ГОДОВОЙ ОТЧЕТ АО «БАНК АСТАНЫ» ЗА 2017 Г. - KASE

255

1 AO “Банк Астаны” 2017 ГОДОВОЙ ОТЧЕТ АО «БАНК АСТАНЫ» ЗА 2017 Г. г. Алматы, 2018

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of ГОДОВОЙ ОТЧЕТ АО «БАНК АСТАНЫ» ЗА 2017 Г. - KASE

1

AO “Банк Астаны” 2017

ГОДОВОЙ ОТЧЕТ АО «БАНК АСТАНЫ» ЗА 2017 Г.

г. Алматы, 2018

2

AO “Банк Астаны” 2017

Оглавление

ОБРАЩЕНИЕ ПРЕДСЕДАТЕЛЯ ПРАВЛЕНИЯ АО «БАНК АСТАНЫ» 3

ИСТОРИЯ И КРАТКАЯ ИНФОРМАЦИЯ О БАНКЕ 5

АКЦИОНЕРЫ БАНКА 6

ОСНОВНЫЕ ЦЕННОСТИ НАШЕГО БАНКА 6

ОПИСАНИЕ ТЕКУЩЕЙ ПРОДУКТОВОЙ ЛИНЕЙКИ БАНКА 7

НАИБОЛЕЕ ВАЖНЫЕ СОБЫТИЯ, ПРОИЗОШЕДШИЕ В ЖИЗНИ БАНКА В 2017 ГОДУ: 8

ПОЛИТИКА В ОБЛАСТИ РЕКЛАМЫ И PR 12

ИТ АРХИТЕКТУРА И СТРАТЕГИЯ БАНКА 13

ОПЕРАЦИОННАЯ ДЕЯТЕЛЬНОСТЬ 13

ФИНАНСОВО-ЭКОНОМИЧЕСКИЕ ПОКАЗАТЕЛИ 23

УПРАВЛЕНИЕ РИСКАМИ 27

СОЦИАЛЬНАЯ ОТВЕТСТВЕННОСТЬ 33

КОРПОРАТИВНОЕ УПРАВЛЕНИЕ 34

ОРГАНИЗАЦИОННАЯ СТРУКТУРА 35

ВНУТРЕННИЙ КОНТРОЛЬ И АУДИТ 42

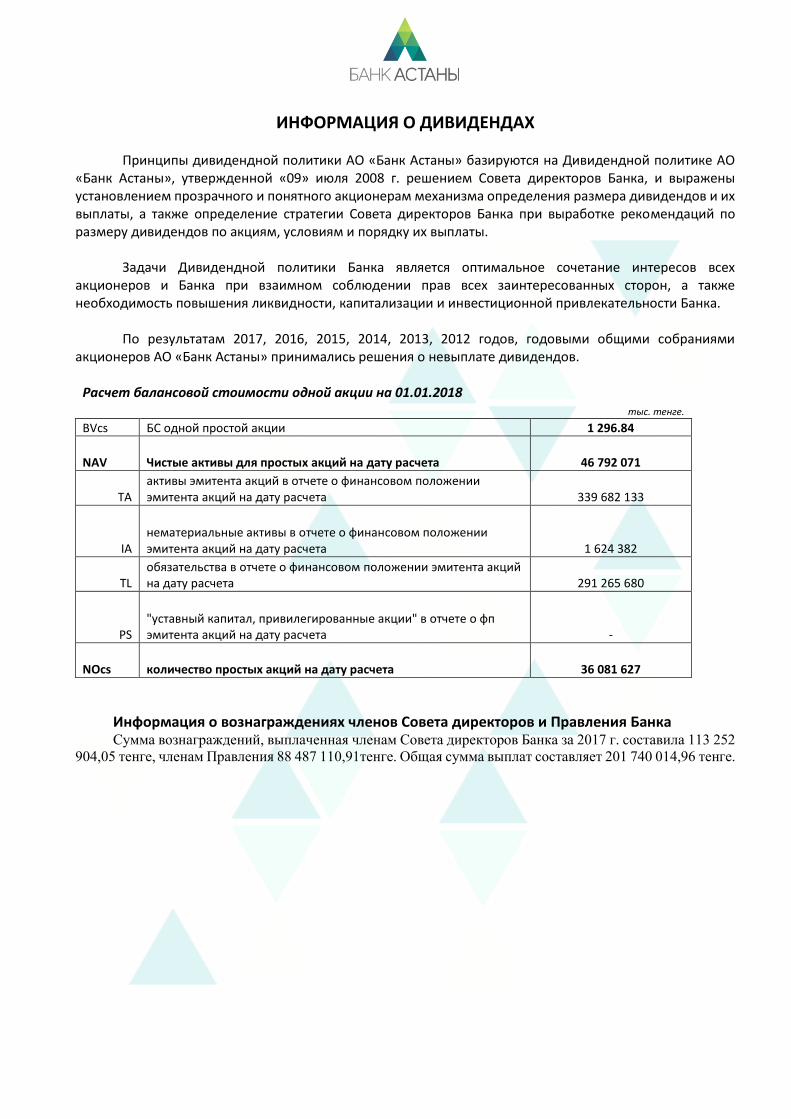

ИНФОРМАЦИЯ О ДИВИДЕНДАХ 44

ОСНОВНЫЕ ЦЕЛИ И ЗАДАЧИ НА СЛЕДУЮЩИЙ ГОД 45

КОНТАКТНАЯ ИНФОРМАЦИЯ 46

АУДИРОВАННАЯ ФИНАНСОВАЯ ОТЧЁТНОСТЬ ЗА 2017 Г. 47

3

AO “Банк Астаны” 2017

ОБРАЩЕНИЕ ПРЕДСЕДАТЕЛЯ ПРАВЛЕНИЯ АО «БАНК АСТАНЫ»

Дорогие друзья!

Выражаю искреннюю благодарность за Вашу поддержку и внимание, которые Вы оказываете Банку Астаны все это время. Хочется отметить, что прошлый 2017 год стал для Банка плодотворным и богатым на события. Были закреплены позиции Банка Астаны как карточного лидера на рынке Казахстана, постепенно введены инновации в обслуживание клиентов, улучшена продуктовая линейка, проведены успешные IPO (первичное размещение акций) на Казахстанской фондовой бирже (KASE) и SPO (вторичное размещение акций) на Московской фондовой бирже (MOEX). В этом же году влиятельное мировое издание Global Finance присудило Банку Астаны премию «Лучший цифровой банк Казахстана» (Best Digital Bank of Kazakhstan).

На протяжении последних двух лет Банк Астаны является трендсеттером во внедрении на казахстанский рынок инновационных услуг и продуктов, к которым относятся персональная доставка карт, заказ карты онлайн, мобильный офис Light-office, открытие депозитов онлайн, разработка платформы детских карт с добавлением развивающих учебных материалов. Одним из успешных инновационных внедрений стал запуск в отделениях Банка мобильного обслуживания пришедших клиентов - Light-office, где весь сервис осуществляется на планшете. При его помощи проводятся кассовые операции, переводные операции, открытие счетов, и многое другое, в зависимости от нужд клиента. Данный сервис получил много позитивных откликов от клиентов, так как его внедрение позволило сократить время обслуживания в два раза.

Банк по-прежнему уделяет большое внимание сотрудничеству с общепризнанными международными лидерами, такие как Warner Bros., Wargaming, Rovio Studio. Благодаря успеху по карточным коллаборациям, был продлён глобальный договор с легендарной киностудией Warner Bros. на два года.

В 2017 году также были достижения на социальном фронте. В марте был запущен социально ориентированный проект в поддержку женского предпринимательства «Розовые воротнички», напрямую связанный с женскими картами Банка Астаны. Так, при проведении безналичной оплаты за товары и услуги с женской платежной карты, банк направлял 0,7% от потраченной клиентом суммы из собственных средств для поддержки и развития женского предпринимательства в стране. В итоге, клиент, совершая покупки, вносил вклад в развитие женского бизнеса, и получал кэшбек в привычном размере. В результате данного проекта, в Казахстане было проведено шесть женских бизнес конференций, охвативших более 600 женщин, желающих стать бизнеледи или уже являющихся таковыми.

4

AO “Банк Астаны” 2017

Мы считаем, что диджитализация – единственно правильный вектор развития,

который был определен несколько лет назад. Банк продолжает неукоснительно придерживается политики инновационности, клиентоориентированности и финансовой устойчивости. Доказательством служат следующие показатели: рост чистой прибыли, наличие достаточной капитализации и ликвидности, сотрудничество с государственным и квазигосударственным сектором и высокая поддержка со стороны акционеров. Мы продолжаем развивать наш продуктовый ряд, совершенствовать услуги и удобство в использовании мобильного и интернет-банкинга.

Ушедший 2017 год показал, что благодаря стратегии и выполнению поставленных задач, а также сплоченной командной работе, Банк Астаны реализовал смелые проекты, усовершенствовал сервис и продукты для блага клиента. Особо подчеркну, что в успехе Банка Астаны неоценимую роль сыграла поддержка и вера клиентов, партнеров и акционеров.

С уважением, Председатель Правления

АО «Банк Астаны» Искендер Майлибаев

Июнь 2018 год

5

AO “Банк Астаны” 2017

ИСТОРИЯ И КРАТКАЯ ИНФОРМАЦИЯ О БАНКЕ

АО «Банк Астаны» (далее – Банк) ранее являлось 100% дочерней структурой АО «Астана-финанс». В настоящее время крупным акционером Банка является Тохтаров О.Т. (52,39%). Банк зарегистрирован в качестве юридического лица 26.05.2008г. - свидетельство о государственной перерегистрации № 5052-1900-АО. Юридический адрес: Республика Казахстан, 050040, г. Алматы, Бостандыкский район, мкр. Коктем-2, 22. Лицензия на проведение банковских и иных операций №1.1.257 от 24.08.2011г. Банк осуществляет свою деятельность с 2008 года, а с начала 2014 года под новым торговым знаком «Банк Астаны». Вдохновившись мировыми тенденциями банковского бизнеса и технологиями сервиса, весной 2014 года мы решили вывести на рынок Казахстана - Банк, который будет простым, понятным и удобным. Банк предлагает весь спектр

банковских услуг, как частным, так и бизнес клиентам.

С 01.01.2009г. Банк является членом Объединения юридических лиц «Ассоциация финансистов Казахстана» (Свидетельство Серия А №268).

Банк осуществляет финансовую деятельность с 07.08.2008г. и является вновь созданным.

Мы обслуживаем клиентов в 8 регионах Казахстана – Алматы, Астана, Атырау, Актау и Караганда, Шымкент, Усть-Каменогорск, Павлодар. В среднесрочной перспективе банк планирует значительно увеличить региональную сеть в крупных областных центрах и городах промышленного значения Республики.

Мы привлекли лучших специалистов из разных стран мира, погрузили их в нашу финансовую лабораторию и создали Банк нового поколения.

6

AO “Банк Астаны” 2017

АКЦИОНЕРЫ БАНКА

Актуальный состав акционеров Банка Астаны:

Олжаc Тохтаров - 52,39%.

Миноритарные акционеры – 47,61%

В рамках планового развития Банка в соответствии с новой бизнес-стратегией за 2017 год уставный капитал банка был увеличен акционерами на 7,3 млрд. тенге, что придало новый импульс для деятельности Банка.

ОСНОВНЫЕ ЦЕННОСТИ НАШЕГО БАНКА

Наша миссия

Превосходить ожидания клиентов, предоставляя финансовый сервис высшего качества.

Наше видение

Стать лидером в области сервиса, качества и инноваций, а также занять лидирующую позицию на рынке факторинга.

Финансовые показатели

Согласно финансовой отчётности за 2017 год, аудированной компанией ТОО «BDO Kazakhstan», активы Банка Астаны составили 339,7 млрд тенге, собственный капитал — 48,4 млрд тенге, кредитный портфель — 169,9 млрд тенге, при уровне обязательств – 291,3 млрд. тенге.

Рейтинги Кредитоспособность Банка подтверждена международным рейтинговым агентством Standard & Poor's в виде присвоения долгосрочного и краткосрочного кредитного рейтинга контрагента на уровне «D»

КЛИЕНТООРИЕНТИРОВАННОСТЬ

ПРОФЕССИОНАЛИЗМ ПРОЗРАЧНОСТЬ ИННОВАЦИОННОСТЬ

АМБИЦИОЗНОСТЬ КАЧЕСТВЕННЫЙ

СЕРВИС

7

AO “Банк Астаны” 2017

ОПИСАНИЕ ТЕКУЩЕЙ ПРОДУКТОВОЙ ЛИНЕЙКИ БАНКА Приоритетные направления Банка – развитие клиент ориентированных бизнес-

направлений – корпоративный бизнес, малый и средний бизнес, розничный бизнес и банковские карточки, а также успешная реализация государственных программ. Основной клиентский сегмент Банка составляют юридические лица. В этой связи Банк располагает следующей продуктовой линейкой для юридических лиц:

расчетно-кассовое обслуживание:

открытие и ведение счетов;

кассовые операции;

банковские переводы;

обменно-валютные операции;

быстрые расчеты;

прием депозитов;

кредитование;

банковские и тендерные гарантии;

аккредитивы;

интернет-банкинг для юридических лиц;

аренда сейфовых ячеек. В этой связи продуктовая линейка Банка для физических лиц в настоящее время

представлена следующими продуктами:

расчетно-кассовое обслуживание:

открытие счетов;

кассовые операции;

обменно-валютные операции;

прием депозитов;

кредитование;

системы денежных переводов:

быстрые расчеты;

оплата коммунальных платежей;

платежные карточки;

интернет-банкинг для физических лиц;

мобильный банкинг;

аренда сейфовых ячеек.

Обслуживание в POS терминалах/ Банкоматах Банка

8

AO “Банк Астаны” 2017

НАИБОЛЕЕ ВАЖНЫЕ СОБЫТИЯ, ПРОИЗОШЕДШИЕ В ЖИЗНИ БАНКА В

2017 ГОДУ:

Первое полугодие 2017 г. – Банк увеличил уставной капитал на 5,300,000 тысячи тенге путем размещения простых акций Банка на IPO неограниченному кругу инвесторов на АО «Казахстанская фондовая биржа». Увеличение сети банкоматов.

Второе полугодие 2017 г. – Банк вторично размещал свои акции на SPO неограниченному кругу инвесторов на МОЕХ (Московская фондовая биржа) в количестве 2 881 835 по цене 215 рублей за каждую акцию. Окончание всех сертификационных работ и получение от МПС одобрения по выводу собственного эквайринга (POS/ATM) в промышленную эксплуатацию.

Филиальная сеть Банка в 2017 г.

Филиальная сеть Банка состоит из 8 филиалов которые представлены в следующих регионах РК (г. Алматы, г. Астана, г. Караганда, г.Павлодар, г.Усть-Каменогорск, г.Актау, г.Атырау, г. Шымкент)

В 2017 году открыты операционные кассы в 6 Отделах

НАО Государственная корпорация "Правительство для граждан" г. Астана и Алматы, где принимаются платежи в бюджет, оплата за медосмотр и т.д.

Филиальная сеть Банка

Наименование 2017 2018 (план)

Филиалы 8 9

Отделения 17 19 (+2)

1. Нам доверяют:

- более 640 000 клиентов;

- около 2 500 партнеров.

2. На первом месте по количеству выпуска

бесконтактных карт по всему Казахстану.

3. На первом месте по привлечению

кобрендовых карт по всему Казахстану.

4. На 4 м месте среди эмитентов платежных

карточек Master Card по всему Казахстану.

5. Завершена сертификация в Master Card в

части торгового и Ecom-эквайринга.

6. Пройден аудиты безопасности хранению

и защите карточных данных PIN Security и

PCI DSS.

7. На банкоматах запущена функция взноса

наличных на карты Банка Астаны.

8. Доставка карт осуществляется в руки

клиенту по указанному адресу.

9. Запущен проект E-PIN, т.е.

самостоятельная установка ПИН-кода

клиентом, выпуск карт без ПИН конвертов

10. Запущен проект по Международному

стандарту безопасности - 3D Secure.

9

AO “Банк Астаны” 2017

Модернизация и разработка новых продуктов срочных и условных счетов для бизнес-клиентов:

«Текущий счет с ежедневным начислением вознаграждения»

«Срочный»;

«Корпоративный»;

«Рабочая сила»;

«Недропользование».

Модернизация и разработка новых продуктов для клиентов розничного бизнеса:

Депозит «Астана»;

Депозит «Детский»

Кобрендовая карта Wargaming

«Кобрендовая карточка Al Saqr Finance»

«Социальная карта»

«Карта Forbes»

Данные депозиты рассчитаны для всех сегментов и категорий вкладчиков и предусматривают различные условия накоплений. Банк Астаны также продолжает полноценно оказывать населению следующие услуги:

Открытие и ведение счетов;

Операции с наличными деньгами;

Обменные операции;

Денежные переводы;

Аренда сейфовых ячеек;

Оплата платежей в бюджет;

Прием коммунальных платежей.

Активное и успешное участие в государственных программах, включая: Программу финансирования субъектов МСБ за счет пенсионных активов АО «Единый

накопительный пенсионный фонд»; Программу регионального финансирования субъектов малого и среднего

предпринимательства Мангистауской области; программу регионального финансирования субъектов малого и среднего

предпринимательства Алматинской области; Программу регионального финансирования субъектов малого и среднего

предпринимательства г. Алматы; Программу обусловленного размещения средств в банках второго уровня для

последующего финансирования франчайзинговых проектов субъектов малого и среднего предпринимательства;

Программу финансирования субъектов среднего и малого предпринимательства на цели пополнения оборотных средств через АО «Банк Развития Казахстана»;

Ежегодную программу поддержки субъектов агропромышленного комплекса на проведение весенне-полевых, уборочных работ по бюджетной программе Кредитование

10

AO “Банк Астаны” 2017

АО «НУХ «КазАгро» для проведения мероприятий по поддержке субъектов агропромышленного комплекса»;

Программа рефинансирования ипотечных жилищных займов/ипотечных займов. Совершенствованы механизмы и процедуры предоставления действующих продуктов по

корпоративному, малому и среднему бизнесу:

кредитные операции;

документарные операции;

предоставление займов;

предоставление овердрафтов;

предоставление условных обязательств.

Совершенствованы механизмы и процедуры предоставления действующих продуктов по кредитования физических лиц на приобретение товаров и/или услуг партнеров Банка в рассрочку.

Представленная в Банке продуктовая линейка, по сути, покрывает необходимые потребности клиентов, но в случае внедрения в мировой практике новых продуктов они, после соответствующей адаптации и привязки к местным условиям, будут внедряться в Банке.

Разработана концепция по развитию партнерской сети в рамках Программы лояльности Банка Астаны.

Проведены активные мероприятия по привлечению компаний оказывающие услуги для сегмента Премиум класса. В течение 2017 года было заключено партнерское соглашение с 2200 компаниями, оказывающими услуги в различных отраслях во всех регионах, где присутствуют региональная сеть Банка;

Продлены сроки проведения акций с крупными международными компаниями Uber, foodpanda, Lamoda. Социальные проекты с НАО «Государственная корпорация «правительство для

граждан» АО «Банк Астаны» продолжает активно сотрудничать с НАО «Государственная корпорация

«Правительство для граждан» по ряду важных проектов. Партнерство финансовой организации и государственного предприятия началось в середине прошлого года года и уже вылилось в целую программу долгосрочного взаимодействия и системной помощи гражданам Казахстана. Так, одним из важнейших проектов, запущенных совместно с НАО «Государственная корпорация «Правительство для граждан», является проект по платежным кобрендинговым картам, в том числе для начисления социальных выплат, к которым относятся пенсионные выплаты и пособия по рождению ребенка. К слову сказать, проект по кобрендинговым картам своевременен и актуален, так как карточные продукты Банка Астаны на рынке являются одними из выгодных и обладают рядом преимуществ. Одним из них является мультивалютность, так как на картах можно хранить до пяти валют: тенге (основная валюта), доллар США, евро, российский рубль и британский фунт. Кобрендинговые карты можно заказать на территории всех ЦОНов (Центр обслуживания населения) Алматы и Астаны, после выпуска карту доставят бесплатно клиенту в руки на дом или в офис. По социальным картам снятие наличных денег в любых банкоматах всех банков на

11

AO “Банк Астаны” 2017

территории Республики Казахстан бесплатное. Карты Банка Астаны универсальны, ими можно пользоваться по всему миру.

Открытие стоек в ЦОНах Алматы и Астаны Одним из первых результатов сотрудничества финансового института и госструктуры

стало открытие на территории ЦОНа Медеуского района Алматы мобильной стойки Банка Астаны и операционной кассы, где можно оплачивать все виды платежей в бюджет (налог, госпошлина), услуги ЦОНа, коммунальные услуги, штрафы и т.д. Кроме того, здесь любой желающий – как физическое, так и юридическое лицо – может получить информацию по банковским продуктам, а также подать заявку на кредитование МСБ, на выпуск дебитной, кредитной платежной карты с бесплатной доставкой.

В Банке Астаны понимают, как важно помогать предпринимателям, особенно в начале их пути, поэтому было принято решение об открытии подобной мобильной стойки в ЦОНе. На протяжении последних месяцев посетители Медеуского ЦОНа уже оценили все выгодные преимущества банковских услуг от Банка Астаны.

В декабре открылось отделение в специализированном ЦОНе по ул. Майлина в Алматы, где действуют операционные кассы Банка Астаны, в которых можно оплачивать штрафы, медосмотр, производить платежи в бюджет (налог, госпошлина), за постановку на учет, за ВИП-номера, сделать пересчет наличных денег, также произвести проверку банкнот на подлинность и получить другие услуги. В ближайшем будущем планируется посадить здесь специалистов, которые будут осуществлять все виды переводов, открытие и ведение депозитов и банковских счетов, также будут принимать заявки на выпуск платежных карточек.

В ноябре и декабре открылись отделения «ЦОН» в Сарыаркинском и Есильском районах Астаны, где клиенты могут оплатить все платежи в бюджет, услуги центра, штрафы и коммунальные платежи. Совместные проекты с ЦОНами важны для банка в первую очередь из-за того, что услуги становятся доступными для всех.

Обслуживание населения в ЦОНах в Алматы и Астаны – это пилотный проект. После его успешной реализации в этих городах планируется открывать такие отделения в других регионах Казахстана.

Студенческий ЦЦОС в КазНПУ имени Абая В ноябре прошлого года при университете КазНПУ (бывший АГУ) им. Абая открылся

студенческий Цифровой центр обслуживания студентов (ЦЦОС), где студенты и их родители могут получить весь спектр услуг, от регистрации на учебные дисциплины, получения академических справок, дубликатов дипломов и до постановки на воинский учет. Также здесь действуют такие структурные подразделения, как: офис студента, центр карьеры, сектор обеспечения международной академической мобильности, паспортный отдел, отдел управления бухгалтерского учета и отчетности, военно-мобилизационный отдел. В Центре сотрудник Банка Астаны занимается предоставлением кредитных платежных карт, которые можно использовать для оплаты учебы. Они удобны, особенно в случаях, когда происходит задержка выплат финансовых средств, а надо срочно оплатить учебу. Кредит выдается сроком до 72 месяцев, при этом льготный период по начислению вознаграждения за пользование кредитом составляет 55 дней, максимальная сумма займа доходит до 3 миллионов тенге. Родители студентов при помощи кредитной карты, удобного мобильного приложения и доступного интернет-банкинга имеют возможность оплачивать учебу из отдаленных регионов Казахстана.

12

AO “Банк Астаны” 2017

Являясь инновационным финансовым институтом, Банк Астаны считает своим долгом сотрудничать по таким проектам, как открытие студенческого ЦЦОСа, направленного на улучшение условий для казахстанской молодежи.

ПОЛИТИКА В ОБЛАСТИ РЕКЛАМЫ И PR

В рамках общей бизнес стратегии банка была разработана маркетинговая стратегия на 2017 год, в которой были продолжены ранее обозначенные линии развития:

Было продолжено развитие двух флагманских продукта Банка: платежные карты, мобильный банкинг; Была продолжена работа с основной целевой аудиторией Банка: адептами и

прогрессистами (молодыми людьми, городскими жителями в возрасте 25-35 лет, с доходом от 150 000 т, пользователями мобильных приложений, смартфонов).

В течение 2017 года путём маркетинговых кампаний были закреплены позиции Банка

Астаны как карточного Банка. Был продлён двухгодичный контракт со студией Warner Bros. на выпуск лимитированной карточной серии Wonder Woman, что стало продолжением успешной выпуска карт с оригинальными изображениями The Batman, The Superman, The Joker.

В 2017 году ещё больше внимания стало уделяться формированию и укреплению

положительных имиджа и репутации Банка. На регулярной основе такие издания как Forbes, Курсив и Капитал публиковали информационные материалы, интервью с топ менеджментом Банка Астаны. Кроме того, Банк участвовал в независимых обзорах и рейтингах, велась активная работа с казахстанским и международными СМИ. В прошлом году у председателя правления Искендера Майлибаева брали эксклюзивные интервью издания Japan Times, бизнес канал РБК. В 2017 году продолжилось позиционирование Банка Астаны как цифрового и инновационного Банка Казахстана в соответствии с бизнес-стратегией Банка на 2014-2018 года.

Благодаря маркетинговой стратегии Банка за 2017 год были реализованы карточные

проекты, подписаны международные договора, поддержаны спортивные и культурные инициативы, связанные с социальной ответственностью финансового института.

Осенью 2017 года был достигнут выпуск более 500 тысяч карт, что стало

перевыполнением годового плана на два месяца. Успешная реализация проектов и продуктов Банка состоялась благодаря грамотно

продуманной маркетинговой стратегии, в основе которой лежит креативный подход к решению бизнес задач.

Правильность стратегии Банка Астаны подтвердило международное признание со

стороны авторитетного издания Global Finance. Банк был удостоен награды «Лучший цифровой банк Казахстана».

13

AO “Банк Астаны” 2017

ИТ АРХИТЕКТУРА И СТРАТЕГИЯ БАНКА В течении 2017 года были проведены следующие работы:

1. Система АБС БИСквит a. Развитие интеграционных сервисов, на базе технологии SOAP – БИСквит интегрирован с

мини хранилищем (по обеспечению выгрузки данных в регуляторную отчетность, ПКБ/ГКБ, КФГД), системой GCentre (выгрузка данных для создания маркетинговых компаний и Soft Collection), терминальной сетью (прием платежей, пополнение счетов, погашение кредитов), система управления бизнес процессами (запуск операционных процессов), интернет банкинг для юридических и физических лиц, карточная система.

b. Внедрены новые продукты по депозитам и кредитам. 2. Модернизация текущей инфраструктуры

a. Подняты инфраструктуры для новых систем банка: i. Процессинг терминалов QP;

ii. Корпоративное хранилище данных. 3. Модернизирована Система управления бизнес-процессами SpringDoc. 4. Модернизирован процесс кредитования без залоговых займов ФЛ.

a. версии интернет банкинга для юридических лиц. b. Реализация возможности регистрация ИП в ИБ ЮЛ в SpringDoc.

5. Развитие карточной системы банка - WAY4:

ОПЕРАЦИОННАЯ ДЕЯТЕЛЬНОСТЬ Анализ рынка В 2017 году в рамках повышения устойчивости банковской системы Национальный Банк

приступил к реализации Программы повышения финансовой устойчивости банковского сектора. Участие банков в программе оздоровления основано на принципах солидарного участия акционеров в докапитализации и возвратности государственной помощи. После успешной реализации антикризисных мер, мы переходим к усилению надзора со стороны Национального Банка. Целью рискориентированного надзора является стимулирование высокоосмотрительной политики банков. Соответствующие поправки в законодательство Национальным Банком уже разработаны.

Банковский сектор представлен 32 банками второго уровня, из которых 14 банков с иностранным

участием, в том числе 12 дочерних банков, доля активов по пяти Банкам составляет 56,1%. Жизненный цикл банковских продуктов достаточно велик, т.к. продукты не «умирают», а модифицируются и «заворачиваются» в новую оболочку. Прогноз развития банковской отрасли в целом – оптимистичен.

На конъюнктуру рынка будут оказывать влияние три основных фактора, вызывая изменения

макроэкономического масштаба и требуя от участников рынка выработки соответствующей стратегии: регуляторные требования, информационные технологии и демографические изменения.

Наблюдается снижение ставки по депозитам, путем снижение годовой эффективной ставки через

КФГД, данное снижение будет стимулировать кредитование на рынке.

Анализ конкурентов Банковскую систему в целом можно поделить на 4 категории банков: крупные банки (Казком,

Халык Банк, Цесна Банк, Центр-Кредит Банк), средние банки (Kaspi Банк, АТФ Банк, Форте Банк, Евразийский Банк, BankRBK, Жилстройсбербанк Казахстана, Delta Bank, Нурбанк, Qazaq Banki), дочерние организации крупных зарубежных банков (ДБ АО «Сбербанк России», Альфа Банк, ВТБ, HomeCredit банк),

14

AO “Банк Астаны” 2017

небольшие и быстроразвивающиеся частные банки (AsiaCredit Bank, BankRBK, Казинвестбанк, Capital Bank Kazakhstan).

Конкуренты Банка в краткосрочном периоде — это банки четвертой категории. Банки данной

категории имеют недолгую историю (от 5 до 7 лет), демонстрируют стремительный и агрессивный рост активов (около 50-70%), имеют пользующуюся спросом продуктовую линейку. Данная категория банков в основном сфокусирована на корпоративном и МСБ секторе и имеет небольшую долю розничного бизнеса. Фондирование банков осуществляется в основном за счет депозитов юридических лиц (порядка 80%). Сильными сторонами банков этой категории являются индивидуальный подход к клиентам, быстрый рост за счет небольшой базы, новое позиционирование в качестве инновационных банков, получение кредитных рейтингов. При этом имеются и значительные недостатки: балансовые ограничения по кредитованию крупных клиентов, короткое и дорогое фондирование, небольшой спектр продуктов. Банк может дифференцироваться от данной категории банков путем развития розничного банка и предложения высокого уровня и качества обслуживания.

В долгосрочной перспективе (10 лет) Банк видит конкурентов среди банков среднего уровня.

Данная категория банков сфокусирована на обслуживании розничного сегмента. Фондирование за счет розничных депозитов (42%). Сильными сторонами данной категории банков являются: высокая эффективность процессов, наработанность клиентов, широкий ассортимент простых и понятных продуктов, упор на карточные продукты, высокий уровень кросс-продаж, хороший уровень риск-менеджмента, активные вложения в маркетинг, разработка инновационных каналов продаж. Слабыми сторонами являются: отсутствие фокуса на корпоративном и МСБ сегментах, высокие затраты на поддержание широкой сети филиалов и отделений, низкий уровень качества и скорости обслуживания. Банк может дифференцироваться внутри данной категории от банков-конкурентов путем предложения спектра инновационных продуктов с развитыми каналами продаж, а также предложения высокого и быстрого уровня обслуживания.

Продукты Банка Депозиты юридических лиц Линейка срочных депозитов для бизнес-клиентов представлена следующими депозитами:

«Срочный»;

«Корпоративный»;

«Рабочая сила»;

«Недропользование»;

«Сейфовые ячейки».

Основными преимуществами вкладов юридических лиц являются:

выгодные процентные ставки; привлекательные условия размещения; возможность пополнения вклада; возможность частичного снятия суммы вклада с сохранением вознаграждения; гибкие условия при досрочном расторжении договора вклада.

В 2017 году Банком актуализированы Тарифные пакеты по комплексному банковскому

обслуживанию.

15

AO “Банк Астаны” 2017

В целях повышения экономической привлекательности Банка для иностранных банков, осуществляющих услуги по обслуживанию расчётно-переводных операций Банка в иностранных валютах, за счёт повышения оборотов SWIFT-переводов, Банком запущена Акция по переводам SWIFT.

На период акции по SWIFT переводам установлены льготные тарифы: Перевод на сумму до 10 000 долларах США - 25 долларов США за перевод; Перевод на сумму от 10 001 до 200 000 долларах США - 30 долларов США за перевод; Перевод на сумму свыше 200 000 долларах США - 60 долларов США за перевод.

Депозиты физических лиц. VIP обслуживание. Компенсация курсовой разницы. Аренда сейфовых ячеек. За 2017 год Банк предоставлял следующие виды депозитов и условного вклада:

Депозит «Астана»;

Депозит «Детский»;

«Сейфовые ячейки».

Данные депозиты рассчитаны и предусматривают различные условия накоплений. Преимущества быть с Банком Астаны:

Высокодоходный: максимальные ставки; Супермультивалютный: 1 депозит - 4 валюты, при этом пополнение вклада в любой валюте; Открытие вклада с нулевым остатком.

В целях увеличения депозитного портфеля по физическим лицам, Банком был запущен Акции по поощрению вкладчиков. По вкладам, открытым в период действия Акции через систему Интернет-банкинг для физических лиц предусмотрены:

повышенный акционный cashback до 10% на карту Банка; в подарок 5 МРП на счет, открытый в Банке (с удержанием ИПН); в подарок предоставление услуги «Аренда сейфовых ячеек» сроком на 3 месяца.

Кроме того, продолжается работа по организации комфортных условий для обслуживания VIP-

клиентовVIP-центра в г.Алматы. Введены отдельные единицы менеджеров для обслуживания VIP-клиентов.

Для улучшения качества предоставления сервиса клиентам по рассчетно-кассовым операциям

Банком был запущен проект Light-office. Новый формат обслуживания Light-office направлен на улучшение качества предоставления сервиса

клиентам по рассчетно-кассовым операциям. В данный момент данный проект является уникальным на рынке Казахстана, то есть, таких дистанционных услуг нет у других банков второго уровня. Банк Астаны уже не в первый раз становится первопроходцем услуг и продуктов на местном рынке, поэтому идею с дистанционными офисами Light-office многие клиенты восприняли с восторгом, ведь мало кому нравится тратить дорогое время в очередях в отделении банка.

Проект Light-office подразумевает под собой фронт-офисное приложение для обслуживания

физических и юридических лиц на платформе интернет-банкинга. Все обслуживание клиента осуществляется на планшете. При помощи планшета специалист Банка Астаны проводят кассовые операции, переводные операции, открытие счетов, в зависимости от нужд клиента. Такой новый формат позволяет значительно экономить время клиента: за счет компонентного и качественного обслуживания

16

AO “Банк Астаны” 2017

почти в два с половиной раза сокращается время работы с каждым клиентом, также для удобства клиентов в банке было увеличено количество менеджеров в два раза, работающих по расчётно-кассовым операциям. Соответственно, повышается и лояльность. При этом сотрудник банка улучшает показатели работы за счет единовременного и оперативного решения всех вопросов с клиентом. Новый формат также предполагает обслуживание не за операционной стойкой, а на удобных креслах, расположенных в кофейных зонах банка, что позволит клиентам общаться с сотрудниками на одном уровне, создаст атмосферу доверия и комфорта. Кроме того, в рамках Light-office сотрудники будут обучать клиентов работать с устройствами самообслуживания.

Мобильные офисы Light-office масштабированы во всех отделениях Банка Астаны в Казахстане начиная с 01-января 2018 года.

В целях повышения экономической привлекательности Банка для иностранных банков, осуществляющих услуги по обслуживанию расчётно-переводных операций Банка в иностранных валютах, за счёт повышения оборотов SWIFT-переводов, Банком запущена Акция по переводам SWIFT. На период акции по SWIFT переводам установлены льготные тарифы:

Перевод на сумму до 10 000 долларах США - 25 долларов США за перевод; Перевод на сумму от 10 001 до 200 000 долларах США - 30 долларов США за перевод; Перевод на сумму свыше 200 000 долларах США - 60 долларов США за перевод.

В филиалах в г. Усть-Каменогорск и г. Павлодар запущены автоматизированные сейфовые

депозитарий. Расположение автоматизированного сейфового депозитария в зоне круглосуточного самообслуживания (24/7) дает возможность клиентам воспользоваться услугой сейфового хранения в любое время суток.

Преимущества автоматизированного сейфового депозитария: круглосуточный доступ с возможностью закладки и изъятия ценностей в удобное для Вас время,

24 часа в сутки, семь дней в неделю система самообслуживания - работа с сейфовыми ячейками без участия работников Банка безопасный доступ посредством пластиковой магнитной карточки, ПИН-кода, по отпечаткам

пальцев руки (при наличии) и замка от ячейки дополнительная идентификация путем сканирования отпечатка клиента широкий выбор ячеек различного объема возможность хранения предметов весом до 20 кг простота использования удобное расположение сейфового депозитария в центральной части города

Корпоративное кредитование

Корпоративный кредит в Банке Астаны может привлечь любое эффективно действующее

юридическое лицо. Кредиты предоставляются на срок до 84 месяцев в соответствии с определенными внутренними

требованиями Банка в тенге и иностранной валюте в денежной форме и в виде условных обязательств под определенные Банком виды обеспечения. В целом, вопрос о необходимости предоставления обеспечения, его структуре и объеме решается в индивидуальном порядке в зависимости от соответствия клиента параметрам, установленным внутренними нормативными документами Банка. Процентная ставка определяется исходя из конъюнктуры финансового рынка, а также индивидуальных условий кредитования и платежеспособности Клиента. Размер и состав комиссионных платежей устанавливаются

17

AO “Банк Астаны” 2017

с учетом режима кредитования, особенностей кредитуемой сделки и других факторов. Источником погашения кредита является денежный поток от текущей производственной и финансовой деятельности Клиента.

Банк Астаны следит за мировыми тенденциями бизнес финансирования, адаптируя лучшие из них

для рынка Казахстана. Банк в 2017 году активно участвовал в поддержки государственных программ финансирования

через «Фонд развития предпринимательства «ДАМУ», «Национальный управляющий холдинг «КазАгро», «Аграрная кредитная корпорация».

Предпринимателям, участвующим в тендерах по закупкам, чаще всего, Банк предлагает бланковые

тендерные гарантии. Потенциальный поставщик имеет право предоставить банковскую гарантию в качестве обеспечения заявки для участия в тендере в соответствии с Законом Республики Казахстан «О государственных закупках», а потом и заказчику в качестве гарантии исполнения обязательств по договору. Удобство процесса заключается в том, что предприниматель может не блокировать свои денежные средства, что необходимо для участия в тендере, а также не отвлекать их из оборота. Необходимо отметить, что в частности, в соответствии с действующими условиями продукта, бланковые тендерные гарантии выпускаются с целью участия в тендере по государственным закупкам, по закупкам национальных холдингов, его дочерних организаций.

Дополнительно хотелось бы сообщить, что в начале 2017 года Банком были подведены итоги

запуска пилотного проекта «Тендерные гарантии с доставкой в офис клиента», учитывая положительный эффект от реализации данного пилотного проекта в апреле 2017 года Банк успешно тиражировал проект на все региональные филиалы.

Также особое внимание будет уделяться «кросс-продажам», которое предполагает повышение

лояльности клиентов за счет реализации комплексного обслуживания в виде удовлетворения всех финансовых потребностей клиентов.

Кредитование малого и среднего бизнеса

Банковские кредиты по малому бизнесу — один из эффективных инструментов развития

предпринимательства. Оперативное получение средств позволяет владельцам компаний быстро реагировать на изменения ситуации. Кредиты малому бизнесу — это возможность расширять производственную или товарную базу, внедрять инновационные технологии, оборудовать новые рабочие места и т. д. Программы кредитов для индивидуальных предпринимателей рассчитаны на разные потребности.

Банком запущен уникальный продукт «Микробизнес», специально разработанный для

индивидуальных предпринимателей, долгое время остававшихся за бортом интересов коммерческих банков.

Кредитование малого бизнеса, а точнее микробизнеса, было заложено в стратегию развития

Банка Астаны. Практически весь 2017 год ушёл на автоматизацию процессов, написание скоринговой модели, интеграцию наших систем с различными платформами, реализацию планшетных решений от получения заявки до выдачи займа и обслуживания после получения кредита. Программа в пилотном режиме работала в нескольких регионах, тем временем мы наблюдали за качеством портфеля для получения полной картины. Только после этого мы пришли уже подготовленными к промышленному запуску нашего сервиса для казахстанского рынка.

18

AO “Банк Астаны” 2017

Следуя выбранной стратегии по цифровизации процессов, Банк в первую очередь, разработал систему проверки потенциальных клиентов, где имеется возможность принимать предварительное решение в течение двух минут. Далее провел интеграцию с соответствующими программными обеспечениями, чтобы клиент мог открыть текущий счёт в автоматическом режиме, без походов от кредитного эксперта к операционисту и обратно. Также провел интеграцию с платформой по лидогенерации (генерации заявок потенциальных клиентов), на основании которого может управлять трафиком и целенаправленно направлять его по тем регионам, где есть потребность в объёмах. Все процессы были адаптированы под планшетные решения. Кроме того, с онлайн кредитным комитетом Банк построили трекинг – систему отслеживания в реальном времени, что позволило получить первые результаты.

Преимущество цифрового подхода в том, что можно таргетированно направить онлайн-трафик

нескольких тысяч клиентов в регионы по востребованности в продукте. То есть теперь не нужно идти на рынок и раздавать буклеты, не надо пускать «радиорубки», Банк управляет трафиком в интернете в режиме реального времени. Многие процессы состоялись благодаря сильной IT-команде банка, которая позволяет выстроить и интегрировать данные решения. В век цифровизации это действительно важно.

Индивидуальные предприниматели (ИП) – это клиенты, которые попали в серую зону. Банки

разрабатывают продукты для физических лиц (экспресс-кредиты, ипотека, автокредитование, кредитные карты) и для юридических лиц (кредитование малого и среднего бизнеса (МСБ) и корпоративный сектор), но практически никто не работает с ИП, а если даже и работают, то рассматривают мелких предпринимателей как физических лиц, считая их доходы по заработной плате в рамках декларации, либо как юридическое лицо – ТОО, где формат и объём бизнеса не подходят под условия продукта.

Хотя на самом деле потенциал у рынка есть и составляет свыше 1 млн ИП, которые остаются без

должного внимания банков, на откуп микрокредитным организациям. Во многих развитых странах индивидуальные предприниматели являются основой для экономического благосостояния многих семей и сообществ.

При реализации скоринга Банк сделали возможным предоставить предварительное решение

клиенту онлайн, чтобы сэкономить его время и время менеджера. Индивидуальный предприниматель может путём ввода своих данных онлайн (ИИН и номера телефона), не посещая банк, узнать: одобрят ему кредит или нет. И если одобрят, то на какую сумму. В других коммерческих банках, клиенты для получения ответа собирают полный пакет документов и получают отказ в лучшем случае через неделю ожидания.

При положительном решении, клиент может дистанционно выслать документы, после которого

сотрудники Банка выезжают по его адресу для подтверждения бизнеса. Завершает процесс кредитования решение онлайн-комитета, что позволяет получить заём всего за 1-2 дня.

Вместе с тем, Банк Астаны в средне и долгосрочной перспективе осуществляет реализацию

государственных программ финансирования субъектов МСБ за счет средств, выделенных из АО «Фонд развития предпринимательства «Даму», в рамках выделенных средств активно идет освоение по программам Жибек-жолы, Даму-регионы III. Возвратные средства от клиентов будут заново переразмещаться с целью поддержания внутренней экономики, а также поддержка будет осуществляться за счет субсидирования части ставок вознаграждения государством с целью снижения уровня долговой нагрузки клиента.

Кредитование розничного бизнеса

19

AO “Банк Астаны” 2017

Развитие розничного бизнеса в Банке в 2017 году обусловлено наличием лицензии НБРК на осуществление операции, связанные с розничными продуктами и услугами. В 2017 году наблюдается стабильный рост портфеля как по депозитам для физических лиц, так и розничного кредитования.

В рамках развития розничного кредитования в прошедшем году в Банке проведены следующие мероприятия:

Автоматизация стадий прохождения кредитной заявки – исключение человеческого фактора- снижение операционных рисков;

начаты процедуры по оптимизации продуктовой линейки принятия решений по стандартным проектам; реализация мероприятий по оптимизации процессов посткредитного обслуживания займов.

Платежные карточки

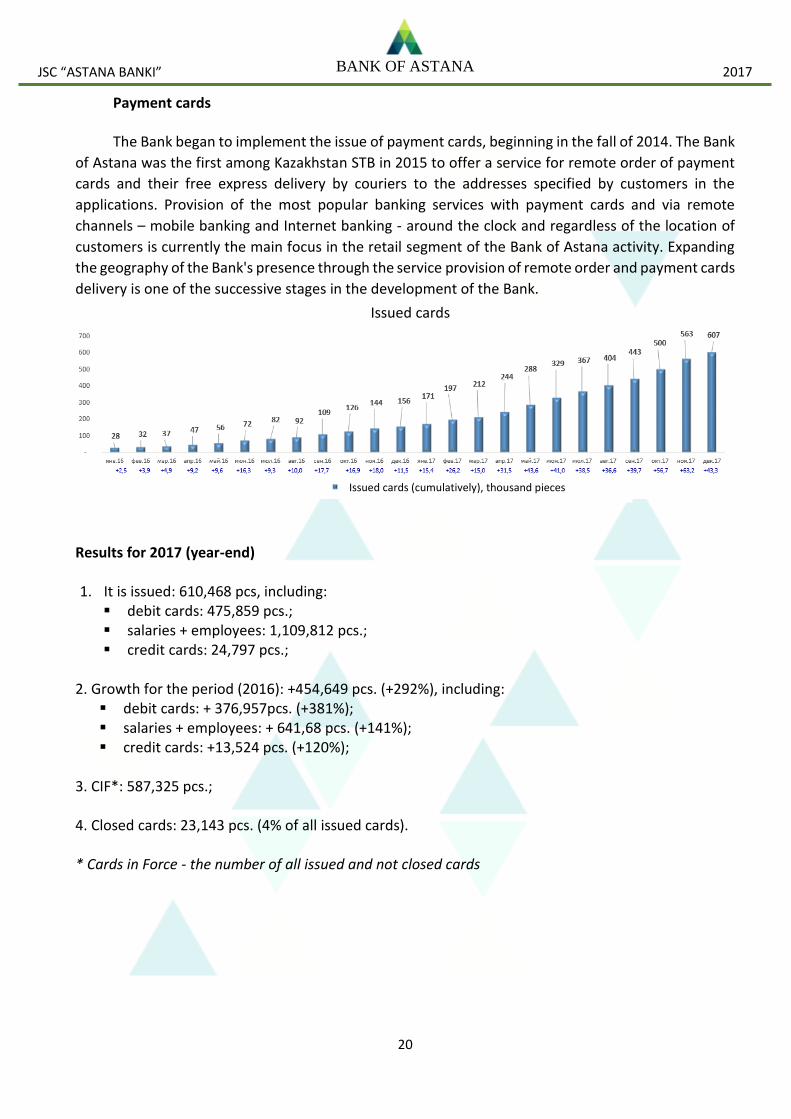

Выпуск платежных карточек Банк начал осуществлять, начиная с осени 2014 года. Банк Астаны

первым среди казахстанских БВУ в 2015 году предложил услугу по дистанционному заказу платежных карт и их бесплатной экспресс-доставке курьерами по адресам, указанным клиентами в заявках. Предоставление самых востребованных банковских услуг с помощью платежных карт и через дистанционные каналы – мобильный банкинг и интернет-банкинг – в круглосуточном режиме и вне зависимости от местонахождения клиентов является на данный момент основным направлением в розничном сегменте деятельности Банка Астаны. Расширение географии присутствия банка благодаря предоставлению услуги по дистанционному заказу и доставке платежных карт является одним из последовательных этапов в развитии банка.

Итоги за 2017 (на конец года)

1. Выпущено: 610 468 шт. В т.ч.: дебетовые карты: 475 859 шт.; ЗП + сотрудники: 1 109 812 шт.; кредитные карты: 24 797 шт.;

2. Рост за период (2016): +454 649шт. (+292%). В т.ч.: дебетовые карты: + 376 957шт. (+381%); ЗП + сотрудники: + 641 68 шт. (+141%); кредитные карты: +13 524 шт. (+120%);

3. CIF*: 587 325 шт.; 4. Закрыто карт: 23 143 шт. (4% от всего выпущенных карт). *Cards in Force – количество всех выпущенных и не закрытых карт

20

AO “Банк Астаны” 2017

Банк Астаны фокусирует особое внимание на повышении лояльности со стороны действующих и

потенциальных клиентов и с этой целью делает свои услуги более выгодными, внедряет новые бонусные программы. В 2017 г. были внедрены сразу несколько приятных для клиентов инструментов:

Держатели платежных карт банка получают возможность сгенерировать собственный ПИН –код

при помощи функции e-pin. Внедрено обслуживание в собственных POS- терминалах Банка

В течение года реализовано ряд проектов, которые позволят значительно повысить уровень

сервиса и расширить спектр предлагаемых услуг:

- Запущена Кобрендовая карта Wargaming, позволяющая держателям получать игровую валюту в игре World of Tanks, осуществляя безналичные транзакции по картам.

- Запущена карта с уникальным дизайном Wonder Women - Запущена первая в Казахстане «Кобрендовая карточка Al Saqr Finance» - дебетная

платежная мультивалютная карточка, соответствующая нормам и принципам Шариата. - Запущен проект «Социальная карта» – продукт, предназначенный для зачисления пенсий

и пособий из Республиканского бюджета с льготными условиями обслуживания.

- Запущена «Карта Forbes» - это дебетная платежная мультивалютная карточка, созданная для успешных людей. Часть от потраченных денег клиентами Банк направляет в фонд журналистики.

- Окончание всех сертификационных работ и получение от МПС одобрения по выводу собственного эквайринга (POS/ATM) в промышленную эксплуатацию

Целью Банка также остается предоставление выгодных банковских продуктов в сочетании с качественным и доступным сервисом для клиентов.

Согласно новой стратегии в среднесрочной перспективе Банк Астаны должен стать лидирующим

казахстанским банком, предлагающим своим клиентам расширенные возможности удаленного обслуживания, максимально используя инновационные технологии и IT-решения. Дистанционные каналы обслуживания. Интернет и мобильный банкинг для физических лиц.

Розничный банкинг уже становится цифровым бизнесом, благодаря быстрому распространению безграничного доступа и доступности мобильных устройств. Глобально, в среднем более чем половина клиентских транзакций идут через онлайн или через мобильный телефон. Большая часть этих операций идет на продвинутых Северных рынках и в Австралии.

Согласно исследованию компании, Bain&Company, сделанному в прошлом году (в исследовании

приняли участие 78 самых крупных банков в мире), если добавить также использование ATM-банкоматов, которые все чаще подключают к интернету, сейчас доля цифровых транзакций достигла 85% в наиболее продвинутых странах и в ближайшем будущем эта цифра приблизиться к 95%.

Но до сих пор еще очень много банков, которые находятся только в начале этого пути. Менее чем

половина потребителей в развивающихся странах не использует свои смартфоны для интернет-банкинга, а в развитых странах 30%.

В новой стратегии в среднесрочной перспективе Банк Астаны должен стать первым казахстанским

банком, работающим в формате 24/7, предлагающим своим клиентам расширенные возможности удаленного обслуживания, максимально используя инновационные технологические и IT-решения. Исходя из данного позиционирования приоритетная целевая аудитория — это малый и средний бизнес, физические лица со среднем и выше среднего уровнем дохода – будущая основа бизнеса Банка.

При создании мобильного приложения команда банка изучила внимательно существующие

приложения в Казахстане, России, ознакомилась с аналогами в США и Европе. При запуске проекта был предусмотрен достаточно широкий набор функциональности в web и в мобильной версии, рассчитанный для клиентов Банка Астаны и клиентов, имеющих счета в других Банках. Система Интернет банкинга с мобильным приложением для физических лиц была запущена в боевую эксплуатацию с 2015 года, за полгода развития уже имеется более 5 000 активных пользователей, при этом большинство из них не являются держателями зарплатных карт Банка Астаны, но с успехом пользуются приложением.

Сейчас приложение банка Астаны доступно и для пользователей устройств на платформах IPhone и

Android. Предусмотрен простой и быстрый способ регистрации (достаточно лишь адреса электронной почты и номера мобильного телефона). В рамках исполнения стратегии Банка, пользователям было предложено совершать любые платежи в мобильном банкинг в режиме 24/7.

В мобильном приложении для пользователя предложены все виды внутрибанковских переводов,

в том числе в иностранной валюте. Конвертация и конверсия производятся без комиссий круглосуточно, в том числе конвертация внутри депозита. Немаловажное дополнение - все виды платежей без комиссий – 0 тенге. Пользователь с помощью мобильного приложения также может осуществить покупку страхования ОГПО с бесплатной доставкой.

Неотъемлемой частью стратегии развития является предоставление банковских продуктов с

доставкой клиенту, исключающее необходимость обращаться в банк. С помощью нашего приложения, пользователь сможет осуществить заказ на выпуск платежной карты с доставкой «в руки». В ближайшее время будут доступны услуги дистанционного открытия вкладов и получения розничных кредитов, револьверных карт.

В течение года планируются внедрить следующие функции, которые в настоящее время проходят

испытания и тестирование:

Межбанковские переводы в пользу юридических и физических лиц, Быстрые международные переводы, Покупка всех видов страхования с доставкой клиенту, Сложные банковские сервисы: дистанционный выпуск платежных карты с доставкой клиенту,

открытие депозитов и получение беззалоговых кредитов.

В сложных сервисах будет использоваться ЭЦП НУЦ. Акцент в 2015 году будет также сделан

на безопасность системы, в связи с чем будет запущен проект по внедрению специального ПО, используемого в европейских банках, без аналогов в СНГ. Интернет банкинг для юридических лиц

В рамках мобильной стратегии развития Банка Астаны, с середины 2014 году активно велась работа по разработке новой системы дистанционного обслуживания и для юридических лиц, которая была запущена в работу с января 2015 года. Основные принципы построения новой системы - это широкий функционал с учетом потребностей клиентов МСБ и простота в использовании. За достаточно короткий срок удалось создать конкурентоспособный продукт, к основным отличиям от аналогичных систем на рынке банковских услуг можно отнести:

Работа системы в режиме on-line; Работа с универсальным ЭЦП НУЦ, который многие клиенты уже используют в работе с НК РК и

egov, это исключает необходимость получения отдельных специальных ключей/устройств; Минимальные на рынке тарифы на услуги в дистанционных каналах; Все виды платежей, в том числе валютные платежи, особый подход к тарифам по валютным

переводам; Операции конвертации/ конверсии валюты; Заявки на продукты банка из приложения; Удобство использования за счет «легкого» интерфейса; Интеграция с системами бухгалтерского учета; Контроль за дочерними предприятиями (структура холдинга). Владелец нескольких компаний

имеет возможность работать со счетами каждой из них в одной системе, также реализованы разные уровни доступов, от просто «наблюдателя» до первой и второй подписи документов.

Система предусматривает все виды услуг для владельцев ИП, это достаточно большой сегмент на нашем рынке.

В настоящее время ведется работа над созданием первого в Казахстане мобильного приложения для юридических лиц с возможностями просмотра счетов и подписания документов. Учитывая, что это позволит руководителям компаний поддерживать свой бизнес в любой точке мира, то думаем данная услуга будет востребована на рынке. Также до конца года планируется развитие в направлении унификации каналов, системы для физических и юридических лиц должны иметь общие принципы работы. Когда клиент заходит в одно мобильное приложение и имеет доступ и к своим личным счетам, и к счетам компании, проводя все виды банковских операций. Таким образом, в полной мере достигается цель создания мобильного банкинга без необходимости посещения отделений.

ФИНАНСОВО-ЭКОНОМИЧЕСКИЕ ПОКАЗАТЕЛИ

Активы Банка за 2017 г. по факту составили 339,7 млрд. тенге, отток за год на 21,3 млрд. тг или на

6%. Денежные средства и их эквиваленты в 2017г. сократились на 73,4 млрд. тенге и составили 65,6 млрд. тенге, что выразилось в оттоке в 53%. Основные средства и прочие активы за 2017 г. составили 95 млрд. тенге, тем самым выросли по сравнению с предыдущим годом на 64,3 млрд. тенге.

Динамика ссудного портфеля

01.01.2017 01.07.2017 01.10.2017 01.01.2018

Розница 44 751 32 907 25 403 24 684

карточки 960 1 285 1 419 1824

Корпорейт/МСБ 132 472 141 979 148 399 134 039

Итого 177 223 176 172 175 220 160 548

34 102 60851 996 783

139 080 652

65 632 908

81 204 263

131 824 973

181 668 650

169 889 325

127 439 395

223 670 469

361 004 637

339 682 133

2014 2015 2016 2017

АКТИВЫ БАНКАПрочие активы

Основные средства и нематериальные активы

Кредиты, выданные клиентам

Кредиты и авансы, выданные банкам и прочим финансовым институтам

Финансовые активы, имеющиеся в наличии для продажи

Финансовые инструменты, оцениваемые по справедливой стоимости

Денежные средства и их эквиваленты

Итого, активы

44 75132 907 25 403 24 684

132 472 141 979 148 399 134 039

0

40 000

80 000

120 000

01.01.2017 01.07.2017 01.10.2017 01.01.2018

Розница Корпорейт/МСБ

тыс. тенге

Ссудный портфель за 2017 гг. уменьшился на 9,5% до 170,4 млрд.тенге. Рост кредитного портфеля связан в основном за счет увеличения кредитного портфеля по КБ/МСБ и РБ;

По состоянию на 01.01.2018 г. ссудный портфель занимает 16 позицию среди банков Казахстана опустившись с 15 позиции в сравнении 01.01.2017 г., доля на рынке за указанный период составила 1,32%;

Совокупные обязательства Банка за 2017г. составили 291,3 млрд. тенге, отток за год на 38 млрд. тенге. или 12%. Превалирующая доля фондирующей базы формируется за счёт текущих счетов и депозитов клиентов, составляющих на 01.01.2018 г. 90,9% от общей суммы обязательств Банка. Иные обязательства Банка представлены счетами и депозитами банков и прочих финансовых учреждений, а также прочие пассивы.

7 477 346 13 340 011 6 611 745 527 738

81 204 263

131 824 973

181 668 650

169 889 325

88 681 609

145 164 984

188 280 395

170 417 063

2014 2015 2016 2017

Динамика ссудного портфеля

Кредиты, выданные клиентам

Кредиты и авансы, выданные банкам и прочим финансовым институтам

13 844 44845 844 884 31 099 930 20 097 849

94 973 470

145 182 100

295 582 457

264 810 845109 844 887

200 181 275

329 278 632

291 265 680

2014 2015 2016 2017

СТРУКТУРА ОБЯЗАТЕЛЬСТВПрочие обязательства

Отложенное налоговое обязательство

Субординированные облигации

Кредиторская задолженность по сделкам «РЕПО»

Текущие счета и депозиты клиентов

Счета и депозиты банков и прочих финансовых учреждений

Итого, обязательства

тыс. тенге

тыс. тенге

Фондирующая база Банка показывает естественный прирост параллельно показателям темпов роста активов Банка. За 2017 г. депозитный портфель Банка в виде текущих счетов и депозитов юридических и физических лиц сформировал отток в величине 10,4% что в суммарном выражении составляет 30,8 млрд. тенге. Большую долю обязательств Банка перед клиентами составляют текущие счета и депозиты юридических лиц с долей 73,1 % от общей совокупной суммы депозитного портфеля.

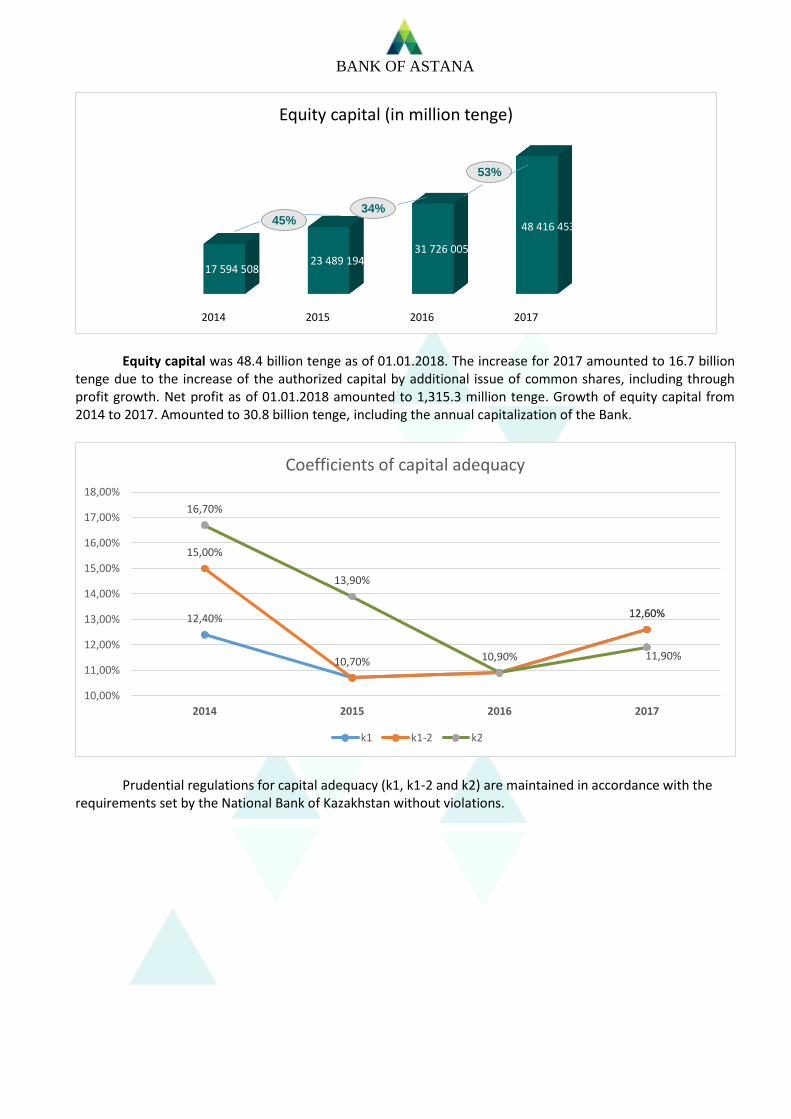

Собственный капитал на 01.01.2018 г. составил 48,4 млрд. тенге. Прирост за 2017 год составил 16,7 млрд. тенге за счет увеличения уставного капитала путем дополнительной эмиссии простых акций, в том числе за счет роста прибыли. Чистая прибыль на 01.01.2018г. составила 1 315,3 млн. тенге. Прирост собственного капитала с 2014 по 2017 гг. составил 30,8 млрд. тенге, в том числе за счет ежегодной докапитализации Банка.

6 760 89327 285 666

44 013 37071 128 486

88 212 577

117 896 434

251 569 087 193 682 359

94 973 470

145 182 100

295 582 457

264 810 845

2014 2015 2016 2017

Депозитный портфель (обязательства перед клиентами)

Текущие счета и депозиты юридических лиц

Текущие счета и депозиты физических лиц

Итого, обязательств перед клиентами

2014 2015 2016 2017

17 594 50823 489 194

31 726 005

48 416 453

Собственный капитал (в млн.тг.)

45%34%

53%

тыс. тенге

Пруденциальные нормативы по достаточности капитала (k1, k1-2 и k2) выдерживаются в соответствии с требованиями, предъявляемыми НБРК, без нарушений.

В 2017 г. в сравнении с 2016 г. процентные доходы выросли на 7 323 млн. тенге, или на 103,73%;

Чистый комиссионный доход Банка за 2017 г. составил 1 889 млн. тенге, тем самым увеличившись по сравнению с 2015 г. на 281 млн. тенге;

12,40%

10,70% 10,90%

12,60%

15,00%

12,60%

16,70%

13,90%

11,90%

10,00%

11,00%

12,00%

13,00%

14,00%

15,00%

16,00%

17,00%

18,00%

2014 2015 2016 2017

Коэффициенты достаточности капитала

k1 k1-2 k2

4 156 596

6 237 1437 059 250

14 381 931

477 040 1 009 712 1 608 197 1 889 483

5 030 906

8 879 0427 951 561

19 554 279

1984 074 1394 686 994 940

6218 856

2014 2015 2016 2017

Структура дохода

Чистый процентный доход Чистый комиссионый доход Операционные доходы Совокупный доход

тыс.тенге

Рентабельность активов Банка за 2017 г. отражает снижение с 0,6% до 0,4% Рентабельность собственного капитала за 2017 г. уменьшение с 6% до 3,9%

УПРАВЛЕНИЕ РИСКАМИ Управление рисками лежит в основе банковской деятельности и является существенным

элементом операционной деятельности Банка. Основной задачей Банка в области риск-менеджмента является совершенствование системы управления рисками, соответствующей характеру, масштабности деятельности и долгосрочным задачам Банка, профилю принимаемых Банком рисков, а также отвечающей потребностям дальнейшего развития бизнеса и соответствующей требованиям регулятора. Система управления рисками представляет собой систему организации, политик, процедур и методов, принятых Банком с целью своевременного выявления, измерения, контроля и мониторинга рисков Банка для обеспечения его финансовой устойчивости, и стабильного функционирования.

Политика и процедуры по управлению рисками Политика Банка по управлению рисками нацелена на определение, анализ и управление

рисками, которым подвержен Банк, на установление лимитов рисков и соответствующих контролей, а также на постоянную оценку уровня рисков и их соответствия установленным лимитам. Политика и процедуры по управлению рисками пересматриваются на регулярной основе с целью отражения изменений рыночной ситуации, предлагаемых банковских продуктов и услуг, и появляющейся лучшей практики.

Совет Директоров несет ответственность за надлежащее функционирование системы контроля по

управлению рисками, за управление ключевыми рисками и одобрение политик и процедур по управлению рисками, а также за одобрение крупных сделок.

Правление несет ответственность за мониторинг и внедрение мер по снижению рисков, а также

следит за тем, чтобы Банк осуществлял деятельность в установленных пределах рисков. В обязанности руководителя Департамента рисков входит общее управление рисками и осуществление контроля за соблюдением требований действующего законодательства, а также осуществление контроля за

11,2%

4,4%

3,5%

1,6%1,4% 1,1%0,6% 0,4%

10,6%

7,7%

6,0%

3,9%4,6%

3,2%

2,0% 1,8%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

01.01.2015 01.01.2016 01.01.2017 01.01.2018

Рентабельность Банка

Ro (рентабельность общая) ROA (рентабельность активов)

ROE (рентабельность собственного капитала) ROIC (рентабельность инвестированного капитала)

применением общих принципов и методов по обнаружению, оценке, управлению и составлению отчетов как по финансовым, так и по нефинансовым рискам.

Обеспечение «трех линий защиты». В процессе осуществления деятельности по управлению рисками обеспечивается вовлеченность

всех структурных подразделений Банка в оценку, принятие и контроль рисков: Принятие рисков (1 -я линия защиты): структурные подразделения Банка, непосредственно

подготавливающие и осуществляющие операцию, вовлечены в процесс идентификации, оценки и мониторинга рисков, и соблюдают требования внутренних нормативных документов в части управления рисками, а также учитывают уровень риска при подготовке операции;

Управление рисками (2-я линия защиты): структурные подразделения Банка и коллегиальные

органы, ответственные за управление рисками, разрабатывают механизмы управления рисками, методологию, проводят оценку и мониторинг уровня рисков, подготавливают сводную отчетность по рискам, осуществляют агрегирование рисков, рассчитывают размер требований по рискам к совокупному капиталу;

Внутренний аудит (3-я линия защиты): проводит независимую оценку качества действующих

процессов управления рисками, выявляет нарушения и дает предложения по совершенствованию системы управления рисками.

Риски, которым подвержен Банк. В процессе осуществления своей деятельности Банк управляет следующими видами риска:

кредитный, рыночный, операционный риски, риск ликвидности и другие риски. Кредитный риск

Кредитный риск – это риск финансовых потерь, возникающих в результате неисполнения

обязательств заемщиком или контрагентом Банка. Банк управляет кредитным риском посредством применения утвержденных политик и процедур, включающих требования по установлению и соблюдению лимитов концентрации кредитного риска, а также посредством создания Кредитных комитетов, в функции которых входит активный мониторинг кредитного риска. Для повышения эффективности процесса принятия решений Банк создал иерархическую структуру кредитных комитетов в зависимости от типа и величины подверженности риску. Кредитная политика рассматривается и утверждается Советом директоров.

При управлении кредитными рисками Банк учитывает лимиты, установленные на одного заемщика/группу взаимосвязанных заемщиков, контролирует уровень концентрации рисков по отраслям деятельности заёмщиков, регионам.

При анализе кредитных проектов осуществляется всесторонняя оценка рисков, в том числе финансовых и юридических; проводится оценка залогового обеспечения, анализируются качественные и количественные показатели проекта.

В целях минимизации возможных убытков, связанных с финансированием проектов клиентов, Банком осуществляется постоянный мониторинг кредитного портфеля на предмет наличия тревожных сигналов и, при необходимости, применяются превентивные меры по снижению рисков.

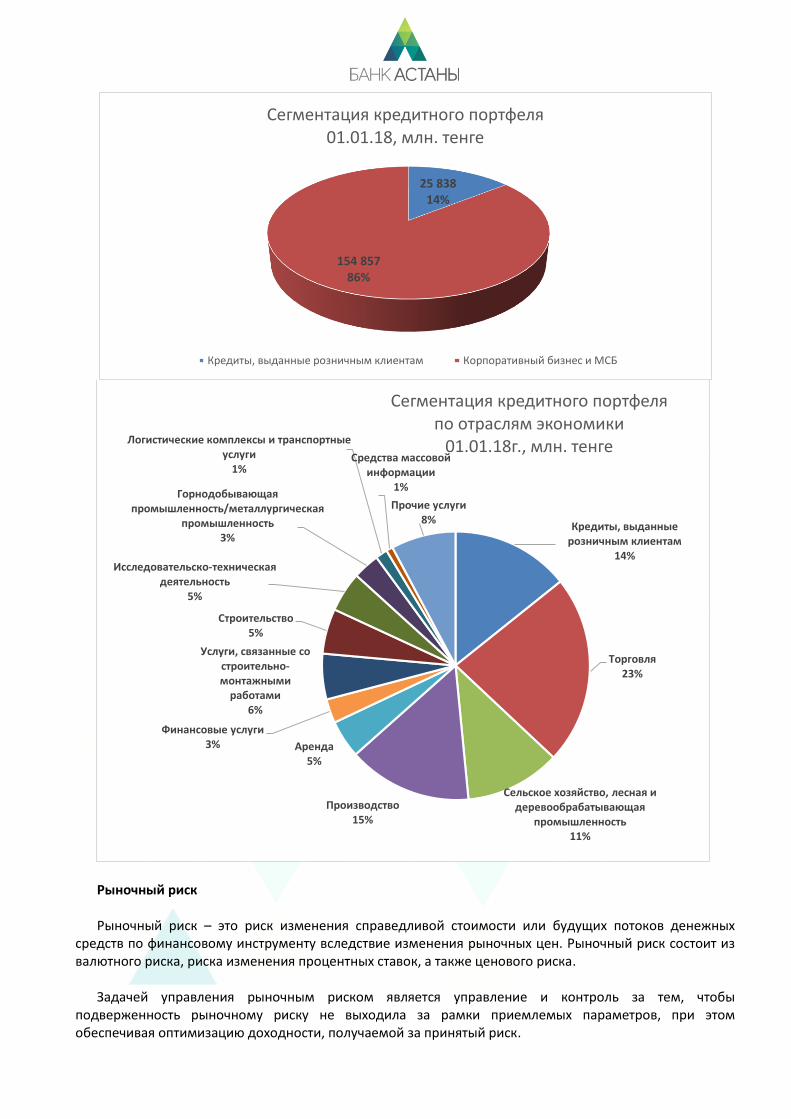

По состоянию на 01.01.2018г. значительный удельный вес в структуре ссудного портфеля Банка занимает корпоративный бизнес и МСБ (86%).

Рыночный риск Рыночный риск – это риск изменения справедливой стоимости или будущих потоков денежных

средств по финансовому инструменту вследствие изменения рыночных цен. Рыночный риск состоит из валютного риска, риска изменения процентных ставок, а также ценового риска.

Задачей управления рыночным риском является управление и контроль за тем, чтобы

подверженность рыночному риску не выходила за рамки приемлемых параметров, при этом обеспечивая оптимизацию доходности, получаемой за принятый риск.

25 83814%

154 85786%

Сегментация кредитного портфеля01.01.18, млн. тенге

Кредиты, выданные розничным клиентам Корпоративный бизнес и МСБ

Кредиты, выданные розничным клиентам

14%

Торговля23%

Сельское хозяйство, лесная и деревообрабатывающая

промышленность11%

Производство15%

Аренда5%

Финансовые услуги3%

Услуги, связанные со строительно-монтажными

работами6%

Строительство5%

Исследовательско-техническая деятельность

5%

Горнодобывающая промышленность/металлургическая

промышленность3%

Логистические комплексы и транспортные услуги

1%Средства массовой

информации1%

Прочие услуги8%

Сегментация кредитного портфеля по отраслям экономики

01.01.18г., млн. тенге

Рыночный риск управляется и контролируется Комитетом по управлению активами и пассивами (КУАП), как на уровне Банка в целом, так и на уровне отдельных сделок.

В процессе управления рыночным риском Банк руководствуется требованиями, установленными

нормативными актами и рекомендациями регуляторного органа. Банк выявляет рыночные риски, анализируя различные количественные и качественные показатели,

используя специальные модели и методики. Применяемые модели и методики измерения рыночных рисков пересматриваются на периодической основе для обеспечения адекватности и приемлемости используемых инструментов.

Банк управляет рыночным риском путем установления лимитов по открытой позиции в отношении

величины портфеля по отдельным финансовым инструментам, сроков изменения процентных ставок, валютной позиции, лимитов потерь и проведения регулярного мониторинга их соблюдения, результаты которого рассматриваются и утверждаются Правлением.

Риск ликвидности Риск ликвидности – это риск того, что Банк может столкнуться со сложностями в привлечении

денежных средств для выполнения своих обязательств. Риск ликвидности возникает при несовпадении по срокам погашения активов и обязательств. Совпадение и/или контролируемое несовпадение по срокам погашения и процентным ставкам активов и обязательств является основополагающим моментом в управлении риском ликвидности.

Для оценки и анализа риска потери ликвидности Банк использует различные системы и инструменты,

позволяющие объективно определить размер и степень влияния риска потери ликвидности на деятельность Банка. Например, действенным методом стратегического анализа ликвидности является GAP анализ, который позволяет увидеть разрывы между активами и обязательствами Банка в разрезе сроков. GAP анализ также позволяет выделить проблемные зоны, препятствующие развитию Банка. Банк проводит GAP анализ процентных, тенговых, долларовых активов и обязательств на ежемесячной основе. А общий GAP анализ позволяет увидеть полную картину ликвидности Банка и по необходимости регулировать её.

Банк поддерживает необходимый уровень ликвидности с целью обеспечения постоянного наличия

денежных средств, необходимых для выполнения всех обязательств по мере наступления сроков их погашения. Политика по управлению ликвидностью рассматривается и утверждается Советом директоров.

Банк стремится активно поддерживать диверсифицированную и стабильную структуру источников

финансирования, а также диверсифицированный портфель высоколиквидных активов для того, чтобы Банк был способен оперативно и без резких колебаний реагировать на непредвиденные требования в отношении ликвидности.

«Подушка» ликвидности на 01.01.2018г.

Запас ликвидности Банка представлен непосредственно ликвидными денежными средствами, обеспечивающими мгновенную ликвидность Банка (наличные деньги, корреспондентские счета, неинвестированные остатки), а также ликвидными активами, способными трансформироваться в денежные средства до 7 дней (операции «обратное РЕПО», ЦБ, имеющиеся в наличии для продажи, операции «валютный своп» со сроком овернайт), и краткосрочными межбанковскими вкладами. Совокупный объем ликвидных средств по состоянию на 1 января 2018 г. составляет 66 606 млн. тг. Заданный объем краткосрочной ликвидности позволяет Банку поддерживать свою платежеспособность, своевременно исполнять принятые на него обязательства и осуществлять инвестиции в инструменты размещения краткосрочной ликвидности

01.01.2018 В млн.тг.

7 810 НАЛИЧНЫЕ ДЕНЬГИ

24 357

КОРРЕСПОНДЕНТСКИЙ СЧЕТ В НБ РК и ВКЛАДЫ В НБРК (НА ОДНУ НОЧЬ)

13 045

КОРРЕСПОНДЕНТСКИЕ СЧЕТА В ДРУГИХ БАНКАХ

722 ГОСУДАРСТВЕННЫЕ ЦЕННЫЕ БУМАГИ

19 222 ОПЕРАЦИИ «ОБРАТНОЕ РЕПО», СВОП

1 450

ВКЛАДЫ, РАЗМЕЩЕННЫЕ В ДРУГИХ БАНКАХ

66 606 ИТОГО, ЛИКВИДНОСТИ

Банк обеспечивает соответствие регуляторным требованиям по уровню ликвидности, включая

коэффициенты срочной и валютной ликвидности. Казначейство ежедневно проводит мониторинг позиции по ликвидности. Также на регулярной основе

Департаментом рисков и Казначейством проводятся «стресс-тесты» с учетом разнообразных возможных сценариев состояния рынка как в нормальных, так и в неблагоприятных условиях.

Риск ликвидности управляется и контролируется КУАП, как на уровне Банка в целом, так и на уровне

отдельных сделок. Решения относительно политики по управлению ликвидностью принимаются КУАП и исполняются Казначейством.

Операционный риск Управление операционным риском в Банке осуществляется на постоянной основе с помощью

следующих инструментов операционного риск-менеджмента: 1. разработка, внедрение и постоянное развитие системы управления операционным риском; 2. мониторинг и оценка уровня операционного риска банка, в том числе на основе информации,

получаемой от других линий защиты; 3. формирование и предоставление отчетности или иной информации совету директоров банка,

УКО и (или) правлению банка по управлению операционным риском; 4. взаимодействие и консультирование структурных подразделений по вопросам управления

операционным риском; 5. осуществление формирования сводной отчетности о событиях операционного риска и

отслеживание исполнения плана мероприятий по их устранению; 6. осуществление контроля за своевременным занесением информации по событиям

операционных рисков в базу данных по операционным рискам риск-координаторами; 7. планирование, координация проведения и анализ результатов самооценки операционных

рисков;

8. разработка совместно со структурными подразделениями ключевых индикаторов операционного риска и пороговых значений по ним;

9. планирование и координация работ по проведению сценарного анализа; 10. разработка и формирование карты рисков; 11. осуществление на периодической основе (не реже 1 раза в год) сравнительного анализа

инструментов оценки операционного риска. В Банке внедрена система риск-координаторов по управлению операционными рисками. В

каждом структурном подразделении Банка и в филиалах назначены риск-координаторы, которые обеспечивают работу по выявление и доведению до Департамента рисков информации об инцидентах операционного риска.

Все инциденты операционного риска заносятся в Базу данных, где подробно анализируются причины

возникновения рисков, ущерб, нанесенный Банку, а также предпринятые или планируемые мероприятия по минимизации/устранению операционных рисков. Также Департаментом рисков ведется надлежащий контроль над выполнением всех мероприятий по снижению рисков.

Все инциденты операционного риска доводятся до сведения Правления Банка в рамках ежемесячных

отчетов и до сведения Совета директоров посредством ежеквартальной информации. Риск информационных технологий Управление риском информационных технологий и информационной безопасности в Банке

осуществляется на постоянной основе с помощью следующих инструментов риск-менеджмента: 1. разработка, внедрение и постоянное развитие системы управления рисками ИТ и ИБ; 2. мониторинг и оценка уровня рисков ИТ и ИБ банка, в том числе на основе информации,

получаемой от других линий защиты; 3. формирование и предоставление отчетности или иной информации совету директоров банка,

УКО и (или) правлению банка по управлению рисками ИТ и ИБ; 4. Участия в проектах Банка, выявление возможных рисков ИТ и ИБ, взаимодействие и

консультирование структурных подразделений по вопросам управления рисков ИТ и ИБ; 5. разработка и формирование карты рисков; 6. осуществление на периодической основе (не реже 1 раза в год) анализа рисков ИТ и ИБ. Менеджмент рисков информационных технологий и информационной безопасности в Банке

осуществляется посредством внедренной системы управления рисками информационных технологий и информационной безопасности, включающую выявление, оценку, минимизацию и мониторинг инфраструктурных рисков, рисков уязвимых ИТ-процессов и ИТ-систем. Выявление угроз и уязвимостей ИТ и ИБ производится при тесном взаимодействии с подразделением ИТ и Службой Информационной Безопасности.

В целях совершенствования внутренних моделей и информационных систем управления рисками ИТ

и ИБ, Банк проводит мероприятия по оснащению необходимым программным обеспечением, автоматизации внутренних процессов учета и автоматизированному формированию ключевых риск-показателей Банка.

СОЦИАЛЬНАЯ ОТВЕТСТВЕННОСТЬ

Благотворительность и спонсорство

Являясь инновационным финансовым институтом, Банк Астаны активно проводил политику социальной активности в Казахстане. Для Банка важно оставаться не только передовым, технологичным и цифровым, но и социально активным, поддерживающим различные инициативы в обществе. Спорт, культура, образование, финансовая грамотность среди детей - это не полный список областей, поддерживаемых Банком.

Доступный спорт для всех желающих на спортивных открытых площадках Стрит воркаут. В 2017

году площадки для занятий спортом были открыты в Алматы, Астане, Актау и Жанаозене. Поскольку в Банке Астаны считают, что занятия спортом укрепляют здоровье нации, открытие спортивных площадок является приоритетным в социальной политике финансового института. Также в Банке поддержали занятия хоккеем среди детей и юношества, поэтому в 2017 году были выпущены платежные кобрендинговые карты КХЛ.

В 2017 году Банк Астаны принял декларацию ООН в отношении гендерного равенства на рабочих

местах. В Банке Астаны всецело поддерживают идею гендерного равенства, как на рабочих местах, так и в обществе в целом.

С целью поддержки и развития женского предпринимательства в 2017 году был запущен

социальный проект "Розовые воротнички" и перевыпущены Ladies (женские) карты. С каждой транзакции по данной карте, банк из собственных средств перечислял определенный процент на развитие женского бизнеса в Казахстане. В результате, проведены обучающие конференции для более 600 начинающих и практикующих бизнес леди в Алматы, Астане, Шымкенте, Усть-Каменогорске, Караганде и Актау.

В прошлом году Банк Астаны выделил гранты для обучения талантливых студентов в Назарбаев

Университет, а также поддержал университетский персонал через покупку автобусов для них. В конце 2016 года был запущен социальный проект по детским картам совместно с финской студией Rovio, создателем популярной игры Angry Birds. Карты предназначены для детей от 7 до 16 лет. Благодаря использованию карт, у детей появляются первые навыки обращения с деньгами, они обучаются основам финансовой грамотности, учатся ценить и копить средства.

В рамках государственной культурной программы «Рухани Жангыру», Банк Астаны проспонсировал ряд культурных мероприятий, включая проведение детской выставки одаренных учащихся детской школы им. А. Кастеева в Париже в штаб-квартире Юнеско во время презентации проекта.

Банк выделил средства для строительства нового помещения театра современного искусства

"АРТиШОК", в старом центре Алматы. Также в 2017 году Банк поддержал проведение крупнейшего в Центральной Азии джазового фестиваля Jazzistan. Осенью прошлого года в Алматы прошло дизайнерское мероприятие, где Банк Астаны выступил основным спонсором и провел конкурс среди художников и дизайнеров на разработку дизайнов платежных карт, авторы лучших работ согласно результатам голосования, получили денежные призы от Банка.

Банк Астаны выступает соучредителем фонда Astana Film Fund и поддерживает молодых

отечественных кинематографистов. В копилке кинокартин, созданных благодаря помощи Банка, такие фильмы Ахана Сатаева как «Дорого к матери», «Районы» и др.

КОРПОРАТИВНОЕ УПРАВЛЕНИЕ

Система корпоративного управления Система корпоративного управления АО «Банк Астаны» определяет основные стандарты и

принципы, применяемые в процессе управления Банком, включая отношения между Советом директоров и Правлением, акционерами и должностными лицами Банка, порядок функционирования и принятия решений органами Банка. Принципы корпоративного управления – это исходные начала, которыми руководствуется Банка в процессе формирования, функционирования и совершенствования своей системы корпоративного управления.

Корпоративное управление Банка основывается, прежде всего, на уважении прав и законных интересов всех его акционеров и статуса самого Банка и направлено на достижение роста эффективности деятельность Данка, в том числе роста активов Банка, создание рабочих мест и поддержание финансовой стабильности и прибыльности Банка. Банком придерживаются следующие принципы корпоративного управления, направленные на создание доверия в отношениях, возникающих в связи с управлением Банка:

обеспечение акционерам реальной возможности для реализации их права на участие в управлении Банком;

создание для акционеров Банка реальной возможности участвовать в распределении чистого дохода Банка (получение дивидендов);

обеспечение своевременного и полного представления акционерам Банка достоверной информации, касающейся финансового положения Банка, экономических показателей, результатов деятельности, структуры управления Банком, в целях обеспечения возможности принятия обоснованных решений акционерами Банка и инвесторами;

обеспечение равного отношения ко всем категориям акционеров Банка;

обеспечение максимальной прозрачности деятельности должностных лиц Банка;

обеспечение осуществления Советом директоров Банка стратегического управления деятельностью и эффективный контроль с его стороны за деятельностью исполнительного органа общества, а также подотчетность директоров его акционерам;

обеспечение Правлению Банка возможности добросовестно осуществлять эффективное руководство текущей деятельностью Банка, а также установление подотчетности Правления Банка Совету директоров Банка и его акционерам;

определение этических норм для акционеров Банка;

обеспечение функционирования эффективной системы внутреннего контроля Банка и ее объективной оценки.

Акционерный капитал По состоянию на 29 декабря 2017 года, разрешенный к выпуску акционерный капитал Банка

состоял из 100,000,000 акций (в 2016 году: 32,000,000 обыкновенных акций), а разрешенный к выпуску, выпущенный и полностью оплаченный капитал состоял из 36,081,627 обыкновенных акций (в 2016 году: 26,882,601 обыкновенных акций).

В течении 2017 года Банк увеличил количество разрешенных к выпуску акций до 100,000,000

акций, 7 июня 2017 года г-н Тохтаров О.Т. приобрел дополнительно 1,739,131 обыкновенных акций Банка за возмещение в размере 2,000,001 тысячи тенге, расчет по которым был осуществлен денежными средствами.

30 июня, 2017 года, Банк увеличил уставной капитал на 5,300,000 тысячи тенге путем размещения простых акций Банка на IPO неограниченному кругу инвесторов на АО «Казахстанская фондовая биржа».

14 декабря, 2017 года Банк вторично размещал свои акции на SPO неограниченному кругу

инвесторов на МОЕХ (Московская фондовая биржа) в количестве 2 881 835 по цене 215 рублей за каждую акцию.

ОРГАНИЗАЦИОННАЯ СТРУКТУРА Организационная структура Банка построена по линейно-функциональному типу и обеспечивает:

оперативное осуществление действий по распоряжениям и указаниям, отдающимся вышестоящими руководителями нижестоящим;

рациональное сочетание линейных и функциональных взаимосвязей;

стабильность полномочий и ответственности за персоналом;

единство и четкость распорядительства;

более высокая, чем в линейной структуре, оперативность принятия и выполнения решений;

личная ответственность каждого руководителя за результаты деятельности;

профессиональное решение задач специалистами функциональных служб. Основные подразделения участвующие в операционной деятельности:

Подразделение по развитию и поддержке бизнеса (малый и средний бизнес, розничный бизнес);

Подразделение корпоративного кредитования;

Подразделение каналов продаж;

Подразделение платежных карт;

Подразделение операционного управления.

Совет директоров Банка

Совет директоров - орган управления АО «Банк Астаны», осуществляющий общее руководство деятельностью АО «Банк Астаны», за исключением решения вопросов, отнесенных к исключительной компетенции Общего собрания акционеров.

Члены Совета директоров Банка