Management, Finance and Cost Control in the Midlands charcoal iron industry

29

PLEASE SCROLL DOWN FOR ARTICLE This article was downloaded by: [King, Peter] On: 6 January 2011 Access details: Access Details: [subscription number 931809571] Publisher Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37- 41 Mortimer Street, London W1T 3JH, UK Accounting, Business & Financial History Publication details, including instructions for authors and subscription information: http://www.informaworld.com/smpp/title~content=t713683750 Management, finance and cost control in the Midlands charcoal iron industry P. W. King Online publication date: 04 January 2011 To cite this Article King, P. W.(2010) 'Management, finance and cost control in the Midlands charcoal iron industry', Accounting, Business & Financial History, 20: 3, 385 — 412 To link to this Article: DOI: 10.1080/09585206.2010.514410 URL: http://dx.doi.org/10.1080/09585206.2010.514410 Full terms and conditions of use: http://www.informaworld.com/terms-and-conditions-of-access.pdf This article may be used for research, teaching and private study purposes. Any substantial or systematic reproduction, re-distribution, re-selling, loan or sub-licensing, systematic supply or distribution in any form to anyone is expressly forbidden. The publisher does not give any warranty express or implied or make any representation that the contents will be complete or accurate or up to date. The accuracy of any instructions, formulae and drug doses should be independently verified with primary sources. The publisher shall not be liable for any loss, actions, claims, proceedings, demand or costs or damages whatsoever or howsoever caused arising directly or indirectly in connection with or arising out of the use of this material.

Transcript of Management, Finance and Cost Control in the Midlands charcoal iron industry

PLEASE SCROLL DOWN FOR ARTICLE

This article was downloaded by: [King, Peter]On: 6 January 2011Access details: Access Details: [subscription number 931809571]Publisher RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Accounting, Business & Financial HistoryPublication details, including instructions for authors and subscription information:http://www.informaworld.com/smpp/title~content=t713683750

Management, finance and cost control in the Midlands charcoal ironindustryP. W. King

Online publication date: 04 January 2011

To cite this Article King, P. W.(2010) 'Management, finance and cost control in the Midlands charcoal iron industry',Accounting, Business & Financial History, 20: 3, 385 — 412To link to this Article: DOI: 10.1080/09585206.2010.514410URL: http://dx.doi.org/10.1080/09585206.2010.514410

Full terms and conditions of use: http://www.informaworld.com/terms-and-conditions-of-access.pdf

This article may be used for research, teaching and private study purposes. Any substantial orsystematic reproduction, re-distribution, re-selling, loan or sub-licensing, systematic supply ordistribution in any form to anyone is expressly forbidden.

The publisher does not give any warranty express or implied or make any representation that the contentswill be complete or accurate or up to date. The accuracy of any instructions, formulae and drug dosesshould be independently verified with primary sources. The publisher shall not be liable for any loss,actions, claims, proceedings, demand or costs or damages whatsoever or howsoever caused arising directlyor indirectly in connection with or arising out of the use of this material.

Accounting, Business & Financial HistoryVol. 20, No. 3, November 2010, 385–412

Management, finance and cost controlin the Midlands charcoal iron industry

P.W. King∗

Hagley, Worcestershire, England

The iron industry was fully industrialized by the seventeenth century. The initial ironmasters were landowners,with clerks managing their ironworks. Professional ironmasters emerged from the clerks by the 1600s. The largestiron businesses (such as that of the Foley family described here) had general managers. Loans (secured by bonds)were important for business finance, including for paying up share capital. Accounting varied between chargeand discharge-oriented systems of double entry bookkeeping and those maintained according to the classic Italianmethod. Cost accounting was not systematically practised, but yields from raw materials were monitored and theinformation contained in the financial accounts contained data relevant to performance decision making. Managerswere trained on the job by experienced managers.

Keywords: Foley; iron production; double entry; Italian method; management; cost accounting; bonds

1. Introduction

The inherent problems of management inevitably depend on the nature of the business being man-aged. The accounting system for any particular business should be designed to assist with the moredifficult issues of control. Many manufacturers before the industrial revolution (particularly tex-tiles) were organized on the domestic system, often in a dual economy (‘proto-industrialization’),where people divided their time between agriculture and manufacture (Hudson 1989). In these,the greatest difficulty for an entrepreneur, like the mid-eighteenth century Essex clothier ThomasGriggs who put out materials for manufacture, was perhaps stock control to help prevent embez-zlement by out-workers (Burley 1958). During the industrial revolution, textile businesses weremechanized, and the workers were gathered in a mill (or factory) where power was available todrive the machinery. This produced new management problems, which required new solutions.Various studies have focused on the response to these problems of manufacturing business duringthe industrial revolution (e.g. Pollard 1965; Hudson 1986; Wilson 1995). However, the type ofproblems they faced were not new. Iron production by ironmasters was probably fully industrial-ized from the sixteenth century, in that it used water-powered plant (furnaces and finery forges)and occupied its artisans full-time. Its main products (bar and rod iron) were then sold to ironmon-gers, who organized their manufacture into nails and a host of other consumer goods under the

∗Email: [email protected]

ISSN 0958-5206 print/ISSN 1466-4275 online© 2010 Taylor & FrancisDOI: 10.1080/09585206.2010.514410http://www.informaworld.com

Downloaded By: [King, Peter] At: 13:25 6 January 2011

386 P.W. King

proto-industrial domestic system (Rowlands 1975, 1989; Hey 1975, 1990). The inherent problemsof an ironmonger’s business differed little from those of other putting-out businesses. However,ironmasters had to address some issues of plant-based production, including the control of produc-tion costs, long before the textile manufacturers did. To help clarify matters in this article, the termsproduction and manufacture will consistently be used as antonyms to distinguish the two iron busi-nesses: first ironmasters produced iron; then ironmongers organized its manufacture into ironware.

A quarter of a century ago little archival research had been undertaken into accounting methodsup to and during the industrial revolution, authors having generally relied on what appeared incontemporary treatises. The work of Jones (1985), Fleischman and Parker (1997; also 1990, 1992),Boyns and Edwards (2007; also 1992, 1996, 1997), Edwards and Newell (1991), Oldroyd (2009)and others, has revolutionized understanding of cost and management accounting in the industrialrevolution. However, few studies have considered accounting methods in the preceding period.Grassby’s work (1995) mainly considered the mercantile business community in London. Jones’valuable work (1985) is limited in its scope to Wales, where the economy remained relativelyunsophisticated until the industrial revolution, with the result that he identified, as new, devel-opments that can be traced in England considerably earlier. Edwards, Hammersley, and Newell(1990) considered the operations of the Society of Mines Royal at the turn of the seventeenth cen-tury, whose records were found to contain several cost statements. Boyns and Edwards (1992)1

examined an English ironmasters’ business (near Sheffield) from 1690 to 1783, and they found itto be using a sophisticated accounting system according to the classic Italian method. The contextof that business has also been considered by historians (Hopkinson 1954; King forthcoming).The Italian method was similarly used by the Backbarrow Company in north Lancashire. Theiraccounts are similar in structure to those found near Sheffield, with the stock and consumption ofiron ore and charcoal carefully recorded, so that the yield and the production costs could easilyhave been extracted, but nothing suggests that they in fact did so (Lancs. RO, DDMc/30/2–5).Fleischman and Parker (1997, 61, 140), who dismissed the company’s accounts as valueless,appear only to have examined a (preliminary) record book for a single blast in the furnace (Lancs.RO, DDMc 30/1).

This article focuses on a group of ironmaking businesses in the Midlands, in which successivemembers of the Foley family were concerned. Its most important source is accounts, which survive(not quite continuously) from 1667 to 1751. They, and other documents preserved by the family,are now deposited in Herefordshire Record Office. These were used by Johnson (e.g. 1951, 1952),by Schafer (1971, 1978, 1990), and by Hammersley (1979), mostly to consider issues of economichistory.2 This paper will concentrate on who managed the business and how it was run (section 2),and the accounting systems used (section 3). This will be followed by shorter sections on costaccounting (section 4), finance (with an emphasis on bonds in the commercial life of the period)(section 5), and the inter-generational transmission of knowledge (section 6). Before these matterscan be addressed, it is first necessary to contextualize the material by describing the productionprocesses, the structure of the industry in the region, the origins of the Foley business, and theirmethods of fuel cost control. In doing so, it will also draw analogies from other charcoal ironworks.However, these are often much less well recorded, and are in some cases hardly known exceptfrom pleadings (and so on) in the Chancery and other courts.

1.1. The production processes

From the mid sixteenth to the mid eighteenth century, most iron was made (using charcoal as fuel)in a two-stage process involving a blast furnace and finery forge. The furnace was a large structure

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting, Business & Financial History 387

which operated a continuous process. Iron ore and charcoal were fed at the top and molten pigiron (also called sow iron) and slag flowed from the bottom. The forge had two kinds of hearth,fineries (usually two of them) where pig iron was remelted so that its carbon content (4–5%)could be oxidized, and a chafery for reheating during forging. The blast furnace and both kindsof hearth were blown by water-powered bellows, and the hammer (whose head weighed about aquarter of a ton) was lifted by another waterwheel. The forge process was batch-based, processingas much iron at a time as would make a single bar, and usually provided a fulltime occupationfor its artisans (Schubert 1957, 157–291; Tylecote 1991, 1992, 95–9 and 102–4). Rod iron fornailmaking was then produced by cutting bars in a slitting mill, a variety of mill introduced toKent in 1590 and to the Midlands in c.1611 (Schubert 1957, 304–12; Tylecote 1991, 248–52,1992, 105; King 1999, 62–4, 71–4). The business of an ironmaster was thus mainly concernedwith relatively few successive processes – the operation of blast furnaces, forges and sometimesslitting mills – and with procuring charcoal to fuel these.

Iron commodities were measured in tons shortweight (2240lb) or tons longweight (2400lb).Charcoal was invariably measured in loads (or dozens) and sacks (or shems or seams). Thesesound vague, but were, at least in theory, precise measures of volume. A sack contained eightbushels (or strikes), and a load (evidently a cart load) consisted of a dozen sacks. The practice wasno doubt somewhat less precise, because of charcoal settling in transit (Jones and Harrison 1978,802; Mott 1957–9, 85–6; FIW, KL/12; WRO, BA 10470/3, passim). Ironstone was measured inloads (or blooms or dozens) usually of 12 bushels (or strikes); again a precise measure in theory(Mott 1957–9, 86; FIW, KL/12; Schafer 1978, 86).3

1.2. Regional structure of the industry

Initially, ironmaking entrepreneurs were magnates or landed gentry, whose prime object was toexploit unsaleable wood on their estates, by using it to produce iron (Stone 1965, 349).4 Thus themanor of Wentsland and Bryngwyn near Pontypool (Gwent) was described as ‘overgrown withgreat woods worth nothing for want of use of the same’ until Richard Hanbury built an ironworksin 1576 (TNA, E 134/13 Jas. I/Hil. 15; E 134/13 Jas. I/Mich. 16; cf. Donald 1961, 99–100).Similarly Ralph Tomlins (a minor landowner) was induced to build a furnace in Burford (southShropshire) in the 1590s, because he had ‘there great store of woods and underwoods, which atthat time and in that country would not yield any great profit by reason of the great store of woodsthereabouts’ (TNA, REQ 2/393/12).

The ironworks were usually managed by a clerk who was accountable to the landowner. For thispurpose, a simple charge and discharge account was used. For example, the accounts of the Earl ofShrewsbury’s ironworks at Shifnal in Shropshire are in this form. The charge consisted of the ironmade and previously in stock. The discharge included expenses incurred at the ‘hammers’(forges),the furnace, and in obtaining ironstone (Watts 2000). This ensured that the clerk accounted properlyfor the assets passing through his hands, but it did not provide an efficient tool for controllingcosts.

Major landowners had heavy calls on their time (such as politics and hunting) and tended to beill equipped to oversee a complicated business, and to ensure that they obtained the best returnfrom it, even if they had the necessary ability. A convenient answer was to avoid managementproblems by leasing the works. The landowner then agreed in advance what return would bereceived. This usually consisted of a rent for the works and a payment for every cord (128ft3) ofwood consumed. There might in addition be a payment for every load of ‘mine’ (ironstone) usedwhere the landowner had a mine on his land. The landowner might also provide the working capital

Downloaded By: [King, Peter] At: 13:25 6 January 2011

388 P.W. King

as a loan, whose repayment was secured by a bond. Such bonds were important as a source offinance, and will be discussed later. In these cases, the clerk in charge of the ironworks became anironmaster in his own right. The management problem remained, but the risk fell on a person morelikely to have the ability to manage it. Thus, Walter Colman and others ran ironworks on CannockChase in the 1600s under a series of short leases (King 1999, 68). Henry Wallop (himself a lesseefrom the crown) let Bringewood ironworks (Herefordshire) to Robert Steward and others in 1605(TNA, C 2/Jas. I/A3/31; E 134/10 Chas. I/Mich. 18). The Earl of Kingston’s arrangement withMartin Ash at Whaley Furnace (Derbyshire) and Cuckney Forge (Nottinghamshire) in 1617 tookthe form of a partnership. However, when Ash could not perform his bargain and absconded, theEarl had to take the works in hand (TNA, C2/Chas. I/C6/37).

Businesses could become more complicated. One man could manage a furnace and forge onnearby sites, but certain businesses had several of each – usually equal numbers of furnaces andtwo finery forges in the early periods. Thomas Parkes (an ironmaster) and William Whorwood(a gentleman) had a furnace and forge, at each of Perry Barr, Wednesbury, and West Bromwich.Parkes had further furnaces at Deepmore (in Saredon) and Moddershall (in Stone) with twomore forges and perhaps other works. All these places were in Staffordshire. A dispute thatarose between them (indicted as a riot) was evidently resolved by Whorwood retiring, and thebusiness was continued until the death of Thomas’ son Richard in 1618, when it was sold (byRichard’s son another Thomas) to Middleton, Nye, Goreinge & Co. Their business was split upin 1622, with Thomas Nye taking over most of the works. He was subsequently in partnershipwith ‘one Mr Ffolie’, almost certainly Richard Foley of Dudley, and later of Stourbridge, bothin Worcestershire, who was probably previously simply a nail ironmonger. The other part of thebusiness was continued by Middleton, Goreinge & Co., until 1627 when Goreinge alone renewedthe lease of the one remaining ironworks – Chartley (Burne 1932, 194, 279–301; King 1999,64–8, 2006, 74–7).

1.3. Origins of the Foley business

Richard Foley (see Figure 1) continued several of Nye’s ironworks after Thomas Nye’s death in1631, and leased others from Lord Dudley and other landowners. Few records survive from theearlier periods of the Foley business, how it was managed and what form its accounts took remainsuncertain. Richard handed over his ironworks to his son Thomas, beginning with WhittingtonForge in 1637, when he was aged 21. Thomas expanded the business by acquiring ironworks inand around the Forest of Dean (Gloucestershire), starting at Tintern in c.1648 (King 1999, 67–8,74–5). This evidently became an immensely profitable business in the 1650s and 1660s, as ThomasFoley invested over £140,000 in the purchase of landed estates in that period (FIW, C/1). Thissuccess was almost certainly the result of owning all the ironworks in the area, enabling him todictate the price he would pay for wood to be turned into charcoal. In 1669, Thomas sold his SouthStaffordshire works (which included some in Worcestershire and Shropshire) to his youngest sonPhilip (then aged 21) for the colossal sum of £60,000. This was the culmination of an inter-generational transmission process going back to 1666. He passed those in Gloucestershire on tohis second son Paul at about the same time. The business arrangements of Paul and Philip almostcertainly reflect those employed by their father, and perhaps even their grandfather (Schafer 1971,19–23, 1978, xi–xix; Rowlands 2008; original bonds etc: FIW, KBf/72–87; and P/15/1–6.). Eachironworks (or small group of them) had a clerk, who was responsible for its management (Schafer1978, passim). The clerks had substantial assets under their control and probably all entered intobonds ‘to render a true just account’, though only one example of such (for Flaxley furnace and

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting, Business & Financial History 389

________________

A simplified family tree of the Foley family

Richard(1580-1657)

Richard I of Longton Thomas I of Witley Priscilla = Robert Samuel John (1608-78) (1616-77) (1615-67) (1626-76) (1631-84)

| Henry Glover (d. 1689)Richard II of Longton

(1632-81) Robert IIThomas II of Witley Paul Philip (c.1651-1702)

(1641-1701) (1645-99) (1648-1716) | |

Thomas III of Witley Thomas Icreated Lord Foley 1712 of Stoke Edith

(1673-1733) (c.1670-1737)| |

Thomas IV of Witley Thomas II 2nd Lord Foley of Stoke Edith (1703-66) (c.1695-1749)

| Thomas

III of Stoke EdithV of Witley (from 1766) created Lord Foley 1776

(1716-77)

Figure 1. A simplified family tree of the Foley family.

forges in Gloucestershire) has been found (FIW, DCc/9). The accounts show substantial sumsas due from them, but this could be reconciled with sums due to them for goods sold on credit(Schafer 1978, passim); an issue that will be further explored below.

1.4. Methods of fuel cost control

The largest variable cost was for charcoal (Hammersley 1973, 608–11; Hyde 1973, 407–10, 1974,191–6), so that control of its price was important. Iron ore and other raw materials, of course, hadto be obtained, but generally their availability was not a limiting factor on iron output. As Schaferhas shown, in the early 1670s Philip found his profits squeezed by his brother Paul, a supplierwho was raising his price for Forest of Dean pig iron, and by John Finch, a new competitor whosepresence was forcing up the price of charcoal. The end of the local monopoly for fuel requireda new solution. Philip and Finch came to an agreement, which (though framed as an agreementfor sale) was essentially restrictive in character. It gave each party liberty to buy wood and makeiron in certain places, but it required sales at uncompetitive prices if they went beyond the agreedlimits. In Foley’s case the buyers were to be his clerks John Wheeler and Richard Avenant (ofwhom more below) (FIW, KE/31 and 50; Schafer 1971, 30; King 2002, 49).5 A few monthslater, Finch sold his works to Alderman John Foorth and Sir Clement Clerke, and Philip later soldthem certain works in the upper Stour catchment. Unusually, he obtained a payment for goodwill(though not so-described) of £2000 beyond the value of the net assets (FIW, KD series; Schafer1971, 29; King 2002, 49–50, 2008, 49–50). This is the only ‘goodwill’ payment which this writerhas observed in the charcoal iron industry. In 1676, Foley sold ironworks in the Tame valley toHumfrey Jennens of Birmingham (HRO, E12/KG/5 cf. KG/1–15; Schafer 1971, 29), who hadhis ironworks to the east of Foley’s.

When Philip sold certain works to Foorth and Clerke (FIW, KD series; Schafer 1971, 29),boundaries for buying wood were agreed (FIW, KD/11), securing a continuing monopoly over

Downloaded By: [King, Peter] At: 13:25 6 January 2011

390 P.W. King

the fuel supply. Following Foley’s 1676 sale of ironworks in the Tame valley to Humfrey Jennens,the boundaries were to be fixed by the party’s clerks (HRO, E12/KG/5 cf. KG/1–15; Schafer1971, 29). In 1682, Hales Furnace at Halesowen (which had been included in this sale) passedto John Wheeler and Richard Avenant, with the clerk there called John Downing (FIW, KH/31;Schafer 1971, 31). At the same time, Jennens agreed to buy 150 tons of pig iron per year fromHales. In 1692, John Downing and his son Zachary leased the furnace. They then agreed to sell100 tons per year to Jennens, and continued the boundary agreement. This arrangement brokedown in acrimony about ten years later. Due to war, the import of foreign iron had become moreexpensive, and the price of English iron rose with it. The price of cordwood had increased withthat of iron, from five to six shillings per cord to ‘nine shillings or more’ (TNA, E 112/880/41).Zachary Downing was thus tied to a fixed-price sale agreement for pig iron when his charcoalcosts were rising, and suffered the inevitable consequences.

The 1692 boundary agreement is the last one so far discovered. However, the boundary systemwas inherently unstable, since any agreement was for a fixed term that expired (such as that of anironworks lease). By the 1720s, the system had been replaced by one where the ironmasters agreedamongst themselves the price at which they would sell iron. Hendrik Kahlmeter reported that theironmasters met at Stourbridge on the first Friday after Twelfth Night and monthly thereafter(Hildebrand 1958, 28). This in turn determined the price that ironmasters could afford to pay forwood and other commodities.6 This system continued far into the nineteenth century and probablygrew out of regular quarterly meetings at Stourbridge for settling accounts, perhaps going backat least to the 1670s (Ashton 1963, chapter VII; Birch 1967, 104–18; Smith 1978; King 1996,28–31; Evans 1997, 126–31; FIW, KBf/62–71).

2. General managers of the Foley Ironworks

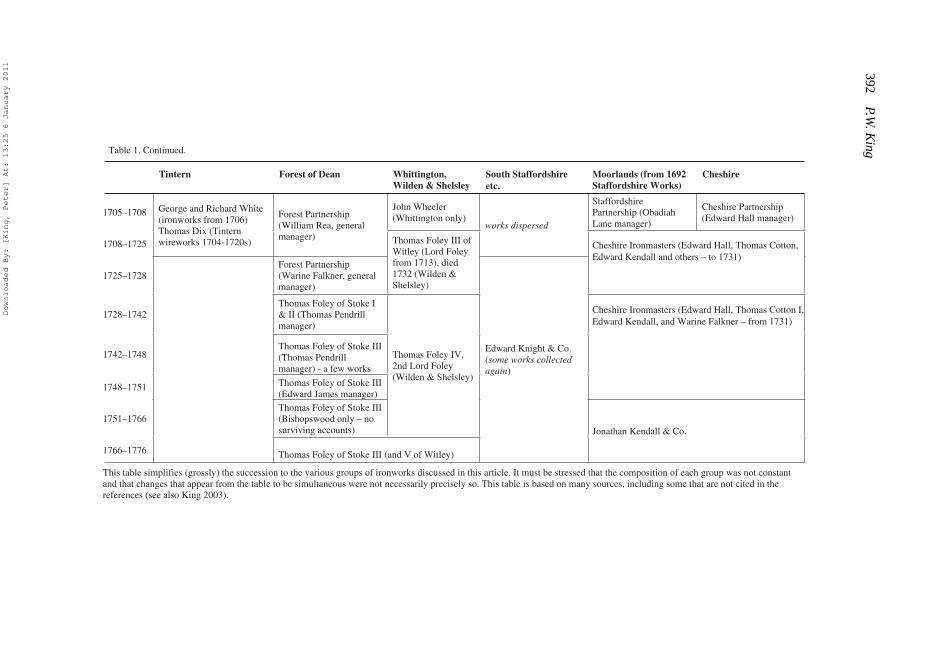

The Foley iron businesses were managed by a succession of general managers or managingpartners (not contemporary terms). Reference will be made below to several different businessesin which members of the Foley family were concerned. Table 1 seeks to portray the ownership ofthe various groups of works and, although quite complicated, it is still a simplification of the fullpicture.

2.1. Henry Glover

Thomas Foley employed Henry Glover as his general manager, probably from 1646 (HRO,E12/S/106, 1 Jun. 1646), but perhaps earlier, and Glover subsequently served Thomas’ sons. In1654, Glover married Thomas’ widowed sister ‘Pryssylla’ Wallis at Kidderminster.7 Glover alsohad business interests of his own, being involved in mining ironstone and coal (FIW, KAc/49;HRO, E12/IV/18/8/1). He was also from 1660 in partnership with Thomas, Thomas’ brotherRobert Foley, ‘Josuah’ Newborough (the other forge partner in Wolverley Forge) and others insupplying ironware down the Severn and into the southwest of England, including Exeter (TNA,C 6/161/57). Glover’s partnership with Robert Foley and George Gibbons may have been in hisown right and in continuation of this 1660 firm. Thomas (and then his son Paul) collected bonddebts due to them from Bristol ironmongers in the late 1660s and the 1670s (FIW, DAf/3–15).However, except in collecting payments, Glover was probably not active as a partner in these busi-nesses. He kept Philip Foley’s Stourbridge cash (Schafer 1978, 61–4), and he inspected Paul’sworks in the Forest of Dean in 1679 on his way back from Bristol fair (FIW, DCc/11). He contin-ued to manage the Tintern Works for Thomas’ son for the rest of his life (FIW, Ac and Af series;

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting,B

usiness&

FinancialH

istory391

Table 1. Business ownership.

Tintern Forest of Dean Whittington, Wilden & Shelsley

South Staffordshire etc.

Moorlands (from 1692 Staffordshire Works)

Cheshire

1590s–1618Parkes family

Middleton Nye & Co.Thomas Nye (RichardFoley a partner?)

Richard Foley (possiblywith Humfrey Jennens)

1640s

Sir Basil Brooke, GeorgeMynne, Thomas Hackett(from c.1627)

1648–1669Thomas Foley (Henry Glover general manager)Forest of Dean from late 1650s or later

1669–1674

1631–1638

1621–1631

1618–1621

Paul Foley (ThomasFoley perhaps initially apartner)

yeloFpilihPdnaluaP

Philip FoleyFoorth & Clerke(to 1676)

(from c. 1651) Richard Foley of Longton I(died 1678)

1678–1681

1674–1678

Cornish, Langworth &Sergeant

Richard Foley of Longton II (died 1681)

1681–1685Paul Foley

John Foley (died 1684)As Moorland (?)

(Continued)

1685–1689

Thomas Foley (died 1677)and Thomas Foley II ofWitley (Henry Glovermanager)

Henry Glover (died1689)

1689–1692John Wheeler and Richard Avenant

1692–1698Ironworks in Partnership(Paul Foley "Chairman"; John Wheeler "Cashkeeper")

Hayford & Cotton(manager Thomas Hall)

1698–1705

Thomas Foley II ofWitley; (Obadiah Lanemanager - Whitebrookwireworks only)Duke of Beaufort (Tintern) Richard Wheeler

(bankrupt 1703)

John Wheeler (Obadiah Lane manager); Philip Foley declared a partner in 1698 Cheshire Partnership

(manager Thomas Hall)

Downloaded By: [King, Peter] At: 13:25 6 January 2011

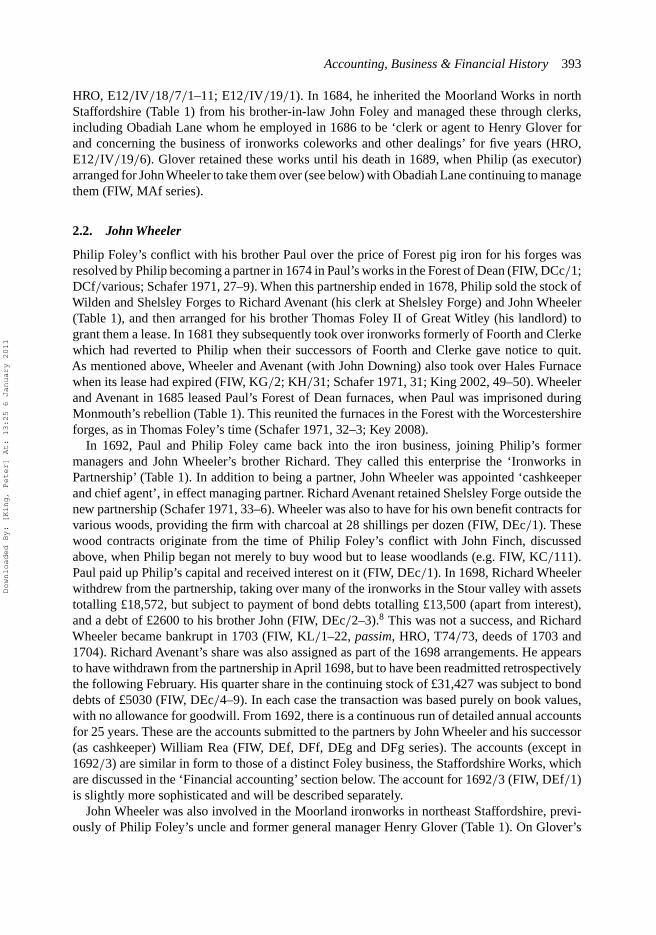

392P.W

.King

Tintern Forest of Dean Whittington,

Table 1. Continued.

Wilden & Shelsley South Staffordshire etc.

Moorlands (from 1692 Staffordshire Works)

Cheshire

1705–1708John Wheeler (Whittington only)

StaffordshirePartnership (Obadiah Lane manager)

Cheshire Partnership (Edward Hall manager)

1708–1725

George and Richard White (ironworks from 1706) Thomas Dix (Tintern wireworks 1704-1720s)

Forest Partnership (William Rea, general manager)

works dispersed

1725–1728 Forest Partnership (Warine Falkner, general manager)

Thomas Foley III of Witley (Lord Foley from 1713), died 1732 (Wilden & Shelsley)

1728–1742 Thomas Foley of Stoke I & II (Thomas Pendrill manager)

1742–1748Thomas Foley of Stoke III (Thomas Pendrill manager) - a few works

1748–1751 Thomas Foley of Stoke III (Edward James manager)

Cheshire Ironmasters (Edward Hall, Thomas Cotton I,Edward Kendall, and Warine Falkner – from 1731)

Cheshire Ironmasters (Edward Hall, Thomas Cotton,Edward Kendall and others – to 1731)

1751–1766Thomas Foley of Stoke III (Bishopswood only – no surviving accounts)

Thomas Foley IV, 2nd Lord Foley (Wilden & Shelsley)

1766–1776 ekotS fo yeloF samohT III (and V of Witley)

Edward Knight & Co. (some works collected again)

Jonathan Kendall & Co.

This table simplifies (grossly) the succession to the various groups of ironworks discussed in this article. It must be stressed that the composition of each group was not constant and that changes that appear from the table to be simultaneous were not necessarily precisely so. This table is based on many sources, including some that are not cited in the references (see also King 2003).

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting, Business & Financial History 393

HRO, E12/IV/18/7/1–11; E12/IV/19/1). In 1684, he inherited the Moorland Works in northStaffordshire (Table 1) from his brother-in-law John Foley and managed these through clerks,including Obadiah Lane whom he employed in 1686 to be ‘clerk or agent to Henry Glover forand concerning the business of ironworks coleworks and other dealings’ for five years (HRO,E12/IV/19/6). Glover retained these works until his death in 1689, when Philip (as executor)arranged for John Wheeler to take them over (see below) with Obadiah Lane continuing to managethem (FIW, MAf series).

2.2. John Wheeler

Philip Foley’s conflict with his brother Paul over the price of Forest pig iron for his forges wasresolved by Philip becoming a partner in 1674 in Paul’s works in the Forest of Dean (FIW, DCc/1;DCf/various; Schafer 1971, 27–9). When this partnership ended in 1678, Philip sold the stock ofWilden and Shelsley Forges to Richard Avenant (his clerk at Shelsley Forge) and John Wheeler(Table 1), and then arranged for his brother Thomas Foley II of Great Witley (his landlord) togrant them a lease. In 1681 they subsequently took over ironworks formerly of Foorth and Clerkewhich had reverted to Philip when their successors of Foorth and Clerke gave notice to quit.As mentioned above, Wheeler and Avenant (with John Downing) also took over Hales Furnacewhen its lease had expired (FIW, KG/2; KH/31; Schafer 1971, 31; King 2002, 49–50). Wheelerand Avenant in 1685 leased Paul’s Forest of Dean furnaces, when Paul was imprisoned duringMonmouth’s rebellion (Table 1). This reunited the furnaces in the Forest with the Worcestershireforges, as in Thomas Foley’s time (Schafer 1971, 32–3; Key 2008).

In 1692, Paul and Philip Foley came back into the iron business, joining Philip’s formermanagers and John Wheeler’s brother Richard. They called this enterprise the ‘Ironworks inPartnership’ (Table 1). In addition to being a partner, John Wheeler was appointed ‘cashkeeperand chief agent’, in effect managing partner. Richard Avenant retained Shelsley Forge outside thenew partnership (Schafer 1971, 33–6). Wheeler was also to have for his own benefit contracts forvarious woods, providing the firm with charcoal at 28 shillings per dozen (FIW, DEc/1). Thesewood contracts originate from the time of Philip Foley’s conflict with John Finch, discussedabove, when Philip began not merely to buy wood but to lease woodlands (e.g. FIW, KC/111).Paul paid up Philip’s capital and received interest on it (FIW, DEc/1). In 1698, Richard Wheelerwithdrew from the partnership, taking over many of the ironworks in the Stour valley with assetstotalling £18,572, but subject to payment of bond debts totalling £13,500 (apart from interest),and a debt of £2600 to his brother John (FIW, DEc/2–3).8 This was not a success, and RichardWheeler became bankrupt in 1703 (FIW, KL/1–22, passim, HRO, T74/73, deeds of 1703 and1704). Richard Avenant’s share was also assigned as part of the 1698 arrangements. He appearsto have withdrawn from the partnership in April 1698, but to have been readmitted retrospectivelythe following February. His quarter share in the continuing stock of £31,427 was subject to bonddebts of £5030 (FIW, DEc/4–9). In each case the transaction was based purely on book values,with no allowance for goodwill. From 1692, there is a continuous run of detailed annual accountsfor 25 years. These are the accounts submitted to the partners by John Wheeler and his successor(as cashkeeper) William Rea (FIW, DEf, DFf, DEg and DFg series). The accounts (except in1692/3) are similar in form to those of a distinct Foley business, the Staffordshire Works, whichare discussed in the ‘Financial accounting’ section below. The account for 1692/3 (FIW, DEf/1)is slightly more sophisticated and will be described separately.

John Wheeler was also involved in the Moorland ironworks in northeast Staffordshire, previ-ously of Philip Foley’s uncle and former general manager Henry Glover (Table 1). On Glover’s

Downloaded By: [King, Peter] At: 13:25 6 January 2011

394 P.W. King

death in 1689, Philip (as an executor of Glover) arranged for Wheeler to take them over. Wheelerleased further works in Staffordshire (as far south as Cannock Chase), together making upthe Staffordshire Works. They occupied an area to the north of Philip Foley’s earlier SouthStaffordshire Works. He also in 1695 rented the Staveley ironworks (Derbyshire), which includedCarburton Forge (Nottinghamshire). Philip Foley acted as guarantor for that bargain, until in 1698these works were transferred to variousYorkshire ironmasters.9 In 1698, Foley and Wheeler madean agreement to the effect that they had been partners since Glover’s death in 1689. This was per-haps a partnership previously, but a secret one because of Foley’s position as executor. It was adifficult executorship, because Glover had given legacies to the limit of his assets. He assumedthat a disputed debt relating to trade with Smyrna and Leghorn (inherited from his brother-in-lawJohn Foley, a Turkey merchant) was good, but it was not.10 Obadiah Lane managed these works,and he was granted a share in them. Lane also invested part of the money in his charge in apartnership in certain Cheshire ironworks (managed by Thomas Hall). This was no doubt donefor sound commercial reasons relating to the supply of Cheshire pig iron to Staffordshire forges,but has had the archival consequence that copies of the Cheshire Ironmasters’ accounts are inthe Foley archive (FIW, MDf/1–36; MDc/2; Awty 1957, 87–9, 92–100). A discussion of thesevarious accounts will form the bulk of the later section on accounting methods.

2.3. William Rea

John Wheeler was presumably growing old by 1705 (he died in 1708) and seeking to drawback from his responsibilities (TNA, PROB 11/508, q. 103, f.115). Under the new partnershipagreement in 1705 – the ‘Forest Partnership’ (see Table 1) – for the Forest Ironworks (near theForest of Dean), William Rea became ‘chief manager and cashier’, with a salary of £120 per year(and expenses), and with a small share in the partnership. The other shares were retained by thepartners in the Ironworks in Partnership (Thomas Foley of Stoke Edith, Philip Foley, John Wheelerand RichardAvenant).William Rea was clerk atWilden in the 1690s, sometimes jointly with others(FIW, DEf series), but subsequently settled in Monmouth to assist Wheeler in managing ironworksin and around the Forest of Dean, including a group of forges that Wheeler, Lane, and he acquiredin 1702. He also managed Redbrook Furnace in the Wye valley from 1702/3 and Monmouth Forgefrom 1704/5. The 1705 agreement appointed Richard Avenant ‘to go once a month to the Forestof Dean to inspect the business and take a view of the works and assist in making any considerablecontracts for wood and cinders’with a salary of £50 per year. (Bloomery cinders were used as a rawmaterial there to supplement iron ore.) The negotiations for this were apparently prolonged andonly completed in 1706, as a lease of July 1706 is listed in its schedule (FIW, DEf/8–11; DEc/10–13, 38). After Avenant’s death, Richard Knight, the prominent ironmaster who owned (amongstothers) the Bringewood works west of Ludlow (Ince 1991, 2–3; Page 1979, 8–11), bought a sharein the partnership and took over Avenant’s management role in inspecting the works. The deedwas dated 18 March 1709, but effective from 29 September 1707 (Worcs. RO, r899:228 BA 1970).He retired from the partnership in 1717, shortly after Philip Foley’s death when Philip’s executorsalso withdrew. That left just Thomas Foley of Stoke Edith (Paul’s son), William Rea, and JohnWheeler II (son of the other John Wheeler) as partners (TNA, E 112/1127/5; HRO, E12/II/2/16).

William Rea was until 1726 also a partner of the Cunsey Company, which built ironworks in theFurness Fells in 1711. He was a partner in the Cheshire Ironworks, which succeeded the businessin which Wheeler, Lane, and Philip Foley were earlier concerned. This was a network (includingwhat had been their Staffordshire Works) stretching from Bodfari in Flintshire to Cannock Chasein east Staffordshire. Rea was also an ‘agent and cashier’ for it (but not the chief manager), until

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting, Business & Financial History 395

1719 when he was found to have drawn out his capital (TNA, E 112/957/107, answer of EdwardHall). He also assisted John Wheeler’s widow Mary in her acquisition of the Cradley ironworks,near Stourbridge, following the bankruptcy of Zachary Downing (DALHS, DE 4/3, Rowleyleases, 1713), and married one of her daughters (Worcs. RO, Consistory wills, Mary Wheeler, 7Jan. 1714). Mary’s business had previously consisted of Hales Furnace and Whittington Forge(also near Stourbridge), which her husband had taken over in 1705. Before that, these were thelast works of the Foley Forest Partnership in the Stour valley (FIW, DEc/13). Edward Kendall,who had been John Wheeler’s clerk, managed the business for her and then for her two youngersons. In 1725, Rea and Kendall bought the Cradley Works from the sons. Rea had to withdraw acouple of years later, but Kendall continued them for the rest of his life.11 Kendall was a significantinvestor in the iron industry, with a share in the Cunsey Company (from 1711) and in the CheshireIronworks, perhaps from 1712 when he married Anne, daughter of William Cotton. He passedthese interests on to his sons, who were still partners in the 1770s (Awty 1957, 98–9, 110–7; TNA,E112/957/107, Answer of Edward Hall). From 1729, Kendall and John Williams (then also ofStourbridge) were partners in Little Clifton Furnace (Cumberland) and in associated foundries atGateshead and Newcastle (Anon 1907–8, 170–1); possibly at Little Clifton from its erection in1723 (cf. Lancaster and Wattleworth 1977, 19–20).

Rea’s great mistake was his purchase of a large quantity of wood from Lady Scudamore’s estatesat Holme Lacy (Herefordshire). She apparently insisted on him buying not only the cordwood(to be converted into charcoal), but also the timber. Rea realised this was too big a transactionfor him, and asked his ironworks partner Thomas Foley of Stoke Edith (Paul’s son) to join him.This contract was agreed during the embargo on Swedish trade (of 1717–19) when the priceof iron and hence of wood (for charcoal) were high; it proved to be too high for the ‘Homtimber’ partnership to be profitable, once the embargo ended and prices fell back. Furthermore,timber (as opposed to cordwood) was not a commodity in which Rea would normally havedealt, and he may have misestimated its value. Certainly, the partnership made a great loss, andits result was to ruin Rea financially (FIW, DGd/1–39; TNA, E 112/957/94–6, 107, 110–1;E134/1 Geo. II/East. 2; E134/ 3 Geo. II/Tr. 4; cf. E 112/1127/4–5; E 134/4 Geo. II/Hil. 8;E 134/5 Geo. II/Hil. 8 and 11; for embargo see King 1996, 30–1; for the price relationshipsee note 6).

2.4. Warine Falkner

On 1 October 1725, the other Forest Partners met at the Cock Inn in Wolverhampton and sackedWilliam Rea (TNA, E 112/1127/4, answer of Warine Falkner). He was seriously in arrears insubmitting annual accounts, having produced none since Michaelmas 1722 (TNA, E 112/957/94).The other partners were little involved in management, but (like a modern shareholder) neededannual accounts in order to monitor their investment and guard against embezzlement by themanagers. Thomas Foley seems to have moved to secure such subsidiary accounts as existed,as (exceptionally) a number of such accounts survive for 1723 and 1724 (FIW, DGf/36/1–36).Litigation followed as Foley sought to recover debts owed by Rea. This was conducted in theCourt of Exchequer, because Foley was an Auditor of the Imprests, and (in theory) had to attendthe Exchequer constantly; in practice, it was a valuable sinecure, the work being done by a clerk(Funnell 2008). The litigation dragged on, until it was eventually compromised in 1732 (TNA,E126/25, 1732 Mich. 2). By that stage, Foley and his son (yet another Thomas) had bought outthe two other partners, John Wheeler II and Cecilia Lane (FIW, DGc/1–5). The latter was thewidow of Obadiah’s son Nathaniel, and had joined the firm in March 1725 (FIW, DGc/3). The

Downloaded By: [King, Peter] At: 13:25 6 January 2011

396 P.W. King

main ironworks accounts for 1717–25 are missing due to their being sent to London in connectionwith this litigation (TNA, E 134, various as in preceding paragraph).

In 1725, the partners needed a manager to replace the sacked Rea. Cecilia Lane suggestedher brother-in-law Warine Falkner (TNA, E 112/1127/4, answer of Warine Falkner). He hadbeen a servant of Obadiah Lane and then of his widow Anne, and he married their daughterPriscilla. They lived with her mother, who in about 1714 transferred to him £500 of her stock ofthe Cheshire Ironworks.12 Falkner accepted the appointment (in place of Rea) as cashkeeper at asalary of £200 per year (Table 1). Rea was persuaded to prepare the missing accounts (TNA, E112/1127/5, answer; E 112/957/110, bill). Warine Falkner resigned at Midsummer 1728, partlybecause Foley distrusted him, and was constantly calling for payment faster than was possible(TNA, E 112/1127/4, answer of Warine Falkner). He returned to Staffordshire where he hadproperty at Rugeley, bought from Anne Lane.13 In 1731, a new partnership agreement was madefor the Cheshire Ironworks between Edward Hall, Warine Falkner, Edward Kendall and ThomasCotton.14 Perhaps, the more lucrative opportunities there also provided an incentive for Falknerto leave the Foleys.

2.5. Decline

Accounts for the Foley Forest Works survive again from Warine Falkner’s arrival in 1725 (FIW,DGf/1–2). Thomas Pendrill (the next manager – from 1728) continued the business (Table 1),but ironworks leases were not renewed when they expired, so that the business shrank in scale(FIW, DGf/3–16). At the point where Pendrill gave up (or perhaps died), there is a gap in theaccounts and subsequent ones are less detailed (FIW, DGf/17–35; cf. Hammersley 1979). Thesurviving accounts finally end in 1751 under Edward James’ managership. The last account forElmbridge Furnace suggests its closure, but Paul’s great-grandson Thomas III may have continuedBishopswood Furnace longer, as he appears as a purchaser of cordwood from the Forest of Deanuntil at least 1764.15 Shortly after that, he inherited the Great Witley estate from his distant cousinThomas, the second Lord Foley. The two Lords Foley had successively operated Wilden andShelsley Forges since 1708 when the 1678 lease to Wheeler and Avenant had expired. Thomas(the heir) continued these until the autumn of 1776.16

3. Financial accounts

At least two accounting systems were in use in the iron industry in the period discussed here,apart from charge and discharge accounts. Both have a double entry ledger, but what is referredto here as the classic Italian method is distinguished by the maintenance of a further book, thejournal. In the latter situation, information from books of first entry is systemically collected and‘journalised’by setting out the detail of each transaction (or group of them) and indicating to whatledger folios it should be posted. Thence it was posted to two pages of the ledger. Ledgers for thissystem can often be recognised by the presence of two sets of page or folio references: one (oftento the right of the date) to the journal page; the other (typically to the left of the money column)to the other ledger folio. This description applies to the system which John Fell & Co. used fortheir ironworks at Sheffield by 1690 (SA, SIR/1–6 and 12–20; cf. Boyns and Edwards 1992), butwas also used for many other businesses, including the Backbarrow Company from 1712 (Lancs.RO, DDMc 30/2–5) and the Coalbrookdale Company from 1718 (King 2010). In contrast, theaccounts of most of the Foley businesses use a double entry system consisting largely of personalaccounts though, sometimes, other classes of account are included, as will become clear below.

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting, Business & Financial History 397

3.1. A double entry method

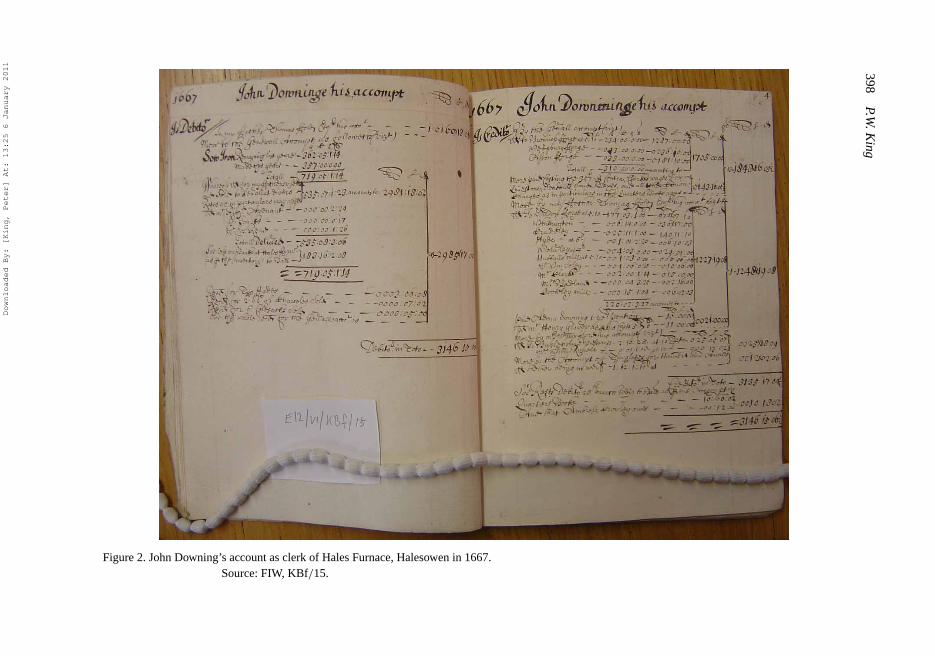

The annual accounts of the Philip Foley’s South Staffordshire Works survive for 1667–72. Theseconsist of charge and discharge accounts for each clerk (such as that for John Downing to ThomasFoley in Figure 2), with personal accounts also in double entry format headed ‘debtor’ and ‘cred-itor’ for other people. The latter include outside partners in certain forges (such as Lady Blountat Shelsley Forge, Worcestershire), and neighbouring ironmasters such as Hester Brindley whoslitted Philip’s iron at her Hyde mill. The clerks’ accounts also include those of Thomas Foley’sbrother-in-law Henry Glover (the general manager) for Stourbridge cash, Joshua Hall for Londoncash, and John Baldwin who kept their storehouse at Bewdley, the north Worcestershire riverport (FIW, KBf/15–19; Schafer 1978). Following a ‘tabula’ (index), the volume starts with PhilipFoley’s account with his father where the largest item is four bonds for the £60,000 purchase price(Schafer 1978, 58). This is followed by Philip Foley’s own account, listing the opening balances,to which he added the years profit (£2165 – although not named as such), enabling him to deter-mine that he had net assets in the business (before bad debts) of £11,051 (Schafer 1978, 60–1).The profit (again not named as such) was the balance of an account near the end called ‘generalaccount’, the result of posting to it the balances of the individual clerks’ (and other) accounts;finally, there is a trial balance, ‘the proofe of the whole account’(Schafer 1978, 108–11). These aredouble entry accounts in the sense that every credit has a corresponding debit entered elsewherein them, but with no separate nominal or real accounts, though costs are of course recognised asallowable expenses incurred by clerks in the same way that the revenues they collect are chargedto them. Some entries result from one clerk having made payments on behalf of another, so thata book transfer between their respective accounts was necessary. There are occasional passingreferences to a ‘Quarter’s Book’ and to a ‘Debt Book’, but it is not clear from what subsidiarybooks this annual account was compiled (Schafer 1978, mainly 57–111). However, in the 1680swhen Henry Glover owned the Moorland Works in north Staffordshire, he kept a ‘debt book’ (apersonal ledger) and a ‘cash book’ (which records the receipts and payments of various clerks).The debt book was small enough to live in Glover’s pocket (HRO, E12/IV/19/2–3). The existenceof a Quarter’s Book may imply that performance was monitored quarterly, but it could merely beconcerned with the quarterly settlement of ironmongers’ and other debts, for which a series ofstatements survive from the 1670s (FIW, KBf/63–71).

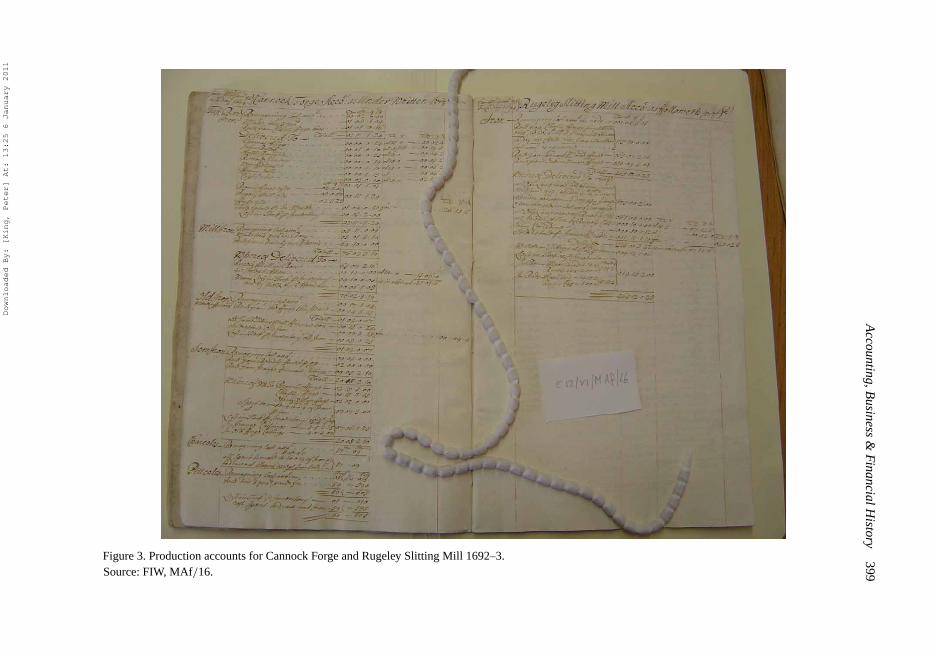

The accounts of John Wheeler’s Staffordshire ironworks from 1689 (FIW, MAf series) alsocomprise a balanced ledger of double entry accounts, wholly within a single book (for each year)and without a journal. However, they differ from Philip Foley’s accounts of 20 years earlier inthat the ledger starts with memorandum production accounts for each furnace, forge and so on(Figure 3 reproduces those for Cannock Forge and the Rugeley Slitting Mill 1692–3). These arenot part of the double entry system, but preliminary statements concerned with the consumption ofmaterials and the production and disposal of iron from each ironworks, probably derived from lessformal records kept by the clerks. No records from individual clerks survive for the StaffordshireWorks, but some kept by the clerks or stocktakers of works in the Forest of Dean survive for 1723and 1724 (FIW, DGf/36/1–36). The yields of the main raw materials were usually calculated inthe production account, but the space for the yield of sow iron has been left blank in Figure 3.Related to this is the clerk’s account for each works, a charge and discharge account in bilateralform, but with folio references appear on the left pointing to corresponding entries elsewhere.The sales data from each works was posted to an ‘abstract of several chapmen’s accounts forbar iron’, also bringing in payment information (presumably from a debt book – a ledger). Fromthere, totals were collected in a sales account and carried to the ‘General Account’.

Downloaded By: [King, Peter] At: 13:25 6 January 2011

398P.W

.King

Figure 2. John Downing’s account as clerk of Hales Furnace, Halesowen in 1667.Source: FIW, KBf/15.

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting,B

usiness&

FinancialH

istory399

Figure 3. Production accounts for Cannock Forge and Rugeley Slitting Mill 1692–3.Source: FIW, MAf/16.

Downloaded By: [King, Peter] At: 13:25 6 January 2011

400 P.W. King

The accounts of the Ironworks in Partnership (mainly in the Forest of Dean and the valley of theWorcestershire Stour) are very similar. These end with the balance of the ‘General Account’beingdivided among the partners (FIW, DEf/2–11). However, for the Staffordshire Works separateprivate accounts between Philip Foley and John Wheeler were prepared after Philip was declaredto be a partner in 1698 (FIW, MCc/1; MCf/1–4). The similarity of all these accounts to PhilipFoley’s in the years around 1670 is hardly surprising with Wheeler involved and Lane havingbeen Glover’s clerk. The Staffordshire accounts were probably prepared by John Wheeler, asEdward Kendall described the 1708 account as being in the writing of Wheeler, whose clerk hehad been.17 The accounts of William Rea for the Forest Works are in the same form as Wheeler’sin the preceding period with two minor exceptions: pig iron sales (as well as bar iron sales)were dealt with in a sales abstract (rather than in personal accounts for each customer); and thefolio numbers of the corresponding entries are not given. Each annual account is neverthelesspresented as a balanced ledger containing accounts in the broad format described above (FIW,DFf/1–13). Warine Falkner’s accounts also used much the same form (FIW, DGf/1–2), as do thoseof his successor Thomas Pendrill (FIW, DGf/3–16). In Warine Falkner’s accounts, an auditors’objections are annotated in red (FIW, DGf/1–2). After his time, the quality of the Foley Forestaccounts (though similar in structure) markedly deteriorates. Thomas Pendrill (the next manager)often only recorded who money was paid to, rather than what it was paid for, so that the natureof the costs is less apparent (FIW, DGf/3–16). At the point where he gave up (or perhaps died),there is a gap in the accounts and subsequent ones are even less detailed (FIW, DGf/17–35; cf.Hammersley 1979).

3.2. The 1692/3 account

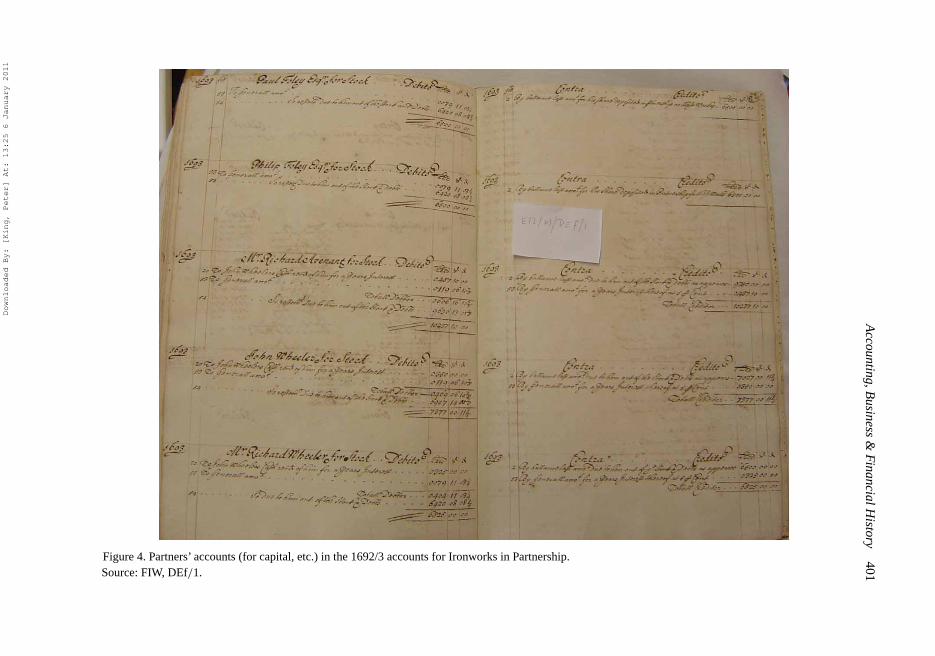

The account for 1692/3 (FIW, DEf/1) for the Ironworks in Partnership (1692–1705, see Table 1)starts in the same way, leading as usual to a ‘General Account’ – in which the profit or lossappears – and a ‘Balance’account. The General Account is balanced by transferring each partner’sshare of the surplus (the profit of the whole business) to his personal ‘account for stock’ aftercharging interest on capital. Thus, for example, John Wheeler receives £350 for interest on his£7000 capital, but allows £118.6.10 1

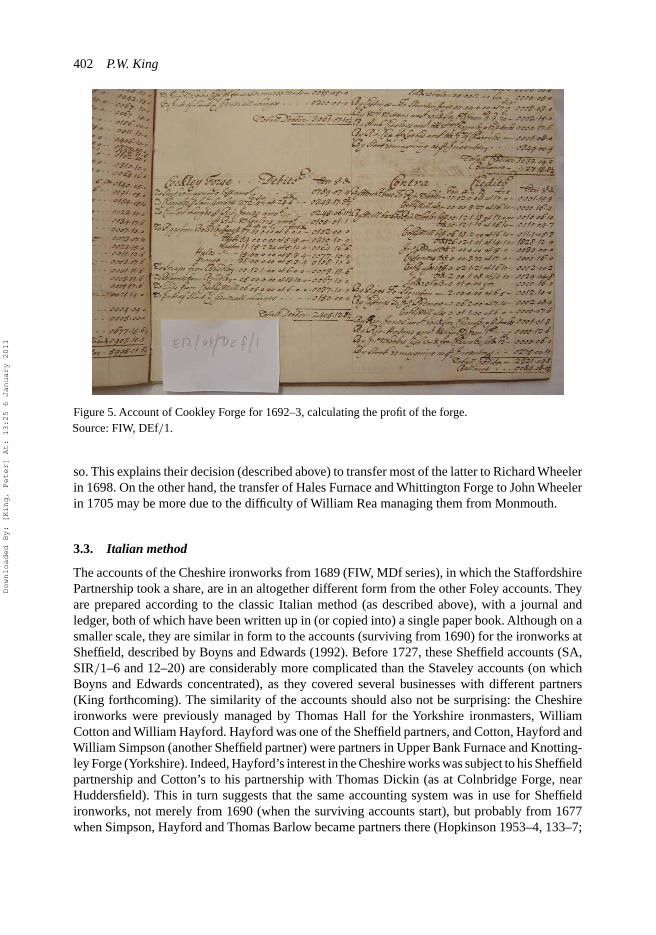

2 d for his quarter share of the loss (fourth ledger accountreproduced in Figure 4). This system is common to most annual accounts both for the Ironworksin Partnership (1692–1705) and its successor the Forest Partnership (from 1705) as well as theStaffordshire Partnership. However, the 1692/3 account differs from its successors in that theseaccounts are followed by a series of accounts (probably outside this double entry system) in whichthe costs and sales of each ironworks were brought together to calculate the individual profit orloss of each works (as for the Cookley Forge in Figure 5 which shows a loss of £84.8.0 1

4 ). Each ofthese accounts takes quantities from the preliminary production memorandum accounts, which arelargely concerned with the quantities of each commodity consumed or produced. It then appliesprices to them. Transfer prices used were probably the market prices of each commodity. Thecosts charged included a round-sum contribution (whose basis is not stated) from each towards‘interest and general charges’, thus distributing these between the works. This provides the profitor loss of each works. Only Wilden Forge, Bewdley Storehouse, and two of the furnaces wereprofitable. Blakeney Furnace would also have been, but for its rebuilding cost, written off thatyear. All the rest made losses (FIW, DEf/1). It is not clear why this more sophisticated systemof production accounts is not used for subsequent years, but it shows that John Wheeler was ableto work out the profitability of each ironworks. However, its use suggests that the partners wereaware that their Forest of Dean furnaces were profitable and their forges in the Stour valley less

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting,B

usiness&

FinancialH

istory401

Figure 4. Partners’ accounts (for capital, etc.) in the 1692/3 accounts for Ironworks in Partnership.Source: FIW, DEf/1.

Downloaded By: [King, Peter] At: 13:25 6 January 2011

402 P.W. King

Figure 5. Account of Cookley Forge for 1692–3, calculating the profit of the forge.Source: FIW, DEf/1.

so. This explains their decision (described above) to transfer most of the latter to Richard Wheelerin 1698. On the other hand, the transfer of Hales Furnace and Whittington Forge to John Wheelerin 1705 may be more due to the difficulty of William Rea managing them from Monmouth.

3.3. Italian method

The accounts of the Cheshire ironworks from 1689 (FIW, MDf series), in which the StaffordshirePartnership took a share, are in an altogether different form from the other Foley accounts. Theyare prepared according to the classic Italian method (as described above), with a journal andledger, both of which have been written up in (or copied into) a single paper book. Although on asmaller scale, they are similar in form to the accounts (surviving from 1690) for the ironworks atSheffield, described by Boyns and Edwards (1992). Before 1727, these Sheffield accounts (SA,SIR/1–6 and 12–20) are considerably more complicated than the Staveley accounts (on whichBoyns and Edwards concentrated), as they covered several businesses with different partners(King forthcoming). The similarity of the accounts should also not be surprising: the Cheshireironworks were previously managed by Thomas Hall for the Yorkshire ironmasters, WilliamCotton and William Hayford. Hayford was one of the Sheffield partners, and Cotton, Hayford andWilliam Simpson (another Sheffield partner) were partners in Upper Bank Furnace and Knotting-ley Forge (Yorkshire). Indeed, Hayford’s interest in the Cheshire works was subject to his Sheffieldpartnership and Cotton’s to his partnership with Thomas Dickin (as at Colnbridge Forge, nearHuddersfield). This in turn suggests that the same accounting system was in use for Sheffieldironworks, not merely from 1690 (when the surviving accounts start), but probably from 1677when Simpson, Hayford and Thomas Barlow became partners there (Hopkinson 1953–4, 133–7;

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting, Business & Financial History 403

Awty 1957, 79–89; King forthcoming). It could have begun even earlier under the previous owner,Lionel Copley, and conceivably in 1639 when Copley and others (including two London partners)rented land from the Earl of Arundel to build the works at Sheffield (SA, ACM/SD 180; Kingforthcoming).

3.4. Depreciation and goodwill

Most of the financial accounts described above contain no reference to fixed assets. This is becauseironmasters usually leased the plant they used such as furnaces and forges (cf. Jones 1985, 100–1).For example, this applied to the Foley ‘Ironworks in Partnership’. The 1691 partnership articlesprovided for Paul Foley to receive rent for the furnaces that he let to the firm (FIW, DEc/1).Perhaps partly because of the absence of fixed assets, the issue of depreciation rarely surfaces. Itwas often the contemporary practice to write off expenditure on fixed assets immediately againstrevenue, as when Blakeney Furnace was rebuilt in 1692 at a cost of £324 (FIW, DEf/1, f.38).However John Wheeler was allowed £50 per year for seven years over and above the lease rentsin lieu of a ‘fine [premium] formerly paid by him and for erecting Cookley Forge’ (FIW, DEc/1).And when the Ironworks in Partnership bought Grange Furnace from Philip Foley after RichardWheeler’s bankruptcy (paying £300 for the furnace and £55 for Richard’s stock), a dead rent of£20 was charged against profits for some years until the cost was written off, although the furnacewas never used (FIW, DEf/12–13 and DFf/1–6; King 2008, 50). A similar charge, perhaps morelike amortisation than depreciation, was made in the accounts for Attercliffe Mill at Sheffieldfrom 1748 (Boyns and Edwards 1992, 163–4).

There is little evidence of premium payments for goodwill on the sale of businesses or sharesin them. For example, the transactions when Richard Wheeler withdrew from the Ironworks inPartnership in 1698 are all at the book values of net assets (FIW, DEc/4–9). The only case (notedabove), which this writer has observed in the charcoal iron industry,18 of a premium payment wason Philip Foley’s sale of Grange Furnace and four forges in 1674. Foorth and Clerke entered intoa bond for the future payment of £2000 beyond the value of the net assets transferred (FIW, KDseries; Schafer 1971, 29; King 2002, 49–50, 2008, 49–50).

3.5. Summary

There were thus two separate systems of double entry bookkeeping in use in the iron industry inthe late seventeenth and early eighteenth centuries. Both are more sophisticated than the chargeand discharge systems used earlier in estate accounting. The Cotton, Hayford and Simpson groupin Cheshire,Yorkshire and the east Midlands made use of a journal; the Foleys and their associatesin the west Midlands and the Forest of Dean did not. In neither case is it possible to determine theorigin of the system. Each system was already fully formed by the time of the earliest survivingaccounts. The only change observable is that Wheeler’s method differed slightly from PhilipFoley’s. As Philip was able to obtain similar data on the Brewood and Grange Works (in southStaffordshire) back to 1650 (Schafer 1990, 31, printing FIW, KBf/47), it is likely that Gloverused much the same system for Philip’s father Thomas, and that one of them taught it to Philip.Unfortunately, nothing is known of Glover’s origins or of who (if not his own father Richard)trained Thomas. However, Thomas could have adopted his double entry system while livingat Austin Friars in London in the 1650s.19 The Italian method could have been introduced toSheffield soon after 1639 by Copley’s London partners. In both cases, the absence of archivalevidence renders the question of origins a matter of pure speculation.

Downloaded By: [King, Peter] At: 13:25 6 January 2011

404 P.W. King

4. Cost accounts

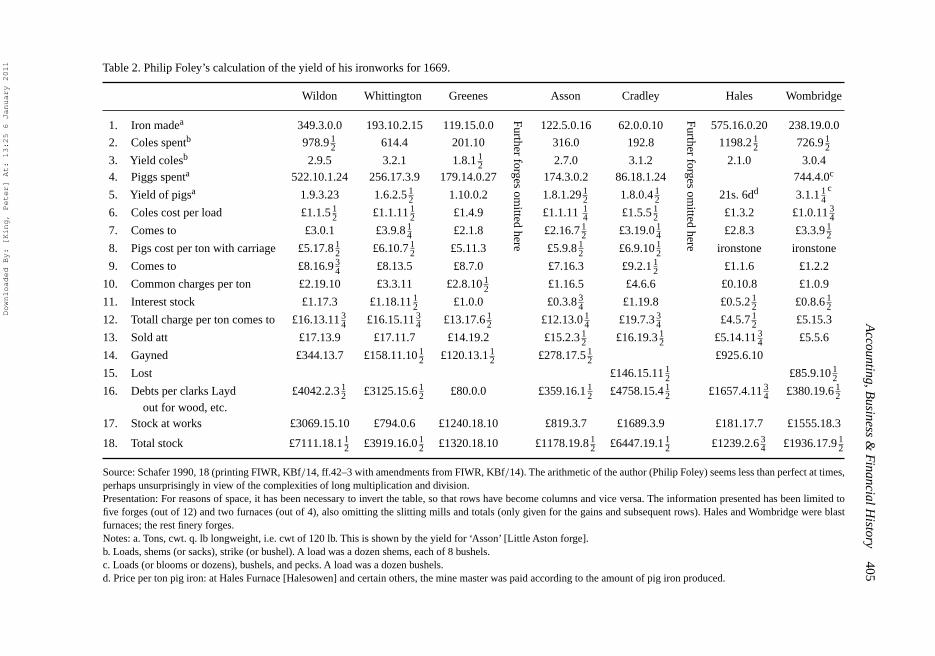

As mentioned above, the earliest surviving complete set of accounts for any Foley business arePhilip Foley’s in the late 1660s (FIW, KBf/15–18; Schafer 1978, 1990). Those for 1669 showno attempt to work out the profit of individual works within the financial accounts. However, atthe end of each annual account there is a separate ‘account of the yield’ (see Table 2), which listsfor each works the amount of iron made, the ‘coles’ and pigs spent, and the yield of each. Itsnext section converts these into money, multiplying the cost of ‘coles’ per load and pigs per tonby the yield to produce the fuel and metal cost per ton of iron made. To this is added a sum perton for common charges and interest of stock, to produce a total charge per ton, which is thencompared with the average sale price. Further columns then show the total gain (or loss) of eachworks, the clerks’ debts, and the stock remaining. Some accounts end by adding up the profitsand losses, to produce a different figure from that in the ‘General Account’ in the main accounts(Schafer 1990, 19, printing FIW, KBf/16, ff. 42–4). The reasons for the difference have not beendetermined. Caustic comments are written against the 1674 account of yield (which deals onlywith quantities), explaining the performance and in several cases blaming the workmen (Schafer1990, 22, printing FIW, KBf/49). An account of the Brewood and Grange Works, giving theprofit in each of nine works annually from 1650 to 1673 also survives, suggesting that similarcost statements were prepared for or by Philip’s father from at least 1650, and that the accountingsystem was in use by then (Schafer 1990, 31 printing FIW, KBf/47). These cost statements onlyseem to have been prepared post factum, when the annual accounts were complete, as a tool forexamining the efficiency of each works.

Surviving evidence of formal cost accounting (as such) is very scarce.20 Certain ex ante state-ments exist for Carey Forge (Herefordshire) about 1630, based on the performance of nearbyforges (British Library, Add. Ms. 11052, ff. 60–70; cf. van Laun 1979, 55; Taylor 1986, 450–67).There is a similar statement in 1759, probably for Lizard Forge (StRO, D 641/3/E/5/32 – identitydeduced from provenance). Their rarity suggests that they were unusual. However, as Boyns andEdwards (1992) showed, cost data is readily obtainable from financial accounts kept accordingto the classic Italian method, when production is dealt with in a separate account. Cost data cansimilarly be extracted from double entry accounts kept by the Foleys and their managers. Thisenabled Philip Foley to append a cost statement to his financial accounts and John Wheeler towork out the profit of each works in his 1692/3 accounts.

In contrast, performance was more routinely monitored by examining the yield from the rawmaterials of each process, often as a note in the financial accounts. The achievable yields wereknown and were evidently useful as a management tool. For example, around 1700, an account offour ‘blasts’ at Grange Furnace (near Wolverhampton) goes as far as to calculate the yield downto pecks (half bushels) (FIW, KL/12). Nevertheless, it is not possible to say how far costs (orat least the yields from raw materials) were monitored over shorter periods as a routine tool ofmanagement. However, that objective was also addressed by giving the workmen incentives toachieve a good yield. Forgemen were usually paid a piecework rate, according to the amount ofiron they made. If the hammerman did better, he was paid a bonus for his ‘overplus yield’. Hewas probably expected produce a ton of bar iron (20 cwt) from a ton of blooms (22 cwt).21 Inthe same way, Thomas Cooke the slitter of iron at Wolverley Lower Mill (Worcestershire) wasallowed five shillings per ton of iron slit and 14 shillings per cwt. for half the loss (of weight)under 1 cwt per ton, ‘Thomas Cooke not putting any more ends in a bundle of rod than is usual’(Birmingham City Archives, Z10).

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting,B

usiness&

FinancialH

istory405

Table 2. Philip Foley’s calculation of the yield of his ironworks for 1669.

Wildon Whittington Greenes Asson Cradley Hales Wombridge

Furtherforges

omitted

here

Furtherforges

omitted

here

1. Iron madea 349.3.0.0 193.10.2.15 119.15.0.0 122.5.0.16 62.0.0.10 575.16.0.20 238.19.0.0

2. Coles spentb 978.9 12 614.4 201.10 316.0 192.8 1198.2 1

2 726.9 12

3. Yield colesb 2.9.5 3.2.1 1.8.1 12 2.7.0 3.1.2 2.1.0 3.0.4

4. Piggs spenta 522.10.1.24 256.17.3.9 179.14.0.27 174.3.0.2 86.18.1.24 744.4.0c

5. Yield of pigsa 1.9.3.23 1.6.2.5 12 1.10.0.2 1.8.1.29 1

2 1.8.0.4 12 21s. 6dd 3.1.1 1

4c

6. Coles cost per load £1.1.5 12 £1.1.11 1

2 £1.4.9 £1.1.11 14 £1.5.5 1

2 £1.3.2 £1.0.11 34

7. Comes to £3.0.1 £3.9.8 14 £2.1.8 £2.16.7 1

2 £3.19.0 14 £2.8.3 £3.3.9 1

2

8. Pigs cost per ton with carriage £5.17.8 12 £6.10.7 1

2 £5.11.3 £5.9.8 12 £6.9.10 1

2 ironstone ironstone

9. Comes to £8.16.9 34 £8.13.5 £8.7.0 £7.16.3 £9.2.1 1

2 £1.1.6 £1.2.2

10. Common charges per ton £2.19.10 £3.3.11 £2.8.10 12 £1.16.5 £4.6.6 £0.10.8 £1.0.9

11. Interest stock £1.17.3 £1.18.11 12 £1.0.0 £0.3.8 3

4 £1.19.8 £0.5.2 12 £0.8.6 1

2

12. Totall charge per ton comes to £16.13.11 34 £16.15.11 3

4 £13.17.6 12 £12.13.0 1

4 £19.7.3 34 £4.5.7 1

2 £5.15.3

13. Sold att £17.13.9 £17.11.7 £14.19.2 £15.2.3 12 £16.19.3 1

2 £5.14.11 34 £5.5.6

14. Gayned £344.13.7 £158.11.10 12 £120.13.1 1

2 £278.17.5 12 £925.6.10

15. Lost £146.15.11 12 £85.9.10 1

2

16. Debts per clarks Layd £4042.2.3 12 £3125.15.6 1

2 £80.0.0 £359.16.1 12 £4758.15.4 1

2 £1657.4.11 34 £380.19.6 1

2out for wood, etc.

17. Stock at works £3069.15.10 £794.0.6 £1240.18.10 £819.3.7 £1689.3.9 £181.17.7 £1555.18.3

18. Total stock £7111.18.1 12 £3919.16.0 1

2 £1320.18.10 £1178.19.8 12 £6447.19.1 1

2 £1239.2.6 34 £1936.17.9 1

2

Source: Schafer 1990, 18 (printing FIWR, KBf/14, ff.42–3 with amendments from FIWR, KBf/14). The arithmetic of the author (Philip Foley) seems less than perfect at times,perhaps unsurprisingly in view of the complexities of long multiplication and division.Presentation: For reasons of space, it has been necessary to invert the table, so that rows have become columns and vice versa. The information presented has been limited tofive forges (out of 12) and two furnaces (out of 4), also omitting the slitting mills and totals (only given for the gains and subsequent rows). Hales and Wombridge were blastfurnaces; the rest finery forges.Notes: a. Tons, cwt. q. lb longweight, i.e. cwt of 120 lb. This is shown by the yield for ‘Asson’ [Little Aston forge].b. Loads, shems (or sacks), strike (or bushel). A load was a dozen shems, each of 8 bushels.c. Loads (or blooms or dozens), bushels, and pecks. A load was a dozen bushels.d. Price per ton pig iron: at Hales Furnace [Halesowen] and certain others, the mine master was paid according to the amount of pig iron produced.

Downloaded By: [King, Peter] At: 13:25 6 January 2011

406 P.W. King

5. Finance

It has been shown above that the earliest ironworks clerks were previously managers employedby landowners. As such people are unlikely to have had substantial capital available to investin a business, working capital was sometimes made available to them by their former masters.Similarly, Thomas Parkes in 1640 sued Henry Goreinge for over £3000 on a bond dated 1627,where he was a guarantor for John Middleton and Thomas Nye, perhaps the balance of a largersum left on loan, when Parkes sold them his father’s ironworks in 1618 (King 1999, 66–7).Thomas Foley’s business was also partly financed by debt. In 1673, Philip Foley reduced his debtto his father by agreeing to ‘free and clear’ his father from debts (probably on bonds) totalling£20,000.22 The extent to which the shares of John and Richard Wheeler and Richard Avenant inthe Ironworks in Partnership were financed by bonds in the 1690s has also been mentioned (FIW,DEc/2–9). Three decades later, the settlement of the dispute over the Hom timber partnershipinvolved Thomas Foley paying off debts that he had guaranteed for William Rea. Foley had thosebonds assigned to a nominee, to keep them on foot, and he retained the documents (FIW, DGd/12;P/9–12). In all, the Foley archive contains several hundred discharged bonds, most of which seemto have financed the ironworks stock (FIW, P series).

Bonds were ubiquitous in the commercial life of the period. They were used to secure theperformance of articles of agreement for the sale of wood (e.g. FIW, KAc/6 17–9); and ofindentures conveying or leasing land; as well as to secure the repayment of loans.A bond consistedof the formal obligation (usually in Latin) for a penal sum of money (which is usually exactlydouble the actual consideration). This was followed by a provision that the bond should be void ifa condition was met. The condition varied according to the nature of the transaction, most usuallythat the indentures (or articles) were duly performed, or that the loan was repaid with interest.For the creditor, bonds had the advantage that the debtor had no defence if sued at law, so that thecreditor could quickly obtain judgment, whether or not the condition had been met: this was anaction for debt for ‘a fixed sum promised by a sealed document’. However, the equity courts wouldintervene and restrain the creditor from enforcing a bond, if he put it in suit when the conditionhad been performed (Jacobs and Tomlins 1810, I, 350–61; Holdsworth II (1923 edition), 366–8;V (1924), 325–30; Browne 1589, 51).

These bonds for loan capital may be regarded as fulfilling a similar role to loan stock in alate nineteenth or twentieth century company or corporate bonds today. However, they often didnot appear in the accounts of the firm. Rather, they were used by the partners to finance theirpaid-up capital in the firm. Many partnership agreements and accounts show interest being paidto the partners on their paid up capital (e.g. Downes 1950; FIW, DEc/1; DEf-DGf series; SA,SIR/1–29). This was evidently to enable the partners respectively to keep down the interest dueto their bond creditors. Foley’s Staffordshire Partnership is exceptional in that details of the loansappear in the accounts, but only in private accounts between John Wheeler and Philip Foley, whichshow £10,960 due in 1699, including £3000 to Foley, (FIW, MCf/2, f.2; cf. MCf/1–3, each at f.2;Johnson 1952, 328). This reflects the view, expressed by Hamilton in 1777, that gain was onlythe excess profit over common interest (Mepham 1988). Similarly, when Edward Knight & Co.expanded their business by taking over Wolverley Old Forge in 1727 and then Lower Mitton Forgein 1733, they obtained loans for additional working capital, probably on bonds. This appears frombalance sheets at the end of each account (Worcs. RO, BA 10470/3, passim; Downes 1950).

Iron production was a profitable business. It seems not to have been difficult for a creditworthyironmaster to borrow capital on bonds. This provided a means for the gentry (and widows) toobtain a return on sums that they had available without investing in land. This was no doubt

Downloaded By: [King, Peter] At: 13:25 6 January 2011

Accounting, Business & Financial History 407

particularly important in the period before the financial revolution of the 1690s made investmentin government debt an acceptable alternative. In Philip Foley’s main accounts in 1669–72, eachclerk’s account ends with a balance due from him at the year-end. Sometimes this is specified ‘asin the debt book’, but in other cases, the account lists debts for which the clerk was accountable(Schafer 1978). This was probably because the debt arose from a sale, made by the clerk and anysecurity for the debt would have been taken in the clerk’s name: the securities (probably bonds)would have been given up and cancelled (or destroyed) when the debt was paid, and so they do notusually survive. However, similar bonds are referred to in another context. Robert Foley (Thomas’brother), Henry Glover and George Gibbons were (as mentioned) in partnership as ironmongersat Stourbridge, and had evidently bought iron from Thomas Foley. Some of their products weresold to Bristol ironmongers (such as John Stibbins) from whom they took bonds. They assignedthese bonds to Thomas Foley, apparently as security but also to enable him to receive paymentdirect from their debtors (FIW, DAf/3–13). Similar bonds are mentioned in litigation betweenJohn Stibbins and Robert Foley in the late 1650s (TNA, C 10/51/153).

In some firms, the clerks seem to have had a considerable freedom of action. Purchases of pigiron for Longnor and Sheinton Forges (Salop. – of Boycott & Co.), appearing in a later seriesof Foley accounts, were invariably in the name of the clerks of those forges (FIW, DEf and DFfseries, passim). One would not know that the clerks were not their own masters, had it not beenfor the survival of various partnership agreements and accounts.23 This is perhaps an extremecase, but clerks were evidently authorized to enter into substantial contracts on behalf of theirmasters for the purchase of wood and sale of iron. Thus Thomas Lowbridge (clerk of WildenForge, Worcestershire) made an agreement on behalf of Thomas Foley with John Wheeler ofAstwood (Worcestershire) in 1656. Similarly, Henry Shaw (Thomas Foley’s wood clerk) boughtwood on his behalf from Sir William Whitmore at Claverley and Quatford in 1658; and JohnWoodder on behalf of Thomas Lord Windsor in 1678 sold 10 tons of iron from Redditch UpperForge to Philip Foley (FIW, KAc/22 33; KBc/55). On the other hand, when Henry Glover in1686 employed Obadiah Lane as his clerk, Lane was forbidden to deliver more than two tons ofiron to any customer on trust (i.e. on credit) without Glover’s consent (HRO, E12/IV/19/6).

6. Transmission of knowledge

Textbooks for mercantile accounts began to appear in the period covered here, and there is ampleevidence of academies teaching commercial subjects in the eighteenth century, for aspiring mer-chants and their clerks, particularly in London (Edwards 2009). Such training will have provideda young man with the rudiments for a commercial life, but its application was learned in theworkplace from an experienced practitioner, whom the apprentice was encouraged to imitate.Knowledge was thus transmitted visually and orally (Grassby 1995, 194–6, 411; Pollard 1965,104–26; Oldroyd 2009, 60–6). This article has shown that several successful ironmasters andsenior ironworks managers began their career and obtained their training in the workplace. WarineFalkner was a servant in the household of Obadiah Lane (see note 12). Obadiah Lane was a clerkto Henry Glover (HRO, E12/IV/19/6), and Edward Kendall to John Wheeler (see note 17). PhilipFoley was probably trained by Henry Glover, and clerks under him. His father’s gift to him of theprofit of Hales Furnace suggests that he acted as understudy to John Downing, its clerk (Schafer1978, xvi). Henry Glover may also have trained John Wheeler, and John Wheeler may have trainedWilliam Rea, but there is no evidence, except that Rea was living at Wollaston in 1703, near (if notin) Wheeler’s Wollaston Hall (HRO, T74/73, deeds of 1703 and 1704). This finding differs little

Downloaded By: [King, Peter] At: 13:25 6 January 2011

408 P.W. King

from that reached (as to cost accounting) by Boyns and Edwards (1996), who concluded that themain mechanism for the transmission of accounting methods was apprenticeship and the recruit-ment of trained personnel. However the period considered here was a century or more earlier thanmost of what they considered. The dearth of literature on cost accounting is analogous to thatof contemporary descriptions of technology (Harris 1976, 167–9; reprint, 18–20), with the resultthat the travel diaries of tourists are a significant source for its history. The reason is the same ineach case: the subject was taught by practice in the workplace through the apprenticeship system.

7. Conclusion

It is clear that those who managed ironworks understood the costs of the processes in which theirbusiness was engaged. They were particularly concerned to control their fuel cost, which was thelargest item, and they monitored the yield from each raw material. They were evidently competentmanagers, who were usually able to generate a profit beyond the interest payable on any borrowedcapital. This enabled various ironmasters to become rich men, entering the gentry, and in latergenerations, sometimes (as with the Foleys) the peerage. They knew how to calculate their costs,but apparently rarely did so (based on surviving evidence), being content with monitoring theyields from raw materials.

Business succession was often achieved by a manager training a servant, who in turn became acompetent manager and later a partner or an entrepreneur in his own right, sometimes succeedingto his master’s business. No doubt marrying a boss’s daughter sometimes helped (as with WarineFalkner and Edward Kendall). However, records of training are elusive, so that a ‘business geneal-ogy’ from master to apprentice cannot be reconstructed as easily as that from father to son, forwhich we have parish registers.

The immediate source of their accounting systems is also elusive, but may derive from thesystems used by overseas merchants. The Italian method was common in merchants’ accounts,such as those of Marescoe and of Phill (Roseveare 1987, 11–2; Grassby 1995, 184–8). A variant ofit (in use at Coalbrookdale from 1718) may have been introduced by Thomas Goldney III, the sonof a Bristol merchant in partnership there (Stembridge 1998, 29; King 2010). The Foleys’ doubleentry system could have been begun when Thomas Foley lived in London in the mid-seventeenthcentury. Loan finance was readily obtainable. An ambitious (and creditworthy) manager couldeasily raise working capital, by borrowing money on bonds. Where (as often) he was in partner-ship, this was used to pay up his share capital in the firm, and so does not appear in the firm’saccounts.

This article has presented some evidence on these matters for one industry – charcoal iron-making. Oldroyd (2009) has recently done the like for mining near Newcastle. Researchers areinvited to assemble similar information on other industries.

Acknowledgements