Issues-paper-pharmaceutical-sector-Tunisia-april ... - OECD

22

Promoting investment and business climate reforms in Tunisia’s pharmaceutical sector Issues paper Tunis, 5 April 2022 This note aims to guide the discussions of a meeting on “Promoting investment and business climate reforms in Tunisia’s pharmaceutical sector” on 5 th April 2022 in Tunis. The meeting will bring together Tunisian policymakers, representatives from the pharmaceutical sector and development partners to share their views and perspectives on the next steps to promote the development of the pharmaceutical sector in Tunisia, including the need for co-ordination of policies and initiatives. This note is a draft document. Please do not quote or cite. Contact [email protected] OFDE

-

Upload

khangminh22 -

Category

Documents

-

view

9 -

download

0

Transcript of Issues-paper-pharmaceutical-sector-Tunisia-april ... - OECD

Promoting investment and business climate reforms in Tunisia’s pharmaceutical sector

Issues paper Tunis, 5 April 2022 This note aims to guide the discussions of a meeting on “Promoting investment and business climate reforms in Tunisia’s pharmaceutical sector” on 5th April 2022 in Tunis. The meeting will bring together Tunisian policymakers, representatives from the pharmaceutical sector and development partners to share their views and perspectives on the next steps to promote the development of the pharmaceutical sector in Tunisia, including the need for co-ordination of policies and initiatives. This note is a draft document. Please do not quote or cite. Contact [email protected]

OFDE

2 |

Promoting investment and business climate reforms in Tunisia’s pharmaceutical sector

The pharmaceutical industry is an important and growing sector for many economies worldwide. In 2020, global revenues from the pharmaceutical sector surpassed USD 1.3 trillion and are expected to reach USD 1.6 trillion by 2025 (IQVIA Institute, 2021[1]). While the sector remains dominated by the United States, the European Union, and Japan (EFPIA, 2020[2]), there are increasing opportunities for emerging markets. A stronger pharmaceutical sector can help drive economic development, achieve positive health outcomes, including COVID-19 recovery, and overall country resilience.

Promoting more investment in pharmaceuticals has been a priority for Tunisia as well as other economies of the Middle East and North Africa (MENA) region. With a market of over USD 32 billion, the pharmaceutical sector in MENA is expected to have a growth rate of almost 10% yearly, roughly twice as fast as the global market (IQVIA, 2019[3]). Such demand is driven by growing populations, longer life expectancy, new therapeutics and vaccines, as well as the rise of lifestyle related diseases, such as cancer, cardiovascular diseases, chronic respiratory tract diseases, diabetes, strokes, and increased prioritisation of healthcare services by governments in the region (Burton, 2019[4]).

The post-pandemic recovery presents an opportunity for Tunisia to advance on the necessary reforms to make its pharmaceutical market more attractive for investments. Tunisia has the potential to play an important role in the future mRNA technology transfer hub aiming to empower low- and middle-income countries to produce their own vaccines, medicines and diagnostics to address health emergencies and reach universal health coverage (WHO, 2022[5]).

In recent years, a number of initiatives were introduced in Tunisia to foster investments in the pharmaceutical sector, including a roadmap documentcalled “Pacte de Partenariat Public Privé pour le développement de la compétitivité du secteur pharmaceutique” (Pacte sectoriel) developed in 2019. While the Pacte sets concrete objectives for the development of the sector and was developed through a process of consensus among all relevant stakeholders, the majority of its recommendations have yet to be implemented. Further areas of reform include improving investment strategies and business climate reforms, fostering intellectual property rights protection (IPRs), and enhancing trade and participation in value chains. A comprehensive industrial strategy as well as a stronger governance system for the sector is also needed.

The OECD has developed best practice tools to support policy makers in decision making on key questions concerning access and pricing of medicines, handling of property rights and developing innovation in the pharmaceutical sector. This includes recommendations (OECD Recommendation of the Council on the Licensing of Genetic Inventions), reports (OECD Report on Pharmaceutical Innovation and Access to Medicines) and assessment frameworks (OECD Policy Guidance for Pharmaceutical Pricing in a Global Market) to evaluate the impact of health and R&D policies and options to address current challenges for policy-makers in this sector. These tools can help Tunisia design appropriate reforms to meet public health objectives and support the development of its pharmaceutical sector.

| 3

The pharmaceutical industry is a key sector for Tunisia’s growth and competitiveness

Although it represents only 1.5% of gross domestic product (GDP) and has a market size of USD 681 million (in terms of sales), the pharmaceutical sector is one of the fastest growing industries in Tunisia (Fitch Solutions, 2021[6]). The market is expected to expand at a compound annual growth rate of 11.1% from 2021 to 2025 to reach USD 747 million (ibid). The government allocates a sizeable portion of its expenditures towards health spending, currently standing at 7.3% of GDP, higher than its regional neighbours such as Algeria (6.2%), Egypt (4.9%) and Morocco (5.3%) (World Bank, 2018[7]).

Despite its small market size, Tunisia is a suitable destination for pharmaceutical investors looking to export to African and European markets. Currently, there are over 70 companies in Tunisia active across all segments of the pharmaceutical value chain, from research and development activities, manufacturing inputs for the pharmaceutical industry, to production and distribution channels (Tunisia Investment Authority, 2022[8]). In 2020, total local production of pharmaceutical companies was estimated at over USD 474 million (ibid). The market is shared between companies that produce drugs for human use (29%), followed by single use pharmaceutical products (27%), and other pharmaceutical products (16%) (Figure 1).

Figure 1: Breakdown of pharmaceutical companies in 2021

By segment

Source: Tunisia Investment Authority

The pharmaceutical market is shared between local manufacturing firms (53% of total market value) and multinational enterprises (47%). Together, these companies employ over 13,000 people (FIPA, 2020[9]). A significant portion of the jobs are high skilled labour, including pharmacists, doctors, engineers, and veterinarians, with average salaries that are among the highest in the country (World Bank, 2016[10]). Generic medicines dominate the market with more than two thirds of the local production (by volume) while the remaining part is patented pharmaceuticals (Oxford Business Group, 2019[11]).

Drugs for human use29%

Single use pharmaceutical products

27%

Other pharmaceutical products

16%

Veterinary medicinal products

12%

Bandages16%

4 |

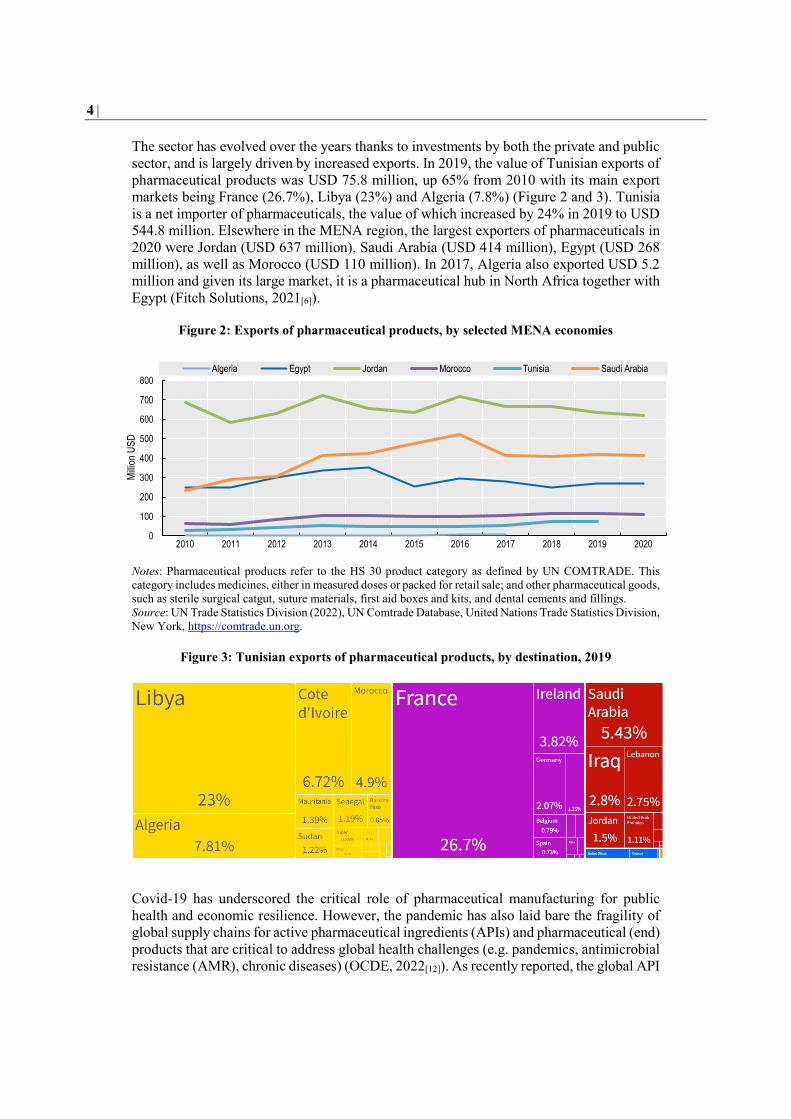

The sector has evolved over the years thanks to investments by both the private and public sector, and is largely driven by increased exports. In 2019, the value of Tunisian exports of pharmaceutical products was USD 75.8 million, up 65% from 2010 with its main export markets being France (26.7%), Libya (23%) and Algeria (7.8%) (Figure 2 and 3). Tunisia is a net importer of pharmaceuticals, the value of which increased by 24% in 2019 to USD 544.8 million. Elsewhere in the MENA region, the largest exporters of pharmaceuticals in 2020 were Jordan (USD 637 million), Saudi Arabia (USD 414 million), Egypt (USD 268 million), as well as Morocco (USD 110 million). In 2017, Algeria also exported USD 5.2 million and given its large market, it is a pharmaceutical hub in North Africa together with Egypt (Fitch Solutions, 2021[6]).

Figure 2: Exports of pharmaceutical products, by selected MENA economies

Notes: Pharmaceutical products refer to the HS 30 product category as defined by UN COMTRADE. This category includes medicines, either in measured doses or packed for retail sale; and other pharmaceutical goods, such as sterile surgical catgut, suture materials, first aid boxes and kits, and dental cements and fillings. Source: UN Trade Statistics Division (2022), UN Comtrade Database, United Nations Trade Statistics Division, New York, https://comtrade.un.org.

Figure 3: Tunisian exports of pharmaceutical products, by destination, 2019

Covid-19 has underscored the critical role of pharmaceutical manufacturing for public health and economic resilience. However, the pandemic has also laid bare the fragility of global supply chains for active pharmaceutical ingredients (APIs) and pharmaceutical (end) products that are critical to address global health challenges (e.g. pandemics, antimicrobial resistance (AMR), chronic diseases) (OCDE, 2022[12]). As recently reported, the global API

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Millio

n USD

Algeria Egypt Jordan Morocco Tunisia Saudi Arabia

| 5

market is projected to grow at a compound annual growth rate of 6.1 % from 2021-2030 (Kenneth Research, 2022[13]).

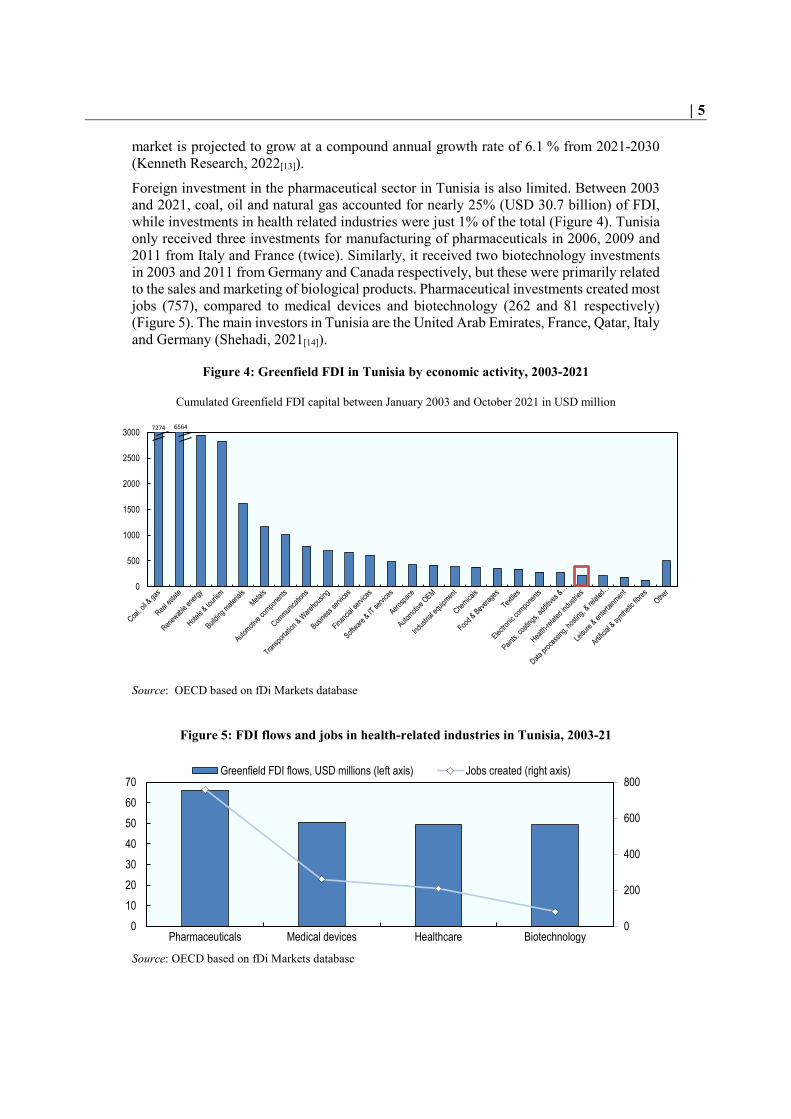

Foreign investment in the pharmaceutical sector in Tunisia is also limited. Between 2003 and 2021, coal, oil and natural gas accounted for nearly 25% (USD 30.7 billion) of FDI, while investments in health related industries were just 1% of the total (Figure 4). Tunisia only received three investments for manufacturing of pharmaceuticals in 2006, 2009 and 2011 from Italy and France (twice). Similarly, it received two biotechnology investments in 2003 and 2011 from Germany and Canada respectively, but these were primarily related to the sales and marketing of biological products. Pharmaceutical investments created most jobs (757), compared to medical devices and biotechnology (262 and 81 respectively) (Figure 5). The main investors in Tunisia are the United Arab Emirates, France, Qatar, Italy and Germany (Shehadi, 2021[14]).

Figure 4: Greenfield FDI in Tunisia by economic activity, 2003-2021

Cumulated Greenfield FDI capital between January 2003 and October 2021 in USD million

Source: OECD based on fDi Markets database

Figure 5: FDI flows and jobs in health-related industries in Tunisia, 2003-21

Source: OECD based on fDi Markets database

0

500

1000

1500

2000

2500

3000 7274 6564

0

200

400

600

800

010203040506070

Pharmaceuticals Medical devices Healthcare Biotechnology

Greenfield FDI flows, USD millions (left axis) Jobs created (right axis)

6 |

The low level of FDI in the pharmaceutical industry is partly due to the country’s relatively small domestic market, and a high level of perceived political risk, which deters multinational pharmaceuticals from investing in Tunisia (Fitch Solutions, 2021[6]). As a result, most multinational companies operate through joint ventures with domestic firms. For example, Novartis, Roche, GlaxoSmithKline, Abbott and Pfizer have contracts with the Tunisian company Teriak Laboratories to manufacture their products (ibid).

But it has yet to achieve its potential

Tunisia presents attractive opportunities for pharmaceutical companies thanks to its strategic location, abundance of university graduates, and presence of a qualified work force. Growth in the pharmaceutical sector could offer more employment opportunities for Tunisia’s unemployed or under-employed health professionals (Box 1). The overall unemployment rate among Tunisia’s university graduates has hovered at around 30% since 2016 (World Bank, 2022[15]) and led to emigration and brain drain. Possible avenues to explore opportunities in the pharmaceutical sector could include schemes that Tunisia has been developing since 2015 to improve employment opportunities for graduates. This includes the Decent Work Country Programme in Tunisia for 2017-2022 and the PAX-co scheme, under which training programmes are co-constructed by private companies and public universities (UNESCO, 2015[16]).

Box 1. Pharmaceutical sector role in women’s economic empowerment in Tunisia

Growth in the pharmaceutical sector can create new business and employment opportunities for women in Tunisia, who suffer from high unemployment rates among graduates and high-skilled workers (ILO, 2015[17]).

• Women account for a smaller share of students studying engineering (44%) than men, but they make up a high share of students studying the Natural Sciences (77%) and Health and Welfare (75%) (UNESCO, 2019[18]).

• In 2018, women in Tunisia made up 56% of scientific researchers in the country, far exceeding the global share of women in research of 33.3% and the European Union share of 33.8% (UNESCO, 2019[19]). However, Tunisia’s share of women among researchers in the business enterprise sector is 30%.

• Of the 6,757 pharmacists registered as members of the Tunisian National Council of Pharmacists in 2019, 56% were women (CNOP, 2019[20]).

Expanding exports is directly tied to improving local manufacturing capacities to compete successfully with other regional hubs such as Egypt and Algeria. During consultations with pharmaceutical business associations in Tunisia, stakeholders have repeatedly emphasised the need for greater policy coherence to enable Tunisia to develop as a hub for the African pharmaceutical industry (Box 2).

| 7

Box 2. Pharmaceutical sector in Africa

Africa has relatively few local or regional pharmaceutical manufacturing companies. As of 2019, there were about 375 drug manufacturers on the continent, the majority of them in North Africa (McKinsey, 2019[21]). In sub-Saharan Africa, only Nigeria, Kenya and South Africa have a relatively large market with most of the companies producing for domestic markets and in some cases exporting to neighbouring countries (ibid). By comparison, China and India, each home to roughly 1.4 billion in population, have as many as 5,000 and 10,000 drug manufacturers, respectively (McKinsey, 2019[22]). However, not all these manufacturers meet international standards of Good Manufacturing Practice and thus can only sell in domestic markets.

Tunisia’s healthcare system includes over 90% health insurance coverage, healthcare infrastructure at both primary and tertiary levels and a relatively strong local pharmaceutical industry, with biosimilar and generic production (WHO, 2016[23]). The pharmaceutical industry manufactures in line with international quality standards (IPEMED, 2015[24]). The National Authority for Assessment and Accreditation in Healthcare (INEAS) established in 2012 under the auspices of the Tunisian Ministry of Health, is further mandated with the regulation and evidence-based assessment of the health system through quality and efficiency (Decree No. 1709) (INEAS, 2019[25]). This strong framework has led to a significant increase in the coverage of the pharmaceutical market’s needs by local production, from 14% in 1990 to over 52% in 2019 (de Sinta, 2021[26]).

In recent years, the government has prioritised improving the regulatory framework for investment, including for the pharmaceutical sector. In 2014, a new legal framework was put in place to govern clinical trials. This was followed in 2016 with a revamped of its investment legal framework, starting with a new Investment Law (OECD, 2021[27]). Since then, the government has continuously pursued legislative reforms to progressively strengthen investor rights, create a more investor-friendly environment and narrow the policy gap between foreign and domestic investors (ibid).

Another aim of the Pacte Sectoriel is to further enhance the potential of the sector with concrete reform objectives through 2023. Developed with the support of the World Bank, the Pacte aims to improve the national ecosystem in terms of infrastructure, governance, training, and investment. Its objectives include maintaining a growth higher than 8% in local production, creating an additional 4,000 jobs, increasing exports of locally produced pharmaceutical products from 17 to 30% of total exports, as well as increasing the total pharmaceutical market coverage by local manufacturing from 53 to 62% by 2023.

Still there is more that Tunisia’s private and public sectors could do to realise the potential of the country as a pharmaceutical hub attracting global investors to supply neighbouring markets and integrate the economy into international chains of pharmaceutical production.

Key challenges continue to dampen investments in the pharmaceutical sector

While the public-private dialogue process and the resulting Pacte sectoriel in 2019 identified key policy priorities and actions to make the sector more competitive for investors, several challenges remain that are negatively affecting investments in the sector. In this context, the consultation will focus on three main challenges hindering the potential impact of the sector on economic development: (i) inadequate business and regulatory

8 |

environment; (ii) weak intellectual property protection and limited research and development (R&D); and (iii) limited trade and integration in value chains.

Inadequate business and regulatory environment Tunisia made progress in improving its overall business and regulatory environment for investors through the 2016 Investment Law, which simplified investment procedures and removed a screening requirement for foreign majority owned projects (OECD, 2021[27]). Foreign investors are also allowed to hold up to 100% of the capital for the construction of pharmaceutical plants and private clinics, guaranteed free transfer of capital and offered a reduction of customs duties for equipment and raw materials (TABC, 2018[28]). In 2019, the government also tax reductions for companies operating in the pharmaceutical sector (Fitch Solutions, 2021[6]). Overall, these reforms are reflected in the OECD FDI Regulatory Restrictiveness Index, where Tunisia displays a relatively open environment for investment (Figure 6).

Figure 6: OECD FDI Regulatory Restrictiveness Index, selected sectors

Closed =1, Open=0, 2019

Source: OECD, 2020.

Yet, despite this progress, there remain several challenges specific to the pharmaceutical sector, including unclear pricing and reimbursement procedures, and long timeframes for marketing authorization.

Distorted price-setting procedures and delays in payment for imported products

Currently, the Central Pharmacy of Tunisia (PCT) has the monopoly over all imported pharmaceutical products, at a price and procedure established by the Ministries of Health, Social Affairs and Commerce. The government determines the price based on, in part, a reference to the price in the exporting country reduced by 12.5%. Other factors, such as the price of other products in the same therapeutic category, are also part of the pricing calculation. The price is not adjusted on a regular basis to inflation (although this holds true for many countries that do not routinely adjust prices with inflation) and the devaluation of the Tunisian dinar (Fitch Solutions, 2021). An additional challenge foreign companies face is the obligation to carry the risk of dinar depreciation for a period of four years from the moment they receive the marketing authorisation (MA).

0

0.2

0.4

0.6

0.8

1

1.2

OECD average Algeria Egypt Jordan Lebanon Libya Morocco Palestinian Authority Tunisia

Total Manufacturing Oil ref. & Chemicals Distribution Transport

| 9

While it is normal practice to have high levels of government price controls on pharmaceutical products to meet public health objectives (OECD, 2008[29]), the multiplicity of Tunisian actors involved in this process and lack of coordination have led to unclear and inconsistent pricing procedures. It is also reported that pricing procedures lack transparency and low trust between ministries (ITES, 2022[30]). Overall, such procedures have led to sub-optimal conditions for the industry and resulted in a distortive impact on the international trade of Tunisian pharmaceutical products (World Bank, Ministere de la santé and CNIP, 2017[31]).

Payment for imported pharmaceutical products is also assured by the PCT which currently faces significant payment arrears to foreign suppliers creating significant impediments to business continuity for international investors. This issue has been ongoing for the past four years creating an unpredictable environment for the marketing of new products (Fitch Solutions, 2021[6]). As of September 2020, arrears totalled more than USD 27.1 million. According to interviews with private sector stakeholders, payment delays by the PCT are now an important risk to companies’ (primarily importing ones) ability to continue to supply the market.

The Pacte sectoriel identified pricing reforms that could improve the sector’s performance, including establishing a single price mechanism to replace the current fragmented process, but such reforms have not yet been undertaken. While the impact of payment arrears from sales to the PCT on business continuity is primarily felt by international investors that largely import their products, similar difficulties have an impact on national companies struggling with commercial viability resulting from the delay in aligning the local, fixed price with raw material and other costs.

Delays in granting Marketing Authorisation

Tunisia also faces important delays in granting marketing authorisation (MA) for pharmaceutical products. Interviews with pharmaceutical business associations in Tunisia reveal that it can still take as long as three years to obtain the MA (Figure 7). This process is applicable to all products and is longer than Morocco’s 13 months with similar submission procedures (Ministère de la Santé Marocain, 2015[32]). In Tunisia, pricing is also part of the MA process, which takes an additional year, compared to 2-3 months in Morocco. Reasons for this long timeframe include frequent price negotiations during the entire process (at least four rounds and sometimes leading to 90% price decrease), and delays in processing the files at various levels of government without a transparent timeline.

Today, to register a drug and obtain marketing authorisation, an application must be first reviewed by the Directorate of Pharmacy and Medicine, then approved by the National Laboratory for the Control of Medication (LNCM), which takes around 24 months. The file is subsequently sent to other committees such as technical, drug procurement, pricing, and reimbursement committees with several rounds of price negotiations that can take numerous years.

According to OECD interviews, such complex price negotiation processes and overall delays could be addressed by setting up a medicine agency (Agence du Medicament) to supervise the overall MA process, and establish a unique price committee (Comité Unique de Fixation des Prix) to avoid numerous price negotiations along the process. Moreover, prioritising the use of digital platforms (e.g digitising the LNCM) could further help to accelerate the MA process.

10 |

Figure 7: Timeline of marketing authorisation, pricing and reimbursement process for Tunisia’s pharmaceutical products

Source: SEPHIRE

Given that local manufacturers produce mostly generic products, such delays and procedures primarily affect foreign companies, leading to fewer novel products marketed in Tunisia compared to other countries in the region. For instance, in 2010-2018, the number of approvals of novel medicines, known as new molecular entities (NMEs) in Tunisia was 11, compared to 94 in the United Arab Emirates, 92 in Lebanon, or 29 in Morocco (Figure 8).

Figure 8: Number of NMEs registered, launched and reimbursed between 2010 and 2018, selected countries

Source: PhRMA, Assessment of access to medicines timelines in selected countries in Middle East and Africa, Project Report, December 2018

Finally, a major challenge facing Tunisia and directly affecting the pharmaceutical sector is the need to align the priorities of various ministries. The ministries involved in regulating the market include the Ministry of Health, the Ministry of Industry and Trade, and the Ministry of Social Affairs. Currently there is no governance mechanisms providing any leading role to a Ministry in the development and implementation of a pharmaceutical strategy. The government has been discussing the creation of a Drug Agency to bring together existing structures and regulate the pharmaceutical sector but this has not yet materialised. In this process, current development partners involved in proposing sectoral reforms, should also make efforts to eliminate overlap and duplication.

0102030405060708090

100

UAE Lebanon Saudi Arabia Egypt Jordan Kuwait Morocco Algeria Tunisia

Number of NMEs registered Number of NMEs launched Number of NMEs reimbursed

| 11

Weak intellectual property protection and limited research and development Tunisia has yet to establish a research policy and promote more R&D to consolidate its pharmaceutical industry. Currently, the bulk of investment from multinational companies focuses on upgrading manufacturing capabilities rather than on actual research (Fitch Solutions, 2021[6]). Limited R&D can reduce the interest of companies focusing on new generation medicines, such as the ones based on biotechnology, which are expected to represent more than half of top 100 selling medicines by 2026 (Evaluate Pharma, 2021[33]).

One particular challenge is weak protection of intellectual property rights (IPRs), which, according to the private sector, is hampering innovation in the sector. The International Property Rights Index (IPRI) currently ranks Tunisia 80th globally, and 11th out of 15 countries in the region in terms of property rights protection (evaluating patent, trademark and copyright protection, as well as perception of IP rights) (Property Rights Alliance, 2021[34]). The private sector reveals that there are often cases of patent infringement where generic versions of patented medicines are launched while the patent is still in effect. This includes infringement of two of Novartis’s innovative medicines in Tunisia. According to Fitch’ Solutions' Innovative Pharmaceuticals Risk/Reward Index, Tunisia is the least attractive country in the MENA region for patent respect, pricing regime, and protectionism (together with Algeria) (Table 1).

Table 1. Pharmaceutical Industry Risk Scores 2021, selected MENA countries

0-100 (lower risk)

Patent Respect Pricing Regime Protectionism

UAE 77.3 70.8 81.5

Saudi Arabia 38.9 38.4 33.3

Morocco 89.4 38.4 51.9

Egypt 38.9 19.0 17.6

Lebanon 38.9 38.4 51.9

Jordan 54.2 38.4 51.9

Algeria 21.3 38.4 17.6

Tunisia 21.3 38.4 17.6

Regional average 49.1 50.2 41.6

Global average 50.4 50.4 50.3

Notes on the methodology for calculation of the scores. Patent respect: markets with fair and enforced intellectual property regulations score higher than those with endemic counterfeiting; Pricing regime: markets with a free pricing environment score higher than markets where governments and private sector payers put downward pressure on pharmaceutical prices as a mechanism to control expenditure; Protectionism: High scores are awarded to markets which have realised the economic and social benefit of pharmaceuticals, in turn modernising the provision of healthcare through reforms and essential drug lists and encouraging local manufacturing and research and development by foreign firms.

Source: Fitch Solutions' Innovative Pharmaceuticals Risk/Reward Index, 2021

12 |

Currently, R&D is driven largely by the public sector but the government intends to encourage more contribution from the private sector, in particular though university-industry R&D collaboration (Figure 9) (WIPO, 2021[35]). Often, research collaboration between universities and Tunisian firms is implemented only in the short-term with objectives of achieving limited activities related to R&D or to use equipment that exist in universities. Tunisia has 35 research centers with, more than 600 units focusing on scientific research and some 150 laboratories (de Sinta, 2021[26]). To promote more university-industry R&D collaboration, Tunisia established BiotechPoles, a technopark focusing on biotechnologies and pharma industries among others, to strengthen collaboration between private companies, R&D institutions and universities (Biotechpole, 2022[36]).

Figure 9: Global Innovation Index, selected economies

(0-100=most innovative), 2021

Source: Global Innovation Index 2021, World Intellectual Property Organisation.

More R&D can also be supported by blended finance mechanisms, where development finance can be used for the production and manufacturing of pharmaceutical products. One practical example of this mechanism is the Investment Fund for Health in Africa, a private equity fund focused on privately backed healthcare SMEs. The fund targets, among others, healthcare product manufacturing and supply, and wholesale and distribution of pharmaceutical products in sub-Saharan Africa. The fund includes guarantees and insurance from public and philanthropic investors (IFHA, 2020[37]).

Limited trade and integration in value chains Currently, pharmaceutical manufacturers in Tunisia face several challenges including the lack of infrastructure to allow direct air routes and maritime connections, and high logistics costs that hinder their domestic and cross-border operations (Grand View Research, 2021, 2020[38]). Almost 50% of exporting firms in Tunisia identify transport costs as a major constraint on their activity (Figure 10) (World Bank, 2020[39]). This is a higher share compared to Tunisia’s neighbours in the Mediterranean, adding to logistics costs and further limiting its integration in value chains (OECD, 2018[40]). The Tunisian airline company (Tunisair) also reportedly lacks the fleet to export pharmaceuticals (IPEMED, 2015[41]).

0

5

10

15

20

25

30

35

40

45

Turkey Tunisia Morocco Jordan Lebanon Egypt Algeria

Global innovation index Innovation linkages

| 13

More efforts are needed to focus on shortening average time spent at the border by all firms, notably in the country’s main ports (OECD, 2015[42]). Such delays can impact all segments of a global value chain and limit its competitiveness. Delays in importing raw materials can negatively impact the export potential of Tunisian pharmaceutical firms, which are mostly specialised at the fabrication and distribution stages.

Figure 10: Exporting firms identifying transport costs as a major constraint, selected MENA economies

As % of manufacturing firms

Source: World Bank, Enterprise surveys, 2020

Tunisia can also do more to actively promote business partnerships between foreign investors and domestic firms that can act as suppliers or local partners, so as to facilitate knowledge transfer and higher participation in value chains. For instance, such business linkages can contribute to increasing the share of domestic value-added in Tunisia’s pharmaceutical exports. According to the OECD Trade in Value Added database, in 2018, Tunisia’s domestic value added share of gross pharmaceutical exports1 amounted to 53.7% of total gross exports, lower than Morocco (77.2%), Saudi Arabia (77.9%) or South Africa (74.9%) (OECD, 2018[43]). Successful experiences by other countries show that coordination of investment and trade promotion activities could play a critical role in enhancing such value chains.

Despite its geographic proximity to Europe, sub-Saharan Africa and the Middle East countries, Tunisia lags behind major exporters, such as Jordan, in terms of development of a robust, export-oriented national industry (in addition, Jordan has a Free Trade Agreement with the United States) (Grand View Research, 2021, 2020[38]). While it has signed Free Trade Agreements with the European Union and other markets, (Tunisia Investment Authority, 2022[8]), deeper agreements that include trade and investment provisions could increase exports of pharmaceutical products. The implementation of the African Continental Free Trade Agreement could also support intra-regional trade of pharmaceutical products (UN, 2020[44]).

Promoting better representation of the private sector in Tunisia’s pharmaceutical decision making process

The Tunisian pharmaceutical industry is well represented through multiple business associations and chambers of industry/commerce (Figure 11). Since the first sectoral

14 |

dialogue in 2014, facilitated by the World Bank, the private sector has become more organised through strengthened collaboration of two main organisations: the National Chamber of Local Manufacturing Companies (CNIP) and the Union for Innovating Pharmaceutical Research Enterprises (SEPHIRE), which represents multinational pharmaceutical firms. Tunisia is also one of the few countries in the region to participate in the Middle East and Africa Code of Promotional Practices (MEACPP) that provides guiding principles for companies to self-regulate marketing and promotional practices (often associated with lobbying) (Salhout and Bechter, 2018[45])(Box 3).

Box 3. Lobbying practices in the pharmaceutical sector

Pharmaceutical lobbying is the set of measures implemented by manufacturers in the sector to influence public health decisions according to certain interests or causes. In the United States where data on lobbying is widely available, the pharmaceutical is the sector with the largest expenditure dedicated to lobbying, estimated at more than USD 300 million1 (OECD, 2021[46]). For the European Union this number is lower with estimates around EUR 36 million, which still makes the pharmaceutical industry part of the largest lobbying sectors in terms of expenditure (Corporate Europe Observatory, 2021[47]).

While lobbying is legal, it needs to be honest, transparent and fair and avoid being unethical by encouraging policy makers to defend other interests than the public good (OECD, 2013[48]). For instance, pharmaceutical lobbies were found to engage in unethical lobbying when promoting medicines with limited clinical gains, no cost-effectiveness or that have cheaper alternatives (Vilhelmsson and Mulinari, 2017[49]) as well as to defend an intellectual property rights regime at the expense of competition (Glasgow, 2001[50]) and consumer welfare (Hawksbee, McKee and King, 2022[51]).

In 2011, the preparation of a Middle East and Africa Code of Promotional Practices in the Pharmaceutical Industry (MEACPP) was an attempt to limit lobbying drifts by setting guiding principles for pharmaceutical industries in the region to self-regulate their promotion practices. As opposed to the European self-regulation system or the US law, the code fails to enforce pharmaceutical companies to provide data on their lobbying expenditure. In Tunisia, elements of this code on promotional practices are overseen by SEPHIRE (Salhout and Bechter, 2018[45]). 1 This number covers both the pharmaceutical and health products industries and includes drug manufacturers, dealers in medical products and nutritional and dietary supplements.

Private organisations In Tunisia, businesses are mainly represented by the Tunisian Union of Industry, Trade and Handicrafts (UTICA), which is the private sector’s leading trade association. The pharmaceutical industry is represented within the UTICA by the Chambre Nationale de l'Industrie Pharmaceutique (CNIP). It plays a major role with both public and private institutions towards the sector’s development in Tunisia and abroad. Around 35 manufacturers are represented by the CNIP, from domestic manufacturing companies to international firms with production units in Tunisia.

SEPHIRE was created after the 2011 revolution and it currently represents 20 multinational firms established under Tunisian law (with or without manufacturing plants in the country).

| 15

The association is not registered under UTICA, but it plays an important role in bringing novel medicines and promoting medical research in the country. SEPHIRE also participates in the Middle East and Africa Code of Promotional Practices in the Pharmaceutical Industry (MEACPP) that promotes guiding principles for pharmaceutical companies’ self-regulation on promotional practices.

Other specialised actors are also part of the pharmaceutical ecosystem, such as the Conseil National de l’Ordre des Pharmaciens en Tunisie (CNOP) and the Syndicat des pharmaciens d’officine en Tunisie (SPOT) (under UTICA) which are both active and represent dispensary pharmacists.

Between 2014 and 2017, the World Bank supported the Tunisian pharmaceutical sector through a series of public private dialogues (PPDs), which identified the main reforms to be implemented. The PPD discussions led to the creation of additional organisations:

• Pharma In, a new cluster of pharmaceutical companies created in 2017, aims to implement collaborative projects, foster innovation, and promote “Made in Tunisia” medicine. This cluster is made up of pharmaceutical companies, the Biotech hub of Sidi Thabet, as well as research centres and academic institutes.

• The Tunisian Association of Generic Medicine (ATMG), created in 2018 promotes the use of generic drugs. This association (not affiliated with UTICA) has a heterogeneous composition, counting among its members pharmaceutical manufacturers, business executives, and media companies, as well as representatives from the order of pharmacists.

• The Tunisia Health Alliance (THA), an economic interest group of 15 firms representing the healthcare value chain in Tunisia and operating in the main sub-sectors: the pharmaceutical industry, medical devices, healthcare services, medical education and health technologies. This alliance aims to promote the export of healthcare products and services in Africa.

• The National Chamber of Contract Research Organizations (CROs), under UTICA, represents CROs in Tunisia and promotes an enabling environment for clinical trials. This group emerged from the Pacte sectoriel and the PPD working group organised on the topic of clinical trials.

16 |

Figure 11: Mapping of main private sector stakeholders and current initiatives in Tunisia

Involvement in Government’s Decision-Making As a result of the PPD, a series of dialogues and public - private sector consultations has developed through two main channels:

First Channel: Senior Government Officials Meetings with the Private Sector

Due to the frequent change of governments in recent years, the private sector took a leadership role to ensure continuity and progress of the reforms identified in the Pacte sectoriel and follow-on initiatives. CNIP, SEPHIRE, and other business associations regularly invite ministers and senior government officials to discuss and advance work on specific agreed agendas.

Second Channel: Inclusion of Private Sector in Decision-making Committees

Other initiatives under the Ministry of Industry (Dialogue sectoriel Horizon 2035), the Ministry of Economy & Planning (Plan Triennale), and the Ministry of Health (Politique nationale pharmaceutique), also include consultations with the private sector, whereby the ministries invite private sector representatives to meetings of specific committees. As it is the national representative of the pharmaceutical industry in Tunisia with the greatest number of members, CNIP tends to be invited most often to attend such Government committee meetings.

| 17

OECD policy tools can support Tunisia’s efforts to improve the competitiveness and attractiveness of its pharmaceutical sector

This note aims to guide a first discussion among the relevant public private sector stakeholders in the pharmaceutical sector in Tunisia. In this discussion, stakeholders may want to consider some policy tools developed by the OECD when engaging in policy reforms. A few examples of such tools include instruments to improve the quality of health care (e.g. OECD Health Care Quality Framework), to understand the role of the biopharmaceutical industry and the process, risks, and returns of R&D investments in pharmaceuticals (e.g. OECD Report on Pharmaceutical Innovation and Access to Medicines), as well as tools to assess the impact of pharmaceutical pricing on innovation, healthcare initiatives, etc. (e.g., Policy Guidance for Pharmaceutical Pricing in a Global Market).

In addition, the OECD has developed useful policy recommendations on the pharmaceutical sector. These can help Tunisia improve the competitiveness of its pharmaceutical sector and its attractiveness for international investors.

• The OECD Policy Guidance for Pharmaceutical Pricing in a Global Market assesses how pharmaceutical pricing and reimbursement policies have contributed to the achievement of certain health policy initiatives. It examines the national and transnational effects of these policies, in particular, their implications for the availability of medicines in other countries, the prices of these medicines, and innovation in the pharmaceutical sector (OECD, 2008[29]).

• The OECD Recommendation of the Council on the Licensing of Genetic Inventions (2006). The recommendation provides for greater collaboration in the handling of intellectual property that affect basic genetic discoveries, inventions, and the development of drugs and diagnostics, in areas of science with high relevance to COVID-19 (OECD, 2006[52]).

• The OECD Report on Pharmaceutical Innovation and Access to Medicines assesses current challenges in pharmaceutical markets, based on the best available evidence and looks at pharmaceutical industries' activities and performance. The report also describes the role of the biopharmaceutical industry, examines the process of R&D and its financing, and looks at the risks, costs and return from R&D investment for the industry. The final section is dedicated to a set of policy options to support the development of effective and coordinated responses to the pressing challenges (OECD, 2018[53]).

Finally, the OECD Policy Framework for Investment (PFI) brings together key guidelines to help governments create the right conditions to attract domestic and foreign investment. Investment policies can participate in enhancing connectivity, notably through enhancing market openness, investment promotion and facilitation, and by enhancing the impact of FDI on sustainability (OECD, 2015[54]).

18 |

References

Biotechpole (2022), Overview, https://www.biotechpole.tn/en/presentation.php. [36]

Burton, P. (2019), “MENA Pharma Market Set to Grow to USD 60 Billion”, Pharma Boardroom, https://pharmaboardroom.com/articles/mena-pharma-market-set-to-grow-to-usd-60-billion/.

[4]

CNOP (2019), Rapport de l’ordre des pharmaciens tunisiens, https://www.cnopt.tn/cnoptMTD/uploads/2020/07/RAPPORT-MORAL-2019-A-IMPRIMER-1.pdf.

[20]

Corporate Europe Observatory (2021), , Big Pharma’s lobbying firepower in Brussels: at least €36 million a year (and likely far more), https://corporateeurope.org/en/2021/05/big-pharmas-lobbying-firepower-brussels-least-eu36-million-year-and-likely-far-more.

[47]

de Sinta, T. (2021), “Tunisia : the ambitions of the pharmaceutical industry”, African News Agency, https://www.africanewsagency.fr/tunisie-les-ambitions-du-secteur-pharmaceutique/?lang=en.

[26]

EFPIA (2020), The Pharmaceutical Industry in Figures, https://www.efpia.eu/media/554521/efpia_pharmafigures_2020_web.pdf.

[2]

Evaluate Pharma (2021), World Preview 2021: Outlook to 2026, https://info.evaluate.com/rs/607-YGS-364/images/WorldPreviewReport_Final_2021.pdf.

[33]

fDi Markets (2021), fDi Markets Database. [55]

FIPA (2020), Le secteur des industries pharmaceutiques en Tunisie. [9]

Fitch Solutions (2021), Tunisia Pharmaceuticals & Healthcare Report, https://store.fitchsolutions.com/all-products/tunisia-pharmaceuticals-healthcare-report.

[6]

Glasgow, L. (2001), Stretching the Limits of Intellectual Property Rights: Has the Industry Gone Too Far?, pp. 227-258, https://ipmall.law.unh.edu/sites/default/files/hosted_resources/IDEA/2.Glasgow01.pdf.

[50]

Grand View Research, 2021 (2020), Tunisia Pharmaceutical Market Size Report, 2021-2028, https://www.grandviewresearch.com/industry-analysis/tunisia-pharmaceutical-market.

[38]

Hawksbee, L., M. McKee and L. King (2022), Don’t worry about the drug industry’s profits when considering a waiver on covid-19 intellectual property rights, https://www.bmj.com/content/376/bmj-2021-067367.

[51]

IFHA (2020), Investment Funds for Health in Africa, https://www.ifhafund.com/. [37]

ILO (2015), Labour market entry in Tunisia: The gender gap, http://ilo.org/wcmsp5/groups/public/---ed_emp/documents/publication/wcms_440855.pdf.

[17]

| 19

INEAS (2019), INEAS. [25]

IPEMED (2015), Co-production in Tunisia: Context, realisations and perspectives, http://www.ipemed.coop/adminIpemed/media/fich_article/1487264405_co-production-tunisia-v1.pdf.

[41]

IPEMED (2015), Moving towards a North African pharmaceutical market, http://www.ipemed.coop/fr/publications-r17/collection-construire-la-mediterranee-c49/moving-towards-a-north-african-pharmaceutical-market-a2517.html.

[24]

IQVIA (2019), Middle East and Africa Pharmaceutical Market Insights, https://www.iqvia.com/locations/middle-east-and-africa/library/presentations/mea-pharmaceutical-market-quarterly-report-edition-14.

[3]

IQVIA Institute (2021), Global Medicine Spending and Usage Trends: Outlook to 2025, https://www.iqvia.com/insights/the-iqvia-institute/reports/global-medicine-spending-and-usage-trends-outlook-to-2025.

[1]

ITES (2022), La sécurité sanitaire à l’horizon 2025: vision et manoeuvre stratégique, https://www.admin.ites.tn/api/uploads/6204f5b196563a695d76cbc5.pdf.

[30]

Kenneth Research (2022), Active Pharmaceutical Ingredients (API) Market Report, https://www.kennethresearch.com/report-details/active-pharmaceutical-ingredients-api-market/10352347.

[13]

McKinsey (2019), Should sub-Saharan Africa make its own drugs?, https://www.mckinsey.com/industries/public-and-social-sector/our-insights/should-sub-saharan-africa-make-its-own-drugs.

[21]

McKinsey (2019), Should sub-Saharan Africa make its own drugs?, https://www.mckinsey.com/industries/public-and-social-sector/our-insights/should-sub-saharan-africa-make-its-own-drugs.

[22]

Ministère de la Santé Marocain (2015), Bulletin Officiel numéro 6388, Décret 2-14-841 du 18 chaoual 1436, https://www.sante.gov.ma/Reglementation/REGLEMENTATIONAPPLICABLEAUPRODUITSDESANTE/2-14-841.pdf.

[32]

OCDE (2022), Shortages of medicines in OECD countries, https://www.oecd-ilibrary.org/social-issues-migration-health/shortages-of-medicines-in-oecd-countries_b5d9e15d-en.

[12]

OECD (2021), Lobbying in the 21st century, https://www.oecd-ilibrary.org/docserver/c6d8eff8-en.pdf?expires=1648213692&id=id&accname=ocid84004878&checksum=AD904B0DD541AE947EC7FECB108418CC.

[46]

OECD (2021), Middle East and North Africa Investment Policy Perspectives, OECD Publishing, https://doi.org/10.1787/6d84ee94-en.

[27]

OECD (2020), FDI Regulatory Restrictiveness Index, https://stats.oecd.org/Index.aspx?datasetcode=FDIINDEX#.

[56]

20 |

OECD (2018), Making Global value chains more inclusive in the MED region: The role of MNE-SME linkages, Draft Background paper, https://www.oecd.org/mena/competitiveness/BN-Making-global-value-chains-more-inclusive-Beirut-04201.

[40]

OECD (2018), Pharmaceutical Innovation and Access to Medicines, OECD Health Policy Studies, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264307391-en.

[53]

OECD (2018), Trade in Value Added (TiVA) 2021 ed: Principal Indicators, https://stats.oecd.org/Index.aspx?DataSetCode=TIVA_2021_C1#.

[43]

OECD (2015), A reform agenda to support competitiveness and growth, https://www.oecd.org/economy/Tunisia-a-reform-agenda-to-support-competitiveness-and-inclusive-growth.pdf.

[42]

OECD (2015), Policy Framework for Investment, https://www.oecd.org/investment/pfi.htm. [54]

OECD (2013), The 10 Principles for Transparency and Integrity in Lobbying, https://www.oecd.org/gov/ethics/Lobbying-Brochure.pdf.

[48]

OECD (2008), Pharmaceutical Pricing Policies in a Global Market, OECD Health Policy Studies, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264044159-en.

[29]

OECD (2006), Recommendation of the Council on the Licensing of Genetic Inventions, https://legalinstruments.oecd.org/en/instruments/OECD-LEGAL-0342.

[52]

Oxford Business Group (2019), Investments aimed at overhauling Tunisia’s public health system increase quality of services, Oxford Business Group, https://oxfordbusinessgroup.com/overview/path-recovery-investments-are-aimed-overhauling-public-health-system.

[11]

Property Rights Alliance (2021), International Property Rights Index, https://www.internationalpropertyrightsindex.org/.

[34]

Salhout, S. and C. Bechter (2018), The Middle East and Africa Code of Promotional Practices in the Pharmaceutical Industry, https://doi.org/10.3390/admsci8030053.

[45]

Shehadi, S. (2021), “The state of play: FDI in Tunisia”, Investment Monitor, https://www.investmentmonitor.ai/tunisia/the-state-of-play-fdi-in-tunisia#:~:text=FDI%20to%20Tunisia%20has%20not,UNCTAD)%20World%20Investment%20Report%202020.

[14]

TABC (2018), How public policy could enable the Knowledge Economy: The Case of Healthcare Sector in Tunisia, http://tabc.org.tn/wp-content/uploads/2018/11/Public-policy-to-enable-KBE-in-Africa.-The-case-of-Healthcare-sector-in-Tunisia.pdf.

[28]

Tunisia Investment Authority (2022), Pharmaceutical Sector, Tunisia Investment Authority, https://tia.gov.tn/storage/app/media/ARGUMENTAIRES/TIA_TUNISIA_PHARMA/AG%20PHARMA%20ANG.pdf.

[8]

| 21

UN (ed.) (2022), WHO announces first technology recipients of mRNA vaccine hub with strong support from African and European partners, https://www.un.org/africarenewal/magazine/february-2022/who-announces-first-technology-recipients-mrna-vaccine-hub-strong-support.

[5]

UN (2020), Ways Africa’s Free Trade Area could help mitigate effects of COVID-19, https://www.un.org/africarenewal/web-features/coronavirus/ways-africa%E2%80%99s-free-trade-area-could-help-mitigate-effects-covid-19.

[44]

UNESCO (2019), Share of female tertiary graduates by field, http://uis.unesco.org/en/country/tn. [18]

UNESCO (2019), Women as a share of total researchers (HC) & Share of women among researchers in the business enterprise sector, http://uis.unesco.org/en/country/tn.

[19]

UNESCO (2015), UNESCO Science report: towards 2030, https://unesdoc.unesco.org/ark:/48223/pf0000235406.

[16]

Vilhelmsson, A. and S. Mulinari (2017), Pharmaceutical lobbying and pandemic stockpiling of Tamiflu: a qualitative study of arguments and tactics, pp. 646-651.

[49]

WHO (2016), Tunisia: Health Systems Profile - Key Health system indicators, WHO, https://applications.emro.who.int/docs/Country_profile_2013_EN_15402.pdf.

[23]

WIPO (2021), Global Innovation Index, World Intellectual Property Organization, https://www.wipo.int/edocs/pubdocs/en/wipo_pub_gii_2021/tn.pdf.

[35]

World Bank (2022), Unemployment with advanced education (% of total labor force with advanced education) - Tunisia, https://data.worldbank.org/indicator/SL.UEM.ADVN.ZS?locations=TN.

[15]

World Bank (2020), Enterprise Surveys, https://www.enterprisesurveys.org/en/enterprisesurveys. [39]

World Bank (2018), “Current health expenditure (% of GDP)”, World Bank Indicators, https://data.worldbank.org/indicator/SH.XPD.CHEX.GD.ZS.

[7]

World Bank (2016), Dialogue boosts competitiveness of Tunisia’s pharmaceutical sector, https://blogs.worldbank.org/arabvoices/dialogue-tunisia-pharmaceutical.

[10]

World Bank, Ministere de la santé and CNIP (2017), Pharmaceuticals sector: Tunisia’s sector competitiveness enhancement through PPDs, http://www.publicprivatedialogue.org/workshop%202017/2017%20-%20Public%20Private%20Dialogue%20in%20Tunisia1.pdf.

[31]

22 |

1 This value takes into account pharmaceuticals, medicinal, chemical and botanical products.