Family of teen thrown to ground in violent arrest by Rialto ...

Upload

khangminh22Category

view

0download

0

I""·

IN THE SPECIAL COURT (TRIAL OF OFFENCES RELATING TO

TRANSACTIONS IN SECURITIES) AT BOMBAY.

SPECI""�L CASE NO 5 OF 1993

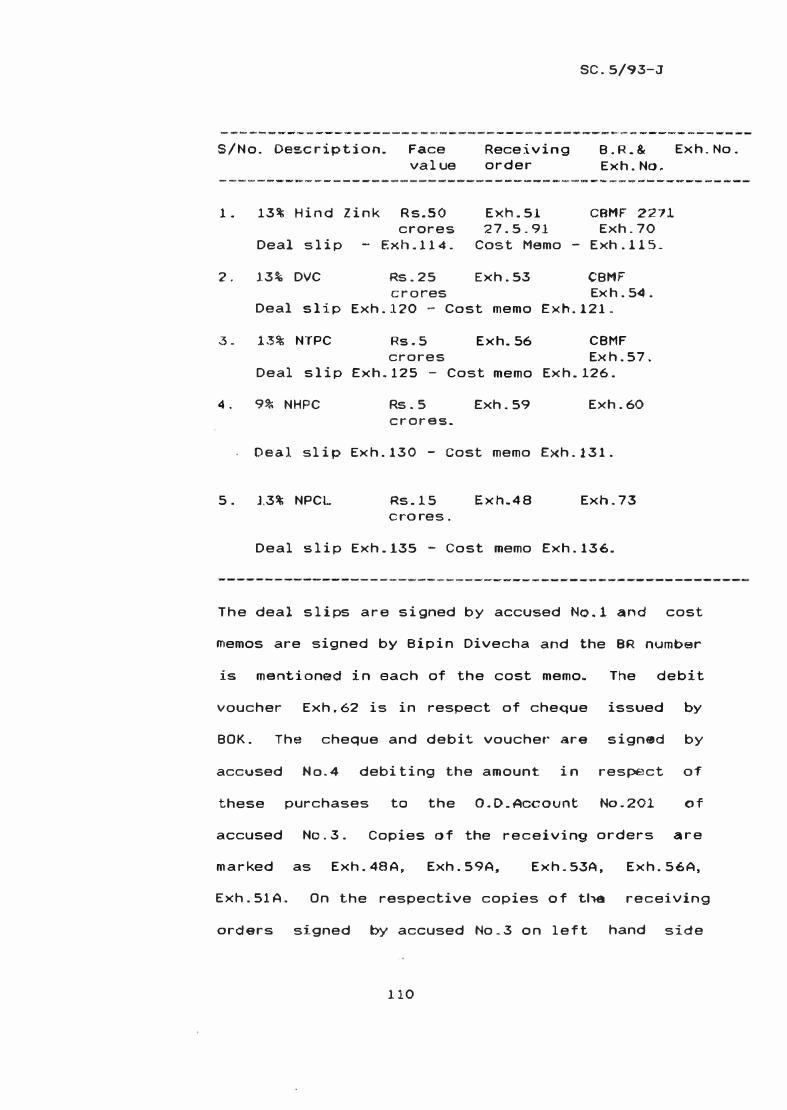

CENlRAL BUREAU OF

INVF.STIGA TION.

VERSUS 1. ANJL MOHANLAL NARICHANIA,

36 Pushpanjali,

Goshala Road, Mulund (West),

Bombay 400 080.

2. HITEN PRASAN .DALAL,

201, Shanti Towers,

Military Road, Marol,

Andheri (East),

Bombay 400 059.

3. ABHA Y DHARAMSEY NAROTIAM,

186, Walkeshwar Road,

1st Floor, Teen Bathi,

Malbar Hill,

Bombay 400 006

COMPLAINANT

j

CHANDRASHEKHAR SIT ARAiv1 RAJE.

'Shiv Gaurav, Plot No.16,

Shiv Ganga Nagar,

A1nbemath (East),

Dist Thane 421 501. ACCUSED

Mr.V.C.Gupte with Mr.RB.Thakare, Special Public Prosecutor for

CBI.

Ivtr.A.G.Pawar for Accused No.1.

Mr.R.D.Ovlekar with Mrs.M.N.Karandikar and Mr.Swill Kale i/by

M/s. Purnand & Co. for accused No.2.

Mr.Manoj Mohite with Mr.S.P.KotwaJ for accused No.3.

Mr.N.K.Thakore with Mr.P.D.Naik for accused No.4.

CORAM:A.B.PALKAR,J DA1ED:31st January, 2003

JUDG1v1E1'TT.

,,

L

1991-92.

SC.5/93-J

This case arise$ out of security scam of

The compl aint (FIR) was lodged by

K.R.Acharya, P .W.8, the then Chief E�ecutive of the

Canbank Mutual Fund ("C8MF"' for short).

2. Accused No.1- Anil Mohanlal Narichania

was at the r elevan t time the Asstt.General manager

of C8MF. He had joined some time in Augus t 1990

after resigning from Canara Bank and as Asstt.

General Manager. He was also a dealer for CBMF and

as such was looking after the money market

transactions specially transactions in sale and

purchase of Securities.

.3. Accused No.2-Hiten Prasan Dalal ("HPO"

for short) was stock broker and a member of the

Bombay Stock Exchange and at the relevant time he

was broker for CBMF as well as for Ci tibank ("Citi"

for short) and Standard Chartered Bank ("SCB" for

s hort).

4. Accused No.3-Abhay Dharamsingh Narottam

("AON" for short) was also a stock broker and a

member of the Bombay Stock Exchange. He had his

dealings in securities through Bank of Karad ("BOK"

3

l

SC.5/93-J

for short). He was also a constituent o f BOK and at

the relevant time was one o f the Di rectors of the

BOK. He had obtained membership of Bombay Stock

Exchange long back and was maintaining one

overdraft account i.e.O.D.No.201 and one cur rent

account with BOK.

5. Accused No.4-Chandrashekhar Sitaram Raje

("Raje" for short) was working as Agent of BOK

incharge o·f Securities Department. and was

authorized to deal in securities on behalf of BOK

for transactions of bank as well as for the

transactions of its constituents. one of whom was

accused No . 3-ADN. Accused No.4 was given power of

attorney by

transactions

constituents.

BOK for

on behalf

dealing in

of the bank

security

and its

6. The charge against the accused in brief

can be stated as below; The charge runs into 20

pages under 19 different heads . However. suffice

it to state in brief as to what the charges are

under the different heads:

(i.) Accused Nos.1 to 4 are charged unde r

section 1208 of IPC for having entered into a

criminal conspiracy in order· to secure pecuniary

4

r

li..:

SC . 5/93-J

advantage to accused No . 3 -AON and ul timately to

accused No . 2-HPD by means o f ostensible

t ransactions in securities for cheating CBMF by

concealing from the said fund and from one Bipin

Divecha (PW-5) co-signatory to RBI cheque for a sum

of Rs . 103 ,82,47, 295.65 ps. issued on 27. 5 . 1991 the

fact that it was issued against two false

Subsidiary Ge11eral Ledger transfer forms (SGL T Fs)

issued on behal f o f BOK by accused No.4 and i n

pursuance o f the same accused No . l bei ng a public

servant by abuse o f his pos i t i o n as a publ ic

servant, by corr upt or i l legal means dishonestly

pu rchased secur i ties i n the a fo re$aid ostensible

transacti ons th rough accused H.2-HPD.

The Securities were (i) ll . 5% GOI 2008 face

value Rs . 58 . 39 crores, and ( i i ) 1 1 . 5% GOI 2009 face

v a l ue Rs.44. 5805 crores. Aforesaid two false and

forged SGLTFs were issued by accused No. 4-Raje on

27 . 5 . 1991 . These SGLTFs were purported to be

issued by BOK and were issued without authority and

without disclosing t liat they are being i ssued on

behalf of accused Na.3-AON . the constituent of BOK

and without there being secu r i ties sufficient to

cove r the said transactions purpo rted to have been

entered into. The SGLTFS were issued in SGL account

BYSL-0107 of BOK maintai ned wi th Reserve Bank o f

5

SC.5/93-J

India ("RBI for short) for constituents of the bank

and for this accused No. 1, dealer· and A$stt. General

Manage r of CBMF issued the aforesaid cheque of

Rs . 103 and odd crores i.n favour of BOK. the

proceeds c>f which accused No. 4-Raje ultimately

credited to the account of accused No.3-ADH in

violation of the banking practice and implied

contract touching the mode of discharge of such

t rust which resulted in co rresponding gain to

accused No.3-ADN and ultimately to accused No.2-

HPD. These transactions were entered into by

Accused knowing fully well that these transactions

were ostensible. dishonest , and i l legal a11d i n

pursuance of the said ostensible and non-existent

t ransactions, accused No.3-ADN issued two delivery

o rde rs on 27.5.1991 to BOK directing the Bank to

del iver the aforesaid securities to CBMF although

there were no securities i n his account to satisfy

the claim under the said two SGLTFs and the reby all

the four accused committed offence under section

1208 r/w.section 420 of the IPC and also under

section 1 3 ( 1)(d) r/w. section 13(2) of the

Prevention of Corruption Act 1988 and sections 411,

467, 468. 471 and 477A of the IPC. There is also

a l ternative charge of c riminal breach of trust

punishable under section 409 r/w. 1208 !PC.

6

,

S C . 5/93-J

However. the a l ternative charge of section 409

r/w . 1208 lPC as against a l l the four accused is not

pressed by the prosecution. The cha rge o f

o ffence under section 409 i s pressed only against

accused No. 4-Raje for having committed criminal

br-each of t ru$t by crediting the proceeds of sale

to the account of Accused N o . 3-ADN, although he had

issued SGLTFs creating l iabi l i ty against the BOK.

In vi ew of these a l l egations there is

i ndividual charge of offence under section !3(1)(d)

r/w. 13(2) of the Prevention of Corruption Act

against accu$ed No.l. There i s ind:ividual c:ha rge

against each of the accused o f offence under

section 420 IPC and similarly alternative charge

under section 409 IPC. There is also charge

against accused No . l for of fence under sections

467, 468, 471 of IPC for fraudulently and dishon-

estly using as genuine the two SGLTFs dated

27 . 5 . 1991 which he knew were false and forged.

There is i ndividual charge of o ffence under section

47 1 , 467 and 468 as against accused No. 2-HPD.

Accused Nos . 2 and 3 are also separately charged for

o ffence under section 4 1 1 IPC for receivi ng stolen

property i . e . the proceeds of the cheque. Accused

No.3 i5 separately charged for of fence under sec

t i on 47 1 , 468 and 467 !PC for_ dishonestly using as

7

SC.S/93-J

genuine the two SGL.TFs mentioned above . There is

also charge for offence punishabl e under section

409 IPC against accused No . 4-Raje for having com

mi tted c r iminal breach of trust against BOK by

issuing false and forged SGLTFs as s tated above on

27 . 5 . 1991 w i t hout there being backing of securities

i n the concerned accoun t . Simi l arly there i s

charge under section 467 and 468 against accused

No . 4 . There is also specific charge of falsifica

tion of accounts punishable under section 477A

against accused No.4-Raje.

7. The charge was framed by Justice Variava.

Judge Special Court , (as he then was ) . I t was

amended by him by making charge o:r offence under

section 409 al ternative to of fence under section

420 IPC and later on during the course of trial,

after I took over, additional charge of offence

under section 41 1 IPC was framed against accused

Nos . 2 and 3 by refering speci fically to the five

transactions of PSU Bonds . Charge was amended on

27.10. 2002 after hearing accused and they were

given opportuni ty to recal l any of the wi tness

earlier examined by the prosec ution for

crossexamination. i f they so desired. The accused

did not reca l l any o f tha w i t nesses examined by the

8

SC. S/93-J

prosecution, probably because the charge was on the

basis of the allegations contained i n the charge

sheet and the documents pertaining to the various

transactions and the statemen� o f witnesses.

8 . The a l l egatic:rns o f the prosecution can

be stated in brief as below:

The starting point is 27 . 5 . 1991. On that day

accused No . 4-Raja entered into two transactions of

sale of secu riti es (i) 1 1 . 5% GOI 2008 face value

Rs . 58 . 39 crores , and ( i i ) 1 1 .5% GOI 2009 face value

Rs . 4� . 5805 crores. These transactions were

apparently of sale by BOK to CBMF but are in fact

transactions of accused No . 3-ADN. Se cur i t ies were

delivered by issuance of SGLTFs , Exh.33 and Exh . 37 .

BYSL-107 is the number of SGL account for const i tu

ents maintained by the BOK. SGL account of BOK

ma i ntained with the RBI bears account No . 098. On

behalf of the CBMF the tran!>act ion was entered into

by accused No . 1 , dealer of CBMF through b roker

accused No. 2-HPD. It is not disputed at this stage

that on the date of issuance of the two SGLTFs by

accused No.4, there were no securities either in

the account of BOK in t he SGL Account maintai ned by

the Bank or i n the account maintai ned by it for its

9

SC . 5/93-J

consti tuents . It is also not disputed that RBI had

permitted BOK to maintain separate account for its

const i t uents and the same was maintained for all

the consti tuents of the bank and not for accused

No . 3-AD N .

9 . These transfer forms were presented on

29 . 5 . 1991 for the f i rst time and were returned a$

the account number was riot mentioned and on

31 . 5 . 1991 when presented again were returned for

want o f suf ficient balance i n the account. It

needs to be pointed out at this stage only that at

no time e i the r before or after the issuance of SGL

transfer forms. the said secur i t ies were in credit

with BOK ' s SGL account or wi th the consti tuent"s

SGL account maintained by BOK . Af'ter the SGL

transfer forms were ret urned or were dishonoured

for want of sufficien t balance i n the account no

att.empt was rnade on the part of BOK or on beha l f o f

accused No . 3-ADN by accused No . 4 to get the same

rectified by providing sufficient credit i n the

account_ By issuance of these two SGL t ransfer

fonos. liability was created agai nst BOK and i n

favour of CBMF to the extent o f Rs . 103,82,47,295 . 60

ps . According to the prosecution there was no

genuine sale transaction as such and the documents

1 0

SC. 5/93-J'

of sale i n favour o f CBMF were created w i t h a view

to s i phoning the amount of Rs . 1 03 and odd crores

stated above f rom CBMF and a l l the accused having

entered i nto conspi racy for the aforesaid purpose,

accused No . 1 issued ch eque which was immediatel y

credited to the account of BOK with RBI and the

proceeds thereof were credi ted by accused N o . 4 to

the O . D . Account No.201 of accused No. 3-ADN and i n

this transaction accused N o . 2 represented CBMF as

broker. As a resul t of this CBMF suffered wrongful

loss of the said amount and accused No.3 got

wrongful gain when the proceeds were credi ted to

h is O . D . Account. I n pursuance of this accused

No . 3-ADN issued delivery orders to BOK for delivery

of the aforesaid securities to CBMF but in fact he

was fully aware that there wer·e no secu rities i n

cred i t i n the aforesaid account .

issued cost

t ransact ions

memos for the said

i n favour of CBMF .

Accused No.4

ostensible

Balance o f

securi ties i n the concerned account BYSL-107 on

that day i n respect of 1 1 . 5% GOI 2008 was 1300 only

and i.n respect of 11 .5% GOI 2009 the balance was

ni l . Accused No . 1 issued deal s l i ps and the cheque

of Rs. 103 and odd c rores signed by himself and

Bi pi n Divecha1 P . W . 5 .

1 1

SC.5/93-J

10 . Accused No . 3-ADN used the aforesaid

amount for purchase of five different PSU Bonds on

the same day i . e . ?.7 . 5 . 1991 . On the aforesaid date

opening balance i n the . D . Account o·r accused No . 3-

AdN was Rs.3,17 , 9 5 , 216 . 76 ps. and this amount of

Rs . 103 , 82 , 47 , 295 . 60 ps. was credited by

fraudulently obtaining the cheque o f the said

amount f rom CBMF. The five PSU Bonds having total

face value of Rs . 100 croras were purchased in

similar ·fraudulent a.REI .a�tHZll'i ltt;;e t ransactions . The

details o f the PSU bonds are -

( i ) 13% Hind Z i nk Bonds face val ue Rs.SO crores;

( i i) 13% DVC Bonds face value Rs . 25 crores ;

( i i i ) 13% NTPC Bonds face val ue Rs . 5 croras;

( i v ) 9% NHPC 0onds face value Rs . 5 cro res:

(v) 9% NP CL Bonds face value Rs . 15 cro res;

and cheque was debited to the 0 . 0 . Account No . 201 of

accused No. 3-ADN for making payment to CSMF and

CBMF i n t u r n issued five d i f fe rent bank rece i pts

towards delivery of the secur i t i es to BO K . These

transact ions were reversed on 26/27 . 7 . 1991 and the

five BRs issued by CBMF were discha rged. The

amount of these transactions of sale ( reve rsal ) was

paid by CBMF to BOK by cheque.

11 . According to the prosecution on the same

12

...

SC.5/93-J'

day i.e. 27 . 5 . 1991 accused No.l entered into two

transactions of sale o f the aforesaid GOI

sec u r i t ies w i t h Citibank and i ssued SGLTFs . These

securit ies were sold at slightly higher price

thereby to show

Rs.103 , 84 , 53 , 2 56 . 65

profit and a cheque

ps . was issued by Citi bank

of

i n

faVOUt' of CBMF . Citibank•s cheque was credi ted

but as the C i t i bank failed to get the securities as

the SGLTFs issued by accused for and on behalf o f

CBMF were dishonoured. Al though accused No.1 kept

quiet inspite o f dishonour of SGLTFs issued by

BOK, Citibank did not keep quiet and on beha l f of

C i t i bank V . N . Shenoy ( P . W.16) took up the matter

with accused No.1-Narichania. Accused No . 1 assured

him to give credit for clearance o f the SGLTFs, but

the said securities were never ar ranged for by

accused No.1 and as such SGLTFs were not cleared at

any time by RBI PDQ.

12 . I t is further case o f prosecution that

i n order to cover up the dishonour o f SGLTf's issued

i n favour of Citibank accused No. 1 entered i nto

further transactions. On 26 . 7 . 1991 he purchased

1 1 . 5% GO! 2008 o f face value o f Rs . 60 crores from

SCB through accused No.2-HPD. This purchase was i n

CBHF scheme CAN aocc 90 and delivery of the

13

SC . 5/93-J

securi ties was given by see by issuing BR No . 0970

(Exh.198). On 27 . 7 . 1991 i . e . o n the very next day

he again purchased 1 1 . 5% GOI 2008 from C i t i i n

CANSTAR Scheme and Citi issued i ts 8R No.474

(Exh . 1 92 ) . Both these transactions were through

HPD-accused No . 2 . Accused No. 1 then i nter n a l l y

exchanged BR 0970 Exh.198 dated 26 . 7 . 1991 o f sea

with BR 474 o f Citi between two Schemes CAN 80CC 90

and CANSTAR. BR of sea Exh. 188 was re-sold to scs

on 2 7 . 7 . 1991 .

1 3 . I n the ear l i er transaction o n 2 7 . 5 . 1991

C i t i bank was holding bounced SGL (Exh.183) o f CSMF',

face value o f which was Rs. 58.39 crores and for

getting the SGL discharged and C i t i bank gave the

dishonoured SGL of CBMF for GOI 2008 Exh . 183 and

issued i ts own SGL for Rs. 1 . 61 crores aga i nst the

return of BR Exh . 1 92 on 20 . 8 or 21 . 8 . 1991 . I n these

transactions accused No . 2-HPD was the broke r for

SCB as wel l as for Citi.. So far as SGL issued by

C i t i for Rs . 1 . 61 c1·ore i s concerned , it was

honoured when presented. There was no other

independent transaction o f Rs . 1 . 6 1 crore with C i ti,

still this SGL was given i n order to make up the

amount o f face value Rs . 60 crores.

14

SC . S/93-J

14 . As the bounced SGL of Rs . 58 . 39 c rores of

BOK and one val i d SGL of Rs . 1 . 6 1 crores o f C i t i

came to CBMF, accused No. 1 had to show some

transactions and to see that bounced SGL goes out

of CBMF . Therefore, accused No . l sold securities

1 1 . 5% GOI 2008 on three different dates i.e. on

23 . 8 . 1991 Rs . 1 0 crores, 26- 8 . 1991 Rs . 7 crores and

4 . 9 . 1991 Rs. 4·3 crores and issued fresh SGL t ransfe r

forms backed by the bounced SGL of 27 . 5 . 1991 and in

addition gave one fresh SGL transfer form for

Rs.1.61 crores by bifurcating one o f the SGLs of

seven crores . Since the SGL t ransfe r forms which

were issued by CBMF were not backed by the securi

ties i n the account , they were di s honou red although

repeatedly presented .

.15 . The re was a n arrangement of 15% between

see a nd acc1Jsed No . 2-HPD, whereby SCB was commi tted

a retur·n of 15% on a l l the deals of sale and

purchase entered into through accused No . 2-HPD. I n

November 1991 interest became due. However, SCB had

not received valid delivery o f secur i ties . Accused

No.2-HPD was the common broker. SCB could not get

the due interest . Therefore. accused No . 2 paid

i n terest t o sea amounti ng to Rs . 3,45 , 000 . 00 I t is

further the case o f the prosecution that accused

1 5

SC . 5/93-J

No.1 gave the SGL t ransfer forms of GO! 2008 and

GOI 2009 back to ac cused No.2 for 3ettling the

issue and accused N o . 2 handed over the same to

accused No. 3-ADN wh o i n turn handed over the same

t o BOK or accused No . 4-Raj e and the dishonoured SGL

transfer forms were ultirnately found i n t he custody

of BOK duri ng searc h . The said SGLTFs were be a r ing

endorsements of80K that the same have been d is-

charged.

16. As regards the second security GOI 2009

Rs . 44 . 5805 o f which SGL was also

dishonoured, accused No . 1 did not take any ·Follow

lup action. At the instance of accused No . 2-HPD,

SCB t hrough accused No.2 , purchased GOI 1 1 . 5% 2009

face value Rs . 42 c rores a n 19. 9 . 1991 from Citi and

GOI 2009 11.5% face value Rs . 8 crores on 1 8 . 9 . 1991

and C i t i issued two 8Rs to SC B . One Jaideep

Patha k who was i n-charge of the back up department

of SCB asked Investment O f f icer o f SCB Santosh

Mulgaonkar to w r i te a letter· to C i t i bank cal l ing

for the SGL transfer forms of CBMF i n exchange o f

Cit i bank BRs a nd ret u r n�the bounced SGL o f 1 1 . 5%

GOI 2009 (Exh.188) dated 27.5 . 1991 face value

Rs.44.5805 c rores and issued i ts own SGL for the

balance o f Rs . 5 . 4195 crores.

16

SC . 5/93-J

1 7 . I n the case o f GOI 2009 also interest

became due as interest date of both the sec u r i ties

were i n November but SCB did not get interest from

RBI . Accused No . 2-HPD paid i nterest to see

amounting to Rs . 2,56 , 33 , 787 . 50 ps . Howeve r , SCB --\ ,...,.�"(

had a l ready sold securities o f 11 . 5% GOI 2009 to ,/.

Bank of America and State Bank of India. see then

passed on the i nterest paid by accused N o . 2-HPD to

these banks .

1 8 . It i s also prosecution case that on

27 . 5 . 1991 when the amount o f Rs . 103 and odd crores

was credi ted to the O . D. account No. 201 of accused

N . 3-ADN, accused No.4-Raje at the instance o f

accused N o . 3-ADN had called cal l money o f Rs . 1 0

crores from Federal Bank and that amount was also

credi ted to the account o f accused N o . 3 -ADN namely

0 . 0 . Account No. 201 by accused N o . 4 . I n addition

ear l i e r on 23 . 5 . 1991 accused No . 4 had given credi t

o f about Rs . 5 crores o f simi l a r c a l l money received

f rom Karur Vyasa Bank to the account of accused

No.3-ADN . Accused No . 3-ADN purchased five d i fferent

PSU Bonds with t hese funds from CBMF. These trans-

actions were also done similarly i n BoK•s name.

17

,..

19 -

SC . 5/93-J

For five PSU Bonds transactions. there

were five BRs iss ued by CBMF in favour of BOK on

27 . 5 . 1991 . There was reveral on 26/7 and 27/7 and

the bonds ( i n fact 8Rs) were sold by BOK to CBMF.

These transactions were also of accused No. 3-ADN

only. 'The BRs issued by CBMF were retunrned i . e.

exchanged and delivay wae completed by such e�-

change . The cost memos were issued by accused

N o . 2-HPD. He cl ai ms to have issued the cost memos

as broker (agen t ) of CBMF. In respect o f one of

the Bonds vi z . 13% OVC Bonds, accused No . 2-HPD

asked for issuance of cheque i n favour of Andhra

Bank whereas in respect o·f other 4 PSU Bonds. he

asked the cheque ta be issued i n the name of SOK.

The cheque for that amount of R s . 25 and odd cro res

was issued in favour of Andhra Bank and not i n

favour o f 80K a l though BOK was the counter party on

record . Accused No . 1 did not stop at this. He

gave a letter in favour of Andhra Bank c a l l ing upon

Andhra Bank to c redi t the proceeds of the cheque t o

the join t account of accused N o . 2-HPD and his wi fe

and thus accused No . 2 took away Rs . 25 crores and

In orde r to make up the face value of Rs . 100

crores of the S PSU Bonds , accused No. 3-ADN asked

BOK to deliver " f ree" four other PSU Bonds of the

face value of Rs . 25 crores and thus the amount of

18

SC. 5/93-J

Rs.101 , 75 , 1 7 , 808 . 18 ps. for which cheque was issued

by CBMF i n favour o f BOK was credi ted to the ac

count o f BOK with RBI and proceeds thereof were

then credited to the 0.0.Account No . 201 of Accused

No.3-AON . The entire amount credi ted to the ac-

count o f accused No. 3-ADN was used by him for

making payme nt to d i f ferent banks like Uni ted

Western Bank, Corporation Bank, Punjab National

Bank, Indian Overseas Bank etc. towards the dues of

his ear l i e r t ransactions. Therefore, i t appears

that transaction of PSU Bonds on 27 . 5 . 1991 between

CBMF and BOK or AO N were i n the nature o f ready

forward although on record they are not shown as

ready forward. but a l l the transactions were re

versed and BRs were taken back on 26th and

27 . 7.1991 out of which i n respect of one BR i . e .

13% DVC Bond, the amount was taken away by

No . 2-HPD by get t i ng the same credi ted

accused

to

personal account with the active assis tance

his

o f

accused No . 1 by iss uance of cheque and issuance of

l e t ter to Andhra Bank.

20 . In respect of B R o f 13% DVC Bond.

amount of Rs . 25 crores having taken by accused

No . 2-HPD and got transferred to his account w i t h

Andhra Bank, the! same was substi tuted by four

19

SC .5/93-J

earlier BRs issued by CBMF for 14% REC Bonds of

Rs . 2 . 50 crores. 14% MTNL Bonds of R s . l crores and

14% MTNL Bonds of Rs. 1 1 . 5 crores and another BR

for 13% OVC Bonds face value Rs. 10 cro res dated

24.7.1991 total of Rs.25 crores face value.

21. The ent i re transactions reveal that

accused Nos.1 to 4 conspired togethe r and siphoned

of an amount of Rs.103 and odd crores from CBMF and

commi tted various of fences

lodging

as detailed

complaint by

i n the

P.W.8 charge. Before

K.R.Acharya, there was an i n-house inquiry conduct

ed by P.W.13 K.V.Hegde i n which certain facts came

to l i gh t . P.W.8 had visited the Bombay Office on

22.5.1992 and also on 28.5.1992. Accused No.1 was

called upon to explain and he told that he wou l d

contact. accused No. 2-HPD and get the SGLs recti-

fied . He cou ld not. P . W.8 visi ted the of fice of

BOK i n company of Mr. Gopalkri shnan and in�uired

from accused No. 4-Raje as to what had happened.

Raje showed them the SGLs Exh.33 and Exh . 37 and

also told that the transaction was settled and SGLs

were discha rged by BOK and cross mark was shown and

photo copies were also given. They met accused

No . 2-HPD i n his office and sough t his explanation as

CBMF had suf fered huge loss. On 23.5.1992 accused

20

SC . 5 /93-J

No . 2 HPD submitted explanation i n the form o f

affidavi t Exh. 250 sworn before a Notary Public and

one Subbarao. P.W.ll. Accused No . l also gave

explanation i n w r i ting Exh. 244 to P.W.8 K.R.Acharya

and Gopalk rishnan . Action was taken forthwith

against accused No . 1 o n 22 . 5 . 1992 by cal l i ng upon

him to hand over charge t o 8 . R . Acharya, General

Manage r . On 28 . 5 . 1992 his explanation was taken.

P . W . 13 . K . V . Hegde submitted repor t o f i nquiry.

Accused No . 1 was suspended and was lat�r on dis

missed. Complaint was lodged by K . R . Acharya after

about a month on 1 9 . 6 . 1991 w i t h C . 8. I . D u r i ng

investigation various documents. bank acocunt

books, as wel l as account books of accused No . 3-ADN

and diary o f accused N o . l and various other doc u

ments i nc l uding cor respondence were seized and

statements o f number o f w i tnesses were recorded.

Disputed documents regarding handw r i t i ng and s igna

ture part were sent to the Gover nment Expe rt for

exam i nation and his opinion was sought. At the

t r i a l none o f the accused disputed the signature o r

handwri t i ng and that evidence has not been adduced.

Sanction was obtai ned for prosecution of accused

No . 1 for o ffences under section 13(1 ) (d ) r/w. 1 3 (2)

o f the Prevention of Corruption Act , 1988. P . W . 46

A. M. Prabhu i s the sanctioning autho r i ty . ·

2 1

SC. 5/93-J

22. In order to appreciate the evidence on

record i t i s necessary to point out the defence of

the accused . Although all the four accused have

denied existence o·f any criminal cons pi racy. each

of the accused raised i ndepende n t pleas i n his own

defence and even contradictory stands have been

taken i n respect o f particular t ransaction o r

documents by the accused. I n view o f this i t i s

necessary to refer to the defence o f each of the

accused.

2 3 . Accu�.ed No . 1 has i n addition to the

detailed replies given to various questions put to

him while examining under section 3 1 3 C r . P . C .

filed a brief written statement i n reply to the

general question whether he has to say anything

mo r e . Admitting that he was working as dealer i n

CBMF for money market transac t i ons , he stated that

CBMF is a Trust registe red under the Indian T rusts

Act and i s not a subsidiary of Canara Bank. He was

given powe r o f attorney to deal i n money market

operations i . e . sel l i ng and purchasing of Govern

ment securities, PSU Bonds , call money deposits

etc . I t is wel l known that every mutual fund has

d i fferent schemes which are declared a t a

22

SC. 5/93-J

particular p0i nt of time and subscription is open

for a par ticul ar per i od . Accord i ng accused No . 1-

Na richa nia each scheme had a Funds Manager and each

Fund Manage r was required to submit daily statement

o f cas h flow to the dealer showing the surplus of

funds by the scheme or requirement of funds by the

schEJme and o n that basis accused No . l used to take

decision regarding the sa le or purchase o f securi

ties. The head office was at Bangalore and brokers

were being appointed by the head office. Accused

No.l was holding power of at torney . His powers

were restricted up to the l i m i t o f Rs . 10 crores and

i f the transaction was of hig hsr amount then Gener

al Manager was requi red to ratify and in case i t

exceeded Rs . 25 crores, ratification by the Board

was required . Statements of the transactions were

being sent to Bangalore dai l y . He has fo l lowed

l.ns t ructions o·r the General Manage r and the Board

meticulously . There was also a system of dai ly

audit by i nterna l auditors M/$.C.S.Choksi & Co. I t

i s his specific case that as a dealer his duty wa$

to deal i n money market operations meaning thereby

that his duty was to deploy funds i n purchase or to

generate funds by sale o r call money etc. Howeve r ,

once the deal is struck, he used to prepare a deal

s l i p i n duplicate and pass it to the Funds Manager

23

SC . 5 /93-J

o f the Scheme and after processi ng work by the

sec retarial staff, the respons i bi l i ty of follow up

is of the Funds Manager.

24 . On 27 . 5.1991 BOK sold to CBMF 11.5% GOI

2008 and 1 1 . 5 % GOI 2009 and same secu ri ties were

sold on the same day to C i tibank whereby CBMF

secured pro f i t of more than Rs . 2 lakhs . Two SGLs

were given by SOK which were deposited with PDO RBI

on 29 . 5 . 1991 by the Funds Manager Bipin O i vecha ,

P .W . 5 . SGL transfer forms were resubmi t ted on

31. 5 .1991 . The letter sent to RBI (Ex h . 1 1 1 ) i s

s igned by Bipin Oivecha . Thereafter neither RBI

sent SGLTFs to CBMF nor Mr . Bipin Di vecha i n formed

him about the fate of t he two SGL tr·ansf e r forms

and he had no occasion to see these documents after

27.5.1991. The question o f his handing over o f the

SGL transfer forms to accused No . 2-HPD does not

arise and he has not handed ove r the same.

Evidence i n this regard is not supported by any

documents and is contradicted by Exh . 45 which

clearly shows that SGL transfer forms were returned

back direc tly to BOK by RBI on 3 1 . 5 . 1991 .

25 . 26. 7 . 1991 was a repo r t i ng F r i day and

transactions on such raPo rti ng Friday are to be

24

SC . 5/93-.J

completed i n order to give report o n the next day.

The t ransaction of buying o f PSU Bonds worth

Rs.100 crores was therefore s upposed to be

completed on 26 . 7 .1.991 and report thereof was to be

given o n the next day i . e . Saturday 27 . 7 . 1991 .

Howeve r , on that day due to heavy rain the local

trains were not running and he could not attend the

office . I n his absence General Manager

M r . 8 .R. Acharya and Funds Manager Bipin Di vecha

{P.W.5) accepted delivery from accused No. 2-HPD

contrary to the deal settled by him.

26. As regards information note Exh. 244, i t

i s his specifi c contention that this note was

prepared by CBMF people {of ficers) themselves and

they obt ai ned his signature on i t under threat and

by "force . The said i nformation note is a computer

ger1erated document and he does not know how to

handle computer. He was called by Mr . B . R . Acharya,

General Manager on the 2nd floor of Orient House

Bui lding and at that time three other higher

o f ficers, name ly

Mr . C . S . Gopalak rishna n ,

Mr . K . R . Acharya

General

(P.W�8).

Manager,

M r . S . V . Kamath, Deputy General Manager of Canara

Bank were present. Typed i n formation note was ready

wi th them and under threat of dismissal from

25

SC . 5 /93-J

service, they obtained his signature by force.

Contents therefore are not true . I n the said state

ment there is reference to 19. 5 . 1992 and acco rding

to him on 1 9 . 5 . 1992 Ci ti bank never communicated to

him about SGL because and on that date also he was

on leave as he was sick (he was suffering f rom

Herpes ) . He used t o deal in money market operations

of high value and i n a period of about one year the

transactions were o f about R s . 50 , 000 crores. As

regards BOK ' s c redence same was examined by

C . S.Gopalakrishnan i n his v i s i t during the year

1990 and BOK was recommended for dea l i ng with and

he had fol lowed inst ructions of supe r io r s . Cheque

is requi red to be signed not only by the dea ler but

also by the Funds Manager and he ( funds Manager) is

expected to check every thing before signing t he

cheq u e . Accused No . 1 in fact generated profit for

CBMF . He has however bee11 falsely i nvolved.

Further transactions are not connected or conce r ned

with the transactions of 27 . 5 . 1991 regarding GOI

sec u r i ties .

27 . Accused No . 2-HPD spec i f ical ly contended

i n his defence

sec u r i ties dated

that the t ransactions

27 . 5 . 1991 and the

t ransactions are totally u nconnected.

26

of GO!

further

Al l the

SC . 5/93-J

further t ransactions are i ndependent transactions

which are done i n usual course of business.

Accused No . 2 is ne>t at a l l connected w i th accused

No . 3 and he is no t aware about the dealings of

accused No . 3 . He was merely a broker of CBMF as

wel l as SCB and C i t i bank. Accused No.2 admitted

the existence o f 15% a r rangement with SCB i n re

spect o f sale and purchase of sec u r i t i es through

him. On 27. S.1991 t here was also t ransac tions

between CBMF and BOK i n respect o f sale of PSU

Bonds by CBMF to BOK and co11sideration was paid by

cheque by BOK . At that time there was market

practice o f deali ng in third party BRs and such

t ransactions used to take place regu l a r l y . On

26 . 6 . 1991 he received Rs.25 crores in re�pec t o f

t ransaction of 13% DVC Bonds f rom accused No. 3-AD N .

This was by way o f a BR issued by CBMF i n favour o f

BOK. It was a payment made to him by accused No . 3

i n lieu of or as conside ration o f transacti on of

Rs.28 crores pertai ning to 9 . 25% 1992 securi ties.

28 . On 27 . 7 . 1 991 pursuant to a purchase

transac tion by C BMF of PSU Bonds from BOK he issued

cost memos to fac i l i tate CBMF and as the transaction

was w i t h BOK he made a speci fie note in tt1e cost

memo i ns truc ting CBMF to issue RBI cheque i n favour

27

SC. 5/93-J

of BOK and t he refore � cheques Exh . 83 and 88 were

issued i n favour of BOK . There was abso l u tely no

i n tention on his part to dive r t the funds or to

defraud anybody and the cost memos were issued to

fac i l i tate CBMF to give delivery. In the documents

of accused No. 3-AON i ncluding recei v i ng orders ,

delivery orders and the account books sei zed by the

CBI the mention o f HPD i s not a t his i n$ tance and

at the most i t would suggest that s i nce he was a

broker h i g name a ppears. There was no other reason

for mentioning his name and they ware not his

transactions. He never received money from accused

No . 3 and w henever he received, it was by way o f

lawful consideration under genuine transactions .

He was never i n formed of di shonour o f SGL transfer

forms o f BOK and he never received any dishonoured

SGL from anybody. He has not denied the signature

on the affidav i t but according to him the contents

thereof are fals e . Simila r l y the contents o f

information note o f accused No . l are also false.

The signature on the said affidavi t was obtained by

o f f icers of the CBMF by pract i c i ng coercion. He

was not even aware that BOK was en te r i ng into

transaction� on beha l f o f ADN o r on account o f AON.

Therefore. there was no question of supp ressi o n o f

facts by him o r even by accused No . l . A l l the

28

SC . 5/93-J

t ransactions were genuine and have been ente red

i nto i n the normal course o f business w i thout any

i ntention o f practicing fraud on CBMF. The 6GLs

issued by BOK were not false and forged and he was

not routing transactions through somebody else • s

account but he was routing his transactions through

his own account with Andhra Bank , Fort Branch.

There were t ransactions of about Rs . 27 , 000 crores

i n his account with Andhra Bank during the relevant

pe riod and he has paid more than Rs . 1 c r o re as

banking charges. The funds generated by accused

No . 3 i n these t ransactions have been u t i U. zed by

him and i n fact he (accused No . 3 ) gave evidence i n

Special Case No . 7 o f 1993 for having u t i l i zed the

funds on 27: 7 . 1 99 1 . Al though he stated that he

would be f i l ing wri tten statement , he has f i l ed

only a note of missing l i nks after the arguments

were ove r .

29 . Accused No . 3-ADN has taken a

contradictory stand to that o f accused No . 2-HPO i n

reply to · d i f fe rent questions put to h i m under

section 313 C r . P . C . and has also f i led w r i t ten

s tatement as supplement to oral repl ies to question

put to him under section 313 C r . P . C . . I n the

w r i t ten statement f i led on 27 . 8 . 2002 he has s ta ted

29

SC. 5/93-J

that he i s aged 70 years. He joined the f i rm o f

Champaklal Devidas i n 1961 as a C l e r k . Champaklal

Devidas and J . P . Gandhi were partners o f the f i rm

and the f i rm was dea l i ng i n Government sec u r i t i es

with various banks and financial i ns t i tutions .

Champaklal Devidas and J . P . Gandhi were members o f

the Bombay Stock Exchange . He was wor k i ng as an

Assistant to J . P . Gandhi and was attending to the

bank work regarding deali ngs i n secur i ties. I n

1995 Champaklal arranged for membership card o f

Bombay Stock Exchange fo r h i m . I t was however

dormant si nce he was only working wi t h the f i rm and

was not doing i ndependent busi ness o f his own .

A$te-rlft na rrat� detailed history of the f i rm and

haw he was made di rec to r by Bhupen Da lal . when

Bhupen could no more corlti nue as di rec tor due to

RBI regulations.

30 . Regardi ng the t ransactions of 27 . 5 . 1 99 1

in GOI securi t ies of 2ooa and 2009 . he has

speci fically stated that i t was HPO who di rected

him to deliver through BOK the said SGL transfer

forms and even the detai ls of the transactions were

not given to him and he was led t<' believe that i t

was a simul taneous transac ti ons entered into as i n

t� pas t therefore . amount of

30

SC . 5/93-J

Rs . 103.82 , 47 , 295 .60 was credi ted to his account . On

the same day H i ten Dalal di rected him to purchase

PSU Bonds o f Rs . 1 00 c rores face value and be l i ev i ng

him (HPD) he entered into these t ransacti ons . As

even i n the past simi l a r simul taneous t ransactions

were done, some of which are quoted by him (about

1 0 ) . Thus he di rected SOK to i�sue SGL t rans fe r

forms on the i nstructi ons of Accused No . 2-HPD on

understanding that the secu r i t ies of the same value

would be procured i n simultaneous traneactions by

accused No . 2 and as secu r i t i es were not brought, he

was constantly reminding accused No . 2 and was after

him to comple te the t ransactions . Accused N . 2 on

his part kept on promising to b r i ng the said

secu ri t i es and went on givirig one excuse or the

othe r . Accused No . 2 even promised that SGL transfer

forms dated 2 7 . 5 . 1 99 1 w i l l not be lodged by CBMF

with RBI and when repeatedly remi nded by him.

accused No . 2 i n formed him that CBMF would return

the SGL t ransfer forms dated 2 7 . 5 . 1991 and the BRs

purchased out of the said amount would be returned

f ree of cost to CBMF and the transactions would be

squared o f .

31 . Thereafter on 26 . 6 . 1991 accused No . 2-HPD

took away one BR of Rs . 25 crores regarding 13% DVC

3 1

SC . 5/93-J

Bonds free and without informing accused No . 3 he

sold the said BR under his cost memo to C8MF and

diverted the proceeds to his account i n Andhra

Bank. Accused No. 2-HPO returned two SGLs o·r BOK

and took away remai ning BRs o f PSU Bonds of C8MF on

27 . 5 . 1991 i nforming accused No . 4-Raje that the

transactions of two SGL transfer forms dated

27 . 5 . 1991 i n favour of C8MF had been $quared o f .

He has mai ntained regula r account books and his

statement i n defence i s supported by those account

books. He was never informed by the officers of

BOK that the SGLs were lodged with RBI and were

sent back with objections, nor had the CBMF taken

up the mater with BOK a t any time . Thus he was not

aware rega rding the i l legal sale o f BRs to CBMF by

H i ten Dalal i nstead of returning them free as

promised. Large amounts were brought by Hiten

Dalal and credi ted to his account and he has routed

certain transactions through the account of <�ccused

No . 3 and these amounts were used on di rections o f

accused No . 2-HPD for ostensible purchases on behal f

of Dhanraj Mi l l s for about Rs . 1 12 crores and

balance of Rs . 9 crores was taken away by HPO and

deposited i n his own account w i t h Andhra Bank and

this is also shown by him in hi s account books . He

is not aware about Rs . 101 . 75 crores brought i nto

SC . 5/93-J

his account on 27 . 7 . 1991 by HPO from CBMF by i l le

gal sale of BRs o·r CBMF unde r his own cost memo.

Looking to the past conduct o f HPO-accused No . 2 i n

bringing large amounts t o h i s account ha had no

reason to suspect any i l l ega l i t y . The amount o f

Rs . 101 . 75 crores received from C B M F and Rs . 20

crores received f r om Andhra Bank were brought by

accused No. 2-HPD and were used for purchase on

account of Dhanraj M i l l s by HPD. When he was i n

Police Custody . he came to know about i l l egality i n

these transactions . HPD-accused No . 2 had no busi

ness to sel l the aforesaid BRs. under his own cost

memos and CBMf should not have purchased these BRs

under the cost memo HPD and should have i nsisted on

the cost memo of BOK. Thus HPD has i n fact cheated

him (accused No . 3 ) (broken his fai th) for ul te rior

motive. He did not deliver the SGLs on 27 . 5 . 1991

a l t hough he ( HPD ) was claiming that he was holding

the same and this is stated by him i n his affidavit

Exh . 250 . After squa ring of the transactions .

accused No . 2 had no right to sell the BRs or PSU

Bonds under his own cost memo to CBMF having ob

tained the same free of cost from accused No . 3 for

the purpose of squa ring o f the transactions of

27 . 5 . 1991 . While depos i t i ng Rs . 1 0 1 . 75 crores on

27 . 7 . 1991 neither accused No . 2-HPD nor did the

33

..

SC . 5/93-J

o f f i cers of BOK i n form him that the amount was

obtained by HPD i l lega l l y and dishonestly by sel l

ing the BRs o f CBMF i nstead o f delive r i ng the same

free o f cost. HPD was involved i n further transac-

t i ons pertaining to sale of two SGLs to C i t i and to

SCB as he was common broker i n a l l these transac

tions . Accused No . 3 had however no role to play i n

a l l these t ransact ions . The real bene f i c i a r ies o f

t ransactions are not made accused by the CBI for

reasons be$t kno�n to them. He neve r had any

dishonest intent i o n . He is a victim of c i rcum-

stances .

32 . Defence of accused No . 4 i s that he

started his career as a small employee and was at

the relevant time Agent o f BOK . He was holding

power o f attorney to deal i n secur i ties

transactions on behalf o f BOK. Accused N o . 3 was

di rector o f the bank and he was bound to obey

i nstructions given by accused No . 3 and the refore,

o n the instructions o f accused No. 3 , he issued the

SGL transfer forms a l t hough there was no secu r i ty

i n the account o f accused No . 3 . Accused No . 3

promised him that securi ties of the same value

would be simul taneously purchased by evening o f

2 7 . 5 . l 991 f r o m SCB and he be l i eved i n that

34

SC . S/93-J

sta tement and assurance of accused N o . 3 and even

otherwise accused No . 3 being Di recto r . he had no

cho ice than to obey accused No . 3 . Rega rd i ng

t ransactions o f GOI securi ties dated 27 . 5 . 1991

postings a r e no t made in the accounts of BOK as

accused N . 3 had promised to bring in the secur i ties

and there was no provision for any suspense

accoun t . He has no connection w i t h accused No . 2 or

accused No . 1 and there was no question o f his being

a conspi rator al ong with them . The material

account books wa re always at SOK ' s head o f f ice ,

Fort Branch. He had credited call money to the

account of accused No . 3 on the inst ruc t ions of

Chairman of BOK and he credited the cheque on

2 7 . 5 . 1991 to the account o f accu$ed No . 3 as the

transactions were of accused No . 3 and not of BOK .

He has not himse l f received any advantage and he

has been impl icated only because certai n documents

are signed by him at the ins tance of accused No . 3 .

He has mentioned the cor rect account number of

consti tuents i n the SGL t ransfer forms when they

were returned for want of account numbe r . He also

admi. ts that SGL transfer forms were brought back by

accused No . 3 th rough accused No . 2 from CBMF and the

SGL transfer fo rms were discharged as the

transactions were squared of and when P . W . 8

35

SC . S/93-J

K . R . Acharya and M r . Gopalakrishnan visited his

office on 22 . 5 . 1992 he had shown them discharged

SGL transfer forms and also gave them photostat

copies thereo f . He is not aware of the further

transactions . He i s not even concerned w i t h those

transactions at a l l .

33. I n view of the controversy the point�

that arise for determination are along w i th the

findings thereon are as below and reasons for the

fi ndings are stated in the paragraphs that follow:

( 1 ) Does the prosecution prove that accused

Nos . 1 to 4 o r any o f them entered into

criminal conspiracy dur i ng the period May

1991 to December 1991 w i t h the object of

obtaining pecuniary advantage to accused

No . 3-ADN and ultimately to accused No . 2-

HPD t o cheat CBMF and for that purpose

suppressed from CBMF and/or from Bipin

Divecha ( P . W . 5 ) certain material facts,

v i z . that SGL transfer forms were issued

on account of accused No . 3-ADN and that

there was no backing of secu r i t ies for

36

SC . 5 /93-J

issuance o f SGL transfer form$ i n the

concerned account o f ADN and that cheque

o f Rs . 103 , 82 , 4 7 , 295 . 60 ps. was be i ng

issued against two false and forged SGLs

issued by accused No . 4 C . S . Raje ?

F i nd i ng : Yes . The conspi racy was to s i phon the money by ostensible make beli eve sale f rom CBMF and cause wrongful loss to i t and w rong f ul gain to accused No . 2-HPD and accused No . 3-ADN.

( 2 ) Does the prosecution prove that accused

No . 1 -Narichania being a public :servant by

abuse of his p0si tion and/or by corrupt

or i l legal means dishonestly purchased

through accused No. 2-HPD securities 1 1 . 5%

GOI 2008 and 1 1 . 5% GOI 2009 face value

Rs . 58 . 39 crores and Rs . 44. 5806 c rores

respectively against the above desc ribed

two SGL t ra nsfe r forms ?

Finding: Yes.

(3) Does the prosecution prove that accused

No . 4 -Raje having dominion over o r being

ent rusted with the f unds of BOK comm i t ted

c r i mi nal breach o f trust by dishones t l y

credi t i ng the proceeds o f the account

37

SC. S/93-J

payee cheque dated 27 . 5 . 199.l bea r i ng

No . 160319 payable to BOK i n the

O . D . Account No . 201 of aCCU$9d No . 3-ADN

maintai ned by BOK i n violation of the

banking r·ules and practice and/or express

or implied t rust touching the mode o f

discharge of such trust causing thereby

i l legal loss to CBMF and cor respondi ng

i l legal gain to accused No . 3 and

ul timately to accused No . 2 knowing f u l l y

w e l l that the t ransactions were only

ostensible t ransactions i n securi t ies ?

F i nding: Yes. I llegal gain to accused Nos . 2 and 3 .

( 4 ) Does the prosecution prove that accused

No . 1 concealed from CBMF that the

aforesaid cheque was being issued against

two false and forges SGl$ thereby causing

cor responding wrongful loss to CBMF and

wrongful gain to accused Nos . 2 a�d 3 ?

Finding : Yes. However the SGLs though false are not forged documents .

( 5 ) Against which af the accused individually

the offence of cheating punishable under

38

SC . 5/93-J

section 420 !PC is proved . ?

Findi ng ; Against a l l the accused Nos . 1 to 4 .

(6) Does the prosecution prove that accused

No . 4 issued the aforesaid two false and

forged SGL transfer forms knowing f u l l y

wel l that they were not backed by

securities and neither BOK nor ADN were

i n a position to deliver the said

secur i ties at any time ?

F i nding: SGLs are false but not forged docume n t s .

(7) Does the prosecution prove that accused

Nos . 1 , 2 , 3 and 4 used the aforesaid two

false and forged SGL transfer forms as

genuin� knowing them to be false and

forged '?

Finding: SGLs are not forged document$ a l though they <�re false.

( 8 ) Does the prosec ution prove that i n

pursuance o f the aforesaid conspi racy

accused No . 4-C . S . Raje · falsi fied the

accounts of BOK ?

F i nding: Yes.

39

•

SC . 5/93-J

(9) Does the prosecution prove that accused

Nos . 2 and 3 rece i ved stolen property

knowing or having reason to believe that

tha same to be stolen by �ecei v i ng the

proceeds of the aforesaid RBI cheque

issued by accused No . 4 i n the name o f

CBMF ?

Fi.riding: No.

( 1 0 ) Does the prosecution prove that accused

Nos . 2 , 3 and 4 abetted the commission o f

offence o f criminal misconduct comm i t ted

by acct1sed No . 1 i n pursuance o f the

aforesaid c r i minal conspiracy ?

F i nding: Yes.

( 1 1 ) What offences are co m�i t ted and by which

of the accused and what sentence ?

F i nding: As stated i n the concluding paras. Sentence to be passed after hea r i ng the accused .

40

SC. 5/93-J

.34 . Before I proceed to discuss . scan, and

appr·eci.ate the evidence. i t is 11ecessary to point

out the nature and type of evidence adduced by the

prosecu tion. The oral evidence consi!it o f 47

witnesses including the investigating officer and

the compl ainant . There are volumi nous documents

mos tly consisting o f records of the transactions

be tween di fferent banks, concerned account books ,

and records of the Reserve Bank o f India. certa i n

correspondence exchanged between banks, reports

submitted by the accused and by some others to the

head o f f i ce o r to their suped.ors. In addi tion

there is a separate huge record of the account

books maintai ned by accused No . 3 regarding which

one o f his employee has given evidence and p roved

the concerned entr ies . Apart f rom the above , the

personal diary o f accused No . 1 is also produced by

the prosecution i n which details regarding the

t ransactions are recorded mostly by accused No. 1 .

These records were sei zed during i nvestiga t i o n .

Simi l a r l y certain part o f the account books or

computer records of the accounts maintai ned by

accused No . 2 is also seized and is relied upon by

the prosecution. Apart from this, there is a w r i t

ten note dated 2"J-. 5 . 199l_si9ned by accused No . l and

given to hi s superiors as his explanation and there

4 1

SC. 5/93-J

i s an a f f i davit of accused No . 2 sworn before Notary

Public coupled with the evidence of notary. These

two documents al though they are statement of ac-

cused, they a re given long back when even lodging

of F I R was not i n contemplation and there is no

challenge to t he i r admissibi l i ty i n evidence i n

view o f this s i tuation.

35 . The oral evidence can be gro uped

insti tution wise and it would help i n referring to

the evidence and thei r appreciation al�o. List of

w i t nesses insti tution wise are as below:

� i!D.d Designation Qi Witness.

� Q.E. KARAP LIMITED

l . Shri Vilas Damodar Rajadnya , Vo l - I . 1 -44 Reti red officer working w i t h BOK i n 1991 in Advance Department and he was also General Manager .

2 . Shri Mukund K rishnaj i Khe r . Agent o f BOK , Fort Branch. Vo l - I . 45-173

i4 . Mrs. Meena Mohan Arbune, Worki ng i n 1991 i n Karur Vaishya Bank , . Mumbai as Manage r , Head Office. Vol-IV. 629-661

CANBAMK MUTUAL �

5. Sl1ri Bipin Pushpasen Oivecha, Vol - 1 1 . 1 89-322 Funds Manager wit h Can Bank Mutual Fund at the relevant time.

42

6 . Shri Rajesh Pitambardas Bhatija, working with Can Bank Mutual Fund under M r . An i l Narichania-

SC . 5/93-J

Accused No . l i n Secretarial Staf f . Vol - I l l . 383-41 1

7 . Ms . Nandi ta Nitin Rao . ( Nayak . ) , working with Can Bank Mutual Fund i n Secreta rial staff (Canstar Scheme) at the rel evant t i m e . Vol-I I I . 412-471

8. Shri Kundapur Rarnkrishna Acharya. workin9 with Canara Bank, Bangalore Office and thereafter promoted and posted in Bombay . He was Chief Executive Officer of Can Bank Mutual Fund, Bangalore . Vol• I I I . 472-537

9. Shri S . N . Satish, working with Can Bank Mutual Fund as Manager upto 1994 and also working as Manager i n Canstar Scheme Ni t h Bipin Divecha. Vol-IV. 538-561

1 1 . Shri P . 3 . Subbarao, working with Can Bank Mutual Fund during relevant period as Astt. General Manager and t ransferred to Mumbai and was working under B . R. Achar·ya . Vol - I V . 580-590

1 2 . Shri Ramesh Suryakant Parab. working as Peon with Can Bank Mutual Fund at the relevant time . Vol -IV . 591 -614

13. Shri K . V . Hegde, working as As t t . General Manage r . Canara Bank Regional office was asked to come to Bombay to look into the transactions o f the Can Bank Mutual Fund. Vol -IV. 615-628

20. Shri Jyotimani Nallaiah, working with Can Bank Mutual Fund and looking after misce l laneous work l i ke , reconc i l i a tion of bank account and i n Novembe r , 1990 as Manager of Ca nstock scheme . Vol-V. 751 -804

2 1 . Mrs. Jyoti Ashok Bhatt, working with Can Bank Mutual Fund i n Secre tarial s t a f f and was working i n Can 80 CC 90 Scheme .

43

Vol-V. 805-834

46 . Shri A . M . Prabhu, working as General Manager , Canara Bank and Chief Executive of Can Bank Mutual Fund. He g ranted sanction o f prosecution .

SC . 5/�3-J

Vol - I X . 1402-1406

RESERVE .etlliK QE �

22 . Shri Vardhanapu V i l l iam Raj u , working with Reserve Bank o f India as S t a f f Of ficer maintaining accounts of the Banks and f i nancial institutions. Vol-V I . 835-848

23. Mrs. Snehal Suhar Muley, working w i t h RBI as Clerk in RBI PDO office Mumbai at the relevant time and was in correspondence secti o n . Vol-VI . 849-854

26 . Shri Abdus Samad U . Khan, working w i t h RBI PDO as Staff Officer. Vol-V I . 906-913

31 . Shr i Shri ram Khadilkar. working w i th RBI PDO Department as Clerk. Vol-V I I ! . 1 1 72-1 1 75

32 . Shri J . R . P . Ratnarao, working w i t h RBI PDO in cor respondence section.

3 3 .

34.

3 5 .

Shri Dahyabhai S . Patel , wo r k i ng with RBI PDQ i n lndustr-ial and Export Credit Department.

Shri N . D . Parme�.>hwaran , working w i th RBI , Bombay i n Banking Operations.

Shri A . L . Verma , working w i t h R . B . I . as Di rector and monito ri ng of money marke t .

36 . Shri Peter W . D " souza, working w i t h RBI as Staff O f ficer i n ·

the Accounts Department .

44

Vol-VII I . 1 1 76-1185

Vol-V I I I . 1 186-1187

Vol-VI I I . 1 188-1 192 Vol-VI I I . 1207-1214

Vol-VIII . 1 1 93-1 197

Vol-VI I I . 1 198-1201

3 7 . S h r i wi. t h

' .

A . Mastan Reddy, working RBI a t the relevant time

i.n Deposit Account Department .

38 . Shri A . V . Raghuraman, working wi t h RBI Staff O f f i ce r .

39 . Shri Ravindra Raghunath Jos h i . working w i t h RBI as Clerk .

40. Shri L . M . Fonsaca, working w i t h RBI as Chief General Manager in charge of Non-banking operation.

4 1 . Shri Nayan Vi nayak Samant , working as C l e r k Grade- I , RBI .

43 . Shri Manohar Pandurang P i tka r ,

SC . 5/93-J

Vol-VI I I . 1202-1206

Vol-V I I I . 1215-1218

Vol-VII I . 1219-1234

Vol-V I I I . 1235-·1240

Vol-VI I I . 1 24 1 - 1 257

working w i t h RBI as Staff Office r . Vol-VI I I . 1 262-1271

STANDARD � BANK.

24 . Shri Manoj Rane , working with Standard Chartered Bank in the front office and was hand l i ng cal l money t ransactions under Mohanlal and Jaideep Pathak and was also dea l e r . Vol-VI . 855-872

27 . Shri Sri kant Hanumant Sheth. working with Standard Chartered Bank as Clerk. Vol-VI . 91 4-1011

28 . S h r i Sanjay Natwa r la l Shah.working wi. th Standard Charte red Bank as C l e r k i n the Money Market Department under Jaideep Pathak and Santosh Mulgaonkar. Vol-VI I . 10 1 2-1051

29. Shri Ganesh Atmaram Hatka r , working with Standard Chartered Bank as Clerk i n the Money Market Department as Clerk under Jaideep Pathak, Santosh Mulgaonkar and Benu Chaterjee. Vol-VI I . 1052-1062

30. Shri Santosh S i taram Mulgaonkar , working i n Standard Chartered Bank i n Investment Department at the relevant time under Jaideep Pathak. Vol -V I l . 1063- 1 1 7 1

45

1 5 . M r s . Annapurna Narayanmoorthy. working with C i ti bank as

S C . 5 /93-J

Receptionist-cum-Clark i n 1991 . Vol - IV . 662-687

1 6 . Shri Vishwanath N . Shenoy. working with C i t i bank as Asstt . Vice President i n T reasury Department . Vol-V. 688-725

1 7 . Sh ri Prashant Madhusudan Purkar·, working as Peon in the o f fice of M r . Hiten P . Dala l-Accused No . 2 . Vol -V. 726·�732

19. M rs . Sa r i ta Desai , working w i t h Ci tibank a s Special Assistant and at the rel evan t time was i n Sec u r i t i e s Department. Vol-V. 742-750

2 5 .

ANDHRA lA.lilS.

Shri Ramesh Gangadhar Ramteka. working with Andhra Sank, Bombay Branch. Fort i n cur rent account department .

� QE, AMERICA

45 . Sh ri Mohan D�t tat raya Kokane , working i n Bank of Ame rica, Treasury Operation Department looking after sec u r i ties department.

KeRUR VAISHYA BA�K.

3 . Shri Achis Sunderrajan Vasudevan . working i n 1991 i n Kar u r Vaishya Bank, Mumbai , as Manage r .

Vol-VI. 873-905

Vol - I X . 1 384-1401

Head O f f i c e . Vol-l . 1 74-179

FEDERAL �

4 . Shri Balgopal Ramkr ishnan , working as Deputy Manager i n May 1991 with Federal Bank , Mumbai . Vol-I . 180-188

46

OTHER WITNESSES

44. Shri Bharat S . Da rj i , working with M r . Abhay Narottam-Accused No . 3 upto 1992 i n Accounts Section, w r i t i ng account books , prepa r i ng vouche rs, receipts etc. along with Naval Kishore Pand i t , Arun Sudhale, Manisha

SC . S/93-J

Rawal and K i ran Sur t i . Vol - I X . 1 272-1383

18. Shri Tushar Jagannath Pati l , working as Peon i n the o f f ice of M r . �iten P . Dalal-Accused No . 2 . Vol-V. 733-741

4 7 . Shri B . N . P . Azad, Investigating O f ficer. Vol-IX . 1 407-1429

.36 . So far as documentary evidence i s

conce rned, various seizure memos and panchanamas

a re admitted i n evidence under section 294 o f

Cr . P . C . However, the other documents are not

admi tted. The documents are proved and in case o f

some documents when only a pa r t i cular portion of

the document was proved that portion alone was

admitted i n evidence a t that stage. The objections

raised to the admissibi l i ty of the documents have

been dea l t with whi l e recording the evidence.

Al though not adm i tted , accused are not disputing in

general the documents or the contents thereof i n

case o f bank documents and the bank account books

whereas accused No. 2-HPD has seriously cha l lenged

the entire account books of accused No . 3-ADN.

Al though evidence is lengthy running i n to 1500

pages ( i n 9 typed volumes) and documents are also

47

SC . S/93-J

voluminous refe rence can be restricted only to the

relevant portions as most of the o ra l evidence

consists of depots i tions pertaining to the desc rip

tion of the documents and the proof thereof, which

at thi s stage generally is not i n dispute and

wherever i t is chal lenged , refe rence would be made

to the same . With this background I propose to

deal w i t h the evidence on record and i n my view i t

i s convenient to refer to the evidence transaction

wise.

37 . Sefore I refer to the docuMents and the

material evidence i n respect thereof , i t is neces

sary to point out what i s "BR" and what is "SGL" .

SGL transfer form i s a document by which transfer

if effected from SGL account of bank or f i nancial

i nsti tution to the account of another bank o r

f i nancial insti tution. I t i s issued by the bank

which sel l s sec u r i t ies which are i n credit i n i ts

SGL account maintained with Public Debt O f fice

( PDO) of RBI . and as can be seen in the present

case, i t may be SGL Account sepa rately maintained

for a constituent, inasmuch as BOK was permitted to

open a separate SGL account for i ts constituents.

I n fact during the course of argument M r . R.D.Ovle

k a r , learned Counsel appea r i ng for accused N . 2 has

48

SC . 5/93-J

made a reference to the contents of one o f the SGL

transfer forms used in this case . SGL Transfer

form Exh.33 is issued by BOK fo r the transaction of

GOI 2008 dated 27 . 5 . 1991 and the format of the form

i s as below:

FORM OF TRANSFER FOR OPERATION ON S . G . L. ACCOUNT .

We, The Bank o f Ka rad Ltd . , Bombay do hereby assign and t ransfer our i n terest or sha re i n the Subs i d i ary ledger account No.BYSL: . . . . . • . . . . . . . . . . . For Rupees . . . . . . . . . . . . . . . . ( Rupees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . • . . . . .

being the portion outstanding at the credit o f the aforesaid account for Rs. • . . . . . . • • . . . . . . . . . . as registered i n the books of the Re�erve Bank o f India, Public Debt. O f fice, at Bombay together w i t h the accrued i nterest thereto rUp to . . . . . . . . . . . . . . . . . . . . . . . . . . . • . . . . . . . their

administrators or assigns and we • • . . • • . . . . . . • • • . • . . . . • . . • . . . . • . . . • • . • . • . do freely accept t he above amount t rans ferred t o us .

As W i tness our hand the thousand. nihe hundred Ninety

day o f

For THE BANK OF KARAD LTD . ,

One

Si gned by the above named transferor in

the presence of

Reg . Ma nager/Agent/Of f i ce r , 0ombay Se l ler

Signature

The Bank of Karad Ltd . , Raja Bahadur Compound,

Ambalal Doshi Marg, ( Hamam Stree t ) Post Box No . 1347 , Fo r t , Bombay 400 023.

Signed by the above named t rans fe ree i n the presence o f

49

Buyer

Signature : Occupa tion : Address o f : Wi tness

SIGNATORY

S C . S/95-J

For CANARA BANK TRUSTEE CANBANK MUTUAL FUND

AUTHORISED

FOR THE USE I N PUBLIC DEBT . OFFICE

I ndia

P . Manager ,

Reserve Bank o f

Publ ic Debt. Office, Bombay 400 001 .

I t i s clear from the above wordings of the SGLTF

that the sel l i ng bank makes a ·firm statement

regarding the assignment o f the i r interest i n the

particular SGL account mentioning the face value

with the desc r i ption o f the secu r i ties with a

f u rther statement that the said securi ties are

outstanding at the credit o f the aforesaid account

as registered i n the RBI booke with Publ i c Debt

Office and agrees to transfe r i t with interest to

the purchasing bank or f i nancial institution and

the purchasing bank accepts securi ties as

transferred to i t . I t i s also not disputed that i t

was requi red to be signed by two o f ficers in case

of SGL issued by CBMF. Howeve r , i n case of BOK

accused N . 4-Raje alone coul d issue the SGL transfer

form. The purchasing bank has to sign in place of

transferee.

so

38.

sel l i ng

SC. 5/93-J

Bank receipt acknowl 9d9es receipt by the

bank o f the amou nt i n favour o f

counterparty the l!>ecu rities w i th particular

desc r i ption mentioning the exact value as we l l as

face value , rate with a statement that the

securities or the bonds o f the face value

mentioned. There is a clear unde r taking that the

secur i ties wi l l be delivered when ready i n exchange

of the rece i p t . Thus the normal mode of discharge

of BR is by physical delivery o f securi ties. The

evidence of t r·ansac t i o n has to be considered on

this background.

Broker

FORMAT OF BANK RECE I PT .

JiQI TBANSFERABLE Tel : 262 0165-66-67-68

(Taken from form Exh . 86 )

CANARA fu1tlli

Trustee : CANBANK MUTUAL FUND . Orient House, 2nd f l oo r ,

Adi Marzban Pat h , BOMBAY 400 038.

No . 2272 Rs • . • • • • • • • • • • • • •

Received f rom • . • . . . . . . . . . . . • . . . . . . . . . . . . . . . . . . . . . .

the sum of Rupees . • . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

be i ng the cost o f . . . . . . . per cant . . . . . . . . . . . . . . . .

Securities/Debentures/Bonds of the face value o f

5 1

SC . 5/9:!-J

Rs . . . • . . . . . . . . . @ . . . . . . . . . . . . . . . . . . % w i t h interest

Rs . . . . . . . . . . . . . . . . . . . . . . less i ncome Tax Rs . . . . . . . . .

f r om . . . . . . . . . . . . . . . to date.

The Sec u r i t i es/Debentures/Bonds of the face value

of Rs . . . . . . . . . . . . . a re delivered herewi t h and Secu-

rities/Det>entures/Bonds

Rs .. 0 •••••• -••••• will Qn deliyered � r�ady in

exchange fQr. ..t.b..1.§. receipt � discharged.

39 .

T rustee For CANARA BANK. Canbank Mutual Fund

Managef" (Unde r l i n i ng is m i ne . )

The first two transactions are on paper

at least transac t i ons of sale between BOK and CBMF ,

but as a matter o f fact i t was accused No. 3-ADN who

was counter party and sold the sec u r i t i es to CBMF.

At the cost of repeti t ion transactions are ( i ) sale

of 1 1 . 5% GOI 2008 to CBMF by BOK (ADN) face val ue

Rs . 58 . 39 crores on 27 . 5 . 1991 and ( i i ) sale of 1 1 . 5%

GOI 2009

c rores .

to CBMF by

Evidence o f

'\i':-J.) BOK� face val ue Rs . 44 . 5805 " ..,.

P . W . 1 Vi las Rajadnya is of

general type desc r i bi ng the procedure in sale and

purchase transactions of the bank (BOK) and the

general procedure of bankers a l t hough ever-y bank

has i ts own pecu l i a r i ties. the basic requirements

52

SC . 5/93-J

and the concerned documents are of same type.

P . W . 1 Rajadnya has stated that in case of sale and

purchase o f securi ties head of fice af BOK was to

give i nst ructions to the sec u r i ties department that

the bank is holding in excess or short ce r t a i n

secur i ties f o r the purpose o f Stat1,,1tory Liquidity

Ratio (SLR) . Howeve r , i t needs to be noted here

o n l y that this would not apply i f the

is of a congtituent of the bank

transac tion

and not a

transaction by the bank as such. He has stated

that BOK was having Subsidiary General Ledger (SGL)

account with PDO RBI and subseque n t l y the SGL

accou n t was opened for the transactions i n

sec u r i t i es o n behalf o f i t s c l ients constituents.

40. The documents pertaining t o the

transaction are proved through P . W . 2 Mukund Kher a t

the relevant time working as Agent of the Fort

Branch of B O K . Evidence t h a t accused No.4 being

agent was i n -charge of sec u r i tie$ t ransactions and

was given power of at torney fo r that purpose and

had therefore powers to issue SGL i n sec u r i t y

transactions i s n o t i n dispute a l though t he extent

of his authority for entering i n to the transactions

on beha l f of the bank is a dispu ted quest ion . I t

is not necessary to go into that aspect of the

5..3

SC. 5/93-J

matter i n this case as the transaction even

acco rding to the prosecu t i o n , were of accused No . 3-

ADN, a consti tuent of the bank, a l t hough on

i t was shown to be a ban k ' s transaction.

pape rs

There

can be no monetary l im i t to a t ransaction ente red

into on behal f of the consti tuent but at the same

time i t cannot be even disputed that the

cons t i t uent can enter i nto transaction only when he

possesses concerned securi ties and i s i n a pos i tion

e i ther to give physical delivery or otherwise

securi ties a re held by h i m i n the SGL account fo r

which separate account was maintai ned wit h RBI PDO

by BOK No. BY-SL-107. I t needs to be noted that

this sepa rate account was not an independent

account for one consti tuent, vi z . AON-Accused No . 3 ,

but i t was an account for a l l the cons t i t uents of

the bank i n which the secu r i t ies held by

particular consti tuent were separately shown i n

his name .

4 1 . P . W . 2 Mukund Kher has deposed that i n

regard to broker • s (cons t i tuent ' s ) own

t ransactions . I f he wants to purchase sec u r i t i es he

would issue receiving order i n favour o f BOK

desc r i bi ng the particular sec u r i t y , face value,

rate and i ndicate the due date o f i nterest and also

54

a

SC . S/93-J

11ame of the counter party. Thereafter the

concerned person from the secur i t i es depa r tment

w i l l confirm from the Fort branch whether the

concerned broker has sufficient funds i n tha

account to purchase such secu r i t ies and i n case o f

sale by such broke r , he w i l l give del i very order

men t i o n i ng the aforesaid deta i ls as wel l as mode of

delivery v i z . SGL , physical o r BR and on the basis

of the said delivery order cost memo w i l l be

prepared by the securi ties department and o n the

original cost memo the name of the broker or his

account number are not mentioned whereas o n the

remaining three copies , the name o f the broker is

menti oned along with his account number and the

second copy is treated as advise to the broker and

the third copy is the office copy which i s to be

sent to the Fort Branch and one copy wi l l remain

with the secur i ties depa r tmen t . As stated earlier

evidence i n proof of the documents pertaining to

the transaction is not i n dispute. I t would be

convenient to refer to the evidence and documents

togethe r . Referring to Exh. 30 delivery order of

accused No . 3-ADN dated 27 . 5 . 1991 , he stated that on

the top of :i. t the words " N P " are mentioned which

means " not posted" or " no t to be posted " . This

different terminology he has used at two places

55

SC . S /93-J

but u l t imately i t is clear that i t was meant for

not posting the entry of the said docume nt i n the

account books o f BOK , which aspect of the matter

even accused No . 4 has not disputed but has given

explanation for the same. This delivery order i s

i n respect of GOI 2008 and simi lar i s the delivery

order in respect o f GOI 2009 Exh . 34 containing

simi lar endorsement as " N P " i n red i nk on t he top

as also the word "SGL" in red i n k . He deposed that

in the secur i ty l edger maintai ned by BOK for

Accused No . 3 in the concerned folio$ Exh . 32

Exh . 36 , there were no secu r i t i es i n balance.

the folio pe r taining to GOI 2008 balance was

1300 whereas i n the folio pertaining to GOI

AON

and

I n

only

2009

balance was ni l , which is not in dispute as wel l

as the fact that there were no sufficient

secu r i ties of aforesaid desc r i pt ion in the account

of BOK i ts e l f on that particular date.

4 2 . By issuing the delivery order Exh . 30 on

27 . 5 . 1991 accused N o . 3-ADN di rected the BOK to

deliver to CBMF 1 1 . S GOI 2008 a t the rate of

Rs . 10 0 . 78 face value Rs . 58 . 39 crores w i t h inte rest

t i l l date against SGL conveying thereby that the

sec u r i ties were held i n the SGL account maintained

with the RBI PDO. The delivery orders and SGLs

56

SC . 5 /93-J

pertaining to t ransaction o f GOI 2009 o f t he same

date are simi l a r ( Ex h . 34 and Exh . 37 ) . The ot he r

wi tnesses on the same point are P . W . 1 4 Meena

Arbune, P . W . 44 Bharat Dar j i , a l t hough P . W . 44 does

riot know what happened at BOK .

43 . Cost memo o f t h i s transaction Ex h . 3 1 i �

signed by accused No . 4 -Raje . I t i s prepared by

P . W . 14 M r s . Meena A r bune and she has stated that i n

the copies o f the cost memo Ex h . 3 1-A and 31-8

mentioning o f " ADN " means the amount has been

credited to O . D . Account No . 20 1 o f AON and that the

del i very o rder was given to he r by accused No . 4-

Raj e . I t is her speci fic evidence that whenever

she was required to work i n the de pa r tment in the

absence of regular C l e r k of Sudhakar A i l , she had

occas i o n to prepare SGL t rans fe r forms as well as

cost memos i n such transactions. Accused No . 4 gave

her delivery order Exh . 30 o f accused No. 3-AdN and

asked her to prepare the cost memos, she veri fied

the ledger f o l i o Exh . 32 pertaining to the securi-

ties and found that there was no balance and a.c-

cordingly i nformed Accused No . 4- Raje that there was

no balance pe rtai n i ng to the sec u r i t i es i. n the

account of bro ker ( AON) . Inspi te o f t hat Raje

asked her to prepare the cost memo and del ivery

57

SC . S/93-J

document and acco rdingly she prepared the same .