National Electrification Master Plan for Lesotho - Amazon AWS

200

The Government of Lesotho National Electrification Master Plan for Lesotho Final Report October 2007

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of National Electrification Master Plan for Lesotho - Amazon AWS

The Government of Lesotho

National Electrification Master Plan for Lesotho Final Report

October 2007

The Government of Lesotho

National Electrification Master Plan for Lesotho Final Report

October 2007

Report no. 64131-0-13

Issue no. 3.2

Date of issue 20 October 2007

Prepared NBP

Checked DH/ABR/CW/GB

Approved NBP

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

1

.

Table of Contents

1 Executive Summary 6 1.1 Introduction 6 1.2 Electrification Target 6 1.3 Settlements 7 1.4 Load Forecast 8 1.5 Technical Standards 9 1.6 Systems in Remote Areas 10 1.7 Transmission System 11 1.8 Distribution Systems 11 1.9 Financial Aspects 13 1.10 Prioritisation of Settlements 14 1.11 Project Schedule Years 1 to 5 - Distribution 15 1.12 Project Schedule for Years 6 - 15 - Distribution 18 1.13 Allocation of Responsibilities 19 1.14 Future Service Models for Electricity Supply 21 1.15 Tariffs and Connection Fee 21 1.16 Subsidies 22 1.17 Institutional Development and Training 23 1.18 Monitoring and Evaluation Framework 23 1.19 Environmental Issues 25

2 Introduction 27 2.1 Electrification Target for Lesotho 27 2.2 Balancing Policy Objectives 28 2.3 Planning Criteria and Approach 29 2.4 Report Structure and Terminology 32

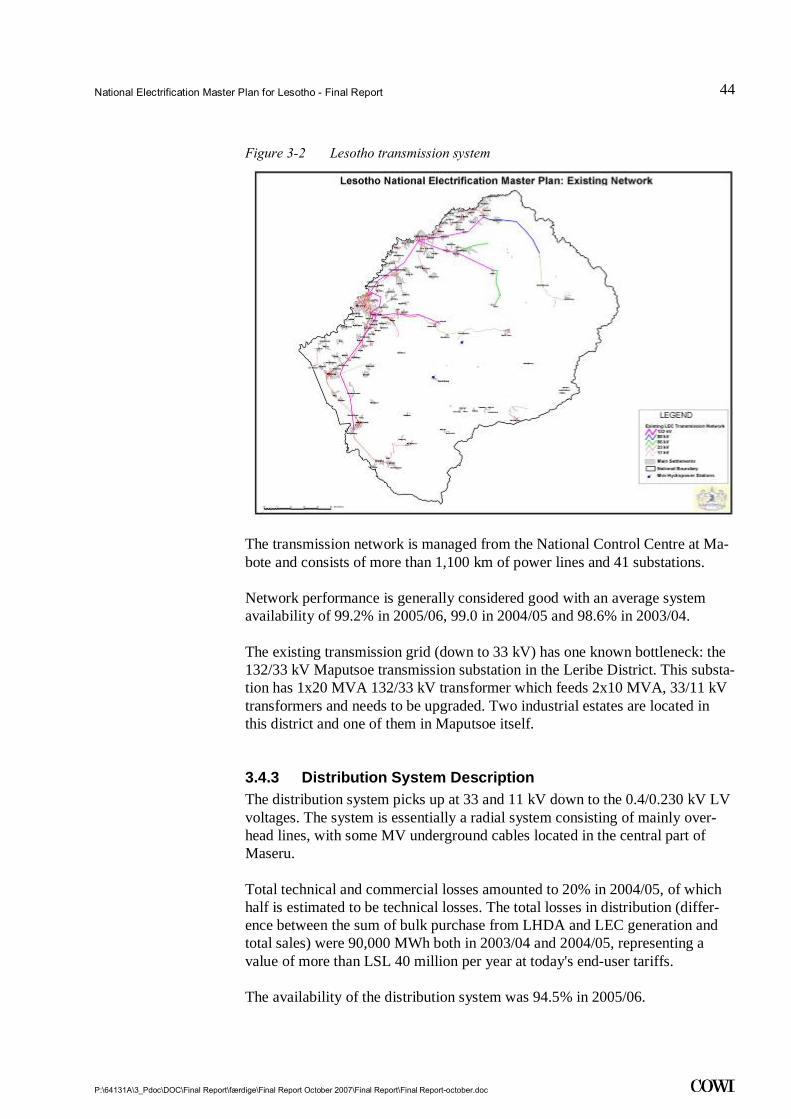

3 Background 34 3.1 Context 34 3.2 Energy Policy and Power Sector Reform 35 3.3 Institutions Involved in Electrification 37 3.4 Existing Power System 42

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

2

.

4 Socio-Economic Data and Analysis 51 4.1 Demography and Settlement Identification 51 4.2 Poverty Mapping and Energy Demand Surveys 62 4.3 WAP Studies for Electricity 63 4.4 Social Impact of Household Electrification 65 4.5 Conclusions Regarding Socio-Economic Information 66

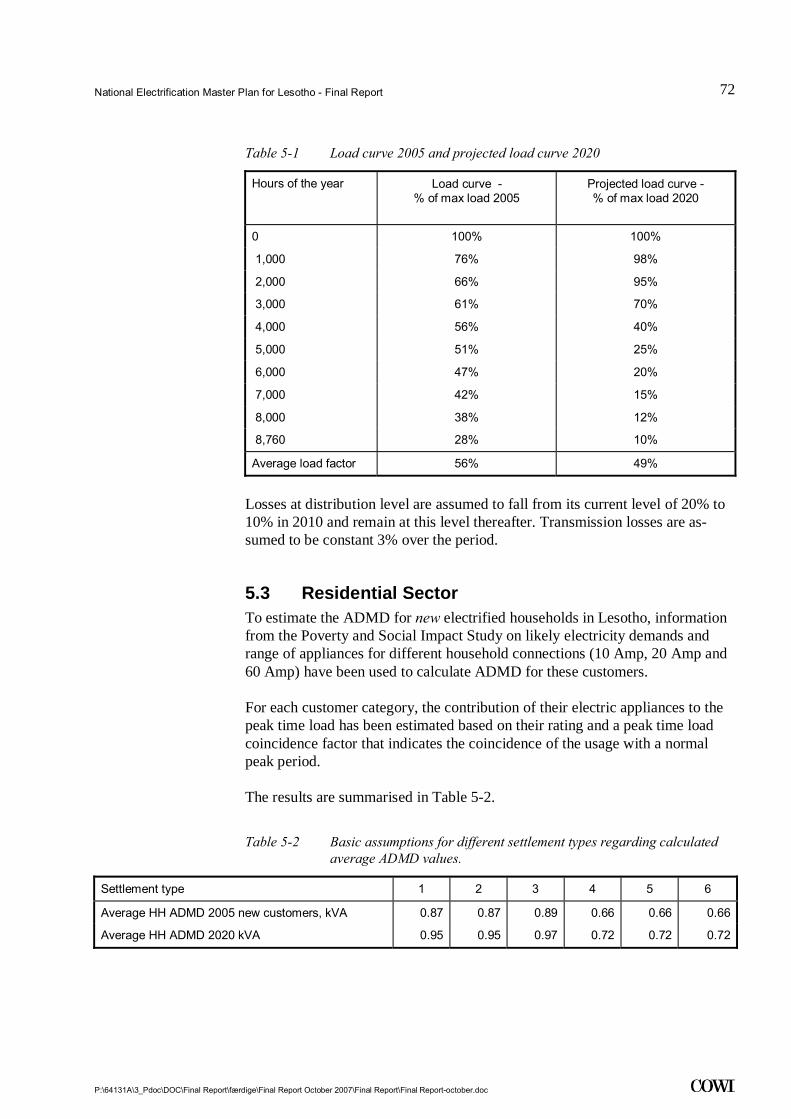

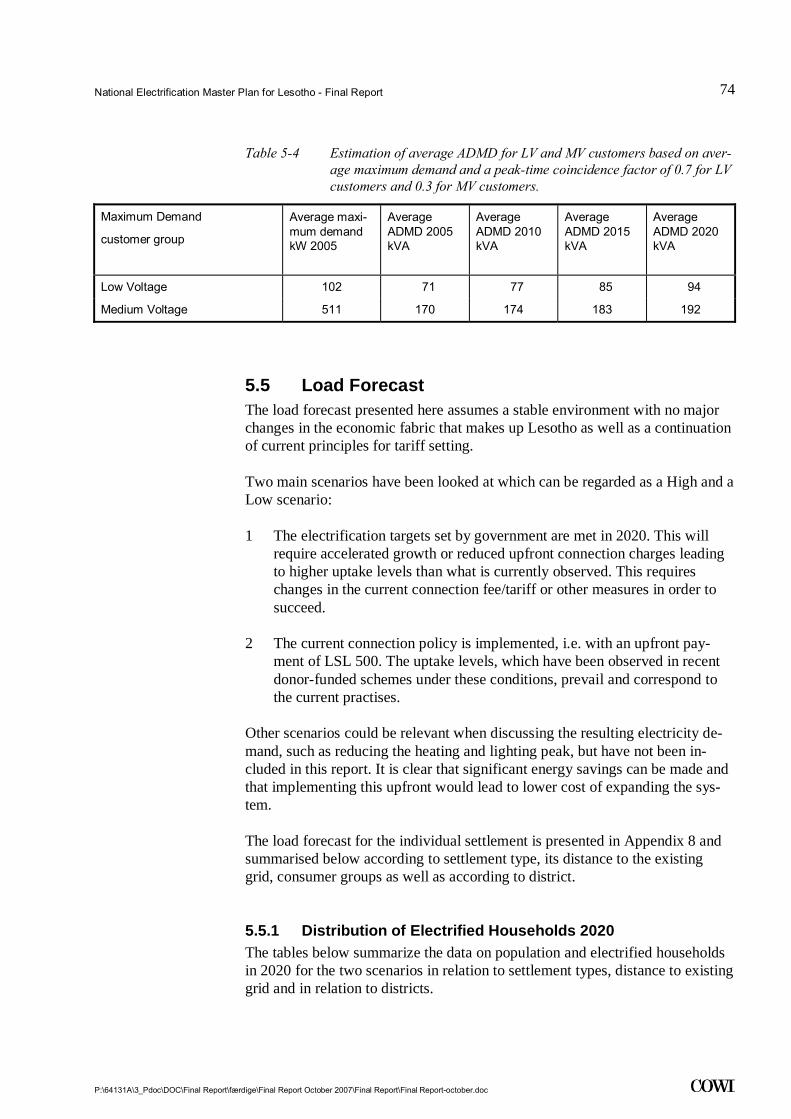

5 Load Demand Forecast 70 5.1 Methodology and General Assumptions 70 5.2 System Load Curve and Losses 71 5.3 Residential Sector 72 5.4 Other Customer Groups 73 5.5 Load Forecast 74

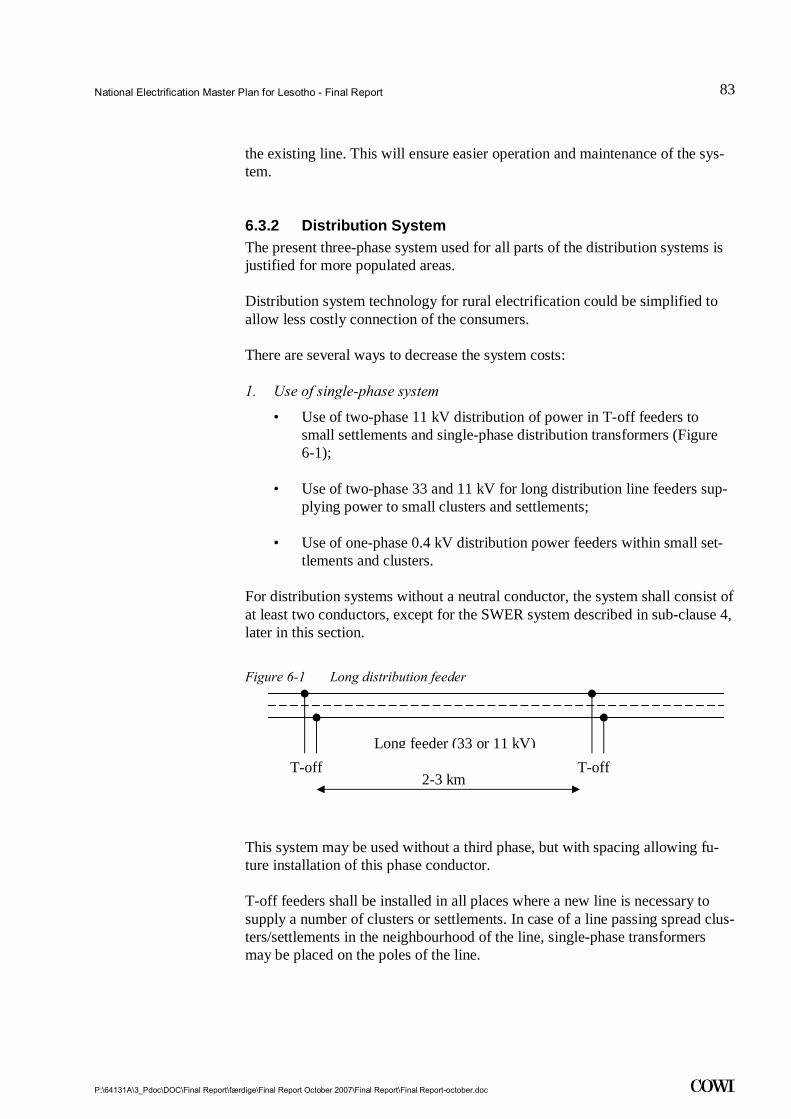

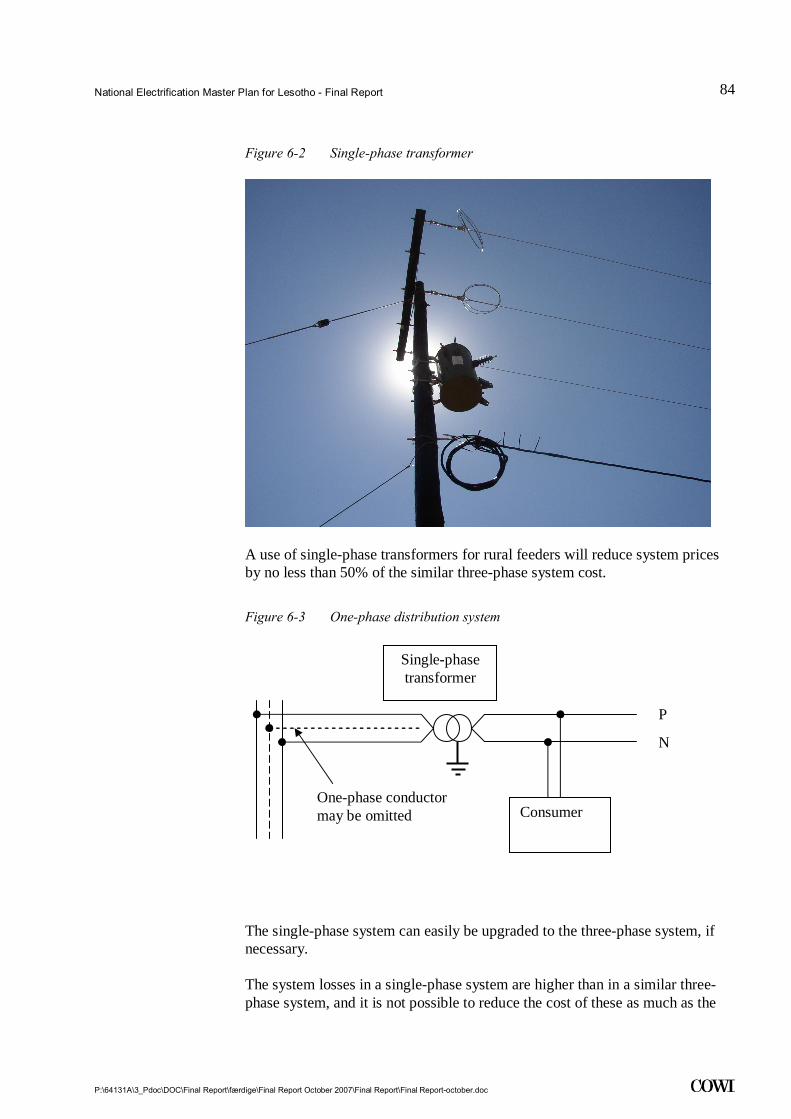

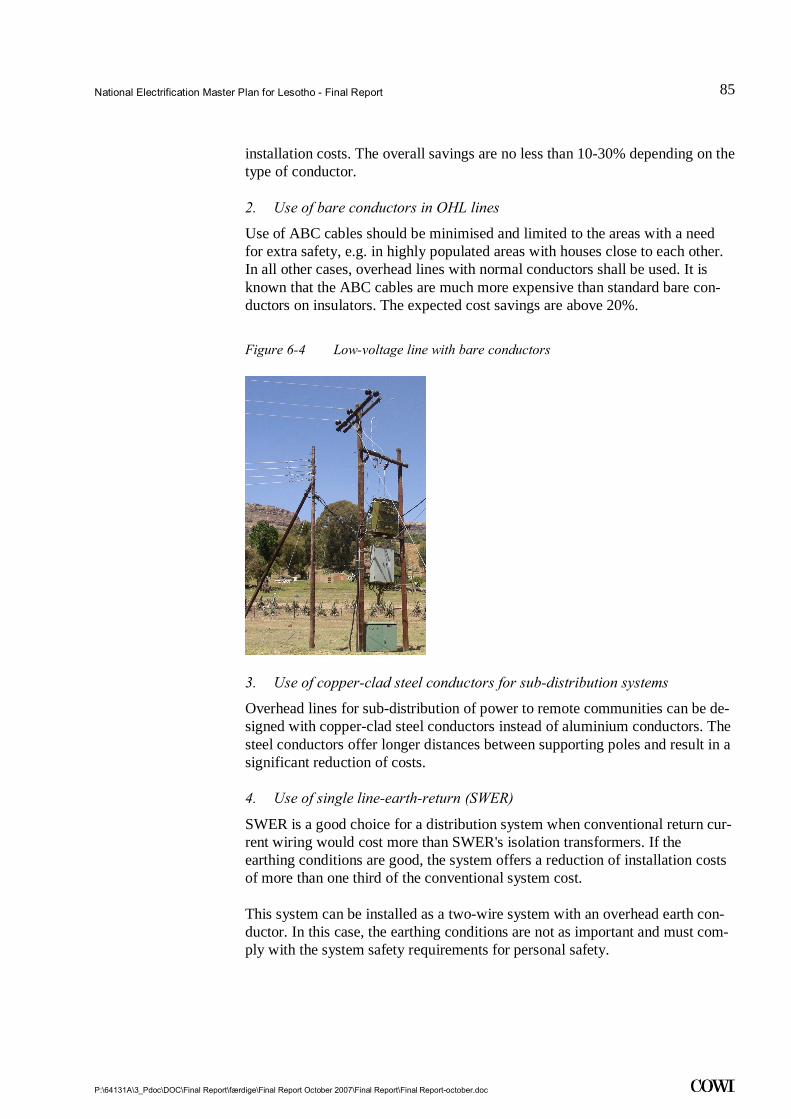

6 Electrical Design Issues 79 6.1 Technical Standards used in LEC 79 6.2 Power Supply Quality 81 6.3 Recommendations 82

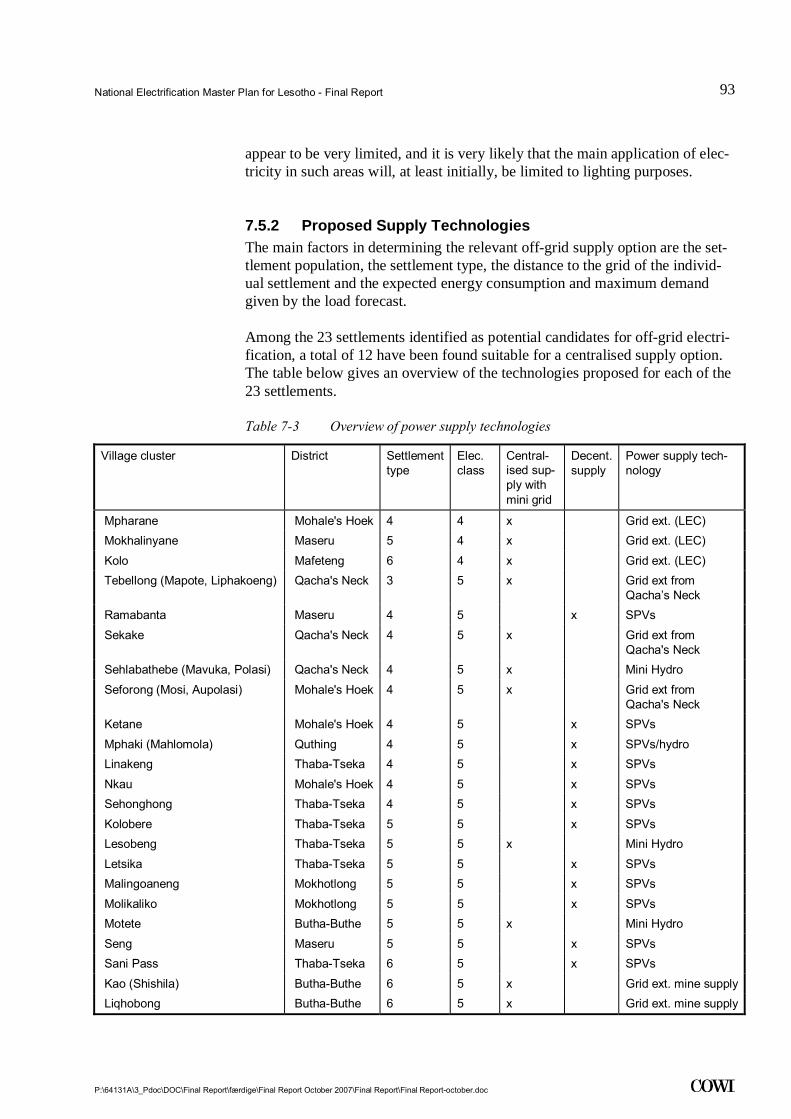

7 Off-grid Power Supply Options and Standards 87 7.1 Decentralised Options 87 7.2 Centralised Options 88 7.3 Suitability of Power Supply Options in the Context of

Lesotho 88 7.4 Standards 91 7.5 Supply of Off-grid Schemes 91 7.6 Cost per Settlement (Off-Grid) 97

8 System Design and Cost Estimates in Transmission and Distribution 98

8.1 Transmission System 98 8.2 Distribution System 104 8.3 Investment Costs 109

9 Economic and Financial Analyses 114 9.1 Financial Analyses 114 9.2 Results of the Financial Analysis 118

10 Prioritisation and Scheduling of Electrification Projects 121

10.1 Outline of Electrification Projects 121 10.2 Ranking of Settlements by Viability 122

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

3

.

10.3 Outline of Settlements included in the Plan for the First Five Years 123

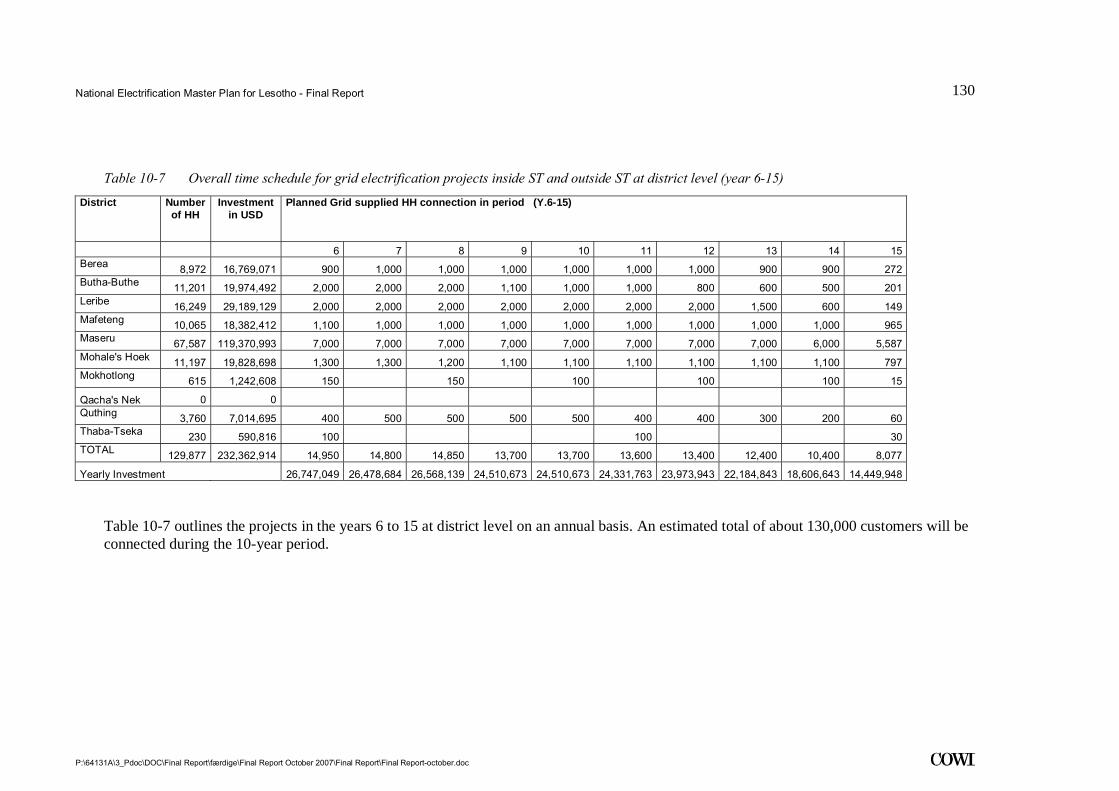

10.4 Outline of Settlements Included in the Plan for the Next 10 Years 129

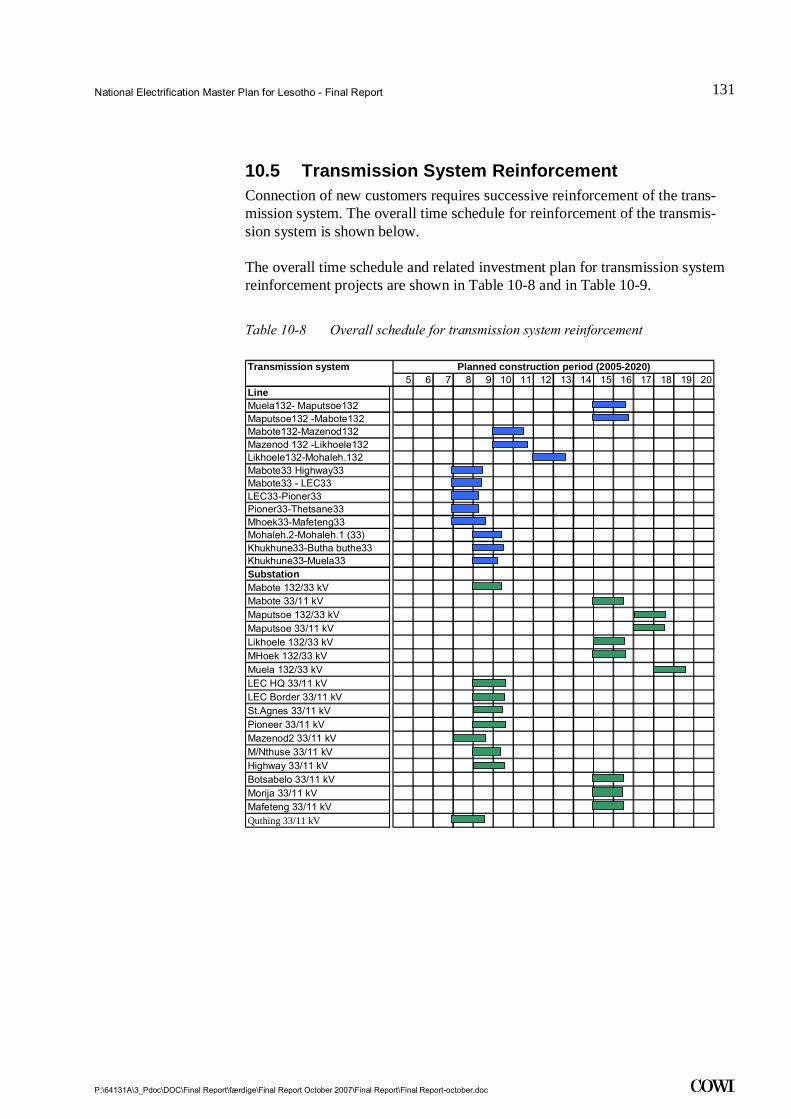

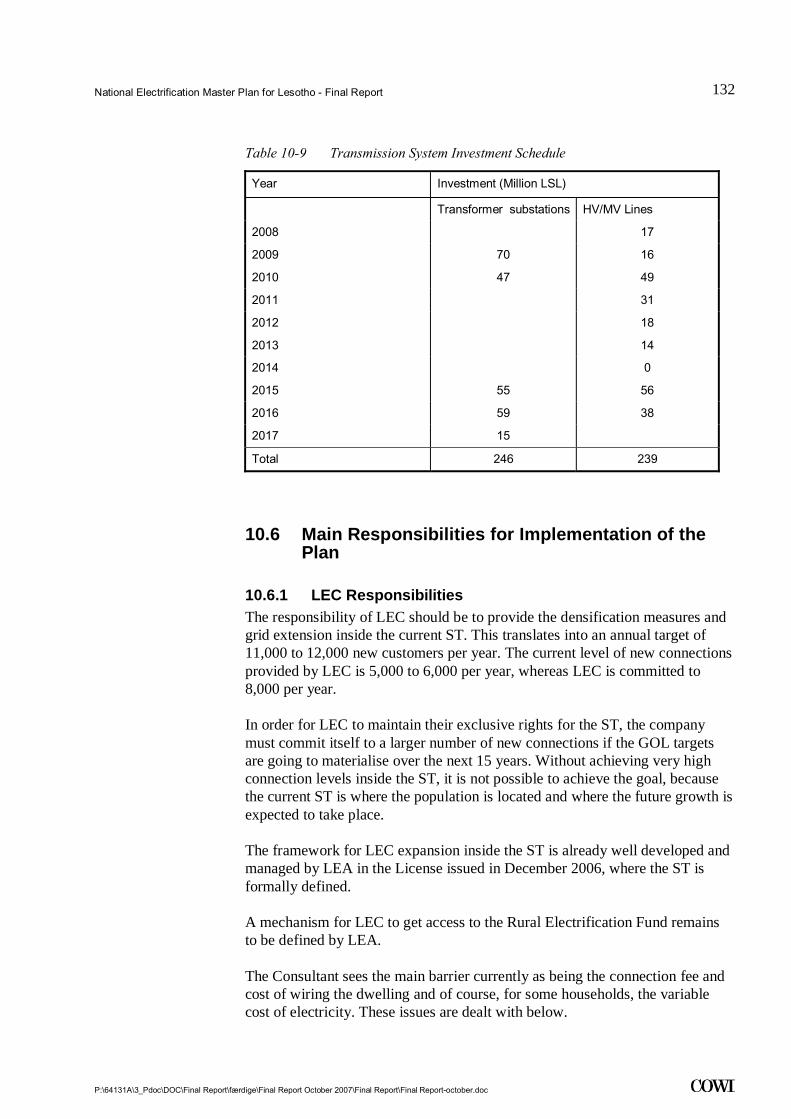

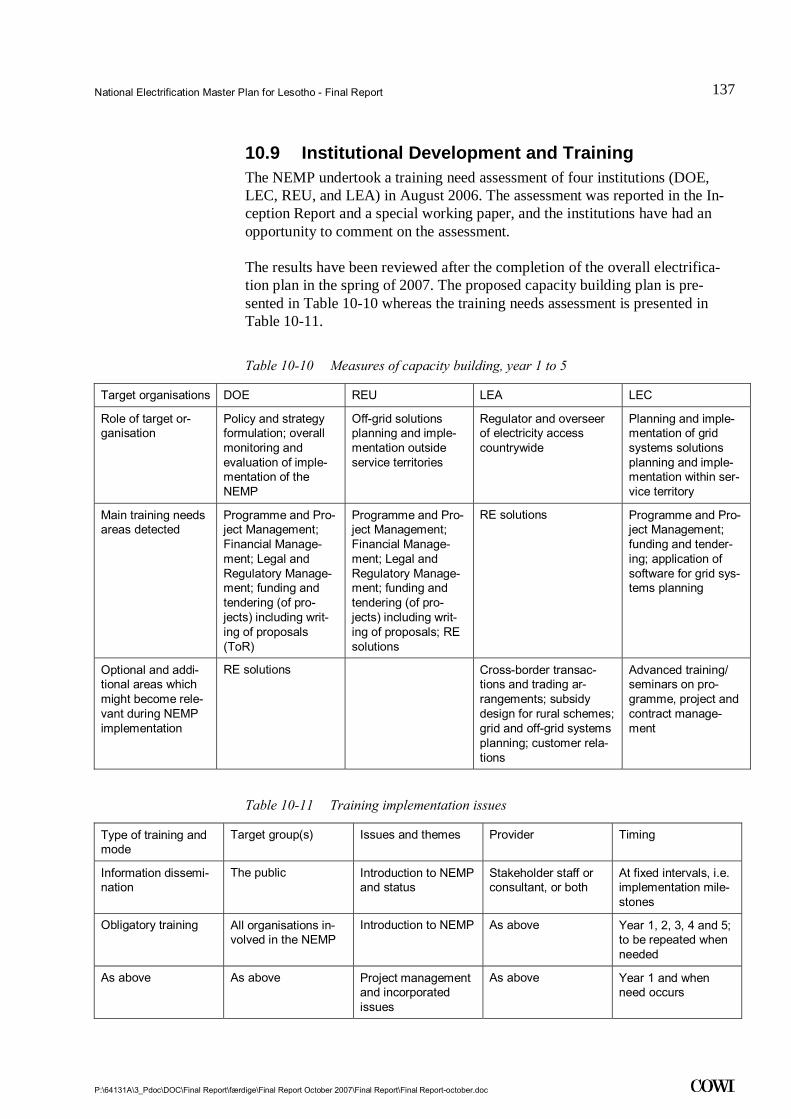

10.5 Transmission System Reinforcement 131 10.6 Main Responsibilities for Implementation of the Plan 132 10.7 Connection Fee and Tariff 135 10.8 Densification Measures 136 10.9 Institutional Development and Training 137 10.10 Monitoring and Evaluation Framework 139

11 Future Service Delivery in Lesotho 143 11.1 Problems Facing the Power Sector 143 11.2 Inside the ST - Future Role of LEC 144 11.3 Concession Model Approach for Lesotho 145 11.4 Outside the ST Areas – Grid Connection 146 11.5 Delivery Models Off-grid 149 11.6 Conclusions 150

12 Environmental Issues 151 12.1 Impact and Mitigation 151 12.2 Impacts from Transmission and Distribution 152

Table of Appendices

Appendix 1 – NEMP Reports Appendix 2 – References Appendix 3 – Price Levels for Transmission and Distribution Appendix 4 – Cost of Distribution Overview per Settlement Appendix 5 – Viability Score by Settlement Appendix 6 – Financial Model Appendix 7 – Settlements Ranked by Balance Price Appendix 8 – Load Forecast per Settlement Appendix 9 – Transmission Network Model for 2005 and 2020 Appendix 10 – Overview at Constituency Level Appendix 11 – Maps and Description of Settlements

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

4

.

Abbreviations

ABC Arial Bundled Cables

ACSR Aluminium Conductor Steel Reinforced

ADMD After Diversity Maximum Demand

AES Access to Electricity Study

AfDB African Development Bank

AGOA African Growth and Opportunity Act

BEC-meter Budget Energy Controller - (Prepaid meter system)

BOS Bureau of Statistics (Lesotho)

CCA Community Council Areas

DOE Department of Energy

EAPPs Electricity Access Pilot Projects

GOL Government of Lesotho

GIS Geographical Information System

HH Households

HV High Voltage - a nominal phase-to-phase voltage between the range 11 kV and 132 kV both inclusive

ICB International Competitive Bidding

IEC International Electro-technical Commission

IMTF Interim Management Task Force

kV kilo Volt

kWh kilo Watt hours

LCB Local Competitive Bidding

LDHS Lesotho Demographic and Health Survey, 2004

LEA Lesotho Electricity Authority

LEC Lesotho Electricity Company

LHDA Lesotho Highlands Development Authority

LHWP Lesotho Highlands Water Project

LURP Lesotho Utilities Reform Project

LRMC Long Run Marginal Cost

LSL Lesotho Maloti = 100 Lisente (l), 1 USD = 7.5 LSL

LV Low Voltage

MCB Miniature Circuit Breaker

MHPP Muela Hydro Power Plant

MNR Ministry of Natural Resources

MV Medium Voltage

MW Mega Watt

NEMP National Electrification Master Plan

NREF National Rural Electrification Fund

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

5

.

NREP National Rural Electrification Programme

OHL Overhead Line

OPGW Optical Grounding Wire

PSIA

RE

Poverty and Social Impact Assessment

Rural Electrification

REF Rural Electrification Forum

REU Rural Electrification Unit

REWG Rural Electrification Working Group

RSA Republic of South Africa

SABS South African Bureau of Standards

SPV (or PV) Solar Photovoltaic

ST Service Territory

TNA Training Needs Assessment

WASA Water and Sewerage Authority

WAP Willingness to Pay

WB World Bank

XLPE Cross-linked polyethylene

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

6

.

1 Executive Summary

1.1 Introduction The objective of this National Electrification Master Plan Study (NEMP) is to provide clear guidelines and establish priorities for providing access to electric-ity in Lesotho in a co-ordinated and cost-effective manner, which will enable the Government of Lesotho (GOL) to meet its electrification targets in particu-lar, and rural development goals in general. The NEMP study has been organ-ised in three distinct steps:

1 Inception;

2 Electrification Master Planning;

3 Electrification Master Plan Implementation Strategy.

This Final Report presents the outcome and results of the study.

1.2 Electrification Target The target of the Government of Lesotho is to ensure that in 2020 at least 40% of all households have access to electricity either from the national power grid, from an isolated system or from individual solutions (solar PV/generators). The table below shows the projection of population and number of households in Lesotho and specifies the number of electrified households required to achieve the electrification target.

Table 1-1 Population, households and electrification targets

Year 2005 2010 2015 2020

Total population 2,200,000 2,300,000 2,320,000 2,320,000

Total number of households 564,000 590,000 595,000 595,000

Electrification level 8% 20% 35% 40%

No. of domestic customers 42,610 118,000 208,000 238,000

Source: Consultant's calculations. The electrification level of 2005 as well as the projections are based on an average household size of 3.9

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

7

.

Briefly, the number of electrified households should increase from 42,000 to 238,000. This corresponds to an annual average of new connections of ap-proximately 13,000. Currently, 5,000-6,000 new customers are added annually to the system. The commercialised LEC is foreseen to connect 8,000 new cus-tomers within its service territory (ST). Through the Rural Electrification Unit (REU), the Government is foreseen to be in charge of the remaining.

In order to achieve this goal, Lesotho faces two main challenges: (1) to moti-vate LEC to fulfil their commitment, and (2) to establish a parallel structure that can plan for and handle approximately 5,000 connections per year outside the ST.

This National Electrification Master Plan provides a framework for the actions over the next 15 years, including the following:

• The cluster approach (see Section 1.3) identifies large and viable planning areas for electrification of Lesotho over the next 15 years;

• The plan establishes a clear priority of settlements to be electrified;

• The plan includes an estimate of the investment and operational cost of the plan using recommended technologies and projects;

• The plan demonstrates that considerable subsidies are required for its im-plementation;

• The plan clearly identifies the role and responsibilities of LEC, REU, Le-sotho Electrification Authority (LEA) and Department of Energy (DOE);

• The plan provides a capacity building framework that will enable the key players to fulfil their role.

1.3 Settlements The viability of the constituencies and type of settlement has been used as a starting point for the ranking of the settlements to be electrified. The ranking was both based on economic and social criteria, with emphasis on the potential for economic development. There are a number of settlements that are already served with electricity, but where only few households have been connected to the grid. The potential for densification of these underserved electrified settle-ments is important and should be met concurrently with grid extension to new areas.

To maximise the number of electricity customers in each area in a cost-effective way, a ‘cluster’ approach was used. This entailed identifying groups of villages or neighbourhoods that are situated within no more than one kilome-tre from each other, forming a continuous area of settlement. These ‘settle-ments’, which form distinct types ranging from the capital city down to clusters of relatively small villages, have been analysed and described in some detail.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

8

.

Recommendations have been made on how each one should be served, taking into account its type, population, level of poverty, economic viability, number of social services and distance from the grid.

A total of 140 clusters have been identified: 106 settlements in the Lowlands, with a population of 2,500 or more, and further 34 settlements in the Highlands or as special cases. The 140 settlements have been divided into 6 categories re-flecting their characteristics (Capital City, Industrial Towns, Large Institutional Towns, Medium Settlements, Small Settlements and Special Cases). Each set-tlement has been described in terms of electrification status, local resources and distance to the national grid and assessed with the most updated socio-economic information that can be provided currently. Population data have been estimated using a "block building" approach to population estimates, as the results of the census from 2006 have not been available.

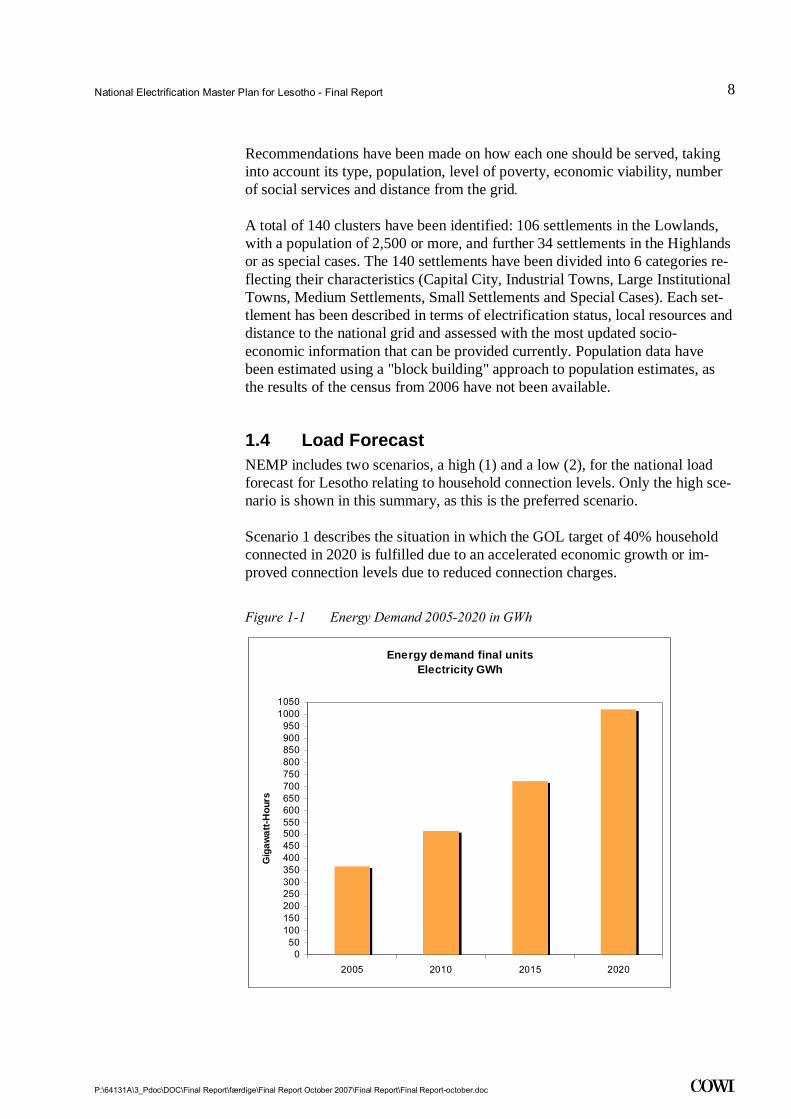

1.4 Load Forecast NEMP includes two scenarios, a high (1) and a low (2), for the national load forecast for Lesotho relating to household connection levels. Only the high sce-nario is shown in this summary, as this is the preferred scenario.

Scenario 1 describes the situation in which the GOL target of 40% household connected in 2020 is fulfilled due to an accelerated economic growth or im-proved connection levels due to reduced connection charges.

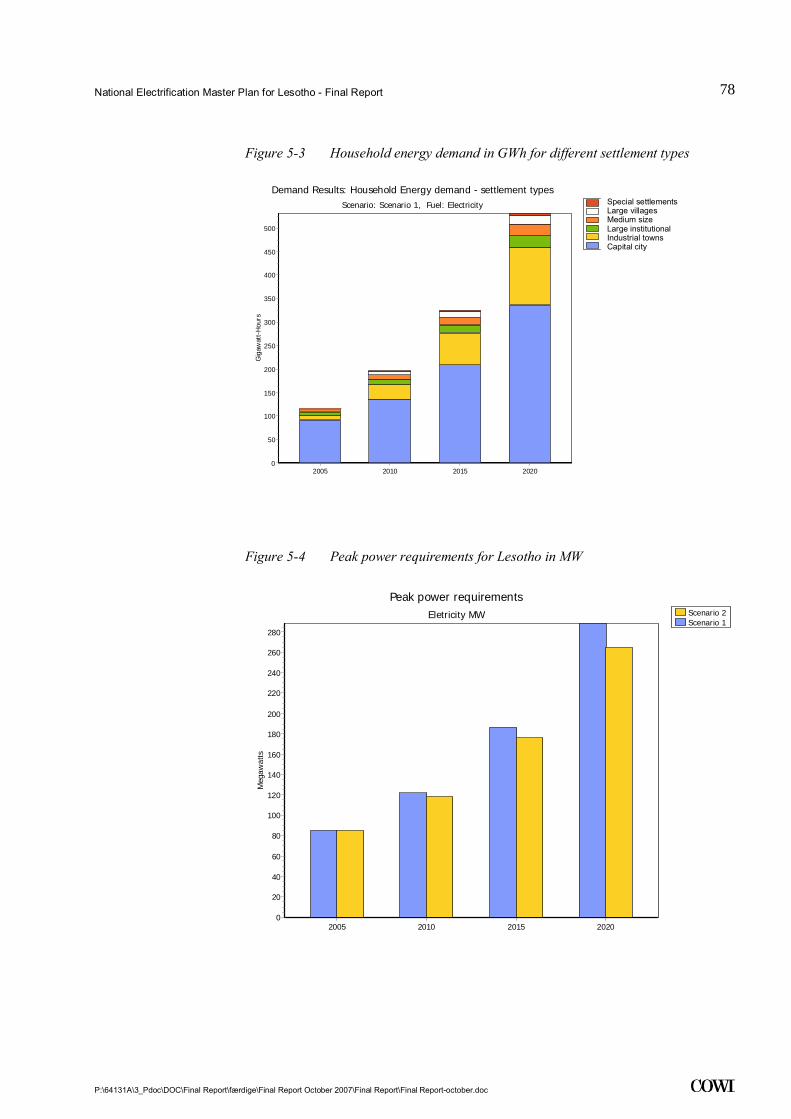

Figure 1-1 Energy Demand 2005-2020 in GWh

Energy demand final unitsElectricity GWh

050

100150200250300350400450500550600650700750800850900950

10001050

2005 2010 2015 2020

Gig

awat

t-Hou

rs

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

9

.

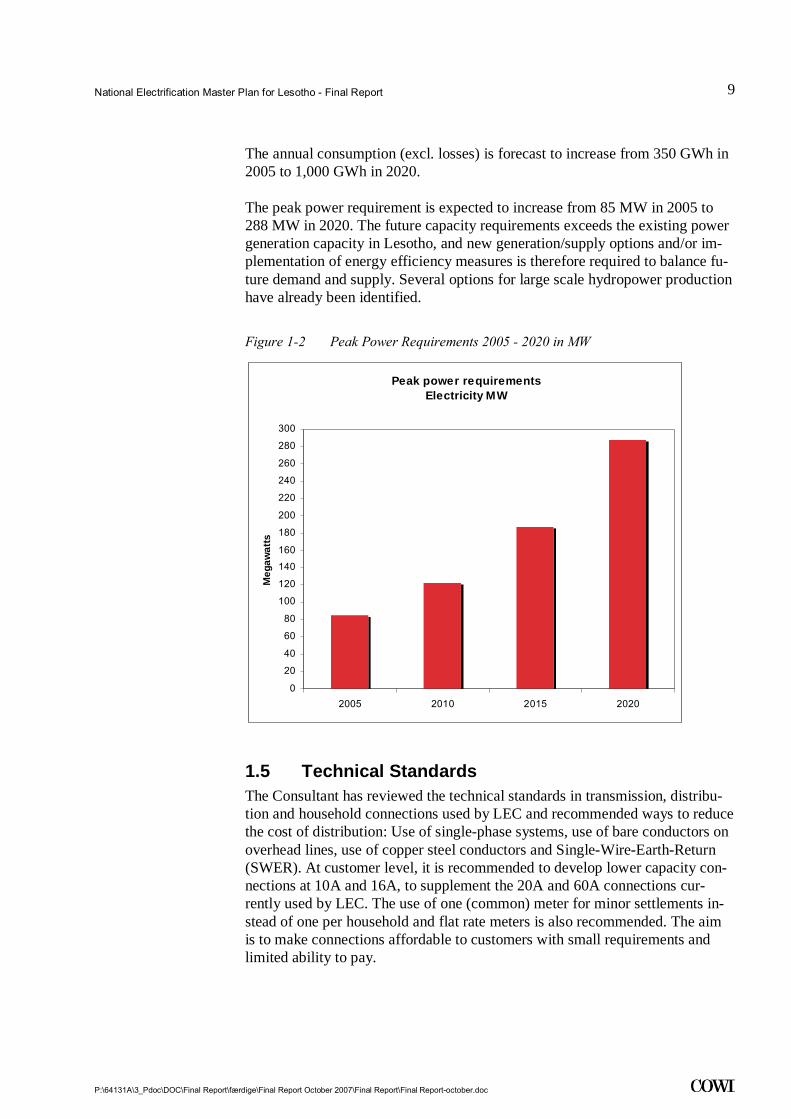

The annual consumption (excl. losses) is forecast to increase from 350 GWh in 2005 to 1,000 GWh in 2020.

The peak power requirement is expected to increase from 85 MW in 2005 to 288 MW in 2020. The future capacity requirements exceeds the existing power generation capacity in Lesotho, and new generation/supply options and/or im-plementation of energy efficiency measures is therefore required to balance fu-ture demand and supply. Several options for large scale hydropower production have already been identified.

Figure 1-2 Peak Power Requirements 2005 - 2020 in MW

Peak power requirementsElectricity MW

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

2005 2010 2015 2020

Meg

awat

ts

1.5 Technical Standards The Consultant has reviewed the technical standards in transmission, distribu-tion and household connections used by LEC and recommended ways to reduce the cost of distribution: Use of single-phase systems, use of bare conductors on overhead lines, use of copper steel conductors and Single-Wire-Earth-Return (SWER). At customer level, it is recommended to develop lower capacity con-nections at 10A and 16A, to supplement the 20A and 60A connections cur-rently used by LEC. The use of one (common) meter for minor settlements in-stead of one per household and flat rate meters is also recommended. The aim is to make connections affordable to customers with small requirements and limited ability to pay.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

10

.

1.6 Systems in Remote Areas Off-grid supply options and standards have been reviewed. Settlements located more than 15 km from the existing grid have been identified, and the power supply options (grid extension, off-grid) for the next 15 years have been ana-lysed taking local resources into consideration.

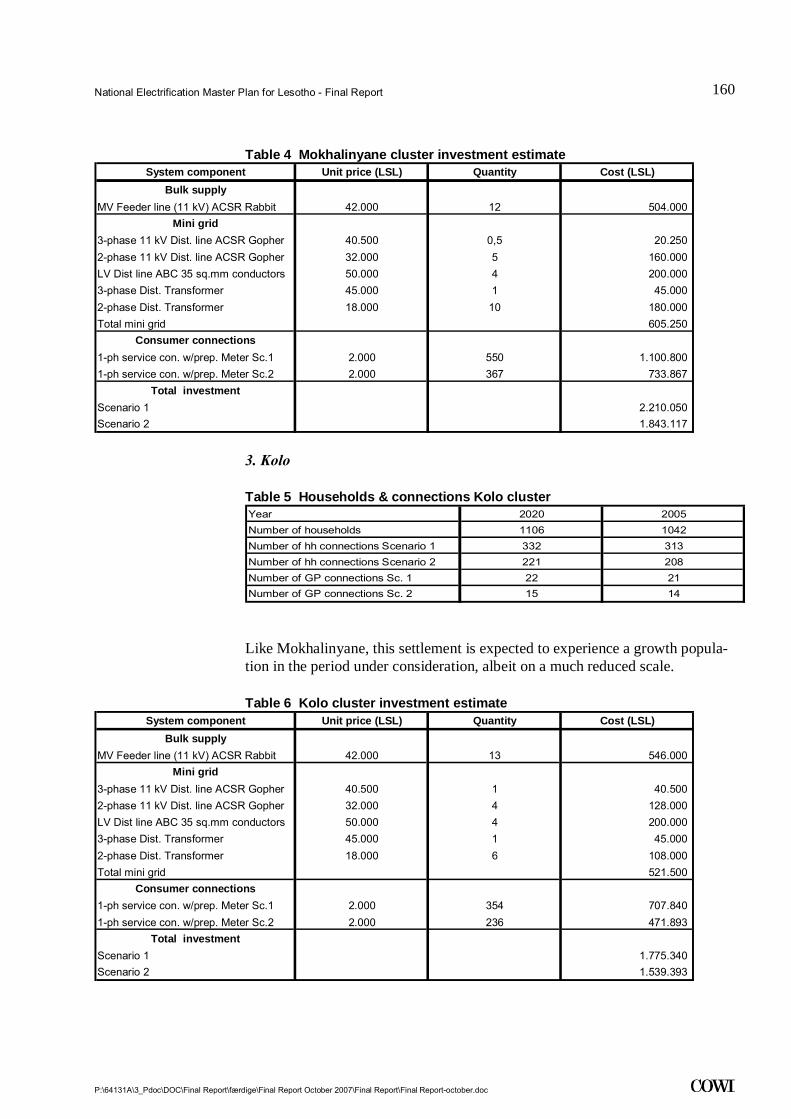

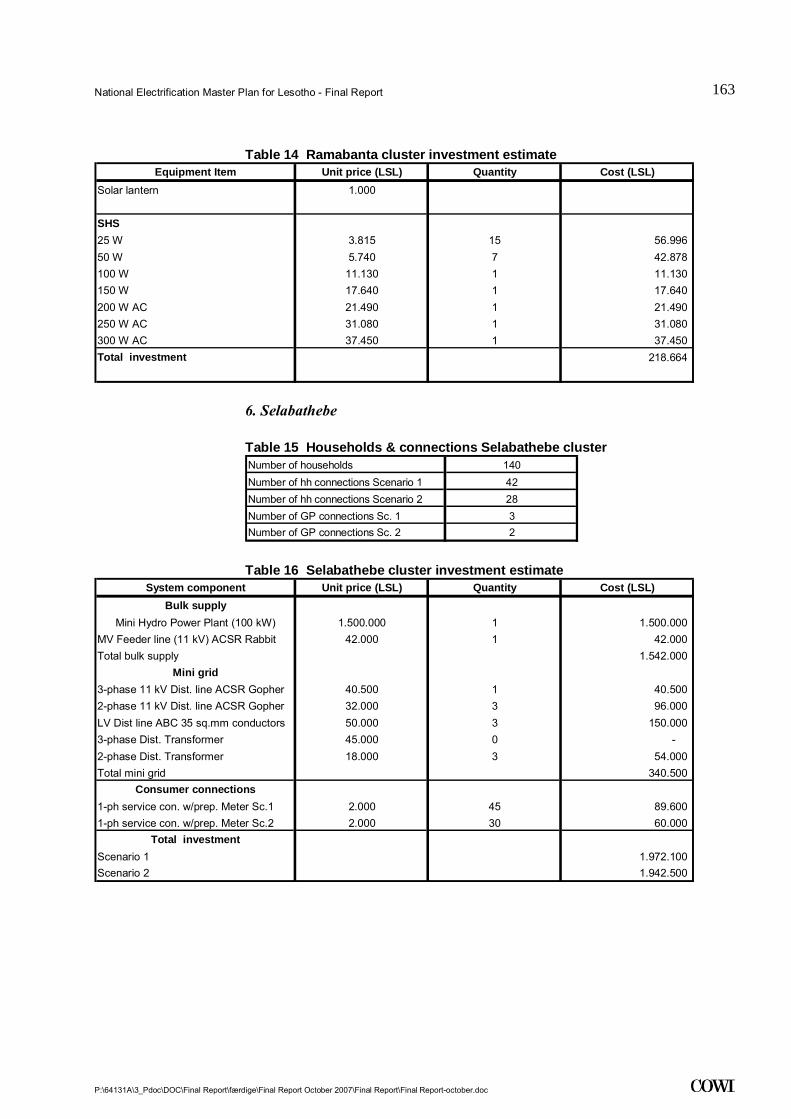

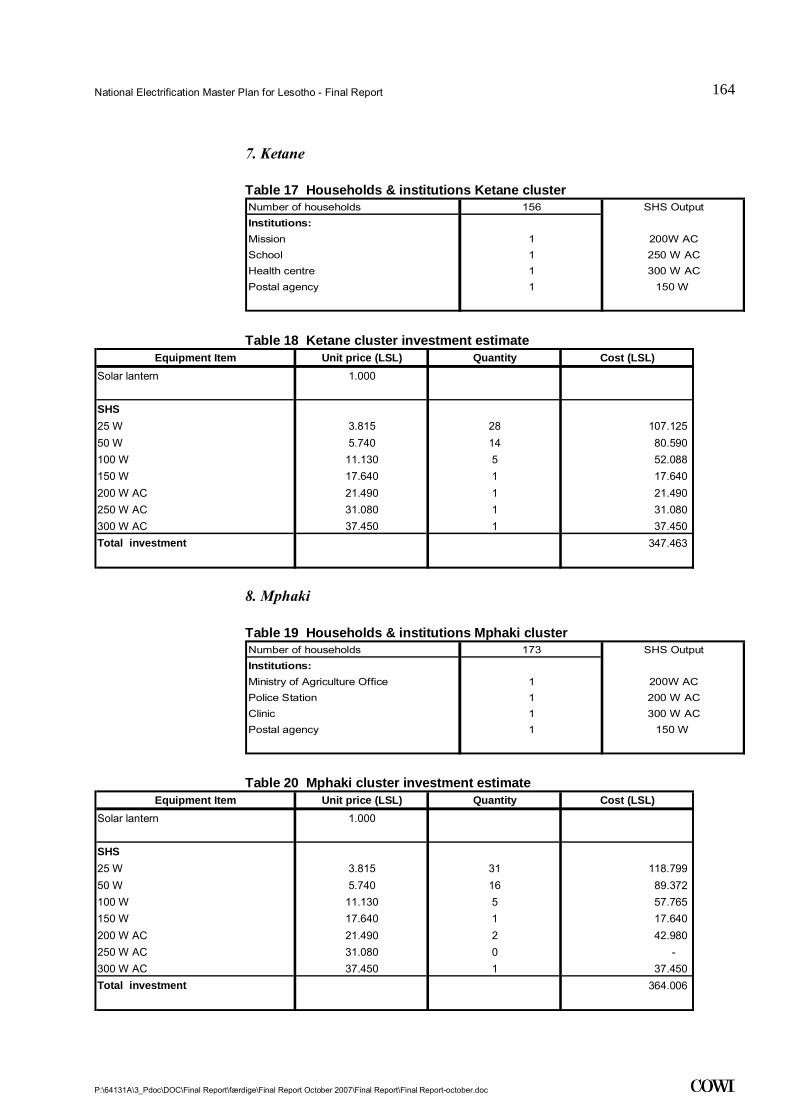

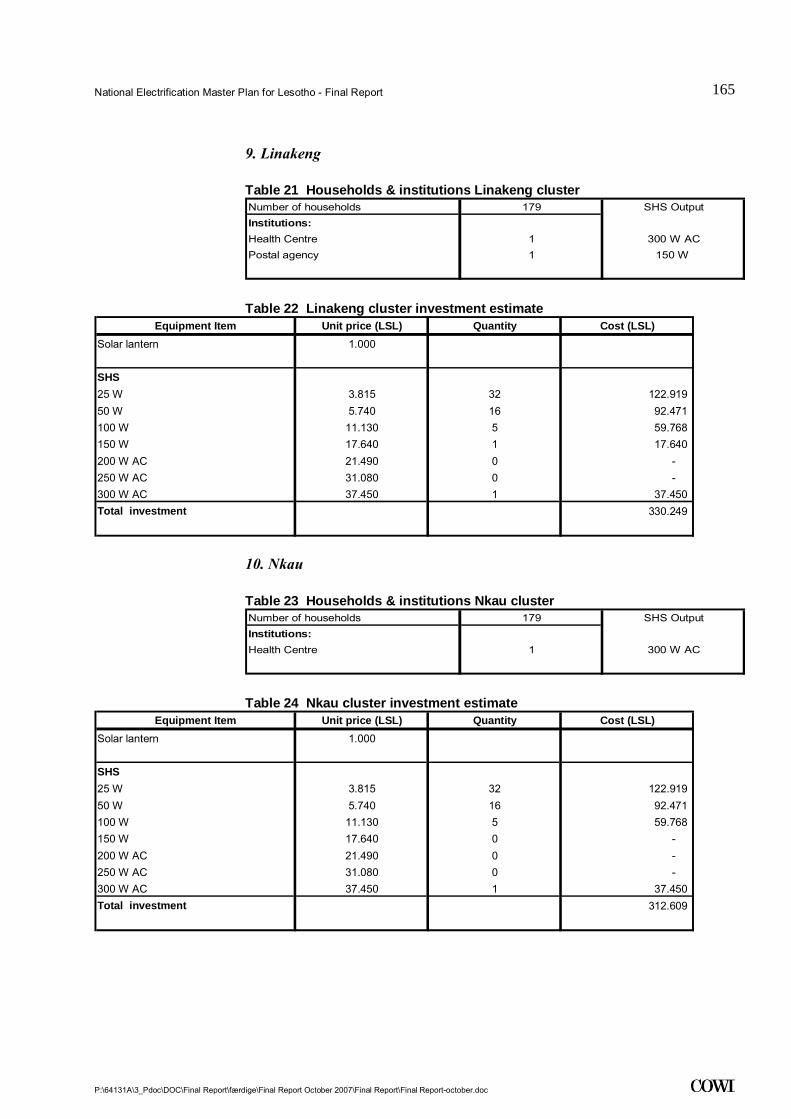

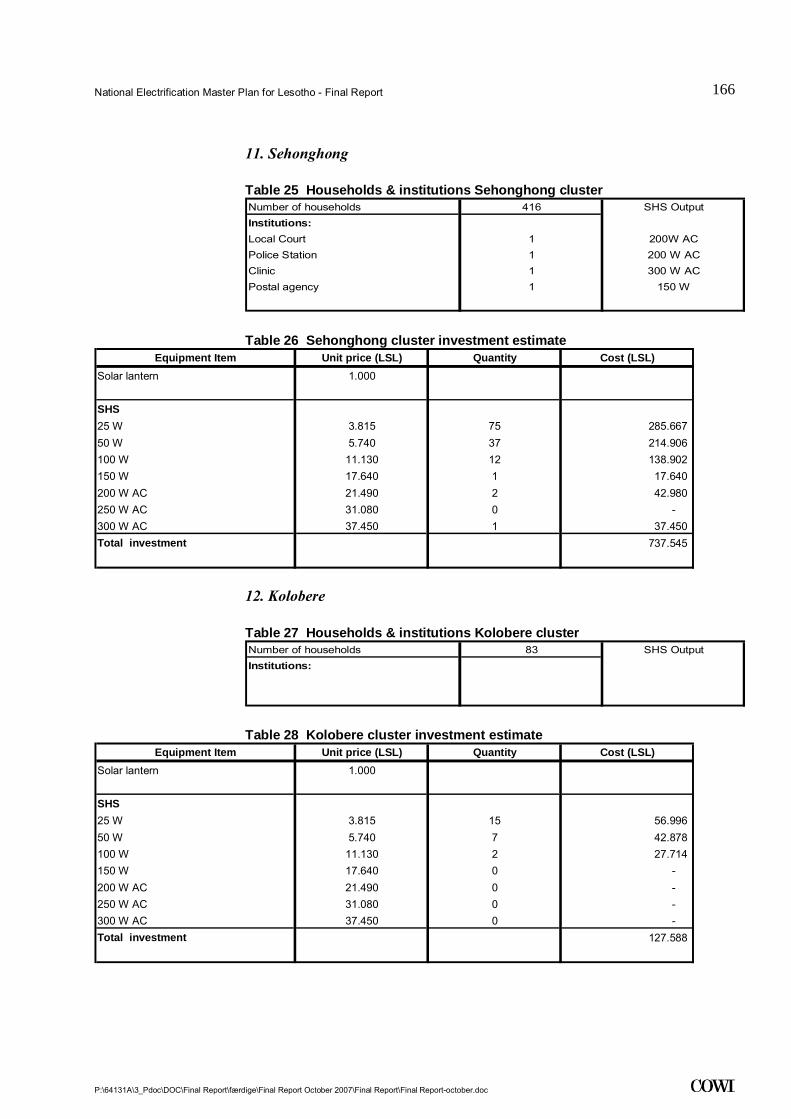

Table 1-2 Settlements far from existing grid that have been analysed for potential off-grid supply

Settlement/Village cluster District Technology Investment Cost

in 1000 LSL

Mpharane Mohale's Hoek Grid Extension 1,447

Mokhalinyane Maseru Grid Extension 2,210

Kolo Mafeteng Grid Extension 1,775

Tebellong (Mapote, Liphakoeng) Qacha's Neck Grid Extension* 1,765

Ramabanta Maseru Grid Extension/ SPV 218

Sekake Qacha's Neck Grid Extension* 1,180

Sehlabathebe (Mavuka, Polasi) Qacha's Neck Mini Hydro 1,972

Seforong (Mosi, Aupolasi) Mohale's Hoek Grid Extension* 943

Ketane Mohale's Hoek SPV 347

Mphaki (Mahlomola) Quthing SPV/hydro 364

Linakeng Thaba-Tseka SPV 330

Nkau Mohale's Hoek SPV 312

Sehonghong Thaba-Tseka SPV 737

Kolobere Thaba-Tseka Grid Extension/SPV 127

Lesobeng Thaba-Tseka Mini Hydro 1,954

Letsika Thaba-Tseka SPV 127

Malingoaneng Mokhotlong SPV 127

Molikaliko Mokhotlong SPV 165

Motete

Kao

Liqhobong** Butha-Buthe

Mini Hydro/Grid Ext

9,392

Seng Maseru SPV 127

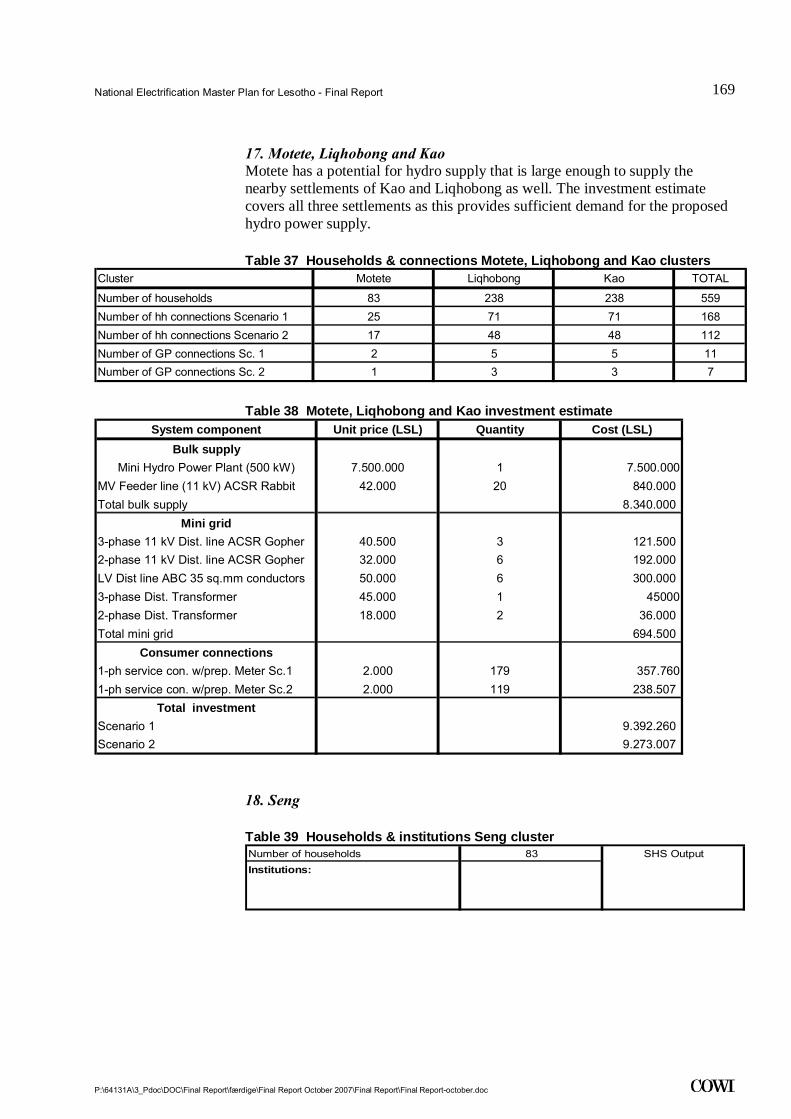

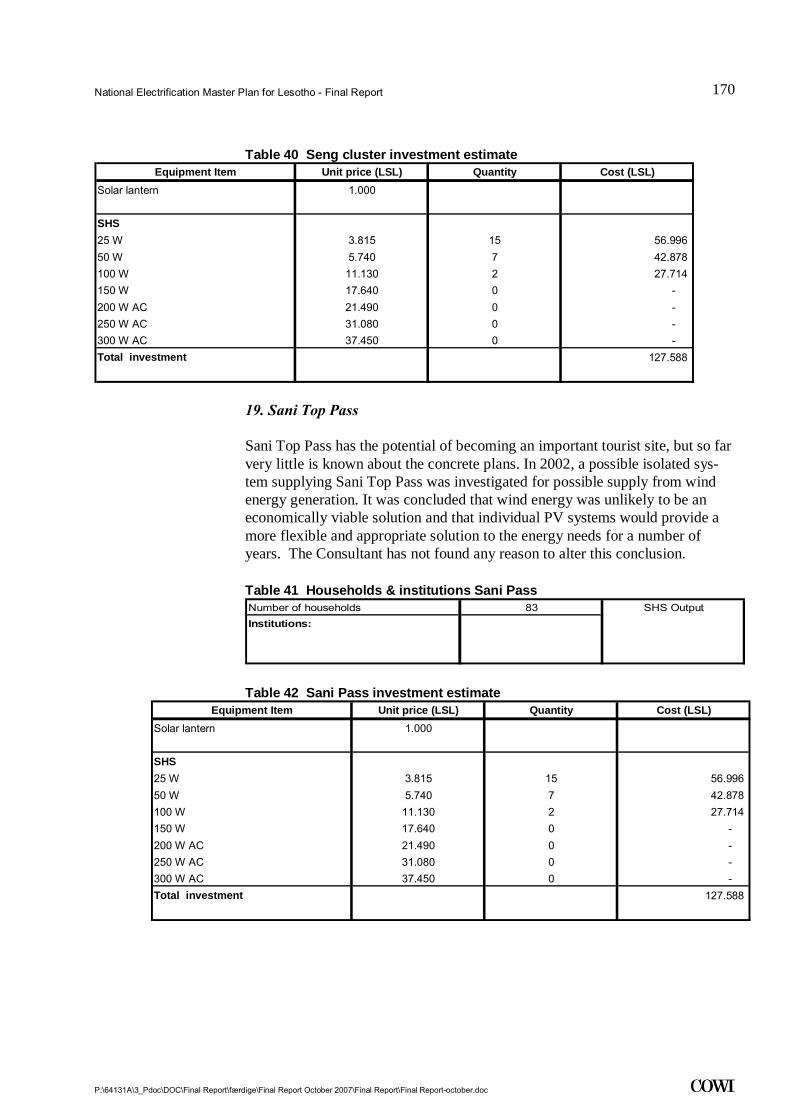

Sani Pass Thaba-Tseka SPV 127* From Qacha's Neck ** Motete has a potential for hydro supply that is large enough to supply the nearby settlements of

Kao and Liqhobong as well. The investment estimate covers all three settlements as this provides sufficient demand for the proposed hydro power supply.

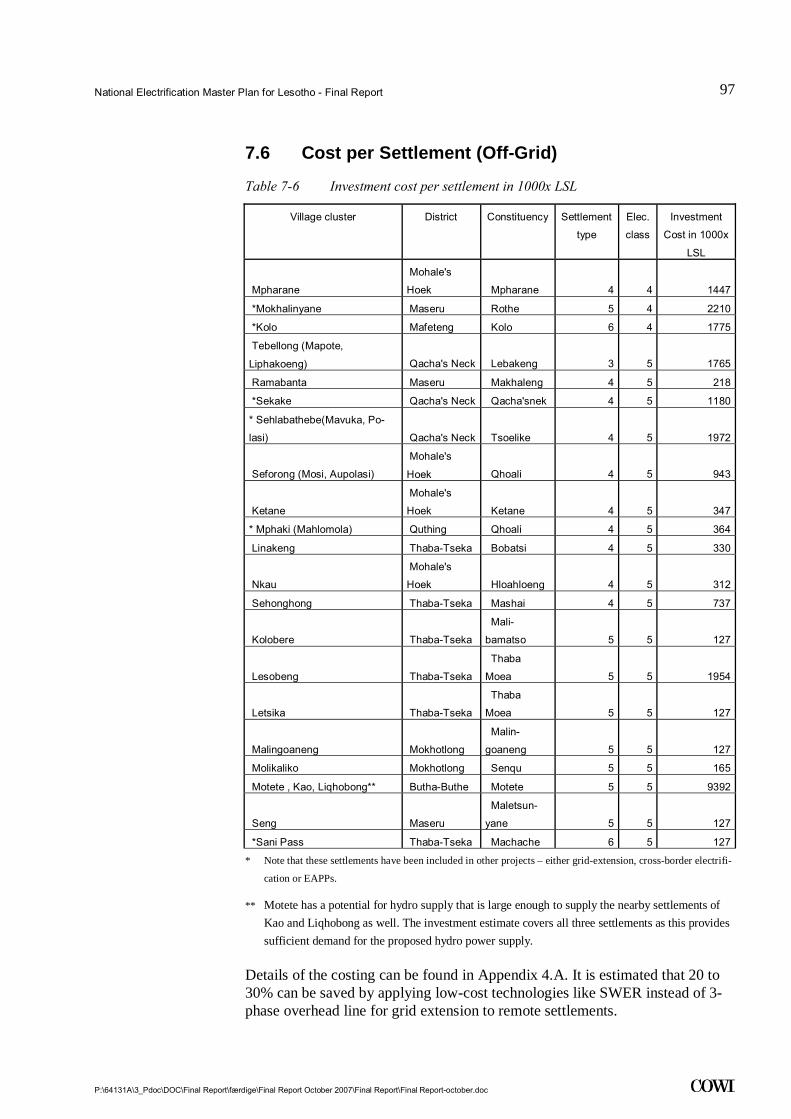

The table above shows the recommended technology and investment cost for 23 settlements of interest for isolated supply. Some of these settlements form part of planned projects, such as Electricity Access Pilot Projects or RSA Vil-lage Border Projects. Mphaki Rural Electrification Project is scheduled for grid extension by DOE.

It is estimated that 20 to 30 per cent can be saved on investment costs by apply-ing low-cost technologies like SWER instead of 3-phase overhead line for grid extension to remote settlements.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

11

.

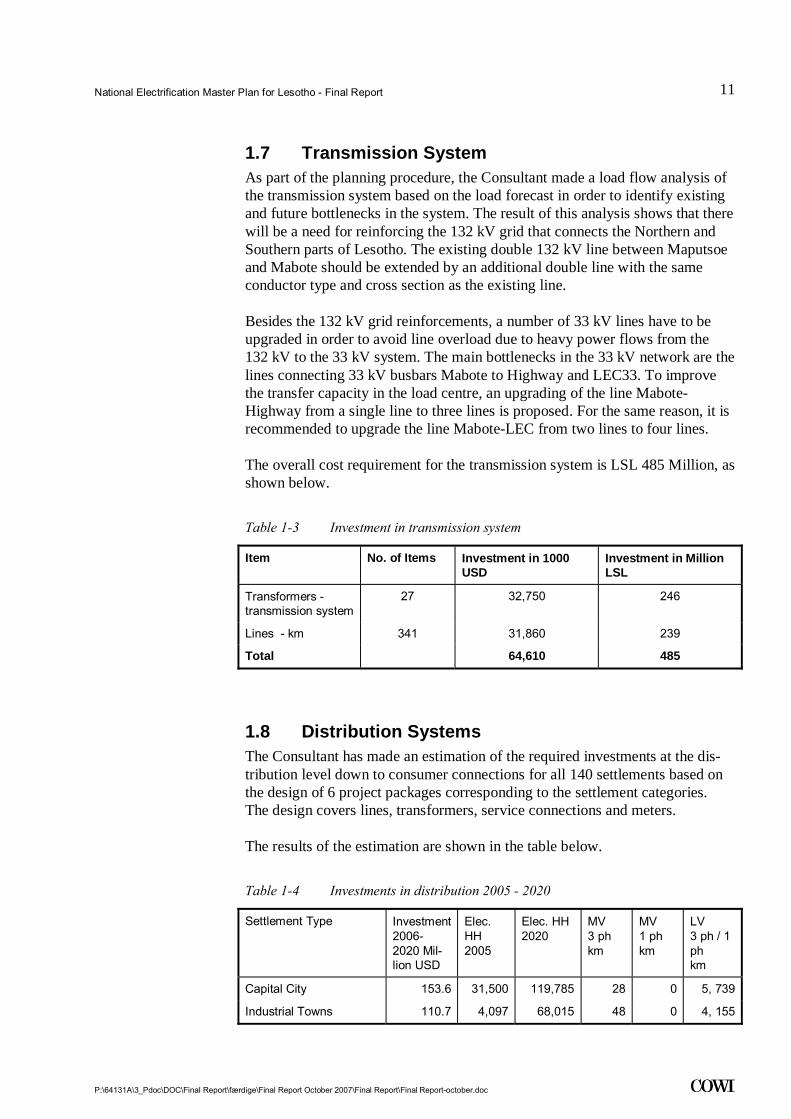

1.7 Transmission System As part of the planning procedure, the Consultant made a load flow analysis of the transmission system based on the load forecast in order to identify existing and future bottlenecks in the system. The result of this analysis shows that there will be a need for reinforcing the 132 kV grid that connects the Northern and Southern parts of Lesotho. The existing double 132 kV line between Maputsoe and Mabote should be extended by an additional double line with the same conductor type and cross section as the existing line.

Besides the 132 kV grid reinforcements, a number of 33 kV lines have to be upgraded in order to avoid line overload due to heavy power flows from the 132 kV to the 33 kV system. The main bottlenecks in the 33 kV network are the lines connecting 33 kV busbars Mabote to Highway and LEC33. To improve the transfer capacity in the load centre, an upgrading of the line Mabote-Highway from a single line to three lines is proposed. For the same reason, it is recommended to upgrade the line Mabote-LEC from two lines to four lines.

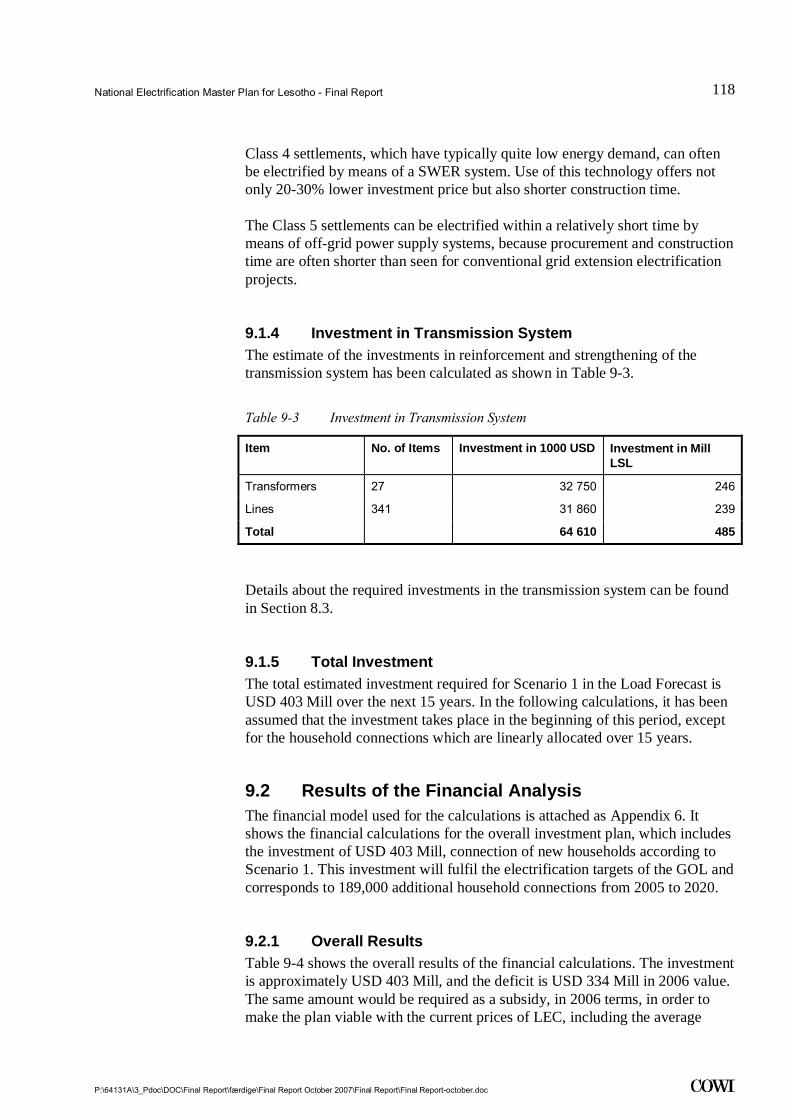

The overall cost requirement for the transmission system is LSL 485 Million, as shown below.

Table 1-3 Investment in transmission system

Item No. of Items Investment in 1000 USD

Investment in Million LSL

Transformers - transmission system

27 32,750 246

Lines - km 341 31,860 239

Total 64,610 485

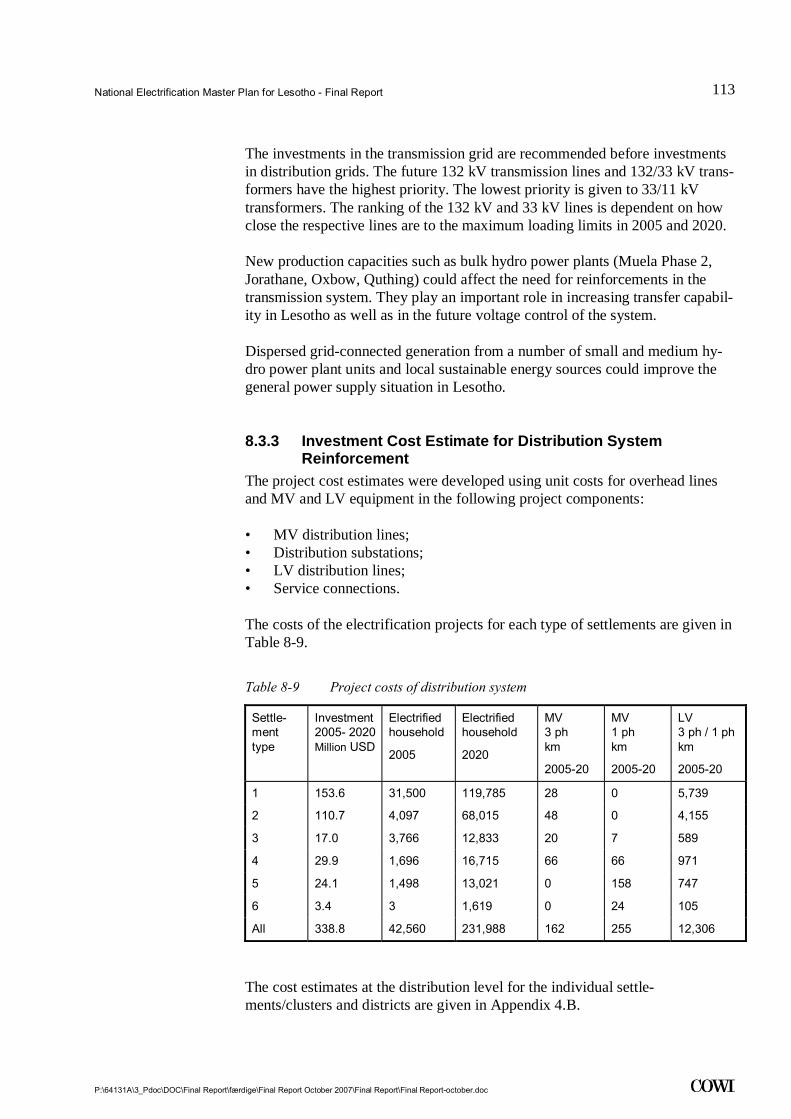

1.8 Distribution Systems The Consultant has made an estimation of the required investments at the dis-tribution level down to consumer connections for all 140 settlements based on the design of 6 project packages corresponding to the settlement categories. The design covers lines, transformers, service connections and meters.

The results of the estimation are shown in the table below.

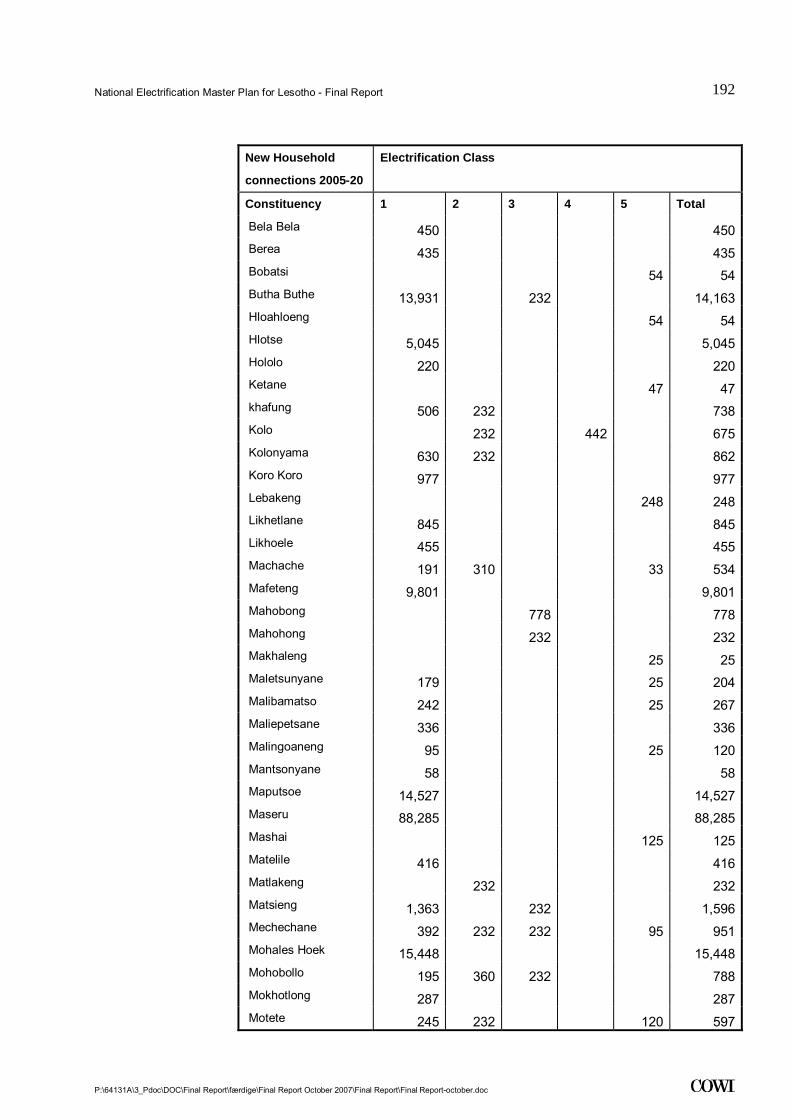

Table 1-4 Investments in distribution 2005 - 2020

Settlement Type Investment 2006- 2020 Mil-lion USD

Elec. HH 2005

Elec. HH 2020

MV 3 ph km

MV 1 ph km

LV 3 ph / 1 ph km

Capital City 153.6 31,500 119,785 28 0 5, 739

Industrial Towns 110.7 4,097 68,015 48 0 4, 155

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

12

.

Institutional Towns 17.0 3,766 12,833 20 7 589

Medium-size Settlements 29.9 1,696 16,715 66 66 971

Large villages 24.1 1,498 13,021 0 158 747

Special Cases 3.4 3 1,619 0 24 105

All 338.8 42,560 231,988 162 255 12,306

The investment required over the next 15 years is USD 339 Million or LSL 2,543 Million, of which the bulk is targeted Maseru and the large industrial towns.

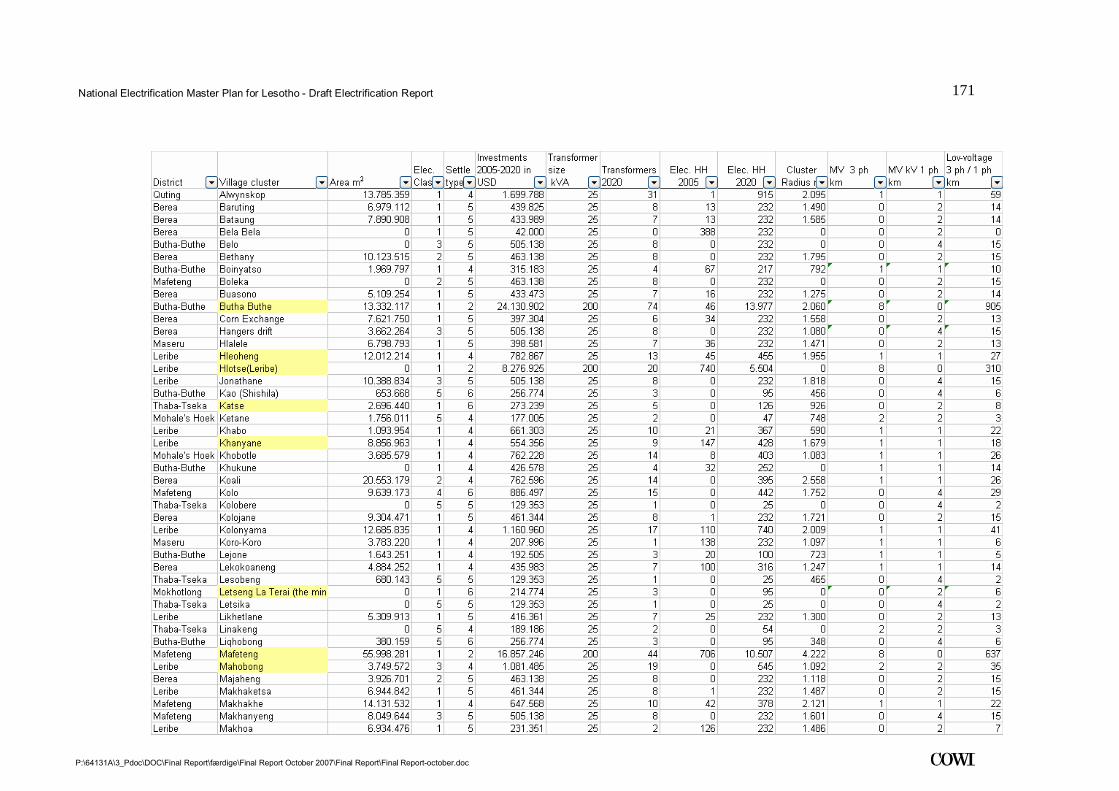

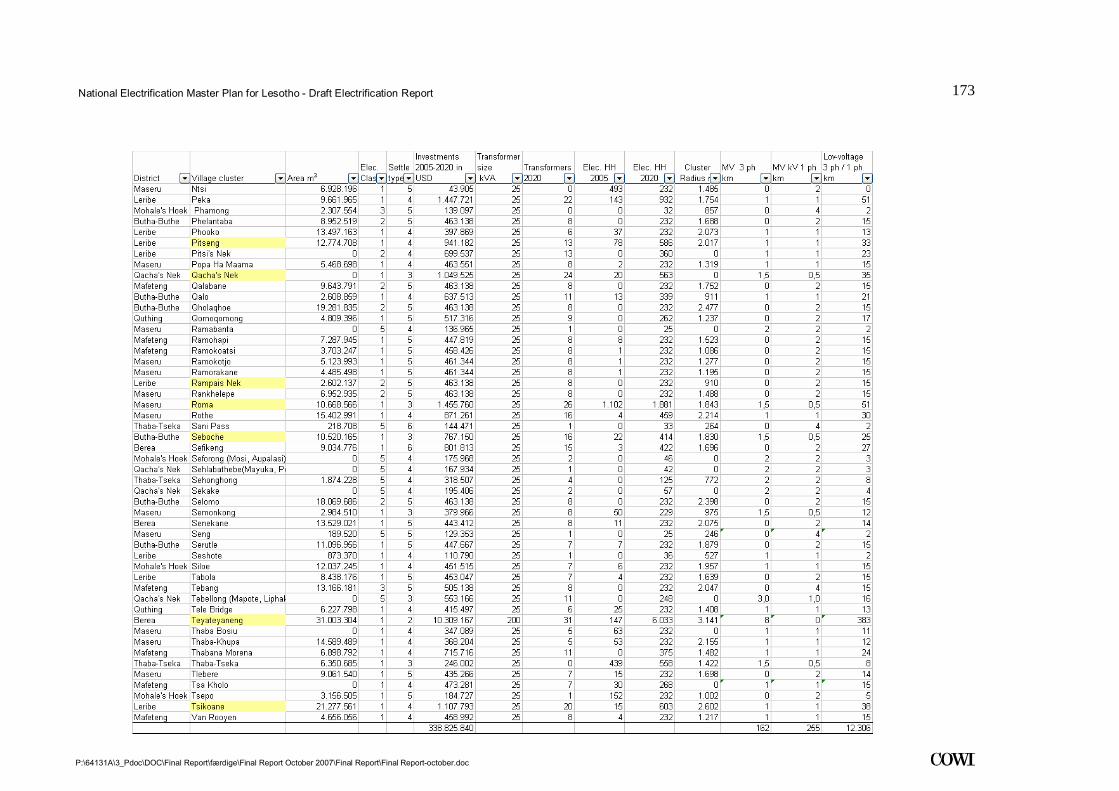

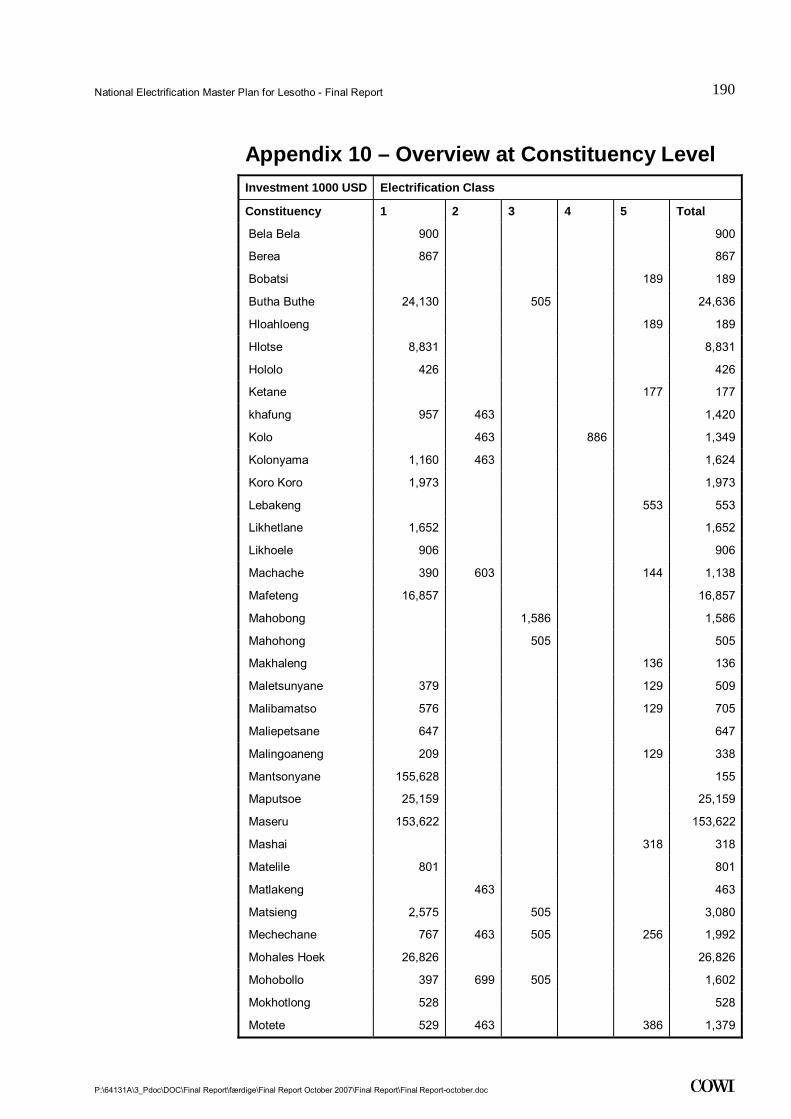

The following table shows the investment allocated on districts and electrifica-tion status. Appendix 10 displays similar information at the constituency level.

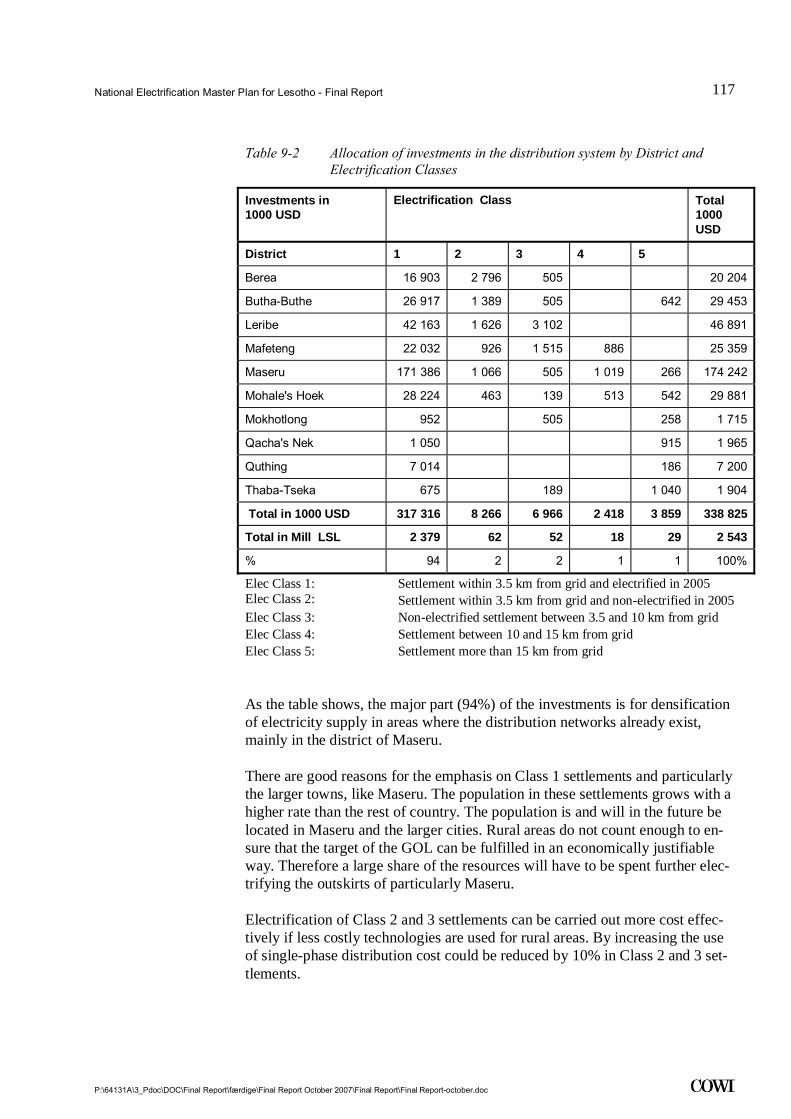

Table 1-5 Investment in distribution by District and Electrification Class

Electrification Class

1000 USD

District

1 2 3 4 5 Total

Berea 16,903 2,796 505 20,204

Butha-Buthe 26,917 1,389 505 642 29,453

Leribe 42,163 1,626 3,102 46,891

Mafeteng 22,032 926 1,515 886 25,359

Maseru 171,386 1,066 505 1,019 266 174,242

Mohale's Hoek 28,224 463 139 513 542 29,881

Mokhotlong 952 505 258 1,715

Qacha's Neck 1,050 915 1,965

Quthing 7,014 186 7,200

Thaba-Tseka 675 189 1,040 1,904

Total 1000 USD 317,316 8,266 6,966 2,418 3,859 338,825

Total in Million LSL 2 ,379 62 52 18 29 2,543

% 94 2 2 1 1

Elec Class 1: Settlements within 3.5 km from grid and electrified in 2005 Elec Class 2: Settlements within 3.5 km from grid and non-electrified in

2005 Elec Class 3: Non-electrified settlements between 3.5 and 10 km from grid Elec Class 4: Settlements between 10 and 15 km from grid Elec Class 5: Settlements more than 15 km from grid

94 per cent of the investment are in areas less than 3.5 km from the existing grid and already electrified. These areas should undergo 'densification', i.e. in-creasing the number of connections within already serviced areas.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

13

.

There are good reasons for the emphasis on Class 1 settlements and particularly the major towns, such as Maseru. The population in these settlements grows by a higher rate than the rest of the country. A very large portion of the population is and will in the future be located in Maseru and the major cities. The number of households in the rural areas is not high enough to ensure that the electrifica-tion target of 40 per cent can be fulfilled in an economically justifiable way. In order to meet the target, a large share of the resources will therefore have to be spent on further electrifying the peri-urban areas of particularly Maseru and the larger towns.

Electrification of Class 2 and 3 settlements can be carried out more cost-effectively if less costly technologies are used in the rural areas. By increasing the use of single-phase distribution, the costs could be reduced by 10% in Class 2 and 3 settlements.

Class 4 settlements, which typically have a quite low energy demand, can often be electrified by means of a SWER system. The use of this technology offers not only 20-30% lower investment costs but also shorter construction time.

The Class 5 settlements can be electrified within a relatively short time by means of off-grid power supply systems, because procurement and construction time are often shorter than seen for conventional grid extension electrification projects.

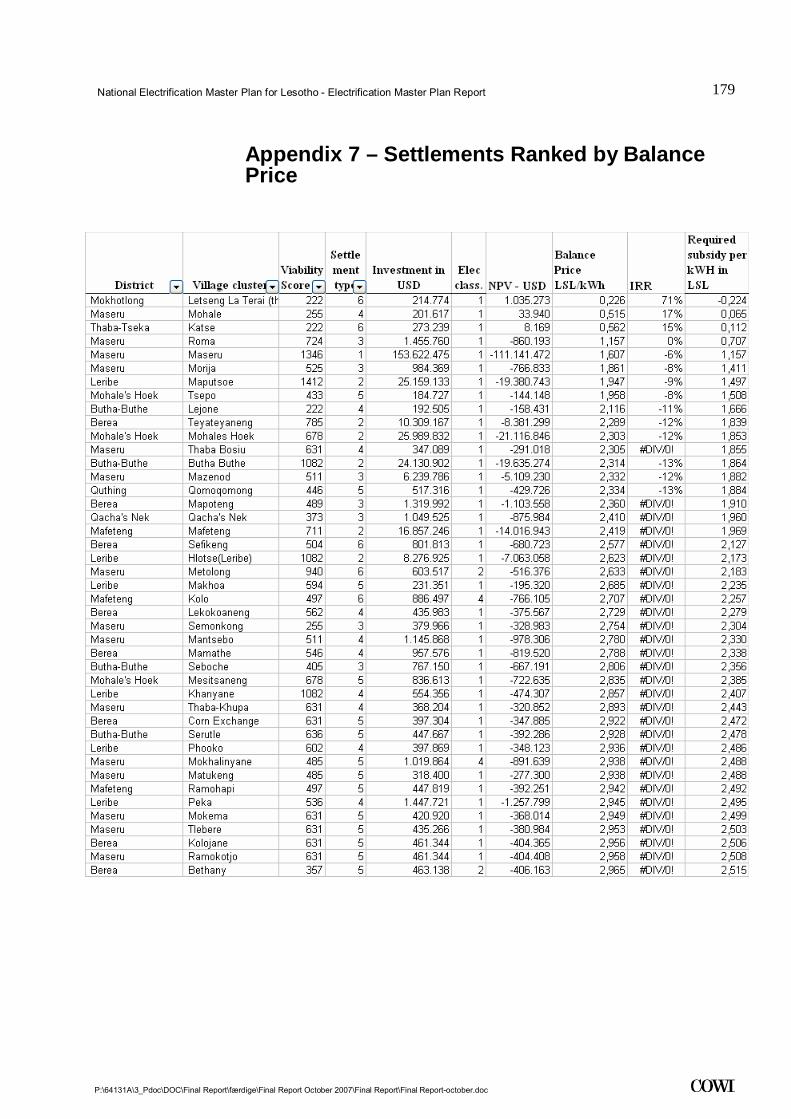

1.9 Financial Aspects The financial analysis of the complete package and each settlement indicates that the investments in nearly all individual settlements are non-viable, and very few are viable from a commercial point of view. The overall package is not viable either.

The total investment is LSL 3,022 Million over the next 15 years.

The financial deficit of the projects is LSL 2,505 Million for the entire package, including the reinforcement of the transmission system, and LSL 1,943 Million for the distribution system only. The key financial figures are presented in Table 1-6.

Table 1-6 Results of the Financial Calculations for the Electrification Plan

Unit Including Trans-mission Invest-ments of USD 65 Million

Excluding Trans-mission Invest-ments of USD 65 Million

New Households connected

No. 189 000 189 000

Investment Million USD/ Million LSL 403 / 3,022 339 / 2,543

Net Present Value of the 'project'

Million USD/ Million LSL -334 / -2,505 -259 / -1,943

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

14

.

Balance Price LSL/kWh 2.29 1.92

IRR % n.a. -9%

Subsidy Require-ment

LSL/kWh 1.58 1.20

Subsidy Require-ment (NPV)

Total Million LSL 2,505 1,943

The financial deficit is the amount needed in order to finance all costs (invest-ments, operational expenditure, purchase of power, losses, interest and depre-ciations) taking the expected revenue over the next 15 years into consideration. This deficit will need to be financed either by the GOL, the service providers or donor organisations. The scope of financing possibilities will largely determine at what speed the implementation of the plan can proceed.

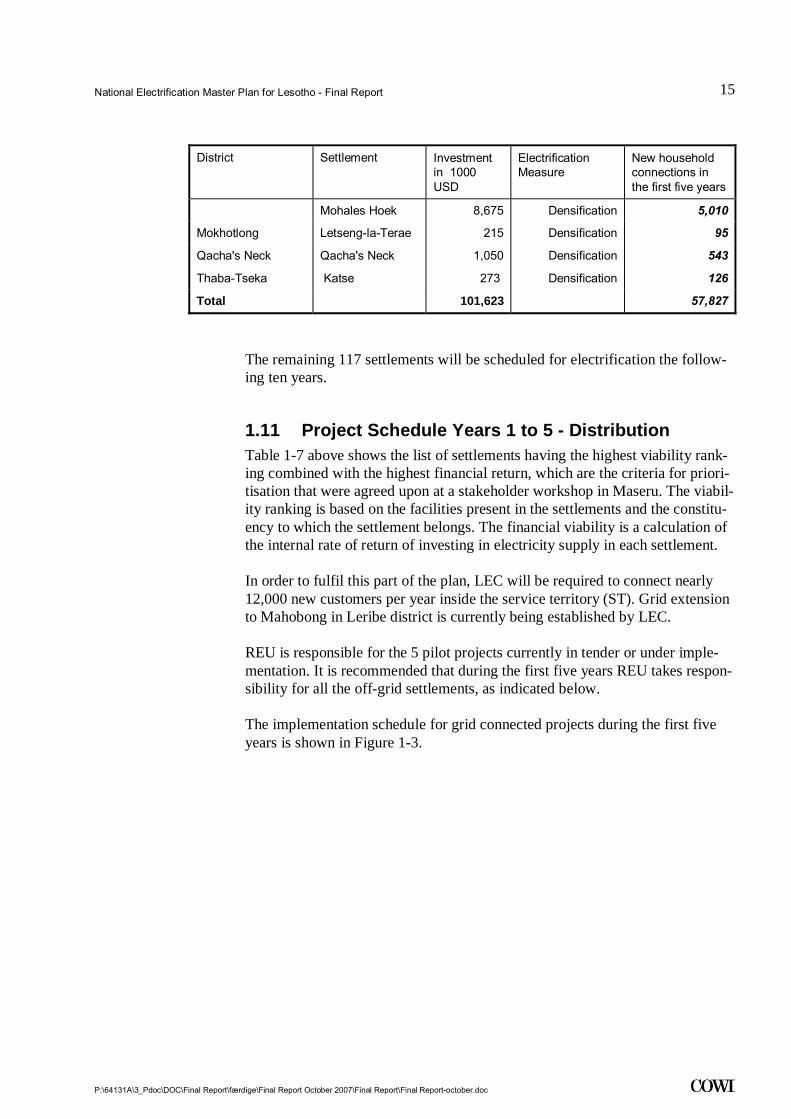

1.10 Prioritisation of Settlements Based on the agreed viability criteria, the following 23 settlements have been selected to comprise the project packages for the first five years.

Table 1-7 Priority settlements for the first five years

District Settlement Investment in 1000 USD

Electrification Measure

New household connections in the first five years

Berea Teyateyaneng 3,437 Densification 1,962

Butha-Buthe Butha Buthe 8,070 Densification 4,659

Seboche 767 Densification 392

Leribe Hleoheng 783 Densification 410

Hlotse(Leribe) 3,648 Densification 2,100

Khanyane 555 Densification 281

Mahobong 1,081 Grid Extension 545

Maputsoe 8,660 Densification 5,000

Mohlokaqala 463 Grid Extension 232

Pitseng 942 Densification 508

Rampais Nek 463 Grid Extension 232

Tsikoane 1,107 Densification 588

Mafeteng Mafeteng 6,019 Densification 3,500

Maseru Maseru 51,332 Densification 29,500

Metolong 604 Grid Extension 310

Mohale 203 Densification 88

Morija 985 Densification 528

Roma 1,455 Densification 779

Mohale's Hoek Mesitsaneng 837 Densification 439

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

15

.

District Settlement Investment in 1000 USD

Electrification Measure

New household connections in the first five years

Mohales Hoek 8,675 Densification 5,010

Mokhotlong Letseng-la-Terae 215 Densification 95

Qacha's Neck Qacha's Neck 1,050 Densification 543

Thaba-Tseka Katse 273 Densification 126

Total 101,623 57,827

The remaining 117 settlements will be scheduled for electrification the follow-ing ten years.

1.11 Project Schedule Years 1 to 5 - Distribution Table 1-7 above shows the list of settlements having the highest viability rank-ing combined with the highest financial return, which are the criteria for priori-tisation that were agreed upon at a stakeholder workshop in Maseru. The viabil-ity ranking is based on the facilities present in the settlements and the constitu-ency to which the settlement belongs. The financial viability is a calculation of the internal rate of return of investing in electricity supply in each settlement.

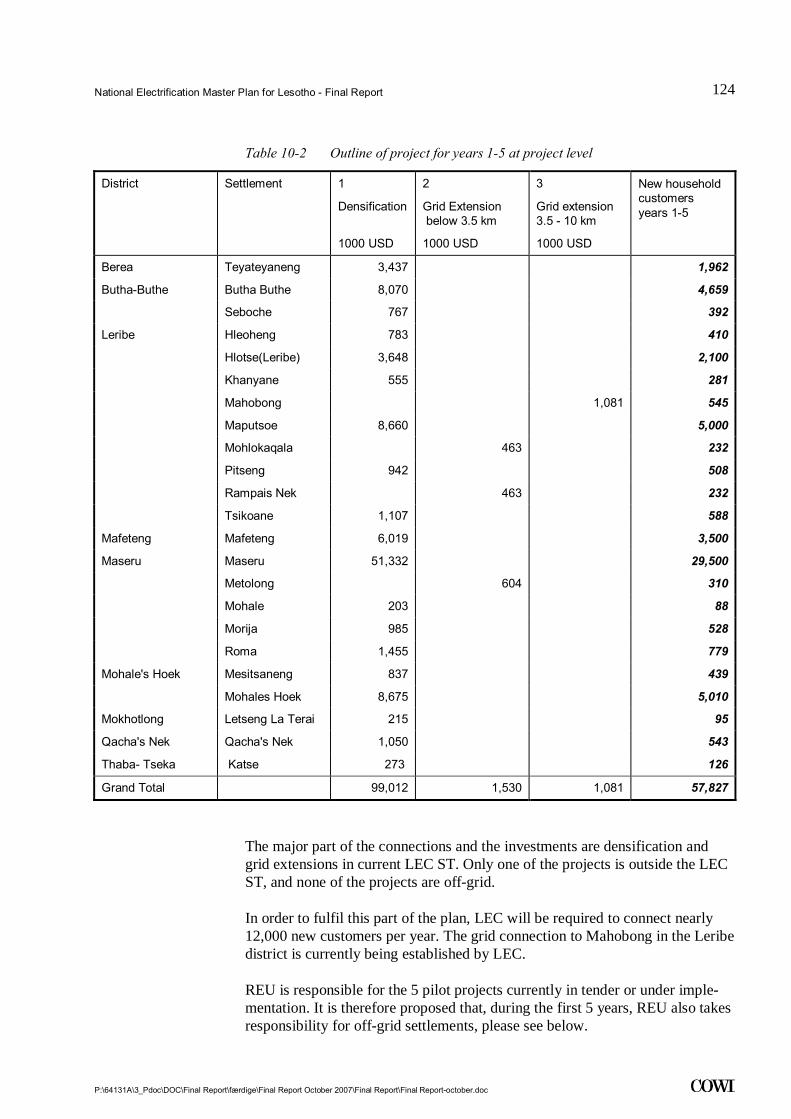

In order to fulfil this part of the plan, LEC will be required to connect nearly 12,000 new customers per year inside the service territory (ST). Grid extension to Mahobong in Leribe district is currently being established by LEC.

REU is responsible for the 5 pilot projects currently in tender or under imple-mentation. It is recommended that during the first five years REU takes respon-sibility for all the off-grid settlements, as indicated below.

The implementation schedule for grid connected projects during the first five years is shown in Figure 1-3.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

16

.

Figure 1-3 Implementation schedule for grid connection, years 1- 5 District Works Pack. Year 1 Year 2 Year 3 Year 4 Year 5

No. 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 Months

DesignTenderPre-constr.Works for: Pack.1 22

Berea Teyateyaneng 6.5Butha-Buthe Butha Buthe 15

Seboche 1.3DesignTenderPre-constr.Works for: Pack. 2 23

Leribe Hleoheng 1.4Hlotse(Leribe) 7Khanyane 0.9Mahobong 1.8Maputsoe 16.7DesignTenderPre-constr.Works for: Pack.3 17Mohlokaqala 0.8Pitseng 1.7Rampais Nek 0.8Tsikoane 2

Mafeteng Mafeteng 11.7DesignTenderPre-constr.Works for: Pack.4 56

Maseru Maseru 50DesignTenderPre-constr.Works for: Pack.5 24Metolong 1Mohale 0.3Morija 1.8Roma 2.6

Mohale's Hoek Mesitsaneng 1.5Mohales Hoek 16.7

Mokhotlong Letseng La Terai 0.3Qacha's Nek Qacha's Nek 1.8Katse Katse 0.5

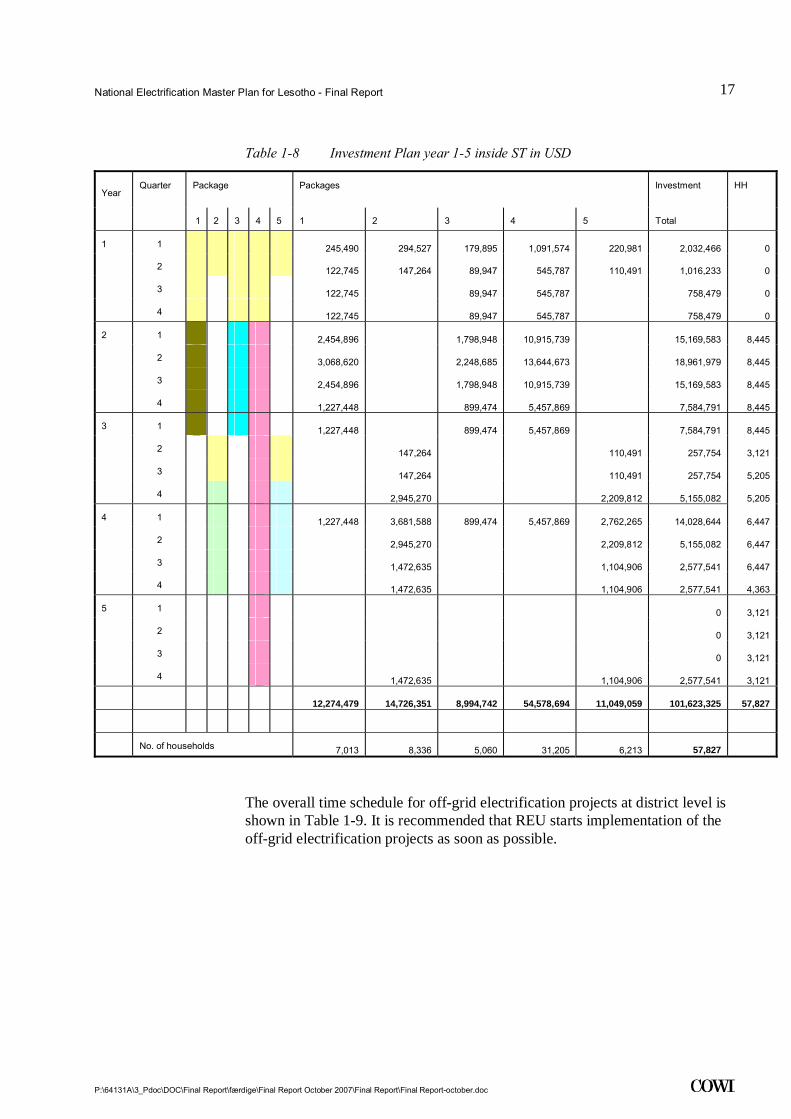

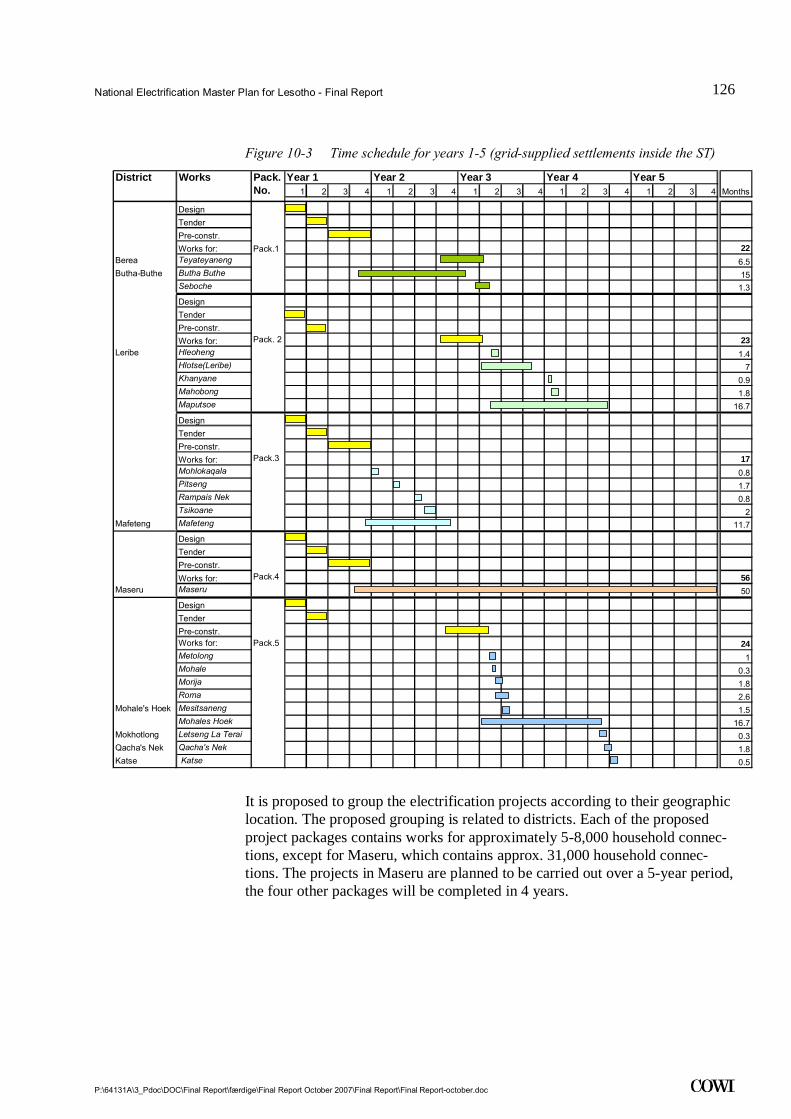

The electrification projects are grouped following their geographic location. The proposed grouping is related to districts. Each of the five proposed project packages contains works for approximately 5-8,000 household connections, except Maseru, which contains approx. 31,000 house connections.

The works are expected to be finalised in year four, except for Maseru which will run in all five years. The number of connections in Maseru made in year five will increase in order to keep a stable overall number of new connections per year. The table below shows the sequence of these packages.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

17

.

Table 1-8 Investment Plan year 1-5 inside ST in USD

Year Quarter Package Packages Investment HH

1 2 3 4 5 1 2 3 4 5 Total

1 1 245,490 294,527 179,895 1,091,574 220,981 2,032,466 0

2 122,745 147,264 89,947 545,787 110,491 1,016,233 0

3 122,745 89,947 545,787 758,479 0

4 122,745 89,947 545,787 758,479 0

2 1 2,454,896 1,798,948 10,915,739 15,169,583 8,445

2 3,068,620 2,248,685 13,644,673 18,961,979 8,445

3 2,454,896 1,798,948 10,915,739 15,169,583 8,445

4 1,227,448 899,474 5,457,869 7,584,791 8,445

3 1 1,227,448 899,474 5,457,869 7,584,791 8,445

2 147,264 110,491 257,754 3,121

3 147,264 110,491 257,754 5,205

4 2,945,270 2,209,812 5,155,082 5,205

4 1 1,227,448 3,681,588 899,474 5,457,869 2,762,265 14,028,644 6,447

2 2,945,270 2,209,812 5,155,082 6,447

3 1,472,635 1,104,906 2,577,541 6,447

4 1,472,635 1,104,906 2,577,541 4,363

5 1 0 3,121

2 0 3,121

3 0 3,121

4 1,472,635 1,104,906 2,577,541 3,121

12,274,479 14,726,351 8,994,742 54,578,694 11,049,059 101,623,325 57,827

No. of households 7,013 8,336 5,060 31,205 6,213 57,827

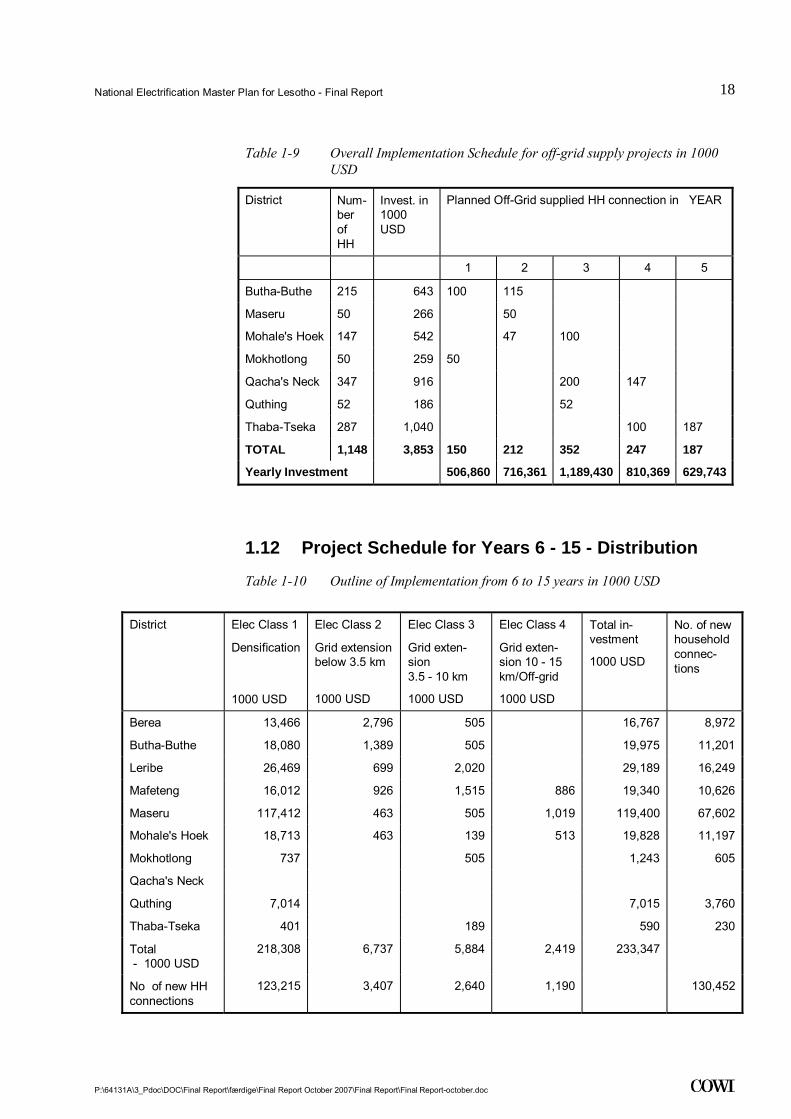

The overall time schedule for off-grid electrification projects at district level is shown in Table 1-9. It is recommended that REU starts implementation of the off-grid electrification projects as soon as possible.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

18

.

Table 1-9 Overall Implementation Schedule for off-grid supply projects in 1000 USD

District Num-ber of HH

Invest. in 1000 USD

Planned Off-Grid supplied HH connection in YEAR

1 2 3 4 5

Butha-Buthe 215 643 100 115

Maseru 50 266 50

Mohale's Hoek 147 542 47 100

Mokhotlong 50 259 50

Qacha's Neck 347 916 200 147

Quthing 52 186 52

Thaba-Tseka 287 1,040 100 187

TOTAL 1,148 3,853 150 212 352 247 187

Yearly Investment 506,860 716,361 1,189,430 810,369 629,743

1.12 Project Schedule for Years 6 - 15 - Distribution

Table 1-10 Outline of Implementation from 6 to 15 years in 1000 USD

District Elec Class 1

Densification

1000 USD

Elec Class 2

Grid extensionbelow 3.5 km

1000 USD

Elec Class 3

Grid exten-sion 3.5 - 10 km

1000 USD

Elec Class 4

Grid exten-sion 10 - 15 km/Off-grid

1000 USD

Total in-vestment

1000 USD

No. of new household connec-tions

Berea 13,466 2,796 505 16,767 8,972

Butha-Buthe 18,080 1,389 505 19,975 11,201

Leribe 26,469 699 2,020 29,189 16,249

Mafeteng 16,012 926 1,515 886 19,340 10,626

Maseru 117,412 463 505 1,019 119,400 67,602

Mohale's Hoek 18,713 463 139 513 19,828 11,197

Mokhotlong 737 505 1,243 605

Qacha's Neck

Quthing 7,014 7,015 3,760

Thaba-Tseka 401 189 590 230

Total - 1000 USD

218,308 6,737 5,884 2,419 233,347

No of new HH connections

123,215 3,407 2,640 1,190 130,452

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

19

.

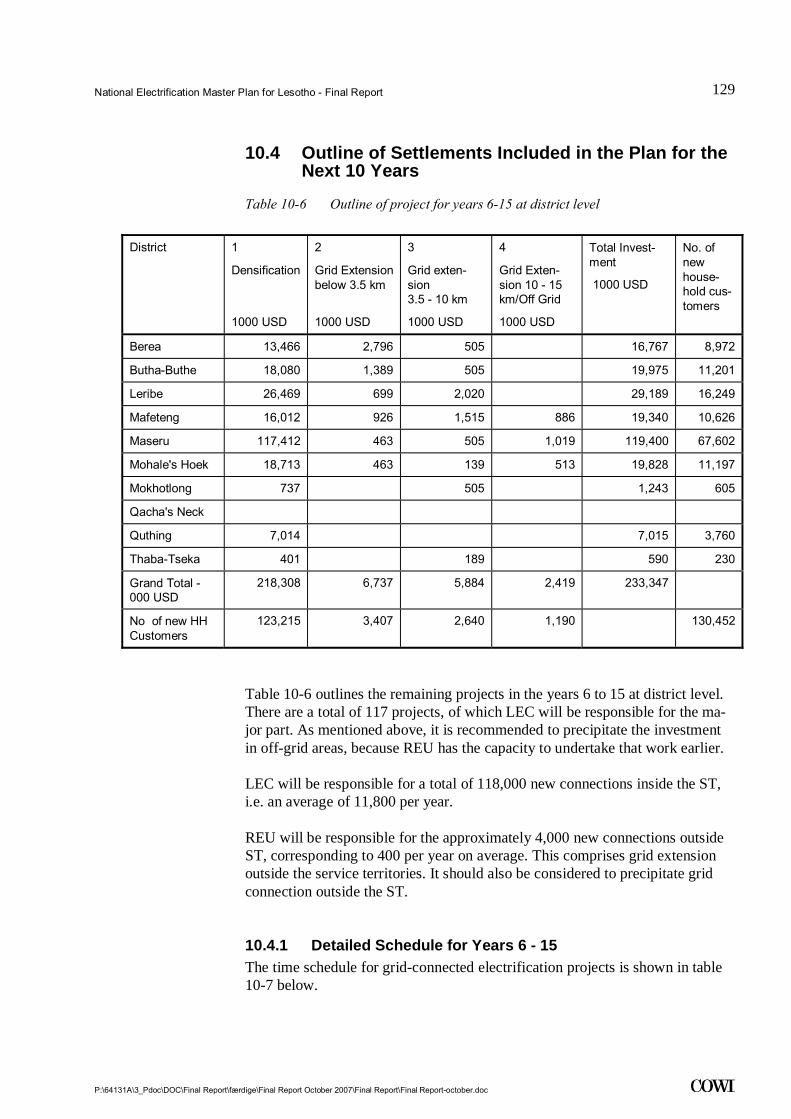

Table 1-10 outlines the remaining projects in the years 6 to 15 at district level. There are a total of 117 projects, of which LEC will be responsible for the ma-jor part.

As mentioned above, it is recommended to precipitate the investments in off-grid areas, because REU has the capacity to undertake that work now. LEC will be responsible for a total of 118,000 new connections inside the ST, i.e. an av-erage of 11,800 per year.

REU will be responsible for the approximately 4,000 new connections outside ST, corresponding to 400 per year, on average. It is also recommended to pre-cipitate grid connections outside ST, if proper arrangements can be made with LEC.

1.13 Allocation of Responsibilities LEC The responsibility of LEC should be to provide the densification measures and grid extensions inside the current ST. This translates into an annual target of 11,000 to 12,000 new customers per year. The current level of new connections provided by LEC is 5,000 to 6,000 per year, whereas LEC is committed to 8,000 per year. Without achieving very high connection levels inside the ST, it is not possible to achieve this goal, because the current ST is where the popula-tion is located and where the future growth is expected to take place.

The framework for LEC expansion inside the ST is already well developed and managed by LEA in the License issued in December 2006, where the ST is formally defined.

A mechanism for LEC to get access to the Rural Electrification Fund remains to be defined by LEA.

REU REU will be responsible for the grid extension outside the LEC ST and off-grid parts of the plan. The responsibility of REU, in terms of number of connec-tions, will be relatively small, but can be increased by taking on a number of small projects not identified in this report.

REU will implement two types of projects: grid extension beyond 3.5 km and off-grid. The operational mode will be tendering of construction and implemen-tation of project and administration of subsidies to projects where required, i.e. corresponding to the current responsibilities of REU.

For the grid extension projects, an interface with LEC has to be defined. A mechanism for works inside the ST with the aim of extending lines to REU projects has to be defined. Should REU or LEC select the contractors? An ef-fective mechanism could be that REU uses LEC as contractors, i.e. enters into binding agreements with LEC about the works to be made, and LEC selects the contractors.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

20

.

Power Purchase Agreements (PPA) and points of metering have to be consid-ered in the case of grid extension projects. One option is that the operators/REU go into contractual relationships with LEC on a case-to-case basis and LEA in each case approves the PPA. Another option would be that LEC defines tariffs for bulk supply, which are regulated by LEA. Finally, there is also the option that LEC defines tariffs for transportation and supplies at various voltage lev-els, again regulated by LEA. The main issue is that it is important that the regu-lator ensures a stable and lasting set of agreements which are secure and trans-parent for the operators/investors.

REU should also administer applications from villages that, based on their own initiative, have provided a basis for grid extension or off-grid supply. For in-stance in cases where the CCA or other local operators have made the prepara-tions for electrification of one of more areas, but subsidies are required.

Further, it could be considered whether REU should be responsible for supply-ing individual solutions, i.e. SPV/Gen-sets, inside ST. During the next 10 years, there will still be many villages/settlements left without grid supply, and it makes sense to make an authority responsible for the existence of credible al-ternatives for these households until the grid is extended.

1.13.2 Private Sector The overall capacity needs to be increased significantly in the short term by using foreign contractors and in the longer term by education and training of Basotho technicians and engineers.

One way of increasing the capacity and keeping the benefits inside Lesotho is to select Basotho consultants and contractors. The problem in Lesotho is that there are only few local consultants and few contractors. It is important that the Basotho private sector is strengthened in terms of numbers of staff/companies and capacity. In the longer term, the scope of maintenance work on electrical supply systems will increase significantly, and LEC will also require external capacity to cope with the upkeep. As a result of the NEMP, the room for the private sector will increase dramatically, and strategies to ensure that the local private sector is capable of assisting and benefiting from this development are necessary.

International Competitive Bidding (ICB) disadvantages the local expertise, be-cause it not always results in transfer of skills. Experience shows that external contractors/consultants may yield expected results, but the method is not effec-tive for transfer of skills. Adoption of partnership models will result in an effec-tive capacity building in the Basotho community. Partnerships between Baso-tho and foreign companies should be encouraged, and advantage should be given to partnerships with local firms in the tender evaluation criteria.

It is highly desirable that the design of new extensions and supply systems are made by local consultants. In order to ensure that the projects are implemented, a mixture of ICB and Local Competitive Bidding (LCB) is recommended. Tar-

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

21

.

gets and indicators for Basotho participation should be developed and moni-tored. It is recommended to allocate 80% of the design Basotho consultants, and a mix of ICB and LCB should be used in contracting the actual implemen-tation.

1.14 Future Service Models for Electricity Supply It is the formulated goal of the government to promote competition and effi-ciency in power distribution by involving the private sector and Local Govern-ment more in operation of utilities. Until recently, LEC was the only supplier in the country, and therefore there is only limited experience of involving other players.

Due to the low viability and low ability to pay among the Basotho households, power distribution is only attractive, if investors are guaranteed access to large institutional/commercial/industrial customers. Therefore, a system of conces-sions in order to provide some security for the investments is required. The Consultant recommends investigating a concession model with four sustainable areas as soon as possible. The four areas could be the districts of Mokhotlong, Qacha's Neck, Mohales Hoek and Thaba-Theka.

Outside the Service Territories, the Consultant recommends a "lease and trans-fer model", which has already been proposed as a suitable solution for Lesotho, where private operators lease the generation/distribution facilities from the Government (REU) for a specific period of time. The Government provides the assets for the operators against a fee. In the long run, this system will also en-able the Government to involve the Local Government actively in the power supply. REU could play an important role in capacitating and supporting the Local Government in this effort.

For the individual solutions (SHS and SPV), a number of options for involving the private sector exist. These are currently being tested by REU.

1.15 Tariffs and Connection Fee The Consultant recommends the connection fee to be lowered to a maximum level of 500 LSL, because the current connection fee seems to be an important barrier for increasing the connection level in Lesotho.

The current method of setting tariffs is based on LRMC, and tariffs are cost-reflective. The advantage of cost-reflective tariffs is that the LEC will obtain the resources to support and maintain the current and new system from its reve-nue, and therefore can operate on commercial conditions without any direct subsidies. Instead, subsidies, where needed, are provided directly to projects on a case-to-case basis, or directly to the customers. The Consultant strongly sup-ports this approach to tariff setting.

Collection and billing by LEC consist mainly of pre-payment that basically works well, i.e. limits the commercial losses - it is, however expensive in in-

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

22

.

vestment and require a certain volume of customers. The conditions of the fu-ture electrification areas are different from the existing areas, and with lower population and lower average demand, the cost of the system will increase. Therefore, ideas of using simpler and less expensive metering systems are re-quired.

The following methods have been used with success in other countries in terms of accelerating connection levels:

• Paying a premium to existing consumers who get new consumers to con-nect;

• Financing the connection of new consumers over the electricity bill (dis-tribute the payment of connection fee plus interest over 10 years);

• Financing of internal house wiring and basic appliance packages;

• Extending the network to a village only if 70% of the potential consumers will connect and pay in advance;

• Giving introduction discounts or connection discounts, which decrease over a period, so that it is cheapest to connect at the beginning;

• Providing discount in selected areas in 3-month to one-year campaigns;

• Using a system of differentiated tariffs according to quality, for instance introducing a special low tariff for power supply to a basic 5 A installation with a load limiter, instead of a meter. This is suitable for households with limited ability to pay and limited power requirements.

1.16 Subsidies It is clearly demonstrated in the financial analysis, that a subsidy is required to achieve the aims of the NEMP. In most cases, when analysing the individual settlement, the subsidy requirement exceeds the capital investment, i.e. there is also a need for subsidies on operational costs.

Special funding mechanisms therefore need to be put in place (levies, fiscal al-locations, donor funds, Output-based Aid), consolidated in a rural electrifica-tion fund, and linked to electrification planning with a transparent fund alloca-tion process.

The pricing system needs to accommodate tariffs that are affordable for poor households, yet also sustainable for the electricity supply industry and the gov-ernment budget, e.g. through cross-subsidization from large consumers. The pricing system for poor households also needs to be targeted - this can be done through restricting lifeline or social tariffs to those consumers who consume less than 50 kWh per month, or they could be targeted to consumers who accept current-limited supply systems or pre-paid systems, provided these are proxies for poverty.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

23

.

1.17 Institutional Development and Training A training needs assessment of four institutions, DOE, LEC, REU and LEA was made as part of the NEMP, focusing on the skills needed for monitoring and implementation of the NEMP. It is assessed that approximately LSL 4 Mil-lion should be allocated annually for training and institutional development over the 15-year period.

Only at the end of the period would it be relevant to include the Local Govern-ment into the programme due to their focus on other tasks in the coming 10 to 15 years.

1.18 Monitoring and Evaluation Framework National/ Central Requirement The NEMP provides indicators for monitoring electrification progress and im-pact in Lesotho, i.e. number of households electrified at national and district level. This information should be collected for monitoring at monthly or quar-terly intervals.

The key provider of data will be LEC, which must operate its customer data-base so that detailed customer data can be provided on a regular basis. All other future service providers (including REU) should also be required to submit data on the number and types of connections achieved over a given period of time.

National monitoring should focus on the extent to which the targets of the NEMP are fulfilled. This implies comparing coverage records with national population trends to derive the percentage served. It is important that this is done by settlement type as the population growth rates will differ significantly according to type. The BOS should provide population updates on an annual basis, based on the 2006 census data. They should also be used to improve the accuracy of the data on the population and the number of households for the base year (2005).

At the national level, it is important to monitor the extent to which the provi-sion of electricity contributes to the Poverty Reduction Strategy of the Gov-ernment, in particular the extent to which new jobs are created and education and health services are improved. The key objective here will be to look at the long-term benefits or outcomes of electrification.

Ministry/ Sector At the sector level, indicators for the impact of rural electrification on the use of other sources of energy and the environment need to be identified. Of particular importance will be the environmental data about use of wood and scrubs. In addition, indicators measuring the effect on business in rural centres, effect on development of institutions and effects on schools should be established. It will be necessary to carry out regular surveys to collect this information and this need to be budgeted for by sector institutions.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

24

.

Strategic/ Corporate level (LEC / REU) At this level, the focus will primarily be on matching resources requirements with demand. Demand estimates will have to be revised on a regular basis, par-ticularly if any adjustments are made to tariffs or connection fees. National economic trends, notably employment, should also be monitored as these will have a major influence on the demand.

Indicators will address the extent to which funding and human resources are made available to meet demand. Progress and efficiency indicators will include coverage by district and constituency and degree to which these are achieved within the estimated NEMP budget.

Planning/ Operational Level (LEC / REU) Indicators should cover both implementation and impact/results, and include number of projects, costing, implementation schedules and performance indica-tors.

Project Level Individual project indicators will deal with inputs, outputs, implementation tar-gets, and milestones.

District Level At district level, key indicators will address:

• Number and percentage of households with electricity;

• Number and percentage of villages/towns with electricity;

• Presence of schemes in the district;

• Local representation in institutions in charge of electricity services in the district etc;

• Amounts collected by schemes;

• Total funds generated for electrification.

Communities/ Consumers At the community levels/ service recipient’s key indicators will include:

• Number of applications;

• Processing time for applications;

• Number of applications approved;

• Time between approval and contractor starting;

• Time between payment and construction; construction and connection.

At consumer level, citizen report cards could be used to measure consumer per-ceptions of service efficiency, for example number of power cuts or surges, speed of response and response efficiency, cost of power cuts (inconveniences).

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

25

.

Institutional Arrangements The responsibility for monitoring and evaluation of the electricity sector is rec-ommended to continue to lie with the LEA. The LEA will probably need to es-tablish an M&E unit. Different types of monitoring will need to be undertaken using different or a mix of methodologies. Although some of these activities will probably be sub-contracted to private expertise, some capacity building for the M&E Unit should be foreseen.

Institutionally, the monitoring and evaluation role of LEA will be performed through a number of structures. In particular, the Rural Electrification Unit will advise the Board through an Advisory Committee on Rural Electrification. Among other things, the Advisory Committee will advise on implementation of the Electrification Master Plan and monitoring of projects. Membership of the Board of the proposed National Electrification Fund and the participation in planning of the electrification policy will provide further tools for LEA to fulfil its mandate.

LEA expects the monitoring and evaluation function to be housed in one of the departments, possibly the Technical Department or the Economics Department. In this way, the Authority will play a very active role in the overall M&E of the NEMP.

At the national level, the Lesotho Electricity Company will be the major im-plementing agency and data provider, while the Rural Electrification Unit (Agency) will also take responsibility for M&E of the rural electrification pro-gramme, and may require a unit for M&E, as well as a related programme of capacity building.

1.19 Environmental Issues Impact and Mitigation Major constructions should be avoided in protected areas. Lesotho has few and small national parks and protected areas. A new protected area along the north-eastern border is under development, and parts of this will be protected as re-serves.

It is a prerequisite for tourism that electricity is available, but large pylons and power lines can be a sore to the eye. In tourism development areas, special care must be taken to either avoid (high tension) transmission lines or to be very careful with the blending into the landscape.

In the sandstone areas, it is a good idea to screen for archaeological finds, rock paintings etc. before constructing new alignments in order to avoid delays when inspections and possible excavation are taking place.

Lesotho houses a number of rare animal species; some of these are legally pro-tected. Most of the species occur in the highlands where the impact from people is the least. One species of fish is not protected by the law but is only found in

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

26

.

Lesotho in the upper parts of the Orange River. The construction of a dam here must be avoided.

The Wetlands attract large (protected) species of birds that are especially prone to collisions with power lines.

Impact from Distribution and Transmission Lines The same houses that benefit from having electricity will also experience a number of disadvantages, such as loss of small tracts of land for pylons, risk of lightning and health hazards. Most of these can be ameliorated through a careful planning of the pylons and raising of awareness.

The pylons for the transmission networks are galvanized with zinc, which also contains elements of heavy metals. Lead and cadmium will normally leak in quantities that might damage aquatic life. Pylons must be avoided in the wetlands.

The negative impacts of the proposed transmission lines are caused during the construction phase when surface areas become exposed due to vegetation clear-ing, and this may in turn give rise to erosion. Clearing of vegetation from the site, access roads and tower pads may also give rise to negative impacts.

Un-insulated overhead lines are more prone to lightning strikes and short-circuit incidents than insulated overhead lines. Insulated overhead lines should be used in areas of Lesotho that are known to be prone to lightning strikes, as well as to ensure a more reliable energy supply.

Potential sources of waste include lead acid batteries that are used particularly in the rural areas to power televisions, video casette players, radios and satellite systems. The appropriate disposal of spent lead acid batteries is a potential impact as Lesotho does not currently have a registered hazardous waste disposal facility.

The use of diesel generators gives rise to spent oil, the disposal of which is regarded as problematic as there are no companies in Lesotho recycling used oil.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

27

.

2 Introduction The objective of this National Electrification Master Plan Study is to provide clear guidelines and establish priorities for providing access to electricity in Lesotho in a co-ordinated and cost-effective manner, which will enable the Government of Lesotho (GOL) to meet its electrification targets in particular, and rural development goals in general.

The plan provides prioritised electrification schedules that indicate the annual number of connections to be made and systems to be installed, as well as cost.

The contract for preparing the National Electrification Master Plan (NEMP) has been granted to COWI A/S, Denmark, in association with Sechaba Consultants of Lesotho. The contract was carried out from 1 July 2006 to 15 March 2007 and was extended to 31 July 2007.

The NEMP has been organised in three distinct steps:

• STEP 1: Inception;

• STEP 2: Electricity Master Planning;

• STEP 3: Electricity Master Plan Implementation Strategy.

This Final Report captures the results of all three steps of the study.

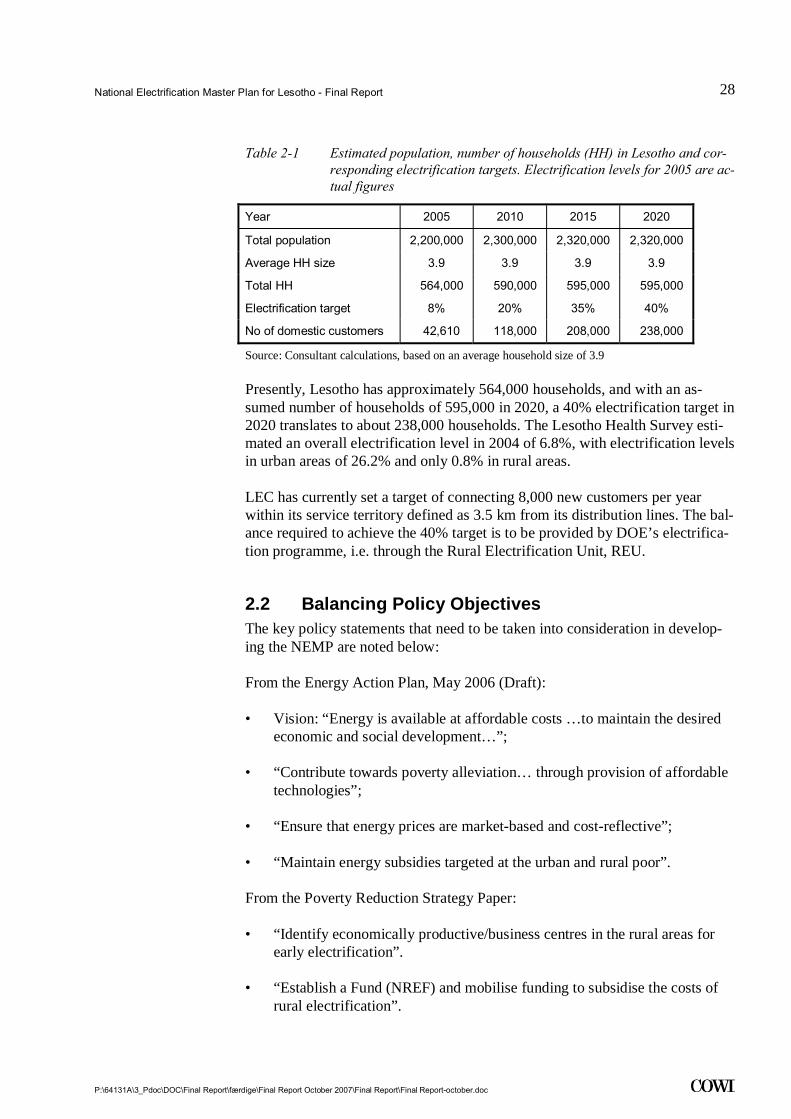

2.1 Electrification Target for Lesotho The overall electrification target for Lesotho is a minimum of 35% by 2015 and 40% by 2020. The target is defined as the number of households actually con-nected to the grid or supplied by off-grid means (e.g. hydro/diesel mini-grid or PV solar home systems).

While awaiting the results of the 2006 census, estimates based on current in-formation have been used to estimate the number of households in Lesotho to-wards 2020 and the targeted number of electrified households, when meeting the Government's electrification targets.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

28

.

Table 2-1 Estimated population, number of households (HH) in Lesotho and cor-responding electrification targets. Electrification levels for 2005 are ac-tual figures

Year 2005 2010 2015 2020

Total population 2,200,000 2,300,000 2,320,000 2,320,000

Average HH size 3.9 3.9 3.9 3.9

Total HH 564,000 590,000 595,000 595,000

Electrification target 8% 20% 35% 40%

No of domestic customers 42,610 118,000 208,000 238,000

Source: Consultant calculations, based on an average household size of 3.9

Presently, Lesotho has approximately 564,000 households, and with an as-sumed number of households of 595,000 in 2020, a 40% electrification target in 2020 translates to about 238,000 households. The Lesotho Health Survey esti-mated an overall electrification level in 2004 of 6.8%, with electrification levels in urban areas of 26.2% and only 0.8% in rural areas.

LEC has currently set a target of connecting 8,000 new customers per year within its service territory defined as 3.5 km from its distribution lines. The bal-ance required to achieve the 40% target is to be provided by DOE’s electrifica-tion programme, i.e. through the Rural Electrification Unit, REU.

2.2 Balancing Policy Objectives The key policy statements that need to be taken into consideration in develop-ing the NEMP are noted below:

From the Energy Action Plan, May 2006 (Draft):

• Vision: “Energy is available at affordable costs …to maintain the desired economic and social development…”;

• “Contribute towards poverty alleviation… through provision of affordable technologies”;

• “Ensure that energy prices are market-based and cost-reflective”;

• “Maintain energy subsidies targeted at the urban and rural poor”.

From the Poverty Reduction Strategy Paper:

• “Identify economically productive/business centres in the rural areas for early electrification”.

• “Establish a Fund (NREF) and mobilise funding to subsidise the costs of rural electrification”.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

29

.

As can be seen from the above, there is a trade-off between provision of mar-ket-based/least cost and cost-reflective services (demand-driven, by those able to pay) and services that can be afforded by the poor (i.e. subsidized, targeting the poor) and that sustain social development. The selection criteria for new areas to be electrified will have to reflect these different policy objectives to achieve a balanced approach to service provision.

2.3 Planning Criteria and Approach

2.3.1 Current LEC Practice Traditionally, the criterion for a community to be considered for electrification by LEC is the creation of a “scheme” (an organised group of potential custom-ers) and a registration of this with LEC.

The priority of the schemes is then primarily made according to the estimated average cost per connection, but is often subject to inexplicit political priorities. The ranking is determined by the distance to the grid connection point, the number of scheme members and the amount of funds collected from scheme members. Ability and willingness-to-pay assessments are sometimes made by LEC to determine the group’s financial viability. Thus, the approach is based on a mix of the cost of the scheme, the number of potential customers and the ability of the scheme members to pay.

2.3.2 Approach of Other Planning Projects In the Lesotho Lowlands Water Supply Feasibility Study, LLWSFS, a cluster approach was used to identify viable areas for supply. The cluster approach means that instead of taking the village name as a point of departure, an effort was made to group minor villages situated within short distances (less than 1 km) of each other into a cluster of min. 2,500 inhabitants.

The clusters were identified in eight zones in the Lowlands and indicated on maps. The approach was later accepted for telecommunications development planning and extended to cover also the Highlands.

The villages or clusters of villages were then classified according to the Na-tional Settlement Plan into 6 settlement types: Capital city, industrial towns, large “institutional” towns, medium-sized settlements, large villages and small villages, each with different expectations regarding population growth.

The study, Access to Electricity (2001), used a large number of socio-economic variables for the ranking of settlements for electrification that were more than 10 km from LEC distribution lines. The point score was used to select five elec-trification pilot projects to test different approaches to rural electrification. Al-though surveys were carried out on indications of ability and willingness to pay, this did not form part of the selection criteria.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

30

.

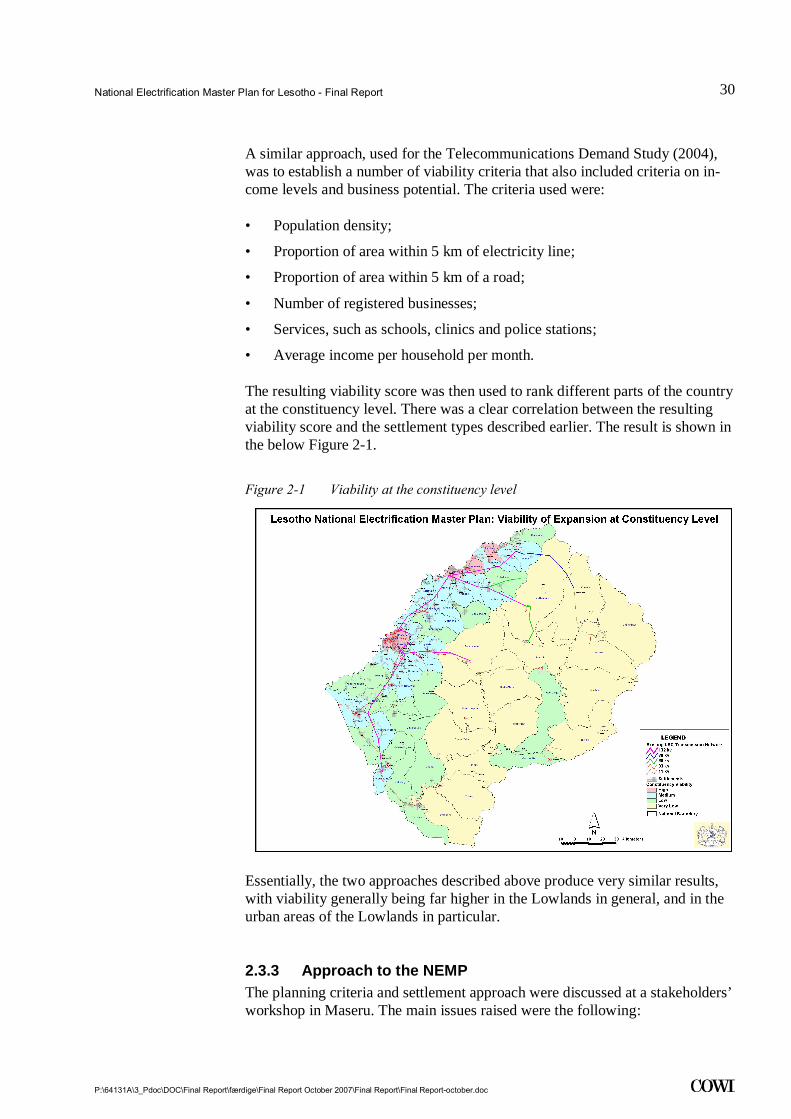

A similar approach, used for the Telecommunications Demand Study (2004), was to establish a number of viability criteria that also included criteria on in-come levels and business potential. The criteria used were:

• Population density;

• Proportion of area within 5 km of electricity line;

• Proportion of area within 5 km of a road;

• Number of registered businesses;

• Services, such as schools, clinics and police stations;

• Average income per household per month.

The resulting viability score was then used to rank different parts of the country at the constituency level. There was a clear correlation between the resulting viability score and the settlement types described earlier. The result is shown in the below Figure 2-1.

Figure 2-1 Viability at the constituency level

Essentially, the two approaches described above produce very similar results, with viability generally being far higher in the Lowlands in general, and in the urban areas of the Lowlands in particular.

2.3.3 Approach to the NEMP The planning criteria and settlement approach were discussed at a stakeholders’ workshop in Maseru. The main issues raised were the following:

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

31

.

Selection Criteria It was stressed that the plan is a national plan, meaning that a settlement falling within or outside the service territory of LEC should not be a criterion for se-lection.

Several participants stressed that the electrification plan should contribute to economic development in general and income generation in the rural areas in particular. Focus should therefore be on criteria, such as the existence of private sector development opportunities, e.g. mining, tourism and agriculture. The number of registered businesses in a settlement area could be an indicator for this.

The national development plan should be consulted to identify plans for new activities.

A special issue to be looked at was resettled communities, as these are normally not indicated on maps, but have funds for infrastructure development, such as electrification.

Planning Assumptions It is important that electrification contributes to the creation of wealth, espe-cially in the rural areas. The planning should take potential for productive uses into account as an important parameter in the planning, e.g. the presence of other infrastructure, such as roads, telecommunication and water.

Design and Standards The current practice of LEC only to offer 20 and 60 A underground connec-tions does not provide future consumers with the possibility of choosing a cheaper solution. If people were provided with the choice of a cheaper connec-tion, such as 10 A, overhead connection, ready-board, more people would be able to afford the connection charges.

Other Issues Raised Environmental considerations should be made upfront. A strategic environ-mental impact assessment of the electrification plan is programmed and would deal with both placement of electricity lines (sensitive areas, proximity to houses, etc.) and assessment of production facilities (hydro dams, generators).

2.3.4 Conclusions The discussion above of the various factors that need to be taken into consid-eration in developing the Master Plan suggests that a new approach is needed, which is not purely demand-driven and takes into consideration social criteria without being driven solely by development requirements (balance).

For the sake of cost effectiveness, it is important to optimize the uptake (get as many customers at the lowest costs). For this reason, the ‘cluster approach’ to scheme choice is proposed, in which small settlements situated close to each other are grouped into “clusters”. Chapter 4.1 presents the cluster approach in

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

32

.

more detail. Each settlement or cluster of settlements of a certain size has been analysed and recommendations made on how it should be served, taking into consideration population, settlement type, social services, levels of poverty and distance from the grid. These issues are described further in Chapters 6 and 7.

The NEMP has taken the ranking of viability of the constituencies as a starting point for the settlement analysis. Priority is therefore given to the more devel-oped settlement types that are unconnected at present, as well as to reaching existing schemes registered with LEC, especially in cases where payments have already been made. The refining of the proposed sequencing of electrifying the settlements of Lesotho is based on an analysis of the future electricity demand of each settlement, technical considerations and cost as well as a financial analysis. The ranking is therefore both based on economic and social criteria, with emphasis on the potential for economic development.

There are a number of settlements that are already served with electricity, but where only few households have been connected to the grid. The potential for densification of these underserved electrified settlements is clear and should be concurrent with the grid extension to new areas.

2.4 Report Structure and Terminology

2.4.1 Reporting The reporting of this NEMP study allows for five major reports:

1 Inception Report: Captured the results of STEP 1 of the project with the main outputs being an agreement on the planning criteria, the need for fur-ther socio-economic surveys and the further process. A detailed work plan for the completion of the project was included, serving as the basis for the entire project.

2 Electrification Master Planning Report: Captured the results of STEP 2 with the main outputs being: A national load forecast, design of electrical systems, selection of and prioritisation of settlements, investment schedule for 15 years, financial analysis, assessment of future delivery systems and environmental analysis.

3 Implementation Strategy Report: Captured the outcomes of STEP 3 and includes a project schedule for 15 years and details from the first five years as well as recommendations for a monitoring and evaluation framework for the project implementation.

4 Stakeholder Consultation Report: Captured the outcome of Stakeholder Consultations undertaken in Maseru from 11 to 14 June 2007.

5 Final Report: This report, which summarises the results of the master planning process.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

33

.

During the project, a number of Working Papers have been issued. A list of the Working Papers can be found in Appendix 1.

2.4.2 Terminology Used In this report, “up-take levels” and “connection levels” are used interchangea-bly, referring to the number of electrified households in an area or settlement in relation to the total number of households in the same area. At national level, this translates into the share of all households in Lesotho using electricity sup-plied from the electricity mains, a generator or solar panels for their electricity needs (thus excluding households using car batteries for television or lighting or small batteries for radio cassettes, etc).

The electrification level refers to the share of households using electricity as their main source of lighting. It should the noted that the Government’s electri-fication target is not defined as access to supply, but as actually connected households.

All cost and prices items are provided in fixed 2006 prices.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

34

.

3 Background

3.1 Context Lesotho is a small, mountainous, landlocked country covering an area of ap-proximately 33,000 square kilometres entirely surrounded by the Republic of South Africa (RSA). Lesotho’s economy is dependent on its close relationship with the RSA, which supplies the bulk of consumer goods and significant em-ployment opportunities for Lesotho workers. Historically, agricultural and pas-toral productions have sustained many rural communities, with very limited surplus produce being sold, other than wool and mohair. More recently, light manufacturing, notably of textiles, has become important and now forms the bulk of Lesotho’s exports. Lesotho is currently the biggest exporter in Sub-Saharan Africa of denim jeans to the United States and the country has suc-ceeded in maintaining relatively high levels of foreign direct investments at a time of rapid global changes in the garment sector. Garment factories, located primarily in Maseru and Maputsoe, are the largest employers in the country.

The economy is supplemented by large, but declining, remittances from Leso-tho miners in RSA and, recently, the receipt of royalties from supplying water to RSA through the Lesotho Highlands Water Project (LHWP). The LHWP played an important role in opening up previously inaccessible parts of the country, allowing for new infrastructure, particularly roads, electricity and tele-communications.

In a country that is largely mountainous, it is not surprising that the bulk of the population and of economic activity is concentrated in the more accessible Lowlands areas in general, and in the urban areas in particular. Utility services are largely focused on these areas, with electricity being no exception.

So far, about 51,000 customers are connected to the network, and between 2,000 and 3,000 use PV systems for electricity supply. Although no statistics exist on generators, it was estimated in 1999 that less than 500 households were supplied from generators. According to the Demographic and Health Survey from 2004, 18% of the household use either batteries/generator or solar energy, but it has not been possible to identify the split between the three sources.

The difficult mountainous terrain with low population density increases the cost of grid electrification.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

35

.

3.2 Energy Policy and Power Sector Reform Through its energy policy and poverty reduction strategy, the Government of Lesotho (GOL) is geared for the ultimate goals of sustainable rapid economic growth, job creation and poverty reduction through development of the private sector. The key challenge of the Government in the energy sector is to increase access to electricity for both the urban and the rural population. Through the Department of Energy (DOE), the Ministry of Natural Resources (MNR) is the Government’s principal entity charged with the national energy planning and policy development.

The major energy policy elements of the GOL are to:

1 Increase access to electricity for economic, social and environmental rea-sons;

2 Introduce competition in the power sector;

3 Encourage private sector participation;

4 Restructure 'Muela Hydropower Plant and LEC and then privatise them;

5 Charge the customer with cost-reflective tariffs;

6 Develop appropriate institutional energy sector framework.

The decision to privatise LEC is currently under review.

Before the independence in 1966, electricity supply was very limited, confined essentially to cross-border supply from South Africa to the administrative and commercial centres of the main Lowland towns and off-grid systems run by missionaries and traders in the more remote areas.

A key point in the history of Lesotho’s electrification came in 1969 with the establishment of the Lesotho Electricity Company (LEC) in terms of the Elec-tricity Act of 1969. LEC was mandated by the Act for the generation, transmis-sion, distribution and supply of electricity in the entire country. Subsequently, under provisions of the Treaty (between GOL and RSA) for the LHWP, GOL established an autonomous body, Lesotho Highlands Development Authority (LHDA), as the implementing agency for the LHWP, which included the gen-eration of hydroelectricity at Muela.

GOL has approved a policy statement, stating that LEC will purchase the elec-tricity generated at the 'Muela Hydro Power Plant (MHPP) from LHDA and will act as the distributor of electricity within Lesotho. LHDA will own MHPP and the related transmission lines. LEC will operate and maintain the transmis-sion lines owned by LHDA as a contractor of LHDA. Currently, this policy statement is being changed through the reforming and restructuring of the elec-tricity sector, including a provision to transfer the transmission assets to LEC.

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

36

.

The table below shows the number of connections per district in 2003.

Table 3-1 LEC connections as per 2003 by district

District Population Number of households

Connections end of 2003

Electrification level in %

Butha-Buthe 150,815 30,163 977 3

Leribe 280,766 56,153 4,338 8

Berea 201,852 40,370 1,735 4

Maseru 441,741 88,348 29,106 33

Mafeteng 190,301 38,060 1,983 5

Mohale's Hoek 159,939 31,988 1,544 5

Quthing 102,429 20,486 345 2

Qacha's Neck 127,179 25,436 337 1

Mokhotlong 106,286 21,257 216 1

Thaba-Tseka 167,176 33,435 352 1

Total 1,928,484 385, 697 40, 933 11

Source: DOE 2006, using an average household size of 5.

In 2003, the Lesotho Government estimated that only about 11% of the house-holds in Lesotho had access to electricity. This prompted GOL to set an ambi-tious target of 40% electrification by 2020 and to embark on reforming and re-structuring the electricity sector with a view to introducing private sector par-ticipation.

Currently, LEC is adding 5,000-6,000 new customers per year to their customer base. LEC has, however, a commitment to connect 8,000 new customers per year within its Service Territory (ST). A considerable increase in the resources and changes in policies towards new connections are required to achieve this target.

The restructuring process started with the restructuring of LEC in early 2001 through the appointment of an Interim Management Task Force (IMTF). The Management Contract Team succeeded the IMTF and is currently managing LEC. The ultimate aim is privatisation, but this is currently on hold, although the commercialisation process continues. LEC was transformed into a Com-pany in December 2006 and licensed for import, transmission and distribution in December 2006.

Lesotho Electricity Authority (LEA), the regulator of the electricity sector, be-came operational in August 2004 (in conformity with the LEA Act 2002).

GOL has reviewed its institutional framework for Rural Electrification (RE) and approved an implementation strategy, which involves the implementation of Electricity Access Pilot Projects (EAPPs) at five locations outside the Ser-vice Territory of the LEC; initially, to test various grid and off-grid institutional

National Electrification Master Plan for Lesotho - Final Report

P:\64131A\3_Pdoc\DOC\Final Report\færdige\Final Report October 2007\Final Report\Final Report-october.doc

37

.

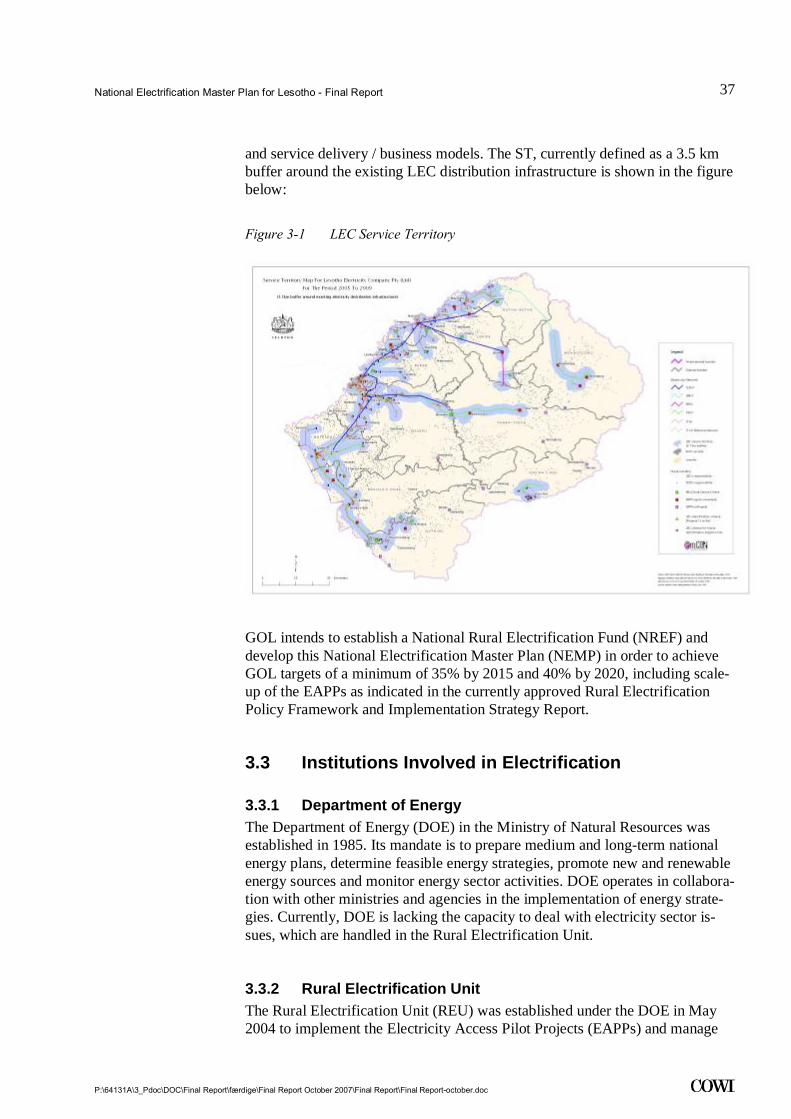

and service delivery / business models. The ST, currently defined as a 3.5 km buffer around the existing LEC distribution infrastructure is shown in the figure below:

Figure 3-1 LEC Service Territory

GOL intends to establish a National Rural Electrification Fund (NREF) and develop this National Electrification Master Plan (NEMP) in order to achieve GOL targets of a minimum of 35% by 2015 and 40% by 2020, including scale-up of the EAPPs as indicated in the currently approved Rural Electrification Policy Framework and Implementation Strategy Report.

3.3 Institutions Involved in Electrification