Negotiation, Risk and Russia

30

Negotiation Styles, Risk and Russia by Dr Leslie J. Shaw Associate Professor of Negotiation ESCP-EAP European School of Management and Nino Mendiburu External Consultant Mendex GmbH

-

Upload

escpeurope -

Category

Documents

-

view

0 -

download

0

Transcript of Negotiation, Risk and Russia

Negotiation Styles, Risk and Russia

by

Dr Leslie J. Shaw

Associate Professor of Negotiation

ESCP-EAP European School of Management

and

Nino Mendiburu

External Consultant

Mendex GmbH

Abstract

Negotiation styles in North-West and South-East Europe. The

concept of risk in negotiation. Russia - a case study in risk.

Transition from Communism to Capitalism. How to mitigate risk

when negotiating with Russians.

Key Words: Negotiation, Russia, risk.

Contacts:

Dr Leslie J. Shaw

Associate Professor

ESCP-EAP, 79 avenue de la République, 75011 PARIS

Email: [email protected]

Nino Mendiburu

External Consultant

Mendex GmbH, Markomannenstr. 13, 12524 BERLIN

Email: [email protected]

Culture and Negotiation

The mindsets and approaches negotiators bring to the table

shape their behaviour. It follows from this that in order to

negotiate effectively, their preparation should focus not on

substance alone but also on cultural, institutional and

behavioural differences.

Our experience over the last two decades has led us to identify

a fault-line running through Europe, dividing the continent

into two parts that we label North-West (Scandinavia, Denmark,

the British Isles, Holland, Belgium, Germany, Switzerland,

Austria) and South-East (France, Spain, Portugal, Italy,

Greece, the former Soviet Union and its satellites). Anecdotal

evidence collected by the authors suggests that these two

regions are radically different in terms of their approach to

negotiating.

The table below, based on the relative importance attached to

twelve key negotiation parameters, illustrates the two

contrasting approaches :

NW Europe SE Europe

1. Preparation high low

2. Structure/Agenda/Protocol high

low

3. Time management high low

4. Openness & Directness high low

5. Conflict & Emotion low high

6. Relationships low high

7. Listening & Feedback high low

8. Ambiguity low high

9. Empowerment high low

10. Position gap low

high

11. Contractual detail high

low

12. Packaging flexibility high

low

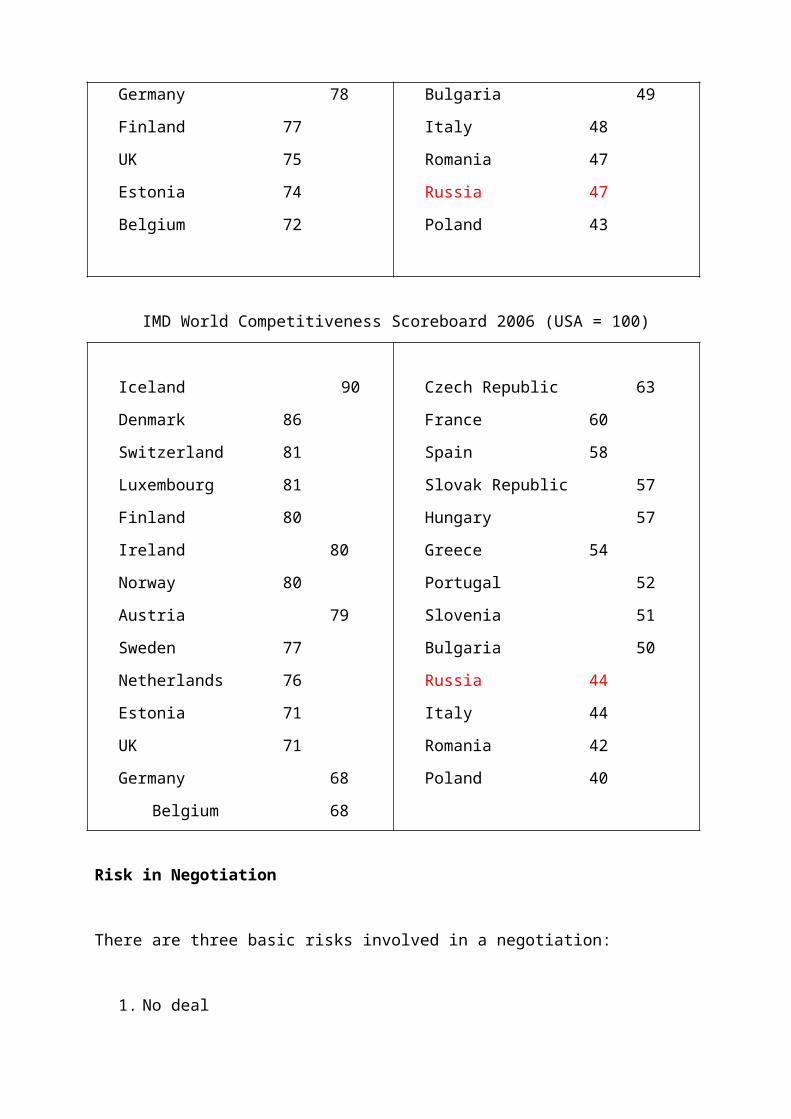

This fault line corresponds closely with the rankings of EU

member states in the IMD World Competitiveness Report over the

past ten years and a strong correlation is found between

negotiating styles and economic competitiveness. We find the NW

countries are consistently ranked at the top of the IMD league

table, while the SE countries come in lower down.

IMD World Competitiveness Scoreboard 2007 (USA = 100)

Luxembourg 92

Denmark 92

Switzerland 90

Iceland 89

Netherlands 86

Sweden 84

Austria 83

Ireland 82

Norway 82

France 62

Spain 61

Lithuania 61

Czech Republic 60

Slovak Republic 58

Hungary 58

Greece 57

Slovenia 56

Portugal 56

Germany 78

Finland 77

UK 75

Estonia 74

Belgium 72

Bulgaria 49

Italy 48

Romania 47

Russia 47

Poland 43

IMD World Competitiveness Scoreboard 2006 (USA = 100)

Iceland 90

Denmark 86

Switzerland 81

Luxembourg 81

Finland 80

Ireland 80

Norway 80

Austria 79

Sweden 77

Netherlands 76

Estonia 71

UK 71

Germany 68

Belgium 68

Czech Republic 63

France 60

Spain 58

Slovak Republic 57

Hungary 57

Greece 54

Portugal 52

Slovenia 51

Bulgaria 50

Russia 44

Italy 44

Romania 42

Poland 40

Risk in Negotiation

There are three basic risks involved in a negotiation:

1. No deal

2. A bad deal

3. A good deal that is not respected

These risks are covered by the degree of expertise and

professionalism of the negotiator, comprising thorough

preparation (including an understanding of cultural

differences) and a mastery of strategy and tactics. A good

negotiator is able to dovetail talent, experience and knowledge

of his counterpart in order to arrive at an optimal deal. He

also knows when to walk away from the table and avoid signing

an unfavourable or unworkable agreement.

As well as these three basic risks, which we shall term macro-

risks, there are other risks inherent in business negotiation

(micro-risks) that we can categorize as follows:

Intrinsic External

Technology

Cost

Delays

Volume

Commercial

Operational

Supply

Political

Act of God

Force Majeure

Legal stability

Regulatory stability

Exchange rate

Crime

Intrinsic risks can be covered in the negotiation itself. For

commercial risk, provision may be made to ensure acceptable

trading terms and bad debt recovery. External risks are more

unpredictable and difficult to manage. The negotiator may have

recourse to export credit insurance, and hedge against

fluctuating exchange rates.

All of these risks impact on profitability and need to be

anticipated during the preparation phase, so understanding the

other party’s cultural background is a key factor. We shall

illustrate this point with reference to Russia.

Russia - Opportunity and Risk

EU trucks queuing to get into Russia

In November 2006, hundreds of trucks loaded with goods from the

EU queued up at Terehova on the Latvian-Russian frontier.

Following a dispute with Poland over border controls, the

Kremlin had decided to delay truckers importing EU goods into

Russia. Some truckers waited for days to get through. Similar

queues built up at border controls at every other entry point

into Russia from the Baltic states.

This backlog of trucks symbolised the mood within Russia's

corridors of power. The Putin administration seemed keen on

pursuing its strategic objectives by putting pressure on

selected nations and corporates. While that perception had

existed for some time, investors feared the situation was

getting worse. In early December Royal Dutch Shell gave in to

Kremlin pressure and sold a majority stake in the $22bn

Sakhalin-2 oil project to Russia's state-owned energy group

Gazprom. Who would be next? Was any Russian asset safe from the

hands of the authorities?

In the short term, the Russian state's interest does seem to be

restricted to the resources sector. But if you look five or

seven years ahead there's no telling what will happen. If you

had said five years ago that the state would even consider

requisitioning these oil assets no one would have believed you.

- Stephen O'Sullivan, Deutsche UFG Moscow

The UK's collective involvement with Russia is huge. In 2006

the UK exported almost £2bn worth of goods to Russia. The same

year the net book value of UK foreign direct investment in

Russia amounted to over £2bn. The Russian embassy estimates

that the UK provided 10% of the cumulative external investment

into the post-Soviet Russian economy. Only Cyprus (where

several Russian companies are registered), the Netherlands and

Luxembourg have contributed more.

Since the collapse of Communism, some British companies have

developed huge businesses in Russia. Shell's £10bn Sakhalin

project was the biggest foreign investment in Russia. When the

project was launched in the mid 1990s Russia lacked the know-

how and cash to implement such a scheme. Ten years later Shell

was forced to give up much of the upside over claims that it

was breaching environmental laws. Gazprom, who had been

negotiating with Shell to buy shares in the venture,

eventually got the controlling interest. The grievances of the

Russian environmental protection agencies gradually

disappeared.

BP is another Russian flag-bearer, through TNK-BP, its Russian

joint venture. BP invested over $10bn in Russia between 2003

and 2006. Tony Blair called the deal a “concrete testament” to

Britain’s long-term confidence in Russia. Although much of the

original investment was clawed back in dividends, the company's

interest soon came under threat. TNK-BP had 10.5 billion

barrels of reserves, provided a quarter of BP’s production and

brought in 15% of BP’s net income. BP had no other major

projects coming on stream that could take the place of TNK-BP

if production dropped over the short term.

Russian authorities held TNK-BP to a target of producing 9bn

cubic metres of gas from the Kovykta deposit in Itkutsk region

by the end of 2006. Kovykta is a strategic reserve with some 3

trillion cubic meters of gas. TNK-BP claimed that total demand

for gas in the Itkutsk region would only reach 2.5bn cubic feet

by 2008. More ominously, Rosprirodnadzor, the state

environmental regulator, accused TNK-BP of illegal logging and

drilling at the Kovykta Siberian gas field. TNK-BP stood to

lose its licences unless it could reach a deal with Gazprom. A

deal with Gazprom would give TNK-BP access to Russian gas

consumers and enable it to reach the rated capacity at Kovykta

and abide by the terms of the license agreement.

BP appointed Russian oligarch Viktor Vekselberg to negotiate

with the Russians to resolve the dispute, and offered Gazprom a

controlling stake in the Kovytka deposit, but he was unable to

reach a deal on a partnership agreement. Gazprom claimed

Kovytka was not a priority project, although according to

informal sources it badly needs more gas both for domestic

consumption and exports. Would it be unreasonable to assume

that Gazprom is playing hard to get in order to enter the

project on more favourable terms?

It would appear so. On the eve of the regulatory agency meeting

on June 1 2007, which was expected to announce the revocation

of TNK-BP’s license, BP CEO Tony Hayward held another round of

talks with Gazprom CEO Alexei Miller. The subject of discussion

was not disclosed in full, but it probably motivated Russian

officials to suspend a decision on the revocation of the

license for 2 weeks and then for a further 2 to 3 months.

No reason was given for this reprieve, but it looked like a

diplomatic manoeuvre. The Russians did not want to revoke the

license of a Russian-British joint venture prior to the G8

summit in Germany and the International Economic Forum in St.

Petersburg, both scheduled for June 2007.

In another showdown between the Russian state and Western

investors, Oleg Mitlov, the junior environmental minister who

had conducted a concerted campaign against Shell, threatened to

revoke the licences of Peter Hambro Mining, but the crisis was

averted due to the company’s good relations with the Putin

administration.

The Russian government sees mining and energy resources as

particularly strategic assets. It could attempt to revoke those

assets, even if it does have to resort to environmental

rationales. One need only look to the AIM market to see the

exposure of UK investors to that threat. Dozens of AIM

companies are targeting Russia, such as Highland Gold, Imperial

Energy, Bema, Petroneft and Victoria Oil & Gas. Analysts say

that assets held by any company that is not state-owned are

potentially at risk, despite vehement statements to the

contrary by Russian officials.

There's no well-defined rule book in Russia, and the sands can

shift right in front of you. The rule of law is relatively

primitive. It is very difficult to go to court to enforce a

contract. That's not exclusive to Russia; there are many

countries in the world where a contract is just the beginning

of a negotiation, and Russia happens to be one of them.

- Bill Browder, CEO of Hermitage Capital Management.

(Browder was exiled from Russia for speaking out on corporate

governance issues).

Yet Browder says the potential rewards for investors outweigh

the risks for those who know what they are doing. His own fund

is proof: $1,000 invested 10 years ago is worth $25,000 today.

Although resources are where Russia's wealth lies, the booming

Russian economy is also attracting European and US consumer

goods companies. Gallaher, the tobacco company, generates over

50% of its sales from the former Soviet bloc. Retailers

including Kingfisher and Alliance Boots have made inroads into

Russia. Dixons is considering a move into Russia through an

option to buy into Eldorado, a Russian electrical retailer.

Scottish & Newcastle is Russia’s largest brewer, through Baltic

Beverage Holdings (BBH), a 50/50 joint venture with Carlsberg.

BBH accounts for over 35% of S&N group profits and growth in

Russia outstrips that in its established markets. KFC, Pizza

Hut, Coca-Cola, Heineken, Ikea, Ford and Renault have also

invested in Russia.

Many observers believe that the political risk inherent in

dealing with Russia at present is not being sufficiently

factored into company valuations. The market underestimates

this factor and investors are not paid sufficient risk

premiums, a result of the current environment of low spreads

and excess cash in the money markets.

People have underestimated the risks in Russia quite

substantially. There's an implicit understanding among

investors in the UK that large Russian companies won't be

allowed to renege on their commitments because they have an

implicit guarantee of the Russian state. But that guarantee is

only there while the Russian state is playing ball.

- Mark Otto, MD of New Europe Strategic Advisers

Russia’s Gas War

The recent signs that Russia may not always play ball have been

put down to one thing: high oil prices. Russia has grown

arrogant on the back of the resources boom, analysts say, much

in the way that Iran and Venezuela have done.

The Kremlin's decision to cut off gas supplies to Ukraine in

2006 demonstrated Putin's willingness to play hardball with the

power this affords. He subsequently punished Lithuania after

the government's decision to sell a refinery to a Polish

company rather than a Russian one. In December 2005. Russia and

Belarus signed a one-year contract for 2006 gas deliveries at

$46.68 per 1,000 cubic meters. In return, Belarus agreed to

complete on schedule its section of the Yamal-Europe pipeline,

which would transport gas to Germany via Poland. Belarus also

agreed to resolve problems regarding the leases for land on

which Russian compressor stations were to be built. But in

March 2006 the Russians went back on their commitment and gave

notice that in 2007 Belarus would be charged European rates for

Russian gas deliveries. ($230 per 1,000 cubic meters) The

official reason for this was later explained by the Russian

ambassador to Belarus, Aleksandr Surikov, who said that the

price increase was needed in order for Russia to be accepted

into the World Trade Organization, At the end of 2006

Belarusian Energy Minister Nikolai Ozerets announced that

Beltransgaz and Gazprom would set up a joint venture in 2007.

In January 2007 Gazprom pursued its aggressive strategy and

partly suspended cooperation with the operator of the Polish

segment of a major pipeline after its request for lower transit

fees was rebuffed.

Gazprom CEO Aleksei Miller with Vladimir Putin

Russia's strategic goal regarding energy is to maximize the

role of its resources in the world market and thereby increase

its geopolitical influence. To do this, it must reduce

competition and maximize dependency on its own energy

resources, as well as ensure a stable supply.

But if oil prices were to fall further, Russia would once again

become heavily dependent on foreign direct investment to keep

the economy going.

The Russian economy is fuelled by oil. The reason the Soviet

Union fell apart was not because of Ronald Reagan or Star Wars

or the Pope, but because oil prices fell below $10 a barrel.

The reason why Russia is so strong right now is that oil prices

are at $60 a barrel.

- Bill Browder, December 2006

The Russians disagree strongly and consider such concerns as

misplaced.

Publicity around Sakhalin and a handful of other cases should

not mask the opportunities that are being realised in Russia.

Substantial successful British investments are taking place

throughout the country, not least in the energy sector. It is

clear that the economic turbulence of Russia's post-Soviet

transition is over. The reform programme continues, with new

legislation being passed to strengthen the rule of law and

further liberalise the economy.

- Yury Fedotov, Russian ambassador to the UK

But actions speak louder than words. Recent interventions by

from the Kremlin have given business plenty of cause for

concern.

Working with Russia is frustrating. Russia does seem regularly

to shoot itself in the foot in terms of international PR -

something the evidence suggests that the Russian state does not

consider a high-priority problem. Russia resolutely, and on

occasion brutally, goes its own economic and political way. We

may disagree with that way or see it as self-destructive, but

the business partnership with Russia - which in the 90 years of

RBCC's existence has survived revolution, Communism, Stalin and

two world wars - will continue. As RBCC members know, the

purely business case for careful investment based on an eyes-

open understanding of the risks remains compelling.

- Godfrey Cromwell, executive director of the Russo-British Chamber of Commerce

Control over oil and gas supplies has made Russia more powerful

than it was during the Cold War, when it possessed a nuclear

arsenal capable of annihilating Western Europe. That

destruction was mutually assured, but today all of Europe is

dependent on Russia for oil and gas and the balance of power

has shifted with the boom in energy prices. Even during the

Soviet era, oil supply was used as a weapon; supplies were cut

off to Yugoslavia, Israel, China, Cuba and Finland.

Vladimir Putin’s popularity can be attributed to the structural

reforms achieved and to the fact that a middle class has

emerged under his presidency. However, these reforms were

mainly fuelled by energy exports. Russia now has the world’s

third largest foreign currency reserves, after China and Japan.

Putin’s re-nationalization of state assets and moves against

the economic oligarchs who wielded enormous power under Boris

Yeltsin have also been popular. He has restored Russia’s pride

and prevented the Federation from disintegrating.

The turnaround since Russia defaulted on its debt obligations

in 1998 has been exceptional. Russian debt now enjoys

investment-grade status with the major credit rating agencies.

Stock prices have trebled since the start of 2005 and the yield

on long term government bonds is just over one point higher

than that available on comparable US treasuries.

The collapse of the Soviet Union was followed by an economic

catastrophe far worse than the Depression of the 1930s in the

US. Output fell by 40% in a decade while stock prices fell by

over 90%. Since 1999 the economy has grown by an average 6.5% a

year and inflation has been cut by over 50%. The state’s

budgetary position has gone from a deficit of 4% to a surplus

of 8%. Foreign exchange reserves now exceed external debt.

Yet it must be noted that the surge in energy prices in recent

years accounts for one half of economic growth and that oil and

gas represent more than two thirds of market capitalisation.

On the downside, Russia’s investment rate is less than 20%,

seriously insufficient considering the crumbling infrastructure

and the average age of plant and equipment (20 years, three

times the OECD average). Russia is competitive in only two

industries - military hardware and nuclear power. Roads,

railways, pipelines, power networks and water supply all

require upgrading. Future growth is also hampered by a

declining working population, a high dependency ratio (as is

the case in Western Europe) as well as low immigration.

Despite the turnaround in Russia’s fortunes, many analysts

consider the country an unattractive location for investment.

The World Economic Forum ranked Russia 62nd in its 2006 Global

Competitiveness Report, while the IMD World Competitiveness

Yearbook places Russia in 54th place, just behind Mexico,

Brazil and Turkey. Transparency International ranked Russia

129th in its Corruption Perception Index. The World Bank put

Russia behind Uganda and Zambia in its 2006 corporate

governance ratings.

It has been estimated that protection money, bribes and

kickbacks increased from $26bn in 2000 to $316bn in 2005,

almost one half of GDP.

The high risks inherent in Russia’s capital markets are

compounded by political risk, such as disputes with

neighbouring states and murders, the most striking examples

being the assassinations of Anna Politkovskaya and Alexander

Litvinenko.

Ex-spy Yuri Shvets said Litvinenko had been employed by Western

companies to provide information on potential Russian clients

before they committed to investment deals in the former Soviet

Union. He said Litvinenko was asked by an unnamed British

company to write reports on five Russians. The report, which

apparently contained damaging personal details about a highly

placed member of Putin's administration, led to the British

company pulling out of a deal, losing the Russian figure

potential earnings of dozens of millions of dollars.

Global capital investment is highest in places and in projects

with low perception of risk, and high rates of return. Further

reducing risk for potential investors by establishing a rule of

law and further opening its markets will help Russia keep more

capital at home and attract more from abroad.

Post Soviet Russia

In 1991 the first democratically elected President Boris

Yeltsin, supported by a small group of Russian advisors and by

foreign consultants like the economists Jeffrey Sachs from

Harvard, tried to introduce democracy and market economy to

Russia.

President Boris Yeltsin and his acting prime minister, Yegor

Gaidar, adopted a program of "shock therapy," involving abrupt

deregulation of prices, privatization of state-owned

enterprises, and the shift to a market economy.

- Findling, Thackeray, Ziegler The History of Russia (1999), p.176

However, this “shock therapy” caused hyperinflation and the

majority of Russians lost their savings overnight. In addition,

the process of privatization was characterized by a high level

of corruption.

In actuality, most of the new business elite, the wealthy "New

Russians," were former Communist Party and government officials

who were ideally positioned to take advantage of the economic

transition.

- idem

In 1998, after a period of 8 years of straight economic

decline, the rouble collapsed, the Russian stock market index

dropped by 90% and most Russians again lost again the bulk of

their savings.

The increasingly unpopular Yeltsin was replaced in March 2000

by Vladimir Putin, who is the second elected president of

Russia and who has since run the country in a more centralized

and autocratic way.

Putin started his second term of office after winning 71 per

cent of the votes, which shows the high degree of acceptance of

his policy by the Russian public.

During Putin’s governance several governmental actions reduced

democracy. The Kremlin took control of most of the media

broadcasting stations and restricted press freedom. Although

his leadership style is seen to be autocratic, at least under

Putin stability has returned.

Putin closed tax loopholes for natural-resource companies and

the super-rich elite commonly called “oligarchs” and reduced

the tax burden on everyone else (flat rate tax of 13% on

personal income).

Due to their substantial economic power and influence, the

oligarchs are a major pressure group on the Russian government.

The imprisonment of Russia’s richest man, Michael Chodorkovsky,

for fraud and tax evasion was supposed to be politically

motivated and that increased concerns in the West about the

real level of democracy in Russia..

In 2006, the most important drivers of Russia’s economy were

again high oil prices and the relatively cheap rouble. Russia’s

high dependency on the export of natural resources (80% of all

exports are oil, natural gas, metals and timber) represents a

major structural weakness of the country’s economy due to the

vulnerability to price changes on world markets. In addition,

as we have already mentioned, manufacturing plant is in dire

need of modernization.

Since 2000, consumer-driven demand has played a growing role.

Real personal income has risen by over 12% and there is an

increasingly affluent middle class. Yet 25% of the Russian

population is still living below the poverty line. The majority

of poor people can be found in cities, whereas the majority of

those living in extreme poverty is situated in the rural areas.

The main reason for this still very high number of poor

Russians can be found in the transition from a planned to a

market economy and the resulting structural unemployment.

Despite widespread poverty the literacy rate of 99.6% is

extremely high. Russia still has an excellent educational

system and Russian negotiators are highly skilled

intellectually. Years of isolation means many Russians over 40

do not speak English, but this is not the case for the younger

generation.

Russia is an attractive export market for many Western

companies, because at the end of the day it is an economy that

combines strong growth and scale. Mastering negotiations with

Russian business people is thus becoming increasingly

important.

From our own experience we can state that Westerners trading

with Russia usually do not need to fear the arbitrariness of

the Russian authorities. However, if a Westerner is planning to

set up a business there, he will not only be confronted with

the formidable Russian bureaucracy and the associated bribery,

but will need what the Russians call a krysha (roof). This is a

minder, who will protect the entrepreneur from criminal

elements or state interference. It can be likened to lobbying,

but unlike in Western Europe where it is mainly used to secure

interests, in Russia it is a form of private rule of law and

hence mitigates the specific risks of doing business.

Even if reforms have been made, Russia has so far failed to

establish a strong and enforced legal framework, which is the

cornerstone of Western market economies. Institutional capacity

remains weak and corruption is still a serious issue that needs

to be addressed. The main reason for the high level of bribery

in Russia is the fact that civil servants are badly paid,

forcing them to accept bribes in order to survive.

Unfortunately this results in a serious problem which affects

the whole Russian economy. Western companies who provide

Foreign Direct Investment are confronted with requests for

kickbacks from Russian officials, usually in excess of 15% of

the contract value. The outcome of this is that initial

investments are artificially inflated, so that many business

ventures take a long time to show a profit.

The absence of rule of law in Russia after the dissolution of

the Soviet Union represents a serious problem for Western

business. Deals still very often rely on handshakes or the

threat of retaliation, but there is so far no real legal

recourse.

Nevertheless, that does not mean at all that Russians are risk-

takers. Taking Hofstede’s cultural dimension, Russians seem to

have a high level of uncertainty avoidance. This explains the

plethora of laws, rules and regulations that aim to provide

security and reduce risk. The only problem at the current stage

is that the executive authority is neither strong enough nor

willing to enforce the existing laws.

Until the end of the 20th century Russia was led by extremely

autocratic and brutal leaders. A totalitarian monarchy was

replaced by a communist dictatorship, then in 1991 the Russians

were confronted with a very tough version of a free-market

economy combined with lawlessness, often referred to as

“bandit-capitalism”.

The most obvious result is that Russians today have very little

trust in the politicians who are governing their country and

they are usually rather pessimistic, a trait for which they are

renowned. Almost no Russian work of classical literature has a

happy ending.

A second consequence is that the hardships endured by Russians

throughout history (and especially in the last 15 years or so

when most of them lost their savings due to two financial

crises) make them averse to planning ahead. This is a clear

hint that, according to Hofstede’s cultural dimensions,

Russians seem to have a very low long-term orientation.

This phenomenon is reflected in the low savings rate, as well

as in the fact that Russians prefer a bird in the hand to two

in the bush and do not really believe in the future outcome of

today’s hard work. That is why it is unfortunately very common

in Russia for employees and also managers to steal money from

their company even if that puts the future of the company at

risk and compromises higher rewards. On the other hand, a low

long-term approach facilitates change, which is definitely the

case in Russia, especially considering the tremendous

transformations that have taken place since 1991.

An additional observation that can be traced to their

historical experience is that Russian business people seldom

have a “win-win” attitude in business. They are rather zero-sum

players, which could result from the fact that in the past the

ruling class were always the winners and the people were the

losers.

The work environment in Russia is very specific. The work ethic

is practically non-existent, due to a millennium of autocratic

rule and a communist history that undermined nearly every

private initiative.

However, the status of an employee inside an organisation is

usually of enormous importance for the individual. That is why

even new Russian private companies have complex organigrams

and multilayered hierarchies. Decision-making is extremely slow

compared to Western companies and many employees are still

afraid to take any responsibility.

This attachment to status and hierarchy is a relic from the

autocratic past and the present situation of the country.

Despite a professed egalitarianism, enormous differences

existed between the ruling class and the people in the Soviet

era and these inequalities were exacerbated with the advent of

capitalism.

In contrast to the weak work ethic among employees, many

Russians have developed a remarkable entrepreneurial spirit.

Some individuals have built up business empires from scratch.

This phenomenon mainly derived from the disappearance of the

national welfare system in the beginning of the 1990s, when

many Russians simply had to become entrepreneurs in order to

secure the economic survival of their families.

Relationships and trust are a crucial factor for doing business

in Russia; hence personal contact has to be established, even

in times of constant e-mail traffic, conference calls and video

conferences.

This phenomenon may have its roots in the centuries of

oppression and scarcity, when interdependence and survival were

closely linked.

According to Hall’s cultural framework Russians would be

clearly characterised as a high-context culture. Russians are

typified by extensive information networks among family,

friends, associates and clients. All events are connected in a

meaningful context, while relationships are close and personal.

Therefore, once Western business people build trust with a

Russian, it is worth far more than any contract, which is

mainly seen as a set of guidelines for a business that is

subject to adjustment as a result of changing circumstances.

Failure to understand the importance attached to the personal

dimension will make it virtually impossible to overcome the

main impediments to progress that characterize the Russian

negotiating ethos: lack of a strong legal tradition, suspicion

of outsiders (and particularly Westerners), limited flexibility

at the table due to the control exercised by superiors, the

lack of initiative and consequent tendency to negotiate by

responding and their unhurried approach.

There is a remarkable similarity between the negotiating style

of people raised under the Bolshevik code and the younger

generation, for whom nationalism has replaced Marxism-Leninism

as an ideological driving force. They have a greater tendency

to behave irrationally, meaning they can take risky decisions

since they are less skilful at assessing risk. The chronic

instability that marked both the Soviet era and the transition

to capitalism has made Russians excessively pessimistic and

suspicious, but on the positive side they have a great ability

to adapt to a changing situation.. Relationships continue to

play a key role. Opening positions tend to be extreme and they

are quick to exploit weaknesses in the other party. Despite

this tough stance, they move rapidly to a conclusion once they

realize that they have extracted sufficient concessions to meet

their objectives and that putting further pressure on the other

party is likely to lead to a shutdown.

How to Mitigate Risk when Negotiating with Russians

It would be naive to suppose that we can produce a list of key

success factors to follow when negotiating with Russian

partners. Nevertheless, we believe that the following

guidelines will be useful in mitigating both the macro-risks

(no deal, a bad deal, a good deal that is not respected) as

well as the intrinsic and external micro-risks associated with

contractual negotiations.

10 Guidelines for mitigating risk

1. Establish a strong personal relationship with the other

party and seek out a krysha who will minimize the risks

associated with the absence of a strong rule of law.

2. Don’t adopt an explicitly win-win approach as Russians

tend to be zero-sum players and might interpret this as a

sign of weakness.

3. Be sensitive to Russian problems and address those

problems during the negotiation by using incentives.

4. Treat the Russian party with respect, even when behaviour

borders on the unacceptable (inconsistency, rigidity,

dissimulation, emotiveness).

5. Insist on agreed rules and show them a line that must not

be crossed.

6. Define timelines and back them up with penalties.

7. Never rely on verbal agreements.

8. Do not be destabilized by delays and unexpected changes.

Be ready to adapt.

9. Russians love using artful strategies and tactics. Pay

close attention to their manoeuvres.

10. Do not transfer know-how too soon.

Russia is undoubtedly a high-risk environment for the business

negotiator. Only time will tell if the positive trends in this

great country - an increasingly dynamic economy and the

development of an entrepreneurial spirit in the younger

generation - will lead to the emergence of a level playing

field. An open and competitive marketplace backed up by a

stable, equitable legal environment and a free press will

enable Russia to consolidate and extend its transition from

communism to capitalism.

Sources

Books

Findling, Thackeray, Ziegler: The History of Russia (Westport, 1999)

Hall, E.T. and M.R., Understanding Cultural Differences (Yarmouth,

1990)

Press

Daily Telegraph, New York Times, International Herald Tribune,

St. Petersburg Times

Websites

http://www.geert-hofstede.com/

http://www.imd.ch

Interviews

Michael Stern, founder and Executive Vice President of PRN in-

store TV network.

Wilfried Freund, MD of AKW A+V PAB BAUTZEN, an engineering

company selling to Russia and Central Asia.

Irina Borisova, Director of the Russian Advertising Agency I-

MEDIA.

Eduard Gershman, Director of Mendex GmbH in Moscow.