Issues Paper on Conduct of Business in Inclusive Insurance

55

ISSUES PAPER ON CONDUCT OF BUSINESS IN INCLUSIVE INSURANCE November 2015

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Issues Paper on Conduct of Business in Inclusive Insurance

ISSUES PAPER ON CONDUCT OF BUSINESS

IN INCLUSIVE INSURANCE

November 2015

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 2 of 55

About the IAIS The International Association of Insurance Supervisors (IAIS) is a voluntary membership organisation of insurance supervisors and regulators from more than 200 jurisdictions in nearly 140 countries. The mission of the IAIS is to promote effective and globally consistent supervision of the insurance industry in order to develop and maintain fair, safe and stable insurance markets for the benefit and protection of policyholders and to contribute to global financial stability. Established in 1994, the IAIS is the international standard setting body responsible for developing principles, standards and other supporting material for the supervision of the insurance sector and assisting in their implementation. The IAIS also provides a forum for Members to share their experiences and understanding of insurance supervision and insurance markets. The IAIS coordinates its work with other international financial policymakers and associations of supervisors or regulators, and assists in shaping financial systems globally. In particular, the IAIS is a member of the Financial Stability Board (FSB), member of the Standards Advisory Council of the International Accounting Standards Board (IASB) and partner in the Access to Insurance Initiative (A2ii). In recognition of its collective expertise, the IAIS also is routinely called upon by the G20 leaders and other international standard setting bodies for input on insurance issues as well as on issues related to the regulation and supervision of the global financial sector.

Issues Papers provide background on particular topics, describe current practices, actual examples or case studies pertaining to a particular topic and/or identify related regulatory and supervisory issues and challenges. Issues Papers are primarily descriptive and not meant to create expectations on how supervisors should implement supervisory material. Issues Papers often form part of the preparatory work for developing standards and may contain recommendations for future work by the IAIS.

This paper was prepared by the Financial Inclusion Subcommittee in cooperation with the Access to Insurance Initiative and the MicroInsurance Network.

The publication is available on the IAIS website (www.iaisweb.org).

© International Association of Insurance Supervisors 2015. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 3 of 55

Issues Paper on Conduct of Business in Inclusive Insurance

Contents 1. Introduction ....................................................................................................................... 4 2. Features of the Inclusive Insurance Market ....................................................................... 7

2.1 The Inclusive Insurance Customer’s Profile ................................................................. 7 2.2 Country specific Context and Conditions ..................................................................... 9 2.3 Distribution features and risks common to inclusive insurance .................................. 11 2.4 Digitalisation of inclusive insurance transactions ....................................................... 19

3. The Inclusive Insurance Product Life Cycle ..................................................................... 22 3.1 Product Development ................................................................................................ 22 3.2 Distribution ................................................................................................................ 29 3.3 Disclosure of Information ........................................................................................... 34 3.4 Customer Acceptance ............................................................................................... 38 3.5 Premium Collection ................................................................................................... 43 3.6 Claims Settlement ..................................................................................................... 45 3.7 Complaints handling .................................................................................................. 48

4. Conclusions and Recommendations ............................................................................... 51 Annex - Background information on risks relating to the business models .......................... 53

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 4 of 55

1. Introduction 1. The International Association of Insurance Supervisors (IAIS), through the Insurance Core Principles (ICPs)1, provides a globally accepted framework for the supervision of the insurance2 sector. Its mission is to promote effective and globally consistent supervision of the insurance industry in order to develop and maintain fair, safe and stable insurance markets for the benefit and protection of policyholders3; and to contribute to global financial stability.

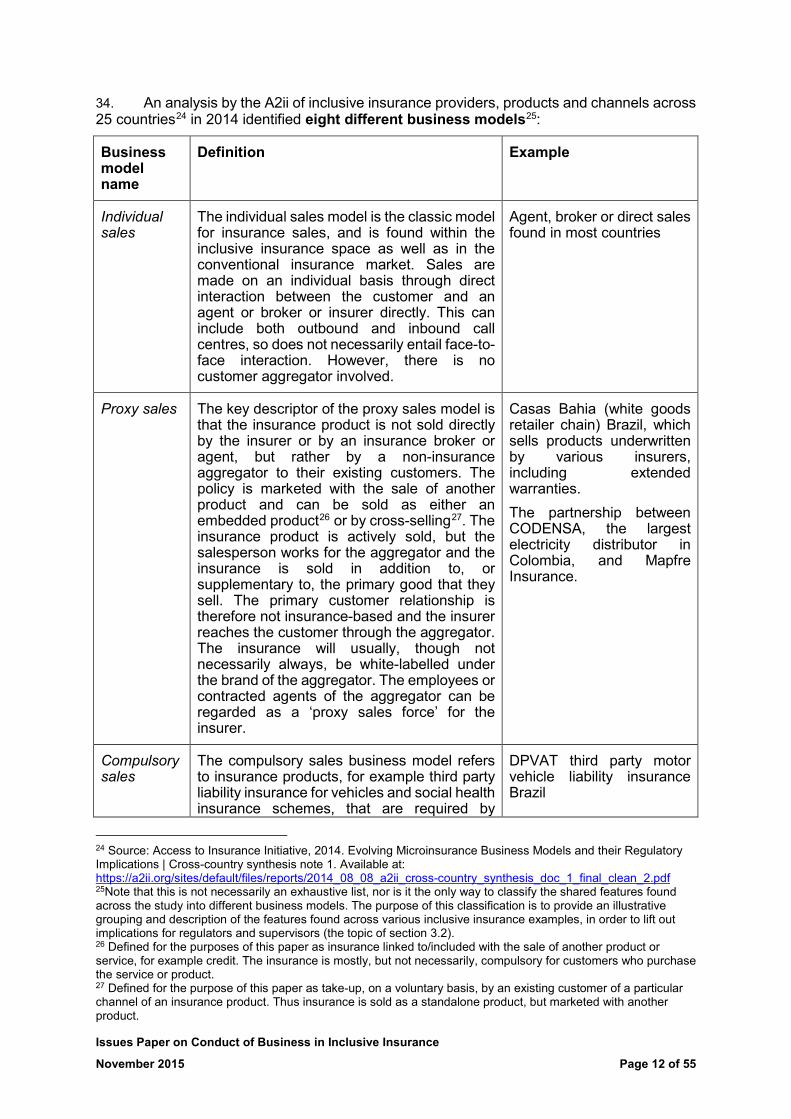

2. There is a general recognition that enhanced access to insurance services helps reduce poverty, improve social and economic development and supports major public policy objectives such as improving health conditions for the population, dealing with the effects of climate change and food security. Insurance supervisors in emerging markets and developing economies are increasingly looking for an appropriate balance between regulation, enhancing access to insurance services and protecting policyholders. Insurers and intermediaries4 are seeing the business potential of the low-income population and are offering innovative products and entering into distribution partnerships.

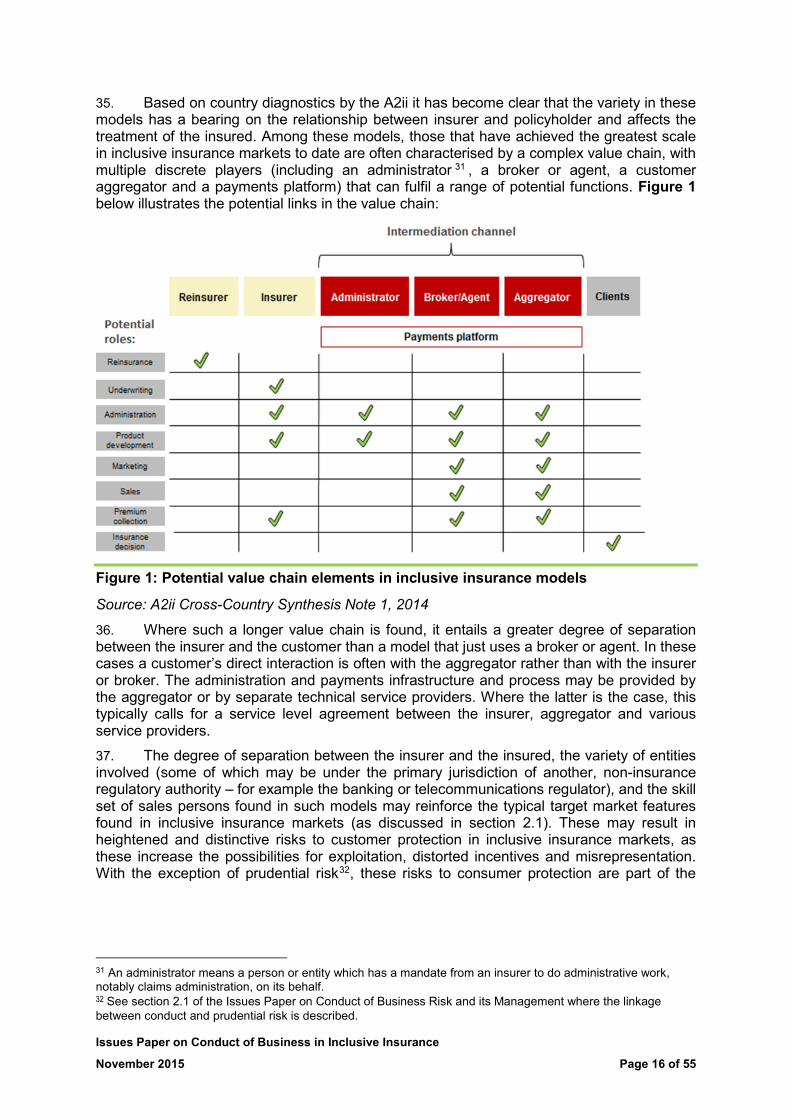

3. To support supervisors in their efforts to deal with these challenges, the IAIS has been working on its “access agenda” since 2006 by way of the IAIS-CGAP5 Joint Working Group on Microinsurance, succeeded by the IAIS-Microinsurance Network Joint Working Group on Microinsurance, and, since 2009, the Access to Insurance Initiative (A2ii). Prior to this paper, two Issues Papers and one Application Paper have been adopted:

• Issues in Regulation and Supervision of Microinsurance (June 2007): This paper discusses regulation and supervision as well as provides background to microinsurance concepts. The paper also contains a preliminary analysis of the ICPs that were in place at the time and concluded that the ICPs cover the essential aspects. However, when applying these principles in practice the outcomes could be positive or negative for inclusive markets depending on the approach taken whilst still observing the ICPs.

• Issues Paper on the Regulation and Supervision of Mutuals, Cooperatives and other Community-based Organisations in increasing access to Insurance Markets (October 2010): Recommended as a follow-up from the work of the first paper, this paper discusses the key elements of such organisations that are relevant to considering the approach to their regulation and supervision.

• Application Paper on Regulation and Supervision supporting Inclusive Insurance Markets (October 2012): The purpose of this paper is to provide application guidance supporting inclusive insurance markets. It provides examples of how relevant principles and standards can be practically applied. Where enhancing inclusive insurance markets is a policy objective, this document elaborates guidance for supervisors. It is directed at the objectives of implementing the ICPs in a manner that protects policyholders, contributes to local and global financial stability, and enhances inclusive insurance markets.

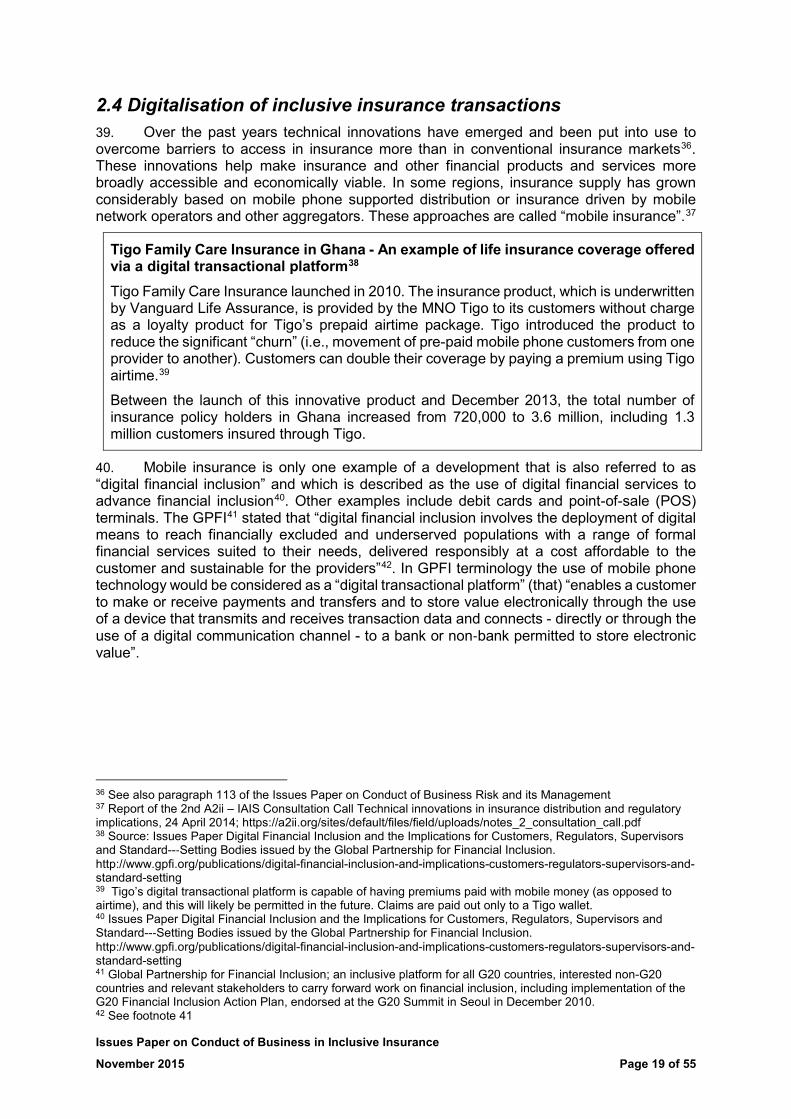

1 The complete set of ICPs including introduction, Principles, Standards and Guidance can be found on the public section of the IAIS website (http://www.iaisweb.org/ICP-on-line-tool-689) 2 Insurance refers to the business of insurers and reinsurers, including captives. 3 The IAIS Glossary defines a “customer” as a “policyholder or prospective policyholder with whom an insurer or insurance intermediary interacts, and includes, where relevant, other beneficiaries and claimants with a legitimate interest in the policy”. The glossary does not define “policyholder” although earlier papers had noted that “Policyholders includes beneficiaries”. 4 "Intermediaries" refers to any natural person or legal entity that engages in insurance intermediation. The ICPs do not normally apply to the supervision of intermediaries but where they do, this is specifically indicated in the ICPs, Standards and Guidance (refer to paragraph 9 of the Introduction to the ICPs). 5 The Consultative Group to Assist the Poor

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 5 of 55

4. About the paper. This Issues Paper on Conduct of Business in Inclusive Insurance is about the fair treatment of customers6 in inclusive insurance markets. The paper gives an overview of the issues in respect of conduct of business in inclusive insurance markets that affect the extent to which customers are treated fairly, both before a contract is entered into and through to the point at which all obligations under a contract have been satisfied. Recognising the increased vulnerability of the typical customer in this market segment and based on the typical characteristics of the business and distribution models that have emerged in inclusive insurance – as described further on in this paper – the objective of this paper is to promote the understanding of these particular issues among regulators and supervisors and other organisations and parties with an interest in this area. This understanding can furthermore inform further initiatives to address these issues in the area of conduct of business as a follow-up to this paper, possibly by developing application guidance on proportionate regulation and supervision.

5. The term “inclusive insurance” is used in this paper in the broad sense of the word, denoting all insurance products aimed at the excluded or underserved market, rather than just those aimed at the poor or a narrow conception of the low-income market. In developing countries, the majority of the population often classifies as un- or underserved. Thus inclusive insurance is a mainstream topic of relevance to the development of the retail insurance market as a whole. While the term “inclusive insurance” is aimed at excluded or underserved markets the term “microinsurance” has been defined as insurance that is accessed by low-income populations, provided by a variety of different entities, but run in accordance with generally accepted practices (which include the Insurance Core Principles) 7 . This paper looks specifically at insurance aimed at the low-income or lowers middle income due to specific requirements in term of service and consumer protection.

6. In inclusive insurance the need for providing customer value is particularly relevant. An insurance product in an inclusive insurance market can add value to the private objectives of the customer as well as to the overall public policy objective(s) of the country or region. The public policy objectives of a country – for example social development, food security, dealing with climate change, improving health and education of the population – are thwarted if the insurance products that should play a supporting role in achieving these objectives do not produce the desired outcome. If for example the cover of the basis risk in an index-based agricultural insurance8 is not well understood and actual losses are not paid, the customer will lose its trust in the product which will also negatively affect public policy objectives such as food security. Or, if payment of claims is taking too long, the insured when coping with the effects of a natural disaster might need to resort to the sale of their assets depriving them of future income or to taking children from school to save money. This would also be at the detriment of public policy objectives. It is therefore essential to provide insurance services that add value in the light of the specific context / living conditions of the inclusive insurance customer.

7. The primary focus of this paper is on the fair treatment of customers which as such belongs to the domain “conduct of business”9. However, this paper also touches upon issues that affect the treatment of customers outside of conduct of business in a strict sense, for example in respect of financial integrity, for which sometimes the term “market conduct” is also used. It is however noted that supervisors sometimes use both terms interchangeably.10

8. Throughout the paper examples or observed responses have been included. It is important for the reader of this paper to understand that - as this is an Issues Paper providing 6 See footnote 3. 7 See paragraph 1.32 of the Application Paper on Regulation and Supervision supporting Inclusive Insurance Markets 8 Insurance linked to an index, such as rainfall, temperature, humidity or crop yields, rather than actual loss 9 See ICP 19 10 As is also recognised in section 2.2.1 of the Application paper on Approaches to Conduct of Business Supervision and paragraph 11 of the Issues Paper on Conduct of Business Risk and its Management.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 6 of 55

background information, describing current practices, examples and case studies – these examples and observed response have been included for illustrative purposes only and should not be considered to provide preferred solutions or best practices in addressing the issue(s) concerned.

9. Structure of the paper. This Issues Paper is structured as follows: The first part (section 2) gives a description of the features of the inclusive insurance market. This is important as it is essential to understand the setting in which the contractual relationship will exist11 to gain an appreciation of how the concept of fair treatment of the customer plays out in an inclusive insurance market. This will include the profile of the typical inclusive insurance customer, the country-specific legal framework and roles of customer organisations and insurance associations / authorities, the business and distribution models that are typical for inclusive insurance markets and the digital means of interaction between insurer and policyholder that often characterise inclusive insurance business and distribution models.

The second part (section 3) will subsequently discuss the various elements of the inclusive insurance life cycle and present the issues that have been identified from a conduct of business perspective. The term “life cycle” is used as reference to the specific elements of an insurance product from its development as a product, its distribution, disclosure of information, customer acceptance, premium collection, and claims settlement to the handling of complaints by the insurer.

The paper ends with conclusions and recommendations in section 4.

11 The relevance of a jurisdictions’ tradition, culture, legal regime and the degree of development of the insurance sector as well as of the nature of the customer and type of contract is also recognised in Guidance 19.0.2 and 19.0.3.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 7 of 55

2. Features of the Inclusive Insurance Market 10. This section provides an overview of aspects outside the direct relationship between insurer and policyholder that nevertheless affect the overall level of conduct of business protection afforded to them. It considers the unique features of inclusive insurance markets that confront supervisors with conduct of business considerations that differ from more conventional insurance markets. The features outlined here give rise to the issues raised for each element of the product life cycle in the rest of the document, in particular in respect of:

• the inclusive insurance customer’s profile;

• the country specific context and conditions;

• the distribution models typical for inclusive insurance; and

• the digitalisation of inclusive insurance transactions.

2.1 The Inclusive Insurance Customer’s Profile 11. Low-income customers are generally more vulnerable than higher-income customers because of the deprivations they face as consequence of poverty12. Low-income households are also more vulnerable to risk as they are more exposed and have limited access to the whole range of risk mitigating tools13. Besides financial exclusion and the lack of access to effective mechanisms of risks transfer, low-income customers lack other basic necessities such as education, employment, housing, and access to justice.

12. In order to illustrate the relevance of conduct of business protection for the customers in inclusive insurance markets, it is important to understand the features of the typical inclusive insurance customer profile.

13. Low education levels and low insurance awareness. The low-income population might not always be sufficiently aware or informed about the risks it faces and the basic concept of insurance. Even if they are aware then still lack of knowledge and information may negatively affect decisions. No or low literacy and numeracy is a big issue. Many people simply can't read policy conditions and other written material. Studies consistently find education levels, awareness of insurance in general and understanding of the specific features of insurance in particular to be low. The low-income customer typically has very little, if any, experience with insurance. Customers also often confuse savings with insurance (expecting a return of premium). In addition, their risk mitigation strategies otherwise used can be inefficient and damaging for their economic and social development, as people may get more indebted, not send their children to school, deplete their long-term savings, or sell their productive assets. Also, low income customers will likely have limited experience with insurance contracts, and therefore are unlikely to be aware of their rights and obligations or those of their counterparty and the available mechanisms for seeking redress when they believe that they have been wronged. Customers will therefore not know to whom to turn to complain or to seek enforcement of the contract or generally, how to settle disputes14.

14. Low levels of disposable income. Low-income customers’ patterns of income are different from other income segments. Incomes are often seasonal and subject to fluctuation.

12 Drawing on focus group discussions and demand-side survey data analysis conducted as part of access to insurance diagnostics 13 GIZ, 2013. Discussion Paper: Customer Protection in Microinsurance. Available at: http://www.mfw4a.org/documents-details/discussion-paper-customer-protection-in-microinsurance.html?dl=1 14 See on financial education: Organisation for Economic Co-operation and Development (OECD). 2011. G20 High-level Principles on Financial Customer Protection. Paris: OECD. http://www.oecd.org/daf/fin/financial-markets/48892010.pdf; Organisation for Economic Co-operation and Development (OECD). 2013. Advancing National Strategies for Financial Education: A joint publication by Russia’s G20 Presidency and the OECD. http://www.oecd.org/daf/fin/financial-education/advancing-national-strategies-for-financial-education.htm.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 8 of 55

Disposable incomes are small and trade-off choices have to be made. Cash-flow fluctuations are common, limiting the ability to regularly pay premiums.

15. Nature of expenditures. The low levels of income affect the affordability of insurance. Most of the customer’s income is spent on basic requirements such as food and shelter15. Features of available insurance options are often perceived not to be appropriate to customers’ needs, not to be readily available at community level, and not to be affordable, even if perceptions of cost and affordability are not necessarily aligned with actual costs of available product options in the market.

16. Difficult to reach customers. A substantial proportion of the low-income population live in rural areas and poorer parts of urbanised areas. It tends to make a living in the informal sector and/or is self-employed. Thus it might be insufficiently covered by state social protection schemes. It is also often out of easy reach of traditional distribution touch-points. These elements challenge distribution to the low-income market.

17. A lack of trust in insurance providers and negative perception of insurance. The low-income segment generally has little trust in formal insurance provided by commercial insurers or conventional intermediaries such as banks or brokers. Also culture plays a role in the (mis)perception of insurance, such as beliefs that talking about a risk will cause that risk to happen. Though most respondents in focus group research16 have not personally had a claims experience, word of mouth from others in the community has a powerful impact. Rumours of delayed claims pay-outs travel fast and claim rejections, even if valid, exacerbate the limited understanding of terms and conditions. The result is that trust in insurance is negatively affected. In some countries specific negative experiences in the past, for example an insurer going bankrupt, continue to shape customer distrust. However, those respondents that do have insurance policies tend to be more positive about it than those who do not, especially if they had a good claims experience.

18. These features suggest that low-income customers are likely to be less financially sophisticated than conventional customers and more difficult to reach and therefore to protect. They are also likely to be more prone to mis-selling or customer abuse. Thus, the need for insurance to provide value for money and engender trust becomes even more pronounced for this segment of the population. All of this underlines the importance of proper conduct of business with regard to disclosure, advice and claims payment, coupled with effective customer redress, to ensure customer protection is effective for inclusive insurance customers.

19. There is however more to it than the application of proportionate conduct of business principles to promote greater access to insurance. Insurance should be seen as an essential element in an optimal financial strategy for the customer. The customers need to be made aware of the risks to which they are exposed and if and how insurance can play a role. For example, funeral insurance may cover the burial expenses but what if the breadwinner of the family deceases? Are there loans to be repaid and how is income for food, health and education arranged? It is not to be said, however, that all these risks need to be covered by insurance. When affected by a disaster various coping mechanisms come into play including donations from neighbours and relatives, reduction of spending or using the prospect of an insurance payment as “collateral” for obtaining formal or informal loans. It is the understanding of these aspects that needs to find its way into for example education of customers, product development, the providing of suitable advice by providers and claims handling.

15 Application Paper on Regulation and Supervision Supporting Inclusive Insurance Markets. Available at: www.iaisweb.org 16 This paragraph is based on insights from qualitative market research, in the form of focus group discussions, included in various inclusive insurance diagnostic studies, conducted under the umbrella of the Access to insurance Initiative. For more information, see https://a2ii.org/en/knowledge-centre/reports,

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 9 of 55

2.2 Country specific Context and Conditions 20. National regulatory framework. The scope and extent of involvement of the supervisor in conduct of business supervision in a specific jurisdiction is dependent on its mandate as determined by the jurisdictional regulatory framework. This affects the nature and level of customer protection provided by the supervisor. National public policy considerations in respect of the need for conduct of business protection and on the role of the supervisor are fundamental for the establishment of the regulatory framework. These considerations can vary across jurisdictions and could be based on political or economic positions regarding the role and responsibility of the public sector versus those of the “market” or the private sector. At policy level the objective could be to limit involvement of the public sector in the contractual relationships between private parties and leave - within boundaries – these relationships subject to economic market forces. In that case private sector initiatives – for example customer organisations - could fill that void.

21. Possible roles of the supervisor. A regulatory framework that provides a conduct of business mandate to a supervisor could have various modalities. The mandate could assign supervisory duties towards insurers at entity level rather than transaction level. This means that the supervisor does not protect individual policyholders directly but rather checks that an insurer in general acts in line with the laws and other regulatory requirements which protect policyholders as a whole so that the insurer’s conduct of business leads to fair treatment of customers. In this case the supervisor’s activities are aimed at processes, structures or general business practices within the supervised entities rather than at transaction level (individual contracts), although complaints by individual customers could point at an issue within the supervised entities processes and/or structures or business practices.

22. Additionally, the supervisor could be responsible for alternative dispute resolution (ADR). This could take the form of either dealing with customer complaints itself directly or managing / supervising a mechanism or entity that deals with ADR17.

23. Also, the regulatory framework could give the supervisor responsibilities in the area of financial education of the public18. Financial education has become a key pillar of financial reform, a complement to conduct of business and prudential regulation, on which financial sector development can rely. Such recognition has, notably, led to the development of a wide range of financial education initiatives by public authorities, including supervisors, and various other private and civil stakeholders over the past years. At policy level a jurisdiction may have initiated a financial inclusion strategy that includes financial education efforts by the supervisor or other public or private bodies.

24. Initiatives in practice. Specific microinsurance regulations date back to the year 2005, when India issued the first ever Microinsurance Regulations. Shortly thereafter, Philippines, Peru and Mexico followed, all providing for microinsurance-related conduct of business clauses, starting with the definition of microinsurance. Other important areas specifically regulated are distribution (intermediary licensing, registration or training), policy documents or certificates, products (covers, simplicity, exclusions, fees), and the related processes and services (disclosure to the customer, commissions, customer acceptance; premium collection, claims settlement, complaints handling and recourse).

25. In the past decade, at least 17 jurisdictions have adopted specific microinsurance regulations, all with a focus on conduct of business. Many of them have been revising and adjusting the initial regulations, and some have even issued a series of complementary regulations to advance the regulatory framework continuously, for example covering alternative dispute resolution. Another 18 jurisdictions are currently developing such a

17 See section 2.2.6 of the Application paper on Approaches to Conduct of Business Supervision. 18 See section 2.2.2 of the Application paper on Approaches to Conduct of Business Supervision.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 10 of 55

framework. Some jurisdictions have introduced, or are planning to introduce a new tier for a dedicated microinsurance provider.

26. Existence and operations of customer protection associations and authorities. In some jurisdictions, strong customer protection associations exist. They check and compare insurance contracts, do mystery shopping19 and challenge insurers. Often national legislation provides these associations with the right to sue insurers on behalf of the customer. Not only the achievements but all relevant court cases, professional opinions, reports etc. are published regularly. Also, customer associations offer seminars on customer topics. In other jurisdictions, customer protection authorities are in charge of monitoring customer relations in general and have the authority to impose administrative sanctions. For inclusive insurance customers, the role of these associations and authorities is particularly important due to the vulnerability described in the previous section.

27. Contributions of insurance associations. In some jurisdictions insurance associations may issue “model contracts” for their members. These model contracts are drafted in line with the applicable customer protection legislation in a jurisdiction. Insurance associations can participate in the development of and inform their members about all regulatory developments, including those regarding customer protection.

28. Functioning of the court system. Courts serve as a last resort for customers in case their disputes with the insurer/intermediary cannot be resolved out-of-court. This requires that customers are aware of such facilities, dare to approach them, and can afford an attorney and court fees that they need to pay for sometimes even if they win their case. To assure this, many court systems provide legal aid if the relevant party cannot afford the costs but – on a preliminary view – has sufficient prospect of success. In the case of inclusive insurance markets, affordability of court procedures is an issue. Inclusive insurance markets could benefit from alternative approaches such as accessible and low-cost and low-threshold court system or ADR system with mediators who are willing and trained to deal with this type of client.

29. Conclusion. The conditions as outlined above often do not hold in markets where inclusive insurance is a mainstream topic. For example, many developing countries may not have a clear conduct of business mandate or the supervisory capacity to fully act out such mandate as supervisory agencies are often new and under-capacitated, plus there typically will not be such strong consumer protection agencies/bodies as discussed here. Also, typically, insurance associations are nascent or even non-existent and face severe capacity constraints. Thus model contracts do not as a rule exist.

30. All of this means that the typical structures for consumer protection and conduct of business are challenged in the inclusive insurance sphere, meaning that the country-specific context and conditions that prevail in many developing countries (where inclusive insurance is most relevant) may reinforce consumer vulnerabilities. This reinforces the imperative for considering conduct of business in the inclusive insurance space. Likewise, the typical distribution and business models and digitalisation often found (described in sections 2.3. and 2.4) strengthen this imperative, as it confronts supervisors with new players, channels and considerations that may not be fully accommodated in the conventional regulatory and supervisory framework.

19 A tool used to gauge quality of service or compliance with regulation by purchasing a good or service without revealing the test buyer’s true identity.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 11 of 55

2.3 Distribution features and risks common to inclusive insurance 31. The characteristics of the low-income target market make its customers vulnerable to mis-selling, reduced value of products and customer abuse. These vulnerabilities manifest in different ways, depending on the specific inclusive insurance business model followed.

32. Generally, a business model is defined as the method or means through which a company captures value from its business. This can be based on many different aspects, including how products are designed, priced, marketed and distributed 20 . Similar to conventional insurance a business model within the inclusive insurance space can be defined as a composite of a number of elements:

• The product or service that is underwritten.

• The various parties involved in the insurance value chain and their functions. Importantly, in inclusive insurance the value chain often involves a so-called customer aggregator.21

• Who the policyholder is (the end-customer, versus another party as master policyholder).

• How and by whom the insurance is underwritten22.

• Who decides to buy the insurance and how such a decision is made (for example: is it compulsory/mandatory or voluntary, opt-in or opt-out).

• The manner in which the policy is sold to the policyholder, including how information about the policy is communicated to the policyholder.

• The manner in which the premium is paid and collected.

• The manner in which the claims are paid (claims payment systems).

33. Some of these elements relate to distribution. Distribution23 includes the channels and actions through which an insurance company sells a policy to the policyholder as well as services the policy on an ongoing basis. Alternative modes of distribution are of particular relevance in the inclusive insurance market and a core consideration in distinguishing between different inclusive insurance business models. Due to low premiums and thus low margins, the emphasis within inclusive insurance falls strongly on reducing distribution costs. Furthermore, the relative difficulties in reaching the lower income market due to limited infrastructure, poor connectivity, low education levels and limited experience with insurance underline the importance of distribution innovation in inclusive insurance.

20 Source: http://lexicon.ft.com/Term?term=business-model 21 Aggregators can be defined as entities that bring together people for non-insurance purposes (for example retailers, service providers, utility companies, membership based organizations or civil society organisations) and that are then utilised by insurers, with or without the intervention of agents or brokers, to distribute insurance and, depending on the model, fulfil additional functions such as administration and/or claims pay-out. 22 For example: on a group or individual basis; by a commercial insurer, a mutual, cooperative or other community-based group, or in-house on an informal basis by for example a Micro Finance Institution or funeral service provider 23 Note: the term distribution is used interchangeably in this paper with that of intermediation, which is defined in the IAIS glossary as: The activity of soliciting, negotiating or selling insurance contracts through any medium. Where: “Solicit" means attempting to sell insurance or asking or urging a person to apply for a particular kind of insurance from a particular company for compensation. "Negotiate" means the act of conferring directly with, or offering advice directly to, a purchaser or prospective purchaser of a particular contract of insurance concerning any of the substantive benefits, terms or conditions of the contract, provided that the person engaged in that act either sells insurance or obtains insurance from insurers for purchasers. "Sell" means to exchange a contract of insurance by any means, for money or its equivalent, on behalf of an insurance company.”

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 12 of 55

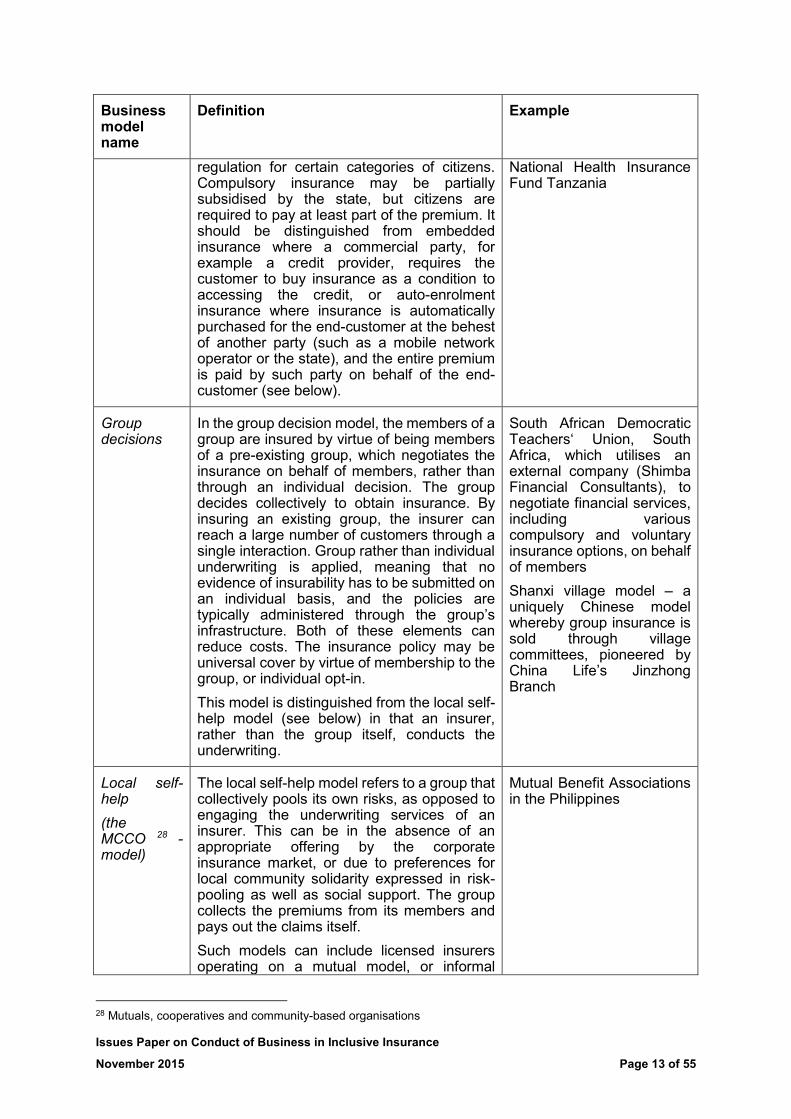

34. An analysis by the A2ii of inclusive insurance providers, products and channels across 25 countries24 in 2014 identified eight different business models25:

Business model name

Definition Example

Individual sales

The individual sales model is the classic model for insurance sales, and is found within the inclusive insurance space as well as in the conventional insurance market. Sales are made on an individual basis through direct interaction between the customer and an agent or broker or insurer directly. This can include both outbound and inbound call centres, so does not necessarily entail face-to-face interaction. However, there is no customer aggregator involved.

Agent, broker or direct sales found in most countries

Proxy sales The key descriptor of the proxy sales model is that the insurance product is not sold directly by the insurer or by an insurance broker or agent, but rather by a non-insurance aggregator to their existing customers. The policy is marketed with the sale of another product and can be sold as either an embedded product26 or by cross-selling27. The insurance product is actively sold, but the salesperson works for the aggregator and the insurance is sold in addition to, or supplementary to, the primary good that they sell. The primary customer relationship is therefore not insurance-based and the insurer reaches the customer through the aggregator. The insurance will usually, though not necessarily always, be white-labelled under the brand of the aggregator. The employees or contracted agents of the aggregator can be regarded as a ‘proxy sales force’ for the insurer.

Casas Bahia (white goods retailer chain) Brazil, which sells products underwritten by various insurers, including extended warranties. The partnership between CODENSA, the largest electricity distributor in Colombia, and Mapfre Insurance.

Compulsory sales

The compulsory sales business model refers to insurance products, for example third party liability insurance for vehicles and social health insurance schemes, that are required by

DPVAT third party motor vehicle liability insurance Brazil

24 Source: Access to Insurance Initiative, 2014. Evolving Microinsurance Business Models and their Regulatory Implications | Cross-country synthesis note 1. Available at: https://a2ii.org/sites/default/files/reports/2014_08_08_a2ii_cross-country_synthesis_doc_1_final_clean_2.pdf 25Note that this is not necessarily an exhaustive list, nor is it the only way to classify the shared features found across the study into different business models. The purpose of this classification is to provide an illustrative grouping and description of the features found across various inclusive insurance examples, in order to lift out implications for regulators and supervisors (the topic of section 3.2). 26 Defined for the purposes of this paper as insurance linked to/included with the sale of another product or service, for example credit. The insurance is mostly, but not necessarily, compulsory for customers who purchase the service or product. 27 Defined for the purpose of this paper as take-up, on a voluntary basis, by an existing customer of a particular channel of an insurance product. Thus insurance is sold as a standalone product, but marketed with another product.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 13 of 55

Business model name

Definition Example

regulation for certain categories of citizens. Compulsory insurance may be partially subsidised by the state, but citizens are required to pay at least part of the premium. It should be distinguished from embedded insurance where a commercial party, for example a credit provider, requires the customer to buy insurance as a condition to accessing the credit, or auto-enrolment insurance where insurance is automatically purchased for the end-customer at the behest of another party (such as a mobile network operator or the state), and the entire premium is paid by such party on behalf of the end-customer (see below).

National Health Insurance Fund Tanzania

Group decisions

In the group decision model, the members of a group are insured by virtue of being members of a pre-existing group, which negotiates the insurance on behalf of members, rather than through an individual decision. The group decides collectively to obtain insurance. By insuring an existing group, the insurer can reach a large number of customers through a single interaction. Group rather than individual underwriting is applied, meaning that no evidence of insurability has to be submitted on an individual basis, and the policies are typically administered through the group’s infrastructure. Both of these elements can reduce costs. The insurance policy may be universal cover by virtue of membership to the group, or individual opt-in. This model is distinguished from the local self-help model (see below) in that an insurer, rather than the group itself, conducts the underwriting.

South African Democratic Teachers‘ Union, South Africa, which utilises an external company (Shimba Financial Consultants), to negotiate financial services, including various compulsory and voluntary insurance options, on behalf of members Shanxi village model – a uniquely Chinese model whereby group insurance is sold through village committees, pioneered by China Life’s Jinzhong Branch

Local self-help (the MCCO 28 -model)

The local self-help model refers to a group that collectively pools its own risks, as opposed to engaging the underwriting services of an insurer. This can be in the absence of an appropriate offering by the corporate insurance market, or due to preferences for local community solidarity expressed in risk-pooling as well as social support. The group collects the premiums from its members and pays out the claims itself. Such models can include licensed insurers operating on a mutual model, or informal

Mutual Benefit Associations in the Philippines

28 Mutuals, cooperatives and community-based organisations

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 14 of 55

Business model name

Definition Example

schemes. There is also a distinction between local self-help initiatives which only provide insurance to members and those which also offer insurance to non-members.

Auto-enrolment

The auto-enrolment model is characterised by the fact that a third party 29 purchases insurance on behalf of a pre-determined group of people. The insurance is underwritten by commercial insurers and the premiums are paid directly to the insurer by the third party. The contractual relationship within the auto-enrolment model is usually between the third party and the insurer, rather than between the end-customer and the insurer.

This model has two separate embodiments:

• State-provided: Where the state subsidises insurance on behalf of a defined group of people. A public procurement process is normally followed to appoint an insurer, unless a state-owned insurer is used

• Loyalty benefits: Where a provider of retail services such as a mobile network operator (MNO) 30 or bank purchases insurance for its customers as a loyalty benefit.

State-provided: Rashtriya Swasthya Bima Yojana (RSBY) India – a fully-subsidised national health insurance scheme, underwritten by various insurers. Loyalty benefits: Tanzania’s National Microinsurance Bank (NMB) offers automatic free funeral insurance, underwritten by African Life, to all active holders of the NMB Personal Accounts. Various “freemium” loyalty insurance schemes by MNOs, for example the pioneering case of Tigo Ghana.

Passive sales

In the passive sales model, the insurer relies on the customer to actively buy the insurance. The potential customer uses a passive sales outlet, such as the internet or a supermarket shelf, provided by the insurer to purchase the product. The insurer promotes the product through brochures or mass market advertising. The onus is upon the customer, rather than a salesperson or intermediary, to inform him/herself about the product as there is no individual communication prior to the sale. There is an individual but not an active in-person sales transaction. There may be communication following the sale, for example where a call centre contacts the customer to confirm their details and complete the transaction.

Pep (a clothing retailer chain) selling insurance products by Hollard Life off the shelf in its network of stores in South Africa.

29 A “third party” is defined for the purpose of this paper as a person or organisation that is neither the insurer nor the end-customer. 30 Where it is often known as the “freemium” model. Note that not all MNO models are characterised by auto-enrolment, with such schemes increasingly reverting to explicit opt-in by the customer.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 15 of 55

Business model name

Definition Example

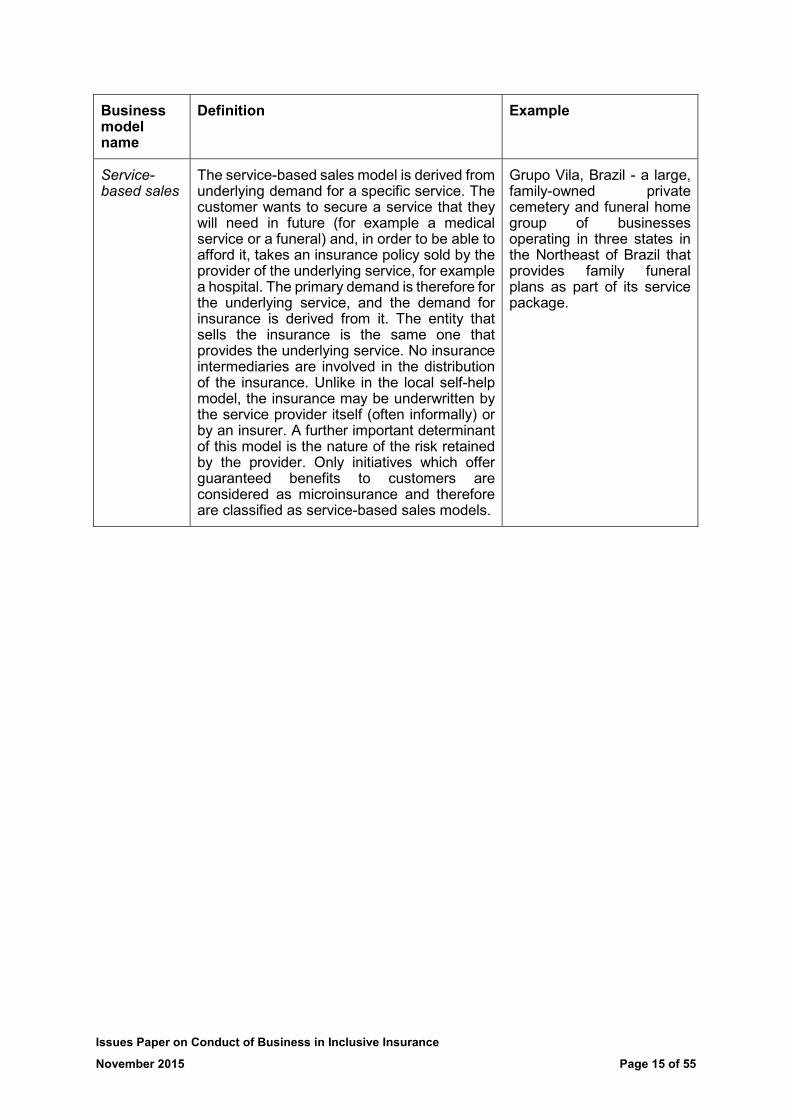

Service-based sales

The service-based sales model is derived from underlying demand for a specific service. The customer wants to secure a service that they will need in future (for example a medical service or a funeral) and, in order to be able to afford it, takes an insurance policy sold by the provider of the underlying service, for example a hospital. The primary demand is therefore for the underlying service, and the demand for insurance is derived from it. The entity that sells the insurance is the same one that provides the underlying service. No insurance intermediaries are involved in the distribution of the insurance. Unlike in the local self-help model, the insurance may be underwritten by the service provider itself (often informally) or by an insurer. A further important determinant of this model is the nature of the risk retained by the provider. Only initiatives which offer guaranteed benefits to customers are considered as microinsurance and therefore are classified as service-based sales models.

Grupo Vila, Brazil - a large, family-owned private cemetery and funeral home group of businesses operating in three states in the Northeast of Brazil that provides family funeral plans as part of its service package.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 16 of 55

35. Based on country diagnostics by the A2ii it has become clear that the variety in these models has a bearing on the relationship between insurer and policyholder and affects the treatment of the insured. Among these models, those that have achieved the greatest scale in inclusive insurance markets to date are often characterised by a complex value chain, with multiple discrete players (including an administrator 31 , a broker or agent, a customer aggregator and a payments platform) that can fulfil a range of potential functions. Figure 1 below illustrates the potential links in the value chain:

Figure 1: Potential value chain elements in inclusive insurance models

Source: A2ii Cross-Country Synthesis Note 1, 2014

36. Where such a longer value chain is found, it entails a greater degree of separation between the insurer and the customer than a model that just uses a broker or agent. In these cases a customer’s direct interaction is often with the aggregator rather than with the insurer or broker. The administration and payments infrastructure and process may be provided by the aggregator or by separate technical service providers. Where the latter is the case, this typically calls for a service level agreement between the insurer, aggregator and various service providers.

37. The degree of separation between the insurer and the insured, the variety of entities involved (some of which may be under the primary jurisdiction of another, non-insurance regulatory authority – for example the banking or telecommunications regulator), and the skill set of sales persons found in such models may reinforce the typical target market features found in inclusive insurance markets (as discussed in section 2.1). These may result in heightened and distinctive risks to customer protection in inclusive insurance markets, as these increase the possibilities for exploitation, distorted incentives and misrepresentation. With the exception of prudential risk32, these risks to consumer protection are part of the

31 An administrator means a person or entity which has a mandate from an insurer to do administrative work, notably claims administration, on its behalf. 32 See section 2.1 of the Issues Paper on Conduct of Business Risk and its Management where the linkage between conduct and prudential risk is described.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 17 of 55

overarching concept of conduct of business risk33. To enable a better understanding of the nature and impact of risks to consumer protection in the inclusive space and as these risks are the result of different risk drivers found in inclusive insurance market contexts these risks have been defined as subsets of conduct of business risk in the box below.

Typical risks found in inclusive insurance business models Six common risks 34 can be identified that have a distinct manifestation in inclusive insurance distribution:

• Prudential risk35 is the risk that the insurer as risk manager is not able to keep its promises and deliver benefits to the beneficiaries. Prudential risk derives largely from the features of the insurer’s operations and management and therefore a lack of capacity of the insurer and a lack of regulation and oversight regarding the management of insurers heightens prudential risk.

• Aggregator risk is the risk of reduced customer value and inappropriate products being sold to customers when an insurer accesses the aggregated customer base of a non-insurance third party to sell its products through that channel.

• Sales risk is the risk that the salesperson will misrepresent the product to the customer or sell a product that the customer does not need. Reduced customer value or inappropriate product choice can also be the result of sales risk.

• Policy awareness risk is the risk that the insured is not aware that he or she has insurance cover and is therefore unable to lodge a claim should the risk event occur. The manner in which insurance is sold through certain inclusive insurance business models can heighten the risk that policyholders are unaware that they have insurance coverage. There is also the risk that the insured is not fully aware of the terms and conditions of the insurance or does not know how to make a claim.

• Payments risk is the risk that the premium will not reach the insurer, that the premium will not be paid on the due date or that the cost of collecting the premium is disproportionate. Payments risk means there is a heightened possibility that premiums are not regularly received by the insurer.

• Post-sales risk is the risk that customers face unreasonable post-sale barriers to maintain their cover, change between products, make enquiries, submit claims, receive benefits or make complaints. It therefore refers to the risk of poor service and the potential disincentive for insurers and intermediaries to be efficient in claims processing and service provision.

See the annex for more details.

33 Paragraph 11 of the Issues Paper on Conduct of Business Risk and its Management indicates that Conduct of business risk can be described as “the risk to customers, insurers, the insurance sector or the insurance market that arises from insurers and/or intermediaries conducting their business in a way that does not ensure fair treatment of customers.” 34 Note that inclusive insurance initiatives may also be subject to other risks that are not distinctive to the inclusive insurance market. Similarly, the risks listed here are not unique to inclusive insurance. For example: prudential risk is universal across insurance, as is payments risk, policy awareness risk or post-sales risk. The discussion here centres on those risks that are particularly manifest in inclusive insurance markets or that take on a distinct nature in inclusive insurance models, as identified in the 2014 Access to Insurance Initiative cross-country synthesis exercise. 35 Note that, while prudential risk is present in all insurance models and by no means unique to inclusive insurance, it manifests in specific ways in inclusive insurance business models and therefore warrants discussion.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 18 of 55

38. These market features and risks confront regulators and supervisors with new considerations in conduct of business that are often not fully addressed in conventional regulatory and supervisory frameworks. Section 3.2 considers the distribution-related issues arising in the inclusive insurance market and the implications for regulators and supervisors.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 19 of 55

2.4 Digitalisation of inclusive insurance transactions 39. Over the past years technical innovations have emerged and been put into use to overcome barriers to access in insurance more than in conventional insurance markets36. These innovations help make insurance and other financial products and services more broadly accessible and economically viable. In some regions, insurance supply has grown considerably based on mobile phone supported distribution or insurance driven by mobile network operators and other aggregators. These approaches are called “mobile insurance”.37

Tigo Family Care Insurance in Ghana - An example of life insurance coverage offered via a digital transactional platform38 Tigo Family Care Insurance launched in 2010. The insurance product, which is underwritten by Vanguard Life Assurance, is provided by the MNO Tigo to its customers without charge as a loyalty product for Tigo’s prepaid airtime package. Tigo introduced the product to reduce the significant “churn” (i.e., movement of pre-paid mobile phone customers from one provider to another). Customers can double their coverage by paying a premium using Tigo airtime.39

Between the launch of this innovative product and December 2013, the total number of insurance policy holders in Ghana increased from 720,000 to 3.6 million, including 1.3 million customers insured through Tigo.

40. Mobile insurance is only one example of a development that is also referred to as “digital financial inclusion” and which is described as the use of digital financial services to advance financial inclusion40. Other examples include debit cards and point-of-sale (POS) terminals. The GPFI41 stated that “digital financial inclusion involves the deployment of digital means to reach financially excluded and underserved populations with a range of formal financial services suited to their needs, delivered responsibly at a cost affordable to the customer and sustainable for the providers”42. In GPFI terminology the use of mobile phone technology would be considered as a “digital transactional platform” (that) “enables a customer to make or receive payments and transfers and to store value electronically through the use of a device that transmits and receives transaction data and connects - directly or through the use of a digital communication channel - to a bank or non‐bank permitted to store electronic value”.

36 See also paragraph 113 of the Issues Paper on Conduct of Business Risk and its Management 37 Report of the 2nd A2ii – IAIS Consultation Call Technical innovations in insurance distribution and regulatory implications, 24 April 2014; https://a2ii.org/sites/default/files/field/uploads/notes_2_consultation_call.pdf 38 Source: Issues Paper Digital Financial Inclusion and the Implications for Customers, Regulators, Supervisors and Standard--‐Setting Bodies issued by the Global Partnership for Financial Inclusion. http://www.gpfi.org/publications/digital-financial-inclusion-and-implications-customers-regulators-supervisors-and-standard-setting 39 Tigo’s digital transactional platform is capable of having premiums paid with mobile money (as opposed to airtime), and this will likely be permitted in the future. Claims are paid out only to a Tigo wallet. 40 Issues Paper Digital Financial Inclusion and the Implications for Customers, Regulators, Supervisors and Standard--‐Setting Bodies issued by the Global Partnership for Financial Inclusion. http://www.gpfi.org/publications/digital-financial-inclusion-and-implications-customers-regulators-supervisors-and-standard-setting 41 Global Partnership for Financial Inclusion; an inclusive platform for all G20 countries, interested non-G20 countries and relevant stakeholders to carry forward work on financial inclusion, including implementation of the G20 Financial Inclusion Action Plan, endorsed at the G20 Summit in Seoul in December 2010. 42 See footnote 41

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 20 of 55

EcoLife in Zimbabwe – example of a failure in a mobile insurance scheme43

EcoLife was a partnership between Econet Wireless (the largest MNO in Zimbabwe), First Mutual Life (an insurer in Zimbabwe) and Trustco (a third party technical service provider based in Namibia). EcoLife reached 20% of the adult population within 7 months of launch, but due to a dispute between two of the non-insurance entities, Trustco and Econet, the scheme was discontinued overnight. In undertaking a survey of the discontinued customers of EcoLife, 63% ruled out the use of similar products in future, 42% were dissatisfied with insurance and 30% felt there were better ways to protect against future problems than insurance. Considering the product had reached 20% of the adult population, the impact was significant.

41. The potential for scale in mobile insurance brings significant opportunity to increase financial inclusion as demonstrated by several mobile insurance ‘sprinters’. For example, Tigo Ghana reached almost one million lives in 12 months, Airtel Zambia reached an estimated two million adults at launch and Telenor Pakistan reached over a million lives in six months.

42. Mobile-phone technology can play a role in various stages of the insurance product life cycle 44. It can play a role in the enrolment of policyholders, premium collection, claims processing and renewals. At the enrolment stage mobile phones can process some or all of the customer and other details needed. This could also be carried out by the agent. In some cases additional paper information or a non-digital signature needs to be arranged separately. As part of the enrolment photographs can be taken by mobile phone – for example of livestock – and transmitted to the insurer. As to the premium collection often payment takes place through the airtime of the customer, or through a mobile money account accessible via a mobile phone referred to as “mobile wallet” allowing non-cash payments45. In respect of claims processing the mobile phone can be used to make the claim and – through photographs – provide proof of loss. In index-insurance there can even be a link with other technological developments such as weather stations and satellites as is described in the next box.

For Kilimo Salama, the claims payment is linked to an indexed parameter. At the time of purchasing the insurance product, farmers decide on the automated weather station that is closest to their land and their policy is based on the parameters recorded at that weather station. Farmers’ phone numbers are collected at the time of the policy purchase. When that parameter is triggered (based on weather station data), all farmers’ phone numbers that are linked to that weather station receive a pay-out directly via M-Pesa. The farmers receive a confirmation of their payment via SMS. If the farmer does not have a mobile phone, then the dealer through whom the insurance was purchased receives the pay-out and passes it on to the farmer. The dealer provides a physical receipt to the insurer to document the pay-out to the farmer.

Tata AIG uses a mobile phone application to approve and settle claims for its cattle insurance product. Through an application developed especially for claims, the agent sends photographs of the dead animal to the central server. The central server sends an email to the claims team with the on-the-spot survey report for the customer immediately. Previously, it used to take up to 20 days for the documentation and survey report to reach

43 Source: Report of the 2nd A2ii – IAIS Consultation Call Technical innovations in insurance distribution and regulatory implications, 24 April 2014; https://a2ii.org/sites/default/files/field/uploads/notes_2_consultation_call.pdf 44 See: Microinsurance Innovation Facility, Mobile Phones and Microinsurance, Microinsurance Paper 26, November 2013 45 The terms “digital wallet”, “mobile wallet,” “e-wallet,” and “electronic wallet” are sometimes used to refer to this ability to carry, access, and use value stored in or via a digital device. When issued or distributed by an MNO, this stored value is often referred to as “mobile money” (source: Issues Paper Digital Financial Inclusion and the Implications for Customers, Regulators, Supervisors and Standard--‐Setting Bodies issued by the Global Partnership for Financial Inclusion)

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 21 of 55

the claims team. Claims assessors compare the photographs with those taken at the time of enrolment. Specific features like the distance between the horns, or coloured patches on the skin are compared to verify the identity of the animal. Once the claim is approved, confirmation is sent to the customer by SMS. This process has reduced the claims turnaround time to 6 days from about 30 days earlier. However, the biggest challenge currently is ensuring that the assessors are comfortable with the process. There is a need to have the software in the local language, so that there is better understanding in the implementation phase.46

43. Mobile-phone technology can also be an important instrument for data management and analysis. Customer and premium details can be stored on the mobile phone of the agent and then transmitted to the server of the insurer. The mobile phone user data can also inform the customer profile of the insurer.

44. According to the Application Paper on Regulation and Supervision Supporting Inclusive Insurance Markets innovations in technology can be required and should be permitted in regulation and supervision to overcome barriers to access while protecting the policyholders47.

45. These developments come with certain challenges. The customer will need to understand and be able to perform the required (trans)actions by mobile phone. Where literary and numeracy are an issue customers may trust others, for example the agent, to perform the necessary actions creating a risk of abuse. There are also privacy and cybercrime risks. Large inclusive insurance schemes using modern digital means of communication quickly reach millions of people. Data leakage and misuse can take a very large scale very quickly. Moreover, low income customers are often uninformed about the importance of data protection, potential of abuse etc. Offerings via mobile phone might give opportunity for misinformation to the customer if the (correct) product information is not properly disclosed.

46. Ensuring the proper quality of agents through training is also a point of attention, even more so if there is a high turnover in agents. Where there is no or limited face-to-face contact between customer and agent the risk of misuse or misinformation is exacerbated.

47. For the insurer reliance on a digital network will create various IT-related risks. The computer server capacity should be such that the insurer can manage and process the volume of data entered into the system without negatively affecting the continuity of the system. Also, the use of third party providers to which the development, operation or maintenance of the IT systems has been outsourced should be properly managed. Furthermore, the integrity of the system should be safeguarded against any forms of cybercrime, including malware.

48. The use of mobile phone technology in insurance will likely affect multiple supervisors. One or more insurance supervisors are involved in respect of the prudential and conduct of business aspects of the insurance business. Regarding payments also banking supervisors and/or authorities responsible for oversight of the payment systems will have a responsibility. The use of mobile phone technology and digital networks will entail the involvement of telecom supervisors/regulators. These categories of supervisors and regulators will need to coordinate and cooperate to the greatest extent possible to avoid initiatives that unnecessarily interfere with and harm the interests of the customer.

49. Supervisors need to keep up with the speed at which technical innovations in insurance distribution are being deployed.

46 Source: Microinsurance Innovation Facility, Mobile Phones and Microinsurance, Microinsurance Paper 26, November 2013, p. 9 47 Paragraphs 3.2 and 3.3 of the Application Paper on Regulation and Supervision Supporting Inclusive Insurance Markets

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 22 of 55

3. The Inclusive Insurance Product Life Cycle 50. Following the description of the features of the inclusive insurance market in the previous section, this section presents the issues that have been identified from a conduct of business perspective for each of the elements of the inclusive insurance product life cycle. The term “life cycle” is used to refer to the passage of an insurance product from inception to conclusion; it includes the following stages: development of the product, distribution, disclosure of information, customer acceptance, premium collection, claims settlement and the handling of complaints by the insurer.

3.1 Product Development 51. Fair treatment of customers encompasses achieving outcomes such as developing and marketing products in a way that pays due regard to the interests of customers48. Although the group of inclusive insurance customers is very heterogeneous, its commonalities require particular attention at the inception stage of a new insurance product, with a view to ensuring fair treatment of the customer. This applies in particular but is not limited to:

• Covered risks - Are the risks being covered relevant to the target market?

• Terms and Conditions – Are the terms and conditions appropriate for the customer profile?

• Pricing - Is the product appropriately priced and structured for the premium paying capacity of the customer?

52. Various initiatives have emerged to address these issues. The Microinsurance Centre promotes for example the principle that every microinsurance product needs to be S.U.A.V.E. i.e. simple, understood, appropriate, valuable and efficient. 49 In various jurisdictions the supervisors have been made responsible for product oversight as a means to achieving the regulatory objectives in increasing access to insurance. The role of the supervisor in respect of product oversight in these instances is to control the launch of products by overseeing that they meet certain standards or parameters and offer appropriate value to customers50.

53. Covered risks. Without research into the requirements of the specific target market, as would be the case when product design is supply driven, the product is less likely to meet the needs and cover the risks relevant to the target market and more likely to give rise to sub-optimal customer protection and value, to lead to mis-selling or customer abuse. Whether product design is demand or supply driven will give rise to differing customer protection concerns. For example, when consumer goods are purchased the supplier often sells insurance against loss or damage of that good or for an extended warranty. This type of attached sales products is often offered to generate revenues for the retailer rather than address the needs of the customer.

54. It is important for supervisors to be aware that insurers may oblige customers of certain services or products to purchase linked insurance. In inclusive insurance this is for instance the case with credit life insurance. Due to the compulsory nature of these products, the value offered to the customer may frequently be of secondary concern to the provider, with the product primarily designed to mitigate the risk of the service provider rather than the customer or with the provider just making use of a cross-selling opportunity. Whilst supervisors will aim to protect the value offered to customers through compulsory products, they also need to

48 Guidance 19.2.4; see also paragraph 76 onwards of the Issues Paper on Conduct of Business Risk and its Management 49 Microinsurance product development for microfinance providers, Microinsurance Centre and the International Fund for Agricultural Development, October 2012, p. 14.; http://www.ifad.org/ruralfinance/pub/manual.pdf 50 For more information see: Report of the 5th A2ii – IAIS Consultation Call, Product Oversight in Inclusive Insurance, 28 August 2014; https://a2ii.org/sites/default/files/field/uploads/notes_5th_iais-a2ii_consultation_call_product_oversight_in_inclusive_insurance_0.pdf

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 23 of 55

recognise the important role such products play in developing a nascent inclusive insurance or credit market.

Observed response(s) to the indicated issue: A number of jurisdictions require that customers be given a choice of insurance provider when required to buy mandatory embedded cover. Specific conduct of business and disclosure requirements may also apply to the intermediation of compulsory products. Regulation in Peru provides contract conditions for credit/mortgage life insurance, specifying the obligations of the financial company to accept the insurance that the customer chooses when it complies with established policies. Also, the client is free to decide to replace the policy during their term by another of the same or better features, being that if the premiums have been financed, the customer is entitled to a refund of future interest payments.

55. Combination(s) of cover offered – Sometimes insurance is sold together or as a package with other financial or non-financial products, for example with banking or credit products or with consumer goods such as household equipment and furniture or air tickets. This concept is known as bundling51. Also, the term “embedded” is used to indicate insurance covers tagged along with other products52. The differentiation between life, non-life and health products, and to what extent different elements may be bundled in one policy, as well as the conditions for embedded products, are further important product-related issues for supervisors in inclusive insurance markets. Below, each is discussed in turn.

56. Demarcation between life and non-life lines in the case of bundled products53 - A statutory demarcation between the provision of life and asset/general insurance can preclude the provision of cross-over products with both a life and a non-life element, unless different insurers underwrite different components or composite insurers are permitted. The demand for asset insurance is typically very low in the low-income market. A composite product containing funeral cover and asset insurance, for example, is likely to have more of an allure to customers than a free-standing asset insurance product. Hence the distribution of non-life policies to the low-income market is likely to be more feasible if sold in one offering with life components. However, in countries with different prudential requirements for life and non-life products (for example, more reserves have to be maintained for longer term life products than for non-life products) the bundling of a life and a non-life product gives rise to regulatory challenges. In response, regulators may set certain product parameters that both life and non-life microinsurance products need to adhere to in order to ensure that they are underwritten on the same basis.

Observed response(s) to the indicated issue: The Microinsurance Regulations in India allow bundling of life and non-life components only if life and non-life insurers underwrite the respective components and if there is clear separation of premiums and risk between the components. Similarly, in the Philippines (Insurance Memorandum Circular 1-2010), bundled microinsurance products in life and non-life may be provided by insurers (commercial and cooperative) and mutual benefit associations as long as each component is underwritten separately.

51 See paragraphs 44 and 77 of the Issues Paper on Conduct of Business Risk and its Management 52 See paragraph 1.23 of the Application Paper on Regulation and Supervision supporting Inclusive Insurance Markets 53 See paragraph 3.12 onwards and 4.41.4 of the Application Paper on Regulation and Supervisions supporting Inclusive Insurance Markets.

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 24 of 55

The statutory demarcation between general and life insurance in countries such as Zambia, Tanzania and South Africa precludes the offering of bundled products. Proposed microinsurance regulations in South Africa and Zambia aim to address this by allowing bundled products where the life and non-life covers have similar risk profiles.

57. Classification of health insurance - How health insurance is classified is a particularly relevant issue in a number of countries. For example, where regulation excludes health insurance from the ambit of insurance or is not clear on the definition, it may create a grey area for informal operators outside the jurisdiction of the insurance supervisor. In other instances, strict demarcation between the business of medical schemes and that of other insurers, coupled with prescribed minimum benefits for medical schemes, may reduce affordability and inhibit innovation in the low-income health insurance space. The grey area in the case of the supervision of health insurance could not only occur if medical services firms are unregulated or unsupervised but also if there is an additional supervisor in this area.

Observed response(s) to the indicated issue: In the Philippines private insurance companies are allowed by the Insurance Commission to offer health insurance. Many companies are currently offering hospital cash benefits (some of which are approved as microinsurance products) and HMO-type health insurance products. In South Africa there is a clear demarcation between the business of a medical scheme and health insurance, with implications for microinsurance-relevant products such as hospital cash plans that provide a pay-out to the customer with a medical trigger, but not related to the underlying medical cost.

For example, Peru has a national supervisory authority of public and private entities providing health services (SUSALUD), which seeks to promote and protect the access of people to health care services. SUSALUD’s field of competence on insurance companies covers processes associated with the provision of health services to policyholders, and the compliance of medical dispositions agreed by contract such as medical audit or treatment guidelines.

58. Insurance bundled with non-insurance - Examples include credit life insurance, or funeral or personal accident insurance embedded free of charge in a savings product or deposit account, a mobile network subscription (the latter is also known as loyalty insurance) or an insurance attached to the purchase of consumer goods. The non-insurance element of the embedded insurance cover is not supervised for insurance purposes and the insurance supervisor would normally not have jurisdiction over the delivery of this underlying product or service. However, it can have significant implications for the insurance policy. As the insurance cover is the secondary product it may offer limited value to the customer as the product design would frequently be supply driven and may, as in the case of credit life, be designed to meet the needs of the lender (supplier, or distributor,) rather than the customer. The interests of the distribution channel – the product in which the insurance cover is embedded – can dominate over the interests of the insured. The embedded nature of the insurance also increases the risk that customers may be unaware of the insurance cover as they are likely primarily purchasing the non-insurance product with the insurance cover automatically added.

59. Terms and Conditions. Are the terms and conditions of the product appropriate for the customer profile? A term that is excessively short can exacerbate policy awareness risk – where the insured individual is unaware that they have the insurance or that it needs to be renewed. Very low claims ratios have been observed in some massively provided accident policies, which run for a few weeks only. Shorter terms can also increase the prevalence of adverse selection, in turn increasing the prudential risk to the insurer itself. On the other hand, restricting the maximum term length (as is the case of some microinsurance specific legislation such as proposed in South Africa and existing in India) and the need for frequent renewal that it entails may also help in creating awareness of the policy. Furthermore, a relatively short

Issues Paper on Conduct of Business in Inclusive Insurance

November 2015 Page 25 of 55

term provides customers with the flexibility to change insurers and/or products if they are unhappy with the value offered.