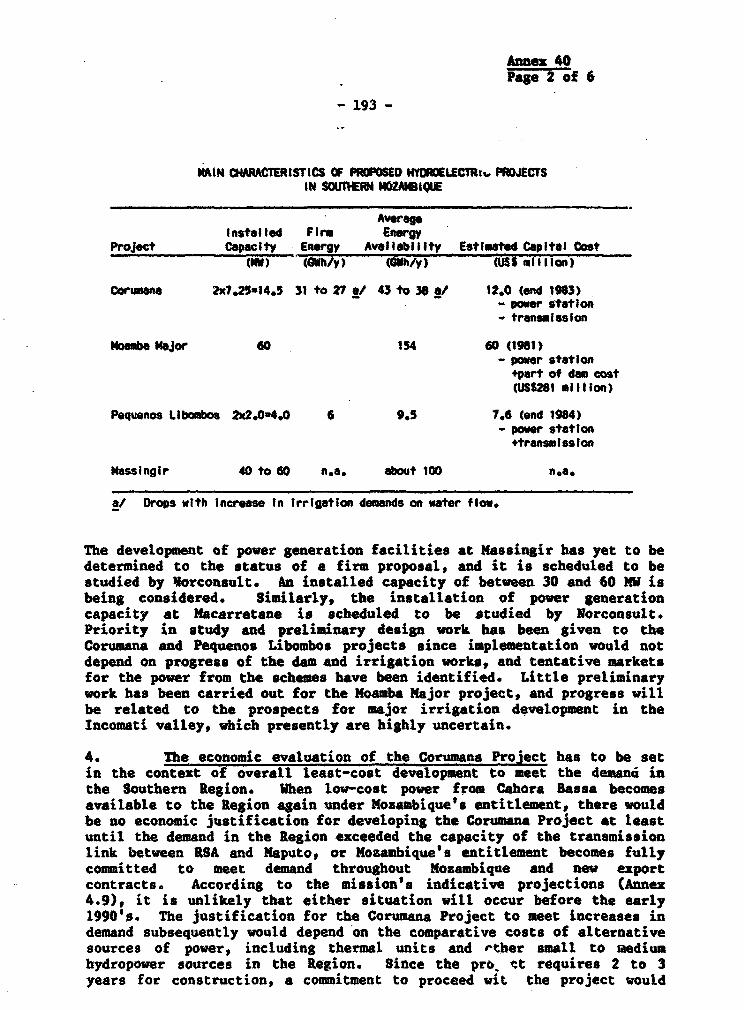

Defense Contracting in Iraq: Issues and Options for Congress

Upload

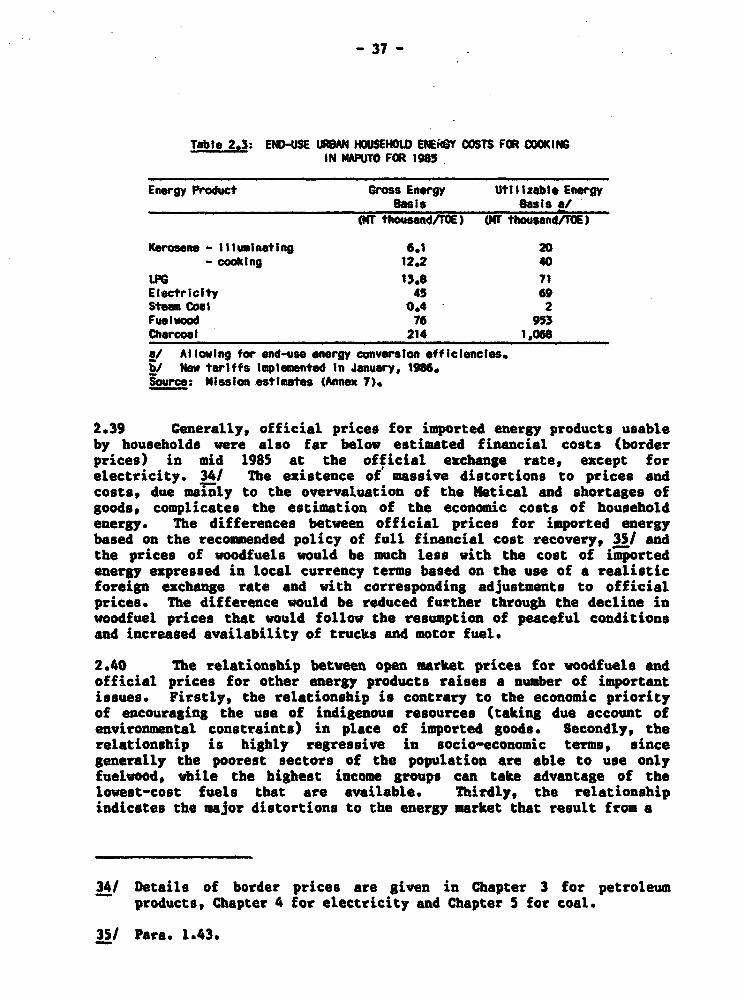

khangminh22Category

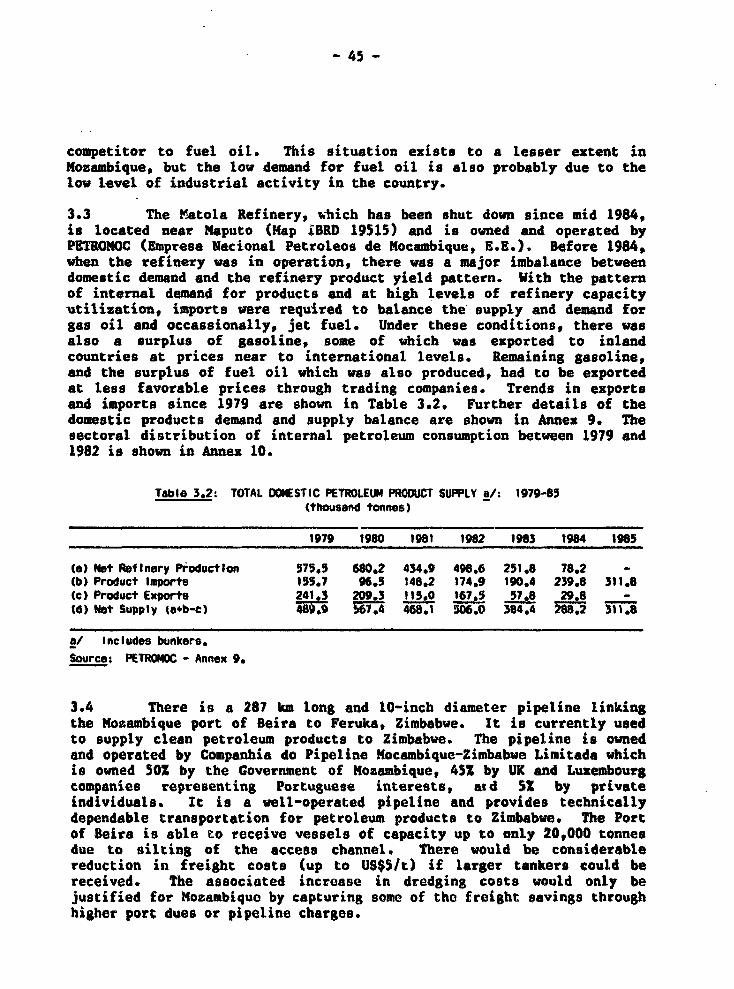

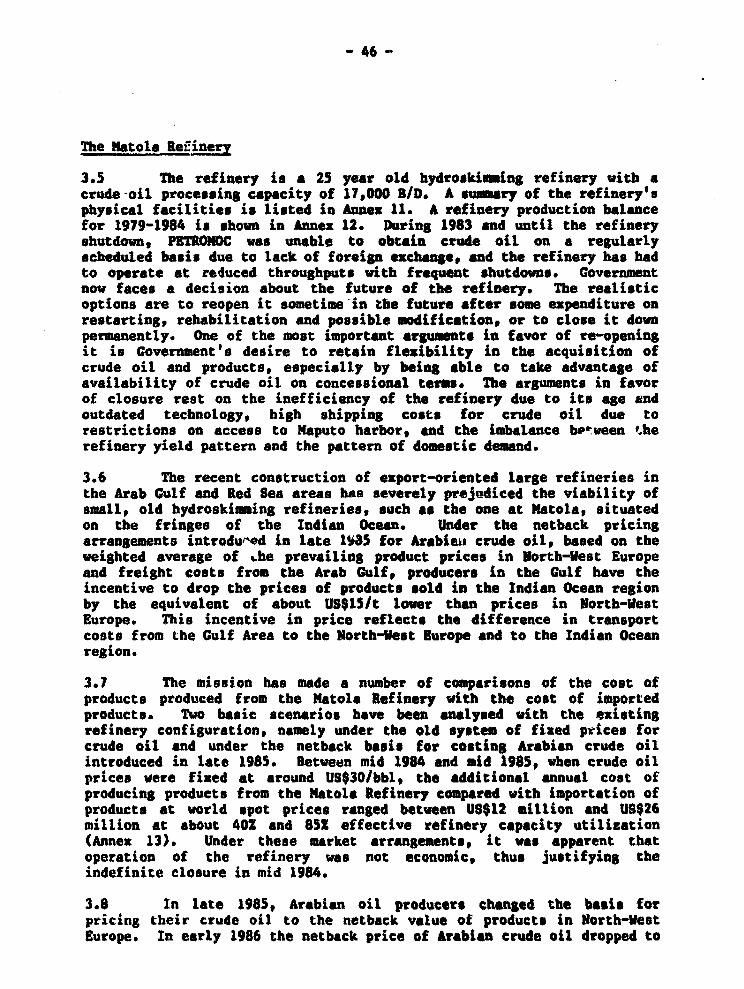

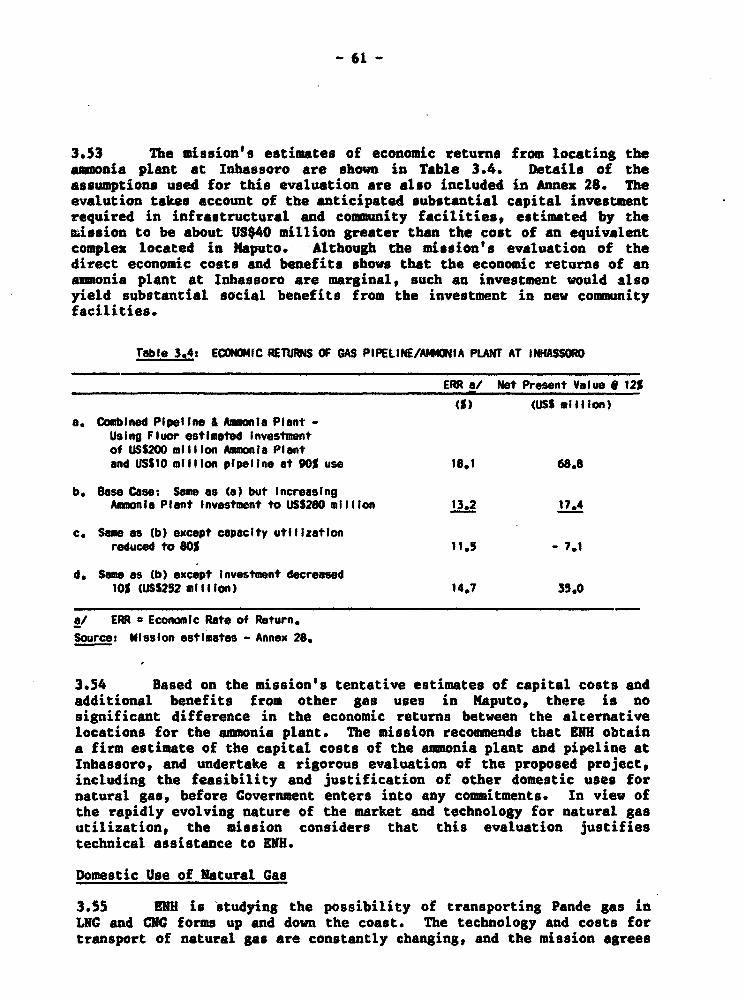

view

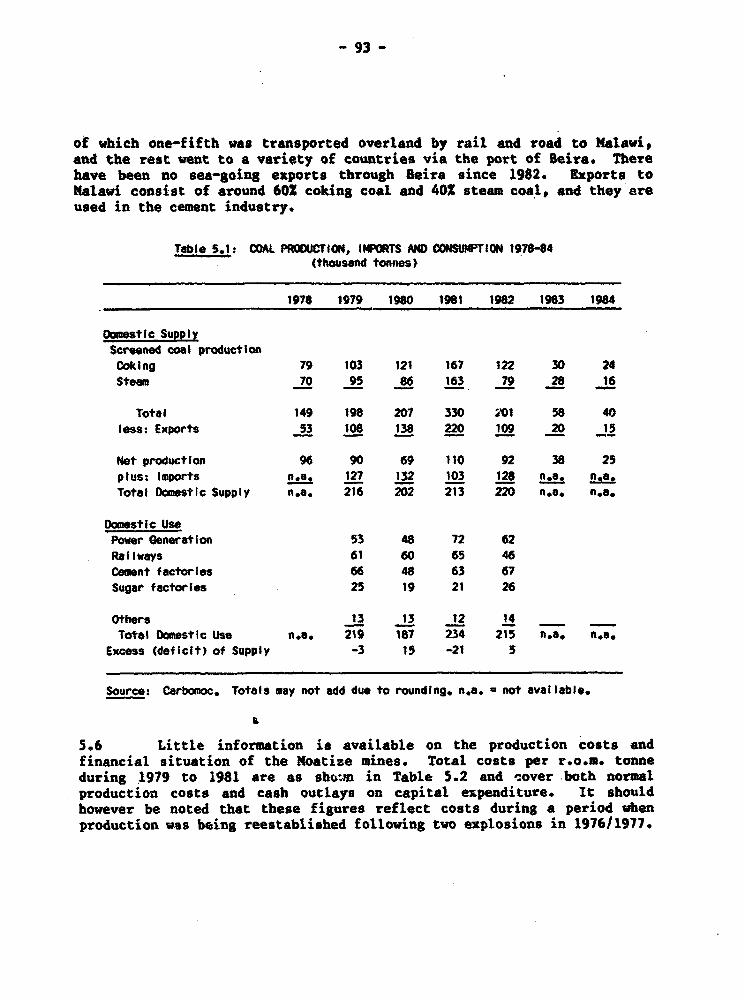

7download

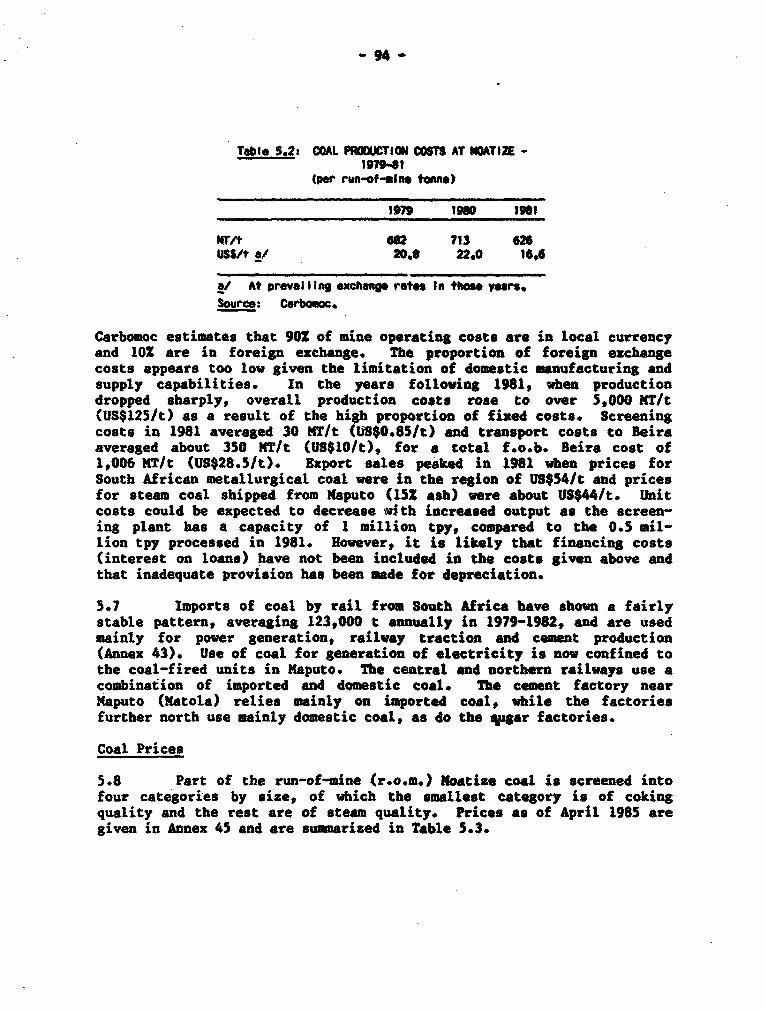

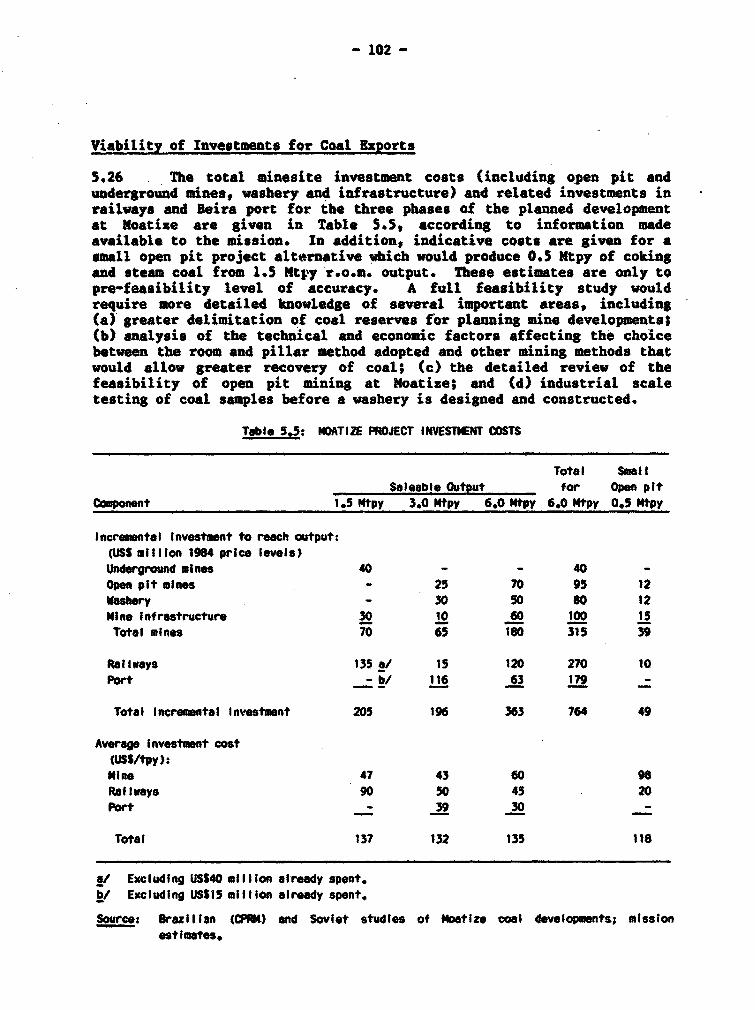

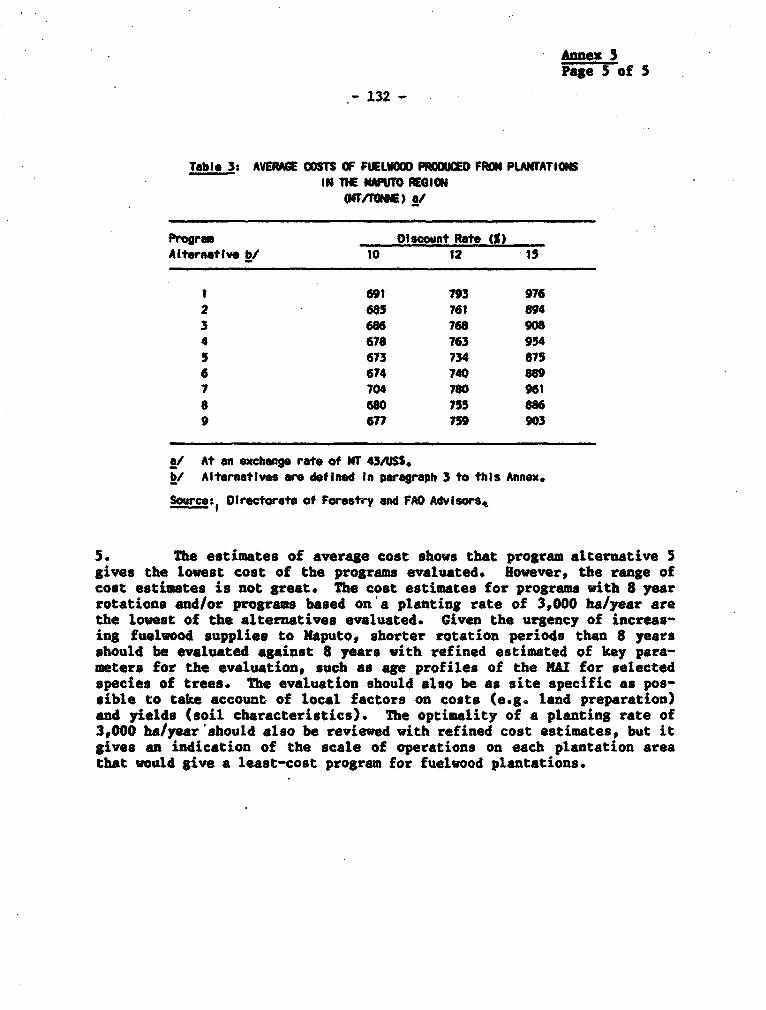

0

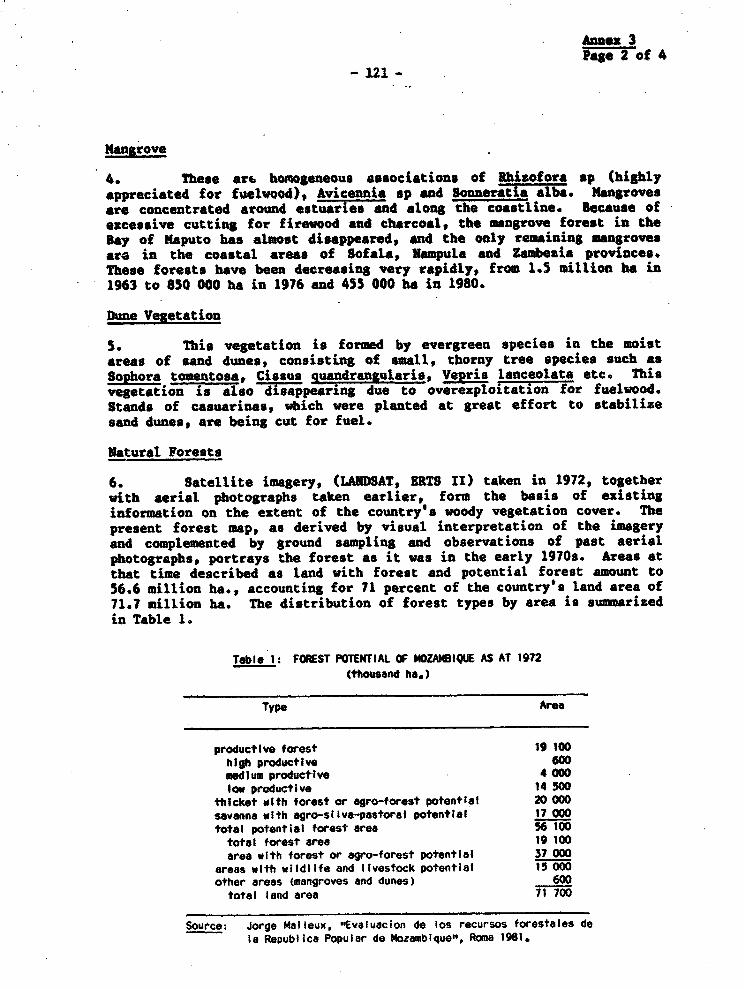

Report No. 6128-MOZ

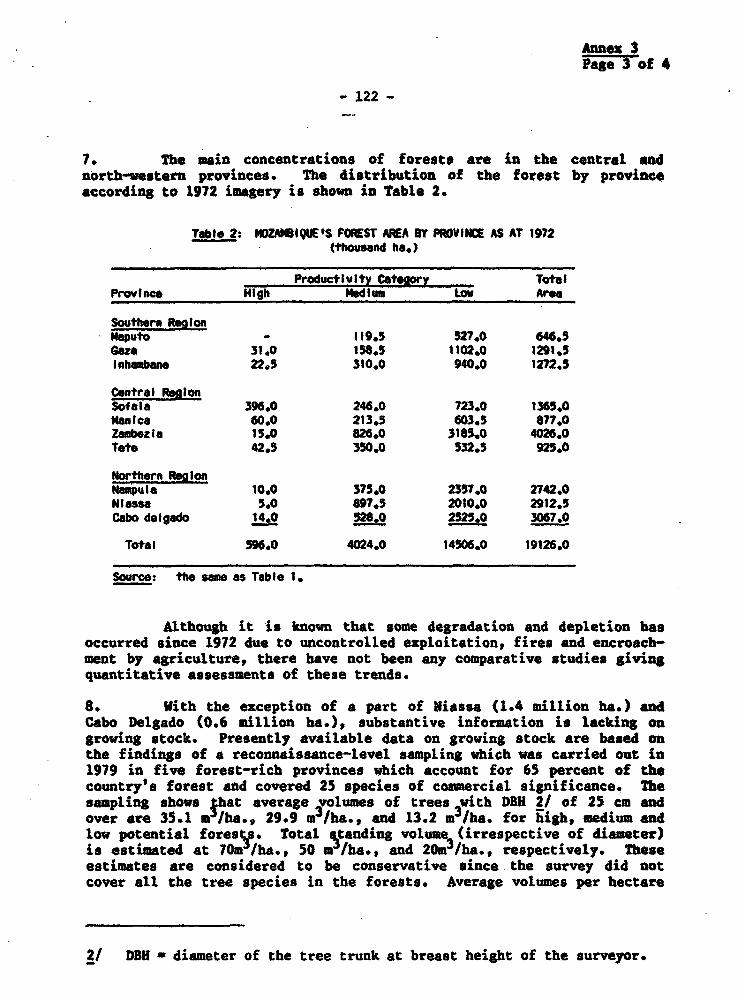

Mozambique: Issues and Optionsin the Energy Sector

January 1987

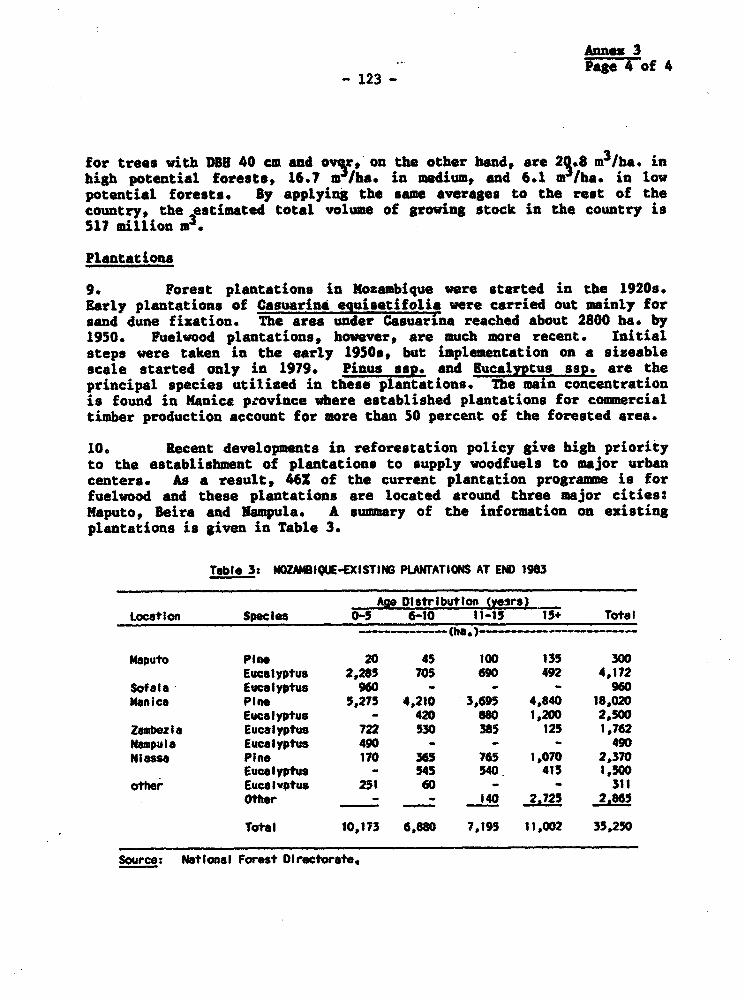

~. . ..

.. 2.

: .~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~..~~~~~~~~~~~~~~~~~~~~~~~

.: . . . ., i t

. .. . . . . . .~~~~~~~~~~~~~~~~~~~~~~14

Pub

lic D

iscl

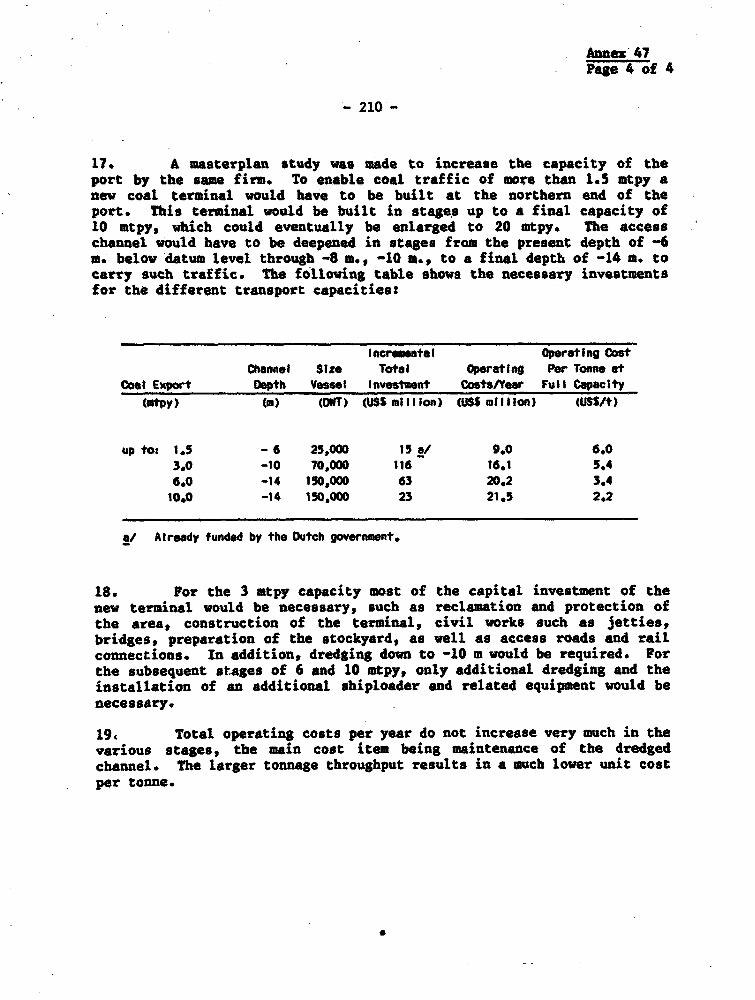

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

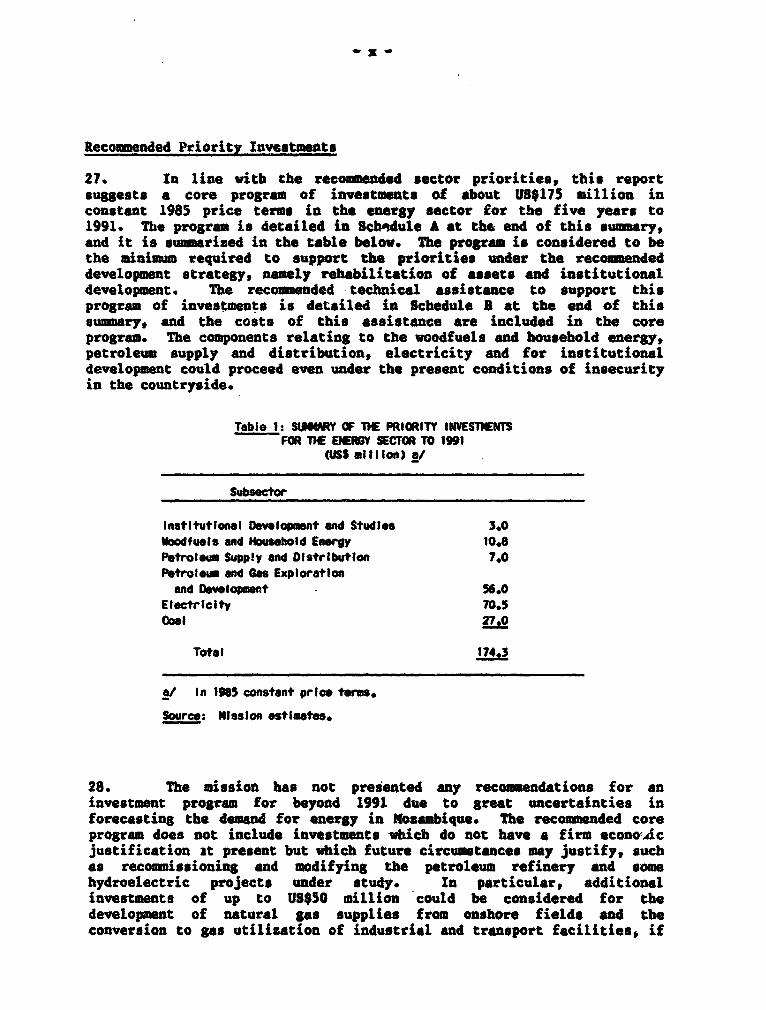

rized

Pub

lic D

iscl

osur

e A

utho

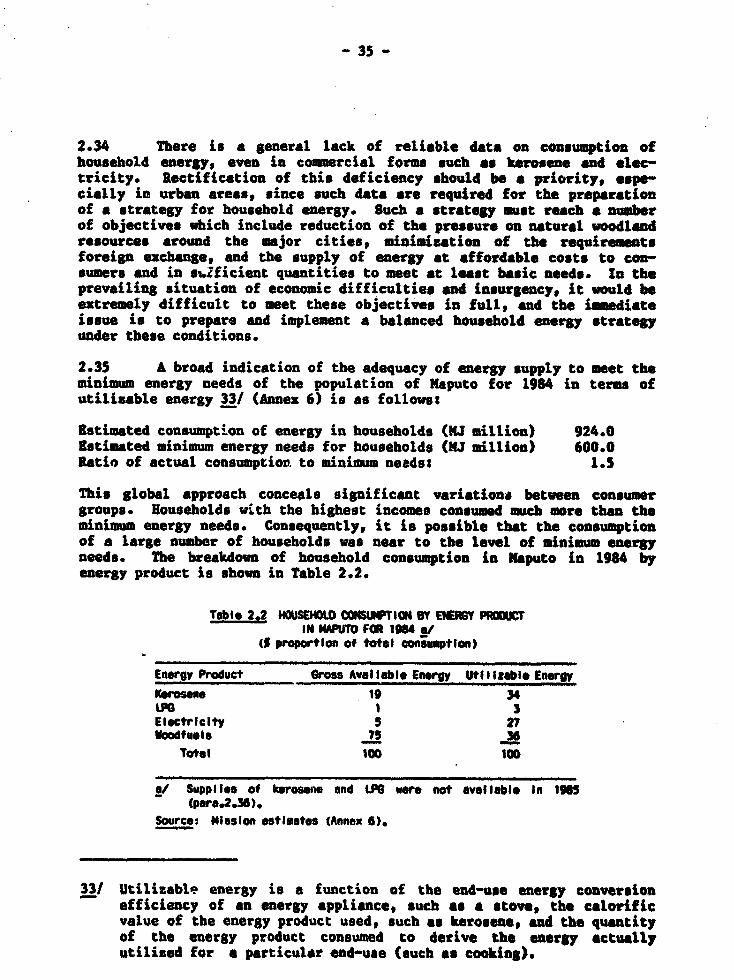

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

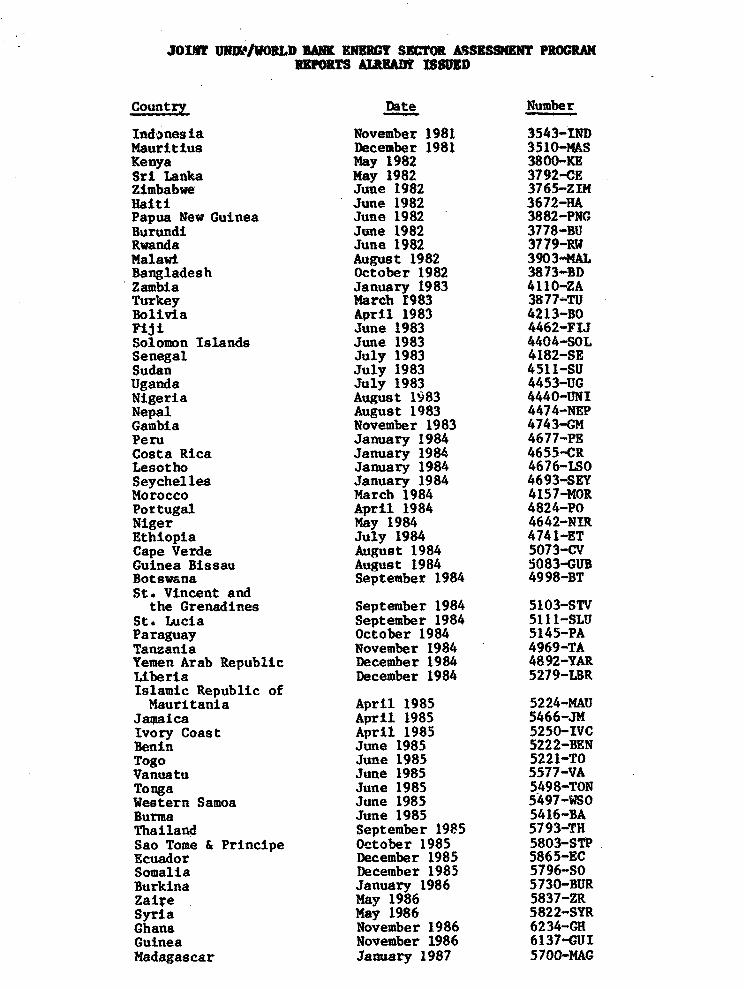

JOIMT UNW/WOULD RAW ENICRY SSCTOR ASS3SSNENT PROGRHMREPORTS AJREADY ISSUED

Country Date Number

Indonesia November 1981 3543-INDMauritius December 1981 3510-MASKenya May 1982 3800-KESri Lanka May 1982 3792-CEZimbabwe June 1982 3765-ZIMHaiti June 1982 3672-HAPapua New Guinea June 1982 3882-PNGBurundi June 1982 3778-BURwanda June 1982 3779-RWMalawi August 1982 3903-MALBangladesh October 1982 3873-BDZambia January 1983 4110-ZATurkey March I983 3877-TUBolivia April 1983 4213-BOFiji June 1983 4462-FIJSolomon Islands June 1983 4404-SOLSenegal July 1983 4182-SESudan July 1983 4511-SUUganda July 1983 4453-UGNigeria August 1983 4440-UNINepal August 1983 4474-NEPGambia November 1983 4743-GMPeru January 1984 4677-PECosta Rica January 1984 4655-CRLesotho January 1984 4676-ISOSeychelles January 1984 4693-SEYMorocco March 1984 4157-MORPortugal April 1984 4824-PoNiger May 1984 4642-NIREthiopia July 1984 4741-ETCape Verde August 1984 5073-CVGuinea Bissau August 1984 5083-GUBBotswana September 1984 4998-BTSt. Vincent andthe Grenadines September 1984 5103-STV

St. Lucia September 1984 5111-SLUParaguay October 1984 5145-PATanzania November 1984 4969-TAYemen Arab Republic December 1984 4892-YARLiberia December 1984 5279-LBRIslamic Republic ofMauritania April 1985 5224-MAU

Jaiiaica April 1985 5466-JMIvory Coast April 1985 5250-IVCBenin June 1985 5222-BENTogo June 1985 5221-TOVanuatu June 1985 5577-VATonga June 1985 5498-TONWestern Samoa June 1985 5497-WSOBurma June 1985 5416-BAThailand September 1985 5793-THSao Tome & Principe October 1985 5803-STPEcuador December 1985 5865-ECSomalia December 1985 5796-SOBurkina January 1986 5730-BURZaire May 1986 5837-ZRSyria May 1986 5822-SYRGhana November 1986 6234-GHGuinea November 1986 6137-GUIMadagascar January 1987 5700-MAG

FM O"ICIAL USE OILYREPORT 10. 6128-MUo

MlOZAMBIQUE

ISSUES AiD OPTIONS IN THE ENECY SCTOR

JANUARY 197

This report is based on the findings of an energy assssmnt missionwhich visited Mozambique in April/lNy 1985. The mission consisted ofMessrs. J. Besant-Jones, Mi-uion Leader; M. Del muono, Deputy MissionLeader; A. Alberti, Manpower and Training; H. Chaves* Power Engineer;D.C. Krishnamurthy, Refinery Engineer; J. Rochet, Geologist;I. Rodriguea, Researcher; and A. Bellasoug (Consultant) Gas Expert;Sroukhorst (Consultant) Coal Mining Expert; and Mrs. S. Carbonnier,(Consultant) Forestry Expert. Messrs. Sesant-Jones and Del Buono werethe principal authors of this report, which benefited also fromcontributions by Ms. D. Williamon (Economist), Messrs. C. Warren (CoalEconomist), K. Rornby (Consultant), E. Roumeni (Consultant) endR. Williams (Consultant). The draft report was discussed several timeswith the Mozambican authorities, most notably in July and November, 1986.

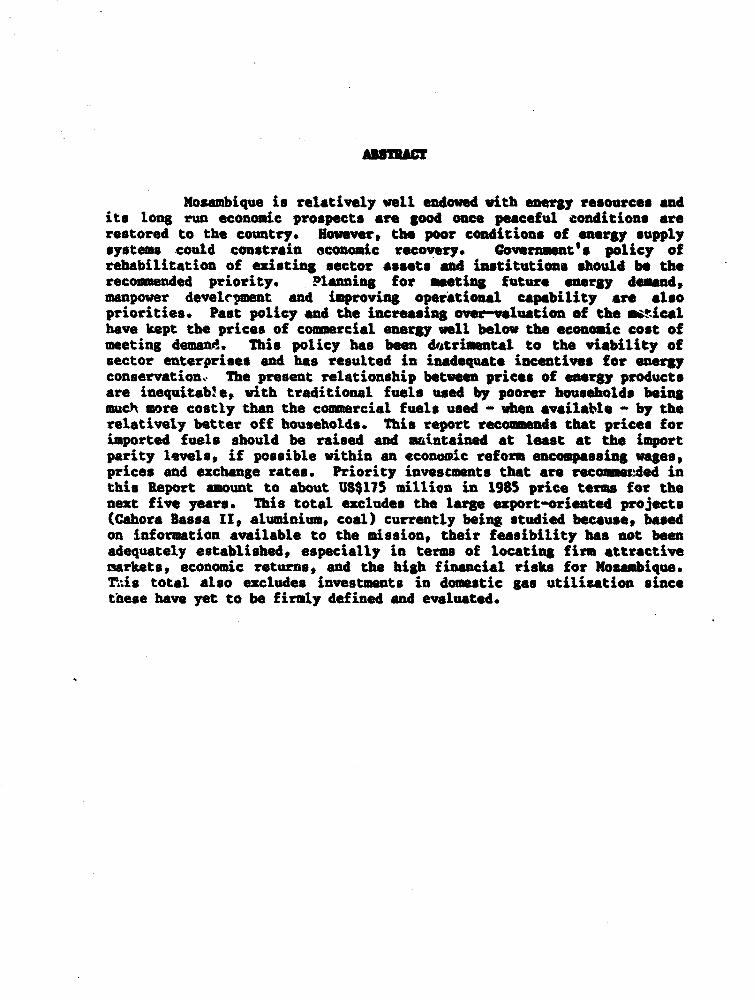

Mosambique is relatively well endowed with energy resourc e andits long run economic prospects are good once peaceful conditions arerestored to the country. However, the poor conditions of energy supplysystems could constrain economic recovery. Gover t s policy ofrehabilitation of ezisting sector assets and institutions should be therecommended priority. Planning for meting future energy demand,manpower develeimsnt and improving operational capability are alsopriorities. Past policy and the incrasing over-valuation of the m_icalhave kept the prices of comercial energy well below the economic cost ofmeeting demand. This policy has been dvitrimetal to the viability ofsector enterprises and has resulted in inadequate incentives for energyconservation, The present relationship betwee prices of energy productsare inequitab'e, with traditional fuels used by poorer households beingmuch more costly than the commercial fuels used - when available - by therelatively better off households. This report recommends that prices forimported fuels should be raised and maintaine at least at the importparity levels, if possible within an economic reform encompassing wages,prices and exchange rates. Priority invescaets that are recommetIed inthis Report amount to about US$175 million in 1985 price terms for thenext five years. This total excludes the large export-oriented projects(Cahora Bassa IIt aluminium, coal) currently being studied because, basedon information available to the mission,, their feasibility has not beenadequately established, especially in terms of locating firm attractivemarkets, economic returns, and the high financial risks for loambique.rhis total also excludes iLnvestments in domestic gas utilisation sincetnese have yet to be firmly defined and evaluated.

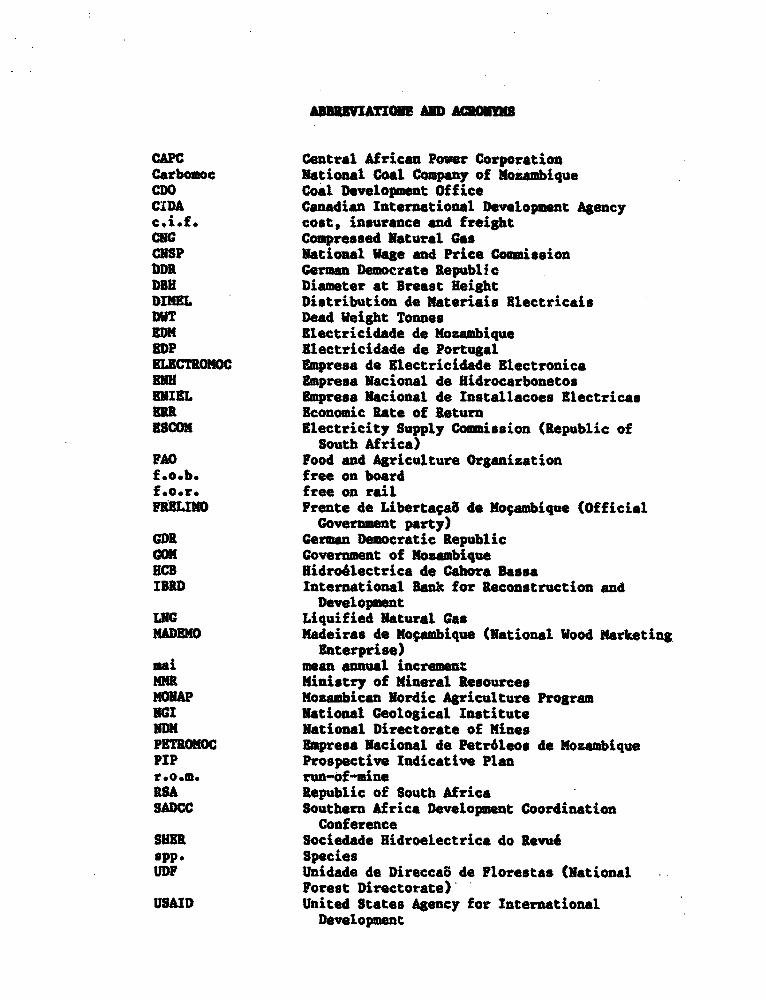

ARDRIYATU SAND ACUUS

CAPC Central African Power CorporationCarboamoc National Coal Companry of MozambiqueCDO Coal Development OfficeCIDA Canadian International Development Agencyc.i.f. cost, insurance and freightCNG Compressed Natural GasCUSP National Wage and Price CommissionDDR German Democrate RepublicDBH Diameter at Breast HeightDIMEL Distribution de Materiais ElectricaisDWT Dead eipght TonnesEDM Electricidade de MozambiqueEDP Electricidade de Portugal8LECTROMOC Empresa de Electricidade Electronicamm Empresa Nacional de RidrocarbouetosEVIEL Empresa Nacional de Installacoes BlectricasERR Economic Rate of ReturnBROOM Electricity Supply Commission (Republic of

South Africa)PAO Food and Agriculture Organizationf.o.b. free on boardf.o.r. free on railFuELIaG Prente de Liberta,a8 de Mogambique (Official

Government party)CDR German Democratic RepublicGMI Government of MozambiqueBCB Hidroelectrica de Cahora BassaIBID International Bank for Reconstruction and

DevelopmentLNG Liquified Natural GasMADEMO Madeiras de Mogambique (National Wood Marketing

Enterprise)mai mean annual incrementRUE Ministry of Mineral ResourcesMONAP Mozambican Nordic Agriculture ProgramNCI National Geological InstituteNDM National Directorate of MinesPETROKOC EMpresa acional de Petr6leos de KozambiquePIP Prospective Indicative Planr.o.m. run-of-mineBBA Republic of South Africa

SADCC Southern Africa Development CoordinationConference

SHER Sociedade Hidroelectrica do Rev%Aspp. speciesUDP Unidade de Direccab de Florestas (National

Forest Directorate)USAID United States Agency for International

Development

WIN W

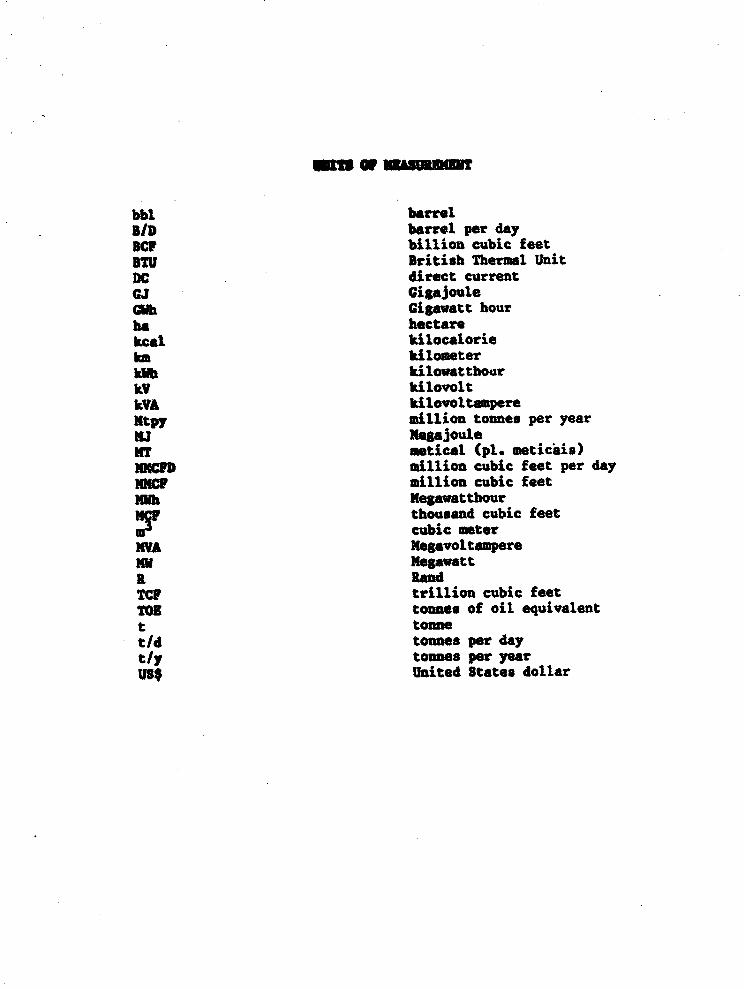

bbl barrelB/D barrel per dayBCP billion cubic feetBTU British Thermal UnitDC direct currentcJ GigajouleGCh Gigawatt hourha hectarekcal kilocaloriekm kilometerkWh kilowatthoorkV kilovoltkA kilovoltamperemtpy million tonmes per yearHJ emgajouleUT meticl (pl. meticais)

million cubic feet per day.NP ahmillion cubic feetHa Megawatthour

thousand cubic feet'V cubic meterIWA NegavoltempereMW megawattX RandTCP trillion cubic feetTOG tonnes of oil equivalentt tonnet/d tonnes per dayt/y tonnes per yearU8 United States dollar

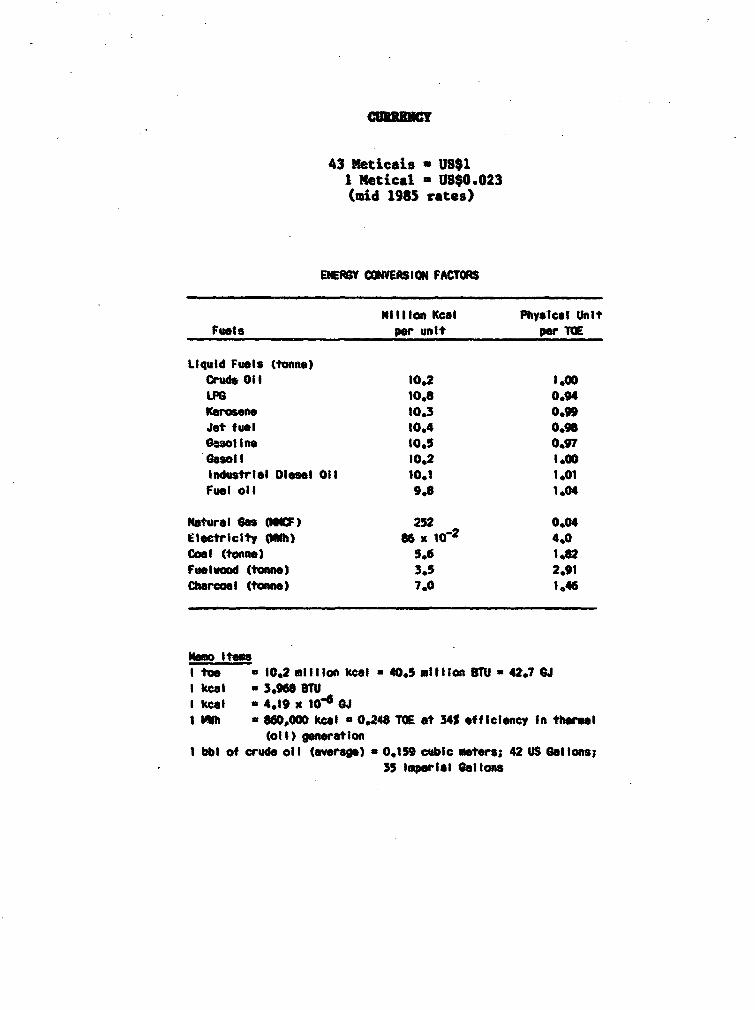

43 Meticais a US$1I J4etical - US$0.023(mid 1985 rates)

ENEMY CONVERS ION FACTOR

4I llon tKcal Physical UnitFuets per unit per TOE

Liquid Fuels (tonne)Crude 011 10.2 .00OLPG 10.8 0.94Kerosene 10.3 0.99Jet fuel 10.4 0.96sao lne 10.5 0.97

S.i1 10.2 1.00Industrial Diesel Ol 10.1 1.01Fuel oIl 9.8 1.04

Natural GOs O ) 252 0.04Electricity 0Ih) 86 x o12 4.0cool Itoene) 5.6 1.82Fueluood (tone) 3.5 2.91Charcoal (tono.) 7.0 1,46

mo Ito"I toe a 10,2 mi lIon kcal u 40.5 ml I I Ion OBM 427 U JI keal 3.968 STUI keal I 4.19 x 104 @1 Ywh a 60,000 kcal a 0.248 TOE at 34S of filency In thermal

(ol) genration1 bbl of crude oll (averge) a 0.159 cubic atets; 42 US Gallons;

35 Im_eial Gotllns

TAM, OF c .ToTV

?sge

EXECUTIVE sUMARY......................................... i

It SCTOR R..................... ...... 1Macro-economic Trendse.................* ........o...*o 1Energy 2sources............. .. , 2Overview of Energy in the Economy..................... 2Energy Supply and Consumptio 4n......................... 4Woodfuels and Household Energy.0 ...................... SPetroleum and Cas..................................... 5Electric Power ........................ e.o .*eeee 7

7The Inotutional Framework for the Energy Sector....... 8Policies and Investments in the Last Ten Years ........ 9Energy Planning Issues...................................... 10Operational Efficiency and Institutional

Strengtheninge .................................................11Future Large Energy Projects .................... 11Large Energy-Intensive Industrial Projects............ 12Energy .............................. ................. 14Energy Conservation, Fuel Substitution and

Rural Enela............. 18Energy Development Strategies and Policies............ 18Rec ded Prioritie s 20.....................**.. 20Recommended Technical Assistance Priorities

for the Energy Sector ....................... ..... 21

II. WOODFUELS AND HOUSEHOLD ENERGY .......... .*e .... 23Voodfuel Supply and Demand............................ 23Woodfuel Situation in Urban Areaa..................... 23Voodfuel Situation in Rural Ares..................... 25Voodfuel Resources .................................... 25Puelwood Nantstsons......., .......................... 27Priorities for Increasing Puelwood Supply .............*- 30Institutional Issues for Woo6fuels and

Household Eergy.................................... 3234

Urban Household Energy Consumption.........e ....* .. 34Comparative Costs of Household Energy................. 36Household Energy Supply Options ....................... 38Priorities for Household Eergy....................... 39Priorities for Development ............................ 41

Summary of the Mission's Recommendations for theVoodfuels and Household Energy.. 42

III. PETROLEUM AND CAS*......................................... 44Crude Oil and Petroleum ProductSfe,..................... 44Petroleum Products Supply end Demandt... ............., 44The Matola Refinery.................... ............... 46Product Pricing....................................... 48Product Supply, Storage and Distribution .............. 49Petroleum Supply, Procurement and Planning............ 51PERIROMOC's Manpower................................... 52Corporate Accounting................ .... .......... 52Indicative Investment Program.....,.................. 52

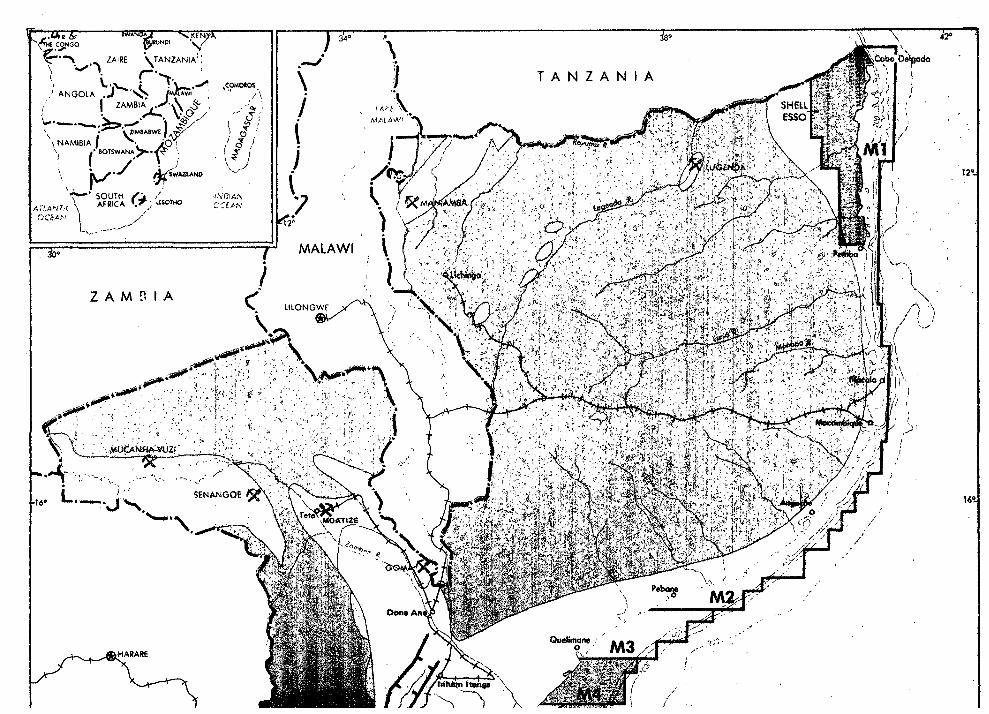

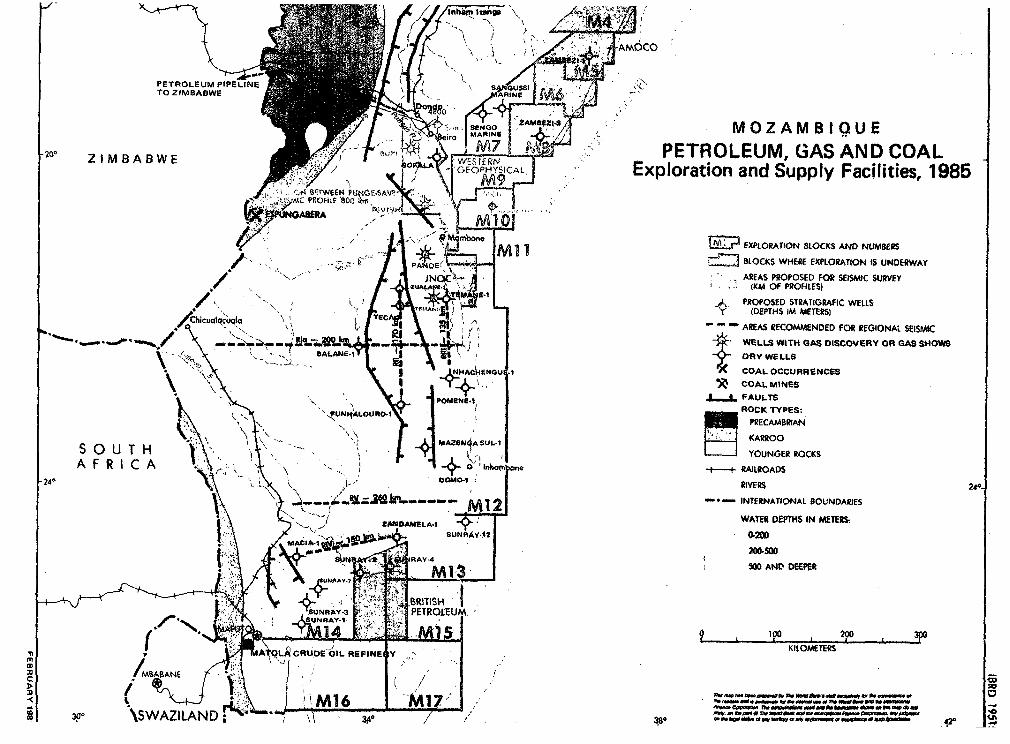

Petroleum ard Gas Exploration and Development ........... 53Geological Framework.................................. 53Past Exploration Activity............................. 53Petroleum Promotion Strategy.......................... 54Current and Proposed Exploration Work................. 54Manpower and Organizational Needs..................... 55

Gas Demand and Utilization ......... 5.........* ..... 57Use of Pande Field Gas ................................ 57Ammonia Project .............................. 58Domestic Use of Natural Gas........................... 61Use of Busi Field Gas................................. 62Export Market Potential for Natural Gas.............. 63Priority Investment Program. ...... .... ..... ....*...... 63

Summary of the Mission's Recommendations forthe Petroleum Supply Sector ........................*. 64

Swumary of the Mission's Recommendations forPetroleum and Gas Exploration and Development ........ 65

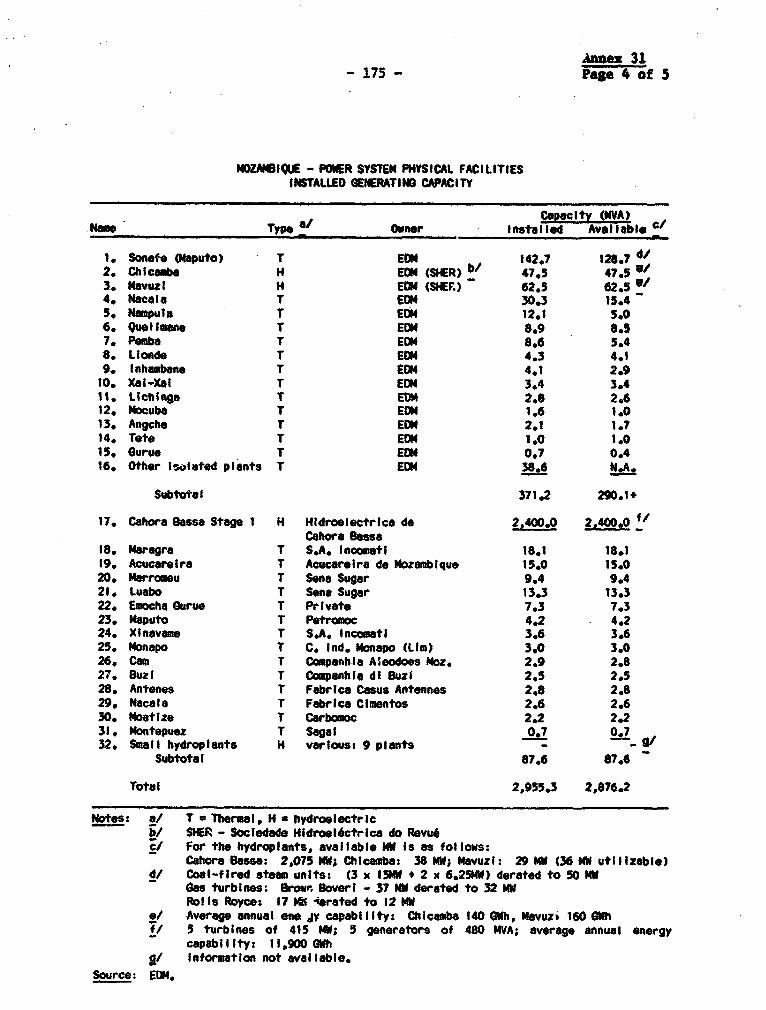

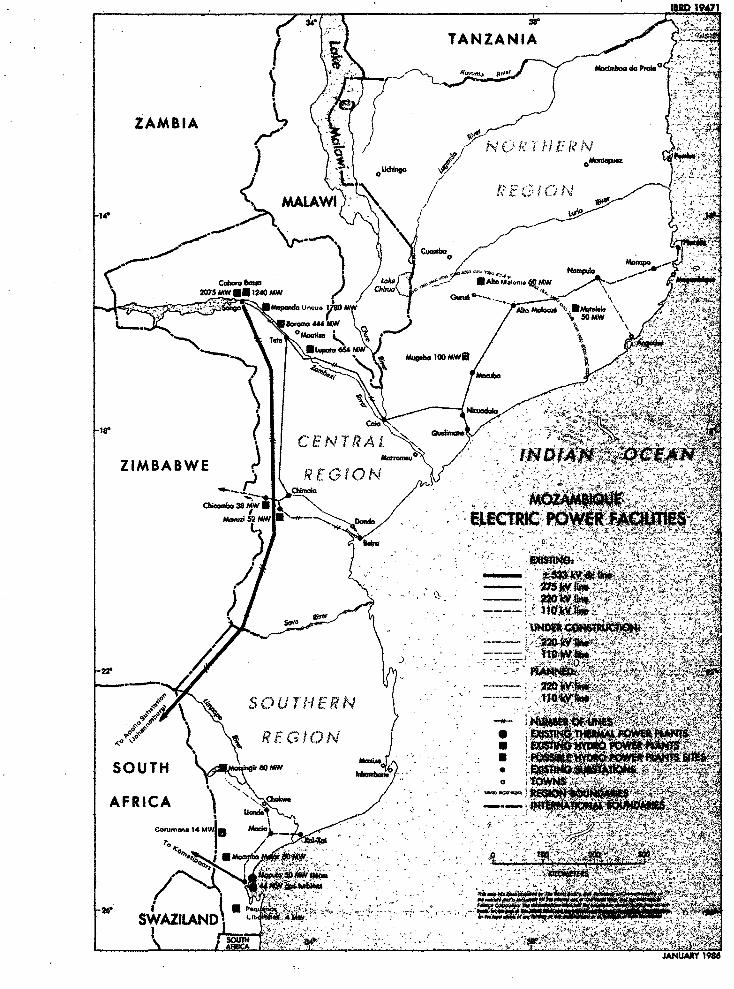

IV. ELECTRIC ..................... *....................... 67Organization of the Power Sector...................... 67Physical Facilities ........ *. 68

71Historic Demand and Supply....................... 72Present Supply/Demand Situation....................... 73-RED's Taif ...........................75EDM's Financial Position and Practices................ 78Power Resources.............. . 80Cabora Bassa Developments ..... .... . ................... 81Prospective Demand for Power .......................... 84Power Exports................................. 85Power Supply to Southern Mozambique.................. 86Power Supply to Central-Northern Mozambiquee........... 88Priority Investments.................................. 88

Sumary of the Mission's Recommendationsfor the Power Sector.................................. 89

Ve O ............................. 91Introductionooeoo*oooooooo*to*ooeotoooe* * ........... 91

Cosl Resources........................................ 91Supply and Demand..................................... 92ColPrcst.......................... 94

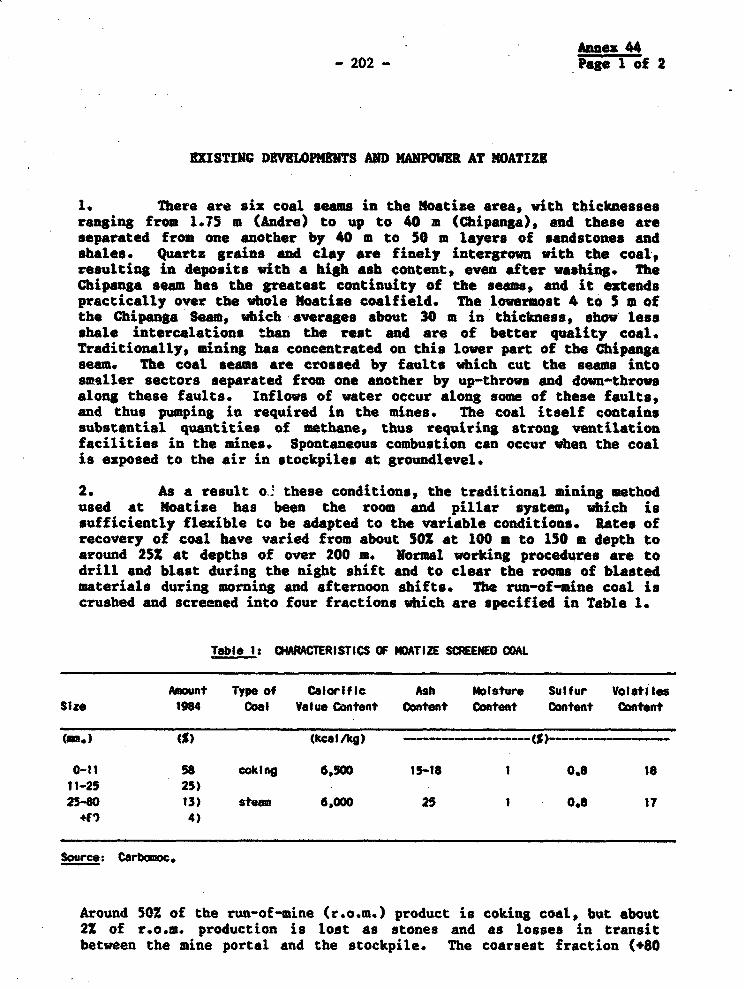

Sector Organi:ation.....................,.. 96Mbnpower ..... 4 ~~~~~~~97

Domestic Market Prospects......e..................e... 98Rehabilitation of Existing Moatize Mines ............. 99Planned Coal Developments.....0. *. ......*.** *. .. , 99Coal Transport Facilities.eee................e........ 101Viability of Investments for Coal Exports 102

Past and Projected Investment in the Coal Sectors.....,* 105Summary of Mission's Recommendations for theCoal Setr105

VI, INSTITUTIONAL I ES .............. . 107Sector Organization and Institutions............s..... 107Sector Coordination 108National Energy Council ....... 109Department of E ner g y 110Management .................... 111Manpower Development....... 112Technical Assistance ...... 112Mul-wti-sectoral Developments*********oeo*o 113

Summary of the Mission's Recommendationson I n s t i t u t i o n s 114

TABLES

Table 1 Summary of Priority Investments for theEnergy Sector to 1991 x

Schedule A Recommended Sub-Sectoral Priority Investmentsto 19919.......................... xii

Schedule B Recommended Sub-Sectoral Priorities forTechnical Assistance......94444 4@*494444444@444 Xiv

Table 1.1 Evolution of CDP 1973-1983.... 1Table 1.2 Summary of Energy Balances, 1981 and 1984. 8 4.......... 4Table 1.3 Sammory of Trends in the Fetroleum Subsector

1978-1985 .................... 6Table 1.4 Energy Prices in Mid-1985....... ..................... 16Table 2.1 Estimated Forest Resources in 19 8 2 26Table 2.2 Household Consumption by Energy Product in

Maputo for 1984 35Table 2.3 End-Use Urban Household Energy Costs for Cooking

in Ma-uto for 1985 ..... 37Table 2.4 Priority Investments for Woodfuels and

Household Energy to 1991.... 42Table 3.1 Internal Consumption of Petroleum Products:

1979-85 .... w ~~~~~~~44Table 3.2 Total Domestic Petroleum Product Supply: 1979-85 ..... 4Table 3.3 Economic Retutas of Gas Pipeline/Ammonia

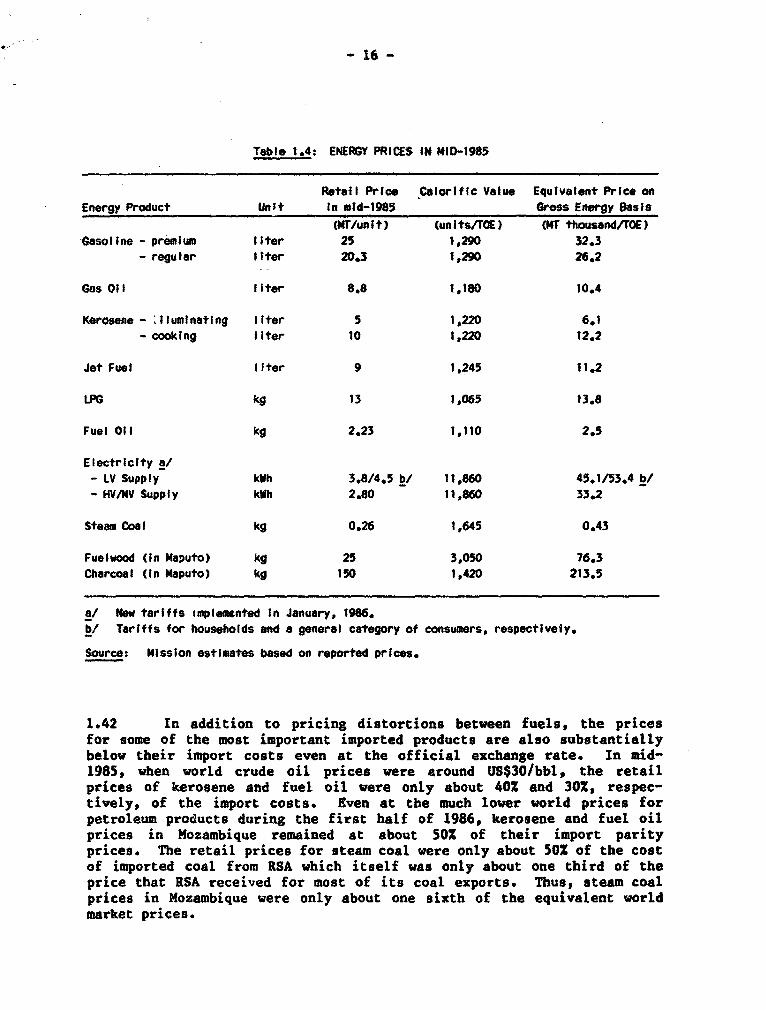

Plant at Maputo............ 4 60Table 3.4 Economic Returns of Gas Pipeline/Ammonia Plant

at Inbassoro ..... .... e a 61

Table 3.5 Economic Returns of Buxi Pipeline/Gas Utilisationat Ber ....* ...63

Table 3.6 Priority 'vtavesents for Petroleum and CasExploration and Development to 199 1 64

Table 4.1 Main Power Supply Facilities to EDN's System....... 69Table 4.2 Production, Imports and Exports of Power

in Mozambique 1978-1985........ 73Table 4.3 ESM's Tariffs....... 77Table 4.4 Comparison of EDM's Tariff with Bulk Supply Tariffs... 77Table 4.5 Capabilities of the Cahora Bassa Complex.......... 82Table 4.6 Possible Phased Development of Cahora Bassa -

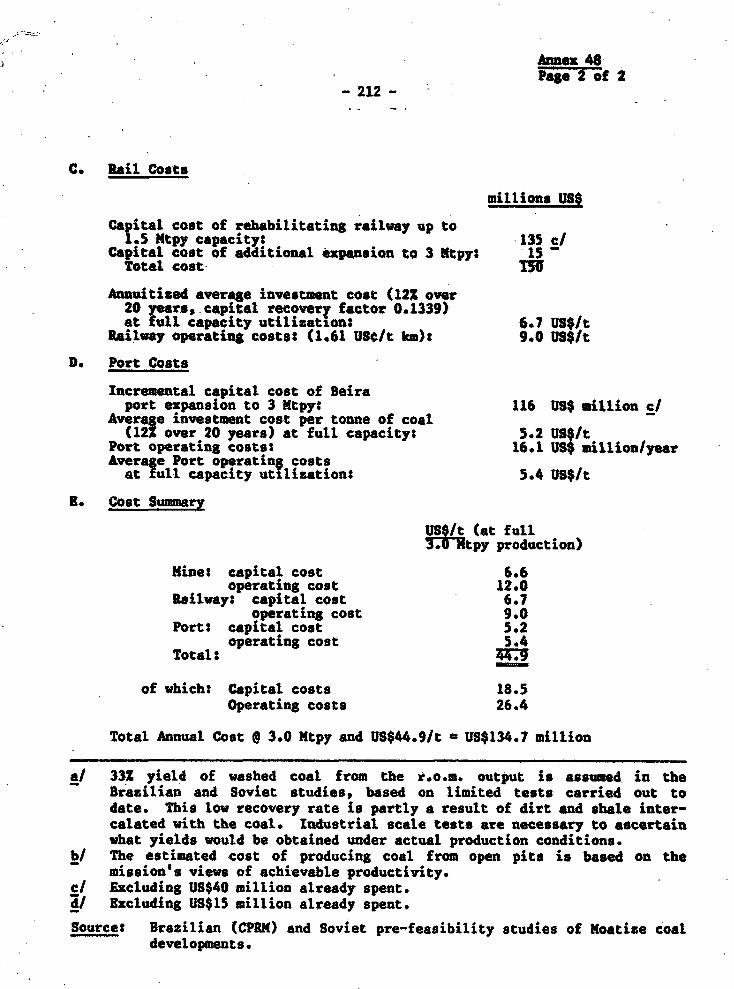

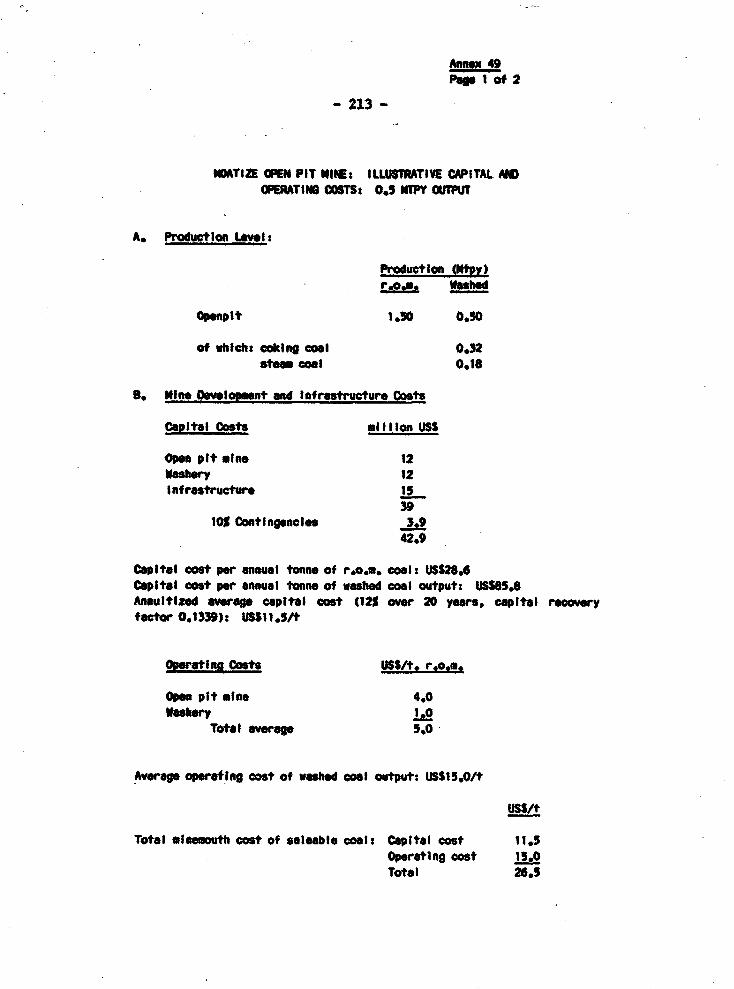

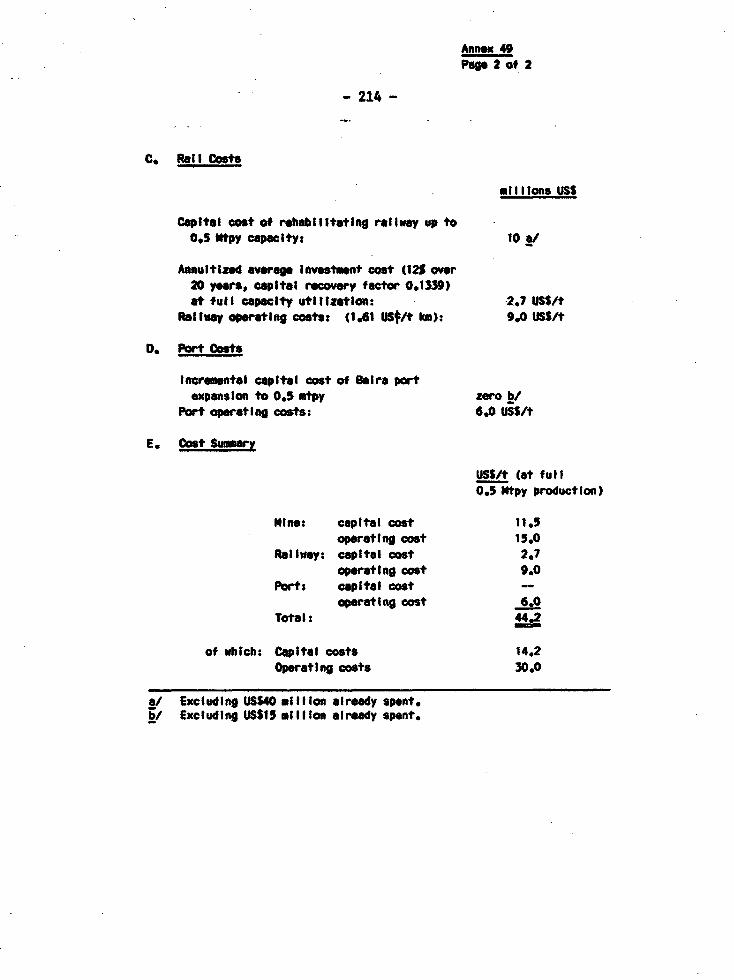

Stage 2............ 83Table 4.7 Priority Investments ^or Electric Power to 1991....... 89Table 5.1 Coal Production, Imports and Consumption, 1978-84..... 93Table 5.2 Coal Production Costs at Moatize - 1979-819........... 94Table 5.3 Coal Prices in 1985................ <. .......... 95Table 5.4 Moatize Expansion Projeet Coal Characteristics******* 100Table 5.5 Moatise Project Investment Costs....... t s............. 102Table 5.6 Priority Investments for Coal to 1991................. 105

ANNEXES

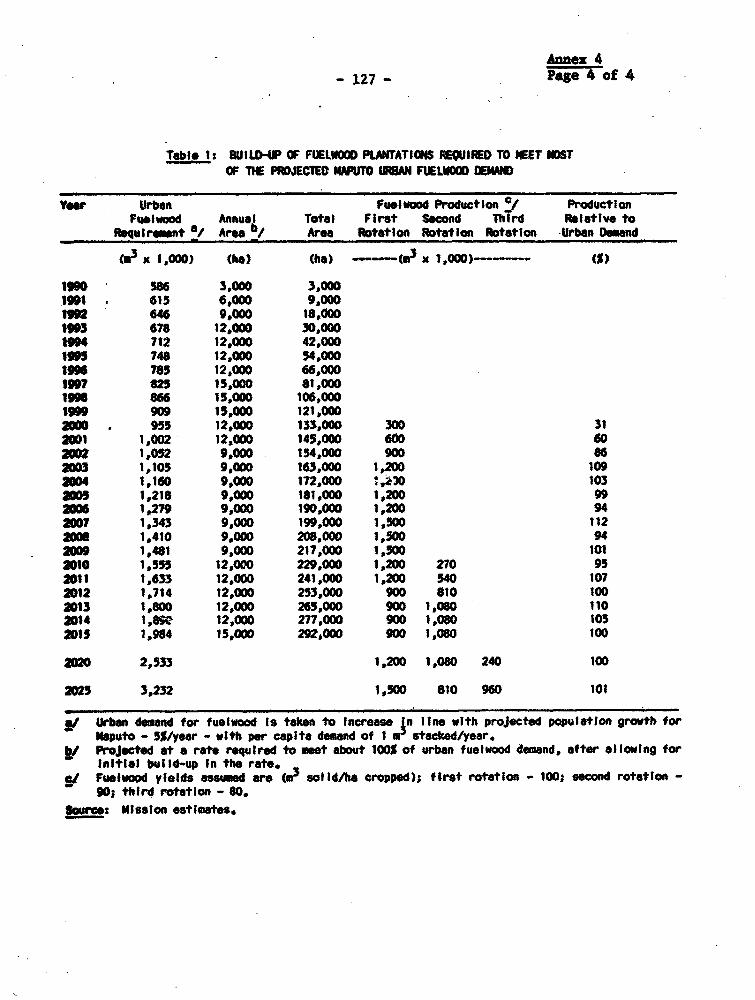

Annex I Mozambique Energy Balance: 19797 99.................... 115Annex 2 Woodfuel Costs and Prices for Maputo in 1985.,.......o 118Annex 3 Forest Resources in Mozambique.... 120Aniex 4 Estimated Requirement for Puelwood Plantations to

Supply Maputo Urban Households... 124Annex 5 Evaluation of Alternative Programs for Fuelwood

Plantations in the Region of Maputo................. 128Aunex 6 Household Energy Consumption in Maputo for 1984 4...... 133Annex 7 End-Use Urban Household Energy Costs in Maputoo....... 135Annex 8 Consumption of Energy and Non-Energy Petroleum

Producta, l7 98 136Annex 9 Domestic Products Demand and Supply

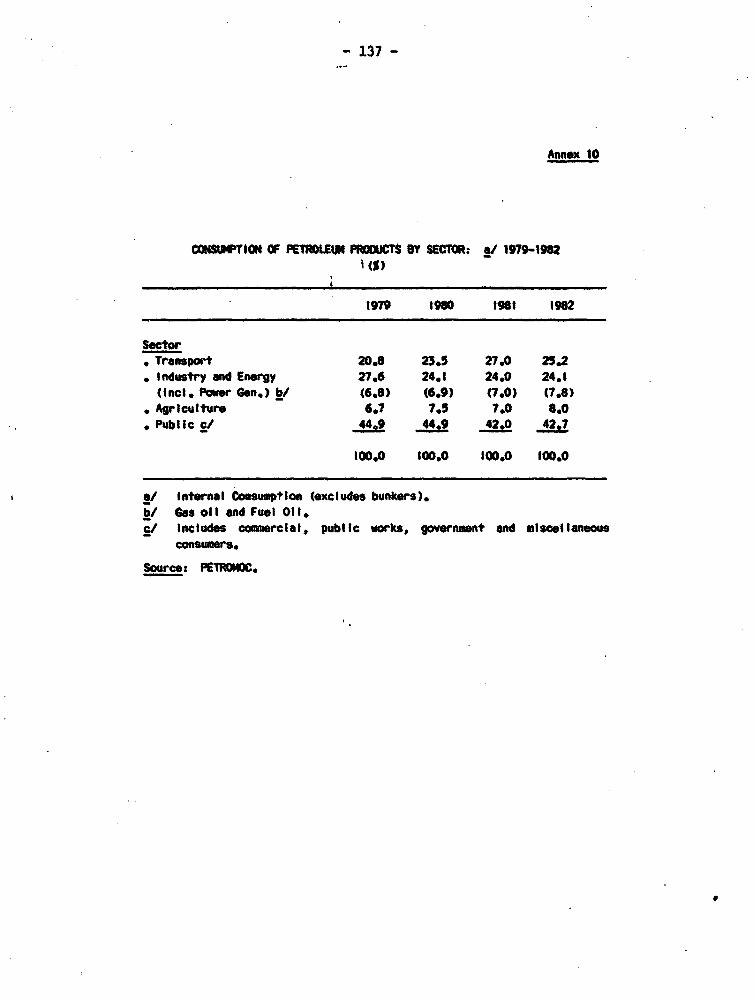

Balance - 1991 9-........... 137Annex 10 Consumption of Petroleum Products by

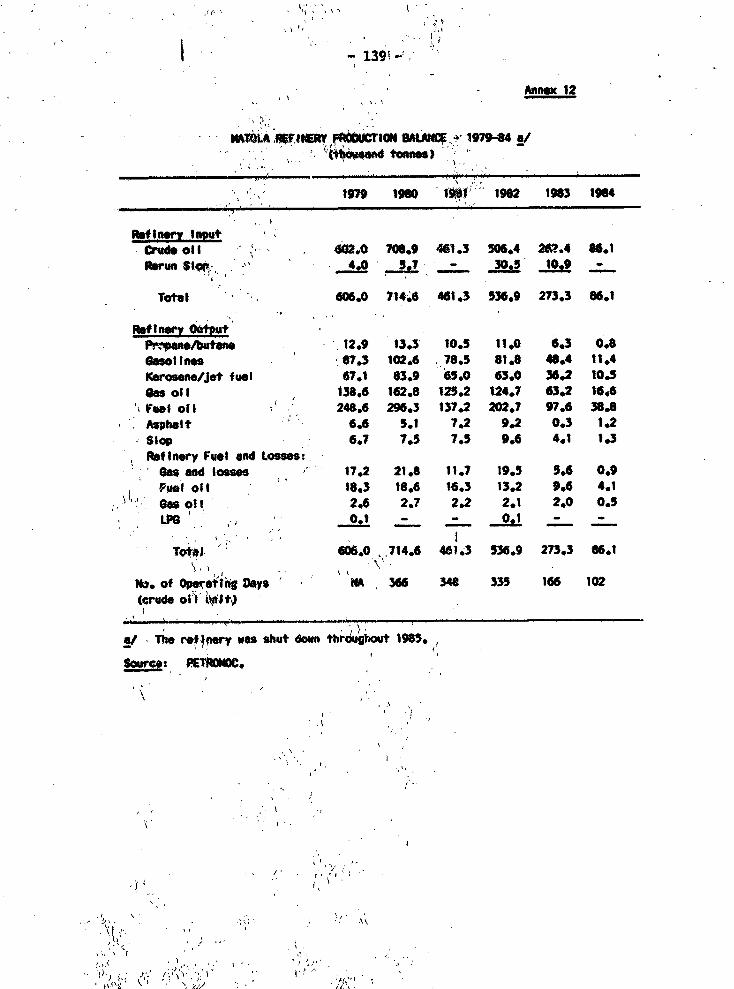

Sector: 9918 138Annex 11 Sumary of Matola Refinery Physical Pacilities........ 139Annex 12 Matola Refinery Production Balance - 1979-84 .... 140Annex 13 Comparison of Costs of Meeting Mozambican Demand

for Petroleum Products from Operating the MatolaRefinery Versus Importing Products in Pre Mid1985 Vorld Market Conditionstit..............ons... 141

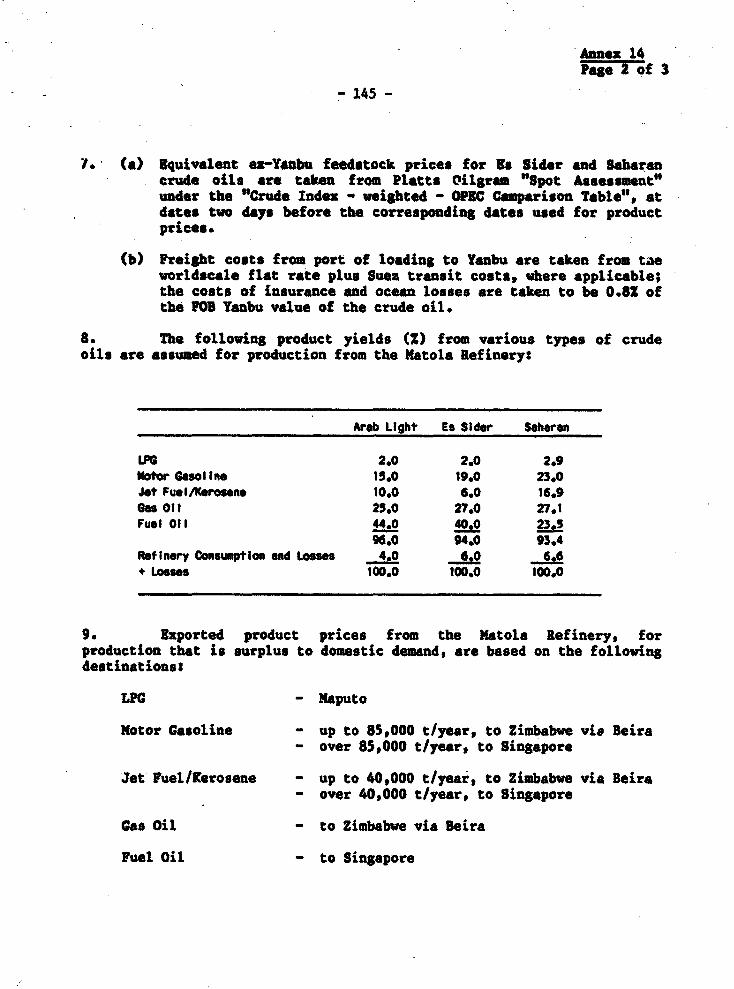

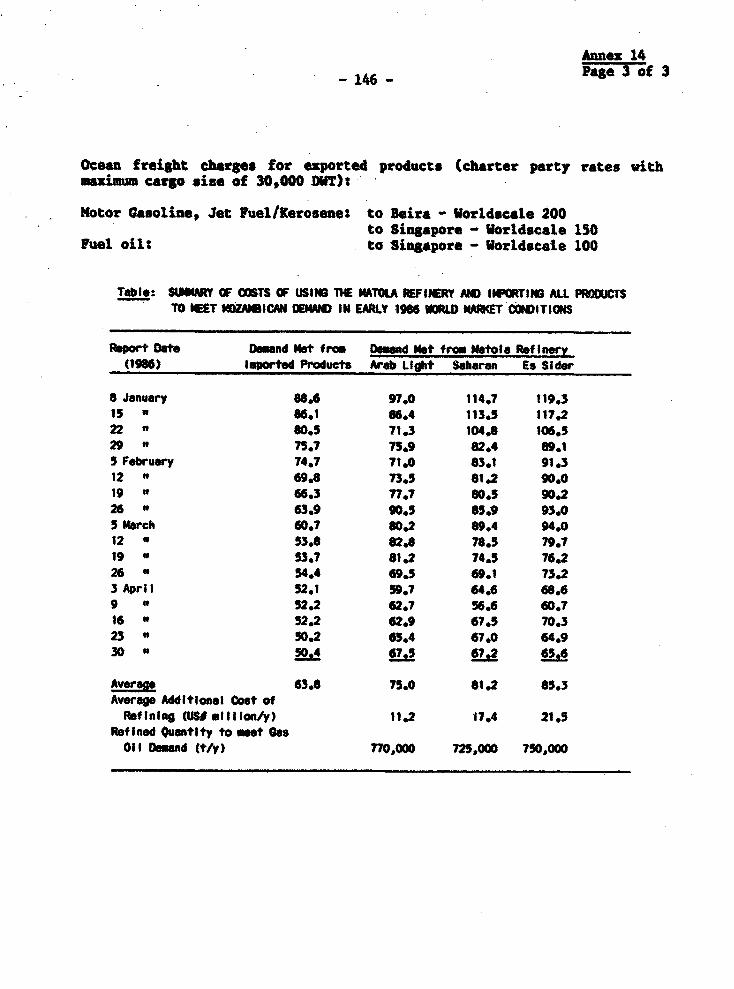

Annex 14 Comparison of Costs of Meeting Mozambican Demandfor Petroleum Products from Operating the MatolaRefinery Versus Importing Products in Early 1986World Market Conditions ... 145

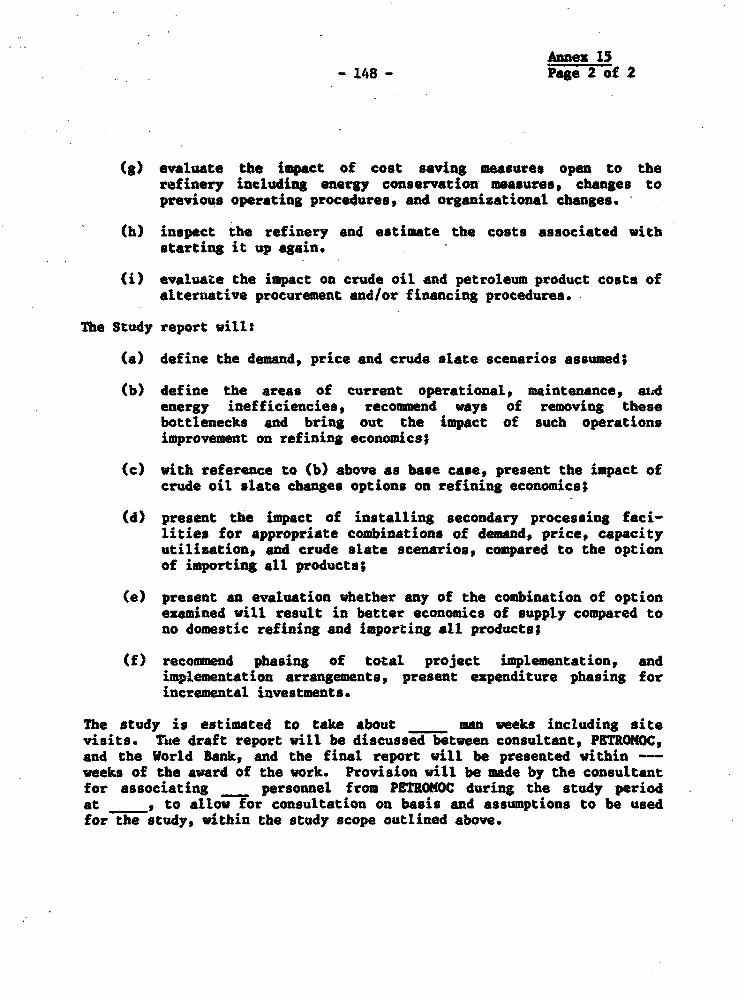

Annex 15 Proposed Objectives for the Supply of PetroleumProducts to the Marine Terminals Includingtke Feasibility of Operating the Natola Refinery.... 148

Annex 16 Structure of Refinery Prices.......................... 1SOAnnex 17 Crude Oil and Products Storage Capacities

- BY Pr1no........................... SAnnex 18 Proposed Objectives for Study into the Internal

Storage Internal and Transportation of PetroleumProdueto ..... P ........... ~152

Annex 19 Proposed Objectives for Technical Assistance toPETROMOC for Corporate Accounting...............o... 153

Annex 20 Petroleum and Gas Sector Investments in Mozambique

Annex 21 Mozambique Geological Framework and Interpretationfor Petroleum and Gas Exploration ...... o.......... 155

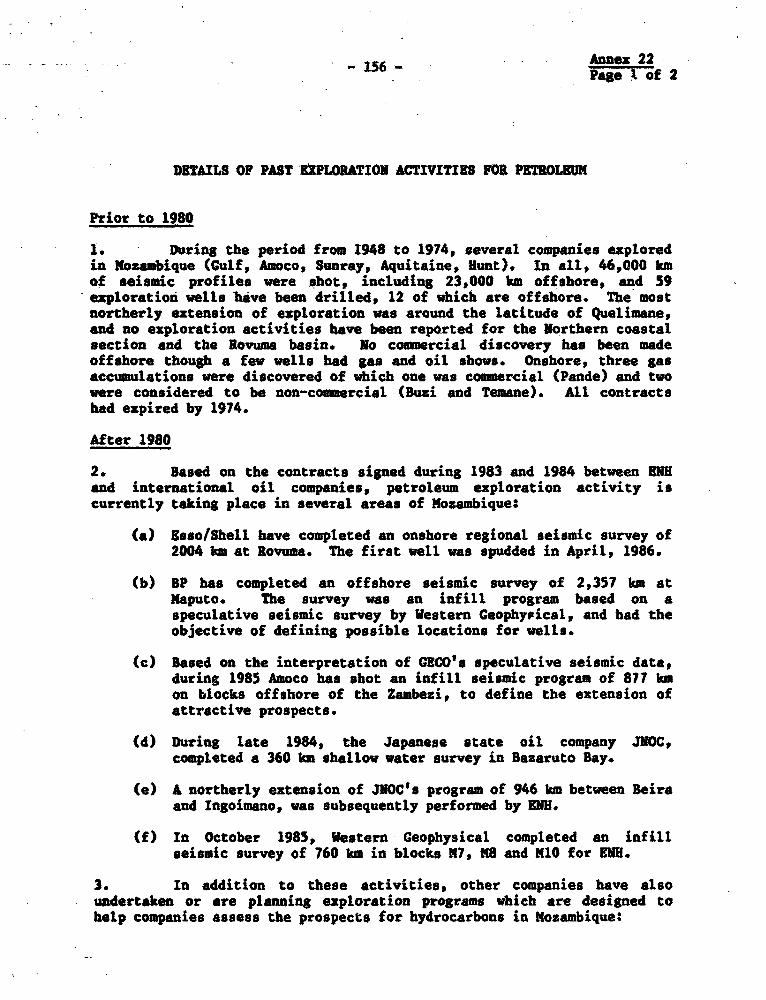

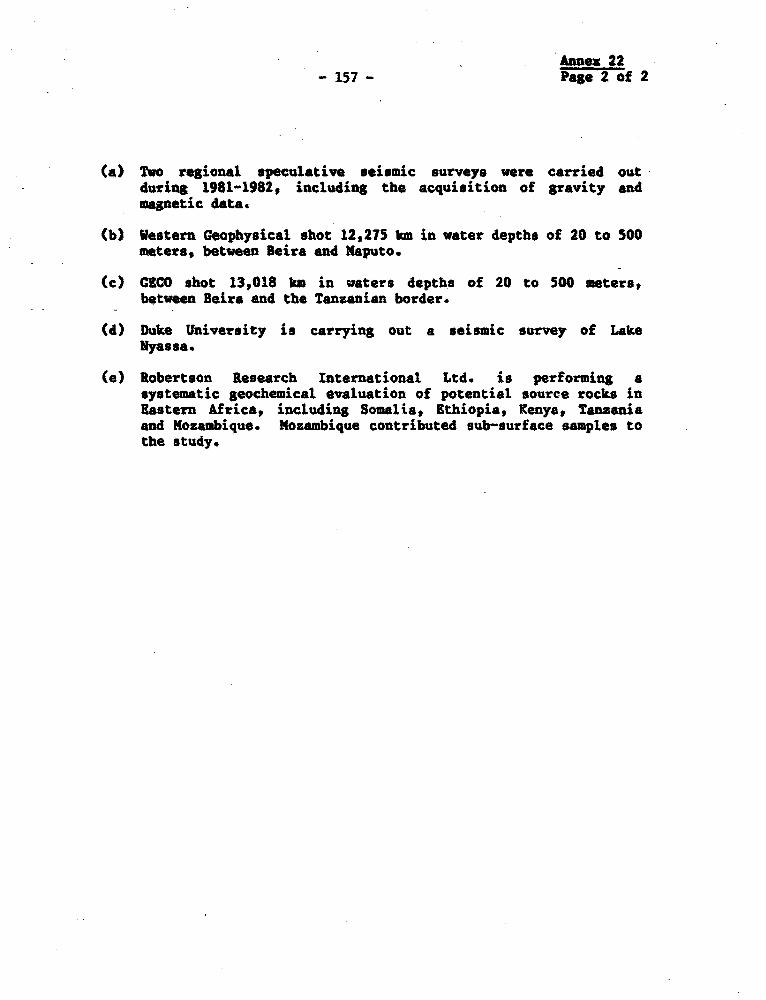

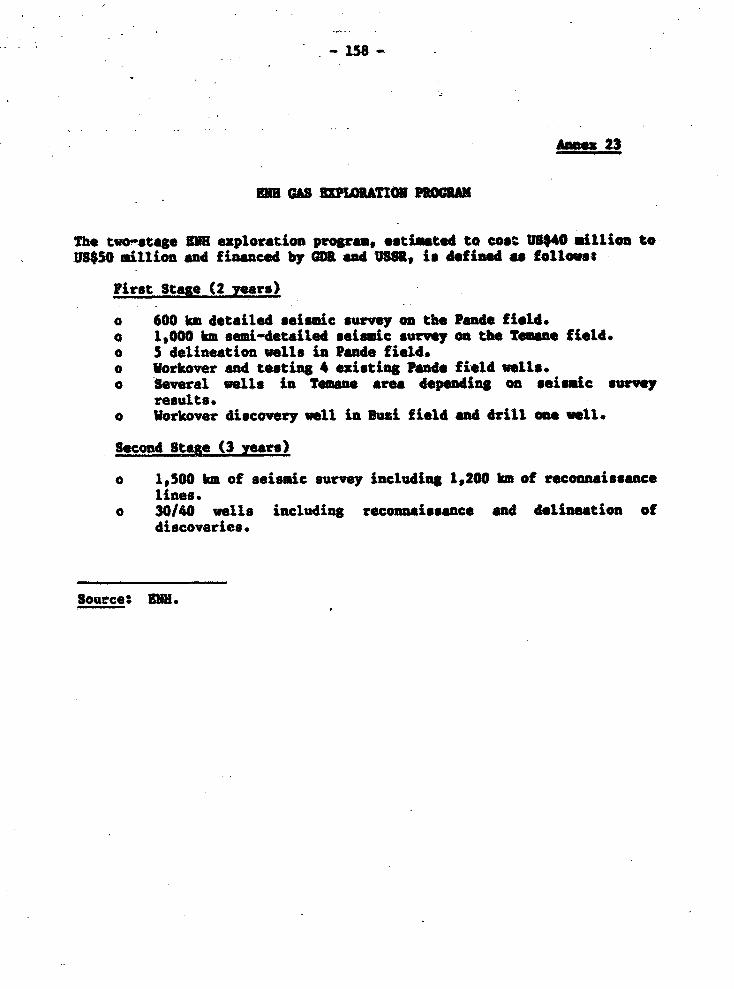

Annex 22 Details of Past Exploration Activitiesfor Petroleum...... .. eo.oo...ooe.ooo.@ . .. o....... 157

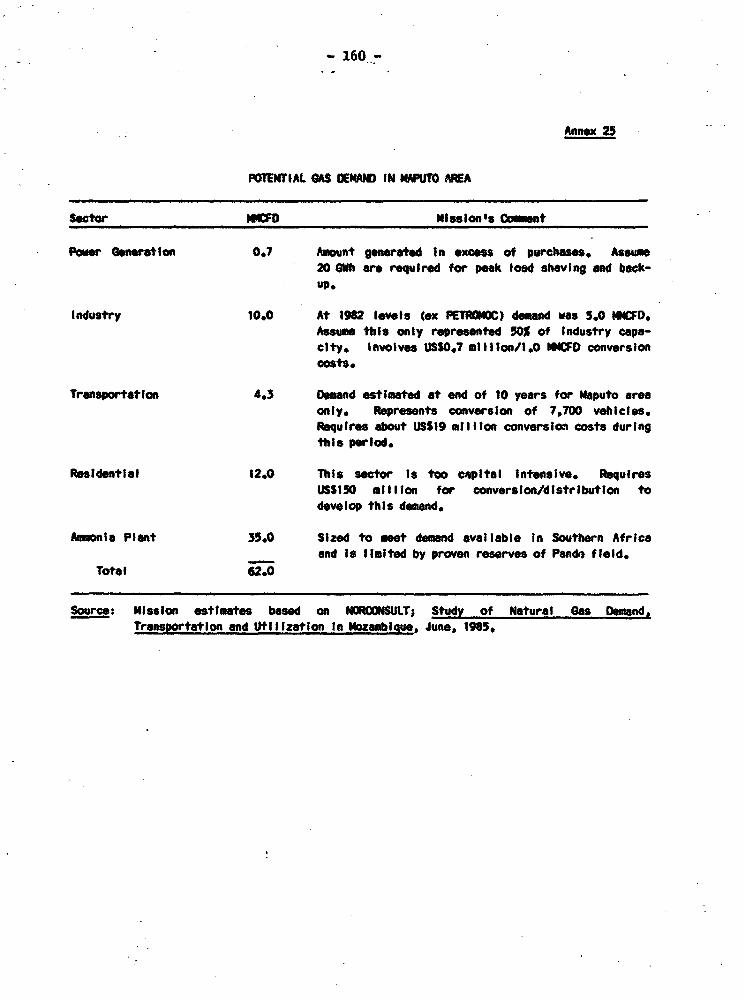

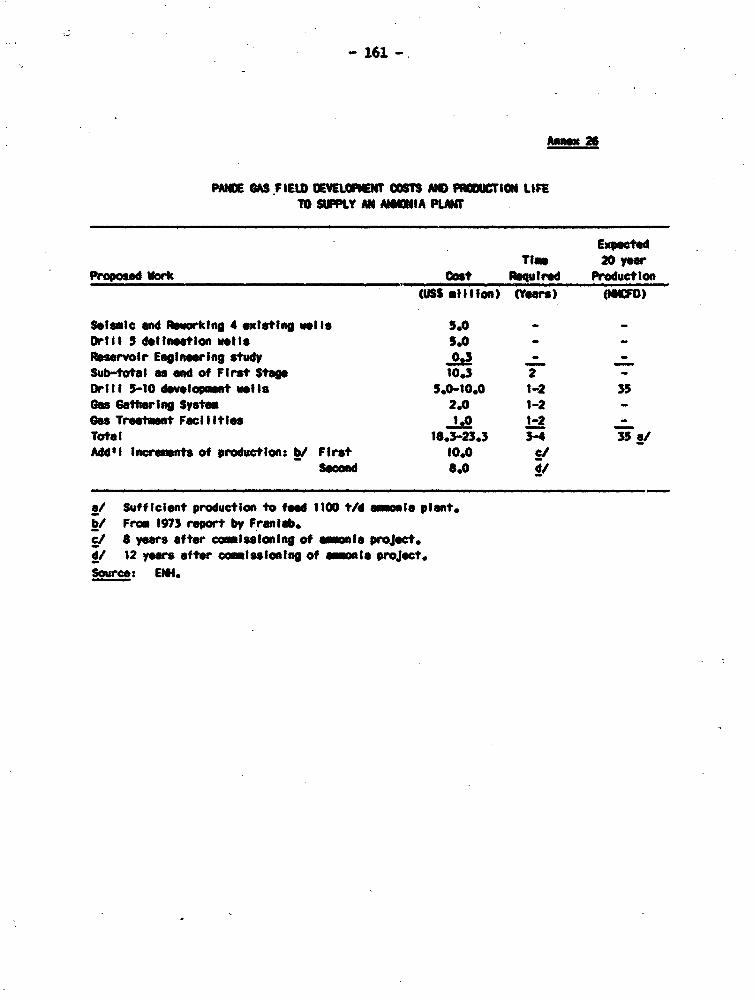

Annex 23 E HGas Exploration Programs.......................... 159Annex 24 SUE's Technical Staff in Mid 1986 ........... 4*....... 160Annex 25 Potential Gas Demand in Mapoto Area ...................0 161Annex 26 Pande Gas Field Development Costs and Production

Life to Supply an Ammonia Plant..................... 162Annex 27 Comments on Awmonia Project Assumption

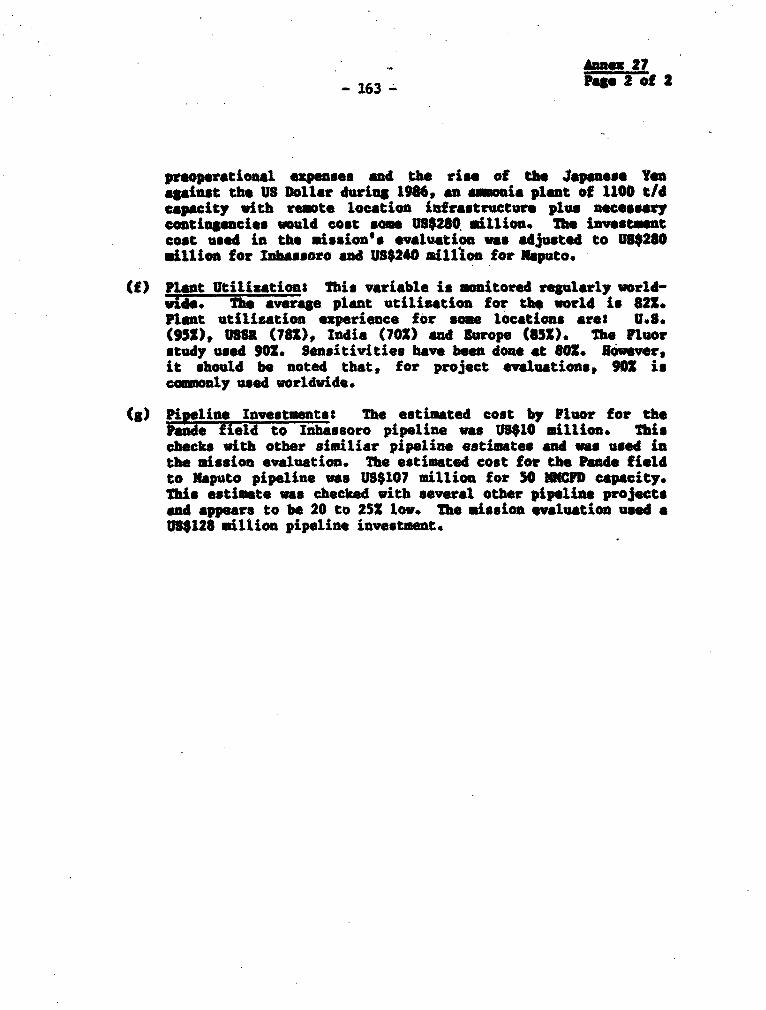

used by Fluor e.go. g......ee.e.......... ........... 163Annex 28 Assumptions to Evaluate Ammonia

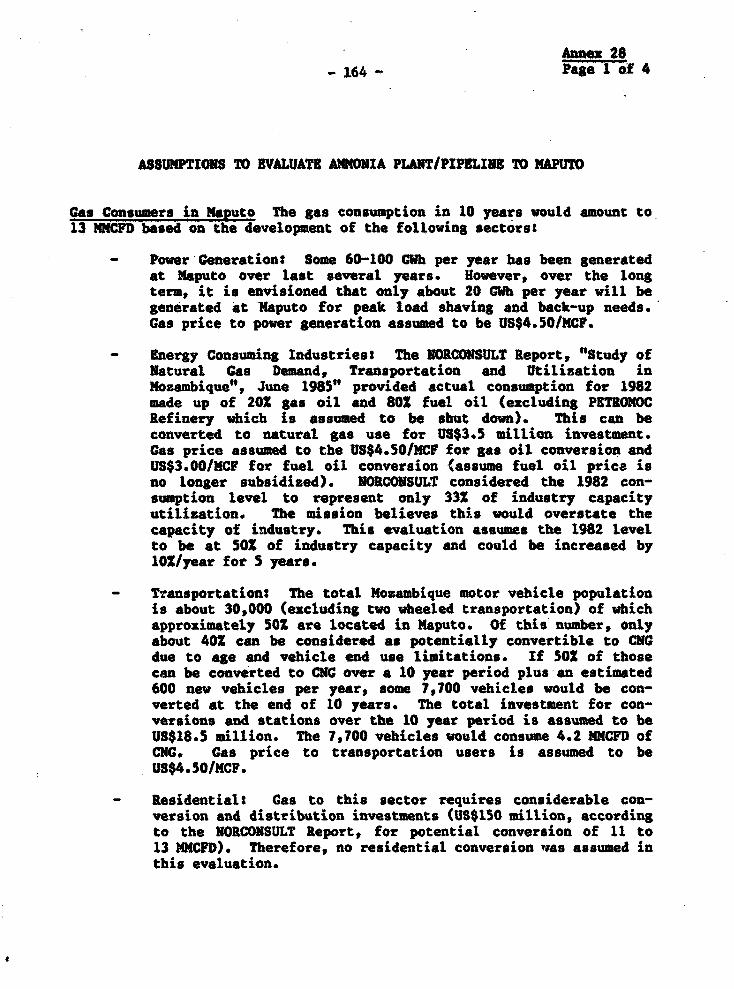

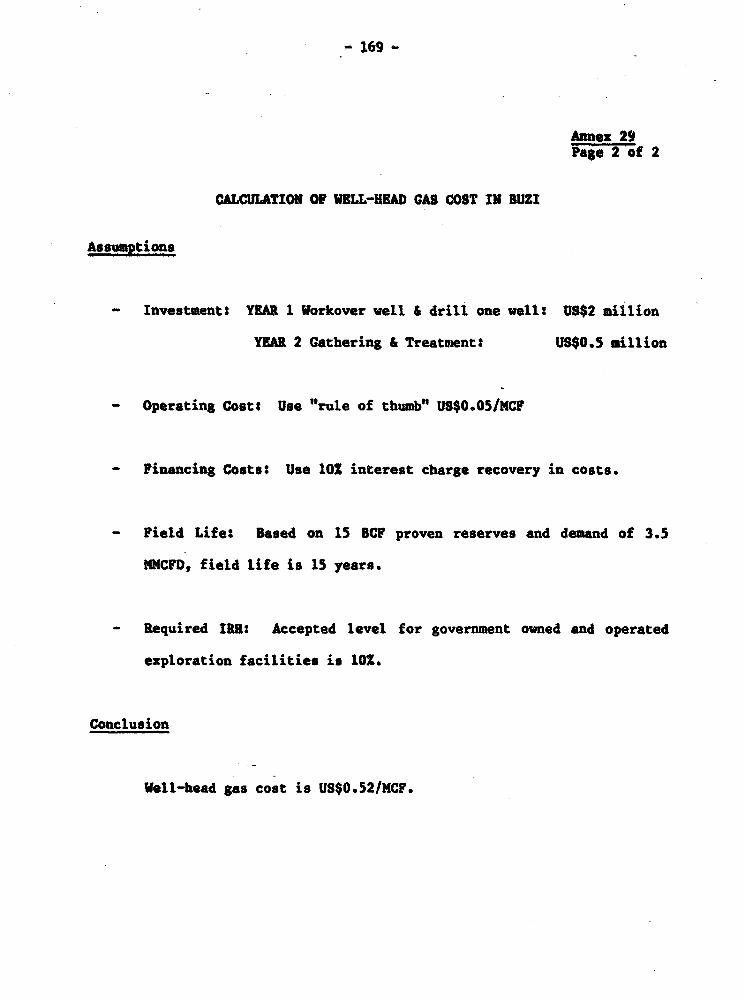

Plant/Pipeline to Naputo.e.**.**.. *..***o.. .. .....*- 165Annex 29 Summary of Base Case Cost and Benefits Streams for

Buzi Pipeline/Utilization in Beira.................. 169Annex 30 Major Gas Consuming Possibilities...............g..... 171Annex 31 Existing Power Facilities in Mozambique............... 173Annex 32 Power Sector Investments in Mozambique 1980-1985...... 178Annex 33 Maputo Thermal Power Station Recumnended

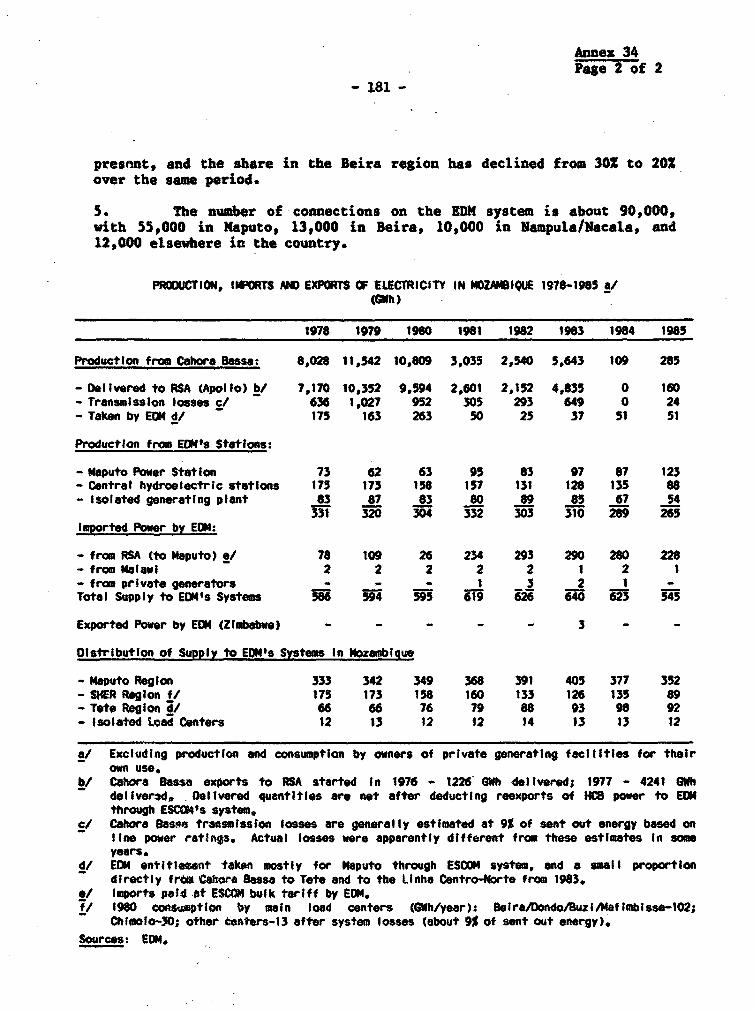

Remedial Vorks.................gge......eeg... 179Annex 34 Historic Production and Consumption of Power in

Mozaimbique. g.gs.......e.g....... g e.g...... .....geg...... 181Annex 35 Capabilities and Costs of Existing Power Sources

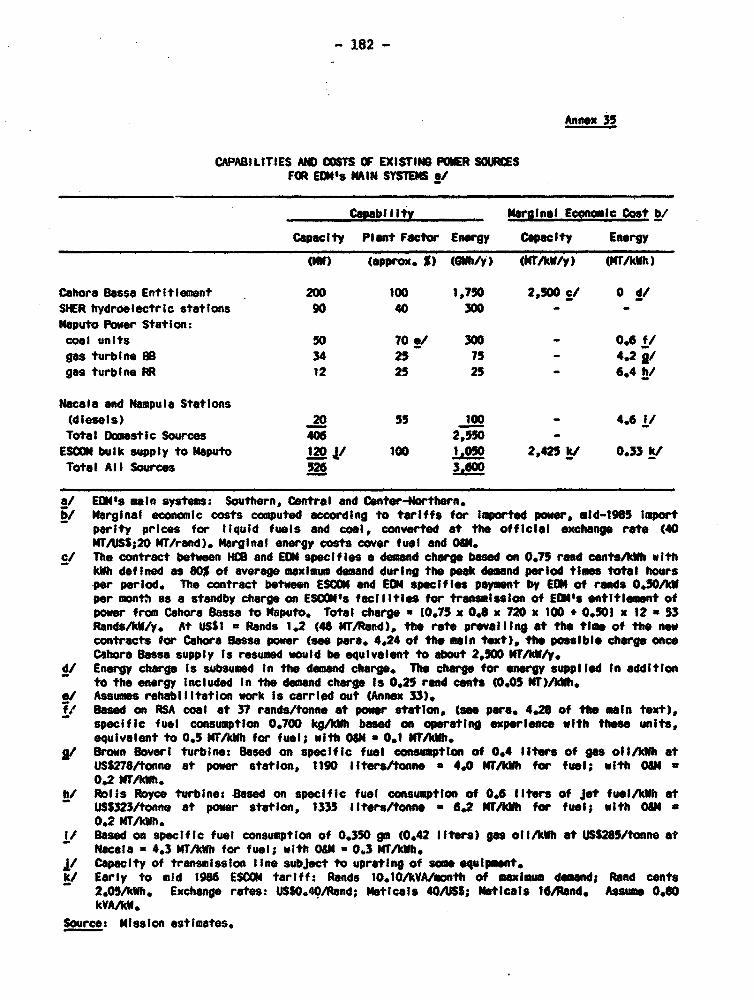

for EDM's Main Systems .............................. 183Annex 36 EDK's Tariff - Assessment Mission's Coments*****e*.......... 184Annex 37 Possible Scenarios for Evolution of Domestic Demand

for Power on EDN's Main Systess......e.............. 185Annex 38 Export Potential for Mozambican Power................. 186Annex 39 Projected Availability of Power for Export from

Existing Surplus and Low-Cost Sources............... 190Annex 40 Proposed Small Hydroelectric Projects in Southern

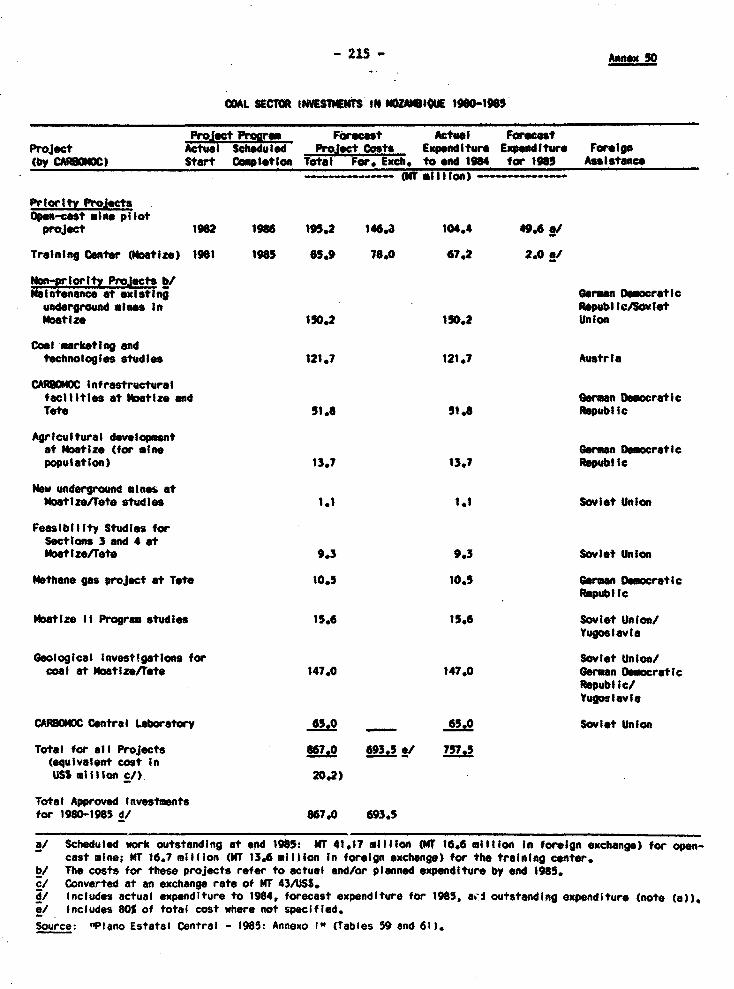

Mozambique........g................................ ,193Annex 41 Minor Coal Occurrences in Mozambique.................. 199Annex 42 Coal Reserves in the Moatize Region .................. 200Annex 43 Mozambique Coal Supply and Use: 1978-1984 ........ .* 202Annex 44 Existing Dev4lopments and Manpower at Moatiiez.e*e**,& 203Annex 45 Domestic and Export Prices of Coal 205

Anne" 46 Illustrative Economic Cost of Ele^tricity from a60 NW Thermal Power Plant Burning Moatize Coal...... 206

Annex 47 Coal Related Transport Facilities..................... 208Annex 48 Noaitixe Projects Illustrative Capital and

Operating Costs* *,** 212Annex 49 Noatise Open Pit Mine: Illustrative Capital and

Operating Costs 214Annex 50 Coal Sector Investments in Mozambique 1980-19959... 216

MAPS

IBiD 19471 - Mozambique$ Electric Power FacilitiesIBRD 19515 - Mozambique: Petroleum, Gas and Coal - Exploration

and Supply Facilities, 1985

EXECUTm SUNU&RY

Present Situation in the Energy Sector

Adverse Factors for the Energy Sector

1. Recent trends in the energy sector of Mozambique reflect theprevailing conditions throughout the economy, particularly disruption toeconomic activity by armed bands, acute scarcity of foreign exchange andtrained manpower, and shortcomings in management and operationalcapability and in financial performance. The continuous decline ineconomic activity since 1981, as indicated in estimates of GDP, has beencause and effect of a fall in Mozambican consumption of commercial energyforms (petroleum products, electricity and coal) of about 40X between1981 and 1984. Government attributes the main cause of this decline tothe activities of armed bands.

Disruption to Energy Supply

2. Acts of sabotage and attacks on the local populace by armedbands have severely disrupted energy production and supply, especiallyfor electricity transmission since 1981 and for coal transportaticr since1983. Consequently, the two major facilities for the production ofenergy in Mozambique, the Cahora Bassa hydroelectric power station andthe coal mines at Noatize. are virtually out of operation at present.The direct annual cost to Mozambique of this disruption is aboutUS$20 million in terms of foregone earnings from exported energy andadditional costs of imported energy. The activities of armed bands aredisrupting supplies of woodfuels to urban areas with grave socio-economicconsequences for the urban population. These activities are alsopreventing the exploration and development of natural gas resources andthe implementation of major new developments to exploit Mozambique'sconsiderable energy resources.

Woodfuels and Household Energy

3. Shortages of energy supplies to urban households are the mostserious problem in the energy sector. These shortages have a greatersignificance to the national socio-economic fabric than even the con-sequences for economic activity arising from interruptions of commercialenergyXsupplies to the productive sectors of the economy. The problemhas been manifested by the rising cost of woodfuels as degradation of thenatural forests and savanna-land around towns becomes more acute.Evidence of this problem is the ten-fold increase in woodfuel prices inMaputo since the early 1980's, compared to a three-fole increase ingeneral prices. Loss of supplies has also been due to the activities ofarmed bands. This burden is causing major social and economic hardshipfor lower and even middle-income urban households. Restoration ofpeaceful conditions to the country would bring some relief to this

- ii -

situation, but a significant impact on household energy suppi.es throughthe development of indigenous energy resources (woodfuels, electricity,coal and natural gas) would take many years and require large amounts offinancial resources and skilled manpower. For the short-term, Governmentconsiders the only technically available option to be importation ofkerosene and LPG, but there was a shortage of these products during 1985and 1986 due to scarcity of foreign exchange.

Shortage of Foreign Bzchange

4. Shortages of foreign exchange have periodically interrupted thesupply of petroleum products since 1983. PETRONC has not been able topurchase petroleum products on the best terms with the small andunpredictable amounts of foreign exchange that are put at its disposal,thus leading to an increase in procurement costs. Government has createda Petroleum Funds, operated by PETROMOC at the Bank of Mozambique, tochannel foreign exchange for increasing procurement efficiency andstabilising the supply of petroleum products at least to key consmers.Consumption of petroleum products in 1984 and 1985 was abuout 251 belowthe level in the period 1970-1982 due to constraints on supply, as notedabove, and a fall in demand due to the decline in economic activity.

5. Lack of foreign exchange has contributed to a decline inoperational efficiency by causing shortages of spare parts, materials andequipment required for system operation, maintenance andrehabilitation. These constraints are particularly evident in thedistribution systems for electricity and petroleum products. Thedistribution systems of Electricidade de Mocambique (1DM) have been keptin operation largely through substantial donor support for importedgoods. The handling and distribution facilities owned by PETRONOC andprivate sector oil companies need to be rehabilitated urgently. Thetransport fleets of EDM and PETRONOC are inadequate to sustain efficientoperations. In the main urban areas, there are frequent power outagesand inefficient distribution of petroleum products, while many areas ofthe country do not receive any petroleum supplies or electricity fromlocal diesel generators. One of the results is loss of agroindustrialproduction and interruption of other produtive activities.

6. Lack of foreign exchange threatens to delay rehabilitation workon major coal and petroleum production facilities. Once securityconditions allow normal operations at the Noatize coal mines, foreignexchange will be required for rehabilitation of the mines (US$14 million)and the railway link from the mines to the main railway system(US$10 million) to allow a resumption of production at historic maximumlevels (S50,000 tpy). Likewise, foreign exchange would be required forthe recommissioning of PETROMOC's Matola refinery, if justified.However, the mission's review supports Government's present policy ofimporting petroleum products for meeting domestic demand instead ofoperating the Natola Refinery. A comprehensive study into the supply anddistribution of petroleum products is required before any commitments aremade on the refinery.

- iii

Shortage of Trained Manpower

7. The shortage of trained manpower that resulted from the exodusof Portuguese managers and technicians in the mid 1970s has been a majorimpediment to achieving the Government's objective for its manpowerpolicy of improving the operational performunce of the sector insti-tutions and to support -sustained economic development. Government wasfaced at Independence with a national illiteracy rate of about 98X, andit has hsd to allocate a substantial proportion of its scarce resourcesto education. Past and probable future levels of output of trainedpersonnel in Mozembique are low relative to the needs of the economy andthe sector. There is also a shortage of teachers and educationalmaterials. In addition, emigration of skilled manpower has been andstill is occurring. Consequently, there is a reliance on expatriateworkers for the operation of energy sector facilities, who are generallyprovided under bilateral agreements. Government has attempted to stemthe outflow of skilled personnel by issuing a new labor law in December,1985 that allows enterprises to offer wages and incentives to motivateand retain such personnel.

Institutional Weaknesses

8. The sector organizations responsible for production and distri-bution of energy share common institutional and management problems.Nany of the problems stem from the newness of these organisations and theshortages of skilled manpower. Broadly, these problems fall into thefollowing categories: (a) inadequate financial data; (b) absence ofoperating, financial and accounting systems; (c) lack of manag_emntinformation systems; (d) minimal planning and budgeting; (e) absence ofinternal auditing; (f) little or no technical and management training;(g) inadequate computer facilities; and (h) little coordination withrelated enterprises. Presently, the management of these organizations is'supported by some assistance from expatriates.

Energy Pricing

9. The Government has a general policy of maintaining pricestability and enterprise viability. Electricity prices were not changedbetween the mid 1960's and January 1986. Petroleum product prices havenot been changed since 1979. The economic costs of meeting energy demandare not generally considered in setting energy prices, so that changes inimport parity prices or the long run marginal costs of meeting demand arenot reflected in corresponding changes in the retail prices for energyproducts. Consequently, consumers of these products aave becomeincreasingly subsidized. Thus, there is little incentive for improvingthe efficiency of energy consumption and for economically justifiedsubstitution between fuels to reduce costs.

10. The policy of keeping the metical grossly overvalued hasfacilitated the maintenance of official prices of petroleum products,electricity and coal at artificially low levels. On the other hand,

- iv -

prices for woodfuels which are market determined, are substantiallyincreased by supply constraints and by general inflation due to excessivemonetary expansion. At present, these official prices are only afraction of the prices of fuelwood and charcoal, whose prices aremarket-determined. For example, charcoal is about 500 times moreexpensive than steam coal and 85 times more expensive than fuel oil on agross energy basis, while fuelwood is nearly 13 times more expensive thanilluminating kerosene. The comparison of the costs of fuels to consumerswhich takes account of the conversion efficiencies of energy appliancesshows even greater differences. For household cooking, charcoal is about53 times more expensive than kerosene and 15 times more expensive thanelectricity on a useful energy basis. Likewise, fuelwood is 24 and 14times more expensive than kerosene and electricity respectively. Theseexceedingly large price differentials are not justifiable in terms ofeconomic efficiency or social equity.

11. Prices for some of the most important energy products aresubstantially below their imported cost even at the overvalued officialexchange rate. In mid-1985, when world crude oil prices were aroundUS~30/bbl, the retail prices of kerosene and fuel oil were only about 402and 30X respectively of the imported costs. Even at the much lower worldprices for petroleum products during the first half of 1986, kerosene andfuel oil prices in Mozambique remained below their imported costs, beingabout 50S of these prices. The retail prices for steam coal were onlyabout one sixth of the equivalent world market prices.

Enterprise Financial Viability

12. Government's policy an energy pricing has prejudiced theviability of the energy supplying agencies, with detrimental consequencesfor operating efficiency. EDM was making increasing losses from 1981onwards, and it may at best only break even in 1986 on a cash accrualbasis after the major tariff increase in January 1986. PETRONOC andCARBONOC are also extremely short of financial resources, but theirfinancial position cannot be analysed until they start to producefinancial accounts. The failure of prices to cover the actual costs ofthe enterprises has been accommodated through subsidies from the centralbudget and credit from the banking system. The Government decreed in1984 that all enterprises should produce full sets of accounts from PY86,which will require technical assistance to fulfill by the energyagencies.

Policy Issues

13. The present assessment of the energy sector in Mozambique hasidentified aiany policy issues concerning investments, pricing, manpowerand institutional development. Covernment's investment strategy is basedon two principles which it considers to be complementary, namely tomaintain viable productive assets in operation through rehabilitation and

maintenance programs, and to promote sustained economic developmentthrough exploitaticn of natural resources. The basic issue concerns thepriority between these two principles given the country's financial andeconomic difficulties in the short to medium term.

Investment Policy

14. Government has expended in the last few years substantialamounts of scarce financial and trai}ed manpower resources on thepreparation and promotion of a number of very large export-orientedenergy and energy-intensive projects. This work forms part ofGovernment's strategy for placing Mozambique in a position from which itcould exploit regional and international market opportunities should theyoccur. The present activities of armed bands in the country limitGovernment's scope for starting in the near future any of the majordevelopments. The combined investment in these projects (inhydroelectricity, coal, natural gas, asmonia and aluminum) would be morethan US $2 billion in constant price terms of the early 1980's, andrepresent massive comitments relative to the size and ebsorptivecapacity of the Mozambican economy.

15. The mission's reviews in this report conclude that the strategyof large-scale development of known energy resources specifically forexport by Mozambique has not been shown to be viable for the foreseeablefuture, with the possible exception of the ammonia project, mainly due toconstraints or lacK of competitiveness in export markets. A major changein the circumstances of the project environment would be required tomodify this general conclusion, including improved project preparationand a substantial and sustained increase in world commodity prices. Themission supports government's criteria for acceptability before enteringinto commitments for large investments in export-oriented projectsnamelys (a) viability at world market prices with secure marketprospects; and (b) satisfactory economic benefits to Mozambique from theexploitation of its resources. The mission also recommends thatGovernment's policy of taking steps to reduce the risks to the Mozambicaneconomy be strengthened through the use of foreign capital, marketing,management and technical expertise and long-term commitments to theproject by foreign partners.

Rehabilitation Policy

16. The mission agrees with Government that the main objective inthe short and medium term for the energy sector should be the improvementof operational efficiency and the strengthening of sectoralinstitutions. Improvements to operational efficiency cover a wide rangeof activities. Individually, many are relatively small, but togetherthey comprise a major program. The main activities cover manpowertraining, davelopment of improved management, financial and operationalprocedures, rehabilitation of facilities, improvements in the efficiencyof energy utilization and supply, and fuel substitution. This objectiveis a vital component of any strategy for economic recovery in Mozambique

- vi -

and for enabling the country to benef it from its locational advantage forproviding transit services to inland countries. The effort ofrehabilitating energy and transport facilities would fully absorbMosambican institutional capacity and available financial and manpowerresources for many years to come. In fact, substantial inputs fromabroad will also be required, making technical assistance a vitalcomponent of this strategy. Any allocation of resources for large newdevelopmnets should not be at the expense of sector operatingperformance.

Knergy Pricing Policy

17. The essential objectives of energy pricing in Mozambique shouldbe the efficient use of economic resources, the financial viability ofsector enterprises and the satisfaction of demand for energy at leastcost to the economy. The main issues are the need to: (a) eliminategross distortion in prices between energy products; (b) take account ofeconomic factors in pricing policy, especially to cover import parityprices and to provide incentives for efficient utiliuation of energy; and(c) make the institutional procedures for price-setting more responsiveto changes in economic and financial circumstances, and thus establish abetter balance between the objectives of price stability and theobjectives listed above.

18. Implementation of a new policy for energy pricing in Mozambiqueis complicated by the major distortions in the foreign exchange rate ofthe domestic currency and prices and wages throughout the economyrelative to economic costs. Thus, energy pricing policy is bound up witheconomy-wide pricing issues. Without subbtantial investigation, it isnot possible to estimate reliably the import parity prices at a realisticexchange rate. Preparation of least-cost development programs would alsobe required to set the economic basis for energy pricing throughderivation of the long run marginal costs of meeting demand. While theseparameters are being researched and until new policies are implemented,there is a strong economic case for raising imuediately the prices ofimported energy at least to import parity levels based on the presentofficial exchange rate. This adjustment would substantially improve thefinancial position of the energy supplying enterprises and would givemore appropriate indications of economic costs to energy consumers. Ingeneral, the mission recommends that Government should implement apricing policy of at least full financial cost recovery from energyconsumers, thus maintaining import parity levels for initernationallytraded energy products.

Manpower Policy

19. The challeage to energy sector enterprises posed by theshortages of trained manpower is to develop low-cost and efficienttraining systems that will meet their requirements and reduce the needfor expensive expatriate support. The enterprises must be able 1* stemthe emigration of skilled manpower. Recent labor legislation allows

- vii -

enterprises to offer wages and incentives to motivate and retain staffwith key skills. However, there is still a need to give employersgreater scope for recruiting and laying-off labor to improve operationalperformance. These issues are economy-wide, but they require attentionurgently to support the training efforts to bring about sustainedimprovements in the manpower situation.

Institutional Policy

20. The need to redress the institutional weaknesses noted above(pars. 8) requires a stronger adhereuce to policies already laid down.For example, sector enterprises are required to submit financial reportsat specified frequencies and standards in their decrees of establishment,yet they have not fulfilled this requirement. The capabilities of theMinistry of Industry and Energy and the Ministry of Mineral Resourcesneed to be strengthened to monitor and coordinate the activities in theirsectors and to liaise with other ministries.

21. The role of the prospective National Energy Council will beimportant for development of the energy sector through itsresponsibilities for recommending policies, setting priorities andensuring the adequacy of investment planning for the sector. The missionfully supports the proposal to set up the Council. The mission alsoconsiders that the role of the Department of Energy should be critical inthe formulation of energy policies through its responsibility forcoordination and monitoring in the energy sector and support to theNational Energy Council. One important area that requires thepolicy-based perspective and coordinating role of the National EnergyCouncil is the planning of large, multi-sectoral projects and programs,taking into account explicitly the linkages between the energy sector andthe agricultural, industrial, and transport sectors.

Strategy and Priorities

Develoo_ nt Stretegy

22. The evaluation of issues and options in this Report indicatesthat the order of priorities for energy development in Mozambique in theshort to medium term should be determined through the following strategy:

First: to satisfy Mozambique's own energy needs by using primarilydomestic sources, if economic, and by rehabilitating and improvingexisting sector assets.

Second: to develop Mosambique's potential to benefit from transit tradeTn energy products for inland countries and trade in electricity, and tocooperate with neighbouring countries in development of solutions toco on energy issues.

- viii -

Third: to invest in energy or energy intensive industries for export;Wl yif a number of important conditions are met, especially economic,financial and market criteria.

23. The mission's recommended strategy for development gives alower priority to large scale export-oriented projects than torehabilitation of existing facilities to meet the domestic demand forenergy. While security constraints exist, even investments that satisfyall the proposed criteria will not be feasible. While the conditions ofinsecurity and scarcity of financial and human resource persist, themission recommends that Government focus resources on rehabilitation andinstitutional strengthening. The mission's reconmendations on prioritiesare given at the end of this Summary. Furthermore, before entering intoany major commitments, Government should strengthen its coordination forthe planning of large-scale developments in energy, industry andtransportation.

Regional Cooperation

24. Development of Mozambique's potential for transit trade inenergy products (petroleum products and coal) conforms to the generalstrategy for regional cooperation under the auspices of SADCC. Otherimportant areas are trade in electricity, natural gas utilization,cooperation in developing regional solutions to common issues such asfuelwood plantations, improving efficiencies of cooking stoves andcharcoal manufacture, and development of coal as a household fuel. Themission supports these efforts. On the other hand, concerningGovernment's policy towards energy trade with the Republic of SouthAfrica (RSA), the right balance is required between taking advantage ofthe availability of low-cost energy (coal, electricity) from RSA andmaintaining the capability to supply key energy consumers in the Maputoregion in the event of prolonged disruption to transportation andtransmission links between the coast and inland areas.

Recommended Sector Priorities

25. Sumuaries of the mission's recommendations concerning policiesand strategies and for technical assistance are given for each of themain energy subsectors at the end of the chapters in this Report. Takentogether, general themes emerge from these recommendations and constitutethe following recommended priorities for the Government in the energysector.

(a) remedy shortages of energy products and secure stable supplyconditions;

(b) improve the reliability of energy supply facilities throughrehabilitation;

(c) carry out institutional strengthening and manpower developmentof the energy suppliers (EDM, PITROMOC, and CARBONOC) end also

- is -

ENH* the Ministry of Industry and Energy and the Ministry ofNatural Resources;

(d) remove distortions to energy pricing, at least by increases inofficial prices to import parity levels at the prevailing offi-cial exchange rate; account should be taken of the rela-tionship between eaergy prices and other prices in the economy,and to the structure of economic costs of meeting energydemand;

(e) strengthen the capacity for planning in energy sector agenciesto meet domestic demand for energy and to evaluate large energyprojects;

(f) address the urban household energy crisis to arrest the des-truction of natural forests around cities (especially Maputo,Beira and Nampula) and to ameliorate socio-economic hardshipthrough a combination of measures to manage demand and increasesupply of energy; and

(g) continue promotional efforts to stimulate the interest offoreign oil companies in petroleum exploration.

Generally, these priorities reflect Governrii's own priorities, and themission considers that Government could proceed with the implementationof most of these recommendations. Some of the measures required toimprove the reliability of energy supply may not be feasible whilst theactivities of the armed bands persist.

Recommended Technical Assistance Priorities

26. The following priorities for technical assistance emerge fromthis assessment of the energy sector:

(a) to strengthen the management, financial and operatingperform-n'ce of the main sector agencies;

(b) to develop manpower resources at all levels of skills;

(c) to improve the planning capability of the main supply agenciesand assist in the preparation of sub-sector developmentprograms;

(d) to improve sector-wide planning and coordination throughdevelopment of the capability of the Department of Energy;

(e) to assist with specific important studies covering thestructure of energy prices, household energy demand, mappingand forest inventories, petroleum procurement, natural gasutilization, electricity tariffs, rehabilitation requirementsfor existing operating facilities (petrolem, electricity andcoal), energy conservation, fuel substitution and the use ofenergy in rural communities.

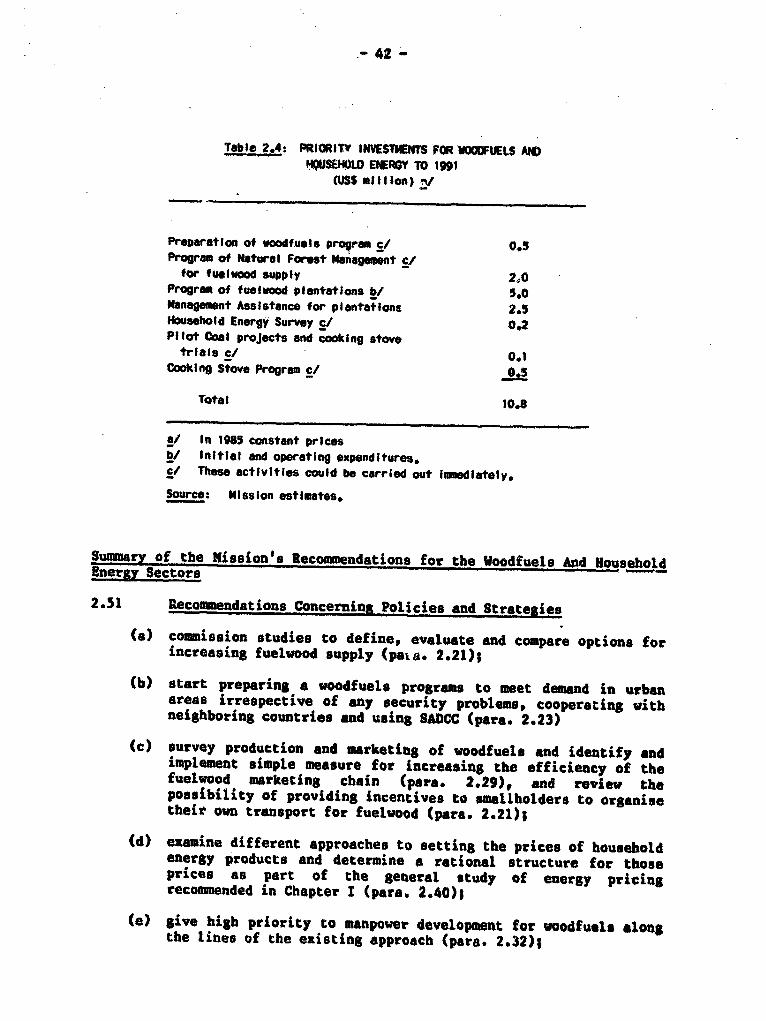

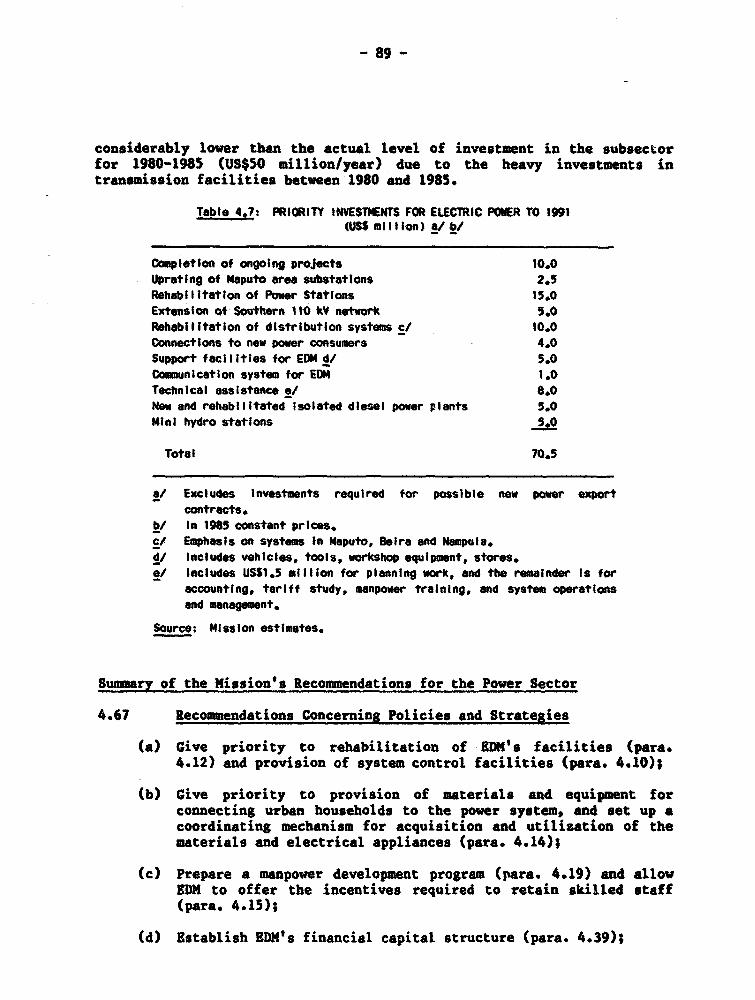

Recommended Priority Investments

27. In line witb the recommended sector priorities, this reportsuggests a core program of investments of about US$175 million inconstant 1985 price terms in the energy sector for the five years to1991. The program is detailed in Scb,dule A at tba end of this summary,and it is summarized in the table below. The program is considered to bethe minimum required to aupport the priorities under the recommendeddevelopment strategy, namely rehabilitation of assets and institutionaldevelopment. The recommended technical assistance to support thisprogram of investments is detailed in Schedule 3 at the end of thissummary, and the costs of this assistance are included in the coreprogram. The components relating to the woodfuelu and household energy,petroleum supply and distribution, electricity and for institutionaldevelopment could proceed even under the present conditions of insecurityin the countryside.

Table 1: SUIUIRY OF THE PRIORITY INWESTMENTSFOR THE ENEMY SECTOR TO 1991

(1110 million) a

Subsector

lnstitutional DOvelopment ond Studies 3.0Woodfuels and Household Energy 10.8Petroleum Supply and Distribution 7.0Petroleum and Gas Exploration

and Oevelopment 56.0Electricity 70.5Coal 27.0

Total 174.3

a/ In 1985 constant price terms.

Source: NIsslon estImates.

28. The mission has not presented any recommendations for aninvestment program for beyond 1991 due to great uncertainties inforecasting the demand for energy in Mozambique. The recommended coreprogram does not include investments which do not have a firm econo,dcjustification it present but which future circumstances may justify, suchas recommisuioning and modifying the petroleum refinery and somehydroelectric projects under study. In particular, additionalinvestments of up to US$50 million could be considered for thedevelopment of natural gas supplies from onshore fields and theconversion to gas utilization of industrial and transport facilities* if

- xi -

shown to be economically justified. Large energy-intensive projects,such as the proposed _aoia plant, are not included since they would beclassified as induttial sector development. Large energy resourcedevelopments, such as for coal, are not included due to the presentunfavorable international market prospects and the lack of economicjustification based on inforation available to the mission, and to thegreat uncertainty concerning the availability of funds and the securitysituation. In addition to surmounting the difficulties enumerated above,interested foreign investors would have to satisfy themselves of thefinancial and technical feasibility of these projects under the stringentcriteria of the private sector.

xii -

Schedule A: RECCOMENDED ENER6Y SUE-SECTORAL PRIORITY INNESTIMENTS TO 1991(USS million) 8/

Voodfuels and Househrld EneMr2Preparation of woodfu*ls program 0.5Progra of Natural Forest Managementfor fuelwood supply 2.0

Program of fuelwood plantations 5.0Managemont Assistance for plantatlons 2.5Household Energy Survey 0.2Plirt Coat projects and cooking stovetrials O.1

Cooking Stove Program 0.Total for Sub-Sector 10.8

Petroleum SUDPIY and DistributionRehabilitation of Storage and Distribution FaciIlties 4.0Technical assistance for institutlonal strengthening 3.0

Petroleum and Gas Exploration and DevelopmentPromotion and preparation 1.5Driling/f lolJ development 3.0

Gas ExplorationPande Field 10.0Temane Flold and others 14.0

Gas Fleld DevelopmentPands Field 13.0

ans f&oectsPipelIne Pande-Inhassoro 10.009 Pilolt ProJect 1.0

Assistance and Training to ENHManagement and Administration 1.0Technical staff for gas proJects 2.5

Total for Sub-Sector 63.0

ElectricityCompletion of ongoing projects 10.0Uprating of teputo area substations 2.5RehabilIltation of Power Stations 1S.0Extension of Southern 110 kV network 5.0Rehabilitation of distribution systems 10.0Connections to new power consumers 4.0Support facilities for EOM 5.0Coinunicatton system for EON 1.0Technical assistance for Institutional strengthening 8.0New and rehabilitated Isolated diesel power plants 3.0Nini-"ydro stations -fi0

Total for Sub-Sector 70.

- Aii -

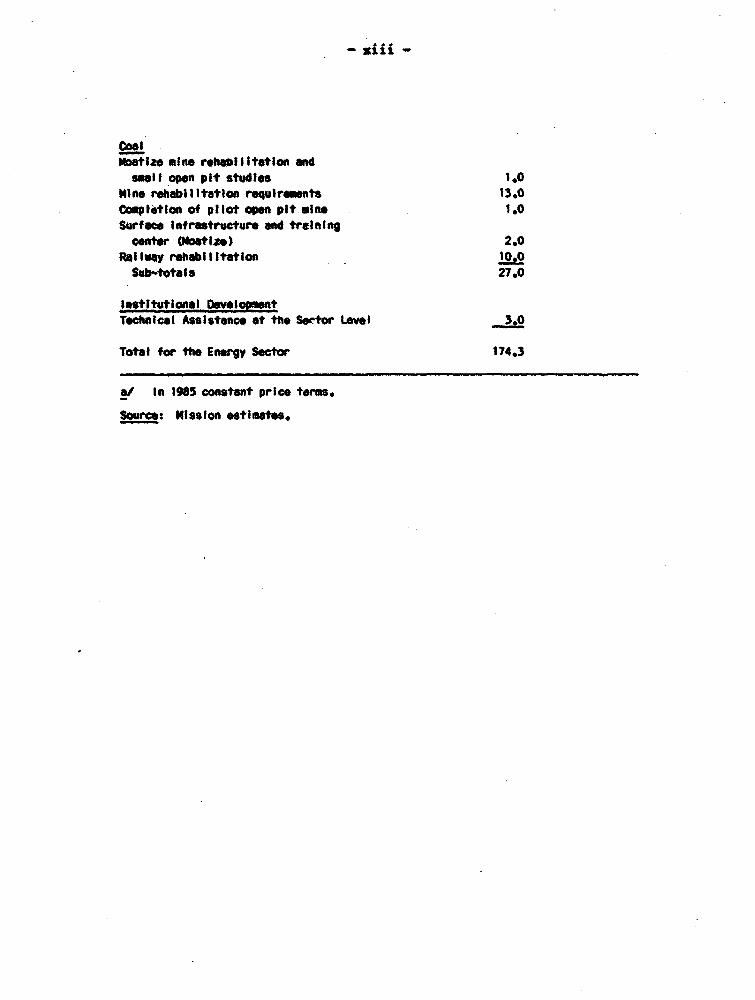

coalNcotize mine rehai itetatlo ands"ll open pit studies 1.0

Nine rehSabIltation requirsemnts 13.0Compltilon of pilot open pit sine 1.0Surface Infrastructure and trainingcenter (Ioatlze) 2.0

Railway rehbilIltation f0.Sub-totals 27.0

Institutional DeveloPoentTchnical Assistance at the Sertor Level 3.0

Total for the Energy Sector 174.3

a/ In 1985 constant price terms.

Source: mission estimates.

z-iv -

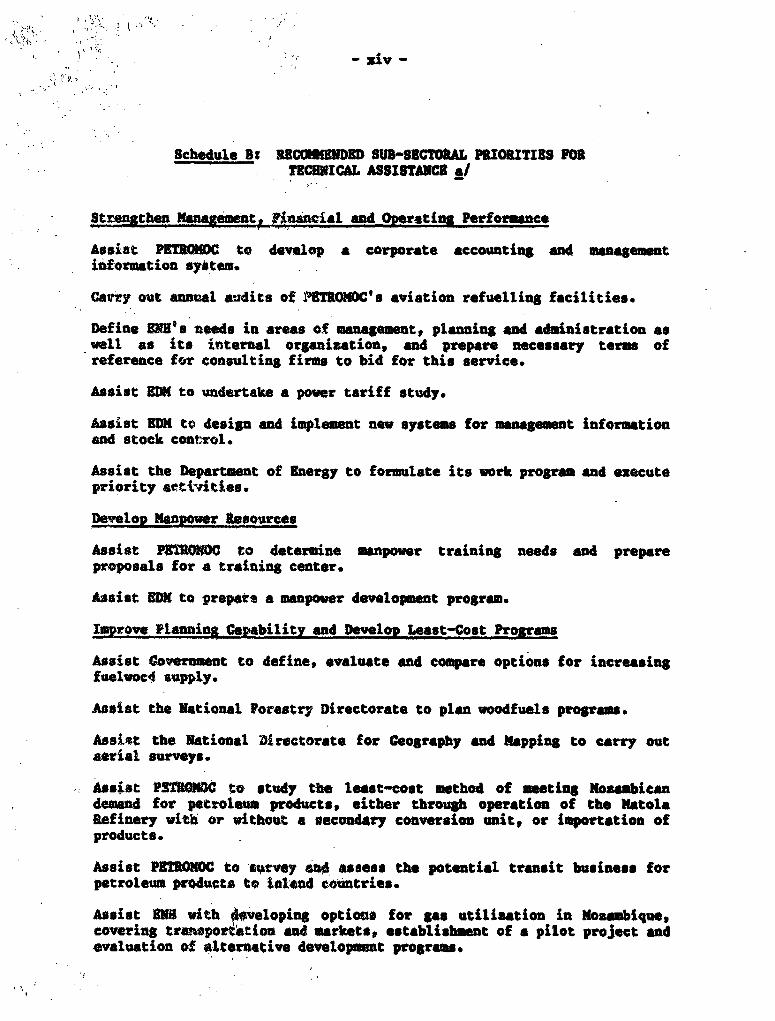

Schedule Bs RBCHMQSNDED SUB-SECTOftL PRIORITIES FORTECHNICAL ASSISTANCE */

Stgrengtben Management Financial and Overatins Performance

Assist PETROMC to develop a corporate accounting and managementinfcrumtion syitem.

Carry out annual audits of IMETRONOC's aviation refuelling facilities.

Define INK's needs in areas of managemnt, planning and administration aswell as its internal organisation, and prepare necessary terms ofreference for consulting firms to bid for this service.

Assist EDM to undertake a power tariff study.

Assist RDO to design and implement new systems for management iniormationand stock control.

Assist the Department of Energy to formulate its work program and executepriority act;b'ities.

Develop Mlaenpwr ftesoureas

Assist PSTRO WO to determine manpower training needs and prepareproposals for a training center.

Assist EDM to prepate a manpower development program.

Improve Flanni Capability and Develop Least-Cost Program

Assist Covernment to define, evaluate and compare options for increasingfuelvoc4 supply.

Assist the National Forestry Directorate to plan woodfuels programs.

Assist the National Dirctorate for Geography and Mapping to carry outserial surveys.

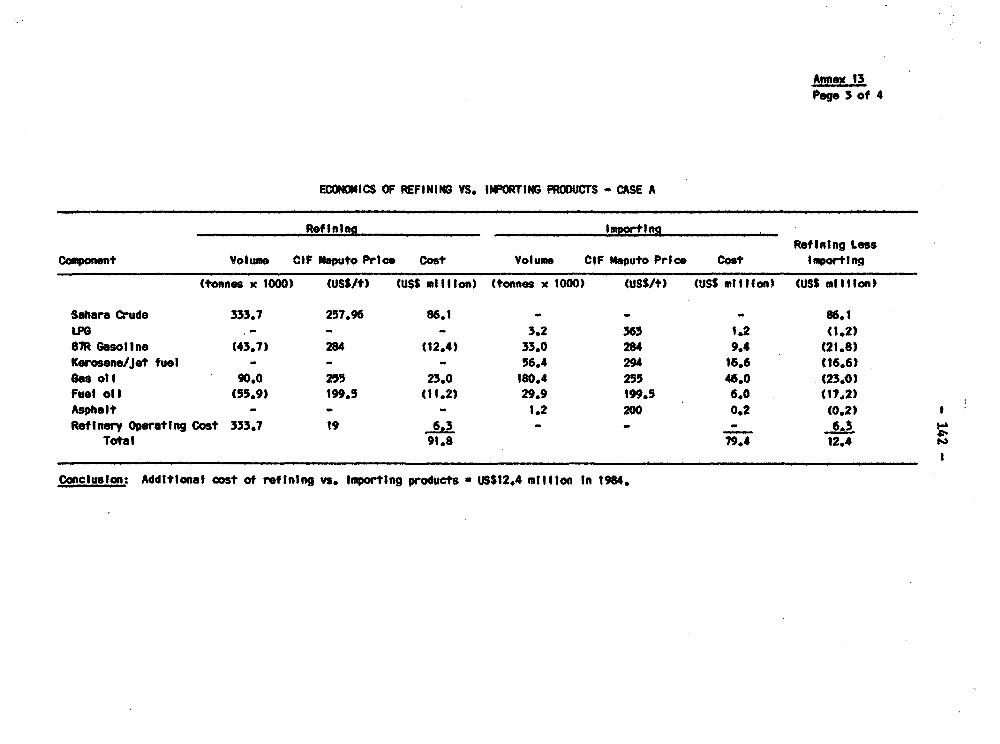

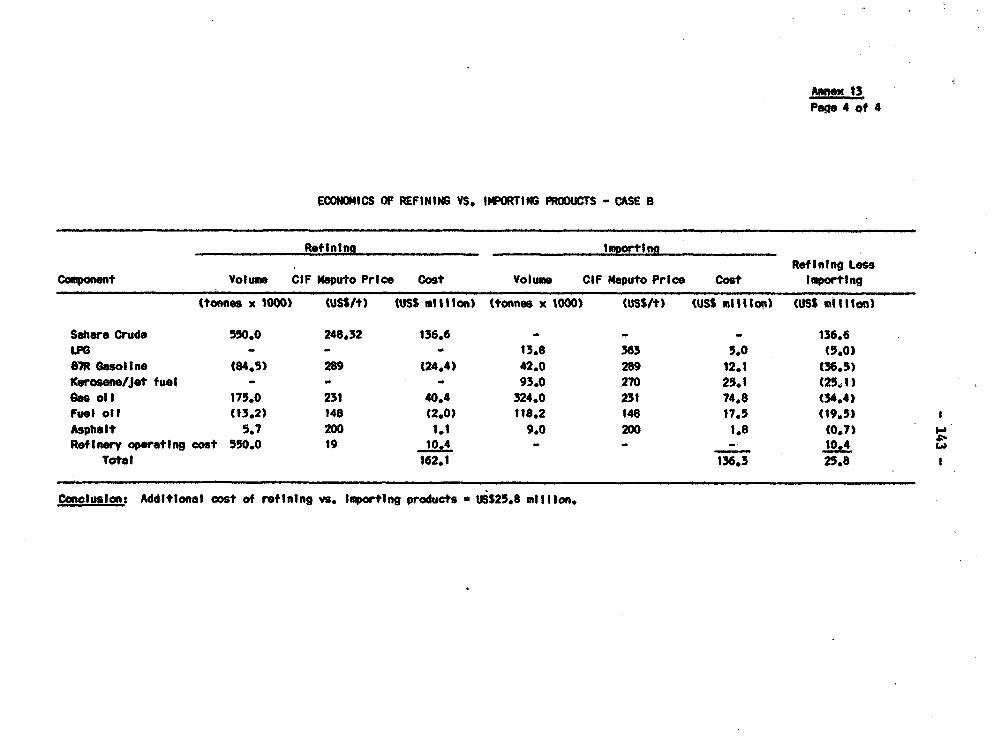

Assist PSTnOMWo to study th least-cost method of eeting Kos abicandemand for petroleum products, either through operation of the KatolaRefinery with or without a secondary conversion unit, or importation ofproducts.

Assist PETROMOC to stgrvey mo assess the potential transit business forpetroleum products to blotnd countries.

Assist BIP with 4veloping options for gSa utilization in Kozambique,covering tranwpo erion and markets, establishment of a pilot project andevaluation of alternative development programs.

- xv

Assist 5DM to establish a program for overhauling the standards fordistribution systems.

Assist EDM to evaluate the scope for extending electricity supply tourban households.

Assist EDM to evaluate the least-cost method of meeting demand for powerin 1DM's Southern Region.

Evaluate the power potentially available from conjunctive use of theKariba and Cabora Bassa complexes.

Assist CARBONOC to carry out a pre-feasibility study of therehabilitation needs of the Moatise coal mines.

Assist the Natural Geological Institute to carry out basic geologicalinvestigation and exploratory drilling for coal in Southern Noxambique.

Assist the Ministry of Industry and Energy to review the optionsavailable to Mosambique in international markets for the exploitation ofthe country's energy resources.

Assist the Ministry of Industry and Energy in studying various approachesto setting the prices of energy products under the prevailing distortionsin prices, wages and foreign exchange rate.

Assist the Ministry of Industry and Energy in identifying andimplementing economically justified measures for energy conservation,fuel substitution and the use of energy in rural communities.

a/ The estimated costs for the recommended technical assistance areincluded in the core investment program given in Schedule A.Outline terms of reference for some of the technical assistanceactivities are given in Annexes to this report, and the objectivesof some of the activities are sumuarised in the main text of thereport.

I. 8SCTOR OVRVIYD

Macro-economic Trends

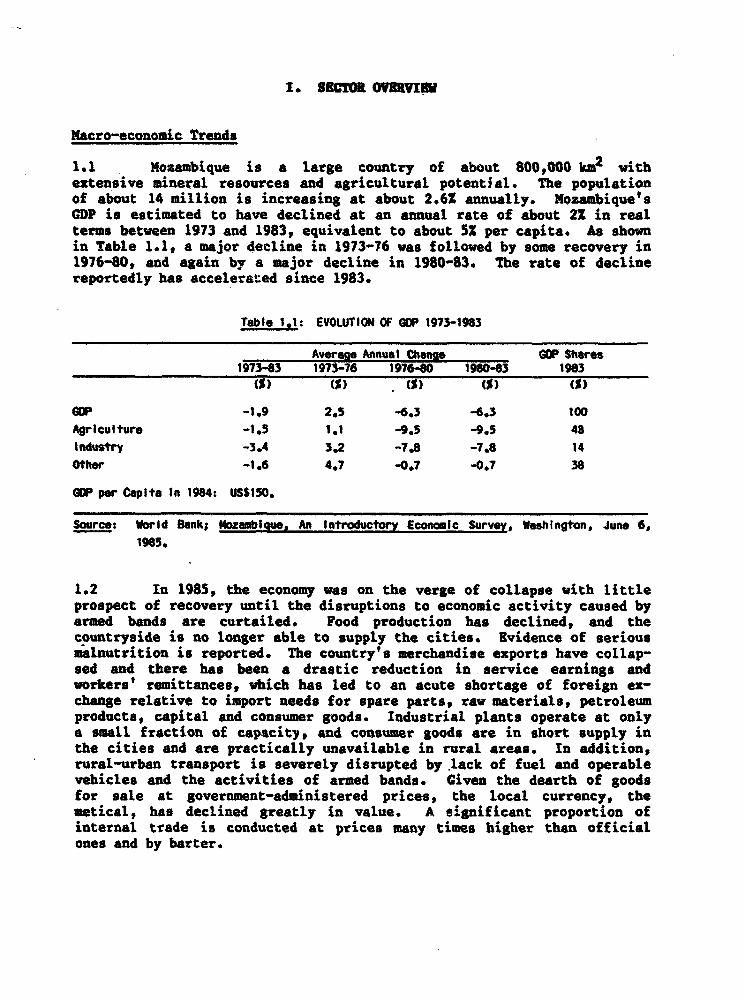

1.1 Mozambique is a large country of about 800,000 km2 withextensive mineral resources and agricultural potential. The populationof about 14 million is increasing at about 2.62 annually. Mozambique'sCDP is estimated to have declined at an annuAl rate of about 2X in realterms between 1973 and 1983, equivalent to about 52 per capita. As shownin Table 1.1, a major decline in 1973-76 was followed by some recovery in1976-80, and again by a major decline in 1980-83. The rate of declinereportedly has accelerated since 1983.

Table 1.1: EVOLUTION OF GOP 1973-1983

Averan4 Annua I Chang. GOP Shares1973-83 1973-76 1976-80 1980-83 1963'O) CS) (5) (5i) (5)

GOP -1.9 2.5 -6.3 -6.3 100Agriculture -1.5 1.1 -9.5 -9.5 43Industry -3.4 3.2 -7.8 -7.8 14Other -1.6 4.7 -0.7 -0.7 38

GOP per Capita In 1984: US$150.

Source: World Bank; Mozambigue, An Introductory Economic Survey, Washington, June 6,1985.

1.2 In 1985, the economy was on the verge of collapse with littleprospect of recovery until the disruptions to economic activity caused byarmed bands are curtailed. Food production has declined, and thecountryside is no longer able to supply the cities. Evidence of seriousmalnutrition is reported. The country's merchandise exports have collap-sed and there has been a drastic reduction in service earnings andworkers' remittances, which has led to an acute shortage of foreign ex-change relative to import needs for spare parts, raw materials, petroleumproducts, capital and consumer goods. Industrial plants operate at onlya small fraction of capacity, and consumer goods are in short supply inthe cities and are practically unavailable in rural areas. In addition,rural-urban transport is severely disrupted by lack of fuel and operablevehicles and the activities of armed bands. Given the dearth of goodsfor sale at government-administered prices, the local currency, themetical, has declined greatly in value. A eignificant proportion ofinternal trade is conducted at prices many times higher than officialones and by barter.

-2-

1.3 Pac%ors beyond Government's control have been instrumentat inthe decline of the economy. The main factors are the vacuum in skilledand semi-skilled manpower left by the mass exodus of Portuguese residentsin the mid 1970, various natural calamities, spreading of disruption byarmed bands since the early 19809 and the fall in revenues from transittrade and worker's remittances from the Republic of South Africa (RSA).However, the economic decline has also resulted from shortcomings inAovernment's economic and financial policies and institutionalweaknesses, especially the severe shortage of trained manpower.

Energy Resources

1.4 Mozambique has substantial energy resources which, have beenidentified fro exploration work undertaken largely since Independence toassist Government in the identification of investment opportunities.Hydroelectric potential is estimated at about 11,000 MW, of which onlyabout 2,200 NW have been developed. Coal deposits abound although provenreserves are only about 5 million tonnes and probable reserves areestimated at 82 million tonnes, but estimates of possible reserves exceed3 billion tonnes. On-shore gas has been discovered, and estimates ofdiscovered reserves vary between 0.4 TCF and 1.4 TCP. Many other areasare considered to be prospective for gas. Petroleum has not bendiscovered but several international oil companies have been exploring,mainly in off-shore areas. Existing forests are still substantial(19 million ha) even though they have been depleted during the last twodecades. The country's locational advantage for offering transitservices to inland countries also provides substantial potential fordevelopment. Good examples of the potential for transit tradt in thesector are the exports of coal and importation of petroleum products.

Overview of Energy in the Economy

1.5 Developments in the energy sector have been both cause and con-sequence of the depressed macro-economic situation. The sector agenciessuffer from institutional weaknesses and shortages of trained anpowerthat are endemic throughout the economy. Shortages of petroleum productshave contributed to a decline in production in many sectors, while thedepressed state of the economy has reduced the demand for energy. Thecollapse of exports and consequent dearth of foreign exchange areresponsible for the shortage of petroleum products, but there is excesssupply capacity of electricity at the national level when all supplyfacilities are in operation. The use of commercial sources of energy byhouseholds has been receding because of supply constraints, andincreasing reliance is being placed on traditional fuels. The lack offoreign exchange has reduced the supply of kerosene, and supplies during1985 and 1986 have been negligible. The activities of armed bands in thecountryside have constrained supplies of fuelwood, charcoal and evenelectricity, or made supply less ru'iable and more costly. Consequently,there are inadequate supplies of woodfuels to meet the urban demand.

-3-

1.6 In an average year of the early 1980s, the gross energy avail-able to Mozambique from all energy forms was About 3 million tofnes ofoil equivalent (T08) or roughly 250 kgoe per capita (of which about 80Xwas from woodfuels). This compares with about 560 kgoe for Malawi,470 kgo. for Tonmania, 760 kgoe for Zimbabwe, 350 kgoe for Uganda, and270 kgoe for Ethiopia. Mozambique's per capita energy consumption wasthus at the lower end of the average for Eastern Africa, although agreater share of total supply came from comercial sources. I1 Of the20S provided from commercial sources, 7O1 to 752 was from petroleum, 1Sto 202 was from primary electricity, and 51 to 101 was from coal.

1.7 In the early 1980s, the distribution of commercial energyconsumption on an oil equivalent basis in Nozambique was approximately271 in industry, 271 in transportation, 311 in households and publicinstitutions, and 151 in agriculture and other sectors. Consumption ofcommercial and traditional forms of energy together in households andpublic institutions averaged about 901 of national consumption. Inoverall terms, Nozambique required about 1.4 toe of energy per thousandUS$ of CDP, while for commercial energy only the intensity of consumptionwas about 280 kgoe per thousand US$ of GDP. Compared to some neighboringcountries, 2/ Mozambique requires more commercial energy (most of whichis importeds) relative to economic output, which possibly reflects acombination of differences in structure of demand and lower efficiency inenergy utilization.

1.8 Energy used to play a much larger role in the country's foreigntrade than it. does presently. Power exports from the Cahora Bassahydroelectric complex were reduced in 1981 and halted in 1984 due tosabotage to transmission lines at a cost to Mozambique in foregoneforeign exchange earnings of about US$8.4 million annually. Nationalcoal production is a fraction of its level in the late 19709 due to theseverance of transport links from the coal mines, and the country islosing about US$4 million annually in revenues from coal exports. 3/

1/ Commercial ene gy sources here mean electricity, petroleum, gas, andcoal, even though sizeable quantities of "traditional' fuels (mainlyfirewood and charcoal) are traded in markets for cash. Zimbabweconsumes a higher share of commercial energy, essentially because ofthe importance of mining and heavy industries.

2/ Comparable numbers for Tanzania are:- all energy sourcest 1.6 TOE per US$1,000 of GDP- commercial energy : 126 kgoe per n n "and for Ethiopia:- all energy sources: 1.8 TOE per US$1,000 of GDP- commercial energy s 116 kgoe per n n

3/ In 1985 total merchandise exports by Mozambique were aboutUS$70 million.

-.4-

Imports of crude oil have been replaced by imports of refined produActs,and the total volume and value of imported petroleum has declinedsubstantially from 1981 onwards. With the closure of the petroleumrefinery in Maputo, excess refined products ceased to be exported during1984. 4/

Energy Supply and Consumption

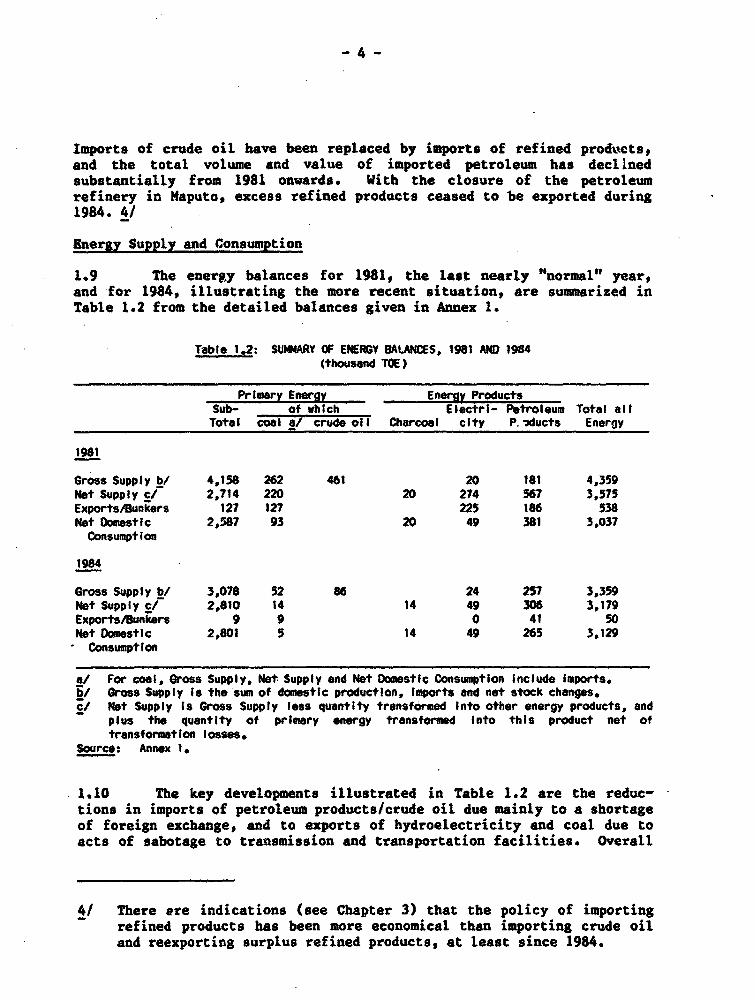

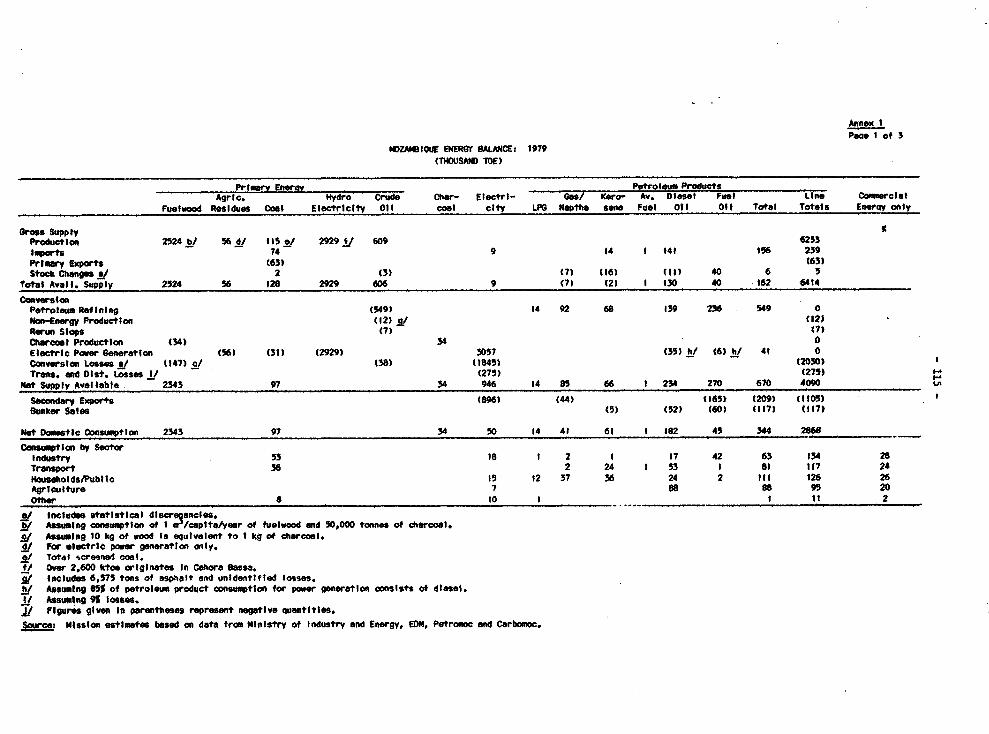

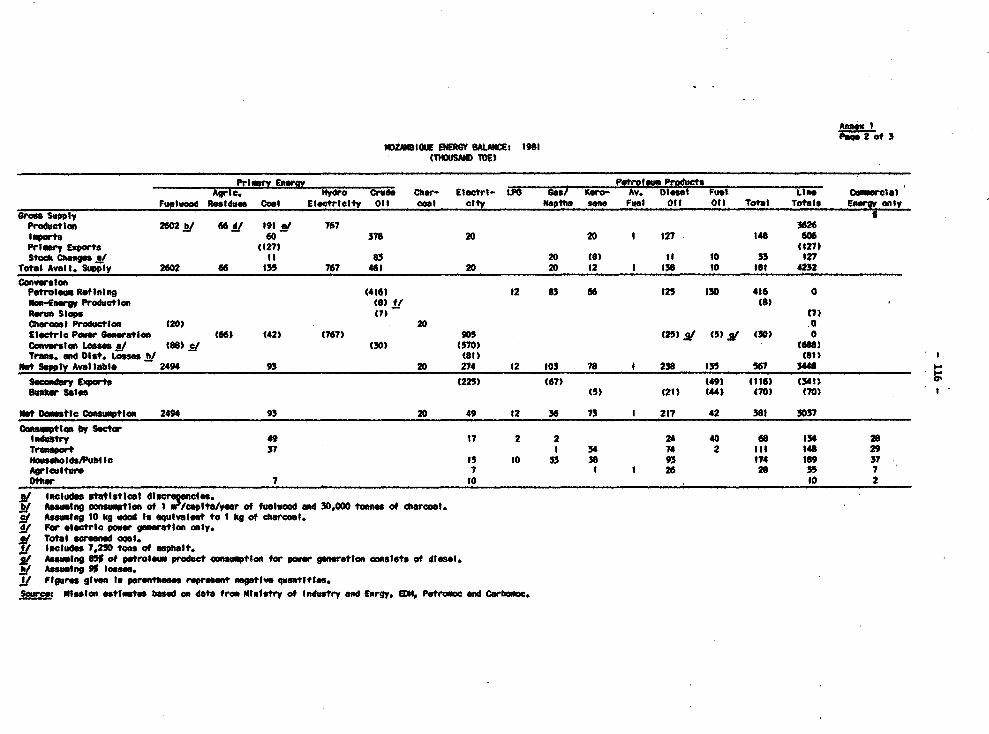

1.9 The energy balances for 1981, the last nearly "normal" year,and for 1984, illustrating the more recent situation, are summarized inTable 1.2 from the detailed balances given in Annex 1.

Table 1.2: SUOWARY OF ENEtGY BALANCES, 1981 AND 1984(thousand TOE)

Primary Energy Energy ProductsSub- of whIch ElectrI- Petroleum Total allTotal coal a/ crude oil Coarcoal city P.'ducts Energy

190?'

Gross Supply b/ 4,158 262 461 20 181 4,359Net Supply cl 2,714 220 20 274 567 3,575Exports/Bunkers 127 127 225 186 538Net Domestic 2,587 93 20 49 381 3,037Consumption

1984

Gross Supply b/ 3,078 52 86 24 257 3,359Net Supply c/ 2,810 14 14 49 306 3,179ExportsABunkers 9 9 0 41 50Net Domestic 2,801 5 14 49 265 3,129

Consumptlon

a/ For coal, Gross Supply, Net Supply end Net Domestic Consumption Include Imports.b/ Gross Supply Is the sum of domestic production, Imports and net stock changes.cl Net Supply Is Gross Supply less quantity transformed Into other energy products, and

plus the quantity of primary energy transformed into this product net oftransformation losses.

Source: Annex 1.

1.10 The key developments illustrated in Table 1.2 are the reduc-tions in imports of petroleum products/crude oil due mainly to a shortageof foreign exchange, and to exports of hydroelectricity and coal due toacts of sabotage to transmission and transportation facilities. Overall

4/ There are indications (see Chapter 3) that the policy of importingrefined products has been more economical than importing crude oiland reexporting surplus refined products, at least since 1984.

-5-

net 4omestic consumption of energy increased marginally assuming that percapita fuelwood consumption remained roughly constant as the populationincreased. As a result, it is estimated that traditional fuels accountedfor about 80Z of net domestic energy consumption in 1981 and 90% in 1984,a significant increase attributable mainly to the decline in consumptionof commercial fuels.

Woodfuels and Household Energy

1.11 Woodfuels are the main source of energy for households (thecategory with the largest consumption of energy), and nearly allwoodfuels- originate from natural forests and savanna-land around townsand villages. These resources are badly degraded and cannot sustainpresent levels of urban consumption in the long term. Deforestationaround the main urban areas will continue due to demand for woodfuels.The prices of woodfuels in urban markets are extremely high relative toofficial prices for other commodities and wages, causing major economicand social hardship. Further deterioration in the urban energy situationduring the next few years is unavoidable, and the major issue facingGovernment is the need to implement measures to reverse this trend assoon as possible.

1.12 On the national scale, consumption of fuelwood and smalldiameter poles in 1980 was estimated to be roughly equivalent to thenatural growth of the total standing volume of wood in the country. How-ever, the balance between supply and demand varied greatly over thecountry, with most of the population living in areas of woodfuelsscarcity. Government embarked on a program of fuelwood plantations inthe late 19709, investing about US$31.5 million. The results from theprogram have been poor due to unforeseen natural factors, inadequateplanning, preparation and management, and disruption by armed bands.

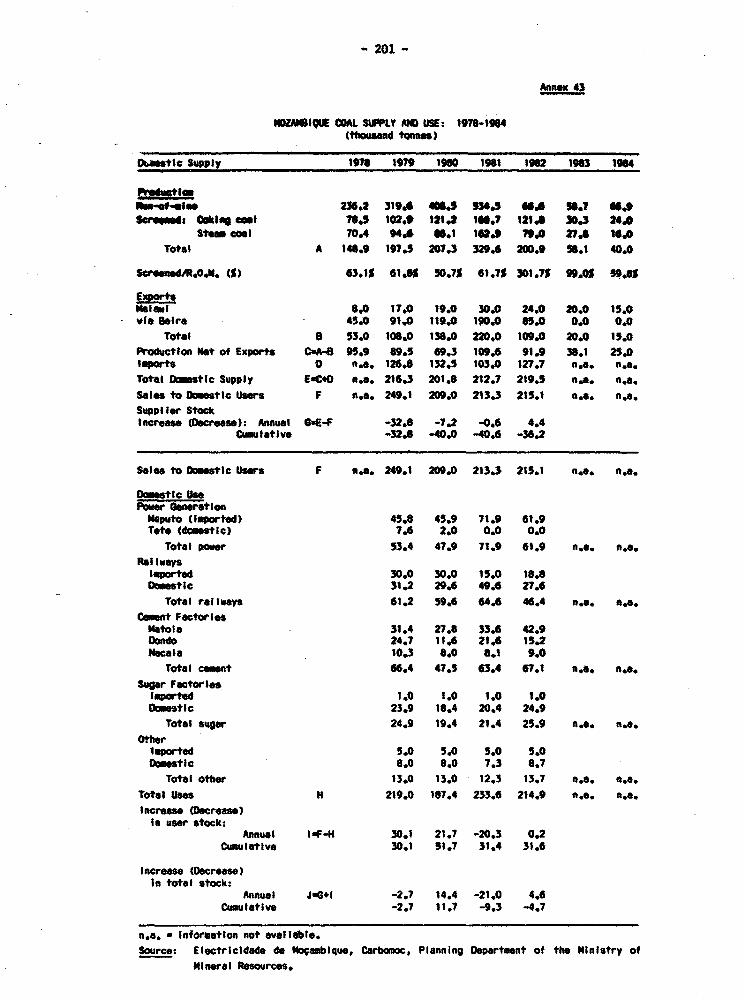

Petroleum and Gas

1.13 In an average year in the early 19809, petroleum supplied about751 of the commercial energy used in Mozambique. Consumption of petro-leum energy products fell by about 21Z over the period 1978 to 1985, from384,373 tons in 1979 to 303,820 tons in 1985. The structure of supplyhowever, changed markedly. Up to 1980, Mozambique refined sizeablequantities of imported crude oil (600,000-700,000 tpy), exported morethan 200,000 tpy of products (mostly gasoline and heavy fuels), andimported gas oil because of a mismatch between refinery yield compositionand the pattern of demand for products. 5/ In the most recent years, incontrast, crude oil imports were drastically cut (to 250,000 tons in1983, 86,000 t in 1984), while product imports rose substantially, from

5/ The historical pattern of demand, skewed towards gasoil and awayfrom gasoline, has also been partly the result of a policy ofkeeping gasoil prices much lower than gasoline prices.

-6-

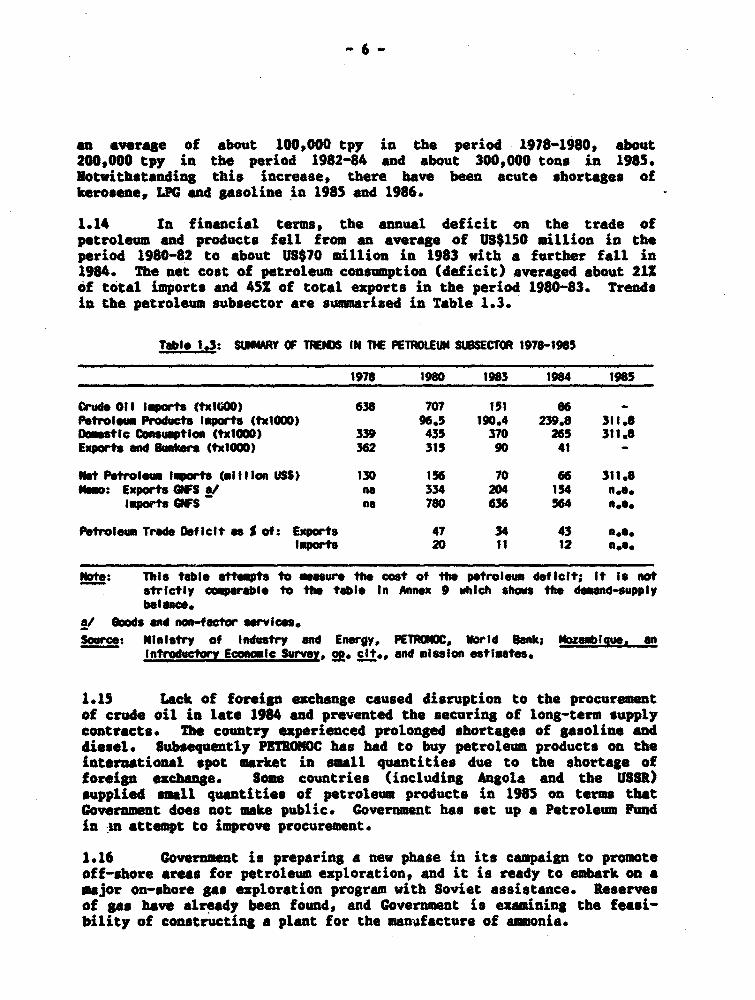

an average of about 100,000 tpy in the period 1978-1980, about200,000 tpy in the period 1982-84 and about 300,000 tons in 1983.Notwithstanding this increase, there have been acute shortages ofkerosene, LPG and gasoline in 1985 and 1986.

1.14 In financial terms, the annual deficit on the trade ofpetroleum and products fell from an average of US$150 million in theperiod 1980-82 to about US$70 million in 1983 with a further fall in1984. The net cost of petroleum consumption (deficit) averaged about 212of total imports and 45Z of total exports in the period 1980-83. Trendsin the petroleum subsector are summarized in Table 1.3.

Table 1.3: SUIIRY OF T1EN16 IN T1E PETRMOUM SUBSECTOR 1978-1965

1978 1980 1963 1964 1985

Coudroil Imports (txlCOO) 638 707 151 86 -Petroleum Products lpowts (txlOOO) 96.5 190.4 239.8 311.8Yomestic Consumption (txwIOo) 339 435 370 265 311.8Exports and Sunkews (txlOOO) 362 315 90 41 -

Not Petroleum Imports (millon USS) 130 156 70 66 311.8'_g: Exports GFS a/ na 334 204 154 n.a.

Imporfts NFS na 760 636 56 n.ea.

Petroleum Trade Deficit es £ of: Exports 47 34 43 na..Imports 20 11 12 n.o.

Note: This table ettempts to asesure the cost of the petroleum def let; It ts notstrictly cmoparable to the table In Annex 9 which shows the domend-supplybelance.

G/ oods and non-fector services.Source: Ministry of Industry and Energy, FETPROOC, World Sank; Nozambigue. an

Introductory Economic Sur"ey, g. i-t.. and mission estimates.

1.15 Lack of foreign e"change caused disruption to the procurementof crude oil in late 1984 and prevented the securing of long-term supplycontracts. The country experienced prolonged shortages of gasoline anddiesel. Subsequently P3TRONOC has had to buy petroleum products on theinternational spot market in small quantities due to the shortage offoreign exchange. Some countries (including Angola and the USSR)supplied small quantities of petroleum products in 198S on terms thatGovernment does not mke public. Government has set up a Petroleum Fudin nm attempt to improve procurement.

1.16 Covernmeut is preparing a new phase in its campaign to promoteoff-shore areas for petroleum exploration, and it is ready to embark on amajor on-shore gas exploration program with Soviet assistance. Reservesof gas have already been found, and Government is examining the feasi-bility of constructing a plant for the manafacture of ammonia.

Eloctric Power

1.17 Rlectri,idade de Mo9ambique (EDM) was created in 1977 and givenexclusive responsibility for the public supply of electricity includinggeneration, transmission and distribution. 3DM operates a considerablearray of facilities including about 250 HU of available generatingcapacity, 3,000 km of high and medium tension transmission lines, andthree grid systems. In addition, EDM has at its disposal up to 200 MI ofpower from Cahora Bassa as Mozambique's entitlement. Production fromDU's own facilities has oscillated around 300 GWh annually in the lastfive years, while anual consumption (served in part by imports) hasvaried between 600 and 650 CUh. The 2,075 MW Cahora Bassa hydroelectriccomplex and D.C. transmission link to Pretoria in the Republic of SouthAfrica (RSA) are owned and operated by Hidroelectrica de Cahora Bassa(ICB), an international public corporation owned by Portuguese interests(821) and the Government of Mozambique (18X). The status of the contractbetween MCB and the Electricity Supply Commission (ESCOM) of RSA greatlyaffects the price that 8DM pays for the power it receives from ES8OM. 6/

coal

1.18 There are three major, known coal deposits, all around Tete inthe western-central part of the country located at substantial distancesfrom the coast and the main domestic markets. Coal has been producedsince the 1940 from the Moatise underground mines near Tete. Productionof coal has virtually ceased with the cutting of the railway link betweenNoatise and Beira, impeding most domestic and export sales. Productionpeaked in 1981 at about 330,000 t (screened), of which 220,000 t/y wereexported and 110,000 tons sold domestically. In addition, Mosambiquenormally imports 120,000 tons of coal from RSA at very low prices tosupply the Maputo area. Domestic consumption averaged about 215,000 tpyin the period 1979-1982 7/ but has declined subsequently because ofdisruption by sabotage to coal transportation facilities from Moatize andthe general decline in economic activity.

1.19 The Government is investigating a major expansion in coalproduction capacity to an annual level of 6 million tonnes of saleablecoal in two trenches of 3 million tonnes. Implementation of these plonsdepends on the restoration of peaceful conditions in the country and

6/ lhen the supply contract is in force, EDM effectively "reimports"Cahora Bassa power via ESCOM's grid to supply Maputo; when the con-tract is not in force, as when the DC link is interrupted due tosabotage, 3DM imports power from ESCOM. The link has been out ofservice since 1984.

7/ The main coal users in Mozambique are the railwayst cementfactories, sugar mills and the Maputo Power Plant (which uses coalimported from RSA).

progress in arranging the huge amounts of finance for capital investrzentsin new mines, rehabilitation and upgrading of railway and portfacilities. 8/

The Institutional Framework for the Energy Sector 9/

1.20 The economy of Mozambique is managed through central plan-ning. Economic decision-making, including the allocation of resources,is highly centralized. The planning and administrative structure isstrictly hierarchical and is dominated by vertical linkages. The focusof planning has so far been the implementation of development projectsconsidered strategic to the country's development, establishing outputtargets, and allocating the corresponding requirements for inputs.Government intends to modify the system of economic management in thenear future to include the use of fiscal, monetary and pricing policiesin resource allocation. The official exchange rate massively overvaluesthe domestic currency, and the State has nearly total control of foreigntrade.

1.21 Central agencies are assigned exclusive responsibility for thedefinition of principles, objectives, norms, methods and procedures forthe allocation of resources, and for their implementation through controlof planning, budgeting, credit and prices. Within the framework of theCentral State Plan, these tasks are coordinated by the National PlanningCommission (which has formal responsibility for ensuring theintersectoral consistency of investments and the compatibility of pro-duction plans for enterprises with resource availability), the Ministryof Finance, the Bank of Mozambique, and the National Wage and PriceCommission. Sectoral ministries are responsible for the coordination andsubmission to these agencies of proposals made by the enterprises undertheir supervision regarding production targets, requirements for rawmaterials and spare parts and output prices, and for transmitting tothese enterprises the decisions of the central agencies on these matters.

8/ The estimated capital cost, excluding price escalation, of the fulldevelopment to 6 million tpy is about US$1 billion. Financing forthe first tranche of the mine development program has been securedfrom the USSR; France, Italy and Portugal are reportedly interestedin the second 3 million tpy tranche.

9/ The reviews of the institutional framework and of development andpolicy issues in this chapter are based on: World Bank; Mozsambique- An Introductory Economic Survey, June 6, 1985.

9

Policies and Investments in the Last Ten Years

1.22 Since the late 1970s, highest priority in the allocation ofresources has been given to implementing projects envisaged- in theProspective Indicative Plan. 10/ The Prospective Indicative Planenvisaged projects for the production of agricultural commodities,textiles, iron and steel, machinery, aluminium, gas, basic chemicals,coal, electr5.city and construction materials; dams, br^iges and roads;and oil exploration. Government's policy was to create the infra--structure expected to stimulate investment in productive capacity.Implementation of new investments during the years following Independence(on state farms and, since the late 1970s, on major development projects)has claimed the bulk of the available financial and quelified manpowerresources. The major electrification works are now almost complete, butthe envisaged associated agricultural and industrial developments havenot taken place. Investments in the energy sector (including fuelwood)since the late 1970s (based on data given in the Central State Plan)amounted to about US$335 million, or 20% of total investment expendi-tures.

1.23 Government's policy was established before armed bands startedto cause major disruption to the economy. However, shortcomings in theexecution of this policy have also been recognized as a contributoryfactor to non-fulfillment of the objectives. ll/ Some investments havebeen undertaken without a realistic assessment of the physical andfinancial resources available in the short to medium-term, or an adequateevaluation of the benefits and costs. These factors, aggravated by thedisruption caused by armed bands, have contributed to the critica! under-performance of these investments.

1.24 Existing installations and equipment have either deterioratedor been utilized below capacity because of poor management and lack ofraw materials, spare parts, maintenance and qualified manpower, andbecause of the focus on new investments. In addition, efficiency inresource use has been discouraged by pricing and credit policies.

1.25 Present prices, the most important of which are fixed orregulated by the Council of Ministers and the National Wage and PriceCommission (CNSP), reflect neither costs- of supply nor scarc;ty inrelation to demand. The price structure is highly distorted, between aswell as within sectors. Covernment has so far allowed the metical tobecome grossly overvalued, which has facilitated maintaining official

10/ Rep6blica Popular de Mocambique, "Linhas Fundamentais do PlanoProspectivo Indicativo para 1981-1990" (Maputo: Imprensa Nacionaln.d.).

11/ These shortcomings were openly discussed at the Fourth PartyCongress in 1°°

10 -

prices of petroleum products, electricity and coal at artificially lowlevels. While inflation has been substantial (about 30X/year between1983 and 1985), nominal wages and salaries have not changed for severalyears. However, wage bills have risen as a result of overemployment ofunskilled labor. The fall in real wages has discouraged the labor forceand promoted the emigration of semi-skilled and skilled workers. TheGo .trnment has attempted to stem the outflow of skilled personnel byissu-n- a new labor law (December 1985) that allows enterprises to offerwages and incentives to motivate and retain skilled personnel.

1.26 The failure of prices to cover the actual costs of the enter-prises has been accommodated through subsidies from the central budgetand credit from the banking system. Although subsidies are reportedlygranted only to enterprises of social, rather than economic, interest,other loss-making enterprises have obtained credit even when their repay-ment prospects were poor. Interest rates have not changed since 1980 andthey do not have an allocative role because credit is allocated withinthe framework of the Central State Plan.

1.27 The negative impact of these development orientations on theeconomy has been substantial. The impact of the financial, physical andparticularly, manpower constraints on one sector of the economy cannot beresolved in the context of that sector alone. Managing the transition toan economic system wbich includes fiscal, monetary and price policies inthe allocation of resources is a major task facing Government. Since theFourth Party Congress in 1983, the Government has undertaken somemeasures to address these problems, although the depth of the crisis andthe activities of armed bands will hinder recovery. It would go beyondthe scope of this Report to make recommendations on such generalissues. However, the Report does assess the impact of these issues onthe performance of the energy sector.

Energy Planning Issues