FNDACT2 Of Theory and Accounts

11

/FNDACT2 Of Theory and Accounts Page 1 of 11 I. ACCOUNTING FOR CORPORATION 1. Corporation Artificial being created by law Having the right of succession, and powers, attributes, and properties expressly authorized by law or incident to its existence 2. Batas Pambansa Blg. 68 The Corporation Code of the Philippines – the law governing the corporations in the Philippines. 3. Securities and Exchange Commission (SEC) The government agency regulating the corporation and other associations in the Philippines. 4. Major Classifications 4.1. Stock Corporation –corporations which have share capital divided into shares and are authorized to distribute to the shareholders dividends or allotments of the surplus profits on the basis of the shares held. 4.2. Non-stock Corporation –is one where no part of its income is distributable as dividends to its members, trustees or officers. Any profit accruing to the corporation, whenever necessary or proper, be used for the furtherance of the purpose or purposes for which the corporation was organized. 5. Other types of corporations Public corporations – created for political or public purpose & connected with the administration of government. (e.g. barangay, cities, provinces) Private Corporations are owned by individuals or other corporations for private purpose and benefit. (e.g. private corporations and government-owned and controlled corporations) Open Corporations – Shares of stocks are available to the public. (e.g. corporations whose shares are available in the stock exchange or over the counter security brokers) Closed Corporations – Shares of stocks are held by few individuals and ownership is not available to the public. (e.g. family corporations) Publicly Listed Corporations – Shares are traded on an organized stock exchange. (e.g. corporations whose shares are traded in Philippine Stock Exchange) Non-listed Corporations – Shares are not actively traded over organized stock exchange. (e.g. corporations whose shares are traded over the counter by brokers) 6. Steps in the Creation of a Corporation 6.1. Promotion involves the process of bringing together the incorporators or the persons interested in the business, procuring subscriptions or capital that leads to the incorporation of the corporation. Underwriters – investment banking or stockbrokers often facilitate the promotion and subsequent sale of shares to prospective investors. 6.2. Incorporation involves filing the articles of corporation with the Securities and Exchange Commission (SEC) together with treasurer’s affidavit, statement of financial position, certificate of bank deposit, and certificate as to the name of the corporation; payment of filing and publication fees; and ultimately the issuance by the SEC of the certificate of incorporation. Note: Generally, the corporation does not acquire its juridical personality until the SEC issues to it its certificate of incorporation. 6.3. Formal organization and commencement requires the adoption of by-laws and the election of the board of directors (BOD) and of administrative officers including taking such other steps to enable it to transact the legitimate business or accomplish the purpose for which it was created. Note: If a corporation does not formally organize and commence the transaction of its business within two (2) years from the date of its incorporation, its corporate powers shall cease and the corporation shall be deemed dissolved. However, if a corporation has commenced business but subsequently becomes continuously inoperative for a period of at least five (5) years, the same shall be a ground for the suspension or revocation of its certificate of incorporation. 7. Why or why not a corporation? 7.1. Advantages of a corporation Ease of raising capital resources Limited liability Ease of transfer of ownership Continuous life Centralized management 7.2. Disadvantages of a corporation Difficult/costly to establish Strict government regulation 8. Contents of Articles of Incorporation 8.1. Name of the corporation 8.2. Purpose of the corporation 8.3. Place of principal office (must be within the Philippines) 8.4. Term of existence (not more than 50 years) 8.5. Names, residences and addresses of the incorporators 8.6. The amount of share capital, its par value and the no. of shares into which it is divided. If the share has no par value, the articles shall state only the no. of shares but the fact that the shares is without par shall be stated therein

Transcript of FNDACT2 Of Theory and Accounts

/FNDACT2

Of Theory and Accounts Page 1 of 11

I. ACCOUNTING FOR CORPORATION 1. Corporation

Artificial being

created by law Having the right of succession, and

powers, attributes, and properties expressly authorized by law or incident to its existence 2. Batas Pambansa Blg. 68

The Corporation Code of the Philippines – the law governing the corporations in the Philippines. 3. Securities and Exchange Commission (SEC)

The government agency regulating the corporation and other associations in the Philippines.

4. Major Classifications

4.1. Stock Corporation –corporations which have share capital divided into shares and are authorized to distribute to the shareholders dividends or allotments of the surplus profits on the basis of the shares held.

4.2. Non-stock Corporation –is one where no part of its income is distributable as dividends to its members, trustees or officers. Any profit accruing to the corporation, whenever necessary or proper, be used for the furtherance of the purpose or purposes for which the corporation was organized.

5. Other types of corporations

Public corporations – created for political or public purpose & connected with the administration of government. (e.g. barangay, cities, provinces)

Private Corporations are owned by individuals or other corporations for private purpose and benefit. (e.g. private corporations and government-owned and controlled corporations)

Open Corporations – Shares of stocks are available to the public. (e.g. corporations whose shares are available in the stock exchange or over the counter security brokers)

Closed Corporations – Shares of stocks are held by few individuals and ownership is not available to the public. (e.g. family corporations)

Publicly Listed Corporations – Shares are traded on an organized stock exchange. (e.g. corporations whose shares are traded in Philippine Stock Exchange)

Non-listed Corporations – Shares are not actively traded over organized stock exchange. (e.g. corporations

whose shares are traded over the counter by brokers) 6. Steps in the Creation of a Corporation

6.1. Promotion involves the process of bringing together the incorporators or the persons interested in the business, procuring subscriptions or capital that leads to the incorporation of the corporation. Underwriters – investment banking or stockbrokers often facilitate the promotion and subsequent sale of

shares to prospective investors.

6.2. Incorporation involves filing the articles of corporation with the Securities and Exchange Commission (SEC) together with treasurer’s affidavit, statement of financial position, certificate of bank deposit, and certificate as to the name of the corporation; payment of filing and publication fees; and ultimately the issuance by the SEC of the certificate of incorporation. Note: Generally, the corporation does not acquire its juridical personality until the SEC issues to it its

certificate of incorporation.

6.3. Formal organization and commencement requires the adoption of by-laws and the election of the board of directors (BOD) and of administrative officers including taking such other steps to enable it to transact the legitimate business or accomplish the purpose for which it was created. Note: If a corporation does not formally organize and commence the transaction of its business within two

(2) years from the date of its incorporation, its corporate powers shall cease and the corporation shall be deemed dissolved.

However, if a corporation has commenced business but subsequently becomes continuously inoperative

for a period of at least five (5) years, the same shall be a ground for the suspension or revocation of its certificate of incorporation.

7. Why or why not a corporation? 7.1. Advantages of a corporation

Ease of raising capital resources

Limited liability

Ease of transfer of ownership Continuous life Centralized management

7.2. Disadvantages of a corporation Difficult/costly to establish Strict government regulation

8. Contents of Articles of Incorporation

8.1. Name of the corporation 8.2. Purpose of the corporation 8.3. Place of principal office (must be within the Philippines) 8.4. Term of existence (not more than 50 years) 8.5. Names, residences and addresses of the incorporators

8.6. The amount of share capital, its par value and the no. of shares into which it is divided. If the share has no par value, the articles shall state only the no. of shares but the fact that the shares is without par shall be stated therein

/FNDACT2

Of Theory and Accounts Page 2 of 11

8.7. The amount if share capital or number of no-par shares subscribed with indication of the amount or number of no-par shares subscribed and paid by each

9. By-laws

9.1. Rules of action adopted by the corporation for its internal government and for the government of its officers, shareholders or members.

9.2. To be adopted and filed with SEC within one (1) month from the date of incorporation. Typical contents of by-laws are: Conduct of meeting of shareholders and directors Rules for directorship (i.e. owner of at least 1 share and majority are residents of the Phil.) Rules for officership Rules for issuing shares Method of amending by laws

Others

10. Organization Costs 10.1. Preliminary expenses incurred upon forming a corporation including legal fees, incorporation fees and share

issuance costs. 10.2. Generally, organization costs shall be expensed as incurred with the exception for share issuance cost which

shall be debited to share premium arising from share issuance with any excess to retained earnings.

11. Components of a Corporation

11.1. Corporators –are those who compose a corporation whether as shareholders or members. A corporation or a partnership can be a corporator, but cannot be an incorporator. A partnership can be a corporator in a corporation but a corporation cannot be a general partner in a

partnership.

11.2. Incorporators –are shareholders or members mentioned in the articles of incorporation as originally forming and composing the corporation and are signatories to said articles of incorporation. They must be natural persons (human beings) as distinguished from artificial beings such as corporations or partnerships.

Note: Five or more persons, not exceeding fifteen, may form a private corporation provided they are of legal age; owners or subscribers to at least one share of capital stock and that majority are residents of the Philippines.

11.3. Shareholders/Members –shareholders are corporators in stock corporation while members are corporators of

a non-stock corporation. 11.4. Subscribers –are persons who have agreed to take and pay for original, unissued shares of a corporation

formed or to be formed. 12. Rights of a Shareholder

12.1. Vote in elections for directors and on actions requiring shareholder approval. 12.2. Share in company’s profits through the receipt of dividends.

12.3. Preemptive right to keep the same percentage of ownership when new shares are issued. 12.4. Residual claim to share in assets upon liquidation in proportion to their holdings.

13. Typical Records used by a corporation

13.1. Minutes book – Contains the minutes of the meetings of the directors and stockholders. 13.2. Stock and transfer book – A record of the names of shareholders, installments paid and unpaid by shareholders

and dates of payment, transfers of shares and dates thereof. 13.3. Shareholder’s ledger – Subsidiary record of share capital issued indicating the number of shares issued to

each shareholder. 13.4. Subscriber’s ledger – Subsidiary record of subscriptions made indicating the individual subscriptions of the

subscribers. 14. Classes of Shares in General

14.1. Par value shares one in which a specific amount is fixed in the articles of incorporation and appearing on the certificate of

stock. This amount is the minimum issue price of the shares. Preference/preferred shares may be issued only as par value shares.

14.2. No-par value shares one without any value appearing on the face of the certificate of stock. A no-par value share may have a

stated value which may be fixed in the articles of incorporation or by the board of directors or the

shareholders. However, the minimum stated value of a no-par share is five pesos (P5.00) and is deemed to be fully paid

when issued. Note that the following are not permitted to issue no-par value shares: (BPI-TB)

a. Banks b. Public utilities

c. Insurance companies d. Trust Companies; and e. Building and Loan Associations

14.3. Voting and Non-voting shares 14.4. Ordinary Shares –entitle the holder to an equal pro-rata division of profits without any preference. 14.5. Preference shares –entitle the holder to certain advantages or benefits over the holders of ordinary shares. 14.6. Treasury shares –A share that has been issued by the corporation as fully paid and later reacquired but not

retired.

/FNDACT2

Of Theory and Accounts Page 3 of 11

15. Par value vis-à-vis Market value of shares 15.1. Par value is a nominal amount indicated on the share certificate and fixed in the articles of incorporation. Most

often than not, it is not the price at which the corporation sells the share though this amount reflects the minimum issue price of the shares. The selling price of the share or its market value will be usually higher

than a share’s par value and is influenced by a number of factors, such as: Anticipated future earnings of the company

Expected dividend rate per share Current financial position Current state of the economy Current state of the securities market

16. Minimum Subscription and Paid-In Capital (The 25%-25% Rule)

At the time of incorporation, at least twenty-five (25%) percent of the authorized share capital as stated in the

articles of incorporation must be subscribed, and At least twenty-five (25%) percent of the total subscription must be paid upon subscription, the balance to be

payable on a date or dates fixed in the contract of subscription without the need of a call (demand), or in the absence of a fixed date or dates, upon call for payment by the Board of directors.

In no case shall the paid-in capital be less than five thousand (P5,000.00) pesos.

17. Shareholder’s Equity

17.1. Share Capital a. Ordinary Share Capital or Common Stock b. Preference Share Capital or Preferred Stock Note: Trust Fund Doctrine mandates that the corporation must maintain its Legal Capital for the protection

of its creditors. It is not available for distribution to shareholders until the claims of corporate creditors are

satisfied. Legal Capital –is that portion of the contributed capital or the minimum amount of paid-in capital, which

must remain in the corporation for the protection of corporate creditors. In case of par value shares, legal capital is the aggregate par value of all issued and subscribed shares. In case of no-par shares, legal capital is the total consideration received by the corporation for the issuance

of its shares including the excess of issue price over the stated value. 17.2. Share Capital Not Yet Fully Paid (Subscribed Share Capital)

the portion of the authorized share capital that has been subscribed but not yet fully paid. Note: Subscription Receivable is a shareholders’ equity account. It is presented in the statement of

financial position as a deduction from the related subscribed ordinary shares; HOWEVER, when it is collectible within twelve months from the date of statement of financial position, this is presented as current asset in the current asset portion of the statement of financial position. Thus, it is ignored in the computation of Shareholder’s equity.

17.3. Share Premium or Additional Paid-In Capital the portion of the paid-in capital representing amounts paid by shareholders in excess of par. It may also

result from transactions involving treasury shares, retirement of shares, donated capital, share dividends and any other “gain” on the corporation’s own share transactions.

17.4. Other Appropriation Reserves These include revaluation and other reserves properly appropriated by the corporation. These items will

be discussed in the financial accounting courses.

17.5. Accumulated Profits/Losses or Retained Earnings represent the component of the shareholders’ equity arising from the retention of assets generated from

profit-oriented activities of the corporation. 18. Accounting for Issuance of Shares

18.1. Measure of Capital When Issued:

a. With Par –credit share capital at par any excess to Share Premium

b. Without Par but with a Stated Value – Share Capital is credited at stated value with the excess to Share Premium

Measure of the Consideration Received on the Issue of Share Capital 1. For Cash or Receivable –at Face value 2. For Non-Cash Consideration –at Fair Market Value (FMV) of non-cash or FMV of the shares issued

whichever is clearly determinable 3. For Services Rendered –at FMV of the services rendered or market value of the shares issued

whichever is clearly determinable Fair Value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. (IFRS 13 par. 9)

19. Accounting for Delinquent Subscriptions 19.1. When the subscriber fails to settle the subscriptions in full on the date specified in the subscription contract

or in the call made by the board of directors, the subscribed shares are declared delinquent.

Illustration:

If the authorized share capital is P2,000,000, the subscribed share capital must be P500,000 (P2,000,000 authorized share capital X

25%) of which P125,000 (P500,000 subscribed X 25%) must be paid upon subscription.

Suppose that the authorized share capital is P50,000; the subscribed portion should be P12,500 (P50,000 X 25%). However the

amount to be paid will no longer be P3,125 (Applying the 25-25 rule i.e. P12,500 X 25%) but P5,000 because this is the minimum

paid-in capital required by law.

/FNDACT2

Of Theory and Accounts Page 4 of 11

19.2. The remedy of the corporation in this case is to dispose of the shares in a public auction for the account of the delinquent subscriber. These shares will be sold to the highest bidder –the person who is willing to pay the “offer price” which includes the full amount of the subscription balance plus accrued interest, cost of advertisement and expenses of auction sale in exchange for the smallest number of shares.

19.3. If there is no bidder, the corporation may bid for the delinquent shares and the total amount due shall be credited as paid in full in the books of corporation. These shares shall be considered as treasury shares.

20. Accounting for Treasury Shares

20.1. Treasury shares are shares of stock which have been issued and fully paid for, but subsequently reacquired by the issuing corporation either by purchase, redemption, donation or through other lawful means. Such shares may again be disposed of for a reasonable price fixed by the board of directors.

20.2. Treasury share is reported as a deduction from total shareholders’ equity. (contra-equity account) 20.3. The Cost Method is the preferred method of accounting for treasury shares. Under this method, treasury

share is recorded at cost of purchase regardless of whether it is acquired below or above par. 20.4. The purchase of treasury shares does not decrease the number of shares issued; only the outstanding shares

decrease. Thus:

20.5. Therefore, unless retired, treasury shares remain to be considered issued. 20.6. Treasury share is always debited for the cost of the shares purchased or credited for the cost of the shares

reissued. Par value is ignored. If the reissue price exceeds the cost of the treasury, the excess over cost is not regarded a “gain” but component of share premium (Share Premium–Treasury).

20.7. On the other hand, if the cost exceeds the reissue price, the difference should be debited to share premium –treasury to the extent of its balance. In the absence of any balance in this account, or if it has already been

depleted, the “loss” is debited to retained earnings. 20.8. Observe that Retained Earnings account may be debited, but is never credited for treasury share transactions. 20.9. Retirement of treasury shares.

Cancel the carrying value of the share and the cost of treasury. The carrying value includes the Par and the Share Premium at the time the shares were originally issued.

The ordinary shares account and the share premium attaching to it when it was originally issued are debited and the corresponding credit is the treasury share at cost. Any positive excess (excess debits over

credits) is credited to share premium account (Share Premium –Retirement). Any negative excess (excess credits over debits) is debited to Retained Earnings.

21. Accounting for Donated Capital

21.1. Contributions from shareholders are measured and recorded at Fair Market Value of the items received with the credit going to a share premium account. If significant, separate share premium account may be set up

designated as Donated Capital.

21.2. If the donation is in the form of shares of the corporation, the receipt of the donated shares is recorded by means of memorandum entry only. The account share premium or donated capital is credited at the time the shares are to be reissued.

22. Book value per share 22.1. Book value per share represents the equity a shareholder has in the net assets of the corporation from owning

one share. 22.2. Book value per share formula:

23. Retained Earnings

23.1. The account Retained Earnings represents the firm’s accumulated profit or loss, including prior-period adjustments less the dividends declared and other amounts transferred to the contributed capital accounts.

23.2. A debit balance in retained earnings account is referred to as a deficit.

Illustration:

Finest Inc.’s 1,000 shares of P10 par value ordinary shares were sold on subscription at P15 per share on Oct. 17, 2010 to Kanor.

Subscription installments of P7,000 and P8,000 will be due on Nov. 1 and 15, respectively.

Kanor was able to pay the first installment; however, he failed to settle the latter one due to his ensuing financial problems. After

complying with the legal procedures pertaining to delinquency sale, a public auction was held. The offer price is P12,000 including

P500 accrued interest and P3,500 expenses of sale. Three bidders are willing to pay the offer price:

Norina Salvador 900 shares

Bryan Trinidad 600 shares

Rian Soliman 750 shares

Required: Who is the highest bidder?

Ans: Bryan Trinidad is the highest bidder, agreeing to pay the full price of P12,000 for the smallest number of shares. Consequently,

the 1,000 shares are deemed fully paid. Kanor, the original subscriber, gets 400 shares and Bryan T. receives the 600 shares.

Authorized Shares – Unissued Shares = Issued Shares

Issued Shares = Outstanding Shares (without the presence of treasury)

Issued Shares = Outstanding Shares + Treasury Shares (with Treasury shares)

Book value per share = Total Shareholder’s Equity ÷ No. of shares outstanding

/FNDACT2

Of Theory and Accounts Page 5 of 11

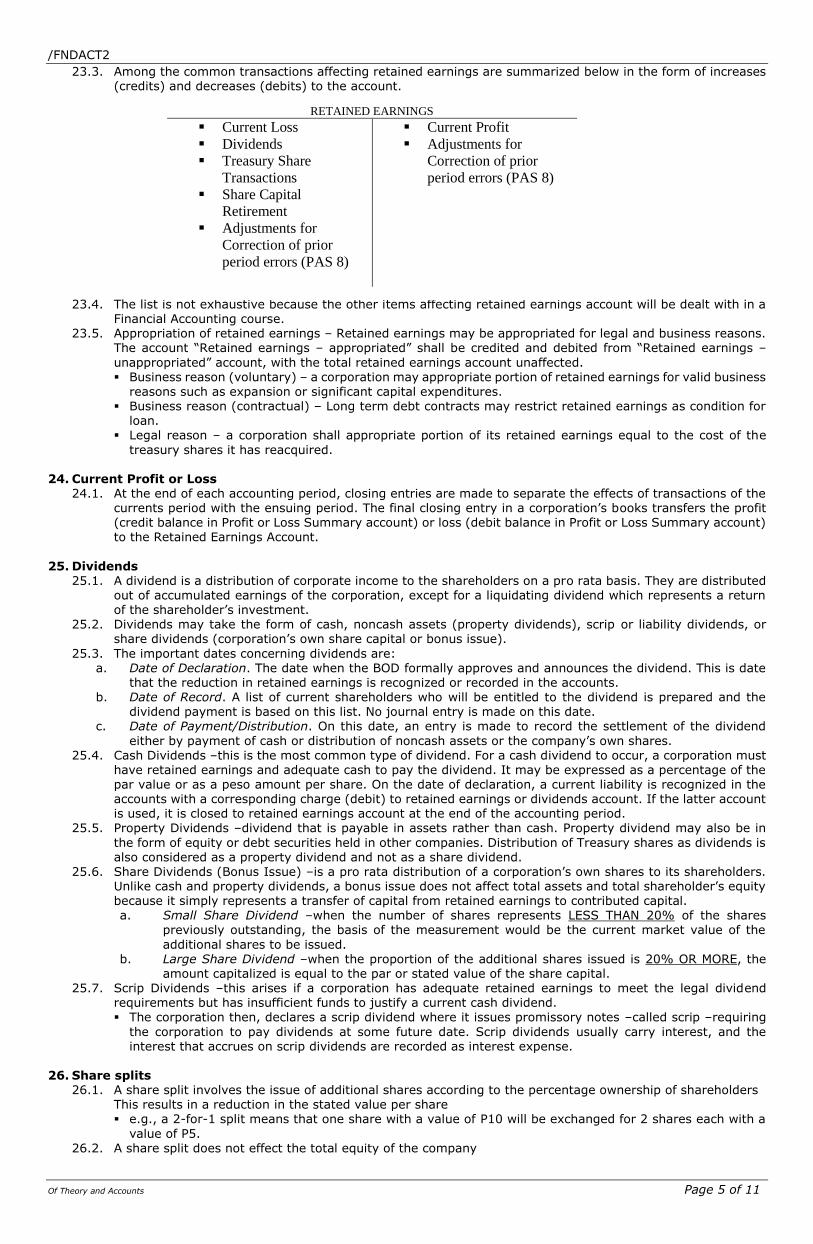

23.3. Among the common transactions affecting retained earnings are summarized below in the form of increases (credits) and decreases (debits) to the account.

23.4. The list is not exhaustive because the other items affecting retained earnings account will be dealt with in a

Financial Accounting course. 23.5. Appropriation of retained earnings – Retained earnings may be appropriated for legal and business reasons.

The account “Retained earnings – appropriated” shall be credited and debited from “Retained earnings –

unappropriated” account, with the total retained earnings account unaffected. Business reason (voluntary) – a corporation may appropriate portion of retained earnings for valid business

reasons such as expansion or significant capital expenditures. Business reason (contractual) – Long term debt contracts may restrict retained earnings as condition for

loan. Legal reason – a corporation shall appropriate portion of its retained earnings equal to the cost of the

treasury shares it has reacquired.

24. Current Profit or Loss 24.1. At the end of each accounting period, closing entries are made to separate the effects of transactions of the

currents period with the ensuing period. The final closing entry in a corporation’s books transfers the profit (credit balance in Profit or Loss Summary account) or loss (debit balance in Profit or Loss Summary account) to the Retained Earnings Account.

25. Dividends

25.1. A dividend is a distribution of corporate income to the shareholders on a pro rata basis. They are distributed out of accumulated earnings of the corporation, except for a liquidating dividend which represents a return of the shareholder’s investment.

25.2. Dividends may take the form of cash, noncash assets (property dividends), scrip or liability dividends, or share dividends (corporation’s own share capital or bonus issue).

25.3. The important dates concerning dividends are: a. Date of Declaration. The date when the BOD formally approves and announces the dividend. This is date

that the reduction in retained earnings is recognized or recorded in the accounts. b. Date of Record. A list of current shareholders who will be entitled to the dividend is prepared and the

dividend payment is based on this list. No journal entry is made on this date. c. Date of Payment/Distribution. On this date, an entry is made to record the settlement of the dividend

either by payment of cash or distribution of noncash assets or the company’s own shares. 25.4. Cash Dividends –this is the most common type of dividend. For a cash dividend to occur, a corporation must

have retained earnings and adequate cash to pay the dividend. It may be expressed as a percentage of the par value or as a peso amount per share. On the date of declaration, a current liability is recognized in the accounts with a corresponding charge (debit) to retained earnings or dividends account. If the latter account is used, it is closed to retained earnings account at the end of the accounting period.

25.5. Property Dividends –dividend that is payable in assets rather than cash. Property dividend may also be in

the form of equity or debt securities held in other companies. Distribution of Treasury shares as dividends is also considered as a property dividend and not as a share dividend.

25.6. Share Dividends (Bonus Issue) –is a pro rata distribution of a corporation’s own shares to its shareholders. Unlike cash and property dividends, a bonus issue does not affect total assets and total shareholder’s equity because it simply represents a transfer of capital from retained earnings to contributed capital. a. Small Share Dividend –when the number of shares represents LESS THAN 20% of the shares

previously outstanding, the basis of the measurement would be the current market value of the

additional shares to be issued. b. Large Share Dividend –when the proportion of the additional shares issued is 20% OR MORE, the

amount capitalized is equal to the par or stated value of the share capital. 25.7. Scrip Dividends –this arises if a corporation has adequate retained earnings to meet the legal dividend

requirements but has insufficient funds to justify a current cash dividend. The corporation then, declares a scrip dividend where it issues promissory notes –called scrip –requiring

the corporation to pay dividends at some future date. Scrip dividends usually carry interest, and the interest that accrues on scrip dividends are recorded as interest expense.

26. Share splits

26.1. A share split involves the issue of additional shares according to the percentage ownership of shareholders This results in a reduction in the stated value per share e.g., a 2-for-1 split means that one share with a value of P10 will be exchanged for 2 shares each with a

value of P5. 26.2. A share split does not effect the total equity of the company

RETAINED EARNINGS

Current Loss

Dividends

Treasury Share

Transactions

Share Capital

Retirement

Adjustments for

Correction of prior

period errors (PAS 8)

Current Profit

Adjustments for

Correction of prior

period errors (PAS 8)

/FNDACT2

Of Theory and Accounts Page 6 of 11

26.3. The purpose of a share split is to increase the marketability of the shares by lowering the market price per share.

26.4. A share split does not affect the balance in shareholders’ equity accounts and therefore a formal journal entry is not required.

27. Allocation of Cash Dividends Between Preference Shares and Ordinary Shares

27.1. Preference shares have priority over ordinary shares in terms of dividends. 27.2. The amount of dividend payment to preference shares depends on the type and preferential rights attached

to the share, which could be cumulative or non cumulative and participating or non-participating. a. A cumulative preference share has a right to receive current dividends in arrears before ordinary

shareholders receive any dividends. b. A participating preference share provides for additional dividends to be paid to its holder after

dividends of a specified amount or rate are paid to ordinary shareholders.

27.3. If the problem is silent, the preference shares are assumed to be noncumulative and nonparticipating. 27.4. Dividends for the current year are called current dividends, while dividends that were not declared in the

previous years are called dividends in arrears. Dividends not declared on the previous years are usually considered forfeited unless the preference shares are cumulative in nature. Dividends in arrears must be specifically disclosed, otherwise, no dividends in arrears shall be assumed.

27.5. In case there are two or more classes of participating preference shares with different rates, the LOWER rate shall be the basis of allocation to the ordinary shares. If only one of them is participating, then that rate shall

be used regardless whether the other preference share but nonparticipating shall have a lower rate.

28. Correction of Prior Period Errors 28.1. Prior period errors are omissions from, and misstatements in, the entity’s financial statements for one or

more periods arising from failure to use, or misuse of, reliable information that was available when financial statements for those periods were authorized for issue and could reasonably be expected to have been

obtained and taken into account in the preparation of those financial statements. 28.2. Such errors encompass effects of mathematical mistakes, mistakes in applying accounting policies, oversights

or misinterpretation of facts, and fraud. 28.3. They may result to either a net understatement or net overstatement of the balance in the retained earnings

account. The adjustment that should be taken up in the retained earnings is net of the related income tax.

II. ILLUSTRATIVE EXERCISES

PROBLEM 1. Pre-incorporation subscription requirement Determine the minimum pre-incorporation subscription requirement on the following cases independently: Minimum Subscription Minimum Paid-In (In Php) (In Php)

A. The authorized share capital

is P5,000,000 divided into 50,000

shares with par value of P100 per share.

B. The authorized number of shares is

30,000 with par value of P50 per share.

C. Authorized share amounts to P60,000

divided into 60,000 shares of P1 par value each.

PROBLEM 2. Accounting for share capital Far East Corporation, a newly registered corporation had the following transactions during the year:

a) On January 2, Philippine SEC authorized the entity to issue 500,000 shares with par value of ten peso per share.

b) The entity received subscription to 150,000 shares at par.

c) The entity collected 30% on the above subscription.

d) Received full payment for 90,000 shares originally subscribed.

e) The entity then issued the share certificates for 90,000 shares which were fully paid.

f) Received a cash subscription for 6,000 shares at par.

REQUIRED: 1. Journalize the transactions above using:

a. Memorandum entry method

b. Journal entry method

2. Present the shareholder’s equity portion to be shown on the entity’s statement of financial position under

a. Memorandum entry method

b. Journal entry method

PROBLEM 3. Issuance of share capital for cash

1. With Par value

Avalanche Corporation sold 20,000 ordinary shares of P100 par value for P130 per share.

2. Without Par value

Vague Company sold 40,000 ordinary shares with stated value of P80 for P120 each.

/FNDACT2

Of Theory and Accounts Page 7 of 11

REQUIRED: Prepare journal entries based on above transactions. (From this moment, use memorandum method if the problem is silent)

PROBLEM 4. Issuance of shares for noncash consideration Prepare the journal entries for the following independent situations:

a. Algeria Corp. issued 15,000 ordinary shares of P100 par value in exchange of for land and building with total fair value of P2,000,000 of which 25% is attributable to the land.

b. Nortek Corporation exchanged 25,000 shares of its P100 par value share for a land. A few months ago, the land was appraised by an independent appraiser at P4,000,000. Nortek is currently trading at the Philippine Stock Exchange (PSE) at P140 per share.

c. Atty. Pao received 1,000 ordinary shares of P100 par value from Secador Corp. after rendering legal services in getting the corporation organized. The fair value of such services is reliably determined to be P125,000.

d. Dientes Corp. issued 5,000 shares of its P100 par ordinary share to Atty. Harvey as compensation for 1,200

hours of legal services performed. Atty. Harvey usually bills P500 per hour for legal services. On this date of issuance, the share was selling at a public trading at P140 per share.

PROBLEM 5. Incorporation of a proprietorship The December 31, 2013 condensed statement of financial position of Django Services, an individual proprietorship,

follows: Current assets P150,000 Equipment (net) 140,000 P290,000

Liabilities P 90,000 Django, Capital 200,000 P290,000

Fair values at December 31, 2013 are as follows:

Current assets P170,000 Equipment 200,000 Liabilities 90,000

On January 2, 2014, Django Services was incorporated with 5,500, P10 par value, ordinary shares issued. REQUIRED:

Prepare the journal entry to account for above transaction on the books of the corporation. PROBLEM 5. Issuance of two classes of shares

Hologram Corporation issued 20,000 shares of its P10 par value ordinary share and 40,000 shares of its P10 par value preference share for a total amount of P1,800,000. At this date, Hologram’s ordinary shares was selling P20 per share and the preference share was selling for P30 per share REQUIRED: Prepare the journal entry to record the above transaction.

PROBLEM 6. Organization cost Harlem Corporation issued 50,000 ordinary shares with par value of P100 for P150 per share. Costs incurred related to the issuance which were paid cash are as follows: Cost of drafting articles of incorporation and by laws P25,000 Other legal costs 5,000 Incorporation fees 15,000

Cost of printing share certificate 10,000 Other share issuance cost (cost of stock and transfer book, seal of corporation, underwriting fees and legal

fees related to share issuance) 25,000 REQUIRED: Prepare the journal entries to account for:

a) Issuance of shares b) Incurrence of organization cost

PROBLEM 7. Computation of legal capital CASE A The shareholder’s equity of Lovely Company revealed the following information on December 31, 2012:

Preference share (P100 par), P2,500,000; share premium in excess of par-preference, P750,000; Ordinary share (P10 par), P5,000,000; share premium in excess of par-ordinary, P2,800,000; Subscribed ordinary share, P65,000; Accumulated profits and losses, P2,000,000; and Subscription receivable-ordinary, P350,000.

/FNDACT2

Of Theory and Accounts Page 8 of 11

CASE B The shareholder’s equity of Aranque Inc. revealed the following information on December 31, 2012: Preference share (P80 stated value), P1,200,000; share premium in excess of stated value-preference, P900,000;

Ordinary share (P15 stated value), P3,000,000; share premium in excess of stated value-ordinary, P2,800,000; Subscribed ordinary share, P80,000; Accumulated profits and losses, P1,950,000; and Subscription receivable-ordinary,

P200,000. REQUIRED: Compute for the legal capital based on each of the case above. PROBLEM 8. Delinquent subscription and highest bidder Macchiato Corp. had the following transactions with one of its subscribers during the year:

a) On January 2, Olive subscribes for 25,000 shares at par P50 to be paid within 60 days from the date of subscription.

b) On February 28, Olive pays P750,000 of her subscription to the corporation. c) On March 5, The corporation called Olive’s subscription balance but she defaulted. Consequently the subscription

was declared to be delinquent. d) Macchiato paid P38,000 for expenses incurred in connection with the auction of the delinquent shares. The offer

price was P560,000 which includes the balance still due on the subscription, interest and costs of the sale.

e) Three bidders offered to pay the offer price in exchange for the following shares: Rey 4,000 shares, Paul 5,500 shares and Joven 6,000 shares. Accordingly the auction was awarded to the highest bidder. The corporation

then received cash representing the offer price on March 15. f) Macchiato issued the shares to the subscribers on March 18.

REQUIRED:

1. Journalize above transactions. 2. Who was the highest bidder? 3. How many shares were actually issued to (a) Olive and to the (b) highest bidder?

PROBLEM 9. Treasury shares

On August 10, Cultura Corporation reacquired 8,000 shares of its P100 par value ordinary shares at P134. The share was originally issued at P110. The shares were resold on November 21 at P145.

REQUIRED: Provide the entries required to record the reacquisition and the subsequent resale of the share using the: (1) Par value method of accounting for treasury share. (2) Cost method of accounting for treasury share.

PROBLEM 10. Treasury shares – Cost method Medley Inc. had the following information during the year:

a) Medley issued 10,000 ordinary shares (P100 par) for P120 per share. b) Medley reacquired 3,000 ordinary shares at P150 per share. c) The corporation then reissued 1,000 of the treasury shares for P170 per share. d) Finally, the remaining treasury shares were issued at P100 per share.

REQUIRED: Prepare the journal entries to record above transactions. PROBLEM 11. Treasury share presentation Bucks Corp. have the following information as of December 31, 2012:

Ordinary share capital, 60,000 shares, P100 par; Share premium, P60,000; Retained earnings, 2,000,000 and Treasury shares, 5,000 at cost of P140 each. REQUIRED: Present the shareholder’s equity portion to be shown on the entity’s statement of financial position.

PROBLEM 12. Donated capital

Pashmina Inc. is a corporation incorporated in the Philippines, during the year, certain shareholder donated to the entity an aggregate of 10,000 ordinary shares with par value of P100. Subsequently, the 10,000 donated shares were sold for P130 per share. REQUIRED:

1. Prepare the journal entries to record:

a. The receipt of the donated shares b. The subsequent sale of the donated shares

2. How would the donated capital be accounted for in the shareholder’s equity of Pashmina? PROBLEM 13. Contributed capital Nathaniel Corporation is authorized to issue 100,000 ordinary shares, P17 par value. At the beginning of 2012, 18,000 ordinary shares were issued and outstanding. These shares had been issued at P24. During 2012, the company entered

into the following transactions: Jan. 16 - Issued 1,300 ordinary shares at P25 per share. Mar. 21 - Exchanged 12,000 ordinary shares for a building. The ordinary shares were selling at P27 per share.

/FNDACT2

Of Theory and Accounts Page 9 of 11

May 7 - Reacquired 500 ordinary shares at P26 per share to be held in treasury. July 1 - Accepted subscriptions to 1,000 ordinary shares at P28 per share. The contract called for 10% down

payment with the balance due on December 1. Sept. 20 - Sold 500 treasury shares at P29 per share.

Dec. 1 - Collected the balance due on July 1 subscriptions and issued the shares.

REQUIRED: Compute for the total contributed capital for December 31, 2012. PROBLEM 14. Retirement of treasury shares

a) The corporation holds as treasury, 30,000 ordinary shares with P10 par value per share, at cost amounting P250,000. The shares were subsequently retired.

b) West Corporation has the following information: Ordinary share capital, 200,000 shares, P10 par, P2,000,000; Share premium – original issuance, P400,000; Share premium – treasury, P80,000; Retained earnings P500,000; Treasure shares, 20,000 shares, at cost P350,000. West Corporation subsequently decided to retire all of its treasury shares.

REQUIRED: Journalize above transactions relating to retirement of treasury shares. (Treat each case independently).

PROBLEM 15. Share premium Hello Corporation was organized on January 1, 2013, with an authorization of 1,000,000 ordinary shares with a par value of P5 per share.

During 2013, the corporation had the following equity transactions:

Jan. 4 - Issued 200,000 shares @ P5 per share. April 8 - Issued 100,000 shares @ P7 per share. June 9

- Issued 30,000 shares @ P10 per share

July 29

- Purchased 50,000 shares @ P4 per share.

Dec. 31

- Sold 50,000 shares held in treasury @ P8 per share.

REQUIRED: What should be the total Share Premium as of December 31, 2012?

PROBLEM 16. Comprehensive

The following transactions relate to the stockholders' equity transactions of Monique Corporation for its first year of existence. Jan. 7 Articles of incorporation are filed with the Philippine SEC. SEC authorized the issuance of 10,000

shares of P50 par value preferred stock and 200,000 shares of P10 par value common stock. Jan. 28 40,000 shares of common stock are issued for P14 per share. Feb. 3 80,000 shares of common stock are issued in exchange for land and buildings that have an

appraised value of P250,000 and P1,000,000, respectively. The stock traded at P15 per share on that date on the over-the-counter market.

Feb. 24 2,000 shares of common stock are issued to Specter and Ross, Attorneys-at-Law, in payment for legal services rendered in connection with incorporation. The company charged the amount

to organization costs. The market value of the stock was P16 per share. Sep. 12 Received subscriptions for 10,000 shares of preferred stock at P53 per share. A 40 percent down

payment accompanied the subscriptions. Oct. 1 Reacquired 5,000 ordinary shares for a total cost of P80,000 Nov. 5 Reissued 3,000 ordinary shares at P18 per share. Dec. 10 Shareholders holding an aggregate of 5,000 shares donated their shares to Lindsay. The

company was able to reissue them at P12 per share.

Dec. 31 Profit and loss summary to be closed to retained earnings amounted to P300,000 (credit). REQUIRED:

1. Prepare journal entries to record the foregoing transactions. 2. How much is the contributed capital? 3. How much is the share premium as of December 31?

4. How much is the total shareholder’s equity as of December 31? 5. How much is the legal capital?

PROBLEM 17. Comprehensive

Casio Corp. registered with SEC and was authorized to issue 120,000 ordinary shares at P15 par value per share. During the first year of operations, 40,000 shares were sold at P28 per share. 600 shares were issued in payment of a current operating debt of P18,600. In the first year, the net income was P142,000.

During the year, dividends of P36,000 were paid to shareholders. At the end of the year, total liabilities were P82,000. Use the given data to compute the following items at the end of the first year (show all computations):

/FNDACT2

Of Theory and Accounts Page 10 of 11

REQUIRED: (1) Total liabilities and shareholders' equity (2) Shareholders' equity

(3) Contributed capital (4) Issued share capital (par)

(5) Outstanding share capital (par) (6) Unissued share capital (number of shares) (7) Share premium

Problem 18. Book value per share The shareholder’s equity of Dancing Queen Co. in the statement of financial position on December 31, 2014 is as follows:

Share capital, P10 par, 110,000 shares P1,000,000 Share premium 500,000 Retained earnings 250,000 Treasury shares 10,000 shares, cost – 50,000 50,000

REQUIRED: Compute the book value per share as of December 31, 2014 of Dancing Queen Co.?

PROBLEM 19. Dividends

Journalize each transaction below independently: a. During the May 31, 2014, the Board of Directors of Cashew Corporation declared a dividend of P5 per share,

payable September 30, 2014, to shareholders of record July 31, 2014. The entity has 10,000 shares issued and outstanding with par value of P100. Give the journal entries on (a) May 31, (b) July 31, and (c)

September 30.

b. During the May 31, 2014, the Board of Directors of Cool Corporation declared a 10% dividend, payable September 30, 2014, to shareholders of record July 31, 2014. The entity has 10,000 shares issued and outstanding with par value of P100. Give the journal entries on (a) May 31, (b) July 31, and (c) September 30.

c. Libra Co.’s board of directors decided to declare a dividend on June 30, 2014 to be distributed on August 1, 2014. The company will give inventories worth P1,500,000 to its shareholders of record July 10, 2014. Give the journal entries on (a) June 30, (b) July 10, and (c) August 1.

d. Twins Corporation declared on July 1, 2014 dividends to its stockholders of record as of September 1, 2014. However, due to shortage of cash, the corporation issued scrip dividends at the time of declaration amounting to P100,000 with 12% interest payable on December 31, 2014. Give the journal entries on (a)

July 1, (b) September 1, and (c) December 31.

e. Consider the following information: Share capital, P10 par, 100,000 shares authorized, 50,000 shares issued

P500,000

Share premium 200,000

Retained earnings 300,000 The Board of Directors declared a “bonus issue” on March 1, 2014 to be distributed on April 1, 2014. Fair value of shares is P14 per share. Prepare the entries on March 1, 2014 and April 1, 2014 assuming the company declared (a) 20% issue and (b) 10% issue.

f. The company holds 15,000 shares in treasury costing P7.00 each with market value of P12 per share. The

BOD declared such treasury shares as dividend on February 14, 2014 to be issued on May 1, 2014. Prepare the journal entries to record the foregoing transactions.

PROBLEM 20. Allocation of Dividends

The shareholder’s equity in the statement of financial position on December 31, 2014 of Quijones Corporation showed

the following: Preference share capital, 10% P50 par, 40,000 shares P2,000,000 Ordinary shares capital, P100 par, 30,000 shares 3,000,000 Share premium 500,000 Retained earnings 2,500,000

Total shareholder’s equity P8,000,000 No dividends are in arrears up to December 31, 2012. The company declared P1,000,000 dividend at the end of 2014 at the appropriate rate for preference shares and the remainder to ordinary. REQUIRED: Determine the allocation of the dividend to (1) preference and (2) ordinary, assuming the following cases independently:

a. Preference share is noncumulative and nonparticipating. b. Preference share is cumulative and nonparticipating.

/FNDACT2

Of Theory and Accounts Page 11 of 11

c. Preference share is cumulative and participating. d. Preference share is cumulative and participating up to 12%.

PROBLEM 21. Allocation of Dividends – more than one class of preference shares

The shareholder’s equity in the statement of financial position on December 31, 2014 of Quijones Corporation showed the following:

Class “A” Preference share capital, 10% P50 par, 40,000 shares P2,000,000 Class “B” Preference share capital, 14% P50 par, 20,000 shares P1,000,000 Ordinary shares capital, P100 par, 30,000 shares 3,000,000 Share premium 500,000 Retained earnings 2,500,000 Total shareholder’s equity P9,000,000

No dividends are in arrears up to December 31, 2012. The company declared P1,100,000 dividend at the end of 2014 at the appropriate rate for preference shares and the remainder to ordinary. Determine the allocation of the dividend to (1) preference and (2) ordinary assuming both class of preference shares are cumulative and participating.

**END OF MATERIAL**

“The more you sweat during peacetime, the less you bleed in war” -Sun Tzu

REFERENCES:

BP. BLG. 68 The Corporation Code of the Philippines

Principles of Accounting, Wegandt Kieso et al © John Wiley and Sons

Philippine Financial Reporting Standards (PFRS) © Financial Reporting Standards Council (FRSC)

Partnership and Corporation Accounting, Ballada & Ballada

Financial Accounting and Reporting Vol. 2, Cabrera & Ocampo

Intermediate Accounting Vol. 2., Robles & Empleo

Intermediate Accounting, Stice, Stice, & Skousen

Practical Accounting 1, Uberita

Practical Accounting 1, Valix

Auditing Problems, Ocampo