Final End Term Paper

62

Value versus Growth: Evidence in NEPSE Value versus Growth: Evidence in NEPSE PAPI Fund Page 1 Submitted to: Sabin Bikram Panta Submitted by: Prajol Joshi Pralin Raj Regmi Ashish Bahadur Silwal End Term

Transcript of Final End Term Paper

Value versus Growth: Evidence

in NEPSE

Value versus Growth: Evidence in NEPSE

PAPI Fund Page 1

Submitted to:

Sabin Bikram Panta

Submitted by:

Prajol JoshiPralin Raj RegmiAshish Bahadur

Silwal

End Term

Table of ContentsBackground:....................................................1Purpose of Study...............................................2Scope of Study.................................................3Limitations of Study...........................................3Conceptual Framework...........................................4Growth Stocks:................................................4Value Stocks:.................................................4Book-to-market equity (B/M) ratio:............................5Earnings to Price (E/P) ratio:................................5Cash Flow to Price (C/P) Ratio:...............................5Dividends to Price (D/P) Ratio:...............................6Value versus Growth:..........................................6

Literature Review..............................................7Diagrammatic Presentation of Concept of Study:.................8Input.........................................................9Process.......................................................9Output.......................................................10

Analysis:.....................................................10Conclusion:...................................................14Scope for further study:......................................15References:...................................................17Annex:........................................................18

Value versus Growth: Evidence in NEPSE

Background:

“As Buffet said in the speech, He’s not looking at quarterly earnings projections,

he’s not looking at next year’s earnings, he’s not thinking about what day of the

week it is, he doesn’t care what investment research from any place says, he’s not

interested in price momentum, volume or anything. He’s simply asking: What is

the business worth?”

Investors generally subscribe to the conventional wisdom that

growth stocks outperform value stocks. But a study of

international portfolios by professors at the University Of

Chicago Graduate School Of Business and the Yale School of

Management has shown that in reality the reverse is true: Value

stocks reap higher returns than growth stocks in markets around

the world.

"Value Versus Growth: The International Evidence," a 1997 working

paper co-written by finance professor Eugene Fama of the

University of Chicago Graduate School of Business and Kenneth R.

French, a former Chicago faculty member now at the Yale School of

Management, argues that the conventional wisdom is wrong. Fama

and French have concluded that Value Stocks have higher returns

than growth stocks in markets around the world. For the period

1975 through 1995, the difference between the average returns on

global portfolios of high and low book-to-market stocks is 7.68

percent per year, and value stocks outperform growth stocks in

twelve of thirteen major markets. Speaking about growth stocks,

PAPI FUND Page 1

Fama says "people think because these are good companies, their

stock returns will be high. But in fact, their prices are pegged

so high by the market that their returns actually tend to be

low."

Fama and French define value stocks as those stocks that have

high ratios of book value to market value and growth stocks as

those that have low ratios of book value to market value. "The

intuition is that value stocks have low prices relative to their

book value, so the market feels they're relatively distressed,"

says Fama. "The intuition is the opposite for growth stocks."

Investment managers classify firms that have high ratios of book-

to-market equity (B/M), earnings to price (E/P), or cash flow to

price (C/P) or Dividends to price (D/P) as value stocks because

they tend to have persistently low earnings and low B/M, E/P, C/P

and D/P stocks tend to be strong (growth) firms with persistently

high earnings.

The sharp rise and decline in recent years of technology and

other growth-oriented stocks calls into question the argument

that growth stocks are less risky investments. Rather, the

evidence suggests that value stocks are not more risky than

growth stocks, based on a variety of indicators including beta

and return volatility. Indeed, using one popular risk indicator

which focuses on performance in down markets, value stocks suffer

less severely than growth stocks when the stock market or the

overall economy does poorly. (Chan & Lakonishok, 2002).

In Nepal stock exchange (NEPSE) also, there are number of stocks

that provide regular income and are valued high in the market as

well as there exists another pool of stocks that doesn’t provide

regular incomes. This study has identified three stocks as value

and other three as growth stocks based on the ratios of book-to-

market (B/M) ratios as done by Fama and French in their study.

Based on the classified, returns has been calculated for last 60

months and based on calculated returns the difference in average

returns is calculated. As studied by Fama and French, value

stocks outperform growth stocks in twelve of thirteen major

markets and this study seeks to examine if the value stock

outperform growth stocks in NEPSE as in major stocks market.

Purpose of Study

A large body of empirical research indicates that value stocks on

average earn higher returns than growth stocks. The reward to

value investing is more pronounced for small stocks but it is

also present in the larger stocks. The value premium also exists

in equity markets outside the U.S.

The primary purpose of this study is to examine if the value

stocks of NEPSE even outperform the performance of growth stocks

of NEPSE. This also intends to examine if there is difference in

average returns on portfolios of high and low book-to-market

stocks. To achieve this primary objective, there are several

other specific objectives of this study:

To classify the stocks listed in NEPSE into value and

growth stocks based on book-to-market (B/M) equity ratio

and examine its possibility and applicability

Calculate the average returns on the portfolio of value

stocks and portfolio of growth stocks based on data

available from NEPSE

To examine if their exist a significant difference in

annual returns of value and growth stocks

Scope of Study

This study exclusively focuses on the comparison of annual

returns of value and growth stocks of NEPSE based on technique

used by Fama and French in their working paper: Value versus

Growth: Thee International Evidence (Fama & French, Value versus

Growth: The International Evidence, 1998). The value stock

portfolio includes three value stocks i.e. KIST bank, Prime Life

Insurance and Citizen Bank International. The growth stock

portfolio includes three growth stocks i.e. Standard Chartered

Bank Nepal, Everest Bank and Nabil Bank. The selection of value

and growth stocks was based on book-to-market equity ratio of ten

stocks listed in NEPSE i.e. KIST bank, Prime Life Insurance,

Citizen Bank International, Standard Chartered Bank Nepal,

Everest Bank, Nabil Bank, Himalayan Bank Nepal, Siddhartha Bank

Limited, Nepal SBI Bank Limited and Butwal Power Ltd. The book-

to-market equity ratio was calculated based on annual reports of

last five fiscal years 2007/8 – 2012/13. The annual returns of

value and growth stocks was for last 60 months data available

i.e. 2065 Shrawan to 2070 Asadh. During this period, NEPSE soared

to its record high index (in 2008) as well plummeted record low

(in 2011) which could possibly have impact on our study of

calendar anomalies due to those extremes. This analysis is based

on descriptive statistics (mean and standard deviations).

Limitations of Study

The limitations for this study are as follow:

The selection of growth and value stock was done from the

pool of ten different stocks listed in NEPSE (KIST bank,

Prime Life Insurance, Citizen Bank International, Standard

Chartered Bank Nepal, Everest Bank, Nabil Bank, Himalayan

Bank Nepal, Siddhartha Bank Limited, Nepal SBI Bank Limited

and Butwal Power Ltd.)

The selection criterion for value and growth stock was book-

to-market equity (B/M) ratio as used by Fama and French in

their working paper: Value versus Growth.

To calculate the book-to-market equity ratio, last five

fiscal year data was used.

The return calculation was based on 60 months month end

closing price of each stock i.e. 2065 Shrawan to 2070 Asadh.

Within this period, few stocks’ were not traded so, only few

data were available for them.

Conceptual Framework

When evaluating which stocks to include in our portfolio, we are

likely to run across two labels that may be confusing: Growth

stocks and Value stocks. Both types of stocks seek to provide the

best possible returns. The difference is in the approach they

take, the way they pick stocks, and the types of markets for

which they are best suited.

Growth Stocks:Growth stocks refer to those companies that investors believe

will experience faster than average growth as measured by

revenues, earnings, or cash flow. Growth companies by definition

are those that have substantial potential for growth in the

foreseeable future. Growth companies may currently be growing at

a faster rate than the overall markets, and they often devote

most of their current revenue toward further expansion. Every

sector of the market has growth companies, but they are more

prevalent in some areas such as technology, alternative energy

and biotechnology. Most growth stocks tend to be newer companies

with innovative products that are expected to make a big impact

in the market in the future, but there are exceptions. Some

growth companies are simply very well-run entities with good

business models that have capitalized on the demand for their

products.

Value Stocks:Undervalued companies can often provide long-term profits for

those who do their homework. The goal of value stock investors is

to find proverbial diamonds in the rough; that is, companies

whose stock prices don’t necessarily reflect their fundamental

worth. The reasons for these stocks being undervalued by the

market can vary. Sometimes a company or industry has fallen on

hard times. Other times a poor quarterly earnings report or some

external event can temporarily depress a company’s stock price

and create a longer-term buying opportunity. In searching for

these companies, managers look for what many experts call a

"margin of safety." This means that the market has discounted a

security more than it should have and that its market value, the

price at which it is trading, is less than its intrinsic value,

the present value of its future cash flows. One example would be

a stock that is trading at Rs. 900, but whose intrinsic value is

Rs. 1000. The stock price may also have dropped due to public

perception regarding factors that have little to do with the

company’s current operations. Smart investors know that this is a

good time to buy the stock, as the public will soon forget about

the incident and the price will most likely revert to its

previous level.

Book-to-market equity (B/M) ratio:A ratio used to find the value of a company by comparing the book

value of a firm to its market value. Book value is calculated by

looking at the firm's historical cost, or accounting value.

Market value is determined in the stock market through its market

capitalization. The book-to-market ratio attempts to identify

undervalued or overvalued securities by taking the book value and

dividing it by market value. A high ratio is often interpreted as

a value stock (the market is valuing equity relatively cheaply

compared to book value). This is the same as a low price-to-book

value ratio.

Formula:

Earnings to Price (E/P) ratio:The annual earnings of a security per share at a given time

divided into its price per share. It is the inverse of the more

common price-earnings ratio. Often, the earnings one uses are

trailing 12-month earnings, but some analysts use other forms.

The earnings-price ratio is a way to help determine a security's

stock valuation, that is, the fair value of a stock in a perfect

market. It is also a measure of expected, but not realized,

growth. A measure indicating the rate at which investors will

capitalize a firm's expected earnings in the coming period.

Earnings¿PriceRatio=Earningspershare

MarketPriceperShare

Cash Flow to Price (C/P) Ratio:C/P ratio is a measure of the market's expectations of a firm's

future financial health. Because this measure deals with cash

flow, the effects of depreciation and other non-cash factors are

removed. Cash flow is the sum of earnings and depreciation which

is divided by outstanding number of shares to calculated the cash

flow to price ratio per share.

Cashflow¿PriceRatio=(NetIncome+Depreciation )pershare

MarketPriceperShare

Dividends to Price (D/P) Ratio:The other measure is dividends to price ratio which compares the

dividends paid by the companies each period against the market

price per share. If the ratio is high then, it means the company

is distributing income to shareholders than retaining them which

reduces the probability of growth.

Dividends¿PriceRatio= DividendpershareMarketPriceperShare

Value versus Growth: “Value versus Growth” debate has been there since very long and

different academic researchers have pointed down several findings

regarding the returns offered by value stocks or growth stocks

which are always contradicting. Investors have the conventional

thought that growth stocks outperform value stocks and thus,

offer higher returns for them But, Contrary to this wisdom Fama

and French in their working paper (Fama & French, Value versus

Growth: The International Evidence, 1998) has claimed that value

stocks outperform the growth stocks. The implication for

investors is that value stocks have higher returns than growth

stocks in markets around the world. Looking at book-to-market

equity, Fama and French found that value stocks outperformed

growth stocks in 12 of 13 developed countries from 1975 to 1995,

and that the difference between average returns on global

portfolios of high and low book-to-market stocks was 7.6 percent

per year. Furthermore, when earnings-to-price, cash flow-to-price

and dividend-to-price were examined, the value premium continued

to be evident. In our study, we thus, intend to examine if the

same applies in Nepal Stock exchange (NEPSE) thus, we have

calculated the differentials in earnings between value and growth

stocks.

Literature Review

Value stocks are usually defined as those traded at low price-to-

earnings ratios (stock prices divided by earnings per share), low

price-to-book ratios (stock prices divided by book value per

share) or high dividend yields (dividends per share divided by

stock prices). Growth stocks, on the other hand, are traded at

high price-to-earnings ratios, high price-to-book ratios or low

dividend yields.

The explosion of academic interest in value and growth investment

strategies can be traced back to Fama and French (1992), and

Lakonishok, Shleifer and Vishny (1994). The results of Fama and

French delivered a stunning blow to the explanatory power of the

Capital Asset Pricing Model, and sparked debates about the “death

of beta.” In the wake of this study, academics shifted their

attention to the ratio of book-to-market value of equity, and

firm size as the leading explanatory variables for the cross-

section of average stock returns. In turn, this work built on

earlier studies of stock market “anomalies.” Basu (1977), for

example, showed that stocks with low price-to-earnings ratios

subsequently tend to have higher average returns than stocks with

high ratios. Chan, Hamao and Lakonishok (1991) study Japanese

data and find strong support for the superior performance of

value investment strategies.Based on the accumulated weight of

the evidence from studies on the book-to-market effect and

related anomalies, the academic community has generally come to

PAPI Fund Page 11

agree that value strategies on average outperform growth

investment strategies. There is much less consensus, however, on

the underlying reasons for the superior returns. On the one hand,

Fama and French take the position of the efficient markets

hypothesis, and attribute the higher returns of value strategies

to their increased risk. On the other hand, Lakonishok, Shleifer

and Vishny suggest that cognitive biases underlying investor

behavior, and the agency costs of professional investment

management are at the root of the rewards to value investing. Yet

another explanation for the returns to value investing rests on

methodological issues of data selection bias (see Kothari,

Shanken and Sloan (1995)). A careful study by Chan, Jegadeesh and

Lakonishok (1995), however, suggests that any such bias cannot

explain the differential performance of value and growth

investing.

Investment manager classify firm that have high ratios of book-

to-market equity (B/M), earnings to price (E/P), or cash flow to

price (C/P) as value stocks. Fama and French (1992, 1996) and

Lakonishok, Shleifer, and Vishny (1994) show that for U.S. stocks

there are a strong value premium in average returns. High B/M,

E/P, or C/P stocks have higher average returns than low B/M, E/P,

or C/P stocks. Fama and French (1995) and Lakonishok et al.

(1994) also show that the value premium is associated with

relative distress. High B/M, E/P, and C/P firms tend to have

persistently low earnings; low B/M, E/P, and C/P stocks tend to

be strong (growth) firms with persistently high earnings.

PAPI Fund Page 12

Month-End Closing price of each individual Stock from 2065 Shrawan to 2070 Asadh then, mean annual return of value & growth stock returnsTools & Techniques: - Statistical tools Comparative Analysis

Average Return difference in Value and Growth stocks of NEPSE

Lakonishok et al. (1994) and Haugen (1995) argue that the value

premium in average returns arises because the market undervalues

distressed stocks and overvalues growth stocks. When these

pricing errors are corrected, dis-tressed (value) stocks have

high returns and growth stocks have low re-turns. In contrast,

Fama and French (1993, 1995, and 1996) argue that the value

premium is compensation for risk missed by the capital asset

pricing model (CAPM) of Sharpe (1964) and Lintner (1965). This

conclusion is based on evidence that there is common variation in

the earnings of distressed firms that is not explained by market

earnings, and there is common variation in the returns on

distressed stocks that is not explained by the market return.

Most directly, including a risk factor for relative distress in a

multifactor version of Merton's (1973) inter temporal capital

asset pricing model (CAPM).

The Journal of Finance or Ross's (1976) arbitrage pricing theory

(APT) captures the value premiums in U.S. returns generated by

sorting stocks on B/M, E/P, C/P, or D/P (dividend yield). Still

another position, argued by Black (1993) and MacKinlay (1995), is

that the value premium is sample-specific. Its appearance in past

U.S. returns is a chance result unlikely to recur in future

returns.

Diagrammatic Presentation of Concept of Study:

PAPI Fund Page 13

The input-output model gives a glimpse of the overall study. The

main output of this study is to find whether there is significant

difference in annual returns of value and growth stocks in long

run in NEPSE listed stocks based on empirical studies on stock

market from developed and emerging countries. The research on U.S

stocks market and other International major stocks markets of

World has shown the evidence that value stocks generally

outperform the growth stocks. Thus, this study intends to examine

if same is the case in Nepal and the only stock market of Nepal

(NEPSE). To understand this, we need to analyze the returns of

number of different value and growth stocks over a long

historical period and compare the average returns between value

and growth stocks. Statistical tools like mean and standard

deviation has been used and finally comparative analysis is

conducted to interpret the final outcome.

InputThe inputs for our analysis include two levels of data. First of

all, to calculate the book-to-market ratio so as to differentiate

growth and value stocks, we used the annual reports of last five

fiscal years of all the companies which were available in their

PAPI Fund Page 14

corporate website. After distinction between growth and value

stock, the second step was to calculate the average returns of

value and growth stocks. For this, we used the month end closing

price of last 60 months from 2065 Shrawan to 2070 Asadh retrieved

from the website www.nepalstock.com.np

Book to market ratio was calculated using:

And, the average monthly returns on each stock =Pt−Pt−1

Pt−1

ProcessThere involved two steps of calculation in our analysis. First of

all, growth and value stocks were identified based on book to

market equity ratio. This was calculated from the data retrieved

from company’s annual reports and its financial performance. We

calculated the book-to-market equity ratio of 10 stocks out of

which stocks having book-to-market equity ratio fall in top 30%

was the portfolio of value stocks. In contrast, stocks having

book-to-market equity ratio fall in bottom 30% was the portfolio

of growth stocks. After then, monthly return on all the

individual stocks was extracted from which average monthly return

of each individual stock was calculated and finally, the average

of all three value and three growth stocks was calculated and

annualized to get the average annual returns in value and growth

stocks of NEPSE.

PAPI Fund Page 15

OutputThe main outcome of the study was to examine the annual average

returns of value and growth stocks in Nepal. In International

context, different research on various key stock markets revealed

that value stocks outperform the growth stocks in average so,

this study intends to evaluate if same is applicable in the

Nepal’s stock market. This can tell if the country’s only stock

market is following the general trend or as claimed by critics is

manipulated by few big investors for their personal benefit.

Analysis:

Our analysis was based on an article published on 1998 after a

research by Eugene Fama and Kenneth French regarding the returns

of value stocks and growth stocks in various capital markets

around the world. Originally, Fama-French had found that the US

capital market data proved that value stocks provided higher

average returns compared to growth stocks. Then Fama-French tried

to apply this same conclusion to thirteen capital markets around

the world. Their conclusion was that for the study period of 20

years (1975-1995), value stocks outperformed growth stocks in

twelve out of thirteen countries, and the difference between

average returns of value stocks and growth stocks was 7.68%.

In Nepalese context, awareness level among general investors is

very low about the concepts of value or growth stocks, which seem

to be limited among only a small proportion of individuals who

have educational background about the issue. As such, we still

PAPI Fund Page 16

wanted to see if the value and growth stocks performed in a

similar way with the global market patterns. We used the same

criterion applied by Fama-French, i.e. book-to-market ratio

(B/M), earning to price (E/P), cash flow to price (C/P), and

dividend to price (D/P), to separate between value stocks and

growth stocks. All of these calculations and their significance

have been explained in detail in the structural framework of this

research earlier.

In order to do all the calculations, we needed representative

stocks from the Nepalese capital market (NEPSE). We chose to

study the returns of 10 sample stocks over a period of five years

from 2008 to 2013.

The selection of these sample stocks from NEPSE needed to

accurately represent the structure of the overall market. Hence,

we separated NEPSE’s structure into three categories according to

their capital size: banking stocks, insurance stocks, and other

stocks. The overall banking sector has commanded in average

around 80 percent of the total share of Nepalese capital market

over the study period of 2008-2013. Furthermore, insurance sector

has held around 10 percent level over the same period and other

sectors made up the remaining 10 percent. Within those

categories, the stocks were chosen at random by the study team.

These were the representative stocks from the Nepalese stock

market with their respective categories in our study:

Category S.No. Name

PAPI Fund Page 17

Banking

1 Standard Chartered Bank (SCB)

2 KIST Bank (KIST)

3 Nabil Bank (Nabil)

4 Himalayan Bank (HBL)

5 Siddhartha Bank (SBL)

6 Citizens Bank International (CBIL)

7 Everest Bank (EBL)

8 Nepal SBI Bank (SBI)

Insurance 9 Prime Life Insurance (PLI)

Others 10 Butwal Power Company (BPC)

In order to collect the necessary data, we first went to the

respective companies and received annual reports from them for

five years from 2008 to 2013. These annual reports provided data

like annual book value per share, annual closing market value per

share, annual earnings per share, annual increment/decrement in

cash flow per share, annual dividends per share (including

monetary adjustments for shares and cash dividends), and other

financial data.

All of the aforementioned data were used in calculation purposes

to come to arithmetic mean and standard deviation of B/M, E/P,

C/P, and D/P for the selected ten stocks from NEPSE. The

PAPI Fund Page 18

calculation is attached in annexure. The summary of the

calculated data is also included in annexure.

With the comparison of the second table, Fama-French model

suggests that the top 30 percent of the sample stocks in that

calculation justify as being the value stocks, as explained in

the structural framework. Furthermore, the bottom 30 percent of

sample stocks in that calculation in Table B justify as being

growth stocks.

After above mentioned calculations, we find the representative

value and growth stocks in NEPSE over the period of 2008-2013 as

follows:

Value Stocks:

KIST Bank

Prime Life Insurance

Citizen Bank International

Growth Stocks:

Everest Bank

Standard Chartered Bank

Nabil Bank

Unlike in the case of five years annual reports, for which we had

to go to the companies to get them as they were not fully

available in the internet, we were able to find NEPSE’s index

values and stock prices of all those companies over the five

PAPI Fund Page 19

years period between 2008-2013 in NEPSE’s official website. All

of the data we have used are publicly available for free of cost.

In order to know whether the value stocks gave better returns

than growth stocks, we listed monthly returns data of NEPSE index

between 2008-2013. Although daily data was available, we wanted

to minimize the effect of noise in the daily data, leading to a

choice of monthly data. We also listed monthly price of the three

value and three growth stocks so that they can be compared for

being the prices of the same days.

With a change in the NEPSE index prices between each of the

consecutive months of the study period, we computed average NEPSE

return in percentage form. Similarly, we calculated the returns

of all six stocks to come to average monthly returns in

percentage form for the same months under study.

To find the total average monthly returns by NEPSE, three value

stocks, and three growth stocks, we took an arithmetic mean of

the sixty months study period, and found out the average returns

by each of those companies. The monthly returns were then

adjusted into annual terms for easier comparison.

As the study period consisted of a time of decline in the capital

market performance for NEPSE, the average returns over the five

years under study were bound to come in negative values. The mean

NEPSE index return was -11.97% per year between 2008 and 2013. In

regards to the companies being studied, only one stock (value)

had given a positive annual return, i.e. Prime Life InsurancePAPI Fund Page 20

Company with 0.28%. Other two value stocks had the following

annual returns: KIST Bank with -10.26% and Citizens Bank

International with -8.02%. Three growth companies had the

following annual returns: Nabil Bank with -11.81%, Standard

Chartered Bank with -22.52% and Everest Bank with -8.25%.

Fama-French had calculated the collective average annual returns

of their calculated value and growth stocks. Hence, the

collective mean annual return of the three value stocks from

NEPSE was -6.0007%. Similarly, the collective mean annual return

of growth stocks from NEPSE was -14.1926%.

PAPI Fund Page 21

NEPSEReturnin %

KISTReturnin %

PrimeLife

Insurance Return

in %

Citizens

Intl.Bank

Returnin %

NabilBank

Returnin %

Std.Chartered BankReturnin %

EverestBank

Return in%

Mean Return (Monthly)

-0.9975%-

0.8549%

0.0229%-

0.6681%

-0.9844

%-1.8766% -0.6871%

Mean Return (Annual)

-11.9700%

-10.259

3%0.2751%

-8.0178

%

-11.812

8%

-22.5196% -8.2454%

Average Return ofValue Stocks (H)

-6.0007%

Average Return ofGrowth Stocks (L)

-14.1926%

High - Low Return

8.1919%

Looking at the difference between the returns of value and growth

stocks in NEPSE, we found a spread of significant 8.19%. This

premium for value stocks compared to growth stocks is consistent

with the findings of Fama-French where they had concluded a

spread of 7.68% in the global capital market. This spread is

justified by the higher risk level associated with the value

stocks, which are usually ignored by mainstream investors.

Conclusion:

PAPI Fund Page 22

Value stocks have more than double returns than growth stocks in

the Nepalese capital market. Value stocks also outperform the

overall market by a significant proportion in Nepalese context.

Due to various reasons, the market was continuously going down

so, Investors are actually losing their investment in these last

60 months trend but, the amount they are losing is less with the

value stocks than with the growth stocks. The investors are

losing more with the growth stocks i.e. -14.20% whereas they are

just losing -6% with the value stocks.

Sorting on book-to-market ratio, and other three calculations,

value stocks are proven to be better investment opportunities in

NEPSE rather than otherwise-popular growth stocks. Although

globally value stocks gave 7.68 percent higher returns than

growth stocks, in Nepalese context we found an even higher

premium for investing in value stocks, with a higher returns of

8.19 percent. All of the calculations clearly conclude that the

return premium for value stocks is higher than other stocks,

especially growth stocks.

Our study even supports the conclusion drawn by Fama and French

in their highly appreciated working paper (Fama & French, Value

versus Growth: The International Evidence, 1998) where they

concluded that globally value stocks gave 7.68% higher returns

than growth stocks. This was because, most of investors think

because these are good companies, their stock returns will be

high. But in fact, their prices are pegged so high by the market

PAPI Fund Page 23

that their returns actually tend to be low in compare to their

market price. But, the value stocks are usually priced very low

by the market and in many occasions are undervalued in the market

so, with slight increase in their price value investors can gain

more. With value investment, risk is usually higher as returns

are uncertain so, investors must be offered higher return to

compensate for higher risk.

Our conclusion backs up the rationale of investors who choose to

invest in value stocks that are ignored by major investors in our

markets. While making portfolio decisions in Nepalese equity

market, it is advisable to have a higher proportion of value

stocks in terms of B/M, E/P, C/P, and D/P in a portfolio to get

higher returns than the market in average.

Scope for further study:

Due to various limitations, we could only calculate the book-to-

market equity ratio of ten stocks listed in NEPSE but, the

conclusion would be more relevant if we could calculate the book-

to-market equity ratio of all the listed stocks and based on that

data, we could chose stocks with 30% top B/M ratio as value

stocks and bottom 30% as growth stocks. In future, there remains

a scope to include all the stocks listed in NEPSE in this study

and find a conclusion of Value versus Growth and evaluate if the

Nepalese stocks also follow the same trend like in Global stock

market. It would provide a concrete answer of if the NEPSE also

PAPI Fund Page 24

provide higher premium for bearing the higher risk of holding the

value stocks in place of growth stock.

Instead of using just last five fiscal years as our base to

calculate the book-to-equity ratio, we can use all the data of

trading available to us for all the stocks listed since inception

of stock market, that got de-listed in the middle and some other

new stocks got listed in the stock market. If we could use all

these data to calculate the book-to-equity ratio then, the

conclusion drawn would be more concrete. So, there is a scope of

the detail research in this field of stock market.

PAPI Fund Page 25

References:

2005 Growth and Value Stocks: Risks Associated With Value’s Outperformance of Growth California State University

Income, Value and Growth Stocks

Nepal Stock Exchange. (2065/66, 2066/67, 2067/68, 2068/69, 2069/70). Annual Reports: NEPSE. Retrieved from NEPAL Stock Exchange Ltd.: http://nepalstock.com/reports/annual.php

Rethinking Stock Returns: New Evidence on Value Versus Growth

Value and Growth Investing: A review and update 2002

Value versus Growth: The International Evidence 1998 The Journal of Finance

Prime Life Annual Reports (2007, 2008, 2009, 2010, 2011, 2012, 2013)

Butwal Power Company (2007, 2008, 2009, 2010, 2011, 2012, 2013)

Nepal SBI Bank (2007, 2008, 2009, 2010, 2011, 2012, 2013)

Himalayan Bank Limited (2007, 2008, 2009, 2010, 2011, 2012, 2013)

KIST Bank Limited (2007, 2008, 2009, 2010, 2011, 2012, 2013)

Nabil Bank Limited (2007, 2008, 2009, 2010, 2011, 2012, 2013)

Standard Chartered Bank (2007, 2008, 2009, 2010, 2011, 2012, 2013)

Siddhartha Bank Limited (2007, 2008, 2009, 2010, 2011, 2012, 2013)

Citizens Bank International Limited (2007, 2008, 2009, 2010, 2011, 2012, 2013)

PAPI Fund Page 26

Everest Bank Limited (2007, 2008, 2009, 2010, 2011, 2012, 2013)

Annex:

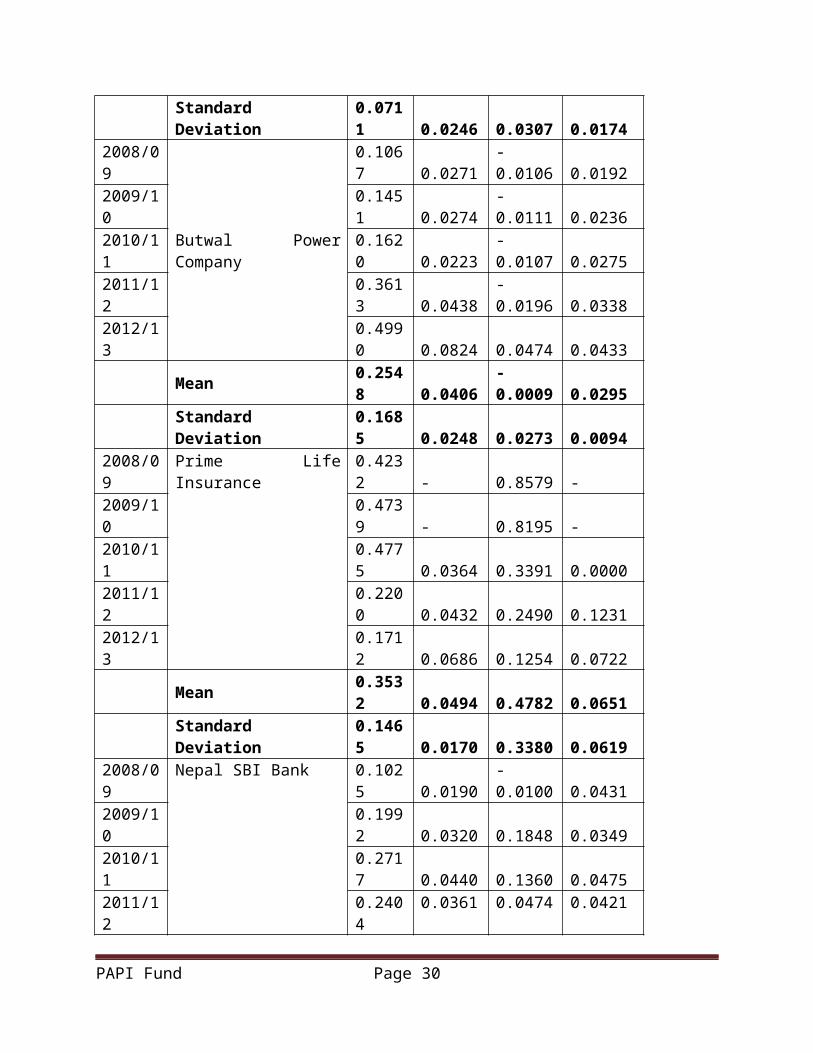

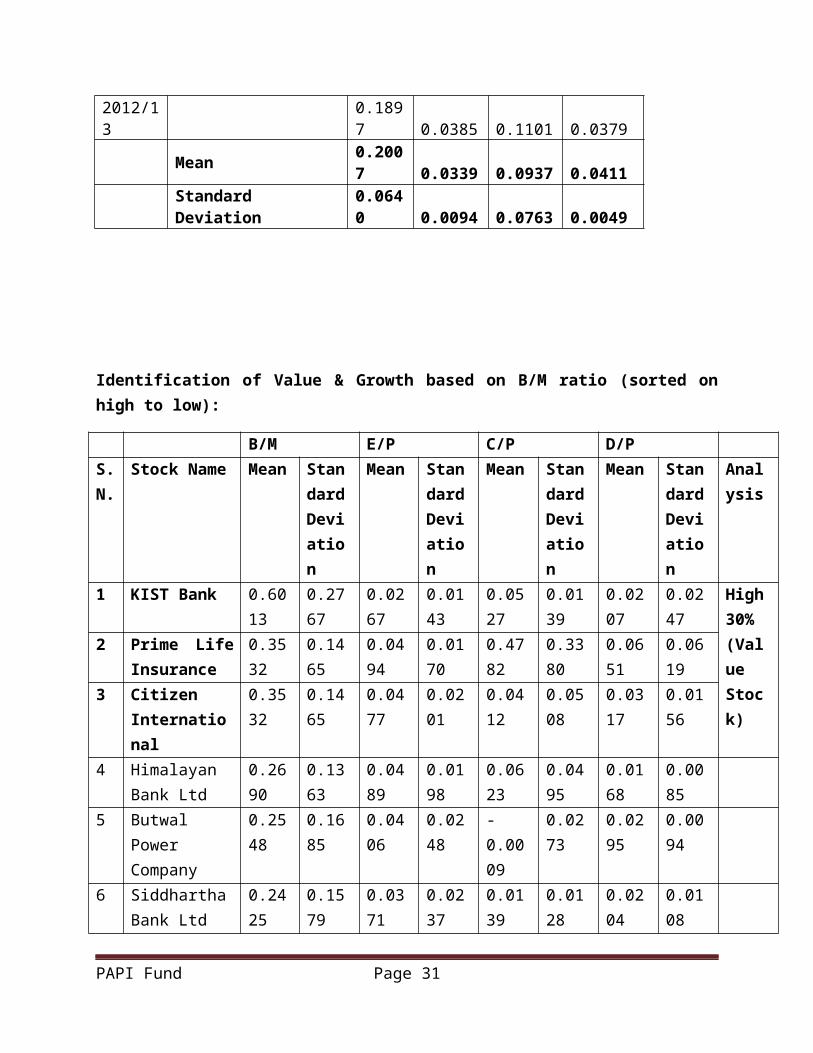

Calculation of B/M, E/P, C/P, & D/P for 10 stocks:

FiscalYear Stock Name B/M

Earnings toprice

Cashflowtoprice

Dividends toPrice

2008/09

StandardChartered Bank

0.0545 0.0183 0.0187 0.3053

2009/10

0.0639 0.0237 0.0212 0.3341

2010/11

0.1269 0.0386 0.0395 0.2189

2011/12

0.1237 0.0404 0.0358 0.2695

2012/13

0.1244 0.0361 0.0333 0.2208

Mean 0.0987 0.0314 0.0297 0.2697

StandardDeviation

0.0362 0.0098 0.0092 0.0510

2008/09

KIST Bank 0.2730 0.0119 0.0526 0.0339

2009/10

0.5138 0.0362 0.0425 0.0489

2010/11

0.6914

0.0174 0.0432 0.0000

PAPI Fund Page 27

2011/12

0.9271 0.0414 0.0724 0.0000

2012/13 N/A N/A N/A N/A

Mean 0.6013 0.0267 0.0527 0.0207

StandardDeviation

0.2767 0.0143 0.0139 0.0247

2008/09

Nabil Bank

0.0441 0.0232 0.0154 0.3934

2009/10

0.0793 0.0352 0.0250 0.3701

2010/11

0.1797 0.0564 0.0566 0.1333

2011/12

0.1649 0.0617 0.0547 0.2684

2012/13

0.1210 0.0524 0.0421 0.2960

Mean 0.1178 0.0458 0.0388 0.2923

StandardDeviation

0.0570 0.0161 0.0182 0.1026

2008/09

Himalayan BankLtd

0.1252 0.0317 0.0212 0.0126

2009/10

0.1458 0.0352 0.0230 0.0068

2010/11

0.2779 0.0390 0.0350 0.0145

2011/12

0.3473 0.0777 0.1172 0.0293

2012/13

0.4487 0.0612 0.1152 0.0206

Mean 0.2690 0.0489 0.0623 0.0168

StandardDeviation

0.1363 0.0198 0.0495 0.0085

2008/09

Siddhartha BankLtd

0.1662

0.0222 0.0122 0.0203

PAPI Fund Page 28

2009/10

0.1143 0.0210 0.0025 0.0138

2010/11

0.1460 0.0220 0.0045 0.0084

2011/12

0.2860 0.0446 0.0156 0.0226

2012/13

0.5000 0.0756 0.0347 0.0370

Mean 0.2425 0.0371 0.0139 0.0204

StandardDeviation

0.1579 0.0237 0.0128 0.0108

2008/09

CitizenInternational

0.1712 0.0186 0.0052 0.0152

2009/10

0.2200 0.0431 0.0045 0.0257

2010/11

0.4775 0.0568 0.0056 0.0249

2011/12

0.4739 0.0465 0.0791 0.0366

2012/13

0.4232 0.0736 0.1118 0.0562

Mean 0.3532 0.0477 0.0412 0.0317

StandardDeviation

0.1465 0.0201 0.0508 0.0156

2008/09

Everest Bank

0.0252 0.0293 0.0038 0.0064

2009/10

0.0449 0.0407 0.0056 0.0122

2010/11

0.0577 0.0419 0.0213 0.0126

2011/12

0.1350 0.0760 0.0570 0.0457

2012/13

0.1944 0.0857 0.0711 0.0015

Mean 0.0915 0.0547 0.0318 0.0157

PAPI Fund Page 29

StandardDeviation

0.0711 0.0246 0.0307 0.0174

2008/09

Butwal PowerCompany

0.1067 0.0271

-0.0106 0.0192

2009/10

0.1451 0.0274

-0.0111 0.0236

2010/11

0.1620 0.0223

-0.0107 0.0275

2011/12

0.3613 0.0438

-0.0196 0.0338

2012/13

0.4990 0.0824 0.0474 0.0433

Mean 0.2548 0.0406

-0.0009 0.0295

StandardDeviation

0.1685 0.0248 0.0273 0.0094

2008/09

Prime LifeInsurance

0.4232 - 0.8579 -

2009/10

0.4739 - 0.8195 -

2010/11

0.4775 0.0364 0.3391 0.0000

2011/12

0.2200 0.0432 0.2490 0.1231

2012/13

0.1712 0.0686 0.1254 0.0722

Mean 0.3532 0.0494 0.4782 0.0651

StandardDeviation

0.1465 0.0170 0.3380 0.0619

2008/09

Nepal SBI Bank 0.1025 0.0190

-0.0100 0.0431

2009/10

0.1992 0.0320 0.1848 0.0349

2010/11

0.2717 0.0440 0.1360 0.0475

2011/12

0.2404

0.0361 0.0474 0.0421

PAPI Fund Page 30

2012/13

0.1897 0.0385 0.1101 0.0379

Mean 0.2007 0.0339 0.0937 0.0411

StandardDeviation

0.0640 0.0094 0.0763 0.0049

Identification of Value & Growth based on B/M ratio (sorted onhigh to low):

B/M E/P C/P D/P S.N.

Stock Name Mean StandardDeviation

Mean StandardDeviation

Mean StandardDeviation

Mean StandardDeviation

Analysis

1 KIST Bank 0.6013

0.2767

0.0267

0.0143

0.0527

0.0139

0.0207

0.0247

High30%(ValueStock)

2 Prime LifeInsurance

0.3532

0.1465

0.0494

0.0170

0.4782

0.3380

0.0651

0.0619

3 CitizenInternational

0.3532

0.1465

0.0477

0.0201

0.0412

0.0508

0.0317

0.0156

4 HimalayanBank Ltd

0.2690

0.1363

0.0489

0.0198

0.0623

0.0495

0.0168

0.0085

5 ButwalPowerCompany

0.2548

0.1685

0.0406

0.0248

-0.0009

0.0273

0.0295

0.0094

6 SiddharthaBank Ltd

0.2425

0.1579

0.0371

0.0237

0.0139

0.0128

0.0204

0.0108

PAPI Fund Page 31

7 Nepal SBIBank

0.2007

0.0640

0.0339

0.0094

0.0937

0.0763

0.0411

0.0049

8 Nabil Bank 0.1178

0.0570

0.0458

0.0161

0.0388

0.0182

0.2923

0.1026

Low30%(GrowthStock)

9 StandardCharteredBank

0.0987

0.0362

0.0314

0.0098

0.0297

0.0092

0.2697

0.0510

10 EverestBank

0.0915

0.0711

0.0547

0.0246

0.0318

0.0307

0.0157

0.0174

PAPI Fund Page 32

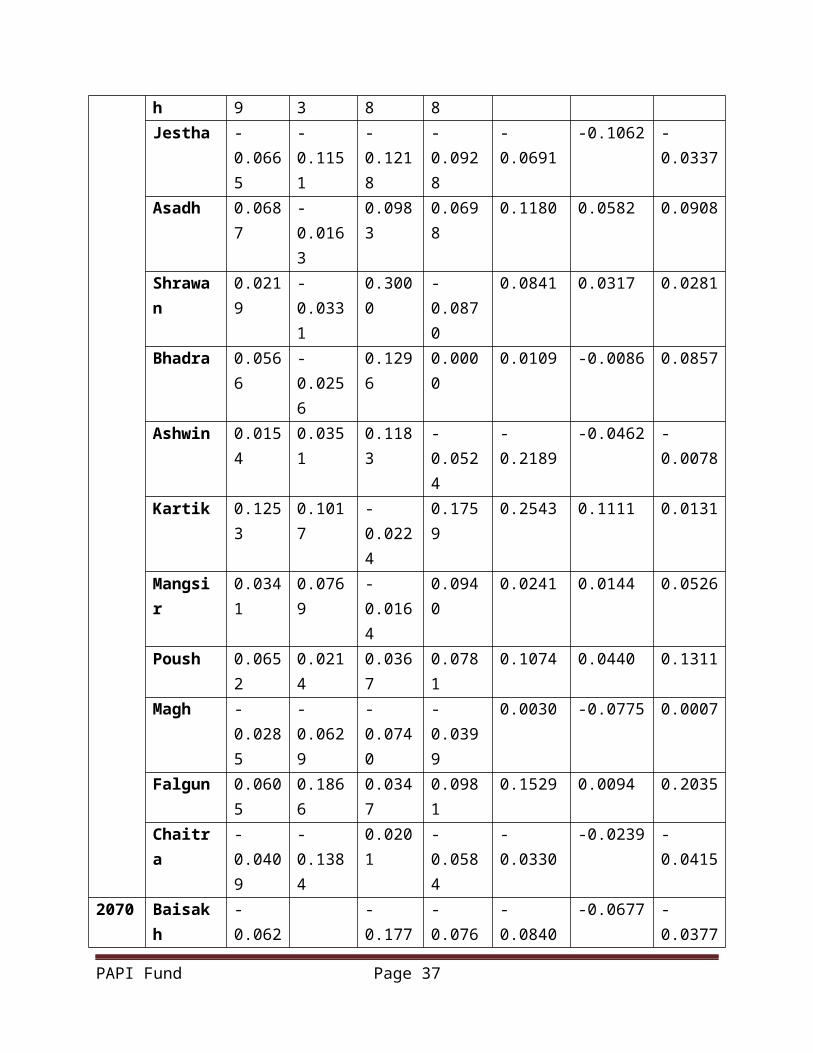

Detail Calculation of Monthly Returns on each stock:

NEPSEReturn in%

KISTReturn in%

PrimeLifeInsuranceReturn in%

CitizensIntl.BankReturn in%

NabilBankReturnin %

Std.Chartered BankReturnin %

Everest BankReturnin %

2065 Shrawan

Bhadra -0.1003

-0.3280

-0.0783 -0.0766

Ashwin -0.0431

-0.0293

-0.0137 -0.0254

Kartik -0.1361

-0.0515

-0.3432 -0.2245

Mangsir

-0.0893

-0.0196

-0.0422 -0.1093

Poush -0.1021

-0.0948

-0.0291 -0.0329

Magh 0.0056

0.0627 -0.0260 -0.0054

Falgun 0.0055

-0.0112

-0.0022 0.0124

Chaitra

-0.0089

0.0114 0.0215 0.0931

2066 Baisak - 0.0281 0.0268 -

PAPI Fund Page 33

h 0.0005

0.0471

Jestha 0.0269

0.1519 0.1554 0.1035

Asadh 0.1037

0.0107

0.2022

0.1620 0.0780 0.0469

Shrawan

-0.0426

0.0714

0.0758

0.0092 0.0293 0.0794

Bhadra -0.1218

-0.1481

-0.0310

-0.4296

-0.1537 -0.1358

Ashwin -0.0323

0.0696

-0.0102

0.0213 -0.2970 0.0437

Kartik -0.0699

-0.0325

-0.0822

-0.0625

-0.0304 -0.2690

Mangsir

-0.0323

-0.0728

-0.0272

-0.0407

-0.0163 -0.0143

Poush -0.0298

-0.0483

-0.0625

0.0039 -0.0584 -0.0685

Magh -0.0737

-0.2603

-0.1053

-0.1077

-0.0862 -0.0143

Falgun -0.0254

0.1159

-0.0471

-0.0254

0.0351 -0.0196

Chaitra

-0.0655

-0.1808

-0.1584

-0.0977

-0.0739 -0.0652

2067 Baisak - - 0.073 0.0784 0.0086 -

PAPI Fund Page 34

h 0.0190

0.0986

3 0.0738

Jestha 0.0797

0.1563

0.1390

0.0455 0.0959 0.1833

Asadh 0.0044

-0.1036

-0.0180

0.0365 0.0247 0.0264

Shrawan

-0.0503

-0.0201

-0.3622

-0.3890

-0.1103

-0.1235 -0.0442

Bhadra -0.1086

-0.1128

-0.1695

-0.0333

-0.0736

-0.2589 -0.2850

Ashwin 0.0392

0.2312

0.0306

0.0069

-0.2351

0.1366 -0.0350

Kartik 0.0110

-0.0939

0.1089

0.0274

-0.0546

-0.1152 0.0781

Mangsir

-0.0774

-0.1140

-0.0982

-0.1567

-0.1823

-0.1335 -0.1372

Poush 0.0298

0.0409

-0.0099

-0.0119

0.1446 0.0911 0.1000

Magh 0.0019

-0.0112

0.0450

-0.0320

0.0165 0.0025 -0.0273

Falgun -0.0667

-0.0398

-0.0766

-0.1033

-0.1191

-0.1074 -0.0196

Chaitra

-0.0114

-0.2130

-0.0881

-0.0968

0.0227 -0.0453 0.0686

2068 Baisak - - - 0.061 - -0.0480 -

PAPI Fund Page 35

h 0.0605

0.0376

0.1136

2 0.1043 0.1338

Jestha -0.1343

-0.1953

-0.1026

-0.2404

-0.2044

-0.1900 -0.0525

Asadh 0.1954

0.5049

0.2214

0.4051

0.4424 0.3493 0.1891

Shrawan

-0.0262

0.0323

-0.0994

-0.1036

-0.0168

-0.0611 -0.1088

Bhadra -0.0910

-0.0813

-0.0844

-0.1156

-0.2486

-0.1953 0.0051

Ashwin 0.0305

-0.0408

0.1844

-0.0682

0.0249 0.0809 -0.0357

Kartik -0.0163

-0.0638

0.0180

0.0244

-0.0770

-0.0816 -0.1746

Mangsir

-0.0287

-0.0530

-0.0059

-0.0119

-0.0754

-0.0237 -0.0192

Poush 0.0517

0.0480

-0.0178

0.0663

0.1174 0.0698 -0.0484

Magh -0.0624

0.4885

-0.0120

-0.0678

-0.0675

-0.0553 -0.0618

Falgun 0.0065

-0.4513

-0.1646

-0.0061

0.0439 0.0360 -0.0190

Chaitra

0.0192

0.1215

0.1533

0.1646

0.1227 0.0507 0.1209

2069 Baisak 0.220 0.158 0.246 0.240 0.3178 0.3117 0.3049

PAPI Fund Page 36

h 9 3 8 8Jestha -

0.0665

-0.1151

-0.1218

-0.0928

-0.0691

-0.1062 -0.0337

Asadh 0.0687

-0.0163

0.0983

0.0698

0.1180 0.0582 0.0908

Shrawan

0.0219

-0.0331

0.3000

-0.0870

0.0841 0.0317 0.0281

Bhadra 0.0566

-0.0256

0.1296

0.0000

0.0109 -0.0086 0.0857

Ashwin 0.0154

0.0351

0.1183

-0.0524

-0.2189

-0.0462 -0.0078

Kartik 0.1253

0.1017

-0.0224

0.1759

0.2543 0.1111 0.0131

Mangsir

0.0341

0.0769

-0.0164

0.0940

0.0241 0.0144 0.0526

Poush 0.0652

0.0214

0.0367

0.0781

0.1074 0.0440 0.1311

Magh -0.0285

-0.0629

-0.0740

-0.0399

0.0030 -0.0775 0.0007

Falgun 0.0605

0.1866

0.0347

0.0981

0.1529 0.0094 0.2035

Chaitra

-0.0409

-0.1384

0.0201

-0.0584

-0.0330

-0.0239 -0.0415

2070 Baisakh

-0.062

-0.177

-0.076

-0.0840

-0.0677 -0.0377

PAPI Fund Page 37

8 6 6Jestha 0.007

8 0.012

00.0040

0.0225 0.0291 -0.0013

Asadh 0.0485

0.0672

0.0512

0.0503 0.0105 0.0392

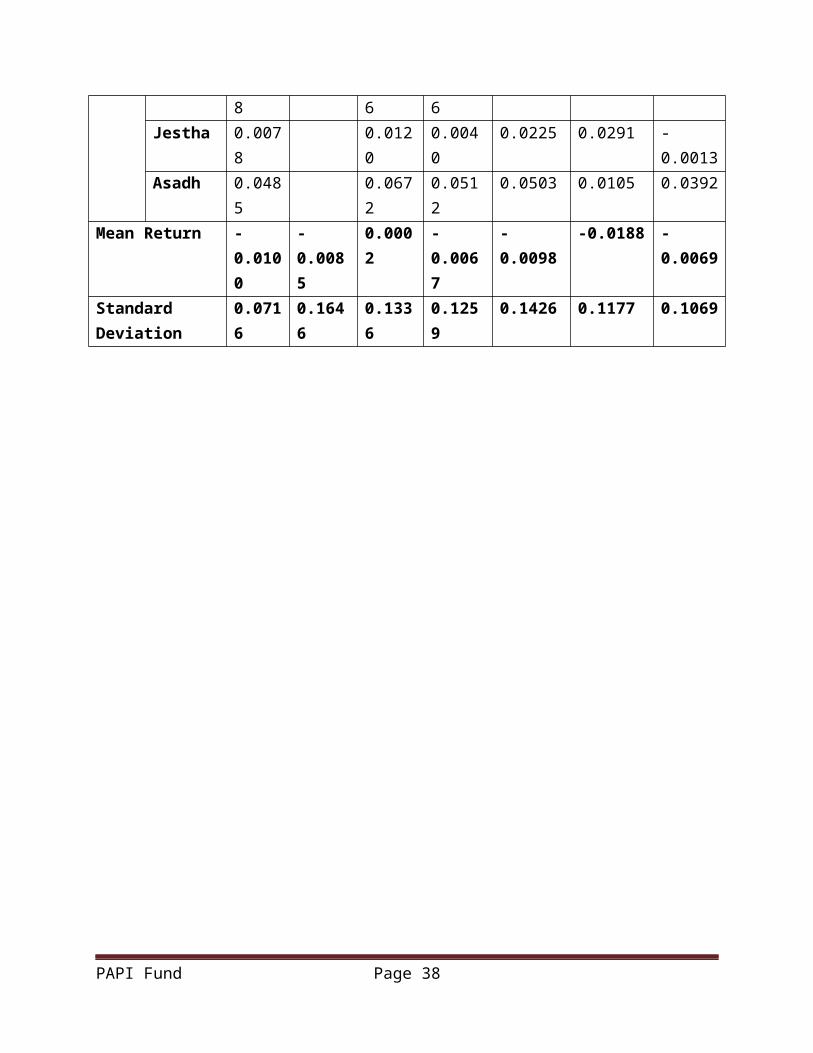

Mean Return -0.0100

-0.0085

0.0002

-0.0067

-0.0098

-0.0188 -0.0069

StandardDeviation

0.0716

0.1646

0.1336

0.1259

0.1426 0.1177 0.1069

PAPI Fund Page 38

Average Annual Return Calculation and difference in return ofGrowth and Value Stock:

NEPSEReturnin %

KISTReturnin %

PrimeLifeInsuranceReturnin %

CitizensIntl.BankReturnin %

NabilBankReturnin %

Std.Chartered BankReturnin %

Everest BankReturnin %

Mean Return(Monthly)

-0.9975%

-0.8549%

0.0229%

-0.6681%

-0.9844%

-1.8766%

-0.6871%

Mean Return(Annual)

-11.97% -10.25% 0.2751%

-8.0178%

-11.8128%

-22.5196%

-8.2454%

AverageReturn ofValue Stocks(H)

-6.0007%

AverageReturn ofGrowthStocks (L)

-14.1926%

High - LowReturn 8.1919%

PAPI Fund Page 39

Detail Calculation of Return based on Month End Closing Price:

NEPSEKIST Bank (ValueStock)

MonthEndNEPSEIndex

MonthlyReturn

Returnin %

MonthEndClosingPrice

MonthlyReturn

Returnin %

2065Shrawan

1084.76

Bhadra 976.01

-108.75

-0.100253

Ashwin 933.97-42.04

-0.043073

Kartik 806.9

-127.07

-0.136054

Mangsir 734.85-72.05

-0.089292

Poush 659.81 - -

PAPI Fund Page 40

75.040.102116

Magh 663.52 3.710.0056228

Falgun 667.2 3.680.0055462

Chaitra 661.27 -5.93

-0.008888

2066

Baisakh 660.97 -0.3

-0.000454

Jestha 678.74 17.770.0268847 374

Asadh 749.1 70.360.1036627 378 4

0.01069519

Shrawan 717.2 -31.9

-0.042584 405 27

0.07142857

Bhadra 629.88-87.32

-0.121751 345 -60

-0.1481481

Ashwin 609.55-20.33

-0.032276 369 24

0.06956522

Kartik 566.94-42.61

-0.069904 357 -12

-0.0325203

Mangsir 548.61-18.33

-0.032331 331 -26

-0.0728291

Poush 532.26 -16.35

-0.029803

315 -16 -0.0483384

PAPI Fund Page 41

Magh 493.02-39.24

-0.073723 233 -82

-0.2603175

Falgun 480.49-12.53

-0.025415 260 27

0.11587983

Chaitra 449.04-31.45

-0.065454 213 -47

-0.1807692

2067

Baisakh 440.53 -8.51

-0.018952 192 -21

-0.0985915

Jestha 475.65 35.120.0797222 222 30 0.15625

Asadh 477.73 2.080.004373 199 -23

-0.1036036

Shrawan 453.7-24.03

-0.0503 195 -4

-0.0201005

Bhadra 404.43-49.27

-0.108596 173 -22

-0.1128205

Ashwin 420.3 15.870.0392404 213 40

0.23121387

Kartik 424.93 4.630.0110159 193 -20

-0.0938967

Mangsir 392.04-32.89

-0.077401 171 -22

-0.1139896

Poush 403.71 11.670.0297674 178 7

0.04093567

Magh 404.47 0.76 0.0018 176 -2 -

PAPI Fund Page 42

8250.011236

Falgun 377.5

-26.97

-0.06668 169 -7

-0.0397727

Chaitra 373.2 -4.3

-0.011391 133 -36

-0.2130178

2068

Baisakh 350.62

-22.58

-0.060504 128 -5

-0.037594

Jestha 303.53

-47.09

-0.134305 103 -25

-0.1953125

Asadh362.85 59.32 0.1954

337155 52 0.50485

437

Shrawan 353.33 -9.52

-0.026237 160 5

0.03225806

Bhadra 321.18

-32.15

-0.090991 147 -13

-0.08125

Ashwin 330.99 9.81

0.0305436

141 -6

-0.0408163

Kartik 325.61 -5.38

-0.016254 132 -9

-0.0638298

Mangsir 316.27 -9.34

-0.028685 125 -7

-0.0530303

Poush332.62 16.35 0.0516

963131 6 0.048

Magh 311.88 - - 195 64 0.48854

PAPI Fund Page 43

20.740.062353 962

Falgun 313.92 2.040.006541 107 -88

-0.4512821

Chaitra 319.95 6.030.0192087 120 13

0.12149533

2069Baisakh 390.63 70.68

0.2209095 139 19

0.15833333

Jestha 364.67-25.96

-0.066457 123 -16

-0.1151079

Asadh 389.74 25.070.0687471 121 -2

-0.0162602

Shrawan 398.28 8.540.021912 117 -4

-0.0330579

Bhadra 420.83 22.550.0566185 114 -3

-0.025641

Ashwin 427.3 6.470.0153744 118 4

0.03508772

Kartik 480.85 53.550.1253218 130 12

0.10169492

Mangsir 497.27 16.420.0341479 140 10

0.07692308

Poush 529.69 32.420.065196 143 3

0.02142857

Magh 514.57-15.12

-0.028545 134 -9

-0.0629371

Falgun 545.72 31.15 0.060536

159 25 0.18656716

PAPI Fund Page 44

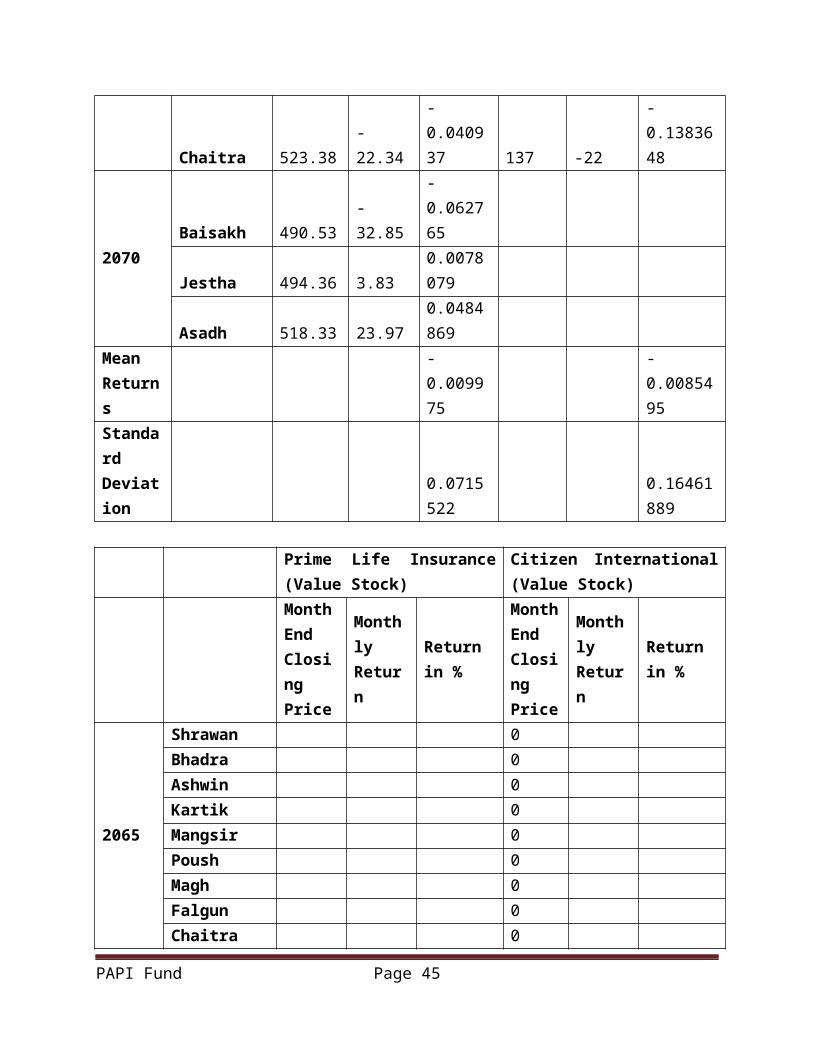

Chaitra 523.38-22.34

-0.040937 137 -22

-0.1383648

2070Baisakh 490.53

-32.85

-0.062765

Jestha 494.36 3.830.0078079

Asadh 518.33 23.970.0484869

MeanReturns

-0.009975

-0.0085495

StandardDeviation

0.0715522

0.16461889

Prime Life Insurance(Value Stock)

Citizen International(Value Stock)

MonthEndClosingPrice

MonthlyReturn

Returnin %

MonthEndClosingPrice

MonthlyReturn

Returnin %

2065

Shrawan 0 Bhadra 0 Ashwin 0 Kartik 0 Mangsir 0 Poush 0 Magh 0 Falgun 0 Chaitra 0

PAPI Fund Page 45

2066

Baisakh 0 Jestha 549

Asadh 660 1110.20218579

Shrawan 710 500.07575758

Bhadra 688 -22

-0.0309859

Ashwin 681 -7

-0.0101744

Kartik 625 -56

-0.082232

Mangsir 608 -17 -0.0272Poush 570 -38 -0.0625

Magh 510 -60

-0.1052632

Falgun 486 -24

-0.0470588

Chaitra 409 -77

-0.1584362

2067Baisakh 439 30

0.07334963

Jestha 500 610.13895216

Asadh 370 491 -9 -0.018Shrawan 236 -134 -

0.3621622

300 -191 -0.389002

PAPI Fund Page 46

Bhadra 196 -40

-0.1694915 290 -10

-0.0333333

Ashwin 202 60.03061224 292 2

0.00689655

Kartik 224 220.10891089 300 8

0.02739726

Mangsir 202 -22

-0.0982143 253 -47

-0.1566667

Poush 200 -2

-0.009901 250 -3

-0.0118577

Magh 209 9 0.045 242 -8 -0.032

Falgun 193 -16

-0.076555 217 -25

-0.1033058

Chaitra 176 -17

-0.0880829 196 -21

-0.0967742

2068

Baisakh 156 -20

-0.1136364 208 12

0.06122449

Jestha 140 -16

-0.1025641 158 -50

-0.2403846

Asadh 171 310.22142857 222 64

0.40506329

Shrawan 154 -17

-0.0994152 199 -23

-0.1036036

Bhadra 141 -13 -0.0844156

176 -23 -0.1155779

PAPI Fund Page 47

Ashwin 167 260.18439716 164 -12

-0.0681818

Kartik 170 30.01796407 168 4

0.02439024

Mangsir 169 -1

-0.0058824 166 -2

-0.0119048

Poush 166 -3

-0.0177515 177 11

0.06626506

Magh 164 -2

-0.0120482 165 -12

-0.0677966

Falgun 137 -27

-0.1646341 164 -1

-0.0060606

Chaitra 158 210.15328467 191 27

0.16463415

2069Baisakh 197 39

0.24683544 237 46

0.2408377

Jestha 173 -24

-0.1218274 215 -22

-0.092827

Asadh 190 170.0982659 230 15

0.06976744

Shrawan 247 57 0.3 210 -20

-0.0869565

Bhadra 279 320.12955466 210 0 0

Ashwin 312 33 0.11827957

199 -11 -0.052381

PAPI Fund Page 48

Kartik 305 -7

-0.0224359 234 35

0.1758794

Mangsir 300 -5

-0.0163934 256 22

0.09401709

Poush 311 110.03666667 276 20

0.078125

Magh 288 -23

-0.073955 265 -11

-0.0398551

Falgun 298 100.03472222 291 26

0.09811321

Chaitra 304 60.02013423 274 -17

-0.0584192

2070Baisakh 250 -54

-0.1776316 253 -21

-0.0766423

Jestha 253 3 0.012 254 10.00395257

Asadh 270 170.06719368 267 13

0.0511811

Mean Returns

0.00022923

-0.0066815

StandardDeviation

0.13358531

0.125939

Nabil Bank (GrowthStock)

Standard CharteredBank (Growth Stock)

MonthEnd

Monthly

Returnin %

MonthEnd

Monthly

Returnin %

PAPI Fund Page 49

ClosingPrice

Return

ClosingPrice

Return

2065

Shrawan 6101 8526

Bhadra 4100 -2001

-0.327979 7858 -668

-0.0783486

Ashwin 3980 -120

-0.0292683 7750 -108

-0.013744

Kartik 3775 -205

-0.0515075 5090 -2660

-0.3432258

Mangsir 3701 -74

-0.0196026 4875 -215

-0.0422397

Poush 3350 -351

-0.0948392 4733 -142

-0.0291282

Magh 3560 2100.06268657 4610 -123

-0.0259877

Falgun 3520 -40

-0.011236 4600 -10

-0.0021692

Chaitra 3560 40

0.01136364 4699 99

0.02152174

2066 Baisakh 3660 100

0.02808989 4825 126

0.02681422

Jestha 4216 5560.15191257 5575 750

0.15544041

Asadh 4899 683 0.1620019

6010 435 0.07802691

PAPI Fund Page 50

Shrawan 4944 45

0.00918555 6186 176

0.02928453

Bhadra 2820 -2124

-0.4296117 5235 -951

-0.1537342

Ashwin 2880 600.0212766 3680 -1555

-0.2970392

Kartik 2700 -180 -0.0625 3568 -112

-0.0304348

Mangsir 2590 -110

-0.0407407 3510 -58

-0.0162556

Poush 2600 100.003861 3305 -205

-0.0584046

Magh 2320 -280

-0.1076923 3020 -285

-0.086233

Falgun 2261 -59

-0.025431 3126 106

0.03509934

Chaitra 2040 -221

-0.0977444 2895 -231

-0.0738964

2067 Baisakh 2200 160

0.07843137 2920 25

0.00863558

Jestha 2300 1000.04545455 3200 280

0.09589041

Asadh 2384 840.03652174 3279 79

0.0246875

Shrawan

2121 -263 -0.11031

2874 -405 -0.12351

PAPI Fund Page 51

88 33

Bhadra 1965 -156

-0.0735502 2130 -744

-0.2588727

Ashwin 1503 -462

-0.2351145 2421 291

0.13661972

Kartik 1421 -82

-0.0545576 2142 -279

-0.1152416

Mangsir 1162 -259

-0.182266 1856 -286

-0.1335201

Poush 1330 1680.14457831 2025 169

0.09105603

Magh 1352 220.01654135 2030 5

0.00246914

Falgun 1191 -161

-0.1190828 1812 -218

-0.1073892

Chaitra 1218 27

0.02267003 1730 -82

-0.0452539

2068

Baisakh 1091 -127

-0.1042693 1647 -83

-0.0479769

Jestha 868 -223

-0.2043996 1334 -313

-0.1900425

Asadh 1252 3840.44239631 1800 466

0.34932534

Shrawan 1231 -21

-0.0167732 1690 -110

-0.0611111

PAPI Fund Page 52

Bhadra 925 -306

-0.2485784 1360 -330

-0.1952663

Ashwin 948 230.02486486 1470 110

0.08088235

Kartik 875 -73

-0.0770042 1350 -120

-0.0816327

Mangsir 809 -66

-0.0754286 1318 -32

-0.0237037

Poush 904 950.11742892 1410 92

0.06980273

Magh 843 -61

-0.0674779 1332 -78

-0.0553191

Falgun 880 370.04389087 1380 48

0.03603604

Chaitra 988 108

0.12272727 1450 70

0.05072464

2069 Baisakh 1302 314

0.31781377 1902 452

0.31172414

Jestha 1212 -90

-0.0691244 1700 -202

-0.106204

Asadh 1355 1430.1179868 1799 99

0.05823529

Shrawan 1469 114

0.08413284 1856 57

0.03168427

Bhadra 1485 160.01089176 1840 -16

-0.0086207

Ashwin 1160 -325 -0.21885

1755 -85 -0.04619

PAPI Fund Page 53

52 57

Kartik 1455 2950.25431034 1950 195

0.11111111

Mangsir 1490 35

0.02405498 1978 28

0.01435897

Poush 1650 1600.10738255 2065 87

0.04398382

Magh 1655 50.0030303 1905 -160

-0.0774818

Falgun 1908 2530.15287009 1923 18

0.00944882

Chaitra 1845 -63

-0.0330189 1877 -46

-0.023921

2070

Baisakh 1690 -155

-0.0840108 1750 -127

-0.0676612

Jestha 1728 380.02248521 1801 51

0.02914286

Asadh 1815 870.05034722 1820 19

0.01054969

Mean Returns

-0.009844

-0.0187663

StandardDeviation

0.14264467

0.11766251

Everest Bank (GrowthStock)

PAPI Fund Page 54

MonthEndClosingPrice

MonthlyReturn

Returnin %

2065

Shrawan 3370

Bhadra 3112 -258

-0.0765579

Ashwin 3033 -79

-0.0253856

Kartik 2352 -681

-0.2245302

Mangsir 2095 -257

-0.1092687

Poush 2026 -69

-0.0329356

Magh 2015 -11

-0.0054294

Falgun 2040 250.01240695

Chaitra 2230 1900.09313725

2066 Baisakh 2125 -105

-0.0470852

Jestha 2345 2200.10352941

PAPI Fund Page 55

Asadh 2455 1100.04690832

Shrawan 2650 1950.07942974

Bhadra 2290 -360

-0.1358491

Ashwin 2390 1000.04366812

Kartik 1747 -643

-0.2690377

Mangsir 1722 -25

-0.0143102

Poush 1604 -118

-0.068525

Magh 1581 -23

-0.0143392

Falgun 1550 -31

-0.0196078

Chaitra 1449 -101

-0.0651613

2067Baisakh 1342 -107

-0.073844

Jestha 1588 2460.18330849

Asadh 1630 420.02644836

PAPI Fund Page 56

Shrawan 1558 -72

-0.0441718

Bhadra 1114 -444

-0.2849807

Ashwin 1075 -39

-0.035009

Kartik 1159 840.07813953

Mangsir 1000 -159

-0.1371872

Poush 1100 100 0.1

Magh 1070 -30

-0.0272727

Falgun 1049 -21

-0.0196262

Chaitra 1121 720.0686368

2068

Baisakh 971 -150

-0.1338091

Jestha 920 -51

-0.0525232

Asadh 1094 1740.18913043

Shrawan 975 -119

-0.1087751

PAPI Fund Page 57

Bhadra 980 50.00512821

Ashwin 945 -35

-0.0357143

Kartik 780 -165

-0.1746032

Mangsir 765 -15

-0.0192308

Poush 728 -37

-0.048366

Magh 683 -45

-0.0618132

Falgun 670 -13

-0.0190337

Chaitra 751 810.12089552

2069Baisakh 980 229

0.30492676

Jestha 947 -33

-0.0336735

Asadh 1033 860.09081309

Shrawan 1062 290.02807357

Bhadra 1153 910.08568738

Ashwin 1144 -9 -

PAPI Fund Page 58

0.0078057

Kartik 1159 150.01311189

Mangsir1220 61 0.05263

158

Poush1380 160 0.13114

754

Magh1381 1 0.00072

464

Falgun1662 281 0.20347

574

Chaitra 1593 -69

-0.0415162

2070

Baisakh 1533 -60

-0.0376648

Jestha 1531 -2

-0.0013046

Asadh 1591 600.03919007

Mean Returns

-0.0068712

StandardDeviation

0.10693141

PAPI Fund Page 59