IT GOVERNANCE ACCORDING TO COBIT - CiteSeerX

67

Master Thesis IT GOVERNANCE ACCORDING TO COBIT How does the IT performance within one of the largest investment banks in the world compare to COBIT? JOEL ETZLER Stockholm, Sweden XR-EE-ICS 2007:14

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of IT GOVERNANCE ACCORDING TO COBIT - CiteSeerX

Master Thesis

IT GOVERNANCEACCORDING TO COBIT

How does the IT performance within one ofthe largest investment banks in the world

compare to COBIT?

JOEL ETZLER

Stockholm, Sweden

XR-EE-ICS 2007:14

1

ABSTRACT

To improve the governance of IT and comply with regulatory demands,

organizations are using best practice frameworks to facilitate the work. One of

these IT governance frameworks is COBIT (The Control Objectives for

Information and related Technology). COBIT provides guidance on what could be

done within an IT organization in terms of controls, activities, measuring and

documentation. This framework is however large and require specific knowledge in

order to enable full use of its potential. This project was initiated to use a

straightforward method of working with COBIT while assessing the maturity of an

organization. The method was developed by myself and my advisor at The Royal

Institute of Technology in Stockholm and describes one way of using COBIT. The

organization under evaluation is one of the largest, most well known investment

banks in the world, in this project referred to as The Firm.

A specific part of the IT organization within The Firm was evaluated with COBIT

as a starting point and the gap between the framework and the organization was

underlined. COBIT provides an incremental measurement scale, where the internal

processes are measured in terms of how defined and structured they are. The scale

expresses levels of maturity and The Firm reached a level 3.3 out of 5.

The strongest and weakest areas have been emphasized and improvements on the

weaker areas have been suggested. These improvement actions could enable

organizations to better govern IT and facilitate compliance to regulatory

requirements.

Keywords: IT Governance, IT Management, COBIT, ITIL, Align IT to business,

Sarbanes and Oxley.

2

PREFACE

This is my Master Thesis and it constitutes the final part in my Master of Science

education in Electrical Engineering at the Royal Institute of Technology in

Stockholm. Conducting this project has been a great experience for me. I have met

many, very kind and helpful people and would like to express my gratitude to all

involved. Above all I would like thank, my advisor at ICS, Mårten Simonsson and

key stakeholders at The Firm; Moss, Nikki, Andrew and Trevor. Thank you!

Joel Etzler

Stockholm, 16th of May, 2007

3

TABLE OF CONTENTS

1 INTRODUCTION ................................................................................................................... 5

1.1 BACKGROUND ....................................................................................................................... 5

1.2 PROBLEM ............................................................................................................................... 7

1.3 PURPOSE ................................................................................................................................ 7

1.4 DELIMITATIONS ..................................................................................................................... 7

1.5 THESIS DISPOSITION AND READING ADVICES ......................................................................... 7

2 METHODOLOGY .................................................................................................................. 9

2.1 INITIATION ............................................................................................................................ 9

2.2 CASE STUDY .......................................................................................................................... 9

2.3 THEORETICAL STUDY .......................................................................................................... 10

2.4 EVALUATION METHOD......................................................................................................... 11

3 THEORETICAL FRAMEWORK ....................................................................................... 12

3.1 CORPORATE GOVERNANCE .................................................................................................. 12

3.2 IT GOVERNANCE .................................................................................................................. 18

3.3 IT GOVERNANCE FRAMEWORKS .......................................................................................... 20

3.4 COBIT ................................................................................................................................ 22

3.5 COBIT FACILITATES COMPLIANCE WITH SARBANES-OXLEY .............................................. 31

4 ANALYTICAL FRAMEWORK.......................................................................................... 33

4.1 DATA COLLECTION .............................................................................................................. 33

4.2 MODELING .......................................................................................................................... 37

4.3 ANALYSIS ............................................................................................................................ 38

5 EMPIRICAL STUDY ........................................................................................................... 39

5.1 PROCEDURE ......................................................................................................................... 39

5.2 THE FIRM ............................................................................................................................ 39

5.3 PROJECT DEFINITION ........................................................................................................... 40

5.4 CASE STUDY AT THE FIRM................................................................................................... 41

6 RESULTS ............................................................................................................................... 43

6.1 GENERAL RESULTS WITHIN THE MARKETS DIVISION ............................................................. 43

6.2 WEAKNESSES AT THE FIRM ................................................................................................. 47

7 DISCUSSION......................................................................................................................... 49

7.1 DISCUSSING THE RESULTS ................................................................................................... 49

7.2 HOW TO IMPROVE THE WEAKNESSES ................................................................................... 51

7.3 VALIDITY ............................................................................................................................ 53

7.4 RELIABILITY ........................................................................................................................ 53

4

8 CONCLUSION ...................................................................................................................... 54

LIST OF FIGURES

FIGURE 1 – FRAMEWORK LINKING CORPORATE GOVERNANCE TO IT GOVERNANCE8 ............................ 13

FIGURE 2 – POSITIONING OF IT GOVERNANCE AND IT MANAGEMENT. SOURCE: PETERSON, SEE

GREMBERGEN, 2004. ............................................................................................................................................... 19

FIGURE 3 – COBIT, OVERLYING FRAMEWORK PRINCIPLES. SOURCE: IT GOVERNANCE INSTITUTE,

COBIT 4.0 ................................................................................................................................................................. 23

FIGURE 4 – COBIT, STRUCTURE AND INTERRELATIONSHIP OF PROCESSES. SOURCE: IT GOVERNANCE

INSTITUTE, COBIT 4.0 ........................................................................................................................................... 24

FIGURE 5 – COBIT, OVERALL FRAMEWORK. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0 ........ 25

FIGURE 6 – METRICS. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0 ................................................. 28

FIGURE 7 – RACI-CHART. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0 ......................................... 30

FIGURE 8 – DOCUMENTS. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0 ......................................... 30

FIGURE 9 – MAPPING TO PCAOB TO COBIT. SOURCE: ITGI (2006), IT CONTROL OBJECTIVES FOR

SARBANES-OXLEY, THE ROLE OF IT IN THE DESIGN AND IMPLEMENTATION OF INTERNAL CONTROL

OVER FINANCIAL REPORTING. ............................................................................................................................... 31

FIGURE 10 – WEIGHTED RESULTS ON ALL COBIT PROCESSES...................................................................... 44

FIGURE 11 – TOP AND BOTTOM PROCESSES EMPHASIZED .............................................................................. 45

FIGURE 12 – THE STRONGEST AREAS .................................................................................................................. 45

FIGURE 13 – THE WEAKEST AREAS ...................................................................................................................... 47

FIGURE 14 – SUGGESTED IMPROVEMENTS, CONTROLS AND METRICS ......................................................... 51

5

1 INTRODUCTION

This chapter gives the reader an introduction to the subject of matter. I present

background to the research, a problem description, the purpose of my thesis where

I display my research question, then delimitations of this thesis and finally, my

thesis disposition.

1.1 BACKGROUND

Companies growing and merging with other businesses demand great changes to

their infrastructure. The equities market space is constantly evolving and the

implications to the IT systems and processes within the organizations are

substantial. Companies today depend to a great extent on the information stored

and managed through IT and many would not be able to operate without a

functional IT structure. The increasing regulatory demands also put a pressure on

the accounting, documenting and reporting through IT. The systems are required

not only to support the operations of the companies, but to report and store

financial and organizational data to meet external demands. It is no longer enough

to look at talented individuals to manage IT projects, the projects regularly need to

be structured as sustainable processes, where documentation and measuring is

standardized. Many companies acknowledge this need and put more effort into

standardizing the IT structure, policies and procedures and focus on aligning them

to the business objectives. This practice is called IT governance and will be further

explained and discussed throughout this report.

To facilitate the governing of IT there are several frameworks available on the

market. One of the most frequently used and chosen in this work is called COBIT1,

the Control Objectives for Information and Related Technology, further described

1 IT governance institute (2005), Control objectives for Sarbanes-Oxley

6

in section 3.4. COBIT gives guidance from “best practices” derived from major

global IT-related standards, practices and frameworks on processes and its

constituents to aid in the work of governing IT. The framework defines a set of

processes, to which there is a number of activities, suggested documentation and

measuring. It provides a high level view of an IT organization and what could be

done within it. COBIT also associates a maturity model that can be used to

benchmark the performance and level of definition to each process in a

standardized manner. The scale, which is obtained from the Capability Maturity

Model (CMM), described in section 3.3.3 spans from 0 to 5, with 5 being the

highest.

To many organizations, the help of external best practices is a cost efficient and

effective alternative to creating own frameworks and standards. This thesis will

highlight the work with one of these frameworks, namely COBIT and look at the

possibilities to improve the governance on a specific IT organization through the

help of that framework. The project has been performed at one of the largest

investment banks in the world at a global division on the IT side. The project has

followed the organization’s desire to externally assess their IT performance with

COBIT as a frame for benchmarking.

The organization is in this thesis referred to as The Firm and the specific part of

The Firm that the project is focused on is called The Markets division. This is

further described in section 5.2. My advisor at the department of Industrial

Information and Control Systems (ICS) at the Royal Institute of Technology is PhD

student Mårten Simonsson. My advisor at The Firm is the European Head of

Technology Business Development. Key stakeholders at The Firm are the

European Head of Technology Business Development, the Head of Development at

The Markets Division and the people responsible for the scope and implementation

phase of the COBIT initiative at The Firm. The Head of Development did

participate in interviews, but when referred to as “key personnel”, they do not

represent a respondent’s view.

7

1.2 PROBLEM

How should IT be governed and how could COBIT be used as guidance? In this

project, there are two key issues I have addressed.

• The framework itself does not say how it should be used; it merely states

guidance on its defined processes.

• The Markets division wanted to know how it compared to industry

standards and see how the effectiveness and efficiency of the IT

organization could be improved.

1.3 PURPOSE

The purpose of the project was to do an assessment of The Markets division at The

Firm with COBIT serving as a starting point. The assessment could be resembled

by a gap analysis where the difference between the framework and the actual

organization is emphasized. Derived from that assessment is the information about

strengths and weaknesses within the IT organization, in comparison to COBIT. The

four strongest and weakest areas should be emphasized and suggestions on how to

improve the weaker areas should be presented. The question I tried to answer was:

How does the IT procedures and processes at The Markets division compare to

COBIT- how big are the gaps, what could be improved and how?

1.4 DELIMITATIONS

The project was decided to be a high level assessment and was limited to gathering

information on the COBIT processes from one person per process. The definition

of a process is described in section 3.4 COBIT.

This project covers what is being done in respect to COBIT, not processes outside

those borders. The project was also limited to The Markets division which is further

described in section 5.2.

1.5 THESIS DISPOSITION

1. Introduction –

8

This chapter gives the reader an introduction to the subject of matter. I

present background to the research, a problem description, the purpose of

my thesis where I display my research question, then delimitations of this

thesis and finally, my thesis disposition

2. Methodology –

This chapter provides the projects course of action and motivates why I

have chosen this approach to address the given problem. I describe the

initiation, the method of collecting data, required theoretical knowledge and

finally how I evaluated the data

3. Theoretical framework –

This chapter provides the theoretical foundation of the thesis. Initially I will

discuss theory around corporate and IT governance, leading up to the ways

IT could be governed. Brief reviews of possible IT governance frameworks

are presented to facilitate the governing of IT and the framework used in

this study, COBIT, will be described closer.

4. Analytical framework -

In this chapter I explain the method of collecting data in detail, the analysis

of the collected data and the method I have chosen to derive my results.

5. Empirical study -

This chapter portrays the data collection specific for the assessment at The

Firm and a description of the organization.

6. Results -

In this chapter I reveal my results of the assessment beginning with general

results. I then explain the results for the stronger and weaker areas closer.

7. Discussion -

This chapter will discuss the results of the assessment and highlight relevant

and interesting findings throughout the project.

8. Conclusion -

This chapter describes the conclusions that can be drawn from this

assessment and answers the question posed in the purpose section.

9

2 METHODOLOGY

This chapter provides the projects course of action and motivates why I have

chosen this approach to address the given problem. I describe the initiation, the

method of collecting data, required theoretical knowledge and finally how I

evaluated the data.

2.1 INITIATION

The reason why the project was initiated relates to the research of PhD student

Mårten Simonsson and the department of Industrial Information and Control

Systems at the Royal Institute of Technology, previously described in section 1.1.

The purpose, also prior described, is evaluating a part of an IT organization with

COBIT as a starting point. The first problem of the thesis project was to find a

sponsoring company that would be willing to participate in this project. During a

previous employment, I came in contact with The Firm and proposed my project.

The Firm felt as a suitable sponsor where my project could be of value. This is

further described in section 5.2. The project was also further limited to The Markets

division, also described in section 5.2 as that area seemed to be just the right size

for my study.

2.2 CASE STUDY

“The case study is but one of several ways of doing social

science research. Other ways include experiments, surveys,

10

histories, and the analysis of archival information (as in

economic studies).”2

The way to fulfill the purpose of this project has mainly been through a case study.

A more quantitative method, like questionnaires would possibly have been

applicable to this project as well. According to Holme & Solvang3 the qualitative

and quantitative methods both have their advantages and disadvantages. As COBIT

was new to many of the participants in the study, explanations were in several

cases necessary.

“In general, case studies are the preferred strategy when

“how” or “why” questions are being posed”2

The study required the presence of someone with knowledge in COBIT to facilitate

the questions- and answering process. This is the reason why I chose to do

interviews. That way I could participate as an interviewer with specific knowledge

in the COBIT framework and easier get accurate answers from the respondents. I

used COBIT as a starting point and asked the respondent to evaluate the maturity

on each activity within one process. I also asked them to answer how many of the

suggested documents and metrics The Markets division was actually using. Finally

I asked how the role assignment suggested in the RACI-chart corresponded to the

structure at The Markets division. COBIT specifics can be found in section 3.4.

2.3 THEORETICAL STUDY

After determining the method of gathering information there were a few areas I

needed more theoretical knowledge in. This also constitute a part of the curriculum

of a master thesis and motivates chapter 3, Theoretical framework where the

research is presented as needed to understand the empirical study. The research is

partly about corporate governance and its constituents. This along with the

relationship to IT governance depicts the foundation for the thesis subject. The way

to govern IT is suggested with help and guidance from an assessment framework

and the currently available frameworks are presented briefly as a benchmark for

2Yin, Robert K. (1994), Case study research, Design and methods, second edition.

3 Holme & Solvang (1997).

11

comparative analysis in respect to COBIT, the framework of choice in this project.

COBIT was chosen because it is considered

“arguably the most appropriate control framework to help

an organization ensure alignment between use of

Information Technology (IT) and its business goals”4

The analysis shows the competitive advantages of COBIT compared to its

alternatives. COBIT is then described in detail in section 3.4, COBIT, as it

constitutes a large portion of the required theoretical knowledge in this thesis. The

way COBIT can be useful to organizations will be presented and examined in terms

of what drives the implementation of the framework in general. It will be shown

that COBIT is an effective framework as to assure compliance to regulatory

requirements and provide a way to enhance efficiency within the IT organization

and for the company as a whole. Various regulatory requirements will be described

along with their relationship to COBIT.

2.4 EVALUATION METHOD

After collecting the data from the interviews I needed a way to aggregate them into

results. Discussions with my advisor from ICS lead to the evaluation method. We

decided to take all results from all parts of the data collection and add them

together. The mean value generated the maturity on each process, and the mean

value on all 34 COBIT processes gave the overall maturity level.

4Ridley G. et al (2004), COBIT and its Utilization: A framework from the literature.

Proceedings of the 37th Hawaii International Conference on System Sciences, IEEE

12

3 THEORETICAL FRAMEWORK

This chapter provides the theoretical foundation of the thesis. Initially I will discuss

theory around corporate and IT governance and the regulatory demands in that

space. This leading up to the ways IT could be governed. Brief reviews of possible

IT governance frameworks are presented to facilitate the governing of IT and the

framework used in this study, COBIT, will be described closer.

3.1 CORPORATE GOVERNANCE

In order to understand the concept of IT governance one needs insight into the

principles of corporate governance and its constituents.

"Corporate Governance is concerned with holding the

balance between economic and social goals and between

individual and communal goals. The corporate governance

framework is there to encourage the efficient use of

resources and equally to require accountability for the

stewardship of those resources. The aim is to align as

nearly as possible the interests of individuals, corporations

and society" 5

The Organization for Economic Cooperation and Development’s 1999 published

the “OECD Principles for Corporate Governance” which defines corporate

governance as providing the structure through which the objectives for the

company is set and the ways to align and achieve those objectives and monitor the

performance is determined. It also set the relationships between an organization’s

5 Sir Adrian Cadbury (2000), in 'Global Corporate Governance Forum', World Bank.

13

board, management, shareholders and additional key stakeholders.6 IT governance

closely relates to corporate governance, the structure of the IT organization and its

objectives and alignment to the business objectives.

”Corporate Governance issues cannot be addressed without

considering IT Governance issues”7

Weill and Ross8 have created a framework for linking the corporate governance

and IT governance principles together, which can be seen in figure 1. The areas that

relates to IT governance are marked in grey.

Figure 1 – Framework linking corporate governance to IT governance8

There are several ways of looking at the connection between corporate governance

and IT governance. Another is described by Van Grembergen, De Raes and

6 OECD (1999), Principles of Corporate Governance.

7 Van Grembergen, De Raes o Guldentops (2004), Structures, Processes and Relational

Mechanisms for IT Governance, Idea Group inc. 8 Weill & Ross (2004), IT Governance

8 Van Grembergen, De Raes o Guldentops (2004), Structures, Processes and Relational

Mechanisms for IT Governance, Idea Group inc.

14

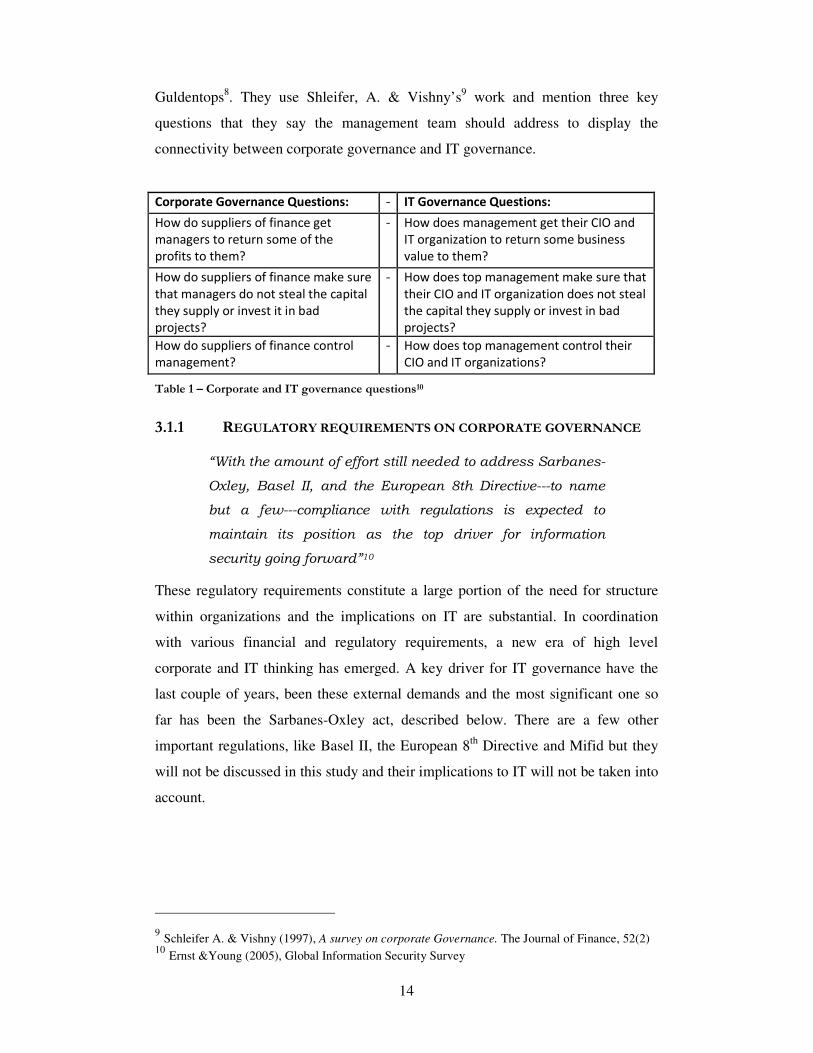

Guldentops8. They use Shleifer, A. & Vishny’s9 work and mention three key

questions that they say the management team should address to display the

connectivity between corporate governance and IT governance.

Corporate Governance Questions: - IT Governance Questions:

How do suppliers of finance get

managers to return some of the

profits to them?

- How does management get their CIO and

IT organization to return some business

value to them?

How do suppliers of finance make sure

that managers do not steal the capital

they supply or invest it in bad

projects?

- How does top management make sure that

their CIO and IT organization does not steal

the capital they supply or invest in bad

projects?

How do suppliers of finance control

management?

- How does top management control their

CIO and IT organizations?

Table 1 – Corporate and IT governance questions10

3.1.1 REGULATORY REQUIREMENTS ON CORPORATE GOVERNANCE

“With the amount of effort still needed to address Sarbanes-

Oxley, Basel II, and the European 8th Directive---to name

but a few---compliance with regulations is expected to

maintain its position as the top driver for information

security going forward”10

These regulatory requirements constitute a large portion of the need for structure

within organizations and the implications on IT are substantial. In coordination

with various financial and regulatory requirements, a new era of high level

corporate and IT thinking has emerged. A key driver for IT governance have the

last couple of years, been these external demands and the most significant one so

far has been the Sarbanes-Oxley act, described below. There are a few other

important regulations, like Basel II, the European 8th Directive and Mifid but they

will not be discussed in this study and their implications to IT will not be taken into

account.

9 Schleifer A. & Vishny (1997), A survey on corporate Governance. The Journal of Finance, 52(2) 10 Ernst &Young (2005), Global Information Security Survey

15

THE SARBANES-OXLEY ACT OF 2002

The Sarbanes-Oxley act of 2002, SOX, has changed the world of reporting

accountabilities as we know it. A number of corporate and accounting scandals,

most notably Enron, Tyco International and WorldCom reinvigorated the debate on

regulating corporate governance. The loss of trust in large corporations accounting

and reporting practices became apparent. To restore the lack of trust investors and

shareholders experienced, the Sarbanes-Oxley act was created. The act was passed

on as United States federal law on July 30, 2002 initiated by the naming sponsors,

Senator Paul Sarbanes and Representative Michael G. Oxley.

All companies, including subsidiaries, American or not, listed on American stock

exchanges like NYSE, the New York Stock Exchange, or NASDAQ are required to

comply with the Sarbanes-Oxley act. The act establishes standards for all such

company’s boards, managements and public accounting firms. Containing eleven

titles, details in appendix 1, the act ranges from describing the increased corporate

board responsibilities to criminal penalties for corporate wrongdoing. It also

obligates the SEC, Securities and Exchange Commission, to implement rulings and

accounting standards for compliance. The titles or sections of the act can be seen

below and are of varying importance in regards to this thesis.

Title I – “Public Company Accounting Oversight Board”

Title II – “Auditor Independence”

Title III – “Corporate Responsibility”

Title IV – “Enhanced Financial Disclosures”

Title V – “Analyst Conflicts of Interest”

Title VI – “Commission Resources and Authority”

Title VII – “Studies and Reports”

Title VIII – “Corporate and Criminal Fraud Accountability”

Title IX – “White Collar Crime Penalty Enhancements”

Title X – “Corporate Tax Returns”

Title XI – “Corporate Fraud Accountability”

Title III and IV are the titles that are closest related to this work.

16

“The two sections that should concern IT executives the

most are 302 and 404(a) because they deal with the

internal controls that a company has in place to ensure the

accuracy of their data. This relates directly to the software

systems that a company uses to control, transmit and

calculate the data that is used in their financial reports.”11

Section 302 is characterized mainly by the CEO’s and CFO’s responsibility of

internal control regarding the annual financial reporting.

Section 404 demands each annual report to contain an internal control report which

shall

(1) state the responsibility of management for establishing and

maintaining an adequate internal control structure and procedures for

financial reporting; and

(2) contain an assessment, as of the end of the most recent fiscal year

of the issuer, of the effectiveness of the internal control structure and

procedures of the issuer for financial reporting.12

Even though the act is focused on accounting and financial reporting, the

importance of appropriate IT systems as an integral part in the reporting procedure

is evident. The systems ensure the validity of information and provide fundamental

structure to the reporting standards and assessments of financial data. Section 409

of the act expresses the real time accounting demands and is central to the IT

systems involved.

11 Dietrich, Robert (2004). Sarbanes-Oxley and the Need to Audit Your IT Processes, MKS

12 ”Sarbanes and Oxley act of 2002” Section 404. PUBLIC LAW 107–204

17

”REAL TIME ISSUER DISCLOSURES.—Each issuer reporting

under section 13(a) or 15(d) shall disclose to the public on a

rapid and current basis such additional information

concerning material changes in the financial condition or

operations of the issuer, in plain English, which may

include trend and qualitative information and graphic

presentations, as the Commission determines, by rule, is

necessary or useful for the protection of investors and in the

public interest.]”13

The relationship between IT systems and section 409 is described by Rob Smith,

Co-Chair of Industry Solutions – SOX Committee and Michael Kuhbock, Co-

Chairman and Founder of the Integration Consortium.

”The only way for issuers to be aware of real time

information and trends on operations or the physical

activities of their organization is for the issuers systems to

report on anomalies and trends in real time and on an

exception basis. As well, the integration of any new system

into an organization will have to pass SOX compliancy

before it is either selected or ‘plugged in’. Failure of control

process, due to a systems failure will strictly fall under the

409 clause regarding “material change”.14

This could very well be the most grueling challenges in the compliance work and

one of the reasons corporations struggle to find easily adopted, implemented and

administered frameworks to facilitate the process of compliance. A framework is

required by the act; however the choice of version is free. One such framework is

provided by COBIT and another by COSO, described in section 3.4 and 3.3.2

respectively.

13 ”Sarbanes and Oxley act of 2002” Section 409. PUBLIC LAW 107–204

14Smith R. Kuhbock M.. Sarbanes Oxley 404/409-Integration Organizations and SOX.

www.integrationconsortium.org

18

COSO’s framework is the most frequently used when implementing compliance

procedures today.15 It is also recommended by the SEC to aid in such tasks. COSO,

does not provide a great deal of guidance to assist companies in the design and

implementation of IT controls.16 COBIT on the other hand has its main focus on

controls within the IT organization.

The auditing standards are set by the PCAOB, The Public Company Accounting

Oversight Board. The PCAOB is created by Sarbanes-Oxley and described in title I

of the act. The purpose is to supervise and regulate the work done by auditing

companies. It also sets the working principles for the auditing companies.

3.2 IT GOVERNANCE

“IT Governance is the organisational capacity exercised by

the Board, executive management and IT management to

control the formulation and implementation of IT strategy

and in this way ensure the fusion of business and IT.”17

These are the words of well renowned, IT governance theorist, Grembergen in

2002. There have been several different ways of defining IT governance, below are

a few additional of the more famous displayed.

“IT governance is the responsibility of the board of directors

and executive management. It is an integral part of

enterprise governance and consists of the leadership and

organisational structures and processes that ensure that

the organisation’s IT sustains and extends the

organisation’s strategies and objectives.”18

“The organisational capacity to control the formulation and

implementation of IT strategy and guide to proper direction

15IT Governance Institute (2005), IT Control objectives for Sarbanes-Oxley

16 IT governance institute (2006), IT control objectives for Sarbane-Oxley

17 Grembergen, (2002)

18 IT governance institute (2003)

19

for the purpose of achieving competitive advantages for the

corporation”19

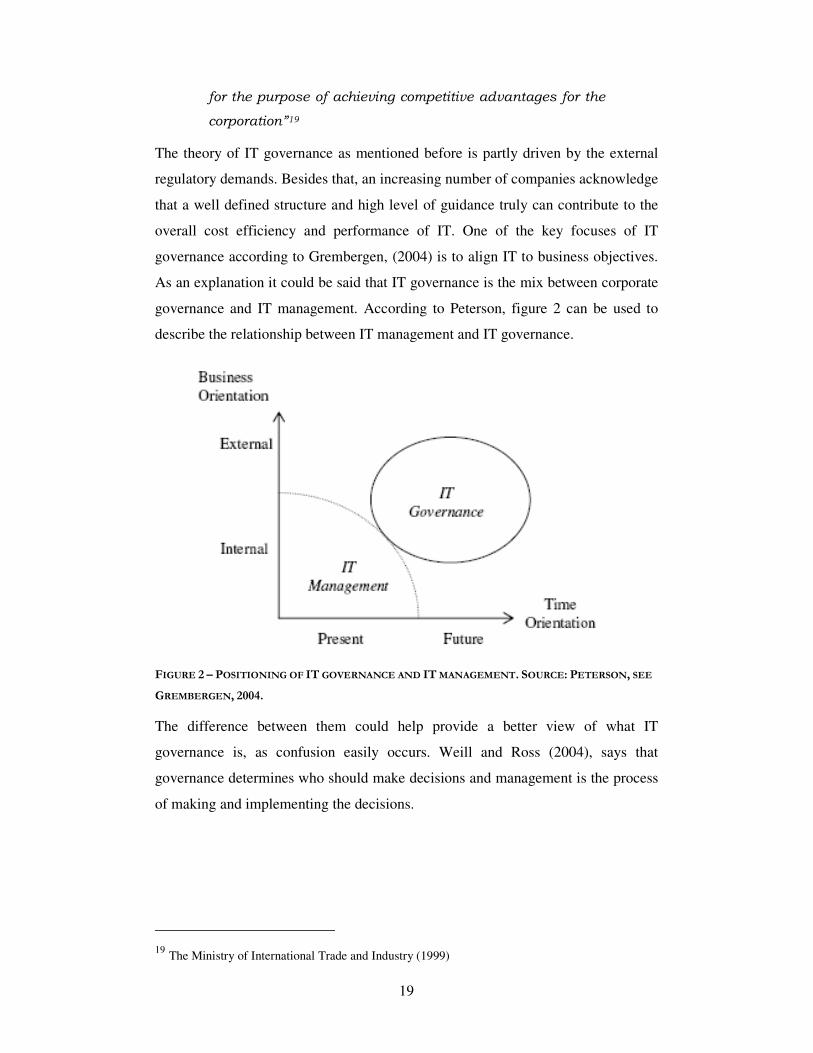

The theory of IT governance as mentioned before is partly driven by the external

regulatory demands. Besides that, an increasing number of companies acknowledge

that a well defined structure and high level of guidance truly can contribute to the

overall cost efficiency and performance of IT. One of the key focuses of IT

governance according to Grembergen, (2004) is to align IT to business objectives.

As an explanation it could be said that IT governance is the mix between corporate

governance and IT management. According to Peterson, figure 2 can be used to

describe the relationship between IT management and IT governance.

FIGURE 2 – POSITIONING OF IT GOVERNANCE AND IT MANAGEMENT. SOURCE: PETERSON, SEE

GREMBERGEN, 2004.

The difference between them could help provide a better view of what IT

governance is, as confusion easily occurs. Weill and Ross (2004), says that

governance determines who should make decisions and management is the process

of making and implementing the decisions.

19 The Ministry of International Trade and Industry (1999)

20

3.3 IT GOVERNANCE FRAMEWORKS

3.3.1 ITIL

The IT Infrastructure Library, ITIL, was created by the British Office of

Government Commerce, OGC, to more effectively manage IT within British

authorities as well as public companies. The principles of the ITIL framework were

derived out of best practice with regards to observed companies within the IT

sector. It is now a fully documented set of best practice documents for IT service

management and “the most widely accepted approach to IT service management in

the world.”20 It consists of several books, hence the term library. At the moment

there are eight books:

1. Service Delivery

2. Service Support

3. ICT Infrastructure Management

4. Security Management

5. The business perspective

6. Application management

7. Software Asset Management

8. Planning to Implement Service Management

ITIL’s main objectives are to provide best practice definitions and criteria for

operations management within two key areas, namely Service Support and Service

Delivery2122. In these areas ITIL focuses on the operational, organizational and

functional attributes required for optimized operations management. These areas

also have a number of supporting subcategories. ITIL, however does not cover the

strategic impact of IT and the relation between IT and the business.2021

20 Office of Government Commerce, OGC. http://www.itil.co.uk/

21 Office of Government Commerce: IT Infrastructure Library Service Support. The

Stationery Office (2002) 22 Office of Government Commerce: IT Infrastructure Library Service Delivery. The

Stationery Office (2002)

21

3.3.2 COSO

COSO or the Committee of Sponsoring Organizations of the Treadway

commission was established in 1985. In 1992 COSO released the Internal Control

– Integrated framework. It was originally developed to cope with the fraudulent

financial reporting present in the world of corporate accounting.23 The framework

COSO consists of five interrelated Internal control components and three

Enterprise risk management components. The ERM components and the Enterprise

Risk Management – Integrated Framework, were created in collaboration with

PriceWaterhouseCoopers in 2004. All components are shown below with risk

management components in bolded fonts.

− Internal Environment

− Objective Setting

− Event Identification

− Risk Assessment

− Risk Response

− Control Activities

− Information and Communication

− Monitoring

“COSO is a voluntary private sector organization dedicated

to improving the quality of financial reporting through

business ethics, effective internal controls, and corporate

governance.”23

The five components of internal control that COSO identifies can be resembled by

the guidance COBIT provides for IT.24

23 COSO-The Committee of Sponsoring Organizations of the Treadway commission, www.coso.org

24 Damianides, Marios (2005), Sarbanes–Oxley and IT governance: New guidance on it control and

compliance http://www.infosectoday.com/SOX/Damianides.pdf

22

3.3.3 CMMI

“Capability Maturity Model® Integration (CMMI) is a process

improvement approach that provides organizations with the

essential elements of effective processes. It can be used to

guide process improvement across a project, a division, or

an entire organization.”25

CMMI, (Capabilities Maturity Model Integration), previously CMM developed by

the Software Engineering Institute (SEI), provides a model to improve the

efficiency in processes across an organization. As the name implies, a key element

in the model is the evaluation of maturity through a maturity model. This maturity

model is further described in section 3.4.1.

3.4 COBIT

COBIT is short for the Control Objectives for Information and Related Technology

and was developed by the Information Systems Audit and Control Foundation,

ISACF in 1996. ISACF, founded 1969 later became ISACA, Information Systems

Audit and Control Association. ISACA, is now a global organization with over 50

000 members in more than 140 countries. The founders, a group of IT auditors,

recognized the increasing need for control within IT organizations and decided to

create a network for information and guidance in the field. In 1998 ISACA

established the IT Governance Institute, ITGI, who is now responsible for COBIT.

During the fall of 2005, ITGI released a version 4.0 of COBIT which constitutes

the framework of reference in this thesis.

COBIT was originally developed as a tool to control IT and reduce risk within IT

organizations, primarily in the banking and e-business industries. It has evolved to

become more business oriented and now gives a high level image on what to

accomplish within an organization rather than how. It is designed to provide

fundamental guidance to management and process owners to in best way possible

allocate the assets of the organization. Figure 3 shows the overlying framework

principles.

25Software Engineering Institute (SEI) http://www.sei.cmu.edu/cmmi/general/general.html

23

The COBIT framework has the aspiration to be both responsive and practical in the

sense of the business needs, while at the same time being independent to the

technical and structural differences within various organizations.

COBIT uses ideas from all frameworks above and even more standards when

creating its definitions and controls.

“For this COBIT update (COBIT 4.0), six of the major global IT-

related standards, frameworks and practices were focused

on as the major supporting references to ensure appropriate

coverage, consistency and alignment”26

The standards, frameworks and practices mentioned in the quote above are:26

Committee of Sponsoring Organisations of the Treadway Commission (COSO):

− Internal Control—Integrated Framework, 1994

− Enterprise Risk Mangement—Integrated Framework, 2004

Office of Government Commerce (OGC®):

− IT Infrastructure Library® (ITIL®), 1999-2004

International Organisation for Standardisation:

− ISO/IEC 17799:2005, Code of Practice for Information Security Management

Software Engineering Institute (SEI®):

− SEI Capability Maturity Model (CMM®), 1993

− SEI Capability Maturity Model Integration (CMMI®), 2000

Project Management Institute (PMI®):

26IT Governance Institute (2005), COBIT 4.0

FIGURE 3 – COBIT, OVERLYING FRAMEWORK PRINCIPLES.

SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0

24

− Project Management Body of Knowledge (PMBOK®), 2000

Information Security Forum (ISF):

− The Standard of Good Practice for Information Security, 2003

Originally the framework was based on three separate documents:

Control Objectives is the first of the documents that describes the 34 processes

and the control objectives to each process employed by COBIT. The maturity

levels are not regarded in this section.

Management Guidelines presents the maturity levels and the two measurable

indicators connected to each process type.

Audit Guidelines is based on Management Guidelines and provide advice on who

to interview and what kind of information is demanded to each process type.

THE COBIT FRAMEWORK

COBIT provides a detailed and easily used model to govern IT. The structure and

interrelationship of the processes that COBIT treats is shown in Figure 4. The

COBIT control objectives document is divided into four domains that describe the

risks and activities within IT that needs to be managed. The domains in turn are

divided, in all into 34 different high level control objectives or processes. The

processes each encompass detailed control objectives, activities, roles, different

metrics and an incremental measurement scale. The roles in turn have

responsibilities associated to the activities.

FIGURE 4 – COBIT, STRUCTURE AND INTERRELATIONSHIP OF PROCESSES. SOURCE: IT

GOVERNANCE INSTITUTE, COBIT 4.0

25

The processes apply at different levels of the IT organization and each domain

could help to provide an understanding of the purpose of the processes. The names

of all the COBIT processes are displayed in Figure 5.

The four COBIT domains; Plan and Organise, Acquire and Implement, Deliver and

Support and Monitor and Evaluate as shown in figure 5, are clarified below.

− Plan and Organise (PO) describes how the business

objectives are best reached through the use of IT. This

domain administrates the use of tactics and strategy to

FIGURE 5 – COBIT, OVERALL FRAMEWORK. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0

26

plan, communicate and manage the different perspectives

throughout the organization.

− Acquire and Implement (AI) depicts the identifying and

acquiring of IT solutions. Furthermore this domain

explains the solutions integration to the business processes

and how to manage and upkeep the existing systems.

− Deliver and Support (DS) handles the actual delivery of

the information at hand and see to the management of

service levels, performance and capacity, configurations,

operations and the physical environment, to name a few.

This domain is also responsible for the identification and

allocation of costs and the training of users.

− Monitor and Evaluate (ME) describes the monitoring

and evaluation of all the processes employed by the IT

organization. This domain also delivers the final statement

to “provide IT governance”

3.4.1 ASSESSMENT WITH THE COBIT FRAMEWORK

MATURITY MODEL

It is not easy to know how to benchmark an organization and to what grade of

accuracy the evaluation should be scaled. COBIT suggests an incremental

measurement scale of six maturity levels. Going from 0, Non-existent to 5,

Optimized, COBIT covers the entire spectrum of maturity in a process. The

structure and design of the scale is the same as the one used by Capability Maturity

Model, (CMM), described in section 3.3.3. These maturity levels are individually

explained for each of the 34 processes but the general structure could be seen in

table 2.

27

ACTIVITIES

The activities are a significant part of the suggested guidance COBIT describes for

each process. They say what should be done and they are also associated to the

roles, further described under “Roles and Responsibilities”. An example of

activities is shown in figure 7, RACI-chart. As previously mentioned; COBIT also

describe detailed control objectives. The detailed control objectives often

correspond to the activities and their purpose is the same. COBIT is not entirely

consistent about this but in many cases, the activities are just simplified detailed

control objectives.

METRICS

To improve the efficiency and effectiveness of the processes, COBIT suggest a set

of metrics to use as measurement to each process. The metrics are different for

each process but some of the outlines are similar. The metrics are in the version

used in this study, COBIT 4.0, Key Performance Indicators, Process Key Goal

0 Non-ExistentComplete lack of any recognisable processes. The organisation has not even

recognised that there is an issue to be addressed.

1 Initial

There is evidence that the organisation has recognised that the issues exist

and need to be addressed. There are however no standardised processes but

instead there are ad hoc approaches that tend to be applied on an individual

or

2 Repeatable

Processes have developed to the stage where similar procedures are followed

by different people undertaking the same task. There is no formal training or

communication of standard procedures and responsibility is left to the

individual. There is a high degree of reliance on the knowledge of individuals

and therefore errors are likely.

3 Defined

Procedures have been standardised and documented, and communicated

through training. It is however left to the individual to follow these processes,

and it is unlikely that deviations will be detected. The procedures themselves

are not sophisticated but are the formalisation of existing practices.

4 Managed

It is possible to monitor and measure compliance with procedures and to take

action where processes appear not to be working effectively. Processes are

under constant improvement and provide good practice. Automation and tools

are used in a limited or fragmented way.

5 Optimised

Processes have been refined to a level of best practice, based on the results

of continuous improvement and maturity modelling with other organisations.

IT is used in an integrated way to automate the workflow, providing tools to

improve quality and effectiveness, making the enterprise quick to adapt.

TABLE 2 – MATURITY MODEL. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0

28

Indicators and IT Key Goal Indicators. For the process, “Manage the IT

investment” the metrics are shown in figure 6.

Just to clarify what is shown in the image, one metric COBIT suggests could be to

measure the “percentage of projects with benefit defined upfront”. That metric can

be seen in the upper left corner of the Key Performance Indicators box in figure 6.

According to Guldentops27 the primary purpose of the guidelines is to enable

corporate management to:

− Measure Performance – What are the indicators of good

performance?

− Profile their IT control – What’s important? What are the

critical success factors for control?

− Enhance their awareness – What are the risks of not

achieving our objectives?

− Benchmark the organization – What do others do? How do

we measure and compare?

The indicators are the key inputs in the benchmarking process. The Management

guidelines indicators are Key Goal Indicators (KGIs), Key Performance Indicators

(KPIs) and maturity models.

The Key Goal Indicators represents what has to be accomplished in order to

achieve the process goals. They define measures that tell if business objectives

27Guldentops, E in Van Grembergen, W (2004). Strategies for Information Technology Governance.

Idea Group Inc. Chapter 11 Governing Information Technology through COBIT.

FIGURE 6 – METRICS. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0

29

have been met for a specific process and are often defined as the target to achieve.

Business requirements are generally expressed in terms of information criteria:

− Availability of information needed to support the business needs

− Absence of integrity and confidentiality risks

− Cost-efficiency of processes and operations

− Confirmation of reliability, effectiveness and compliance

The Key Performance Indicators define measures to explain to what extent the

process is fulfilling its objectives, how well it’s performing. They are the most

important indicators in revealing whether or not a goal will be reached and are

often used to in an early stage tell if the KGIs will be difficult to achieve.

ROLES AND RESPONSIBILITIES

COBIT describes a number of different roles that an IT organization should use.

The roles suggested by COBIT can be seen below.

− Chief executive officer (CEO)

− Chief information officer (CIO)

− Business executives

− Chief financial officer (CFO)

− Head operations

− Chief Architect

− Head development

− Head IT administration

− The project manager office (PMO)

− Compliance, audit risk and security

To every process there are a number of activities with the responsible employee or

employees conveyed in a chart, called a RACI-chart, see figure 7. To be more

precise COBIT defines four different ways in which a person or role should be

connected to an activity. The different ways are Responsible, Accountable,

Consulted and Informed, hence the name RACI. The Responsible person is the one

responsible for the execution of an activity while Accountable is the one who

authorizes it. Consulted is someone who should be asked or consulted when an

30

activity is performed while the function of Informed is merely one who should

know about the activity. Figure 7 shows the roles as functions and their relationship

to the activities of the process “Manage the IT investment”. The activities extend

the understanding of the process and its purpose. To each activity there is either a

Responsible or an Accountable role to see to that the activity is executed in a proper

manner.

DOCUMENTS

Relevant documentation renders repetition and effective feedback of the processes

possible. COBIT defines which documents should exist at the initiation stage and

which should be produced during the process. They are referred to as Inputs and

Outputs, shown in figure 8.

FIGURE 7 – RACI-CHART. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0

FIGURE 8 – DOCUMENTS. SOURCE: IT GOVERNANCE INSTITUTE, COBIT 4.0

31

3.5 COBIT FACILITATES COMPLIANCE WITH SARBANES-OXLEY

As mentioned above, COBIT is one applicable assessment framework that could

help in the compliance of SOX. COBIT aligns 12 of the IT control objectives with

the PCAOB Auditing standards No 2, displayed in figure 9. COBIT focuses on IT

as opposed to COSO which is focused on controls for financial processes. This

means that COBIT’s guidance is centered on the IT processes which in reality are

the way through which financial auditing is conducted.

“COBIT enables clear policy development and good practice

for IT control throughout organizations. ITGI’s latest version

COBIT 4.0 emphasizes regulatory compliance, helps

organizations to increase the value attained from IT,

enables alignment and simplifies implementation of the

COBIT framework.”28

Appendix 2 shows the IT Governance Institute’s compliance to SOX, roadmap.

28 www.Isaca.org

FIGURE 9 – MAPPING TO PCAOB TO COBIT. SOURCE: ITGI (2006), IT

CONTROL OBJECTIVES FOR SARBANES-OXLEY, THE ROLE OF IT IN THE

DESIGN AND IMPLEMENTATION OF INTERNAL CONTROL OVER FINANCIAL

REPORTING.

32

While implementing procedures to comply with SOX regulations, many companies

choose to overlook the IT structure to see what else could be improved during the

reconstructuring. Ernst & Young have interviewed 1300 companies regarding

information security practice. They experienced a surprisingly low 41 percent of

the interviewees using the opportunity of restructuring IT while complying with

external regulatory requirements. According to Ernst & Young it’s the ideal time to

improve and streamline the business structure while a structural change still is

inevitable due to the external regulatory demands.29

29 Ernst&Young (2005), Global Information Security Survey

33

4 ANALYTICAL FRAMEWORK

In this chapter I explain the method of collecting data in detail, the analysis of the

collected data and the method I have chosen to derive my results.

4.1 DATA COLLECTION

There are no rules that govern the way to use COBIT and to what extent it is to be

implemented. Each organization may adopt the framework to meet their business

objectives in which way they see fit.

COBIT works as a helping hand, providing guidance to the management on how,

according to best practice to use the assets and people within the organization.

However, the complexity of COBIT could make the usage difficult and time

consuming. Furthermore it leaves room for interpretation, which means that two

interviewers could obtain incomparable results on the same assessment. It is not a

given that for instace the COBIT-defined activities, are interpreted the same way

by two separate people. While the purpose of COBIT is to provide guidance on IT

governance, it does require a substantial amount of expertise with regards to the

framework. This has led to the creation of a tool through which COBIT can be used

in a more formalized and straightforward way. This improves the validity and

makes the framework more usable. It was created by PhD student Mårten

Simonsson at the department of Industrial Information and Control Systems (ICS)

at the Royal Institute of Technology. I will here describe how the data can be

collected, the modeling tool used and how to analyze the results.

34

As presented in section 2.4 the interviews will provide the input information to the

project. The vast majority of the respondents should be executives with

management functions as their knowledge is most likely to correspond to the kind

of strategic information COBIT deals with. The descriptions below explains the

steps to take when working with COBIT and conducting the interviews.

1. Who to speak to about what

With key personnel, map each of the suggested roles in COBIT to

corresponding person at the organization under evaluation. From that

mapping, talk to the person with the highest responsibility on each

COBIT process. Through this method some individuals could easily

become potential respondents to many processes. To even out the

time spent with each individual, discuss together with key

stakeholders at the organization under evaluation and try to find other

people that could answer questions on some of those processes.

2. Short introduction to the project.

Send by email a short PowerPoint briefing about the project and also

information regarding the subject of the interview. This generally makes the

face-to-face introduction shorter. Many times the respondent will not have

time to review the material beforehand, which leads to the need of a

background description of the project and COBIT anyway.

3. Explanation of respondents role

Ask the respondent to explain his/hers role at the organization under

evaluation. This could make it easier to appreciate from where the answers

come.

4. Evaluation of a process

The respondents should be asked about the activities within each process he/she is

either Accountable or Responsible to, according to the RACI-chart. The question is

on what level of maturity in terms of the maturity model the respondent places that

activity, section 3.4.1.

35

The respondent should also be asked about the documents associated to the process

and the measured KPI’s and KGI’s. This will be yes or no questions, adding up to a

total which later in the analysis is compared to the maximum number of metrics

defined by COBIT. In more detail the interviews can be done as follows.

1. The respondents should be asked to assess the maturity on each activity

suggested by COBIT. Table 3 could be used to assign maturity for each

activity: (For help and guidance, the maturity model provided on each

process in the COBIT document can be used)

MATURITY

LEVEL

ACTIVITY EXECUTION

LEVEL 0 NO AWARENESS OF THE IMPORTANCE OF ISSUES RELATED TO THE ACTIVITY. NO MONITORING IS PERFORMED. NO

DOCUMENTATION EXISTS.

NO ACTIVITY IMPROVEMENT ACTIONS TAKE PLACE.

LEVEL 1 SOME AWARENESS OF THE IMPORTANCE OF ISSUES RELATED TO THE ACTIVITY. NO MONITORING IS PERFORMED. NO

DOCUMENTATION EXISTS. NO ACTIVITY IMPROVEMENT ACTIONS TAKE PLACE.

LEVEL 2 INDIVIDUALS HAVE KNOWLEDGE ABOUT ISSUES RELATED TO THE ACTIVITY AND TAKE ACTIONS ACCORDINGLY. NO

MONITORING IS PERFORMED. NO DOCUMENTATION EXISTS. NO ACTIVITY IMPROVEMENT ACTIONS TAKE PLACE.

LEVEL 3 AFFECTED PERSONNEL ARE TRAINED IN THE MEANS AND GOALS OF THE ACTIVITY. NO MONITORING IS PERFORMED.

DOCUMENTATION IS PRESENT. NO ACTIVITY IMPROVEMENT ACTIONS TAKE PLACE.

LEVEL 4 AFFECTED PERSONNEL ARE TRAINED IN THE MEANS AND GOALS OF THE ACTIVITY. MONITORING IS PERFORMED.

DOCUMENTATION IS PRESENT. THE ACTIVITY IS UNDER CONSTANT IMPROVEMENT. AUTOMATED TOOLS ARE

EMPLOYED IN A LIMITED AND FRAGMENTED WAY

LEVEL 5 AFFECTED PERSONNEL ARE TRAINED IN THE MEANS AND GOALS OF THE ACTIVITY. MONITORING IS PERFORMED.

DOCUMENTATION IS PRESENT. AUTOMATED TOOLS ARE EMPLOYED IN AN INTEGRATED WAY, TO IMPROVE QUALITY

AND EFFECTIVENESS OF THE ACTIVITY

TABLE 3 – ACTIVITY ASSESSMENT

A mean value for all activities within a process, the average activity

maturity (AM), should then be calculated. The values are threshold values,

i.e. all criteria for level 3 have to be fulfilled in order to achieve level 3

maturity.

2. The RACI-chart should be discussed on each point to see how well it

corresponds to the role assignment of the organization under evaluation. It

is broadly visualized in table 4. For more details, see appendix 5, Role

assignment

36

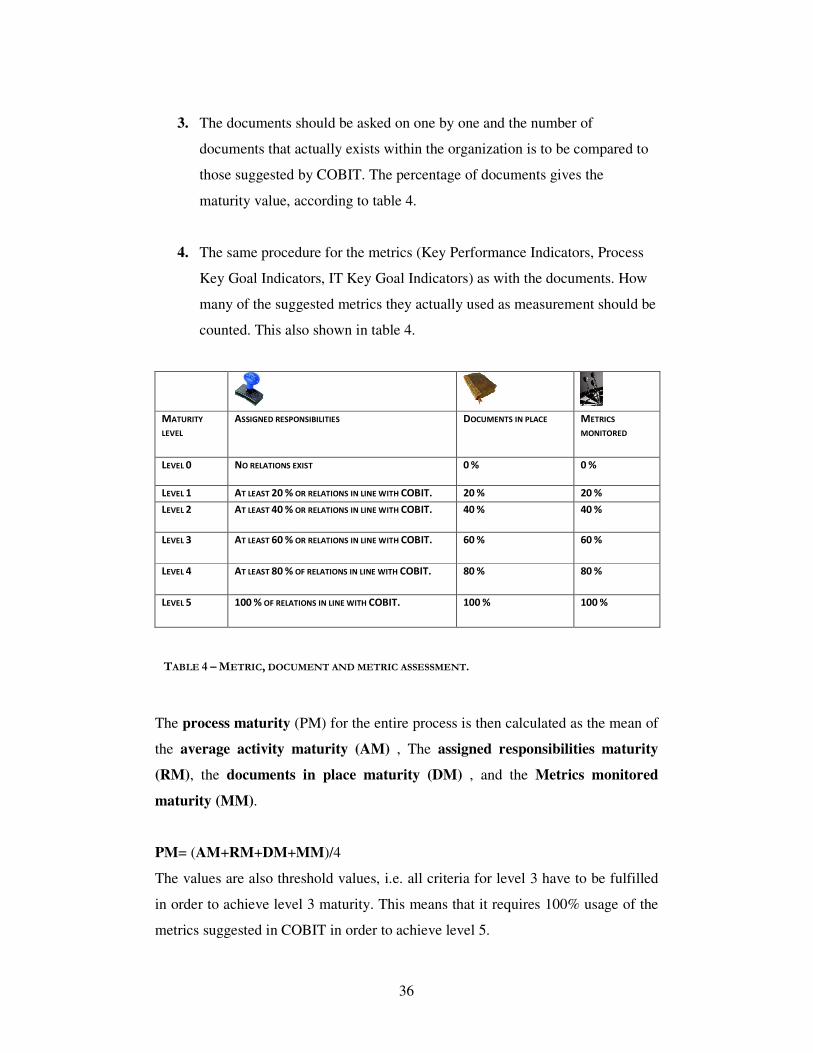

3. The documents should be asked on one by one and the number of

documents that actually exists within the organization is to be compared to

those suggested by COBIT. The percentage of documents gives the

maturity value, according to table 4.

4. The same procedure for the metrics (Key Performance Indicators, Process

Key Goal Indicators, IT Key Goal Indicators) as with the documents. How

many of the suggested metrics they actually used as measurement should be

counted. This also shown in table 4.

TABLE 4 – METRIC, DOCUMENT AND METRIC ASSESSMENT.

The process maturity (PM) for the entire process is then calculated as the mean of

the average activity maturity (AM) , The assigned responsibilities maturity

(RM), the documents in place maturity (DM) , and the Metrics monitored

maturity (MM).

PM= (AM+RM+DM+MM)/4

The values are also threshold values, i.e. all criteria for level 3 have to be fulfilled

in order to achieve level 3 maturity. This means that it requires 100% usage of the

metrics suggested in COBIT in order to achieve level 5.

MATURITY

LEVEL

ASSIGNED RESPONSIBILITIES

DOCUMENTS IN PLACE

METRICS

MONITORED

LEVEL 0 NO RELATIONS EXIST

0 % 0 %

LEVEL 1 AT LEAST 20 % OR RELATIONS IN LINE WITH COBIT. 20 % 20 %

LEVEL 2 AT LEAST 40 % OR RELATIONS IN LINE WITH COBIT. 40 % 40 %

LEVEL 3 AT LEAST 60 % OR RELATIONS IN LINE WITH COBIT. 60 % 60 %

LEVEL 4 AT LEAST 80 % OF RELATIONS IN LINE WITH COBIT. 80 % 80 %

LEVEL 5 100 % OF RELATIONS IN LINE WITH COBIT. 100 % 100 %

37

Regarding weights for separate metrics, the basic assumption is that all metrics

have the same weight. It is up to each organization to do their own weighting but a

guideline could be that activities should have the highest weight followed by the

metrics.

As an optional final step, the respondent should be asked to evaluate where he/she

thinks the entire organization or the suggested silo would land on the maturity

scale. This should not be used in the assessment but is interesting to collected for

future benchmarking and evaluation of the maturity assessment method.

4.2 MODELING

The modeling phase represents the aggregation of all the collected data and the

creation of a map showing all the COBIT processes and its relations to the

activities, metrics, roles and documents used by the organization. The reason for

creating an architectural map is to easier get an overview of the processes and their

relationships and to set definitions so that information about the model more easily

can be derived. The map in this case study was created with a modeling program

called Metis, a Troux technologies30 product. Metis is the software chosen by ICS,

which is why I used it for this study. User specific functionality in Metis is done

through an application Programming Interface (API) that supports Visual Basic and

Java script. At ICS an own Meta model that incorporates the definitions, rules and

restrictions of the model I used in this project has previously been created. That

Meta model describes what could be modeled, which processes, metrics,

documents and relations could be used in the model. It holds a reference model of

the complete COBIT framework to which the model of the organization under

evaluation could be compared. The gap between the reference model and the model

under evaluation generates the basis for the results and give the maturity to the

processes. The complete map can be seen in appendix 4, Model of The Firm. The

modeling in Metis is a method that is still under evaluation by ICS. It will be used

to a greater extent in future research as the benefit of using it increases the more

defined this method gets. One of the key beneficial aspects of the model, is that it

can be used to easier change relations to the processes.

30 Troux Technology, Metis http://www.troux.com

38

4.3 ANALYSIS

The analysis is where the results are reviewed from the modeling and which

conclusions could be drawn from the work. As one of the goals in the thesis was to

find areas or processes with lower and higher maturity level and suggest

improvements, the conclusion of the modeling was crucial in this study. The

processes with more and less mature nature have been examined in detail. This is

further described in chapter 6, Results. From the interviews I have tried to figure

out which are the key gaps or specific strengths within those areas. To find out

more about the current state and the reason for the strong or weak procedures and

policies within those areas, key personnel from The Firm was involved and

questioned.

39

5 EMPIRICAL STUDY

This chapter portrays the data collection specific for the assessment at The Firm

and a description of the organization.

5.1 PROCEDURE

This project will initially be described with a short introduction of the company

where the study was done. After that follows in chronological order the phases of

the project with the Initiation followed by Project definition and Case study at The

Firm.

5.2 THE FIRM

For security reasons the name of the company where the study took place will not

be revealed, it will instead be given a fictitious name, The Firm. The company I

have chosen to call The Firm is one of the largest and most well known investment

banks in the world. It operates on a global basis and house more than 50 000

employees. The Firm has taken a silo like approach to enterprise structure, which

means that each division functions almost as a separate organization. Each silo has

got roles equivalent to what a normal company would have, like CIO (Chief

Information Officer) and CFO (Chief Financial Officer). As this thesis mainly is

about IT governance and the structure around IT processes, the following

description is focused on the IT organization at The Firm.

Many roles are clearly defined within each silo. Their responsibilities are most

often tied to the area they are “stationed” in but their superior officer’s

responsibilities could vary from central isolated groups to officers controlling

40

several silos. As many separate groups perform functions that are of use to all areas

at The Firm, those groups are in a way a part of all the silos. As will be described in

section 1.5 the purpose of this project is to do an assessment of a specific division

or silo at The Firm called The Markets division. The silo I, together with key

stakeholders from The Firm, chose for this project is not really a silo but a mixture

of three silos. The reason for choosing The Markets division was a result of several

discussions with people who later became key stakeholders in the project.

Because many external auditors and regulators use COBIT, The Firm’s internal

audit section has chosen to use it. Thereby they “talk the same language”. COBIT

is also the basis for the structure of their new global IT policy program31, which is

why I found this company to be a suitable sponsor of this project.

5.3 PROJECT DEFINITION

As the need for structure and definition of the project was evident, many

introductory interviews contributed to the project layout. These interviews along

with discussions with my advisor at The Firm lead to the definition of the project.

The assessment really had two different possible ways of being performed. One

being a very high-level with the role mapping on European executive’s level. The

COBIT roles, CEO, CIO, and CFO would correspond to the level of The Firm’s

European CEO, CIO, and CFO and so on. As The Firm’s IT organization keeps a

silo like structure, each silo functions as a small organization with between 200-

1000 employees within IT. A proper high-level assessment would require

interviews with respondents within each silo and from those with responsibilities

spanning the entire organization. My advisor at The Firm and I agreed that this

project was too large within the given timeframe so we turned to the second

alternative, to focus on one division within The Firm. Discussions throughout the

organization resulted in a desire to assess The Markets division. It seemed to

present a reasonably sized IT organization, 33 employees globally, where this

relatively small, and short project could find interesting results and still deal with

complex systems and structures, much like the other silos.

31 Information from a global IT policy conference at The Firm the 24th of April, 2007

41

5.4 CASE STUDY AT THE FIRM

This project was performed at the company’s European headquarter in London

between the 15th of January 2007 and the 27th of April 2007. The method I used in

this study is described in chapter 4, Analytical framework. As previously

mentioned, the case study was based on interviews with selected personnel at The

Firm. Every interview was conducted in the same way and the questions were

posed in a standardized manner, but to different subject areas. The areas were

represented by the COBIT processes. In most cases the interviewee was the most

responsible within that area. For instance I interviewed the European Head of

Operational Risk when talking about the “Assess and manage IT risk” process, the

CFO of The Markets division regarding the “Manage the IT investment” process

and the CIO of The Markets division regarding the “Manage Operations” process.

In this example the “Assess and manage IT risk” process was managed by a central

group and the maturity on that process would be the same for a different silo since

that work is done across the board. In some cases one individual answered

questions on several processes, which meant that we had to be clear that the role

had been change since the last interview and that this new process required a

different focus. On average, one process took around 30 minutes to go through,

which was good since I could often get a one hour meeting and do two interviews,

when it was necessary.

As COBIT has a way of describing processes that was not familiar to all

respondents, explanations were often required. The problem occurred most

frequently when discussing the maturity on the activities. COBIT describes detailed

control objectives to each process that often corresponds to the activities. The

framework does not provide a consistent approach to this. Some of the activities

cannot be explained by a corresponding detailed control objective. Below is an

example of when an activity can be further explained by a detailed control

objective associated to the same process. It is taken from process PO5 - “Manage

the IT investment”.

Activity: Establish and maintain IT budgeting process

Detailed control objective: IT budgeting process

42

Described by the detailed control objective as:

Establish a process to prepare and manage a budget reflecting the priorities established

by the enterprise’s portfolio of IT-enabled investment programmes, and including the

ongoing costs of operating and maintaining the current infrastructure. The process should

support development of an overall IT budget as well as development of budgets for

individual programmes, with specific emphasis on the IT components of those

programmes. The process should allow for ongoing review, refinement and approval of

the overall budget and the budgets for individual programmes.

Some interviewees suggested ways to improve the COBIT framework with ideas

that made sense to the work they were doing at The Firm. One suggestion was to

include a Quality Assurance role to the RACI-chart. This was motivated by the fact

that in all the work done at The Firm there is interaction from a Quality Assurance

function that makes sure that the quality policies are followed. There were also

numerous suggestions on metrics and documents that could be added to improve

the framework. One example could be to add a document called “space planning”

to the process “Procure IT resources”. That document would describe the

available space within each area of company so that there was adequate space for

the manpower and hardware.

The results of this assessment will be described in the next chapter in the way they

have been weighted in this study. Together with the group responsible for the

initiation phase of the COBIT initiative at The Firm, I decided to give more weight

to the activities and metrics. The activities received weight 4 and the metrics

weight 2, the documents and role assignment stayed at weight 1. This meaning that

the activities were four times as important as the documents to the results.

43

6 RESULTS

In this chapter I reveal my results of the assessment beginning with general results.

I then explain the results for the stronger and weaker areas closer.

6.1 GENERAL RESULTS WITHIN THE MARKETS DIVISION

As described in chapter 1.5 and 5.2, the assessment was done at a specific division

within The Firm, called The Markets division. There were however difficulties

keeping the assessment to only The Markets division since many of the areas or

functions are centrally governed and managed. In those cases where one of the

COBIT processes was managed at a central level, the interview was conducted with

personnel working in that group, i.e. outside The Markets Division. Table 5 shows

where each process belongs.

Central at The Firm Both Local within The Markets division

PO2 PO1 PO5

PO4 PO3 PO8

PO6 AI2 PO10

PO7 AI6 AI1

PO9 ME1 AI4

AI3 ME2 AI7

AI5 DS3

DS1 DS4

DS2 DS9

DS5 DS10

DS6 DS11

DS7 DS13

DS8

DS12

ME3

ME4

TABLE 5 – PROCESS LOCATION AT THE FIRM

44

As shown in the table, almost half of the processes are managed on a central level

and operate across the board. Another relevant issue to consider, when revealing

the results, is the fact that The Markets division is a mix of three silos within The

Firm. That contributes to the rather high amount of centrally managed processes

which in some cases only stretches to the boundaries of these three silos and not the

entire company.

The complete results of this assessment can be seen in detail in appendix 4, where

the maturity level, (the result) is displayed and specified by activities, metrics,

documents and role assignment for each process. Since The Firm had desires to

weight the final results, the activities have weight 4, the metrics weight 2, the

documents and role assignment weight 1. The aggregated process maturity results

after weighting can be seen in figure 10. The average maturity across all processes

was 3.3 after weighting. The activity maturity was 3.1, metrics 2.9, documents 4.0

and role assignment 3.9. Since the activities and metrics were heavier weighted, the

result sank to 3.3, from an un-weighted result of 3.5.

Figure 11 shows the maturity on all the processes, with the top and bottom four

highlighted. Their definition according to COBIT can be seen in appendix 6.

FIGURE 10 – WEIGHTED RESULTS ON ALL COBIT PROCESSES.

Average maturity, 3.3.

45

These processes will be described further in the following sections to clarify how

big the gaps to COBIT are in these areas, which was a part of the purpose of this

project. The results and information are based on the interviews.