Italy - Regulatory Reform in Electricity, Gas and Railroads 2000

Upload

independentCategory

view

0download

0

Global Regulatory Reform

The world of financial instruments just got more complex. Time to take note.Capital markets reform: MiFID II

Contents

Introduction 1

MiFID II summary 2

Key considerations 4

Impacts and opportunities 6

What’s next? 10

Contacts 12

1The world of financial instruments just got more complex Capital Markets Reform: MiFID II

Introduction

Following the financial crisis, a mass of global regulatory reform continues to take shape and as the debate progresses, the evolving landscape of the financial services sector remains challenging.

Markets in Financial Instruments Directives (MiFID II) represents one of the centerpieces of the upcoming financial markets reform and it is far from an incremental change. Since the publication of the first draft in October 2011, well over 2,000 amendments have been submitted. MiFID II will dramatically change almost the entire marketplace as we know it today, with far-reaching impacts on everyone engaged in the dealing and the processing of financial instruments. As MiFID II currently stands, we expect no business or operating model — especially in the over-the-counter (OTC) space — to remain untouched. In particular, MiFID II will not only completely change the way almost all OTC products are priced, traded and reported, but it will also bring further changes to the exchange traded equity market. This will lead to a raft of implications for investment banks, private banks, asset managers, retail banks, insurance firms, market infrastructure providers and non-financial firms such as energy providers — in short: everyone!

Most importantly, MiFID II is not just a compliance exercise. There are major strategic implications that could bring market opportunities and competitive advantage for those who start to plan in advance or potential revenue loss and market share for those who fail to react.

MiFID II must be aligned to a number of other regulations that are being debated and concluded at a global, European and local and domestic level. Most market participants are currently focused on running their regulatory change agenda on a regulation-by-regulation basis. Only a few organizations are considering subsuming, e.g., Dodd Frank, Basel III/Capital Requirements Directive (CRD) IV, European Market Infrastructure Regulations (EMIR), Market Abuse Directive (MAD) II and MiFID II under one regulatory change program and are building out workstreams on a topical basis. Requirements from local regulators further add to the complexity. Firms need to orchestrate analysis efficiently, planning, development and delivery of all regulations relevant to their organization in order to meet challenging deadlines and to minimize implementation costs.

The opportunities for firms will start to crystallize if they can coordinate regulatory overlaps and start to identify overarching changes to their business early on. With all this complexity and degree of change, firms will need to start assessing the impact of MiFID II in 2013 to ensure compliance by 2015.

Key issuesThose areas causing heightened concern and discussion across the industry include:

► ►High-frequency trading (HFT): it has proven difficult to differentiate between HFT and algorithmic (algo) trading in order to avoid slowing down trades in general and thereby potentially damaging the supply of liquidity. The proposed resting period of 500ms is not based on scientific analysis and has proven controversial.

► Position limits and trading restrictions for commodity derivatives: disagreement on whether to implement hard position limits or a more flexible position management approach and who will be impacted by any imposed restrictions.

► Ban of inducement: it has also proven difficult to agree whether to either remove third-party commissions or limit the requirements to an increased up-front disclosure regime on any received inducements.

► Organized trading facilities (OTF): retention of the OTF category for non-equity trades only (bonds and derivatives) and limited to professional investors with impacts on broker crossing networks.

2 The world of financial instruments just got more complex Capital Markets Reform: MiFID II

What is driving MiFID II?

Since its implementation in November 2007, MiFID has been the cornerstone of capital markets regulation in Europe. However, since its inception, not all benefits have fed down to the end investor as envisaged. MiFID II is aiming to address the shortcomings of the original MiFID release. The diagram below highlights the key objectives and core measure of MiFID II.Figure 1

MiFID II objectives and core measures

MiFID II summary

► Appropriateness and suitability regime applicable for all asset classes (specifically for complex products)

► “Best Execution” regime applicable for OTC products

► Ban of inducements removed and replaced with a stringent disclosure regime

► Trading bans and position limits for commodity derivatives

► Restrictions on commodity derivatives positions

► Taking into account whether national regulators need to intervene to approve, authorize or ban products sold to retail classified investors

► Passporting and harmonized third-country equivalence regime vs. “Substituted Compliance”

► Strengthening of internal control function specifying rules on time commitment and criteria for board directors

► Increased scope and role of compliance (semi- independence)

► “Tone from the top”

► Significant portion of OTC products to move to RM, MTF or OTF

► Treatments of single- and multi-dealer platforms; dark pools; algo-trading provisions

► Increased regulatory and client reporting requirements for all asset classes on RM, MTF, OTF and SI

► Near real-time reporting requirements to regulators

► Increased transparency requirements on received commissions

► European Consolidated Tape (ECT) approaches

MiFID II

External controls/reporting

Internal controls/

governance

Market structure

Market transparency

Investor protection

“Firms are underestimating the challenges of MiFID II and the far-reaching impact it will have on their organization. Understandably, there are still areas that require further clarity, but firms will have no option but to start modeling scenarios soon or they risk being caught on the back foot.”John Liver, Partner, Head of Global Regulatory Reform, Ernst & Young UK LLP

3The world of financial instruments just got more complex Capital Markets Reform: MiFID II

Scope and impact of MiFID II

MiFID II will command significant changes in business and operating models, systems, data, people and processes. As a result, a fundamental transformation will emerge. The biggest impact will be felt by banks, broker dealers and trading venues. Additionally, investment managers, insurance firms, independent

financial advisors (IFAs), custodian banks and other asset servicing entities will also need to undertake a substantial effort.

The level of impact of MiFID II differs in most areas for investment banks, investment managers, insurance, private banking and retail banking:

Figure 2

Preliminary heat map of MiFID II impacts

Market structure

Market transparency

Investor protection

Internal and external controls/reporting

New

mar

ket

stru

ctur

es

Pre-

/pos

t tra

de

tran

spar

ency

eq

uity

-like

Trad

e tr

ansp

ar.

Non

-equ

ity

Trad

e tr

ansp

ar.

com

mod

s.

Bes

t exe

cutio

n/lia

bilit

ies

Provision of investment services and protection of client interests

Reg

. sup

ervi

sion

Thir

d co

untr

ies

Reg

ulat

ory

pow

ers

Systems and controls/record-

keeping

MTF

/OTF

/SI c

hang

es

Dark

poo

ls/S

D/M

D pl

atfo

rms

HFT

pro

visi

ons

Ord

er h

andl

ing

IOI m

anag

emen

t

Euro

pean

con

solid

ated

tape

Pre-

trad

e tr

ansp

.

Post

-tra

de d

iscl

osur

e

Pre-

trad

e tr

ansp

.

Post

-tra

de d

iscl

osur

e

Equi

ty-li

ke

Non

-equ

ity in

cl. O

TC

Reve

rse

burd

en o

f pro

of/l

iabi

litie

s?

Clie

nt c

lass

ifica

tion

Clie

nt in

form

atio

n

TCF/

COI m

anag

emne

t

Suita

bilit

y

App

ropr

iate

ness

Clie

nt a

sset

s/m

oney

Indu

cem

ents

Clie

nt re

port

ing

Inte

r-re

gula

tory

coo

pera

tion

Reci

proc

al th

ird-c

ount

ry a

cces

s

Bans

/res

tric

tions

/lim

its

Ord

er re

port

ing

Tran

sact

ion

repo

rtin

g

Syst

ems/

reco

rds

Gov

erna

nce/

com

plia

nce

cont

rols

Out

sour

cing

Investment banksInvestment managers/ insuranceCustodian banks

Private and retail banking

How will the implementation timeline emerge?

MiFID II will take the form of a regulation, MiFIR, backed up by a directive. The EC introduced MiFIR to ensure that a “maximum harmonization” framework was implemented centrally from Brussels with limited scope for national discretions, derogations or divergent interpretations. The European Securities and Markets Authority (ESMA) will play a central role in coordinating and specifying implementation details of MiFID II. In particular, ESMA is expected to draw much of the monitoring and supervisory support from the national regulatory authorities.

The timing of MiFID II is set to coincide with the issue of adjacent regulations, such as the revised Market Abuse Directive (MAD II), the revised Insurance Mediation Directive (IMD II) and the impending Packaged Retail Investment Products Directive (PRIPs).

The target MiFID II implementation timeline is moving toward 2015.

Key:High MediumLow

4 The world of financial instruments just got more complex Capital Markets Reform: MiFID II

Outlined below are some of the provisions under MiFID II that are particularly in the spotlight.

Market structure

By way of impact, various issues relating to trading mechanisms, venues and products would need to be considered.

► Market structure: there has been an intense debate as to how the rules on market structure might be amended. The options include a new category of trading venues called organized trading facilities (OTFs) alongside regulated markets, multilateral trading facilities (MTFs), and the amended scope of systematic internalizers (SIs).

In contrast to regulated markets (RM) and MTFs, OTF operators will have discretion over order execution, although orders will not be executable against their own capital, which will effectively limit the usability of OTFs to dealers, unless OTFs are moved to a separate entity. Members of European Parliament have also agreed to limit the use of OTFs to non-equities such as bonds, derivatives and emissions allowances (equities being mandatorily traded on either RMs or MTFs). The OTF category has a particular relevance for derivatives, given its eligibility for open contracts as long as they are sufficiently liquid and as long as no MTF or regulated market is available for that instrument. ESMA will need to define what “sufficiently liquid” derivatives are, according to specific criteria such as size, trade frequency and number of market participants. Since the transparency requirements will only apply to

those instruments that have been determined to be sufficiently liquid, illiquid instruments and block trades could be exempted from any of the pre-trade transparency requirements. Following the European Parliament’s Economic and Monetary Affairs Committee (ECON) vote in September, it seems that broker crossing networks (BCNs) will have to be reclassified as MTFs or SIs instead of OTFs. This is against original expectations and has significant consequences for order flow and liquidity, as a result of the non-discretionary order execution provisions on MTFs.

SIs have received further refinement, requiring firm quotes as a response to client RFQs, with the obligation to publish and share that quote with other investors, as long as it is below a certain volume threshold. This is very similar to the market-maker obligations for exchange-traded equities. However, SIs will be allowed to withdraw quotes and establish “commercial policy” protections, allowing them to consider counterparty credit and settlement risk and thereby giving them greater control over who they are trading with.

► Position limits and trading restrictions: MiFID II implements trade restrictions and position limits on commodity derivative contracts that any given market members or participants can enter into over a specified period of time. These limits and restrictions, which target excess speculation, will be determined by ESMA and, as adopted in the text by the European Parliament, applied on a net position basis. These restrictions

will not be imposed on positions built for hedging purposes by non-financial service firms. However, these exempted firms could, after all, be significantly impacted due to an overall decrease in demand and supply for commodity derivatives as a result of the position limits. Furthermore, should — as it currently stands — the limits not be set across the various marketplaces (i.e., regulated markets, MTFs and OTFs), it would benefit those organizations with access to a large number of trading venues. It would also benefit smaller market places since the execution quality will not be the deciding factor, but simply the access to multiple independent limit-setting trading venues. Given the economic consequences of the restrictions, firms need to start modeling scenarios, assess the impact and, where necessary, reassess their strategies before these trading restrictions are enforced.

► HFT/Algo trading: a more restrictive regime coupled with enhanced disclosure covering high frequency and algo trading will be introduced. Business resilience and continuous liquidity provision will be areas of focus. It is envisioned that non-broker intermediated direct market access (DMA) will no longer be permitted. A rest time of half a second might be applied to all orders that are delivered to market via HFT mechanisms. Coupled with the introduction of cancellation fees, it could force HFT traders having to rethink their trading strategies. Firms engaged in HFT will need to review the implications and their business options.

Key considerations

5The world of financial instruments just got more complex Capital Markets Reform: MiFID II

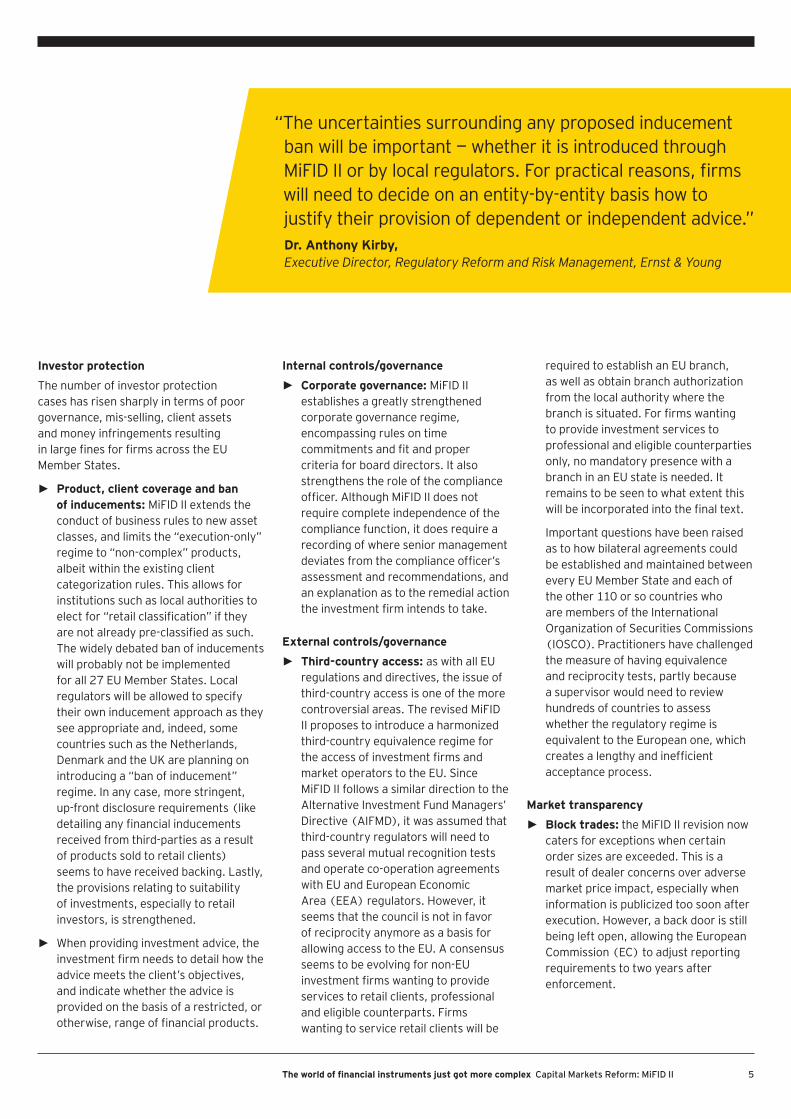

Investor protection

The number of investor protection cases has risen sharply in terms of poor governance, mis-selling, client assets and money infringements resulting in large fines for firms across the EU Member States.

► Product, client coverage and ban of inducements: MiFID II extends the conduct of business rules to new asset classes, and limits the “execution-only” regime to “non-complex” products, albeit within the existing client categorization rules. This allows for institutions such as local authorities to elect for “retail classification” if they are not already pre-classified as such. The widely debated ban of inducements will probably not be implemented for all 27 EU Member States. Local regulators will be allowed to specify their own inducement approach as they see appropriate and, indeed, some countries such as the Netherlands, Denmark and the UK are planning on introducing a “ban of inducement” regime. In any case, more stringent, up-front disclosure requirements (like detailing any financial inducements received from third-parties as a result of products sold to retail clients) seems to have received backing. Lastly, the provisions relating to suitability of investments, especially to retail investors, is strengthened.

► When providing investment advice, the investment firm needs to detail how the advice meets the client’s objectives, and indicate whether the advice is provided on the basis of a restricted, or otherwise, range of financial products.

Internal controls/governance

► Corporate governance: MiFID II establishes a greatly strengthened corporate governance regime, encompassing rules on time commitments and fit and proper criteria for board directors. It also strengthens the role of the compliance officer. Although MiFID II does not require complete independence of the compliance function, it does require a recording of where senior management deviates from the compliance officer’s assessment and recommendations, and an explanation as to the remedial action the investment firm intends to take.

External controls/governance

► Third-country access: as with all EU regulations and directives, the issue of third-country access is one of the more controversial areas. The revised MiFID II proposes to introduce a harmonized third-country equivalence regime for the access of investment firms and market operators to the EU. Since MiFID II follows a similar direction to the Alternative Investment Fund Managers’ Directive (AIFMD), it was assumed that third-country regulators will need to pass several mutual recognition tests and operate co-operation agreements with EU and European Economic Area (EEA) regulators. However, it seems that the council is not in favor of reciprocity anymore as a basis for allowing access to the EU. A consensus seems to be evolving for non-EU investment firms wanting to provide services to retail clients, professional and eligible counterparts. Firms wanting to service retail clients will be

required to establish an EU branch, as well as obtain branch authorization from the local authority where the branch is situated. For firms wanting to provide investment services to professional and eligible counterparties only, no mandatory presence with a branch in an EU state is needed. It remains to be seen to what extent this will be incorporated into the final text.

Important questions have been raised as to how bilateral agreements could be established and maintained between every EU Member State and each of the other 110 or so countries who are members of the International Organization of Securities Commissions (IOSCO). Practitioners have challenged the measure of having equivalence and reciprocity tests, partly because a supervisor would need to review hundreds of countries to assess whether the regulatory regime is equivalent to the European one, which creates a lengthy and inefficient acceptance process.

Market transparency

► Block trades: the MiFID II revision now caters for exceptions when certain order sizes are exceeded. This is a result of dealer concerns over adverse market price impact, especially when information is publicized too soon after execution. However, a back door is still being left open, allowing the European Commission (EC) to adjust reporting requirements to two years after enforcement.

“The uncertainties surrounding any proposed inducement ban will be important — whether it is introduced through MiFID II or by local regulators. For practical reasons, firms will need to decide on an entity-by-entity basis how to justify their provision of dependent or independent advice.”Dr. Anthony Kirby, Executive Director, Regulatory Reform and Risk Management, Ernst & Young

6 The world of financial instruments just got more complex Capital Markets Reform: MiFID II

Impacts and opportunities

Many valuable lessons have been taken from MiFID I. These inevitably will help reduce costs in relation to the upcoming implementation of MiFID II. However, the cost will be substantial given product scope, impact on business models, degree of European harmonization and the need to align with other parallel regulatory developments. Figure 3

MiFID I and MiFID II comparisons

Equities Equity-likeproducts

MiFID I MiFID IIEquities

Extends to other asset classes

Extends to other asset classes

Addition of OTFs (broker crossing networks, dark pools)

Extends to other asset classes (revision of independent advice)

Mar

ket

tran

spar

ency

Treatment of SDPs/MDPs/ dark pools

European consolidated tape

Inve

stor

prot

ectio

n

Extends to other asset classesComplex products

Inte

rnal

and

ex

tern

al c

ontr

ols Third-country access

Product intervention (banning of products by ESMA)Position limits for products

Extends to other asset classesExtends to other asset classes

Extends to other asset classes and new services

Conditions for waivers will be revised

Mar

ket

stru

ctur

e

Extends regulatory transparency requirement tailored to asset classes

Governance/strengthening internal compliance functions

Algo trading provisions (HFTs)

Fixedincome

Commods/energy

Structuredproducts Derivatives

Transparency — pre- and post- trade

Best execution

Market structures RMs, MTF, SIs

Waivers to large-scale trade reporting

Reporting to clients

Requirements on marketing/sales materials

Suitability and appropriateness tests

Treatment of inducements

Passporting

Business model

► Revenue impact: the migration of trading to regulated markets (MTFs or OTFs), coupled with increased transparency requirements, should in principle increase competition and reduce spreads. In other words, the long-term direction will be toward a transparent, higher volume, lower margin, more commoditized market. As was seen in the equity market with MiFID I, fragmentation of liquidity across multiple venues could, at least in the short term, lead to mixed results — greater competition, equally greater fragmentation, and increased market impact costs (particularly for the buy-side). There are significant opportunities for banks, trading venues and market infrastructure providers to capture market share, particularly for those that invest in scalable platforms and are able to reduce operational complexity for their client base.

In addition, a drive toward greater transparency may deter some investment banks from making quotes. This will drive valuable liquidity away from the market and concentrate the business on a smaller number of pricemakers, which would not be so beneficial for the buy-side.

7The world of financial instruments just got more complex Capital Markets Reform: MiFID II

► Cost impact: despite the opportunities to capture market share, there are also significant cost impacts of MiFID II. The EC estimated initial MiFID II one-off implementation costs to be between €512m and €732m, with ongoing compliance costs in the region of €312m to €586m. This is significantly lower than the overall €2b implementation cost of MiFID I.1

Given the cost of the investment required to meet regulatory demands, coupled with increased capital and liquidity requirements due to Basel III and CRD IV, some businesses will no longer be profitable. The return on capital employed (ROCE) figures may struggle to reach double digits. This may apply to many mid-tier banks that do not have capital available to invest. Firms wishing to design, approve and service products with different, or complex, financial characteristics for retail-classified clients in different countries, may find the cross-border challenges a step too far. There could be a migration of the business toward more streamlined client take-on structures accompanied by products that are more disclosable, fungible and above all, liquid.

► Outsourcing: MiFID II could present a shift in the industry toward more outsourcing providers. The move to execution on trading venues is likely to result in higher volumes of smaller value transactions in quote-driven markets, just as those that occurred with equity trades across Europe from 2007–12. Enhancing the scalability of OTC derivative trading, trade confirmation, as well as novation and netting systems will be imperative. Many asset managers and other intermediaries who lack the scale to invest in systems, may look toward new outsourcing service providers as a way to provide support services and facilitation at the appropriate price points. Parties who outsource will still need to perform the necessary regulatory due diligence and manage operational complexities in the front, middle and back offices.

Systems, processes and controls

► Front-to-back infrastructure impact: the implementation of MiFID II, MAD II and EMIR may usher in significant market microstructure changes by introducing auction systems competing with dealer pricing, as “former OTC products” become more “equity like.” A whole array of system and process changes would be required to cater for the auction models impacting both the sell-side and buy-side.

However, early movers on the sell-side will be able to achieve a competitive advantage and attract market share. Specifically in areas like collaterization, it will be possible for early movers to capitalize on regulation. Also, firms with the capabilities for processing market and reference data will enjoy a distinct advantage when executing effective trading strategies or reporting to clients, regulators and senior management.

1 Source: MiFID II data European Commission MiFID II draft of 20 October 2012; MiFID I costs Ernst & Young estimates.

► Trading impacts: MiFID II and Dodd Frank will stimulate a high degree of trading process changes over the next five years. This includes multiple competing trading venues with the potential for a) order-driven models (both continuous-auction and batch-auction systems in the secondary OTC market) and b) quote-driven models (the evolution of OTC dealers to full market makers or a more hybrid system).

Additionally, in the case of trading bans for instance, it would allow competent authorities, in coordination with ESMA, to temporarily or permanently prohibit or restrict the trading of financial products or services. As a result, systems and processes will need to be adjusted accordingly to allow for time efficient implementation and monitoring of these restrictions. Each financial institution will also have to implement internal risk assessment measures to minimize the impact of these restrictions.

Data and reporting

MiFID II will essentially mirror the scope of MAD II, which will require further adjustments (due to its ongoing review) as well as major changes in both operational and reference data — unique trade identifiers, counterparty and legal entity identifiers and product identifiers. Those firms that have already invested in enhancing their data architecture across multiple asset classes will be best placed, while others will need to investigate this infrastructure as an immediate priority.

8 The world of financial instruments just got more complex Capital Markets Reform: MiFID II

► Record-keeping and documentation: most firms have already implemented their transaction-reporting capabilities to comply with MiFID I, resulting in robust arrangements in which to store their records on machine-readable and durable media for five years.2 However, because there were several high-profile cases in recent years where firms were fined for misdemeanors, audit trails will need to be more robust. They should now include on-demand documentary retrieval for more complex instruments, such as OTC derivatives, to evidence best execution with regard to the broader OTC-traded markets. In addition, some Member States, such as the UK, will remove the exemption for mobile phone conversations for reasons of market abuse prevention. As a result, MiFID II will strengthen the treatment of client assets and money, which will necessitate further investments in data management.

2 Five years constitutes the minimum record-keeping duration with the option to impose more stringent requirements at a national level by local regulators.

► Near real-time reporting: the near real-time post-trade reporting requirements will drive system, process and cultural change. This will enhance timing of trade capture down to 15 minutes after trade execution, for trading venues and single dealer platforms (SDPs) of investment banks. To improve the quality and consistency, the amendment requires firms to publish their trade reports through approved publication arrangements (APAs) for all asset classes of MiFID II, with harmonized reporting standards across all Member States and alignment with EMIR trade reporting.

9The world of financial instruments just got more complex Capital Markets Reform: MiFID II

10 The world of financial instruments just got more complex Capital Markets Reform: MiFID II

Aligning MiFID II with other regulations

Depending on the type of financial services offered by an organization and the degree of internationalization, a number of other regulations need to be considered in conjunction with MiFID II. Figure 4

Cross-regulation impact assessment

Coordination of new regulatory

implementation

Legal entity/business model

Business conduct and compliance

Trade execution/client advisory

Clearing and settlements

Trade reporting

Reference data and identifiers

Collateral and margin

Risk management

Capital

Regulatory reporting

Pricing and valuations

Product control and accounting

Tax

FTT MIFID II EMIR DF OTC AMLFATCAVolcker

Common global programs are essential for those organizations impacted by related US measures, such as Dodd Frank (DF). However, the differences in the timing of implementation and emergence of detailed rules will prove challenging, as will the evaluation of potential extra-territorial impacts. Organizations that aim to establish one platform covering swap execution under DF and OTF trading will have to manage the different requirements of each jurisdiction and ensure that their platform is flexible enough to cater for each set of requirements. Independent platform providers may be placed at an advantage over dealers providing pricing for standardized swaps on their SDP as they appear to be banned, requiring a significant change in the dealer’s business model.

In addition, non-banking organizations, such as insurance firms, will need to start aligning any MiFID II analysis with PRIPs and IMD II, especially in relation to investor protection measures and commission prohibitions, as these could significantly change business models by reducing the choice of products for policyholders.

What’s next?

Illustrative approach will vary from organization to organization and may be subject to changes as regulatory requirements evolve

11The world of financial instruments just got more complex Capital Markets Reform: MiFID II

National regulations will come into play earlier and potentially interact with MiFID II; in the UK, for instance, the Retail Distribution Review (RDR) is implementing many of the original MiFID II requirements on the ban of inducements.

With the sheer number of upcoming regulations that overlap in key areas, it is inefficient to look at their impacts independently, but rather identify all relevant regulations and determine commonalities and overlapping themes. This will ensure a more cost-effective implementation of the requirements, as it reduces the duplication of work in the overlapping areas.

Overall priority actions

► Conduct initial impact assessment for MiFID to determine budget requirements

► Establish cross-regulatory reform agenda and ensure that MiFID II analysis is joined up with other regulatory projects

► ►Conduct overall market impact analysis to identify suitable opportunities

► Review validity of current business model (e.g., SDP)

► Assess MiFID II impact on revenue structure, fees and commissions (i.e., independent vs. dependant advice)

► Conduct asset class-specific MiFID II front-to-back impact analysis

► Review MiFID II impact specifically from a risk and compliance management point of view (e.g., managing times of prohibited or restricted trading (commodity derivatives))

“Organizations will need a plan that spans across individual regulations. Managing them one-by-one will incur significant costs and duplications and will simply stretch even large organizations beyond their capabilities.”John Kersten, Senior Manager, Financial Services Advisory, Ernst & Young

12 The world of financial instruments just got more complex Capital Markets Reform: MiFID II

Contacts

How Ernst & Young can help

Ernst & Young has extensive experience in helping organizations navigate through regulatory initiatives. Our global regulatory reform team is a dedicated, cross-functional team with years of relevant industry experience advising clients in derivatives risk management, regulatory matters and process or systems changes. The team is composed of core members, as well as those drawn from across the broader global regulatory team.

Belgium

Wouter Van den KerkhoveTel: +32 2 774 9429Email: [email protected]

Jean-Francois HubinTel: +32 2 774 9266Email: [email protected]

Greece

Alexandros ChristidisTel: +30 210 288 6043Email: [email protected]

Ilias Argyriou Tel: +30 210 288 6237Email: [email protected]

Poland

Pawel Preuss Tel: +48 22 557 7530Email: [email protected]

Pawel FlakTel: +48 22 557 6224Email: [email protected]

Denmark

Henrik AxelsenTel: +45 35 87 26 63E-mail: [email protected]

Emil WillumsenTel: +4551582538Email: [email protected]

Italy

Maurizio GrigoloTel: +39 02 722 12412Email: [email protected]

Federico MaschioTel: +39 02 722 12317Email: [email protected]

SpainFrancisco Javier Ruiz GarciaTel: +34 915 727 811Email: [email protected]

Victor Manuel Martín Giménez Tel: +34 915 727 096Email: [email protected]

Finland

Antti HakkarainenTel: +358 405924433E-mail: [email protected]

Mikko ReiniläTel: +358400477980Email: [email protected]

Luxembourg

Christophe WintgensTel: +352 42 124 8402Email: [email protected]

Romain Leroy-CastilloTel: +352 42 124 8804Email: [email protected]

Sweden

Pehr AmbuhmTel: +46 8 520 59682Email: [email protected]

Peter FranksTel: +46 8 520 58973Email: [email protected]

France

Tanguy CoatmellecTel: +33 1 46 93 80 74Email: [email protected]

Olivier BiteauTel: +33 1 46 93 72 53Email: [email protected]

Netherlands

Alexander FiliusTel: +31 88 40 70412Email: [email protected]

Lizette BruidegomTel: +31 88 40 71550Email: [email protected]

Switzerland

Christian RöthlinTel: +41 58 286 3538Email: [email protected]

Bruno PatusiTel: +41 58 286 4690Email: [email protected]

Germany

Ralf TemporaleTel: +49 89 14331 22191Email: [email protected]

Thomas WenzelTel: +49 89 14331 13511Email: [email protected]

Norway

Kjetil RimstadTel: +47 24 00 27 83E-mail: [email protected]

Erik KlausenTel: +47 24 00 27 76E-mail: [email protected]

UK

John KerstenTel: +44 20 7951 7965Email: [email protected]

Dr. Anthony KirbyTel: +44 20 7951 9729Email: [email protected]

Ernst & Young

Assurance | Tax | Transactions | Advisory

About Ernst & Young

Ernst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 167,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

© 2013 EYGM Limited. All Rights Reserved.

EYG no. CQ0062

In line with Ernst & Young’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

1264883.indd (UK) 01/13. Creative Services Group Design.

ED None

Copyright © 2022 FDOKUMEN