IRDA Journal July Issue - Irdai

96

July 2010 Volume VIII, No. 7 Ë ÿ• § ı U • § • § U Ever Ready to Help - Policyholder Protection

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of IRDA Journal July Issue - Irdai

July 2010

Volume VIII, No. 7

’Ë◊Ê ÁflÁŸÿÊ◊∑§ •ı⁄U Áfl∑§Ê‚ ¬̋ÊÁœ∑§⁄Uá Ê

Ever Ready to Help- Policyholder Protection

Editorial BoardJ. Hari NarayanR. KannanS.V. MonyS.B. MathurS.L. MohanVepa KamesamAshvin Parekh

EditorU. JawaharlalHindi CorrespondentKamal ChowlaPrinted by G. Venugopala Krishna andpublished by J. Hari Narayan on behalf ofInsurance Regulatory and Development Authority.Editor: U. JawaharlalPrinted at Vamsi Art Printers Pvt. Ltd.(with design inputs from Efforts)11-6-872, Red Hills, Lakdikapul, Hyderabad.and published from

rdParishram Bhavan, 3 FloorBasheer BaghHyderabad - 500 004Phone: +91-40-23381100Fax: +91-40-66823334e-mail: [email protected]

© 2010 Insurance Regulatory and Development Authority.Please reproduce with due permission.Unless explicitly stated, the information and views published in this Journal may not be construed as those of the Insurance Regulatory and Development Authority.

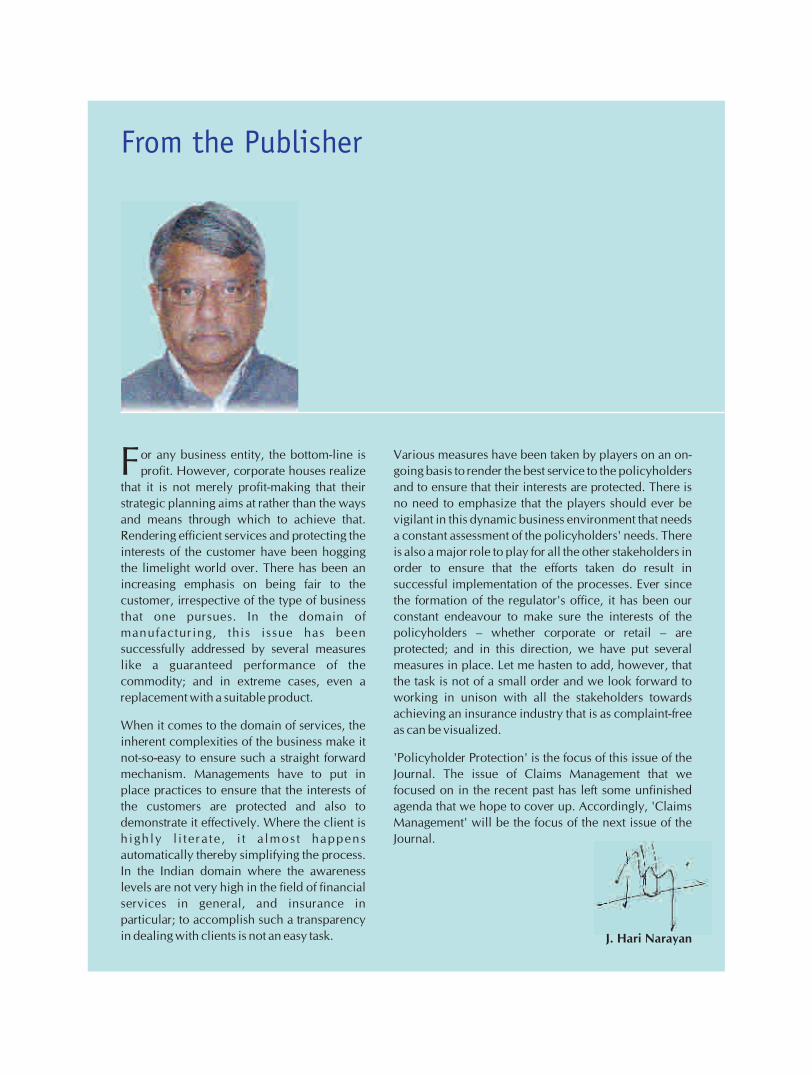

From the Publisher

or any business entity, the bottom-line is

profit. However, corporate houses realize Fthat it is not merely profit-making that their

strategic planning aims at rather than the ways

and means through which to achieve that.

Rendering efficient services and protecting the

interests of the customer have been hogging

the limelight world over. There has been an

increasing emphasis on being fair to the

customer, irrespective of the type of business

that one pursues. In the domain of

manufacturing, this issue has been

successfully addressed by several measures

like a guaranteed performance of the

commodity; and in extreme cases, even a

replacement with a suitable product.

When it comes to the domain of services, the

inherent complexities of the business make it

not-so-easy to ensure such a straight forward

mechanism. Managements have to put in

place practices to ensure that the interests of

the customers are protected and also to

demonstrate it effectively. Where the client is

h ighly l i te ra te , i t a lmost happens

automatically thereby simplifying the process.

In the Indian domain where the awareness

levels are not very high in the field of financial

services in general, and insurance in

particular; to accomplish such a transparency

in dealing with clients is not an easy task.

Various measures have been taken by players on an on-

going basis to render the best service to the policyholders

and to ensure that their interests are protected. There is

no need to emphasize that the players should ever be

vigilant in this dynamic business environment that needs

a constant assessment of the policyholders' needs. There

is also a major role to play for all the other stakeholders in

order to ensure that the efforts taken do result in

successful implementation of the processes. Ever since

the formation of the regulator's office, it has been our

constant endeavour to make sure the interests of the

policyholders – whether corporate or retail – are

protected; and in this direction, we have put several

measures in place. Let me hasten to add, however, that

the task is not of a small order and we look forward to

working in unison with all the stakeholders towards

achieving an insurance industry that is as complaint-free

as can be visualized.

'Policyholder Protection' is the focus of this issue of the

Journal. The issue of Claims Management that we

focused on in the recent past has left some unfinished

agenda that we hope to cover up. Accordingly, 'Claims

Management' will be the focus of the next issue of the

Journal.

J. Hari Narayan

Editorial BoardJ. Hari NarayanR. KannanS.V. MonyS.B. MathurS.L. MohanVepa KamesamAshvin Parekh

EditorU. JawaharlalHindi CorrespondentKamal ChowlaPrinted by G. Venugopala Krishna andpublished by J. Hari Narayan on behalf ofInsurance Regulatory and Development Authority.Editor: U. JawaharlalPrinted at Vamsi Art Printers Pvt. Ltd.(with design inputs from Efforts)11-6-872, Red Hills, Lakdikapul, Hyderabad.and published from

rdParishram Bhavan, 3 FloorBasheer BaghHyderabad - 500 004Phone: +91-40-23381100Fax: +91-40-66823334e-mail: [email protected]

© 2010 Insurance Regulatory and Development Authority.Please reproduce with due permission.Unless explicitly stated, the information and views published in this Journal may not be construed as those of the Insurance Regulatory and Development Authority.

From the Publisher

or any business entity, the bottom-line is

profit. However, corporate houses realize Fthat it is not merely profit-making that their

strategic planning aims at rather than the ways

and means through which to achieve that.

Rendering efficient services and protecting the

interests of the customer have been hogging

the limelight world over. There has been an

increasing emphasis on being fair to the

customer, irrespective of the type of business

that one pursues. In the domain of

manufacturing, this issue has been

successfully addressed by several measures

like a guaranteed performance of the

commodity; and in extreme cases, even a

replacement with a suitable product.

When it comes to the domain of services, the

inherent complexities of the business make it

not-so-easy to ensure such a straight forward

mechanism. Managements have to put in

place practices to ensure that the interests of

the customers are protected and also to

demonstrate it effectively. Where the client is

h ighly l i te ra te , i t a lmost happens

automatically thereby simplifying the process.

In the Indian domain where the awareness

levels are not very high in the field of financial

services in general, and insurance in

particular; to accomplish such a transparency

in dealing with clients is not an easy task.

Various measures have been taken by players on an on-

going basis to render the best service to the policyholders

and to ensure that their interests are protected. There is

no need to emphasize that the players should ever be

vigilant in this dynamic business environment that needs

a constant assessment of the policyholders' needs. There

is also a major role to play for all the other stakeholders in

order to ensure that the efforts taken do result in

successful implementation of the processes. Ever since

the formation of the regulator's office, it has been our

constant endeavour to make sure the interests of the

policyholders – whether corporate or retail – are

protected; and in this direction, we have put several

measures in place. Let me hasten to add, however, that

the task is not of a small order and we look forward to

working in unison with all the stakeholders towards

achieving an insurance industry that is as complaint-free

as can be visualized.

'Policyholder Protection' is the focus of this issue of the

Journal. The issue of Claims Management that we

focused on in the recent past has left some unfinished

agenda that we hope to cover up. Accordingly, 'Claims

Management' will be the focus of the next issue of the

Journal.

J. Hari Narayan

inside

Issu

e F

oc

us

Changing the Way Insurance is Transacted

Yegnapriya Bharat

Need to Demonstrate and Deliver

Vishwavijay Singh

Contours of World Class Organizations

Prof. Rajni M. Shah

Pro-active Customer Service

Anand Pejawar

Commitment towards Protection

CP Udayachandran

A Myth or a Reality?

K.Nagaraja Rao and Dr Y.Raja Ram

Statistics - Life Insurance 04

In the Air 06

Vantage Point U. Jawaharlal 17

thou chek esa xzkgd fgr j{kkS>m°. gw~moY Hw$‘ma, hare MÝÐ aVyS>r 41

Statistics - Non-Life Insurance 47

Round up 48

Statistical Supplement (Monthly) 49

from the editor

- Essential Management Imperative

There is an increasing emphasis world over on

ensuring that the customer is rendered the best

of services, irrespective of whether it is

demanded or not. This puts the onus on the

providers to be proactive on assessment of the

client's needs; and then put in place an

efficient mechanism to enable the fulfillment

of those needs. The urge to be perfect led to the

evolution of such business management

strategies as Six Sigma which has become

synonymous with corporate managements

seeking perfection. While it would not be easy

to emulate these models in the services

industry entirely, several organizations still set

their benchmarks at a high pedestal so that they

hardly leave any space for consumer

disenchantment.

In the domain of financial services in India,

several service providers have defined pre-set

goals in terms of quality and timelines; and

these are re-visited and reviewed from time to

time to be in tune with the developments

taking place in the corporate world. The

performance of the organizations is assessed

vis-à-vis these standards in order to gauge the

level of their accomplishment and it functions

as a good tool to ensure that there is a constant

attempt to perform well. It necessarily

presupposes that the customer is literate and

capable of taking care of his need-fulfillment,

at least to some extent. However, in a domain

where the financial literacy levels are not very

high, there is need for organizations to be

additionally devoted to render the best

services. Policyholder protection in the

insurance industry occupies even a more

important place considering the fact that

despite the growth in volumes of business,

insurance is still not greatly understood by the

masses.

Further, the need for legal intervention in several disputes pertaining

to the insurance industry bears silent testimony to the fact that the

degree of consumer dissatisfaction is still high. And if a majority of the

verdicts go against the insurers, it gradually leads to a situation where

the policyholder begins to lose confidence in the system. This trend is

detrimental to the growth of the industry and should be arrested

forthwith. Insurers and other stakeholders of the industry should

realize the importance of the spirit of the contracts rather than what is

merely stated in the documents; in order that policyholder protection

in its truest sense is achieved.

'Policyholder Protection' is the focus of this issue of the Journal. As the

regulator of the industry, IRDA has been taking several measures

constantly to ensure the protection of the policyholders' interests.

Could there be a better way of opening the debate than looking at

some of the regulator's initiatives? Ms. Yegnapriya Bharat gives a vivid

account of the various steps taken by the regulatory authority towards

ensuring policyholder protection. In the next article, Mr. Vishwavijay

Singh lays emphasis on the importance of transparency in dealing

with the policyholder at every stage of the policy lifecycle. Prof. Rajni

M Shah brings in the concept of adding value to the customer and

speaks about how to bring it out.

Mr. Anand Pejawar is the author of the next article in which he gives

details of the various services rendered to a life insurance

policyholder; and on how to attain the best degree of client servicing.

In the next article, Mr. C.P. Udayachandran speaks about the punitive

measures to be adopted in case the service providers deliberately

default on rendering the desired service to the customer. In the last

article of the issue, Mr. K. Nagaraja Rao and Dr. Y. Raja Ram throw

light on what the rural policyholder feels about the services being

rendered by insurers.

It was not long ago that the focus of the Journal was on Claims

Management. However, looking at the various issues associated with

the hugely important aspect of insurance business, it is proposed to

focus on 'Claims Management' once again in the next issue of the

Journal.

U. Jawaharlal

Ensuring Wholesome Protection

18

22

24

29

32

34

inside

Issu

e F

oc

us

Changing the Way Insurance is Transacted

Yegnapriya Bharat

Need to Demonstrate and Deliver

Vishwavijay Singh

Contours of World Class Organizations

Prof. Rajni M. Shah

Pro-active Customer Service

Anand Pejawar

Commitment towards Protection

CP Udayachandran

A Myth or a Reality?

K.Nagaraja Rao and Dr Y.Raja Ram

Statistics - Life Insurance 04

In the Air 06

Vantage Point U. Jawaharlal 17

thou chek esa xzkgd fgr j{kkS>m°. gw~moY Hw$‘ma, hare MÝÐ aVyS>r 41

Statistics - Non-Life Insurance 47

Round up 48

Statistical Supplement (Monthly) 49

from the editor

- Essential Management Imperative

There is an increasing emphasis world over on

ensuring that the customer is rendered the best

of services, irrespective of whether it is

demanded or not. This puts the onus on the

providers to be proactive on assessment of the

client's needs; and then put in place an

efficient mechanism to enable the fulfillment

of those needs. The urge to be perfect led to the

evolution of such business management

strategies as Six Sigma which has become

synonymous with corporate managements

seeking perfection. While it would not be easy

to emulate these models in the services

industry entirely, several organizations still set

their benchmarks at a high pedestal so that they

hardly leave any space for consumer

disenchantment.

In the domain of financial services in India,

several service providers have defined pre-set

goals in terms of quality and timelines; and

these are re-visited and reviewed from time to

time to be in tune with the developments

taking place in the corporate world. The

performance of the organizations is assessed

vis-à-vis these standards in order to gauge the

level of their accomplishment and it functions

as a good tool to ensure that there is a constant

attempt to perform well. It necessarily

presupposes that the customer is literate and

capable of taking care of his need-fulfillment,

at least to some extent. However, in a domain

where the financial literacy levels are not very

high, there is need for organizations to be

additionally devoted to render the best

services. Policyholder protection in the

insurance industry occupies even a more

important place considering the fact that

despite the growth in volumes of business,

insurance is still not greatly understood by the

masses.

Further, the need for legal intervention in several disputes pertaining

to the insurance industry bears silent testimony to the fact that the

degree of consumer dissatisfaction is still high. And if a majority of the

verdicts go against the insurers, it gradually leads to a situation where

the policyholder begins to lose confidence in the system. This trend is

detrimental to the growth of the industry and should be arrested

forthwith. Insurers and other stakeholders of the industry should

realize the importance of the spirit of the contracts rather than what is

merely stated in the documents; in order that policyholder protection

in its truest sense is achieved.

'Policyholder Protection' is the focus of this issue of the Journal. As the

regulator of the industry, IRDA has been taking several measures

constantly to ensure the protection of the policyholders' interests.

Could there be a better way of opening the debate than looking at

some of the regulator's initiatives? Ms. Yegnapriya Bharat gives a vivid

account of the various steps taken by the regulatory authority towards

ensuring policyholder protection. In the next article, Mr. Vishwavijay

Singh lays emphasis on the importance of transparency in dealing

with the policyholder at every stage of the policy lifecycle. Prof. Rajni

M Shah brings in the concept of adding value to the customer and

speaks about how to bring it out.

Mr. Anand Pejawar is the author of the next article in which he gives

details of the various services rendered to a life insurance

policyholder; and on how to attain the best degree of client servicing.

In the next article, Mr. C.P. Udayachandran speaks about the punitive

measures to be adopted in case the service providers deliberately

default on rendering the desired service to the customer. In the last

article of the issue, Mr. K. Nagaraja Rao and Dr. Y. Raja Ram throw

light on what the rural policyholder feels about the services being

rendered by insurers.

It was not long ago that the focus of the Journal was on Claims

Management. However, looking at the various issues associated with

the hugely important aspect of insurance business, it is proposed to

focus on 'Claims Management' once again in the next issue of the

Journal.

U. Jawaharlal

Ensuring Wholesome Protection

18

22

24

29

32

34

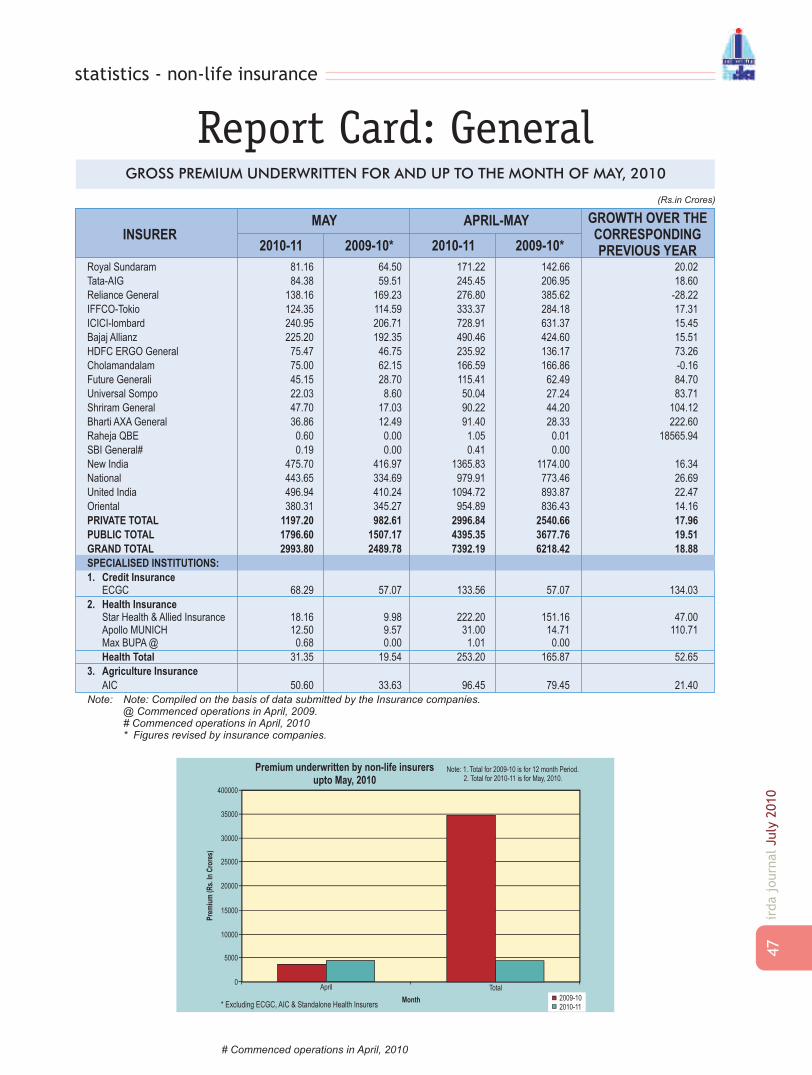

statistics - life insurance

04

irda

journ

alJuly

2010

Repo

rt C

ard:

LIFE

Firs

t Ye

ar P

rem

ium

of

Life

Ins

urer

s fo

r th

e Pe

riod

Ende

d M

ay, 20

10No

. of l

ives c

over

edun

der G

roup

Sche

mes

Sl No.

Insu

rer

Prem

ium

u/w

(Rs.

inCr

ores

)No

. of P

olici

es/ S

chem

es

May

, 10

May

May

May

May

May

May

May

May

Upto

, 10

Upto

, 09

, 10

Upto

, 10

Upto

, 09

, 10

Upto

, 10

Upto

, 09

1In

divi

dual

Sin

gle

Pre

miu

m58

.62

85.2

723

.98

8168

1350

980

87In

divi

dual

Non

-Sin

gle

Pre

miu

m13

0.30

248.

2123

4.60

1218

8522

8264

1960

89G

roup

Sin

gle

Pre

miu

m4.

939.

723.

697

82

9036

1503

768

4G

roup

Non

-Sin

gle

Pre

miu

m15

.67

30.3

578

.58

151

257

8011

9253

228

3940

910

4919

9

2In

divi

dual

Sin

gle

Pre

miu

m0.

020.

031.

081

317

1In

divi

dual

Non

-Sin

gle

Pre

miu

m29

.12

58.0

672

.08

1387

528

284

4094

2G

roup

Sin

gle

Pre

miu

m0.

831.

371.

350

00

148

254

520

Gro

upN

on-S

ingl

eP

rem

ium

0.00

0.00

0.08

00

027

7090

2

3In

divi

dual

Sin

gle

Pre

miu

m15

.63

23.8

28.

8329

0450

6328

04In

divi

dual

Non

-Sin

gle

Pre

miu

m16

7.26

278.

0721

6.60

1483

0623

9555

2305

56G

roup

Sin

gle

Pre

miu

m0.

692.

4628

.90

1337

123

343

6456

976

Gro

upN

on-S

ingl

eP

rem

ium

1.61

13.3

36.

1926

4397

1688

420

806

2240

64

4In

divi

dual

Sin

gle

Pre

miu

m39

.81

59.1

531

.99

5318

7760

6294

Indi

vidu

alN

on-S

ingl

eP

rem

ium

139.

1822

6.56

279.

2739

505

6212

787

933

Gro

upS

ingl

eP

rem

ium

3.01

7.07

30.3

40

10

474

735

2304

8G

roup

Non

-Sin

gle

Pre

miu

m26

0.50

335.

1144

2.34

89

2213

2019

1521

3814

7066

5In

divi

dual

Sin

gle

Pre

miu

m2.

554.

843.

0328

460

591

8In

divi

dual

Non

-Sin

gle

Pre

miu

m56

.00

117.

4610

7.95

3560

778

087

9140

5G

roup

Sin

gle

Pre

miu

m2.

274.

332.

760

01

3955

7783

4607

Gro

upN

on-S

ingl

eP

rem

ium

6.48

7.64

5.61

714

1646

2017

803

2098

7

6In

divi

dual

Sin

gle

Pre

miu

m8.

2312

.08

15.7

720

4040

3826

55In

divi

dual

Non

-Sin

gle

Pre

miu

m19

5.86

312.

9319

6.08

4586

775

426

7898

2G

roup

Sin

gle

Pre

miu

m0.

601.

9820

.98

1839

3521

093

4341

364

906

Gro

upN

on-S

ingl

eP

rem

ium

33.0

474

.08

1.03

39

017

289

3872

322

5

7In

divi

dual

Sin

gle

Pre

miu

m1.

492.

6022

.87

1165

2299

Indi

vidu

alN

on-S

ingl

eP

rem

ium

283.

2554

9.67

282.

5910

5760

2049

5922

3655

Gro

upS

ingl

eP

rem

ium

44.1

654

.40

29.3

052

140

113

1461

4624

1353

1657

41G

roup

Non

-Sin

gle

Pre

miu

m13

1.07

156.

9714

8.78

6019

018

949

007

1660

3922

4386

8In

divi

dual

Sin

gle

Pre

miu

m3.

845.

768.

2739

1425

679

1886

9In

divi

dual

Non

-Sin

gle

Pre

miu

m11

2.18

182.

9218

3.36

9874

922

4616

1787

88G

roup

Sin

gle

Pre

miu

m0.

300.

520.

090

00

5613

746

Gro

upN

on-S

ingl

eP

rem

ium

46.3

658

.93

50.7

913

3534

8820

913

3531

6870

7

9In

divi

dual

Sin

gle

Pre

miu

m1.

832.

9312

.41

5912

119

21In

divi

dual

Non

-Sin

gle

Pre

miu

m40

.39

63.7

861

.64

1561

226

782

2456

8G

roup

Sin

gle

Pre

miu

m0.

020.

030.

000

00

5382

0G

roup

Non

-Sin

gle

Pre

miu

m2.

935.

464.

938

1612

1061

5128

5478

1471

18

10In

divi

dual

Sin

gle

Pre

miu

m5.

4610

.75

1.29

515

952

172

Indi

vidu

alN

on-S

ingl

eP

rem

ium

44.4

476

.57

64.9

618

311

2861

127

197

Gro

upS

ingl

eP

rem

ium

6.59

10.5

23.

420

00

2495

341

830

1074

7G

roup

Non

-Sin

gle

Pre

miu

m11

.34

19.5

58.

6887

137

109

1119

2321

3441

9785

5

11In

divi

dual

Sin

gle

Pre

miu

m13

.43

26.0

936

.01

179

281

2306

Indi

vidu

alN

on-S

ingl

eP

rem

ium

107.

4122

6.61

239.

0859

170

1245

6215

3236

Gro

upS

ingl

eP

rem

ium

0.42

1.59

0.05

28

659

689

4254

3820

6232

Gro

upN

on-S

ingl

eP

rem

ium

12.6

218

.01

2.73

8724

819

515

5995

017

6116

320

5792

12In

divi

dual

Sin

gle

Pre

miu

m1.

412.

700.

5331

163

279

Indi

vidu

alN

on-S

ingl

eP

rem

ium

34.8

854

.58

62.7

213

652

2215

822

812

Gro

upS

ingl

eP

rem

ium

1.85

3.75

0.00

00

096

718

790

Gro

upN

on-S

ingl

eP

rem

ium

3.42

7.40

12.2

258

7836

3234

7036

7518

6847

3

Baj

ajA

llian

z

ING

Vys

ya

Rel

ian

ceL

ife

SB

I Lif

e

Tata

AIG

HD

FC

Sta

nd

ard

ICIC

I Pru

den

tial

Bir

laS

un

life

Avi

va

Ko

tak

Mah

ind

raO

ldM

utu

al

Max

New

Yo

rk

Met

Lif

e

05

irda

journ

alJuly

2010

Not

e:1.

Cum

ulat

ive

prem

ium

/No.

ofpo

licie

sup

toth

em

onth

isne

tofc

ance

llatio

nsw

hich

may

occu

rdu

ring

the

free

look

perio

d.2.

Com

pile

don

the

basi

sof

data

subm

itted

byth

eIn

sura

nce

com

pani

es3.

@S

tart

edop

erat

ions

inF

ebru

ary ,

2009

4.#S

tart

edop

erat

ions

inN

ovem

ber ,2

009

13In

divi

dual

Sin

gle

Pre

miu

m1.

562.

282.

6644

462

080

6In

divi

dual

Non

-Sin

gle

Pre

miu

m3.

545.

596.

8046

8969

2072

45G

roup

Sin

gle

Pre

miu

m0.

000.

000.

000

00

00

0G

roup

Non

-Sin

gle

Pre

miu

m0.

000.

004.

380

00

00

5544

12

14In

divi

dual

Sin

gle

Pre

miu

m15

.51

28.7

05.

5217

7232

6093

3In

divi

dual

Non

-Sin

gle

Pre

miu

m14

.66

27.3

029

.73

6086

1085

818

289

Gro

upS

ingl

eP

rem

ium

4.31

6.11

0.00

00

018

738

2616

50

Gro

upN

on-S

ingl

eP

rem

ium

1.52

1.52

0.00

22

016

2190

1621

900

15In

divi

dual

Sin

gle

Pre

miu

m0.

461.

020.

4835

673

459

Indi

vidu

alN

on-S

ingl

eP

rem

ium

28.7

248

.81

39.3

013

239

2109

019

482

Gro

upS

ingl

eP

rem

ium

1.36

2.84

2.50

00

210

2120

3824

58G

roup

Non

-Sin

gle

Pre

miu

m0.

000.

000.

000

00

00

0

16In

divi

dual

Sin

gle

Pre

miu

m0.

370.

530.

8448

7214

5In

divi

dual

Non

-Sin

gle

Pre

miu

m27

.46

40.5

722

.60

2551

436

081

2068

6G

roup

Sin

gle

Pre

miu

m0.

020.

040.

000

00

440

1044

0G

roup

Non

-Sin

gle

Pre

miu

m2.

084.

145.

987

1420

3337

6483

1945

7039

7

17In

divi

dual

Sin

gle

Pre

miu

m6.

089.

9212

.64

1182

2023

1792

Indi

vidu

alN

on-S

ingl

eP

rem

ium

15.5

027

.91

22.0

559

4497

4968

48G

roup

Sin

gle

Pre

miu

m0.

000.

000.

000

00

00

0G

roup

Non

-Sin

gle

Pre

miu

m0.

030.

060.

010

52

8239

1567

352

30

18In

divi

dual

Sin

gle

Pre

miu

m0.

551.

230.

7642

7354

Indi

vidu

alN

on-S

ingl

eP

rem

ium

34.0

187

.19

75.4

552

3411

619

7619

Gro

upS

ingl

eP

rem

ium

2.26

3.28

0.00

00

012

8918

630

Gro

upN

on-S

ingl

eP

rem

ium

0.00

0.00

0.00

00

00

00

19In

divi

dual

Sin

gle

Pre

miu

m0.

811.

180.

1231

5416

Indi

vidu

alN

on-S

ingl

eP

rem

ium

11.6

317

.92

6.78

3275

4924

2669

Gro

upS

ingl

eP

rem

ium

0.06

0.11

0.00

00

012

823

80

Gro

upN

on-S

ingl

eP

rem

ium

0.00

0.00

0.00

00

00

00

20In

divi

dual

Sin

gle

Pre

miu

m0.

090.

360.

008

520

Indi

vidu

alN

on-S

ingl

eP

rem

ium

3.51

8.99

2.17

1846

4151

1576

Gro

upS

ingl

eP

rem

ium

0.00

0.00

0.00

00

00

00

Gro

upN

on-S

ingl

eP

rem

ium

0.00

0.00

0.00

00

00

00

21In

divi

dual

Sin

gle

Pre

miu

m12

.26

17.6

62.

6187

712

1244

7In

divi

dual

Non

-Sin

gle

Pre

miu

m10

.45

15.0

95.

9235

9949

1924

12G

roup

Sin

gle

Pre

miu

m2.

895.

270.

000

00

1660

2232

0G

roup

Non

-Sin

gle

Pre

miu

m0.

110.

620.

006

70

9006

1454

20

22In

divi

dual

Sin

gle

Pre

miu

m8.

6415

.13

711

1366

Indi

vidu

alN

on-S

ingl

eP

rem

ium

17.1

746

.15

6620

1557

7G

roup

Sin

gle

Pre

miu

m0.

200.

202

267

8267

82G

roup

Non

-Sin

gle

Pre

miu

m0.

000.

000

20

0

198.

6531

4.04

191.

6929

175

6817

450

827

1506

.92

2720

.95

2211

.75

7923

4514

6931

914

4298

976

.74

115.

6012

3.38

9423

516

031

9971

8828

7247

9065

528.

7973

3.17

772.

3252

310

6681

241

1528

070

2046

928

8481

3

23In

divi

dual

Sin

gle

Pre

miu

m23

48.5

539

59.2

312

01.1

837

9548

6483

7232

2389

Indi

vidu

alN

on-S

ingl

eP

rem

ium

1827

.79

3273

.81

2130

.94

1819

657

3269

264

2983

085

Gro

upS

ingl

eP

rem

ium

1039

.77

2076

.77

2022

.80

1154

1986

1993

1561

108

2425

687

1990

944

Gro

upN

on-S

ingl

eP

rem

ium

693.

0477

3.04

0.00

8181

039

3170

4472

950

2547

.20

4273

.26

1392

.87

4087

2371

6546

3732

1633

34.7

159

94.7

543

42.6

926

1200

247

3858

344

2607

411

16.5

121

92.3

621

46.1

812

4822

2121

5318

8107

933

0855

924

7000

912

21.8

315

06.2

177

2.32

604

1147

812

4508

450

7467

764

2884

813

Sah

ara

Lif

e

Sh

rira

mL

ife

Bh

arti

Axa

Lif

e

Fu

ture

Gen

eral

i Lif

e

IDB

I Fo

rtis

Lif

e

Can

ara

HS

BC

OB

CL

ife

Aeg

on

Rel

igar

e

DL

FP

ram

eric

a

Sta

rU

nio

nD

ai-i

chi@

Ind

iaF

irst

#

Pri

vate

Tota

lIn

div

idu

alS

ing

leP

rem

ium

Ind

ivid

ual

No

n-S

ing

leP

rem

ium

Gro

up

Sin

gle

Pre

miu

mG

rou

pN

on

-Sin

gle

Pre

miu

m

LIC

Gra

nd

Tota

lIn

div

idu

alS

ing

leP

rem

ium

Ind

ivid

ual

No

n-S

ing

leP

rem

ium

Gro

up

Sin

gle

Pre

miu

mG

rou

pN

on

-Sin

gle

Pre

miu

m

in the air

06

irda j

ourn

al Ju

ly 2

010

EXPOSURE DRAFT

Re: Exposure draft regarding proposed amendment to IRDA

Regulations for Protection of Policyholders Interests, 2002 -

Issuance of Key Feature Documents for insurance products.

In line with the nation's approach to economic reforms, the IRDA has

initiated reform measures around the principle of sustainable growth

along with public accountability. Therefore protecting the interests of

policyholders is the main mission of IRDA and the Authority's efforts

have been constantly directed towards this end.

In 2002, the Authority brought out the IRDA (Protection of

Policyholders' Interest) Regulations. The Regulations define the

obligation of insurers and intermediaries and lay down time-frames

for compliance that cover the entire life cycle of a product, starting

from its sale to servicing, including at the point of claim.

The opening up of the insurance sector has given insurers the

opportunity to bring about many innovative designs and concepts in

product development. Spurred by competition triggered by this

opportunity, the market has seen a plethora of new products. This has

raised new concerns regarding availability of information to prospects

and policyholders.

While IRDA has made continuous efforts to demystify complex

products by requiring insurers to follow certain guidelines relating to

disclosures especially in respect of the new breed of products such as

ULIPs and carry out adequate safeguards while advertising about

products etc, there is a need to constantly scale up the efforts to ensure

that the required information is made available to prospects and

policyholders and that the “information gap” between them and the

insurers is reduced or removed.

The Authority is sensitive to the fact that information asymmetry is a

reality in the market and that it is necessary for all stakeholders to

work towards its removal. In this backdrop, the importance of giving

policyholders clear and precise information with regard to insurance

products needs no further emphasis. The Authority has brought out

the IRDA (Insurance Advertisement and Disclosure) Regulations in

2000 to ensure that asymmetry is addressed. It has been IRDA's

constant endeavour to permit only correct, easily understood

depiction of the product features. Apart from the Regulations, IRDA

has also issued guidelines in this regard.

Ensuring fair treatment to policyholders: There should be utmost

transparency at the time of sale and promotion so that the

policyholder is made to feel confident that he or she is being given

complete information regarding the product. Provision of clear and

complete information about products is not only a fundamental

expectation but also a necessity to ensure fair treatment to

policyholders by insurance companies. It is a necessary disclosure

obligation of insurance companies.

Contractual documents issued by insurers: Contractual documents

developed by insurance companies should take care of the interests of

policyholders by giving them the required information in a clear and

4th June, 2010 ALL INSURERS/CONSUMER BODIES/GENERAL PUBLIC

simple manner. Legal documents are complex

and not comprehensible to the insured

persons. It is observed that insurance policy

documents are long and run into several pages

making it almost impossible for policyholders

to read them.

While, more than 30% of the Indian

population is illiterate, even the literate

population will not understand complex legal

language. In view of this, providing product

information in a simple and easy to understand

manner is very crucial.

Key Feature Documents: To ensure fair

treatment to policyholders, it is necessary for

insurers to bring out Key Feature Documents in

simple language. This document will have the

same legal sanction that a comprehensive

policy document will have. Towards this end,

it is proposed to incorporate a provision in

IRDA Regulations for Protection of

Policyholders Interests that would require

insurance companies to issue Key Feature

Documents for various insurance products to

policyholders.

Format of Key Feature Document: It is

necessary that the proposed Key Feature

Documents are developed in a clear format

with an appropriate title and sub-titles that

makes it easy for policyholders to

comprehend. The language used should be

simple. Illustrations relating to cover/benefits

offered should be part of the Key Feature

Document. The ultimate test of a Key Feature

Document is whether or not the target

customer for a particular product understands

its main features and is able to take a decision

as to whether the product is suitable for

him/her. A good example of a Key Feature

Document is one that clearly captures the aim

of the product or in other words, what the

product seeks to cover. It would clearly bring

out the risks involved for the policyholder and

the obligations or commitments required of

him/her. A Key Feature document should not

be too long as to lose the precision nor should

it be too short thereby missing out on key facts.

The document should avoid jargon, should be

easy to read and most of all be attractive for the

consumer to peruse. It should be titled

prominently and should use easy to

07

irda j

ourn

al Ju

ly 2

010

EXPOSURE DRAFT4th June, 2010

understand language. It should be in at least 14

size font (of Times New Roman, as an

indication). Key Feature Document shall be

available in local languages depending on the

region where the policy holder resides.

It is necessary to have the Key Feature

Document as a separate item and not part of

other literature. Model Key Feature

Documents in respect of 4 products are

enclosed as indicative formats to communicate

the intention behind the proposed regulations.

Insurers, general public and consumer bodies are requested to

respond by 20th June, 2010. E-mails may be forwarded to

Encl: Model Key Feature Documents 1. Jeevan Anand 2. Wealth Plus 3. Forever Life 4. Family Care

Sd/-

(A.Giridhar)

Executive Director, IRDA

Re: Exposure Draft on Guidelines on Distance

Marketing and Sale Process Verification of

Insurance Products

The Authority proposes to come out with the

Guidelines on Distance Marketing and Sale of

Insurance Products to streamline the manner of

sale of insurance products and to address some

of the issues which are specific to protection of

interests of policyholders buying insurance

over distance modes such as telephone and the

internet.

The exposure draft on the above guideline is

hereby published to elicit opinion of

policyholders, consumer organisations, general public, distributors,

insurers and various other stakeholders.

It is therefore requested that the comments may be forwarded to Mr. V.

Sai Kumar, OSD (Life) or e-mail to [email protected] in on or before

20th June, 2010.

Encl: Exposure Draft on Guidelines on Distance Marketing and Sale

Process Verification of Insurance Products

Sd/-

(A. Giridhar)

ED (Admin)

CIRCULARDate: June 10, 2010 Ref: IRDA/F&I/CIR/DATA/091/06/2010

To,

The CEOs of All Insurance Companies

Dear Sir,

Section 31B(2) of the Insurance Act, 1938

Attention is drawn to section 31B(2) of the

Insurance Act, 1938 by virtue of which “Every

insurer shall before the close of the month

following every year, submit to the Authority [a

statement, in the form specified by the

Regulations made by the Authority,] showing

the remuneration paid, whether by way of

commission or otherwise, to any person in

cases where such remuneration exceeds (such

sum as may be specified by the regulations

made by the Authority.)”

2. The Authority has now decided that the

details of remuneration paid whether by

way of commission or otherwise to any person, in cases where

such remuneration exceeds Rs. 1 lakh per annum may be furnished

to the Authority in the format prescribed in the Annexure.

3. The said details pertaining to the financial year ending 31st March

may be furnished by 30th April of every year. However, for the year

ending 31st March 2010, details may be furnished by 30st June

2010.

4. Employee remuneration details which are being furnished as part

of the Director's Report as required under Section 217 (2A) (a) of

the Companies Act, 1956 read with the Companies (Particulars of

Employees) Rules, 1975 may continue to be provided along with

Director's Report.

5. This circular supersedes the circular dated 9th May 2003 on the

subject.

Sd/-

(R. K. Nair)

Member (F&I)

in the air

06

irda j

ourn

al Ju

ly 2

010

EXPOSURE DRAFT

Re: Exposure draft regarding proposed amendment to IRDA

Regulations for Protection of Policyholders Interests, 2002 -

Issuance of Key Feature Documents for insurance products.

In line with the nation's approach to economic reforms, the IRDA has

initiated reform measures around the principle of sustainable growth

along with public accountability. Therefore protecting the interests of

policyholders is the main mission of IRDA and the Authority's efforts

have been constantly directed towards this end.

In 2002, the Authority brought out the IRDA (Protection of

Policyholders' Interest) Regulations. The Regulations define the

obligation of insurers and intermediaries and lay down time-frames

for compliance that cover the entire life cycle of a product, starting

from its sale to servicing, including at the point of claim.

The opening up of the insurance sector has given insurers the

opportunity to bring about many innovative designs and concepts in

product development. Spurred by competition triggered by this

opportunity, the market has seen a plethora of new products. This has

raised new concerns regarding availability of information to prospects

and policyholders.

While IRDA has made continuous efforts to demystify complex

products by requiring insurers to follow certain guidelines relating to

disclosures especially in respect of the new breed of products such as

ULIPs and carry out adequate safeguards while advertising about

products etc, there is a need to constantly scale up the efforts to ensure

that the required information is made available to prospects and

policyholders and that the “information gap” between them and the

insurers is reduced or removed.

The Authority is sensitive to the fact that information asymmetry is a

reality in the market and that it is necessary for all stakeholders to

work towards its removal. In this backdrop, the importance of giving

policyholders clear and precise information with regard to insurance

products needs no further emphasis. The Authority has brought out

the IRDA (Insurance Advertisement and Disclosure) Regulations in

2000 to ensure that asymmetry is addressed. It has been IRDA's

constant endeavour to permit only correct, easily understood

depiction of the product features. Apart from the Regulations, IRDA

has also issued guidelines in this regard.

Ensuring fair treatment to policyholders: There should be utmost

transparency at the time of sale and promotion so that the

policyholder is made to feel confident that he or she is being given

complete information regarding the product. Provision of clear and

complete information about products is not only a fundamental

expectation but also a necessity to ensure fair treatment to

policyholders by insurance companies. It is a necessary disclosure

obligation of insurance companies.

Contractual documents issued by insurers: Contractual documents

developed by insurance companies should take care of the interests of

policyholders by giving them the required information in a clear and

4th June, 2010 ALL INSURERS/CONSUMER BODIES/GENERAL PUBLIC

simple manner. Legal documents are complex

and not comprehensible to the insured

persons. It is observed that insurance policy

documents are long and run into several pages

making it almost impossible for policyholders

to read them.

While, more than 30% of the Indian

population is illiterate, even the literate

population will not understand complex legal

language. In view of this, providing product

information in a simple and easy to understand

manner is very crucial.

Key Feature Documents: To ensure fair

treatment to policyholders, it is necessary for

insurers to bring out Key Feature Documents in

simple language. This document will have the

same legal sanction that a comprehensive

policy document will have. Towards this end,

it is proposed to incorporate a provision in

IRDA Regulations for Protection of

Policyholders Interests that would require

insurance companies to issue Key Feature

Documents for various insurance products to

policyholders.

Format of Key Feature Document: It is

necessary that the proposed Key Feature

Documents are developed in a clear format

with an appropriate title and sub-titles that

makes it easy for policyholders to

comprehend. The language used should be

simple. Illustrations relating to cover/benefits

offered should be part of the Key Feature

Document. The ultimate test of a Key Feature

Document is whether or not the target

customer for a particular product understands

its main features and is able to take a decision

as to whether the product is suitable for

him/her. A good example of a Key Feature

Document is one that clearly captures the aim

of the product or in other words, what the

product seeks to cover. It would clearly bring

out the risks involved for the policyholder and

the obligations or commitments required of

him/her. A Key Feature document should not

be too long as to lose the precision nor should

it be too short thereby missing out on key facts.

The document should avoid jargon, should be

easy to read and most of all be attractive for the

consumer to peruse. It should be titled

prominently and should use easy to

07

irda j

ourn

al Ju

ly 2

010

EXPOSURE DRAFT4th June, 2010

understand language. It should be in at least 14

size font (of Times New Roman, as an

indication). Key Feature Document shall be

available in local languages depending on the

region where the policy holder resides.

It is necessary to have the Key Feature

Document as a separate item and not part of

other literature. Model Key Feature

Documents in respect of 4 products are

enclosed as indicative formats to communicate

the intention behind the proposed regulations.

Insurers, general public and consumer bodies are requested to

respond by 20th June, 2010. E-mails may be forwarded to

Encl: Model Key Feature Documents 1. Jeevan Anand 2. Wealth Plus 3. Forever Life 4. Family Care

Sd/-

(A.Giridhar)

Executive Director, IRDA

Re: Exposure Draft on Guidelines on Distance

Marketing and Sale Process Verification of

Insurance Products

The Authority proposes to come out with the

Guidelines on Distance Marketing and Sale of

Insurance Products to streamline the manner of

sale of insurance products and to address some

of the issues which are specific to protection of

interests of policyholders buying insurance

over distance modes such as telephone and the

internet.

The exposure draft on the above guideline is

hereby published to elicit opinion of

policyholders, consumer organisations, general public, distributors,

insurers and various other stakeholders.

It is therefore requested that the comments may be forwarded to Mr. V.

Sai Kumar, OSD (Life) or e-mail to [email protected] in on or before

20th June, 2010.

Encl: Exposure Draft on Guidelines on Distance Marketing and Sale

Process Verification of Insurance Products

Sd/-

(A. Giridhar)

ED (Admin)

CIRCULARDate: June 10, 2010 Ref: IRDA/F&I/CIR/DATA/091/06/2010

To,

The CEOs of All Insurance Companies

Dear Sir,

Section 31B(2) of the Insurance Act, 1938

Attention is drawn to section 31B(2) of the

Insurance Act, 1938 by virtue of which “Every

insurer shall before the close of the month

following every year, submit to the Authority [a

statement, in the form specified by the

Regulations made by the Authority,] showing

the remuneration paid, whether by way of

commission or otherwise, to any person in

cases where such remuneration exceeds (such

sum as may be specified by the regulations

made by the Authority.)”

2. The Authority has now decided that the

details of remuneration paid whether by

way of commission or otherwise to any person, in cases where

such remuneration exceeds Rs. 1 lakh per annum may be furnished

to the Authority in the format prescribed in the Annexure.

3. The said details pertaining to the financial year ending 31st March

may be furnished by 30th April of every year. However, for the year

ending 31st March 2010, details may be furnished by 30st June

2010.

4. Employee remuneration details which are being furnished as part

of the Director's Report as required under Section 217 (2A) (a) of

the Companies Act, 1956 read with the Companies (Particulars of

Employees) Rules, 1975 may continue to be provided along with

Director's Report.

5. This circular supersedes the circular dated 9th May 2003 on the

subject.

Sd/-

(R. K. Nair)

Member (F&I)

in the air

08

irda

journ

alJuly

2010

CIRCULAR

June 16, 2010 Ref: Ref:IRDA/F&I/CIR/100/06/2010

To

Authority vide its Circular No. IRDA/F&A/064/JAN/05 dated 12th

January, 2005 and IRDA/CIR/F&A/073/FEB-05 dated 22nd February,

2005 had mandated all the insurers to submit the detail of the

shareholding of the insurance company and the Indian promoter (s) of

the insurance company in the prescribed format.

The prescribed format for the submission of the shareholding pattern

is revised to capture the information about the pledge or any other

encumbrance, if any created on the shares. The revised format is

The CMDs/ CEOs of All Insurance Companies

Details of Equity Holding Pattern of Insurance Companies

attached herewith. The revision in the format

shall come into force with immediate effect

and the reporting as per the revised formats

shall start from the quarter ending 30th June,

2010.

All insurers are requested to take note of the

above for compliance.

Sd/-

Member (F&I)

(R. K .Nair)

To

In order to streamline the system of Issue/Renewal of License to

Corporate Agents, the Authority has, in addition to the Regulations

and Guidelines already in force, decided to issue the following

instructions under Section 14 of the IRDA Act, 1999 for compliance

by the Insurers while issuing / renewing Licence to Corporate Agents.

These guidelines shall for part of Cir.No.017/IRDA Circular/CA

Guidelines/2005, dated 14.07.2005 and further circulars/

clarifications issued from time to time.

The following procedure shall be adopted by all the Insurers for

seeking prior approval from the Authority, before issuing Fresh

Licence / Renewal of Licence to the Corporate Agents:

1. All the Insurers shall send to the Authority, the Checklist-cum-

Certification as per Annexure-1, in respect of all Fresh Licences

and the Renewals to obtain prior approval of the Authority.

2. The Checklist shall be duly filled in and signed by the Corporate

Compliance Officer, who shall be designated as the Corporate

Designated Person of the Insurer.

3. The scanned copy (.pdf document) of Checklist along with

Certification shall be mailed to the Authority at the email address

[email protected] for the purpose of processing at the office

All the Insurers

Subject: Guidelines on Issue/Renewal of Licence to Corporate

Agents.

CORPORATE AGENTS - GUIDELINES

of the Authority.

4. The relevant documents supporting the

facts of the Checklist shall be maintained at

the Corporate/Head Office of the Insurer

and shall be made available to the Officers

of the Authority for Inspection, as and when

required by the Authority.

5. On receipt and scrutiny of the Checklist-

cum-Certification from the Insurer, the

Authority shall intimate its decision of

Approval or otherwise with in 7 (seven)

working days from the date of receipt, to the

Insurer in respect of the Fresh/Renewal of

Licence to act as Corporate Agent.

6. Fresh/Renewal Licence shall be issued by

the Corporate Designated Person of the

Insurer from the IRDA portal (as per the

existing procedure) only after obtaining

prior approval of the Authority.

These Guidelines will apply with immediate

effect.

Sd/-

Executive Director

(A Giridhar)

28th June, 2010 Ref: IRDA/CAGTS/GTL/LCE/106/06/2010

09

irda

journ

alJuly

2010

Guidance notes on recent regulatory changes

related to unit linked insurance products

(ULIPs)

Introduction:IRDA has, from time to time, taken various

initiatives for protecting the interests of

policyholders by bringing out Regulations,

Guidelines, Circulars etc applicable to insurers

and intermediaries covering the various stages

in the lifecycle of an insurance product,

commencing from solicitation, sale, policy

servicing, to claims servicing and grievance

redressal.

With expansion of the insurance sector and

more and more innovative insurance products,

in particular the Unit Linked Insurance

Products coming into the life insurance

market, IRDA has been sensitive to the

changing scenario and the challenges that go

with it. In particular, IRDA has been conscious

of how these changes have been impacting the

policyholder and has taken several steps to

bring in changes in the regulatory framework

to address various concerns of the

policyholder.

IRDA had stipulated that insurers must provide

the prospect/policyholder all relevant

information regarding amounts deducted

towards various charges for each policy year so

that the prospect could take an informed

decision. Insurers were required to provide

Benefit Illustrations giving two scenarios of

interest rates, 6% and 10% respectively. The

prospect was required to sign on the

illustration while signing the proposal form.

This was done to ensure transparency and

proper disclosures by the insurers.

It is necessary to demystify complex products

and ensure that proper product disclosures are

made to the prospect/policyholder. Towards

this end, IRDA has already come out with an

exposure draft on need to issue Key Features

Documents. Responses received by the

Authority are under examination and the

initiative will be taken forward further.

Similarly, Needs Analysis is another initiative

identified by IRDA as a step in curbing wrong

advice and mis-selling. An exposure draft on

this requirement is already circulated and

responses are coming in. Whilst on mis-

UNIT LINKED INSURANCE PRODUCTS

selling, IRDA has identified Distance Marketing as yet another area of

concern and draft guidelines in this regard have been put up as an

exposure note for all stakeholders to respond to.

Mention must be made of what is perhaps the most important step that

the Authority has taken keeping in view the interests of policyholders.

IRDA set up an exclusive Consumer Affairs Department that focuses

on consumer related issues and initiatives including grievance

redressal and consumer education through Insurance Awareness

Campaigns. With a view to creating a central repository of industry-

wide insurance grievance data and facilitating monitoring of disposal

of grievances by insurers, IRDA is on the verge of implementing the

Integrated Grievance Management System (IGMS). IGMS will not

only help monitor the redress systems of insurers but also create a

gateway for policyholders to register complaints with insurance

companies first and if need be escalate them to the IRDA Grievance

Cells. The Consumer Affairs department goes beyond facilitation and

works towards taking grievances to their logical end by calling for

explanations where required, carrying out enquiries and inspections

etc. It is proposed to make the institution of the Insurance

Ombudsman handle all types of complaints including those relating

to policy sale and servicing rather than just restricting it to claims.

IRDA is also shortly making its Call Centre operational for

policyholders to lodge their grievances and also seek their status over

phone/e-mail.

Further, keeping in view the need for efficient functioning of the

insurance sector for protecting the interests of policyholders, it is

necessary to have reliable, timely and accurate data relating to

insurance. In order to ensure that proper data is collected, processed

and disseminated in the manner required, IRDA has set up an

independent body, namely the Insurance Information Bureau (IIB).

The IIB has started functioning and has already made good progress.

More recently, IRDA has taken a holistic view of the features of ULIPs

and addressed issues impacting the policyholders including the way

such products are sold/bought; how ULIPs can be better financial

instruments for providing risk coverage; how sale by unlicensed

personnel and several other malpractices existing in this market may

be curbed by plugging legal loopholes and tightening of the

regulatory ambit; legal mandate to initiate direct penal action against

Corporate Agents etc. IRDA therefore initiated exposure drafts

covering these areas and received considerable feedback from

various stakeholders on the issues put forth. The issues were then

presented to and discussed with the members of the Insurance

Advisory Committee as well as the members of the Board of the

Authority. The following regulatory initiatives have been approved by

the Authority during the Board meeting on 31.05.10.

1. IRDA has amended the IRDA (Insurance Advertisements and

Disclosure) Regulations to remove any scope for the involvement

of unlicensed personnel/entities in the sale of insurance products.

Recent Regulatory Initiatives

I. Distribution channel related changes:

Date : 28th June, 2010

in the air

10

irda j

ourn

al Ju

ly 2

010

2. IRDA has amended the IRDA (Licensing of Corporate Agents)

Regulations to further tighten the Code of Conduct of corporate

agents to ensure that the prospect does not deal with any

unlicensed person. The Regulations have also been amended to

ensure that there is no scope for any kind of remuneration other

than commission where sale has been effected. This measure will

reduce the expenses of the insurer, thereby lowering premiums to

be paid by the policyholder.

3. Regulations for referrals: IRDA has also addressed the issue of

Referrals by bringing out separate Regulations leaving no scope for

misuse of the system. Companies which wish to share their

database of customers with insurers would need to get approval

from IRDA after having conformed to the requirements as laid

down in the Regulations. Further, there are restrictions on the

business activities of the referral company to ensure that there is no

misuse of the system. For instance, the referral company shall not

be in any business of extending loans and advances or accepting

deposits etc though there are exceptions such as for Regional

Rural Banks, Co-operative banks etc. The Regulations cast

obligations on the referral company as well as the insurer

including submission of data as and when called for by the

Authority.

II. ULIP Structure Related Changes:

(1) Lock in period increased to five years:

IRDA has increased the lock-in period for all Unit Linked Products

from three years to five years, including top-up premiums, thereby

making them long term financial instruments which basically provide

risk protection.

(2) Level Paying Premiums:

Further, all regular premium/limited premium ULIPs shall have

uniform/level paying premiums. Any additional payments shall be

treated as single premium for the purpose of insurance cover.

(3) Even Distribution of Charges:

Charges on ULIPs are mandated to be evenly distributed during the

lock in period, to ensure that high front ending of expenses is

eliminated.

(4). Minimum Premium Paying Term Of Five Years:

All limited premium unit linked insurance products, other than single

premium products shall have premium paying term of at least five

years.

(5). Increase In Risk Component:

Further, all unit linked products, other than pension and annuity

products shall provide a mortality cover or a health cover thereby

increasing the risk cover component in such products.

(i) The minimum mortality cover should be as follows:

Minimum Sum assured for age at entry of below 45 years

Minimum Sum assured for age at entry of 45 years and above

Single Premium (SP) contracts: 125 percent of single premium.

Regular Premium (RP) including limited premium paying (LPP)

contracts: 10 times the annualized premiums or (0.5 X T X annualized

premium) whichever is higher. At no time the death benefit shall be

11

irda j

ourn

al Ju

ly 2

010

less than 105 percent of the total premiums

(including top-ups) paid.

Single Premium (SP) contracts: 110 percent

of single premium

Regular Premium (RP) including limited

premium paying (LPP) contracts: 7 times the

annualized premiums or (0.25 X T X

annualized premium) whichever is higher. At

no time the death benefit shall be less than 105

percent of the total premiums (including top-

ups) paid.

(In case of whole life contracts, term (T) shall be

taken as 70 minus age at entry)

(ii)The minimum health cover per annum

should be as follows:

Minimum annual health cover for age at entry

of below 45 years

Minimum annual health cover for age at entry

of 45 years and above

Regular Premium (RP) contracts: 5 times the

annualized premiums or Rs.100,000 per

annum whichever is higher,

At no time the annual health cover shall be less

than 105 percent of the total premiums paid.

Regular Premium (RP) contracts: 5times the

annualized premiums or Rs.75,000 per annum

whichever is higher.

At no time the annual health cover shall be less

than 105 percent of the total premiums paid

(6). Minimum Guaranteed Return for Pension

Products:

As regards pension products, all ULIP

pension/annuity products shall offer a

minimum guaranteed return of 4.5% per

annum or as specified by IRDA from time to

time. This will protect the life time savings for

the pensioners, from any adverse fluctuations

at the time of maturity.

(7). Rationalisation of Cap on Charges:

With a view to smoothening the cap on

charges, the capping been rationalized to

ensure that the difference in yield is capped

from the 5th year onwards. This will not only

reduce the overall charges on these products,

but also smoothen the charge structure for the

policyholder.

III. Discontinuance Of Charges:

IRDA has also addressed the issue of

discontinuance of charges for surrender of

ULIPs. The IRDA (Treatment of Discontinued

Linked Insurance Policies) Regulations

brought out by IRDA in this regard ensure that

policyholders do not get overcharged when

they wish to discontinue their policies for any

emergency cash requirement. The Regulations

stipulate that an insurer shall recover only the

incurred acquisition costs in the event of

discontinuance of policy and that these

charges are not excessive. The discontinuance

charges have been capped both as percentage

of fund value and premium and also in

absolute value. The Regulations also clearly define the Grace Period

for different modes of premium payment. Upon discontinuance of a

policy, a policyholder shall be entitled to exercise an option of either

reviving the policy or completely withdrawing from the policy

without any risk cover. Further, the regulations also enable IRDA to

order refund of discontinuance charges in case they are found

excessive on enquiry.

These regulations are applicable to all new ULIP products approved

by IRDA after these regulations are notified.

J Hari Narayan

Chairman

CIRCULARDATE: 16/06/2010 REF: IRDA/F&I/CIR/AML/99/06/2010

To

THE CEOs OF ALL INSURERS

Anti Money Laundering (AML) Guidelines

A review of AML guidelines has been carried

out to address various issues identified out of

inspections carried out, interactions with FIU-

IND and FATF's Mutual Evaluation and

Assessment process.

2. The following amendments to/clarifications

on the guidelines are issued:

a. Know Your Customer (KYC):Various queries have been raised by insurers

on who can be termed as customer(s) for the

purposes of AML guidelines. Keeping the

objective of the PMLA and AML guidelines in

view, it is hereby clarified that details of the

person who funds/pays for an insurance

contract, either as beneficial owner or

otherwise become relevant and important

Stipulations under clause 3.1 of the AML

guidelines will therefore have to be applied to

such persons. The term customers also refer to

the Proposer/policyholder; Beneficiaries and

Assignee for the purposes of AML guidelines.

At any point in time during the contract period,

where an insurance company is no longer

satisfied that it knows the true identity of the

customer, an STR should be filed with FIU-

IND.

There have been queries on whether due

diligence requirements under clause 3.1.1 (ii)

are to be applied on 'other than individual

entities'. It is clarified that reference to

'individual' policies' to be read to mean

'individual' business. (As 'group' insurance

business falls under clause 3.1.4 and is not covered under AML.

guidelines). It is emphasized that no distinction be made between

'individuals' and 'other than individual entities' for the purposes of

clause 3.1.1

b. Guidance on 'Detailed due diligence':Guidance has been sought on what constitutes detailed due diligence

under clause 3.1.1 (ii) of the AML guidelines. Conducting detailed

due diligence would mean having measures and procedures which

are more rigorous and robust than normal KYC. These measures

should be commensurate to the risk. While it is not intended to be

exhaustive, the following are some of the reasonable measures in

carrying out detailed due diligence:

lMore frequent reviews of the customers activities/

profile/transactions

lApplication of additional measures like gathering information

from Public available. Sources or otherwise

lReview of the proposal/contract by a senior official of the

insurance company etc.,

It is further clarified that detailed due diligence should not be limited

to merely documenting income proofs. Measures laid down should

be in such a way that it would satisfy competent authorities

(Regulatory/enforcement authorities), if need be at a future date, that

due diligence was in fact observed by the insurer in compliance with

the guidelines and the PML Act based on the assessed risk involved in

a transaction/contract.

c. Reduced Customer Due Diligence (CDD) measures:

It is reiterated that while deciding on the extent of due diligence to be

carried out on any customer, risk profile of the product and the

customer should be taken into consideration as indicated at

dause3.1.3 of the AML guidelines.

Notwithstanding the above, detailed due diligence measures should

be applied in the event where there are suspicions of money

laundering or terrorist financing, or where there are factors to indicate

a higher risk.

in the air

10

irda j

ourn

al Ju

ly 2

010

2. IRDA has amended the IRDA (Licensing of Corporate Agents)

Regulations to further tighten the Code of Conduct of corporate

agents to ensure that the prospect does not deal with any

unlicensed person. The Regulations have also been amended to

ensure that there is no scope for any kind of remuneration other

than commission where sale has been effected. This measure will

reduce the expenses of the insurer, thereby lowering premiums to

be paid by the policyholder.

3. Regulations for referrals: IRDA has also addressed the issue of

Referrals by bringing out separate Regulations leaving no scope for

misuse of the system. Companies which wish to share their

database of customers with insurers would need to get approval

from IRDA after having conformed to the requirements as laid

down in the Regulations. Further, there are restrictions on the

business activities of the referral company to ensure that there is no

misuse of the system. For instance, the referral company shall not

be in any business of extending loans and advances or accepting

deposits etc though there are exceptions such as for Regional

Rural Banks, Co-operative banks etc. The Regulations cast

obligations on the referral company as well as the insurer

including submission of data as and when called for by the

Authority.

II. ULIP Structure Related Changes:

(1) Lock in period increased to five years:

IRDA has increased the lock-in period for all Unit Linked Products

from three years to five years, including top-up premiums, thereby

making them long term financial instruments which basically provide

risk protection.

(2) Level Paying Premiums:

Further, all regular premium/limited premium ULIPs shall have

uniform/level paying premiums. Any additional payments shall be