NCR, Uttar Pradesh and East India

24

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd. © Your success is our success Emkay . India Equity Research | Cement February 8, 2016 Emkay Ground Speak Cement- Road Trip NCR, Uttar Pradesh and East India ACC HOLD CMP Target Price 1,271 1,394 Ambuja Cements HOLD CMP Target Price 196 224 UltraTech Cement BUY CMP Target Price 2,843 3,281 Grasim BUY CMP Target Price 3,463 4,302 Shree Cements BUY CMP Target Price 10,350 12,900 Ramco Cements BUY CMP Target Price 382 432 India Cement HOLD CMP Target Price 84 104 JK Lakshmi Cement HOLD CMP Target Price 276 303 JK Cement ACCUMULATE CMP Target Price 465 705 OCL India BUY CMP Target Price 477 671 Orient Cement HOLD CMP Target Price 138 152 Prism Cement HOLD CMP Target Price 72 98 Mangalam Cement BUY CMP Target Price 179 257 Sanjeev Kumar Singh [email protected] +91 22 66121255 Tejashwini Kumari [email protected] +91 22 66121285 We travelled 3,200 kms (primarily by rail & road) across the NCR, Uttar Pradesh and East regions to get a firsthand idea of the logistical issues involved, met up with around 50 industry participants (cement marketing officials, sales promoters/C&F agents & stockists) to - a) Assess the cement demand and pricing situation in NCR, UP (West/Central/East) and East India, and b) Understand market size and behavior of various cement players in these regions Areas covered: NCR- Delhi, Gurgaon, Ghaziabad, Noida (Prices in Noida are kept Rs 5/bag lower than in Ghaziabad, primarily to offset movement from Delhi. The difference, till a year ago, was Rs 3/bag) and Meerut, the most competitive market in West UP (Supply from non- trade to trade segment is rampant); Central UP – Lucknow (the largest consumption centre in the state) & Kanpur; Eastern UP: Varanasi; East India: Bihar (Patna, South Bihar/Muzaffarpur, North Bihar), Jharkhand (Ranchi), Orissa (Bhubaneswar, Cuttack, Durg), West Bengal (Kolkata) and Chhattisgarh (Raipur, Bilaspur) Robust volume growth partially led by better demand; However, inventory stockings have been higher: During December, cement companies in the regions we visited, reported robust volume growth, led by a) slight improvement in demand, and, b) inventory stockings. Most of the people were of the view that empty godowns facilitated inventory pile up and secondary sale remains tepid (except in Bihar, where the feedback was different) Lower prices remain a cause of worry; Companies focus on market share gains: Cement prices remain tepid and this has worried industry. Many of them were of the opinion that this type of worrisome trend has not been witnessed in the last 10years. Most of the people believe that companies are not willing to compromise on market share, which coupled with year-end volume push by Ambuja/ACC/Lafarge, has led to pressure on cement prices North: December despatches at all-time high: In the North, December despatches were 7.2mn tonnes against the normal run-rate of 5.5-5.9mn tonnes/month in the last 4 years. Almost all the companies have registered highest ever despatches. Before Dec’15, highest despatches in the region were 6.5mn tonnes reported in the month of March, when the government led demand is usually very high Maintain Buy on Shree: Based on the cash flow & discussions with equipment suppliers, it is estimated that Shree Cement can add another 10 million tonnes capacity in the next 4 years. Combo mill (capacity: 1.6 million tons) in Aurangabad, Bihar is expected by Q1FY17- end, because as per the existing industrial policy of the state, VAT incentives are valid till June’16. Shree Cement is the first and the only company till date to have set up split location cement GU in Bihar. We believe that one should look beyond near-term concerns and factor in the sharp jump in capacities. We maintain Buy. Company Financials EPS EV/EBITDA (x) P/E (x) Companies FY16e FY17e FY16e FY17e FY16e FY17e ACC 42.6 60.2 15.7 11.5 29.9 21.1 Ambuja Cements 7.0 10.0 15.8 10.8 27.9 19.5 Grasim Industries 224.7 289.0 6.9 5.6 15.2 11.8 India Cements 4.4 10.0 6.9 5.1 19.3 8.4 Madras Cements 17.7 24.3 12.8 10.2 21.6 15.7 Shree Cements 107.8 339.2 26.3 15.0 96.0 30.5 UltraTech Cement 85.2 115.1 17.7 13.7 33.4 24.7 JK Lakshmi Cement 0.8 7.6 18.4 11.7 359.9 36.3 JK Cement 18.3 45.8 11.5 7.1 25.4 10.2 Orient Cement 4.1 6.2 20.3 9.7 33.7 22.1 OCL India 34.7 51.3 5.4 3.8 13.7 9.3 Mangalam Cement 8.7 28.8 9.5 4.9 20.6 6.2 Prism Cement 0.5 4.4 14.3 8.5 154.2 16.2 Source: Company, Emkay Research

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of NCR, Uttar Pradesh and East India

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

.

India Equity Research | Cement

February 8, 2016

Emkay Ground Speak

Cement- Road Trip

NCR, Uttar Pradesh and East India

ACC HOLD

CMP Target Price

1,271 1,394

Ambuja Cements HOLD

CMP Target Price

196 224

UltraTech Cement BUY

CMP Target Price

2,843 3,281

Grasim BUY

CMP Target Price

3,463 4,302

Shree Cements BUY

CMP Target Price

10,350 12,900

Ramco Cements BUY

CMP Target Price

382 432

India Cement HOLD

CMP Target Price

84 104

JK Lakshmi Cement HOLD

CMP Target Price

276 303

JK Cement ACCUMULATE

CMP Target Price

465 705

OCL India BUY

CMP Target Price

477 671

Orient Cement HOLD

CMP Target Price

138 152

Prism Cement HOLD

CMP Target Price

72 98

Mangalam Cement BUY

CMP Target Price

179 257

Sanjeev Kumar Singh [email protected] +91 22 66121255

Tejashwini Kumari [email protected] +91 22 66121285

We travelled 3,200 kms (primarily by rail & road) across the NCR, Uttar Pradesh and East

regions to get a firsthand idea of the logistical issues involved, met up with around 50 industry

participants (cement marketing officials, sales promoters/C&F agents & stockists) to - a)

Assess the cement demand and pricing situation in NCR, UP (West/Central/East) and East

India, and b) Understand market size and behavior of various cement players in these regions

Areas covered: NCR- Delhi, Gurgaon, Ghaziabad, Noida (Prices in Noida are kept Rs 5/bag

lower than in Ghaziabad, primarily to offset movement from Delhi. The difference, till a year

ago, was Rs 3/bag) and Meerut, the most competitive market in West UP (Supply from non-

trade to trade segment is rampant); Central UP – Lucknow (the largest consumption centre

in the state) & Kanpur; Eastern UP: Varanasi; East India: Bihar (Patna, South

Bihar/Muzaffarpur, North Bihar), Jharkhand (Ranchi), Orissa (Bhubaneswar, Cuttack, Durg),

West Bengal (Kolkata) and Chhattisgarh (Raipur, Bilaspur)

Robust volume growth partially led by better demand; However, inventory stockings

have been higher: During December, cement companies in the regions we visited, reported

robust volume growth, led by a) slight improvement in demand, and, b) inventory stockings.

Most of the people were of the view that empty godowns facilitated inventory pile up and

secondary sale remains tepid (except in Bihar, where the feedback was different)

Lower prices remain a cause of worry; Companies focus on market share gains:

Cement prices remain tepid and this has worried industry. Many of them were of the opinion

that this type of worrisome trend has not been witnessed in the last 10years. Most of the

people believe that companies are not willing to compromise on market share, which coupled

with year-end volume push by Ambuja/ACC/Lafarge, has led to pressure on cement prices

North: December despatches at all-time high: In the North, December despatches were

7.2mn tonnes against the normal run-rate of 5.5-5.9mn tonnes/month in the last 4 years.

Almost all the companies have registered highest ever despatches. Before Dec’15, highest

despatches in the region were 6.5mn tonnes reported in the month of March, when the

government led demand is usually very high

Maintain Buy on Shree: Based on the cash flow & discussions with equipment suppliers, it

is estimated that Shree Cement can add another 10 million tonnes capacity in the next 4

years. Combo mill (capacity: 1.6 million tons) in Aurangabad, Bihar is expected by Q1FY17-

end, because as per the existing industrial policy of the state, VAT incentives are valid till

June’16. Shree Cement is the first and the only company till date to have set up split location

cement GU in Bihar. We believe that one should look beyond near-term concerns and factor

in the sharp jump in capacities. We maintain Buy.

Company Financials

EPS EV/EBITDA (x) P/E (x)

Companies FY16e FY17e FY16e FY17e FY16e FY17e

ACC 42.6 60.2 15.7 11.5 29.9 21.1

Ambuja Cements 7.0 10.0 15.8 10.8 27.9 19.5

Grasim Industries 224.7 289.0 6.9 5.6 15.2 11.8

India Cements 4.4 10.0 6.9 5.1 19.3 8.4

Madras Cements 17.7 24.3 12.8 10.2 21.6 15.7

Shree Cements 107.8 339.2 26.3 15.0 96.0 30.5

UltraTech Cement 85.2 115.1 17.7 13.7 33.4 24.7

JK Lakshmi Cement 0.8 7.6 18.4 11.7 359.9 36.3

JK Cement 18.3 45.8 11.5 7.1 25.4 10.2

Orient Cement 4.1 6.2 20.3 9.7 33.7 22.1

OCL India 34.7 51.3 5.4 3.8 13.7 9.3

Mangalam Cement 8.7 28.8 9.5 4.9 20.6 6.2

Prism Cement 0.5 4.4 14.3 8.5 154.2 16.2

Source: Company, Emkay Research

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 2

Earnings for JKLC to remain impacted, downgrade to Hold: JKLC’s inability to gain a

strong foothold in Jharkhand, West Bengal and Orissa markets, will impact its NCR till the

time Cuttack GU gets commissioned. Cuttack Grinding unit (GU) which was expected to get

commissioned by Q3FY17 earlier is now expected to come by Q3FY18e. Railway siding at

Durg, Chhattisgarh unit has also been delayed and is now expected after 6-9 months.

Minimum time for WHRS to get commissioned at Durg Plant will be 18 months (assuming

company places order in February itself). 80% of Durg plant serves two of the lowest cement

priced markets – Chhattisgarh and Orissa – with proportion of non-trade being higher (50:50

trade: non-trade) in the Orissa market. We believe that East capacity will be a drag for the

company for at least 18 months. Though, the stock has corrected in last 6-7 months, we

believe that the concerns related to East plant will continue to keep the stock under pressure

for some time. We downgrade our rating on the stock to Hold from Buy with revised PT of

Rs303 based on 8x FY18e EV/EBITDA and Rs14/share for its stake in Udaipur Cement

Work.

Key features of markets visited

Bihar

It is an ex (depot/rake point) market. Shree Cement remains the only company to operate

on FoR basis.

The incremental volume growth has been captured almost entirely by Shree

Cement (Shree & Bangur).

Shree Cement (SCL) is the only company to have operational cement unit in the state. The

primary advantage is slag as blending material. The only cement company in the state is

Kalyanpur Cement, which is a BIFR case.

It is primarily a trade market. Lafarge “Concreto” is the highest priced brand. Lafarge is the

price & volume leader in 'A' segment, & Birla Gold (Century Textiles) is the highest priced

'B' grade brand and does the largest volume in the state.

Almost every company has separate brands for PPC & PSC (slag cement) with different

schemes. The market consists of 40+ brands.

For the first time in the last 6 years, January'16 saw no price hike.

Shree Cement has introduced the concept of small sized godowns. As a result, there is no

difference between despatches & sales, as holding capacity of godowns is very limited.

Planned Capacities in the state:

Exhibit 1: Capacity addition in Bihar

Company Capacity

(Mn Tons) Estimated

Commissioning Comments

Shree Cement (Aurangabad)

1.60 By end of June-16

UltraTech (Patliputra)

1.63 Mar-16

Will, be the closest unit to the largest consumption centre in the state, Patna. Delay of almost a year compared to original schedule.

Prism Cement 1.16 Jun-16 Located on border of E.UP & Bihar. On "rent/conversion basis".

Total 4.39

Source: Emkay Research, Industry

Orissa

The state cement market is sub-divided into:

Coastal Orissa (Bhubneshwar/Cuttack/Jajpur/Balasore/Angul): Estimated size is 0.18

million tons/month. Serious recovery related issues. Very difficult market. Being primarily a paper

bag market, loading/unloading charges are high.

Western Orissa (Sambalpur/Jharsuguda/Sundergarh): It is on Jharkhand border. Same size

as Coastal Orissa.

Southern Orissa: Attached to Andhra border. Size :0.1-01.3 million tonnes/month market.

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 3

Key features:

Very strong transport unions. The ratio of private: union truck is 1:1.

Same district in Coastal Orissa will have multiple billing.

Shree Cement has introduced the concept of paper depots. It effectively results in

secondary freight getting adjusted in primary freight itself.

Uttar Pradesh

Lucknow (Central U.P.)

ACC remains the highest priced brand in Lucknow, the largest consumption center.

Despite having the unit (Kundanganj GU) located closest to border of Lucknow district,

Reliance is not a relevant player in the trade segment.

Kanpur (Central U.P.)

ACC & JP are price & volume leaders respectively.

Reportedly, Reliance remains primarily a non-trade player & that too, the lowest priced

brand in Non-trade segment.

Varanasi (E. UP)

The largest market in E. UP (larger than Allahabad).

Jharkhand

Dalmia (paper bags) is being sold at par with Shree (WSP). It effectively indicates discount of Rs

20/bag compared to Shree Cement.

West Bengal

Extremely local brand conscious market. For any significant presence, cement grinding unit in

the state is a must. It does not have limestone reserves & hence, can’t have clinker capacity

Chhattisgarh

It is F.o.R. market. No Ex-price anywhere in Chhattisgarh. At best, even NTPC gets ex-rake rate.

For rest of non-trade buyers, pricing is F.o.R.

NCR (Delhi, Ghaziabad and Gurgaon): Robust volume growth, but at the cost of

pricing

Volume in the month of December’15 was 7.2 mn tonnes, which was the highest ever

volume recorded in the northern region. Average volume run–rate was 5.5-5.9mt/month in

the last 4 years. Before Dec ’15, highest despatches in the region were 6.5mn tonnes

reported in the month of March, when the government led demand is usually very high

Increase in volume is led by two factors: a) Partly demand push- infrastructure projects

have shown initial signals of pick-up and b) Partly stocking of inventories: Godowns were

empty (only 20-25% of storage capacity was utilized) and hence, inventory was piled up

due to low prices

Every player has done highest ever volume. Chances are that most of the volume increase

is due to stocking of inventories, as in last 10 days of Decemeber, despatches picked up

significantly (3x of normal volume). However, industry view is that if on an average, Jan &

Feb’16 volumes are 10% lower than that of Dec’15, start of demand recovery in the region

can safely be considered.

Secondary sale is lacking and major improvement in demand is still some time away. Boost

in confidence will come only after 3-4 months of consistent demand, as reason for demand

pick up in December is not very clear- actual demand, pent up demand or stocking of

inventory in anticipation of price hikes in January, which did not materialize

Market size of Gurgaon is normally 8-9 lakh tonnes/month. However, December volume

was between 10-11 lakh tonnes. Shree Cement and UltraTech despatches in Gurgaon

should be at 3 lakh tonnes and 2.4-3 lakh tonnes respectively.

Most of the people expect pickup in demand from infra segment from Mar-April, but as of

now, nothing much is happening on ground. There has not been any material procurement

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 4

of cement for road projects. Recently also, few companies were asked to submit bids, which

they refused as no timeline for order was given.

Price in Delhi is Rs10-20/bag lower than Western UP and in Noida, it is Rs5/bag lower than

Ghaziabad.

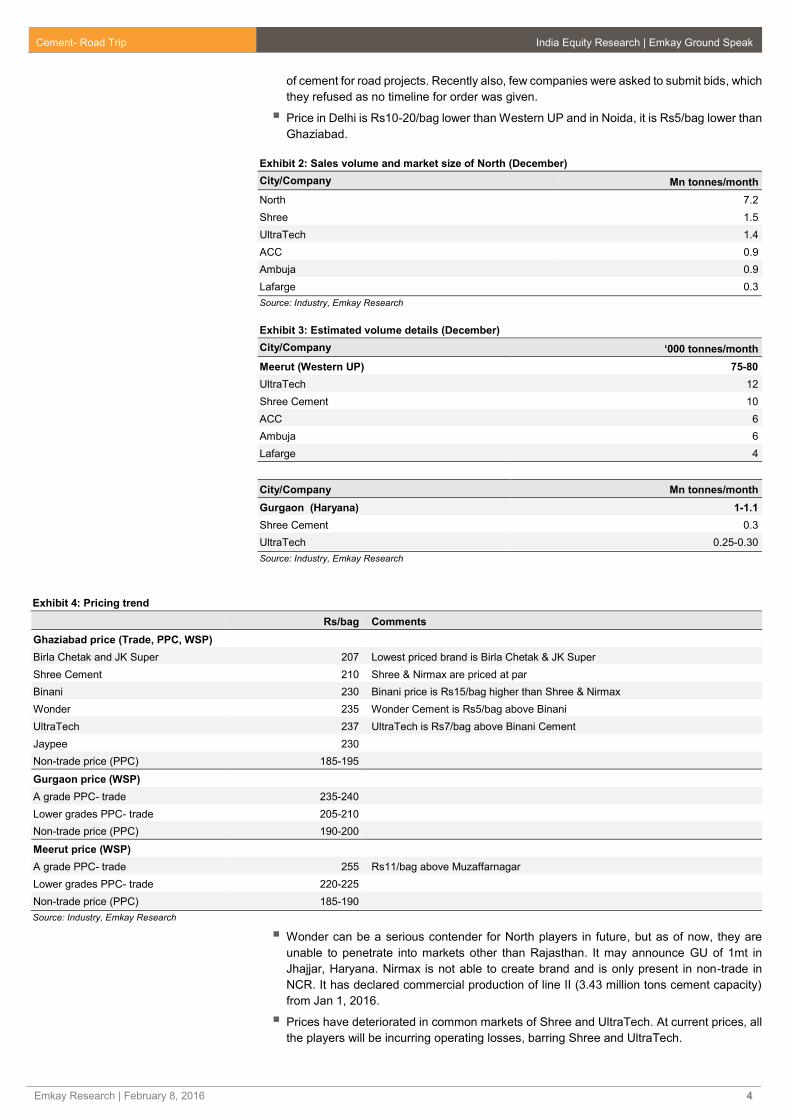

Exhibit 2: Sales volume and market size of North (December)

City/Company Mn tonnes/month

North 7.2

Shree 1.5

UltraTech 1.4

ACC 0.9

Ambuja 0.9

Lafarge 0.3

Source: Industry, Emkay Research

Exhibit 3: Estimated volume details (December)

City/Company ‘000 tonnes/month

Meerut (Western UP) 75-80

UltraTech 12

Shree Cement 10

ACC 6

Ambuja 6

Lafarge 4

City/Company Mn tonnes/month

Gurgaon (Haryana) 1-1.1

Shree Cement 0.3

UltraTech 0.25-0.30

Source: Industry, Emkay Research

Exhibit 4: Pricing trend

Rs/bag Comments

Ghaziabad price (Trade, PPC, WSP)

Birla Chetak and JK Super 207 Lowest priced brand is Birla Chetak & JK Super

Shree Cement 210 Shree & Nirmax are priced at par

Binani 230 Binani price is Rs15/bag higher than Shree & Nirmax

Wonder 235 Wonder Cement is Rs5/bag above Binani

UltraTech 237 UltraTech is Rs7/bag above Binani Cement

Jaypee 230

Non-trade price (PPC) 185-195

Gurgaon price (WSP)

A grade PPC- trade 235-240

Lower grades PPC- trade 205-210

Non-trade price (PPC) 190-200

Meerut price (WSP)

A grade PPC- trade 255 Rs11/bag above Muzaffarnagar

Lower grades PPC- trade 220-225

Non-trade price (PPC) 185-190

Source: Industry, Emkay Research

Wonder can be a serious contender for North players in future, but as of now, they are

unable to penetrate into markets other than Rajasthan. It may announce GU of 1mt in

Jhajjar, Haryana. Nirmax is not able to create brand and is only present in non-trade in

NCR. It has declared commercial production of line II (3.43 million tons cement capacity)

from Jan 1, 2016.

Prices have deteriorated in common markets of Shree and UltraTech. At current prices, all

the players will be incurring operating losses, barring Shree and UltraTech.

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 5

Uttar Pradesh (Kanpur, Lucknow and Varanasi)

The demand scenario continues to remain weak in Kanpur, due to low demand from real

estate and government projects. Dealers in Lucknow and Varanasi were of the opinion that

government projects are driving cement consumption.

Demand in Lucknow was impacted in Nov-Dec’15 due to ongoing panchayat and municipal

elections. Now, dealers believe that the allocated funds for infrastructure expenditure will

start flowing to the panchayat from the government, which would help cement consumption.

Varanasi is also witnessing good demand from the new projects announced by the

government, which includes construction of National Highways, bypasses, sewage and

other projects.

Overall, the dealers are positive on the demand pick up in the state of UP and believe that

the state elections, which are to be held in 2017 would drive growth in the state. Also, the

MNREGA funds, which were not given since last one and half years, is anticipated to start

flowing in directly to the beneficiaries, which will help improvement in demand in rural areas.

Despite the good demand from government projects, which aided strong volume growth,

prices were low in the region as along with the actual demand, lot of hoarding happened

by the dealers in order to take benefit of full year incentive schemes. Also, the

competitiveness among various players to maintain/gain market share has put pressure on

cement prices. The market can absorb price hikes, but companies are not willing to take

price hikes, leaving prices to remain subdued.

Prices in North region are much lower compared to Central region, even after adjusting for

freight of Rs15-20/bag. Hence, brands like Shree, Bangur, JK Lakshmi Cement and Nirma

are being transported to Central market (other than W. UP) through Agra route. However,

this is not sale by the concerned companies.

In Central U.P., Non-trade material of Prism Cement is being sold into trade and also, much

lower quantity is being supplied in non-trade. The company has same colour of bags for

trade and non-trade. It may be a one-off. However, 40/200 bags of non-trade were also

sold at Rs230/bag (Kanpur and Lucknow).

Location-wise, Reliance cement is best placed to serve Central U.P. However, it is not able

to penetrate the market. It is not able to create much impact in the trade segment, even in

its near-by markets (e.g. Raibareli, Lucknow and Kanpur). Reliance sells 70-80% in non-

trade in Lucknow and Kanpur.

Exhibit 5: Market size and region-wise volume (December)

City/Company ‘000 tn/month

Kanpur 120

ACC 8-10

JP 12-15

Prism 10-12

Mycem 12-15

Birla Corp 12-15

Reliance 8-10

Lafarge 5

Lucknow 200

ACC 34

JP 37-38

Mycem 37-38

Birla Corp 20 -22

Reliance 15

Prism 28

Century 10-12

Varanasi 40

ACC 15-16

JP 7-8

Prism 3.5-4

Source: Industry, Emkay Research

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 6

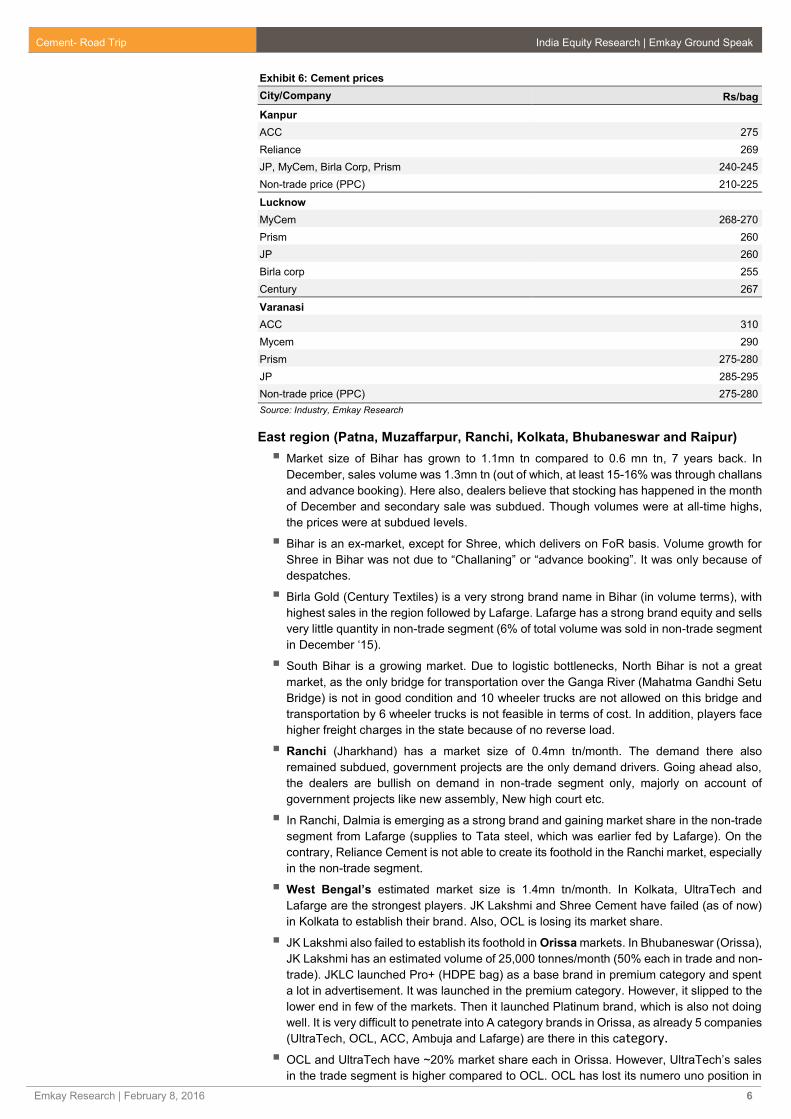

Exhibit 6: Cement prices

City/Company Rs/bag

Kanpur

ACC 275

Reliance 269

JP, MyCem, Birla Corp, Prism 240-245

Non-trade price (PPC) 210-225

Lucknow

MyCem 268-270

Prism 260

JP 260

Birla corp 255

Century 267

Varanasi

ACC 310

Mycem 290

Prism 275-280

JP 285-295

Non-trade price (PPC) 275-280

Source: Industry, Emkay Research

East region (Patna, Muzaffarpur, Ranchi, Kolkata, Bhubaneswar and Raipur)

Market size of Bihar has grown to 1.1mn tn compared to 0.6 mn tn, 7 years back. In

December, sales volume was 1.3mn tn (out of which, at least 15-16% was through challans

and advance booking). Here also, dealers believe that stocking has happened in the month

of December and secondary sale was subdued. Though volumes were at all-time highs,

the prices were at subdued levels.

Bihar is an ex-market, except for Shree, which delivers on FoR basis. Volume growth for

Shree in Bihar was not due to “Challaning” or “advance booking”. It was only because of

despatches.

Birla Gold (Century Textiles) is a very strong brand name in Bihar (in volume terms), with

highest sales in the region followed by Lafarge. Lafarge has a strong brand equity and sells

very little quantity in non-trade segment (6% of total volume was sold in non-trade segment

in December ‘15).

South Bihar is a growing market. Due to logistic bottlenecks, North Bihar is not a great

market, as the only bridge for transportation over the Ganga River (Mahatma Gandhi Setu

Bridge) is not in good condition and 10 wheeler trucks are not allowed on this bridge and

transportation by 6 wheeler trucks is not feasible in terms of cost. In addition, players face

higher freight charges in the state because of no reverse load.

Ranchi (Jharkhand) has a market size of 0.4mn tn/month. The demand there also

remained subdued, government projects are the only demand drivers. Going ahead also,

the dealers are bullish on demand in non-trade segment only, majorly on account of

government projects like new assembly, New high court etc.

In Ranchi, Dalmia is emerging as a strong brand and gaining market share in the non-trade

segment from Lafarge (supplies to Tata steel, which was earlier fed by Lafarge). On the

contrary, Reliance Cement is not able to create its foothold in the Ranchi market, especially

in the non-trade segment.

West Bengal’s estimated market size is 1.4mn tn/month. In Kolkata, UltraTech and

Lafarge are the strongest players. JK Lakshmi and Shree Cement have failed (as of now)

in Kolkata to establish their brand. Also, OCL is losing its market share.

JK Lakshmi also failed to establish its foothold in Orissa markets. In Bhubaneswar (Orissa),

JK Lakshmi has an estimated volume of 25,000 tonnes/month (50% each in trade and non-

trade). JKLC launched Pro+ (HDPE bag) as a base brand in premium category and spent

a lot in advertisement. It was launched in the premium category. However, it slipped to the

lower end in few of the markets. Then it launched Platinum brand, which is also not doing

well. It is very difficult to penetrate into A category brands in Orissa, as already 5 companies

(UltraTech, OCL, ACC, Ambuja and Lafarge) are there in this category.

OCL and UltraTech have ~20% market share each in Orissa. However, UltraTech’s sales

in the trade segment is higher compared to OCL. OCL has lost its numero uno position in

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 7

the trade segment in the state. Coastal Orissa gets significant “consignment sale” from

Andhra Pradesh based manufacturers. My Home (Brand:Mahashakti) is the key player.

Chhattisgarh remains FoR market and there is no ex-rate applicable in the state. Demand

from infrastructure and government projects is very low in the state. UltraTech has the

strongest brand equity in the region and it is the only brand, which is spread across the

state. JK Lakshmi Cement has capitalized on volume loss of JP Associates and has

become aggressive to gain market share. Lafarge is losing market share in the state and

in trade segment. Now, it is priced at Rs10/bag lower, compared to UltraTech, which was

earlier only Rs5/bag.

Raipur also witnessed lowest pricing in the month of December. Government project

demand remains low coupled with slowdown in the rural demand (due to low rainfall).

Exhibit 7: Company-wise volume details (December)

Company mt/month

Bihar 1.3

Lafarge 0.17

Birla gold 0.2

Shree 0.15

UltraTech 0.09

ACC 0.15

Prism 0.1

Konark 0.1

Birla Corp 0.06

Kalyanpur 0.05

JP 0.09

Samrat 0.06

Ambuja 0.04

Star 0.03

Mycem 0.01

Reliance 0.02

Ranchi 0.4

Lafarge 0.1

UltraTech 0.05

ACC 0.07

Birla Corp 0.02

JP 0.01

Ambuja 0.03

OCL 0.02

Century 0.03

Dalmia 0.05

West Bengal 1.4

Lafarge 0.25

UltraTech 0.3

ACC 0.1

Birla Corp 0.07

Ambuja 0.25

OCL 0.1

Century 0.09

Dalmia 0.03

Ramco 0.09

Source: Industry, Emkay Research

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 8

Exhibit 8: Company-wise volume details (December)

Company mt/month

Orissa 0.7

Bhubaneshwar 0.08

Cuttack 0.07

Birla gold 0.04

UltraTech 0.12

OCL 0.12

Shree + Bangur 0.03

Chhattisgarh 0.5

Raipur 0.13

Durg 0.05

Bilaspur 0.07

Lafarge 0.1

Shree 0.03

UltraTech 0.16

Century 0.08

JK Lakshmi 0.07

Bangur 0.03

Source: Industry, Emkay Research

Exhibit 9: Pricing trend

Region/Company Trade (Rs/bag) Non-trade (Rs/bag)

Bihar

Lafarge (Duraguard) 320 275-280

Concreto 335-340

UltraTech 298 265

ACC 315 275-280

Birla gold 265 260

Prism 245-250

Konark 290 240-245

Satna 250 240

Shree (PSC) 260

Prism 230-240

Ranchi

Lafarge 275-280

UltraTech 240-245

ACC 240-245

Birla gold 220-230 265

Dalmia 240-250 285

Ambuja 240-245

Birla corp 220-230

Konark 265-270

Kolkata

Lafarge 310-320 280

UltraTech 280-285 280

ACC 290

Birla gold 240-260

Ambuja 305-315

Birla corp 240-260

Raipur

Lafarge 225-226 195

Shree 212 185

JKLC 215-218 185

Bhubaneshwar

Lafarge 280 250

UltraTech 305 250

Ambuja 280 250

Ramco 285

OCL 305 250

Source: Industry, Emkay Research

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 9

Key Takeaways: Cement Companies

Shree Cement (SCL)

Road distance from Chhattisgarh to Bihar is lesser by almost 300 km as compared to rail.

Shree is the only company to transfer clinker from Chhattisgarh to Bihar (almost entire

quantity) by road. Chhattisgarh players are at a disadvantage compared to Satna players

for supply of cement to Bihar because of lead distance. It is more economical to supply

clinker from Chhattisgarh & use slag as blending material.

As per a large transporter of Bihar, despite no reverse load, freight/ton-km of SCL is lower,

primarily because of competitive bidding & owned fleet.

It had ~11.6% market share in Bihar in December’15. It is supplying only in trade segment.

It does not sell OPC, only PPC & PSC. Bihar is an ex-depot/rake-point market, except for

Shree, which delivers on FoR basis. It may be noted that in North (including W. UP), non-

trade segment accounts for almost 40% of volume sale of Shree.

Volume growth for Shree in Bihar was not due to “Challaning” or “advance booking”. It was

only because of despatches.

West Bengal is a difficult market to enter and non-locals find it difficult to enter there. Shree

Cement’s volume is also negligible in the state. (Non-local means without cement GU in

the state). West Bengal does not have limestone reserves & hence, can’t have clinker

capacity.

Bihar remains the focus market for the company in the East region. It has not been able to

create much impact in Jharkhand too. As per our estimate, Bihar market is more profitable

(on per ton basis) than North. The primary advantage is NOT cost of clinker but slag.

Already operational WHRS & self-sufficiency of captive power for clinker in Chhattisgarh

will improve the profitability.

Despite not having Flue Gas Desulphurisation (FGD) unit, Eastern unit is entirely on pet

coke. FGD is required to handle high sulphur pet coke.

JK Cement

The company need not pay VAT for cement sales in Rajasthan from Mangrol plant. The

VAT is exempted for 7 years.

The company is using road transport for inter-unit clinker transfer from Mangrol, Rajasthan

to Jhajjar, Haryana unit, even though railway siding and wagon tippler is operational on

both sides. This is due to steep increase in rail freight (up 27% yoy) and hence, road

transportation cost is lower than rail transport. The capex for this siding was Rs1.5bn and

the company was expecting savings of Rs200/tn in clinker transportation earlier.

One kiln at the old plant continues to remain shut due to higher operational cost. The

company will operate this kiln only if the demand improves.

It is increasing Wall Putty capacity by 0.2mtpa to 0.7mtpa. Capex cost for the same will be

Rs1.25bn. It is also establishing Dolomite grinding unit, and capex for the same will be

Rs400mn.

UAE unit of the company (Capacity - white cement 0.6mtpa or grey cement 1 mtpa) is

impacted negatively because of lower crude prices, as Saudi Arabia has shelved growth

plans.

In UAE, the grid power is available now, but the company is facing some issues in 2nd

circuit, which needs to be rectified.

There should be a saving of Rs100/tn in energy cost due to recent correction in pet coke

prices.

JK Lakshmi Cement

JKLC has tied up for a grinding unit on Bihar- Uttar Pradesh border. This was a constant

feedback from our meetings in Patna and Muzaffarpur.

The company has not been able to create much impact in Jharkhand. Sales volume of the

company is 3,000 - 4,000 tonnes/month.

In Kolkata too, the feedback was that JK Lakshmi has not been able to create much impact.

Its volume in December was ~9,000 tonnes (2,500 trade and 6,500 non-trade). JK Lakshmi

is mostly supplying OPC in the non-trade market.

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 10

West Bengal is a market where only those companies have succeeded, who are having

grinding unit in the state. 60% market is with local players and it is on the rise.

JKLC’s quality and packaging is appreciated. Higher distance is a negative. It will take

some time to create an impact in West Bengal markets.

In Bhubaneswar (Orissa), JK Lakshmi does volume of 25,000 tonnes/month (50% each in

trade and non-trade). JKLC launched Pro+ (HDPE bag) as a base brand in premium

category and spent a lot in advertisement. It was launched in the premium category.

However, it slipped to the lower end in few of the markets. Then it launched Platinum brand,

which is also not doing well. It is very difficult to penetrate into A category brands in Orissa

as already 5 companies (UltraTech, OCL, ACC, Ambuja and Lafarge) are present in this

category.

Raipur: JK Lakshmi is very aggressive in non-trade markets and is looking to gain volume

only. Shree and JKLC are the lowest priced brands in the non-trade segment (Rs180-

185/bag). We believe that this is primarily to gain market share as the company has recently

entered Chhattisgarh markets.

In Chhattisgarh, UltraTech is the only company, whose products are spread across the

state (except few specific Naxal affected areas). JKLC too, wants to spread its materials in

each and every corner. For e.g. in places like Bijapur, Dantewada and Sukuma, only

UltraTech and JKLC have presence. It will help the company to gain market share, though

NCR (naked cement realization) is likely to come down.

Prism Cement

In Central U.P, non-trade material is being sold into trade and also, much lower

quantity is being supplied in non-trade. The company has same colour of bags for trade

and non-trade. It may be a one-off. However, reportedly 40/200bags of non-trade were also

sold at Rs230/bag (Kanpur and Lucknow respectively).

The same feedback about selling of non-trade material into trade was received in Patna

(Bihar) too.

The company is taking one grinding unit on rent near Bihar-Uttar Pradesh border (within 10

kms of Eastern UP-Bihar border). Our interaction with equipment suppliers indicates that

the company is taking a GU of capacity of 175 TPH (or 1.16 mn tonnes) on rent from

Kanoria Cement. The unit is estimated to be operational in June’16.

OCL & Dalmia Bharat

OCL is supplying material from Orissa to Bihar. Dalmia Bharat is supplying from Bokaro,

Jharkhand.

Both these players have higher proportion of sales in the non-trade segment. In the non-

trade segment, the price of these brands is on the lower side. For e.g. non-trade price is

Rs240/bag FoR in Patna, compared to Rs235/bag ex-price of Prism and Rs240/bag ex-

price of Birla Corp

OCL had ~8% market share in Bihar, whereas Dalmia had 2.5% market share in Bihar in

December ’15.

OCL & Dalmia combined had ~20% market share in Jharkhand in December’15. Dalmia

Bharat sells 60-65% in non-trade segment in the state.

Dalmia Bharat has become an aggressive player and is fighting for volume share in West

Bengal. OCL has ~7% market share in West Bengal.

OCL and UltraTech have ~20% market share each in Orissa. However, UltraTech’s sales

in the trade segment is higher compared to OCL. OCL has lost its numero uno position in

the trade segment in the state.

Emami Cement

Emami Cement’s grinding unit of 335 TPH (or 2.2mt/year) capacity is expected to get

commissioned in this month. The company is expected to source first rake of clinker from

Reliance Cement to start trial-run of the plant.

Clinkerization plant (9,000 TPD or capacity 2.97 mtpa) will get commissioned only after 6-

7 months and hence, it will have to procure clinker from outside to operate the grinding unit

till clinkerisation unit stabilises.

Cement- Road Trip India Equity Research | Emkay Ground Speak

Emkay Research | February 8, 2016 11

None of the people seemed to be worried about this plant and believe that the company

will find it difficult to create market as the marketing team, C&Fs and dealers are not in

place.

Other two grinding units of the company with similar capacity of 335 TPH (or 2.2 mt/year)

each in Durgapur (West Bengal) and Baigunea (Orissa) will get commissioned by

Q4FY17e.

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

India Equity Research | Cement

February 8, 2016

Company Update

Shree Cements

Look beyond near-term challenges

CMP Target Price

Rs10,350 Rs12,900 (■)

Rating Upside

BUY (■) 24.6 %

Change in Estimates

EPS Chg FY16E/FY17E (%) NA

Target Price change (%) NA

Previous Reco BUY

Emkay vs Consensus

EPS Estimates

FY16E FY17E

Emkay 107.8 339.2

Consensus 171.4 361.3

Mean Consensus TP Rs 10,813

Stock Details

Bloomberg Code SRCM IN

Face Value (Rs) 10

Shares outstanding (mn) 35

52 Week H/L 13,360 / 9,350

M Cap (Rs bn/USD bn) 361 / 5.33

Daily Avg Volume (nos.) 16,258

Daily Avg Turnover (US$ mn) 2.5

Shareholding Pattern Dec '15

Promoters 64.8%

FIIs 13.6%

DIIs 15.4%

Public and Others 6.2%

Price Performance

(%) 1M 3M 6M 12M

Absolute (7) (14) (11) (6)

Rel. to Nifty (3) (8) 2 10

Relative price chart

Source: Bloomberg

Sanjeev Kumar Singh

+91 22 66121255

Tejashwini Kumari

+91 22 66121285

-10

-2

6

14

22

30

9500

10175

10850

11525

12200

12875

Feb-15 Apr-15 Jun-15 Aug-15 Oct-15 Dec-15 Feb-16

%Rs

Shree Cements (LHS) Rel to Nifty (RHS)

All set to become 34 mn tonnes capacity company by FY18-end. Though no incremental

capacity is on order as on date (except for 1.6mt common Ball mill in Aurangabad, Bihar),

our interaction with various industry people indicate that next phase of expansion is on

company’s radar

The reason being- the free cash flow generation and near completion of earlier planned

capex. It has received in-principal approval for 4mt of capacity in Karnataka in the Board

meeting yesterday. We believe that the company may reach to 40mt capacity in next 4

years

We have estimated next phase of Brownfield capex to be US$100, which is higher than

the capex cost of last few years. We believe that the company will not need any debt/equity

dilution for the next phase of expansion (Capacity increased 2.5x between FY10 to till date

and at the same time, gross debt has come down by 56%

Though, there could be near-term risk to earnings estimates, we believe that one should

look beyond near-term concerns and factor in sharp jump in capacities. We value the

company at 14xFY18e EV/EBITDA and maintain Buy with a TP of Rs 12,900

Next phase of capacity expansion is on radar

The company may plan capacity expansion in the North and East regions in the next 5-6

months. Industry people believe that 2 kilns of the capacity of 2mt will be ordered for Ras,

Rajasthan and Baloda Bazar, Chhattisgarh in the next 3-4 months. The Chhattisgarh unit may

have two grinding units- West Bengal and Orissa. We believe that if the demand remains

strong or the company is able to maintain profitability in excess of Rs600-700/tn, then it will

look at expansions in the North region very soon. East plant may see announcement of

capacity expansion once the company is able to achieve capacity utilization of ~70%. It has

received in-principal approval for 4mt of capacity in Karnataka in the Board meeting

yesterday. We expect it to become a 34.2mt capacity company by FY18e.

East plants: Profits to improve with commissioning of captive power plants

During Oct’15, Shree started commercial generation from 27.5MW WHRS (Waste Heat

Recovery System) at Chhattisgarh. Also, the company has plans to shift 18 MW CPP from

Ras to Baloda Bazar by September’16. Post transfer, even Chhattisgarh will be 100% on

captive power at current capacities.

Look beyond near-term concerns; maintain Buy

Though, there could be near-term risk to earnings estimates, we believe that one should look

beyond near-term concerns and factor in sharp jump in capacities and company’s ability to

fund capex without incremental debt/equity dilution. We value the company at 14xFY18e

EV/EBITDA and maintain Buy with a target price of Rs12,900.

Financial Snapshot (Standalone)

(Rs mn) FY14 FY15 FY16E* FY17E FY18E

Net Sales 58,759 64,399 55,132 92,014 110,609

EBITDA 13,784 13,302 13,091 23,605 30,258

EBITDA Margin (%) 23.5 20.7 23.7 25.7 27.4

APAT 8,677 4,618 3,755 11,816 15,918

EPS (Rs) 249.1 132.6 107.8 339.2 456.9

EPS (% chg) (14.6) (46.8) (18.7) 214.7 34.7

ROE (%) 20.3 9.3 6.9 19.4 21.6

P/E (x) 41.6 78.1 96.0 30.5 22.7

EV/EBITDA (x) 25.3 26.3 26.3 15.0 11.2

P/BV (x) 7.7 6.8 6.5 5.4 4.4

Source: Company, Emkay Research, *FY16e numbers are only for 9 months and hence, are not comparable with

FY15/FY17e numbers

Shree Cements (SRCM IN) India Equity Research | Management Meet Update

Emkay Research | February 2, 2016 13

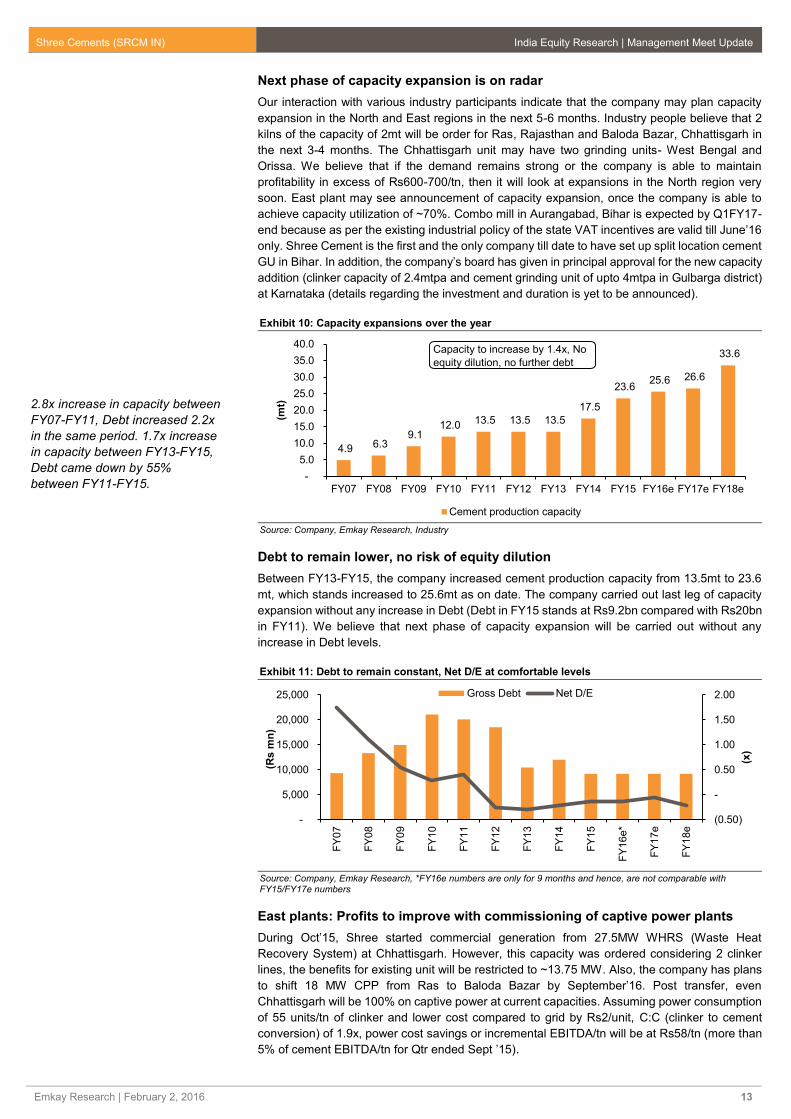

Next phase of capacity expansion is on radar

Our interaction with various industry participants indicate that the company may plan capacity

expansion in the North and East regions in the next 5-6 months. Industry people believe that 2

kilns of the capacity of 2mt will be order for Ras, Rajasthan and Baloda Bazar, Chhattisgarh in

the next 3-4 months. The Chhattisgarh unit may have two grinding units- West Bengal and

Orissa. We believe that if the demand remains strong or the company is able to maintain

profitability in excess of Rs600-700/tn, then it will look at expansions in the North region very

soon. East plant may see announcement of capacity expansion, once the company is able to

achieve capacity utilization of ~70%. Combo mill in Aurangabad, Bihar is expected by Q1FY17-

end because as per the existing industrial policy of the state VAT incentives are valid till June’16

only. Shree Cement is the first and the only company till date to have set up split location cement

GU in Bihar. In addition, the company’s board has given in principal approval for the new capacity

addition (clinker capacity of 2.4mtpa and cement grinding unit of upto 4mtpa in Gulbarga district)

at Karnataka (details regarding the investment and duration is yet to be announced).

Exhibit 10: Capacity expansions over the year

Source: Company, Emkay Research, Industry

Debt to remain lower, no risk of equity dilution

Between FY13-FY15, the company increased cement production capacity from 13.5mt to 23.6

mt, which stands increased to 25.6mt as on date. The company carried out last leg of capacity

expansion without any increase in Debt (Debt in FY15 stands at Rs9.2bn compared with Rs20bn

in FY11). We believe that next phase of capacity expansion will be carried out without any

increase in Debt levels.

Exhibit 11: Debt to remain constant, Net D/E at comfortable levels

Source: Company, Emkay Research, *FY16e numbers are only for 9 months and hence, are not comparable with

FY15/FY17e numbers

East plants: Profits to improve with commissioning of captive power plants

During Oct’15, Shree started commercial generation from 27.5MW WHRS (Waste Heat

Recovery System) at Chhattisgarh. However, this capacity was ordered considering 2 clinker

lines, the benefits for existing unit will be restricted to ~13.75 MW. Also, the company has plans

to shift 18 MW CPP from Ras to Baloda Bazar by September’16. Post transfer, even

Chhattisgarh will be 100% on captive power at current capacities. Assuming power consumption

of 55 units/tn of clinker and lower cost compared to grid by Rs2/unit, C:C (clinker to cement

conversion) of 1.9x, power cost savings or incremental EBITDA/tn will be at Rs58/tn (more than

5% of cement EBITDA/tn for Qtr ended Sept ’15).

4.9 6.3 9.1

12.0 13.5 13.5 13.5

17.5

23.6 25.6 26.6

33.6

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16e FY17e FY18e

(mt)

Cement production capacity

Capacity to increase by 1.4x, No

equity dilution, no further debt

(0.50)

-

0.50

1.00

1.50

2.00

-

5,000

10,000

15,000

20,000

25,000

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16e*

FY

17e

FY

18e

(x)

(Rs m

n)

Gross Debt Net D/E

2.8x increase in capacity between

FY07-FY11, Debt increased 2.2x

in the same period. 1.7x increase

in capacity between FY13-FY15,

Debt came down by 55%

between FY11-FY15.

Shree Cements (SRCM IN) India Equity Research | Management Meet Update

Emkay Research | February 2, 2016 14

Bihar: Company has gained double digit market share

Based on our interaction with Cement dealers and industry people, we believe that the company

had ~12% market share in Bihar in Dec ’15 which reflects the company’s ability to establish its

brand in new areas. It is to be noted here that the company started sales in Bihar in June ’14.

Free cash flow yield to improve to 4.6% in FY18e

We expect the company to generate Operating cash of Rs58bn over FY16e-FY18e, which will

be sufficient to meet capacity addition of at least 7mt in this period, even if we assume capex of

US$120/tn. Shree’s capital cost has been on the lower side compared to industry benchmark

and though, people argue that it was primarily due to expansion in a particular area, the company

proved its ability to commission capacities at lower cost in Chhattisgarh (capex of Rs8-10bn for

similar sized kiln of 2.6mt). Considering the fact that these capacities are expected to be through

Brownfield expansion, capital cost should be lower than US$120/tn. We expect free cash flow

yield of the company to be 4.9% in FY18e.

Exhibit 12: Free cash flow and capex trend

Source: Company, Emkay Research, *FY16e numbers are only for 9 months and hence, are not comparable with

FY15/FY17e numbers

Lower pet coke prices to protect margins when cement prices are under pressure

Pet Coke price basic cost has come down by 36% between Jan ’15 to Dec ’15, which would help

the company to protect margins at a time when cement prices are under pressure in its key

markets. Cement price in North India was down to Rs225/bag (as of mid-January 2016).

Exhibit 13: Pet coke price declined sharply

Source: Industry, Emkay Research

Look beyond near-term concerns; maintain Buy

Though lower cement prices and subdued demand environment pose uncertainty in the near-

term, we believe that one should look beyond near-term concerns and to factor in sharp jump in

capacities. The company’s ability to expand capacities at a much lower capex and its ability to

control operating costs would help it in gaining market share and improving profitability going

ahead. In the North region, no new kiln capacity is on order as of now and only few players will

look forward to commission capacities in this challenging environment. We value the company

at 14x FY18e EV/EBITDA and maintain Buy rating on the stock. We believe that any near-term

correction in the stock is a Buying opportunity considering its sound business fundamentals with

TP of Rs12,900.

(20,000)

(10,000)

-

10,000

20,000

30,000

40,000F

Y07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16e*

FY

17e

FY

18e

(Rs m

n)

Free cash flow Capex

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Jan

-15

Fe

b-1

5

Ma

r-15

Ap

r-15

Ma

y-1

5

Jun

-15

Jul-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

Nov-1

5

Dec-1

5

(Rs/t

n)

Shree Cements (SRCM IN) India Equity Research | Management Meet Update

Emkay Research | February 2, 2016 15

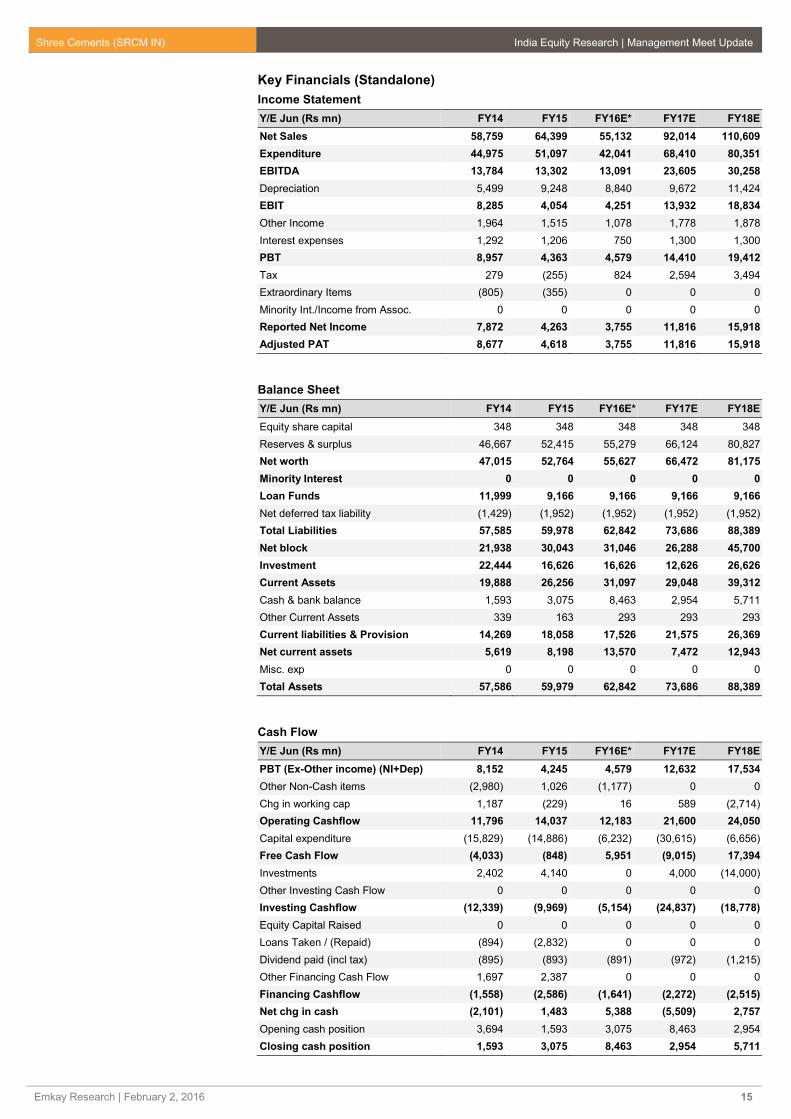

Key Financials (Standalone)

Income Statement

Y/E Jun (Rs mn) FY14 FY15 FY16E* FY17E FY18E

Net Sales 58,759 64,399 55,132 92,014 110,609

Expenditure 44,975 51,097 42,041 68,410 80,351

EBITDA 13,784 13,302 13,091 23,605 30,258

Depreciation 5,499 9,248 8,840 9,672 11,424

EBIT 8,285 4,054 4,251 13,932 18,834

Other Income 1,964 1,515 1,078 1,778 1,878

Interest expenses 1,292 1,206 750 1,300 1,300

PBT 8,957 4,363 4,579 14,410 19,412

Tax 279 (255) 824 2,594 3,494

Extraordinary Items (805) (355) 0 0 0

Minority Int./Income from Assoc. 0 0 0 0 0

Reported Net Income 7,872 4,263 3,755 11,816 15,918

Adjusted PAT 8,677 4,618 3,755 11,816 15,918

Balance Sheet

Y/E Jun (Rs mn) FY14 FY15 FY16E* FY17E FY18E

Equity share capital 348 348 348 348 348

Reserves & surplus 46,667 52,415 55,279 66,124 80,827

Net worth 47,015 52,764 55,627 66,472 81,175

Minority Interest 0 0 0 0 0

Loan Funds 11,999 9,166 9,166 9,166 9,166

Net deferred tax liability (1,429) (1,952) (1,952) (1,952) (1,952)

Total Liabilities 57,585 59,978 62,842 73,686 88,389

Net block 21,938 30,043 31,046 26,288 45,700

Investment 22,444 16,626 16,626 12,626 26,626

Current Assets 19,888 26,256 31,097 29,048 39,312

Cash & bank balance 1,593 3,075 8,463 2,954 5,711

Other Current Assets 339 163 293 293 293

Current liabilities & Provision 14,269 18,058 17,526 21,575 26,369

Net current assets 5,619 8,198 13,570 7,472 12,943

Misc. exp 0 0 0 0 0

Total Assets 57,586 59,979 62,842 73,686 88,389

Cash Flow

Y/E Jun (Rs mn) FY14 FY15 FY16E* FY17E FY18E

PBT (Ex-Other income) (NI+Dep) 8,152 4,245 4,579 12,632 17,534

Other Non-Cash items (2,980) 1,026 (1,177) 0 0

Chg in working cap 1,187 (229) 16 589 (2,714)

Operating Cashflow 11,796 14,037 12,183 21,600 24,050

Capital expenditure (15,829) (14,886) (6,232) (30,615) (6,656)

Free Cash Flow (4,033) (848) 5,951 (9,015) 17,394

Investments 2,402 4,140 0 4,000 (14,000)

Other Investing Cash Flow 0 0 0 0 0

Investing Cashflow (12,339) (9,969) (5,154) (24,837) (18,778)

Equity Capital Raised 0 0 0 0 0

Loans Taken / (Repaid) (894) (2,832) 0 0 0

Dividend paid (incl tax) (895) (893) (891) (972) (1,215)

Other Financing Cash Flow 1,697 2,387 0 0 0

Financing Cashflow (1,558) (2,586) (1,641) (2,272) (2,515)

Net chg in cash (2,101) 1,483 5,388 (5,509) 2,757

Opening cash position 3,694 1,593 3,075 8,463 2,954

Closing cash position 1,593 3,075 8,463 2,954 5,711

Shree Cements (SRCM IN) India Equity Research | Management Meet Update

Emkay Research | February 2, 2016 16

Key Ratios

Profitability (%) FY14 FY15 FY16E* FY17E FY18E

EBITDA Margin 23.5 20.7 23.7 25.7 27.4

EBIT Margin 14.1 6.3 7.7 15.1 17.0

Effective Tax Rate 3.1 (5.8) 18.0 18.0 18.0

Net Margin 14.8 7.2 6.8 12.8 14.4

ROCE 19.4 9.5 8.7 23.0 25.6

ROE 20.3 9.3 6.9 19.4 21.6

RoIC 38.1 13.3 11.9 41.6 45.0

Per Share Data (Rs) FY14 FY15 FY16E* FY17E FY18E

EPS 249.1 132.6 107.8 339.2 456.9

CEPS 406.9 398.0 361.5 616.8 784.8

BVPS 1,349.6 1,514.6 1,596.8 1,908.1 2,330.1

DPS 22.0 24.0 22.0 24.0 30.0

Valuations (x) FY14 FY15 FY16E* FY17E FY18E

PER 41.6 78.1 96.0 30.5 22.7

P/CEPS 25.4 26.0 28.6 16.8 13.2

P/BV 7.7 6.8 6.5 5.4 4.4

EV / Sales 5.9 5.4 6.3 3.8 3.1

EV / EBITDA 25.3 26.3 26.3 15.0 11.2

Dividend Yield (%) 0.2 0.2 0.2 0.2 0.3

Gearing Ratio (x) FY14 FY15 FY16E* FY17E FY18E

Net Debt/ Equity (0.3) (0.2) (0.3) (0.1) (0.3)

Net Debt/EBIDTA (0.9) (0.8) (1.2) (0.3) (0.8)

Working Cap Cycle (days) 25.0 29.0 33.8 17.9 23.9

Growth (%) FY14 FY15 FY16E* FY17E FY18E

Revenue 5.5 9.6 (14.4) 66.9 20.2

EBITDA (11.1) (3.5) (1.6) 80.3 28.2

EBIT (25.6) (51.1) 4.9 227.7 35.2

PAT (21.6) (45.8) (11.9) 214.7 34.7

Quarterly (Rs mn) Q2FY15 Q3FY15 Q4FY15 Q1FY16 Q2FY16

Revenue 15,419 15,733 17,194 17,235 18,268

EBITDA 3,035 3,375 3,516 4,108 4,240

EBITDA Margin (%) 19.7 21.5 20.4 23.8 23.2

PAT 937 1,197 1,041 1,287 1,029

EPS (Rs) 26.9 34.4 29.9 36.9 29.5

Shareholding Pattern (%) Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Promoters 64.8 64.8 64.8 64.8 64.8

FIIs 11.3 11.9 13.5 13.6 13.6

DIIs 5.6 5.2 4.7 4.9 15.4

Public and Others 18.3 18.1 17.0 16.7 6.2

*FY16e numbers are only for 9 months and hence, are not comparable with FY15/FY17e numbers

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

India Equity Research | Cement

February 8, 2016

Company Update

JK Lakshmi Cement

East plant to remain under pressure, downgrade to Hold

CMP Target Price

Rs276 Rs303 ()

Rating Upside

HOLD () 9.6 %

Change in Estimates

EPS Chg FY16E/FY17E (%) (89)/(63)

Target Price change (%) (33.2)

Previous Reco BUY

Emkay vs Consensus

EPS Estimates

FY16E FY17E

Emkay 0.8 7.6

Consensus 2.4 16.9

Mean Consensus TP Rs 390

Stock Details

Bloomberg Code JKLC IN

Face Value (Rs) 5

Shares outstanding (mn) 118

52 Week H/L 410 / 258

M Cap (Rs bn/USD bn) 33 / 0.48

Daily Avg Volume (nos.) 62,535

Daily Avg Turnover (US$ mn) 0.3

Shareholding Pattern Sep '15

Promoters 45.9%

FIIs 14.4%

DIIs 18.2%

Public and Others 21.5%

Price Performance

(%) 1M 3M 6M 12M

Absolute (17) (23) (24) (30)

Rel. to Nifty 1 (18) (13) (18)

Relative price chart

Source: Bloomberg

Sanjeev Kumar Singh

+91 22 66121255

Tejashwini Kumari

+91 22 66121285

-20

-14

-8

-2

4

10

250

280

310

340

370

400

Feb-15 Apr-15 Jun-15 Aug-15 Oct-15 Dec-15 Feb-16

%Rs

JK Lakshmi Cement (LHS) Rel to Nifty (RHS)

Continuous pricing pressure in the company’s key markets (North and West regions) and

weakening cement prices in Chhattisgarh markets too, have forced us to downgrade our

realization assumptions. Also, Cuttack grinding unit has been delayed by 12 months and

WHRS has not yet been ordered.

Our interaction with various industry participants suggest that JK Lakshmi (JKLC) has

been unable to create markets in Jharkhand, West Bengal and Orissa, which is a reason

for concern in the near-term

In Chhattisgarh, the company has gained ~13% market share in December ’15 as per our

channel checks. However, the price for JKLC remains on the lower side. We believe that

this could be company’s strategy to gain market share

Based on our channel checks and delay in commissioning of Cuttack GU, railway siding

and WHRS, we have revised FY16e/FY17e/FY18e EBITDA estimates downwards by

24.4%/29.4%/29.1%. Downgrade our rating on the stock to Hold from Buy.

Cement prices under pressure, delay in capex plans

Weak demand coupled with aggressive volume push (by ACC, Ambuja, Lafarge, Shree

Cement), led to continued pressure on cement prices during the month of January’2016,

leading to a 6.0%/4.5% MoM correction in prices in West/North region. Cuttack GU which was

earlier expected to get commissioned by Q3FY17 has now been delayed to Q3FY18e.

Railway siding has also been delayed by 6-9 months and WHRS capacity has not yet been

ordered. These factors will continue to keep the profitability of East plant under pressure at

least for next 18 months.

Difficult to gain market share in West Bengal, Jharkhand and Orissa markets;

Chhattisgarh market share at ~13%

Our interactions with various industry people suggest that the company has not been able to

gain market share in the West Bengal, Jharkhand and Orissa markets, which remains a

concern in the near-term. We believe that brand creation in Orissa markets would take some

time and Cuttack GU (estimated commissioning in Q3FY17e) would help the company to

make some impact. The company had ~13% market share in Chhattisgarh in December ’15,

but realizations are low there too (215-218/bag in Raipur).

Have sharply downgraded estimates owing to weak cement prices & delay in

Cuttack grinding unit

We have revised FY16e/FY17e/FY18e EBITDA estimates downwards by

24.4%/29.4%/29.1%, factoring in a) delay in commissioning of grinding unit at Cuttack, Orissa;

b) pressure on realization in the company’s key markets and c) the difficulty being faced by

the company to establish foothold in the market of Jharkhand and Kolkata. We downgrade

our rating on the stock to Hold from Buy with revised PT of Rs303.

Financial Snapshot (Standalone)

(Rs mn) FY14 FY15 FY16E FY17E FY18E

Net Sales 20,559 23,011 26,378 31,060 35,656

EBITDA 3,013 3,434 2,889 4,314 5,741

EBITDA Margin (%) 14.7 14.9 11.0 13.9 16.1

APAT 1,115 1,587 90 894 2,195

EPS (Rs) 9.5 13.5 0.8 7.6 18.7

EPS (% chg) (41.9) 42.4 (94.3) 890.1 145.5

ROE (%) 8.7 12.1 0.7 6.5 14.8

P/E (x) 29.2 20.5 359.9 36.3 14.8

EV/EBITDA (x) 16.1 15.0 18.4 11.7 8.2

P/BV (x) 2.5 2.4 2.4 2.3 2.1

Source: Company, Emkay Research

JK Lakshmi Cement (JKLC IN) India Equity Research | Management Meet Update

Emkay Research | February 8, 2016 18

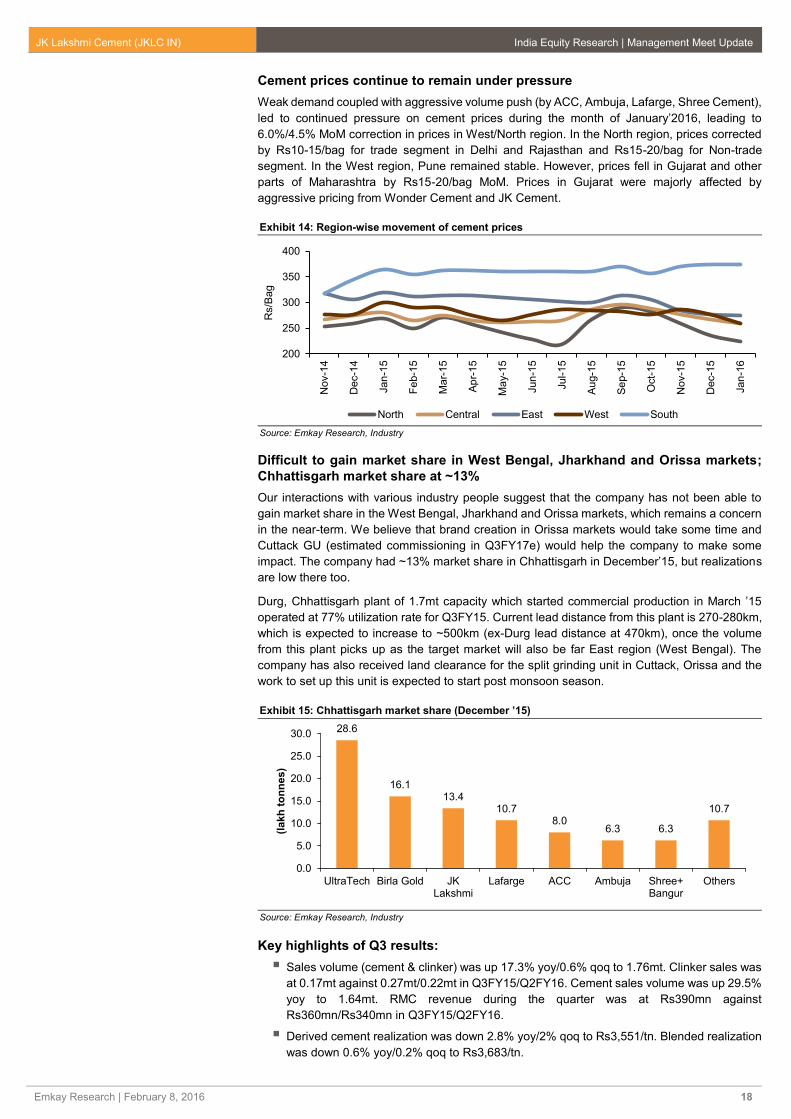

Cement prices continue to remain under pressure

Weak demand coupled with aggressive volume push (by ACC, Ambuja, Lafarge, Shree Cement),

led to continued pressure on cement prices during the month of January’2016, leading to

6.0%/4.5% MoM correction in prices in West/North region. In the North region, prices corrected

by Rs10-15/bag for trade segment in Delhi and Rajasthan and Rs15-20/bag for Non-trade

segment. In the West region, Pune remained stable. However, prices fell in Gujarat and other

parts of Maharashtra by Rs15-20/bag MoM. Prices in Gujarat were majorly affected by

aggressive pricing from Wonder Cement and JK Cement.

Exhibit 14: Region-wise movement of cement prices

Source: Emkay Research, Industry

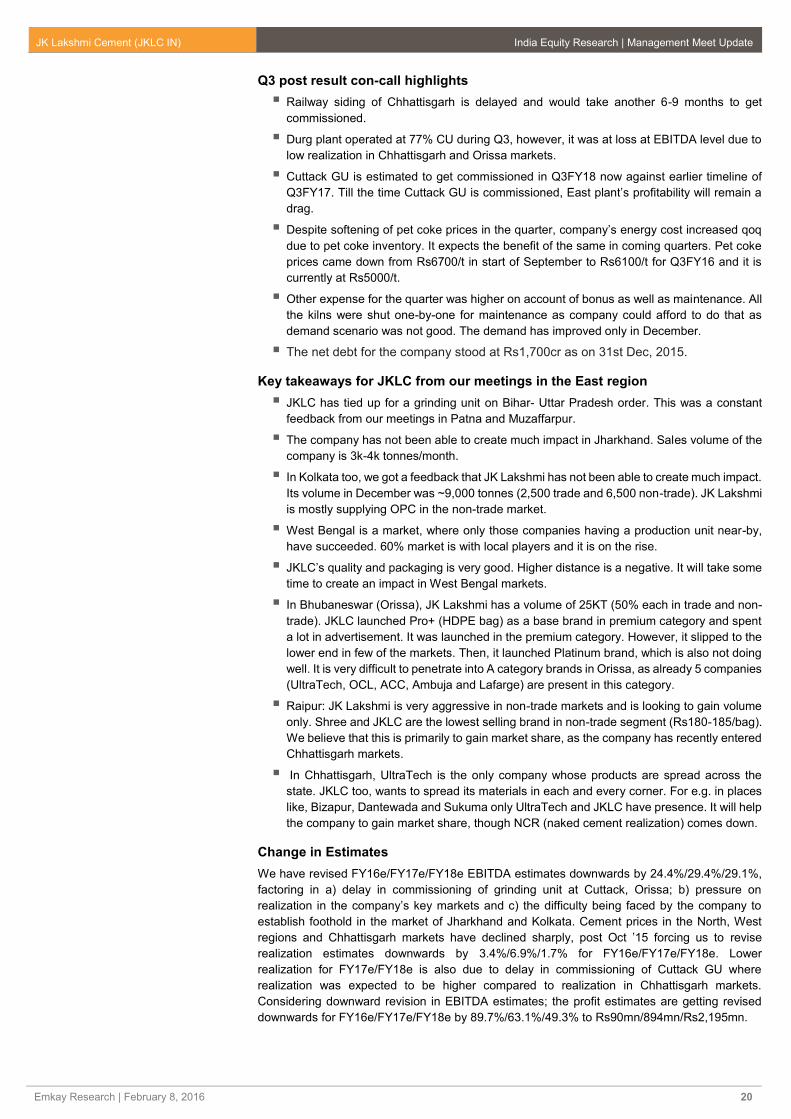

Difficult to gain market share in West Bengal, Jharkhand and Orissa markets;

Chhattisgarh market share at ~13%

Our interactions with various industry people suggest that the company has not been able to

gain market share in the West Bengal, Jharkhand and Orissa markets, which remains a concern

in the near-term. We believe that brand creation in Orissa markets would take some time and

Cuttack GU (estimated commissioning in Q3FY17e) would help the company to make some

impact. The company had ~13% market share in Chhattisgarh in December’15, but realizations

are low there too.

Durg, Chhattisgarh plant of 1.7mt capacity which started commercial production in March ’15

operated at 77% utilization rate for Q3FY15. Current lead distance from this plant is 270-280km,

which is expected to increase to ~500km (ex-Durg lead distance at 470km), once the volume

from this plant picks up as the target market will also be far East region (West Bengal). The

company has also received land clearance for the split grinding unit in Cuttack, Orissa and the

work to set up this unit is expected to start post monsoon season.

Exhibit 15: Chhattisgarh market share (December ’15)

Source: Emkay Research, Industry

Key highlights of Q3 results:

Sales volume (cement & clinker) was up 17.3% yoy/0.6% qoq to 1.76mt. Clinker sales was

at 0.17mt against 0.27mt/0.22mt in Q3FY15/Q2FY16. Cement sales volume was up 29.5%

yoy to 1.64mt. RMC revenue during the quarter was at Rs390mn against

Rs360mn/Rs340mn in Q3FY15/Q2FY16.

Derived cement realization was down 2.8% yoy/2% qoq to Rs3,551/tn. Blended realization

was down 0.6% yoy/0.2% qoq to Rs3,683/tn.

200

250

300

350

400

Nov-1

4

Dec-1

4

Jan

-15

Fe

b-1

5

Ma

r-15

Ap

r-15

Ma

y-1

5

Jun

-15

Jul-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

Nov-1

5

Dec-1

5

Jan

-16

Rs/B

ag

North Central East West South

28.6

16.113.4

10.78.0

6.3 6.3

10.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

UltraTech Birla Gold JKLakshmi

Lafarge ACC Ambuja Shree+Bangur

Others

(lakh

to

nn

es)

JK Lakshmi Cement (JKLC IN) India Equity Research | Management Meet Update

Emkay Research | February 8, 2016 19

Opex/tn was up 3.2% yoy, but down 0.3% qoq to Rs3,303/tn. Though, energy cost was

down 7.6% yoy, it increased 4.1% qoq despite decline in pet coke prices. The company

was carrying high cost inventory which restricted the benefits in the quarter and the

management expects the benefits to accrue in subsequent quarters. Employee cost/tn was

up 22.3% yoy led by capacity increase at Durg, Chhattisgarh. Freight cost/tn was up 8%

yoy/4.7% qoq to Rs911.

Led by higher cost and decline in realization, EBITDA/tn declined 24.3% yoy to Rs380

during the quarter. EBITDA was down 11.2% yoy to Rs669mn. OPM declined 324bps yoy

to 10.3%.

Depreciation was up 49.3% yoy to Rs419mn and interest cost was up 128% yoy to Rs497

mn primarily due to new capacity additions.

Exhibit 16: Quarterly results

(Y/E Mar, Rs mn) Q3FY15 Q4FY15 Q1FY16 Q2FY16 Q3FY16 YoY (%) QoQ (%) YTD FY16 YTD FY15 YoY (%)

Net Sales 5,559 5,782 5,908 6,457 6,483 16.6 0.4 18,848 17,289 9.0

Expenditure 4,805 5,067 5,401 5,791 5,814 21.0 0.4 17,005 14,509 17.2

as % of sales 86.4% 87.6% 91.4% 89.7% 89.7% 90.2% 83.9%

Consumption of RM 900 817 1,052 1,303 1,145 27.3 -12.1 3,501 2,745 27.5

as % of sales 16.2% 14.1% 17.8% 20.2% 17.7% 18.6% 15.9%

Employee Cost 349 392 489 496 501 43.4 0.9 1,486 1,069 39.1

as % of sales 6.3% 6.8% 8.3% 7.7% 7.7% 7.9% 6.2%

Power, Oil & Fuel 1,268 1,304 1,357 1,312 1,374 8.3 4.8 4,042 3,644 10.9

as % of sales 22.8% 22.5% 23.0% 20.3% 21.2% 21.4% 21.1%

Transportation & Handling 1,267 1,382 1,495 1,522 1,604 26.6 5.4 4,621 3,780 22.2

as % of sales 22.8% 23.9% 25.3% 23.6% 24.7% 24.5% 21.9%

Other expenditure 1,021 1,173 1,008 1,157 1,189 16.5 2.8 3,355 3,271 2.6

as % of sales 18.4% 20.3% 17.1% 17.9% 18.3% 17.8% 18.9%

EBITDA 754 715 507 667 669 -11.2 0.4 1,843 2,780 -33.7

Depreciation 281 270 392 417 419 49.3 0.6 1,228 905 35.7

EBIT 473 445 115 250 250 -47.2 0.0 615 1,875 -67.2

Other Income 67 178 44 60 157 133.8 164.0 260 104 150.0

Interest 218 255.9 453 477.7 497 128.0 4.0 1,428 651 119.3

PBT 322 367 -295 -168 -90 n/m n/m -553 1,328 n/m

Total Tax 37 -12 -114 -72 -53 n/m n/m -239 173 n/m

Adjusted PAT 285 378 -180 -97 -37 n/m n/m -314 1,155 n/m

Extra ordinary items 100 318 55 53 0 107 259

Reported PAT 185 61 -235 -150 -37 n/m n/m -421 896 n/m

Adjusted EPS 2.42 3.21 -1.53 -0.82 -0.31 n/m n/m -2.67 9.81 n/m

Margins (%)

EBIDTA 13.6 12.4 8.6 10.3 10.3 -324 0 9.8 16.1 -630

EBIT 8.5 7.7 1.9 3.9 3.9 -465 -2 3.3 10.8 -759

EBT 5.8 6.3 (5.0) (2.6) (1.4) -718 122 (2.9) 7.7 -1,062

PAT 5.1 6.5 (3.1) (1.5) (0.6) -570 93 (2.2) 5.2 -742

Effective Tax rate 11.5 (3.1) 38.8 42.5 59.2 4,774 1,671 43.3 13.0 3,021

Source: Company, Emkay Research

Exhibit 17: Operating cost on per tonne basis

Per ton costs Q3FY15 Q4FY15 Q1FY16 Q2FY16 Q3FY16 YoY (%) QoQ (%) YTD FY16 YTD FY15 YoY (%)

Cement volumes 1.50 1.55 1.66 1.75 1.76 17.3 0.6 5.16 4.40 17.3

Raw Material 599 527 636 745 651 8.5 -12.7 636 594 6.9

Employee 233 253 295 284 285 22.3 0.3 295 259 14.2

Power and fuel 845 841 820 750 781 -7.6 4.1 820 844 -2.8

Freight 844 891 903 870 911 8.0 4.7 903 873 3.5

Other Expenses 680 756 609 662 676 -0.7 2.1 609 803 -24.1

Net Realisation 3704 3730 3569 3692 3683 -0.6 -0.2 3569 4158 -14.2

Total cost per tonne 3201 3269 3263 3311 3303 3.2 -0.2 3263 3372 -3.2

EBIDTA per tonne 502 461 306 381 380 -24.3 -0.3 306 786 -61.0

Source: Company, Emkay Research

JK Lakshmi Cement (JKLC IN) India Equity Research | Management Meet Update

Emkay Research | February 8, 2016 20

Q3 post result con-call highlights

Railway siding of Chhattisgarh is delayed and would take another 6-9 months to get

commissioned.

Durg plant operated at 77% CU during Q3, however, it was at loss at EBITDA level due to

low realization in Chhattisgarh and Orissa markets.

Cuttack GU is estimated to get commissioned in Q3FY18 now against earlier timeline of

Q3FY17. Till the time Cuttack GU is commissioned, East plant’s profitability will remain a

drag.

Despite softening of pet coke prices in the quarter, company’s energy cost increased qoq

due to pet coke inventory. It expects the benefit of the same in coming quarters. Pet coke

prices came down from Rs6700/t in start of September to Rs6100/t for Q3FY16 and it is

currently at Rs5000/t.

Other expense for the quarter was higher on account of bonus as well as maintenance. All

the kilns were shut one-by-one for maintenance as company could afford to do that as

demand scenario was not good. The demand has improved only in December.

The net debt for the company stood at Rs1,700cr as on 31st Dec, 2015.

Key takeaways for JKLC from our meetings in the East region

JKLC has tied up for a grinding unit on Bihar- Uttar Pradesh order. This was a constant

feedback from our meetings in Patna and Muzaffarpur.

The company has not been able to create much impact in Jharkhand. Sales volume of the

company is 3k-4k tonnes/month.

In Kolkata too, we got a feedback that JK Lakshmi has not been able to create much impact.

Its volume in December was ~9,000 tonnes (2,500 trade and 6,500 non-trade). JK Lakshmi

is mostly supplying OPC in the non-trade market.

West Bengal is a market, where only those companies having a production unit near-by,

have succeeded. 60% market is with local players and it is on the rise.

JKLC’s quality and packaging is very good. Higher distance is a negative. It will take some

time to create an impact in West Bengal markets.

In Bhubaneswar (Orissa), JK Lakshmi has a volume of 25KT (50% each in trade and non-

trade). JKLC launched Pro+ (HDPE bag) as a base brand in premium category and spent

a lot in advertisement. It was launched in the premium category. However, it slipped to the

lower end in few of the markets. Then, it launched Platinum brand, which is also not doing

well. It is very difficult to penetrate into A category brands in Orissa, as already 5 companies

(UltraTech, OCL, ACC, Ambuja and Lafarge) are present in this category.

Raipur: JK Lakshmi is very aggressive in non-trade markets and is looking to gain volume

only. Shree and JKLC are the lowest selling brand in non-trade segment (Rs180-185/bag).

We believe that this is primarily to gain market share, as the company has recently entered

Chhattisgarh markets.

In Chhattisgarh, UltraTech is the only company whose products are spread across the

state. JKLC too, wants to spread its materials in each and every corner. For e.g. in places

like, Bizapur, Dantewada and Sukuma only UltraTech and JKLC have presence. It will help

the company to gain market share, though NCR (naked cement realization) comes down.

Change in Estimates

We have revised FY16e/FY17e/FY18e EBITDA estimates downwards by 24.4%/29.4%/29.1%,

factoring in a) delay in commissioning of grinding unit at Cuttack, Orissa; b) pressure on

realization in the company’s key markets and c) the difficulty being faced by the company to

establish foothold in the market of Jharkhand and Kolkata. Cement prices in the North, West

regions and Chhattisgarh markets have declined sharply, post Oct ’15 forcing us to revise

realization estimates downwards by 3.4%/6.9%/1.7% for FY16e/FY17e/FY18e. Lower

realization for FY17e/FY18e is also due to delay in commissioning of Cuttack GU where

realization was expected to be higher compared to realization in Chhattisgarh markets.

Considering downward revision in EBITDA estimates; the profit estimates are getting revised

downwards for FY16e/FY17e/FY18e by 89.7%/63.1%/49.3% to Rs90mn/894mn/Rs2,195mn.

JK Lakshmi Cement (JKLC IN) India Equity Research | Management Meet Update

Emkay Research | February 8, 2016 21

Exhibit 18: Earnings revision

FY16e FY17e FY18e

Particulars/Rs mn Earlier Revised Chg (%) Earlier Revised Chg (%) Earlier Revised Chg (%)

Sales Volume 7.3 7.2 (1.2) 8.7 8.1 (6.6) 9.5 8.6 (9.2)

Net Realisation 3,854 3,722.9 (3.4) 4,169 3,881.4 (6.9) 4,205 4,133.2 (1.7)

Revenue 27552 26,378 (4.3) 36,031 31,060 (13.8) 40,870 35,656 (12.8)

EBITDA 3822 2,889 (24.4) 6,112 4,314 (29.4) 8,096 5,741 (29.1)

EBITDA m (%) 13.9 11.0 (292) 17.0 13.9 (307) 19.8 16.1 (371)

PAT 873 90 (89.7) 2,426 894 (63.1) 4,331 2,195 (49.3)

EPS (Rs) 7 0.8 (89.7) 20.6 7.6 (63.1) 36.8 18.7 (49.3)

Source: Company, Emkay Research

East plant to continue to strain the financials, downgrade to Hold

Cuttack Grinding unit (GU) which was expected to get commissioned by Q3FY17 earlier is now

expected to come by Q3FY18e. Railway siding at Durg, Chhattisgarh unit has also been delayed

and is now expected after 6-9 months. Minimum time for WHRS to get commissioned at Durg

Plant will be 18 months (assuming company places order in February itself). 80% of Durg

plant serves two of the lowest cement priced markets – Chhattisgarh and Orissa – with

proportion of non-trade being higher (50:50 trade: non-trade) in the Orissa market. We

believe that East capacity will be a drag for the company for at least 18 months. Though, the

stock has corrected in last 6-7 months, we believe that the concerns related to East plant will

continue to keep the stock under pressure for some time. We downgrade our rating on the stock

to Hold from Buy with revised PT of Rs303 based on 8x FY18e EV/EBITDA and Rs14/share for

its stake in Udaipur Cement Work.

JK Lakshmi Cement (JKLC IN) India Equity Research | Management Meet Update

Emkay Research | February 8, 2016 22

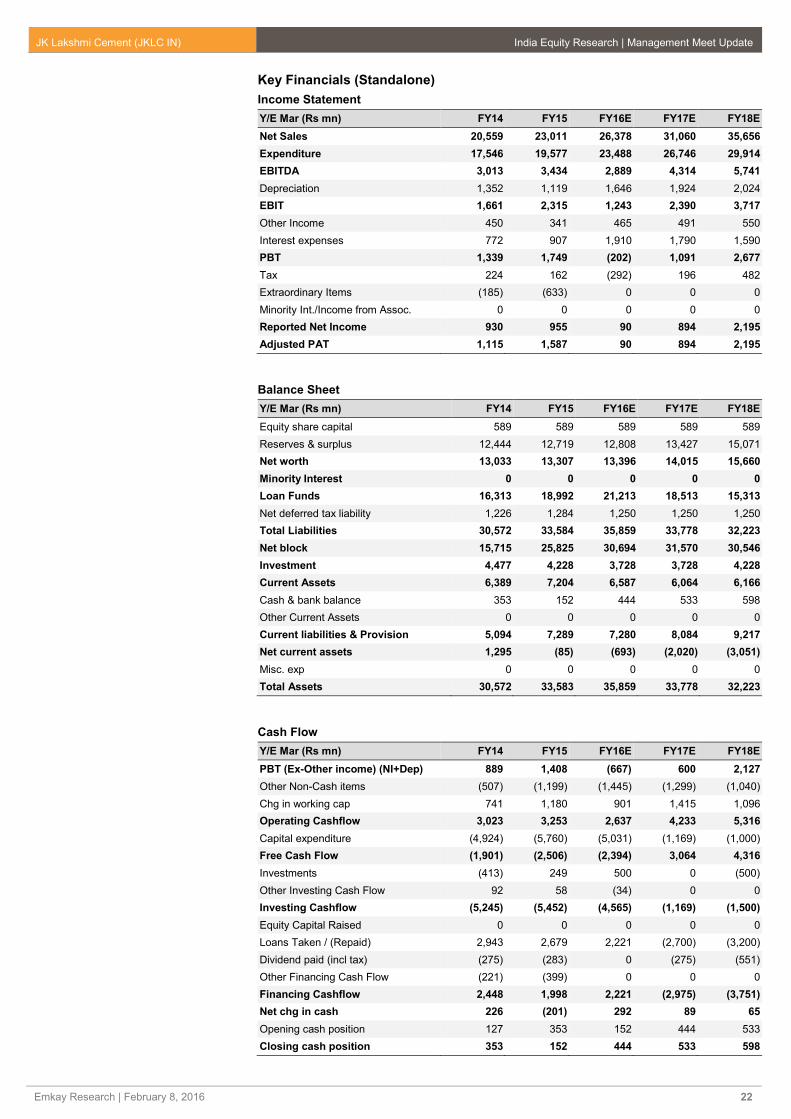

Key Financials (Standalone)

Income Statement

Y/E Mar (Rs mn) FY14 FY15 FY16E FY17E FY18E

Net Sales 20,559 23,011 26,378 31,060 35,656

Expenditure 17,546 19,577 23,488 26,746 29,914

EBITDA 3,013 3,434 2,889 4,314 5,741

Depreciation 1,352 1,119 1,646 1,924 2,024

EBIT 1,661 2,315 1,243 2,390 3,717

Other Income 450 341 465 491 550

Interest expenses 772 907 1,910 1,790 1,590

PBT 1,339 1,749 (202) 1,091 2,677

Tax 224 162 (292) 196 482

Extraordinary Items (185) (633) 0 0 0

Minority Int./Income from Assoc. 0 0 0 0 0

Reported Net Income 930 955 90 894 2,195

Adjusted PAT 1,115 1,587 90 894 2,195

Balance Sheet

Y/E Mar (Rs mn) FY14 FY15 FY16E FY17E FY18E

Equity share capital 589 589 589 589 589

Reserves & surplus 12,444 12,719 12,808 13,427 15,071

Net worth 13,033 13,307 13,396 14,015 15,660

Minority Interest 0 0 0 0 0

Loan Funds 16,313 18,992 21,213 18,513 15,313

Net deferred tax liability 1,226 1,284 1,250 1,250 1,250

Total Liabilities 30,572 33,584 35,859 33,778 32,223

Net block 15,715 25,825 30,694 31,570 30,546

Investment 4,477 4,228 3,728 3,728 4,228

Current Assets 6,389 7,204 6,587 6,064 6,166

Cash & bank balance 353 152 444 533 598

Other Current Assets 0 0 0 0 0

Current liabilities & Provision 5,094 7,289 7,280 8,084 9,217

Net current assets 1,295 (85) (693) (2,020) (3,051)

Misc. exp 0 0 0 0 0

Total Assets 30,572 33,583 35,859 33,778 32,223

Cash Flow

Y/E Mar (Rs mn) FY14 FY15 FY16E FY17E FY18E

PBT (Ex-Other income) (NI+Dep) 889 1,408 (667) 600 2,127

Other Non-Cash items (507) (1,199) (1,445) (1,299) (1,040)

Chg in working cap 741 1,180 901 1,415 1,096

Operating Cashflow 3,023 3,253 2,637 4,233 5,316

Capital expenditure (4,924) (5,760) (5,031) (1,169) (1,000)

Free Cash Flow (1,901) (2,506) (2,394) 3,064 4,316

Investments (413) 249 500 0 (500)

Other Investing Cash Flow 92 58 (34) 0 0

Investing Cashflow (5,245) (5,452) (4,565) (1,169) (1,500)

Equity Capital Raised 0 0 0 0 0

Loans Taken / (Repaid) 2,943 2,679 2,221 (2,700) (3,200)

Dividend paid (incl tax) (275) (283) 0 (275) (551)

Other Financing Cash Flow (221) (399) 0 0 0

Financing Cashflow 2,448 1,998 2,221 (2,975) (3,751)

Net chg in cash 226 (201) 292 89 65

Opening cash position 127 353 152 444 533

Closing cash position 353 152 444 533 598

JK Lakshmi Cement (JKLC IN) India Equity Research | Management Meet Update

Emkay Research | February 8, 2016 23

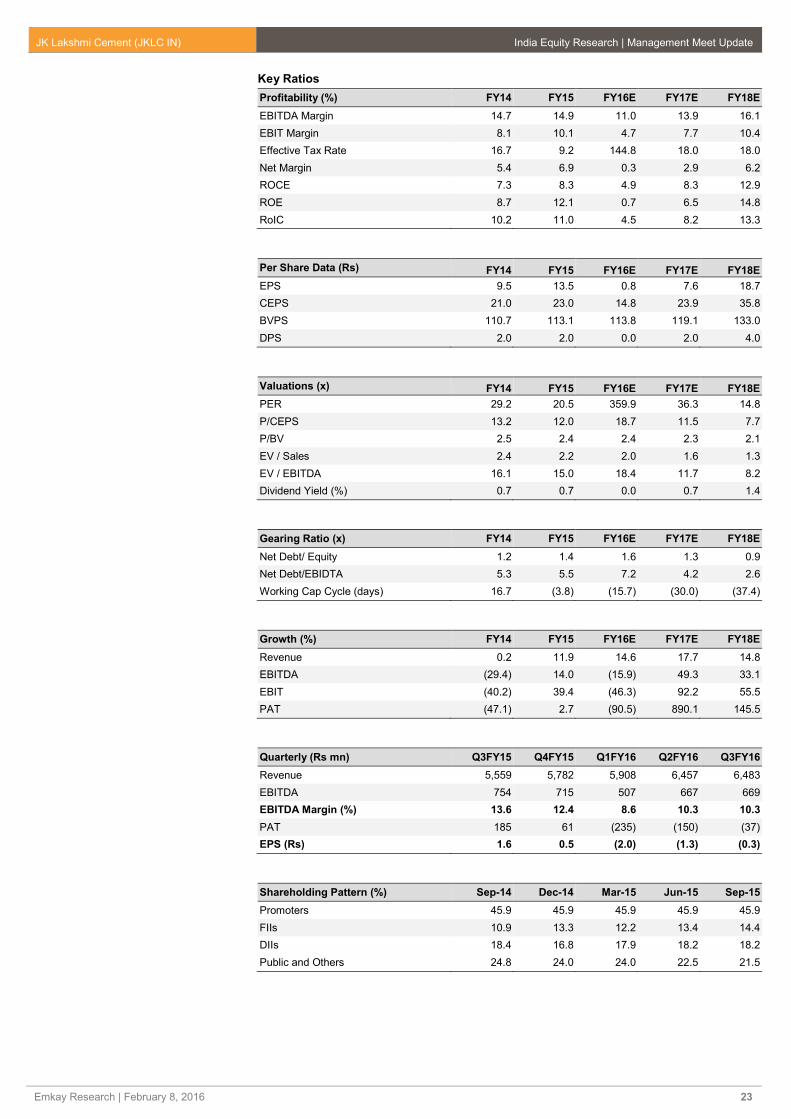

Key Ratios

Profitability (%) FY14 FY15 FY16E FY17E FY18E

EBITDA Margin 14.7 14.9 11.0 13.9 16.1

EBIT Margin 8.1 10.1 4.7 7.7 10.4

Effective Tax Rate 16.7 9.2 144.8 18.0 18.0

Net Margin 5.4 6.9 0.3 2.9 6.2

ROCE 7.3 8.3 4.9 8.3 12.9

ROE 8.7 12.1 0.7 6.5 14.8

RoIC 10.2 11.0 4.5 8.2 13.3

Per Share Data (Rs) FY14 FY15 FY16E FY17E FY18E

EPS 9.5 13.5 0.8 7.6 18.7

CEPS 21.0 23.0 14.8 23.9 35.8

BVPS 110.7 113.1 113.8 119.1 133.0

DPS 2.0 2.0 0.0 2.0 4.0

Valuations (x) FY14 FY15 FY16E FY17E FY18E

PER 29.2 20.5 359.9 36.3 14.8

P/CEPS 13.2 12.0 18.7 11.5 7.7

P/BV 2.5 2.4 2.4 2.3 2.1

EV / Sales 2.4 2.2 2.0 1.6 1.3

EV / EBITDA 16.1 15.0 18.4 11.7 8.2

Dividend Yield (%) 0.7 0.7 0.0 0.7 1.4

Gearing Ratio (x) FY14 FY15 FY16E FY17E FY18E

Net Debt/ Equity 1.2 1.4 1.6 1.3 0.9

Net Debt/EBIDTA 5.3 5.5 7.2 4.2 2.6

Working Cap Cycle (days) 16.7 (3.8) (15.7) (30.0) (37.4)

Growth (%) FY14 FY15 FY16E FY17E FY18E

Revenue 0.2 11.9 14.6 17.7 14.8

EBITDA (29.4) 14.0 (15.9) 49.3 33.1

EBIT (40.2) 39.4 (46.3) 92.2 55.5

PAT (47.1) 2.7 (90.5) 890.1 145.5

Quarterly (Rs mn) Q3FY15 Q4FY15 Q1FY16 Q2FY16 Q3FY16

Revenue 5,559 5,782 5,908 6,457 6,483

EBITDA 754 715 507 667 669

EBITDA Margin (%) 13.6 12.4 8.6 10.3 10.3

PAT 185 61 (235) (150) (37)

EPS (Rs) 1.6 0.5 (2.0) (1.3) (0.3)

Shareholding Pattern (%) Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

Promoters 45.9 45.9 45.9 45.9 45.9

FIIs 10.9 13.3 12.2 13.4 14.4

DIIs 18.4 16.8 17.9 18.2 18.2

Public and Others 24.8 24.0 24.0 22.5 21.5

JK Lakshmi Cement (JKLC IN) India Equity Research | Management Meet Update

Emkay Research | February 8, 2016 25

DISCLAIMERS AND DISCLOSURES: Emkay Global Financial Services Limited (CIN-L67120MH1995PLC084899) and its affiliates are a full-service, brokerage, investment banking, investment

management and financing group. Emkay Global Financial Services Limited (EGFSL) along with its affiliates are participants in virtually all securities trading markets in India. EGFSL was established in