India Pharmaceuticals

84

Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it. Issuer of report: HSBC Securities and Capital Markets (India) Private Limited View HSBC Global Research at: https://www.research.hsbc.com Secular growth in domestic India pharma market to continue, despite short-term regulatory issues Companies with emerging focus on chronic therapies likely to sustain India growth; lower US exposure limits US FDA risk Initiate on Alkem Lab with a Buy (TP INR1,945) and Alembic Pharma with a Hold (TP INR645) Tough times: The past 15-18 months have been difficult for Indian pharma players. The numerous regulatory red flags raised by the US FDA have hurt sentiment and growth. Domestic price controls haven’t helped either, so little wonder that the sector has underperformed in the last year. Despite this, we think long-term growth opportunities remain intact in India, while a US recovery will depend on resolving FDA issues. Better India prospects: Strong growth – the Indian pharma market has tripled in the last 10 years – is being driven by a higher incidence of lifestyle diseases, growing healthcare awareness and increasing affordability. Chronic therapies for lifestyle-related disorders (e.g. diabetes) are likely to contribute to higher sales for emerging players like Alkem Lab (current share c15%) and Alembic Pharma, the focus of this report. Home advantage: The two companies have a much lower share of sales from the US (c25%) than larger peers like Sun Pharma, Lupin and Dr Reddy’s (c45%). We believe this makes them less exposed to regulatory risk (to date they have a good US FDA record). We think better compliance, quality control and increased spending on R&D make a case for the US being a long-term driver for these companies. We forecast Alkem’s earnings will rise at a CAGR of 22.5% over FY16-19e and Alembic’s c11%. Initiate coverage: We initiate on Alkem Lab with a Buy (TP INR1,945) and Alembic Pharma with a Hold (TP INR645). We prefer Alkem for its sustained growth outlook in India due to its strong brand positioning and expected market share gains in chronic therapies, as well as product launches in the US. We like Alembic’s long-term story but see limited upside from current levels. We value Alkem at 22x Sep-18 EPS of INR95.2 and Alembic at 22x Sep-18 EPS of INR31.6 and discount back the values to derive our TPs. Key risks: higher-than-expected price cuts in India and regulatory issues in the US. 21 September 2016 Damayanti Kerai* Analyst, Healthcare & Hospitals HSBC Securities and Capital Markets (India) Private Limited [email protected] +9122 3396 0692 Girish Bakhru*, CFA Analyst, South East Asia Healthcare HSBC Securities and Capital Markets (India) Private Limited [email protected] +9122 2268 1638 *Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations India Pharmaceuticals EQUITIES PHARMACEUTICALS India Summary: Alkem Lab and Alembic Pharma Ticker Company Mcap (USDb) 3m ADTV (USDm) TP (INR) Rating Upside/ Downside EPS FY16 EPS FY17e EPS FY18e PE FY16 PE FY17e PE FY18e ALKEM IN Alkem Lab 3.0 1 1,945 Buy 14.6% 56.3 70.9 86.8 30.2 23.9 19.6 ALPM IN Alembic Pharma 1.8 1 645 Hold -1.3% 26.4 21.6 27.9 24.7 30.2 23.4 Source: HSBC estimates, Thomson Reuters DataStream. Based on closing prices as of 20 Sep 2016. Look for home advantage: initiate on Alkem, Alembic

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of India Pharmaceuticals

Disclaimer & Disclosures

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Securities and Capital Markets (India) Private Limited

View HSBC Global Research at:

https://www.research.hsbc.com

Secular growth in domestic India pharma market to continue,

despite short-term regulatory issues

Companies with emerging focus on chronic therapies likely to

sustain India growth; lower US exposure limits US FDA risk

Initiate on Alkem Lab with a Buy (TP INR1,945) and Alembic

Pharma with a Hold (TP INR645)

Tough times: The past 15-18 months have been difficult for Indian pharma players.

The numerous regulatory red flags raised by the US FDA have hurt sentiment and

growth. Domestic price controls haven’t helped either, so little wonder that the sector

has underperformed in the last year. Despite this, we think long-term growth

opportunities remain intact in India, while a US recovery will depend on resolving

FDA issues.

Better India prospects: Strong growth – the Indian pharma market has tripled in the

last 10 years – is being driven by a higher incidence of lifestyle diseases, growing

healthcare awareness and increasing affordability. Chronic therapies for lifestyle-related

disorders (e.g. diabetes) are likely to contribute to higher sales for emerging players like

Alkem Lab (current share c15%) and Alembic Pharma, the focus of this report.

Home advantage: The two companies have a much lower share of sales from the US

(c25%) than larger peers like Sun Pharma, Lupin and Dr Reddy’s (c45%). We believe

this makes them less exposed to regulatory risk (to date they have a good US FDA

record). We think better compliance, quality control and increased spending on R&D

make a case for the US being a long-term driver for these companies. We forecast

Alkem’s earnings will rise at a CAGR of 22.5% over FY16-19e and Alembic’s c11%.

Initiate coverage: We initiate on Alkem Lab with a Buy (TP INR1,945) and Alembic

Pharma with a Hold (TP INR645). We prefer Alkem for its sustained growth outlook in

India due to its strong brand positioning and expected market share gains in chronic

therapies, as well as product launches in the US. We like Alembic’s long-term story

but see limited upside from current levels. We value Alkem at 22x Sep-18 EPS of

INR95.2 and Alembic at 22x Sep-18 EPS of INR31.6 and discount back the values to

derive our TPs. Key risks: higher-than-expected price cuts in India and regulatory

issues in the US.

21 September 2016

Damayanti Kerai*

Analyst, Healthcare & Hospitals

HSBC Securities and Capital Markets (India) Private Limited

+9122 3396 0692

Girish Bakhru*, CFA Analyst, South East Asia Healthcare

HSBC Securities and Capital Markets (India) Private Limited

+9122 2268 1638

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

India Pharmaceuticals EQUITIES PHARMACEUTICALS

India

Summary: Alkem Lab and Alembic Pharma

Ticker

Company

Mcap (USDb)

3m ADTV (USDm)

TP (INR)

Rating Upside/ Downside

EPS FY16

EPS FY17e

EPS FY18e

PE FY16

PE FY17e

PE FY18e

ALKEM IN Alkem Lab 3.0 1 1,945 Buy 14.6% 56.3 70.9 86.8 30.2 23.9 19.6 ALPM IN Alembic Pharma 1.8 1 645 Hold -1.3% 26.4 21.6 27.9 24.7 30.2 23.4

Source: HSBC estimates, Thomson Reuters DataStream. Based on closing prices as of 20 Sep 2016.

Look for home advantage: initiate on Alkem, Alembic

2

EQ

UIT

IES

P

HA

RM

AC

EU

TIC

AL

S

21

Se

pte

mb

er 2

01

6

Exhibit 1: India Healthcare coverage

Companies BBG Mcap (USDb) Rating CMP (INR) TP (INR) _____________ EPS (INR) ______________ ______________ PE (x) ________________ ___________ EV/EBITDA (x) ____________ FY16 FY17e FY18e FY16 FY17e FY18e FY16 FY17e FY18e

Generics Alkem Lab ALKEM IN 3.0 Initiate at Buy 1,698 1,945 56.3 70.9 86.8 30.2 23.9 19.6 23.3 18.3 14.1 Alembic Pharma ALPM IN 1.8 Initiate at Hold 653 645 26.4 21.6 27.9 24.7 30.2 23.4 11.9 19.9 15.5 Cipla CIPLA IN 7.2 Buy 603 586 20.6 21.3 26.9 29.2 28.3 22.4 20.9 18.8 15.0 Dr Reddy's DRRD IN 7.8 Reduce 3,158 2,700 138.9 110.6 147.9 22.7 28.6 21.4 15.8 20.4 16.0 Lupin LPC IN 10.4 Buy 1,548 1,846 47.4 61.9 79.5 32.7 25.0 19.5 21.1 16.7 13.1 Sun Pharma SUNP IN 28.0 Hold 779 815 21.3 27.8 35.8 36.6 28.0 21.7 22.1 16.4 13.5 Aurobindo ARBP IN 7.0 Buy 806 880 33.9 42.1 50.4 23.7 19.2 16.0 17.1 19.2 14.5 Cadila Healthcare CDH IN 6.0 Hold 393 369 15.0 14.7 18.9 26.2 26.6 20.8 18.6 11.7 8.8 Glenmark Pharma GNP IN 3.8 Hold 905 900 27.1 46.8 53.2 33.3 19.3 17.0 10.2 16.3 13.5 Ipca Lab IPCA IN 1.1 Buy 591 761 15.2 32.2 41.7 38.9 18.3 14.2 25.0 20.6 16.4 Torrent Pharma TRP IN 4.1 Buy 1,606 1,571 100.8 69.1 84.7 15.9 23.2 18.9 25.5 20.1 15.0 Biocon BIOS IN 2.9 Hold 960 780 19.6 26.5 31.1 48.9 36.2 30.9 24.2 19.1 15.9 Divi's Lab DIVI IN 5.3 Hold 1,336 1,077 41.7 47.7 58.1 32.0 28.0 23.0 25.0 20.6 16.4 Hospitals Apollo Hospitals APHS IN 2.7 Buy 1,297 1,565 23.8 24.7 37.2 54.5 52.5 34.9 26.9 24.4 19.3 Fortis Healthcare FORH IN 1.2 Buy 172 224 -0.5 0.9 1.7 NM 195.0 100.8 42.5 25.0 19.4

Source: HSBC estimates, Thomson Reuters DataStream (as of 20 Sep 2016 closing price)

3

EQUITIES PHARMACEUTICALS

21 September 2016

Investment summary 5

India secular growth to continue

despite challenges 5

Chronic therapies lead growth 6

Low US exposure reduces FDA-

related risks 7

Initiating coverage 8

Valuation and performance 12

Growth drivers are intact 15

Revisiting the sector 15

Industry trends 18

Domestic regulatory challenges 29

Company Section 37

Alkem Laboratories 38

Alembic Pharma 59

Disclosure appendix 80

Disclaimer 83

Contents

EQUITIES PHARMACEUTICALS

21 September 2016

4

Exhibit 2: Alkem Lab and Alembic Pharma snapshot

Parameters Alkem Lab Alembic Pharma

Bloomberg ticker ALKEM IN ALPM IN Year of establishment 1973 1907 Public listing on: Dec 2015 Sep 2011* Shareholding pattern** Major shareholders (66.88%), Institutional (6.91%),

non-institutional (26.21%) Major shareholders (74.13%), Institutional (13.54%), non-institutional (12.33%)

Market cap (USDbn) 3.1 1.8 3m ADTV (USDm) 1 1 Initiate with Buy Hold Target price (INR) 1,945 645 CMP (INR) 1,698 653 FY16 sales split (%) India:73, US:20, RoW: 7 India:38, US:38, RoW:7, API:17 India (acute: chronic/specialty mix)

86:14 40:60

FY16-19 adj. core EPS CAGR

22.5% 11%

Strength Sixth largest player in highly fragmented

India pharma market with leadership positions in key acute therapies of anti-infectives, gastrointestinal and pan/analgesics

Rapidly changing product mix towards specialty products in India

Strong brand recognition in industry with multiple power brands like Clavam, Pan, Pan D, Taxim, Taxim O

Demonstrated execution in the US on gAbilify success

Robust sales & distribution network with wide reach in small towns and rural markets

One of best asset turnover ratios in the industry

Weakness Yet to be proven capabilities in developing niche/complex generics in the US & execution record in regulated markets

Below industry average sales force productivity in India

Heavy inclination of its India portfolio towards low margin acute products

Yet to be proven capabilities in developing niche/complex generics in the US

Opportunities New launches and consistent market share gain in key chronic segments (anti-diabetic, neuro, cardiac, derma etc), OTC and new areas of growth in India

New launches and consistent market share gain in key chronic segments (anti-diabetic, neuro, cardiac, derma etc), OTC and new areas of growth in India

US sales ramp-up on consistent new launches

US sales ramp-up on consistent new launches and ongoing R&D for niche/complex opportunities coming to fruition faster

Threats Product & concentration risks in India (top 10 products contribute c46% of sales in India, top four therapies account for c80%)

Facility concentration risk-It has single formulation facility (Panelav) for the US market

Heavy tilt of its India portfolio towards acute therapies (c85% of total India sales) hence more prone to government-mandated price cuts which generally cover acute therapies

Exposure to foreign currency fluctuations given exports contribute for c55% of total sales

Adverse observations from regulatory bodies like the USFDA, EMA at key facilities

Adverse observations from regulatory bodies like the USFDA, EMA at key facilities

Key catalysts 1) Strong growth in India formulations sales; 2) Successful FDA inspection of Daman and Ankaleshwar facilities

Recovery in India formulations sales

Source: Company data, HSBC estimates (*Alembic Pharma was separately listed from parent Alembic Ltd in Sep 2011, **Major shareholders are mainly company promoters)

5

EQUITIES PHARMACEUTICALS

21 September 2016

India secular growth to continue despite challenges

The India pharma market (IPM) is one of the fastest growing drug markets in the world,

increasing from cUSD5bn in 2005 to current sales of cUSD15bn. This growth has been driven

by a higher incidence of lifestyle diseases, better healthcare awareness and increasing

affordability. Despite this, healthcare spending in India remains low – expenditure per capita is

just cUSD74 p.a. vs the global average of USD1,061.

Similarly, India’s pharma expenditure per capita at cUSD20 p.a. is far lower than in the US

(cUSD1,100), other developed nations like Japan, Canada, Germany and France (USD500-800),

and emerging markets such as Brazil, Russia and Mexico (USD150-200). This implies continued

significant growth opportunities in India and CRISIL Research forecasts that India’s pharma market

will grow at a CAGR of c13-15% to reach cUSD20bn by 2019-20.

While the secular growth story remains intact due to favourable demographics and healthcare

demand, recent regulatory events have slowed down overall market growth. In India, the

government has issued a series of regulatory updates in the last 8-10 months. These include

putting additional drugs under price controls as well as reducing prices for certain drugs in line

with the negative wholesale price inflation (WPI) for 2015. The government has also proposed

banning several hundred fixed dose combination (FDC) medicines on health grounds.

These regulatory changes have created uncertainty among manufacturers and trade channel

participants who have reduced/delayed product uptake from manufacturers, impacting sales

growth. As a result, sector growth has fallen from the historical trend of 12-15% to single digits

in recent quarters. See page 29 for the full list of recent regulatory changes.

The overall Indian pharma sector has also been faced with a series of regulatory issues raised

by the US Food and Drug Administration (US FDA) and other global regulatory agencies with

regard to the some of the larger companies’ facilities. These regulatory issues, as well as a

challenging pricing environment due to channel consolidation and increasing competition, have

slowed sales growth in the US, an important market for most of the Indian pharma companies.

While investor sentiment has remained cautious due to these concerns, we believe growth

prospects in the domestic Indian market continue to be bright, while a recovery in US sales is

largely dependent on the resolution of FDA-related issues.

Investment summary

We expect sustained growth for emerging chronic players in India,

driven by a chronic therapies sales ramp-up and a stable base in the

acute segment

Lower exposure to US limits near-term FDA related risks

Initiate with a Buy on Alkem Lab and a Hold on Alembic Pharma

Recent regulatory events

have slowed down overall

market growth

EQUITIES PHARMACEUTICALS

21 September 2016

6

We believe government-mandated price revisions are scheduled every two to three years and

therefore the next round of revisions will likely take place in India in 2018-19. Additionally, companies

are consciously launching brands in discretionary areas where pricing may be flexible.

We now take a more detailed look at what pharma categories are driving India pharma and

introduce the two companies highlighted in this report, Alkem Lab and Alembic Pharma.

Exhibit 3: India pharma growth trend

Source: AIOCD, HSBC

Chronic therapies lead growth

The India pharma market is dominated by acute therapies used for short-term treatments. They

account for 66% of total sales versus 34% for chronic treatments, which need to be taken for a

longer period (e.g. cardiac, anti-diabetic, oncology and neurology). However it is the chronic

category that is growing fastest – recording a CAGR of 15% over the last 10 years compared to

10% for the overall market.

There are several reasons for this, ranging from an increasing incidence of lifestyle related

diseases and better awareness about healthcare, to greater penetration in small towns and rural

areas and general affordability. We expect the chronic category to represent 40-45% of sales by

2020, up from 34%. Growth in sales of acute therapies will continue, but the pace of increase

will be slower than for chronic therapies.

Given the significant growth potential and better margin profile, it is little surprise that most

companies have enhanced their focus on the chronic segment. We believe this trend will

continue to be the key driver for India sales growth.

Presence across categories

We have mapped the domestic sales of leading companies across acute, sub-chronic and

chronic therapies to assess areas of strength and growth opportunities. This is what we found:

Chronic: Sun Pharma, Lupin, Torrent and Cadila Healthcare have an established presence

in cardiac therapies. In diabetes treatments, Sun Pharma, Lupin and Glenmark are the

leading names. Neuro/central nervous system (CNS) is an important segment for

Sun Pharma and Torrent Pharma, while oncology treatments are among the top therapies

for Dr Reddy’s and Cadila (mainly biosimilars). Respiratory remains the biggest segment

for Cipla, where it has maintained leadership status in inhalers.

10.8%

14.6%

12.8%

17.0%

11.3%13.0%

11.5%

13.8%12.1%

14.9%

11.9%

6.2%

10.8%

13.7%

11.1%

16.8%

14.8%

11.9%

14.9%

9.5%6.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

1QF

Y15

2QF

Y15

3QF

Y15

4QF

Y15

1QF

Y16

2QF

Y16

3QF

Y16

4QF

Y16

1QF

Y17

IPM growth

Impact of new DPCO 2013

Combined impact ofNLEM expansion, WPI-related price revisions,propsoed FDC ban

7

EQUITIES PHARMACEUTICALS

21 September 2016

Sub-chronic: Derma, pain management and gynaecology therapies offer opportunities to

increase market share. Derma is a focus therapy for Glenmark, and pain for Sun Pharma,

Alkem Lab, Torrent and Ipca Lab.

Acute: Anti-infectives remain key revenue contributors for Alkem, Cipla, Lupin, GSK and

Mankind, while gastro remains a major therapy for Sun Pharma, Abbott, Alkem, Cadila and

Dr Reddy’s.

Growth areas for Alkem Lab and Alembic Pharma

As shown in the table below, Alkem Lab trails its bigger rivals in terms of sales of cardiac,

anti-diabetes and neuro therapies. Alkem, which makes most of its sales from acute therapies

(anti-infectives, gastrointestinal, pain/analgesics) is deploying more resources to try to close the

gap in the chronic segment. Alembic Pharma is also ramping up major chronic segment sales

(cardiac and anti-diabetic) through launches in high-growth molecules.

We believe Alkem Lab and Alembic Pharma will see strong growth in their chronic sales from

the current low base, supported by their established presence in acute therapies. They also

have less exposure to the US market than their larger peers, which in the current environment

we see as a definite advantage, as discussed in the next section.

Exhibit 4: Therapy sales split for key companies

Company ________________________________ Therapy share in India sales _________________________________ Anti-

infective Cardiac Gastro VNM Anti-

diabetic Respiratory pain Neuro Derma Gynae Oncology Others

Sun + Ranbaxy

11.8% 18.2% 12.0% 4.0% 9.0% 3.7% 7.3% 17.2% 4.7% 4.0% 0.5% 7.6%

Abbott 11.1% 10.4% 18.7% 12.6% 4.9% 7.7% 5.6% 11.8% 6.0% 4.0% 0.0% 7.1%

Cipla 26.8% 11.8% 7.9% 1.8% 1.0% 30.2% 3.1% 3.5% 2.5% 1.5% 0.7% 9.1%

Zydus Cadila 7.4% 16.8% 13.6% 4.2% 1.3% 10.5% 9.6% 1.3% 8.0% 10.7% 5.3% 11.1%

Mankind 23.3% 8.8% 11.2% 14.5% 5.4% 6.3% 5.0% 3.0% 4.6% 6.2% 0.0% 11.6%

Alkem 42.8% 2.7% 17.8% 12.0% 2.5% 2.8% 6.9% 5.1% 3.7% 2.2% 0.7% 0.8%

Lupin 21.1% 25.0% 7.9% 5.5% 11.3% 12.3% 4.4% 5.0% 0.5% 3.5% 0.3% 3.2%

Glaxo Pharma

23.0% 1.9% 5.6% 7.6% 0.0% 8.1% 9.2% 0.3% 18.8% 1.1% 0.4% 23.9%

Glenmark 13.1% 22.7% 2.4% 2.8% 8.4% 15.3% 2.1% 0.4% 29.2% 1.8% 0.1% 1.8%

Dr. Reddy’s 8.0% 14.5% 22.0% 2.7% 6.7% 8.6% 7.8% 3.2% 6.8% 0.2% 6.7% 12.9%

Torrent 4.2% 29.2% 14.6% 15.7% 6.0% 0.3% 7.8% 16.3% 2.6% 1.6% 0.0% 1.6%

Alembic 23.5% 13.9% 13.9% 7.7% 6.1% 12.7% 3.8% 1.0% 2.0% 10.8% 0.0% 4.6%

Ipca Lab 5.9% 17.2% 8.2% 2.2% 5.3% 4.1% 26.1% 3.4% 2.9% 0.0% 4.1% 20.6%

Source: AIOCD, HSBC analysis (red cell indicates chronic therapies, grey cell indicates acute therapies while pale red cells indicate sub-chronic therapies; focus areas shown in bordered cells for Alkem and Alembic)

Low US exposure reduces FDA-related risks

The US remains the largest market for the majority of Indian pharma companies. In the past 15-18

months multiple US FDA regulatory issues have slowed/delayed new product approvals and

impacted product supplies from the key facilities of several large companies in the sector.

Alkem and Alembic generate about 20-25% of their sales in the US, much lower than the c45-50%

for larger companies like Sun, Lupin and Dr Reddy’s. This makes them less exposed to the US

FDA risk that is currently troubling the sector. Alkem and Alembic have a good record with the US

FDA so far, hence their long-term focus on maintaining high quality standards and increasing front-

end investments make the case for the US market becoming a long-term driver for these

companies.

EQUITIES PHARMACEUTICALS

21 September 2016

8

Exhibit 5: Alkem and Alembic have less exposure to US than peers (FY16 sales)

Company India formulations US Russia Japan EU Others

Alkem Lab 72.5% 20.3% 7.2% Alembic Pharma 37.6% 38.3%* 24.2% Aurobindo Pharma 21.0% 43.7% 22.3% 13.0% Cadila Healthcare 30.8% 41.5% 3.1% 24.6% Cipla 38.2% 15.3% 4.4% 42.0% Dr Reddy's 13.8% 48.8% 9.2% 11.0% 17.3% Glenmark 27.6% 31.6% 9.4% 31.4% Lupin 24.8% 43.3% 10.0% 3.1% 18.8% Sun Pharma 25.9% 48.3% 25.8% Torrent Pharma 27.3% 40.0% 9.5% 23.2%

Source: Company data, HSBC analysis (*Higher due to gAbilify in FY16, otherwise 20-25% on a normalized basis)

Despite being late entrants in the US both companies have ambitious plans to expand in that

market. Alembic has demonstrated its execution capabilities by securing FDA approval and

launching the generic Abilify (aripiprazole) in FY15-16 ahead of many front-line generics. Alkem,

through strategic acquisitions and product launches (including in-licensed products), has a

leading market share in areas like mycophenolate, benzonatate, silver sulfadiazine. Both

companies are investing in R&D and we expect them to reap the benefits in the next two to

three years.

Initiating coverage

Alkem Lab (ALKEM IN, Initiate at Buy, TP INR1,945). See full company write-up

commencing on page 38.

Alkem Lab is the sixth largest player by sales in the highly fragmented India pharma market,

with leadership positions in key acute therapies like anti-infectives (consistently No 1 for the last

10 years), gastrointestinal and pain/analgesics. Alkem has established industry recognition for

creating strong brands like Clavam, Pan, Pan D and Taxim in a crowded market and is one of

the fastest growing pharma companies among the top 10 players in India. India formulations

accounted for c72% of overall sales in FY16. After establishing a leadership position in acute

therapies, Alkem is aiming to repeat this success in better margin, high-growth chronic therapies

(e.g. cardiac, anti-diabetes, derma), leveraging on its strong sales and distribution network and

strong reach to the medical fraternity.

India growth to sustain: Despite the challenging regulatory environment, we believe Alkem

can sustain above market growth for its India formulations business, driven by volume growth in

power brands, increasing marketing share in the chronic segment and new product launches.

An increasingly competitive pricing environment in segments like anti-infectives and gastro may

continue to impact the prices of its key brands. However, this will also provide opportunities for

higher volume growth in price-sensitive segments. The company has been able to hold/increase

market share in several of its biggest brands, which should sustain the growth of its domestic

formulations business, along with increasing share in chronic therapies products. We expect

India formulations sales to grow at a CAGR of c18% over FY16-19e (acute therapies c16% and

chronic therapies c29%).

US to grow from a small base: Alkem’s US sales have increased from USD14m in FY11 (from

less than 10 products) to cUSD150m in FY16 (19 products, of which five are in-licensed). We

believe several factors will drive further growth in the US growth – its Abbreviated New Drug

Application (ANDA) pipeline, strong market share in key products, the company’s own front-end

commercial and manufacturing infrastructure and strong channel reach.

We forecast that US sales will increase at a CAGR of c23% over FY16-19e which will be driven

by continued traction in existing products, new product launches and a gradual shift towards

9

EQUITIES PHARMACEUTICALS

21 September 2016

Paragraph-IV (P-IV) ANDA and specialty launches. (Under a P-IV filing, a company can seek

FDA approval to market a generic drug in the US before the expiration of a patent protecting the

reference brand drug. P-IV certifies that the patent in question is either invalid or is not infringed

by the generic product. If the generic filer successfully invalidates the patent in the subsequent

legal battle which follows after P-IV filing, it can launch the generic before the expiry of the

patent.)

Margin improvements: Alkem has historically lagged behind peers in terms of gross margins

and subsequent operating margins due to a heavy dependence on acute therapies. In the long

term it aims to bridge this gap in EBITDA margins – Alkem’s c17% vs 23-25% for key peers – by

increasing the sales share of chronic therapies in India and growing sales in the US. We

estimate that gross margin improvement, coupled with increasing operating efficiency, should

drive the EBITDA margin up at least 260bps over FY16-19e. Overall, we expect earnings CAGR

of 22.5% between FY16-19e. Moreover a healthy balance sheet, with cash and equivalents of

cINR8bn in FY16 and net debt/equity of -0.06, should enable the company to make strategic

acquisitions to support its growth plans.

Valuation: We value the stock at a PE of 22x (Gordon Growth based PE) September 2018e

EPS of INR95.2, and we discount this value to arrive at our TP of INR1,945. Our TP implies

FY17, FY18, FY19 PE of 27.4x, 22.4x and 18.8x, compared to peer averages of 26.4x, 20.8x

and 17.8x. Our TP offers 14.6% upside; at this level, according to HSBC’s rating system, the

stock could be rated either as a Hold or a Buy. We rate Alkem a Buy, however, based on its

sustained growth outlook in India on strong brand positioning and expected market share gain

in chronic therapies products, as well as increasing sales in the US which should lead to margin

expansion.

Our Gordon Growth Model assumes 22% ROE, 7.7% cost of equity and a 4% long-term growth

rate. ROE is based on our explicit forecast average of FY17-19e period, while the cost of equity

of 7.7% is based on our in-house view of a global risk free rate of 3% and a 6.5% equity risk

premium for India.

Key catalysts: 1) Strong recovery in India formulations sales; 2) successful US FDA inspection

of its Daman and Ankaleshwar facilities.

Key downside risks: 1) Concentration risk from dependence on top brands; 2) price cuts and

other regulatory challenges in India; 3) delay/failure to receive drug approvals in the US;

4) regulatory risks (US FDA and other regulatory agencies like EMA, UK MHRA); 5) lack of

vertical integration in the US market.

For more detailed risks, see page 52 in the company section.

HSBC vs Consensus: We are in-line with Bloomberg consensus on FY17 EPS estimates while

we are 5-6% ahead of consensus on FY18 and FY19 estimates (see Exhibit 6 below).

Alembic Pharma (ALPM IN, Initiate at Hold, TP INR645). See full company write-up

commencing on page 59.

Alembic Pharma, a mid-sized pharma company, has successfully transitioned from being

predominantly an acute player to becoming a specialty therapy focused player after the current

management team re-aligned their strategies towards the high-growth specialty segment in

2007-08. These specialty products will be key drivers for its India formulations business, which

contributed c60% of total India sales in FY16. We forecast c21% FY16-19e CAGR for its India

specialty formulations sales (vs 14% CAGR for total India sales). Overall, we forecast c11%

adjusted core PAT CAGR for FY16-19e.

EQUITIES PHARMACEUTICALS

21 September 2016

10

US investment ongoing: After the success of exclusive gAbilify (an anti-psychotic treatment)

sales during FY16, Alembic expects core US sales (excluding any one-off benefits) momentum

to continue with y-o-y sales growth of c30-35%, driven by new launches. Its pipeline of c35

pending ANDAs (of which 40% are P-IV opportunities) has an attractive maturity profile based

on their filing dates as they all could be approved in the next three to four years. The company

has ramped-up its R&D efforts to increase the width and quality of its pipeline. It is targeting

niche areas like injectables (including oncology injectables) and derma and we believe these

R&D investments will start to bear fruit in two to three years. With a front-end marketing

infrastructure now in place we expect margins to improve (it previously had to share revenues

with marketing partners). On the back of seven to eight expected new launches a year, we

expect core US sales to grow at a FY16-19e CAGR of c29%.

Strong management team: We believe the management team deserves credit for making

structural changes to the company. These include shifting the focus to specialty therapies in

India, de-merging Alembic Pharma from its parent to unlock the value of the India business,

putting a greater focus on the US and ramping up its R&D investment. We think this will take the

company to the next level of growth and profitability.

Valuation: We value the stock at 22x (Gordon Growth based PE) September 2018e EPS of

INR31.6 and discount this value to arrive at our TP of INR645. Our TP implies FY17, FY18 and

FY19 PE of 29.8x, 23.1x and 18.0x compared to peer averages of 26.4x, 20.8x and 17.8x.

Our model assumes c25% sustainable ROE, 7.9% cost of equity and 4% long-term growth rate.

ROE is based on our explicit forecast average of the FY17-19e period, while the cost of equity

is based on a global risk-free rate of 3% and a 6.5% equity risk premium for India.

We are positive about Alembic’s long-term growth prospects, which will be driven by increasing

specialty market share in India, the ramp-up of US sales and R&D investment. However, we

believe the current stock price, which implies forward multiples of 28.4x FY17 and 21.3x FY18

consensus earnings estimates, reflects the long-term positives from ongoing R&D initiatives and

we don’t have much upside in our numbers. Hence, we initiate with a Hold rating.

Key downside risks: 1) Higher margin pressure due to higher R&D expense; 2) regulatory risks,

especially the US FDA); 3) delay/failure to receive US FDA approvals in the US; 4) price cuts

and other regulatory challenges in India; c18% of its domestic branded formulations portfolio

comes under the National List of Essential Medicines, which are subject to price caps by

regulatory bodies; 5) foreign currency fluctuations: export sales contribute c55% of company

revenues.

Key upside risks: 1) Strong recovery in India formulations sales after a muted 1Q FY17; 2)

faster than expected pick-up of US sales from new launches.

For more detailed risks, see pages 70-71 in the company section.

HSBC vs Consensus: We are 6.5-7.5% below Bloomberg consensus on FY17-19 earnings

(see Exhibit 6 below) due to our assumption of a more gradual improvement in margins.

11

EQUITIES PHARMACEUTICALS

21 September 2016

Exhibit 6: HSBC vs Consensus estimates

Company Estimates (INRm except EPS) FY17e FY18e FY19e

Alkem Lab HSBC Sales 60,202 72,738 83,308 EBITDA 10,717 13,709 16,319 PAT 8,477 10,382 12,386 EPS 70.9 86.8 103.6 Bloomberg Sales 57,544 67,898 78,634 EBITDA 10,132 12,514 15,647 PAT 8,448 9,783 11,759 EPS 70.7 81.8 98.4 % difference HSBC vs BBG Sales 4.6% 7.1% 5.9% EBITDA 5.8% 9.5% 4.3% PAT 0.4% 6.1% 5.3% EPS 0.3% 6.1% 5.3% Alembic Pharma FY17e FY18e FY19e HSBC Sales 30,365 36,479 43,667 EBITDA 6,105 7,865 9,990 PAT 4,080 5,266 6,747 EPS 21.64 27.94 35.79 Bloomberg Sales 31,667 36,507 41,341 EBITDA 6,411 8,159 10,376 PAT 4,379 5,695 7,221 EPS 23.23 30.20 38.28 % difference-HSBC vs BBG Sales -4.1% -0.1% 5.6% EBITDA -4.8% -3.6% -3.7% PAT -6.8% -7.5% -6.6% EPS -6.8% -7.5% -6.5%

Source: HSBC estimates, Bloomberg

Exhibit 7: Valuation comparison

Alkem Lab Alembic Pharma Remarks

Target price (INR) 1,945 645 Implied PE FY17e 27.4 29.8 FY18e 22.4 23.1 FY19e 18.8 18.0 Average 12-m forward PE 3-yr average na 18.3 Alembic has significantly rerated in FY16 on gAbilify

success in the US. Alkem went public in Dec 2015 5-yr average na 14.8 Current 22.1 24.2 Comps average FY17e 26.4 Range 17-34x FY18e 20.8 Range 16-30x FY19e 17.8 Range 14-25x

Source: HSBC estimates, Thomson Reuters DataStream

EQUITIES PHARMACEUTICALS

21 September 2016

12

The Indian pharma sector has gone through a difficult time in the last 15-18 months as a result

of US FDA regulatory issues. This has resulted in slower approvals, launches and sales in the

US for many of the larger companies in the sector. After years of outperformance, it is not a

surprise that India healthcare has underperformed other sectors in the past 12 months

(see Exhibit 8).

Additionally, increasing competition and channel consolidation in the US have led to price

erosion, which has had a material impact (see our report Cherry picking amidst consolidation,

16 September 2015). In India, domestic sales have been hurt by pricing controls, while

emerging market sales have been impacted by currency volatility.

Exhibit 8: India healthcare has underperformed other sectors in the past 12 months

Source: Thomson Reuters DataStream

70.0

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16

Basic Mat. Energy FMCG Finance Healthcare

Industrials IT Telecom Utilities Sensex

Valuation and performance

Regulatory issues are the major overhang for the sector

Resolving problems raised by the US FDA will be a key trigger for

sector rerating

A strong recovery in India sales for domestic focused players like

Alkem and Alembic will be key to strong performance

13

EQUITIES PHARMACEUTICALS

21 September 2016

Exhibit 9: US sales growth has slowed for major Indian generics

US Sales (USDm) FY11 FY12 FY13 FY14 FY15 FY16 1QFY17

Aurobindo Pharma 261 247 322 567 773 940 255 Dr Reddy's Lab 417 670 738 921 1,055 1,168 237 Lupin 441 507 693 803 891 887 322 Sun Pharma 481 725 1,132 1,620 2,244 2,064 609 Sun Pharma ex Taro 266 291 524 922 1,450 1,208 399 Cadila Healthcare 212 260 277 366 551 609 129 Glenmark Pharma 182 250 310 336 333 371 104 Torrent Pharma 24 44 64 128 133 403 65 % y-o-y Aurobindo Pharma 35.8% -5.2% 30.4% 75.9% 36.3% 21.6% 20.3% Dr Reddy's Lab 17.5% 60.7% 10.1% 24.8% 14.5% 10.7% -19.7% Lupin 26.7% 15.0% 36.7% 15.9% 11.0% -0.4% 56.7*% Sun Pharma 108.2% 50.7% 56.1% 43.1% 38.5% -8.0% 5.3**% Sun Pharma ex Taro 15.2% 9.4% 80.1% 76.0% 57.3% -16.7% 0.3**% Cadila Healthcare 49.3% 22.6% 6.5% 32.1% 50.5% 10.5% -18.4% Glenmark Pharma 19.6% 37.4% 24.0% 8.4% -0.9% 11.4% 17.4% Torrent Pharma 25.5% 83.6% 45.5% 100.7% 3.5% 203.0% -53.2%

Source: Company data, HSBC analysis (*Appear high on very low base, **Showing base sales growth excluding one-offs)

Exhibit 10: 2016 ytd Stock performance

Source: Thomson Reuters DataStream (as of 20 Sep 2016 closing price)

Biocon

Cadila Healthcare

Alkem Lab

Sensex

Torrent Pharma

Dr Reddy's

Glenmark

Sun Pharma

Alembic Pharma

Cipla

Aurobindo Pharma

Lupin

Ipca Lab

-40.0% -20.0% 0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

EQUITIES PHARMACEUTICALS

21 September 2016

14

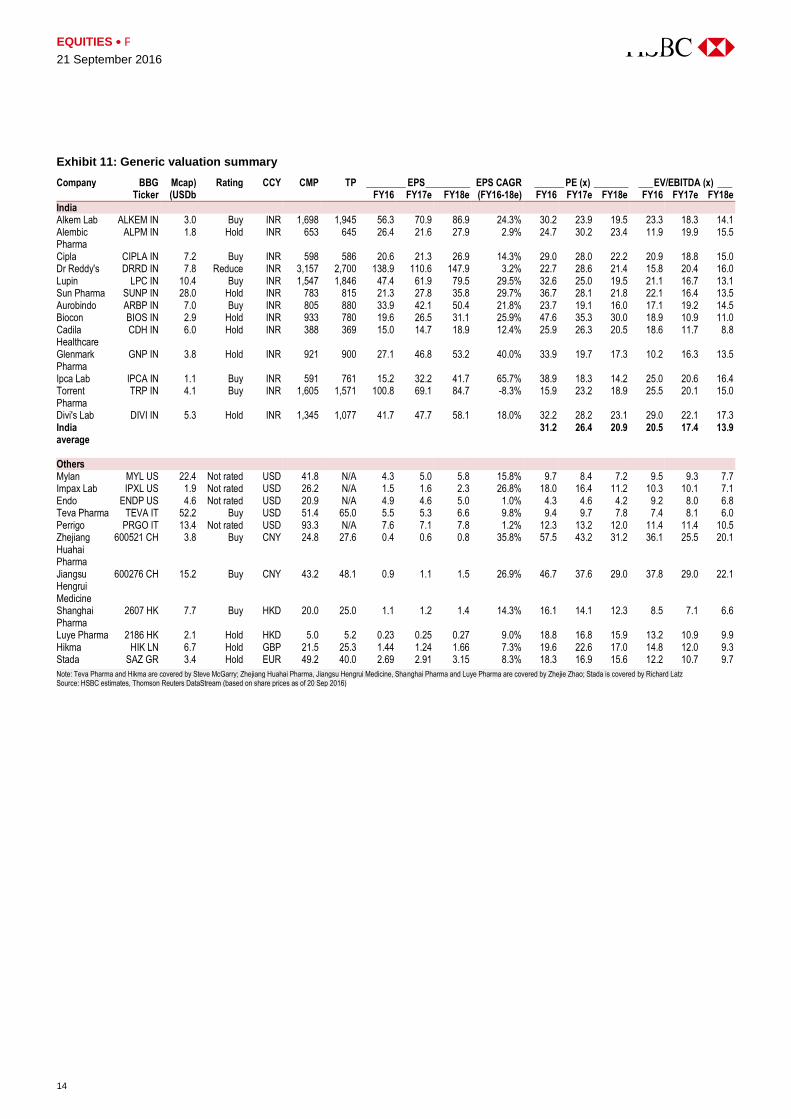

Exhibit 11: Generic valuation summary

Company BBG Mcap) Rating CCY CMP TP ________ EPS _________ EPS CAGR ______ PE (x) _______ ___ EV/EBITDA (x) ___ Ticker (USDb FY16 FY17e FY18e (FY16-18e) FY16 FY17e FY18e FY16 FY17e FY18e

India Alkem Lab ALKEM IN 3.0 Buy INR 1,698 1,945 56.3 70.9 86.9 24.3% 30.2 23.9 19.5 23.3 18.3 14.1 Alembic Pharma

ALPM IN 1.8 Hold INR 653 645 26.4 21.6 27.9 2.9% 24.7 30.2 23.4 11.9 19.9 15.5

Cipla CIPLA IN 7.2 Buy INR 598 586 20.6 21.3 26.9 14.3% 29.0 28.0 22.2 20.9 18.8 15.0 Dr Reddy's DRRD IN 7.8 Reduce INR 3,157 2,700 138.9 110.6 147.9 3.2% 22.7 28.6 21.4 15.8 20.4 16.0 Lupin LPC IN 10.4 Buy INR 1,547 1,846 47.4 61.9 79.5 29.5% 32.6 25.0 19.5 21.1 16.7 13.1 Sun Pharma SUNP IN 28.0 Hold INR 783 815 21.3 27.8 35.8 29.7% 36.7 28.1 21.8 22.1 16.4 13.5 Aurobindo ARBP IN 7.0 Buy INR 805 880 33.9 42.1 50.4 21.8% 23.7 19.1 16.0 17.1 19.2 14.5 Biocon BIOS IN 2.9 Hold INR 933 780 19.6 26.5 31.1 25.9% 47.6 35.3 30.0 18.9 10.9 11.0 Cadila Healthcare

CDH IN 6.0 Hold INR 388 369 15.0 14.7 18.9 12.4% 25.9 26.3 20.5 18.6 11.7 8.8

Glenmark Pharma

GNP IN 3.8 Hold INR 921 900 27.1 46.8 53.2 40.0% 33.9 19.7 17.3 10.2 16.3 13.5

Ipca Lab IPCA IN 1.1 Buy INR 591 761 15.2 32.2 41.7 65.7% 38.9 18.3 14.2 25.0 20.6 16.4 Torrent Pharma

TRP IN 4.1 Buy INR 1,605 1,571 100.8 69.1 84.7 -8.3% 15.9 23.2 18.9 25.5 20.1 15.0

Divi's Lab DIVI IN 5.3 Hold INR 1,345 1,077 41.7 47.7 58.1 18.0% 32.2 28.2 23.1 29.0 22.1 17.3 India average

31.2 26.4 20.9 20.5 17.4 13.9

Others Mylan MYL US 22.4 Not rated USD 41.8 N/A 4.3 5.0 5.8 15.8% 9.7 8.4 7.2 9.5 9.3 7.7 Impax Lab IPXL US 1.9 Not rated USD 26.2 N/A 1.5 1.6 2.3 26.8% 18.0 16.4 11.2 10.3 10.1 7.1 Endo ENDP US 4.6 Not rated USD 20.9 N/A 4.9 4.6 5.0 1.0% 4.3 4.6 4.2 9.2 8.0 6.8 Teva Pharma TEVA IT 52.2 Buy USD 51.4 65.0 5.5 5.3 6.6 9.8% 9.4 9.7 7.8 7.4 8.1 6.0 Perrigo PRGO IT 13.4 Not rated USD 93.3 N/A 7.6 7.1 7.8 1.2% 12.3 13.2 12.0 11.4 11.4 10.5 Zhejiang Huahai Pharma

600521 CH 3.8 Buy CNY 24.8 27.6 0.4 0.6 0.8 35.8% 57.5 43.2 31.2 36.1 25.5 20.1

Jiangsu Hengrui Medicine

600276 CH 15.2 Buy CNY 43.2 48.1 0.9 1.1 1.5 26.9% 46.7 37.6 29.0 37.8 29.0 22.1

Shanghai Pharma

2607 HK 7.7 Buy HKD 20.0 25.0 1.1 1.2 1.4 14.3% 16.1 14.1 12.3 8.5 7.1 6.6

Luye Pharma 2186 HK 2.1 Hold HKD 5.0 5.2 0.23 0.25 0.27 9.0% 18.8 16.8 15.9 13.2 10.9 9.9 Hikma HIK LN 6.7 Hold GBP 21.5 25.3 1.44 1.24 1.66 7.3% 19.6 22.6 17.0 14.8 12.0 9.3 Stada SAZ GR 3.4 Hold EUR 49.2 40.0 2.69 2.91 3.15 8.3% 18.3 16.9 15.6 12.2 10.7 9.7

Note: Teva Pharma and Hikma are covered by Steve McGarry; Zhejiang Huahai Pharma, Jiangsu Hengrui Medicine, Shanghai Pharma and Luye Pharma are covered by Zhejie Zhao; Stada is covered by Richard Latz Source: HSBC estimates, Thomson Reuters DataStream (based on share prices as of 20 Sep 2016)

15

EQUITIES PHARMACEUTICALS

21 September 2016

Revisiting the sector

India’s pharmaceutical market (IPM) has tripled in size from cUSD5bn in 2005 to around

USD15bn currently. It’s highly fragmented, with the top 10 companies accounting for c44% of

the market (source: AIOCD MAT July 2016). Acute therapies dominate the market and

contribute for 66% of total sales while chronic therapies account for 34% sales. We expect this

to change due to changes in lifestyle, demographics and healthcare demand. Chronic therapies,

which need to be taken for a longer period, continue to be the key growth drivers for India’s

pharma market.

India formulations account for an average of 30-35% of total company sales for major

companies. The figure is generally lower for US-focused generic companies like Lupin, Sun

Pharma, Glenmark and Dr Reddy’s.

See Exhibits 12-14 for more details on market and growth trends.

Growth drivers are intact

We look at the categories and segments which are driving growth in

a difficult, fragmented market

We also take a detailed look at the regulatory problems facing the

industry in India

Despite these challenges, double-digit annual growth is still possible

due to favourable demographics and strong healthcare demand

EQUITIES PHARMACEUTICALS

21 September 2016

16

Exhibit 12: Top players in the fragmented market (INRbn)

Rank INRbn Type of company MAT July 2016 (AIOCD basis)

Jul13-16 CAGR Market share

IPM 1009.0 11.7% 100.0% 1 Sun + Ranbaxy Public/Indian 87.9 9.6% 8.7% 2 Abbott + Novo Public/MNC 63.2 8.6% 6.3% 3 Cipla Public/Indian 50.0 11.0% 5.0% 4 Zydus + Biochem Public/Indian 42.5 9.4% 4.2% 5 Mankind Private/Indian 38.9 13.7% 3.9% 6 Alkem + Cachet + Indchemie Public/Indian 34.7 11.2% 3.4% 7 Lupin Public/Indian 33.8 15.6% 3.3% 8 Glaxo Public/MNC 32.5 0.8% 3.2% 9 Macleods Private/Indian 29.5 16.3% 2.9% 10 Pfizer+Wyeth Public/Indian 29.1 9.8% 2.9% 11 Intas Private/Indian 28.9 17.1% 2.9% 12 Emcure Private/India 26.8 16.1% 2.7% 13 Aristo Private/Indian 25.0 13.6% 2.5% 14 Glenmark Public/Indian 24.3 18.7% 2.4% 15 Sanofi India Public/Indian 24.3 16.2% 2.4% 16 Dr. Reddys Public/MNC 24.1 14.6% 2.4% 17 Torrent Public/Indian 22.8 21.9% 2.3% 18 USV Private/Indian 20.3 15.7% 2.0% 19 Micro + Bal Private/India 19.6 14.4% 1.9% 20 Alembic Public/Indian 14.2 13.5% 1.4% Top 10 share in IPM 43.8% Top 20 share in IPM 66.6%

Source: AIOCD, HSBC analysis

Exhibit 13: India formulations growth trend for key companies

Company FY16 reported

sales India as % of

sales FY12 FY13 FY14 FY15 FY16 ___________________________ % y-o-y ____________________________

Sun+Ranbaxy 72.5 25.9% 10.6% 13.1% 11.0% 14.4% 8.0% Cipla 51.1 38.2% 14.0% 14.6% 12.0% 17.0% 5.9% Zydus Cadila 29.7 30.8% 10.6% 22.6% 6.1% 8.6% 11.1% Alkem 35.4 72.5% 18.6% 16.8% 14.6% 20.3% 30.4% Lupin 33.9 24.8% 22.8% 21.4% 4.9% 19.7% 14.3% Glaxo 27.3 100.0% 8.6% 11.2% -3.1% 4.8% -16.1% Glenmark 21.1 27.6% 18.6% 30.7% 15.3% 15.8% 20.6% Dr. Reddys 21.3 13.8% 10.6% 12.6% 7.9% 13.7% 19.2% Torrent 18.3 27.3% 9.0% 13.2% 12.6% 38.6% 13.4% Alembic 11.9 40.6% 12.9% 13.2% 10.7% 12.5% 8.3% Ipca Lab 12.1 42.5% 8.2% 16.6% 10.4% 16.4% 6.9%

Source: Company data, HSBC analysis

17

EQ

UIT

IES

P

HA

RM

AC

EU

TIC

AL

S

21

Se

pte

mb

er 2

01

6

Exhibit 14: Snapshot of top companies (INRm)

Source: AIOCD, HSBC analysis (*Abbott doesn’t include anti-diabetic brands which it distributes in India under agreement with Novo Nordisk)

Company Sun Pharma Sales Abbott* Sales Cipla Sales Zydus Cadila Sales Mankind Sales Alkem Sales

Rank (previous year) 1 (1) 2 (2) 3 (3) 4 (4) 5 (5) 6 (6)

Top 5 brands Volini 2,303 Phensedyl Cough Linctus 2,473 Foracort 2,007 Skinlite 1,822 Manforce 1,767 Clavam 2,453

Rosuvas 1,760 Thyronorm 1,824 Budecort 1,646 Atorva 1,304 Moxikind CV 1,674 Pan 2,005

Istamet 1,624 Duphaston 1,745 Asthalin 1,391 Mifegest Kit 1,234 Unwanted Kit 1,224 Taxim O 1,948

Gemer 1,605 Vertin 1,270 Seroflo 1,328 Deriphyllin 1,034 Glimestar M 739 Pan D 1,634

Levipil 1,539 Udiliv 1,259 Duolin 1,267 Pantodac 1,022 Amlokind-AT 722 Taxim 1,425Total no of brands 1,323 919 1,027 1,247 703 954% Sales contribution

Top 15 brands 22.7% 31.4% 30.6% 29.9% 29.1% 48.9%

Top 16-50 brands 20.5% 26.2% 26.7% 22.9% 25.9% 18.5%

Top 51-100 brands 15.1% 18.2% 17.2% 14.2% 17.3% 10.3%

Remaining brands 41.6% 24.2% 25.5% 33.0% 27.7% 22.3%

Total India sales 87,380 52,531 49,668 42,470 38,281 34,720

Acute: Chronic mix 40:60 39:61 59:41 67:33 57:43 86:14

Company Lupin Sales Glaxo Sales Glenmark Sales Dr Reddy's Sales Torrent Sales Alembic Sales

Rank (previous year) 7 (7) 8 (8) 14 (16) 16 (17) 17 (15) 20 (20)

Top 5 brands Gluconorm-G 1,464 Augmentin 3,025 Telma 1,772 Omez 1,312 Shelcal 1,856 Azithral 1,371

Tonact 965 Synflorix 1,985 Telma H 1,437 Omez D 987 Chymoral Forte 1,111 Althrocin 818

Budamate 855 Calpol 1,785 Ascoril Plus 1,059 Econorm 730 Nikoran 856 Roxid 579

Rablet-D 547 Zinetac 1,575 Candid 1,004 Nise 720 Dilzem 634 Gestofit 557

Esiflo 517 Betnovate C 1,539 Candid-B 928 Stamlo 665 Nebicard 616 Wikoryl 465Total no of brands 829 225 350 379 490 441% Sales contribution

Top 15 brands 25.8% 60.7% 42.9% 38.9% 40.5% 45.0%

Top 16-50 brands 26.9% 25.4% 29.3% 28.2% 27.4% 28.9%

Top 51-100 brands 18.6% 10.7% 15.8% 16.8% 16.8% 16.7%

Remaining brands 28.7% 3.1% 12.1% 16.0% 15.4% 9.3%

Total India sales 33,524 1,014 2,913 3,822 3,491 1,308

Acute: Chronic mix 42:58 87:13 40:60 52:48 38:62 40:60

EQUITIES PHARMACEUTICALS

21 September 2016

18

Industry trends

We now look at therapies, molecules and brands to assess recent industry trends.

A. Therapeutic overview

Anti-infectives remains the leading therapeutic segment, with a market share of c15%. Its share

has though gradually come down due to the increased growth in chronic therapies.

Exhibit 15: Anti-infectives continue its dominance in IPM

Therapy Sales (INRb) CAGR ___________________ Market share ____________________ MAT Jul 16 MAT Jul 13-16 MAT Jul 13 MAT Jul 14 MAT Jul 15 MAT Jul 16

IPM 1,009 11.7% 100.0% 100.0% 100.0% 100.0% Anti-Infectives 152 5.9% 17.7% 16.1% 15.5% 15.1% Cardiac 125 12.7% 12.1% 12.3% 12.5% 12.4% Gastro Intestinal 119 13.1% 11.4% 11.4% 11.6% 11.8% Vitamins/Minerals/Nutrients 89 11.7% 8.8% 9.0% 9.0% 8.8% Anti-Diabetic 85 20.0% 6.7% 7.2% 7.9% 8.4% Respiratory 78 11.9% 7.7% 7.8% 7.8% 7.8% Pain / Analgesics 70 9.5% 7.3% 7.2% 6.9% 6.9% Neuro/CNS 62 11.9% 6.1% 6.2% 6.1% 6.2% Derma 60 16.3% 5.3% 5.8% 5.9% 5.9% Gynaecological 51 2.9% 6.4% 5.2% 4.9% 5.0% Ophthal / Otologicals 19 13.2% 1.8% 1.8% 1.8% 1.9% Hormones 17 10.7% 1.7% 1.7% 1.7% 1.7% Anti-Neoplastics 15 18.0% 1.3% 1.6% 1.7% 1.5% Vaccines 17 24.4% 1.2% 1.5% 1.7% 1.7% Others 50 15.9% 4.4% 5.2% 4.9% 4.9%

Source: AIOCD, HSBC analysis

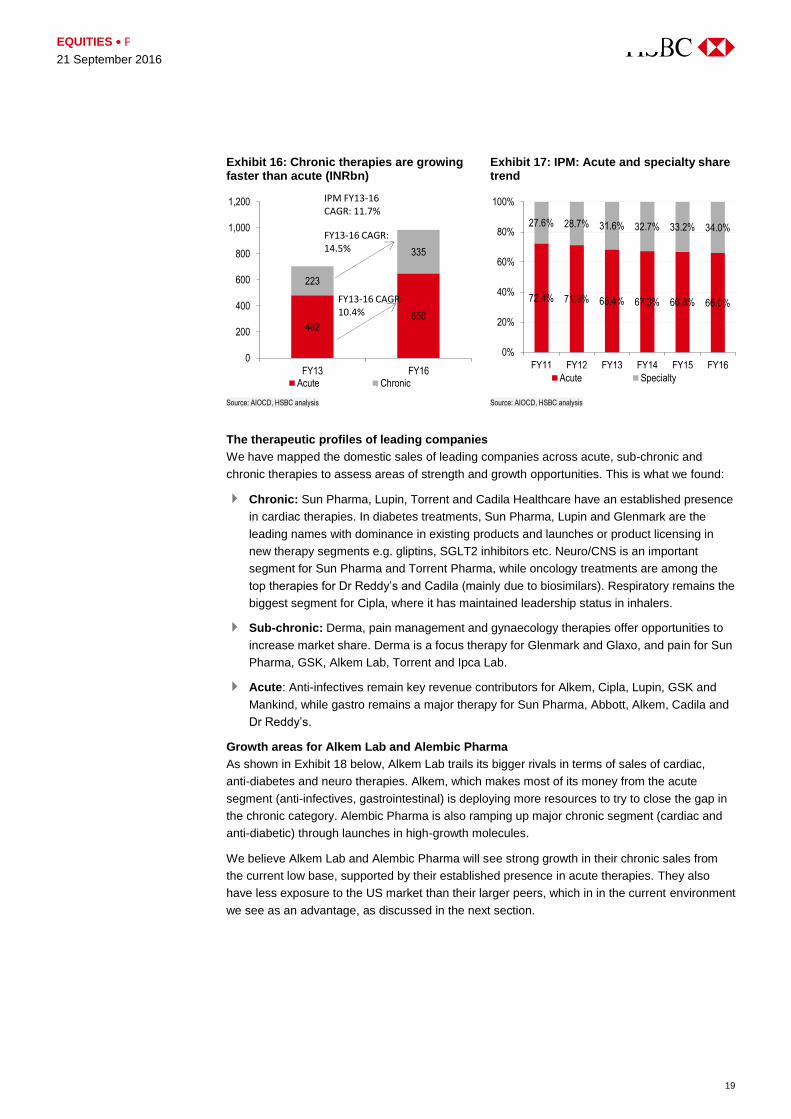

Chronic/specialty therapies including areas such as anti-diabetic, respiratory (inhalers), cardiac

and the CNS (central nervous system) have grown significantly in recent years, driven by

increasing incidence of lifestyle related diseases. For example, anti-diabetic treatments have

gained c160bps in market share in the last four years.

Given the strong growth and better margin profile, most companies have increased their focus

on chronic therapies. This will continue to be the key driver for India sales growth and we expect

the share of chronic therapies sales to reach 40-45% by 2020 from the current level of c34%.

We expect sales of acute therapies to grow in high single-digits on the back of poor healthcare

facilities, including poor hygiene/sanitation for the majority of the population.

19

EQUITIES PHARMACEUTICALS

21 September 2016

Exhibit 16: Chronic therapies are growing faster than acute (INRbn)

Exhibit 17: IPM: Acute and specialty share trend

Source: AIOCD, HSBC analysis Source: AIOCD, HSBC analysis

The therapeutic profiles of leading companies

We have mapped the domestic sales of leading companies across acute, sub-chronic and

chronic therapies to assess areas of strength and growth opportunities. This is what we found:

Chronic: Sun Pharma, Lupin, Torrent and Cadila Healthcare have an established presence

in cardiac therapies. In diabetes treatments, Sun Pharma, Lupin and Glenmark are the

leading names with dominance in existing products and launches or product licensing in

new therapy segments e.g. gliptins, SGLT2 inhibitors etc. Neuro/CNS is an important

segment for Sun Pharma and Torrent Pharma, while oncology treatments are among the

top therapies for Dr Reddy’s and Cadila (mainly due to biosimilars). Respiratory remains the

biggest segment for Cipla, where it has maintained leadership status in inhalers.

Sub-chronic: Derma, pain management and gynaecology therapies offer opportunities to

increase market share. Derma is a focus therapy for Glenmark and Glaxo, and pain for Sun

Pharma, GSK, Alkem Lab, Torrent and Ipca Lab.

Acute: Anti-infectives remain key revenue contributors for Alkem, Cipla, Lupin, GSK and

Mankind, while gastro remains a major therapy for Sun Pharma, Abbott, Alkem, Cadila and

Dr Reddy’s.

Growth areas for Alkem Lab and Alembic Pharma

As shown in Exhibit 18 below, Alkem Lab trails its bigger rivals in terms of sales of cardiac,

anti-diabetes and neuro therapies. Alkem, which makes most of its money from the acute

segment (anti-infectives, gastrointestinal) is deploying more resources to try to close the gap in

the chronic category. Alembic Pharma is also ramping up major chronic segment (cardiac and

anti-diabetic) through launches in high-growth molecules.

We believe Alkem Lab and Alembic Pharma will see strong growth in their chronic sales from

the current low base, supported by their established presence in acute therapies. They also

have less exposure to the US market than their larger peers, which in in the current environment

we see as an advantage, as discussed in the next section.

482650

223

335

0

200

400

600

800

1,000

1,200

FY13 FY16Acute Chronic

FY13-16 CAGR:14.5%

FY13-16 CAGR:10.4%

IPM FY13-16 CAGR: 11.7%

72.4% 71.3% 68.4% 67.3% 66.8% 66.0%

27.6% 28.7% 31.6% 32.7% 33.2% 34.0%

0%

20%

40%

60%

80%

100%

FY11 FY12 FY13 FY14 FY15 FY16

Acute Specialty

EQUITIES PHARMACEUTICALS

21 September 2016

20

Exhibit 18: Therapy sales split for key companies

Company ________________________________ Therapy share in India sales _________________________________ Anti-

Infective Cardiac Gastro VNM Anti-

diabetic Respiratory Pain Neuro Derma Gynae Onco. Others

Sun + Ranbaxy

11.8% 18.2% 12.0% 4.0% 9.0% 3.7% 7.3% 17.2% 4.7% 4.0% 0.5% 7.6%

Abbott 11.1% 10.4% 18.7% 12.6% 4.9% 7.7% 5.6% 11.8% 6.0% 4.0% 0.0% 7.1%

Cipla 26.8% 11.8% 7.9% 1.8% 1.0% 30.2% 3.1% 3.5% 2.5% 1.5% 0.7% 9.1%

Zydus Cadila 7.4% 16.8% 13.6% 4.2% 1.3% 10.5% 9.6% 1.3% 8.0% 10.7% 5.3% 11.1%

Mankind 23.3% 8.8% 11.2% 14.5% 5.4% 6.3% 5.0% 3.0% 4.6% 6.2% 0.0% 11.6%

Alkem 42.8% 2.7% 17.8% 12.0% 2.5% 2.8% 6.9% 5.1% 3.7% 2.2% 0.7% 0.8%

Lupin 21.1% 25.0% 7.9% 5.5% 11.3% 12.3% 4.4% 5.0% 0.5% 3.5% 0.3% 3.2%

Glaxo 23.0% 1.9% 5.6% 7.6% 0.0% 8.1% 9.2% 0.3% 18.8% 1.1% 0.4% 23.9%

Glenmark 13.1% 22.7% 2.4% 2.8% 8.4% 15.3% 2.1% 0.4% 29.2% 1.8% 0.1% 1.8%

Dr. Reddy’s 8.0% 14.5% 22.0% 2.7% 6.7% 8.6% 7.8% 3.2% 6.8% 0.2% 6.7% 12.9%

Torrent 4.2% 29.2% 14.6% 15.7% 6.0% 0.3% 7.8% 16.3% 2.6% 1.6% 0.0% 1.6%

Alembic 23.5% 13.9% 13.9% 7.7% 6.1% 12.7% 3.8% 1.0% 2.0% 10.8% 0.0% 4.6%

Ipca Lab 5.9% 17.2% 8.2% 2.2% 5.3% 4.1% 26.1% 3.4% 2.9% 0.0% 4.1% 20.6%

Source: AIOCD, HSBC analysis (red cell indicates chronic therapies, grey cell indicates acute therapies while pale red cells indicate sub-chronic therapies; focus areas shown in bordered cells for Alkem and Alembic)

B. Molecules overview

In India, the top 10 molecules account for 9.9% of the total market, down from c10.2% in 2012,

indicating increasing competition. Of the top 10 molecules, four are in the anti-infectives

category of the acute segment. However in terms of growth, chronic therapies have

outperformed acute therapies.

Exhibit 19: Dominance of anti-infective molecules continues in IPM

Top ranked molecules Therapy MAT Jul'16 sales (INRb)

MAT Jul 12-16 CAGR

MAT Jul 14-16 CAGR

% share of IPM

1.Amoxycillin + Clavulanic acid Anti-infectives 17 9.0% 10.5% 1.7% 2. Glimepiride + Metformin Anti-diabetes 16 22.8% 15.6% 1.6% 3.Multivitamins + Minerals Vitamins/minerals

/nutrients 12 11.8% 15.6% 1.2%

4.Atorvastatin Cardiac 8 4.4% 8.0% 0.8% 5.Cefixime Anti-infectives 8 0.6% 5.5% 0.8% 6.Human Premix Anti-diabetes 8 3.9% 9.0% 0.8% 7.Ceftriaxone Anti-infectives 8 7.8% 12.1% 0.8% 8.Paracetamol Pain/analgesics 8 13.1% 17.3% 0.8% 9.Pantoprazole Gastro-intestinal 8 10.5% 14.9% 0.8% 10.Cefpodoxime Anti-infectives 7 9.2% 12.2% 0.7% Top 10 100 9.6% 12.1% 9.9% Top 11-25 88 12.5% 14.2% 8.8% Top 26-50 107 11.7% 13.7% 10.6% Top 51-100 136 11.0% 11.3% 13.5% 100+ 577 9.5% 11.8% 57.2% IPM 1,009 10.2% 12.2% 100.0%

Source: AIOCD, HSBC analysis

21

EQUITIES PHARMACEUTICALS

21 September 2016

Exhibit 20: Positioning of top 20 molecules over the last five years

Rank MAT July 2012 MAT July 2013 MAT July 2014 MAT July 2015 MAT July 2016

1 Amoxycillin + Clavulanic Acid

Amoxycillin + Clavulanic Acid

Amoxycillin + Clavulanic Acid

Amoxycillin + Clavulanic Acid

Amoxycillin + Clavulanic Acid

2 Cefixime Glimepiride + Metformin Glimepiride + Metformin Glimepiride + Metformin Glimepiride + Metformin

3 Multivitamins + Minerals

Multivitamins + Minerals

Multivitamins + Minerals

Multivitamins + Minerals

Multivitamins + Minerals

4 Glimepiride + Metformin Cefixime Cefixime Human Premix Atorvastatin

5 Atorvastatin Atorvastatin Atorvastatin Atorvastatin Cefixime

6 Human Premix Human Premix Human Premix Cefixime Human Premix

7 Ceftriaxone Ceftriaxone Chlorpheniramine + Codeine

Ceftriaxone Ceftriaxone

8 Pantoprazole Chlorpheniramine + Codeine

Ceftriaxone Pantoprazole Paracetamol

9 Cefpodoxime Paracetamol Methylcobalamin Combinations

Chlorpheniramine + Codeine

Pantoprazole

10 Chlorpheniramine + Codeine

Cefpodoxime Pantoprazole Methylcobalamin Combinations

Cefpodoxime

11 Methylcobalamin Combinations

Pantoprazole Cefpodoxime Cefpodoxime Chlorpheniramine + Codeine

12 Azithromycin Methylcobalamin Combinations

Paracetamol Paracetamol Methylcobalamin Combinations

13 Paracetamol Azithromycin Cefuroxime Domperidone + Pantoprazole

Domperidone + Pantoprazole

14 Cefuroxime Ranitidine Ranitidine Protein Supplements Rosuvastatin

15 Ranitidine Cefuroxime Protein Supplements Azithromycin Protein Supplements

16 Protein Supplements Glimepiride + Metformin + Pioglitazone

Azithromycin Rosuvastatin Ranitidine

17 Ferrous Combination Protein Supplements Domperidone + Pantoprazole

Ranitidine Meropenem

18 Glimepiride + Metformin + Pioglitazone

Ferrous Combination Ferrous Combination Domperidone + Rabeprazole

Telmisartan

19 Piperacillin + Tazobactam

Domperidone + Pantoprazole

Rosuvastatin Cefuroxime Domperidone + Rabeprazole

20 Diclofenac Diclofenac Domperidone + Rabeprazole

Calcium Carbonate + Vit D3 (Cholecalciferol)

Azithromycin

Source: AIOCD, HSBC analysis (Red cells are chronic therapy molecules; grey cells are acute/sub-chronic therapies products)

B1. Chronic therapy molecules are growing fastest

We have looked at fastest growing molecules among the top 100 (selection criteria of CAGR of

more than 20% in last two and four years). As expected, majority of these molecules were in

anti-diabetics, followed by cardiac, derma and anti-infectives. See Exhibit 21 below.

Exhibit 21: Fastest growing molecules within the top 100

Molecules Therapy MAT July

16 sales (INRbn) MAT July

12-16 CAGR MAT July

14-16 CAGR

Rosuvastatin Cardiac 6.4 23.5% 20.6% Meropenem Anti-infectives 6.0 23.1% 29.2%

Vildagliptin + Metformin Anti-diabetes 5.3 40.4% 37.6% Sitagliptin + Metformin Anti-diabetes 4.6 40.3% 46.8% Levetiracetam Neuro/CNS 4.5 30.6% 27.4% Vitamin D3 (Cholecalciferol) Vitamins/minerals/

nutrients 4.5 41.7% 25.0%

Voglibose + Metformin + Glimepiride Anti-diabetes 3.8 141.4% 46.9% Telmisartan + Amlodipine Cardiac 3.3 24.0% 23.3% Dicyclomine + Paracetamol + Tramadol Gastro-intestinal 3.1 259.0% 49.3% Terbinafine + Clobetasol + Ofloxacin + Ornidazole

Derma 2.7 65.0% 51.1%

Clotrimazole Derma 2.6 18.4% 24.3% Paracetamol + Tramadol Pain/analgesics 2.6 21.8% 20.0% Itraconazole Anti-infectives 2.2 72.9% 111.3%

Source: AIOCD, HSBC analysis (shaded cells represent chronic/sub-chronic therapy molecules)

The fastest growing

molecules within the top 100

EQUITIES PHARMACEUTICALS

21 September 2016

22

Alkem and Alembic’s standing: In Vitamin D3 (cholecalciferol), Alkem’s Uprise D3 brand

maintains a leading position with c13% market share. In Voglibose+metformin+glimperide

combination and the meropenem market, Alkem is gradually stepping up its presence with a

market share of 6.3% and 4.5% respectively. Alembic is expanding in telmisartan+amlodipine

through brand Tellzy MT.

B2. New molecules that have grown most

We have analysed new molecules launched in the last three years that have achieved

significant sales growth. Sofosbuvir and combinations indicated for hepatitis C (Hep C) and a

new glitpin class of teneligliptin and combinations for diabetes treatment stand out in terms of

new launches and sales growth.

Sofosbuvir & combinations: Gilead Sciences (GILD US, Not Rated) in September 2014

entered a licensing agreement with multiple generic players for the launch of its new Hep C

drug in India (sofosbuvir mono or in combination with ledipasvir or in combination with each

other). Since March 2015, 14 companies have launched brands in the sofosbuvir mono

segment. In sofosbuvir+ledipasvir combination, nine new brands have been launched.

Gliptin class: This now represents c25% of overall anti-diabetic sales (INR84.5bn) in India.

In October 2015, the Delhi high court ruled in favour of MSD for patents covering its gliptin

drug, Sitagliptin (brand Januvia/Januvia) and restrained the litigating counterpart, Glenmark

Pharma, from marketing its brands (Zita/Zita-Met) in India. While sitaglitpin is under patent

protection, most companies have focused on another glitpin class, teneligliptin, which is not

protected by any patent in India. To date, there have been 33 teneliglitpin molecule brands

launches and 21 for teneligliptin+metformin combination.

Which new molecules have

grown most?

23

EQUITIES PHARMACEUTICALS

21 September 2016

Exhibit 22: Teneligliptin and combination brand launches

Molecule Brand Company Launch date MAT Jul'16 sales (INRm)

Teneligliptin Zita Plus Glenmark 6/1/2015 331 Ziten Glenmark 6/1/2015 213 Tenglyn Zydus Cadila 11/1/2015 154 Tenepride Micro Labs 11/1/2015 107 Teniva Intas 10/1/2015 88 Tendia Eris Life Sciences 10/1/2015 79 Dynaglipt Mankind 11/1/2015 73 Inogla Wockhardt 10/1/2015 71 Eternex T Alembic 10/1/2015 52 Tiban Ajanta Pharma 8/1/2015 48 Tenlimac Macleods 12/1/2015 46 Teneza Unichem 12/1/2015 38 Tglip Intas 10/1/2015 31 Tenepure Unichem 10/1/2015 27 Tenebite Corona 10/1/2015 16 Olymprix Alkem Lab 3/1/2016 10 Tenali Cadila Pharma 1/1/2016 9 Afoglip Torrent Pharma 3/1/2016 9 Glytrin Medley Pharma 2/1/2016 7 Megagliptin Aristo 5/1/2016 6 Tenuvia Precia Pharma 11/1/2015 5 Ten (Centaur) Centaur Pharma 11/1/2015 4 Teneliglip Akumentis 4/1/2016 3 Glipijub Jubilant Life Sciences 5/1/2016 2 Zilenta Indoco Remedies 4/1/2016 2 Jring Indoco Remedies 4/1/2016 1 Janisha UTH Healthcare 4/1/2016 1 Eliptin HBC Lifesciences 4/1/2016 1 Tenepan Panacea Biotec 6/1/2016 1 Tenlin Lincoln Pharma 6/1/2016 0 Ecoglip T Ozone Pharma 6/1/2016 0 Telnimac Macleods 3/1/2016 0 Ten DC FDC 7/1/2016 0 Teneligliptin + Metformin Zitamet Plus Glenmark 10/1/2015 231 Ziten M Glenmark 10/1/2015 126 Tendia M Eris Life Sciences 3/1/2016 28 Totaglipt M Mankind 3/1/2016 14 Teniva M Intas 4/1/2016 10 Tglip M Intas 4/1/2016 9 Eternex M Alembic 4/1/2016 9 Tenepride M Micro Labs 5/1/2016 8 Tenglyn M Zydus Cadila 6/1/2016 6 Afoglip M Torrent Pharma 5/1/2016 4 Tiban M Ajanta Pharma 4/1/2016 3 Tenebite M Corona 4/1/2016 2 Zilenta M Indoco Remedies 5/1/2016 1 Jring M Indoco Remedies 5/1/2016 1 Glytrin Met Medley Pharma 5/1/2016 1 Tolnim Delcure Life Sciences 12/1/2015 1 Tenepure M Unichem 7/1/2016 1 Teneza M Unichem 7/1/2016 1 Inogla M Wockhardt 7/1/2016 1 Ten M Centaur 5/1/2016 0 Olymprix M Alkem Lab 7/1/2016 0

Source: AIOCD, HSBC analysis

First-in market molecules: Patented launches by multinationals have focused on diabetes

treatments like SGLT2 inhibitors (Boehringer’s Jardiance, Janssen’s Invokana and

AstraZeneca’s Forxiga) and Novo’s insulin degludec (Tresiba and Ryzodeg). These are the

fastest growing molecules, indicating increased demand for new and improved treatments

in anti-diabetes segment. Sales of Saroglitazar, Zydus Cadilla’s indigenously developed

novel drug for treatment of type 2 diabetes and dyslipidemia, have grown to cINR400m

(145% y-o-y).

EQUITIES PHARMACEUTICALS

21 September 2016

24

Exhibit 23: First-in class launches focus on anti-diabetes and cardiac

Company Brand Molecule Therapy Launched Patented? Remark

GSK Priorix Tetra Quadravalent MMRV vaccine

Vaccine Jul'16 Combined vaccine for measles, mumps, rubella and varicella

Merck Rebif Interferon beta 1-a Multiple sclerosis Jun'16 Sanofi India Lyxumia Lixisenatide Anti-diabetes May'16 Yes GLP-1 inhibitor Novartis Jakavi Ruxolitinib Oncology May'16 Yes Sanofi India Zemiglo Gemigliptin Anti-diabetes Apr'16 DPP-4 inhibitor (gliptin) AstraZeneca Forxiga Dapagliflozin SGLT2 inhibitors

for anti-diabetes May'15 Yes Agreement in Mar'16 with

Sun Pharma marketing its product under brand name Oxra/Oxramet

Boehringer Ingelheim

Jardiance Empagliflozin SGLT2 inhibitors for anti-diabetes

Oct'15 Yes

Janssen Invokana Canagliflozin SGLT2 inhibitors for anti-diabetes

June'15 Yes

Pfizer Inlyta Axitinib Oncology May'15 MSD Variped Varicella vaccine Vaccine May'15 Novo Nordisk Ryzodeg Insulin

degludec+insulin Anti-diabetes Jan'15

Cadila Healthcare Lipaglyn Saroglitazar Diabetes combined with high cholesterol

Sep’13 Yes World’s first drug for treatment of diabetes and high cholesterol

Source: AIOCD, Company data, HSBC analysis

Biosimilars: Only a few companies have technical expertise in monoclonal antibodies

biosimilars. Sales of adalimumab (a biosimilar version of AbbVir’s auto-immune biologic

drug, Humira) have grown to cINR330m. There are four brands, one from Zydus Cadila and

three from Torrent Pharma, which it has licensed from Reliance LifeSciences.

Exhibit 24: Key recent monoclonal antibodies biosimilar launches

Brand Molecule Company MAT Jul'16 sales (INRm)

Launch date

Cizumab Bevacizumab Hetero Pharma 1 Jul-16 Adfrar P Adalimumab Torrent Pharma 1 Jul-16 Vivitra Trastuzumab Zydus Cadila 194 Apr-16 Mabtas N Rituximab Intas Pharma 1 Mar-16 Adfrar IB Adalimumab Torrent Pharma 1 Mar-16 Adfrar Adalimumab Torrent Pharma 5 Feb-16 Toritz Rituximab Torrent Pharma 13 Dec-15 Lupiximab Rituximab Lupin 2 Dec-15 Toritz RA Rituximab Torrent Pharma 1 Dec-15 Toritz MS Rituximab Torrent Pharma 0 Dec-15 Infimab Infliximab Sun Pharma 82 Jun-15 Maball Rituximab Hetero Pharma Feb-15 Mabtas T Rituximab Intas Pharma 9 Jan-15 Exemptia Adalimumab Zydus Cadila 326 Dec-14 Mabtas RA Rituximab Intas Pharma 12 Dec-14 Reditux RA Rituximab Dr. Reddys Lab 30 Sep-14

Source: Company data, AIOCD, HSBC analysis

Combination molecules: Other molecules which have grown rapidly in the last three years

include triple combination drugs for cardiac ailments like aspirin+rosuvastatin+clopidogrel

and olmesartan+clinidipine+chlorthalidone and neurological disorders (e.g.

pregabalin+nortriptyline).

Alkem and Alembic’s standing in fastest growing new molecules:

In sofosbuvir and combinations, Alkem has launched its own brands during FY16.

In teneligliptin and combination molecules, both Alkem and Alembic have introduced their

brands, emphasising their focus on entering new segments.

During FY16, Alkem launched its first biosimilar (rituximab).

25

EQUITIES PHARMACEUTICALS

21 September 2016

Alkem and Alembic are increasing their focus on combinations molecules. Alkem is now the

second largest player in telmisartan+clinidipine+chlorthalidone and olmesratn+

clinidipine+chlorthalidone molecules. Both companies have recently entered the

aspirin+rosuvastatin+clopidogrel combination market.

B3. Overview of launches by top 25 companies

The launch of new products (including line extensions) is one of the key growth drivers. On

average there are more than 3,000 brand launches a year in the India pharma market.

Exhibit 25: Number of brand launches Exhibit 26: New product growth: the contribution is consistent

Source: AIOCD, HSBC analysis Source: AIOCD, HSBC analysis

Launch quality: In view of ever increasing competition, most companies are focusing on quality

rather than quantity. They tend to compete of their areas of strength and segments where they

can gain a viable share of the market.

Exhibit 27: New launches by key players in IPM

Company FY11 FY12 FY13 FY14 FY15 FY16 FY17 ytd

Abbott 68 70 40 30 41 48 11

Alembic 30 23 25 22 29 44 11

Alkem 62 45 51 32 41 53 15

Aristo 11 10 18 19 5 7 2

Cadila 60 90 90 75 55 40 18

Cipla 72 46 39 47 30 57 21

Dr Reddy's 35 24 19 22 20 31 3

FDC 17 12 10 10 9 18 6

Glenmark 28 28 29 31 25 29 17

GSK 25 8 14 6 8 4 2

Intas 76 43 53 48 34 43 39

Ipca 32 19 19 31 26 11 2

Lupin 67 47 58 46 36 48 18

Macleods 30 42 32 31 26 44 14

Mankind 58 44 42 27 39 42 24

MSD 2 6 1 5 0 0 0

Pfizer 30 46 15 11 8 2

Ranbaxy 77 45 18 32 22 23 20

Sanofi 29 11 32 6 7 6 4

Sun Pharma 47 35 25 24 21 19 7

Torrent Pharma 34 26 19 11 17 30 5

USV 15 17 9 12 6 4 2

Source: AIOCD, Company data, HSBC analysis

0

100

200

300

400

500

600

700

800

Jul'15 Sep'15 Nov'15 Jan'16 Mar'16 May'16 Jul'16

No. of brands launches No. of SKUS launches

8.36.7

4.16.7

1.5

-1.0

3.2

5.24.8

4.6

5.0

5.04.4

3.3

3.3

3.4

3.1

3.1

3.0

3.1

3.1

-2

0

2

4

6

8

10

12

14

16

18

4QF

Y15

1QF

Y16

2QF

Y16

3QF

Y16

4QF

Y16

1QF

Y17

Jul'1

6

Vol growth Price growth NP growth

EQUITIES PHARMACEUTICALS

21 September 2016

26

Launches by the top 25: We have looked at launches by the top 25 companies over the last

two years. Excluding the “Others” category, which includes unspecified molecules such as anti-

allergies, laxatives, non-medicated skin-care products, parasitic worm treatments, and smoking

cessation chewing gum; anti-infectives led with 11%, closely followed by

vitamins/minerals/nutrients supplements, cardiac and derma.

Exhibit 28: Top 25 companies’ new launches by therapy in last two years (n=1,174)

Source: AIOCD, HSBC analysis (“All others” include urology, hormones, sex stimulants, vaccines, anti-malarials, etc.)

Exhibit 29: Top companies’ launches* in the last two years

Company No of launches

Anti-Infectives

Anti-diabetic

Cardiac GI VNM Neuro Derma Gynae Resp. Onco. Pain Others

Cipla 104 14 8 7 5 7 7 2 14 4 4 32

Intas Pharma 102 12 4 7 2 9 16 2 4 6 10 5 25

Sun Pharma 94 11 1 10 13 11 8 7 2 10 3 7 11

Mankind 90 5 2 2 9 19 4 7 5 5 5 27

Alkem 90 11 2 6 13 5 9 9 2 12 2 3 16

Lupin 86 8 6 16 3 5 4 6 6 6 2 6 18

Abbott 79 11 1 2 5 1 12 2 3 4 12

Macleods 75 6 3 12 7 15 5 8 3 5 3 8

Zydus Cadila 73 7 2 8 6 9 1 5 4 8 8 4 11

Glenmark 58 5 6 6 2 3 1 15 10 1 2 7

Dr Reddy's 45 6 3 4 2 3 2 6 2 4 2 11

Torrent 42 4 3 6 2 3 8 2 1 3 3 5 2

Alembic 40 2 4 9 3 4 3 2 6 3 4

Ipca Lab 29 3 3 5 2 12 1 3

GSK 11 1 1 1 1 2 2 3

Source: AIOCD, HSBC analysis (*Last 24 months launches as of MAT Jul’16 data.)

Differentiated, better margin products: In view of aggressive launches by new entrants, more

stringent rules for new product approvals and a proposed ban on certain combinations, leading

companies have shifted their focus to new/differentiated launches, including biosimilars and

in-licensed products. Higher-margin over the counter (OTC) and consumer healthcare products,

including derma, pain, hair loss and nutritional products, are also popular.

12%11%

10% 10% 10%

8% 8%

7%6%

5%3% 3%

2%

5%

0%

2%

4%

6%

8%

10%

12%

14%

27

EQUITIES PHARMACEUTICALS

21 September 2016

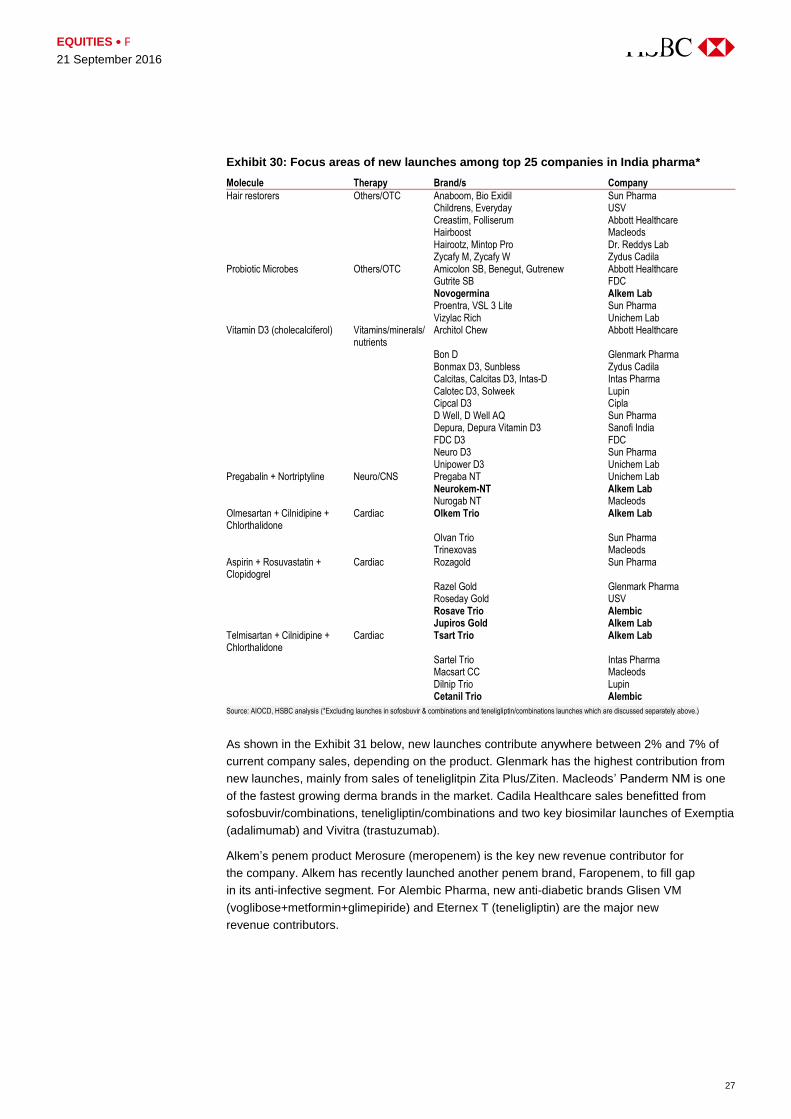

Exhibit 30: Focus areas of new launches among top 25 companies in India pharma*

Molecule Therapy Brand/s Company

Hair restorers Others/OTC Anaboom, Bio Exidil Sun Pharma Childrens, Everyday USV Creastim, Folliserum Abbott Healthcare Hairboost Macleods Hairootz, Mintop Pro Dr. Reddys Lab Zycafy M, Zycafy W Zydus Cadila Probiotic Microbes Others/OTC Amicolon SB, Benegut, Gutrenew Abbott Healthcare Gutrite SB FDC Novogermina Alkem Lab Proentra, VSL 3 Lite Sun Pharma Vizylac Rich Unichem Lab Vitamin D3 (cholecalciferol) Vitamins/minerals/

nutrients Architol Chew Abbott Healthcare

Bon D Glenmark Pharma Bonmax D3, Sunbless Zydus Cadila Calcitas, Calcitas D3, Intas-D Intas Pharma Calotec D3, Solweek Lupin Cipcal D3 Cipla D Well, D Well AQ Sun Pharma Depura, Depura Vitamin D3 Sanofi India FDC D3 FDC Neuro D3 Sun Pharma Unipower D3 Unichem Lab Pregabalin + Nortriptyline Neuro/CNS Pregaba NT Unichem Lab Neurokem-NT Alkem Lab Nurogab NT Macleods Olmesartan + Cilnidipine + Chlorthalidone

Cardiac Olkem Trio Alkem Lab

Olvan Trio Sun Pharma Trinexovas Macleods Aspirin + Rosuvastatin + Clopidogrel

Cardiac Rozagold Sun Pharma

Razel Gold Glenmark Pharma Roseday Gold USV Rosave Trio Alembic Jupiros Gold Alkem Lab Telmisartan + Cilnidipine + Chlorthalidone

Cardiac Tsart Trio Alkem Lab

Sartel Trio Intas Pharma Macsart CC Macleods Dilnip Trio Lupin Cetanil Trio Alembic

Source: AIOCD, HSBC analysis (*Excluding launches in sofosbuvir & combinations and teneligliptin/combinations launches which are discussed separately above.)

As shown in the Exhibit 31 below, new launches contribute anywhere between 2% and 7% of

current company sales, depending on the product. Glenmark has the highest contribution from

new launches, mainly from sales of teneliglitpin Zita Plus/Ziten. Macleods’ Panderm NM is one

of the fastest growing derma brands in the market. Cadila Healthcare sales benefitted from

sofosbuvir/combinations, teneligliptin/combinations and two key biosimilar launches of Exemptia

(adalimumab) and Vivitra (trastuzumab).

Alkem’s penem product Merosure (meropenem) is the key new revenue contributor for

the company. Alkem has recently launched another penem brand, Faropenem, to fill gap

in its anti-infective segment. For Alembic Pharma, new anti-diabetic brands Glisen VM

(voglibose+metformin+glimepiride) and Eternex T (teneligliptin) are the major new

revenue contributors.

EQUITIES PHARMACEUTICALS

21 September 2016

28

Exhibit 31: Contribution from new launches* to sales of leading companies

Source: AIOCD, HSBC analysis (*New launches for last 24 months as of MAT Jul’16 data.)

C. Brand positioning

The key to success is to create strong brands which have strong recall value among doctors

and patients. Alkem is strong in this area. It has five brands in the top 50, more than bigger

companies like Cipla and Sun Pharma.

Exhibit 32: Brand positioning in India

Company Total brands ________________________ Brands in: _________________________ Top 50 Top 100 Top 300

Sun + Ranbaxy 1,323 3 11 29 Abbott + Novo 919 5 11 28 Cipla 1,027 3 6 23 Zydus Cadila 1,247 0 4 11 Mankind 703 2 2 11 Alkem 954 5 5 15 Lupin 829 0 1 4 Glaxo 225 7 10 14 Macleods 507 1 1 6 Pfizer+Wyeth 209 3 7 13 Intas 967 0 1 11 Emcure 752 0 1 5 Aristo 305 1 5 11 Glenmark 350 1 2 8 Dr. Reddys 379 0 1 9 Sanofi India 195 2 4 10 Torrent 490 1 1 7 USV 196 2 4 8 Micro + Bal 775 0 1 1 Alembic 441 1 1 5

Source: IMS Health, HSBC analysis

7.3%

5.2%

4.4% 4.3% 4.3% 4.1% 4.0% 3.8%3.5% 3.3% 3.1%

2.4% 2.3% 2.3% 2.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Gle

nmar

k

Mac

leod

s

Cad

ilaH

thca

re

Ale

mbi

c

MS

D

Man

kind

Sun

Pha

rma

Uni

chem

Lupi

n

Inta

s

Dr

Red

dy's

Cip

la

Alk

em

Aris

to

Tor

rent

Strong brand positioning

leads to better brand recall

by doctors & patients. Hence,

companies strive to create

strong brands in the market

29

EQUITIES PHARMACEUTICALS

21 September 2016

Domestic regulatory challenges

Volume growth accounts for c60% of total growth in the Indian pharma market. The market is

very price sensitive and the government has established the National Pharmaceutical Pricing

Authority (NPPA) to control drug prices.

Under the government drug policy, certain drugs on the National List of Essential Medicines

(NLEM) are subject to price controls. In May 2013, the Department of Pharmaceuticals released

the Drugs Price Control Order (DPCO), 2013 governing the price control mechanism for 348

drugs listed in the NLEM.

DPCO 2013 replaced DPCO 1995 which earlier controlled the price of 74 drugs. With DPCO

2013, the government has moved from a cost to market-based pricing mechanism. Under

DPCO 1995, companies were allowed to make a nominal profit over manufacturing costs.

Under DPCO 2013, the price of a brand can’t exceed the average price of various brands of the

same underlying formulation with a market share of 1% or more.

In March this year, three separate regulatory announcements either capped drug prices or

banned certain drugs. As Exhibits 33 and 36 show, these changes have increased the volatility

of sector growth.

Summary of key regulatory changes in India:

May 2013: The government implemented DPCO 2013, which governs the price control

mechanism for 348 drugs listed on the NLEM.

December 2015: The government issued a proposal to list certain additional drugs on

the NLEM.

March 2016: The maximum prices of various drugs were subject to reduction as a result of

negative inflation measured by India’s Wholesale Price Index (WPI) which declined

2.7105% y-o-y during 2015.

March 2016: The Department of Pharmaceuticals issued Drugs Price Control Amendment

Order (DPCAO), 2016. A total of 106 drugs were added and 70 drugs were deleted from

the NLEM, which now contains 376 drugs.

March 2016: The Department of Health and Family Welfare proposed a ban on 344 fixed

dose combination (FDC) drugs. Drug manufacturers have received an interim stay on the

ban from the high court in Delhi. A final decision is awaited.

Looking ahead, government-mandated price revisions are scheduled every 2-3 years, so the

next round of revisions will likely take place in 2018-19 in our understanding.

Impact

Drugs on the NLEM constitute c12% of total sales and FDC products c3% (source: AIOCD July

2016) in IPM. The frequent regulatory changes with regard to drug prices have created