Chapter 13 Responsibility Accounting, Support Department ...

Upload

khangminh22Category

view

0download

0

1

LIBBY CHAPTER 12 PRERECORDED LECTURE

A Statement of Cash Flows (SCF) is a crucial financial statement that provides

important information about a company, and it is the only financial statement

prepared on a cash basis.

The Balance Sheet, Income Statement, Statement of Comprehensive Income, and

Statement of Stockholder’s Equity are all accrual basis documents.

The Operating Activities section of a SCF prepared on the indirect method is not

intuitive.

Students must learn the format and understand how accrual accounting

works in order to understand, and prepare, the Operating Activities section.

2

Cash or Cash and Cash Equivalents

A statement of cash flows can be prepared either on a (1) cash or (2) cash and cash

equivalents basis.

A cash equivalent is a short-term, highly-liquid investment with an original

maturity of less than three months.

For an example, both the American Eagle Outfitters Statement of Cash Flows on

text p. B-25 and Urban Outfitters Statement of Cash Flows on p. C-8 are prepared

on a cash basis and cash equivalent basis.

We will use the cash basis when preparing a SCF, which means that the statement of cash flows foots (totals) to the increase (decrease) in cash.

3

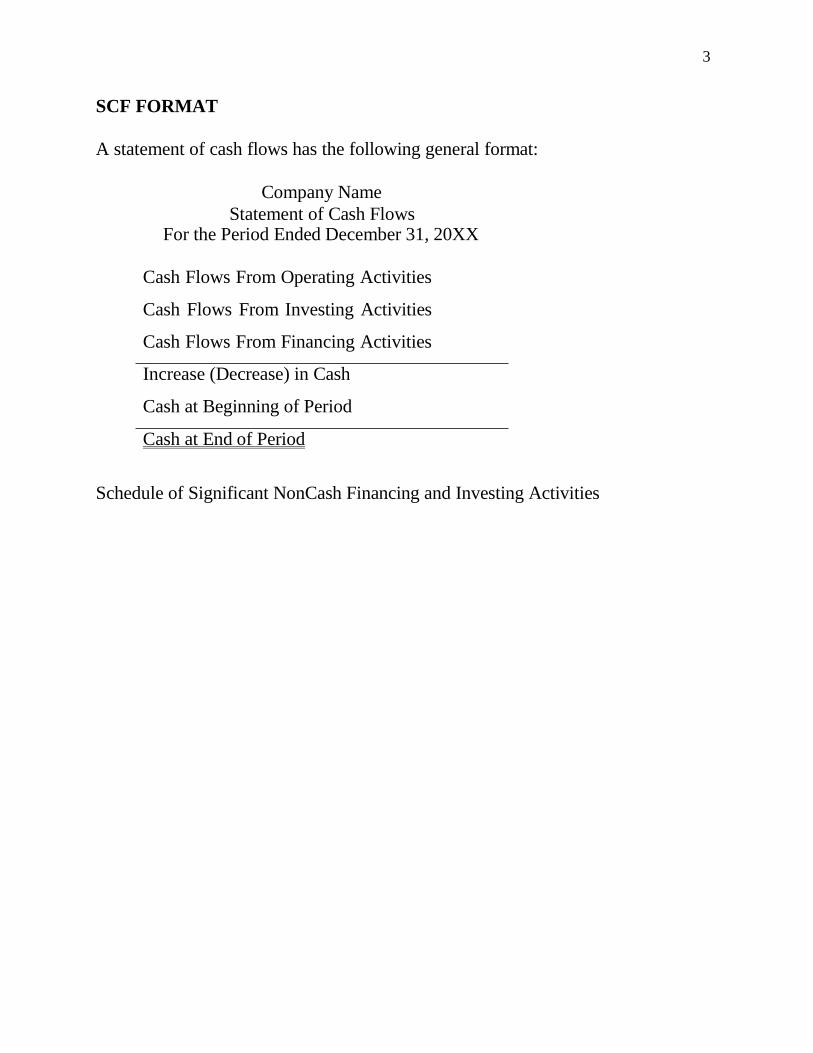

SCF FORMAT

A statement of cash flows has the following general format:

Company Name

Statement of Cash Flows For the Period Ended December 31, 20XX

Cash Flows From Operating Activities

Cash Flows From Investing Activities

Cash Flows From Financing Activities

Increase (Decrease) in Cash

Cash at Beginning of Period

Cash at End of Period

Schedule of Significant NonCash Financing and Investing Activities

4

SCHEDULE OF SIGNIFICANT NONCASH INVESTING AND FINANCING

ACTIVITIES

Some important transactions may be significant investing and financing

transactions but may not involve cash.

For example, a company might purchase property, plant, and equipment (investing

activity) in exchange for a note payable (financing activity).

If a company has these types of noncash transactions, then they are

reported on as supplement to the statement of cash flows as an attached

schedule.

HOW BALANCE SHEET CLASSIFICATIONS MAP INTO

STATEMENT OF CASH FLOWS CLASSIFICATIONS

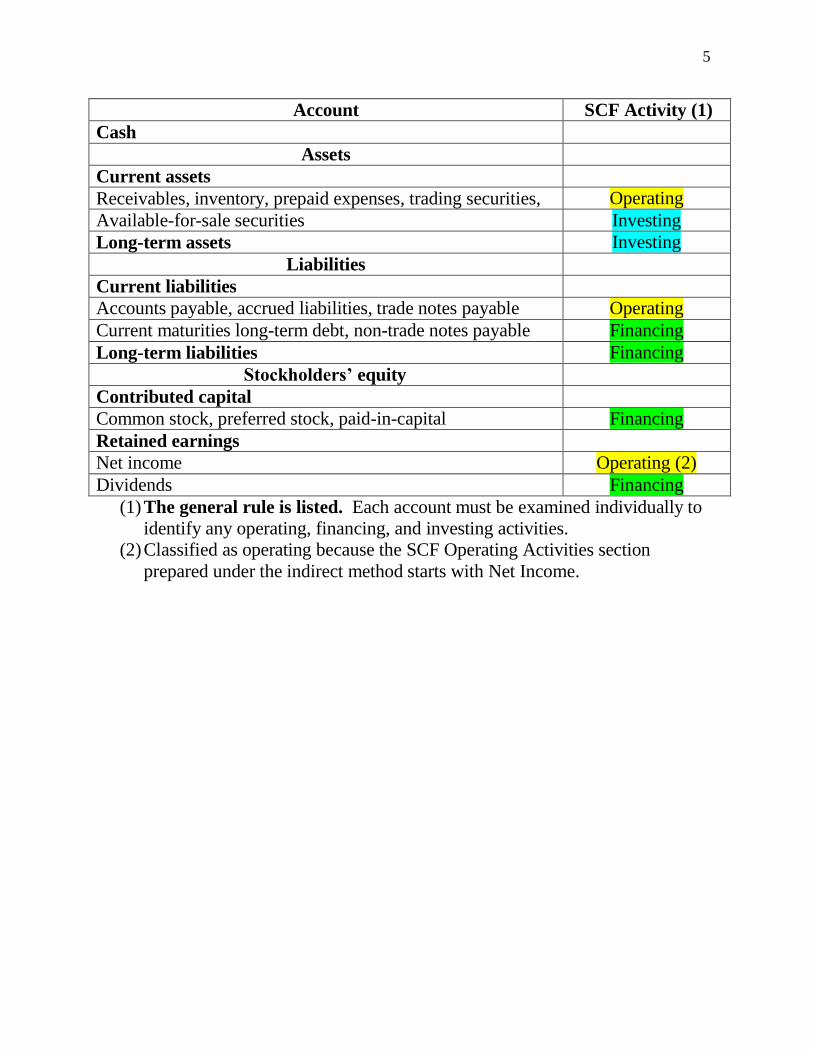

A listing of each general balance sheet account and the type of statement of cash

flow activity associate with each account is shown below. In this format, the

general classification is used. Some items within a classification could be treated

differently.

5

Account SCF Activity (1)

Cash

Assets

Current assets

Receivables, inventory, prepaid expenses, trading securities,

cash equivalents

Operating

Available-for-sale securities Investing

Long-term assets Investing

Liabilities

Current liabilities

Accounts payable, accrued liabilities, trade notes payable Operating

Current maturities long-term debt, non-trade notes payable Financing

Long-term liabilities Financing

Stockholders’ equity

Contributed capital

Common stock, preferred stock, paid-in-capital Financing

Retained earnings

Net income Operating (2)

Dividends Financing

(1) The general rule is listed. Each account must be examined individually to

identify any operating, financing, and investing activities.

(2) Classified as operating because the SCF Operating Activities section

prepared under the indirect method starts with Net Income.

6

INVESTING AND FINANCING ACTIVITIES SECTIONS

In these sections, the SCF lists inflows of cash (e.g., sales of assets, issuance of

debt) and outflows of cash (e.g., purchase of investments, dividends paid).

Note: in the investing and financing activities section, cash inflows may be

aggregated and cash outflows may be aggregated, but cash inflows and cash

outflows may not be netted together.

7

INDIRECT METHOD IN THE OPERATING ACTIVITIES SECTION

Almost all U.S. companies present the operating activities section using the

indirect method.

BECAUSE ALMOST ALL COMPANIES USE THE INDIRECT METHOD, WE WILL

CONCENTRATE ON IT.

In the indirect method, the operating activities section starts with net income.

However, net income is an accrual-based measure, not a cash-based

measure.

Thus, adjustments are made to reconcile from net income to cash flow

from operations.

Those adjustments include adjusting for

1. noncash expenses (income)*

2. losses (gains)*

3. changes in operational current asset and current liability accounts,

including interest receivable**

*Because noncash expenses (income) and losses (gains) reduced (increased) net

income but did not affect cash, the adjustment to add back (subtract) the amount

of the noncash expense (income) is apparent.

**But, the adjustment for changes in operational current asset and liability

accounts is not apparent.

The adjustments work because the operational current asset and liability

accounts have an accrual basis side, which is reflected in net income, and a

cash basis side, which is not reflected in net income.

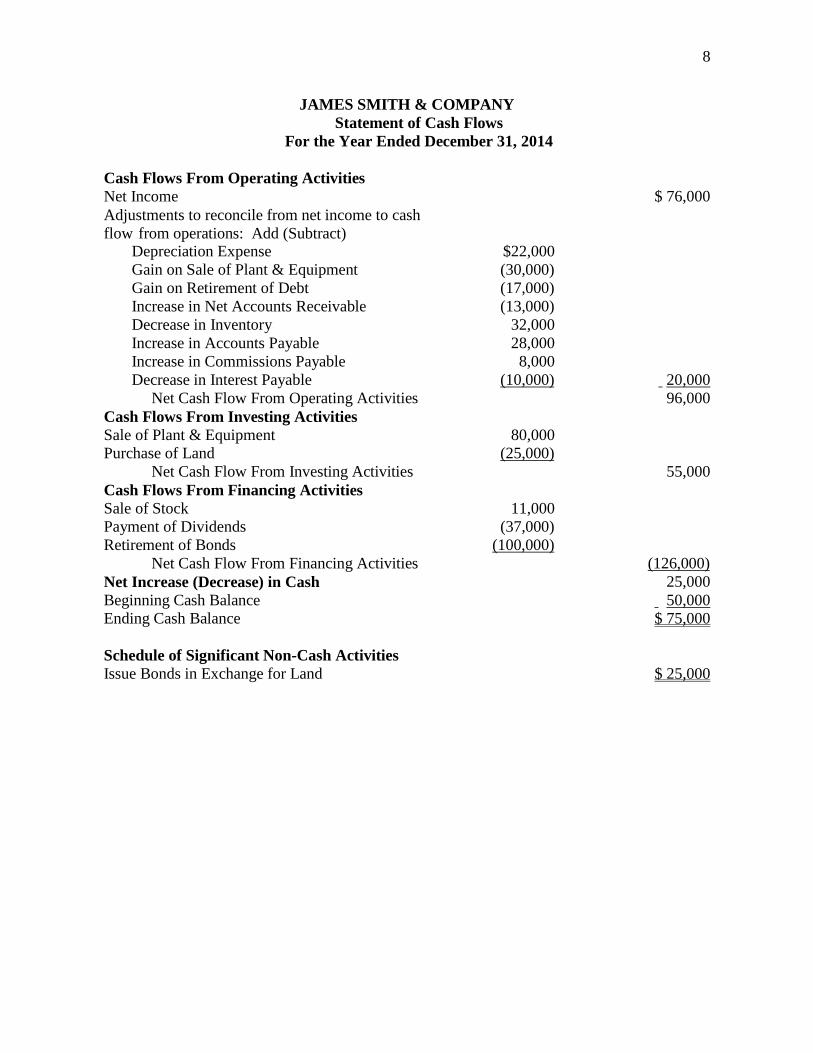

The Jim Smith Co. Statement of Cash Flow under the Indirect Method is attached.

8

JAMES SMITH & COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities

Net Income $ 76,000

Adjustments to reconcile from net income to cash

flow from operations: Add (Subtract) Depreciation Expense $22,000 Gain on Sale of Plant & Equipment (30,000) Gain on Retirement of Debt (17,000) Increase in Net Accounts Receivable (13,000) Decrease in Inventory 32,000 Increase in Accounts Payable 28,000 Increase in Commissions Payable 8,000 Decrease in Interest Payable (10,000) 20,000

Net Cash Flow From Operating Activities 96,000

Cash Flows From Investing Activities

Sale of Plant & Equipment 80,000 Purchase of Land (25,000)

Net Cash Flow From Investing Activities 55,000

Cash Flows From Financing Activities

Sale of Stock 11,000 Payment of Dividends (37,000) Retirement of Bonds (100,000)

Net Cash Flow From Financing Activities (126,000)

Net Increase (Decrease) in Cash 25,000

Beginning Cash Balance 50,000

Ending Cash Balance $ 75,000

Schedule of Significant Non-Cash Activities

Issue Bonds in Exchange for Land $ 25,000

9

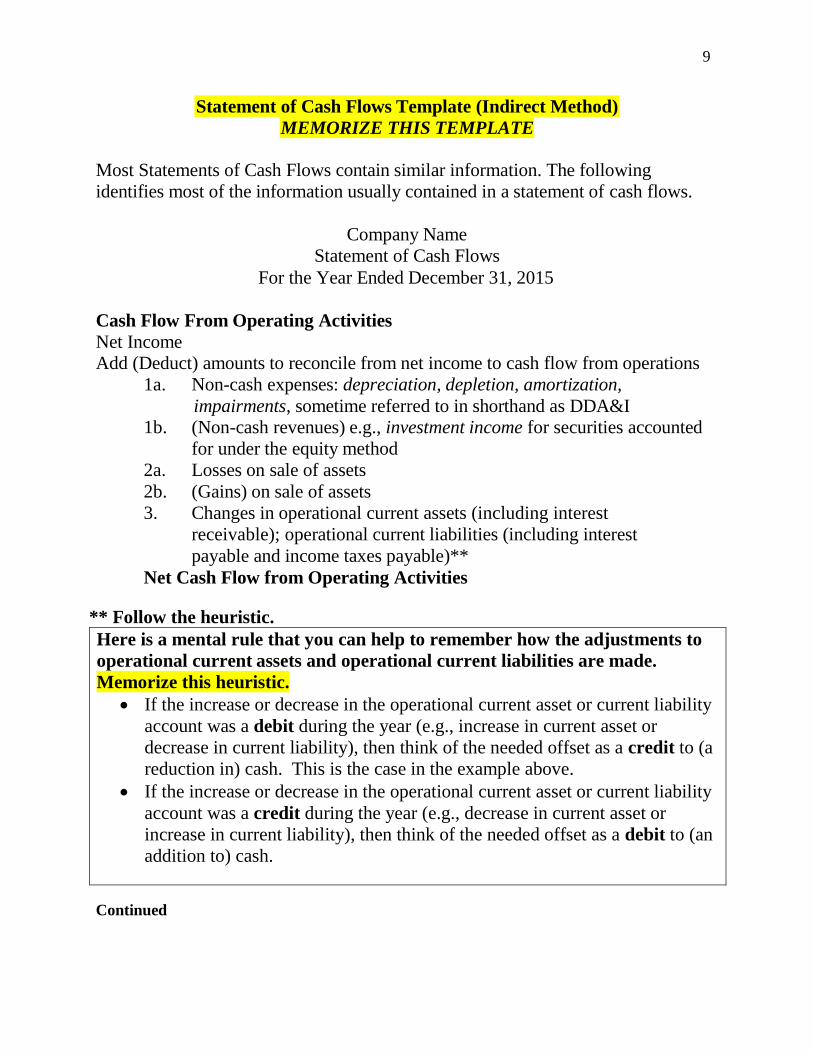

Most Statements of Cash Flows contain similar information. The following

identifies most of the information usually contained in a statement of cash flows.

Company Name

Statement of Cash Flows

For the Year Ended December 31, 2015

Cash Flow From Operating Activities

Net Income

Add (Deduct) amounts to reconcile from net income to cash flow from operations

1a. Non-cash expenses: depreciation, depletion, amortization,

impairments, sometime referred to in shorthand as DDA&I

1b. (Non-cash revenues) e.g., investment income for securities accounted

for under the equity method

2a. Losses on sale of assets

2b. (Gains) on sale of assets

3. Changes in operational current assets (including interest

receivable); operational current liabilities (including interest

payable and income taxes payable)**

Net Cash Flow from Operating Activities

** Follow the heuristic.

Here is a mental rule that you can help to remember how the adjustments to

operational current assets and operational current liabilities are made.

Memorize this heuristic.

If the increase or decrease in the operational current asset or current liability

account was a debit during the year (e.g., increase in current asset or

decrease in current liability), then think of the needed offset as a credit to (a

reduction in) cash. This is the case in the example above.

If the increase or decrease in the operational current asset or current liability

account was a credit during the year (e.g., decrease in current asset or

increase in current liability), then think of the needed offset as a debit to (an

addition to) cash.

Continued

Statement of Cash Flows Template (Indirect Method)

MEMORIZE THIS TEMPLATE

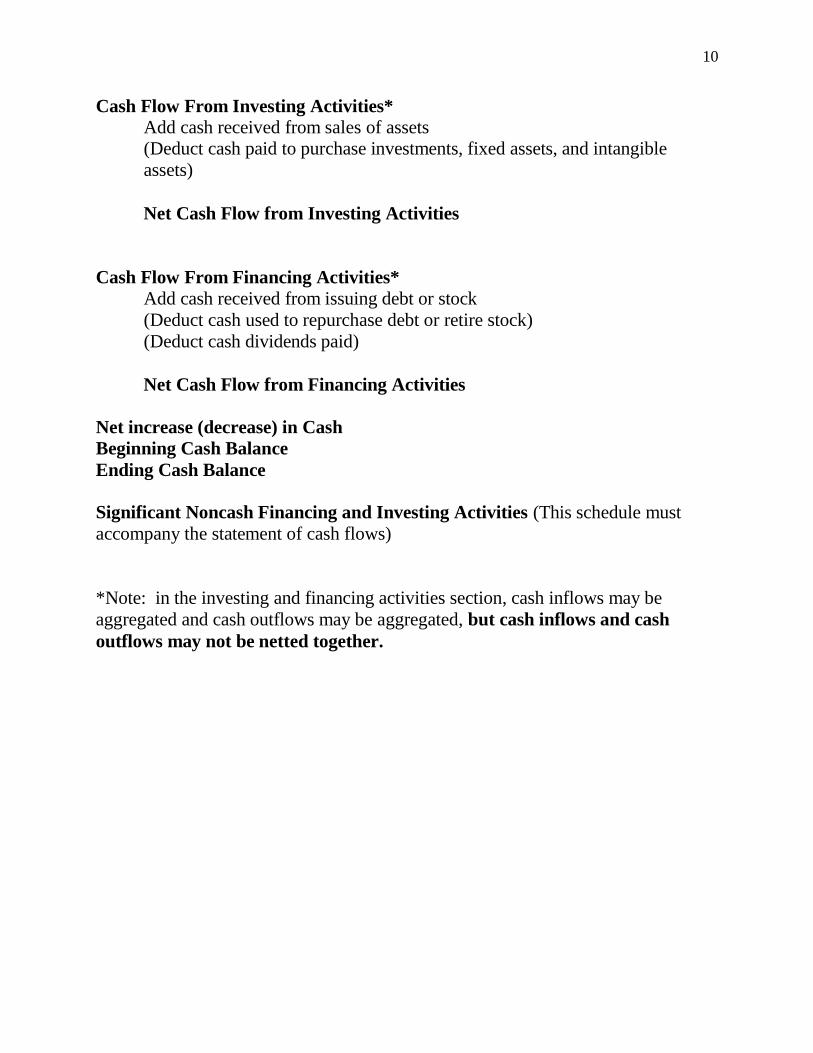

10

Cash Flow From Investing Activities* Add cash received from sales of assets

(Deduct cash paid to purchase investments, fixed assets, and intangible

assets)

Net Cash Flow from Investing Activities

Cash Flow From Financing Activities*

Add cash received from issuing debt or stock

(Deduct cash used to repurchase debt or retire stock)

(Deduct cash dividends paid)

Net Cash Flow from Financing Activities

Net increase (decrease) in Cash

Beginning Cash Balance

Ending Cash Balance

Significant Noncash Financing and Investing Activities (This schedule must

accompany the statement of cash flows)

*Note: in the investing and financing activities section, cash inflows may be

aggregated and cash outflows may be aggregated, but cash inflows and cash

outflows may not be netted together.

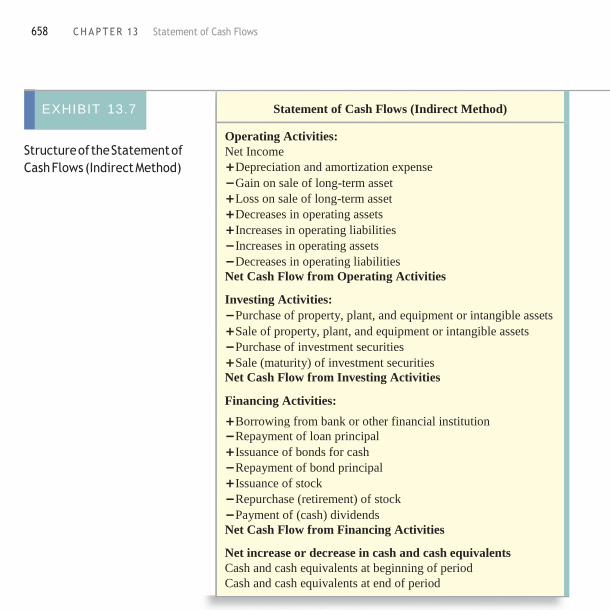

658 C H A P T E R 13 Statement of Cash Flows

EXHIBIT 13.7

Structure of the Statement of

Cash Flows (Indirect Method)

Statement of Cash Flows (Indirect Method)

Operating Activities:

Net Income

+Depreciation and amortization expense

−Gain on sale of long-term asset

+Loss on sale of long-term asset

+Decreases in operating assets

+Increases in operating liabilities

−Increases in operating assets

−Decreases in operating liabilities

Net Cash Flow from Operating Activities

Investing Activities:

−Purchase of property, plant, and equipment or intangible assets

+Sale of property, plant, and equipment or intangible assets

−Purchase of investment securities

+Sale (maturity) of investment securities

Net Cash Flow from Investing Activities

Financing Activities:

+Borrowing from bank or other financial institution

−Repayment of loan principal

+Issuance of bonds for cash

−Repayment of bond principal

+Issuance of stock

−Repurchase (retirement) of stock

−Payment of (cash) dividends

Net Cash Flow from Financing Activities

Net increase or decrease in cash and cash equivalents

Cash and cash equivalents at beginning of period

Cash and cash equivalents at end of period

12

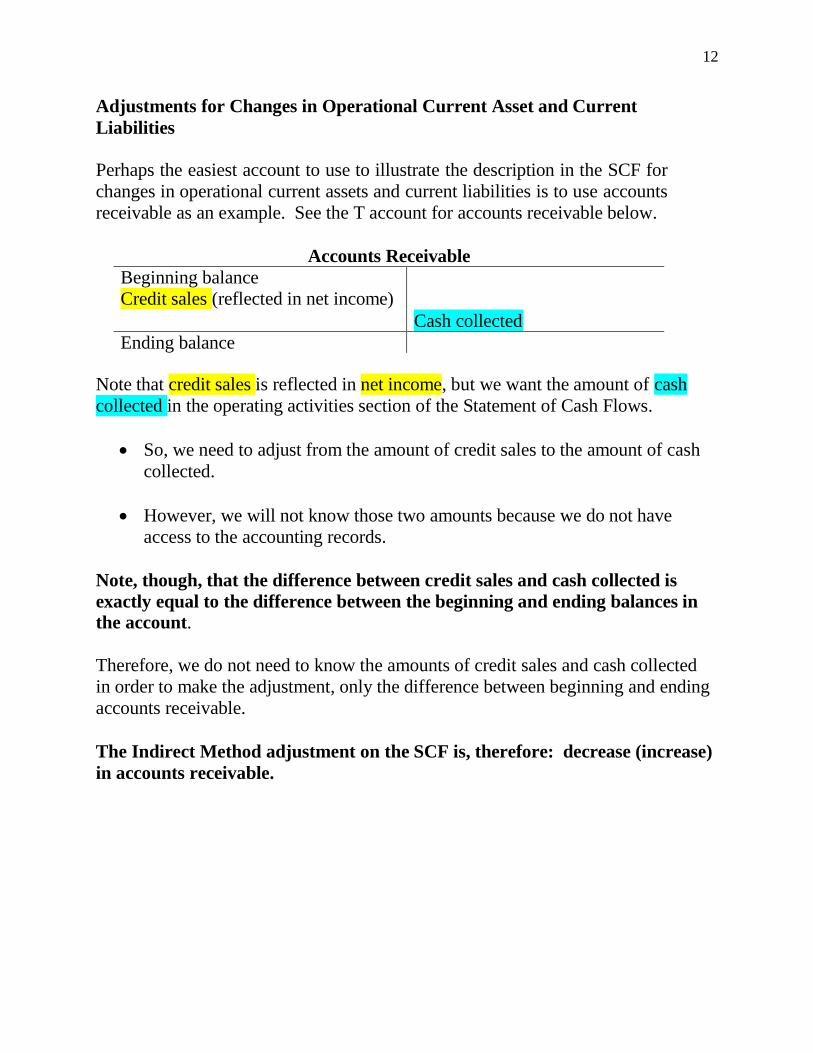

Adjustments for Changes in Operational Current Asset and Current

Liabilities

Perhaps the easiest account to use to illustrate the description in the SCF for

changes in operational current assets and current liabilities is to use accounts

receivable as an example. See the T account for accounts receivable below.

Accounts Receivable

Beginning balance

Credit sales (reflected in net income)

Cash collected

Ending balance

Note that credit sales is reflected in net income, but we want the amount of cash

collected in the operating activities section of the Statement of Cash Flows.

So, we need to adjust from the amount of credit sales to the amount of cash

collected.

However, we will not know those two amounts because we do not have

access to the accounting records.

Note, though, that the difference between credit sales and cash collected is

exactly equal to the difference between the beginning and ending balances in

the account.

Therefore, we do not need to know the amounts of credit sales and cash collected

in order to make the adjustment, only the difference between beginning and ending

accounts receivable.

The Indirect Method adjustment on the SCF is, therefore: decrease (increase)

in accounts receivable.

13

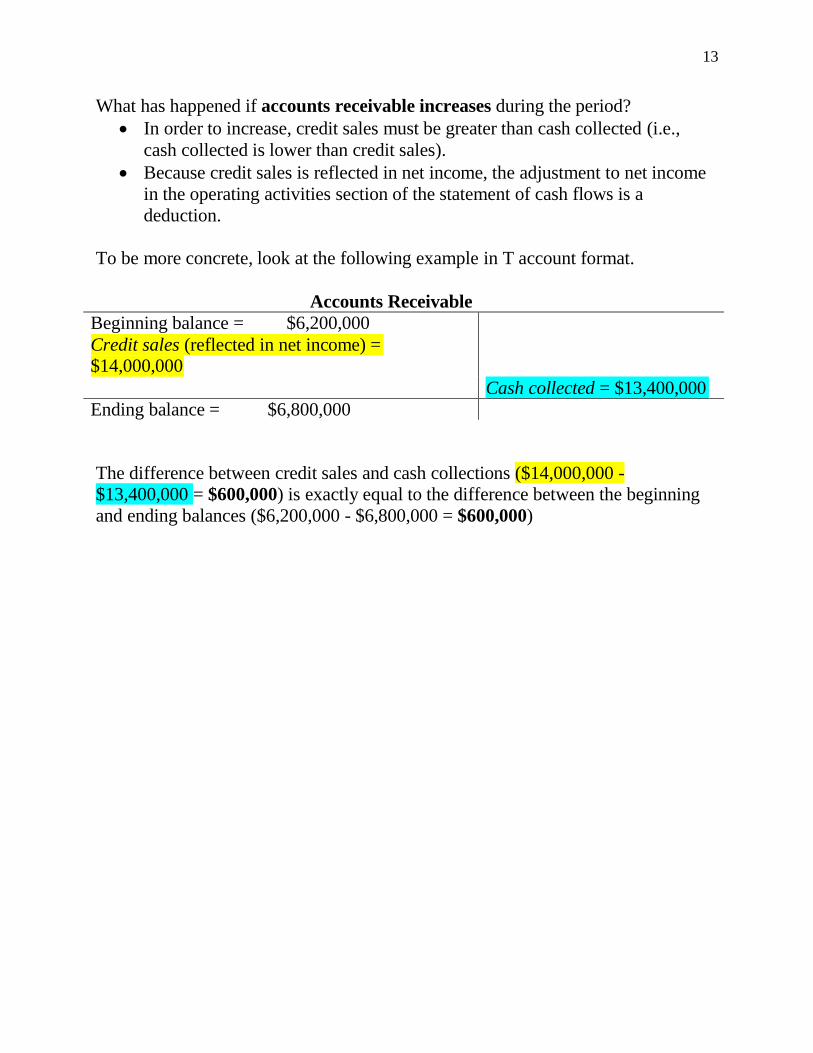

What has happened if accounts receivable increases during the period?

In order to increase, credit sales must be greater than cash collected (i.e.,

cash collected is lower than credit sales).

Because credit sales is reflected in net income, the adjustment to net income

in the operating activities section of the statement of cash flows is a

deduction.

To be more concrete, look at the following example in T account format.

Accounts Receivable

Beginning balance = $6,200,000

Credit sales (reflected in net income) = $14,000,000

Cash collected = $13,400,000

Ending balance = $6,800,000

The difference between credit sales and cash collections ($14,000,000 -

$13,400,000 = $600,000) is exactly equal to the difference between the beginning

and ending balances ($6,200,000 - $6,800,000 = $600,000)

14

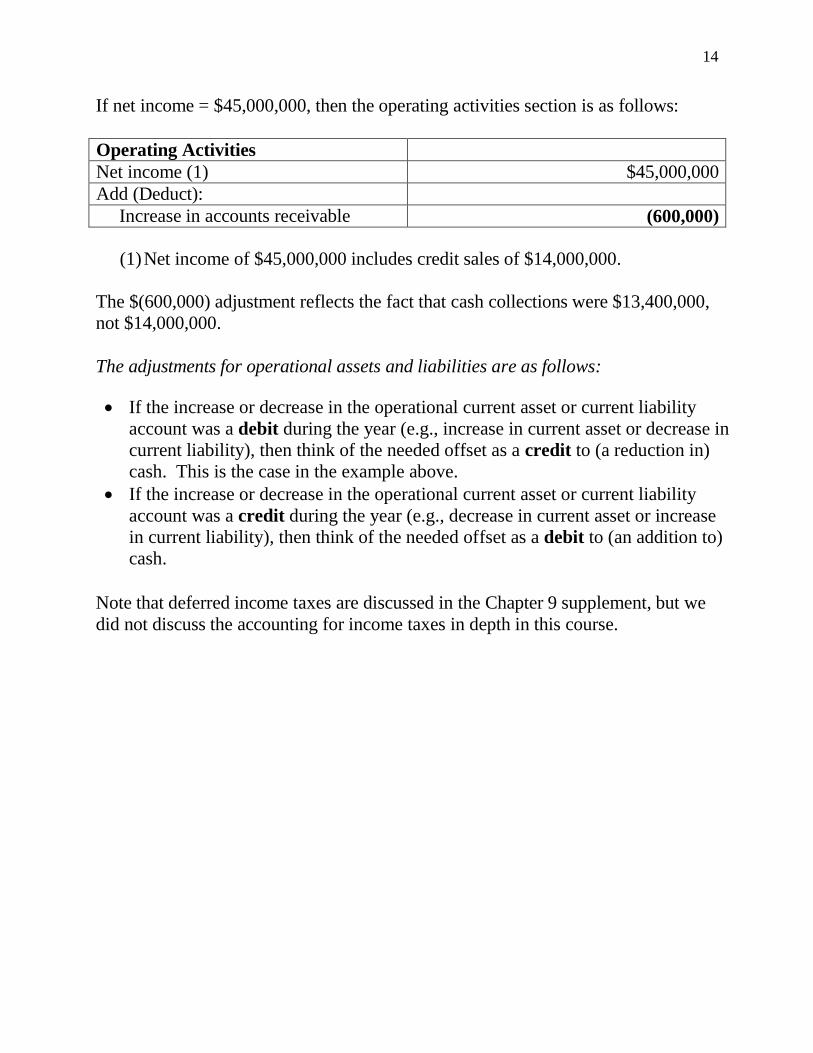

If net income = $45,000,000, then the operating activities section is as follows:

Operating Activities

Net income (1) $45,000,000

Add (Deduct):

Increase in accounts receivable (600,000)

(1) Net income of $45,000,000 includes credit sales of $14,000,000.

The $(600,000) adjustment reflects the fact that cash collections were $13,400,000,

not $14,000,000.

The adjustments for operational assets and liabilities are as follows:

If the increase or decrease in the operational current asset or current liability

account was a debit during the year (e.g., increase in current asset or decrease in

current liability), then think of the needed offset as a credit to (a reduction in)

cash. This is the case in the example above.

If the increase or decrease in the operational current asset or current liability

account was a credit during the year (e.g., decrease in current asset or increase

in current liability), then think of the needed offset as a debit to (an addition to)

cash.

Note that deferred income taxes are discussed in the Chapter 9 supplement, but we

did not discuss the accounting for income taxes in depth in this course.

15

Disclosures for Interest Paid and Income Taxes Paid

GAAP requires that when using the indirect method, the company must report the

amounts of cash paid for income taxes and for interest.

These amounts may be reported at the bottom of the statement of cash flows,

but usually presented in the notes to the financial statements. Therefore, these

amounts are not required to be on the SCF.

16

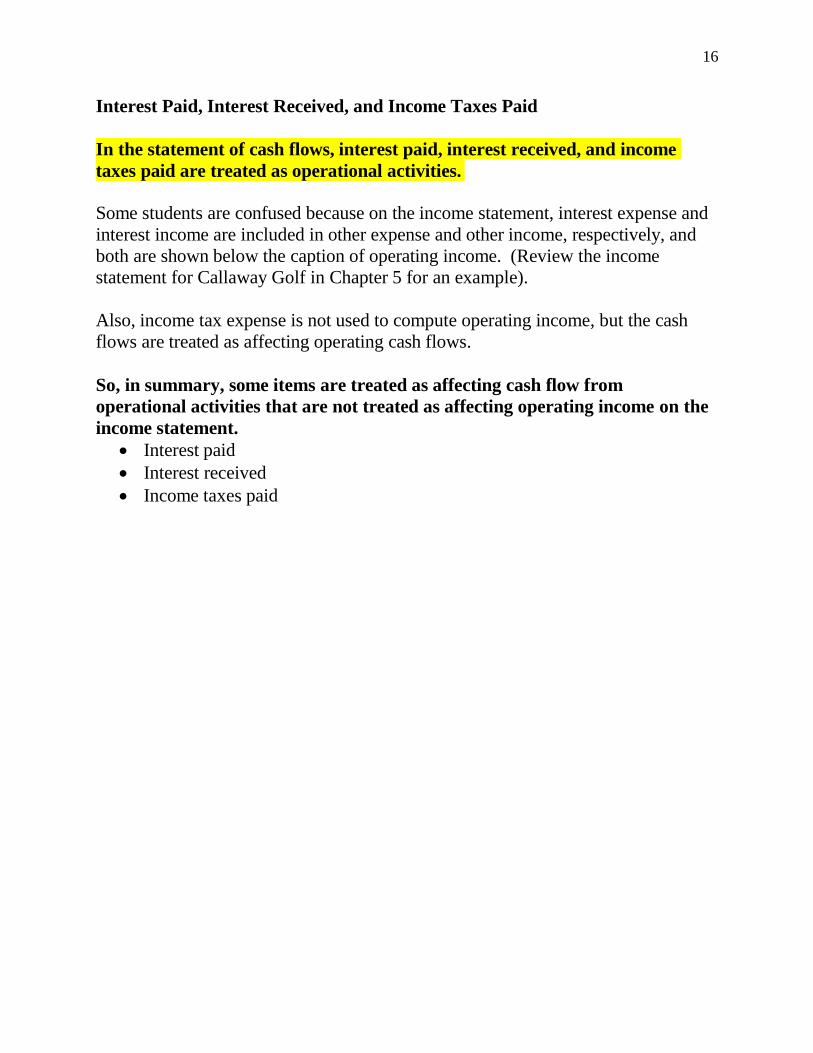

Interest Paid, Interest Received, and Income Taxes Paid

Some students are confused because on the income statement, interest expense and

interest income are included in other expense and other income, respectively, and

both are shown below the caption of operating income. (Review the income

statement for Callaway Golf in Chapter 5 for an example).

Also, income tax expense is not used to compute operating income, but the cash

flows are treated as affecting operating cash flows.

So, in summary, some items are treated as affecting cash flow from

operational activities that are not treated as affecting operating income on the

income statement.

Interest paid

Interest received

Income taxes paid

In the statement of cash flows, interest paid, interest received, and income

taxes paid are treated as operational activities.

17

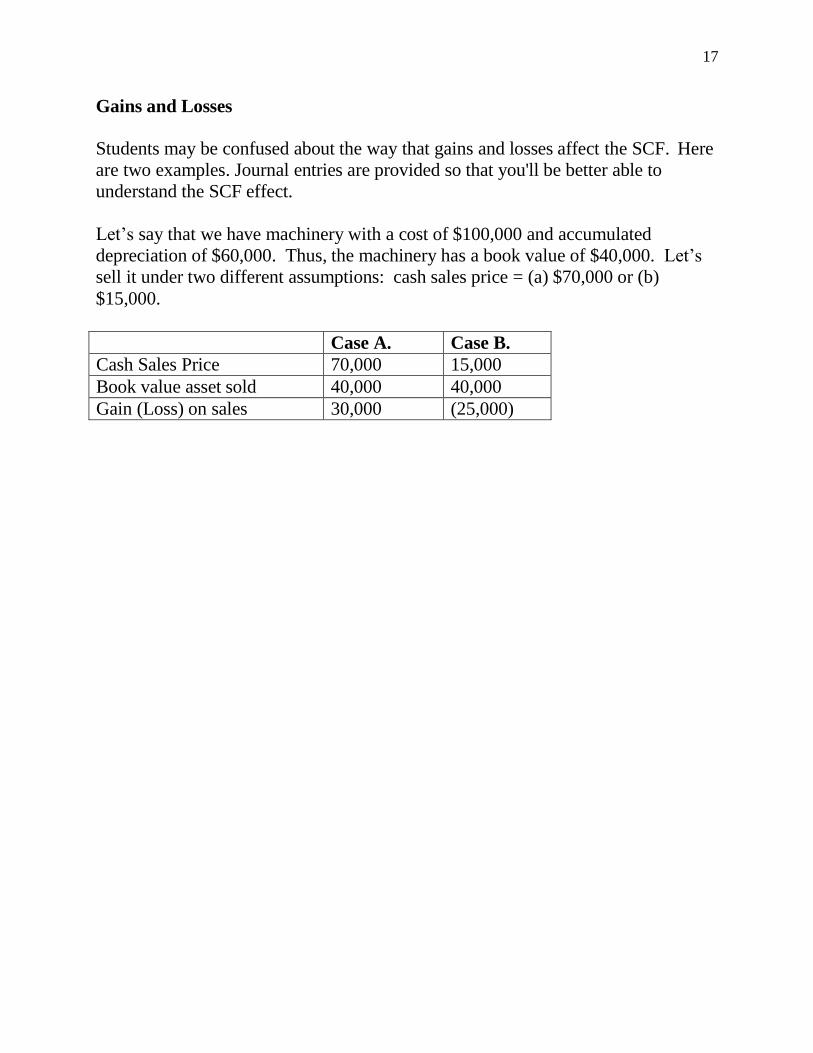

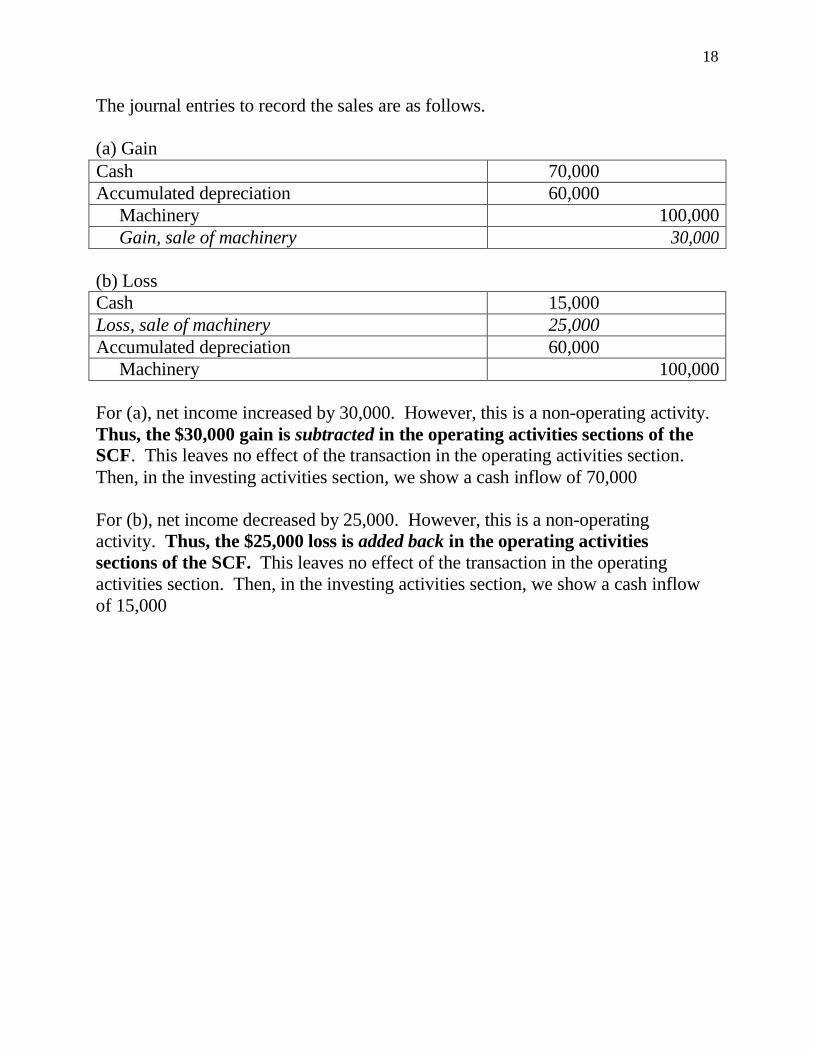

Gains and Losses

Students may be confused about the way that gains and losses affect the SCF. Here

are two examples. Journal entries are provided so that you'll be better able to

understand the SCF effect.

Let’s say that we have machinery with a cost of $100,000 and accumulated

depreciation of $60,000. Thus, the machinery has a book value of $40,000. Let’s

sell it under two different assumptions: cash sales price = (a) $70,000 or (b)

$15,000.

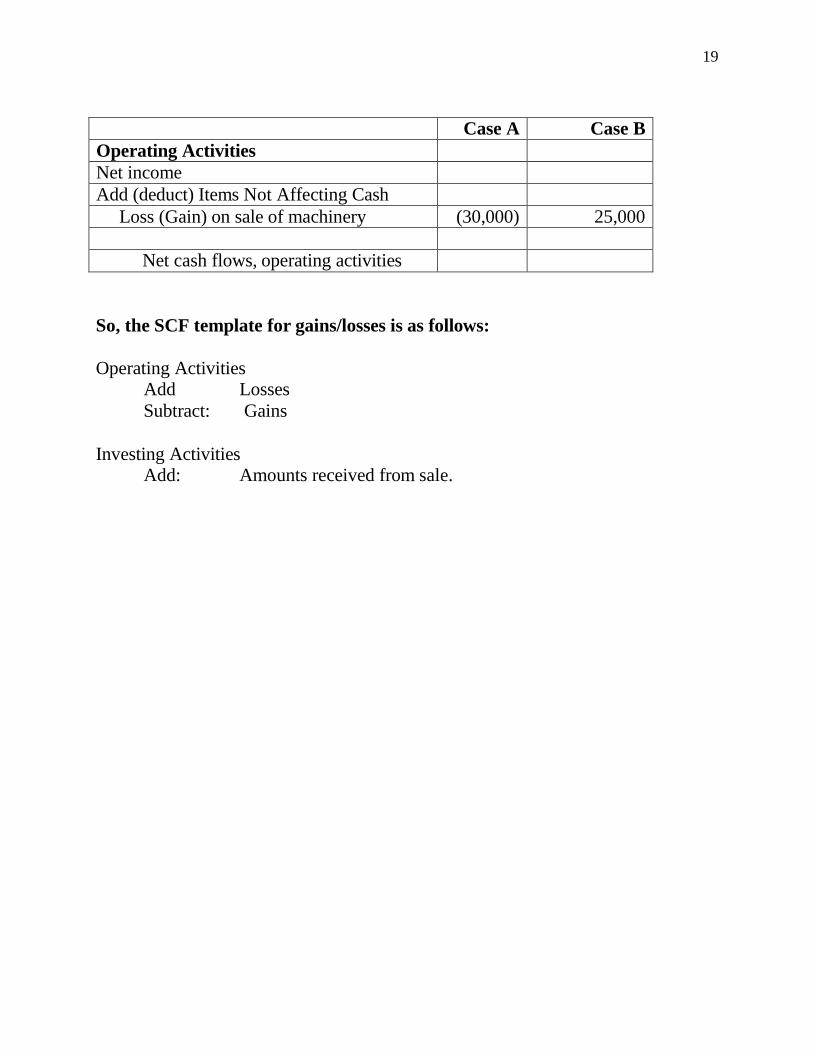

Case A. Case B.

Cash Sales Price 70,000 15,000

Book value asset sold 40,000 40,000

Gain (Loss) on sales 30,000 (25,000)

18

The journal entries to record the sales are as follows.

(a) Gain

(b) Loss

Cash 15,000

Loss, sale of machinery 25,000

Accumulated depreciation 60,000

Machinery 100,000

For (a), net income increased by 30,000. However, this is a non-operating activity.

Thus, the $30,000 gain is subtracted in the operating activities sections of the

SCF. This leaves no effect of the transaction in the operating activities section.

Then, in the investing activities section, we show a cash inflow of 70,000

For (b), net income decreased by 25,000. However, this is a non-operating

activity. Thus, the $25,000 loss is added back in the operating activities

sections of the SCF. This leaves no effect of the transaction in the operating

activities section. Then, in the investing activities section, we show a cash inflow

of 15,000

Cash 70,000

Accumulated depreciation 60,000

Machinery 100,000

Gain, sale of machinery 30,000

19

Case A Case B

Operating Activities

Net income

Add (deduct) Items Not Affecting Cash

Loss (Gain) on sale of machinery (30,000) 25,000

Net cash flows, operating activities

So, the SCF template for gains/losses is as follows:

Operating Activities Add Losses

Subtract: Gains

Investing Activities Add: Amounts received from sale.

20

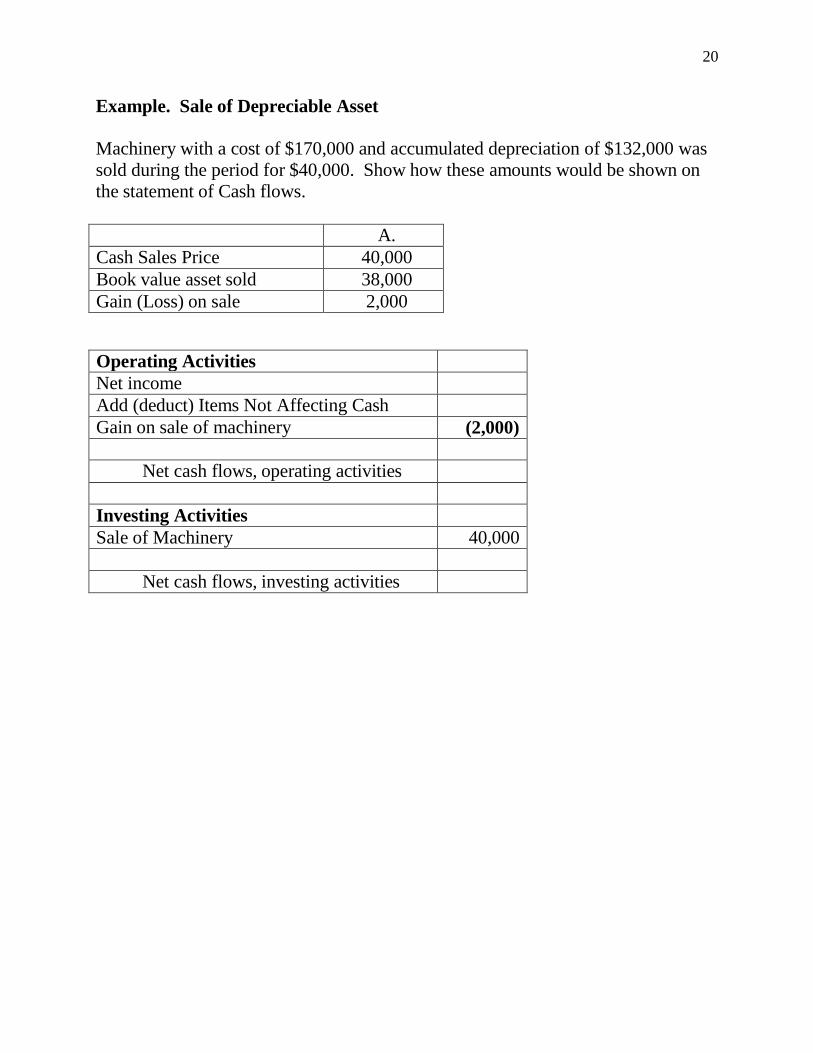

Example. Sale of Depreciable Asset

Machinery with a cost of $170,000 and accumulated depreciation of $132,000 was

sold during the period for $40,000. Show how these amounts would be shown on

the statement of Cash flows.

A.

Cash Sales Price 40,000

Book value asset sold 38,000

Gain (Loss) on sale 2,000

Operating Activities

Net income

Add (deduct) Items Not Affecting Cash

Gain on sale of machinery (2,000)

Net cash flows, operating activities

Investing Activities

Sale of Machinery 40,000

Net cash flows, investing activities

21

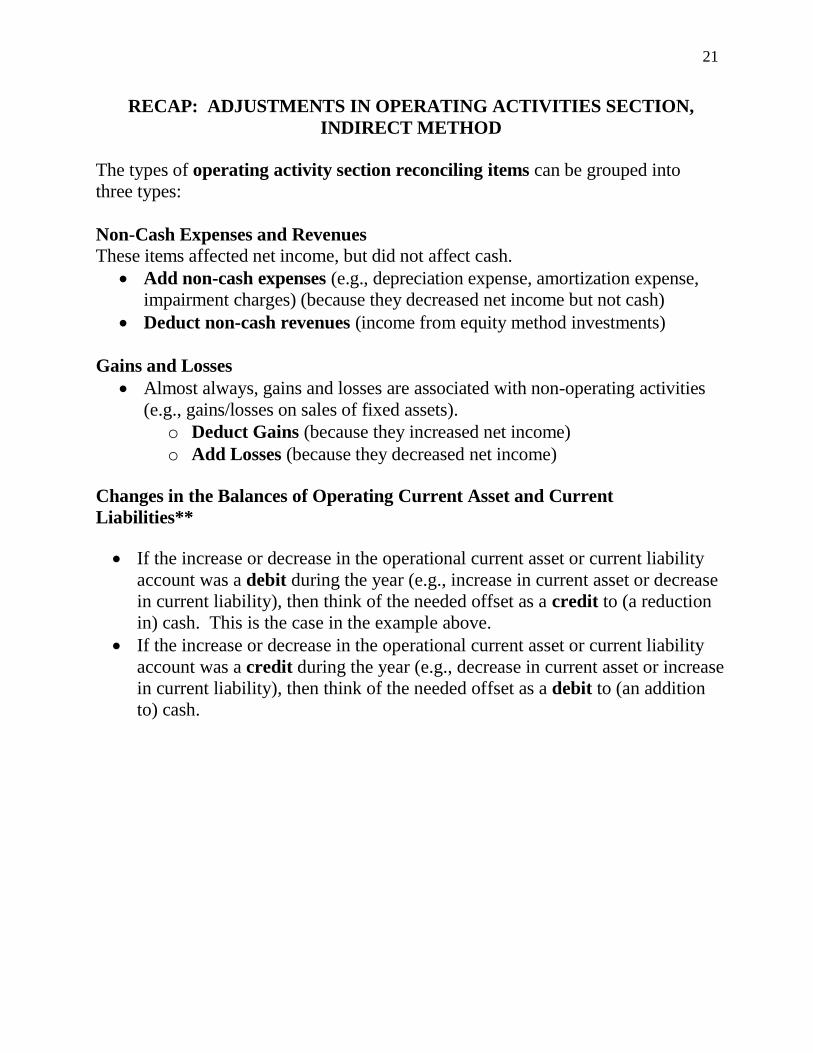

RECAP: ADJUSTMENTS IN OPERATING ACTIVITIES SECTION,

INDIRECT METHOD

The types of operating activity section reconciling items can be grouped into

three types:

Non-Cash Expenses and Revenues

These items affected net income, but did not affect cash.

Add non-cash expenses (e.g., depreciation expense, amortization expense,

impairment charges) (because they decreased net income but not cash)

Deduct non-cash revenues (income from equity method investments)

Gains and Losses

Almost always, gains and losses are associated with non-operating activities

(e.g., gains/losses on sales of fixed assets).

o Deduct Gains (because they increased net income)

o Add Losses (because they decreased net income)

Changes in the Balances of Operating Current Asset and Current

Liabilities**

If the increase or decrease in the operational current asset or current liability

account was a debit during the year (e.g., increase in current asset or decrease

in current liability), then think of the needed offset as a credit to (a reduction

in) cash. This is the case in the example above.

If the increase or decrease in the operational current asset or current liability

account was a credit during the year (e.g., decrease in current asset or increase

in current liability), then think of the needed offset as a debit to (an addition

to) cash.

22

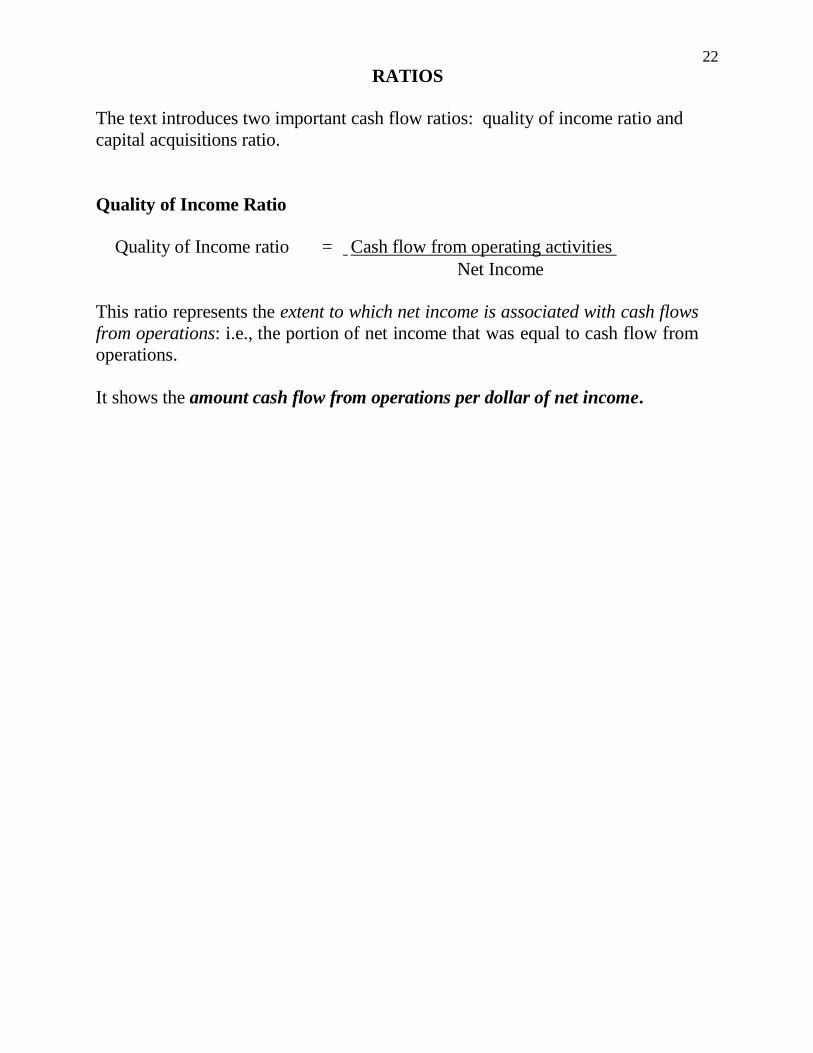

RATIOS

The text introduces two important cash flow ratios: quality of income ratio and

capital acquisitions ratio.

Quality of Income Ratio

Quality of Income ratio = Cash flow from operating activities

Net Income

This ratio represents the extent to which net income is associated with cash flows

from operations: i.e., the portion of net income that was equal to cash flow from

operations.

It shows the amount cash flow from operations per dollar of net income.

23

Capital Acquisitions Ratio

Capital Acquisitions Ratio = Cash flow from operating activities

Cash paid for property, plant, and

equipment

The capital acquisitions ratio reflects the amounts of cash paid to expand

productive capacity that could have been paid out of operating cash flows.

If the ratio is greater than 1.0, then the company is generating enough operating

cash flow to cover its investments in new property, plant, and equipment.

Note: the denominator in the ratio can be expanded to include amounts paid for

natural resources and intangible assets.

24

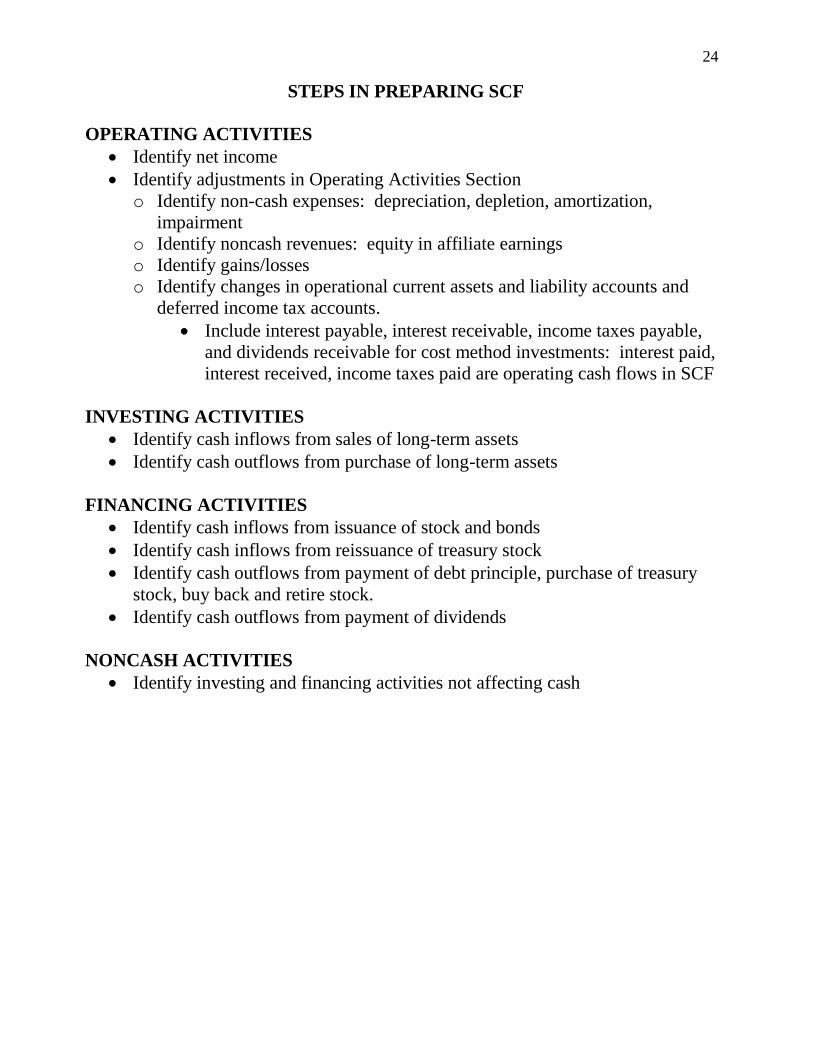

STEPS IN PREPARING SCF

OPERATING ACTIVITIES

Identify net income

Identify adjustments in Operating Activities Section

o Identify non-cash expenses: depreciation, depletion, amortization,

impairment

o Identify noncash revenues: equity in affiliate earnings

o Identify gains/losses

o Identify changes in operational current assets and liability accounts and

deferred income tax accounts.

Include interest payable, interest receivable, income taxes payable,

and dividends receivable for cost method investments: interest paid,

interest received, income taxes paid are operating cash flows in SCF

INVESTING ACTIVITIES

Identify cash inflows from sales of long-term assets

Identify cash outflows from purchase of long-term assets

FINANCING ACTIVITIES

Identify cash inflows from issuance of stock and bonds

Identify cash inflows from reissuance of treasury stock

Identify cash outflows from payment of debt principle, purchase of treasury

stock, buy back and retire stock.

Identify cash outflows from payment of dividends

NONCASH ACTIVITIES

Identify investing and financing activities not affecting cash

25

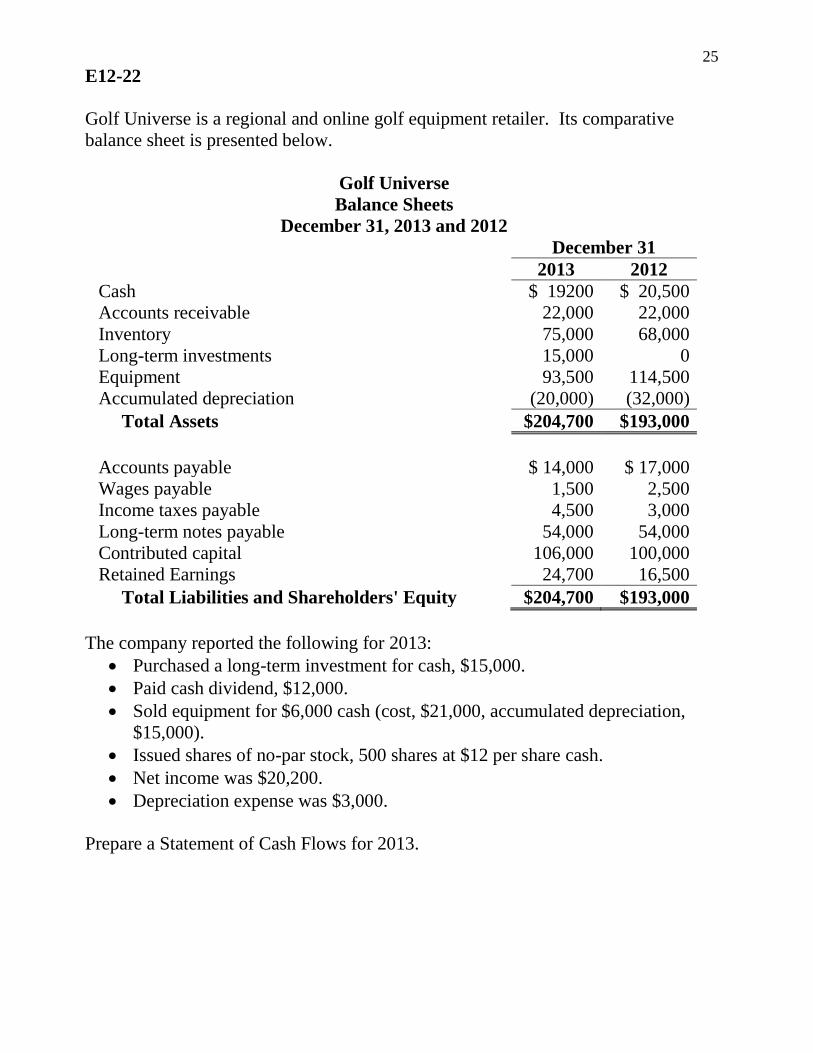

E12-22

Golf Universe is a regional and online golf equipment retailer. Its comparative

balance sheet is presented below.

Golf Universe

Balance Sheets

December 31, 2013 and 2012

December 31

2013 2012

Cash $ 19200 $ 20,500

Accounts receivable 22,000 22,000

Inventory 75,000 68,000

Long-term investments 15,000 0

Equipment 93,500 114,500

Accumulated depreciation (20,000) (32,000)

Total Assets $204,700 $193,000

Accounts payable $ 14,000 $ 17,000

Wages payable 1,500 2,500

Income taxes payable 4,500 3,000

Long-term notes payable 54,000 54,000

Contributed capital 106,000 100,000

Retained Earnings 24,700 16,500

Total Liabilities and Shareholders' Equity $204,700 $193,000

The company reported the following for 2013:

Purchased a long-term investment for cash, $15,000.

Paid cash dividend, $12,000.

Sold equipment for $6,000 cash (cost, $21,000, accumulated depreciation,

$15,000).

Issued shares of no-par stock, 500 shares at $12 per share cash.

Net income was $20,200.

Depreciation expense was $3,000.

Prepare a Statement of Cash Flows for 2013.

26

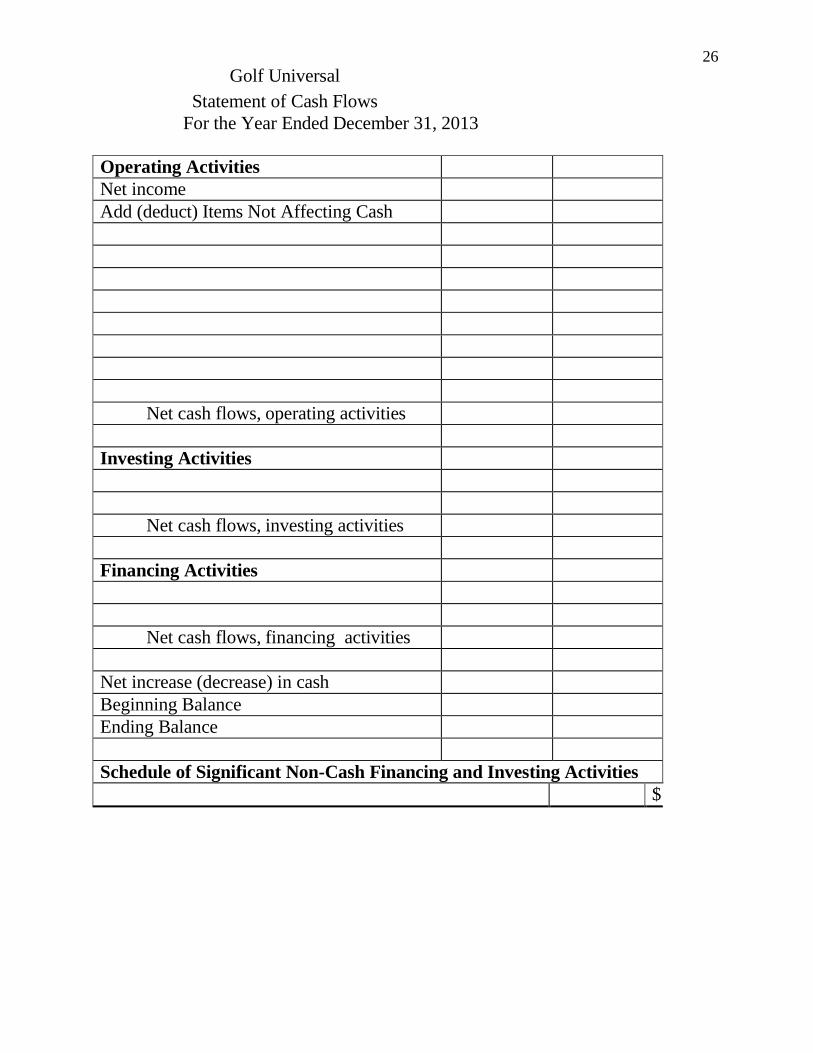

Golf Universal

Statement of Cash Flows

For the Year Ended December 31, 2013

Operating Activities

Net income

Add (deduct) Items Not Affecting Cash

Net cash flows, operating activities

Investing Activities

Net cash flows, investing activities

Financing Activities

Net cash flows, financing activities

Net increase (decrease) in cash

Beginning Balance

Ending Balance

Schedule of Significant Non-Cash Financing and Investing Activities

$

27

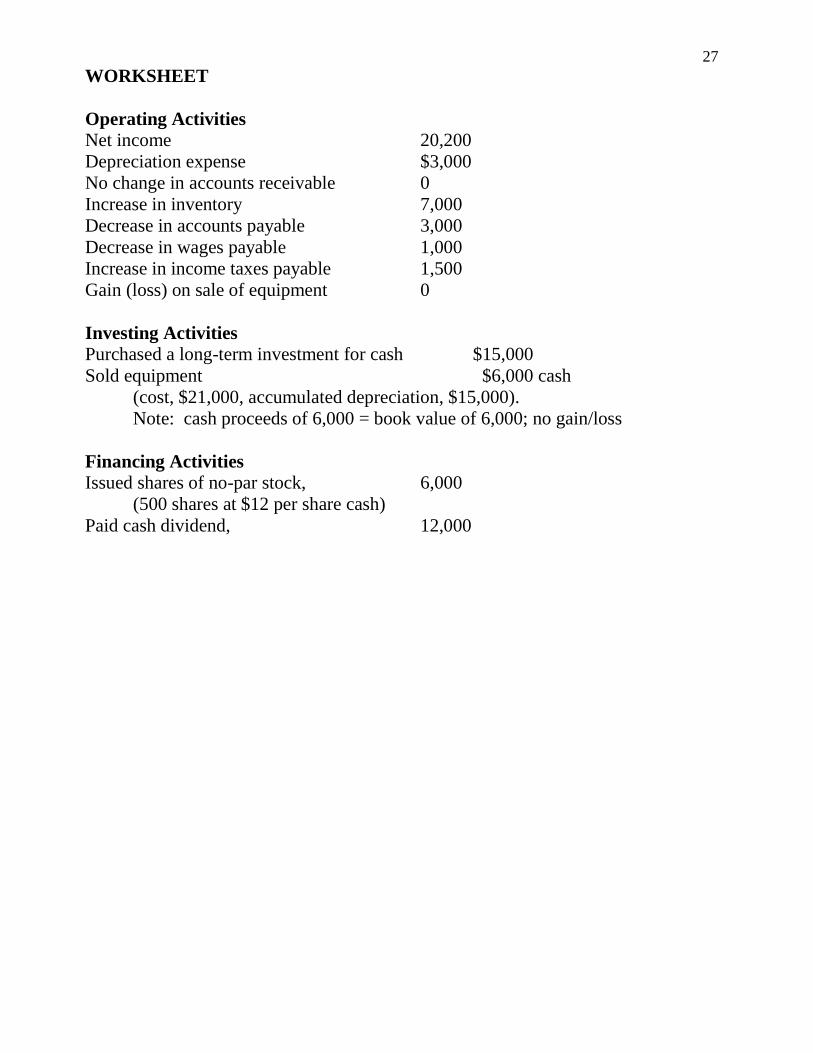

WORKSHEET

Operating Activities

Net income 20,200

Depreciation expense $3,000

No change in accounts receivable 0

Increase in inventory 7,000

Decrease in accounts payable 3,000

Decrease in wages payable 1,000

Increase in income taxes payable 1,500

Gain (loss) on sale of equipment 0

Investing Activities

Purchased a long-term investment for cash $15,000

Sold equipment $6,000 cash

(cost, $21,000, accumulated depreciation, $15,000).

Note: cash proceeds of 6,000 = book value of 6,000; no gain/loss

Financing Activities

Issued shares of no-par stock, 6,000

(500 shares at $12 per share cash)

Paid cash dividend, 12,000

28

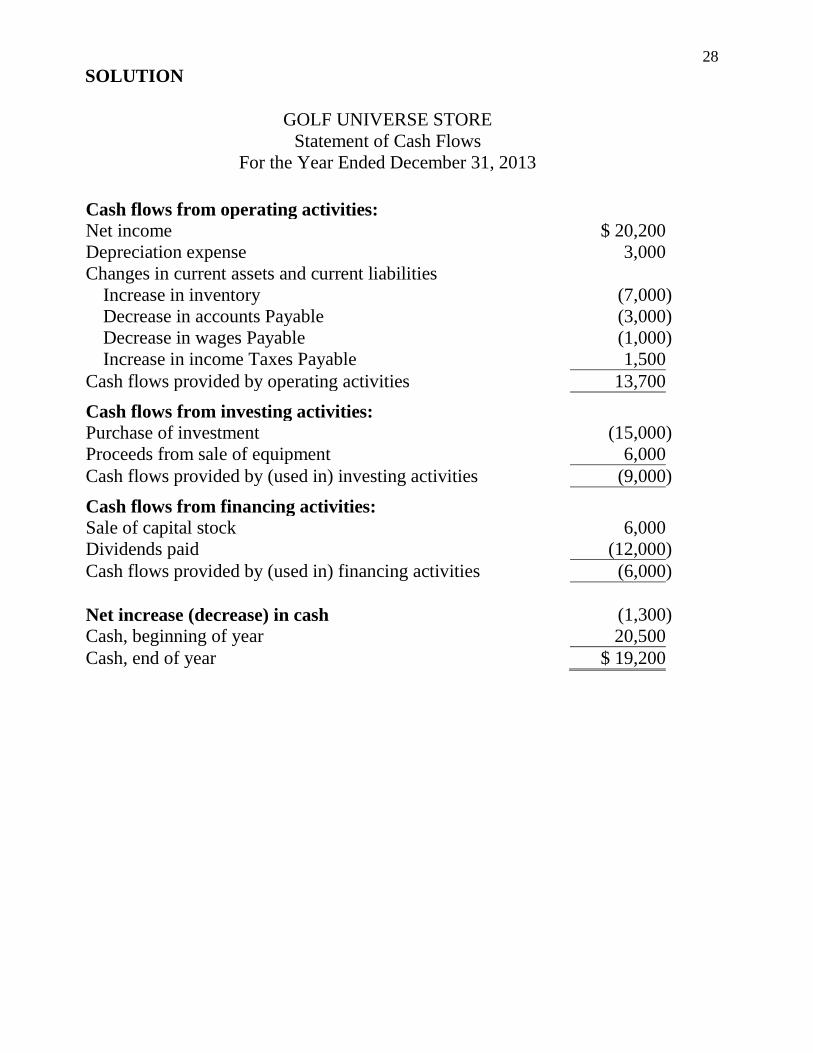

SOLUTION

GOLF UNIVERSE STORE

Statement of Cash Flows

For the Year Ended December 31, 2013

Cash flows from operating activities:

Net income $ 20,200

Depreciation expense 3,000

Changes in current assets and current liabilities

Increase in inventory (7,000 )

Decrease in accounts Payable (3,000 )

Decrease in wages Payable (1,000 )

Increase in income Taxes Payable 1,500

Cash flows provided by operating activities 13,700

Cash flows from investing activities:

Purchase of investment (15,000 )

Proceeds from sale of equipment 6,000

Cash flows provided by (used in) investing activities (9,000 )

Cash flows from financing activities:

Sale of capital stock 6,000

Dividends paid (12,000 )

Cash flows provided by (used in) financing activities (6,000 )

Net increase (decrease) in cash (1,300 )

Cash, beginning of year 20,500

Cash, end of year $ 19,200

Copyright © 2022 FDOKUMEN