Finding the “Democratic Advantage” in Sovereign Bond Ratings: The Importance of Strong Courts,...

21

Finding the “Democratic Advantage” in Sovereign Bond Ratings: The Importance of Strong Courts, Property Rights Protection, and the Rule of Law Glen Biglaiser and Joseph L+ Staats Abstract Much scholarship in the political economy literature has investigated the influence of the democratic advantage on sovereign bond ratings by credit rating agencies ~CRAs!+ Missing from earlier work, however, is inquiry into the effects on bond ratings of factors that lower political risk, such as adherence to the rule of law, the presence of a strong and independent judicial system, and protection of property rights+ Using panel data for up to thirty-six developing countries from 1996 to 2006, we find that rule of law, strong and independent courts, and protection of property rights have significant positive effects on bond ratings+ Policymakers wanting to obtain higher bond ratings and increased revenue from bond sales would do well to heed the message contained in these findings+ This article seeks to show that strong courts, adherence to the rule of law, and protection of property rights are important factors used by the three main credit rating agencies ~CRAs! —Moody’s Investor Services ~ Moody’s!, Standard and Poor’s ~S&P!, and Fitch Ratings ~ Fitch! —when assessing the quality of bonds issued by sovereign nations+ Building on scholarly literatures that have shown a “democratic advantage” for countries seeking to attract foreign direct investment ~ FDI ! and foreign portfolio investment ~ PI !, 1 we demonstrate that a democratic advantage also exists for receiving higher sovereign bond ratings+ Although our findings contrast with previous studies that suggest the limitations of the demo- cratic advantage argument for sovereign debt repayment, 2 the honoring by sover- We thank Karl DeRouen and Paul Vaaler for providing us with valuable insights on bond ratings research+ We also greatly appreciate the advice of the two anonymous reviewers of our manuscript+ 1+ See Biglaiser and Staats 2010; Biglaiser, Hicks, and Huggins 2008; Busse 2004; Feng 2001; Henisz 2000; Jensen 2003, 2006, and 2008; Li 2006 and 2009; Li and Resnick 2003; North and Wein- gast 1989; Schultz and Weingast 1996, 1998, and 2003; and Staats and Biglaiser 2011 and 2012+ 2+ Saiegh 2005+ International Organization 66, Summer 2012, pp+ 515–35 © 2012 by The IO Foundation+ doi:10+10170S0020818312000185

Transcript of Finding the “Democratic Advantage” in Sovereign Bond Ratings: The Importance of Strong Courts,...

Finding the “Democratic Advantage”in Sovereign Bond Ratings:The Importance of Strong Courts,Property Rights Protection, andthe Rule of LawGlen Biglaiser and Joseph L+ Staats

Abstract Much scholarship in the political economy literature has investigatedthe influence of the democratic advantage on sovereign bond ratings by credit ratingagencies ~CRAs!+ Missing from earlier work, however, is inquiry into the effects onbond ratings of factors that lower political risk, such as adherence to the rule of law,the presence of a strong and independent judicial system, and protection of propertyrights+ Using panel data for up to thirty-six developing countries from 1996 to 2006,we find that rule of law, strong and independent courts, and protection of propertyrights have significant positive effects on bond ratings+ Policymakers wanting to obtainhigher bond ratings and increased revenue from bond sales would do well to heedthe message contained in these findings+

This article seeks to show that strong courts, adherence to the rule of law, andprotection of property rights are important factors used by the three main creditrating agencies ~CRAs!—Moody’s Investor Services ~Moody’s!, Standard andPoor’s ~S&P!, and Fitch Ratings ~Fitch!—when assessing the quality of bondsissued by sovereign nations+ Building on scholarly literatures that have shown a“democratic advantage” for countries seeking to attract foreign direct investment~FDI! and foreign portfolio investment ~PI!,1 we demonstrate that a democraticadvantage also exists for receiving higher sovereign bond ratings+ Although ourfindings contrast with previous studies that suggest the limitations of the demo-cratic advantage argument for sovereign debt repayment,2 the honoring by sover-

We thank Karl DeRouen and Paul Vaaler for providing us with valuable insights on bond ratingsresearch+ We also greatly appreciate the advice of the two anonymous reviewers of our manuscript+

1+ See Biglaiser and Staats 2010; Biglaiser, Hicks, and Huggins 2008; Busse 2004; Feng 2001;Henisz 2000; Jensen 2003, 2006, and 2008; Li 2006 and 2009; Li and Resnick 2003; North and Wein-gast 1989; Schultz and Weingast 1996, 1998, and 2003; and Staats and Biglaiser 2011 and 2012+

2+ Saiegh 2005+

International Organization 66, Summer 2012, pp+ 515–35© 2012 by The IO Foundation+ doi:10+10170S0020818312000185

eigns of international financial commitments,3 and the outcomes of sovereign bondratings,4 such research did not consider institutional characteristics that tend tolower political risk+ Put simply, the democratic advantage for obtaining higher bondratings comes from democratic regimes’ tendency to have strong courts, adhere tothe rule of law, and protect property rights compared to authoritarian regimes+Our findings, based on regression results for as many as thirty-six developing coun-tries rated by Fitch, Moody’s, and S&P from 1996 to 2006, show that countrieshigh on judicial strength, respect for the rule of law, and protection of propertyrights receive significantly higher bond-rating scores than countries low on judi-cial strength and rule of law+

The results present important implications+ First, and contrary to earlier studiesshowing that politics and political institutions appeared to have a minimal influ-ence on ratings,5 our findings suggest that political factors play a key role for CRAs+Unlike previous research, we find that political institutions tied to political risk,which in this case means strong and independent courts, respect for the rule oflaw, and protection of property rights, strongly influence bond ratings+ Second,the results are consistent with information about methodologies published on CRAweb pages and confirm disclosures made by bond raters during interviews con-ducted by one of the authors+6 However, the results do much more than confirmwhat is publicly known about bond ratings+ CRAs are private firms that competewith each other to attract business, and are very guarded about disclosing theweighting they give to the multiple factors they consider in their rating assess-ments+ Our research offers clear evidence that judicial strength, rule of law, andprotection of property rights have great significance to the raters+ Third, the find-ings reinforce previous political economy work on the impact of political risk oninvestment decisions+7 Finally, the results provide added incentive for govern-ments in developing countries to do whatever it takes to build respect for rule oflaw+ The work by Tomz,8 Simmons,9 and Mosley10 suggest that a reputation inone area can have spillover advantages in other areas+ Hence, a country with areputation for honoring commitments to the rule of law at home can be seen aslikely to honor other commitments, including promises to pay sovereign debts whenthey come due+ Developing countries, especially, should be interested in building

3+ Tomz 2002 and 2007+4+ See Archer, Biglaiser, and DeRouen 2007; and Biglaiser and DeRouen 2007+5+ See ibid+6+ Phone interviews with two Fitch bond raters, 20 December 2005; phone interviews with four

Moody’s bond raters, 30 November and 14 December 2005; and phone interviews with two S&P bondraters, 12 December 2005+

7+ See Biglaiser and Lektzian 2011; Biglaiser and Staats 2010; Henisz 2000; Jensen 2003, 2006,and 2008; Li 2006; Li and Resnick 2003; Malesky 2007; and Pinto and Pinto 2008+

8+ Tomz 2007+9+ Simmons 2000+

10+ Mosley 2003+

516 International Organization

good reputations, because, as Mosely argues,11 they encounter great difficulties inconvincing the international financial system that they make reliable borrowers+

We discuss CRAs’ importance to developing countries and propose theories forwhy judicial strength and rule of law adherence should have positive effects onbond ratings+ We then present model specification issues and the results of ourdata analysis+

CRAs, Bond Ratings, and Judicial Strength andAdherence to the Rule of Law

During the past four decades, bond financing by developing countries has expandedexponentially+ In 1983, only 14 countries, nearly all from the developed world,issued sovereign debt, but by 2008, 108 countries issued sovereign bonds+12 Cor-porate and sovereign bond sales for the developing world alone rose from $10+8million in 1970 to nearly $50 trillion in 1996+13 Although bond purchases fell afterthe 1997 Asian financial crisis, by 2005 sales in the developing world again boomedto record levels, with more than $52 trillion in bonds sold+14

The expansion of CRA sovereign debt services mirrors the growth in bond sales+15

In 1975, S&P rated only Canada and the United States, while Moody’s rated Can-ada, the United States, and Australia, and Fitch did not exist+16 Sovereign ratings,focused mainly on developed countries, grew steadily during the 1980s+ By 1990,S&P rated 35 countries and Moody’s 33+17 The numbers swelled with the entry ofemerging countries into bond markets after the turn of the century+ By mid-2002,S&P rated 93 countries, Moody’s 109, and Fitch 77+18

CRAs rate sovereign bonds and provide potential investors with information toassess the probability of debt repayment and hopefully increase prospective buy-ers’ interest+19 The value to investors of bond ratings can be seen by the relative

11+ Ibid+12+ “Sovereign Bond Ratings,” The Economist, 2 April 2009+ Available at ^http:00www+

economist+com0node013415397&+ Accessed 24 April 2012+13+ World Bank 2008+14+ Ibid+15+ CRAs are also involved in activities beyond rating sovereign issues+ CRAs supply information

relevant to the investment climate in a country and therefore affect FDI and nonsovereign PI inflows~see Ferri, Liu, and Stiglitz 1999; Kaminsky and Schmukler 2002; and Setty and Dodd 2003!+ CRAsalso are seen as a potential weapon in preventing future financial global crises ~Biglaiser, DeRouen,and Archer 2011!, because the 1999 Basel Capital Accord ~Basel II! uses CRAs as a financial regula-tion source ~Bank for International Settlements 1999!+ More recently, CRAs have received negativepress following the U+S+ subprime crisis and their role in issuing bond ratings on mortgage-backedsecurities ~White 2009!+ For the context of this article, we focus on the role of CRAs in rating sover-eign issues+

16+ Bhatia 2002, 6+17+ Ibid+18+ Ibid+19+ Schwarcz 2001, 299+

Finding the ‘Democratic Advantage’ in Sovereign Bond Ratings 517

fortunes of highly rated countries relative to lowly rated ones+ No country receiv-ing an AAA, AA, or A rating from S&P has ever defaulted within a fifteen-yearperiod subsequent to the rating, and nearly 98 percent of countries rated AAAwere rated as at least AA fifteen years later+20 On the other hand, from 1991 to2004, sovereign bond default occurred fourteen times, all in the developing world,21

increasing the need for CRA ratings by both investors and issuers+ Bond ratingsthus are especially critical for emerging countries, which in recent years have begunto see sovereign bond debt as a vital component to supply capital+ Indeed, as Sin-clair22 notes, CRAs are guardians of the gates of capital to developing countries+As Schwarcz similarly remarks, CRAs have “huge powers to move markets+”23

Since sovereign ratings are critical for drawing in foreign capital, the factorsCRAs rely on in reaching their determinations are matters of great interest+ Thechallenge for scholars and issuing countries is that it is not obvious how ratingsare determined+ Although each CRA publicly lists numerous categories and sub-categories of political and economic variables that influence its ratings methodol-ogy, details about how the political and economic measures are weighted relativeto other factors are not made public+ Moreover, the stated political criteria arequite vague and not easily operationalized for measurement purposes+ Much ofthe reason for the secrecy and vagueness is that CRAs are for-profit companieslargely motivated by the premiums they charge investors for the information+ CRAsare often privy to insider information legally obtained from government financeofficials, which enables them to offer credible and proprietary information to theirclients that each CRA claims is more accurate than its competitors+ Based on theircontacts, the CRAs hope that their arguably better assessments will attract moreclients+

Despite the relative secrecy of ratings methodologies, we do know certain basicsabout the ratings process+ First, the government interested in issuing bonds invitesthe rating agency ~and not necessarily all agencies! to perform a risk analysis tohelp determine the degree to which the government is likely to fulfill its debt obli-gations+ Such risk analyses affect the interest rate that governments offer potentialinvestors+ After agreeing to work with a government, CRAs collect economic dataon the country and obtain domestic political and policy information through ques-tionnaires and interviews of relevant government officials and leaders in opposi-tion political parties+ From the CRA’s perspective, the goal is to assess the investorrisk environment and identify problems that might lead to future bond default overa three- to five-year time horizon+ The government’s goal is to obtain a rating highenough to assure investors about the safety of its bonds and to keep interest ratesas low as possible to reduce capital costs+

20+ “The Grim Rater: Countries Don’t Like Bad News About Their Creditworthiness,” The Econo-mist, 4 March 2010+Available at ^http:00www+economist+com0node015606329&+Accessed 24 April 2012+

21+ Borensztein and Panizza 2008, 29+22+ Sinclair 2005+23+ Schwarcz 2001, 297+

518 International Organization

Given the importance of sovereign ratings for attracting capital, a large litera-ture exists on assessing the determinants of bond ratings, with much of it focusedon macroeconomic conditions,24 economic reforms ~for example, trade commit-ment!, resource endowments, and bond default history+25 The economic consider-ations rest squarely on the factors that influence the likelihood of debt repayment+Research on the effect of political factors on bond ratings, by contrast, has receivedless attention+26 In the political economy literature, much debate has focused onthe impact of regime type on government credibility, with scholars claiming thereis a “democratic advantage” that supports democracies making good on debt obli-gations27 while others find that a democratic advantage does not exist+28 Beyondregime type, a few scholars have tested several political institutional factors oftentied to elections, executive ideology, or other variables identified with politicalstability that are expected to affect whether a country will likely institute eco-nomic policies and reforms that tend to enhance or diminish the ability or willing-ness of a government to honor debt obligations+29

Despite the many political factors assessed in the bond ratings literature, miss-ing from the discussion are those political institutions and practices more directlytied to risk, including adherence to the rule of law and whether a country has inplace a politically independent court system that is fair, impartial, and willing andable to protect property rights+ We posit that there are theoretical reasons linkingjudicial strength, rule of law, and protection of property rights to sovereign bondratings, and by this we mean theory that transcends the mere fact that the ratingagencies may say they take these factors into account+

The fact that rating agencies may take judicial strength, rule of law, and protec-tion of property rights into account does not tell us how much the CRAs considerthese things, nor necessarily why they do so+ While the bond rating agencies intheir public statements may hint at some of the why, we want to go beyond this tounderstand why it would be reasonable for the CRAs to consider these factors iftheir mission is to assess the likelihood of a country defaulting on its debt+ Inessence, we are presenting a theory that explains why judicial strength, adherenceto the rule of law, and protection of property rights will increase the likelihoodthat countries honor their sovereign bond debts+We start this process by first look-

24+ See Afonso 2003; Cantor and Packer 1996; Eichengreen and Mody 1998; Nogués and Grandes2001; and Rowland and Torres 2004+

25+ See Afonso 2003; Archer, Biglaiser, and DeRouen 2007; Biglaiser and DeRouen 2007; Cantorand Packer 1996; Eichengreen and Mody 1998; Nogués and Grandes 2001; and Rowland 2004+

26+ The political studies are limited perhaps because of the challenges in testing political factorsthat are relatively unchanging or do not lend themselves to quantitative testing+ An example is Sin-clair’s ~2005! compelling discussion of “mental frameworks” that helps to explain the mindsets ofraters but is not easily quantified+

27+ See North and Weingast 1989; and Schultz and Weingast 1996, 1998, and 2003+28+ See Archer, Biglaiser, and DeRouen 2007; Saiegh 2005; and Tomz 2007+29+ See Block and Vaaler 2004; Vaaler and McNamara 2004; and Vaaler, Schrage, and Block 2005+

See Archer, Biglaiser, and DeRouen 2007 for determinants commonly tested in the political institu-tions literature+

Finding the ‘Democratic Advantage’ in Sovereign Bond Ratings 519

ing at what the CRAs say about the factors they consider because this will helpmake a prima facie case for the theoretical assertions that we advance later+

Moody’s, S&P, and Fitch all have published statements on their web pagesdescribing in some detail their bond-rating processes and methodologies+Moody’sstates that it first assesses the economic strength of the issuing country, focusingmainly on gross domestic product ~GDP! per capita as well as diversification andsize of the economy and long-term trends+ It then examines the country’s institu-tional strength and this is where judicial strength, adherence to the rule of law,and protection of property rights come into play+According to Moody’s, “the qual-ity of a country’s institutional framework and governance is a key considerationin the rating process+ + + + This factor considers the extent to which a nation’s polit-ical, social, and legal institutions act as a constraint on sudden and adverse changesin a country’s ability and willingness to repay its debt+ The stronger the institu-tions, the greater the constraint+”30 Moody’s also mentions that it relies on infor-mation contained in the Worldwide Governance Indicators ~WGI! published bythe World Bank, and uses from these indicators three metrics: rule of law, gover-nance, and transparency+ Moody’s also notes that institutional respect for propertyrights is important+31

Similarly, among the nine separate categories used in its ratings, S&P includespolitical risk, “which encompasses institutions as well as systems and process-es+”32 S&P states that, “the stability, predictability, and transparency of a country’spolitical institutions are important considerations in analyzing the parameters foreconomic policymaking, including how quickly policy shortcomings are identi-fied and addressed+While a democratic tradition is usually supportive of the open-ness and accountability that preclude political shocks, the most important factorsare probably an independent judiciary and a civil society, particularly a freepress+”33 S&P also states that, “Well established institutions provide transparencyand predictability, particularly with regard to property rights, in an efficientmanner+”34

Fitch35 similarly lists political risk among thirteen separate areas involved in itssovereign ratings+ Under political risk, three things specifically mentioned by Fitchstand out as relevant to our analysis: ~1! description of the constitution and therelationship of the principal institutions including the courts; ~2! durability of thegovernment’s policy directions; and ~3! description of the legal framework for pri-vate property and contract settlement+36 The relevance of the first and third of theseis self-evident+ We will discuss policy durability subsequently+

30+ Moody’s 2008, 8+31+ Ibid+32+ Standard and Poor’s 2008+33+ Ibid+34+ Ibid+35+ Fitch n+d+, 9–14+36+ Ibid+

520 International Organization

Supplementing the foregoing, we also have insights into the ratings agenciesderived from interviews conducted in an earlier project by one of the authors withraters employed by Moody’s and Fitch+37 These raters specifically stated that theyconsult the WGI+38 This is important to know because one of the important met-rics in WGI is a rule of law measure, which is ~along with judicial strength andproperty rights protection! a factor of principal interest in this article+ Notably, theraters said that they do not give much weight to regime type ~democracy or author-itarian! when conducting their assessments+What they want to know is whether aregime is stable, and the mere fact that a country is democratic or authoritarian isnot determinative to this issue+ Such an approach is in line with the idea that weargue in this article—that institutional strength as nested within democracy is impor-tant, not the mere fact that a country is democratic+

From a theoretical standpoint there are a number of reasons why we expectjudicial strength, rule of law, and protection of property rights to be important forincreasing the likelihood that countries will honor their sovereign bond debts+39

First, strong courts and adherence to the rule of law contribute to political stabil-ity, a matter of concern for foreign investors of all kinds, including those holdingsovereign bonds+ Governments subject to political instability are more inclined toengage in policies detrimental to their ability, or willingness, to repay sovereigndebt+ Two theoretical strands connect strong courts0rule of law with politicalstability—insurance policy theory and a variation of credible commitment theory+Insurance policy theory suggests that opposing political forces operating undercompetitive conditions are motivated to install strong and independent courts toenforce a democratic bargain between the governing party and its challengers+Because of competitive balance, even a governing party must contemplate the pos-sibility of some day entering the opposition+ It is better for those currently gov-erning to give up prerogatives while in office as the price to pay to avoid havingseriously diminished rights in the future when out of power+40 This promotes polit-ical stability by encouraging both those in power and in the opposition to play bycourt-enforced legal rules of the game+ Commitment theory also comes into playin the form of an agreement between all political participants, backed by the courts~which makes the commitment credible!, to continue playing the democratic gamerather than defect to extra-legal regime change+41

37+ Phone interviews with two Fitch bond raters, 20 December 2005; and phone interviews withfour Moody’s bond raters, 30 November and 14 December 2005+

38+ Kaufmann, Kraay, and Mastruzzi 2009 developed the WGI+ The data set is available at ^http:00info+worldbank+org0governance0wgi0index+asp&+ Accessed 24 April 2012+

39+ For political economy studies that stress the benefits of quality courts, rule of law, and stableproperty rights for attracting capital, see Biglaiser and Staats 2010; Brunetti, Kisunko, and Weder 1997;Feng 2001; Globerman and Shapiro 2002; Jensen 2003 and 2006; Levine 1998; Li 2006 and 2009; Liand Resnick 2003; North 1990; Sherwood, Shepherd, and De Souza 1994; and Staats and Biglaiser2011 and 2012+

40+ See Ginsburg 2003, 73, 78; Finkel 2004 and 2005; and Chavez 2004+41+ Ginsburg 2003, 73, 78+

Finding the ‘Democratic Advantage’ in Sovereign Bond Ratings 521

Second, a country less committed to the rule of law is not as prone to repaysovereign debt+ Governments that ignore the rule of law are more likely to engagein arbitrary policy changes and politically driven policy choices, especially dur-ing election years, that include unsustainable social welfare plans that harm busi-ness interests+42 Outright corruption is a concern but so are the possibilities thatgovernment will impose high business taxes to finance social welfare initiativesor strictly regulate business operations to satisfy populist demands+ Systems com-mitted to the rule of law, especially when courts are given effective powers, areexpected to constrain arbitrary and extra-legal actions by governmental decisionmakers and policymakers+43 Governments bring credibility to their commitmentsby delegating to courts the authority to force current and future governments toconduct themselves in accordance with the law+44 This does not guarantee thatcurrent policies will persist, or that government will totally refrain from enactingpolicies harmful to business or the economy generally+ However, courts can requiregovernment to follow established legal procedures when it wants to do some-thing that affects business interests+45 It might have to give advance notice ofproposed changes, conduct public hearings, make formal findings, get legislationpassed, or even in some cases amend the constitution+ This court-enforced “con-stitutionalization” of rights46 makes change more difficult and costly, and tendsto slow things down, which supports investor confidence in the stability of poli-cies+47 S&P seems to have something like this in mind when describing its ratingmethodology: “Due to its decentralized decision-making processes, a market econ-omy with legally enforceable property rights tends to be less prone to policyerror and more respectful of the interests of creditors than one where the publicsector dominates+”48 Moody’s also takes a similar approach, and “considers theextent to which a nation’s political, social, and legal institutions act as a con-straint on sudden and adverse changes in a country’s ability and willingness torepay its debt+”49

A final theoretical reason why countries high in judicial strength, adherence tothe rule of law, and protection of property rights are expected to pay back theirsovereign debts relates to reputation+ Tomz50 contends that a loss of reputation inone area may have negative spillover effects in other areas of importance to a

42+ Brunetti, Kisunko, and Weder 1997, 10–11+43+ See Landes and Posner 1975, 882; North and Weingast 1989, 819; and Brunetti and Weder

1997, 2+ The courts complement Tomz’s ~2007! notion of the fair-weather debtor, who repays in goodtimes and potentially defaults in bad economic circumstances+

44+ See Landes and Posner 1975, 882; North and Weingast 1989, 819; and Brunetti and Weder1997, 2+

45+ See North 1990, 34, 58; and Olson 1993, 572+46+ See, for example, Schneiderman 2001, 521; and Hirschl 2004, 146– 47+47+ See Henisz 2000; Jensen 2003, 2006, and 2008; and Li 2006 and 2009+48+ Standard and Poor’s 2008+49+ Moody’s 2008, 8+50+ Tomz 2007+

522 International Organization

country+ Applying this principle to specifics, Simmons51 writes: “It seems clearthat governments that provide for a stable framework of law and system of prop-erty rights domestically are more likely to do the same for the purposes of facili-tating international transactions+” Thus, we would expect that a country with areputation for rule of law and protection of property rights will honor its inter-national obligations, including sovereign debts+ Adherence to the rule of law sug-gests a consistent and enduring commitment to honor all obligations+ Although acountry may encounter unexpected conditions in the future that virtually force itto default on an obligation, at least creditors will know that a country will noteven entertain the thought of default except under the most extraordinary of cir-cumstances+ Creditors prefer “stalwart” debtors, but at the very least they want toavoid “lemons+”52

Based on this discussion, we propose the following hypothesis:

Hypothesis: Countries that adhere to the rule of law and have in place a politi-cally independent court system that is fair, impartial, and willing and able to pro-tect property rights are likely to receive higher bond ratings than countries withoutsuch legal protections+

Research Design

We collect annual data for up to thirty-six developing countries from 1996 to 2006+The data represent all years for which data are available for our main explanatoryvariables of interest ~that is, adherence to the rule of law, judicial independence,impartial courts, and protection of property rights! as well as for CRAs+ Our cov-erage of 1996 to 2006 is useful for comparison since bond ratings and global cap-ital markets greatly increased during this period+

For the dependent variables, we use annual bond ratings published by Fitch,Moody’s, and S&P+ While our data represents all ratings during the years of cov-erage, not all the countries in our study are rated by all three agencies during theentire eleven years which creates an unbalanced data set+53 We follow previousresearch54 and convert the agency sovereign rating lettering system into ordinalvalues measured on a seventeen point ~0–16! scale, with 16 as the highest bondrating ~“AAA”! and 0 as the lowest ~“C”!+ We obtain bond-rating data using theservices of Bloomberg International+55 In instances where a bond rating changedin a given year, we use the rating that the country held for the most months+

51+ Simmons 2000, 15+52+ Tomz 2007, 18–19+53+ Fitch is especially prone to missing data in mid-to-late 1990s as it grew significantly as a result

of its mergers with International Bank Credit Analysis, Duff & Phelps Credit Rating Company, andThomson Bank Watch between 1997 and 2000+

54+ See Afonso 2003; Block and Vaaler 2004; and Vaaler, Schrage, and Block 2006+55+ Bloomberg International 2006+

Finding the ‘Democratic Advantage’ in Sovereign Bond Ratings 523

For one of our main explanatory variables, adherence to the rule of law, weemploy the WGI+ The WGI rule of law measure is defined as the “extent towhich agents have confidence in and abide by the rules of society, and in particu-lar the quality of contract enforcement, property rights, the police, and the courts,as well as the likelihood of crime and violence+”56 The various measures con-tained in WGI are derived from “several hundred individual variables measuringperceptions of governance, drawn from 35 separate data sources constructed by33 different organizations from around the world+”57 The data begins in 1996, butuntil 2002 the WGI authors collected data every two years+ To account for miss-ing data, we use a linear interpolation equation to calculate values in 1997, 1999,and 2001+ The rule of law measure is scaled from �2+5 to 2+5, with highervalues indicating better rule of law outcomes+ For our other independent variablesof interest, we rely on the judicial independence, impartial courts, and pro-tection of property rights measures contained in the Legal Structure and Secu-rity of Property Rights section of the Economic Freedom of the World ~EFW!report+58 EFW is now published annually, but prior to the 2000 report it was issuedevery five years only—the last five-year report was for 1995+We use a linear inter-polation equation to calculate values for the missing years between 1995 and 1999+Each of these measures is recorded on a 0–10 scale, with 0 representing the low-est performance and 10 the highest+

We also include controls for political factors commonly used in the bond rat-ings literature such as the democratic advantage, executive party tenure, undividedgovernment, executive ideology, years left in office, electoral year, and honey-moon periods+59 Based on limited government and the dangers of lost constituentsupport if a country neglects to repay its debts, many scholars claim that there is a“democratic advantage” that allows democracies to draw in more capital,60 whileothers question the benefits of democracy for repayment+61 Some studies suggestthat election cycles and executive ideology are important determinants of bondratings+62 These authors argue that election cycles affect CRA assessments, asincumbents are expected to implement election-year policies detrimental to debtrepayment to help win re-election+ The authors also claim that the president’s ide-ology matters for CRA assessments—leftist executives oppose economic reformsthat may help with meeting debt obligations because such policies weigh mostheavily on their constituents+63 In contrast, newly elected officials often experi-

56+ Kaufmann, Kraay, and Mastruzzi 2009, 6+57+ Ibid+, 2+58+ Fraser Institute various years+59+ See Archer, Biglaiser, and DeRouen 2007; and Biglaiser and DeRouen 2007+60+ See North and Weingast 1989; and Schultz and Weingast 1996, 1998, and 2003+61+ See Saiegh 2005; and Tomz 2002 and 2007+ See also Stasavage 2002, who notes the importance

not necessarily of veto players but of cross-issue coalitions that help promote debt repayment underlimited government+

62+ See Block and Vaaler 2004; Vaaler and McNamara 2004; and Vaaler, Schrage, and Block 2005+63+ See Johnson and Crisp 2003, who argue that ideology influences policymaking+

524 International Organization

ence a honeymoon period, where they have more freedom to implement painfulreforms+ Other research suggests that the executive party’s tenure in office andundivided government are expected to affect bond ratings: an executive party thathas held power for a long time or is in a situation of undivided government isexpected to have fewer veto players that enable them to institute unpopular eco-nomic reforms to help avert bond default+ To test the “democratic advantage” argu-ment, we use the democracy measure from Polity IV,64 rescaled from a 10-pointplus and minus scale to 0–20, after which we created dummy variables of 0 forcountries scoring less than 17, representing nondemocratic regimes, and 1 for scoresof 17 or more, representing democracies+65 For executive party tenure, we assesshow many years the current executive’s party has held the executive branch+ Forundivided government, we code 1 for undivided governments and 0 for dividedgovernment+ Presidential ideology is coded 1 for leftist presidents and 0 other-wise+ Years left in office counts how many years remain in the executive’s term,while the honeymoon effect counts how long the executive has held power, andelection year assesses if it is an election year or not+ All political variables arelagged a year because it takes time for political issues to filter down to investmentpolicies+66

We control for macroeconomic conditions that include GDP growth rates, GDP,GDP per capita, total external debt, inflation, and current account balance+ HigherGDP, growth, and income levels suggest more prosperous countries, lesseningbond default risk+67 In contrast, rising external debt, inflation, and current accountdeficits increase bond default risk+ GDP and GDP per capita ~both in constant2000 dollars!, GDP growth rates, external debt and current account balance ~bothas a percent of GDP!, and inflation ~using the consumer price index! come fromthe World Bank+68 All economic controls are lagged a year, as is conventionallydone+

We also control for bond default history, trade levels, and natural resource endow-ments+ Recent bond default history suggests the probability that a bond issuer willdefault in the future+69 Higher trade and larger resource endowments are expectedto increase revenues to support debt repayment+ We follow earlier studies70 bymeasuring default history on long-term foreign currency denominated debt in thelast five years ~lagged a year! using a 0–1 indicator ~1 if default; 0 if no default!+71

To measure trade level, we use exports plus imports as a percent of GDP ~lagged!

64+ Marshall and Jaggers 2006+65+ The results remain unchanged for variables of significance if the 21-point scale is used in place

of a dummy measure for democracy+ The results are available from the authors+66+ We obtain the political data from Beck et al+ 2001+67+ Cantor and Packer, 1996, 39+68+ World Bank 2008+ See Vaaler and McNamara 2004; Vaaler, Schrage, and Block 2006; and Block

and Vaaler 2004, who also use World Bank economic measures+69+ See Archer, Biglaiser, and DeRouen 2007; and Biglaiser and DeRouen 2007+70+ Block and Vaaler 2004, 925+71+ Data come from Standard and Poor’s 2008+

Finding the ‘Democratic Advantage’ in Sovereign Bond Ratings 525

that is typically used in the literature+72 We assess natural resource endowmentsby adding lagged measures of annual ores and metals exports ~as a percent ofmerchandise exports! to fuel exports ~as a percent of merchandise exports!+73 Tradeand natural resource measures are from the World Bank+74 We also include a laggeddependent variable on the right-hand side of the equation because bond ratings arenotoriously sticky, with previous bond ratings likely to affect future ratings+75

We detected heteroskedasticity in our data using the Breusch-Pagan0Cook Weis-berg test and therefore use panel-corrected standard error parameter estimates+76

We conducted Hausman and Wald tests and determined the need to model for coun-try and year fixed-effects, which we accomplish by including dummy variablesfor each country and year+ Because we noted autocorrelation in our dependent vari-ables, we include a lagged dependent variable in all models, which, as noted before,is reasonable from a theoretical standpoint based on ratings stickiness+

Findings

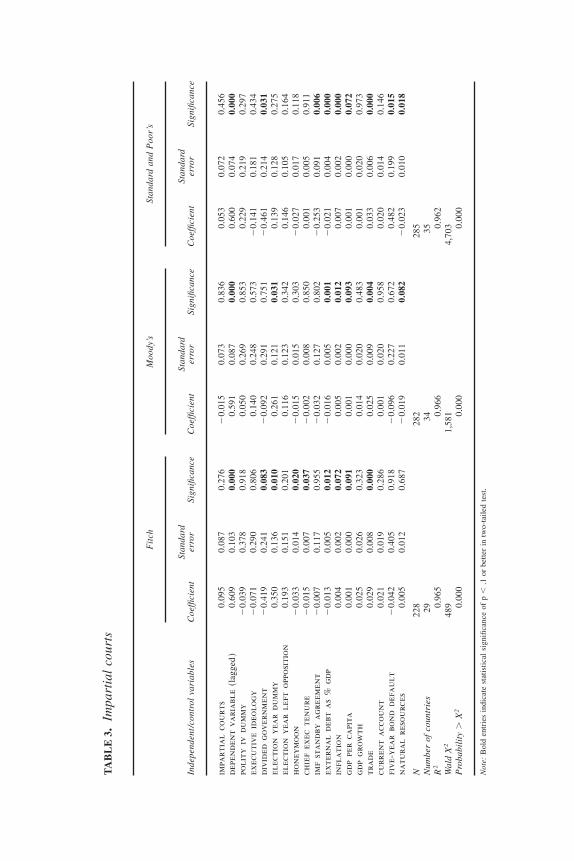

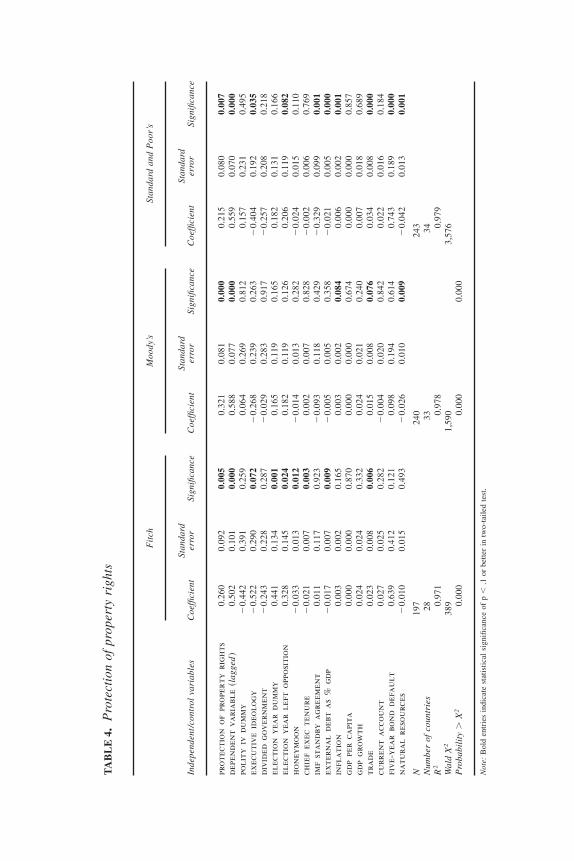

We report findings for twelve separate models, one for each of the three CRAsmatched up with each of the four independent variables of interest in Tables 1, 2,3, and 4+77 The independent variable of interest in Table 1 is rule of law+ We testthis measure in conjunction with dependent variable ratings provided by Fitch,Moody’s, and S&P along with the economic and political controls commonlyapplied in the literature+ The results in Table 1 show rule of law is statisticallysignificant for each of the rating agencies+ In terms of substantive importance,regarding Fitch, we see a 15+4 percent ~0+91 rating point! increase in rating if weincrease rule of law by one standard deviation, an 8+4 percent ~0+45! increase forMoody’s, and 17+0 percent ~0+91! for S&P+ To clarify further the substantive impor-tance of the results, a one standard deviation increase in rule of law for both Fitchand S&P would on its own move the rating of a country to almost the next highestlevel+ For Moody’s, it would move a country halfway to the next highest level+

Table 2 contains the results of judicial independence on ratings from the threeCRAs+ The results in each case again are statistically significant+ For substantiveimportance, a one standard deviation increase in judicial independence means a4+0 percent ~0+24 rating point! increase in rating by Fitch, 3+4 percent ~0+18! byMoody’s, and 6+9 percent ~0+37! by S&P+While these numbers are much less than

72+ See Jensen 2003; Li and Resnick 2003; and Tomz 2004+73+ See an approach used by Jensen 2003 who uses a similar approach+74+ World Bank 2008+75+ In the interest of conserving space, we do not report summary statistics but they are available

from the authors+76+ Beck and Katz 1996+77+ We provide separate models for each of the independent variables of interest because they are

highly correlated with each other, ranging from an r of 0+69 to 0+85+

526 International Organization

TA

BL

E1.

Rul

eof

law

Fit

chM

oody

’sSt

anda

rdan

dP

oor’

s

Inde

pend

ent/

cont

rol

vari

able

sC

oeffi

cien

tSt

anda

rder

ror

Sign

ifica

nce

Coe

ffici

ent

Stan

dard

erro

rSi

gnifi

canc

eC

oeffi

cien

tSt

anda

rder

ror

Sign

ifica

nce

rule

of

law

1+55

60+

426

0.00

00+

769

0+42

50.

070

1+52

90+

303

0.00

0d

epen

den

tv

ari

abl

e~l

agge

d!

0+57

50+

105

0.00

00+

612

0+08

20.

000

0+57

60+

076

0.00

0po

lity

ivd

um

my

�0+

237

0+35

40+

503

0+00

40+

287

0+99

00+

084

0+21

10+

691

exec

uti

ve

ideo

log

y�

0+02

40+

287

0+93

40+

094

0+23

20+

684

�0+

110

0+16

20+

500

div

ided

go

ver

nm

ent

�0+

315

0+19

20+

101

�0+

106

0+30

30+

726

�0+

374

0+17

90.

036

elec

tio

ny

ear

du

mm

y0+

335

0+13

50.

013

0+20

90+

127

0.09

90+

069

0+12

20+

576

elec

tio

ny

ear

left

opp

osi

tio

n0+

209

0+14

90+

160

0+12

90+

125

0+30

10+

160

0+10

60+

132

ho

ney

mo

on

�0+

036

0+01

50.

014

�0+

015

0+01

50+

315

�0+

029

0+01

70.

093

chie

fex

ecte

nu

re�

0+02

30+

007

0.00

1�

0+00

30+

008

0+70

1�

0+00

30+

005

0+54

0im

fst

an

dby

ag

reem

ent

0+05

30+

120

0+66

1�

0+07

20+

133

0+59

0�

0+24

20+

098

0.01

4ex

tern

al

deb

ta

s%

gd

p�

0+00

80+

004

0.04

5�

0+01

00+

004

0.01

8�

0+01

70+

004

0.00

0in

fla

tio

n0+

003

0+00

30+

230

0+00

40+

002

0.02

60+

006

0+00

20.

001

gd

ppe

rca

pita

0+00

00+

000

0+23

00+

000

0+00

00+

192

0+00

00+

000

0+19

4g

dp

gro

wth

0+04

20+

021

0.04

60+

031

0+01

90.

092

0+01

80+

018

0+33

1tr

ad

e0+

028

0+00

70.

000

0+02

50+

009

0.00

40+

029

0+00

60.

004

curr

ent

acc

ou

nt

0+01

90+

018

0+27

40+

000

0+02

00+

981

0+02

00+

014

0+15

4fi

ve

yea

rbo

nd

def

au

lt�

0+34

30+

392

0+38

1�

0+26

40+

226

0+24

30+

345

0+18

30.

060

na

tura

lre

sou

rces

0+02

20+

012

0.08

0�

0+00

50+

010

0+62

20+

001

0+01

00+

940

N23

729

129

4N

umbe

rof

coun

trie

s30

3536

R2

0+96

70+

969

0+96

4W

ald

X2

568

45,6

146,

022

Pro

babi

lity

�X

20+

000

0+00

00+

000

Not

e:B

old

entr

ies

indi

cate

stat

isti

cal

sign

ifica

nce

ofp

,+1

orbe

tter

intw

o-ta

iled

test+

was the case with rule of law, they still show the importance of an independentcourt system in the overall makeup of bond ratings+ In Table 3, we see that merelyhaving an impartial court system does not in any statistically significant way affectratings from any of the companies+ Table 4 presents the results of property rightsprotection on ratings+ As we see, protection of property rights is statistically sig-nificant for each CRA+ Substantively, a one standard deviation increase in protec-tion of property rights means a 5+6 percent ~0+33! increase in a Fitch rating, 7+8percent ~0+42! in Moody’s, and 5+2 percent ~0+28! in S&P+

Among the economic controls, in support of the literature, trade and external debtappear to be most critical and statistically significant in nearly all the models, withhigher trade seen positively by bond raters while growing debt is perceived nega-tively+ Inflation is also significant in several models but, surprisingly, it positivelyinfluences bond ratings+ Among the political controls, few are consistently statis-tically significant+ The election year dummy, which reflects the political businesscycle, is significant in half the models+ The honeymoon effect and chief executivetenure are significant and negative for all the Fitch models but generally not forMoody’s or S&P+ Interestingly, the democracy variable is not significant in any ofthe twelve models, confirming previous work78 suggesting that the democraticadvantage based on regime type appears to have little influence on bond ratings+

Conclusion

Previous empirical research on the effects of political institutions on CRA bondratings has generally found that political variables have minimal impact comparedto economic factors+ However, missing from earlier work is the effect of institu-tional factors that tend to minimize investor risk, including adherence to the ruleof law, strength, and independence of the judicial sector, and protection of prop-erty rights+ The fact that bond raters in interviews and in written work assert thatpolitical risk influences their ratings—and in the case of Fitch and Moody’s, ana-lysts even mention that rule of law measures from the WGI are consulted—makesit even more important to assess the effects of political risk on bond ratings+

Our findings indicate that political risk factors strongly influence CRA ratings+Complementing political risk research on FDI79 and building on political econ-omy work,80 these findings should send a clear message to developing countriesof the profound benefits they might realize by reforming and strengthening judi-cial institutions and otherwise paying heed to the need for respecting the rule oflaw and protecting property rights+ To accomplish change in political risk factorsrequires that elected leaders be convinced of the payoffs that can be achieved+We

78+ See Archer, Biglaiser, and DeRouen 2007; and Biglaiser and DeRouen 2007+79+ See Biglaiser and Staats 2010; Henisz 2000; Jensen 2003, 2006, and 2008; Li 2006; Li and

Resnick 2003; Malesky 2007; and Pinto and Pinto 2008+80+ See Mosley 2003; Simmons 2000; and Tomz 2007+

528 International Organization

TA

BL

E2.

Judi

cial

inde

pend

ence

Fit

chM

oody

’sSt

anda

rdan

dP

oor’

s

Inde

pend

ent/

cont

rol

vari

able

sC

oeffi

cien

tSt

anda

rder

ror

Sign

ifica

nce

Coe

ffici

ent

Stan

dard

erro

rSi

gnifi

canc

eC

oeffi

cien

tSt

anda

rder

ror

Sign

ifica

nce/

i&

jud

icia

lin

dep

end

ence

0+13

30+

063

0.03

50+

101

0+05

70.

075

0+20

40+

054

0.00

0d

epen

den

tv

ari

abl

e~l

agge

d!

0+53

00+

105

0.00

00+

574

0+08

70.

000

0+57

00+

069

0.00

0po

lity

ivd

um

my

�0+

453

0+43

20+

295

�0+

025

0+27

70+

927

0+13

80+

218

0+52

6ex

ecu

tiv

eid

eolo

gy

�0+

486

0+30

30+

108

�0+

209

0+26

90+

438

�0+

410

0+16

90.

015

div

ided

go

ver

nm

ent

�0+

276

0+23

60+

241

�0+

057

0+32

30+

860

�0+

315

0+20

60+

127

elec

tio

ny

ear

du

mm

y0+

436

0+13

10.

001

0+17

10+

122

0+16

20+

176

0+12

30+

153

elec

tio

ny

ear

left

opp

osi

tio

n0+

365

0+15

00.

015

0+18

20+

108

0.09

10+

223

0+11

40.

051

ho

ney

mo

on

�0+

031

0+01

40.

031

�0+

014

0+01

40+

296

�0+

020

0+01

50+

177

chie

fex

ecte

nu

re�

0+01

70+

007

0.02

40+

005

0+00

80+

537

0+00

30+

005

0+51

2im

fst

an

dby

ag

reem

ent

�0+

034

0+12

20+

779

�0+

133

0+12

30+

278

�0+

390

0+10

50.

000

exte

rna

ld

ebt

as

%g

dp

�0+

018

0+00

70.

008

�0+

006

0+00

50+

287

�0+

021

0+00

50.

000

infl

ati

on

0+00

30+

002

0+15

90+

002

0+00

20+

257

0+00

60+

002

0.00

0g

dp

per

capi

ta0+

000

0+00

00+

873

0+00

00+

000

0+46

00+

000

0+00

00+

763

gd

pg

row

th0+

018

0+02

70+

499

0+01

50+

023

0+49

60+

005

0+01

80+

773

tra

de

0+02

40+

008

0.00

30+

016

0+00

80.

052

0+03

60+

007

0.00

0cu

rren

ta

cco

un

t0+

023

0+02

60+

376

�0+

017

0+02

10+

426

0+02

10+

016

0+19

3fi

ve

yea

rbo

nd

def

au

lt0+

772

0+51

40+

133

0+10

70+

223

0+63

30+

766

0+18

00.

000

na

tura

lre

sou

rces

�0+

004

0+01

50+

779

�0+

017

0+01

30+

169

�0+

033

0+01

30.

010

N19

623

924

2N

umbe

rof

coun

trie

s28

3334

R2

0+96

90+

973

0+97

8W

ald

X2

738

4,01

694,3

44P

roba

bili

ty.

X2

0+00

00+

000

0+00

0

Not

e:B

old

entr

ies

indi

cate

stat

isti

cal

sign

ifica

nce

ofp

,+1

orbe

tter

intw

o-ta

iled

test+

TA

BL

E3.

Impa

rtia

lco

urts

Fit

chM

oody

’sSt

anda

rdan

dP

oor’

s

Inde

pend

ent/

cont

rol

vari

able

sC

oeffi

cien

tSt

anda

rder

ror

Sign

ifica

nce

Coe

ffici

ent

Stan

dard

erro

rSi

gnifi

canc

eC

oeffi

cien

tSt

anda

rder

ror

Sign

ifica

nce

impa

rtia

lco

urt

s0+

095

0+08

70+

276

�0+

015

0+07

30+

836

0+05

30+

072

0+45

6d

epen

den

tv

ari

abl

e~l

agge

d!

0+60

90+

103

0.00

00+

591

0+08

70.

000

0+60

00+

074

0.00

0po

lity

ivd

um

my

�0+

039

0+37

80+

918

0+05

00+

269

0+85

30+

229

0+21

90+

297

exec

uti

ve

ideo

log

y�

0+07

10+

290

0+80

60+

140

0+24

80+

573

�0+

141

0+18

10+

434

div

ided

go

ver

nm

ent

�0+

419

0+24

10.

083

�0+

092

0+29

10+

751

�0+

461

0+21

40.

031

elec

tio

ny

ear

du

mm

y0+

350

0+13

60.

010

0+26

10+

121

0.03

10+

139

0+12

80+

275

elec

tio

ny

ear

left

opp

osi

tio

n0+

193

0+15

10+

201

0+11

60+

123

0+34

20+

146

0+10

50+

164

ho

ney

mo

on

�0+

033

0+01

40.

020

�0+

015

0+01

50+

303

�0+

027

0+01

70+

118

chie

fex

ecte

nu

re�

0+01

50+

007

0.03

7�

0+00

20+

008

0+85

00+

001

0+00

50+

911

imf

sta

nd

bya

gre

emen

t�

0+00

70+

117

0+95

5�

0+03

20+

127

0+80

2�

0+25

30+

091

0.00

6ex

tern

al

deb

ta

s%

gd

p�

0+01

30+

005

0.01

2�

0+01

60+

005

0.00

1�

0+02

10+

004

0.00

0in

fla

tio

n0+

004

0+00

20.

072

0+00

50+

002

0.01

20+

007

0+00

20.

000

gd

ppe

rca

pita

0+00

10+

000

0.09

10+

001

0+00

00.

093

0+00

10+

000

0.07

2g

dp

gro

wth

0+02

50+

026

0+32

30+

014

0+02

00+

483

0+00

10+

020

0+97

3tr

ad

e0+

029

0+00

80.

000

0+02

50+

009

0.00

40+

033

0+00

60.

000

curr

ent

acc

ou

nt

0+02

10+

019

0+28

60+

001

0+02

00+

958

0+02

00+

014

0+14

6fi

ve-

yea

rbo

nd

def

au

lt�

0+04

20+

405

0+91

8�

0+09

60+

227

0+67

20+

482

0+19

90.

015

na

tura

lre

sou

rces

0+00

50+

012

0+68

7�

0+01

90+

011

0.08

2�

0+02

30+

010

0.01

8

N22

828

228

5N

umbe

rof

coun

trie

s29

3435

R2

0+96

50+

966

0+96

2W

ald

X2

489

1,58

14,

703

Pro

babi

lity

.X

20+

000

0+00

00+

000

Not

e:B

old

entr

ies

indi

cate

stat

isti

cal

sign

ifica

nce

ofp

,+1

orbe

tter

intw

o-ta

iled

test+

TA

BL

E4.

Pro

tect

ion

ofpr

oper

tyri

ghts

Fit

chM

oody

’sSt

anda

rdan

dP

oor’

s

Inde

pend

ent/

cont

rol

vari

able

sC

oeffi

cien

tSt

anda

rder

ror

Sign

ifica

nce

Coe

ffici

ent

Stan

dard

erro

rSi

gnifi

canc

eC

oeffi

cien

tSt

anda

rder

ror

Sign

ifica

nce

pro

tect

ion

of

pro

pert

yri

gh

ts0+

260

0+09

20.

005

0+32

10+

081

0.00

00+

215

0+08

00.

007

dep

end

ent

va

ria

ble

~lag

ged

!0+

502

0+10

10.

000

0+58

80+

077

0.00

00+

559

0+07

00.

000

poli

tyiv

du

mm

y�

0+44

20+

391

0+25

90+

064

0+26

90+

812

0+15

70+

231

0+49

5ex

ecu

tiv

eid

eolo

gy

�0+

522

0+29

00.

072

�0+

268

0+23

90+

263

�0+

404

0+19

20.

035

div

ided

go

ver

nm

ent

�0+

243

0+22

80+

287

�0+

029

0+28

30+

917

�0+

257

0+20

80+

218

elec

tio

ny

ear

du

mm

y0+

441

0+13

40.

001

0+16

50+

119

0+16

50+

182

0+13

10+

166

elec

tio

ny

ear

left

opp

osi

tio

n0+

328

0+14

50.

024

0+18

20+

119

0+12

60+

206

0+11

90.

082

ho

ney

mo

on

�0+

033

0+01

30.

012

�0+

014

0+01

30+

282

�0+

024

0+01

50+

110

chie

fex

ecte

nu

re�

0+02

10+

007

0.00

30+

002

0+00

70+

828

�0+

002

0+00

60+

769

imf

sta

nd

bya

gre

emen

t0+

011

0+11

70+

923

�0+

093

0+11

80+

429

�0+

329

0+09

90.

001

exte

rna

ld

ebt

as

%g

dp

�0+

017

0+00

70.

009

�0+

005

0+00

50+

358

�0+

021

0+00

50.

000

infl

ati

on

0+00

30+

002

0+16

50+

003

0+00

20.

084

0+00

60+

002

0.00

1g

dp

per

capi

ta0+

000

0+00

00+

870

0+00

00+

000

0+67

40+

000

0+00

00+

857

gd

pg

row

th0+

024

0+02

40+

332

0+02

40+

021

0+24

00+

007

0+01

80+

689

tra

de

0+02

30+

008

0.00

60+

015

0+00

80.

076

0+03

40+

008

0.00

0cu

rren

ta

cco

un

t0+

027

0+02

50+

282

�0+

004

0+02

00+

842

0+02

20+

016

0+18

4fi

ve-

yea

rbo

nd

def

au

lt0+

639

0+41

20+

121

0+09

80+

194

0+61

40+

743

0+18

90.

000

na

tura

lre

sou

rces

�0+

010

0+01

50+

493

�0+

026

0+01

00.

009

�0+

042

0+01

30.

001

N19

724

024

3N

umbe

rof

coun

trie

s28

3334

R2

0+97

10+

978

0+97

9W

ald

X2

389

1,59

03,

576

Pro

babi

lity

.X

20+

000

0+00

00+

000

Not

e:B

old

entr

ies

indi

cate

stat

isti

cal

sign

ifica

nce

ofp

,+1

orbe

tter

intw

o-ta

iled

test+

know from the judicial literature that survival-minded political leaders will del-egate power to the courts for two reasons: independent courts, by protectingeverybody’s rights, can convince opposition parties to join or continue playing thedemocratic game rather than attempting to overthrow the existing regime by force;and courts can protect the rights of the current ruling party when they ultimatelybecome the party in opposition+81 To these two reasons we can now suggest athird+ Economic success goes a long way toward continuing electoral success forthose holding political office; economic failure can surely lead to electoral ruin+For developing countries in dire need of outside capital to achieve economic suc-cess, the benefit to political leaders derived from moving toward strong and inde-pendent courts, adherence to the rule of law, and protection of property rightsseems altogether clear+ But political leaders need to be convinced of this connec-tion+ In an interview conducted by one of the authors with Uruguay’s ex-presidentJulio María Sanguinetti less than three years after he left office82 ~who at the timewas still influential in politics throughout South America!, the former leader dis-missed the connection between judicial strength and rule of law and the ability ofa country to attract foreign capital+While he admitted that foreign holders of cap-ital made such assertions, Sanguinetti said he strongly believed that such pro-nouncements were issued as a pretext to extract concessions out of prospectiveborrowers+ Political leaders have to be convinced of the connection between polit-ical risk factors and their ability to obtain higher bond ratings before deciding tochange things very much+ The message for policymakers in the developing worldis clear: developing countries need to respect rule of law and maintain politicalinstitutions conducive to stable democracies if they hope to attract future bondhold-ers at relatively low capital costs+

References

Afonso, Antonio+ 2003+ Understanding the Determinants of Sovereign Debt Ratings: Evidence for theTwo Leading Agencies+ Journal of Economics and Finance 27 ~1!:56–74+

Archer, Candace C+, Glen Biglaiser, and Karl DeRouen, Jr+ 2007+ Sovereign Bonds and the “Demo-cratic Advantage”: Does Regime Type Affect Credit Rating Agency Ratings in the Developing World?International Organization 61 ~2!:341– 65+

Bank for International Settlements ~BIS!+ 1999+ A New Capital Adequacy Framework+ Basel, Switzer-land: Bank for International Settlements+

Beck, Nathaniel, and Jonathan N+ Katz+ 1996+ Nuisance vs+ Substance: Specifying and Estimating Time-Series-Cross-Section Models+ Political Analysis 6 ~1!:1–36+

Beck, Thorsten, George Clarke, Alberto Groff, Philip Keefer, and Patrick Walsh+ 2001+ New Tools inComparative Political Economy: The Database of Political Institutions+ World Bank Economic Review15 ~1!:165–76+

Bhatia,Ashok Vir+ 2002+ Sovereign Credit Ratings Methodology:An Evaluation+Working Paper 020170+Washington, D+C+: IMF+

81+ See Ginsburg 2003, 73, 78; Finkel 2004 and 2005; and Chavez 2004+82+ Interview with the former president in Montevideo, Uruguay, 21 April 2003+

532 International Organization

Biglaiser, Glen, and Karl DeRouen, Jr+ 2007+ Sovereign Bond Ratings and Neoliberalism in Latin Amer-ica+ International Studies Quarterly 51 ~1!:121–38+

Biglaiser, Glen, Karl DeRouen, Jr+, and Candace C+ Archer+ 2011+ Politics, Early Warning Systems,and Credit Rating Agencies+ Foreign Policy Analysis 7 ~1!:67–87+

Biglaiser, Glen, Brian Hicks, and Caitlin Huggins+ 2008+ Sovereign Bond Ratings and the DemocraticAdvantage: Portfolio Investment in the Developing World+ Comparative Political Studies 41 ~8!:1092–116+

Biglaiser, Glen, and David Lektzian+ 2011+ The Effect of Sanctions on U+S+ Foreign Direct Investment+International Organization 65 ~3!:531–51+

Biglaiser, Glen, and Joseph Staats+ 2010+ Do Political Institutions Affect Foreign Direct Investment? ASurvey of U+S+ Corporations in Latin America+ Political Research Quarterly 63 ~3!:508–22+

Block, Steven A+, and Paul M+ Vaaler+ 2004+ The Price of Democracy: Sovereign Risk Ratings, BondSpreads and Political Business Cycles in Developing Countries+ Journal of International Money andFinance 23 ~6!:917– 46+

Bloomberg International+ 2006+ International Bond Series: Bloomberg On-Line Data Services+ NewYork: Bloomberg International+

Borensztein, Eduardo, and Ugo Panizza+ 2008+ The Costs of Sovereign Default+ IMF Working Paper080238+Washington, D+C+: International Monetary Fund+Available at ^www+imf+org0external0pubs0ft0wp020080wp08238+pdf&+ Accessed 24 April 2012+

Brunetti, Aymo, and Beatrice Weder+ 1997+ Investment and Institutional Uncertainty: A ComparativeStudy of Different Uncertainty Measures+ Washington, D+C+: World Bank+

Brunetti,Aymo, Gregory Kisunko, and Beatrice Weder+ 1997+ Credibility of Rules and Economic Growth:Evidence from a Worldwide Survey of the Private Sector+World Bank Policy Research Paper 1760+Washington, D+C+:World Bank+ Available at ^http:00go+worldbank+org0FOWNFWGUZ0&+ Accessed24 April 2012+

Busse, Matthias+ 2004+ Transnational Corporations and Repression of Political Rights and Civil Liber-ties: An Empirical Analysis+ Kyklos 57 ~1!:45– 65+

Cantor, Richard, and Frank Packer+ 1996+ Determinants and Impact of Sovereign Credit Ratings+ Eco-nomic Policy Review 2 ~2!:37–53+

Chavez, Rebecca Bill+ 2004+ The Rule of Law in Nascent Democracies: Judicial Politics in Argentina+Palo Alto, Calif+: Stanford University Press+

Eichengreen, Barry, and Ashoka Mody+ 1998+ What Explains Changing Spreads on Emerging-MarketDebt: Fundamentals or Market Sentiment? Working Paper 6408+ Cambridge,Mass+: National Bureauof Economic Research+

Feng, Yi+ 2001+ Political Freedom, Political Instability, and Policy Uncertainty: A Study of PoliticalInstitutions and Private Investment in Developing Countries+ International Studies Quarterly 45~2!:271–94+

Ferri, Giovanni, Li-Gang Liu, and Joseph E+ Stiglitz+ 1999+ The Procyclical Role of Rating Agencies:Evidence from the East Asian Crisis+ Economic Notes 28 ~3!:335–55+

Finkel, Jodi+ 2004+ Judicial Reform in Argentina in the 1990s: How Electoral Incentives Shape Insti-tutional Change+ Latin American Research Review 39 ~3!:56–80+

———+ 2005+ Judicial Reform as Insurance Policy: Mexico in the 1990s+ Latin American Politics andSociety 47 ~1!:87–113+

Fitch+ n+d+ Fitch IBCA Sovereign Ratings: Rating Methodology+Available at ^www+docstoc+com0docs0document-preview+aspx?doc_id�33179468&+ Accessed 24 April 2012+

Fraser Institute+ Various years+ Economic Freedom of the World+ Vancouver, Canada+ Available at^www+freetheworld+com0release+html&+ Accessed 24 April 2012+

Ginsburg, Tom+ 2003+ Judicial Review in New Democracies: Constitutional Courts in Asian Cases+New York: Cambridge University Press+

Globerman, Steven, and Daniel Shapiro+ 2002+ Global Foreign Direct Investment Flows: The Role ofGovernance Infrastructure+ World Development 30 ~11!:1899–1919+

Henisz, Witold J+ 2000+ The Institutional Environment for Multilateral Investment+ Journal of Law,Economics, and Organization 16 ~2!:334– 64+

Finding the ‘Democratic Advantage’ in Sovereign Bond Ratings 533

Hirschl, Ran+ 2004+ Towards Juristocracy: The Origins and Consequences of the New Constitutional-ism+ Cambridge, Mass+: Harvard University Press+

Jensen, Nathan M+ 2003+ Democratic Governance and Multinational Corporations: Political Regimesand Inflows of Foreign Direct Investment+ International Organization 57 ~3!:587– 616+

———+ 2006+ Nation-States and the Multinational Corporations: A Political Economy of Foreign DirectInvestment+ Princeton, N+J+: Princeton University Press+

———+ 2008+ Political Risk, Democratic Institutions, and Foreign Direct Investment+ Journal of Pol-itics 70 ~4!:1040–52+

Johnson, Gregg B+, and Brian F+ Crisp+ 2003+ Mandates, Powers, and Policies+ American Journal ofPolitical Science 47 ~1!:128– 42+

Kaminsky, Graciela, and Sergio L+ Schmukler+ 2002+ Emerging Market Instability: Do Sovereign Rat-ings Affect Country Risk and Stock Returns? World Bank Economic Review 16 ~2!:171–95+

Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi+ 2009+ Governance Matters VIII: Aggregateand Individual Governance Indicators 1996–2008+ World Bank Policy Research Paper 4978+ Wash-ington, D+C+: World Bank+

Landes, William M+, and Richard A+ Posner+ 1975+ The Independent Judiciary in an Interest-GroupPerspective+ Journal of Law and Economics 18 ~3!:875–901+

Levine, Ross+ 1998+ The Legal Environment, Banks, and Long-Run Economic Growth+ Journal ofMoney, Credit, and Banking 30 ~3!:596– 613+

Li, Quan+ 2006+ Democracy, Autocracy, and Tax Incentives to Foreign Direct Investors: A Cross-National Analysis+ Journal of Politics 68 ~1!:62–74+

———+ 2009+ Democracy, Autocracy, and Expropriation of Foreign Direct Investment+ ComparativePolitical Studies 42 ~8!:1098–127+

Li, Quan, and Adam Resnick+ 2003+ Reversal of Fortunes: Democratic Institutions and Foreign DirectInvestment Inflows to Developing Countries+ International Organization 57 ~1!:175–211+

Malesky, Edmund J+ 2007+ Provincial Governance and Foreign Direct Investment in Vietnam+ In TwentyYears of Foreign Investment in Vietnam: Reviewing and Looking Forward, edited by Pham TuyetNga and Nguyen Binh Thuy, 147– 62+ Hanoi, Vietnam: Knowledge Publishing House+

Marshall, Monty G+, and Keith Jaggers+ 2006+ Polity IV Project: Political Regime Characteristics andTransitions, 1800–2004+ Severn,Md+: Center for Systemic Peace+Available at ^www+systemicpeace+org0polity0polity4+htm&+ Accessed 24 April 2012+

Moody’s+ 2008+ Rating Methodology: Sovereign Bond Ratings+ September 2008 ~Doc+ 109490!+ NewYork: Moody’s+

Mosley, Layna+ 2003+ Global Capital and National Governments+ Cambridge: Cambridge UniversityPress+

Nogués, Julio, and Martín Grandes+ 2001+ Country Risk: Economic Policy, Contagion Effect or Polit-ical Noise+ Journal of Applied Economics 4 ~1!:125– 62+

North, Douglass C+ 1990+ Institutions, Institutional Change and Economic Performance+ New York:Cambridge University Press+

North, Douglass C+, and Barry R+ Weingast+ 1989+ Constitutions and Commitment: The Evolution ofInstitutional Governing Public Choice in Seventeenth-Century England+ Journal of Economic His-tory 49 ~4!:803–32+

Olson, Mancur+ 1993+ Dictatorship, Democracy, and Development+ American Political Science Review87 ~3!:567–76+

Pinto, Pablo M+, and Santiago Pinto+ 2008+ The Politics of Investment: Partisanship and the SectoralAllocation of Foreign Direct Investment+ Economics and Politics 20 ~2!:216–54+

Rowland, Peter+ 2004+ Determinants of Spread and Credit Ratings and Creditworthiness for EmergingMarket Sovereign Debt: A Follow-Up Study Using Pooled Data Analysis+ Bogotá, Colombia: Bancode la República+ Available at ^www+banrep+gov+co0docum0ftp0borra296+pdf&+ Accessed 24 April2012+

Rowland, Peter, and José L+ Torres+ 2004+ Determinants of Spread and Creditworthiness for EmergingMarket Sovereign Debt:A Panel Data Study+ Bogatá, Colombia: Banco de la República+Available at^www+banrep+gov+co0docum0ftp0borra295+pdf&+ Accessed 24 April 2012+

534 International Organization

Saiegh, Sebastian M+ 2005+ Do Countries Have a ‘Democratic Advantage’? Political Institutions,Multi-lateral Agencies, and Sovereign Borrowing+ Comparative Political Studies 38 ~4!:366–87+

Schneiderman, David+ 2001+ Investment Rules and the Rule of Law+ Constellations 8 ~4!:521–37+Schultz, Kenneth A+, and Barry R+Weingast+ 1996+ The Democratic Advantage: The Institutional Sources

of State Power in International Competition+ Stanford, Calif+: Hoover Institution Press+———+ 1998+ Limited Governments, Powerful States+ In Strategic Politicians, Institutions, and For-

eign Policy, edited by Randolph M+ Siverson, 15–50+ Ann Arbor: University of Michigan Press+———+ 2003+ The Democratic Advantage: Institutional Foundations of Financial Power in Inter-

national Competition+ International Organization 57 ~1!:3– 42+Schwarcz, Steven L+ 2001+ The Role of Credit Agencies in Global Market Regulation+ In Regulating

Financial Services and Markets in the 21st Century, edited by Eilís Ferran and Charles A+E+ Goodhart,297–310+ Portland, Ore+: Hart+

Setty, Gautam, and Randall Dodd+ 2003+ Credit Rating Agencies: Their Impact on Capital Flows toDeveloping Countries+ Special Policy Report 6+ Washington, D+C+: Financial Policy Forum, Deriv-atives Study Center+ Available at ^www+financialpolicy+org0FPFSPR6+pdf&+ Accessed 24 April 2012+

Sherwood, Robert M+, Geoffrey Shepherd, and Celso Marcos De Souza+ 1994+ Judicial Systems andEconomic Performance+ Quarterly Review of Economics and Finance 34 ~suppl+ 1!:101–16+

Simmons, Beth A+ 2000+ Money and the Law: Why Comply with the Public International Law ofMoney? Yale Journal of International Law 25 ~2!:323– 62+

Sinclair, Timothy J+ 2005+ The New Masters of Capital: American Bond Rating Agencies and the Pol-itics of Creditworthiness+ Ithaca, N+Y+: Cornell University Press+

Staats, Joseph L+, and Glen Biglaiser+ 2011+ The Effects of Judicial Strength and Rule of Law on Port-folio Investment in the Developing World+ Social Science Quarterly 92 ~3!:609–30+

———+ 2012+ “Foreign Direct Investment in Latin America: The Importance of Judicial Strength andRule of Law+” International Studies Quarterly 56 ~1!:193–202+

Standard and Poor’s ~S&P!+ 2008+ Sovereign Credit Ratings: A Primer+ Available at ^www+standardandpoors+com0ratings0articles0en0us0?assetID�1245227841398&+Accessed 24 April 2012+

Stasavage, David+ 2002+ Credible Commitment in Early Modern Europe: North and Weingast Revis-ited+ Journal of Law, Economics, and Organization 18 ~1!:155–86+

Tomz, Michael+ 2002+ Democratic Default; Domestic Audiences, and Compliance with InternationalAgreements+ Paper presented at the 98th Annual Meeting of the American Political Science Associ-ation, August0September, Boston+

———+ 2004+ Finance and Trade: Issue Linkage and the Enforcement of International Debt Contracts+Paper presented at the 100th Annual Meeting of the American Political Association,August, Chicago+

———+ 2007+ Reputation and International Cooperation: Sovereign Debt Across Three Centuries+Princeton, N+J+: Princeton University Press+

Vaaler, Paul M+, and Gerry McNamara+ 2004+ Crisis and Competition in Expert Organizational Deci-sion Making: Credit-Rating Agencies and Their Response to Turbulence in Emerging Economies+Organization Science 15 ~6!:687–703+

Vaaler, Paul M+, Burkhard N+ Schrage, and Steven A+ Block+ 2005+ Counting the Investor Vote: Polit-ical Business Cycle Effects on Sovereign Bond Spreads in Developing Countries+ Journal of Inter-national Business Studies 36 ~1!:62–88+

———+ 2006+ Elections, Opportunism, Partisanship and Sovereign Ratings in Developing Countries+Review of Development Economics 10 ~1!:154–70+

White, Lawrence J+ 2009+ The Credit-Rating Agencies and the Subprime Debacle+ Critical Review 21~2–3!:389–99+

World Bank+ 2008+ World Development Indicators 2008+ Washington, D+C+: World Bank+ Available at^http:00data+worldbank+org0sites0default0files0wdi08+pdf&+ Accessed 24 April 2012+

Finding the ‘Democratic Advantage’ in Sovereign Bond Ratings 535