FIRE & POLICE - City of Pasadena

424

PASADENA PASADENA FIRE & POLICE RETIREMENT SYSTEM FIRE & POLICE RETIREMENT BOARD - REGULAR MEETING Wedn es day, February 21, 2018 RETIREMENT SYSTEM City Council Chamb e rs , 100 N. Garfield Ave., #5249 10:15 a.m. AGENDA 1. Call to Order 2. Public Comment 3. Minutes: November 15, 2017 (Regular Meeting) CONSENT CALENDAR 4. Approve the monthly retirement allowance roll of $1,073,865.44 for November 2017, $ 1, 071,271.25 for December 2017, and $1 ,069,560.74 for January 2018. 5. Approve additions/removals of the following members/beneficiaries to/from the manthl II II 1y a owance ro : Effective Add/ Pension Pension Name Date Remove Continuance Amount a. G. Kenney 10/26/17 remove No $1,936.31 6. Receive and file the 4th Quarter 2017 Asset Manager Performance Reports from the fo ll owing asset managers: a. Atlanta Capital Investment Managers b. Capital Group, American Funds EuroPacific Growth Fund c. Dodge & Cox International Stock Fund d. Dodge & Cox Stock Fund e. Invesco Core Real Estate, USA - LP f. PIMCO All Asset Fund g. T CW MetWest Fi xed In come Review h. Vanguard Inflation-Protected Securities Fund i. Vanguard Growth Index Fund j. Vanguard Short-Term Investment-Grade Fund k. Voya Senior Loan Trust Fund Review 7. Schedule the CalPERS Service Pending Industrial Disability Retirement hearing application for Salvador Vidales, Police Officer, for the March 21, 2018 regular meeting of the FPRS Board. 8. Adopt Resolution No. 326 setting the cost of living adjustment at an increase of 3% for all eligible retires and beneficiaries per Charter Section 1509.8 to become effective July 1, 2018, as determined by Bartel Associates, System actuary. Page 1 of 3

-

Upload

khangminh22 -

Category

Documents

-

view

32 -

download

0

Transcript of FIRE & POLICE - City of Pasadena

PASADENA PASADENA FIRE & POLICE RETIREMENT SYSTEM FIRE & POLICE

RETIREMENT BOARD - REGULAR MEETING

Wednesday, February 21, 2018 RETIREMENT SYSTEM City Council Chambers, 100 N. Garfield Ave. , #5249

10:15 a.m.

AGENDA

1. Call to Order 2. Public Comment 3. Minutes: November 15, 2017 (Regular Meeting)

CONSENT CALENDAR 4. Approve the monthly retirement allowance roll of $1,073,865.44 for November

2017, $1,071,271.25 for December 2017, and $1 ,069,560.74 for January 2018. 5. Approve additions/removals of the following members/beneficiaries to/from the

man thl II II 1y a owance ro : Effective Add/ Pension Pension

Name Date Remove Continuance Amount a. G. Kenney 10/26/17 remove No $1,936.31

6. Receive and file the 4th Quarter 2017 Asset Manager Performance Reports from the fo llowing asset managers: a. Atlanta Capital Investment Managers b. Capital Group, American Funds EuroPacific Growth Fund c. Dodge & Cox International Stock Fund d. Dodge & Cox Stock Fund e. Invesco Core Real Estate, USA - LP f. PIMCO All Asset Fund g. TCW MetWest Fixed Income Review h. Vanguard Inflation-Protected Securities Fund i. Vanguard Growth Index Fund j. Vanguard Short-Term Investment-Grade Fund k. Voya Senior Loan Trust Fund Review

7. Schedule the CalPERS Service Pending Industrial Disability Retirement hearing application fo r Salvador Vidales, Police Officer, for the March 21, 2018 regular meeting of the FPRS Board.

8. Adopt Resolution No. 326 setting the cost of living adjustment at an increase of 3% for al l eligible retires and beneficiaries per Charter Section 1509.8 to become effective July 1, 2018, as determined by Bartel Associates, System actuary.

Page 1 of 3

CLOSED SESSION

A. CONFERENCE ON PUBLIC EMPLOYMENT (Government Code Section 54957) Title: Retirement Administrator/Secretary (Management Analyst IV) System Representative: Keith Jones

B. CONFERENCE ON PUBLIC EMPLOYMENT (Government Code Section 54957) Title: City Temporary Worker System Representative: Keith Jones

ACTION ITEMS - The Board may discuss and take action on the following items: 9. Receive, discuss, and possibly take action on the presentations by prospective

auditing financial services firms: a. Brown Armstrong b. Moss Adams, LLP c. Macias Gini & O'Connell , LLP

10. Discuss and take action on Amendment to Agreement No. 20,823, assignment of beneficial interest in 275 East Cordova Street.

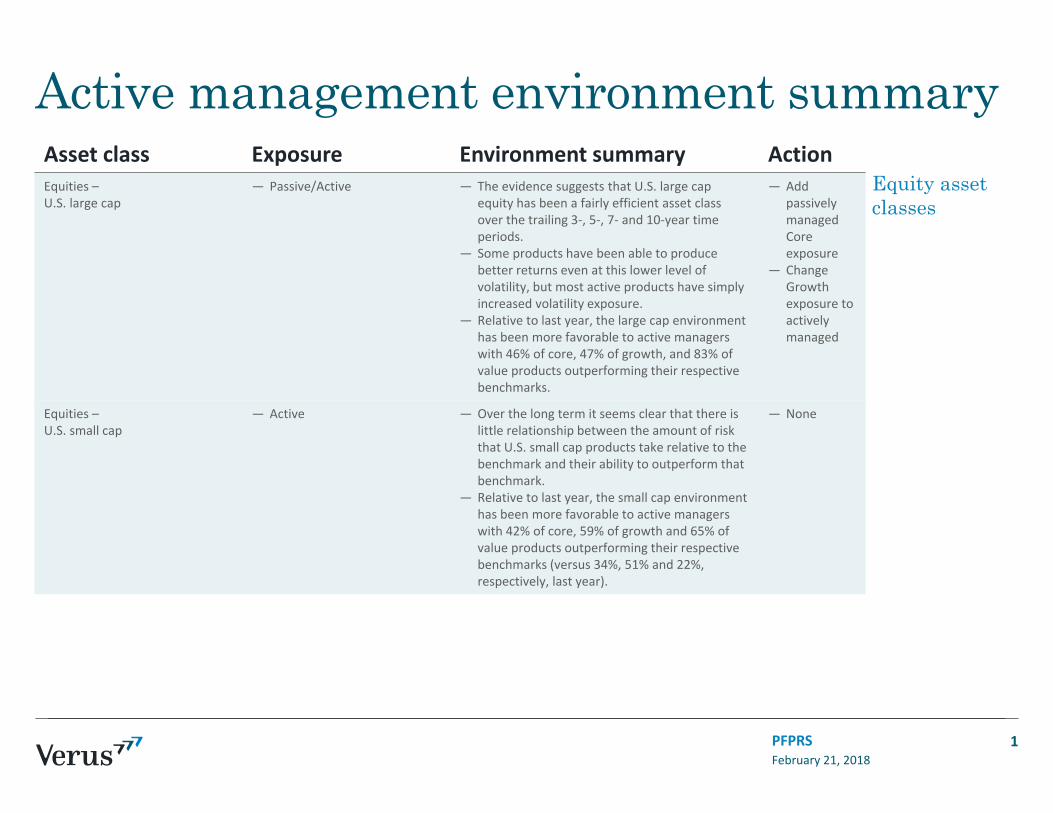

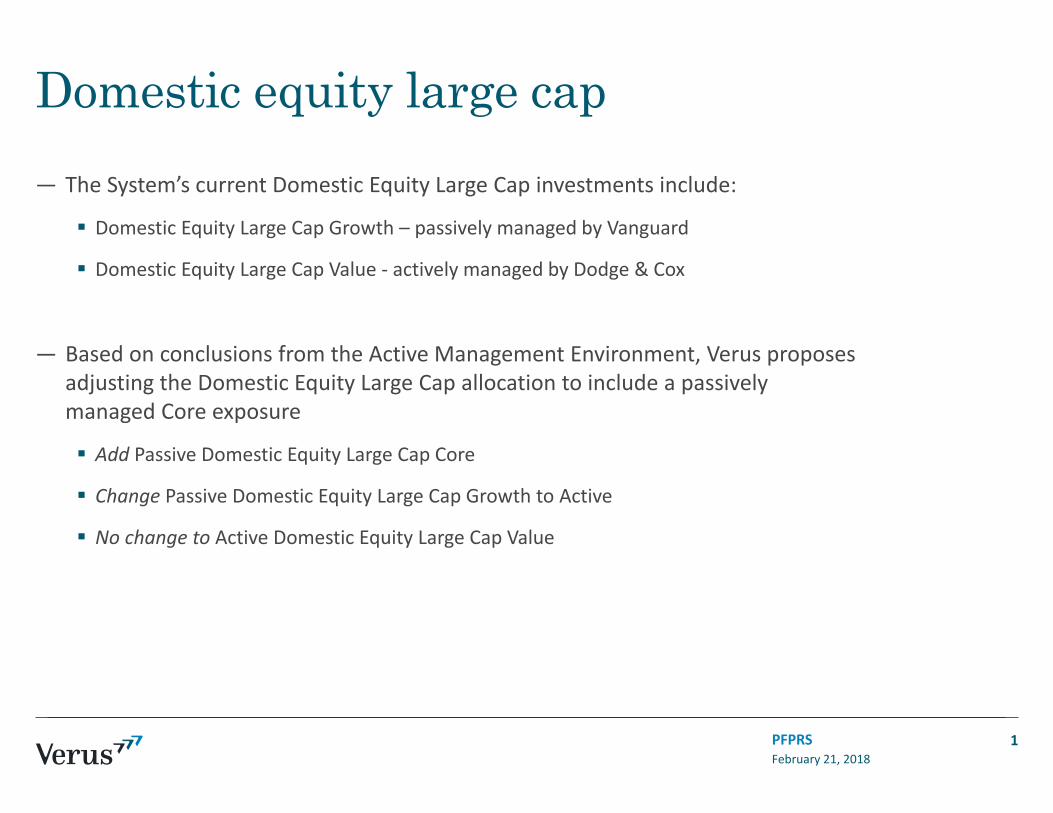

11. Discuss and possibly take action on the following investment reports submitted by Verus Investments: a. Receive and file, Active Management Environment Summary b. Discuss, and possibly take action, US Large Cap Equity Passive vs.

Active Analysis c. Receive and file, November 2017 -January 2018 Withdrawal and

Rebalance Transaction Summary d. Receive and file, 4th Quarter 2017 Investment Performance Review e. Receive and file, January 2018 Performance Update f. Review and approve, February-April 2018 Rebalance and Withdrawal g. Review and approve, Invesco Core Real Estate - U.S.A., L.P. Ratification

of Advisory Committee Members

INFORMATION ITEMS 12. Staff Report

a. January 2018 Budget/Expense Report 13. Counsel Report 14. Articles/Newsletters/Conferences

COMMENTS FROM BOARD MEMBERS

ADJOURN

Page 2 of 2

POSTING STATEMENT: I HEREBY CERTIFY that this Agenda was posted in its entirety at the City Kiosk and on the City Council Chamber bulletin board, Room S249, on February 15, 2018 at 5:00 p.m., and a copy was sent to the Central Library for posting.

Jill ;b.Jt~ Administrator/Secretary to the Board

In compliance with the Americans with Disabilities Act of 1990, listening assistive devices are avai/able.fi-om the City Clerk's Office with a 24-hour advance notice. Please call (626) 744-4320 to request use of a listening device.

Any documents distributed to a majority of the Pasadena Fire & Police Retirement Board regarding any item on this agenda will be made available at the office of the Fire & Police Retirement System, located at 100 N. Garfield Avenue, #N204, Pasadena, CA 91101. To make arrangements to view items, during normal business hours, please contact the Retirement office at (626)744-4320.

DISTRIBUTION Board Members Bartel Associates A. Taylor, Verus I. Safie, City Atty

Police Dept (Admin Srv) Fire Chief Director of Finance City Treasurer

P. Fuleihan S. Lebovitz A. Snitzer

Page 3 of 3

T. Phillips, CPA D. Barba, AdminSure D. Sullivan, AdminSure R. Lennon, AdminSure

L. Derderian, Interim PIO Library, NIS City Controller

PASADENA FIRE & POLICE RETIREMENT SYSTEM RETIREMENT BOARD - REGULAR MEETING

Wednesday, November 15, 2017 City Council Chambers S249

Pasadena City Hall, 100 N. Garfield Avenue 10:15 a.m.

MINUTES

1. Call to Order

The regular meeting of the Pasadena Fire & Police Retirement Board was called to order by the Chair, Mr. Keith Jones, on Wednesday, November 15, 2017 at 10:16 a.m. in the City Council Chambers at City Hall.

Members - Present K. Jones, Chair P. Boyle, Vice Chair (departed 11:15) J. Brinsley J. Milligan T. Tomek

Staff - Present

J. Fosselman, Administrator/Secretary E. Wong, Sr. Office Assistant I. Safie, City Attorney Representative

Others Present A. Taylor, J. Godsey, A. Chiang, R. Ridley

2. Public Comment

None noted.

Not Present

Not Present

3. Minutes: Approve the minutes for the regular meeting of September 20 and the special meeting of October 9, 2017.

MOTION by Mr. Milligan, seconded by Mr. Brinsley, to approve the Minutes for the regular meeting of September 20 and the special meeting of October 9, 2017. (Motion unanimously carried)

Page 1of6

CONSENT CALENDAR

4. Approve the monthly retirement allowance roll of $1,073, 179.24 for September 2017, and $1,067,418.15 for October 2017.

5. Approve additions/removals of the following members/beneficiaries to/from the man thl II II 1y a owance ro :

Effective Add/ Pension Pension Name Date Remove Continuance Amount

a. J. Galligan 10/13/17 remove Yes, 100% $4,075.40

b. F. Galligan 10/14/17 remove No $4,075.40

6. Receive and file the 3rd Quarter 2017 Asset Manager Performance Reports from the following asset managers: a. Atlanta Capital Investment Managers b. Capital Group, American Funds EuroPacific Growth Fund c. Dodge & Cox International Stock Fund d. Dodge & .Cox Stock Fund e. Invesco Core Real Estate, USA- LP f. PIMCO All Asset Fund g. TCW MetWest Fixed Income Review h. Voya Senior Loan Trust Fund Review

MOTION by Mr. Boyle, seconded by Mr. Milligan, to approve items 4-6 on the Consent Calendar. (Motion unanimously carried)

CalPERS HEARINGS 7. CalPERS scheduled hearing on the Service Pending Industrial Disability

Retirement application for Salvador Vidales, Police Officer. (Remove from calendar)

The Chair announced it was the time for the hearing on the CalPERS Service Pending Industrial Disability Retirement application, filed by Salvador Vidales, Police Officer. However, the Board received notification from the City on November 2, 2017 that the applicant filed an additional claim. Thus, the City requested (with concurrence from the applicant) to remove the scheduled hearing from the Board's calendar.

ACTION ITEMS - The Board may discuss and take action on the following items:

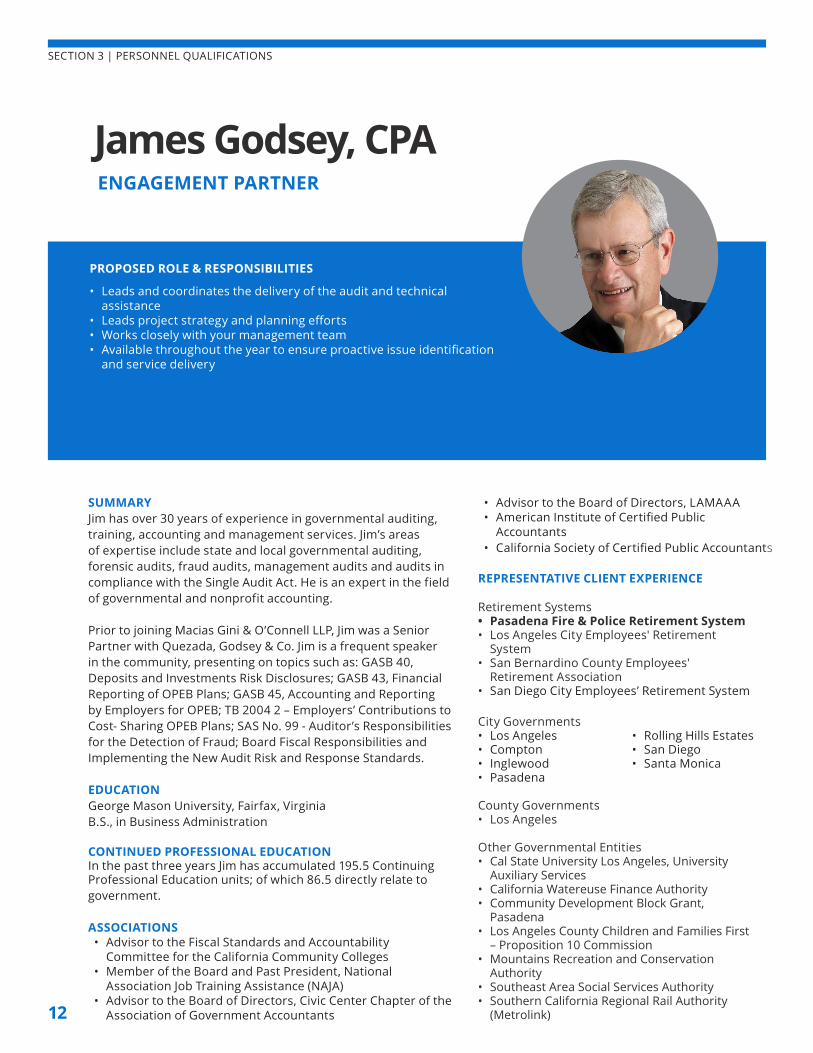

8. Review, discuss and approve the June 30, 2017 Annual Report and Audited Financial Statements, as prepared by System Auditor Macias Gini & O'Connell.

Engagement Partner James Godsey of Macias Gini & O'Connell ("MGO") reviewed the reports and significant information in the financial statements and notes. He reported that there were no findings, and that MGO had issued an unmodified opinion on the financial statements. Although MGO was not engaged

Page 2 of 6

to provide an opinion on internal controls, if they had discovered any, they would have disclosed them to the Board. No such deficiencies in internal control were found, and MGO believes that adequate checks and balances are in place to maintain control.

MOTION by Mr. Boyle, seconded by Mr. Tomek, to approve the June 30, 2017 Annual Report and Audited Financial Statements. (Motion unanimously carried)

Following action on this item, Chair Jones moved to Item 10 on the Agenda.

10. Receive presentation, discuss and possibly take action on the City's assignment of beneficial interest to the System in 275 East Cordova Street (The Concord).

Jill Fosselman provided a verbal update on the staff efforts to develop mutually agreed memorialization of the System's beneficial interest. She briefly iterated the key tenants of the System's beneficial interest: 100% of the rent, past-due rent, and interest on the past due rent until 2031 or until the City sells the property; 93% interest in the original "Concord" land parcel, including 93% of any proceeds realized from the sale or leasing of any part of the property, until the City is no longer fee title owner to the land, and; the City maintains all control over all decisions to be made regarding the sale, lease, or use of the property.

The Board generally discussed a tentative review and approval process for the beneficial interest, and further expressed their preference to develop a separate agreement to memorialize the beneficial agreement rather than amend the current contribution agreement between the City and System.

MOTION by Mr. Brinsely, seconded by Mr. Milligan, to approve in concept, the key tenants of the beneficial interest presented verbally, and directed counsel to draft the framework for a memorandum of understanding memorializing the System's beneficial interest in the Concord. (Motion unanimously carried)

Following action on this item, Chair Jones returned to Item 9 on the Agenda.

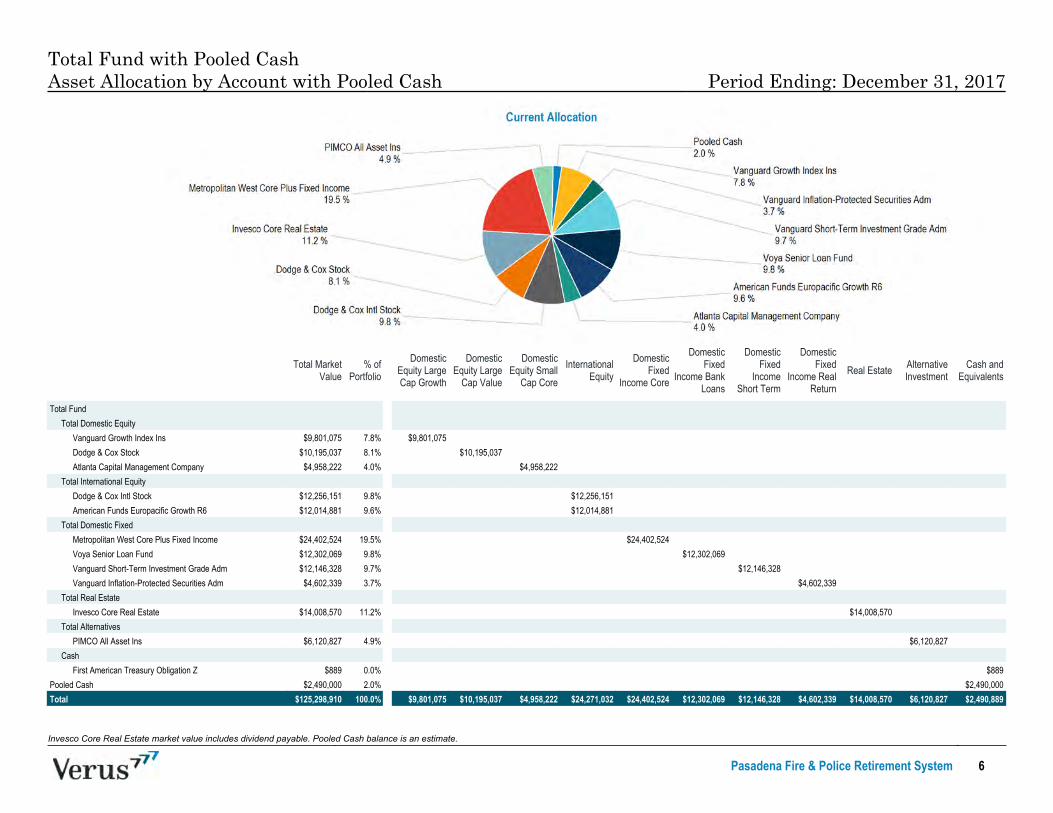

9. Discuss and possibly take action on the following investment reports submitted by Verus Investments: a. Receive and file, 3rct Quarter 2017 Investment Performance Review

Annie Taylor reviewed the research report. In view of the broader economy, Verus believes the moderate overweight to risk is warranted as interest rates are expected to increase in December. The net change in the portfolio for the quarter was -$785,798, bringing the value to $123,370,489 on September 30, 2017. The fund returned 3.0% net of fees (v. the benchmark of 2.6%) for the quarter). Over each of the earnings periods in the report (3 month, Fiscal YTD, YTD, and 1/3/5 Years), the fund outperformed its policy index. The fund's overall overperformance relative to the benchmark for the quarter was largely driven by earnings in international equities. Including pooled cash with the City,

Page 3 of 6

total market value at the end of the quarter was $125.8 million. The fund's cumulative performance for the quarter ranked in the 59th percentile relative to its peer universe (lnvestorForce Public DB $50mm-$250mm Gross).

MOTION by Mr. Brinsley, seconded by Mr. Milligan, to receive and file the 3rd Quarter 2017 Investment Performance Review, as recommended by Verus Investments. (Motion unanimously carried)

b. Receive and file, October 2017 Performance Update

Ms. Taylor reviewed the performance update reflecting performance without pooled cash. The total fund returned 0.8% net of fees for October (compared to the index of 0.7%), bringing the fiscal year-to-date return to 3.8% net of fees (vs. the index of 3.4%). Domestic Equities provided the strongest returns for the month with cumulative earnings of 1.8%, next followed by International Equities with cumulative earnings of 1.4% for these asset categories. Total market value at the end of October was $125.6 million, including pooled cash with the City.

Vice Chair Boyle departed the meeting at 11:15 a.m.

All asset classes were within the policy ranges specified in the Investment Performance Statement. However, given Verus' recommendation that the portfolio's moderate overweight to risk continues to be warranted, Ms. Taylor suggested a rebalance over time from Private Real Estate (current percentage is 11.1 %, and the target allocation is 10.0%). Ms. Taylor further recommended the Board request to redeem $1,000,000 from Invesco (to be reinvested or withdrawn for benefit payments).

MOTION by Mr. Tomek, seconded by Mr. Milligan, to approve the recommended withdrawal of $1,000,000 from Private Real Estate asset manager Invesco and rebalance as practicable, as recommended by Verus Investments. (Motion unanimously carried, 4-0, Boyle absent)

c. Receive and file, Liquidity Analysis

Ms. Taylor reviewed the liquidity analysis of the fund's portfolio, focusing on the individual assets and categories of assets held by liquidity. The System's portfolio is predominantly highly liquid: 80% of the assets have daily or weekly liquidity. Such liquidity is sufficient to meet the quarterly withdrawal needs for payment of benefits and administration, and no changes in asset managers or asset classes were recommended.

MOTION by Mr. Milligan, seconded by Mr. Brinsley, to receive and file the Liquidity Analysis, as recommended by Verus Investments. (Motion unanimously carried, 4-0)

Page 4 of6

d. Receive and file, September - October 2017 Withdrawal and Rebalance Transaction Summary

Ms. Taylor briefly reviewed the transaction summary for the rebalance and withdrawal for September-October pension benefits and administration of $2,200,000. The majority of the withdrawal was taken from international equities, followed next by domestic equities.

MOTION by Mr. Brinsley, seconded by Mr. Milligan, to receive and file the Transaction Summary, as recommended by Verus Investments. (Motion unanimously carried, 4-0)

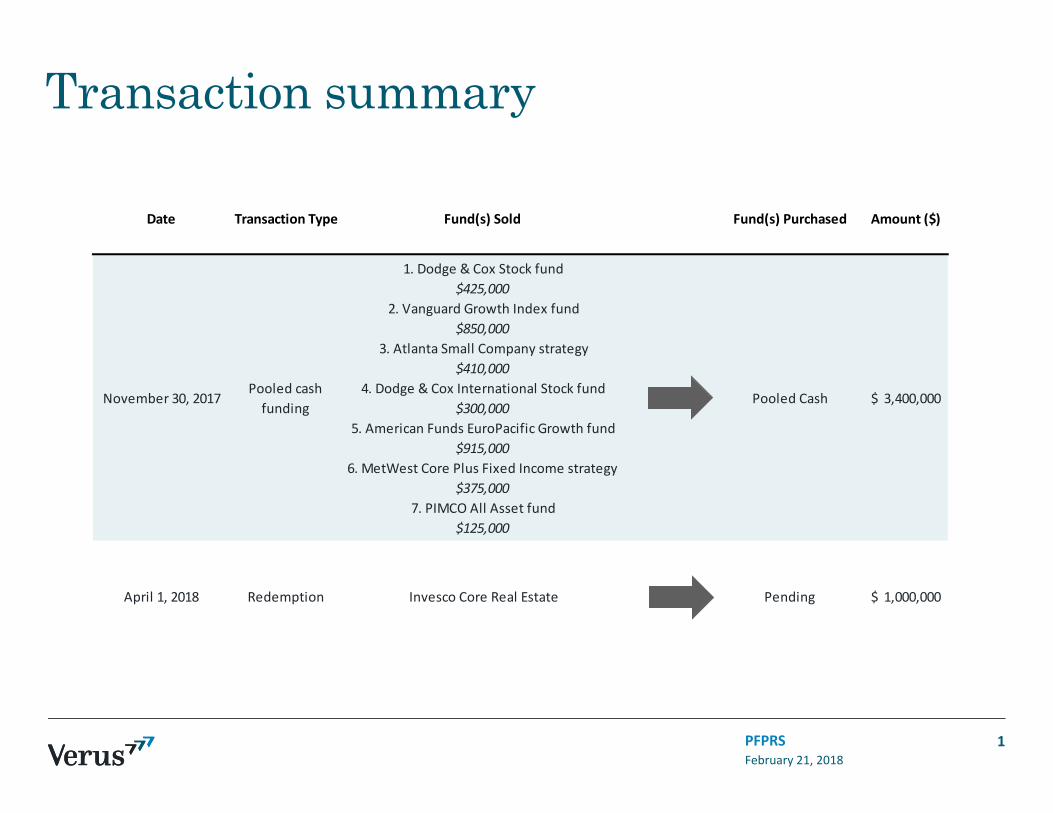

e. Review and approve, November 2017 - January 2018 Withdrawal and Rebalance

Ms. Taylor reviewed the proposed preliminary withdrawal and rebalance of $3.4 million for benefits and administration for the months of November, December and January. Funds will be predominantly withdrawn from earnings in the Fund's equity assets, followed next by the fixed income asset manager, and a smaller amount from liquid alternatives.

MOTION by Mr. Brinsley, seconded by Mr. Milligan, to approve the preliminary rebalance and withdrawal of $3,400,000, as recommended by Verus Investments. (Motion unanimously carried, 4-0)

INFORMATION ITEMS

11. Staff Report - Ms. Fosselman provided a brief update on the US Bank payroll system (new 2018 medical rates), auditing financial services RFP, and noted the Board meeting break over the holidays until February. a. October 2017 Budget/Expense Report- noted. b. 2018 Board Meeting Schedule - noted.

12. Counsel Report- none noted. 13. Articles/Newsletters/Conferences - none noted.

COMMENTS FROM BOARD MEMBERS

None noted.

ADJOURNMENT

MOTION by Mr. Tomek, seconded by Mr. Milligan, to adjourn the meeting at 11 :38 a.m. (Motion unanimously carried, 4-0)

Page 5 of 6

Respectfully submitted,

Ji~~ifiYJL Keith Jones Secretary to the Board/Administrator Chair, Retirement Board

Details of this meeting are contained on a DVD recording of the meeting and will be kept in the archives for two years, per Board policy.

DISTRIBUTION: Board Members City Attorney Director of Finance

Fire & Police Retirees Assn. Police Chief Fire Chief

P. Fuleihan S. Lebovitz

Page 6 of 6

A. Snitzer D. Barba

DATE V2 1//€3 ITEM# t

PASADENA FIRE AND POLICE RETIREMENT SYSTEM

MONTHLY ALLOWANCE ROLL-TOTALS

MONTH 2016-2017 2017-2018 Notes

JULY 1, 113,678.65 1,080,895.48 a. AUGUST 1,114,712.51 1,072,450.04 d., e. SEPTEMBER 1,11 0,857.14 1,073, 179.24 d. , OCTOBER 1,110,857.14 1,067,418.15 q. NOVEMBER 1,110,857.14 1,073,865.44 q. DECEMBER 1,105,747.36 1,071,271.25 q., h. JANUARY 1,089, 152.42 1,069,560.74 FEBRUARY 1,076,066.67 MARCH 1,086,444.43 APRIL 1,072, 755.90 MAY 1,066,511.65 JUNE 1,062,779.72 Refund Checks -2,697.45 Prior Year Accruals Paid -2,859.76 b., c., f. FY TOTALS 13, 117,723.28 7,505, 780.58

COL BENEFITS INCLUDED ABOVE 6,930 , 154.22 3,971 ,080.46

COL- % Of Total 53% 53%

a. 2% COLA applied to all members and beneficiaries. b. T. Smith passed 6/4/2017. Final amount of $606.75 (accrued in June '17 - FY17) paid 7/31/17. c. A.J. Bergeson passed 6/12/2017. Final amount $1,878.40 (accrued in June '1 7 - FY17) paid

7/31/2017. d. B. Mcintyre passed 8/8/2017. Final amount $1,307.58 paid 9/30/17. No Survivor. e. R. McCray passed 8/16/2017. Surviving Spouse continuance 60%. Final amount $2,382.47

paid 8/31/17. Surviving Spouse normal amount $2 ,769 .62. Surviving Spouse initial August payment $1,340. 14 paid 8/31/2017. be paid when paperwork is complete. Surviving Spouse initial payment will be paid with her November payment.

f. H. Quinan passed 4/16/2017. Final amount $374.61 (accrued in June '17 - FY 17) paid 9/30/17. g. J. Galligan passed 10/13/17. Surviving Spouse continuance 100%. Final amount $1, 710.51

paid 12/31/2017. Surviving Spouse initial payment was paid with her November payment. h. G. Kenney passed 10/26/17. No continuance. Overpaid 5 days October and all of November.

Received refund check 2/5/2018 (after January payroll).

January 10, 2018

Bill Hackney, CFA(404) 876-9411

www.atlcap.com

OPINION AND ANALYSIS OF KEY ECONOMIC AND INVESTMENT ISSUES Page One

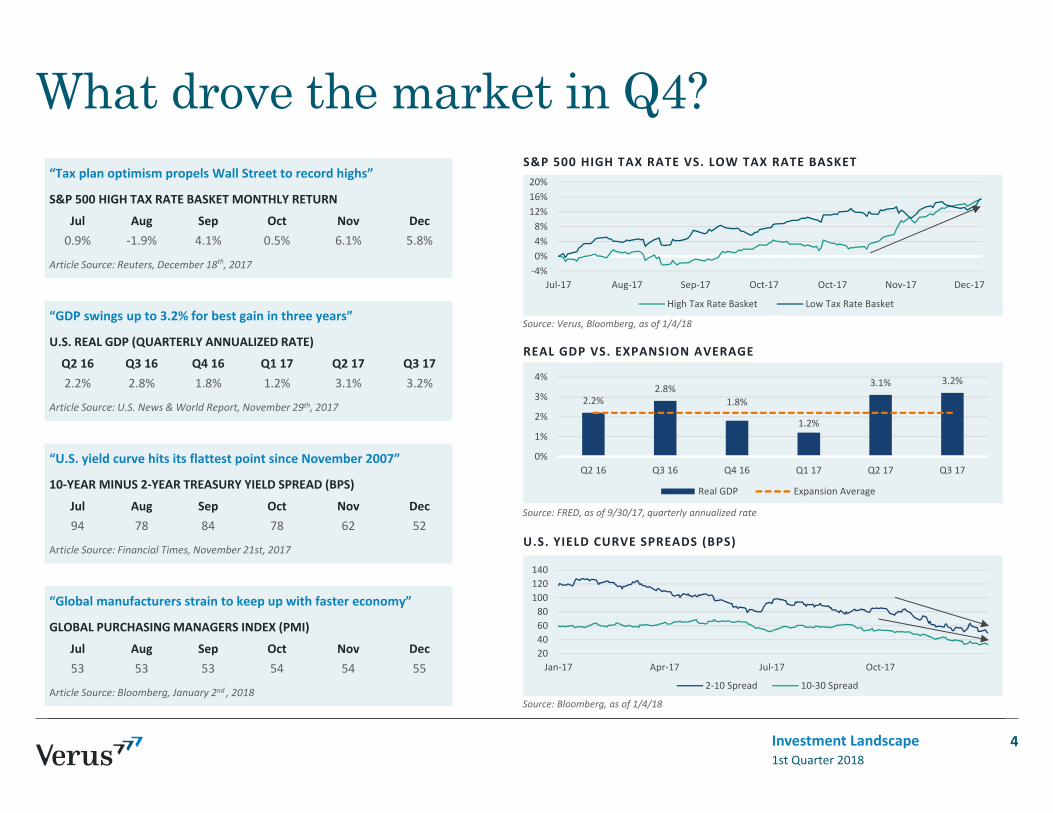

What’s up with tax reform? The stock market seems to like it. Most Republicans seem to like it. But public opinion polls show that over half of the American populati on doesn’t like it.

Economist Larry Summers predicts that 10,000 people per year will die due to tax reform. New York governor Andrew Cuomo calls it “a dagger at the economic heart of New York.” A study by the University of Chicago found that only one of 42 economists surveyed said the tax bill would increase economic growth substanti ally.

Of course Republicans and their favorite economists—apparently few of whom were interviewed by the University of Chicago—have a diff erent take on tax reform. They claim that the Tax Cuts and Jobs Act will result in more jobs, higher wages, greater business investment, faster economic growth and a fl ood of money fl owing back to the US from American companies’ $2 trillion overseas cash hoard.

“Finding Waldo” in this forest of economic hyperbole and jabbering punditry is diffi cult. But, as one might expect, the kernels of truth are probably found somewhere in between the prognosti cati ons of the opti mists and the naysayers.

What follows is my take on the tax bill, with parti cular focus on what’s important for investors to know in 2018.

First, some general observati ons. This legislati on is more a straightf orward tax cut than tax reform. Tax reform is usually viewed as revenue neutral, with the loss of tax revenues from the rate cuts being off set by the gain in revenues from the eliminati on of tax deducti ons and loopholes and from base broadening. This bill should cut taxes by about $1.5 trillion over the next ten years, with the cut about evenly distributed between individuals and corporati ons. Some of the lost tax revenues will likely be off set by gains generated from additi onal economic acti vity. Just how much growth will off set the revenue loss is, of course, the great debate between Democrats and Republicans.

An important feature of this legislati on is that the tax cuts for corporati ons are permanent, but most of the personal tax cuts expire in 2026. Beginning in 2018, the US federal corporate tax rate will be cut from 35% to 21%, the largest corporate tax cut in history and the fi rst cut since 1986.

For individuals, the top personal tax rate goes from 39.5% to 37%. All other personal tax rates are cut as well, with lower income earners benefi ti ng from a near doubling in the standard deducti on and a hike in the child tax credit. Between now and 2025, about 80% of Americans will get a tax cut, about 15% will see litt le or no change, and 5% will experience a tax increase (mostly the higher earners in high tax states like New York, New Jersey and California).

What You Wish For!Be Careful

OPINION AND ANALYSIS OF KEY ECONOMIC AND INVESTMENT ISSUES Page Two

Are the personal tax cuts distributed fairly across the income spectrum? Alas, “fairness” like “beauty” is in the eye of the beholder. Many opponents of the bill say that the majority of the benefi ts will accrue to the highest earners. This is true: mostly because top earners in America pay the lion’s share of the income taxes, so it’s diffi cult to implement a tax cut without benefi ti ng top earners. For example, the top one percent pay about 40% of total federal income taxes, despite generati ng only 20% of the taxable income. The top 50% of earners pay 97% of the total income taxes. As Congress fi ddled with income taxes over the past four decades, they have steadily eliminated lower income earners from the tax rolls.

From an investor point of view, there are six key conclusions that can be gleaned from these tax cuts.

1. US economic growth will be signifi cantly enhanced in 2018 and 2019. I don’t buy the argument that this legislati on is likely to have a negligible eff ect on US economic growth. It consti tutes a signifi cant dose of fi scal sti mulus. Not only does it cut tax rates for both corporati ons and individuals, it also provides a fi ve-year window for companies to fully expense their investments in capital equipment. A boost, if not a boom, in capital investment spending is likely to follow. What’s more, many companies have recently announced $1000 bonuses for their employees. Soon, most employees will see a bump in take home pay due to lower withholding. I think 3% plus economic growth can conti nue at least through 2018. The tax cuts will increase the defi cit and thereby push up interest rates, which will eventually slow the economy. But that likely won’t become a problem in the next year or so.

2. The internati onal competi ti veness of American manufacturers will improve. Prior to this legislati on, the US had the highest corporate tax rate among major developed world economies. High US corporate taxes have been a major impediment to manufacturers located in the US. Currently, the world average corporate rate is about 29%. Adding in 4% for state and local taxes, the new US corporate tax rate will be about 25%. This lower tax rate will reduce, but not eliminate, corporate desires to take advantage of tax havens such as Ireland, Bermuda and the Cayman Islands. Most importantly, it will substanti ally improve the US manufacturers’ competi ti ve positi on in world markets. (At least unti l foreign countries begin to match our tax cuts.)

3. Corporate earnings will jump in 2018. Earnings will be about 10% higher in 2018 just because of the tax bill. However, as corporati ons adjust to the new legislati on, there will be “noise” in 4th quarter 2017 and 1st quarter 2018 earnings when some companies take write-downs to adjust to the new tax code. Using the S&P 500® index as a benchmark, 2017 earnings are esti mated to be about $130. Prior to the tax cut, 2018 earnings were expected to advance about 5 to 7%. Since the bill’s passage, analysts have been scrambling to raise their 2018 esti mates to about $155, a gain of about 19% over 2017. Using the S&P 500 close of $2674 at year-end, the stock market sells at 20.5 ti mes 2017 earnings, but for 2018 earnings it sells at a more reasonable 17.2 ti mes.

4. The tax bill’s corporate benefi ts will vary. The tax bill will benefi t companies and economic sectors with a large US base of business. As such, smaller capitalizati on companies will benefi t more than the larger multi nati onals, which usually have higher foreign sales. Among economic sectors, Consumer

~ The Huffi ngton PostDecember 18, 2017

The average household would pay $1600 less in taxes next year,

increasing after-tax incomes 2.2 percent according to the

nonpartisan Tax Policy Center . . . In 2025, the last year before the individual tax cuts expire, 76 percent of households would pay about $2500 less in taxes. But by 2027, only a quarter of taxpayers

would see a cut.

The Republican tax-overhaul plan will send about 10% of a

net $1.5 trillion tax cut directly to middle-income households . . . Households that earn $20,000 to $100,000 a year in wages, dividends and benefi ts will get

$144 billion in tax cuts in all over a decade, with most of those cuts coming in the early years of the decade and then petering out or reversing as tax cuts expire . . .

~Wall Street JournalSeptember 19, 2017

OPINION AND ANALYSIS OF KEY ECONOMIC AND INVESTMENT ISSUES Page Three

Discreti onary (retailers), Telecom Services, Industrials and Regional Banks are expected to be major benefi ciaries. The sectors benefi ti ng the least should be Energy, Technology and Materials, because of their relati vely high foreign sales content. Despite their domesti c orientati on, most Uti liti es are also unlikely to benefi t because their earnings power is heavily regulated.

5. Repatriati on of corporate cash held overseas won’t meet investor expectati ons. Many analysts predict a fl ood of cash being repatriated from the $2 trillion corporate cash hoard held overseas. This presumed fl ood will enable corporati ons to pay increased dividends, buyback stock, reti re debt and fund additi onal capital investment. It might even increase the value of the US dollar. The opti mists oft en base their predicti on on what happened in 2004, when legislati on opened up a window of opportunity to bring overseas cash back at a low 5.5% rate. The new tax bill should cause overseas corporate cash to fl ow back to the US, but it won’t be a fl ood—more likely a steady trickle. The new tax bill treats cash repatriati on diff erently than the 2004 legislati on. It taxes all unrepatriated foreign earnings at 15.5% over a period of eight years, whether the company brings cash back to the US or not. There is no window of opportunity to spur companies to take immediate acti on.

6. Debt-laden companies are likely to suff er, with negati ve implicati ons for the junk bond market. Historically, companies have been able to deduct from their taxes all interest payments on debt. In 2021, the amount of interest expense companies can deduct will be limited to 30% of EBITDA—earnings before interest, taxes, depreciati on and amorti zati on. This rule stays in eff ect unti l 2025, then the interest deducti on becomes even more onerous. As a result, the new rule will restrain credit availability to lower quality companies as well as make them more vulnerable to any rise in interest rates.

There is a lot to like in the new tax bill. But, with all major legislati on, there will be unintended consequences. The one I worry about is infl ati on. The Tax Cut and Jobs Act of 2017 applies a powerful dose of fi scal sti mulus to our economy which is already doing well. The US unemployment rate is a low 4.1%, with an increasing number of businesses citi ng shortages of skilled labor.

~ NFIB Jobs ReportNational Federation of Independent Business

January 4, 2018

The shortage of qualifi ed workers reached a record high

in December, and the number of small business owners who made plans to raise compensation was the second highest in history. . .

“Finding qualifi ed workers is now the second biggest concern

for small business owners,” said NFIB Chief Economist Bill

Dunkelberg. “Taxes occupied the top spot all of last year, but that

may drop as the recently enacted tax reform law takes effect. The worker shortage could very well become the number-one problem

for small businesses.”

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Perc

enta

ge (%

)

Atlanta Fed’s Wage Growth Tracker

Recessions

Source: Federal Reserve Bank of Atlanta

My #1 Economic Indicator for 2018: Wage Growth

Source: Federal Reserve Bank of Atlanta

OPINION AND ANALYSIS OF KEY ECONOMIC AND INVESTMENT ISSUES Page Four

Atlanta Capital Management Co., LLC1075 Peachtree Street NESuite 2100Atlanta, GA 30309

This material is presented for informati onal and illustrati ve purposes only and should not be construed as investment advice, a recommendati on to purchase or sell specifi c securiti es, or to adopt any parti cular investment strategy. The opinions expressed herein are those of the author and do not necessarily refl ect the views of other employees at Atlanta Capital Management. Any current investment views and opinions/analyses expressed consti tute judgments as of the date of this material and are subject to change at any ti me without noti ce. Index and commodity changes are based on price-only percentage change. This material has been prepared on the basis of publicly available informati on, internally developed data, and other third party sources believed to be reliable. However, no assurances are provided regarding the reliability of such informati on and Atlanta Capital has not sought to independently verify informati on taken from public and third party sources. This material may contain statements that are not historical facts, referred to as forward-looking statements. Future results may diff er signifi cantly from those stated in forward-looking statements, depending on factors such as changes in securiti es or fi nancial markets or general economic conditi ons. Investi ng entails risks and there can be no assurance that any forecasts or opinions expressed in this material will be realized. It is not possible to directly invest in an index. Past performance does not predict future results.

So far, infl ati on pressures in the US have been benign—a big benefi t to stock and bond prices. The Consumer Price Index (CPI) is running at 2.2%, up from 1.6% last summer due to higher energy prices. Core CPI (CPI excluding food and energy) has fl atlined at a low 1.7% since last spring. As US economic acti vity conti nues to improve, there is a growing possibility that the markets could experience an infl ati on scare, which causes the Fed to raise interest rates more aggressively.

My favorite early warning indicator of infl ati on is the trend in wages and salaries as measured by the Atlanta Fed’s wage tracker on page three. When wage growth gets to 4% or more, the Fed tends to become more serious about raising interest rates. As the chart on wage growth shows, the uptrend stalled in 2017. That’s the key reason that core infl ati on remained steady throughout last year.

The table above shows fi ve indicators I monitor to gauge the health of the equity market. When two or three turn red, I get worried about the outlook for stocks. Currently, only one, the S&P 500 price/earnings rati o, is fl ashing a negati ve signal.

My big concern is that infl ati on pressures are lurking right below the surface of US economic acti vity. If they breakout, interest rates could spike and credit conditi ons could quickly deteriorate. So for those opti mists raging about the tax bill’s benefi cial impact on our economy, be careful what you wish for.

Indicator Commentary Current Reading

❶ Short-term vs. long-terminterest rates

When short-term interest rates rise to meet or exceed long-term rates, monetary policy is usually tight enough to eventually cause a recession.

Fed funds rate isbelow 10-year T note, but

gap is narrowing

❷ High-quality vs. low-qualitybond yields

A widening gap between junk bond yields and Treasuries indicates deteriorating credit market conditions. Credit Spreads are still

narrow

❸ Wage inflationWhen wages rise at a 4% annual rate, it is difficult for the Fed to keep core inflation near its 2% goal. So the Fed usually tightens policy aggressively. Wage growth is 3% and

beginning to accelerate

❹ S&P 500 P/E ratio Price/earnings ratios over 20 times makes stocks vulnerable to rising interest rates and inflation.

P/E is 20.5 times

❺ The leading economic indicators

The Conference Board’s LEI has peaked and turned down in advance of each recession since 1960.

Strong uptrend

~ Financial TimesJanuary 5, 2017

Drug makers have imposed price rises of several times

the rate of infl ation on more than a thousand products in

the US, a New Year move that risks a political backlash at a time of intense scrutiny on

healthcare costs.

The recent string of natural catastrophes will lead to

across-the-board increases in insurance prices, according to Swiss Re’s chief fi nancial offi cer. Prices for specialist insurance and reinsurance has been falling for years,

but hopes are rising that the estimated $100bn in claims

from hurricanes Harvey, Irma and Maria, combined with earthquakes in Mexico, will

reverse the trend, allowing the industry to put up prices again.

~Financial TimesNovember 3, 2017

Data as of December 31, 2017.

Your Atlanta Capital Team

Michael Jaje, CFA Investment Specialist & Principal (404) 682-2498 [email protected]

Cheryl lnnerarity Portfolio Administrator (404) 682-2552 cheryl. [email protected]

ATLANTA CAPITAL INVESTMENT MANAGERS

1075 Peachtree Street NE I Suite 2100 I Atlanta I GA I 30309

Atlanta Capital Management Co., LLC As of December 31, 2017

• Founded in 1969 in Atlanta, Georgia

• Singular focus on High Quality stocks and bonds

• Owned by employees & Eaton Vance Corporation

• Employ 41 professionals (17 are equity partners)

Investment Franchises ($20.6 Billion)

Core Equity Management ($16.1 Billion)

Fixed Income SMID Cap

s13.2 bn I 2004

Core Equity

Growth Equity llllim Small Cap $2.1 bn I 1992 Select Equity

$818 mm I 2006

Assets under management I inception data of strategy.

ATLANTA CAPITAL INVESTMENT MANAGERS

Seasoned & Stable Investment Team

A focused team that combines the benefit of conducting independent fundamental research with the ability to make timely investment decisions.

11

Portfolio Managers

Matt Hereford, CFA 22 Yrs I 2002

Investment Specialist

• Portfolio managers are generalists and serve as both research analyst and portfolio manager • Our team does not rely on a research staff to generate ideas or perform fundamental research • Each portfolio manager conducts his own research while decisions are made on a consensus basis

Years industiy experience as of 12131/17 I year joined Atlanta Capital.

2

ATLANTA CAPITAL INVESTMENT MANACiERS

Consistent Growth & Stability in Earnings Key Tenet of Our Investment Philosophy

15%

12%

9%

6%

3%

Five-Year Rolling CAGR of As Reported Earnings Russell 2000® Index by Earnings Stability

0% ...... J L L l •r• "L LJQC! ' L J l J J L L .,...., Z:t " ~Y"Y J J L L l rnT y: ~~ J L J J J ~

(3%)

• •

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Earnings Stability Above-Average Below-Average

Avg. 5-Year CAGR 6.9% 3.9%

Earnings Variability 1.7% 3.4%

# Positive Periods 120or100% 105 or88%

# Negative Periods Oor0%

15or12%

*Time period: January 1, 1988 - December 31, 2017. The Earnings Stability portfolios are modal portfolios formed and rebalanced monthly by Atlanta Capital based on Iha stocks in Iha Russell 2000® Index sorted by quality rankings. The Above-Average Earnings Stability and Below-Average Earnings Stability portfolios are provided to compare the aggregate of all companies in the index with High Quality S&P Rankings (B+ or Better) to those with Low Quality S&P Rankings (B or Below). The universe includes all Russell 2000® Index constituents with S&P Quality Rankings and prices greater than $1. Five-year historical earnings growth rates are calculated using a market capitalization-weighted methodology. The Russell 2000® Index is a widely-accepted measure of the U.S. small cap stock market. Indexes are unmanaged and it is not possible to directly invest in an index. The Above-Average Earnings Stability and Below-Average Earnings Stability portfolios were derived in part from the Russell Index Data and Frank Russell Company remains the source and owner of the Russell Index Data contained or reflected and all trademarks and copyrights. Sources: Russell, Standard & Poor's, Wilshire Atlas, Atlanta Capital. The material is based upon information that Russell, S&P, Wilshire and Atlanta Capital considers to be reliable, but neither Russell, S&P, Wilshire nor Atlanta Capital warrants its completeness, accuracy or adequacy and it should not be relied upon as such. This information is provided for illustrative purposes only and does not reflect historical results or predict future results for any particular Atlanta Capital investment strategy. The chart demonstrates the long-term trend; individual client results may vary. The material should not be considered investment advice or a recommendation to invest in a particular strategy. Reproduction or redistribution of this page in any form without express permission from Atlanta Capital is prohibited. Above-average earnings stability does not guarantee outperformance. Past performance does not predict future results.

ATLANTA CAPITAL INVESTMENT MANAGERS

3

Investment Objective April 1, 1992 - December 31, 2017

40%

30%

20%

10%

0%

Our objective is to participate in rising markets, protect capital during declining markets, and outperform over the long term ...

RISING MARKETS DECLINING MARKETS SINCE INCEPTION* (70 Positive Quarters)

Net of Fees (33 Negative Quarters)

Net of Fees (103 Total Quarters)

Net of Fees

Upside Reward + Downside Protection = Long-Term Results

0%

·10%

·20%

-30%

-40%

Beta • HQ Small I R2000® •

0.71 11.00

13%

11%

9%

7%

5%

Standard Deviation • HQ Small I R2000® •

14.9% 119.3%

... without the volatility typically associated with small cap investing. 'Inception data of the High Quality Small Capitalization Composite is April 1, 1992. For illustrative purposes only. The charts above illustrate the average (annualized) return of the High Quality Small Capitalization Composite during both rising and declining markets since inception. Results for other time periods may differ from the long-term trend shown above. Rising markets are defined as quarters where the return of the Russell 2000® index was positive. Declining markets are defined as quarters where the return of the Russell 2000® index was negative. These positive and negative quarters are separated out from the intervening quarters, cumulated across the period, and annualized. Long-term investment returns include both rising and declining periods. Composite performance is shown in US dollars and reflects reinvestment of all income and capital gains. Composite performance is shown net of investment advisory fees using a maximum annual investment management fee of 0.80% applied monthly; client results will be reduced by custody fees and other client expanses. Performance during certain periods reflects strong stock market performance that is not typical and may not be repeated. Individual client returns will vary due to fees, client-imposed investment constraints and client inception date. Beta measures the historical sensitivity of portfolio excess returns to movements in the excess return of the market index. Standard Deviation is a measure of absolute volatility of returns. The Russell 2000® index is unmanaged and does not incur management fees or other expanses associated with managed accounts. It is not possible to directly invest in an index. This material is supplemental to the GIPS® presentation included at the and of this presentation. Please sea the GIPS® composite presentation for important additional information and disclosure. Past performance does not predict or guarantee future results. Source: aVestment and Atlanta Capital. ATLANTA CAPITAL

INVESTMENT MANAGERS

4

Disciplined Investment Process High Quality Small Cap Equity

Step 1. Create a 'Focus List' of High Quality Companies

Exclude companies with:

• Volatile earnings streams

• Short operating histories

• High levels of debt

• Weak cash flow generation

.... +~ ...

Step 3. Construct a Focused Yet Well-Diversified Portfolio

* 3-year average turnover based on a single representative client portfolio and subject to change; individual client results may vary.

• Low returns on capital

Step 2. Conduct 'Onsite' Fundamental Research

5

Step 4. Monitor Holdings & Review Focus List

ATLANTA CAPITAL INVESTMENT MANAGERS

Summary of Guidelines City of Pasadena Fire & Police Retirement System

Objective • Over rolling three-year periods, the account will be expected to achieve the following:

Outperform the return of the Russell 2000® Index.

Provide a rate of return which ranks in the top half of the Mercer US Small Mid Cap Core Equity Universe.

Generate a standard deviation of quarterly returns which does not exceed that of the Russell 2000® Index by more than 50% without a proportionate percentage increase in return achieved.

Guidelines • No more than 7% of the portfolio's total market value shall be invested in cash.

• The market cap of securities held will generally be within the range of stocks comprising the Russell 2000® Index. Atlanta Capital defines a small cap company as one with a market capitalization greater than the market capitalization of the smallest company in the Russell 2000® Index and less than three times the weighted average market capitalization of companies in that Index. The portfolio management team will generally not initiate a position in a company unless it has a market capitalization between $200 million and $3.0 billion.

• The account's exposure to the securities of any one issuer is limited to the greater of 7.5% of the total account at market value or the benchmark weight of the security plus 2%.

• Portfolio sector allocations is limited to a maximum of 200% of the weight of the sector in the benchmark index or 30%, whichever is greater, with the exception of sectors whose benchmark allocation is less than 5%, where the maximum allocation shall be 15%.

• The account may hold non-U.S. companies up to a maximum of 10% of the total account at market value. All issues must be denominated in US dollars.

Trading • Investment Managers shall effect all purchases and sales of securities for the account in a manner consistent with the

principals of best execution, taking into account net price (including commissions), execution capability and other services which the broker or dealer may provide.

ATLANTA CAPITAL INVESTMENT MANAGERS

6

Summary of Guidelines City of Pasadena Fire & Police Retirement System

Proxy Voting • All proxies shall be voted at the Investment Managers' discretion in the best interests of the participants of the system's

constituent base.

Investment Policy Date: July 2011. Amended February 2015

ATLANTA CAPITAL INVESTMENT MANAGERS

7

Annualized Performance As of December 31, 2017

City of Pasadena Fire and Police Retirement System

QTD (%)

YTD (%)

1 Yr (%)

3 Yrs*

(%) 5 Yrs*

(%)

7 Yrs*

(%)

10 Yrs*

(%)

Since Inception*

(%)

High Quality Small Cap 5.40 15.15 15.15 13.37 16.45 14.83 - 17.83

Russell 2500 - 2000 (03/01/15) Periods < 03/01/15 represent SMID

3.34 14.65 14.65 10.40

Account Summary

Performance Inception Date:

Net Investment Contributions:

Investment Dollars Earned:

Market Value (12/31/17):

"Time periods greater than one year are annualized. Performance reflects reinvestment of all income and capital gains (realized and unrealized). Results are based on the accrual method of accounting as well as trade dale valuation. Returns are gross of fees unless otherwise noted.

14.54

June 30, 2009

($5,565,985)

$10,524,021

$4,958,036

Gross of fee returns do not reflect the deduction of management and custodial fees. Net of fee returns reflect the deduction of the management fee accrued on a monthly basis. Returns are based on the total assets of the client's account, calculated on a daily basis, and geometrically linked to calculate returns for longer periods of time. The unmanaged indexes shown for comparative purposes do not reflect the subtraction of any fees or transaction costs. II is not possible to directly invest in an index. Past performance does not guarantee or predict future results.

8

12.39 16.34

ATLANTA CAPITAL INVESTMENT MANAGERS

Performance Drivers & Detractors As of December 31, 2017 City of Pasadena Fire and Police Retirement System

Total Portfolio

vs. Russell 2000® Index

Sector Allocation

Stock Selection

Excess Return

Last3-Mos. Attribution

(%)

I o.6

" 1.5

- 2.1

+ Positive stock selection in Technology, Financials, Health Care, and Consumer Discretionary

+ Overweight in Consumer Staples, Consumer Discretionary, Industrials

+ Underweight Real Estate, Utilities, Telecom, and Health Care

- Negative stock selection in Industrials and Materials

- Overweight Technology

Underweight Energy

Sector Allocation

Stock Selection

Excess Return

Last 12-Mos. Attribution

(%)

I 0.1

I 0.3

I 0.4

+ Positive stock selection in Industrials, Consumer Staples, Real Estate, and Energy

+ Underweight in Energy, Real Estate, Financials, and Telecom

+ Overweight Industrials

- Negative stock selection in Consumer Discretionary, Materials, Technology, and Health Care

Underweight in Health Care

- Overweight in Consumer Staples and Technology

Stock Selection + Sector Allocation = Excess Return Source: Factset The above attribution results are based on each day's ending holdings, and linked to generate attribution over longer periods. Cash in the portfolio is included in the analysis. Portfolio returns do not reflect applicable expenses and trading costs, or variations in transaction prices from end of day values.

9

ATLANTA CAPITAL INVESTMENT MANAGER$

Portfolio Transactions Last 3-Months Ending December 31, 2017 City of Pasadena Fire and Police Retirement System High Quality Small Cap

New Purchases none this quarter

10

ATLANTA CAPITAL INVESTMENT MANAGERS

Portfolio Transactions Last 3-Months Ending December 31, 2017 City of Pasadena Fire and Police Retirement System High Quality Small Cap

Complete Sales Health Care

Advisory Board Co.

Bio-Rad Labs

Industrials

Provides best practice consulting for Health Care and Educational clients. The company's previously announced acquisition was completed during the quarter.

Produces reagents, apparatus, and instruments used in life sciences and Clinical Laboratories. We sold as the company's market capitalization has appreciated to the high end of our threshold.

Graco Produces equipment used to pump, meter, mix and dispense a wide variety of fluids. We sold the position as the company's market capitalization has appreciated to the high end of our threshold.

HEICO Corp. A Designs and manufactures parts and performs repairs for aerospace and aviation end markets. We sold as the company's market capitalization has appreciated to the high end of our threshold.

Knight-Swift Transportation Inc Offers trucking and logistical solutions. We sold the position after the completed merger between Knight and Swift drove the market cap to the high end of our threshold.

ATLANTA CAPITAL INVESTMENT MANAGERS

11

Portfolio Characteristics As of December 31, 2017 City of Pasadena Fire and Police Retirement System High Quality Small Cap

Top Ten Holdings o/o Portfolio Metrics

Manhattan Associates 4.2 WEX 3.7 Metrics Corelogic 3.3

#of Holdings AptarGroup 2.9 Black baud 2.9 Wtd. A\g. Mkt. Cap (billions)

Choice Hotels lnt'I 2.9 Historical Earnings Growth

Morningstar 2.8 Forecasted Earnings Growth Exponent 2.7 Return on Equity Fair Isaac Corp. 2.7 Price/Earnings (NTM) Columbia Sportswear 2.6 Dividend Yield

Sector Exposure

Russe II 2000® Index

1,983 $2.4 9% 13% 6%

18.7x 1.2%

45

40

35

30

• Total Portfolio • Russell 2000® Index

25 23.2

Total Portfolio

56 $3.4 6% 11% 17%

22.4x 0.9%

20 1 16.6 17.9 17.717.8 16.1 15.4 15.3 15 12~

10 7.3 6.2 5 7 6.7 : 111 1111 ·~ .I m; ~· ~: ·~ ... . .. : : ... Information Industrials Financials Consumer Consumer Health Care Materials Real Estate Energy Technology Discretionary Staples

Source: FactSet. Sector weight percentages shown are percentages of total equities.

12

Tele comm Services

Utilities Cash

ATLANTA CAPITAL INVESTMENT MANAGERS

Current Portfolio Holdings As of December 31, 2017

City of Pasadena Fire and Police Retirement System High Quality Small Cap

Sector

Consumer Discretionary

Bright Horizons (BFAM)

Oloice Hotels lnt'I (CHH)

Colurrt>ia Sportswear (COLM)

Domen A"oducts (DORM)

IVbnro (~RO)

Pool Corp. (POOL)

Sally Beauty Hldgs. (SBH)

Sonic Corp. (SONG)

Wolverine World Vllide (WWW)

Consumer Staples

Casey's General Stores (CASY)

.,ter Parfums (IPAR)

J&J Snack Foods Corp. (JJSF)

Lancaster Colony Corp. (LANG)

Dril-Quip (DRQ)

Financials

Artisan Partners (APAM)

BERlb.BANK Corp. (IBKC)

IVbrningstar (II/ORN)

Navigators Group (NAVG)

Pinnacle Fin'I Partners (PNFF?

A"osperily Bancshares (PB)

RU Corp. (RLO

Ending Weight

lmlml 1.3%

2.9%

2.6%

1.8%

1.4%

2.1%

1.7%

1.1%

1.1% ~~ ~ llllllYi&I

2.3%

2.0%

1.8%

1.3%

m'IEI 0.9% ~ mft'!'!!'ll ~~

1.5%

1.5%

2.8%

1.6%

1.5%

1.8%

1.2%

South State Corp. (SSB) 1.2%

State Bank Financial (SlBZ) 1.7%

Urrpqua Holdings Corp. (l.M'Q) 1.2%

Westarrerica Bancorp. (WABC) 1.5%

Source: FactSet.

Health Care

Bio-Techne (TECH)

ICU Medical (ICUO

.,tegra LifeSciences (IARl)

Patterson Corrpanies (PDCO)

Industrials

AAON(AAON)

Beacon Roofing Supply (BECN)

Exponent (EXPO)

Forward Air (FWRD)

Huron Consulting Group (HURN)

Kirby Corp. (KEX)

Landstar System (LSTR)

IVbog (11/0G.A)

Raven Industries (RAVN)

UniFirst Corp. (UNF)

US Ecobgy (ECOL)

13

IBl•fJi'4! 2.1%

1.2%

1.7%

1.1%

ID!l•fJ!f4! 1.0%

1.6%

2.7%

1.8%

1.0%

2.2%

1.8%

2.1%

0.9%

1.8%

1.0%

• High Quality Small Cap

• Russell 2000® Index

Information Technology

Blackbaud (BLKB)

Cass lnforrretion Sys (CASS)

CoreLogic (CLGX)

Envestnet (ENV)

ePius (PLUS)

Fair Isaac Corp. (Fro)

Manhattan Associates (MANH)

National .,strurrents (NA TO

Pow er lnteg rations ( POV'v1)

ScanSource (SCSC)

WCX(WCX)

Materials

AptarGroup (A TR)

Balchem Corp. (BCPC)

Sensient Technologies Corp. (SXT)

Stepan Co. (SCL)

Real Estate

Universal Health Realty (UHT)

Telecommunication Services

Utilities

Cash

aunm 2.9%

0.9%

3.3%

1.3%

1.0%

2.7%

4.2%

1.4%

1.1%

0.9%

3.7%

•t•mm 2.9%

1.0%

1.0%

0.8% ., .... 1.0%

•·n•m::.11 •M•llm •is·•mi!ll

ATLANTA CAPITAL INVESTMENT MANAGERS

Investment Outlook & Strategy As of December 31, 2017

High Quality Small Cap

Outlook

• U.S. equity investors had a lot to cheer about as 2017 drew to a close. Economic growth has been accelerating both here and abroad, inflation and interest rates remain low, and recently passed U.S. tax law should provide a meaningful one-time boost to corporate earnings in 2018.

• Small cap U.S. markets (represented by the Russell 2000® Index) gained 3.3% during the quarter, reaching new all-time highs.

• As small cap markets continue to move higher, valuations continue to be a major challenge. While positive economic growth and low interest rates continue to drive markets higher, they also increase the risk of inflationary surprises that could cause the Fed to become more aggressive.

Portfolio Positioning

• During the quarter, we sold five positions entirely from the portfolio. Four of the sales were due to the stocks reaching the high end of our market cap threshold, and the fifth stock was acquired.

• At quarter end, the portfolio held 56 stocks representing nine of the eleven economic sectors in the Russell 2000®.

• Relative to the benchmark, the portfolio was overweight Technology, Consumer Staples, Consumer Discretionary, Industrials, and Materials.

• The portfolio was underweight Health Care, Real Estate, Energy, and Financials. There are no positions in Utilities or Telecom Services.

ATLANTA CAPITAL INVESTMENT MANAGERS

14

GIPS® Performance Information and Disclosure High Quality Small Capitalization Composite (E7)

January 1, 2007 through December 31, 2017

Period Composite Composite Russell 2000® Composite Russell 2000®

Gross Return(%) Nat Return (%) Return(%) 3-yr Std. Dav. (%) 3-yr Std. Dav. (%)

2017(1) 14.77 13.87 14.65 10.95 13.91

2016 19.00 18.07 21.31 12.69 15.76

2015 5.12 4.29 -4.41 12.68 13.96

2014 3.60 2.78 4.89 10.52 13.12

2013 42.34 41.24 38.82 12.80 16.45

2012 12.24 11.36 16.35 16.63 20.20

2011 10.31 9.44 -4.18 21.88 24.99

2010 25.98 24.99 26.86 24.41 27.69

2009 27.17 26.18 27.17 21.69 24.83

2008 -19.41 -20.06 -33.79 16.62 19.85

2007 6.77 5.92 -1.57 10.66 13.17

(1) Period- 01/01/2017 through 12131/2017. Past performance does not predict or guarantee future results.

Number of Internal Composite Firm Portfolios Dispersion (%) Assets ($mil) Assets ($mil)

49 0.21 1,551 20,606

53 0.19 1,544 17,646

54 0.16 1,259 16,054

56 0.24 1,235 16,707

57 0.51 1,294 18,082

60 0.22 996 14,235

60 0.25 1,023 11,964

49 0.19 737 9,845

36 0.34 639 7,748

38 0.34 494 6,199

37 0.25 551 8,828

Atlanta Capital Management Company, LLC claims compliance with the Global Investment Performance Standards (GIPS") and has prepared and presented this report in compliance with the GIPS Standards. Atlanta Capital Management has bean independently verified for the periods January 1, 1999 through December 31, 2016.

Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm's policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. The High Quality Small Capitalization Composite has bean examined for the periods January 1,1999 through December 31, 2016. The verification and performance examination reports are available upon request.

Composite Description: The investment objective of this style is to seek long-term capital growth. Accounts in this composite invest in common stocks of companies having market capitalizations within the range of companies comprising the Russell 2000®. Management seeks to invest in quality companies in strong financial condition whose equities are priced below their estimate of fair value. Characteristics of high quality companies include a history of sustained growth in earnings and operating cash flow, high returns on capital, attractive profit margins and leading industry positions. Investments are determined based primarily on fundamental analysis of a company's financial trends, products and services, and other factors. Financial quality rankings provided by nationally-recognized rating services may be utilized as part of the investment analysis but are not solely relied upon. The portfolios are broadly diversified. All fully discretionary accounts that are managed in this style and do not pay a bundled or SMA wrap fee are eligible for inclusion in the composite. Benchmark: The Russell 2000® Index includes the smallest 2000 companies in the Russell 3000® and is a widely accepted measure of the small-cap segment of the U.S. equity universe. The index is the benchmark used to evaluate the strategy's performance and characteristics within the small-<:ap U.S. equity universe. Strategy investments differ from the benchmark due to active management, exclusion/inclusion of securities held/not held in the index, over/underweighting specific sectors or securities, limitations in market cap, and/or client constraints. Prior to July 1, 2005, the composite was also compared to the Russell 2000® Value Index as the portfolio construction process produced both core and value characteristics. Our high quality investment philosophy tends to be defensive in nature and does consider valuation metrics, but ii is more consistent with the philosophy and process of a core manager than a value manager. As of July 1, 2015, to clarify our process for potential clients, we determined that it was most appropriate to benchmark our performance results against the Russell 2000® Index only. Indexes include the reinvestment of dividends and earnings, are unmanaged, and do not incur management fees, transaction costs or other expenses associated with separately managed accounts. It is not possible to directly invest in an index. Gross and Nat Returns: Performance reflects reinvestment of all income and capital gains. Composite returns and market values are reported in U.S. dollars. Gross-<Jf-fees performance returns are presented before management and custodial fees but after all trading expenses. Returns ara presented net of withholding taxes. Net-of-fees performance returns are calculated by deducting the highest management fee of 0.80% from the monthly gross-of-fees returns. Other expenses will reduce a client's returns. The annual fee schedule for this composite is as follows: 0.80% on the first $50 million in assets; 0. 70% on the next $50 million in assets; 0.60% on the next $150 million. Actual management fees incurred by clients may vary. Dispersion: The annual internal composite dispersion is calculated using the asset-weighted standard deviation of annual gross returns of those portfolios that were included in the composite for the entire year. The three-year annualized standard deviation measures the variability of the composite and the benchmark returns over the preceding 36-month period. Notes: The creation date of this composite is July 1992. Effective July 1, 2010, the composite was redefined to include both taxable and tax-exempt institutional accounts. The composite up to that time included only tax-exempt institutional accounts. The change provides increased transparency to prospective clients by reducing the number of separate composites maintained for this strategy. There has been no change in investment objective or management style. Clients or prospective clients should not assume that they will have an investment experience similar to that indicated by past performance results, as shown on the Schedule. Returns may vary based upon differences in account size, timing of transactions and market conditions at the lime of investment. Performance during certain lime periods reflects the strong stock market performance and/or the strong performance of stocks held during those periods. This performance is not typical and may not be repeated. Firm Definition: Atlanta Capital Management Company, LLC (Atlanta Capital or the Firm) is an SEC-registered investment adviser located in Atlanta, Georgia. The Firm became a majority-owned subsidiary of Eaton Vance Corp. in 2001. Atlanta Capital operates as an independent subsidiary of Eaton Vance and provides professional investment advisory services to a broad range of institutional and individual clients, and sub-advisory investment management to mutual funds and separately managed sub-advisory account programs. Atlanta Capital includes all discretionary accounts under management in its composites; firm assets include nondiscretionary accounts as well. The Firm's list of composite descriptions and policies for valuing portfolios, calculating performance and preparing compliant presentations ara available upon request. To request any additional information, please contact the Atlanta Capital Management Performance Department at 404-876-9411 or write to Atlanta Capital Management Company, LLC, 1075 Peachtree Street NE, Suite 2100, Atlanta, Georgia 30309, Attention Performance Department.

Atlanta Capital High Quality Small Capitalization Composite

Composite Gross of Faas

Composite Nat of Faas

Russell 2000® Index

"Inception date is April 1, 1992. 01.10.18

1 Year 3Years

14.77 12.81

13.87 11.93

14.65 9.96

Annualiud Returns (%) for Periods Ending December 31, 2017 Cumulative (%)

5Years 7Yaars 10 Years Since Inception• Since Inception•

16.19 14.76 12.97 12.96 2204.57

15.27 13.86 12.08 12.06 1777.32

14.12 11.62 8.71 9.67 975.98

ATLANTA CAPITAL INVESTMENT MANAGERS

15

co .....

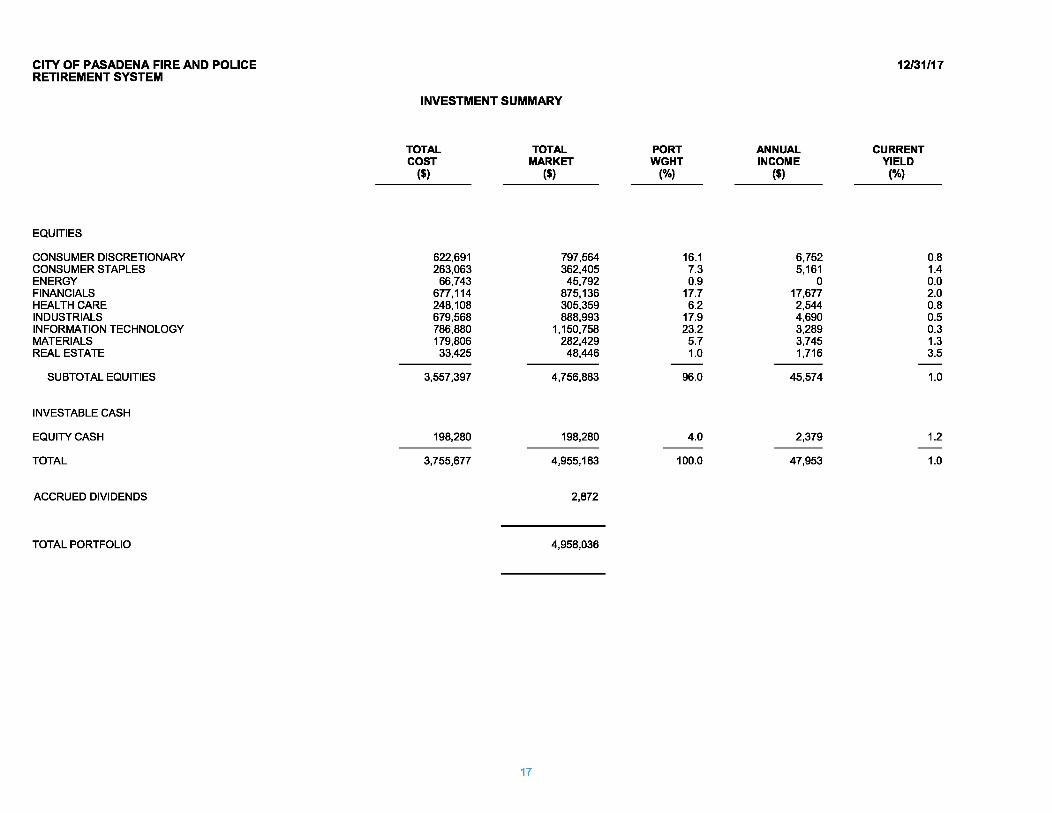

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

EQUITIES

CONSUMER DISCRETIONARY CONSUMER STAPLES ENERGY FINANCIALS HEALTH CARE INDUSTRIALS INFORMATION TECHNOLOGY MATERIALS REAL ESTATE

SUBTOTAL EQUITIES

INVESTABLE CASH

EQUITY CASH

TOTAL

ACCRUED DIVIDENDS

TOTAL PORTFOLIO

INVESTMENT SUMMARY

TOTAL COST

($)

622,691 263,063

66,743 677,114 248,108 679,568 786,880 179,806 33,425

3,557,397

198,280

3,755,677

TOTAL MARKET

($)

797,564 362,405

45,792 875,136 305,359 888,993

1, 150,758 282,429

48,446

4,756,883

198,280

4,955,163

2,872

4,958,036

17

PORT WGHT

(%)

16.1 7.3 0.9

17.7 6.2

17.9 23.2

5.7 1.0

--96.0

4.0 ---

100.0

ANNUAL INCOME

($)

6,752 5,161

0 17,677 2,544 4,690 3,289 3,745 1,716

45,574

2,379

47,953

12/31/17

CURRENT YIELD

(%)

0.8 1.4 0.0 2.0 0.8 0.5 0.3 1.3 3.5

--1.0

1.2 --

1.0

CITY OF PASADENA FIRE AND POLICE 12/31/17 RETIREMENT SYSTEM

ASSET STATEMENT

SECURITY COST/ MARKET/ TOTAL TOTAL PORT ANNUAL CURRENT DESCRIPTION SHARE SHARE COST MARKET WHTG INCOME YIELD

SHARES ($) ($) ($) ($) (%) ($) (%) --

EQUITIES

CONSUMER DISCRETIONARY

BRIGHT HORIZONS FAMILY SOL 687 64.94 94.00 44,614 64,578 1.3 0 0.0 CHOICE HOTELS INT'L INC 1,880 60.26 77.60 113,285 145,888 2.9 1,617 1.1 COLUMBIA SPORTSWEAR CO 1,775 38.87 71.88 68,985 127,587 2.6 1,349 1.1 DORMAN PRODUCTS INC 1,469 47.49 61.14 69,766 89,815 1.8 0 0.0 MONRO INC 1,250 63.19 56.95 78,992 71, 188 1.4 900 1.3 POOL CORP 797 69.18 129.65 55,138 103,331 2.1 1,180 1.1 SALLY BEAUTY HOLDINGS INC 4,602 19.92 18.76 91,657 86,334 1.7 0 0.0 SONIC CORP 2,049 24.90 27.48 51,025 56,307 1.1 1,311 2.3 WOLVERINE WORLD WIDE INC 1,648 29.87 31.88 49,228 52,538 1.1 396 0.8

-- --- --622,691 797,564 16.1 6,752 0.8

CONSUMER STAPLES

CASEY'S GEN'L STORES INC 1,017 91.46 111.94 93,017 113,843 2.3 1,058 0.9 INTER PARFUMS INC 2,277 28.87 43.45 65,732 98,936 2.0 1,913 1.9 J&J SNACK FOODS CORP 577 101.45 151.83 58,535 87,606 1.8 1,039 1.2 LANCASTER COLONY CORP 480 95.37 129.21 45,780 62,021 1.3 1,152 1.9

-- -- --- -263,063 362,405 7.3 5, 161 1.4

ENERGY

DRIL-QUIP INC 960 69.52 47.70 66,743 45,792 0.9 0 0.0

FINANCIALS

ARTISAN PARTNERS ASSET MGMT INC 1,869 46.40 39.50 86,720 73,826 1.5 4,486 6.1 IBERIABANK CORP 987 63.28 77.50 62,460 76,493 1.5 1,461 1.9 MORNINGSTAR INC 1,450 50.67 96.97 73,470 140,607 2.8 1,450 1.0 NAVIGATORS GROUP INC 1,661 45.43 48.70 75,467 80,891 1.6 399 0.5 PINNACLE FINANCIAL PARTNERS 1, 110 43.56 66.30 48,355 73,593 1.5 622 0.8 PROSPERITY BANCSHARES INC 1,293 54.57 70.07 70,558 90,601 1.8 1,862 2.1 RU CORP 1,003 49.72 60.66 49,866 60,842 1.2 843 1.4 SOUTH STATE CORP 681 90.06 87.15 61,328 59,349 1.2 899 1.5 STATE BANK FINANCIAL CORP 2,877 20.14 29.84 57,942 85,850 1.7 1,611 1.9 UMPQUA HOLDINGS CORP 2,917 13.00 20.80 37,924 60,674 1.2 2,100 3.5

18

CITY OF PASADENA FIRE AND POLICE 12/31/17 RETIREMENT SYSTEM

ASSET STATEMENT

SECURITY COST/ MARKET/ TOTAL TOTAL PORT ANNUAL CURRENT DESCRIPTION SHARE SHARE COST MARKET WHTG INCOME YIELD

SHARES ($) ($) ($) ($) (%) ($) (%) --

EQUITIES -cont.

FINANCIALS - cont.

WESTAMERICA BANCORPORATION 1,216 43.60 59.55 53,023 72,413 1.5 1,946 2.7 -- --

677,114 875,136 17.7 17,677 2.0

HEALTH CARE

BIO-TECHNE CORP 823 98.30 129.55 80,903 106,620 2.2 1,053 1.0 ICU MEDICAL INC 284 126.11 216.00 35,815 61,344 1.2 0 0.0 INTEGRA LIFESCIENCES HOLDINGS 1,789 42.62 47.86 76,253 85,622 1.7 0 0.0 PATTERSON COMPANIES INC 1,433 38.48 36.13 55,137 51,774 1.0 1,490 2.9

-- --- --248,108 305,359 6.2 2,544 0.8

INDUSTRIALS

AAON INC 1,405 23.90 36.70 33,580 51,564 1.0 365 0.7 BEACON ROOFING SUPPLY INC 1,210 31.07 63.76 37,590 77,150 1.6 0 0.0 EXPONENT INC 1,876 45.00 71.10 84,419 133,384 2.7 1,576 1.2 FORWARD AIR CORP 1,537 52.98 57.44 81,438 88,285 1.8 922 1.0 HURON CONSUL TING GROUP INC 1,230 58.00 40.45 71,338 49,754 1.0 0 0.0 KIRBY CORP 1,632 54.58 66.80 89,069 109,018 2.2 0 0.0 LANDSTAR SYSTEM INC 862 57.62 104.10 49,670 89,734 1.8 345 0.4 MOOG INC CL A 1,203 76.00 86.85 91,428 104,481 2.1 0 0.0 RAVEN INDUSTRIES INC 1,327 20.35 34.35 27,000 45,582 0.9 690 1.5 UNIFIRST CORP 544 123.67 164.90 67,276 89,706 1.8 82 0.1 US ECOLOGY INC 987 47.38 51.00 46,760 50,337 1.0 711 1.4

- -- --679,568 888,993 17.9 4,690 0.5

INFORMATION TECHNOLOGY

BLACKBAUD INC 1,535 23.40 94.49 35,921 145,042 2.9 737 0.5 CASS INFORMATION SYSTEMS INC 793 46.19 58.21 36,627 46,161 0.9 692 1.5 CORELOGIC INC 3,510 36.60 46.21 128,461 162, 197 3.3 0 0.0 ENVESTNET INC 1,254 48.18 49.85 60,424 62,512 1.3 0 0.0 EPLUS INC 652 90.40 75.20 58,943 49,030 1.0 0 0.0 FAIR ISAAC CORP 863 15.59 153.20 13,454 132,212 2.7 69 0.1

19

CITY OF PASADENA FIRE AND POLICE 12/31/17 RETIREMENT SYSTEM

ASSET STATEMENT

SECURITY COST/ MARKET/ TOTAL TOTAL PORT ANNUAL CURRENT DESCRIPTION SHARE SHARE COST MARKET WHTG INCOME YIELD

SHARES ($) ($) ($) ($) (%) ($) (%) --

EQUITIES -cont.

INFORMATION TECHNOLOGY -cont.

MANHATTAN ASSOCIATES INC 4,186 48.20 49.54 201,778 207,374 4.2 0 0.0 NATIONAL INSTRUMENTS CORP 1,636 30.72 41.63 50,261 68,107 1.4 1,374 2.0 POWER INTEGRATIONS INC 744 59.40 73.55 44,192 54,721 1.1 417 0.8 SCANSOURCE INC 1, 171 37.27 35.80 43,640 41,922 0.8 0 0.0 WEXINC 1,285 88.08 141.23 113,179 181,481 3.7 0 0.0

-- --- --786,880 1,150,758 23.2 3,289 0.3

MATERIALS

APTARGROUP INC 1,691 44.40 86.28 75,078 145,899 2.9 2,164 1.5 BALCHEM CORP 608 58.49 80.60 35,564 49,005 1.0 255 0.5 SENSIENT TECHNOLOGIES CORP 674 73.34 73.15 49,430 49,303 1.0 890 1.8 STEPAN CO 484 40.77 78.97 19,735 38,221 0.8 436 1.1

-- -- --- --179,806 282,429 5.7 3,745 1.3

REAL ESTATE

UNIVERSAL HEAL TH RL TY INCOME TR 645 51.82 75.11 33,425 48,446 1.0 1,716 3.5 -- --

3,557,397 4,756,883 96.0 45,574 1.0

INVESTABLE CASH

20

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

SECURITY DESCRIPTION

EQUITY CASH

TOTAL

ACCRUED DIVIDENDS

TOTAL PORTFOLIO

COST/ SHARE

SHARES ($) -

198 0.00

ASSET STATEMENT

MARKET/ TOTAL SHARE COST

($) ($)

1000.00 198,280

3,755,677

21

12/31/17

TOTAL PORT ANNUAL CURRENT MARKET WHTG INCOME YIELD

($) (%) ($) (%)

198,280 4.0 2,379 1.2 --- --

4,955,163 100.0 47,953 1.0

2,872

--4,958,036

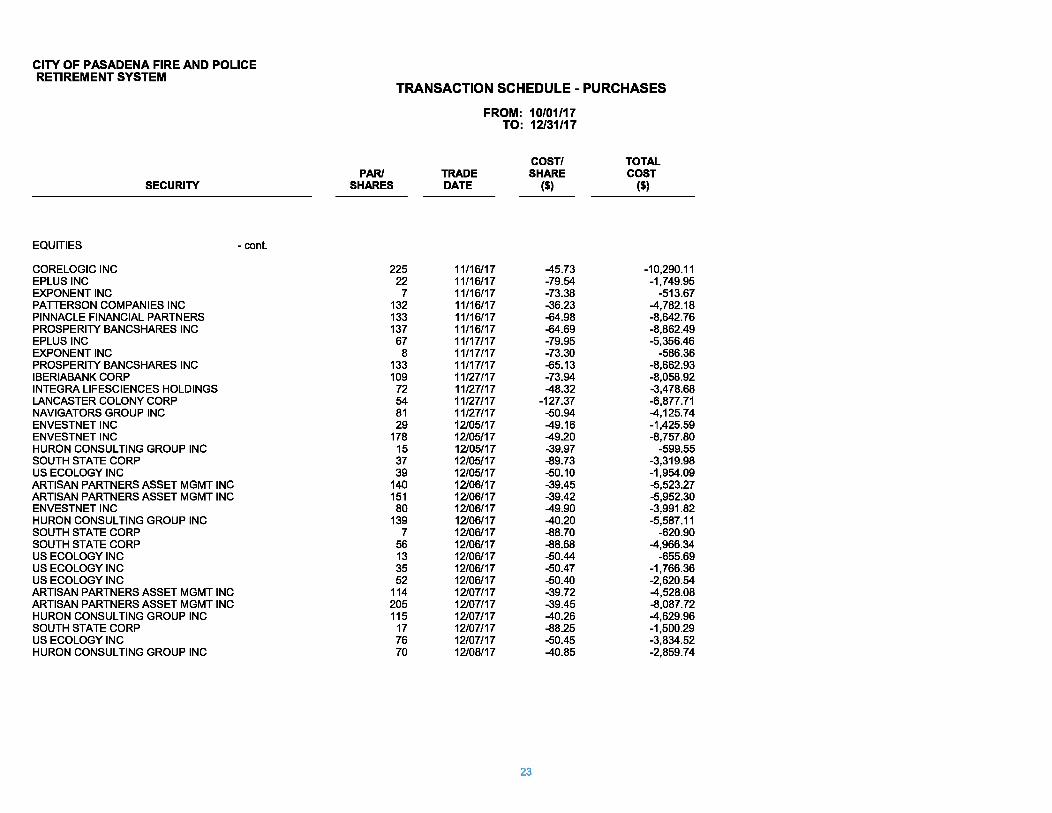

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

SECURITY

EQUITIES

SONIC CORP SONIC CORP SOUTH STATE CORP SOUTH STATE CORP EPLUS INC PATTERSON COMPANIES INC PATTERSON COMPANIES INC PATTERSON COMPANIES INC SONIC CORP SONIC CORP SONIC CORP SOUTH STATE CORP EPLUS INC SONIC CORP SOUTH STATE CORP EPLUS INC SOUTH STATE CORP EPLUS INC SOUTH STATE CORP DORMAN PRODUCTS INC DORMAN PRODUCTS INC DORMAN PRODUCTS INC DORMAN PRODUCTS INC DORMAN PRODUCTS INC EPLUS INC EPLUS INC PATTERSON COMPANIES INC SONIC CORP SOUTH STATE CORP SONIC CORP SONIC CORP SOUTH STATE CORP SOUTH STATE CORP

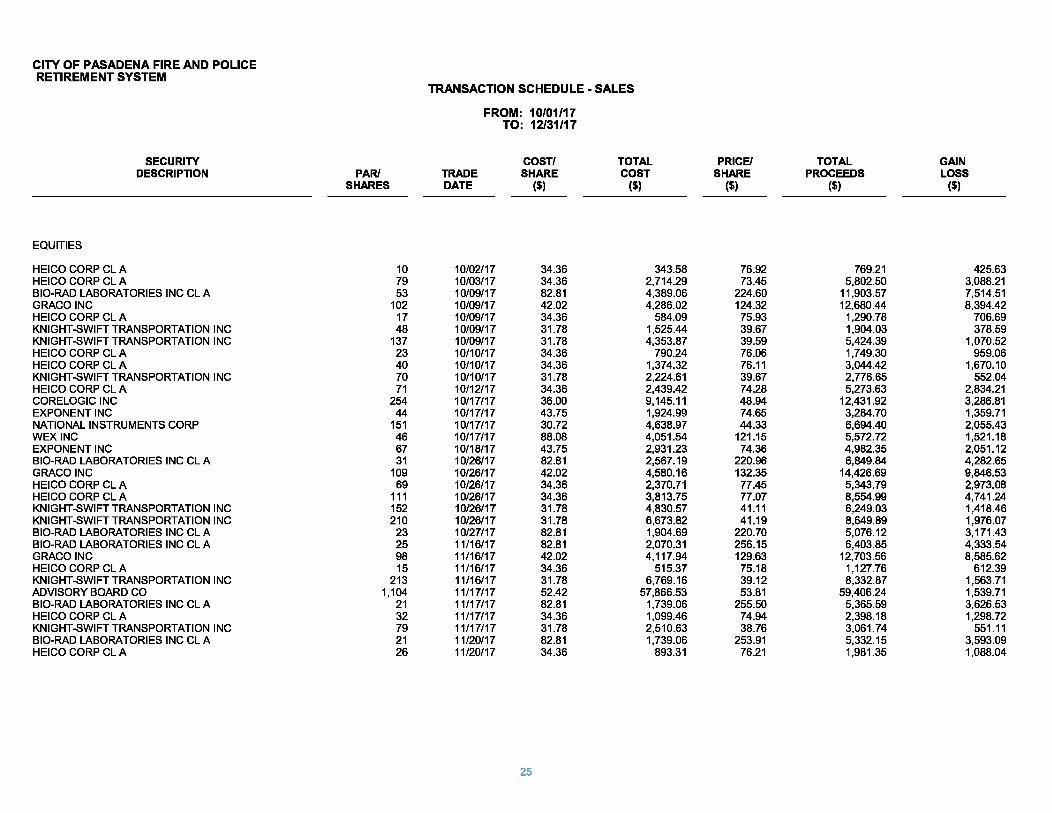

TRANSACTION SCHEDULE - PURCHASES

PAR/ SHARES

73 166 46 50

9 1

44 336

62 88

317 34 18

121 15 18 26 82 55

3 13 10 17 14 61 88

264 190

51 75

168 27 61

FROM: 10/01/17 TO: 12/31/17

TRADE DATE

10/02/17 10/02/17 10/02/17 10/03/17 10/09/17 10/09/17 10/09/17 10/09/17 10/09/17 10/09/17 10/09/17 10/09/17 10/10/17 10/10/17 10/10/17 10/11/17 10/11/17 10/12/17 10/12/17 10/17/17 10/17/17 10/18/17 10/18/17 10/19/17 10/26/17 10/26/17 10/26/17 10/26/17 10/26/17 10/27/17 10/27/17 10/27/17 10/30/17

COST/ SHARE

($)

-24.92 -25.25 -90.55 -91.40 -94.09 -37.80 -37.58 -37.76 -24.09 -24.09 -24.00 -91.85 -95.59 -23.93 -92.23 -96.62 -92.44 -97.05 -92.22 -70.02 -71.16 -72.34 -72.33 -72.11 -92.49 -92.41 -40.23 -25.69 -93.54 -25.68 -25.73 -91.99 -90.49

22

TOTAL COST

($)

-1,819.08 -4, 192.15 -4, 165.22 -4,570.17

-846.82 -37.80

-1,653.72 -12,686.39

-1,493.68 -2, 120.18 -7,609.33 -3, 122.76 -1,720.58 -2,895.23 -1,383.49 -1,739.17 -2,403.31 -7,958.05 -5,071.93

-210.06 -925.03 -723.39

-1,229.59 -1,009.56 -5,641.90 -8, 131.69

-10,621.86 -4,881.86 -4,770.41 -1,925.63 -4,322.22 -2,483.60 -5,520.04

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

SECURITY

EQUITIES - cont.

CORELOGIC INC EPLUS INC EXPONENT INC PATTERSON COMPANIES INC PINNACLE FINANCIAL PARTNERS PROSPERITY BANCSHARES INC EPLUS INC EXPONENT INC PROSPERITY BANCSHARES INC IBERIABANK CORP INTEGRA LIFESCIENCES HOLDINGS LANCASTER COLONY CORP NAVIGATORS GROUP INC ENVESTNET INC ENVESTNET INC HURON CONSUL TING GROUP INC SOUTH STATE CORP US ECOLOGY INC ARTISAN PARTNERS ASSET MGMT INC ARTISAN PARTNERS ASSET MGMT INC ENVESTNET INC HURON CONSUL TING GROUP INC SOUTH STATE CORP SOUTH STATE CORP US ECOLOGY INC US ECOLOGY INC US ECOLOGY INC ARTISAN PARTNERS ASSET MGMT INC ARTISAN PARTNERS ASSET MGMT INC HURON CONSUL TING GROUP INC SOUTH STATE CORP US ECOLOGY INC HURON CONSUL TING GROUP INC

TRANSACTION SCHEDULE - PURCHASES

PAR/ SHARES

225 22

7 132 133 137

67 8

133 109

72 54 81 29

178 15 37 39

140 151 80

139 7

56 13 35 52

114 205 115

17 76 70

FROM: 10/01/17 TO: 12/31/17

TRADE DATE

11/16/17 11/16/17 11/16/17 11/16/17 11/16/17 11/16/17 11/17/17 11/17117 11/17117 11/27/17 11/27/17 11/27/17 11/27/17 12/05/17 12/05/17 12/05/17 12/05/17 12/05/17 12/06/17 12/06/17 12/06/17 12/06/17 12/06/17 12/06/17 12/06/17 12/06/17 12/06/17 12/07/17 12/07/17 12/07/17 12/07/17 12/07/17 12/08/17

COST/ SHARE

($)

-45.73 -79.54 -73.38 -36.23 -64.98 -64.69 -79.95 -73.30 -65.13 -73.94 -48.32

-127.37 -50.94 -49.16 -49.20 -39.97 -89.73 -50.10 -39.45 -39.42 -49.90 -40.20 -88.70 -88.68 -50.44 -50.47 -50.40 -39.72 -39.45 -40.26 -88.25 -50.45 -40.85

23

TOTAL COST

($)

-10,290.11 -1,749.95

-513.67 -4,782.18 -8,642.76 -8,862.49 -5,356.46

-586.36 -8,662.93 -8,058.92 -3,478.68 -6,877.71 -4,125.74 -1,425.59 -8,757.80

-599.55 -3,319.98 -1,954.09 -5,523.27 -5,952.30 -3,991.82 -5,587.11

-620.90 -4,966.34

-655.69 -1,766.36 -2,620.54 -4,528.08 -8,087.72 -4,629.96 -1,500.29 -3,834.52 -2,859.74

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

EQUITIES

US ECOLOGY INC US ECOLOGY INC EXPONENT INC EXPONENT INC

SECURITY

STATE BANK FINANCIAL CORP

- cont.

PAR/ SHARES

TRANSACTION SCHEDULE - PURCHASES

26 37 70

2 18

FROM: 10/01/17 TO: 12/31/17

TRADE DATE

12/11/17 12/12/17 12/13/17 12/14/17 12/27/17

COST/ SHARE

($)

-50.01 -50.38 -70.54 -71.42 -30.11

24

TOTAL COST

($)

-1,300.21 -1,864.05 -4,937.45

-142.83 -541.98

-273,842.03

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

EQUITIES

HEICO CORP CL A HEICO CORP CL A

SECURITY DESCRIPTION

BIO-RAD LABORATORIES INC CL A GRACO INC HEICO CORP CL A KNIGHT-SWIFT TRANSPORTATION INC KNIGHT-SWIFT TRANSPORTATION INC HEICO CORP CL A HEICO CORP CL A KNIGHT-SWIFT TRANSPORTATION INC HEICO CORP CL A CORELOGIC INC EXPONENT INC NATIONAL INSTRUMENTS CORP WEXINC EXPONENT INC BIO-RAD LABORATORIES INC CL A GRACO INC HEICO CORP CL A HEICO CORP CL A KNIGHT-SWIFT TRANSPORTATION INC KNIGHT-SWIFT TRANSPORTATION INC BIO-RAD LABORATORIES INC CL A BIO-RAD LABORATORIES INC CL A GRACO INC HEICO CORP CL A KNIGHT-SWIFT TRANSPORTATION INC ADVISORY BOARD CO BIO-RAD LABORATORIES INC CL A HEICO CORP CL A KNIGHT-SWIFT TRANSPORTATION INC BIO-RAD LABORATORIES INC CL A HEICO CORP CL A

PAR/ SHARES

10 79 53

102 17 48

137 23 40 70 71

254 44

151 46 67 31

109 69

111 152 210

23 25 98 15

213 1,104

21 32 79 21 26

TRANSACTION SCHEDULE - SALES

FROM: 10/01/17

TRADE DATE

10/02/17 10/03/17 10/09/17 10/09/17 10/09/17 10/09/17 10/09/17 10/10/17 10/10/17 10/10/17 10/12/17 10/17/17 10/17/17 10/17/17 10/17/17 10/18/17 10/26/17 10/26/17 10/26/17 10/26/17 10/26/17 10/26/17 10/27/17 11/16/17 11/16/17 11/16/17 11/16/17 11/17/17 11/17/17 11/17/17 11/17/17 11/20/17 11/20/17

TO: 12/31/17

COST/ SHARE

($)

34.36 34.36 82.81 42.02 34.36 31.78 31.78 34.36 34.36 31.78 34.36 36.00 43.75 30.72 88.08 43.75 82.81 42.02 34.36 34.36 31.78 31.78 82.81 82.81 42.02 34.36 31.78 52.42 82.81 34.36 31.78 82.81 34.36

25

TOTAL COST

($)

343.58 2,714.29 4,389.06 4,286.02

584.09 1,525.44 4,353.87

790.24 1,374.32 2,224.61 2,439.42 9, 145.11 1,924.99 4,638.97 4,051.54 2,931.23 2,567.19 4,580.16 2,370.71 3,813.75 4,830.57 6,673.82 1,904.69 2,070.31 4,117.94

515.37 6,769.16

57,866.53 1,739.06 1,099.46 2,510.63 1,739.06

893.31

PRICE/ SHARE

($)

76.92 73.45

224.60 124.32

75.93 39.67 39.59 76.06 76.11 39.67 74.28 48.94 74.65 44.33

121.15 74.36

220.96 132.35

77.45 77.07 41.11 41.19

220.70 256.15 129.63

75.18 39.12 53.81

255.50 74.94 38.76

253.91 76.21

TOTAL PROCEEDS

($)

769.21 5,802.50

11,903.57 12,680.44

1,290.78 1,904.03 5,424.39 1,749.30 3,044.42 2,776.65 5,273.63

12,431.92 3,284.70 6,694.40 5,572.72 4,982.35 6,849.84

14,426.69 5,343.79 8,554.99 6,249.03 8,649.89 5,076.12 6,403.85

12,703.56 1,127.76 8,332.87

59,406.24 5,365.59 2,398.18 3,061.74 5,332.15 1,981.35

GAIN LOSS

($)

425.63 3,088.21 7,514.51 8,394.42

706.69 378.59

1,070.52 959.06

1,670.10 552.04

2,834.21 3,286.81 1,359.71 2,055.43 1,521.18 2,051.12 4,282.65 9,846.53 2,973.08 4,741.24 1,418.46 1,976.07 3,171.43 4,333.54 8,585.62

612.39 1,563.71 1,539.71 3,626.53 1,298.72

551.11 3,593.09 1,088.04

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

EQUITIES

HEICO CORP CL A HEICO CORP CL A APTARGROUP INC

SECURITY DESCRIPTION

ARTISAN PARTNERS ASSET MGMT INC BEACON ROOFING SUPPLY INC BIO-TECHNE CORP BLACKBAUD INC BRIGHT HORIZONS FAMILY SOL CASEY'S GEN'L STORES INC CHOICE HOTELS INT'L INC COLUMBIA SPORTSWEAR CO CORELOGIC INC ENVESTNET INC EXPONENT INC FAIR ISAAC CORP FORWARD AIR CORP HEICO CORP CL A HURON CONSUL TING GROUP INC ICU MEDICAL INC INTER PARFUMS INC J&J SNACK FOODS CORP LANDSTAR SYSTEM INC MOOG INC CLA MORNINGSTAR INC NATIONAL INSTRUMENTS CORP PINNACLE FINANCIAL PARTNERS POWER INTEGRATIONS INC PROSPERITY BANCSHARES INC RAVEN INDUSTRIES INC SALLY BEAUTY HOLDINGS INC STATE BANK FINANCIAL CORP UMPQUA HOLDINGS CORP UNIFIRST CORP

- cont.

PAR/ SHARES

46 15

150 465 318 172 272 172 176 249 365 174 113 128 107 168 27

328 72

521 92

175 137 143 120

79 177 101 293 325 188 361

66

TRANSACTION SCHEDULE - SALES

FROM: 10/01/17

TRADE DATE