India's Growth Story - NCAER

34

India’s Growth Story India Policy Forum July, 2018 Junaid Ahmad, Florian Blum, Poonam Gupta, Dhruv Jain 1

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of India's Growth Story - NCAER

India’s Growth Story India Policy Forum

July, 2018

Junaid Ahmad, Florian Blum, Poonam Gupta, Dhruv Jain

1

(i) India’s long term growth (last 40-50 years)

(ii) Growth dynamics in the last decade and a half (since 2003)

(iii) Recent economic developments

(iv) Lingering challenges and emerging policy priorities

2

Plan of the paper/presentation

Long term growth has consistently accelerated and stabilized--declining standard deviation or coefficient of variation.

3

GDP growth has accelerated over the long run

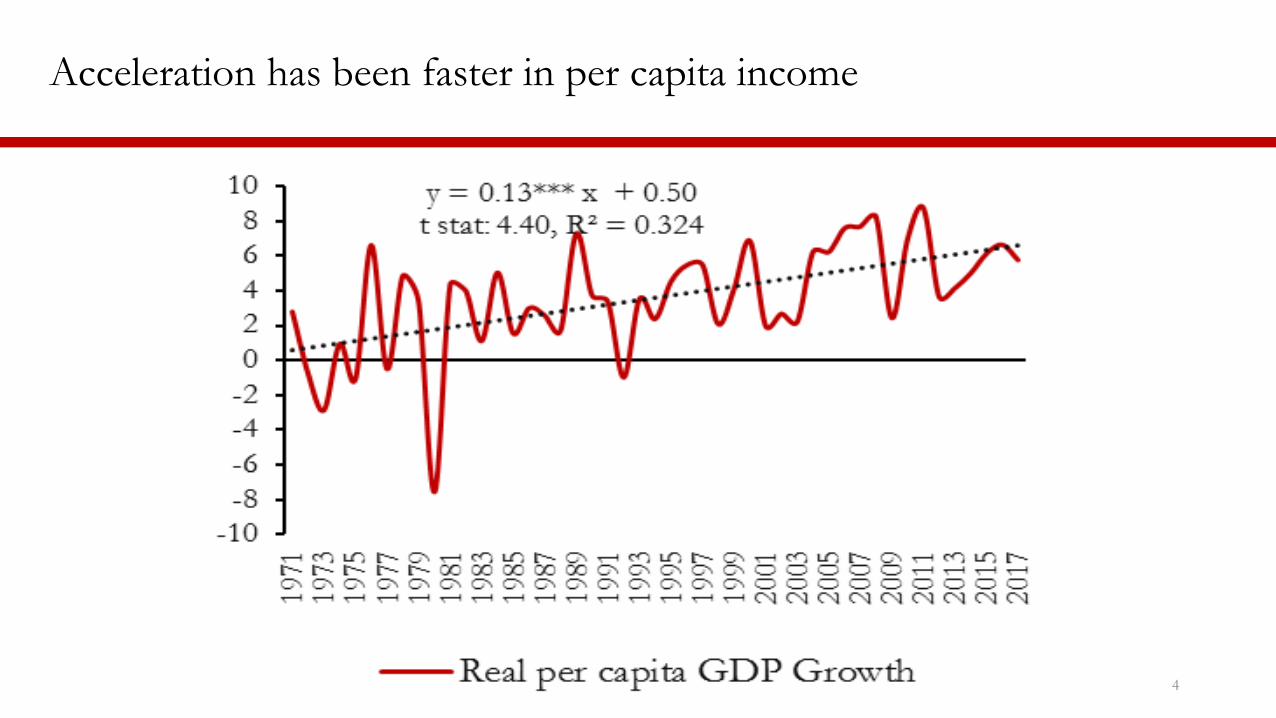

Acceleration has been faster in per capita income

4

Decomposition of GDP growth

Acceleration and stability across sectors: Agriculture, Industry and Services

• Agricultural growth : has become more stable, no definite acceleration.

• Services growth: has become more stable, fastest acceleration.

• Industrial growth: too has become more stable, some acceleration

Consumption, Investment, and Exports

• Acceleration in their contribution to growth over long run

• Share of consumption in GDP has declined, of investment and exports increased

Contribution of factor inputs and productivity growth

• A balanced narrative: TFP has increased slowly, as has the labor productivity (Bosworth, Collins and Virmani, 2007; Bosworth and Collins, 2008)

5

Inter state experience: growth has accelerated, stabilized on average, across states

6

(1) (2) (3) (4) (5)

VARIABLES Growth

Rate Growth

Rate Growth

Rate

Coefficient of

Variation

Coefficient of

Variation

Trend 0.089*** 0.099** 0.089*** -2.96*** -3.56***

(9.27) (2.47) (5.99) (4.53) (3.22)

Ag. Share (1981) X Trend -0.0002

(0.251)

GDP per capita > Median x Trend -0.0012

1.28

(0.064) (1.03)

State Fixed Effects Yes Yes Yes Yes Yes

Observations 734 734 734 567 567

R-squared 0.062 0.063 0.063 0.628 0.636

Inter state experience: growth has accelerated across states

7

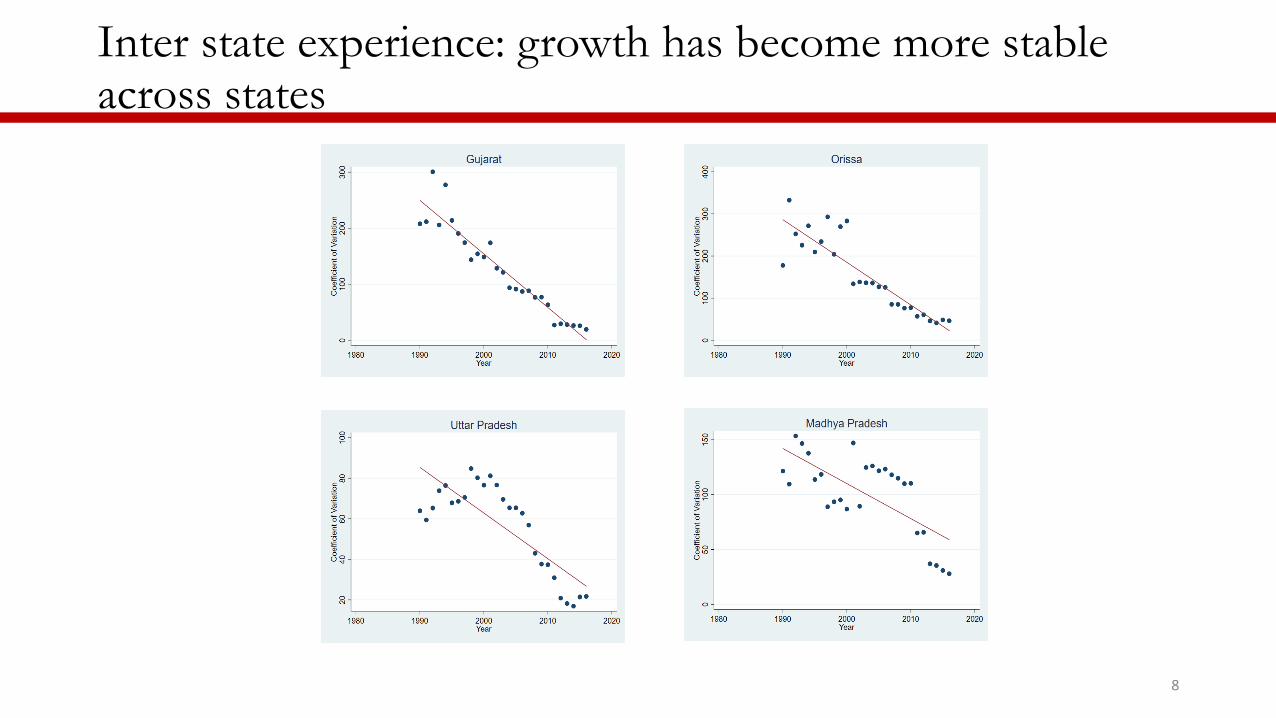

Inter state experience: growth has become more stable across states

8

(ii) Growth rates in the last decade and a half: Parsing the long run to understand when slowdown started

9

4.4

5.48.8

7.1

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

FY

Real GDP Growth Average 1970-90 Average 1991-2003Average 2004-08 Average 2009-17

Growth faster than before in 2004-2008; and somewhat faster than in many other emerging markets.

Prominently reflected in investment and credit growth, coincided with rapid inflows of capital. Features of unsustainable boom?

• External factors clearly contributed to it (Shankar Acharya; Mohan and Kapur); India specific features too—impact of economic reforms (Shankar Acharya; Arvind Panagariya)

• Policy response during the GFC impacted the pace of recovery (Mohan and Kapur; and Mundle, Rao and Bhanumurthy)

10

(ii) A distinct cycle in the Indian economy around the global financial

crisis: High growth rates in 2003-08, and a slowdown thereafter

Global growth and trade outlook have implications for India

India’s growth rate correlates strongly with advanced economies’ and global growth

India’s goods exports growth are strongly correlated with world imports growth

11

0

0.2

0.4

0.6

0.8

1

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Rolling correlation

International comparisons—EM7 or a larger set of EMDE

Credit growth was far more rapid in India prior

to the GFC

Investment growth in India outpaced growth in

the EM7, and the correction was sharper…

12

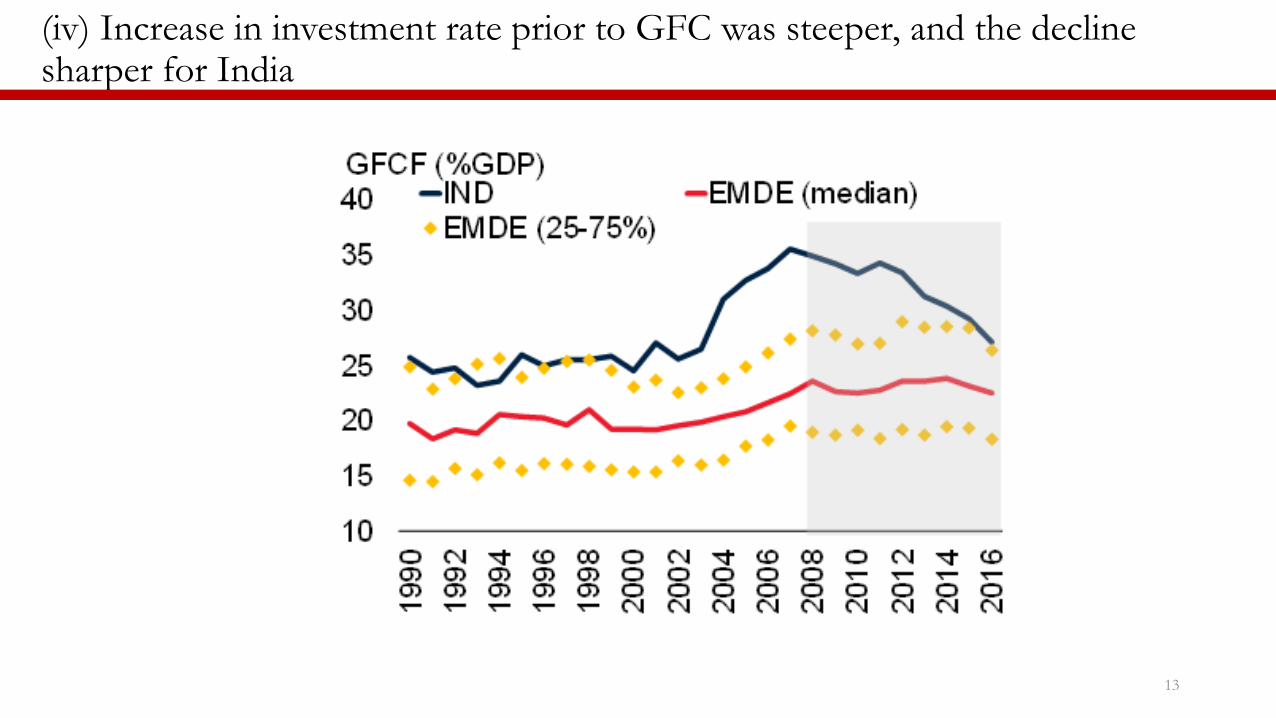

(iv) Increase in investment rate prior to GFC was steeper, and the decline sharper for India

13

• Slowdown in India coincided with the global financial crisis.

• Subsequent investment slowdown and credit slowdown sharper in India than in other large emerging markets—related to the extent of increase in prior years and the specific policy mix during 2008-09 and thereafter.

• The policy response consisted of increased spending, monetary policy easing, tax rebates, regulatory forbearance in the banking sector, evergreening. Coincided with a pre election spending spree.

14

Slowdown since 2008-09

Investment rate has been slowing after peaking in 2007-08

15

Credit growth has been declining after peaking in 2007

16

Exports and trade as percent of GDP have been declining since the global financial crisis

17

• Demonetization and implementation of GST had an impact on growth when it declined below 7 percent

• Growth temporarily decelerated to 5.6 percent in Q1, 2017-18; but rebounded to 6.3 percent in Q2, 2017-18; 7.0 in Q3, 2017-18 and 7.7 percent in Q4, 2017-18

• High frequency indicators such as trade, credit, investment, IIP, PMI, point to a continuing rebound in the economy

18

(iii) Recent Economic Developments

Continuing rebound…

19

Continuing rebound……. (contd.)

20

Continuing rebound… … (contd.)

21

Credit growth has picked up Investment growth accelerates sharply

Economy shows signs of recovery… (contd.)

22

Export show signs of recovery; imports remain stronger

Manufacturing output expands

(iv) Investment rate has declined for corporate and household sectors

23

investment rate has declined since the GFC… decline is evident in household investments…

…and private corporate sector While public investment fell after GFC, it has

increased modestly in recent years

(iv) India’s share in world exports has stagnated/declined for goods and services

24

Service and merchandise export growth has

slowed down

India’s share in goods exports has plateaued in

the recent years

(iv) India’s share in world exports has stagnated/declined across destinations and products

25

Contribution of different destinations to export

growth

Difference in Growth Rates between 2003-08

and 2012-16

(iv) Public sector banks have fared differently/less well

26

NPA Credit growth

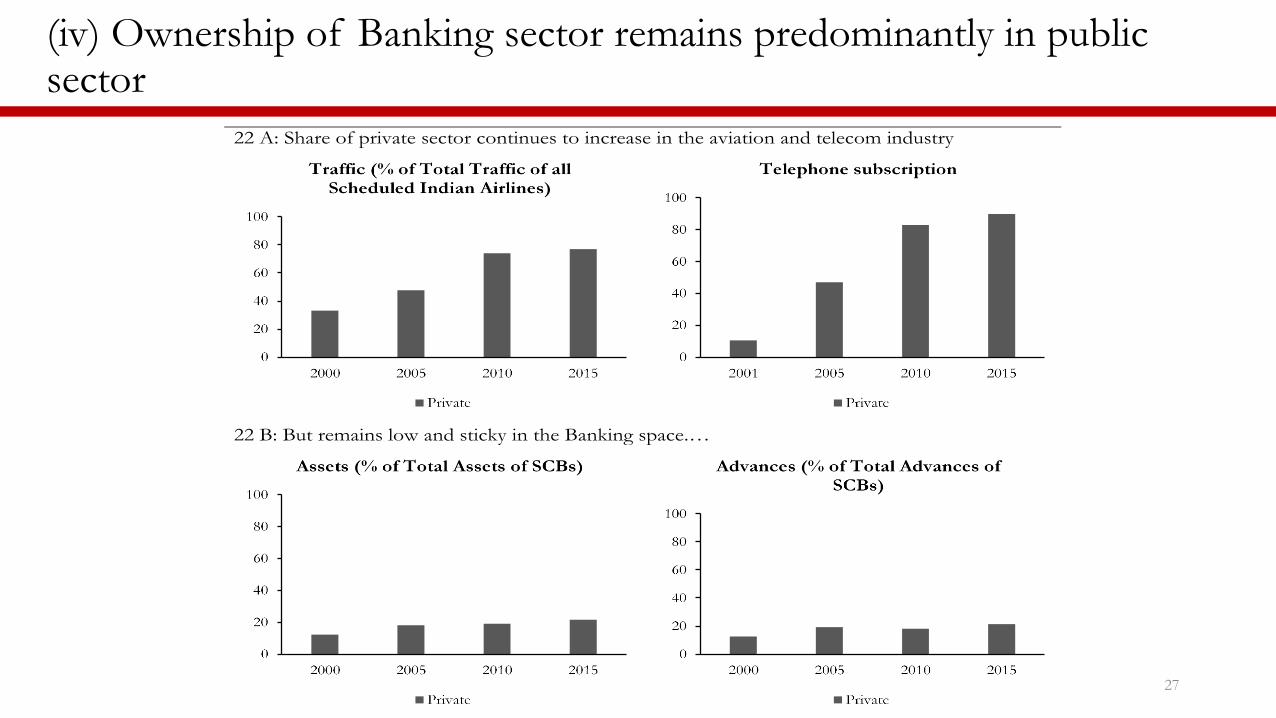

(iv) Ownership of Banking sector remains predominantly in public sector

27

22 A: Share of private sector continues to increase in the aviation and telecom industry

22 B: But remains low and sticky in the Banking space.…

Summary

• India’s growth has been credible over the long run: accelerated, steadier, diversified, balanced.

• Growth averaged 7 percent in the last decade, as growth decelerated after the global financial crisis.

• A slowdown below that was seemingly transitory and now signs of revival.

• Growth at higher levels would require a supportive global economy, reversing declining trends in investment and exports; an efficient and resilient financial sector; and continuing reform momentum.

28

Thank you

29

Policy certainty—how does one ensure it in an evolving policy paradigm

A financial sector for a 2.5 trillion economy, growing at double digit nominally.

Wisely handling global integration—maximizing gains and withstanding volatility. Easier said than done.

Public vs private goods and their provision, skills for the changing nature of jobs (is it a private or public good. Who finances and who provides), regulation of markets and sectors that have a healthy presence of public and private or only private providers,

Land/labor (silent reforms by stealth?)

30

Emerging policy priorities

Correlates and Policy Framework for sustained growth rate

31

• A conducive global economy, increasing integration while being cautious on capital flows.

• Given the structural nature of the slowdown little rationale or room for countercyclical policies. Macroeconomic stability—hard won macroeconomic stability should not be compromised

• Financial sector (some but perhaps insufficient progress on Recognize, Resolve, and Recapitalize; and missing Reforms)

• Reinstating the competitiveness of exports—real competitiveness; nominal competitiveness. Role of exchange rate. Policy tools?

• Inflation targeting framework, Policy tools available to central banks

• Increasing decentralization

• Fiscal architecture.

Global Integration of the Indian Economy

• India is a large emerging market:• Increasingly integrated on trade and capital account

• An oil importer

• Impacted by: • Global growth

• Global trade volumes

• Oil prices

• Monetary policy in advanced economies

• Global liquidity and risk aversion

32

• A distinct cycle in the Indian economy, around the global financial crisis

• External factors clearly contributed to it—somewhat similar cycles in other countries (Shankar Acharya; Mohan, and Kapur)

• India specific features too—impact of economic reforms, and the pre crisis boom (Shankar Acharya; Arvind Panagariya)

• Policy response during the GFC impacted the pace of recovery (Mohan, and Kapur; and Mundle, Rao and Bhanumurthy)

33

(ii) Growth rates in the last decade and a half

• External factors clearly contributed to it—somewhat similar cycles in other countries (Shankar Acharya; Mohan and Kapur)

• India specific features too—impact of economic reforms, and the pre crisis boom (Shankar Acharya; Arvind Panagariya)

• Policy response during the GFC impacted the pace of recovery (Mohan and Kapur; and Mundle, Rao and Bhanumurthy)

34

(ii) A distinct cycle in the Indian economy, around the global financial

crisis: High growth rates in 2003-08, and a slowdown thereafter