Fixed Satellite Services Addressing structural question marks CONTENTS

68

Equity Research 30 September 2014 Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. This research report has been prepared in whole or in part by equity research analysts based outside the US who are not registered/qualified as research analysts with FINRA. PLEASE SEE ANALYST CERTIFICATION(S) AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 61. Fixed Satellite Services Addressing structural question marks The market has focused in the past two years on key areas of structural concern for the Fixed Satellite Services (FSS) industry. Year-to-date, good short-term delivery and a market preference for bond-like equities have led Eutelsat and SES to outperform. But we believe the structural debate continues to hold back investor interest. We address three areas: 1) compression in Video, 2) government budget impacts, and 3) oversupply risks in Data (including High Throughput Satellites – HTS). We aim to separate out where there could be real reasons for concern and the timeframes involved. We then model what could be a sensible “normal year” revenue and EBITDA growth for FSS operators within each subcategory in Video, Government and Data. Looking at mix, we conclude that SES can grow EBITDA at 4.0% in a “normal year”, while Eutelsat can achieve 3.8%. We use these growth rates to consider what multiples could be sensible, based on a regression of valuation vs growth for “peers” in infrastructure, telco and media. On EV/EBITDA vs EBITDA growth, Eutelsat looks better value but 1) SES has a major tax advantage; 2) SES’s cash flow momentum and dividend growth give it advantages; and 3) we still have some short-term government concerns at Eutelsat. So we reiterate our Overweight on SES and Equal Weight on Eutelsat. Compression – not as big a problem as has been suggested: We have investigated the issue of compression vs the shift from SD to HD to Ultra HD. We conclude: 1) the shift to MPEG-4 only matters when removing the last MPEG-2 box and early indications suggest planning for Ultra HD will at least offset MPEG-2 removal; 2) this is less relevant in EM (operators went straight to MPEG-4) or free-TV (unlikely to invest in new boxes). Government – concerns on growth, but expect fewer shocks: We split government revenues into component parts and use industry forecasts where possible (e.g. for Unmanned Aerial Vehicles – UAVs) to model future growth. While we do not expect strong growth over the medium term, with US budget pressures here to stay, we do see room for modest growth, with more reliability. Governments beyond the US should support growth over time. Oversupply – new operators can impact Data; HTS a problem for specific uses: Supply should outstrip demand over the next few years due to small national operators and High Throughput Satellites. But 1) this is unlikely to impact Direct-To-Home (DTH); 2) HTS impacts are likely to be specific and somewhat smaller than has been suggested; and 3) the key risks from oversupply are in fairly small corners of revenue for the FSS operators. SES – reiterate Overweight: We expect solid delivery, and maintain our view that 10% dividend growth makes this one of the most attractive income stories in the market. Eutelsat – reiterate Equal Weight: Trends have started to improve, and valuation is not stretched, but some further short-term risks around Data and Multi-Usage prevent us from being more positive here. INDUSTRY UPDATE European Media POSITIVE Unchanged European Media Nick Dempsey +44 (0)20 3134 5888 [email protected] Barclays, London Andrew Ross +44 (0)20 7773 3023 [email protected] Barclays, London Julien Roch +44 (0)20 3134 3323 [email protected] Barclays, London

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Fixed Satellite Services Addressing structural question marks CONTENTS

Equity Research30 September 2014

Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.

Investors should consider this report as only a single factor in making their investment decision.

This research report has been prepared in whole or in part by equity research analysts based outside the US who are not registered/qualified as research analysts with FINRA.

PLEASE SEE ANALYST CERTIFICATION(S) AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 61.

Fixed Satellite Services

Addressing structural question marks The market has focused in the past two years on key areas of structural concern for the Fixed Satellite Services (FSS) industry. Year-to-date, good short-term delivery and a market preference for bond-like equities have led Eutelsat and SES to outperform. But we believe the structural debate continues to hold back investor interest. We address three areas: 1) compression in Video, 2) government budget impacts, and 3) oversupply risks in Data (including High Throughput Satellites – HTS). We aim to separate out where there could be real reasons for concern and the timeframes involved. We then model what could be a sensible “normal year” revenue and EBITDA growth for FSS operators within each subcategory in Video, Government and Data. Looking at mix, we conclude that SES can grow EBITDA at 4.0% in a “normal year”, while Eutelsat can achieve 3.8%. We use these growth rates to consider what multiples could be sensible, based on a regression of valuation vs growth for “peers” in infrastructure, telco and media. On EV/EBITDA vs EBITDA growth, Eutelsat looks better value but 1) SES has a major tax advantage; 2) SES’s cash flow momentum and dividend growth give it advantages; and 3) we still have some short-term government concerns at Eutelsat. So we reiterate our Overweight on SES and Equal Weight on Eutelsat.

Compression – not as big a problem as has been suggested: We have investigated the issue of compression vs the shift from SD to HD to Ultra HD. We conclude: 1) the shift to MPEG-4 only matters when removing the last MPEG-2 box and early indications suggest planning for Ultra HD will at least offset MPEG-2 removal; 2) this is less relevant in EM (operators went straight to MPEG-4) or free-TV (unlikely to invest in new boxes).

Government – concerns on growth, but expect fewer shocks: We split government revenues into component parts and use industry forecasts where possible (e.g. for Unmanned Aerial Vehicles – UAVs) to model future growth. While we do not expect strong growth over the medium term, with US budget pressures here to stay, we do see room for modest growth, with more reliability. Governments beyond the US should support growth over time.

Oversupply – new operators can impact Data; HTS a problem for specific uses: Supply should outstrip demand over the next few years due to small national operators and High Throughput Satellites. But 1) this is unlikely to impact Direct-To-Home (DTH); 2) HTS impacts are likely to be specific and somewhat smaller than has been suggested; and 3) the key risks from oversupply are in fairly small corners of revenue for the FSS operators.

SES – reiterate Overweight: We expect solid delivery, and maintain our view that 10% dividend growth makes this one of the most attractive income stories in the market.

Eutelsat – reiterate Equal Weight: Trends have started to improve, and valuation is not stretched, but some further short-term risks around Data and Multi-Usage prevent us from being more positive here.

INDUSTRY UPDATE

European Media POSITIVE Unchanged

European Media Nick Dempsey +44 (0)20 3134 5888 [email protected] Barclays, London

Andrew Ross +44 (0)20 7773 3023 [email protected] Barclays, London

Julien Roch +44 (0)20 3134 3323 [email protected] Barclays, London

Barclays | Fixed Satellite Services

30 September 2014 2

CONTENTS

EXECUTIVE SUMMARY .................................................................................... 3 1: How will compression impact Video growth? ................................................................................ 3 2: What will the trends be in Government going forward? ............................................................... 6 3: Are there oversupply risks from new operators and HTS? ........................................................... 8 Putting it together – revenue and EBITDA growth by segment .................................................... 10

VALUATION: ETL LOOKS CHEAPER BUT IT’S NOT THE FULL PICTURE12

PAY-OFF BETWEEN COMPRESSION AND RESOLUTION: ACCRETIVE OR DILUTIVE? ................................................................................................... 17 Quick summary of our conclusions ..................................................................................................... 17 Intro: BSkyB slide showed capacity reduction as HD increased .................................................... 17 1) Channel growth running ahead of revenue growth – why? .................................................. 19 2) Practicalities of how compression could affect FSS players .................................................. 21 DTH market growth: assuming 2% for Europe and 8% for EM .................................................... 27

GOVERNMENT: SHORT-TERM WEAKNESS; RETURN TO GROWTH OVER TIME ........................................................................................................ 29 What will be the short-term trends in US gov satcom spend? ...................................................... 31 What are the long-term trends for FSS operators? .......................................................................... 34 Building a model to forecast growth in US military satcom ........................................................... 36 Gov market revenue growth: expect 2.5% in a normal year .......................................................... 43

DO WE NEED TO WORRY ABOUT OVERSUPPLY? .................................. 44 Transponder supply set to outstrip demand on a global basis ...................................................... 44 How can we predict where there could be problems? .................................................................... 46 Potential impact on different areas of Data revenue from HTS..................................................... 49 Conclusion on Data: 1-3% growth overall in this area .................................................................... 55 Implications for normal year growth at ETL and SES ....................................................................... 55

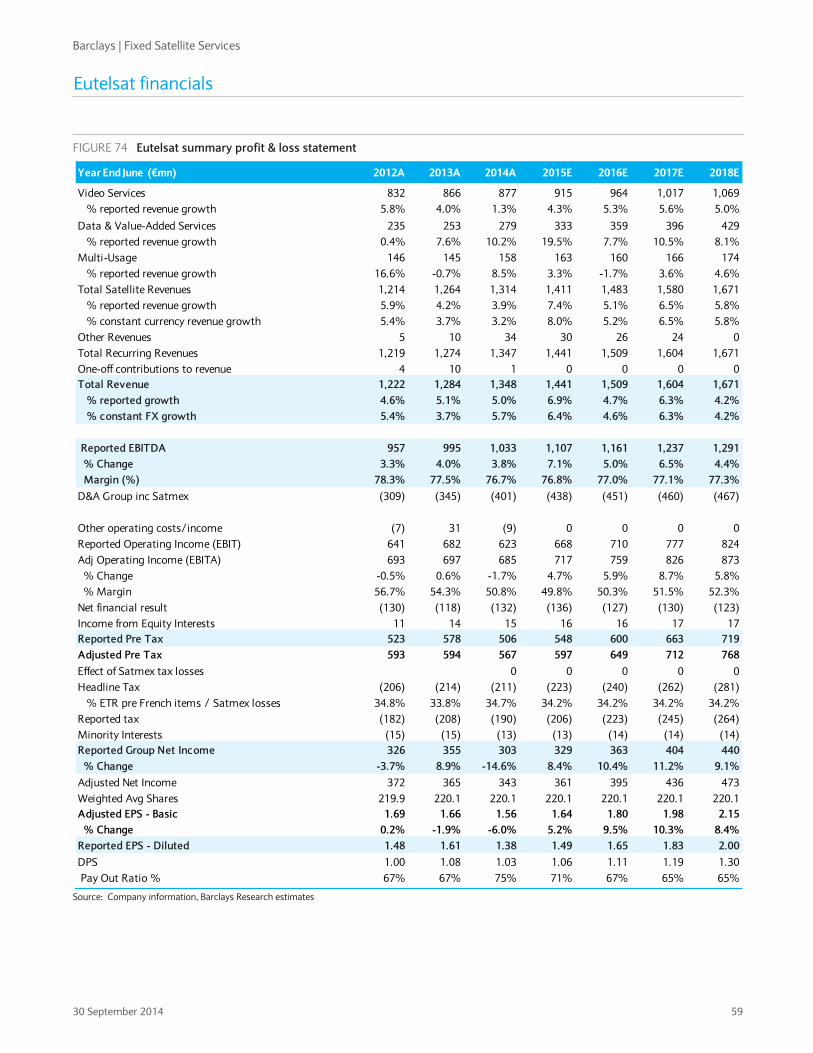

KEY FINANCIALS .............................................................................................. 57 SES financials ............................................................................................................................................. 57 Eutelsat financials ..................................................................................................................................... 59

Barclays | Fixed Satellite Services

30 September 2014 3

EXECUTIVE SUMMARY

Sentiment on Eutelsat and SES took a hit in 2012 and 2013, as Eutelsat in particular saw significant downgrades. During that period of weak momentum, it became easier for investors to listen to structural bear arguments on these names. This year, delivery has been more solid and sentiment has gradually improved, driving a rerating. But structural questions remain critical for these stories. We believe that that there are clear attractions in a business model with 1) multi-year contracts driving visibility, 2) reducing capex per transponder and 3) high dividend yields with relatively predictable dividend growth. But those attractions are only worth focusing on if we can get comfortable with the structural question marks.

So in this note, we get under the skin of three areas of structural concern: 1) the impact of compression technology on growth in the Video segment; 2) likely mid-term progress in Government, which has recently been weak; and 3) risks from oversupply, especially in the broad Data segment, from High Throughput Satellites and new operators. We do not just debate these issues, we model out the likely “normal year” revenue and EBITDA growth potential in each subsegment of the industry – and then look at mix to see what kind of “normal year” growth each of Eutelsat and SES can realistically achieve.

We use this growth to cross-check our valuation for both Eutelsat and SES. Benchmarking the performance of Fixed Satellite Services (FSS) operators in terms of growth can be challenging, given they are at different stages of their internal capex/launch/revenue cycles. And taking a historical growth average may not capture future structural concerns. So we run a regression of EV/EBITDA vs EBITDA growth for comparable sectors such as Infrastructure, Telco and Cable – and then we compare the “normal year” EBITDA growth for Eutelsat and SES.

We show below our conclusions on the key structural question marks. Below that, we show our assumptions on “normal year” growth for the different satellite revenue streams and the implications for SES and Eutelsat – and our thoughts on valuation.

1: How will compression impact Video growth? We have investigated the issue of compression vs the shift from SD to HD to Ultra HD. This has been a hot topic in the investment community in the last year or more.

This is the bear argument (as we understand it):

1. FSS operators have been saying for years that the payoff between increasing compression and the shift to HD and Ultra HD will be accretive for transponder demand.

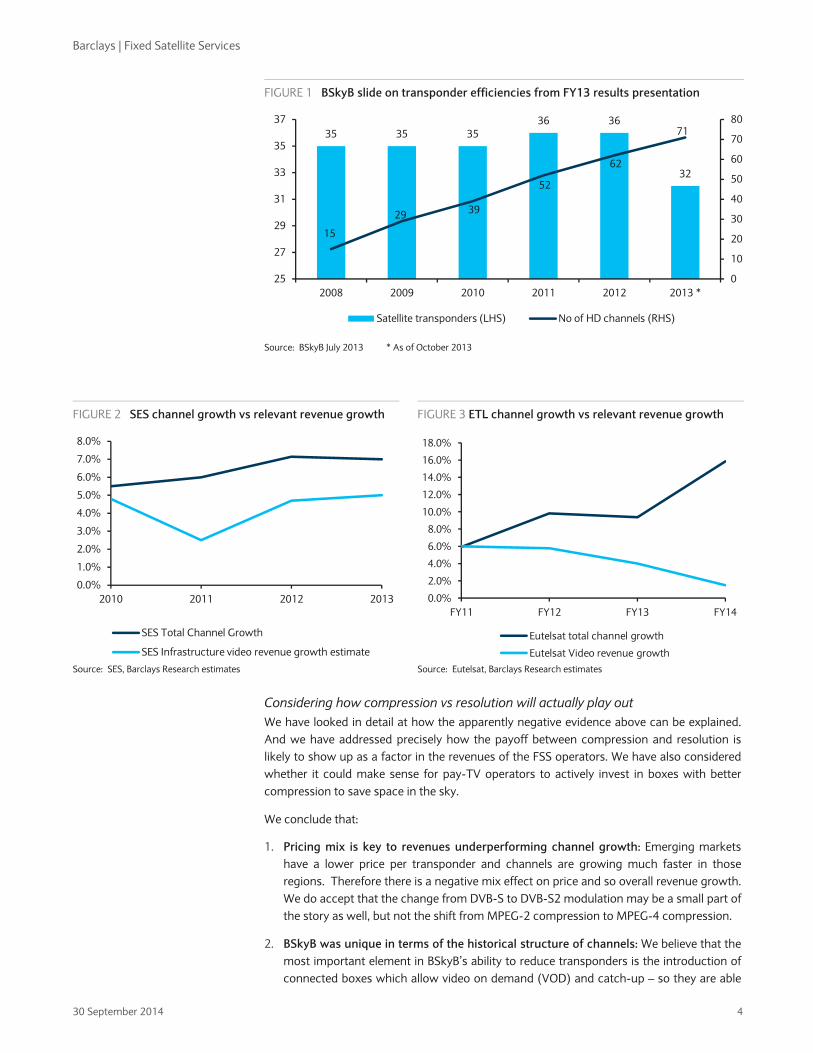

2. But as shown below in Figure 1, BSkyB has recently been able to reduce its transponder needs despite a major increase in HD channels, while revenue growth at SES and Eutelsat (even adjusted for some factors like German analogue switch-off) has underperformed channel growth in the past few years (as shown in Figure 2 and Figure 3 below).

3. HEVC (High Efficiency Video Coding) compression is coming and there could be a scenario where better compression starts to impact the industry before Ultra HD demand arrives.

4. Therefore it seems likely that compression is actually winning the battle and industry-wide Video growth will be lower than many expect going forward.

Barclays | Fixed Satellite Services

30 September 2014 4

FIGURE 1 BSkyB slide on transponder efficiencies from FY13 results presentation

Source: BSkyB July 2013 * As of October 2013

FIGURE 2 SES channel growth vs relevant revenue growth

FIGURE 3 ETL channel growth vs relevant revenue growth

Source: SES, Barclays Research estimates Source: Eutelsat, Barclays Research estimates

Considering how compression vs resolution will actually play out We have looked in detail at how the apparently negative evidence above can be explained. And we have addressed precisely how the payoff between compression and resolution is likely to show up as a factor in the revenues of the FSS operators. We have also considered whether it could make sense for pay-TV operators to actively invest in boxes with better compression to save space in the sky.

We conclude that:

1. Pricing mix is key to revenues underperforming channel growth: Emerging markets have a lower price per transponder and channels are growing much faster in those regions. Therefore there is a negative mix effect on price and so overall revenue growth. We do accept that the change from DVB-S to DVB-S2 modulation may be a small part of the story as well, but not the shift from MPEG-2 compression to MPEG-4 compression.

2. BSkyB was unique in terms of the historical structure of channels: We believe that the most important element in BSkyB’s ability to reduce transponders is the introduction of connected boxes which allow video on demand (VOD) and catch-up – so they are able

35 35 3536 36

32

15

29 39

52

62

71

0

10

20

30

40

50

60

70

80

25

27

29

31

33

35

37

2008 2009 2010 2011 2012 2013 *

Satellite transponders (LHS) No of HD channels (RHS)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2010 2011 2012 2013

SES Total Channel Growth

SES Infrastructure video revenue growth estimate

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

FY11 FY12 FY13 FY14

Eutelsat total channel growth

Eutelsat Video revenue growth

Barclays | Fixed Satellite Services

30 September 2014 5

to switch off quite a few carousel channels (the ones with films starting every 15 minutes) and “+1” channels, replicating channels an hour later. Our work suggests that BSkyB was an outlier in terms of having so many of those channels, so its ability to reduce space in the sky is more or less unique among pay-TV operators.

3. Timing of MPEG-4 impact is complex – we care about the number of channels broadcast: The shift to MPEG-4 only matters when removing the last MPEG-2 box, which has not happened anywhere yet. It is not true that as MPEG-4 boxes start to increase in the customer mix there are gradual negative effects. Satellite operators care about the number of channels broadcast and if you switch the SD channels to MPEG-4 compression in the broadcast, then no one with an MPEG-2 box can see them. So you need to wait until there are no more MPEG-2 customers (or until there are so few that it makes sense to squeeze them out).

That might suggest that there is a “cliff” still to come when TV groups remove the last MPEG-2 box and have the double benefit of A) no longer simulcasting channels in both SD and HD, and B) being able to apply MPEG-4 compression to SD channels. However, early indications from CanalSat and Sky Deutschland suggest that this “cliff” will be smoothed out by the renewal process for multi-year contracts. We think that TV operators will plan for significantly increased numbers of HD channels and the start of Ultra HD, at least offsetting MPEG-2 removal in their transponder demand expectations.

4. HEVC boxes – it is exactly the same as the move from MPEG-2 to MPEG-4: We will see a rise in the number of set-top boxes with HEVC compression (the next step in compression which is now becoming available, and goes hand in hand with Ultra HD). But this is not particularly relevant to satellite operators until MPEG-4 boxes are replaced in very large numbers (which will be many years in the future, we think). Because, following the example of SD/MPEG-2 and HD/MPEG-4, as long as there are significant numbers of customers with MPEG-4 boxes, then channels that are shown in Ultra-HD (viewable only by customers with HEVC boxes) will need to be simulcast in HD.

FIGURE 4 Forecasts for HD and Ultra HD as % of total channels in 2022 vs 2012

Source: Euroconsult 2013 (as shown in Eutelsat presentation from December 2013)

5. You only need a suggestion that Ultra HD will ultimately be important: Satellite operators do not need to see major take-up of Ultra HD channels any time soon, in order to remain relaxed about future Video transponder demand. They just need to see the early signs of take-up in the next five years to encourage TV customers to plan ahead for the kind of capacity that will be needed in an Ultra HD world. Figure 4 above shows Euroconsult’s expectations for HD and Ultra HD channels, with Ultra HD established in

85%

38%

91%

67%

95%

78% 92

%

78% 97

%

80% 90

%

68%

15%

60%

9%

32%

5%

21%

8%

21%

3%

19% 10

%

31%

2.4% 1.4% 1.5% 1.0% 0.8% 1.0%

0%

20%

40%

60%

80%

100%

SD HD Ultra HD

Barclays | Fixed Satellite Services

30 September 2014 6

the mix in 2022, in developed markets, but still small. This does not look great, but it is all you need (along with a further ramp-up in HD as shown).

6. Box replacement in order to save on satellite capacity makes little economic sense: We have looked at whether an operator like BSkyB could look to change the pattern discussed above by investing in a complete switch to HEVC boxes, purely to save space in the sky. We calculate that rolling out HEVC boxes in one go to all of Sky’s subscribers would cost BSkyB c.£1bn (c.£100 per box to 10m subscribers). And we assume that the benefits offered by enhanced compression would save c.£60m per year. This assumes no change at all in the current mix of channels between SD, HD and Ultra HD. So that would be a <6% return on investment, or put another way, the NPV of the savings would be c.£500-600m vs the £1bn investment.

7. This is all less relevant in EM where operators went straight to MPEG-4. It is also less important for free-TV customers, who are unlikely to invest in new boxes to squeeze out the last MPEG-2 customers.

Expect 2% European Video growth; 8% EM Video growth In developed markets, which essentially means Europe for the major satellite operators, we expect only modest underlying growth in channels, driven by the effects of HD/Ultra HD (partially offset by compression effects) as discussed above. We also see only very small increases coming from price. So we assume “normal year” growth of 2% for developed market Video revenues.

In developing markets, we note a number of strong forecasts for channel growth and expected transponder demand from DTH (pay and free-to-air) in Latin America, South Asia, South East Asia and Africa (as discussed at the end of our section on Video and compression below). We assume “normal year” revenue growth of 8% in developing market Video.

2: What will the trends be in Government going forward? We have looked to size the market for Government spending on commercial satellite capacity and break it down into its component parts. We base our estimates for the total pie and the share of each player below on comments from Intelsat on its share of this market – and then the comments from Eutelsat, SES and Intelsat about how much of their revenues derive from Government.

FIGURE 5 US dominates government satellite spend (2013)

FIGURE 6 Estimated share of US gov satellite spend (2013)

Source: Company information, Barclays Research Source: Company information, Barclays Research

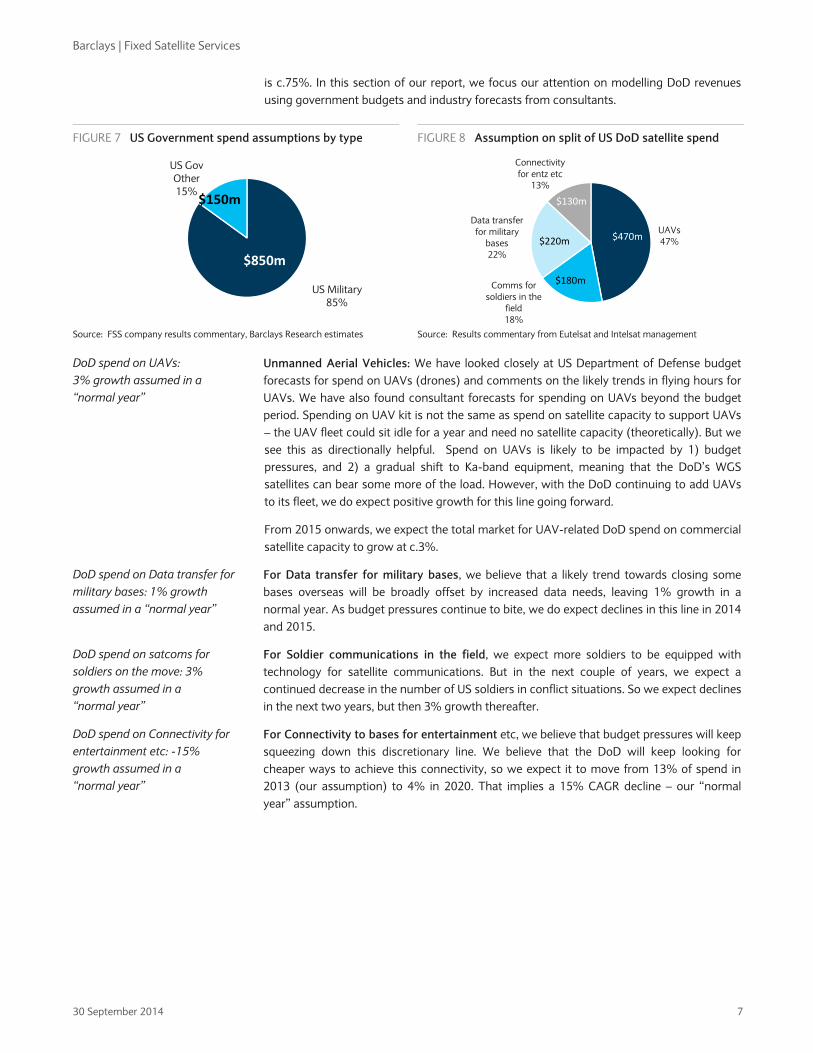

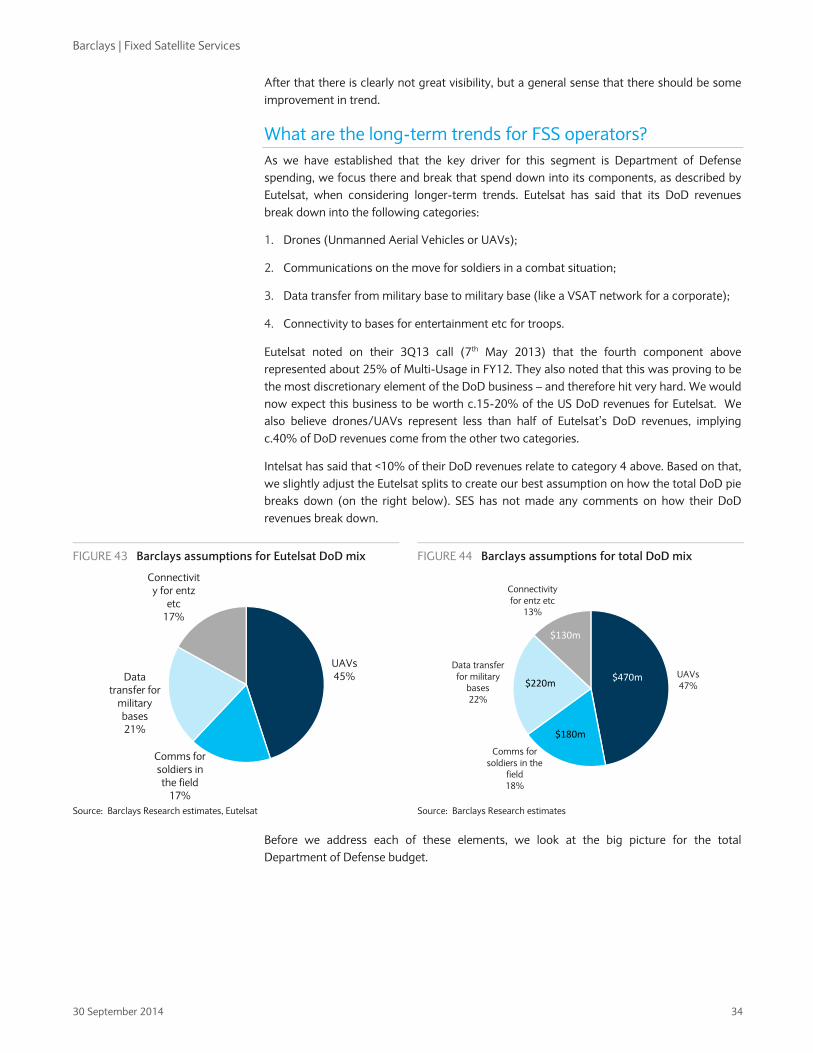

We segment the US Department of Defense (DoD) spend on commercial satellite capacity in Figure 8 below based on comments made by Eutelsat on the different components of its Multi-Usage revenues. The DoD is by far the largest part of this global market: we assume it

US Gov91%

Other Govs9%

$1bn

$100m

Intelsat45%

SES15%

Eutelsat12%

Others28%

$447m$294m

$154m

$120m

Barclays | Fixed Satellite Services

30 September 2014 7

is c.75%. In this section of our report, we focus our attention on modelling DoD revenues using government budgets and industry forecasts from consultants.

FIGURE 7 US Government spend assumptions by type

FIGURE 8 Assumption on split of US DoD satellite spend

Source: FSS company results commentary, Barclays Research estimates Source: Results commentary from Eutelsat and Intelsat management

Unmanned Aerial Vehicles: We have looked closely at US Department of Defense budget forecasts for spend on UAVs (drones) and comments on the likely trends in flying hours for UAVs. We have also found consultant forecasts for spending on UAVs beyond the budget period. Spending on UAV kit is not the same as spend on satellite capacity to support UAVs – the UAV fleet could sit idle for a year and need no satellite capacity (theoretically). But we see this as directionally helpful. Spend on UAVs is likely to be impacted by 1) budget pressures, and 2) a gradual shift to Ka-band equipment, meaning that the DoD’s WGS satellites can bear some more of the load. However, with the DoD continuing to add UAVs to its fleet, we do expect positive growth for this line going forward.

From 2015 onwards, we expect the total market for UAV-related DoD spend on commercial satellite capacity to grow at c.3%.

For Data transfer for military bases, we believe that a likely trend towards closing some bases overseas will be broadly offset by increased data needs, leaving 1% growth in a normal year. As budget pressures continue to bite, we do expect declines in this line in 2014 and 2015.

For Soldier communications in the field, we expect more soldiers to be equipped with technology for satellite communications. But in the next couple of years, we expect a continued decrease in the number of US soldiers in conflict situations. So we expect declines in the next two years, but then 3% growth thereafter.

For Connectivity to bases for entertainment etc, we believe that budget pressures will keep squeezing down this discretionary line. We believe that the DoD will keep looking for cheaper ways to achieve this connectivity, so we expect it to move from 13% of spend in 2013 (our assumption) to 4% in 2020. That implies a 15% CAGR decline – our “normal year” assumption.

US Military85%

US Gov Other15%

$850m

$150m

UAVs47%

Comms for soldiers in the

field18%

Data transfer for military

bases22%

Connectivity for entz etc

13%

$220m

$180m

$470m

$130m

DoD spend on UAVs: 3% growth assumed in a “normal year”

DoD spend on Data transfer for military bases: 1% growth assumed in a “normal year”

DoD spend on satcoms for soldiers on the move: 3% growth assumed in a “normal year”

DoD spend on Connectivity for entertainment etc: -15% growth assumed in a “normal year”

Barclays | Fixed Satellite Services

30 September 2014 8

FIGURE 9 Barclays assumptions for growth in DoD spend on satellite capacity

Source: Barclays Research estimates

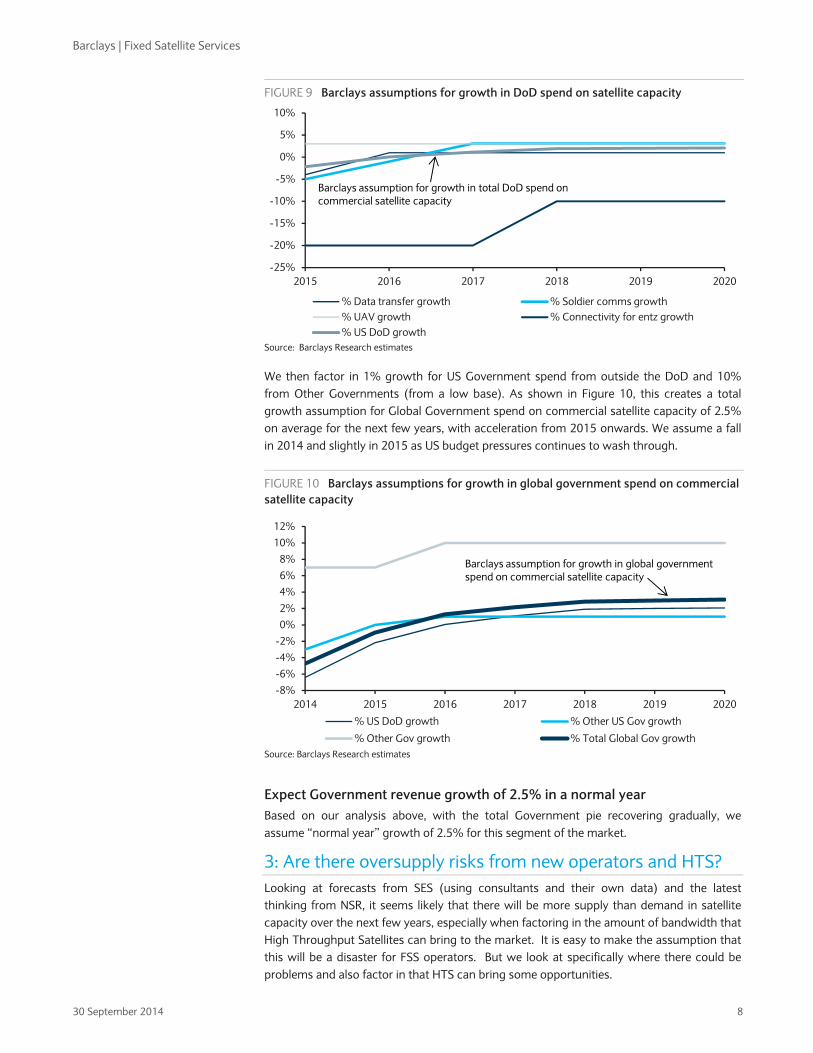

We then factor in 1% growth for US Government spend from outside the DoD and 10% from Other Governments (from a low base). As shown in Figure 10, this creates a total growth assumption for Global Government spend on commercial satellite capacity of 2.5% on average for the next few years, with acceleration from 2015 onwards. We assume a fall in 2014 and slightly in 2015 as US budget pressures continues to wash through.

FIGURE 10 Barclays assumptions for growth in global government spend on commercial satellite capacity

Source: Barclays Research estimates

Expect Government revenue growth of 2.5% in a normal year Based on our analysis above, with the total Government pie recovering gradually, we assume “normal year” growth of 2.5% for this segment of the market.

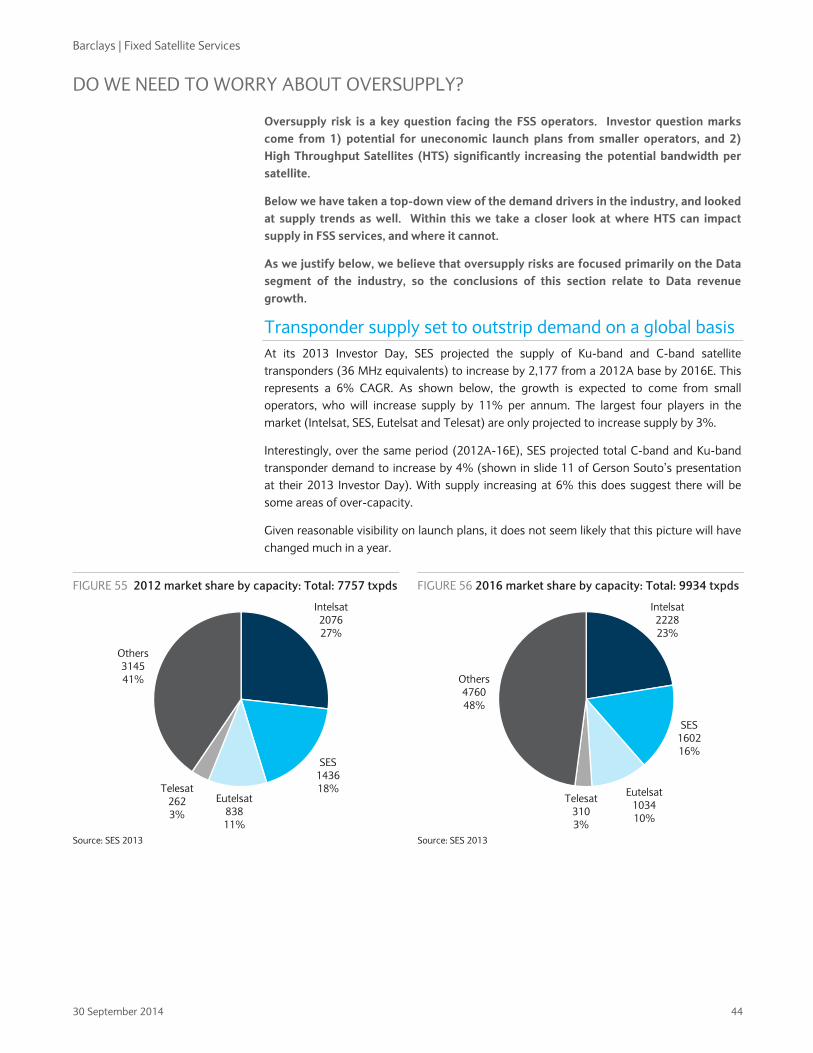

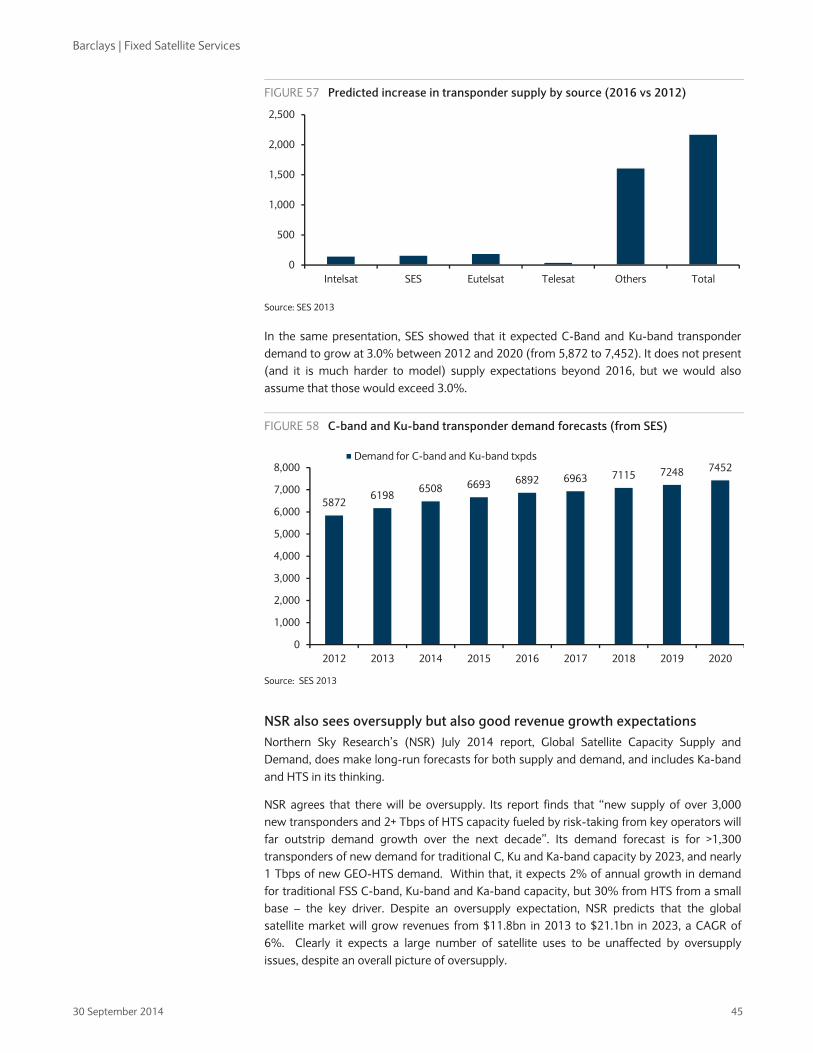

3: Are there oversupply risks from new operators and HTS? Looking at forecasts from SES (using consultants and their own data) and the latest thinking from NSR, it seems likely that there will be more supply than demand in satellite capacity over the next few years, especially when factoring in the amount of bandwidth that High Throughput Satellites can bring to the market. It is easy to make the assumption that this will be a disaster for FSS operators. But we look at specifically where there could be problems and also factor in that HTS can bring some opportunities.

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

2015 2016 2017 2018 2019 2020

% Data transfer growth % Soldier comms growth% UAV growth % Connectivity for entz growth% US DoD growth

Barclays assumption for growth in total DoD spend on commercial satellite capacity

-8%-6%-4%-2%0%2%4%6%8%

10%12%

2014 2015 2016 2017 2018 2019 2020

% US DoD growth % Other US Gov growth

% Other Gov growth % Total Global Gov growth

Barclays assumption for growth in global government spend on commercial satellite capacity

Barclays | Fixed Satellite Services

30 September 2014 9

We conclude that the main area of risk from oversupply is Data, given that 1) DTH requires long-term contracts and is very sticky (so is hard for smaller operators to break into), and it is also not an application appropriate for High Throughput Satellites; and 2) Government applications would face some strategic risks using space on smaller, government-owned operators (but HTS could have an impact within Government over time).

We consider the various different FSS satellite applications within the Data umbrella below, and our assumptions on exposure to these for Eutelsat and SES. We see most risk to growth from HTS oversupply in IP Trunking and Mobile Backhaul. But in the latter we do actually expect strong underlying demand growth. We expect some risks to pricing at Enterprise VSAT from smaller operator launches, but conclude that HTS are not well-suited to most VSAT configurations, given that HTS works better for point-to-point, not a network containing multiple locations over a wide area.

In the area of Mobility, in particular, we see potential for good growth from a low base for the FSS players, although competition is likely to be intense. We also see some potential for further growth in consumer broadband.

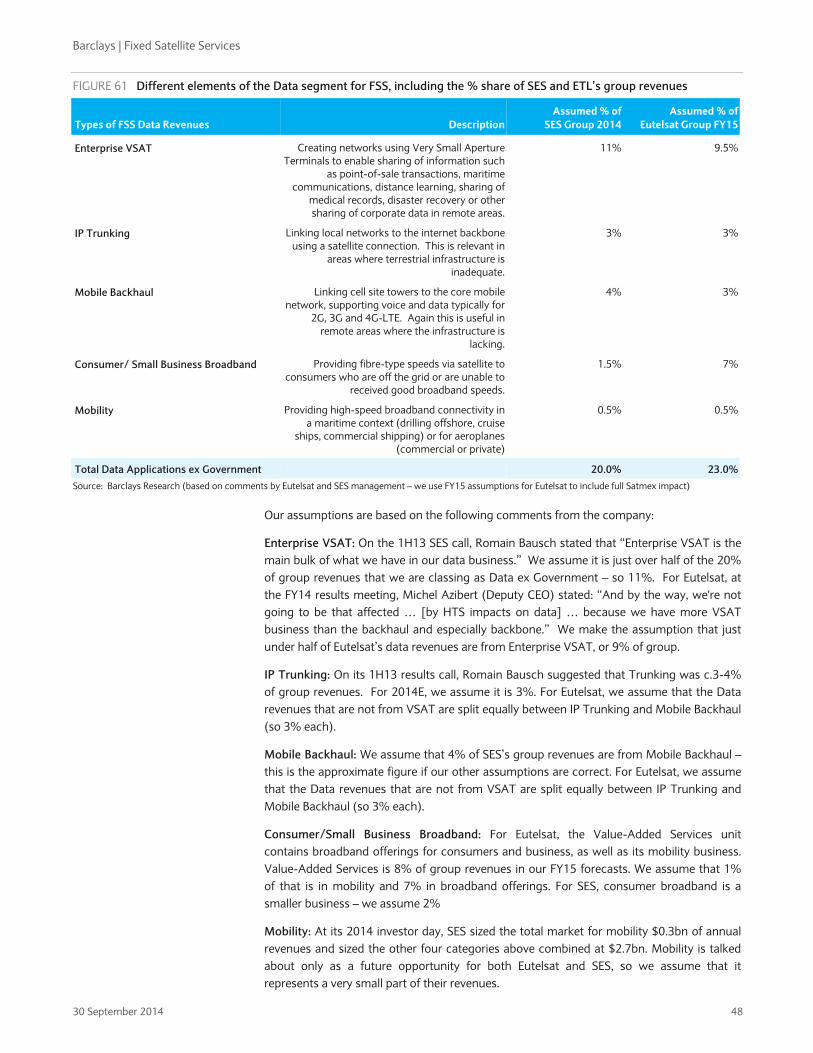

FIGURE 11 Different elements of the Data segment for FSS, including the % share of SES and ETL’s group revenues

Types of FSS Data Revenues DescriptionAssumed % of

SES Group 2014 Assumed % of

ETL Group FY15

Enterprise VSAT Creating networks using Very Small Aperture Terminals to enable sharing of information such as point-of-sale

transactions, maritime communications, distance learning, sharing of medical records, disaster recovery or other sharing

of corporate data in remote areas.

11% 9%

IP Trunking Linking local networks to the internet backbone using a satellite connection. This is relevant in areas where terrestrial

infrastructure is inadequate.

3% 3%

Mobile Backhaul Linking cell site towers to the core mobile network, supporting voice and data typically for 2G, 3G and 4G-LTE. Again this is

useful in remote areas where the infrastructure is lacking.

4% 3%

Consumer/ Small Business Broadband Providing fibre-type speeds via satellite to consumers who are off the grid or are unable to received good broadband speeds.

1.5% 7%

Mobility Providing high-speed broadband connectivity in a maritime context (drilling offshore, cruise ships, commercial shipping)

or for aeroplanes (commercial or private)

0.5% 1.0%

Total Data Applications ex Government 20.0% 23.0%Source: Barclays Research estimates (based on comments by Eutelsat and SES management – we use FY15 assumptions for Eutelsat to include full Satmex impact)

Expect Data revenue growth of 1-3% in a normal year Based on our analysis of oversupply risks from new operators and HTS, but strong transponder demand in areas, we expect “normal year” growth rates by application shown below. Depending on mix, this implies Data revenue growth of 1-3% in a “normal year”.

FIGURE 12 Normal year revenue growth potential for different Data applications

Normal year growth

Enterprise VSAT 2%

Trunking -15%

Mobile Backhaul 3%

Consumer Broadband 6%

Mobility 15%Source: Barclays Research estimates

Barclays | Fixed Satellite Services

30 September 2014 10

Putting it together – revenue and EBITDA growth by segment In the table below, we show our “normal year” revenue assumptions for each sub-sector of Fixed Satellite Services. We assume very little operational gearing – as there is not much in this model. So the EBITDA growth rates are only very slightly ahead of the revenue growth.

FIGURE 13 Barclays assumptions for “normal year” growth by FSS revenue stream

Sector Subsector Revenue growth EBITDA growth

Data Applications Enterprise VSAT 2.0% 2.0%

Trunking -15.0% -17.0%

Mobile Backhaul 3.0% 3.0%

Consumer Broadband 6.0% 6.0%

Mobility 15.0% 15.0%

Government Government applications 2.5% 3.0%

Video Developed markets 2.0% 2.5%

Emerging markets 8.0% 8.5%

Source: Barclays Research estimates

Assumed “normal year” EBITDA growth for Eutelsat and SES

FIGURE 14 ETL splits by type Our weighted average “normal year” EBITDA growth assumption for Eutelsat is 3.9%. Clearly

there are some assumptions on the splits here. We have discussed the Data splits in moredetail above (and in the Data section). Within Video Services, we have assumed that theyhave substantial EM revenues, but that they are still weighted to developed markets. Given fairly low assumptions on transponder demand in Eastern Europe, we class that as adeveloped market.

The table below shows that when applying Eutelsat’s splits (containing some assumptions) toour suggested “normal year” growth rates in Figure 13 above, the weighted average EBITDA growth is 3.8%.

Source: Barclays Research estimates

FIGURE 15 Barclays assumptions on Eutelsat revenue splits – and weighted ave growth

Category Split of revenues

Enterprise VSAT 9.0%

IP Trunking 3.0%

Mobile Backhaul 3.0%

Consumer/ Small Business Broadband 7.0%

Mobility 1.0%

Total Data Applications ex Government 23.0%

Developed markets 41.0%

Emerging markets 23.0%

Video Services 64.0%

Government 11%

Other 2.0%

Weighted Average Growth

Eutelsat Group Weighted Revenue Growth 3.5%

Eutelsat Group Weighted EBITDA Growth 3.8%Source: Barclays Research estimates

Video Servs64%

Value-Added Servs8%

Data15%

Multi-Usage (DoD)11%

Other2%

Barclays | Fixed Satellite Services

30 September 2014 11

At SES, we run the same analysis for the Infrastructure business and then deal with Services separately. We make an assumption on the splits for Infrastructure, as shown below, based on their 2012 revenues (the list time this pie chart was provided). We assume that Services is more weighted to Government and Network Services, and less to Media.

FIGURE 16 SES revenue splits 2012 inc Services

FIGURE 17 SES revenue splits 2012 just in Infrastructure

Source: SES (Investor Day 2013) Source: SES, Barclays Research estimates

FIGURE 18 Barclays assumptions on SES Infrastructure splits – and weighted ave growth

Category Split of revenues

Enterprise VSAT 11.0%

IP Trunking 2.5%

Mobile Backhaul 3.5%

Consumer/ Small Business Broadband 1.5%

Mobility 0.5%

Total Data Applications ex Government 19%

Developed markets 44%

Emerging markets 28%

Video Services 71%

Government 10%

Weighted Average Growth

Weighted average revenue growth 3.6%

Weighted average EBITDA growth 3.9%Source: Barclays Research estimates

As our thinking on the different revenue categories within the FSS business is mostly relevant for SES’s Infrastructure business, we have made an extra step to factor in their Services business as well. We assume continued strong growth in the European Services business (including HD+), but low growth in the US Government Services business, implying 4.5% EBITDA growth in a “normal year”. This means that the implied “normal year” growth for SES Group is very similar to the Infrastructure number – 4.0%.

FIGURE 19 Factoring in Services as well

Split of revenues "Normal year" EBITDA growth

SES Infrastructure 79% 3.9%

SES Services 21% 4.5%

SES Group 100% 4.0%Source: Barclays Research estimates

Media67%

Network Services

20%

Govt & Institutions

13%

Media71%

Network Services

19%

Govt & Institutions

10%

Barclays | Fixed Satellite Services

30 September 2014 12

VALUATION: ETL LOOKS CHEAPER BUT IT’S NOT THE FULL PICTURE

So we have devoted this report to creating what we believe to be “normal year” EBITDA growth for Eutelsat and SES. How can we use those numbers to consider valuation for the two names?

We have run a regression of 2014 EV/EBITDA vs 2014-16 EBITDA growth for the areas of the market which we think are comparable to the satellite names: EU telecoms, US cable and satellite and EU infrastructure (primarily toll roads and airports). We do not put the current multiples and growth for the Fixed Satellite Services names on this chart. Instead we look at where they “should” be valued based on the 3.8% “normal year” EBITDA growth at Eutelsat and the 4.0% at SES.

FIGURE 20 EV/EBITDA vs EBITDA growth regression exercise for comparable sectors

Source: Barclays Research estimates (Barclays forecasts used for the other sectors)

As shown in the table below, the implied EV/EBITDA multiple for SES is 8.0x and for Eutelsat 7.9x. Eutelsat is not too far off that, whereas SES is clearly higher at 9.6x. This already factors in a value of €600m for O3b. So why are we Overweight on SES and Equal Weight on Eutelsat?

FIGURE 21 ETL looks broadly in-line; SES more expensive

2014E EV/EBITDA implied Actual trading 2014E EV/EBITDA

SES 8.0x 9.6x

Eutelsat 7.9x 8.4x

Source: Barclays Research estimates

Looking at sustainable tax advantage SES has a sustainable 15% tax rate. It might well vary slightly from that level, but its location in Luxembourg gives it good protection on a low tax rate. At the same time, Eutelsat is based in France and has a high tax rate. Again that could vary over time, but we would expect a substantial difference between the two to persist over time. Based on Eutelsat at 37% and SES at 15%, an NPV of the difference implies that we should remove €3.6bn from SES’s EV to make a fairer comparison. On that basis, SES would be on 7.2x EV/EBITDA. Perhaps investors will not be ready to assume that the tax disparity continues forever, but we clearly need to build it into our thinking.

EU Telco Incumbents

EU Telco Challengers

US Cable & Satellite

EU Infrastructurey = 52.195x + 5.8695R² = 0.8076

6.0x

6.5x

7.0x

7.5x

8.0x

8.5x

9.0x

9.5x

10.0x

10.5x

2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0%

Eutelsat

SES

Barclays | Fixed Satellite Services

30 September 2014 13

FIGURE 22 SES’s tax advantage is worth 2.4x on EV/EBITDA multiple

Tax calculation details

SES Tax Rate 15%

Eutelsat Tax Rate 37.0%

Difference 22.5%

Discount Rate 8.0%

NPV 3599

Multiple of EBITDA 2.4Source: Barclays Research estimates

We would also suggest that the average tax rate for the sectors shown above is in the 30% region, so SES has a sustainable advantage compared to nearly all comparable companies. An NPV of the difference between a 15% and 30% tax rate at SES points to €2.5bn or 1.6x SES EBITDA. So when making a comparison with the regression chart above, a tax-adjusted 2014E EV/EBITDA for SES would be 8.0x – or in other words broadly in line with where it “should be” on the chart.

So when adjusting for tax, SES looks more or less fairly valued for its growth potential vs its peer group sectors. And the tax gap is significant when valuing SES and Eutelsat.

Infrastructure peers are above the line on the regression The sector that is probably the most comparable to satellites in terms of long-term contracts and broad resilience is the European Infrastructure sector. In the regression of EV/EBITDA vs EBITDA growth above, that sector is perched above the line. We suggest that reliability vs telco sectors should argue for a higher multiple for the same growth rate for both infrastructure and satellite players. Clearly satellites have not been as reliable in the past few years as they were previously – primarily driven by the US Government. But our work on the structural issues in this report suggests to us that there are large parts of the business that should deliver reliable growth for many years.

So SES’s position on the line when adjusted for tax still looks attractive to us, given that the higher-quality business models in this group appear to be above the line.

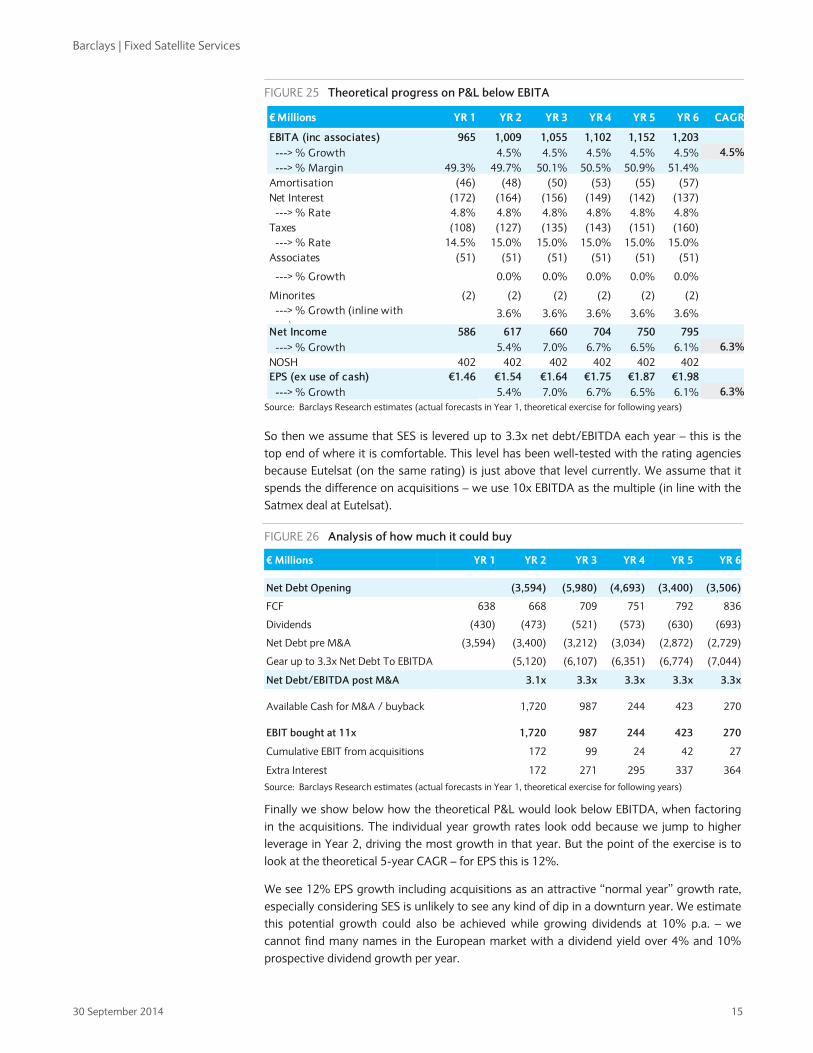

Looking at the power of SES’s balance sheet Because the progress of FSS players in terms of revenue and capex is lumpy, we show a theoretical exercise below, modelling out the potential EPS growth SES could achieve with normal year EBITDA growth of 4.0%. Starting with our forecasts in Year 1, we show a five-year theoretical forecast period with 3.6% revenue growth and 4.0% EBITDA growth each year. Given all of the FSS operators are gradually seeing lower capex per transponder, we also assume that depreciation grows slightly slower than revenue, leaving 4.5% EBITA growth.

Barclays | Fixed Satellite Services

30 September 2014 14

FIGURE 23 Theoretical progress on revenues, EBITDA and EBITA

Source: Barclays Research (actual forecasts in Year 1, theoretical exercise for following years)

Then we model out what we would expect to be a standard cash flow scenario as well, with 1) cash interest and tax matching our P&L interest and tax (shown further down), 2) capex higher than in the current year and higher than our short-term forecasts because there will be some replacement capex from 2019 or 2020 onwards, and 3)dividends growing 10% p.a. as management has guided. On that basis, the model delevers by 0.2x each year.

FIGURE 24 Theoretical progress on cash flow for the SES model

€Millions Y1 Y2 Y3 Y4 Y5 Y6

EBITDA 1,448 1,506 1,566 1,629 1,694 1,761

Cash interest (172) (163) (154) (146) (139) (133)

Cash tax (108) (127) (135) (143) (151) (160)

Capital Expenditure (494) (548) (568) (589) (610) (633)

Free Cash Flow 638 668 709 751 792 836

Dividends (430) (473) (521) (573) (630) (693)

Net Cash / (Debt) (3,594) (3,400) (3,212) (3,034) (2,872) (2,729)

Net Debt/EBITDA 2.5x 2.3x 2.1x 1.9x 1.7x 1.5xSource: Barclays Research estimates (actual forecasts in Year 1, theoretical exercise for following years)

We then show the rest of the theoretical P&L before the impact of uses of cash. We leave a €51m negative in the associates line each year, which is what we model for its share of O3b losses this year. If this number reduces, it will clearly support SES’s EPS growth in the short term, but this is a “normal year” exercise so we leave the same number each year.

€ Millions YR 1 YR 2 YR 3 YR 4 YR 5 YR 6 CAGR

Revenues 1,959 2,030 2,104 2,181 2,260 2,343 ---> % Growth 3.6% 3.6% 3.6% 3.6% 3.6% 3.6%Operating Costs (511) (524) (538) (552) (567) (582) ---> % Revenues 26.1% 25.8% 25.6% 25.3% 25.1% 24.8%EBITDA (ex associates) 1,448 1,506 1,566 1,629 1,694 1,761 ---> % Growth 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% ---> % Margin 73.9% 74.2% 74.4% 74.7% 74.9% 75.2%Depreciation (483) (497) (511) (527) (542) (558) ---> % Growth 2.9% 2.9% 2.9% 2.9% 2.9%EBITA (inc associates) 965 1,009 1,055 1,102 1,152 1,203 ---> % Growth 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% ---> % Margin 49.3% 49.7% 50.1% 50.5% 50.9% 51.4%

Barclays | Fixed Satellite Services

30 September 2014 15

FIGURE 25 Theoretical progress on P&L below EBITA

Source: Barclays Research estimates (actual forecasts in Year 1, theoretical exercise for following years)

So then we assume that SES is levered up to 3.3x net debt/EBITDA each year – this is the top end of where it is comfortable. This level has been well-tested with the rating agencies because Eutelsat (on the same rating) is just above that level currently. We assume that it spends the difference on acquisitions – we use 10x EBITDA as the multiple (in line with the Satmex deal at Eutelsat).

FIGURE 26 Analysis of how much it could buy

€ Millions YR 1 YR 2 YR 3 YR 4 YR 5 YR 6

Net Debt Opening (3,594) (5,980) (4,693) (3,400) (3,506)

FCF 638 668 709 751 792 836

Dividends (430) (473) (521) (573) (630) (693)

Net Debt pre M&A (3,594) (3,400) (3,212) (3,034) (2,872) (2,729)

Gear up to 3.3x Net Debt To EBITDA (5,120) (6,107) (6,351) (6,774) (7,044)

Net Debt/EBITDA post M&A 3.1x 3.3x 3.3x 3.3x 3.3x

Available Cash for M&A / buyback 1,720 987 244 423 270

EBIT bought at 11x 1,720 987 244 423 270

Cumulative EBIT from acquisitions 172 99 24 42 27

Extra Interest 172 271 295 337 364

Source: Barclays Research estimates (actual forecasts in Year 1, theoretical exercise for following years)

Finally we show below how the theoretical P&L would look below EBITDA, when factoring in the acquisitions. The individual year growth rates look odd because we jump to higher leverage in Year 2, driving the most growth in that year. But the point of the exercise is to look at the theoretical 5-year CAGR – for EPS this is 12%.

We see 12% EPS growth including acquisitions as an attractive “normal year” growth rate, especially considering SES is unlikely to see any kind of dip in a downturn year. We estimate this potential growth could also be achieved while growing dividends at 10% p.a. – we cannot find many names in the European market with a dividend yield over 4% and 10% prospective dividend growth per year.

€ Millions YR 1 YR 2 YR 3 YR 4 YR 5 YR 6 CAGR

EBITA (inc associates) 965 1,009 1,055 1,102 1,152 1,203 ---> % Growth 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% ---> % Margin 49.3% 49.7% 50.1% 50.5% 50.9% 51.4%Amortisation (46) (48) (50) (53) (55) (57)Net Interest (172) (164) (156) (149) (142) (137) ---> % Rate 4.8% 4.8% 4.8% 4.8% 4.8% 4.8%Taxes (108) (127) (135) (143) (151) (160) ---> % Rate 14.5% 15.0% 15.0% 15.0% 15.0% 15.0%Associates (51) (51) (51) (51) (51) (51)

---> % Growth 0.0% 0.0% 0.0% 0.0% 0.0%

Minorites (2) (2) (2) (2) (2) (2) ---> % Growth (inline with

)3.6% 3.6% 3.6% 3.6% 3.6%

Net Income 586 617 660 704 750 795 ---> % Growth 5.4% 7.0% 6.7% 6.5% 6.1% 6.3%NOSH 402 402 402 402 402 402 EPS (ex use of cash) €1.46 €1.54 €1.64 €1.75 €1.87 €1.98 ---> % Growth 5.4% 7.0% 6.7% 6.5% 6.1% 6.3%

Barclays | Fixed Satellite Services

30 September 2014 16

FIGURE 27 Theoretical progress in P&L including impact of acquisitions

Source: Barclays Research estimates

Conclusion on valuation So though SES looks like it has too high an EV/EBITDA multiple for its “normal year” EBITDA growth potential, we think that this comparison is unfair because 1) SES has a sustainably low tax rate; 2) we see strong cash generation and balance sheet headroom as having the potential to drive much stronger EPS growth than you would expect for 4% EBITDA growth; and 3) the Infrastructure sector is the best comp, in our view, and it trades on a premium within the regression analysis above. We therefore believe that SES can rerate further, as solid delivery underpins the reliability of the business.

For both SES and Eutelsat, we use a DCF to drive our price targets – we think this works well for satellites, given relatively visible mid-term cash flow growth. Our DCF drives a price target of €26.50 for Eutelsat and €31.40 for SES.

€ Millions YR 1 YR 2 YR 3 YR 4 YR 5 YR 6 CAGR

EBITDA post M&A 1,448 1,678 1,837 1,924 2,031 2,126 D&A post M&A (529) (545) (562) (579) (597) (615)EBIT post M&A 919 1,133 1,275 1,345 1,434 1,510 Net Interest post M&A (172) (216) (237) (238) (243) (246)Taxes post M&A (108) (138) (156) (166) (179) (190)Associates (51) (51) (51) (51) (51) (51)Minorities (2) (2) (2) (2) (2) (2)Net Income (inc M&A) 586 727 829 888 959 1,021 ---> % Growth 24.1% 14.1% 7.1% 8.0% 6.5% 11.8%NOSH 402 402 402 402 402 402 EPS (inc M&A) €1.46 €1.81 €2.06 €2.21 €2.39 €2.54 ---> % Growth 24.1% 14.1% 7.1% 8.0% 6.5% 11.8%

Barclays | Fixed Satellite Services

30 September 2014 17

PAY-OFF BETWEEN COMPRESSION AND RESOLUTION: ACCRETIVE OR DILUTIVE?

The likely impact of changes in compression technology on the FSS business has been one of the hottest areas of debate in the last couple of years. In this section, we look at this issue from several angles:

1) Has channel growth clearly outstripped Video revenue growth for the big players? If so, what could be the reasons for that?

2) Where could compression actually impact the business of FSS players in the next few years? (It’s not straightforward!)

3) Could it ever make sense for a pay TV group to invest in better compression to save space in the sky?

4) What are the prospects for Ultra HD?

Quick summary of our conclusions We make the following conclusions:

1. For Eutelsat and SES, revenue growth in the areas closest to DTH has been underperforming channel growth – but the key reasons are mix (lower priced geographies growing faster), timing of renewals, and probably the shift from DVB-S to DVB-S2 modulation. But it is not because of the shift from MPEG-2 to MPEG-4 compression;

2. The shift to MPEG-4 only matters when you remove the last MPEG-2 box – that is achievable for some pay TV groups in the next couple of years but the example of CanalSat suggests that when customers renew, their expectations for future increases in HD and then Ultra HD channels will more than offset the short-term benefits of applying MPEG-4 compression to the SD channels;

3. The issue of removing the last MPEG-2 box is only really relevant for pay TV customers in Europe: in many EM territories, operators moved straight to MPEG-4 boxes and therefore the next compression issue will only come when they move to HEVC boxes in quite a few years’ time, while Eutelsat (for example) has just under half of its DTH revenues from free TV customers, who are much less likely to make a major investment to squeeze out remaining MPEG-2 boxes.

Overall we do not see compression as a drag on revenue growth for SES and Eutelsat in the next few years. The moment to worry would be if the customers of satellite operators had been taking more capacity with a view to offering Ultra HD in the future, but then Ultra HD never takes off. Based on predictions for Ultra HD take-up, that seems unlikely but is clearly not impossible.

Intro: BSkyB slide showed capacity reduction as HD increased We start with background on the debate over compression. SES and Eutelsat have suggested for years that the shift from Standard Definition to High Definition is a growth driver, while the future shift to Ultra HD would also be accretive. The idea is that an HD channel takes up more space on a transponder, and Ultra HD more again, even factoring in better compression technologies (pay TV businesses have rolled out boxes with MPEG-4 compression as they have moved into HD). And then those benefits get partially offset because when SD channels are broadcast in MPEG-4 compression, they take up less space in the sky (but you can only get this benefit in practice when the last MPEG-2 customer has

Barclays | Fixed Satellite Services

30 September 2014 18

migrated). The net effect of all of this should be positive for satellite operator revenues, according to SES and Eutelsat.

A slide in BSkyB’s FY13 results (July-13) suggested this was not working. Sky has reduced transponders, while HD channels have gone to 71 from 15 in the past five years.

FIGURE 28 BSkyB slide on transponder efficiencies from FY13 results presentation

Source: BSkyB July 2013 * As of October 2013

So what was actually going on here? In its FY13 annual report, BSkyB noted that it has a contract with SES for 32 transponders and that until 3 October 2013 it would have a contract with Arqiva for a further four transponders, with Arqiva acting as an intermediary (the four transponders were on the Eutelsat 28A satellite). So first of all the drop from 36 to 32 transponders in 2013 is due to the four Arqiva transponders dropping out. That fact is relevant for SES but clearly does not alter the point that BSkyB now needs fewer transponders.

We see several reasons for Sky’s ability to reduce capacity in the sky:

• The upgrade from the DVB-S diffusion mode to DVB-S2 (a separate area where changes in compression can have an effect) has enabled BSkyB to squeeze more channels on to a transponder. For example, using MPEG-4 compression you can fit 26 channels on to a transponder with DVB-S2 vs 20 transponders with DVB-S. This is separate from the debate about the shift from MPEG-2 to MPEG-4. We think this has had a modest effect.

• But there is another important factor: BSkyB has been reducing their number of catch-up channels (+1) and pay-per-view carousels (with movies starting every 15 minutes to replicate an on-demand environment). As it has moved to using connected boxes to support catch-up services like iPlayer, and to deliver on-demand movies and box sets, it has been able to reduce the number of channels needed.

It is difficult to know how much these “one-off” channel reductions have driven the reduction in capacity needed, but the satellite operators believe that this is the most important reason. Can other payTV operators make similar savings? We have not done a comprehensive review, but looking at the channels on Sky Deutschland and Sky Italia, for example, there are far fewer of either category of channel (+1 or pay-per-view carousels). And moving into emerging markets, use of channels for these purposes is very rare. So it looks as though this is a legacy issue relating specifically to BSkyB.

35 35 3536 36

32

15

29 39

52

62

71

0

10

20

30

40

50

60

70

80

25

27

29

31

33

35

37

2008 2009 2010 2011 2012 2013 *

Satellite transponders (LHS) No of HD channels (RHS)

BSkyB’s reduction in transponders probably relates more to reductions in catch-up channels and carousel channels than to compression

Barclays | Fixed Satellite Services

30 September 2014 19

1) Channel growth running ahead of revenue growth – why? This has been a thorny issue in the last year. The bear argument in relation to channel growth goes like this:

• Every quarter we can track the growth in the number of channels on the FSS players’ services, and we can also see Video revenues for Eutelsat and Infrastructure revenues for SES (which are clearly weighted to Video);

• Revenue growth has been underperforming channel growth;

• Something is driving this differential and it seems likely that this relates to compression.

Below we have attempted to match recent channel growth to the most relevant revenue growth number for Eutelsat and SES. The channel growth is a simple number, but we have made the following adjustments on the revenue growth:

Eutelsat: small adjustments to Video growth this year due to SES dispute We use the Video revenue growth only on a constant FX basis. We have also adjusted this year’s growth to reflect the negative impact of the dispute with SES at 28.5E (which effectively switches revenue out of Video into the Other line). Michel Azibert (Deputy CEO) showed on the 3Q call that the nine-month Video growth number would be slightly positive excluding that effect, and they reiterated this at the FY results. We also see a timing issue here, with more channels added in Q4 due to launches, which have not been fully felt in the numbers.

SES: we adjust for German analogue switch-off We have created our estimates of video revenue growth within the Infrastructure revenue line for SES, adjusted for the German analogue switch-off effect. So we have used the constant FX Group Infrastructure revenues, as adjusted for the analogue switch-off effect (a number that management gave during 2012 and 2013). This is because the revenues were being significantly impacted by the loss of a small number of channels (as each analogue channel occupied one transponder).

We have then made an assumption, based on commentary at the time, regarding the difference between Video Infrastructure growth and total Infrastructure growth.

FIGURE 29 Adjustments made to SES growth to make it comparable to channel growth

2010 2011 2012 2013

SES Infrastructure growth at constant FX 4.4% 2.0% -2.0% 2.8%

SES Infrastructure growth adj for switch-off and FX 4.4% 2.0% 4.0% 4.3%

SES Infrastructure video revenue growth estimate 4.8% 2.5% 4.7% 5.0%Source: SES, Barclays Research estimates

Barclays | Fixed Satellite Services

30 September 2014 20

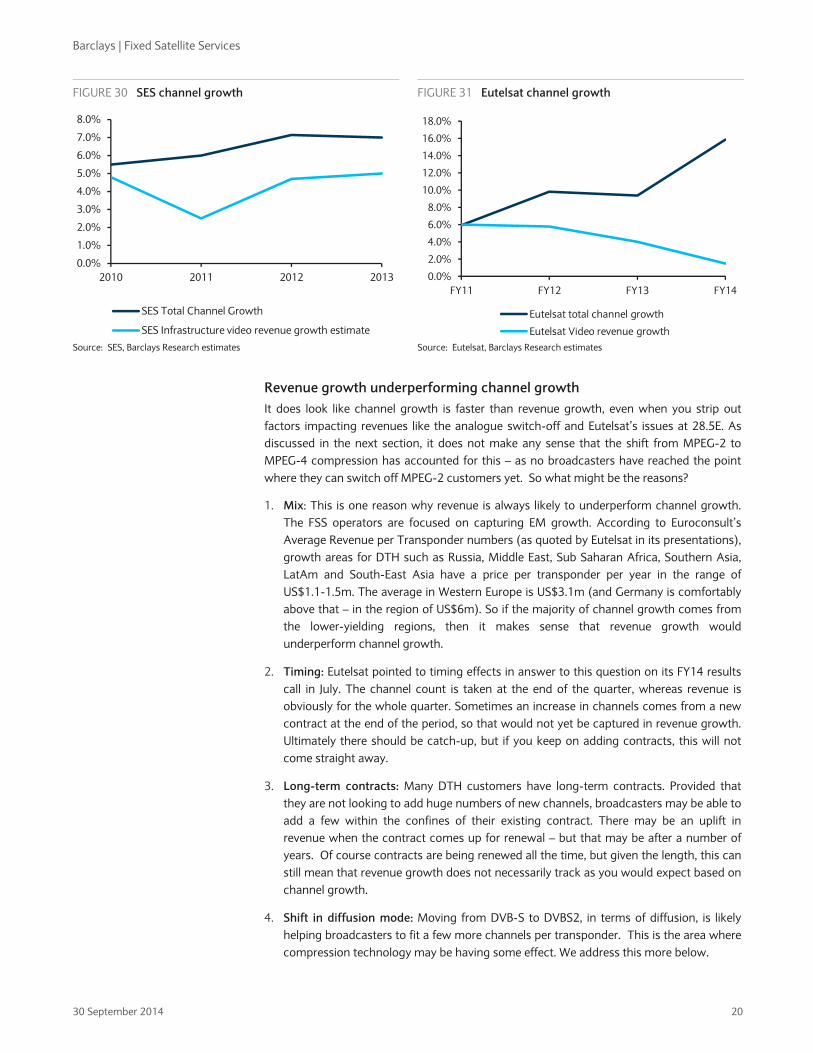

FIGURE 30 SES channel growth

FIGURE 31 Eutelsat channel growth

Source: SES, Barclays Research estimates Source: Eutelsat, Barclays Research estimates

Revenue growth underperforming channel growth It does look like channel growth is faster than revenue growth, even when you strip out factors impacting revenues like the analogue switch-off and Eutelsat’s issues at 28.5E. As discussed in the next section, it does not make any sense that the shift from MPEG-2 to MPEG-4 compression has accounted for this – as no broadcasters have reached the point where they can switch off MPEG-2 customers yet. So what might be the reasons?

1. Mix: This is one reason why revenue is always likely to underperform channel growth. The FSS operators are focused on capturing EM growth. According to Euroconsult’s Average Revenue per Transponder numbers (as quoted by Eutelsat in its presentations), growth areas for DTH such as Russia, Middle East, Sub Saharan Africa, Southern Asia, LatAm and South-East Asia have a price per transponder per year in the range of US$1.1-1.5m. The average in Western Europe is US$3.1m (and Germany is comfortably above that – in the region of US$6m). So if the majority of channel growth comes from the lower-yielding regions, then it makes sense that revenue growth would underperform channel growth.

2. Timing: Eutelsat pointed to timing effects in answer to this question on its FY14 results call in July. The channel count is taken at the end of the quarter, whereas revenue is obviously for the whole quarter. Sometimes an increase in channels comes from a new contract at the end of the period, so that would not yet be captured in revenue growth. Ultimately there should be catch-up, but if you keep on adding contracts, this will not come straight away.

3. Long-term contracts: Many DTH customers have long-term contracts. Provided that they are not looking to add huge numbers of new channels, broadcasters may be able to add a few within the confines of their existing contract. There may be an uplift in revenue when the contract comes up for renewal – but that may be after a number of years. Of course contracts are being renewed all the time, but given the length, this can still mean that revenue growth does not necessarily track as you would expect based on channel growth.

4. Shift in diffusion mode: Moving from DVB-S to DVBS2, in terms of diffusion, is likely helping broadcasters to fit a few more channels per transponder. This is the area where compression technology may be having some effect. We address this more below.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2010 2011 2012 2013

SES Total Channel Growth

SES Infrastructure video revenue growth estimate

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

FY11 FY12 FY13 FY14

Eutelsat total channel growth

Eutelsat Video revenue growth

Barclays | Fixed Satellite Services

30 September 2014 21

So in conclusion, when you make an apples-for-apples comparison, channel growth has been somewhat higher than revenue growth. But there are a number of reasons why we should expect that – and only one of those relates to compression.

2) Practicalities of how compression could affect FSS players It is not true that every time a broadcaster moves a customer to a box with MPEG-4 compression it reduces the space needed in the sky. What matters is what you are broadcasting, not the receiving equipment of the viewers.

For example, when BSkyB broadcasts Sky Sports 1 SD, they need to broadcast it in MPEG-2 because otherwise customers who do not yet have an MPEG-4 box cannot see it. Then they also broadcast Sky Sports 1 HD in MPEG-4. The industry refers to this as simulcasting. The HD channel in MPEG-4 is incremental revenue for a satellite operator (compared to before there were MPEG-4 boxes or demand for HD). So in practical terms, the proportion of boxes that have MPEG-4 can move from 10% to 95% within the mix of subscribers, without impacting the spend of that broadcaster on satellites. At 90% or 95%, the pay TV business might look to actively squeeze out the remaining MPEG-2 boxes.

So the moment where compression changes could matter is when broadcasters (pay TV or free TV) are able to stop simulcasting MPEG-2 and MPEG-4 broadcasts – and can instead move to broadcasting all the channels (SD and HD) in MPEG-4. That moment comes when the last MPEG-2 box has gone. None of the major European pay TV or free TV platforms has made that change yet.

So do we need to worry about a “cliff” when MPEG-2 boxes are removed? We consider a theoretical worked example to address this question.

Broadcaster A has 50 channels of content and currently has half of its viewers using MPEG-2 boxes and half using MPEG-4 boxes. Broadcaster A shows 10 of its channels in HD, which means that it needs to broadcast 60 channels: 50 in SD and 10 in HD, as shown below.

FIGURE 32 Broadcaster A’s initial mix of channels and the no of transponders needed

Under current conditions

Channels Compression used for broadcast

Channels per txpd

Transponders needed

No of channels (in terms of content) 50

No of channels shown in SD 50 MPEG-2 12 4.2

No of channels shown in HD 10 MPEG-4 7 1.4

Total 60 5.6 Source: Barclays Research

The channels per transponder shown in the table above derive from Eutelsat’s guide to how many channels fit on a transponder based on a range of combinations of compression and resolution. We show this below.

FIGURE 33 Channels per transponder (36Mhz) with different compression/resolution

Format Diffusion Mode MPEG-2 MPEG-4 HEVC

SD DVB-S 12 20

DVB-S2 - 26 50?

HD DVB-S 2 to 3 5

DVB-S2 3 to 4 6 to 8 12 to 15

Ultra HD (4K) DVB-S2 1 to 2 3 to 4Source: Eutelsat 2013

Move from MPEG-2 to MPEG-4 is not about mix – you only get an effect when the last MPEG-2 box has gone

Barclays | Fixed Satellite Services

30 September 2014 22

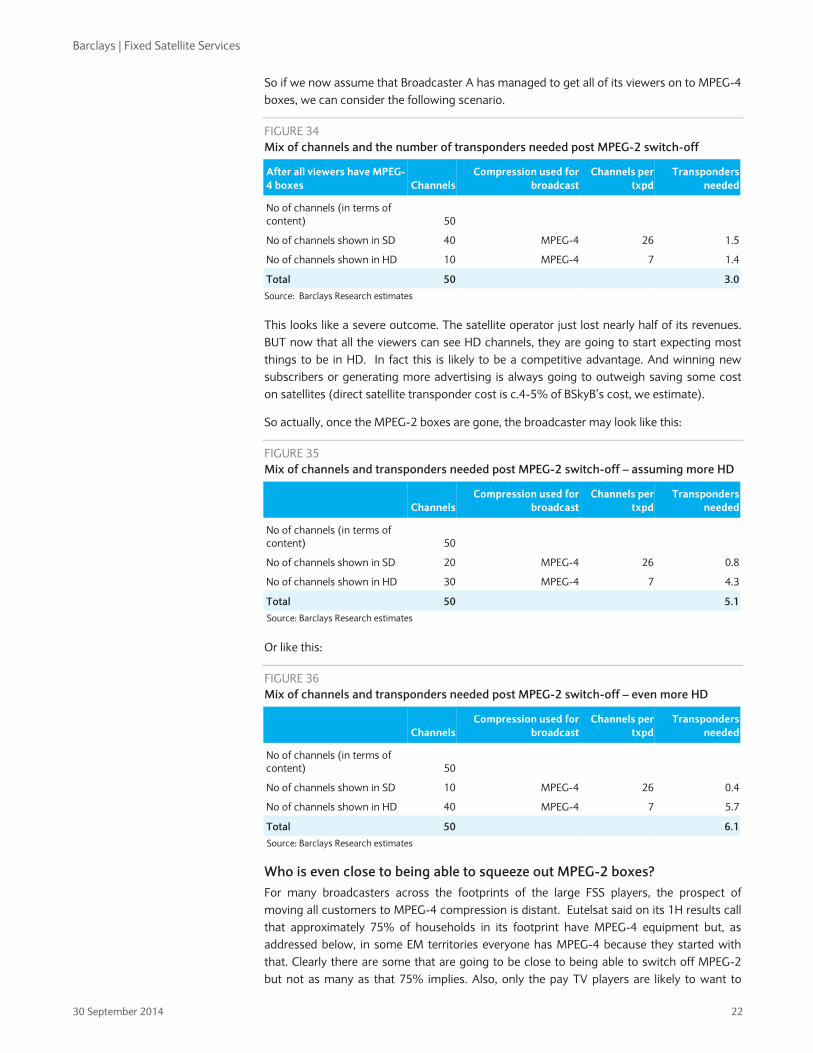

So if we now assume that Broadcaster A has managed to get all of its viewers on to MPEG-4 boxes, we can consider the following scenario.

FIGURE 34 Mix of channels and the number of transponders needed post MPEG-2 switch-off

After all viewers have MPEG-4 boxes Channels

Compression used for broadcast

Channels per txpd

Transponders needed

No of channels (in terms of content) 50

No of channels shown in SD 40 MPEG-4 26 1.5

No of channels shown in HD 10 MPEG-4 7 1.4

Total 50 3.0Source: Barclays Research estimates

This looks like a severe outcome. The satellite operator just lost nearly half of its revenues. BUT now that all the viewers can see HD channels, they are going to start expecting most things to be in HD. In fact this is likely to be a competitive advantage. And winning new subscribers or generating more advertising is always going to outweigh saving some cost on satellites (direct satellite transponder cost is c.4-5% of BSkyB’s cost, we estimate).

So actually, once the MPEG-2 boxes are gone, the broadcaster may look like this:

FIGURE 35 Mix of channels and transponders needed post MPEG-2 switch-off – assuming more HD

ChannelsCompression used for

broadcast Channels per

txpdTransponders

needed

No of channels (in terms of content) 50

No of channels shown in SD 20 MPEG-4 26 0.8

No of channels shown in HD 30 MPEG-4 7 4.3

Total 50 5.1 Source: Barclays Research estimates

Or like this:

FIGURE 36 Mix of channels and transponders needed post MPEG-2 switch-off – even more HD

ChannelsCompression used for

broadcast Channels per

txpdTransponders

needed

No of channels (in terms of content) 50

No of channels shown in SD 10 MPEG-4 26 0.4

No of channels shown in HD 40 MPEG-4 7 5.7

Total 50 6.1 Source: Barclays Research estimates

Who is even close to being able to squeeze out MPEG-2 boxes? For many broadcasters across the footprints of the large FSS players, the prospect of moving all customers to MPEG-4 compression is distant. Eutelsat said on its 1H results call that approximately 75% of households in its footprint have MPEG-4 equipment but, as addressed below, in some EM territories everyone has MPEG-4 because they started with that. Clearly there are some that are going to be close to being able to switch off MPEG-2 but not as many as that 75% implies. Also, only the pay TV players are likely to want to

Barclays | Fixed Satellite Services

30 September 2014 23

make the relevant investment to squeeze out MPEG-2 boxes: free TV players have never been in the business of spending heavily to subsidise boxes. Lastly, we believe that the risk of churn increases when pay TV operators choose to make changes to equipment – so there are some risks involved in squeezing out the last boxes as well.

CanalSat is a very interesting example: it is talking about being all MPEG-4 by July 2015, so is the pioneer here. So where does it fit in terms of the theoretical example above? According to SES, it renewed two years ago with 24 transponders, which included two incremental transponders – and it has doubled the number of HD channels in the past two years. So it is not expecting to make savings in the sky when it removes the last MPEG-2 box – or at least it is not expecting to make savings over time: its renewal was for 10 years.

Sky Deutschland has talked about removing its last box next year. It has said that it is so far undecided about whether to use this situation to make cost savings or to expand its HD line-up. Given Sky D’s focus on growth, we see the latter as the more likely option.

What will the revenue pattern be before MPEG-2 switch-off? For broadcasters who have both MPEG-2 and MPEG-4 subscribers, spend on satellite capacity is likely to increase modestly, as they choose to simulcast a few more of their SD channels in HD, to improve the offering for customers who have MPEG-4 boxes. This is assuming that they cannot pull off the same “tricks” as BSkyB in terms of removing catch-up and carousel channels. It also assumes that they do not change their diffusion from DVB-S to DVB-S2 (we address this below).

Compression not as widespread an issue among FSS customers as you think There are two factors here: 1) Free TV broadcasters are important customers for FSS operators; and 2) Emerging Markets Pay TV broadcasters have often started off in MPEG-4.

1. We tend to think of FSS operators as servicing pay TV operators because there are obvious large customers like BSkyB, Canal+, Sky Deutschland, Sky Italia and Cyfrowy Polsat. But Eutelsat management has noted that just under 50% of their customers are free-to-air broadcasters. SES is less exposed to free at c.[X%]. HD channels are still rare on free TV but are starting (e.g. the BBC). And free-to-air broadcasters are not in the business of subsidising boxes so will not be looking to aggressively squeeze out customers with MPEG-2 equipment. So we would expect free TV broadcasters to continue in their current pattern for a very long time.

2. In regions like Latin America, Indonesia, the Philippines and parts of sub-Saharan Africa, pay TV is still a fairly new business and so when set-top boxes were rolled out, they were all MPEG-4 from the start. Therefore there is no “cliff” to worry about – the benefits in terms of satellite capacity that comes with MPEG-4 are already being felt by these customers. The geographies where MPEG-2 boxes are likely to be prevalent (where the FSS operators also have DTH customers) are: Western Europe, Eastern Europe and Russia, and the Middle East.

Who is exposed where? Eutelsat has more exposure to free TV but less to EM regions where all the boxes are MPEG-4 already, while SES is the opposite. It is difficult to tell whether these two factors balance each other out: so we cannot say that one of these two is more exposed to compression risks than the other. Intelsat has fairly limited DTH business in the regions where there are still MPEG-2 boxes.

What about shifting from DVB-S to DVB-S2? Changing the “diffusion mode” from DVB-S to DVB-S2 can be done through software updates and this can somewhat reduce the capacity that broadcasters need on satellites.

CanalSat is looking to switch off MPEG-2 but increased transponders at last renewal

Sky Deutschland is approaching the same situation – undecided whether to make savings or expand HD

Barclays | Fixed Satellite Services

30 September 2014 24

Referring to Figure 33 above, the place to focus is on HD delivered in MPEG-4. Using DVB-S, you can fit five channels on to a transponder. But using DVB-S2 you can fit six to eight. Why should we not be focused on the difference between 20 channels in DVB-S vs 26 channels in DVB-S2 for SD in MPEG-4? Because as shown in our example above, most TV groups are not broadcasting SD channels in MPEG-4 – they will not be able to do that until they squeeze out MPEG-2 boxes. For Eutelsat, 10% of channels currently broadcast are in HD, while for SES it is 30%.

So moving to DVB-S2 from DVB-S still has the capacity to be a modest headwind to transponder demand as more operators update software across customer boxes and save on the space taken up by HD channels specifically.

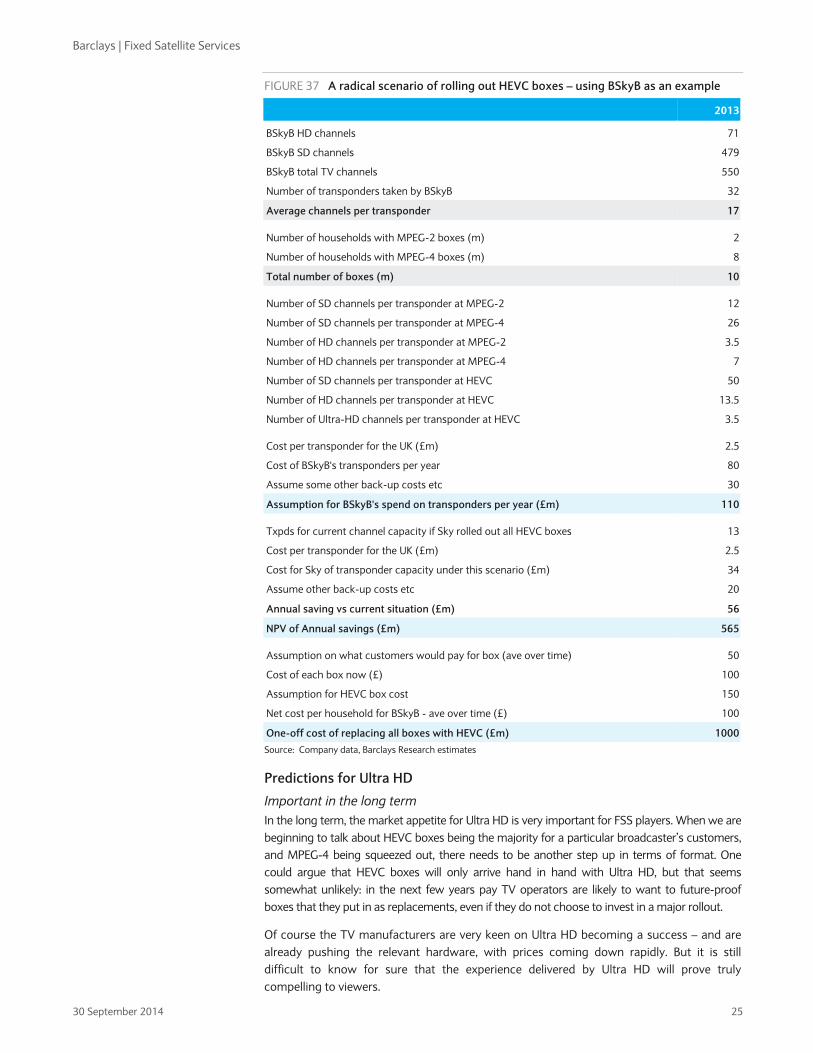

It makes no economic sense to invest in boxes to reduce satellite capacity Our work below, using BSkyB as an example, suggests that investment in new set-top boxes specifically to save spending on satellite capacity does not make economic sense. We use a radical example. We calculate that rolling out HEVC boxes in one go to all of Sky’s subscribers would cost c.£1bn. And we assume that the benefits offered by enhanced compression would save c.£60m per year. This assumes no change at all in the current mix of channels between SD, HD and Ultra HD. So that would be a <6% return on investment, or put another way, the NPV of the savings would be £500-600m vs the £1bn investment.

We think it is important to stress this – as it seems unlikely that any TV operator would set about replacing boxes just to save satellite costs. So pay TV operators are likely to roll out boxes with better compression for two reasons: 1) because they want to offer better resolution to their customers (e.g. HD or Ultra HD); or 2) because they need to replace old boxes anyway, and they want to future-proof the new boxes.

Barclays | Fixed Satellite Services

30 September 2014 25

FIGURE 37 A radical scenario of rolling out HEVC boxes – using BSkyB as an example

2013

BSkyB HD channels 71

BSkyB SD channels 479

BSkyB total TV channels 550

Number of transponders taken by BSkyB 32

Average channels per transponder 17

Number of households with MPEG-2 boxes (m) 2

Number of households with MPEG-4 boxes (m) 8

Total number of boxes (m) 10

Number of SD channels per transponder at MPEG-2 12

Number of SD channels per transponder at MPEG-4 26

Number of HD channels per transponder at MPEG-2 3.5

Number of HD channels per transponder at MPEG-4 7

Number of SD channels per transponder at HEVC 50

Number of HD channels per transponder at HEVC 13.5

Number of Ultra-HD channels per transponder at HEVC 3.5

Cost per transponder for the UK (£m) 2.5

Cost of BSkyB's transponders per year 80

Assume some other back-up costs etc 30

Assumption for BSkyB's spend on transponders per year (£m) 110

Txpds for current channel capacity if Sky rolled out all HEVC boxes 13

Cost per transponder for the UK (£m) 2.5

Cost for Sky of transponder capacity under this scenario (£m) 34

Assume other back-up costs etc 20

Annual saving vs current situation (£m) 56

NPV of Annual savings (£m) 565

Assumption on what customers would pay for box (ave over time) 50

Cost of each box now (£) 100

Assumption for HEVC box cost 150

Net cost per household for BSkyB - ave over time (£) 100

One-off cost of replacing all boxes with HEVC (£m) 1000Source: Company data, Barclays Research estimates

Predictions for Ultra HD

Important in the long term In the long term, the market appetite for Ultra HD is very important for FSS players. When we are beginning to talk about HEVC boxes being the majority for a particular broadcaster’s customers, and MPEG-4 being squeezed out, there needs to be another step up in terms of format. One could argue that HEVC boxes will only arrive hand in hand with Ultra HD, but that seems somewhat unlikely: in the next few years pay TV operators are likely to want to future-proof boxes that they put in as replacements, even if they do not choose to invest in a major rollout.

Of course the TV manufacturers are very keen on Ultra HD becoming a success – and are already pushing the relevant hardware, with prices coming down rapidly. But it is still difficult to know for sure that the experience delivered by Ultra HD will prove truly compelling to viewers.

Barclays | Fixed Satellite Services

30 September 2014 26

Not dramatically important in the next five years If some Ultra HD channels arrive on TV platforms in developed markets in the next few years and the number of compatible devices continues to ramp up, that will be taken as a good indicator for the long term. And potentially when broadcasters come to renew long-term contracts, the satellite operators may benefit from mid-term planning, which would include thoughts on Ultra HD. As Ultra-HD ready TVs start to move below $1,000, this scenario of early progress seems likely.

Though Ultra HD channels are unlikely to become significant in number in the next five years, it seems highly likely that these would be incremental, with broadcasters simulcasting the same channels in HD/MPEG-4 and Ultra HD/HEVC (just as they do currently with SD in MPEG-2 and HD in MPEG-4). But we would not expect the number of channels to be large enough to generate game-changing revenue. It is more important that we can gain confidence regarding Ultra HD’s place within the future mix.

Consultant forecasts on Ultra HD point to fairly slow take-up Euroconsult’s forecasts below point to a very small proportion of channels being in Ultra HD, even by 2022. But they do expect a big increase in HD by that time and it is important to remember that it only matters that Ultra HD is shown to be “here to stay” – not really how many channels there are. Because broadcasters will be planning for a time when Ultra HD becomes a more important part of the mix.

FIGURE 38 Forecasts for HD and Ultra HD as % of total channels in 2022 vs 2012

Source: Euroconsult 2013 (as shown in Eutelsat presentation from December 2013)

Separately, as shown in SES’s 2014 Investor Day presentation, IHS predicts that there will be 200 Ultra HD channels and 100m Ultra HD screens by 2020 globally and 1,000 Ultra HD channels and >500m Ultra HD screens by 2025. Again this shows that the numbers will be small but that Ultra HD is expected at least to be an established part of the mix.

Conclusion: Slightly accretive in next five years; longer-term Ultra HD is key So we have narrowed the debate on compression vs resolution to the following positives and negatives:

Positives:

1. More simulcasting of HD and SD channels by broadcasters who will have MPEG-2 boxes in their mix for some time;

2. Major ramp-up of HD channels when broadcasters move to all MPEG-4 boxes;

3. Broadcasters planning for Ultra HD in the future when renewing contracts.

85%

38%

91%

67%

95%

78% 92

%

78% 97

%

80% 90

%

68%

15%

60%

9%

32%

5%

21%

8%

21%

3%

19% 10

%

31%

2.4% 1.4% 1.5% 1.0% 0.8% 1.0%

0%

20%

40%

60%

80%

100%

SD HD Ultra HD

Barclays | Fixed Satellite Services

30 September 2014 27

Negatives:

1. Ongoing shift from DVB-S to DVB-S2 modulation (which does not need a box roll-out);

2. When MPEG-2 boxes are eliminated, double negative of a) no longer needing to simulcast channels and b) applying MPEG-4 compression to SD channels.

Neutral factors:

1. Anything that happens in DTH regions that started with all boxes carrying MPEG-4 and DVB-S2 (some emerging markets).

Small positive contribution to annual growth in relevant areas The key swing factors here are how aggressively pay TV groups ramp up HD channels within their mix when they do finally remove MPEG-2 boxes, and what their future views are on Ultra HD. We believe that as broadcasters renew their capacity, the primary motivation will be to have enough capacity to deliver HD and later Ultra HD – and that this motivation will smooth out the bump of squeezing out MPEG-2 boxes. Our view is therefore that there should be modest increases in capacity demands. But the shift from DVB-S to DVB-S2 will likely take the edge off those increases. So we expect a very small positive contribution to growth from the balance between compression and new formats over the next five years.

Beyond the next five years, Ultra HD take-up becomes critical. If broadcasters start to think that Ultra HD will not be a differentiator, then they will gradually replace existing boxes with HEVC ones and simply reduce demand in the sky. If Ultra HD takes off as the consultants suggest (becoming a small but permanent part of the mix with more significant growth beyond 2020) then we believe that this balancing act can continue to fall on the side of positive growth for the FSS operators.