Mohammad Tahir Sabit Haji Mohammad , (2015) "Theoretical and trustees’ perspectives on the...

39

Humanomics Theoretical and trustees’ perspectives on the establishment of an Islamic social (Waqf) bank Mohammad Tahir Sabit Haji Mohammad Article information: To cite this document: Mohammad Tahir Sabit Haji Mohammad , (2015),"Theoretical and trustees’ perspectives on the establishment of an Islamic social (Waqf) bank", Humanomics, Vol. 31 Iss 1 pp. 37 - 73 Permanent link to this document: http://dx.doi.org/10.1108/H-05-2013-0032 Downloaded on: 07 February 2015, At: 20:00 (PT) References: this document contains references to 66 other documents. To copy this document: [email protected] The fulltext of this document has been downloaded 44 times since 2015* Users who downloaded this article also downloaded: Professor Masudul Alam Choudhury, Farhana Mohamad Suhaimi, Asmak Ab Rahman, Sabitha Marican, (2014),"The role of share waqf in the socio-economic development of the Muslim community: The Malaysian experience", Humanomics, Vol. 30 Iss 3 pp. 227-254 http:// dx.doi.org/10.1108/H-12-2012-0025 Professor Masudul Alam Choudhury, Muhammad Abbas, Rayan S Hammad, Mohamed Fathy Elshahat, Toseef Azid, (2015),"Efficiency, productivity and Islamic banks: an application of DEA and Malmquist index", Humanomics, Vol. 31 Iss 1 pp. 118-131 http://dx.doi.org/10.1108/H-03-2013-0022 AbulHasan M. Sadeq, (2002),"Waqf, perpetual charity and poverty alleviation", International Journal of Social Economics, Vol. 29 Iss 1/2 pp. 135-151 http://dx.doi.org/10.1108/03068290210413038 Access to this document was granted through an Emerald subscription provided by 581774 [] For Authors If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service information about how to choose which publication to write for and submission guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information. About Emerald www.emeraldinsight.com Emerald is a global publisher linking research and practice to the benefit of society. The company manages a portfolio of more than 290 journals and over 2,350 books and book series volumes, as well as providing an extensive range of online products and additional customer resources and services. Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation. Downloaded by UNIVERSITI TEKNOLOGI MALAYSIA At 20:00 07 February 2015 (PT)

Transcript of Mohammad Tahir Sabit Haji Mohammad , (2015) "Theoretical and trustees’ perspectives on the...

HumanomicsTheoretical and trustees’ perspectives on the establishment of an Islamic social(Waqf) bankMohammad Tahir Sabit Haji Mohammad

Article information:To cite this document:Mohammad Tahir Sabit Haji Mohammad , (2015),"Theoretical and trustees’ perspectives on theestablishment of an Islamic social (Waqf) bank", Humanomics, Vol. 31 Iss 1 pp. 37 - 73Permanent link to this document:http://dx.doi.org/10.1108/H-05-2013-0032

Downloaded on: 07 February 2015, At: 20:00 (PT)References: this document contains references to 66 other documents.To copy this document: [email protected] fulltext of this document has been downloaded 44 times since 2015*

Users who downloaded this article also downloaded:Professor Masudul Alam Choudhury, Farhana Mohamad Suhaimi, Asmak Ab Rahman,Sabitha Marican, (2014),"The role of share waqf in the socio-economic development of theMuslim community: The Malaysian experience", Humanomics, Vol. 30 Iss 3 pp. 227-254 http://dx.doi.org/10.1108/H-12-2012-0025Professor Masudul Alam Choudhury, Muhammad Abbas, Rayan S Hammad, Mohamed FathyElshahat, Toseef Azid, (2015),"Efficiency, productivity and Islamic banks: an application of DEA andMalmquist index", Humanomics, Vol. 31 Iss 1 pp. 118-131 http://dx.doi.org/10.1108/H-03-2013-0022AbulHasan M. Sadeq, (2002),"Waqf, perpetual charity and poverty alleviation", International Journalof Social Economics, Vol. 29 Iss 1/2 pp. 135-151 http://dx.doi.org/10.1108/03068290210413038

Access to this document was granted through an Emerald subscription provided by 581774 []

For AuthorsIf you would like to write for this, or any other Emerald publication, then please use our Emeraldfor Authors service information about how to choose which publication to write for and submissionguidelines are available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comEmerald is a global publisher linking research and practice to the benefit of society. The companymanages a portfolio of more than 290 journals and over 2,350 books and book series volumes, aswell as providing an extensive range of online products and additional customer resources andservices.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of theCommittee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative fordigital archive preservation.

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

*Related content and download information correct at time ofdownload.

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

Theoretical and trustees’perspectives on the

establishment of an Islamicsocial (Waqf) bank

Mohammad Tahir Sabit Haji MohammadDepartment of Real Estate, Faculty of Geoinformation and Real Estate,

Universiti Teknologi Malaysia, Johor Bahru, Malaysia

AbstractPurpose – This paper aims to present an alternative to current banking systems. The purpose of thepaper is the optimisation of the concept of cash waqf and its management in the framework of a waqfbank and its viability.Design/methodology/approach – The study is doctrinal and empirical. Several assumptionsconcerning the structure and operation of the bank are made, surveyed and descriptively analysed.Findings – The concept of cash waqf could be used for the operation of a waqf bank. There was atendency among the given group of practitioners towards a corporate international social bank,capitalised by the waqf and non-waqf assets, sought after from the public and private sectors, as well asthe Muslims and non-Muslims.Research limitations/implications – Assumptions are basic. Empirical findings are based on theperspective of waqf trustees. Other stakeholders’ perspectives need further research.Practical implications – The study is expected to persuade for, and assist in the establishment of awaqf bank.Social implications – This paper could contribute to the effectiveness of waqf institutions in theirdelivery of public good to the poor and society. These implications are not restricted to a specificcountry. Charities and the poor of any society may benefit from this study if the idea of total socialbanking is upheld.Originality/value – This study is the first to address the structure and operation of a waqf bankempirically.

Keywords Microcredit, Cash waqf, Social bank, Socioeconomic development

Paper type Research paper

IntroductionThere is worrying gap, 30-60 on the Gini coefficients (HDR, 2009), between the rich andthe poor globally, particularly in the Islamic world, despite various efforts made by theinternational community and the existence of various banks. Out of 104 countries, abouta billion people live in multidimensional poverty. There are 1372.8 million poor (UNDP,2001; Hassan, 1999), 915 million people live in hunger (FAO, 2010) and half a billionpeople live in urban slums (UN-HABITAT, 2003). To escape from such a state of gloom,the man in the street will need financial assistance. Banks, however, work for thewell-to-do, and the micro-financing entities are controversial (Morduch and Haley, 2002;Amin et al., 2003; Roodman and Morduch, 2009; Young, 2010) or accused of

The current issue and full text archive of this journal is available on Emerald Insight at:www.emeraldinsight.com/0828-8666.htm

Establishmentof an Islamicsocial (Waqf)

bank

37

HumanomicsVol. 31 No. 1, 2015

pp. 37-73© Emerald Group Publishing Limited

0828-8666DOI 10.1108/H-05-2013-0032

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

hyper-profits (Mishra, 2006; Vakulabharanam, 2005; Mitias, 2009). Developmentprograms in the rich countries, too, are problematic (Grodach, 2011), and those in theThird World economies, carried out by the International Monetary Fund and the WorldBank, have a negative impact on poverty (Dreher, 2006; Easterly, 2010). This begs forsocial capitalism.

As poverty in Islamic countries is more serious, an Islamic social bank could be asolution to alleviate poverty. Such a bank can be perceived to be a controlled,interest-free and non-profit waqf institution (charity), dedicated mainly to thesocioeconomic welfare of the community, with special attention to providingmicro-financing and economic development for the poor and the under-privileged. Theimmediate benefit of this bank would be to enable waqf institutions to create wealth andhave access to adequate liquid funds for financing the development of waqf properties,and to finance and participate in major socioeconomic projects. It may also serve as anincome-generating arm of the waqf institutions, a social banking enterprise and analternative to privately owned micro-financing (Ahmed, 2007) and private banks orfinancial institutions.

The author looks at the Islamic solutions, namely, the duty of giving alms (zakat),optional charities and fiats, for the redistribution of wealth. It is said that:

[…] [p]rograms that make poverty reduction an explicit goal and make it a part of theirorganisational culture are far more effective at reaching poor households than those that valuefinance above all else (Hassan, 1999).

Accordingly, however, the indigenous Islamic charitable trust (hereafter referred to aswaqf), an income-generating charity with “some bank-like features” (Kuran, 2005),which is an empowering tool for Muslims and non-Muslims alike, also has inadequatefunds; its properties are predominantly illiquid while very few are productive. Many ofsuch properties face ruin and dilapidation. Overall, the trust is not only incapable ofsustaining itself as one can wish for, but it is also unable to effectively and universallysolve the abovementioned problems. Nevertheless, this tool is “valuable” (Kahf, 1998), asit has the potential of shaping the future of microcredit and sustainable development, ifthis idea is explored, examined and developed further. This paper focuses on such anexamination.

The social bank can create adequate liquid wealth and make it available for financingthe development of waqf properties, as well as various other socioeconomic projects. Aconventional bank earns by collecting deposits, granting loans, providing liquidity andtransferring funds and payment system, selling insurance and investment products andstock broking (Peng, 1998). They also charge transaction fees on financial or overdraftservices and earn interest on lending. Islamic banks do earn in the same way but avoidusury, uncertainty (gharar), gambling and investment in prohibited businesses. A socialbank would do business in the same way as a conventional bank, but it would complywith the rules of waqf. It can be a strong source of income to waqf institutions. Theincome from services, fees and investment will enable the waqf institutions to developwaqf properties and participate in even more social welfare and microcredit andfinancing projects. However, the fundamental question is whether or not such a bank isviable.

In light of the above question, this paper focuses on two issues: the possibility of awaqf bank from perspective of Islamic law, and the likelihood of the Islamic social bank

HUM31,1

38

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

from perspective of the practitioners entrusted with managing waqf properties. In thefirst part, the author argues on the basis of Islamic law and its jurisprudence attemptingto deduce a general idea about the viability of a waqf bank. Few assumptions are madeabout possible organisational and management of the bank. In the second part of thispaper, results of a preliminary survey are given which can add a minimum rate ofcertainty, given that the survey was conducted among a group of eight state officerswho used to deal with day-to-day affairs of waqf.

The paper begins with the literature review, theoretical discussion on the viability ofwaqf bank, followed by the discussion on its likelihood according to a select group ofpractitioners.

Literature reviewNo comprehensive literature about the validity of waqf bank and its establishment hasbeen advanced yet. Previous waqf studies, in the field of economics and financing(Zarqa, 1994; Sabit and Abdul Hamid, 2006; Magda, 2009), have focused on technicallysound solutions for financing the development of waqf properties and their investment,the success of which depends on geo-religious tendencies. These solutions presuppose agreat number of non-existent, income-generating fixed properties. Other stream in thesame field has focused on cash waqf (Magda, 2009; Cizakca, 2004a, 2004b; Mannan,2000) and its investment methods. Few went further by proposing waqf funds (Cizakca,2004a, 2004b; Zuhaili, 2004), and a benevolent-lending bank (Zuhaili, 2004; El-Gari,2004). Generally, they looked at waqf as a tool to use it for fixing the conventionalfinancial and micro-financing systems. However, these studies provide neithersufficient details nor effective solutions for dealing with under-developed andabandoned waqf properties, as well as illiquid and inadequate waqf assets.Consequently, there is still more to be explored to make the waqf institutions participatein a large number of diverse welfare projects of the community.

This paper is the extension of the above thought, as it builds on the old Islamicpractice of socioeconomic welfare and entrepreneurship, which provides an example forZahra et al. (2009) theory of maximisation of total wealth creation. The paper joins theidea of cash waqf and waqf bank which will enable waqf institutions to use waqf andnon-waqf funds for the development of its own properties on one hand and for providingthrough the bank affordable microcredit and microfinance to the unbankable class of thecommunity on the other. Such an Islamic social bank will be different from the existingprivately owned micro-financiers and socially responsible investment houses. Theproposed bank cannot follow the various micro-financiers and socially responsibleinvestment models of Yemen, Bahrain, India, Bangladesh and England. Unlike waqffunds, conventional institutions are private and pay for the costs of their capital. Thesecosts are then transferred to consumers. Even the private corporate Islamic Social Bankof Bangladesh is profit-optimizing organisation that collects and manages cash forcharitable purposes. However, it is only part of the bank’s business and does not shareprofits with waqf institutions. One can consider it fulfilment of a part of corporate socialresponsibility (CSR) of the bank that benefits the bank. Although it is substantiallyowned by charitable foundations, and manages their “cash revenues and expenditures”(Vakifbank Annual Report, 2009), the non-profit VakifBank of Turkey, is not intendedas a model because it is an interest-based state-owned institution. Social banking, i.e. theCharity Bank and the Industrial Common Ownership Finance of England may be

39

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

similar to the proposed waqf bank in some aspects, but they would have fundamentaldifferences. These institutions accept, with or without interest, deposits from variousparties and lend it with interest to groups who otherwise would be unqualified to getfinance for lack of collateral, predominantly charities (Buttle, 2007). Depositors may ormay not have the intention of pursuing social or ethical objectives and some may notexpect the suboptimal financial performance of their investment (Renneboog et al.,2008). The waqf bank if established, therefore, may share some aspects of theseorganisations, however, it has to be entirely non-usurious, which may lend toindividuals, as well as institutions including charities, Islamic or otherwise. The capitalof the bank, investment deposits, and the disbursement of the funds would make waqfbank clearly different from British social banking in various aspects. Put it differently,waqf bank needs to be founded on the fundamental principles of waqf first. This isexplored in the next sections.

TheoryBecause this paper relates to pro-poor financing alternative, it is vital to look at thegeneral framework of poverty eradication in Islam, the role of waqf (charitable trust) andits central theme to justify the creation of waqf bank. This is necessary because for apracticing Muslim, religious legitimacy is a precondition for stepping in any act ofsocioeconomic significance, especially charity. Therefore, this section includes thegeneral framework of poverty eradication in Islam, the role and objective of waqf, i.e.pro-poor assistance and finance, the permissibility of cash waqf and other forms ofliquid properties, and the advantages of cash waqf. Accepting the validity of cash waqfis considered to pave way for the validity of waqf bank in Islamic law. The legalframework of a waqf bank, its structure including the ownership, the capital and itsmanagement follows this.

The Islamic framework of poverty eradication and the role of waqfThe Quran pronounces that there should not be perpetual distribution of wealth amongthe rich in the society (see Chapter 59: verse 7). This presupposes the recognition anddivision of a community into rich and poor, the recognition of the ills of poverty, the needfor its eradication, the strategy for its alleviation and enforcing it. Hence, Islam treats theill of poverty through the proper belief system, causing Muslims to be responsible fortheir individual economic empowerment, responsible partnership between individualsand the State, responsible private ownership and compassionate management of publicresources, which would lead to the modest transfer of wealth to the poor sometimes fromthe rich and other times from the State.

Al-Quran, chapter 13, verse 11, enjoins Muslims to strive for individual economicempowerment, to be the drivers of their own spiritual and economic developmentwithout which their misfortunes could persist[1]. Disregard for material gains is notencouraged, and, at times, it may lead to a sin. This is so because it may result in aself-inflicted death[2], regret and so forth[3] or a total dependence on others.

To uplift themselves, Muslims have to follow the guidance of al-Quran, andal-Sunnah (al Quran, 59:7). As Islam rejects the scarcity of resource (15: 19-21) for Allahhas created no creature without providing its sustenance (11:6), individuals do not haveto be restrained by such a thinking, and instead need to seek them through work andeffort. The Holy Quran enjoins Muslims to seek the grace of Allah by earning through

HUM31,1

40

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

trade and labour (al-Quran, 59:8, 62:10, 67:15; al-Bukhari, Hadith No. 1,470, 1,471, 2072,2073; al-Muslim, Hadith No. 1,042, 2,379). It is the duty of a Muslim to seek his ownlife-sustenance means within the legal framework provided by al-Quran and al-Sunnah.

As understood from the Quranic concept of istikhlaf (vicegerency) (2:30; 6: 165; 35: 39;24: 55), individuals and the State are enjoined to manage land resources responsibly thatis to seek such resources, enjoy them and dispose them within the Islamic framework ofjustice. Responsible management of land resources by an individual and the state inaddition to personal sustenance of an individual also includes care for the present andfuture generations. Individuals and the State are having the duty to consumemoderately and assist the poor of their generation, thus creating a partnership betweenpublic and private sectors for the eradication of poverty. Both have to manage theresources under their control justly and in belief that God Almighty has created them inabundance (15: 19-21) and being sufficient for the survival of all creatures (11: 6)including men.

In the context of individual and State partnership, individuals have to fulfil theirobligation of zakat and other pro-poor atonements or expiations. Not only this, butfurther, al-Quran (59:10) has praised those who had donated their property to others,preferring them over themselves and even when they needed it the most. These includevoluntary alienation of one’s own property to the poor and needy through sadaqat andawqaf. The State has been enjoined to be the custodian of the resources and to distributeanfal, baitul mal assets and virgin resources justly (land alienating grants andreservation of it for the benefit of the poor). This makes it the duty of the State to planeconomic empowerment of the masses, according to the three levels of Shariahobjectives, whereby it can fairly allocate resources for a particular poor-friendlydevelopment activity and create employment opportunities for them.

The aforementioned framework implies the rights of poor and needy in the statetreasury on one hand and the spiritual duty of care to other individuals[4], and to begenerously kind to them out of love to Allah (swt)[5]. This is based on other Islamicconcepts, which are mentioned below.

Morally, there is unity between spiritual and economic development, and betweenindividuals[6] and the community[7]. Individual restriction or responsibility, towardshimself, family, community, being local or international, is discharged through thefreedom to perform it in disregard for material self-interest, and thus help others receivespiritual good and, economic independence from others, family, community or the state,through labour, trade and investments[8]. In Islam, disregard for material gains in thecourse of discharging one’s spiritual responsibility is relatively more appreciated if thedisregard for material gains is spent for the economic and spiritual good of one himselfand other fellow members of the community[9]. It is spiritual for one to decently sustainhis livelihood; it is also spiritual to assist others to live and sustain their life with dignity.This creates a determined productive agent moving forward the engine of economicdevelopment, for his own interest and for the well-being of others, without expectingmonetary reward, recognition and admiration. The sense of responsibility and freedomof an agent not only make him altruist[10] but also less consumptive[11].

Morally and legally, transactions involving work, labour, trade, investments and thelike form the economic system of Islam, coupled with altruism being mandated,recommended and promoted. If these principles are achieved, it will help the poor havefair access to economic growth, and they are not marginalised and exploited by those

41

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

who could dominate them. Altruist participation in market activities is not just a legalduty but also means to achieve the pleasure of God the Almighty. Thus, one should entertransactions while upholding taqwa (righteousness), respecting the rights of others(huquq al-ibad); doing justice and being fair (adl); and avoiding usury, betting, fraud,misrepresentation, and other forms of deceit. Additionally, one has to fulfil themandatory infaq (various forms of regular and irregular charity), give sadaqa to thosewho ask for and to the deprived. On top of that, one has to do ihsan (doing good withoutbeing asked for) ta’awun (aid, and cooperation), contribute to takaful (mutual security)and justice. Each of these principles has their own subsidiary rules, the explanation ofwhich is beyond the limits of this paper.

Putting it plainly, the Islamic framework, for removing poverty and creatingsustainable community, among others, emphasises on two inner grids and two exteriormeasures. The former includes individual motivation to work and recommendation ofmodest living. The two exterior measures are assistance of the poor and needy throughprivate property (i.e. zakat, waqf and others) and allocation of public resources by statefor the same reasons so that there “will not be a perpetual distribution among the richfrom among” members of society (al-Quran, 59:7). In either case, the man has toremember Allah, and fear him (see al-Quran, 62: 10; 59:8).

Among the redistributive measures for the eradication of poverty, Islam providedzakat, kafart, qard hasan and sadaqat. The former is consumptive in nature and thelatter may include sustainable measures for eradication of poverty, as discussed below.

Waqf as a sustainable poverty eradication toolThe beauty of waqf is that it provides support to the poor and needy in a sustainablemanner, and its main contributors are the concepts of perpetuity and inalienability.Other subsidiary and unrealised aspect of its sustainability is the capability of waqfasset to generate or regenerate income or capital. Both are significant today and forever.Hence, constant work is needed to enlarge the scope of income generation of waqf assets.This work is an attempt to that direction.

The sustainable nature of waqf is clear from its inception in Islam. Most of awqafduring the time of the Prophet (p.b.u.h.) and during the time of his companions werelanded properties. These according to al-Khassaf (261 AH) included orchards, lands,buildings and water well and fountain. There were also moveable properties such as warequipment and animals[12].

There is no specific verse about waqf in the Quran; it is, however, one of the charitiesthat might be understood from Quranic verses regarding infaq and sadaqt (3: 92; 2: 177).This is clear and confirmed by the saying of the Prophet (p.b.u.h.): “A man’s work endsupon his death except for three things: on-going charity (sadaqah jariyah); acontribution to beneficial knowledge; and faithful child”[13]. Ongoing charity issustainable, as it can be illustrated by the hadith of Ibn Umar: the Prophet of Islam(p.b.u.h.) said to Umar: retain the corpus [of the land] and let its fruit (income) [for thepoor and the needy][14]. This hadith, therefore, has created a habs, as expressed by theProphet, or waqf, as known today […] to be a self-reliant, sustainable, charitable trustentity. Unlike object given under other Islamic redistributive ideas i.e. zakah, sadaqat,kafart and qard hasan, waqf properties remain charitable assets throughoutgenerations. This is so because it is perpetual, irrevocable and is not subject to transferor transmission. Thus, it is capable of generating income to sustain itself […] and to

HUM31,1

42

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

provide direct assistance to the poor and the needy, under the supervision of anappointed trustee, court, state and other entities. Both real-estate waqf and cash waqfwere utilised for the above function.

The geopolitical events in the Islamic world after the eighteenth century and theadministration of Islamic trusts by the state[15], especially in occupied territories, hadcertainly dented their utility (Cizakca, 1998). With the demise of colonial era, Muslimscholarship and some states have revived it, but attention was predominantly paid toreal-estate waqfs. The idea of cash waqf has not been enthusiastically pursued becauseof the controversial nature of such waqf (Cizakca, 1998) until recently, when its potentialwas emphasised on either as remedy to the ills of Islamic banking (Cizakca, 1998, 2004a)or as independent welfare and financial assistance provider. For this reason, thejustification of cash waqf, not only for its validity in Islamic law but also for thedevelopment of such an idea into future Islamic financial institutions, is still relevant.

The permissibility of cash waqf and other liquid assetsCash waqf is the best means of income generation and capital growth for awqaf. It istherefore instrumental in the creation of sustainable communities. However, for somereasons, it has remained controversial throughout centuries. This is because of the factthat there is no express text in the Quran or sunnah enjoining or prohibiting cash waqf.The lack of express text in the two main sources of Islamic law, therefore, has moved theearly scholars to allow or prohibit cash waqf based on principles of analogical reasoning(qiyas). This paper relies on the opinions of those who permitted cash waqf, consideringcash as moveable property, categorised as comparable (mithli) asset and used forlending and trade.

The main text of Shariah (i.e. the Sunnah) allows moveable property (Sabit et al.,2006) as the object of waqf. Few classical jurists recognise cash waqf among them,provided that it is used for loans or investment (Bukhari, 256 A. H.; Ibn Humam, 861A. H.; Ibn Abidin, 1252 A. H.; Ibn Taymiyah, 728 A. H.; Dunya, 2002). Somecontemporary scholars did so because it is in the interest of the waqf, its beneficiariesand the society. The Shafi’i School is less inclined to allow cash waqf (Dunya, 2002),despite a report from Imam Shafi’i to the contrary (Mawardi, 450 A. H). Nevertheless, theprinciple that a waqf object shall be capable of recurrent benefit or use (Khatib, 968 A. H.;Nawawi, 676 A. H.) in the school can justify the validity of cash waqf if used forinvestment and loans. As such, it can have both perpetuity and recurrent use (AbuZahrah, 1971; Ibn Abidin, d. 1252 A. H.). The Hanafis considered the cash waqf to beused in mudarabah trade, the income of which to be distributed among the beneficiaries(Ibn Humam, 861 A. H.; Ibn Abidin, 1252 A. H.; Ibn Nujaim, 970 A. H.). The Maliki andHanbali schools reportedly recognised cash waqf for the purposes of loans andinvestment (Dirdir, 1201 A.H.; Ibn Taymiyah, 728 A. H). These opinions leave no roomfor alleged usurious piety (Mandaville, 1979) of the Ottoman period that seems to besomething similar to bai’ al-wafa or istiqlal, as Cizakca (1998) has called it[16].

Contemporary jurists agree with the rule on permissibility of cash waqf (Abu Zahrah,1971; Fatwa 140(6/l5) 11/3/, 2001; Tabtaba’i, 2003), for the purpose of loans andinvestment (Tabtaba’i, 2003; El-Gari, 2004). They go further by allowing it forinvestment in banks and bonds (Dawwabah, 2005; Sabit and Abdul Hamid, 2006;Dunya, 2002; Zuhaili, 2004). Although recognised early, (Arnawut, 2005; Cizakca, 1998,2004a; Dunya, 2002; Sabit et al., 2006; Magda, 2009), Ammar (2006), Maiman (2006) and

43

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

others (Cizakca, 1998)[17] systematically extended the rule from coins to currency andother liquid assets such as company shares, certificates and bonds.

The advantages of cash waqfContemporary jurists listed some utilities of cash waqf as follows: it is the best way forcreating joint waqf; it creates more economic stimulus and social development; and itsinvestment can be diversified, and it has a greater revenue generation ability and higherchances for growth (Ammar, 2006; Dunya, 2002). It is liquid (Sabit et al., 2006; Ammar, 2006).

Permissibility of the coins of the old, the paper currency of today, or any other formof liquid asset, under modem banking practice, if accepted as the object of waqf (Ammar,2006; Maiman, 2006), can be effective tools of attracting more funds and creatingliquidity. For the purpose of loans and investment, currency will be more useful to awaqf fund, but not other forms of liquid assets, unless prudent deeds of waqf are inplace, empowering the fund to use certificates of shares, sukuk and others as currency.

The cash waqf fund may be the best tool in the Islamic trusts to alleviate poverty, ifthese trusts could manage the fund. A substantial part of income will not go to anon-trust manager. Waqf institution will have control. The true potential of cash waqfwould not be wasted. Indeed, sharing its income with capitalist entities, or using it as atool to cure the ills of such entities is damaging and may not even succeed. To avoid this,and to realise the full potential of cash waqf, the author proposes the creation of waqfbank that not only could have control over the investment and management of the cashwaqf but also offer services that can attract more funds.

The establishment of waqf bank and Islamic lawBennett (1998) has suggested making conventional financial institutions linked to thetarget group (i.e. the poor) and the provision of microcredit through non-governmentalorganisations (NGOs), government agencies, cooperatives and development financeinstitutions. Waqf bank falls in the second category, which can be run by Islamic NGOs(i.e. waqf institutions), state organisations in charge of waqf affairs […] or corporatebody, partially private and partially owned by a non-private entity.

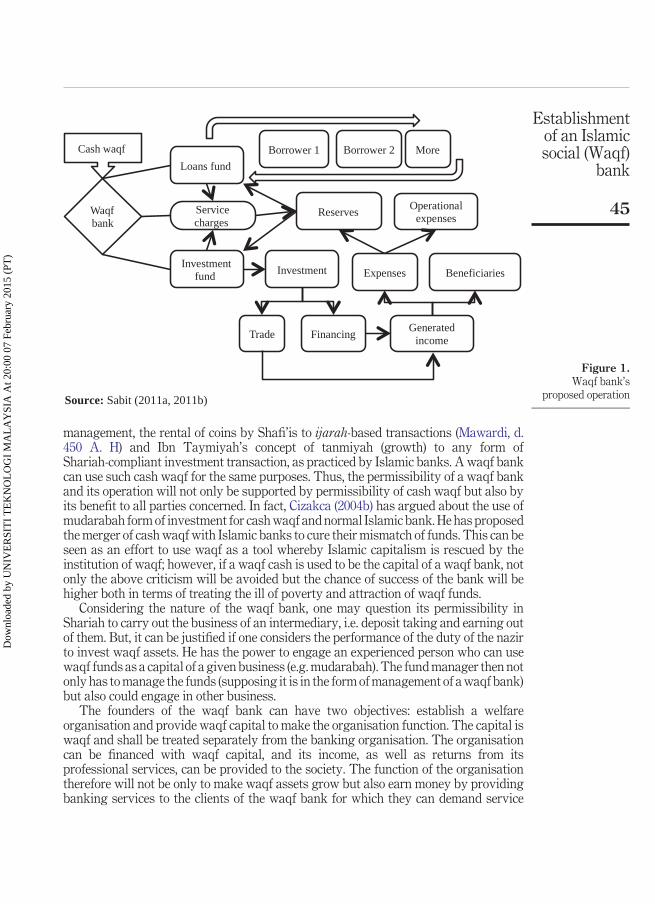

Regardless of who controls the bank, its main function would be to extend loans withless cost to the poor and the needy, and to invest its funds in ethical projects that arebeneficial to the poor and other good causes or at least not to contradict the generalwell-being of the society at large. The income from the investment would be recycled,used or distributed on the beneficiaries (Figure 1).

This will be permissible in Islamic law analogically and on its merits and utilityaccording to the established principles of Islamic jurisprudence.

Analogical reasoning. According to Cizakca (1998), “a cash waqf could function in realityjust like a bank”. Equally, a waqf bank can function just like a cash waqf; thus, a waqf bankcan be allowed in Islam by applying to it the rule of permissibility of cash waqf.

In the absence of primary texts in the Islamic law prohibiting the establishment ofwaqf bank, almost all waqf issues being rational, and as, ultimately, the bank will havewaqf capital, the permissibility of cash waqf then can be extended to waqf bank. Thetwo functions of cash waqf, i.e. benevolent credit to the poor and investment ofthe productive funds, is in conformity with the main function of banks. This is possibleif the mudarabah based investment proposed by Hanafis (Ibn Humam, d. 861 A. H.; IbnAbidin, d. 1252 A. H.; Ibn Nujaim, d. 970 A. H.) can be broadened to include fund

HUM31,1

44

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

management, the rental of coins by Shafi’is to ijarah-based transactions (Mawardi, d.450 A. H) and Ibn Taymiyah’s concept of tanmiyah (growth) to any form ofShariah-compliant investment transaction, as practiced by Islamic banks. A waqf bankcan use such cash waqf for the same purposes. Thus, the permissibility of a waqf bankand its operation will not only be supported by permissibility of cash waqf but also byits benefit to all parties concerned. In fact, Cizakca (2004b) has argued about the use ofmudarabah form of investment for cash waqf and normal Islamic bank. He has proposedthe merger of cash waqf with Islamic banks to cure their mismatch of funds. This can beseen as an effort to use waqf as a tool whereby Islamic capitalism is rescued by theinstitution of waqf; however, if a waqf cash is used to be the capital of a waqf bank, notonly the above criticism will be avoided but the chance of success of the bank will behigher both in terms of treating the ill of poverty and attraction of waqf funds.

Considering the nature of the waqf bank, one may question its permissibility inShariah to carry out the business of an intermediary, i.e. deposit taking and earning outof them. But, it can be justified if one considers the performance of the duty of the nazirto invest waqf assets. He has the power to engage an experienced person who can usewaqf funds as a capital of a given business (e.g. mudarabah). The fund manager then notonly has to manage the funds (supposing it is in the form of management of a waqf bank)but also could engage in other business.

The founders of the waqf bank can have two objectives: establish a welfareorganisation and provide waqf capital to make the organisation function. The capital iswaqf and shall be treated separately from the banking organisation. The organisationcan be financed with waqf capital, and its income, as well as returns from itsprofessional services, can be provided to the society. The function of the organisationtherefore will not be only to make waqf assets grow but also earn money by providingbanking services to the clients of the waqf bank for which they can demand service

Cash waqf

W

Source: Sabit (2011a, 2011b)

aqf bank

Loans fund

Investmentfund

Borrower 1 Borrower 2 More

Reserves

Investment

Generated income

Expenses Beneficiaries

Trade Financing

Operationalexpenses

Servicecharges

Figure 1.Waqf bank’s

proposed operation

45

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

charges. There is no Shariah impediment to such an arrangement, and therefore, thebank shall be permitted to accept deposits from the general public.

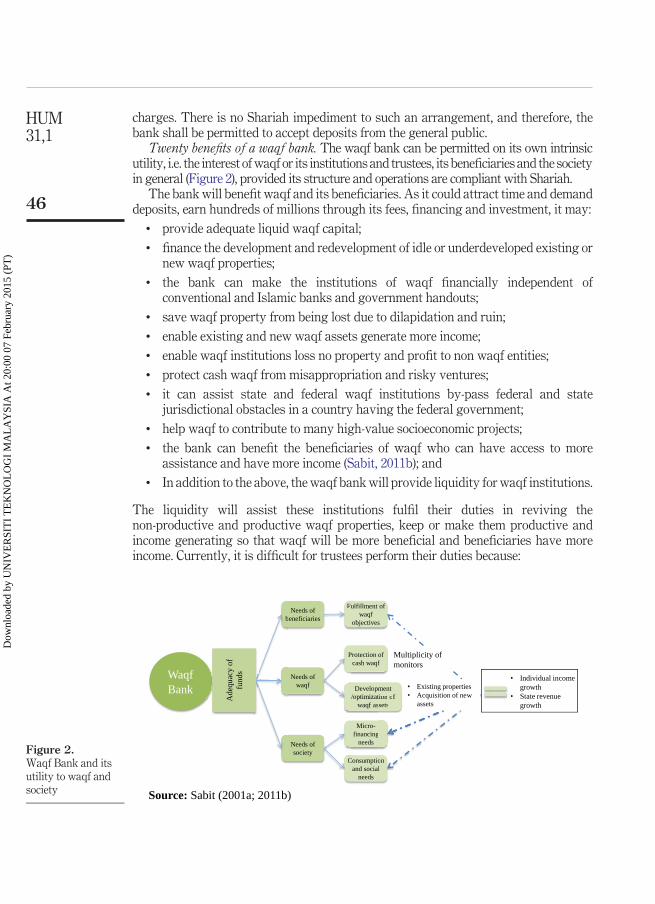

Twenty benefits of a waqf bank. The waqf bank can be permitted on its own intrinsicutility, i.e. the interest of waqf or its institutions and trustees, its beneficiaries and the societyin general (Figure 2), provided its structure and operations are compliant with Shariah.

The bank will benefit waqf and its beneficiaries. As it could attract time and demanddeposits, earn hundreds of millions through its fees, financing and investment, it may:

• provide adequate liquid waqf capital;• finance the development and redevelopment of idle or underdeveloped existing or

new waqf properties;• the bank can make the institutions of waqf financially independent of

conventional and Islamic banks and government handouts;• save waqf property from being lost due to dilapidation and ruin;• enable existing and new waqf assets generate more income;• enable waqf institutions loss no property and profit to non waqf entities;• protect cash waqf from misappropriation and risky ventures;• it can assist state and federal waqf institutions by-pass federal and state

jurisdictional obstacles in a country having the federal government;• help waqf to contribute to many high-value socioeconomic projects;• the bank can benefit the beneficiaries of waqf who can have access to more

assistance and have more income (Sabit, 2011b); and• In addition to the above, the waqf bank will provide liquidity for waqf institutions.

The liquidity will assist these institutions fulfil their duties in reviving thenon-productive and productive waqf properties, keep or make them productive andincome generating so that waqf will be more beneficial and beneficiaries have moreincome. Currently, it is difficult for trustees perform their duties because:

Waqf Bank

Needs of waqf

Needs of society

Needs of beneficiaries

Protection of cash waqf

Development /optimization of

waqf assets

Micro-financing

needs

Consumption and social

needs

Fulfillment of waqf

objectivesb

P

/

C onl

tion ofsets

g

• Individual income growth

• State revenue growth

Multiplicity of monitors

• Existing properties• Acquisition of new

assets

Ade

quac

y of

fu

nds

Source: Sabit (2001a; 2011b)

Figure 2.Waqf Bank and itsutility to waqf andsociety

HUM31,1

46

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

• waqf has overwhelmingly fixed assets that can be used only for cultivation orlease, which are relatively less and inadequate to finance new investments; and

• financing their development through conventional banking system is not easy dueto non-collateralisation of these properties.

A waqf bank can certainly save these institutions from both failures to make waqf asource of great utility and failure to give adequate income to the beneficiaries (Sabit,2011b).

Above all the above, even if waqf has no weaknesses, the proposal for attracting morefunds through a waqf bank is needed. The bank will enable the institutions of waqf tohave access to more funds, which will enable them to provide low-cost credit with nocollateral and no distress to the borrowers. The bank can offer employmentopportunities within the bank or within the workplaces of the borrowers. All these willcertainly enhance the gross domestic product of a nation (Sabit, 2011b).

The establishment of the waqf bank as a social bank is the need of today. The gapbetween the rich is going wider, inequality of income, the concentration of wealth in asmall 20 per cent of the global population, the high level of poverty in Muslim and otherdeveloping countries and the increase in the number of old people in advanced societymakes the need for a social bank urgent even more. The waqf bank can fill this gap andcan be a true pro-poor by redistributing the national wealth management tool for micro-and macro-economic planning of a nation. The proposed waqf bank can lessen theburden of the State in the provision of decent living standards to its citizens includingshelter, education, health care, employment and the like (Sabit, 2011b).

To sum, a waqf bank is possible to set up, as it will be valid based on the validity ofcash waqf and its own utility according the principles of Islamic jurisprudence. Whetherit is viable legally, the following section will explain.

Legal frameworkA waqf bank can be established and then be operated under the current legalframework, if any, of a given country, provided that it has standard companies andbanking laws for its registration and licensing. The bank can register normally as acompany, which can have its own legal personality, independent of its shareholders, cansue or be sued in its own name, and can hold land and other assets in its own name. Itmay also register itself as a cooperative, if the law permits it […] which will have thesame legal personality as a company and be limited in terms of liability. Law needs to beamended to enable waqf institutions to form a cooperative of their own. The bank can belicensed, upon incorporation or registration as a society, in accordance to rules andregulations set by the Central Bank and the existing laws of a country. The main lawsapplicable to waqf bank could be Islamic Banking laws, the conventional banking andfinancial Institutions law, the Company law, Cooperative and Societies law and otherstatutes and regulations.

Because waqf bank would necessarily be an Islamic bank, it has to be regulated bythe legal framework of the Islamic banks. This framework includes issues such as thelicensing of the Islamic bank, financial requirements and duties of an Islamic bank,ownership, control and management of the Islamic banks, restriction on business,powers of supervision and control over the Islamic banks and others. A license to do thebusiness of Islamic banking could be conditioned on two things: its business should not

47

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

involve any element contrary to the Islamic law and the need for the establishment of aShariah Advisory Council under the articles of association of the bank, to advise thebank and to ensure compliance with the principles of Islamic law, particularly waqflaws. […]

Because the bank will be a new entity, it may give rise to new legal issues. In light ofthis understanding, there would be a need for the amendment and enactment of newlaws or additional provisions to the existing laws.

The management of a waqf bankThis section discusses the management of the waqf bank by explaining the capitalstructure of a bank, the investment and the protection of its assets. The discussion alsoincludes the distribution of income among the shareholders, beneficiaries of waqf andreserves. The management of funds for purpose of micro financing is discussedseparately.

The waqf bank will have the capacity to collect, distribute and manage charitable ornon-charitable funds. It can also be involved in recollection of such funds.

The bank can offer profit-generating and service-based products regardless of thenature of the bank as corporate or otherwise. Income-generating products will includethe capital invested by non-waqf persons, as well as income-generating waqf assets.Service-based products will be specifically useful when added to the non-productivewaqf capital[18]. These will include the provision of benevolent loans with minimumcharges for financial and non-financial assistance to the poor and welfare organisations.

The structure of the bank. The structure of an Islamic social bank can take variousforms under the existing legal framework of a country. Depending on the capital and thetype of ownership, it can be formed as a sole waqf bank, cooperative or a corporate entitybased on profit-sharing between waqf and the investors of the banks.

Raising capital and other funds. A waqf bank can raise funds consisting of its capitaland funds of other forms. The latter could be in the form of deposits, investment,donations, grants and loans. The capital of the bank can be liquid waqf assets, donatednew cash waqf funds, bank’s shareholders’ funds (waqf and non waqf), grants andbenevolent loans (qard hasan). The bank can also attract profit- and loss-sharinginvestment funds or demand and time deposits after it is established.

Like any other bank, waqf bank has to maintain capital fund[19], reserve fund andminimum amount of liquid asset. The minimum capital requirement can be satisfied bysuccessfully attracting the above-mentioned funds, capital maintenance would bepossible through wise management of funds investment and microfinance. Liquiditycould be kept through having a sufficient pool of reserves and other funds, which wouldbe discussed later.

To enable waqf bank to have more resources for helping the underprivileged groupsof the society, it could collect zakat, waqf and sadaqa donations. The bank can alsoaccept other types of donations, from any willing individual or body. These funds canhelp the bank contribute to poverty eradication on a wider scale.

In addition to the role as intermediary and entrepreneur, the waqf bank could play therole of an administrator of charitable funds, i.e. zakat, sadaqat and other donationsmarked as CSR funds. The bank will have the power to use them for the designatedpurpose, invest them and collect them if loaned to the poor and needy, when specified bythe donors.

HUM31,1

48

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

The sources of funds. Capital of the bank and other funds may be raised from varioussources and in different forms.

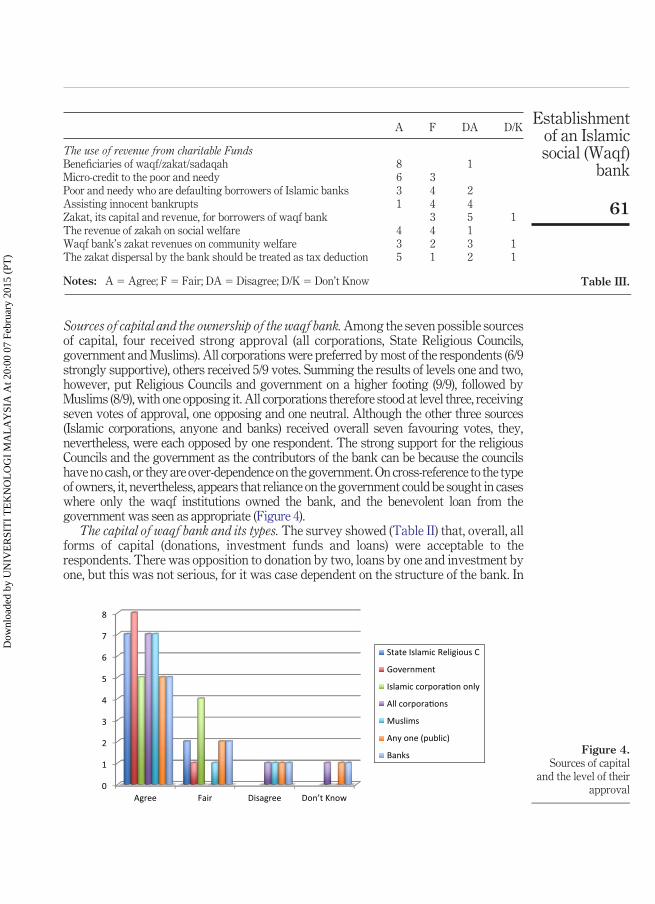

There are seven sources of raising funds in terms of capital or deposits which can beused by a waqf bank: State or Federal Religious Councils (the trustees of waqf assets),State or Federal government, all corporations and banks, members of public includingnon-Muslims (Figure 3).

The State or Federal Religious Councils can contribute either by way of depositingwaqf funds for safekeeping or investment. The investment can be made either as asubscription for the shares of the bank or in the form of normal fixed deposits. Only thesubscription for the shares of the waqf bank can be considered as a contribution to thecapital of the bank. Others will be bank’s liabilities only.

All waqf funds, either cash waqf or the proceeds of other waqf properties, can bemixed. As mentioned by Dunya (2002) and Ammar (2006), cash waqf may be individualor group donations dedicated for one or more causes for a specific project or otherwise.If there is will on the part of all waqf institutions, self-capitalisation of the waqf bankfrom their existing liquid assets could be possible. This does not mean they cannot raisefunds through new cash waqf and other charitable donations.

Where waqf institutions are unable to raise capital for the bank, raising new cashwaqf would be the first step towards that objective. If invested prudently, the incometogether with its principle of cash waqf can be used as capital for the waqf bank later.For instance, it is now established that waqf institutions are asking each member of thepublic to donate a minimum of RM10. If this amount is promoted aggressively, and theyhave a pool of two million donors for five years who can contribute the same amount ona monthly basis, there will be enough cash waqf funds to establish a waqf bank. In casethe waqf bank is established early as a joint venture between waqf institutions and acorporate entity, the institutions of waqf will be able to purchase all subscribers’ sharesin the waqf bank.

The bank could get capital or other funds from the government (state and/or federal),in terms of loans, cash waqf grants, demand or investment deposits or both. Similarly,government-linked companies (GLCs) and private bodies including Islamic banks (local

Waqf

institutions

Banks

Donations

Waqffunds

LoansG

overnment

and GLC

s

Private com

panies and individuals

Waqf bank

Private companies

Waqfinstitutions and

individuals

Waqf funds

Loans

Banks (local / international)

Government and GLCs

InvestmentsDemand/Time deposits

Figure 3.Capital of waqf bank,

its sources and itstypes

49

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

and international) can be the participants, in terms of capitalisation, donors andinvestors. Other sources, irrespective of who they are and to what group they belong to,can contribute by way of waqf donations or investment in the above manner. Wherewaqf funds are insufficient, the bank could opt for benevolent loans and investmentsfrom governmental, semi-governmental and corporate bodies.

The capitalisation of the bank would be a business venture. This business venturecan be between the various states and federal waqf institutions or between theseinstitutions and government-linked companies and other entities, financial or otherwise.

Management of bank’s assets. The balance sheet and income statement of a waqfbank should measure its success. The balance sheet of a waqf bank would consist of itsassets and liabilities, including its own share capital (waqf and/or investment), waqfdeposits and deposits of its clients. The bank can balance its funds’ allocation againstthe adequacy of its funds. It should invest its share capital in low-risk and highly liquidinstruments and the deposits in long-term, low-risk investment products. The formulafor debt to equity ratio needs to be based on security of assets, liquidity and capitaladequacy and not greed for high profits. It should measure its balance sheet by theachievement of the objectives of waqf rather the sheer maximisation of profits of thebank. Although the maximisation of profits and social benefits would be ideal,nevertheless, as long as the bank has no losses to show, the generation of social valueshould set off its profits. Such a management of funds would be needed in activities asmentioned below.

The capital of a waqf bank. The capital of a waqf bank will include contributedcapital (which will be largely waqf properties) part of earnings (e.g. reinvested profitsand service charges). Another could be debt or invested capital from the shareholder ofthe waqf bank, which requires the duty of utmost care under the principle of trust(amanah), and it carries liability for negligent acts of the bank under Islamic law.

Some principles of conventional banking systems may apply to the management ofassets. For instance, the bank can invest its capital in short-term, highly liquid products.Nevertheless, the management of these funds could be realistic and based on the realability and strength of the bank on one hand and capturing good investmentopportunities for waqf on the other. The investment of these funds must be Shariah, andwaqf – compliant, and must be in accordance with the existing laws and regulations ofa given jurisdiction. A similar rule should be applied to investment funds.

Waqf bank may have capital or waqf deposits earmarked for loans to the needysections of the society. These funds need to be managed according to the wishes of thedonors and used for pro-poor activities. Because these funds are prone to higherborrower risk, adequate funds need to be earmarked for offsetting losses and providingliquidity.

Deposits. The main attractive feature of waqf bank to waqf institutions would be itsability to utilise the entrusted deposits for maintenance and development of waqf assets(movable and immovable). For this, a waqf bank needs to be a full bank. Its businessshould include accepting deposits and using them for trade and investment in diversebusinesses including waqf properties. A waqf bank, in this way, can use its own capital,and two other sources of funds:

(1) transaction deposits in current and saving accounts, which are normally riskfree for the depositors, but yield to depositors no return.

HUM31,1

50

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

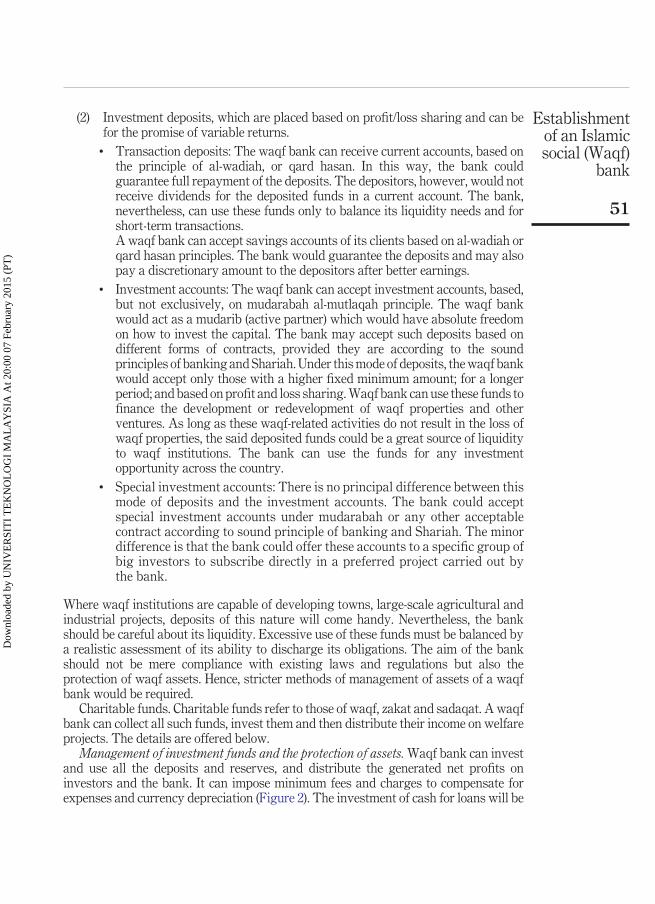

(2) Investment deposits, which are placed based on profit/loss sharing and can befor the promise of variable returns.

• Transaction deposits: The waqf bank can receive current accounts, based onthe principle of al-wadiah, or qard hasan. In this way, the bank couldguarantee full repayment of the deposits. The depositors, however, would notreceive dividends for the deposited funds in a current account. The bank,nevertheless, can use these funds only to balance its liquidity needs and forshort-term transactions.A waqf bank can accept savings accounts of its clients based on al-wadiah orqard hasan principles. The bank would guarantee the deposits and may alsopay a discretionary amount to the depositors after better earnings.

• Investment accounts: The waqf bank can accept investment accounts, based,but not exclusively, on mudarabah al-mutlaqah principle. The waqf bankwould act as a mudarib (active partner) which would have absolute freedomon how to invest the capital. The bank may accept such deposits based ondifferent forms of contracts, provided they are according to the soundprinciples of banking and Shariah. Under this mode of deposits, the waqf bankwould accept only those with a higher fixed minimum amount; for a longerperiod; and based on profit and loss sharing. Waqf bank can use these funds tofinance the development or redevelopment of waqf properties and otherventures. As long as these waqf-related activities do not result in the loss ofwaqf properties, the said deposited funds could be a great source of liquidityto waqf institutions. The bank can use the funds for any investmentopportunity across the country.

• Special investment accounts: There is no principal difference between thismode of deposits and the investment accounts. The bank could acceptspecial investment accounts under mudarabah or any other acceptablecontract according to sound principle of banking and Shariah. The minordifference is that the bank could offer these accounts to a specific group ofbig investors to subscribe directly in a preferred project carried out bythe bank.

Where waqf institutions are capable of developing towns, large-scale agricultural andindustrial projects, deposits of this nature will come handy. Nevertheless, the bankshould be careful about its liquidity. Excessive use of these funds must be balanced bya realistic assessment of its ability to discharge its obligations. The aim of the bankshould not be mere compliance with existing laws and regulations but also theprotection of waqf assets. Hence, stricter methods of management of assets of a waqfbank would be required.

Charitable funds. Charitable funds refer to those of waqf, zakat and sadaqat. A waqfbank can collect all such funds, invest them and then distribute their income on welfareprojects. The details are offered below.

Management of investment funds and the protection of assets. Waqf bank can investand use all the deposits and reserves, and distribute the generated net profits oninvestors and the bank. It can impose minimum fees and charges to compensate forexpenses and currency depreciation (Figure 2). The investment of cash for loans will be

51

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

on short term. Productive waqfs can be allocated for short or long term, provided that agood management practice dictates it.

All funds including the capital of waqf bank, deposits, donations, reserves and theundistributed revenue from investment and banking services shall be invested orreinvested, risks have to be minimised, all in accordance to the principles of Shariah andprevailing law.

As a rule, productive waqf must be kept invested and income-generating which canbe best achieved by going to the business of banking. The contemporary Islamicbanking practice provides evidence of successful cash investment methods that are notonly good for expected good returns on the investment but also for protection of theassets.

Sound investment. Similar to cash waqf, the bank has to use the entrusted funds in apermissible income-generating business, and not for other purposes. Their protectionand growth shall be the main function of the bank. Income from the invested funds andloans has to be used for the benefit of the society according to the wishes of the donors.

A waqf bank should adopt a sound investment strategy. It should have a diversifiedportfolio based on a reliable analysis of markets and monitoring. It should take decisionsabout asset allocation for waqf and the clients of the bank. Following the principles ofcash waqf and normal banking standards there shall be various types of reserves for thepurpose of risk aversion. The bank should not invest in activities that are risky. It shouldinvest reserves in activities that do not affect liquidity according to banking industry.

Risk aversion. A waqf bank should be responsible for the protection of its capital anddeposits. For capital security, normal hedging against risks associated with bankingsystem be in place. There shall exist higher standards of sound banking, capitaladequacy and liquidity of bank assets. Adequate measures have to be taken againstrisks of possible loss of deposits, over leveraging and illiquidity, borrowers’ default,capital adequacy, settlement of claims and taxes. In addition, the bank has to considerthe rules preserving the perpetuity of waqf capital. In other works, two major measuresare needed: preventive and compensatory.

As a preventive measure, highly risky products have to be avoided. Minimised riskcould be tolerated. For this, the bank can choose investment products of low-to-mediumrisk used by Islamic banks. Attention has to be paid to products suggested for theinvestment of cash waqf[20]. The bank should act as a responsible agent of theinvestors. It should be liable for its negligence and misappropriation. In the case ofsavings and current accounts deposits, the bank as a borrower should bear the losses.For avoiding liability, various types of reserves accounts from the income of its halaland non-halal trading be opened. Additionally, the Basel II pillars of sound banking, i.e.minimum capital requirement, transparency and effective supervision, have to becomplied with. These should be observed in all risk-prone activities of the bank, i.e.financial, business and operational activities[21].

For compensatory purposes, there should exist an internal mechanism for theprotection of waqf assets and depositors’ accounts. This should revolve around havingreserve accounts, insurance (takaful), a government guarantee and, in rare cases, theincome of the waqf deposits, but not its capital. This will help the bank to not lose waqfand other assets. The bank can draw appropriate mechanisms for the use of either ofthese measures, in an order of priorities.

HUM31,1

52

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

The management of revenues and distributable income. The bank should annuallyassess its revenues and determine its losses and profits. If the bank has made profits, itcan distribute them among shareholders and the bank. The distribution should takeplace according to an agreed ratio. The bank has to distribute the net profit of the waqfamong the beneficiaries according to a sound formula, whereby there shall remain anamount reserved and reinvested in income generating financial activities.

A waqf bank can create revenues through trade or investment and by providingbanking services such as wakalah, kafalah, custody and safe deposits, management andplacement, advice, consultations, micro-credit and other products. The bank can usethese revenues for operational expenses and risk management purposes. If there is asurplus, the bank can share it with investors according to the initial agreement of theparties. Because the objective of waqf is to offer social and economic benefits to the poorand disadvantaged persons, a waqf bank has to save costs and generate more income.For this reason, the bank needs to operate efficiently so that the expenses of the waqfbank are at minimum. Efficiency and sound ratio of income distribution may help thebank to save the income and accumulate it in the course of time. This will later make theinstitutions of awqaf more effective in carrying out their socioeconomic projectsnationally and internationally.

The revenues from investments and services can be distributed according to theterms and conditions stipulated in agreements between the investors, depositors anddonors on one hand and the constitution of the bank on the other. The investors andcontributors should expect return on their investments. The ratio of entitlement to theincome has to be stipulated in advance. The income of waqf however has to be managedin a way that provides sustainability of waqf bank and benefits the beneficiaries ofwaqf. Therefore, the bank shall keep a substantial part of such profits, and the balanceshall be transferred to the beneficiaries of waqf or other funds.

The profits of the bank, after allocation of dividends to its investors and non-waqfshareholders, along with zakat, can be distributed on welfare projects, andmicro-financing according to Islamic law. The funds marked for loans can be used formicrocredit offered by the bank to its nonperforming clients according to the principle ofzakat. Additionally, the bank can offer zakat, sadaqat, waqf and other donated funds tothe needy. The bank can automatically transfer such loans to their accounts, if any, orgiven based on applications received by the bank, or channelled to a collaboratingpartner. The funds can be directed to micro-financing and other welfare projectssponsored or run by the subsidiaries of waqf bank according to a framework that ismentioned below.

Waqf bank and the microfinance for the unbankablesAs mentioned at the outset of this paper, the proposed waqf bank is aimed to overcomethe shortcomings of the current financial system, not only for the benefit of waqfinstitutions but also for the benefit of a great majority of unbankles Muslims and othersequally.

Waqf institutions. The bank can finance various development projects on waqfproperties. This is not easy normally because waqf institutions are charitableorganisations, which are unbankable. They lack collaterals, and conventional banksconsider loans to them risky. Nevertheless, waqf institutions, like any normalincome-generating business, need such services, for millions of its real estates that need

53

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

development, reinvention and redevelopment. Waqf institutions can do all these if theycould have their own bank. It can help the institutions of waqf to develop and redeveloptheir existing landed assets, and, additionally, it could enable them to buy newproperties. It can also facilitate cash waqf capital investments and acquire new liquidassets. The waqf bank can use waqf capital and proceeds for short-term bridging loans,working capital loans and other normal banking services such as underwriting facilitiesfor fund-raising purposes and many more. This will enable waqf institutions to save onthe cost of capital and yet generate income for waqf purposes, thus making themsustainable and ever more capable of contributing to the welfare of the society. This isclear from the ability of the bank to provide microfinance to others as explained below.

Provision of cheap microfinances. Without prejudice to the power of waqf bank toenter into normal business transactions, it can prioritise micro-financing and run it ontwo platforms: qard hasan and profit-sharing, as proposed by Ahmed (2007, 2004) andObaidullah (2008). This is in line with cash waqf principles: to use the capital forbenevolent loans (qard hasan) or invest it in business operations. These are discussedbelow.

Microcredit or qard hasan. As illustrated in Figure 1, once deposits dedicated tolending are made, the bank can disburse the cash to the indebted, needy and a welfareorganisation, as the case may be. Additionally, part of profits of the bank can also beallocated for microcredit purposes and disbursed subsequently. Once borrowerssettle the loan, the recovered amount can be recycled and loaned to another. This will berepeated whenever an amount is available in a given fund. The bank has to maintain thecash waqf perpetually by providing compensations for losses and market fluctuations.For this, a special reserves account will be needed. As the loan fund will be disbursedinterest free, a minimum service charge will be imposed on borrowers, a portion of whichcan be allocated for making good on losses. The balance of the service charges could beused for other expenses.

The waqf bank, as an intermediary and an agent of waqf institutions, its clients andmember of public or organisation, has to allocate cash waqf to the needy for theirexpenses or businesses. The bank can loan it to individuals to finance their householdneeds or to give it as capital goods or as working capital for a small enterprise. Theborrowers can apply for either short- or long-term loans. The bank, in assessing theperiod of repayment of the loan, would need to weigh not only the possibility of recoveryof loan but also has to consider the capability of the borrower whether he/she could payit within a given period.

The bank should keep the cost of the credit cheap, at least at par with mainstreamcredit rates offered by ordinary banks. The bank can subsidise some of its servicesthrough other businesses, and because the capital is free and there are no expectations ofearning from these funds, offering cheap microcredit to the poorest of the poor should bethe main attraction of the bank. This will substitute the current exploitation of the poorby the existing MFIs.

The paramount task of the bank would be to collect the loans and recycle it for thebenefits of the underprivileged class of the community. To collect the full amount ofloans without security or collaterals would need sound strategy for risk management.The main risk can be attributed to borrowers. For this, reserves and other measures ofpreserving the waqf capital need to exist.

HUM31,1

54

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

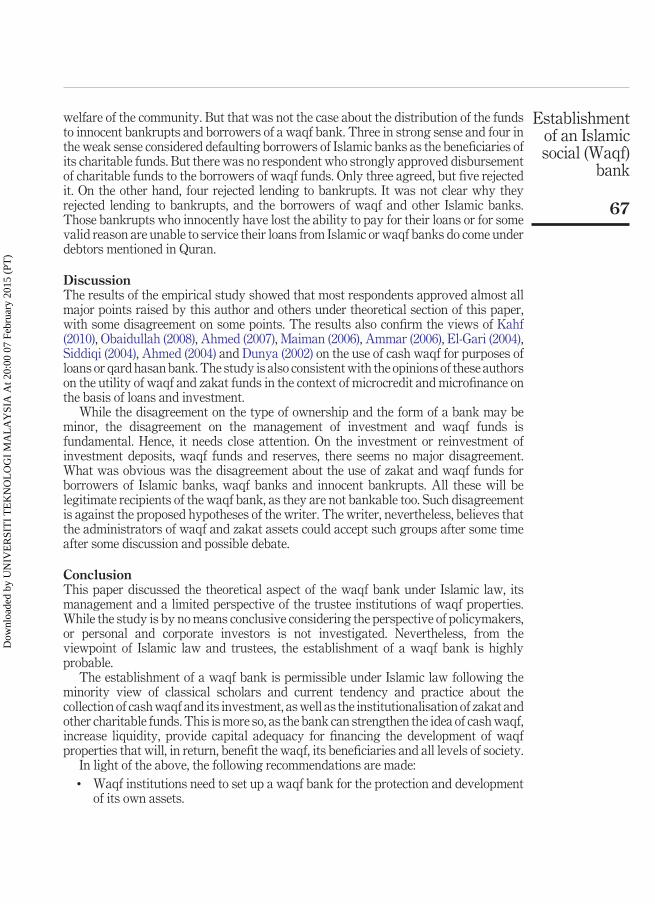

There are, arguably, few risk-free products in the market, which incorporate groupguarantees and individual insurances in addition to regular savings. If proven so, thebank needs to use them. In theory, and mathematically, this appears to be workable. TheIslamic MFIs, offering such product, also claim to have a high rate of recovery (80-99 percent). However, fresh study is needed to investigate the real statistics of repayment ofshort-term loans by the first-time borrowers from the stratum of the poor. There is alsono study on the verification of claims by the Islamic MFIs about the 99 per cent recoveryof their loans. This writer finds the 99 per cent claim of repayment difficult to be true,considering the burden of repaying the principle loan in a very short time, plus anamount for saving account and insurance policy. The writer presumes that there wouldbe group pressure and shaming which is not in accordance with the spirit of benevolentloan (qard hasan). It is feared that the so-called successful borrowers, in the eyes ofIslamic MFIs, might not be better off. They might be in the same place as those underconventional MFIs, pushed into the debt trap for a long time. In case the fear of thiswriter is proven to be a reality, then the waqf bank has to avoid the existing methods ofrecovery and find alternative ones.

As an alternative, and as suggested by Obaidullah (2008), waqf bank can use fundsthat could be written off. These types of funds would be zakat and other funds that canbe given to the borrowers in parallel with loans from waqf funds. These non-waqf fundswould be used for the purpose of servicing waqf loans, as well as for subsistence andother needs. At least three categories of beneficiaries (poor of the poor, destitute andindebted and in the cause of Islam or fi sabilillah) can benefit from zakat in terms ofconsumable grants to the borrowers. In addition, distressed borrowers could ask forreadjustment of instalments without penalty and additional burden. All these may workfor the security of cash waqf funds, if the bank could have a good monitoring andsupervision mechanism in place.

Microfinance. Waqf bank can disburse cash waqf funds earmarked for trade to thepoor, as well as part of its profits to the needy, particularly those who are below thepoverty line. Cash waqf collected by the bank or received from Religious Councils andwaqf institutions could be used too.

There are various products in the market offered by Islamic institutions that can beincorporated by the bank, used when disbursing waqf funds. The predominant productsare murabahah, ijarah, istisna’, salam, musharakah, mudarabah and others.

The bank can use murabahah contracts to purchase capital goods for smallbusinesses. This contract would be useful and compliant to Islamic law if there iswaqf-owned wholesale business and goods, which are sold to the microbusinesses forcheap. Some of costs of the financing may be subsidised in this way. Further, it ispossible to tie up with managers of waqf commercial assets such as shops and otherlanded properties and offer them to micro-entrepreneurs for doing their businesses onsuch premises. These premises can be rented to them on subsidised rates, with strictrules for the entrepreneurs to pay the rent, as well as their loan repayment instalments.Similar to microcredit, the funds from zakah can be brought in, thereby assisting thepoor in repayment of the waqf loans, as well as providing for their family needs.

To sum the above discussion, the waqf bank has to follow the rules of Islamic law andbanking regulations. It has to comply with Islamic Banking laws, and has to do businessaccordingly. The bank, as a manager of waqf funds, also has to invest according to thespecial characteristic of waqf properties and in line with duties of trustees that is to

55

Establishmentof an Islamicsocial (Waqf)

bank

Dow

nloa

ded

by U

NIV

ER

SIT

I T

EK

NO

LO

GI

MA

LA

YSI

A A

t 20:

00 0

7 Fe

brua

ry 2

015

(PT

)

safeguard waqf capital and increase its income. It would have the duty to retain theprincipal, distribute its income, minimise investment risk, take contingency measuresfor depreciation and other risks and apply for tax exemption. It must give priority toprojects that are in line with Shariah objectives (maqasid Shariah), beneficial to the localpopulation and in the interest of beneficiaries. Investment that involves high risk can beavoided (Dunya, 2002). The bank can reserve a portion of the income for contingenciesand invest them to generate income to increase its reserved funds. The bank can alsoliquidate some of the waqf properties as and when they are considered profitable and donot clash with the interests of the waqf and its beneficiaries. This will not be againstIslamic law, for the principle of perpetuity will apply to the capital […]

Waqf bank would be required to maintain its capital. Several measures againstmisappropriation and mismanagement of the funds will be in place. The restrictionsimposed by the founders of the waqf, the principles of Islamic law, adherence to the bestpractice and banking regulation will enable the waqf bank to maintain its capital. It willbe required to have and maintain reserve fund including statutory reserves, and to havein possession minimum liquid assets. The bank will be subjected to annual audit.

The bank will be subject to the supervision of the Sharia Advisory Board,shareholders and the Central Bank. All these entities will scrutinise the performance ofthe bank and, thus, the dismissal of negligent and incompetent individuals will be easywhen it can be proven that the bank has suffered losses because of their maliciousintentions or negligence. It will be easy to hire and fire fund managers when they do notdeliver what are expected of them.

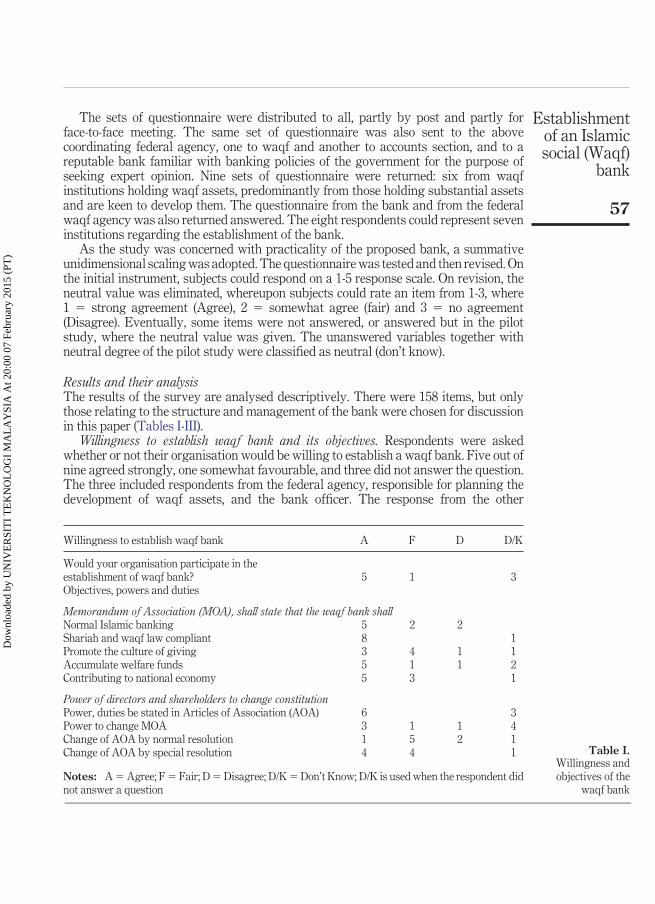

Empirical studyIn this section, the writer discusses the result of a preliminary survey about theperspective of the waqf institutions represented by their midlevel executives. Thediscussion is divided into two main subsections: research methodology and the resultsof data analysis and discussion.

Research methodologyTo test the practicality of the idea about waqf bank, in Malaysia, views of practitionersin the waqf institutions, the policymakers, lenders, the potential investors and otherexpert would have made this study more reliable. However, limited by cost and time, thewriter explores the views of those in waqf institutions, familiar with waqf affairs and itsneeds, which were considered sufficient to indicate a degree of willingness among thepractitioners. A questionnaire was also distributed to a banker to seek his expert advice.

The total number of population of the investigation ought to be 15, comprising 13states and 2 federal waqf institutions, from west and east Malaysia. However, because oftime and cost factors, the sample comprised institutions located in west Malaysia only.