Module 2: Understanding Financial Management

35

Public Housing Authority Financial Management Training Module 2: Understanding Financial Management

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Module 2: Understanding Financial Management

Public Housing Authority Financial Management Training

Module 2:

Understanding Financial Management

Module 2 Topics • National – Portfolio Snapshot

– PHA & Program Type– Public Housing– Housing Choice Voucher

• Common PHA Audit Findings– Annual “Outside” Audits– HUD’s Office of Inspector General (OIG) Audits– Other HUD Reviews

• The Financial Management Concept

Module 2

PORTFOLIO SNAPSHOT

Portfolio Snapshot: PHA Type National Level – Public Housing Authorities

# PHA Type PHA Count % of PHAs # of Units % of Units

1 Combined 1,394 36% 2,635,236 74%

2 PH Only 1,648 42% 22,782 6%

3 S8 Only 844 22% 716,321 20%

Total 3,886 100% 3,580,339 100%

• Nationally, there are 3,886 PHAs that in total administer more than 3.5 million PH units andHousing Choice Vouchers

• 78% of all PHAs (3,042 of 3,886) manage the Public Housing program• 58% of all PHAs (2,238 of 3,886) manage the Housing Choice Voucher program• Nationally, there are 604 PHAs with a COCC (managing 60% of all PH and HCV units)• There are 39 Moving-to-Work PHAs nationally; most manage both the PH and HCV

programs

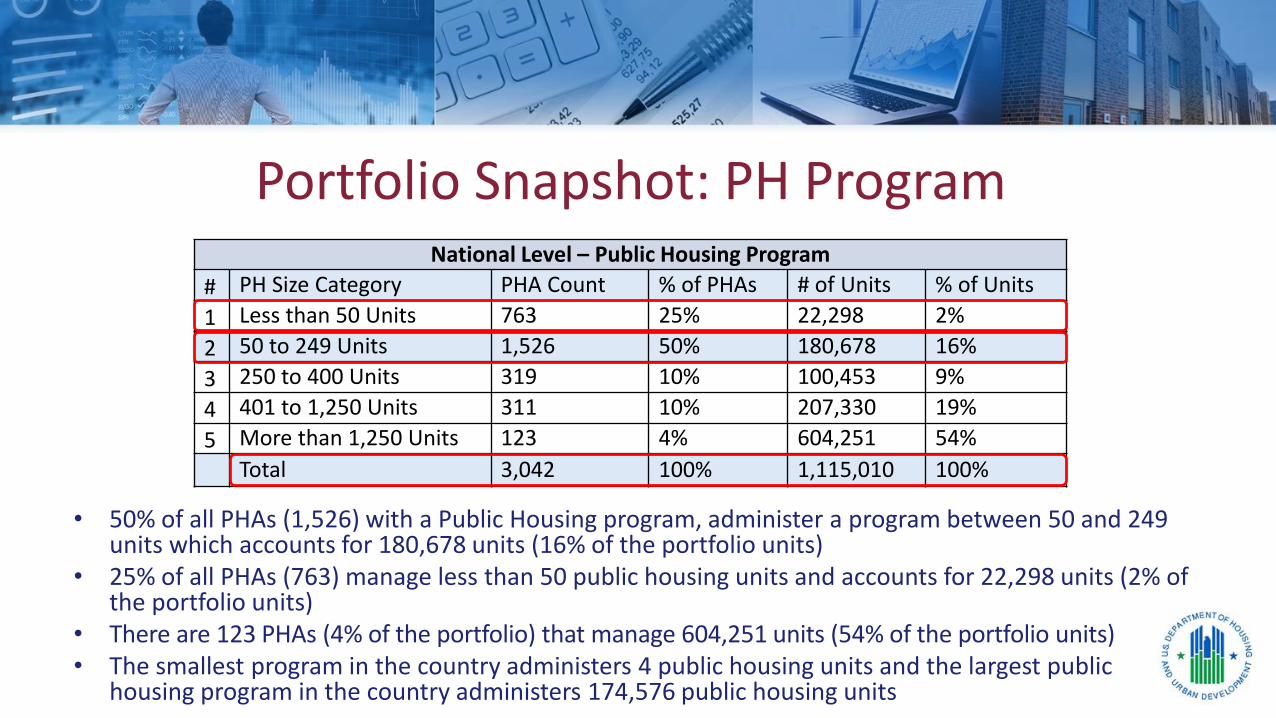

Portfolio Snapshot: PH Program National Level – Public Housing Program

# PH Size Category PHA Count % of PHAs # of Units % of Units

1 Less than 50 Units 763 25% 22,298 2%

2 50 to 249 Units 1,526 50% 180,678 16%

3 250 to 400 Units 319 10% 100,453 9%

4 401 to 1,250 Units 311 10% 207,330 19%

5 More than 1,250 Units 123 4% 604,251 54%

Total 3,042 100% 1,115,010 100%

• 50% of all PHAs (1,526) with a Public Housing program, administer a program between 50 and 249units which accounts for 180,678 units (16% of the portfolio units)

• 25% of all PHAs (763) manage less than 50 public housing units and accounts for 22,298 units (2% ofthe portfolio units)

• There are 123 PHAs (4% of the portfolio) that manage 604,251 units (54% of the portfolio units)• The smallest program in the country administers 4 public housing units and the largest public

housing program in the country administers 174,576 public housing units

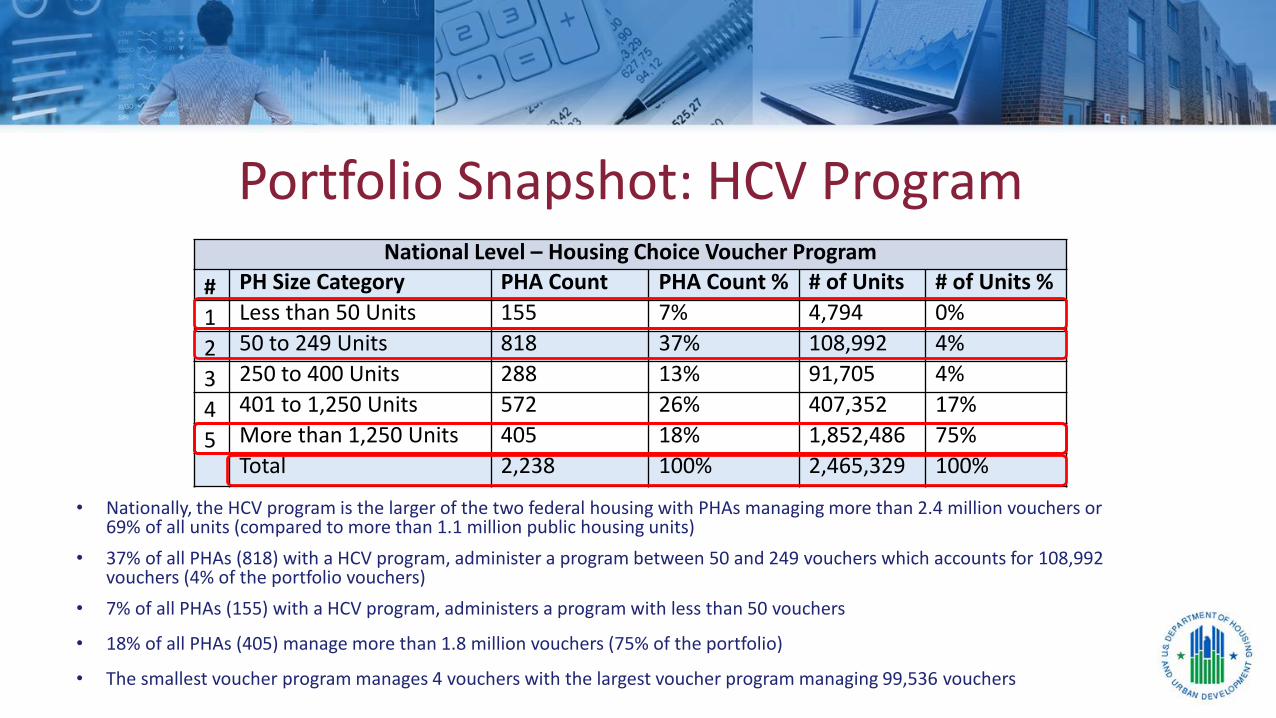

Portfolio Snapshot: HCV Program National Level – Housing Choice Voucher Program

# PH Size Category PHA Count PHA Count % # of Units # of Units %

1 Less than 50 Units 155 7% 4,794 0%

2 50 to 249 Units 818 37% 108,992 4%

3 250 to 400 Units 288 13% 91,705 4%

4 401 to 1,250 Units 572 26% 407,352 17%

5 More than 1,250 Units 405 18% 1,852,486 75%

Total 2,238 100% 2,465,329 100%

• Nationally, the HCV program is the larger of the two federal housing with PHAs managing more than 2.4 million vouchers or69% of all units (compared to more than 1.1 million public housing units)

• 37% of all PHAs (818) with a HCV program, administer a program between 50 and 249 vouchers which accounts for 108,992vouchers (4% of the portfolio vouchers)

• 7% of all PHAs (155) with a HCV program, administers a program with less than 50 vouchers

• 18% of all PHAs (405) manage more than 1.8 million vouchers (75% of the portfolio)

• The smallest voucher program manages 4 vouchers with the largest voucher program managing 99,536 vouchers

Module 2

COMMON PHA AUDIT FINDINGS

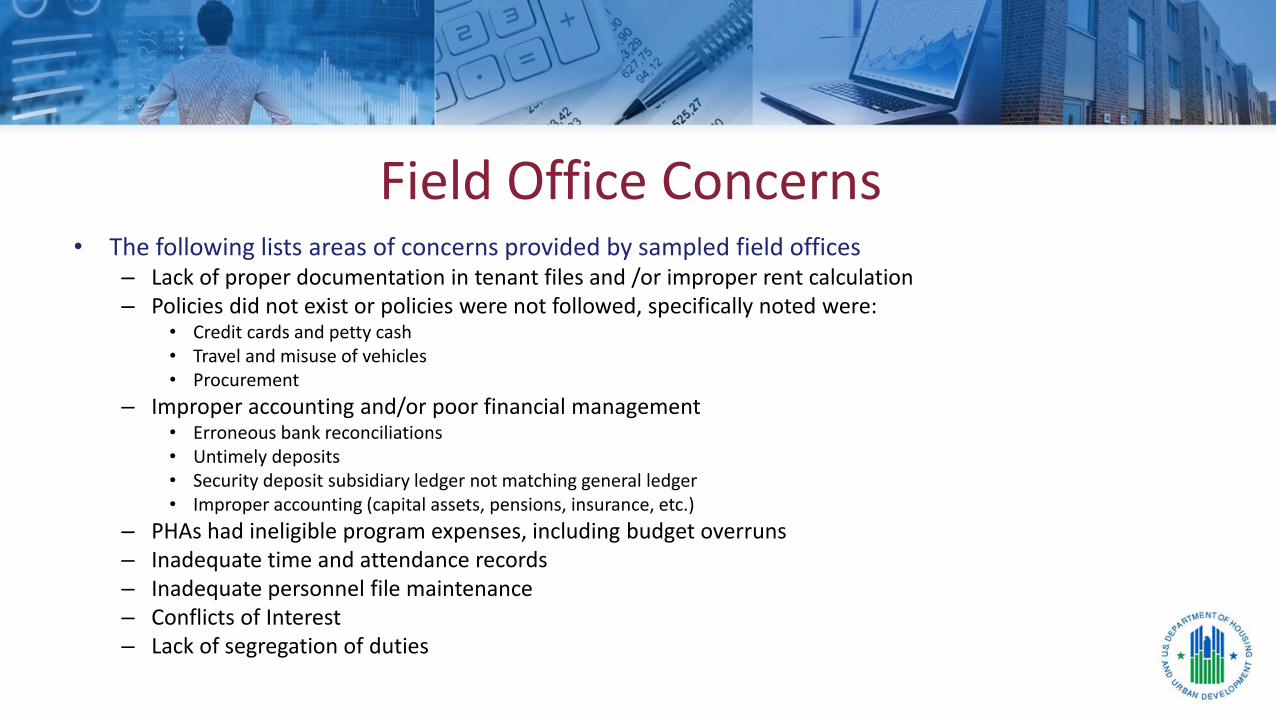

Field Office Concerns • The following lists areas of concerns provided by sampled field offices

– Lack of proper documentation in tenant files and /or improper rent calculation– Policies did not exist or policies were not followed, specifically noted were:

• Credit cards and petty cash• Travel and misuse of vehicles• Procurement

– Improper accounting and/or poor financial management• Erroneous bank reconciliations• Untimely deposits• Security deposit subsidiary ledger not matching general ledger• Improper accounting (capital assets, pensions, insurance, etc.)

– PHAs had ineligible program expenses, including budget overruns– Inadequate time and attendance records– Inadequate personnel file maintenance– Conflicts of Interest– Lack of segregation of duties

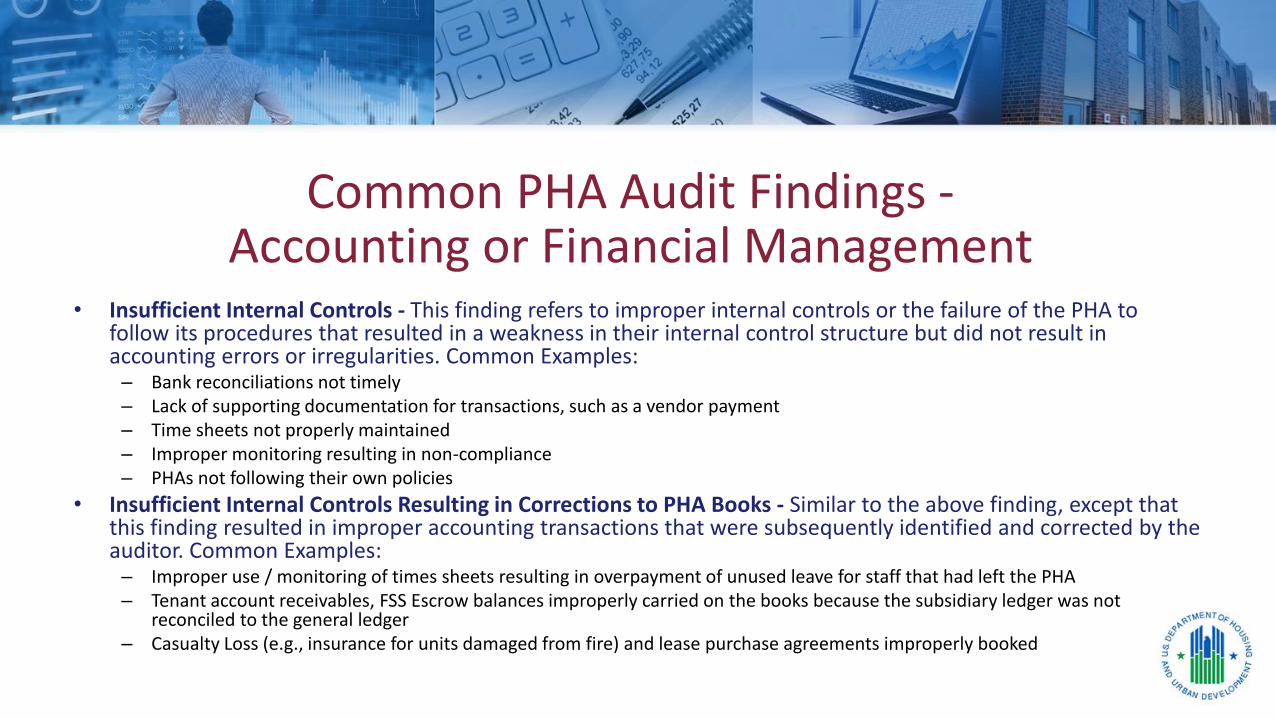

Common PHA Audit Findings - Accounting or Financial Management

• Insufficient Internal Controls - This finding refers to improper internal controls or the failure of the PHA tofollow its procedures that resulted in a weakness in their internal control structure but did not result inaccounting errors or irregularities. Common Examples:– Bank reconciliations not timely– Lack of supporting documentation for transactions, such as a vendor payment– Time sheets not properly maintained– Improper monitoring resulting in non-compliance– PHAs not following their own policies

• Insufficient Internal Controls Resulting in Corrections to PHA Books - Similar to the above finding, except thatthis finding resulted in improper accounting transactions that were subsequently identified and corrected by theauditor. Common Examples:– Improper use / monitoring of times sheets resulting in overpayment of unused leave for staff that had left the PHA– Tenant account receivables, FSS Escrow balances improperly carried on the books because the subsidiary ledger was not

reconciled to the general ledger– Casualty Loss (e.g., insurance for units damaged from fire) and lease purchase agreements improperly booked

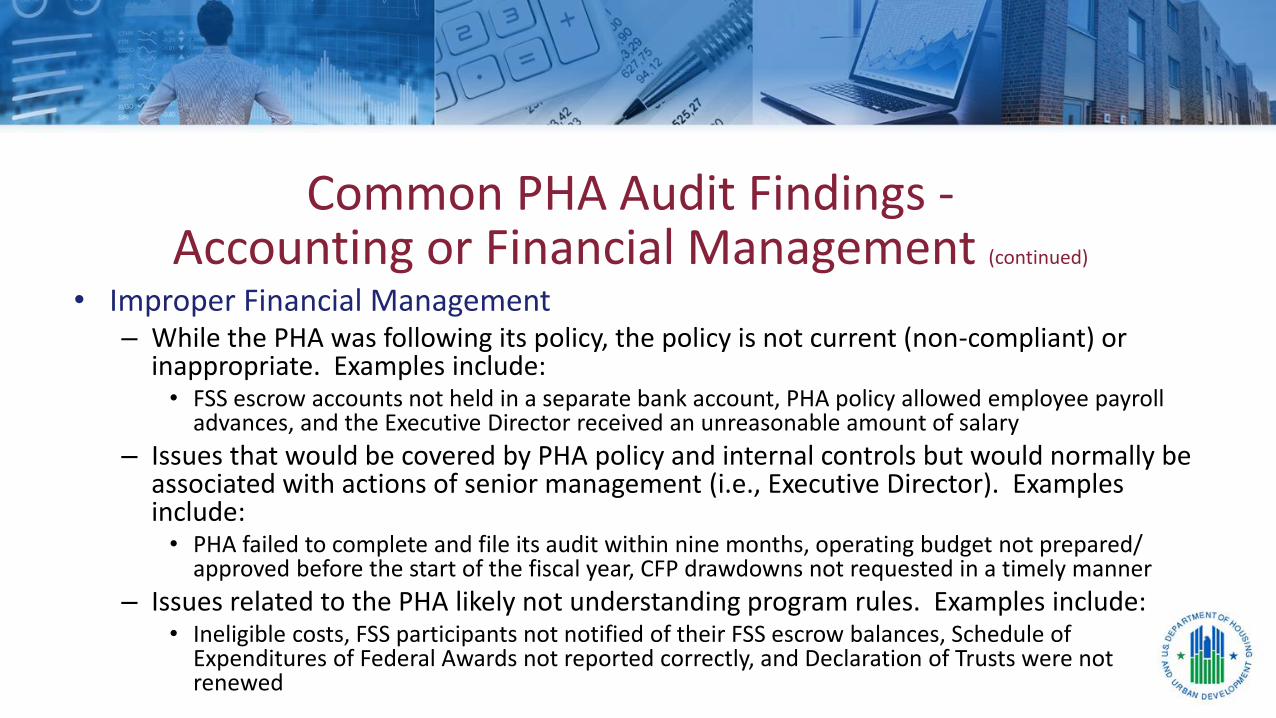

Common PHA Audit Findings - Accounting or Financial Management (continued)

• Improper Financial Management– While the PHA was following its policy, the policy is not current (non-compliant) or

inappropriate. Examples include:• FSS escrow accounts not held in a separate bank account, PHA policy allowed employee payroll

advances, and the Executive Director received an unreasonable amount of salary

– Issues that would be covered by PHA policy and internal controls but would normally beassociated with actions of senior management (i.e., Executive Director). Examplesinclude:• PHA failed to complete and file its audit within nine months, operating budget not prepared/

approved before the start of the fiscal year, CFP drawdowns not requested in a timely manner

– Issues related to the PHA likely not understanding program rules. Examples include:• Ineligible costs, FSS participants not notified of their FSS escrow balances, Schedule of

Expenditures of Federal Awards not reported correctly, and Declaration of Trusts were notrenewed

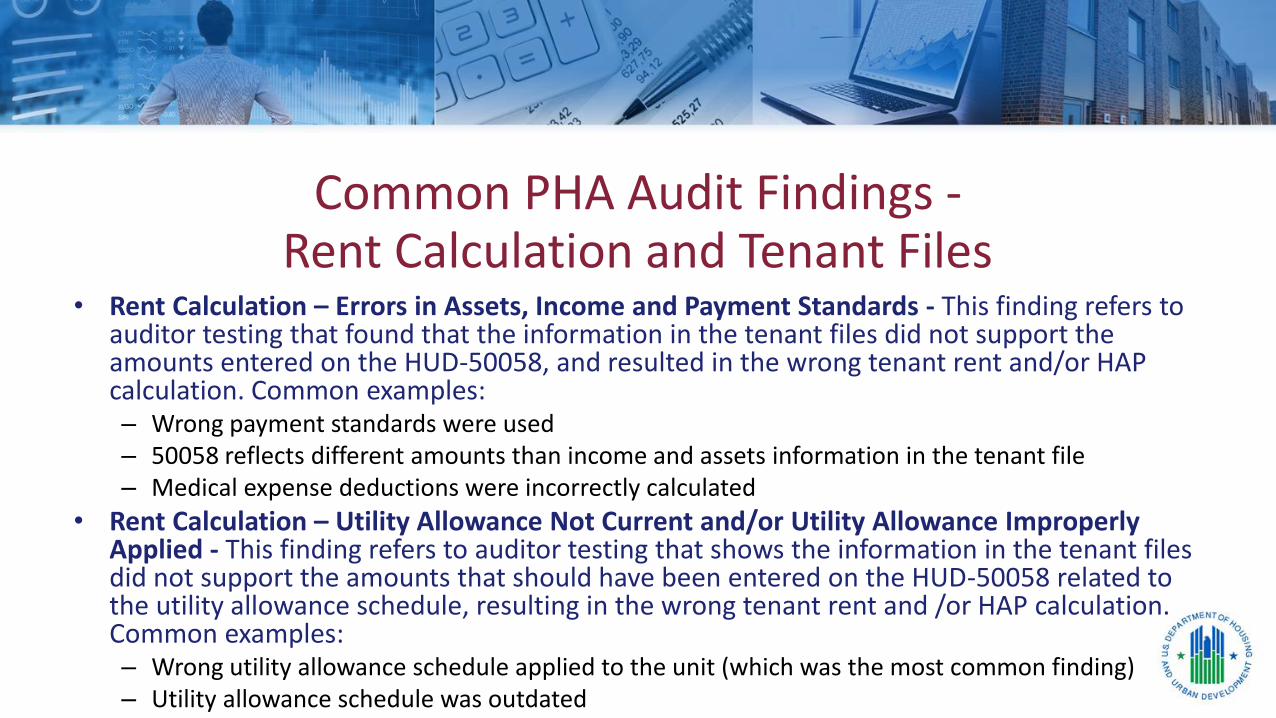

Common PHA Audit Findings - Rent Calculation and Tenant Files

• Rent Calculation – Errors in Assets, Income and Payment Standards - This finding refers toauditor testing that found that the information in the tenant files did not support theamounts entered on the HUD-50058, and resulted in the wrong tenant rent and/or HAPcalculation. Common examples:– Wrong payment standards were used– 50058 reflects different amounts than income and assets information in the tenant file– Medical expense deductions were incorrectly calculated

• Rent Calculation – Utility Allowance Not Current and/or Utility Allowance ImproperlyApplied - This finding refers to auditor testing that shows the information in the tenant filesdid not support the amounts that should have been entered on the HUD-50058 related tothe utility allowance schedule, resulting in the wrong tenant rent and /or HAP calculation.Common examples:– Wrong utility allowance schedule applied to the unit (which was the most common finding)– Utility allowance schedule was outdated

Common PHA Audit Findings - Rent Calculation and Tenant Files (continued)

• Rent Calculation – Other Errors - This finding refers to other rent calculation errors:– Findings are related to rent reasonableness standards that were not properly applied resulting in

overpayments of HAP to the landlords– Ineligible person allowed into the program

• Tenant Files – Improper Documentation in Tenant Files /Recertification's Not Timely - Thisfinding refers to missing documentation in the tenant file and /or annual recertification notcompleted in a timely manner. Common examples of missing items include:– 3rd party income verification not in the file– Income discrepancies not documented– No community service documentation– No background check information– No lease

12

OIG Audits

• HUD’s Office of Inspector General (OIG)

– HUD’s OIG has a dual and independent reporting relationship to theHUD Secretary and Congress

– HUD’s OIG scope of activities are provided in an annual Audit Plan.The Audit Plan covers audits mandated by Congress, areas identifiedby the OIG as HUD’s management challenges, and external audits

• External audits focus on activities based on complaints, HUD andcongressional staff requests, and media attention

13

OIG Audits (continued)

• HUD’s OIG Report: Oversight of Small PHAs (2015-FW-0802)– Report concluded that there was a high risk associated with small and very

small PHAs– Of the 26 PHAs that were reviewed, 24 had common violations of HUD and

other requirements• Did not have adequate financial controls (18 housing agencies); including mis-use of

funds, financial conflicts of interest, and other similar issues, some of which resultedin criminal charges

• Did not follow procurement regulations or maintain documentation to support thePHA’s procurement functions (15 housing agencies)

• Did not properly administer tenant rents (7 housing agencies)

14

OIG Audits (continued)

• Common PHA audit findings in the Southwest Region and Michigan– Travel policies were not followed– Misuse of credit cards and vehicles– Procurement policy and procedures

were not followed or out of date– PHAs had ineligible program expenses,

including• Use of funds for personnel use• Unsupported costs• Unsupported / unreasonable cost

allocation plans• Unreasonable salaries

– Conflict of interest– Inadequate time and leave tracking– Rent calculation errors including

• Use of incorrect payment standards• Use of incorrect utility allowances• Missing documentation• Unexplained / unsupported payments

to landlords• Lack of policies and procedures

Other HUD Reviews – Departmental Enforcement Center (DEC)

• The Departmental Enforcement Center (DEC) is part of HUD’s Office of GeneralCounsel. The reviews initiated by the DEC are typically based on referrals fromHUD’s field offices regarding internal controls or non-compliance items

• DEC Findings− Lack of internal control policies or policies were not

followed − Travel policies were not followed − Improper cost allocation (lack of adequate

documentation); federal programs were charged for more than the program’s fair share of expenses

− Procurement policy was not followed or needs to be updated

− PHAs had ineligible program expenses (i.e., eligible costs) some of which resulted from inter-program activities

− Lack of segregation of duties − Inadequate time and attendance records (leave tracking) − Conflict of interest − Misuse use of credits cards and petty cash − Lack of Board oversight

Other HUD Reviews – PIH - Quality Assurance Division Reviews

• Quality Assurance Division (QAD) Reviews– A division within HUD’s HCV office

– Performs onsite reviews of the PHA data submitted into the VoucherManagement System (VMS)

– A VMS review focuses on determining:• If the VMS data submitted by the PHA accurately reflects the PHA’s HCV program

• If the data is reported in accordance with VMS instructions and definitions

• If the PHA has appropriate procedures in place to ensure accurate reporting

– Once the review is concluded, QAD will issue a report17

PIH - Quality Assurance Division Reviews (continued)

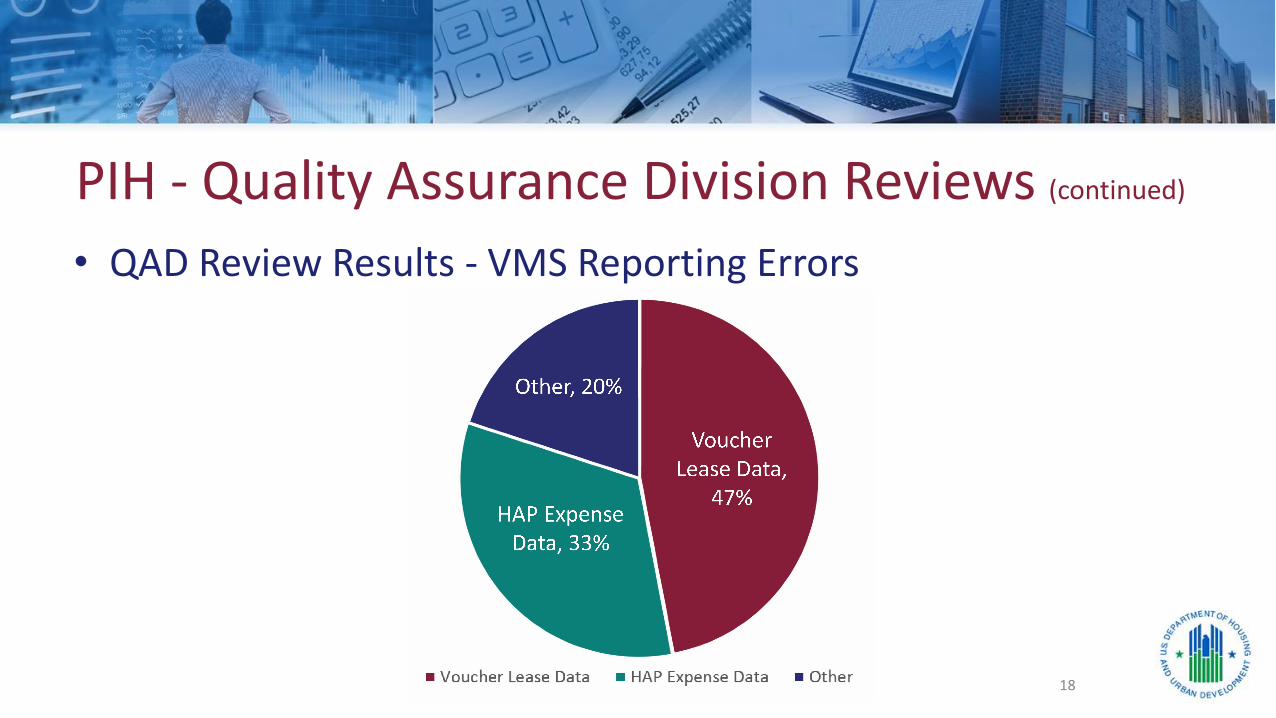

• QAD Review Results - VMS Reporting Errors

18

PIH - Quality Assurance Division Reviews (continued)

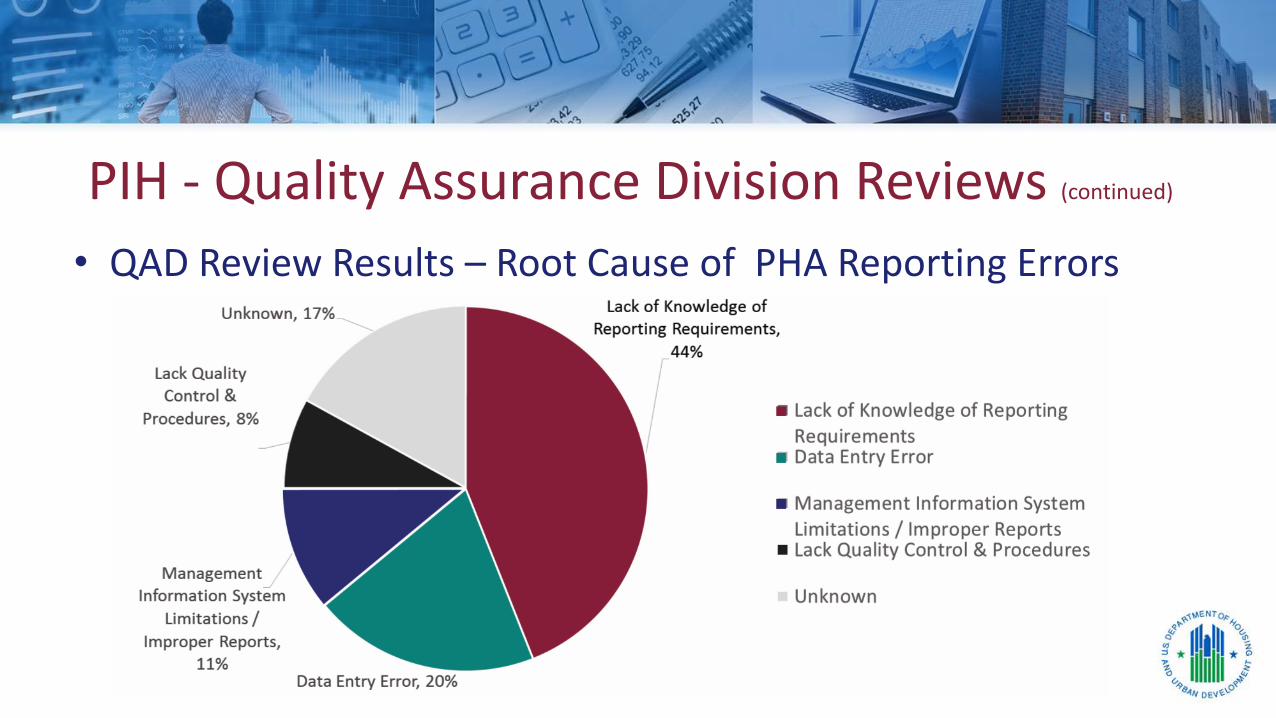

• QAD Review Results – Root Cause of PHA Reporting Errors

Module 2

THE FINANCIAL MANAGEMENT CONCEPT

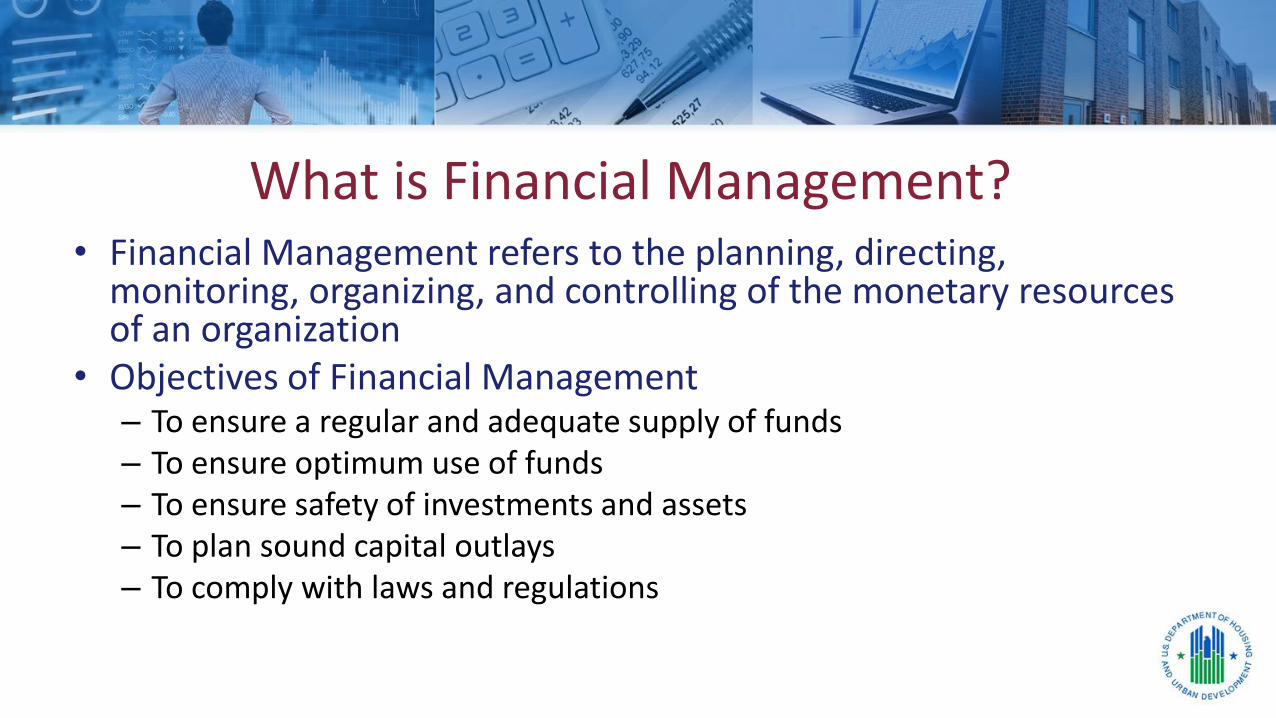

What is Financial Management? • Financial Management refers to the planning, directing,

monitoring, organizing, and controlling of the monetary resourcesof an organization

• Objectives of Financial Management– To ensure a regular and adequate supply of funds– To ensure optimum use of funds– To ensure safety of investments and assets– To plan sound capital outlays– To comply with laws and regulations

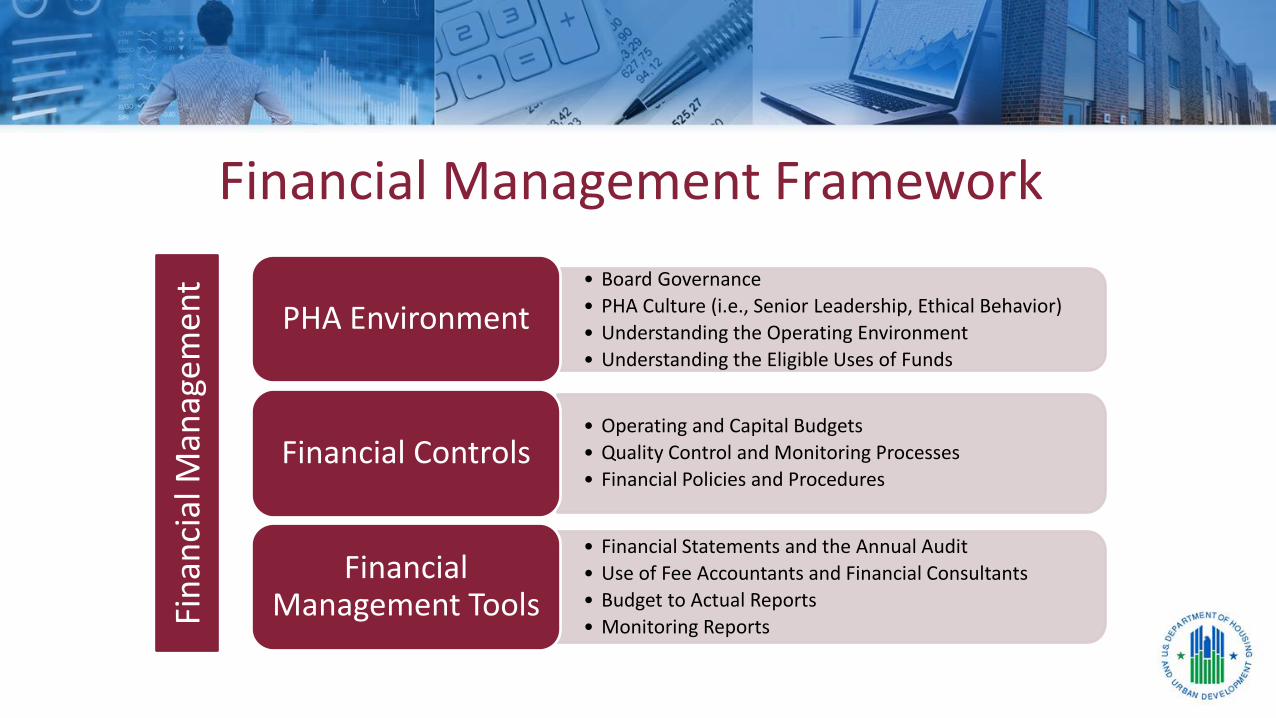

Financial Management Framework Fi

nan

cial

Man

agem

ent

PHA Environment • Board Governance

• PHA Culture (i.e., Senior Leadership, Ethical Behavior)

• Understanding the Operating Environment

• Understanding the Eligible Uses of Funds

Financial Controls • Operating and Capital Budgets

• Quality Control and Monitoring Processes

• Financial Policies and Procedures

Financial Management Tools

• Financial Statements and the Annual Audit

• Use of Fee Accountants and Financial Consultants

• Budget to Actual Reports

• Monitoring Reports

End of Module

This Ends the Training Module on

Understanding Financial Management

Public Housing Authority Financial Management Training

Module 2: Understanding Financial Management

Learning Activity 1:

Initial Identification of Risk

Learning Activity 1: Initial Identification of Risk Background

• In this learning activity, you are assuming the role of a new BoardCommissioner of the fictitious Anywhere Housing Authority

• While you have not attended your first board meeting, you have beenintroduced to most staff, including the Executive Director, Eric Davidson,and have talked with some of the other Board members

• To help you prepare for your first board meeting, Eric Davidson and someof the other Board members have given you a couple of documents to helpyou better understand the PHA and provided you with some backgroundand history on the Anywhere Housing Authority

Learning Activity 1: Initial Identification of Risk Instructions

• Download and print – Learning Activity 1: Identification of Risk

• Read the General Background of the Anywhere Housing Authority(Pages 2 -7 of the document)

• As you read, highlight any part of the general background, whichseems to be a warning flag or risk to the PHA

• When finished reading, answer the three questions on Page 1 ofthe document and return to the webinar for the answers andexplanations

End of Learning Activity 1

This Ends Learning Activity 1:

Initial Identification of Risk

Public Housing Authority Financial Management Training

Module 2: Understanding Financial Management

Learning Activity 1:

Solutions to Initial Identification of Risk

Goal of Learning Activity 1

• The goal of the learning activity is to help those charged withgovernance and in key leadership roles to understand the needto identify operational and financial risk at their own PHA

• Further learning activities in this training course will build onthis exercise by helping course participates develop skills to:– Identify risk and root causes of identified problems

– Implement policies and procedures for proper monitoring andcontrol

General Solution • The solutions provided in the next slides can also be found on page

7 of the Learning Activity 1 of the document and are not the onlyanswers to this exercise– Many responses by other participates were common

– However, there were areas that some participants thought were risk itemsand others did not, and

– There were differences in opinion as to the degree of risk on many of theitems noted

• Illustrates that the determination of risk by any one individualcan differ significantly

Solution to Question 1 Question 1: List those items in the “General Background of the Anywhere Housing Authority” which you would consider a risk to the PHA or a warning flag. • East Farm Road Apartments seems to have little contact with the central office• The working relationship between Paul Moore, property manager and Eric

Davidson, the ED, seems to be strained• AHA may be overstaffed for maintenance• There may be a conflict of interest as Ed Lincoln, maintenance staff at East Farm

Roads is supervised by Mark Lincoln, maintenance supervisor• AHA’s service model provides property managers with authorization to procure

up to $20,000 in material and services with no further approval• Rent can be paid in cash and a manual receipt is issued

Solution to Question 1 (continued)

• The property managers and Eric Davidson, the ED have credit cards with a veryhigh limit of $20,000

• Hope Collins, the HCV coordinator does not have much in the way of support /backup and likely is not up to date on all the rules and regulations for the HCVprogram

• Questions can be raised as to the quality of audit services, Johnson, CPA isproviding

• 40% of CFP funds is used to support operations• Comments made by Board members call into question Board governance as the

statements seem to indicate a hands-off approach to monitoring and a highreliance on the fact that everything is OK because of the program’s highperformance status, no audit findings, and little contact with the field office

Solution to Question 2 Question 2. Based on the information provided do you consider AHA to have any serious management or financial issues? • With the information provided as part of the learning activity, it is difficult to

determine if AHA has serious management or financial issues• A certain number of improvements are needed at East Farm Road Apartments

and some of the policies that are currently used by AHA are questionable• These issues may or may not raise to a serious management or financial

condition• Other Board members seem to have confidence in Eric Davidson and are

generally OK with the results of the operations• At this time, you have not been provided enough information to really form an

opinion on how serious some of the issues may be at AHA

Solution to Question 3

Question 3. As a Board member, what other information would you need to better understand the issues?

• Board Meeting package, with program metrics and dashboards

• 2017 Budget package

• Current financial statements, including budget to actuals

• Similar historical information / data at the project / program levelin order to determine the “norm” and for trending purposes

End of Learning Activity 1 Solutions

This Ends Learning Activity 1:

Initial Identification of Risk