FtC red Flags and Address Discrepancy rules:

96

A DEALER GUIDE TO THE FTC Red Flags and Address Discrepancy Rules: Protecting Against Identity Theft L50 L50 Driven NADA MANAGEMENT SERIES

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of FtC red Flags and Address Discrepancy rules:

A DeAler GuiDe to tHe

FtC red Flags and Address Discrepancy rules:Protecting Against identity theft

L50L50Driven

NADA MANAgeMeNt ser ies

the National Automobile Dealers Association (NADA) has prepared this management guide to assist its dealer members in being as efficient as possible in the operation of their dealerships. the presentation of this information is not intended to encourage concerted action among competitors or any other action on the part of dealers that would in any manner fix or stabilize the price or any element of the price of any good or service.

this guide explains a Federal trade Commission (FtC) rule that requires automobile dealers and other creditors to develop, implement, and maintain a comprehensive written identity theft Prevention Program. it also addresses a separate FtC rule involving the receipt of notices of address discrepancies from a consumer reporting agency when requesting a consumer report. the guide provides a sample template to assist dealers in preparing their identity theft Prevention Program as well as step-by-step instructions for using the template.

Nothing in the guide is intended as legal advice. the requirements of the laws and rules covered in this guide are too complex and the circumstances of each dealership are too varied simply to adopt our model sample identity theft Prevention Program without proper modifications. in addition, this guide discusses only the federal red Flags and Address Discrepancy rules. it does not discuss state or local law that may impose additional requirements, or other federal laws pertaining to other aspects of identity theft. it is essential that you draft a written identity theft Prevention Program that is appropriate to your dealership and that you have it reviewed by qualified legal counsel. Dealers must be in full compliance with the requirement to have an identity theft Prevention Program in place by November 1, 2008.

Table of Contents

SECTION ONE

InTroduCTIon ...................................................................................................................................................................................1

The Red Flags and Address Discrepancy Rules .....................................................................................................................................1Using this Guide ...........................................................................................................................................................................................2Compliance Requirements Not Covered in this Guide .......................................................................................................................3

THE FTC rEd FLAGS ruLE ..............................................................................................................................................................4

The Basics ......................................................................................................................................................................................................4Appointing a Team to Develop and Implement the ITPP ..................................................................................................................4Identifying “Covered Accounts” ...............................................................................................................................................................5 Application to Commercial Truck Dealers .............................................................................................................................................7Substantive Elements of the ITPP ............................................................................................................................................................7

Identifying Relevant Red Flags ..........................................................................................................................................................8Developing the Means to Detect Red Flags and Verify Identity............................................................................................... 10Developing Policies and Procedures for Responding to Detected Red Flags ........................................................................ 11Developing Policies and Procedures to Update the ITPP ......................................................................................................... 12

Administrative Elements of the ITPP ................................................................................................................................................... 12Training ................................................................................................................................................................................................ 12Overseeing Service Providers .......................................................................................................................................................... 13Board Approval of the ITPP ............................................................................................................................................................ 14Management Oversight ..................................................................................................................................................................... 14Reporting ............................................................................................................................................................................................. 14

THE FTC AddrESS dISCrEPAnCY ruLE ..............................................................................................................................15

Duty to Implement Policies and Procedures to Confirm Identity upon Receipt of Notice from CRA .................................. 15Policies to Furnish Address to Consumer Reporting Agency ........................................................................................................ 16 Application to Commercial Truck Dealers .......................................................................................................................................... 16

FrEQuEnTLY ASKEd QuESTIonS ...........................................................................................................................................17

FTC rEd FLAGS ruLE CoMPLIAnCE CHArT: STEP BY STEP ....................................................................................20

EndnoTES ..............................................................................................................................................................................................22

Driven FTC Red Flags and Address Discrepancy Rules

A DeAleR GuiDe To THe

SECTION TWO

SAMPLE IdEnTITY THEFT PrEVEnTIon ProGRAM (ITPP) ..................................................................................23

AttACHMEnTS

A. Account Identification and risk Assessment WorksheetsInstructions ........................................................................................................................................................................................... 41 Worksheet Template ........................................................................................................................................................................... 43 Example Worksheets (A-I) ................................................................................................................................................................ 44

B. red Flag Identification, detection, and response WorksheetsIntroduction .......................................................................................................................................................................................... 53 Worksheet Template ........................................................................................................................................................................... 55Worksheet Instructions ...................................................................................................................................................................... 56The 26 FTC Example Red Flags: Identification of Methods of Detection and Specific Response .................................... 57Dealer-Specific Red Flags ................................................................................................................................................................. 74Other Dealership-Specific Red Flags .............................................................................................................................................. 81

APPEndICES

A. Sample Clauses to Include in Service Provider Agreements .............................................................................................83

B. Sample Compliance report .......................................................................................................................................................... 85

l50 NADA Management Series driven 1

FTC Red Flags and Address Discrepancy Rules

Many automobile dealers are all too familiar with identity theft. Maybe it’s happened to you:

A customer walks into the showroom, expresses interest in a vehicle, and completes a credit application to learn about financing options. You enter into a deal with the customer, who drives his new vehicle off the lot, and you send the deal over to the finance source that conditionally agreed to take assignment of the credit contract. Later, the finance source notifies you that there is a problem—the customer is not who he claimed to be. By that time, the vehicle is gone, you are on the hook for the loss, and you have only the fraudulent information the customer provided you to track him down. You quickly conclude that you have just been victimized by identity theft to the tune of tens of thousands of dollars.

While this problem remains relatively rare, it is growing, and the victims include not only the dealer but also the unsuspecting individual whose iden-tity has been stolen. Because of these risks, and simply as a good business practice, most dealers already have extensive policies and procedures in place to confirm the identity of their customers. Many businesses and other industries, however, have not been as diligent. As a result, Congress stepped in and enacted several new requirements with which all financial institutions and creditors, including most dealers, must comply.

The red Flags and Address discrepancy rules

According to the Federal Trade Commission (FTC), identity theft “occurs when someone uses your personally identifying information, like your name, Social Security number, or credit card number, without your permission, to commit fraud or other crimes.”1 In an attempt to combat this growing problem, Congress directed the FTC and other federal agencies to issue several new identity theft regulations and guidelines pursuant to the Fair and Accurate Credit Transactions Act of 2003 (FACT Act).2 On November 9, 2007, the FTC and federal banking agencies fulfilled this mandate by issuing their final Red Flags Rule and Address Discrepancy Rule.3

The basic idea behind the Red Flags Rule is that identity theft can be reduced if businesses have policies and procedures in place to spot and prevent it. Recognizing that each business is different, the regulators determined that each business subject to the rule should create its own policies and pro-cedures based on its specific circumstances and then set forth those policies and procedures in a formal written program, known as an Identity Theft Prevention Program (“ITPP” or “Program”).

In short, the Red Flags Rule4 generally requires each dealer who offers or maintains consumer credit, such as installment sale contracts and

InTroduCTIon

SECT ION ONE

A DeAleR GuiDe To THe

2 driven NADA Management Series l50

vehicle leases, and business credit where a rea-sonably foreseeable risk of identity theft exists to the dealer or its customers, to do three things. These are:

1) Identify relevant Red Flags that apply to these types of credit (known as “covered accounts”).

2) Develop reasonable policies and procedures to identify, detect, and respond to those relevant Red Flags.

3) Ensure that those policies and procedures are updated periodically to reflect new risks from identity theft.

Dealers must develop, adopt, and implement a written ITPP that contains these policies and procedures no later than November 1, 2008.

The Address Discrepancy Rule is a separate but related identity theft prevention regulation that also has a November 1, 2008 mandatory com-pliance date. It requires dealers and other users of consumer credit reports to adopt policies and procedures to verify that a consumer report relates to the correct individual when the user receives a Notice of Address Discrepancy from a consumer reporting agency (CRA). Nationwide CRAs must submit this notice to a dealer who orders a con-sumer credit report when the consumer’s address as submitted by the dealer to the CRA substantially differs from the address the CRA has on file for the consumer.

While sharing a similar goal, these new rules should not be confused with another current identity theft prevention rule, the FTC Safeguards Rule under the Gramm-Leach-Bliley (GLB) Act. This ongoing requirement, which took effect in May 2003,

requires dealers and other financial institutions to develop a written program to protect customer information at the dealership from would-be iden-tity thieves. Simply put, the Safeguards Rule seeks to prevent data maintained by the dealer from being stolen, while the Red Flags and Address Discrepancy Rules seek to prevent would-be iden-tity thieves from using stolen data (from whatever source) to fraudulently obtain credit.5

using This Guide

Section One of this guide explains the basic require-ments of the Red Flags and Address Discrepancy Rules, contains answers to frequently asked questions arising under these rules, and provides a step-by-step guide to complying with the Red Flags Rule. Section Two contains a Sample ITPP and Worksheets at Attachments A and B to assist you in developing your ITPP. The appendices con-tain additional templates to assist you with your compliance responsibilities and include Sample Clauses to Include in Service Provider Agreements (Appendix A) and a Sample Compliance Report (Appendix B).

The Sample ITPP is designed to be a starting point from which you can develop your own writ-ten Program specific to your dealership. It is not intended to be a readymade program that you simply reproduce as your own. In fact, because each dealer’s operations are different, it is unlikely that any two written Programs will be the same.

What is a “Red Flag”?

A Red Flag is a pattern, practice, or specific activity that indicates the possible existence of identity theft.

l50 NADA Management Series driven 3

Compliance requirements not Covered in this Guide

Please note that this guide focuses exclusively on the federal requirements under the Red Flags and Address Discrepancy Rules. The guide does not cover the numerous other federal laws and regulations dealing with other aspects of identity theft, such as:

• TheFACTActrequirementsfor

• Respondingtofraudalertsandactiveduty alerts that appear on credit reports

• Disposalofinformationfromconsumercredit reports (also known as the FTC Disposal Rule)

• PreventingtherefurnishingofreportstoCRAs after a claim of identity theft

• Providinginformationtoandhandlingtheclaims of victims of identity theft, includ-ing complying with prohibitions regarding the sale, transfer, and placement for col-lection of certain debts claimed to have resulted from identity theft

• Debitandcreditcardtruncation

• Protectingmedicalinformationinthecredit application process (also known as the Federal Reserve Board’s Regulation FF)

• TheGLBrequirementscontainedintheFTCPrivacy Rule governing the sharing and use of personally identifiable information with third parties

• TheGLBrequirementscontainedintheFTCSafeguards Rule governing the safeguarding of customer information

In addition, the guide does not cover any appli-cable state or local law requirements, such as state “credit freeze” laws placed on creditors by states and localities. ■

4 driven NADA Management Series l50

The Basics

As mentioned above, the idea behind the Red Flags Rule is to require businesses that offer credit to establish policies to detect and thwart identity thieves. The primary goal of the Red Flags Rule in the dealership context is to prevent an identity thief from financing or leasing a vehicle in some-one else’s name.

With that said, however, the Rule applies to much more than just automobile finance or lease transactions. It applies to all consumer finance accounts and may apply to some business accounts throughout the dealership. Indeed, the first requirement under the Rule is for dealers to review all of the different types of accounts they offer to identify those that could be subject to identity theft. After dealers have determined each account type that could be at risk of identity theft, they must then figure out what indicators of identity theft may be relevant to those types of accounts, implement procedures to detect those indicators, determine what reasonable steps the dealer should take if they are detected, and then create a Program that administers and updates these and other steps on an ongoing basis.

With all that in mind, let’s take a closer look at the Rule and the guidance the FTC provides on how to comply.

Appointing a Team to develop and Implement the ITPP

The first step that a dealer should take in com-plying with the Red Flags Rule is to appoint the internal personnel who will be responsible for the dealership’s ITPP.

Board of Directors/Senior Management

The Rule requires the dealership’s board of direc-tors, an appropriate committee of the board, or a designated employee at the level of senior management to be involved in the Program’s oversight, development, implementation, and administration. The oversight function should include assigning specific responsibility for the Program’s implementation, reviewing required compliance reports by staff who are assigned implementation functions (discussed below), and approving material changes to the Program as new identity theft risks emerge.

In addition, the board of directors or an appropriate board committee must approve the initial written Program. If the dealership does not have a board of directors, the approval must come from a designated employee at the level of senior management.

Staff

The Rule contemplates that “staff” will be respon-sible for implementing the Program and drafting and presenting compliance reports to the board.

THE FTC rEd FLAGS ruLE

l50 NADA Management Series driven 5

Team Approach

Thus, establishing the ITPP lends itself to a task force or team approach not only because of the multiple duties involved, but also because the Red Flags Rule envisions a division of responsibility between management and staff.

The approach followed in the Sample ITPP is to appoint a member of senior management as the “Compliance Officer” as early as possible in the process. The Compliance Officer will be responsible for the oversight, development, implementation, administration, and approval of material changes to the Program. There is no requirement to use this title, but the Rule does require a member of senior management (or the board or board com-mittee) to fulfill this role.

To fulfill the staff roles mentioned in the Rule, the Sample ITPP calls for designation of a “Program Coordinator” (or, where necessary, a team of Program Coordinators). Again, the Rule does not require use of this title, but it does require assignment of specific responsibility for comple-tion of these tasks. It may be advisable to name as Program Coordinator the same employee who serves as Program Coordinator under your Customer Information Safeguards Program under the FTC Safeguards Rule.

More important than the actual titles used is the timing of the appointments. The Compliance Officer and Program Coordinator(s) should be identified as early as possible to allow them to be involved in developing and drafting the Program, as well as in administering it after it is completed and approved.

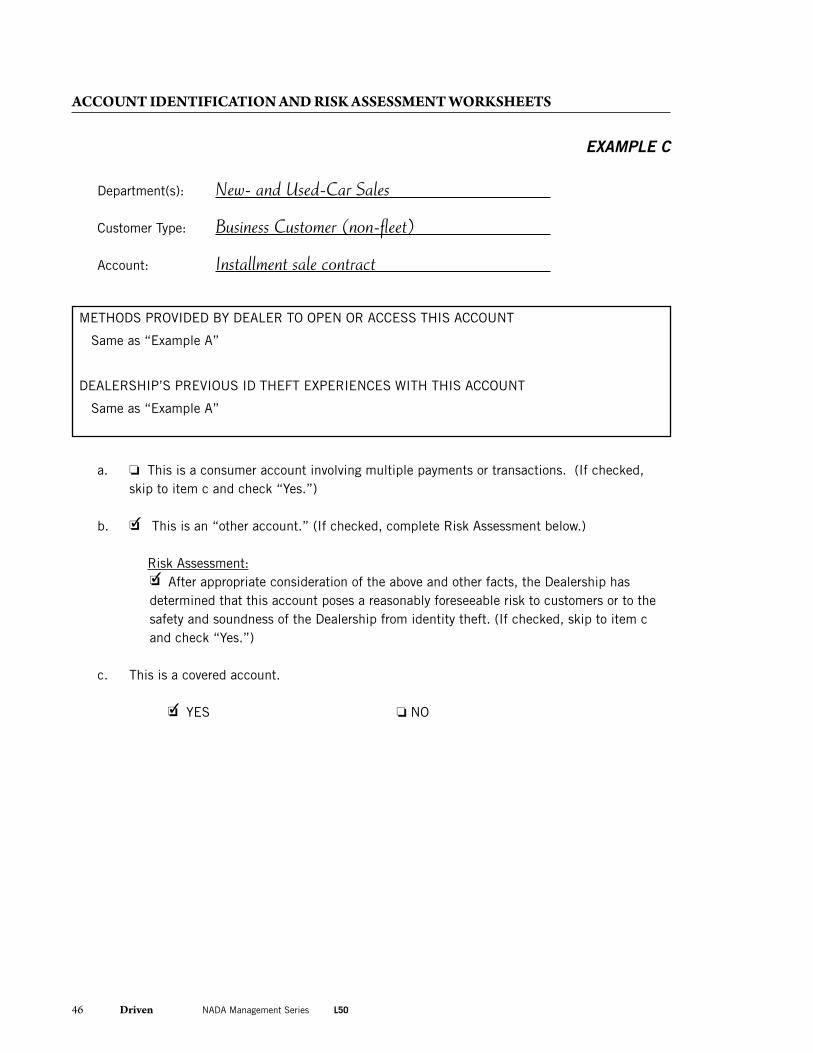

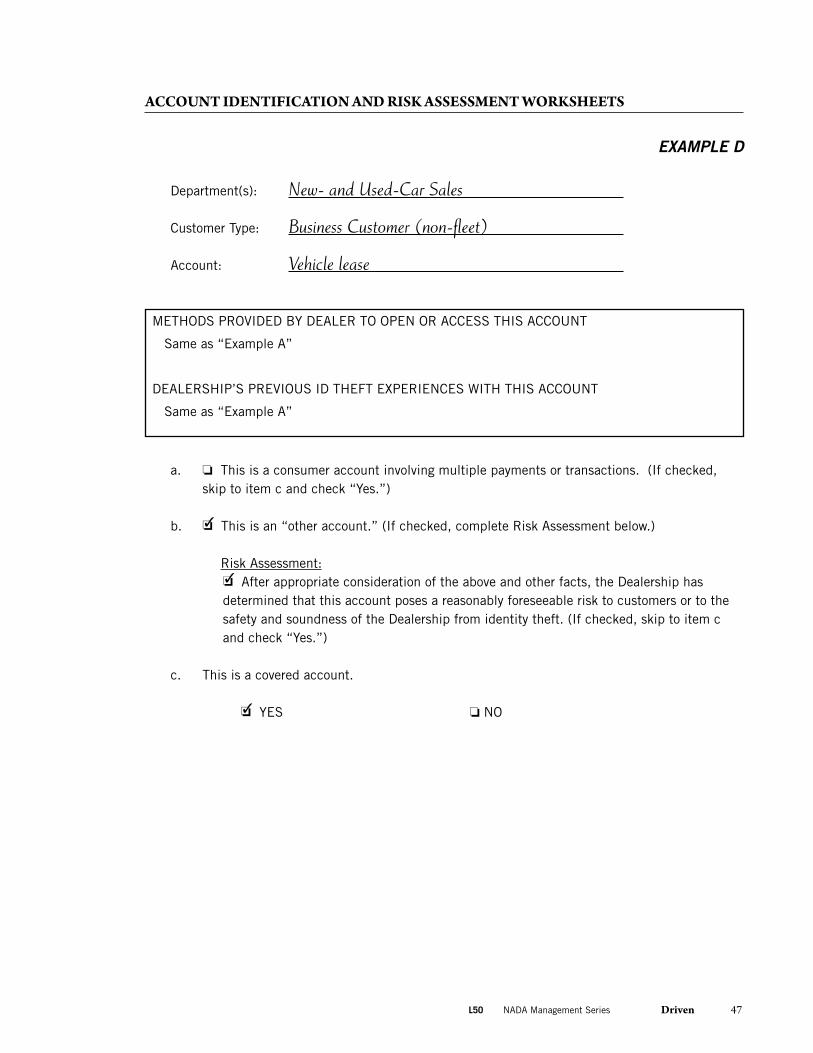

Identifying “Covered Accounts”

Once the compliance personnel are in place and their duties are outlined, the first step they should take is to review all of the different types of “accounts” the dealership offers or maintains and determine whether any of them are “covered accounts.” (As a threshold matter, you are only

required to develop and implement an ITPP if you offer or maintain one or more “covered accounts.”)

What is an Account?

The Rule defines “account” as “a continuing relationship established by a person with a finan-cial institution or creditor to obtain a product or service for personal, family, household or business purposes.” This includes “an extension of credit, such as the purchase of property or services involv-ing a deferred payment.”

This definition casts a wide net over any extensions of credit—whether for personal or business pur-poses. The reference to “continuing relationship,” however, appears to exclude from consideration those one-time transactions that may have an element of credit risk to them, but which are not intended to continue for any length of time. For example, paying off a trade-in vehicle prior to receipt of the title certificate or accepting a per-sonal check or credit card for parts, service, or as full payment for a vehicle all involve a degree of credit risk. However, the commentary to the Rule explains that one-time transactions such as these are not covered because “the burden that would be imposed upon financial institutions and creditors by a requirement to detect, prevent and mitigate identity theft in connection with single, non-continuing transactions by non-customers would outweigh the benefits of such a requirement.”6

What is a Covered Account?

The Red Flags Rule does not apply to all accounts, but rather only to “covered accounts.” If you offer or maintain any covered accounts, then you must implement an ITPP that applies to those covered accounts. The Red Flags Rule’s definition of covered account is two-pronged and any account that falls within either prong is included. The two types of covered accounts are:

1. Consumer Accounts. Accounts offered or maintained for personal, family, or household purposes that involve or are designed to

6 driven NADA Management Series l50

permit multiple payments or transactions, such as a consumer automobile installment sale contract or lease; and

2. Other Accounts. Other accounts (such as commercial or business accounts) offered or maintained by the dealer for which there is a reasonably foreseeable risk to customers or to the safety and soundness of the dealer-ship from identity theft, including financial, operational, compliance, reputation, or litiga-tion risks.

The first part of this definition includes accounts where consumers make multiple payments, includ-ing consumer retail installment sales contracts and leases. Most dealers offer these accounts even if they do not maintain them (because they routinely assign them to a third-party finance source or leasing company). Others, such as dealers with Buy-Here, Pay-Here financing or in-house leasing companies, both offer and maintain consumer accounts. Dealers that engage in either type of transaction with consumers (entering into and assigning finance and lease contracts to finance sources or holding the paper themselves) will be required to develop and implement an ITPP because they offer and/or maintain covered accounts.

The second part includes “other accounts,” which are not covered accounts unless there is a reason-ably foreseeable risk from identity theft. These “other accounts” consist of (a) business accounts and, apparently, (b) non-multiple payment con-sumer accounts that still involve a continuing

relationship (see Frequently Asked Questions for possible examples of b).

Risk Assessment

Most of a dealer’s accounts will be easily catego-rized as covered or not covered. However, there may be some “other” accounts offered or maintained where it is not readily apparent. Under the Rule, you must review these accounts to determine whether enough risk exists to elevate any of them to the status of a covered account. This process is referred to in the Rule as a “Risk Assessment.” The Risk Assessment must take the following fac-tors into consideration:

• Themethodsthedealershipemploystoopen its accounts

• Themethodsthedealershipemploystoaccess its accounts

• Thedealership’sprevious experiences with identity theft

The types of risk at issue in evaluating these factors are reasonably foreseeable financial, operational, compliance, reputational, or litigation risks to customers or to the safety and soundness of the dealership from identity theft.

In other words, considering the way you open or provide access to your non-consumer accounts, would an identity theft attempt against any of those accounts pose risks to your customers or to the dealership? For example, what are the chances that an identity thief could:

• Costyouoryourcustomersmoney?

• Harmyourreputationorthatofyourcustomers?

• Resultinlawsuitsagainstyouoryourcustomers?

Or, has the dealership experienced an incident of iden-tity theft in relation to that account in the past?

If any of these risks are reasonably foreseeable, your Risk Assessment may conclude that the account is a covered account.

Practice Tip

You should assume that a covered account includes any and all extensions

of credit—beyond a single payment transaction—offered or maintained by

your dealership to consumers and, if there is a reasonably foreseeable risk of identity

theft, to business customers as well.

l50 NADA Management Series driven 7

You must conduct an initial Risk Assessment prior to November 1, 2008, and periodic Risk Assessments thereafter to determine whether any of your non-consumer accounts are associated with a reasonably foreseeable risk of identity theft and thus are covered accounts that must be included in your ITPP.

The Sample ITPP in Section Two is followed by Attachment A, “Account Identification and Risk Assessment Worksheets,” to assist you in identify-ing your covered accounts.

The Worksheets include the following account types, some of which may not be offered by your dealership:

• Consumerinstallmentsalecontracts

• Consumervehicleleases

• Businessinstallmentsalecontracts

• Businessvehicleleases

• Businessopenaccountsforparts,service,and daily rentals

• Businessreceivableaccountsforpartsandlabor supplied to vehicle manufacturers under warranty and to service contract obligors

• Consumerpartsorservicechargeaccounts issued by the dealership

• Employeechargeaccountsissuedbythedealership

• Anyotherextensionofcreditordeferredpayment program, except those involving no continuing relationship

Keep in mind that any multiple-payment con-sumer account is considered a covered account, whereas other accounts depend on the identity theft risk posed. To the extent that your business and consumer vehicle installment sales and leases are handled in a similar manner and are open for business to the public generally, including those business accounts as covered accounts should not impose any significantly increased burden on the dealership.

Substantive Elements of the ITPP

With all of your covered accounts identified and the scope of your Program defined, you can now assemble the Program. As discussed below, your ITPP must consist of reasonable policies and procedures to:

• Identify relevant patterns, practices, and specific forms of activity signaling the possible existence of identity theft (Red Flags) for each of your covered accounts

• Detect relevant Red Flags that you identify

Application to Commercial Truck Dealers

Medium- and heavy-duty truck dealers that engage solely in business-to-business transactions may determine that they do not offer or maintain any covered accounts and thus do not need to develop and implement an ITPP. If this determination is correct, the dealer nonetheless must conduct an initial Risk Assessment to verify that it does not offer or maintain any covered accounts, and the dealer must conduct periodic Risk Assessments thereafter to determine if any changes to the accounts it offers or maintains or new identity theft risks elevate any of its accounts to the status of a covered account (which would then require the dealer to develop and implement an ITPP). In addition, as discussed below, the dealer still must comply with the Address Discrepancy Rule if it orders consumer credit reports.

8 driven NADA Management Series l50

• Respond appropriately to any relevant Red Flags that are detected to prevent and mitigate identity theft

• Review and update the Program peri-odically to reflect changes in risks from identity theft

Identifying relevant red Flags

In determining which Red Flags are relevant to each of your covered accounts, you must consider the following areas:

• Riskfactors

• CategoriesofRedFlags

• OthersourcesofRedFlags

Risk factors

The risk factors for purposes of identifying relevant Red Flags are the same as those used in your Risk Assessment to identify your covered accounts (i.e., for each covered account, you must analyze the methods the dealership employs to open and access the account and the dealership’s previous experiences with identity theft).

Because of the overlap between the Risk Assessment involved in identifying covered accounts and the risk factors analysis required to determine relevant Red Flags for each cov-ered account, the previously mentioned Account Identification and Risk Assessment Worksheets are designed to be used for both purposes.

Categories of Red Flags

The second area you must consider are the fol-lowing categories of Red Flags:

• Alerts,notifications,orotherwarningsreceived from CRAs or service providers, such as fraud detection services

• Thepresentationofsuspiciousdocuments

• Thepresentationofsuspiciouspersonalidentifying information, such as a suspi-cious address change

• Theunusualuseof,orsuspiciousactivityrelated to, a covered account

• Noticefromcustomers,victimsofiden-tity theft, law enforcement authorities, or other persons regarding possible identity theft in connection with your covered accounts

The FTC sets forth 26 illustrative examples of Red Flags (“Example Red Flags”) from these categories, which you should analyze and, if you determine them to be relevant, incorporate into your ITPP. The “Red Flag Identification, Detection, and Response Worksheets” (Attachment B) to the Sample ITPP in Section Two lists each Example Red Flag.7

When analyzing the relevance of the 26 Example Red Flags, keep in mind that this list was devel-oped jointly by the FTC and the federal banking regulatory agencies with all financial institutions and creditors in mind, not just dealers. Therefore, while many are likely to be relevant to your covered accounts, others are not likely to be relevant.

For example, certain Example Red Flags, such as Number 5 (“documents provided for identification appear to have been altered or forged”) and Number 6 (“the photograph or physical description on the identification is not consistent with the appear-ance of the applicant or customer presenting the identification”), would appear highly relevant to most dealers’ covered accounts (and, in these instances, are likely already part of your existing policies and procedures to prevent identity theft). In contrast, others, such as Number 20 that pertains to revolving credit accounts, clearly are not relevant to dealers that do not offer such accounts.

The larger challenge exists with Example Red Flags that appear to provide useful information but perhaps are not reasonable to adopt in light of their cost, burden, and the fact that you currently possess or will adopt other customer identifica-tion procedures that diminish their relevance.

l50 NADA Management Series driven 9

For example, Number 10b (“the Social Security Number (SSN) has not been issued, or is listed on the Social Security Administration’s Death Master File”) mentions useful information. However, as noted in the “General Guidance on Identifying Relevant Red Flags” (see below), the FTC is not expected to suggest that a Red Flag is “relevant” (and therefore required to be included in the ITPP) simply because it could theoretically be helpful in preventing identity theft. The FTC might ask, however, whether the Red Flag would realistically increase your chances of detecting and prevent-ing identity theft. With respect to Number 10b, the answer to that question would be “no” if you determine from your Risk Assessment that it is highly unlikely that an identity thief could use a deceased person’s or non-issued SSN to circum-vent your customer identification procedures and your other Red Flag detection methods. Keep in mind, however, that circumstances can change and that if implementation of Number 10b (or any other Red Flag) should become less expensive or less difficult for whatever reason, your relevance determination may change. You should review your assessments when you review and update your program.

Other Sources of Red Flags

The third area you must consider are other sources of Red Flags, including:

• Incidentsinvolvingidentitytheftthe dealership has experienced

• Methodsofidentitytheftthedealershiphas identified that reflect changes in identity theft risks

• Applicablesupervisory(FTC)guidance

Another source of Red Flags may come from the dealership’s existing policies and procedures for preventing identity theft.

These requirements recognize that past identity theft incidents at the dealership are clear indicators of the threat of identity theft in the future, and that the tactics used by identity thieves are constantly evolving. The dealership must account for these changing tactics when developing and updating its ITPP. Because the list of relevant Red Flags must be updated periodically, the dealership should adopt a procedure that will include in the Program update any information the dealership maintains concern-ing identity theft incidents and changed methods

General Guidance on identifying Relevant Red Flags

In determining what Red Flags are relevant to your covered accounts and thus must be incorpo-rated into your ITPP, keep in mind:

• EvenwiththeRule’sdirectivesregardingriskfactorsandcategoriesandsourcesofRedFlags, there is very little guidance in the Rule concerning exactly how to create a set of “relevant” Red Flags for incorporation into your ITPP.

• Thelackofdefinitiveandbright-linerulesisacknowledgedbytheregulators,whoreferto the Rule’s Red Flag identification provisions as taking “a risk-based, non-prescriptive approach.”

• TheFTCisnotexpectedtosuggestthataRedFlagis“relevant”simplybecauseitcouldtheoretically be helpful in preventing identity theft.

• TheRedFlagsRulecallsforthedealershiptoadoptreasonable policies and procedures for the identification of relevant Red Flags. Although you should take a cautious approach toward your regulatory obligations, there is no prohibition against considering factors such as feasibility and cost when developing your ITPP policies and procedures.

10 driven NADA Management Series l50

of identity theft. The Sample ITPP suggests that the Program Coordinator develop a log of dealership identity theft incidents for this purpose.

In the end, the Example Red Flags and other potential Red Flags identified by your dealership should be evaluated in light of the risk factors for covered accounts; the categories and sources of Red Flags; the dealership’s size, complexity, and the nature and scope of its activities; the dealer-ship’s existing identity theft prevention policies; the cost and availability of establishing methods to detect a particular Red Flag; and whether, in light of these considerations and other relevant facts, it would be reasonable and appropriate for you to identify the Red Flag as relevant and include it in your ITPP.

developing the Means to detect red Flags and Verify Identity

Once you have identified Red Flags that are rel-evant for each type of your covered accounts, the next step under the Rule is to develop reasonable policies and procedures to detect those relevant Red Flags by appropriate means, such as:

• Obtainingidentifyinginformationabout,and verifying the identity of, a person opening a covered account

• Wherethedealershipmaintainsacoveredaccount after it is opened, authenticating customers, monitoring transactions, and verifying the validity of change of address requests

The Red Flags and Address Discrepancy Rules each identify the Customer Information Program (CIP) rules under section 326 of the USA PATRIOT Act (also known as the “Know Your Customer” rules) as a means of verifying a customer’s identity.8 The CIP rules require (and to a great extent provide) reasonable procedures for verifying the identity of any person seeking to open an account; maintaining records of the information used to verify the per-son’s identity, including name, address, and other

identifying information; and determining whether the person appears on any lists of known or sus-pected terrorists or terrorist organizations provided to financial institutions by the government.

Dealers presently are not required to adopt the identity verification procedures contained in the CIP rules.9 Nonetheless, should dealers choose to adopt and implement them, they would serve as a permissible Red Flag detection method under the Red Flags Rule and also, as discussed below, one of several means of satisfying your customer identification responsibilities under the Address Discrepancy Rule.

If you choose not to adopt the CIP procedures, you must develop other identity verification procedures for persons opening an account. For purposes of complying with the detection component of the Red Flags Rule, consider applying the procedures you develop to respond to Notices of Address Discrepancy to any situation involving the open-ing of a covered account, even those not involving the receipt of a Notice of Address Discrepancy from a CRA. Although the procedures may vary depending on the type of account involved, identity verification should become (if it is not already) a standard operating procedure for your dealership to use for any person seeking to conduct business with your dealership.

Beyond identity verification, you also should consider additional means that may be useful in detecting each of the relevant Red Flags that you have identified. The approach suggested in the Sample ITPP is to use the Red Flag Identification, Detection, and Response Worksheets for this purpose. The Worksheets provide space to set forth specific detection methods for each relevant Red Flag. After you complete the process for all relevant Red Flags, the detection methods can be collected and edited, and you can develop a list of customized detection methods. This list, along with the identity verification procedures you adopt, should allow you to establish an effective detection mechanism for the relevant Red Flags you have identified.

l50 NADA Management Series driven 11

developing Policies and Procedures for responding to detected red Flags

The Rule also requires the ITPP to include reasonable policies and procedures to respond appropriately to detected Red Flags to prevent and mitigate identity theft. The responses are to be commensurate with the degree of risk posed, considering aggravating factors.

The approach suggested in the Sample ITPP is to list the response approach you will follow for each relevant Red Flag you detect on the Red Flag Identification, Detection, and Response Worksheets.

Again, the responses will depend in large part on the nature and severity of the Red Flag detected, and

should take into account the quality and quantity of the Red Flags present in any one transaction. Further, your approach should provide for a range of responses based on the circumstances and the judgment of the personnel involved. Because not every response is appropriate in every circum-stance, the Sample ITPP takes a three-pronged approach to response policies and procedures.

First, to give the dealership maximum flexibility, the Sample ITPP establishes General Response Procedures that permit a range of possible responses, based on the facts and circumstances that exist when a Red Flag is detected.

Second, the General Response Procedures recog-nize that there are many detected Red Flags that can be cleared through a reasonable investigation.

examples of Detection Methods

The detection method describes exactly what steps dealer personnel need to take to detect a relevant Red Flag. Again, Red Flags that are extremely difficult or impossible to detect are not likely to be deemed “relevant,” so to an extent, the detection determination is closely connected to the identification of relevant Red Flags. In the end, it should include any reasonable method available to the dealer to detect a relevant indicator of identity theft.

For example, some detection methods include:

• Closelyinspectingdocumentsprovidedforidentification

• Comparingtheinformationprovidedbytheconsumerwithotherinformationthedealer-ship has on file about that consumer

• Reviewingtheconsumercreditreportforsuchthingsasfraudalerts,activedutyalerts,or notices of address discrepancy

• Reviewingthecreditreportforunusualpatternsoractivity

• Askingverificationquestionsbasedoninformationcontainedinthecreditreport

• Listeningcarefullyforsuspiciousstatementsbythecreditapplicant

• Comparingsignatures

Of course, not all detection methods make sense for all Red Flags. A review of the Red Flag Identification, Detection, and Response Worksheets provides numerous examples. Dealership personnel with experience in confirming identity and/or requesting and reviewing credit reports should be consulted when developing the detection methods. You should keep track of which detection methods are effective and which are ineffective, and update your ITPP accordingly.

12 driven NADA Management Series l50

Consequently, it establishes a procedure where the employee who detects the Red Flag works with his or her manager to assess the level of risk present. If they cannot negate their suspicion of identity theft, they will not open the account and the matter will be referred to the Program Coordinator for any further response. If, on the other hand, the inves-tigation removes their suspicion of identity theft, they will proceed with opening the account.

Third, the Sample ITPP recognizes that the detec-tion of some Red Flags requires the dealership to take specific actions, such as following the procedures to respond to a fraud or active duty alert (which is a separate duty under section 112 of the FACT Act and also is set forth by the FTC as Example Red Flag Number 1) or to a Notice of Address Discrepancy (which, as discussed below, is a separate duty under section 315 of the FACT Act and also is set forth by the FTC as Example Red Flag Number 3). The Sample ITPP contains sample Specific Response Procedures, intended to supplement the General Response Procedures, for these and other situations.

developing Policies and Procedures to update the ITPP

Once you have established your procedures for identifying, detecting, and responding to relevant Red Flags, you must develop policies and proce-dures to update your ITPP periodically.

The Red Flags Rule directs that updates appro-priately reflect changes in risks, based on factors such as:

• Theexperiencesofthedealerwithiden-tity theft

• Changesinmethodsofidentitytheft

• Changesinmethodstodetect,prevent,and mitigate identity theft

• Changesinthetypesofaccountsthatthedealership offers or maintains

• Changesinthebusinessarrangementsof the dealership, including mergers, acquisitions, alliances, joint ventures, and service provider arrangements

In light of the Rule’s requirement for an annual compliance report (discussed below), it should be reasonable to perform your Program update annually after the compliance report has been reviewed and considered. As part of the updat-ing process, you should review the identification of covered accounts and relevant Red Flags and reassess the effectiveness of your current detection and response procedures. You also should address necessary changes to the administrative elements of your ITPP (see discussion below).

In addition, should you encounter a significant change in circumstances, such as a serious incident of identity theft or installation of a new credit report retrieval system, you should immediately update the Program (at least to the extent relevant to the changed circumstance).

Administrative Elements of the ITPP

After the written Program has been developed in accordance with the guidelines above, the Red Flags Rule sets forth certain steps that dealers must take to administer it.

Training

The ITPP should include policies for training all relevant dealership personnel. Relevant personnel include those who perform functions covered by the ITPP, including employees involved in opening covered accounts, working with existing accounts (if any), or, as required by the Address Discrepancy Rule, requesting or using credit reports.

See the Sample ITPP in Section Two for sample policies and procedures applicable to training.

l50 NADA Management Series driven 13

Overseeing Service Providers

The Rule also requires dealers to “oversee service pro-vider arrangements effectively and appropriately.”

When engaging a service provider to perform an activity in connection with one or more covered accounts, the dealer should ensure that the activity of the service provider is conducted in accordance with reasonable policies and procedures designed to detect, prevent, and mitigate the risk of iden-tity theft. As an example, the Rule notes that the service provider could be asked to sign a contract requiring the service provider to have policies and procedures in place to detect relevant Red Flags that may arise in the performance of the service provider’s activities, and either report the Red Flags to the dealer or take appropriate steps to prevent or mitigate identity theft. Appendix A contains sample clauses that may be appropriate to include in your contracts with your service providers.

Under the Rule, a service provider means a person who provides a service directly to the dealership in connection with one or more covered accounts. This is an extremely broad definition.

Despite the breadth of the definition and of the triggering event that requires service provider oversight (engaging a service provider to perform “an activity” in connection with covered accounts), it appears the regulators are concerned here with a set of circumstances that may be somewhat infrequent among automobile dealers.

The intent of this requirement is twofold: to make it clear that a creditor or financial institution cannot escape duties under the Red Flags Rule simply by delegating or outsourcing them to outside entities, and to ensure that any entity performing such duties observes the requirements of the Rule. Therefore, there would be no point in including an entity within the “service provider” definition unless the activities it performs are, at least in part, activities implicated by the Rule, such as opening covered accounts or having some responsibility for servicing or maintaining covered accounts in a manner involving a relevant Red Flag.

Dealers whose covered accounts are limited to installment sale contracts and leases and who immediately assign those agreements to finance sources do not maintain or service covered accounts, and thus do not retain service provid-ers to maintain or service those accounts. And, with respect to opening such accounts, most of those dealers do not outsource the actual account opening functions.

However, the following arrangements may be examples of the use of service providers in the opening of covered accounts:

• Abrokerorotherthirdpartyactingonbehalf of the dealer secures the cus-tomer’s signature on installment sale contracts or leases.

• Avendorofidentitytheftpreventionservices retained by the dealer performs the duties of the dealer under the Red Flags Rule with respect to each potential covered account.

On the other hand, a vendor that creates and hosts dealer websites—even those that contain an online credit application—would not appear to be a service provider who would be required to detect relevant Red Flags unless that vendor is actually engaged by the dealer to make some use of the information obtained through the website (such as information contained in the online credit application) as part of the process of opening the account. For example, the vendor may be a service provider subject to the regulations if the dealer engages the vendor to review the credit application or other information supplied by the consumer for certain information that would otherwise be reviewed internally at the dealership as part of the account opening process.

Dealers who hold covered accounts for a period of time after they are opened may engage service providers to perform activities on the accounts that would trigger the service provider requirement. For example, outsourced customer service centers or other agents serving as the customer’s principal

14 driven NADA Management Series l50

point of contact on the account would likely be considered “service providers” under the Rule.

In the event your dealership outsources to or relies on service providers as part of the account open-ing or maintenance process, you should exercise appropriate and effective oversight of them. This includes carefully selecting the vendor and, as contemplated by the Rule, obtaining a contractual commitment that the service provider will have policies and procedures in place to detect relevant Red Flags that may arise in the performance of the service provider’s activities, and either report the Red Flags to the dealer or take appropriate steps to prevent or mitigate identity theft.

Board Approval of the ITPP

Once the ITPP has been drafted, the Rule requires that it be approved by the dealer’s board of direc-tors or an appropriate board committee. For dealers that do not have a board of directors, the Rule requires approval by a “designated employee at the level of senior management.”

Management Oversight

The Rule requires that the board of directors, an appropriate committee of the board, or a designated employee at the level of senior management also perform the functions listed below:

Assigning specific responsibility for imple-mentation of the ITPP

This is addressed above under “Appointing a Team to Develop and Implement the ITPP.”

Reviewing compliance reports

The board, board committee, or senior management employee must also review the staff compliance reports (see below under “Reporting”).

Approving material changes to the ITPP as necessary to address changing identity theft risks

The board, board committee, or senior management employee is responsible for ap-

proving changes to the Program either at the time of the periodic update or when required by the circumstances (for example, follow-ing an incidence of identity theft at your dealership).

Reporting

The Rule also requires that staff who are responsible for developing, implementing, and administering the ITPP report to the board of directors, board committee, or senior management employee at least annually on the dealership’s compliance with the Red Flags Rule.

The report, which should be in writing, must address material matters related to the Program and evaluate issues such as:

• Theeffectivenessofthepoliciesandprocedures of the dealership in address-ing the risk of identity theft in connection with the opening of covered accounts and with respect to existing covered accounts

• Serviceproviderarrangements

• Significantincidentsinvolvingidentitytheft and management’s response

• Recommendationsformaterialchangestothe Program

Appendix B contains a Compliance Report template to assist you with this obligation. ■

l50 NADA Management Series driven 15

duty to Implement Policies and Procedures to Confirm Identity upon receipt of notice from CRA

As mentioned above, the FACT Act also requires nationwide CRAs to inform users of consumer credit reports when a substantial difference exists between the consumer address the user provided when requesting a credit report and the address(es) the CRA has on file for the consumer. Determining whether such a notice should be issued to the dealer is entirely up to the CRA.

The Address Discrepancy Rule requires a dealer to develop and implement reasonable policies and procedures to be followed when it receives a Notice of Address Discrepancy from a CRA. These policies and procedures must enable the dealer to form a reasonable belief that a credit report relates to the consumer about whom it has requested the report or determine that it cannot do so.

The Rule applies only with respect to consumer credit reports—that is, credit reports respecting an individual. (This includes consumer credit reports obtained for hiring or other employment purposes as well those obtained for vehicle financing pur-poses.) The Rule has no application with respect to business credit reports, unless they include a consumer credit report on the business owner.

What is a Reasonable Policy to Confirm Identity?

The Address Discrepancy Rule provides the fol-lowing examples of reasonable policies and pro-cedures a dealer could implement to confirm the applicant’s identity:

1. Comparing the information in the consumer credit report with:

A. Information the dealer obtains to verify the consumer’s identity in accordance with the CIP rules;

B. Information the dealer maintains in its own records, such as applications, change of address notifications, other customer account records, or retained CIP docu-mentation; or

C. Information the dealer obtains from third-party sources; or

2. Verifying the information in the credit report with the consumer.

As mentioned above, the CIP rules are a series of policies and procedures regarding customer iden-tification and verification set forth in a separate federal statute known as the USA PATRIOT Act. Although dealers presently are not subject to the CIP rules, you may, if you have or intend to put CIP procedures in place, use those procedures as one means of verifying that you obtained the correct credit report.

THE FTC AddrESS dISCrEPAnCY ruLE

16 driven NADA Management Series l50

If you do not have CIP procedures in place, sev-eral reasonable alternatives exist. Item 1B above, for example, allows dealer personnel to compare the credit report against information the dealer maintains in its own records, such as the credit application, driver’s license, and other data gath-ered as part of the dealer’s ITPP. Item 2 allows dealer personnel to verify or “test” the consumer on information contained in the consumer credit report. In other words, dealership personnel can verify the customer’s identity by asking the customer questions about the information in the credit report, such as former addresses, amounts on credit lines, names of creditors, etc.

Whatever policies the dealer adopts, the credit report should not be used and the account opening process should not proceed unless and until dealer personnel have followed the procedures and have formed a reasonable belief that the credit report relates to the correct customer. If such a belief is formed, the report may be used and, subject to any other requirements of the ITPP (detailed below), the account may be opened. If such a belief cannot be formed—because there is still suspicion—the account should not be opened and any further responses provided for in the ITPP should be followed.

Policies to Furnish Address to Consumer reporting Agency

Although unlikely to apply to many dealers, there is a second component of the Address Discrepancy Rule that requires certain users of credit reports to report back an accurate address for a consumer to the CRA from which it received a Notice of Address Discrepancy.

This second component applies only to dealers who regularly and in the ordinary course of business furnish information to the CRA that issued the Notice of Address Discrepancy. If you are a fur-nisher of information to the CRA, you must develop and implement policies and procedures to furnish the address you have for the consumer to the CRA when all the following conditions are met:

• Youformareasonablebeliefthatthecredit report relates to the consumer about whom you requested the report.

• Youestablishacontinuingrelationshipwith the consumer—that is, you sell on credit or lease a vehicle to the consumer or otherwise open an account.

• Youreasonablyconfirmthattheaddressisaccurate.

Examples of reasonable confirmation methods set forth in the Rule are:

• Verifyingtheaddresswiththeconsumerabout whom you have requested the report;

• Reviewingyourrecordstoverifytheaddress of the consumer;

• Verifyingtheaddressthroughthird-partysources; or

• Usingotherreasonablemeans

Your policies and procedures must provide that you will furnish the address that you have reasonably confirmed is accurate to the CRA as part of the information you regularly furnish for the reporting period in which you establish a relationship with the consumer (in other words, the period in which you sell a vehicle on credit, enter into a lease transaction, or otherwise open an account). ■

Application to Commercial Truck Dealers

Medium- and heavy-duty truck dealers that obtain consumer credit reports must

comply with the Address Discrepancy Rule even if they determine that they are not required to develop and implement

an ITPP under the Red Flags Rule (which dealers may only determine after

conducting a mandatory Risk Assessment concerning the accounts they offer).

l50 NADA Management Series driven 17

1. What dealers are subject to the Red Flags Rule?

The Rule casts an extremely wide net that brings within its coverage a very large share of the nation’s business economy. Not only are financial institu-tions subject to the Rule, but so are creditors. In that sense, virtually all dealers are covered by the Red Flags Rule because virtually all dealers are creditors. In fact, the Red Flags Rule spe-cifically identifies automobile dealers in its list of creditors. However, the requirement to develop and implement an ITPP only applies to financial institutions or creditors that open or maintain “cov-ered accounts.” As discussed under “Identifying Covered Accounts,” this includes multiple-payment transactions with consumers, such as retail install-ment sale contracts and lease agreements (even if they are immediately assigned to a third-party finance source), and also includes other accounts where there is a reasonably foreseeable risk to customers or to the dealership from identity theft. If you are a medium- and/or heavy-duty truck dealer, see the information under “Application to Commercial Truck Dealers” on page 7.

2. What dealers are subject to the Address Discrepancy Rule?

The rule applies to dealers who order consumer credit reports from a CRA.

3. Does each dealership in a dealer group need to comply individually?

Each legal entity subject to the Red Flags Rule must comply, whether or not it is owned by a dealer group that owns other dealerships. However, nothing in the Rule prohibits the dealer group from developing an ITPP for use by its individual dealer entities, provided that any unique circumstances relevant to the development and operation of the Program at the dealer-entity level is accounted for and provided that the board of directors (or appropriate board committee or, if there is no board, a designated senior management employee) for each dealer-entity approves the Program for use by that entity.

4. Am I required to have a written Address Discrepancy policy?

There is no express requirement to have a written policy to comply with the Address Discrepancy Rule. However, you must have policies and procedures to verify the identity of customers for whom you receive a Notice of Address Discrepancy, and it would be prudent to set forth those procedures in writing. The Sample ITPP contains procedures at Section 13 for this purpose.

5. Can we combine our ITPP with our Customer Information Safeguards Program under the FTC Safeguards Rule?

Yes, and doing so may have the benefit of encouraging comprehensive training for both

FrEQuEnTLY ASKEd QuESTIonS

18 driven NADA Management Series l50

your safeguarding policies and your identity theft detection policies. However, the complexity of both Rules could hamper any effort to compose a unified program that complies with both Rules. In addition, although there are similarities between the Rules, they have significant differences, such as being the products of entirely separate legislative enactments with different sets of defined terms.

6. If we fall victim to identity theft, have we automatically violated the Red Flags Rule?

No. The Rule does not impose strict liability for failing to detect identity theft in any particular instance. Instead, the FTC would, upon inves-tigation, examine the particular circumstances surrounding the incident. The focus of the Rule is on having financial institutions and creditors create and follow reasonable policies and proce-dures designed to prevent and mitigate identity theft, but it does not require perfect policies that eliminate the possibility of identity theft from ever occurring (hence the need to develop reasonable policies and procedures under the Rule). If the dealership does fall victim to identity theft, the Rule would require you to take everything learned from that experience into consideration in revising and updating your Program.

7. What are the penalties for violating the Red Flags or Address Discrepancy Rules?

There is no federal private right of action for vio-lating either the Red Flags Rule or the Address Discrepancy Rule. Enforcement falls to the FTC as the agency responsible for interpreting and enforcing the Rules as they pertain to dealers. All enforcement matters begin with an investigation. When the facts point to law violations, these inves-tigations can lead to administrative settlements. These settlements can include both injunctions that require the company to comply with the Rule, other reporting obligations, and civil penalties of up to $2,500 for each “knowing” violation of the Rule(s). If the dealer fails to comply with that order, the FTC could file a federal lawsuit seeking fines of up to $11,000 for each future violation, injunctive

relief, and/or a long-term consent decree. Keep in mind that the civil penalties (up to $2,500) that may be required to resolve the investigation could apply to past violations, while fines stemming from a lawsuit apply only to future violations. If the parties do not reach a settlement, the FTC can bring an action in Federal district court for civil penalties and injunctive relief.

In addition, it is also possible that violations of these Rules could subject a dealer to state law claims (including class action claims) under state “unfair and deceptive acts and practices” (UDAP) statutes. These laws typically permit actual and punitive damages, as well as attorneys’ fees and costs.

8. What are some examples of non-multiple payment consumer accounts involving a continuing relationship that may be considered covered accounts under the Red Flags Rule?

While the Red Flags Rule provides no definitive answer, one example might be a zero-down install-ment contract that calls for only one payment—a balloon payment—at the end of the contract term. In such an extension of credit, the continuing rela-tionship could be seen to result from the contractual terms unrelated to payment that the buyer must observe over the duration of the contract, such as maintaining the vehicle, keeping it insured, and renewing registration. Another possible example would be a rental car contract for an extended term where only one payment is due at the end of the term even though the renter is obligated to various contractual duties during the term.

9. Under what circumstances, if any, do we need to notify law enforcement under the Red Flags Rule?

The Rule does not directly identify any circum-stances that require you to notify law enforcement. The Rule includes notification of law enforcement as a possible response if such a response would prevent or mitigate identity theft considering the degree of risk posed by the Red Flag(s) you detect

l50 NADA Management Series driven 19

and any aggravating factors. For example, if an identity thief presents identification documents that you determine are clearly counterfeit and your review of the consumer credit report reveals overwhelming evidence of ongoing identity theft, in addition to not opening the account, your Program Coordinator may determine it appropriate in accordance with state and local law to notify law enforcement. Another example where notify-ing law enforcement may be appropriate would be if the dealership finds that it has been targeted by a ring of identity thieves in the dealer’s com-munity that law enforcement has been attempting to apprehend.

10. Do these Rules mean that we cannot conduct transactions with persons who never come to the dealership, such as someone in another state who contacts us by phone after visiting our website?

No. The Rules do not in any way prohibit telephone, online, or interstate transactions. However, a dealer that enters into installment sale contracts or leases with customers who never come to the dealer-ship or meet dealership employees in person will require an ITPP that takes that method of open-ing an account into consideration in identifying, detecting, and responding to relevant Red Flags. For example, for accounts opened remotely and without meeting the customer in person, the dealer may determine that additional Red Flags and/or customer identification methods are necessary due to the inability to physically inspect identification documents and determine, for example, if the customer’s appearance matches the photograph on the identification documents. As noted in our discussion of “Substantive Elements of the ITPP,” the CIP rules contain examples of “non-documentary” identity verification procedures that allow verification of identity without reliance on identification cards and other documents.

11. What documents should we retain to demonstrate compliance with these Rules and how long should we retain them?

You should retain all of the following:

• Theinitialandallsubsequentversionsandupdates of your ITPP

• Alldocumentsusedintheprocessofcreatingand updating your ITPP, such as worksheets and annual compliance reports

• All documents supporting your Programadministration responsibilities, such as training outlines, training attendance sheets, and documents related to your oversight of service providers

These documents may be necessary if you are ever called upon to verify that you followed the required processes to develop and update your ITPP.

These documents should be retained indefinitely, or at least for the full statute of limitations (SOL) period under the laws mentioned above. Regarding the FCRA and the FTC Act, the FCRA has the longer SOL, which can extend up to five years from the date of a FCRA violation. Your state UDAP statute may impose a longer SOL period. ■

20 driven NADA Management Series l50

Appoint an iTPP Compliance officer and an iTPP Program Coordinator.

Appoint a senior manager to serve as the ITPP Compliance Officer who will be responsible for the Program’s over-sight, development, implementation, and administration. If necessary, appoint an ITPP Program Coordinator to manage and coordinate the Program under the supervi-sion of the Compliance Officer.

See Section 3 and the final page of Sample ITPP (entitled “Appointments and Approval”) and narrative discussion at pp. 4 - 5.

Determine the “covered accounts” that you offer or maintain.

Identify all of the “accounts” that you offer or maintain and determine which ones are “covered accounts” that must be addressed in your ITPP. Covered accounts gen-erally consist of (1) all of your consumer transactions involving multiple payments (even if you immediately assign the contract to a third party) and (2) your other multiple payment accounts (including business accounts) where there is a reasonably foreseeable risk of identity theft to your dealership or your customers.

See Sections 4-6 and 9 of Sample ITPP and narrative discussion at pp. 5 - 7.

Use Account Identification and Risk Assessment Worksheets.

identify relevant indicators of possible identity theft (“Red Flags”) for each covered account.

For each of the covered accounts you identified, deter-mine what patterns, practices, or activities may indicate a possible attempt at identity theft. Keep in mind that “relevant” Red Flags are reasonable (as opposed to theo-retical) indicators of ID theft. You must consider several sources of Red Flags, such as vulnerabilities in how you open and maintain your covered accounts, your prior experiences with identity theft (consider also methods of identity theft at other dealerships that you have learned

about), and guidance from the FTC, including its list of 26 Example Red Flags.

The Worksheets to the Sample ITPP set forth the 26 Example Red Flags and other Red Flags that may apply to your cov-ered accounts. Determine which of these, and other Red Flags that are not set forth in the Worksheets, are relevant to your covered accounts, and list them in your ITPP.

See Sections 7 and 10 of Sample ITPP and narrative discussion at pp. 7 - 10.

Use Red Flag Identification, Detection, and Response Worksheets.

Develop procedures for detecting those Red Flags.

For each relevant Red Flag that you have identified, de-termine what reasonable methods dealership personnel must follow to detect that Red Flag. Include procedures to verify the identity of a customer who wishes to open or access a covered account, and additional detection procedures for certain Red Flags that you identify.

See Sections 8 and 11 of Sample ITPP and narrative discussion at pp. 10 - 11.

Use Red Flag Identification, Detection, and Response Worksheets.

Develop procedures for responding to relevant Red Flags that you detect.

For each relevant Red Flag that you identify and detect, determine what reasonable response procedures deal-ership personnel must follow. The procedures should be flexible and should provide for a range of possible responses depending on the Red Flag detected and the specific facts and circumstances involved. The Sample ITPP sets forth “General Response Procedures” to be followed when any Red Flag is detected as well as ad-ditional “Specific Response Procedures” to be followed when certain Red Flags are detected.

See Section 12 of Sample ITPP and narrative discussion at pp. 11- 12

Use Red Flag Identification, Detection, and Response Worksheets.

FTC ReD FlAGS Rule CoMPliANCe CHART: STeP BY STePThis chart may assist you in developing and implementing a written iTPP by the final date for complying with the Red Flags Rule (November 1, 2008). The chart highlights the general compliance steps you must take with cross-references to the Sample iTPP and the narrative portion of the guide.

2STeP

3STeP

1STeP

4STeP

5STeP

l50 NADA Management Series driven 21

10STeP

9STeP

8STeP

7STeP

6STeP

Train your employees.

Your ITPP should include policies for training all dealership personnel involved in opening or maintaining covered accounts or performing any duty set forth in your Program, including your procedures for complying with the Address Discrepancy Rule.

See Sections 13, 14 (if applicable), and 15 of Sample ITPP and narrative discussion at page 12.

oversee your service providers.

If you outsource to a service provider any activity necessary for opening or maintaining covered accounts, or any duty under your ITPP (e.g., functions related to identifying, detecting, or responding to relevant Red Flags that exist with your covered accounts), ensure that your service provider has appropriate policies and procedures in place to perform these functions and agrees to do so contractually.

Note that the Sample ITPP assumes the dealership does not retain service providers for this purpose. If you retain service providers to which you have outsourced ITPP duties, ensure that your ITPP reflects that arrangement.

See Section 16 of Sample ITPP, narrative discussion at pp. 13 - 14, and Appendix A entitled “Sample Clauses to Include in Service Provider Agreements.”

Draft an iTPP that details the procedures set forth above.

Consolidate the information gathered and produced to comply with each of these steps, including the information from the Sample ITPP Worksheets, and incorporate it into a formal written Program. Ensure that your ITPP is comprehensive and includes the procedures you will adopt to comply with the Address Discrepancy Rule. In addition, ensure that you document all of your compliance efforts.

ensure that your board of directors or a committee of the board approves your iTPP by November 1, 2008.

Once your ITPP is drafted, it must be approved by the dealership’s board of directors or an appropriate board committee by November 1, 2008. If your dealership does not have a board of directors, the ITPP must be approved by a designated senior management employee.

See Sections 1 and 3 and the “Appointments and Approval” page of Sample ITPP and narrative discussion at page 14.

Comply with the ongoing Program requirements.

Your compliance duties under the Red Flags Rule do not end on November 1, 2008. The Program must be continuously administered and you must adhere to a series of ongoing administrative requirements designed to ensure that your ITPP is responsive to the latest trends in identity theft.

The Program Coordinator (or staff responsible for administration of the ITPP) must submit compliance reports at least annually as detailed in the ITPP, while the Compliance Officer (or the board of directors, a board committee, or a designated senior management employee) must ensure the ITPP is updated periodically. The dealership should update its list of covered accounts, relevant Red Flags, and detection and response procedures as part of this process or sooner if warranted by the circumstances (such as if an identity theft incident occurs). The dealership also must stay current with its training obligations and service provider oversight responsibilities.

See Sections 17 and 18 of Sample ITPP, narrative discussion at page 14, and Appendix B entitled “Sample Compliance Report.”

This chart is offered for informational purposes only and is not intended as legal advice. Consult your legal counsel concerning the full range of your Red Flags Rule compliance responsibilities.

FTC ReD FlAGS Rule CoMPliANCe CHART: STeP BY STeP

22 driven NADA Management Series l50

EndnoTES

1 FTC publication, “Fighting Back Against Identity Theft,” at http://ftc.gov/bcp/edu/microsites/idtheft/consumers/about-identity-theft.html.

2 15 U.S.C. §§ 1681 et seq. 3 72 Fed. Reg. 63,718 – 63,775 (Nov. 9, 2007). The FTC Red Flags and Address Discrepancy Rules

are set forth at 16 C.F.R. Part 681. These Rules implement sections 114 and 315 of the FACT Act of 2003, respectively.

4 The Red Flags Rule includes an Appendix containing “Interagency Guidelines on Identity Theft Detection, Prevention, and Mitigation,” which “are intended to assist financial institutions and credi-tors” in formulating and maintaining an Identity Theft Prevention Program, and reflect the agen-cies’ recommendations for doing so. Section 681.2(f) of the Rule states any entity that is required to implement an identity theft prevention program must consider the guidelines and include in its Program those guidelines that are appropriate. Therefore, this guide does not distinguish between the Red Flags Rule itself and these guidelines found at Appendix A to 16 C.F.R. part 681.

5 For an overview of dealers’ responsibilities under the FTC Safeguards Rule, see the NADA publication, A Dealer Guide to Safeguarding Customer Information (2003). See also the FTC publication, “Financial Institutions and Customer Information: Complying with the Safeguards Rule,” (2006) at www.ftc.gov/bcp/conline/pubs/buspubs/safeguards.pdf.

6 72 Fed. Reg. at 63,721.7 The Example Red Flags are also set forth at Supplement A to Appendix A of the FTC Red Flags Rule,

which is available on page 58 of the Final Rule (identified at the top of the page as 63,774) at www.ftc.gov/os/fedreg/2007/november/071109redflags.pdf.

8 31 U.S.C. § 5318(l); 31 C.F.R. Part 103, Subpart I. 9 See 31 C.F.R. 103.170 (as to section 352).

L50 NADA Management Series Driven 23

Sample Identity Theft Prevention Program (ITPP)

1. Effective Date