How do agency problems and information asymmetry moderate investment-cash flow sensitivity-Evidence...

30

1 How do agency problems and information asymmetry moderate investment-cash flow sensitivity- Evidence from China’s listed firms Pei-Gi Shu*, Ya-wei Yang**, Yin-Hua Yeh***, and Shean-Bii Chiu**** * Graduate Institute of Business Administration, Fu Jen Caholic University ** Department of Finance and International Business, Fu Jen Catholic University *** Institute of Finance, National Chiao Tung University **** Department of Finance, National Taiwan University Abstract In this study we investigate the investment-cash flow sensitivity of the listed firms in China and verify that investment is strongly sensitive to cash flow. We explore whether this sensitivity is a result of agency problems that managers with high discretion overinvest, or information asymmetry that market demands a high risk premium to result in underinvestment. We use alternative variables of ownership structure and board structure to capture agency problems and alternative variables to capture information asymmetry. We find that investment-cash flow sensitivity results mainly from agency problems embedded in variables of ownership structure and board structure. Specifically, we find that the wedge between voting rights and cash flow rights and state control accentuate investment-cash flow sensitivity, while CEO/chairman duality and board size attenuate investment-cash flow sensitivity. Moreover, the result is more saliently found in the subsample of firms with high cash flow and low growth potentials. Finally, we contrast the impact of agency problems on investment-cash flow sensitivity before and after share reform of the split share structure. The result indicates that the moderating effect of agency problems is heightened after the share reform.

Transcript of How do agency problems and information asymmetry moderate investment-cash flow sensitivity-Evidence...

1

How do agency problems and information asymmetry moderate investment-cash

flow sensitivity- Evidence from China’s listed firms

Pei-Gi Shu*, Ya-wei Yang**, Yin-Hua Yeh***, and Shean-Bii Chiu****

* Graduate Institute of Business Administration, Fu Jen Caholic University

** Department of Finance and International Business, Fu Jen Catholic University

*** Institute of Finance, National Chiao Tung University

**** Department of Finance, National Taiwan University

Abstract

In this study we investigate the investment-cash flow sensitivity of the listed firms in

China and verify that investment is strongly sensitive to cash flow. We explore

whether this sensitivity is a result of agency problems that managers with high

discretion overinvest, or information asymmetry that market demands a high risk

premium to result in underinvestment. We use alternative variables of ownership

structure and board structure to capture agency problems and alternative variables to

capture information asymmetry. We find that investment-cash flow sensitivity results

mainly from agency problems embedded in variables of ownership structure and

board structure. Specifically, we find that the wedge between voting rights and cash

flow rights and state control accentuate investment-cash flow sensitivity, while

CEO/chairman duality and board size attenuate investment-cash flow sensitivity.

Moreover, the result is more saliently found in the subsample of firms with high cash

flow and low growth potentials. Finally, we contrast the impact of agency problems

on investment-cash flow sensitivity before and after share reform of the split share

structure. The result indicates that the moderating effect of agency problems is

heightened after the share reform.

2

1. Introduction

In a perfect market a firm’s investment decisions should be independent from its

financial condition (Modigliani and Miller, 1958). However, the excess sensitivity of

investment to cash flow, initially documented by Fazzari, Hubbard, and Petersen

(1988), has triggered numerous academic attentions ever since. Literature exploring

the underlying factors is mainly in two threads: agency problems (e.g. Jensen and

Meckling, 1976; Grossman and Hart, 1982; Jensen, 1986) and information asymmetry

(e.g. Myers and Majluf, 1984; Greenwald, Stiglitz, and Weiss, 1984). The agency

problems indicate that owners-managers of levered firms tend to overinvest in risky

while negative-NPV projects due to their limited liability (Jensen and Meckling,

1976). The information asymmetry between firms and outside investors imply that

good investment opportunities many be forsaken because the costs of issuing

undervalued securities exceed the benefits from profitable project investments (Myers

and Majluf, 1984). A similar argument proposed by Stiglitz and Weiss (1981)

indicates that asymmetric information may result in the rationing of debt finance.

Prior studies tracing investment-cash flow sensitivity mainly focus on financing

constraint that is based on regressions of investment on cash flow and Tobin's Q.

However, challenges remain on the issue of how financial constraint is defined. For

example, Kaplan and Zingales (1997) use multiple qualitative and quantitative criteria

to define financial constraint and find firms that are less likely to be financially

constrained are associated with higher cash flow sensitivity. Kaplan and Zingales

(1997) and Hovakimian (2009) indicate that the sensitivity is non-monotonic with

respect to financial constraint. Another thread of studies illustrates the impact of

agency problems on investment-cash flow sensitivity. For example, Huang et al.

(2011) using the data from Chinese listed companies examine the effect of agency

cost on the relation between top executives' overconfidence and investment-cash flow

3

sensitivity. They find that the positive effect of top executives' overconfidence1 on

investment-cash flow sensitivity holds only for companies that exhibit high agency

cost. Pawlina and Renneboog (2005) simultaneously include agency problems and

information asymmetry into examination and conclude that investment-cash flow

sensitivity results mainly from the agency costs of free cash flow.

In this study we also include both agency problems and information asymmetry

into the examination of investment-cash flow sensitivity. Alternative proxies were

used to serve as surrogates of agency problems and information asymmetry. More

importantly, we use both cash holdings and Tobin’s Q (a proxy of growth potentials)

to illustrate the condition that are specifically applied to the empirical test of agency

problems and of information asymmetry. If agency problems are the key issue to

result in a sensitive investment-cash flow relation, the sensitivity is expected to be

more saliently found in firms with high internal cash holdings and low Tobin’s Q. In

contrast, if information asymmetry are the key issue, the sensitivity is applied to firms

with low internal cash holdings and high Tobin’s Q.

The reasons why we choose China’s listed firms as our sample for the

investigation of investment-cash flow sensitivity are elaborated as follows. First, the

majority of China’s listed firms had been centrally controlled by the government and

then were transformed into or established as state owned enterprises (SOEs), where

the government held a majority of firms' shares and therefore served as the controlling

owner. Due to inadequate internal governance mechanisms and an ineffective market

1 Another thread of studies illustrate that managerial overconfidence could result in investment-cash

flow sensitivity even without invoking any assumptions on agency cost and information asymmetry

(Heaton, 2002). That is, overconfident managers increase their investment sensitivity to cash flow

under the belief that market undervalues the firm's projects and that the cost of external finance is too

high. Malmendier and Tate (2005) use managers’ personal portfolio in firms to serve as proxies of

managerial overconfidence. They find that overconfident managers show significantly higher

investment sensitivity to free cash flow, particularly for equity-dependent firms. Lin et al. (2005) find

the sensitivity is more salient for financing constrained firms. Nevertheless, this thread of studies relies

crucially on finding convincible surrogates of managerial overconfidence that is not readily observable.

4

of corporate control, the government plays an important role in affecting firm’s

investment in the sense that state control associated with severe agency problems (Qi

et al., 2000) is expected to heighten investment-cash flow sensitivity. Second, China’s

economic modernization was in tandem with its share reform which gradually

transformed state controlled mechanism into market mechanism. The share reform

provides a splendid forum to contrast the impact of agency problems on

investment-cash flow sensitivity before and after the share reform. Third, the issue of

wealth expropriation from minority shareholders is more relevant in economies with

weak legal protection or poorer governance structure (La Porta et al., 1999, 2000;

Johnson et al., 2000; Peng et al., 2011). The ownership structure of China’s listed

companies is characterized as highly concentrated and the ultimate shareholder

usually has effective control. The unique characteristics of China’s listed firms could

be further incorporated in the research design.

Our investigation of the investment-cash flow sensitivity of the listed firms in

China could be easily summarized as follows. First, a strong link between firm’s

investment and cash flow is verified. Second, the investment-cash flow sensitivity

results mainly from agency problems embedded in ownership structure and board

structure than information asymmetry. Specifically, we find agency problems

accentuate the investment-cash flow relation particularly for the subsample of high

cash flow and low Tobin’s Q when agency problems are severe. In contrast, the

impact of information asymmetry on the investment-cash flow relation was not found

for the subsample of low cash flow and high Tobin’s Q where information asymmetry

is severe. For the variables of agency problems we find that the wedge between

voting rights and cash flow rights and state control accentuate investment-cash flow

sensitivity, while CEO/chairman duality and board size attenuate investment-cash

flow sensitivity. Finally, we contrast the impact of agency problems on

5

investment-cash flow sensitivity before and after share reform and find that the

moderating effect of agency problems is heightened after the share reform.

This study bears some resemblances to previous studies. First, Pawlina and

Renneboog (2005) also explore how information asymmetry and agency cost affect

the investment-cash flow relationship. They use ownership and control patterns to

capture agency cost, and the impact of technical efficiency to capture information

asymmetry. They drew a similar conclusion with ours that investment-cash flow

sensitivity results mainly from the agency costs though our proxies of agency costs

contain some ownership structure variables that pertain to China, namely, wedge, state

control, CEO/chairman duality, and board size. Huang, Jiang, Liu, and Zhang (2011)

use the data from China’s listed firms to explore the effect of agency cost on the

relation between top executives' overconfidence and investment-cash flow sensitivity,

and conclude that the positive impact of executives' overconfidence on

investment-cash flow sensitivity only sustains for state-owned entities but not for

non-state controlled firms. Using the ratio of managerial expenses to total assets to

serve as a proxy of agency cost they find that the investment distortion due to top

executives' overconfidence behavior may be alleviated by reducing agency cost

through elevated supervision. In contrast, we use four variables to capture agency

problems and conclude a similar story that agency cost accentuates the positive

investment-cash flow relationship. However, we additionally cover information

asymmetry and illustrate conditions that would be differently applied to agency cost

and information asymmetry in moderating the investment-cash flow relationship.

Another similar finding is found in Kuo and Hung (2012) who use the sample of

Taiwan’s listed firms and find that excess control rights and board independence

moderate the relationship between family control and investment-cash flow

sensitivity.

6

The potential contributions of this paper are multifold. First, we revisit the issue of

investment-cash flow sensitivity by using the data of the listed firms in China that is

characterized as weak in investor protection and illiquid in market trading. An

emerging market that exhibits severe agency problems and information asymmetry

makes it a splendid forum to revisit the issue. Second, we do not only identify the

proxy variables relating to the special attributes of China but also identify conditions

that would separately better fit for the test of how agency problem affects the

investment-cash flow sensitivity and for the test of how information asymmetry

affects the investment-cash flow sensitivity. Third, as most listed firms in China have

been through share reform that corrects the split-share structure, we explore the issue

of how share reform affects the moderating effect of agency problems on

investment-cash flow sensitivity. We find that the moderating effect is applied more to

the sample after share reform than the sample before share reform. This implies that

the share reform transforming into market mechanism sharpens the moderating effect

of agency costs on investment-cash flow sensitivity. The rest of this paper is

organized as follows. Section 2 is literature review and hypothesis development.

Section 3 depicts the data, variables, and empirical models. Section 4 reports the

empirical findings. Section 5 concludes.

2. Literature Review and Hypothesis Development

2.1. Agency Problems and Investment-Cash Flow Sensitivity

In a perfect market without agency problems, external funds provide a perfect

substitute for internal funds and that makes firm's investment decisions independent

of its financial condition. However, in the presence agency costs a firm’s investment

is affected by changes in its net worth or internal funds, holding constant investment

opportunities (Hubbard, 1998). In this study we include four variables to illustrate

how agency problems affect the investment-cash flow sensitivity. The first variable is

7

the wedge between cash flow and control rights. Prior studies indicate that the wedge

negatively affects firm value (Claessens et al., 2002; Lemmon and Lins, 2003; Laeven

and Levine, 2008; Gompers et al., 2010). The wedge mainly through the common

practice of cross shareholdings and pyramidal structure allows controlling owners to

exercise excess control despite having relatively small proportional cash flow rights.

Therefore, the wedge gives controlling owners an incentive to pursue their own

interests at the expense of the wealth of other investors (Chen et al., 2011). Moreover,

the wealth expropriation is especially relevant in economies with weak legal

protection or poorer governance standards (La Porta et al., 1999, 2000; Johnson et al.,

2000; Peng et al., 2011). We therefore expect to find that the wedge positively

moderates the investment-cash flow relation.

The second variable is state control. This is common attribute for many

transitional economies where government has a profound impact on how the firms

operate. Many Chinese listed companies have the state, a state agency, or city or

regional government as the controlling shareholder. The debate remains as to whether

state control is a reason for the poor efficiency (Allen et al., 2005; Chen et al., 2009).

One of reasons why state control could have a positive impact on investment-cash

flow sensitivity is because government has multiple socio-economic objectives so that

some not-that promising investments would still be taken suffice that the perceived

marginal benefits exceed the marginal costs. Firth et al. (2012) indicate that the listed

firms under government control are associated with greater investment-cash flow

sensitivities than do privately controlled listed companies. Moreover, the difference in

sensitivities appears only in firms with few profitable investment opportunities.

The third variable is CEO/chairman duality. Jensen (1993) indicates that

chairman-CEO duality gives the CEO excessive power over the decision-making

process and therefore fails internal control systems. It is therefore suggested that good

8

corporate governance in the UK separates the two roles (Cadbury, 1992). However,

the case applied to China’s listed firms is somewhat different. First, China’s corporate

governance is relatively weak and many firms are subject to insider control. The

CEO/chairman duality increases the possibility of power concentration and therefore

gives CEOs more negotiation power. Second, some empirical findings of China

support for a positive relationship between CEO duality and firm performance (Tian

and Lau, 2001). Because CEO duality is associated with better performance and

therefore lower likelihood of CEO turnover, CEOs simultaneously chairs the board

would be somewhat exonerated from the burden of short-term performance and

therefore a lower inclination of overinvestment. We therefore postulate that

CEO/chairman duality is expected to attenuate the investment-cash flow sensitivity.

The fourth variable is board size. There are two opposing arguments relating to

board size. From the perspective of agency theory, large boards are usually associated

with ineffective monitoring and poor coordination (Jensen, 1993; Lipton and Lorsch,

1992). In contrast, the resource dependence theory indicates that large boards provide

greater access to outside recourses, expertise, industry experience, and legitimacy

(Pfeffer, 1972; Zahra and Pearce, 1989). Moreover, guanxi referring to the durable

social connections and networks a firm uses to exchange favors for organizational

purposes is a special attribute of China’s listed firms (Gu, Hung, and Tse, 2008). Xin

and Pearce (1996) indicate that guanxi could serve as a substitute for formal

institutional support since it goes deep as a governance mechanism and even

dominates business activities throughout China. In this sense, board size could

attenuate the investment-cash flow relation.

In general, we would expect to find that variables of agency problems would

accentuate the investment-cash flow relation. Moreover, the close tie due to agency

problems implies the overinvestment on negative-NPV projects, we would expect to

9

find that the moderating effect of agency problems would be more saliently found in

condition that firms with high cash holdings while low growth opportunity.

Hypothesis 1: Agency problem accentuates the investment-cash flow sensitivity and

the tightened sensitivity is more saliently found in firms with high cash

holdings while low growth potentials.

2.2. Information Asymmetry and Investment-Cash Flow Sensitivity

In a perfect market without frictions Modigliani and Miller (1958) postulate that a

firm’s investment decisions should be independent from its financing decisions.

Numerous studies indicate that information asymmetry results in costly external

financing because it contains a “lemons” premium (e.g., Myers and Majluf, 1984;

Amihud and Mendelson, 1988; Brennan and Subrahmanyam, 1996; Easley and

O’Hara, 2004). Fazzari et al. (1988) indicate that the investment of firms that have

exhausted internal funds would become more sensitive to the fluctuations of their cash

flows. Cleary et al. (2007) present a theoretical model that predicts that firms facing

greater asymmetric information problems would be associated with greater

investment-cash flow sensitivity.

Fazzari et al. (1988) use low-dividend payout as the proxy of financial constraint,

and argue firms with low-dividend payout should have higher investment-cash flow

sensitivity. Kaplan and Zingales (1997) indicate that dividend policy is a choice

variable and might not directly relate to financial constraint. Instead, they use

qualitative and quantitative information from financial statements to classified firms

into three categories: never constrained, likely constrained, and constrained. However,

they find that the investment-cash flow relation is less sensitive for likely- constrained

firms than for never-constrained firms, therefore whether the investment-cash flow

10

sensitivities provide a good measure of financing constraint was questioned (e,g,

Kaplan and Zingales, 1997, 2000). Consistent with Kaplan and Zingales (1997),

Cleary (1999) also finds the investment-cash flow relation is most sensitive for firms

being classified in the most credit-worthy group. Cleary et al. (2007) try to reconcile

the seemingly irreconcilable findings of Fazzari et al. (1988) with those of Kaplan and

Zingales (1997, 2000) by arguing that some firms being classified as constrained

firms with the classification based on measures of information asymmetry are in

general not distressed.

Since information asymmetry remains a primary cause of financial constraints and

higher external capital costs, we use alternative measures of asymmetric information

to explore the moderating effect of information asymmetry on the investment-cash

flow relation. The first variable is big 4 auditors that are demanded because greater

assurance is seen to reduce information asymmetry (Carey, Simnett, and Tanewski,

2000; DeFond, 1992; Knechel, Niemi, & Sundgren, 2008). The second variable is

illiquidity measured by the average across stocks of the daily ratio of absolute stock

return to dollar volume. Aminud (2002) indicates that expected market illiquidity

positively affects ex-ante stock excess return, suggesting that expected stock excess

return partially reflects an illiquidity premium. Kaplan and Zingales (1997) indicate

that the degree of financial constraints affecting the sensitivity of investment to

changes in liquidity is ambiguous. Almeida and Campello (2002) argue that an

increase in liquidity will relax the constraints less for more constrained firms. We

postulate that firms have more liquid balances would be associated with lower

investment-cash flow sensitivity. This is because firms are less likely to be financially

constrained in the future if the liquid balances can be carried into future periods. The

third variable is discretionary accruals, as estimated using the modified Jones model

(Dechow et al., 1995). Most of the studies regarding information disclosure indicate a

11

negative relation between disclosure quality and information asymmetry (e.g. Brown

and Hillegeist, 2007, Healy et al., 1999, Heflin et al., 2005 and Welker, 1995). As the

discretionary accruals increase, the firm becomes less transparent, and therefore the

information between firm and investors increases. The fourth variable is share

turnover which is computed as the mean daily trading volume scaled by shares

outstanding during the fiscal year (e.g., Leuz and Verrecchia, 2000), suggesting that

higher values of share turnover indicate more transparency and less opacity.

Since information asymmetry is a key to result in a close investment-cash flow tie,

we would expect to find that variables of information asymmetry would accentuate

the investment-cash flow relation. Moreover, the close tie due to information

asymmetry implies underinvestment or renouncement of profitable projects. The

condition is more saliently found in condition that firms with low cash holdings while

high growth opportunity.

Hypothesis 2: Information asymmetry accentuates the investment-cash flow sensitivity

and the tightened sensitivity is more saliently found in firms with

low cash holdings while high growth potentials.

2.3. Share Reform and Investment-Cash Flow Sensitivity

Share reform initially launched by the Chinese authorities in 2005 aimed at

eliminating non-tradable shares. The reform obliged the non-tradable shareholders to

compensate the tradable shareholders for gaining transferability. The reform is

deemed an advancement of the privatization process and an improvement on

corporate governance which in turn should enhance the value of the firm (e.g. Doidge

et al., 2007; Gompers et al., 2003). Furthermore, the reform increases the supply of

tradable shares and therefore has a positive effect on liquidity (see Amihud, 2002;

12

Pastor and Stambaugh, 2003; Acharya and Pedersen, 2005). Overall, the reform

moves the capital market toward market mechanism. We therefore postulate that the

impact of agency problems or information asymmetry on the investment-cash flow

sensitivity would be much salient after share reform than before share reform.

Hypothesis 3: The impact of agency problems or information asymmetry on the

investment-cash flow sensitivity would be much salient after share

reform than before share reform.

3. Data, Variables, and Models

Our sample covers Chinese companies listed on both Shanghai and Shenzhen

stock exchanges during the period of 2003 to 2012. Financial firms and loss-making

firms in the process of delisting (i.e. being noted as special treatment) were excluded

from the sample. Moreover, the final sample was winsorized at 1% to ameliorate the

impact of extreme observations. The final sample contains 2,255 listed firms and

13,486 firm-year observations. The subsample of firms that have involved in share

reform consist 1,243 listed firms and 10,623 firm-year observations. The data was

jointly collected from the China Stock Market Trading Database (CSMAR) and

Taiwan Economic Journal (TEJ).

Table 1 reports the summary statistics of the variables. The dependent variable is

firm’s investment normalized by the beginning capital stock (I/K). On average, the

investment is 0.0712. The independent variable of cash flow is defined as income

before extraordinary items plus depreciation and amortization normalized by the

beginning capital stock (Cash/K). The average cash flow is 0.2011.

For agency problems, we include four variables. Wedge (wedge) is the difference

13

between controlling owner’s control rights and cash flow rights2. The average wedge

is 0.0596. Board size (board size) is measured as the natural logarithm of number of

board membership. Duality (duality) is a dummy that is assigned the value of 1 when

CEO simultaneously chairs the board and 0 otherwise. On average, 16.45% of the

listed are associated with CEO/chairman duality. State control (state) is a dummy that

is assigned the value of 1 when the listed firm is ultimately controlled by the

government and 0 otherwise. The sampling firms comprise 57.85% of state-control

firms.

For information asymmetry, we also include four variables. Big 4 auditor (big 4)

is a dummy that is assigned the value of 1 when the listed firm’s accounting report is

attested by the big 4 auditors (Deloitte, PwC, Ernst & Young, and KPMG) and 0

otherwise. Only 6.11% of the sampling firms having their financial reports attested by

the big 4 auditors. Discretionary accrual (DA) is measured by the modified Jone’s

model as follows:

TACt = αt (1/TAt–1) + βt (ΔSALESt – ΔARt) + γt PPEt + ζt ROAt–1 + εt, … (1)

where TACt denotes total accruals in year t, calculated using the statement of cash

flow approach recommended by Hribar and Collins (2002) as income before

discontinued operations and extraordinary items less cash from operations and

discontinued operations and extraordinary items from the statement of cash flows);

TAt–1 denotes total assets at the end of year t-1; ΔSALESt denotes the change in sales

revenue between year t and year t-1; ΔARt denotes the change in accounts receivable

between year t and year t-1; PPEt denotes the gross amount of property, plant and

equipment at the end of year t; and ROAt–1 denotes return on assets in year t-1,

calculated as the ratio of income before discontinued operations and extraordinary

2 The defintion of control rights and cash flow rights refers to La Porta et al. (1999) and Claessens et al.

(2002). Control rights are the sum of the weakest link in the chain of ownership. Cash flow rights are

the sum of the product of ownership stakes along each chain of ownership.

14

items to total assets. We note that TACt, ΔSALESt, ΔARt, and PPEt are scaled by

lagged total assets (TAt–1). The average discretionary accrual is 0.0645. Illiquidity

(Illiq), referred to Aminud (2002), is defined as the daily ratio of absolute stock return

to its dollar volume, averaged over the sampling period. On average the illiquidity is

0.0026.

⁄ ∑| |

, (2)

Where denotes the number of trading days for stock i in year t, | |

denotes the absolute return for stock i in year t, and denotes the dollar

volume which is the multiplication of price and trading volume for stock i in year t.

Finally, turnover (turnover) is defined as measured by daily trading divided by

outstanding shares.

∑

⁄ , (3)

For control variables, Tobin’s Q (Q), referred to Chung and Pruitt (1994), is

defined as follows.

) ) ) ) ) )

) , (4)

where MV(X) and BV(X) indicate the market and book variable of the argument

X, respectively. CS is common stock, PS is preferred stock, LTD is long-term debt,

INV is inventory, CL is capital leases, CA is current assets, and TA is total assets. The

average Tobin’s Q is 1.3665. Firm size (firm size) being defined as the natural

logarithm of firm’s assets is 9.3636 on average. Firm age (firm age) is defined as the

natural logarithm of the time lapse in months since the inception of the firm. Leverage

(lev) being defined as the ratio of total debt to total assets is 0.4881 on average.

The empirical model is specified as follows.

15

(

)

(

) , (5)

Where Agency denotes the proxies for agency problems (including wedge, board

size, duality, and state control), and IA denotes the proxies for information asymmetry

(including big-4 auditor, discretionary accruals, illiquidity, and turnover). In this

equation, the most important ones, and , are expected to be positive, implying

that agency problems and information asymmetry attentuate the investment-cash flow

relation.

<<Insert Table 1 Here>>

4. Empirical Findings

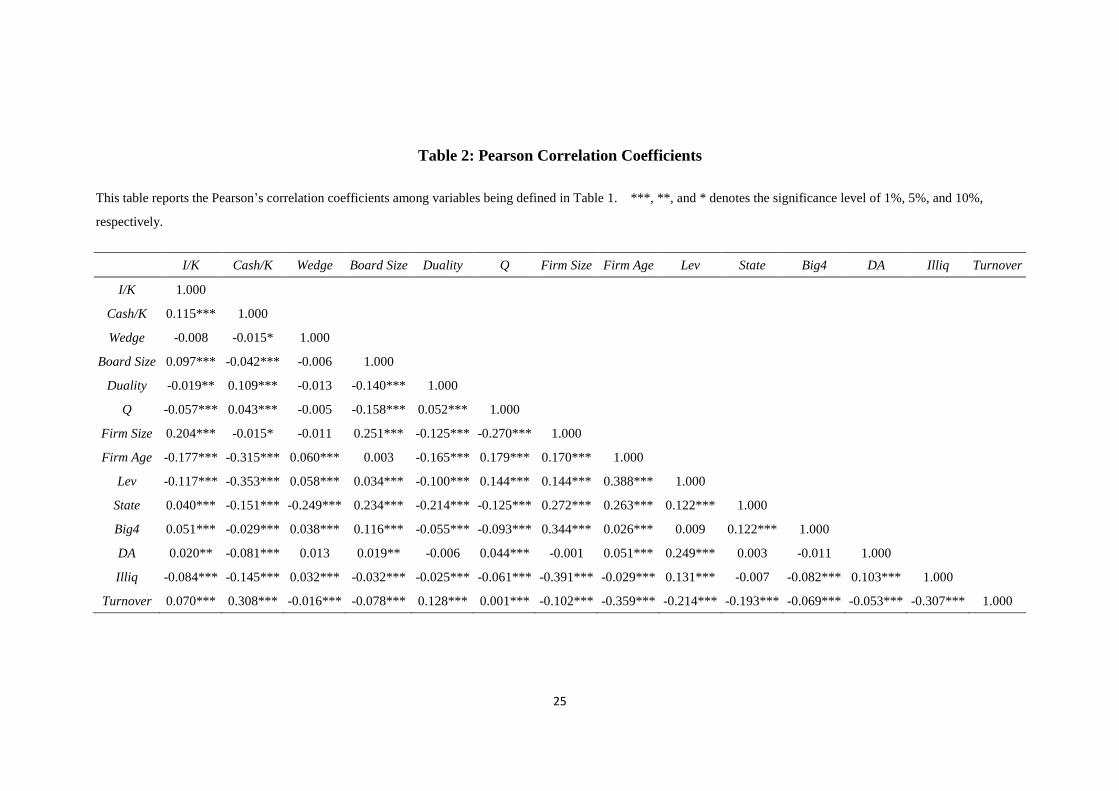

Table 2 reports the Pearson correlation coefficients among variables. The result

indicates that firm’s investment is strictly connected with its cash flows, with the

correlation coefficient of 0.115 and significant at 1% level. Moreover, a firm’s

investment is positively correlated with board size, assets, state control, attestation by

big 4 auditors, discretionary accruals, and turnover, while is negatively correlated

with duality, Tobin’s Q, firm age, leverage, and illiquidity measure.

<<Insert Table 2 Here>>

In Table 3 we explore the impact of governance variables (which imply agency

problems) on investment cash flow relation. The result from model 1 indicates that

wedge is negatively correlated with firm’s investment (-0.0437), significant at 1%

level. More importantly, the interaction between wedge and cash flow is 0.2738,

significant at 1% level. This support prior findings that wedge is negatively affects

16

firm value (Claessens et al., 2002; Lemmon and Lins, 2003; Laeven and Levine, 2008;

Gompers et al., 2010), a proxy of controlling owner’s wealth expropriation (Chen et

al., 2011), and particularly relevant in economies with weak legal protection or poorer

governance standards (La Porta et al., 1999, 2000; Johnson et al., 2000; Peng et al.,

2011). The significance of the moderating effect prevails across different model

specifications. More importantly, we find that the regression coefficient of the

interative term is higher for all the subsample comprising firms with high cash flow

and low Tobin’s Q (0.8216 in model 4) than for the full sample (0.2807 in model 3)3.

That is, the impact of wedge on investment-cash flow relation is more saliently found

for the subsample of firms confronting severe agency problems.

In model 2 we include state control in the regression and find that state-controlled

firms are associated with higher investment-cash flow sensitivity. The interactive term

of state control and cash flow is 0.0296, significant at 5% level. This is consistent

with prior findings of Qi et al. (2000) that government plays an important role in

affecting firm’s investment, and of Firth et al. (2012) that the listed firms under

government control are associated with greater investment-cash flow sensitivities than

do privately controlled listed companies.

In model 3 we include CEO/chairman duality and its interaction with cash flow

into the regression analysis. The result indicates that firms whose CEO

simultaneously chair the boards are associated with higher investment. However, the

interaction between duality and cash flow is significantly negative, indicating that

3 We use F test to verify whether the regression coefficients are significantly different in different

sample compositions and model specifications. The F statistics is specified as ) ⁄

) )⁄,

where RSSfull and RSSsub denotes residual sum of square for the full sample and subsample, respectively.

K denotes the number of parameters.

17

CEO/chairman duality attenuates the positive investment-cash flow relation. The

finding is inconsistent with the findings from the western societies (e.g. Jensen, 1993;

Cadbury, 1992), while is consistent with the findings using the forum of China. For

example, Tian and Lau (2001) find that CEO/chairman duality is positively correlated

with firm performance for the listed firms in China. If this is the case, firms with

CEO/chairman duality are less likely to be replaced due to better performance. These

CEOs are therefore less burdened with short-term performance and therefore a lower

inclination of overinvestment. Our empirical finding basically supports this

postulation in the sense that the interaction between duality and cash flows is

significantly negative for the full sample (-0.0616), and the moderating effect of

CEO/chairman duality is more pronounced for the subsample of high-cash and low-Q

firms in which agency problems are severe (-0.1133).

In model 4 we include board size and find that board size attenuates the positive

investment-cash flow relation. The regression coefficient of the interaction between

board size and cash flows is -0.1491, significant at 5% level. Again, this finding is

inconsistent with the findings or postulations from the western societies (e.g. Jensen,

1993; Lipton and Lorsch, 1992). Our finding probably resembles the argument that

board size implies guanxi that is durable social connections and networks (Gu, Hung,

and Tse, 2008) and therefore serves as substitution for formal governance mechanism

(Xin and Pearce, 1996). However, the moderating effect of board size is insignificant

for the subsample of high-cash and low-Q firms.

For the control variables, we find that Tobin’s Q is positively correlated with

investment. This is consistent with setting of Fazzari, Hubbard, and Petersen, (1988)

and previous findings (e.g. Fazzari, Hubbard, and Petersen, 1988; Hoshi, Kashyap,

and Scharfstein, 1991; Lamont, 1997). We find that firm size is positively correlated

with investment. This is consistent with prior finding that larger firms are associated

18

with lower transaction costs and are less susceptible to information asymmetry effects

(e.g. Zarzeski, 1996). Firm age is negatively correlated with investment. Prior studies

(e.g., Rauh, 2006; Brown et al., 2009) indicate that firm age is strongly correlated

with asymmetric information problems and has been used as a proxy for the presence

of financing frictions. Finally, we find that leverage is negatively correlated with

investment, which is consistent with Habib and Ljungqvist (2005).

In general, our first hypothesis that agency problem accentuates the

investment-cash flow sensitivity receive supporting evidence from the listed firms in

China. Specifically, wedge and state control accentuate while CEO duality and board

size attenuate the positive investment-cash flow relation. Moreover, the moderating

effect of agency problem embedded in corporate governance is more pronounced in

the subsample of firms with high cash holdings while low growth potentials.

<< Insert Table 3 Here>>

In Table 4 we investigate how information asymmetry affect investment-cash

flow relation. The proxy variables for information asymmetry include big-4-auditor

dummy, discretionary accruals, illiquidity measure, and turnover. In model 1 we

include big-4 dummy and discretionary accruals. The result indicates that

discretionary accruals heighten the investment-cash flow relation because firms with a

high level of discretionary accruals are negatively associated with disclosure quality

and therefore a higher level of information asymmetry (e.g. Brown and Hillegeist,

2007, Healy et al., 1999, Heflin et al., 2005 and Welker, 1995). The interaction

between big-4 dummy and cash flow is positive, albeit insignificant.

In model 2 we include illiquidity measure, turnover, and their interaction with

cash flow. The result indicates that illiquidity measure accentuates while turnover

19

attenuates the investment-cash flow relation. The moderating effect of illiquidity

measure supports Almeida and Campello’s (2002) argument that an increase in

liquidity will relax the constraints less for more constrained firms. The moderating

effect of turnover is in supportive to Leuz and Verrecchia (2000) in the sense that

higher values of share turnover indicate more transparency and less opacity. In model

3 we include the four proxy variables of information asymmetry and find the result

basically intact. In general, the empirical results for the full sample lend support to the

postulation that information asymmetry has a positive impact on the investment-cash

flow relation.

However, if information asymmetry is the key to drive investment-cash flow

sensitivity, we would expect to find that the moderating effect of information

asymmetry is applied more to the condition of financial constraint. We use the

subsample of low cash flow and high Tobin’s Q as the proxy for financial constraint.

Unfortunately, the subsample fails to provide a more promising picture of the

moderating effect of information asymmetry on the investment-cash flow relation. In

general, we do find that information asymmetry positively moderate the

investment-cash flow relation. However, the moderating effect of information

asymmetry is insignificant for the subsample of financially constrained firms.

In general, our second hypothesis receives partial support from the empirical

evidence: the part that information asymmetry accentuates the investment-cash flow

sensitivity is supported while the part that the tightened sensitivity is more saliently

found in firms with low cash holdings while high growth potentials is unsupported.

<<Insert Table 4 Here>>

In Table 5 we contrast the moderating effect of agency problem before and after

20

share reform. The literature of split-share reform indicates that the share reform

increases market liquidity (Amihud, 2002; Pastor and Stambaugh, 2003; Acharya and

Pedersen, 2005) and improves corporate governance (e.g. Doidge et al., 2007;

Gompers et al., 2003). More importantly, Liao, Liu, and Wang (2014) indicate that the

reform adopted a market mechanism that played an effective information discovery

role in aligning the interests of the government and public investors. We therefore

assume that the reform is a milestone moving the capital market toward market

mechanism, and therefore expect that the moderating effect of agency problems is

more pronounced after than before the share reform. The result in Table 5 verifies this

postulation by showing that wedge positively moderates while CEO/chairman

negatively moderates the investment-cash flow sensitivity. In contrast, board size is

significant in moderating the investment-cash flow relation before share reform, and

becomes insignificant after the share reform. This could be explained that as the

market moves toward market mechanism, the facilitation of board connection in

alleviating financial constraint was effectual before the share reform while ineffectual

after the share reform.

We also conduct the test whether the moderating effect of information

asymmetry is more significant for the subsample after the share reform than before

the share reform. The result (unreported) fails to illustrate any significant contrast

between samples in the two sub-periods. Therefore, our third hypothesis receives

partial support that the impact of agency problems on the investment-cash flow

sensitivity is much salient after share reform than before share reform.

<<Insert Table 5 Here>>

5. Concluding Remark

21

This paper investigates the investment-cash flow sensitivity of using a sample of

firms listed of China. In general, we confirm earlier findings that investment is strictly

tied to cash flow. Moreover, we find that a cash flow-dependent investment policy

results mainly from agency problems. The significantly positive relationship between

investment-cash flow sensitivity is moderated by the wedge between controlling

owner’s voting rights and cash flow rights, state control, CEO/chairman duality, and

board size. Moreover, the moderating effect of agency problems is more saliently

found for the subsample of firms with high cash flows and low growth potentials.

Secondly, we find that the positive investment-cash flow relation is also moderated by

information asymmetry using the proxies such as big-4 auditors dummy, discretionary

accruals, illiquidity measure, and stock turnover. The result basically supports the

argument that information asymmetry sharpens the linkage between investment and

cash flows. However, we fail to find that the moderating effect of information

asymmetry is more pronounced for the subsample consisting firms with low cash

flows and high growth potentials. Finally, we find that the moderating effect of

agency problems is more salient after share reform than before share reform.

The results of this paper indicate that the agency costs of free cash flow appear to

be the main source of the investment-cash flow sensitivity of the UK listed

corporations in the post-Cadbury period. Therefore, from a policy perspective, it

seems essential to pursue the further alignment of interests of managers and

shareholders by stimulating effective shareholder monitoring and

pay-for-performance schemes.

Furthermore, our results indicate promising avenues for future research. First, one

can attempt to incorporate managerial remuneration and turnover in the investment

model to analyze to what extent the disciplining devices have already translated into

efficient investment policies. Second, an interesting research opportunity is to analyze

22

the changes in the cash flow sensitivity of investment in the aftermath of (voluntary)

changes in corporate disclosure.

23

Brown, J.R., Fazzari, S.M., Petersen, B.C., 2009. Financing innovation and growth: Cash flow, external

equity and the 1990s R&D boom. Journal of Finance, 64 (1), 151-185.

Cadbury, A. (1992). A report of the committee on the financial aspects of corporate governance.

London: Gee.

Doidge, C., Karolyi, G.A., Stulz, R., 2007. Why do countries matter so much for corporate governance?

Journal of Financial Economics 86, 1–39.

Gompers, P.A., Ishii, J.L., Metrick, A., 2003. Corporate governance and equity prices. Quarterly

Journal of Economics 118, 107–155.

Gu, F. F., Hung, K., and Tse, D. K. 2008. When does Guanxi matter? Issues of capitalization and its

dark sides. Journal of Marketing, 72, 12-28.

Habib, M. A. and Ljungqvist, A. P., 2005. Firm value and managerial incentives: A stochastic

frontier’, Journal of Business, 78 (6), 2053-2094.

Leuz, C., Verrecchia, R.E., 2000. The economic consequences of increased disclosure. Journal of

Accounting Research 38, 91–124.

Liao, Liu, and Wang, 2014. China's secondary privatization: Perspectives from the split-share structure

reform, Journal of Financial Economics, forthcoming.

Rauh, J.D., 2006. Investment and financing constraints: Evidence from the funding of corporate

pension plans. Journal of Finance 61, 33–72.

Tian, J.J., Lau, C., 2001. Board composition, leadership structure and performance in Chinese

shareholding companies. Asia Pacific Journal of Management 18, 245–263.

Zarzeski, M.T., 1996. Spontaneous harmonization effects of culture and market forces on accounting

disclosures practices. Accounting Horizons 10 (1), 18-37.

24

Table 1: Summary Statistics

Investment ratio (I/K) is investment scaled by beginning capital stock. Cash flow ratio (Cash/K) is cash

flow scaled by beginning capital stock. Wedge (Wedge) denotes the discrepancy between controlling

owner’s voting rights and cash flow rights. Board size (Board size) is measured by the natural

logarithm of the number of board members. Duality (Duality) is a dummy that is assigned the value of

1 when the CEO simultaneously chairs the board and 0 otherwise. The state dummy (State) is assigned

the value of 1 when the firm is ultimately controlled by the State and 0 otherwise. The audit quality is

measured by the big-4 dummy (Big4) that is assigned the value of 1 when the firms is attested by

auditors in the big 4 auditing firms and 0 otherwise. Earnings quality is measured by discretionary

accruals from the modified Jone’s model. Illiquidity measure, referred to Aminud, is defined as the

daily ratio of absolute stock return to its dollar volume, averaged over some period. Turnover

(Turnover) is measured by daily trading divided by outstanding shares. Tobin’s Q (Q) is measured by

Chung and Pruitt (1994) at the beginning of the period t. Firm size (Firm Size) is the natural logarithm

of beginning total assets. Firm Age (Firm Age) is the natural logarithm of the time lapse since inception.

Leverage (Lev) is the total debt scaled by beginning total assets.

Variable Mean Q1 Median Q3 S.D.

I/K 0.0712 0.0087 0.0401 0.1005 0.0712

Cash/K 0.2011 0.0848 0.1525 0.2678 0.2011

Wedge 0.0596 0 0 0.1138 0.0596

Board size 0.9551 0.9542 0.9542 1 0.0903

Duality 0.1645 0 0 0 0.3708

State 0.5785 0 1 1 0.4938

Big4 0.0611 0 0 0 0.2395

DA 0.0645 -0.1599 0.0339 0.2332 0.6959

Illiq 0.0026 0.0005 0.0010 0.0028 0.0040

Turnover 0.2737 0.0777 0.1735 0.3665 0.2915

Q 1.3665 0.8016 1.0333 1.5371 0.9821

Firm Size 9.3636 9.0151 9.3114 9.6516 0.5176

Firm Age 0.8221 0.6021 0.9031 1.0792 0.3513

Lev 0.4881 0.3283 0.4892 0.6314 0.2327

25

Table 2: Pearson Correlation Coefficients

This table reports the Pearson’s correlation coefficients among variables being defined in Table 1. ***, **, and * denotes the significance level of 1%, 5%, and 10%,

respectively.

I/K Cash/K Wedge Board Size Duality Q Firm Size Firm Age Lev State Big4 DA Illiq Turnover

I/K 1.000

Cash/K 0.115*** 1.000

Wedge -0.008 -0.015* 1.000

Board Size 0.097*** -0.042*** -0.006 1.000

Duality -0.019** 0.109*** -0.013 -0.140*** 1.000

Q -0.057*** 0.043*** -0.005 -0.158*** 0.052*** 1.000

Firm Size 0.204*** -0.015* -0.011 0.251*** -0.125*** -0.270*** 1.000

Firm Age -0.177*** -0.315*** 0.060*** 0.003 -0.165*** 0.179*** 0.170*** 1.000

Lev -0.117*** -0.353*** 0.058*** 0.034*** -0.100*** 0.144*** 0.144*** 0.388*** 1.000

State 0.040*** -0.151*** -0.249*** 0.234*** -0.214*** -0.125*** 0.272*** 0.263*** 0.122*** 1.000

Big4 0.051*** -0.029*** 0.038*** 0.116*** -0.055*** -0.093*** 0.344*** 0.026*** 0.009 0.122*** 1.000

DA 0.020** -0.081*** 0.013 0.019** -0.006 0.044*** -0.001 0.051*** 0.249*** 0.003 -0.011 1.000

Illiq -0.084*** -0.145*** 0.032*** -0.032*** -0.025*** -0.061*** -0.391*** -0.029*** 0.131*** -0.007 -0.082*** 0.103*** 1.000

Turnover 0.070*** 0.308*** -0.016*** -0.078*** 0.128*** 0.001*** -0.102*** -0.359*** -0.214*** -0.193*** -0.069*** -0.053*** -0.307*** 1.000

26

Table 3: Impact of Corporate Governance on Investment-Cash Flow Sensitivity

This table reports the regression of firm’s investment on cash flow, and variables of corporate

governance, including wedge, the state dummy, and duality. All variables are defined in Table 1. In

each cell the regression coefficient and t-statistics in parentheses are reported in the upper and lower

case, respectively. ***, **, and * denote the significance level of 1%, 5%, and 10%, respectively.

Full Sample Subsample: High-Cash Low-Q

(1) (2) (3) (4)

Intercept -0.4310***

(-20.92)

-0.4215***

(-20.06)

-0.4623***

(-18.71)

-0.4357***

(-6.03)

Cash/K 0.0219***

(2.88)

0.0207*

(1.87)

0.1666***

(2.63)

0.0295

(0.19)

Wedge -0.0437***

(-2.37)

-0.0481**

(-2.51)

-0.0452**

(-2.35)

-0.2072***

(-3.71)

State

-0.0034

(-1.04)

-0.0034

(-1.00)

-0.0129

(-1.22)

Duality

0.0085**

(2.04)

0.0409***

(3.26)

Board Size

0.0572***

(3.38)

0.0241

(0.43)

Wedge*Cash/K 0.2738***

(3.79)

0.3105***

(4.20)

0.2807***

(3.75)

0.8216***

(4.93)

State*Cash/K

0.0296**

(2.44)

0.0213

(1.63)

0.0530*

(1.69)

Duality*Cash/K

-0.0616***

(-4.32)

-0.1133***

(-3.39)

Board Size*Cash/K

-0.1491**

(-2.20)

-0.0758

(-0.45)

Q 0.0096***

(8.47)

0.0096***

(8.43)

0.0096***

(8.40)

0.0119***

(0.77)

Firm Size 0.0617***

(28.11)

0.0610***

(27.03)

0.0593***

(25.76)

0.0638***

(11.1)

Firm Age -0.0608***

(-19.01)

-0.0625***

(-18.94)

-0.0627***

(-18.91)

-0.07358***

(-10.03)

Lev -0.0352***

(-7.28)

-0.0354***

(-7.31)

-0.0354***

(-7.33)

-0.0603***

(-4.07)

Industry YES YES YES YES

Year YES YES YES YES

27

Adjusted R2 0.1355 0.1358 0.1377 0.107

28

Table 4: Impact of Information Asymmetry on Investment-Cash Flow Sensitivity

This table reports the regression of firm’s investment on cash flow, and variables of information

asymmetry, including the big-4 dummy, discretionary accruals, illiquidity, and turnover. All variables

are defined in Table 1. In each cell the regression coefficient and t-statistics in parentheses are reported

in the upper and lower case, respectively. ***, **, and * denote the significance level of 1%, 5%, and

10%, respectively.

Full Sample Subsample: Low-Cash and High Q

(1) (2) (3) (4)

Intercept -0.4610***

(-21.27)

-0.5010***

(-21.02)

-0.5263***

(-21.30)

-0.3780***

(-8.85)

Cash/K 0.0365***

(5.49)

0.0534***

(6.86)

0.0517***

(6.47)

0.1401**

(2.34)

Big4 -0.0195***

(-3.03)

-0.0187***

(-2.92)

-0.0267

(-1.30)

DA 0.0055***

(3.25)

0.0055***

(3.24)

-0.0002

(-0.06)

Illiq

1.3395***

(4.27)

1.3062***

(4.17)

1.2145**

(2.50)

Turnover 0.0343***

(5.90)

0.0332***

(5.73)

0.0230

(1.19)

Big4*Cash/K -0.0151

(-0.59)

-0.0211

(-0.82)

0.0433

(0.20)

DA*Cash/K 0.0192***

(5.66)

0.0186***

(5.51)

0.0503

(1.58)

Illiq*Cash/K 1.4140***

(4.54)

1.4496***

(4.67)

-0.2413

(-0.17)

Turnover*Cash/K -0.0596***

(-5.48)

-0.0574***

(-5.28)

0.2208

(1.21)

Q 0.0096***

(8.48)

0.0105***

(9.12)

0.0105***

(9.12)

0.0078***

(4.54)

Firm Size 0.0651***

(27.42)

0.0672***

(27.17)

0.0706***

(27.22)

0.0544***

(12.45)

Firm Age -0.0608***

(-18.65)

-0.0580***

(-17.00)

-0.0580

(-17.03)

-0.0716***

(-10.64)

Lev -0.0439***

(-8.87)

-0.0394***

(-8.04)

-0.0478

(-9.55)

-0.0501***

(-6.77)

State 0.0022

(1.01)

0.0017

(0.78)

0.0021

(0.98)

0.0070**

(1.97)

29

Industry YES YES YES YES

Year YES YES YES YES

Adjusted R2 0.1411 0.1394 0.1458 0.1926

30

Table 5: Investment-Cash Flow Sensitivity- Before and After Share Reform

This table reports the investment-cash flow regression results for firms involving share reform. All

variables are defined in Table 1. ***, **, and * denote the significance level of 1%, 5%, and 10%,

respectively.

Before Share Reform After Share Reform Full Sample

(1) (3) (4)

Intercept -0.7367***

(-10.56)

-0.5362***

(-15.20)

-0.5831***

(-18.67)

Cash/K 0.4640***

(2.71)

0.2026**

(2.71)

0.3374***

(4.13)

Wedge -0.0343

(-0.76)

-0.0224

(-0.87)

-0.0316

(-1.41)

State -0.0045

(-0.56)

0.0115**

(2.52)

0.0100**

(2.51)

Duality 0.0150

(1.40)

0.0032

(0.56)

0.0010

(0.20)

Board Size 0.1260***

(3.52)

0.0179

(0.61)

0.0532***

(2.77)

Wedge*Cash/K 0.1152

(0.57)

0.2240**

(2.01)

0.2199**

(2.25)

State*Cash/K -0.0011

(-0.03)

-0.0471**

(-2.52)

-0.0427**

(-2.55)

Duality*Cash/K -0.0344

(-0.71)

-0.0396*

(-1.65)

-0.0388*

(-1.80)

Board Size*Cash/K -0.4789***

(-2.72)

-0.0645

(-0.65)

-0.2336***

(-2.70)

Q 0.0029

(0.75)

0.0104***

(7.27)

0.0089***

(6.86)

Firm Size 0.0830***

(12.21)

0.0688***

(21.55)

0.0708***

(24.28)

Firm Age -0.1009***

(-12.5)

-0.0753***

(-10.24)

-0.0873***

(-16.71)

Lev 0.0184***

(4.05)

0.0191***

(7.51)

0.0178***

(8.04)

Industry YES YES YES

Year YES YES YES

Adjusted R2 0.1608 0.1594 0.1552