goVernAnce, risK & etHics

150

GOVERNANCE, RISK & ETHICS Paper P1 OpenTuition Course Notes can be downloaded FREE from www.OpenTuition.com Copyright belongs to OpenTuition.com - please do not support piracy by downloading from other websites. Visit opentuition.com for the latest updates, watch free video lectures and get free tutors’ support on the forums ACCA QUALIFICATION COURSE NOTES DECEMBER 2013 EXAMINATIONS

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of goVernAnce, risK & etHics

goVernAnce, risK & etHicsPaper

P1

OpenTuition Course Notes can be downloaded FREEfrom www.OpenTuition.com

Copyright belongs to OpenTuition.com - please do not support piracy by downloading from other websites.

Visit opentuition.com for the latest updates, watch free video lectures and get free tutors’ support on the forums

ACCA QuAlifiCAtionCourse notes

December 2013 examinations

For the latest free course notes, free lectures and forum support please visit opentuition.com/acca

The besT Things in life are free

Free ACCA resourCes By PAPer

(free course notes / lectures / revision lectures / tests / flashcards and more - on line on http://opentuition.com/acca/)

F1 Accountant in Business / FAB Foundations in Accountancy

F2 Management Accounting / FMA Foundations in Accountancy

F3 Financial Accounting / FFA Foundations in Accountancy

F4 Corporate & Business Law (English & Global)

F5 Performance Management

F6 Taxation (UK)

F7 Financial Reporting

F8 Audit and Assurance

F9 Financial Management

P1 Governance, Risk & Ethics

P2 Corporate Reporting

P3 Business Analysis

P4 Advanced Financial Management

P5 Advanced Performance Management

P7 Advanced Audit & Assurance

To fully benefit from these notesdo not forget to watch free ACCA Lectures

on OpenTuition.com website

a Paper P1

December 2013 Examinations

OpenTuition Course Notes can be downloaded FREE from www.OpenTuition.com

Copyright belongs to OpenTuition.com - please do not support piracy by downloading from other websites.

Visit opentuition.com for the latest updates, watch free video lectures and get free tutors’ support on the forums

Contents

Aims and Objectives i

1 Corporate Governance 1

2 Approaches to Corporate Governance 9

3 The Board of Directors 17

4 Board committees 35

5 Corporate Governance and Corporate Social Responsibility 49

6 Corporate governance – control systems 57

7 Auditors and Internal Controls 61

8 Management Information Systems 65

9 The Risk Management Process 67

10 Controlling Risk 81

11 Ethics and Social Responsibility 91

12 Deontology and Teleology 97

13 Social Responsibility 99

14 Professions and the Public Interest 107

15 Professional Practice and Codes of Ethics 117

16 Ethical Characteristics of Professionalism 133

17 Social and Environmental and Ethical Behaviour 137

Paper P1

Paper P1December 2013 Examinations

i Paper P1

December 2013 Examinations

Paper P1

Aims And Objectives

Aim

• Toapply relevantknowledge,skillsandexerciseprofessional judgement incarryingout the roleof theaccountantrelatingtogovernance,internalcontrol,complianceandthemanagementofriskwithinanorganisation,inthecontextofanoverallethicalframework.

Objectives

• Onsuccessfulcompletionofthispaper,candidatesshouldbeableto:

• Definegovernanceandexplainitsfunctionintheeffectivemanagementandcontroloforganisationsandoftheresourcesforwhichtheyareaccountable

• Evaluatetheprofessionalaccountant’sroleininternalcontrol,reviewandcompliance

• Explaintheroleoftheaccountantinidentifyingandassessingrisk

• Explainandevaluatetheroleoftheaccountantincontrollingandmitigatingrisk

• Demonstratetheapplicationofprofessionalvaluesandjudgementthroughanethicalframeworkthatisinthebestinterestsofsocietyandtheprofession,incompliancewithrelevantprofessionalcodes,lawsandregulations.

Position of the paper in the overall syllabus

• ThesyllabusforPaperP1,Governance,RiskandEthics,actsasthegatewaysyllabusintotheprofessionallevel.ItsetstheotherEssentialsandOptionspapersintoawiderprofessional,organisational,andsocietalcontext.

• The syllabus assumesessential technical skills and knowledgeacquiredat the Fundamentals levelwhere the coretechnicalcapabilitieswillhavebeenacquired,andwhereethics,corporategovernance,internalaudit,control,andriskwillhavebeenintroducedinasubject-specificcontext.

• TheP1syllabusbeginsbyexaminingthewholeareaofgovernancewithinorganisationsinthebroadcontextoftheagencyrelationship.Thisaspectof thesyllabus focusesontherespectiverolesandresponsibilitiesofdirectorsandofficerstoorganisationalstakeholdersandofaccountingandauditingassupportandcontrolfunctions.

• The syllabus thenexplores internal review, control, and feedback to implementand supporteffectivegovernance,includingcomplianceissuesrelatedtorisk,decision-makinganddecision-supportfunctions.Thesyllabusalsoexaminesthewholeareaofidentifying,assessing,andcontrollingriskasakeyaspectofresponsiblemanagement.

• Finally,thesyllabuscoverspersonalandprofessionalethics,ethicalframeworks–andprofessionalvalues–asappliedinthecontextoftheaccountant’sdutiesandasaguidetoappropriateprofessionalbehaviourandconductinavarietyofsituations.

Paper P1December 2013 Examinations

detailed syllabusA Governanceandresponsibility

1. Thescopeofgovernance2. Agencyrelationshipsandtheories3. Theboardofdirectors4. Boardcommittees5. Directors’remuneration6. Differentapproachestocorporategovernance7. Corporategovernanceandcorporatesocialresponsibility8. Governance:reportinganddisclosure

B Internalcontrolandreview1. Managementcontrolsystemsincorporategovernance2. Internalcontrol,auditandcomplianceincorporategovernance3. Internalcontrolandreporting4. Managementinformationinauditandinternalcontrol

C Identifyingandassessingrisk1. Riskandtheriskmanagementprocess2. Categoriesofrisk3. Identification,assessmentandmeasurementofrisk

D Controllingrisk1. Targetingandmonitoringrisk2. Methodsofcontrollingandreducingrisk3. Riskavoidance,retentionandmodelling

E Professionalvaluesandethics1. Ethicaltheories2. Differentapproachestoethicsandsocialresponsibility3. Professionsandthepublicinterest4. Professionalpracticeandcodesofethics5. Conflictsofinterestandtheconsequencesofunethicalbehaviour6. Ethicalcharacteristicsofprofessionalism7. Socialandenvironmentalissuesintheconductofbusinessandofethicalbehaviour

Approach to examining the syllabus

• Thesyllabuswillbeassessedbyathree-hourpaper-basedexamination.Theexaminationpaperwillbestructuredintwosections.SectionAwillbebasedonacasestudystylequestioncomprisingacompulsory50markquestion,withrequirementsbasedonseveralpartswithallpartsrelatingtothesamecaseinformation.Thecasestudywillusuallyassessarangeofsubjectareasacrossthesyllabusandwillrequirethecandidatetodemonstratehighlevelcapabilitiestoevaluate,relateandapplytheinformationinthecasestudytoseveraloftherequirements.

• SectionBcomprisesthreequestionsof25markseach,ofwhichcandidatesmustanswertwo.Thesequestionswillbemorelikelytoassessarangeofdiscretesubjectareasfromthemainsyllabussectionheadings,butmayrequireapplication,evaluationandthesynthesisofinformationcontainedwithinshortscenariosinwhichsomerequirementsmayneedtobecontextualised.

• TheexaminerisDavidCampbell

1 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click hereChapter 1

CorPorate GovernanCe

• thesystembywhichorganisationsaredirectedandcontrolled(CadburyReport)

• corporategovernance(cg)isasetofrelationshipsbetweenanentity’sdirectors,shareholdersandotherstakeholders

• alsoprovidesthestructurethroughwhichtheobjectivesoftheentityaresetanddeterminesthemeansofachievingthoseobjectivesandmonitoringperformance

• cgisanissueforallentities,whethertheybe

• largequotedentities

• commercialentities

• not–for–profitorganisationsincluding:

- publicsector

- non–governmentalorganisations

Chapter 1 Paper P1Corporate Governance December 2013 Examinations

2

Corporate governance - elements

• management,awareness,evaluationandmitigationofrisk

• includestheoperationofanadequateandappropriatesystemofcontrol

• overallperformanceisimprovedbygoodsupervisionandmanagementwithinsetbestpracticeguidelines

• frameworkforanorganisationtopursuestrategyinanethicalandeffectiveway

• offerssafeguardsagainstmisuseofresources–human,financial,physicalandintellectual

• involvesmorethanfollowingexternallyestablishedcodesofgoodpracticeAlsorequiresawillingnesstoapplythespiritaswellastheletterofthelaw

• canattractnewinvestmentintoentities,particularlyindevelopingnations

• accountabilitytoshareholdersandalsootherstakeholders

• underpinscapitalmarketconfidenceinentities,government,regulatorsandtaxauthorities

3Chapter 1 Paper P1Corporate Governance December 2013 Examinations

Corporate governance – concepts

• honesty / probity – not simply telling the truth but also not being guilty of issuingmisleading statements orpresentinginformationinaconfusingordistortedway

• accountability–emphasisofthedirectors’accountabilitytoshareholders,butopensthedoorfordiscussionabouttheextentoftheiraccountabilitytootherstakeholders

• independence–strongemphasisontheappointmentofindependentnon–executivedirectorswhoarefreefromconflictsofinterestandarethusabletomonitoreffectivelytheentity’sandexecutivedirectors’activities,ideallyworkingcloselywiththeexternalauditors

• responsibility–asystemofresponsibilityshouldexistwherebyentitydirectorsacknowledgetheirresponsibilitiestothestakeholders,andwilltakewhatevercorrectiveactionisnecessaryinordertokeeptheentityfocussed

• decisiontaking/judgement–theskillwithwhichmanagementmakedecisionswhichwillimprovethewealth/prosperityoftheorganisation

• reputation–builtbydirectors,oftenasaresultoftheirabilitytocomplywithothercgconcepts

• integrity–straightforwarddealing,honesty,andbalanceForfinancialstatementstohavethecharacteristicofintegrity,thisdependsupontheintegrityofthosepeoplewhopreparethemIntegrityinvolvesapersonwhodemonstrateshighmoralcharacter,isprincipled,professional,honestandtrustworthy

• fairness–takingintoaccounttheinterests,rightsandviewsofeveryonewhohasalegitimateinterestintheentity

• transparency /openness – involves full disclosure ofmaterialmatterswhich could influence thedecisions ofstakeholders This means not simply openness in the reporting of information required by IFRS in the financialstatements It also involvesother information suchas cashandmanagement forecasts, environmental reports andsustainabilityreports

Chapter 1 Paper P1Corporate Governance December 2013 Examinations

4

Corporate governance and agency theory

• directorsactasagentsoftheshareholders

• cg tries to ensure that agency responsibilities are fulfilled as agents by requiring disclosure and by suggestingperformance-relatedrewards

• definition:anagencyrelationshipisacontractunderwhichoneormorepersons(theprincipals)engageanotherperson(theagent)toperformsomeserviceontheirbehalfthatinvolvesdelegatingsomedecision–makingauthoritytotheagent

• fiduciarydutiesdefinition:adutyimposeduponcertainpersonsbecauseofthepositionoftrustandconfidenceinwhichtheystand in relationtoanotherTheduty ismoreonerousthangenerallyarisesunderacontractualor tortrelationshipItrequiresfulldisclosureofinformationheldbythefiduciary,astrictdutytoaccountforanyprofitsreceivedasaresultoftherelationship,andadutytoavoidconflictsofinterest

• fiduciarydutiesareowedtotheentity,nottoindividualshareholders

• directorsmustexercisetheirpowersfortheproperpurpose

5Chapter 1 Paper P1Corporate Governance December 2013 Examinations

Duties of directors as agents

• performance–ifpaid,directorshaveacontractualobligationtoperformasagreed(ifunpaid,nosuchobligation)

• obedience–directorsshouldactstrictlyinaccordancewiththeprincipal’sinstructions

• skillandcare–directorsshouldactwithsuchadegreeofskillandcareasmayreasonablybeexpectedfromapersonwithsuchexperienceandqualifications

• personalperformance–directorsshouldonlydelegatetheirassignmentswheretheyhavenoreasontobelievethatthepersontowhomtheworkisdelegatedisnotcapableofproperperformance

• avoidconflictsofinterest–egshouldnotsellhisownpropertytotheentity,eventhoughitmaybeatanindependent,arm’slengthvaluation

• confidence–agentsshouldnotdiscloseconfidentialmattersabouttheprincipal,evenaftertheagencyagreementhasended

• accountingforbenefits–agentsmustaccounttotheprincipalforanyundisclosedbenefitwhichtheyreceiveasaresultoftheirofficeasagent

• becauseownershipofanentityisnecessarilyseparatedfromthemanagement,problemsmayresult

Chapter 1 Paper P1Corporate Governance December 2013 Examinations

6

Corporate governance – Potential Problems

• directorsmaychoosetopursuestrategiesmorebeneficialfortheirowninterestratherthantheentity’s

• directorswillalmostcertainlyhaveadifferentattitudetorisk,andriskmanagement,sinceitisnottheirowninvestmentwhichtheyarerisking

• ifmanagementhaveonlyasmallbeneficial interest intheentity(orevennoneatall )thentheymaywellpursueactivitieswhichimproveshorttermresults(thereforeimprovingtheircurrentbonuses)totheexclusionofmorefar–sightedstrategieswhichwouldbeofgreaterbenefittotheentityinthelongerterm

• ultimately,shareholdershavetherighttodecidewhoshall(andwhoshallnot)bedirectorsoftheirentityButthisis,inpracticalterms,verymuchatheoreticalpowerGenerallyshareholdersneitherhavethedynamismnororganisationtoeffectsuchachangeinthecompositionoftheboard

overcoming the problem – alignment of interests ( goal congruence )

• incentivesdesignedtoaligninterestsinclude:

• profitrelatedpay

• shareissueschemes,forinstanceontheoccasionofamanagementbuy–out

• shareoptionschemes

• butforallofthesethereisanaturaltendencyformanagementtoadoptcreativeaccountingtomanipulatetheprofitfigureuponwhichtheseincentivesarebased

7Chapter 1 Paper P1Corporate Governance December 2013 Examinations

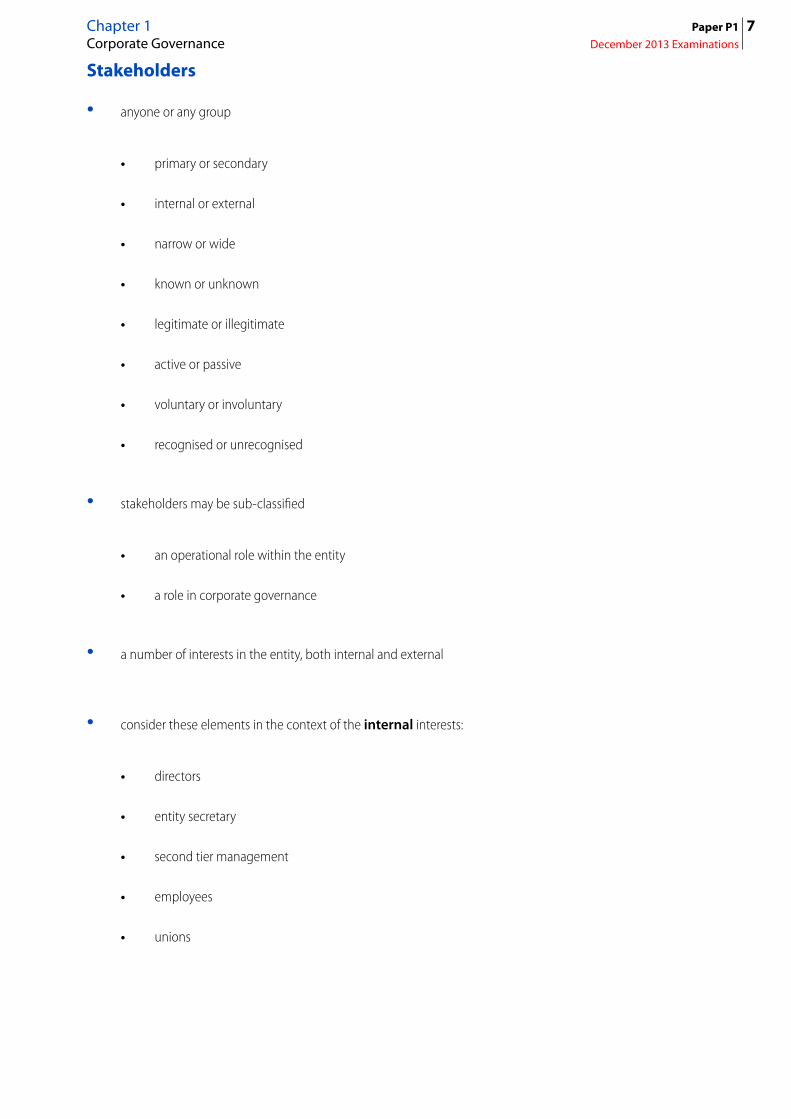

Stakeholders

• anyoneoranygroup

• primaryorsecondary

• internalorexternal

• narroworwide

• knownorunknown

• legitimateorillegitimate

• activeorpassive

• voluntaryorinvoluntary

• recognisedorunrecognised

• stakeholdersmaybesub-classified

• anoperationalrolewithintheentity

• aroleincorporategovernance

• anumberofinterestsintheentity,bothinternalandexternal

• considertheseelementsinthecontextoftheinternalinterests:

• directors

• entitysecretary

• secondtiermanagement

• employees

• unions

Chapter 1 Paper P1Corporate Governance December 2013 Examinations

8

• Eachexternalstakeholderhas:

• aroletoplayininfluencingtheoperationsoftheentity

• theirowninterestsandclaimsintheentity

• considertheseinthecontextoftheexternalinterests:

• auditors

• regulators

• government

• stockexchange

• smallinvestors

• institutionalinvestors

• ReferencetoDavidCampbellStudentAccountantarticles:“Rules,principlesandSarbanes-Oxley”April2008

Spread the word about OpenTuition.comso that all ACCA Students can benefit

from free ACCA resources

Print and share our poster

Free resources for ACCA students

100% Free

250,000 members can’t be wrong

Free course notes, Free lecturesFree Tests and FlashcardsFree Forums with tutor supportStudyBuddy FinderChat and Study Groupsand much more

9 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click hereChapter 2

APProAChes to CorPorAte GovernAnCe

two distinct approaches to corporate governance

• rulesbased,and

• principlesbased

Characteristics of the rules based approach

• prescribedsetofcgrequirements

• quickwayofensuringcompliance

• adoptsachecklistapproach

• cleardistinctionbetweencomplianceandnon–compliance

• easytoseethatentityiscomplying

• reductionofflexibilityonthepartofmanagementandauditors

• difficulttosetrulestocoverallsituations

• possibletomisinterpretrules

• samerulesapplytoall,whatevertheirsize

Chapter 2 Paper P1Approaches to Corporate Governance December 2013 Examinations

10

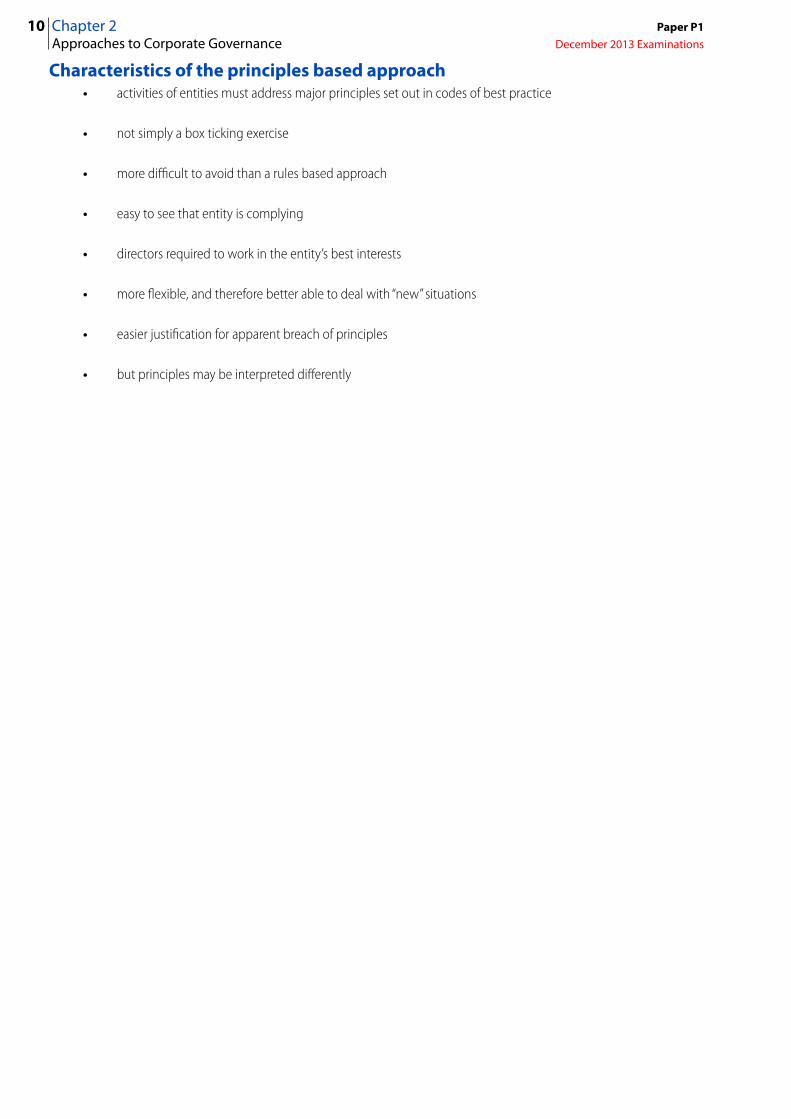

Characteristics of the principles based approach• activitiesofentitiesmustaddressmajorprinciplessetoutincodesofbestpractice

• notsimplyaboxtickingexercise

• moredifficulttoavoidthanarulesbasedapproach

• easytoseethatentityiscomplying

• directorsrequiredtoworkintheentity’sbestinterests

• moreflexible,andthereforebetterabletodealwith“new”situations

• easierjustificationforapparentbreachofprinciples

• butprinciplesmaybeinterpreteddifferently

11Chapter 2 Paper P1Approaches to Corporate Governance December 2013 Examinations

• Arrivalofcorporategovernance

• headlinehittingcorporatefailuresinEurope,USAandUKledtorecognitionoftheneedforsomesortofcontrolinanattempttopreventsimilarfailures

• commonelementsidentifiedas:

• poorentitymanagementbydirectors

• singledominantindividual

• unreliablefinancialreporting

• ineffectiveinternalcontrols

• incompetentdirectors

• lackofcloseinvolvementofinstitutionalshareholders

• directorsinterestedmoreinpersonalpositionratherthaninthewelfareoftheentity

Chapter 2 Paper P1Approaches to Corporate Governance December 2013 Examinations

12

Development of the UK Corporate Governance Code 2010 ( CGC )

• 1992,theCadburyReport

• followedbyGreenburyreportondirectors’remuneration

• thenHampelreport–alistofprinciplesof“goodcorporategovernance”

• 1998,thesethreemergedintotheCombinedCodeonCorporateGovernance

• 2003,HiggsReport,effectivenessofnon-executivedirectors(neds)

• 2005,Turnbullreport,guidanceoninternalcontrols

• 2006,newCGCpublished

• 2010,revisedandre-named–TheUKCorporateGovernanceCode(CGC)

• CGCappliestoallUKquotedentitieswhichmuststate:

• howithasappliedCGCprinciples

• whetherornotithascompliedwithCGCthroughouttheaccountingperiod,and…

• …ifnot,whynot

13Chapter 2 Paper P1Approaches to Corporate Governance December 2013 Examinations

rules based approach

• USApassedlegislation-SarbanesOxley(SOX)

• appliestoallUSquotedentities

• butalsotoanyentity,anywhereintheWorld,ifithasanAmericanquotedparententity

• mainprovisionsofSOX

• allquotedentitiesmustprovideacertificatetotheSecuritiesExchangeCommissionconfirmingtheaccuracyoftheirfinancialstatements

• wherefinancialstatementshavetoberestatedfollowingmaterialnon-compliance,CEOandCFOmustrepayanybonusesreceivedintheprevioustwelvemonths

• auditorsrestrictedtoauditwork(andtax)

• seniorauditpartnermustrotateofftheauditafternomorethanfiveyears

• PublicEntityOversightBoard–responsibleforenforcingprofessionalstandardsinaccountingandauditing

• directorsforbiddenfromdealinginentitysharesduring“sensitive”times

Chapter 2 Paper P1Approaches to Corporate Governance December 2013 Examinations

14

oeCD and ICGn have both issued principles on corporate governance

• theseprinciplesservemultiplepurposes:

• assistgovernmentsintheireffortstointroducecgprinciples

• provideguidanceandadvicetoregulatorybodiessuchasstockexchanges,investorgroupsandinstitutions

• althoughaimeddirectlyatlistedentities,recognisedthatallentitiescouldbenefitfromadoptionofprinciples

• theprincipleshavenolegalstatus

summary of oeCD principles

• ContentsoftheOECDPrinciples:

• identificationofthebasisforaneffectivecgframework

• fairtreatmentforallshareholders

• identifiestherightsofshareholders

• andtheroleofstakeholders

• detailsdisclosurerequirements

• andtransparencyarrangements

• establisheskeyownershipfunctions

• andboardresponsibilities

15Chapter 2 Paper P1Approaches to Corporate Governance December 2013 Examinations

summary of ICGn principles

• identifiescorporateobjectiveofprovidingreturnstoshareholdersontheirinvestments

• disclosureandtransparencymatters

• independentaudit

• detailsshareholders’ownership,responsibilities,rightsandremedies

• detailsprovisionsrelatingtoboardsofdirectors

• prescribesboardremunerationpolicies

• providesguidanceoncgimplementation

• prescribessocialawareness

• recommendsentity/stakeholderrelationship

• establishesneedforbusinessethics

Chapter 2 Paper P1Approaches to Corporate Governance December 2013 Examinations

16

17 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click hereChapter 3

The Board of direCTors

directors

• anyonewhooccupiesthepositionofdirector

• shadowdirectorsare‘anyoneinaccordancewithwhoseinstructionsthedirectorsareaccustomedtoact’

• cgcestablishesrolesandresponsibilities:

• provideleadershipfortheentity

• representtheentityinitsdealings,andtothepublicgenerally

• settheagendasforboardmeetings

• decidethosematterswhicharetobedeterminedbytheboard,andnotthereforetobedelegated

• decideuponastrategyfortheentity

• selectadirectortobeCEO,and…

• …anotheronetobeChair

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

18

• directors’rolesandresponsibilitiescontinued

• establishacorporateculture

• ensurethatthosechargedwithtakingoperatingdecisionsaredoingtheirjobproperly

• establishandimplementaneffectivesystemofinternalcontrolscapableofriskassessmentandmanagement

• ensurethataimsandobjectivesoftheentityarerealisticandachievable

• ensurethatallemployeesareawareoftheentity’sresponsibilitiestoitsstakeholders

• holdregularandfrequentboardmeetings

• assessownperformance,andreportannuallytoshareholders

• submitthemselvesforre–electioneverythreeyears(FTSE350entity?re-electALLdirectorseveryyear)

• forlistedentitiesthereare“additionalrequirements”

19Chapter 3 Paper P1The Board of Directors December 2013 Examinations

Listed entity requirements and the higgs report contents

• listedentitiesshould:

• appointappropriateandindependentneds

• establishsub-committees

- audit

- remuneration

- risk

- nomination

• Higgsidentifiedfourfactorswhichaffecttheeffectivenessoftheboard:

• timeavailabletodevotetoentitymatters

• personalcompetence

• qualityofinformation

• boardroomculture

• othermajorpointsaddressedbyHiggswere:

• theroleofneds,and

• performancemeasurementfortheboardasawholeandforindividualdirectors

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

20

Corporate Governance Code sub-divisions

• CGCbreaksdownneatlyintofoursub-divisions:

• directors

• directors’remuneration

• accountsandaudit

• investorrelations

21Chapter 3 Paper P1The Board of Directors December 2013 Examinations

CGC sub-divisions - directors

• everylistedentityshouldhaveaneffectiveboard

• positionsofChairandCEOshouldbeheldbydifferentindividuals

• boardshouldcomprisebothexecutiveandnon–executivedirectors

• thereshouldbeatleastasmanynedsasexecutivedirectors

• appointmenttotheboardshouldbeformalandtransparent

• informationshouldbeprovidedtotheboard

• thereshouldbeaformalassessmentoftheboard’sperformanceannually

• shouldsubmitthemselvesforre–electiononaregularbasis

• withintervalsnotgreaterthanthreeyears

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

22

CGC sub-divisions – directors’ remuneration

• shouldbesufficienttoattract,retainandmotivate

• aproportionshouldbeperformancerelated

• nodirectorshouldbeinvolvedindeterminingtheirownremuneration

• remunerationcommitteeshouldpublishareportoftheiractivitiesintheannualfinancialstatements

CGC sub-divisions – accounts and audit

• boardshouldpresentabalancedassessmentoftheentity’sposition

• theboardshouldmaintainasoundsystemofinternalcontrolinordertosafeguardshareholders’investments

• formalarrangementsshouldbeinplaceforconsideringhowtoapplyfinancialreportingandinternalcontrolprinciples

• theboardshouldmakearrangementsformaintaininganappropriaterelationshipwiththeauditors

• thiswillinvolveestablishinganauditcommittee

23Chapter 3 Paper P1The Board of Directors December 2013 Examinations

CGC sub-divisions – investor relations and potential problems with implementation of CGC

• directorsshouldhaveregulardialoguewithinstitutionalinvestors

• directorsshouldencourageactiveparticipationofallshareholdersattheannualgeneralmeeting

• toadoptalltherecommendationsoftheCGCsoundslikeanexcellentidea,buttherecanbeproblems!

• potentialproblems

• possiblethatexecutiveboardcouldlackskillorexperience

• when daily management team report to executive, their failings could mean that problems are not fullyappreciatedoropportunitiescouldbeoverlooked

• directorsmaymeetinfrequentlyandarenotnecessarilycloseacquaintancesThiscouldmakeitdifficultforthemeffectivelytoquestionthedailymanagementteam

• CEOsareoftenpeoplewithforcefulpersonalitieswhosometimesexerciseadominantinfluenceovertheboard

• CEO’sperformanceis judgedbythesamepeoplewhoappointedhimCouldbeverydifficult forthemtobeunbiasedintheirevaluationofCEO’sperformance

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

24

structure of the board - single tier ( unified ) or two-tier?

• singletierstructurecharacteristics:

• bothcontrolandmanagementareinthehandsofasinglegroupofdirectors

• commonintheUSandtheUK

• thecgcrecommendsthatatleasthalftheboardshouldbeneds

• anotherrecommendationconcernsthesplitoftherolesofCEOandChair

• theeffectistosplitthemanagement(CEO)fromcontrol(anon–executiveChair)

• inpractice,thenedsnotonlymonitormanagementbutalsocontributetostrategydevelopment

• inlargerentities,managementisoftendevolvedtosub–committees

• alldirectors,whethermanagementorneds,haveequallegalandexecutivestatusAllarethereforeaccountableandresponsibleforboarddecisions

• nedsmayalsotaketheinitiativeinmanagementdecisionsandarenotrestrictedtopost–decisionapproval

• alldirectorsowethesamefiduciarydutiestotheentity

25Chapter 3 Paper P1The Board of Directors December 2013 Examinations

structure of the board - two-tier structure

• twotierstructurecharacteristics:

• consistsofasupervisoryboardandamanagementboard

• entitiesinFrance,GermanyandotherpartsofEuropeoftenhaveatwo–tierboard

• managementisresponsibleforthegeneralrunningofthebusiness

• managementboardisledbyCEO

• supervisory board is responsible for the appointment, supervision and removal of members from themanagementboard

• alsoresponsibleforoverseeingtheactivitiesofthemanagementboard,anditscompliancewithlaw,regulationandtheentity’sconstitution

• also,ageneraloverseeingoftheentityanditsbusinessstrategies

• supervisoryboardisledbytheChair

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

26

directors - structure of the board

• thestructureshouldtakeaccountofthefollowingfactors:

• aneffectiveboardisessentialforgoodcorporategovernance

• abalancebetweenexecutiveandnedssothatnosinglegroupcandominate

• theboardshouldnotbedominatedneitherbyanyindividual

• norbyanygroup/section

• thereneedstobeasplitofpowerbetweenCEOandChair

• executivedirectorsshouldeachbeanexpertintheirownfield

27Chapter 3 Paper P1The Board of Directors December 2013 Examinations

directors - sub-division of roles

• Executivedirectors

• involvedindaytodaymanagement

• usuallyremuneratedasfull–timeemployees

• dedicatetheirworkinglivestofulfillingtheirdutiesasdirector

• takeresponsibilityforthedaytodayrunningoftheentity

• Non-executivedirectors

• membersoftheboard,butnotinvolvedinthedaytodayrunningoftheentity

• neitherafull–timeemployee,norconnectedinanyotherwaywiththeentity

• serveonthevariousboardsub-committees:

- audit

- remuneration

- risk

- nominations

- socialand

- ethical

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

28

functions of neds• constructivelychallengeandcontributetodevelopmentofstrategy

• overseeandevaluatemanagement’sperformanceinmeetingagreedobjectives

• satisfythemselvesthatfinancialinformationisaccurate

• satisfythemselvesthatfinancialcontrolsandsystemsofriskmanagementarestrongandappropriate

• roleonremunerationcommittee

• constantlyseektoestablishandmaintainconfidenceintheconductoftheentity

• beindependentinjudgement,andinquisitive

• trytounderstandtheviewsofthemajorinvestors

• beofferedtheopportunitytoattendmeetingswithmajorshareholders

29Chapter 3 Paper P1The Board of Directors December 2013 Examinations

statutory duties of all directors

• Wehavealreadycomeacrosssomeofthedutiesofdirectors,butthefollowinglistincludessomenewones:

• actingoodfaith,intheinterestsoftheentityasawhole,by:

- treatingallshareholdersequally

- declaringanyconflictsofinterest

- notmakingpersonalprofitsattheentity’sexpense

• ensurethattheentitymaintainsproperaccountingrecords

• produceproperfinancialstatementsanddirectors’report

• filethefinancialstatementswiththeGovernmentdepartment

• obeyotherlawsandregulationssuchashealthandsafetylegislation

• Individually,eachdirectormust:

• discloseanyinterestinanentitycontract

• discloseanyinterestinsharesordebenturesoftheentity

• disclosedetailsofanyoptionswhichareheld

• Inaddition,directorshaveacommonlawdutytodemonstratesuchdegreeofskillandcareasmayreasonablybeexpectedfromapersonofthatage,experienceandqualification.FailuretodosomayresultinthedirectorbeingfoundliablefornegligencewiththeconsequencethataCourtmayholdthedirectorpersonallyliableforanylosswhichtheentityhassufferedasaresultofthatnegligence.

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

30

directors - appointment and service contracts

• Appointment

• Therulesfortheappointmentandremovalofdirectorsarefoundintheconstitutionofanentityandtypicallyprovidethefollowing:

- thefirstdirectorsareappointedatthetimeofformationoftheentity

- subsequentdirectorsarenormallyappointedbythedirectorsinthetimebetweengeneralmeetings,butsuchappointeesmustseektobere–electedbytheshareholdersatthenextannualgeneralmeeting

- directorsarerequiredtoretirebyrotation

- directorsshouldstepdownfromofficeatleasteverythreeyears,butmayseekre–election

- iftheentityisanFTSE350entity,alldirectorsmustbere-electedeveryyear

• Directors’servicecontracts

• Thesearelegaldocumentscontainingthetermsofserviceforeachdirectorandwillnormallyinclude:

- keydates

- duties

- remunerationdetails

- terminationprovisions

- constraints

- anyother“normal”employmentprovisions

• Thecontractshouldnotbeforaperiodinexcessofoneyear

31Chapter 3 Paper P1The Board of Directors December 2013 Examinations

directors – removal and disqualification

• Directorsmaybe removed fromofficeat any timeby thevoteof themajorityofmembers ingeneralmeeting Inaddition,theofficeofdirectorshallbevacatedaccordingtotherulessetoutintheentity’sconstitutionTypicallythiswillprovidethatadirectorshallloseofficeif:

• becomesdisqualifiedbylaw

• dies

• isremovedbyshareholders

• becomespersonallybankrupt

• resignsfromofficebynoticeinwriting

• isabsentfromboardmeetingswithoutpermissionforaperiodinexcessofsixmonths

• Disqualificationunderthelawcanhappenwhenadirectorisguiltyof:

• allowingtheentitytocontinuetotradewhilstitisinsolvent

• notkeepingproperaccountingrecords

• failuretopreparefinancialstatements

• threedefaults(withinafiveyearperiod)offailingtofilerelevantdocumentswiththeGovernmentdepartment

• failuretofiletaxreturns(orpaytax)

• takingactionswhicharedeemedbytheCourttobeinappropriateforthemanagementoftheentity

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

32

directors – insider dealing

• Insider – a personwho has a business connectionwith an entity as a result ofwhich theymay acquire relevantinformation

• Dealing–buyingorsellingsharesorsecuritiesinanentity

• Unpublishedprice–sensitiveinformationisinformationabouttheentitywhichisnotinthepublicdomain

• islessthan6monthsold,and…

• is,onpublication,likelytohaveamaterialimpactonthemarketpriceoftheentity’sshares

• Aninsiderinpossessionofunpublishedprice–sensitiveinformationshouldnotdeal

• Anoffenceisalsocommittediftheinsiderencouragesanotherpersontodeal

• Apersondealingasaresultofthatencouragement,andbelievingthesourcetobeaninsider,isalsocommittinganoffence

• Disclosureofinsideinformation,otherthaninthepropercourseofemploymenttoanauthorisedperson,isalsoanoffence

• Somedefencesareavailabletobeclaimed

33Chapter 3 Paper P1The Board of Directors December 2013 Examinations

directors - induction and education

• TheCGCestablishesprinciplesfortheeducationofanewdirectorintheactivitiesoftheentityItisclearlyimportantthatthenewdirectorshouldbecomeacquaintedwiththeexecutiveboardassoonaspossibleaftertheirappointment,sotheentity’sinductionprocedureshould:

• becomprehensive

• betailoredtotheneedsoftheentityandindividualdirectors

• containwritteninformationpluspresentationsandappropriateactivities(egsitevisits)

• givenewappointeesabalancedoverviewoftheentity

• notoverloadthedirectorwithanexcessofinformation

• attheendoftheinductionprocess,thenewdirectorshouldhave:

- anunderstandingofthenatureoftheentity,itsbusinessandthemarketsinwhichitoperates

- alinkwiththeentity’semployees

- anunderstandingoftheentity’smainrelationshipsincludingtherelationshipwiththeauditors

Chapter 3 Paper P1The Board of Directors December 2013 Examinations

34

directors – performance evaluation

• TheCGCcontainsaframeworkforassessingtheperformanceofindividualdirectorsaswellasoftheboardasawhole:

• thereshouldbeanannualevaluationoftheperformanceoftheboardasawholeandofeachmemberoftheboard

• theevaluationexerciseshouldbetailoredtosuittheentity’sneeds

• entitiesshouldpublishinthefinancialstatementswhethersuchanevaluationexercisehasbeencarriedout

• theChairisresponsiblefortheselectionofaneffectiveprocess,andfortakingappropriateactiononcompletion

• theuseofanindependentthirdpartywouldbringadditionalobjectivitytotheexercise

• theevaluationexerciseshouldconsistofanumberofquestionsandanswersdesignedtoassessperformanceandidentifyhowperformancecouldbeimproved

• thewholeprocessshouldbeusedconstructivelyasameanstoimproveboardeffectiveness,maximisestrengthsandminimiseweaknesses

• theresultsoftheboardevaluationshouldbesharedwiththewholeboard,but

• theresultsofindividualevaluationsshouldremainconfidentialbetweentheChairandtheindividualdirector

35 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click here Chapter 4

Board Committees

audit committee

• auditcommitteeisasub–committeeoftheboardandiscomprisedentirelyofneds

• inalistedentity,thereshouldbeatleastthreenedsontheauditcommittee,oneofwhomhashadrecentrelevantfinancialexperience

• keyrolesfortheauditcommitteeare:

• oversight

• assessment

• reviewoftheotherfunctionsandsystemsintheentity

• mostoftheboard’sobjectivesrelatingtointernalcontrolwillprobablybedelegatedtotheauditcommittee

• theauditcommitteeshould:

• reviewtheentity’sinternalfinancialcontrols

• reviewalltheentity’sicandriskmanagementsystems

• approvethewordinginthefinancialstatementsrelatingtoicandriskmanagementsystems

• receivereportsfrommanagementabouttheeffectivenessofthecontrolsystems

• receivereportsconcerningtheconclusionofanytestscarriedoutonthecontrolsbyeitherinternalorexternalauditors

Chapter 4 Paper P1Board committees - audit committee December 2013 Examinations

36

internal control systems

• foranicsystemtobeeffectiveitneedstominimisesuccessfullythebusinessrisksidentifiedbymanagement:

• playsanimportantrole inmanagingthoseriskswhichmostthreatentheattainmentoftheentity’sbusinessobjectives

• contributes significantly to protecting shareholders’ investment, safeguarding the assets and ensuringcompliancewithlawandregulation

• shouldalsoseektopreventandtodetectfraudInapoorcontrolenvironmentfraudcouldmoreeasilydevelop

• shouldbereviewedcontinuallyandimprovedasappropriate

• thecostsofimplementingacontrolshouldnotexceedthebenefittobegainedfromthereducedrisk

• suitabilityofacontrolwillvaryfromentitytoentity

• shouldbeanintegralpartofanyentity’sriskmanagementstrategy–itshouldnotbeanafter–thought

• effectivefinancialcontrols(includingmaintenanceofproperaccountingrecords)areanimportantelementofasystemofic

37Chapter 4 Paper P1Board committees - audit committee December 2013 Examinations

internal controls -categorisation

• canberememberedbythemnemonicoapspasm

o organisational

A Arithmeticandaccounting

P Personnel

s segregationofduties

P Physical

A Authorisation

s supervision

m management

Chapter 4 Paper P1Board committees - audit committee December 2013 Examinations

38

internal controls - categorisation

• theseeightcontrolscannowbecategorisedintothreeheadings–

Structure Transactions Staff

Organisational•controlovertheorganisationstructureincludingmanagershavingspecificresponsibilitiesanddelegationtasks

Physical•protectionofassetsagainsttheft,unauthorisedaccessoruse

Personnel•controlsthat:-suitablepeoplearerecruited

foreachjob,and-appropriatetrainingispro-

videdforthatjob

Segregationofduties•foreachtransactiondifferentpeople:

-authoriseit-recordit-maintainphysicalcustodyof

anyassets-payforit

Arithmeticandaccounting•checkingaccountingtransac-tionsforaccuracy

•includesuseofcontrolaccountsandreconciliations(egbankreconciliation)

Supervision•oversightofworkofotherindividualstoensuretasksarecarriedoutcorrectly

Authorisationandapproval•controlstoensurethattransac-tionsdonotproceeduntilanappropriateindividualhasgivenapproval(normallyinwriting)

Management•controlactiontakenbyman-agementdependingonthecontentsofreportsreceived

39Chapter 4 Paper P1Board committees - audit committee December 2013 Examinations

audit committee and internal audit ( ia )

• aspartoftheirobligationtoensureadequateandeffectivecontrolsauditcommitteeisresponsiblefortheactivitiesofia

• theauditcommitteeshould:

• monitorandassesstheroleoftheiafunctionwithintheentity’soverallriskmanagementsystem

• checktheefficiencyofia

• approvetheappointment(orremoval)ofthechiefinternalauditor

• ensurethattheiafunctionhasdirectaccesstotheChairandisaccountabletotheauditcommittee

• reviewandassesstheannualiaworkplan

• receivereportsconcerningtheworkoftheiafunction

• reviewandmonitormanagement’sresponsetoiafindings

• ensureia’srecommendationsareimplemented

• helptopreservetheiafunctionfrompressureswhichmightotherwiseimpairtheirobjectivity

• auditcommitteeshouldmeetwithiaatleastonceeachyeartodiscussaudit–relatedmatters

• possiblethatevenalistedentitydoesnothaveaniafunction

• ifnoauditcommittee,shouldreviewthesituationannuallyandmakeanyappropriaterecommendation

• ifthereisnoiadepartment,thisfactmustbedisclosedinthefinancialstatements

Chapter 4 Paper P1Board committees - audit committee December 2013 Examinations

40

audit committee and the external auditors ( ea )

• auditcommitteeisresponsibleforoverseeingtheentity’srelationshipwiththeea

• responsibilityisgivenbytheCGCwhichalsostatesthattheauditcommitteeshould:

• havetheprimaryresponsibilityforrecommendingeasforappointment,re–appointmentorevenremoval

• overseetheselectionprocesswhenreplacementauditorsarebeingconsidered

• approvetheterms(notnecessarilynegotiate)oftheea’sengagement,andtheirremuneration

• developprocedureswherebytheycanannuallyensuretheea’scontinuingindependenceandobjectivity

• reviewthescopeoftheauditwithea,andsatisfythemselvesthatthescopeissufficient

• ensurethatappropriateplansareinplacefortheauditatthecommencementoftheaudit

• carryoutapostauditreview

41Chapter 4 Paper P1Board committees - audit committee December 2013 Examinations

reporting on internal controls to shareholders

• CGCrequiresthatanentity’sboardshouldmaintainasoundsystemofinternalcontrolstosafeguardtheentity’sassetsandtoprotectshareholders’investments

• issueishowmuchtheentityshouldtellitsshareholdersabouttheinternalcontrolsystem

• asownersof theentity, shareholdersareentitled toknowwhether the internalcontrol system issufficientlystrongtosafeguardtheentity’sassets

• boardshould,atleastonceeachyear,reviewtheeffectivenessoftheinternalcontrolsystem,andreporttotheshareholderstheresultsofthatreview

• reviewshouldcoverallmaterialcontrolsincludingfinancial,operationalandcompliancecontrolsaswellastheriskmanagementsystem

• in addition, the shareholders shouldbe told, through the financial statements, about thework of the auditcommittee

• attheannualgeneralmeetingtheChairoftheauditcommitteeshouldbeavailabletoansweranyshareholderquestions

Chapter 4 Paper P1Board committees - audit committee December 2013 Examinations

42

internal audit reporting Report section Reason Example

Objectivesofauditwork •Setsthesceneforreportaudiencebydescribingpurposeofreview

•Forapayrollaudit‘checkwhether:-wagesarepaidtothecorrect

individuals-deductionsfromgrosspayare

properlycalculated’

Summaryofprocessunder-takenbyauditor

•Describeshowtheevidencetosupporttheopinionandrecom-mendationswasgathered

•‘Recalculationofdeductionswasperformedforasampleof50monthlyand50weeklywagespayments’

Auditopinion(ifrequired) •Summaryofwhetherthecontrolreviewedisworkingornot

•‘Inouropinion,thecontroliswork-ingasintended’

Recommendations •Highlightareasofcontrolweaknessandsuggestcourseofremedialaction

•‘Werecommendthatnewemploy-eesareonlyaddedtothepayrollsystemonreceiptofanappropri-atelyauthorisedForm1a’

43Chapter 4 Paper P1Board committees - audit committee December 2013 Examinations

role and function of an audit committee

• createaclimateofdisciplineandcontrolleadingtoareductionofopportunitiesforfraud

• lendanairofcredibilityandobjectivityinthefinancialstatementstherebyincreasingpublicconfidence

• assistCFObyprovidingaforum

• reviewfinancialstatementstoimprovethequalityofreporting

• independentjudgement

• strengthenpositionoftheinternalauditor

• strengthenpositionoftheexternalauditor

• assistintheresolutionofdisputesbetweenexternalauditorandexecutiveboard

• rememberClarissa

Chapter 4 Paper P1Board committees - remuneration committee December 2013 Examinations

44

remuneration committee

• importance:

• executivedirectorsshouldnotberesponsiblefordeterminingtheirownremuneration

• remunerationdecisionscanbeseentobetakenbythosewhowillnotbenefitfromthosedecisions

• thereisaneedforformal,transparentproceduresfordevelopingpolicyandforindividualpackages

• role

• the committee determines appropriate packages for the executive directors, and the composition of thosepackages

• composition

• inlistedentitiesthecommitteewilltypicallycompriseneds

• accountability

• reportstothemainboard

45Chapter 4 Paper P1Board committees - remuneration committee December 2013 Examinations

strategy of the remuneration committee may consider:

• greaterbenefitsinkindtocompensateforlowerbasicsalaries

• offeringnon–cashmotivationforsome(orall)oftheentity’semployees.Non–cashmotivatorscouldincludethingslikecrèchefacilities,carsandadditionalholidays

• availabilityofentityresources.Forexample,theentitymaynothavesufficientcashresourcetopayanannualbonus,butmayofferashareincentiveschemeinstead

• encouragementoflong–termloyaltybyofferingshare–purchaseschemes

Chapter 4 Paper P1Board committees - remuneration committee December 2013 Examinations

46

remuneration committee responsibilities

• determine, and regularly review, the framework, broadpolicy and specific terms for the remuneration, terms andconditionsofemploymentoftheChairandoftheexecutivedirectors

• recommendandmonitorthelevelandstructureoftheremunerationofseniormanagement

• setdetailedremunerationforallexecutivedirectorsandtheChairincludingpensionrightsandcompensationpayments

• ensurethatexecutivedirectorsandseniormanagementarefairlyrewardedfortheir individualcontributionstotheoverallperformanceoftheentity

• demonstratetoshareholdersthattheremunerationofexecutivedirectorsandseniormanagementissetbyindividualswithnopersonalinterestintheoutcomeofthecommittee’sdecisions

• agreecompensationforlossofoffice

• ensurethatprovisionsfordisclosureofremuneration,includingpensions,assetoutinlawandintheCGCarefollowed

47Chapter 4 Paper P1Board committees - nominations committee December 2013 Examinations

Nominations committee

• importance:

• needstobeseentobeunbiasedandimpartial

• needstobeobjectiveinordertoensurethatappointmentsaremadeinlinewithpre–agreedspecifications

• role

• identifyappropriatepeopletobeinvitedtojointheboard

• thecommitteedeterminesappropriatepackagesfortheprospectiveexecutivedirectors,andthecompositionofthosepackages

• composition

• executivedirectorsandneds,butnedsshouldbethemajority

• accountability

• makesrecommendationstothemainboard,but

• finaldecisionsaremadebythemainboardasawhole

• overallresponsibilitiesofthenominationscommitteeareto:

• reviewregularlythestructure,sizeandcompositionoftheboard,andmakerecommendationstotheboardofnewnominees

• givefullconsiderationtosuccessionplanningfordirectors

• regularlyevaluatethebalanceofskills,knowledgeandexperienceoftheboard

• prepareadescriptionoftheroleandcapabilitiesrequiredforanyparticularboardappointment

• identify,andnominateforapproval,candidatestofillboardvacanciesastheyarise

• recommendtotheboardconcerningexistingdirectorsstandingforre–appointment

Chapter 4 Paper P1Board committees - risk management committee December 2013 Examinations

48

risk management committee

• boardisresponsibleforriskidentificationandriskmanagement,bothofwhichinvolvetheestablishmentofasoundsystemofinternalcontrol

• importance:

• givesanobjectiveviewontheentity’sriskprofile

• role

• assessesinternalcontrols

• performsriskassessmentsoftheentity’skeyoperations

• oftenoverseestheimplementationandeffectiveoperationofriskstrategy,policiesandprocedures

• composition

• executivedirectorsandneds,butnedsshouldbethemajority

• accountability

• makesrecommendationstothefullboardofinternalcontrolandriskstrategy,or

• totheauditcommittee,buttheyinturnwillreporttothefullboard

• mainresponsibilitiesanddutiesoftheriskmanagementcommitteeareto:

• advisethefullboardonriskmanagementissues,strategyandpolicy

• emphasiseanddemonstratethebenefitsofarisk–basedapproachtointernalcontrols

• setappropriateinternalcontrolpolicies

• regularlyassurethatthesystemisfunctioning

• reviewtheeffectivenessofinternalcontrols

• providerelevantdisclosuresaboutinternalcontrolsinthefinancialstatements

• reviewthesystemofinternalcontrolspayingparticularattentiontothecontrolenvironment,riskassessment,informationsystems,controlproceduresandmonitoring

49 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click here Chapter 5

CorPorate GovernanCe and CorPorate SoCial reSPonSibility

• entitiesareincreasinglyacceptingthattheyhavesocialandenvironmentalresponsibilities

• whoarethepeoplewhoareaffectedbyanentity’sactions?

• thereare,ofcourse,manyincluding:

- employees

- customers,suppliersandthelocalcommunity

- theenvironmentmaybeaffectedasaresultofourproductionprocesses

• CGvsCSR

• cgisnotthesameascorporatesocialresponsibility(csr)

• csristheprinciplethatanentitywillthinkaboutitsimpactonthewiderenvironmentandwilltakedocumentedstepstominimisethedamageandmaximisethebenefitsofitsactions

• strategyofanorganisationisshapedbymanyfactors,includingthedemandsofstakeholders

• eachdifferentstakeholder,orclassofstakeholder,willtypicallyhavedifferentobjectivesaswellasdifferentlevelsofinfluence

• expression stakeholder is applied to anyonewhohas anything todowith thebusiness,whetherdirectlyorindirectly

• cgframeworkofanentityshouldrecognisetherightsofstakeholdersestablishedbylaworbyseparateagreement

• becausedifferentstakeholdershavedifferentobjectives,itisnecessaryfortheboardtobalancetheseconflictinginterests

• anentity’sstrategyisoftentomanage,ratherthansatisfy,stakeholderobjectives

• inevitably,themoreinfluentialthestakeholder,thegreaterwillbetheattentiondirectedtotheirinterests

Chapter 5 Paper P1Corporate Governance and Corporate Social Responsibility December 2013 Examinations

50

the most important group of stakeholders is ( normally ) the shareholders

• theyarethelegalownersoftheentity,andcontrolitthroughvotescastattheannualgeneralmeeting

• eventhoughtheyowntheentity,theydonotownthepropertyoftheentity–thisreinforcesthelegalconceptofanentitybeingaseparatelegalperson

• shareholdershaveanumberofstatutoryrights:

• therighttotransfertheirshares

• therighttoreceivenoticeofmeetings

• therighttoattend,speakandbeheardatthosemeetings

• therighttoreceiveadividend(whenapprovedbythegeneralmeeting)

• therighttoacopyoftheentity’sfinancialstatements

• oncetheyhavepaidthefullfacevalueofthesharesheldbythem,they(normally)willhavenofurtherobligationtocontributetoashortfallinaninsolventliquidation(butthereareexceptions)

• theydoNOThavetoremainloyaltotheentityandmayselltheirsharesatanytime

• nordotheyhaveanydutytoensurethattheentityoperatesinasociallyresponsibleway

51Chapter 5 Paper P1Corporate Governance and Corporate Social Responsibility December 2013 Examinations

Corporate social responsibility and disclosure

• isasuccessfulbusinessalsoagoodcorporatecitizen?

• onlyifitpaysattentiontoitsenvironmentandstakeholders

• forexample:

• aswellasmakingproductsorsupplyingservices, resulting inprofitability, it shouldalso try tomaximise thebenefitsof,andminimisetheharmcausedby,itsoperatingactivities

• it should achieve a balance between its legal responsibilities, its commercial responsibilities and its socialresponsibilities

• itshouldconstantlybereviewingitssocialresponsibilityposition

• asaconsequenceofacknowledgingitssocialresponsibility,andbeingseentobeactinginaresponsibleway,anentitycouldverywellfindthatdemandforitsproductsincreases

• disclosure

• generalprinciples

- becauseshareholdersaretheownersofanentity,theyareentitledtobegivensufficientinformationtoenablethemtomakeinvestmentdecisions

- theAnnualGeneralMeetingisseenasthemostopportunetime(oftentheONLYtime!)fordirectorstobeabletocommunicatedirectlywiththeentity’sshareholders

- inaddition,thefinancialstatementsareoftentheonlyprintedinformationwhichshareholdersreceivefromtheentity

• commonsensewilltellusthat:

• moreregularandconstructivedialoguewithourshareholderswillleadto:

- betterunderstandingofshareholders’interestsandconcerns

- betterunderstandingbytheshareholders’ofwhattheentityistryingtoachieve

- increaseinshareholderinterestthereforeencouragingchecksonthemanagersoftheentity

- potentialbenefitresultingfromthecloserinterestintheentitybythemajorshareholders

Chapter 5 Paper P1Corporate Governance and Corporate Social Responsibility December 2013 Examinations

52

CGC disclosure recommendations

• disclosure

• itallowstheentity’sboardtoprovideinformationongovernancematterstoshareholdersandotherstakeholders

• disclosuredemonstratesthatgoodcgprinciplesarebeingappliedbytheentity

• alsoameansofcommunicatingmattersofinterestandvalue

• CGCcontainspoliciesandprovisionswithwhichlistedentitiesareexpectedtocomply

• thesepoliciesandprovisionsrepresent“bestpractice”intermsofdisclosure

• CGCrequirements

• alistedentityisrequiredtostatewithinthefinancialstatements:

- howithasappliedtheprinciplesoftheCGC,and

- whetherithascompliedwiththeCGCthroughouttheaccountingperiod

- andifnot,whynot

53Chapter 5 Paper P1Corporate Governance and Corporate Social Responsibility December 2013 Examinations

CGC – additional disclosures

• astatementbytheboardacknowledgingtheirresponsibilityforthefinancialstatements

• astatementbytheboardtoconfirmtheirviewthattheentityisagoingconcern

• detailsofeachboardmembertogetherwithdetailsoftheirresponsibilitiesandtheirrecordofattendanceatboardmeetings

• theidentityoftheChair,theCEOandwhichdirectorssitonwhichofthesub–committees(audit,socialresponsibility,nominations,remunerationandriskmanagement)aswellastheirattendancerecordsatmeetingsofthosecommittees

• reportsontheactivitiesofthecommittees

• ifthereisnointernalauditfunction,therelevantsectionoftheannualreportshouldexplainwhynot

• astatementthatthedirectorshaveundertakenareviewoftheeffectivenessoftheinternalcontrolsystem

• areportonthemethodsusedtoevaluateperformanceoftheboardanditscommittees

• informationaboutthemeasurestakenbytheboardtoensurethatitunderstandstheviewsofitsmajorshareholders

• informationaboutthestepstakentoensurethecontinuingindependenceoftheexternalauditors

• wheretheboarddoesnotacceptarecommendationfromtheauditcommittee,thereshouldbeastatementbytheauditcommitteeexplainingtheirrecommendationandwhytheboardhastakenadifferentview

Chapter 5 Paper P1Corporate Governance and Corporate Social Responsibility December 2013 Examinations

54

annual General Meetings

• everyentitymustholdanannualgeneralmeetingonceineverycalendaryear(Thisisnottechnicallycorrect–privateentitiesmaydispensewiththisrequirementbut,forourpurposes,whendealingwithcorporategovernanceofpublicentities,thestatementistrue)

• somequickpointsaboutAGMs

• theyarealegalrequirement

• eachissuemustbeapprovedbyseparateresolution

• themeetingrequiresnotlessthan21days’notice

• thefirstmeetingmustbeheldwithin18monthsoftheentity’sincorporationdate

• eachsuccessivemeetingshallbeheldnolaterthan15monthsafterthepreviousmeeting

• allshareholderswhoareentitledtoattendmustbegivennoticeofthemeeting

• theboardshouldusetheAGMtocommunicatewithshareholders,andshouldencouragetheirparticipation

• thepurposeofthemeetingistoapprovethe“ordinarybusiness”oftheentitytogetherwithanyothermatterswhichrequireshareholderapproval

• “ordinarybusiness”comprises:

- thereceivingoftheannualfinancialstatements

- thereappointmentofdirectorsretiringbyrotation

- thereappointmentoftheauditorsforanotherfullyear

- theformalapprovalofthedividendwhichhasbeenproposedbythedirectors

• theboardshouldarrangefortheChairofthesub–committeestobepresentattheAGMtoansweranyquestionsfromtheshareholders,andforalldirectorstobepresent

55Chapter 5 Paper P1Corporate Governance and Corporate Social Responsibility December 2013 Examinations

other general meetings and proxy votes

• entitiesmayalsofindthattheyneedtoholdgeneralmeetingswhicharenotAGMsTheseareOtherGeneralMeetings(OGMs)

• somequickpointsaboutOGMs

• heldirregularly,andonlywhensomethingurgentariseswhichneedsshareholderapproval

• separateresolutionsshouldbepassedforeachdifferentmatter

• lengthofnoticeofthemeetingdependsonwhattypeofresolutionistobeproposed

• itistheoreticallypossibleforanentitytogofrombirthtodeathwithoutanyneedtoholdanOGM

• proxyvoting

• ashareholderwhoisunabletoattendageneralmeetingmayappointapersontoattendthemeetingontheirbehalf

• suchapersoniscalleda“proxy”andthedocumentwhichappointsthemisa“proxyform”

• wheretheshareholderisanentity,theywillappointa“representative”andnotaproxy

Chapter 5 Paper P1Corporate Governance and Corporate Social Responsibility December 2013 Examinations

56

CGC and proxies

• CGCsaysaboutproxies:

• foreachresolutiontobeproposed,theproxyformshallprovidetheshareholderwiththeoptionsofdirectingtheirproxytovoteinfavour,against,orwithholdtheirvote

• avotewhichiswithheldisnotcountedasavote–neitherinfavournoragainst

• theentityshouldensurethatallproxyformsreceivedareproperlyrecordedandcounted

• foreachresolution,afteravotehasbeentaken,theentityshouldpublishonitswebsitethedetailsofthevotesand,inparticular:

- thenumberofsharesinrespectofwhichvalidproxieshavebeenreceived

- thenumberofvotesforeachresolution

- thenumberofvotesagainsttheresolution

- thenumberofsharesinrespectofwhichthevotewaswithheld

57 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click hereChapter 6

CorPorate governanCe – Control systems

• Internalcontrolisakeyprocesswithinanorganisationconcernedwiththemanagementofriskandtheachievementofobjectives

• byinternalcontrolismeantnotonlyinternalcheckandinternalauditbutthewholesystemofcontrols,financialandotherwise,establishedbythemanagementinorderto

• carryonthebusinessoftheentityinanorderlyandefficientmanner

• ensureadherencetomanagementpolicies

• safeguardtheassets

• preventanddetectfraudanderror

• secureasfaraspossiblethecompletenessandaccuracyoftheaccountingrecordsenabling

• thetimelypreparationofreliablefinancialinformation

• Internalcontrolandriskmanagementincg

• bothelementsofinternalcontrolandriskmanagementarefundamentalpartsofsoundcgbecause:

- cghaskeylinkstorisksandtointernalcontrols

- whilstitisnotpossibletopreventcorporatefailures,goodcgcangoalongwaytominimisetherisk,andwell–runentitiestendtoachievetheirobjectivesinalessriskyway

- sowecanseethatcgisakeytoriskreduction

- theCGC requiresentities tooperateappropriatesystemsof internalcontrol,and toensure that thosesystemsareregularlyreviewedandimproved

Chapter 6 Paper P1Corporate governance – control systems December 2013 Examinations

58

turnbull report and internal controls

• requiresthatinternalcontrolsshouldbeestablishedusingarisk–basedapproach

• specificallyanentityshould:

• establishitsbusinessobjectives

• identifytheassociatedkeyrisks

• designcontrolstoaddressthoserisks

• establishasystemtoimplementthecontrols,includingtheprovisionofregularfeedback

• objectivesofinternalcontrolsystems

• managetheriskswhichhavebeenidentifiedwithinanentityincludingtheriskthattheentityfailstoachieveitsobjectives

• internalcontrolsystemsshouldbedesignedsothattheygivereasonableassurancethat:

- operationsarerunningefficientlyandeffectively

- financialreportingisreliable

- applicablelawsandregulationsarebeingadheredto

• iftherewerenointernalcontrolsystem,managementwouldbeunabletomonitortheeffectivenessoftheirriskmanagementstrategy,andwouldcertainlynotbeinanypositiontorespondtonewthreatsastheyarose

59Chapter 6 Paper P1Corporate governance – control systems December 2013 Examinations

• Executivemanagementrolesinriskmanagement

• in any entity the board is ultimately responsible for all matters concerning the entity However, it is notunreasonabletoexpecttheboardtodelegatedutiesdowntoindividualexecutivedirectorlevel

• CEO(ultimatelyresponsiblefortheentiresystemandoperationsoftheentity)shouldbeseentobeincontrolofriskmanagement

• CEOistheoneindividualmorethananyotherwhosetsthestandardforethicsandacceptanceofresponsibility

• boardofdirectors,asawhole,isresponsibleforensuringtheadequacyoftheinternalcontrolsystemandtheyshouldthereforeensurethatexecutivedirectorsmonitortheinternalcontrolsystemeffectively

• senior executivemanagement is responsible for setting the internal control policies and formonitoring theadequacyandeffectivenessoftheinternalcontrolsystemTheyalsoreporttothefullboardthatthishasbeendone

• lower levelmanagement ( not executive directors ) will typically find that these responsibilities have beendelegated to them! But executive directors remain the ones responsible for confirming adequacy andeffectiveness

• employeesgenerallyhave the taskof carryingout thedirectors’ orders, andare therefore theoneswhoarechargedwiththeresponsibilityofensuringthecorrectapplicationoftheinternalcontrols

Chapter 6 Paper P1Corporate governance – control systems December 2013 Examinations

60

61 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click hereChapter 7

Auditors And internAl Controls

Function and importance of internal audit

• internalaudit(ia)isanindependentappraisalactivityestablishedwithinanorganisationasaservicetoit

• itisacontrolwhichfunctionsbyexaminingandevaluatingtheadequacyandeffectivenessofothercontrols

• inalargeorganisationiawillbeaseparatedepartment

• insmallerentities,itcouldbethatanindividualisallocatedtocarryoutspecifictasksofanianature

• itmaybethattheiafunctionisoutsourced

• ifitisanin-housedepartment,itisimportantthatthefunctionisstructuredinanappropriateway

• scopeofinternalaudit

• managementwillprescribethescopeandobjectivesoftheiadepartment,butthesewilltypicallyinclude:

- reviewoftheaccountingandinternalcontrolsystems

- detailedtestingoftransactionsandbalances

- reviewoftheeconomy,efficiencyandeffectivenessofoperations

- reviewoftheimplementationofentitypolicies

- specialinvestigations

- assistingtheexternalauditors

Chapter 7 Paper P1Auditors and Internal Controls December 2013 Examinations

62

independence of internal audit

• foranauditfunctiontooperatesuccessfully,itisnecessarythattheauditorisindependent

• appliesequallywelltointernalauditorsastoexternalauditors

• for internal audit to be effective, the reviews which they carry out must be conducted and reported on on anindependentbasis

• theequivalentoftheconfidencewhichisgivenbytheexternalauditorbeingindependent

• Comparisonofinternalandexternalauditors

External Internal

Requiredby statute management

Appointedby shareholders management

Reportsto shareholders,andmanagement management

Reportson financialstatements internalcontrols

Opinionabout truthandfairness,properpresentation adequacyofintconts,valueformoney

Scope asnecessary prescribedbyexecutiveboard

63Chapter 7 Paper P1Auditors and Internal Controls December 2013 Examinations

Potential threats to independence

• inthesyllabusfortheearlierauditingpaper,

• seehowmanyyoucanremember!

• f

• f

• c

• l

• b

• g

Chapter 7 Paper P1Auditors and Internal Controls December 2013 Examinations

64

65 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click here Chapter 8

ManageMent InforMatIon SySteMS

• informationflowsarevitalifmanagementaretobeabletomanageriskandmonitorinternalcontrols

• threeelementswhichshouldbeapparent:

• bothinternalandexternalinformationisrequiredinorderthatinformeddecisionscanbemade

• theinformationshouldbeprovidedonaregularbasisinorderthatmanagementcanmonitorperformanceofeconomy,efficiencyandeffectiveness

• there needs to be clearly defined, effective channels of communication within the organisation so thatmanagementreceivetheinformationonatimelybasis

Chapter 8 Paper P1Management Information Systems December 2013 Examinations

66

Information characteristics

• a accessible

• a adequate

• c complete

• c concise

• c consistent

• i integrated

• o objective

• p provable

• r relevant

• r reliable

• t timely

• u unbiased

• u understandable

67 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click hereChapter 9

The Risk ManageMenT PRoCess

Risk and corporate governance

• goodcginvolveseffectiveriskmanagement,andthateffectiveriskmanagementinturninvolvesasoundsystemofinternalcontrol(TurnbullReport)

• goodcorporategovernancewilleliminateordecreasemanyoftherisksfacinganentity

• fairtreatmentofshareholders

• rightsofshareholders

• theroleofstakeholders

• disclosurerequirementsandtransparencyarrangements

• boardresponsibilities

Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

68

First three principles of good corporate governance

• Fairtreatmentofshareholders

• preferentialtreatmentshouldnotbegiventoanyonegroupofshareholders

• othershareholderscouldresentthisanditcouldresultinbadpublicityfortheentity

• Rightsofshareholders

• theentitymaynotallowshareholderstheirrights

• forexample, if theentity fails toallowashareholder to join indiscussionsatanAGM,or if theentity fails tocommunicatethedetailsoftheAGM

• Theroleofstakeholders

• entitiesmayignorestakeholders

• astakeholdergroupcouldbetreatedinappropriately

• forexample,ifanentitytriestomakeanemployeeredundantwithoutfollowingestablishedlegalprocedure

69Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

Final two principles of good corporate governance

• Disclosurerequirementsandtransparencyarrangements

• directorspossiblyfailtoprovideappropriatereports

• directorsfailtoreportthetruefinancialpositionoftheentity

• itisnecessarilythecasethat,forproperdisclosureandtransparency,asoundsystemofinternalcontrolintheentityshouldexist

• Boardresponsibilities

• theboardpossiblydoesnotcontroltheentityadequately

• theboardattemptstoruntheentityfortheirownbenefitratherthanforthebenefitofshareholdersandotherstakeholders

Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

70

Management’s responsibility for risk management

• Riskisdefinedas“thechanceofexposuretotheadverseconsequencesofuncertainfutureevents”

• Itcanthereforebeseenthat:

• riskcanadverselyaffecttheachievementoftheentity’sobjectives

• byreducingthelikelihoodofanevent,oritspotentialimpact,theriskismanaged

• theresponsibility formanagingtherisk ismanagement’sandtheydosobyestablishingariskmanagementsystem

• Processofriskmanagementsystemestablishment

• identify–preparelistofpotentialrisks

• analyse–prioritisethepotentialrisks

• reporttomanagementabouttherisksidentified

• designriskmanagementsystem–prepareavoidanceandcontingencyplans

• recommenddesignedsystemforimplementation

• implement–putinplacetheacceptedsystem

• evaluate–monitorand,ifnecessary,re-analyse

71Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

Risk management

• necessarytomanagerisk:

• identifynewrisksthatmayaffecttheentitysoanappropriatemanagementstrategycanbedesigned

• identifychangestoexistingorknownriskssoanamendmentmaybemadetoexistingstrategy

• ensurethatbestuseismadeofchangingopportunities

• managingtheupside

• riskappliesequallyto“goodnews”

• thisupsideriskneedstobemanagedjustasmuchasdownsiderisk

• managementoftheupsideriskisviewedinadifferentwaythanthedownsidebecause:

• risksareseenasopportunitiestobeusedtoadvantage

• organisationsareprepared toaccept someuncertainty inorder togaingreaterbenefitsandhigher rewardsassociatedwithhigherrisk

• riskmanagementisusedtoidentifyrisksassociatedwithnewopportunitiesleadingtoanincreaseinprobabilityofprofitabilityandmaximisedreturns

• effectiveriskmanagementisseenasawayofimprovingshareholdervaluebyimprovingperformance

• ALARPattitudetoriskmanagement

• manageriskdowntoalevelaslowasreasonablypossible

• basically,acostbenefitanalysis

Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

72

• strategicoroperational?

• strategic risksarethosewhicharisefromthepossibleconsequencesofstrategicdecisionstakenwithintheorganisation

- examplewouldbewhereoneentitypursuesastrategyofgrowthbyacquisitionwhereasanotheraimstogroworganically

- “acquisition”entityisexposedtoagreaterdegreeofrisk,butthepotentialreturnsarelikelytobegreater

• operational risks aretherisksoflossesresultingfrominadequateorfailedinternalprocesses,peopleandsystems,orfromexternalevents

- referstothepotentiallosseswhichmightariseinbusinessoperations

- includesriskoffraudortheftbyemployees

- canbemanagedbyinternalcontrolsystems

73Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

sources and impacts of business risks

• businessesfaceriskfromanumberofdifferentsources:

• market–risksassociatedwiththesectororindustryinwhichtheentityoperates

• credit–relatestothecreditratingofthebusiness,andthereforeitsabilitytoraisefinance

• liquidity–theriskofbeingunabletomeetdebtsastheyfallduebecauseofinsufficientcash

• technological–relatestotherisksassociatedwhereafast–changingtechnologyaffectsthemarketorproducts

• legal–riskassociatedwiththeneedtocomplywithlawandregulation

• healthandsafetyandenvironmentalissues

• reputation–thepossibilityofdamagetotheentity’simagearisingfrompoorperformanceoradversepublicity

• businessprobity–relatestothegovernanceandethicsoftheentity

• derivatives–risksduetotheuseoffinancialinstruments

Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

74

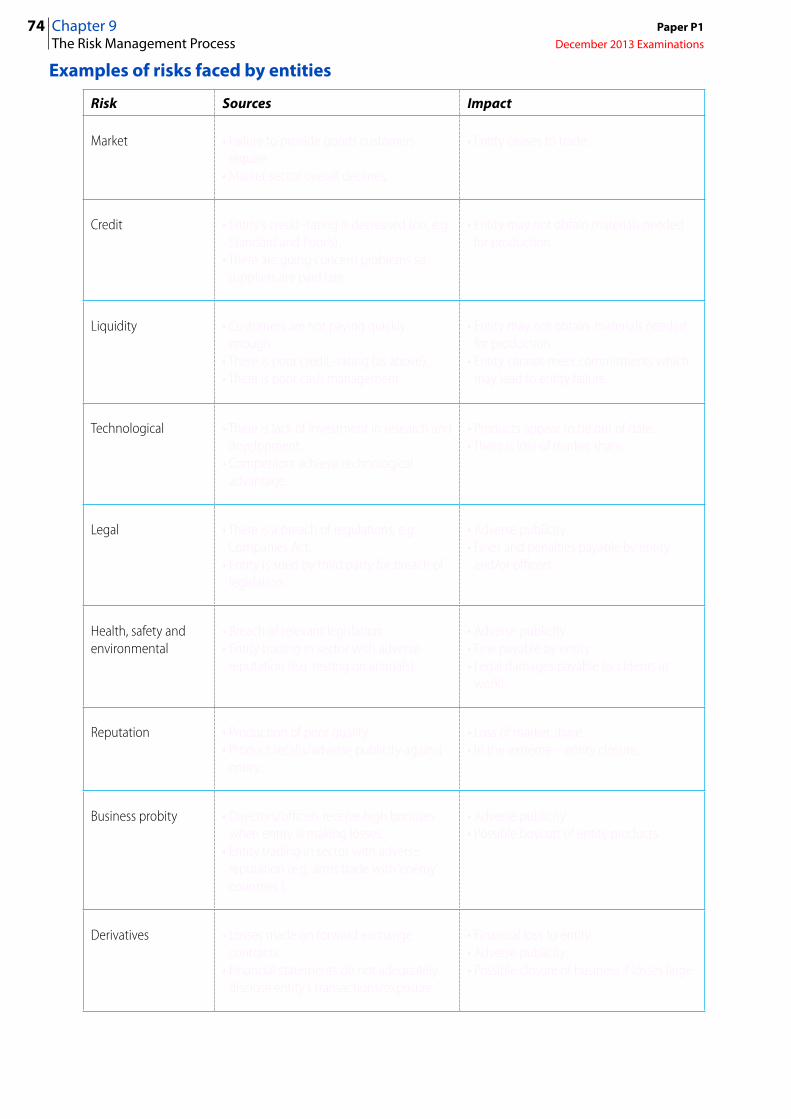

examples of risks faced by entities

Risk Sources Impact

Market •Failuretoprovidegoodscustomersrequire

•Marketsectoroveralldeclines.

•Entityceasestotrade.

Credit •Entity’scredit–ratingisdecreased(on,e.g.StandardandPoor’s).

•Therearegoingconcernproblemssosuppliersarepaidlate.

•Entitymaynotobtainmaterialsneededforproduction.

Liquidity •Customersarenotpayingquicklyenough.

•Thereispoorcredit–rating(asabove).•Thereispoorcashmanagement.

•Entitymaynotobtainmaterialsneededforproduction.

•Entitycannotmeetcommitmentswhichmayleadtoentityfailure.

Technological •Thereislackofinvestmentinresearchanddevelopment.

•Competitorsachievetechnologicaladvantage.

•Productsappeartobeoutofdate.•Thereislossofmarketshare.

Legal •Thereisabreachofregulations,e.g.CompaniesAct.

•Entityissuedbythirdpartyforbreachoflegislation.

•Adversepublicity•Finesandpenaltiespayablebyentityand/orofficers.

Health,safetyandenvironmental

•Breachofrelevantlegislation.•Entitytradinginsectorwithadversereputation(e.g.testingonanimals).

•Adversepublicity•Finepayablebyentity•Legaldamagespayable(accidentsatwork).

Reputation •Productionofpoorquality•Productrecalls/adversepublicityagainstentity.

•Lossofmarketshare•Intheextreme–entityclosure.

Businessprobity •Directors/officersreceivehighbonuseswhenentityismakinglosses.

•Entitytradinginsectorwithadversereputation(e.g.armstradewith‘enemy’countries).

•Adversepublicity•Possibleboycottofentityproducts.

Derivatives •Lossesmadeonforwardexchangecontracts.

•Financialstatementsdonotadequatelydiscloseentity’stransactions/exposure

•Financiallosstoentity.•Adversepublicity.•Possibleclosureofbusinessiflosseslarge

75Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

sector specific risks

• businessrisksmaybesimplygeneralrisksfacinganybusiness

• butsomeriskswillbespecifictoaparticularentity,market,orindustry

• genericrisksincludechangesininterestrates,ornon–compliancewithlaw

• inaddition,althoughariskmaybegeneral,itcanaffectdifferentbusinessesindifferentways

• aboveexampleofachangeininterestrateswillclearlyhaveoppositeaffectsforoneentitywithasubstantialdepositaccountatthebankandanotherwithalargeoverdraft!

• sectorspecificrisksrelatetoaparticularsector,andpotentiallynottoanyothersector

• forexample,sectorspecificrisksfacingaprivatehospitalcouldbe:

• inabilitytoemploysufficientnumberofjuniordoctors(orevenseniorconsultants)

• increaseincompetitionfromanotherprivatehospitalopeninginthesamearea

• improvementinstatehealthcaresystemleadingtofalloffindemandforprivatetreatment

• collapseofstatehealthcaresystemthroughlackoffunding(remember,riskcanbe“upside”aswellas“downside”)

Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

76

analysis of risk

• onewayofanalysingriskistoacknowledgethattheprobabilityofriskcouldbe“high”or“low”,andthatconsequences(impact)couldalsobe“high”or“low”

• amatrixcanbepreparedshowingthefourpossiblecombinationsof“high”/“high”,“high”/“low”etc

• whenariskisseenas“high”/“high”,itneedsurgentattention/immediateactioninordertomanagetherisk

• if the risk is“high”probability,but“low” impact, then thepositionneeds tobemonitored,and theentityneeds topreparetomeetthechange

• a“low”probability,“high”impactcombinationneedsactiontobeconsideredand,attheveryleast,acontingencyplan

• “low”probabilityand“low”impact–keepaneyeonthesituation,andbepreparedtoadapttoanychange

IMPACT/CONSEQUENCE

HIGH LOW

PROBABILITY

HIGH

LOW

77Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

Role of the board in risk analysis

• boardhasanimportantroletoplayinriskmanagement,becausethey:

• considerriskatthestrategiclevel,andthendefinetheentity’sattitudeandapproachtorisk

• areresponsibleforimplementingtheriskmanagementprocess,andthereforeforensuringthatthosechargedwithadministeringithaveappropriateresources

• arealsoresponsibleforensuringthattheriskmanagementpoliciessupporttheoverallstrategicobjectivesoftheentity

• determinethelevelofriskwhichtheentityispreparedtoacceptinordertomeetitsstrategicobjectives

• communicatetheriskmanagementstrategytotherestoftheentityandwillensurethatitisintegratedwithallotherentityactivities

• reviewtherisks,andthenidentifyandmonitortheprogressoftheriskmanagementpolicies

• determine the riskswhichwillbeaccepted,butwhichcannotbemanaged,orwhere it is tooexpensive tomanage.Thesearecalledresidualrisks

Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

78

external reporting

• Shouldreportsbemadetopeopleotherthanmanagementconcerningtheinternalcontrolsandriskmanagement?

• Pointstoconsider:

• reportingmayberequired,ormaybevoluntary

• inanextremesituation,itmaybethatthirdpartieshavetobereportedtowheremanagementisunawareofreportingrequirementsorsimplyrefusestoreportvoluntarily

• manyreportsareintendedforinternaluseonly–forexample,reportstotheauditcommittee–buttherecanbesituationswhereexternalreportingisrequired

• suchexternalreportingwillnormallyonlybedoneasarequirementofcompliancewithlaworregulation,orcompliancewithethicalguidelinesapplicableeithertotheentityitselfortotheexternalregulator

• Reportingmethods

• threeobviouswaysinwhichentityinformationcanbereportedexternally:

- annualfinancialstatements

- auditors

- auditcommittee

79Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

Reporting methods

• annualfinancialstatements-internalcontrols

• disclosureisrequiredbytheprinciplesoutlinedincgregulationsforlistedentities

• detailtobegivenisastatementofthedirectors’assessmentoftheadequacyoftheinternalcontrolsystem,andofhowthedirectorsmaintainthesystem

• annualfinancialstatements–risk

• disclosureshouldbemadeexplaininghowthedirectorshaveaddressedsomeoftherisksfacingtheentity

• disclosurewouldbemade,forinstance,intheCorporateandSocialResponsibilityReport

• auditors–internalcontrols

• wheretheinternalcontrolsystemisweak,thiscouldleadtotheauditorsissuingamodifiedauditreport

• thismodifiedreportmaythereforeincludedetailsoftheparticularareasofthecontrolsystemwhichhavegiventheauditorscauseformajorconcern

• auditors–risk

• theauditorswouldonlyreportonrisksfacingtheentityinthesituationthattheriskhasgivenrisetoamaterialerrorinthefinancialstatements

• auditcommittee–internalcontrols

• inthenormalcourseofevents,theauditcommitteewillreportitsrecommendationsaboutcontrolweaknessestotheboard

• onlyinanextremesituation(forinstance,wheretheboardignorestherecommendationsandthesituationisserious)willtheauditcommitteereportexternally(called“whistleblowing”)

• auditcommittee–risk

• itwouldbeunusualforanauditcommitteetoreportexternallyonmattersconcerningrisk

Chapter 9 Paper P1The Risk Management Process December 2013 Examinations

80

81 Paper P1December 2013 Examinations

Free lectures available for Paper P1 - click hereChapter 10

Controlling risk

• risk targeting

• riskmanager

• riskmanagementcommittee

• audit(internalandexternal)

• risk reduction

• riskawareness

• embeddingriskinsystems

• embeddingriskinculture

• diversification

• risk avoidance / retention / modelling

• riskavoidanceandretention

• riskattitude

• needforrisk

• attitudetorisk–doessizematter?

Chapter 10 Paper P1Controlling Risk December 2013 Examinations

82

risk targeting – risk manager

• leaderoftheriskmanagementcommittee

• reportsdirectlytotheboard

• roleisprimarilytooverseeimplementationoftheboard’sriskmanagementpolicies

• supportedbyriskmanagementcommittee

• notnormallyinvolvedindeterminingstrategy

• moreofanoperationalrole

• policiestobeimplementedaredecidedbyboardandriskmanagementcommittee