Financial Empowerment and Credit Accessibility: A Business Model for Poverty Alleviation in Egypt

40

Financial Empowerment and Credit Accessibility: A Business Model for Poverty Alleviation in Egypt By Ali A. Massoud* * The author is an associate professor at Economics Department, Faculty of Commerce, Sohag University, Sohag, Egypt. Email: [email protected] Phone: ++20-1148482200. 1

Transcript of Financial Empowerment and Credit Accessibility: A Business Model for Poverty Alleviation in Egypt

Financial Empowerment and Credit Accessibility:A Business Model for Poverty Alleviation in

EgyptBy

Ali A. Massoud*

* The author is an associate professor at Economics Department, Faculty of Commerce, Sohag University, Sohag, Egypt.

Email: [email protected]

Phone: ++20-1148482200.

1

Keywords: Financial Empowerment, Financial Inclusion, Credit Accessibility, and Poverty alleviation.

Financial Empowerment and Credit Accessibility:

A Business Model for Poverty Alleviation in Egypt

By

Ali A. Massoud

Associate Professor at the Economics Department, Faculty of Commerce,

Sohag University, Sohag, Egypt

Abstract:

Using finance in order to alleviate poverty is a major topic in

development. Microfinance has received tremendous attention over

the last four decades. The main business models for microfinance

did not deliver the desired outcomes. Both the Grameen Bank model

and the Self-Help Groups (SHGs) Model did not have a significant

impact on poverty alleviation.

The main goal of this paper is to develop a new business model to

deal with poverty in Egypt that can be an alternative for Grameen

and the SHGs models. The main contribution of this paper is

emphasizing the importance of the business environment as a

2

complement to the financial aspect of poverty alleviation. The

new concept that the proposed model is built on is “Financial

Empowerment.” This concept includes both financial inclusion in

its broad term and the business environment as an important

aspect for poverty alleviation. The proposed model was

implemented in Tahta Sohag and proved to be a great success so

far.

Introduction:

Poverty is a major global problem. The United Nations, the World

Bank, and international donors have been allocating huge sums of

financial resources for poverty alleviation. Poverty is not a

problem for poor countries only. Rather, it is a problem that

faces developing countries as well. Egypt is not an exception. It

is very important to emphasize that feeding the poor does not

alleviate poverty nor does it solve the challenges that the poor

face. For this reason, the best approach to deal with poverty is

enabling the poor to generate their own income that is enough to

meet their basic needs of food, shelter, clothes, education, and3

health. The poor suffer from challenges that make them worse off

over time. Financial difficulties, low levels of human capital,

and the inability to access financing puts the poor in a vicious

cycle of poverty. I argue that poverty alleviation efforts should

be a part of comprehensive policies for economic growth for the

poor and for social justice. In the short-run the social justice

dimension has to be given more attention in order to deal with

urgent needs for the poor, i.e. food, shelter, health, and

clothes. However, over the medium and long-run, more attention

has to be given to accumulating human capital for the poor and

empowering them financially. Governments must play a vital role

in poverty alleviation because the market fails to provide a

safety net for the poor.

The main business models that have been used by local

governments, international institutions, and donors are the

Grameen Bank Model and the Self-Help Groups (SHGs) Model. Many

studies have shown that both models are not effective in poverty

alleviation. As a matter of fact, instead of leading to

improvement of the financial situation for the poor, they lead to

an increase in the financial vulnerability of the poor. This has

been the case in Egypt as well. As mentioned before, many studies

have shown that the business models for microfinance that have

been used in India, Bangladesh, Bolivia, and other countries did

not have a significant impact on poverty alleviation, Bateman and

Change (2012). This makes the development of a new business model

of poverty alleviation, built on financial empowerment of the

4

poor, as an important contribution to the current literature and

policymaking efforts that target poverty alleviation. All current

models concentrate only on the financial aspect of poverty

alleviation. They do not give enough attention to the other

aspects with which small businesses and entrepreneurs deal, such

as the business environment. Credit availability and financial

inclusion have not proven to have a significant impact on poverty

alleviation. Thus, financial empowerment provides a feasible

alternative for the credit availability and financial inclusion

that have been used in the existing financial models of poverty

alleviation.

This paper proceeds as follows. Section (1) sheds light on the

magnitude of poverty in Egypt. Section (2) explains financial

empowerment as a tool for poverty alleviation. Section (3)

discusses the main characteristics of banks as the main credit

providers in Egypt. Section (4) assesses financial empowerment in

Egypt. Section (5) presents a business model for financial

empowerment and poverty alleviation in Egypt. Section (6)

summarizes with a conclusion and policy recommendations.

(1) The magnitude of poverty in Egypt:

According to the Human Development Report, 2013, published by the

United Nations Development Program (UNDP): 22% of Egyptians are

below income poverty line; the percentage of population who live

on PPP $1.5 or less is 1.7%; the percentage of population who

live in severe poverty is 1%; and the percentage of those who are

vulnerable to poverty is 7.2% of the total population. These5

numbers did not change substantially from what they were in the

Egypt Human Development Report in 2010. According to the latter

report, the percentage of poor people in Egypt in 2008/2009 was

21.6% of the total population. In rural areas this percentage

increased to 28.9% of the total population while in the urban

areas the percentage of poor people was 11% of the population.

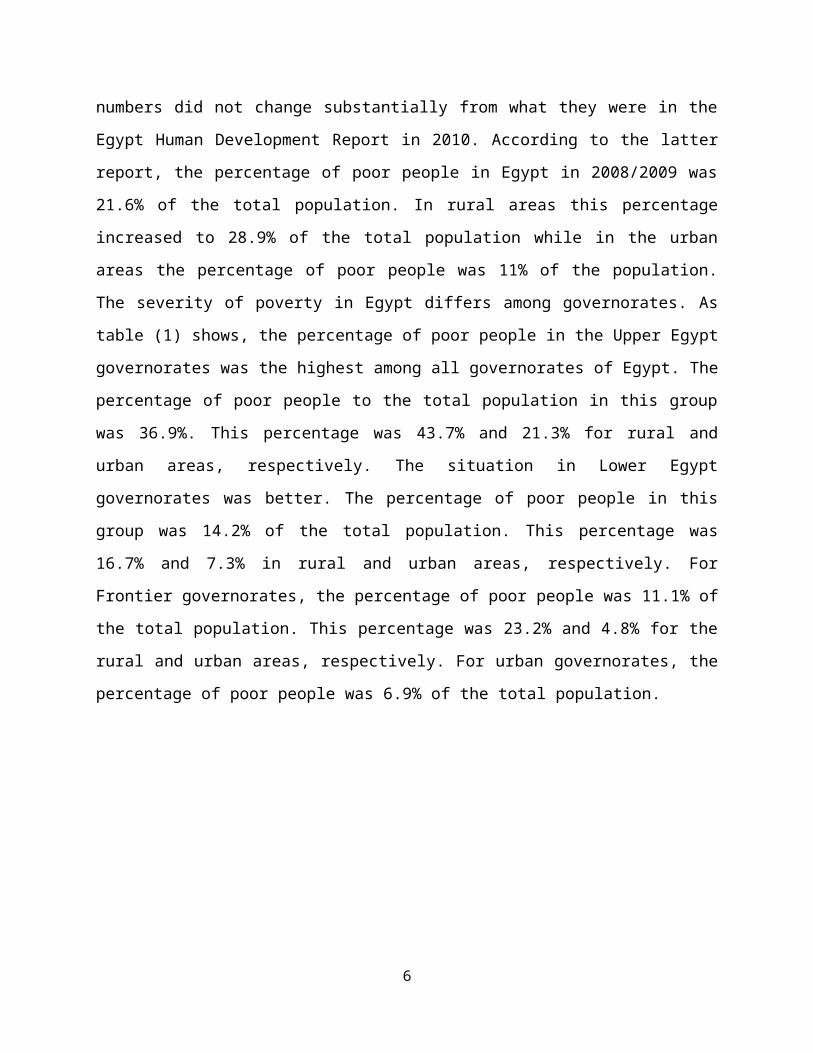

The severity of poverty in Egypt differs among governorates. As

table (1) shows, the percentage of poor people in the Upper Egypt

governorates was the highest among all governorates of Egypt. The

percentage of poor people to the total population in this group

was 36.9%. This percentage was 43.7% and 21.3% for rural and

urban areas, respectively. The situation in Lower Egypt

governorates was better. The percentage of poor people in this

group was 14.2% of the total population. This percentage was

16.7% and 7.3% in rural and urban areas, respectively. For

Frontier governorates, the percentage of poor people was 11.1% of

the total population. This percentage was 23.2% and 4.8% for the

rural and urban areas, respectively. For urban governorates, the

percentage of poor people was 6.9% of the total population.

6

Table (1)

Poverty indicators in Egypt (2008/2009)

Region Poor People to the total population(%)

Total Rural UrbanEgypt 21.6 28.9 11Urban Governorates 6.9 - -Lower Egypt Governorates 14.2 16.7 7.3Upper Egypt Governorates 36.9 43.7 21.3Frontier Governorates 11.1 23.2 4.8Source: Egypt Human Development Report, UNDP, 2010.

We conclude from the above analysis that even though poverty is a

major problem in Egypt, its severity differs among areas and

governorates. Poverty is more severe in the rural areas and in

the Upper Egypt governorates than it is in the urban areas and in

the Lower Egypt governorates.

(2) Understanding financial empowerment as a tool for poverty alleviation:

In 1970s, Dr. Muhamed Yunus put the foundation of a comprehensive

model of microfinance in Bangladesh. His experiment in micro-

financing evolved to the establishment of the Grameen Bank in

1983. Since that, microfinance has become a major topic in

development and poverty alleviation. Many studies have emphasized

the role of microfinance in the process of poverty alleviation.

Microfinance provides an economic opportunity for the poor to

change their economic situation. Economic opportunity is strongly

linked to access in financial services. Increasing access to

finance for the poor, citizens of the rural areas, and SMEs could

7

help to reduce poverty, enhance economic growth, and diversify

national economies. This approach can be classified as a bottom-

up development model. Shetty (2005) examined the impact of

microfinance on households, welfare, income, employment,

expenditure, assets, and human & social capital. He designed a

field survey and applied it on two rural areas in India in order

to determine the impact of microfinance on the above elements. By

comparing the status of the surveyed households, he found a

positive and significant impact of microfinance credit plus

services on all variables. Mosely (2001) found that microfinance is

effective in reducing poverty for those who are close to the

poverty line, but it is not effective in reducing extreme

poverty.

This view of the effectiveness of microfinance in poverty

alleviation has been challenged by Bateman and Change who have

argued that the positive expected impact of microfinance on

poverty is very limited.

“We argue that any positive outcomes are very limited in number and swamped by

much wider longer run downsides and opportunity costs at the community and

national level. Our view is that microfinance actually constitutes a powerful institutional

and political barrier to sustainable economic and social development, and to poverty

reduction. Finally, we suggest that continued support for microfinance cannot be

divorced from its supreme serviceability to the neoliberal/globalization agenda.”

As a result of the shortcomings of the microfinance models that

have been used since the 1970s, new concepts emerged to emphasis

8

the importance of the financial aspect in dealing with poverty

alleviation. This concept is known as financial inclusion. The

concept of financial inclusion has been given tremendous

attention recently. Even though there is increasing interest of

international economic institutions, policymakers, and academics

in financial inclusion, there is no unified definition for this

concept, i.e. while Allen, et.al (2012) provides a narrow definition of

financial inclusion by defining it as holding a formal account at

a financial institution. The Center for Financial Inclusion

provides a broader definition for this concept as follows:

“Full financial inclusion is a state in which all people who can use them have access to a

full suite of quality financial services, provided at affordable prices, in a convenient

manner, and with dignity for the clients. Financial services are delivered by a range of

providers, most of them private, and reach everyone who can use them, including

disabled, poor, rural, and other excluded population.”

In this paper, I introduce a new concept for dealing with poverty

through: better access to finance; a better business environment;

and a more comprehensive strategy. I call this concept “Financial

Empowerment” which is defined as the ability of individuals and

SMEs to have access to credit instruments and financial services

such as insurance, savings, and payment at reasonable costs

within a comprehensive government strategy to deal with the

business environment and other challenges that face individuals

and SMEs, i.e. marketing and economies of scale. This concept

fits the situation in Egypt where financial institutions cover

all Egypt; the cost of holding an account at banks are reasonably

9

low; and the documents required to open an account are available

for any citizen. Opening an account at an Egyptian bank only

requires the national number ID. However, the major challenge in

Egypt is getting a loan. For individuals and SMEs to get a loan

in order to start a new business or to extend an existing

business they have to get through a complicated process that ends

in most cases by refusing the loan application. On one hand, bank

loans require collateral and documentation requirements that are

very difficult for individuals and SMEs to meet. On the other

hand, banks prefer to invest in government treasury bills and

other instruments where the associated risks associated are very

low and their returns are high.

(3) The characteristics of banks as credit providers in Egypt:

To enhance the ability of individuals and MSEs in getting the

financial resources and services they need, the Egyptian

government established the Social Fund for Development (SDF), the

Development & Agriculture Credit Bank (DACB), and the Local

Development Fund (LDF). SDF provides finance, marketing, and

capacity building for individuals who want to start their own

business. DACB provides finance for farmers in order to increase

the productivity of their farms or to establish agricultural

projects. It extended its work to finance small business in all

areas. LDF was established at the Ministry of Local Development

in order to provide very low-cost finance to poor farmers.

Moreover, the Egyptian government allows business associations

and NGOs to work in the area of microfinance. Even though the

10

establishment of SDF, DACB, and LDF is very important for

providing finance to individuals and SMEs, their impact on

poverty alleviation and unemployment is very low. This can be

attributed to three main reasons. First, the fact that these three

credit providers do not follow specific business models in

providing their services which have led to channeling most of

their finance into consumption needs not into establishing new

projects or extending existing projects. Second, the absence of a

unified business model used in providing microfinance and related

services for individuals and SMEs that is connected directly to

the national development plan leads to repeating the same

mistakes by all microfinance providers. Also, it leads to

excessive lending for some sectors and activities and minimal

lending to other sectors and activities. Third, Egyptian bank

engagement in providing credit to individuals and SMEs is very

limited compared with the magnitude of finance needed to

alleviate poverty in Egypt. Moreover, resources that are

available in the SDF, DACB, and LDF are not enough to deal with

poverty alleviation in Egypt. The whole financial system in Egypt

must be re-regulated in order to play an active role in providing

finance and other related services for individuals and SMEs.

Demirguc-Kunt and Klapper (2013) differentiate between two types of

financial systems. The first are the well-functioning financial

systems which have a vital role in offering savings, credit,

payment, and risk management products to people with a range of

needs. The second is the more-inclusive financial systems which

11

allow broad access to appropriate financial services. They argued

that the latter are more likely to benefit the poor and other

disadvantaged groups. Providing access to credit and financial

services to these groups of people enhances entrepreneurship and

helps to alleviate poverty.

To investigate the current and the future role of Egyptian banks

in providing finance and other related services to individuals,

the rest of this section is allocated to examining the structure

of banks and their current role as credit providers. The source

of data used in this section is the Central Bank of Egypt (CBE).

As figure (1) shows, while the total number of operating banks in

Egypt was declining over time, the number of branches was

increasing. In 2004, the total number of banks was 61 banks. This

number declined to 39 banks by June 2011 as a result of the

decisions of some foreign banks to end their business in Egypt.

In June 5, 2012, the registration of the Arab International Bank

under the supervision of the Central Bank of Egypt increased the

number of operating banks to 40 banks instead of 39. The number

of operating banks continues to be 40 until the end of June 2013.

The number of branches was 2783 branches in 2004 and increased to

3651 branches by June 2013.

12

Figure (1)

Total number of banks and their branches operating in Egypt from2004 to 2013

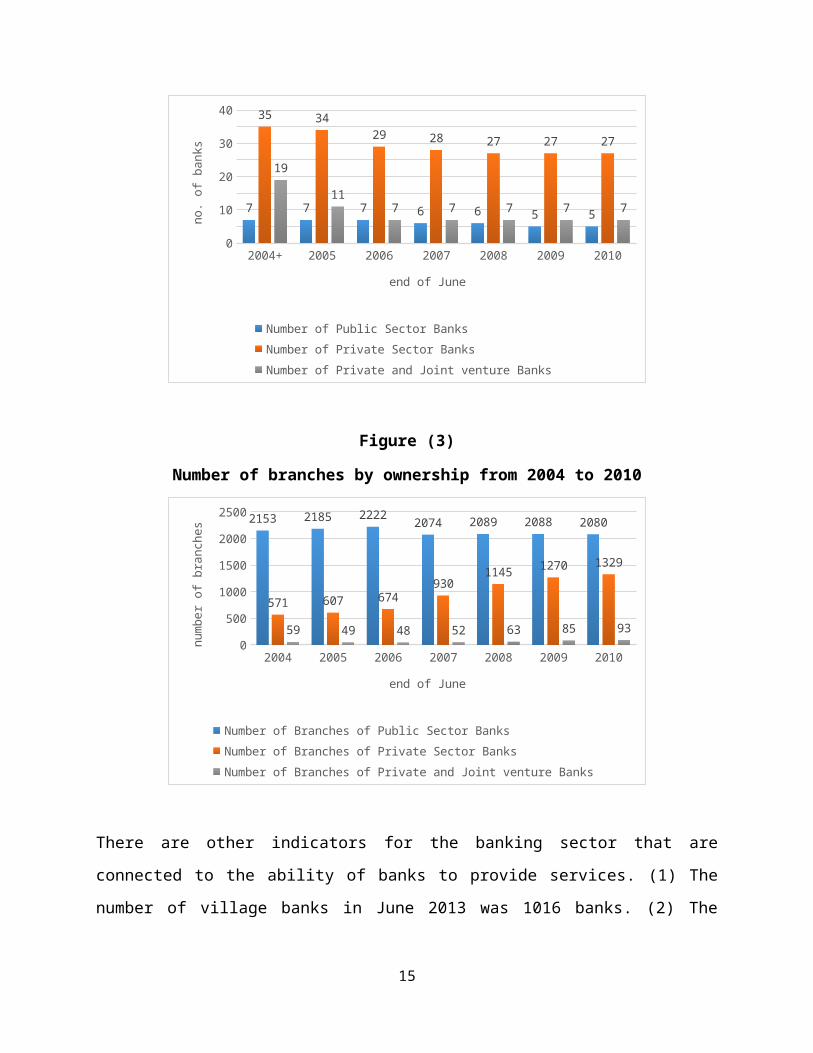

Figure (2) shows the distribution of the ownership of banks in

Egypt. As this figure shows, the majority of banks in Egypt are

13

private banks. However, when we look at the branches of the

banks, figure (3) shows that the majority of branches / banking

units are owned by the public sector. Also we note from figure

(3) that while the number of branches for public banks declined

from 2153 branches in 2004 to 2080 branches in 2010 by a

percentage decrease of 3.3%, the number of branches for private

banks increased from 571 branches to 1329 branches during the

same period with a percentage increase of 133%.

Figure (2)

Number of operating banks in Egypt by the ownership from 2004 to2010

14

2004+ 2005 2006 2007 2008 2009 20100

10

20

30

40

7 7 7 6 6 5 5

35 3429 28 27 27 27

19

117 7 7 7 7

Number of Public Sector Banks Number of Private Sector Banks Number of Private and Joint venture Banks

end of June

no. of banks

Figure (3)

Number of branches by ownership from 2004 to 2010

2004 2005 2006 2007 2008 2009 20100

500

1000

1500

2000

25002153 2185 2222 2074 2089 2088 2080

571 607 674930

1145 1270 1329

59 49 48 52 63 85 93

Number of Branches of Public Sector Banks Number of Branches of Private Sector Banks Number of Branches of Private and Joint venture Banks

end of June

number of branches

There are other indicators for the banking sector that are

connected to the ability of banks to provide services. (1) The

number of village banks in June 2013 was 1016 banks. (2) The

15

numbers of debit cards, credit cards, ATMs, and points of sale

were 12,677,275; 2,100,471; 6,283; and 45,716 respectively.

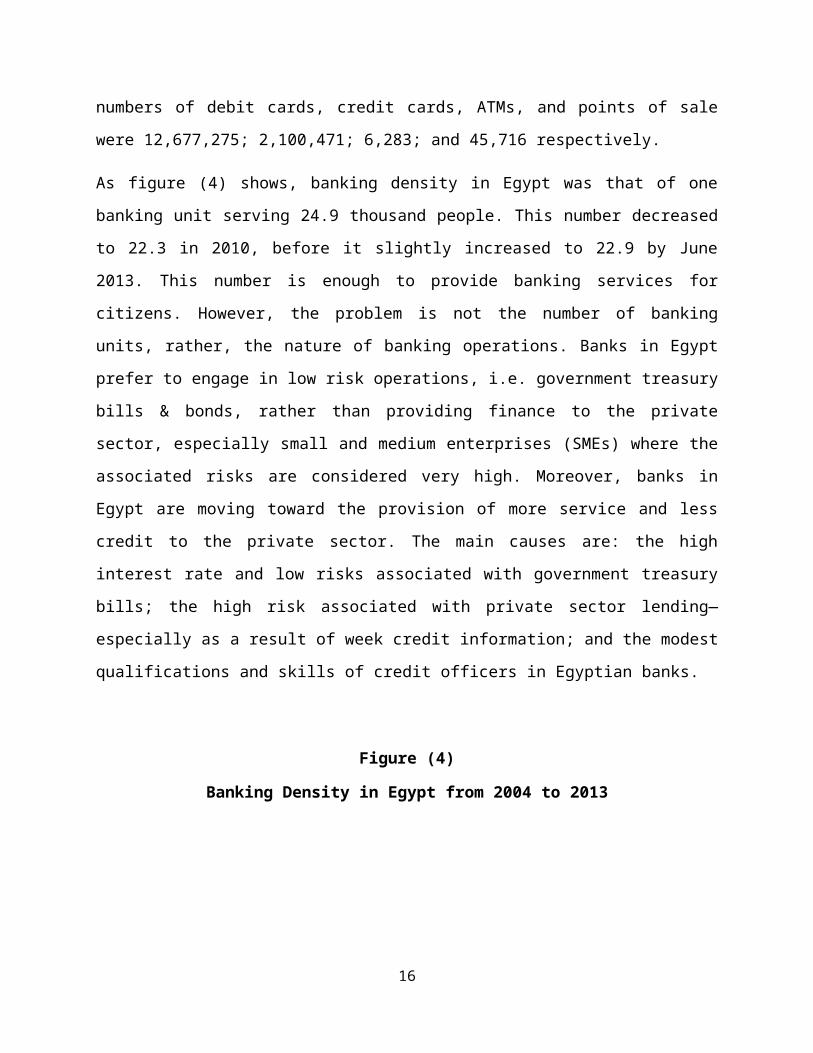

As figure (4) shows, banking density in Egypt was that of one

banking unit serving 24.9 thousand people. This number decreased

to 22.3 in 2010, before it slightly increased to 22.9 by June

2013. This number is enough to provide banking services for

citizens. However, the problem is not the number of banking

units, rather, the nature of banking operations. Banks in Egypt

prefer to engage in low risk operations, i.e. government treasury

bills & bonds, rather than providing finance to the private

sector, especially small and medium enterprises (SMEs) where the

associated risks are considered very high. Moreover, banks in

Egypt are moving toward the provision of more service and less

credit to the private sector. The main causes are: the high

interest rate and low risks associated with government treasury

bills; the high risk associated with private sector lending—

especially as a result of week credit information; and the modest

qualifications and skills of credit officers in Egyptian banks.

Figure (4)

Banking Density in Egypt from 2004 to 2013

16

2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 321

21.522

22.523

23.524

24.525

25.524.9 24.8

24.524.2

22.9

22.3 22.3 22.5 22.722.9

end of June

Population in thousands per

banking unit

Source of data: the Central Bank of Egypt.

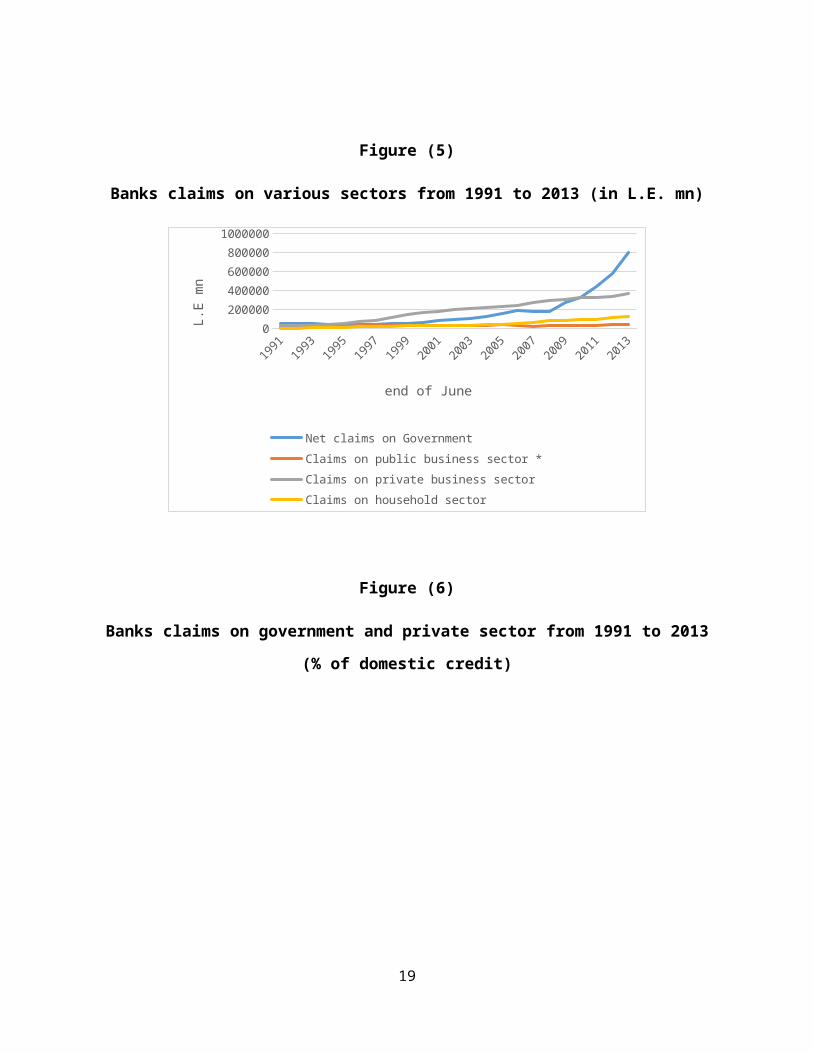

By reviewing figure (5), we can differentiate among three periods

regarding bank preferences of lending to the government versus

the private sector. The first period is before the adoption of the

Economic Reform Program in Egypt. In this period banks were

lending to the government more than to the private sector. As

figure (6) shows, in 1991 bank claims on the government accounted

for 53.5% of domestic credit, while bank claims on the private

sector only accounted for 29.9% of domestic credit. This trend

continued until 1995. One explanation for the high percentage of

bank claims on the government relative to the private sector is

the structure of the ownership of banks in Egypt during this

period. Another explanation is that risks associated with

government credit are lower than those associated with private

sector credit. The second period is from 1995 until 2010. During

this period bank claims on the private sector exceeded the bank

17

claims on the government. Over this period, bank claims on the

private sector exceeded bank claims on the government. As figure

(6) shows, in 2000, bank claims on the private sector accounted

for 56.6% of domestic credit, while bank claims on government

only accounted for 22% of domestic credit. However, after 2000

bank claims on government were increasing by rates higher than

the rate of increase of bank claims on private sector. This can

be attributed to the increasing size of treasury bills that were

issued in order to finance public budget deficit. The third period

starts from 2010. Starting from this year bank claims on

government increased steadily to account for 59.8% of domestic

credit compared with 27.5% for the private sector in June 2013.

As a result of political unrest and economic instability after

the 25th of January 2011, the risk of lending to the private

sector increased which made banks prefer to lend to the

government more than to the private sector. The increasing size

of government treasury bills, their high rate of return, and the

low level of risk associated with them, made government treasury

bills better investment tools than loans to the private sector.

18

Figure (5)

Banks claims on various sectors from 1991 to 2013 (in L.E. mn)

02000004000006000008000001000000

Net claims on Government Claims on public business sector *Claims on private business sectorClaims on household sector

end of June

L.E

mn

Figure (6)

Banks claims on government and private sector from 1991 to 2013

(% of domestic credit)

19

010203040506070

Banks Claims on Governoment Bank Claims on Private Sector Business

end of June

% of

dom

esti

c cr

edit

(4) Assessing the financial empowerment in Egypt:

Financial empowerment goes beyond financial inclusion. Financial

empowerment has two dimensions. The first dimension is financial

inclusion in its broad definition, which implies the ability of

individuals and SMEs to have access to financial resources and

services at a reasonably low cost. The second dimension is the

business environment. A good business environment is a

prerequisite for providing economic opportunity for individuals

and SMEs to manage successful businesses—the right strategy for

poverty alleviation. To assess the current situation of financial

empowerment in Egypt, the rest of this section is allocated to

examining the two dimensions of financial empowerment.

Shanakar (2013) found out that barriers to financial inclusion can

be attributed to the supply side and/or the demand side. For the

20

supply side, physical barriers, lack of suitable products, and

documentation are the main barriers. For the demand side,

psychological & cultural barriers and the lack of financial

literacy were found to be the main barriers. Allen, et.al (2012) found

out that the main reasons for not holding accounts in financial

institutions are: high costs, lack of necessary documentation,

and the long distance from banks. Singh and Yadav (2012) identified

seven reasons for banks to limit their lending to poor people.

These reasons are: irregular income patterns; inadequate credit

information; lack of collateral; illiteracy; high transaction

costs due to small sized loans; psychological & cultural

barriers; and lack of popular knowledge of financial services.

In Egypt, it is very difficult for individuals and SMEs to get

financing from financial institutions. The reason for the low

level of financial inclusion and credit accessibility in Egypt

can be attributed to two sets of factors. First, factors that are

related to the supply side. Second, factors that are related to

the demand side. The factors that are related to the supply side

are: underdeveloped financial structure, i.e. the weakness of

credit information and the lack of a clear framework for non-bank

financial institutions; the legal framework of microfinance;

limited availability and diversity of specialized financial

products and services; high fixed costs; macroeconomic

instability; low population density in some areas; high risk; the

crowding out effects of government tools; high transaction costs;

and the difficulties in managing loans to SMEs. Factors that are

21

related to the demand side are: financial illiteracy; rules and

regulations, i.e. requirements for getting a loan; high fees and

interest rates; the low level of income and savings.

The business environment in Egypt does not provide enough support

for small entrepreneurs and SMEs. One of the main indicators for

the business environment is the “ease of doing business

indicator,” published by the World Bank. According to this

indicator, Egypt ranked 128 among countries regarding the ease of

doing business in 2014. This indicator has ten sub-indicators.

The first sub-indicator is starting a business. According to this

indicator, Egypt in 2014 was ranked 50 among countries. Its rank

in 2013 was 44. Egyptian authorities have taken many steps in

order to make it easier for investors and entrepreneurs to start

business in Egypt. The number of procedures and the numbers of

days to start a business declined from 13 and 37 respectively in

2004 to 7 and 8 respectively in 2014. The second sub-indicator is

dealing with construction permits. According to this indicator,

Egypt ranked 149 among countries in 2014. In 2013, Egypt ranked

144. The Egyptian authorities decreased the number of procedures

and the number of days to finish construction permits from 25 and

211 respectively in 2004 to 21 and 179 respectively in 2014. The

third sub-indicator is getting electricity. According to this

indicator, Egypt was ranked 105 among countries in 2014. Seven

procedures and 54 days are required for a business in order to

get electricity. The fourth sub-indicator is registering property.

According to this indicator, Egypt was ranked 105 among countries

22

in 2014. Even though the number of procedures required to

register a property has not changed from being 8 procedures in

2004 until 2014, the Egyptian authorities have managed to

decrease the number of days required to register a property from

194 in 2004 to 63 in 2014. The fifth sub-indicator is getting credit.

According this indicator, Egypt was ranked 86 among countries in

2014. The sixth sub-indicator is protecting investors. According to

this indicator, Egypt ranked 147 among countries in 2014. The

seventh sub-indicator is paying taxes. According to this indicator,

Egypt was ranked 148 among countries in 2014. The eighth sub-indicator

is trading across borders. According this indicator, Egypt was

ranked 83 among countries in 2014. In this regard, the number of

days for exporting declined from 27 in 2005 to 12 in 2014. The

ninth sub-indicator is enforcing contracts. According to this

indicator, Egypt was ranked 156 among countries in 2014. The tenth

sub-indicator is resolving insolvency. According to this indicator,

Egypt was ranked 146 among countries in 2014. Table (2)

summarizes the performance of Egypt according to the ease of

doing a business indicator and its sub-indicators. We conclude

from this table that the legislative framework for business must

be changed in order to encourage investors to establish new

business. This is very important issue in the process of

enhancing financial empowerment as a strategy to alleviate

poverty in Egypt.

Table (2)

Ease of doing business in Egypt

23

Indicator RankEase of doing business 128Starting a business 50Dealing with construction permits 149Getting electricity 105Registering a property 105Getting credit 86Protecting investors 147Paying taxes 148Trading across borders 83Enforcing contracts 156Resolving insolvency 146The source: Doing business indicator, the World Bank.

Besides the factors mentioned above, SMEs face major challenges

that affect negatively the number of established SMEs in Egypt

which has a negative impact on poverty alleviation. The first major

challenge that SMEs face is the high interest margin. While the

average interest rate on deposit during the last decade was

around 10%, banks and other credit providers lend to SMEs at

interest rates that exceed, in most cases, 20%. The high interest

margin can be attributed to the high risk levels that are

associated with loans to SMEs and the high level of transaction

costs of these loans. Poghosyan (2012) provides explanations for

the high level of interest margins in low-income countries. The

high interest margins is one of the main reasons for a low level

of banks’ loans to SMEs. According to the Global Financial

24

Development Report published by the World Bank, only 5.1% of

small firms in Egypt held bank loans or bank lines of credit in

2009. Barajas, et.al (2013) attributes the limited access of SMEs

to credit in some financial systems to two main reasons. First,

economies of scale at all levels lead to high transaction costs

in providing credit to SMEs. Second, high default risks. They

distinguished between two types of default risks. (1) Contract

specific / idiosyncratic risks such as agency frictions arising

from asymmetric information between debtors and creditors; the

high cost of contract enforcement; and limits to the possibility

of diversifying risks. (2) Systemic risks such as non-

diversifiablity that affects all financial contracts and the

ability of financial institutions to manage idiosyncratic risks.

(5) A business model for financial empowerment as a tool for

poverty alleviation in Egypt:

The most common model of microfinance is the Grameen Bank model

that has been used in Bangladesh and other countries. The main

characteristics of this model are: (1) It is a non-profit

oriented model. (2) Credit for beneficiaries is provided by

forming groups that consist of members that will be collectively

responsible for paying back loans that are given to all members

in the group to which they belong. (3) It allows the microfinance

institutions to receive deposits. The other well-known model of

microfinance is the Self-Help Groups (SHGs) that have been used

in India and many other countries in Asia and Latin America. What

differentiates the SHGs model from the Grameen model are: (1)

25

SHGs follow a profit oriented model. (2) It does not allow

microfinance institutions to receive deposits. Ghosh (2013) has

provided a detailed review of literature that has dealt with the

microfinance topic. This review concluded that the current

microfinance models suffer from major shortcomings and do not

lead to poverty reduction in the communities in which they work.

As a matter of fact, instead of increasing income-generating

activities for the poor and supporting their financial situation,

they have led to an increase in financial vulnerability of the

poor.

In this section, I will develop a business model for financial

empowerment as a tool for poverty alleviation in Egypt.

Developing a business model that enhances financial empowerment

in Egypt, as defined in this paper, requires providing a clear

answer for the following questions: What services should be

provided? How should these services be provided? Who provides

these services? To whom should these services be directed?

First question: What services should be provided?

Based on the current situation of financial inclusion and the

main challenges that face individuals and SMEs in Egypt, the

proposed model suggests that four services be provided to

targeted people. These services are credit instruments,

insurance, marketing, and capacity building. Beside these

services, the proposed model enhances the business environment

for people who want to start their own businesses; it coordinates

26

among them in order to achieve economies of scale; it solves the

problem of a replication of successful business; and it deals

with the obstacle of centralization by making the local

government take the lead in project supervision.

Second question: How should services be provided?

In order to benefit from economies of scale to reduce transaction

costs and to reduce the marginal cost of production, the proposed

model encourages the provision of credits for small or medium

enterprises that formed from targeted people. These people are

supposed to work for firms where all the value is added by people

within the target area. In this way, people in the firm are going

to watch over each other’s behavior to prevent misuse of credit.

Simply said, the firms have a self-supervision mechanism. Beside

the above rationale, forming small and medium firms for targeted

people has the following benefits: (1) It allows for the

provision of other services, insurance, marketing and capacity

building. These services are very costly to be provided for

individuals. (2) It solves the dilemma of microfinance in Egypt

where people obtained loans to finance business but instead

financed personal consumption needs. This happens in most of

cases in Egypt and, in most cases, the creditors know of this

abuse in advance. However, they approved the loans either to

achieve their targets or because of personal connections between

credit officers and the borrowers. Many of these fake projects

lead to insolvency and put pressures the government to write off

these loans. (3) It encourages entrepreneurship. A government

27

entity in every area provides support in getting easier access to

all documentation and permits. (4) It allows for the best use of

central government resources within a decentralized framework.

(5) It deals with the informal sector problem in Egypt. Forming

such firms attracts people who work in the informal sector to

join the formal economy.

Third question: Who provides these services?

This model proposed a joint private-public provision of suggested

financial services. On one hand, depending on markets to provide

these services faces the possibility of market failure in

financial markets. These failures are because of: insufficient

collateral; lack of credit history information; and incomplete

markets or not deep enough markets. On the other hand, depending

only on government to provide such services leads to the

following problems: (1) Distortionary, excessive or otherwise

improperly designed interventions that may be generated by

bureaucratic incentives. (2) Prevalent inefficiencies, including

politically connected lending. (3) Beneficiaries may exercise

organized political pressure aimed at the change of signed credit

contracts, Ratnovski and Narain (2007).

In this business model for financial empowerment, the major role

of the government is not limited to providing credit to

individuals and SMEs. Private financial institutions, business

associations, and NGOs should be encouraged or pushed to take the

lead in this function. For government institutions that provide

28

credits for individuals and SMEs, i.e. SDF, DACB, and LDF, these

institutions cover all villages and remote areas and they have a

direct contact with poor people and small entrepreneurs. In order

for these institutions to do their job more efficiently, they

have to be restructured. For instance, DACB has branches that

cover all Egyptian villages. However, it lacks financial

technology, skilled people, and a clear vision that is needed in

order for it to play a vital role in credit accessibility and

poverty alleviation in rural areas. The role of government in

this model is the following: (1) Designing and implementing a

strategic plan for poverty alleviation that is built on financial

inclusion and enhancement of credit accessibility. (2)

Coordinating and supervising the role of all stakeholders of this

plan. (3) Granting loans that are provided by private financial

institutions to firms that participate in this program. (4)

Enhancing the business environment by improving the ranking on

the indicator of doing business in Egypt and its sub-indicators.

This means that according to the proposed model for financial

empowerment, the Egyptian government must have a strong

commitment to increase financial inclusion and credit

accessibility for individuals and SMEs. This commitment makes the

government adopt a proactive approach in addressing policy and

regulatory issues; gathering and publishing data regarding

financial inclusion and credit accessibility; enhancing financial

literacy; and improving the environment of doing business in

Egypt for SMEs. Chowdhury (2009) have emphasized the role of

29

government in supporting poverty alleviation through establishing

state-owned financial institutions that provide credit for

individuals and SMEs. G20 (2010) provides a comprehensive review

of the role of governments in financial inclusion in many

developing countries across the world.

In order to enhance financial empowerment as a tool for poverty

alleviation, the Egyptian government must improve the business

environment by making it easier to do business in Egypt. This

requires the following steps: (1) Easing the process of starting

business by decreasing the number of procedures, documents, and

days that are required to start business. All procedures should

be decentralized. (2) Dealing with construction permits is an

area which government must revisit. As mentioned above, the

second worst performance for Egypt in the ease of doing business

indicator is its performance in dealing with construction

permits. New laws and regulations are needed in order to make

getting construction permits less of an obstacle in starting

business. (3) Enforcing contracts is the worst performance in the

indicator of the ease of doing business in Egypt, as mentioned

above. In order to improve the business environment, the Egyptian

government must change the judicial system to make enforcement of

contracts faster and less costly and to provide the necessary

protection for investors. (4) Registering a property is one area

where the government of Egypt must make processes easier. Many

individuals have properties that can be used as collateral for

loans. However, they cannot use them because of the difficult and

30

long procedures in order to register property. Dealing with this

problem will allow many individuals to get access to credit for

financing their businesses. (5) Fighting corruption is one area

in which the government must work very hard. Corruption hurts

entrepreneurs, especially the small ones, and put constraints on

them in getting started with business and getting the financing

that is needed.

Fourth question: To whom should these services be directed?

According to the financial empowerment business model for poverty

alleviation that is suggested in this paper, two main groups of

beneficiaries are targeted. The first group of beneficiaries are

people who have skills in producing a specific product, however

they cannot start their own businesses because of their inability

to get financing or their inability to complete the procedures of

starting a business. In this case, local governments should adopt

project under which these groups of people can start their own

business with the support of local government. Local government

can mobilize the needed finance and overcome the obstacles that

face small entrepreneurs in starting their businesses. Another

advantage of doing so is making sure that the new businesses are

not exceeding market capacity which has led to the failure of

many small businesses in Egypt over the last two decades. The

second group of beneficiaries are SMEs. According to the financial

empowerment model for poverty alleviation, local governments must

group all SMEs producing the same products or produce

complementary products together under the umbrella of projects

31

that are supported by the government. Government in this case co-

ordinates with credit providers and these groups of SMEs under

supported projects in order to provide low cost financing and

financial services. Local governments may even need to grant

loans for these SMEs under the supported projects. This model

enables the local government to provide capacity building

activities for the supported projects and to benefit from the

central government resources that are available for supporting

business.

The proposed model has many advantages. First, it insures the

coordination among all government units that deal with

microfinance, credit accessibility, and poverty allocation at all

levels. This is a very important issue in Egypt given its heavily

centralized system. Second, it emphasizes the crucial role of

scale economies by getting many of the small production units

together to work under the umbrella of a large project. Thus, it

also deals with the problem that is responsible for the failure

of many small projects, that microenterprises have the tendency

to replicate successful activities which ends up by collapsing

both new and old projects. Third, it allows microenterprises to

connect with each other, allowing for synergies to develop in

productive activities. Fourth, it emphasizes local community

ownership and control. Fifth, it solves the problem of collateral

which faces the SMEs in getting credits. Sixth, it targets people

who have a high propensity to start a new business. Thus, it

deals with a major problem that faces the microfinance providers

32

which is that poor people in most of the cases use financing to

increase their spending on consumption goods, particularly non-

durables such as food. This behavior has made the role of

microfinance in generating income very low. Instead, it worsened

the financial situation for poor people who used microfinance

tools. For instance, the DACB was forced to write off credit that

it provided to poor farmers. Seventh, it deals with the problem of

the duplication of providing credits from different microcredit

providers. Eighth, it leads to a better usage of local resources

that can be sued as bases for new businesses.

In the appendix, I will discuss the application of this model on

the home furniture sector in the city of Tahta, Sohag, Egypt.

(6) Conclusion and policy recommendations.

As a result of the shortcoming that the business models used in

microfinance suffer from and their limited impacts on reducing

poverty, developing a new business model for microfinance is a

very important issue in the field of economic development and for

policy making that target poverty alleviation. What was missing

in the previous business models that all of them concentrate on

financial inclusion or/and credit accessibility and they ignore

33

other aspects such as: institutional capacity and business

environment.

In this paper, I developed a business model for financial

empowerment as a tool for poverty alleviation in Egypt.

Developing a business model that enhances financial empowerment

in Egypt, as defined in this paper, requires providing a clear

answer for the following questions: What services should be

provided? How should these services be provided? Who provides

these services? To whom should these services be directed?

The proposed business model include four main aspects: financial

inclusion; credit accessibility; enhancing institutional capacity

in designing a comprehensive strategy for poverty alleviation;

and improving business environment. The main policy

recommendation for policy makers in Egypt is to implement this

model in all governorates.

34

References:

Allen, F., A. Demirguc-Kunt, L. Klapper, M. Peria (2012). “The

Foundations of Financial Inclusion: Understanding the Ownership

and Use of Formal Accounts.” The World Bank, Policy Research Working Paper,

WPS 6290.

Baragas, A., T. Beck, E. Dabla-Norris, and S. Yousefi (2013).

“Too Cold, Too Hot, Or Just Right? Financial Sector Development

Across the Globe.” IMF Working Paper, WP/13/81.

Bateman, M. and H.-J. Chang (2012). “Microfinance and the

illusion of development: from hubris to nemesis in their years.”

World Economic Review, Vol.1, 13-36.

Chowdhury, A. (2009). “Microfinance as a Poverty Reduction Tool –

A Critical Assessment.” United Nation, Department of Economic & Social

Affairs, DESA Working Paper No. 89.

Demirguc-Kunt, A. and L. Klapper (2013). “Measuring Financial

Inclusion: Explaining Variation in Use of Financial Services

across and Within Countries.” Brookings Papers on Economic Activity.

Duvendack, M., R. Palmer-Jones, J.G. Copestake, L. Hooper, Y.

Loke, and N. Rao (2011). “What is the evidence of the impact of

the microfinance on the well-being of poor people?” EPPI-Center,

Social Science Research Unit, Institute of Education, University of London.

35

Ghosh, J. (2013). “Microfinance and the challenge of financial

inclusion for development.” Cambridge Journal of Economics.

G20 (2010). “Innovative Financial Inclusion.” G20 financial inclusion

experts group.

Mosely, P. (2001). “Microfinance and Poverty in Bolivia.” The

Journal of Development Studies, vol. 37.pp101-132.

Poghosyan, T. (2012). “Financial Intermediation Costs in Low-

Income Countries: The Role of Regulatory, Institutional, and

Macroeconomic Factors.” IMF Working Papers, WP/12/140.

Ratnovski, L. and A. Narain (2007). “Public Financial

Institutions in Developed Countries-Organization and Oversight.”

IMF Working Paper, WP/07/227.

Shankar, S. (2013). “Financial Inclusion in India: Do

Microfinance Institutions Address Access Barriers? ACRN Journal of

Entrepreneurship Prospectives, Vol.2 no.2, pp 60-74.

Shetty, N. (2005). “The Microfinance Promise in Financial

Inclusion and Welfare of the Poor: Evidence from India.” Center for

Economic Studies and Policy.

Singh, J. and P. Yadav (2012). “Micro Finance As A Tool For

Financial Inclusion & Reduction Of Poverty.” Journal of Business

Management & Social Sciences Research, Vol. 1 no.1.

36

Appendix A case study for implemented the proposed business model.

This model was implemented in the governorate of Sohag in Egypt.

Sohag is one of the poorest governorates in Egypt. With 43 % of

37

its population under the poverty line, Sohag is ranked as the

second poorest governorate among all governorates of Egypt, after

Assiut. The idea started when the governor of Sohag, Gen.

Elnoumany, decided to work on poverty alleviation and improving

the economic conditions for the people of Sohag. With all

stakeholders, we developed a comprehensive strategy to enhance

economic growth and development in Sohag. One dimension of this

strategy is to make use of financial resources that are available

at financial institutions and the central government in reducing

poverty and enhancing economic growth & development in Sohag. In

order to encourage our partners, we have to provide visible and

profitable project proposals that meet the objectives of all

stakeholders. We start our mission by identifying all connected

small businesses that suffer from financial and other problems.

At the same time there is a large number of people who are

willing to start their own businesses in this area if they could

obtain financing. The first experimental case for the model is

establishing an industrial compound for home furniture products

in Tahta. Tahta has around 370 home furniture products workshops.

In this city, there is a large number of people with very high

skills in this business. The problem was that most of these

workshops are very small, only 15m2; they have financial

difficulties; they have problems in marketing their products; and

even most of them do not have licenses and permits. The

authorities used to close some of these workshops from time to

time. After holding several meetings with the owners of these

38

workshops and with financial institutions, we developed a plan to

transfer these businesses from very small and informal workshops

to a medium size industry. A protocol among the Sohag

governorate, SDF, the General Authority for Industrial

Development, the Ministry of Local development, and the Ministry

of Industry & Trade was signed. According to this protocol, the

governorate of Sohag provides the land for this project and

coordinates among targeted people and all other stakeholders. The

General Authority for Industrial Development is responsible for

the infrastructure of this project, i.e. roads, electricity, and

water. The Ministry of Industry & Trade finances a training

institute for this project. The Ministry of Local Development

coordinates among all central government entities that are

involved in this project. The SDF finances the buildings and the

equipment. It is also responsible for stimulating marketing for

the products. The infrastructure for the project is expected to

be finished by the end of 2014. The number of units to be built

is 1200 units in three models. The first model is for units with

a size of 250 m2. The second model is for units 400 m2. The third

model is for units 600 m2 or more. The beneficiaries will pay

back the cost of the new units to the SDF over a long period of

time at a very low interest rate. The expected outcomes of this

project are: (1) it is expected to create 8500 job opportunities

for poor, but skilled people. (2) Transferring 370 small,

informal, and inefficient workshops to small & medium and formal

manufacturing businesses and establishing 830 new businesses that

39

would otherwise have not gotten financing. The lessons learned

from this project are: (1) Poor people and small business can

benefit from the financial resources that are available from

central government programs for industrial development. (2)

Coordination among all governmental units at all levels ease the

doing of business for poor people and young entrepreneurs. (3)

Financial institutions are willing to provide credit for poor

people and for SMEs if it is granted that they will get their

money back. Once this project is finished and proves successful,

it will be replicated in the other 49 areas with similar activity

as that of the poor Sohag cities and villages.

40