FORM NO. FORM

30

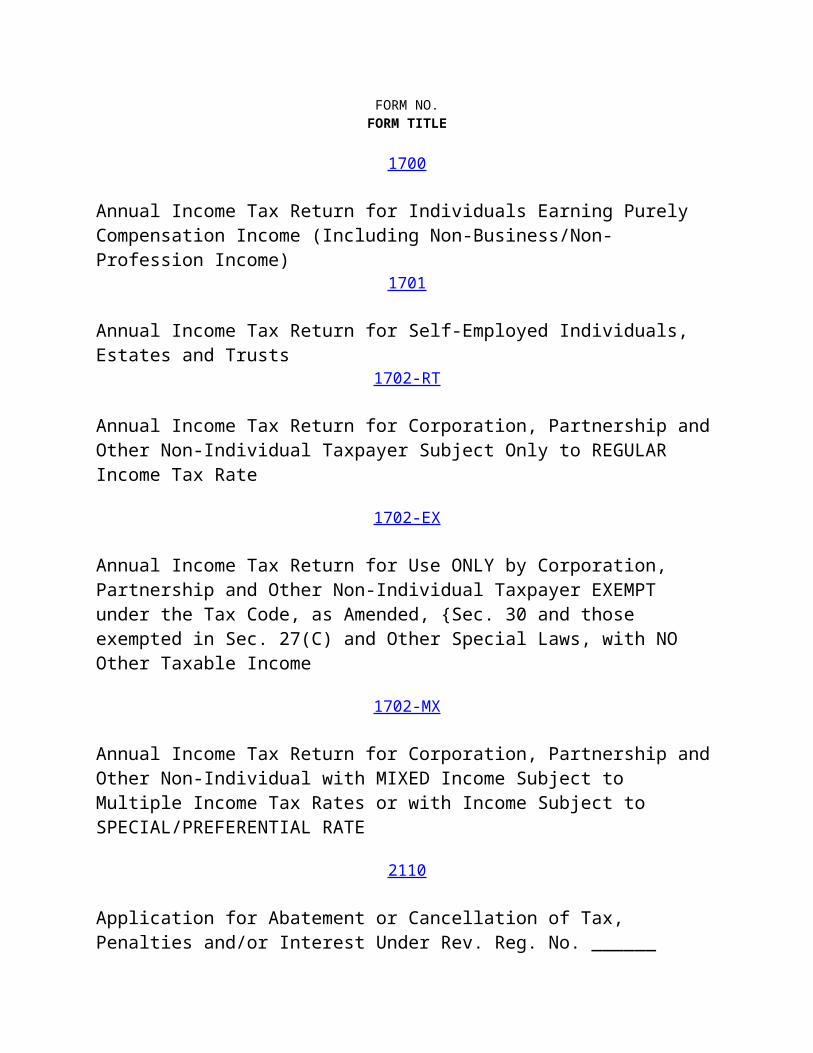

FORM NO. FORM TITLE 1700 Annual Income Tax Return for Individuals Earning Purely Compensation Income (Including Non-Business/Non- Profession Income) 1701 Annual Income Tax Return for Self-Employed Individuals, Estates and Trusts 1702-RT Annual Income Tax Return for Corporation, Partnership and Other Non-Individual Taxpayer Subject Only to REGULAR Income Tax Rate 1702-EX Annual Income Tax Return for Use ONLY by Corporation, Partnership and Other Non-Individual Taxpayer EXEMPT under the Tax Code, as Amended, {Sec. 30 and those exempted in Sec. 27(C) and Other Special Laws, with NO Other Taxable Income 1702-MX Annual Income Tax Return for Corporation, Partnership and Other Non-Individual with MIXED Income Subject to Multiple Income Tax Rates or with Income Subject to SPECIAL/PREFERENTIAL RATE 2110 Application for Abatement or Cancellation of Tax, Penalties and/or Interest Under Rev. Reg. No. ______

Transcript of FORM NO. FORM

FORM NO.FORM TITLE

1700

Annual Income Tax Return for Individuals Earning Purely Compensation Income (Including Non-Business/Non-Profession Income)

1701

Annual Income Tax Return for Self-Employed Individuals, Estates and Trusts

1702-RT

Annual Income Tax Return for Corporation, Partnership andOther Non-Individual Taxpayer Subject Only to REGULAR Income Tax Rate

1702-EX

Annual Income Tax Return for Use ONLY by Corporation, Partnership and Other Non-Individual Taxpayer EXEMPT under the Tax Code, as Amended, {Sec. 30 and those exempted in Sec. 27(C) and Other Special Laws, with NO Other Taxable Income

1702-MX

Annual Income Tax Return for Corporation, Partnership andOther Non-Individual with MIXED Income Subject to Multiple Income Tax Rates or with Income Subject to SPECIAL/PREFERENTIAL RATE

2110

Application for Abatement or Cancellation of Tax, Penalties and/or Interest Under Rev. Reg. No. ______

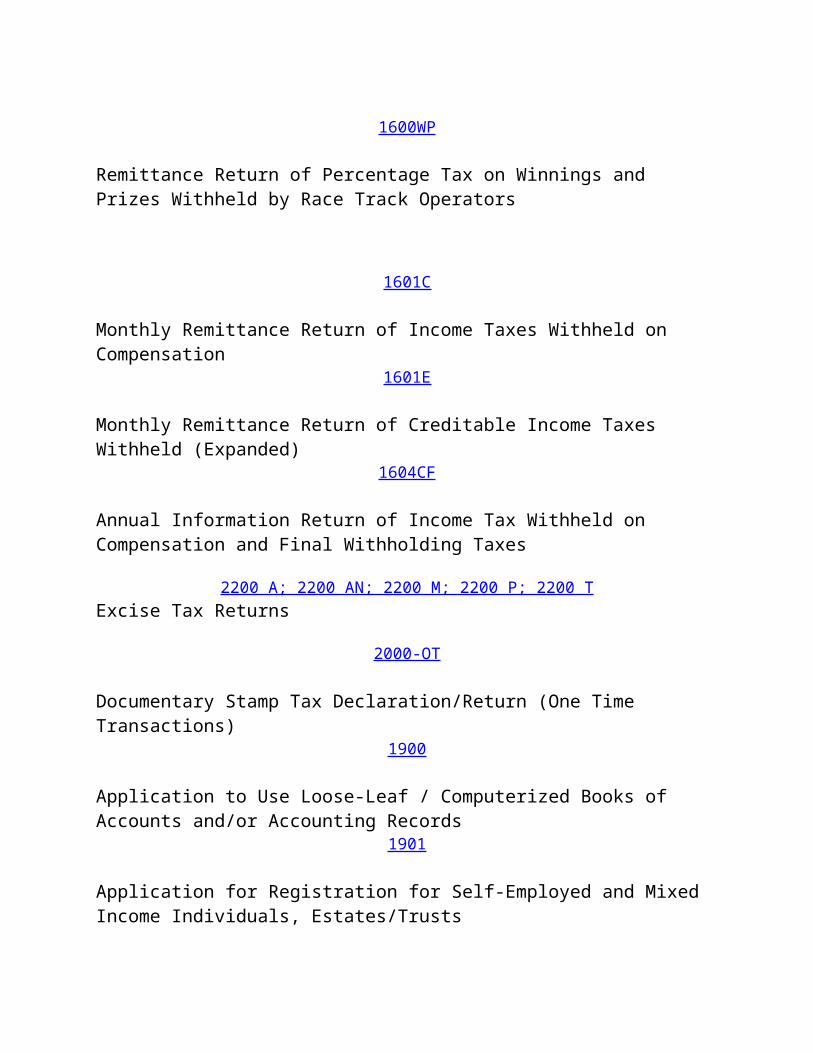

1600WP

Remittance Return of Percentage Tax on Winnings and Prizes Withheld by Race Track Operators

1601C

Monthly Remittance Return of Income Taxes Withheld on Compensation

1601E

Monthly Remittance Return of Creditable Income Taxes Withheld (Expanded)

1604CF

Annual Information Return of Income Tax Withheld on Compensation and Final Withholding Taxes

2200 A; 2200 AN; 2200 M; 2200 P; 2200 TExcise Tax Returns

2000-OT

Documentary Stamp Tax Declaration/Return (One Time Transactions)

1900

Application to Use Loose-Leaf / Computerized Books of Accounts and/or Accounting Records

1901

Application for Registration for Self-Employed and Mixed Income Individuals, Estates/Trusts

0605Payment Form

1701Q

Quarterly Income Tax Return for Self-employed Individuals, Estates, and Trusts (Including Those with both Business and Compensation Income)

1703

Annual Income Information Return for Non-Resident Citizens / OCWs and Seamen (for foreign-sourced income)

1704

Improperly Accumulated Earnings Tax Return

1706

Capital Gains Tax Return for Onerous Transfer of Real Property Classified as Capital Asset (both Taxable and Exempt)

1707

Capital Gains Tax Return for Onerous Transfer of Shares of Stocks Not Traded Through the Local Stock Exchange

1707-A

Annual Capital Gains Tax Return for Onerous Transfer of Shares of Stock Not Traded Through the Local Stock Exchange

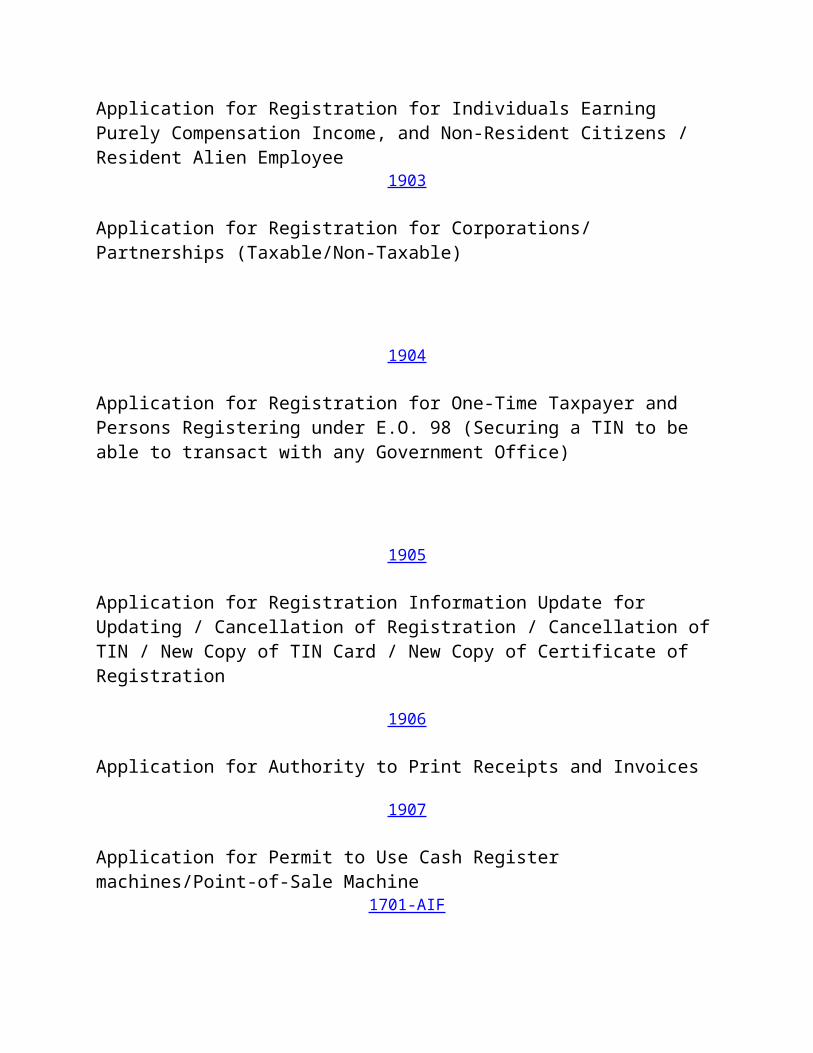

1902

Application for Registration for Individuals Earning Purely Compensation Income, and Non-Resident Citizens / Resident Alien Employee

1903

Application for Registration for Corporations/ Partnerships (Taxable/Non-Taxable)

1904

Application for Registration for One-Time Taxpayer and Persons Registering under E.O. 98 (Securing a TIN to be able to transact with any Government Office)

1905

Application for Registration Information Update for Updating / Cancellation of Registration / Cancellation ofTIN / New Copy of TIN Card / New Copy of Certificate of Registration

1906

Application for Authority to Print Receipts and Invoices

1907

Application for Permit to Use Cash Register machines/Point-of-Sale Machine

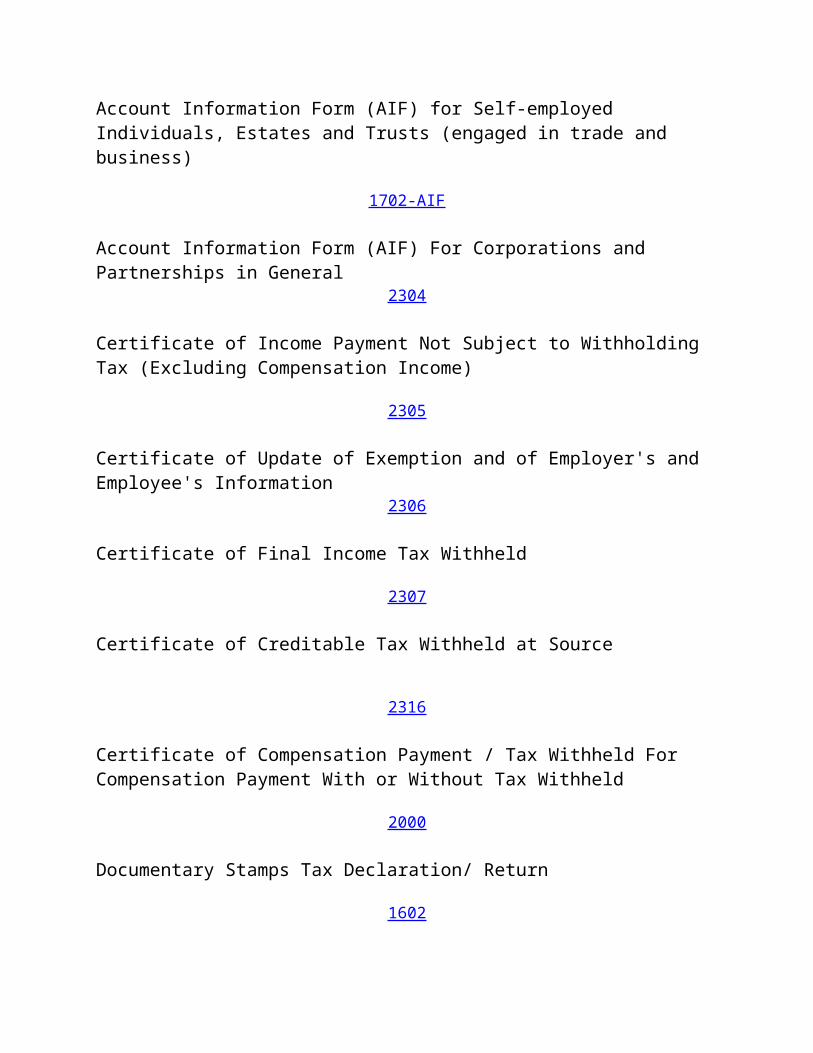

1701-AIF

Account Information Form (AIF) for Self-employed Individuals, Estates and Trusts (engaged in trade and business)

1702-AIF

Account Information Form (AIF) For Corporations and Partnerships in General

2304

Certificate of Income Payment Not Subject to Withholding Tax (Excluding Compensation Income)

2305

Certificate of Update of Exemption and of Employer's and Employee's Information

2306

Certificate of Final Income Tax Withheld

2307

Certificate of Creditable Tax Withheld at Source

2316

Certificate of Compensation Payment / Tax Withheld For Compensation Payment With or Without Tax Withheld

2000

Documentary Stamps Tax Declaration/ Return

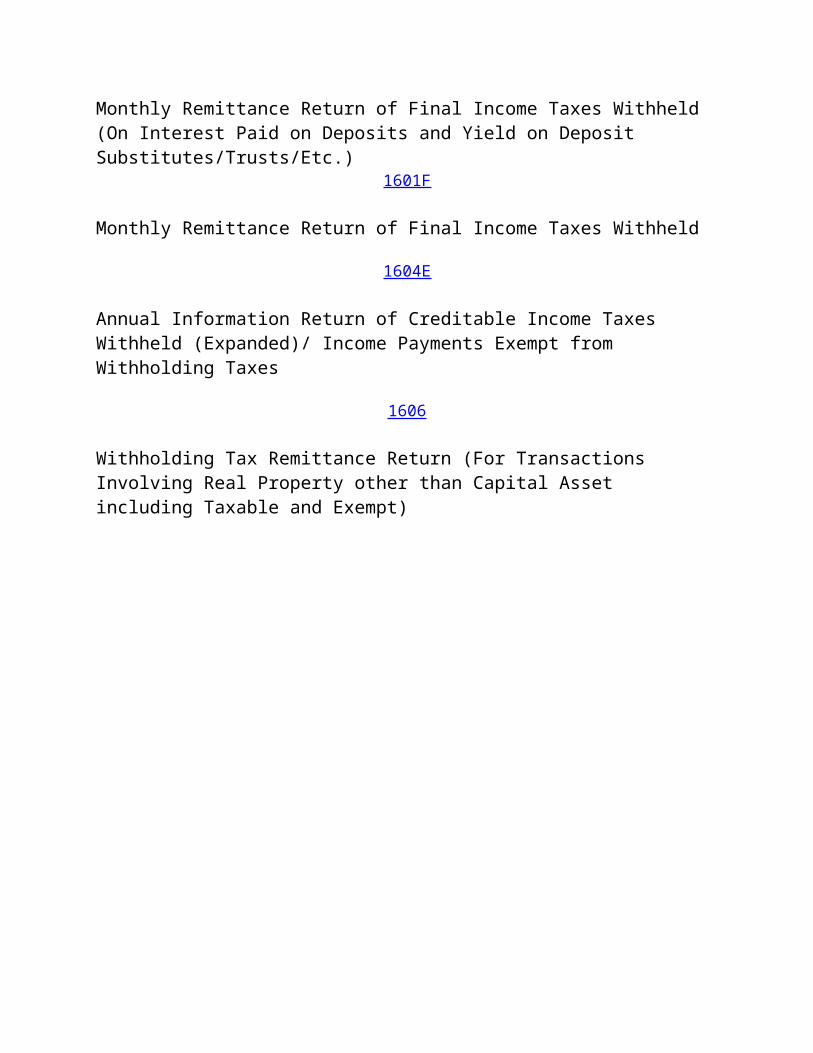

1602

Monthly Remittance Return of Final Income Taxes Withheld (On Interest Paid on Deposits and Yield on Deposit Substitutes/Trusts/Etc.)

1601F

Monthly Remittance Return of Final Income Taxes Withheld

1604E

Annual Information Return of Creditable Income Taxes Withheld (Expanded)/ Income Payments Exempt from Withholding Taxes

1606

Withholding Tax Remittance Return (For Transactions Involving Real Property other than Capital Asset including Taxable and Exempt)

Internship or on the job training is one way by which we students are given an opportunity to apply the theories and computations that we have learned from school. It also helpsus to obtain applicable knowledge and skills by performing in actual work setting. Colleges and universities require their students to undergo such training within a specific number of hours as part of the curriculumFor us students, an OJT or internship program provides opportunities to go through the actual methodologies of a specific job using the real tools, equipments, and documents. In effect, the work place becomes a development venue for us student trainee to learn more about our chosen field and practice what we have learn from academy.On the other hand, a valuable OJT program also profits the companies who accept trainees. First OJT or intern provides extra manpower for a less significant labor cost than a regular employee. Most of them are all eager to learn the ropes so chances are high that they’ll be given a chance to work on the same company as an employee after graduating.Employers can use this internship strategy as method in recruiting employees. Since the trainer or supervisor can follow the trainees’ progress, he can gauge based on performance, behavior and attitude if the trainee will make good recruit after the completion of his internship.We trainees can bring fresh ideas into the organization. Given the opportunity to converse our minds freely and without fear, we may be able to contribute significantly in brainstorming sessions or research and eventually help improve the organizations productivity.

While training the interns, employers are in fact also teachtheir employees to guide the trainees by stretching their patience, develop teaching skills and make them more sensitive to the needs and mind set of the younger generation. The course of supervision also teaches them how to share what they know and be receptive to questions.

Hence, the internship also becomes an avenue in training forfuture managers of the company.

First Month of OJTJuly 2, 2012. Welcome to my first day of On the Job Training. I was upset at the very first day because I have noticed that the company which will be my first place to work with, is no percentage connection in my choosen course. TRAVEL SAVER (PHILS.) INC., a company that caters International & Domestic tickets, proccess visa, passport and also package tours around the world. I am sure that you will agree with me that from the nature of business the company have, my course is out of way. But stillmy journey should continue.

At first, I have the hardship of familiarizing all the work they are giving me. Maybe because Idon't find it connected with my course, they askme to file all the documents and transactions they are doing.

I don't find my self productive if I will just file the whole day. But as days goes by they

tough me how to use their system. Abacus system used in their accounting department. It helps a bit in their accounting task. In a click of a number or a letter all the pertinent documents will be displayed. At this time, I know that I can use their system to have a fruitfull OJT.

As a IT student, all the new knowledge I will get from this company will be of great help to my future career. All their transactions are automated, invoicing and checking of payments can be done in their system. Hi – tech compare to other agencies.

My 2nd month of OJT. My workflow is the same as my first month of stay in this office. But at this time I can say that I am more familliar to my duties and at the same time less supervion isgiven to me. I can now work farter than before, I am no longer hesitant to do all the assigned work because I'm already used to it.

During this month, I have experience the strike of "habagat" here in manila. Flood all over the

are, and because of this most of the employees of Travel Saver are absent, so I was assigned tohelp in their reservation department. Another first time experience. I'm amazed how the reseravtion officers manage to answer all those calls and still they do some paper works and assist passengers. At first I am reluctant to answer the phone because I'm afraid I might givethem the wrong information and this may cause the company a bad name to their passengers. Withproper teaching from the employees, I was able to help them and also I'm enjoying this work.

Because of the flood their system they are usingis not working, so they need to prepare all the documents manually and I have observe that it istime consuming. The use of hightech system greatly affect their nature of work.

Introduction:

Our school, General de Jesus College let us students to

engage and experience the things happening in the actual world of

Business through our On-The-Job-Training(Internship) in banks,

auditing firms, and other business establishments related. We

have given 250 hours to undergo and pursue this training that

will help us to acquire knowledge and skills that will serve as a

tool to face the challenges of life in the future. It will set

our mind of what does a real world of accounting is all about.

Others think that accounting matters only on numbers or

quantitative information; however, it also matters or related in

decision making and business operations. It also somewhat related

to the development of our skills in communication, leadership and

management. Thus, experience is vital to one’s improvement and

preparing students to their career is the best way to set them on

success.

To hold this On-The-Job-Training( Charis A.

Pillarina, an Business administration) has chosen (Rural Bank of

Jaen) as a training ground in promoting professionalism.

Goals/Objectives of the On-The-Job-Training:

On the Job Training is one method by which students

ar exposed with different work situation designed to give

students an opportunity to experience and a chance to apply the

theories and computation that they have learned from the school.

It also helps the students to acquire relevant knowledge and

skills by performing in actual work setting.

During and after training, It should be able to gain

both Office Management and Personal skills to be acquired:

A. Office Management Skills:

1. Provided opportunities to go through the actual methodologies

of a specific job using the real tools, equipments and documents.

2. To learn more about his/her chosen field and practice what

he/she have learned from the academy.

3. To provide the students with a venue to achieve efficient

knowledge to the use of office management skills in industry,

government and academy.

4. Build up the student’s competence, professionalism in dealing

with people, quality awareness, collaboration skills, critical

thinking abilities, discipline, ingenuity and independence.

5. Provide agencies with opportunities to observed and evaluate

potential staff.

6. Strong organizational skills and high ethical standards.

7. Ability to communicate with people at all levels.

8. Good judgement, discretion and initiatives.

B. Personal Skills:1. To gain self confidence and maturity through attention to

qualities which are needed in the word of work to prepare us.2. To learn how to communicate with others.3. To acquire ability to work harmoniously with employers,

workers and customers.

Core Values of the Organization Being Observed:

The following are the organizational values, knowledge andability that I have taken and developed during our OJT to becomeProductive Individuals.

CommitmentWe will be responsible in the performance of our assigned

tasks as we dedicate ourselves to the vision and mission of thecompany and also to the goals of our school to have thistraining.

Integrity

We are committed to uphold ourselves to the principles ofhonesty and transparency in all our actions. Furthermore, weshould not be easily influence by others and to take unnecessaryactions that will let us in breaking our integrity.

Interpersonal RelationshipIn order to have better communication with the

employees/workers, they are always open to us whenever we havequestions or we need some help. And because of regularcommunication with the employees, officials and co-traineesthrough daily encounter is one of the nice practices in order todevelop not only our skills but in improving our relationshipwith them and to others.

TeamworkTeamwork is really important in any organizations existing.

We are committed to work as one family to achieve our common goalin the spirit of cooperation, mutual respect and trust; thus,teamwork must always be present.

ConfidentialityAll financial and non financial date are confidential in

nature. So we should not disclose it with third parties. Thetransactions are all about thousands and even millions of peso sothat we should not disseminate it to the public particularly thewithdrawals or deposits taken by the NRLBSL or the client

involved. What we have heard or seen in the bank, will leave inthe bank.

Professional BehaviourWe are in the actual workplace, so we are practicing the

world of professionalism that’s why we must act as professionalsand we should maintain our behaviour in and outside theestablishment. And I think we have complied with relevant lawsand regulations of NRBSL and avoided any action that discreditsus from our internship.

EnthusiasmOn my training session, I have given more importance on it. Atfirst, I thought that it’s not easy to take OJT because there arelots of tasks and activities to be assigned and performed. But inenthusiastic way, “Even if you are tired, don;t stop on yourwork, stop when you’re done”, and that’s really true to becomeProductive.

PolitenessWe should respect our employee/ co-workers all the time. Alwaysgreet the clients, employees, officials, and co-trainees or smileat them at chances.

PunctualityTo be a productive person you need to be punctual. There shouldbe no space of being late as the saying goes by that “Time isgold”. Every seconds of our life counts and is really important.We don’t need to waste our time and we should have proper time

for each specific action. Honestly, I go to NRBSL on or before8:00 in the morning to practice this important value.

An Evaluation of My Training:

A. Office Producers I Learned and Applied:During our On-The-Job training. I learned some things that reallyhelped me to improve my skills.

I learned to manage time. I learned how to use photocopy machine that I didn’t know how to

use before. I become familiarize in the nature of banking. I learned to ask someone’s help whenever I don’t know how to do.

Because in my mind there’s a saying “ marunong ang nagtatanong”. I become responsible. I become more polite to others in the way to greet them. I become more patience in the tasks given to us. I learned to have confidence and strength to overcome my fears.

B. Activities or Tasks Performed at the New RuralBank of Jaen

This present the entire training period with the activitiesdone by the trainee. It also shows the accomplishments and skillsbeing enhanced during the Internship period that gave them thebest training ground as a beginner.

In doing a task, we must exert our full effort into themaximum level in order to do what the task requires. Thefollowing are the tasks that I have peformed during my 250 hoursof On-The-Job training.

Problems Encountered During Training andSolution Everyone has a problem, even in school, family andorganization. When I was on my training at Rural Bank of Jaen, Iencountered problem which is the feeling of being not welcome intheir company, I felt that some employees don’t like me, maybethey don’t want me to be part of their tasks. This problem isn’ta big deal, I didn’t say to anyone about my feeling I just keptit on my own because I’m not sure if my feelings is true. Maybemy interpretation was wrong that’s why I persuade to do my bestto finish my tasks that they given. Maybe God was testing mypatience at that time. As the day passes, I realized that myanalysis about them was wrong. They’re just only serious duringworking hours.

Self Assessment Intelligence is one of the key to succeed. No one cantake it away from us. But having knowledge isn’t enough tosucceed. We need to use it on the right way. We have to persistto anything undertaken to attain our goals. On my training Ilearned a lot such as improving my whole personality in terms ofsocialization and vision towards life. I’d realized that problems in life are like problemsin work, we must search for the best solution. We couldn’t solveit without co-workers, co-trainees and employees. It’s like thesaying “No man is an island” in other words, we couldn’t liveonly with ourselves we need the help of other people to overcomethe problems in life. During the days of my training I’d familiarized whatare the transactions in the bank was. But just like in real lifewe couldn’t avoid to commit mistakes. No one is perfect, Iremember one time that I committed a mistake, they didn’t blameme instead they teach me how to do the task correctly. Sometimesthe more we commit mistakes the more we learned the lessonbecause as what they said we’ll learn a lot from our ownmistakes. SO in the near future I’ll apply those things that Ilearned during my OJT time. In this training I can say that I’m transformed intoa real better person.

A NARRATIVE REPORT ON ON-THE-JOB TRAINING UNDERTAKEN AT MARKETING DEPARTMENT OF PAG-IBIG FUND-ILIGAN, ILIGAN CITY I, Van Loven S. Semborio, an Information Technology student from STI Iligan, had completed a total of Four Hundred (400) hours of office practicum with Marketing Department in Home Development Mutual Fund also known as Pag-ibig Fund , Iligan City from July 02,2013 toSeptember 20,2013. On the first day of my internship, I met the Manager and the Marketing Department Head. I felt a bit of nervous but I stayed calm and cool. I didn’tknow anyone so I was on my own, concentrating to my assigned work and askingquestions for clarification. I gave all my best not to commit mistakes but neverthelessthe following day I made an error. Good thing is I used a pencil so whatever mistakethat I did was able to be corrected. As dayswent by, I improved myself, eager to learn to show to them I am able, that I can handle

whatever task they want me to do and to prove I can do it. In a couple of days, someof my classmates were also given the opportunity to be a student trainee. There are also students from other schools like Lyle, JM, Joy, and Yang who are from St. Michael’s College, while Mark is from Tesda.Lyle, JM, Mark and I are in the same department. Since they started ahead of me, they already know some of the basic work so I, as a starter, usually ask for their help and ask for further clarifications. During my training days, traveling from Naawan to Iligan City, I always set my alarm 5AM just to be on-time. I was in the front line so most of the time I face clients, assessing them for their online registration, asking them personal questions, encoding and updating oral or

written information, doing tag forms, arranging files, and other office related activities. In doing all this work, I keep

in mind to always do my best even if it’s just a small task and always do what is right. I deal with different types of clients; mostly I enjoy dealing with them, treating them as I would want to be treated.There are few that are difficult to handle, especially the “Maranao” who can’t understand “tagalog”. There is this one timethat I was mental blocked by a client. He was spelling the letters of a name. I, who can’t hear him clearly, ask him to repeat the letters. In response, he gets annoyed and starts to shout at me. I was shocked andbegan to mental block. I control myself not to return his anger and shout back. I just charge that as an experience. Anyway, it helps me develop my self-control. I really like and enjoy my On-the-job training or OJTin Pag-ibig Fund. It served as the beginning, a stepping stone to the real lifeof being an employee. It helped me acquire relevant knowledge and skills by performing in an actual work setting. Pag-ibig Fund

Iligan became my development venue as a student to learn more about my chosen field which is Information Technology and practicewhat I learned from school. I am blessed andthankful to my OJT Supervisor Mrs. Ma Beverly Adsuara for extending her patience, for sharing what she knew, and for the guidance and training at the company. To allstaff of the company, thank you, whose kindness and support in the training was overwhelming. To my co-trainee for the roller coaster experience, to my Guardian for the moral and financial support, and last but not the least, to God, for giving me the strength and power of mind, protection and skills. Thank you! God bless!

MISSION

The Bureau of Internal Revenue is committed to collect taxes for nation-building through excellent, efficient and transparent service, just and fairenforcement of tax laws, uplifting the life of every Filipino.

LAYUNIN

Ang Kawanihan ng Rentas Internas ay walang pasubaling lilikom ng buwis parasa pagpapaunlad ng ating bansa sa pamamagitan ng mahusay, masinop at tapat napaglilingkod, walang kinikilingan at patas na pagpapatupad ng mga batas sa

pagbubuwis upang maiangat ang antas ng pamumuhay ng bawat mamamayang Pilipino.

VISION

The Bureau of Internal Revenue is an institution of service excellence, apartner in nation-building, manned by globally competitive professionals withintegrity and patriotism.

PANANAW

Ang Kawanihan ng Rentas Internas ay institusyon na tinitingala sa laranganng paglilingkod at kaagapay sa pagpapaunlad ng ating bansa, na pinaglilingkuran

ng mga kawani na may sapat na kaalaman, karanasan, paninindigan atpagkamakabansa.

GUIDING PRINCIPLE

"Service Excellence with Integrity and Professionalism"

VALUES

God-fearing Innovativeness Respect Consistency Accountability Fairness

Competency Synergy Transparency

BIR History

Spanish Era

During the 17th and 18th centuries, the Contador de' Resultas served as the Chief RoyalAccountant whose functions were similar to the Commissioner of Internal Revenue. He wasthe Chief Arbitrator whose decisions on financial matters were final except when revokedby the Council of Indies. During these times, taxes that were collected from theinhabitants varied from tribute or head tax of one gold maiz annually; tax on value ofjewelries and gold trinkets; indirect taxes on tobacco, wine, cockpits, burlas and powder.From 1521 to 1821, the Spanish treasury had to subsidize the Philippines in the amount ofP 250,000.00 per annum due to the poor financial condition of the country, which can beprimarily attributed to the poor revenue collection system.

American Era

In the early American regime from the period 1898 to 1901, the country was ruled byAmerican military governors. In 1902, the first civil government was established underWilliam H. Taft. However, it was only during the term of second civil governor Luke E.Wright that the Bureau of Internal Revenue (BIR) was created through the passage ofReorganization Act No. 1189 dated July 2, 1904. On August 1, 1904, the BIR was formallyorganized and made operational under the Secretary of Finance, Henry Ide (author of theInternal Revenue Law of 1904), with John S. Hord as the first Collector (Commissioner).The first organization started with 69 employees, which consisted of a Collector, Vice-Collector, one Chief Clerk, one Law Clerk, one Records Clerk and three (3) DivisionChiefs.

Following the tenure of John S. Hord were three (3) more American collectors, namely:Ellis Cromwell (1909-1912), William T. Holting (1912-1214) and James J. Rafferty (1914-1918). They were all appointed by the Governor-General with the approval of the PhilippineCommission and the US President.

During the term of Collector Holting, the Bureau had its first reorganization on January1, 1913 with the creation of eight (8) divisions, namely: 1) Accounting, 2) Cash, 3)Clerical, 4) Inspection, 5) Law, 6) Real Estate, 7) License and 8) Records. Collections bythe Real Estate and License Divisions were confined to revenue accruing to the Cityof Manila.

In line with the Filipinization policy of then US President McKinley, Filipino Collectorswere appointed. The first three (3) BIR Collectors were: Wenceslao Trinidad (1918-1922);Juan Posadas, Jr. (1922-1934) and Alfredo Yatao (1934-1938).

On May 1921, by virtue of Act No. 299, the Real Estate, License and Cash Divisions wereabolished and their functions were transferred to the City ofManila. As a result of thistransfer, the Bureau was left with five (5) divisions, namely: 1) Administrative, 2) Law,3) Accounting, 4) Income Tax and 5) Inspection. Thereafter, the Bureau established thefollowing: 1) the Examiner's Division, formerly the Income Tax Examiner's Section whichwas later merged with the Income Tax Division and 2) the Secret Service Section, whichhandled the detection and surveillance activities but was later abolished on January 1,1951. Except for minor changes and the creation of the Miscellaneous Tax Division in 1939,the Bureau's organization remained the same from 1921 to 1941.

In 1937, the Secretary of Finance promulgated Regulation No. 95, reorganizing theProvincial Inspection Districts and maintaining in each province an Internal RevenueOffice supervised by a Provincial Agent.

Japanese Era

At the outbreak of World War II, under the Japanese regime (1942-1945), the Bureau wascombined with the Customs Office and was headed by a Director of Customs and InternalRevenue.

Post War Era

On July 4, 1946, when the Philippines gained its independence from the United States, theBureau was eventually re-established separately. This led to a reorganization on October1, 1947, by virtue of Executive Order No. 94, wherein the following were undertaken: 1)the Accounting Unit and the Revenue Accounts and Statistical Division were merged intoone; 2) all records in the Records Section under the Administrative Division wereconsolidated; and 3) all legal work were centralized in the Law Division.

Revenue Regulations No. V-2 dated October 23, 1947 divided the country into 31 inspectionunits, each of which was under a Provincial Revenue Agent (except in certain special unitswhich were headed by a City Revenue Agent or supervisors for distilleries and tobaccofactories).

The second major reorganization of the Bureau took place on January 1, 1951 through thepassage of Executive Order No. 392. Three (3) new departments were created, namely: 1)Legal, 2) Assessment and 3) Collection. On the latter part of January of the same year,Memorandum Order No. V-188 created the Withholding Tax Unit, which was placed under theIncome Tax Division of the Assessment Department. Simultaneously, the implementation ofthe withholding tax system was adopted by virtue of Republic Act (RA) 690. This method ofcollecting income tax upon receipt of the income resulted to the collection ofapproximately 25% of the total income tax collected during the said period.

The third major reorganization of the Bureau took effect on March 1, 1954 through RevenueMemorandum Order (RMO) No. 41. This led to the creation of the following offices: 1)Specific Tax Division, 2) Litigation Section, 3) Processing Section and the 4) Office ofthe City Revenue Examiner. By September 1, 1954, a Training Unit was created through RMONo. V-4-47.

As an initial step towards decentralization, the Bureau created its first 2 RegionalOffices in Cebu and in Davao on July 20, 1955 per RMO No. V-536. Each Regional Office washeaded by a Regional Director, assisted by Chiefs of five (5) Branches, namely: 1) TaxAudit, 2) Collection, 3) Investigation, 4) Legal and 5) Administrative. The creation ofthe Regional Offices marked the division of the Philippine islands into three (3) revenueregions.

The Bureau's organizational set-up expanded beginning 1956 in line with theregionalization scheme of the government. Consequently, the Bureau's Regional Officesincreased to (8) eight and later into ten (10) in 1957. The Accounting Machine Branch wasalso created in each Regional Office.

In January 1957, the position title of the head of the Bureau was changed from Collectorto Commissioner. The last Collector and the first Commissioner of the BIR was Jose Aranas.

A significant step undertaken by the Bureau in 1958 was the establishment of the TaxCensus Division and the corresponding Tax Census Unit for each Regional Office. This was

done to consolidate all statements of assets, incomes and liabilities of all individualand resident corporations in the Philippines into a National Tax Census.

To strictly enforce the payment of taxes and to further discourage tax evasion, RA No. 233or the Rewards Law was passed on June 19, 1959 whereby informers were rewarded the 25%equivalent of the revenue collected from the tax evader.

In 1964, the Philippines was re-divided anew into 15 regions and 72 inspection districts.The Tobacco Inspection Board and Accountable Forms Committee were also created directlyunder the Office of the Commissioner.

Marcos Administration

The appointment of Misael Vera as Commissioner in 1965 led the Bureau to a "new direction"in tax administration. The most notable programs implemented were the "Blue MasterProgram" and the "Voluntary Tax Compliance Program". The first program was adopted to curbthe abuses of both the taxpayers and BIR personnel, while the second program was designedto encourage professionals in the private and government sectors to report their trueincome and to pay the correct amount of taxes.

It was also during Commissioner Vera's administration that the country was furthersubdivided into 20 Regional Offices and 90 Revenue District Offices, in addition to thecreation of various offices which included the Internal Audit Department (replacing theInspection Department), Administrative Service Department, International Tax Affairs Staffand Specific Tax Department.

Providing each taxpayer with a permanent Tax Account Number (TAN) in 1970 not onlyfacilitated the identification of taxpayers but also resulted to faster verification oftax records. Similarly, the payment of taxes through banks (per Executive Order No. 206),as well as the implementation of the package audit investigation by industry areconsidered to be important measures which contributed significantly to the improvedcollection performance of the Bureau.

The proclamation of Martial Law on September 21, 1972 marked the advent of the New Societyand ushered in a new approach in the developmental efforts of the government. Several taxamnesty decrees issued by the President were promulgated to enable erring taxpayers tostart anew. Organization-wise, the Bureau had also undergone several changes during theMartial Law period (1972-1980).

In 1976, under Commissioner Efren Plana's administration, the Bureau's National Officetransferred from the Finance Building in Manila to its own 12-storey building in QuezonCity, which was inaugurated on June 3, 1977. It was also in the same year that PresidentMarcos promulgated the National Internal Revenue Code of 1977, which updated the 1934 TaxCode.

On August 1, 1980, the Bureau was further reorganized under the administration ofCommissioner Ruben Ancheta. New offices were created and some organizational units wererelocated for the purpose of making the Bureau more responsive to the needs of thetaxpaying public.

Aquino Administration

After the People's Revolution in February 1986, a renewed thrust towards an effective taxadministration was pursued by the Bureau. "Operation: Walang Lagay" was launched topromote the efficient and honest collection of taxes.

On January 30, 1987, the Bureau was reorganized under the administration of CommissionerBienvenido Tan, Jr. pursuant to Executive Order (EO) No. 127. Under the said EO, two (2)major functional groups headed and supervised by a Deputy Commissioner were created, andthese were: 1) the Assessment and Collection Group; and 2) the Legal and InternalAdministration Group.

With the advent of the value-added tax (VAT) in 1988, a massive campaign program aimed topromote and encourage compliance with the requirements of the VAT was launched. Theadoption of the VAT system was one of the structural reforms provided for in the 1986 TaxReform Program, which was designed to simplify tax administration and make the tax systemmore equitable. It was also in 1988 that the Revenue Information Systems Services Inc.(RISSI) was abolished and transferred back to the BIR by virtue of a Memorandum Order fromthe Office of the President dated May 24, 1988. This transfer had implications on thedelivery of the computerization requirements of the Bureau in relation to its functions oftax assessment and collection.

The entry of Commissioner Jose Ong in 1989 saw the advent of the "Tax AdministrationProgram" which is the embodiment of the Bureau's mission to improve tax collection andsimplify tax administration. The Program contained several tax reform and enhancementmeasures, which included the use of the Taxpayer Identification Number (TIN) and theadoption of the New Payment Control System and Simplified Net Income Taxation Scheme.

Ramos Administration

The year 1993 marked the entry into the Bureau of its first lady Commissioner, LiwaywayVinzons-Chato. In order to attain the Bureau's vision of transformation, a comprehensiveand integrated program known as the ACTS or Action-Centered Transformation Program wasundertaken to realign and direct the entire organization towards the fulfillment of itsvision and mission.

It was during Commissioner Chato's term that a five-year Tax Computerization Project (TCP)was undertaken in 1994. This involved the establishment of a modern and computerizedIntegrated Tax System and Internal Administration System.

Further streamlining of the BIR was approved on July 1997 through the passage of EONo.430, in order to support the implementation of the computerized Integrated Tax System.Highlights of the said EO included the: 1) creation of a fourth Revenue Group in the BIR,which is the Legal and Enforcement Group (headed by a Deputy Commissioner); and 2)creation of the Internal Affairs Service, Taxpayers Assistance Service, InformationPlanning and Quality Service and the Revenue Data Centers.

Estrada Administration

With the advent of President Estrada's administration, a Deputy Commissioner of the BIR,Beethoven Rualo, was appointed as Commissioner of Internal Revenue. Under his leadership,priority reform measures were undertaken to enhance voluntary compliance and improve theBureau's productivity. One of the most significant reform measures was the implementationof the Economic Recovery Assistance Payment (ERAP) Program, which granted immunity fromaudit and investigation to taxpayers who have paid 20% more than the tax paid in 1997 forincome tax, VAT and/or percentage taxes.

In order to encourage and educate consumers/taxpayers to demand sales invoices andreceipts, the raffle promo "Humingi ng Resibo, Manalo ng Libo-Libo" was institutionalizedin 1999. The Large Taxpayers Monitoring System was also established under CommissionerRualo's administration to closely monitor the tax compliance of the country's largetaxpayers.

The coming of the new millennium ushered in the changing of the guard in the BIR with theappointment of Dakila Fonacier as the new Commissioner of Internal Revenue. Under hisadministration, measures that would enhance taxpayer compliance and deter tax violationswere prioritized. The most significant of these measures include: full utilization of taxcomputerization in the Bureau's operations; expansion of the use of electronic DocumentaryStamp Tax metering machine and establishment of tie-up with the national governmentagencies and local government units for the prompt remittance of withholding taxes; andimplementation of Compromise Settlement Program for taxpayers with outstanding accountsreceivable and disputed assessments with the BIR.

Memoranda of Agreement were also forged with the league of local government units andseveral private sector and professional organizations (i.e. MAP, TMAP, PCCI, FFCCCI, etc.)to help the BIR implement tax campaign initiatives.

In September 1, 2000, the Large Taxpayers Service (LTS) and the Excise Taxpayers Service(ETS) were established under EO No. 175 to reinforce the tax administration andenforcement capabilities of the BIR. Shortly after the establishment of said revenueservices, a new organizational structure was approved on October 31, 2001 under EO No. 306which resulted in the integration of the functions of the ETS and the LTS.

In line with the passage of the Electronic Commerce Act of 2000 on June 14, the Bureauimplemented a Full Integrated Tax System (ITS) Rollout Acceleration Program to facilitatethe full utilization of tax computerization in the Bureau's operations. Under the Program,seven (7) ITS back-end systems were released in stages in RR 8 - Makati City and the LargeTaxpayers Service.

Arroyo Administration

Following the momentous events of EDSA II in January 2001, newly-installed PresidentGloria Macapagal-Arroyo appointed a former Deputy Commissioner, Atty. René G. Bañez, asthe new Commissioner of Internal Revenue.

Under Commissioner Bañez's administration, the BIR’s thrust was to transform the agency tomake it taxpayer-focused. This was undertaken through the implementation of changeinitiatives that were directed to: 1) reform the tax system to make it simpler and suitthe Philippine culture; 2) reengineer the tax processes to make them simpler, moreefficient and transparent; 3) restructure the BIR to give it financial and administrativeflexibility; and 4) redesign the human resource policies, systems and procedures totransform the workforce to be more responsive to taxpayers' needs.

Measures to enhance the Bureau's revenue-generating capability were also implemented, themost notable of which were the implementation of the Voluntary Assessment Program andCompromise Settlement Program and expansion of coverage of the creditable withholding taxsystem. A technology-based system that promotes the paperless filing of tax returns andpayment of taxes was also adopted through the Electronic Filing and Payment System (eFPS).

With the resignation of Commissioner Bañez on August 19, 2002, Finance UndersecretaryCornelio C. Gison was designated as interim BIR Commissioner. Eight days later (on August27, 2002), former Customs Commissioner, Guillermo L. Parayno, Jr. was appointed as the newCommissioner of Internal Revenue (CIR).

Barely a month since his assumption to duty as the new CIR, Commissioner Parayno offered aVoluntary Assessment and Abatement Program (VAAP) to taxpayers with under-declaredsales/receipts/income. To enhance the collection performance of the BIR, CommissionerParayno adopted the use of new systems such as the Reconciliation of Listings forEnforcement or RELIEF System to detect under-declarations of taxable income by taxpayers

and the electronic broadcasting system to enhance the security of tax payments. It wasalso under Commissioner Parayno’s administration that the BIR expanded its electronicservices to include the web-based TIN application and processing; electronic raffle ofinvoices/receipts; provision of e-payment gateways; e-substituted filing of tax returnsand electronic submission of sales reports. The conduct of special operations on highprofile tax evaders, which resulted to the filing of tax cases under the Run After TaxEvaders (RATE) Program marked Commissioner Parayno’s administration as well as the conductof Tax Compliance Verification Drives and accreditation and registration of cash registermachines and point-of-sale machines. To improve taxpayer service, the Bureaualso established a BIR Contact Center in the National Office and eLounges in RegionalOffices.

On October 28, 2006, Deputy Commissioner for Legal and Inspection Group, Jose Mario C.Buñag was appointed as full-fledged Commissioner of Internal Revenue. Under hisadministration, the Bureau attained success in a number of key undertakings, whichincluded the expansion of the RATE Program to the Regional Offices; inclusion of newpayment gateways, such as the Efficient Service Machines and the G-Cash and SMART Moneyfacilities; implementation of the Benchmarking Method and installation of the Bureau’s e-Complaint System, a new e-Service that allows taxpayers to log their complaints againsterring revenuers through the BIR website. The Nationwide Rollout of Computerized Systems(NRCS) was also undertaken to extend the use of the Bureau’s Integrated Tax System acrossits non-computerized Revenue District Offices. In 2007, the National Program Support forTax Administration Reform (NPSTAR), a program funded by various international developmentagencies, was launched to improve the BIR efficiency in various areas of taxadministration (i.e. taxpayer compliance, tax enforcement and control, etc.).

On June 29, 2007, Commissioner Buñag relinquished the top post of the BIR and was replacedby Deputy Commissioner for Operations Group, Lilian B. Hefti, making her the second ladyCommissioner of the BIR. Commissioner Hefti focused on the strengthening of the use ofbusiness intelligence by embarking on data matching of income payments of withholdingagents against the reported income of the concerned recipients. Information sharingbetween the BIR and the Local Government Units (LGUs) was also intensified through the LGURevenue Assurance System, which aims to uncover fraud and non-payment of taxes. To enhancethe Bureau’s audit capabilities, the use of Computer-Assisted Audit Tools and Techniques(CAATTs) was also introduced in the BIR under her term.

With the resignation of Commissioner Hefti in October 2008, former BIR Deputy Commissionerfor Legal and Enforcement Group, Sixto S. Esquivias IV was appointed as the newCommissioner of Internal Revenue. Commissioner Esquivias’ administration was marked withthe conduct of nationwide closure of erring business establishments under the “OplanKandado” Program. A Taxpayer Feedback Mechanism (through the eComplaint facilityaccessible via the BIR Website) was also established under his term where complaints onerring BIR employees and taxpayers who do not pay taxes and do not issue ORs/invoices canbe reported. In 2009, the Bureau revived its “Handang Maglingkod” Project where the bestfrontline offices were recognized for rendering effective taxpayer service.

When Commissioner Esquivias resigned in November 2009, Senior Deputy Commissioner, Joel L.Tan-Torres assumed the position of Commissioner of Internal Revenue. Under hisadministration, Commissioner Tan-Torres pursued a high visibility public awarenesscampaign on the Bureau’s enforcement and taxpayers’ service programs. He institutionalizedseveral programs/projects to improve revenue collections, and these include Project R.I.P(Rest in Peace); intensified filing of tax evasion cases under the re-invigorated RATEProgram; conduct of Taxpayers Lifestyle Check and development of Industry Champions.Linkages with various agencies (i.e. LTO, SEC, BLGF, PHALTRA, etc.) were also establishedthrough the signing of several Memoranda of Agreement to improve specific areas of taxadministration.

P-Noy Aquino Administration

Following the highly-acclaimed inauguration of President Benigno C. Aquino III on June 30,2010, a former BIR Deputy Commissioner, Atty. Kim S. Jacinto-Henares, was appointed as thenew Commissioner of Internal Revenue. During her first few months in the BIR, CommissionerHenares focused on the filing of tax evasion cases under the RATE Program, in compliancewith the SONA pronouncements of President Aquino.

BIR Mandate

The Bureau of Internal Revenue is mandated by law to assess and collect all national internal revenue taxes, fees and charges, and to enforce all forfeitures, penalties and fines connected therewith, including the execution of judgements in all cases decided in its favor by the Court of Tax Appeals and the ordinary courts (Sec. 2 of the National Internal Revenue Code of 1997).