JANUARY 2022 - Global Economic Prospects - Open ...

240

A World Bank Group Flagship Report Global Economic Prospects JANUARY 2022

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of JANUARY 2022 - Global Economic Prospects - Open ...

A World Bank Group Flagship Report

Global Economic Prospects

JANUARY 2022

Global Economic Prospects

JANUARY 2022

Global Economic Prospects

© 2022 International Bank for Reconstruction and Development / The World Bank

1818 H Street NW, Washington, DC 20433

Telephone: 202-473-1000; Internet: www.worldbank.org

Some rights reserved

1 2 3 4 25 24 23 22

This work is a product of the staff of The World Bank with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy, completeness, or currency of the data included in this work and does not assume responsibility for any errors, omissions, or discrepancies in the information, or liability with respect to the use of or failure to use the information, methods, processes, or conclusions set forth. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Nothing herein shall constitute or be construed or considered to be a limitation upon or waiver of the privileges and immunities of The World Bank, all of which are specifically reserved.

Rights and Permissions

This work is available under the Creative Commons Attribution 3.0 IGO license (CC BY 3.0 IGO) http://creativecommons.org/licenses/by/3.0/igo. Under the Creative Commons Attribution license, you are free to copy, distribute, transmit, and adapt this work, including for commercial purposes, under the following conditions:

Attribution—Please cite the work as follows: World Bank. 2022. Global Economic Prospects, January 2022. Washington, DC: World Bank. doi: 10.1596/978-1-4648-1758-8. License: Creative Commons Attribution CC BY 3.0 IGO.

Translations—If you create a translation of this work, please add the following disclaimer along with the attribution: This translation was not created by The World Bank and should not be considered an official World Bank translation. The World Bank shall not be liable for any content or error in this translation.

Adaptations—If you create an adaptation of this work, please add the following disclaimer along with the attribution: This is an adaptation of an original work by The World Bank. Views and opinions expressed in the adaptation are the sole responsibility of the author or authors of the adaptation and are not endorsed by The World Bank.

Third-party content—The World Bank does not necessarily own each component of the content contained within the work. The World Bank therefore does not warrant that the use of any third-party-owned individual component or part contained in the work will not infringe on the rights of those third parties. The risk of claims resulting from such infringement rests solely with you. If you wish to re-use a component of the work, it is your responsibility to determine whether permission is needed for that re-use and to obtain permission from the copyright owner. Examples of components can include, but are not limited to, tables, figures, or images.

All queries on rights and licenses should be addressed to World Bank Publications, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; e-mail: [email protected].

ISBN (paper): 978-1-4648-1758-8

ISBN (electronic): 978-1-4648-1760-1

DOI: 10.1596/978-1-4648-1758-8

Cover design: Bill Pragluski (Critical Stages).

The Library of Congress Control Number has been requested.

The cutoff date for the data used in this report was December 20, 2021.

v

Summary of Contents

Statistical Appendix ............................................................................................................................ 201

Selected Topics ................................................................................................................................... 208

Chapter 1

Special Focus

Chapter 2

Chapter 3

Chapter 4

Global Outlook ......................................................................................................... 1

Box 1.1 Regional perspectives: Outlook and risks ................................................. 17

Box 1.2 Recent developments and outlook for low-income countries ..................... 22

Resolving High Debt after the Pandemic: Lessons from Past Episodes

of Debt Relief ........................................................................................................ 47

Regional Outlooks .................................................................................................. 63

East Asia and Pacific ............................................................................................ 65

Europe and Central Asia ...................................................................................... 73

Latin America and the Caribbean ......................................................................... 81

Middle East and North Africa .............................................................................. 89

South Asia .......................................................................................................... 95

Sub-Saharan Africa ............................................................................................ 101

Commodity Price Cycles: Drivers and Policies ....................................................... 111

Box 3.1 Drivers of commodity cycles ................................................................ 125

Impact of COVID-19 on Global Income Inequality ............................................... 155

Box 4.1 Within-country inequality around recessions, financial crises,

and epidemics ................................................................................................... 164

Box 4.2 Evidence on the distributional effects of past policy initiatives ................. 181

Acknowledgments ................................................................................................................................ xv

Foreword ........................................................................................................................................... xvii

Executive Summary ............................................................................................................................. xix

Abbreviations ...................................................................................................................................... xxi

vii

Contents

Chapter 1

Global Outlook ....................................................................................................... 1

Summary ................................................................................................................. 3

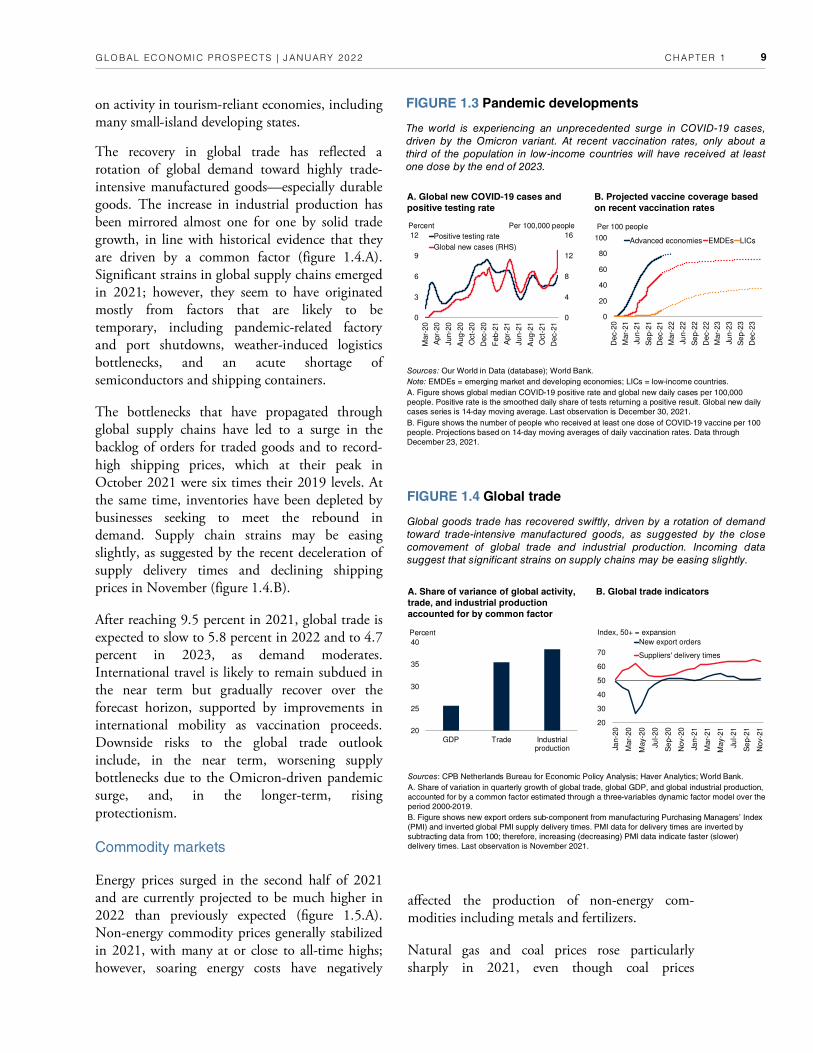

Global context.......................................................................................................... 8

Pandemic developments ..................................................................................... 8

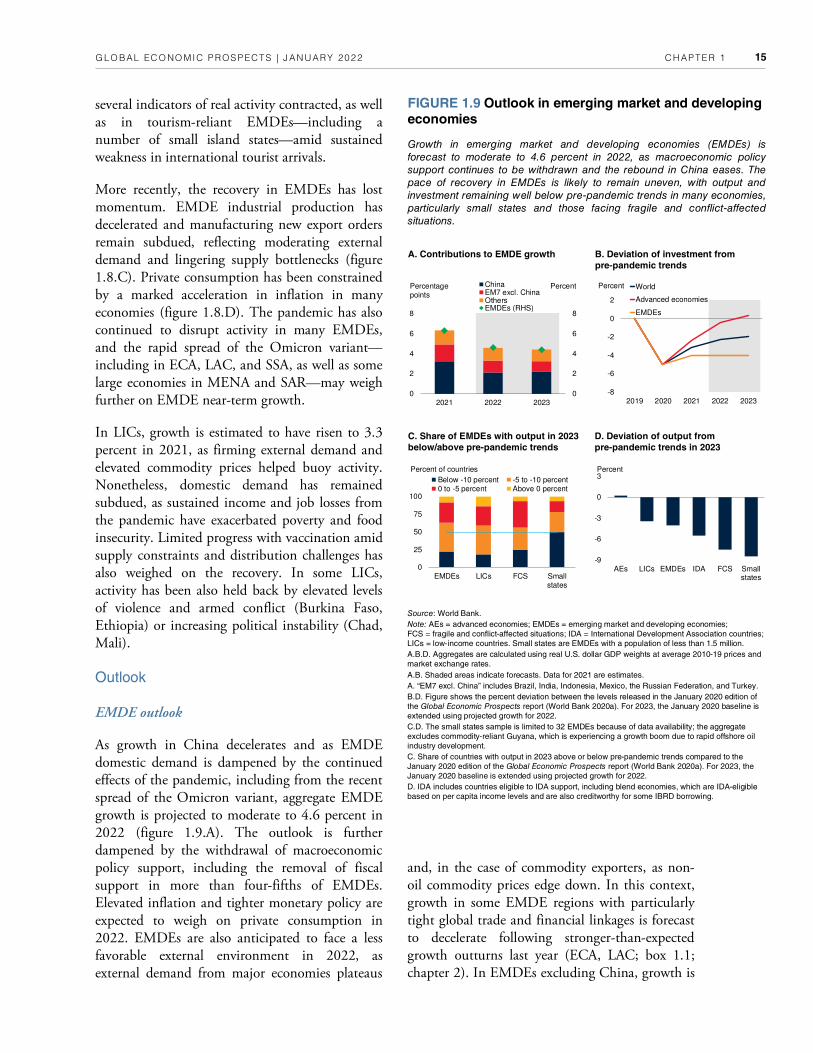

Global trade ....................................................................................................... 8

Commodity markets ........................................................................................... 9

Global inflation and financial developments ...................................................... 11

Major economies: Recent developments and outlook ................................................ 12

Advanced economies ........................................................................................ 12

China .............................................................................................................. 13

Emerging market and developing economies ............................................................ 14

Recent developments ........................................................................................ 14

Outlook ........................................................................................................... 15

Per capita income growth, poverty, and inequality ............................................. 20

Global outlook and risks ......................................................................................... 21

Global outlook ................................................................................................. 21

Risks to the outlook.......................................................................................... 27

Policy challenges..................................................................................................... 32

Key global challenges ........................................................................................ 32

Challenges in advanced economies .................................................................... 33

Challenges in emerging market and developing economies ................................. 34

References .............................................................................................................. 41

Acknowledgments ................................................................................................................................ xv

Foreword ........................................................................................................................................... xvii

Executive Summary ............................................................................................................................. xix

Abbreviations ...................................................................................................................................... xxi

Resolving High Debt after the Pandemic: Lessons from Past Episodes

of Debt Relief ........................................................................................................ 47

Introduction .......................................................................................................... 49

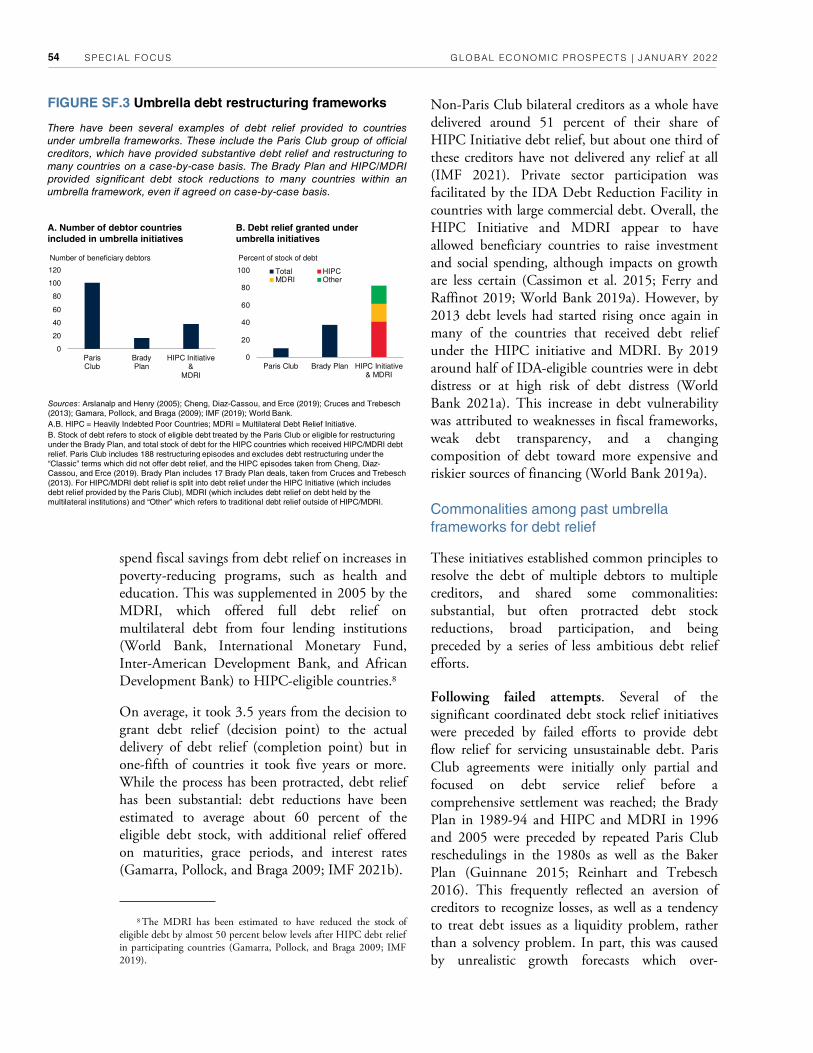

Lessons from past debt resolutions ........................................................................... 51

Past debt resolution .......................................................................................... 51

Past umbrella facilities for debt relief ................................................................. 51

Special Focus

viii

Regional Outlooks ................................................................................................. 63

East Asia and Pacific ............................................................................................. 65

Recent developments ........................................................................................... 65

Outlook .............................................................................................................. 66

Risks ................................................................................................................... 68

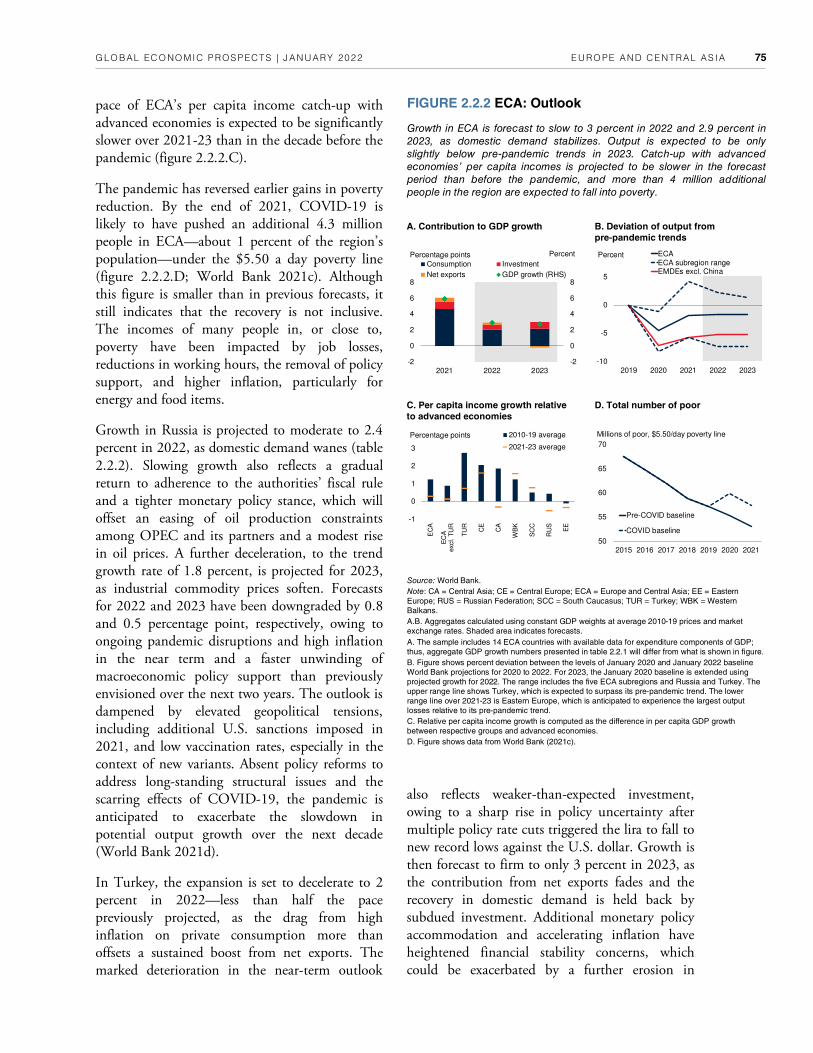

Europe and Central Asia ......................................................................................... 73

Recent developments.......................................................................................... 73

Outlook ............................................................................................................ 74

Risks ................................................................................................................. 76

Latin America and the Caribbean ........................................................................... 81

Recent developments.......................................................................................... 81

Outlook ............................................................................................................ 82

Risks ................................................................................................................. 84

Middle East and North Africa ................................................................................ 89

Recent developments.......................................................................................... 89

Outlook ............................................................................................................ 90

Risks ................................................................................................................. 92

South Asia .............................................................................................................. 95

Recent developments.......................................................................................... 95

Outlook ............................................................................................................ 96

Risks ................................................................................................................. 98

Sub-Saharan Africa .............................................................................................. 101

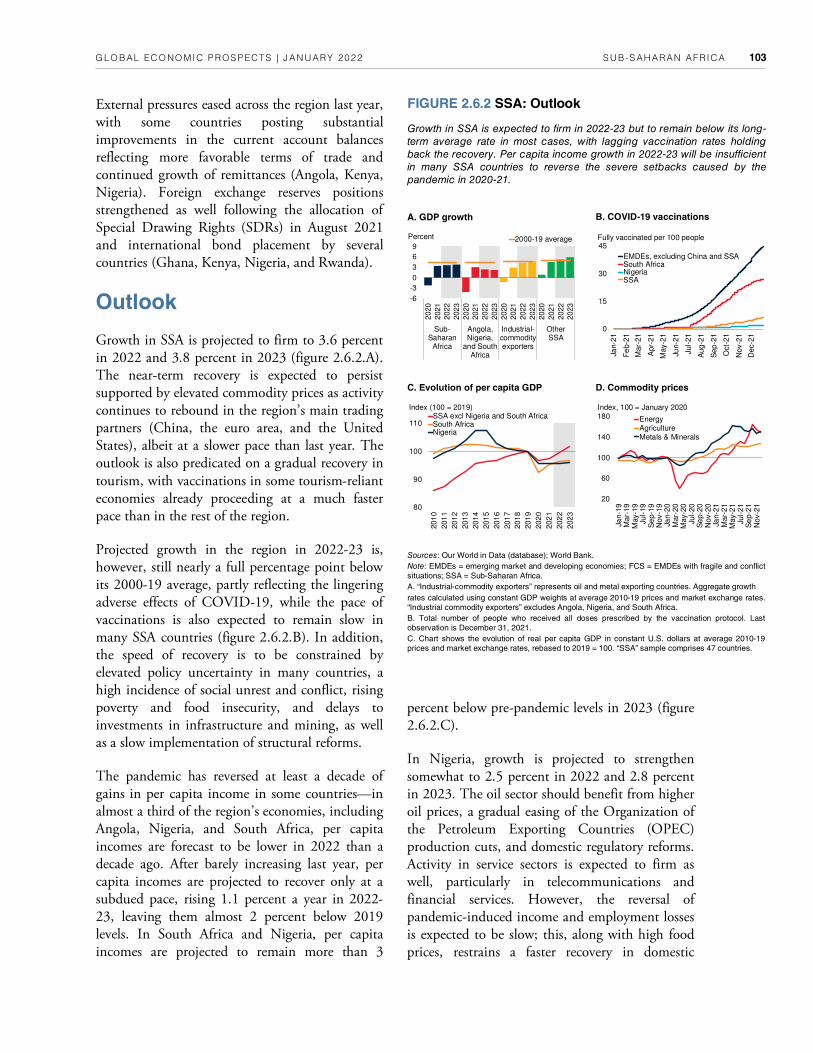

Recent developments........................................................................................ 101

Outlook .......................................................................................................... 102

Risks ............................................................................................................... 104

References ............................................................................................................ 108

Chapter 2

Chapter 3 Commodity Price Cycles: Drivers and Policies ...................................................... 111

Introduction......................................................................................................... 113

Commonalities among past umbrella frameworks for debt relief .......................... 54

Differences among past umbrella frameworks for debt relief ................................ 55

Changes in debt resolution and the emergence of collective action clauses ............ 56

The Common Framework in historical comparison ............................................ 57

Implications for future debt reduction and resolution ............................................... 59

References .............................................................................................................. 60

Special Focus

ix

Chapter 4

Impact of COVID-19 on Global Income Inequality ............................................. 155

Introduction .........................................................................................................157

Recent trends in global income inequality ..............................................................159

Distributional impacts of disruptive events .............................................................161

Transmission channels ....................................................................................162

Empirical estimates from the literature .............................................................162

Event study ....................................................................................................163

Effects of COVID-19 on income inequality ...........................................................163

COVID-19 pandemic: Aggravating factors.......................................................163

Policies deployed during the COVID-19 pandemic ..........................................169

High-frequency phone surveys to assess the distributional impact

of the pandemic ..............................................................................................172

Impact of COVID-19 on within-country income inequality: Simulations ..........175

Chapter 3 Main features of commodity cycles ........................................................................ 116

Empirical approach ......................................................................................... 116

Features of commodity price cycles .................................................................. 117

Recent commodity price movements compared with historical experience ......... 119

Evolution of commodity cycles .............................................................................. 119

Crude oil........................................................................................................ 120

Coal ............................................................................................................... 121

Aluminum ..................................................................................................... 122

Copper .......................................................................................................... 122

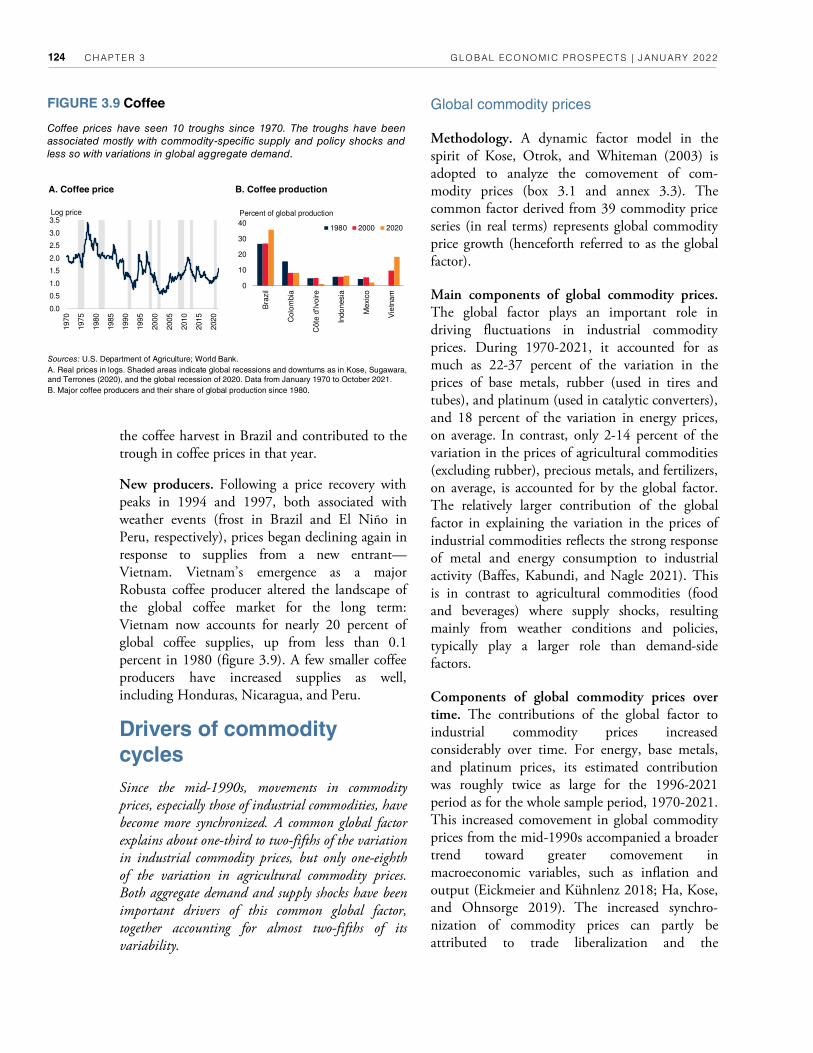

Coffee ............................................................................................................ 123

Drivers of commodity cycles .................................................................................. 124

Global commodity prices ................................................................................ 124

Drivers of commodity prices ........................................................................... 130

Policy options ....................................................................................................... 131

Need for policy action..................................................................................... 131

Macroeconomic and regulatory policies ........................................................... 132

Structural policies ........................................................................................... 135

Conclusion ........................................................................................................... 138

Annex 3.1 Methodology for dating turning points .................................................. 140

Annex 3.2 Methodology for estimating concordance ............................................... 140

Annex 3.3 Methodology: Factor-augmented vector autoregression ........................... 141

Annex 3.4 Additional tables................................................................................... 145

References ............................................................................................................ 147

x

Statistical Appendix .............................................................................................................................201

Data and Forecast Conventions ........................................................................................................... 207

Selected Topics ...................................................................................................................................208

1.1 Global prospects ...................................................................................... 5

1.2 Global risks and policy challenges ............................................................. 7

1.3 Pandemic developments ........................................................................... 9

1.4 Global trade ............................................................................................ 9

1.5 Commodity markets .............................................................................. 10

1.6 Global inflation and financial developments ............................................ 11

1.7 Major economies: Recent developments and outlook ............................... 13

1.8 Recent developments in emerging market and developing economies ....... 14

1.9 Outlook in emerging market and developing economies .......................... 15

B1.1.1 Regional outlook ................................................................................... 18

B1.1.2 Regional risks ........................................................................................ 19

1.10 Per capita income, poverty, and inequality .............................................. 20

1.11 Global outlook ...................................................................................... 21

B1.2.1 LICs: Recent developments .................................................................... 23

B1.2.2 LICs: Outlook and risks ......................................................................... 24

1.12 Downside risks: Simultaneous Omicron-driven economic disruptions ...... 28

1.13 Downside risks: Worsening supply bottlenecks and de-anchored

inflation expectations ............................................................................. 29

Figures

Boxes 1.1 Regional perspectives: Outlook and risks ................................................ 17

1.2 Recent developments and outlook for low-income countries .................... 22

3.1 Drivers of commodity cycles ................................................................ 125

4.1 Within-country inequality around recessions, financial crises,

and epidemics ..................................................................................... 164

4.2 Evidence on the distributional effects of past policy initiatives ................ 181

Implications for between-country and global inequality .................................... 177

Empirical evidence from the literature ............................................................. 178

Policy implications ............................................................................................... 179

Conclusion........................................................................................................... 184

Annex 4.1 Data challenges .................................................................................... 184

Annex 4.2 Technical details on the simulation exercises .......................................... 187

Annex 4.3 Additional results ................................................................................. 190

References ............................................................................................................ 191

Chapter 4

xi

Figures 1.14 Downside risks: Financial stress ..............................................................30

1.15 Downside risks: Natural disasters and climate change...............................31

1.16 Policy challenges in advanced economies .................................................33

1.17 Monetary policy challenges in emerging market and developing

economies .............................................................................................34

1.18 Fiscal policy challenges in emerging market and developing economies .....36

1.19 Longer-term policy challenges in emerging market and developing

economies .............................................................................................37

SF.1 Debt .....................................................................................................50

SF.2 Debt increases and composition before and after the Brady Plan

and HIPC/MDRI ..................................................................................52

SF.3 Umbrella debt restructuring frameworks .................................................54

SF.4 Economic growth before and after debt relief ..........................................55

2.1.1 China: Recent developments ..................................................................66

2.1.2 EAP excluding China: Recent developments ...........................................67

2.1.3 EAP: Outlook........................................................................................68

2.1.4 EAP: Risks ............................................................................................69

2.2.1 ECA: Recent developments ....................................................................74

2.2.2 ECA: Outlook .......................................................................................75

2.2.3 ECA: Risks ............................................................................................77

2.3.1 LAC: Recent developments ....................................................................82

2.3.2 LAC: Outlook .......................................................................................83

2.3.3 LAC: Risks ............................................................................................85

2.4.1 MENA: Recent developments ................................................................90

2.4.2 MENA: Outlook ...................................................................................91

2.4.3 MENA: Risks ........................................................................................92

2.5.1 SAR: Recent developments .....................................................................96

2.5.2 SAR: Outlook........................................................................................97

2.5.3 SAR: Risks ............................................................................................98

2.6.1 SSA: Recent developments ................................................................... 102

2.6.2 SSA: Outlook ..................................................................................... 103

2.6.3 SSA: Risks ........................................................................................... 105

3.1 Commodity prices ............................................................................... 114

3.2 Importance of commodities .................................................................. 115

3.3 Duration, amplitude, and slope ............................................................ 118

3.4 Synchronization of commodity price cycles ........................................... 119

3.5 Commodity prices around global recessions and downturns ................... 120

3.6 Crude oil ............................................................................................. 121

xii

3.7 Coal ................................................................................................... 121

3.8 Aluminum and copper......................................................................... 123

3.9 Coffee ................................................................................................ 124

B3.1.1 Global commodity prices ..................................................................... 126

B3.1.2 Contributions of global shocks to commodity prices ............................. 128

3.10 Structural policies and capital flow volatility in EMDEs ........................ 134

A3.1.1 Commodity prices ............................................................................... 140

4.1 Within-country income inequality and poverty, 2000-09 and 2010-19 .. 159

4.2 Within-country income inequality and poverty, by region and

country group, 2000-09 and 2010-19 .................................................. 161

4.3 Between-country and global income inequality, 2000-20 ....................... 162

B4.1.1 Literature review: Studies indicating an increase or decrease in

inequality after an event ....................................................................... 165

B4.1.2 Event study: Inequality around recessions, crises, and epidemics,

1970-2019 .......................................................................................... 167

4.4 Shares of countries implementing social protection measures

in response to COVID-19, 2020-21 ..................................................... 170

4.5 Shares of countries implementing social protection measures

in response to COVID-19, by EMDE region, 2020-21 ......................... 171

4.6 Government support spending on COVID-19 ..................................... 172

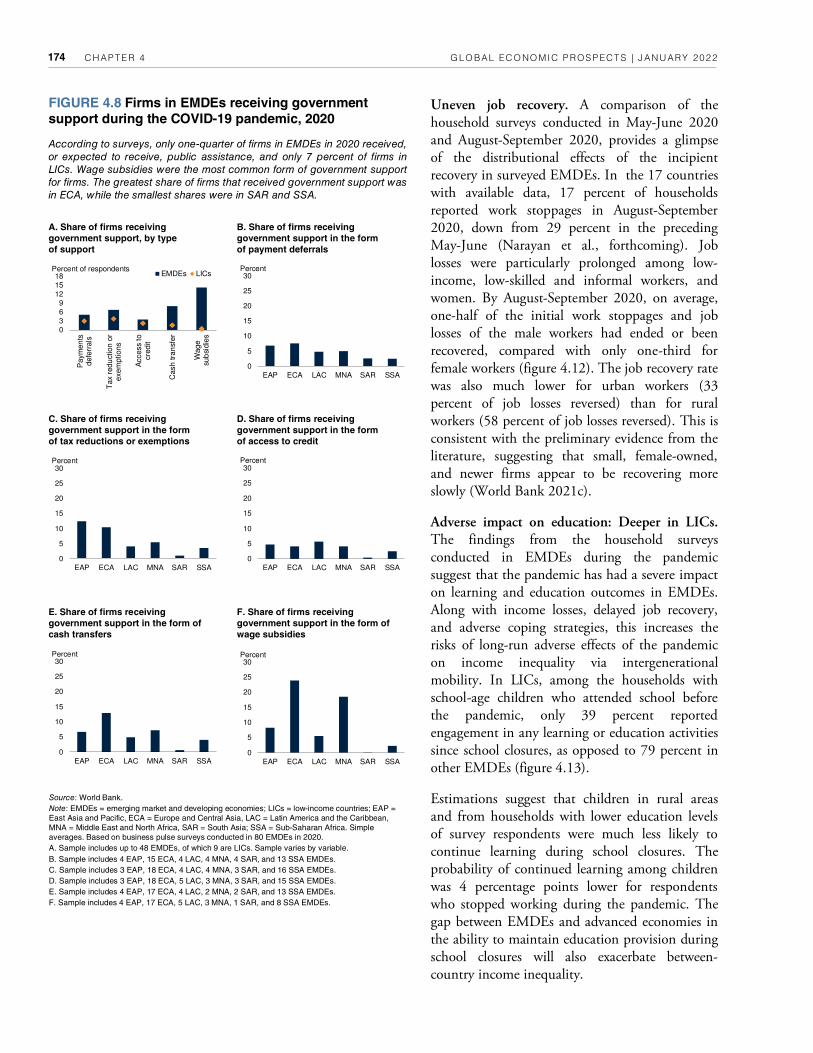

4.7 Households in EMDEs receiving government assistance during

the COVID-19 pandemic, 2020 .......................................................... 173

4.8 Firms in EMDEs receiving government support during the COVID-19

pandemic, 2020 .................................................................................. 174

4.9 Households reporting income losses in EMDEs since the beginning

of the pandemic, 2020 ......................................................................... 175

4.10 Households reporting work stoppages in EMDEs since the beginning

of the pandemic, 2020 ......................................................................... 176

4.11 Firms reporting cuts in working hours or wages in EMDEs since the

beginning of the COVID-19 pandemic, 2020 ...................................... 177

4.12 Job recovery in EMDEs, 2020 ............................................................. 177

4.13 Impact of COVID-19 on education in EMDEs, 2020 .......................... 178

4.14 Distributional impacts of COVID-19 in EMDEs, 2019-20 ................... 179

4.15 Estimated changes in between-country income inequality ...................... 180

B4.2.1 Pre- and post-tax Gini indices, 1990-2018 ............................................ 182

A4.1.1 Within-country income inequality and poverty (5-year averages)

1990-2019 .......................................................................................... 185

A4.1.2 Within-country income inequality and poverty (population-weighted

averages), 2000-19 .............................................................................. 186

Figures

xiii

Tables 1.1 Real GDP ................................................................................................ 4

B1.2.1 Low-income country forecasts ................................................................. 25

1.2 Emerging market and developing economies ............................................ 40

2.1.1 East Asia and Pacific forecast summary .................................................... 71

2.1.2 East Asia and Pacific country forecasts ..................................................... 71

2.2.1 Europe and Central Asia forecast summary .............................................. 78

2.2.2 Europe and Central Asia country forecasts ............................................... 79

2.3.1 Latin America and the Caribbean forecast summary ................................. 86

2.3.2 Latin America and the Caribbean country forecasts .................................. 87

2.4.1 Middle East and North Africa forecast summary ...................................... 94

2.4.2 Middle East and North Africa economy forecasts ..................................... 94

2.5.1 South Asia forecast summary ................................................................. 100

2.5.2 South Asia country forecasts .................................................................. 100

2.6.1 Sub-Saharan Africa forecast summary .................................................... 106

2.6.2 Sub-Saharan Africa country forecasts ..................................................... 107

A3.1.1 Peaks and troughs in price cycles for selected commodities since 1970 ..... 139

A3.2.1 Concordance matrix of real commodity prices........................................ 141

A3.4.1 Characteristics of commodity price cycles .............................................. 145

A3.4.2 Global recessions and downturns since 1970 .......................................... 147

A4.2.1 Sample of countries used in simulations ................................................. 189

A4.3.1 Impact of COVID-19 on income inequality: Main transmission channels..190

A4.3.2 Additional results from the event study .................................................. 191

A4.3.3 Estimated probability of income losses ................................................... 191

xv

Global and regional surveillance work was coordi-nated by Carlos Arteta. The report was prepared by a team that included Amat Adarov, John Baffes, Tom Bundervoet, Alexandru Cojocaru, Justin-Damien Guénette, Jongrim Ha, Osamu Inami, Alain Kabundi, Sergiy Kasyanenko, Sinem Kilic Celik, Wee Chian Koh, Christoph Lakner, Daniel Gerszon Mahler, Peter Nagle, Ambar Nara-yan, Lucia Quaglietti, Franz Ulrich Ruch, Naotaka Sugawara, Ekaterine Vashakmadze, Garima Vasishtha, Dana Vorisek, Collette Wheeler, Take-fumi Yamazaki, and Nishant Yonzan.

Research assistance was provided by Lule Bahtiri, Giovanni Borraccia, Hrisyana Doytchinova, Jiayue Fan, Dhruv Gandhi, Arika Kayastha, Maria Hazel Macadangdang, Muneeb Ahmad Naseem, Julia Roseman Norfleet, Vasiliki Papagianni, Lorëz Qehaja, Juan Felipe Serrano, Shijie Shi, Kaltrina Temaj, Jingran Wang, Yujia Yao, and Juncheng Zhou. Modeling and data work were provided by Rajesh Kumar Danda and Shijie Shi.

Online products were produced by Graeme Littler. Alejandra Viveros managed communications and media outreach with a team that included Joe Rebello and Nandita Roy, and extensive sup-port from the World Bank’s media and digital communications teams. Graeme Littler provided

editorial support, with contributions from Adriana Maximiliano.

The print publication was produced by Adriana Maximiliano, in collaboration with Andrew Berghauser, Cindy Fisher, Michael Harrup, Maria Hazel Macadangdang, and Jewel McFadden.

Regional projections and write-ups were produced in coordination with country teams, country directors, and the offices of the regional chief economists.

Many reviewers provided extensive advice and comments. The analysis also benefited from comments and suggestions by staff members from World Bank Group country teams and other World Bank Group Vice Presidencies as well as Executive Directors in their discussion of the report on December 14, 2021. However, both forecasts and analysis are those of the World Bank Group staff and should not be attributed to Executive Directors or their national authorities.

The research for Chapter 3 “Commodity Price Cycles: Drivers and Policies” was generously funded by the Government of Japan through the Policy and Human Resources Development (PHRD) Fund, administered by the World Bank Group.

Acknowledgments This World Bank Group Flagship Report is a product of the Prospects Group in the Equitable Growth, Finance and Institutions (EFI) Vice Presidency. The project was managed by M. Ayhan Kose and Franziska Ohnsorge, under the general guidance of Indermit Gill.

xvii

As the world enters the third year of the COVID-19 crisis, economic developments have been both encouraging and troubling, clouded by many risks and considerable uncertainty.

The good news is that output in many countries rebounded in 2021 after a sharp decline in 2020. Advanced economies and many middle-income countries have reached substantial vaccination rates. International trade has picked up, and high commodity prices are benefiting many developing countries. Domestic financial crises and foreign debt restructurings have been less frequent than might have been expected in a time of severe global shocks.

Yet, for many developing countries, progress toward recovery has been hampered by daunting challenges. This edition of Global Economic Prospects analyzes three of them.

Macroeconomic imbalances have reached un-precedented proportions. Government spending, deficits, and debt in several advanced economies have reached record highs relative to GDP. Central bank balance sheets have absorbed unprecedented amounts of long-term assets financed by bank reserves, resulting in an inequitable allocation of capital. Spending in developing countries surged to support economic activity during the crisis, but many countries are now facing record levels of external and domestic debt. Adding to these debt-related risks is the potential for higher interest rates: it is difficult to predict how rapidly interest rates will rise as advanced economies slow down their expansion in monetary policies. With fiscal and monetary policy in uncharted territory, the implications for exchange rates, inflation, debt sustainability, and economic growth are unlikely to be favorable for developing countries.

The world is facing growing income inequality across and within countries. The COVID-19 crisis wiped out years of progress in poverty

reduction. As government’s fiscal space has narrowed, many households in developing countries have suffered severe employment and earning losses—with women, the unskilled, and informal workers hit the hardest. School closures and sustained disruptions to healthcare services can do lasting damage to human capital, espe-cially among children and the most vulnerable. At the other end of the income scale, booming asset prices are boosting the wealth of richer segments of the population, adding to inflation. This increasing divergence of fortunes is especially troubling given the possibility of social discontent in developing countries.

Compounding this rising inequality, the world is undergoing a phase of exceptional uncertainty. The emergence of the Omicron variant is a stark reminder that the COVID-19 pandemic is not over. New variants of the virus can put even highly vaccinated countries under pressure and threaten to wreak havoc in those with low vaccination rates—which are the poorest and most vulnerable of all. Supply bottlenecks have hit developing countries hard—these countries are often the last in the global supply line, outbid by countries with greater financial resources and larger orders. Ports operating below capacity, pandemic-related delays in orders for new vessels, and containers stranded in the “wrong” ports have increased shipping costs and supply constraints to unprecedented levels. Volatile commodity prices and extreme weather events driven by climate change are aggravating food insecurity risks, further burdening health and nutrition.

Progress in vaccination is key to restoring mobility and overcoming supply-chain disrup-tions. For most of 2021, the main obstacle was the limited access to vaccine doses, with low-income countries suffering the most. At the start of 2022 the supply of vaccines is increasing appreciably, but new variants and vaccine deployment bottlenecks remain major obstacles,

Foreword

xviii

causing the uncertainty over health to persist well into the future.

In response, this edition of Global Economic Prospects charts a policy agenda for the world to address these three major challenges.

To soften the increased global inequality, this report calls for a concerted effort to mobilize external resources and accelerate debt relief efforts. The recent $93 billion replenishment of the International Development Association (IDA)—the World Bank’s fund for the poorest countries—is a key milestone in this respect. More progress, however, is needed on the implementation of the G20’s Common Frame-work for debt restructuring for low-income countries under stress. In 2022 alone, around $35 billion in bilateral and private debt-service payments will become due on the public and publicly guaranteed debt of IDA countries. Given that burden, vulnerable countries will find it increasingly difficult to support recovery or direct resources to health, education, social protection, and climate.

Some of the most important steps to contain inequality can come from domestic growth and innovation. The digital revolution offers an opportunity to strengthen social protection systems and health and education services. It can enable access to finance and help create new jobs and economic opportunities. E-government initiatives can facilitate access to public services for the poor and encourage entrepreneurs. Greater access to continuous electricity supply will be a

vital first step. In addition, policy measures to facilitate cross-border trade and investment—especially if combined with reforms in developing countries to improve business climates, human and physical capital—can help these countries generate the productivity growth needed to catch up to advanced-economy per capita incomes.

To enable social spending while investing more in infrastructure, climate adaptation and clean energy will require a careful review and pri-oritization of public spending, subsidies, and measures to expand the tax base. It will be equally important to strengthen financial systems, and to reprofile debt to spread out repayments and reduce exchange-rate risks.

Food-price inflation and supply shortages call for heightened attention to food security, particularly in fragile and conflict-affected countries. Access to clean water and better nutrition are vital to reduce stunting. Carbon taxes and the reduction of fossil-fuel subsidies are important steps in reducing greenhouse gas emissions, but high energy prices are making the implementation of these policies more challenging.

Against this mix of encouraging and troubling news, it is clear that challenging times lie ahead for the global economy—and particularly for developing countries—as economic stimulus slows and credit conditions tighten. Putting more countries on a favorable growth path will require concerted international action and a compre-hensive set of national policy responses.

David Malpass

President

World Bank Group

xix

Executive Summary

The global recovery is set to decelerate markedly amid continued COVID-19 flare-ups, diminished policy support, and lingering supply bottlenecks. In contrast to that in advanced economies, output in emerging market and developing economies (EMDEs) will remain substantially below the pre-pandemic trend over the forecast horizon. The global outlook is clouded by various downside risks, including renewed COVID-19 outbreaks due to Omicron or new virus variants, the possibility of de-anchored inflation expectations, and financial stress in a context of record-high debt levels. If some countries eventually require debt restructuring, this will be more difficult to achieve than in the past. Climate change may increase commodity price volatility, creating challenges for the almost two-thirds of EMDEs that rely heavily on commodity exports and highlighting the need for asset diversification. Social tensions may heighten as a result of the increase in between-country and within-country inequality caused by the pandemic. Given limited policy space in EMDEs to support activity if needed, these downside risks increase the possibility of a hard landing. These challenges underscore the importance of strengthened global cooperation to foster rapid and equitable vaccine distribution, proactive measures to enhance debt sustainability in the poorest countries, redoubled efforts to tackle climate change and within-country inequality, and an emphasis on growth-enhancing policy interventions to promote green, resilient, and inclusive development and on reforms that broaden economic activity to decouple from global commodity markets.

Global Outlook. After rebounding to an estimated 5.5 percent in 2021, global growth is expected to decelerate markedly to 4.1 percent in 2022, reflecting continued COVID-19 flare-ups, diminished fiscal support, and lingering supply bottlenecks. The near-term outlook for global growth is somewhat weaker, and for global inflation notably higher, than previously envisioned, owing to pandemic resurgence, higher food and energy prices, and more pernicious supply disruptions. Global growth is projected to soften further to 3.2 percent in 2023, as pent-up demand wanes and supportive macroeconomic policies continue to be un-wound. Although output and investment in advanced economies are projected to return to pre-pandemic trends next year, in emerging market and developing economies (EMDEs)—particularly in small states and fragile and conflict-afflicted countries—they will remain markedly below, owing to lower vaccination rates, tighter fiscal and monetary policies, and more persistent scarring from the pandemic.

Various downside risks cloud the outlook, including simultaneous Omicron-driven econom-ic disruptions, further supply bottlenecks, a de-anchoring of inflation expectations, financial

stress, climate-related disasters, and a weakening of long-term growth drivers. As EMDEs have limited policy space to provide additional support if needed, these downside risks heighten the possibility of a hard landing. This underscores the importance of strengthening global cooperation to foster rapid and equitable vaccine distribution, calibrate health and economic policies, enhance debt sustainability in the poorest countries, and tackle the mounting costs of climate change. EMDE policy makers also face the challenges of heightened inflationary pressures, spillovers from prospective advanced-economy monetary tighten-ing, and constrained fiscal space. Despite budge-tary consolidation, debt levels—which are already at record highs in many EMDEs—are likely to rise further owing to sustained revenue weakness. Over the longer term, EMDEs will need to buttress growth by pursuing decisive policy actions, including reforms that mitigate vulner-abilities to commodity shocks, reduce income and gender inequality, and enhance preparedness for health- and climate-related crises.

Regional Prospects. Growth in most EMDE regions in 2022-23 is projected to revert to the average rates during the decade prior to the pandemic, with the exception of East Asia and

xx

Pacific. This pace of growth will not be enough to recoup output setbacks during the pandemic, however. By 2023, annual output is expected to remain below the pre-pandemic trend in all EMDE regions, in contrast to advanced econ-omies, where the gap is projected to close. The pace of recovery will be uneven across and within regions, with downside risks dominating the outlook. On a per capita basis, the recovery may leave behind those in economies that experienced the deepest contractions in 2020, such as tourism-reliant island economies. Half or more of economies in East Asia and Pacific, Latin America and the Caribbean, and the Middle East and North Africa, and two-fifths of economies in Sub-Saharan Africa, will still be below their 2019 per capita GDP levels by 2023.

This edition of Global Economic Prospects also includes analytical pieces on the features and implications of global commodity price cycles, the impact of the COVID-19 pandemic on global income inequality, and the experience with past coordinated debt restructurings.

Commodity Price Cycles: Drivers and Policies. Commodity prices soared in 2021 following the broad-based decline in early 2020, with prices of several commodities reaching all-time highs. In part, this reflected the strong rebound of demand from the 2020 global recession. Energy and metal prices generally move in line with global econom-ic activity, and this tendency has strengthened in recent decades. Looking ahead, global macro-economic developments and commodity supply factors will likely continue to cause recurring commodity price swings. For many commodities, these may be amplified by the transition away from fossil fuels. To dampen the associated macroeconomic fluctuations, the almost two-thirds of EMDEs that are commodity exporters need to strengthen their policy frameworks and reduce their reliance on commodity-related revenues by diversifying exports and, more importantly, national asset portfolios.

Impact of COVID-19 on Global Income Inequality. The COVID-19 pandemic has raised global income inequality, partly reversing the

decline that was achieved over the previous two decades. Weak recoveries in EMDEs are expected to return between-country inequality to the levels of the early 2010s. Preliminary evidence suggests that the pandemic has also caused within-country income inequality to rise somewhat in EMDEs because of particularly severe job and income losses among lower-income population groups. Over the medium and long term, rising inflation, especially food price inflation, as well as pandemic-related disruptions to education may further raise within-country inequality. Within-country inequality remains particularly high in EMDE regions that account for about two-thirds of the global extreme poor. To steer the global recovery onto a more equitable development path, a comprehensive package of policies is needed. A rapid global rollout of vaccination and redoubled productivity-enhancing reforms can help lower between-country inequality. Support targeted at vulnerable populations and measures to broaden access to education, health care, digital services and infrastructure, as well as an emphasis on supportive fiscal measures, can help lower within-country inequality. Assistance from the global community is essential to expedite a return to a green, resilient, and inclusive recovery.

Resolving High Debt after the Pandemic: Lessons from Past Episodes of Debt Relief. In the pandemic-induced global recession of 2020, global debt levels surged. The rise in debt has led to several countries initiating debt restructurings, while many others are in or at high risk of debt distress and may also eventually need debt relief. Historically, several umbrella frameworks coordinated debt relief to multiple debtor countries from multiple creditors on common principles. They offered substantial—but pro-tracted—debt stock reductions that were typically preceded by a series of less ambitious debt relief efforts. The G20 Common Framework provides a structure to initiate debt restructuring for low-income IDA eligible countries, but largely avoids the issue of outright debt reductions. Future umbrella frameworks for debt restructuring will face greater challenges than those in the past due to a more fragmented creditor base.

xxi

AE

CAC

CPI

DSSI

EAP

ECA

EMBI

EMDE

EU

FAVAR

FCS

FDI

G7

G20

GCC

GDP

GEP

HIPC

IDA

IEA

LHS

LIA

LIOA

ILO

IMF

LAC

LIC

MDRI

MNA/MENA

NBER

OECD

OPEC

OPEC+

PMI

PPP

RHS

SAR

SSA

UN

WAEMU

WDI

Abbreviations

advanced economy

collective action clause

consumer price index

Debt Service Suspension Initiative

East Asia and Pacific

Europe and Central Asia

Emerging Market Bond Index

emerging market and developing economy

European Union

factor-augmented vector autoregression

fragile and conflict-affected situations

foreign direct investment

Group of Seven: Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States

Group of Twenty: Argentina, Australia, Brazil, Canada, China, France, Germany, India, Indonesia, Italy, Japan, Republic of Korea, Mexico, Russian Federation, Saudi Arabia, South Africa, Turkey, the United Kingdom, the United States, and the European Union

Gulf Cooperation Council

gross domestic product

Global Economic Prospects

heavily indebted poor countries

International Development Association

International Energy Agency

left-hand scale

lending into arrears

lending into official arrears

International Labour Organization

International Monetary Fund

Latin America and the Caribbean

low-income country

Multilateral Debt Relief Initiative

Middle East and North Africa

National Bureau of Economic Research

Organisation for Economic Co-operation and Development

Organization of the Petroleum Exporting Countries

OPEC and Azerbaijan, Bahrain, Brunei Darussalam, Kazakhstan, Malaysia, Mexico, Oman, Russian Federation, South Sudan, and Sudan

Purchasing Managers’ Index

purchasing power parity

right-hand scale

South Asia

Sub-Saharan Africa

United Nations

West African Economic and Monetary Union

World Development Indicators

CHAPTER 1

GLOBAL OUTLOOK

CHAPTER 1 GLOBAL ECONOMIC PROSPECTS | JANUARY 2022 3

After rebounding to an estimated 5.5 percent in 2021, global growth is expected to decelerate markedly to 4.1 percent in 2022, reflecting continued COVID-19 flare-ups, diminished fiscal support, and lingering supply bottlenecks. The near-term outlook for global growth is somewhat weaker, and for global inflation notably higher, than previously envisioned, owing to pandemic resurgence, higher food and energy prices, and more pernicious supply disruptions. Global growth is projected to soften further to 3.2 percent in 2023, as pent-up demand wanes and supportive macroeconomic policies continue to be unwound. Although output and investment in advanced economies are projected to return to pre-pandemic trends next year, in emerging market and developing economies (EMDEs)—particularly in small states and fragile and conflict-afflicted countries—they will remain markedly below, owing to lower vaccination rates, tighter fiscal and monetary policies, and more persistent scarring from the pandemic. Various downside risks cloud the outlook, including simultaneous Omicron-driven economic disruptions, further supply bottlenecks, a de-anchoring of inflation expectations, financial stress, climate-related disasters, and a weakening of long-term growth drivers. As EMDEs have limited policy space to provide additional support if needed, these downside risks heighten the possibility of a hard landing. This underscores the importance of strengthening global cooperation to foster rapid and equitable vaccine distribution, calibrate health and economic policies, enhance debt sustainability in the poorest countries, and tackle the mounting costs of climate change. EMDE policy makers also face the challenges of heightened inflationary pressures, spillovers from prospective advanced-economy monetary tightening, and constrained fiscal space. Despite budgetary consolidation, debt levels—which are already at record highs in many EMDEs—are likely to rise further owing to sustained revenue weakness. Over the longer term, EMDEs will need to buttress growth by pursuing decisive policy actions, including reforms that mitigate vulnerabilities to commodity shocks, reduce income and gender inequality, and enhance preparedness for health- and climate-related crises.

Summary

Global growth is estimated to have surged to 5.5 percent in 2021—its strongest post-recession pace in 80 years, as a relaxation of pandemic-related lockdowns in many countries helped boost demand. Notwithstanding this annual increase, resurgences of the COVID-19 pandemic and widespread supply bottlenecks weighed appreciably on global activity in the second half of last year. Moreover, emerging market and developing economies (EMDEs) are experiencing notably weaker and more fragile recoveries compared to those in advanced economies as a result of slower vaccination progress, a more limited policy response, and the pandemic’s scarring effects (figure 1.1.A). In particular, these scarring effects on potential output reflect the pandemic’s adverse impact on EMDE physical and human capital. Among the most vulnerable countries, the impact of the pandemic will reverse several years of income gains.

Global COVID-19 infection rates have soared, driven by the rapid spread of the Omicron variant. Advanced economies and a growing number of EMDEs have fully vaccinated a majority of their populations. But despite expansive vaccine coverage, some countries have been forced to reintroduce strict lockdown measures recently to alleviate acute pressures on their health systems. Vaccine coverage remains highly uneven around the world, and stubbornly limited across low-income countries (LICs). At recent vaccination rates, only about a third of the LIC population will have received even one vaccine dose by the end of 2023 (figure 1.1.B).

Recent data point to solid but moderating global growth. The surge in infections in 2021 related to the Delta variant sapped consumer demand, but to a much more limited degree than previous waves. Persistent supply bottlenecks have weighed on global production and trade. In advanced economies, high vaccination rates and sizable fiscal support have helped cushion some of the adverse economic impacts of the pandemic. In EMDEs, however, the pace of recovery has been further dampened by waning policy support and a tightening of financing conditions.

Note: This chapter was prepared by Carlos Arteta, Justin-Damien Guénette, Lucia Quaglietti, and Collette Wheeler, with contributions from Jongrim Ha, Osamu Inami, Sergiy Kasyanenko, Peter Nagle, and Ekaterine Vashakmadze.

CHAPTER 1 GLOBAL ECONOMIC PROSPECTS | JANUARY 2022 4

TABLE 1.1 Real GDP1

(Percent change from previous year)

2019 2020 2021e 2022f 2023f 2021e 2022f 2023f

World 2.6 -3.4 5.5 4.1 3.2 -0.2 -0.2 0.1

Advanced economies 1.7 -4.6 5.0 3.8 2.3 -0.4 -0.2 0.1

United States 2.3 -3.4 5.6 3.7 2.6 -1.2 -0.5 0.3

Euro area 1.6 -6.4 5.2 4.2 2.1 1.0 -0.2 -0.3

Japan -0.2 -4.5 1.7 2.9 1.2 -1.2 0.3 0.2

Emerging market and developing economies 3.8 -1.7 6.3 4.6 4.4 0.2 -0.1 0.0

East Asia and Pacific 5.8 1.2 7.1 5.1 5.2 -0.6 -0.2 0.0

China 6.0 2.2 8.0 5.1 5.3 -0.5 -0.3 0.0

Indonesia 5.0 -2.1 3.7 5.2 5.1 -0.7 0.2 0.0

Thailand 2.3 -6.1 1.0 3.9 4.3 -1.2 -1.2 0.0

Europe and Central Asia 2.7 -2.0 5.8 3.0 2.9 1.9 -0.9 -0.6

Russian Federation 2.0 -3.0 4.3 2.4 1.8 1.1 -0.8 -0.5

Turkey 0.9 1.8 9.5 2.0 3.0 4.5 -2.5 -1.5

Poland 4.7 -2.5 5.1 4.7 3.4 1.3 0.2 -0.5

Latin America and the Caribbean 0.8 -6.4 6.7 2.6 2.7 1.5 -0.3 0.2

Brazil 1.2 -3.9 4.9 1.4 2.7 0.4 -1.1 0.4

Mexico -0.2 -8.2 5.7 3.0 2.2 0.7 0.0 0.2

Argentina -2.0 -9.9 10.0 2.6 2.1 3.6 0.9 0.2

Middle East and North Africa 0.9 -4.0 3.1 4.4 3.4 0.6 0.8 0.1

Saudi Arabia 0.3 -4.1 2.4 4.9 2.3 0.0 1.6 -0.9

Iran, Islamic Rep. 3 -6.8 3.4 3.1 2.4 2.2 1.0 0.2 -0.1

Egypt, Arab Rep. 2 5.6 3.6 3.3 5.5 5.5 1.0 1.0 0.0

South Asia 4.4 -5.2 7.0 7.6 6.0 0.1 0.8 0.8

India 3 4.0 -7.3 8.3 8.7 6.8 0.0 1.2 0.3

Pakistan 2 2.1 -0.5 3.5 3.4 4.0 2.2 1.4 0.6

Bangladesh 2 8.2 3.5 5.0 6.4 6.9 1.4 1.3 0.7

Sub-Saharan Africa 2.5 -2.2 3.5 3.6 3.8 0.7 0.3 0.0

Nigeria 2.2 -1.8 2.4 2.5 2.8 0.6 0.4 0.4

South Africa 0.1 -6.4 4.6 2.1 1.5 1.1 0.0 0.0

Angola -0.6 -5.4 0.4 3.1 2.8 -0.1 -0.2 -0.7

Memorandum items:

Real GDP1

High-income countries 1.7 -4.6 5.0 3.8 2.4 -0.3 -0.2 0.2

Developing countries 4.0 -1.4 6.5 4.6 4.5 0.2 -0.2 0.0

EMDEs excluding China 2.5 -4.2 5.2 4.2 3.8 0.8 0.0 0.1

Commodity-exporting EMDEs 1.8 -3.9 4.5 3.3 3.1 0.9 0.0 0.0

Commodity-importing EMDEs 4.9 -0.5 7.2 5.2 5.0 -0.1 -0.2 0.0

Commodity-importing EMDEs excluding China 3.3 -4.5 6.1 5.3 4.6 0.7 0.0 0.1

Low-income countries 4.6 1.3 3.3 4.9 5.9 0.2 0.0 0.0

EM7 4.5 -0.6 7.2 4.8 4.7 0.0 -0.3 0.0

World (PPP weights) 4 2.9 -3.0 5.7 4.4 3.6 0.0 -0.1 0.1

World trade volume 5 1.1 -8.2 9.5 5.8 4.7 1.2 -0.5 0.3

Commodity prices 6

Oil price -10.2 -32.8 67.2 7.2 -12.2 16.9 7.2 -13.1

Non-energy commodity price index -4.2 3.0 31.9 -2.0 -4.0 9.4 0.5 -1.3

Source: World Bank.

1. Headline aggregate growth rates are calculated using GDP weights at average 2010-19 prices and market exchange rates. The aggregate growth rates may differ from the previously

published numbers that were calculated using GDP weights at average 2010 prices and market exchange rates. Data for Afghanistan and Lebanon are excluded.

2. GDP growth rates are on a fiscal year basis. Aggregates that include these countries are calculated using data compiled on a calendar year basis. Pakistan's growth rates are based on

GDP at factor cost. The column labeled 2019 refers to FY2018/19.

3. GDP growth rates are on a fiscal year basis. Aggregates that include these countries are calculated using data compiled on a calendar year basis. The column labeled 2019 refers to

FY2019/20.

4. World growth rates are calculated using average 2010-19 purchasing power parity (PPP) weights, which attribute a greater share of global GDP to emerging market and developing

economies (EMDEs) than market exchange rates.

5. World trade volume of goods and nonfactor services.

6. Oil price is the simple average of Brent, Dubai, and West Texas Intermediate prices. The non-energy index is the weighted average of 39 commodity prices (7 metals, 5 fertilizers, and 27

agricultural commodities). For additional details, please see https://www.worldbank.org/commodities.

Note: e = estimate; f = forecast. World Bank forecasts are frequently updated based on new information. Consequently, projections presented here may differ from those contained in other

World Bank documents, even if basic assessments of countries’ prospects do not differ at any given date. For the definition of EMDEs, developing countries, commodity exporters, and

commodity importers, please refer to table 1.2. EM7 includes Brazil, China, India, Indonesia, Mexico, the Russian Federation, and Turkey. The World Bank is currently not publishing

economic output, income, or growth data for Turkmenistan and República Bolivariana de Venezuela owing to lack of reliable data of adequate quality. Turkmenistan and República

Bolivariana de Venezuela are excluded from cross-country macroeconomic aggregates.

Percentage point

differences from June 2021 projections

CHAPTER 1 GLOBAL ECONOMIC PROSPECTS | JANUARY 2022 5

Global energy prices surged in the second half of 2021, particularly for natural gas and coal, owing to recovering demand and constrained supply. Meanwhile, non-energy commodity prices have stabilized, with some at or close to record highs. After rising briskly earlier last year, global trade has plateaued, owing to softening growth of demand for traded goods and supply bottlenecks caused by pandemic-related factory and port shutdowns, weather-induced logistical obstacles, and shortages of semiconductors and shipping containers. Reflecting these bottlenecks, as well as the recovery in global demand and rising food and energy prices, global consumer price inflation and its near-term expectations have increased more than previously anticipated (figure 1.1.C). Labor markets in advanced economies have tightened, supporting a rebound in wage inflation, in contrast to their uneven recovery in EMDEs. Although financial conditions continue to be broadly accommodative at the global level, they have tightened for EMDEs as risk sentiment has deteriorated.

Against this backdrop, the global economy is set to experience its sharpest slowdown after an initial rebound from a global recession since at least the 1970s. Global growth is projected to decelerate from 5.5 percent in 2021 to 4.1 percent in 2022, reflecting continued COVID-19 flare-ups, diminished policy support, and lingering supply disruptions. Growth is envisioned to slow further in 2023, to 3.2 percent, as pent-up demand is depleted and supportive macroeconomic policies continue to be unwound.

Growth in advanced economies is forecast to decelerate from 5 percent in 2021 to 3.8 percent in 2022 as the unwinding of pent-up demand only partly cushions a pronounced withdrawal of fiscal policy support. Growth is projected to moderate further in 2023 to 2.3 percent as pent-up demand is exhausted. Despite the slowdown, the projected pace of expansion will be sufficient to return aggregate advanced-economy output to its pre-pandemic trend in 2023 and thus complete its cyclical recovery. A solid rebound is projected for investment, based on sustained aggregate demand and broadly favorable financing conditions.

In contrast to advanced economies, most EMDEs are expected to suffer substantial scarring to

FIGURE 1.1 Global prospects

Emerging market and developing economies (EMDEs) are experiencing a

weaker recovery than advanced economies, owing to slower vaccination

progress, more muted policy support, and more pronounced scarring

effects from the pandemic. Vaccine access remains unequal, with very low

rates in low-income countries. After surprising to the upside in 2021, global

inflation is expected to remain above its pre-pandemic rate this year.

Investment is expected to be sharply more subdued in EMDEs than in

advanced economies. In 2023, per capita incomes in nearly 40 percent of

EMDEs will remain below their 2019 levels. Omicron-related economic

disruptions could substantially reduce growth in 2022.

Sources: Consensus Economics; Our World in Data (database); Oxford Economics; World Bank.

Note: AEs = advanced economies; EMDEs = emerging market and developing economies; FCS =

fragile and conflict-affected situations; LICs = low-income countries. Small states are EMDEs with a

population of less than 1.5 million. Unless otherwise noted, aggregates are calculated using real U.S.

dollar GDP weights at average 2010-19 prices and market exchange rates. Data for 2021 are

estimates.

A.C.D. Shaded areas indicate forecasts.

A.D. Figure shows the percent deviation between the latest projections and forecasts released in the

January 2020 edition of the Global Economic Prospects report (World Bank 2020a). For 2023, the

January 2020 baseline is extended using projected growth for 2022.

B. Number of people who received at least one COVID-19 vaccine dose per 100 people. Projections

based on 14-day moving averages of daily vaccination rates. Data through December 23, 2021.

C. Figure shows the Consensus forecast for median headline CPI inflation for 2021-22 based on

December 2021 and May 2021 surveys of 32 advanced economies and 50 EMDEs.

E. Sample includes 36 AEs, 145 EMDEs, 32 FCS, and 34 small states. The small states sample

excludes commodity-reliant Guyana which is experiencing a growth boom due to rapid offshore oil

industry development.

F. Yellow lines denote the range of the downside scenario in which economies (18 advanced

economies and 22 EMDEs) face a range of unanticipated pandemic shocks, scaled from about one-

tenth to about two-tenths of the size of those from the first half of 2020.

A. Deviation of output from

pre-pandemic trends

B. Projected vaccine coverage based

on recent vaccination rates

C. Consensus median inflation

forecasts D. Deviation of investment from

pre-pandemic trends

E. Share of economies with lower per

capita GDP levels than in 2019

F. Possible Omicron-driven growth

outcomes for 2022

0

20

40

60

80

100

Dec-2

0

Mar-

21

Jun

-21

Sep

-21

Dec-2

1

Mar-

22

Jun

-22

Sep

-22

Dec-2

2

Mar-

23

Jun

-23

Sep

-23

Dec-2

3

Advanced economies EMDEs LICs

Per 100 people

0

1

2

3

4

2019 2020 2021 2022

December 2021 May 2021Percent

-8

-6

-4

-2

0

2

2019 2020 2021 2022 2023

World

Advanced economies

EMDEs

Percent

0

20

40

60

80

100

World AEs EMDEs FCS Smallstates

2022 2023Percent of economies

0

1

2

3

4

5

World AEs EMDEs

Baseline Scenario rangePercent

-8

-6

-4

-2

0

2

2019 2020 2021 2022 2023

World

Advanced economies

EMDEs

EMDEs excl. China

Percent

CHAPTER 1 GLOBAL ECONOMIC PROSPECTS | JANUARY 2022 6

This forecast assumes that COVID-19 will continue to flare up across the globe this year—including in EMDEs where substantial proportions of the population remain unvacci-nated—but that the virus will cause outbreaks of steadily diminishing economic impact. Supply bottlenecks and labor shortages are assumed to gradually dissipate through 2022, while inflation and commodity prices are assumed to gradually decline in the second half of the year. Wage pressures are assumed to moderate thereafter in advanced economies while remaining contained in most EMDEs. Monetary policy is assumed to be tightened at a measured pace in advanced economies over the forecast horizon, but at a faster pace in EMDEs. These shifts are expected to result in a steady tightening of EMDE financing conditions. The withdrawal of fiscal support around the world is expected to continue, with fiscal policy being tightened in the vast majority of countries over 2022-23.

These forecasts imply that per capita income growth in EMDEs will decelerate from an estimated 5.1 percent in 2021 to 3.4 percent in 2022 and 3.3 percent next year. In 2023, per capita incomes in nearly 40 percent of EMDEs will remain below their 2019 levels—including over half of countries facing fragile and conflict-affected situations and three-fourths of small states (figure 1.1.E). Average growth of per capita income during 2021-23 will be insufficient to allow progress in catching up with advanced economies in nearly 70 percent of EMDEs. Rising food prices will hit the poorest populations the hardest, increasing food insecurity and accentuating the pandemic’s impact on income inequality.

The global outlook is subject to various downside risks. Critically, the continued spread of COVID-19 amid unequal distribution of vaccines across countries opens the door to new concerning strains, as exemplified by the Omicron variant first detected in November. While Omicron infections may cause less severe disease, the variant’s ability to spread quickly through vaccinated populations could overwhelm exhausted health systems and force governments to tighten control measures, causing a significant slowdown in near-term growth (figure 1.1.F).

output from the pandemic, with growth trajectories not strong enough to return investment or output to pre-pandemic trends over the forecast horizon of 2022-23 (figure 1.1.D). EMDE growth is projected to slow from 6.3 percent in 2021 to 4.6 percent in 2022, as the ongoing withdrawal of macroeconomic support, together with COVID-19 flare-ups amid the spread of the Omicron variant and continued vaccination obstacles, weigh on the recovery of domestic demand. In one-third of EMDEs, many of which are tourism-reliant economies or small states, output this year is expected to remain lower than in 2019. Growth in China is expected to ease to 5.1 percent this year, reflecting the lingering effects of the pandemic and additional regulatory tightening. Growth in LICs is anticipated to firm to 4.9 percent in 2022—below its historical average, as limited policy space constrains the recovery and as high inflation, including of food prices, and continued conflict in some cases dampen consumption.

In 2023, EMDE growth is forecast to edge further down to 4.4 percent—notably below the 5.1 percent average of the past decade—as domestic demand stabilizes and commodity prices moderate. Despite the continued recovery, the pandemic is expected to scar EMDE output for a prolonged period, in part through its adverse effects on human and physical capital accumulation. Aggregate output in 2023 is expected to be about 4 percent below its pre-pandemic trend—and, in fragile and conflict-affected EMDEs, over 7 percent below, as they face heightened uncertainty, security challenges, weak investment prospects, and anemic vaccination progress.

The near-term global outlook is a touch below previous forecasts, with a modest downgrade to growth in both advanced economies and EMDEs. Although the forecast for EMDE growth in 2022 is only slightly weaker than previous projections, this masks notable divergences across regions. Downgrades in Europe and Central Asia and Latin America and the Caribbean, due to faster removal of policy support, are accompanied by upgrades in the Middle East and North Africa and Sub-Saharan Africa amid higher-than-expected oil revenues.

CHAPTER 1 GLOBAL ECONOMIC PROSPECTS | JANUARY 2022 7

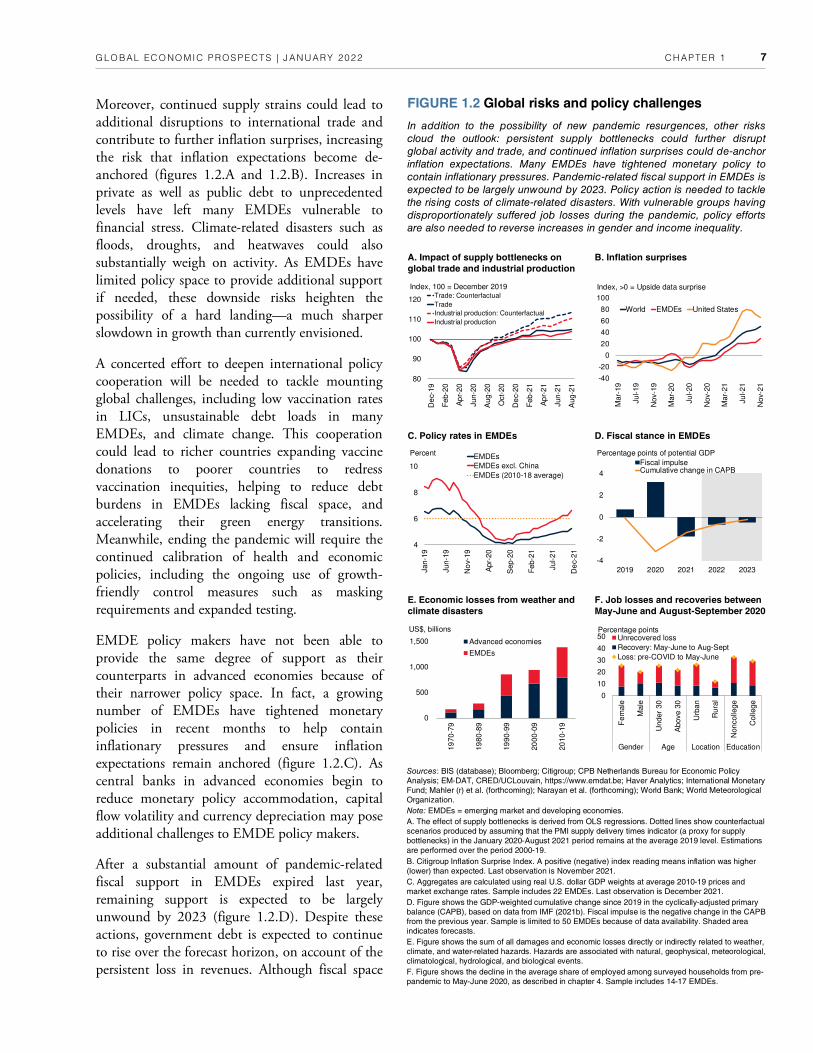

Moreover, continued supply strains could lead to additional disruptions to international trade and contribute to further inflation surprises, increasing the risk that inflation expectations become de-anchored (figures 1.2.A and 1.2.B). Increases in private as well as public debt to unprecedented levels have left many EMDEs vulnerable to financial stress. Climate-related disasters such as floods, droughts, and heatwaves could also substantially weigh on activity. As EMDEs have limited policy space to provide additional support if needed, these downside risks heighten the possibility of a hard landing—a much sharper slowdown in growth than currently envisioned.

A concerted effort to deepen international policy cooperation will be needed to tackle mounting global challenges, including low vaccination rates in LICs, unsustainable debt loads in many EMDEs, and climate change. This cooperation could lead to richer countries expanding vaccine donations to poorer countries to redress vaccination inequities, helping to reduce debt burdens in EMDEs lacking fiscal space, and accelerating their green energy transitions. Meanwhile, ending the pandemic will require the continued calibration of health and economic policies, including the ongoing use of growth-friendly control measures such as masking requirements and expanded testing.

EMDE policy makers have not been able to provide the same degree of support as their counterparts in advanced economies because of their narrower policy space. In fact, a growing number of EMDEs have tightened monetary policies in recent months to help contain inflationary pressures and ensure inflation expectations remain anchored (figure 1.2.C). As central banks in advanced economies begin to reduce monetary policy accommodation, capital flow volatility and currency depreciation may pose additional challenges to EMDE policy makers.

After a substantial amount of pandemic-related fiscal support in EMDEs expired last year, remaining support is expected to be largely unwound by 2023 (figure 1.2.D). Despite these actions, government debt is expected to continue to rise over the forecast horizon, on account of the persistent loss in revenues. Although fiscal space

FIGURE 1.2 Global risks and policy challenges

In addition to the possibility of new pandemic resurgences, other risks

cloud the outlook: persistent supply bottlenecks could further disrupt

global activity and trade, and continued inflation surprises could de-anchor

inflation expectations. Many EMDEs have tightened monetary policy to

contain inflationary pressures. Pandemic-related fiscal support in EMDEs is

expected to be largely unwound by 2023. Policy action is needed to tackle

the rising costs of climate-related disasters. With vulnerable groups having

disproportionately suffered job losses during the pandemic, policy efforts

are also needed to reverse increases in gender and income inequality.

Sources: BIS (database); Bloomberg; Citigroup; CPB Netherlands Bureau for Economic Policy

Analysis; EM-DAT, CRED/UCLouvain, https://www.emdat.be; Haver Analytics; International Monetary

Fund; Mahler (r) et al. (forthcoming); Narayan et al. (forthcoming); World Bank; World Meteorological

Organization.

Note: EMDEs = emerging market and developing economies.

A. The effect of supply bottlenecks is derived from OLS regressions. Dotted lines show counterfactual

scenarios produced by assuming that the PMI supply delivery times indicator (a proxy for supply

bottlenecks) in the January 2020-August 2021 period remains at the average 2019 level. Estimations

are performed over the period 2000-19.

B. Citigroup Inflation Surprise Index. A positive (negative) index reading means inflation was higher

(lower) than expected. Last observation is November 2021.

C. Aggregates are calculated using real U.S. dollar GDP weights at average 2010-19 prices and

market exchange rates. Sample includes 22 EMDEs. Last observation is December 2021.

D. Figure shows the GDP-weighted cumulative change since 2019 in the cyclically-adjusted primary

balance (CAPB), based on data from IMF (2021b). Fiscal impulse is the negative change in the CAPB

from the previous year. Sample is limited to 50 EMDEs because of data availability. Shaded area

indicates forecasts.

E. Figure shows the sum of all damages and economic losses directly or indirectly related to weather,

climate, and water-related hazards. Hazards are associated with natural, geophysical, meteorological,

climatological, hydrological, and biological events.

F. Figure shows the decline in the average share of employed among surveyed households from pre-

pandemic to May-June 2020, as described in chapter 4. Sample includes 14-17 EMDEs.

A. Impact of supply bottlenecks on

global trade and industrial production

B. Inflation surprises

C. Policy rates in EMDEs D. Fiscal stance in EMDEs

E. Economic losses from weather and

climate disasters

F. Job losses and recoveries between

May-June and August-September 2020

-40

-20

0

20

40

60

80

100

Mar-

19

Jul-19

Nov-1

9

Mar-

20

Jul-20

Nov-2

0

Mar-

21

Jul-21

Nov-2

1

World EMDEs United States

Index, >0 = Upside data surprise

4

6

8

10

Jan-1

9

Jun-1