Industry Internship and Report on “FMCG & LARGE CAP

75

Industry Internship and Report on “FMCG & LARGE CAP – FUND ANALYSIS FOR LONG TERM BENEFITS” BY Sumant Kumar 1NZ16MBA64 Submitted to DEPARTMENT OF MANAGEMENT STUDIES NEW HORIZON COLLEGE OF ENGINEERING, OUTER RING ROAD, MARATHALLI, BANGALORE In partial fulfillment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION Under the guidance of INTERNAL GUIDE EXTERNAL GUIDE Niviya Feston Nandakishore Appanaboyina Sr. Asst. Professor Dir. -Operations & Talent Acquisition 2016-2018

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Industry Internship and Report on “FMCG & LARGE CAP

Industry Internship and Report on

“FMCG & LARGE CAP – FUND ANALYSIS FOR LONG TERM

BENEFITS”

BY

Sumant Kumar

1NZ16MBA64

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BANGALORE

In partial fulfillment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

INTERNAL GUIDE EXTERNAL GUIDE

Niviya Feston Nandakishore Appanaboyina

Sr. Asst. Professor Dir. -Operations & Talent Acquisition

2016-2018

CERTIFICATE

This is to certify that Sumant Kumar bearing USN 1NZ16MBA64, is a bonfide student of

Master of Business Administration course of the Institute Batch 2016-2018, autonomous

program, affiliated to Visvesvaraya Technological University, Belgaum. Internship report

on “FMCG & LARGE CAP – FUND ANALYSIS FOR LONG TERM BENIFITS” is

prepared by him under the guidance of Niviya Feston (Sr. Asst. Professor), in partial

fulfillment of requirements for the award of the degree of Master of Business

Administration of Visvesvaraya Technological University, Belgaum Karnataka.

Signature of Internal Guide Signature of HOD Signature of Principal

DECLARATION

I, Sumant Kumar, hereby declare that the Internship report entitled “FMCG & LARGE

CAP – FUND ANALYSIS FOR LONG TERM BENIFITS” with reference to “Dvija

Digital Pvt. Ltd., Whitefield” prepared by me under the guidance of Niviya Feston (Sr.

Asst. Professor), faculty of M.B.A Department, New Horizon College of Engineering and

external assistance by Dr. Nandakishore Appanaboyina (Director-Operations and Talent

Acquisition), Dvija Digital Pvt. Ltd.

I also declare that this Internship work is towards the partial fulfillment of the university

regulations for the award of the degree of Master of Business Administration by

Visvesvaraya Technological University, Belgaum.

I have undergone an industry internship for a period of Twelve weeks. I further declare that

this report is based on the original study undertaken by me and has not been submitted for

the award of a degree/diploma from any other University / Institution.

Signature of Student

Place:

Date

ACKNOWLEDGEMENT

I Sumant Kumar take this opportunity to express my deep sense of gratitude and whole

hearted thanks along with my profound respect to all those who guided and inspired me in

the completion of project.

First of all I would like to extend my gratitude to our Principal, Dr. Manjunatha for giving

me the opportunity to prepare this project work.

I am thankful to the head of department, Dr. Sheelan Mishra for being the guiding light of

this project.

I am greatly indebted to my internal guide, Ms. Niviya Feston for extending her support

and valuable guidance, without which this project would have not possible.

Lastly, I appreciate the patience and support of my parents, teachers and friends for always

maintaining their faith in me, and have enriched my life with their knowledge and

guidance.

Above all, I would like to thank the amity for making this project a reality.

SUMANT KUMAR

1NZ16MBA64

TABLE OF CONTENTS

Chapter Title Page Nos.

Executive Summary

1 Theoretical Background of the study 1-7

2 Industry and Company Profile 8-41

3 Methodology 42-48

4 Data Analysis and interpretation 49-58

5 Summary of Findings, Suggestion and Conclusion 59-62

6 Learning Experience 63

Bibliography

Annexure

FORMAT OF LIST OF CHARTS AND TABLES

List of Charts

Fact Sheet

No. Particulars Page Nos.

Fact Sheet-4.1 Fact Sheet showing SBI FMCG Fund -

Direct Plan Growth Analysis 50

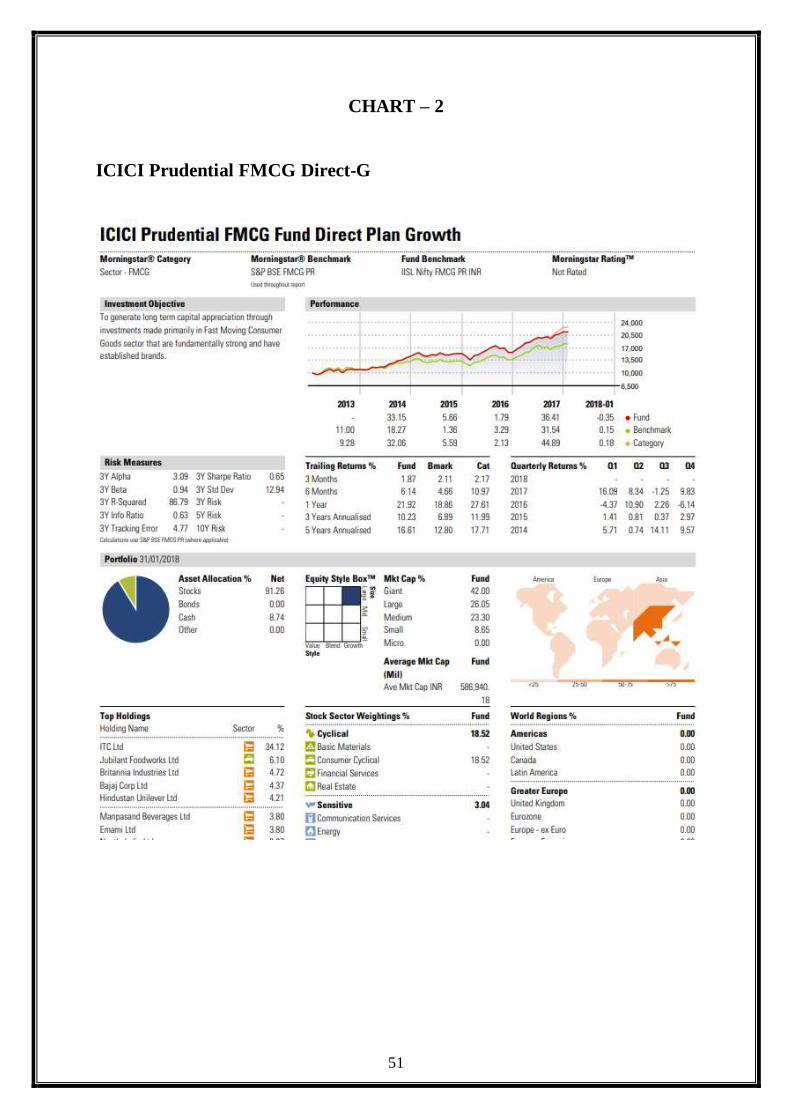

Fact Sheet-4.2 Fact Sheet showing ICICI Prudential

FMCG Fund Direct Plan-G Analysis 51

Fact Sheet-4.3 Fact Sheet showing Reliance Large Cap

Fund - Direct 52

Fact Sheet-4.4 Fact Sheet showing ICICI Prudential

Balanced Fund Direct Plan Growth 53

List of Tables

Table No. Particulars Page Nos.

Table-4.1 Table showing SBI FMCG Fund - Direct

Plan Growth Analysis 55

Table-4.2 Table showing ICICI Prudential FMCG

Fund Direct Plan-G Analysis 56

Table-4.3 Table showing Reliance Large Cap Fund -

Direct 57

Table-4.4 Table showing ICICI Prudential Balanced

Fund Direct Plan Growth 58

EXECUTIVE SUMMARY

A mutual fund is a collective investment scheme, which specializes in investing a pool of money

collected from many investors for the purpose of investing in securities such as stocks, bonds,

money market instruments and similar assets. It is indirect mode of investing. There are three types

of mutual funds by structure, by investment objective and other fund. This paper is focused FMCG

and Large Cap fund. A Mutual Fund is a trust that pools the savings of a number of investors who

share a common financial goal. It throws the light on how FMCG and Large Cap Mutual funds

really work, how much risk involved in it and how they diversify themselves. Investing involves

risk of loss of principal and is more concerned on the return of investment.

The main objective of the study is to analysis of FMCG and Large Cap Fund for long term and

give investors a basic idea of investing into the FMCG and Large Cap Mutual Funds and encourage

them to invest in those areas where they can maximize the return on their capital. The research

provided an interesting insight into awareness about the mutual funds, differences in risk taking

ability of individuals, investment options preferred etc.

There are 7 parameters taken for calculating risk and return Standard Deviation, Beta, R-squared,

Jensen’s Alpha, Portfolio Turnover Ratio, Sharpe’s Index and Treynor’s Ratio. In this study the

data collected are secondary that is through the factsheets of top funds as on February 2018. The

report is based on the data provided in the factsheets of SBI FMCG Mutual fund &ICICI Prudential

FMCG Mutual Fund and Reliance Large Cap fund & ICICI Prudential Balanced Fund.

BIBLIOGRAPHY

REFERENCE

Prasanna Chandra, Investment Analysis and Portfolio Management.

Fund fact Sheet of a company

www.moneycontrol.com

www.nseindia.com

www.google.com

www.investopedia.com

www.rathi.com

Association of Mutual Funds in India

https://www.pwc.in/assets/pdfs/publications/2017/mutual-funds-2-0-expanding-

into-new-horizons.pdf

www.learn.tradimo.com

www.morningstar.com

RELakhs.com

ANNEXURE

SBI FMCG Fund - Direct Plan

ICICI Prudential FMCG Direct-G

Reliance Large Cap Fund

Report as of 6 May 2018

Reliance Large Cap Fund - Direct Plan - Growth Plan Morningstar® Category Morningstar® Benchmark Fund Benchmark Morningstar Rating™ Large-Cap S&P BSE 100 India TR INR S&P BSE 100 India TR INR QQQQQ

Used throughout report Investment Objective

The primary investment objective of the scheme is to

seek to generate long term capital appreciation by

investing predominantly into equity and equity related

instruments of large cap companies. The secondary

objective is to generate consistent returns by investing

in debt, money market securities, REITs and InvITs.

However, there can be no assurance that the investment

objective of the Scheme will be realized.

Risk Measures 3Y Alpha 0.76 3Y Sharpe Ratio 0.65 3Y Beta 1.04 3Y Std Dev 14.78 3Y R-Squared 93.63 3Y Risk abv avg 3Y Info Ratio 0.28 5Y Risk abv avg 3Y Tracking Error 3.78 10Y Risk - Calculations use S&P BSE 100 India TR INR (where applicable)

Performance

27,000 22,750 18,500 14,250 10,000 5,750

2013 2014 2015 2016 2017 2018-04

- 55.70 1.85 3.43 39.91 -1.26 Fund 7.56 34.21 -1.95 5.02 33.27 1.49 Benchmark 4.26 40.45 -0.86 4.42 31.60 0.54 Category

Trailing Returns % Fund Bmark Cat Quarterly Returns % Q1 Q2 Q3 Q4 3 Months -2.78 -0.73 -1.21 2018 -6.67 - - - 6 Months -0.38 1.27 0.64 2017 15.20 6.33 2.40 11.54 1 Year 14.24 14.46 12.54 2016 -5.47 6.58 8.54 -5.41 3 Years Annualised 11.66 10.64 9.65 2015 5.12 -2.02 -3.21 2.17 5 Years Annualised 19.11 14.66 14.67 2014 8.38 22.39 6.36 10.36

Portfolio 31/03/2018

Asset Allocation % Net Stocks 98.50 Bonds 0.00 Cash 1.26 Other 0.24

Equity Style Box™ S

ize

Large

Sm

all Value Blend Growth Style

Mkt Cap % Fund Giant 44.94 Large 40.55 Medium 13.27 Small 1.24 Micro 0.00 Average Mkt Cap Fund (Mil)

Ave Mkt Cap INR 809,870. 06

America Europe Asia <25 25-50 50-75 >75

Top Holdings

Holding Name Sector %

HDFC Bank Ltd y 6.44 State Bank of India y 6.23 Larsen & Toubro Ltd p 4.46 ITC Ltd s 4.17 Infosys Ltd a 3.69

ICICI Bank Ltd y 3.63 Bajaj Finance Ltd y 3.01 Tata Steel Ltd r 2.97 Divi's Laboratories Ltd d 2.96 ACC Ltd r 2.56

Assets in Top 10 Holdings % 40.11 Total Number of Equity Holdings 54 Total Number of Bond Holdings 0

Operations

Fund Company Reliance Nippon Life Asset Management Ltd Phone +91 22 30994600/30301111 Website www.reliancemutual.com Inception Date 01/01/2013 Manager Name Sailesh Raj Bhan Manager Start Date 08/08/2007 NAV (04/05/2018) INR 33.83 Total Net Assets (mil) 88,251.43 INR (31/03/2018)

Stock Sector Weightings % Fund World Regions % Fund

hCyclical 50.27 Americas 0.00

rBasic Materials 7.73 United States 0.00

tConsumer Cyclical 11.60 Canada 0.00

yFinancial Services 30.93 Latin America 0.00

uReal Estate - Greater Europe 0.00

jSensitive 30.40 United Kingdom 0.00

iCommunication Services 2.04 Eurozone 0.00

oEnergy 6.85 Europe - ex Euro 0.00

pIndustrials 14.02 Europe - Emerging 0.00

aTechnology 7.49 Africa 0.00

kDefensive 19.34 Middle East 0.00

Greater Asia 100.00

sConsumer Defensive 7.48

dHealthcare 8.56 Japan 0.00

fUtilities 3.29 Australasia 0.00

Asia - Developed 0.00

Asia - Emerging 100.00

Share Class Size (mil) - Minimum Initial Purchase 5,000 INR

Domicile India Minimum Additional Purchase 1,000 INR

Currency INR Exit Load 1.00% - 0-1 years

UCITS - 0.00% - >1 years

Inc/Acc Acc Expense Ratio 1.13%

ISIN INF204K01XI3

© 2018 Morningstar. All Rights Reserved. The information, data , analyses and opinions (“Information”) conta ined here in: (1) inc lude the proprie ta ry information of Morningstar and Morningstar’s third party licensors; (2) may

ß ®

not be copied or redistributed except as specifica lly authorised;(3) do not constitute investment advice;(4) a re provided sole ly for informationa l purposes; (5) are not warranted to be comple te, ac cura te or time ly; and (6) may

be drawn from fund da ta published on various da tes. Morningsta r is not responsible for any trading dec isions, damages or other losses rela ted to the Information or its use . Please verify a ll of the Information before usin g it

and don’t make any investment dec ision except upon the advice of a professiona l financ ia l adviser. Past pe rformance is no guarantee of future results. The va lue and income derived from investments may go down as well

as up.

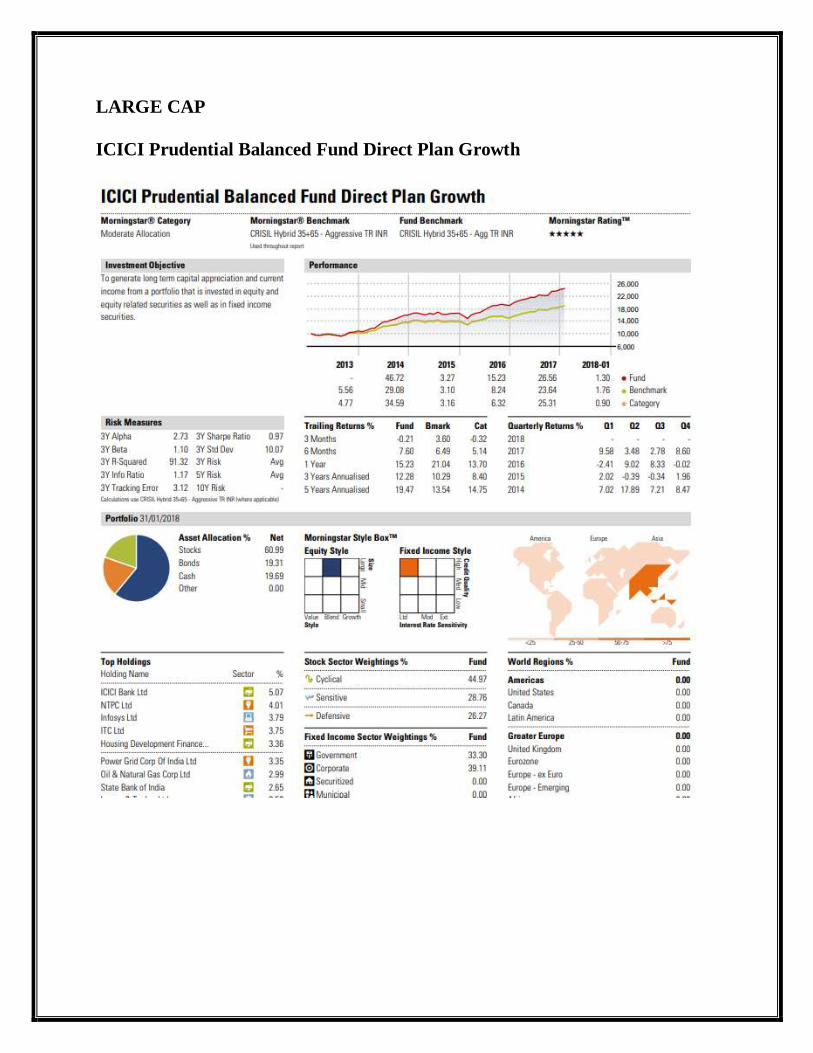

LARGE CAP

ICICI Prudential Balanced Fund Direct Plan Growth

CHAPTER - 1

INTRODUCTION

1. What is Mutual Fund?

Mutual funds are a collective investment vehicle that is they show an indirect way in which

investors can invest in capital market. The objective is to collect the funds, from the investors

and then invest these fund insecurities permitted under the regulations, such kind of

investment is ideal for small investors who want to invest in stock market but cannot in most

of the scrips because of limited amount of capital at their disposal. Mutual funds are suitable

for those investors who do not have sufficient knowledge of capital market and by investing

through a mutual fund. Mutual fund is one of the money related instrument in capital market

here the examination depends on the observational examination on the execution of common

fund schemes, fundamental motivation behind the investigation is to recognize which of the

month and year plot give by most astounding return and limit the hazard. The governing body

of trust gives direction, control, and also manages the overall affairs of the mutual fund. The

trustee has to be a person of high reputation and integrity. One of the member of governing

body becomes a full-time executive of the trust and heads a company known as Asset

Management Company (AMC). Asset Management Company design fund goods,

international financial instrument. So mutual fund industry is high competitive and fund

manager investment style and research team also affecting risk and return of the fund. An

important practical motivation for mutual fund performance evaluation is to help an investor

decide in which mutual funds to invest.

2. What is a FMCG company?

In this study, the aim is to check on how funds focusing on the FMCG sector are performing.

FMCG or Fast Moving Consumer Goods companies deal in manufacture, packing and

distribution of goods that are bought by customers frequently and hence are sold quickly and

relatively at a lower cost.

Sector specific mutual funds invest in specific category of companies only and in this case a

FMCG fund would invest in many companies but only within the FMCG category.

2

3. What are Large Cap funds?

Companies with market capitalization higher than $10 billion are termed as Large Cap

companies. Market capitalization is simply the number of a company's shares outstanding by

its stock price per share.

Sector specific mutual funds invest in specific category companies only and in this case a

Large Cap fund would invest in many companies but only within the Large Cap category.

THE HYPOTHESIS to prove in this study is Long term Equity funds deliver higher returns

in the long term (5yrs for this study) in comparison to FMCG funds.

4. Measuring tools and Techniques:

4.1. Return: Return on a typical investment consists of two components. The basic is the

periodic cash receipts (or income) on the investment, either in the form of interest or

dividends. The second component is the change in the price of the assets-commonly called

the capital gain or loss. This element of return is the difference between the purchase price

and the price at which the assets can be or is sold; therefore, it can be a gain or a loss.

The return has been calculated as under:

NAVt – NAVt-1

Portfolio return: Rit = ---------------------------------

NAV t-1

Where Rit is the difference between Net Asset Values for two consecutive days dividend by

the NAV of the preceding day.

M.indt – M.indt-1

Market return: Rmt = ------------------------

M.indt-1

Where Rmt is the difference between market indices of two consecutive day’s dividend by

the market index for the preceding day.

4.2. Risk: Risk is neither good nor bad. Risk in holding securities is usually related to the

likelihood that completed returns are going to be but expected returns. The difference

between the required rate of returns on mutual fund investment and the risk free return is the

risk premium. Risk can be measured in terms of Beta & standard deviations.

4.3. Standard deviation: - It is wont to measure the variation in individual returns from the

average expected returns over a particular amount. Standard deviation is employed within

the construct of risk of a portfolio of investments. Higher standard deviation suggests

that a bigger fluctuation in expected come.

Standard deviation may be a measure of the dispersion of a collection of data from its

mean. It’s calculated because the root of variance by determinative the variation

4

between every data point relative to the mean. If the data points area unit away from the

mean, there's higher deviation within the data set.

In finance, standard deviation may be an applied mathematics measurement; once applied to

the annual rate of return of an investment, it sheds lightweight on the historical volatility of

that investment. The bigger the standard deviation of a security, the bigger the variance

between every worth and also the mean, indicating a bigger worth vary. As an example, a

volatile stock features a high variance, whereas the deviation of a stable ordinary shares is

sometimes rather low.

4.1. What's Standard Deviance Used For?

Standard deviation is associate degree particularly great tool in investment and

commercialism methods, because it helps measure market and security volatility and predict

performance trends. As it relates to investment, for instance, associate degree open-end

fund may be expected to have a low standard deviation versus its benchmark index, because

the fund's goal is to duplicate the index. Aggressive growth funds on the opposite hand, may

be expected to possess a high standard deviation from relative stock indices, as their portfolio

managers build aggressive bets in an endeavor to get higher-than-average returns. A

lower standard deviation is not essentially desirable. It all depends on the type of investments

one is creating, and also the one's disposition to assume risk. Once coping with the number of

deviation in their portfolios, investors ought to take into account each their personal tolerance

for volatility and their overall investment objectives. A lot of aggressive investors could also

be snug with associate degree investment strategy that opts for vehicles with higher-than-

average volatility, whereas a lot of conservative investors might not.

4.2. Calculating a Standard Deviation

The formula for standard deviation uses 3 variables. The primary variable is to be the

worth of every purpose inside the data set, historically listed as x, with a sub-number

denoting every extra variable (x, x1, x2, x3, etc.). The mean, or average, of the data points is

applied to the worth of the variable M, and therefore the range of

information points concerned is appointed to the variable n.

To determine the mean, the values of the data points should be additional along, which total

is then divided by the quantity of data points that were enclosed? For instance, if the

data points were 5, 7, 3 and 7, the entire would be 22. That total of twenty-two would then be

5

divided by the quantity of data points, during this case four, leading to a mean of 5.5.

This ends up in the subsequent determinations: M = 5.5 and n = 4.

The variance is decided by subtracting the worth of the mean from every information, leading

to -0.5, 1.5, -2.5 and 1.5. Every of these values area unit then square, leading to 0.25, 2.25,

6.25 and 2.25. The sq. values area unit then additional along, leading to a complete of 11

that is then divided by the worth of n-1 that is 3 during this instance leading to a variance or

so of 3.67.The root of the variance is then calculated, leading to the quality deviation of

roughly 13.46.

5. Beta: - Beta measures the systematic risk and shows how prices of securities respond to

the market forces. It is calculated by relating the return on a security with return for the

market. By convention, market will have beta 1.0.Mutual fund is said to be volatile, more

volatile or less volatile. If beta is greater than 1 the stock is said to be riskier than market. If

beta is less than 1, the indication is that stock is less risky in comparison to market. If beta is

zero then the risk is the same as that of the market. Negative beta is rare.

ß = Covariance / (SD) 2

Where, Covariance is the average of the products of deviations for each data point pair. And,

covariance is calculated as:

Covariance = 1/n Σ (xi –µ x) (yi - µy)

Where, x = scheme returns. y = market returns.

µ = mean. β = n Σxy - (Σx) (Σy) nΣx 2 -(Σx)

Where, n = number of years, X = rolling returns of the BSE index, Y = rolling returns of the

schemes

5.2. Using Beta

A security's beta should only be used when a security has a high R-squared value in relation

to the benchmark. The R-squared measures the percentage of a security's historical price

movements that could be explained by movements in a benchmark index.

6

6. Sharpe index

Sharpe index measures risk premium of a portfolio, relative to the total amount of risk in the

portfolio. Sharpe index summarizes the risk and return of a portfolio in a single measure that

categorizes the performance of funds on the risk adjusted basis. The larger the Sharpe’s index

the portfolio over performs the market and vice versa.

6.1. Formula to calculate Sharpe’s measure is:

Where, St = Sharpe’s index Rp= portfolio return, Rf= Risk free rate of return (5%) SD=

Standard Deviation of the portfolio.

6.2. Applications of the Sharpe Ratio

The Sharpe proportion is frequently used to think about the adjustment in a portfolio's general

hazard return attributes when another advantage or resource class is added to it. For instance,

a portfolio director is thinking about adding a flexible investments allotment to his current

50/50 venture arrangement of stocks and bonds which has a Sharpe proportion of 0.67. In the

event that the new portfolio's assignment is 40/40/20 stocks, securities and an expanded

support investments allotment (maybe a reserve of assets), the Sharpe proportion increments

to 0.87. This demonstrates despite the fact that the support stock investments venture is

dangerous as an independent introduction, it really enhances the hazard return normal for the

consolidated portfolio, and in this way includes a broadening advantage. On the off chance

that the option of the new speculation brought down the Sharpe proportion, it ought not to be

added to the portfolio.

The Sharpe proportion can likewise help clarify whether a portfolio's overabundance returns

are because of savvy speculation choices or a consequence of an excess of hazard. Albeit one

portfolio or reserve can appreciate higher returns than its associates, it is just a decent

speculation if those higher returns don't accompany an abundance of extra hazard. The more

7

prominent a portfolio's Sharpe proportion, the better its hazard balanced execution. A

negative Sharpe proportion shows that a hazard less resource would perform superior to

anything the security being broke down.

7. Treynor’s Index

The Treynor proportion, otherwise called the reward-to-unpredictability proportion, is a

metric for restores that surpass those that may have been picked up on a hazard less

speculation, per every unit of market chance. The Treynor proportion, created by Jack

Treynor, is computed as takes after:

(Normal Return of a Portfolio – Average return of the Risk-Free Rate)/Beta of the Portfolio.

It quantifies portfolio chance as far as beta, which is weighted normal of individual security

beta. The proportion is financial specialists, for who the store speaks to just a small amount of

their aggregate resources. The higher the proportion better is the execution.

At the point when the estimation of the Treynor proportion is high, it means that a speculator

has created exceptional yields on every one of the market dangers he has taken. The Treynor

proportion takes into consideration a comprehension of how every venture inside a portfolio

is performing. It likewise gives the financial specialist a thought of how effectively capital is

being utilized.

8. Alpha

The Jensen's measure is a hazard balanced execution measure that speaks to the arrival on

venture above or beneath that anticipated this metric is likewise generally alluded to as

Jensen's alpha, or just alpha.

The measure of the alpha shows the stock's unsystematic return and its normal return free of

market return. If the fund produces the expected return at the level of risk assumed, the fund

would have an alpha equal to zero. A positive alpha indicates that the manager produced

return greater than expected for the risk taken. Alpha is calculated by comparing the fund’s

actual performance with the risk adjusted expected return.

Jensen's alpha is calculated using the following four variables:

R(i) = the realized return of the portfolio or investment

R(m) = the realized return of the appropriate market index

R(f) = the risk-free rate of return for the time period

B = the beta of the portfolio of investment with respect to the chosen market index

8

Using these variables, the formula for Jensen's alpha is:

Alpha = R(i) - (R(f) + B x (R(m) - R(f))

9. R-squared

R-squared may be an applied math measure that represents the proportion of a fund or

security's movements which will be explained by movements in index. R-squared

values vary from zero to one and square measure unremarkably explicit as percentages

from 0 to 100 percent. An R-squared of 100 percent means that all movements of a

security square measure fully explained by movements within the index. A high R-squared,

between 85th and 100 percent, indicates the fund's performance patterns are in line with the

index. A fund with a low R-squared, at 70th or less, indicates the safety doesn't act very

like the index. If a fund incorporates an R-squared worth of near 100 percent however has a

beta below1, it's presumably giving higher risk-adjusted returns.

10. Portfolio turnover ratio

Portfolio turnover is a measure of how habitually resources inside a store are purchased and

sold by the chiefs. Portfolio turnover is ascertained by taking either the aggregate sum of new

securities obtained or the measure of securities sold - whichever is less - over a specific

period, separated by the aggregate Net Asset Value of the reserve. The estimation is typically

detailed for a year day and age. The portfolio turnover estimation ought to be considered by a

speculator before choosing to buy a given shared store or comparable money related

instrument. All things considered, a firm with a high turnover rate will acquire more

exchange costs than a reserve with a lower rate. Unless the prevalent resource choice renders

benefits that counterbalance the additional exchange costs they cause, a less dynamic

exchanging stance may produce higher store returns.

Moreover, cost cognizant store speculators should observe that the value-based business

charge costs are excluded in the count of a reserve's working cost proportion and in this way

speak to what can be, in high-turnover portfolios, a noteworthy extra cost that diminishes

venture return.

9

CHAPTER - 2

INDUSTRY PROFILE AND COMPANY PROFILE

2.1. INTRODUCTION TO MUTUAL FUND

A Mutual Fund gets investment from investors and invests it on behalf of the investors into

diversified Securities thus providing investors with both diversification of their portfolio and

professional management of their funds. Mutual fund may launch many such mutual funds to

investment in different sectors and different combination of factors namely developing

market companies, or new age companies, stable and very minimal risk sectors, high risk and

high return sectors etc.

A mutual fund invests in stocks, bonds, options, money market securities, and commodities,

to name a few depending on the fund’s investment objectives. An investor may choose from

many different mutual funds currently in the market based on his or her risk profile and

investment criteria. Mutual fund is an ideal investment route for individuals who are not

aware or well aware of the investing techniques, limited or no financial literacy regards to

investment tools, techniques and hence cannot invest in the equity or other financial

instruments directly. Investor can invest directly in a mutual fund or hire the services of a

mutual fund advisor.

Over the past decade, mutual funds have increasingly become the investor’s vehicle of choice

for long term investing. As of late, the rising pattern in the common store industry is the

forceful development of the remote claimed shared reserve organizations and the decrease of

the organizations glided by nationalized banks and little private segment players.

What is a Mutual Fund?

Mutual fund is the most popular investment avenue for general public or retail investors.

These are simple to understand and easy to invest compared to other investment options

available in the financial markets. A Mutual Fund pools the funds contributed by a number of

investors who may share a common profile on their investment choice which primarily

concerns with risk taking ability and return expected and the size of investment is also

comparatively smaller. The primary concerns of the small investors the security of their

investment.

10

The cash hence gathered is then put resources into capital market instruments, for example,

offers, debentures and different securities. These funds are like baskets where each basket

holds a certain type of instruments or a blend of multiple instruments like stocks, bonds or a

combination of stocks and bonds for one portfolio. The wage earned through these ventures

and the capital gratefulness acknowledged is shared by its unit holders in extent to the

quantity of units possessed by them Thus a Mutual Fund is most suitable investment for the

common man as it offers an opportunity to invest in a diversified, professionally managed

basket of securities at a relatively low cost.

The value of investment is calculated on a day to day basis and the same value is reported

using Net Asset Value as declared by the fund house. This NAV can change due to change in

the value of bond and equity market and therefore a diversified portfolio would balance out

the risk where some stocks may be doing very well and some not so well. The fund managers

make alteration in the portfolio time to time secure higher return as compare to the other

financial assets.

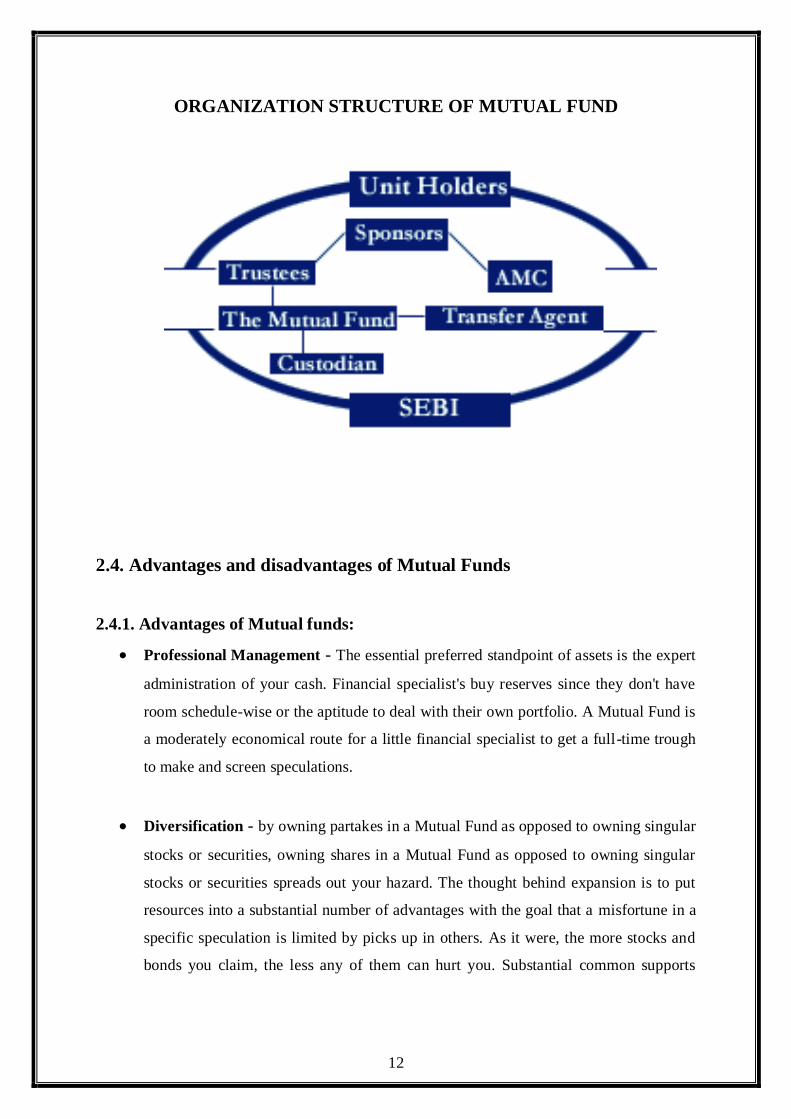

The flow chart below describes broadly the working of a Mutual fund.

2.2. Mutual Fund Operation Flow Chart

11

2.3. Organization structure of a Mutual Fund Company

Sponsors – One or more persons who come together to establish a mutual fund and

register the same with Securities and Exchange Board of the respective country. For

e.g. in India it is SEBI. The person(s) may also consider setting the mutual fund

jointly with another corporate. Sponsor’s track record of staying actively engaged

with the stock market along with running profitable operations will be considered

while evaluating the registration.

The sponsors then form a Trust as per the Trust Act in the respective country. In India

the Trust Act of 1882 is used for the formation of trust. Mutual Fund is also the trust

which holds the investments. A trust deed is prepared detailing the intended activities

of the trust with the underlying principles and actions needed to protect the interest of

investors is filed with Securities and Exchange Board.

Trustees –Sponsors then appoint the Trustees who chief responsibility is to protect

the financial interests of the mutual fund holders. As a rule there will be restrictions to

appoint trustees who are connected with Sponsor. In India, 2/3rd of Trustees should

not be connected with Sponsors and are addressed as Independent directors.

Asset Management Company (AMC) –Asset Management Company is

appointed by the Trustees as the investment manager of the Mutual Fund. The AMC

can in turn appoint the Registrar and Transfer Agent for the Mutual Fund.

Registrar & Transfer Agent –The registrar and transfer agent stay in touch with

the investors and periodically share reports or account statements.

Custodian – The custodian is a bank, a trust company, or an agent who holds and

safeguards investor’s mutual funds.

12

ORGANIZATION STRUCTURE OF MUTUAL FUND

2.4. Advantages and disadvantages of Mutual Funds

2.4.1. Advantages of Mutual funds:

Professional Management - The essential preferred standpoint of assets is the expert

administration of your cash. Financial specialist's buy reserves since they don't have

room schedule-wise or the aptitude to deal with their own portfolio. A Mutual Fund is

a moderately economical route for a little financial specialist to get a full-time trough

to make and screen speculations.

Diversification - by owning partakes in a Mutual Fund as opposed to owning singular

stocks or securities, owning shares in a Mutual Fund as opposed to owning singular

stocks or securities spreads out your hazard. The thought behind expansion is to put

resources into a substantial number of advantages with the goal that a misfortune in a

specific speculation is limited by picks up in others. As it were, the more stocks and

bonds you claim, the less any of them can hurt you. Substantial common supports

13

ordinarily claim several distinct stocks in a wide range of businesses. A speculator

wouldn't be able to fabricate this sort of portfolio with a little measure of cash.

Economies of Scale - Because a shared reserve purchases and offers a lot of

securities at any given moment, its exchange costs are lower than you as an individual

would pay.

Liquidity - Just like an individual stock, a common store enables you to ask for that

your offers be changed over into money whenever.

Simplicity – Buying a shared store is simple! Really well any bank has its own

particular line of common assets, and the base speculation is little. Most organizations

additionally have programmed buy designs whereby as meager as $100 can be

contributed on a month to month premise.

2.4.2. Disadvantages of Mutual Funds:

Poor Management – Did you see how we qualified the upside of expert

administration with the word" hypothetically"? Numerous financial specialists banter

about whether or not the alleged experts are any superior to you or I at picking stocks.

Administration is in no way, shape or form trustworthy, and, regardless of whether the

reserve loses cash, the director still takes his/her cut.

Costs - Mutual Funds don't exist exclusively to make your life less demanding all

assets are in it for a benefit. The shared reserve industry is awesome at purchasing

costs under layers of language. These expenses are complicated to the point that in

this instructional exercise we have given a whole segment to the subject

Dilution - It's conceivable to have excessively expansion. Since stores have little

possessions in such a large number of various organizations, exceptional yield from a

couple of ventures regularly don't have much effect on the general return. Weakening

likewise the aftereffect of a win finance getting too enormous. At the point when cash

14

fills subsidizes that have had solid achievement, the chief regularly experiences

difficulty finding a decent speculation for all the new organization.

Taxes - when profiting, subsidize supervisors don't think about your own duty

circumstance. For instance, when a reserve administrator offers a security, a capital-

pick up charge is activated, which influences how productive the individual is from

the deal. It may have been more invaluable for the person to concede the capital

additions risk. Amid an average year, most effectively oversaw common assets offer

somewhere in the range of 20 to 70% of the securities in their portfolios. In the event

that your store makes a benefit on its business, you will pay imposes on the pay you

get, regardless of whether you reinvest the cash you made.

2.5. Mutual Funds have their drawbacks and may not be for everyone:

No Guarantees: No investment is risk free. On the off chance that the whole

securities exchange decreases in esteem, the estimation of common reserve offers will

go down also, regardless of how adjusted the portfolio. Investors encounter fewer

risks when they invest in mutual funds than when they buy and sells stocks on their

own. In any case, any individual who contributes through a common store risks losing

cash.

Charges and commissions: All assets charge authoritative charges to cover their

everyday costs. Some funds also charge sales commission or “loads” to compensate

brokers, financial consultants, or financial planners. Even if you don’t use a broker or

other financial adviser, you will pay a sales commission if you buy shares in a Load

Funds

Management Risk: When an individual invest in Mutual Fund, depend on the fund’s

manager to make the right decisions regarding the fund’s portfolio. If the manager

does not perform as well individual had hoped, he might not make as much money on

individual investment as he expected. Of course, if individual invest in Index Funds,

he forego management risk, because these funds do not employ managers.

15

2.6. Types of Mutual Funds In India

Wide variety of Mutual Fund Schemes exists to cater to the needs such as financial position,

risk tolerance and return expectations etc. The table below gives an overview into the existing

types of Schemes in the industry.

Types of Mutual Fund Schemes

2.6.1. By Structure

i. Open –Ended Schemes

ii. Close-Ended Schemes

iii. Interval Schemes

2.6.2 By investment Objective

i. Growth Schemes

ii. Income Schemes

iii. Balanced Schemes

iv. Money market Schemes

2.6.2. Others Schemes

i. Tax Saving Schemes

ii. Special Schemes

iii. Index Schemes

iv. Sector Specific Schemes

Classification of Mutual Fund

Mutual Fund Scheme can be classified into open-ended scheme and close-ended scheme

depending on its maturity period.

2.6.1. By Structure

i. Open-ended Scheme

An Open-ended scheme is one that is available for subscription and repurchase on a

continuous basis. These schemes do not have a fixed maturity period. Investors can

16

conveniently buy and sell units at Net Asset Value (NAV) related process, which are

declared on a daily basis. The key features of open-ended Schemes are liquidity.

ii. Close-ended Scheme

A Close-ended scheme has a stipulated maturity period e.g. 5-7 years. The fund is

open for subscription only during a specified period at the time of launch of the

scheme. Investors can invest in the scheme at the time of the initial public issue and

thereafter they can buy or sell the units of the scheme on the stock exchanges where

the units are listed. In order to provide an exit route to the investors, some close-ended

funds give an option of selling back the units to the mutual fund through periodic

repurchase at NAV related prices. SEBI Regulations stipulate that at least one of the

two exit routes is provided to the investor either repurchase facility or through listing

on stock exchanges. These mutual funds schemes disclose NAV generally on weekly

basis.

iii. Interval Scheme

Interval Schemes are those that join the highlights of open-ended and close-

ended fund. The units might be exchanged on the stock trade or might be open

available to be purchased or recovery amid pre-decided interims at NAV

related costs.

2.6.2. Categorization by Investment Objective

A Scheme can also be classified as growth scheme, income scheme, or balanced scheme

considering its investment objective. Such schemes may be open-ended or closed-ended

schemes as described earlier. Such schemes may be classified mainly as follows

i. Growth/ Equity Oriented Schemes

The point of development reserves is to give capital increase over the medium to long

haul. Such plans typically invest a major part of their corpus in equities. Such funds

have comparatively high risks. These schemes provide different options to the

investors like dividend option, capital appreciation etc. and the investors may choose

an option depending on their preferences. The financial specialists must show the

choice in the application frame. The common supports additionally enable the

17

financial specialists to change the choices at a later date. Growth schemes are good

for investors to change the options at a later date. Development plans are useful for

speculators having a long haul viewpoint looking for increase over some stretch of

time.

ii. Income/ Debt Oriented Scheme

The point of pay stores is to give customary and relentless salary to investors. Such

plans by and large put resources into settled salary securities, for example, securities,

corporate debentures, Government securities and currency showcase instruments.

Such subsidizes are less risky than contrast of equity schemes. These funds are not

affected because of fluctuation in equity markets. However, opportunities of capital

appreciation are also limited in such funds. The NAVs of such funds affected because

of change in interest rates in the country. On the off chance that the financing costs

fall, NAVs of such subsidizes are probably going to increment in the short run and the

other way around. Nonetheless, long haul investors may not make a fuss over these

variances.

iii. Balanced Fund or Hybrid Fund or Asset Allocation Funds

The aim of balanced funds is to provide both growth and regular income as such

schemes invest both in equities and fixed income securities in the proportion indicated

in their offer documents. These are acceptable for investors looking for moderate

growth. They generally invest 40-60 per cent in equity and debt instruments. These

funds a re also affected because of fluctuations in share prices in the stock markets.

Be that as it may, NAVs of such funds are probably going to be less unstable

contrasted with pure equity fund.

iv. Money Market or Liquid Fund

These funds are also income funds and their aim to provide easy liquidity,

preservation of capital and moderate income. These plans put only in more secure

here and now instruments, for example, Treasury Bills, Certificates of Deposits, and

Commercial Paper and between banks call cash, Government Securities, and so on.

Returns on these schemes fluctuate much less compared to other funds. These funds

18

are fitting for corporate and singular financial specialists as a way to stop their surplus

supports for brief periods.

2.5.3. Others Funds

i. Gilt fund

These funds invest exclusively in government securities. Government Securities have

no default risk. NAVs of these schemes also fluctuate due to change in interest rates

and other economic factor as is the case with income or debt oriented schemes.

ii. Index Funds

Index Funds replicate the portfolio of a particular index such as the BSE Sensitive

index, S&P NSE 50 index (Nifty), etc. These schemes invest in the securities in the

same weightings comprising of an index. NAVs of these plans likewise vary because

of progress in financing costs and other monetary factor similar to the case with wage

or obligation arranged plans. Though not exactly by the same percentage due to some

factors known as “tracking error” in technical terms. Necessary disclosures in this

regard are made in the offer document of the mutual fund scheme. There are also

exchange traded index funds launched by the mutual funds which are traded on the

stock exchanges.

iii. Sector specific funds / Schemes

These are the assets or plans, which put resources into the securities of just those

segments or enterprises as indicated in the offer archives e.g. Pharmaceuticals,

programming, Fast Moving Consumer Goods (FMCG), Petroleum stocks, and so

forth. The profits in these assets are subject to the execution of the separate

parts/ventures. While these assets may give higher returns, they are more dangerous

contrasted with enhanced assets. Financial specialists need to keep a watch on the

execution of those divisions/ventures and should exit at a proper time. They may

likewise look for counsel of a specialist.

iv. Expense Saving Schemes

These plans offer assessment discounts to the financial specialists under particular

arrangements of the Income Tax Act.1962 as the administration offers impose

19

motivators for interest in determined roads e.g. Value Linked Saving Schemes

(ELSS). Annuity Schemes propelled by the common supports additionally offer tax

cuts. These plans are development situated and contribute pre-overwhelmingly I

values. Their development openings and dangers related resemble any value situated

plan.

v. Load or no-heap Fund

A Load finance is one that charges a level of NAV for passage or exit. That is, each

time one purchases or offers units in the store, a charge will be payable. This charge is

utilized by the common store for advertising and dissemination costs. Assume the

NAV per unit is Rs.10. In the section and in addition leave stack charged is.1%, at

that point the speculators who purchase would be required to pay RS.10.10 and these

who offer their units for repurchase the common store will get just Rs.9.90 per unit.

The financial specialists should mull over the heaps while making venture as these

influence their yields/returns. Nonetheless, the financial specialists ought to likewise

consider the execution reputation and administration gauges of the common reserve,

which are more imperative. Proficient assets may give higher returns regardless of

burdens.

A no-heap finance is one that does not charge for passage or exit. It implies the

financial specialists can enter the reserve/plot at NAV and no extra charges are

payable on buy or offer of units.

vi. Guaranteed return plot

Guaranteed return plans are those plans that guarantee a particular come back to the

unit holders regardless of execution of the plan. A plan can't guarantee returns unless

such returns are completely ensured by the support or AMC and this is required to be

revealed in the offer record. Speculators should deliberately read the offer report

whether return is guaranteed for the whole time of the plan or just for a specific

period. A few plans guarantee returns one year a period and they survey and change it

toward the start of the following year.

20

2.7. Key Terminology

Net plus worth (NAV)

Net plus worth is value of the assets of the theme minus its liabilities. The per unit

NAV is that the internet plus worth of the theme divided by the amount of units

outstanding on the Valuation Date.

Redemption worth

Redemption price is that the worth at which open-ended schemes repurchase their

units and close- Sales Load could be a charge collected by a scheme when it sells the

units. Additionally called “Front-end” load. Schemes that do not charge a load area

unit called “No Load” Schemes.

Repurchase or “Back-end” Load

Is a charge collected by a scheme when it buys back the units from the unit holders?

Ended schemes redeem their units on maturity. Such prices are NAV related.

Evaluating Performance

Repurchase or “Back-end” Load is a charge gathered by a plan when it purchases back the

units from the unit-holders?

Ended schemes redeem their units on maturity. Such prices are NAV related.

2.8. Evaluating Performance

Perhaps you've got detected those mutual fund ads that quote amazingly high one-year rates

of return? Your first thought could be, "wow, that mutual fund did great!" Well, yes it did

great last year, but then you look at the three-year performance, which is lower, and also the

five years, which is yet even lower. What’s the underlying story here? Let's inspect associate

actual example from a large mutual fund's performance:

1-year return – 53%

3-year return – 20%

5-year return – 11%

First year, this mutual fund had excellent performance, returning 53 to investors. But, over

the past 3 years the common annual return was just 200th. What did the fund return in years 1

and 2 to bring the average return down to 20%? Simple math shows North American country

that the fund made an average return of 3.5% over those 1st 2 years: 200th = (53% + 3.5% +

3.5%)/3. Since this 3.5% figure is merely an average, it is very doable that the fund lost

money in one or more of those years.

21

It gets more dismal if we glance at the five-year performance. We know that in the last year

the fund returned 53 and in years two {and three and three} we have a tendency to area unit

guessing it returned around 3.5%. So, what happened in years 4 and 5 to bring the average

return all the way down to just 11%? again, by doing some simple calculations we find that

the fund must have lost money, on average -2.5% each year of those 2 years: Martina’s =

(53% + 3.5% + 3.5% - 2.5% - 2.5%)/5. with that in mind the fund's performance does not

look quite therefore spectacular.

2.9. There are 5 ways to evaluate performance of mutual fund

Investing in mutual funds has associate degree inherent risk assumed upon the possession.

However, performance of the mutual funds will be quantified with the mathematical

calculation of the historical returns. The correlation of the potential risk and also the potential

returns perpetually place forth the opportunities to speculate in mutual funds and drive most

potential returns with minimum underlying risk.

Risk adjusted returns- Risk adjusted returns are the shrewd returns your

funds build compared to the chance indicated over the amount of your time. If

compared, some of mutual funds that drive identical share of returns

over identical amount of your time, the lesser risk funds have a better Risk Adjusted

Returns.

Benchmark- Benchmarking is that the activity of quality of the funds against the

quality measurements. It’s a degree of reference compared to the funds peer

markets. Regardless of the objectives of investment in mutual funds, benchmark helps

you gauge the performance of your investment against the market competition.

Considering historical returns against the market conditions can assist

you verify the connation of the performance benchmark for your investments.

However, historical come back isn't a reliable indicator of future results.

Relative performance with peers may be a yardstick of the effectiveness of

your investment company of identical class. Mutual Funds actively try and high the

ranking of the fund universe. Supposed towards a better come for the

determined amount important learning, the relative peer performance is usually

recommended.

Quality of stocks within the portfolio - Quality of stocks within the portfolio

is mirrored in its ability to drive superior returns on capital invested with for a

22

selected amount of your time. It’s knowing check the trade leadership position of

the investment company. Quality of the stocks within the portfolio would mirror in

returns thus within the performance. Qualitative statistics and historical performance

of mutual funds would facilitate evaluating the performance.

Documentation and competency of the fund manager

Your fund manager is a crucial one who makes investment choices and

stock choice within the portfolio. Perceive your fund manager’s competency in

keeping with his/her fund management data and skill. Your fund manager’s past

performance would be a decent parameter to trace his/her record and

will communicate be of an excellent worth for your investments.

2.10. How to buy or purchase and invest in mutual funds?

There are 5 ways by which we can invest in mutual funds.

Through a Financial Advisor: This the oldest and most popular way of investing in

mutual funds in India. AMFI, an industry association of all the SEBI approved AMCs,

provides licenses to financial advisor to advice customers on mutual fund

investments. The financial advisor provides end to end to services, including

collecting KYC (Know your Customer) documents, filling the application forms and

getting your signatures and submitting them for processing. Most financial advisors

do not charge any fee from their customers. They are paid commissions by the mutual

fund companies. If you are new investor it is recommended that you invest through a

financial advisor. Before investing through financial advisors, you should check if

they have a valid AMFI license.

Investing directly with the Mutual Fund companies: You can visit the office of the

mutual fund companies and invest directly at their office. If you are investing for the

first time, you need to submit the necessary documentation for KYC (identity proof,

address proof, PAN card etc.) along with the duly filled application form at the mutual

fund. Once a folio number is generated for you, you can invest online in any scheme

of the mutual company by going to the website of the company.

Investing through registrars (CAMS or Karvy): CAMS or Karvy are registrars who

process the mutual fund transactions and keep records on behalf of the mutual fund

companies. You can visit CAMS or Karvy workplaces and present the shared reserve

23

application shapes there, much the same as contributing specifically with common

store organizations.

Investing through online portals: There are several online portals like

fundsindia.com and fundsupermart.com through you can invest in mutual funds. To

invest through the online portals your KYC has to be registered. Some of the portals

can also help you with getting your KYC registered. One of the advantages of

investing through an online portal is that you can view your entire portfolio

(investment in mutual funds of different companies) in one place. However, you be

aware of to that amount this online portals are registered mutual fund distributors as

you monetary guide and attain commissions beside the mutual resources companies.

Investing through your online demat account: Some brokers who provide online

trading and demat services, also offer online investment in mutual funds.

2.11. Performance of Mutual Fund in India

Let us begin the discussion of the performance of investment companies in India Bharat

Asian country Asian nation from the day the idea of mutual fund took birth in India. The year

was 1963. Investment Company of Asian nation invited investors or rather to people

who believed in savings, to park their cash in UTI Investment Company.

For thirty years it goaled while not a sing second player. Although the 1988-year saw some

new investment company corporations, however UTI remained in a very monopoly position.

The performance of mutual funds in Asian nation within the initial part wasn't even nearer to

satisfactory level. Individuals seldom understood, and after all infesting was out of question.

But yes, some twenty four million shareholders were accustomed with bonded high returns

by the start of relaxation of the business in 1992. This smart record of UTI

became promoting tool for brand spanking new entrants. The expectations of investors

touched the sky in profitableness issue. However, individuals were miles far away from

the state of risks issue when the relaxation. The Assets below Management of UTI was

PRs. 67 billions by the top of 1987. Let, concentrate regarding the performance of mutual

funds in Asian nation through Figures. From PRs. 67 billions the quality below Management

rose to Rs.470 bn. In March 1993 and therefore the figure had a 3 time higher performance

by April 2004. It rose as high as Rs.2.54bn. The net quality worth of mutual funds in Asian

nation declined once stock costs started falling within the year 1992. Those days, the

market laws didn't enable portfolio shifts into different investments. There was rather

24

no alternative excluding holding the money or to any continue investment in shares. An

added factor to be noted, since solely closed-end funds were floated within the market, the

investors disinvested by merchandising at a loss within the secondary market. The

performance of mutual funds in Asian nation suffered qualitatively.

The 1992 exchange scandal, the losses by disinvestments and after all the dearth of clear rules

within the wherever regarding rocked confidence among the investors. Part owning to a

comparatively weak exchange performance, mutual funds haven't however recovered, with

funds commercialism a median discount of 1020% of their NAV. The superordinate authority

adopted a collection of measures to make a clear and competitive surroundings in mutual

funds. A number of them were like reposeful investment restrictions into the market,

introduction of open-ended funds, and paving the entrance for mutual funds to launch pension

schemes. The live was taken to create mutual funds the key instrument for long saving

.The additional the variability offered, the quantitative are going to be investors. At last to

say, as long as investment company corporations area unit performing arts with lower risks

and better profitableness at intervals a brief span of your time, additional and additional

individuals are going to be inclined to take a position till and unless they are totally educated

with the dos and don’ts of mutual funds. Average Assets Under Management (AAUM) of

Indian investment company business for the month of Dec 2017 stood at INR 22,

60,000 large integer. Assets Under Management (AUM) as on day, 2017stood at INR 21,

27,000 large integer.

The Aum Shinrikyo of the Indian MF business has mature from INR 3.26 trillion as

on 31st March 2007 to INR21.27 trillion as on 31st Dec 2017, regarding six and fold

increase in a very span of regarding ten and half years!!

The MF Industry’s Aum Shinrikyo has mature from INR 5.87 trillion as on thirty first March,

2012 to INR twenty one.27 trillion as on thirty first Dec, 2017, regarding 3 and fold

increase in a very span of regarding five and years!! The Industry’s Aum Shinrikyo had

crossed the milestone of INR10 Trillion (INR10 hundred thousand Crore) for the

primary time in might 2014 and in a very short span of regarding 3 and half years, the Aum

Shinrikyo size has exaggerated over 2 folds and stood at INR21.27 Trillion (INR twenty

one.27 hundred thousand Crore) as on thirty first Dec, 2017. The whole variety of accounts

(or folios as per investment company parlance) as on day, 2017 stood at vi.65 large

integer (66.5 million), whereas the amount of folios below Equity, ELSS and Balanced

schemes, whereby the utmost investment is from retail phase stood at five.46 large

integer (54.6 million).

25

2.12. Future of mutual fund in India

As mindfulness expands, MFs could end up one of the principal decisions for both here and

now and long haul ventures. While MF products are not suitable for all kinds of investors, the

sector has shown tremendous growth by exceeding 17 lakh crore INR in assets under

management (AUM), with inflows worth almost 4 lakh crore INR over the most recent 2

years alone. With the demonetization effect, rapid digitization, government incentives,

regulatory initiatives, and a deliberate push for improving investor education, the next 2–3

years should see the AUM reaching another great milestone. "In the prompt future, with loan

fees declining, it is sensible to anticipate that obligation assets will be the drivers of

development in the main portion of 2017, while the effects of the Goods and Services Tax

(GST) will be felt in the second half.

SEBI and Assets Management Organizations (AMCs) themselves have tried a few endeavors

to build the recognition retail financial specialists have with speculation language. This has

made them more comfortable with the idea of investing in MFs over traditional alternatives

such as real estate and gold. The cost of MFs is likewise falling as the business keeps on

building scale. Innovation has assumed a critical part, with numerous open doors for the

business to use.

2.13. Some Facts

Investment companies determine the price of a Mutual Fund on a daily basis. Mutual

Fund companies are monitored by SEBI.

There are several types of Mutual Funds: Equity, Diversified, Gilt, Debt Hybrid,

Index, Debt, and more.

Equity funds include equity diversified funds, sector specific funds, and tax-saving

funds.

Debt funds include income funds, liquid funds, and short-term funds.

Hybrid funds include equity-oriented hybrid funds, arbitrage funds, and debt-oriented

hybrid funds.

Mutual fund investment is similar to investing in a stock except a fund manager does

it for you.

A fund is considered an Equity Fund if more than 65% of the money is invested in

equities (stocks).

Investment companies determine the price of a mutual fund on a daily basis

26

Mutual fund companies are monitored by SEBI

There are four types of Mutual Funds: Stock, Bond, Money Market, and Hybrid

Mutual fund investment is similar to investing in a stock except a fund manager does

it for you

A fund is considered an Equity Fund if more than 65% of the money is invested in

equities (stocks)

Indian shared reserve industry right now midpoints at Rs.19.47 lakh crores

Indexed fund are less many dangerous when contrasted with non-index funds.

27

2.14. PROFILE OF THE COMPANY

2.14.1. MUTUAL FUNDS

2.14.1.1. SBI MUTUAL FUND

History

The investment company business in India originally began in 1963 with the investment

trust of India (UTI) as a Government of India and also the Federal Reserve Bank of India

initiative. Launched in 1987, SBI Investment Company became the primary non-

UTI investment company in Republic of India. In July 2004, bank of Republic of India

determined to divest 37 per cent of its holding in its investment company arm, SBI Funds

Management Pvt. Ltd, to Society General Quality Management, for associate

degree quantity in way over $35 million. Post-divestment, bank of India's stake within

the investment company arm diminished to sixty seven. In could 2011, Amundi picked

up 37thstake in SBI Funds Management that was command by Society

General plus Management, as a part of a worldwide move to merge its quality management

business with Credit Gnaeus Julius Agricola. As of Sept 2015, the fund house claims to serve

around 5.8 million investors through 130 points of acceptance, 29capitalist service

centers, 59 capitalist service desks and 6 capitalist Service Points. As of July 2017,

assets below management of SBI investment company area unit valued at Rs. 1, 82,916 large

integer ($28.4 billion).

SBI Mutual Fund

SBI investment firm may be a bank sponsored fund house with its company headquarters

in Mumbai, India. It’s a venture between the bank of Asian country, Associate in

Nursing Indian international, Public Sector banking and monetary services company and

Amundi, a European quality management company.

With 30years of wealthy expertise in fund management, SBI Funds Management Pvt. Ltd.

brings forward experience by systematically delivering price to investors. They need a

powerful and proud lineage that traces back to the bank of Asian country (SBI) - India's

largest bank. SBI investment firm may be a venture between SBI and AMUNDI

(France), one in all the world's leading fund management firms. With a network of over 222

points of acceptance across Asian country, they aim to deliver price and nurture the trust of

our huge and varied family of investors.

28

Key Information

Mutual Fund SBI Mutual Fund

Setup Date Jun-29-1987

Incorporation Date Feb-07-1992

Sponsor State Bank of India

Trustee SBI Mutual Fund Trustee Company Private Limited

Chairman Mrs. Arundhati Bhattacharya

CEO / MD Mrs. Anuradha Rao

CIO Mr. Navneet Munot

Compliance Officer Ms. Vinaya Datar

Investor Service Officer Mr. Rohidas Nakashe

Assets Managed Rs. 205272.78 crore (Dec-31-2017)

Products and Services

SBI Mutual Fund offers mutual fund schemes such as Debt Schemes, Equity Schemes,

Hybrid Schemes, Exchange-traded fund, Liquid Schemes and Fixed Maturity Plans. It also

offers Portfolio Management and Advisory Services to financial institutions and asset

management companies.

Major competitors

SBI Mutual Fund offers common store plans, for example, Debt Schemes, Equity Schemes,

Hybrid Schemes, Exchange-exchanged reserve, Liquid Schemes and Fixed Maturity Plans. It

likewise offers Portfolio Management and Advisory Services to money related establishments

and resource administration organizations.

29

VISION

“To be the most preferred and the largest fund house for all asset classes, with a consistent

track record of excellent returns and best standards in customer service, product innovation,

technology and HR practices.”

SERVICES

1) Mutual Funds

Financial specialists are need. The mission has been to build up Mutual Funds as a

feasible venture choice to the majority in the nation. Working towards it, they claim to

have created inventive, require particular items and taught the financial specialists

about the additional advantages of putting resources into capital markets by means of

Mutual Funds.

Today, the assets have been currently dealing with financial specialist's benefits not

just through venture mastery in residential shared assets, yet in addition seaward

supports and portfolio administration warning administrations for institutional

speculators.

This makes SBI MF one of the largest investment management firms in India,

managing investment mandates of over 5.4 million investors.

2) Portfolio Management and Advisory Services

SBI Funds Management has risen as one of the biggest player in India exhorting

different money related organizations, benefits assets, and neighborhood and

worldwide resource administration organizations.

They likewise give an incorporated end-to-end redid resource administration answer

for organizations as far as warning administration, optional and non-optional portfolio

administration administrations.

3) Offshore Funds

SBI Funds Management has been effectively overseeing and exhorting India's

devoted seaward subsidizes since 1988. SBI Funds Management was the first bank

supported resource administration organization reserve to dispatch a seaward store

called 'SBI Resurgent India Opportunities Fund' with a goal to give speculators open

30

doors for long haul development in capital, through all around investigated interests in

a broadened container of loads of Indian Companies.

4) Alternative Investment Funds (AIF)

As a component of the different resource administration bundles of items offered by

the SBI Funds Management Private Limited, interchange resource venture items

through Alternative Investment Funds is likewise advertised. To begin with elective

speculation subsidize in 2015 was propelled and more supports are on the iron block

as the space is as yet early and a great deal of chances exist. With a characterized

administrative structure set up, we see AIFs becoming speedier and boosting interests

in the nation with cooperation from local and in addition remote financial specialists.

5) Investment Solutions

Equity Schemes

Medium and long term equity investments for capital growth

Hybrid Schemes

Mix of debt and equity investments to offer income and growth

Exchange Traded Schemes

Stock exchange trading of investments in baskets of securities

Debt Schemes

Debt asset investments aimed at regular and steady income

Liquid Schemes

Focused investments in short-term instruments and cash assets

Fund of Funds

Schemes that invests in other schemes of the same or another fund

New Fund Offer

Subscriptions open for our New Fund Offer

Fixed Maturity Plans

Close ended debt schemes with a fixed maturity date

31

4.10.1.2. ICICI Mutual Fund

History

The AMC is a joint wander between ICICI Bank in India and Prudential Plc, one of

UK's biggest players in the monetary administrations segments.

With its Corporate Office situated in Bandra Kurla Complex, Mumbai, India the

AMC has seen generous development in scale; from 2 areas and 6 workers at the

commencement of the joint wander in 1998, to a present quality of in excess of 1000

representatives with around 120 areas contacting a financial specialist base of in

excess of 1.9 million speculators.

Items and Services

The AMC oversees critical Assets under Management (AUM) in the Mutual Fund

portion crosswise over resource classes. The AMC additionally takes into account

Portfolio Management Services and Real Estate Division for financial specialists,

spread the nation over, alongside International Advisory Mandates for customers

crosswise over worldwide markets.

Shared Fund

The Mutual Fund caters essentially to retail speculators. ICICI Prudential AMC has

acquainted items lined up with address client issues prompting an all-around

expanded arrangement of shared store items.

Portfolio Management Services

The Portfolio Management Services enable high total assets financial specialists to

put resources into a more amassed portfolio going for higher returns. In the year 2000,

ICICI Prudential AMC was the principal institutional member to offer the

administration, and has now got an effective reputation of more than 10 years.

Land Business

The Real Estate division takes into account high total assets financial specialists and

local institutional speculators, with ICICI Prudential AMC beginning the Real Estate

Investment Series Portfolio in the year 2007.

Real Competitors

A couple of the contenders for ICICI Prudential Mutual Fund in the shared store

division are HDFC Mutual Fund, Reliance Mutual Fund, SBI Mutual Fund, and Birla

Sun Life Mutual Fund and UTI Mutual Fund.

32

ICICI Mutual Fund

ICICI Prudential Asset Management Company Ltd. is a main resource administration

organization (AMC) in the nation concentrated on overcoming any issues between funds and

ventures and making long haul riches for financial specialists through a scope of

straightforward and applicable speculation arrangements. The AMC is a joint wander

between ICICI Bank, an outstanding and trusted name in money related administrations in

India and Prudential Plc, one of UK's biggest players in the monetary administrations

divisions. During these time of the joint wander, the organization has produced a place of

pre-greatness in the Indian Mutual Fund industry. The AMC oversees huge Assets under

Management (AUM) in the shared store section. The AMC additionally takes into account

Portfolio Management Services for financial specialists, spread the nation over, alongside

International Advisory Mandates for customers crosswise over universal markets in resource

classes like Debt, Equity and Real Estate. The AMC has seen considerable development in

scale; from 2 areas and 6 workers at the initiation of the joint wander in 1998, to a present

quality of 1476 representatives with a span crosswise over more than 215 areas contacting a

financial specialist base of in excess of 2.5 million speculators (As on March 31, 2017). The

organization's development force has been exponential and it has constantly centered around

expanding availability for its financial specialists. Driven by a totally financial specialist

driven approach, the association today is an appropriate blend of speculation ability, asset

transmission capacity and process introduction. The AMC attempts to streamline its

speculator's excursion to meet their money related objectives, and give a decent financial

specialist encounter through development, consistency and supported hazard balanced

execution.

Sponsors

ICICI Bank is India's biggest private area manage an account with add up to resources of Rs.

7,206.95 billion (US$ 109 billion) at March 31, 2016 and benefit after expense Rs. 97.26

billion (US$ 1,468 million) for the year finished March 31, 2016. ICICI Bank at present has a

system of 4,608 Branches and 14,052 ATM's crosswise over India.

33

Prudential plc is a global money related administrations assemble with huge tasks in Asia, US

and the UK. The organization serves in excess of 24 million protection clients and has £599

billion of advantages under administration (as at 31 December 2016).

Key Information

Mutual Fund ICICI Prudential Mutual Fund

Setup Date Oct-13-1993

Incorporation Date Jun-22-1993

Sponsor Prudential Plc and ICICI Bank Ltd.

Trustee ICICI Prudential Trust Ltd.

Chairman Ms. Chanda Kochhar

CEO / MD Mr. Nimesh Shah

CIO Mr. S Naren

Compliance Officer Ms. Supriya Sapre

Investor Service Officer Mr. Yatin Suvarna

Assets Managed Rs. 293337.55 crore (Dec-31-2017)

Prudential Corporation Asia (PCA)

Prudential is a main life back up plan that traverses 13 advertises in Asia, covering

Cambodia, China, Hong Kong, India, Indonesia, Korea, Laos, Malaysia, the Philippines,

Singapore, Taiwan, Thailand and Vietnam. Prudential has a strong multi-channel dispersion

stage giving a complete scope of funds, speculation and assurance items. East spring

Investments oversees speculations crosswise over Asia in the interest of an extensive variety

of retail and institutional speculators, with about portion of its benefits sourced from life and

annuity items sold by Prudential plc. It is one of the locale's biggest resource administrators

with a nearness in 10 noteworthy Asian markets and in addition dissemination workplaces in

34

the US and Europe. It has £104.9 billion in resources under administration (as at 30 June

2016), overseeing reserves over a scope of advantage classes including values and settled

pay.

Prudential UK and Europe (PUE)

Prudential UK is a main life and benefits' supplier to around 6 million clients in the United

Kingdom. Their mastery in zones, for example, life span, hazard administration and multi-

resource venture, together with our budgetary quality and profoundly regarded mark, implies

that the business is firmly situated to keep seeking after an esteem driven methodology

worked around our center qualities in with-benefits and annuities.

M&G

M&G is Prudential's UK and European reserve administration business with add up to

resources under administration in abundance of £255.4 bn (as at 30 June 2016). M&G has

been contributing cash for individual and institutional customers for more than 80 years.

Today it is one of Europe's biggest dynamic speculation supervisors and in addition being a

powerhouse in settled pay.

Principal Mutual Fund

Main PNB Asset Management Company is the speculation supervisor to Principal Mutual