Floor Rules: The Unwritten Code of the Exchange

21

Floor Rules: The Unwritten Code of the Exchange Mark W. Geiger Paper presented at the Society for the Advancement of Socio-Economics Annual Conference, July, 2014 in Chicago, IL. ABSTRACT This paper presents research from a book in progress on the customary, unwritten code of conduct on exchanges and linked financial institutions. Floor rules are not necessarily illegal, but legality is irrelevant; floor rules are how things get done. But the legality issue complicates research, since people will not admit to illegal acts. This paper avoids the problem by examining floor rules in an episode that occurred before government regulation existed: a great wheat corner on the Chicago Board of Trade in 1888. [SLIDE 1] I’m going to talk today about the unwritten rules that financial insiders use in dealings with one another. “Floor rules,” in the title of this paper, is the term Chicago commodities traders formerly used to describe the customary practices in their business. “The floor” is the exchange floor. Today, exchange floors have almost disappeared, though financial insiders are still around. [SLIDE 2] By “insiders” I mean people working close to the center of the market: traders, portfolio managers, investment bankers and Wall Street and City of London executives—vice presidents and up. I belonged to this last group myself, in an earlier stage of my working career. [SLIDE 3] Outsiders include anyone on the retail side of the business— stockbrokers, branch bankers, and financial planners; also securities analysts and swindlers. I mention this last group to make it clear that this paper is not about people like Bernard Madoff or the Wolf of Wall Street. Along with insiders themselves, floor rules have also survived the end of brick-and- mortar exchanges, and have remained remarkably consistent over time and geography. But legality is largely irrelevant in floor rules, which makes researching them tricky: People do not give straightforward answers to questions about illegal acts they have committed. So I’m researching the topic by looking at market disturbances that are especially well documented, and where floor rules played a crucial role. [SLIDE 4] In a moment I’ll talk about one of these disturbances, a great wheat corner on the Chicago Board of Trade in 1888. But first, so as not to make you wait, I’ll tell you what I found. First: for exchange members in 1888, the market was a system of concentric rings. [SLIDE 5] A few well-connected, long-term members were at the core: On the inside, as it were. The great majority of members occupied the outer rings of this system. Money mattered, but what really determined a member’s placement was how many personal connections he had. The member would receive market information through these connections, including advance notice on price movements, and what was real, and what was a feint or a ploy. Besides getting market news faster than anyone else, the 1 geiger_SASE_2014_ppr_1 7/11/2014

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Floor Rules: The Unwritten Code of the Exchange

Floor Rules: The Unwritten Code of the Exchange

Mark W. Geiger

Paper presented at the Society for the Advancement of Socio-Economics Annual Conference, July, 2014 in Chicago, IL.

ABSTRACT

This paper presents research from a book in progress on the customary, unwritten code of conduct on exchanges and linked financial institutions. Floor rules are not necessarily illegal, but legality is irrelevant; floor rules are how things get done. But the legality issue complicates research, since people will not admit to illegal acts. This paper avoids the problem by examining floor rules in an episode that occurred before government regulation existed: a great wheat corner on the Chicago Board of Trade in 1888.

[SLIDE 1] I’m going to talk today about the unwritten rules that financial insiders use in dealings with one another. “Floor rules,” in the title of this paper, is the term Chicago commodities traders formerly used to describe the customary practices in their business. “The floor” is the exchange floor.

Today, exchange floors have almost disappeared, though financial insiders are still around. [SLIDE 2] By “insiders” I mean people working close to the center of the market: traders, portfolio managers, investment bankers and Wall Street and City of London executives—vice presidents and up. I belonged to this last group myself, in an earlier stage of my working career. [SLIDE 3] Outsiders include anyone on the retail side of the business— stockbrokers, branch bankers, and financial planners; also securities analysts and swindlers. I mention this last group to make it clear that this paper is not about people like Bernard Madoff or the Wolf of Wall Street.

Along with insiders themselves, floor rules have also survived the end of brick-and-mortar exchanges, and have remained remarkably consistent over time and geography. But legality is largely irrelevant in floor rules, which makes researching them tricky: People do not give straightforward answers to questions about illegal acts they have committed. So I’m researching the topic by looking at market disturbances that are especially well documented, and where floor rules played a crucial role. [SLIDE 4] In a moment I’ll talk about one of these disturbances, a great wheat corner on the Chicago Board of Trade in 1888. But first, so as not to make you wait, I’ll tell you what I found.

First: for exchange members in 1888, the market was a system of concentric rings. [SLIDE 5] A few well-connected, long-term members were at the core: On the inside, as it were. The great majority of members occupied the outer rings of this system. Money mattered, but what really determined a member’s placement was how many personal connections he had. The member would receive market information through these connections, including advance notice on price movements, and what was real, and what was a feint or a ploy. Besides getting market news faster than anyone else, the

1 geiger_SASE_2014_ppr_1

7/11/2014

Floor Rules: The Unwritten Code of the Exchange

Mark W. Geiger

insiders also manipulated prices up or down, to their advantage. Insiders, or cliques of them, mainly competed against one another, rather than against outer-ring members. But what the insiders fought over was who would get the outer-ring members’ money. Money, which fueled the whole system, flowed from the outside toward the center.

Outer-ring members, which meant nearly all the members of the exchange, had fewer connections and were, relatively speaking, in the dark. Most of them didn’t survive long on the exchange - only two to four years. When a member’s money ran out, he exited the exchange and a hopeful newcomer would take his place.

As to the rules of play, the wheat corner shows the great lengths of trickery that insiders resorted to. They did not try to fool one another, but instead inflicted their shenanigans against outer-ring members. These innocents were subjected to an unending barrage of sharp practices that would have been unacceptable in any other setting, business or social. Insider trading was the least of it. Insiders invented elaborate plots and routinely spread disinformation, going so far as to print fake trade circulars and price lists. Common strategies, such as bear raids, corners and stock pools, all hinged on deception. The market then was what nineteenth-century Americans called a brace game—that is, rigged.

That outer-ring members would knowingly play a game rigged against them might seem odd. But the exchange was the central collection point for all market information, and any member had an edge in the market over non-members. Second, the exchange was a casino and it drew gamblers. Only a few members would ever win big, but they all hoped for that.

Despite all this, the 1888 financial market was not amoral. The unwritten rules the members followed made a separate, partitioned ethical space, like a poker game. Poker bans certain kinds of deception, but allows other kinds that would be unacceptable outside of the game. And as in poker, inside the exchange a kind of equal opportunity prevailed, since all members had access to the same repertoire of tricks. Outsiders, however, had trouble when they entered this world. On nineteenth-century U.S. exchanges, members referred to outside investors as lambs—to be shorn or slaughtered.

I’ll now speak about the wheat corner itself, then end with some further comments on what the corner shows us.

What happened is this. [SLIDE 6] In late September 1888 a great struggle over control of the wheat market broke out at the Chicago Board of Trade, rattling produce exchanges from San Francisco to Liverpool. The Board of Trade (which I will occasionally refer to as CBOT) was already the world’s largest grain market, [SLIDE 7] and the fight was nationwide front-page news for days. Business in other U.S. commodities markets virtually stopped until things quieted down. When I say this was

2 geiger_SASE_2014_ppr_1

7/11/2014

Floor Rules: The Unwritten Code of the Exchange

Mark W. Geiger

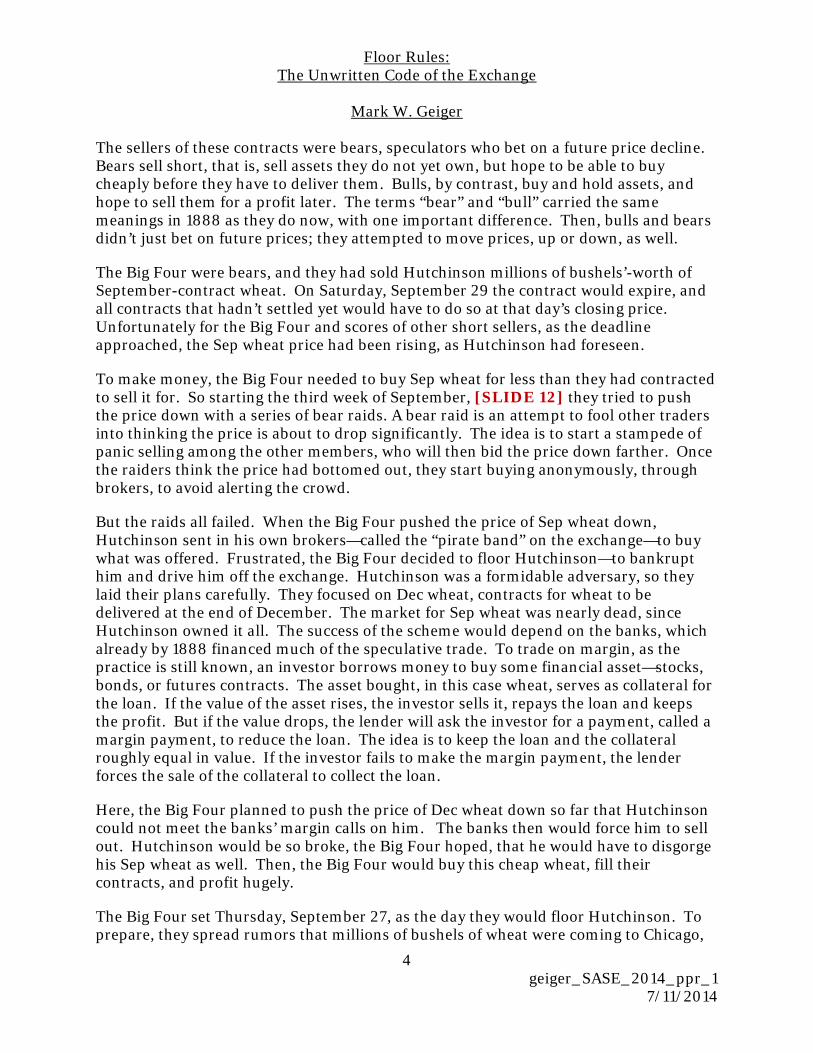

a struggle over the wheat market, it was specifically a struggle over the wheat price, and this slide shows how that played out. [SLIDE 8] Wheat prices on CBOT had risen gradually throughout September until the last week. But in the last half of that last week, all hell broke loose. As you see, over the span of a week, the price more than doubled. This was an unprecedented increases, both in percentage and in absolute terms. By Saturday September 29, at $2.00 a bushel, the price of wheat was higher than at any time since the Civil war. The next trading day, Monday October 1, the price crashed back down to $1.08.

Price graphs make the whole business appear impersonal and abstract, but the floor scene was anything but. Here is an account from the Chicago Tribune, describing how these prices were set. I quote:

“In the wheat pit several hundred men are packed together so tightly in an immense dished space that simply to stand there for a few minutes entails little short of suffocation, and makes one perspire as if he were in a hot bath. Then add to this the fact that the great majority are in a state of the wildest excitement, gesticulating fiercely, and shouting till hoarse in the effort to make themselves heard above the din, which is little short of infernal. The hope of immense gain or the fear of ruinous loss adds to the feverishness of the system, and if to this be added the fact that not a few of those in the pit yesterday had been up nearly all the previous night trying to balance up their books and see just where they stood the acme of exhaustion may perhaps be conceived but scarcely be described.”1

It was not a decorous scene.

All this melodrama revolved around a conflict among five men, out of nearly 2000 CBOT members. [SLIDE 9] On one side was the “Big Four,” the most powerful clique of speculators on the exchange. Here are three of them; I couldn’t find a picture for the fourth. Opposing them was a brilliant loner [SLIDE 10] named Benjamin Peters Hutchinson.

The conflict had originated in mid-August, right about here. [SLIDE 11] Then, and well before anybody else did, Hutchinson realized that year’s U.S. wheat crop would be disastrous, and the short supply would push prices way up. He proceeded to buy all the wheat he could—actual wheat in Chicago’s grain elevators, and every available contract for wheat for September delivery—“Sep wheat.” These were contracts in which the seller agreed to deliver a stated quantity of wheat by the end of September at a set price. By mid-September, two weeks before the settlement date, Hutchinson owned contracts to receive millions of bushels more wheat than existed in fact. Such contracts traded for speculation, and were in effect bets on what the future price would be. Speculative contracts were settled by check, rather than delivery of the physical good.

3 geiger_SASE_2014_ppr_1

7/11/2014

Floor Rules: The Unwritten Code of the Exchange

Mark W. Geiger

The sellers of these contracts were bears, speculators who bet on a future price decline. Bears sell short, that is, sell assets they do not yet own, but hope to be able to buy cheaply before they have to deliver them. Bulls, by contrast, buy and hold assets, and hope to sell them for a profit later. The terms “bear” and “bull” carried the same meanings in 1888 as they do now, with one important difference. Then, bulls and bears didn’t just bet on future prices; they attempted to move prices, up or down, as well.

The Big Four were bears, and they had sold Hutchinson millions of bushels’-worth of September-contract wheat. On Saturday, September 29 the contract would expire, and all contracts that hadn’t settled yet would have to do so at that day’s closing price. Unfortunately for the Big Four and scores of other short sellers, as the deadline approached, the Sep wheat price had been rising, as Hutchinson had foreseen.

To make money, the Big Four needed to buy Sep wheat for less than they had contracted to sell it for. So starting the third week of September, [SLIDE 12] they tried to push the price down with a series of bear raids. A bear raid is an attempt to fool other traders into thinking the price is about to drop significantly. The idea is to start a stampede of panic selling among the other members, who will then bid the price down farther. Once the raiders think the price had bottomed out, they start buying anonymously, through brokers, to avoid alerting the crowd.

But the raids all failed. When the Big Four pushed the price of Sep wheat down, Hutchinson sent in his own brokers—called the “pirate band” on the exchange—to buy what was offered. Frustrated, the Big Four decided to floor Hutchinson—to bankrupt him and drive him off the exchange. Hutchinson was a formidable adversary, so they laid their plans carefully. They focused on Dec wheat, contracts for wheat to be delivered at the end of December. The market for Sep wheat was nearly dead, since Hutchinson owned it all. The success of the scheme would depend on the banks, which already by 1888 financed much of the speculative trade. To trade on margin, as the practice is still known, an investor borrows money to buy some financial asset—stocks, bonds, or futures contracts. The asset bought, in this case wheat, serves as collateral for the loan. If the value of the asset rises, the investor sells it, repays the loan and keeps the profit. But if the value drops, the lender will ask the investor for a payment, called a margin payment, to reduce the loan. The idea is to keep the loan and the collateral roughly equal in value. If the investor fails to make the margin payment, the lender forces the sale of the collateral to collect the loan.

Here, the Big Four planned to push the price of Dec wheat down so far that Hutchinson could not meet the banks’ margin calls on him. The banks then would force him to sell out. Hutchinson would be so broke, the Big Four hoped, that he would have to disgorge his Sep wheat as well. Then, the Big Four would buy this cheap wheat, fill their contracts, and profit hugely.

The Big Four set Thursday, September 27, as the day they would floor Hutchinson. To prepare, they spread rumors that millions of bushels of wheat were coming to Chicago,

4 geiger_SASE_2014_ppr_1

7/11/2014

Floor Rules: The Unwritten Code of the Exchange

Mark W. Geiger

and would swamp the market and crash the price. They arranged with friendly speculators in New York, London, and Liverpool to launch simultaneous bear raids in those places. They had these same confederates send cables to Chicago full of gloomy (and false) news about their home markets. The Big Four spread rumors, too, that Hutchinson was broke, and would dump millions of bushels of wheat on the market on Thursday, and crash the price. Everyone holding wheat should sell now to save themselves, they whispered.

This would be the mother of all bear raids, and the greatest assemblage of clout seen on the exchange up to that time—all directed against one man. And incidental to getting their way, the Big Four would engineer a nationwide and transatlantic drop in the price of wheat.

The day came, and everybody in the wheat pit expected a big sell-off. To launch the raid, the Big Four sent their brokers into the pit to make so-called “wash sales.” These are phony sales between confederates, who sell something back and forth to set an artificial market price. Here, the Big Four's brokers sold Dec wheat to one other at progressively lower prices, hoping to set off a more general wave of selling in the crowd. But after they had put the price down a few cents, Hutchinson again had the pirates buy up what was offered. The Big Four realized, to their horror, that they had based their whole strategy on a false premise. Hutchinson had not borrowed money to buy his wheat; he had bought it outright. Even worse, he still had cash reserves.

The crowd saw that Hutchinson's brokers were buying, and the bear raid stopped dead. There was a moment of indecision, and near silence in the pit. Then one of Hutchinson's pirates shouted out, “Buy Sep at eleven!” signaling something like this [demonstration]. He was offering to buy any amount of Sep wheat at $1.11 per bushel, three and a half cents over the last quoted price. No one took the bid, but it was a shock and a wake-up call: Three and a half cents was a huge jump. The bears’ brokers looked to their principals for direction, but got none. The bears were in complete disarray, and didn’t know what to do.

With that, the whole market started to turn. The bidding spooked the crowd in the pit, most of whom were bears and just as trapped as the Big Four. Wheat prices started to rise, at first slowly then faster and faster. Traders lost their heads and bid wildly against one another, pushing the price up without further help from Hutchinson’s pirates. By the end of the day [SLIDE 13], Sep wheat had risen twenty-two cents a bushel, to $1.25—a record increase. Over the next two days, Hutchinson first put the price to $1.50, then to $2.00. When it was over, the lowest estimate of Hutchinson’s profit was $1.5 million ($37 million in 2013). He also destroyed the Big Four: They never again did business again as a team.

5 geiger_SASE_2014_ppr_1

7/11/2014

Floor Rules: The Unwritten Code of the Exchange

Mark W. Geiger

[SLIDE 14] I now want to recap what I said earlier about the informal rules of the marketplace, and what this episode shows us. Hutchinson and the Big Four are insiders, at the center of the system of concentric rings that I described earlier. The wheat corner also showcases insider trickery. Actually, the plotting by the Big Four was even more baroque than I described, but I didn’t have time to go into it. But—one feature of the wheat corner seemingly contradicts something I said earlier about market dynamics: Hutchinson and the Big Four were after each other’s money, not that of outer-ring members. I think that things happened as they did because Hutchinson violated an unspoken rule that I haven’t mentioned yet, namely, that insiders stayed out of one another’s business. But because of Hutchinson’s insight about the coming failure of the wheat crop, he stood to take a great pile of money off the Big Four. In another parallel to poker, professional gamblers have a similar kind of détente. Card sharps avoid one another in a poker room, and instead target weaker players. Here, Hutchinson had overstepped a line, as the Big Four saw it, and they would make him pay. And so they turned on him, even though they had all done business with him for over a decade.

Except that he fought them off. Which brings me to the final point I want to make, which is this: Members competed for more than money. Hutchinson could have made even more money than he did, if he had held all the short sellers to their contracts. But he did not. Instead, he made a great public show of scratching scratched the trades of nearly all the members who had shorted Sep wheat. Meanwhile, he insisted on full payment from the Big Four and their cronies. The fight was about money, of course, but also about turf, reputation, and payback. Hutchinson wanted to show that he controlled the market and to publicly humiliate the Big Four, as a warning to would-be challengers. Any street-corner gangster would understand the stakes.

I’ll close with a comment on Michael Lewis’s recent book, Flash Boys, in which Lewis caused something of a stir when he asserted that modern-day financial markets are rigged. In the nineteenth century, no one thought the market was anything else—and they were right.

Thanks for listening.

6 geiger_SASE_2014_ppr_1

7/11/2014

Floor Rules: The Unwritten Code of the Exchange

Mark W. Geiger

ENDNOTES

1 Chicago Tribune, June 16, 1887, 1.

7 geiger_SASE_2014_ppr_1

7/11/2014

Floor Rules: The Unwritten Code of the Exchange

Mark W. Geiger7/11/2014 1geiger_SASE_2014_ppr_1

Who’s In:

• Traders

• Portfolio Managers

• Investment Bankers

• Wall Street and City Executives: ≥ VPs

7/11/2014 2geiger_SASE_2014_ppr_1

Who’s Out:

• Retail Anything

• Securities Analysts

• Swindlers

7/11/2014 3geiger_SASE_2014_ppr_1

Four Case Studies:

• New York markets, 1866

• Chicago Board of Trade, 1888

• Australian Exchanges, 1969-70

• City of London, 2012-present

7/11/2014 4geiger_SASE_2014_ppr_1

CBOT Grain Trade, 1890 :Member Relationships

57/11/2014 geiger_SASE_2014_ppr_1

CBOT Trading Floor, 1888

7/11/2014 6geiger_SASE_2014_ppr_1

Front-Page NewsFriday, September 28, 1888

Chicago San Francisco New York

7/11/2014 7geiger_SASE_2014_ppr_1

7/11/2014 8

$0.92 $0.93 $0.94 $0.95

$2.00

$1.08

$0.80

$1.20

$1.60

$2.00

9/1 9/8 9/15 9/22 9/29Week Ending (Saturday)

Sep Wheat Price9/1 - 10/1/1888

geiger_SASE_2014_ppr_1

The Big Four

7/11/2014

Jack Cudahy Norman Ream Nat Jones

(Not pictured: Charlie Singer)9geiger_SASE_2014_ppr_1

Benjamin P. Hutchinson, “Old Hutch”

7/11/2014 10geiger_SASE_2014_ppr_1

Cash Wheat Price per BushelFirst Trading Day of each Month, 1888

$0.79 $0.76 $0.76 $0.73 $0.82 $0.86

$0.80 $0.84 $0.93

$1.08 $1.17

$1.04

$0.70

$0.90

$1.10

$1.30

$1.50

$1.70

$1.90

$2.10

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

7/11/2014 11geiger_SASE_2014_ppr_1

7/11/2014 12

$0.92 $0.93 $0.94 $0.95

$2.00

$1.08

$0.80

$1.20

$1.60

$2.00

9/1 9/8 9/15 9/22 9/29Week Ending (Saturday)

Sep Wheat Price9/1 - 10/1/1888

geiger_SASE_2014_ppr_1

7/11/2014 13

$0.99 $1.02 $1.04

$1.25

$1.50

$2.00

$0.80

$1.20

$1.60

$2.00

9/24 9/25 9/26 9/27 9/28 9/29

Sep Wheat Price9/24 - 9/29/1888

geiger_SASE_2014_ppr_1

Floor Life, Up Close

7/11/201414

geiger_SASE_2014_ppr_1