SHT vrfcf/Passed by: Shri MohitAgrawal, ADDITIONAL COMMISSIONER *******************************************************************************

W&r W/Order-In-Original No.24/CGST/Ahmd-South/ADC/MA/2020*******************************************************************************

(^ff) ^ 3tr%9T ^rrft Rv4i trt ^h41<i % f%tr

This copy is granted free of charge for private use of the person(s) to whom it is sent.

3n^tF(3pfttT),-15 # 7TW?.TT.-1 t spfler | | SpftrT WTTT TT 3H^«r cmftTT ftfr

odTp w 3ti%?r ^ ?«nr ^1 ^>rtri'jflt(+tfl VWH, dtiaiqijfl,SRt^T apiT^T ^ SKRTfT ^1 mfly ^ % 4htT 'Jit’fl I 2.00/-

epnr^hrr^rf^tr i

Any person deeming himself aggrieved by this Order may appeal against this order in Form E.A.I to Commissioner (Appeals), Central GST, Central GST Bhavan, Near Government Polytechnic, Ambawadi, Ahmedabad -15 within sixty days from date of its communication. The appeal should bear a court fee stamp of Rs.2.00/-only. '

apfhr vi(cl4) viicH 'Jii4l I d«H<, ^JcTT? ^<t+(3i41<H) Pi<1*11=141, 2001 %R'-trs%%sr^mrsrfhr^crf^f^Rrrarf%tr«rr^rrf^tTi RviRtPaci ti<i« f^rr'Jim:

The Appeal should be filed in form No. E.A.-l in duplicate. It should be filed by the appellants in accordance with provisions of Rule 3 of the Central Excise (Appeals) Rules, 2001. It shall be accompanied with the following:

apftcT # ICopy of the aforesaid appeal.

trsp sn%9T vl^iRld yRRlR Rpa% SEfNl cPl<ii t) arq'gT3tr^?T^ 2.00/-4fT R+e al^OT.ennui'll I

Copies of the Decision (one of which at least shall be certified copy of the order appealed against) or copy of the said Order bearing a court feestamp of Rs.2.00/-.

W sntw % atrjcKiapflw) # % 7.5% srft trt^nRr ^r | ami % qft^+dH spOr qr cHcfl f 1R=li<i f 'Stl+l

An appeal against this order shall lie before the Commissioner (Appeal) on payment of 7.5% of the duty demanded where duty or duty and penalty are in dispute, or penalty, where penalty alone is in dispute."

tTT^/Reference TT-tt. F.No. VI/l(b)/CTA/Tech-42/SCN/GIDC/18-19 dated 14.10.2019issued to M/s. Gujarat Industrial Development Corporation, Fadia Chambers, 3rd Floor, Ashram Road, Ahmedabad

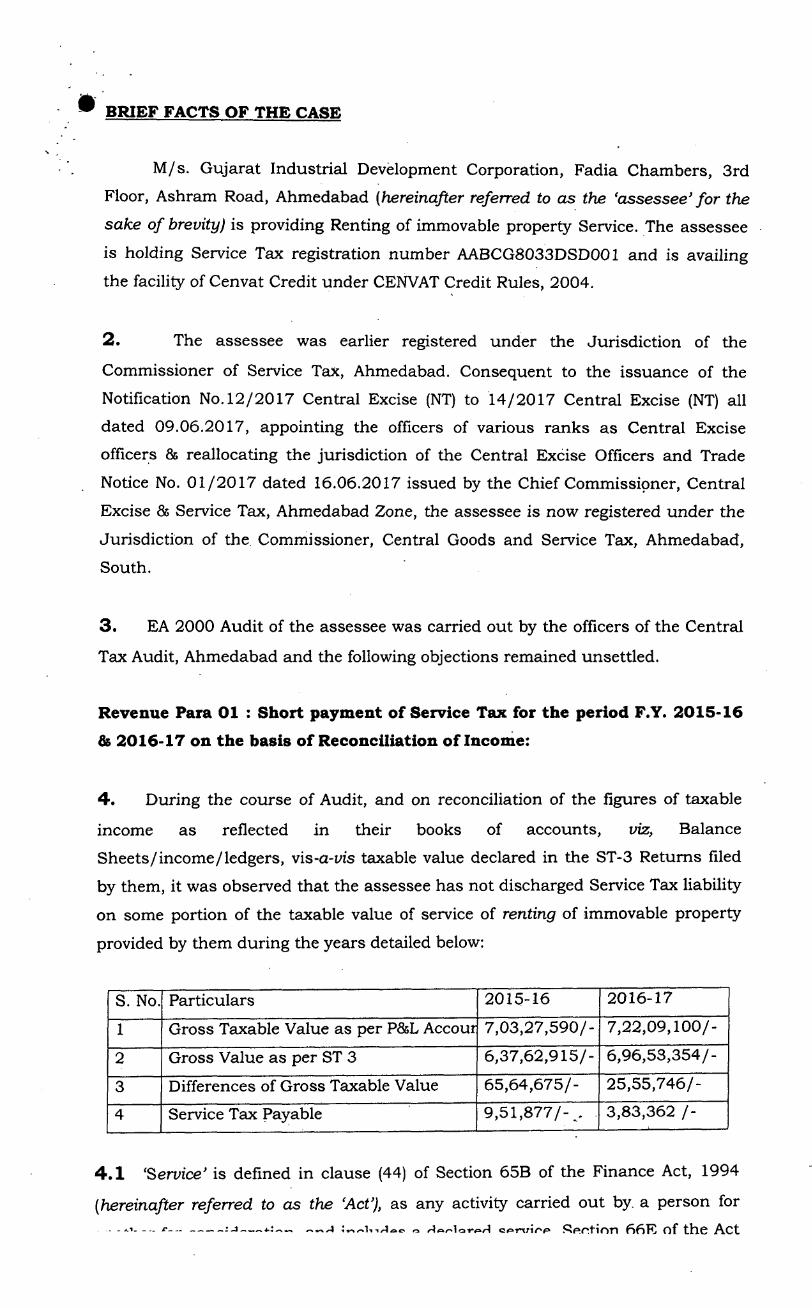

BRIEF FACTS OF THE CASE

M/s. Gujarat Industrial Development Corporation, Fadia Chambers, 3rd

Floor, Ashram Road, Ahmedabad {hereinafter referred to as the ‘assessee’ for the

sake of brevity) is providing Renting of immovable property Service. The assessee

is holding Service Tax registration number AABCG8033DSD001 and is availing

the facility of Cenvat Credit under CENVAT Credit Rules, 2004.

2. The assessee was earlier registered under the Jurisdiction of the

Commissioner of Service Tax, Ahmedabad. Consequent to the issuance of the

Notification No. 12/2017 Central Excise (NT) to 14/2017 Central Excise (NT) all dated 09.06.2017, appointing the officers of various ranks as Central Excise

officers 8b reallocating the jurisdiction of the Central Excise Officers and Trade

Notice No. 01/2017 dated 16.06.2017 issued by the Chief Commissioner, Central

Excise 8b Service Tax, Ahmedabad Zone, the assessee is now registered under the

Jurisdiction of the Commissioner, Central Goods and Service Tax, Ahmedabad, South.

3. EA 2000 Audit of the assessee was carried out by the officers of the Central

Tax Audit, Ahmedabad and the following objections remained unsettled.

Revenue Para 01 : Short payment of Service Tax for the period F.Y. 2015-16

& 2016-17 on the basis of Reconciliation of Income:

4. During the course of Audit, and on reconciliation of the figures of taxable

income as reflected in their books of accounts, viz, Balance

Sheets/income/ledgers, vis-a-vis taxable value declared in the ST-3 Returns filed

by them, it was observed that the assessee has not discharged Service Tax liability

on some portion of the taxable value of service of renting of immovable property

provided by them during the years detailed below:

2016-172015-16ParticularsS. No.7,22,09,100/-7,03,27,590/-Gross Taxable Value as per P8bL Accour16,96,53,354/-6,37,62,915/-Gross Value as per ST 3225,55,746/-65,64,675/-Differences of Gross Taxable Value33,83,362 /-9,51,877/-Service Tax Payable4

4.1 ‘Service" is defined in clause (44) of Section 65B of the Finance Act, 1994

{hereinafter referred to as the ‘Act"), as any activity carried out by. a person for—i/4ao o oof* the Act_ xi-

defines ‘declared service’ as any activity carried out by a person for anoth^

person for consideration and declared as such under Section 66E of the Act. Renting of immovable property is a declared service, specified in clause (a) of

Section 66E of the Act which reads as follows:

66E. The following shall constitute declared service, namely:

Renting of immovable property;(a)

(b)

4.2 Renting is defined in Section 65B(41) as follows :

(41) “renting” means allowing, permitting or granting access, entry, occupation, use or any such facility, wholly or partly, in an immovable property, with or without the transfer of possession or control of the said immovable

property and includes letting, leasing, licensing or other similar arrangements in

respect of immovable property;

4.3 Section 67(i) of the Act provides that “in a case where the provision of

service is for a consideration in money, be the gross amount charged by the

service provider for such service provided or to be provided by him”.

5. When the above provisions were read together it was clear that any activity

of renting, when carried out by a person for another, for consideration, would

amount to provision of service, which would be taxable. The activity of renting of

immovable property was not covered under the Negative List specified in Section

66D of the Act and were, therefore taxable services. Further, no exemption had

been provided to the services under the Mega Exemption Notification No 25/2012-

ST dated 20.6.2012, as amended or any other Notification issued under the Act. It, therefore, appeared that by providing the service of renting of immovable

property to business entities, for a consideration, the assessee had provided a

declared service under clause (a) to Section 66(E) of the Act. Accordingly, it appeared that the services provided by the assessee were leviable to service tax

under Section 66B.

6. From a reconciliation of the ST-3 returns filed by the assessee with the

financial records for the period 2015-16 and 2016-17, it appeared that theassessee had provided the taxable service of renting of immovable property; had

shown less gross value of Rs.91,20,421/- in their ST-3 returns as compared to

their financial statements and had, therefore, short paid service tax of

4

Rs. 13,35,239/- on differential gross amount charged by them from their

customers.

7. It appeared that the assessee had contravened the provisions of

Section 67 of the Finance Act, 1994 read with Rule 6(1) of the Service

Tax Rules, 1994 inasmuch as they have failed to correctly self-assess

their Service Tax Liability at the specified rates and in such manner

and within such period as discussed supra;Section 68 of the Finance Act, 1994 read with Rule 6 of the Service Tax

Rules, 1994 inasmuch as they failed to pay the Service Tax on the gross

amount of Rs.91,20,421/- to the credit of the Central Government, by

the 5 th of the quarter immediately following the calendar quarter, in

which the payments are received, towards the value of taxable services; Section 70 of the Finance Act, 1994 read with Rule 7 of the Service Tax

Rules, 1994 inasmuch as they failed to submit a correct half-yearly

return incorporating the details of the Service Tax discussed supra, along with a copy of the Challan in form GAR-7, for the quarters

covered in the half-yearly returns.

(a)

(b)

(c)

8. It also appeared that the assessee had not disclosed the full amount of

consideration received by them on renting of immovable property in the ST-3

returns filed by them for 2015-16 and 2016-17 and had therefore, suppressed the

material facts from the department. The assessee had shown an income of Rs

14,25,36,690/- from renting of immovable property in their financial records in

2015-16 and 2016-17 whereas in ST-3 returns filed during the same period, the

income from renting of immovable property was shown as Rs.13,34,16,269/-. In

view thereof, unpaid service tax of Rs. 13,35,239/- on the differential gross value

of Rs.91,20,421/- was liable to be demanded and recovered from the assessee

under the proviso to Section 73(1) of the Finance Act, 1994 alongwith interest under Section 75 of the Act, ibid. It also appeared that by the act of not disclosing

the full amount of consideration received on account of renting of immovable

property, the assessee was liable for penal action under Section 78(1) of the Act,

ibid.

The assessee agreed with the observation of the audit party and voluntarily

paid the tax of Rs. 13,35,239/- vide debit entry no. DI2406180282757 dated

19.06.2018, but refused to pay the interest and penalty.

9.

As per section 75 of the Finance Act, 1994 every person, liable to pay the

tax in accordance with the provisions of section 68 or rules made there under,10.

who fails to credit the tax or any part thereof to the account of the Cental

Government within the period prescribed, shall pay simple interest at rate as

prescribed by the Central Government. Since the assessee had failed to make - payment of service tax in the prescribed time limit framed under the rules and

provisions of the Finance Act, 1994, they were liable to pay interest at appropriate

rate on the unpaid Service Tax for the period 2015-16 and 2016-17.

11. Further, as per Section 78(1) of the Finance Act, 1994, where any service

tax had not been levied or paid, or had been short-levied or short-paid, or

erroneously refunded, by reason of fraud or collusion or wilful mis-statement or

suppression of facts or contravention of any of the provisions of Chapter V of the

Finance Act, 1994 or of the rules made thereunder with the intent to evade

payment of service tax, the person who had been served notice under the proviso

to sub-section (1) of section 73 shall, in addition to the service tax and interest

specified in the notice, be also liable to pay a penalty which shall be equal to

hundred per cent of the amount of such service tax. As the assessee had not paid

the service tax within the prescribed time limit and had suppressed the material facts from the department and had contravened the provisions of Chapter V of the

Finance Act, 1994 and the rules made thereunder with intent to evade payment of

service tax, the assessee would also be liable for penal action under the provisions

of Sections 78(1) of the Act, in addition to the service tax and interest under

Section 75 of the Act.

Revenue Para 06: Non payment of Service Tax on other taxable services:

12. On verification of the financial records of the assessee, it was observed that

the assessee had collected fees/ charges from their customers during the F. Y.2015-16 and 2016-17, reflected under the head Misc. Income in their Financial records, as under:

Fees/ charges 2016-172015-16Sr. No.

Collateral Security Fees 41,36,30624,32,88301

Subletting Fees02 91,59,849 51,41,026

Sub Division Fees 8,67,300 210,96,53903

Adjoining Charges04 15,13,182 95,90,174

Amalgamation fees05 20,383 468,59,684

Total Income 1,39,93,597 8,68,23,729

The reasons cited by the assessee for collecting the above Fees and the

nature of such fees are discussed below:

6

Collateral Security Fees:If any person to whom a plot had been allotted by the assessee wishes to avail a

loan by mortgaging the Plot/Shed allotted to them, then he has to take permission

of the assessee. If the Plot allotted to him is mortgaged to a third Party, then the

assessee collects 1% Fees from the original allottee which is termed as “Collateral Fees”. These charges are collected only if property belonging to original allottee is

offered as collateral by any third party.

(i)

(ii) Subletting Fees:GIDC allots plots on lease hold basis. If any allottee of the corporation wants to

sub-let the property allotted to them, they have to take permission of the

corporation for the same. The Corporation collects prescribed charges from the

allottee as per policy of the corporation for such permission, which is termed as

“Subletting Charges”. These charges are collected only at the time of giving

approval of sub-letting of plot/ shed.”

(iii) Sub Division Fees:If any allottee of GIDC wants to sub divide the plot allotted to them then it has to

apply to the corporation for sub division of the plot. The Corporation collects

prescribed charges from the allottees as per the policy of the corporation for such

division of plot, which is termed as “Sub-Division Fees”. These charges are

collected only at the time of giving approval of sub-division of plot.

(iv) Adjoining Charges:If any allottee of GIDC wants expansion and applies to the corporation for

allotment of plot adjoining to their existing unit, the corporation allots the same

after charging extra premium over and above regular allotment price of the

particular plot as per the policy of GIDC, which is termed as “Adjoining Charges”. These charges are collected only at the time of allotment of adjoining plot.

(v) Amalgamation Fees:If any allottee of GIDC wants to merge the various plots allotted to them into a

single plot then they have to apply to the corporation for amalgamation of their

plots. The corporation collects prescribed charges from the allottee as per the

policy of the corporation for such merger of plots, which is termed as

“Amalgamation fees/ charges”. These charges are collected only at the time of

giving approval of amalgamation of plot.

12.1 From the description provided by the assessee on the nature of fees

allottees/plot holders in lieu of permitting such allottees to use the plots allotted

to them for expansion or furtherance of their respective business. Thus, collateral

security fees were collected in lieu of facilitating the plot holder to avail loans \

against mortgaging of property. Similarly, subletting fees, Sub division fees, r " Adjoining fees and Amalgamation fees were collected for permitting the plot holders to sub-let plots, sub-divide plots, acquire the plots adjoining their own

plots and to merge the plots allotted to them.

12.2 It appears that the ‘Misc Income’ reflected in the Balance Sheet consisting

of collateral security fees, subletting fees, Sub division fees, Adjoining fees and

Amalgamation fees, etc., was actually consideration received by the assessee from

the plot holders, in return for facilitating the expansion of their businesses.

13. Whereas, the definitions of taxable services and classification of service as

provided under section 65 of the Finance Act, 1994 has been done away with

effect from 01.07.2012. The Government, vide Notification No. 19/2012-S.T. dated 05.06.2012, appointed 01.07.2012 as the date with effect from which the

provisions of Section 65B of the Finance Act, 1994, as inserted vide clause (C) of

Section 143 of the Finance Act, 2012, came into force. Under the negative list regime of service tax effective from July 1, 2012, as per the definition of service

under Section 65B (44) of the Finance Act, 1994, every activity for a consideration

by any person for another shall be liable to service tax, unless excluded under the

negative list or is specifically exempted.

o

The activities of the assessee insofar as they facilitate and aid the business

of their clientele, in return for consideration, comes within the ambit of service as

per Section 65B(44) of the Act. The term ‘service’ is defined in clause (44) of

Section 65B of the Finance Act, 1994 as under :

14.

(44) “service” means any activity carried out by a person for another for consideration, and includes a declared service, but shall not include—

(a) an activity which constitutes merely,—

(i) a transfer of title in goods or immovable property, by way of sale, gift or in any other manner; or

(ii) such transfer, delivery or supply of any goods which is deemed to be a sale within the meaning of clause (29A) of Article 366 of the Constitution, or

(iii) a transaction in money or actionable claim;

(b) a provision of service by an employee to the employer in the course of or in relation to his employment;

8

(c) fees taken in any Court or tribunal established under any law for the time being in force.

15. Thus service means any activity carried out by a person for another for

consideration, and includes a declared service. The concept ‘activity for a

consideration’ involves an element of contractual relationship wherein the person

doing an activity does so at the desire of the person for whom the activity is done

in exchange for a consideration. In this particular instance, collateral security

fees, subletting fees, Sub division fees, Adjoining fees and Amalgamation fees were

collected by the assessee in lieu of permitting or allowing the plot holders to

mortgage, sub-let, sub-divide, acquire adjoining plots and amalgamate plots, for

use in the course or furtherance or expansion of their business. Collateral security

fees were collected by the assessee in lieu of facilitating the plot holders to avail loans against mortgaging of rented property. Similarly, subletting fees, Sub

division fees, Adjoining fees and Amalgamation fees were collected as

consideration for permitting the plot holders to sub-let plots, sub-divide plots, acquire the plots adjoining their own plots and to merge the plots allotted/rented

to them. All the arrangements such as mortgaging, sub-dividing, sub-letting, adjoining and amalgamating, affects the nature of the rented plots and directly

affects occupation, enjoyment or exploitation of an immovable property, in this

case, plots allotted by the assessee to holders. The service provided by the

assessee had also resulted in acquisition of rented plots which had enhanced the

value of the plots and made easy availability of loans to the plot holders as a

result of mortgaging the plots. Thus, all such activities for which the assessee has

charged fees have affected the nature of the plots rented out to such plot holders/allottees by the assessee on lease hold basis. Besides, such plots have

been used by the allottees in the course or furtherance of business or commerce.

16. As per Section 66B of the Finance Act, 1994, there shall be levied a tax at

the rate of fourteen per cent on the value of all services, other than those services

specified in the negative list, provided or agreed to be provided in the taxable

territory by one person to another and collected in such manner as may be

prescribed. Taxable service is defined under section 65B(51) of Finance Act, 1994

as any service on which service tax is leviable under Section 66B.

Section 67(i) of the Act ibid provides that where service tax is chargeable on

any taxable service with reference to its value, then such value, in a case where

the provision of service is for a consideration in money, be the gross amount

charged by the service provider for such service provided or to be provided by

him. As per Explanation (a) to section 67 of the Act “consideration” includes any

amount that is payable for the taxable services provided or to be provided.

17.

18. Thus, it seemed that the various fees such as Collateral Security fee®

Subletting fees, Sub-division fees, Adjoining fees and amalgamation fees, etc., shown under the head ‘Misc Income' in the financial records was consideration. received by the assessee from the plot holders/allottees for services provided by

the assessee to the plot holders, who had undertaken such acts which were in

addition to the purpose for which they were allotted plots in the first place. It, therefore, appeared that by allowing or permitting usage of such plots by the plot holders and thus, enabling and facilitating their businesses, in return for a

consideration, the assessee had provided a service as defined in Section 65B(44) of

the Act, leviable to Service tax in terms of Section 66B of the Finance Act, 1994.

19. Further, Section 66E of the Finance Act, 1944 defines 'declared service' as

any activity carried out by a person for another person for consideration and

declared as such under Section 66E of the Act. Clause (e) of Section 66E of the

Finance Act, 1994 covers under the ambit of ‘Declared Services’, “agreeing to the

obligation to refrain from an act, or to tolerate an act or a situation, or to do an

act”. It is clear that 'agreeing to the obligation to tolerate an act or a situation'for a

consideration, qualifies as a 'service' and therefore, attracts service tax. It also

appeared that the assessee had agreed to the obligation to tolerate an act of the

plot holders, mortgaging / sub-letting / sub-dividing / amalgamating the plots

allotted to them for which the assessee had charged fees as per the terms and

conditions agreed upon by both the parties. On the part of the plot holders, it was

obligated that they shall apply to the Corporation before embarking on such acts

of mortgaging, sub-letting, sub-dividing, amalgamating the plots already allotted

to them by the assessee or before acquiring adjoining plots. In other words, the

assessee had agreed to tolerate the above acts of the plot holders subject to the

plot holders paying the agreed upon consideration. It, therefore, appeared that by

agreeing to tolerate the acts of the plot holders and thus, enabling and facilitating

their businesses, the assessee had also provided a declared service as defined in

Section 66E (e) of the Act, leviable to Service tax in terms of Section 66B of the

Finance Act, 1994.

20. During the period 2015-16 and 2016-17, the assessee had rendered taxable

services for a consideration of Rs. 10,08,17,326/-, but had not paid service tax

amounting to Rs. l,50,52,631/-(Rs. 20,29,072/- + Rs. 1,30,23,559/-).

21. It, therefore, appeared that the assessee had contravened the provisions of

Sections 67, 68, & 70 of the Finance Act, 1994 and Rules 6 and 7 of the Service

Tax Rules, 1994 as under(a) Section 67 of the Finance Act, 1994 read with Rule 6(1) of the Service

Tax Rules, 1994 inasmuch as they had failed to correctly self-assess

10

their Service Tax Liability on the consideration received by them for

provision of taxable services, as discussed supra;(b) Section 68 of the Finance Act, 1994 read with Rule 6 of the Service Tax

Rules, 1994 inasmuch as they failed to pay the Service Tax to the

credit of the Central Government, by the 5th of the quarter

immediately following the calendar quarter, in which the payments

were received, towards the value of taxable services;(c) Section 70 of the Finance Act, 1994 read with Rule 7 of the Service Tax

Rules, 1994 inasmuch as they failed to submit a correct half-yearly

return incorporating the details of the Service Tax discussed supra, along with a copy of the Challan in form GAR-7, for the quarters

covered in the half-yearly returns.

22. It appeared that the assessee had not disclosed the full amount of

consideration received by them on provision of services in the ST-3 returns filedby them for the period 2015-16 and 2016-17 and had therefore, suppressed the

material facts from the department. Hence, it appeared that there was a

deliberate withholding of essential material information from the departmentabout the taxable services provided and consideration received by them, and

such facts came to the notice of the department only during audit. With the

introduction of self-assessment and filing of ST-3 returns online, no documents

were submitted by the assessee to the department and therefore, the department

would come to know about such non-payment of service tax only during audit or

preventive/other checks. Hence, it appeared that all these information had been

concealed from the department deliberately, consciously and purposefully to

evade payment of service tax. Therefore, in this case all essential ingredients exist to invoke the extended period under proviso to Section 73(1) of Finance Act, 1994

to demand the service tax not paid along with interest under Section 75 of the Act ibid.

It appeared that unpaid Service Tax amounting to Rs. 1,50,52,631/-

required to be recovered from the assessee under proviso to Section 73(1) of the

Finance Act, 1994 along with interest under Section 75 of the said Act. It further

appeared that the assessee had suppressed the material fact of rendering such

service from the department with intent to evade payment of service tax. By the

act of not disclosing the full amount of consideration received on account of

provision of service, and by the acts of contravention of the provisions of Sections

67, 68 & 70 of the Finance Act, 1994, the assessee had also rendered themselves

liable for penal action under Section 78(1) of the Act.

23. was

24. Pre-SCN Consultation in terms of instructions issued from File N#

1080/09/DLA/MISC/15 dated 21.12.2015, F.No. 1080/DLA/CC

Conference/2016 dated 13.10.2016 and Master Circular No. 1053/02/2017-CX

dated 10.03.2017, was granted on 21.02.2019, before the Additional Commissioner, Central Tax Audit, Ahmedabad. Subsequent to the Pre-SCN

consultation, the assessee vide letter dated 22/2/2019, informed that they had

undergone service tax audit for the period from 2011-12 to 2014-15 and a show

cause notice was issued to them but the demand under the said show cause

notice was dropped by the Hon. Commissioner, Ahmedabad South and

Ahmedabad Zone Commissionerate has also accepted the same by relying on

Entry No.39 of the Mega Exemption Notification No.25/2012-ST dated

20.06.2012, the relevant extract of which is reproduced below:

“39. Services by a governmental authority by way of any activity in

relation to any function entrusted to a municipality under article 243Wof the

Constitution”

24.1 In view of the above, it was submitted by the assessee that various fees

such as Collateral Security fees, Subletting fees, Sub-division fees, Adjoining fees

and amalgamation fees, etc., collected by the assessee would not attract service

tax.

25. The submissions of the assessee were examined. It was seen that after

conclusion of the audit for the period from 2011-12 to 2014-15, a show cause

notice was issued to the assessee on (i) inadmissible cenvat credit (ii) short

payment of service tax on reconciliation (iii) short payment of service tax on

“infrastructure Up gradation Fund”,(iv) non-payment of service tax on ‘penalty on

non-utilisation’ (v) non-payment of service tax on “water charges” and (vi) nonpayment of service tax on ‘transfer fees’.

25.1 It was seen that the assessee had already accepted their liability and made

payments against inadmissible cenvat credit, against short payment of service tax

on reconciliation and the interest thereon but had refused to pay the penalty. The

Commissioner, Ahmedabad South under his adjudication order had upheld the

imposition of penalty on the assessee for both the above issues. However, in the

matter of short payment of service tax on “Infrastructure Up gradation Fund”, ‘penally on non-utilisation’, ‘transfer fees’, and on Vater charges’, the

Commissioner has dropped the demand w.e.f. 1.7.2012 by relying on Entry No.39

of the Mega Exemption Notification No.25/2012-ST dated 20.06.2012.

12

26. In the present case the assessee had already admitted his liability and paid

the service tax, noticed on reconciliation of financial records vis-a-vis the ST-3

Returns filed by them during the period 2015-16 and 2016-17. The facts of the

present case are distinguishable from the facts of the previous audit and order

passed by the Commissioner, Ahmedabad South. The issue of Collateral Security

fees, Subletting fees, Sub-division fees, Adjoining fees and amalgamation fees, etc., have not been decided in the Order passed by the Commissioner, Ahmedabad South.

27. The contentions of the assessee, therefore, appear to be unacceptable as

Collateral Security fees, Subletting fees, Sub-division fees, Adjoining fees and

amalgamation fees, etc. have a direct correlation with the activity of renting of

immovable property and support and facilitation of the businesses of plot holders

undertaken by the assessee. Hence, there is an implied contractual reciprocity of a

consideration. As long as the payment was made (or fee charged) for getting a

service in return (i.e., as a quid pro quo for the service received), it had to be

regarded as a consideration for that service and taxable irrespective of whatever

name such payment was called. Therefore, it appeared that the assessee had

rendered taxable services as defined under clause (44) of Section 65B of the

Finance Act, 1994, but failed to discharge service tax in the manner prescribed

under Finance Act, 1994. Further, it appeared that service of renting of

immovable property provided to business entities and fees/charges collected in

connection with such immovable property from business entities would not fall under the function of Regulation of land-use and construction of buildings

entrusted to a municipality under article 243W of the Constitution.

28. In the regime of self-assessment, the liability of self-assessment and correct

payment of tax was cast upon the assessee by the law. It is the assessee who has

to ascertain his correct tax liability and discharge it as per the time and manner

prescribed under Service tax law. From the evidences, it appeared that the

assessee has knowingly evaded the payment of service tax. Had audit not been

conducted in due course, the lapse would not have come to the notice of the

department. The deliberate non-payment of tax 8b suppression of value of taxable

services provided is in disregard to the requirements of law and also not in line

with the government’s efforts to create a voluntary tax compliance regime. In the

case of Mahavir Plastics versus CCE Mumbai, 2010 (255) ELT 241, it was held

that if facts are gathered by department in subsequent investigation extended

period can be invoked. In 2009 (23) STT 275, in case of Lalit Enterprises Vs. CST

Chennai, it was held that extended period can be invoked when department

comes to know of service charges received by appellant on verification of his

accounts. It, therefore, appeared that unpaid Service Tax of Rs. 1,63,87,870/-^

was required to be recovered from the assessee under proviso to Section 73(1) of

the Finance Act, 1994 along with interest under Section 75 of the Act ibid. The

assessee was also liable for penal action under Section 78(1) of the Act for

contravention of the provisions of applicable law by not ascertaining the correct assessable income and not making payment of service tax on that income.

29. Therefore, M/s. Gujarat Industrial Development Corporation, Fadia

Chambers, 3rd Floor, Ashram Road, Ahmedabad was issued a show cause notice

dated 27.09.2019 asking them to Show Cause to the Joint/Additional Commissioner of Central GST, Ahmedabad South Commissionerate having his

office at 7th Floor, CGST Bhawan, Near Panjarapole, Ambawadi, Ahmedabad as to

why:-

Short paid service tax of Rs.l3,35,239/-(Rupees thirteen lakhs thirty five

thousand two hundred and thirty nine only) should not be demanded and

them under the proviso to Section 73(1) of the Finance Act, 1994 and the amount of Rs. 13,35,239/- already paid by them should not

adjusted and appropriated against the above demand(Revenue Para No.01);

(i)

recovered from

Unpaid Service tax of Rs. 1,50,52,631/- (Rupees one crore fifty lakhs fifty

thousand six hundred and thirty one only) should not be demanded and

from them under proviso to Section 73(1) of the Finance Act, 1994(Revenue Para No. 06);

(ii)tworecovered

(iii) Interest at the applicable rate should not be charged and recovered from

them under Section 75 of the Finance Act, 1994 on the demand at (i) & (ii) above;

Penalty should not be imposed upon them under Section 78(1) of the

Finance Act, 1994 on the demand at (i) 86 (ii) above.(iv)

Defence reply of the noticee:30. The assessee M/s. Gujarat Industrial Development Corporation vide their

reply dated 25.02.2020 have stated that they are established under the Gujarat

Industrial Development Act, 1962 (hereinafter referred to as the GID Act) by the

State Government of Gujarat for the purpose of securing orderly establishment and organization of industries in industrial areas and industrial estates in the

State of. Gujarat and establishing commercial centres in connection with the

establishment and organization of such industries; that GID Act and Gujarat

Industrial Development Rules, 1963 (hereinafter referred to as the ‘GID Rules’) govern the functioning of the GIDC and have submitted a copy of the GID Act and GID Rules’ that after the establishment of the GIDC, various areas in

14

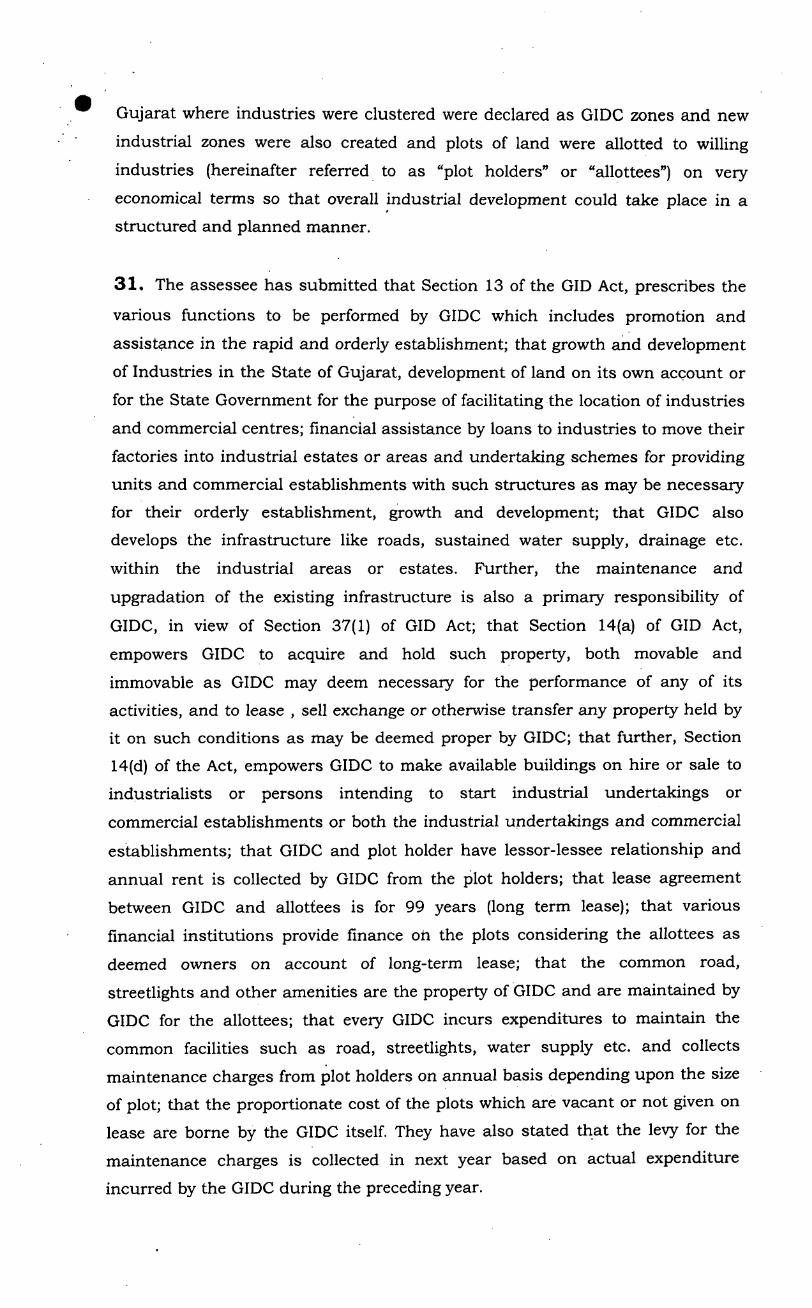

Gujarat where industries were clustered were declared as GIDC zones and new

industrial zones were also created and plots of land were allotted to willing

industries (hereinafter referred to as “plot holders” or “allottees”) on very

economical terms so that overall industrial development could take place in a

structured and planned manner.

31. The assessee has submitted that Section 13 of the GID Act, prescribes the

various functions to be performed by GIDC which includes promotion and

assistance in the rapid and orderly establishment; that growth and development of Industries in the State of Gujarat, development of land on its own account or

for the State Government for the purpose of facilitating the location of industries

and commercial centres; financial assistance by loans to industries to move their

factories into industrial estates or areas and undertaking schemes for providing

units and commercial establishments with such structures as may be necessary

for their orderly establishment, growth and development; that GIDC also

develops the infrastructure like roads, sustained water supply, drainage etc. within the industrial areas or estates. Further, the maintenance and

upgradation of the existing infrastructure is also a primary responsibility of

GIDC, in view of Section 37(1) of GID Act; that Section 14(a) of GID Act, empowers GIDC to acquire and hold such property, both movable and

immovable as GIDC may deem necessary for the performance of any of its

activities, and to lease , sell exchange or otherwise transfer any property held by

it on such conditions as may be deemed proper by GIDC; that further, Section

14(d) of the Act, empowers GIDC to make available buildings on hire or sale to

industrialists or persons intending to start industrial undertakings or

commercial establishments or both the industrial undertakings and commercial establishments; that GIDC and plot holder have lessor-lessee relationship and

annual rent is collected by GIDC from the plot holders; that lease agreement between GIDC and allottees is for 99 years (long term lease); that various

financial institutions provide finance oh the plots considering the allottees as

deemed owners on account of long-term lease; that the common road, streetlights and other amenities are the property of GIDC and are maintained by

GIDC for the allottees; that every GIDC incurs expenditures to maintain the

common facilities such as road, streetlights, water supply etc. and collects

maintenance charges from plot holders on annual basis depending upon the size

of plot; that the proportionate cost of the plots which are vacant or not given on

lease are borne by the GIDC itself. They have also stated that the levy for the

maintenance charges is collected in next year based on actual expenditure

incurred by the GIDC during the preceding year.

32. The assessee has submitted that at the outset, they deny all the charge^

and allegations made in the notice and also denied that the assessee is liable to

tax, penalty or interest as proposed in the notice; that before showing causes as

required in the impugned notice, it was imperative to submit that all allegations

made therein are baseless, capricious and nondescript. The said assessee has

stated that the notice bears allegations that are liable to be squashed based on

grounds submitted hereinbelow and in the light of the facts mentioned as under:

Miscellaneous Receipts:No Service tax is payable under the income head ^Miscellaneous

Receipts’ under the service category of ‘renting of immovable property

service’.(i) SCN has alleged demand on the income head 'Miscellaneous Receipts’

under the service category of “Renting of Immovable Property” for the

period from April, 2016 to June, 2017 without understanding the

nature of the transaction and as the Department is unaware of the

nature of the transaction as carried out by GIDC as alleged in SCN, the

same needs to be set aside.

Governmental Authority:

Notwithstanding to the arguments as stated in the above paras, GIDC

being a governmental authority w.e.f. 01.07.2012 pursuant to entry 39

of Mega Exemption Notification, service shall not be leviable on the

collection done by GIDC under various income heads.

(ii) CBEC has issued mega exemption notification No.25/2012-ST dated

20.06.2012 and the relevant extract is reproduced below:

“39. Services by a governmental authority by way of any activity in relation to

any function entrusted to a municipality under Article' 243W of the

Constitution. *

As per the said exemption entry, any services provided by government authority in relation to any function entrusted to municipality under Article

243W of the Constitution are exempted from the levy of service tax. The term

‘governmental authority’ is defined under clause2(s) of the mega exemption

notification which was amended vide notification No.2/2014-ST dated

30.01.2014 and for the sake of reference, the definition of ‘governmental

authority’ pre and post amendment is as reproduced below:

16

From 01.07.2012 to 29.01.2014 w.e.f. 30.01.2014(s) “governmental authority” means a board, or an authority or any other body established with 90% or more participation by way of equity or control by Government and set up by an Act of the Parliament or a State Legislature to carry out any function entrusted to a municipality under Article 243W of the Constitution;_____________________

(s) ‘governmental authority’ means and authority or a board or any other body;(i) set up by an Act of Parliament or a State Legislature; or(ii) established by Government, with 90% or more participation by wayof equity or control, to carry out

any function entrusted to a municipality under Article 243W of the Constitution;’.

In order to ascertain, whether GIDC can be termed as Governmental Authority, the following essentials are being fulfilled by GIDC:Set up by an Act of Parliament or a State Legislature or established bythe Government:

(i) GIDC has been established by the Legislature of State of Gujarat under

the Act and the GIDC performs its functions in accordance with the

provisions contained in the Act and the said Rules. Section 3 of GID Act reads as follows:

“3. (1) For the purpose of securing and assisting in the rapid and

orderly establishment, and organisation of industries in industrial

areas and industrial estates in the State of Gujarat and for the

purpose of establishing commercial centres in connection with the

establishment and organisation of such industries], there shall be

established by the State Government by notification in the OfficialGazette, a Corporation bv the name of the Guiarat IndustrialDevelopment Corporation.(2) The Corporation shall be a body corporate with perpetual succession and a common seal, and may sue and be sued in its

corporate name, and shall be competent to acquire, hold and

dispose of property, both movable and immovable, and to

contract, and do all things necessary, for the purpose of this Act. “(ii) Further, item 29 of the subjects allotted to Industries and Mines

Department of First Schedule to Gujarat Government Rules of Business, 1990 mentions about GIDC. Moreover, the Gujarat Government Rules of

Business, 1990 is made under article 166 of Constitution of India. Therefore, in the light of the above legal provisions, this essential is

fulfilled by GIDC.

90% or more participation of the Central or State Government, by wayof equity or control;

(iii) Section 4 of GID Act lays down the constitution of GIDC, wherein it-has %

been stated that GIDC shall consist of twelve directors, out of which

three official directors shall be nominated by the State Government, of

whom one shall be financial adviser to GIDC. Further, six directors

would be nominated by the State Government, from amongst persons

appearing to it either to be qualified by reason of experience of, and

capability in, industry or trade or finance or to be suitable to represent

the interest of persons engaged or employed therein. Moreover, subsection (2) of section 4 of GID Act specifies that the State Government shall appoint one of the Directors of GIDC to be Chairman of the

Corporation and may appoint one of the other Directors as Vice-

Chairman.

Section 12(1) of GID Act states that the State Government shall appoint a

Managing Director and a Chief Accounts Officer of GIDC and section 15

of GID Act states that all permissions, orders, decisions, notices and

other documents of the GIDC shall be authenticated by the signature of

the Managing Director of the GIDC. Further, section 16 of GID Act empowers the State Government to notify any area as ‘notified area’ under the provisions of the Act and the provisions of the Gujarat

Municipalities Act, 1963 shall not apply to such ‘notified area’. Moreover, section 17 of GID Act empowers the State Government to issue general or

special directions of policy to the GIDC, as it thinks necessary or

expedient for the purposes of carrying out the purposes of the Act and

the GIDC shall be bound to follow and act upon such directions.

(iv)

(v) Section 23(1) of GID Act states that the GIDC shall make provision for

such reserve and other specially denominated funds and in such manner

and to such extent as the State Government may, from time to time, direct

Further, sub section (3) of section 23 of GID Act states that none of the

funds referred to in sub-section (1) shall be utilised for any purpose other

than that for which it was constituted, without the previous approval of

the State Government.

(vi) Section 25 of GID Act prescribes that the GIDC has to prepare and

submit an annual financial statement (budget) and the programme of

work for the succeeding financial year, to the State Government for

approval. Further, the GIDC shall be competent to make variations in the

programme of work in the course of the year, with the approval of the

State Government. Section 26(2) of GID Act prescribes that the accounts

of the GIDC shall be audited bu an auditor appointed bu the State

18

Government in consultation with the Comptroller and Auditor General of

India.

(vii) Section 27 of GID Act empowers the State Government to conduct

concurrent and special audit of the accounts of the GIDC, by such

persons as it may thinks fit. Further, the State Government may pass

such orders on the reports of the special audit and the GIDC shall be

bound to comply with such order.

(viii) Section 45(1) of GID Act states that the GIDC shall furnish to the State

Government such returns, statistics, reports, accounts and other

information with respect to its conduct of affairs, properties or activities

or in regard to any proposed work or scheme as the State Government may from time to time require. Further, section 45(2) of GID Act requires

the GIDC to furnish an. annual report on its working as soon as may be

after the end of financial year in the form and manner prescribed by the

State Government.

(ix) Moreover, section 46 of GID Act empowers the State Government to

withdraw any particular industrial area, estate or part thereof from the

jurisdiction of the GIDC. If, the State Government is satisfied that in

respect of any particular industrial estate or area, the purpose for which

the GIDC was established has been substantially achieved, so as to

render the continued existence of such industrial; estate or area under

the GIDC unnecessary.

\(x) Section 48 of GID Act empowers the State Government to dissolve the

GIDC, if the State Government is satisfied that the purposes for which

the GIDC was established under the Act, has been substantially

achieved.

I

(xi) The provisions contained in the Act, makes it clear that the State

Government of Gujarat controls the function of the GIDC either directly

or indirectly. Thus, this condition is also satisfied by the GIDC.

To carry out any function entrusted to a municipality under Article243W of the Constitution.

(xii) Article 243W of the Constitution of India reads as follow:

243W. Powers, authority and responsibilities of Municipalities, etc

Subject to the provisions of this Constitution, the Legislature of a

State may, by law, endow -(a) the Municipalities with such powers and authority as may be

necessary to them to function as institutions of self government and such law may contain provisions for the devolution of powers

and responsibilities upon Municipalities, subject to such

conditions as may be specified therein, with respect to(i) the preparation of plans for economic development and social justice:(ii) the performance of functions and the implementation of

schemes as may entrusted to them including those in relation tothe matters listed in the Twelfth Schedule:(b) the Committees with such powers and authority as may be

necessary to enable them to carry out the responsibilities

conferred upon them including those in relation to the matters

listed in the Twelfth Schedule

(underlining supplied)

(xiii) Further, Schedule XII of the Constitution of India, lists out the following

functions to be performed by the municipalities:TWELFTH SCHEDULE (Article 243W)1. Urban planning including town planning.2. Regulation of land-use and construction of buildings.3. Planning for economic and social development.4. Roads and bridges.5. Water supply for domestic, industrial and commercialpurposes.6. Public health, sanitation, conservancy and solid waste

management.7. Fire services.8. Urban forestry, protection of the environment and promotion of

ecological aspects.9. Safeguarding the interests of weaker sections of society, including the handicapped and mentally retarded.10.Slum improvement and upgradation.11 .Urban poverty alleviation.12. Provision of urban amenities and facilities such as parks, gardens, playgrounds.13. Promotion of cultural, educational and aesthetic aspects.

20

14. Burials and burial grounds; cremations, cremation

grounds and electric crematoriums.15. Cattle pounds; prevention of cruelty to animals.16. Vital statistics including registration of births and deaths.17. Public amenities including street lighting, parking lots, busstops and public conveniences.18.Regulation of slaughter houses and tanneries,

(underlining supplied)

(xiv) Section 3 of GID Act, as discussed hereinabove, lays down that the GIDC

has been established for securing and assisting in the rapid and orderly

establishment and organisation of industries in industrial areas and

industrial estates in the State of Gujarat. Further, section 13 of GID Act states the functions to be performed by the GIDC which includes

establishment, development and management of industrial estates in the

State of Gujarat. Thus, the GIDC has been established for managing and

developing the industrial areas and estates, in order to increase the

number of industries established in State of Gujarat.

(xv) On conjoint reading of Article 243W of the Constitution of India and

section 3 and 13 of GID Act, makes it clear that the GIDC has to prepare

and execute plans for economic development. Since, the growth in the

number of industries is directly proportional to the economic

development of any State. Moreover, the establishment of the GIDC has

resulted in exponential growth in the number of industries in the State of

Gujarat.

(xvi) Section 14 of GID Act, lists out the general powers entrusted to the

GIDC, which includes provision of amenities and common facilities in

industrial estates, commercial centres and industrial areas and

construction and maintenance of buildings, amenities and common

facilities. The amenities include road, supply of water or electricity, street lighting, drainage, sewerage, conservancy and such other convenience as

the State Government may specify. Further, section 37 of GID Act, empowers the GIDC to lay down, maintain, alter, remove, or repair any

pipes, pipelines, conduits, supply or service lines, posts, or other

appliances or apparatus in, on, under over, along or. across any land in

the industrial area or estate for carrying gas, water electricity or

construction of sewers or drains necessary for carrying off workings and

waste liquids of an industrial process. The aforesaid functions qualify as_,ui:~

health, sanitation conservancy and solid waste management’; and ‘public^

amenities including street lighting, parking lots, bus stops and public

conveniences’.

(xvii) The GIDC is also empowered to make available buildings on hire or sale

to industrialists or persons intending to start industrial undertakings or

commercial establishments. Moreover, the GIDC can also construct

buildings for housing of the employees of such industries or commercial establishments and allot factory sheds or buildings and shops etc. to

suitable persons in the industrial estates or commercial centres

established by the GIDC. The aforesaid functions qualify as ‘regulation of

land use and construction of buildings’.

(xviii) Section 16 of GID Act, empowers the State Government of Gujarat to

notify any area as industrial area and the provisions of Gujarat

Municipalities Act, 1963 shall not be in force, in such industrial area. Thus, in light of the above, we are of the view that the GIDC has been

entrusted to carry out functions of the municipality as contained under

Article 243W of the Constitution of India and Schedule XU of the

Constitution of India.

(xix) Their view is also supported by the decision of the HonTile Apex Court in

the GIDC’s own case, GIDC vs. CIT AIR 1997 SC 3275, wherein the

Hon’ble Apex Court held that the industrial development is enveloped

within the expression “planning, development or improvement of cities, towns and villages or for both” in section 10(20A) of the Income-Tax Act, 1961. The relevant part of the said judgment is reproduced hereinbelow:

“9. The Gujarat Act was enacted “to make special provision for securing

the orderly establishment of industries in industrial areas and industrial estates in the State of Gujarat, and to assist generally in the organisation

thereof and for that purpose to establish an Industrial Development Corporation, and for purposes connected with the matters aforesaid” as

can be discerned from the preamble thereof

10. Section 2(g) of the Act defines “industrial area” as any area declared

to be an industrial area by the State Government by notification in the

Official Gazette which is to be developed and where industries are to be

accommodated. Section 2(n) defines “industrial estate” as any site

selected by the State Government where the Corporation builds factories

and other buildings and makes them available for any industries or class

of industries. Section 13 of the Gujarat Act enumerates the function of the

Corporation and they contain, inter alia, “to promote and assist in the

22

rapid and orderly establishment, growth and development of industries in

the State of Gujarat”.

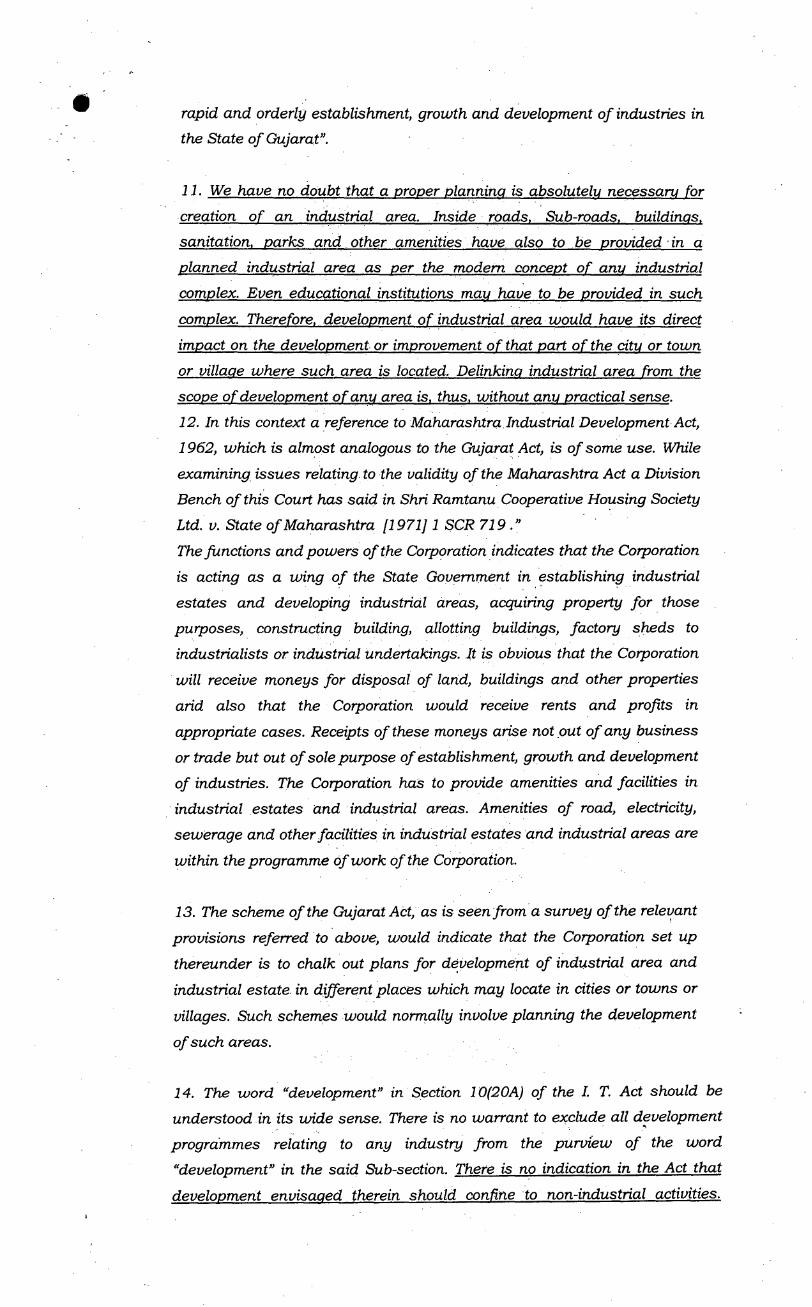

11. We have no doubt that a proper planning is absolutely necessary forcreation of an industrial area. Inside roads. Sub-roads, buildings,sanitation, parks and other amenities have also to be provided in aplanned industrial area as ver the modem concept of anu industrialcomplex. Even educational institutions may have to be provided in suchcomplex. Therefore, development of industrial area would have its directimpact on the development or improvement of that part of the city or townor village where such area is located. Delinking industrial area from thescope of development of anu area is. thus, without anu practical sense.12. In this context a reference to Maharashtra Industrial Development Act, 1962, which is almost analogous to the Gujarat Act, is of some use. While

examining issues relating to the validity of the Maharashtra Act a Division

Bench of this Court has said in Shri Ramtanu Cooperative Housing Society

Ltd. v. State of Maharashtra [1971] 1 SCR 719.”The functions and powers of the Corporation indicates that the Corporation

is acting as a wing of the State Government in establishing industrial estates and developing industrial areas, acquiring property for those

purposes, constructing building, allotting buildings, factory sheds to

industrialists or industrial undertakings. It is obvious that the Corporation

will receive moneys for disposal of land, buildings and other properties

arid also that the Corporation would receive rents and profits in

appropriate cases. Receipts of these moneys arise not put of any business

or trade but out of sole purpose of establishment, growth and development of industries. The Corporation has to provide amenities and facilities in

industrial estates and industrial areas. Amenities of road, electricity, sewerage and other facilities in industrial estates and industrial areas are

within the programme of work of the Corporation.

13. The scheme of the Gujarat Act, as is seen from a survey of the relevant provisions referred to above, would indicate that the Corporation set up

thereunder is to chalk out plans for development of industrial area and

industrial estate in different places which may locate in cities or towns or

villages. Such schemes would normally involve planning the development

of such areas.

14. The word “development” in Section 10(20A) of the I. T. Act should be

understood in its wide sense. There is no warrant to exclude all development programmes relating to any industry from the purview of the word

“development” in the said Sub-section. There is no indication in the Act that development envisaged therein should confine to non-industrial activities.

Development of a place can be accelerated through varieties of schemes and mestablishment of industries is one of the modes of developing an area.

15. One of the reasons for incorporating a specific provision of exemptionfrom income-tax such as Section 10(20A) is to protect public bodies createdunder law for achieving the purpose of developing urban or rural areas forpublic good. When the object is such, an interpretation which wouldpreserve it should be accepted even if the provision is capable of morethan one interpretation. The principle of interpretation is very much

applicable to fiscal statutes also, (vide State of Tamil Nadu v. M.K. Kandaswami [1976] 1 SCR 38. This Court has reiterated the said principle

in Calcutta Jute Manufacturing Co: 1997 (93) ELT 657 (SC).

16. The position is, therefore, clear that authorities constituted by law for

facilitating all kinds of development of cities, towns and villages for public

purposes shall not be subjected to the liability to pay income-tax. The

Division Bench of the High Court seems to have interpreted the exemption

clause too rigidly and narrowly which resulted in the anomaly of bringing

authorities like appellant Corporation within the tentacles of income-tax

liability while the authorities dealing with housing schemes which provide

houses to private individuals would stand outside the taxing sphere.

17. In the result, we allow these appeals, set aside the judgment under

challenge. The answer to the question will, therefore, be in favour of the

assessee and against the Revenue. ”

(xx) Therefore, GIDC qualifies as a governmental authority and performs

various functions which are entrusted to a municipality under Article

243W of the Constitution and Schedule XII of the Constitution. Thus, in

the light of the above referred decision of the Supreme Court in the

GIDC’s own case, it can be said that any activity performed by the

Querist, in relation to the purpose for which, GIDC has been established,

would qualify for exemption from service tax under entry 39 of. the Mega

Exemption Notification No. 25/2012-ST dated 20.06.2012 and hence

service tax shall not be levied for the period from 01.07.2012 on the

amount of transfer fees collected by GIDC from its allottees.

(xxi) As GIDC is exempted from the levy of service tax, demand as alleged in

the SCN needs to be set aside.

33. The assessee has referred to the judgement of Honorable Bombay High Court in case of CCE Nasik v/s Maharashtra Industrial Development Corporation(2017-TIOL-2629-HC-MUM-ST). Part 12 of the judgement of

24

Honorable Bombay High Court in the case of CCE Nasik vs. M/s. MIDC is produced as under:

"We have already referred to Section 14 of the MID Act which provides that the function

of the MIDC is not only to develop industrial areas but to establish and manage

industrial estates. The role of MIDC is not limited only to establishing industrial estates

and allotting the plots or buildings or factory sheds to industrial undertakings. The

function and obligation of the MIDC is also to manage and maintain the said industrial estates as provided in Section 14. Therefore, it is the statutory obligation of the MIDC to

provide amenities as defined in clause(a) of Section 2 of the MID Act to the industrial estates established by it. Thus, it is the statutory obligation of MIDC to provide and

maintain amenities in its Industrial estates such as roads, water supply, street lighting, drainage etc. Thus, we find that the activities for which the demand was made are

part of the statutory functions of the MIDC under MID Act. As stated earlier, the

demand is in respect of service charges collected from plot holders for providing them

various facilities including maintenance, management and repairs. As provided in the

circular dated 18th December, 2006, for providing amenities to the plot holders, the

service fees or service charges collected by MIDC are obviously in the nature of compulsory levy which is used by MIDC in discharging statutory obligations under

Section 14. We find that even in the Order-in-Original, there is no finding of fact recorded that the service rendered for which service tax was sought to be levied was

not in the nature of statutory obligation.”

34. The assessee has submitted that the Honorable Bombay High Court has

relied upon the Circular No.89/7/2006-ST dated 18th December, 2006(copy

submitted). Point No.2 of the Circular is produced as under:

"2. The issue has been examined. The Board is of the view that the activity

performed by the sovereign/public authorities under the provision of the law are

in the nature of statuary obligations which are to be fulfilled in accordance with

the law. The fee collected by them for performing such activates is in the nature

of compulsory levy as per the provisions of the relevant statute, and it is

deposited into the Government Treasury. Such activity is purely in the public

interest and it is undertaken as mandatory and statutory function. These are not in the nature of service to any particular individual for any consideration. Therefore, such activity performed by a sovereign/public authority under the

provisions of law does not constitute provision of taxable service to a person and,

therefore, no service tax is leviable on such activities. ”

35. The assessee has submitted that in their own case Honorable

Commissioner of Ahmedabad South has relied upon the decision of Bombay

High Court in the case of M.I.D.C. and resultantly had dropped the demand of

GIDC, Ahmedabad for the period prior to 01.07.2012. They have submitted a

copy of the Order-in-Original No.AHM-EXCUS-COM-Ol 1-18-19 dated

LiicxL in uic atuu uiuei , ior ine income oi postt?

negative list i.e. from 01.07.2012, Honorable Commissioner of Ahmedabad £

South has relied upon the entry No.39 of the Mega Exemption Notification

No.25/2012 dated 20.06.2012 by considering GIDC as a Governmental Authority and resultantly has dropped the demand of G.I.D.C., Ahmedabad

w.e.f. 01.07.2012.

HCiVVy OLCXLt/Va

36. The assessee has submitted that in their own case, Honorable

Commissioner of Rajkot has relied upon the entry No.39 of the Mega

Exemption Notification No.25/2012 dated 20.06.2012 by considering GIDC as

a Governmental Authority and resultantly has dropped the demand of

G.I.D.C., Rajkot w.e.f. 01.07.2012 and that in addition, there is no

departmental appeal filed against this order which has been accepted by the

Honorable Chief Commissioner, Central GST and Central Excise, Ahmedabad

Zone. They have submitted a copy of the Order-in-Original No.RAJ-EXCUS-

000-CGM-04-17-18 dated 25.10.2018.

37. The assessee has submitted that in their own case, service tax demand

has been dropped by the Department in the case of GIDC, Gandhinagar and

GIDC, Mehsana and GIDC Head Office by relying upon the entry No.39 of the

Mega Exemption Notification No.25/2012 dated 20.06.2012 by considering

GIDC as a Governmental Authority; that in their own case in GIDC, Mehsana

Region, Commissioner(Appeals), CGST, Ahmedabad has dropped the demand

of ‘Miscellaneous Receipts’ income head and has submitted a copy of the said

order.

38. The assessee has submitted that: (a) no interest is payable u/s. 75 of

the Act, as assessee is not liable to pay service tax as demanded in the

impugned SCN as submitted in the above paras. (b)No Penalty is payable

u/s. 78 of the Act as SCN has raised demand for the period from April, 2015

to March, 2017 by invoking larger period of limitation i.e. beyond normal

period of limitation of 30 months. As per section 78 of the Act, larger period of

limitation can be invoked only in case where there is fraud, collusion, willful misstatement, suppression of facts or contravention of provision of any Excise

law with 'an intent to evade payment of duty'. Only in such circumstances

demand can be raised beyond the normal period of limitation. The onus to

provide that there is 'an intent to evade payment of duty' is upon the

department, (c) There is 'no intent to evade payment of duty as SCN has

invoked larger period of limitation only on the ground that assessee has

suppressed/concealed the value of taxable service with an intent to evade

payment of service tax. Only in unusual circumstances, demands for extended

26

m period are to be invoked, with a very serious allegation of suppression of factsSuch serious allegations ofand intention to evade payment of service tax,

suppression can be invoked only if assessee has deliberately done an actionwith an intention to hide certain facts from the department and department

has confirmed it beyond doubt with aid of corroborative evidence that there

was a deliberate act on part of assessee to evade tax. There is no finding in

impugned SCN which can allege that GIDC has intended to evade payment of

tax. In the absence of any finding of “intend to evade” demand cannot be

sustained. Reliance is placed on the following decisions:Continental Foundation v. CCE [2007 1216) E.L.T. 177 (S.C.)]CCE v. Pioneer Scientific Glass Works [2006 1197) E.L.T. 308

(S.C.)]Pahwa Chemicals Pvt. Ltd. v. CCE [2005 1189) E.L.T. 257 (S.C.)]

Anand Nishikawa Co Ltd. v. CCE [2005 1188) E.L.T. 149]

(i)(ii)

(iii)

(iv)

39. The assessee has submitted that in the present case, GIDC is a body

corporate of the Government of Gujarat for performing statutory functions in

accordance with the provisions of Gujarat Industrial Act, 1962 and one of its

functions is the allotment of vacant land to various persons for industrial

purposes on long term lease basis. Thus, GIDC being a government body

could not have a malafide intention for non-payment of service tax. Reliance is

put on the following judgments:CCE v. Bharat Petroleum Corporation Ltd. (2016) 344 ELT 657 (Tri. -(i)

Hyd.)(ii) Karnataka State Tourism Dev. Corpn. Ltd. v. CST (2011) 21 STR 51 (Tri.-

Bang.)(iii) Maharashtra State Seed Certification Agency v. CC&CE (2016) 37 STR

655 (Tri.-Mumbai)(iv) Gujarat Narmada Valley Fertilizers 86 Chem. Ltd. v. CCE (2016) 37 STR

796 (Tri.-Ahmd.)

40. The said assessee has submitted that in a very recent decision by

Karnataka High Court, the Hon’ble HC in case of CST Bangalore Vs. Motor

World and other vide 2012-TIOL-418-HC-KAR-ST has appropriately dealt

with the issue of penalty and applicability of Section 80, the crux of the

decision is as under:

“The ingredients mentioned in the Section should exist. In respect of

Sections 76, 77 and 78 of the Act, not only the ingredients of those Sections

should exist, but also there should be absence of reasonable cause for the said

Section 78, Section 76 is not attracted. Therefore, no penalty can be imposed for^

the same failure under both the provisions; Even if the ingredients stipulated in

Sections 76 and 78 of the Act are established, if the Assessee shows reasonable

cause for such failure, then the authority has no power to impose penalty in view

of Section 80 of the Act; Even after holding that the ingredients stipulated in

Sections 76 and 78 exist, and there is no reasonable cause shown for failure to

comply with the said provisions, the authority has the discretion regarding the

quantity of the penalty to be imposed.”

41. The assessee has submitted that in case of CCE, Meerut-II v. On Dot

Couriers & Cargo Ltd. (2006) 6 STJ 337 (CESTAT, New Delhi) held that no

penalty shall be imposable on assessee for any failure referred to in the said

provisions if assessee proves that there was reasonable cause for said failure.

42. The assessee has submitted that though reasonable cause has not been

defined, it has been interpreted by various courts. In Municipal Corporation

of Delhi v. Jagannath Ashok Kumar, (1987) AIR 2316 (Supreme Court), Apex Court observed that the reasons given by the Arbitrator are cogent and

based on materials on record. Reason varies in its conclusions according to

the idiosyncrasy of the individual, and the time and circumstance in which he

thinks. In Commissioner of Wealth Tax v. Jagdish Prasad Choudhary, (1996) AIR 58 (Patna), it was held that the context of penalty provision, the

word, 'reasonable cause' would mean a cause which is beyond the control of

the assessee. 'Reasonable cause' obviously means a cause which prevents a

reasonable man of an ordinary prudence acting under normal circumstances, without negligence or inaction or want of bona fide from furnishing the return

in time. In Gujarat Water Supply & Sewerage Board v. Unique Erectors

(Gujarat) Pvt. Ltd. (1989) AIR 973 (Supreme Court), it was held that it is

difficult to give an exact definition of the word, 'reasonable'. Reason varies in

its conclusions according to the idiosyncrasy of the individual and the times

and the circumstances of which the actor, called upon to act reasonably, knows or ought to know. In Ram Krishna Travels Pvt. Ltd. v. CCE, Vadodara, [2007 -TMI - 977 - CESTAT, MUMBAI] it was held that bonafide

belief is a reasonable cause under section 80 and as such, penalty was set

aside following ETA Engineering Ltd. v. CCE [2005 -TMI - 165 - CESTAT, NEW DELHI].

43. The assessee has submitted that according to section 67(2) of the

Finance Act, 1994 where the gross amount charged by a service provider, for

the service provided or to be provided is inclusive of service tax payable, the

value of such taxable service shall be such amount as, with the addition of tax

28

period are to be invoked, with a very serious allegation of suppression of facts

and intention to evade payment of service tax. Such serious allegations of

suppression can be invoked only if assessee has deliberately done an action

with an intention to hide certain facts from the department and department

has confirmed it beyond doubt with aid of corroborative evidence that there

was a deliberate act on part of assessee to evade tax. There is no finding in

impugned SCN which can allege that GIDC has intended to evade payment of

tax. In the absence of any finding of “intend to evade” demand cannot be

sustained. Reliance is placed on the following decisions:(i) Continental Foundation v. CCE [2007 (216) E.L.T. 177 (S.C.)](ii) CCE v. Pioneer Scientific Glass Works [2006 (197) E.L.T. 308

(S.C.)](iii) Pahwa Chemicals Pvt. Ltd. v. CCE [2005 (189) E.L.T. 257 (S.C.)](iv) Anand Nishikawa Co Ltd. v. CCE [2005 (188) E.L.T. 149]

39. The assessee has submitted that in the present case, GIDC is a body

corporate of the Government of Gujarat for performing statutory functions in

accordance with the provisions of Gujarat Industrial Act, 1962 and one of its

functions is the allotment of vacant land to various persons for industrial

purposes on long term lease basis. Thus, GIDC being a government body

could not have a malafide intention for non-payment of service tax. Reliance is

put on the following judgments:CCE v. Bharat Petroleum Corporation Ltd. (2016) 344 ELT 657 (Tri. -(i)

Hyd.)(ii) Karnataka State Tourism Dev. Cqrpn. Ltd. v. CST (2011) 21 STR 51 (Tri.-

Bang.)(iii) Maharashtra State Seed Certification Agency v. CC&CE (2016) 37 STR

655 (Tri.-Mumbai)(iv) Gujarat Narmada Valley Fertilizers & Chem. Ltd. v. CCE (2016) 37 STR

796 (Tri.-Ahmd.)

40. The said assessee has submitted that in a very recent decision by

Karnataka High Court, the HonTile HC in case of CST Bangalore Vs. Motor

World and other vide 2012’TIOL-418-HC-KAR-ST has appropriately dealt

with the issue of penalty and applicability of Section 80, the crux of the

decision is as under:

“The ingredients mentioned in the Section should exist. In respect of

Sections 76, 77 and 78 of the Act, not only the ingredients of those Sections

should exist, but also there should be absence of reasonable cause for the said

Section 78, Section 76 is not attracted. Therefore, no penalty can be imposed for^

the same failure under both the provisions; Even if the ingredients stipulated in

Sections 76 and 78 of the Act are established, if the Assessee shows reasonable

cause for such failure, then the authority has no power to impose penalty in view

of Section 80 of the Act; Even after holding that the ingredients stipulated in

Sections 76 and 78 exist, and there is no reasonable cause shown for failure to

comply with the said provisions, the authority has the discretion regarding the

quantity of the penalty to be imposed. ”

41. The assessee has submitted that in case of CCE, Meenit-II v. On Dot

Couriers & Cargo Ltd. (2006) 6 STJ 337 (CESTAT, New Delhi) held that no

penalty shall be imposable on assessee for any failure referred to in the said

provisions if assessee proves that there was reasonable cause for said failure.

42. The assessee has submitted that though reasonable cause has not been

defined, it has been interpreted by various courts. In Municipal Corporation

of Delhi v. Jagannath Ashok Kumar, (1987) AIR 2316 (Supreme Court), Apex Court observed that the reasons given by the Arbitrator are cogent and

based on materials on record. Reason varies in its conclusions according to

the idiosyncrasy of the individual, and the time and circumstance in which he

thinks. In Commissioner of Wealth Tax v. Jagdish Prasad Choudhary, (1996) AIR 58 (Patna), it was held that the context of penalty provision, the

word, 'reasonable cause' would mean a cause which is beyond the control of

the assessee. 'Reasonable cause' obviously means a cause which prevents a

reasonable man of an ordinary prudence acting under normal circumstances, without negligence or inaction or want of bona fide from furnishing the return

in time. In Gujarat Water Supply & Sewerage Board v. Unique Erectors

(Gujarat) Pvt. Ltd. (1989) AIR 973 (Supreme Court), it was held that it is

difficult to give an exact definition of the word, 'reasonable'. Reason varies in

its conclusions according to the idiosyncrasy of the individual and the times