INSIDE PAGE FINAL-23-10-2017 Hindi 1

152

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of INSIDE PAGE FINAL-23-10-2017 Hindi 1

Hkkjr esa vkokl dh izo`fÙk ,oa izxfr fjiksVZ

2016

01

jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

03

varj.k i=jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

04

jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016

fo"k; lwph

05

fo"k; lwph

fooj.k i`"B la-

1-1 vkoklh; ra=&,d n`f"Vdks.k 09

1-2 oSf’od vkfFkZd ifjn`’; 10

1-3 Hkkjrh; vFkZO;oLFkk ,oa vkokl dk fogaxkoyksdu 13

1-4 jk"Vªh; vkokl cSad dh Hkwfedk 15

2-1 vkokl izsjd ds :i esa 19

2-2 Hkkjr esa vkokl laca/kh igysa 19

2-3 foÙkh; lq/kkj 37

2-4 fof/kd lq/kkj 39

2-5 Hkw lEink ¼fofu;e ,oa fodkl½ vf/kfu;e] 2016 vkSj izHkkfor {ks= 40

3-1 vkokl foRr esa izkFkfed _.knkrk laLFkku 43

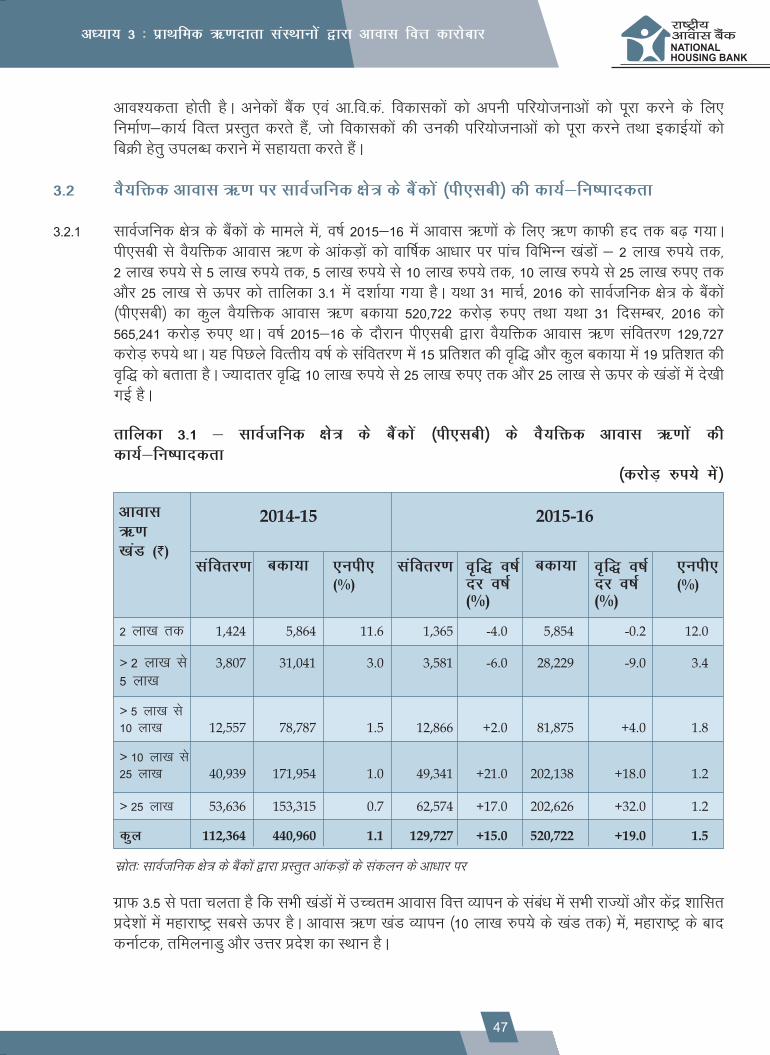

3-2 oS;fäd vkokl _.k ij lkoZtfud {ks= ds cSadksa ¼ih,lch½ dh dk;Z&fu"ikndrk 47

3-3 vkokl foÙk daifu;ka ,oa mudk dkjksckj 49

3-4 vkokl foRr esa vU; i{k 61

4-1 i`"BHkwfe 66

4-2 o"kZ 2022 rd lcds fy, vkokl 66

rkfydk la- 1-1% foxr rhu o"kksZa esa laLFkku&okj iqufoZÙk laforj.k 16

rkfydk la- 2-1 % xzkeh.k {ks=ksa esa vkoklksa dh deh ds fofHkUu dkj.k 20

rkfydk la- 2-2 % 'kgjh {ks=ksa esa vkokl dh deh ds dkj.k 23

rkfydk la- 2-3 % lh,y,l,l ds rgr bZMCY;w,l@,yvkbZth Jsf.k;ksa ds ykHkkfFkZ;ksa ij ykxw ekunaM 25

rkfydk la- 3-1 % lkoZtfud {ks= ds cSadksa ¼ih,lch½ ds oS;fäd vkokl _.kksa dh dk;Z&fu"ikndrk 47

rkfydk la- 3-2 % vkokl foÙk daifu;ksa ds eq[; foÙkh; ladsrd 51

rkfydk la- 3-3 % vk-fo-da- dh tek,a Lohdkj djus dh fLFkfr ds vk/kkj ij vk-fo-da- ds eq[; foRrh; ekinaM 52

v/;k; 1% n`f"Vdks.k ,oa uhfrxr ekgkSy

v/;k; 2% Hkkjr esa vkokl

v/;k; 3% izkFkfed _.knkrk laLFkkuksa }kjk vkokl foÙk dkjksckj

v/;k; 4% o"kZ 2022 rd lcds fy, vkokl

v/;k; 5% Hkkoh ifjn`’; 70

rkfydk

jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

fooj.k i`"B la-

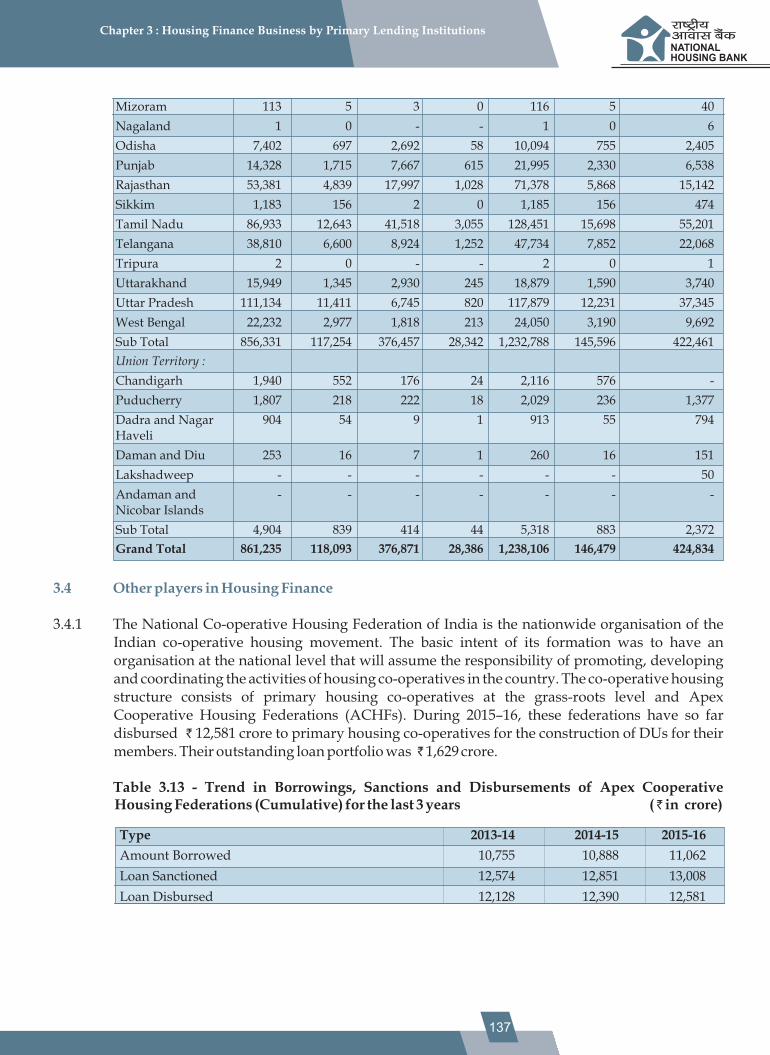

Rkkfydk 3-4 % vkokl foRr daifu;ksa dh m/kkj jkf'k;ksa dk la?kVu 54

rkfydk la- 3-5 % vkokl foÙk daifu;ksa ds cdk;k _.k ,oa vfxze rFkk fuos’k 56

rkfydk la- 3-6 % vkokl foÙk daifu;ksa ds dqy _.kksa ds lkFk vkokl _.kksa dh rqyuk 57

rkfydk la- 3-7 % vkokl foÙk daifu;ksa ds [kaM&okj oS;fäd vkokl _.k 57

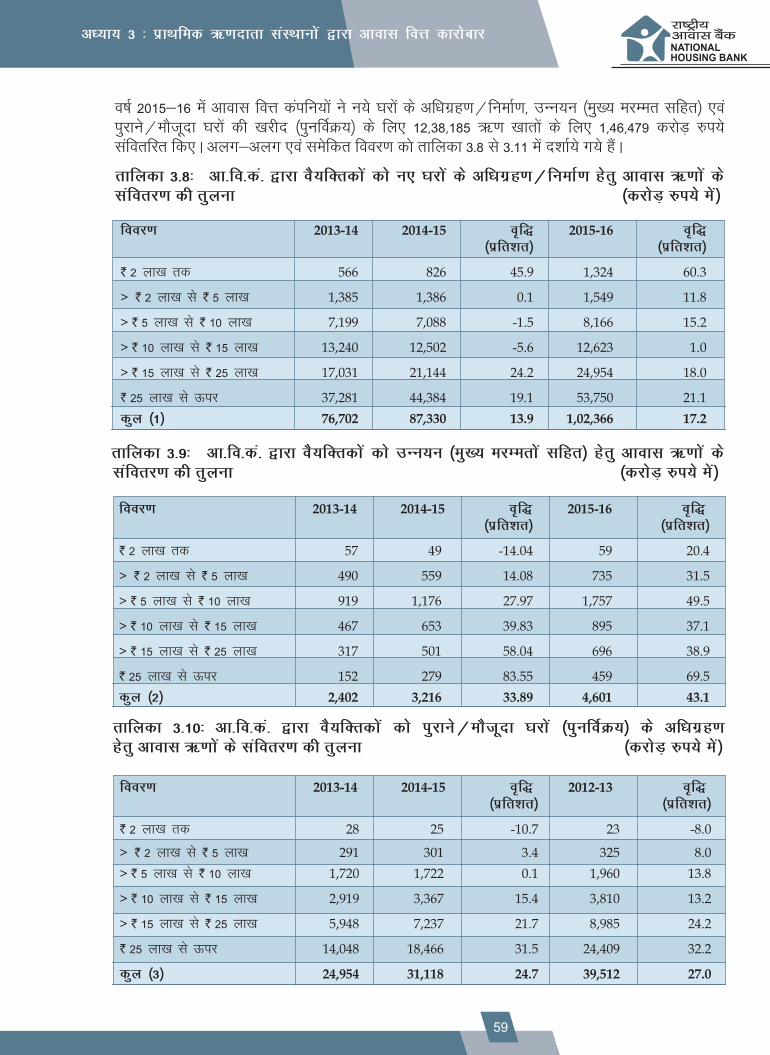

rkfydk la- 3-8 % vk-fo-da- }kjk oS;fDrdksa dks u, ?kjksa ds vf/[email protected] gsrq vkokl _.kksa 59ds laforj.k dh rqyuk

rkfydk la- 3-9 % vk-fo-da- }kjk oS;fDrdksa dks mUu;u ¼eq[; ejEerksa lfgr½ gsrq vkokl _.kksa ds 59laforj.k dh rqyuk

rkfydk la- 3-10 % vk-fo-da- }kjk oS;fDrdksa dks iqjkus@ekStwnk ?kjksa ¼iqufoZØ;½ ds vf/kxzg.k 59gsrq vkokl _.kksa ds laforj.k dh rqyuk

rkfydk la- 3-11 % vk-fo-da- }kjk oS;fDrdksa dks vkokl _.kksa ds dqy laforj.k dh rqyuk 60

rkfydk la- 3-12 % vkokl _.kksa dk jkT;@dsUnz 'kkflr&okj laforj.k 60

rkfydk la- 3-13 % foxr rhu o"kksZa dh 'kh"kZ lgdkjh vkokl ifjla?kksa ¼lap;h½ ds m/kkj 61jkf’k;ksa] laLohd`fr;ksa ,oa laforj.kksa dh izo`fÙk

rkfydk la- 3-14 % foxr rhu o"kksZa ds laforfjr vkokl _.k ,oa ,lh,p,Q ¼jkT; okj½ }kjk 62fufeZr bdkbZ;ksa dh izo`fÙk

xzkQ 1-1 % laoguh;rk c<+kus ds rjhds 13

xzkQ 1-2 % lhvkjvkj] cSad nj] jsiks nj ,oa 10 o"kZ ds ljdkjh {ks= ds izfrQy esa izo`fÙk 14

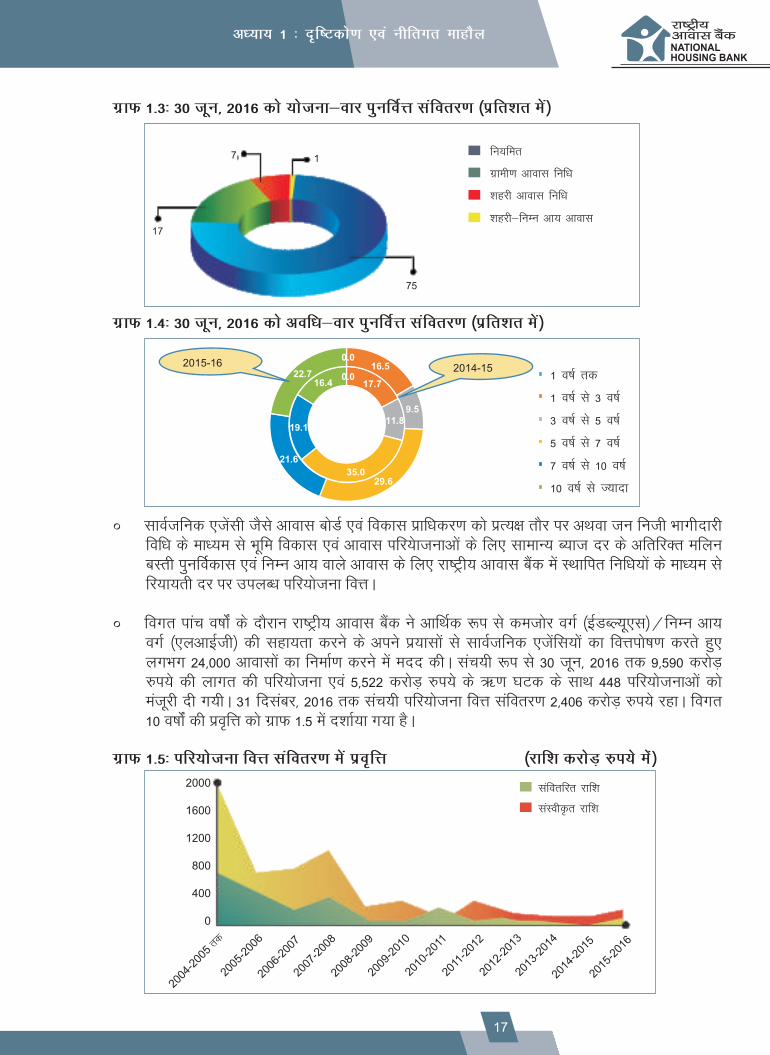

xzkQ 1-3 % 30 twu] 2016 dks ;kstuk&okj iqufoZÙk laforj.k ¼izfr’kr esa½ 17

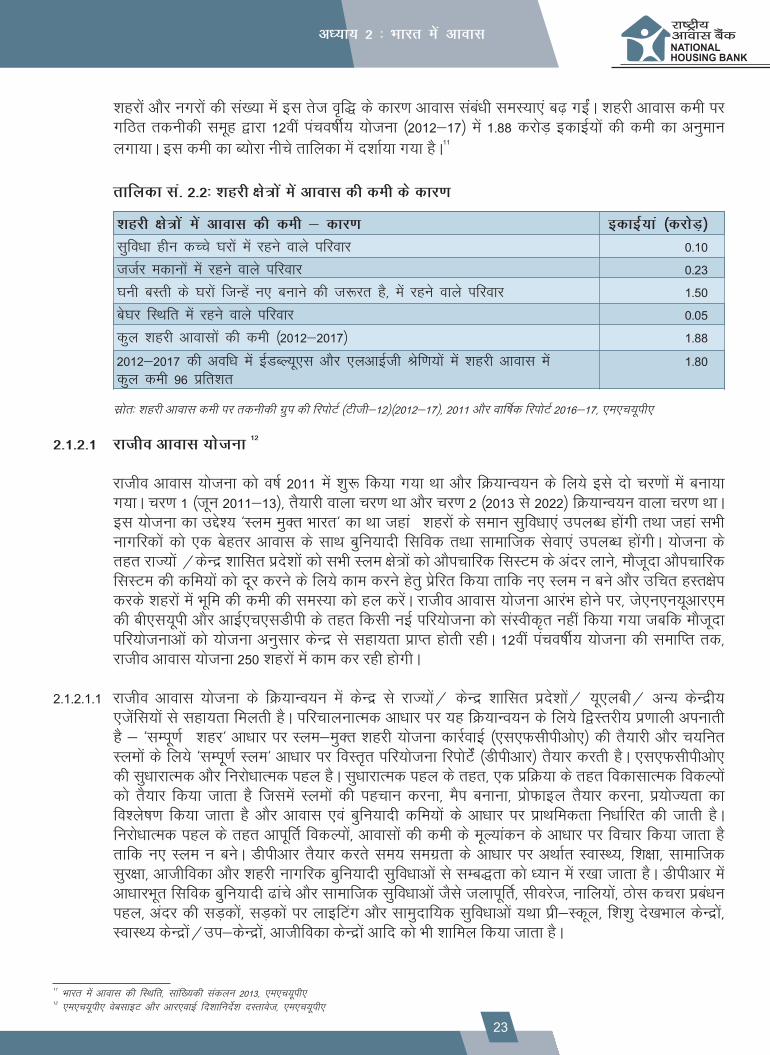

xzkQ 1-4 % 30 twu] 2016 dks vofèk&okj iqufoZÙk laforj.k ¼izfr’kr esa½ 17

xzkQ 1-5 % ifj;kstuk foÙk ds laforj.k esa izo`fÙk 17

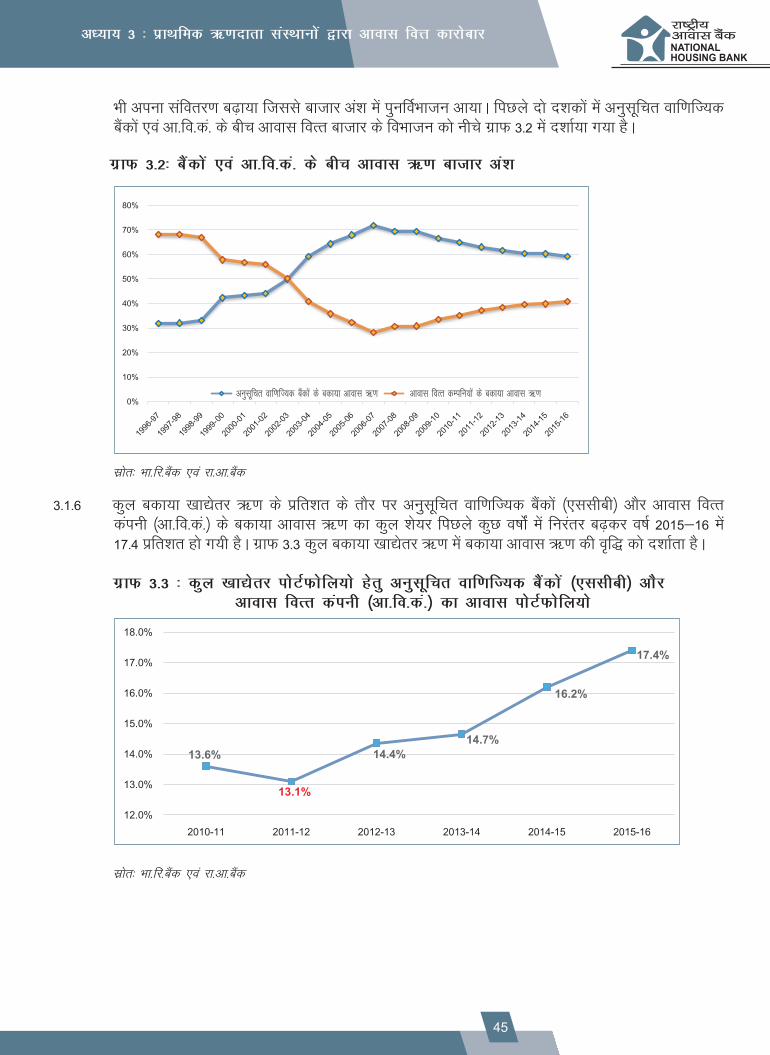

xzkQ 3-1 % cSadksa ,oa vk-fo-da- ds vkokl _.k cdk;k 44

xzkQ 3-2 % cSadksa ,oa vk-fo-da- ds chp vkokl _.k cktkj va’k 45

xzkQ 3-3 % dyq [kk|rs j ikVs QZ kfs y;k s grs q vulq fw pr okf.kfT;d cdaS k as ¼,llhch½ vkjS 45vkokl foRr dia uh ¼vk-fo-d-a ½ dk vkokl iksVZQksfy;ks

xzkQ 3-4 % cSadksa vkSj vk-fo-daifu;ksa ds cdk;k vkokl _.kksa esa ço`fÙk 46

xzkQ 3-5 % ;Fkk 31-03-2016 dks 'kh"kZ lkoZtfud {ks= ds cSadksa ¼ih,lch½ ds oS;fäd vkokl _.k cdk;k ¼[kaM&okj½ 48

xzkQ 3-6 % lkoZtfud {ks= ds cSadksa ¼ih,lch½ dk [kaM&okj cdk;k oS;fäd vkokl _.k vkadM+s 49

xzkQ 3-7 % iathd`r vkokl foÙk daifu;ksa dk oxhZdj.k 49

xzkQ 3-8 % foxr 2 o"kksaZ eas iathd`r vk-fo-da- dh 'kk[kkvksa@dk;kZy;ksa dk jkT;@dsUn 'kkflr izns’k&okj forj.k 50

xzkQ 3-9% foxr rhu o"kksZa esa vk-fo-da- ds cdk;k lalkèkuksa dh izo`fÙk 53

xzkQ 3-10% foxr rhu o"kksZa esa vk-fo-da- dh lkoZtfud tekvksa dh vkdkj&okj izo`fÙk 54

la-

xzkQ

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016

06

jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

fooj.k i`"B la-

xzkQ 3-11% foxr rhu o"kksZa esa vk-fo-da- dh lkoZtfud tekvksa dh C;kt nj&okj izo`fÙk 55

xzkQ 3-12% foxr rhu o"kksZa esa vk-fo-da- dh lkoZtfud tekvksa dh ifjiDork izo`fÙk 55

xzkQ 3-13% foxr rhu o"kksZa esa vk-fo-da- ds cdk;k _.k ,oa vfxze rFkk fuos’k dh izo`fÙk 56

xzkQ 3-14% vk-fo-da- ds oS;fDrdksa gsrq vkokl _.kksa dh ifjiDork Lo:i&okj izo`fÙk 57

xzkQ 3-15% vk-fo-da- ds oS;fDrdksa gsrq vkokl _.kksa dh mÌs’;&okj izo`fÙk 58

xzkQ 3-16% vkokl _.kksa dh m/kkjdrkZ ds izdkj&okj laforj.k dh izo`fÙk 58

xzkQ 3-17% foÙkh; o"kZ 2015&16 ds nkSjku oS;fDrdksa dks vkokl _.kksa ds laforj.k dk jkT;&okj foHkktu 63

xzkQ 3-18% oS;fDrdksa gsrq cdk;k vkokl _.kksa dk jkT;&okj foHkktu 63

xzkQ 3-19% foÙkh; o"kZ 2015&16 ds nkSjku Hkou fuekZrkvksa dks vkokl _.kksa ds laforj.k dk jkT;&okj foHkktu 64

xzkQ 3-20% Hkou fuekZvksa gsrq cdk;k vkokl _.kksa dk jkT;&okj foHkktu 64

xzkQ 3-21% foÙkh; o"kZ 2015&16 ds nkSjku oS;fDrdksa dks u, ?kjksa ds vf/kxzg.k@ 65fuekZ.k gsrq vkokl _.kksa ds lafoj.k dk jkT;&okj foHkktu

xzkQ 4-1% ?kVd ftlds ek/;e ls ih,e,okbZ&’kgjh dk;kZfUor fd;k x;k gS 68

xzkQ 4-2% ;Fkk frfFk 31 fnlEcj] 2016 dk s ih,e,okb&Z lh,y,l,l d s rgr jkT;@dUs n z 'kkflr inz ’s k okj inz ’kuZ 69

xzkQ 5-1 % ^^o"kZ 2022 rd lcds fy, vkokl fe’ku** ds rgr u, ra= dk mn~Hko 71

ckWDl 1-1% oSf’od vkokl 10

ckWDl 1-2% oSf’od 'kgjhdj.k dh izo`fÙk 11

ckWDl 1-3% vkokl ds fy, fuos’k ,oa foÙkh; lgk;rk 14

ckWDl 1-4% vkokl {ks= ds fy, dsUnzh; ctV dh ?kks"k.kk,a 14

ckWDl 1-5% vkokl {ks= ds fy, uhfrxr <kapk ,oa foèkk;h leFkZu 14

ckWDl 1-6% vkokl ds fy, uoksUes"kh izkS|ksfxdh ,oa {kerk fuekZ.k esa lgk;rk 15

ckWDl 2-1% xqtjkr 27

ckWDl 2-2 % jktLFkku 29

ckWDl 2-3 % vksfM'kk 30

ckWDl 2-4 % egkjk"Vª 31

ckWDl 2-5 % if’pe caxky 32

ckWDl 2-6 % NÙkhlx<+ 34

ckWDl 2-7 % dukZVd 35

ckWDl 2-8 % e/; izns’k 36

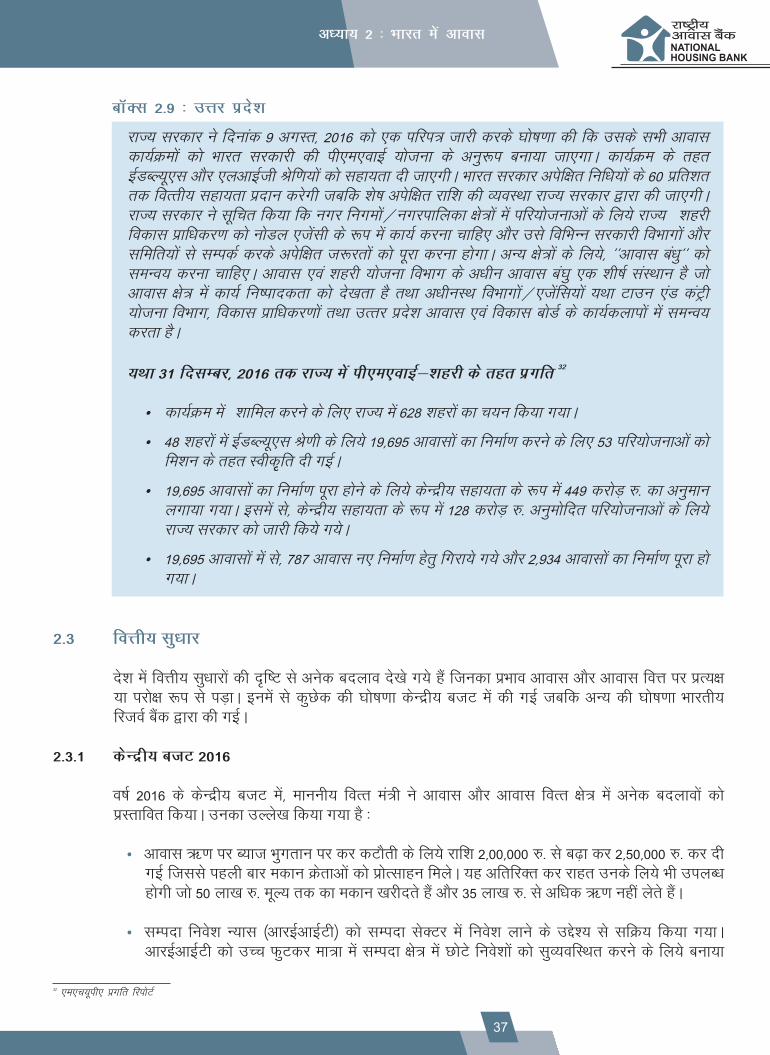

ckWDl 2-9 % mÙkj izns’k 37

ckWDl 3-1 % vkokl foÙk daifu;ksa dk dk;Z&fu"iknu 50

ckWDl

fo"k; lwph

07

jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

1 Hkkjr i;kZokl III jk"Vªh; fjiksVZ] 2016 vkokl ,oa 'kgjh xjhch mi’keu ea=ky;

vè;k;

1-1 vkoklh; ra=&,d n`f"Vdks.k

1 % n`f"Vdks.k ,oa uhfrxr ekgkSy

ekuuh; foÙk ea=h us vius dsUnzh; ctV Hkk"k.k 2015&16 esa Hkkjr ds gj ifjokj dks vn~n Nr dh igqap rd leFkZ cukus ds egRo dks js[kkafdr fd;k Fkk ,oa ̂ ^o"kZ 2022 rd lcds fy, vkokl** ds y{; ds izfr Hkkjr ljdkj dh izfrc)rk nksgjkbZ ftlds fy, Vhe bafM;k dks 'kgjh {ks=ksa esa 2 djksM+ vkokl ,oa xzkeh.k {ks=ksa esa 4 djksM+ vkoklksa dk fuekZ.k djus dh vko’;drk gksxhA

vkokl dh deh esa vlj Mkyus okys dqN egRoiw.kZ dkjdksa] eas vkokl fo’ks"k rkSj ij fdQk;rh vkokl ds fy, Hkwfe dh i;kZIr vkiwfrZ ,oa ekax ds vykok vkiwfrZ i{k ds o`gr Lrj ij fufèk;ksa dh nh?kkZofèk o vYi ykxr ds lzksrksa dh vuqiyCèkrk 'kkfey gSA vr% ,slh uhfr;ka ,oa dk;ZØe ftudk mn~ns’; lexz rjhds esa bu leL;kvksa dk fuokj.k djuk gS] ns’k ds fdQk;rh vkokl LVkWd esa mUu;u dh fn’kk esa O;kid izHkko MkysaxsA

dsUnzh; ctV esa dh xbZ gky dh uhfrxr ?kks"k.kkvksa ds vykok dsUnz ljdkj vFkok jkT; ljdkj@Hkkjrh; fjtoZ cSad@jk"Vªh; vkokl cSad }kjk 'kq: fd, x;s vU; fofu;ked ,oa foÙkh; igyksa dk mn~ns’; bl {ks= dks mPpre Lrj rd igq¡pkus ds fy, vko’;d izksRlkgu nsuk gSA izR;sd Hkkjrh; ifjokj dks iDdk vkokl miyCèk djkus dh lksp dks iwjk djus ds fy, ̂o"kZ 2022 rd lcds fy, vkokl fe’ku* dk 'kqHkkjaHk lfgr dbZ i.kèkkjd 'kkfey djuk ,oa fdQk;rh vkokl {ks= dks izHkkfor djus okys fofHkUu eqn~nksa dk fuokj.k djuk] tSls cgq&vk;keh n`f"Vdks.k viuk;s x;s gSaA

iqufoZÙk iznku djus okys laLFkku ,oa ^^izèkkuea=h vkokl ;kstuk ¼ih,e,okbZ½** ds rgr _.k lgc) lfClMh ;kstuk ¼lh,y,l,l½ ds dk;kZUo;u ds fy, dsUnzh; uksMy ,tsalh ds rkSj ij jk"Vªh; vkokl cSad ns’k esa vkokl foÙk dh miyCèkrk] vfHkxE;rk ,oa laoguh;rk lqfuf’pr djus esa egRoiw.kZ Hkwfedk fuHkk jgk gSA

1-1-1 vkokl dk O;fDr ,oa jk"Vª ij O;kid izHkko gksrk gS pwafd bldk vkfFkZd] lkekftd ,oa jktuhfrd ifjos’k ls xgjk lacaèk gksrk gSA foxr n’kd ds nkSjku izeq[k oSf’od ifjfLFkfr;ksa ls oSf’od vkfFkZd fodkl ij dkQh izHkko iM+k gSA blfy, tc Hkkjr esa vkokl dh fLFkfr dh tkap dh tk jgh gS rks oSf’od vFkZO;oLFkk ,oa vkokl ifjn`’; dks lanHkZ esa j[kuk vR;ar vko’;d gks tkrk gSA

1-1-2 vkokl {ks= us Hkkjr ds uhfr fuekZrkvksa dk è;ku viuh vksj vkdf"kZr fd;k gSA bls vf/kdkfjd ekU;rk nh x;h fd vkokl {ks= ds fodkl dk ns’k ds vkfFkZd fodkl ij lh/kk izHkko iM+rk gS] yksxksa dh lkekftd fLFkfr] lqj{kk ,oa laj{kk ds vuqlkj ;g etcwr lkekftd izHkko iSnk djrk gS] ns’k dh fodkl ;k=k esa ns’k dh vkcknh ds cM+s oxZ ds lekos’ku dks lqfoèkkijd cukrk gS ,oa blds vykok ;g xjhch mUewyu o ekuo

1fodkl lwpdkad esa lqèkkj ds izfr dkQh ;ksxnku nsrk gSA Hkw&laink ,oa vkokl esa fd;s x;s fuos’k dk 250 ls vfèkd vuq"kaxh m|ksxksa ij ;k rks izR;{k rkSj ij vFkok vizR;{k rkSj ij izHkko iM+rk gSA blds nwjxkeh izHkko dks ns[krs gq, vkokl {ks= esa fodkl lkekftd ,oa foÙkh; lekos’ku dks lqfoèkkijd cukrs gq, o dbZ yksxksa ds vk; Lrj esa lqèkkj ykrs gq, lexz fodkl dks c<+kok nsrh gSA Bhd blh rjg vkokl {ks= esa eanh lexz vkfFkZd fodkl dh j¶rkj de dj nsrk gSA

1-1-3 Hkkjr esa vkokl dh fLFkfr dks okLrfod :i ls le>us ds fy, mu pqukSfr;ksa dh lhek le>uk vR;ar vko’;d gks tkrk gS ftudk lkeuk ns’k dj jgk gSA vkokl dh c<rh ekax ds lkFk Hkkjr vkokl dh deh dk

09

vè;k; 1 % n`f"Vdks.k ,oa uhfrxr ekgkSyjk"Vªh; vkokl cSadNATIONAL HOUSING BANK

2 'kgjh vkokl dh deh ij rduhdh lewg dh fjiksVZ ¼Vhth&12½&¼o"kZ 2012&2017½3 ckjgoha iapo"khZ; ;kstuk ds fy, xzkeh.k vkokl ij dk;Zdkjh ny

lkeuk dj jgk gSA ns’k esa cnyrs lkekftd ,oa tulkaf[;dh Lo:i] lkaLd`frd o vkfFkZd fofoèkrk ,oa c<+rh vkcknh tSls dkjdksa us Hkkjr esa vkokl dh fLFkfr dks vkSj Hkh tfVy cuk fn;k gSA 'kgjhdj.k] ewy ifjokjksa dk ,dhdj.k] f’k{kk] vk; Lrj ,oa laoguh;rk bR;kfn us ns’k esa vkokl dh ekax dks vkSj Hkh c<+k fn;k gSA ckjgoha iapo"khZ; ;kstukofèk ¼o"kZ 2012&2017½ esa Hkkjr esa 'kgjh {ks=ksa ,o xzkeh.k {ks=ksa esa Øe’k% 1-88

2 3djksM+ ,oa 4-37 djksM+ vkokl bdkbZ;ksa dh deh dk vuqeku yxk;k x;k gSA a

1-1-4 Hkkjr ljdkj us Hkkjr dh Lora=rk dh 75oha o"kZxkaB ij izR;sd Hkkjrh; ifjokj dks vkokl ds LokfeRo dh lqfo/kk iznku djus ds fy, ̂o"kZ 2022 rd lcds fy, vkokl fe'ku* vkjaHk fd;k gSA vrhr esa Øexr ljdkjksa }kjk fd;s x;s fofHkUu mik;ksa us vkokl dh fLFkfr esa lqèkkj ykus ds vusd fØ;kdykiksa dks xfr iznku dh ysfdu vlyh pqukSfr;ka tks vkt Hkh ekStwn gSa muesa tehuh Lrj ij ;kstukvksa ds izHkkoh fu"iknu ds fy, lHkh iz;klksa ,oa lalkèkuksa dk ,dhdj.k 'kkfey gSA

oSf’od foÙkh; ladV ftlus o"kZ 2007&08 dh vofèk esa iwjs fo’o dks izHkkfor fd;k] dk fofHkUu ns’kksa dh vkokl ifjfLFkfr;ksa ij nh?kZdkfyd izHkko iM+kA vkokl dh dherksa esa gksus okys mrkj&p<+ko ,oa izo`fÙk ls fo’o Hkj dh vFkOZ ;oLFkkvk as e as fofoèkrk Hkjh vkokl i)fÙk n[s kh x;hA vkb,Z e,Q Xykcs y okpW fjikVs Z fo’o dh vFkOZ ;LFkk dk s rhu vyx&vyx oxk aZs e as oxhdZ r̀ djrh g S ,o a vFkOZ ;oLFkk dh mu oxk aZs d s lca èa k e as vkokl dher lwpdkad dh izo`fÙk dk fo’ys"k.k djrh gSA mDr dk lkj fuEufyf[kr ckWDl 1-1 esa izLrqr fd;k tkrk gSA

Û vkbZ,e,Q dh oSf’od vkokl dher lwpdkad ds vuqlkj o"kZ 2016 esa lHkh ns’kksa esa okLrfod vkokl dher dk vkSlr yxHkx mlh Lrj ij vk x;k gS tks foÙkh; ladV dh 'kq:vkr ls iwoZ FkkA

Û 21 vFkZO;oLFkk,a ,slh Fkh ftUgsa ̂ rsth* okyh vFkZO;oLFkkvksa ds rkSj ij lanfHkZr fd;k x;k] tgka o"kZ 2007&2012 dh foÙkh; ladV dh vofèk esa dherksa esa ekewyh fxjkoV Fkh ,oa blds i’pkr fQj ls Rofjr mNky vk x;k FkkA Hkkjr dks ̂rsth* okyh vFkZO;oLFkkvksa esa oxhZd`r fd;k x;k FkkA

Û 18 vFkOZ ;oLFkk, a ,ls h Fkh ftUg as ^[kjkc ,o a rts h* okyh vFkOZ ;oLFkkvk as da s rkjS ij lna fHkrZ fd;k x;k tgk a o"k Z2007&2012 dh vofèk e as rts h l s fxjkoV vku s d s i’pkr o"k Z 2013 d s i’pkr fQj l s mNky vk;kA

Û 18 vFkZO;oLFkk,a ,slh Fkh ftUgsa ^fujk’kkHkjh* vFkZO;oLFkkvksa ads rkSj ij lanfHkZr fd;k x;k ftlesa ladV ds 'kq:vkr esa gh vkokl dh dherksa esa Hkkjh fxjkoV vkbZ ,oa fujarj fxjrh gh jghA

Û vU; vFkZO;oLFkkvksa dh rqyuk esa ̂rsth* okyh vFkZO;oLFkkvksa esa vfèkd rsth ls _.k iznku fd;kA

Û o"kZ 2007 ls o"kZ 2012 dh vofèk esa ̂/kheh ,oa rsth* okyh vFkZO;oLFkkvksa esa fuekZ.k {ks= esa ;ksftr ldy ewY; ,oa tkjh Hkou ijfeVksa dh la[;k esa rsth ls fxjkoV vkbZ ,oa o"kZ 2013 ds i’pkr ml Lrj ij vfèkd ;k de jguk tkjh jgkA

Û ^fujk’kkHkjh* vFkZO;oLFkkvksa esa o"kZ 2013 dh ckn dh vofèk esa fuekZ.k {ks= esa ;ksftr ldy ewY; ,oa Hkou ijfeVksa dh la[;k esa fxjkoV vkbZA blls igys Hkh bu vFkZO;oLFkkvksa esa o"kZ 2000 ds ckn ds o"kksZa esa dsoy lhekar Lrj dh o`f) ns[kh x;h ,oa muesa o"kZ 2008 ls fxjkoV vkuh 'kq: gks x;hA

1-2 oSf’od vkfFkZd ifjn`’;

ckWDl 1-1% oSf’od vkokl

L=ksr % vkbZ,e,Q Xykscy gkWmflax okWp% tqykbZ] 2016 rFkk vkbZ,e,Q Xykscy gkmflax okWp] uoEcj 2016

10

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

1-2-1 'kgjhdj.k ,oa vkokl

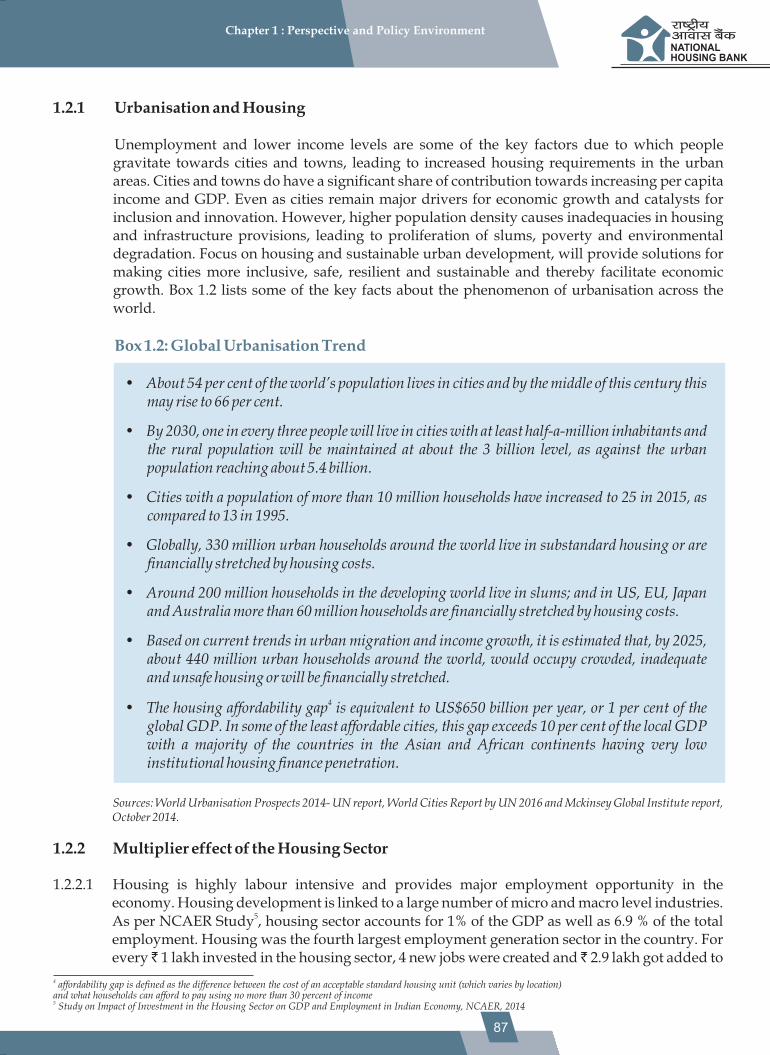

csjkstxkjh ,oa fuEu vk; Lrj dqN ,sls egRoiw.kZ dkjdksa esa ls ,d gSa ftuds dkj.k yksx 'kgjksa o uxjksa dh vksj vkdf"kZr gksrs gSa ftlds ifj.kkeLo:i 'kgjh {ks=ksa esa vkokl dh ekax c<+rh gSA 'kgjksa ,oa uxjksa dh izfr O;fDr vk; ,oa ldy ?kjsyw mRikn ¼thMhih½ ds izfr ;ksxnku esa egRoiw.kZ fgLlsnkjh gksrh gSA 'kgj fujarj vkfFkZd fodkl ds izeq[k dkjd ,oa lekos’ku o uoksUes"k ds mRizsjd cus gq, gSaA gkykafd vR;fèkd ?kuh vkcknh ds dkj.k vkokl ,oa cqfu;knh lqfoèkkvksa ds izkoèkkuksa esa vi;kZIrrk vkrh gS ftlds ifj.kkeLo:i efyu cfLr;ksa dk izlkj] xjhch ,oa i;kZoj.k lacaèkh {kj.k gksrk gSA vkokl ,oa lrr 'kgjh fodkl ij è;ku dsfUnzr djus ls 'kgjksa dks vkSj vfèkd lekos’kh] lqjf{kr ,oa fVdkÅ cukus okys lekèkku miyCèk gksaxs tks vkfFkZd fodkl dks Hkh lqfoèkkijd cuk,axsA ckWDl 1-2 esa fo’o Hkj esa 'kgjhdj.k ds fo"k; ls lacafèkr dqN izeq[k rF;ksa dh lwph iznku dh x;h gSA

Û fo’o dh yxHkx 54 izfr’kr vkcknh 'kgjksa esa jgrh gS ,oa bl lnh ds eè; rd blesa 66 izfr’kr rd dh c<ksÙkjh gks ldrh gSA

Û o"kZ 2030 rd de ls de ikap yk[k fuokfl;ksa ds lkFk gj rhu O;fDr esa ls ,d O;fDr 'kgjksa eas jgsxk ,oa yxHkx 5-4 fcfy;u 'kgjh vkcknh dh rqyuk esa 'kgjh vkcknh yxHkx 3 fcfy;u ds Lrj rd jgsxhA

Û 10 fefy;u ifjokj ls vfèkd dh vkcknh okys 'kgj o"kZ 1995 esa 13 dh rqyuk esa o"kZ 2015 esa 25 rd c<+sA

Û oSf’od Lrj ij fo’o Hkj ds 330 fefy;u 'kgjh ifjokj fuEu vkokl esa jgrs gSa vFkok vkfFkZd :i ls vkokl dh ykxrksa ds vuqlkj QSys gq, gSaA

Û fodkl’khy fo’o esa yxHkx 200 fefy;u ifjokj efyu cfLr;ksa eas fuokl djrs gSa ,oa la;qDr jkT; vesfjdk] ;wjksih; la?k] tkiku ,oa vkWLVªsfy;k esa 60 fefy;u ls vfèkd ifjokj vkfFkZd :i ls vkokl dh ykxrksa ds vuqlkj QSys gq, gSaA

Û 'kgjh iyk;u ,oa vk; o`f) esa orZeku izo`fÙk;ksa ds vkèkkj ij ;g vuqeku yxk;k tkrk gS fd o"kZ 2025 rd fo’o Hkj esa yxHkx 440 fefy;u 'kgjh ifjokj HkhM+HkkM+ Hkjs] vi;kZIr ,oa vlqjf{kr vkokl esa jgsaxs vFkok vkfFkZd :i ls QSys gksaxsA

4 Û vkokl laoguh;rk varj izfro"kZ 650 fcfy;u vejhdh MkWyj vFkok oSf’od ldy ?kjsyw mRikn dk 1 izfr’kr ds cjkcj gksrk gSA dqN lcls de fdQk;rh 'kgjksa esa ;g varj LFkkuh; ldy ?kjsyw mRikn ls 10 izfr’kr ls vfèkd gS tSls ,f’k;k o vÝhdk egk}hiksa esa vfèkdka’k ns’kksa esa laLFkkxr vkokl foÙk fuos’k cgqr de gSA

lzksr% oYMZ vcZukbts’ku izkWlisDV~l] 2014& ;w,u fjiksVZ] ;w,u 2016 }kjk fo’o ds ‘kgjksa dh fjiksVZ ,oa eSfdUls Xykscy baLVhV~;wV fjiksVZ] vDrwcj] 2014

1-2-2 vkokl {ks= dh fofo/k izHkko

1-2-2-1 vkokl vR;fèkd Je&izèkku {ks= gS ,oa vFkZO;oLFkk esa O;kid jkstxkj ds volj miyCèk djkrk gSA vkokl 5fodkl cM+h la[;k esa lw{e ,ao lef"V Lrjh; m|ksx ls tqM+k gqvk gSA ,ulh,bZvkj vè;;u ] ds vuqlkj

ckWDl 1-2% oSf’od 'kgjhdj.k dh izo`fÙk

4 laoguh;rk varj fdlh Lohdk;Z ekud vkokl bdkbZ dh ykxr ¼tks vofLFkfr ds vuqlkj fHkUu gks ldrh gS½ ,oa ifjokj 30 izfr’kr ls vufèkd vk; dk bLrseky djrs gq, Hkqxrku djus esa [kpZ dj ldrkk gS ds chp varj ds rkSj ij ifjHkkf”kr fd;k tkrk gSA 5 Hkkjrh; vFkZO;oLFkk esa ldy ?kjsyw mRikn ,oa jkstxkj ij vkokl {ks= esa fuos’k ds izHkko ij vè;;u] ,ulh,bZvkj] 2014A

11

vè;k; 1 % n`f"Vdks.k ,oa uhfrxr ekgkSyjk"Vªh; vkokl cSadNATIONAL HOUSING BANK

vkokl {ks= ldy ?kjsyw mRikn dk 1 izfr’kr ds vykok dqy jkstxkj dk 6-9 izfr’kr cSBrk gSA vkokl ns’k esa jkstxkj iSnk djus okyk pkSFkk lcls cM+k {ks= gSA vkokl {ks= esa fd;s x;s izR;sd ,d yk[k #i;s ds fuos’k us pkj u;s jkstxkj iSnk fd, ,oa blds xq.kd izHkko ls ldy ?kjsyw mRikn esa 2-9 yk[k #i;s tqM+sA blfy, Hkkjr esa vkokl fuekZ.k dks izksRlkgu nsus ds ifj.kkeLo:i blls tqM+s m|ksxksa esa cM+s jkstxkj ,oa vk; iSnk djus ds vykok vkS|ksfxd mRiknu dh {kerk Hkh c<+sxhA tSlk fd iwoZ esa ifjppkZ dh x;h gS] vkokl us vkfFkZd xfrfofèk dks c<+kok nsus esa ,oa 269 lgk;d m|ksxksa ds mRiknu esa ;k rks izR;{k rkSj ij vFko vizR;{k rkSj ij

6dbZ xquk izHkko Mkyk gSA fuekZ.k {ks= ftlesa vkokl {ks= Hkh 'kkfey gS] dk Hkkjr ds ldy ?kjsyw mRikn esa 8-2 dk ;ksxnku gSA

1-2-2-2 ^o"kZ 2022 rd lcds fy, vkokl* fe’ku ds 'kqHkkjaHk ls ns’k Hkj esa xzkeh.k o 'kgjh nksuksa {ks=ksa esa vkokl dh xfrfofèk dks nks ;kstukvksa ;Fkk ih,e,okbZ ¼’kgjh½ ,oa ih,e,okbZ ¼xzkeh.k½ ds rgr lkFkZd c<+kok feysxkA bl fe’ku dk eq[; mn~ns’; yf{kr ifjokjksa dks cqfu;knh ukxfjd lq[k&lqfoèkkvksa ds lkFk Lo;a dk leqfpr ,oa LFkk;h vkokl bdkbZ dh igqap iznku djus esa l{ke cukuk gSA blesa o"kZ 2022 rd lHkh ik= ykHkkFkhZ ifjokjksa dks lkeF;Zdkjh fdQk;rh vkokl dk dk;kZUo;u djus okyh ,tsafl;ksa ds ekè;e ls iwathxr vFkok C;kt lfClMh ds Lo:i esa dsUnzh; lgk;rk iznku djus dk igys ls gh vuqeku yxk;k x;k gSA ih,e,okbZ esa lfClMh] izksRlkgu] izkS|ksfxdh ,oa dkS’ky fodkl ds ekè;e ls ekax ds vykok vkiwfrZ dh ckèkkvksa dk lekèkku djus] LFkkuh; lalkèkuksa ds iz;ksx ,oa fofHkUu i.kèkkjdksa dh lgHkkfxrk bR;kfn dks c<+kok nsus okys lexz cgq&vk;keh n`f"Vdks.k dks viuk;k x;k gSA ;g fe’ku dsfUnzr n`f"Vdks.k ds lkFk ns’k esa vkokl dh deh dk fuokj.k djus esa izeq[k izsj.kk 'kfDr ds rkSj ij dk;Z dj jgk gSA

1-2-3 fdQk;rh vkokl

1-2-3-1 'kgjh {ks=ksa esa c<+rh vkcknh ds ifj.kkeLo:i iyk;u djus okyksa dh cM+h vkcknh efyu cfLr;ksa vFkok fuEu vkokl esa cl tkrh gSaA ,slk gksus dk eq[; dkj.k ;g gS fd vfèkdka’k yksx viuh laoguh;rk ds Hkhrj vkokl izkIr djus esa la?k"kZjr gSaA bl lanHkZ esa Hkkjr ds ekuuh; jk"Vªifr] laln ds nksuksa lnuksa dks lacksfèkr djrs le; ;g dgrs gq, vkokl dh egÙkk ij cy fn;k fd vkokl lEekutud thou ;kiu ds fy, ewyHkwr vko’;drk gS ,oa ljdkj gekjh Lora=rk ds 75 o"kZ iwjs gksus ds miy{; esa ̂o"kZ 2022 rd lcds fy, vkokl* fe’ku ds rgr lHkh ifjokj] fo’ks"k rkSj ij xjhc ls xjhc yksxksa dh viuh vkokl bdkbZ gksus dh vkdka{kk,a iwjh djus ds fy, izfrc) gSA mudh ;g n`f"V o"kZ 2022 rd lcds fy, vkokl fe’ku esa ifjyf{kr gqbZA ;|fi bl lacaèk esa ljdkj }kjk fofHkUu igysa dh xbZ rFkkfi vkokl dh dherksa ,oa yksxksa dh laoguh;rk ds chp dh [kkbZ dks ikVuk vHkh Hkh cgqr cM+k dk;Z gS ftldk fuokj.k fe’ku dks iwjk djrs gq, fd;s tkus dh vko’;drk gSA

1-2-3-2 eSfdUls Xykscy baLVhV~;wV }kjk fd;k x;k fo’ys"k.k n’kkZrk gS fd fdQk;rh vkokl lqiqnZ djus dh ykxr de djus ds pkj rjhds gSa ,oa ;s fofèk;ka ekud vkokl bdkbZ dh dqy ykxr esaa 20 izfr’kr ls 50 izfr’kr rd dh deh yk ldrh gSaA ;s fofèk;ka fuEukuqlkj gSa%

Û lgh vofLFkfr ij Hkwfe [kksyuk(Û uoksUes"kh ,oa rnuqdwy rduhd ds ekè;e ls fuekZ.k ykxr esa deh ykuk(Û ifjpkyu c<+kuk ,oa n{krk cuk;s j[kuk] ,oa Û miHkksDrkvksa ,oa fodkldksa ds fy, foÙkiks"k.k dh ykxrksa dks de djuk

xzkQ 1-1 esa ekud bdkbZ dh dqy ykxr ij bu izR;sd dk;Z ;kstukvksa ds izHkko dh ek=k fuèkkZfjr dh xbZ gS@n’kkbZ x;h gSA tSlk fd fuEu xzkQ esa fn[kkbZ nsrk gS Hkwfe dh vkiwfrZ [kksyus ls ykxr esa 8 ls 23 izfr’kr

6 Hkkjr i;kZokl III jk"Vªh; fjiksVZ] 2016 vkokl ,oa 'kgjh xjhch mi’keu ea=ky;

12

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

dh fxjkoV vk ldrh gS ,oa fuekZ.k ykxr dks rdZlaxr cukus ls laoguh; {kerk 12 ls 16 izfr’kr rd c<+ ldrh gSA mUur ifjpkyu ,oa foÙkh; ykxr dks de j[kus ls ykxr esa Øe’k% 2 izfr’kr ,oa 7 izfr’kr rd dh fxjkoV vk ldrh gSA

xzkQ 1-1% laoguh;rk c<+kus ds rjhds ¼çfr'kr esa½

lzksr% eSfdUls Xykscy baLVhV~;wV dk fo’ys”k.k] fdQk;rh vkokl dh oSf’od pquksfr;ksa dk lekèkku djus dk [kkdk] vDrwcj] 2014

1-3-1 vis{kkd`r èkheh fodkl nj ls oSf’od ifjos’k dh i`"BHkwfe ds le{k o"kZ 2015&16 esa Hkkjrh; vFkZO;oLFkk esa 77-6 izfr’kr dh i;kZIr ldy ?kjsyw mRikn nj ntZ dh x;hA ;g nh?kZdkfyd fodkl laHkkoukvksa ds lkFk

lcls rsth ls c<+us okyh izeq[k vFkZO;oLFkk ds rkSj ij mHkjh gSA vkfFkZd xfrfofèk us xfr idM+h ,oa fodkl dh xfr dks etcwr uhfr;ka ,oa vk’kkoknh iqu#)kj dh enn ls lhfer jktdks"kh; o pkyw [kkrk ?kkVk] detksj iM+rh eqnzkLQhfr esa lfUufgr lef"Vxr vkfFkZd fLFkjrk dks etcwrh feyhA nf{k.k&if’pe ekulwu dk vkxeu d`f"k ,oa xzkeh.k vFkZO;oLFkk ds fy, 'kqHk ladsr gSA lkrosa osru vk;ksx dk fu.kZ; ljdkjh miHkksx O;; ds xq.kd izHkkoksa ds ekè;e ls yf{kr jktdks"kh; ?kkVs ds Hkhrj miHkksx O;; dks c<+k ldrh gSA gkykafd fofHkUu dkjdksa ij vkfFkZd fodkl dh fLFkjrk dkQh egRo j[krh gSA i;kZIr] fdQk;rh ,oa lqjf{kr vkokl Hkh ,slk gksus ds egRoiw.kZ dkjdksa esa ls ,d gSA blesa ns’k dk cM+k ,oa ukStoku dk;Zcy vfèkd mRiknd gks ldrk gS ,oa i;kZIr vkokl nsrs gq, gekjs ns’k ds vkfFkZd fodkl esa vfèkd ls vfèkd ;ksxnku ns ldrk gSA

1-3-2 foÙkh; cktkjksa ds lacaèk esa Hkkjrh; fjtoZ cSad us vizSy] 2016 esa uhfrxr nj ?kVk nhA foÙk o"kZ 2015&16 esa lhihvkbZ eqnzkLQhfr 4-9 izfr’kr jgh ftlls Hkkjrh; fjtoZ cSad dks eq[; njsa ?kVkus esa enn feyhA jsiks nj esa Hkkjrh; fjtoZ cSad }kjk dh xbZ dVkSrh ls cSadksa dks viuk _.k nj vkSj vfèkd ?kVkus esa enn feyhA fiNys dqN o"kksZa ls Hkkjrh; fjtoZ cSad us èkhjs&èkhjs uhfrxr njksa ,oa vkjf{kr ekax dks ?kVk fn;k ftlds ifj.kkeLo:i vkokl foÙk {ks= esa mPprj +_.k ds mBko dks lqfoèkkijd cukrs gq, izkFkfed _.knkrk laLFkkuksa ¼ih,yvkbZ½ us C;kt njksa esa dVkSrh dhA C;kt nj esa dh xbZ dVkSrh ls vkokl ifj;kstukvksa esa fufèk ds izokg dks lqfoèkkijd cukrs gq, Hkw laink {ks= esa _.k mBko esa Hkh lgk;rk feyhA xzkQ 1-2 esa o"kZ 2012 ls o"kZ 2016 rd dh vofèk esa jsiks nj] cSad nj] 10 o"kZ dh ljdkjh {ks= dh izfrQy nj ,oa lhvkjvkj esa ?kVrh gqbZ izo`fÙk dks n’kkZ;k x;k gSA jsiks nj esa o"kZ 2012 esa 8-5 izfr’kr ls o"kZ 2016 esa 6-25 izfr’kr rd dh fxjkoV vkbZA cSad nj esa o"kZ 2012 esa 9-5 izfr’kr ls o"kZ 2016 esa 6-75 izfr’kr rd dh fxjkoV vkbZA lhvkjvkj esa o"kZ 2012 esa +6 izfr’kr ls o"kZ 2016 esa 4 izfr’kr rd dh fxjkoV vkbZA 10 o"kksZa ljdkjh {ks= ds izfrQy esa Hkh 8-47 izfr’kr ls o"kZ 2016 esa 6-73 izfr’kr rd dh fxjkoV vkbZA

1-3 Hkkjrh; vFkZO;oLFkk ,oa vkokl dk fogaxkoyksdu

7 vkfFkZd losZ{k.k] 2015&16

13

100%

80%

8 ls 23%

12 16%ls

2%

7%

52 78%ls

ekud bdkbZ dh ykxr

60%

40%

20%

100%

Hkwfe vkiwfÙkZ [kksyuk

fuekZ.k ykxr esa deh

mUur ifjpkyu,oa vuqj{k.k

foÙkh; ykxrde djuk

vuqdwfyr ykxr

vè;k; 1 % n`f"Vdks.k ,oa uhfrxr ekgkSyjk"Vªh; vkokl cSadNATIONAL HOUSING BANK

8 Hkkjr i;kZokl III jk"Vªh; fjiksVZ] 2016] vkokl ,oa 'kgjh xjhch mi'keu ea=ky; rFkk Hkkjrh; fjtoZ cSad

10,00

9,00

8,00

7,00

6,00

5,00

4,00

3,002012 2013 2014 2015 2016

xzkQ 1-2% lhvkjvkj] cSad nj] jsiks nj ,oa 10 o"kZ ds ljdkjh {ks= ds izfrQy esa izo`fÙk

lzksr% Hkkjrh; fjtoZ cSad

81-3-3 vkokl ds fodkl ds fy, gky dh igysa

fuEufyf[kr ckWDl esa Hkkjr ljdkj }kjk 'kq: dh xbZ dqN igysa nh xbZ gSa tks vkokl LVkWd esa lqèkkj ykus ds fy, izklafxd gSaA

Û izR;{k fons’kh fuos’k ¼,QMhvkbZ½% U;wure {ks=Qy ,oa iwathdj.k vis+{kkvksa ,oa vU; 'krksZa dks gVkuk] ljdkjh ekè;e ds ctk; Lopkfyr ekè;e ls ns’k esa fons’kh fuos’k dk ljyhdj.k djuk

Û cká okf.kfT;d mèkkj ¼bZlhch½% fodkldksa@Hkou fuekZrkvksa ,oa jk"Vªh; vkokl cSad@fofufnZ"V vkokl foÙk daifu;ksa dks nh?kZdkfyd fufèk miyCèk djkrs gq, fdQk;rh vkokl ,oa efyu cLrh dk mUu;u djus ds fy, leFkZ cukukA

Û Hkw laink fuos’k U;kl ¼vkjbZvkbZVh½% fuos’kdksa dks fu;fer vk; ds lzksr] fofoèkrkHkjh ,oa nh?kZdkfyd iwath o`f) miyCèk djkrs gq, Hkw laink esa fuos’k tqVkus dks vuqefr nsukA

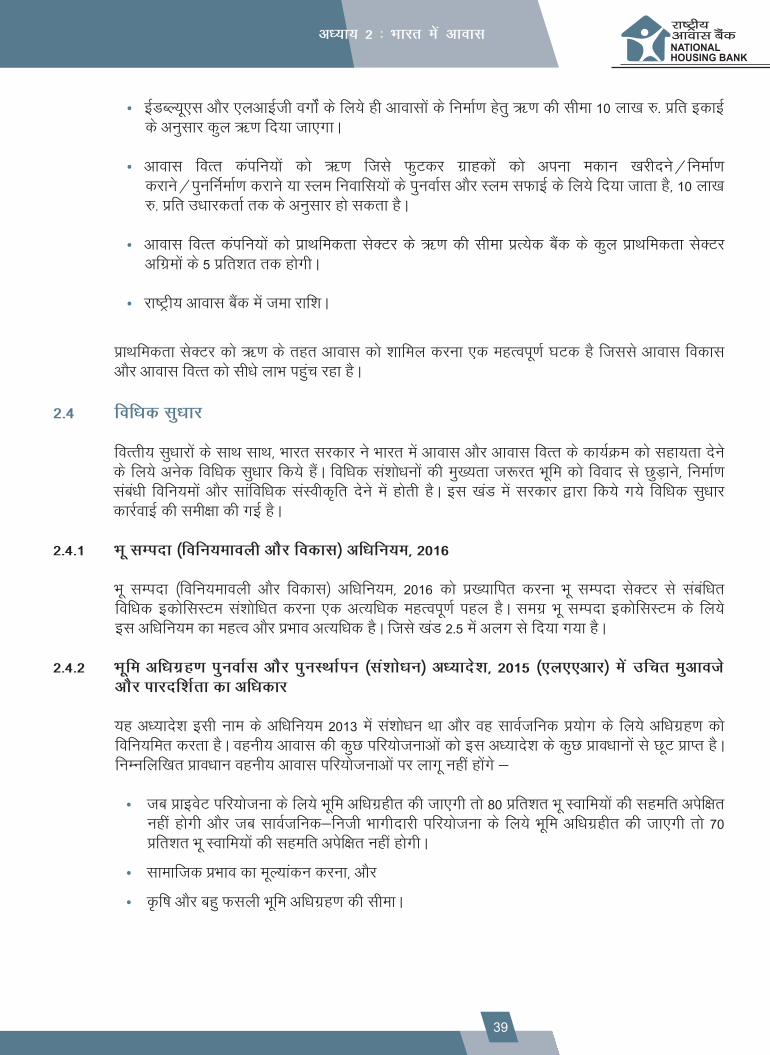

Û dsUnzh; ctV 2016 esa C;kt Hkqxrku dVkSrh dh vuqefr] fdQk;rh vkokl bdkbZ;ksa dk fuekZ.k djus okys Hkou fuekZrkvksa dks ykHk] fdjk;s okys vkokl ds fy, ykHk] vkjbZvkbZVh ds fy, ykHkka’k forj.k dj ¼MhMhVh½ ls NwV bR;kfn ds {ks= esa dbZ ennxkj ?kks"k.kk,a dh x;hA d`i;k dsUnzh; ctV 2016 esa vkokl {ks= ls lacafèkr ?kks"k.kkvksa ds fofufnZ"V fooj.k ds fy, [kaM 2-3-1 dk lanHkZ ysaA

Û Hkw laink ¼fu;eu ,oa fodkl½ vfèkfu;e] 2016% miHkksDrk ds fgrksa dh j{kk djus esa leku fofu;ked ekgkSy iznku djus] fooknksa dk Rofjr fu.kZ; ysus esa enn djus ,oa Hkw laink {ks= dk lqO;ofLFkr fodkl lqfuf’pr djus ds mn~ns’; ls Hkw laink ¼fofu;eu ,oa fodkl½ vfèkfu;e] 2016 dks vfèkfu;fer fd;kA

Û ekWMy Hkou fuekZ.k mi&fu;e] 2016% Hkkjr ljdkj us ekpZ] 2016 esa i;kZoj.k lacaèkh lqj{kk ds izkoèkku lfgr ekWMy Hkou fuekZ.k mi&fu;e izdkf’kr fd;k gS ftls jkT;ksa }kjk Hkh viuk;k tkuk gSA ;s Hkou fuekZ.k mi&fu;eksa dks muds vfèkd ls vfèkd lekos’kh ,oa mi;ksxdrkZ vuqdwy cukus ds mn~ns’; ls le&lkef;d 'kgjh izo`fÙk;ksa ds vuqlkj vn~;rhr fd;k x;k gSA

ckWDl 1-3% vkokl ds fy, fuos’k ,oa foÙkh; lgk;rk

ckWDl 1-4% vkokl {ks= ds fy, dsUnzh; ctV dh ?kks"k.kk,a

ckWDl 1-5% vkokl {ks= ds fy, uhfrxr <kapk ,oa foèkk;h leFkZu

vkjf{kr udn fuf/k vuqikr uhfr jsiks nj cSad nj 10 o"kZ ljdkjh çfrHkwfr;ka çfrQy

14

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

Û fdjk;s dk vkokl% vkokl ,o a 'kgjh xjhch mi’keu e=a ky; u s jk"Vhª ; 'kgjh fdjk;k vkokl uhfr] 2016 dk elknS k r;S kj fd;k tk s vyx&vyx vk; ox Z d s ykxs k as d s fy, fdjk; s dk s ikz Rs lkgu nxs h ,o a lkekftd fdjk;k vkokl ¼,lvkj,p½ dk s c<k+ ok nrs s g,q i;kIZ r fdjk;k vkokl LVkdW r;S kj djxs hA vfr fiNM s+ ox Zd s ykxs k as dk s vkokl dh lfq oèkkvk as dk s c<k+ ok nrs s g,q ,o a fofufn"Z V yf{kr ox Z d s ykxs k as d s fy, fdjk;k vkokl dh vko’;drk d s vkèkkj ij vfr fiNM s+ ox Z d s ykxs k as dh loa guh;rk ij fo’k"s k è;ku fn;k x;k gAS

Û ekMW y jkT; vkokl uhfr jkT; ,o a dUs n z 'kkflr inz ’s kk as dk s viu s uhfr;k as dk l=w hdj.k dju@s leh{kk dju se as leFk Z cuku s d s mnn~ ’s ; l s tuw ] 2016 e as 'kgjh {k=s k as e as vkokl uhfr dk ueuw k tkjh fd;k x;kA

Û dkjksckj djus dks vklku cukuk ¼bZvksMhch½ RkFkk Hkou fuekZ.k&;kstuk&vuqeksnu izfØ;k dks ;qfDrlaxr cukuk vkokl ,oa fuekZ.k ifj;sktukvksa dh vuqeksnu izfØ;k dks vU; lacafèkr ea=ky; tSls i;kZoj.k] ou ,oa tyok;q ifjorZu] ukxj foekuu] laLd`fr] j{kk ,oa miHkksDrk ekeys ds lkFk ijke’kZ djrs gq, ljy ,oa ;qfDrlaxr cuk;k x;k gSA bl fn’kk esa ih,e,okbZ ds fn’kk&funsZ’kksa eas Hkh dqN vkns’k fn;s x;s gSa tSls fuekZ.k ds ijfeVksa ds fy, ,dy f[kM+dh dh LFkkiuk djuk] ekun Hkou fuekZ.k dh vueq fr dh voèkkj.kk ,o a [kkl ifjfLFkfr;k as e as uD’k s dk vueq kns u bR;kfnA

Û izkS|ksfxdh mi&fe’ku% mUur fuek.Z k ikz |S kfs xdh ,o a dk;iZ )fr vkokl ifj;kts ukvk as dk s vfèkd l{kerk l s ,o a de l s de le; e as ijw k dju s e as lgk;rk dj ldrh gAS iow fZ uferZ ,o a ekMW ;~ yw j fuek.Z k tlS h fuek.Z k rduhdh ,o a uokUs e"s kh fuek.Z k lkexhz ifj;kts ukvk as dk s de l s de le; e as rFkk cgrq de lla kèkuk as d s lkFk ijw k dju s e as lgk;rk dj ldrh gAS bl fn’kk e as rts h ,o a x.q koÙkkijd vkoklk as dk fuek.Z k dju s d s fy, vkèkfq ud] uokUs e"s kh ,o a gfjr rduhdh o Hkou fuek.Z k lkexhz viuku s dh lfq oèkk inz ku djr s g,q ièz kkue=a h vkokl ;kts uk ¼’kgjh½ d s rgr ikz |S kfs xdh mi&fe’ku dh LFkkiuk dh x;h gAS

Û izn’kZu ifj;kstuk,a% ns’k esa ukS jkT;ksa us LFkkuh; lw{e&tyok;q ifjfLFkfr;ksa dks è;ku esa j[krs gq, ubZ ,oa mUur fuekZ.k izkS|ksfxfd;ksa ds izn’kZu esa #fp fn[kkbZ gSA cM+s ea=ky;@foHkkx ¼jsyos] j{kk] dsUnzh; yksd fuekZ.k foHkkx ,ao lkoZtfud {ks= ds miØe½ deZpkfj;ksa ds vkokl ,oa vU; dkexkjksa ds fy, ubZ rduhdh viukus ds fy, vkxs c<+ jgs gSaA p;fur izkS|ksfxfd;ksa ds fy, njksa dh ekudhd`r vuqlwph fodflr dh tk jgh gSA

Û fuekZ.k ls lacafèkr dkexkjksa dk dkS’ky fodkl% ;g vueq ku yxk;k x;k g S fd fuek.Z k {k=s e a s dke dju s oky s45 fefy;u ykxs k a s e a s l s 6 ifz r’kr ykxs k a s d s ikl gh lOq ;ofLFkr ifz ’k{k.k ,o a dk’S ky fuek.Z k dh lfq oèkk gAS bl fLFkfr dk s n[s kr s g,q oreZ ku e as c<h+ gbq Z mRikndrk ,o a 'kgjh vFkOZ ;oLFkk e as dk; Z cy dk vfèkd l s vfèkd ;kxs nku nus s e a s fuek.Z k dkexkjk a s d s dk’S ky fodkl ifz ’k{k.k ij T;knk l s T;knk è;ku dfs Unrz fd;k tk jgk gAS

lzksr% Hkkjr i;kZokl III jk”Vªh; fjiksVZ] 2016 vkokl ,oa ‘kgjh xjhch mi’keu ea=ky;

jk"Vªh; vkokl cSad dh LFkkiuk jk"Vªh; vkokl cSad] 1987 ds rgr dh x;h Fkh ftldk mn~ns’; vkokl foÙk laLFkkuksa dks c<+kok nsus ds fo’ks"kkfèkdkj ds lkFk&lkFk bu laLFkkuksa dks Hkkjr esa vkokl foÙk iz.kkyh ds fodkl dh fn’kk esa fofu;ked ekxZn’kZu] foÙkh; lgk;rk] tkudkjh o 'kksèk dh lgk;rk nsuk gSA Hkkjrh; fjtoZ cSad ds iw.kZLokfeRokèkhu jk"Vªh; vkokl cSad vkokl {ks= ds fy, cgq&vk;keh fodkl foÙk laLFkku gSA blds fØ;k&dykiksa esa vkokl foÙk daifu;ksa dk fofu;eu ,oa i;Zos{k.k] Hkkjr esa vkokl foÙk dk foÙkiks"k.k ,oa laoèkZu o fodkl 'kkfey gSA jk"Vªh; vkokl cSad ds mn~ns’;ksa esa lHkh oxZ ds yksxksa dh vkokl dh vko’;drkvksa dh iwfrZ djus esa lqn`<+] ;Fks"V] vFkZ{ke ,oa fdQk;rh vkokl foÙk dk laoèkZu djuk ,oa vkokl foÙk dk lexz foÙkh; iz.kkyh ds lkFk ,dhdj.k djuk 'kkfey gSA

ckWDl 1-6% vkokl ds fy, uoksUes"kh izkS|ksfxdh ,oa {kerk fuekZ.k esa lgk;rk

1-4 jk"Vªh; vkokl cSad dh Hkwfedk

15

vè;k; 1 % n`f"Vdks.k ,oa uhfrxr ekgkSyjk"Vªh; vkokl cSadNATIONAL HOUSING BANK

fofu;eu ,oa i;Zos{k.k

å vkokl foÙk daifu;ksa ¼vk- fo- da-½ dk iathdj.k ,oa fuxjkuh

å vkokl foÙk daifu;ksa dks LFkk;h ,oa lqn`<+ vkokl foÙk iz.kkyh ds fodkl ds fy, funsZ’k] fn’kk&funsZ’k] lafgrk bR;kfn tkjh djukA

å LFkyh; fujh{k.k ,oa LFkysÙkj fuxjkuh ds ekè;e ls i;Zos{k.kA

å miHkksDrkvksa dks tkx:d djuk ,ao muds fgrksa dh j{kk djukA

å varj&fofu;ked leUo;

o"kZ 2015&16 ds nkSjku jk"Vªh; vkokl cSad us 11 vkokl foÙk daifu;ksa dks iathdj.k izek.ki= ¼lhvksvkj½ iznku fd;sA 31 fnlacj] 2016 rd 82 vkokl foÙk daifu;ka jk"Vªh; vkokl cSad ls iathd`r FkhaA ;g lqfuf’pr djus ds fy, fd vkokl foÙk daifu;ka vius dkjksckjh ekeyksa ds lapkyu ls tekdrkZvksa] xzkgdksa ,oa tu lkèkkj.k ds fgr ds izfr vfgrdj u gksa] jk"Vªh; vkokl cSad vkokl foÙk daifu;ksa ds fu"iknd ,oa vfHk’kklu <kaps esa gLr{ksi djrk gSA vkokl foÙk daifu;kasa ds fofu;ked ds rkSj ij jk"Vªh; vkokl cSad vkokl foÙk daifu;ksa dk ekxZn’kZu] fuxjkuh o fujh{k.k djrk gS rkfd muds lHkh iz;kl mlh fn’kk esa gksaA i.kèkkjdks dks egRo nsus ds mn~ns’; ls jk"Vªh; vkokl cSad us vkol foÙk daifu;ksa ds fo#) xzkgdksa dh f’kdk;rk as dk irk yxku s d s fy, vkuW ykbu f’kdk;r ita hdj.k ,o a lpw uk MkVkcls i.z kkyh ¼fxMz l~ ½ dh LFkkiuk dh gSA ,d vU; izeq[k {ks=] tgka jk"Vªh; vkokl cSad lfØ; :i ls gLr{ksi djrk gS og vkokl foÙk m|ksx esa èkks[kkèkM+h dks dkcw esa j[kuk gSA jk"Vªh; vkokl cSad vkokl foÙk m|ksx esa gksus okyh èkks[kkèkfM+;ksa ds ckjs esa tkudkjh ,df=r djrk gS ,oa psrkouh lwpuk ds ekè;e ls lHkh vkokl foÙk daifu;ksa dks fu;fer :i ls /kks[kkèkM+h ij lesfdr lwpuk dk izlkj djrk gSA blls vkokl foÙk daifu;ksa dks cktkj dh ifjfLFkfr;ksa ,oa vius fuos’k dh lqj{kk ds izfr vkSj tkx:d gksus esa enn feyrh gSA jk"Vªh; vkokl cSad lwpuk lk>k djus ,oa leUo; djus ds fy, ns’k ds vU; fofu;kedksa ds lkFk fu;fer rkSj ij ifjppkZ djrk gSA

foÙkiks"k.k

å iqufoZÙk ds ekè;e ls lrr vkokl foÙk iz.kkyh ftlesa lkekU; C;kt nj ij miyCèk dsUnzh; iqufoZÙk ;kstuk ds vfrfjDr jk"Vªh; vkokl cSad esa LFkkfir fufèk;ksa ds ekè;e ls fj;k;rh C;kt nj ij miyCèk fo’ks"k iqufoZÙk ;kstuk,a 'kkfey gSA

å o"kZ 2015&16 ds nkSjku vkokl foÙk daifu;ksa ,oa vuqlwfpr okf.kfT;d cSadksa ds chp vfèkd vFkok de ;k cjkcj fgLlsnkjh ds lkFk dqy 21]590 djksM+ #i;s dk iqufoZÙk laforfjr fd;k x;kA foxr rhu o"kksZa ds nkSjku fd;s x;s iqufoZÙk laforj.k ds laLFkku&okj fo’ys"k.k dks fuEufyf[kr rkfydk 1-1 e as n’kk;Z k x;k gAS ;kts uk&okj ,o a vofèk&okj fooj.k fuEufyf[kr xkz Q 1-3 ,o a 1-4 e as n’kk;Z k x;k gAS

rkfydk 1-1% foxr rhu o"kksZa esa laLFkku&okj iqufoZÙk laforj.k ¼jkf’k djksM+ #i;s eas½

Û

Û

16

izkFkfed _.knkrk laLFkku

2013-14 2014-15 2015-162016-17 (01.07.2016-

31.12.2016)

laforfjr jkf’k

laforfjr jkf’k

dqy dk izfr’kr

dqy dk izfr’kr

dqy dk izfr’kr

laforfjr jkf’k

laforfjr jkf’k

dqy dk izfr’kr

vkokl foÙk daifu;ka 9,633 53.9 7,390 33.8 10,852 50.3 4,614 88.0

vuqlwfpr okf.kfT;d cSad 7,943 44.5 14,114 64.6 10,275 47.6 600 11.4

{ks=h; xzkeh.k cSad 280 1.6 253 1.2 463 2.1 30 0.6

lgdkjh {ks= - - 90 0.4 - - -

dqy 17,856 100.0 21,847 100.0 21,590 100.0 5,244 100.0

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

2000

1600

1200

800

400

0

2004

-200

5 rd

2005

-200

6

2006

-200

7

2007

-200

8

2008

-200

9

2009

-201

0

2010

-201

1

2011

-201

2

2012

-201

3

2013

-201

4

2014

-201

5

2015

-201

6

laLohÑr jkf'k

laforfjr jkf'k

1 o"kZ rd

1 o"kZ ls 3 o"kZ

3 o"kZ ls 5 o"kZ

5 o"kZ ls 7 o"kZ

7 o"kZ ls 10 o"kZ

10 o"kZ ls T;knk

xzkQ 1-3% 30 twu] 2016 dks ;kstuk&okj iqufoZÙk laforj.k ¼izfr’kr esa½

xzkQ 1-4% 30 twu] 2016 dks vofèk&okj iqufoZÙk laforj.k ¼izfr’kr esa½

lkoZtfud ,tsalh tSls vkokl cksMZ ,oa fodkl izkfèkdj.k dks izR;{k rkSj ij vFkok tu futh Hkkxhnkjh fof/k ds ekè;e ls Hkwfe fodkl ,oa vkokl ifj;sktukvksa ds fy, lkekU; C;kt nj ds vfrfjDr efyu cLrh iqufoZdkl ,oa fuEu vk; okys vkokl ds fy, jk"Vªh; vkokl cSad esa LFkkfir fufèk;ksa ds ekè;e ls fj;k;rh nj ij miyCèk ifj;kstuk foÙkA

å foxr ikap o"kksZa ds nkSjku jk"Vªh; vkokl cSad us vkfFkZd :i ls detksj oxZ ¼bZMCY;w,l½@fuEu vk; oxZ ¼,yvkbZth½ dh lgk;rk djus ds vius iz;klksa ls lkoZtfud ,tsafl;ksa dk foÙkiks"k.k djrs gq, yxHkx 24]000 vkoklksa dk fuekZ.k djus esa enn dhA lap;h :i ls 30 twu] 2016 rd 9]590 djksM+ #i;s dh ykxr dh ifj;kstuk ,oa 5]522 djksM+ #i;s ds _.k ?kVd ds lkFk 448 ifj;kstukvksa dks eatwjh nh x;hA 31 fnlacj] 2016 rd lap;h ifj;kstuk foÙk laforj.k 2]406 djksM+ #i;s jgkA foxr 10 o"kksZa dh izo`fÙk dks xzkQ 1-5 esa n’kkZ;k x;k gSA

xzkQ 1-5% ifj;kstuk foÙk laforj.k esa izo`fÙk ¼jkf’k djksM+ #i;s eas½

å

75

17

17

fu;fer

xzkeh.k vkokl fuf/k

'kgjh vkokl fuf/k

'kgjh&fuEu vk; vkokl

17

vè;k; 1 % n`f"Vdks.k ,oa uhfrxr ekgkSyjk"Vªh; vkokl cSadNATIONAL HOUSING BANK

Û

Û

Û

Û

laoèkZu ,oa fodkl

bfDoVh lgHkkfxrk ds ekè;e ls u;s i{kksa dk l`tu

å _.knkrk laLFkkuksa ds ekStwnk usVodZ dk lqn`<+hdj.kA

å {ks= dk {kerk fuekZ.k

å izf’k{k.k] laxks"Bh bR;kfn ds ekè;e ls miHkksDrkvksa esa tkx:drk QSykukA

å fofHkUu i.kèkkjdksa dk Kku dk lk>hnkj cuukA

å fofHkUu ljdkjh ;kstukvksa ds fy, uksMy ,tsalh cuuk] ,oa

å mRikn fodkl esa lgk;rk djuk ,oa {ks= dk ekxZn’kZu djukA

bfDoVh lgHkkfxrk% ns’k esa vkokl foÙk iz.kkyh ds laoèkZu ,oa fodkl ds fy, jk"Vªh; vkokl cSad dks fn;s x;s vfèkns’k ds vuqlkj jk"Vªh; vkokl cSad vkokl foÙk daifu;ksa ,oa vU; lacafèkr daifu;ksa dh bfDoVh 'ks;j iwath esa lgHkkfxrk djrk gSA orZeku esa jk"Vªh; vkokl cSad dh ikap daifu;ksa dh bfDoVh 'ks;j iwath esa lgHkkfxrk gSA

ljdkjh ;kstukvksa dk dk;kZUo;u% jk"Vªh; vkokl cSad Hkkjr ljdkj dh ;kstukvksa ds dk;kZUo;u ds fy, dsUnzh; uksMy ,tsalh ¼lh,u,½ ds rkSj ij dk;Z djrk gSA os ;kstuk,a ftuesa jk"Vªh; vkokl cSad bl Hkwfedk dk fuoZgu djrk gS muesa fuEufyf[kr 'kkfey gS%

vkokl ,oa 'kgjh xjhch mi’keu ea=ky; dh 'kgjh xjhc ds vkokl gsrq C;kt lfClMh ;kstuk] jktho +_.k ;kstuk ,oa ̂o"kZZ 2022 rd lcds fy, vkokl fe’ku* ds rgr izèkkuea=h vkokl ;kstuk ¼’kgjh½A

foÙk ea=ky; ds vèkhu ,d izfr’kr C;kt jkgr ;kstuk] ,oa

uohu ,oa uohdj.kh; ÅtkZ ea=ky; ds vèkhu ?kjksa es lkSj ty rkid ,oa lkSj izdk’k iz.kkfy;ksa ds vfèk"Bkiu gsrq iwathxr lfClMh ;kstuk

blds vfrfjDr jk"Vªh; vkokl cSad vkokl ,oa 'kgjh xjhch mi’keu ea=ky; dh vksj ls fuEu vk; vkokl ds fy, _.k tksf[ke xkjaVh fufèk U;kl dk Hkh lapkyu djrk gSA

{kerk fuekZ.k% jk"Vªh; vkokl cSad bl {ks= ds fofHkUu i.kèkkjdksa ds izf’k{k.k ,oa {kerk fuekZ.k dh fn’kk esa fu;fer rkSj ij fofHkUu mik; djrk gSA blesa eq[; dk;Zikyd vfèkdkjh ¼lhbZvks½ cSBd ,oa xksy est lEesyu tSls eapksa esa fofHkUu izkFkfed _.knkrk laLFkkuksa ds lkFk fu;fer ifjppkZ djus ds vykok izf’k{k.k dk;ZØeksa esa Hkkx ysuk o lapkyu djuk 'kkfey gSA o"kZ 2015&16 esa jk"Vªh; vkokl cSad us lewps Hkkjr o"kZ esa 11 izf’k{k.k dk;ZØe vk;ksftr fd;s ftuesa fofHkUu izkFkfed _.knkrk laLFkkuksa ds 443 izfrHkkfx;ksa us Hkkx fy;kA bu 11 izf’k{k.k dk;ZØeksa esa ls eè; izns’k esa dke dj jgs nks {ks=h; xzkeh.k cSadksa ds fy, nks rnuqdwy dk;ZØe fganh esa vk;ksftr fd;s x;sA izkFkfed _.knkrk laLFkkuksa ,oa jkT; Lrjh; uksMy ,stsafl;ksa ¼,l,y,u,½ esa tkx:drk iSnk djus ,oa laosnu’khy cukus ds mn~ns’; ls jk"Vªh; vkokl cSad us o"kZ 2015&16 esa izèkkuea=h vkokl ;kstuk & +_.k lgc) lfClMh ;kstuk ij vfHk;ku pyk;k ,oa 12 {ks=h; dk;’Z kkyk, a vk;kfs tr dhA tu tkx:drk vfHk;ku dk s fiVaz ] byDS Vkª fW ud ,o a lk’s ky ehfM;k e as Hkh pyk;k x;kA

1-4-1 bu lg;ksxiw.kZ ,oa ikjLifjd lqn`<+ Hkwfedkvksa dk fuoZgu djrs le; jk"Vªh; vkokl cSad us vkokl foÙk cktkj ds fodkl ,oa foLrkj ds vykok bldh fLFkjrk esa Hkh Hkkjh ;ksxnku fn;kA dsUnz ,oa jkT; Lrj ij vU; laLFkkuksa o uhfr fuekZrkvksa ds lkFk lk>snkjh djrs gq, jk"Vªh; vkokl cSad us vusd ;kstuvksa o dk;ZØeksa dk lw=ikr fd;k tks fuEu ,oa eè;e&vk; oxZ ds yksxksa esa iSB cukus ij yf{kr gSaA

å

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016

18

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

vè;k;

2-1 vkokl izsjd ds :i esa

2-2 Hkkjr esa vkokl laca/kh igysa

2 % Hkkjr esa vkokl ljdkj us 'kgjh vkSj xzkeh.k xjhcksa ds fy, lLrs edkuksa dh vkiwfrZ c<+kus ds fy, vusd ;kstuk,a ykxw dh gSa] fdarq budh vkiwfrZ vf/kdka’kr% ljdkjh ,tsafl;ksa ds ek/;e ls gh dh tkrh gSA ns’k esa vkokl dh cM+h pqukSrh dk lkeuk djus ds fy, futh {ks= dks 'kkfey djus dh vko’;drk gSA ns’k ds lkekftd& vkfFkZd <kaps esa fHkUurk ds dkj.k bl leL;k dks lexzrk ds lkFk gy djus dh t:jr gSA ljdkjh ra= 'kgjh vkokl ds fy, iz/kkuea=h vkokl ;kstuk&’kgjh vkSj xzkeh.k vkokl ds fy, iz/kkuea=h vkokl ;kstuk&xzkeh.k ds fØ;kUo;u esa lfØ; :i ls dk;Z dj jgk gSA vusd jkT; ljdkjksa us fo’ks"k :i ls viuh LFkkuh; vkokl ekaxksa dks iwjk djus ds fy, futh {ks= ds lg;ksx ls vkSj lg;ksx ds fcuk vusd ;kstuk,a vkjaHk dh gSaA ljdkjksa }kjk vusd foRrh; izksRlkguksa dh ?kks"k.kk dh xbZ gS vkSj Hkkjrh; fjtoZ cSad dh ekSfnzd uhfr ls vkokl foRr iz.kkyh esa _.k tksf[ke rFkk O;ogk;Zrk esa larqyu cuk;s j[kus esa lgk;rk feyrh gS ftlls fdQk;rh vkokl vf/kd ek=k esa miyC/k djkus dks izksRlkgu feykA ^jsjk^ dkuwu cuus ds ckn vkokl lsDVj dks dkuwuh bdksflLVe ls cgqr etcwrh feyh gS ftlesa Hkou fuekZrkvksa dks viuh ;kstuk ds vuqikyu vkSj fd;s x;s ok;ns iwjs djus ds izfr tckonsg cuk;k x;k gSA

2-1-1 vkokl {ks= vU; vusd m|ksxksa ds lkFk cgqr vf/kd tqM+k gqvk gS vkSj vkokl esa o`f) ls mu lHkh m|ksxksa esa Hkh o`f) gksrh gSA blds lkFk&lkFk] vkokl izR;sd euq"; dh vko’;drk gS] vkokl ij fopkj djrs le; ns’k esa O;kIr vusd eqÌksa dh tfVyrk ij Hkh /;ku j[kuk gksxk tSls csjkstxkjh] xjhch] vk;] 'kSf{kd vlekurk vkSj ogu{kerkA blh dkj.k vkokl laca/kh xfrfof/k;ksa ls ns’k esa] izR;{k ;k ijks{k :i ls] jkstxkj ds volj c<+rs gSa] csgrj f’k{kk] csgrj vk; Lrj ikus vkSj xjhch nwj djus esa enn feyrh gSA

2-1-2 ns’k esa vkokl laca/kh leL;kvksa dks nwj djus ds fy;s cgqeq[kh dk;Z djus vkSj futh {ks= dks 'kkfey djus dh t:jr gS] ljdkj us fofHkUu Jsf.k;ksa ds yksxksa dh t:jrksa dks iwjk djus ds fy;s oSfo/; fo’ks"k vkokl dk;ZØeksa dks 'kq: fd;k gSA xzkeh.k {ks=ksa ds fy;s rS;kj dk;ZØeksa dks 'kgjh {ks=ksa ds dk;ZØeksa ls fHkUu izdkj ls rS;kj fd;k x;k gSA blds vfrfjDr] ljdkj us vkokl {ks= ds fodkl esa lqfo/kk gsrq vusd foRrh; vkSj fof/kd lq/kkj Hkh fd;s gSa vkSj ljdkj ?kksf"kr dk;ZØeksa ds lQy fØ;kUo;u esa lgk;rk Hkh dj jgh gSA

2-2-1 dsUnz ljdkj }kjk 'kq: dh xbZ xzkeh.k vkokl igysa

2-2-1-1 xzkeh.k vkokl dk vusd dkj.kksa ls cgqr vf/kd egRo gSA lHkh cs?kj yksxksa dks vkSj fo’ks"kdj mu yksxksa dks tks ttZj edkuksa esa jg jgs gSa] lqjf{kr vkSj csgrj vkokl miyC/k djkuk igyh vkSj lokZf/kd egRoiw.kZ t:jr gSA lqjf{kr vkokl feyus ds ckn O;fDr vius thou ds nwljs igyqvksa ij /;ku nsrk gS tSls vk; c<+kuk] ifjokj ds fy;s f’k{kk vkSj LokLF; dh ns[kHkkyA nwljh ckr] Hkkjrh; xzkeh.k vFkZO;oLFkk eq[;r% d`f"k rFkk lacaf/kr fØ;kdykiksa tSls i’kqikyu o erL; ikyu ij vk/kkfjr gSA d`f"k ls xzkeh.kksa dks jkstxkj feyus esas u dsoy lgk;rk feyrh gS fdarq mls Hkkjrh; vFkZO;oLFkk dh jh<+ Hkh ekuk tkrk gS D;ksafd vFkZO;oLFkk ds vU; {ks=ksa ls mldh Hkkjh ekax vkSj vkiwfrZ tqM+h gksrh gSA vFkZO;oLFkk ds fodkl ds fy;s d`f"k esa o`f) egRoiw.kZ gksrh gSA blesa lgk;rk ds fy;s ,d lqjf{kr mik; ;g lqfuf’pr djuk gS fd fdlkuksa vkSj [ksrksa esa dke djus okys Jfedksa dks jgus ds fy;s lqjf{kr vkokl miyC/k gksaA rhljh ckr] pwafd d`f"k {ks= ds egRo dks ekU;rk nh xbZ gS] xkaoksa esa d`f"k ls brj Hkh voljksa dks ryk’kuk pkfg, rkfd os vU; vkfFkZd xfrfof/k;ksa ls lEc) gksdj

{ks=

19

vè;k; 2 % Hkkjr esa vkokl jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

viuh vk; c<+k ldsaA xkaoksa esa vk; ds vU; lk/kuksa dh vuqiyC/krk ds dkj.k xzkeh.k yksx jkstxkj ds fy;s 'kgjksa dh vksj Hkkxrs gSaA bl ifjizs{; esa] xzkeh.k {ks=ksa esa vkokl ds fodkl ds QyLo:i vkfFkZd xfrfof/k;ksa esa Hkkjh o`f) gksxh D;ksafd mlds fiNM+s gksus vkSj fodkl gksus dk vFkZO;oLFkk ls xgjk laca/k gksrk gSA xzkeh.k {ks=ksa esa xjhch mUewyu ds fy;s fd;s x;s iz;klksa esa vkoklh; xfrfof/k;ksa ls cgqr lgk;rk feysxhA

2-2-1-2 ckjgoha iapo"khZ; ;kstuk ds fy;s dk;Z lfefr ds izkDdyu ds vuqlkj] dqy xzkeh.k vkoklksa dh deh vuqekur% 4-37 djksM+ bdkbZ;ka FkhA blesa xjhch js[kk ls uhps ifjokjksa ds fy;s deh yxHkx 3-93 djksM+ bdkbZ;ksa dh FkhA bl deh ds fofHkUu dkj.kksa dks n’kkZus okyh rkfydk uhps nh xbZ gSA

rkfydk la- 2-1 % xzkeh.k {ks=ksa esa vkoklksa dh deh ds fofHkUu dkj.k

lzksr% ckjgoha iapo"khZ; ;kstuk ds fy;s xzkeh.k vkokl ij xfBr dk;Z xzqi dh fjiksVZ] xzkeh.k fodkl ea=ky;] 2011

2-2-1-3 xzkeh.k vkoklksa dh deh dks nwj djus ds fy,] bafnjk vkokl ;kstuk ¼vkbZ,okbZ½] xzkeh.k vkokl ds fy;s igyh ;kstuk] Hkkjr ljdkj] xzkeh.k fodkl ea=ky; }kjk twu 1985 esa 'kq: dh xbZA ;kstuk dk izeq[k mÌs’; xjhch js[kk ls uhps ds ifjokjksa dks lqjf{kr vkSj iDdk vkokl miyC/k djkus esa lgk;rk djuk FkkA twu 2015 esa] ljdkj us ̂ ^2022 rd lc ds fy;s vkokl^^ fe’ku dh ?kks"k.kk dhA bl fe’ku dh ?kks"k.kk ds ckn vkSj xzkeh.k vkokl dh ekax vkSj vkiwfrZ esa Hkkjh varj dh pqukSrh dk lkeuk djus ds fy;s] bafnjk vkokl ;kstuk dks iqu% rS;kj fd;k x;k vkSj mls ̂iz/kkuea=h vkokl ;kstuk & xzkeh.k^ ds vUrxZr 01 vizSy] 2016 ls 'kq: dj fn;k x;kA

2-2-1-4 bafnjk vkokl ;kstuk & bafnjk vkokl ;kstuk ,d lkoZtfud vkokl ;kstuk Fkh tks cs?kj vkSj xjhc ifjokjksa dks tks ttZj ;k dPps ?kjksa esa jg jgs Fks] ljdkj }kjk mUgssa vkcafVr Hkwfe ij iDdk edku cukus ds fy;s volj iznku djus gsrq FkhA ;g ;kstuk] fØ;kUo;u dh j.kuhfr ds Hkkx Lo:i] ,sls ykHkkfFkZ;ksa dks ljdkj ls rduhdh vkSj foRrh; lgk;rk miyC/k djkrh FkhA tqykbZ 2013 esa bafnjk vkokl ;kstuk ds la’kksf/kr fn’kkfunsZ’kksa ds vuqlkj] ;kstuk ds vUrxZr fufnZ"V ifjokjksa dks u;s vkokl ds fuekZ.k gsrq lgk;rk miyC/k djkbZ tkrh gS] lgk;rk vof/k de ls de 30 o"kZ gksrh gSA blds vUrxZr ttZj vkSj dPps edkuksa dk mUu;u djkus ds fy;s iqu%iz;ksT; lkexzh dk bLrseky fd;k tkrk gSA blesa mu Hkwfeghu xjhcksa dks Hkwfe miyC/k djkus dk Hkh izko/kku gS ftuds ikl dksbZ vkJ; ugha gS vkSj u gh edku fuekZ.k gsrq Hkwfe gSA bl ;kstuk esa uohu vkSj xzhu izkS|ksfxdh dk iz;ksx djds lLrs edku fuekZ.k djus dk Hkh izLrko gSA iz/kkuea=h vkokl ;kstuk&xzkeh.k vkjaHk gksus ij] bafnjk vkokl ;kstuk dks blesa 'kkfey dj fn;k x;kA bafnjk vkokl ;kstuk dh fo’ks"krkvksa dks lq/kkjksa ds lkFk iz/kkuea=h vkokl ;kstuk&xzkeh.k esa lfEefyr dj fn;k x;kA

20

xzkeh.k {ks=ksa esa vkoklksa dh deh ds fofHkUu dkj.k bdkbZ;ka ¼djksM+½

ifjokjksa dh la[;k ftuds ikl 2012 esa vkokl ugha Fkk 0-42

2012 esa vLFkk;h vkoklksa dh la[;k 2-02

2012 esa HkhM+HkkM+ ds dkj.k deh 1-13

2012 esa vkokl viz;ksT; gksus ds dkj.k deh 0-75

2012 ls 2017 ds nkSjku vfrfjDr vkoklksa dh deh 0-05

2012&2017 esa dqy xzkeh.k vkoklksa dh deh 4-37

2012&2017 esa chih,y ifjokjksa ds fy;s dqy xzkeh.k vkoklksa dh vuqekfur 3-9390 izfr’kr deh

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

9 xzkeh.k fodkl eaa=ky;] okf"kZd fjiksVZ 2016&17] vkSj dk;kZUo;u gsrq ] ih,e,okbZ&th] ,evks;wMh] flrEcj 2016ÝseodZ

92-2-1-5 iz/kkuea=h vkokl ;kstuk &xzkeh.k ¼ih,e,okbZ&xzkeh.k½

ih,e,okbZ&xzkeh.k dk mÌs’; xzkeh.k {ks=ksa esa fuokl dj jgs lHkh cs?kj ifjokjksa vkSj ttZj gkyr esa fuokl dj jgs ifjokjksa dks lHkh cqfu;knh lqfo/kkvksa ls ;qDr iDds edku miyC/k djkuk gSA dk;ZØe dk mÌs’; xzkeh.k {ks=ksa ds lHkh ifjokjksa dks o"kZ 2022 rd vkokl miyC/k djkuk gSA bl dk;ZØe dh eq[; fo’ks"krk,a fuEukuqlkj gSa %

ih,e,okbZ&xzkeh.k dk iz;kstu xzkeh.k {ks=ksa esa ,d djksM+ vkokl o"kZ 2016&17 ls 2018&19 rd 3 o"kZ ds nkSjku miyC/k djkuk gSA bu ,d djksM+ vkoklksa dh fuekZ.k ykxr dk vuqeku 1]30]075 djksM+ :i;s gS ftlesa Hkkjr ljdkj vkSj jkT; ljdkj dh fgLlsnkjh 60%40 ds vuqikr esa gksxhA ;|fi] iwoksZRrj jkT;ksa ds ekeys esa] jkT; ljdkj dh fgLlsnkjh dsoy 10 izfr’kr gksxhA dsUnz }kjk 'kkflr izns’kksa esa Hkkjr ljdkj }kjk iw.kZ foRr iks"k.k fd;k tk,xkA

eSnkuh bykdksa esa foRrh; lgk;rk 1]20]000 #i;s izfr bdkbZ vkSj igkM+h {ks=ksa esa 1]30]000 #i;s izfr bdkbZ nh tk,xhA

ykHkkFkhZ 'kkSpky; fuekZ.k gsrq LoPN Hkkjr vfHk;ku&xzkeh.k] ,eth,uvkjbZth, ;k fdlh vU; foRr iks"k.k lzakssr ls 12]000 #i;s dh lgk;rk jkf’k izkIr djsxkA

edku fuekZ.k ds fy;s eujsxk ds rgr vdq’ky Jfed etnwjh ds crkSj 90@95 O;fDr fnol ikfjJfed ikus dk izko/kku gS tks mDr bdkbZ lgk;rk ds vfrfjDr gksxkA

ykHkkFkhZ edku fuekZ.k ds fy;s 70]000 #- rd ,sfPNd _.k izkIr dj ldsxkA

;kstuk ds rgr bdkbZ dk fuEure vkdkj 25 oxZ ehVj j[kk x;k gSA

ykHkkfFkZ;ksa dh igpku xzke lHkk vk/kkfjr lkekftd&vkfFkZd vkSj tkfrxr tux.kuk ¼,lbZlhlh 2011½ vkadM+ksa ds vk/kkj ij dh tk,xhA blls ykHkkfFkZ;ksa ds p;u esa ikjnf’kZrk vkSj mÌs’; ijdrk vk,xh rFkk p;u esa vyx fu.kZ; dh vk’kadk de gksxhA

dk;ZØe ds rgr y{;ksa dh izkfIr esa rduhdh lgk;rk iznku djus ds fy;s jk"Vªh; Lrj ij ^jk"Vªh; rduhdh lgk;rk ,tsalh& ¼,uVh,l,½ dk xBu djukA ih,e,okbZ&xzkeh.k ds ykHkkfFkZ;ksa dks] ifj;kstukxr lgk;rk ds vfrfjDr] edku fuekZ.k ds fy;s rduhdh lgk;rk Hkh miyC/k djkbZ tk,xhA

vafre ykHkkfFkZ;ksa dks fuf/k;ksa dk 'krizfr’kr bySDVªkWfud fof/k ls varj.k djus ds fy;s] jkT;ksa@dsUnz’kkflr izns’kksa dks ykHkkfFkZ;ksa ds cSad@Mkd[kkuk [kkrs esa foRrh; lgk;rk lh/ks varfjr djus ds fy;s ,d ,dy jkT; uksMy cSad [kkrk [kksyus dk ijke’kZ fn;k x;k gSA blls ykHkkfFkZ;ksa dks Hkqxrku djus esa nsjh ugha gksxh] xM+cM+h ugha gksus dh laHkkouk de gksxhA

edkuksa ds fujh{k.k ds fy;s xzkeh.k fodkl ea=ky; }kjk ,d ,uMªkW;M vk/kkfjr eksckby ,Iyhds’ku ^^vkokl,i^^ ykap fd;k x;k gSA bl ,Iyhds’ku dh lgk;rk ls edku fuekZ.k ds fofHkUu Lrjksa ij rLohjsa Vkbe LVSEi vkSj ft;ks&VSfxax ls yh tk ldsaxh ftuds vk/kkj ij vf/kdkfj;ksa }kjk tkap iM+rky dh tk ldsxhA mlds ckn og fiDpj ̂^vkokllkW¶V^^ ij viyksM dj nh tk,xhA ykHkkfFkZ;ksa dks ;kstuk ds rgr foRrh; lgk;rk tkjh djus ds fy;s ;g 'krZ vfuok;Z gSA

;kstuk ds rgr edku dk vkcaVu ifr vkSj iRuh ds uke la;qDr :i ls fd;k tk,xk ;fn og fo/kok@vfookfgr@lEcU/k foPNsn O;fDr u gksA jkT; ljdkj ;g vkcaVu dsoy iRuh ds uke Hkh dj ldrh gSA

Û

Û

Û

Û

Û

Û

Û

Û

Û

Û

Û

21

vè;k; 2 % Hkkjr esa vkokl jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

edku fuekZ.k dh xq.koRrk dks cuk;s j[kus vkSj xzkeh.k bykdksa esa izf’kf{kr jktfeL=h ugha feyus ds dkj.k] ea=ky; xzkeh.k jkt fefL=;ksa dks fo’ks"k izf’k{k.k nsus esa lgk;rk Hkh djsxhA bl mÌs’; dh izkfIr ds fy;s] xzkeh.k fodkl ea=ky; us Hkkjrh; fuekZ.k n{krk fodkl ifj"kn ¼lh,lMhlhvkbZ½ ls lg;ksx fd;k gS vkSj xzkeh.k jktfeL=;ksa ds fy, ,d DokyhfQds’ku iSd rS;kj fd;k gSA bl DokyhfQds’ku iSd dks jk"Vªh; dkS’ky fodkl fuxe }kjk vuqeksfnr fd;k x;k gSA

;w,uMhih ds lg;ksx ls] xzkeh.k fodkl ea=ky; us ifj;kstuk vfHk’kklu ,oa of/kZr thfodk lgk;rk ¼thvks,,y,l½ ds rgr 18 jkT;ksa esa edkuksa ds fMtkbu tks ogka dh ekSleh ifjfLFkfr;ksa] lkaLd`frd ifjfLFkfr;ksa] ykxr de djus okyh mfpr izkS|ksfxfd;ksa rFkk LFkkuh; miyC/k lkexzh ds iz;ksx tks vkink jks/kh gksrk gS] dk v/;;u djk;k gSA xzkeh.k fodkl ea=ky; us jkT;ksa@dsUnz’kkflr izns’kksa ds lkFk fodflr fMtkbu izkS|ksfxfd;ksa esa tkudkjh gkfly dh tks ykHkkfFkZ;ksa ds fy;s ykHknk;d gS rkfd os vius edku vf/kd etcwr vkSj de ykxr ij cuk ldsaA

bl ;kstuk ds rgr 31 fnlEcj] 2016 rd gqbZ izxfr dks la{ksi esa uhps n’kkZ;k x;k gS %

o"kZ 2016&17 ds fy;s ih,e,okbZ&xzkeh.k ds rgr 15]000 djksM+ #i;s dh vkacfVr jkf'k esa ls 14]290 djksM+ #i;s dh jkf’k tkjh dh tk pqdh gSA bl jkf’k esa ls jkT;ksa@dsUnz 'kkflr izns’kksa }kjk 4645 djksM+ #i;s dh jkf’k dk mi;ksx fd;k x;kA

,lbZlhlh&2011 vkadM+ksa ds vk/kkj ij] bl dk;ZØe ds vUrxZr 1-68 djksM+ ykHkkfFkZ;ksa dks xzke lHkk }kjk lR;kiu vkSj vihyh; izkf/kdj.k }kjk lR;kiu ds ckn ik= ik;k x;kA

xzkeh.k fodkl ea=ky; }kjk jkT;ksa@dsUnz 'kkflr izns’kksa dks 32-64 yk[k vkokl dk y{; lkSaik x;k ftlesa ls 19 jkT;ksa@dsUnz 'kkflr izns’kksa }kjk ftyk vkSj CykWd&okj y{; 24-14 yk[k fu/kkZfjr fd;k x;kA

31 fnlEcj] 2016 rd dqy 21-18 yk[k edkuksa dk fuekZ.k fd;k x;kA

ih,e,okbZ&th ds rgr edkuksa dh eatwjh ds fy;s ̂vkokllkW¶V^ ij 10-44 yk[k ifjokjksa }kjk iathdj.k djk;k x;kA

o"kZ ds nkSjku ih,e,okbZ&th ds rgr 3-5 yk[k vkoklksa dks laLohd`fr nh xbZA

dk;ZØe ds rgr fuekZ.k fd;s tkus okys 4-67 yk[k vkoklksa dks ft;ksVSXM fd;k x;k ¼ykHkkfFkZ;ksa dh ekStwnk vkokl bdkbZ;ksa ds ft;ks&dksvkfMZusV dSIpj lfgr½A

;gka ;g mYys[k djuk vko’;d gS fd ekuuh; iz/kkuea=h us 31 fnlEcj] 2016 dks jk"Vª ds uke vius lacks/ku esa ^xzkeh.k vkokl C;kt lfClMh ;kstuk^ ¼vkj,pvkbZ,l,l½ dks 'kkfey fd;k rkfd lHkh xzkeh.k ifjokj viuk iDdk edku cuok ldsaA xzkeh.k fodkl ea=ky; us bl ;kstuk dks izkFkfed _.knkrk laLFkkuksa ds ek/;e ls fØ;kfUor djkus ds fy;s jk"Vªh; vkokl cSad dks dsUnzh; uksMy ,tsalh ds :i esa mi;qDr ik;kA

2-2-2 dsUnz ljdkj dh 'kgjh vkokl igysa

ns’k esa foxr dqN o"kksZa esa rsth ls 'kgjhdj.k gksrs gq, ns[kkA 1996 ls 2015 dh vof/k esa] 'kgjh tula[;k esa 17-1 djksM+ dh o`f) gqbZA 2011 dh tula[;k ds vkadM+ksa ds vuqlkj] 'kgjh tula[;k dk vuqeku yxHkx 37-7 djksM+ yxk;k x;k Fkk tks fo’o esa nwljh lcls cM+h tula[;k gSA Hkkjr esa 'kgjksa vkSj uxjksa dh la[;k c<+ dj 7]933 gks xbZA egkuxjksa dh la[;k o"kZ 2001 esa 35 Fkh tks o"kZ 2011 esa c<+dj 52 gks xbZ tgka dqy 'kgjh

10tula[;k ds yxHkx 43 izfr’kr yksx gSaA blh vof/k ds nkSjku uxjksa dh la[;k c<+dj 2]532 'kgj gks xbZA

Û

Û

Û

Û

Û

Û

Û

Û

Û

10 Hkkjr esa vkokl dh fLFkfr] lkaf[;dh ladyu 2013] ,e,p;wih,

22

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

'kgjksa vkSj uxjksa dh la[;k esa bl rst o`f) ds dkj.k vkokl laca/kh leL;k,a c<+ xbZaA 'kgjh vkokl deh ij xfBr rduhdh lewg }kjk 12oha iapo"khZ; ;kstuk ¼2012&17½ esa 1-88 djksM+ bdkbZ;ksa dh deh dk vuqeku

11yxk;kA bl deh dk C;ksjk uhps rkfydk esa n’kkZ;k x;k gSA

rkfydk la- 2-2% 'kgjh {ks=ksa esa vkokl dh deh ds dkj.k

lzksr% 'kgjh vkokl deh ij rduhdh xzqi dh fjiksVZ ¼Vhth&12½¼2012&17½] 2011 vkSj okf"kZd fjiksVZ 2016&17] ,e,p;wih,

122-1-2-1 jktho vkokl ;kstuk

jktho vkokl ;kstuk dks o"kZ 2011 esa 'kq: fd;k x;k Fkk vkSj fØ;kUo;u ds fy;s bls nks pj.kksa esa cuk;k x;kA pj.k 1 ¼twu 2011&13½] rS;kjh okyk pj.k Fkk vkSj pj.k 2 ¼2013 ls 2022½ fØ;kUo;u okyk pj.k FkkA bl ;kstuk dk mÌs’; ̂Lye eqDr Hkkjr^ dk Fkk tgka 'kgjksa ds leku lqfo/kk,a miyC/k gksaxh rFkk tgka lHkh ukxfjdksa dks ,d csgrj vkokl ds lkFk cqfu;knh flfod rFkk lkekftd lsok,a miyC/k gksaxhA ;kstuk ds rgr jkT;ksa @dsUnz 'kkflr izns’kksa dks lHkh Lye {ks=ksa dks vkSipkfjd flLVe ds vanj ykus] ekStwnk vkSipkfjd flLVe dh dfe;ksa dks nwj djus ds fy;s dke djus gsrq izsfjr fd;k rkfd u, Lye u cus vkSj mfpr gLr{ksi djds 'kgjksa esa Hkwfe dh deh dh leL;k dks gy djsaA jktho vkokl ;kstuk vkjaHk gksus ij] ts,u,u;wvkj,e dh ch,l;wih vkSj vkbZ,p,lMhih ds rgr fdlh ubZ ifj;kstuk dks laLohd`r ugha fd;k x;k tcfd ekStwnk ifj;kstukvksa dks ;kstuk vuqlkj dsUnz ls lgk;rk izkIr gksrh jghA 12oha iapo"khZ; ;kstuk dh lekfIr rd] jktho vkokl ;kstuk 250 'kgjksa esa dke dj jgh gksxhA

2-1-2-1-1 jktho vkokl ;kstuk ds fØ;kUo;u esa dsUnz ls jkT;ksa@ dsUnz 'kkflr izns’kksa@ ;w,ych@ vU; dsUnzh; ,tsafl;ksa ls lgk;rk feyrh gSA ifjpkyukRed vk/kkj ij ;g fØ;kUo;u ds fy;s f}Lrjh; iz.kkyh viukrh gS & ̂lEiw.kZ 'kgj^ vk/kkj ij Lye&eqDr 'kgjh ;kstuk dkjZokbZ ¼,l,Qlhihvks,½ dh rS;kjh vkSj p;fur Lyeksa ds fy;s ̂lEiw.kZ Lye^ vk/kkj ij foLr`r ifj;kstuk fjiksVsZa ¼Mhihvkj½ rS;kj djrh gSA ,l,Qlhihvks, dh lq/kkjkRed vkSj fujks/kkRed igy gSA lq/kkjkRed igy ds rgr] ,d izfØ;k ds rgr fodklkRed fodYiksa dks rS;kj fd;k tkrk gS ftlesa Lyeksa dh igpku djuk] eSi cukuk] izksQkby rS;kj djuk] iz;ksT;rk dk fo’ys"k.k fd;k tkrk gS vkSj vkokl ,oa cqfu;knh dfe;ksa ds vk/kkj ij izkFkfedrk fu/kkZfjr dh tkrh gSA fujks/kkRed igy ds rgr vkiwfrZ fodYiksa] vkoklksa dh deh ds ewY;kadu ds vk/kkj ij fopkj fd;k tkrk gS rkfd u, Lye u cusA Mhihvkj rS;kj djrs le; lexzrk ds vk/kkj ij vFkkZr LokLF;] f’k{kk] lkekftd lqj{kk] vkthfodk vkSj 'kgjh ukxfjd cqfu;knh lqfo/kkvksa ls lEc)rk dks /;ku esa j[kk tkrk gSA Mhihvkj esa vk/kkjHkwr flfod cqfu;knh <kaps vkSj lkekftd lqfo/kkvksa tSls tykiwfrZ] lhojst] ukfy;ksa] Bksl dpjk izca/ku igy] vanj dh lM+dksa] lM+dksa ij ykbfVax vkSj lkeqnkf;d lqfo/kkvksa ;Fkk izh&Ldwy] f’k’kq ns[kHkky dsUnzksa] LokLF; dsUnzksa@mi&dsUnzksa] vkthfodk dsUnzksa vkfn dks Hkh 'kkfey fd;k tkrk gSA

11 Hkkjr esa vkokl dh fLFkfr] lkaf[;dh ladyu 2013] ,e,p;wih,12 ,e,p;wih, osclkbV vkSj vkj,okbZ fn’kkfunsZ’k nLrkost] ,e,p;wih,

'kgjh {ks=ksa esa vkokl dh deh & dkj.k bdkbZ;ka ¼djksM+½

lqfo/kk ghu dPps ?kjksa esa jgus okys ifjokj 0-10

ttZj edkuksa esa jgus okys ifjokj 0-23

?kuh cLrh ds ?kjksa ftUgsa u, cukus dh t:jr gS] esa jgus okys ifjokj 1-50

cs?kj fLFkfr esa jgus okys ifjokj 0-05

dqy 'kgjh vkoklksa dh deh ¼2012&2017½ 1-88

2012&2017 dh vof/k esa bZMCY;w,l vkSj ,yvkbZth Jsf.k;ksa esa 'kgjh vkokl esa 1-80dqy deh 96 izfr’kr

23

vè;k; 2 % Hkkjr esa vkokl jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

13 okf"kZd fjiksVZ 2016&17 ,e,p;wih,

2-1-2-1-2 ;kstuk ds rgr edkuksa ds Vkbi esa 'kkfey gSa] Lye fuokfl;ksa ftuds ikl iDds edku ugha gS] ds fy;s u, edku] ekStwnk edkuksa esa mUu;u ;Fkk vfrfjDr dejk cukuk ;k 'kkSpky; cukuk] tykiwfrZ vkSj lQkbZ O;oLFkk djukA ;g lqfo/kk mu ?kjksa ds fy;s gS ftudk {ks=Qy 21&27 oxZ ehVj gSA fdjk;s ds edku ,d vU; fodYi gS tks Lye fuokfl;ksa] Jfedksa] 'kgjh xjhcksa vkSj vU; izoklh yksxksa ds fy;s miyC/k gSA csgrj fuxjkuh vkSj dk;kZUo;u ds fy;s vkoklh; bdkb;ksa ds fuekZ.k esa ykHkkfFkZ;ksa dks 'kkfey djus dk izko/kku gSA ykHkkfFkZ;ksa dks vf/kdre pkj fdLrksa esa /ku miyC/k djk;k tkrk gS& 'kq:vkr djus ij 10 izfr’kr] dqlhZ {ks= ¼fIyaFk½ ij 30 izfr’kr] Nr ysoy rd igaqpus ij 40 izfr’kr] vkSj iwjk gksus ij 20 izfr’kr jkf’k nh tkrh gSA ;g dk;Z ;w,ych] vkokl cksMksZa ;k fodkl izkf/kdj.kksa ds ek/;e ls fd;k tkrk gSA izLrko fd;k x;k gS fd izR;sd Lrj ij lkeqnkf;d Hkkxhnkjh gks rkfd yksxksa dh lgHkkfxrk vkSj lkeqnkf;d LokfeRo lqfo/kktud gks rFkk ;kstuk pyrh jgsA

2-1-2-1-3 jktho vkokl ;kstuk }kjk 'kgjh vfHk’kklu esa {kerkvksa dks mUur djds] ekSfnzd fuiq.krk] Hkwfe cSad cukus] lLrs edku cukus dh izfdz;k dks ljy djuk] Iykfuax vkSj vof/k dh lqj{kk c<+kdj lq/kkj djuk gSA dqN izdkj ds lq/kkj vfuok;Z gSa] buesa 'kkfey gSa &

Lye okfl;ksa tks 5 o"kZ ls vf/kd le; ls fuokl dj jgs gksa] dks nh?kZdkyhu iV~Vk vf/kdkj nsuk ftldk uohudj.k gks lds] ftlds fy;s 'kiFk i= vkSj bPNki= fy;k tk,A

bZMCY;w,l@,yvkbZth Jsf.k;ksa ds fy;s vkokl bdkb;ksa dk 35 izfr’kr ;k fjgk;’kh ,Q,vkj@,Q,lvkbZ ds 15 izfr’kr ls vf/kd vkj{k.k gks rFkk lHkh Hkkoh vkokl ifj;kstukvksa esa ,e,p;wih, }kjk izLrkfor fn’kkfunsZ’kksa ds vuqlkj ØkWl lfClMkbts’ku dh O;oLFkk gksA

uxjikfydk ctV esa 'kgjh xjhcksa dks cqfu;knh lqfo/kkvksa ds fy, 25 izfr’kr fu/kkZfjr djukA

;kstuk vof/k ds nkSjku lkekftd@lkeqnkf;d fodkl vkSj 'kgjh xjhch mUewyu ds fy;s ,d uxjikfydk dSMj cukuk vkSj LFkkfir djukA

2-1-2-1-4 jktho vkokl ;kstuk ds Hkkx Lo:i] lLrs edkuksa dh miyC/krk c<+kuk ^Hkkxhnkjh ds lkFk lLrs vkokl^ ¼,,pih½ ds ek/;e ls laHko gks ldsxkA blds rgr bZMCY;w,l@,yvkbZth bdkb;ksa dh Jsf.k;ksa ds fy;s 75]000 #i;s dh dsUnzh; lgk;rk izkIr gksxhA fdQk;rh vkokl ifj;kstukvksa esa vUn:uh fodkl ds fy;s vusd izdkj dh Hkkxhnkjh] futh Hkkxhnkjh lfgr] dh tk,xhA ,,pih ds rgr ifj;kstukvksa esa de ls de 250 vkokl bdkbZ;ka gksuh pkfg,A ,Q,vkj@,Q,lvkbZ dk de ls de 60 izfr’kr vkokl bdkb;ksa ds fy;s iz;ksx fd;k tk,xk ftudk dqlhZ {ks= 60 oxZ ehVj ls vf/kd ugha gksA

132-1-2-2 iz/kkuea=h vkokl ;kstuk & 'kgjh ¼ih,e,okbZ&’kgjh½

2-1-2-2-1 iz/kkuea=h vkokl ;kstuk & 'kgjh ¼ih,e,okbZ&’kgjh½ dh ?kks"k.kk 25 twu] 2015 dks dh xbZA ljdkj dh rRdkyhu jktho vkokl ;kstuk dk;Zdze dks ih,e,okbZ&’kgjh esa 'kkfey dj fn;k x;kA bl dk;ZØe dks 17 twu] 2015 ls 31 ekpZ] 2022 rd dk;kZfUor djuk gS vkSj 'kgjh xjhcksa vkSj Lye fuokfl;ksa ds fy;s tux.kuk 2011 esa lwphc) 4041 lkafof/kd uxjksa esa nks lkS yk[k bdkbZ;ka fuekZ.k djus dk y{; gSA dk;ZØe ds rgr] 'kgjh {ks=ksa esa vkoklh; cqfu;knh <kapk pkj fo’ks"k fu;ksftr mik;ksa }kjk rS;kj fd;k tk,xk tks bl izdkj gSa & d- izkbosV fodkldksa dh Hkkxhnkjh ls Lye iquokZl ftlesa Hkwfe dks lzksr ds :i esa iz;ksx fd;k tk,xk] [k- lLrs edkuksa ds fodkl ds fy;s _.k lgc) lfClMh nsuk] x- lLrh vkoklh; ifj;kstuk ds fodkl gsrq lkoZtfud {ks= vkSj futh {ks= ls Hkkxhnkjh djuk vkSj ?k- ykHkkfFkZ;ksa dks vkokl fuekZ.k vkSj mUu;u ds fy;s lfClMh nsukA

Û

Û

Û

Û

24

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

25

2-1-2-2-2 ih,e,okbZ&’kgjh esa Hkh _.k lgc) lfClMh dk izko/kku dsUnzh; lsDVj dh ;kstuk ds :i esa gS] blds rgr bZMCY;w,l@,yvkbZth Jsf.k;ksa ds fy;s edku [kjhnus vkSj edku fuekZ.k gsrq fy;s x, vkokl _.k ij C;kt esa lfClMh nh tkrh gSA ;gka ;g mYys[k djuk vko’;d gS fd ekuuh; iz/kkuea=h us 31 fnlEcj] 2016 dks jk"Vª ds uke vius lEcks/ku esa ;g Hkh dgk Fkk fd bl ;kstuk esa ,evkbZth Js.kh Hkh 'kkfey gSA ;kstuk ds rgr] ,d ykHkkFkhZ ifjokj esa ifr] iRuh vkSj vfookfgr cPps 'kkfey gSaA ykHkkFkhZ ifjokj dk u rks vius ;k vius ifjokj ds fdlh lnL; ds uke Hkkjr ds fdlh Hkh Hkkx esa iDdk edku ¼lHkh ekSle ;ksX; edku½ ugha gksuk pkfg,A bZMCY;w,l@,yvkbZth Jsf.k;ksa ds ykHkkfFkZ;ksa ij ykxw ekunaM uhps rkfydk esa fn;s x;s gSa%

rkfydk la- 2-3 % lh,y,l,l ds rgr bZMCY;w,l@,yvkbZth Jsf.k;ksa ds ykHkkfFkZ;ksa ij ykxw ekunaM

2-1-2-2-3 jkT;ksa@dsUnz’kkflr izns’kksa dks Hkh dqN vfuok;Z 'krksZa dks iwjk djuk gksrk gS tSls vkoklh; tksuksa ds fy;s vyx xSj d`f"k vuqefr dh t:jr dks gVkuk] lLrs vkoklksa ds fy;s Hkwfe dk fu/kkZj.k djuk] ,dy&foaMks le;c) Lohd`fr] Hkkoh Hkou fuekZ.k dh vuqefr vkSj bZMCY;w,l@,yvkbZth vkokl ds fy, ysvkmV laLrqfr] ekStwnk fdjk;k dkuwuksa esa la’kks/ku] vfrfjDr ,Q,vkj@,Q,lvkbZ@VhMhvkj vkSj Lye fodkl vkSj fuEu ykxr ds vkokl ds fy;s ?kuRo ekunaMksa esa <hy nsukA

14 2-1-2-2-4 ;Fkk 31 fnlEcj] 2016 dks ih,e,okbZ&;w ds rgr gqbZ izxfr uhps n’kkZbZ xbZ gS %

29 jkT;ksa vkSj 5 dsUnz’kkflr izns’kksa ds lkFk 34 djkj Kkiuksa ij gLrk{kj fd;s x;s gSaA

bl dk;ØZ e e as 'kkfey dju s d s fy; s 34 jkT;k as vkjS dUs n’z kkflr inz ’s kk as e as 3]619 'kgjk as dk p;u fd;k x;kA

1]808 'kgjksa esa bZMCY;w,l Js.kh ds fy;s 2]874 ifj;kstukvksa esa 14-7 yk[k edkuksa ds fuekZ.k dks fe’ku ds rgr ljdkj }kjk Lohd`fr iznku dh xbZA

14-70 yk[k edkuksa ds fuekZ.k dk;Z iwjk gksus esa yxHkx 23]239 djksM+ #i;s dh dsUnz ljdkj ls lgk;rk feysxhA blesa ls dsUnzh; lgk;rk ds :i esa 6]478 djksM+ #- dh jkf’k lacaf/kr jkT;ksa dks vuqeksfnr ifj;kstukvksa ds fy;s tkjh dj nh xbZ gSA

Û

Û

Û

Û

14 ,e,p;wih, izxfr fjiksVZ

C;ksjk lh,y,l,l&bZMCY;w,l lh,y,l,l&

1- ykHkkFkhZ ifr $ iRuh vfookfgr cPps

2- ifjokj dh vk; 3]00]000 #i;s rd 3]00]001&6]00]000 #i;s rd

3- dqlhZ {ks= ¼oxZ ehVj½ 30 60

4- vf/kdre _.k jkf’k ftl ij C;kt 6]00]000 #i;s lfClMh miyC/k gS

5- lEifRr dk LFkku tux.kuk 2011 ds vuqlkj lHkh lkafof/kd 'kgj rFkk ckn esa

vf/klwfpr 'kgj

6- iDds edku ij iz;ksT;rk uohuhdj.k@mUu;u ds fy;s ugha

7- efgyk LokfeRo@lg LokfeRo ekStwnk ds fy;s ugha vkSj u;k ysus ds fy, okafNr

8- mi;qDr dk;Z izfØ;k ih,yvkbZ izfØ;k ds vuqlkj

9- ik= _.k jkf’k ih,yvkbZ }kjk ykxw uhfr ds vuqlkj

10- igpku izek.k ;Fkk mfYyf[krA vk/kkj uEcj dks izkFkfedrk

11- vuqikyu vuqeksnu] cqfu;knh flfod cqfu;knh <kapk vkSj ,uchvks] chvkbZ,l rFkk ,uMh,e,] vafre iz;ksx

,yvkbZth

$

vè;k; 2 % Hkkjr esa vkokl jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

15- lhvkjth,Q,yvkbZ,p fn’kkfunsZ’k] okf"kZd fjiksVZ 2016&17] ,e,p;wih,16- ts,u,u;wvkj,e & fn’kkfunsZ’k o VwyfdV] okf"kZd fjiksVZ 2016&17] ,e,p;wih,

Û

Û

Û

Û

Û

Û

Û

Û

Û

14-7 yk[k edkuksa esa ls 2-4 yk[k ?kjksa dks u, fuekZ.k ds fy;s rksM+ fn;k x;k vkSj 44]103 ?kjksa dk fuekZ.k dk;Z iwjk gks x;kA

lh,y,l,l ds rgr] dqy 17]634 nkoksa ds fy;s 316-2 djksM+ #- dh jkf’k laforfjr dj nh xbZA

ih,e,okbZ&’kgjh ds rgr izkS|ksfxdh lc&fe’ku ij] 31 fnlEcj] 2016 rd X;kjg ubZ izkS|ksfxfd;ksa dks viukus ds fy;s fu/kkZfjr dj fn;k x;k gSA

fiNyh jktho vkokl ;kstuk ds rgr 183 ifj;kstukvksa ds izfr nkf;Ro] tks fofHkUu jkT;ksa esa 'kq: gks pqdh Fkha] ih,e,okbZ&’kgjh esa 'kkfey dj fn;k x;kA vizSy 2016 ls fnlEcj 2016 vof/k ds nkSjku] 13]881 vkokl bdkbZ;ksa dk fuekZ.k iwjk gks x;k rFkk 9]940 ij ykHkkfFkZ;ksa dks dCtk ns fn;k x;kA

15 2-1-2-3 fuEu vk; vkokl ds fy;s _.k tksf[ke xkjaVh fuf/k ;kstuk

2-1-2-3-1 fuEu vk; vkokl ds fy;s _.k tksf[ke xkjaVh fuf/k ;kstuk ¼lhvkjth,QVh½ dh LFkkiuk dks dsUnz ljdkj ds eaf=eaMy }kjk 12oha iapo"khZ; ;kstuk ds rgr 1]000 djksM+ #- dh 'kq:vkrh jkf’k ds lkFk laLohd`fr ns nh xbZA ;kstuk ds rgr] U;kl bZMCY;w,l rFkk ,yvkbZth Jsf.k;ksa ds yksxksa dks 8 yk[k #- rd _.kksa ds fy;s fdlh r`rh; i{k dh xkjaVh ;k laikf’oZd izfrHkwfr ds fcuk _.knkrk laLFkkuksa dks _.k tksf[ke xkjaVh iznku djsxkA ;g /;ku fn;k tk, fd ;kstuk ds rgr x`g _.k dh lhek 15 yk[k #- gS] fdarq xkjaVh dsoy 8 yk[k #- dh miyC/k gksxhA 71 cSadksa] vkokl foRr daifu;ksa vkSj ,uch,Qlh us lhvkjth,Q U;kl ds lkFk le>kSrk Kkiu ij gLrk{kj fd;s gSA U;kl us vHkh rd bZMCY;w,l rFkk ,yvkbZth ifjokjksa dks laforfjr 55-85 djksM+ #- ds _.kksa ds fy;s 1]970 vkokl _.kksa ds fy;s xkjaVh doj fn;k gSA jk"Vªh; vkokl cSad fuf/k U;kl dk izca/ku dj jgk gSA

162-1-2-4 tokgjyky usg: jk"Vªh; 'kgjh uohdj.k fe’ku

2-1-2-4-1 ljdkj us tokgjyky usg: jk"Vªh; 'kgjh uohdj.k fe’ku ¼ts,u,u;wvkj,e½ dks 3 fnlEcj] 2005 dks 'kq: fd;k FkkA bl fe’ku dk iz;kstu 'kgjh xjhcksa@Lye fuokfl;ksa ds fy;s vkokl ,oa cqfu;knh lqfo/kk,a miyC/k djkus ds fy;s jkT; ljdkjksa dks lgk;rk iznku djuk FkkA 'kgjh xjhcksa dks cqfu;knh@ewyHkwr lqfo/kkvksa ¼ch,l;wih½ ds rgr lgk;rk ds fy;s 65 'kgjksa dks fpfUgr fd;k x;k tks ts,u,u;wvkj,e ds rgr ,d mi&fe’ku FkkA vU; 'kgjksa vkSj uxjksa ds fy;s] lesfdr vkokl ,oa Lye fodkl dk;ZØe ¼vkbZ,p,lMhih½ ds rgr lgk;rk iznku dh tk,xhA bl fe’ku dh vof/k 2005&06 ls 7 o"kZ Fkh ftls 31 ekpZ] 2017 rd c<+k fn;k x;k rkfd py jgh ifj;kstukvksa dk dke iwjk gks lds ftUgsa 31 ekpZ] 2012 rd eatwjh nh xbZ FkhA

2-1-2-4--2 vkJ; miyC/k djkus ds fy;s fofHku ifj;kstukvksa ds ek/;e ls] fe’ku dk /;ku Lyeksa dk lesfdr fodkl djus dh vksj gS] tgka 'kgjh xjhcksa dks cqfu;knh lqfo/kk,a vkSj lacaf/kr flfod lqfo/kk,a miyC/k djkbZ tk ldsaA fe’ku ds ch,l;wih dk;ZØe ds rgr mÌs’; tSls fd fe’ku VwyfdV esa ifjHkkf"kr fd;k x;k gS] fuEukuqlkj gSa %

'kgjh xjhcksa ds fy;s cqfu;knh lqfo/kkvksa ds lesfdr fodkl ij /;ku dsfUnzr djukA

de dher dks dk;Zdky esa cuk, j[kuk] mUur vkokl] tykiwfrZ] lQkbZA

f’k{kk] LokLF; vkSj lkekftd lqj{kk ds {ks= esa lsok,a miyC/k djkukA

'kgjh xjhcksa dks dk;Z LFky ds lehi] ;Fkk laHko] vkokl miyC/k djkukA

vkfLr l`tu vkSj vkfLr izca/ku ds chp izHkkoh laca/k cukuk rkfd dk;Z{kerk lqfuf’pr gksA

26

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

17- 'kgjh fodkl ,oa 'kgjh vkokl foHkkx] xqtjkr] lEesyu izLrqrhdj.k

Û

Û‘

Û

Û

Û

Û

Û

Û

Û

Û

Û

ckWDl 2-1 % xqtjkr

'kgjh xjhcksa dh ewyHkwr lqfo/kkvksa esa dfe;ksa dks nwj djus ds fy;s i;kZIr fuos’k lqfuf’pr djukA

2-1-2-4-3 mÌs’; ftu ij fe’ku lesfdr vkokl vkSj Lye fodkl dk;ZØe ¼vkbZ,p,lMhih½ ;kstuk ds rgr /;ku nsrk gS] fuEukuqlkj gSa %

lexz Lye fodkl vkSj lewg igaqp

LokLF;izn vkSj mi;qDr 'kgjh okrkoj.k vkSj

Lye fuokfl;ksa ds fy, i;kZIr vkJ; vkSj cqfu;knh lqfo/kk,a

fnlEcj 2016 rd fe’ku ds rgr izxfr fuEukuqlkj gS %

ch,l;wih ds rgr 62 'kgjksa vkSj vkbZ,p,lMhih ds rgr 877 'kgjksa dks 'kkfey fd;k x;k gSA

ch,l;wih ds rgr] 62 'kgjksa esa py jgh 478 ifj;kstukvksa dh dqy ykxr 23]126 djksM+ #- ls 7-89 yk[k vkokl bdkbZ;kas ds fuekZ.k gsrq laLohd`fr nh xbZ gSA

vkbZ,p,lMhih ds rgr] 877 'kgjksa esa 1030 ifj;kstukvksa dh dqy ykxr 9]592 djksM+ #- ls 4-52 yk[k vkokl bdkbZ;kas ds fuekZ.k gsrq laLohd`fr nh xbZ gSA

12-41 yk[k vuqeksfnr vkoklksa esa ls] 10-56 yk[k vkoklksa dk fuekZ.k fd;k tk pqdk gS vkSj buesa ls 8-86 yk[k vkoklksa dk ykHkkfFkZ;ksa }kjk dCtk ys fy;k x;k gSA 1-59 yk[k vkokl bdkbZ;ka fuekZ.kk/khu gSaA

ts,u,u;wvkj,e ¼ch,l;wih ,oa vkbZ,p,lMhih½ dss rgr ifj;kstukvksa ds fy;s jkT;ksa@dsUnz’kkflr izns’kksa dks dsUnzh; fgLlsnkjh dh jkf’k 17]907 djksM+ #- laforfjr dh tk pqdh gSA

vizSy 2016 ls fnlEcj 2016 rd vof/k ds nkSjku] ch,l;wih vkSj vkbZ,p,lMhih ds rgr 47]735 vkoklh; bdkbZ;ksa dk fuekZ.k iwjk gks pqdk gS vkSj fiNys o"kZ ds [kkyh iM+s vkoklksa lfgr 79]197 vkoklksa dks dCtk/khu fd;k tk pqdk gSA

2-2-5 vkokl {ks= esa jkT; Lrjh; igysa

jkT; ljdkjksa us vius Lrj ij viuh uhfr;ksa vkSj dk;ZØeksa ds ek/;e ls vkokl miyC/k djkus ds fy;s vusd igysa dh gSaA ;s uhfr;ka vkSj dk;ZØe dsUnz ljdkj dh uhfr;ksa vkSj dk;ZØeksa ds vuq:i gksaxs ;k muds iwjd gksaxsA dqN jkT;ksa ds jkT; Lrjh; dk;ZØe uhps ckDlksa esa fn;s x;s gSaA

17eq[; ea=h x`g ;kstuk

bZMCY;w,l@,yvkbZth Jsf.k;ksa ds fy;s vkokl bdkbZ;ksa dh ek=k c<+kus dh vksj fo’ks"k /;ku nsus vkSj fdQk;rh edkuksa ds fuekZ.k dk;Z esa futh {ks= dh Hkkxhnkjh dks Hkh c<+kus ds fy;s] xqtjkr ljdkj us o"kZ 2013 esa eq[; ea=h x`g ;kstuk ¼,e,ethokbZ½ vkjaHk dhA ;kstuk ds rgr ykHkkfFkZ;ksa ds fy, bdkbZ;ksa dk dqlhZ {ks= bZMCY;w,l Js.kh ds fy, 30 oxZ ehVj] ,yvkbZth&1 Js.kh ds fy;s 40 oxZ ehVj] ,yvkbZth&2 Js.kh ds fy, 50 oxZ ehVj vkSj ,evkbZth Js.kh ds fy, 65 oxZ ehVj gksxkA ,e,ethokbZ ds rgr fofHkUu uhfrxr igysa bl izdkj gSa %

ukxfjd lqfo/kk,a eqgS;k djkuk vkSj 'kgjh xjhcksa dh loZ= igqqap esa lsokvksa dh vksj /;ku nsuk vkSj

27

vè;k; 2 % Hkkjr esa vkokl jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

18- 'kgjh fodkl ,oa 'kgjh vkokl foHkkx] xqtjkr]] fdQk;rh vkokl uhfr19- jkT; esa vPNs dk;ksZ dk ladyu] 2015] ,e,p;wih,

18fdQk;rh vkokl fe’ku 2014 %

Lye iquokZl uhfr 2013 %

,yvkbZth ds fy;s fdQk;rh vkokl gsrq iwathxr lfClMh %

bl fe’ku dss rgr jkT; ljdkj us ikap o"kZ esa 50 yk[k vkokl fuekZ.k dh ;kstuk rS;kj dh gSA buesa ls 22 yk[k edku 'kgjh {ks=ksa esa cuk, tk,axsA bl ;kstuk ds Hkkx Lo:i] bZMCY;w,l@,yvkbZth&1 o 2 rFkk ,evkbZth&1 Jsf.k;ksa ds rgr vkus okys ykHkkfFkZ;ksa dks fdQk;rh ewY; ij cqfu;knh lqfo/kkvksa ls ;qDr HkyhHkkafr fufeZr edku feysaxsA ifj;kstukvksa ij futh {ks= vkSj xqtjkr vkokl cksMZ ds chp lgHkkfxrk ls dke gksxkA futh {ks= dks izksRlkgu nsus ds fy,] ftu Hkw[kaMksa ij oguh; Jsf.k;ksa ds vkoklksa dk fuekZ.k fd;k tk,xk os 3 rd ,Q,lvkbZ ds fy, ik= gksaxsA dqy Hkwfe esa ls tks iz;ksx gsrq miyC/k gksxh] oguh; vkoklksa ds fy, fpfUgr Hkwfe ls vfrfjDr Hkwfe ij fodkld fdlh Hkh izdkj dk fuekZ.k djkus ds fy, Lora= gksxk ftlesa dqy fufeZr {ks= ds 10 izfr’kr rd okf.kfT;d fuekZ.k djk ldsxkA

Û bl ;kstuk esa Lo&LFkkus ij Lye iquokZl dh lqfo/kk gksxhA bldk edln bZMCY;w,l Js.kh ds fy;s oguh; vkokl dh lqfo/kk iznku djuk gSA bl ;kstuk dk fØ;kUo;u xqtjkr 'kgjh fodkl fe’ku ds vUrxZr fofHkUu uxjikfydkvksa] uxj fuxeksa] {ks=h; fodkl izkf/kdj.kksa vkSj xqtjkr vkokl cksMZ }kjk fd;k tk jgk gSA bdkbZ dk {ks= 25 ls 30 oxZ ehVj gksxk ftlesa nks dejs] jlksbZ] Lukukxkj vkSj 'kkSpky; gksxkA bl fHkUu izdkj dh ihihih ;kstuk ds rgr] futh {ks= dks VhMhvkj ds }kjk Hkkx ysus ds fy;s izksRlkfgr fd;k x;k gSA ljdkj ls foRr iksf"kr ;kstuk ds rgr] foRr iks"k.k esa dsUnz ljdkj] jkT; ljdkj@;w,ych vkSj ykHkkfFkZ;ksa ds chp 50 izfr’kr] 38 izfr’kr vkSj 12 izfr’kr ds vuqikr esa Øe’k% fgLlsnkjh gksxhA ;kstuk ds vUrxZr 1]00]000 #- rd foRrh; lgk;rk dk izko/kku gSA

Û ,yvkbZth ds fy;s fdQk;rh vkokl gsrq iwathxr lfClMh % bl ;kstuk dk mÌs’; ,yvkbZth Js.kh ds fy, fdQk;rh vkokl esa lqfo/kk iznku djuk gSA ;kstuk ds rgr bdkbZ dk vkdkj 50 oxZ ehVj rd gks ldrk gSA ;g ;kstuk iw.kZr;k jkT; ljdkj }kjk foRr iksf"kr gSA ;kstuk ds vUrxZr 1]00]000 #- izfr bdkbZ rd foRrh; lgk;rk dk izko/kku gSA

19Û miyfC/k;ka %

å ,e,ethokbZ ds rgr mldh fofHkUu ifj;kstukvksa ds }kjk 4-71 yk[k ls vf/kd vkoklksa ij dke py jgk gS ftuesa ls 1-37 yk[k vkokl ykHkkfFkZ;ksa dks vkcafVr fd;s tk pqds gSaA

å yxHkx 1-16 yk[k vkoklksa dk fuekZ.k iwjk gks pqdk gSA

å yxHkx 60]500 vkoklksa dk <kapk iwjk cu pqdk gS] yxHkx 79]000 vkoklksa dk fuekZ.k dk;Z py jgk gS vkSj yxHkx 62]800 vkokl fufonk izfØ;k ds v/khu gSaA ;s lHkh dk;Z ,d o"kZ ds nkSjku fd;s x;s gSaA

å ihihih iz.kkyh ds rgr 54]000 vkoklksa esa ls Lye iquokZl ds fy, fu/kkZfjr fd;s x;s gSa] 1]000 ls vf/kd edkuksa dk fuekZ.k iwjk gks pqdk gS] 4]000 vkoklksa dk <kapk iwjk cu pqdk gS vkSj yxHkx 4]600 fuekZ.kk/khu gSaA

å fdQk;rh vkoklksa ds fy, 2]13]000 vkoklksa esa ls] 5]000 ls vf/kd vkokl fufeZr gks pqds gSa] 45]000 vkoklksa dk <kapk iwjk cu pqdk gS vkSj yxHkx 57]600 fuekZ.kk/khu gSaA

å Lo&LFkkus Lye iquokZl ;kstuk ds rgr] 2]04]000 ls vf/kd vkokl iquokZl ds fy;s rS;kj fd;s tk jgs gSaA vf/kdka’kr% dk dk;Z 2013&14 vkSj 2014&15 esa 'kq: fd;k x;kA 88]300 ls vf/kd Lye ifjokjksa dks iDds edkuksa esa iquokZflr fd;k tk pqdk gSA

Û

Lye iquokZl uhfr 2013 %

Û

Lye iquokZl uhfr 2013 %

18fdQk;rh vkokl fe’ku 2014 %

28

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

21 ;Fkk 31 fnlEcj] 2016 dks jkT; esa ih,e,okbZ&’kgjh ds rgr izxfr

20xjhc le`f) ;kstuk

bl ;kstuk dk mÌs’; 'kgjh xjhcksa dks vkoklksa dk LokfeRo iznku djuk gSA bl ;kstuk ds rgr 2]200 djksM+ #- dh jkf’k vkcafVr dh xbZ gSA 2]50]000 bdkb;ksa dk fuekZ.k izLrkfor gSA ;kstuk esa fufeZr izFke vkokl dh Lokfeuh efgyk gksxhA ;kstuk ds vUrxZr ekStwnk bdkb;ksa esa vfrfjDr lqfo/kk,a iznku djuk gS vkSj ;gka cgq eaftyk bekjrsa gkasxhA

21 ;Fkk 31 fnlEcj] 2016 dks jkT; esa ih,e,okbZ&’kgjh ds rgr izxfr

Û bl dk;ZØe ds rgr jkT; esa 171 'kgjksa dk p;u fd;k x;k gSA

Û fe’ku ds rgr 49 'kgjksa esa bZMCY;w,l Js.kh ds fy;s 163 ifj;kstukvksa esa 1]33]347 vkokl fuekZ.k dks Lohd`fr iznku dh xbZ gSA

Û 1]33]347 vkokl fuekZ.k ds fy;s dsUnzh; lgk;rk ds :i esa 1]806 djksM+ #- dk vuqeku yxk;k x;k gSA bl jkf’k esa ls] dsUnzh; lgk;rk ds 695 djksM+ #- jkT; ljdkj dks vuqeksfnr ifj;kstukvksa ds fy, tkjh fd;s tk pqds gSaA

Û 1]33]347 vkoklksa esa ls] 58]824 edkuksa dks uo fuekZ.k ds fy;s fxjk;k x;k vkSj 9]070 vkoklksa dk fuekZ.k dk;Z iwjk gks pqdk gSA

jkT; esa vkokl deh dks nwj djus ds fy,] 'kgjh fodkl vkokl foHkkx vkSj LFkkuh; Lo’kklh ljdkj] jktLFkku us ,d ubZ uhfr & eq[; ea=h tu vkokl ;kstuk&2015 'kq: dhA bl uhfr dh eq[; fo’ks"krk ;g gS fd jkT; esa bZMCY;w,l@,yvkbZth vkokl esa futh {ks= dh Hkkxhnkjh dks c<+kok nsus ds fy;s vusd izko/kku fd;s x;s gSa] blds vfrfjDr vkokl cksMZ] fodkl izkf/kdj.kksa] fodkl U;klksa vkSj 'kgjh LFkkuh; fudk;ksa dh Hkkxhnkjh Hkh gksxhA

22eq[;ea=h tu vkokl ;kstuk&2015

eq[;ea=h tu vkokl ;kstuk&2015 ds eq[; y{; uhps fn;s x;s gSa %

Û jkT; esa bZMCY;w,l@,yvkbZth Js.kh esa vkoklksa dh deh dks nwj djus ds fy, ^lc ds fy, fdQk;rh vkokl^ dk y{; izkIr djukA

Û lekt esa bZMCY;w,l@,yvkbZth oxZ ds fy;s futh fodkldksa dks izksRlkgu nsdj vkoklksa ds fuekZ.k esa futh fuos’k djus ds fy, vkdf"kZr djukA

Û fdQk;rh vkoklksa ds fuekZ.k dk;Z dks djus ds fy, ljdkjh ,tsafl;ksa vkSj futh fodkldksa dks c<+kok nsukA

Û fdQk;rh vkokl ds fy;s Hkwfe dh igpku djuk ftls cM+s vk/kkj ij futh Hkkxhnkjh dks c<+kok nsdj fd;k tk ldrk gSA

Û 'kh?kzrk ds lkFk laLrqfr lqfo/kk nsdj fuekZ.k fodkldksa dh izfØ;k esa rsth ykukA

jkT; ljdkj us bl dk;ZØe ds rgr fodkl ds fuEufyf[kr izk:iksa ds fy, foLr`r fn’kkfunsZ’k rS;kj fd;s gSa &

Û ;w,ych@;wVhvkbZ@fodkl izkf/kdj.k@vkj,pch vkSj futh fodkldksa dh vkoklh; ;kstukA

ckWDl 2-2 % jktLFkku

20- 'kgjh fodkl ,oa 'kgjh vkokl foHkkx] xqtjkr] lEesyu izLrqrh21- ,e,p;wih,] izxfr fjiksVZ22- eq[; ea=h tu vkokl ;kstuk] 2015] uhfr nLrkost 29

vè;k; 2 % Hkkjr esa vkokl jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

Û futh Hkwfe ij izkbosV fodkldksa }kjk Hkkxhnkjh esa oguh; vkoklksa dk fodklA

Û futh Hkwfe ij futh fodkldksa }kjk gh bZMCY;w,l@,yvkbZth ¶ySVksa dk fuekZ.k ¼¶ySV] Hkwry o 3 çk:i ½A

Û futh Hkwfe ij futh fodkldksa }kjk gh bZMCY;w,l@,yvkbZth ¶ySVksa dk fuekZ.k ¼Hkwry o 3 ry ds lkFk IykV rS;kj djuk½

Û Hkwry o 3 eafty vkSj cgq eafty bekjr esa futh Hkou fuekZrk }kjk ljdkjh Hkwfe ij bZMCY;w,l@,yvkbZth vkoklksa dk fuekZ.k djukA

Û 1&3 yk[k vkcknh okys 'kgjksa esa futh fodkldksa }kjk ljdkjh Hkwfe ij fdQk;rh vkoklksa dk fuekZ.kA

futh fodkldksa dks mPp ,Q,vkj vkSj VhMhvkj ds :i esa lqfo/kk nsdj vusd izdkj ls izksRlkgu fn;s tk jgs gSaaA buds vfrfjDr] mUgsa ljdkjh laLohd`fr] laLohd`fr dh QkLV&VªSfdax] Hkwfe ds ØkWl lfClMkbts’ku ds izHkkjksa ls NwV vkSj vkcafVr dqy Hkwfe {ks= ds 10 izfr’kr HkwHkkx dk okf.kfT;d iz;ksx djus vkSj ljdkj dh uksMy ,tsalh }kjk iwoZ fu/kkZfjr njksa ij ¶ySVksa dks okil [kjhnus dh Lohd`fr nh tk jgh gSA

23;Fkk 31 fnlEcj] 2016 dks jkT; esa ih,e,okbZ&;w ds rgr izxfr

Û bl dk;ZØe esa 'kkfey djus ds fy, jkT; esa 183 'kgjksa dk p;u fd;k x;kA

Û bl fe’ku ds rgr 31 'kgjksa esa bZMCY;w,l Js.kh ds fy;s 36]575 vkoklksa ds fuekZ.k gsrq 56 ifj;kstukvksa dks Lohd`fr iznku dh xbZ gSA

Û 670 djksM+ #- dh vuqekfur ykxr ls 36]575 vkoklksa ds fuekZ.k ds fy;s dsUnzh; lgk;rk dks eatwjh nh xbZA bl dsUnzh; lgk;rk jkf’k esa ls 329 djksM+ #- dh jkf’k jkT; ljdkj dks vuqeksfnr ifj;kstukvksa ds fy;s tkjh dj nh xbZA

Û 36]575 vkoklksa esa ls iqufuZekZ.k ds fy, 13]508 edkuksa dks fxjk;k vkSj 9]779 edku cu dj rS;kj gks x;sA

24'kgjh {ks=ksa esa lc ds fy, vkokl uhfr & vksfM'kk 2015

;g uhfr ftldh ?kks"k.kk vksfM'kk ljdkj }kjk dh xbZ] Hkkjr ljdkj dh ^^2022 rd lc ds fy, vkokl^^ dh o`f)r uhfr gSA 12oha iapo"khZ; ;kstuk ¼2012&2017½ esa ’kgjh vkokl deh ij rduhdh xzqi us vksfM'kk jkT; esa yxHkx 4-10 yk[k vkokl bdkbZ;ksa dh deh dk vuqeku yxk;kA bl la[;k esa] Hkqous’oj& dVd {ks= dh yxHkx 3-60 vkokl bdkbZ;ka tqM+ tk,axh D;ksafd vkxkeh n’kd esa bl {ks= esa vkfFkZd o`f) gks pqdh gksxhA vf/kd ekax bZMCY;w,l vkSj ,yvkbZth Jsf.k;ksa esa gksxhA uhfr esa varfuZfgr gh izksRlkgu ç.kkyh dks 'kkfey dj fn;k x;k gS ftlls futh fodkldksa lfgr lHkh i.k/kkjdksa dks vksfM'kk jkT; esa 'kgjh {ks=ksa esa bZMCY;w,l vkSj ,yvkbZth Js.kh ds vkoklksa dk fuekZ.k djus ds fy;s ikz Rs lkgu feyxs kA ljdkj }kjk vkjHa k e as 1]00]000 edkuk as dk fuek.Z k dju s dk y{; fu/kkfZ jr fd;k x;k gAS

uhfr ds rgr fuEufyf[kr igyksa ds }kjk vkokl fuekZ.k gksxk %

Û bZMCY;w,l vkoklksa dk fuekZ.k djuk vfuok;Z gSA

ckWDl 2-3 % vksfM'kk

23- ,e,p;wih, izxfr fjiksVZ 24- 'kgjh {ks=ksa esa lc ds fy, vkokl uhfr] vksfM'kk 2015

30

Hkkjr esa vkokl dh ço`fÙk ,oa çxfr fjiksVZ 2016jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

25- ,e,p;wih, izxfr fjiksVZ 26 egkjk"Vª jkT; ubZ vkokl uhfr ,oa dk;Z ;kstuk 2015

bZMCY;w,l vkSj ,yvkbZth ds vkokl fuekZ.k ds fy,] ljdkj cktkj vk/kkfjr ds fy, izksRlkgu nsrh gSA

Û fdQ;krh vkokl ifj;kstukvksa ds fuekZ.k dh vksj vf/kd /;ku nsukA

Û iqu% vkcaVu vkSj iquokZl

Û fdjk;k vkokl

Û ;Fkk LFkku Lye iqufoZdkl

Û ykHkkFkhZ mUeq[k oS;fDrd vkokl fuekZ.k ;k mUu;u

vksfM'kk vkokl uhfr dh vU; igyksa esa 'kkfey gSa & d½ lHkh izdkj dh vuqefr flaxy foaMks iz.kkyh ls gksxh] [k½ vkosndksa vkSj YkkHkkfFkZ;ksa dk iathdj.k vkWuykbu ck;kseSfVªd oS/krk ls gksxk] blds ckn nLrkostksa dh tkap gksxh] x½ vksfM'kk vkokl fe’ku mu vkosndksa dh lqfo/kk dsUnzksa ds ek/;e ls lgk;rk djsxk ftudh daI;wVj vkSj baVjusV rd igaqp ugha gS vkSj ?k½ lHkh ykHkkFkhZ iathd`r lfefr ds ifj;kstuk Lrj ij lnL; gksaxsA

2531 fnlEcj] 2016 rd ih,e,okbZ&’kgjh ds rgr izxfr

Û bl dk;ZØe esa 'kkfey djus ds fy, jkT; esa 112 'kgjksa dk p;u fd;k x;kA

Û bl fe’ku ds rgr 40 'kgjksa esa bZMCY;w,l Js.kh ds fy;s 46]626 vkoklksa ds fuekZ.k gsrq 63 ifj;kstukvksa dks Lohd`fr iznku dh xbZ gSA

Û 791 djksM+ #- dh vuqekfur ykxr ls 46]626 vkoklksa ds fuekZ.k ds fy;s dsUnzh; lgk;rk dks eatwjh nh xbZA bl dsUnzh; lgk;rk jkf’k esa ls 280 djksM+ #- dh jkf’k jkT; ljdkj dks vuqeksfnr ifj;kstukvksa ds fy;s tkjh dj nh xbZA

Û 46]626 vkoklksa esa ls fuZekZ.k ds fy, 4]025 edkuksa dks fxjk;k x;k vkSj 1]001 edku cu dj rS;kj gq,A

26egkjk"Vª jkT; ubZ vkokl uhfr vkSj dk;Z ;kstuk 2015

ubZ vkokl uhfr dh ?kks"k.kk jkT; ljdkj dh o"kZ 2022 rd 19 yk[k vkokl miyC/k djkus dh i`"BHkwfe esa dh xbZ ftlesa bZMCY;w,l] ,yvkbZth vkSj ,evkbZth vkokl dh vksj vf/kd /;ku fn;k tk,xkA bl uhfr ds rgr eqEcbZ egkuxj {ks= esa 11 yk[k vkoklksa vkSj bl {ks= ls 8 yk[k vkoklksa dk fuekZ.k djus dk y{; fu/kkZfjr fd;k x;kA bl ubZ uhfr dk mÌs’; ̂ ^lc ds fy, vkokl^^ FkkA bl mÌs’; ds vuq:i uhfr ds funsZ’kksa dk uhps n’kkZ;k x;k gS%

Û fdQk;rh vkoklksa ds fy;s Hkwfe cSad dk lrr l`tu ftlesa ljdkjh Hkwfe vkSj futh {ks= dh Hkwfe dks j[kk tk,xkA

Û cktkj esa fdQk;rh vkoklksa dh miyC/krk c<+kuk rkfd miHkksDrk dks fdQk;rh vkokl fey ldsaA

Û iqufoZdkl dks izksRlkgu nsdj miyC/k Hkwfe dk vf/kdre mi;ksxA

Û fuekZ.k

ckWDl 2-4 % egkjk"Vª

31

vè;k; 2 % Hkkjr esa vkokl jk"Vªh; vkokl cSadNATIONAL HOUSING BANK

27 ,e,p;wih, izxfr fjiksVZ

xhrkatfy

Û i;kZoj.k dk /;ku j[krs gq, thou dks mUur cukuk] thou Lrj esa lq/kkj djukA

Û dkjksckj djuk vklku cukukA

bl uhfr ds rgr vusd fo’ks"k mik;ksa dh ?kks"k.kk dh xbZ rkfd bZMCY;w,l@,yvkbZth oxksZa dh vkokl leL;k gy gks ldsA bl oxZ dh lgk;rk gsrq] egkjk"Vª vkokl ,oa {ks= fodkl izkf/kdj.k ¼EgkMk½ 1]000 djksM+ #- ds izkjfEHkd dks"k ds lkFk LFkkiuk djsxkA vkoklksa dh fcØh vkSj [kjhn ij LVkEi M~;wVh vkSj iathdj.k 'kqYd Hkh ?kVkdj bZMCY;w,l] ,yvkbZth vkSj ,evkbZth ds fy, Øe’k% 1 izfr’kr] 2 izfr’kr vkSj 3 izfr’kr dj fn;k x;kA U;wure iathdj.k 'kqYd 1]000 #- olwyk tk,xkA