GIFTS, TICKETS, And NEW REGULATIONS - Cal Cities

45

GIFTS, TICKETS, And NEW REGULATIONS AN FPPC UPDATE League of California Cities City Attorneys Spring Conference Fess Parker’s Doubletree Conference Center May 5 to 7 2010 Presenters: Michele Beal Bagneris City Attorney of Pasadena Michael D. Martello Interim Town Attorney Town of Los Gatos

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of GIFTS, TICKETS, And NEW REGULATIONS - Cal Cities

GIFTS, TICKETS,And

NEW REGULATIONSAN

FPPC UPDATE

League of California CitiesCity Attorneys Spring Conference

Fess Parker’s Doubletree Conference CenterMay 5 to 7

2010

Presenters:

Michele Beal BagnerisCity Attorney of Pasadena

Michael D. MartelloInterim Town AttorneyTown of Los Gatos

1

Political Reform Act

The Local Official’s and Practitioner’s

GIFT GUIDE

Statutes Regulations

Notes and Commentary

Third Draft April 2010

BY

MICHAEL D. MARTELLO Interim Town Attorney

Los Gatos, California ©

2

GIFTS UNDER THE POLITICAL REFORM

ACT

INTRODUCTION The following text analyzes gifts to public officials under the Political Reform Act—a law adopted by the voters in 1974. The practitioner and officials using this guide must be careful not to confuse what the Act permits with what may be proper—or under certain penal statutes, legal. Why is this? It is because the regulations adopted by the FPPC are stuck with the allowances of the Act which, in turn, is stuck in the culture of the 1970’s and before. In 1974 not only was there no gift limit for public officials, those who drafted the initiative measure accepted that gifts and gratuities to government officials were routine and acceptable. Ethics was a yet to be defined term and much of the gift giving and receiving was an accepted perk of public office or employment. Consider that in the mid-1980’s developers would routinely offer discounts to government officials for houses or custom lots—calling the sales price offered to the official the “wholesale price”. In several situations in Ventura County, the officials who accepted the offer, received price discounts of $80K to over $100K. Oddly enough, it wasn’t until well after the fact that these officials learned that the discounts were reportable gifts under the Act. Some never reported it. The point is that it is no longer the 1970’s, and the culture which accepted that type of gratuity, while not gone, is changing. So are the approaches and mindsets of the state and federal prosecutors. Therefore, for the practitioner and official, we must recognize more than ever, that just because it is “legal” under the Act, it may be morally wrong and yes, it may be illegal. Consider this fact situation. A city councilmember annually accepts gifts from several developers. Although different in value each year, the gifts are just below the applicable gift limit. On occasion, his family members also accept gifts that meet the gifts-to-family-exception (18944) and therefore do not count toward the official’s gift limit from the sources. The official accurately reports all the gifts per the FPPC reporting requirements. Over his three terms in office, the official has received thousands of dollars in gifts from these sources.

3

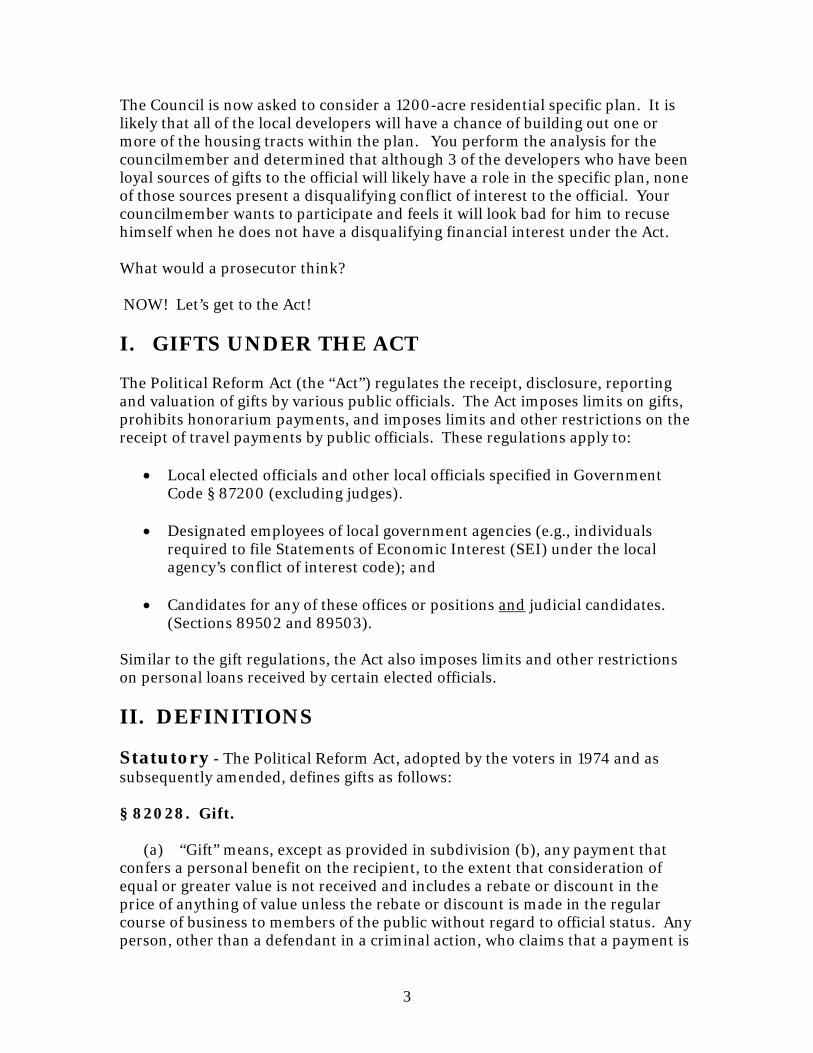

The Council is now asked to consider a 1200-acre residential specific plan. It is likely that all of the local developers will have a chance of building out one or more of the housing tracts within the plan. You perform the analysis for the councilmember and determined that although 3 of the developers who have been loyal sources of gifts to the official will likely have a role in the specific plan, none of those sources present a disqualifying conflict of interest to the official. Your councilmember wants to participate and feels it will look bad for him to recuse himself when he does not have a disqualifying financial interest under the Act. What would a prosecutor think? NOW! Let’s get to the Act!

I. GIFTS UNDER THE ACT The Political Reform Act (the “Act”) regulates the receipt, disclosure, reporting and valuation of gifts by various public officials. The Act imposes limits on gifts, prohibits honorarium payments, and imposes limits and other restrictions on the receipt of travel payments by public officials. These regulations apply to:

• Local elected officials and other local officials specified in Government Code § 87200 (excluding judges).

• Designated employees of local government agencies (e.g., individuals

required to file Statements of Economic Interest (SEI) under the local agency’s conflict of interest code); and

• Candidates for any of these offices or positions and judicial candidates.

(Sections 89502 and 89503). Similar to the gift regulations, the Act also imposes limits and other restrictions on personal loans received by certain elected officials.

II. DEFINITIONS Statutory - The Political Reform Act, adopted by the voters in 1974 and as subsequently amended, defines gifts as follows: § 82028. Gift.

(a) “Gift” means, except as provided in subdivision (b), any payment that confers a personal benefit on the recipient, to the extent that consideration of equal or greater value is not received and includes a rebate or discount in the price of anything of value unless the rebate or discount is made in the regular course of business to members of the public without regard to official status. Any person, other than a defendant in a criminal action, who claims that a payment is

4

not a gift by reason of receipt of consideration, has the burden of proving that the consideration received is of equal or greater value.

(b) The term “gift” does not include:

(1) Informational material such as books, reports, pamphlets, calendars, or periodicals. No payment for travel or reimbursement for any expenses shall be deemed “informational material.” (See also: 18942; and 18942.1)

(2) Gifts which are not used and which, within 30 days after receipt, are either returned to the donor or delivered to a nonprofit entity exempt from taxation under Section 501(c)(3) of the Internal Revenue Code without being claimed as a charitable contribution for tax purposes. (See also 18942)

(3) Gifts from an individual’s spouse, child, parent, grandparent,

grandchild, brother, sister, parent-in-law, brother-in-law, sister-in-law, nephew, niece, aunt, uncle, or first cousin or the spouse of any such person; provided that a gift from any such person shall be considered a gift if the donor is acting as an agent or intermediary for any person not covered by this paragraph. (See also: 18942)

(4) Campaign contributions required to be reporter under Chapter 4

of this title.

(5) Any devise or inheritance.

(6) Personalized plaques and trophies with an individual value of less than $250 (two hundred fifty dollars).

This definition was amended in 1997 to add the concept of “confers a personal benefit on the recipient.” § 82029 – Immediate Family. “Immediate family” means the spouse and dependent children. § 82025.5 – Fair Market Value. “Fair market value” means the estimated fair market value of goods, services, facilities or anything of value other than money. Whenever the amount of goods, services, facilities or anything of value other than money is required to be reported under this title, the amount reported shall be the fair market value, and a description of the goods, services, facilities or other thing of value shall be

5

appended to the report or statement. “Full and adequate consideration” as used in this title means “fair market value.” § 82044 – Payment. “Payment” means a payment, distribution, transfer, loan, advance, deposit, gift or other rendering of money, property, services or anything else of value, whether tangible or intangible. § 82047 – Person. “Person” means an individual, proprietorship, firm, partnership, joint venture, syndicate, business trust, company, corporation, limited liability company, association, committee, and any other organization or group of persons acting in concert. Regulatory § 18229.1 – Dependent Children. The Commission has finally adopted a definition of “dependent child” or “dependent children” and the regulation reads as follows:

“For purposes of the Act and Commission Regulations, “dependent child” or “dependent children” means a child, (including an adoptive child or stepchild) who is under 18 years old and whom the official is entitled to claim as a dependant on his or her federal income tax.”

A draft of this regulation circulated in 2009 did not include the limitation to 18 years of age. Also the definition could be interpreted narrowly to limit the category to those children the official is “entitled to claim” for federal tax purposes and thereby exclude a child the official is not entitled to claim on his or her return due to a child custody agreement. Often, a divorcing couple will agree to let the higher earning spouse claim the deduction even though the other spouse provides the greater support. The result from this interpretation seems unintended, since the goal of the regulation is to define when disclosure, disqualification, and perhaps the gift limit should apply to a child under 18 who lives at home and/or is dependant on the official. This should be read “. . .and whom the official is entitled to claim as a dependant under federal tax law.” This reading mirrors the goals of the definition and excludes external influences such as custody agreements. Also compare the newly revised Gifts to Members of an Official’s or Candidate’s Family (18944). This completely revamped section

6

(discussed more fully on Page 10), introduces the definition of “official’s family” and “family member” and those terms include the spouse and both the dependant children as defined under 18229.1 and “an official’s child” (including and adoptive or step child) who meets all of the following criteria:

(i) Is at least 18 but no more than 23 years old and is a full-time or part-time student; and

(ii) Has the same principal residence as the official. For purposes of this provision, a place, located away from the official’s residence, at which the child resides for the purpose of attending school is not the child’s “principal place of residence”; and

(iii) Does not provide more than one-half of his or her own support.

Other Definitions

• “Face Value” – See 18946 (page 15) • “Ticket/Pass” – See 18946 (page 15) • “Ticket or Pass” – See 18944.1 (Page 17) • “Invitations” - See 18946 (page 15) • “Specific Items” - See 18946 (page 15) • “Payment/Gifts to an Agency” – In addition to 82044(c), see also

18944.2 (page 20) • “Agency Head” – See 18944.2 (page 21) • “Official’s family” – See 18944(b)(2) (page 4) • “Family member” – See 18944(b)(2) (page 4) • “Official” – See 18944(b)(1) • “Financial benefit from a gift” – See 18944(d)(1)(A) (Page 12)

III. GIFT LIMITS § 89503 – Gift Limits. In 1995, the State legislature reorganized many of the gift and honorarium provisions of the government code and extended the dollar limit on gifts (e.g., $420) to public officials at local governmental agencies. Government Code § 89503(a) provides as follows: Statutory Filers

• No elected state officer, elected officer of a local government agency, or other individual specified in 87200 shall accept gifts from any single source in any calendar year with a total value of more than $250 (two hundred fifty dollars).

7

Section 89503 also requires the FPPC to adjust the limitation on January 1st of each odd numbered year to reflect changes in the Consumer Price Index, rounded to the nearest $10 (ten dollars). The gift limitation is currently $420 (four hundred twenty dollars) through December 31, 2010. Non-Statutory Filers Section 89503(c) further provides that no member of a State board or commission or designated employee of a State or local government agency shall accept gifts from any single source in any calendar year with a total value of more than $420 if the member or employee would be required to report the receipt of income or gifts from that source on his or her Statement of Economic Interest. This provides for a split in the gift limit between what we refer to as statutory filers (those enumerated in 872001) and those “designated” by their local conflict of interest code. For non-statutory filers, the gift limit only applies to any source that would be listed on an employee’s or official’s SEI, namely those people located in or doing business in the jurisdiction or with whom the employee or official interacts or is somehow a source of income or other involvement in the employee’s or official’s economic interest.

IV. GIFTS: AN ECONOMIC INTEREST As with most economic interests, there are special regulations which explain or define various terms such as source of gifts, cumulation and aggregation of gifts. The donor of a gift is an economic interest and defined as such in the following regulation: § 18703.4 – Economic Interest, Defined: Source of Gifts - For purposes of disqualification under Government Code §§ 87100 and 87103, a public official has an economic interest in any donor of, or any intermediary or agent for a donor of, a gift or gifts aggregating $420 or more in value provided to, received by, or promised to the public official within twelve (12) months prior to the time when the decision is made.

V. EXCEPTIONS TO “DEFINITION” OF GIFT Both § 82028 which defines gifts and § 89503 which set forth the gift limit, provide for certain exceptions. The Commission has adopted Regulation 18942

1 Section 87200 lists various State agency and Commission members who are considered statutory filers. In addition, it includes the following local agency officials: members of planning commissions, members of board of supervisors, district attorneys, county counsels, county treasurers, and chief administrative officers of counties, mayors, city managers, city attorneys, city treasurers, chief administrative officers and members of city councils of cities and other public officials who manage public investments and to candidates for any of these offices at any election.

8

which spells out those exceptions in greater detail and adds an additional exception or two. The following are listed as exceptions in that regulation:

1. Informational Material – This is defined in a separate regulation, 18942.1, and means any item which serves primarily to convey information which is provided for the purpose of assisting the recipient in the performance of his or her official duties or the elective office he or she seeks. Informational material may include: a) books, reports, pamphlets, calendars, periodicals, videotapes or free or discounted admission to informational conferences or seminars; b) scale models, pictorial representations, maps and other such items provided that where the item has a fair market value in excess of $390 (three hundred ninety dollars), the burden shall be on the recipient to demonstrate the item is informational material; c) on-site demonstrations, tours or inspections designed specifically for the purpose of assisting the recipient public officials or candidates in the performance of either their official duties or the elective office they seek. No payment for transportation to an inspection, tour or demonstration site nor reimbursement for any expenses in connection therewith, shall be deemed “informational material” except insofar as such transportation is not commercially obtainable.

2. Not Used/Returned/Donated - A gift is neither accepted nor received

if, within thirty (30) days after receipt, it is returned or donated unused, or reimbursement is paid. Both returning or donating the gift or reimbursing the gift must be conducted pursuant to § 18943 (discussed below). Tickets to events received under § 18946.1 need not be returned or reimbursed if they are not used or transferred to another person. Also note that returning or donating gifts under 18943 is different than the rules for returning honoraria under 18933.

3. Family Gifts - A gift from an individual’s spouse, child, parent,

grandparent, grandchild, brother, sister, parent-in-law, brother-in-law, sister-in-law, nephew, niece, aunt, uncle or first cousin or the spouse of any such person unless the donor is acting as an agent or intermediary for any person not identified in this subdivision, (a)(3).

4. Campaign Contributions - A campaign contribution required to be

reported under Government Code § 84100.

5. Inheritance - Any devise or inheritance.

6. Plaques/Trophies - A personalized plaque or trophy with an individual value of less than $250 (two hundred fifty dollars).

7. Hospitality - Hospitality, including food, beverages, or occasional

9

a. lodging, provided to an official by an individual in the individual’s home when the individual or a member of the individual’s family is present, is not a gift to the official unless one of the following applies:

i. Any part of the hospitality is paid for by another person. ii. Any person deducts part of that hospitality as a tax

deduction. iii. There is an understanding between the host and any other

person that any amount of compensation that the host receives from that other person includes a portion to provide hospitality in the individual’s home.

b. In trying to adapt to this new change and determine the

applicability of the exception, e.g., whether the exception is available, the regulation allows the official to “presume” that the cost of the hospitality is paid by the host unless he learns otherwise or it is clear from the “surrounding circumstance” that someone other than the host paid the cost (or part of the cost) of the hospitality. This may arise if you go to the individual’s home and find that various companies have sponsored the food, a table you are seated at, or the band.

c. If you are not eligible for the exception, the regulation further

provides that in calculating value received, that the cost of the hospitality does not include any part of the rental value of the home nor depreciation of the home.

d. Note that the rules concerning “home hospitality” for a lobbyist are

far different under 2 Cal. Code Regs. 18630.

8. Exchanged - Gifts exchanged between an individual who is required to file an SEI and another individual, other than a lobbyist, on holidays, birthdays, or similar occasions to the extent that the gifts exchanged are not substantially disproportionate in value.

For purposes of this exception, and notwithstanding 18946.2(b) (Invitation – Only Events), “Gifts Exchanged,” includes food, beverages, entertainment and nominal benefits provided at the occasion by the honoree or another individual, other than a lobbyist, hosting the event. At its April 8, 2010 meeting, the Commission considered a staff-driven amendment to this exception which would have required that the gifts exchanged occur within the same calendar year. The Commission rejected the amendment, in part, as too much of an intrusion into the privacy of the relationship of the individuals involved in the exchanges. Although not of pure legal significance, the Commission’s rejection of the calendar year limitation provides some guidance and the basis for an argument where an

10

official is alleged to not qualify for the exception because of the timing of the exchange.

9. Leave Credits - Leave credits, including vacation, sick leave or

compensatory time off, donated to an official in accordance with a bona fide catastrophic or similar emergency leave program established by the official’s employer and available to all employees in the same job classification or position. This shall not include donations of cash.

Payments received under a government agency program or a program established by a bona fide 501(c)(3) charitable organization designed to provide disaster relief if such payments are available to members of the public without regard to official status.

10. Free admission, common refreshments and similar non-cash nominal

benefits provided to a filer at an event at which the filer gives a speech, participates in a panel or seminar, or provides a similar service, and transportation and any necessary lodging and subsistence that is exempt from disclosure under 18950.3. These items are not payments and need not be reported by any filer.

This section, amended in 2010, formerly included the phrase: “provided directly in connection with the speech, panel, seminar or service, including but not limited to meals and beverages on the day of the activity”, which has now been eliminated in favor of Regulation 18950.3, which also was recently amended.

11. The transportation, lodging and subsistence specified by 2 Cal. Code Regs.

§ 18950.4 (Travel in Connection with Campaign Activity).

VI. EXCEPTIONS TO THE DOLLAR GIFT LIMITS The following items, if they are otherwise gifts, are exempt from the limitation on gifts set forth in Government Code § 89503:

1. Payments for transportation, lodging and subsistence that are exempt from limits on gifts by Government Code § 89506 and 2 Cal. Code Regs. 18950, et seq.

2. Wedding Gifts - The gifts, which are exempt from the limit, are

otherwise reportable on the SEI provided they are gifts. For example, a wedding gift provided by an official’s brother or sister would be an exception to the definition of gift and therefore would not be subject to the gift limit or reportable. Thus, when analyzing wedding gifts, first go to the exceptions (Regulation 18942), then consider reportability (statutory vs. non-statutory filers).

11

VII. SPECIAL GIFT RULES When Is a Gift Received? - 18941 The regulations provide the gift is “received” or “accepted” when the recipient knows that he or she has either actual possession of the gift or takes any action exercising direction or control over the gift. (2 Cal. Code of Regs. 18941). In the case of a rebate or discount that, based on Government Code § 82028, would otherwise be a gift, the gift is “received” or “accepted” when the recipient knows that the rebate or discount is not made in the regular course of business to members of the public without regard to official status. Except for passes or tickets as set forth in § 18946.1(a), discarding a gift does not negate receipt or acceptance of a gift. Neither does turning a gift over to another person unless the other person is a charitable organization or a state, local, or federal government. Payments for Food – 18941.1 This section, which can be confusing, provides that a “… a payment made to an elected officer or candidate for his or her food is a gift.” Since payment is broadly defined, presumably the payment could include a meal or other food provided by a public agency. This section does not contain any exceptions other than the statutory and regulatory exceptions listed above. Source of Gifts – 18945 (AMENDED 4/2010) The general rule is that a person is the source of a gift if the person makes a gift to an official and is not acting as an intermediary. A person is the source of a gift, and a third party is an intermediary of the gift under Sections 87210 or 87313, if the person makes a payment to the third party and the payment is used directly or indirectly by the third party to make a gift to the official under any of the following circumstances:

1. The person (donor) directs and controls the payment at the time it is used by the third party to make a gift to the official; or

2. The person (donor) and the third party have an agreement that the payment will be used by the third party to make a gift to the official; or

3. The person (donor) identifies the official to the third party as the intended beneficiary of the payment prior to the third party making the payment (gift) to the official; or

4. The third party identifies the official as the intended recipient prior to receiving the payment from the donor; or

5. The person knows or has reason to know that the sole or primary purpose of the payment is to make gifts to officials; or

12

6. The official or the official’s agent solicits the payment from the person to the third party for the purpose of making a gift to the official.

For the purpose of categories #3 and #4, above, a person or third party “identifies the official” if the person or third party identifies the official by name or any other designation from which it is clear that the person or third party is referring to the official or group of officials and the official is part of that group. If a person pays dues or makes similar payments for membership in a bona fide association, including any federation, confederation, or trade, labor or membership organization, some portion of which dues or similar payments are used to make gifts to officials, that person is not the source of gifts to those officials unless the sole or primary purpose of the dues or similar payments is to make gifts to officials. 2 Cal. Code Regs. 18945(a)(2). The source of gifts rules also includes a presumption that allows an official to presume that the person delivering the gift or, if the gift is offered but has not been delivered, the person offering the gift to him or her is the source of the gift unless any of the following apply:

1. The person delivering or offering the gift discloses to the official the actual

source of the gift; or 2. it is clear from the surrounding circumstances at the time the gift is

delivered or offered that the person delivering or offering the gift is not the actual source of the gift.

3. the official solicits a payment pursuant to section #6, above and receives or is offered a gift responsive to the solicitation within 12 months of the solicitation. 2 Cal. Code Regs. 18945(b).

The regulation also includes a presumption of source by intermediaries which provides that a third party otherwise qualifying as an intermediary as a result of a payment solicited from an official pursuant to section #6, above may presume that he or she is the source of the gift, and is not required to disclose the actual source of the gift as required by Regulation 18945.3 when both of the following apply:

1. The third party does not know or have reason to know of the official’s

solicitation; and 2. The third party does not qualify as an intermediary under sections #1

through #5, above. Cumulation of Gifts; “Single” Source – 18945.1 The cumulation of gifts is to be distinguished from the “aggregation” of gifts in that this regulation sets forth the standards for determining when gifts must be aggregated when the source may not be the same person or entity.

13

This regulation provides that for purposes of the gift limitations and honoraria limitations in Government Code § 89501 through 89506, two or more gifts are cumulated (more accurately — “aggregated”) as being from a “single” source if any of the following circumstances apply:

a. Gifts from an individual and an entity in which the individual has an ownership interest of more than 50% (fifty percent) shall be cumulated as being gifts from a “single” source.

b. Except as provided in subsection (a), above, gifts from an individual and

an entity shall be cumulated as being gifts from a “single” source if the individual in fact directs and controls the decision of the entity to make the gifts.

c. If the same person or a majority of the same persons in fact directs and

controls the decisions of two or more entities to make gifts to one or more public officials or candidates, gifts by those affiliated entities shall be cumulated as being gifts from a “single” source.

d. Business entities in a parent-subsidiary relationship, or business entities

with the same controlling (more than fifty percent) owner, shall be considered a “single” source unless the business entities act independently in their decisions to make gifts to one or more public officials or candidates. For purposes of the regulation, a parent-subsidiary relationship exists when one business entity owns more than fifty percent of another business entity.

This regulation is helpful although it rests largely on common sense. If, for example, a public official receives a gift from a prominent business person in town who happens to own a business and the initial gift is clearly from the business person and their spouse but that business person and spouse own fifty percent of the business that also gives the official a gift, they obviously must aggregate the gifts for reporting and disqualification purposes if the individual owns fifty-percent or more of the business that furnished the second gift. Intermediary of a Gift – 18945.3

• Amendment of 18945 now requires the practitioner to consider that regulation any time there is the possibility of an intermediary.

• Statutory Filers

This regulation provides that no person shall make a gift totaling $50 (fifty dollars) or more in a calendar year to a public official on behalf of another, or while acting as an intermediary agent of another, without disclosing to the recipient of the gift both his or her own full name, street address, and business activity, if any, and the full name, street address and business

14

activity, if any, of the actual donor. The recipient of the gift should include the information so provided about the intermediary and donor in his or her Statement of Economic Interest (SEI). (See also: 87210; 87313)

• Non-Statutory Filers

Essentially the same rules apply, however, it is limited to the sources of the gift that the intermediary or agent knows or has reason to know may require the recipient to disclose the gift pursuant to a local conflict of interest code.

A Gift From Multiple Donors – 18945.4 A gift that is received from multiple donors must be reported if the gift’s value equals or exceeds $50 (fifty dollars). The name of any donor whose share of the gift is less than $50 in value need not be separately reported; it is sufficient to describe in general terms those who gave the gift. If, however, the share of any donor or his or her agent or intermediary is $50 or more in value, his or her name must be reported. Gifts to an Official’s or Candidate’s Immediate Family - 18944 This section was amended in 2006 and again in late 2009 (operative 2-10-2010). Because of some crossover concerns between this regulation and the common law conflict of interest doctrine as well as state and federal criminal statutes, a caution will be provided after discussion of this gift regulation. The regulation is used to determine whether a gift to a candidate or public official’s family member also constitutes a gift to the candidate or official under the Act. Remember! As discussed on Page 4, under the definition of “dependant children”, this regulation includes its own definition of an “official’s family”, and includes children up to 23 years of age, if they meet certain criteria. Joint Gift—is a gift to the official. The operative part of the regulation begins by providing that a single gift given to either a public official or candidate and one or more members of the official’s immediate family is a gift to the official for the full value of the gift. Direct gift solely to family member. Subdivision (b) of the regulation sets forth the criteria to determine when a gift given solely to a member of the official’s family will be attributed to the official and thus reportable and subject to the gift limits. It provides that a gift given solely to a member’s family is a gift to the official when the gift confers a clear personal benefit on the official. A gift to an official’s family member confers a clear personal benefit on the official in any of the following circumstances:

15

(A) It is reasonably foreseeable at the time the gift is made that the official

will enjoy a financial benefit from the gift. A “financial benefit” includes, but is not limited to, a payment, other than occasional meals, lodging, or transportation, to fulfill a commitment, obligation, or expense of the type normally paid by a family for the ordinary care and support of one of it’s members

(B) It is reasonably foreseeable at the time the gift is made that the official will use the gift, except for minimal use.

(C) The official exercises discretion and control over who will use or dispose of the gift. “Exercises discretion and control” includes, but is not limited to, when an official or his or her agent, requests a gift for, or to be used by, the official’s family member.

Regulatory Presumption: 87200 Filers Only. The regulation goes on to provide that a gift given solely to a member of official’s family and not covered by subdivision (1) is a gift to the official if the gift confers a presumed personal benefit on the official. A gift to an official’s family member confers a presumed personal benefit in any of the following circumstances:

(A) The gift is made to a family member of a state agency official who is

subject to section 87200 by a donor who is a lobbyist, lobbying firm, lobbyist employer, or any other person who is required to file reports under Chapter 6 (commencing with 86100) of the Act.

(B) The gift is made to a family member of a local government agency official who is subject to section 87200 by a donor who is or has been directly involved in a governmental decision, as defined in regulation 18704.1(a), in which the official will foreseeably participate or has participated in the prior 12-month period.

The official can rebut the presumption if he or she can show that there is an established working, social, or similar relationship between the donor and the family member independent of the relationship between the donor and official. The addition of this presumption (18944(d)(2)) is a major change in the regulation and in the theory of the regulation. Under the prior regulation, once you enter the analysis that the gift may not be a gift to an official if given solely to the official’s family, you were done. This new section applies only to 87200 filers and it creates a regulatory “presumption” that there is a gift if the donor has been or will be directly involved in the governmental decision, as defined in regulation 18704.1(a), in the prior 12-month period. The criticism offered by the League and the City Attorneys FPPC Committee to this regulation, in general, was that we often find that public officials, particularly elected officials, gain new friends when they attain public office, sometimes directly disproportionate to the number of friends they had when they were in high school.

16

So for example, a fairly tenured councilmember or planning commissioner has made friends as a result of his or her position. One of the friends happens to be a local developer; another friend may be a supplier of goods and services to the city. On occasion they socialize together and their kids go to the same school. The son or daughter of the public official is asked to go along on a ski trip with the developer’s family and returns home with a brand new $800 snowboard. If you go through the prongs of 18944, it is clear that the official will not enjoy direct benefit from the gift because the snowboard will not be sufficient size to hold his or her weight; the official will not use the gift and the official will not exercise any discretion or control over who will use the gift or dispose of the gift. Likewise, when the prongs evaluating the donor’s intent are considered, there was an existence of a social relationship between the donor and the official’s spouse or immediate family member, etc. The addition of the presumption would operate to attribute the value of the snowboard to the official if the developer/friend had a project before the planning commission within the 12-month window or foreseeably, in the future. The gift would be presumed reportable and subject to the gift limits, unless the official can rebut the presumption by showing that the family member who received the gift had an independent relationship with the donor---not related to or derivative from the official’s relationship with the donor. For example, if the donor had been friends with the official’s spouse and kids before the donor even met the official. Practice Pointer: During the Commission’s discussion on the 2006 amendment, one of the examples used involved a local developer giving a $10,000 check for Junior’s college fund directly to the official’s spouse. If the official did not accept the gift for Junior; did not exercise control over it; and it was used for no other purpose except for Junior’s education, it would be an allowable gift (i.e., not a reportable gift to the public official). The obvious problem is that it may be considered an allowable gift under this regulation; however, a district attorney might see it quite differently. If the public official participates and votes to award a contract to the donor, the penal code could be implicated (and/or common law conflict of interest). If the official votes on the donor’s permit application, an issue of common law conflict of interest can arise. Therefore it is recommended that a public agency attorney advising a public official on this gift exception provide their advice with cautionary note in this regard. The 2009/2010 amendments tighten up this regulation considerably. Nevertheless, the practitioner must be aware that gifts by an applicant to family members of an 87200 official or other official who participates in governmental decisions can present at least the appearance of impropriety, if not the outright common law conflict of interest or susceptibility to criminal sanction. Remember

17

the regulation is aimed at determining when a gift made is reportable by the official or candidate, not necessarily when a gift is appropriate or inappropriate.

VIII. REPORTING AND VALUATION OF GIFTS – 18946 ET SEQ. The regulations provide five specific sections for the valuation of certain types of gifts. All other gifts are to be valued at fair market value as of the date of receipt or promise. 2 Cal. Code Regs. 18946(a). This section also provides the following guidance and definitions:

1. Unique Gifts – Whenever the fair market value cannot readily be ascertained because the gift is unique or unusual, the value shall be the cost to the donor, if known or ascertainable. If unknown or unascertainable, the recipient shall make a reasonable approximation. In making such an approximation, the recipient shall take into account the price of similar items. If similar items are not available as a guide, a good faith estimate shall be utilized. In the Cory, Ken, State Controller Adv. Ltr. 1 FPPC 153 (No. 75-094-B, Oct. 23, 1975), the Commission ruled that the public official may make a reasonable estimate of value based on a good faith effort and that there was no need to retain an appraiser (97-138).

2. Unused/Discarded – As a general rule, a gift must be valued, for

purposes of disclosure and disqualification, even if unused, discarded or given to another person. Special rules apply to gifts under Section 18943 (Returned, Donated or Reimbursed Gifts); 18944 (Gifts to an Official or Candidate’s Immediate Family); and 18946.1 (Tickets or Passes).

Special Gift Valuation Rules (18946.1 through 18946.5) For purposes of these special valuation rules, the following definitions apply:

• “Face Value” – Means the price indicated on the ticket, or if no price is indicated, the price at which the ticket or similar pass would otherwise be offered for sale to the general public by the operator of the venue or the host of the event who offers the ticket for public sale.

• “Ticket/Pass” – Means anything that provides an admission privilege to

an event or function and for which similar tickets or passes are offered for sale to the public.

• “Invitation” – Means a request to attend an event or function by the

sponsor of the event or function, that is not a ticket or pass as defined, above, and where admission to the event is provided by such invitation only.

18

• “Specific Item” – Means a tangible item received by an official or

candidate at an event that is not included among the non-cash nominal items presented to all attendees at the event.

Reporting and Valuation of Gifts: Passes and Tickets – 18946.1 (a) A pass or ticket that provides one-time admission or access to facilities,

goods, services or other incidental tangible or intangible benefits shall be valued at the face value of the pass or ticket provided that the face value is a price that was, or otherwise would have been offered, to the general public.

• A pass or ticket has no value unless it is ultimately used or transferred

to another person.

• This valuation provision applies to a pass to a motion picture theater, amusement park, parking facilities, country clubs and similar places or events and also includes tickets for theater, opera, sporting or similar event but not including travel or lodging.

(b) A pass or ticket that provides repeated admission or access to facilities,

goods, services or other incidental tangible or intangible benefits shall be valued as follows:

1. For Disclosure and Gift Limits – The value shall be the fair market

value of actual use of the pass or ticket by the recipient including guests that may accompany the recipient and who are admitted with the pass or ticket, plus the fair market value of any possible use by any person or persons to whom the privilege of use or the pass or ticket is transferred.

2. For Disqualification – The same valuation applies as for disclosure

and gift limits through the date of the governmental decision in question, plus the fair market value of the maximum reasonable use following the date of the decision. If the official returns the pass or any unused ticket prior to the decision, the value shall be determined based on the actual use prior to the decision.

This is the section that applies to the annual theater passes or similar passes where an official gets an unlimited use and is only charged with the actual use for disclosure and gift limit purposes. However, for disqualification purposes, if the official still holds the, e.g., theater pass, and could use it for the rest of the calendar year or thereafter or for any period after the decision, the maximum allowable use must be considered and that would most likely trigger disqualification.

19

Reporting of Gifts by a Donor –Candidates & Lobbyists As a general rule, donors do not have a reporting obligation, however be aware of Section 18421.7 (Reporting an Expenditure for a Gift, Meal or Travel) if made by a candidate; and Section 18600, et seq., relative to gifts from lobbyists. The Commission has stated that an expenditure of campaign funds to confer a substantial personal benefit on a candidate; pay for a personal gift; or pay for the travel or accommodations of a candidate, elected officer, or anyone with the authority to approve the expenditure of campaign funds must be directly related to a political, legislative or governmental purpose (PLG). Candidates, treasurers and elected officers must maintain detailed accounts for preparation of campaign statements. Candidate controlled committees must describe the PLG for gifts, meals, out-of-state travel expenditures and disclose information such as the dates of the expenditures, the location of the travel or meal, the number of individuals for whom the expenditure was made and the recipient of any gift. See Section 18421.7. In addition, Section 18401 has been amended to require committees to document expenditures for gifts, meals, and out-of-state travel in a dated memorandum and to retain the names of the individuals who engaged in the travel at their expense. Donors also have disclosure obligation and may have to report their role as an intermediary. (See: 87210,87313, and 18945.3).

Recipient of the Gift:

Passes or Tickets Given to an Agency – 18944.1 For entertainment, amusement, recreation, or similar events. NOTE: According to recent advice letters, 18944.1 is limited to tickets given to an agency for “admission to a facility, event, show, or performance for an entertainment, amusement, recreational, or similar purpose.” Scott Adv. Ltr (No. I-09-104 May 11, 2009). Therefore this is not for tickets to lunch or dinner events such as non-profit fundraisers where there is no recreation or entertainment, etc. For nearly fifteen years, Regulation 18944.1 helped to determine whether passes or tickets which provide admission or access to facilities, goods or services, or other tangible or intangible benefits were reportable as “gifts.” This regulation came under fire for perceived excesses by certain cities and, in particular, several state fair boards. Now, the analysis is completely new, with new reporting requirements, new policy mandates, and a new FPPC Form, set forth in a revamped 18944.1.

20

For the purpose of the new regulation, a “ticket” or “pass” is separately defined from regulation 18946, with the principle difference being that the definition in 18944.1 is not limited to tickets or passes offered for sale to the general public. Under this regulation, “ticket or pass” means “admission to a facility, event, show, or performance for an entertainment, amusement, recreational or similar purpose.” Therefore this could be admission to play a free round of golf at a city golf course or admission to a city held event, although the latter may be an unintended consequence of the wording of the regulation. To understand the regulation, it is probably helpful to understand the background of the regulation. It was widely reported in 2008, that members of state appointed fair boards were keeping thousands of tickets for themselves for each day’s state fairs held in their area. The events at the state fair included anything from 4H events to high-end entertainment events. Also considered by the Commission was the fact that many cities had reserved the right to attend events at arenas, ballparks, and concert venues in their jurisdictions when they leased that venue out to operators. Although the Commission could have approached this regulation as a way of “leveling the playing field” (a stated purpose of the PRA) when elected officials were given tickets that challengers were not, they instead wrestled with whether it was a gift, or payment to the official as compensation, or some other form of income. The regulation now provides several different categories for a recipient of a ticket to receive and properly report the ticket and imposes on the agency distributing the ticket certain policy requirements as well reporting and publishing requirements. (a) Admission for ceremonial role A ticket or pass provided by an official’s agency to an official for his or her admission to an event at which the official performs a ceremonial role or function on behalf of an agency is not a gift to the official. (18944.1(a)). (b) Ticket or pass provided by the official’s agency When an agency provides a ticket or pass to an official of that agency, the ticket or pass is not subject to the regulation, provided that the official treats the ticket as income, consistent with applicable state and federal income tax laws and the agency reports the distribution of the ticket or pass as income to the official, complying with subdivision (d) of the regulation. Note that the reporting by the agency of the income distribution is not necessarily to the State Franchise Tax Board or IRS, but rather it is reporting as required by 189974.1(d), which is essentially posting it on the required form (Form 802) and posting it on the agency’s website. The Commission considered requiring the agencies to report income tickets as compensation, but elected not to based on testimony of how difficult it would be for the agency to determine a number of

21

important factors, including the value received---if at all—since unused tickets have no value under the PRA. The Commission adopted this particular section in response to public testimony that when a local agency, like a city, receives tickets as part of its contract it is really receiving “consideration,” which is much like rent. The argument was made that cities are free to do with this consideration as deem appropriate. However, the FPPC wanted to add transparency to have how tickets were distributed and also impose upon the official the obligation to possibly include those tickets as another form of income. Also discussed, but not determined was the fact that if official only takes a couple tickets, it probably falls within the de minimis exception to receive income from your employer, as opposed to taking dozens or hundreds of tickets, which may well be reportable (and taxable) as compensation. (c) Gift Tickets 18944.1(b) and (d) essentially set forth the treatment of “gift tickets” or tickets given to an agency that could not necessarily be considered income to the agency or the official. This is similar to the gifts to an agency rule, but it specifically regulates only tickets. This section provides that when an agency provides a ticket or pass to an official that does meet the definition of gift under section Gov Code 8208 and is not otherwise exempt, the official will meet the burden that equal or greater value has been provided in exchange therefore, provided all of the following requirements are met:

1. The ticket or pass was not earmarked by the original source for use by the agency official who uses the ticket or pass

2. The agency determines, in it sole discretion, which official may use the ticket or pass; and

3. The distribution of the ticket or pass is made in accordance with a policy adopted by the agency in accordance with subdivision (c).

The phrase in the regulation, “and is not exempt under applicable regulations” allows this part of the regulation to integrate with the ticket or pass given to an agency or an official to make a ceremonial or drop in visit, etc. The requirements that the distribution of “gift tickets” must be consistent with 18944.1(c) refers to the requirement that under that subdivision, distribution of tickets to or at the behest of someone must be made pursuant to a written policy, duly adopted by the legislative or governing agency. That policy must state the public purposes to be accomplished by the agency policy and if the agency maintains a website, the written policy must be posted on the website in a prominent fashion. The written policy shall contain, at a minimum:

22

1. A provision setting forth the public purposes of the agency to be accomplished by the distribution of tickets or passes;

2. A provision requiring that the distribution of any ticket or pass by the agency to, or at the behest of an official, accomplish a public purpose of the agency; and

3. A provision prohibiting the transfer by any official of any ticket or pass, distributed to such official pursuant to the agency policy, to any other person, except to members of the official’s family

(d) New Form 802 Concurrent with the adoption of the regulation, the Commission adopted Form 802 and subdivision (d) of the regulation provides that the distribution of a tickets or pass including those distributed under (d) and (b)(2) shall be posted on the form in a prominent fashion on the agency’s website within 30 days of the distribution. If the agency does not maintain a website, the form shall be maintained as a public record, subject to inspection and copying, pursuant to 81008(a) and the form shall be forwarded to the Commission for posting on its website.

The posting shall include:

1. The name of the person receiving the tickets or pass, except if the ticket or pass is distributed to an organization outside the agency, the agency may post the name, address, description of the organization and the number of tickets or passes distributed in lieu of posting the names of each individual receiving a ticket or pass.

2. A description of the event; 3. The date of the event; 4. The face value of the ticket or pass; 5. The number of tickets or passes provided to each person; 6. If the tickets or pass is behested, the name of the official who

behested the tickets or pass; and 7. A description of the public purpose under which the distribution

was made or alternatively that the tickets or pass was distributed as income to the official.

The regulation also includes a statement that the Commission recognizes the discretion of the legislative or governing body of an agency to determine whether the distribution of a tickets or pass serves a legitimate public purpose of the agency, provided that the determination is consistent with state law. This statement was a negotiated compromise with members of the public who provided input to the Commission. The aim of this statement is to say that, provided that the ticket would not be an unlawful gift of public funds, the Commission defers to the judgment of the legislative body as to what may be a qualifying public purpose.

23

Finally, the new regulation provides that the provision of subdivision (b) which regulates tickets received by the public agency and given to the official apply only to the benefits the official receives by admission and are not applicable to any other benefits that the official may receive, such as food or beverages, or any other item presented to the official. The difficulty with this part of the regulation is that certain tickets or passes come with certain privileges. For example, the VIP ticket to the hockey game or concert may come with free admission to the backstage area or free hors d’oeurves presented pre-concert. Likewise, entrance to skyboxes at sporting events may include additional privileges and/or food and beverage. CAUTIONS:

1. If the agency gives some of there tickets to someone other than a public

official (e.g., a charity) at the behest of an official, the tickets are gifts or income to the official unless the provisions of the regulation are invoked (adopting an official policy) and Form 802 was filled out and posted on the website. Walls Adv. Ltr. (No. I-09-064 April 14, 2009).

2. If you agency receives gratuitous tickets (with some value) and distributes them e.g., to employees, the tickets are gifts and may be reportable and the agency becomes an intermediary for gifts over $50 and will have to disclose that role and the name of the donor. Zelenski Adv. Ltr. (No. I-09-066 April 22, 2009).

3. FPPC staff has indicated that tickets which have no value---e.g., where a venue offers bulk tickets to the agency along with other businesses to essentially “paper the house” for a particular event, those tickets are not subject to the Act.

GIFTS TO AN AGENCY – 18944.2 This regulation was extensively amended effective July 1, 2008. The new regulation includes some clarifications and new definitions and importantly, for gifts of travel, lodging and meals prohibits gifts of travel to an elected official and to statutory filers (e.g., 87200) from being accepted under the regulation. Therefore it treats 87200 filers, including elected officials, differently than all other public officials. The regulation establishes the circumstances under which a payment made to a State or local agency that is controlled by the agency and used for official agency business is not considered a reportable or limited gift to an individual public official although the official receives a personal benefit from the payment. The first line in the applicability section of the regulation (18944.2(a)) is significant. It uses the word “payment” and payment is defined in the

24

regulation to include the statutory definition of payment set forth in 82044 and specifically in this regulation includes “a monetary payment to an agency, a loan, gift, or other transfer, and the payment for, or the provision of, goods or services to an agency.” The significance of this wording is that prior to these changes it was unclear whether or not a gift of travel had to be in the form of a payment to the public agency or whether it could be in the form of tickets or vouchers for travel. Two other key points: First, the gift to the agency (and which is then distributed to a public official) must be used for official agency business. Many of the questions received by the FPPC Helpline involve gifts to a public agency that have no official governmental purpose, such as a case of wine, candy, etc. Secondly, if the payment does not provide a personal benefit, by definition, it is not a gift and would therefore not come under this regulation. The regulation only applies to payments that are made to an agency that provide a personal benefit to an official in that agency. The regulation also uses the term “agency head” and it is defined in the regulation to mean an individual in whom the ultimate legal authority of an agency is vested, or who has been delegated authority to make determinations by the agency for purposes of this regulation. This was the subject of much discussion at the Commission level to determine whether or not the city manager or chief operating official should be designated in the regulation or, because this regulation applies to multimember boards who govern an agency, it was left to the discretion of the agency to determine the agency head and they can do so by making such a determination specifically for purposes of this regulation. Operation of the Regulation - Under this regulation, gifts to an agency are defined as: “a payment, that is otherwise a gift to a public official, as defined in Section 82028, shall be considered a gift to the public official’s agency and not a gift to the public official if all the following requirements are met:”

1. Agency Controls Use of Payment – The agency head (or designee) determines and controls the agency’s use of the payment. The donor may specify a purpose for the payment but the donor may not designate by name, title, class, or otherwise, an official who may use the payment. If the payment will provide a personal benefit to an official, the agency head, or his or her designee, shall select the individual who will use it. The agency official who determines and controls the agency’s use of the payment may not select himself or herself as the individual who will use the payment.

2. Official Agency Business – The payment must be used for official

agency business.

25

3. Agency Reports the Gift – Within thirty (30) days after use of the payment, the agency reports the payment on a form prescribed by the Commission (Form 801).

Limitations on Application of this Regulation The exceptions provided under Gifts to an Agency do not apply to the following payments:

1. A payment for travel, including transportation, lodging and meals for State or local elected officers, as defined in Section 82020, or an official specified in Section 87200 (e.g., statutory filers).

2. A payment for travel to the extent that it exceeds the agency’s

reimbursement rates for travel, meals and lodging, and other actual necessary expenses or if the agency has no standard policy or practice concerning reimbursement rates, the State per diem rates set forth in the applicable sections of the State Administrative Manual (see 18944.2(d)(2)).

3. A payment for travel that the agency head, or designee has not

preapproved in writing in advance of the date of the trip.

4. Passes or tickets as described in Regulation 18944.1 which shall be governed by that regulation.

Reporting Requirements—Gifts to an Agency

1. The regulation describes in detail the seven in-depth items which must be reported on form 801.

A. A description of the payment, the date received, the intended purpose, and the amount of the payment (or the actual or estimated amount of the goods or services received.

B. Name and address of the donor. If not an individual the report shall describe the business activity and nature and interests of the entity. If the donor has raised funds from other sources---a complete list of the contributors and amounts.

C. The agency’s use of the payments and the name title and department of the agency for whom the payment was used. The report shall include a breakdown of the date(s) and place(s) of travel and a breakdown of the total expenses for transportation, meals and lodging and other related expenses.

D. Form signed by the “Agency Head” and maintained as a public record.

26

E. State agency sends the form to the FPPC by mail, email, personal delivery or fax within 30 days after use of the payment. Form or the information in the form also posted on the state agency’s website in a prominent fashion (within the same 30 days). If no website, the FPPC will post it on their website. If the FPPC gets gifts--- the forms filed by the FPPC go to the AG.

F. A local agency gives the form to its SEI filing officer within 30 days of use of the payment by mail, email, fax or personal delivery. Same rules for posting on the local agency website except it does not need to be posted “in a prominent fashion” and if no website ---send to the FPPC and they will post it.

G. The individual who has custody of these forms for the agency is the filing office who must maintain a public log of the forms indexed under both the name of the agency receiving the payment and the name of the official and the forms must be kept for at least four (4) years.

Other Exceptions: Gifts to an Agency – 18944.2(e) and (f) There are two additional exceptions, one which relate to a donation to a California public college or university for specific research projects (18944.2(e)) and payments from the federal government such as a grant, reimbursement, funding or other payments received by a State or local agency from a federal government agency for education, training, or other inter-agency programs will not be considered a gift to the public official who receives a benefit from the payment (18944.2(f)). Practice Pointer: Gifts to an agency just got a lot more complicated. The key things to know about the new regulation are as follows: 1. It is probably best to adopt your own official policy as to how you will accept,

monitor and report gifts to an agency. 2. The adopted policy should designate who is the “agency head” and probably

should have an alternate agency head if the city manager may use gifts other than travel.

3. Elected officials and statutory filers (e.g., city attorneys and city managers,

planning commissioners and those who invest public monies) cannot use gifts provided to the agency for travel, including transportation, lodging and meals.

FREQUENTLY ASKED QUESTIONS ABOUT GIFTS TO AN AGENCY

27

On the FPPC’s website, www.fppc.ca.gov, the Commission staff offers answers to frequently asked questions. Some of them are instructive in understanding the regulation just described. They include:

• If the city’s mayor has been invited to visit a Sister City in Mexico, the city may not accept gifts of travel for elected officials and 87200 filers. The city may pay for the mayor’s trip or the mayor may accept the travel payments from the Sister City and disclose them on his or her SEI (Form 700) as gifts. Government Code § 89506 (Travel) describes various travel payments from government, educational, or nonprofit groups that are not subject to limits (although in most circumstances they must be reported as gifts).

• A third party pays for travel for a State employee (or local employee who is

not a statutory filer) and the travel is paid by a third party which would exceed the standard reimbursement rates, no gift will result to the official if the agency follows the established procedures allowing a higher rate for lodging (as if the agency were paying for the lodging itself). If the procedures are not followed, the employee will receive a reportable gift in the amount that exceeds the standard State reimbursement rate.

• There is no required form for ensuring that pre-approval was obtained in

advance of a trip. Local agencies may use their own form. The only official form is Form 801, which is the new State form which records the receipt and distribution of the gift.

• There is no State statute or regulation that defines “official agency

business.” The payment must be used for a legitimate government purpose and must assist the agency in carrying out its mission, programs or goals. The payment may not be for an activity unrelated to the official responsibilities of the agency.

• The donor may make payments directly to vendors instead of the agency

(e.g., the donor can reserve the hotel room or airfare on its own credit card), however, the agency must provide a breakdown of the expenses for transportation, lodging, meals and other related expenses on Form 801. If several agency officials and business leaders attend a meeting and one of the business representatives provides coffees and pastries, this information does not need to be reported on a Form 801 because generally the receipt of food and beverages is considered a gift to the official who consumes them. If the value of the food and beverages to an individual is $50 (fifty dollars) or more, the official may be required to report the gift on his or her Form 700.

• If an agency believes that the provision of food or beverages should be

considered a gift to the agency and not to an official (for example, food

28

provided at a public event sponsored by the agency), the agency should contact the FPPC for advice.

• Where airport parking is provided by one governmental agency to various

elected officials from other governmental agencies, the airport parking is considered a travel payment which cannot be provided as an agency gift if used by elected officials or statutory filers under Gov’t. Code § 87200. Under Government Code § 89506, however, an official may accept free parking from another government agency while on official business. The value of the parking privilege is reportable on the official’s Form 700, though not subject to the gift limit if the requirements of Section 89506 are met. The value of parking privileges used for personal purposes may not exceed $390 (three hundred ninety dollars) in a calendar year. If the parking privileges are provided as an agency gift for use by public officials who are not elected or covered under § 87200, the agency receiving the gift must disclose the payments on Form 801.

GIFTS BY AN AGENCY—(New) 18944.3 This regulation was first added in 2009 and amended later that same year. It provides that except for tickets provided under 18944.1 and gifts to an agency under 18944.2, that a payment by a government agency from that agency’s assets that provide food beverage, entertainment, goods, services, of more than nominal value to an official in that agency, is a gift to the official unless that payment is a lawful expenditure of public funds. The stated purpose of this regulation would be to address any “payment” made to an official which is a misuse of public funds by treating that payment as a “gift” to the official, subject to both the reporting requirements and gift limitations. Said differently, if an expenditure by the agency results in an illegal gift of public funds---it is both illegal as an expenditure and reportable as a gift---provided it is over the $50 threshold and under the gift limit, if applicable. The goal of the regulation is not to second guess the agency when food is provided prior to a council meeting, or door prizes are provided at an employee recognition dinner. It is rather aimed at requiring reporting of gifts of travel for the official or their family when there is no legitimate governmental purpose, and the $20,000 Rolex wristwatch at retirement, etc.

AGENCY RAFFLES AND GIFT EXCHANGES—(New) 189444 At the same meeting where the above regulation was amended, the Commission adopted a new regulation to address gifts given to employees as part of an agency-held raffle or an employee gift exchange.

29

Raffles. When an agency holds an employee raffle and awards an item from an outside source and thus not paid for by the agency or provided by an employee, then the gift (or payment) is a gift to the employee and the agency becomes an intermediary. The value of the gift is the fair market value of the gift minus anything the employee paid to participate in the raffle. If the gift is $50 or more, the employee must list the gift on his/her SEI and list the agency as the intermediary under 87210 and 87313. This promises to be a challenging section to administer unless the employee chooses to err on the side of disclosure, in most instances. Consider that often employee organizations---both formal and informal, contribute gifts to these events and raffles. The regulation also references 18944.3 to the extent that an agency provided gift was an illegal gift of public funds, and exempts gifts provided to the raffle by another employee, provided that the employee is not acting as an intermediary for someone else. Employee Gift Exchanges. The regulation provides that gifts received by an employee in an employee gift exchange is not a gift to the employee so long as the item received came from another employee and the gifts are not substantially disproportionate in value (18944.4(c)) and clarifies that the regulation does not apply to tickets given to the agency.

Testimonial Dinners and Events, Invitation-Only Events, and Ceremonial Functions – 18946.2 Testimonial Dinners – If an official is honored at an event which does not involve campaign fundraising for the official or candidate, the value received is the official’s or candidate’s pro rata share of the cost of the event, plus the value of any specific item that is presented to the official or candidate at the event. Invitation-Only Events – The value received is the official’s or candidate’s pro rata share of the cost of the event, plus the value of any specific item that is presented to the official or candidate at the event. Exceptions: The exceptions to this rule include nonprofit fundraisers under 18946.4; or when an official performs an official or ceremonial function at the event as set forth below; or, where the official merely makes a drop-in visit. Under each of those exceptions, special rules apply as follows:

• Official or Ceremonial Functions – When the official performs an official or ceremonial function at an invitation-only event and where the official is invited to participate by the event’s sponsor or organizer to

30

perform such functions, the value received is the cost of any food or beverages provided to the official plus the value of any specific item that is presented to the official at the event.

• Drop-In Visit – If the official attends an event such as a testimonial

dinner or invitation-only event but does not stay for any meal or entertainment otherwise provided at the event, and receives only minimal appetizers and drinks, the value of the gift received is the cost of the food and beverage consumed by the official and guest accompanying the official, plus the value of any specific item that is presented to the official at the event. For purposes of this subdivision, “entertainment” means a feature show or performance intended for an audience, and does not include music provided for background ambience.

The official or ceremonial function exception and drop-in visit exception were added and clarified in the regulation in 2005 after the Commission became aware that public officials were invited for ceremonial functions but the operation of the regulation for purposes of valuation would eclipse the gift limit rule, even if the official did not stay for the entertainment or dinner. Note that those two exceptions also apply only to officials and not to candidates.

For purposes of 18946.2, “Pro-rata share of the cost of the event” means the cost of all food and beverages, rent of the facilities, decorations, entertainment, and all other costs associated with the event, divided by the number of acceptances or the number of attendees.

Wedding Gifts – Reporting and Valuation – 18946.3 Wedding gifts given to an official and his or her spouse or spouse-to-be are considered as gifts to both spouses equally, and the official is deemed to receive one-half of the value as determined pursuant to valuation provisions of 18946, unless the gift is peculiarly adaptable to the personal use and enjoyment of one spouse or specifically and unequivocally intended exclusively for the use and enjoyment by one spouse, in which event the full value of the gift is attributed to that spouse.

Tickets to Nonprofit and political Fundraisers – 18946.4 This regulation was one of the most widely applied gift regulations because public officials and candidates are invited to countless fundraising events. Often the tickets would be purchased by local businesses, including the local developer or garbage company on behalf of the nonprofit and then handed out to public officials who would attend. Under the prior rules, if the ticket was for a 501(c)(3) fundraising event, it did not matter whether the ticket was provided directly by

31

the nonprofit or by a for-profit business. Pursuant to the terms of the regulation, it had no value. The new regulation adopted by the Commission in August 2008 now provides for the following:

1. The regulation applies to a single ticket or other admission privilege to a specific fundraising event provided to the public official by a nonprofit or political organization holding its own fundraiser and used solely by the public official. If the official takes two tickets, the second one would have to be listed on his/her Form 700.

2. For a 501(c)(3) organization fundraiser, the organization may provide one ticket per event to an official and that ticket shall be deemed to have no value so long as the cumulative value of the non-deductible proportion of the ticket(s), as provided in subdivision (a), received by the official from the same organization during a calendar year, does not exceed the gift limit (currently $390). This means that a 501(c)(3) organization can provide the same elected official with one ticket for each of its yearly events, provided that the non-deductible portion of the tickets, in aggregate, does not exceed the gift limit. If they exceed the gift limit, the official would have to reimburse the nonprofit to bring the gift below the limit.

3. In summary, the “single ticket” is an exception to the reporting

requirements – all tickets are counted toward the gift limit ($420).

4. Other Nonprofits – The value of a gift of a single ticket, pass or other admission privilege to a fundraising event for an entity that is not a committee defined in Section 82013(a) (Campaign Committee) provided by the organization to an official and used by that official shall be determined as follows:

• Where the ticket clearly states that a portion of the ticket price is a

donation to the organization, the value of the gift is the face value of the ticket reduced by the amount of the donation.

• If there is not a ticket indicating a face value or the ticket or other

admission privilege has no stated price or no stated donation portion, the value of the gift is the pro rata share of the cost of any food, and beverages, plus any specific item presented to the attendee at the event.

5. Political Fundraiser – A gift of a ticket, pass or other admission

privilege to a fundraising event for a committee defined in 82013(a), or a

32

comparable committee regulated under federal law holding an event in California, the committee or candidate may provide one ticket per event to an official and that ticket shall be deemed to have no value when used solely by the official.

6. Tickets as Income -- If the agency buys tickets to a charitable or other

event and the official takes the ticket as income, the value is the face value of the ticket without offset of the amount of any donation, if applicable. Scott Adv. Ltr. (No. I-09-104 May 11, 2009).

The big changes in this regulation are obvious. The no value tickets to nonprofit organizations are now limited to one ticket per event per public official provided that the ticket is received directly from the organization or committee. What is also not entirely clear is the fact that, no doubt, the 501(c)(3)’s will adapt to this new rule and instead of the local developer, business or garbage company buying the tickets and handing them out to public officials, they may “buy a table” and allow the nonprofit to distribute the tickets. What may cause some confusion is when the public official goes to the fundraiser for the local music school and believes he or she received a ticket directly from the nonprofit only to sit at a table “sponsored by” the local business.

PRIZES AND AWARDS FROM BONA FIDE COMPETITIONS – 18946.5 A prize or an award received shall be reported as a gift unless the prize or award is received in a bona fide competition not related to the recipient’s status as an official or candidate. A prize or award that is not reported as a gift shall be reported as income. This can arise in a number of circumstances. At some League’s booth functions, public officials throw their business card into a hat at an exhibitor’s booth in the main hall only to learn they won some gift as part of that “competition.” This is not a bona fide competition and it is not unrelated to the recipient’s official status. This gift would therefore be reportable as a gift and subject to the gift limits. If, on the other hand, a candidate entered a nationwide poetry writing contest and won an award, the award (e.g., trophy) and cash prize would be reportable. If the plaque or trophy has a value under $250 (two hundred fifty dollars) it is not reportable as a gift under the gift rule, however, it may be reportable under 18946.5, since it arose from a bona fide competition. Air Transportation – 18946.6 This regulation was amended in August 2008 as it relates to flights on private or chartered aircraft. The new regulation takes a more common sense approach to valuation.

33