International Comparisons of Bank Regulation, Liberalization, and Banking Crises

1.0 Introduction

This internship is a part of the Bachelor of BusinessAdministration (BBA) program that provides an on-the-jobexperience to students. I was placed at Trust Bank Limited,Dhanmondi Branch as an internee officer for three months. Thisinternship program was my very first on-the-job exposure andprovided me with learning experience and knowledge in severalareas. During the first few weeks of my internship period, I wasable to get accustomed to the working environment of Trust BankLimited. As the internship continued, I not only learned aboutthe activities and operations of correspondent Bank, but I alsogathered some knowledge about the basic business activities ofbanking in first one-month of my internship period.

Generally by the word “Bank” we can easily understand that thefinancial institution deals with money. But there are differenttypes of banks such as; Central Banks, Commercial Banks, SavingsBanks, Investment Banks, Industrial Banks, Co-operative Banksetc. But when we use the term “Bank” without any prefix, orqualification, it refers to the ‘Commercial banks’. Commercialbanks are the primary contributors to the economy of a country.So we can say Commercial banks are a profit-making institutionthat holds the deposits of individuals & business in checking &savings accounts and then uses these funds to make loans. Bothgeneral public and the government are dependent on the servicesof banks as the financial intermediary. As, banks are profit-earning concern; they collect deposit at the lowest possible costand provide loans and advances at higher cost. The differencesbetween two are the profit for the bank.

A company can increase efficiency through a number of steps.These include exploiting economies of scale and learning effects,adopting flexible manufacturing technologies, reducing customerdefection rates, getting R&D function to design products that areeasy to manufacture, upgrading the skills of employees throughtraining, introducing self-managing teams, linking pay to

1

performance building a companywide commitment to efficiencythrough strong leadership, and designing structures thatfacilitate cooperation among different functions in pursuit ofefficiency goals.

Efficacy of customer service is related with progression ofoperation. We can identify the efficacy of customer service bystudying the progress of “Trust Bank Ltd.” from starting to atpresent. The progress of “Trust Bank Ltd.” is very rapid with theconcern of its profit making and growth of its operation withinthe country towards the country’s economy.

Trust Bank Limited pursues decentralized management policies andgives adequate work freedom to the employees. This results inless pressure for the workers and acts as a motivational tool forthem, which gives them, increased encouragement and inspirationto move up the ladder of success. Overall, I have experienced avery friendly and supporting environment at Trust Bank Limited,which gave me the pleasure and satisfaction to be a part of themfor a while. While working in different departments of thisbranch I have found each and every employee too friendly to us tocooperate. They have discussed in details about their respectivetasks. I have also participated with their works.

1.1 Objectives of the Report

To present an overview of “Trust Bank Ltd. ”

To get an overall idea of banking from banker’s point of

view.

To apply theoretical knowledge in the practical field.

2

To make a bridge between the theories and practical

procedures of day to day Banking operation.

To assess the decision undertaken by the top-level

management to keep the rein with the

competitiveness of the market.

To relate the theories of banking with the practical banking

activities.

To review the techniques used by the bank to make it

lucrative

Determining the drawbacks of the existing system.

To study existing banker-customer relationship, particularly

the efficacy of customer services of the bank.

Recommending some guidelines to improve the effectiveness

1.2 Scope of the Report

This internship report covers all the trade related productshandled by the “The Trust Bank Ltd.” such as Foreign Exchange,Cash Dept., Dispatch, Account Opening, Remittance, Accounts,Administration and Loans & Advances etc.

This report has been prepared through extensive discussion withbank employees and with the customers. While preparing thisreport, I had a great opportunity to have an in depth knowledgeof all the banking activities practiced by the “The Trust Bank

3

Ltd.” It also helped me to acquire a first-hand perspective of aleading private Bank in Bangladesh

1.3 Methodology of the report

Interview was the basic technique complied to collect primarydata from any people within the organization. Information aboutthe varieties of activities within the Correspondent BankingDepartment was collected through interviews. Data regarding thetypes of product offered to the clients and the descriptions foreach of those products were gathered through interviews. Besides,on-the-job experience has also helped me learn quite a few thingsabout the Correspondent Banking Department and the organizationas well.

On the other hand, secondary sources were used to collect dataregarding the company’s performance over the past five years,Publications, Database, Annual report of Trust Bank Ltd,Different papers of Trust Bank Ltd, Different textbooks, Termpapers of TBL Training manuals, Data have also been collected bygoing through different circulars issued by the head office andBangladesh bank during the tenor of the internship.

1.4 Limitations of the study

The present study was not out of limitations. But it was a greatopportunity for me to know the banking activities of Bangladeshspecially “Trust Bank Ltd.” Some constraints are appended bellow–

The main constraint of the study is inadequate access to

information, which has hampered the scope of analysis

required for the study. As it is a new bank it could not

4

start all its operation, it was unable to provide some

formatted documents data for the study.

Due to time limitations, many of the aspects could not be

discussed in the present report.

Every organization has their own secrecy that is not

revealed to others. While collecting data i.e.

interviewing the employees, they did not disclose much

information for the sake of the confidentiality of the

organization.

Another problem is that creates a lot of confusions

regarding verification of data. In some cases more than one

person were interviewed to clarify each concept as many of

the bankers failed to provide clear-cut idea about the job

they perform.

The clients were too busy to provide me much time for

interview.

I have had no opportunity to compare the general banking

system of the TBBL with that of other contemporary and

common size banks. It was mainly because of the shortage of

time and internship nature.

5

2.0 Origin of Bank

Barter System→ Money→ Bank.

At past, people making transactions by barter system. In thissystem, they transactions products. If someone has enough rice,but his/her required fish & goes to fisherman for collectingfish. On the other hand, fisherman have required rice & theytransfer products one to another. By using this system, they werecontinuing their lives. However, at a time barter system faileddue to divisibility. Due to failure this system, people developmoney. This is now the common medium for transactions. Forsecuring money, people establish bank. By which they aremaintaining their transactions.

2.1 Meaning of Bank

The term Bank derives from the Italian word banco, which means"desk/bench", used to make transactions above a desk covered by agreen tablecloth.

2.2 Definition of Bank

A bank is a financial institution licensed by a government.Its primary activity is to lend money. Many other financialactivities were allowed over time. For example banks areimportant players in financial markets and offer financialservices such as investment funds.

A Bank is a financial intermediaries institution betweenlenders & borrowers,which act as like as pipeline.

6

A Bank is a business organization that receipts & paymentfunds to their customers.

2.3 Banking

The business conducted or services offered by a bank.

All of the activities of bank are called banking

All of the activities of clients that are related with bank

are called banking.

2.4 Banker

Generally, the term banker defined as "a dealer in capital, or,more properly, a dealer in money. He is an intermediate partybetween the borrower and the lender."

According to British Stampt Act, 1881 “any person carrying

on the business of banking is a banker”.

A banker is a person who deals with the money of others; but

he often lends his own money, and when thus acting he is one

of the two original parties.

A public or incorporated bank, like a banker, receives and

lends money. It always has a capital of its own to lend,

besides the money or deposits of individuals.

Some are says that both employee & owner are banker. But,

this is very controversial one.

7

2.5 Objectives of a Bank To facilitate the transferring of fund from the surplus unit

to deficit unit

To accelerate the savings

To accelerate the investment

To enhance the economies development

To facilitate the trades and commerce’s

2.6 Origin of Banking in BangladeshBangladesh is an over populated country, which shares a commonpart with India & Pakistan in respect of development of thebusiness of Banking. With the beginning of Muslim rule in India,the fortune hunting Afghanistan trades started money lendingbusiness in exchange of interest sometime in 1312 AD. They wereknown as “Kabuliwallas”.

During the period of ‘Moguls’ the banking was run by wound / wealfamilies. By the time, the British left the country in 1947, theyhad emerged a large number of banks about 668 in Bengal alone. Atthe time of war in 1965, between India & Pakistan, produced around of disruptions. When the govt. declared most of the banks,which owned by non-muslim, these banks as enemy properties. Mostof the banks were closed down & the responsibility forliquidation was entrusted to the State Bank of Pakistan & laterto the Bangladesh Bank.

8

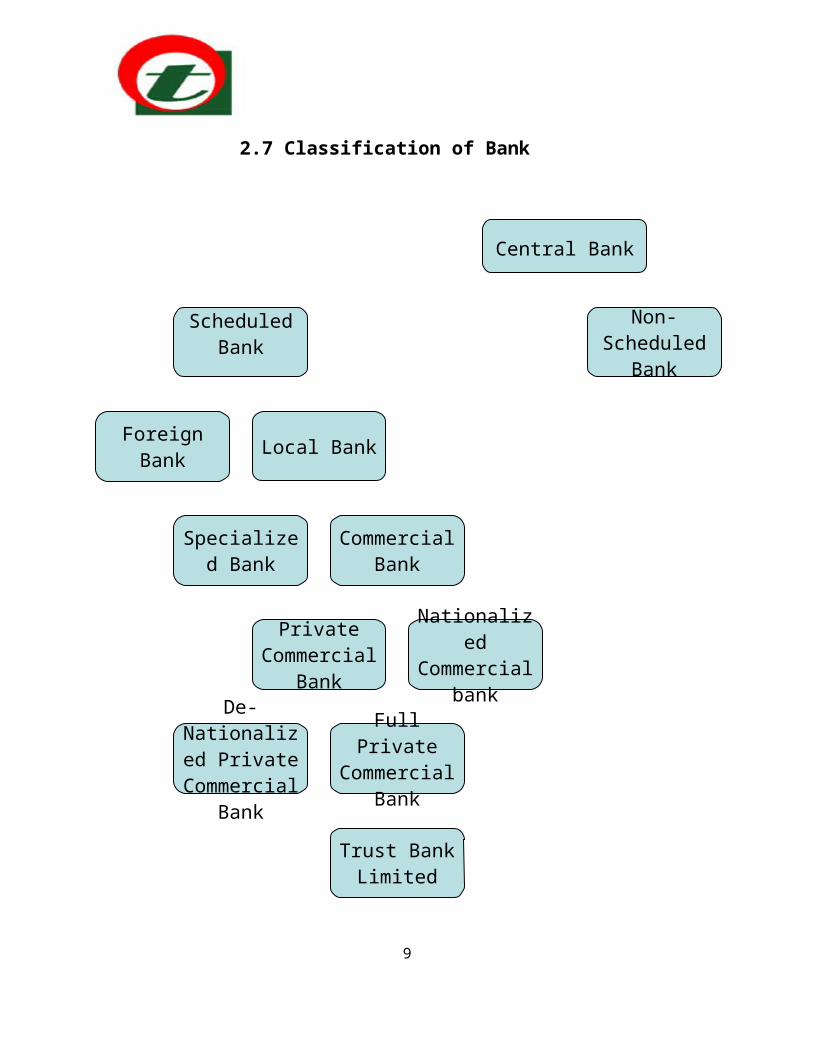

2.7 Classification of Bank

9

Central Bank

ScheduledBank

Non-Scheduled

Bank

Foreign Bank Local Bank

Specialized Bank

Commercial Bank

Private Commercial

Bank

Nationalized

Commercial bankDe-

Nationalized Private Commercial

Bank

Full Private

Commercial Bank

Trust Bank Limited

Figure-1: Classification of bank

2.8 Current Structure of Banks in Bangladesh

The commercial banking system dominates the financial sector ofBangladesh. Where Bangladesh Bank (BB) is the Central Bank ofBangladesh and the chief regulatory authority of this sectorsince the country's independence. Its prime jobs include issuingof currency, maintaining foreign exchange reserve and providingtransaction facilities of all public monetary matters. BB is alsoresponsible for planning the government's monetary policy andimplementing it thereby. The BB has a governing body comprisingof nine members with the Governor as its chief. Apart from thehead office in Dhaka, it has nine more branches, of which two inDhaka and one each in Chittagong, Rajshahi, Khulna, Bogra,Sylhet, Rangpur, and Barisal.

There have 48 banks in our country. An upcoming bank is NonResidence Bank (NRB), which will be the 49th bank of the bankinghistory in Bangladesh. The banking system of BD is consistsof 4 state-owned commercial banks, 5 specialized developmentbanks, 30 private commercial Banks, and 9 foreign commercialbanks.

Sonali Bank is the largest among the state-owned commercial banks,while Pubali Bank Limited is leading in the private ones. Among the 9foreign banks Standard Chartered Bank has become the largest & inleading position in our country.

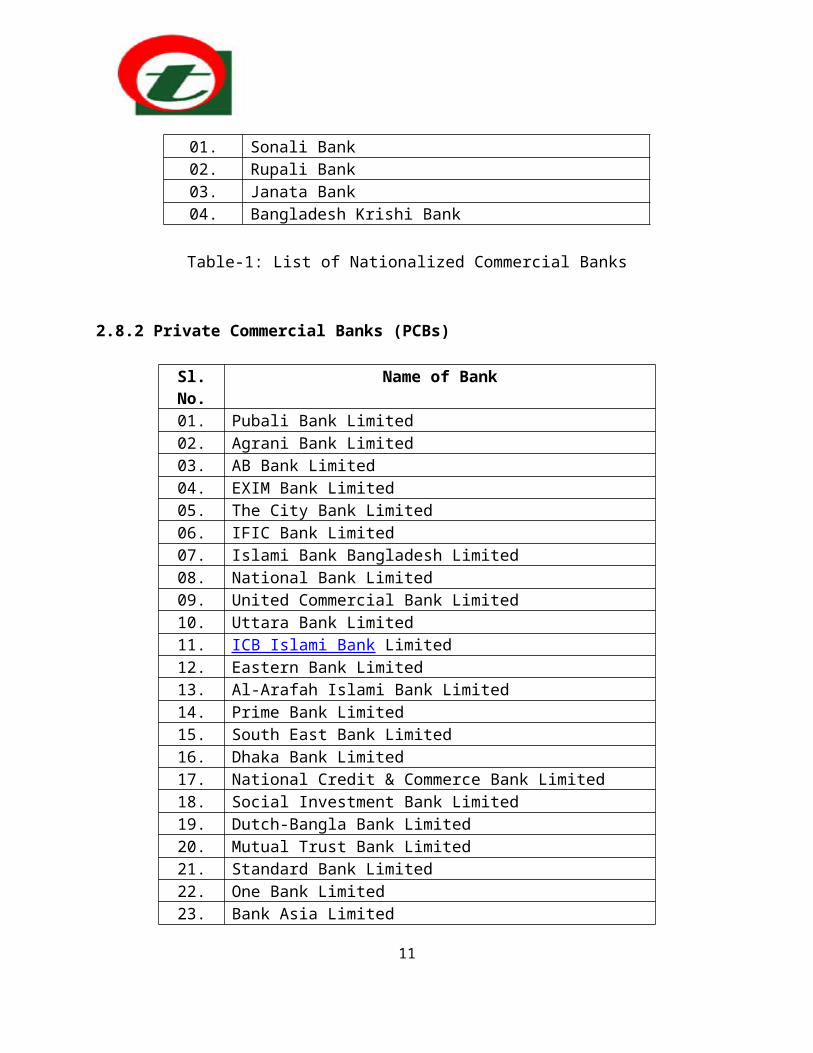

2.8.1 Nationalized Commercial Banks (NCBs)

Sl.No.

Name of Bank

10

01. Sonali Bank02. Rupali Bank03. Janata Bank 04. Bangladesh Krishi Bank

Table-1: List of Nationalized Commercial Banks

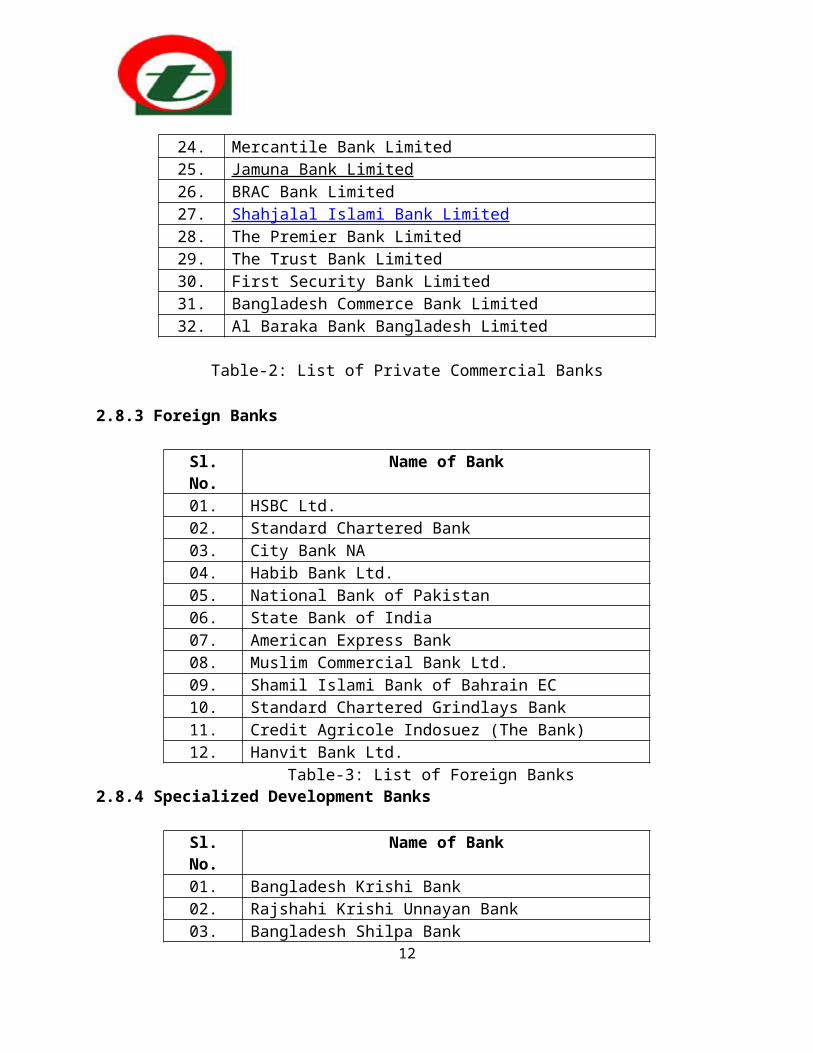

2.8.2 Private Commercial Banks (PCBs)

Sl.No.

Name of Bank

01. Pubali Bank Limited02. Agrani Bank Limited03. AB Bank Limited 04. EXIM Bank Limited 05. The City Bank Limited 06. IFIC Bank Limited07. Islami Bank Bangladesh Limited08. National Bank Limited09. United Commercial Bank Limited 10. Uttara Bank Limited 11. ICB Islami Bank Limited 12. Eastern Bank Limited 13. Al-Arafah Islami Bank Limited 14. Prime Bank Limited 15. South East Bank Limited16. Dhaka Bank Limited 17. National Credit & Commerce Bank Limited 18. Social Investment Bank Limited 19. Dutch-Bangla Bank Limited 20. Mutual Trust Bank Limited 21. Standard Bank Limited22. One Bank Limited 23. Bank Asia Limited

11

24. Mercantile Bank Limited 25. Jamuna Bank Limited 26. BRAC Bank Limited27. Shahjalal Islami Bank Limited 28. The Premier Bank Limited29. The Trust Bank Limited30. First Security Bank Limited31. Bangladesh Commerce Bank Limited32. Al Baraka Bank Bangladesh Limited

Table-2: List of Private Commercial Banks

2.8.3 Foreign Banks

Sl.No.

Name of Bank

01. HSBC Ltd.02. Standard Chartered Bank03. City Bank NA04. Habib Bank Ltd.05. National Bank of Pakistan06. State Bank of India07. American Express Bank08. Muslim Commercial Bank Ltd.09. Shamil Islami Bank of Bahrain EC10. Standard Chartered Grindlays Bank11. Credit Agricole Indosuez (The Bank)12. Hanvit Bank Ltd.

Table-3: List of Foreign Banks2.8.4 Specialized Development Banks

Sl.No.

Name of Bank

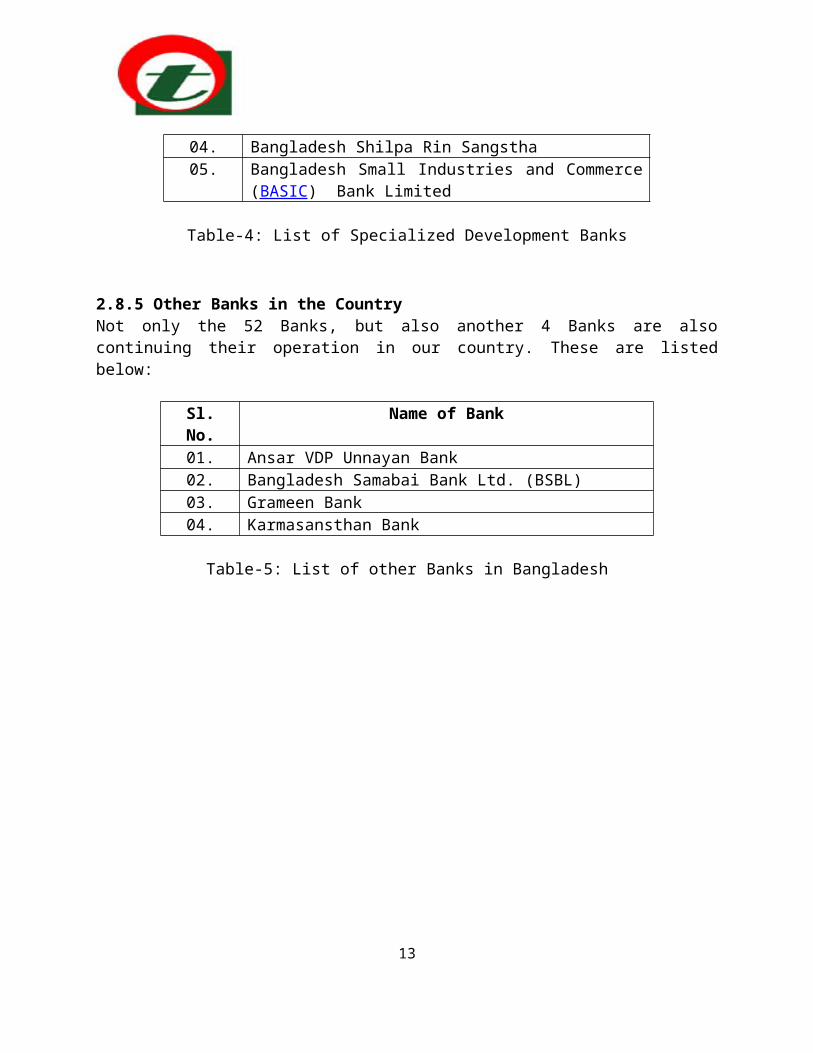

01. Bangladesh Krishi Bank 02. Rajshahi Krishi Unnayan Bank 03. Bangladesh Shilpa Bank

12

04. Bangladesh Shilpa Rin Sangstha 05. Bangladesh Small Industries and Commerce

(BASIC) Bank Limited

Table-4: List of Specialized Development Banks

2.8.5 Other Banks in the CountryNot only the 52 Banks, but also another 4 Banks are alsocontinuing their operation in our country. These are listedbelow:

Sl.No.

Name of Bank

01. Ansar VDP Unnayan Bank 02. Bangladesh Samabai Bank Ltd. (BSBL) 03. Grameen Bank 04. Karmasansthan Bank

Table-5: List of other Banks in Bangladesh

13

3.0 Background of Trust Bank Limited

Trust Bank Ltd. is a private, commercial, scheduled Bank, whichobtained license from Bangladesh Bank on July 15, 1999. PresentlyArmy Welfare Trust is the major shareholder. The authorizedcapital of the Bank is Taka two thousand million and paid-upcapital of Taka five hundred million. Public shares are expectedto be floated in the near future. The Bank was formallyinaugurated and listed as a scheduled Bank on November 1999.

The idea of setting up a Bank by Bangladesh Army was firstconceived in 1987 and on November 29, 1999 the first branch ofTrust Bank Ltd came into operation

Composition of the Board of TBL consists of Ex-officio Directorsof in-service senior Army personnel, with the Chief of Army Staffas its Chairman and the Adjutant General as its Vice-Chairman.

Trust Bank Ltd. having a spread network of 27 branches acrossBangladesh and plans to open few more branches to cover theimportant commercial areas in Dhaka, Chittagong, Sylhet and otherareas in 2013. The Bank sponsored by the Army Welfare Trust(AWT), is first of its kind in the country with a wide range ofmodern corporate and consumer financial products. Trust Bank Ltd.has been operating in Bangladesh since 1999 and has achievedpublic confidence as a sound and stable Bank.

In order to provide up-to-date information on the bank atfingertips to the trade and business communities of the world,their own IT team has developed a E-mail address and a web pagefor the bank. It can be accessed to under the domain: [email protected] and www.trustbankbd.com

In addition to ensuring quality, Customer services related togeneral banking the bank also deals in Foreign Exchange

14

transactions. In the mean time, the bank has extended creditfacilities to almost all the sector of the country’s economy. Thebank has plans to invest extensively in the country’s industrialand agricultural sectors in the coming days.

It has also plans to promote the agro-based industries of thecountry. The bank has already participated in syndicated loanagreement with other banks to promote textile sectors of thecountry. Such participation would continue in the future forgreater interest of the overall economy. Keeping in mind theclient’s financial and banking needs the bank is engaged inconstantly improving its services to the clients and launchingnew and innovative products to provide better services towardsfulfillment of growing demands of its customers.

3.1 Vision Statement of Trust Bank Limited

To build a sustainable and respectable financial

institution.

To be a leading Commercial Bank, with a social focus,

assisting in the economic development of the country.

The Profit of the bank used for the Socio-economic

development of the members of the Bangladesh Army and

thereby the nation as a whole.

3.2 Mission Statement of Trust Bank Limited

Achieving sound and profitable growth in Assets &

Liabilities, with focus to maintain non-performing assets at

acceptable levels.

15

To build long-lasting, credible and mutually dependable

relationships with customers.

Efficiently managing interest and operating costs.

To excel in rendering superior customer service.

To be the preferred employer among Banks in Bangladesh.

3.3 Objectives of TBL

To earn and maintain CAMEL rating strong.

To establish relationship banking and service quality

through development of Strategic Marketing Plan.

To remain one of the best banks in Bangladesh in terms of

profitability and asset quality.

To introduce fully automated systems through integration of

Information Technology.

To ensure an adequate rate of return on investment.

To keep risk position at an acceptable range (including any

off balance sheet risks)

To maintain adequate liquidity to meet maturity obligations

and commitments.

To maintain a healthy growth of business with desired image.

16

To maintain adequate control systems and transparency in

procedures.

To develop and retain a quality work force through an

effective Human Resources Management System.

To ensure optimum utilization of all available resources.

To pursue an effective system of Management by ensuring

compliance to ethical norms, transparency and accountability

at all levels.

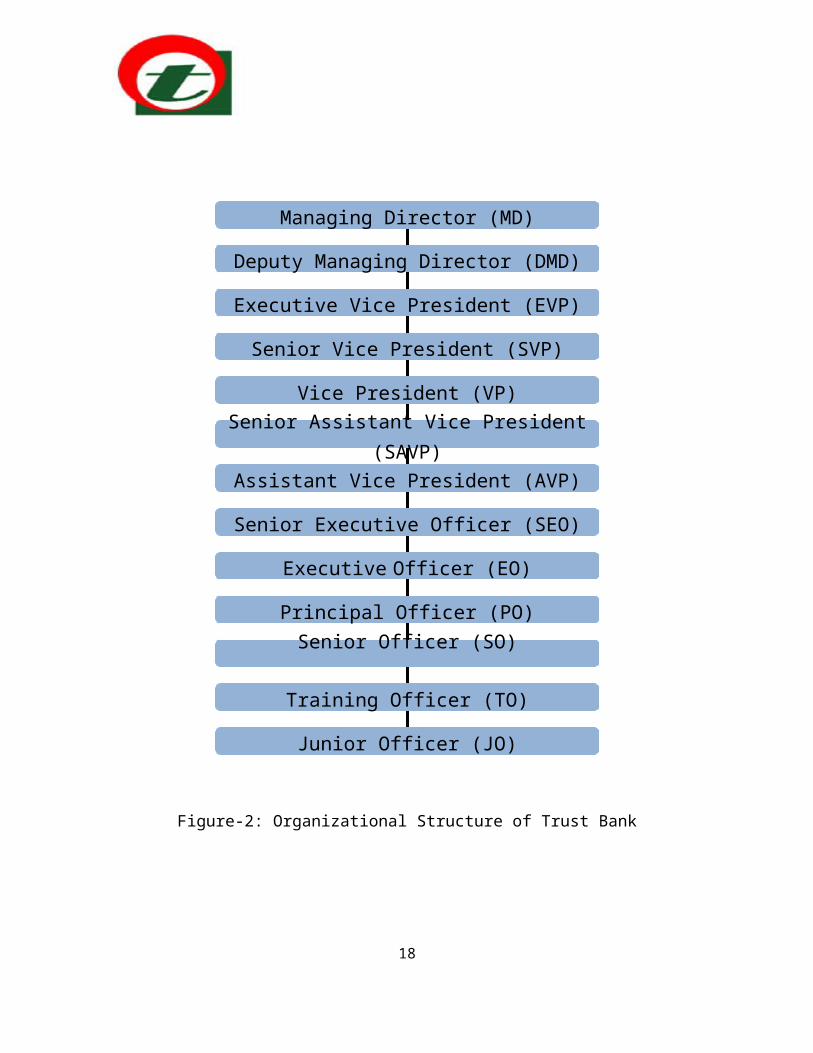

3.4 Organizational Structure of Trust Bank

17

Managing Director (MD)

Deputy Managing Director (DMD)

Executive Vice President (EVP)

Senior Vice President (SVP)

Vice President (VP)Senior Assistant Vice President

(SAVP)Assistant Vice President (AVP)

Senior Executive Officer (SEO)

Executive Officer (EO)

Principal Officer (PO)Senior Officer (SO)

Training Officer (TO)

Junior Officer (JO)

Figure-2: Organizational Structure of Trust Bank

18

3.5 Corporate Culture

Employees of Trust Bank share certain common values, which helps to create a TBL culture.

The client comes first.

Search for professional excellence.

Openness to new ideas &new methods to encourage creativity.

Quick decision‐making.

Flexibility and prompt response.

A sense of professional ethics

3.6 Nature of Business

The Trust Bank Ltd offers full range of banking services that include:

Deposit banking

Loans & advances

Export

Import

Financing inland

International remittance facilities

19

The bank offers a full scale commercial banking includes:

Foreign Exchange transactions

Personal

Credit

Consumer & Corporate Banking

3.7 Corporate Information at a Glance

Banking License received on : 15th July. 1999

Certificate of incorporation received on : 17th June 1999

Certificate of Commencement of business received on : 17th June 1999

First branch licenses on : 9th August 1999

Formal inauguration on : 29th November 1999

Sponsor Shareholders : Army Welfare Trust

SWIFT Code:

Head Office: 36,Dilkusha C/A (2nd, 16th, & 17th Floor Dhaka-1000 )

Phone: 9570261,9570263,9572012-3

Number of Branch : 37

Website: www.trustbankbd.com

20

4.0 General Description of Each Task Completed During Internship

During my practical internship training I was placed NationalBank Limited Shahjalal Upashahar Branch, Sylhet. From this branchI have learned a lot about General Banking activities of theBanks. General Banking consists of different sections. These areaccount opening section, book issue, Remittance section, creditmanagement, clearing and bill section, cash section etc.

4.0.1 Account Opening

A bank has to maintain different types of accounts for differentpurposes. Trust Bank limited offers the general deposit productsin the form of various accounts.

21

4.0.1.1 Savings Account (SB)

Savings bank deposit is popular account maintained in Banks.The different matters relating SB account are described in thefollowing discussion. The summary of the rules and regulationsto open a savings account is as follows:-

Any person or persons of more than 18 years having sound

mind can open and operate this account singly or jointly.

In case of a minor (a person below 18 years), a guardian can

open and operate this account on his or her behalf.

Clubs, Societies, Sole Proprietorship firms, Partnership

firms, Limited Companies either public or private and other

similar organization are eligible to open such account.

More than one account cannot be opened in the same name.

A minimum initial deposit of Tk. 1000.00 is required to open

such account. And the interest rate of SB account is 7.00%

Money will be withdrawn through cheque. Withdrawal cannot be

more than twice a week and generally the amount will not be

more than 25% of the balance available, subject to maximum

Tk. 20,000.00.

In case of closure of any account, the bank deducts Tk.

100.00 as closing charge.

4.0.1.2 Current Account and Short Term Deposit Account (STD)

22

Most businessmen maintain Current Deposit accounts in order tomake their daily business activities. This account’s funds changemost frequently than any other accounts because customers use towithdraw and deposit funds in regular basis. The summary of therules and regulations to open a current account & short termdeposit (STD) account as follows:-

A minimum deposit of Tk. 5000.00 is needed to open a current

account.

The bank charges an incidental charge of Tk 150.00 for every

six (6) months for the maintenance of the account.

In case of the closure, the bank charges Tk. 100.00 as

closing charge of the account.

Withdrawal of money is allowed only through the leaves of

the cheque book issued by the bank.

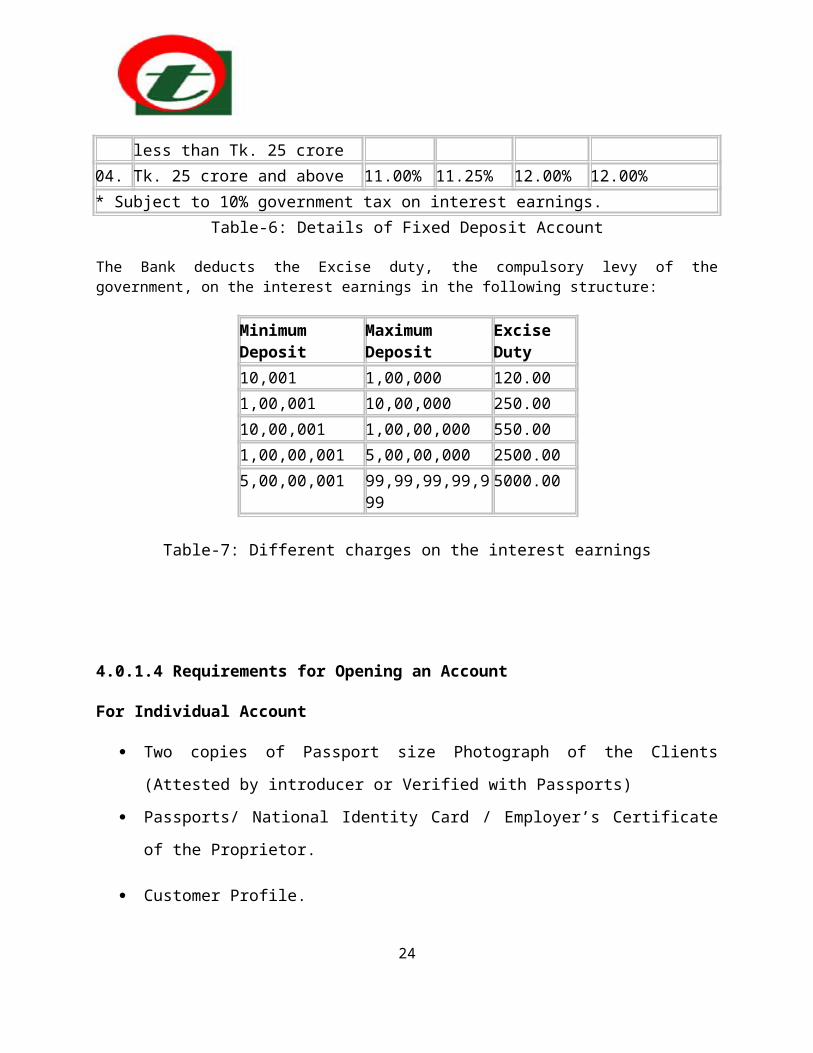

4.0.1.3 Fixed Deposit Account

The bank allows people to keep their idle money secured and profitableas Fixed Deposit. The interest rate that the bank offers to the fixeddepositors is as follows:

SL No

Amount or Slab wise Deposit

Interest rate on Deposit: Maturity wise but based on amount1 Month 3 Months6

months1 Year and above

01. Any amount but less thanTk 5 crore.

10.00% 11.50% 12.00% 12.00%

02. Tk 5 crore & above but less than Tk. 10 crore.

11.00% 11.25% 12.00% 12.00%

03. Tk 10 crore & above but 11.00% 11.25% 12.00% 12.00%

23

less than Tk. 25 crore04. Tk. 25 crore and above 11.00% 11.25% 12.00% 12.00%* Subject to 10% government tax on interest earnings.

Table-6: Details of Fixed Deposit Account

The Bank deducts the Excise duty, the compulsory levy of thegovernment, on the interest earnings in the following structure:

Minimum Deposit

Maximum Deposit

Excise Duty

10,001 1,00,000 120.001,00,001 10,00,000 250.0010,00,001 1,00,00,000 550.001,00,00,001 5,00,00,000 2500.005,00,00,001 99,99,99,99,9

995000.00

Table-7: Different charges on the interest earnings

4.0.1.4 Requirements for Opening an Account

For Individual Account

Two copies of Passport size Photograph of the Clients

(Attested by introducer or Verified with Passports)

Passports/ National Identity Card / Employer’s Certificate

of the Proprietor.

Customer Profile.

24

Transaction Profile.

Photograph of the Nominee(s) attested by the account holder.

TIN Certificate.

Introducer.

For Joint Account

Passports/ National Identity Card / Employer’s Certificate

of the Proprietor.

Two copies of Passport size Photograph of the Clients.

Customer Profile.

Transaction Profile.

Photograph of the Nominee(s) attested by the account holder.

TIN Certificate.

Relationship between the account holders.

Purpose of opening of the Joint account.

Introducer.

For Proprietorship Account

Two copies of Passport size Photograph of the proprietor

(Attested by introducer or Verified with Passports)

25

Passports/ National Identity Card / Employer’s Certificate

of the Proprietor.

Customer Profile.

Transaction Profile.

Photograph of the Nominee(s) attested by the account holder.

TIN Certificate.

Trade License.

VAT Registration (if available)

For Partnership Concern

Two copies of Passport size Photograph of each partner

(Attested by introducer or Verified with Passports)

Passports/ National Identity Card.

Company Profile.

Transaction Profile of the concern.

Personal Profile of the partners.

Photograph of the Nominee(s) attested by the account holder.

TIN Certificate.

Trade License of the concern.

VAT Registration (if available)26

Relationship between the partners.

Attested Photocopy of the Partnership Deed (Deed on Tk

1000.00 stamp)

Resolution regarding opening and operation of the account.

For Company Account

Attested or Certified copy of the Memorandum and Articles of

Association.

Certificate of Incorporation.

Certificate of Commencement of Business.

Two copies of Passport size Photograph of all Directors

(Attested by introducer or Verified with Passports)

Passports/ National Identity Card of all Directors of the

company.

Company Profile.

Transaction Profile of the company.

Personal Profile of all Directors as per enclosed sheet in

the Company’s letterhead pad.

TIN Certificate.

Trade License.

27

VAT Registration (if available).

Board resolution of the company regarding opening and

operation of the account.

For Private School/College/Madrasa

Attested or Certified copy of the Constitution.

Registration Certificate.

List of all Executive Members (as per enclosed format).

Two copies of Passport size Photograph of the account

operators (Attested by introducer or Verified with

Passports)

Passports/ National Identity Card of the account operators.

Personal Profile of all members of the governing body and

Managing Committee.

Board resolution regarding opening and operation of the

account.

For NGO/ Club-Society/Co-operative Account

Registration Certificate from the Joint Stock Company/

Ministry of Social Welfare.

List of all Executive Members (as per enclosed format).

28

Board resolution as per Memorandum regarding opening and

operation of the account.

Attested or Certified copy of the Constitution/Bylaws.

Two copies of Passport size Photograph of all Members

(Attested by introducer or Verified with Passports)

Passports/ National Identity Card of all Members.

Profile of the Firm.

Minor’s Account

Putting the word “MINOR” after the title of the account(with red color).

Recording of the special instruction of operation of theaccount.

The AOF is to be filled in and signed by either the parents orthe legal guardian appointed by the court of law and not by theminor.

“No Objection Certificate” from the Ministry of Social Welfare.

4.0.2 Issuing Cheque Book to the Customer

4.0.2.1 Issue of fresh checkbook

A customer who opened a new a/c initially deposits minimum

required money in the account.

The account opening form is sent for issuance of a

chequebook

29

Respected Officer first draws a chequebook

Officer then sealed it with branch name.

In-charge officer enters the number of the cheque Book in

Cheque Issue Register.

Officer also entry the customer’s name and the account

number in the same Register.

Account number is then writing down on the face of the

Cheque Book and on every leaf of the Chequebook including

Requisition Slip.

There is a special technique to sign every leaf of the

chequebook with the help of carbon paper. So officer’s

signature prints the reverse side of the leaf.

The name of the customer is also written down on the face of

the Chequebook and on the Requisition slip.

4.0.2.2 Issue of Duplicate checkbook

Duplicate checkbook instead of lost one should be issued onlywhen an A/C holder personally approaches the Bank with anapplication Letter of Indemnity in the prescribed Performaagreeing to indemnify the Bank for the lost checkbook. Freshcheck Book in lieu of lost one should be issued afterverification of the signature of the Account holder from theSpecimen signature card and on realization of required Exciseduty only with prior approval of manager of the branch. Checkseries number of the new checkbook should be recorded in ledger

30

card and signature card as usual. Series number of lost checkbookshould be recorded in the stop payment register and cautionshould be exercised to guard against fraudulent payment.

4.0.2.3 Issue of New Cheque book (for old account)

All the procedure for issuing a new Chequebook for old account issame as the procedure of new account. Only difference is thatcustomer has to submit the requisition slip of the old Chequebookwith date, signature and his/her address. Computer posting isthen given to the requisition slip to know the position ofaccount and to know how many leaf/leaves still not used. Thenumber of new Chequebook is entered on the back of the oldrequisition slip and is signed by the officer.

4.0.2.4 Procedure of issuance of a new chequebook

If the cheque is handed over to any other person then the accountholder the bank addressing the account holder with details of theChequebook issues an acknowledgement slip. This acknowledgementslip must be signed by the account holder and returned to thebank. Otherwise the bank will not honor any cheque from thischequebook. At the end of the day all the requisition slips andapplication forms are sent to the computer section to give entryto these new cheque.

4.0.3 Cash/Accounts

Cash section is a very important and busy section of TBLUpashahar Branch, Sylhet. So this section should be handled withextra care. There are two cash officer in this branch as cashreceiving officer and cash payment officer. Operation of thissection begins at the start of the banking hour. Cash officerbegins his transaction with taking money from the vault, which isknown as the opening cash balance. There are several activities

31

under this section such as- cash payment cash received, cashsoling, vault maintenance, posting of information in computer.

4.0.3.1 Cash Payment

Clients may give cheque to other party, bank, self-drawn, for DDissue, or anyone. The payment officer makes the payment. He justcollects any kind of instrument, which verified by the authorizedofficer i.e. signature of the drawer should be, verified andmakes payment. It should be written in the cash payment scrollregister and initiated or signed by authorized officer. Thedenomination is written in the register and also backs side ofthe cheque or other instrument. Then give cash payment seal withdate on that instrument, write the amount in figure and in wordby red ink and denomination on the back of the instrument. Aftercompleting all these it should be posted in the computer by dataentry officer. At the end of the day these scroll numbers of theregister will be compared to ensure the correctness of theentries.

4.0.3.2 Cash Sorting

Receiving amount is sorted i.e. make ail money's edge one sideand scrutinize all the money, one side money is good conditionand other side money is bad condition which will he sent toBangladesh Bank. And also find out the duplicate note.

After that make bundle of money and count by counter machine

Making hole on the bundle for stitch.

Stitch and bind bundles with cotton by using bank's receipts.

32

After this processing money bundles should be kept in vault because there is permission by insurance that counter amountis not above 5 lac.

Lose money should he count and match with cash balance book.

4.0.4 Remittance & Bills

Local remittance is one of the main components of generalbanking. The components of local remittance are-

Telegraphic Transfer (TT)

Demand Draft issue (DD)

Saving Certificate Issue (Sanchaypatra issue),

Pay order.

Works done in the remittance and bill section-

Issue and payment of Pay Order, Pay Slip, Demand Draft, etc.

Execution of Inward and Outward Telegraphic Transfer

Non client services like T.T. and Pay Order

Follow up with clients

Internal and local collection of cheque and bills.

4.0.4.1 Telegraphic Transfer (TT)

It is an order from the issuing branch to the drawee bank /branch for payment of a certain sum of money to the beneficiary.The payment instruction is sent by telephone and funds are paidto the beneficiary through his account maintained with the draweebranch or through a pay order if no account is maintained withthe drawee branch. No charge is required for TT.

33

4.0.4.2 Demand Draft (DD) Issue

Sometimes customers use demand draft for the transfer of moneyfrom one place to another. It is must need for sending moneyoutside Dhaka city. For getting a demand draft, customer has tofill up an application form. The form contains date, name andaddress of the applicant, signature of the applicant, chequenumber (if cheque is given for issuing the DD), draft number,name of the payee, name of the branch on which the DD will bedrawn and the amount of the DD. The form will be duly signed bythe applicant and by the authorized officer. TBL charges 15%commission on the face value of DD as service charge.

4.0.4.3 Shanchaya Patra

Shanchaya patra is received from Bangladesh bank (BB). Peoplepurchasing these bonds by depositing money in this branch andpayment are made on maturity to customers from this branch only.Every transaction is reported to Bangladesh bank. In case ofissuance, report to be reached to BB within 48 hours, otherwisepenalty is imposed. Money is realized from BB after makingpayment to customer.

Various types of Shanchaya Patras are sold here. They are asfollows:

5 years Bangladesh Bank Shanchaya patra (5 BSP):

Duration of this Shanchaya patra is 5 years. Any person whopurchases this Shanchaya patra can withdraw his/her interest onlyafter 5 years at the time of maturity along with capital. Anysingle individual can buy Bangladesh Bank Shanchaya patra for upto TK. 50 lac. And jointly can buy for up to TK.1 Crore. InterestRate: 12.5% after 5 years.

Month Profit Based Sanchaya patra(3MPBSP):

34

Duration of this Shanchaya patra is 3 years. Any person whopurchases this Shanchaya patra can withdraw his/her interest inevery 3 month but capital can be withdrawn after the maturityperiod. Any single individual can buy 3 MPB Shanchaya patra up toTK. 50 lac. And jointly can buy for up to TK.1 Crore.

Interest Rate: 11.5% after 3 year

After every three (03) month 2,875/= Tk. will be given against 1Lac. Taka as interest.

Pensioner’s Sanchaypatra

Duration of this Shanchaya patra is 5 years. Any person (Retired)who purchases this Shanchaya patracanwithdraw his/her interest inevery 3 month but capital can be withdrawn after the maturityperiod. Any single individual can buy Pensioner’s Sanchaypatra upto TK. 30 lac.

Interest Rate: 12.50% after 5 year

After every three (03) month 3,125/= Tk. will be given against 1Lac. Taka.

4.0.4.4 Pay Order

For issuing a pay order, the client has to submit an applicationin the prescribed form. This form should be properly filled upand signed. The procedure of the issuing pay order is similar tothat of the Telegraphic transfer. For issuing pay order TBLcharges commission on the following rate—

Tk. 20/- for non-customers/clientsPay Order[Local] cancellationTk. 20/- per instrument Issuance of Duplicate Instrument Tk. 100/- per instrument plus stamp charges for indemnity at actual.

35

4.0.4.5 Payment of Pay Order

The pay order is presented to the bank either through clearanceor for credit to the client’s account. While payment, relativeentry is given in the pay order register with the date ofpayment.

In case of collecting DD, P0, PS following things is to becarefully checked

Instrument of TBL

Crossing Seal

Clearing Seal

Branch Name

Amount same in word & figure

Signature verification

Avoid the stop order PO, DD

Test key verification. Every TT must have test key.

DD over Tk.50000/- must have test key

Maintenance of PO/TT/DD issue & payable books

Balancing at the end of the month.

4.0.5 Products & Schemes

36

4.0.5.1 Deposit Products

Current Deposit Account

Savings Deposit Account (interest calculated on monthly

minimum balance of Tk.2000 and above)

Fixed Deposit (3 months to 3 years term)

Savings Certificate

Trust Smart Savers Scheme(TSS)

Trust Digoon Laav Scheme(TDLS)

Trust Money Making Scheme(TMMS)

Trust Education Scheme(TES)

4.0.5.2 Investment Products

Corporate Financing

Trust Consumer Durable Scheme (TCDS)

Trust Marriage Loan Scheme (TMLS)

Trust Car Loan Scheme (TCLS)

Trust House Building Loan Scheme (THLS)

Trust Micro Credit for Renovation & Reconstruction of

Dwelling Houses

4.0.5.3 International Trade

37

International Banking

Private Foreign Currency Accounts

Non Resident Foreign Currency Deposit Account

Resident Foreign Currency Deposit Account

Travelers’ Endorsement (Cash and Travelers Cheque)

Remittance of Foreign Currency

Import and Export Transaction

Foreign Exchange Dealing

Purchase of Foreign Currency Drafts, Cheque, Travelers

Cheque

Wage Earner’s Development Bond

4.0.6 Other Services

There are two services offered by the bank exclusively ondistinguishable terms and conditions. The aforesaid services are-

4.0.6.1 Locker Service

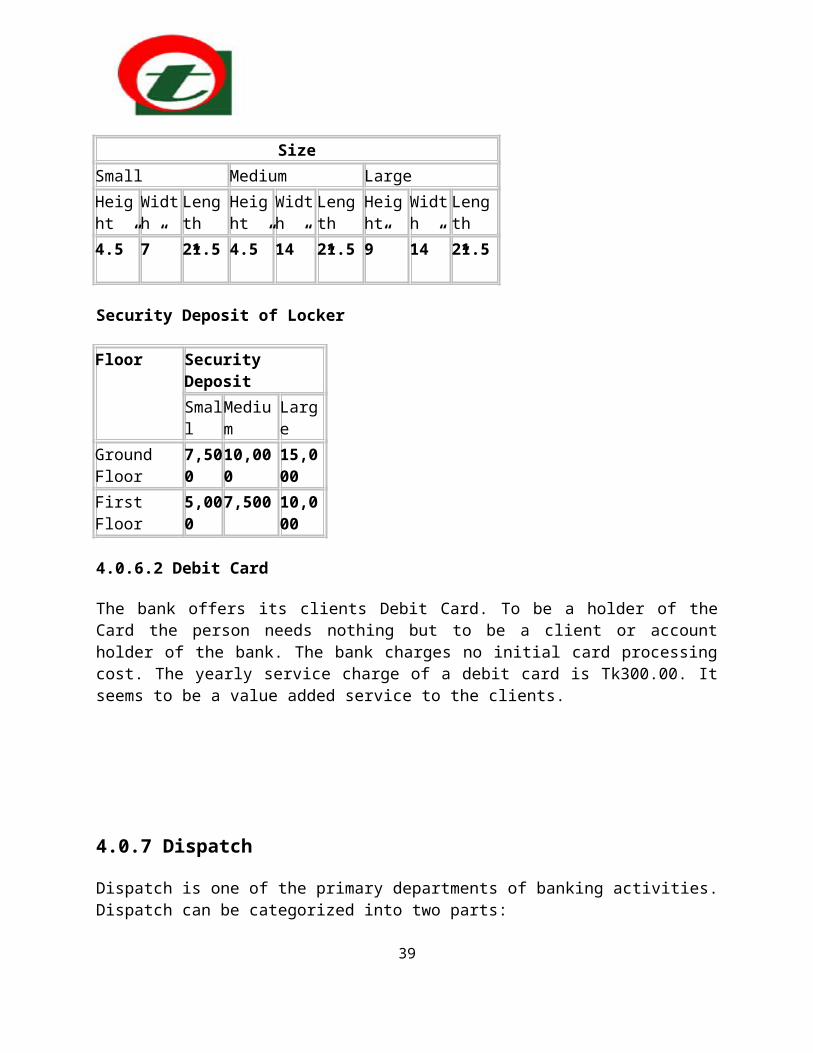

There are some more than 500 lockers at the Dhanmondi Branch ofTBL. The lockers are now rented on Security Deposit Basis insteadof yearly or monthly rental Basis. The lockers are allotted onmost flexible term and meager Security Deposit refundable at thetime of closing the locker.

Size of Locker

38

SizeSmall Medium LargeHeight

Width

Length

Height

Width

Length

Height

Width

Length

4.5” 7” 21.5”

4.5” 14” 21.5”

9” 14” 21.5”

Security Deposit of Locker

Floor Security DepositSmall

Medium

Large

Ground Floor

7,500

10,000

15,000

First Floor

5,000

7,500 10,000

4.0.6.2 Debit Card

The bank offers its clients Debit Card. To be a holder of theCard the person needs nothing but to be a client or accountholder of the bank. The bank charges no initial card processingcost. The yearly service charge of a debit card is Tk300.00. Itseems to be a value added service to the clients.

4.0.7 Dispatch

Dispatch is one of the primary departments of banking activities.Dispatch can be categorized into two parts:

39

4.0.7.1 Inward Register

In inward register all the incoming documents are received andregistered according to date. Then, Documents are transferred todifferent departments according to their destiny.

4.0.7.2 Outward Register

The documents, which are needed to mail to different branches ofTBL in Bangladesh or outside Bangladesh, are registered inoutward register and mailed by courier or by post, which one issuitable.

4.0.8 International Banking

Trust Bank Limited, with its wide correspondent relationship withmajor banks in the world is totally capable to meet your needs offoreign currency transactions and foreign trade services. You canopen and maintain Accounts in foreign currencies like US Dollar,Pound Sterling, and Japanese Yen and even in Euro with us. Withits own Dealing Room, TBL is able to offer competitive ExchangeRate for all major currencies of the world.

FA Account (Foreign Nationals) FC Account (Bangladeshi Nationals)

4.0.8.1 Foreign Exchange

Foreign exchange means the exchange of currency in terms of goodsfrom one country to another. This is the most well-known andwell-organized business uniform in world business. Foreignexchange mainly has two parties:

4.0.8.2 Import Operations

There are different other parties who are also related to thisforeign exchange process. But Bank is the most important of allthe other parties. Bank works as intermediary in case of foreign

40

exchange. So, we can say that the foreign exchange is nothing butthe combination of export and import in international platform.

If an importer wants to buy goods from foreign countries he hasto communicate with the exporter or he may also communicatethrough indenting firms.

4.0.8.3 Export Operations

For becoming an Exporter a person needs

1. Current A/C in TBL2. ERC (Export Registration Certificate) issued by CCI & E

(Chief Controller of Import & Export).

3. Permission from sponsoring Authority such as Board ofInvestment for industries, Department of Textile forgarments etc.

4. Traders Association’s certificate

5. VAT (Value Added Tax) & TIN (Tax Identification Number)certificates.

4.0.9 Credit

Credit is an arrangement whereby bank acting at the request andon the instructions of a customer or on its own behalf to make apayment to or to the order of a third party or is to accept andpay bills of exchange drawn by the beneficiary. In an economybanks play the role of an intermediary that channels resourcesfrom the surplus group to the deficit group. So, one of the corefunctions of Commercial banks is to sanction credit facility toits customers as per requirement. Trust Bank Limited Mission isto actively participate in the growth and expansion of our

41

national economy by providing credit to variable borrowers inmost efficient way of delivery and at a competitive price.

Bank can lend up to 15% of its capital fund without having anyapproval from Bangladesh bank. The maximum limit can go up to100% of the bank’s capital fund. Trust Bank Limited complies withthe ceiling set by Bangladesh Bank.

4.0.9.1 Types Of Loans And Advances Offered By Trust Bank

Basically Trust Bank offers both funded and non-funded creditfacilities.

4.0.9.2 Funded Loan Facility

Any type of credit facility which involves direct outflow ofBank’s fund on account of borrower is termed as funded creditfacility, the funded facilities of loans and advances are:

4.0.9.3 Cash Credit

Cash credit is a continuous credit facility usually provided forworking capital fund requirements purpose of the customer. Cashcredit is generally given to traders, Industrialist for meetingup their working capital requirements. Cash Credit can be givenon Hypothecation of goods or pledge. Trust Bank only practicesCash Credit on Hypothecation.

4.0.9.4 Features of Cash Credit

A certain limit of credit amount is set at the time ofinitiation of Cash Credit facility.

An expiration date is set, which is not more then one year.

The drawings are subject to drawing power.

A service charge, which in effect an interest charge isnormally made as a percentage of the value of purchases.

42

The primary security of Cash credit facility is stock ofgoods, which maybe hypothecated to Trust Bank as collateral.

4.0.9.5 Over Draft

Over draft facility is also a continues loan arrangement on acustomer’s current account permitting him to overdraw up to acertain approved limit for an agreed period. Here the withdrawalof deposits can be made any number of times at the convenience ofthe borrower, provided that the total overdrawn does not exceedthe agreed limit.

Customer can return any amount at any time within the pre-fixedtime of the facility. Turn over of an OD facility is the mostimportant phenomenon on which renewal of the facility depends.Over draft facility is given to the businessman for financingworking capital requirement and high net worth individual toovercome temporary liquidity crisis.

4.0.9.6 Term Loan

Term loans are given to finance the acquisition of capital asset.Loan agreements often contain restrictive covenant and loan isrepayable in accordance to amortization schedule. Collateral ismust for term loan.

Under term loan there are three categories:

Short term loan – less then 1 year falls with this category Midterm – this loan facility is extended formore then 1 year

but less the 3 year. Trust Bank encourages midterm loan.

Long term – tenure of long term loan is more then 5 years

Inland Bill Purchased (IBP)

House Building Loan

Marriage Loan43

Car loan (Staff & Others)

Consumer Durable Scheme (CDS)

Loan Against Trust Receipt (LTR)

Any Purpose Loan

4.0.9.7 Non-funded facilities

Non-funded facilities also known as “contingent facilities” are thosewhere bank fund is not required directly. A non-funded facilitycan turned to a funded facility as per situation creates. Bankreceives commission rather than interest income by providing non-funded facilities.

4.0.9.8 Guarantee

Trust Bank offers guarantee for its reliable and valuablecustomer as per requirements. This is also a Credit facility incontingent liabilities from extended for participation indevelopment work like supply of goods and services.

4.0.9.9 Features of Bank Guarantee

It is a written document on non-judicial stamp Expiry date is mentioned specifically with other terms and

conditions

Trust Bank receives commission quarterly @ 0.50% of theguaranteed amount.

4.0.9.10 Credit Planning at different level of Trust Bank

Credit Planning implies estimating first the total lend ableresources that are likely to be available within the given periodand then allocating the same amongst various alternative uses inconformity with national plan and priorities.

44

Necessity of credit planning in context:

Demand for Credit is much more than its supply. Providing credit at right person at right time at right

quantity.

Getting maximum output as a result of credit allocation.

Ensuring the best of alternative investment opportunities

4.0.10 Modes of Charging Securities by Trust Bank

Securities are the cover against loans and advances. On the otherhand it ensures recovery of loans and advances from the borrowerswho offer properties to the lending banker as security.Properties are converted into securities. But for conversion someconditions are to be full filled as required by the Trust Bankand these are as follows:

a) The properties are to be acceptable to the lending bankers forsecurities.

b) Creation of the charge on the concerned properties.

The Acceptability of properties as securities are mainly

depends on:

Value of property must cover the loan amount with margin.

Consideration of different qualities of properties

Free from credit restrictions of Bangladesh Bank (if any).

Within the credit policy of the bank.

There are two types of securities i.e. primary and collateral.

45

Modes of Creation of charges are of different types. These

are dependable on the basis of nature of loans and advances

and nature of properties for securities.

Charges may be of different types like legal Charge,

Equitable charges, fixed charges, floating charges etc.

Following are the different modes of creation of charges by thebank:

Pledge

Hypothecation

Mortgage

Lien

4.0.10.1 Pledge

When goods and produces are handed over to the lending banker bythe trader or manufacturer who borrow against those goods andproduces for short term i.e. for working capital. But if anygoods and produces are kept with the bank for security purposeswill not be treated as pledge. In otherwise it is the Bailment ofgoods as per Bailment of goods act. In case of Pledge, controland possession of goods and produces will remain with bank butownership will remain with borrower. There will be a storehouseeither of banks or rented for safe keeping of goods. Insurance ofpledged goods are compulsory. And all related expenses would beborn by borrower.

4.0.10.2 Hypothecation

Hypothecation is just opposite of pledge. When a borrowerownership, control and possession of trading goods but legal

46

right and indirect control is created by lending banker forsecurity against short term advances i.e. Equitable charge iscreated is known as Hypothecation. Just control and possession oftrading goods are kept under borrower. In these types ofsecurities lending banker generally asks for collateralsecurities. This type of mode of securities is allowed only forthe case of first class borrowers.

4.0.10.3 Mortgage

When bank create charge on immovable property in the form ofmortgage against any lending to the borrower. Therefore amortgage is a transfer of interest of a specific immovableproperty. The immovable property means land and the propertyattached to land but not grass, trees and crops. Mortgage is tobe created for securing loan or performing any contract. Andthere will be a Mortgagor, Mortgagee, Mortgaged Property andMortgage deed.

4.0.10.4 Lien

A lien is defined as the right to retain property belonging to adebtor until he has discharged a debt due to the retainer of theproperty. Lien may be of two types, General Lien and ParticularLien.

A particular Lien confers a right to retain a property in respectof a particular debt involved in connection with a particulartransaction.

But a General Lien confers a right to retain goods not only inrespect of a debt incurred in connection with a particulartransaction but also in respect of any general balance arisingout of the general dealing between two parties.

Banker’s Lien is defined as an implied pledge. An ordinary liendoes not imply a power of sale, but a pledge implies a power ofsale. A banker’s right of sale is generally regarded as extending

47

only to fully negotiable instrument, with regard to othersecurities.

4.1 Application of Knowledge Gained During BBA Program

There were lots of courses included in the BBA course. I havelearned and acquired a lot of knowledge from these courses. Notonly the text books but also the other curriculum activities likelectures from the teachers, presentation, viva, assignment etc.helped me much to be myself confident enough. The following arethe most important areas which helped me most:

During the BBA program I had to prepare and submit lots ofassignments for the different courses. It gives me a clearidea about how to arrange format the paper. Finally when Iwas preparing my internship report it helped me in variousways.

Different course lectures also helped me to understand andcontinue my job in the bank. Some of them are:

English Language: This course helped me to improvemy ability to speak, listen, read and write, whichhelps me to work in an environment that operatesits activities in English.

Bank management: From this subject lecture I have learndifferent types of risk. Bank risk are capital risk ,credit risk , liquidity risk , market risk , interestrate risk , operating risk , foreign exchange rate risketc.

48

International Business: From this subject lecture Ihave learn international tread, process of LC and import& export.

Principle of accounting: From this subject lecture Ihave learn specially debit and credit. Every task of bankneeded to be Debit and credit.

Organization behaviour: From this subject lecture Ihave learn some special technique to motivate customer,and officer. This is more helpful for me.

Banking and insurance: From this subject lecture Ihave learn different types of account: Saving Account,Current Account, and Fixed Deposit Account. These are themain three types of account. Banks collects deposits bythese types of accounts.

Banking law and practice: From this subject lecture Ihave learn the different rules and regulation of bank.

Business communication: From this subject lecture Ihave learn how to e-mail, write CV, arrange conference,respond the customer e-mail and presentation. In thebeginning I develop CV for internee in the basis offinding knowledge of this subject.

Financial Analysis and Control: From this course lecturesI have understood- Financial statements and reports ofthe bank, it helps me to learn and understandcalculations of different financial statement terms, theproper way to find out the appropriate ratios andcalculate them correctly, the ratio analysis to justifythe financial position of the certain organization.

49

Introduction to Computer Applications: This course helpedme to understand the working procedure of computer, itsdifferent parts and how to deal with them. The placewhere I did my internship was completed computerized.

During the program I had to face viva which made me preparedand feel comfortable to talk to the superiors.

At the end of every semester I had to perform presentations.It helped me to know how to make someone understand mywords. The proper formal way of approach. During myinternship I had to do formal conversation with the co-operatives, customers, managers.

4.2 Recommendations

Giving better customer service, Full computerization of all

activities, Supply of new PC’s in place of old one,

sufficient numbers of PC needed for proper working.

Interior decoration should be introduced for clients

comfort.

The management should impart more emphasis on the

advertisement of the bank in different electronic and

printing media. The Basic goal of the advertisement should

be firstly to make people know and understand that the bank

is universal one and permits any one’s access.

50

Full computerization of the branch will less the time

consumption of manual process. So, that the employees will

able to perform well at the end.

The spread out mechanism of the bank should be faster and

progressive as well. Being established in 1999, the bank has

established only twenty seven branches in eight (8) years.

The mode of extension is much slower than other contemporary

and equivalent banks.

On line banking should be introduced to compete with

multinational banks.

The management should care for the personnel more. At the

recruitment stage, it should go for the best candidate and

after selection the personnel should be allowed with proper

opportunity to be expert on particular task bestowed on

them.

More products of varied interests should be introduced for

the diversified client group.

To enhance the image of the bank and to assume social

responsibility, the bank should engage itself to various

social programs like Scholarship to poor but meritorious

students, Empowerment of the children in abject poverty,

Campaign against dowry and other social evil etc.

51

5.0 Conclusion

Trust Bank limited pursues decentralized management policies and

gives adequate work freedom to the employees. This results in

less pressure for the workers and acts as a motivational tool for

them, which gives them, increased encouragement and inspiration

to move up the ladder of success. The profit earned by the bank

is used to the welfare activities of the Trust. The economic

service of the bank is open to all caste and class of people. The

bank is formatting and accomplishing various welfare projects and

activities for the socio economic infrastructural development of

the country and the active participation to the up gradation of

the comparative feeble class of the society, instead of

accumulating profit. It has also been linked with many foreign

banks to facilitate the foreign currency transfer by the members

of armed forces working in the UN and emigrant Bangladeshi. Trust

Bank Limited has maintained growth in its general banking

business by maintaining and enhancing its relationship with its

clients. The success of Trust Bank limited is largely credited to

its friendly, co-operative approach, understanding the special

banking needs of each and every client and concern for the

benefits and welfare. From the beginning, the prime objective of

52

Trust Bank limited was to increase capitalization, to maintain

disciplined growth and high corporate ethics standard and enhance

the health of the shareholders. So, now Trust Bank limited is in

leading position in Financial Institutional sectors in

Bangladesh. The financial performance of the bank in recent years

is pretty well. Moreover, any laxity in operational ground can

considerably be compensated through the cordial services provided

by a staff of talented officers or employees.

53

Copyright © 2022 FDOKUMEN