Investor-Presentation-FY2020.pdf - The Gym Group plc

32

18 MARCH 2021

-

Upload

khangminh22 -

Category

Documents

-

view

8 -

download

0

Transcript of Investor-Presentation-FY2020.pdf - The Gym Group plc

18 MARCH 2021

This presentation and information communicated

verbally to you may contain certain projections

and other forward-looking statements with respect

to the financial condition, results of operations,

businesses and prospects of The Gym Group plc.

These statements are based on current

expectations and involve risk and uncertainty

because they relate to events and depend upon

circumstances that may or may not occur in the

future. There are several factors which could

cause actual results or developments to differ

materially from those expressed or implied by

these forward-looking statements. Any of the

assumptions underlying these forward-looking

statements could prove inaccurate or incorrect

and therefore any results contemplated in the

forward-looking statements may not actually

be achieved.

Nothing contained in this presentation or

communicated verbally should be construed as

a profit forecast or profit estimate. Investors or

other recipients are cautioned not to place undue

reliance on any forward-looking statements

contained herein.

The Gym Group plc undertakes no obligation

to update or revise (publicly or otherwise) any

forward-looking statement, whether as a result

of new information, future events or other

circumstances. Neither this presentation nor

any verbal communication shall constitute

an invitation or inducement to any person to

subscribe for or otherwise acquire securities

in The Gym Group plc.

FORWARD-LOOKINGSTATEMENT DISCLAIMER

1

A FINANCIALLY RESILIENT BUSINESS THROUGH COVID…

• Entered 2020 in a position of strength

• Membership resilient despite 45% loss of trading days

– Dec20 membership at 73% of Dec19 level

• COVID protocols led to high member satisfaction scores at re-opening

• Traded profitably and cash generatively in open periods after lockdown

• Continued investment in Technology and 8 new site openings in 2020

• £52.7m liquidity with £40m equity raise + £30m increase in bank facility

…WELL-PLACED FOR RECOVERY AND GROWTH

• 8 new sites opening or under construction in H1 2021

• Investment in technology and data driving competitive advantage

• Continue to see high quality sites at attractive rents

– Strong pipeline for 2021 and beyond

INTRODUCTION

Jan Feb Mar Apr

100% 100% 66% 0%

May Jun Jul Aug

0% 0% 17% 91%

Sep Oct Nov Dec

99% 98% 22% 64%

55%

2020

TRADING DAYS IN 2020

2

3

FINANCIAL SUMMARY

4

MEMBERS

578,0001

216,000 VS PY(Dec 2019: 794,000)

1) All members at 31 Dec 20 were frozen whilst gyms were closed

2) Normalised rent is the contractual rent that would have been paid in normal circumstances without any agreed deferments,

recognised in the monthly period to which it relates

ADJUSTED PBT

(£46.5M) £60.5M VS PY(Dec 2019: £14.0m)

GROUP ADJUSTED EBITDA LESS NORMALISED RENT

(£10.2M) £58.7M VS PY(Dec 2019: £48.5m)

LIQUIDITY

£52.7MNet debt of £47.3M vs

£100.0m of debt facilities

REVENUE

£80.5M £72.6M VS PY(Dec 2019: £153.1m)

NON-PROPERTY NET DEBT

£47.3M £0.1M VS PY(Dec 2019: £47.4m)

• Significant reduction in EBITDA and earnings reflecting reduced revenue as a result of closures

• A number of actions taken to manage costs during closures:

– £16m of government relief from rates relief and furlough payments

– Maintenance, cleaning and utilities costs minimised

– Minimal marketing spend

• Central costs flat YOY; restructuring programme reduced costs in H2 after investment in headcount in Q1

• Costs below EBITDA continue to increase with growth in the estate

• LTIP costs reduced with lower expected payout on share plans

GROUP INCOME STATEMENT

5

£'m FY 2020 FY 2019 % Change

Revenue 80.5 153.1 (47.5%)

Cost of sales (2.1) (1.4) 47.3%

Gross profit 78.4 151.7 (48.3%)

Site costs (excl. exceptional costs) (48.5) (64.5) (24.8%)

Central Costs (excl. exceptional costs) (13.0) (12.7) 2.3%

Group Adjusted EBITDA 16.8 74.5 (77.4%)

Normalised rent (27.0) (25.9) 4.1%

Group Adjusted EBITDA less normalised rent (10.2) 48.5 (120.9%)

add back normalised rent 27.0 25.9 4.1%

Depreciation of right of use asset (21.5) (19.1) 12.6%

Other depreciation (23.6) (22.6) 4.8%

Amortisation of IT intangible assets (2.9) (1.9) 49.6%

Finance costs - leases (12.7) (12.9) (1.5%)

Finance costs - borrowing (1.9) (2.6) (25.2%)

Long term employee incentive costs (0.7) (1.9) (64.8%)

Adjusted PBT (46.5) 14.0 (432.2%)

£16.02

£17.19£0.91

£0.21

£0.05

£15.50

£16.00

£16.50

£17.00

£17.50

2019 ARPMM Pricing LIVE IT PT Income 2020 ARPMM

Upward trend in ARPMM from:

• Pricing (including joining fee)

remaining firm with investment in

data and analytics enabling us to

optimise yield at a local market

level;

• Take-up of LIVE IT increasing to

22.5% of members at Dec 20

(Dec 19: 18.9%);

• Increase in PT income would

have been higher (full year of

new PT model in 2020 vs half

year in 2019) but was reduced

due to PTs being offered rent

free periods during closure and

discounted rents after re-opening

* ARPMM calculated on open days only (closures excluded)

YIELD CONTINUES TO GROW

£18.45

£18.81

£17.00

£17.50

£18.00

£18.50

£19.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2019 2020

AVERAGE REVENUE PER MEMBER PER MONTH (EXC. VAT)*

AVERAGE MONTHLY HEADLINE PRICE FOR ‘DO IT’ SUBSCRIPTION

6

COST SAVING INITIATIVES AND GOVT SUPPORT HELP TO MITIGATE LOSS IN REVENUE

GROUP ADJUSTED EBITDA LESS NORMALISED RENT 2020 VS 2019

7

Government support:

• Rates relief £9.6m

• Furlough support £6.1m

Cost saving measures:

• Reduced site costs during closures

• Lower central costs in H2

YOY cost increases:

• 1st full year of new PT model

• Maturation of 2019 sites

• Covid-secure measures

• Inflationary costs

SUMMARY

• £29.2m of cash Capex in year (vs £41.2m in 2019)

-H1: £21.0m primarily on projects committed pre COVID

-H2: £8.2m on strategic investments in Tech, rebuild of 2 easyGym sites plus essential maintenance

1) Contactless entry and gym busyness tracker etc to ensure COVID-19 compliance

CAPEX SCALED BACK IN H2 DUE TO UNCERTAINTY OVER FUTURE LOCKDOWNS

MAINTENANCE

• Maintenance capex significantly scaled back after Q1 in order to preserve cash

• COVID-related purchases for re-opening: e.g. electrostatic handhelds, sanitiser stands (total £0.5m)

EXPANSIONARY

• 8 new gyms at an average build cost per site:

- £1.24m for standard sites

- £0.85m for small box site

• IT capex relating to app update,

data analysis tools and

reopening initiatives1

• New lease agreed for two

former easyGym sites triggered

a deferred consideration

8

H1 2020 H2 2020 2020 2019 % Change

New site Capex 9.2 1.6 10.8 24.1

easyGym rebuilds & consideration 1.7 1.8 3.4 2.6

Tech & Data 2.4 1.9 4.3 3.9

Expansionary Capex 13.3 5.2 18.5 30.6 (39.4%)

Maintenance Capex 4.1 2.0 6.1 10.2 (40.1%)

Total Capex 17.5 7.2 24.6 40.8 (39.6%)

Capex Creditor Unwind:

- Expansionary Capex 2.1 1.2 3.3 0.3

- Maintenance Capex 1.5 (0.2) 1.3 0.1

Total Cashflow Capex 21.0 8.2 29.2 41.2 (29.0%)

1) Group Operating Cash Flow Conversion is calculated as Group Operating Cash Flow as a percentage of Group Adjusted EBITDA

FY19 NET DEBT MAINTAINED WITH EQUITY PLACING AND TIGHT CASH MANAGEMENT

£m

NON-PROPERTY NET DEBT

£47.3M(Dec 2019: £47.4m)

CASH FLOW & NEW DEBT

9

• 547,000 members at the end of Feb 21

• Stronger member retention in this lockdown

vs previous lockdowns (see chart)

• Disciplined cost management during closure

resulting in c.£5m per month cash burn

– Includes c.£2.5m per month of rent

– Ongoing landlord negotiations

• Net debt at end of Feb £58.2m

– £6.9m of deferred rent outstanding

– £1.9m of deferred VAT outstanding

– £1.1m of furlough income from February still to be received

• Waiver agreed with banks for March 21 covenant test

• Gyms in England expected to re-open on 12 April (Scotland 26 April and Wales TBC)

• Additional Government support announced in Budget on 3 March estimated to be worth c.£8m in 2021/22

• We continue to grow our estate:

– 4 sites due to open and 4 more to start on-site in H1

– 6 additional leases exchanged with several more in advanced negotiations

UPDATE & OUTLOOK

MEMBERSHIP RETENTION DURING CLOSURE PERIODS

10

Lockdown 3Lockdown 2Lockdown 1

11

1 2 3 4 5 6 7 8 9 10111213141516171819202122232425262728293031323334353637383940414243444546474849505152

Joiners Leavers

1 2 3 4 5 6 7 8 9 10111213141516171819202122232425262728293031323334353637383940414243444546474849505152

2019 2020

• Membership subscriptions frozen immediately after lockdown announcements

• In a normal year for mature sites, levels of cancellations and new joiners are broadly consistent, with some seasonality

• Joiners in Jan / Feb 2020 surpassed prior year, but overall joiner numbers in the year were significantly lower due to there being no joiners in closure periods

• With each subsequent lockdown the spikes in cancellations at the start of lockdown have reduced

• Rebuilding the membership in 2021 and 2022 will be a strategic priority driven by:

1. Strong demand for health & fitness as well as weakened competitors

2. Market-leading low-price offer with compelling member value proposition

ACTION TAKEN TO REDUCE MEMBERSHIP LOSS IN CLOSURE PERIODS

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

JOINERS AND LEAVERS IN 2020Sites opened up to and including 2018

TOTAL MEMBERS 2020 VS 2019Sites opened up to and including 2018

Lockdown 1 Lockdown 2

12

OF EMPLOYEES WOULD RECOMMEND US AS A GREAT PLACE TO WORK87%

PEOPLE FIRST APPROACH WILL HELP FUEL OUR RECOVERYJAMIE CAN YOU ADD GOLD INVESTORS IN PEOPLE ICON• Launched People First Campaign during lockdown

– Introduced communication & engagement platform

– Employee Forum created for colleagues to share feedback

– Expanded our e-learning platform

– Trained 30 new Wellbeing Champions

• Fitness Trainer part-time employment model enabled use of furlough

• Topped up furlough payments

• Launched 2020 SAYE scheme for all employees

• 461 FTs completed ‘Set for Success’ training programme

• Kickstart programme launched providing employment opportunities to

18-24 year olds previously on universal credits

13

GROWTH DRIVERS FOR HEALTH & FITNESS REINFORCED BY COVID

Prime Minister Boris Johnson attending The Gym, South Ruislip (Aug20)

GYM MEMBERS KEEN TO RETURN BUT NOT ALL WILL DO SO IMMEDIATELY

• Members expected to re-join gyms as confidence increases

• As a result it may take time for membership levels to return to pre-Covid levels

COVID HAS HIGHLIGHTED THE IMPORTANCE OF A HEALTHY LIFESTYLE

• Government initiative to reduce obesity will increase focus on fitness

• Survey data suggests people will exercise more post-Covid

LIKELY REGULARITY OF EXERCISING1

19%

13%

14%26%

22%

6%

I've already done thissince reopening

Haven't done yet butwould be happy to

In a few weeks/months

Not until risk of infectionis much lower

Not until there is avaccine

Never again

CONFIDENCE IN RETURNING TO THE GYM1

65% 27% 5%% of TGG

members

by age

30%45%

30%19%

50%38%

51%58%

6%10% 7%

4%

14%7% 12% 19%

Total 18 - 34 35 - 54 55+

> before = before < before Not exercising

1) Source: Impact of COVID-19 on RCL sectors ‘Strategy&’ (PWC consulting arm)

14

NUMBER OF LOW COST GYMS (DEC 2020)1,2

TWO LARGEST OPERATORS CONTINUE TO GROW WITH REST OF THE LOW COST MARKET STAGNANT

1) Company estimates for the number of sites per low cost operator

2) Low cost defined as majority of membership options <£25 per month and <£30 within London

3) 32 gyms still trading as Xercise4Less

4) Company analysis of average headline rates Dec 2020 (no contract option if available).

5) Market share calculation is the number of TGG open gyms out of the total low cost gyms in the UK estimated by Company as of 31 December 2020

STRONG MARKET POSITION

AVERAGE HEADLINE RATE PER MONTH (NO CONTRACT) DECEMBER 20204,5

F = Franchise

O = Owned

Dec-20Dec-19

22.88

22.71

21.41

19.90

18.81

14.99

energie Fitness

Pure Gym

Everlast Fitness / Sports Direct

JD gyms

The Gym

Xercise4less

WE REMAIN COMPETITIVE IN EACH LOCAL MARKET

Note: Xercise4less and JD Gyms are predominantly located in the north of the UK; in

these regions Gym Group’s gyms are priced substantially lower than our £18.81 national

average ensuring we are highly competitive in every local market

³

UK Low

Cost Gyms

735(727 PY)

TGG ESTIMATED SHARE OF LOW COST MARKET

24.9% (24.0% PY)

15

FAVOURABLE PROPERTY MARKET SUPPORTS HIGH QUALITY GROWTH

The crisis in retail, leisure and hospitality is impacting the

commercial property market. Expect this to be a significant benefit:

RENT LEVELS ON NEW SITES

• Improved rents on sites that were in negotiation pre-COVID

• Favourable rents on new sites coming to market

AVAILABILITY OF NEW SITES

• Volume of sites increasing due to CVAs and insolvencies, combined

with a lack of demand from other retail/leisure/hospitality businesses

ACCESS TO MORE PREMIUM SITES

• Sites that were previously not within our rent threshold, now more

attainable e.g. Cambridge, Oxford and York

• New sites predominantly on high quality retail parks

STRONG PIPELINE DEVELOPING

• 4 new gyms to open and 4 additional sites to start fit-out in H1

• 6 further leases exchanged and several more in advanced stages

• Focus on larger catchments as well as selective small catchment gyms

Chichester, former Lidl

York, former Office Outlet

16

PRODUCT ENHANCEMENT

• Enhanced Group Exercise offer, including trial of Fiit studio and pods

• COVID developments: enhanced cleaning, screens, social distancing

• Ensure offer remains relevant to appeal to post COVID member needs

• Value proposition attractive to members in

economic downturn

– Lowest price high quality offer in the market

– “No contract” offers flexibility

• Ability to run member acquisition at scale;

– Multichannel promotional campaign across TV,

Social, Digital

– Sophisticated CRM with large database of

former members

• Enhanced acquisition capability with new website

– Q4 2021 launch

• Weakened competition

– Closure of site by low cost competitors and

significant distress in mid market / premium

offerings

– Circa 20% of local authority gyms did not

reopen after first lockdown

WILL USE SCALE ADVANTAGES TO TAKE ADVANTAGE OF MARKET DEMAND

TECHNOLOGY & DATA DEVELOPMENTS

• New website planned to improve web merchandising, product upsell, conversionand SEO; continue to evolve app

• COVID developments: QR code entry and busyness tracker

• Further use of data analytics

17

THE GYM: SUSTAINABILITY IN OUR DNA

BREAKING DOWN BARRIERS

TO FITNESS FOR ALL

Robust Risk and

Crisis Management

High standards of

business integrity

Affordable gyms accessible

to 49% of the UK population

Opened first low

carbon gym in 2020

100% of energy purchased

from renewable energy

GOVERNANCE

WE ARE COMMITTED TO ENHANCE STAKEHOLDER ENGAGEMENT, GOAL SETTING AND REPORTING ON ESG TO IMPROVE UNDERSTANDING OF THE GREAT WORK WE ARE DOING

SUSTAINABILITY HAS BEEN AT THE HEART OF OUR BUSINESS SINCE OPENING OUR FIRST GYM IN HOUNSLOW IN 2008; IT’S IN OUR CORE PURPOSE AND IN OUR DNA

Industry-leading employment

model for personal trainers

Created £1.8bn of social

value over past 5 years

90% of waste

diverted from landfill

18

OUR 4 FOCUS AREAS ARE ALIGNED WITH THE UN SUSTAINABLE DEVELOPMENT GOALS

GOOD HEALTH AND WELLBEING

GOOD JOBS, QUALITY EDUCATION & LIFELONG LEARNING

DIVERSITY AND EQUAL OPPORTUNITY

RESPONSIBILITY TO THE ENVIRONMENT

Commissioned 4Global to

calculate Social Value created

‘People First’ campaign

supporting employee wellbeing

Published our Diversity and

Inclusion Manifesto

100% of energy purchased in

2020 from renewable sources

Expanded gym network to

offer access to 49.6% of the

UK population (46.0% in 2019)

High employee engagement

survey scores for

recommending Gym Group and

feeling safe to return to work

Enhanced accuracy of our

equal opportunities

monitoring

Implemented requirements of

the Streamlined Energy and

Carbon Reporting scheme

Provided free online classes

and discounted access to FiiT

during lockdown

New communication and

engagement platform ‘CORE’

and a new e-learning platform

Set targets for 2021 to

improve diversity of our

workforce on all levels

93% of our estate now

operates with full LED lighting

Covid-Secure protocols

developed with the Sheffield

Hallam University

Implemented the Government’s

Kickstart Scheme recruiting 30

young people at risk of long –

term unemployment

Trained 30 employees to

provide additional support to

colleagues

Launched electronic solution

to replace paper-based

process in gyms

SUSTAINABILITY PROGRESS IN 2020

19

0

100

200

300

400

500

600

2016 2017 2018 2019 2020

SOCIAL VALUE GENERATED BY GYM GROUP

£-

£100

£200

£300

£400

£500

2016 2017 2018 2019 2020

SOCIAL VALUE PER MEMBER

£1.8BN SOCIAL VALUE SINCE 2016

SOCIAL VALUE WILL BE CONSIDERED ALONGSIDE COMMERCIAL RETURN IN FUTURE DECISION MAKING

20

• Social Value Calculator developed by

4Global in partnership with Sheffield

Hallam University and used by Sport

England and Government to determine

the social value of regular exercise on

communities through:

- reduced risk of illness and disease

- increased wellbeing

- increased educational attainment

- reduced crime

• Social value lost in 2020 due to closure

of our gyms – £294m

• £3m in Social Value generated per site

in 2019

£m’s

1. GROWING MARKET OPPORTUNITY

2. HIGH QUALITY GYM ESTATE

3. COMPELLINGMEMBERPROPOSITION

4. INNOVATION IN TECHNOLOGY & MARKETING

5. SUSTAINABILITY AT THE CORE OF OUR BUSINESS

6. ATTRACTIVE FINANCIAL MODEL

Investment

rationale

Low cost segment

leading growth

of the UK health

and fitness market

Disciplined site

selection assisted

by strong covenant

for landlords

Attractive low cost

product drives high

levels of member

acquisition

Investment in tech &

marketing capability

enables a low cost,

high margin

business

Supporting communities

with affordable fitness

and flexible careers in a

sustainable way

High returns on

capital, maintained

as the market

develops

Immediate

impact of

COVID

– Gym closures

and wider

restrictions:

decline in gym

membership

– New site growth

limited in 2020 in

order to preserve

cash

+ COVID secure gyms

provided confidence

to our members

+ Launched

partnership with Fiit

to offer at-home

digital classes

+ Tech innovation for

COVID (QR code

entry, gym

busyness tracker)

permanent features

+ Increased focus on the

importance of a healthy

lifestyle, particularly in

lower income

communities

– Significant drop

in revenue from

closures and

EBITDA loss in

2020 : estate

profitable when

open

Medium to

long term

impact of

COVID

+ Increased

focus in health

& fitness

following

COVID

+ Strong value

proposition

means low-cost

gyms will be in

high demand

+ Distressed

property market

improving

availability and

rents of new

sites, enables

more rapid

expansion of our

gym estate

+ Ability to offer multi-

site network will be

attractive to people

with more flexible

working patterns post

COVID

+ Scale advantages

and importance of

market-leading

tech and marketing

continue to

increase

+ COVID has increased

focus on importance of

a healthy lifestyle,

+ Expansion of our

network will bring

affordable fitness to

more communities

+ Target

membership

revenues and

return on capital

to return to pre-

COVID levels

+ Runway of

growth as big as

ever, with

weaker

competition

INVESTMENT CASE STRONGER POST COVID

21

22

23

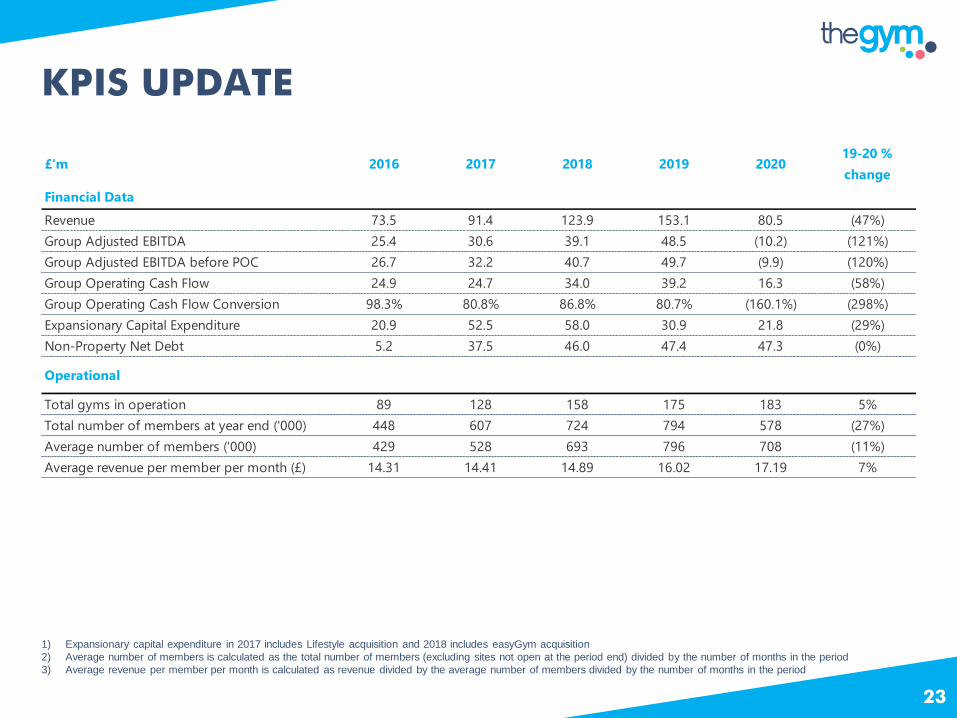

1) Expansionary capital expenditure in 2017 includes Lifestyle acquisition and 2018 includes easyGym acquisition

2) Average number of members is calculated as the total number of members (excluding sites not open at the period end) divided by the number of months in the period

3) Average revenue per member per month is calculated as revenue divided by the average number of members divided by the number of months in the period

KPIS UPDATE

23

£'m 2016 2017 2018 2019 202019-20 %

change

Financial Data

Revenue 73.5 91.4 123.9 153.1 80.5 (47%)

Group Adjusted EBITDA 25.4 30.6 39.1 48.5 (10.2) (121%)

Group Adjusted EBITDA before POC 26.7 32.2 40.7 49.7 (9.9) (120%)

Group Operating Cash Flow 24.9 24.7 34.0 39.2 16.3 (58%)

Group Operating Cash Flow Conversion 98.3% 80.8% 86.8% 80.7% (160.1%) (298%)

Expansionary Capital Expenditure 20.9 52.5 58.0 30.9 21.8 (29%)

Non-Property Net Debt 5.2 37.5 46.0 47.4 47.3 (0%)

Operational

Total gyms in operation 89 128 158 175 183 5%

Total number of members at year end ('000) 448 607 724 794 578 (27%)

Average number of members ('000) 429 528 693 796 708 (11%)

Average revenue per member per month (£) 14.31 14.41 14.89 16.02 17.19 7%

FINANCIAL MODEL:MATURE SITES (2019 PRE COVID)

MATURITY: MEMBERS MATURITY: SITE EBITDA¹

1) Site EBITDA maturity curve is under IFRS 16 for the 2017 cohort

2) Actual Mature gym site metrics in 2019 based off 109 Mature sites open to 31 Dec 2017

3) Fixed property costs include rent, rates, service charge and landlord insurance

4) Other opex includes all other costs below gross profit, the principal costs are marketing, staff, utilities, cleaning, repairs and

maintenance and administration costs such as travel

5) Current capital cost for 2019 excludes small box

Average MatureGym Site Members (#)

Average estateLTM EBITDA

MATURE SITE ECONOMICS²

0

1,000

2,000

3,000

4,000

5,000

6,000

-3 -1 1 3 5 7 9 11 13 1517 192123

• Site EBITDA lags number growth

• Initial losses from pre-opening costs

• Consistent maturity profile with member outcome dependent on sq footage per site

£ m 2018 2019

Revenue £0.97 £1.00

Gross Profit 99% 99%

Fixed Property costs ³ 27% 26%

Other Opex ⁴ 28% 29%

EBITDA £0.44 £0.44

EBITDA margin 45% 44%

Average capital cost £1.44 £1.44

Current Capital cost ⁵ £1.33 £1.27

Mature ROIC 30% 31%

• Mature sites achieve £0.44m

EBITDA from £1.44m investment,

delivering 31% ROIC

• EBITDA % margin diluted slightly

in 2019 due to new PT operating

model which increases revenue

and costs, but not EBITDA

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

-3 -1 1 3 5 7 9 11 13 15 17 19 21 23

£ M

illio

ns

24

SIGNIFICANT OPPORTUNITY FOR GROWTH

• Growth potential in standard catchments across the UK drivenby a broadening of locations inwhich low costs gyms have provento operate successfully(i.e. Horsham or Kilmarnock)

• Further growth potential in small

catchments with a population of

25 – 60k

− we will expand into these areas

using gyms formats of 7,000 –

10,000 sq. ft.

− offering members the core facilities

of our larger gyms and maintaining

high standards of facilities and

service

PwC Analysis (Jan-19)

Total market opportunity

(1)

Existing low cost gyms

(As at Jan-19)

Additional potential gyms (1) (Dec 2020)

Standard

catchments (2) 899 571 328 180

Small catchments (3)

397 83 314 3

Total 1,296 654 642 183

1) As per PwC ‘low cost gym market headroom assessment January 2019’2) Standard catchment include +60k population within and areas 10 – 15 min drive in greater London area3) Small catchment includes <60k of the population

25

UK MARKET IN LONG-TERM GROWTH

• Memberships of health and fitness clubs were in structural growth for many years up until 2019

• During the Global Financial Crisis growth rates flattened but didn’t decline

• The private sector has been driving the increase in penetration since 2012, led by the emergence of low-cost gyms

• Average membership fees remained stable during the Global Financial Crisis and then started to decline with the growth of low cost gyms from 2012/2013.

7.3

10.5

4.6 5.1

11.9

15.6

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

%

% OF UK POPULATION THAT ARE MEMBERS

OF A HEALTH & FITNESS CLUB

Private Public Total Penetration

Source: LDC State of the Industry Report 2019

£42.07 £41.14

£28.39 £30.10

£25.00

£30.00

£35.00

£40.00

£45.00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

AVERAGE MONTHLY RATE FOR HEALTH &

FITNESS CLUBS IN THE UK

Private Public

26

EXTENSIVE RESEARCH BY LEADING ACADEMIC INSTITUTIONS HAS DEMONSTRATED THE LINK BETWEEN PHYSICAL EXERCISE AND

• Reduction in risk of developing non-communicable diseases

• Subjective Wellbeing

• Educational Attainment

• Reduction in crime

SOCIAL VALUE THROUGH PHYSICAL ACTIVITY

BUILDING ON THIS RESEARCH, 4GLOBAL PARTNERED WITH SECTOR LEADING ORGANISATIONS TO BUILD THE SOCIAL VALUE CALCULATOR TO EVIDENCE THE IMPACT OF PHYSICAL ACTIVITY AND SPORTS PARTICIPATION.

The largest socio-economic and credit data

provider in the UK using their lifestyle data at

individual and household level to assess risk

profiles across a range of social indicators.

4global manages the DataHub which is the

largest repository for sport and physical

activity data in the UK, integrated and

enhanced through a suite of participation

and business intelligence modules

Leading academic institution in the UK for

measuring the social value of physical

activity and sports participation in England

on behalf of DCMS and Sport England

created the underlying model.

THE MODEL IS USED BY GOVERNMENT AND KEY SECTOR STAKEHOLDERS

27

THE SOCIAL VALUE CALCULATOR MODEL

• The key outputs of the model are a projection of the total social value into these 4 core categories

• A person has to use the gym at least 4 times per month to contribute to the social value

• The person is then assigned a value based on their age, gender and socioeconomic status

• Increased tenure and frequency of exercise results in higher social value

FACTORS DRIVING SOCIAL VALUE ALIGNED WITH COMMERCIAL VALUE: EXPANSION, MEMBERSHIP LEVELS, VISIT FREQUENCY AND TENURE

VOLUME OF PARTICIPANTS, FREQUENCY OF ACTIVITY, DEMOGRAPHICS AND

SOCIOECONOMIC PROFILE

HEALTH

Reduction in

likelihood of

developing Heart

Disease

Breast Cancer

Colon Cancer

Type 2 Diabetes

Dementia

Depression

CRIME

Crime reduction

for young men

EDUCATION

Increased

educational

attainment and

Improved

starting salaries

SUBJECTIVE WELLBEING

Increased Life

Satisfaction

and Happiness

SOCIAL VALUE GENERATED

28

AVERAGE SQUARE FOOTAGE IN 2020 INCLUDING ALL SITES IN 2020

16,400

MAP OF ALL 183 LOCATIONS ROLLING AVERAGE SQUARE FOOTAGE1

Includes Lifestyle Fitness

& easyGym sites

Increase in average square

footage in 2017 and 2018 is due

to Lifestyle and easyGym

acquisitions which had larger

gyms than typical Gym Group

sites.

Decrease in average square

footage in 2020 is due to three

small box gyms.

PROPERTY

LOCATIONS

Inside M25 61

Outside M25 - South East 29

Outside M25 - Other 93

Total 183

29

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

THE GYM GROUP TEAM

RICHARD DARWIN Chief Executive Officer

• CEO September 2018 (CFO since May 2015)

• Formerly CFO of Essenden plc (now Ten

Entertainment Group plc) and Paramount

Restaurants

• Held senior roles at Diageo plc, Hard Rock

Cafe International and The Rank Group Plc

ANN-MARIE MURPHYChief People Officer

• Joined The Gym Group in May 2018

• Previous roles include HR Director for

New Look, TUI Travel plc

• Currently finishing an Executive Coaching

Qualification at Henley Business School

JASPER MCINTOSHChief Information Officer

• IT Director since June 2014, and primary

IT and digital consultant to The Gym Group since

2011

• Previously co-founded two technology

consultancies and served as a director for three

digital agencies

BARNEY HARRISONChief Commercial Officer

• Joined the team in October 2016

• Previously held several Head of Marketing

and Acquisition roles at Sky

DAVID MELHUISHDevelopment Director

• Joined The Gym Group in April 2013

• Successfully opened c.100 gyms to date

• Previously Head of Development & Facilities

at Central England Co-operative

MARK GEORGEChief Financial Officer

• CFO since October 2018

• Previously Deputy CFO of Auto Trader plc and

Finance director roles at Asos and Tesco

30

OUR PLC BOARD DIRECTORS*

PENNY HUGHES Independent Non-Executive

Chairwoman

• Previously President of Coca-

Cola GB & Ireland

• Current Chairwoman of

Riverstone Living and NED for

Chair Form3

EMMA WOODSNon-Executive Director

• Currently CEO at Wagamama

• Held Director roles at Merlin

Entertainments plc, Pizza

Express and Unilever

JOHN TREHARNEFounder Director

• John founded The Gym in 2007

and retired as CEO in Sep18

• Current Board member of ukactive

• Current Chairman of Frame

DAVID KELLYNon-Executive Director

• Current Chair of Simply Business,

Pure360 and Camelot Global

Lottery Solutions

• Non Exec Director at On the

Beach Group plc, Reach plc,

Forest Holidays and Holiday

Extras

RIO FERDINANDNon-Executive Director

• Former International footballer

• Director at FE Luxury Travel,

Football Escapes and Legacy

Sports and Education Foundation

PAUL GILBERTSenior Independent Non-

Executive Director

• Current Non-Executive Chairman

at Grip-UK Limited

• Previously Non-Executive

Chairman of The Gym from

Feb12 to Sep15

• Previously CFO at TJ Hughes,

National Car Parks and Matalan

31

WAIS SHAIFTANon-Executive Director

• Currently CEO at Push Doctor

• Previous Director roles at

Treatwell and Just Eat

11 MAY 2021Board changes

• Paul Gilbert retiring from The Gym

Group Board in May21

• Emma Woods appointed to Senior

Independent Director and Chair of

Remuneration Committee

• David Kelly to be appointed Chair of

Audit & Risk committee

* Richard Darwin (CEO) and Mark George (CFO) are also PLC Board Directors