Globalisation and Employment in Bangladesh and Kenya ...

32

0 Globalisation and Employment in Bangladesh and Kenya DISCUSSION PAPER 7 By Kunal Sen School of Development Studies and Overseas Development Group, University of East Anglia, Norwich NR4 7TJ, United Kingdom email: [email protected] I would like to thank the Centre for Policy Dialogue (CPD), Dhaka, Bangladesh and the Kenya Institute for Public Policy Research and Analysis (KIPPRA), Nairobi, Kenya, for providing excellent research facilities and logistic support during my visits to Bangladesh and Kenya. In particular, I would like to thank Prof. Mwangi Kimenyi, Executive Director, KIPPRA, and Prof. Mustafizur Rahman, Research Director, CPD, for their support and advice. This paper has benefited considerably from discussions with Md. Akhtaruzzaman, Debapriya Bhattacharya, Enamul Haque, Kapil Kapoor, Rafiqul Islam Molla, Narhari Rao, Zaidi Sattar, Binayak Sen and Rehman Sobhan in the case of Bangladesh, and Graham Glenday , Bernard Kagira, Peter Kimuyu, Kulundu Manda, Eng. Masila , Catherine Masinde, Hezron Nyangitu and Terry Ryan in the case of Kenya. The usual disclaimer applies. This paper has been prepared as part of the DFID-funded project Globalisation, Production and Poverty.

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Globalisation and Employment in Bangladesh and Kenya ...

0

Globalisation and Employment

in Bangladesh and Kenya

DISCUSSION PAPER 7

By

Kunal Sen

School of Development Studies and Overseas Development Group,University of East Anglia, Norwich NR4 7TJ, United Kingdom

email: [email protected]

I would like to thank the Centre for Policy Dialogue (CPD), Dhaka, Bangladesh and the Kenya Institutefor Public Policy Research and Analysis (KIPPRA), Nairobi, Kenya, for providing excellent researchfacilities and logistic support during my visits to Bangladesh and Kenya. In particular, I would like tothank Prof. Mwangi Kimenyi, Executive Director, KIPPRA, and Prof. Mustafizur Rahman, ResearchDirector, CPD, for their support and advice. This paper has benefited considerably from discussionswith Md. Akhtaruzzaman, Debapriya Bhattacharya, Enamul Haque, Kapil Kapoor, Rafiqul IslamMolla, Narhari Rao, Zaidi Sattar, Binayak Sen and Rehman Sobhan in the case of Bangladesh, andGraham Glenday , Bernard Kagira, Peter Kimuyu, Kulundu Manda, Eng. Masila , Catherine Masinde,Hezron Nyangitu and Terry Ryan in the case of Kenya. The usual disclaimer applies.

This paper has been prepared as part of the DFID-funded project Globalisation, Production andPoverty.

1

Globalisation and Employment in Bangladesh and Kenya

By

Kunal Sen

School of Development Studiesand Overseas Development Group,

University of East Anglia,Norwich NR4 7TJ,United Kingdom

email: [email protected]

I would like to thank the Centre for Policy Dialogue (CPD), Dhaka, Bangladesh andthe Kenya Institute for Public Policy Research and Analysis (KIPPRA), Nairobi,Kenya, for providing excellent research facilities and logistic support during my visitsto Bangladesh and Kenya. In particular, I would like to thank Prof. Mwangi Kimenyi,Executive Director, KIPPRA, and Prof. Mustafizur Rahman, Research Director, CPD,for their support and advice. This paper has benefited considerably from discussionswith Md. Akhtaruzzaman, Debapriya Bhattacharya, Enamul Haque , Kapil Kapoor,Rafiqul Islam Molla, Narhari Rao, Zaidi Sattar, Binayak Sen and Rehman Sobhan inthe case of Bangladesh, and Graham Glenday , Bernard Kagira, Peter Kimuyu,Kulundu Manda, Eng. Masila , Catherine Masinde, Hezron Nyangitu and Terry Ryanin the case of Kenya. The usual disclaimer applies.

This paper has been prepared as part of the DFID-funded project, ‘Globalisation,Production and Poverty’.

2

EXECUTIVE SUMMARY

In contrast to the growing empirical literature that examines the labour market effects

of globalisation in middle income developing countries, there are few studies that do

so for the low income countries of South Asia and Sub-Saharran Africa. In this paper,

we study the effects of globalisation on manufacturing employment in Bangladesh

and Kenya, two countries that have witnessed rapid integration of their economies

with the rest of the world in the past two decades. To assess the impact of increased

open-ness on employment, we use the factor content, the growth accounting and

regression-based approaches.

The analysis of the factor-intensity of exports and imports for Bangladesh

suggest a significant increase in labour-intensive manufacturing exports in the 1990s,

along with a corresponding increase in labour-intensive imports. For Kenya, on the

other hand, there is little change in the volume of exports and imports, or in their

factor-content. Employment coefficients for exports and imports suggest that the

structure of exports is marginally more labour-intensive than imports in both

Bangladesh and Kenya. The growth accounting results indicate that in the case

of Bangladesh, the contribution of international trade to total employment growth has

been positive, though less significant both in absolute and relative terms in the 1990s

than in the1980s. For Kenya, the effect of international trade on employment has been

unambiguously negative in the 1990s.

The regression results indicate that in the case of Bangladesh, increased open-

ness led to the adoption of more labour-intensive techniques within the same industry

while in the case of Kenya, there is no evidence that increased open-ness led to any

appreciable changes in the efficiency of labour or shifts in industry-specific

capital/labour ratios. Thus, the paper finds that globalisation has led to a differential

impact on manufacturing employment in the two countries of our study. In the case of

Bangladesh, increased integration with the world economy has led to an increase

(albeit small) in manufacturing employment while in the case of Kenya, the net effect

of globalisation on employment could be considered negative.

1

Introduction

The 1980s and 1990s have witnessed a rapid integration of the global economy,

reflected in reduced trade barriers, increased trade, highly mobile capital and labour

and the rapid transmission of technology across national lines. There is a vast

empirical literature that examines the labour market effects of such a process of

globalisation for developed countries. In contrast, for developing countries, the

limited set of studies that is available is mainly focused on middle income economies

mostly concentrated in Latin America, with few studies on the low- income countries

of South Asia and Sub-Saharran Africa (see Sen 2001 for a critical review of these

studies). This paper attempts to examine the effects of globalisation on manufacturing

employment in two low-income countries, one in South Asia and the other in Africa.

The countries that we study are Bangladesh and Kenya. Both these countries are

appropriate case studies of the subject at hand, having undergone substantial

economic reforms in the past two decades that has led to the rapid integration of these

two economies with the world economy.

In analyzing the relationship between globalisation and manufacturing

employment, the paper employs three approaches. These are the factor content

approach; the growth accounting approach; and a regression-based approach. Factor

content studies have been widely used both in order to test theories of international

trade and to estimate the employment effects of trade, particularly between developed

and developing countries and provide a useful way of analysing the overall effects of

trade changes on the utilisation of labour. The growth accounting approach

decomposes changes in employment into that part which is accounted for by changes

in domestic demand, changes in exports, changes in imports and productivity growth

(Moreira and Najberg 2000). The third approach that has been used in studies of the

impact of trade on employment is to regress employment at the industry level on a

number of explanatory variables, derived from an econometric model. This approach

has been used by Hine and Wright (1998) to analyse the impact of trade on

employment in UK manufacturing and in a developing country context by Milner and

Wright (1998) for Mauritius. Explanatory variables used by Hine and Wright include

output, export penetration, import penetration and the relative cost of labour

(wage/cost of capital ratio). This approach can take account of the indirect impact of

trade on employment via endogenous changes in technology linked to international

2

trade and/or changes in the efficiency of labour use. Further details of these

approaches are provided in Jenkins and Sen (2002).

The remainder of the paper is divided into six sections. Firstly, in Section II,

we provide a brief overview of policies with respect to international trade and foreign

direct investment (FDI) in Bangladesh and Kenya in the past two decades. We follow

this in Section III with an examination of the changing structure of production and

employment in the manufacturing sectors of these two countries in the recent past.

Sections IV, V and VI use the factor content, growth accounting and econometric

approaches respectively to assess the impact of international trade on manufacturing

employment. Section VII concludes.

II. An Overview of Trade and Foreign Direct Investment Policies

This section provides a brief overview of trade reform and foreign investment policies

in each country and the major trends in trade openness and FDI indicators in these two

countries.

Bangladesh: Beginning in the early 1980s, there was slow progress towards a more

liberal economic policy regime in Bangladesh, with the adoption of the New

Industrial Policy in 1982 and the Revised Industrial Policy in 1986. During this

period, the extensive quantitative restrictions on imports and strict exchange control

measures that had existed in the economy of Bangladesh since independence in 1971

were gradually relaxed (Paratian and Torres 2001). The government introduced

measures to promote exports by introducing export subsidies and import duty

reductions on imported inputs used by exporters, and the first export processing zone

(EPZ) was set up in Chittagong in 1983. There was also emphasis on reducing the

level and dispersion of tariffs, simplifying and rationalising the tariff structure, and a

shift from quotas to tariffs. Furthermore, during this period, a positive list of items

that could be imported was replaced with a negative list of items that could not be

imported without a licence, with the negative list being progressively reduced over

time.

The period from 1991 onwards was marked by the acceleration of trade

reforms with peak tariff rates being drastically reduced and the almost complete

3

abolition of quotas.1 The average Effective Rate of Protection (ERP) fell from 75.7

per cent in 1992/93 to 24.5 per cent in 1999/00, with a similar fall in its standard

deviation from 84.4 in 1992/93 to 20.0 in 1999/00. The most dramatic reductions in

ERPs were observed in ready-market garments from 237.2 per cent in 1992/93 to 58.9

per cent in 1999/00, handloom cloth from 157.7 per cent in 1992/93 to 64.6 per cent

in 1999/00, and mill cloth from 189.7 per cent in 1992/93 to 72.7 per cent in 1999/00

(World Bank 1999). The policy measures were also partially successful in reducing

the anti-export bias of the trade regime, with the ratio of the effective exchange rate

for imports to that of exports decreasing from 1.657 in 1991/92 to 1.263 in 1997/98

(op cit.). In addition, the government introduced a unified exchange rate system by

eliminating the ‘Secondary Exchange Market System’ and adopting a moderately

flexible exchange rate policy. By 1994, Bangladesh had accepted the IMF’s Article 8

obligations, thus committing itself to current account convertibility.

The trade liberalisation of the early 1990s seem to have led to a dramatic

increase in the openness of the Bangladesh economy since 1994, with the ratio of

exports plus imports as a ratio of GDP increasing from an average of 24 per cent in

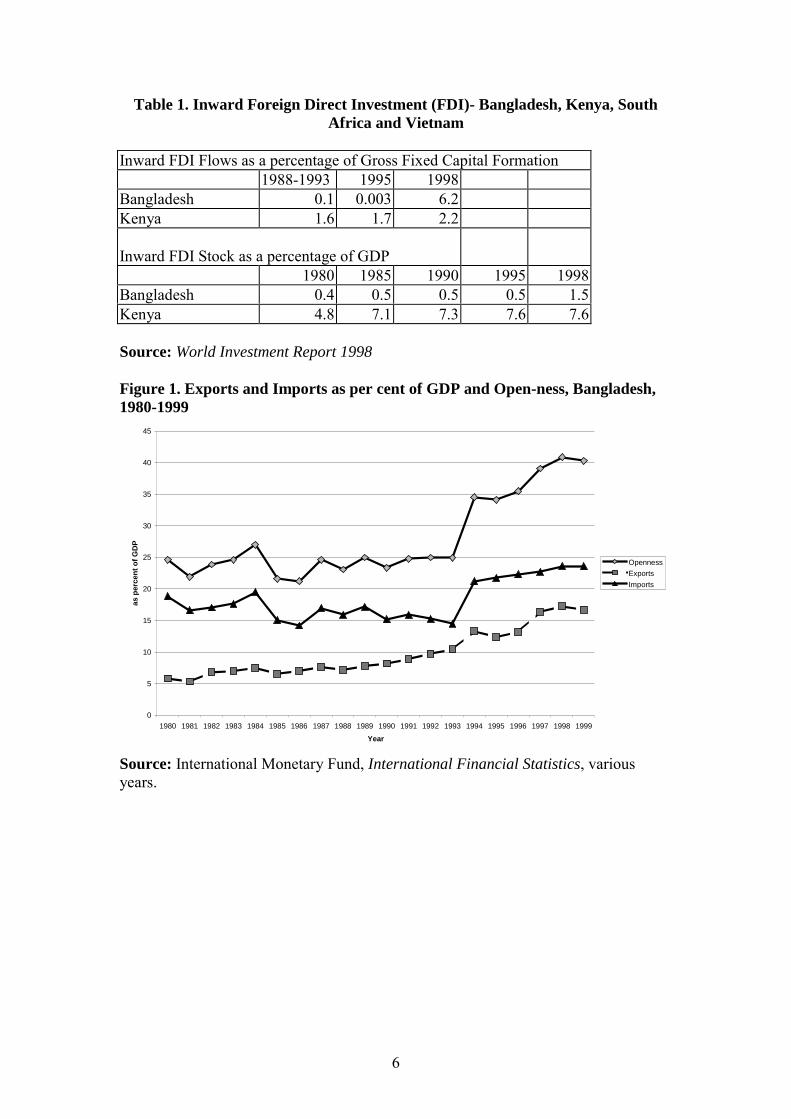

1980-1993 to over 37 per cent in 1994-1998 (Figure 1).

Since 1991, the Bangladesh government has enacted a set of measures to

provide additional incentives to firms to invest in EPZs. A second EPZ was set up in

Savar near Dhaka in 1993 and in October 1996, the government enacted a law

allowing the establishment of EPZs by the private sector. The government also offers

liberal incentives to firms to set up operations in the EPZs – in particular, a ten year

tax holiday, zero duties on the imports of capital and intermediate goods, and the full

repatriation by foreign firms of the principal and profits generated in the EPZs. These

incentives have attracted some foreign investment in the late 1990s, with South Korea

being the largest investor. As a consequence, inward FDI flows as a percentage of

total investment has increased from 0.1 in 1988-1993 to 6.2 in 1998 (Table 1). Much

of this inward foreign investment goes to the EPZs, with the share of EPZs in total

foreign direct investment being 68.1 per cent in 1995/1996 (Paratian and Torres op

cit.). These export processing zones have been critical in the export success of

Bangladesh in recent years, with the bulk of the exports in EPZs originating in the

1 In 1995/97, 115 items were in the negative list, out of which 92 were there for non-trade reasons. Thiscompared to 478 items in 1985/86. With respect to tariffs, the unweighted average tariff rate fell fromover 57 per cent in 1991/92 to 20.7 per cent in 1997/98.

4

ready-made garments sector. A distinctive feature of employment in the EPZs is that a

majority of the workers in the EPZ units are women (approximately 70 per cent

according to Paratian and Torres, op cit.).

Kenya: Since gaining independence from Great Britain in 1963, Kenya followed an

import-substituting industrialisation strategy for the next two decades. The Kenyan

economy performed well in the period 1964-1980 with the GDP growth rate

averaging around 5.5 per cent per annum during this period. The manufacturing sector

grew at a rapid pace, at 10 per cent per annum, fuelled by growth in domestic rural

incomes and the expansion of exports to Tanzanian and Uganda under the common

market created by the East African Community (EAC).

In the late 1970s, the Kenyan economy was hit by several shocks one after

another. First, there was the boom and bust cycle in coffee and tea prices in 1976-

1979. Second, the EAC broke up in 1977, denying Kenyan exporters preferential

access to Ugandan and Tanzanian markets. Third was the oil price shock of 1979.

These shocks contributed to a widening of the current account deficit from 3 per cent

of GDP in 1975-77 to 10-11 per cent in 1978-82.

A structural adjustment programme was introduced in 1979 that, among other

measures, called for eliminating barriers to foreign trade and foreign investment.

Furthermore, steps would be taken to promote export-led growth instead of import

substitution by reducing protection and controls on access to foreign exchange,

adopting a flexible exchange rate policy and providing additional incentives to

exporters. In June 1982, one fifth of restricted items were freed from import licensing

(World Bank 1987). Subsequently, there was limited progress with respect to the

liberalisation of the trade regime with many of the strict controls on the importation of

goods remaining in place. On the exchange rate front, there was a series of

devaluations in 1982, with the exchange rate at the end of 1982 being 14.06 Ksh to 1

US dollar, as compared to 9.66 Ksh to 1 US dollar in 1981.2 Trade reforms started

picking up pace in the late 1980s with the conversion of quantitative restrictions to

tariff equivalents, starting in 1987. In 1990, the government embarked on a phased

tariff reduction (particularly in the high-rate bands) and a rationalisation of tariff

bands (Glenday and Ryan 2000). Perhaps the most significant policy change in the

5

1990s was the revocation of import licensing schedules (other than for health, safety

and security reasons) in May 1993. However, the trade liberalization process was

interrupted by an economic crisis in 1997, following the collapse of an IMF program,

election spending-related budgetary crisis and exchange rate instability (Glenday and

Ndii 1999).

The possible beneficial effects that trade reforms might have had on economic

performance in Kenya has been considerably lessened by major slippages in

macroeconomic policy in the early 1980s and then again in the early 1990s, leading to

high inflation and an appreciation of the real exchange rate during these two periods.

At the same time, the trade reforms have proceeded at an uneven pace, with periods of

rapid opening up followed by periods of stagnancy or reversal in trade liberalisation.3

The openness measure (exports + imports as a per cent of GDP) for Kenya also shows

no clear trend, with an increase in the late 1980s followed by a sharp decline since

1993 (Figure 2). The decline in the open-ness measure in the late 1990s seems to be

driven both by a fall in exports and imports as percentages of GDP.

There has been a negligible flow of FDI into Kenya in the 1980s and 1990s, in

spite of a consistently liberal environment towards FDI by the Kenyan government for

much of the post-independence period. Inward FDI as a ratio of total investment

averaged 1-2 per cent in the period 1988-1998 (Table 1). Since 1988, the Kenyan

government has implemented a series of measures to attract foreign investors into

Kenya, particularly with respect to export platforms such as Manufacturing Under

Bond (MUB) and Export Processing Zones (EPZs). In 1997, 12 out of the 22 firms

operating in Kenya were fully foreign owned and another two had a nominal one per

cent domestic shareholding. However, the performance of these export platforms have

been disappointing with exports from EPZs accounting for 3.5 per cent of total

manufacturing exports and employment in these firms accounting for barely one per

cent of total manufacturing employment in 1997 (Glenday and Ndii op cit.).

2 The sequence of devaluations were in response to a possibility of capital flight following the coupattempt in August 1982.3 As O'Brien and Ryan note, 'Kenya can be made to fit the mould of a reluctant reformer whose overallrecord has been no better than the (Sub-Saharran African) average' (p. 494, 2000).

6

Table 1. Inward Foreign Direct Investment (FDI)- Bangladesh, Kenya, SouthAfrica and Vietnam

Inward FDI Flows as a percentage of Gross Fixed Capital Formation1988-1993 1995 1998

Bangladesh 0.1 0.003 6.2Kenya 1.6 1.7 2.2

Inward FDI Stock as a percentage of GDP1980 1985 1990 1995 1998

Bangladesh 0.4 0.5 0.5 0.5 1.5Kenya 4.8 7.1 7.3 7.6 7.6

Source: World Investment Report 1998

Figure 1. Exports and Imports as per cent of GDP and Open-ness, Bangladesh,1980-1999

Source: International Monetary Fund, International Financial Statistics, variousyears.

0

5

10

15

20

25

30

35

40

45

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999Year

as p

erce

nt o

f GD

P

OpennessExportsImports

7

Figure 2. Exports and Imports as per cent of GDP and Open-ness, Kenya, 1975-1998

Source: International Monetary Fund, International Financial Statistics, variousyears.

III. The Structure of Output and Employment in the ManufacturingSector

Both the manufacturing sectors of Bangladesh and Kenya have witnessed significant

shifts in the patterns of output and employment in the past three decades. In this

section, we highlight the key features of these changing patterns.

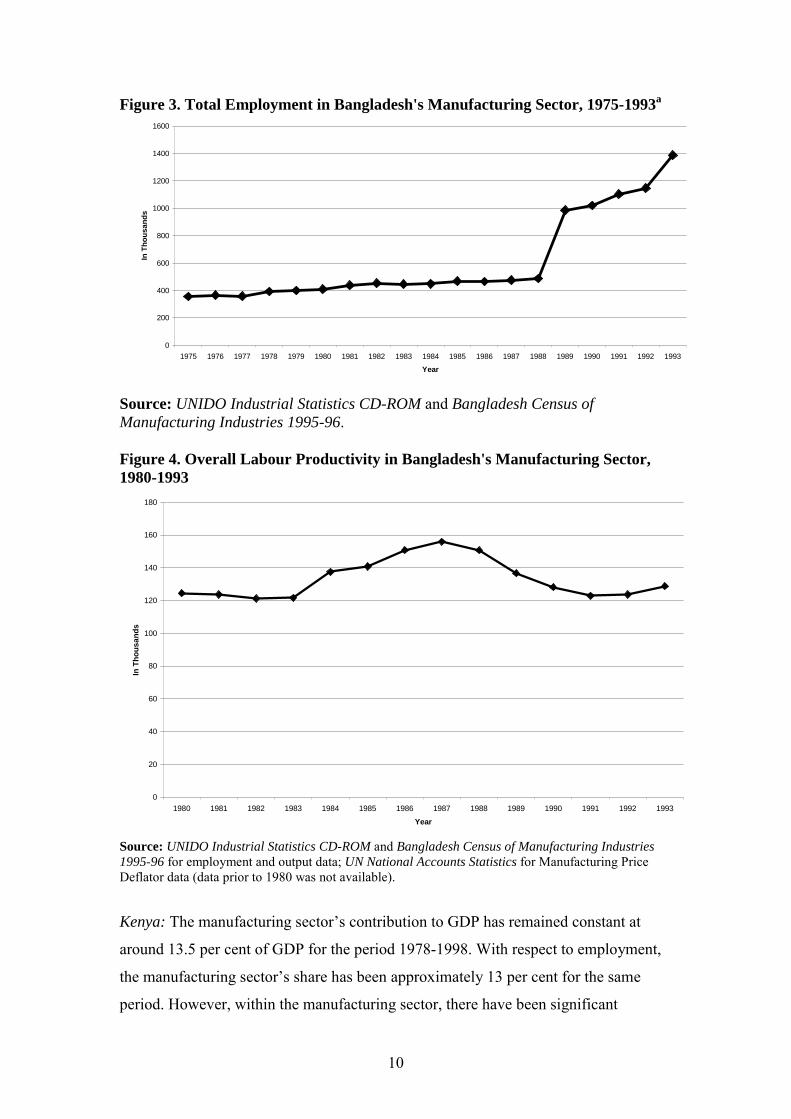

Bangladesh: There has been a marginal increase in the share of the manufacturing

sector in GDP from 12.5 per cent in 1990 to 15 per cent in 1998 (Asian Development

Bank 2000). Within manufacturing, the most dramatic change has been a sharp

decline in the share of textiles from 32.4 per cent in 1975-80 to 19.1 per cent in 1991-

95 in total output, and from 64.9 per cent in 1975-80 to 39.8 per cent in 1991-95 in

total employment (Tables 2 and 3). Food manufacturing, manufacture of wearing

apparel and manufacture of leather products have increased their shares of output in

the period 1975-1995, and in the case of wearing apparel and leather products, there

has also been a dramatic increase in their shares of total employment in the period

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Year

as p

er c

ent o

f GD

P

Open-nessExports Imports

8

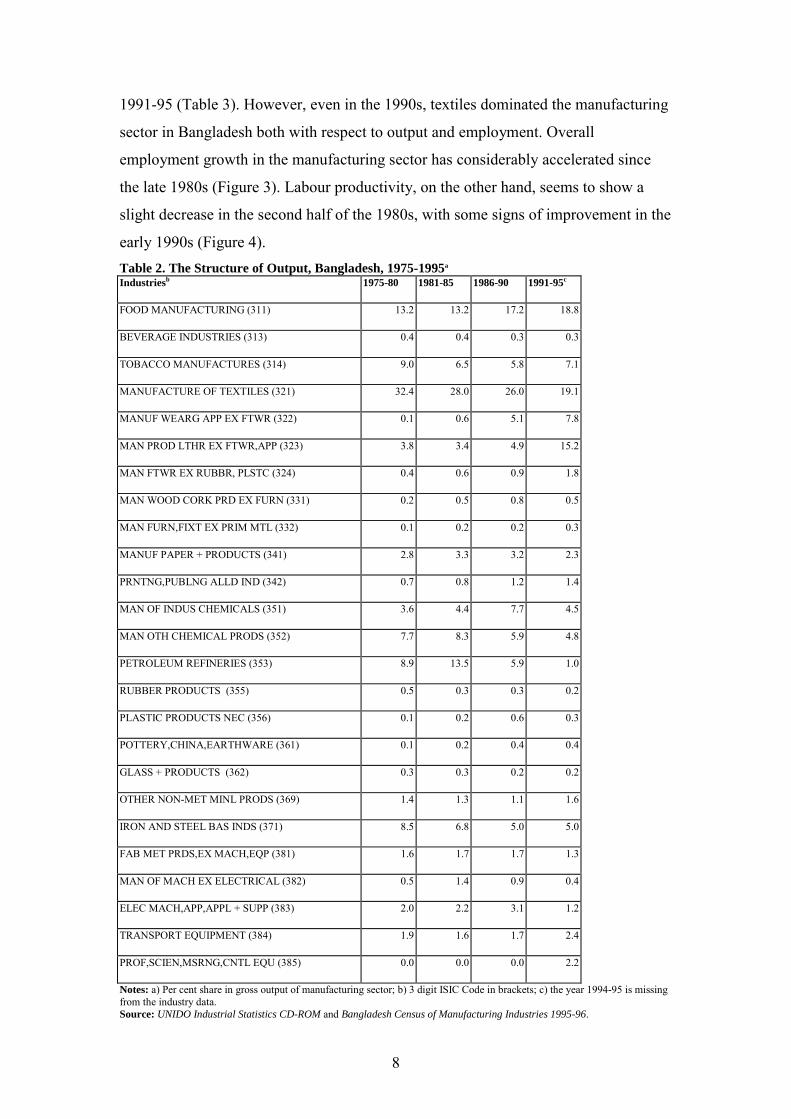

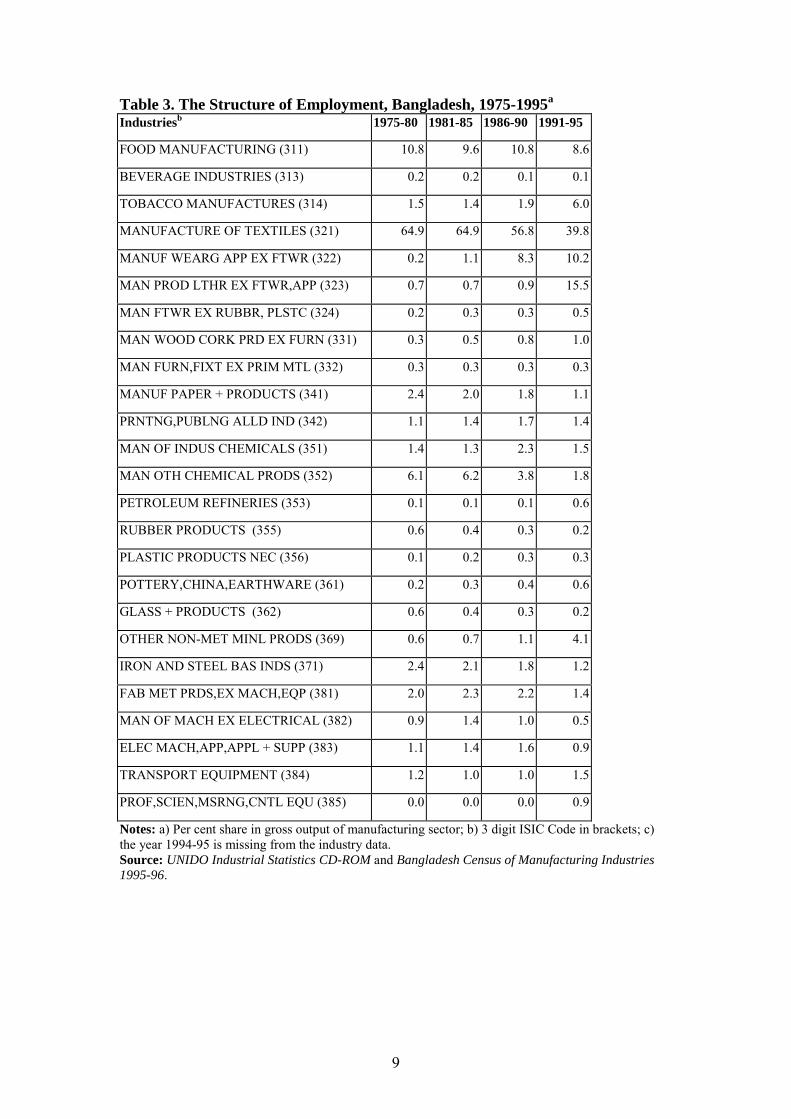

1991-95 (Table 3). However, even in the 1990s, textiles dominated the manufacturing

sector in Bangladesh both with respect to output and employment. Overall

employment growth in the manufacturing sector has considerably accelerated since

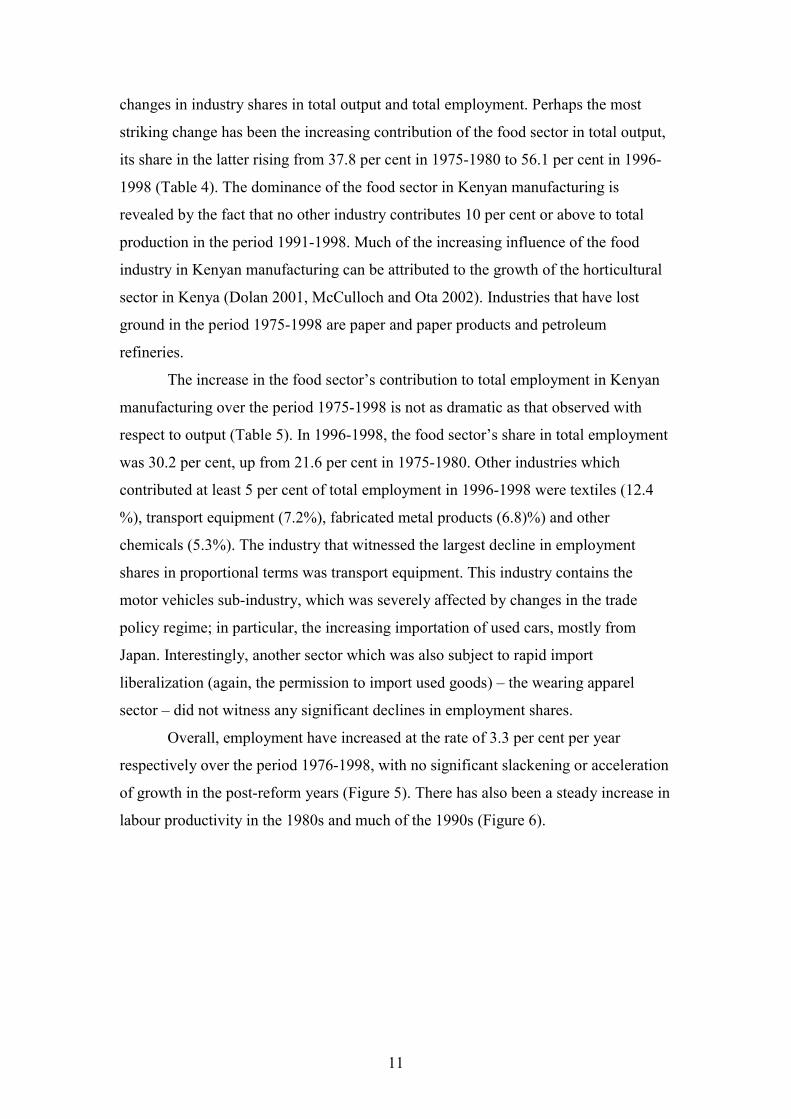

the late 1980s (Figure 3). Labour productivity, on the other hand, seems to show a

slight decrease in the second half of the 1980s, with some signs of improvement in the

early 1990s (Figure 4).Table 2. The Structure of Output, Bangladesh, 1975-1995a

Industriesb 1975-80 1981-85 1986-90 1991-95c

FOOD MANUFACTURING (311) 13.2 13.2 17.2 18.8

BEVERAGE INDUSTRIES (313) 0.4 0.4 0.3 0.3

TOBACCO MANUFACTURES (314) 9.0 6.5 5.8 7.1

MANUFACTURE OF TEXTILES (321) 32.4 28.0 26.0 19.1

MANUF WEARG APP EX FTWR (322) 0.1 0.6 5.1 7.8

MAN PROD LTHR EX FTWR,APP (323) 3.8 3.4 4.9 15.2

MAN FTWR EX RUBBR, PLSTC (324) 0.4 0.6 0.9 1.8

MAN WOOD CORK PRD EX FURN (331) 0.2 0.5 0.8 0.5

MAN FURN,FIXT EX PRIM MTL (332) 0.1 0.2 0.2 0.3

MANUF PAPER + PRODUCTS (341) 2.8 3.3 3.2 2.3

PRNTNG,PUBLNG ALLD IND (342) 0.7 0.8 1.2 1.4

MAN OF INDUS CHEMICALS (351) 3.6 4.4 7.7 4.5

MAN OTH CHEMICAL PRODS (352) 7.7 8.3 5.9 4.8

PETROLEUM REFINERIES (353) 8.9 13.5 5.9 1.0

RUBBER PRODUCTS (355) 0.5 0.3 0.3 0.2

PLASTIC PRODUCTS NEC (356) 0.1 0.2 0.6 0.3

POTTERY,CHINA,EARTHWARE (361) 0.1 0.2 0.4 0.4

GLASS + PRODUCTS (362) 0.3 0.3 0.2 0.2

OTHER NON-MET MINL PRODS (369) 1.4 1.3 1.1 1.6

IRON AND STEEL BAS INDS (371) 8.5 6.8 5.0 5.0

FAB MET PRDS,EX MACH,EQP (381) 1.6 1.7 1.7 1.3

MAN OF MACH EX ELECTRICAL (382) 0.5 1.4 0.9 0.4

ELEC MACH,APP,APPL + SUPP (383) 2.0 2.2 3.1 1.2

TRANSPORT EQUIPMENT (384) 1.9 1.6 1.7 2.4

PROF,SCIEN,MSRNG,CNTL EQU (385) 0.0 0.0 0.0 2.2

Notes: a) Per cent share in gross output of manufacturing sector; b) 3 digit ISIC Code in brackets; c) the year 1994-95 is missingfrom the industry data.Source: UNIDO Industrial Statistics CD-ROM and Bangladesh Census of Manufacturing Industries 1995-96.

9

Table 3. The Structure of Employment, Bangladesh, 1975-1995a

Industriesb 1975-80 1981-85 1986-90 1991-95

FOOD MANUFACTURING (311) 10.8 9.6 10.8 8.6

BEVERAGE INDUSTRIES (313) 0.2 0.2 0.1 0.1

TOBACCO MANUFACTURES (314) 1.5 1.4 1.9 6.0

MANUFACTURE OF TEXTILES (321) 64.9 64.9 56.8 39.8

MANUF WEARG APP EX FTWR (322) 0.2 1.1 8.3 10.2

MAN PROD LTHR EX FTWR,APP (323) 0.7 0.7 0.9 15.5

MAN FTWR EX RUBBR, PLSTC (324) 0.2 0.3 0.3 0.5

MAN WOOD CORK PRD EX FURN (331) 0.3 0.5 0.8 1.0

MAN FURN,FIXT EX PRIM MTL (332) 0.3 0.3 0.3 0.3

MANUF PAPER + PRODUCTS (341) 2.4 2.0 1.8 1.1

PRNTNG,PUBLNG ALLD IND (342) 1.1 1.4 1.7 1.4

MAN OF INDUS CHEMICALS (351) 1.4 1.3 2.3 1.5

MAN OTH CHEMICAL PRODS (352) 6.1 6.2 3.8 1.8

PETROLEUM REFINERIES (353) 0.1 0.1 0.1 0.6

RUBBER PRODUCTS (355) 0.6 0.4 0.3 0.2

PLASTIC PRODUCTS NEC (356) 0.1 0.2 0.3 0.3

POTTERY,CHINA,EARTHWARE (361) 0.2 0.3 0.4 0.6

GLASS + PRODUCTS (362) 0.6 0.4 0.3 0.2

OTHER NON-MET MINL PRODS (369) 0.6 0.7 1.1 4.1

IRON AND STEEL BAS INDS (371) 2.4 2.1 1.8 1.2

FAB MET PRDS,EX MACH,EQP (381) 2.0 2.3 2.2 1.4

MAN OF MACH EX ELECTRICAL (382) 0.9 1.4 1.0 0.5

ELEC MACH,APP,APPL + SUPP (383) 1.1 1.4 1.6 0.9

TRANSPORT EQUIPMENT (384) 1.2 1.0 1.0 1.5

PROF,SCIEN,MSRNG,CNTL EQU (385) 0.0 0.0 0.0 0.9

Notes: a) Per cent share in gross output of manufacturing sector; b) 3 digit ISIC Code in brackets; c)the year 1994-95 is missing from the industry data.Source: UNIDO Industrial Statistics CD-ROM and Bangladesh Census of Manufacturing Industries1995-96.

10

Figure 3. Total Employment in Bangladesh's Manufacturing Sector, 1975-1993a

Source: UNIDO Industrial Statistics CD-ROM and Bangladesh Census ofManufacturing Industries 1995-96.

Figure 4. Overall Labour Productivity in Bangladesh's Manufacturing Sector,1980-1993

Source: UNIDO Industrial Statistics CD-ROM and Bangladesh Census of Manufacturing Industries1995-96 for employment and output data; UN National Accounts Statistics for Manufacturing PriceDeflator data (data prior to 1980 was not available).

Kenya: The manufacturing sector’s contribution to GDP has remained constant at

around 13.5 per cent of GDP for the period 1978-1998. With respect to employment,

the manufacturing sector’s share has been approximately 13 per cent for the same

period. However, within the manufacturing sector, there have been significant

0

200

400

600

800

1000

1200

1400

1600

1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993

Year

In T

hous

ands

0

20

40

60

80

100

120

140

160

180

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993Year

In T

hous

ands

11

changes in industry shares in total output and total employment. Perhaps the most

striking change has been the increasing contribution of the food sector in total output,

its share in the latter rising from 37.8 per cent in 1975-1980 to 56.1 per cent in 1996-

1998 (Table 4). The dominance of the food sector in Kenyan manufacturing is

revealed by the fact that no other industry contributes 10 per cent or above to total

production in the period 1991-1998. Much of the increasing influence of the food

industry in Kenyan manufacturing can be attributed to the growth of the horticultural

sector in Kenya (Dolan 2001, McCulloch and Ota 2002). Industries that have lost

ground in the period 1975-1998 are paper and paper products and petroleum

refineries.

The increase in the food sector’s contribution to total employment in Kenyan

manufacturing over the period 1975-1998 is not as dramatic as that observed with

respect to output (Table 5). In 1996-1998, the food sector’s share in total employment

was 30.2 per cent, up from 21.6 per cent in 1975-1980. Other industries which

contributed at least 5 per cent of total employment in 1996-1998 were textiles (12.4

%), transport equipment (7.2%), fabricated metal products (6.8)%) and other

chemicals (5.3%). The industry that witnessed the largest decline in employment

shares in proportional terms was transport equipment. This industry contains the

motor vehicles sub-industry, which was severely affected by changes in the trade

policy regime; in particular, the increasing importation of used cars, mostly from

Japan. Interestingly, another sector which was also subject to rapid import

liberalization (again, the permission to import used goods) – the wearing apparel

sector – did not witness any significant declines in employment shares.

Overall, employment have increased at the rate of 3.3 per cent per year

respectively over the period 1976-1998, with no significant slackening or acceleration

of growth in the post-reform years (Figure 5). There has also been a steady increase in

labour productivity in the 1980s and much of the 1990s (Figure 6).

12

Table 4. The Structure of Output, Kenya, 1975-1998a

Industriesb 1975-1980 1981-1985 1986-1990 1991-1995 1996-1998FOOD PRODUCTS(311) 37.8 36.7 39.6 44.9 56.1BEVERAGES(313) 4.1 3.3 3.5 2.1 1.1TEXTILES(321) 4.7 4.5 3.5 1.6 1.5WEARING APPAREL,EXCEPTFOOTWEAR(322)

2.4 2.3 2.1 2.0 1.1

LEATHER PRODUCTS(323) 0.5 0.5 0.4 0.2 0.2FOOTWEAR,EXCEPT RUBBER ORPLASTIC(324)

0.8 0.7 0.6 0.4 0.4

WOOD PRODUCTS,EXCEPTFURNITURE(331)

1.8 1.5 1.1 0.6 0.6

FURNITURE,EXCEPT METAL(332) 1.5 0.8 0.4 0.4 0.2PAPER AND PRODUCTS(341) 3.3 3.0 2.2 1.9 1.7PRINTING AND PUBLISHING(342) 3.0 2.5 1.1 1.3 0.9INDUSTRIAL CHEMICALS(351) 2.7 3.1 2.3 2.0 1.9OTHER CHEMICALS(352) 4.9 5.8 10.2 10.4 8.8PETROLEUM REFINERIES(353) 12.1 12.2 12.1 9.8 7.2RUBBER PRODUCTS(355) 1.9 2.1 1.8 1.1 1.1PLASTIC PRODUCTS(356) 1.2 1.3 1.3 1.5 1.4POTTERY,CHINA,EARTHENWARE(361)

0.1 0.0 0.0 0.0 0.0

GLASS AND PRODUCTS(362) 0.4 0.3 0.2 0.1 0.0OTHER NON-METALLIC MINERALPROD.(369)

2.9 3.1 2.5 1.7 2.1

FABRICATED METALPRODUCTS(381)

5.2 5.4 4.9 3.9 4.3

MACHINERY ELECTRIC(383) 2.6 3.6 3.5 6.4 4.1TRANSPORT EQUIPMENT(384) 5.4 6.6 5.8 6.8 4.2PROFESSIONAL & SCIENTIFICEQUIPM.(385)

0.1 0.1 0.1 0.1 0.1

OTHER MANUFACTURING (390) 0.7 0.6 1.0 0.8 1.0Note: a) Per cent share in gross output of manufacturing sector; b) 3 digit ISIC Code in brackets.Source: UNIDO Industrial Statistics CD-ROM

13

Table 5. The Structure of Employment, Kenya, 1975-1998a

Industriesb1975-1980 1981-1985 1986-1990 1991-1995 1996-1998

FOOD PRODUCTS(311) 21.6 23.9 27.2 28.8 30.2BEVERAGES(313) 3.8 3.7 3.7 4.3 3.6TEXTILES(321) 13.4 14.6 14.3 9.7 12.4WEARING APPAREL,EXCEPTFOOTWEAR(322)

4.0 4.6 4.3 2.6 3.6

LEATHER PRODUCTS(323) 1.2 0.8 0.8 1.0 0.9FOOTWEAR,EXCEPT RUBBER ORPLASTIC(324)

1.6 1.4 1.3 2.8 1.2

WOOD PRODUCTS,EXCEPTFURNITURE(331)

6.8 5.9 5.0 3.7 4.7

FURNITURE,EXCEPT METAL(332) 2.3 2.1 2.2 3.0 2.1PAPER AND PRODUCTS(341) 2.9 2.8 3.8 3.9 4.0PRINTING AND PUBLISHING(342) 3.4 3.3 3.5 2.8 3.4INDUSTRIAL CHEMICALS(351) 1.8 2.1 2.0 3.4 2.0OTHER CHEMICALS(352) 3.7 4.2 4.5 3.0 5.3PETROLEUM REFINERIES(353) 0.3 0.2 0.2 0.1 0.1RUBBER PRODUCTS(355) 1.3 1.2 1.2 1.8 1.3PLASTIC PRODUCTS(356) 1.4 1.3 1.5 1.3 2.4POTTERY,CHINA,EARTHENWARE(361)

0.1 0.1 0.1 0.4 0.1

GLASS AND PRODUCTS(362) 0.7 0.8 0.8 1.8 0.8OTHER NON-METALLIC MINERALPROD.(369)

3.2 2.8 3.0 3.1 3.1

FABRICATED METALPRODUCTS(381)

6.7 6.6 6.3 6.9 6.8

MACHINERY ELECTRIC(383) 4.1 4.3 1.7 1.6 1.6TRANSPORT EQUIPMENT(384) 14.3 11.4 9.8 8.7 7.2PROFESSIONAL & SCIENTIFICEQUIPM.(385)

0.1 0.1 0.1 0.1 0.2

OTHER MANUFACTURING (390) 1.0 1.1 1.6 1.9 1.8Notes: a) Per cent share in gross output of manufacturing sector; b) 3 digit ISIC Code in brackets.Source: UNIDO Industrial Statistics CD-ROM

14

Figure 5. Total Employment in Kenya’s Manufacturing Sector, 1975-1998a

Source: UNIDO Industrial Statistics CD-ROM

Figure 6. Overall Labour Productivity in Kenya's Manufacturing Sector, 1975-1998

Source: UNIDO Industrial Statistics CD-ROM for employment and output data andStatistical Abstract, Government of Kenya, various issues, for Manufacturing PriceDeflator data.

0

5

10

15

20

25

30

35

40

45

1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998Year

In T

hous

ands

0

50

100

150

200

250

1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998Year

In T

hous

ands

15

IV. The Factor-Content of Exports and Imports

This section examines the changing factor content of exports and imports in

Bangladesh and Kenya, with a view to identifying the significance of labour-intensive

exports, as opposed to other types of manufactured exports and the way in which this

has changed over time. In order to do so, we have applied Krause’s (1988)

classification of ISIC manufacturing industries according to their dominant factor

input.4 This distinguishes between natural resource intensive, labour intensive,

technology intensive and human capital intensive industries. The natural resource

intensive industries are further sub-divided into agricultural and mineral-based

industries.

Bangladesh: There has been a significant shift into unskilled labour-intensive exports

from agricultural resource intensive exports over the period 1976-1998 (Table 6). The

change in the structure of exports occurred mostly in the 1990s, when total

manufacturing exports increase four fold from $981 million in 1976-80 to $4008

million in 1996-98. By the latter period, unskilled labour intensive exports comprised

around 90 per cent of total manufacturing exports. Much of the exports in this

category was wearing apparel (ISIC 322), which formed 72 per cent of total

manufacturing exports in 1996-98, as compared to 0.08 per cent in 1976-80. This

expansion in ready-made garments was made possible to a great extent by preferential

treatment accorded to Bangladesh’s exports by the European Union under the GSP

scheme, and the substantial quotas made available in the US market, coupled with the

imposition of quota restrictions by the MFA on Bangladesh’s main competitors,

mainly China and India (Spinanger and Wogart 2000).

It is interesting to note, though, that there has also been an increase in the

unskilled labour component of manufacturing imports over the same period (Table 7).

In fact, unskilled labour intensive imports had the largest share in total imports (35.6

per cent) in 1996-98, as compared to the next highest – technology-intensive imports

(24.6 per cent). The increase in unskilled labour intensive imports was due in great

part to the sharp increase in the importation of textiles required for the garments

4 The trade data comes from the International Economic Database of the Australian National Universityand has been reclassified from COMTRADE data according to the International Standard IndustrialClassification (ISIC Rev. 2). Because the trade data is only available at the four digit level and in asmall number of cases, Krause uses a five digit classification, we have had to slightly modify hisgroupings.

16

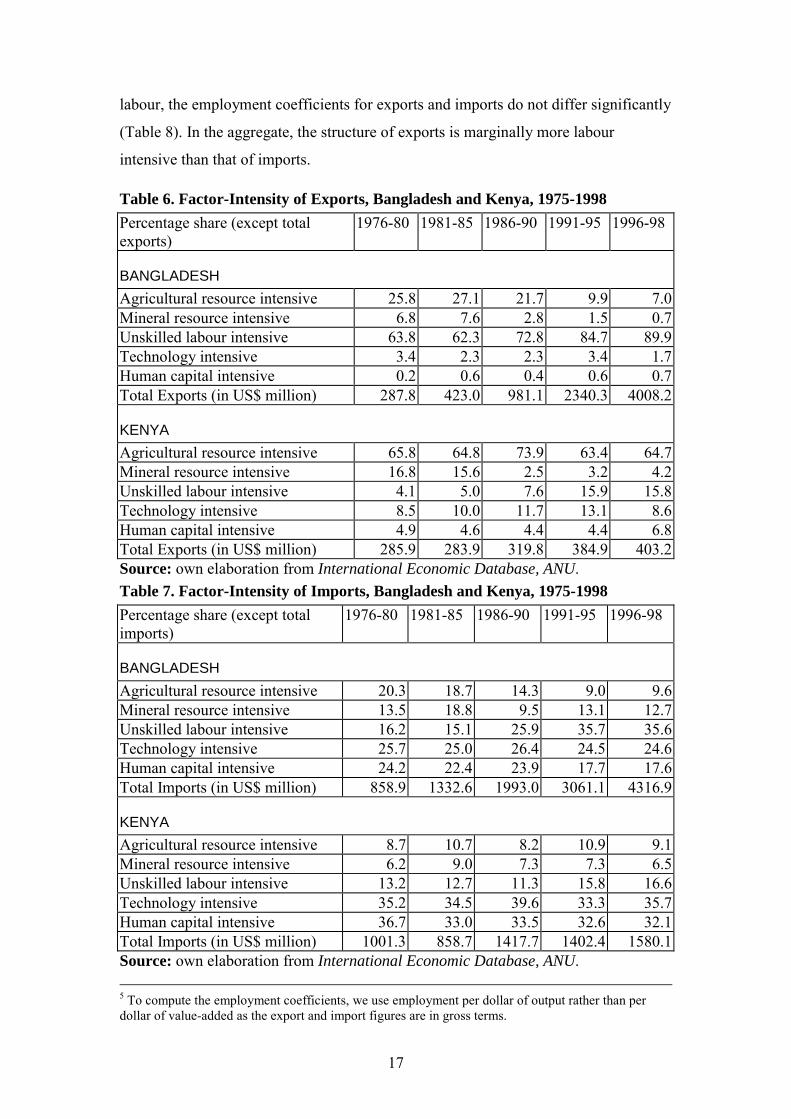

industry, and as we have seen in Section 3, textiles have been the dominant sector in

employment in Bangladesh over the past two decades. This implies that in spite of

Bangladesh’s impressive performance in ready-made garments, it is not obvious that

net employment effects of Bangladesh’s increasing integration with the world

economy have been positive.

To examine the impact of exports and imports on employment, we derive

employment coefficients at the industry level which is then weighted by the share of

each industry in exports and imports. Since the major export industry, the ready-made

garments sector, is female labour intensive, the employment coefficients are

calculated separately for female and male labour (we use 4 digit industry data from

1992, the most recent year for which such data was available). The employment

coefficients are presented in Table 8.5 We find that exports are significantly female

labour intensive than imports; however, the employment coefficient for male labour is

greater for imports than for exports. In the aggregate, the employment coefficient for

exports is marginally higher at 254 versus 226 for imports. This confirms our earlier

finding that the structure of exports in Bangladesh has not been necessarily more

labour-intensive than the structure of its imports, at least till the early 1990s.

Kenya: As noted earlier, Kenya has been a reluctant liberaliser, with slow and uneven

progress in trade reforms. This is also evident in the structure of exports, which does

not display great change over 1976-1998 (Table 6). Agricultural resource intensive

exports remain the most important category of exports, with a share of 64.7 per cent in

total manufacturing exports in 1996-1998. There has been a slight increase in

unskilled labour intensive exports from 4.8 per cent in 1976-80 to 15.8 per cent in

1996-1998. Total manufacturing exports also do not show signs of growth – the

growth rate was 1.9 per cent per annum in 1991-1998 as compared to 7.6 per cent per

annum in 1976-1990.

The structure of imports also does not show significant change in the period under

consideration, with technology and human capital intensive imports remaining the

dominant two components of total manufacturing imports (Table 7). As in the case of

Bangladesh, exports are more female labour intensive than imports, while for male

17

labour, the employment coefficients for exports and imports do not differ significantly

(Table 8). In the aggregate, the structure of exports is marginally more labour

intensive than that of imports.

Table 6. Factor-Intensity of Exports, Bangladesh and Kenya, 1975-1998Percentage share (except totalexports)

1976-80 1981-85 1986-90 1991-95 1996-98

BANGLADESHAgricultural resource intensive 25.8 27.1 21.7 9.9 7.0Mineral resource intensive 6.8 7.6 2.8 1.5 0.7Unskilled labour intensive 63.8 62.3 72.8 84.7 89.9Technology intensive 3.4 2.3 2.3 3.4 1.7Human capital intensive 0.2 0.6 0.4 0.6 0.7Total Exports (in US$ million) 287.8 423.0 981.1 2340.3 4008.2

KENYAAgricultural resource intensive 65.8 64.8 73.9 63.4 64.7Mineral resource intensive 16.8 15.6 2.5 3.2 4.2Unskilled labour intensive 4.1 5.0 7.6 15.9 15.8Technology intensive 8.5 10.0 11.7 13.1 8.6Human capital intensive 4.9 4.6 4.4 4.4 6.8Total Exports (in US$ million) 285.9 283.9 319.8 384.9 403.2Source: own elaboration from International Economic Database, ANU.Table 7. Factor-Intensity of Imports, Bangladesh and Kenya, 1975-1998Percentage share (except totalimports)

1976-80 1981-85 1986-90 1991-95 1996-98

BANGLADESHAgricultural resource intensive 20.3 18.7 14.3 9.0 9.6Mineral resource intensive 13.5 18.8 9.5 13.1 12.7Unskilled labour intensive 16.2 15.1 25.9 35.7 35.6Technology intensive 25.7 25.0 26.4 24.5 24.6Human capital intensive 24.2 22.4 23.9 17.7 17.6Total Imports (in US$ million) 858.9 1332.6 1993.0 3061.1 4316.9

KENYAAgricultural resource intensive 8.7 10.7 8.2 10.9 9.1Mineral resource intensive 6.2 9.0 7.3 7.3 6.5Unskilled labour intensive 13.2 12.7 11.3 15.8 16.6Technology intensive 35.2 34.5 39.6 33.3 35.7Human capital intensive 36.7 33.0 33.5 32.6 32.1Total Imports (in US$ million) 1001.3 858.7 1417.7 1402.4 1580.1Source: own elaboration from International Economic Database, ANU. 5 To compute the employment coefficients, we use employment per dollar of output rather than perdollar of value-added as the export and import figures are in gross terms.

18

Table 8. Employment Coefficients of Imports and Exports, Bangladesh andKenyaBANGLADESHEmployment Coefficient of Imports and Exports, 1992

Exports ImportsEmployment Coefficient per mn. $ of output

Female 139 6Male 114 221Total 254 226

KENYAEmployment Coefficient of Imports and Exports, 1996

Exports ImportsEmployment Coefficient per mn. $ of output

Female 143 89Male 589 597Total 732 686

Source: own elaboration from International Economic Databank (IEDB), ANU andUNIDO data

V. Growth Accounting

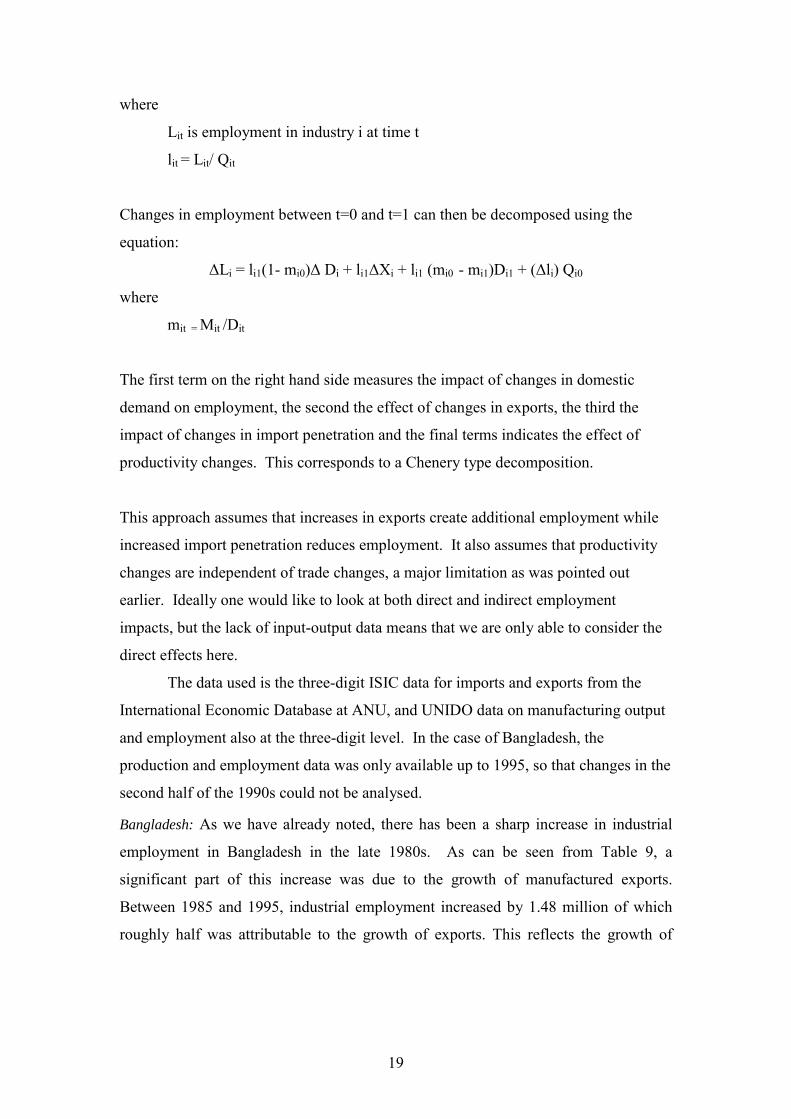

As was seen in Section II, there have been substantial changes in both countries in

terms of openness in recent years. A first stab at estimating the effects of increased

openness on employment can be made using a growth accounting methodology which

divides employment changes over a period of time into that attributable to changes in

domestic demand, exports, import penetration and productivity.

Starting from the basic accounting identity that

Qit = Dit + Xit – Mit

where

Dit is domestic absorption of industry i at time t

Qit is domestic production of industry i at time t

Xit is exports of industry i at time t

Mit is imports of industry i at time t

Employment can be calculated as

Lit = lit(Dit + Xit – Mit)

19

where

Lit is employment in industry i at time t

lit = Lit/ Qit

Changes in employment between t=0 and t=1 can then be decomposed using the

equation:

∆Li = li1(1- mi0)∆ Di + li1∆Xi + li1 (mi0 - mi1)Di1 + (∆li) Qi0

where

mit = Mit /Dit

The first term on the right hand side measures the impact of changes in domestic

demand on employment, the second the effect of changes in exports, the third the

impact of changes in import penetration and the final terms indicates the effect of

productivity changes. This corresponds to a Chenery type decomposition.

This approach assumes that increases in exports create additional employment while

increased import penetration reduces employment. It also assumes that productivity

changes are independent of trade changes, a major limitation as was pointed out

earlier. Ideally one would like to look at both direct and indirect employment

impacts, but the lack of input-output data means that we are only able to consider the

direct effects here.

The data used is the three-digit ISIC data for imports and exports from the

International Economic Database at ANU, and UNIDO data on manufacturing output

and employment also at the three-digit level. In the case of Bangladesh, the

production and employment data was only available up to 1995, so that changes in the

second half of the 1990s could not be analysed.

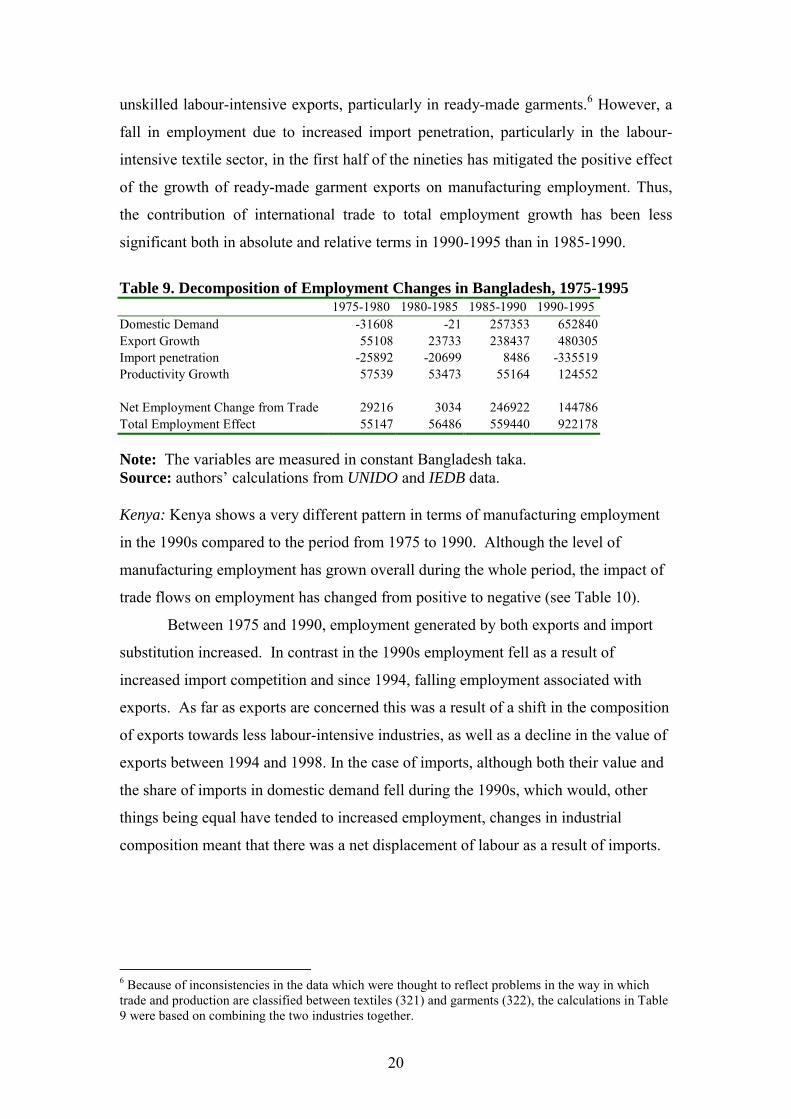

Bangladesh: As we have already noted, there has been a sharp increase in industrial

employment in Bangladesh in the late 1980s. As can be seen from Table 9, a

significant part of this increase was due to the growth of manufactured exports.

Between 1985 and 1995, industrial employment increased by 1.48 million of which

roughly half was attributable to the growth of exports. This reflects the growth of

20

unskilled labour-intensive exports, particularly in ready-made garments.6 However, a

fall in employment due to increased import penetration, particularly in the labour-

intensive textile sector, in the first half of the nineties has mitigated the positive effect

of the growth of ready-made garment exports on manufacturing employment. Thus,

the contribution of international trade to total employment growth has been less

significant both in absolute and relative terms in 1990-1995 than in 1985-1990.

Table 9. Decomposition of Employment Changes in Bangladesh, 1975-19951975-1980 1980-1985 1985-1990 1990-1995

Domestic Demand -31608 -21 257353 652840Export Growth 55108 23733 238437 480305Import penetration -25892 -20699 8486 -335519Productivity Growth 57539 53473 55164 124552

Net Employment Change from Trade 29216 3034 246922 144786Total Employment Effect 55147 56486 559440 922178

Note: The variables are measured in constant Bangladesh taka.Source: authors’ calculations from UNIDO and IEDB data.

Kenya: Kenya shows a very different pattern in terms of manufacturing employment

in the 1990s compared to the period from 1975 to 1990. Although the level of

manufacturing employment has grown overall during the whole period, the impact of

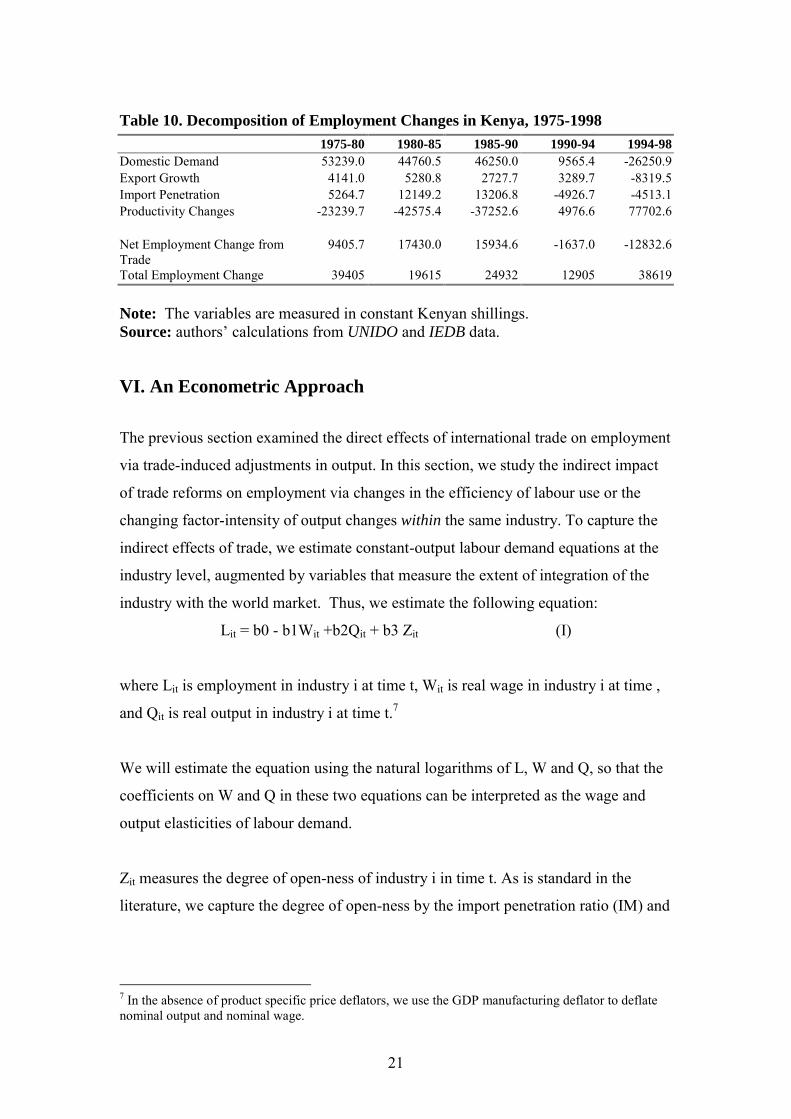

trade flows on employment has changed from positive to negative (see Table 10).

Between 1975 and 1990, employment generated by both exports and import

substitution increased. In contrast in the 1990s employment fell as a result of

increased import competition and since 1994, falling employment associated with

exports. As far as exports are concerned this was a result of a shift in the composition

of exports towards less labour-intensive industries, as well as a decline in the value of

exports between 1994 and 1998. In the case of imports, although both their value and

the share of imports in domestic demand fell during the 1990s, which would, other

things being equal have tended to increased employment, changes in industrial

composition meant that there was a net displacement of labour as a result of imports.

6 Because of inconsistencies in the data which were thought to reflect problems in the way in whichtrade and production are classified between textiles (321) and garments (322), the calculations in Table9 were based on combining the two industries together.

21

Table 10. Decomposition of Employment Changes in Kenya, 1975-19981975-80 1980-85 1985-90 1990-94 1994-98

Domestic Demand 53239.0 44760.5 46250.0 9565.4 -26250.9Export Growth 4141.0 5280.8 2727.7 3289.7 -8319.5Import Penetration 5264.7 12149.2 13206.8 -4926.7 -4513.1Productivity Changes -23239.7 -42575.4 -37252.6 4976.6 77702.6

Net Employment Change fromTrade

9405.7 17430.0 15934.6 -1637.0 -12832.6

Total Employment Change 39405 19615 24932 12905 38619

Note: The variables are measured in constant Kenyan shillings.Source: authors’ calculations from UNIDO and IEDB data.

VI. An Econometric Approach

The previous section examined the direct effects of international trade on employment

via trade-induced adjustments in output. In this section, we study the indirect impact

of trade reforms on employment via changes in the efficiency of labour use or the

changing factor-intensity of output changes within the same industry. To capture the

indirect effects of trade, we estimate constant-output labour demand equations at the

industry level, augmented by variables that measure the extent of integration of the

industry with the world market. Thus, we estimate the following equation:

Lit = b0 - b1Wit +b2Qit + b3 Zit (I)

where Lit is employment in industry i at time t, Wit is real wage in industry i at time ,

and Qit is real output in industry i at time t.7

We will estimate the equation using the natural logarithms of L, W and Q, so that the

coefficients on W and Q in these two equations can be interpreted as the wage and

output elasticities of labour demand.

Zit measures the degree of open-ness of industry i in time t. As is standard in the

literature, we capture the degree of open-ness by the import penetration ratio (IM) and

7 In the absence of product specific price deflators, we use the GDP manufacturing deflator to deflatenominal output and nominal wage.

22

the export-output ratio (EO) defined at the industry level (Hine and Wright 1998).8

The use of these two variables also allows us to separate the effects of import

competition from export orientation on the efficiency of labour use. The exports and

imports data is obtained from the International Economic Databank at the Australian

National University.

The equations are estimated using a pooled dataset drawn from the UNIDO’s

industrial statistics that provides data on output, employment and wages both at the

ISIC three digit and four digit levels from the 1970s. The industry data for Bangladesh

is available at the ISIC 4 digit level for 1982-1992 and allows us to construct a panel

of 660 observations, the panel comprising 60 industries over 11 years. In case of

Kenya, data at the ISIC 4 digit level is not available, but the ISIC 3 digit data is

available for the 1980s and much of the 1990s – the number of industries included in

the panel is 21, and the period of analysis is 1982-1998 (the number of observations is

374).

One econometric problem we face in estimating equation (I) is the possibility

of a high degree of measurement error in the import penetration and export orientation

variables. This is because the output data used in the denominator comes from the

Industrial Census while the trade data used in the numerator (and in the case of IM,

also in the denominator) comes from the Customs or the Directorate of Trade.

Usually, the coverage of the latter is more comprehensive than the coverage of the

former, as the Industrial Census often omits small scale enterprises operating in the

‘informal sector’ (the jua kali sector in Kenya) who may be engaged in international

trade. Thus, inconsistencies in the coverage of the manufacturing sector in the

production and trade data would lead to measurement errors in IM and EO. One way

of addressing this problem is to take first differences of all variables, both dependent

and independent, in equation (I). Under the assumption that the coverage of the

manufacturing sector in the Industrial Census would not change appreciably over

time, first-differencing would give more precise estimates of IM and EO as compared

to using the levels of the latter two variables in the regressions..9

8 We define the import penetration ratio for a particular industry as its imports as a ratio of domesticdemand (i.e, imports+output-exports); while the export-orientation ratio is exports as a ratio of output.9 To see this, suppose the coverage of imports and exports is comprehensive while that for output is not(a defensible assumption, as we have noted earlier). Let q1 be that part of output that is not captured inthe Industrial Census. Let q2 be the output that is reported in the Industrial Census. Then, EO=X/Q,where X is exports and Q is output, and Q=q1+q2. Taking log first differences, we get:

23

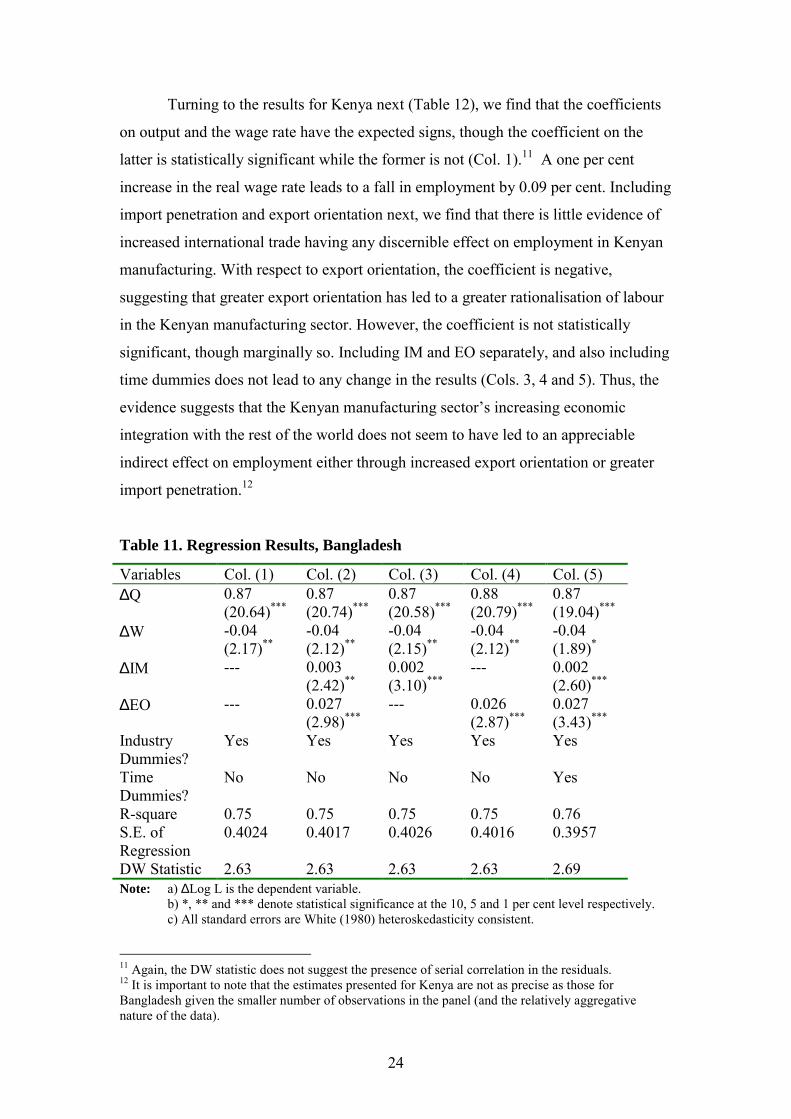

In our estimation procedure, we also introduce industry-specific dummies to

control for unobservable time-invariant differences in across industries (such as in the

rate of technological progress). We experiment with both current and one year lagged

values of W, IM and EO, given the short run rigidities in adjusting employment in a

given year. The regression results for Bangladesh are presented in Table 11 and those

for Kenya in Table 12. In Column 1, we present estimates of the standard labour

demand equation without incorporating the open-ness variables. Column 2 reports the

augmented labour demand equation with the import penetration and export orientation

variables included together. In Columns 3 and 4, we augment the labour demand

equation by including the import penetration and export orientation ratios separately

to incorporate concerns regarding the possible multicollinearity of the two open-ness

variables. In Column 5, we present the augmented labour demand equation, with time

dummies included to control for economy-wide shocks to labour demand (structural

adjustment programmes would fall into this category).

We first discuss the results for Bangladesh (Table 11). From Col. 1, it is clear

that the coefficients on real output and real wage have the expected signs and are

statistically significant. A one per cent increase in output leads to a 0.87 per cent

increase in employment, and an one per cent increase in the real wage rate leads to a

fall in employment by 0.04 per cent. Introducing import penetration and export

orientation, we find that both import penetration and export orientation seem to have a

positive effect on employment, with the coefficient on IM statistically significant at

the 5 per cent level and that for EO significant at the 1 per cent level (Col. 2).10 The

results do not change when we introduce IM and EO separately in the regression

(Cols. 3 and 4). Finally, adding time dummies leads to little change in the coefficients

for IM and EO (Col. 5). Thus, there is clear evidence that increased international trade

(whether due to an increase in imports or in exports relative to output) has led to an

increase in employment (for the same level of output) in Bangladesh’s manufacturing

sector. This could possibly be linked to a shift to labour-intensive techniques in a

given industry following higher degrees of import penetration and/or export-

orientation in that industry, rather than falling labour productivity per se.

21 ˆˆˆˆ qqXOE −−= . Then, as long as 1q̂ is significantly less than 2q̂ (that is, q1 is relatively stableover time), the log first difference of EO will be less subject to measurement error compared to thelevel of EO. A similar argument holds for IM.10 The Durbin-Watson (DW) statistics also suggest a lack of serial correlation in the residuals.

24

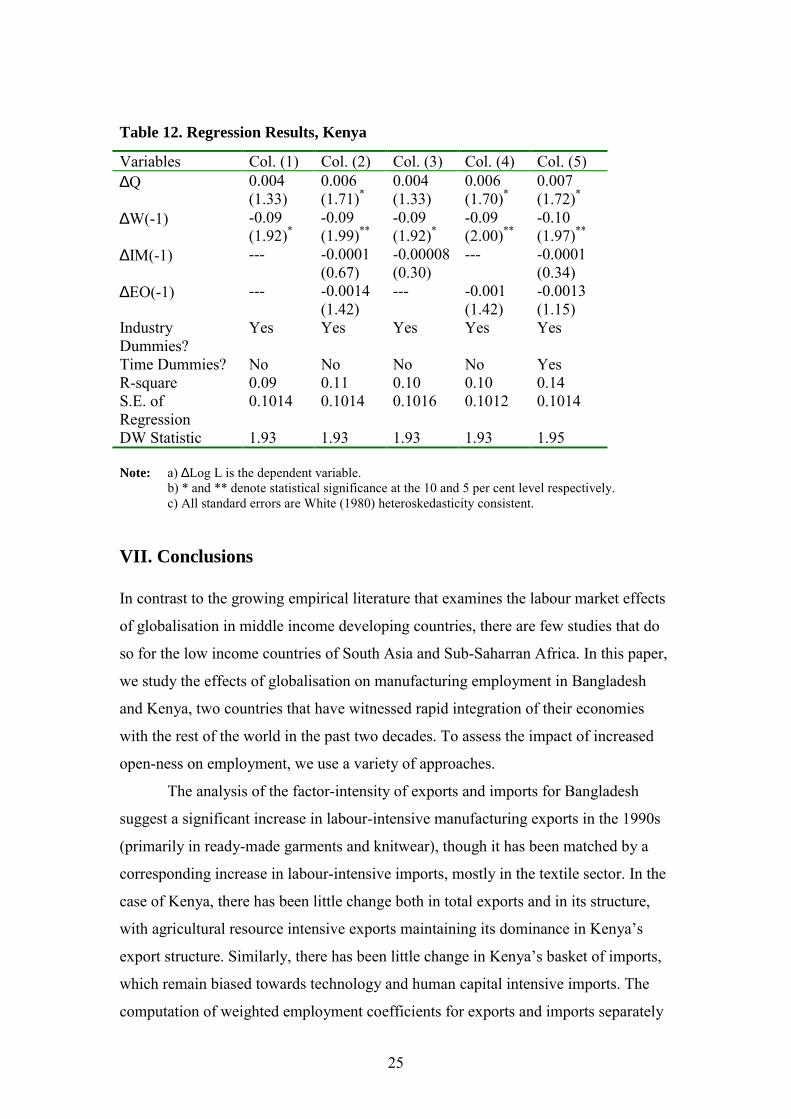

Turning to the results for Kenya next (Table 12), we find that the coefficients

on output and the wage rate have the expected signs, though the coefficient on the

latter is statistically significant while the former is not (Col. 1).11 A one per cent

increase in the real wage rate leads to a fall in employment by 0.09 per cent. Including

import penetration and export orientation next, we find that there is little evidence of

increased international trade having any discernible effect on employment in Kenyan

manufacturing. With respect to export orientation, the coefficient is negative,

suggesting that greater export orientation has led to a greater rationalisation of labour

in the Kenyan manufacturing sector. However, the coefficient is not statistically

significant, though marginally so. Including IM and EO separately, and also including

time dummies does not lead to any change in the results (Cols. 3, 4 and 5). Thus, the

evidence suggests that the Kenyan manufacturing sector’s increasing economic

integration with the rest of the world does not seem to have led to an appreciable

indirect effect on employment either through increased export orientation or greater

import penetration.12

Table 11. Regression Results, Bangladesh

Variables Col. (1) Col. (2) Col. (3) Col. (4) Col. (5)∆Q 0.87

(20.64)***0.87(20.74)***

0.87(20.58)***

0.88(20.79)***

0.87(19.04)***

∆W -0.04(2.17)**

-0.04(2.12)**

-0.04(2.15)**

-0.04(2.12)**

-0.04(1.89)*

∆IM --- 0.003(2.42)**

0.002(3.10)***

--- 0.002(2.60)***

∆EO --- 0.027(2.98)***

--- 0.026(2.87)***

0.027(3.43)***

IndustryDummies?

Yes Yes Yes Yes Yes

TimeDummies?

No No No No Yes

R-square 0.75 0.75 0.75 0.75 0.76S.E. ofRegression

0.4024 0.4017 0.4026 0.4016 0.3957

DW Statistic 2.63 2.63 2.63 2.63 2.69Note: a) ∆Log L is the dependent variable.

b) *, ** and *** denote statistical significance at the 10, 5 and 1 per cent level respectively.c) All standard errors are White (1980) heteroskedasticity consistent.

11 Again, the DW statistic does not suggest the presence of serial correlation in the residuals.12 It is important to note that the estimates presented for Kenya are not as precise as those forBangladesh given the smaller number of observations in the panel (and the relatively aggregativenature of the data).

25

Table 12. Regression Results, Kenya

Variables Col. (1) Col. (2) Col. (3) Col. (4) Col. (5)∆Q 0.004

(1.33)0.006(1.71)*

0.004(1.33)

0.006(1.70)*

0.007(1.72)*

∆W(-1) -0.09(1.92)*

-0.09(1.99)**

-0.09(1.92)*

-0.09(2.00)**

-0.10(1.97)**

∆IM(-1) --- -0.0001(0.67)

-0.00008(0.30)

--- -0.0001(0.34)

∆EO(-1) --- -0.0014(1.42)

--- -0.001(1.42)

-0.0013(1.15)

IndustryDummies?

Yes Yes Yes Yes Yes

Time Dummies? No No No No YesR-square 0.09 0.11 0.10 0.10 0.14S.E. ofRegression

0.1014 0.1014 0.1016 0.1012 0.1014

DW Statistic 1.93 1.93 1.93 1.93 1.95

Note: a) ∆Log L is the dependent variable.b) * and ** denote statistical significance at the 10 and 5 per cent level respectively.c) All standard errors are White (1980) heteroskedasticity consistent.

VII. Conclusions

In contrast to the growing empirical literature that examines the labour market effects

of globalisation in middle income developing countries, there are few studies that do

so for the low income countries of South Asia and Sub-Saharran Africa. In this paper,

we study the effects of globalisation on manufacturing employment in Bangladesh

and Kenya, two countries that have witnessed rapid integration of their economies

with the rest of the world in the past two decades. To assess the impact of increased

open-ness on employment, we use a variety of approaches.

The analysis of the factor-intensity of exports and imports for Bangladesh

suggest a significant increase in labour-intensive manufacturing exports in the 1990s

(primarily in ready-made garments and knitwear), though it has been matched by a

corresponding increase in labour-intensive imports, mostly in the textile sector. In the

case of Kenya, there has been little change both in total exports and in its structure,

with agricultural resource intensive exports maintaining its dominance in Kenya’s

export structure. Similarly, there has been little change in Kenya’s basket of imports,

which remain biased towards technology and human capital intensive imports. The

computation of weighted employment coefficients for exports and imports separately

26

for female and male labour for these two countries suggest that exports are more

female labour intensive than imports in both these countries. However, at the

aggregate, the structure of exports is marginally more labour-intensive than imports

for Bangladesh and Kenya.

The decomposition of employment changes to the different components of

output growth and in productivity indicate that in the case of Bangladesh, the

contribution of international trade to total employment growth has been positive,

though less significant both in absolute and relative terms in the first half of the 1990s

(a period which witnessed rapid trade reforms in Bangladesh) than in the second half

of the 1980s. In the case of Kenya, employment fell in the 1990s as a result of import

competition and since 1994, due also to falling exports. Thus, the effect of

international trade on employment has been unambiguously negative in the 1990s in

Kenya.

The estimation of labour demand equations augmented by variables measuring

open-ness allow us to assess the indirect impact of international trade on employment

via changes in technology or the efficiency of labour use. The results indicate that in

the case of Bangladesh, both greater import penetration and export orientation led to

an increase in employment for the same level of output, suggesting the adoption of

more labour-intensive techniques within the same industry in faced of increased open-

ness. However, for Kenya, there is no evidence that increased open-ness led to any

appreciable changes in the efficiency of labour or shifts in industry-specific capital-

labour ratios.

Thus, the paper finds globalisation has led to a differential impact on

manufacturing employment in the two countries of our study. In the case of

Bangladesh, increased integration with the world economy has led to an increase in

manufacturing employment, both directly via a net expansion in the labour-intensive

industries, and indirectly via changes in industry-specific capital-labour ratios. Even

here, we find that there have also been significant job losses in the labour-intensive

textile sector in Bangladesh due to import competition. In the case of Kenya, labour-

intensive manufacturing exports have not shown signs of significant growth, while

there is evidence of a negative direct impact of import competition on manufacturing

employment. There has also been little indirect impact of international trade on

manufacturing employment. Thus, the net effect of globalisation on employment

could be considered negative, at least in the 1990s.

27

What explains the differences in labour market outcomes following opening

up in these two countries? Two possible reasons may be offered in an answer to this

question. Firstly, there are clear differences in factor endowments between these two

countries, with the labour-land ratio more favourable to the growth of unskilled

labour-intensive manufacturing exports such as garments and knitwear in the case of

Bangladesh as compared to Kenya (Collier and Gunning 1999). Secondly, the reforms

with respect to international trade and foreign investment in the case of Kenya were

implemented in the presence of significant macroeconomic uncertainty and in a

political environment where the relationship between the government and major

bilateral and multilateral donors has not been the most conducive (O’Brien and Ryan

2000). Along with the stop-go nature of the reforms, particularly with respect to

international trade, these factors may have led to a lack of credibility of the reforms

themselves (Reinnika 1996). This may explain why with very similar policies with

respect to the wooing of foreign investment in EPZs, the inflow of FDI in EPZs in

Kenya has been miniscule compared to that in Bangladesh, and may account for the

very different roles that the EPZs have played in their respective countries’ export

drive.

28

References

Asian Development Bank (2000), Country Economic Review, Manila.

Collier, P. and J.W. Gunning (1999), “Why has Africa Grown Slowly?” Journal ofEconomic Perspectives, Vol. 13, No. 2, pp. 3-22.

Dolan, C. (2001), “The ‘Good Wife’: Struggles over resources in the Kenyan

horticultural sector”, Journal of Development Studies, Vol. 37(2), pp. 147-176.

Glenday, G. and D. Ndii (1999), “Export Platforms in Kenya”, mimeo.

Glenday, G. and T.C.I. Ryan (2000), “Trade Liberalization and Growth in Kenya”,

mimeo.

Hine, R. and P. Wright (1998), ‘Trade with Low Wage Economies, Employment and

Productivity in UK Manufacturing’, Economic Journal.

Jenkins, R.O. and K. Sen (2002), “Globalization and Labour Markets in the South”,

paper presented in ESRC Conference on Globalisation and (In)equality,

University of Warwick, April 2002.

Krause, L.B. (1988), U.S Economic Policy Towards the Association of southeast

Asian nations: meeting the Japanese Challenge, Washington D.C., The

Brookings Institution.

McCulloch, N. and M. Ota (2002), “Export Horticulture and Poverty in Kenya”,

mimeo.

Milner, C. and P. Wright (1998), "Modelling Labour Market Adjustment to Trade

Liberalisation in an Industrialising Economy", The Economic Journal, Vol.

108, pp. 509-528.

Moreira, M.M. and S. Najberg (2000), “Trade Liberalisation in Brazil: Creating or

Exporting Jobs?" Journal of Development Studies, Vol. 36, No. 3, pp. 78-99.

O’Brien, F.S. and T.C.I. Ryan (2000), “Kenya” in Devarajan, S. et al. (eds.), Aid and

Reform in Africa, The World Bank, Washington D.C.

Paratian, R. and R. Torres (2001), Bangladesh: Studies on the Social Dimensions of

Globalization, International Labour Office, Geneva.

Reinnika, R. (1996), “The credibility program in trade liberalization: empirical

evidence from Kenya”, Journal of African Economies, Vol. 5(3), ppp. 444-

468.

29

Sen, K. (2001), Globalisation and Labour Market Outcomes in the South: A Critical

Survey, Discussion Paper 1, Project on Golbalisation, Production and Poverty,

Overseas Development Group, Norwich.

Spinanger, D. and J.P. Wogart (2000), “Will the Emperor wear clothes from

Bangladesh in 2005?”, mimeo.

World Bank (1987), Kenya: Industrial Sector Policies for Investment and Export

Growth, Washington D.C.

World Bank (1999), Bangladesh: Trade Liberalization, its Pace and Impacts,

Washington D.C.

White, H. (1980), “A Heteroskedasticity-Consistent Covariance Matrix Estimator and

a Direct Test for Heteroskedasticity”, Econometrica, Vol. 66, pp. 817-838.