Impact of foreign investors on regional and local development: The case of GlaxoSmithKline...

78

-

Transcript of Impact of foreign investors on regional and local development: The case of GlaxoSmithKline...

-

Research project carried out by a team of researchers and doctoral student s from Adam Mickiewicz University and the University of Economics in Poznań

Authors: Prof. Tadeusz Stryjakiewicz (project manager) Prof. Lucyna Wojtasiewicz Dr. Anna Tobolska Dr. Justyna Weltrowska Michał Męczyński Krzysztof Stachowiak Bartosz Stępiński Jacek Wajda Jarosław Jurkiewicz (co-operation)

Reviewed by: Prof. Henryk Rogacki

Translation by: Maria Kawińska

ISBN 83-60247-15-3

Bogucki Wydanictwo Naukowe www.bogucki.com.pl

Druk i oprawa: Uni~druk

Poznań

1. Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2. Beginnings and growth of GlaxoSmithKline Pharmaceuticals (GSK) in Poznań .... 7

3. Place of GSK among other enterprises in Poznań and Wielkopolska in the light of basic economic indicators. . . . . . . . . . . . . . . . . . .

4. Regional multiplier effect of GSK location in Poznań. . . . . . . . . . . . 4.1. Networks of links with suppliers of raw materiais, production components

and semi-finished goods. . . . . . . . . . . . . . . . . . 4.2. Networks of links with product consumers . . . . . . . . . . . . . 4.3. Networks oflinks with firms providing services to GSK ...... . 4.4. Networks of links with scientific and R&D institutions, hospitals,

and the education system . . . . . . . . . . . . . . . . . . . . . . . 4.5. Links of GlaxoSmithKline Pharmaceuticals with enterprises and institutions

. ... 10

· 21

.23 23

. 23

. .. 27

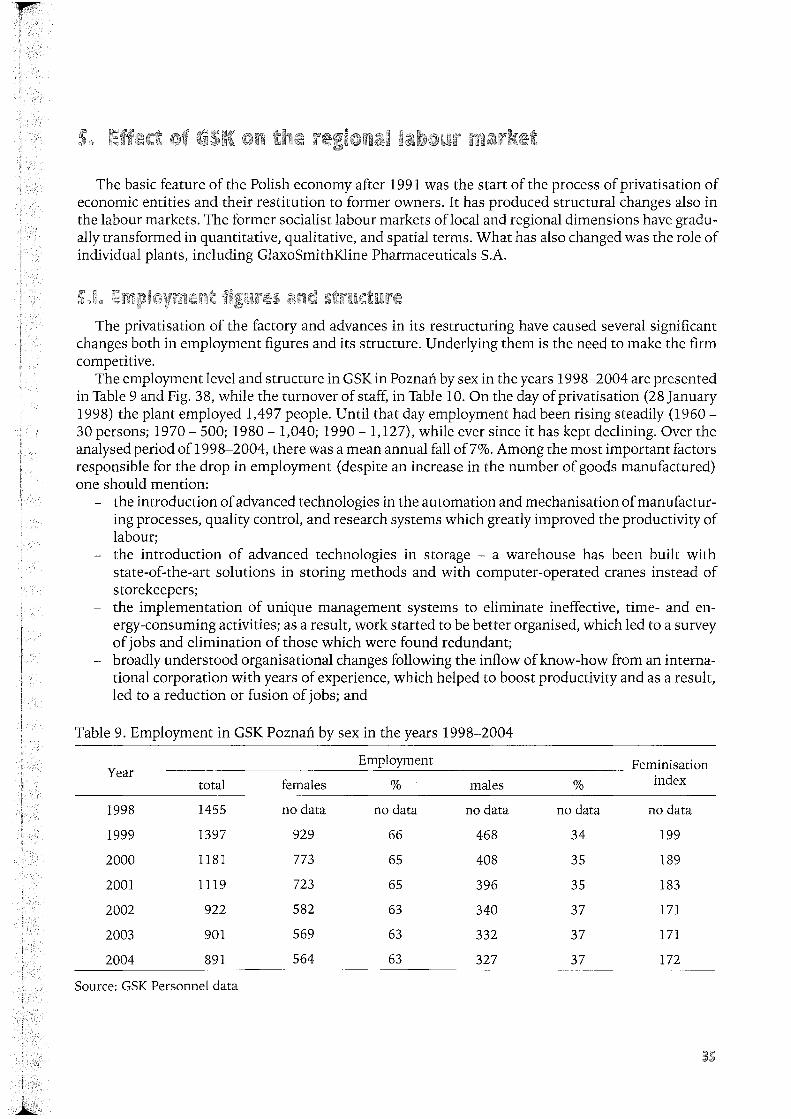

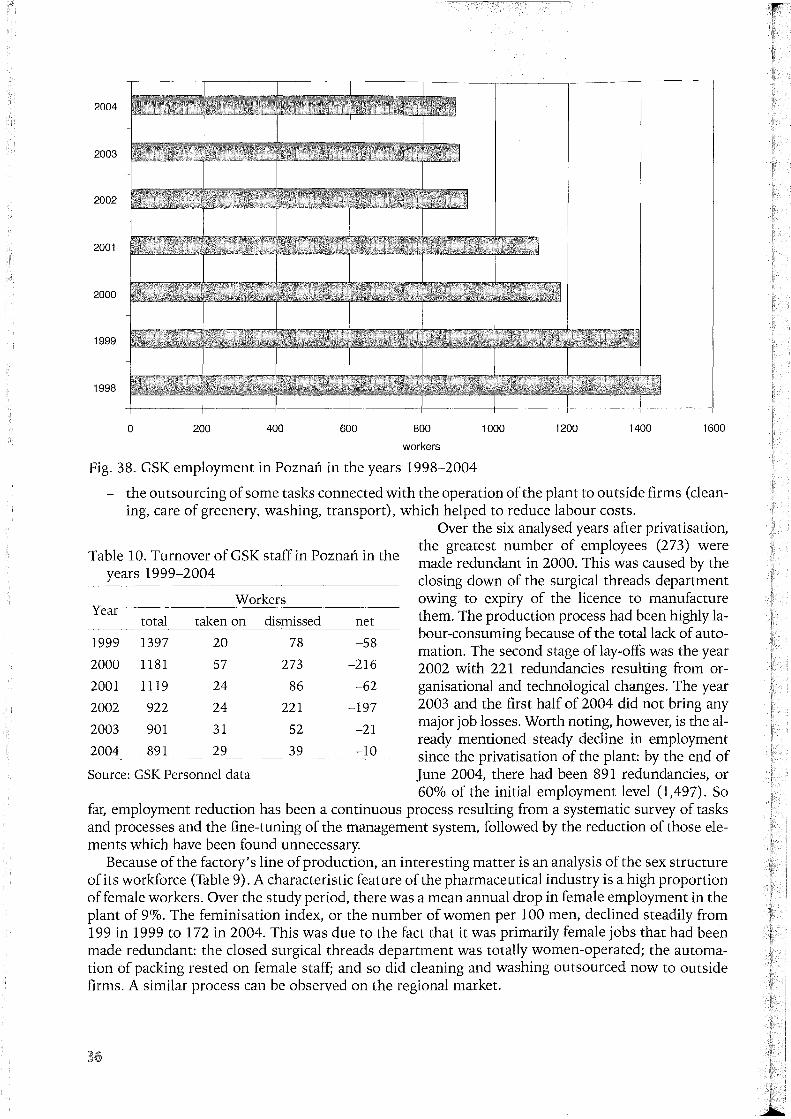

in Wielkopolska in the light of a survey research . . . . .. ......... . 28 5. Effect of GSK on the regionallabour market . . . . . . . . . . . . . . . . . . . . . . 35

5.1. Employment figures and structure . . . . . . 35 5.2. Qualitative changes in the labour market . . 38 5.3. Commuting . . . . . . . . . . . . . . . . . . . . 39 5.4. GSK wages and the regional mean ..... . 43 5.5. Social activi ty . . . . . . . . . . . . . . . . . . . 44 5.6. Competitiveness of GSK on the locallabour market . . . . . . 45

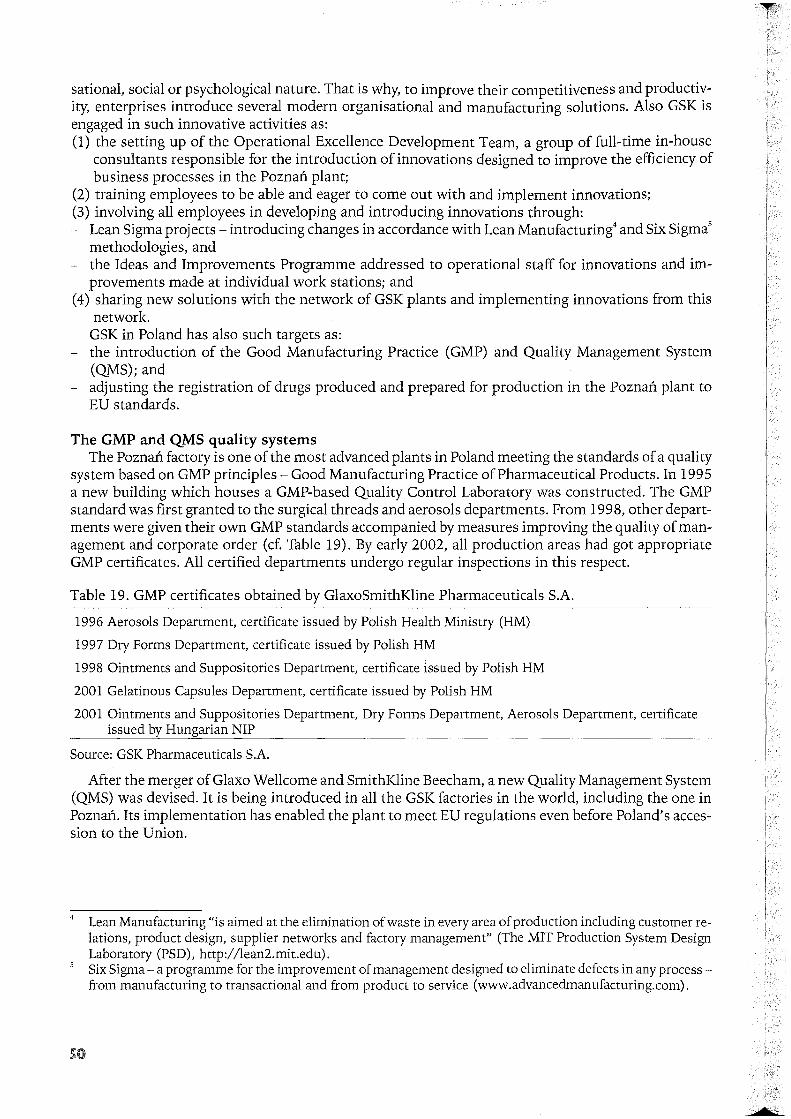

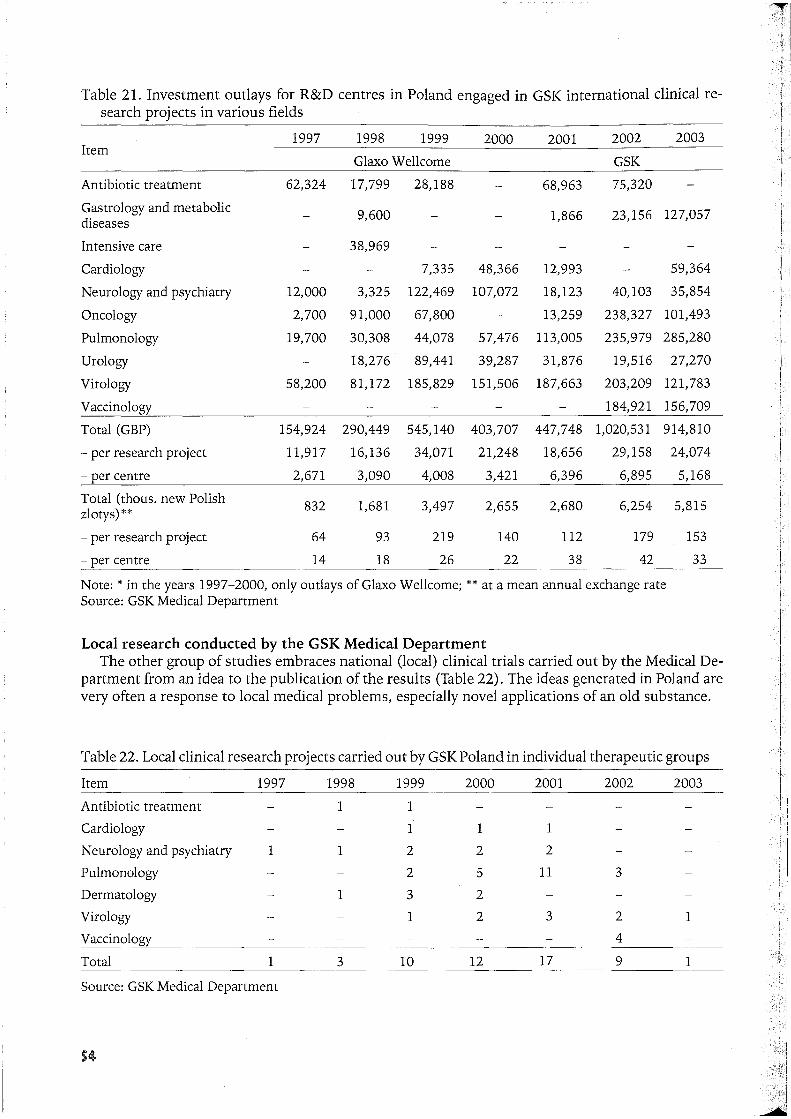

6. Role of GSK in innovative and R&D activity . . . . . . . . . . . . . . . . . . 48 6.1. GSK' s R&D activity . . . . . . . . . . . . . . . . . . . 48 6.2. Innovative, modernising and standardising activity. . . . . . . . . 49 6.3. Clinical trials ......................... 51 6.4. Regional dimension of GSK's innovative and R&D activity ..... . 55

7. Place of foreign corporations (including GlaxoSmithKline) in the network of regional and local institutionallinks ......................... 57 7.1. Development programmes of the city and region - main considerations

for foreign investors ................................ 58 7.2. Policy of the city and region towards foreign investors and its implementation . .. . 59 7.3. Place and role ofGSK in the network oflinks with local government institutions

and local business environment institutions . . . . . . . . . . . . . . . . . 64

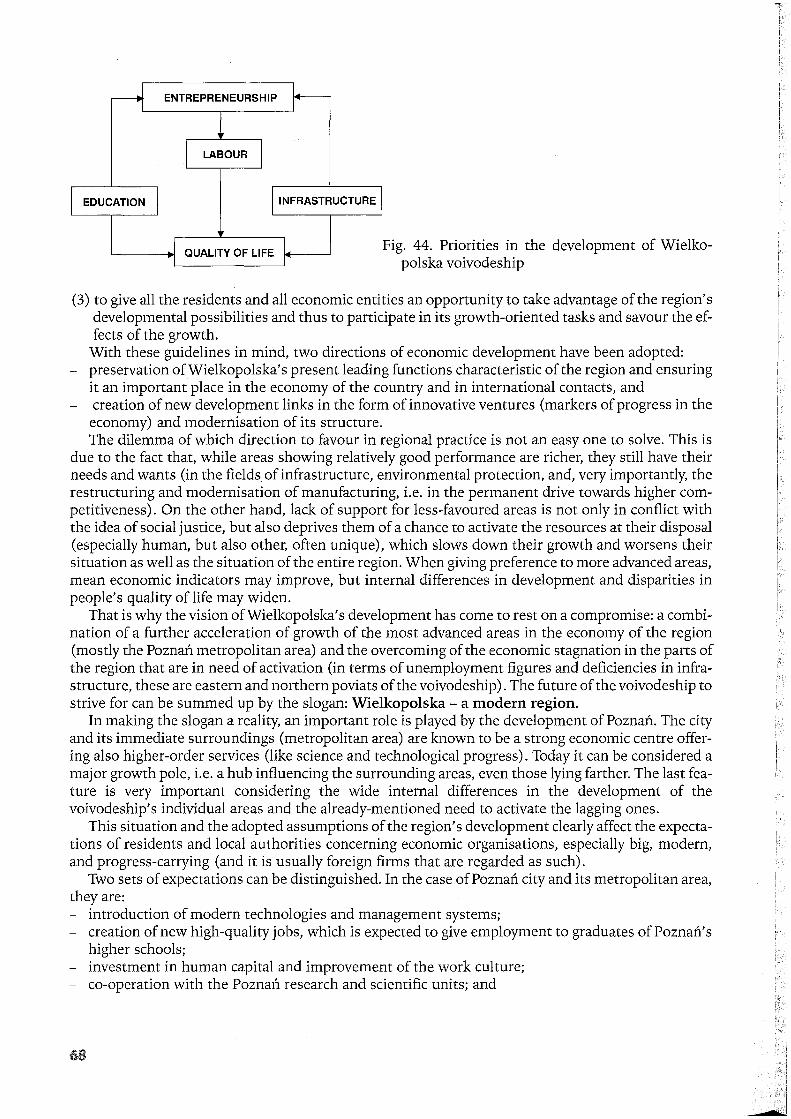

8. Place of foreign corporations (including GSK) in the development strategy of Wielkopolska voivodeship . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67 8.1. Priorities in the development of Wielkopolska voivodeship and its expectations

towards large foreign corporations . . . . . . . . . . . . . ..... 67 8.2. Conclusions and proposals concerning GSK . . . . . . . . . . . . . . . .. . 70

9. Summing up . . . . . . . . . . . . . . .

References and published source materials ..

Appendix - a sample questionnaire . .

List of figures . . . . . . . . . . . . .

List of tables. . . . . . . . . . . . . .

. .. 71

. .. 73

· 76

· 80

· 81

Sinee the very start of the systemic transformation in Poland, foreign enterprises have been an inereasingly important element of the eountry's eeonomy. Their role in eeonomic growth has been the subjeet matter ofmueh diseussion and researeh (ef. e.g. Bąk, Kulawezuk 1996; Błuszkowski, Garlieki 1997; Olesiński 1998; Domański 2001; Durka 2002). However, the researeh usually eoneerns the national eeonomy as a whole and rests on basic eeonomic indicators. It is only to a lesser extent that it foeuses on the effeet that foreign firms have had on the development of towns and regions where they are loeated, Le. on their embeddedness in the regional and loeal eeonomies (ef. Dicken, Forsgren, Malmberg 1994; Pavlinek, Smith 1998; Phelps 2000). There are eonflicting opinions in the world literature about the importanee of foreign eorporations in the eeonomies of their host regions. On the one hand, they are pereeived as 'eathedrals in the desert', or manufaeturing enc1aves with no signifieant links with the loeal eeonomic system (ef. Grabher 1994; Hardy 1998). On the other, many studies have shown them to be highly integrated with their regional and loeal environments. Henee, there is a need for a wide-ranging researeh on the role of foreign firms in regional and loeal development not only from the perspeetive of a firm, but also its town or region, especially in the eountries undergoing asysternic transformation. That is why a team of researehers from Adam Mickiewicz University and the University of Eeonomics in Poznań launehed a projeet whose goal was to define the effeet of GlaxoSmithKline Pharmaeeuticals S.A. (GSK) on the eeonomic growth of the Wielkopolska region1

•

The projeet met with mueh friendly interes t on the part of GSK management, whom we wish to thank here for the researeh grant and assistanee in eolleeting data.

The GSK plant is one the biggest foreign investments in Wielkopolska ereated as a result of the sale on 28 January 1998 ofPoznań's Polfa Pharmaeeutical Works to the British eoneern Glaxo Welleome. The nearly eight years of the eoneern' s operation in the region is a time span long enough to attempt an assessment of the degree of its embeddedness in the loeal eeonomy and its role in the spatial-eeonornic strueture of Wielkopolska voivodeship.

The empirical researeh providing the basi s for this assessment was earried out in the first half-year of2004 by a team ofresearehers and doetoral students from the Institute ofSocio-Eeonomic Geography and Spatial Management, Adam Mickiewicz University in Poznań (Dr Anna Tobolska, Dr Justyna Weltrowska, Michał Męezyński, KrzysztofStaehowiak, Bartosz Stępiński, andJaeek Wajda) under the supervision ofDr Tadeusz Stryjakiewicz, professor at AMU and the University ofEeonomics and head ofthe Institute's Department ofRegional Policy and European Integration. Beeause ofthe regional dimension of the analysis and the neeessary eontaets with the region' s top loeal government officials, the targets of the projeet would have been very diffieult to aehieve without the participation of Prof. Lueyna Wojtasiewicz, head of the Centre of Regional Eeonomie Researeh of the University of Eeonomics in Poznań, who supervised the team that had worked out a strategy for the development ofWielkopoIska voivodeship.

The implementation of the researeh projeet reported here proeeeded in three stages: l. Colleeting data from the following sourees:

(a) appropriate GSK departments following a shopping list provided by the projeet participants; (b) firms and institutions eo-operating with GSK to which questionnaires were sent eoneerning

the role of GSK in their aetivity as a whole as well as an assessment and prospeets of mutual relations (following a list of those firms and institutions supplied by GSK2

; for the questionnaire form, see the Appendix);

l The notions of the Wielkopolska region and Wielkopolska are treated in the present work as identical with Wielkopolska voivodeship, a highest-level administrative unit created on 1 January 1999. Because of the business secret, no names of co-operating firms, hospitals or research centres are given in the present publication.

(c) loeal government institutions (strategies and programmes of the socio-eeonomic development of the city of Poznań and Wielkopolska voivodeship; interviews with representatives of the 10-cal authorities and persons responsible for the region's eeonomic development);

(d) regional and loeal business-environment institutions; and (e) the literature on the subjeet (including eomparative studies); published statistical materiais.

2. Analysing the material eolleeted and presenting the results visually in the form of tables, charts, maps, and diagrams.

3. Drawing up a final report, preparing it for print, and publishing in a book form. The next stage was making the results public at a scientifie session with the participation, among

others, of representatives of GSK, loeal government authorities and loeal media, as well as at other seminars and eonferenees (e.g. the Industrial Spaee Organisation Commission of the International Geographical Union, Regional Studies Association, and the Committee for Spaee Eeonomy and Regional Planning of the Polish Aeademy of Sciences), and business forums. .

The eontents of this book refleet the range of problem s eovered by the researeh projeet. They include: l. The beginnings and growth of GSK in Poznań. 2. The place of GSK among other enterprises in Poznań and Wielkopolska voivodeship in the light of

basic eeonomic indieators. 3. The regional multiplier effeet of GSK loeation in Poznań from the point ofview of:

- networks of links with suppliers of raw materials and semi-finished goods; - networks of links with produet recipients; - networks of links with firms providing services to GSK; - networks oflinks with scientifie and researeh and development (R&D) institutions, hospitals,

and the edueational system. 4. The effeet of GSK on the regionallabour market:

- employment: figures, strueture, and changes - GSK wages and the mean wages in the region; - the level of sodal aetivity; - qualitative changes in the labour market (including training eourses and measures intended to

re-train the employees); - eompetitiveness of GSK on the loeallabour market.

5. The role of GSK in innovative and R&D aetivity. 6. The place of GSK in the network of regional and loeal institutionallinks. 7. The place of GSK in the development strategy of Wielkopolska voivodeship.

Condueting sueh a detailed researeh was only possible thanks to the involvement and help with the eolleetion of material of a lot of people, both in the GSK Warsaw Offiee and the GSK Poznań establishment, firm s eo-operating with GSK which eompleted the questionnaires, representatives of the loeal authorities and institutions who agreed to be interviewed, and AMU students who assisted in polling Poznań residents and in the statistieal processing of a part of the data. Gratefullyaeknowledgin g their help, the present authors would like to express the eonviction that their book will eontribute not only to a deeper view of the effeets of the operation of GlaxoSmithKline Pharmaeeuticals S.A. in Poznań and Wielkopolska, but also to a diseussion about the possibility and eonditions of reinforcing the links between foreign eorporations and their host towns and regions.

The sale of the Poznań Polfa Pharmaceutieal Works to the British concern Glaxo Wellcome was the biggest capital transaction of the State Treasury during the transformation period between 1989 and 1998. The details of the transaction are a good illustration of the strategy of big global corporations towards the so-called emerging markets of East-Central Europe. The information presented in this chapter comes from the interview given to the present author by Simon C. Davidson, Glaxo Wellcome's Director for Central and Eastern Europe, on 20 April 1998 in the company's headquarters in Greenford, Middlesex; materiaIs obtained there (primarily Glaxo Wellcome Annual Report and Accounts and Glaxo Wellcome Key Facts); materiaIs ofthe GlaxoSmithKline Pharmaceutieals Office in Warsaw from 2003; and data collected at a field practiee by 3rd year geography students of Adam Mickiewiez University in Poznań in 1996. Use was also made of studies by Weltrowska (1996), Górski (1998), Olbrot (1998), and Cylwik (2002).

In the estimation ofthe World Bank (after Górski 1998), in 1996 the Polish pharmaceutieal market was worth $1.6 billion, with a relatively low index of drug consumption per head ($49) and hence potentially capable of dynamie growth (at an annual average of 10%)3. The market was largely supplied by more than 300 domestie firms, predominant among which were 14 biggest enterprises once belonging to the Polfa association (their detailed characteristies are presented in Weltrowska 1996). By 1997, four were privatised either through sale to strategie investors or the publie offer of stocks (not counting enterprises embraced by the National Investment Funds program me) . The 1990s saw domestie drug makers facing ever stiffer competition from imports, which reached more than $2 billion in 2002.

Glaxo Wellcome (GlaxoSmithKline since 2001) has been present on the Polish pharmaceutieal market ever since 1978, and its interest in the region greatly increased in the 1990s. In 1984 the firm set up a Glaxo business representation in Poland, while in 1992 an enterprise called Glaxo Wellcome Poland Ltd. was established with a seat in Warsaw to create a distribution network and promote the company' s products in the country. In 1997 the firm opened a drug packaging plant and a storehouse at Duchniee near Warsaw. Thus, it to ok a typieal development path of a multinational corporation: an earlier market penetration through export contacts followed by establishing a sales representation and ending in the launching of its own manufacturing plant. The firm considered taking part in the privatisation of one of the Polfa plants, but not just any one of them. As S.C. Davidson stated candidly, "We had selected three plants in Poland that we were interested in, but in fact we were waiting for the sale of the Poznań establishment". Thus, an element of space played a crucial role in the decision, but not in the traditional sense oflocation factors (like the cost of transport or labour) or other territorially localised investment incentives (e.g. tax relief). The following factors were decisive for the company: 1. Line (specialisation) of production. The Poznań plant was the only producer of anti-asthmatie

aerosol s in the country. It manufactured them relatively cheaply, but using an obsolescent (Freon-based) technology. Glaxo Wellcome produced more modern, Freon-free aerosols. Thus, it achieved a special sort of complementarity: combining lower manufacturing costs with modernised technology, whieh was supposed to let the firm expand also into other Central and Eastern European markets.

2. Good production record: high profitability, the majority of products having international quality certificates (GMP - Good Manufacturing Practiee), and a relatively high productivity oflabour. Un-

In 2001, according to IMS Health data, the Polish pharmaceutical market was worth $2.88 billion.

I

derstandably enough, the company was not going to buy a factory that would only cause trouble (even in return for a larger share of the market).

3. Market-oriented attitude ofthe loeal milieu. The managing organs ofthe Polfa plant in Poznań expressed a wish to have a dynamie strategie investor from the same line ofbusiness (and not, as many other enterprises, one that would merely supply capital, e.g. banks).

4. Complementarity of the distribution network. While Polfa had had a well-developed network supplying pharmacies, in the 1990s Glaxo Wellcome also developed a direct-supply network for hospitals (Polfa' s activity in this field had been restrieted by the centralised hospital-supply system run by a state-owned firm, Cefarm). Besides, Polfa had had an extensive network of links with Central and Eastern European countries from the COMECON times, while Glaxo Wellcome set up a new network in this area. Apart from the above factors related primarily with the plant and its place in the company's ne

twork, equally noteworthy is the firm's motivation for choosing Poland as an East-Central European country with the highest level of its capital investment (the Poznań plant was the first to be bought by Glaxo Wellcome in this part of Europe). According to S.C. Oavidson, the decisive factor, next to the absorptive and rapidly expanding domestie market, was an advanced stage of the transformation of the Polish economy.

The sale of the Polfa Pharmaceutieal Works in Poznań to Glaxo Wellcome stood out among privatisation transactions completed at that time for ensuring the employees the best social conditions. The concern had contracted to keep up employment (of about 1,400 workers) for four years and all the components ofwages and benefits (including the holiday bonus amounting to 1000/0 ofwages and an increase in wages at least by the inflation rate), and to maintain social benefits (including the financing of the modernisation of the plant' s holiday compounds at U stronie Morskie and Sieraków). Besides, each employee received not only the statutory 150/0 of free shares, but also a sort of 'privatisation bonus' to the amount of 10.5 monthly wages ca1culated as for child-care leave. A fitness club for the employees was also set up on the premises. All this sprang from two causes: (a) a wish to arouse a friendly fe eling towards the privatisation and the new owner among the staff (as

Anna Tobolska's 1996 research results listed in Table l show, more than one-third of the Polfa crew had no definite opinion about advantages of the privatisation and its effect on the plant's future); and

(b) a low proportion oflabour costs in total costs ofpharmaceutieal production (in comparison with, e.g., expenditure on R&O and the purchase of raw materiais and packaging) , as a result of whieh the company could afford the above benefits package and employment guarantee, especially in view of the antieipated increase in output. In 2001, Glaxo Wellcome and SmithKline Beecham fused to create the GlaxoSmithKline (GSK)

corporation. In Poland it was registered under the nam e of GlaxoSmithKline Pharmaceutieals S.A., a company in whieh GlaxoSmithKline holds more than 970/0 of shares and the State Treasury, 2.73%. In

Table 1. Employee attitudes towards the privatisation of the Polfa Pharmaceutieal Works in Poznań (per cent of responses)

Thesis

The future of the Works depends primarily on its successful privatisation

Buyout by a Western pharmaceutical firm is achance for acquiring new technologies and markets

I agree

24

16

I rather agree Hard to tell

17 37

19 34

I rather don't agree

8

12

I definitely don't agree

14

19

Source: Results of a survey research carried out by A. Tobolska in 1996 among the crew of the Polfa Pharmaceutical Works in Poznań (unpublished).

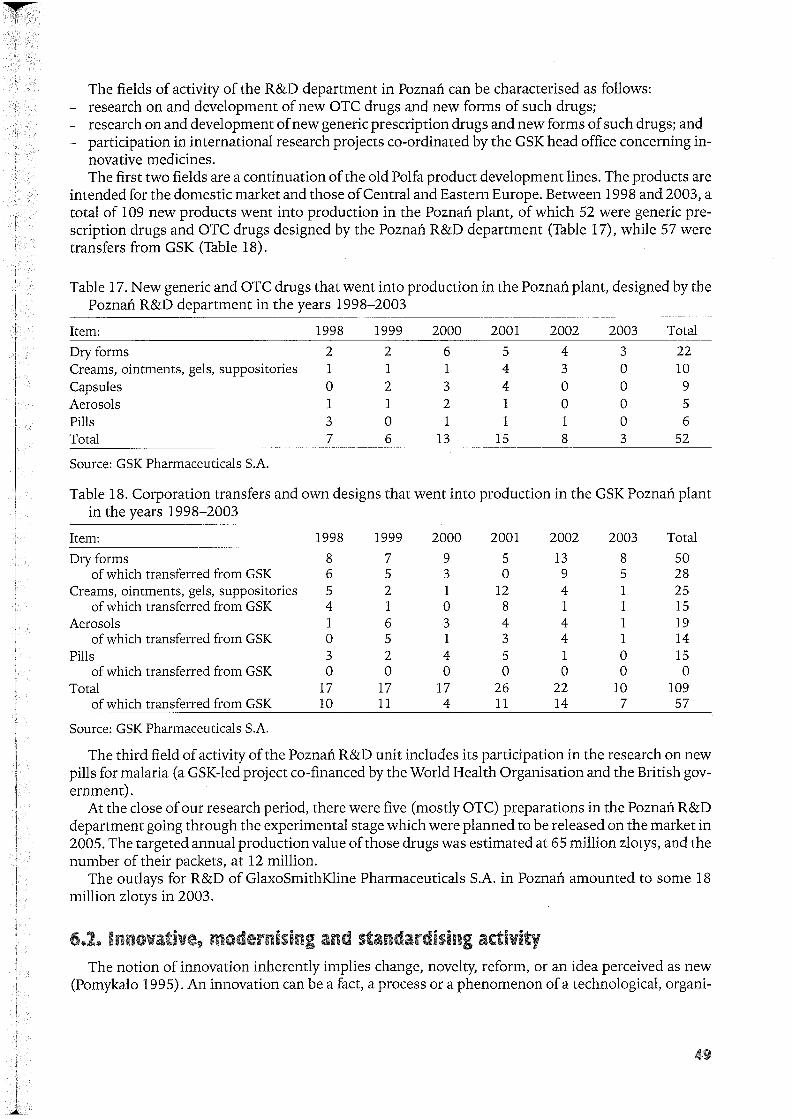

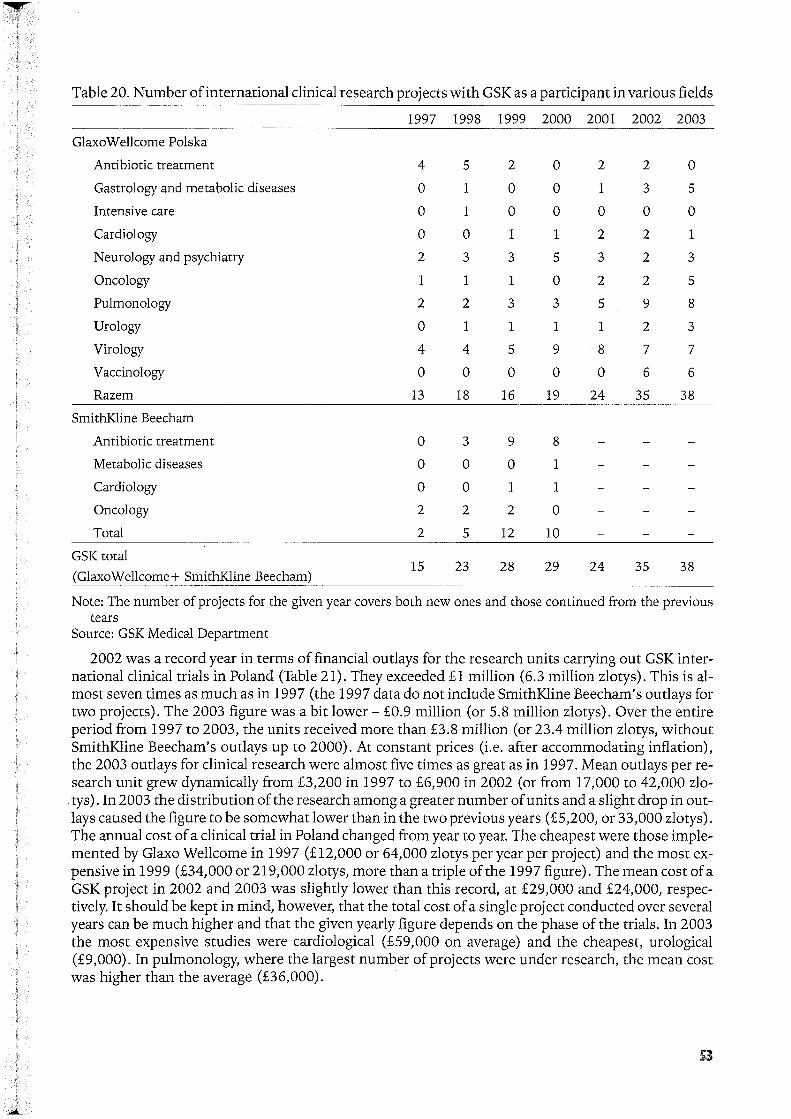

this way Poland has found itself a part of the global network of one of the biggest producers of medicines and health protection products (GSK is estimated to have about a 70/0 share ofthe world pharmaceutical market). The network embraces 108 factories located in 41 countries and 16 research and development centres in 8 countries (including one in Poznań).

The purchase of the Poznań Polfa plant gave the British firm a 7-11 % share of the Polish drug market (the exact figure depends on the indicators employed) and it has kept this market share ever since. The investor has met his privatisation obligations fully, having invested more than US$106 million over the years 1998-2002. In that period atotal of 99 new products started to be manufactured in the Poznań factory, of which 49 were medicines devised by the local R&D Department and 50 were transfers from GSK (Cylwik 2002). Thanks to the investment and the transfer oftechnology, the GSK establishment in Poznań has become the only producer ofFreon-free aerosol s in this part ofEurope and one of the four in the world, and the leading manufacturer of gelatine capsules in the entire GSK group. The foreign investor has also played a big part in product certification by the GMP (Good Manufacturing Practice) standards and adjustment of the drug registration procedure to the European U nion standards.

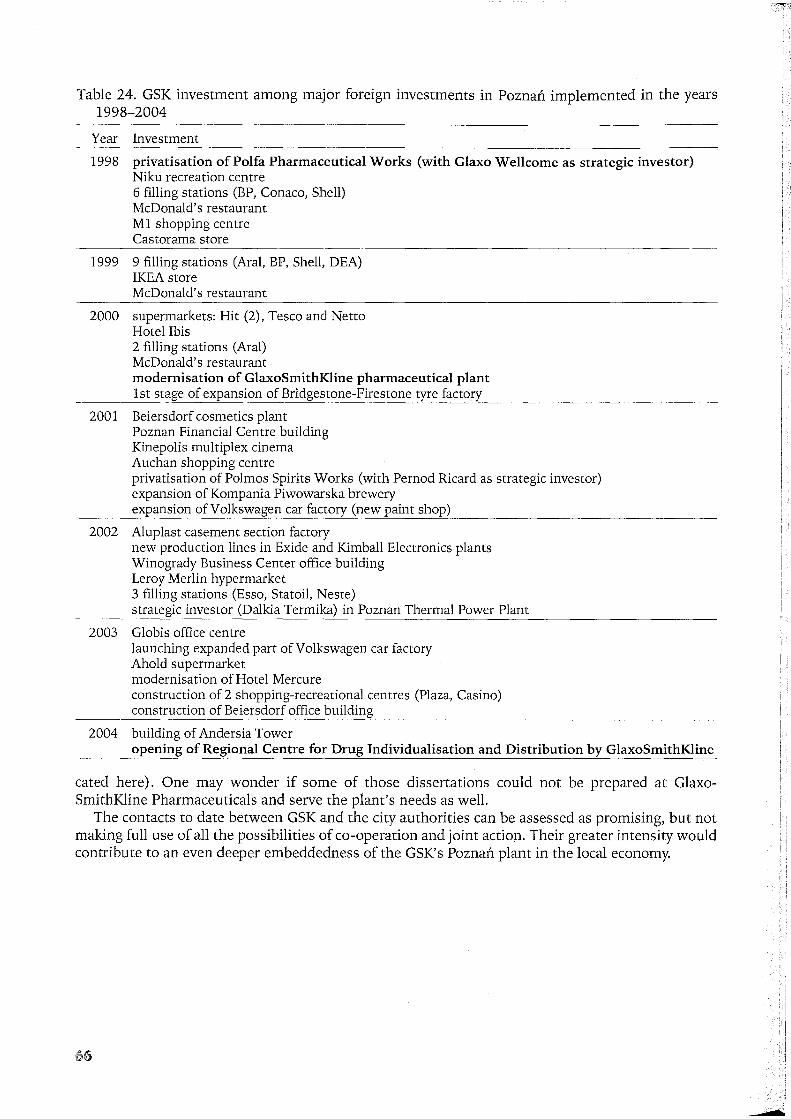

On 28 June 2004 a Regional Centre for Drug Individualisation and Distribution was opened in the Poznań plant, which has enhanced the status ofWielkopolska's capital as one ofthe major European GSK centres responsible for the manufacturing, preparation and distribution of drugs on East-Central European markets.

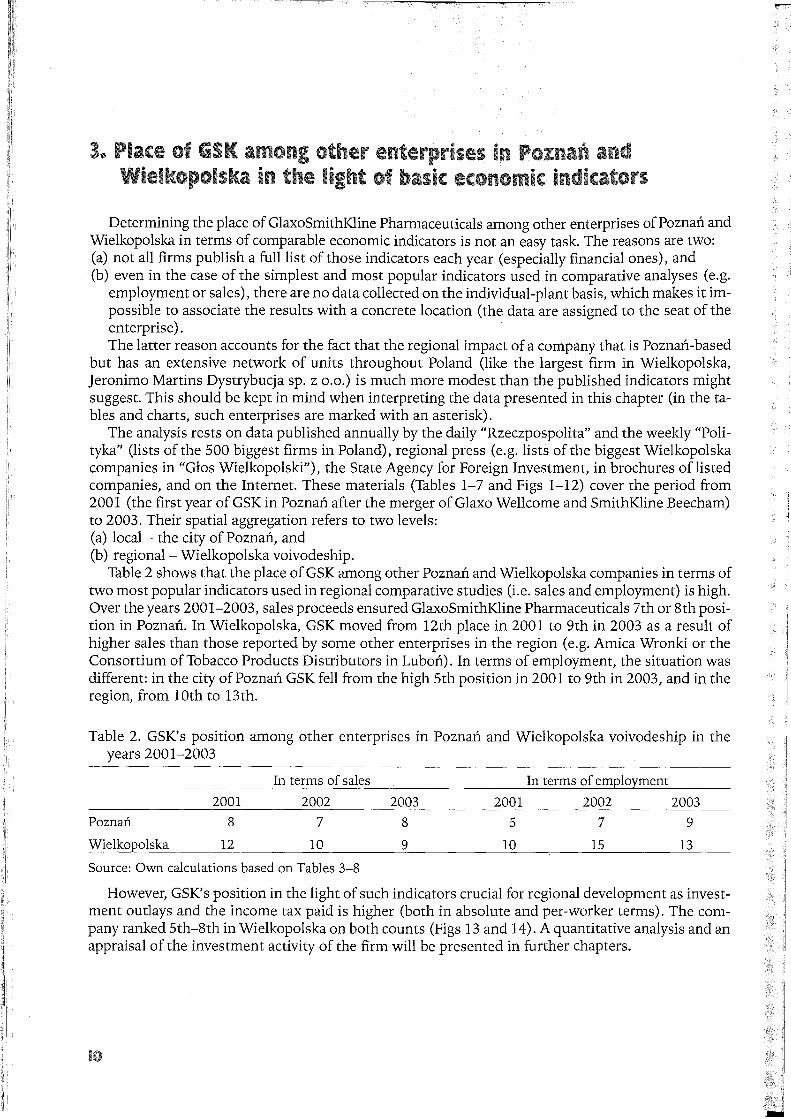

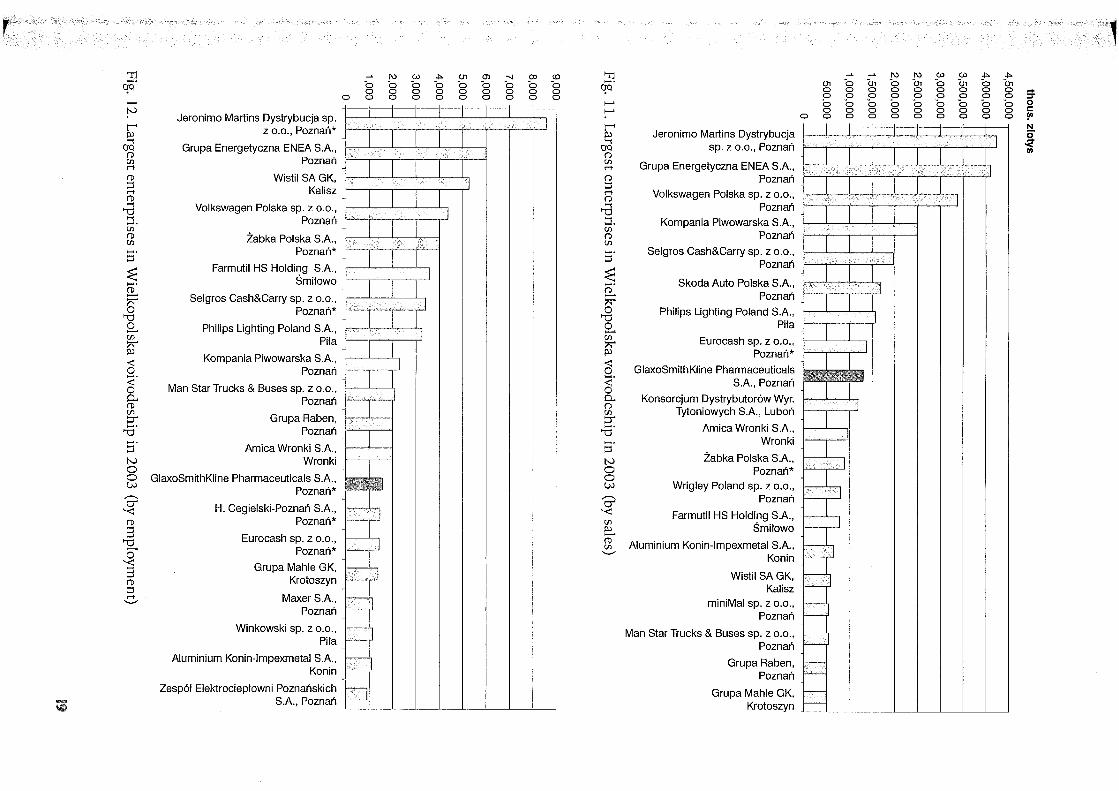

Determining the place of GlaxoSmithKline Pharmaceuticals among other enterprises of Poznań and Wielkopolska in terms of comparable economic indicators is not an easy task. The reasons are two: (a) not all firms publish a fulI list of those indicators each year (especially financial ones), and (b) even in the case of the simplest and most popular indicators used in comparative analyses (e.g.

employment or sales) , there are no data collected on the individual-plant basis, which makes it impossible to associate the results with a concrete location (the data are assigned to the seat of the enterprise) . The latter reason accounts for the fact that the regional impact of a company that is Poznań-based

but has an extensive network of units throughout Poland (like the largest firm in Wielkopolska, Jeronimo Martins Dystrybucja sp. z 0.0.) is much more modest than the published indicators might suggest. This should be kept in mind when interpreting the data presented in this chapter (in the tabIes and charts, such enterprises are marked with an asterisk) .

The analysis rests on data published annually by the daily "Rzeczpospolita" and the weekly "Polityka" (lists ofthe 500 biggest firms in Poland), regional press (e.g.lists ofthe biggest Wielkopolska companies in "Głos Wielkopolski"), the State Agency for Foreign Investment, in brochures of listed companies, and on the Internet. These materiais (Tabies 1-7 and Figs 1-12) cover the period from 2001 (the first year of GSK in Poznań after the merger of Glaxo Wellcome and SmithKline Beecham) to 2003. Their spatial aggregation refers to two levels: (a) local - the city of Poznań, and (b) regional - Wielkopolska voivodeship.

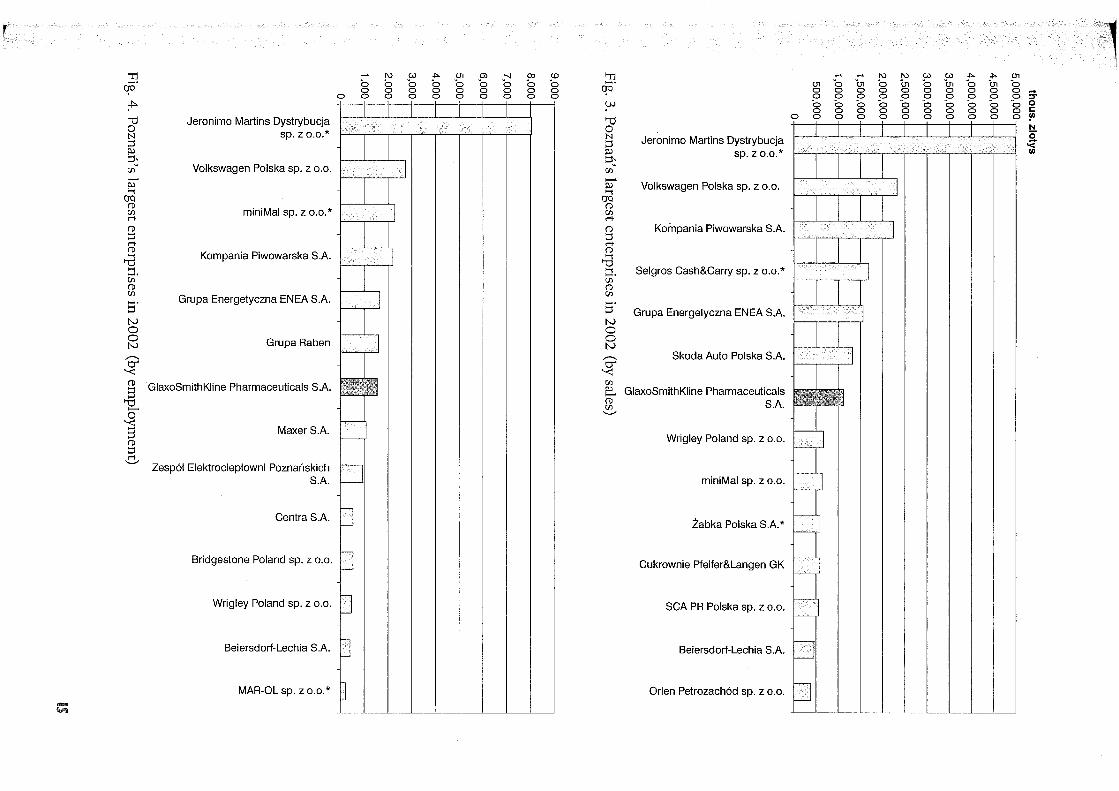

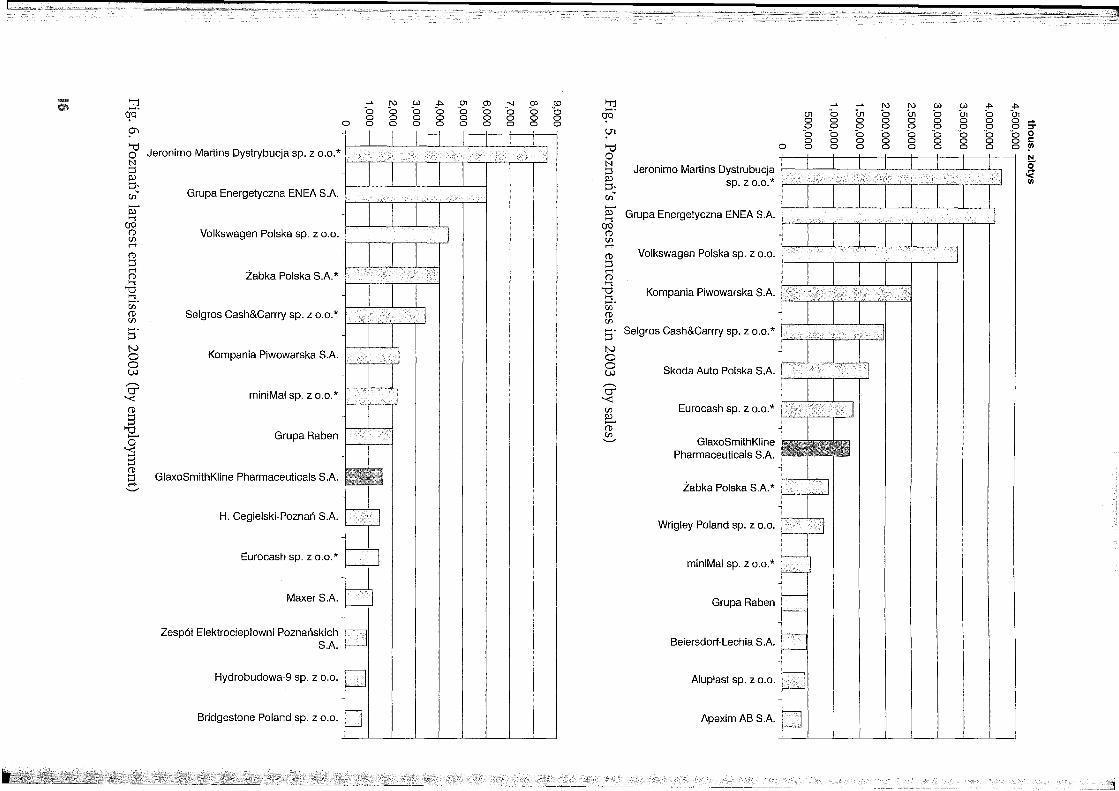

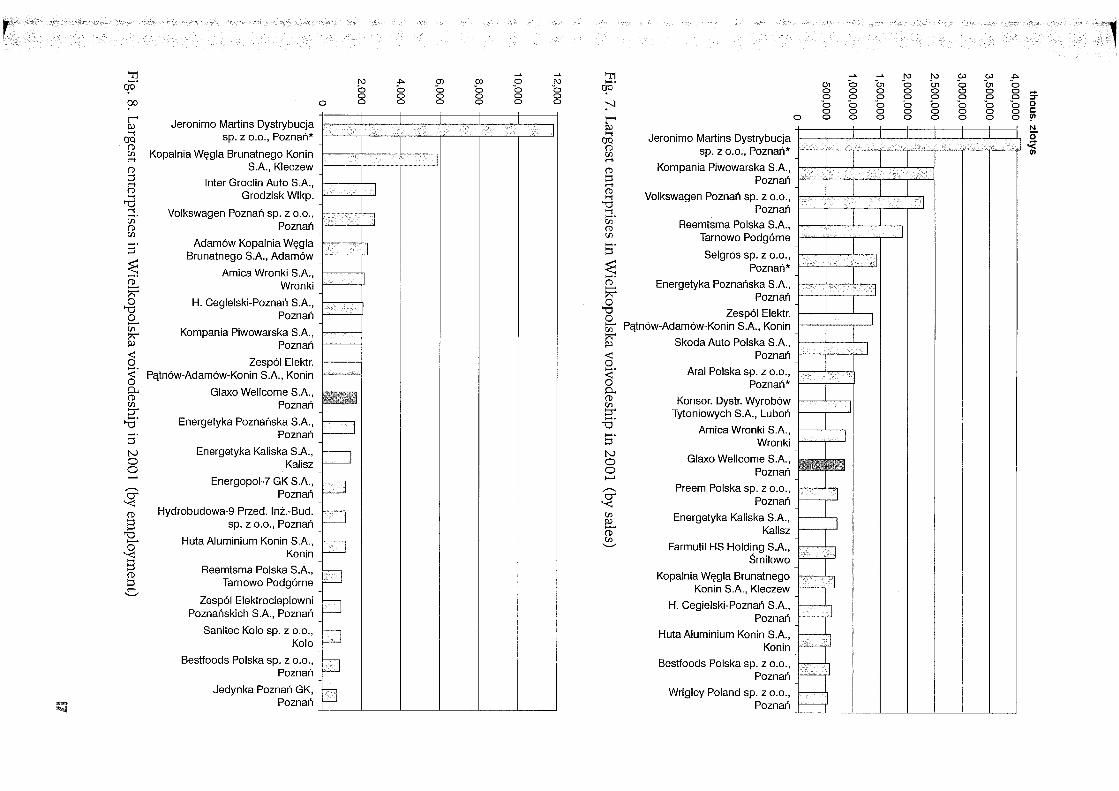

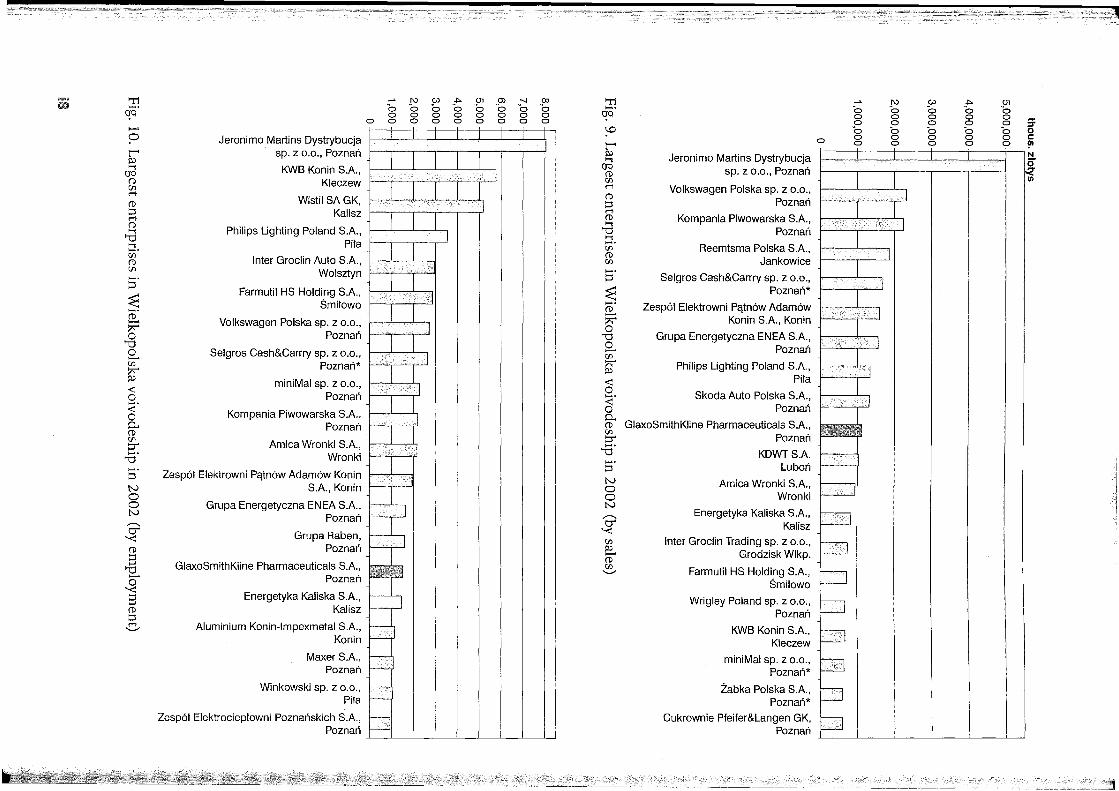

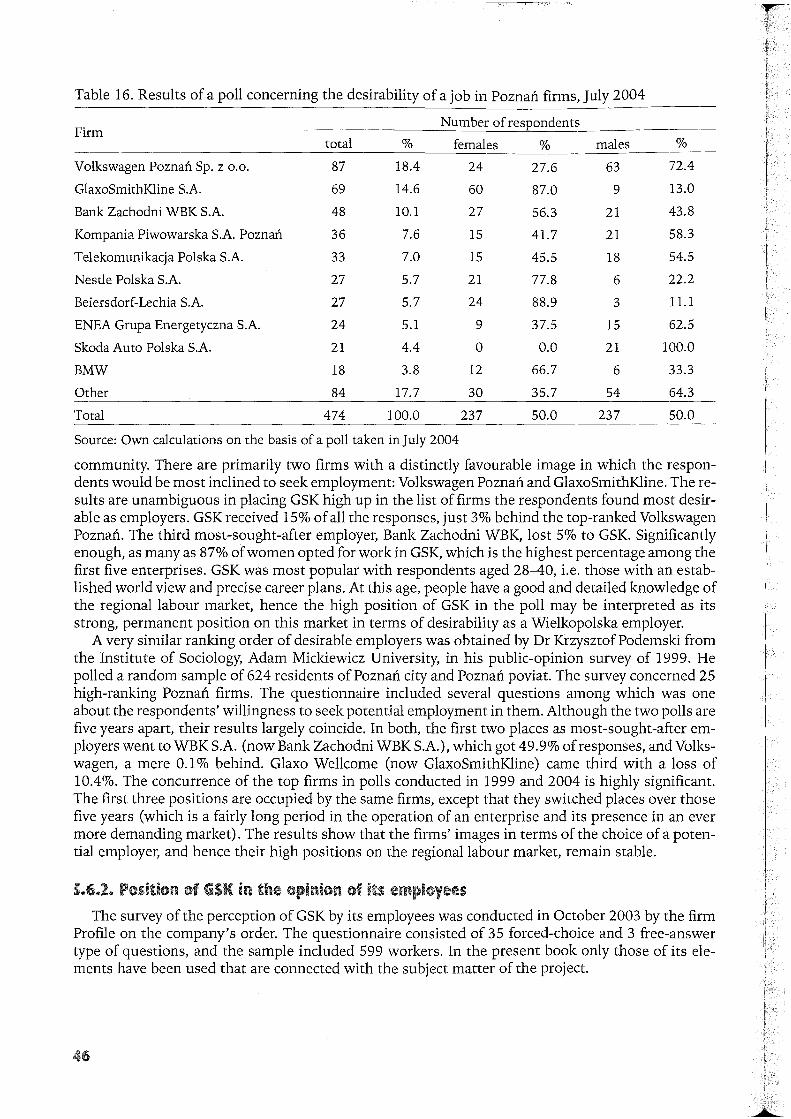

Table 2 shows that the place of GSK among other Poznań and Wielkopolska companies in term s of two most popular indicators used in regional comparative studies (Le. sales and employment) is high. Over the years 2001-2003, sales proceeds ensured GlaxoSmithKline Pharmaceuticals 7th or 8th position in Poznań. In Wielkopolska, GSK moved from 12th place in 2001 to 9th in 2003 as a result of higher sales than those reported by some other enterprises in the region (e.g. Amica Wronki or the Consortium ofTobacco Products Distributors in Luboń). In terms of employment, the situation was different: in the city ofPoznań GSK felI from the high 5th position in 2001 to 9th in 2003, and in the region, from 10th to 13th.

Table 2. GSK' s position among other enterprises in Poznań and Wielkopolska voivodeship in the years 2001-2003

In terms of sales In terms of employment

2001 2002 2003 2001 2002 2003

Poznań 8 7 8 5 7 9

Wielkopolska 12 10 9 10 15 13

Source: Own calculations based on Tables 3-8

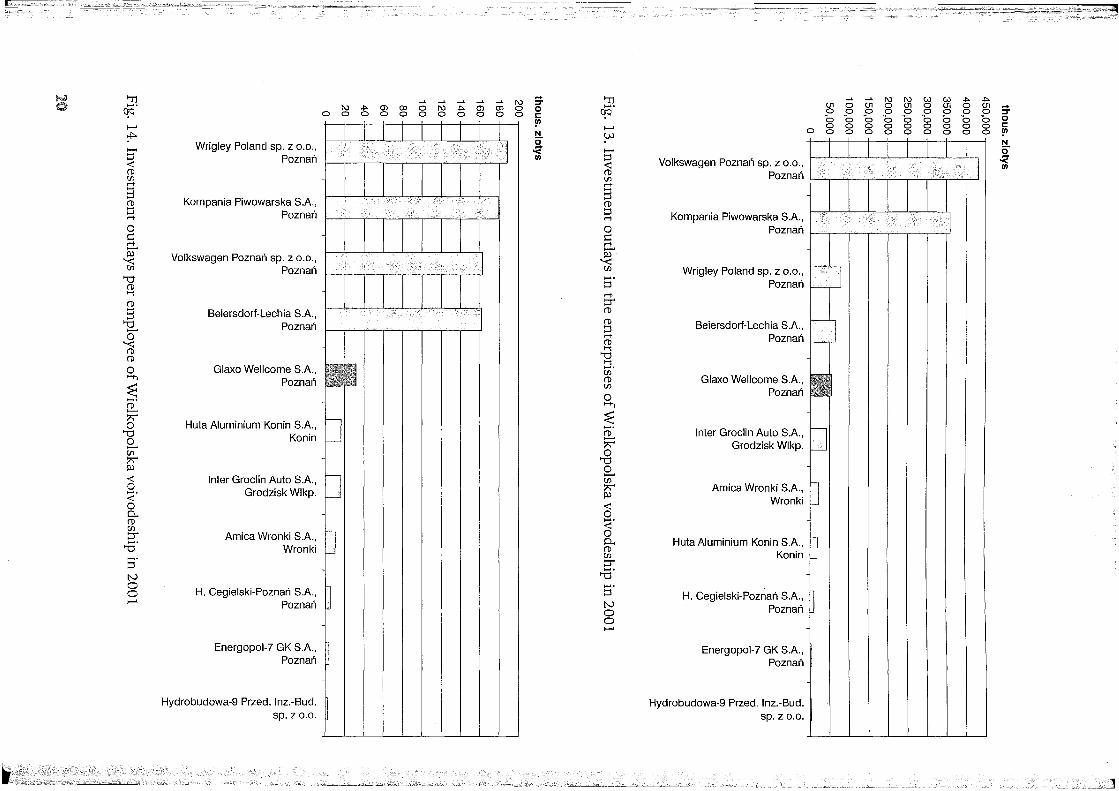

However, GSK's position in the light of such indicators crucial for regional development as investment outlays and the income tax paid is higher (both in absolute and per-worker terms) . The company ranked 5th-8th in Wielkopolska on both counts (Figs 13 and 14). A quantitative analysis and an appraisal of the investment activity of the firm will be presented in further chapters.

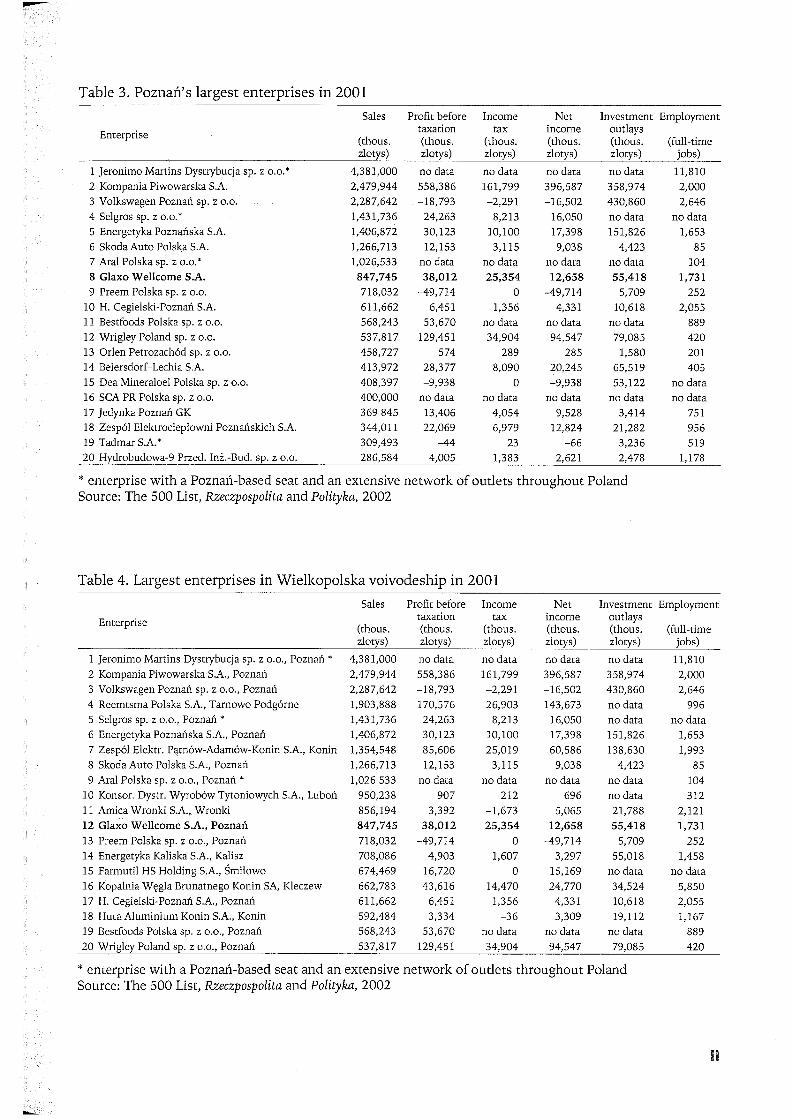

Table 3. Poznań's largest enterprises in 2001

Sales Profit before Income Net Investment Employment

Enterprise taxation tax income outlays (thous. (thous. (thous. (thous. (thous. (full-time zlotys) zlotys) zlotys) zlotys) zlotys) jobs)

l Jeronimo Martins Dystrybucja sp. z 0.0. * 4,381,000 no data no data no data no data 11,810 2 Kompania Piwowarska S.A. 2,479,944 558,386 161,799 396,587 358,974 2,000 3 Volkswagen Poznań sp. z 0.0. 2,287,642 -18,793 -2,291 -16,502 430,860 2,646 4 Selgros sp. z 0.0. * 1,431,736 24,263 8,213 16,050 no data no data 5 Energetyka Poznańska S.A. 1,406,872 30,123 10,100 17,398 151,826 1,653 6 Skoda Auto Polska S.A. 1,266,713 12,153 3,115 9,038 4,423 85 7 Aral Polska sp. z 0.0. * 1,026,533 no data no data no data no data 104 8 Glaxo Wellcome S.A. 847,745 38,012 25,354 12,658 55,418 1,731 9 Preem Polska sp. z 0.0. 718,032 -49,714 ° -49,714 5,709 252

10 H. Cegielski-Poznań S.A. 611,662 6,451 1,356 4,331 10,618 2,055 11 Bestfoods Polska sp. z 0.0. 568,243 53,670 no data no data no data 889 12 Wrigley Poland sp. z 0.0. 537,817 129,451 34,904 94,547 79,085 420 13 Orłen Petrozachód sp. z 0.0. 458,727 574 289 285 1,580 201 14 Beiersdorf-Lechia S.A. 413,972 28,377 8,090 20,245 65,519 405 15 Dea Mineraloel Polska sp. z 0.0. 408,397 -9,938 ° -9,938 53,122 no data 16 SCA PR Polska sp. z 0.0. 400,000 no data no data no data no data no data 17 Jedynka Poznań GK 369845 13,406 4,054 9,528 3,414 751 18 Zespól Elektrociepłowni Poznańskich S.A. 344,011 22,069 6,979 12,824 21,282 956 19 Tadmar S.A. * 309,493 -44 23 -66 3,236 519 20 Hydrobudowa-9 Przed. Inż.-Bud. sp. z 0.0. 286,584 4,005 1,383 2,621 2,478 1,178

* enterprise with a Poznań-based seat and an extensive network of outlets throughout Poland Source: The 500 List, Rzeczpospolita and Polityka, 2002

Table 4. Largest enterprises in Wielkopolska voivodeship in 2001

Sales Profit before Income Net Investment Employment

Enterprise taxation tax income outlays (thous. (thous. (thous. (thous. (thous. (full-time zlotys) zlotys) zlotys) zlotys) zlotys) jobs)

l Jeronimo Martins Dystrybucja sp. z 0.0., Poznań * 4,381,000 no data no data no data no data 11,810 2 Kompania Piwowarska S.A., Poznań 2,479,944 558,386 161,799 396,587 358,974 2,000 3 Volkswagen Poznań sp. z 0.0., Poznań 2,287,642 -18,793 -2,291 -16,502 430,860 2,646 4 Reemtsma Polska S.A., Tamowo Podgórne 1,903,888 170,576 26,903 143,673 no data 996 5 Selgros sp. z 0.0., Poznań * 1,431,736 24,263 8,213 16,050 no data no data 6 Energetyka Poznańska S.A., Poznań 1,406,872 30,123 10,100 17,398 151,826 1,653 7 Zespół Elektr. Pątnów-Adamów-Konin S.A., Konin 1,354,548 85,606 25,019 60,586 138,630 1,993 8 Skoda Auto Polska S.A., Poznań 1,266,713 12,153 3,115 9,038 4,423 85 9 Aral Polska sp. z 0.0., Poznań * 1,026533 no data no data no data no data 104

10 Konsor. Dystr. Wyrobów Tytoniowych S.A., Luboń 950,238 907 212 696 no data 312 11 Amica Wronki S.A., Wronki 856,194 3,392 -1,673 5,065 21,788 2,121 12 Glaxo Wellcome S.A., Poznań 847,745 38,012 25,354 12,658 55,418 1,731 13 Preem Polska sp. z 0.0., Poznań 718,032 -49,714 ° -49,714 5,709 252 14 Energetyka Kaliska S.A., Kalisz 708,086 4,903 1,607 3,297 55,018 1,458 15 Farmutil HS Holding S.A., Śmiłowo 674,469 16,720 ° 15,169 no data no data 16 Kopalnia Węgla Brunatnego Konin SA, Kleczew 662,783 43,616 14,470 24,770 34,524 5,850 17 H. Cegielski-Poznań S.A., Poznań 611,662 6,451 1,356 4,331 10,618 2,055 18 Huta Aluminium Konin S.A., Konin 592,484 3,334 -36 3,309 19,112 1,167 19 Bestfoods Polska sp. z 0.0., Poznań 568,243 53,670 no data no data no data 889 20 Wrigley Poland sp. z 0.0., Poznań 537,817 129,451 34,904 94,547 79,085 420

* enterprise with a Poznań-based seat and an extensive network of outlets throughout Poland Source: The 500 List, Rzeczpospolita and Polityka, 2002

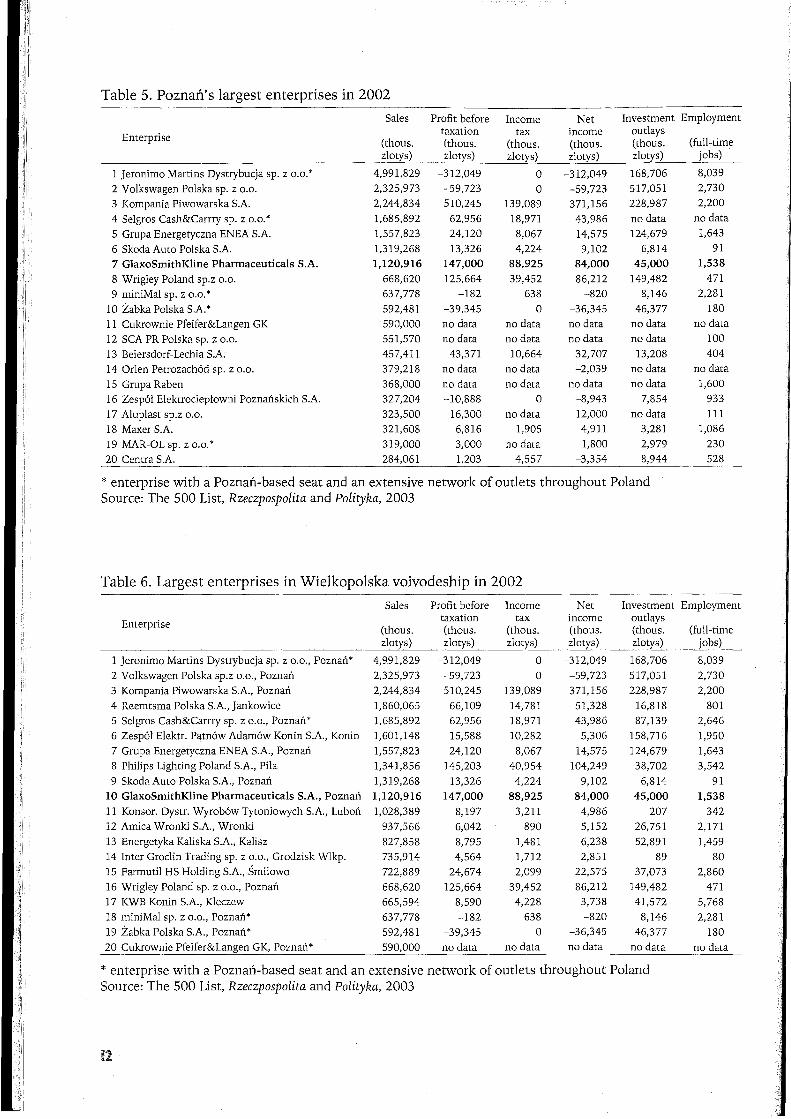

Table 5. Poznań's largest enterprises in 2002

Sales Profit before Income Net Investment Employment

Enterprise taxation tax income outlays

(thous. (thous. (thous. (thous. (thous. (full-time zlotys) zlotys) zlotys) zlotys) zlotys) jobs)

l Jeronimo Martins Dystrybucja sp. z 0.0. * 4,991,829 -312,049 O -312,049 168,706 8,039

2 Volkswagen Polska sp. z 0.0. 2,325,973 -59,723 O -59,723 517,051 2,730

3 Kompania Piwowarska S.A. 2,244,834 510,245 l39,089 371,156 228,987 2,200

4 Selgros Cash&Carrry sp. z 0.0. * 1,685,892 62,956 18,971 43,986 no data no data

5 Grupa Energetyczna ENEA S.A. 1,557,823 24,120 8,067 14,575 124,679 1,643

6 Skoda Auto Polska S.A. 1,319,268 l3,326 4,224 9,102 6,814 91

7 GlaxoSmithKline Pharmaceuticals S.A. 1,120,916 147,000 88,925 84,000 45,000 1,538

8 Wrigley Poland sp.z 0.0. 668,620 125,664 39,452 86,212 149,482 471

9 miniMaI sp. z 0.0. * 637,778 -182 638 -820 8,146 2,281

10 Żabka Polska S.A. * 592,481 -39,345 O -36,345 46,377 180

11 Cukrownie Pfeifer&Langen GK 590,000 no data no data no data no data no data

12 SCA PR Polska sp. z 0.0. 551,570 no data no data no data no data 100

l3 Beiersdorf-Lechia S.A. 457,411 43,371 10,664 32,707 l3,208 404

14 Orlen Petrozachód sp. z 0.0. 379,218 no data no data -2,039 no data no data

15 Grupa Raben 368,000 no data no data no data no data 1,600

16 Zespół Elektrociepłowni Poznańskich S.A. 327,204 -10,888 O -8,943 7,854 933

17 AlupIast sp.z 0.0. 323,500 16,300 no data 12,000 no data 111

18 Maxer S.A. 321,608 6,816 1,905 4,911 3,281 1,086

19 MAR-OL sp. z 0.0. * 319,000 3,000 no data 1,800 2,979 230

20 Centra S.A. 284,061 1,203 4,557 -3,354 8,944 528

* enterprise with a Poznań-based seat and an extensive network of outlets throughout Poland Source: The 500 List, Rzeczpospolita and Polityka, 2003

Table 6. Largest enterprises in Wielkopolska voivodeship in 2002

Sales Profit before Income Net Investment Employment

Enterprise taxation tax income outlays (thous. (thous. (thous. (thous. (thous. (full-time zlotys) zlotys) zlotys) zlotys) zlotys) jobs)

l Jeronimo Martins Dystrybucja sp. z 0.0., Poznań* 4,991,829 -312,049 O -312,049 168,706 8,039

2 Volkswagen Polska sp.z 0.0., Poznań 2,325,973 -59,723 O -59,723 517,051 2,730

3 Kompania Piwowarska S.A., Poznań 2,244,834 510,245 l39,089 371,156 228,987 2,200

4 Reemtsma Polska S.A., Jankowice 1,860,065 66,109 14,781 51,328 16,818 801

5 Selgros Cash&Carrry sp. z 0.0., Poznań* 1,685,892 62,956 18,971 43,986 87,l39 2,646

6 Zespół Elektr. Pątnów Adamów Konin S.A., Konin 1,601,148 15,588 10,282 5,306 158,716 1,950

7 Grupa Energetyczna ENEA S.A., Poznań 1,557,823 24,120 8,067 14,575 124,679 1,643

8 Philips Lighting Poland S.A., Piła 1,341,856 145,203 40,954 104,249 38,702 3,542

9 Skoda Auto Polska S.A., Poznań 1,319,268 l3,326 4,224 9,102 6,814 91 10 GlaxoSmithKline Pharmaceuticals S.A., Poznań 1,120,916 147,000 88,925 84,000 45,000 1,538

11 Konsor. Dystr. Wyrobów Tytoniowych S.A., Luboń 1,028,389 8,197 3,211 4,986 207 342 12 Amica Wronki S.A., Wronki 937,566 6,042 890 5,152 26,751 2,171

l3 Energetyka Kaliska S.A., Kalisz 827,858 8,795 1,481 6,238 52,891 1,459 14 Inter Groclin Trading sp. z 0.0., Grodzisk Wlkp. 735,914 4,564 1,712 2,851 89 80 15 Farmutil HS Holding S.A., Śmiłowo 722,889 24,674 2,099 22,575 37,073 2,860 16 Wrigley Poland sp. z 0.0., Poznań 668,620 125,664 39,452 86,212 149,482 471 17 KWB Konin S.A., Kleczew 665,594 8,590 4,228 3,738 41,572 5,768 18 miniMaI sp. z 0.0., Poznań* 637,778 -182 638 -820 8,146 2,281 19 Żabka Polska S.A., Poznań* 592,481 -39,345 O -36,345 46,377 180 20 Cukrownie Pfeifer&Langen GK, Poznań * 590,000 no data no data no data no data no data

* enterprise with a Poznań-based seat and an extensive network of outlets throughout Poland Source: The 500 List, Rzeczpospolita and Polityka, 2003

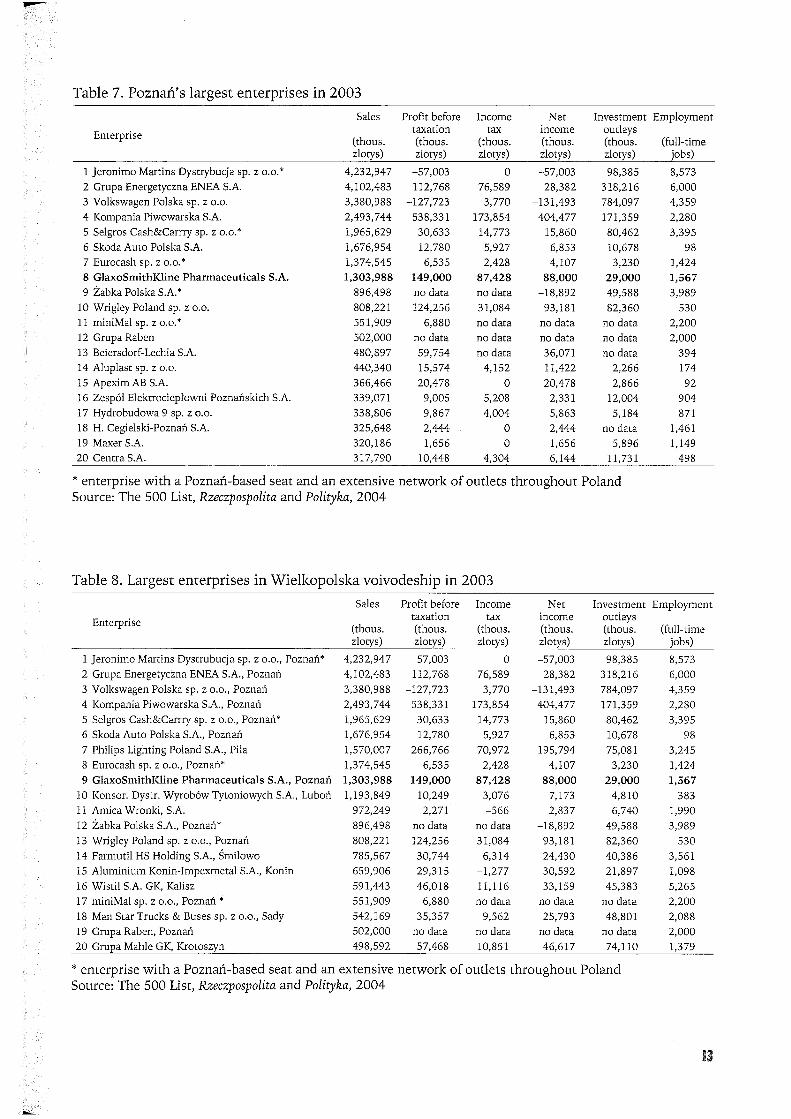

Table 7. Poznań' sIargest enterprises in 2003

Sales Profit before Income Net Investment Employment

Enterprise taxation tax income outlays (thous. (thous. (thous. (thous. (thous. (full-time zlotys) zlotys) zlotys) zlotys) zlotys) jobs)

l Jeronimo Martins Dystrybucja sp. z 0.0.* 4,232,947 -57,003 ° -57,003 98,385 8,573 2 Grupa Energetyczna ENEA S.A. 4,102,483 112,768 76,589 28,382 318,216 6,000 3 Volkswagen Polska sp. z 0.0. 3,380,988 -127,723 3,770 -131,493 784,097 4,359 4 Kompania Piwowarska S.A. 2,493,744 538,331 173,854 404,477 171,359 2,280 5 Selgros Cash&Carrry sp. z 0.0. * 1,965,629 30,633 14,773 15,860 80,462 3,395 6 Skoda Auto Polska S.A. 1,676,954 12,780 5,927 6,853 10,678 98 7 Eurocash sp. z 0.0. * 1,374,545 6,535 2,428 4,107 3,230 1,424 8 GlaxoSmithKline Pharmaceuticals S.A. 1,303,988 149,000 87,428 88,000 29,000 1,567 9 Żabka Polska S.A. * 896,498 no data no data -18,892 49,588 3,989

10 Wrigley Poland sp. z 0.0. 808,221 124,256 31,084 93,181 82,360 530 11 miniMai sp. z 0.0. * 551,909 6,880 no data no data no data 2,200 12 Grupa Raben 502,000 no data no data no data no data 2,000 13 Beiersdorf-Lechia S.A. 480,897 59,754 no data 36,071 no data 394 14 Alupiast sp. z 0.0. 440,340 15,574 4,152 11,422 2,266 174 15 Apexim AB S.A. 366,466 20,478 ° 20,478 2,866 92 16 Zespół Elektrociepłowni Poznańskich S.A. 339,071 9,005 5,208 2,331 12,004 904 17 Hydrobudowa 9 sp. z 0.0. 338,806 9,867 4,004 5,863 5,184 871 18 H. Cegielski-Poznań S.A. 325,648 2,444 ° 2,444 no data 1,461 19 Maxer S.A. 320,186 1,656 ° 1,656 5,896 1,149 20 Centra S.A. 317,790 10,448 4,304 6,144 11,731 498

* enterprise with a Poznań-based seat and an extensive network of outlets throughout Poland Source: The 500 List, Rzeczpospolita and Polityka, 2004

Table 8. Largest enterprises in Wielkopolska voivodeship in 2003

Sales Profit before Income Net Investment Employment

Enterprise taxation tax income outlays (thous. (thous. (thous. (thous. (thous. (full-time zlotys) zlotys) zlotys) zlotys) zlotys) jobs)

l Jeronimo Martins Dystrubucja sp. z 0.0., Poznań* 4,232,947 -57,003 ° -57,003 98,385 8,573 2 Grupa Energetyczna ENEA S.A., Poznań 4,102,483 112,768 76,589 28,382 318,216 6,000 3 Volkswagen Polska sp. z 0.0., Poznań 3,380,988 -127,723 3,770 -131,493 784,097 4,359 4 Kompania Piwowarska S.A., Poznań 2,493,744 538,331 173,854 404,477 171,359 2,280 5 Selgros Cash&Carrry sp. z 0.0., Poznań* 1,965,629 30,633 14,773 15,860 80,462 3,395 6 Skoda Auto Polska S.A., Poznań 1,676,954 12,780 5,927 6,853 10,678 98 7 Philips Lighting Poland S.A., Piła 1,570,007 266,766 70,972 195,794 75,081 3,245 8 Eurocash sp. z 0.0., Poznań* 1,374,545 6,535 2,428 4,107 3,230 1,424 9 GlaxoSmithKline Pharmaceuticals S.A., Poznań 1,303,988 149,000 87,428 88,000 29,000 1,567

10 Konsor. Dystr. Wyrobów Tytoniowych S.A., Luboń 1,193,849 10,249 3,076 7,173 4,810 383 11 Amica Wronki, S.A. 972,249 2,271 -566 2,837 6,740 1,990 12 Żabka Polska S.A., Poznań* 896,498 no data no data -18,892 49,588 3,989 13 Wrigley Poland sp. z 0.0., Poznań 808,221 124,256 31,084 93,181 82,360 530 14 Farmutil HS Holding S.A., Śmiłowo 785,567 30,744 6,314 24,430 40,386 3,561 15 Aluminium Konin-Impexmetal S.A., Konin 659,906 29,315 -1,277 30,592 21,897 1,098 16 Wistil S.A. GK, Kalisz 591,443 46,018 11,116 33,159 45,383 5,265 17 miniMai sp. z 0.0., Poznań * 551,909 6,880 no data no data no data 2,200 18 Man Star Trucks & Buses sp. z 0.0., Sady 542,169 35,357 9,562 25,793 48,801 2,088 19 Grupa Raben, Poznań 502,000 no data no data no data no data 2,000 20 Grupa Mahle GK, Krotoszyn 498,592 57,468 10,851 46,617 74,110 1,379

* enterprise with a Poznań-based seat and an extensive network of outlets throughout Poland Source: The 500 List, Rzeczpospolita and Polityka, 2004

71 ...... qo N

~ O N ::J pJ

::J~ m

p) ""i

CfQ (1) m M

(1)

::J M (1)

~ ::l. m (1) m

5' N O O f-I

,,-.... O""

"<:! (1)

a '"d Q

"<:! a (1)

::J M ~

Jeronimo Martins Dystrybucja sp. z 0.0.*

Volkswagen Poznań sp. z 0.0.

H. Cegielski-Poznań S.A.

Kompania Piwowarska S.A.

Girom Wellcome S.A.

Energetyka Poznańska S.A.

Energopol-7 GK S.A.

Hydrobudowa Przed. Inż.-Bud. sp. z 0.0.

Zespół Elektrociepłowni Poznańskich

S.A.

Bestfoods Polska sp. z 0.0.

Jedynka Poznań GK

Poznańska Energetyka Cieplna S.A.

Tadmar S.A. *

Wrigley Poland sp. z 0.0.

Beiersdorf-Lechia S.A.

o

I\)

o o o

~ o o o

(j)

o o o

ex:> o o o

o o o o

...... I\)

o o o

71 qq' f-I

~ O N ::J pJ

::J~ m

p) ""i

CfQ (1) m M

(1)

::J M (1) ""i

'"d ::l. m (1) m ...... ::J N O O f-I

,,-.... O""

"<:! m e-(1) m ~

I\)

01 o ln o o o o o o o o o o o o o o o o o

o o o o o

Jeronimo Martins Dystrybucja sp. z 0.0.*

Kompania Piwowarska S.A.

Volkswagen Poznań sp. z 0.0.

Selgros sp. z 0.0. *

Energetyka Poznańska S.A.

Skoda Auto Polska S.A.

Aral Polska sp. z 0.0.*

Girom Wellcome S.A.

Preem Polska sp. z 0.0.

H. Cegielski-Poznań S.A.

Bestfoods Polska sp. z 0.0.

Wrigley Poland sp. z 0.0

Orlen Petrozachód sp. z 0.0

Beiersdorf-Lechia S.A

Dea Mineraloel Polska sp. z 0.0

I\) Ul Ul ln o ln o o o o o o o o o o o o o o o

_ ... _-

~ ~ o ln o o o o o o o o o o

-

01 o o _

o :::T o o o s:: o ~

N

i In

r'

~ qq. ~ ""O o N ::J PJ ::J~ CI)

p) '""':

(]Q (D CI) M

(D

::J M (D

:a ~. CI) (D CI)

Er N o o N

".........

c::r' "<:

(D

~ ~ 8 (D

::J M "-'"

Jeronimo Martins Dystrybucja sp. z 0.0.*

Volkswagen Polska sp. z 0.0.

miniMai sp. z 0.0. *

Kompania Piwowarska S.A.

Grupa Energetyczna ENEA S.A.

Grupa Raben

GlaxoSmithKline Pharmaceuticals S.A.

Maxer S.A.

Zespół Elektrociepłowni Poznańskich

S.A.

Centra S.A.

Bridgestone Poland sp. z 0.0.

Wrigley Poland sp. z 0.0.

Beiersdorf-Lechia S.A.

MAR-OL sp. z 0.0. *

I\)

a a o o

o o o

c.u ..p.. a a o o o o

(Jl O) '-I a a a o o o o o o

OJ co a a o o o o

~ qq. w ""O o N ::J PJ ::J~ CI)

I--'

PJ '""':

(]Q (D CI) M

(D

::J M (D

:a ~. CI) (D CI)

5· N O O N

".........

c::r' "<:

CI)

Jeronimo Martins Dystrybucja sp. z 0.0.*

Volkswagen Polska sp. z 0.0.

Kompania Piwowarska S.A.

Selgros Cash&Carry sp. z 0.0.*

Grupa Energetyczna ENEA S.A.

Skoda Auto Polska S.A.

e:.. GlaxoSmithKline Pharmaceuticals ~ S.A.

"-'"

Wrigley Poland sp. z 0.0.

miniMai sp. z 0.0.

Żabka Polska S.A.*

Cukrownie Pfeifer&Langen GK

SCA PR Polska sp. z 0.0.

Beiersdorf-Lechia S.A.

Orlen Petrozachód sp. z 0.0.

o

1 I\) I\) c.u c.u ..p.. ..p.. (Jl

(Jl a c.n a c.n a c.n a c.n a o o o o o o o o o o s: o o o o o o o o o o a a a a a a a a a a o o o o o o o o o o o s::: o o o o o o o o o o !'>

N

9: '< Ul

~"~"S!!l"l!JUNlt!±l,g"'_~_"'\\~'~"''''~'_"J'J""''_l""'_"-''J121''''l""_!l_,',,,"-J"'J"""l"":_':~~~:"""''''~'~_~":""~'~''''-~l'~l",''':~',' ',",'""='~'=',"=l""l""'l"ll'"l"~",'~--'-"""~"""~-- "'-~~":&':''J:'Wl:l''l::a

"Tl ...... qo Q)

I\) UJ .j:>. 01 O) --.j ex> CO O O O O O O O O O O O O O O O O O O

O O O O O O O O O O

~ Jeronimo Martins Dystrybucja sp. z 0.0.* N ~I~~-.--,,~r--.--~--.--.~ ::s p.:l

::s~ (J)

..-. p.:l I-i

ao CD (J) M

CD ::s M CD

~ ::l. (J)

CD (J)

5· tv O O UJ

".-.....

O'" "'<:

CD

8 ~

~ CD ::s M '--"

Grupa Energetyczna ENEA S.A. I

Volkswagen Polska sp. z 0.0. 1-1 -,.--,.--.,.---,-J

Żabka Polska S.A.* 1--......,..-.......... -...,----1

Selgros Cash&Carrry sp. z 0.0.* 1-1 --,---,.--......,..--'

Kompania Piwowarska S.A. I ,l

miniMai sp. z 0.0. * 1-1 -...,--,.J

Grupa Raben

GlaxoSmithKline Pharmaceuticals S.A.

H. Cegielski-Poznań S.A.

Eurocash sp. z 0.0. *

Maxer S.A.

Zespół Elektrociepłowni Poznańskich

S.A.

Hydrobudowa-9 sp. z 0.0.

Bridgestone Poland sp. z 0.0.

1-1 -~---l

"Tl qq. Ul

"i:) O N ::s p.:l

::s~ (J)

..-.

o

Jeronimo Martins Dystrubucja sp. z 0.0.*

01 o 01 o o o o o o o o o o o o o o o

I\) I\) UJ UJ .j:>.

o 01 o 01 o o o o o o o o o o o o o o o o o o o o o o o o o o

p.:l I-i

ao CD (J) M

Grupa Energetyczna ENEA S.A. I I ,

CD ::s M CD

~ ::l. (J)

CD (J)

Volkswagen Polska sp. z 0.0. r-~~~---.--~---.~-r~

Kompania Piwowarska S.A. t

5· Selgros Cash&Carrry sp. z 0.0. * tv O O UJ

".-.....

O'" "'<: (J) p.:l ro (J) '--"

Skoda Auto Polska S.A. 1-1 ~-.--r---......J

Eurocash sp. z 0.0. * 1-1 -':"";---r-..-:..J

GlaxoSmithKline Pharmaceuticals S.A.

Żabka Polska S.A. *

Wrigley Poland sp. z 0.0. 1'-1 _...,.-....J

miniMai sp. z 0.0.*

Grupa Raben

Beiersdorf-Lechia S.A.

Alupiast sp. z 0.0.

Apexim AB S.A.

.j:>.

01 o ..... o :::r o o o t: o !II

N O" -< fil

r'"

'T1 cfQ' 00

~ !lJ """I

ao (D 00 r-t (D

::J r-t (D """I

""d """I 00' (D 00 ....... ::J

~ (D' ~ O

""d O I--' 00 ~ !lJ

<: O <i" O o.. (D 00 p-

..a' S' N O O I--'

,.--.... c:T'

'<: (D

3 ""d O-

'<: 3 (D

::J r-t

........"

I\) .j::::. m co o I\)

a a a a a a o o o o o o

o o o o o o o

Jeronimo Martins Dystrybucja sp. Z 0.0., Poznań*

Kopalnia Węgla Brunatnego Konin S.A., Kleczew

Inter Groclin Auto S.A., Grodzisk Wlkp.

Volkswagen Poznań sp. z 0.0.,

Poznań

Adamów Kopalnia Węgla Brunatnego S.A., Adamów

Amica Wronki S.A., Wronki

H. Cegielski-Poznań S.A., Poznań

Kompania Piwowarska S.A., Poznań

Zespól Elektr. Pątnów-Adamów-Konin S.A., Konin

Girom Wellcome S.A., Poznań

Energetyka Poznańska S.A., Poznań

Energetyka Kaliska S.A., Kalisz

Energopol-7 GK S.A., Poznań

Hydrobudowa-9 Przed. Inż.-Bud. sp. z 0.0., Poznań

Huta Aluminium Konin S.A., Konin

Reemtsma Polska S.A., Tarnowo Podgórne

Zespól Elektrocieplowni Poznańskich S.A., Poznań

Sanitec Kolo sp. z 0.0.,

Koło

Bestfoods Polska sp. z 0.0.,

Poznań

Jedynka Poznań GK: p Poznan

~----~----~----~----~----~----~

'T1 cfQ' :'1 ~ !lJ """I

ao (D 00 r-t (D

::J r-t (D """I

""d """I ....... 00 (D 00

S' ~ (D' ~ O

""d O Ci) ~ !lJ

<: O

8' o.. (D 00 p-.......

""d

S' N O O I--'

,.--.... c:T'

'<: 00 !lJ ro 00

........"

Jeronimo Martins Dystrybucja sp. z 0.0., Poznań*

Kompania Piwowarska S.A., Poznań

Volkswagen Poznań sp. z 0.0.,

Poznań

Reemtsma Polska S.A., Tarnowo Podgórne

Selgros sp. z 0.0.,

Poznań*

Energetyka Poznańska S.A., Poznań

Zespól Elektr. Pątnów-Adamów-Konin S.A., Konin

Skoda Auto Polska S.A., Poznań

Aral Polska sp. z 0.0.,

Poznań*

Konsor. Dystr. Wyrobów Tytoniowych S.A., Luboń

Amica Wronki S.A. Wronk

Girom Wellcome S.A. Poznań

Preem Polska sp. z 0.0.

Poznań

Energetyka Kaliska S.A. Kalisz

Farmutil HS Holding S.A. Śmiłowo

Kopalnia Węgla Brunatnego Konin S.A., Kleczew

H. Cegielski-Poznań S.A. Poznan

Huta Aluminium Konin S.A. Konin

Bestfoods Polska sp. z 0.0

Poznan

Wrigley Poland sp. z 0.0

Pozna

01 a o o o o 'O 'O o o

o o o

I I

I

I

I

I

I

I

l I

I J

I l

I

I I

I I

I\) I\) o, 'O o, o o o o o o 'O a a o o o o o o

I

l

l

j

I

I

l

w w 'O o, o o o o 'O a o o o o

ł

.j::::.

'O o o 'O o o

-::r-o s:::: !II N

~ tli

1

~

qq' f-I

~ tpJ "'i

CJQ (D m M

(D

::l M (D

~ ::t m (D m

5' ~ (D' ~ O ~ O ~

m

~ <:: O ~.

o... (D m p-" ~.

5' N O O N

,..-.... ej

'< (D

S ~

~ S (D

::l .c..-

Jeronimo Martins Dystrybucja sp. z 0.0., Poznań

KWB Konin S.A., Kleczew

Wistil SA GK, Kalisz

Philips Lighting Poland S.A., Piła

Inter Groclin Auto S.A., Wolsztyn

Farmutil HS Holding S.A., Śmiłowo

Volkswagen Polska sp. z 0.0.,

Poznań

Selgros Cash&Carrry sp. z 0.0.,

Poznań*

miniMai sp. z 0.0.,

Poznań

Kompania Piwowarska S.A., Poznań

Amica Wronki S.A., Wronki

Zespół Elektrowni Pątnów Adamów Konin S.A., Konin

Grupa Energetyczna ENEA S.A., Poznań

Grupa Raben, Poznań

GlaxoSmithKline Pharmaceuticals S.A., Poznań

Energetyka Kaliska S.A., Kalisz

Aluminium Konin-Impexmetal S.A., Konin

Maxer S.A., Poznań

Winkowski sp. z 0.0.,

Piła

Zespół Elektrociepłowni Poznańskich S.A., Poznań

o o o o

I\) UJ ..p.. o o o o o o o o o

Ol Ol ...... ex> o o o o o o o o o o o o

~

qq' 1..0

tpJ "'i

CJQ (D m M

(D

::l M (D

~ ::J. m (D m

5' ~ (D' ~ O ~ e.. m ~ pJ

<:: O ~. o... (D m p-" ~.

5' N O O N

~ m pJ

ro m "-"

Jeronimo Martins Dystrybucja sp. z 0.0., Poznań

Volkswagen Polska sp. z 0.0.,

Poznań

Kompania Piwowarska S.A., Poznań

Reemtsma Polska S.A., Jankowice

Selgros Cash&Carrry sp. z 0.0.,

Poznań*

Zespół Elektrowni Pątnów Adamów Konin S.A., Konin

Grupa Energetyczna ENEA S.A., Poznań

Philips Lighting Poland S.A., Piła

Skoda Auto Polska S.A., Poznań

GlaxoSmithKline Pharmaceuticals S.A., Poznań

KDWT S.A. Luboń

Amica Wronki S.A., Wronki

Energetyka Kaliska S.A., Kalisz

Inter Groclin Trading sp. z 0.0.,

Grodzisk Wlkp.

Farmutil HS Holding S.A., Śmiłowo

Wrigley Poland sp. z 0.0.,

Poznań

KWB Konin S.A., Kleczew

miniMai sp. z 0.0.,

Poznań*

Żabka Polska S.A., Poznań*

Cukrownie Pfeifer&Langen GK, Poznań

o o o o

o o o J

I

I

:==J

==:J

~

==:=J

=:J

=:J

=:J

W t=J

I\) UJ o o o o o o o o o o o o

J

I

l

I

l

I

J

..p.. o o o o o o J

Ol o o o o o o

I

I

s: o c: ~ N O' ~ Ul

r'"

'Tj ~.

qo I-i

tv

t-!l) t-o:

aq ('[) fJ) rt ('[)

:::::s rt ('[) t-o: ~

t-o: en· ('[) fJ)

Er ~ (D. ,....... ~ o ~

2-fJ)

~ !l)

<: o <:. o o.. ('[) fJ)

p-' ~.

5· tv o o UJ

".-.... cr' ~

('[)

a ~ ,....... o ~ a

('[)

:::::s rt "-"

Jeronimo Martins Dystrybucja sp. z 0.0., Poznań*

Grupa Energetyczna ENEA S.A., Poznań

Wistil SAGK, Kalisz

Volkswagen Polska sp. z 0.0.,

Poznań

Żabka Polska S.A., Poznań*

Farmutil HS Holding S.A., Śmiłowo

Selgros Cash&Carry sp. z 0.0.,

Poznań*

Philips Lighting Poland S.A., Piła

Kompania Piwowarska S.A., Poznań

Man Star Trucks & Buses sp. z 0.0.,

Poznań

Grupa Raben, Poznań

Amica Wronki S.A., Wronki

GlaxoSmithKline Pharmaceuticals S.A., Poznań*

H. Cegielski-Poznań S.A. Poznań*

Eurocash sp. z 0.0.

Poznań*

Grupa Mahle GK Krotoszyn

Maxer S.A. Poznan

Winkowski sp. z 0.0.

Piła

Aluminium Konin-Impexmetal S.A. Konin

Zespół Elektrociepłowni Poznańskich S.A., Poznań

I\) c..u ~ Ol O) a a a a a a o o o o o o o o o o o o o

I I I

I

I

I

I

j

I

'----T

=J :=J

-....J (Xl

a a o o o o

I I

co a o o

'Tj ~.

qo I-i I-i

t!l) t-o:

aq ('[) fJ) rt ('[)

:::::s rt ('[)

~ ::1. fJ) ('[) fJ)

5· ~ ~.

('[)

~ ~ o ,.......

fJ)

~ <: o ~.

o.. ('[) fJ)

p-' ~.

5· tv o o UJ

".-.... cr' ~

fJ) !l) ro fJ)

"-"

Jeronimo Martins Dystrybucja sp. z 0.0., Poznań

Grupa Energetyczna ENEA S.A., Poznań

Volkswagen Polska sp. z 0.0.,

Poznań

Kompania Piwowarska S.A., Poznań

Selgros Cash&Carry sp. z 0.0.,

Poznań

Skoda Auto Polska S.A., Poznań

Philips Lighting Poland S.A., Piła

Eurocash sp. z 0.0.,

Poznań*

GlaxoSmithKline Pharmaceuticals S.A., Poznań

Konsorcjum Dystrybutorów Wyr. Tytoniowych S.A., Luboń

Amica Wronki S.A., Wronki

Żabka Polska S.A., Poznań*

Wrigley Poland sp. z 0.0.,

Poznań

Farmutil HS Holding S.A., Śmiłowo

Aluminium Konin-Impexmetal S.A., Konin

Wistil SAGK, Kalisz

miniMai sp. z 0.0.,

Poznań

Man Star Trucks & Buses sp. z 0.0.,

Poznań

Grupa Raben, Poznań

Grupa Mahle GK, Krotoszyn

Ol o o a o o o

'<,

"1°':'

I\) I\) Ul Ul ~ ~ a u, a u, a u, a u, o o o o o o o o s: o o o o o o o o a a a a a a a a o o o o o o o o o c o o o o o o o o ~

N O' ~ Ul

"T1 ~.

qo f-I ~ -~ <: (!) Vl M

S (!)

~ M

O C M

Ę Vl

'"d (!) 1-1 (!)

~ ~

O -.....:::

(!) (!)

O

'""'" ~ (D. ~ O

'"d 2-Vl ~ pJ

a 8· o... (!) Vl p-

{j.

5· tv o o f-I

Wrigley Poland sp. z 0.0.,

Poznań

Kompania Piwowarska S.A., Poznań

Volkswagen Poznań sp. z 0.0.,

Poznań

Beiersdorf-Lechia S.A., Poznań

Glaxo Wellcome S.A., Poznań

Huta Aluminium Konin S.A., Konin

Inter Groclin Auto S.A., Grodzisk Wlkp.

Amica Wronki S.A., Wronki

H. Cegielski-Poznań S.A., Poznań

Energopol-7 GK S.A., Poznań

Hydrobudowa-9 Przed. Inz.-Bud. sp. z 0.0.

-oL I\:l :r I\:l +>- O) co o I\:l .j:>. O) co o o o o o o o o o o o o o c:

!'> N O-~ t/)

"T1 q5. f-I W -~ (!) Vl M

S (!)

~ M

O C M

Ę Vl

5· M p-(!)

(!)

~ M (!) 1-1

'"d ::t Vl (!) Vl

O

'""'" ~ ~.

(!)

~ O

'"d 2-Vl ~ pJ

a ~.

<: O o... (!) Vl p-

{j.

5· tv o o f-I

I\:l I\:l tu Ul Ol o Ol o Ol o Ol o o o o o o o a a a a a a a o o o o o o o o o o o o o o o

Volkswagen Poznań sp. z 0.0.,

Poznań

Kompania Piwowarska S.A., Poznań "

Wrigley Poland sp. z 0.0.,

Poznań

Beiersdorf-Lechia S.A., Poznań

Glaxo Wellcome S.A., Poznań

Inter Groclin Auto S.A., Grodzisk Wlkp.

Amica Wronki S.A., Wronki

Huta Aluminium Konin S.A., Konin

H. Cegielski-Poznań S.A., Poznań

Energopol-7 GK S.A., Poznań

Hydrobudowa-9 Przed. Inz.-Bud. sp. z 0.0.

+>- +>-o Ol :r o o a a o o o c: o o !'>

N O-~ t/)

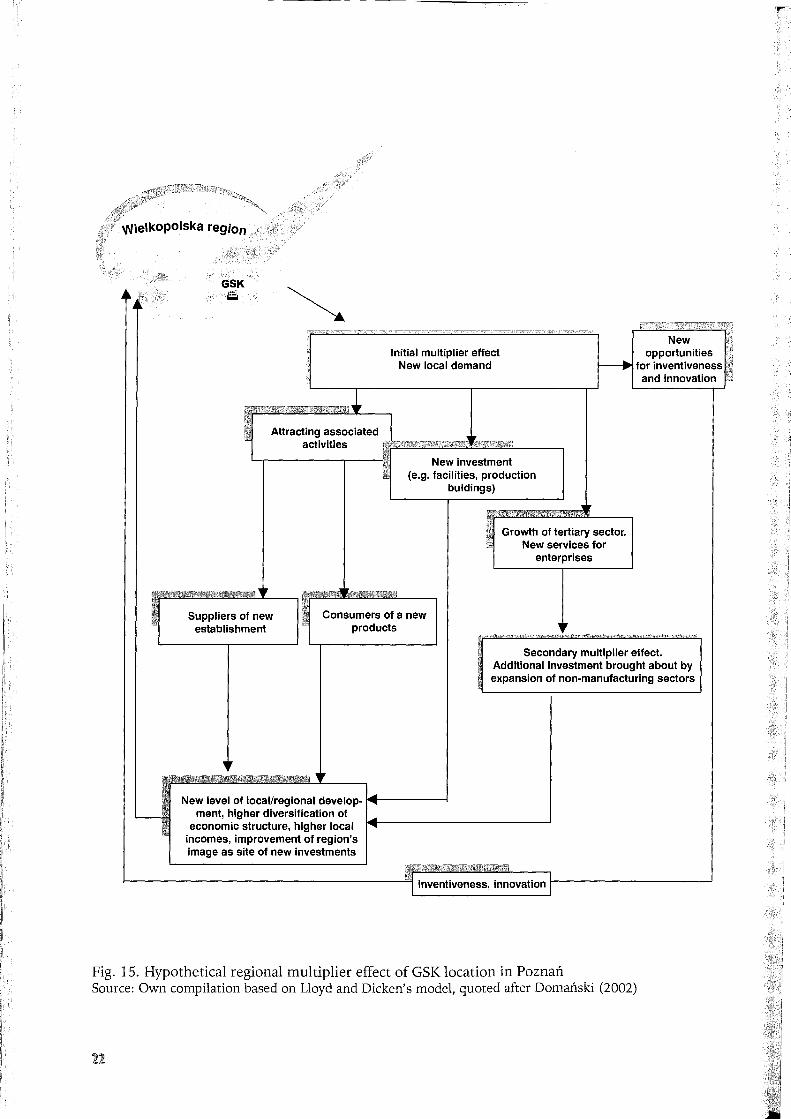

Multiplier effects arise out of links between individual elements of urban and regional systems, in particular enterprise-surroundings relations. S. Marek (1999) distinguishes five groups of such relations:

- enterprise-households (in terms of income earning and spending); - enterprise-other enterprises; - enterprise-authorities; - enterprise-financial institutions; and - enterprise-subjects of economic democracy (e.g. trade unions, employer organisations, con-

sumer organisations, foundations). The relations and multiplier effects associated with them can be beneficial or detrimental, sponta

neous or carefully designed (controlled), they can also be assessed differently by various participants of economic life and when seen in a short- or a long-term perspective.

Multiplier effects spring from a variety of causes (cf. Domański 1983: 305; 2002: 128). Among them can be the construction of a new industrial plant; an extension or change of the line of production of an existing one; or the appearance of a new owner introducing signif1cant changes into the system of management, technological innovativeness and economic links (as has been the case of GSK). A hypothetical diagram of a regional multiplier effect resulting from the location of GSK in Poznań, based on Lloyd and Dicken's (1972) model, is presented in Fig. 15 (after Domański 2002: 128).

The initial multiplier effect of the location of a multinational corporation results from a new pattern of local demand. The demand is shaped in four possible ways: (1) by attracting associated activities, (2) by new investment: building and infrastructure; (3) by introducing new services for the enterprise; and (4) by new opportunities for inventiveness and innovation.

When a firm does not engage in a greenfield type of investment but buys an existing plant, it usually also takes over at least a fragment of the old co-operation network. This was also the case with GSK, although there have developed new links as well due to outsourcing, or the practice of subcontracting some of the factory's old functions to economic entities outside.

As a result of more intensive collaboration among various specialised economic entities, there form micro-markets for unique products and services. Under the influence of globalisation processes, in turn, the operation of each of those micro-markets becomes restricted by a system of standards and detailed technical, commercial and environmental regulations that have to be accommodated in strategies concerning competition on macro-markets. To meet the new market requirements, especially the increase in diversity and efficiency, co-operating firms often establish economic networks based on synergistic effects.

The GSK plant in Poznań has also developed its micro-market for unique products and specialised services. This proces s has produced an initial multiplier effect in the form oflocal dem and for the provision of raw materials, semi-finished goods, and services for the factory. The analysis of the regional multiplier effect of GSK embraces the following issues:

- networks of links with suppliers of raw materiaIs, production components and semi-finished goods;

- networks of links with product consumers; - networks of links with firms providing services to GSK; and - networks oflinks with scientific and R&D institutions, hospitals, and the educational system.

M,"." il

I

I

GSK ~

Initial multiplier effect New local demand

New opportunities

~ for inventiveness and innovation

Attracting associated ... activities .ggggg_ggL __ ---,

Suppliers of new establishment

I

II New investment

(e.g. facilities, production buldings)

-Consumers of a new

products

•• I Growth of tertiary sector. I New services for

enterprises

."

Secondary multiplier effect. Additional investment brought about by expansion of non-manufacturing sectors

New level of local/regional develop- I<IIII~I------ł _ ment, higher diversification of .....

economic structure, higher local 14 ...... ___ --------------'

incomes, improvement of region's image as site of new investments

~--------------------~·I . . . Ir-----------~ I nventlveness, mnovatlon

Fig. 15. Hypothetical regional multiplier effect of GSK location in Poznań Source: Own compilation based on Lloyd and Dicken's model, quoted after Domański (2002)

iF

The analysis is carried out from two perspectives: (1) that ofGlaxoSmithKline Pharmaceuticals, on the basis of data obtained in the company's various

departments, and (2) that of GSK partners, on the basi s of materiaIs collected in a survey research.

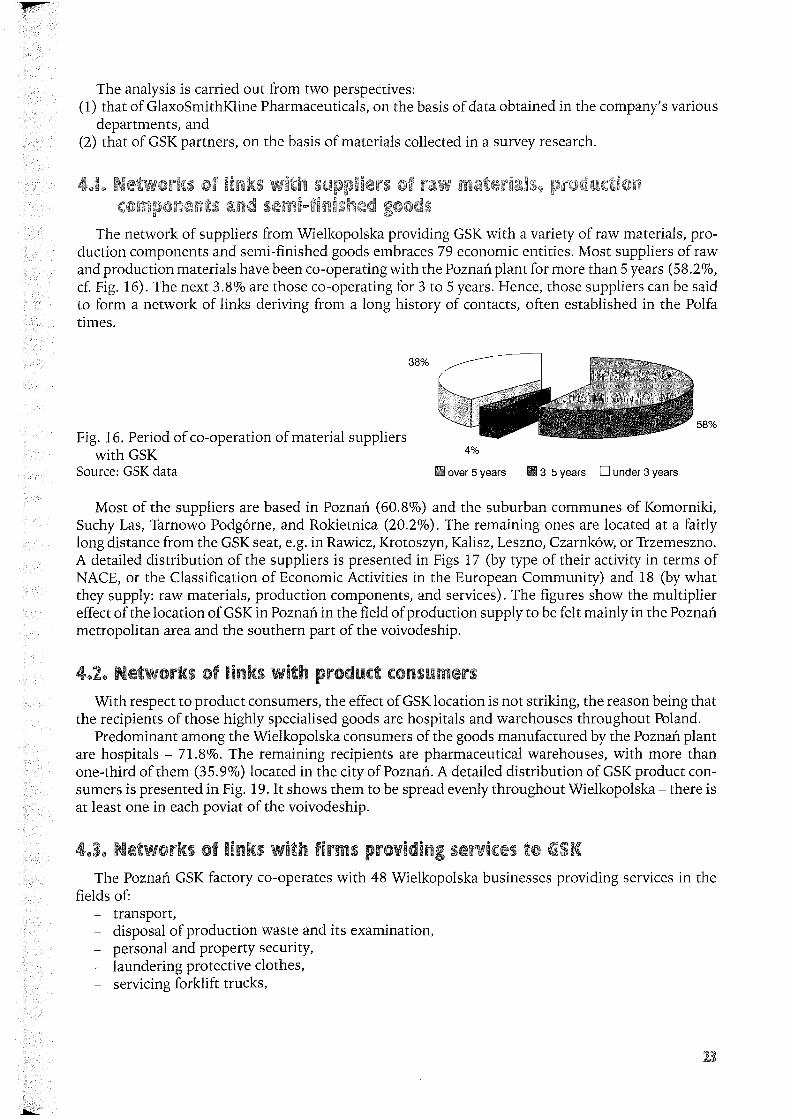

The network of suppliers from Wielkopolska providing GSK with a variety of raw materials, production components and semi-finished goods embraces 79 economic entities. Most suppliers of raw and production materiaIs have been co-operating with the Poznań plant for more than 5 years (58.20/0, cf. Fig. 16). The next 3.8% are those co-operating for 3 to 5 years. Hence, those suppliers can be said to form a network of links deriving from a long history of contacts, often established in the Polfa times.

Fig. 16. Period of co-operation of material suppliers with GSK

Source: GSK data

38%

58%

4%

over 5 years 3-5 years Dunder 3 years

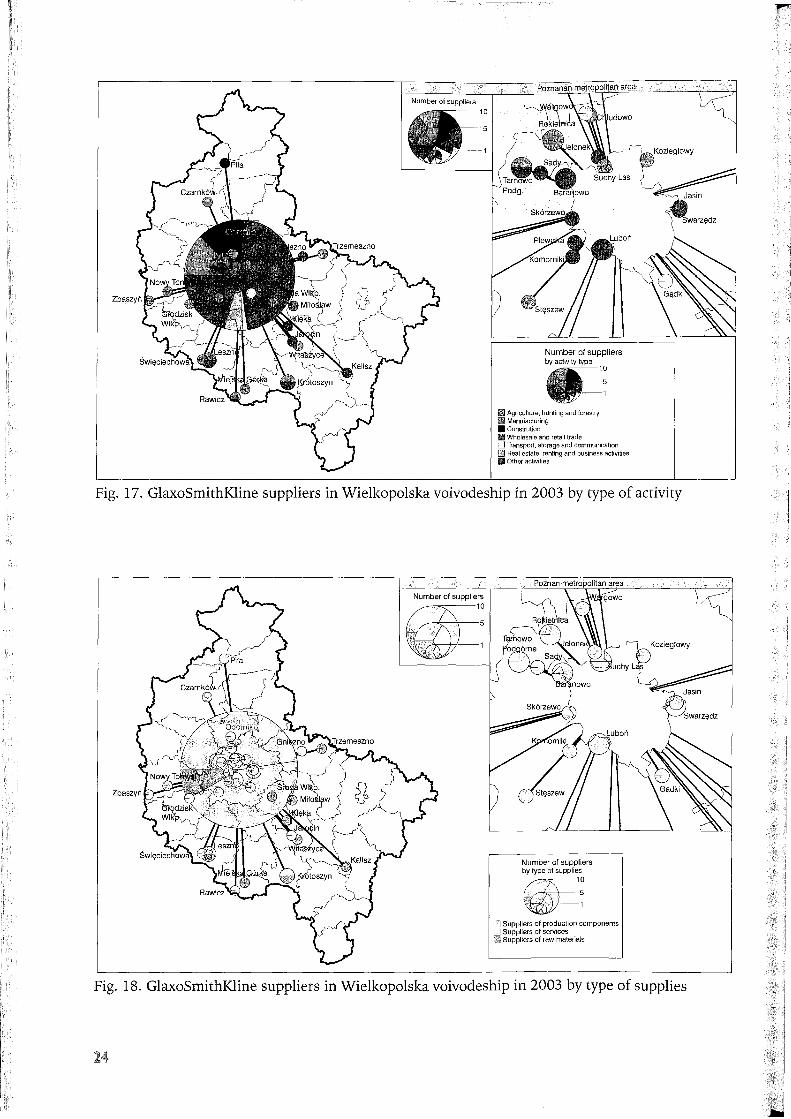

Most of the suppliers are based in Poznań (60.80/0) and the suburban communes of Komorniki, Suchy Las, Tarnowo Podgórne, and Rokietnica (20.2%). The remaining one s are located at a fairly long distance from the GSK seat, e.g. in Rawicz, Krotoszyn, Kalisz, Leszno, Czarnków, or Trzemeszno. A detailed distribution of the suppliers is presented in Figs 17 (by type of their activity in terms of NACE, or the Classification of Economic Activities in the European Community) and 18 (by what they supply: raw materiaIs, production components, and services). The figures show the multiplier effect of the location of GSK in Poznań in the field of production supply to be felt mainly in the Poznań metropolitan area and the southern part of the voivodeship.

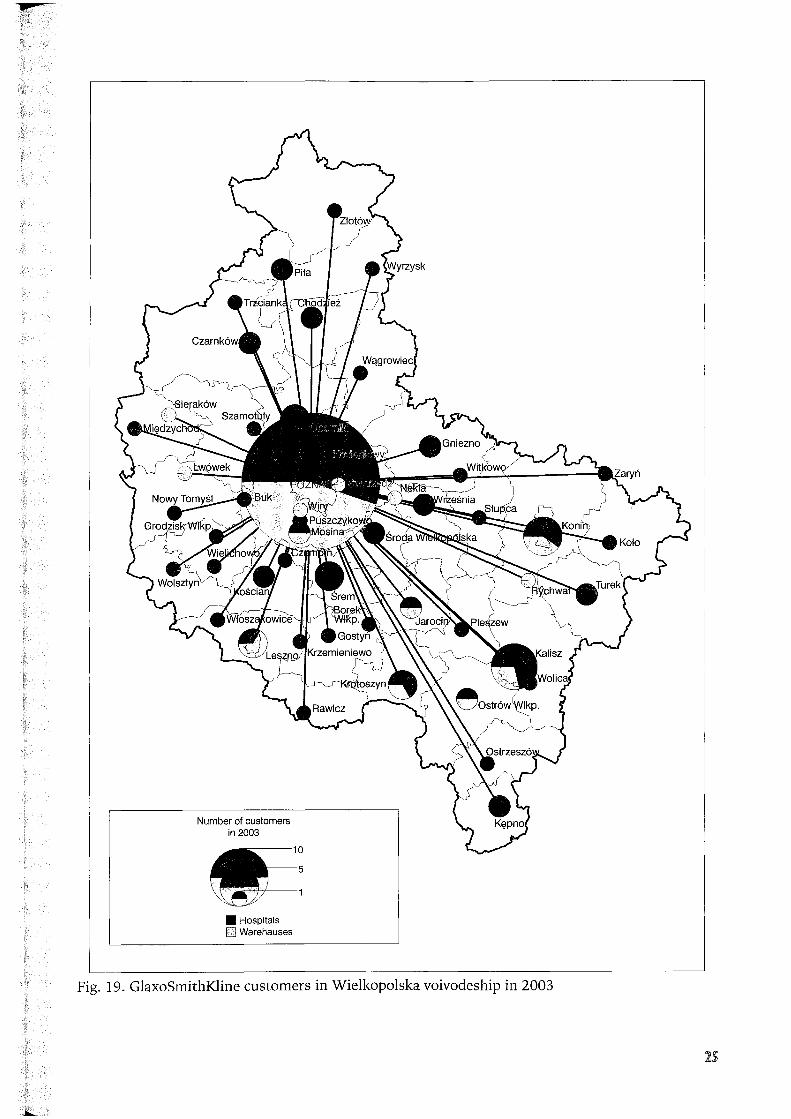

With respect to product consumers, the effect of GSK location is not striking, the reason being that the recipients of those highly specialised goods are hospitals and warehouses throughout Poland.

Predominant among the Wielkopolska consumers of the goods manufactured by the Poznań plant are hospitals - 71.8%. The remaining recipients are pharmaceutical warehouses, with more than one-third of them (35.9%) located in the city ofPoznań. A detailed distribution of GSK product consumer s is presented in Fig. 19. It shows them to be spread evenly throughout Wielkopolska - there is at least one in each poviat of the voivodeship.

The Poznań GSK factory co-operates with 48 Wielkopolska businesses providing services in the fields of:

- transport, - disposal of production waste and its examination,

personal and property security, - laundering protective clothes, - servicing forklift trucks,

Number of suppliers by activity type

III Agriculture, hunting and forestry III Manufacturing • Construlion III Wholesale and retail trade D Transport, storage and communication G:J Real estate, renting and business activities III Other activities

Fig. 17. GlaxoSmithKline suppliers in Wielkopolska voivodeship in 2003 by type of activity

Number ot suppliers by type ot supplies --~--10

D Suppliers ot production components D Suppliers ot services II Suppliers ot raw materials

Fig. 18. GlaxoSmithKline suppliers in Wielkopolska voivodeship in 2003 by type of supplies

·pp. f

Number of customers in 2003

• Hospitals D Warehauses

Fig. 19. GlaxoSmithKline customers in Wielkopolska voivodeship in 2003

- fire prevention monitoring, - construction, - customs clearance, - translations, - document archivisation, - servicing air conditioning systems, lifts, blinds, office equipment, electrical appliances, boilers

(carried out by businesses based in Poznań or its metropolitan area), and - running the factory canteen. GSK is also provided with marketing, legal, financial, insurance and consulting services, but lack of

data makes their detailed analysis impossible. It seems, however, that unlike the services listed above, links of this type often extend beyond the Wielkopolska region. For instance, consulting services concerning the introduction of the ISO 14001 quality management system are offered by a Wrocław-based firm.

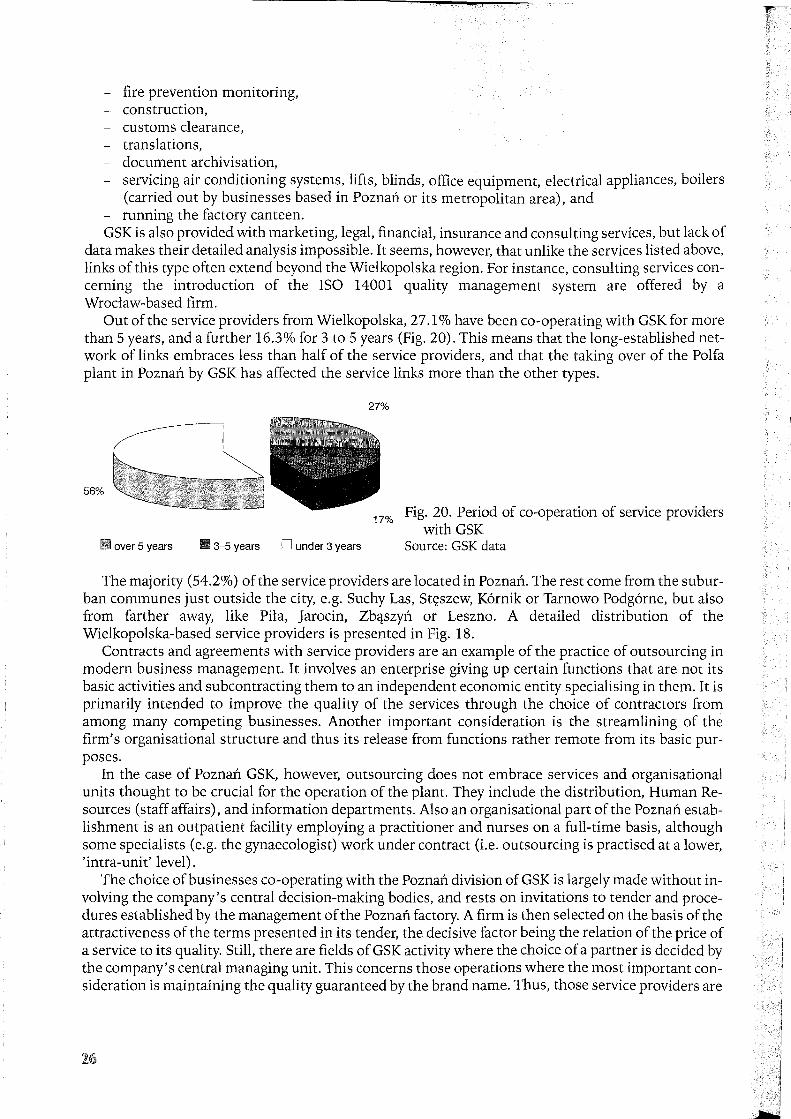

Out of the service providers from Wielkopolska, 27.1 % have been co-operating with GSK for more than 5 years, and a further 16.3% for 3 to 5 years (Fig. 20). This means that the long-established network of links embraces less than half of the service providers, and that the taking over of the Polfa plant in Poznań by GSK has affected the service links more than the other types.

56%

over 5 years 3-5 years Dunder 3 years

27%

17% Fig. 20. Period of co-operation of service providers

with GSK Source: GSK data

The majority (54.20/0) of the service providers are located in Poznań. The rest com e from the suburban communes just outside the city, e.g. Suchy Las, Stęszew, Kórnik or Tarnowo Podgórne, but also from farther away, like Piła, Jarocin, Zbąszyń or Leszno. A detailed distribution of the Wielkopolska-based service providers is presented in Fig. 18.

Contracts and agreements with service providers are an example of the practice of outsourcing in modern business management. It involves an enterprise giving up certain functions that are not its basic activities and subcontracting them to an independent economic entity specialising in them. It is primarily intended to improve the quality of the services through the choice of contractors from among many competing businesses. Another important consideration is the streamlining of the firm's organisational structure and thus its release from functions rather remote from its basic purposes.

In the case of Poznań GSK, however, outsourcing does not embrace services and organisational units thought to be crucial for the operation of the plant. They include the distribution, Human Resources (staff affairs), and information departments. Also an organisational part of the Poznań establishment is an outpatient faci li t y employing a practitioner and nurses on a full-time basi s, although some specialists (e.g. the gynaecologist) work under contract (i.e. outsourcing is practised at a lower, 'intra-unit' level).

The choice ofbusinesses co-operating with the Poznań division of GSK is largely made without involving the company's central decision-making bodies, and rests on invitations to tender and procedures established by the management of the Poznań factory. A firm is then selected on the basis of the attractiveness of the terms presented in its tender, the decisive factor being the relation of the price of a service to its quality. Still, there are fields of GSK activity where the choice of a partner is decided by the company's central managing unit. This concerns those operations where the most important consideration is maintaining the quality guaranteed by the brand name. Thus, those service providers are

favoured who meet the stringent manufacturing standards set by the company. Among such suppliers for the Poznań plant is MAT-OIL, a distributor of specialised oils for machine maintenance, recommended for use in all GSK factories throughout the world and ensuring the proper operation of equipment. Another example of co-operation with a firm handpicked by the company is Marchezzini, an Italian supplier of packaging machines. However, the packaging concerned is not the regular type like cardboard boxes, which are subcontracted to local manufacturers, but specialised, like aerosol botdes. Wherever the prime concern is preserving the established quality of a drug, an original GSK product (whether in term s of raw materials, manufacturing technology, or direct packaging) , the company demands compliance with rigorous standards it has devised which only few centrally selected producers can meet. Hence, in those specific areas also the Poznań branch of the corporation is obliged to use only the services of firms tested and recommended by the headquarters, which means that in this respect the possibilities of developing regional patterns of links are limited.

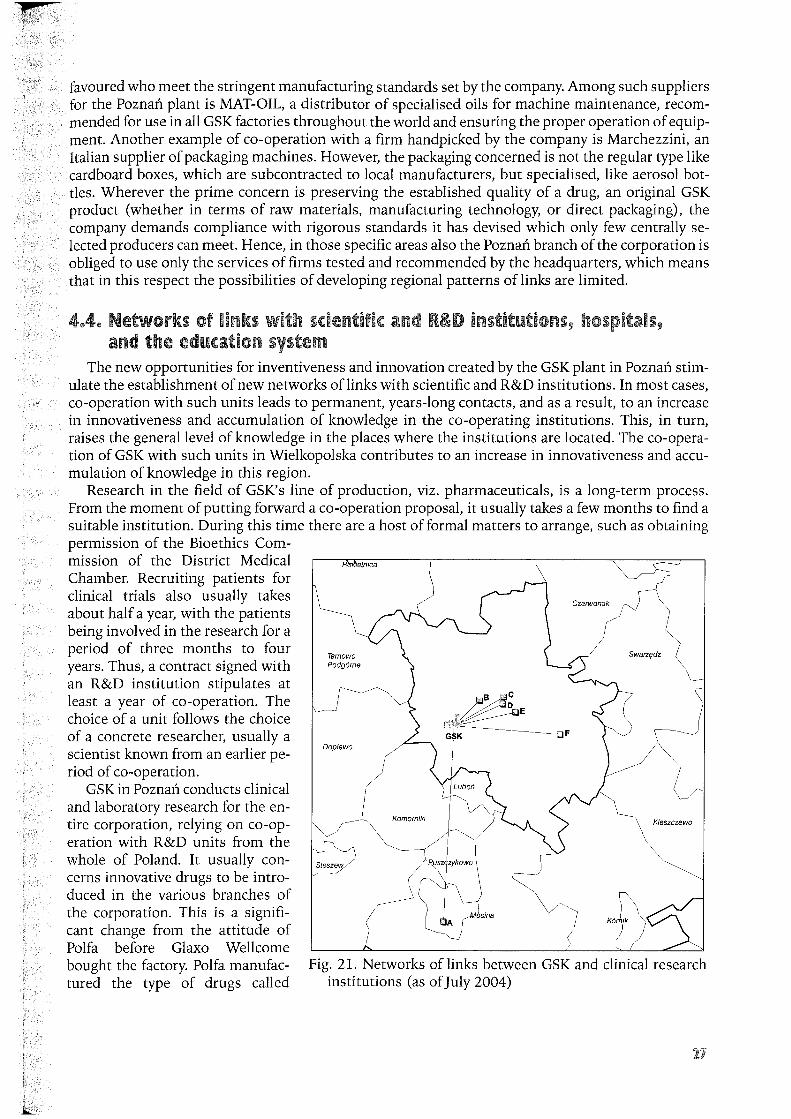

The new opportunities for inventiveness and innovation created by the GSK plant in Poznań stimulate the establishment of new networks oflinks with scientific and R&D institutions. In most cases, co-operation with such unit s leads to permanent, years-Iong contacts, and as a result, to an increase in innovativeness and accumulation of knowledge in the co-operating institutions. This, in turn, raises the generallevel of knowledge in the place s where the institutions are located. The co-operation of GSK with such units in Wielkopolska contributes to an increase in innovativeness and accumulation of knowledge in this region.

Research in the field of GSK's line of production, viz. pharmaceuticals, is a long-term process. From the moment of putting forward a co-operation proposal, it usually takes a few months to find a suitable institution. During this time there are a host of formaI matters to arrange, such as obtaining permission of the Bioethics Commission of the District Medical Chamber. Recruiting patients for clinical triaIs also usually takes about half a year, with the patients being involved in the research for a period of three months to four years. Thus, a contract signed with an R&D institution stipulates at least a year of co-operation. The choice of a unit follows the choice of a concrete researcher, usually a scientist known from an earlier period of co-operation.

GSK in Poznań conducts clinical and laboratory research for the entire corporation, relying on co-operation with R&D units from the whole of Poland. It usually concerns innovative drugs to be introduced in the various branches of the corporation. This is a significant change from the attitude of Polfa before Glaxo Wellcome bought the factory. Polfa manufactured the type of drugs called

R ietnica

Swarzędz

Oopiewo

Kleszczewo

\

Fig. 21. Networks of links between GSK and clinical research institutions (as of July 2004)

generics, and research on them was only intended to test their bio-equivalence, while a study of innovative drugs is mainly designed to prove them to be safe and effective.

In Wielkopolska, the GSK Medical Department is engaged at present Ouly 2004 data) in c1inical triais carried out in 11 units located largely in Poznań, but also at Mosina (Fig. 21). Some of them are working on more than one project. Co-operation rests on a contract signed for the duration ofthe research. Some of the units have been working on the triais unbrokenly for five years.

The GSK Medical Department in Poznań does not collaborate directly with any schools in the training of their staff for tasks performed in the Department. However, as follows from interviews conducted in GSK and various institutions, both sides intend to change this state of affairs. In this respect, Poznań higher schools might be well-advised to show greater activity.

Steps taken by GSK to transfer innovations and technologies as well as the company' s place in the region al innovative system are discussed in greater detail in chapter 6.

From the economic perspective, multiplier effects are usually considered in terms of employment, income, and investment. Their quantification, however, is extremely hard, and moreover, today qualitative aspects are increasingly being seen as no less important.

To assess the regional multiplier effect resulting from the location of the GSK plant in Poznań in a more objective and comprehensive way, the issue was approached not only from the point ofview of the company producing this effect, but also of the entities co-operating with it. To this end, questionnaires were sent to aU GSK partners providing it with materials and services, as well as to consumers of its goods (following a list supplied by GSK). The form (see Appendix) contained detailed questions concerning the nature of co-operation with GSK, its duration, legal status, forms, importance for the performance of the respondent, evaluation, and prospects for further development. The questionnaire consisted of three parts. The first covered a firm' s data, like its address and year of establishment. The second dealt with the firm's links with GSK and contained nine complex questions, usually of the free-answer type. The third concerned the respondent s' perception of GSK's place and role in the region' s economy.

The research was carried out between April andJune 2004 by a team of researchers from the Institute ofSocio-Economic Geography and Spatial Management, Adam Mickiewicz University in Poznań, under the supervision of Prof. Tadeusz Stryjakiewicz.

By assumption, the study of GSK' s links with partners in Wielkopolska was to be exhaustive, i.e. to cover all the firms co-operating with the company. However, since the questionnaire was filled on a voluntary basi s, 62 firms responded, which constituted 240/0 of the total. Among them were 32 suppliers of raw materials and production components (they made up 51.60/0 of all respondents) and 30 consumers of GSK goods (inc1uding 28 hospitals and 2 drug warehouses). Among the suppliers, the largest group (500/0) embraced those from Poznań, and in the consumer group 26.60/0 entities that completed and returned the questionnaire we re Poznań-based.

Forms of links To start with, the firms polled were asked to indicate the most important forms of their links with

GSK, with some respondents choosing more than one type of linko For the largest group (38.70/0), co-operation with GSK involved the provision of services, with maintenance and assembly operations accounting for three-fourths of them. A somewhat smaller group (35.50/0) bought GSK products. For 290/0 of respondents the principallink was the supply of materials and semi-finished products. A few indicated participation in GSK-organised training courses (9.70/0) and drug testing (6.50/0).

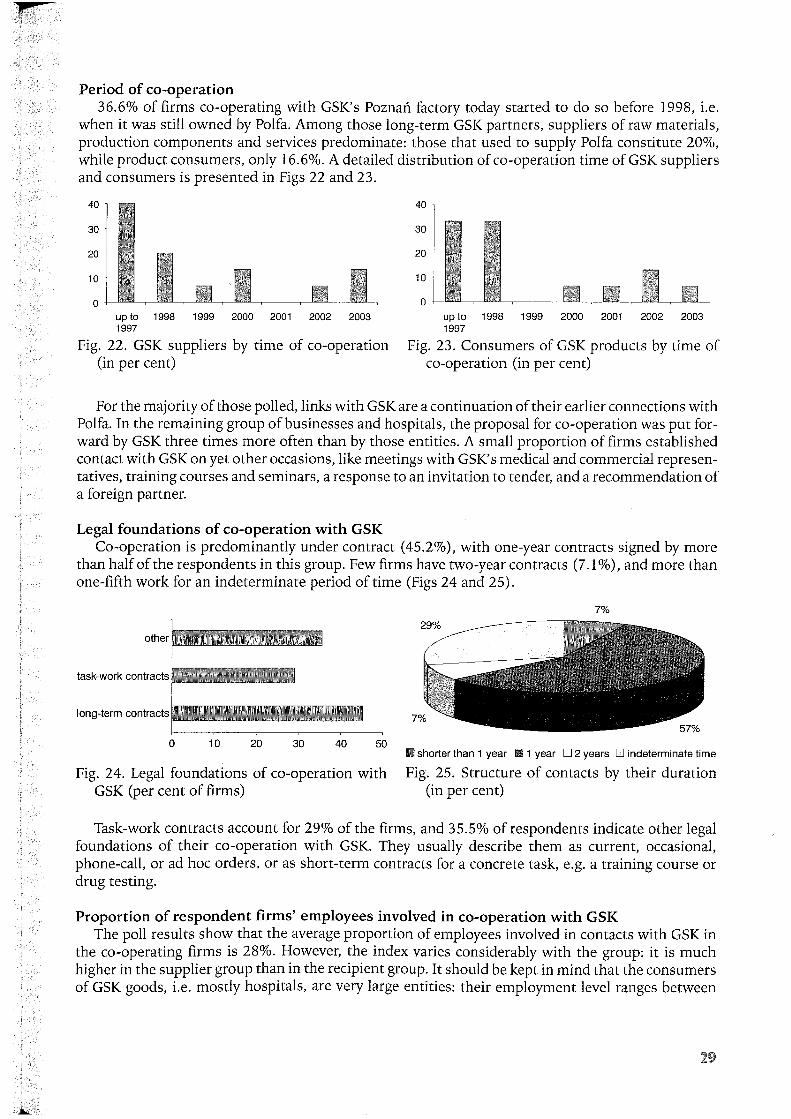

Period of co-operation 36.60/0 of firms co-operating with GSK's Poznań factory today started to do so before 1998, Le.

when it was still owned by Polfa. Among those long-term GSK partners, suppliers of raw materiaIs, production components and services predominate: those that used to supply Polfa constitute 20%, while product consumers, only 16.60/0. A detailed distribution of co-operation time of GSK suppliers and consumers is presented in Figs 22 and 23.

40

30

20

10

o up to 1998 1999 2000 2001 2002 2003 1997

Fig. 22. GSK suppliers by time of co-operation (in per cent)

40

30

20

10

o up to 1998 1999 2000 2001 2002 2003 1997

Fig. 23. Consumers of GSK products by time of co-operation (in per cent)

For the majority of those polled, links with GSK are a continuation of their earlier connections with Polfa. In the remaining group ofbusinesses and hospitals, the proposal for co-operation was put forwar d by GSK three times more often than by those entities. A smalI proportion of firms established contact with GSK on yet other occasions, like meetings with GSK's medical and commercial representatives, training courses and seminars, a response to an invitation to tender, and a recommendation of a foreign partner.

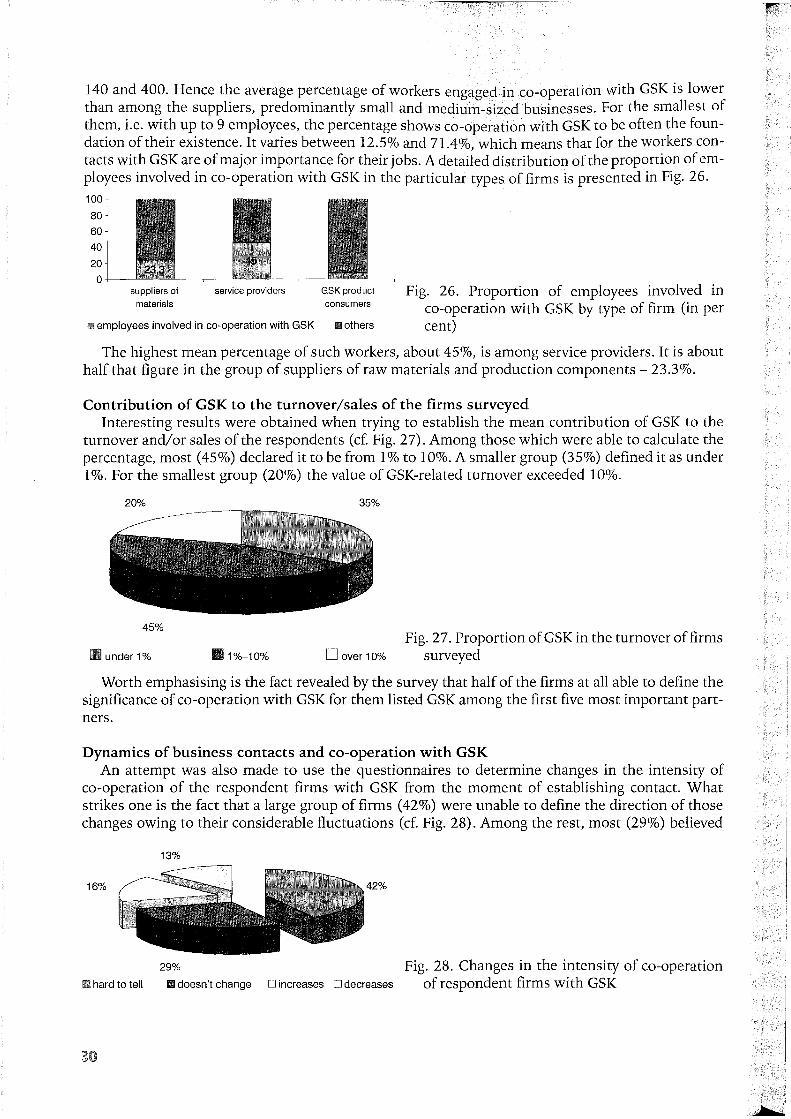

Legal foundations of co-operation with GSK Co-operation is predominantly under contract (45.20/0), with one-year contracts signed by more

than half of the respondent s in this group. Few firms have two-year contracts (7.1 0/0), and more than one-fifth work for an indeterminate period of time (Figs 24 and 25).

other

task-werk contracts

long-term contracts

o 10 20 30 40 50 r

Fig. 24. Legal foundations of co-operation with GSK (per cent of firms)

7%

• shorter than 1 year • 1 year D 2 years D indeterminate time

Fig. 25. Structure of contacts by their duration (in per cent)

Task-work contracts account for 290/0 of the firms, and 35.5% of respondents indicate other legal foundations of their co-operation with GSK. They usually describe them as current, occasional, phone-call, or ad hoc orders, or as short-term contracts for a concrete task, e.g. a training course or drug testing.

Proportion of respondent firms' employees involved in co-operation with GSK The poll results show that the average proportion of employees involved in contacts with GSK in

the co-operating firms is 28%. However, the index varies considerably with the group: it is much higher in the supplier group than in the recipient group. It should be kept in mind that the consumers of GSK goods, Le. mostly hospitals, are very large entities: their employment level ranges between

140 and 400. Henee the average pereentage of workers engaged in eo-operation with GSK is lower than amon g the suppliers, predominantly small and medium-sized businesses. For the smallest of them, Le. with up to 9 employees, the pereentage shows eo-operation with GSK to be often the foundation oftheir existenee. It varies between 12.50/0 and 71.4%, which means that for the workers eontaets with GSK are of major importance for their jobs. A detailed distribution of the proportion of employees involved in eo-operation with GSK in the particular types of firms is presented in Fig. 26. 100

80

60

40

20

o suppliers of

materials

service providers

employees involved in co-operation with GSK

GSK produet

consumers

III others

Fig. 26. Proportion of employees involved in eo-operation with GSK by type of firm (in per cent)

The highest mean pereentage of sueh workers, about 450/0, is among service providers. It is about half that figure in the gro up of suppliers of raw materials and produetion eomponents - 23.30/0.

Contribution of GSK to the turnover/sales of the firms surveyed Interesting results were obtained when trying to establish the mean eontribution of GSK to the

turnover and/or sales ofthe respondents (ef. Fig. 27). Among those whieh were able to ealculate the pereentage, most (45%) declared it to be from 1 % to 10%. A smaller gro up (350/0) defined it as under 10/0. For the smallest group (20%) the value of GSK-related turnover exeeeded 100/0.

20% 35%

45% Fig. 27. Proportion of GSK in the turnover of firms

under 1 % 1 %-1 0% D over 10% surveyed

Worth emphasising is the faet revealed by the survey that half of the firms at all able to define the signifieanee of eo-operation with GSK for them listed GSK amon g the first five most important partners.

Dynamics of business contacts and co-operation with GSK An attempt was also made to use the questionnaires to determine changes in the intensity of

eo-operation of the respondent firms with GSK from the moment of establishing eontaet. What strikes one is the faet that a large gro up of firms (420/0) were unable to define the direetion of those chan ges owing to their eonsiderable tluetuations (ef. Fig. 28). Among the rest, most (290/0) believed

13%

16% 42%

29% Fig. 28. Changes in the intensity of eo-operation • hard to tell • doesn't change D increases D decreases of respondent firms with GSK

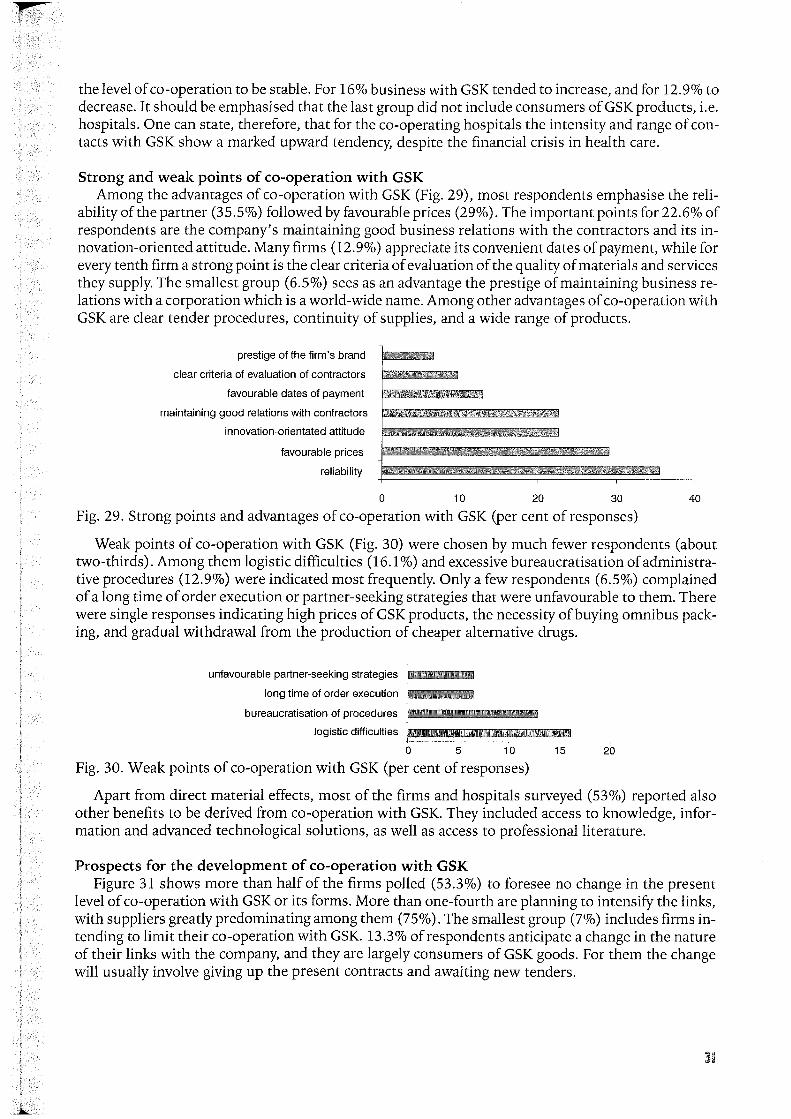

the level of co-operation to be stable. For 16% business with GSK tended to increase, and for 12.90/0 to decrease. It should be emphasised that the last group did not inelude consumers of GSK products, i.e. hospitals. One can state, therefore, that for the co-operating hospitals the intensity and range of contacts with GSK show a marked upward tendency, despite the financial crisis in health care.

Strong and weak points of co-operation with GSK Among the advantages of co-operation with GSK (Fig. 29), most respondents emphasise the reli

ability of the partner (35.50/0) folIowed by favourable prices (29%). The important points for 22.60/0 of respondents are the company's maintaining good business relations with the contractors and its innovation-oriented attitude. Many firms (12.90/0) appreciate its convenient dates of payment, while for every tenth firm a strong point is the elear criteria of evaluation of the quality of materials and services they supply. The smallest group (6.50/0) sees as an advantage the prestige of maintaining business relations with a corporation which is a world-wide name. Among other advantages of co-operation with GSK are elear tender procedures, continuity of supplies, and a wide range of products.

prestige of the firm's brand

elear eriteria of evaluation of eontraetors

favourable dates of payment

maintaining good relations with eontraetors

innovation-orientated attitude

favourable priees

reliability

o 10 20 30 40

Fig. 29. Strong points and advantages of co-operation with GSK (per cent of responses)

Weak points of co-operation with GSK (Fig. 30) were chosen by much fewer respondents (about two-thirds). Among them logistic difficulties (16.10/0) and excessive bureaucratisation of administrative procedures (12.90/0) were indicated most frequently. Onlya few respondents (6.5%) complained of a long time of order execution or partner-seeking strategies that we re unfavourable to them. There were single responses indicating high prices of GSK products, the necessity ofbuying omnibus packing, and gradual withdrawal from the production of cheaper alternative drugs.

unfavourable partner-seeking strategies

long time of order exeeution

bureaueratisation of proeedures

logistie diffieulties

o 5 10

Fig. 30. Weak points of co-operation with GSK (per cent ofresponses) 15 20

Apart from direct material effects, most of the firms and hospitals surveyed (530/0) reported also other benefits to be derived from co-operation with GSK. They ineluded access to knowledge, information and advanced technological solutions, as well as access to professionalliterature.

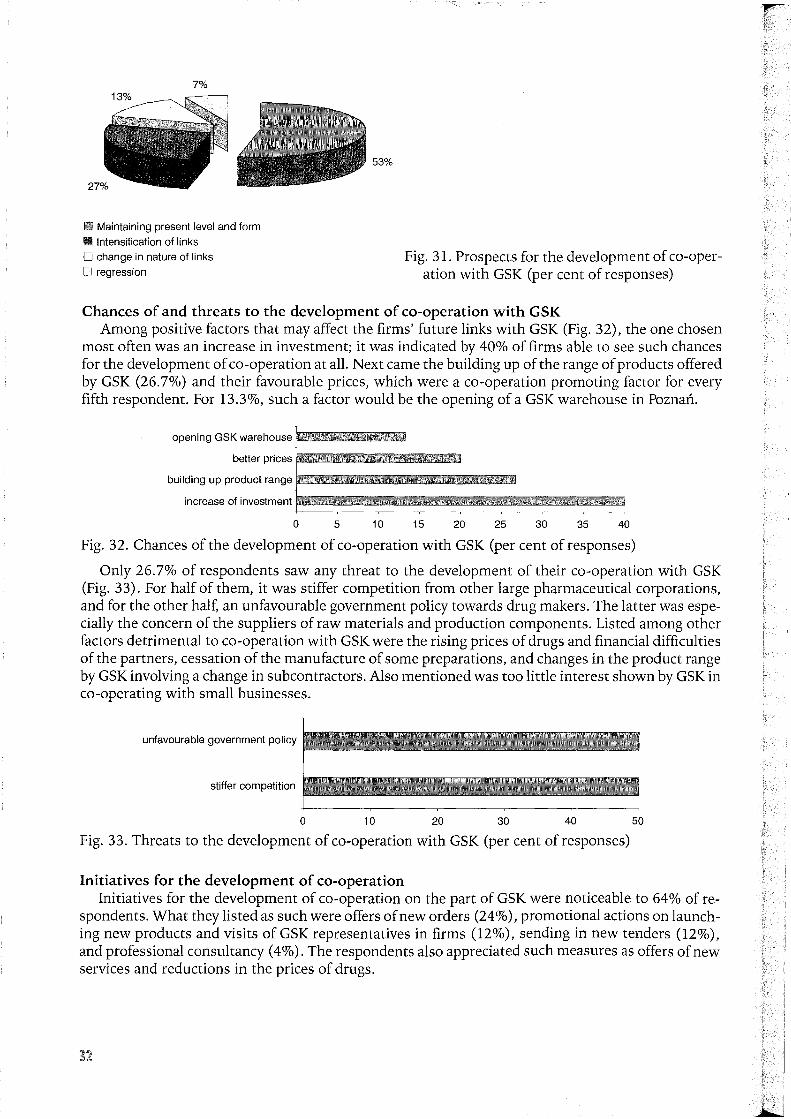

Prospects for the development of co-operation with GSK Figure 31 shows more than half of the firms polled (53.30/0) to foresee no change in the present

level of co-operation with GSK or its forms. More than one-fourth are planning to intensify the links, with suppliers greatly predominating among them (750/0). The smallest gro up (70/0) ineludes firms intending to limit their co-operation with GSK. 13.30/0 of respondents anticipate a change in the nature of their links with the company, and they are largely consumers of GSK goods. For them the change will usually involve giving up the present contracts and awaiting new tenders.

7%

Maintaining present level and form

l1li Intensification of links

53%

D change in nature of links

D regression Fig. 31. Prospects for the development of co-oper

ation with GSK (per cent of responses)

Chances of and threats to the development of co-operation with GSK Among positive factors that may affect the firms' future links with GSK (Fig. 32), the one chosen

most often was an increase in investment; it was indicated by 400/0 of firms able to see such chances for the development of co-operation at alI. Next came the building up of the range of products offered by GSK (26.70/0) and their favourable prices, which were a co-operation promoting factor for every fifth respondent. For 13.30/0, such a factor would be the opening of a GSK warehouse in Poznań.

opening GSK warehouse .l1lil1lil1lil1lil1li11

better prices '-l1lil1lil1lil1lil1lil1lil1lil1li_

building up product range '-l1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1li11

increase of investment .l1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1lil1li_

o 5 10 15 20 25 30 35 40

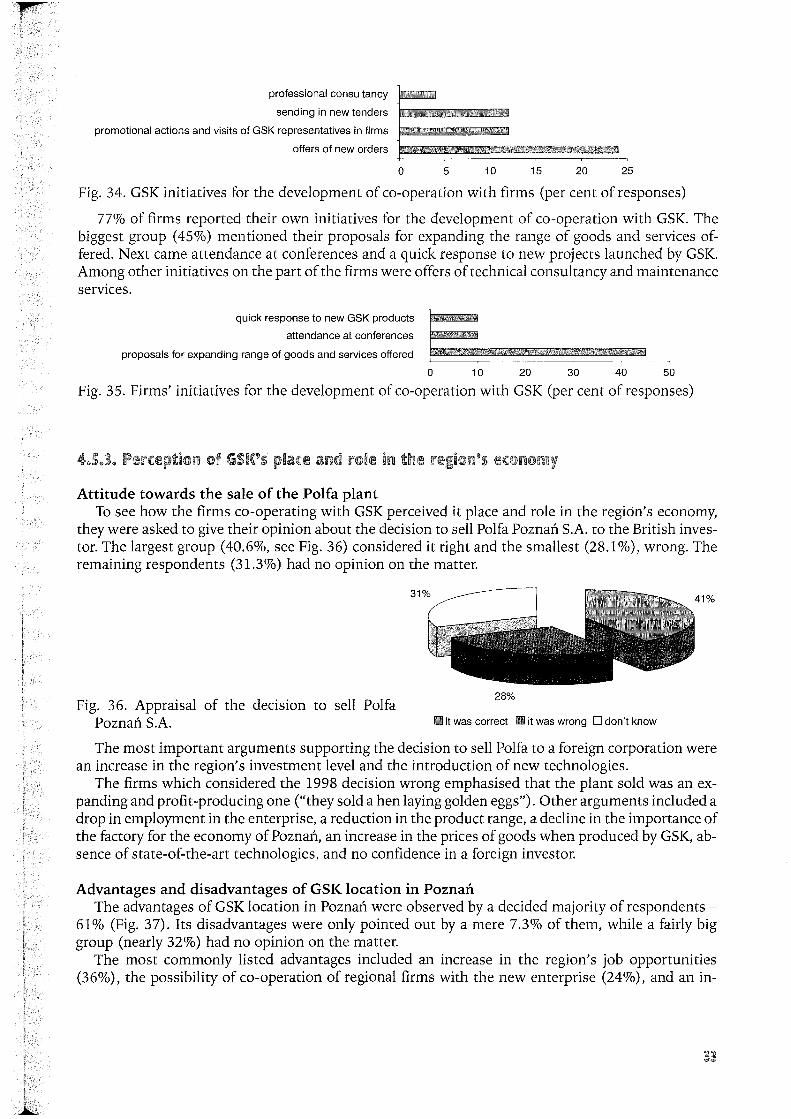

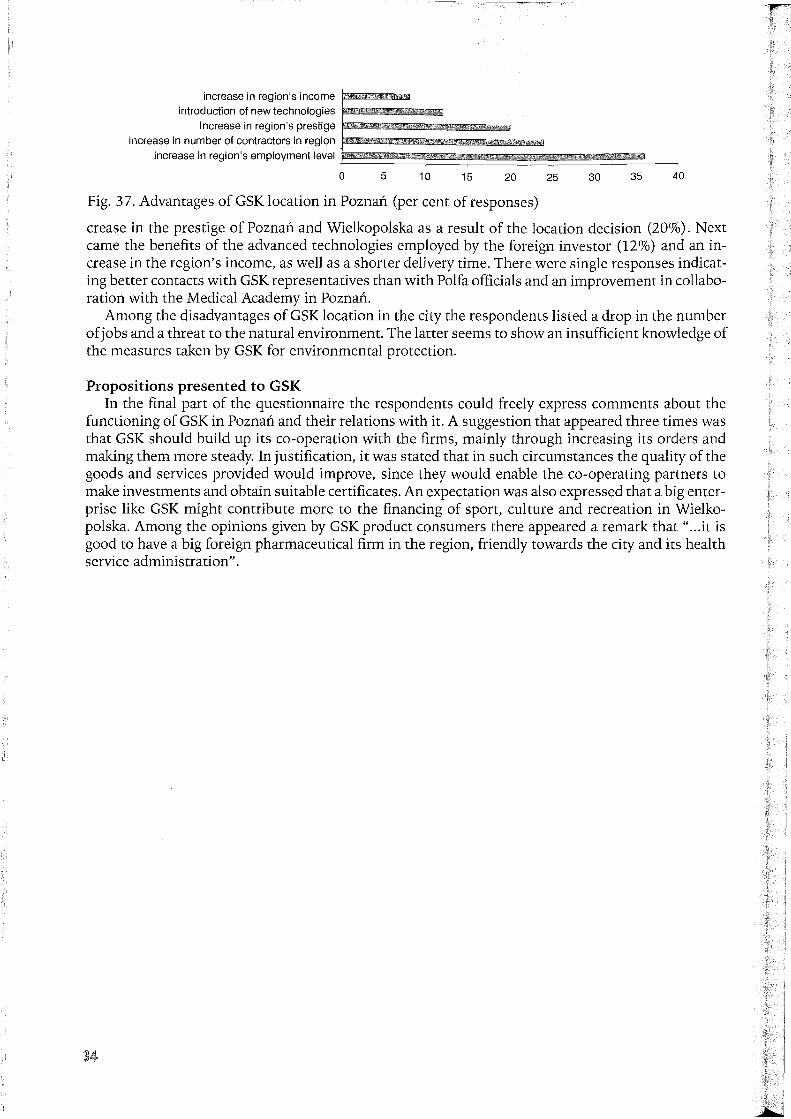

Fig. 32. Chances of the development of co-operation with GSK (per cent of responses)