ICMAP C 2017 DUBAI, UAE.

22

ICMAP GLOBAL MANAGEMENT ACCOUNTANTS C 2017 CONFERENCE 2017 DUBAI, UAE. 1

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of ICMAP C 2017 DUBAI, UAE.

ICMAPGLOBAL MANAGEMENT ACCOUNTANTS

C 2017 CONFERENCE 2017 DUBAI, UAE.

1

GULF CORPORATION COUNCIL (GCC)

GCC Background

WHAT IS MANAGEMENT ACCOUNTING

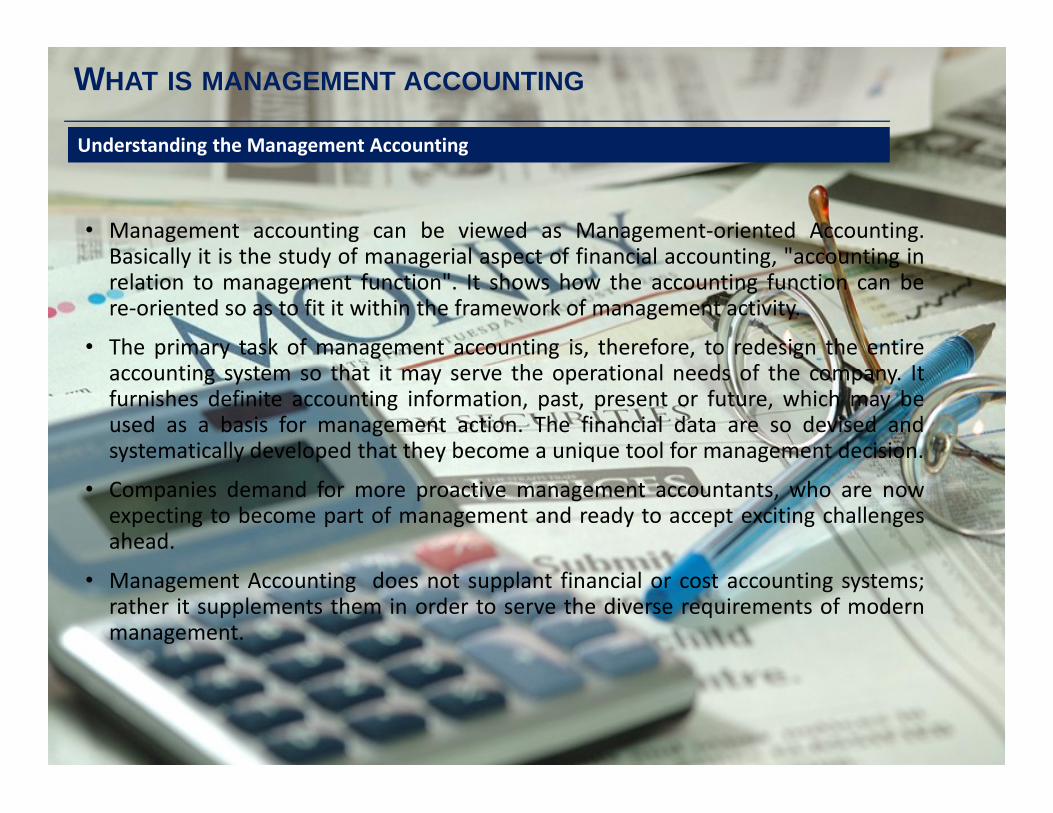

� Management accounting can be viewed as Management-oriented Accounting.Basically it is the study of managerial aspect of financial accounting, "accounting inrelation to management function". It shows how the accounting function can bere-oriented so as to fit it within the framework of management activity.

� The primary task of management accounting is, therefore, to redesign the entireaccounting system so that it may serve the operational needs of the company. Itfurnishes definite accounting information, past, present or future, which may be

Understanding the Management Accounting

furnishes definite accounting information, past, present or future, which may beused as a basis for management action. The financial data are so devised andsystematically developed that they become a unique tool for management decision.

� Companies demand for more proactive management accountants, who are nowexpecting to become part of management and ready to accept exciting challengesahead.

� Management Accounting does not supplant financial or cost accounting systems;rather it supplements them in order to serve the diverse requirements of modernmanagement.

IMPORTANCE OF MANAGEMENT ACCOUNTING

Why Management Accounting is required ?

MANAGEMENT ACCOUNTING IN GCC

Unique mix | Management Accounting Practice | Ownership Structure

CHALLENGES OF MANAGEMENT ACCOUNTING

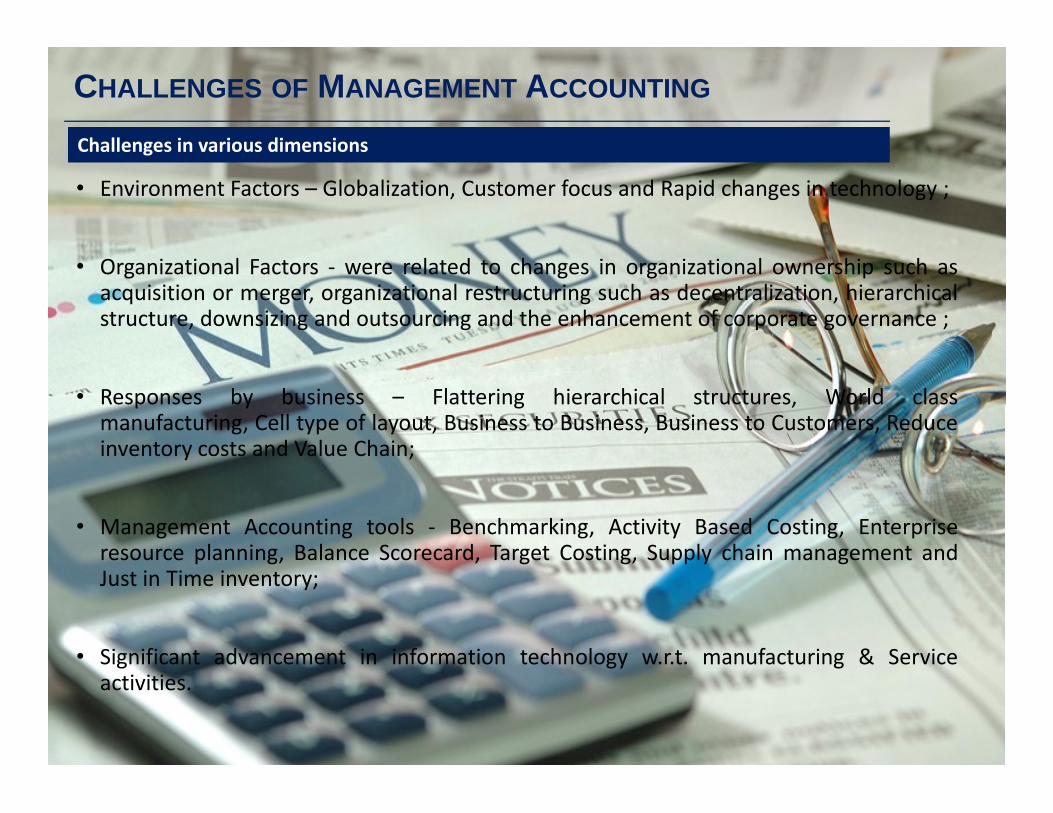

� Environment Factors � Globalization, Customer focus and Rapid changes in technology ;

� Organizational Factors - were related to changes in organizational ownership such asacquisition or merger, organizational restructuring such as decentralization, hierarchicalstructure, downsizing and outsourcing and the enhancement of corporate governance ;

� Responses by business � Flattering hierarchical structures, World class

Challenges in various dimensions

� Responses by business � Flattering hierarchical structures, World classmanufacturing, Cell type of layout, Business to Business, Business to Customers, Reduceinventory costs and Value Chain;

� Management Accounting tools - Benchmarking, Activity Based Costing, Enterpriseresource planning, Balance Scorecard, Target Costing, Supply chain management andJust in Time inventory;

� Significant advancement in information technology w.r.t. manufacturing & Serviceactivities.

VAT IN GCC COUNTRIESVAT IN GCC COUNTRIES

VAT � VALUE ADDED TAX

VAT CONCEPT

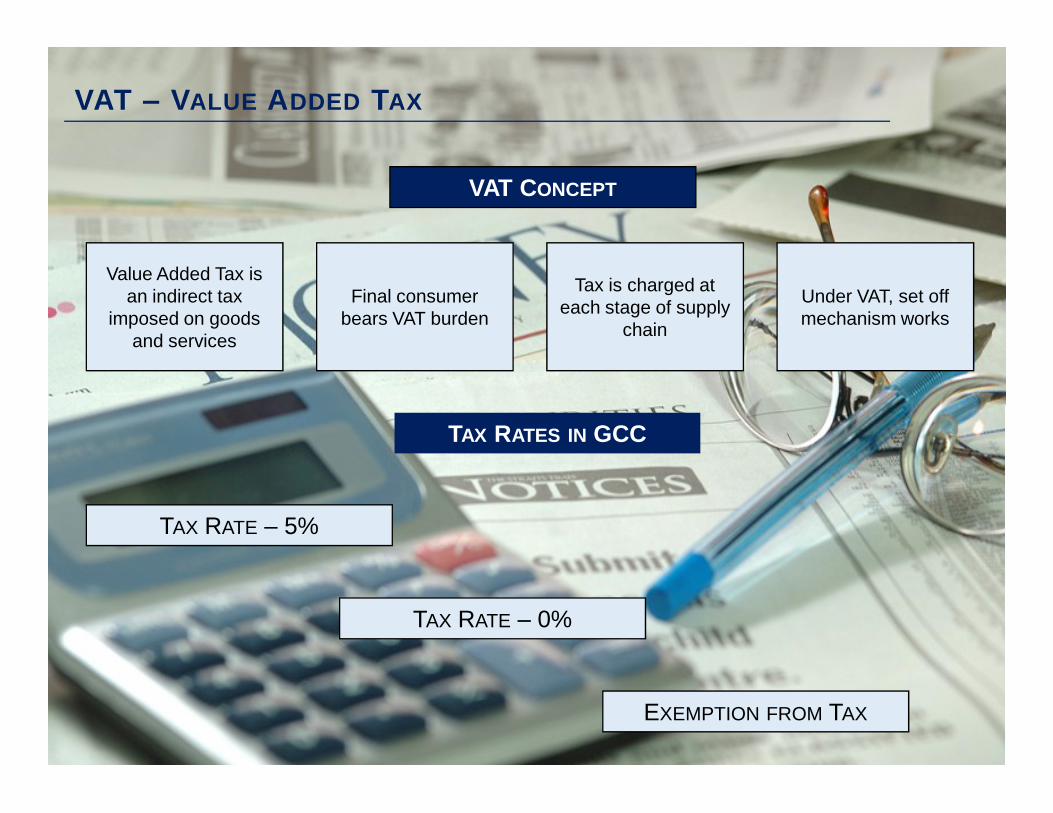

Value Added Tax is an indirect tax

imposed on goods and services

Under VAT, set off mechanism works

Final consumer bears VAT burden

Tax is charged at each stage of supply

chain

TAX RATE � 5%

TAX RATE � 0%

EXEMPTION FROM TAX

TAX RATES IN GCC

VAT - GLOBAL SCENARIO

VAT is already implemented in more than 150 countries in the world.

VAT Countries

No VAT

VAT introduction 2018 (UAE and KSA)

GULF COOPERATION COUNCIL

VAT introduction 2019 (Other GCC States)

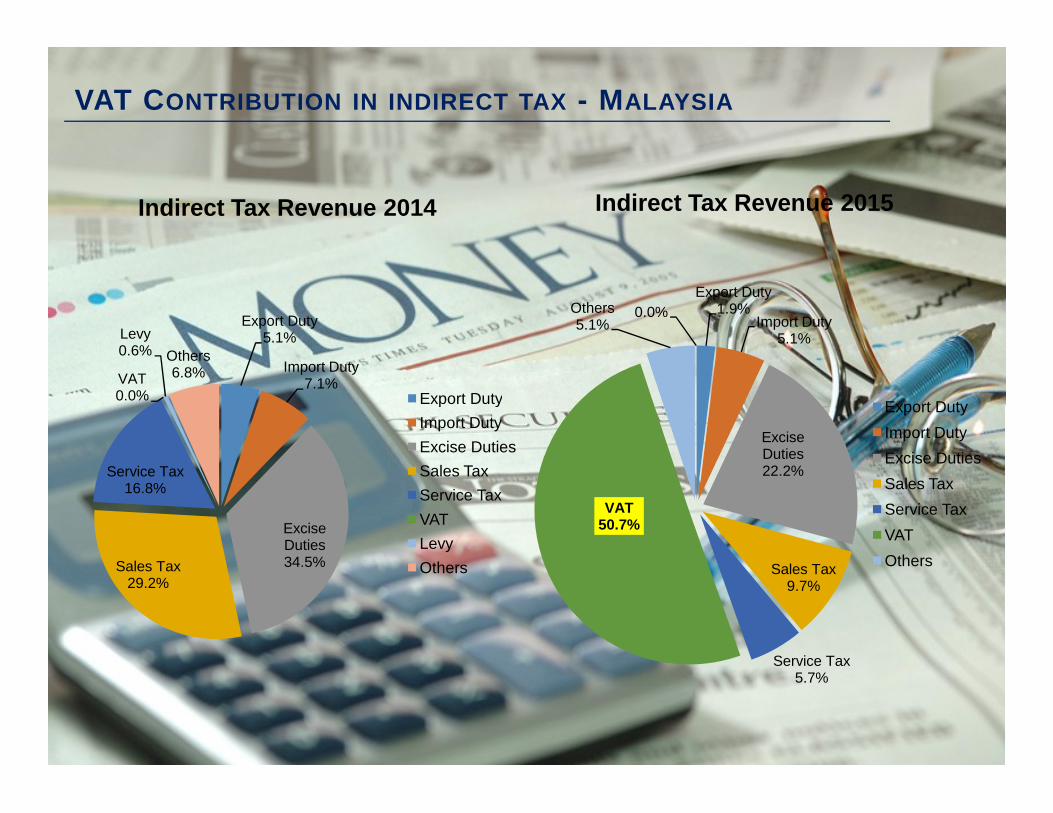

RECENT VAT IMPLEMENTATION - MALAYSIA

VAT CONTRIBUTION IN INDIRECT TAX - MALAYSIA

Export Duty1.9%

Import Duty5.1%

Others5.1%

0.0%

Indirect Tax Revenue 2015

Export Duty

Export Duty5.1%

Import Duty7.1%VAT

0.0%

Levy0.6% Others

6.8%

Indirect Tax Revenue 2014

Export Duty

Excise Duties22.2%

Sales Tax9.7%

Service Tax5.7%

VAT50.7%

Export Duty

Import Duty

Excise Duties

Sales Tax

Service Tax

VAT

Others

Excise Duties34.5%Sales Tax

29.2%

Service Tax16.8%

Export Duty

Import Duty

Excise Duties

Sales Tax

Service Tax

VAT

Levy

Others

GCC AND VAT

What Drives GCC to have common Framework for VAT ?What Drives GCC to have common Framework for VAT ?

GCC AND VAT

Why GCC requires to introduce VAT ?

� Governments provide citizens and residents with many differentpublic services � including hospitals, roads, publicschools, parks, waste control, and police services. These servicesare paid for from the government budgets.

� VAT will provide GCC states a new source of income which will� VAT will provide GCC states a new source of income which willcontribute to the continued provision of high quality publicservices into the future.

� It will also help governments move towards balanced economicrevenue by reducing dependence on oil and other hydrocarbonsas a source of revenue.

KEY HIGHLIGHTS OF GCC VAT AGREEMENT

GCC States | Decision on VAT Rate | Objective of AgreementGCC States | Decision on VAT Rate | Objective of Agreement

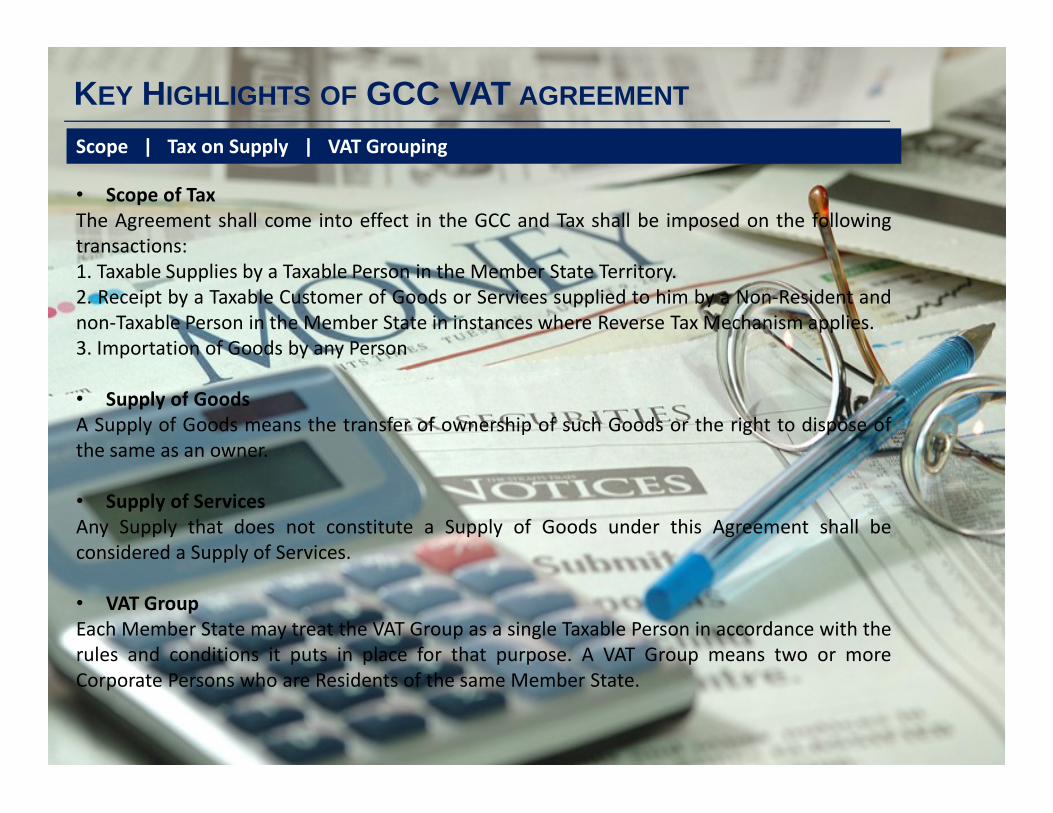

KEY HIGHLIGHTS OF GCC VAT AGREEMENT

� Scope of TaxThe Agreement shall come into effect in the GCC and Tax shall be imposed on the followingtransactions:1. Taxable Supplies by a Taxable Person in the Member State Territory.2. Receipt by a Taxable Customer of Goods or Services supplied to him by a Non-Resident andnon-Taxable Person in the Member State in instances where Reverse Tax Mechanism applies.3. Importation of Goods by any Person

� Supply of Goods

Scope | Tax on Supply | VAT Grouping

� Supply of GoodsA Supply of Goods means the transfer of ownership of such Goods or the right to dispose ofthe same as an owner.

� Supply of ServicesAny Supply that does not constitute a Supply of Goods under this Agreement shall beconsidered a Supply of Services.

� VAT GroupEach Member State may treat the VAT Group as a single Taxable Person in accordance with therules and conditions it puts in place for that purpose. A VAT Group means two or moreCorporate Persons who are Residents of the same Member State.

KEY HIGHLIGHTS OF GCC VAT AGREEMENT

Exceptions and Rights of GCC StatesExceptions and Rights of GCC States

INCREASE IN COST OF DOINGGCC BUSINESS IN GCC COUNTRIES

CHALLENGES IN DOING BUSINESS IN GCC

Region specific challengesRegion specific challenges

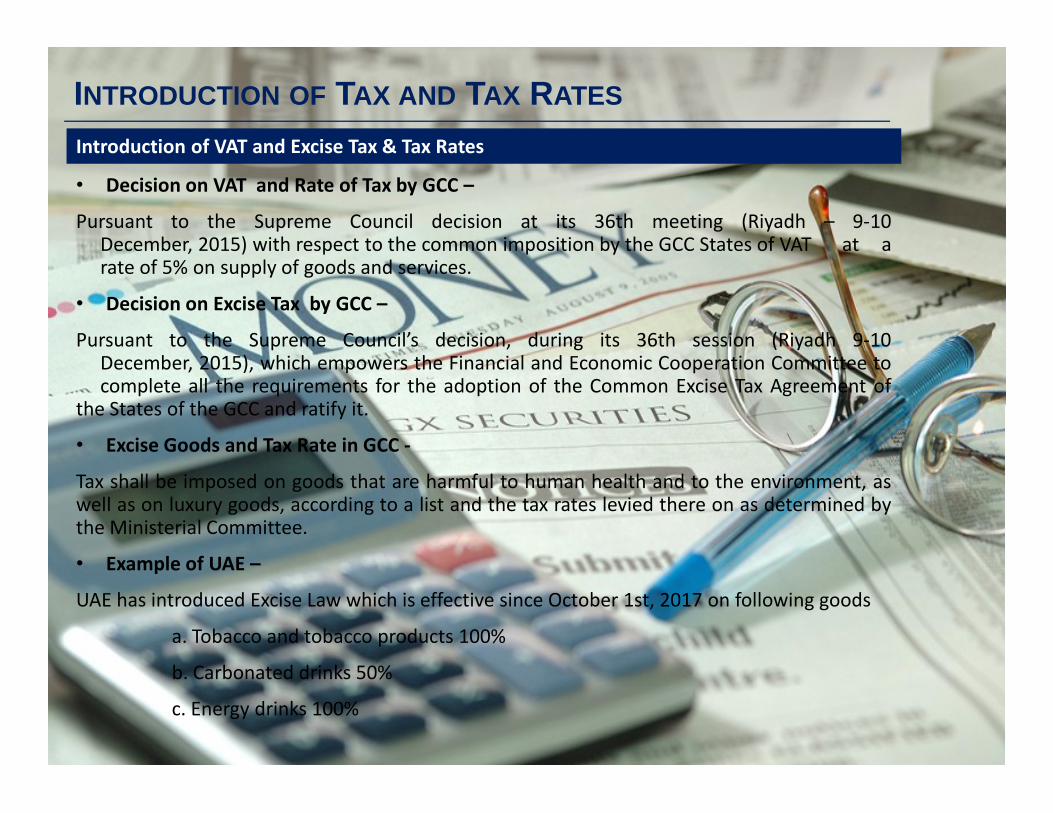

INTRODUCTION OF TAX AND TAX RATES

� Decision on VAT and Rate of Tax by GCC �

Pursuant to the Supreme Council decision at its 36th meeting (Riyadh � 9-10December, 2015) with respect to the common imposition by the GCC States of VAT at arate of 5% on supply of goods and services.

� Decision on Excise Tax by GCC �

Pursuant to the Supreme Council�s decision, during its 36th session (Riyadh 9-10December, 2015), which empowers the Financial and Economic Cooperation Committee tocomplete all the requirements for the adoption of the Common Excise Tax Agreement of

the States of the GCC and ratify it.

Introduction of VAT and Excise Tax & Tax Rates

the States of the GCC and ratify it.

� Excise Goods and Tax Rate in GCC -

Tax shall be imposed on goods that are harmful to human health and to the environment, aswell as on luxury goods, according to a list and the tax rates levied there on as determined bythe Ministerial Committee.

� Example of UAE �

UAE has introduced Excise Law which is effective since October 1st, 2017 on following goods

a. Tobacco and tobacco products 100%

b. Carbonated drinks 50%

c. Energy drinks 100%

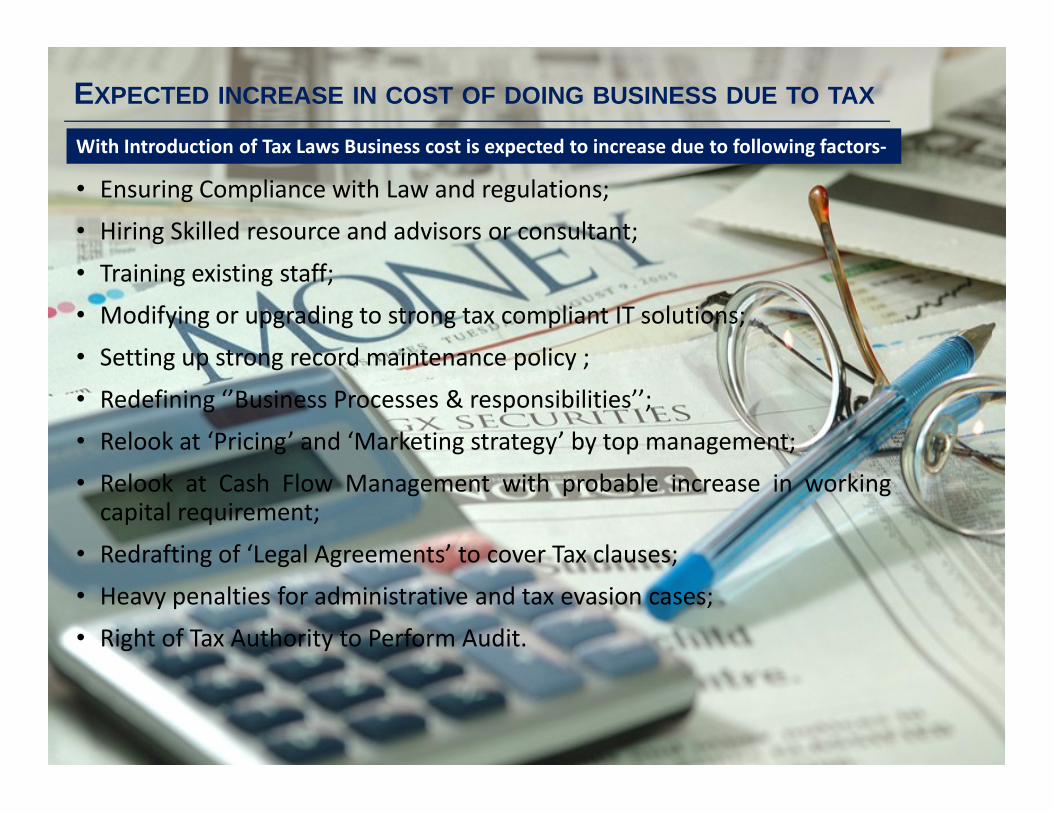

EXPECTED INCREASE IN COST OF DOING BUSINESS DUE TO TAX

� Ensuring Compliance with Law and regulations;

� Hiring Skilled resource and advisors or consultant;

� Training existing staff;

� Modifying or upgrading to strong tax compliant IT solutions;

� Setting up strong record maintenance policy ;

� Redefining ��Business Processes & responsibilities��;

With Introduction of Tax Laws Business cost is expected to increase due to following factors-

� Redefining ��Business Processes & responsibilities��;

� Relook at �Pricing� and �Marketing strategy� by top management;

� Relook at Cash Flow Management with probable increase in workingcapital requirement;

� Redrafting of �Legal Agreements� to cover Tax clauses;

� Heavy penalties for administrative and tax evasion cases;

� Right of Tax Authority to Perform Audit.

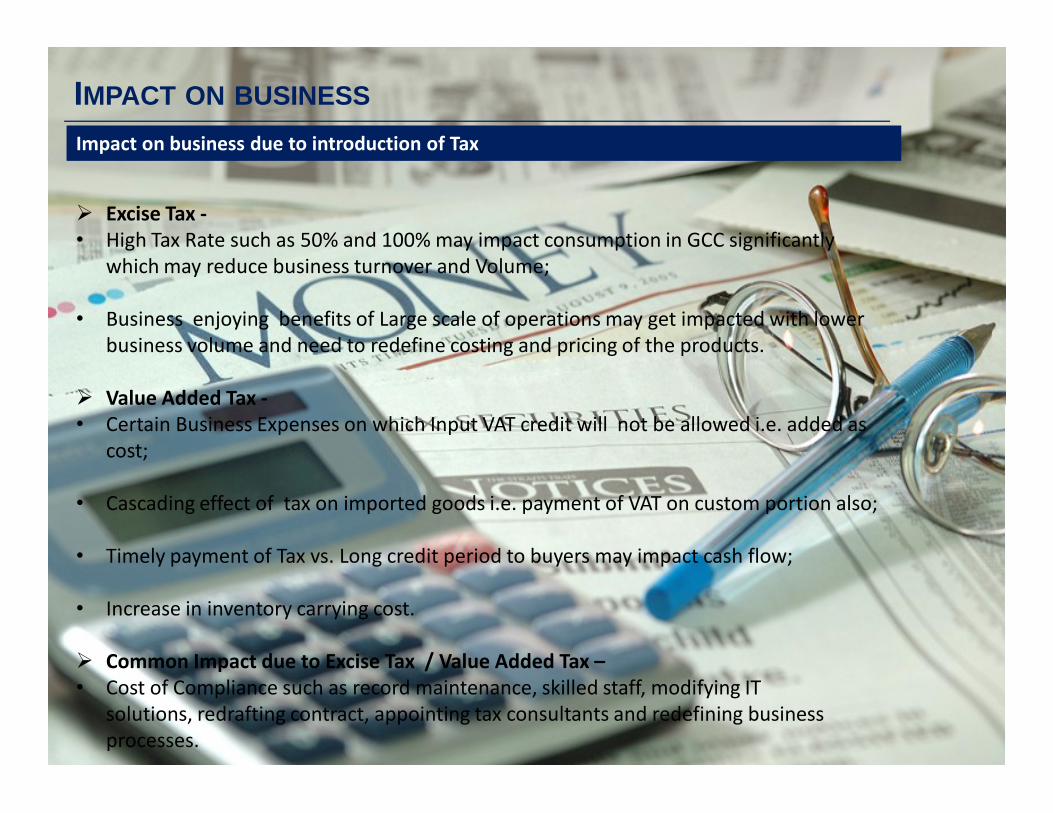

IMPACT ON BUSINESS

Excise Tax -� High Tax Rate such as 50% and 100% may impact consumption in GCC significantly

which may reduce business turnover and Volume;

� Business enjoying benefits of Large scale of operations may get impacted with lower business volume and need to redefine costing and pricing of the products.

Value Added Tax -

Impact on business due to introduction of Tax

Value Added Tax -� Certain Business Expenses on which Input VAT credit will not be allowed i.e. added as

cost;

� Cascading effect of tax on imported goods i.e. payment of VAT on custom portion also;

� Timely payment of Tax vs. Long credit period to buyers may impact cash flow;

� Increase in inventory carrying cost.

Common Impact due to Excise Tax / Value Added Tax �� Cost of Compliance such as record maintenance, skilled staff, modifying IT

solutions, redrafting contract, appointing tax consultants and redefining business processes.

THANK YOU!THANK YOU!