frequently asked question (faq) - National Minorities ...

38

1 FREQUENTLY ASKED QUESTION (FAQ) QUESTION 1 What are the aims and objectives of National Minorities Development and Finance Corporation & when was it incorporated? ANSWER NMDFC was incorporated on 30 th September, 1994 with the objective of promoting economic and developmental activities for the benefit of ‘’backward sections’’ amongst the notified minorities with preference given to occupational groups and women. QUESTION 2 Who are the promoters of the NMDFC? ANSWER The Government of India jointly with the respective State Governments/UT Administrations are the promoters of NMDFC. However initially, State Governments of Andhra Pradesh, Bihar, Karnataka and Uttar Pradesh have promoted NMDFC along with the Central Government. QUESTION 3 What are the activities of NMDFC? ANSWER I. Provision of Term Loans for income generating activities at concessional rate of interest, through the State Channelizing agencies. II. Provision to meet credit requirements of Artisans, both in terms of Working Capital & Fixed Capital requirement under Virasat scheme. III. Providing Micro Finance to the poorest of poor among minorities through SCAs/NGOs & Network of Self Help Groups (SHGs). IV. Providing Educational Loans to persons belonging to minorities. V. Skill Development Training for the welfare of Minority Communities under Kaushal se Kushalta scheme with a view to help them in wage/self-employment. VI. Marketing Assistance to Artisan and Craft persons for sale/display of their products. VII. Mahila Samridhi Yojana aims to provide training to women in employment oriented skills. QUESTION 4 Who comprise the target groups for NMDFC assistance? ANSWER Target groups for NMDFC with regard to direct benefits will be persons belonging to minority communities. At present, Minority communities as per National Minorities Commission Act, 1992 are Muslims, Sikhs,

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of frequently asked question (faq) - National Minorities ...

1

FREQUENTLY ASKED QUESTION (FAQ)

QUESTION 1 What are the aims and objectives of National Minorities

Development and Finance Corporation & when was it incorporated?

ANSWER NMDFC was incorporated on 30th September, 1994 with the objective of

promoting economic and developmental activities for the benefit of

‘’backward sections’’ amongst the notified minorities with preference

given to occupational groups and women.

QUESTION 2 Who are the promoters of the NMDFC?

ANSWER The Government of India jointly with the respective State

Governments/UT Administrations are the promoters of NMDFC.

However initially, State Governments of Andhra Pradesh, Bihar,

Karnataka and Uttar Pradesh have promoted NMDFC along with the

Central Government.

QUESTION 3 What are the activities of NMDFC? ANSWER

I. Provision of Term Loans for income generating activities at

concessional rate of interest, through the State Channelizing agencies.

II. Provision to meet credit requirements of Artisans, both in terms of

Working Capital & Fixed Capital requirement under Virasat scheme.

III. Providing Micro Finance to the poorest of poor among minorities

through SCAs/NGOs & Network of Self Help Groups (SHGs).

IV. Providing Educational Loans to persons belonging to minorities.

V. Skill Development Training for the welfare of Minority Communities

under Kaushal se Kushalta scheme with a view to help them in

wage/self-employment.

VI. Marketing Assistance to Artisan and Craft persons for sale/display of

their products.

VII. Mahila Samridhi Yojana aims to provide training to women in

employment oriented skills.

QUESTION 4 Who comprise the target groups for NMDFC assistance? ANSWER Target groups for NMDFC with regard to direct benefits will be persons

belonging to minority communities. At present, Minority communities as

per National Minorities Commission Act, 1992 are Muslims, Sikhs,

2

Buddhists, Christians, Parsis. Recently Govt. of India vide notification

dtd. 27.01.2014 has included the Jain community amongst Minorities in

addition to already notified five communities.

Families having annual income less than Rs.98,000 in rural areas and

Rs.1,20,000 in urban areas are the target group of NMDFC.

As a special initiative by NMDFC, a new annual household income

eligibility limit of up to Rs.6.00 lacs has been introduced with effect from

September, 2014.

QUESTION 5 How much is the Authorized and Paid-up Share Capital of NMDFC? ANSWER The Authorized Share capital of NMDFC is Rs.3000.00 crores with 73%

(2190.00 crores) contribution from Central Government, 26% (780.00

crores) contribution from various State/UT Governments and 1% (30.00

crores) from individuals/organizations having interest in minorities.

The paid up share capital of NMDFC as on 30/06/2020 is Rs.2143.50

crores with contribution of Rs.1760.00 crores by Government of India

and Rs.383.49 crores by State/UT Governments i.e. 80.37% and 49.17%

respectively.

Amt in Rs/Crs

Shareholders %-age Shares

Share in Authorized

Share Capital

Paid up Capital

%age of

contribution

Amount

yet to be

paid

%age to be

contributed

GOI 73 % 2,190.00 1760.00 80.37% 430.00 19.63%

State/UT Govt.

26 % 780.00 383.49 49.17% 396.51 50.83%

Institutions/ Individuals

1 % 30.00 0.01 0.01% 29.99 99.99

Total 100% 3,000.00 2143.50 71.45% 856.50 28.55

QUESTION 6 Un-like other Apex Corporations, why States are required to

contribute to the equity of NMDFC?

ANSWER Because NMDFC is the joint venture of States and Central Government.

QUESTION 7 What is the earmarked share of each State/UT Government for

contribution to the equity of NMDFC and how much has since been

contributed?

ANSWER Share of each State/UT Governments in the equity of NMDFC has been

earmarked in proportion to its population of minorities. The information

3

of earmarked share and the contribution received by 30/06/2020 is as

given below:

QUESTION 8 How does NMDFC reach the beneficiaries? ANSWER NMDFC has two channels to reach to the ultimate beneficiaries;

(i) through the State Channelizing Agencies (SCAs) nominated by

respective State/UT Government; generally each Channelizing

4

Agency has an office at district level where the beneficiary is

required to make formal application.

(ii). through the network of NGO/SHGs for micro-credit.

QUESTION 9 How many States and UTs have already nominated their Chanelizing

Agencies for NMDFC?

ANSWER NMDFC has 45 State Channelizing Agencies (SCAs) in 27 States and 7

UTs for implementation of NMDFC schemes. Out of total 45 SCAs, 37

SCAs are operational while 8 SCAs are Non-Operational. The following is

the list Operational & Non-Operational SCAs nominated by their

respective States/UTs:-

SR. No. STATES YEAR OF

STARTING NMDFC PROG.

SCAs CHANNELISING AGENCY

Minorities Development & Finance Corporations

1. ANDHRA PRADESH 1995-96 APSMFC 1. ANDHRA PRADESH STATE MINORITIES FINANCIAL

CORPN.

2. ASSAM 1998-99 AMDFC 2. ASSAM MINORITIES DEVELOPMENT & FINANCE

CORPN.

3. BIHAR 1997-98 BSMFC 3. BIHAR STATE MINORITIES FINANCIAL CORPN.

4. GUJARAT 1999-2000 GMFDC 4. GUJARAT MINORITIES FINANCE AND DEVELOPMENT

CORPORATION

5. HIMACHAL PRADESH

1997-98 HPMFDC 5. H.P. MINORITIES FINANCE AND DEVELOPMENT

CORPORATION

6. JHARKHAND 2019-20 JSMFDC 6. JHARKHAND STATE MINORITIES FINANCE &

DEVELOPMENT CORPORATION

7. KARNATAKA 1994-95 KMDC 7. KARNATAKA MINORITIES DEV. CORPN.

8. KERALA 2014-15 KSMDFC 8. KERALA STATE MINORITY DEVELOPMENT &FINANCE

CORPORATION

9. MAHARASHTRA 2001-02 MAAAVN 9. MAULANA AZAD ALPSANKHYAK AARTHIK VIKAS

NIGAM

10. RAJASTHAN 2001-02 RMFDCC 10. RAJASTHAN MINORITIES FINANCE AND

DEVELOPMENT COOP. CORPN.

11. TAMIL NADU 2003-04 TAMCO 11. TAMIL NADU MINORITIES ECONOMIC DEVELOPMENT

CORPORATION

12. TRIPURA 1997-98 TMCDC 12. TRIPURA MINORITIES COOP.DEV.CORPN.

13. UTTAR PRADESH 1994-95 UPMFDC 13. U.P. MINORITIES FINANCIAL DEV. CORPN.

14. UTTRAKHAND 2002-03 UAKTWVN 14. UTTRAKHAND ALPSANKHYAK KALYAN TATHA WAKF

VIKAS NIGAM

5

15. WEST BENGAL 1996-97 WBMDFC 15. WEST BENGAL MINORITIES DEV. & FINANCE CORPN.

State SC & ST Development Corporations

1. CHANDIGARH 1997-98 CSCSTFDC 16. CHANDIGARH SCHEDULED CASTE,BACKWARD

CLASSES & MINORITIES FINANCIAL & DEVELOPMENT CORPORATION

2. CHHATISGARH 2002-03 CSACFDC 17. CHATTISGARH STATE ANTYAVASAYEE COOPERATIVE

FINANCE & DEVELOPMENT CORPORATION

3. DELHI 2002-03 DSCFDC 18. DELHI SC/ST/OBC MINORITIES & HANDICAPPED

FINANCIAL & DEV. CORPN.

4. JAMMU &

KASHMIR (UT) 1995-96 JKSCSTFDC 19. J&K SCs/STs& BCs DEVELOPMENT CORPN.

SR. No.

STATES YEAR OF

STARTING NMDFC PROG.

SCAs CHANNELISING AGENCY

State Backward Classes Development Corporations

1. KERALA 1996-97 KSBCDC 20. KERALA STATE BACKWARD CLASSES DEVELOPMENT

CORPORATION

2. MADHYA PRADESH

1995-96 MPBCDFC 21. M.P. BACKWARD CLASSES & MINORITES FINANCE AND

DEVELOPMENT CORPORATION

3. MANIPUR 2004-05 MOBEDS 22. MANIPUR MINORITIES AND OTHER BACKWARD

CLASSES ECONOMIC DEV. SOCIETY

4. HARYANA 1995-96 HBCKN 23. HARYANA BACKWARD CLASSES & ECONOMICALLY

WEAKER SECTIONS KALYAN NIGAM

5. PUDUCHERRY 2000-01 PBCMDC 24. PUDUCHERRY BACKWARD CLASSES & MINORITIES DEV.

CORPORATION

6. PUNJAB 1995-96 BACKFINCO 25. PUNJAB STATE BACKWARD CLASSES LAND DEV. AND

FINANCE CORPN.

7. ODISHA 2011-12 OBCFDCC 26. ODISHA BACKWARD CLASSES FINANCE DEVELOPMENT

COOPERATIVE CORPORATION

State Women's Development Corporations

1. KERALA 1994-95 KSWDC 27. KERALA STATE WOMEN’s DEVELOPMENT

CORPORATION

2. JAMMU &

KASHMIR (UT) 1995-96 JKWDC 28. J&K STATEWOMEN’s DEV. CORPN.

Handloom & Handicrafts Corporations

1. NAGALAND 2002-03 NHHDC 29. NAGALAND HANDLOOM & HANDICRAFTS

DEVELOPMENT CORPORATION

Other Agencies

1. HARYANA 2009-10 MDA 30. MEWAT DEVELOPMENT AGENCY

2. JAMMU & 2010-11 JKEDI 31. J&K ENTREPRENEURSHIP DEVELOPMENT INSTITUTE

6

KASHMIR

3. MIZORAM 1996-97 MCAB 32. MIZORAM COOPERATIVE APEX BANK

4. MIZORAM 1997-98 ZIDCO 33. ZORAM INDUSTRIAL DEVELOPMENT CORPORATION

5. KERALA 1998-99 KSCFFDC 34. KERALA STATE COOPERATIVE FEDERATION FOR

FISHERIES DEVELOPMENT

6. NAGALAND 1997-98 NIDC 35. NAGALAND INDUSTRIAL DEVELOPMENT CORPN.

7. NAGALAND 2009-10 NSSWB 36. NAGALAND STATE SOCIAL WELFARE BOARD

8. JAMMU &

KASHMIR (UT) 2015-16 JKSFC 37. J&K STATE FINANCIAL CORPORATION

List of Non-operational SCAs of NMDFC

A. STATES S.

No. Name of the State Name of the Non-Operational SCA

1 Arunachal Pradesh 38. Arunachal Pradesh State Coop. Apex Bank 2 Goa 39. Goa State Minorities Finance & Development Corporation 3 Meghalaya 40. Meghalaya Industrial Development Corporation 4 Sikkim 41. Sikkim SC/ST/OBC Development Corporation

B. UNION TERRITORIES

S. No.

Name of the UT Name of the Non-Functional UTs

1 Andaman & Nicobar 42. Andaman &Nicobar Industrial Dev. Corporation 2 Dadra & Nagar Haveli and Daman &

Diu 43. Dadra & Nagar Haveli SC/ST Financial Corporation 44. Daman & Diu SC/ST Financial Corporation

3 Lakshadweep 45. Lakshadweep Development Corporation

QUESTION 10 Which State/UT has so far not nominated SCA for NMDFC? ANSWER State of Telangana & U.T. of Ladakh has not nominated the SCA for

NMDFC so far.

QUESTION11 How many States have established Minorities Development

Corporations?

ANSWER So far, 15 States have nominated Minority Corporations to operate as

State Channelising Agency (SCA) of NMDFC. The name of States who

have nominated Minority Development corporations as SCA of

NMDFC are as follows:-

7

QUESTION 12 Which are the States/UTs who have not availed NMDFC assistance

so far?

ANSWER SCAs in the following States/UTs have not availed NMDFC assistance so far: STATES Arunachal Pradesh, Meghalaya, Telangana, Sikkim and Goa.

UTs : Dadra & Nagar Haveli, Lakshadweep, Daman and Diu,

Andaman and Nicobar.

Financing in UT of Ladakh was carried out when it was part

of J&K State. Now the UT administration of Ladakh is

required to nominate an SCA to implement NMDFC

schemes.

QUESTION 13How many State Channelising Agencies (SCAs) are Functional? ANSWER Out of total 37 operational SCAs, 28 SCAs are functional as they have

availed funds from NMDFC during last six years. The list of Functional

SCAs are as follows:-

Name of the Functional State Channelizing Agencies (SCAs) of NMDFC

STATES S.

no. Name of

State Name of the Functional SCAs

1 Chhattisgarh 1. Chhattisgarh State Antyavasayee Coop. Finance and Dev. Corpn.. 2 Gujarat 2. Gujarat Minorities Finance and Development Corporation 3 Haryana 3. Haryana Backward Classes & Economically Weaker Section

Kalyan Nigam 4. Mewat Development Agency

4 Himachal Pradesh

5. H.P. Minorities Finance and Development Corporation

5 Jharkhand 6. Jharkhand State Minorities Finance & Development Corporation 6 Kerala 7. Kerala State Backward Classes Development Corporation

8. Kerala State Women’s Development Corpn. 9. Kerala State Cooperative Federation for Fisheries Development 10. Kerala State Minorities Development Finance Corpn.

7 Karnataka 11. Karnataka Minorities Development Corporation

1. ASSAM 9. TAMIL NADU

2. ANDHRA PRADESH 10. UTTAR PRADESH

3. BIHAR 11. WEST BENGAL

4. HIMACHAL PRADESH 12. MAHARASHTRA

5. GUJARAT 13. RAJASTHAN

6. JHARKHAND 14. UTTRAKHAND

7. KARNATAKA 15. KERALA

8. TRIPURA

8

8 Maharashtra 12. Maulana Azad AlpsankhyakAarthikVikas Nigam 9 Mizoram 13. Mizoram Cooperative Apex Bank 10 Nagaland 14. Nagaland State Social Welfare Board

11 Punjab 15. Punjab State Backward Classes Land Development & Finance Corporation

12 Rajasthan 16. Rajasthan Minorities Finance and Development Corporation 13 Tamil Nadu 17. Tamil Nadu Minorities Economic Development Corporation 14 Tripura 18. Tripura Minorities Cooperative Development Corporation 15 Uttarakhand 19. Uttranchal Alpsankhyak Kalyan Tatha Wakf Vikas Nigam 16 Uttar

Pradesh 20. U.P. Minorities Financial Development Corporation

17 West Bengal 21. West Bengal Minorities Development and Finance Corporation

UNION TERRITORIES

S. No.

Name of UT

Name of the Functional SCAs

1 Chandigarh 22. Chandigarh SCBC& Minorities Financial & Development Corporation

2 Delhi 23. Delhi SC/ST/OBC& Minorities & Handicapped Fin.& Dev. Corporation

3 Jammu & Kashmir

24. J&K Women’s Development Corporation 25. J&K Entrepreneurship Development Institute (JKEDI) 26. J&K SCs/STs & BCs Development Corporation 27. J&K State Fin Corporation

4 Puducherry 28. Puducherry Backward Classes and Minorities Development Corp.

QUESTION 14How many SCAs of NMDFC are Non- Functional with reasons?

ANSWER Out of total 37 Operational SCAs, 9 SCAs are Non-Functional as they have not availed funds from NMDFC during last six years. The list of Non-Functional SCAs are as follows:-

Name of the Non-Functional State Channelizing Agencies (SCAs) of NMDFC Sr.No Name of the

State Name of the Non-Functional

SCA Reasons for non-functional

1 Andhra Pradesh 1. Andhra Pradesh State Minorities Fin. Corporation

The State Govt. has stopped implementing schemes with Loan component since 2008-09.

2 Assam 2. Assam Minorities Dev & Finance Corporation

Loaning stalled since 2012-13 due to over dues of Rs.13.30 crs.

3 Bihar 3. Bihar State Minorities Financial Corporation

Loaning stalled since 2012-13 due to over dues of Rs.23.74 crs.

4 Mizoram 4. Zoram Industrial Development Corporation

Loaning stalled since 2003-04 due to mounting over dues of Rs.17.29 crs. State Govt. has approached for settlement under OTS. Final approval of State Govt. is

9

pending. 5 Madhya Pradesh 5. M.P. Backward Classes &

Minorities Finance and Development Corporation

Loaning stalled since 2005-06 due to poor repayments in case of MPBCFDC. Over dues since repaid under OTS. SCA has intimated to implement State Govt. schemes only.

6 Manipur 6. Manipur Minorities & Other Backward Classes Economic Development Society

Loaning stalled since 1999-2000 due to over dues. Repaid over dues under OTS. Manipur Minorities & OBC Economic Development Society (MOBEDS) nominated as new SCA. Loaning to start once Govt. Guarantee is furnished.

7 Nagaland 7. Nagaland Handloom & Handicrafts Development Corporation

Loaning stalled since 2013-14 due to mounting over dues of Rs.9.67 crs.

8. Nagaland Industrial Development Corpn

Loaning stalled since 2013-14 due to mounting over dues of Rs.33.55 crs.

8 Odisha 9. Orissa Backward Classes Finance Development Cooperative Corporation

Implementation of NMDFC schemes in Odisha is stalled since 2013-14. The overdues have been settled partially under the OTS and thereafter the State Govt. has decided not to avail loan from NMDFC.

QUESTION 15 How many SCAs of NMDFC are Non-Operational with reasons? ANSWER Out of total 45 SCAs, 28 SCAs are Functional, 9 are Non-Functional while

following 8 SCAs are Non-Operational as the State Govts/SCAs have not

completed codal formalities for availing funds from NMDFC :-

List of Non-operational SCAs of NMDFC STATES

S. No.

Name of the State

Name of the Non-Operational SCA

Reasons for Non-Operationalization of SCA

1 Arunachal Pradesh

1. Arunachal Pradesh State Coop. Apex Bank

Govt. Order towards Govt. Guarantee is pending from the State Government.

2 Goa 2. Goa State SC, OBC Finance & Development Corporation

SCA has signed General Loan Agreement with NMDFC. Govt. guarantee of Rs.2.00 crs. also provided by the Govt. Program is expected to start shortly.

3 Meghalaya 3. Meghalaya Industrial Dev. Corp.

SCA has not signed General Loan Agreement with NMDFC. Also Govt. Order towards Govt. Guarantee is awaited from the State Government.

4 Sikkim 4. Sikkim SC/ST/OBC Dev. Corp.

Govt. Order towards Govt. Guarantee is awaited from the State Government.

10

UNION TERRITORIES S.

No. Name of the

UT Name of the Non-

Functional UTs Reasons for non-functional

1 Andaman & Nicobar

5. Andaman Nicobar Industrial Dev. Corp.

SCA has not signed General Loan Agreement with NMDFC. Also Govt. Order towards Govt. Guarantee is awaited from the UT Administration.

2 Dadra & Nagar Haveli and Daman & Diu

6. Dadra & Nagar Haveli SC/ST Financial Corpn.

--- DO ---

7. Daman & Diu SC/ST Financial Corpn.

--- DO ---

4 Lakshadweep 8. Lakshadweep Development Corpn.

--- DO ---

QUESTION 16 What is the rate of interest structure for NMDFC's schemes? ANSWER

Credit Line-1 Term Loan of up to Rs.20,00,000/- is provided at interest rate of 6% p.a. Under the Educational loan scheme, loan upto Rs.20.00 Lakhs is provided

for domestic courses & loan upto Rs.30.00 lacs is available for courses abroad is given at 3% p.a.

Under Micro credit scheme, loan upto Rs.1.00 lac is available to each member of Self Help Group (SHG) &upto Rs.20.00 lacs to a group of 20 women at interest rate of 7% p.a.

Credit Line-2 Term Loan up to Rs.30,00,000/- is provided at interest rate of 8% p.a. for

male beneficiaries & 6% p.a. for women beneficiaries. Under the Educational loan scheme, loan upto Rs. 20.00 Lakhs is provided

for domestic courses & loan upto Rs.30.00 lacs is available for courses abroad. The Education Loan is available at 8% p.a. for male beneficiaries & 5% p.a. for women beneficiaries.

Under Micro credit, loan upto Rs.1.50 lacs is available to each member of Self Help Group (SHG) &upto Rs.30.00 lacs to a group of 20 women at interest rate of 10% p.a. for male beneficiaries & 8% p.a. for women beneficiaries.

QUESTION 17 What are the financial assistance schemes of NMDFC? ANSWER The following are the financial assistance schemes of NMDFC:-

The concessional credit line of NMDFC is bifurcated into two streams:-

Credit Line 1:- is the existing stream of concessional credit, being disbursed on the basis of income limits of Rs.98,000 p.a. for rural areas & Rs.1.20 lacs in urban areas.

11

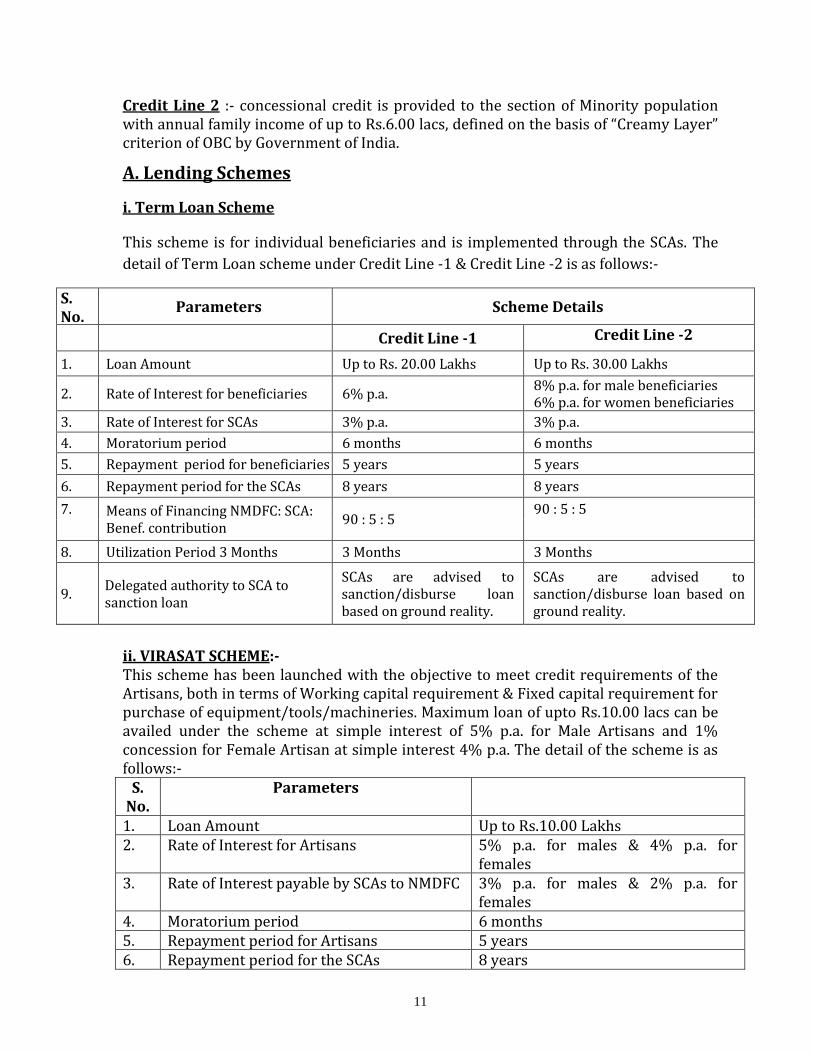

Credit Line 2 :- concessional credit is provided to the section of Minority population with annual family income of up to Rs.6.00 lacs, defined on the basis of “Creamy Layer” criterion of OBC by Government of India.

A. Lending Schemes

i. Term Loan Scheme

This scheme is for individual beneficiaries and is implemented through the SCAs. The

detail of Term Loan scheme under Credit Line -1 & Credit Line -2 is as follows:-

S. No.

Parameters Scheme Details

Credit Line -1 Credit Line -2

1. Loan Amount Up to Rs. 20.00 Lakhs Up to Rs. 30.00 Lakhs

2. Rate of Interest for beneficiaries 6% p.a. 8% p.a. for male beneficiaries 6% p.a. for women beneficiaries

3. Rate of Interest for SCAs 3% p.a. 3% p.a.

4. Moratorium period 6 months 6 months

5. Repayment period for beneficiaries 5 years 5 years

6. Repayment period for the SCAs 8 years 8 years

7. Means of Financing NMDFC: SCA: Benef. contribution

90 : 5 : 5 90 : 5 : 5

8. Utilization Period 3 Months 3 Months 3 Months

9. Delegated authority to SCA to sanction loan

SCAs are advised to sanction/disburse loan based on ground reality.

SCAs are advised to sanction/disburse loan based on ground reality.

ii. VIRASAT SCHEME:- This scheme has been launched with the objective to meet credit requirements of the Artisans, both in terms of Working capital requirement & Fixed capital requirement for purchase of equipment/tools/machineries. Maximum loan of upto Rs.10.00 lacs can be availed under the scheme at simple interest of 5% p.a. for Male Artisans and 1% concession for Female Artisan at simple interest 4% p.a. The detail of the scheme is as follows:-

S. No.

Parameters

1. Loan Amount Up to Rs.10.00 Lakhs 2. Rate of Interest for Artisans 5% p.a. for males & 4% p.a. for

females 3. Rate of Interest payable by SCAs to NMDFC 3% p.a. for males & 2% p.a. for

females 4. Moratorium period 6 months 5. Repayment period for Artisans 5 years 6. Repayment period for the SCAs 8 years

12

7. Pattern of Financing; NMDFC:SCA: Benf. contribution

90:5:5

8. Utilization Period 3 Months

iii. Educational Loan Scheme This scheme is also for the individual beneficiaries and is implemented through the

SCAs. The NMDFC extends Educational Loans with an objective to facilitate job oriented

education for the eligible persons belonging to Minorities. Under this scheme, loan is

available for 'technical and professional courses' of durations not exceeding five

years. The detail of Education Loan scheme under Credit Line -1 & Credit Line -2 is as

follows:-

Sr.

Nos. Parameters Scheme Details as per Credit Line - 1 Scheme Details as per Credit Line - 2

1. Loan Amount Maximum

Loan amount per beneficiary is:- - Up to Rs.20.00 Lacs for 'Professional &

Job Oriented Degree Courses' in India with a maximum duration of 5 years @ Rs.4.00 lacs p.a.

- Up to Rs.30.00 Lacs for 'Courses Abroad' with a maximum duration of 5 years @ Rs.6.00 Lacs per annum.

Loan amount per beneficiary is:- - Up to Rs.20.00 Lacs for 'Professional &

Job Oriented Degree Courses' in India with a maximum duration of 5 years @ Rs. 4.00 lacs per annum.

- Up to Rs.30.00 Lacs for 'Courses Abroad' with a maximum duration of 5 years @ Rs. 6.00 Lacs per annum.

2. Rate of Interest for beneficiaries

3%p.a. 8%p.a.for male beneficiaries

5% p.a. for women beneficiaries

3. Rate of Interest for SCA

1%p.a. 2%p.a.

4. Moratorium period 6 months after completion of the course or getting a job, whichever is earlier

6 months after completion of the course or getting a job, whichever is earlier

5. Delegated authority to SCA to sanction loan

SCAs are advised to sanction/disburse loan based on ground reality.

SCAs are advised to sanction/disburse loan based on ground reality.

6. Repayment period for beneficiaries

5 years 5 years

7. Repayment period for the SCA

5 years 5 years

8. Means of Financing NMDFC : SCA : Beneficiary contribution

90 : 5 : 5 90 : 5 : 5

13

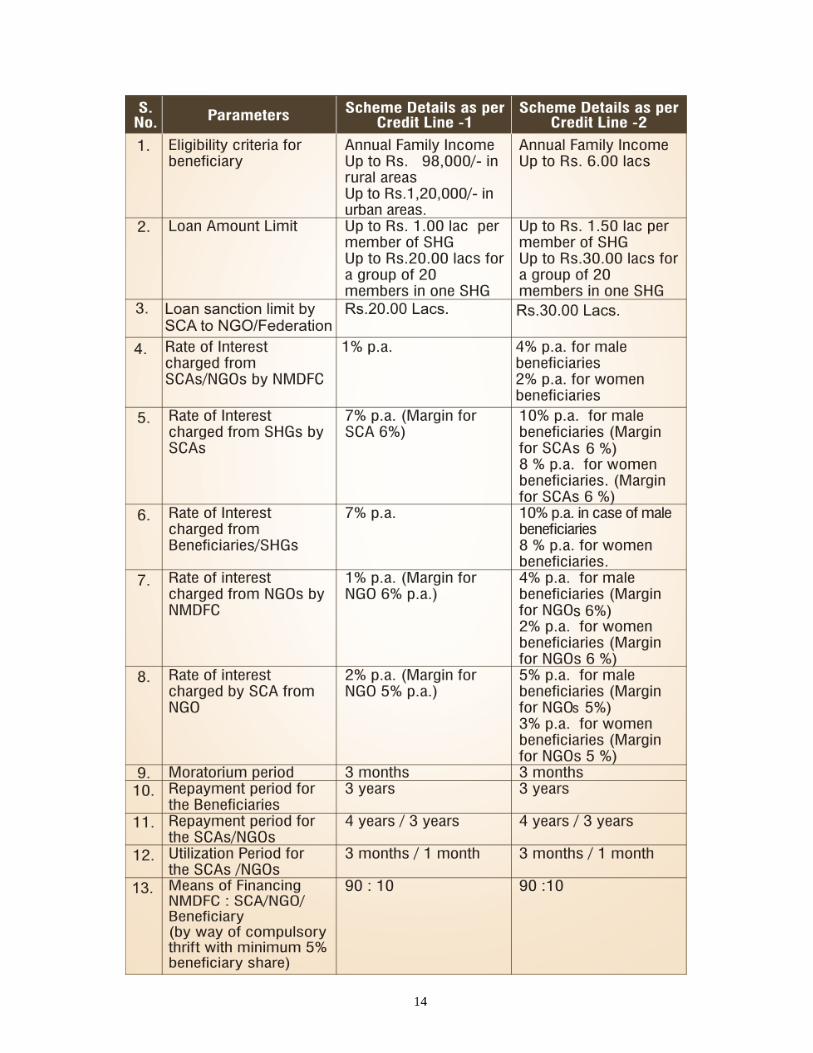

iv. Micro Financing Scheme Under the Micro Financing Scheme, micro-credit is extended to the members of the Self

Help Groups (SHGs), specially the minority women scattered in remote villages and

urban slums, who are not able to take advantage of the formal banking credit as well as

the NMDFC programmes, through its SCAs. The scheme 'requires that the beneficiaries

are organized into Self Help Groups (SHGs) and get into habit of thrift & credit,

however small. The scheme envisages micro-credit to the poorest among the poor

through network of Self Help Groups (SHGs). It is an informal loan scheme which

ensures quick delivery of loan at the door steps of the beneficiaries. The detail of Micro-

Finance scheme under Credit Line -1 & Credit Line -2 is as follows:-

14

15

B.Promotional Schemes

i. Kaushal Se Kushalta Scheme

The Kaushal Se Kushalta Scheme of NMDFC aims at imparting skills to the targeted

individual beneficiaries leading to self/wage employment. The scheme is implemented

through the State Channelising Agencies, which organize need based skill development

training in their States with the help of agencies empanelled by NSDC/ related Sector

Skill Council/ State Skill Mission/ Directorate of Technical Education. Preferably be

accredited through NSDC SMART portal.

The SCAs are required to submit their proposals to NMDFC in the prescribed formats

for approval/release of funds. Brief details of this scheme is as under:

S.

No.

Parameters of the Scheme Particulars of the Parameters

1 Base cost of Training This will be based on per hour fee notified by the

MOSD&E, Govt. of India. The present per hour fee (all

inclusive) is as given below:

Category I – Rs.46.70 per hour

Category II - Rs.40.00 per hour

Category III - Rs.33.40 per hour

The courses having duration between 200 to 250 hours

(theory & practical) would be considered under this

programme. The per hour fee would be subject to

revision by MOSD&E, from time to time.

2 Duration of Training 200 to 250 hours subject to minimum four (4) hours per

day and five days a week training.

3 Stipend Rs. 1,000/- per month per trainee, maximum up to 6

months, to be borne by NMDFC.

4 Means of Financing 100% cost will be borne by the NMDFC including

stipend

5 Placement 70% of pass out trainees with at least 50% of the total

trainees placed in wage employment.

6 Implementing Agency State Channelizing Agencies (SCAs) of NMDFC

ii) Marketing Assistance Scheme

The Marketing Assistance Scheme is meant for individual crafts-persons, beneficiaries of NMDFC as well as SHGs and is implemented through both SCAs as well as NGOs. With a view to support the crafts-persons to promote marketing & sale of their products at remunerative prices, NMDFC assists the SCAs and NGOs in organizing State /District

16

level exhibitions at selected locations. In these exhibitions, hand loom /handicraft products of Minority crafts-persons are exhibited and sold. Such exhibitions also serve the purpose of organizing "buyer seller meet", which is considered very useful for product development and market promotion, for domestic market as well as for exports. NMDFC provides grants for organizing exhibitions, as per the specific guidelines of the scheme, after due appraisal of the proposals as detailed below:-

iii. Mahila Samridhi Yojana

It is a unique scheme linking micro-credit with the training to the women members to

be formed in to SHGs, in the trades such as tailoring, cutting and embroidery, etc. It is

being implemented by NMDFC, through the State Channelizing Agencies of NMDFC.

Under the Mahila Samridhi Yojana, training is given to a group of around 20 women in

any suitable women friendly craft activity. The group is formed into Self Help Group

during the training itself and after the training, micro-credit is provided to the

members of the SHG so formed. The maximum duration of the training is of six months

with maximum training expenses of Rs. 1,500 p.m. per trainee. During the training a

stipend of Rs. 1,000 p.m. is also paid to the trainees. The training cost and stipend is

met by NMDFC as grant. After the training, need based micro credit subject to a

maximum of Rs. 1.00 lac is made available to each member of SHG, so formed at an

interest rate of 7% p.a.

S.No. Parameters Details 1. Cost for organizing exhibition at

SCA level For A Class cities Rs.22,000/stall For B Class cities Rs.18,000/stall For C Class cities Rs.14,000/stall All metros are A class cities, All State Capitals other than Metros are B Class cities, District headquarters/other cities are C Class cities.

2. Travelling Allowance 2nd class sleeper or ordinary bus fare (on actual) by shortest route.

3. Fixed Dearness Allowance to One Artisan/Beneficiary/SHG member only

For A Class cities Rs.700/- For B Class cities Rs. 600/- For C Class cities Rs. 500/-

4. Participants 60 local artisans/beneficiaries and 20 artisans/beneficiaries from outside the state.

5. No. of Stalls in each Exhibition 40 Stalls. If lesser number of stalls are put, then the expenditure would be reduced proportionately.

6. Duration of exhibition 15 days. If exhibition is organised for lesser number of days, expenditure would be reduced proportionately.

7. Sharing of Cost of Exhibition 90% of total cost by NMDFC & 10% by SCAs

17

QUESTION 18 Does NMDFC ask for any security for its loan? ANSWER Yes, the funds are lent by NMDFC to:- a). the State Channelizing Agencies against State Government

Guarantee b). while the funds are provided to NGOs against the concrete

security.

QUESTION 19 What is the Security sought from beneficiaries for availing funds under NMDFC schemes?

ANSWER NMDFC has advised that the SCAs may also seek security from the

beneficiaries for the loans disbursed to them. The type of security to be taken from the beneficiaries is to be decided by the SCAs. The norms of security should be such that the poor beneficiaries are able to meet them while necessary leverage for recovery of loan is also available to the lender. In general following security provisions are advised:-

a) For loans upto Rs.1,00,000

Self-Guarantee & Post Dated Cheques

b)

For loans exceeding Rs.1,00,000 and up to Rs.5,00,000-

Guarantee of one employee of PSU/Govt./Bank or one income tax payee/ Public Representative.

&

Post Dated Cheques.

c) For loans exceeding Rs.5,00,000

Guarantee of two employees of Govt./PSU/Bank or two income tax payee/ Public Representative or Guarantee from owner of property which is pledged as collateral.

OR

Collateral by way of Mortgage of landed property/Immovable Property of not less than the same value.

&

Post Dated Cheques.

Further, the SCAs have also been advised to become member of the Credit Guarantee Fund

Trust for Micro & Small Enterprises (CGTMSE) to help beneficiaries who are not able to

provide collateral security for the loan availed under NMDFC scheme. In such a case, the

interest rate charged from the beneficiary would increase for payment of commission to the

CGTMSE.

18

QUESTION 20 What are the sectoral groups of NMDFC financial assistance?

ANSWER NMDFC finances any viable and bankable proposal with maximum project cost of Rs.20 lac under Credit Line-1 & Rs.30.00 lacs under Credit Line-2. However, proposals could be categorised in the following sectors:-

1. AGRICULTURE & ALLIED This includes schemes such as animal breeding, poultry farming, bee- keeping etc. 2. TECHNICAL TRADES

These include technical trades at village/taluka level such as electrician, plumber, sheet metal, TV/Radio repair, motor mechanic, tyre puncture repair, cycle/taxi/auto rickshaw repairing and vulcanization, refrigeration mechanic etc.

3. SMALL-BUSINESS These include small business/tea shop/pan shop, egg sale/general provision shop/laundry, popcorn/text book shop magazine shop, newspaper, vendor, photocopier service, typewriting and word processing service etc.

4. ARTISAN AND TRADITIONAL OCCUPATIONS Occupation includes Embroidery work, wood carving, safety match box manufacturing, manufacturing of papad, jams, pickles, ready-made garments etc. 5. TRANSPORT & SERVICES SECTOR Includes plying of auto-rickshaws, cycle rickshaws, tempos, bullock and other animal driven carts for hire, cycle hiring service etc.

QUESTION 21What is the sector-wise financial assistance rendered under NMDFC scheme?

ANSWER The sector-wise detail of funds Utilization is given below:-

Name of Sector Percentage of Fund Utilisation by SCAs

Agriculture & Allied 22.49%

Technical Trades 3.44% Small Business 66.81% Artisan & Traditional Occupation

3.26%

Transport & Services Sector 4.00%

19

QUESTION 22How different States and UTs are making use of financial assistance from NMDFC?

ANSWSER So far since inception, NMDFC has disbursed an amount of Rs.5,878.89

crs. to 17,09,656 beneficiaries from Minority communities. State-wise disbursement of funds and the number of beneficiaries assisted up to 30.06.2020 is as given below:

QUESTION23: What is the Community-wise break-up of funds disbursed by

NMDFC? ANSWER Following is the Community-wise break-up of funds utilized under

NMDFC schemes during the 9 years (2010-11 to 2018-19):- In Percentage

Scheme Muslims Christians Sikhs Buddhist Parsis Jains Term Loan 78.10 17.30 3.69 0.73 Nil 0.18 Education 71.60 24.87 0.80 0.05 Nil 2.68

20

Loan Micro-Finance 78.19 21.60 0.07 0.12 Nil 0.02 Total 77.78 19.60 1.93 0.43 Nil 0.26

Question 24 Whether fund disbursement to respective States is in ratio of the

percentage of minority population in the respective State/UT?

Answer The following is the ratio of fund disbursed to respective States vis-à-vis

the ratio of their minority population:-

QUESTION 25What is the Gender-wise break-up of funds disbursed by NMDFC? ANSWER Following is the Gender-wise break-up of funds utilized under NMDFC

schemes during the 9 years (2010-11 to 2018-19):-

21

In Percentage Gender Term Loan Education Loan Micro-Finance Total

Male 66.23 65.95 1.84 38.89 Female 33.77 34.05 98.16 61.11

QUESTION 26What is the Rural-Urban break-up of funds disbursed by NMDFC? ANSWER Following is the Rural-Urban break-up of funds utilised under NMDFC

schemes during the 9 years (2010-11 to 2018-19):-

In Percentage Area Term Loan Education Loan Micro-Finance Total Rural 83.26 76.89 86.23 84.00 Urban 16.74 23.11 13.77 16.00

QUESTION27Who are the Directors on the Board of NMDFC? ANSWER Following are the Directors on Board of NMDFC:

Sr. No

Name of the Directors Telephone Nos.

1 Shri. Siddharth Kishore Dev Verman Addl. Secretary Ministry of Minority Affairs, 11th Floor, Pt. Deendayal ‘Antyodaya’ Bhawan, CGO Complex, Lodhi Road New Delhi-110003

011-24364280, [email protected]

2 Shri. Mohd. Shahbaz Ali Chairman-cum-Managing Director National Minorities Development & Finance Corporation Core 1, 1st Floor, Scope Minar Laxmi Nagar, Delhi -110092.

011- 22441635 [email protected]

3 Shri Subrata Reang Managing Director Tripura Minorities Co-operative Development Corporation Ltd., P.O. Lake Chowmuhani, Agartala West Tripura-799001

0381-2326512 [email protected]

4 Ms. Hema Sharma, IAS Managing Director Haryana Backward Classes & Economically Weaker Sections Kalyan Nigam, SCO 813-14, Sector 22-A CHANDIGARH – 160 022

0172-2701722 [email protected]

22

5. Shri. L.K. Meena Executive Director Rashtriya Mahila Kosh, B-12, Fourth floor, Samaj Kalyan Bhawan, Qutub institutional Area, New Delhi-110016

011-23381851 [email protected]

6 Sh. Ghulam Dar, Director J&K Entrepreneurship Development Institute (JKEDI) Sempora, Pampore Pantha Chowk, Srinagar, UT of J&K – 191 101

01933-224362 [email protected]

7. Sh. R. N. Kuchara, Managing Director Gujarat Minorities Finance and Development Corporation Ground Floor Block No.1, Dr. Jivraj Mehta Bhawan GANDHINAGAR - 382 010 (Guj.)

079- 23254583 [email protected]

8. Syeeda Iisha Managing Director Karnataka Minorities Development Corporation Ltd. 12th Floor, Main Tower Dr. B.R. Ambedkar Veedi BANGALORE – 560 001

080- 22861226 [email protected];

9. Sh. Ravi Tyagi, CGM, Small Industries Development Bank of India, 3rd Floor, Atma Ram House, 1, Tolstoy Marg, New Delhi – 110001.

011-23448422 [email protected]

10. Sh. Malkit Singh, DGM National Bank for Agriculture and Rural Development Plot No. 3, Sector 34-A, Post Box NO. 7 Chandigarh, Haryana – 160022

0172-5046456 [email protected]

11. Smt. Ishrat Mohiuddin Sayed, 320, Neelam Coop, Housing Society Ltd. 14-B Road, Khar, (West), Mumbai – 400052.

9820353069 [email protected]

12. Sh. S. Asim Basha, No. 39, A.A. Road, Kasturibai Gandhi Nagar, Vyasarpadi Chennai - 600039

9841118499 [email protected]

23

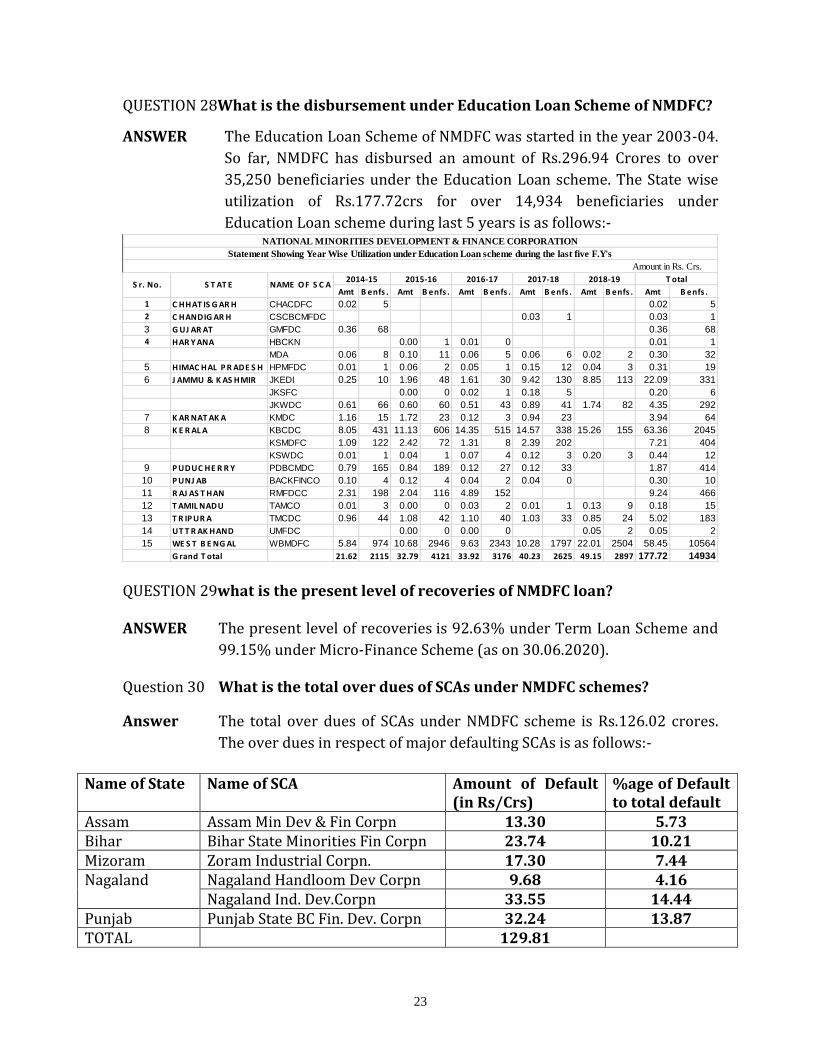

QUESTION 28What is the disbursement under Education Loan Scheme of NMDFC?

ANSWER The Education Loan Scheme of NMDFC was started in the year 2003-04.

So far, NMDFC has disbursed an amount of Rs.296.94 Crores to over

35,250 beneficiaries under the Education Loan scheme. The State wise

utilization of Rs.177.72crs for over 14,934 beneficiaries under

Education Loan scheme during last 5 years is as follows:-

QUESTION 29what is the present level of recoveries of NMDFC loan? ANSWER The present level of recoveries is 92.63% under Term Loan Scheme and

99.15% under Micro-Finance Scheme (as on 30.06.2020).

Question 30 What is the total over dues of SCAs under NMDFC schemes?

Answer The total over dues of SCAs under NMDFC scheme is Rs.126.02 crores.

The over dues in respect of major defaulting SCAs is as follows:-

Name of State Name of SCA Amount of Default

(in Rs/Crs) %age of Default to total default

Assam Assam Min Dev & Fin Corpn 13.30 5.73 Bihar Bihar State Minorities Fin Corpn 23.74 10.21 Mizoram Zoram Industrial Corpn. 17.30 7.44 Nagaland Nagaland Handloom Dev Corpn 9.68 4.16

Nagaland Ind. Dev.Corpn 33.55 14.44 Punjab Punjab State BC Fin. Dev. Corpn 32.24 13.87 TOTAL 129.81

Amt B enfs . Amt B enfs . Amt B enfs . Amt B enfs . Amt B enfs . Amt B enfs .

1 C HHAT IS G AR H CHACDFC 0.02 5 0.02 5

2 C HANDIG AR H CSCBCMFDC 0.03 1 0.03 1

3 G UJ AR AT GMFDC 0.36 68 0.36 68

4 HAR Y ANA HBCKN 0.00 1 0.01 0 0.01 1

MDA 0.06 8 0.10 11 0.06 5 0.06 6 0.02 2 0.30 32

5 HIMAC HAL P R ADE S H HPMFDC 0.01 1 0.06 2 0.05 1 0.15 12 0.04 3 0.31 19

6 J AMMU & K AS HMIR JKEDI 0.25 10 1.96 48 1.61 30 9.42 130 8.85 113 22.09 331

JKSFC 0.00 0 0.02 1 0.18 5 0.20 6

JKWDC 0.61 66 0.60 60 0.51 43 0.89 41 1.74 82 4.35 292

7 K AR NAT AK A KMDC 1.16 15 1.72 23 0.12 3 0.94 23 3.94 64

8 K E R AL A KBCDC 8.05 431 11.13 606 14.35 515 14.57 338 15.26 155 63.36 2045

KSMDFC 1.09 122 2.42 72 1.31 8 2.39 202 7.21 404

KSWDC 0.01 1 0.04 1 0.07 4 0.12 3 0.20 3 0.44 12

9 P UDUC HE R R Y PDBCMDC 0.79 165 0.84 189 0.12 27 0.12 33 1.87 414

10 P UNJ AB BACKFINCO 0.10 4 0.12 4 0.04 2 0.04 0 0.30 10

11 R AJ AS T HAN RMFDCC 2.31 198 2.04 116 4.89 152 9.24 466

12 T AMIL NADU TAMCO 0.01 3 0.00 0 0.03 2 0.01 1 0.13 9 0.18 15

13 T R IP UR A TMCDC 0.96 44 1.08 42 1.10 40 1.03 33 0.85 24 5.02 183

14 UT T R AK HAND UMFDC 0.00 0 0.00 0 0.05 2 0.05 2

15 WE S T B E NG AL WBMDFC 5.84 974 10.68 2946 9.63 2343 10.28 1797 22.01 2504 58.45 10564

G rand T otal 21.62 2115 32.79 4121 33.92 3176 40.23 2625 49.15 2897 177.72 14934

2018-19 T otal

NATIONAL MINORITIES DEVELOPMENT & FINANCE CORPORATION

Statement Showing Year Wise Utilization under Education Loan scheme during the last five F.Y's

Amount in Rs. Crs.

S r. No. S T AT E NAME O F S C A2014-15 2015-16 2016-17 2017-18

24

Question 31 What is the status of settlement of over dues by SCAs?

Answer NMDFC has been following with the State Channelising Agencies (SCAs)

& their respective State Governments for settlement of over dues. Legal

notice was also issued to SCAs with a copy to the State Government,

which stands as Guarantor, for the loan by the SCAs from NMDFC.

The NMDFC has also offered One Time Settlement (OTS) to the State

Channelising Agencies (SCAs) & their respective State Governments for

settlement of overdues. Under the OTS scheme, NMDFC would waive

penal interest/Simple Interest depending on payment terms.

During the last 4 financial years i.e. form 2013-14 to 2016-17,NMDFC has

realized Rs.126.84 crores under the OTS scheme by waiving penal

interest of Rs.53.49 crores as per following detail:-

Amt in Rs/crs. Sr.

Nos. Name of SCA Year of

Settlement Overdue

Amt AmtRealised

under OTS Penal

Interest Waived by

NMDFC under OTS

1 Karnataka Minorities Dev. Corpn (KMDC)

2013-14 19.92 14.24 5.68

2 Punjab BC Dev Corpn (BACKFINCO)

2013-14 2.59 1.40 1.19

3 Manipur Tribal Dev Corpn (MTDC)

2014-15 3.66 2.09 1.57

4 M.P BC Fin Dev Corpn(MPBCFDC)

2015-16 7.59 5.83 1.76

5 JK SCST Fin & Dev Corpn (JKSCSTFDC) (UT)

2015-16 5.62 3.18 2.50

6 Jharkhand ST Fin & Dev Corpn (JHSMFDC)

2015-16 1.01 0.87 0.14

7 Gujarat Minorities Fin &Dev Corpn (GMFDC)

2015-16 23.78 16.10 7.68

8 Haryana BC Kalyan Nigam (HBCKN)

2015-16 14.95 11.08 3.87

9 Odisha BC Dev Corpn (OBCFDC)

2015-16 8.46 4.71 3.75

10 UP Minorities Fin. Dev. Corpn (UPMFDC)*

2016-17 87.11 64.22 22.89

11 Gujarat Backward Classes Dev. Corpn. (GBCDC)

2018-19 5.59 3.12 2.46

T O T A L 180.28 126.84 53.49

* Rs.6.76 crs. pertaining to Uttrakhand has been removed from the overdue of UPMFDC.

25

After settlement of over dues under OTS, NMDFC has been able to

revive the SCAs in the States of Gujarat & Haryana (during F.Y. 2015-

16) and resume financing of poor Minority beneficiaries in these

two States. Further, during the financial year 2016-17 NMDFC has

also resumed financing in JKSCSTFDC, J&K.

Question 32 What is the status of Recovery of SCAs from Beneficiaries & their Repayment to NMDFCs?

Answer The following is the detail of Recovery of SCAs from beneficiaries viz-a- viz their Repayment to NMDFC:-

Sr. No State/UT SCA % Recovery

from Benfs.

Repayment to NMDFC

1 Andhra Pradesh A.P. State Minorities Financial Corporation NR 100%

2 Assam Assam Minorities Development and Finance Corporation NR 20.14%

3 Bihar Bihar State Minorities Financial Corporation NR 63.04%

4 Chandigarh (UT)

Chandigarh SC /BC & Minorities Fin. And Dev. Corp. 44.25 100%

5 Chattisgarh Chattisgarh State A&T. Coop. Fin. & Dev. Corp. 67.99 67.03%

6 Delhi (UT) Delhi SC/ST/OBC Minorities and Handicapped Fin. & Dev. Corp.

91.29 99.21%

7 Gujarat Gujarat Minorities Finance & Development Corporation 38.32 96.57%

8 Haryana Haryana BC and EWS Kalyan Nigam 100.00 100%

Mewat Development Agency 48.53 76.23%

9 Himachal Pradesh

HP Minorities Finance and Development Corporation 85.00 96.37%

10 Jammu & Kashmir (UT)

J&K SCST and BC Development Corporation NR 98.03%

J&K Women’s Development Corporation 99.00 99.12%

J&K Entrepreneurship Development Institute 77.14 91.91%

Jammu & Kashmir State Financial Corporation 100.00 100%

11 Jharkhand Jharkhand State Minorities Fin. & Dev. Corp. NR 98.91%

12 Karnataka Karnataka Minority Development Corp. NR 96.11%

13 Kerala Kerala State BC Dev. Corp. 97.24 97.70%

Kerala State Coop. Federation for Fisheries Dev. 84.00 98.32%

Kerala State Women’s Dev. Corp. 83.00 87.76%

Kerala State Minorities Dev. & Fin. Corp. 75.61 83.20%

14 Madhya Pradesh

M.P. BC & Minorities Fin. & Dev. Corp NR 100%

15 Maharashtra Maulana Azad Alpsankhayak Arthik Vikas Nigam NR 98.89%

16 Mizoram Mizoram Cooperative Apex Bank 100.00 100%

Zoram Industrial Development Corporation NR 34.77%

17 Manipur Manipur Minorities and OBC Economic Dev. Authority NA 100%

18 Nagaland Nagaland Industrial Development corporation 73.00 57.12%

Nagaland Handloom and Handicrafts Dev. Coop. Corp. NR 36.82%

Nagaland State Social Welfare Board NR 99.08%

19 Odisha Orissa BC Fin. Dev. Coop. Corp. NA 94.02%

20 Punjab Punjab State BCs Land Dev. & Fin. Corporation 91.00 67.84%

26

21 Puducherry (UT)

Puducherry BCs and Minorities and Development Corp. NR 62.84%

22 Rajasthan Rajasthan Minorities Finance and Development Crop. 35.94 94.09%

23 Tamilnadu Tamil Nadu Minorities Economic Development Corp.[ 85.00 97.09%

24 Tripura Tripura Minorities Coop Dev Corp. 82.00 89.21%

25 Uttar Pradesh UP Minorities Fin Dev Corp. NR 85.14%

26 Uttrakhand Uttranchal Alpsankhayak Kalyan tatha Waqf Vikas Nigam 55.68 100%

27 West Bengal West Bengal Minorities Dev. & Fin. Corporation 71.11 100%

Question 33 Use of AADHAR Card for sanction/disbursement of loan to beneficiaries

for greater transparency. Answer:-

NMDFC has directed its SCAs to use AADHAR numbers while identifying the

beneficiaries and link their loan accounts with their AADHAR numbers.

Wherever the facility of AADHAR is not available, the SCAs have also been advised to

use any other bio-metric feature of the beneficiary, to avoid duplication /

impersonation and for ensuring greater transparency.

Most of the SCAs have started AADHAR linked financing.

Linking of AADHAR numbers for extending benefits to the notified Minority

beneficiaries has been introduced from 01.01.2015.

Question 34 Transfer of Loan directly in AADHAR/KYC seeded bank account of beneficiaries through NEFT/RTGS for DBT.

Answer:- SCAs have been advised to open Bank Account of beneficiaries under the Jan Dhan

Yojana & link these accounts with AADHAR number or KYC of beneficiaries.

Transfer of loan through RTGS/NEFT directly in bank accounts of beneficiaries has

been made mandatory under the lending policy of NMDFC, for quick delivery of

benefits to the loanee.

SCAs have been directed to ensure DBT from 1st April, 2016.

Question 35 Insurance of beneficiaries & their Assets for safety of loanees & their

families from Loan Liability in the event of any mishap. Answer:-

For safety of the loanees & their family members in the event of any mishap, insurance of beneficiaries & their assets has been made mandatory part of lending policy of NMDFC. The SCAs have been directed to undertake the following:-

Insurance of beneficiaries against death/disabilities and the assets at the time of

financing. For this purpose, the SCA should enter into an understanding with an

insurance company for insuring the beneficiaries and their assets. The SCA

should be made nominee of the insurance claim to the extent of the loan

outstanding and the balance claim amount be given to the nominee of the

beneficiary, in the event of any untoward incident.

27

Beneficiary may also be motivated to subscribe to Pradhan Mantri Suraksha

BimaYojna (PMSBY) & Pradhan Mantri Jeevan Jyoti Bima Yojna (PMJJBY) linked

with their bank account at the time of loaning.

Beneficiaries should also be persuaded to subscribe to Atal Pension Yojana

(APY) as there is guaranteed minimum monthly pension for the subscribers

ranging between Rs.1000 and Rs.5000 per month.

Question 36 Impact Studies Conducted by NMDFC during last 5 years

Answer:

NMDFC conducts “beneficiary verification” and “impact assessment study” through

independent third party organizations / agencies to assess the impact of NMDFC

financing and also to check the mis-utilization, duplicity & diversion of funds.

NMDFC gets verification of beneficiaries every year of at least 10% beneficiaries

financed by it, two years ago.

The study has been conducted through National Institute of Entrepreneurship &

Small Business Development (NIESBUD), NOIDA under Ministry of Small Medium &

Micro Enterprises & Centre for Market Research & Social Development, New Delhi –

an agency empanelled with Ministry of Minority Affairs. Independent empanelled

monitors , mostly retired government officers were also engaged for undertaking

beneficiary work by NMDFC

The detail of impact assessment studies and the beneficiary verification works

carried-out by NMDFC is given below:- Sr. No.

Year Name of Agency Salient observations of the study report.

1 2009-10 By the empanelled Monitors of NMDFC

Most beneficiaries financed were from target income group.

Over 80% beneficiaries reported change in their income level.

65% beneficiaries were repaying loan regularly. 2 2010-11 National Institute of

Entrepreneurship & Small Business Development (NIESBUD), NOIDA. Under Ministry of Small Medium & Micro Enterprises.

52% of beneficiaries financed crossed poverty line Average grass root level recovery of over 60% 12% beneficiaries could provide wage employment

after availing loan.

3. 2011-12 By the empanelled Monitors of NMDFC

54% of the beneficiaries financed crossed poverty line

Nearly 80% beneficiaries created assets from loan 86% of the units were operational.

4. 2012-13 National Institute of Entrepreneurship & Small Business Development (NIESBUD), NOIDA. Under Ministry of Small Medium & Micro Enterprises.

Majority beneficiaries are first time recipient of loan.

Al most all the beneficiaries have opened bank account in the Banks which are located in their locality.

Around 72% beneficiaries have received their loan amount through cheque followed by one-fourth through cash and rest through Demand Draft.

28

95% units were functional. 48% beneficiaries financed have crossed the

poverty line. 5. 2013-14 Centre for Market Research &

Social Development, New Delhi. Agency Empanelled with Ministry of Minority Affairs.

93.5% beneficiaries reported no difficulty in availing the loan

Over 80% beneficiaries indicated that their income/savings has increased and they have now better health & education facilities thereby improving their social prestige.

Majority (67.6%) beneficiaries under micro finance scheme have bank account &possess individual pass book.

Almost all (99.3%) beneficiaries in Self Help Groups have properly utilized loan.

6. 2014-15 Centre for Market Research & Social Development, New Delhi. Agency Empaneled with Ministry of Minority Affairs.

71.9% of the Term Loan beneficiaries are found to be men while 97.1% are women financed under Micro Financing Scheme of NMDFC.

84% of the Term Loan beneficiaries are Muslims, 10.6% are Christians & 5% are Sikhs. Under Micro Financing Scheme 81.5% of the beneficiaries are Muslims, 16.1% are Christians.

99.7% of the sample Term Loan beneficiaries opined that there was no difficulty in availing the loan.

81.8% SCAs are maintaining computerized list of beneficiaries.

The study further suggested to increase the number of functional SCAs in a State with the priority being accorded to those having none of the agencies.

7. 2015-16 APITCO 91% units were found to be operational. 91% beneficiaries had utilized loans properly. 96% beneficiaries have created assets for the

activity for which loan was sanctioned. 97% beneficiaries are satisfied with the financial

assistance process. 71% got loan for the first time and created income

generation capability for the beneficiaries. 29% beneficiaries were existing units and loan was used for expansion of business.

8. 2017-18 Development & Research Service Pvt. Ltd.

96% Term Loan beneficiaries possessed the assets created for which loan was availed from NMDFC.

97% beneficiaries were found to be engaged in the activities for which they had taken the loan.

63% beneficiaries have taken the loan to start a new business, about 34% to expand the existing business.

96% beneficiaries had started repaying the loan amount.

93% beneficiaries faced no difficulty in availing the loan.

On an average 1.5 person per unit were reportedly employed in the operational units of the beneficiaries of term loan scheme as indirect employment.

On an average 7 months of employment was

29

provided per year to the employees working in operational units of beneficiaries under indirect employment.

Question 37 What is the demand for NMDFC Loan?

Answer

The total Minority Population of the country as per 2011 census is 23.47 crores. As per

the poverty line data for the country, it is expected that 22% of the population is below

the poverty line however, the annual family income criterion under NMDFC loaning is

Rs.98,000 for rural areas & Rs.1.20 lacs in urban areas. Thus, it is assumed that about

35% of the minority population fall within the target income criterion of NMDFC. By

the above logic, it works out that 8.20 crores persons amongst the minority population

is within the annual income target group of NMDFC. If the average size of the family

comprise of 5 persons, then there are 1.76 crores members which can be considered as

target group of NMDFC. So far, NMDFC has been able to extend credit to over 17.09 lacs

beneficiaries (as on 30.06.2020) under its financing program.

Question 38 What is Grant-In-Aid Scheme of Ministry of Minority Affairs & how it

has been useful to the SCAs of NMDFC?

Answer

The GIA scheme was started in the year 2007-08.

The objective of the Grant-In-Aid scheme is to strengthen the infrastructure of the

SCAs in order to improve their operations including recovery of loans.

The scheme is implemented by the Ministry of Minority Affairs through NMDFC.

The scheme is available for all performing SCAs of NMDFC.

Assistance is available for following activities:-

a. Awareness Campaign

b. Improvement in Delivery System of SCAs

c. Loan Recovery

d. TA/DA for staff /officers of SCA limited to 5% of total GIA sanctioned in a year.

No Capital Assets or permanent liability can be created under the scheme.

Question 39 How much fund has been disbursed by NMDFC under the Grant-In-

Aid scheme of Ministry of Minority Affairs?

Answer

So far since inception of the GIA scheme in 2008-09, an amount of Rs.25.28 crores

has been released to SCAs.

Year-wise & State wise cumulative funds disbursed by NMDFC to its State

Channelising Agencies (SCAs) under the Grant-In-Aid scheme of Ministry of

Minority Affairs is given below:-

30

Amt. in Rs. Lacs

(As on 30.06.2020)

Sr No Name of State/UT Name of SCA Cumulative amount disbursed since-inception of GIA scheme

2007-08

1 Andhra Pradesh APMFC 30.51

2 Assam AMDFC 97.14

3 Bihar BSMFC 114.97

4 Chandigarh (UT) CHSCSTDFC 4.02

5 Chhatisgarh CACFDC 30.75

6 Delhi (UT) DSCSTMFDC 25.45

7 Gujarat GMDFC 52.74

6 Haryana HBCKN 42.06

MDA 6.26

8 Himachal Pradesh HPMFDC 38.92

9 Jammu & Kashmir (UT) JKWDC 116.98

JKSCSTFDC 11.30

JKEDI 57.13

JKSFC 26.50

10 Jharkhand JSMFDC 13.00

11 Karnataka KMDC 88.06

12 Kerala KSBCDC 208.05

KSWDC 118.77

MATSYAFED 130.06

KSMDFC 33.76

13 Madhya Pradesh MPBCMFDC 18.00

MPHAAVN 2.27

14 Maharashtra MAAAVM 156.48

15 Manipur MOBEDS 11.15

16 Mizoram MCAB 34.43

17 Nagaland NHHDC 17.91

NSSWB 19.32

NIDC 23.14

18 Orissa OSBCDC 25.85

19 Puducherry (UT) PBCMDC 47.64

20 Punjab BACKFINCO 118.34

21 Rajasthan RMDFC 101.68

31

22 Tamil Nadu TAMCO 197.47

23 Tripura TMCDC 107.08

24 Uttar Pradesh UPMFDC 127.23

25 Uttaranchal UAKWVN 15.45

26 West Bengal WBMDFC 279.80

T O T A L 2549.67

Question 40 What are the guidelines issued by NMDFC to the SCAs in implementation

of Term Loan & Micro-Finance scheme?

Answer

NMDFC’s Lending Policy emphasizes on NEED BASED FINANCING i.e. financing as per the need of the beneficiaries (nature of project, quantum of funds) and need of the area (number of units). To achieve this objective, SCAs have been delegated with powers and required freedom and flexibility in working, as given below:- a). For wider coverage of beneficiaries under the financing schemes of NMDFC, the

SCAs may consider to extend mostly small quantum of loans. Out of total disbursement of credit by an SCA, i). 70% of the loans financed must be for loans not exceeding Rs.5.00 lacs

per beneficiary, ii). 20% of the loans financed may be greater than Rs.5.00 lacs but less than

Rs.10.00 lacs and iii). Only 10% of total loan financed could be for projects with loans greater

than Rs.10.00 lacs. b). Number of units to be financed under any scheme at any location will be decided

by the SCA. c). Loan upto Rs.5.00 lacs may be treated as composite loan while for loan beyond

Rs.5.00 lacs, the working capital component must not exceed 40% of total loan amount.

d). Education loan is part of Term Loan & must not exceed beyond 20% of the Term Loan extended by the SCA during a year. Out of this, 10% should be for fresh Education Loan cases & balance 10% for old cases.

e). Preference should be given for Education Loan to students who have secured admission to Government Institutions. Education Loan should be extended only for courses with good employment prospects. Out of total Education Loan cases financed by an SCA in a year, 90% cases should be for domestic courses only. Preference should be given to short duration course with high employment potential.

f). Loans of more than Rs.5.00 lacs should be disbursed in 2 installments. After disbursement of first 50% of the sanctioned loan, verification of its utilization should be conducted by the SCAs before release of further funds to the beneficiaries. Details of all such cases should be uploaded on the website of SCAs before disbursement of loan to the beneficiaries.

g). Beneficiary selection will be the sole-responsibility of the SCAs who fulfill the basic eligibility criteria and are found suitable for their chosen project as well as from socio economic angle through well laid-out selection procedures. The SCAs

32

will also evaluate the techno-economic viability of the project submitted by the beneficiary for final selection of the beneficiary.

h). Follow up with the beneficiaries to check up whether the assets as per the sanctioned scheme have been purchased and are being used for the purpose sanctioned.

i). Effecting recoveries from the beneficiaries for the disbursed amount and making repayments to NMDFC on Quarterly basis.

j). Providing to NMDFC report on the utilization of funds along with the list of beneficiaries from time to time, quarterly report on actual recoveries from the beneficiaries etc.

Question 41 Detail of funds sanctioned under the Vocational Training scheme of

NMDFC.

Answer

So far, NMDFC has sanctioned vocational training program involving outlay of Rs.14.05

crores for over 23,723 trainees. The State-wise detail of sanction accorded by NMDFC is

as follows:-

Amt in Rs/lacs

Sr. Nos. Name of State/UT SANCTION

Amt. Benfs.

1 Andhra Pradesh 7.20 300

2 Assam 5.40 140

3 Bihar 26.40 535

4 Chandigarh (UT) 2.35 55

5 Chhattisgarh 3.60 60

6 Delhi (UT) 0.00 0

7 Gujarat 6.33 498

8 Himachal Pradesh 1.71 44

9 Haryana 21.90 1,500

10 Jammu & Kashmir (UT) 442.22 3,630

11 Jharkhand 7.75 260

12 Kerala 132.14 2,490

13 Karnataka 79.36 1,314

14 Maharashtra 0.00 0

15 Manipur 0.00 0

16 Madhya Pradesh 17.55 440

17 Mizoram 0.00 0

18 Nagaland 8.55 150

19 Orissa 29.34 480

20 Puducherry (UT) 6.93 181

21 Punjab 71.01 1,333

22 Rajasthan 20.74 346

33

23 Tamil Nadu 46.80 910

24 Tripura 1.66 55

25 Uttar Pradesh 60.30 1,395

26 Uttaranchal 30.00 350

27 West Bengal 376.57 7,257

Total 1405.81 23,723

Question 42 Detail of funds disbursed under the Marketing Assistance scheme of

NMDFC.

Answer

So far, NMDFC has sanctioned exhibitions under the Marketing Assistance scheme

involving outlay of Rs.999.28 lacs for over 36,878 artisans/SHG members. The State-

wise detail of sanction accorded by NMDFC is as follows:-

Sr. Nos.

Name of State/UT SANCTION

Amount in Rs.lacs. Beneficiaries 1 ANDHRA PRADESH 𝟎. 𝟏𝟐 𝟔𝟎 2 ASSAM 𝟏. 𝟖𝟎 𝟐𝟎 3 BIHAR 𝟏𝟓. 𝟖𝟒 𝟏, 𝟑𝟐𝟔 4 DELHI (UT) 𝟕𝟔. 𝟒𝟗 𝟐𝟏𝟐 5 GUJARAT 𝟓𝟑. 𝟔𝟓 𝟐𝟐𝟓 6 JAMMU & KASHMIR (UT) 𝟐𝟏𝟐. 𝟗𝟑 𝟏𝟏, 𝟗𝟗𝟖 7 KERALA 𝟒𝟏. 𝟎𝟎 3,640

8

KARNATAKA 𝟒𝟏. 𝟏𝟕 𝟏𝟖𝟎

9 MAHARASHTRA 𝟒𝟕. 𝟏𝟖 𝟖𝟑𝟖 10 MADHYA PRADESH 𝟓. 𝟗𝟐 𝟏, 𝟏𝟎𝟗 11 NAGALAND 𝟔𝟐. 𝟗𝟑 𝟒, 𝟗𝟕𝟏 12 PONDICHERRY (UT) 𝟒𝟔. 𝟑𝟔 𝟑, 𝟏𝟒𝟔 13 RAJASTHAN 23.04 𝟏𝟑𝟎 14 TAMILNADU 𝟒. 𝟐𝟑 𝟓𝟑𝟎 15 UTTAR PRADESH 𝟐𝟏. 𝟖𝟐 𝟏𝟒𝟎 16 UTTARANCHAL 𝟗. 𝟐𝟎 𝟔𝟔𝟑 17 WEST BENGAL 𝟏𝟔𝟎. 𝟔𝟎 𝟕380 18 SURAJKUND MELA 𝟏𝟕𝟓. 𝟎𝟎 𝟑𝟏𝟎

Total 999.28 36,878

Question 43 Detail of funds disbursed under the Mahila Samridhi Yojana scheme of

NMDFC.

Answer

So far, NMDFC has sanctioned training programs under Mahila Samridhi Yojana (MSY)

involving cumulative outlay of Rs.156.41 lacs for 2,164 women from Self Help Groups

34

members. The scheme is implemented through the SCAs & NGOs. The MSY has been

revised in the year 2013-14 by increasing the training cost, cost of raw material &

stipend for trainees. The implementing agencies are being pursued to take up

implementation of the MSY scheme. The State-wise detail of sanction accorded by

NMDFC is as follows:-

Amt in Rs.

STATE/UT

DIST

NAME OF INSTITUE

SCA/NGO

Total Amount (in Rs.)

Benefs.

Andhra Pradesh Kurnool Rubina Women Welfare Association

NGO 180000 40

R.R. Dist. Sri Sai Educational Society NGO 180000 40

Bihar Vaishali Budha Mission of India BSMFC 81000 40

Chandigarh (UT) Chandigarh Chandigarh Child & Women Dev. Corporation

CSCBDDC 107100 28

Delhi (UT) Delhi Chetanalaya NGO 120000 60

Haryana Karnal RashtriyaYuvaSangathan NGO 51000 40

Himachal Pradesh

Nahan ITI Sirmaur HPMFDC 65025 17

J&K (UT) Anantnag Deepak Women, Jammu & J&K Yateem Trust

JKWDC 111000 40

Jammu Kongposh Welfare Society JKWDC 76500 20

Jammu JKWDC JKWDC 1176500 120

New Kashmir Women & Child Welfare Society

JKWDC 76500 20

Rural Artisans Welfare Society NGO 99450 125

Kargil Women Welfare Committee JKWDC 81000 20

Srinagar New Diamond Papier Machine JKWDC 81000 20

Srinagar JKWDC JKWDC 1905000 127

Bandipura JKWDC JKWDC 225000 15

Budgam JKWDC JKWDC 300000 20

Kupwara JKWDC JKWDC 900000 60

Poonch JKWDC JKWDC 300000 20

Kistwar JKWDC JKWDC 330000 22

Baramulla JKWDC JKWDC 390000 26

Udhampur JKWDC JKWDC 270000 18

Ganderbal JKWDC JKWDC 240000 16

Kathua JKWDC JKWDC 225000 15

Rajouri JKWDC JKWDC 300000 20

Hazratbal JKWDC JKWDC 375000 25

Jharkhand Bokaro MahilaKalyanSamiti, Dhori NGO 180000 40

Karnataka Bangalore Mumtaz Fashion Designing Centre KMDC 55500 20

Bhadravathi NayeeDisha Women's Industrial Co-operative Society

KMDC 55500 20

35

Gulbarga Sahara Social Awareness Human Action for Rural Development

KMDC 81000 20

Bidar Hind Education Society, Bidar KMDC 202500 50

Kerala Ernakulam SITW KSWDC 25500 20

Trivandrum GDPM Centre KSWDC 25500 20

Madhya Pradesh

Bhopal Jute Service Centre MPHEHVN 68992 20

Ratlam Jan ShikshanSansthan MPHEHVN 76500 20

Sihore General Facility Centre MPHEHVN 76279 20

Maharashtra Aurangabad MITCON MAAAVN 76500 20

Bhiwandi MITCON MAAAVN 76500 20

Mumbai MITCON MAAAVN 76500 20

Nagpur MITCON MAAAVN 76500 20

Solapur ParishramGraminVikasSanstha MAAAVN 51000 20

Parbhani NabihaShikshanPrasarak Mandal MAAAVN 600000 40

Nagaland Dimapur Nagaland Handloom & Handicrafts Dev. Corporation

NHHDC 76500 20

Orissa Ahmed pur Sroosti OBCFDCC 38250 20

Bhubaneswar Madani Welfare Association NGO 46738 20

Rajasthan Kota Destitute Welfare Trust RMFDCC 600000 40

Tonk Hahnemann Charitable Mission Society

RMFDCC 200000 20

Tamilnadu Chennai Roshini TAMCO 76500 20

Dindigul Social Awareness & Development Organisation for Women

NGO 90000 40

Kancheepuram Centre for Community Development (Mahatma Gandhi Social Service Educational Society)

NGO 180000 40

Kanyakumari Centre for Social Development NGO 180000 40

Kanyakumari Co-Operation League in Development and Employment (COLDE)

NGO 90000 20

Society for Social Development (SOSOD)

NGO 90000 20

YMCA Moolachal TAMCO 76500 20

Pudukkottai Community Action for Rural Development (CARD)

NGO 90000 40

Tirunelveli Arasan Rural Development Society NGO 180000 40

Women and Child Development Society

NGO 180000 40

Tiruvannamalai Arts & Crafts Training School TAMCO 76500 20

Virudhunagar Blossom TAMCO 76500 20

Tripura Agartala TMCDC TMCDC 1800000 120

Uttar Pradesh Barabanki RashtriyaMaholaJagritiSansthan UPMFDC 76500 20

Saharanpur Sharda Devi AudyogikPrakshikshanSansthan

UPMFDC 76500 20

Bareilly NilofarMahilaVikasSamiti UPMFDC 600000 40

36

Uttrakhand Nainital Pahal NGO 90000 40

Kashipur Alpsankhyak Evan PichravargVikasSamiti

NGO 600000 40

Grand Total 15640834 2164

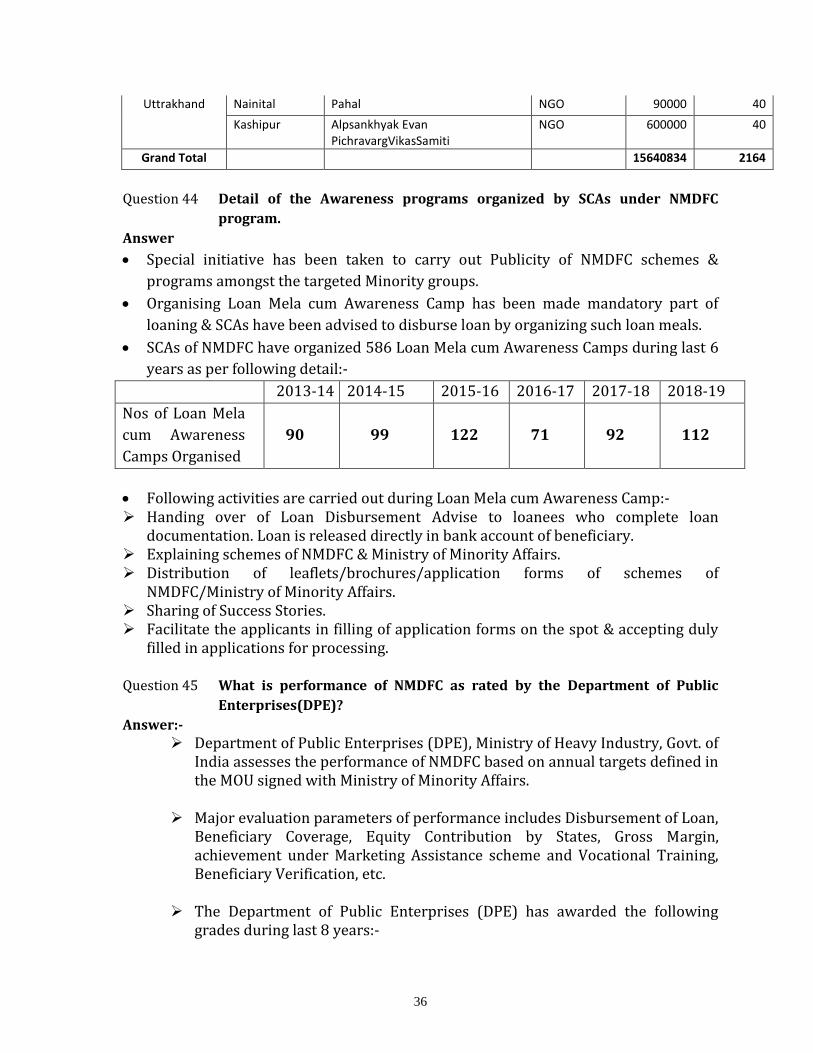

Question 44 Detail of the Awareness programs organized by SCAs under NMDFC

program.

Answer

Special initiative has been taken to carry out Publicity of NMDFC schemes &

programs amongst the targeted Minority groups.

Organising Loan Mela cum Awareness Camp has been made mandatory part of

loaning & SCAs have been advised to disburse loan by organizing such loan meals.

SCAs of NMDFC have organized 586 Loan Mela cum Awareness Camps during last 6

years as per following detail:-

2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Nos of Loan Mela

cum Awareness

Camps Organised

90

99

122

71

92

112

Following activities are carried out during Loan Mela cum Awareness Camp:- Handing over of Loan Disbursement Advise to loanees who complete loan

documentation. Loan is released directly in bank account of beneficiary. Explaining schemes of NMDFC & Ministry of Minority Affairs. Distribution of leaflets/brochures/application forms of schemes of

NMDFC/Ministry of Minority Affairs. Sharing of Success Stories. Facilitate the applicants in filling of application forms on the spot & accepting duly

filled in applications for processing.

Question 45 What is performance of NMDFC as rated by the Department of Public

Enterprises(DPE)?

Answer:-

Department of Public Enterprises (DPE), Ministry of Heavy Industry, Govt. of India assesses the performance of NMDFC based on annual targets defined in the MOU signed with Ministry of Minority Affairs.

Major evaluation parameters of performance includes Disbursement of Loan, Beneficiary Coverage, Equity Contribution by States, Gross Margin, achievement under Marketing Assistance scheme and Vocational Training, Beneficiary Verification, etc.

The Department of Public Enterprises (DPE) has awarded the following

grades during last 8 years:-

37

Financial year

Rating

2010-11 Excellent

2011-12 Excellent

2012-13 Excellent

2013-14 Good

2014-15 Excellent

2015-16 Excellent

2016-17 Very Good

2017-18 Excellent

2018-19 Good

Question 46 What is the total sanctioned staff strength of NMDFC, incumbency position

&vacancies?

Answer:-

Total Sanctioned Staff Strength of NMDFC is 63(including CMD).

Total Incumbency is (32)(including CMD) Executive cadre Including CMD = 15

Supervisory level = 5 Non-executive level = 6 MTS = 6

Total Vacant Positions (31) Executive level = 23 Non-executive level = 8

Question 47 How many students have availed Education loan for Studies Abroad?

Answer:-

Foreign Loan component for studies abroad was introduced in the Education

Loan Scheme of NMDFC from the year 2013-14. So far, an amount of Rs.26.73

crs. for covering 483 beneficiaries has been utilized under the scheme.

The details of the funds utilized by State Channelising Agencies (SCAs) during

the last 5 F.Y’s is given below:-

Amt in Rs./lacs SR. NO.

STATE/SCAs 2014-15 2015-16 2016-17 2017-18 2018-19 Total

AMT. BENES. AMT. BENES. AMT. BENES. AMT. BENES. AMT. BENES. AMT. BENES.

1 HIMACHAL PRADESH (HPMFDC)

0 0 3.39 1 3.48 0 3.35 1 0 0 10.22 2

2 J&K (JKEDI)

(UT)

0 0 4.90 1 27.00 5 629.44 42 661.87 46 1323.2 94

3 J&K (JKWDC) (UT)

51.00 4 13.90 5 9.00 3 35.50 12 0.66 19 110.06 43

4 J&K (JKSFC) (UT)

0.00 0 0.00 0 0.00 0 16.06 3 16.06 3

5 KERALA 4.25 2 68.35 17 94.92 24 97.17 16 0.74 0 265.43 59

38

(KSBCDC)

6 KERALA (KSMDFC)

2.00 1 7.00 3 4.00 1 13 5

7 KARNATAKA (KMDC)

83.60 10 82.65 11 11.40 3 86.54 21 264.19 45

8 TRIPURA (TMCDC)

5.00 1 10.00 2 0.00 0 21.00 3 36 6

9 WEST BENGAL (WBMDFC)

0.00 0 45.45 23 16.65 14 92.31 40 427.83 141 582.24 218

TOTAL

145.85 18 235.64 63 166.45 50 981.37 138 1091.10 206 2620 475

The students have been financed for courses such as MBBS, MSC Computer science,

B.E (mechanical Eng.), MBA, M.S in Electrical Eng, MCA, etc.

The students have got admission in countries such as China, USA, UK, Bangladesh,

Russia, Norway, etc.

Question 48 What is the Status of Indirect Employment generated under loaning

program of NMDFC?

Answer:-

Based on the data furnished by the respective SCAs, the following is the detail of Indirect

Employment generated under loaning schemes of NMDFC during the last 3 F.Y’s.:-

NATIONAL MINORITIES DEVELOPMENT & FINANCE CORPORATION

Data on Direct and Indirect Employment Generated under NMDFC Schemes

SR. NO.

STATEs/UTs SCAs

2016-17 2017-18 2018-19

NO. OF BENEFICIARIES

COVERED

NO. OF PERSONS

EMPLOYED/ INDIRECT

EMPLOYMENT GENERATED

NO. OF BENEFICIARIES

COVERED

NO. OF PERSONS

EMPLOYED/ INDIRECT

EMPLOYMENT GENERATED

NO. OF BENEFICIARIES

COVERED

NO. OF PERSONS

EMPLOYED/ INDIRECT

EMPLOYMENT GENERATED

1 CHANDIGARH CSCBCMFDC 68 30 40 15 61 18

2 DELHI DSFDC 37 37 13 13 16 16

3 HIMACHAL PRADESH

HPMFDC 160 160 95 95 117 117

4 J&K (UT) JKWDC 496 1698 466 1696 539 1771

5 J&K (UT) JKSFC 65 38 279 366 469 816

6 KARNATAKA KMDC 5 10 21 50 41 94

7 KERALA KSBCDC 7688 9823 12404 15821 13214 18156

8 KERALA MATSYAFED 12943 49 15421 182 15736 81

9 KERALA KSMDFC 264 472 420 593 462 601

10 RAJASTHAN RMFDCC 1882 5657 1119 3359 447 1348

11 TRIPURA TMCDC 794 955 843 1037 97 171

12 WEST BENGAL WBMDFC 112300 127620 117308 133074 119118 139127

TOTAL 136702 146549 148429 156301 150317 162316

![rec.autos.vw [W] GENERAL, FREQUENTLY ASKED ...](https://static.fdokumen.com/doc/165x107/63233a18117b4414ec0c3ae3/recautosvw-w-general-frequently-asked-.jpg)