M&A Tax Considerations for Buyers and Sellers When ...

106

M&A Tax Considerations for Buyers and Sellers When Negotiating, Structuring, and Pricing Deals Presented by: Roger Royse Pamela Fuller Clear Law Institute | 4601 N. Fairfax Dr., Ste 1200 | Arlington | VA | 22203 www.clearlawinstitute.com Questions? Please call us at 703-372-0550 or email us at [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of M&A Tax Considerations for Buyers and Sellers When ...

M&A Tax Considerations for Buyers and Sellers When Negotiating, Structuring, and Pricing Deals

Presented by: Roger Royse Pamela Fuller

Clear Law Institute | 4601 N. Fairfax Dr., Ste 1200 | Arlington | VA | 22203

www.clearlawinstitute.com

Questions? Please call us at 703-372-0550 or email us at

All-Access Membership Program

● Earn continuing education credit (CLE, CPE, SHRM, HRCI, etc.) in all states at no additional cost

● Access courses on a computer, tablet, or smartphone

● Access more than 75 live webinars each month

● Access more than 750 on-demand courses

Register within 7 days after the webinar using promo code “7member” to receive a $200 discount off the $799 base price.

Learn more and register here: http://clearlawinstitute.com/member

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 1

Tax Considerations for Buyers and Sellers when Negotiating, Structuring, and Pricing Deals

Roger Royse & Pamela A. Fuller

Royse Law Firm, PC

www.rroyselaw.com

IRS Circular 230 Disclosure: To ensure compliance with the requirements imposed by the IRS, we inform you that any tax advice contained in this communication, including any attachment to this communication, is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to any other person any transaction or matter addressed herein.

Tax Cuts & Jobs Act Changes

• The Tax Cuts & Jobs Act (TCJA) considerations for M&A.

• Changed the rates for Domestic Corporations. • Corporate tax rates were permanently lowed from 35% to 21%.

• New bonus depreciation rules incentivize asset deals

• Limits Corporate NOLs to 80% of TI

• Limited the allowability of interest deductions. • Interest deduction limitation no longer based debt-to-equity ratio.

• Interest is now limited to 30% of an approximation of EBIDTA (EBIT after 2021).

2

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 2

Changes in Corporate Rates

• Changed the rates for Domestic Corporations. • Corporate tax rates were permanently lowed from 35% to 21%.

• US corporate valuations increased

• Asset sales more attractive

• Corporate double federal tax rate is 21% plus 20% dividend rate plus 3.8% NIIT (39.8%)

3

Tax Cuts & Jobs Act Changes

• 100% bonus depreciation for “qualified property” placed into service by the taxpayer after September 27, 2017 (no cap).

• Qualified property is generally acquired tangible depreciable property, under 167(a), and 263A property with a recovery period longer than 10 years (includes films, sound recordings, video tape, book, etc.)

• Cannot be acquired from related parties, members of the same control group, or property with a transferred basis.

• General phase out begins for property placed into service in 2024 with an 80% allowable deduction,

• This phase out continues at a 20% reduction per year until a complete phase out of bonus depreciation for property placed into service in 2028.

• Section 179 deduction was increased to $1,000,000 from $500,000.

4

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 3

Bonus Depreciation and Sec 179

• Incentivizes asset purchases

• Higher value to allocations to depreciable and 179 property

5

Interest Deductions

• Interest deduction limitation no longer based debt-to-equity ratio.

• Interest is now limited to 30% of an approximation of EBIDTA (EBIT after 2021).

• Less leveraged deals

• Interest expense carryforwards

• Gain from assets sales may free up interest expense

6

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 4

NOL Limitation

• Corporate NOLs arising in a taxable year after 2017 can offset up to 80% of current year taxable income

• No NOL carry-back, but unlimited carry-forwards

7

Self Created Intangibles

• After 2017, certain intangible assets can no longer be treated as capital gain assets

• Either (1) created by the taxpayer or (2) acquired from the creating taxpayer in a carryover basis acquisition :

• Patents

• Inventions

• Models and designs (whether or not they are patented)

• Secret formulas or processes

• Places pressure on allocation schedules

8

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 5

Effect of the TCJA

• Asset deals are less costly to seller due to decreased rates

• Buyer will allocate more to tangible property for bonus and additional depreciation

• NOLs not as useful

• Leverage discouraged

• Allocation away from self created intangibles

9

Corporations with NOL’s in a low interest environment

• Section 382 restricts the ability of a “loss corporation” to claim NOLs generated before the sale against income earned after the sale if there has been an “ownership change.”

• A “loss corporation” includes a corporation with an NOL carryover

10

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 6

Section 382 – Ownership Change

• An ownership change occurs if the percentage of stock owned by 1 or more 5 percent shareholders increases by more than 50 percent during a 3 year period.

• The NOL limitation for any year after an ownership change is equal to the value of target immediately prior to the change, multiplied by the long-term tax-exempt rate

• Approximately 2.5% as of early 2016. Was 1.96% in early 2018. At 2.20% for March 2019 Rev. Rul. 2019-07 Table 3

11

Modeling the Tax Aspects

• Suppose Target has NOLs

• In an asset sale, • Target has two levels of tax, maybe be able to soak up some gain with NOLS (now limited)

• Buyer takes a fair market value basis in assets, much of which will be amortizable over 15 years

• In a stock sale, • Seller has one level of tax

• Buyer does not obtain a fair market value basis in assets but does have potential to use Target’s NOLs at the rate of 2% of value of Target per year

12

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 7

SAFEs, SAFTs and Tokens

• A SAFE is a security that converts into shares in a future equity issuance, much like convertible debt but with no interest accrual and no unconditional repayment obligation.

• A SAFT is a security that converts into future tokens to be issued in an initial coin offering (ICO).

• A Token is a digital asset based on distributed ledger technology that may represent a claim to equity, products or services

• Security tokens can be asset backed tokens or digitized stock

13

Treatment as Stock

• IRS defines stock as a permanent interest in the corporation’s equity, i.e. its earnings and or underlying assets

₋ Tracking Stock

₋ Preferred stock

₋ Non qualified preferred

• Debt – debt v. equity ₋ Form of obligation Principle

₋ Debt equity ratio Interest

₋ Intent Management rights

₋ Subordination Credit worthiness

• Partnership Interests ₋ de facto partnerships

₋ analogy to non compensatory partnership options

14

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 8

Stock Rights – Newer Investment Types

• Increasingly, alternative equity derivatives are being used to invest, but their tax status is often uncertain

• This table discusses likely tax treatments

Tax Treatment Note Alternatives (SAFEs, KISSes)

Mandatorily Convertible Debt

Potential Tax Treatment as

Equity?

Like penny warrant, could be deemed exercised from day one depending on certainty of exercise.

If the conversion occurs fairly soon and is certain, and its performance in the debt/equity factors, there is a chance it could be classified as preferred equity.

Potential Tax Treatment as

Warrant?

Probably the best analogy; SAFEs and KISSes are essentially investment stock options exercisable on certain events, rather than at certain times.

Low; the distinction between convertible debt and stock rights under §1223(5) are generally respected.

Potential Tax Treatment as Convertible

Debt?

Low; the distinction between convertible debt and stock rights under §1223(5) are generally respected.

If conversion reasonably far into future and federal tax indicia of debt are generally positive, a likely outcome.

15

TYPE A REORGANIZATIONS – SECTION 368(a)(1)(A) STATUTORY MERGER

Target Acquiror

Shareholders

• Statutory Merger – 2 or more corporations combined and only one survives (Rev. Rul. 2000-5)

• Requires strict compliance with statute

• Target can be foreign; Reg. 1.368-2(b)(1)(ii)

• No “substantially all” requirement

• No “solely for voting stock” requirement

Requirements:

• Necessary Continuity of Interest (40%)

• Business Purpose

• Continuity of Business Enterprise

• Plan of Reorganization

• Net Value

Tax Effect:

• Shareholders – Gain recognized to the extent of boot

• Target – No gain recognition

• Acquiror takes Target’s basis in assets plus gain recognized by Shareholders

• Busted Merger – taxable asset sale followed by liquidation

16

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 9

CONTINUITY OF INTEREST

• IRS – 50% Safe Harbor, Rev. Proc. 77-37

• IRS – 40% in Reg. 1.368-1T(e)(2)(v), example (1)

• John A. Nelson – 38% Stock

• Miller v. CIR – 25% Stock

• Kass v. CIR – 16% Stock is Insufficient

17

Tax Language

The parties acknowledge and agree that for United States federal and state income tax purposes this SAFE is, and at all times has been, intended to be characterized as stock, and more particularly as common stock for purposes of Sections 304, 305, 306, 354, 368, 1036 and 1202 of the Internal Revenue Code of 1986, as amended. Accordingly, the parties agree to treat this Safe consistent with the foregoing intent for all United States federal and state income tax purposes (including, without limitation, on their respective tax returns or other informational statements).

18

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 10

TRIANGULAR OR SUBSIDIARY MERGERS

Target Acquiror

Merger Sub

Acquiror Target

Merger Sub

1. Forward Subsidiary Merger

2. Reverse Subsidiary Merger

19

TRIANGULAR OR SUBSIDIARY MERGERS

Section 368(a)(2)(D) Forward Triangular Merger

• A statutory merger of Target into Merger Sub (at least 80% owned by Merger Sub)

• Substantially all of Target’s assets acquired by Merger Sub

• Would have been a good Type A merger if Target had merged into Merger Sub

Target Acquiror

Target Shareholders

80%

Merger Sub

Tax Consequences • Merger Sub takes Target’s

basis in assets increased by gain recognized by Target

• Acquiror takes “drop down” basis in stock of Merger Sub (same as asset basis)

20

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 11

TRIANGULAR OR SUBSIDIARY MERGERS

Target Acquiror

80%

Merger Sub

Section 368(a)(2)(E) Reverse Triangular Merger

• Merger of Merger Sub into Target where • (i) Target shareholders surrender control (80% of voting and nonvoting classes of stock) for

Acquiror voting stock and

• (ii) Target holds substantially all the assets of Target and Merger Sub

• Shareholder loan issues

Tax Consequences • Non-taxable to Target and carryover

basis • No gain to Acquiror and Merger Sub

under Sections 1032 and 361 • No gain to Target shareholders except

to the extent of boot • Acquiror’s basis in Target stock

generally is the asset basis, but Acquiror can choose to take Target shareholders basis in stock (if it is also a B)

• If transaction is also a 351, Acquiror can use Target shareholders’ basis plus gain

Target Shareholders

21

Double Merger

Acquiror

Target Shareholders

Step 2: A-type Forward Merger Step 1: Reverse Triangular Merger

Target Acquiror

Merger Sub

80%

Merger Sub Target+Sub

Merger Sub Survives

Target Shareholders

Tax Benefit: A taxable reverse merger has just one tax on the shareholders, while a taxable forward merger has two taxes (one on shareholders and one on corporation). Intended that entire transaction be a tax-free A-type merger (where 20% boot limitation does not exist). Pairing the two reduces the risk of incurring the corporate level tax in the event the entire transaction is not treated as an A-type merger.

REV. RUL. 2001-46

22

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 12

Double Merger – Wholly Owned LLC

Acquiror

Target Shareholders

Step 2: A-type Forward Merger Step 1: Reverse Triangular Merger

Target Acquiror

Merger Sub

80%

LLC Target+Sub

Merger LLC Survives

Target Shareholders

REV. RUL. 2001-46

Second step is merger into LLC under Reg 1.368-2(b)(1) (good forward merger)

23

280G GOLDEN PARACHUTE RULES

20% excise tax and loss of deduction on Excess Parachute Payment • “Excess Parachute Payment” means the amount by which the Parachute Payment exceeds the Base

Amount • “Parachute Payment” means a payment, the present value of which, exceeds three times the Base

Amount • “Base Amount” means the average annual compensation for past 5 years • Must be paid to a disqualified individual (meaning employee, officer, shareholder, or highly

compensated individual) • As compensation, AND • Contingent on a change in control (50% change ownership or effective control, or ownership change in

a substantial portion of the company’s assets)

Reduce Excess for reasonable compensation Exclude reasonable compensation for future services Exception for small business corporation and non publicly traded corporation

that has 75% uninterested shareholder approval Withholding requirement

24

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 13

280G – OTHER ISSUES

• Non-Publicly Traded Stock • Approval of 75% of shareholders after adequate disclosure

• Vote determines the right of the shareholder to the payment

• Ignore shares held by persons receiving the payment

• Reduction for Excess (299% of payments)

• Reduction for Reasonable Compensation

• Reduction for Future Services

25

PERSONAL GOODWILL

• Key questions: (1) Who owns the goodwill (individual or company)? And (2) Was that goodwill ever transferred?

• Key case: • Martin Ice Cream – the court held that customer relationships and distribution lists were an asset of the

shareholder because they were never transferred to the company (the business began as a sole proprietorship and then part of the business was specifically transferred to a new company)

26

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 14

PERSONAL GOODWILL

• Issues: • Is a buy/sell non-compete sufficient to satisfy the right to future services?

• What does the scope of the non-compete need to be? (geographic area, time, etc.)

• Is a fiduciary obligation not to compete sufficient?

• Is a non-solicitation and/or non-use of trade secrets provision sufficient?

• Best practice = shareholders should sell their “personal goodwill” separate from the stock/asset sale

27

PERSONAL GOODWILL CASES

• Estate of Franklin Z. Adell v. Comm’r (Tax Court 2014) • Case about the treatment of the goodwill provided by the son of decedent’s company

• The son did not transfer his goodwill through an employment or noncompete agreement

• The Court held that the IRS’s value for the son’s goodwill was not high enough

• Bross Trucking, Inc. – goodwill may be transferred to a company via an employment contract if that employment contract grants the company a right to future services (e.g., through a non-compete provision)

• Note: non-compete provisions are generally invalid in California absent the sale of a business

28

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 15

PERSONAL GOODWILL CASES

• Kennedy v. Comm’r (Tax Court 2010) • Kennedy sold his corporation; 25% of the purchase price was payment for consulting services and 75%

was payment for Kennedy’s goodwill • The Court held that the identification of personal goodwill is not enough to conclude that the goodwill was

sold • The Court found the payments to Kennedy were consideration for services because the contractual allocation

did not genuinely reflect the relative value of his customer relationships compared to the value of the his ongoing personal services

• Solomon v. Comm’r (Tax Court 2008) • Solomon sold its corporate division; the purchase agreement included a customer list and a covenant

not to compete • Nothing in the agreement made reference to the sale of personal goodwill and the acquiring party continued

to do business under its own name • The Court held that the proceeds paid directly to the shareholders were actually attributable to their covenant

not to compete rather than for a customer list or personal goodwill

29

Qualified Small Business Stock (QSBS)

• Benefits • Reduced federal income tax for non-corporate stockholders on capital gains from QSBS held for more

than five years

• Gain exclusion is limited to greater of $10 million or 10x the taxpayer’s aggregate adjusted bases in the stock

• Potential to roll QSBS proceeds into new QSBS and tack holding period

• Eligibility • Stock in a C-corporation originally issued to the taxpayer after August 10, 1993 in exchange for money

or property (not stock) or as compensation for services

• Corporation is a “qualified small business”

• Original issuance exceptions • Acquired on conversion of other stock in the same corporation

• Certain carryover basis transactions

30

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 16

QSBS ISSUE FOR CASH FREE STOCK SALES

• Target companies may be acquired on a cash free/debt free basis, however this often necessitates a cash dividend to shareholders immediately prior to the sale

• During negotiations, both Acquiror and Target shareholders typically treat this dividend as part of the acquisition price, however the form of the transaction is a dividend

• This pre-sale dividend can create problems for shareholders’ QSBS relief: • Under the QSBS rules, the maximum taxable gain considered available for relief is the higher of $10

million or ten times stock basis

• If the dividend payment is treated as a pre-sale distribution then it will reduce the basis of the stock and may therefore reduce the amount of gain available for QSBS relief

• Taxpayer may choose to file on the basis that the dividend is, in substance, part of the sale proceeds, however this could be subject to challenge by the tax authorities

31

ROLLOVER OF GAIN INTO QUALIFIED OPPORTUNITY ZONE FUND

• Within 180 days after the sale of stock or real estate, the capital gain (not tax basis) may be invested in a Qualified Opportunity Zone Fund

• Capital gain deferred until the earlier of the date of sale or 12/31/2026

• 10% of the gain is forgiven for investment held for at least 5 years

• Another 5% of the gain is forgiven for investment held for at least 7 years

• No capital gain on the post reinvestment appreciation after 10 years

32

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 17

EARN OUT PROVISIONS

• Bridge a valuation gap between seller and buyer • Additional financing option • Payment/tax deferral • Reduce risk of overpaying

• Earn outs usually based on • Financial Targets

• Earnings before interest, tax, depreciation and amortization (EBITDA); Revenue; Net income; Earnings per share

• Non-Financial Targets • Regulatory approval; Increase in customer base/sales;

Product development milestones

• Key Considerations: Terms, time period, payout structure, security for payments,

allocation of control of the acquired business, level of support (if any) committed

33

EARN-OUTS TAX AND BOOK TREATMENT

Fair value of contingent earn-out is recorded as a contingent liability by the acquirer at acquisition => increases book goodwill. Earn-out not recognized for tax purposes until the amount is fixed or determinable => book basis but no tax basis at acquisition

Taxable asset acquisition (tax deductible goodwill): Two approaches to account difference at acquisition:

o Earn-out is treated as separate deductible item for tax book purposes:

- Acquisition: no tax basis = gives rise to a deferred tax asset (DTA)

- Over time: contingent payments result in book income or expense and the earn out liability is treated as non-taxable or non-deductible temporary difference which change the associated DTA

- Settlement: goodwill additional tax and additional tax amortization. DTA is reduced over amortization period but the amortization would need to be allocated between goodwill and other tax goodwill.

o Earn-out liability is treated as if its amount was settled at acquisition for tax purpose:

- Acquisition: tax basis is equal to book basis

- Over time: amortization of tax goodwill creates a deferred tax liability (DTL). Subsequent adjustments then affect the earn-out liability and create DTA or DTL because pretax adjustments to earn-out liability that are not measurements period adjustments are treated do not result in adjustments to book goodwill (ASC 805). DTA or DTL is then combined with DTL driven by tax amortization.

- Settlement: goodwill additional tax basis and additional tax amortization

Non-Taxable stock acquisition (non tax deductible goodwill): the initial basis of the shares (outside stock basis) is the purchase price of the stock. Additional goodwill related to earn-out liability does not result in additional tax basis for goodwill or outside stock basis. When subsequent payments are over and earn-out liability is settled there is no immediate tax effect but later adjustments can affect the tax rate.

34

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 18

CONTINGENT PAYMENTS AND EARN-OUTS

• Distinguish Equity vs. Debt

• 3 Issues • (1) allocation between interest and sales proceeds;

• (2) timing of realization of sales proceeds; and

• (3) timing of basis recovery

• Interest • 1.1275-4(b)

• Contingent payment debt for cash or publicly traded property – use non-contingent bond method; projected non-contingent and contingent payments

• 1.1275-4(c) • Contingent debt instrument issued for non-publicly traded property – bifurcate into non-contingent

debt instrument and contingent debt instrument; contingent payment treated as principal based on present value, excess is interest

• Buyer’s basis is non-contingent portion plus contingent payments treated as principal

35

Partnership Structure with Profits Interest

Target

Hold Co, LLC

Target Shareholders

100%

100% 100%

Merger

$$

Merger Co

Acquiror

Hold Co, LLC

Target Shareholders

100%

Issuance of unvested profits

interest

Acquiror

Target, LLC

Acquisition Structure: Post Acquisition:

Target converts to wholly-owned LLC - treated as a tax-free liquidation into Hold Co, LLC if a single member LLC

100% less profits interest

36

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 19

S CORPORATIONS AND 338(h)(10)

T (S Corp) Acquiror

Merger Sub

Target Shareholders

• Character difference – ordinary income assets

• California – 1.5% tax on S corporations

• New York – gain from 338(h)(10) sale of New York S corporation is New York-source income

• All Target shareholders must consent on Form 8023

• Deemed 338 election for subsidiaries

• 1374 – BIG Tax • Minority shareholders in rollover • Hidden tax in liquidation or

deemed liquidation in installment sale.

• 3.8% NIIT Tax

37

S CORP 338(h)(10) ELECTION AND

453B(h) BASIS ALLOCATION ISSUE

• Gain to Shareholders in year of sale: $1 million x 80% = $800,000; A/B of Shareholder = $1.8 million • No 331 liquidation: $1 million cash decreases A/B by $1 million to $800,000; $800,000 A/B in Note = $3.2 million

gain • 331 liquidation – apportion basis: $1.8 million basis apportioned $360,000 to cash and $1,440,000 to Note; Gain

in cash of $640,000 and gain in note of $2,560,000 for a total of $3.2 million gain (GP % on liquidation is 64%) • Defer cash portion and include in installment obligation: gain on liquidation equal to zero; Shareholder A/B in

note of $1 million; profit % is 80%

Target Acquiror

$1 million cash $4 million 453 Note

Stock Sale

$1 million basis

Cash - $1 million / $1 million A/B Assets - $4 million / zero A/B

Reg. 1.338(h)(10) – 1(e) Example 10

Shareholders

38

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 20

S CORP NO 338(h)(10) ELECTION – DISAPPEARING BASIS

T (S Corp) Acquiror

Merger Sub

T Shareholders

Carryover Basis

Liquidate Target into Merger Sub or check the

box Q-Sub

39

Alternative to Section 338(h)(10) S Corp Investment/Acquisition Using LLC

• Target S Corp shareholders form new S Corporation Holding Company

• Target S Corp shareholders contribute their Target stock to the new holding company which immediately elects QSub status

• Target converts to limited liability company and distributes retained assets & liabilities

Steps 1 & 2

S Corporation Holding Company

Target S Corp (QSub)

Target S Corp

Shareholders

Retained Assets and Liabilities

Target LLC

LLC Conversion

40

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 21

S CORP INVESTMENT STRUCTURE

Holdings, Inc. (S Corp)

Target, Inc. (QSSS)

T Shareholders

Step One:

Holdings, Inc. (S Corp)

Target, LLC (QSSS)

Step Two:

T Shareholders

Holdings, Inc. (S Corp)

Target, LLC (QSSS)

T Shareholders

Step Three:

Investor

$$

Membership interest

Step One: Shareholders of Target, Inc. transfer all Target, Inc. stock to Holdings, Inc. in exchange for Holdings, Inc. stock. Holdings, Inc. makes an S election and Target, Inc. elects to be treated as a qualified subchapter S subsidiary (QSSS). Step Two: Target, Inc. converts to an LLC for state law purposes (Target, LLC). Step Three: Investor purchases a membership interest in Target, LLC from Holdings, Inc.

41

Section 336(e)

Acquiror

Shareholder $

Target Stock

$

$ Assets

Assets

= Actual Component

= Deemed Component

Acquiror Shareholder

Target Target 3rd Party

Basic Model (for 80% stock sales): Target is treated as selling all of its assets to an unrelated person while owned by its former shareholders and then reacquiring same upon acquisition by Acquiror.

Section 336(e) does not apply to sales to a “related person.” The attribution rules could give rise to an unexpected “related person” situation where the seller acquires at least 5% of the acquiring partnership as part of the transaction. For example, where an investment partnership acquires a target and provides a modest partnership interest to the selling shareholders.

42

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 22

SECTION 336(E) DETAILS Section 336(e) Basic Model

• Similar to h-10 but can be a non corporate buyer or a distribution

• 336(e) election is made by Seller and “old” Target: they must enter into a binding, written agreement

• “Old” Target is treated as selling all of its assets to an unrelated fictional person while owned by Seller (shareholders) for an amount equal to the “aggregate deemed asset disposition price” (ADADP) which is the sum of the grossed-up amount realized on the disposition (sale, exchange or distribution) plus the liabilities of “old” Target

• “New” Target is treated as acquiring all of the assets from an unrelated fictional person

• After the deemed asset disposition, but before the close of the disposition date, while owned by Seller, “old” Target is treated as transferring to seller all of the consideration deemed received from “new” Target, generally in complete liquidation of “old” Target

• “Old” Target shall recognize all of the gains and losses realized on the deemed asset disposition

• Seller does not recognize gain or loss on the disposition of target stock

• “New” Target is treated as a new corporation for federal income tax purposes but remains liable for the tax liabilities of “old” Target

• Step up in the tax basis of the “old” Target’s assets to fair market value.

• No effect upon a purchaser

• No effect upon minority shareholders, or shareholders other than seller, except in the case of S corporation targets

• For dispositions involving distributions, losses on deemed sales of assets are disallowed to the extent of the net loss, if any, recognized by Target

Tax Consequences

43

International Tax Aspects

of Structuring M&A

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 23

Provisions of the 2017 TCJA that Significantly Altered Cross-Border M&A Stakes

Move to Partial “Territorial Regime”

Lower US Corporate Tax Rate

Broader US Corporate Tax Base for US Shldrs of foreign subs

TCJA Drastically Changes How Foreign Subsidiary Income

of US Corporations is Taxed

BEFORE 2017 US Tax Act

General Rule: United States generally taxes US corporations on a “worldwide” basis—i.e., US corporations taxed currently on both US-source income and foreign source income they receive. (Contrast with a pure “territorial jurisdiction,” which taxes its resident corporations only on income earned within its borders—not on foreign-source dividends and other foreign income ).

Policy for Worldwide (“Residence-Based”) System: Belief that capital is allocated more efficiently when investors’ choices about where to invest are not distorted by tax considerations. Economists believe it is more efficient if investments are made on the basis of pure economic fundamentals.

Deferral “Privilege” Exception: If a FOREIGN corporate Sub (of US corporate parent- as per diagram) earns foreign-source income, US corporate tax is not imposed on the foreign Sub’s income unless and until it is repatriated to the US—in an actual or deemed dividend. (Indefinite tax deferral is tantamount to a complete tax exemption due to time-value of money.)

Policy Rationale: US-owned foreign Subs need a “level playing field” to compete and should not have to pay both foreign and US taxes when their competitors do not. Thus, U.S. tax deferral is allowed so long as the foreign Sub can be viewed as truly competing in an active trade/business in its relevant market abroad. However, to the extent the foreign Sub receives income that is either “passive” or looks like “conduit income” (i.e., earned through an low-tax branch/tax haven), the deferral “privilege” ends w/respect to that income, which is then taxed currently to its US shareholder(s) under one of several statutory anti-abuse regimes. Rationale: Foreign Sub is just there for tax advantages—not to compete in a foreign trade/business (i.e., “capital import neutrality” policy objective no longer being served).

Foreign Tax Credits: The corporate income taxes imposed by U.S. upon actual or deemed repatriation of a foreign Sub’s E&P may generally be offset with the foreign taxes already paid on that E&P via a tax credit (to extent it eliminates double juridical taxation).

US C-Corp

Foreign Corp

U.S.

Foreign Jurisdiction

Foreign-source income

Dividend

46

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 24

TCJA Drastically Changes How Foreign Subsidiary Income of US Corporations is Taxed:

No More Deferral—Sub’s E&P is either taxed currently or exempted

AFTER 2017 US Tax Act

General Rule: United States still generally taxes its US corporations on a “worldwide” basis—but at a much lower rate—i.e., 21% (down from 35%). However, the corporate tax base is broader with more foreign Subs’ E&P subject to US tax. Also, there is some foreign-source income that is completely exempt from U.S. corporate taxation . Thus, new system is still a “hybrid system” exhibiting attributes of both a residence-based AND territorial system.

“Deferral Privilege” Exception is formally eliminated: Now, all income of a foreign subsidiary owned by a U.S. corporation will be either:

Taxed currently by US (either under one of the pre-existing anti-abuse regimes (PFIC or expanded Subpart F ) OR under the new very broad category of §951A “GILTI” income (Global Intangible Low-Taxed Income), which functions as a minimum tax , which can reach a foreign Sub’s income even if it’s not passive or conduit income; OR

EXEMPT from U.S. corporate taxation (forever).

Three categories of foreign-source income of foreign Subs are now EXEMPT . But these may not amount to much due to the breadth of the new GILTI minimum tax. They include:

1. CFC’s earnings attributable to the 10% notional return in the GILTI regime (QBAI), which qualifies for the § 245A DRD when repatriated:

2. Income of 10% corporate “US Shareholders” of foreign Subs that do not qualify as CFCs (but do qualify as “specified foreign corporations” and so get the § 245A DRD); and

3. Pre-1987 E&P accumulated by foreign Subs, but only to extent of the pro rata share owned by 10% U.S. CORPORATE shareholders, since the §965 Transition Tax does not apply to those earnings and the §245A DRD applies when repatriated.

In Sum: U.S. still has a “hybrid system” –i.e., part Residence-based (perhaps more so now) and part Territorial. Despite its new territorial attributes, the purview of US corporate tax is probably greatly expanded… but at a much LOWER rate—21% (vs. the former 35% ).

US C-Corp

Foreign Corp

U.S.

Foreign Jurisdiction

Foreign-source income

Dividend

47

Overview of U.S. Code Provisions

Governing

Cross-Border Reorganizations

IRC § 367

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 25

IRC § 367 - General Overview

• In general, Section 367, when it applies, turns “off” the non-recognition provisions that usually govern tax-free corporate reorganizations, and taxes the shareholders.

• Section 367(a): applies to Outbound tax-deferred reorgs. Applies to outbound transfers of property by U.S. person to a foreign corporation in any transaction to which § § 332, 351, 354, 356, or 361 applies, and turns OFF these non-recognition provisions with respect to built-in gains unless an exception applies, imposing a shareholder-level tax on the gains inherent in the property transferred (as though the property were sold).

• Section 367(b): applies to Inbound reorgs, Inbound § 332 LQs, and foreign-to-foreign reorgs.

• Section 367(d): applies to outbound transfers of “intangibles” by a U.S. person to foreign corporation in an exchange to which § § 351 or 361 would otherwise apply. Treats the intangible property as though it were licensed to the foreign corporation for a deemed royalty stream “commensurate with the income” generated by the intangible. (Thus, 367(d) inserts § 482 transfer-pricing principles.)

• Section 367(e): applies to outbound spin-offs (to which § 355 would otherwise apply) and to outbound liquidations.

49

IRC § 367(a)

Outbound Cross-Border Reorganizations

• § 367(a)(1) – General Rule: “If, in connection with any exchange described in section 332, 351, 354, 356, or 361 , a US person transfers property to a foreign corporation, such foreign corporation shall not, for purposes of determining the extent to which gain shall be recognized on such transfer, be treated as a corporation.”

• General rule is one of taxation unless an exception applies.

• If the transaction does not qualify as a “reorg” under 368, then 367 does not apply (transfer is treated as a sale, which might yield a better result—e.g., installment sale treatment under § 453A).

• Exceptions to Gen. Rule of § 367(a)(1):

• § 367(a)(2): Outbound transfers of stock/securities in a foreign corporation, if that foreign corporation is a “party to the reorg” (and unless an exception in the regs applies)

• Outbound transfers of domestic stock: Regulations provide that generally, gain is recognized unless:

• No more than 50% of stock of foreign Acquiror received by US transferors,

• No more than 50% of stock of foreign Acquiror owned after the transfer by US “control group” (i.e., officers or directors or 5% Target shareholders)

• Gain Recognition Agreement ("GRA") is entered into by 5% US transferee shareholders

• 36 month active trade-or-business test is met,

• No intent to substantially dispose of or discontinue such trade or business,

• FMV of the assets of transferee must be at least equal to the FMV of the US target, and

• Tax reporting obligations are met

• § 367(a)(3) – (Repealed by 2017 TCJA) Transfers of property for use in the foreign transferee corp’s active trade or business.

50

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 26

TCJA Repealed the Foreign Trade/Business Exception of § 367(a)(3)

and Added a new “Recapture” Rule for Foreign Branch Losses –New § 91

• Repeal of § 367(a)(3): Prior to its repeal, subsection (a)(3) provided an exception to the general recognition rule of §367(a)(1) for asset transfers if the assets were used in the active conduct of a trade or business outside the U.S.

• Because of its repeal, all outbound transfers of tangible property (in what would otherwise qualify as an outbound reorg) are subject to tax under § 367(a(1) at the shareholder level.

• Tax may now be recognized in any outbound asset reorg or on the incorporation of a foreign branch.

• New § 91 – Foreign Branch Loss Recapture: § 91 applies if a U.S. corp transfers substantially all of the assets of a foreign branch to a “specified 10 % owned foreign corp(defined in §245A) w/respect to which it is a “US shrldr” after transfer.

• The U.S. corporation must include in gross income the “transferred loss amount” with respect to such transfer, which is any excess of:

• Deductible losses incurred by the foreign branch after Dec. 31, 2017, and before the transfer, over

• Taxable income of the branch for a tax year after the year in which the loss was incurred and through the close of the year of the transfer, plus any amount recognized under § 904(f)(3) on the transfer.

• The transferred loss amount is generally reduced by the amount of gain recognized by the taxpayer on the transfer.

• Recaptured loss amounts are treated as U.S. source income.

51

IRC § 367(d)

Treatment of Intangibles

• § 367(d)(1): “Except as provided in the regulations…if a US person transfers intangible property to a foreign corporation in an exchange described in §351 or § 361,

• (A) subsection (a) does not apply to the transfer and • (B) provisions of 367(d) apply instead.

• § 367(d)(2): Treats outbound transfer of intangible property as though it were sold for a stream of contingent payments—contingent on the productivity of use of the property over its useful life.

• “The amounts taken into account shall be treated as “commensurate with the income attributable to the intangible.”

• Treated as a royalty stream that IRS has the right to adjust under transfer pricing principles and transfer pricing regulations applicable to intangibles.

• What if the intangible is “sold” outright? Can an outright sale avoid the stream of deemed royalties (which is phantom income)m, and also “fix” the value on the date of the putative sale—perhaps locking in a lower value before it appreciates?

• If it is a controlled transaction under § 482, the IRS still has the power to adjust the amount of the royalties in order to prevent the evasion of taxes and to “clearly reflect income.” And, with respect to controlled transactions involving intangibles, the transfer or license must be “commensurate with the income attributable to the intangible.” See § 482 (last sentence).

52

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 27

IRC § 367(d)

Treatment of Intangibles ( continued – 1)

• The TCJA revised the definition of intangible property in § 936(h)(3)(B), which was incorporate by reference in §367(d)(1), and thus applicable to outbound transfers of intangible property under § 367(d).

• Under prior law, §936(h)(3)(B) defined intangible property as any: • patent, invention, formula, process, design, pattern, or know-how;

• copyright, literary, musical, or artistic composition;

• trademark, trade name, or brand name; • franchise, license, or contract;

• method, program, system, procedure, campaign, survey, study, forecast, estimate, customer list, or technical data; or

• any similar item, which has substantial value independent of the services of any individual.

• Missing from the definition was: “foreign goodwill, going concern value, and workforce in place.” • Taxpayers would routinely argue that the legislative history of § 367(d) indicated that Congress did not think these

intangibles should be subject to § 367(a) because their value was ostensibly created outside the U.S. Taxpayers would also argue that if subject to § 367, they should fall under the general rule of 367(a), and thus be eligible for the exception for assets transferred for use in the foreign corporation’s active trade/business (i.e., prior to that exception’s repeal).

53

IRC § 367(d)

Treatment of Intangibles (continued – 2)

• As revised, the definition of intangible property now includes “any goodwill, going concern value, or workforce in place (including its composition and terms and conditions (contractual or otherwise) of its employment).”

• Thus, Congress, in the TCJA, ended the longtime argument; these types of intangible are now clearly subject to § 367(d) deemed royalty treatment rather than § 367(a).

• The revised definition of intangible property is now set forth in § 367(d)(4). And, §936 was repealed in the Consolidated Appropriations Act, 2018 (P.L. 115-141).

• The TCJA also removed “any similar item” in the old definition, replacing it with a more specific catch-all phrase: “any other item the value or potential value of which is not attributable to tangible property or the services of any individual.”

• New grant of strong regulatory authority in § 367(d)(2)(D): an amendment permit Secretary to write regulations and require valuation of intangible property transfers on an aggregate basis or on the basis of realistic alternatives.

• Thus the TCJA confirms the authority of the IRS to require certain valuation methods be applied to intangible property..

54

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 28

IRC § 367(a) and (d)

Planning for Outbound Transfers of Tangible and Intangible Assets

• § 367 now results in income or gain recognition on all outbound transfers of tangible and intangible property.

• But if transferor is a US C-Corp, tax is imposed at a reduced corporate rate of 21%.

• FDII deduction under § 250? If the assets transferred are for “foreign use,” the §367(a) gain or a §367(d) deemed royalty inclusion could be considered “foreign derived intangible income” (FDII) and thus eligible for a deduction under §250 that could further reduce the rate to 13.125%.

• Issue as to “related party” • “Foreign Use” requirement • “Sale” requirement • Foreign Branch Income Exception • Foreign tax treatment of the transfer (basis step-up on the

sale, greater amortization dds) • Also, consider deductibility of actual or deemed royalty

payments by (or US depreciation/amortization dd of) FS in its home jurisdiction.

• Impact on the GILTI calculation

• Assume that USP incorporates its foreign branch, FS, turning it into a corporate sub. USP is deemed to transfer its branch assets to a “foreign corporation”, thus triggering § 367(a) and (d).

55

USP

FS Foreign

Sub

USP transfers tangible and intangible assets to FS

IRC § 250 – FDII Overview

The deduction for “foreign derived intangible income”

• New deduction for U.S. corporations for foreign-derived intangible income (FDII) reduces the U.S. tax rate on income from certain export sales and licenses and services provided to persons outside the United States.

• The current FDII deduction is 37.5%, which produces a 13.125% ETR (the deduction is reduced to 21.875% starting in 2026 for an ETR of 16.406%).

• In general, income is included in the computation of FDII if it is derived from (1) sales of property to any foreign person for foreign use, or (2) services provided to any foreign person or with respect to foreign property.

• The computation of FDII excludes certain types of income, including “foreign branch income,” which is defined in §904(d)(2)(J) as business profits attributable to one or more qualified business units in one or more foreign countries.

• The amount eligible for the FDII deduction is reduced by a fixed 10% return on tangible property.

• The FDII deduction is subject to a taxable income limitation.

• FDII Proposed Regs issued on March 4, 2019, delineating many of the requirements.

• Assume that USP incorporates its foreign branch, FS, turning it into a corporate sub. USP is deemed to transfer its branch assets to a “foreign corporation”, thus triggering § 367(a) and (d).

56

USP

FS Foreign

Sub

USP transfers tangible and intangible assets to FS

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 29

IRC § 250 – FDII Overview (continued)

• “Foreign” use means any use, consumption, or disposition that is not within the United States.

• “Sale” of property includes any lease, license, exchange, or other disposition.

• Related Party Transactions: If property is sold to a related party who is not a U.S. person, the sale is not treated as for a foreign use unless the property is ultimately sold by a related party, or used by a related party in connection with property that is sold or the provision of services, to another person who is an unrelated party who is not a U.S. person, and the taxpayer establishes to the satisfaction of the Secretary that such property is for a foreign use.

• A sale of property is treated as a sale of each of the components thereof.

• If a service is provided to a related party who is not located in the US, taxpayer must establish that the service is not substantially similar to services provided by such related party to persons located within US.

• “Related party” defined by reference to § 1504(a) affiliated group, using a lower 50% threshold and including foreign corps & insurance companies. Any person (other than a corporation) is treated as a member of the affiliated group if the person is controlled by members of the group (including any entity treated as a member of the group by reason of this sentence) or controls any member.

• “Control” is determined under the rules of § 954(d)(3) (definition of “related person” for Subpart F).

57

IRC § 367(b)

Inbound Reorgs & Inbound LQs, Foreign-to-Foreign • Underlying Tax Policy Concern of § 367(b) enunciated in Preamble to 1991 Proposed Regs: US shareholders should not

be allowed to repatriate the earnings and basis of their foreign corporation (which enjoyed deferral) without the imposition of US tax.

• § 367(b)’s policy with respect to Inbound Reorgs: The rules are based on principle that a “domestic acquiror of the foreign corporation’s assets should not succeed to the basis and other attributes of the foreign corporation except to the extent that the U.S. tax jurisdiction has taken account of the U.S. person’s share of the E&P that gave rise to those attributes.”

• Foreign-to-foreign transactions: § 367(b) protects the “1248 taint.” If a CFC is de-controlled in a foreign-foreign reorg, the US shareholder has to recognized a deemed dividend equal to the “1248 amount” as defined.

• Code § 367(b): General rule is no taxation unless provided otherwise in the regulations.

• § 367(b) regulations generally operated to prevent the avoidance of US tax by: • Taxing E&P of foreign subsidiaries in inbound § 381 transactions; and • Preserving such E&P, or accelerating the inclusion of dividend income, in connection with dispositions of stock in

foreign-to-foreign reorganizations.

• The § 367(b) rules can impose tax in the form of a deemed dividend equal to either the “all E&P amount” or the “§ 1248 amount”—two different measures of the foreign corporation’s E&P depending on the transaction and the underlying policy concern (e.g., de-control of a CFC without taxation generally triggers the § 1248 amount as a deemed dividend).

• The deemed dividend recognized under § 367(b) is treated as a “dividend” for all US tax purposes.

58

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 30

IRC § 367(b)

Are purposes underlying § 367(b) and Regs now MOOT?

• What purpose do the § 367(b) regulations continue to serve under current law?

• Under the TCJA:

• Pre-TCJA earnings are taxed under the § 965 deemed repatriation rules.

• No more corporate tax deferral as CFC earnings are subject to current tax under Subpart F or the GILTI rules in § 951A.

• All other CFC earnings generally are exempt from US tax, as § 245A generally provides US corporate shrs with a 100% dividends-received deduction (DRD) on repatriation.

• § 1248(j) treats the § 1248 amount on the sale of stock as a dividend that qualifies for tax-free treatment under § 245A.

• § 964(e) provides for essentially the same treatment to a selling CFC upon a sale by an upper-tier CFC of stock in a lower-tier CFC.

59

Foreign Sub

IRC § 367(b)

Planning for Inbound Asset Transfers in light of § 245A Assumed Facts:

• USP contributes the stock of FS to Newco U.S., after which FS elects to be treated as a disregarded entity for U.S. tax purposes. The transactions should qualify as an inbound “F” reorganization.

• Alternatively, FS elects to be a disregarded entity and is deemed to liquidate directly into USP in a section 332 transaction.

Analysis:

• Pre-TCJA: transaction would generally result in USP including the ”all E&P amount“ with respect to its FS stock in gross income as a dividend (generally, the E&P of FS attributable to the stock held by USP).

• Post-TCJA: Any “all E&P amount” dividend should be eligible for the DRD under §245A and effectively exempt from U.S. tax.

• The result would be the same in a foreign-to-foreign reorganization that resulted in the inclusion of dividend income equal to USP’s “§1248 amount” in the stock of FS (i.e., such amount would be exempt from U.S. tax under §245A).

• Don’t forget about possible impact on the BEAT tax; cf. § 311 distribution of assets from FS to USP.

(1) USP contributes FS stock to NewCo.

(2) FS elects to be treated as a disregarded entity, resulting in a deemed liquidation.

60

USP

NewCo US

Foreign Sub

Foreign Sub

FS liquidates into US NewCo

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 31

JOINT VENTURE STRUCTURES

LLC

US & Foreign Assets

US Company Foreign

Company

• Section 367 Issues

• Disguised Sale ?

• Effect of assumed liabilities

• Possible application of § 721(c) if LLC is treated as a partnership…

• § 721(c) was enacted as a corollary to § 367(a)

61

The U.S.

Anti-Corporate-Inversion

Rules

IRC §7874

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 32

IRC § 7874: Aimed at “corporate expatriations”

• U.S. Congress enacted IRC §7874 in 2004, and has been broadening the purview of its application in recent years with regulatory amendments.

• Senate Report states §7874 is aimed at domestic entities reincorporating offshore with little presence in the foreign acquiring corporation’s country of incorporation (i.e, the home country)…and with business operations conducted in the same manner as before the inversion.

• IRC § 367(a) imposes tax only at the U.S. shareholder level, and failed to stop several waves of high-profile corporate inversions.

• Nothing seemed to work to stop U.S. multinational companies from wanting to effectively reincorporate abroad.

• § 7874 focuses on ownership of the new foreign parent by the historic shareholders of the “inverted” domestic entity—both for purposes of its application and its effects.

63

IRC 7874 – High Level Overview

• Anti-Inversion Rules – tax outbound reorganization and/or tax foreign Acquiror as a U.S. taxpayer; Code § 7874

• If ownership of former U.S. Target shareholders in foreign Acquiror is 80% or more; foreign Acquiror is treated as a U.S. company

• If ownership continuity is between 60-80%; foreign Acquiror is NOT treated as a U.S. company, but U.S. tax attributes cannot be used to offset gains

• 20% excise tax on stock-based compensation upon certain corporate inversion transactions

• § 7874 exception available for companies with “substantial business activities” in the foreign jurisdiction which exist when:

• (1) The number of employees and the amount of employee compensation in the foreign jurisdiction is at least 25% of the number of employees and amount of employee compensation in the total group;

• (2) The value of group assets (only tangible property held for use in the trade or business) located in the foreign jurisdiction is at least 25% of the total group assets; and

• (3) The income derived from the foreign jurisdiction is at least 25% of the group income

64

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 33

What is a Corporate Inversion?

Simple paradigm structure BEFORE inversion

Ireland Co. US Co.

Foreign Sub

SHs SHs

US Co. Stock

UK Co. Stock

• Shareholders of US Co. exchange their stock for stock in Ireland Co.

65

What is a Corporate Inversion?

Paradigm Structure AFTER the Inversion

Ireland Co.

US Co.

Foreign Sub

US SH

SHs Ireland

Focus on ownership of NFP by historic US shrlds

• IRC § 7874 requires that the former US Co. shareholders cannot own 80% or more (value or vote) of Ireland Co.—the “New Foreign Parent” (NFP).

• Otherwise, Ireland Co. (the NFP) will be treated as a U.S. CORPORATION for all U.S. federal tax purposes – a tax disaster (making all the U.S. tax planning obsolete, and also possibly creating double juridical taxation depending on the facts).

66

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 34

Historical Incentives to Invert

(1) Earnings Stripping

Ireland Co.

US Co.

Foreign Sub

US SH

Ireland

SH

Note

• Earnings Stripping has been a main driver for corporate expatriations

• US MNCs have exploited opportunity to “strip-out” earnings from U.S. corp tax free through tax deductions for interest, royalties paid, etc. with little or no tax incurred on receipt by the related party.

• After 1 year, US Co. distributes a note to Ireland Co., creating the opportunity for earnings stripping with reduced withholding tax on the distribution under the US-Ireland treaty.

67

Historical Incentives to Invert

(2) Access Foreign Cash without US Tax Cont.

• Before Notice 2014-52, the foreign acquiror and the former US Co. shareholders could gain access to foreign earnings in Foreign Sub through UK Co. via a “hopscotch” loan.

UK Co.

US Co.

Foreign Sub

US SH

UK SH

“Hopscotch” Loan

68

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 35

Historical Incentives to Invert

(2) Access Foreign Cash without US Tax – (Plenty of it!)

• Since 1960, globalization has caused U.S. multinationals to derive an increasingly greater percentage of their profits from foreign subsidiaries.

• About $2.1 trillion

69

Historical Incentives to Invert

(3) Protect Future Foreign Earnings from U.S. Tax

•High U.S. combined statutory corporate income tax rate

•Earnings of foreign subsidiaries of a U.S. multinational are subject to US tax upon repatriation if not before (e.g., subpart F)

70

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 36

Historical Incentives to Invert

• The foreign acquirer could acquire foreign businesses, make strategic investments abroad, or organically expand its foreign operations without facing U.S. corporate tax on future earnings or trapping foreign earnings under the U.S.

• Inverted U.S. MNCs found ways to migrate their foreign subs so that they were newly situated under the new foreign parent—and thus further removed from the purview of the U.S. income tax net (subject to Subpart F anti-deferral regime).

Ireland Co.

US Co.

Foreign Sub

US SH

Ireland SH

Foreign

(3) Protect Future Foreign Earnings from U.S. Tax

71

How Have Inversions Been Executed?

Simplistic Paradigm Structure BEFORE Inversion

U.S. Co. (i.e., “Domestic Entity” or “DE”) and Foreign Co. (FC) seek to combine under FC or a new foreign holding company—the “Foreign Acquiror” (“FA”).

DE SHs

DE (U.S.)

Foreign Subs

(CFCs)

FC SHs

FC

FC Subs (non-CFCs)

72

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 37

How Have Inversions Typically Been Executed?

Resulting Structure AFTER Inversion

• Here a new foreign entity is formed by contributions of both DE and FC.

• Another variety involves DE becoming a sub of New Foreign Parent (NFP) in a “self inversion”

Legacy DE SHs

DE (U.S.)

Foreign Subs

(CFCs)

Legacy FC SHs

FC

FC Subs (non-CFCs)

New Foreign Parent

(NFP)

< 80% > 20%

73

How Have Inversions Typically Been Executed?

Paradigm inverting merger (BEFORE)

Inversions have often been structured as mergers, where substantially all the assets of the U.S. Target are transferred to a U.S. affiliate of the new Foreign Parent in exchange for Foreign Parent’s stock, which is distributed up to the U.S. Target’s shareholders in a liquidating distribution of the U.S. Target.

DE SHs

DE (U.S. Target)

U.S. Sub 2

U.S.

Sub 1

FC SHs

FA

(Foreign Parent)

U.S.

Affiliate

Merger

Foreign Parent Shares

74

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 38

How Have Inversions Typically Been Executed?

Paradigm inverting merger (After)

After the merger, the U.S. group has effectively been moved under the new Foreign Parent.

DE SHs

DE (U.S. Target)

U.S. Sub 2

U.S.

Sub 1

FC SHs

FA

(Foreign Parent)

U.S.

Affiliate

75

Summary of Key U.S. Restrictions on Corporate Inversions

• Code § 367(a), and § 367 regulations impose tax at U.S. shareholder level. (But these rules did not stop waves of inversions)

• Tax Code §7874 (2004 HIRE Act)—the purview of which has been expanded multiple times by regulation in cat & mouse game between Gov’t and US MNCs. (Slowed down inversions for a while.)

• IRS Notice 2014-52: expanded §7874 guidance to cover transactions after 9/22/2014, impacting calculation of the numerator and denominator in the critical continuity-of-ownership fraction –(key 60% & 80% thresholds)

• IRS Notice 2015-79: Tightened rules and expanded reach of §7874

• Anti-Inversion Regs – 1.7874-1, et seq. (Final & Temp. as of Jan. 2017) implement rules described in the two Notices, and add new ones, including: “serial acquiror rule,” “multi-step acquisition rule,” modifications to SBA test & “spinversion” rules. 2017 Technical Changes.

• §385 Regs (Final as of 10/2016) to Recharacterize “Debt” as “Equity” and vice versa. (Rules attempt to remove earnings stripping incentive for inversions- but rules are very broad)

76

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 39

IRC § 7874

Overview of fundamental statutory 60% and 80% tests

IRC § 7874(a)(2)(B) provides, in its pertinent part, that if pursuant to a plan or series of

related transactions:

(i) a foreign corporation (“FC”) acquires, directly or indirectly, substantially all of the properties held directly or indirectly by a domestic corporation, or substantially all the properties constituting a trade or business of a domestic partnership,

(ii) after the acquisition at least 60 percent of the stock (by vote or value) of FC is held by former shareholders or partners of the domestic entity (“DE”) by reason of their former ownership of DE, and

(iii) after the acquisition, FC’s “expanded affiliated group” (“EAG”) fails to meet the so-called substantial business activities test(which test works as an overall exception to §7874,

then FC will be treated as a “surrogate foreign corporation” and consequently any “inversion gain” will be fully taxable from the date the acquisition begins until ten years after its completion, with only limited offset by losses and tax credits.

[Note: The above is paraphrased from §7874 and emphasis of key statutory terms is supplied.]

77

Overview of statutory 60% and 80% tests (Cont.)

• Section 7874(b) further provides that “notwithstanding §7701(a)(4) (defining “domestic” corporation or partnership) IF conditions (i) and (iii) of § 7874(a)(2)(B) are met and at least 80 percent of the stock of FC (by vote or value) is held by former owners of DE by reason of such historic ownership, the FC will be treated as a domestic US corporation for all federal tax purposes.

• The consequences described in subsections (a) and (b) of § 7874 do not apply, however, if the EAG satisfies the “substantial business activities” test.

78

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 40

§ 7874: Key Operational Rules and Definitions

• Plan or series of related transactions: This is statutory language, but term is left undefined in the Code. Sec. 7874(c)(3) provides that “a plan” is deemed to exist for acquisitions of substantially all of the assets during the 4-year period beginning 2 years before the ownership requirements are met. (But Caution - See Temp. Reg. § 1.7874-8T – “Serial Acquisitions” rule could apply even where no “plan” is found under the facts and circumstances, or within the 4-year statutory presumption period.)

• Substantially All. Undefined in Code. But legislative history states Treasury expects to issue regulations, and is not be bound by interpretations in other contexts (like Subch. C). Subch. C reorg definition is likely to be used as analogous authority.

• Facts & Circumstances or Threshold Percentage? • Gross Assets? Net Assets? Business Assets?

• Stock of the surrogate foreign corporation “held by”: Note that test is not necessarily the stock “received” by historic shldrs of the domestic entity, but rather the stock “held” or owned by them by reason of their ownership in the domestic entity. Attribution rules.

79

§ 7874: Key Rules & Definitions (cont…)

• Inversion Gain: Defined in §7874(d)(3). With respect to “60/<80” transactions, § 7874(a)(1) provides that the “taxable income of the expatriated entity for any taxable year” within the 10 year period following the expatriation (the “applicable period”) can be no less than the “inversion gain.” Inversion gain is primarily any gain realized by the expatriated entity that is related to the transaction (including §78) plus any gains realized by related tax planning occurring during the applicable period. The term includes gains realized by reason of a direct or indirect transfer of stock or other properties, or by reason of a license of any property--either as part of the acquisition described in §7874(a)(2)(B)(i), or, for non-inventory property, after such acquisition if the transfer or license is to a specified related person. Importantly, the use of certain tax attributes, such as NOLs and tax credits, to offset inversion gain is greatly limited. See §7874(e)(1).

• Expatriated Entity: Domestic target (corporation or partnership) for which FA is a “surrogate foreign corporation” and any U.S. person related under §§267(b), 707(b)(1) to the domestic target. This term is relevant to measuring “substantial business activities” in the SBA test.

• Expanded Affiliated Group [EAG]: Use §1504 affiliated group rules, but without regard to §1504(b)(3) and substituting > 50% vote and value instead of 80%. (This term is relevant to measuring “substantial business activities”.)

• Applicable Period: Defined in § 7874(d)(2) as the period beginning on the first date properties are acquired in the acquisition described in § 7874(a)(2)(B)(i), and ending on the date which is 10 years after the last date properties are acquired as part of such acquisition.

80

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 41

Snapshot of Key § 7874 Rules

KEY TEST of IRC § 7874: • If historic Shldrs of US Corp receive > 50% of New Foreign Parent: Deal is generally taxable to U.S. Shrlds of

the U.S. Corp under §367.

• If historic Shldrs of U.S. Corp own at least 60%, but < 80% of NFP: Restrictions are imposed on the inverting U.S. Corp, but NFP is respected for U.S. tax purposes as a foreign (non-U.S.) corporation. However, U.S. Corporate group is taxed on “inversion gain” (as defined).

• If historic Shldrs own 80% or more of NFP: Then NFP will be treated as a U.S. corporation for U.S. TAX purposes (even though it remains a foreign corporation for other legal purposes) -- a tax disaster! (U.S. tax planning is rendered meaningless; multiple juridical taxation could now be a real risk).

==================================================================== • Because the SBA test is so difficult to meet, the key focus has been on the amount of stock the former shareholders

of US Corp OWN in New Foreign Parent (NFP) after the transaction (by reason of their prior ownership in U.S. corp) and the resulting ownership fraction—i.e., 50%, 60%, or 80% of NFP.

• NOTE: Current IRS Regulations are aimed at how this ownership threshold is measured. When the new rules are applied, it can move historic ownership from approx. 55% historic /45%) to say 61% historic/39% --making §7874 applicable!

81

Illustration of 80% and 60% Tests of § 7874

• If, after transaction, historic Shldrs of US Co. own 80% or more (by vote or value) of Ireland Co., Ireland Co. will be treated as a U.S. corporation for U.S. tax purposes – a terrible result. (All tax planning failed; there is also a risk of multiple international taxation.)

• If, after transaction, historic shldrs of US Co own at least 60% but < 80%, then Ireland Co. is respected as a foreign corporation, but the U.S. Co. group is taxed on “inversion gain.”

Ireland Co.

US Co.

Foreign Subs

US SHs

SHs

-- 80% or > -- 60% to 79%

82

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 42

“Substantial Business Activities” Test

• § 7874(b)(2)(iii): If the “expanded affiliated group” (EAG), including the foreign acquiring corp, has “substantial business activities” in the same country where the foreign acquiring corp is created or organized, as compared to the total business activities of the EAG, then the foreign corp is not treated as a “surrogate foreign corp” (and the rules of §7874 do not apply to the transaction).

• Original 2006 SBA Regs: had facts-and-circumstances test and a 10% bright-line safe harbor (requiring at least 10% of tangible assets, employees, compensation, and third party revenues to be in FC’s jurisdiction)..

• July 2012 Regs: imposed a 25% bright-line test as the exclusive SBA test.

• Notice 2015-79: announced requirement that foreign acquiring corporation also be subject to tax as a “tax resident” in the foreign country of its creation or organization in order to meet SBA test.

• Reg. §1.7874-3T(b)(4): implemented the “subject-to-tax as a tax resident” rule of Notice 2015-79, and did not alter the 25% test of the existing regulations. (Result: can no longer arbitrage residency –i.e., having tax residency in a different, more advantageous treaty country that looks to place of “mngmt & control” while §7874 uses “place of incorporation” as corporate residency test.)

SBA is the Big Exception to § 7874, but Difficult to Meet

83

“Substantial Business Activities” Test (Cont. -2)

Meeting the “taxable foreign parent” rule of Reg. §1.7874-3 (originally issued as Temp. Reg – 6/3/2015): • The SBA test will be satisfied only if at least 25% of the

EAG’s “group” employees, group assets and group income are located or derived in the foreign acquiring corporation’s country of incorporation. (Look to EAG’s financial statements for purposes of determining the amount of items of income that are taken into account rather than for the purpose of identifying the members of the EAG. See §1.7874-3(d)(10)

• Reg. §1.7874-3(b)(4) now requires that the foreign acquiring corporation also be a tax resident in the foreign country of its creation or organization.

AND

Tax Resident

UST

(US)

FA

(Country X)

F2

(Country Y)

F1

(Country X)

- At least 25% of employees

- At least 25% of group assets

- At least 25% of group income;

84

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 43

Ownership Rules modifying the Numerator of the Ownership Fraction

Non-Ordinary Course Distributions NOCD – Basic Rules of -10 (final as of 1/13/2017))

• Reg. §1.7874-10 treats former owners of the U.S. target as receiving additional value (not vote) in stock of the foreign acquiring corporation when the U.S. target has made NOCDs.

• Requires excess distributions made by a U.S. target to be “added back” to the value of the U.S. target for purposes of calculating the ownership fraction (but not SBA).

- Excess of total distributions in each look- back year over 110% of the average amount of distributions in the thirty-six month period preceding the start of each look-back “year”.

- 36-month look-back period from closing date divided into three look-back “years”.

UST

(US)

Shareholders A

Shareholders B

<70% >30%

FT

(Country X)

Excess

Distributions

are “added

back”

<85% >15%

FA

(Country X)

Ownership Percentage

After Adding NOCDs

15 %

85

Ownership Rules modifying the Numerator of the Ownership Fraction

Year 1 Year 2 Year 3

Look-Back Period

DHP for LBY 1

DHP for LBY 2

DHP for LBY 3

Steps to determining the amount of NOCD with closing due date of Date X:

1. Identify look-back period.

2. Divide the look-back period into 12 month look-back years (LBYs).

3. Identify the distribution history period (DHP) for each look-back year.

4. Calculate the NOCD threshold for each look-back year.

5. Calculate, for each look-back year, the excess, if any, of all distributions made during the look-back year over the NOCD threshold for the look-back year. Such excess amounts constitute NOCDs.

Non-Ordinary Course Distributions

86

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 44

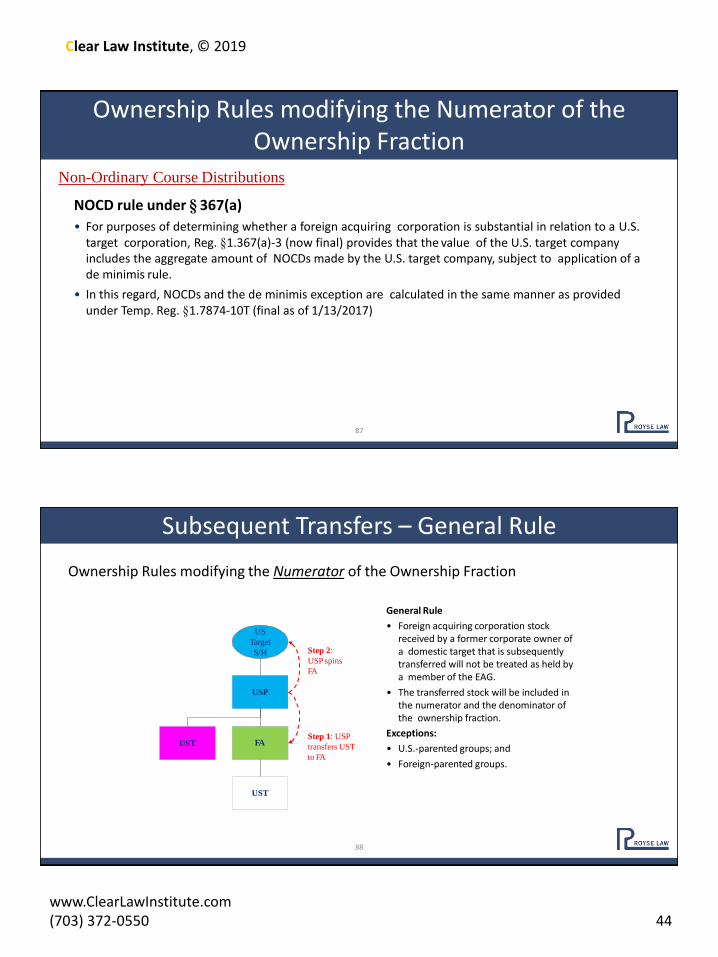

Ownership Rules modifying the Numerator of the Ownership Fraction

NOCD rule under § 367(a)

• For purposes of determining whether a foreign acquiring corporation is substantial in relation to a U.S. target corporation, Reg. §1.367(a)-3 (now final) provides that the value of the U.S. target company includes the aggregate amount of NOCDs made by the U.S. target company, subject to application of a de minimis rule.

• In this regard, NOCDs and the de minimis exception are calculated in the same manner as provided under Temp. Reg. §1.7874-10T (final as of 1/13/2017)

Non-Ordinary Course Distributions

87

Subsequent Transfers – General Rule

Ownership Rules modifying the Numerator of the Ownership Fraction

General Rule

• Foreign acquiring corporation stock received by a former corporate owner of a domestic target that is subsequently transferred will not be treated as held by a member of the EAG.

• The transferred stock will be included in the numerator and the denominator of the ownership fraction.

Exceptions:

• U.S.-parented groups; and

• Foreign-parented groups.

FA

USP

US

Target

S/H

UST

Step 2:

USP spins

FA

Step 1: USP

transfers UST

to FA

UST

88

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 45

Passive Assets/Cash Box Rules

Ownership Rules modifying the Denominator of the Ownership Fraction

• Reg. §1.7874-7T (now final as of 1/13/2017) disregards stock of a foreign acquiring corporation for purposes of calculating ownership continuity if the value of such stock is predominantly (i.e., more than 50%) attributable to certain passive assets (the “passive assets rule”).

• Includes an exception in the case of de minimis ownership continuity.

89

Anti-Stuffing Rules

Ownership Rules modifying the Denominator of the Ownership Fraction

General Rule

•Section 7874(c)(2)(B) provides that stock of a foreign acquiring corporation sold in a public offering related to the acquisition of a U.S. target is excluded from the denominator of the ownership fraction.

•Reg. §1.7874-4T (now final) further excludes certain “disqualified stock” from the denominator of the ownership fraction.

•Defines “avoidance property” as any property (other than specified nonqualified property) acquired with a principal purpose of avoiding 7874, regardless of whether the transaction involves an indirect transfer of specified nonqualified property.

Public

DT

(US)

75% 25%

Treas. Reg. §1.7874-4T(j), Example 3

PRS

(Country X)

PRS Properties

FA

(Country Y)

PRS Properties

Contributed

DT stock in

exchange for

FA stock

Contributed

PRS

properties in

exchange for

FA stock

90

Clear Law Institute, © 2019

www.ClearLawInstitute.com (703) 372-0550 46

End of Corporate Tax Deferral and Expansion of Subpart F

- Expanded purview of CFC Rules

- New Tax on “GILTI” – New § 951A

- One-time “Transition Tax” – New § 965

Expanded Purview of Subpart F’s CFC Rules Post-TCJA

Six ways the 2017 Act broadened Subpart F’s application

1. § 951(b) definition of “US shareholder” was broadened to include a value test -(after TCJA, the test for “US shldr” is a US person owning at least 10% of EITHER vote OR 10% of value of a foreign corporation (directly, indirectly through foreign entities, or constructively through modified § 318 attribution rules).

2. Amended § 951(b) to provide that the new definition of “U.S. shareholder” applies “for purposes of this title,” – (i.e., Title 26—the whole U.S. Internal Revenue Code)—instead of just for purposes of Subpart F as under pre-TCJA law.

3. Repealed IRC § 958(b)(4), which had (prior to repeal) turned-off the downward stock attribution rules of § 318(a)(3)(A) through (C) for purposes of imputing stock owned by a foreign person to a US person (in identifying US shldrs and CFCs).

4. Eliminated from § 951’s income inclusion rule the requirement that a foreign corporation must be a CFC for at least “an uninterrupted period of 30 days” during any taxable year in order for a US shldr to be taxed. (Now a foreign corporation need only be a CFC for 1 day.)