FOR RESTRICTED CIRCULATION S S (DEAP) : 1/99

93

RBI LIBRARY FOR RESTRICTED CIRCULATION S S (DEAP) : 1/99 JUNE 1999

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of FOR RESTRICTED CIRCULATION S S (DEAP) : 1/99

RBI L

IBRA

RY

FOR RESTRICTED CIRCULATION S S (DEAP) : 1/99

JUNE 1999

Previous RBI Staff S tudiesStaff Study No. Subject Author Month / Year

S S (DEAP):1/91 Money Market Mutual Funds (MMMFs) in the USA

S. J. Salvi May 1991

S S (DEAP):2/91 India's Balance of Payments during the Four Decades of Planning

K. R. Holla August 1991

S S (DEAP):l/92 Incidence of Interest Cost on Private Corporate Sector

J. M. Lopez April 1992

S S (DEAP):2/92 Import Intensity in the Indian Economy Vidya Pitre May 1992

S S (DEAP):3/92 Measurement of Inflation Rate : Wholesale Price Index - Revised and Old Series

D. Singh June 1992

S S (DEAP):4/92 Small Scale Industry in India - Its Employment Potential and Productivity

Rajan Goyal June 1992

S S (DEAP):5/92 Credit-Deposit Ratio : Current Status and Future Correction

Rashmi Mehrotra June 1992

S S (DEAP):6/92 Employment, Output and Productivity Trends in India's Small-Scale Industry

Deepak Gupta August 1992

S S (DEAP):7/92 The Role of IMF in External Debt Management in the 'Eighties

A. Prasad August 1992

S S (DEAP):8/92 Surveillance and IMF R. Kannan August 1992

S S (DEAP):9/92 Issue of Instability in Money Demand Analysis : A Perspective

B. K. Bhoi October 1992

S S (DEAP):10/92 Dryland Farming in India - New Thrusts and Prospects

N.K. Inamdar and A.V. Bhuleshkar

October 1992

S S (DEAP):ll/92 Countertrade : A Potential Threat to Multilateralism

B. K. Bhoi November 1992

S S (DEAP):12/92 Industrial Sickness - Issues and Options Deepak Gupta November 1992

S S (DEAP):13/92 Money, Output and Prices : Causality Issues and Evidence

Narendra Jadhav, Himanshu Joshi and Partha Ray

November 1992

S S (DEAP):14/92 Financial Reform and Economic Adjustment in Japan

J. R. Majhee December 1992

S S (DEAP):15/92 Industrialisation in Assam G. T. Vellu December 1992

S S (DEAP):16/92 Industrial Growth and Employment : An Analysis of Labour Absorption in Manufacturing Sector in India

D. Ajit December 1992

S S (DEAP):17/92 Farm Input Subsidies and State Finance (A Case Study of Maharashtra and Uttar Pradesh)

Rashmi Mehrotra December 1992

S S (DEAP):l/93 Developments in the Primary Capital Market During the Eighties and Early Nineties

B. M. Misra March 1993

S S (DEAP):2/93 Quarterly Estimates of GDP : 1970-71 to 1990-91

R. K. Das April 1993

S S (DEAP):3/93 A Short-Term Forecasting Model for India's GDP

S. L. Shetty and Tarlok Singh

June 1993

S S (DEAP):4/93 The Financial Rehabilitation of Public Sector Commercial Banks : Some Conceptual and Policy Aspects

Suman K. Bery September 1993

BUDGET DEFICIT IN INDIA: A PRIMER ON MEASUREMENT

R. K. P ATTN AIK, S. M. PILLAI and SANGEETA DAS’\njJ

The p aper has been designed to fo rm u la te a fe w purpose specific m easures of budget d e fic it inIndia fo r analysing the emerging fisca l developm ents. Due to non a v a ila b ili ty o f da ta in respect o f C) »

Local Governments, the analysis is restricted only to Central and S ta te Governments. The s tu d y has«-----------'

w orked ou t tim e series data for fisca l years 1951 through 1999 for the existing deficit measures. I t has also made some a ttem pt to analyse the PSBR. The stu dy reveals th a t the levels of Grqss Fiscal D eficit (GFD) relative to Gross D om estic Product (GDP) were unsustainable during the '&tg}itie$ as there w as large accum ulation of debt which w a s incurred a t a re la tive ly high rate. T he'^ rgQ J$K£ K^ ^ _ *^ 4 of GFD w ith a siza b le com ponent o f m onetised defic it resulted in excess liq u id ity in the\$ 4j£ t e t i j ^

w h ich in turn has rendered challenges fo r the a tta in m e n t o f the m on etary p o lic y objectW&Ztifc price s ta b i l i ty . S tru ctu ra l d e fic it p redom in a ted the f is c a l s y s te m because o f large f isc a l drag.The im p lica tio n o f th is trend is th a t higher econom ic g ro w th by i ts e lf m a y n o t a u to m a tic a lly reduce defic it. Furthermore, as revealed by the measure o f fisca l stance and f isc a l im pulse, the Government pursued an expansionary fiscal po licy during the 'eighties and m o stly a contractionary fisca l p o lic y during the 'n ineties so far. G iven the borrow ing and taxa tion p ow ers ve s te d w ith the Centre there is a large elem ent of dependence by the S tate Governm ents on the Centre fo r resources.

INTRODUCTION

Reflecting a paradigm shift from the conventional approach of 'single m easure' to the contemporary approach of 'series of m easures', several m easures of budget deficit are currently in discussion and use. In recent years, contemporaneous with the world wide development, it has been widely recognised by the academicians and policy makers in India that a correct measurement of budget deficit is one of the crucial pre-requisites not only to assess the impact of fiscal stance but also for prudent macroeconomic management. Following the publication by Rangarajan et al (1989) which is truly a watershed research effort in the measurement of budget deficit, while discussing the fiscal developments in India, since early 'nineties, a few alternative concepts of budget deficit are widely used. Most of these efforts are, however, restricted to Central Government only and the analysis of the State Governments has not been adequately covered. As a result, the issue of measurement of budget deficit has remained some what underdeveloped and to that extent its analytical significance has not been adequately appreciated in term s of the coverage, usage and analysis.

Recognising this, the present paper has been designed to formulate a few purpose- specific measures which are relevant in the Indian context for analysing the emerging fiscal development. In this context it may be noted that the present paper on methodological issues owes substantially to the paper published by Rangarajan et al (1989); however, in terms of coverage, usage and analysis the scope of the paper has been broadened.* Dr. R.K. Pattnaik is Director, Internal Debt Management Cell, Shri S.M. Pillai is Director and

Smt. Sangeeta Das is Assistant Adviser in the Department of Economic Analysis and Policy. The authors are grateful to Dr. A. Vasudevan and Dr. R. Kannan for their valuable comments. The views expressed are those of the authors and not of the Bank. Computational assistance received from Smt. U.R. Vaidya, Shri. P.A. Shinde and Shri T.R. Vasave is gratefully acknowlfJ

Against the above backdrop, while presenting a 'p rim er' on the measurement of budget deficit in India the objectives have been to (a) analyse some of the concepts which are widely used in contemporary literature but have remained unexplored in India, (b) formulate certain new measures keeping in view the constitutional and accounting practices followed in India, and (c) work out time series data for fiscal years 1951 through 1999 for the existing measures as the same is not available systematically and consistently; emphasis has also been given to provide the data base for the underlying expenditures and receipts of these deficit measures.

The remainder of the paper is organised as follows: Section II presents a review of literature on the methodological issues in the measurement of budget deficit. Section III provides a conceptual framework on the basis of which alternative measures of deficit have been designed and developed in Indian fiscal system. Seetion IV sets out an assessment of the magnitude and implications of these deficit indicators. The major findings by way of concluding observations are presented in Section V.

2

SECTION II

REVIEW OF LITERATURE

The literature on the measurement of budget deficit is prolific and varied. Over the years, a sizeable research effort has been undertaken to examine the underlying issues on this subject. Moreover, in the face of large and persistent deficit during the 'eighties there has been a revival of interest on the topic resulting in a further expansion of the existing body of literature. Notwithstanding these developments, selection of an ap p rop ria te m easure of deficit is still beset w ith difficulties. Recognising this, Tanzi (1993) observes:

"A deficit is like an elephant; one always recognises it when one sees it, even though it may be difficult to measure or design it in a way that is satisfactory to everybody or for every purpose/'

The large body of literature on the measurement of budget deficit has been system atically docum ented in four pioneering surveys viz. (i) B linder and Solow (1974), (ii) H eller et al (1980), (iii) Blejer and Chu (1988), and (iv) Blejer and Cheasty (1991 and 1993). Apart from these surveys, some of the research efforts of individual authors which are worth mentioning are: Chelliah (1973), Chand (1977), Boskin (1982), Buiter (1983 and 1985), P iper and Eisner (1989), Eisner (1989), Blanchard (1990), Kotlikoff (1984 and 1986) and Mackenzie (1989). The underlying issues on m easurem ent of deficit which have been highlighted in these research works may be broadly classified as follows: (a) analysis of a set of purpose-spe- cific deficit indicators reflecting the shift in emphasis from the 'single measure' to 'series of measures'; which includes, the simple budgetary derivative m easures as well as fiscal stance and fiscal impulse measures; (b) analysis of the methodological issues, which includes, the budgetary accounting system and classification procedures; coverage and dimension of Government and the distinction between budgetary and non-budgetary operations while estim ating deficit. These issues are discussed in detail in the following paragraphs.

Analysis of purpose specific deficit indicators

In the absence of a common standardised accounting rule, each country follows a typical conventional measure peculiar to its own budgetary practice1. In respect of cross-country comparison, however, the International M onetary Fund (IMF) has been using the concept of overall deficit which is akin to the fiscal deficit or borrowing requirem ents of the Government. Chelliah (1973) has nam ed it as 'public debt concept of deficit'. According to this concept, a Government deficit represents the portion of expenditure and lending which exceeds receipts from revenues, (foreign) grants and loan repayments and which the Government covers by undertaking obligations for future repaym ent a n d /o r running down its liquidity holdings (IMF 1986). While the budget deficit defined thus, is an useful indicator, there are several limitations on which the policy-oriented economists have been concerned for a long time. This problem was further aggravated during the 'eighties on ac

3

coun t of large m acroeconom ic im balances. W ith the ra p id d e te rio ra tio n in the m acroeconom ic balance, the issue of sustainab ility of b u d g e t deficit has becom e pertinent. C onsequently , the conventional deficit tu rned ou t to be seriously inad equate to exam ine the im pact of deficit on the economy and sustainability related issues. In this context a few concepts w hich have ga ined currency are: p im ary deficit, operational deficit, and quasi-fiscal deficit (Blejer and Cheasty 1991). It was also recognised that the conventional deficit m ay be a m isleading indicator of the th rust of the fiscal policy, unless it is decom posed into its cyclical and structural components. O ver the last tw o decades, this concern has led to the developm ent of various techniques, w hich has been docum ented by Blinder and Solow (1974) and H eller et al (1986). Some of the notable con tribu tions su rveyed by B linder and k>low (1974) are: full em ploym en t su rp lu s by Brow n (1956); fiscal leverage by 4usgrave (1964); w eighted full em ploym ent surplus by Brown (1956) and Gramlich 1966); w eighted average surp lus by H ansen (1969) and Blinder and Solow (1974), and w eighted initial surplus by O akland (1969). Thereafter, Chand (1973) analysed three national m easures viz. U nited States' Full Em ploym ent Balance (FEB), Federal Republic of G erm any's cyclically neutral balance (CNB) and Dutch budget im pulse (BI). H e lle r et al, b e s id e s d isc u ss in g fu ll e m p lo y m e n t b a lan ce m e a su re an d w eigh ted s tan d a rd ised su rp lu s m easures, have also evalua ted som e quan tita tive m easures re lating to the stance and th ru st of fiscal policy tha t have been developed by in ternational agencies, such as In ternational M onetary F und (IMF) and O rganisation for Economic Cooperation and D evelopm ent (OECD).

It is pertinen t to note tha t despite such a vast body of literature on fiscal stance measures, there is some controversy w hether these m easures can be designed w ithou t taking a position on w hether the macroeconom ic structure of the econom y is Keynesian, neo-classical or Ricardian. Furtherm ore, w hile it is conceptually feasible to construct macroeconomic model free fiscal stance and fiscal im pulse measures, it appears that inform ation requirem ents are m any and hence the art of constructing these m easu res rev o lv es a ro u n d u sin g sh o rtcu ts an d com prom ises. F o llow ing Prem chand (1993) a set of alternative deficit indicators which are presently in d iscussion and use in the contem porary literature are set ou t in Exhibit J.

Methodological Issues

A part from form ulating a set of alternative concepts of deficit as discussed in the preceding paragraphs the researchers have also em phasised on the m ethodological issues. For exam ple, Boskin (1988) in his w ork on the U.S. federal G overnm ent deficit has argued th a t the item s w hich are excluded from it can have significant m acroeconom ic effects and certain other item s have no t been properly m easured; Buiter (1985) has a rg u ed for a balance shee t approach to calculate deficit; and Kotlikoff (1984) has proposed a concept called economic deficit. The im portant areas w hich are discussed in this context are (a) accounting system and classification procedures, (b) dim ension and com position of the G overnm ent and (c) distinction betw een budgetary and non-budgetary operations. A brief discussion on these aspects is set o u t in the follow ing paragraphs.

4

Exhibit 1Alternative Budget Balance Concepts

Deficit Indicators Description1. Overall Balance

2. Overall Balance w ithout grants3. Foreign balance

4. Domestic balance5. O perational deficit

6. Prim ary deficit

7. C urrent deficit/Surplus

8. Consolidated Coverage

9. Cyclically neutral balance

10. Cyclical effect of the budget

11. Base year balance12. Structural budget

13. Full em ploym ent balance

14. Liquidity balance

15. Perm anent balance

16. Generational balance

G overnm ent Expenditure minus G overnm ent revenue plus G rantsOverall balance minus grantsGovernment foreign expenditure minus G o v e rn m e n t re v e n u e fro m fo re ig n sourcesOverall balance minus foreign balanceOverall balance minus inflationary part of interest paym entsOverall balance minus all interest paym entsG overnm ent c u rren t rev en u es minus current Expenditures(a) w ith rest of public sector(b) w ith quasi-fiscal accounts of

Central bankG overnm ent expenditure minus cyclically corrected G overnm ent revenueO verall balance minus cyclical neutral balance of the budgetN orm al year balanceCyclical effect of budget plus base-year balanceFull employment Government expenditure minus full em ploym ent revenueO vera ll ba lance m inus n e t dom estic non-bank borrow ing minus net foreign borrow ingPresent value of all G overnm ent balan ces m inus p re s e n t v a lu e o f a ll sources of G overnm ent assets (assets, taxes etc.)P resent value of taxes of an average m em ber of his generation for the rem a in d e r of h is life m inus p re s e n t value of transfers he will receive

5

(a) Accounting System and Classification Procedure

While measuring budget deficit one of the major concerns has been the absence of any uniform accounting rules and practices across the countries. Thus, the adoption of a particular measure is conditioned by the budgetary and accounting procedures followed in a particular country. The differences in the budgetary system and accounting procedures are reflected in the classification of budgetary transactions as well as periodicity in reporting. While classifying the budgetary transactions there are tw o basic approaches viz. G overnm ent debt criterion™and public policy criterion . These two criteria while draw ing a line below and above the budget follow the same classification for most of the budgetary transactions; however, they differ for three types of transactions viz. a) net lending3 (b) external grants4 and (c) debt service . This divergence in approach has led to significant discrepancies in the size of conventional deficit.

A nother area of conceptual variation is the choice betw een cash and accrual accounting which has been discussed in detail by Blejer and Cheasty (1991), Heller et al (1986) and Levin (1993). The two most prevalent Government deficit measures are those prescribed by United Nations (1968) and the International Monetary Fund (1986),w hich are on accrual and cash basis, respectively, (Easterly et al, 1991). In practice, deficit m easures, how ever, lie som ewhere in betw een the complete cash and complete accrual measures. Even in countries which use cash deficit concept, interest paym ents are usually m easured as they accrue, rather than when actually paid (Blejer and Cheasty, 1991). Furtherm ore, difficulties in the m easurem ent of deficit arise w hen attempts are m ade to reconcile the cash and accrual concepts on account of 'arrears '7. In this context D iam ond et al (1988), argued that given the accounting conventions, the presence of 'arrears' may lead to an underestimation of expenditure and correspondingly the impact of Government operations and the size of the fiscal problem facing a country. Moreover, since 'arrears' can be viewed as a form of 'forced saving' to the Government, the Government's borrowing requirement may also be underestimated, resulting in a distorted picture of the sources of credit expansion in an economy.

It is argued by M ansoor (1988) that the problems in measurem ent also aggravate w hen the G overnm ent em barks on p rivatisa tion of public en terp rises th rough disinvestment. In such a situation he observes that the balance sheet approach on the lines suggested by Buiter (1983 and 1985) w ould be more appropriate which w ould take care of the changes in public sector net worth.

(b) Composition of Public Sector

The recent literature em phasises on the deficit of the public sector as a whole which takes into account economic activities of the Central Government, Provincial Government, Local Governm ent and Public Enterprises. In this context the public sector borrowing requirem ent (PSBR) has been widely used (World Bank 1988). At

6

the operational level, however, there are difficulties in defining the scope of the Government for purpose of measuring fiscal deficit because Governments frequently perform operations that are usually carried out in other sectors and also non-Gov- ernm ent agents may be used as instrum ents of Government policy. Recognising this, Blejer and Cheasty (1991), remark that two important aspects are to be distinguished which have a bearing on the proper measurement of the budgetary balance. First, the enterprises that comprise the public sector m ust be selected and second that portion of their operations which has a fiscal impact m ust be identified . While discussing these aspects Stella (1993) observes that public ownership is not a sufficient criterion for distinguishing Government enterprises from private firms. On the contrary, the distinction should be based both on behaviour of enterprises and on their impact on public finance. The discussions on these aspects also cover some of the specific issues such as accrual and cash accounting in public enterprises and netting out of subsidies and tax elements in the enterprise pricing.

Recognising that in many developing countries important quasi-fiscal activities are carried out by the financial public sector institutions, including the Central bank, a large and growing body of literature has emerged on the subject matter of quasifiscal deficit. Some of the im portant research efforts in this respect are: Robinson and Stella (1988), Blejer and Cheasty (1991), A nand and W ijnbergen (1988) and Rocha and Saldanha (1992). In all these research efforts a case has been m ade.for consolidating Central Bank quasi-fiscal operations with those of the Government in order to obtain a deficit measure that will provide a more complete information of the size of the deficit. Another area of extending the coverage of public sector is to include the public financial institutions in the coverage of PSBR. The special nature of the public finance institutions and their relation to public sector deficit is discussed in Leviatan (1993).

(c) Inter-Temporal Budget Constraint of Public Sector

Fiscal developments during the 'eighties have added a completely new dimension to the issue of measurement by focusing the attention towards balance sheet based deficit m easures to exam ine the in ter-tem poral budget constraints (Blejer and Cheasty, 1991 and Buiter 1983 and 1985). This is also otherw ise know n as net worth concept of budget deficit. This has raised a number of methodological issues relating to valuation changes, privatisation proceeds, social insurance program me and guaranteed debt. Some of the im portant research efforts in this regard are: Eisner and Piper (1986), Eisner (1986), Boskin et al (1987) and Kotlikoff (1988 and 1989).

From the above discussion it may be concluded that even though budget deficit has a central role in macroeconomic analysis, yet, a seemingly straight forward concept is difficult to design. Accordingly, the contem porary literature has deemphasised the use of a single measure of deficit and has recommended a family

7

of m easures each w ith its advantages and disadvantages. In addition to the identification of a series of m easures, the research efforts have also focused on the methodological issues relating to accounting and classification procedures, coverage of public sector and tem poral dim ension of Governm ent operations.

Ind ian Experience

The concept of budget deficit or deficit financing as it is popularly know n, has occupied a unique p t e m -tiie designing of fiscal policy and planning in India. Like m any developing economies, in India also, researchers and policy makers relied on the single m easure approach of deficit. D uring the 'eighties, however, contem poraneous w ith the w orld w ide developm ent there has been a fundam ental shift from the conventional approach of single m easure to the series of m easures approach. In this context the research efforts of Rangarajan et al (1989) m ay be truly called as 'epoch making'. In their pioneering work, a range of deficit indicators w ere conceptualised an d w orked o u t for the C entral G overnm ent. Subsequently, some of these deficit indicators were published in the publications of Reserve Bank of India and Government of India. Extending the coverage of the Government, Reserve Bank of India also published a series of deficit indicators for the State Governments and also for the Government Sector (Central and State Governments combined together).

In the context of fiscal stabilisation program me since July 1991, 'fiscal deficit ' (akin to the IMF concept of overall deficit discussed earlier) has become an important fiscal variable and crucial policy target of the Central Government (Chelliah 1993). There has been a debate am ong economists regarding the m erit and usefulness of this deficit indicator as well as the definitional issues; some of the important contributors in this respect are G ulati (1994 and 1995), Gill (1993), Mody (1991, 1992 and 1994) Subba Rao (1994) and K hundrakpam (1996). Gulati (ibid) has expressed reservations against the treatm ent of proceeds from the disinvestment of equity holdings of public sector units as part of receipts in the estimation of fiscal deficit. His contention is that if the strict definition of fiscal deficit was adhered to, the official estim ate of fiscal deficit is underestim ated. M ody (ibid) questioned the validity of treating recoveries of loans and proceeds of public sector disinvestment as part of receipts. He in tu rn argued that recoveries and disinvestment on the contrary w ould reduce the financial assets which in turn increase net financial liability of the Government. The official definition, which takes into account these two components in the receipt side is, therefore, underestim ated to that extent. Subba Rao (ibid) has criticised the inadequacy of fiscal deficit in the context of high Inflationary scenario and its inappropriateness to assess the efficiency of the current fiscal policy. K hundrakpam (ibid) evaluated the alternative measures of Government deficit in India w ith special emphasis on the impact of inflation on budget deficit. According to him fiscal deficit in the official estimates is overestimated on account of the impact of inflation and therefore, may not be a true guide for evaluating fiscal adjustm ent program m es.

8

Another area of controversy relates to the definition of primary deficit (RBI, 1993 and Government of India, 1993). The debate centres around the treatment of 'interest receipts' while defining the gross prim ary deficit. It is pertinent to note that the research efforts relating to the measurement of deficit mostly relate to Central Government. Moreover, as most of the State Governments have not yet introduced alternative m easures in their respective budget documents, this concept is yet to take formal shape. Similarly, the concept of 'structural deficit' which has w ide international applicability has not been systematically developed in the Indian context. The importance of this concept has, however, been recognised in the Reserve Bank of India Annual Report 1993-94, which observes:

"An increasing structural deficit, though has the effect in the short-run of promoting growth and employment, would at the same time tend to bring into the open the rigidities in the fiscal system. Tentative technical exercises show that in the case of India, the cyclical component of the deficit of the Central Government is low, and structural deficit predominates".

Another concept called operational deficit which is more often used in the context of high inflation scenario has also not gained much popularity in Indian context. On the contrary, the concept has been argued to be of no merit in Indian context essentially because of the adm inistered nature of interest rates (Joshi and Little, 1992). The present study, therefore, has been organised to formulate a few purpose specific m easures w hich are relevant in the Indian context. In this context the emphasis has been on (a) estimating structural and cyclical deficit, operational deficit and PSBR, (b) designing a few deficit measures considering the inter-Govern- mental resource transfers. In this respect some of the m easures which have im mense analytical significance but not generally discussed have also been examined. In order to explain these issues a conceptual framework has been designed in the following Section.

9

SECTION III

CONCEPTUAL FRAMEWORK

W hile designing a 'primer' on the m easurem ent of budget deficit the three essential elem ents considered are: (a) level of Government, (b) purpose of analysis and (c) accounting framework. India being a federal setup w ith different layers of G overnm ents (Central, State and Local Governments), in principle, the estimation of alternative m easures should cover all these levels separately and also in their combined position . D ue to n on -availab ility of d a ta in respect of Local Governments, the analysis in the present s tudy is restricted only to Central and State Governments. K eeping in view the em erging fiscal developm ents the purpose of analysis in the present study is confined to the following issues: (a) origin and sources of budget deficit, (b) inter-G ovem m ental resource transfers (c) im pact of deficit on debt, Inflation, balance of paym ents, savings and investm ent, and (d) sustainability of deficit. The budget accounting fram ew ork is comm on for both the Central and State Governm ents. The C onstitu tion , how ever, has g iven separate powers to Central and State G overnm ents in term s of im posing taxes and borrow ings9.

A detailed discussion on the budgetary system is set out in Exhibit 2 and the summ ary position of the budgetary transactions is presented in Exhibit 3. Against the above backdrop a few alternative m easures of deficit are in order which are comm on for the Central as w ell as State Governm ents.

10

Exhibit 2

____________________Indian Budgetary System and Practice____________________

Under Article 112 of the Constitution, a statement of estimated receipts and expenditure of the Government of India has to be laid before Parliament and for the State Governments in the State legislature in respect of the financial year which runs from April 1, to March 31. This statement titled "Annual Financial Statement" (AFS) is the main budget document. The estimates of receipts and disbursements in the AFS and of expenditure in the demand for grants are shown according to the accounting classification prescribed under the Article 150 of the Constitution. The AFS shows the receipts and payments of Government under the three parts in which Government accounts are kept, (i) Consolidated Fund; (ii) Contingency Fund and (iii) Public Account. All revenues received by Government, loans raised by it and also its receipts from recoveries of loans granted by it, form the Consolidated Fund. The Contingency Fund is an imprest placed at the disposal of the President to incur urgent unforeseen expenditure. Besides the normal receipts and expenditure of Government which relate to the Consolidated fund, certain other transactions enter Government account, in respect of which, Government acts more as a banker, viz. transactions relating to provident funds, small savings collections, other deposits etc. The moneys thus received are kept in the account called Public Account.

Under the Constitution of India, Budget has to distinguish expenditure on revenue account from other expenditure. Accordingly, the Government Budget comprises (a) Revenue Budget and (b) Capital Budget. Revenue Budget consists of the revenue receipts of the Government v/hich mainly include tax revenues and interest and dividends on investments made by the Government. Revenue expenditure is for normal running of the Government. Broadly speaking, expenditure which does not result in the creation of assets is treated as revenue expenditure with the exception of grants given to the State Governments. Capital Budget consists of capital receipts and disbursements. Capital receipts consist of non-debt components and debt components. The non-debt item is the recovery of loans disbursed in the past by the Government. The disinvestment proceeds also form part of non-debt capital receipts. The debt portion comprises internal debt (market borrowings), other liabilities (small savings, reserve funds and deposits etc.) and external borrowings. Capital disbursements consist of capital expenditure on acquisition of assets and loans and advances to State Governments. The transactions in the Public Account which include small savings, Provident Fund, deposits and reserve funds are also covered in the Capital Budget.

11

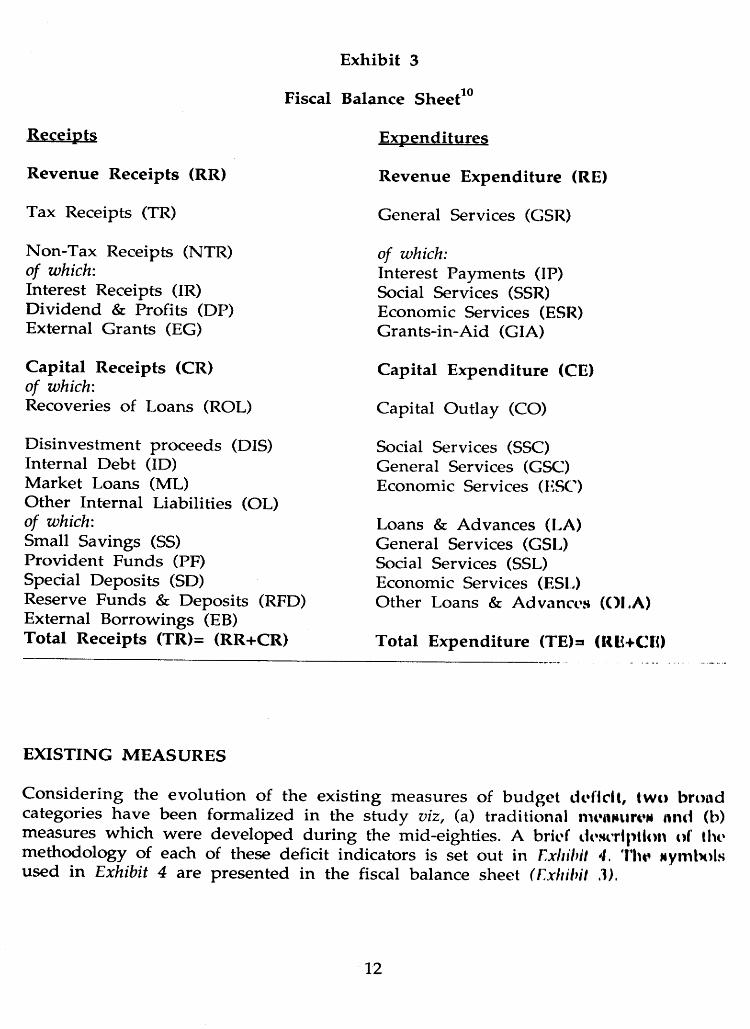

E xhib it 3

Fiscal Balance S heet10

RfcCgipte E xpend itu res

R evenue R eceip ts (RR)

Tax Receipts (TR)

N on-Tax Receipts (NTR) of which:Interest Receipts (IR)D ividend & Profits (DP)External G rants (EG)

C ap ita l R eceip ts (CR)of which:Recoveries of Loans (ROL)

D isinvestm ent proceeds (DIS) Internal D ebt (ID)M arket Loans (ML)O ther In ternal Liabilities (OL) of which:Small Savings (SS)Provident Funds (PF)Special D eposits (SD)Reserve F unds & D eposits (RFD) External B orrow ings (EB)T otal R eceip ts (TR)= (RR+CR)

R evenue E xpend itu re (RE)

G eneral Services (GSR)

of which:Interest Paym ents (IP)Social Services (SSR)Economic Services (ESR) G rants-in-A id (GIA)

C ap ita l E xpend itu re (CE)

C apital O utlay (CO)

Social Services (SSC)G eneral Services (GSC)Economic Services (ESC)

Loans & A dvances (LA)G eneral Services (GSL)Social Services (SSL)Economic Services (ESL)O ther Loans & A dvances (OLA)

T otal E xpend itu re (TE)=* (RLfCK)

EXISTING M EASURES

C onsidering the evo lu tion of the existing m easures of b u d g e t deficit, tw o brood categories have been form alized in the s tudy viz , (a) traditional nnntfiumi and (b) m easures w hich w ere developed during the mid-eighties. A brief do.Hcription of the m ethodology of each of these deficit indicators is set out in Exhibit 4. The sym bols used in Exhibit 4 are p resen ted in the fiscal balance sheet (Exhibit ,1).

12

E xhibit 4

Concepts and Measurement of Existing Deficit Measures

D eficit Indicators (1)

Expenditures(2)

Receipts(3)

M easurement(4)

Traditional Measures

1. Revenue Deficit (RD)2. Capital Account Deficit (CAD)3. Conventional Budget

Deficit (CD)114. Monetised Deficit (MD)

RECE=CO+LA

TE=RE+CE*

RRCR

TR=RR+CR*

RD=RE-RRCAD=CE-CR

CD=TE-TR=RD+CAD*

Measure of Recent Origin

5. Gross Fiscal Deficit (GFD)12 TE-ROL=RE+CO+(LA-ROL)=RE+CO+NL

RR+DIS GFD=(TE-ROL)-(RR+DIS)=(RE+CE-ROL)-(RR+DIS)=(RE+CO+LA-ROL)-(RR+DIS) =(RE+CO+NL) -(RR+DIS) =(RD+CO+NL-DIS)

6. Primary Deficit (PD) (a) PD1

TE-ROL-IP =(RE-IP)+ [CO+(LA-ROL)l =(RE-IP)+ (CO+NL)

RR+DIS PD1 =(RE-ROL-IP) -(RR+DIS)=I(RE-IP)+(CO+LA-ROL)]-(RR+DIS)=[(RE-IP)+(CO+NL)l-(RR+DIS)

(b) PD2 TE-ROL-IP=(RE-IP)+ [(CO+LA-ROL) 1= (RE-IP)+(CO+NL)

(RR-IR)+DIS PD2=(TE-ROL-IP) -[(RR-IR)+DISJ =(RE-IP)+[CO+(LA-ROL)l -[ (RR-IR) +DISJ=[ (RE-IP)+ (CO+NL)]-[(RR-lR)+DIS]

7. Net Fiscal Deficit (NFD) TE - NL=(RE+CE)-(LA-ROL) = (RE+CE)-NL

RR+DIS NFD=(TE-NL)-(RR+DIS) =[(RE+CE)-(LA-ROL)] -(RR+DIS)=[(RE+CE)-NL1 - (RR+DIS)

8. Net Primary Deficit (NPD) TE-NL-IP=(RE-IP)+[CE-(LA-ROL)]=(RE-IP)+(CE-NL)

(RR-IR)+DIS NPD=(TE-NL-IP)- [(RR-IR)+DIS1 =[(RE-IP)+CE-(LA-ROL)] -[(RR-IR)+DIS1=[(RE-IP)+ (CE-NL)M(RR-IP)+DIS]

9. Primary Revenue Balance (PRB)PRB1PRB2

RE - IP RE - IP

RRRR-IR

PRB1=(RE-I P)-RR=RD-IP PRB2=(RE-IP)-(RR-IR)=RD-NIP

* : Since m onetised deficit is essentially a financing item of the Central Government's budgetary gap its measurement through expenditure and receipts approach is not applicable.

Note: Explanation of the notation used in this exhibit is set out in Exhibit 3.

13

The concept and m easu rem en t of the existing m easures becom e self-explanatory follow ing the details set ou t in Exhibit 4. N evertheless, further discussion on the m easurem ent aspects of gross fiscal deficit and prim ary deficit along with the definition of m onetised deficit is presented in the follow ing paragraphs.

Monetised Deficit (MD)

It has been recognised by the Comm ittee to Review the W orking of the M onetary System (Chairm an: Prof. Sukham oy C hakravarty) that there are tw o basic lim itations of the conventional deficit viz.: (a) budgetary deficit defined as such does not reveal the full ex tent of the G overnm ent's reliance on RBI credit and (b) to the extent T reasury Bills are held outside the RBI, the concept tends to overstate the m onetary im pact of the fiscal operation. Accordingly, it recom m ended a m odification in the concept of b u d g e ta ry deficit to include the en tire RBI crcd it to the G overnm ent to capture the m onetary im pact of the fiscal operations13. M onetised deficit is thus denoted by the net RBI credit to the Central Government. Presently, this is defined as the sum of increase in the RBI's holdings of G overnm ent of India dated securities and Treasury Bills and rupee coins and the Ways and Means A dvances to C entral G overnm ent by the Reserve Bank, ad justed for changes in cash balances w ith the Reserve Bank.

Composition and Financing of GFD

W ith the d isc o n tin u a tio n of the au to m atic m o n e tisa tio n of the b u d g e t d efic it th rough the in s tru m en t of ad hoc T reasury Bills w ith effect from the fiscal year 1997-98, the system of conventional deficit has been d iscontinued and the gross fiscal deficit has been introduced in the budget as the benchm ark for assessing the fiscal perform ance.

The analytical advantage of GFD is its com prehensiveness in the presentation of the overall bo rrow ing requ irem en ts position of the G overnm ent. This apart, the GFD can be decom posed into Revenue Deficit (RD), Capital O utlay (CO) and N et Lending (NL) w hich reflects the utilisation of the borrow ed funds by the G overnment. On account of the change in the system of accounting of loans to States and UTs against net Small Savings collections w ith effect from April 1, 1999# these figures do not from p art of GFD. The financing of GFD reveals the extent of G overnm ent borrow ings from different sources viz. external and internal which include non-banking and banking and the level of monetisation of G overnm ent borrowing. It is pertinent to note that the decom position and financing of GFD taken together reflect the sources and uses of borrow ed funds at the disposal of the Government.

Composition of Primary Deficit

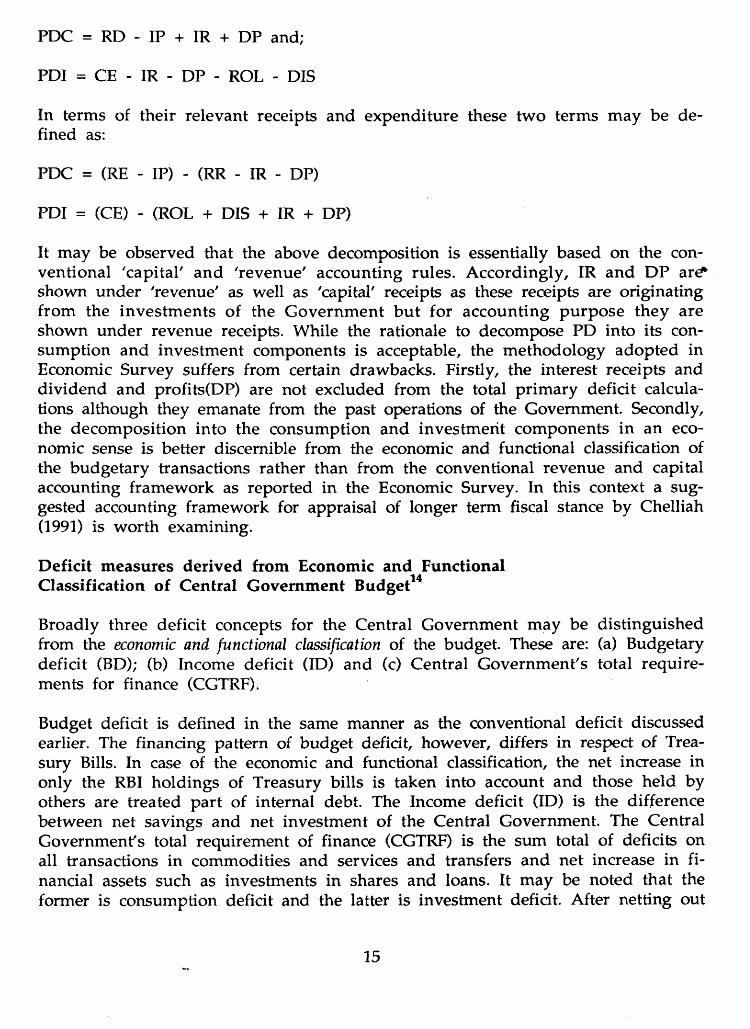

There has been an indication in the Economic Survey, 1995-96 that PD (GFD-IP) m ay be decom posed into its consum ption (PDC) and investm ent (PDI) components. Thus,

14

PDC = RD - IP + IR + DP and;

PDI = CE - IR - DP - ROL - DIS

In terms of their relevant receipts and expenditure these tw o terms m ay be defined as:

PDC = (RE - IP) - (RR - IR - DP)

PDI = (CE) - (ROL + DIS + IR + DP)

It may be observed that the above decomposition is essentially based on the conventional 'capital' and 'revenue' accounting rules. A ccordingly, IR and DP ar£* shown under 'revenue' as well as 'capital' receipts as these receipts are originating from the investm ents of the G overnm ent bu t for accounting purpose they are shown under revenue receipts. While the rationale to decompose PD into its consum ption and investm ent components is acceptable, the methodology adopted in Economic Survey suffers from certain drawbacks. Firstly, the interest receipts and dividend and profits(DP) are not excluded from the total prim ary deficit calculations although they emanate from the past operations of the Government. Secondly, the decom position into the consum ption and investm ent com ponents in an economic sense is better discernible from the economic and functional classification of the budgetary transactions rather than from the conventional revenue and capital accounting framework as reported in the Economic Survey. In this context a suggested accounting framework for appraisal of longer term fiscal stance by Chelliah (1991) is worth examining.

Deficit measures derived from Economic and Functional Classification of Central Government Budget14

Broadly three deficit concepts for the Central Government may be distinguished from the economic and functional classification of the budget. These are: (a) Budgetary deficit (BD); (b) Income deficit (ID) and (c) Central G overnm ent's total requirements for finance (CGTRF).

Budget deficit is defined in the same manner as the conventional deficit discussed earlier. The financing pattern of budget deficit, however, differs in respect of Treasury Bills. In case of the economic and functional classification, the net increase in only the RBI holdings of Treasury bills is taken into account and those held by others are treated part of internal debt. The Income deficit (ID) is the difference between net savings and net investm ent of the Central Government. The Central Government's total requirement of finance (CGTRF) is the sum total of deficits on all transactions in commodities and services and transfers and net increase in financial assets such as investments in shares and loans. It may be noted that the former is consumption deficit and the latter is investment deficit. After netting out

15

interest components from CGTRF the primary deficit (PD) may be worked out and decomposed w ith its consum ption and investment component.

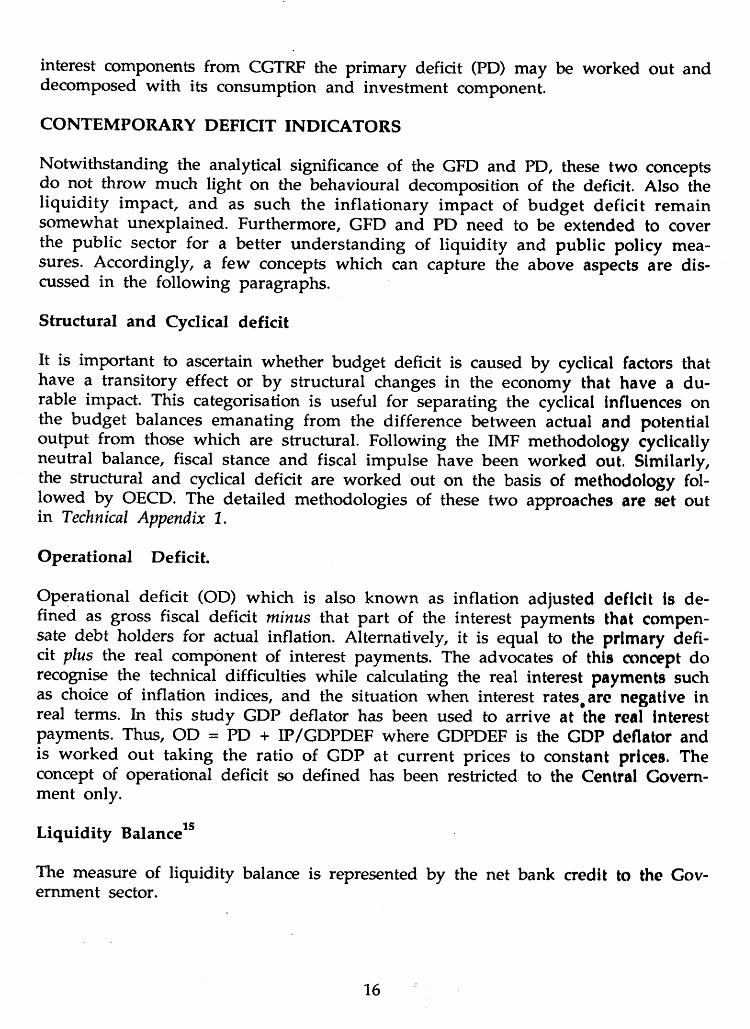

CONTEMPORARY DEFICIT INDICATORS

Notwithstanding the analytical significance of the GFD and PD, these two concepts do not throw much light on the behavioural decomposition of the deficit. Also the liqu id ity im pact, and as such the inflationary im pact of budget deficit rem ain som ew hat unexplained. Furtherm ore, GFD and PD need to be extended to cover the public sector for a better understanding of liquidity and public policy m easures. Accordingly, a few concepts which can capture the above aspects are discussed in the following paragraphs.

Structural and Cyclical deficit

It is im portant to ascertain whether budget deficit is caused by cyclical factors that have a transitory effect or by structural changes in the economy that have a du rable impact. This categorisation is useful for separating the cyclical influences on the budget balances em anating from the difference betw een actual and potential output from those which are structural. Following the IMF methodology cyclically neutral balance, fiscal stance and fiscal im pulse have been worked out. Similarly, the structural and cyclical deficit are worked out on the basis of methodology followed by OECD. The detailed methodologies of these tw o approaches are set out in Technical Appendix 1.

Operational Deficit.

O perational deficit (OD) which is also know n as inflation adjusted deficit is defined as gross fiscal deficit minus that part of the interest paym ents that compensate debt holders for actual inflation. Alternatively, it is equal to the primary deficit plus the real component of interest payments. The advocates of this concept do recognise the technical difficulties while calculating the real interest payments such as choice of inflation indices, and the situation when interest rates#are negative in real terms. In this study GDP deflator has been used to arrive at the real interest payments. Thus, OD = PD + IP/GDPDEF where GDPDEF is the GDP deflator and is w orked ou t taking the ratio of GDP at current prices to constant prices. The concept of operational deficit so defined has been restricted to the Central Governm ent only.

Liquidity Balance15

The measure of liquidity balance is represented by the net bank credit to the Governm ent sector.

16

Liquidity Balance (LB) = Total F inancing of G overnm ent Sector - N on-bankBorrowing

= Net Banking Sector Credit to Government Sector = [Net RBI Credit to Government Sector + N et Other Bank

ing Sector Credit to Government Sector]

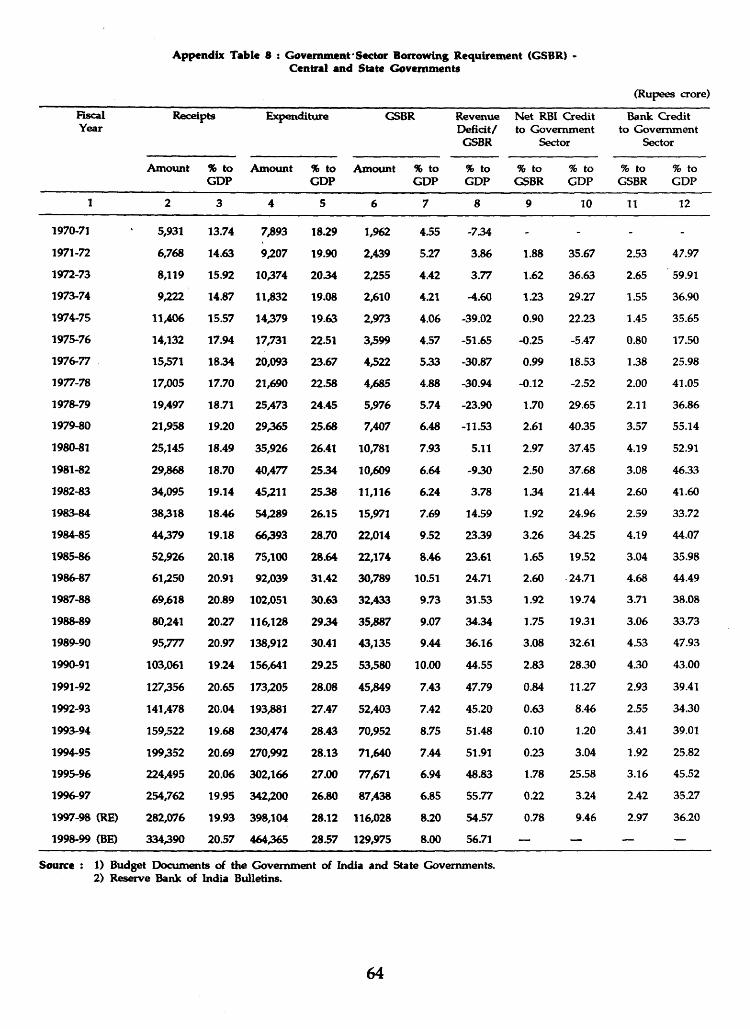

Government Sector Borrowing Requirement (GSBR)

In Indian context public sector deficit has not been studied in its totality because of statistical problems. There is a paucity of information on local Governments and public sector enterprises. Therefore, the Government Sectors Borrowing Requirement (GSBR) has been used as a proxy for Public Sector Borrowing Requirem ents (PSBR). In this context, the present study has developed a database on PSBR and GSBR. The data on PSBR are taken from the Economic Survey of Government of India which include budgetary transactions of the Central Government, State Governments and Union Territories including internal and external budgetary resources of public sector undertakings for their Plans. The data on GSBR have been worked out on the lines worked out in the Reserve Bank of India publications. The detailed methodology is presented in Technical Appendix 2.

INTER-GOVERNMENTAL TRANSACTIONS

The PSBR captures the budgetary constraints of the entire public sector and, therefore, is a useful tool for macroeconomic policy and liquidity management. It does not, however, reveal budgetary transactions between different segments of the Government Sector which have crucial importance in a federal setup like India. The resource flow from the Central Government to State Governments and vice versa is a matter of controversy in the Centre- State financial relations. In this context, it would be useful to derive the budgetary balance for the Central and State Governments taking into account the resource flow before the federal transfers. It may be noted that State Resource Gap (SRG) and Basic Resource Gap (BRG) have been developed in the context of State Governments16. A similar approach has been followed in this study to frame certain deficit indicators taking into account the resources transfer of the Central Government.

State's Resource Gap (SRG)

State's Resource Gap (SRG) = [(RE-IPC)+(CD-DID-RLC)] -[(RR-NSGFC) + (CR-LAC)]

where,RR = Revenue Receipts CR = Capital ReceiptsNSGFC = Non - Statutory Grants from Centre LAC = Loans and Advances from Centre RE = Revenue Expenses

17

IPC = Interest Payments to Centre CD = Capital Disbursement DID = Discharge of Internal Debt RLC = Repayment of Loan from Centre

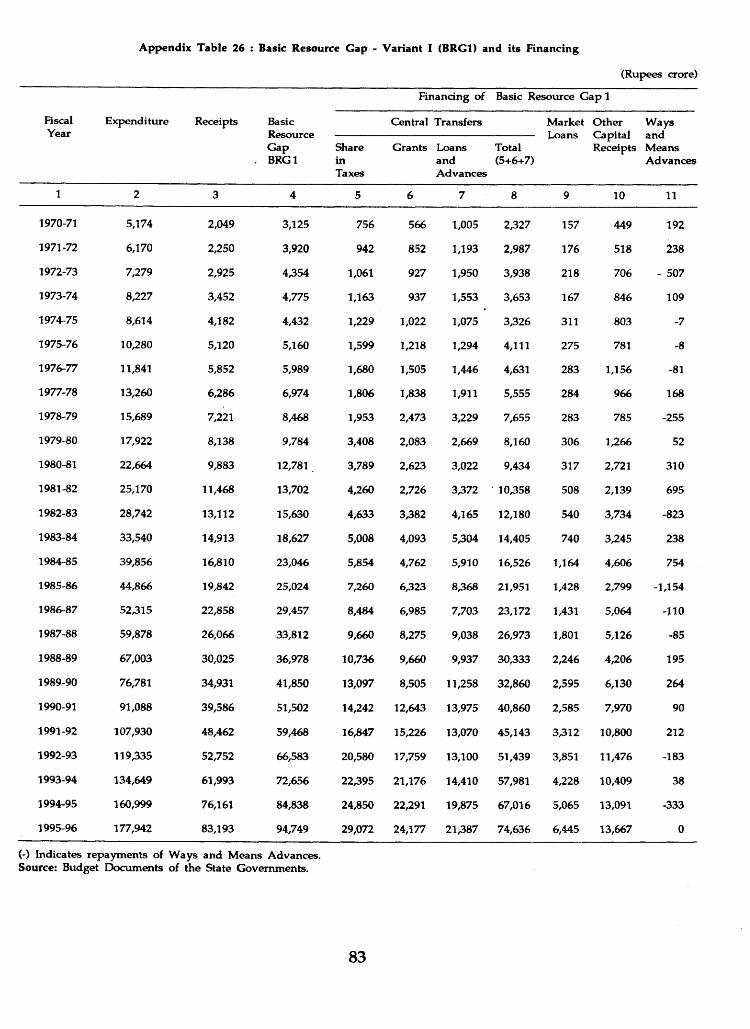

Basic Resource Gap (BRG)

Three variants of Basic Resource Gap have been developed by Pattnaik et al (1994) viz. BRG1, BRG2 and BRG3.

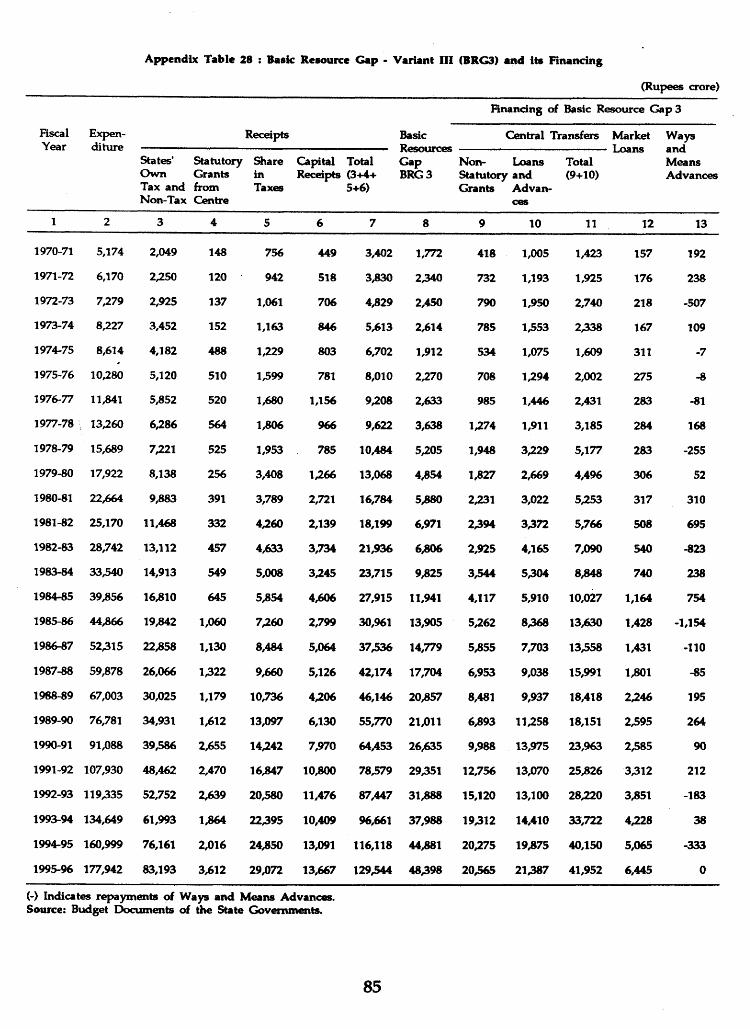

BRG1 = [(TE)-(OTAR + ONTR)]BRG2 = (TE) - [ (OTAR+ONTR) + (ID-ML) + (PFS+RFD+OCR)]BRG3 = (TE) - [(OTAR+ONTR+SCT+SGFC) + (ID-ML)+(PFS+RFD+OCR)] where,

' TE = Aggregate Expenditure OTAR = States Own Tax Receipts ONTR = States Own Non-Tax Receipt ID = Internal Debt ML = Market LoanPFS = Small Savings Provident Fund etc.RFD = Reserve Funds and Deposits OCR = Other Capital Receipts SCT = Share in Central Taxes SGFC = Statutory Grants from Centre

These concepts have the analytical advantage in m easuring the fiscal stress and fiscal dependency of the State Governments [Pattnaik et al (1994)].

Centre's Deficit before Federal Transfers

Three variants of Centre's deficit before federal transfers have been formulated in this study. These are (a) Revenue Deficit Before Federal Transfers (RDBFT), (b) Capital Account Deficit Before Federal Transfers (CDBFT) and (c) Overall DeficitBefore Federal Transfers (ODBFT). The definition of these three deficit indicatorsare given below:

(a) Revenue Deficit before Federal Transfers (RDBFT):(RE - GIA) - (RR - IR) or RD - (GIA- IR)

(b) Capital Account Deficit before Federal Transfers (CADBFT):(CE - LA) - (CR - ROL) or CAD - NL

(c) Overall Deficit before Federal Transfer (ODBFT):[(RE - GIA) + (CE - LA)] - [(RR - IR) + (CR - ROL)]= ODBFT = (RDBFT + CADBFT)

Explanations of the notations used is set out in Exhibit 3.

18

ADVANTAGE OF A TAXONOMY OF DEFICIT INDICATORS

A summary presentation of the deficit indicators explained above in terms of their purpose, level of Government and period of data presentation is set out in Exhibit5. An issue in this context is whether there exists any analytical superiority of one deficit indicator over the other. It may be mentioned that these deficit indicators are mainly contextual. It is, therefore, difficult to discuss the advantage or disadvantage of one concept over the other. As alluded to earlier, these deficit indicators are purpose specific, and the usage of these indicators should be in conformity with the objective for which the analysis has been undertaken. Thus, there lies the advantage in having a series of measures as discussed above than that of a single measure of deficit as the former throw much deeper analytical insights into the assessment of fiscal and macroeconomic management.

EXHIBIT 5 : TAXONOMY OF BUDGET DEFICIT INDICATORSMeasures of deficit

(1)

Purpose

(2)

Level of Government(3)

Period of Data Presentation(4)

1. Conventional Deficit

2. Monetised Deficit

3. Revenue Deficit

Uncovered Gap\ Monetisation Impact

Monetary Impact of Fiscal Operation

Dis-savings of the Government

CentreStatesCombinedGovernment

CentreStates

CentreStatesCombinedGovernment

1950 - 1997 1970 - 1999 1970 - 1997

1951 - 1999 1970 - 1999

1950 - 1999 1970 - 1999 1970 - 1999

4. Gross Fiscal Deficit

5. Government Sector Borrowings Requirement

6. Primary Deficit and Primary Revenue Balance, Net Fiscal Deficit and Net Primary Deficit

Macroeconomic impact of budget deficit

To examine the effects of Government Sector deficits on macroeconomic variables.

Sustainability of deficit

CentreStates

CombinedGovernment

CentreStatesCombinedGovernment

1950 - 1999 1970 - 1999

1970 - 1999

1950 - 1999 1970 - 1999 1970 - 1999

7. Revenue Deficit, Capital Account Deficit and Overall Deficit Before Federal Transfers

8. State Resource Gap and Basic Resource Gap

9. Fiscal Stance, Fiscal Impulse, Cyclical and Structural Deficit

10. Operational Deficit

11. Income Deficit

12. Central Governments Total Requirement of Finance (CGTRF)

13. Liquidity Balance

Inter-Governmental Transfers

Fiscal Dependency and fiscal stress

Autonomous and discretionary effects on Budget Deficit to examine the behavioural decomposition of deficit and growth implications of deficit.

To net out effects of inflation on budget deficit.

Centre

States

CentreCombinedGovernment

CentreCombinedGovernment

To measure saving-investment Centre gap and expansionary effects of the government budgetary operations.

To measure the deficit arising Centre out of Government's net transactions in commodities, services, transfers and transactions in financial assets.

To capture the liquidity impact Centre of the budgetary operations of States the Government sector.

1950 - 1999

1970 - 1996

1970 - 1997 1970 - 1997

1970 - 1997 1970 ~ 1997

1970 1998

1970 199H

1970 19VH 1970 1998

20

SOURCES, RECONCILIATION AND COVERAGE OF DATA

As mentioned earlier, one of the prime objectives of this study is to generate a consistent and comparable time series data for the deficit indicators in the Indian context for undertaking inter-temporal analysis. This requires not only a comprehensive understanding of data base but also a large amount of data reconciliation. Some of these aspects are set out below.

Sources of data mostly relate to the publications of Reserve Bank of India (RBI) and Government of India (GOI) viz. (i) Articles on Central Government Finances and State Government Finances, published in various issues of RBI Bulletin, (ii) Report on Currency and Finance, RBI, (iii) Combined Finance Accounts of Government of India, (iv) Finance Accounts of Government of India, (v) Economic Survey of Government of India and (vi) Budget Documents of Central and State Governments.

It may be noted that there were two major accounting and classification changes in the budget in 1974-75 and in 1986-87; besides the minor changes that had taken place in many other years17. Due to non-availability of detailed data, it is not possible to make a complete adjustment in the time series, however, broad adjustments have been made to make the data consistent and comparable for the purpose of study. In respect of the Central Government, the areas of adjustments relate to financing of conventional deficit, miscellaneous capital receipts, classification and discharge of debt, netting of contra entries, and treatment of external grants and market borrowings18. As regards the State Governments the accounting classification changes during 1974-75 and 1986-87 did not affect the aggregate fiscal variables in the revenue and capital accounts as these data continue to be reported consistently in the RBI documents. The problem relating to State Governments lies in the coverage of the State Governments. On account of coverage changes and reorganisation of States it is difficult to adjust the State Governments data from 1950-51. Therefore, in this study the State Governments data (unlike the Central Government data which are from 1950-51) cover the period 1970-1999. Consequently, the Government sector data (Central and State combined) also cover the same period. Furthermore, the GDP series used in the study are with the base 1980-81.

21

SECTION IV

EMPIRICAL ANALYSIS

The empirical analysis covers the magnitude of the fiscal imbalances of the Central and State Governments separately as well as of the Government sector as a whole. It also examines implications of such imbalances on the economy and budget following the categorisation of deficit indicators set out in the Exhibit 5 in the preceding Section.

RD, CAD, CD and MD

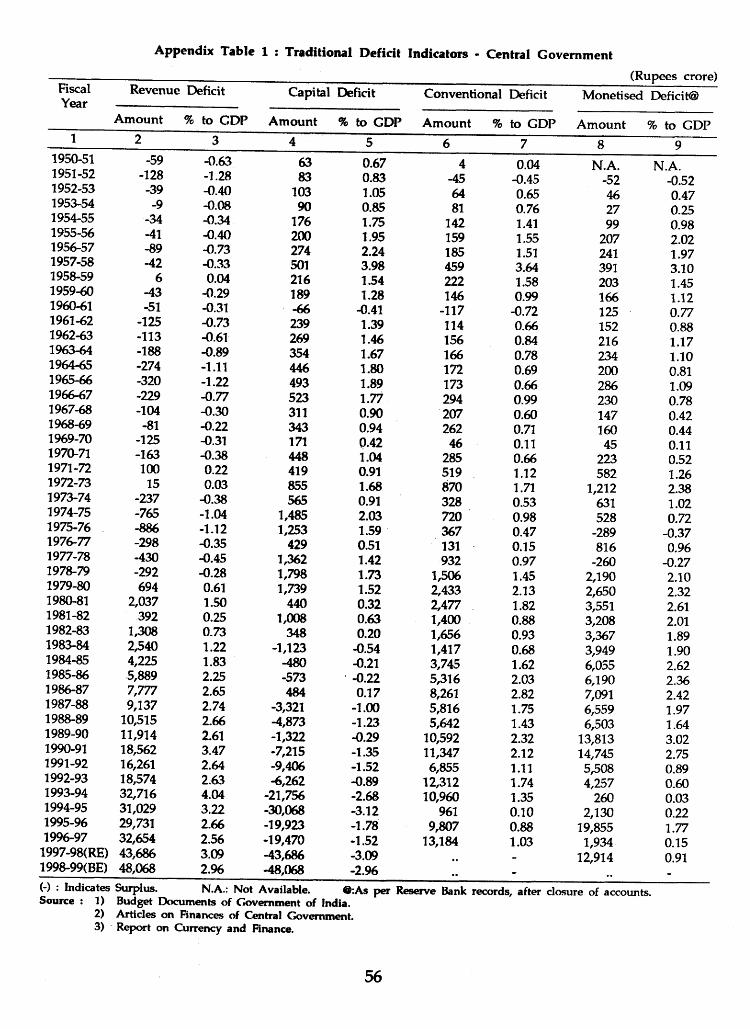

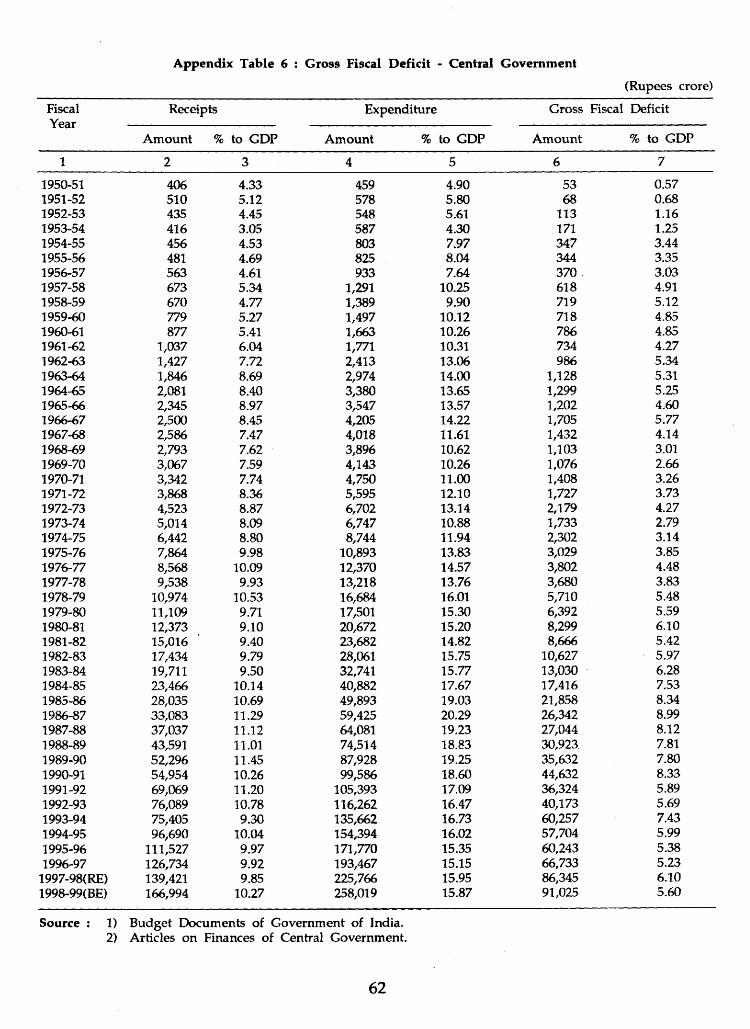

According to the conventional paradigm the revenue account should generate adequate surplus to finance capital expenditure and capital account deficit (if any) is only m eant for financing capital expenditure. The crucial assumption in this regard is that capital expenditure is self balancing and self lim iting.19 In conformity with the above mentioned budgetary principle, the Central as well as the State Governm ents m aintained, by and large, surpluses in their revenue account; the trend in revenue surplus continued in respect of the Central G overnm ent till 1978-79 and for the State Governments upto 1986-87 and for the Government sector till 1981-82 (Appendix Tables 1,2 and 3). Correspondingly, the capital account was in deficit, reflecting a 'm irror im age'. Thus, the conventional deficit of the Central G overnm ent during the period 1950-1979 ranged between 0.04 per cent (1950-51) and 3.64 per cent (1957-58). It is pertinen t to note that the deficit in the year 1957-58 is unusual of the trend and thus w hile presenting the budget the Finance M inister observed "The proposal I have made will still leave the overall deficit for the year at a level somewhat higher than I would consider safe". In respect of the State Governments the deficit ranged betw een 0.04 per cent (1974-75) and 0.66 per cent (1980-81). Reflecting the trends in the Central and State Governments the conventional deficit of the Governm ent Sector also varied in the range of 0.10 per cent (1976-77) and 2.48 per cent (1980-81). The deterioration in the revenue account of the Central and State Governm ents during the 'eighties w as on account of sharp rise in revenue expenditure (Appendix Table 4 and 5). The large gap in revenue account in all levels of G overnm ent also continued during the 'nineties so far. C orrespondingly, there has been a surplus in the capital account m ainly due to cut backs in capital expenditure. The monetised deficit, which reflects the liquidity impact of the budget deficit, deteriorated during the 'eighties on an average of 2.2 per cent of GDP as against 1.1 per cent of GDP in the 'seventies (Appendix Table 1). This deterioration in the monetised deficit eroded the efficacy of monetary policy in controlling inflation. The monetised deficit was, however, contained considerably to below 1 per cent of GDP during the period 1991-95 from the level of 2.75 per cent d u rin g 1990-91. The la test tren d , how ever, is a m atte r of serious concern as m onetised deficit du ring 1995-96 reached a peak level of Rs.19,855 crore or 1.77 per cent of GDP and after coming dow n to Rs.1,934 crore (0.15 per cent of GDP) in 1996-97 shot up to Rs.12,914 crore (0.91 per cent of GDP) in 1997-98.

22

GFD/GSBR/PSBR

Gross fiscal deficit (GFD), Government Sector Borrowing requirements (GSBR) and Public Sector Borrowing Requirements (PSBR) are concepts used for m easuring the total borrowing requirements of Centre and State Governments, Government Sector and Public Sector, respectively. The borrowing requirements of the Central Governm ent w hich w ere, on an average, below 5 per cent of GDP du ring the period 1950-1980 (on a five-yearly average basis) increased to 8.2 per cent during the second half of the 'eighties. The borrow ing requirem ents of the State G overnm ents which were in the neighbourhood of 2 per cent during the 'seventies deteriorated to 3 per cent of GDP during the 'eighties. Correspondingly, the GSBR which was about 5 per cent d u rin g the 'seventies deterio ra ted to 8.5 per cent d u rin g the 'eighties (Table 1 and Appendix Table 6,7 and 8). It is pertinent to note that such large borrowings were necessitated because of huge revenue deficit which is evident in decomposition of GFD (Appendix Table 9 and 10). These borrowings were financed by high cost borrow ed funds as evident in the financing pattern of the GFD (Appendix Table 11 and 12) concomitant with the trends in GSBR, the Public Sector Borrow ing requirem ents (PSBR) also assum ed larger p roportion of GDP during the latter half of the 'eighties as compared with the levels during the seventies (Appendix Table 13). For example, during the latter half of 'eighties PSBR as proportion of GDP, on an average, was about 13 per cent as against around 6 per cent during the 'seventies.

Large and grow ing GFD of the G overnm ent sector w ith a sizable com ponent of m onetised deficit, resulted in a sharp rise in m onetary grow th which was much higher than real economic grow th and thus generating severe dem and pressure. Moreover, the rising GFD and GSBR has resulted in large outstanding debt of the Centre, States and G overnm ent sector. For example, the outstanding liabilities of Central Government increased sharply from Rs.13,379 crore or about 31 per cent of GDP as on end-M arch 1970 to Rs.40,251 crore or 35 per cent as on end-M arch 1980 and further to Rs.2,39,849 crore or 52.5 per cent as on end-M arch 1990. Similarly, the ou ts tand ing liabilities of the State G overnm ents relative to GDP has show n sharp increase (Table 2). A part from generating a high level of debt, the increasing borrow ing requirem ents of the Governm ent Sector during the 'eighties has also p u t pressure on the in terest rate despite the G overnm ents' a ttem pt to borrow in a captive market and from the Reserve Bank of India. Consequently, the interest rate on Government borrowings has shown a sharp rise, the nominal rates on select instrum ents are indicated in Table 3. These rates w ould be m uch higher if fiscal concessions would be taken into account. Large volume of debt along with high rates of in terest has p u t pressure on the budget in term s of large interest payments. As a result interest burden defined as the ratio of interest paym ents to revenue receipts have gone up considerably for all levels of Government (Table 2). Recognising the adverse implications of large borrowings (GFD), the Central Governm ent undertook the fiscal stabilisation measures in July 1991. Consequently, the level of GFD relative to GDP was brought down from its levels in the past except

23

for the bad performance in 1993-94. Since the State Governments are not committed to any fiscal corrections and consolidation, the level of GFD continued at about 3 per cent of GDP; the GSBR, how ever show ed some im provem ent because of Central G overnm ent action in reducing GFD. N otw ithstanding the reduction in GFD of the Central Government and GSBR, the persistence of revenue deficit in all levels of G overnm ent is a m atter of serious concern as it not only reflects the dissavings of G overnm ent sector bu t also m isutilisation of high cost borrow ed funds.

Primary Deficit: PD1, PD2 and NPD

It has been recognised that in the Indian context there is no unanim ity of view regarding the definition of prim ary deficit that is derived from GFD (RBI, 1993). Accordingly, as mentioned earlier, the present study has conceptualised three concepts of prim ary deficit for the Central, States and Government Sector viz. PD1, PD2 and NPD. The trends in PD1, PD2 and NPD of the Central and State Governm ents are set out in Appendix Table 14 through 17. It may be observed that primary balance in any of its variants and for any level of Government depicts a perm anent deficit feature. The persistence of prim ary deficit is clearly evident in the five yearly average trends also (Table 1). For example, in respect of the Central Government PD1, PD2 and NPD, as proportion of GDP, on an average, rose from the levels of 2.01 per cent, 3.26 per cent and 1.58 per cent, respectively, during the period 1970-75 to 4.83 per cent, 6.62 per cent and 3.80 per cent, respectively, during the period 1985-90. It may be noted that the increase has been more than double w ithin two decades. Rapid surge has also been observed in the five- yearly average trends of the State Governments and Government sector (Table 1). As a part of the fiscal stabilisation programme the Central Government undertook the compression of non-interest expenditure. Consequently all the variants of primary deficit are seen to decline over their past levels (Table 1). Similar trend has also been noticed in respect of State Governments though the magnitude of decline has not been sharp. Reflecting the action of the Central Government there has been a substantial decline in the primary deficit of the Government sector. For example, net prim ary deficit has declined by about 2 percentage points from the 1990-91 level and the average level for the latter half of 'eighties. It is pertinent, however, to note that the continuation of deficit in the prim ary balance is a matter of concern as the sustainability of the fiscal policy is seriously questioned.

Primary Revenue Balance: PRB1 and PRB2

In recent years and particularly during the first half of 'nineties the revenue deficit (RD) continued to increase and contributed increasingly to the gross fiscal deficit. It is, therefore, recognised that containing fiscal deficit and more importantly revenue deficit to a sustainable level is essential so that interest payments do not result in large scale pre-em ption of revenue receipts. In this context, there is a need not only to achieve a prim ary surplus derived from GFD but also a primary revenue

24

surplus derived from revenue deficit, which could be adequate enough to meet the entire interest obligations. The trends in PRB1 (revenue deficit minus interest payments) and PRB2 (revenue deficit minus net interest paym ents) for the Central, State and Government Sector are set out in Tables 18, 19 and 19A, respectively. It may be observed that the PRB1 and PRB2 relative to GDP have deteriorated for the Central, State and Government sector during the 'eighties. The deterioration in prim ary revenue balance d u ring the 'e igh ties has been reflected in the low er amount of primary revenue surplus which was not sufficient to absorb the interest payments. Analysis reveals that during the 'seventies, the PRB1 and PRB2 of all levels of Governm ent financed the entire interest expenditures (Table 2). D uring the latter half of the 'eighties, however, the extent of PRB1 financing interest payments deteriorated to the range of 23 to 50 per cent and PRB2 turned out to be negative in the range of 48 to 68 per cent in respect of Central Government. In the case of State Governments a surplus has been m aintained in both the cases (PRB1 and PRB2), however, the magnitude of surplus decelerated during the latter half of 'eighties and the same trend continued during the 'nineties so far (Table 2).

N et Fiscal Deficit

The concept of net fiscal deficit measures the borrowing requirem ents in the absence of the lending operation of the Government. The empirical results indicate that concomitant with the growth in gross fiscal deficit, the net fiscal deficit of the Central Governm ent also sustained sharp increases from 1.9 per cent during the 'seventies to 4.3 per cent in the 'eighties and 4.5 per cent during the 'nineties so far (Table 1 & Appendix Table 20). A similar trend has also been noticed in respect of State Governments (Table 1 and Appendix Table 21). The net fiscal deficit of the State Governments which remained below 1 per cent on an average during the 'seventies relative to GDP increased to around 1.35 per cent during the 'eighties. The underlying trend thus reflects that even after deducting expenditures on loans and advances the net fiscal deficit still continues to grow; this is an indication of larger borrowing requirements essentially to meet the committed expenditures particularly interest payments.

C entre's Deficit Before Transfers: RDBFT, CADFT and ODBFT

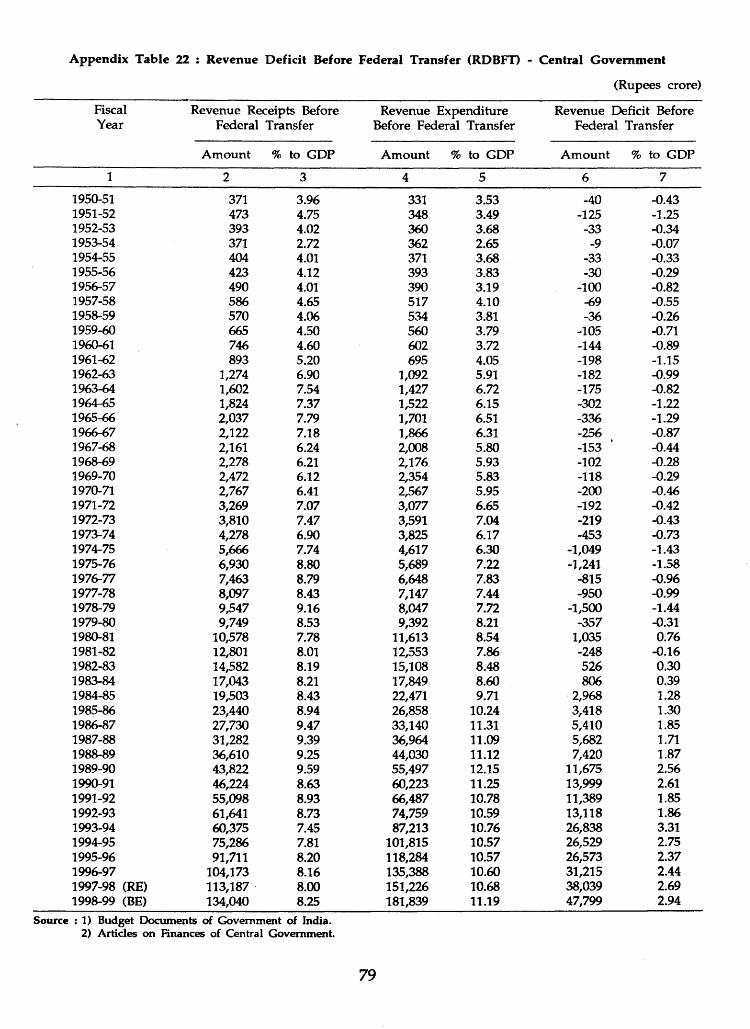

The net fiscal deficit of the Central Government reflects partly the issues relating to inter-Governmental transactions and its im pact on the budgetary balance as it does not cover the grants-in-aid to the State Governments. Given the magnitude of the problem, it is, however, important to examine the full impact of the inter-Gov- ernm ental transactions on the budget. This is more so, as there is an argum ent that inter-Governm ental transfers have contributed to the deterioration in the finances of the Central Government. Accordingly, Revenue Deficit Before Federal Transfers (RDBFT), Capital Account Deficit Before Federal Transfers (CADBFT), O verall D eficit Before Federal Transfers (ODBFT) have been designed in the present study to examine these issues.

25

The em pirical analysis reveals that the revenue account was in surp lus position before transfers to State Governments, during the period 1950-1980. Thereafter, the revenue account was in a deficit even before federal transfers (Table 4 and Appendix Table 22). It is pertinent to note that the surplus before federal transfers were not adequate enough to m eet the net transfers to the State G overnm ents. Thistrend indicates large provisions for the direct expenditures of the Central Government, the grow th of which was not com m ensurate w ith the grow th in revenues. Consequently, there was an elem ent of implicit borrow ing to meet these expenditures even during the period of revenue surplus. The position steadily deteriorated and the revenue account was in the 'red ' even before federal transfers. Thus, borrow ings w ere necessitated for all types of expenditures in the revenue account. The capital account w here loans and advances to States form the basic elem ent of transfers also show ed more or less same trend (Table 4 and A ppendix Table 23). In the capital account, how ever, the G overnm ent has large m anoeuverability in generating surplus through cut backs in capital expenditure. This aspect is quite visible in the m agnitude of generating surplus by compressing capital outlay. Notw ithstanding this m anoeuverability, it has not been possible to fully finance the capital transfer to the State Governments from the CADBFT. On account of relatively larger surplus in the capital account before transfer, the overall deficit before transfers (ODBFT) continued to rem ain surp lus ‘through the period of 'fifties to 'nineties so far (Table 4 and Appendix Table 24). However, these surpluses before transfer were lower than the am ount of transfers from Centre to States. The analysis thus reveals that it is not the resource flow from the Centre to States which is responsible for large budgetary gap of the former, rather it is the outcome of poorexpenditure m anagem ent given the stagnation on the revenue side.

State Resource GAP (SRG) and Basic Resource Gap (BRG)

SRG and BRG are the two deficits indicators exclusively m easuring the budgetary gap of the State Governm ents taking into account the inter-Governm ent transfers. The empirical findings reveal that States' Resources Gap, financed by non-statutory transfers from the Centre (such as non-statutory grants and loans) and Ways and Means Advances from RBI, as a proportion of States' expenditure (total expenditure minus in terest paym ents and repaym ents to Centre) which, on an average, was around 14 per cent in the 'seventies increased to over 18 per cent in the 'eighties (Table 5 and A ppendix Table 25). G iven the level of expenditure, this upw ard trend reflected steady rise in transfer of resources from Centre to the State Governments in the financing of SRG. This trend has reversed in the 'nineties with transfer of resources to States from the Centre show ing declining trend, an inevitable outcome of fiscal correction measures undertaken by the Centre. For instance, the SRG as a proportion to its expenditure during the period 1991-96, averaged 15.6 per cent as against 18.1 per cent in the latter half of the 'eighties, reflecting the steady deterioration in the resource transfers from the Centre (Table 5).

The BRG, on the other hand, m easures the fiscal requirem ents, fiscal dependency

26

and fiscal stress20, The fiscal requirements of the State Governments are reflected by the size of the expenditure which as a proportion to GDP, on an average, amounted to 17.2 per cent during the 'nineties (1990-96) as against 16.8 per cent during the 'eighties and 13.6 per cent during the 'seventies. Given the level of expenditure, fiscal dependency measured in terms of BRG1 (where the entire devolution and transfers from the Centre and capital receipts and market borrowings are treated as exogenous) showed deterioration from 58.7 per cent in the early 'seventies to 55.7 per cent in the 'eighties and further to 54.5 per cent in the 'nineties reflecting the reduced flow of resources from the Centre (Table 5 and Appendix Table 26). The fiscal dependency ratio measured by BRG2 (where excluding capital receipts, devolution and transfers from the Centre, and market borrowings are treated as exogenous), and BRG3 (where devolution and capital receipts are treated as endogenous while transfers from Centre and market borrowings as exogenous) also showed more or less the same trend indicating reduced flow of resources from the Centre (Appendix Table 27 and 28). This is also evident from the fiscal stress ratio (BRG3/BRG1) which on an average stood at 51 per cent both during the 'seventies and 'eighties and reduced by one percentage point to 50 per cent in the 'nineties (Table 5).

The observed trends in SRG and BRG taken together reveal two broad implications for the finances of the States: (a) there has been large reliance on exogenous sources of resources on which States do not have statutory control and (b) absence of perceptible improvement in States resources in relation to the growing expenditure requirements. Given the deceleration in the flow of resource transfers from the Centre because of the fiscal consolidation, the State Governments have to manage their budgets w ith less reliance on Central transfers. Therefore, the underlying solution to the problem is the not the large flow of resources from the Central Government but augmentation of States' resources and prioritisation of expenditure.

Structural and Cyclical Deficit and Government Fiscal Stance

In order to examine the origin of the fiscal deficit in India, the present study has estimated the structural and cyclical deficits using the OECD methodology. The estimation and empirical findings are set out in Technical Appendix 3. While estimating the structural and cyclical components of gross fiscal deficit the year 1977- 78 has been considered as the base year as the actual output in this year was close to the trend output. The calculations show that the growing fiscal deficit of the Central Government originated from large mismatch between receipts and expenditures as reflected in the higher expenditure elasticity (1.217) in relation to the revenue elasticity (1.088) [Table 6]. Besides, there are structural rigidities in the system which were reflected in the predominance of fiscal drag (Appendix Table 29). Consequently, the structural deficit which averaged around 4 percent during the 'seventies, increased to 7 per cent in the first half of the 'eighties and further to about 9 per cent during the latter half of the 'eighties with a peak level of 9.75 per cent in 1986-87 (Table 7 and Appendix Table 29); on account of the predomi-

27

nance of the structural deficit the impact of the cyclical deficit has been minimal. A similar exercise for the primary deficit (GFD minus net interest payments) has been set out in Table 30. It may, therefore, be noted that a move to a highergrowth scenario may not necessarily absorb the deficit.

Apart from estimating the structural and cyclical components, the study has evaluated the fiscal stance to examine whether Government policy is expansionary or contractionary. The estimation of fiscal stance and fiscal impulse for both the Central Government and the Government sector as a whole are presented in Appendix Table 31. Calculations reveal that the fiscal impulse for the Central Government during a larger part of the 'eighties was expansionary and during the reform period it has been mostly contractionary. A similar trend is also visible for the Government sector.

Operational Deficit

Analysis reveals that there has been a sharp fall in the operational deficit in relation to GDP in the recent past (Appendix Table 32). For example, operational deficit (derived from net interest payments) relative to GDP is placed at 2.7 per cent in 1996-97 as compared with 3.9 per cent in 1994-95 and about 4.5 per cent during the period 1991-95. This proportion was about 7 per cent in 1990-91 and around 7.5 per cent during the latter part bf the 'eighties. Given the near stagnation in the revenue receipts, sharp reduction in operational deficit im plies overcorrection of expenditures, particularly in the capital account. Thus, the presentstudy establishes the importance of operational deficit in Indian context which wasrejected by Joshi et al (1994) by stating that 'use of operational deficit would seem to have no merit7. The present study shows that the extent of reduction in the operational deficit which is sharper than the reduction in the GFD indicates that the Government resorted to the soft option of reducing capital expenditure in order to correct fiscal imbalances.

28

SECTION V

CONCLUDING OBSERVATIONS

With the resurgence of interest on budget deficit in recent years, a correct measurement of budget deficit has assumed crucial importance not only for assessing the stance of fiscal policy but also for the overall macroeconomic management. It has been widely recognised that no single indicator provides all information about the fiscal situation. Therefore, while evaluating the fiscal position of the Government it is instructive as well as interesting to look at a range of them to counter balance the shortcoming of each one. Accordingly, several measures of deficit are currently in use reflecting a paradigm shift from the traditional approach of single measure. It is, however, pertinent to note that there is a trade-off between simplicity and comprehensiveness while making a choice among the deficit indicators and the degree and intensity of the trade-off depends essentially on the purpose for which the deficit indicator is used.

Contemporaneous with world wide development alternative concepts of deficits have also been discussed in the Indian context. Much progress, however, has not been made in terms of their coverage and application. The present study is an attempt in this direction. A brief account of the major findings of the study is set out below.

The revenue account gap which broadly reveals the magnitude of the dissavings of the Government was kept within a surplus position till 1979-80 in respect of Central Government, while in respect of State Government this trend was maintained upto 1987-88 and for the Government sector as a whole till 1982-83. Thereafter, revenue deficit continued to show sharp deterioration and became endemic in the system. The study reveals that the levels of GFD relative to GDP were unsustainable during the 'eighties as there was large accumulation of debt which were incurred at a relatively high rate. The burden of debt has thus become a serious concern of the Government particularly in terms of large revenue outgo to finance burgeoning interest payments. The commitments in the budget for such high levels of interest payments have put pressure on the Government budget to allocate resources for income generating expenditure, particularly capital outlay. Apart from this, the persistently large size of GFD with a sizeable component of monetised deficit resulted in excess liquidity in the system which in turn has rendered difficult the attainment of the monetary policy objective of price stability. Analysis reveals that historically there has been a primary deficit (in all its variants) at all levels of Government which necessitated borrowings not only for the current operations but also for debt servicing of the Government. Furthermore, although primary revenue balance (revenue deficit minus interest payments) of Central, State and Government sector continued to remain in surplus the amount so generated showed sharp deterioration in the 'eighties and 'nineties so far and has not been sufficient enough to meet the interest obligations. This development seri

29

ously questions the sustainability of fiscal policy because one of the crucial precondition of having primary surplus which could meet the entire interest obligation is yet to be attained.