INTERNSHIP REPORT ON A STUDY ON WORKING CAPITAL ...

76

INTERNSHIP REPORT ON A STUDY ON WORKING CAPITAL MANAGEMENT AT LARSEN AND TOUBRO By: Mr. MANISH KUMAR SHARMA USN: 1NH14MBA68 Submitted to VISVESVARAYA TECHNOLOGICAL UNIVERSITY, BELGAUM In the partial fulfilment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION Under The Guidance of, Internal Guide External Guide Mr. SHASHI KUMAR Mr. DEEPAK Professor, Dept of Management Studies Regional Manager NEW HORIZON COLLEGE OF ENGINEERING ORR, MARATHALLI, BANGALORE -560103 BATCH-2014-16

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of INTERNSHIP REPORT ON A STUDY ON WORKING CAPITAL ...

INTERNSHIP REPORT ON

A STUDY ON WORKING CAPITAL MANAGEMENT AT

LARSEN AND TOUBRO

By:

Mr. MANISH KUMAR SHARMA

USN: 1NH14MBA68

Submitted to

VISVESVARAYA TECHNOLOGICAL UNIVERSITY, BELGAUM

In the partial fulfilment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under The Guidance of,

Internal Guide External Guide

Mr. SHASHI KUMAR Mr. DEEPAK

Professor, Dept of Management Studies Regional Manager

NEW HORIZON COLLEGE OF ENGINEERING

ORR, MARATHALLI, BANGALORE -560103

BATCH-2014-16

ACKNOWLEDGEMENT

Words are indeed inadequate to convey my profound gratitude and heartiest

thanks to all those who have helped me in making this project report. I will take

this opportunity to thank Dr.Manjunatha, Principal of NEW HORIZON

COLLEGE OF ENGINEERING, Bangalore.

I will take this opportunity to thank Prof. Sheelan Mishra, Head of Management,

for the constant support and encouragement and guidance. I would like to thank

internal guide Prof. SHASHI KUMAR for the valuable inputs provided to this

project, which were immensely helpful in applying various frame works to a

practical situation.

I would also like to thank my external guide Mr. Deepak at KANSBAHAL,

ODISHAwho assisted me and helped me in shaping and execution of the project.

This project has been a great learning experience for me and it would have not

been possible without the support of the guidance of above mentioned people.

Mr. Manish kumar Sharma

USN: 1NH14MBA68

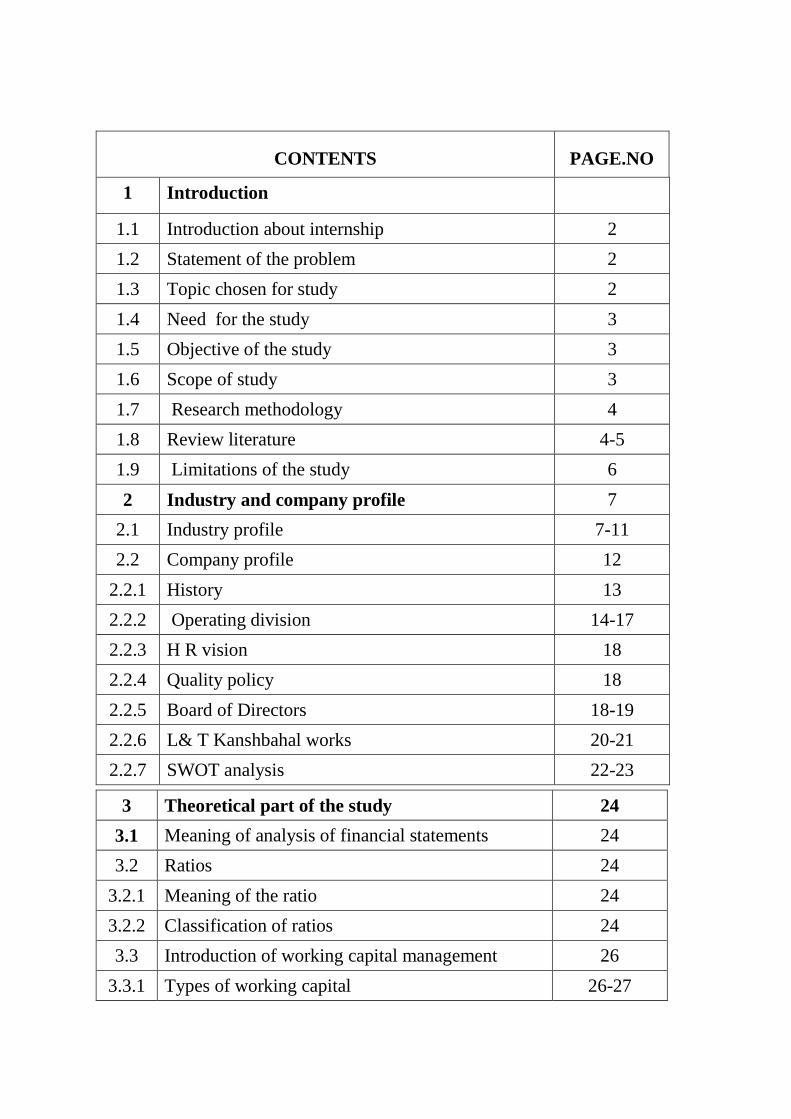

TABLE OF CONTENTS

CONTENTS PAGE.NO

1 Introduction

1.1 Introduction about internship 2

1.2 Statement of the problem 2

1.3 Topic chosen for study 2

1.4 Need for the study 3

1.5 Objective of the study 3

1.6 Scope of study 3

1.7 Research methodology 4

1.8 Review literature 4-5

1.9 Limitations of the study 6

2 Industry and company profile 7

2.1 Industry profile 7-11

2.2 Company profile 12

2.2.1 History 13

2.2.2 Operating division 14-17

2.2.3 H R vision 18

2.2.4 Quality policy 18

2.2.5 Board of Directors 18-19

2.2.6 L& T Kanshbahal works 20-21

2.2.7 SWOT analysis 22-23

3 Theoretical part of the study 24

3.1 Meaning of analysis of financial statements 24

3.2 Ratios 24

3.2.1 Meaning of the ratio 24

3.2.2 Classification of ratios 24

3.3 Introduction of working capital management 26

3.3.1 Types of working capital 26-27

3.3.2 Operating cycle 28

4 Data Analysis And Interpretation 31

4.1 Gross working capital 31

4.2 Net working capital 31-32

4.3 Ratio analysis 32

4.3.1 Current ratio 32-34

4.3.2 Quick ratio 34-35

4.3.3 Activity ratio 35

4.3.4 Stock turnover ratio 36-37

4.3.5 Raw material holding period 38-39

4.3.6 WIP conversion period 39-40

4.3.7 Finished good conversion period 40-41

4.3.8 Inventory to current assets 41-43

4.3.9 Inventory to working capital ratio 43-45

4.3.10 Debtors turnover ratio 45-46

4.3.11 Average turnover ratio 46-47

4.3.12 Working capital turnover ratio 48-49

4.3.13 Asset turnover ratio 49-50

4.3.14 Profitability ratios

A . Net profit ratio

B. Operating ratio

C. Operating profit ratio

D. Expense ratio

50-55

5 FINDIGS, SUGGESTIONS AND CONCLUSION

Findings 56-57

Conclusion 58

Suggestion 59

ANNEXURE 60-64

LIST OF TABLES

Chart No Particulars Page No

4.1 Table on Gross working capital of the company 31

4.2 Table on Net working capital of the company 31-32

4.3 Table on Current Ratio of the company 32-34

4.4 Table on Quick Ratio of the company 32-33

4.5 Table on stock turnover Ratio of the company 36-37

4.6 Table on Raw materials holding period of the

company

38

4.7 Table on Work in progress conversion period

of the company

39

4.8 Table on Finished goods conversion period of

the company

40

4.9 Table on Inventory to current asset of the

company

42-43

4.10 Table on Inventory to working capital of the

company

44

4.11 Table on Debtor turnover ratio of the company 45-46

4.12 Table on Average collection period of the

company

46-47

4.13 Table on Working capital turnover ratio of the

company

48

4.14 Table on Asset turnover ratio of the company 49-50

4.15 Table on net profit ratio of the company 50-52

4.16 Table on Operating ratio of the company

52-53

4.17 Table on Operating profit ratio of the company

53-54

4.18 Table on Expense ratio of the company 54-55

EXECUTIVE SUMMARY

Working cycle is a measure of the working effectiveness and working capital administration

of an organization. A short working cycle is great as it tells that the organization's money is

tied up for a shorter period. Another helpful measure used to survey the working proficiency

of an organization is the money cycle (additionally called the money transformation cycle).

The construction industry is the second largest industry in India after agriculture. It accounts

for about 11% of India as GDP. It makes significant contribution to the national economy and

provides employment to large number of people.

Larsen and Toubro, contracted as L&T is an Indian Multinational Conglomerate whose

headquarters are in Mumbai. It was built up by two Danish engineers in 1938 by Henning

Holck Larsen&Soren Kristen Toubro. L&T is an advancement which has building,

improvement and amassing association. It is one of the greatest and most respected

associations in the Indian private zone.

1

CHAPTER 1

INTRODUCTION

1.1 Introduction about Internship

Internship provides the MBA student a life time opportunity to have an experience of the

corporate world and its atmosphere. The candidates can be able to see how different theories

which they have learnt in their educational period have been executed in the real practical

world of the business organization. The internship candidates fromdifferent specialization

selects the different topic and they can gain more knowledge relating to that topic through the

internship process within the organization. There is need of proper guidance and support from

the organization to the candidates for the successful internship process. The candidates have

the wonderful opportunity to explore the knowledge and contribute something new to the

organization. Internship is an crucial period in the life of a MBA student to learn something

relating to the operating process of the particular organization in which they have completed

their internship. The internship program sometime may end up with a permanent job in future

in most of the cases.

There is no doubt that an internship program is very much important in the carrier of a MBA

graduates as it provide the corporate knowledge, interaction with the corporate culture, proper

knowledge relating to the topic which selected by the candidates and how the theoretical

knowledge been implied, executed and followed in the real business world.

1.2 STATEMENT OF PROBLEM:

The important of working capital management stems from two reasons. The first is the

substantial portion of the investment is invested in current assets and the level of current

assets will change quickly with the variation in sales. Hence in this study, an attempt has been

made to analyze size and composition of working capital and whether such an investment has

increased or declined over a period after determining the requirement of current asset, one of

the important task of the financial is to select a group of appropriate source of finance for

current assets

1.3 Topic chosen for study

I have selected the topic named as “STUDY ON WORKING CAPITAL” in LARSEN and

TOUBRO. As we know every organization is required to have a sufficient level of working

capital in order to meet the current liability, expenses, and contingency in future. The topic I

2

chosen is simple but very much important as it is required to be managed properly in order to

be successful in long run of the business.

1.4 Need for study

Every organization requires a sufficient amount of working capital for the long run and

success of the business. It is important to have a surplus amount of cash or current asset in

order to meet the current obligation and expenses relating to the operation of the business and

maintaining the adequate amount of the inventories and the raw materials for the future time

period of the business.

1.5OBJECTIVES OF THE STUDY

To concentrate on the liquidity position of the association by investigating the

parts of the working capital.

To concentrate on the general working of the organization with connection to

the choice in regards to overseeing working capital.

To recommend the progression to be taken to build the effectiveness in

administration of working capital.

Correlation of different Working Capital Ratios for as long as four years 2010

to 2014. To concentrate on the different segments of working capital.

To dissect the working capital pattern.

To assess the usage of current resource and current liabilities and discover

inadequacies if any.

1.6 SCOPE OF THE STUDY

The focus of the training is on working capital activities at finance department and other

different departments related to this project at L&T ,Kansbahal Works.

3

1.7.RESEARCHMETHODOLOGY

SOURCES OF DATA

Primary sources:

Primary data refers to the data which has been collected for the first time and it has

not been used previously by anyone.

Collection of data from the people of finance department by discussion

Secondary sources:

The information gathered is through the optional source. The optional information are

which collected by another person and which have experienced by measurable

procedure. gathering of data from the yearly records and yearly reports from 2011 to

2015 gathering of information from magazines,journals of L&T ,Kansbahal Gathering

of information through web access .

1.8 LITERATURE REVIEW:

The following are the literature review which given by different authors and research

scholars.

Pass C.L., Pike R.H1(1984):this studied happened before 40 years ago that for the reason to

development in areas of longer-term investment and effective financial decision making.

many of this are new concept which is not used before and effectively implemented on

industrial practice .by contrast less attention given to the short term investment specially to

the working capital management. Such ignorance might be acceptable were give working

capital less importance but effective working capital has a very important and crucial role in

organization profitability and longer growth.

4

Beneda, Nancy; Zhang, Yilei7 (2008): this study about working capital management

describe the overall impact to the firm operating performance and also see the impact

because of growth new public companies.This study also give some light to the relationship

of working capital to debt level, firm risk and industry. Further this study describe that using

the sample of initial public offering (IPO) find significant bond between account receivable

and firm operating performance.

Thomas M. Krueger12 (2005)-:different level working capital studied describes the

performance of different industries which stable over time. This study helps of much industry

to improve their performance and increase their overall turnover. They had faced many

troubles ahead but this show that it takes firm to the continuously improvement stage they

able to achieve their goal which they had decided .this also helps to given top ranked to the

firm belong to the industry and motivate to them their continuously improvement.

Hard castle J5(2009)-:this study define that working capital not always consider gross

working capital but it consider sometimes ,and it simply refer to the company total current

assets, cash, marketable securities ,account receivable and inventory. But the longer term

financial analysis always consider strategic planning for future growth and working capital

management which is to deals with day to day operations, by consider that production do not

stop because of lack of materials and making sure that customer paying enough to pay the due

of the firm . Without working capital no firm can be efficient and profitable.

ThachappillyG6(2009) -: Working capital in cash conversion cycle maintain the cash or

maintain the flow of fund which firm require to carried out needed operation for the firm. i.e.

From the days to paying for raw materials to collecting cash from the customer. A firm buy

raw materials and operating supplies for continue the production process. Wages , salary and

other expenses are paid by the firm to converting the raw materials into the finished goods.

Firm allowed credit to customer for the specific time that is standard in the business which

have to maintain by every firm for future growth .

5

1.9LIMITATIONS

This study led and done is systematic and subject to taking after constraints:-

The study is for the most part completed in light of optional information gave

in the money related explanations.

This study depends on authentic information and data gave in the yearly

reports , in this manner it may not be a future marker .

There might be some partial contrasts in the figured proportions.

We can't do correlations with different organizations unless and until we have

the information of different organizations on the same subject .

A portion of the information's which were required for further examination

were secret and not accessible to the learners .

As the study was for limited ability to focus 06 weeks and because of absence

of time, different zones couldn't be engaged.

6

CHAPTER 2

2.1INDUSTRY PROFILE

The Industrial Revolution has given he birth to the machine and technology. Companies this

relating to this field grew out of iron foundries, shipyards, forges and repair shops.

Sometimes these companies are the combination of machine factory and shipyard. In the

20th century some of themotorcycle and automobile manufacturers started their own machine

manufacturing factories.

Before the industrial revolution a different variety of machines were available such as clocks,

weapons and running gear for mills (watermill, windmill, horse mill etc.) Production of these

machines was very less scale in artisan workshops mostly for the local or regional market.

With the introduction of the industrial revolution manufacturing began of composite tools

with more complex construction, such as steam engines and steam generators for the evolving

industry and transport. In addition, the emerging machine factories started making machines

for production machines as textile machinery, compressors, agricultural machinery, and

engines for ships.

18th century

The first industrial revolution start in England from 1750 before that labor usually was not

yet mechanized factories. In that 18th century there were many type of machines was invented

by the investor themselves also this was the first time that first steam engine was invented.

In the 1770s James watt did some improvement in that engine design which is easily

employable and produce large amount of energy .in England some certain cities concentrated

to manufacture or produce specific products such as textiles and pottery and after this

invention these type of industry also consider the mechanization. In 18th century some

countries are such like England, Britain and Belgium become the first machinery industry.

19th century

In the early of 19th century industrial revolution got boost with the upcoming railways this

because of innovation by the England of mining industry. Here they need for machinery

7

because working in coal mining was very hard and dangerous so they need tools which makes

they work easy and safe. In 1804, Richard made first steam engine and place it to rails, and

in 1825 they start to transport coals from mining to the port. For the apparatus business this

carried a wide range of new work with new hardware for metallurgy, machine instrument for

metalworking, creation of steam motors for trains with every one of its necessities and so on.

In time the business sector for the machine business got to be more extensive, specific items

were made for a more noteworthy national and regularly global business sector. For example,

in the half of the 19th century Americans gave order to England to produce machine or

machinery tools for them which is useful for the to steelmaking because their the techniques

were more advanced and effective compare to others .

20th century -now

The expression "machinery industry" appeared later in the nineteenth century. One of the

primary times this branch of industry was perceived in that capacity, and was researched, was

in a generation insights of 1907 made by the British Ministry of Trade and Industry.

That industry got divided into forty different categories, including for example, agricultural

machinery, machinery for the textile industry and equipment, and parts for train and tram.

The developments of new drive strategies taking into account electric engines, inner ignition

motors and gas turbines brought another era of machines in the twentieth century from autos

to family appliances. Not just the item scope of the machinery business expanded

impressively, particularly smaller machines could conveyed items in much more prominent

numbers created in large scale manufacturing . With the rise of large scale manufacturing in

different parts of the business, there was likewise an appeal for assembling and creation

frameworks, to build or increase the entire production.

Scarcity of availability of labor for agriculture industry in second half of 20th century which

increase the need or requirement for further mechanization of production or specific machine

which is helps in agriculture.

Shortage of labor in agriculture and industry at the beginning of the second half of the 20th

century, raised the need for further mechanization of production, which required for more

specific machines. The rise of the computer made further automation of creation conceivable,

which thusly set new demands on the machinery industry.

8

Product of the machine industry A machinery industry makes very diverse range of the products. A selection:

Engine

Steam turbine

Gas turbine

Pump

9

Compressor

Gear

Bearing of gas turbine

Climate control(of a hospital)

Tractor

10

Machine industry in different countries

Germany

In 2011 around 120,0000 people employed In Germany in which 900,000 people are in

Germany and 300,000are expected from abroad.the combined turnover of that industry in

Germany around €130 billion of which 60% came from exports.at that time there were 6,600

companies are active in that 95% companies strength are less than 500 people.each employee

belong to that industry average generated around 148,000 Euro . the biggest organizations in

Germany are DMG Mori Seiki AG, GEA Group, Siemens AG, and ThyssenKrupp.

France

In the France the machinery industry had generated around 98 billion Euros in 2011.there

were around 650,000 people are employed at that time. The annually turnover had fallen

between 20-15 percent because of the crisis. because of the consumer spending and

continuing demand from the energy sector and transport sector the damage happened with the

crisis is still limited.

Netherlands

In 1996 in the Netherlands approximately 2,500 companies were present and the strength of

people employed over there at that time is around 93,000, in which around 1000 of these

companies having strength of employed people is less then 20 or more employees.according

to the chamber of commerce in 2011 around 15,000 companies were active which belong to

machinery industry some of largest companies in Netherlands like Lely (company) ,Philips

and stork B.V

United states

11

The United States is the world's biggest business sector for machinery, and in addition the

third-biggest supplier.in 2011 U.S machinery industry had total sales of $413.7 billion this is

consider both domestic as well as foreign . American producers held a 58.5 percent offer of

the U.S. household marke

12

2.2COMPANYPROFILE

OVERVIEW

Larsen and Toubro, contracted as L&T is an Indian Multinational Conglomerate whose

headquarters are in Mumbai. It was built up by two Danish engineers in 1938 by Henning

HolckLarsen&Soren Kristen Toubro. L&T is an advancement which has building,

improvement and amassing association. It is one of the greatest and most respected

associations in the Indian private zone. Client centered methodology alongside nonstop

mission for world class quality has made it feasible for the organization to exceed

expectations, accomplish and support initiative in the greater part of its real lines of business.

It has a universal vicinity and it has workplaces and assembling offices in numerous nations.

Because of the International business, the abroad profit have become fundamentally.

L&T has an OK advancing and scattering arrange, and have developed a reputation for strong

customer backing. L&T similarly places stock in down to earth improvement. Progress must

be proficient in congruity with nature. A guarantee to gathering welfare and normal security

are an imperative bit of corporate vision.

13

2.2.1 HISTORY

L&T was established in present day Mumbai (prior knows as Bombay) in 1938 by two

Danish engineers, named H.H Larsen and S.K Toubro. Two were unequivocally dedicated to

building up India's designing capacities to meet the requests of the business.

H.H Larsen

Starting with the import of apparatus from Europe, L&T quickly tackled designing and

development assignments of expanding advancement. Today, the organization sets

worldwide building benchmarks regarding scale and multifaceted nature.

S.K Toubro

14

OPERATING DIVISIONS

L&T organizations have been extensively gathered into six business divisions viz:

Engineering and Construction Projects (E&C)

Heavy Engineering Division (HED)

Electrical and Electronics Business Group (EBG)

Information Technology (IT)

Machinery and Industrial Products Division (MIPD)

L&T Solar

L&T Power

1) ENGINEERING & CONSTRUCTION PROJECTS (E&C):

Largest business portion

Serves to process innovation, essential and definite building, overwhelming

designing and measured creation, acquirement, logistics, development, erection,

appointing and extend administration. It executes ventures on turnkey premise.

L&T has effectively conveyed EPIC administrations for some tasks in the

upstream hydrocarbon division in the course of the most recent two decades in

India, Africa, South-East Asia and Australia.

The organization has effectively finished super undertakings managing underway

of stages, procedure offices, subsea pipelines, seaward and coastal pre-collected

modules,

The organization has additionally effectively finished significant undertakings for

GAIL and OIL India Limited. Worldwide customers of mid and downstream

15

division incorporate Petroleum Development Oman, Dolphin Energy and Saudi

Aramco. L&T has more than 38000 representatives in India.

II) HEAVY ENGINEERING DIVISION (HED):

L&T is asserted to be among the main five manufacture organizations on the planet.

The Heavy building division produces and supplies specially crafted and designed basic

hardware and frameworks to the requirements of center area commercial ventures and the

resistance part. Exercises are sorted out under independent Strategic Business Units (SBUs).

Its pioneer in the field of innovation advancement, hardware, fabricates and site/plant

administrations. It has accomplished the prestigious INS Industrial Excellence

Award' for extraordinary commitment in the atomic segment.

L&T additionally has had a long and close relationship with the Indian Space

Research Association. It built up the Naval Multi-Barrel Rocket Launcher.

III) ELECTRICAL & ELECTRONICS BUSINESS GROUP (EBG):

L&T is a worldwide maker of an extensive variety of electrical and gadgets items and

frameworks.

It's occupied with the matter of low voltage Switchgear items, Electrical Systems,

Energy meters, Medical supplies, Petroleum apportioning pumps, Automation

arrangements and Enterprise organizing.

Largest producer of low voltage switchgear and control gear in India. It fabricates for

modern areas such as force, refineries, petrochemicals and concrete in the electronic

fragment.

EBG items take into account the requirements of different clients including

agriculturists, urban family units and business structures.

16

Its items are required in social insurance types of gear as cutting edge assurance,

control and robotization in various businesses.

IV) INFORMATION TECHNOLOGY:

L&T InfoTech Limited gives far reaching, end-to-end programming answers for

customers in the field of managing an account and budgetary administrations,

protection, vitality and petrochemicals and in addition fabricating everywhere

throughout the world.

It concentrates on: Manufacturing, Banking, Securities and Insurance, Utilities and

Interchanges, Embedded frameworks.

administrations, Strategy Consulting, Value Added administrations.

Larsen and Toubro InfoTech Limited, a 100 for every penny reinforcement of the

L&T, offers programming and organizations with a consideration on Manufacturing,

BFSI and Communications and Embedded Systems. It in like manner gives

organizations in the introduced understanding and e Engineering space.

V)MACHINERY & INDUSTRIAL PRODUCTS DIVISION (MIPD):

Caters to the necessities of the mechanical apparatus, development supplies and

modern items business fragments.

It appreciates market driving capacities in item plan, process innovation, obtainment,

venture administration, promoting and benefits support including charging.

It offers items and administrations for all the business verticals, keeping up stringent

conveyance plans.

17

L&T fabricates advertises and gives administration backing to basic development and

mining hardware surface mineworkers, water driven excavators, total crushers, and

vibratory compactors.

It supplies an extensive variety of elastic handling hardware and fabricates and

advertises mechanical valves and associated items and an extensive variety of use

designed welding combinations.

VI) L&T POWER:

L&T are set up to focused on the opportunities basically from the coal ,gas and

nuclear based power projects.

In 2008-09 firm focus to set up and progress in manufacturing facilities for critical

boilers and turbines at HAZIRA on India’s west coast.

L&T offers turnkey solutions for large i.e. up to 1000 MW for coal based and gas

based power plants.

L&T also signed technical collaboration with CLYDE BERGEMANN.

VII) L&T SOLAR:

This company also takes some solar projects on turn-key on EPC basis.

In April 2012 L&T become a largest photo voltaic based power plant (40

MWp) and the owner for this project is reliance power at jaisalmer Rajasthan.

In 2011 L&T entered with partnership for turn-key EPC in megawatt solar

project and there were planning to construct 100MW in next 12 months in

most of metros and the partnership held between L&T and sharp.

L&T is embraced sun based warm plants and in addition rooftop top

frameworks notwithstanding generally archived sunlight based voltaic taking

into account sun based vitality frameworks.

18

2.2.3HR Vision:

Our HR vision is to develop competent self-motivated team of job owners striving for

excellence in a congenial environment with customer orientation.

2.2.4 Quality Policy:

Adhere strictly to quality parameters at all stages to provide products/services

conforming to customers requirement and satisfaction.

Most requirements of quality management system and strive to continually improve

its effectiveness.

Develop competent human resource through planned training to the employees.

Establish quality objectives and review periodically to achieve continual improvement

2.2.5 BOARD OF DIRECTORS

MR. A. M. NAIK - Group Executive Chairman

MR. K. VENKATARAMANAN - Chief Executive Officer and Managing Director

MR. M. V. KOTWAL - Whole-time Director and President (Heavy Engineering)

MR. S. N. SUBRAHMANYAN - Whole-time Director and Senior Executive Vice

President (Construction and Infrastructure)

MR. R. SHANKAR RAMAN - Whole-time Director and Chief Financial Officer

MR. SHAILENDRA ROY - Whole-time Director and Senior Executive Vice

President (Corporate Affairs and Power)

MR. S. RAJGOPAL - Independent Director

MR. S. N. TALWAR - Independent Director

19

MR. M. M. CHITALE - Independent Director

MR. N. MOHAN RAJ - Nominee of LIC

MR. SUBODH BHARGAVA - Independent Director

MR. A. K. JAIN - Nominee of SUUTI

MR. M. DAMODARAN - Independent Director

MR. VIKRAM SINGH MEHTA - Independent Director

MR. SUSHOBHAN SARKER - Nominee of LIC

Organization Information

Company Secretary - Mr. N. Hariharan

Registered Office - L&T House, Ballard Estate, Mumbai - 400 001

Auditors - M/s. Sharp &Tannan

Solicitors - M/s. ManilalKher Ambalal and Co.

Registrar and Share Transfer Agents - Sharepro Services (India) Private Limited

20

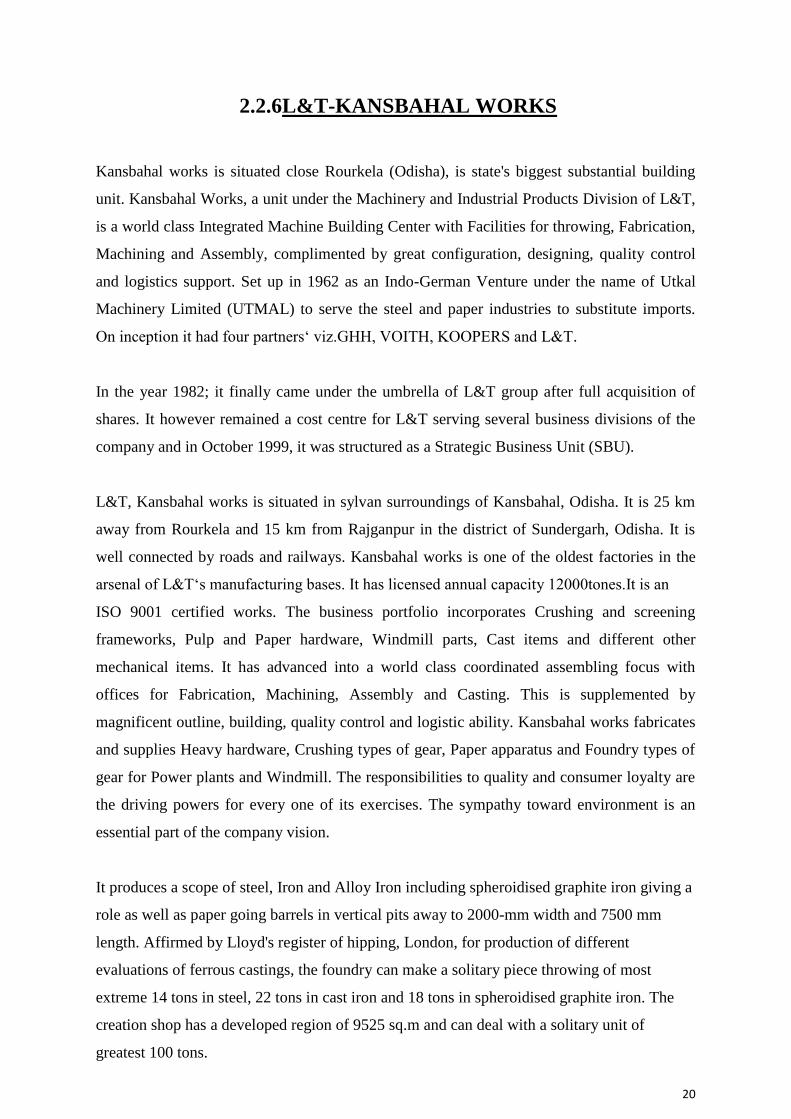

2.2.6L&T-KANSBAHAL WORKS

Kansbahal works is situated close Rourkela (Odisha), is state's biggest substantial building

unit. Kansbahal Works, a unit under the Machinery and Industrial Products Division of L&T,

is a world class Integrated Machine Building Center with Facilities for throwing, Fabrication,

Machining and Assembly, complimented by great configuration, designing, quality control

and logistics support. Set up in 1962 as an Indo-German Venture under the name of Utkal

Machinery Limited (UTMAL) to serve the steel and paper industries to substitute imports.

On inception it had four partners‘ viz.GHH, VOITH, KOOPERS and L&T.

In the year 1982; it finally came under the umbrella of L&T group after full acquisition of

shares. It however remained a cost centre for L&T serving several business divisions of the

company and in October 1999, it was structured as a Strategic Business Unit (SBU).

L&T, Kansbahal works is situated in sylvan surroundings of Kansbahal, Odisha. It is 25 km

away from Rourkela and 15 km from Rajganpur in the district of Sundergarh, Odisha. It is

well connected by roads and railways. Kansbahal works is one of the oldest factories in the

arsenal of L&T‘s manufacturing bases. It has licensed annual capacity 12000tones.It is an

ISO 9001 certified works. The business portfolio incorporates Crushing and screening

frameworks, Pulp and Paper hardware, Windmill parts, Cast items and different other

mechanical items. It has advanced into a world class coordinated assembling focus with

offices for Fabrication, Machining, Assembly and Casting. This is supplemented by

magnificent outline, building, quality control and logistic ability. Kansbahal works fabricates

and supplies Heavy hardware, Crushing types of gear, Paper apparatus and Foundry types of

gear for Power plants and Windmill. The responsibilities to quality and consumer loyalty are

the driving powers for every one of its exercises. The sympathy toward environment is an

essential part of the company vision.

It produces a scope of steel, Iron and Alloy Iron including spheroidised graphite iron giving a

role as well as paper going barrels in vertical pits away to 2000-mm width and 7500 mm

length. Affirmed by Lloyd's register of hipping, London, for production of different

evaluations of ferrous castings, the foundry can make a solitary piece throwing of most

extreme 14 tons in steel, 22 tons in cast iron and 18 tons in spheroidised graphite iron. The

creation shop has a developed region of 9525 sq.m and can deal with a solitary unit of

greatest 100 tons.

21

The L&T Kansbahal Works has four main shops and they are:

1. Foundry shop

2. Machine Shop

3. Fabrication Shop

4. Assembly Shop

5. Wheel loader

Products:

1. Paper and pulp machineries

2. Crushing equipment’s for mining ,limestone and minerals

3. Various Foundry Castings

4. Steel plant equipment

5. Surface Minor

6. Hub Casting and Fabrication items for Windmill power sector

22

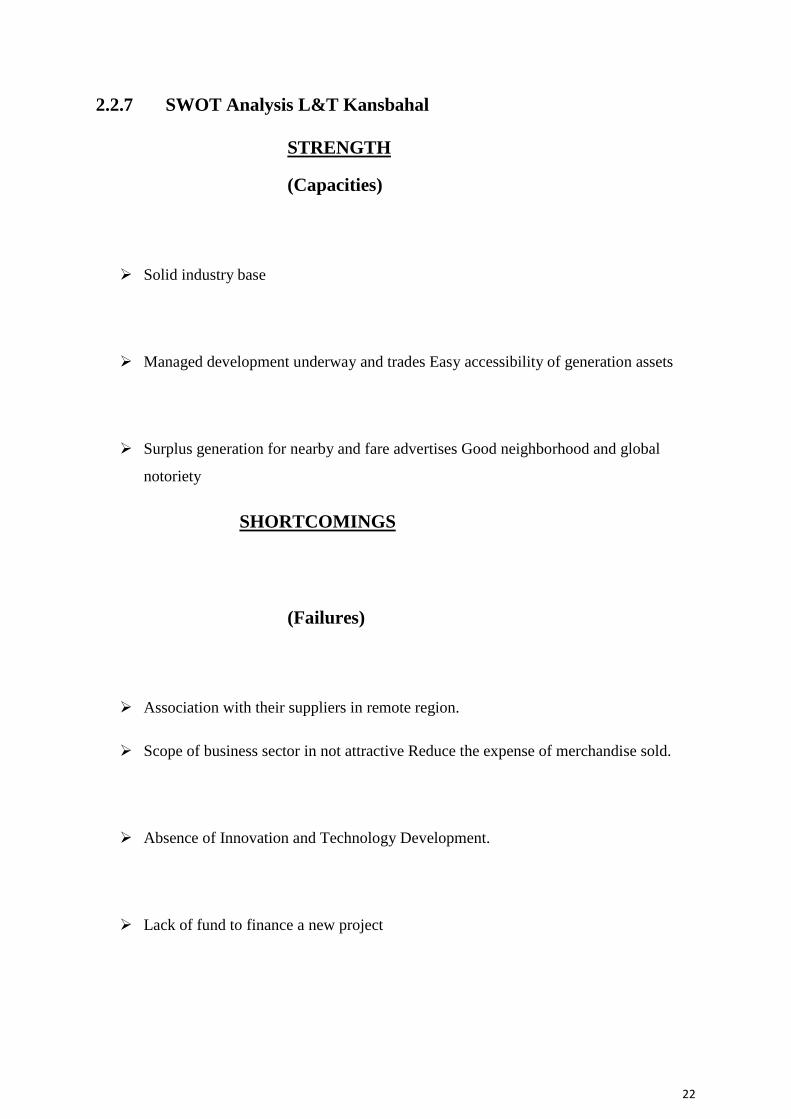

2.2.7 SWOT Analysis L&T Kansbahal

STRENGTH

(Capacities)

Solid industry base

Managed development underway and trades Easy accessibility of generation assets

Surplus generation for nearby and fare advertises Good neighborhood and global

notoriety

SHORTCOMINGS

(Failures)

Association with their suppliers in remote region.

Scope of business sector in not attractive Reduce the expense of merchandise sold.

Absence of Innovation and Technology Development.

Lack of fund to finance a new project

23

OPPORTUNITIES

Future Growth Potential Rising Demand

Developing Export Markets

Adding to a Long Term Vision and Strategy Research to Develop New Products

Concentrate on Cost Optimization Availability of Finance

THREATS

Workforce Challenges (Trade Union) Reduction In deals

Absence of Professional Expertise inside of Industry

Reliance on Cartelization for satisfactory Revenue Lack of Research and

Development.

24

CHAPTER 3

3 THEORTICAL BACKGROUND

3.1MEANING OF ANALYSIS OF FINANCIAL STATEMENTS

The analysis helps the firm to evaluate or interpret financial conditions of the company in

every year so this will helps the company to know the actual positions or performance of the

company. This evaluation can be done according to company profits.

3.2 RATIOS

3.2.1Meaning of the ratio

A ratio is a tools which is used to know the financial performance of the 2 or more years

according to the data given in the balance sheet and profit and loss account. It should be

expressed in the various forms such as quotient, a rate, and a percentage.

3.2.2 CLASSIFICATION OF RATIOS

ON THE BASIS OF TRADITIONAL CLASSIFICATION

A. Balance sheet ratios:

Current ratio

Quick ratio

Proprietary ratio

B. Income statement ratios are:

Gross profit ratio

Operating profit ratio

Net profit ratio

Expenses ratio

C. Composite or Mixed Ratios:

Return on proprietor’s fund ratio

Return on capital employed ratio

Debtors turnover ratio

Creditors turnover ratio

Inventory turnover ratio

25

ON THE BASIS OF FUNCTIONAL CLASSIFICATIONS

Liquidity ratio

Leverage ratio

Activity ratio

Profitability ratio

ON THE BASIS OF SIGINIFANCE OR IMPORTANCE

Liquidity ratios:

Solvency ratios:

Activity ratios:

Profitability ratios:

ACCORDING TO THE CLASSIFICATION OF NATURE IN

FINANCIAL ANALYSIS

Primary ratio

Secondary ratio

ACCORDING TO THE CLASSIFICSTION OF TIME

Structural ratio

Trend ratio

3.3 WORKING CAPITAL MANAGEMENT

Working capital plays an important role for the organization and it is necessary that a proper

plan must be available to manage the firm working capital. It includes both current assets and

the current liability for the calculation of working capital. As per the net working capital

concept the difference between the current assets and current liability is the firms net working

capital. And on the other hand as per the gross working capital concepts the sum total of the

total current asset represents the working capital. A Working capital management plays the

important role by ensuring that an organization has sufficient exchange resource out

solicitation to meet its passing liabilities, responsibilities and working expenses. Having a

sufficient level of working capital management system is a remarkable way for a few

organization to improve their payment capacity. The two essential parts of working capital

management are current asset and current liability.

A couple key execution extents of a working capital management system are the working

capital extent, stock turnover and the social occasion extent. Extent examination will lead

organization to perceive domains of concentrate, for instance, inventory management, cash

management, records of receipts and payment of the organization.

26

If the total of current assets are less than the total amount of current liabilities, it results to the

working capital deficiency, in simple manner it is called as shortage of working capital.

An organization will be having assets and its advantage however short of liquidity if its focal

points can't instantly be converted into cash. Positive working capital is very important to

ensure that a firm is able to continue with its operations and that it has sufficient resources or

the assets to meet the current liability andable to meet the other operating expenses. The

working capital management is useful for directing inventories, cash due and payable.

The key estimation of the working capital is done on the reason of the gross current assets of

the firm.

Gross working capital = Total Current assets

Net working capital = Current assets – Current liabilities.

Net working capital provides the positive or negative results. If the total of current asset is

more than the total of current liability then it means that the firm has the sufficient amount of

working capital to meet its current liability. On the other hand if the current assets is less than

the total current liability then it shows the negative working capital which means that the firm

has not the sufficient amount of current asses to meets its current liability.

Kinds of working capital

27

1) Permanent working capital: it is likewise called settled working capital. It intends

to bear on the everyday costs the firm is required to keep up the base measure of working

capital. For instance the firm is required to keep up the base level of crude material,

completed merchandise or money parity and so forth.

a) Regular working capital-it implies the base sum which the firm needs to keep with

itself to bear on the everyday operation.

b) Reserve working capital-it implies the overabundance sum over the normal working

capital for questionable circumstances such as strike, lock out, misery and so on.

2) Temporary working capital: it is also known variable working capital which is used

to meet occasional requirement and also for additional purpose.

a) Seasonal Working Capital-it is required to meet the regular requirement of the

venture.

b) Special Working Capital- it is required for some uncommon purposes of the

venture. For instance publicizing the result of the firm requires extraordinary working capital.

Brief working capital is for brief period and changes while perpetual working capital is

steady and altered.

28

OPERATING CYCLE

Operating cycle represents the total amount of days an organization requires to convert its

inventories in genuine cash. It levels with the time taken in maintaining inventories not with

standing the time required in recovering cash from trade receivables. This is called as operating

cycle because this is a method of purchasing inventories, offering products in credit, and at the end

recovering cash from customers in exchange of the credit sales, and after that using those cash to

purchase inventories, raw materials etc and it is always keeping going ahead as like circle thus it is

called as the operating cycle.

Operating cycle is helpful for measuring the working effectiveness and efficiency of working

capital management of an organization. A shorter operating cycle is good as it results that the cash

from the credit sale is been received earlier and cash is available to meet other expenses, and

investing in the raw material and inventories.

The accompanying are all elements that impact the term of the operating cycle:

The installment terms reached out to the organization by its suppliers. Longer installment

terms abbreviate the operating cycle, following the organization can defer paying out

money.

The request satisfaction arrangement, since a higher accepted starting satisfaction rate

expands the

measure of stock close by, which expands the operating cycle.

The credit arrangement and related installment terms, subsequent to looser credit compares

to a more drawn out interim before clients pay, which amplifies the operating cycle.

Consequently, a few administration choices (or arranged issues with business accomplices) can

affect the operating cycle of a business.

Analyzing the operating cycle of a potential get can be especially helpful, since doing as such can

uncover courses in which the acquirer can adjust the operating cycle to decrease money

prerequisites, which might balance a few or the greater part of the money expense expected to

purchase the secure.

29

Determination of the length of working and money cycle:

The length of operating cycle of an assembling firm is the whole of

Operating cycle = Inventory change period+ receivable transformation period

= RMCP+WIPCP+FGCP+ Debtors CP- Creditors CP

RMCP(Raw materials conversion period) = Average stock of raw materials

Material consumption/365

30

Average stock of raw materials = (opening stock of RM+ Closing

Stock of RM)/2

Material Consumed during the year= Opening stock of RM + Purchases – closing

stock.

WIPCP (Work in progress conversion period) = Avg. stock of raw material

Total cost of production per day

FGCP (Finished goods conversion period)=Avg. stock of finished goods

Total cost of goods sold per day

RCP (Receivable conversion period) :

It is ordinary time taken to change over obligated people into cash. RCP addresses the

ordinary collection period. It is the time required to assemble the noteworthy aggregate

from the customers.

Hence RCP= Receivable conversion period

= Avg. accounts receivable

Net credit sales per day

PCP(Payables Conversion Period)

It means that credit value according to suppliers and loan bosses ,since it demonstrates to

what extent they are willing to sit tight for installment .

31

CHAPTER 4

DATA ANALYSIS AND INTERPRETATION

4.1 GROSS WORKING CAPITAL

Gross working capital of L&T Kansbahal works for the last four years:

All figures are in Rupees

Current As on As on As on As on Assets 31-3-2012 31-3-2013 31-3-2014 31-3-2015

Inventories 732,891,622 1,292,272,077 1,191,653,112 1,109,372,449

Trade 746,161,152 952,803,991 988,310,861 1,204,042,947 Receivables

Cash and bank 53,316 165,323 92,600 19,386,237 Balances

Short term loans 102,670,535 100,886,250 91,549,829 145,667,051 and advances

Total Current

Assets 1,581,776,625 2,346,127,641 2,271,606,402 2,478,468,684

Sources: Balance sheet Table 1

We know that gross working capital is equal to current asset, hence the respective Gross

Working Capital for the respective years are in the table as shown. From the total working

capital we can see that it is steady over the years. However to study the real short term

financial liquidity, its advised to look at the trends of net working capital. L&T ,Kansbahal

Works always insists on net working capital.

4.2 NET WORKING CAPITAL

The equation for net working capital (NWC), now and again alluded to as essentially working

capital, is utilized to decide the accessibility of an organization's fluid resources by

subtracting its present liabilities. Current Assets are the benefits that are accessible inside of

12 months. Current Liabilities are the liabilities that are expected inside of 12 months.

Net working capital= Current assets- current liabilities

To figure the Net working capital we require the Current resources and current liabilities data

for individual years. Now, from the balancesheet , we see the figures to be

32

All figures are in Rupees

Current As on As on As on As on

Assets 31-3-2012 31-3-2013 31-3-2014 31-3-2015

Inventories 732,891,622 1,292,272,077 1,191,653,112 1,109,372,449

Trade 746,161,152 952,803,991 988,310,861 1,204,042,947 Receivables

Cash and 53,316 165,323 92,600 19,386,237 bank balances

Short term loans 102,670,535 100,886,250 91,549,829 145,667,051 and advances

Total current

Assets 1,581,776,625 2,346,127,641 2,271,606,402 2,478,468,684

(TCA)

Current As on As on As on As on

Liabilities 31-3-2012 31-3-2013 31-3-2014 31-3-2015

Short term (66,755,322) (10,208,686) 1,395,862 307,682 Borrowings

Current 682,260,091 824,015,044 822,123,070 1,107,015,021 maturities of long

term borrowings

Other current 285,125,024 293,472,765 198,080,860 173,821,741 Liabilities

Short term 5,250,000 5,040,000 4,695,600 4,460,400 Provisions

Total current 905,879,793 1,112,319,123 1,026,295,392 1,285,604,844 liabilities(TCL)

Net working 675,896,832 1,233,808,518 1,245,311,010 1,192,863,840

capital (CA-CL)

Sources: Balance sheet Table 2

4.3Ratio Analysis

LIQUIDITY RATIO

4.3 .1 CURRENT RATIO = Current Assets / Current

Liabilities

All figures are in Rupees

Year Current assets Current liabilities CA/CL Ratio

2011-12 1,581,776,626 905,879,793 1.74

33

12-13 2,346,127,640 1,112,319,123 2.10

2013-14 2,271,606,402 1,026,295,392 2.21

2014-15 2,478,468,684 1,285,604,844 1.92

3,000,000,000.00

2,500,000,000.00

2,000,000,000.00

1,500,000,000.00

Current Assets

1,000,000,000.00

Year

500,000,000.00

0.00

1 2 3 4

1,400,000,000.00

1,200,000,000.00

1,000,000,000.00

800,000,000.00

600,000,000.00

400,000,000.00

200,000,000.00

Current Liabilities

0.00

1 2 3 4

ANALYSIS: In below diagram showing current ratio from 2011 t0 2015. In which it

shows the standard ratio is 2.109 which they are getting in 2012 -13 and highest they getting

2013-14 which is 2.213

34

current ratio

2.5

2 2.109 2.213

1.927

1.746

1.5

1 current ratio

0.5

0

2011-2012 2012-2013 2013-2014 2014-2015

INTERPRETATION

Current proportion is a measure of liquidity of an association at a particular date. Current

proportion must be inspected over a time allotment. Increase in current proportion over a time

span may propose improved liquidity of the association or a more preservationist approach to

manage working capital organization. A reducing design in the present proportion may suggest

a disintegrating liquidity position of the business or a leaner working capital push of the

association through the allocation of more viable organization practices. Standard proportion is

2:1. In the year 2011-12 the proportion was 1.74:1 which increments to 2.09:1 in the year

2012-13. Step by step the proportion increments to 2.13:1 in the year 2013-14 lastly reductions

to 1.92:1 in the year 2014-15. It is close to standard proportion which is great and can be

received.

4.3.2 QUICK RATIO = (Current Assets - Inventories) / Current Liabilities

All figures are in Rupees

Year Liquid assets Current liabilities LA/CL Ratio

2011-12 848,885,004 905,879,793 0.93

2012-13 1,053,855,563 1,112,319,123 0.94

2013-14 107,995,3290 1,026,295,392 1.05

2013-15 2,368,096,235 1,285,604,844 1.84

35

ANALYSIS: In 2014-15, the quick ratio is high when contrasted with ideal 1:1. In

different years it was near 1 which was great. In 2011-12 to 2012-13 company

maintain stable quick ratio which is 0.93 to 0.94. 2013-14 company start growing.

QUICK RATIO

2 1.84

1.5

1.05

0.93

0.94

1

QUICK RATIO

0

2011-2012 2012-2013 2013-2014 2014-2015

INTERPRETATION: -quick proportion is a marker of dissolvability of an

element and must be examined over a timeframe furthermore in the connection of the

business the organization works in.In any case, associations must fulfill the right

agreement between liquidity risk rising up out of a low smart proportion and the threat

of mishap coming to fruition on account of a high rapid proportion. In 2014-15 , the

brisk proportion is high when contrasted with ideal 1:1 . In different years it was near 1

which was great .

So it gave adequate influence In 2014-15 it is too high on the grounds that the

organization is seeing to keep up it's position even in extremely capricious business

circumstances . Snappy proportion is in this manner a more dependable measure of

liquidity for assembling organizations and development firms that have moderately

abnormal amounts of stock, work in advancement and receivables than the present

proportion .

4.3.3Activity ratio

Resources are placed assets into various assets in business to make arrangements and

increase advantages. The profitability with which assets are managed particularly impacts

the volume of offer. Movement ratio measure the capability in addition, suitability with

which a firm manages its advantages or assets. These ratio are similarly called turnover

ratio.

36

4.3.4 Stock turnover ratio: Every firm maintain specific level of stock which is

required to finish the products to meet the necessities of the business. Yet the level of stock

of the firm should not be nor too high nor too low.

All figures are in Rupees

Year Net Sales Average inventory Ratio(times)

2012-13 2,782,924,202 1,012,581,850 2.74

2013-14 2,473,640,447 1,241,962,595 1.99

2014-15 2,731,011,684 1,150,512,780 2.37

ANALYSIS: In the below graph we can see that in 2012-13 the proportion was 2.74 &1.99

in the year 2013-2014 and then it increases to 2.37in the year 2014-15, the company holds a

good position without blocking of its money in inventories.

Ratio(times)

2.74

3

1.99

2.37

2.5

2

1.5

Ratio(times)

1

0.5

0

2012-13 2013-14 2014-15

INTERPRETATION: there is no reliable rule or standard stock turnover proportions.

commonly a high stock turnover demonstrates capable organization of stock since more a

great part of the time the stocks are sold, the lesser measure of money is required to back the

stock. A low stock proportion demonstrates an inefficient organization of stock. A low stock

turnover proportion suggests over interest in stocks, poor asset administration. Too high

turnover proportion is likewise not satisfactory as it diminishes benefit by expanding cost.

37

Days of stock holding

=days in a year/stock turnover ratio

All figures are in Rupees

Days of stock Holdings

F.Y No. of days stock Turnover Days of inventory

proportion holdings

2012-13 365 2.74 133.21

2013-14 365 1.99 183.41

2014-15 365 2.37 154.01

ANALYSIS: the below graph show that number of days to holding inventory. In 2013-14 number of

holding inventory was high compared to the other different years. in 2013-14 firm holding stock till

183.41 which was very high.

Days of inventory holdings

200 183.41

180

154.01

160

133.21

140

120

100

Days of inventory holdings

80

60

40

20

0

2012-13 2013-14 2014-15

INTERPRETATION:

The above chart demonstrates that in the year 2013-14 have a high number of days in stock. This

show there is a blockage of Inventory to some extent due to delay in lifting of materials by

customer. But in the year 2012-13 was having a low inventory which indicates the company is

maintain at optimum level of stock on hand to meet demands.

38

4.3.5 RAW MATERIALS HOLDING PERIOD:

Raw materials holding period= 365

Raw materials inventory turnover

All figures are in Rupees

RM Inventory

Year Days Turnover RM holding period

2012-2013 365 1.88 194.14

2013-2014 365 2.52 144.84

2014-2015 365 2.31 158.00

Source: balance sheet

ANALYSIS: The below graph shows that 2012-13 company holding raw material was 194.14

which was very high compared to other different years. In 2013-14 holding period was 144.84

which was increased in 2014-15.

Raw materials holding period

194.14 200

158.01 144.84

150

Raw materials holding

100

Period

50

0

2012-2013 2013-2014 2014-2015

INTERPRETATION:

Raw materials include number of items some of them require to procure longer period

of time and some of them require shorter period of time.

In 2012-13 the raw materials holding period was 194 which is very high.

39

In 2013-14 raw materials holding period was less which shows there is no blockage in

the working capital.

In 2014-15 again the holding period increased to 158 days.

4.3.6 WORK IN PROGRESS CONVERSION PERIOD:

Work in progress conversion period =Average work in progress inventory

Cost of production per day

e.cost of f.WIP a.opening D.Cost of production per conversion

Year WIP b. closing WIP c.Avg(a+b)/2 production day(d/365) period(c/e)

2012-

13 732,891,622 1,292,272,077 1,012,581,850 2,526,210,030 6,921,123 146

2013-

14 1,292,272,077 1,191,653,112 1,241,962,595 2,487,150,476 6,814,110 182 2014-

15 1,191,653,112 1,109,372,449 1,150,512,781 2,385,304,515 6,535,081 176

ANALYSIS: below graph reveals that period of semi-finished work that was 146 in 2012-13

and it increase in 2013-14 and again decreased to 176 in 2014-15.

WIP conversion period

200 182

176

146 150

100

WIP conversion period

50

0

2012-13 2013-14 2014-15

Cost of production amount taken from total expenditure excluding finance cost.

40

INTERPRETATION:

Work in advancement transformation period is the normal regular time taking the work

which is in progress or semi completed.to finish the semi completed work in advancement.

Work in progress conversion period in the year 2012-13 was 146 days .In the year 2013-14 it

is expanded to 182 days and declined in the year 2014-15 i.e. 176 days.

This is thought to be a decent sign as the products are worked upon proficiently and no

addition in the time taken to process merchandise. It is a sign of faster conversion of WIP

into finished goods, resulting in faster sales & better working capital.

4.3.7 FINISHED GOODS CONVERSION PERIOD

Finished Goods Conversion Period = Average finished goods inventory

Cost of goods sold per day

All figures are in Rupees

FG COGS

Year Opening stock Closing stock Avg. FG Inventory

2012-13 81,715,911 55,875,509 68,795,710 1,490,307,168 17

2013-14 55,875,509 41,669,376 48,772,442 1,565,411,024 11

2014-15 22,357,496 19,870,496 21,113,996 1,887,685,903 4

ANALYSIS: Below graph reveals that finished good conversion period , in 2012-13 the finished

goods conversion period was very high it was 17. But in 2014-15 company decreased the finish

goods period to 4 which was good sign for the company.

FG Conversion period

17 18

16

14

11

12

10

FG Conversion period

8

4

6

4

2

0

2012-13 2013-14 2014-15

41

INTERPRETATION:

The completed merchandise transformation period is the normal time taken to

offer completed items. In 2012-13 the average time taken to sell finished

products was 17 days.

In 2013-14 it has decline to 11 days.

However, in 2014-15 the time taken to sell the finished products further decreased to

4 days. So, as we see that time taken to sell the finished goods is decreasing which is

considered to be a good indicator.

The reason for decrease:-

Better advertisement

Improve the facilities e.g transportation and decreasing the time of delivery of good

from manufacture to unit of buyer

In L&T, kansbahal production process is such that maximum of goods are stored as work in

process processed as per customer needs.

4.3.8 INVENTORY TO CURRENT ASSETS

The proportion demonstrates the measure of enthusiasm for stock per rupee of current

assets venture. Generally an extending degree of stock is definite of inefficient stock

organization. The extent may in like manner demonstrate the state of liquidity position of

concern. The lower the stock to current assets cuts down the liquidity when stood out from

other current assets, viz., receivables, cash and attractive securities.

42

Inventory to Current Asset= Total inventory/

Total Current Assets

All figures are in Rupees

Year Inventory Current assets Ratio

2011-12 732,891,622 1,581,776,626 46.33

2012-13 1,292,272,077 2,346,127,640 55.08

2013-14 1,191,653,112 2,271,606,402 52.45

2014-15 1,109,372,449 2,478,468,684 44.76

Source: balance sheet

ANALYSIS: The below graph reveals that the inventory to current asset ratio in 2011-12

was 46.33 and in 2012-13 it was 55.08 and in 2013-14 it 52.45 and in 2014-15 it was 44.76

respectively.

43

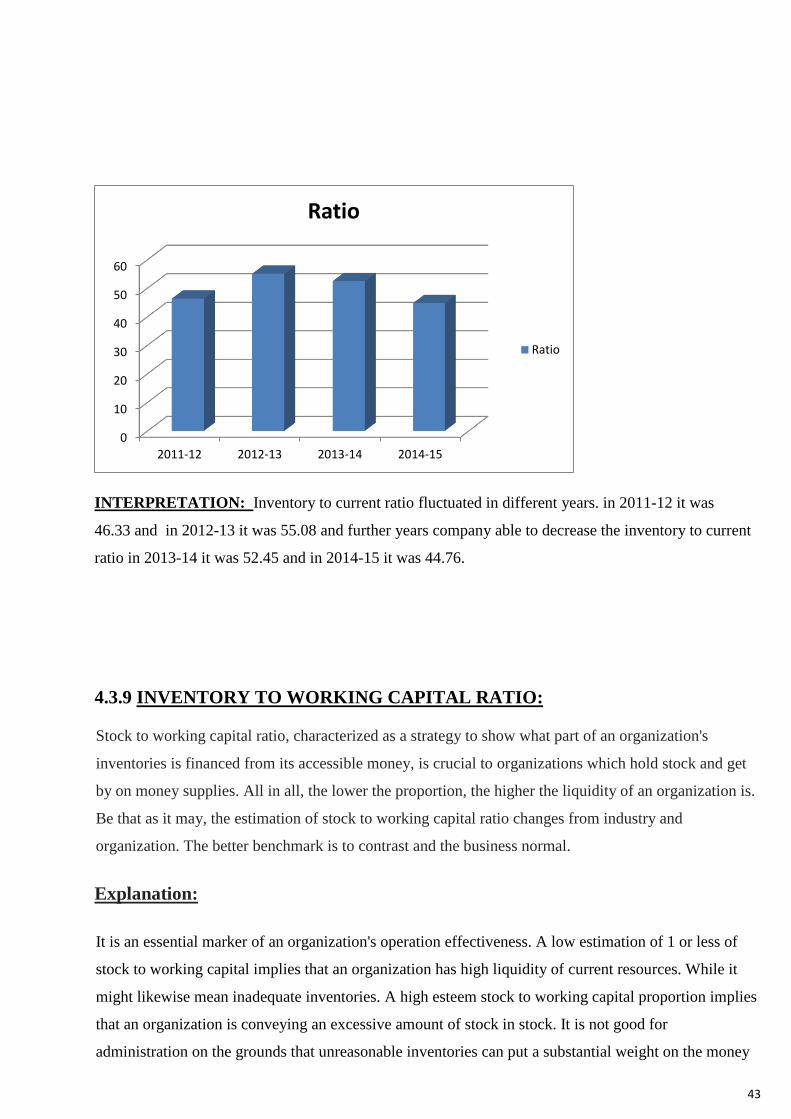

INTERPRETATION: Inventory to current ratio fluctuated in different years. in 2011-12 it was

46.33 and in 2012-13 it was 55.08 and further years company able to decrease the inventory to current

ratio in 2013-14 it was 52.45 and in 2014-15 it was 44.76.

4.3.9 INVENTORY TO WORKING CAPITAL RATIO:

Stock to working capital ratio, characterized as a strategy to show what part of an organization's

inventories is financed from its accessible money, is crucial to organizations which hold stock and get

by on money supplies. All in all, the lower the proportion, the higher the liquidity of an organization is.

Be that as it may, the estimation of stock to working capital ratio changes from industry and

organization. The better benchmark is to contrast and the business normal.

Explanation:

It is an essential marker of an organization's operation effectiveness. A low estimation of 1 or less of

stock to working capital implies that an organization has high liquidity of current resources. While it

might likewise mean inadequate inventories. A high esteem stock to working capital proportion implies

that an organization is conveying an excessive amount of stock in stock. It is not good for

administration on the grounds that unreasonable inventories can put a substantial weight on the money

0

10

20

30

40

50

60

2011-12 2012-13 2013-14 2014-15

Ratio

Ratio

44

assets of an organization. A key issue for an organization to enhance its operation proficiency is to

distinguish the ideal stock levels and in this manner minimize the cost tied up in inventories.

ANALYSIS: Inventory to working capital ratio graph shows that ratio continuously decrease from

2011 to 2015. In 2011-12 company had 1.08 and in 2014-15 company was having 0.93 that means firm

was having enough amount to meet there daily expenses.

All figures are in Rupees

F.Y

C.A C.L

Working capital

prop

ortio

n

Stock

2011-12 1,581,776,626 905,879,793 675,896,833 732,891,622 1.08

2012-13 2,346,127,640 1,112,319,123 1,233,808,517 1,292,272,077 1.04

2013-14 2,271,606,402 1,026,295,392 1,245,311,010 1,191,653,112 0.95

2014-15 2,478,468,684 1,285,604,844 1,192,863,840 1,109,372,449 0.93

Source: balance sheet

Ratio

2014-15

0.93

2013-14

0.95

2012-13

1.04

Ratio

2011-12

1.08

0.85 0.9 0.95 1 1.05 1.1

45

INTERPRETATION–:Working capital is basically difference betwen the current assets

and current liabilities .the lower the stock to working capital company should be in better

position.As the ratio decreases from 2011 to 2015(shown in the above graph) it shows that the

money blocked in inventory reduces and the firm has more amount of cash in hand to meet its

daily expenses.

4.3.10 Debtors turnover ratio: Account holders turnover ratio shows the speed of

obligation gathering of the company. In straightforward words it demonstrates the quantity of

times normal borrowers (receivables) are turned amid a year.

Indebted individuals turnover =net credit yearly deals/normal exchange account holders.

Exchange debtors=sundry debtors + bills receivables and accounts receivables.

On the off chance that appropriate data is not gave then

Indebted individuals turnover can likewise be figured =gross deals/borrowers.

All figures are in Rupees

Year gross sales Debtors DTR

2011-2012 2,915,245,340 746,161,152 3.90

2012-2013 2,970,143,706 952,803,991 3.11

2013-2014 1,727,436,378 988,310,861 1.74

2014-2015 2,778,372,714 1,204,042,947 2.30

Source: balance sheet

ANALYSIS: Debtor’s turnover ratio showed in the below graph in that 2011-12 DTR was

3.90 but it continuously decreases to 2014-15 and in 2014-15 it was 2.30.

46

Ratio

4.5

4 3.9

3.5

3 3.11

2.5 2.3

2

1.74

ratio

1.5

1

0.5

0

2011-2012 2012-2013 2013-2014 2014-2015

INTERPRETATION:DTR shows the amount of times the obligated people are turned over

in the midst of a year. Generally, the higher the estimation of record holders the more successful

is the organization of obliged people/arrangements or more liquid are the borrowers.

Here the DTR decreases from 3.90(2011-12) to 2.30(2014-15)

4.3.11Average collection period=days in year/DTR

All figures are in Rupees

Year Days DTR ratio

2011-12 365 3.90 93

2012-13 365 3.11 117

2013-14 365 1.74 209

2014-15 365 2.30 158

Source: balance sheet

ANANLYSIS: The graph of average collection period showed ratios of the L&T from 2011-

2015. In 2011-12 the average collection period ratio was 93 and it increase next two years but in

2014-15 this was decreased from 209 to 158.

47

ratio

250

209

200

158

150

117

93

ratio

100

50

0

2011-12 2012-13 2013-14 2014-15

INTERPRETATION:

The ordinary aggregation period ratio identifies with the typical number of days for

which a firm needs to hold up before its receivables are changed over to cash.

The shorter it is the better is the way of record holders as a short assembling period

proposes energetic portion by obliged people.

In 2011-12 the average collection period was 93 which increased to 117 in 2012-13 which

further increases to 209 in 2013-14 and finally reduces to 158 in 14-15 It increases in L & T

because to survive in this though competitive world the firmadapts the policy of leniency to

debtors. If the firm will not do so it may loose its customers.

48

4.3.12Working capital turnover ratio:

Working capital of a firm is specifically identified with deals, current resources like account

holders, charges receivables, money stock and so on, working capital=current resources current

liabilities.

Working capital turnover ratio=sales/net working capital.

All figures are in Rupees

Year Current Current

Working capital WCTR Assets Liabilities Net sales

2011- 1,581,776,626 905,879,793

12 2,677,618,516 675,896,833 3.96

2012- 2,346,127,640 1,112,319,123

13 2,782,924,202 1,233,808,517 2.25

2013- 2,271,606,402 1,026,295,392

14 2,473,640,447 1,245,311,010 1.98

2014- 2,478,468,684 1,285,604,844

15 2,731,011,684 1,192,863,840 2.28

Source :balance sheet

ANALYSIS: The graph below it shows L&T working capital turnover ratio. Which increased in

2011-12 to 3.96 and continuously decreased further two years in 2012-2013 it was decreased to

2.25 and in 2013 -14 it was 1.98.but in 2014-15 it increased to 2.28.

WCTR

3.96

4

3.5

3

2.25

2.28

2.5

1.98

2

WCTR

1.5

1

0.5

0

2011-12 2012-13 2013-14 2014-15

49

INTERPRETATION: Thisproportion shows the amount of times the working capital is

turned over in course of one year. This proportions measures the profitability with which the

working capital is being used by the firm .The proportion is 3.96 in the year 2011-12 which

decreases to 2.25 in 2012-13 which again decays to 1.98 in 2013-14 and after that a beam of

trust is seen. That implies the proportion increments to 2.28 in the year 2014-15. This

proportions can, most ideal situation be used by making of close and inclination examination

for different firms in same industry and for different periods.

4.3.13 Assets turnover ratios:

Fixed assets turnover ratio= Net sales

Net fixed assets

The benefit turnover proportion has a tendency to be higher for organizations in a segment like

customer staples, which has a generally little resource base yet high deals volume. Alternately,

firms in segments like utilities and information transfers, which have substantial resource bases,

will have bring down resource turnover.

FATR of L&T Kansbahal works for four years:

All figures in rupees

Year Net sales Net fixed assets FATR

2011-12 2,677,618,516 635,192,333 4.21

2012-13 2,782,924,202 609,296,549 4.57

2013-14 2,473,640,447 612,946,269 4.03

2014-15 2,731,011,684 496,664,908 5.49

Source :balance sheet

ANALYSIS: Fixed assets turnover ratio showing below by graph in that graph shows L&T in

2011-2012 was 4.21 and it increased to 4.57 in 2012-13 that shows here L&T in good position by

the last year. But in next year it was decline to 4.03 that show was in not good position compare to

the last year and it again increased to 5.49 in 2014-2015 that means L&T are in good position

compare to all different years.

50

FATR

6

5.49

5

4.21

4.57

4 4.03

3

FATR

2

1

0

0 1 2 3 4 5

INTERPRETATION The higher the proportion the better high proportion demonstrates the business has less

cash tied up in altered resources for every unit of money of offers income.

Over the four years the ratio is increasing which means that the unit have not over-invested in

plant , machinery and other equipment’s.

4.3.14 Profitability ratio

A Net profit ratio

This proportion measures the relationship of gross benefit to net deals and is normally

spoken to a rate. In this way, it is computed by separating the gross benefit by deals.

Gross profit ratio=(net income/sales)*100

51

All figures are in Rupees

F.Y Net income Net sales

Net

profit ratio

2011-12 250,066,358 2,677,618,516 9.33

2012-13 443,737,101 2,782,924,202 15.94

2013-14 280,154,534 2,473,640,447 11.34

2014-15 402,461,367 2,731,011,684 14.73

Source: balance sheet

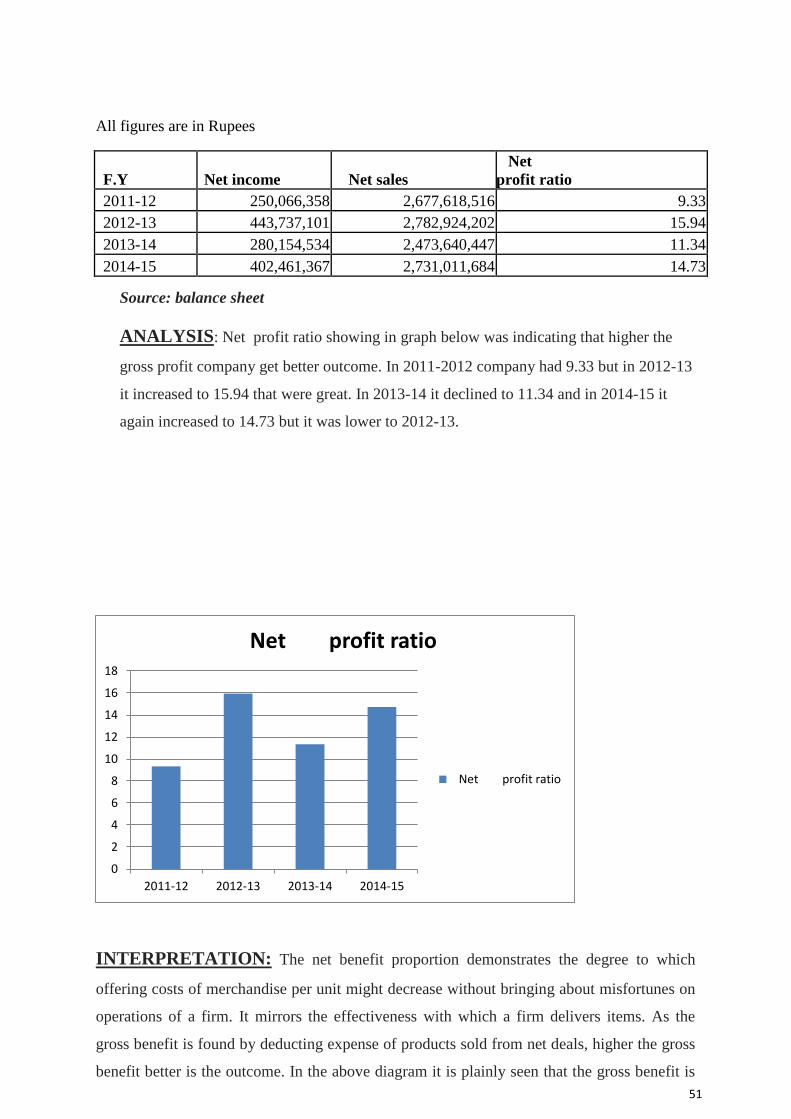

ANALYSIS: Net profit ratio showing in graph below was indicating that higher the

gross profit company get better outcome. In 2011-2012 company had 9.33 but in 2012-13

it increased to 15.94 that were great. In 2013-14 it declined to 11.34 and in 2014-15 it

again increased to 14.73 but it was lower to 2012-13.

14.73

11.34

INTERPRETATION: The net benefit proportion demonstrates the degree to which

offering costs of merchandise per unit might decrease without bringing about misfortunes on

operations of a firm. It mirrors the effectiveness with which a firm delivers items. As the

gross benefit is found by deducting expense of products sold from net deals, higher the gross

benefit better is the outcome. In the above diagram it is plainly seen that the gross benefit is

0

2

4

6

8

10

12

14

16

18

2011-12 2012-13 2013-14 2014-15

Net profit ratio

Net profit ratio

52

most astounding in the year 2012-13.the gross benefit has declined in the year 2013-14 yet

again it is expanding in the year 2014-15 which is a positive sign.

In the event that we deduct net benefit proportion from 100,we acquire the proportion of

expense of products sold to deals. In this manner: proportion of expense of products

sold=100-n.p proportion

Year N.P ratio C.O.G.S ratio

2011-12 9.33 90.67

2012-13 15.94 84.06

2013-14 11.34 88.66

2014-15 14.73 85.27

B.OPERATING RATIO

It is build the relationship between expense of merchandise sold and other working costs on

one hand and the deals on the other.

Operating ratio=(operating cost/net sales)*100

All figures are in Rupees

Year operating cost Net sales operating ratio

2011-12 1,774,260,401 2,677,618,516 66.26

2012-13 1,831,354,258 2,782,924,202 65.8

2013-14 1,789,164,460 2,473,640,447 72.32

2014-15 1,609,267,766 2,731,011,684 58.92

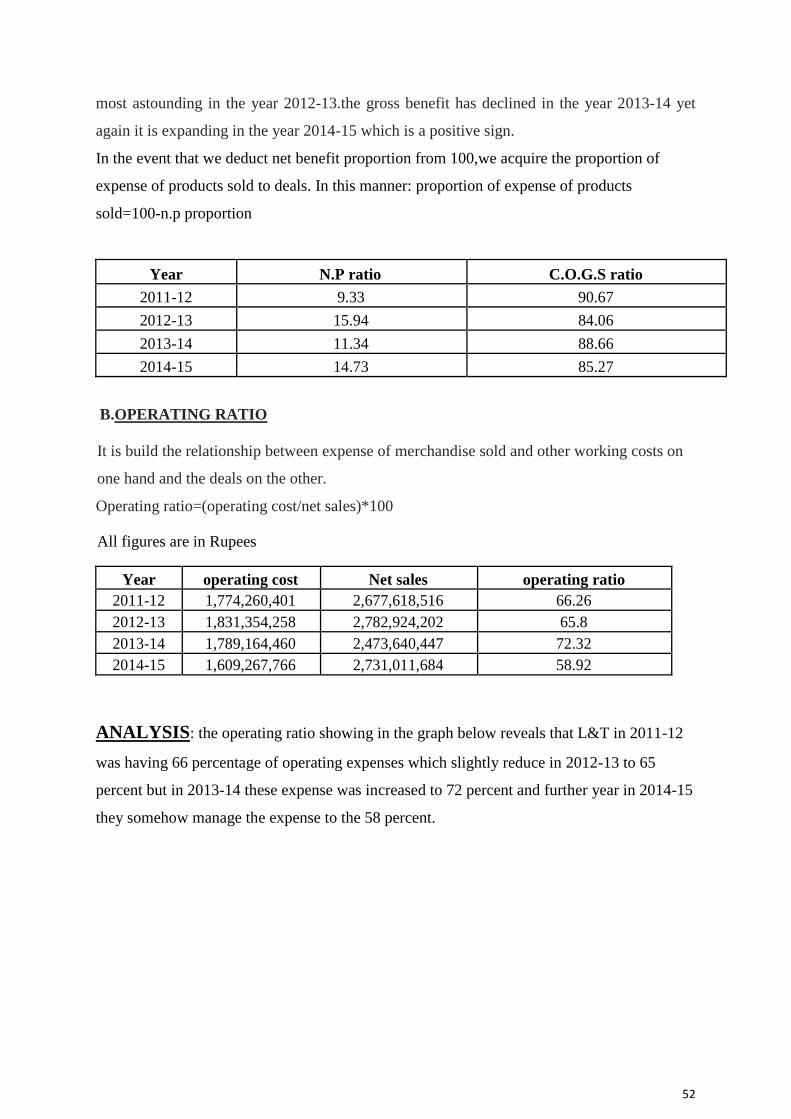

ANALYSIS: the operating ratio showing in the graph below reveals that L&T in 2011-12

was having 66 percentage of operating expenses which slightly reduce in 2012-13 to 65

percent but in 2013-14 these expense was increased to 72 percent and further year in 2014-15

they somehow manage the expense to the 58 percent.

53

operating ratio 80

72.32

70 66.26 65.8

58.92

60

50

40

operating ratio

30

20

10

0

2011-12 2012-13 2013-14 2014-15

INTERPRETATION:This proportion demonstrates the rate of net deals that is devoured

by working expense. Clearly, higher the working proportion, the less ideal it is, on the

grounds that it would have a little edge to cover interest, salarycharge, profit and saves. There

is no general guideline however 75-85% might be viewed as great as far as assembling

endeavors. In L&T Kansbahal works the ratio is quiet less than 75-85%. The ratio is 66% in

the year 2011-12 which declines to 65% in the year 2012-13. The % is highest in the year

2013-14 i.e 72% which again declines to 58% in the year 2014-15. It is lowest in the previous

year which shows that the firm is able to reduce its operating cost.

C. Operating profit ratio All figures are in Rupees

Year Net sales operating cost operating profit o.p ratio

2011-12 2,677,618,516 1,774,260,401 903,358,115 33.73

2012-13 2,782,924,202 1,831,354,258 951,569,944 34.19

2013-14 2,473,640,447 1,789,164,460 684,475,987 27.67

2014-15 2,731,011,684 1,609,267,766 1,121,743,918 41.07

ANALYSIS: operating profit ratio showing in graph that L&T generated profit in 2011 to

2015. In 2011-12 the company profit was 33.73 percent which was decline in 34.19 in 2012-

13 further it was reduced to 27.67 percentage in 2013-14 but in 2014-15 L&T increased their

operating profit to 41.07 percent.

54

o.p ratio

45

34.19

40

33.73

41.07

35

27.67

30

25

o.p ratio

20

15

10

5

0

2011-12 2012-13 2013-14

2014-15

D. Expenses ratio

It demonstrates the relationship of different costs to net deals.

i) Sales, Administrative & other expenses ratio =(sales, administrative & other

expenses)/sales *100

All figures are in Rupees

Year sales & admin

Other Net sales Expense ratio

2011-12 109,751,669 2,677,618,516 4.09

2012-13 115,173,331 2,782,924,202 4.13

2013-14 128,050,270 2,473,640,447 5.17

2014-15 241,437,011 2,731,011,684 8.84

55

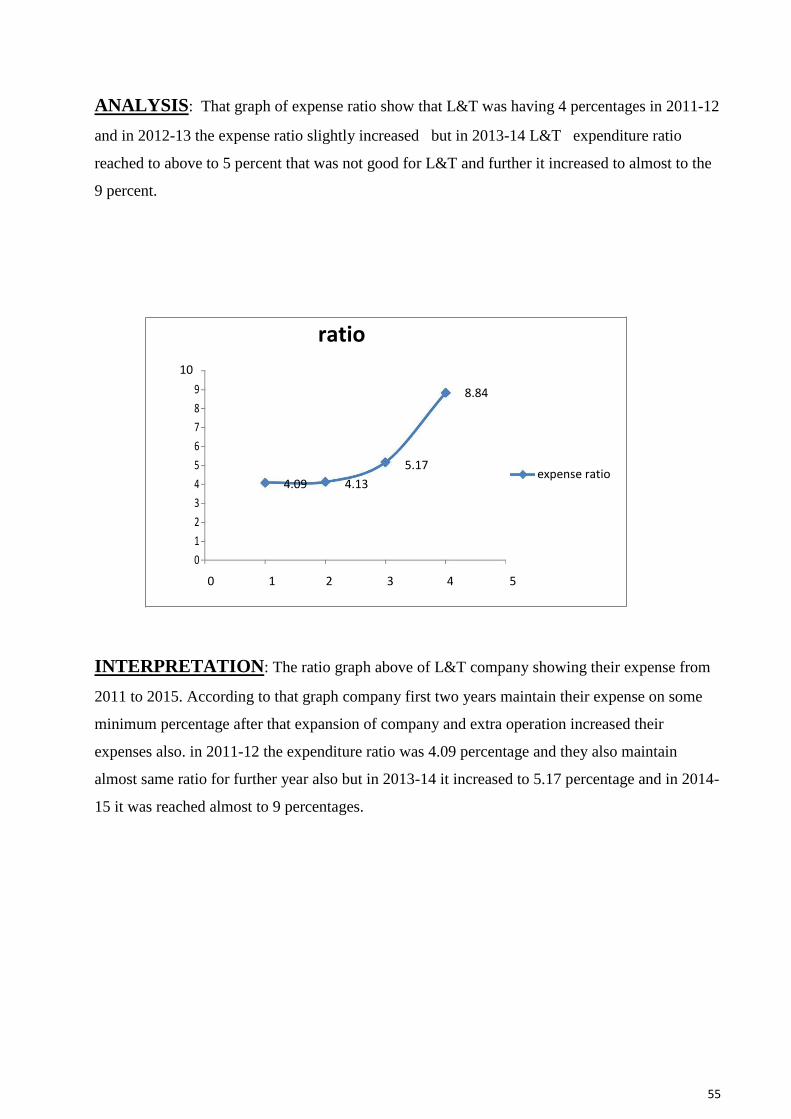

ANALYSIS: That graph of expense ratio show that L&T was having 4 percentages in 2011-12

and in 2012-13 the expense ratio slightly increased but in 2013-14 L&T expenditure ratio

reached to above to 5 percent that was not good for L&T and further it increased to almost to the

9 percent.

ratio

10 9 8.84

8

7

6

5 5.17 expense ratio

4 4.09

4.13

3

2

1

0

0 1 2 3 4 5

INTERPRETATION: The ratio graph above of L&T company showing their expense from

2011 to 2015. According to that graph company first two years maintain their expense on some

minimum percentage after that expansion of company and extra operation increased their

expenses also. in 2011-12 the expenditure ratio was 4.09 percentage and they also maintain

almost same ratio for further year also but in 2013-14 it increased to 5.17 percentage and in 2014-

15 it was reached almost to 9 percentages.

56

CHAPTER 5

FINDINGS, SUGGESTIONS AND CONCLUSION

FINDINGS

In the year 2011-12 the current ratio was 1.74:1 which increases to 2.09:1 in the year

2012-13. Gradually the ratio increases to 2.13:1 in the year 2013-14 and finally

decreases to 1.92:1 in the year 2014-15.

In 2014-15 , the quick ratio is very high as compared to optimal 1:1 . In other years it

was close to 1.

It is seen that in the year 2012-13 the inventory ratio was 2.74 &1.99 in the year 2013-

2014 and then it increases to 2.37in the year 2014-15.the company holds a good

position and does not block its money in inventory.

In 2012-13 the raw materials holding period was 194 which is very high. In 2013-14

raw materials holding period was less which shows there is no blockage in the

working capital. In 2014-15 again the holding period increased to 158 days.

Work in progress conversion period in the year 2012-13 was 146 days. In the year

2013-14 it is increased to 182 days and declined in the year 2014-15 i.e. 176 days.

In 2012-13 the average time taken to sell finished products was 17 days. In 2013-14 it

has reduce to 11 days. However, in 2014-15 the time taken to sell the finished

products further decreased to 4 days

Inventory to working capital ratio decreases from 1.08 in the year 2011-12 to 0.93 in

the year 2014-15

DTR declines from 3.90(2011-12) to 2.30(2014-15)

In 2011-12 the average collection period was 93 which increased to 117 in 2012-13

which further increases to 209 in 2013-14 and finally reduces to 158 in 14-15.

The working capital turnover ratio is 3.96 in the year 2011-12 which reduces to 2.25

in 2012-13 which again declines to 1.98 in 2013-14 and then increases to 2.28 in the

year 2014-15.

57