FACES OF LINN COUNTY SERVING YOU

174

FACES OF LINN COUNTY SERVING YOU www.LinnCounty.org 2014 Annual Budget for Linn County, Iowa Deputy Kevin Louis & K-9 Gompie Debbie Ironside, Recorder’s Office Bill Micheel, Planning & Development Cindy Fiester, Public Health Kim McElree, Attorney’s Office Anastasia Wilson, Attorney’s Office Brock Holub, Secondary Roads

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of FACES OF LINN COUNTY SERVING YOU

FACES OF LINN COUNTYSERVING YOU

www.LinnCounty.org

2014 Annual Budget for Linn County, Iowa

Deputy Kevin Louis & K-9 Gompie

Debbie Ironside, Recorder’s Office

Bill Micheel, Planning & Development

Cindy Fiester, Public Health

Kim McElree, Attorney’s Office

Anastasia Wilson, Attorney’s Office

Brock Holub, Secondary Roads

FACES OF LINN COUNTYSERVING YOU

www.LinnCounty.org

2014 Annual Budget for Linn County, Iowa

Deputy Kevin Louis & K-9 Gompie

Debbie Ironside, Recorder’s Office

Bill Micheel, Planning & Development

Cindy Fiester, Public Health

Kim McElree, Attorney’s Office

Anastasia Wilson, Attorney’s Office

Brock Holub, Secondary Roads

County of Linn, Iowa

Fiscal Year 2014

Annual Budget

Board of Supervisors

John Harris, Chairperson

Lu Barron, Supervisor

Linda Langston, Supervisor

Ben Rogers, Supervisor

Brent Oleson, Supervisor

INTRODUCTION TABLE OF CONTENTS ........................................................................................................................................................... 2 TRANSMITTAL LETTER .......................................................................................................................................................... 4 ORGANIZATIONAL CHART .................................................................................................................................................. 10 COUNTY OFFICIALS ........................................................................................................................................................... 11 COUNTY PROFILE .............................................................................................................................................................. 12

OVERVIEW

SUMMARY MATRIX OF FISCAL YEAR 2014 BUDGET ................................................................................................................ 14 SUMMARY ANALYSIS OF FISCAL YEAR 2014 BUDGET ............................................................................................................... 15 COMBINED FUNDS STATEMENT ........................................................................................................................................... 21 PERSONNEL POSITIONS ...................................................................................................................................................... 22 STAFF ANALYSIS ............................................................................................................................................................... 23

GENERAL FUND

GENERAL FUND NARRATIVE ................................................................................................................................................ 24 GENERAL FUND STATEMENT ............................................................................................................................................... 25 GENERAL FUND BALANCE ANALYSIS ..................................................................................................................................... 26

SPECIAL REVENUE FUNDS SPECIAL REVENUE FUNDS NARRATIVE ................................................................................................................................... 28 SPECIAL REVENUE FUNDS STATEMENT .................................................................................................................................. 29 SPECIAL REVENUE FUND BALANCE ANALYSIS .......................................................................................................................... 30 MH-DD SERVICES FUND ................................................................................................................................................... 32 MH-DD SERVICES FUND STATEMENT .................................................................................................................................. 33 RURAL SERVICES FUND ...................................................................................................................................................... 34 RURAL SERVICES FUND STATEMENT ..................................................................................................................................... 35 SECONDARY ROADS FUND .................................................................................................................................................. 36 SECONDARY ROADS FUND STATEMENT ................................................................................................................................. 37 OTHER SPECIAL REVENUE FUNDS ......................................................................................................................................... 38 OTHER SPECIAL REVENUE FUNDS STATEMENT ........................................................................................................................ 39

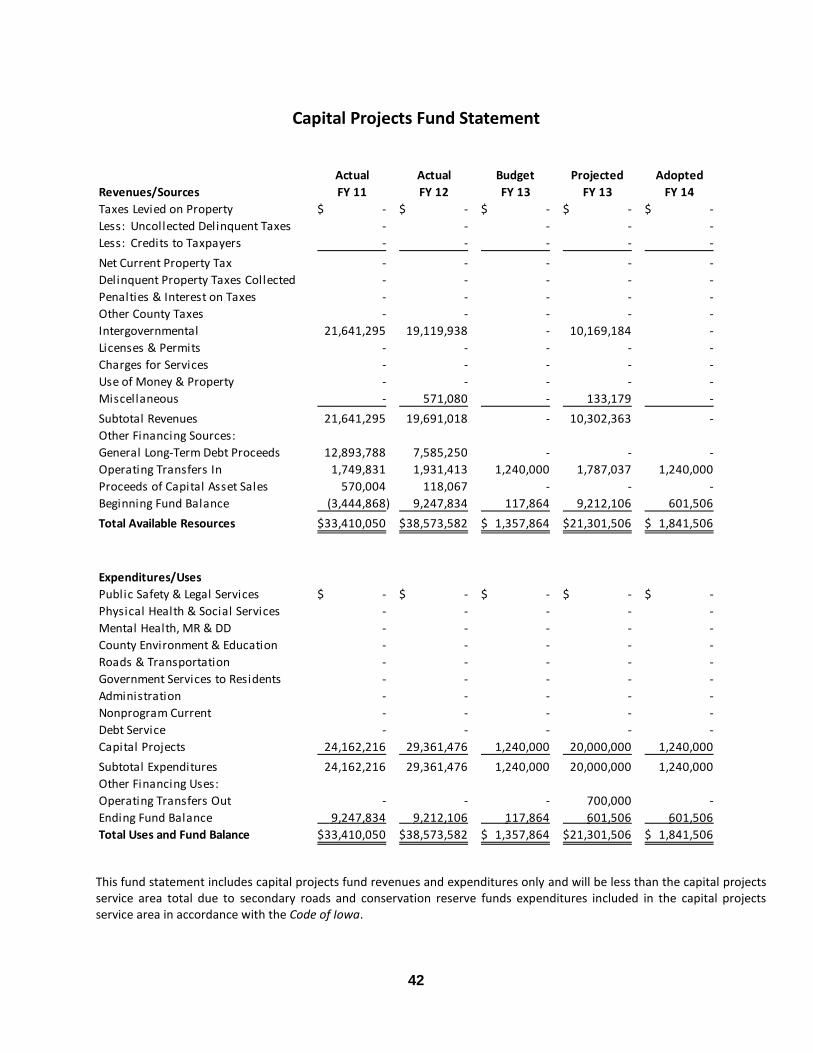

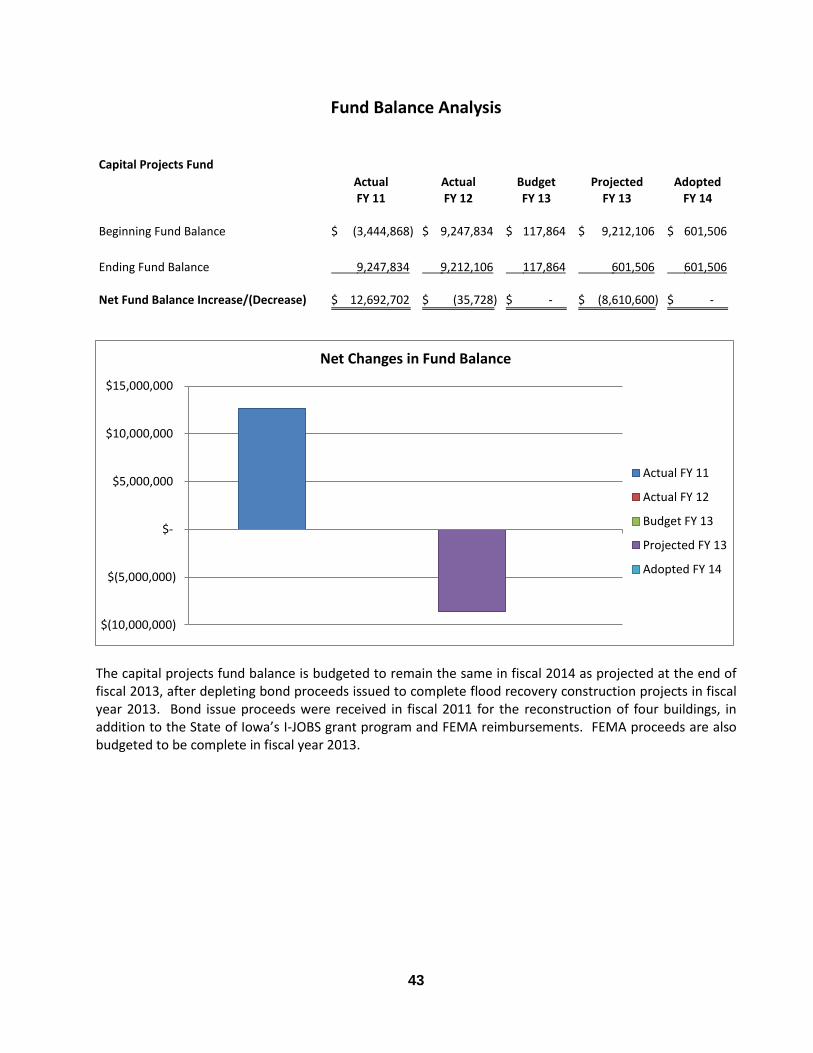

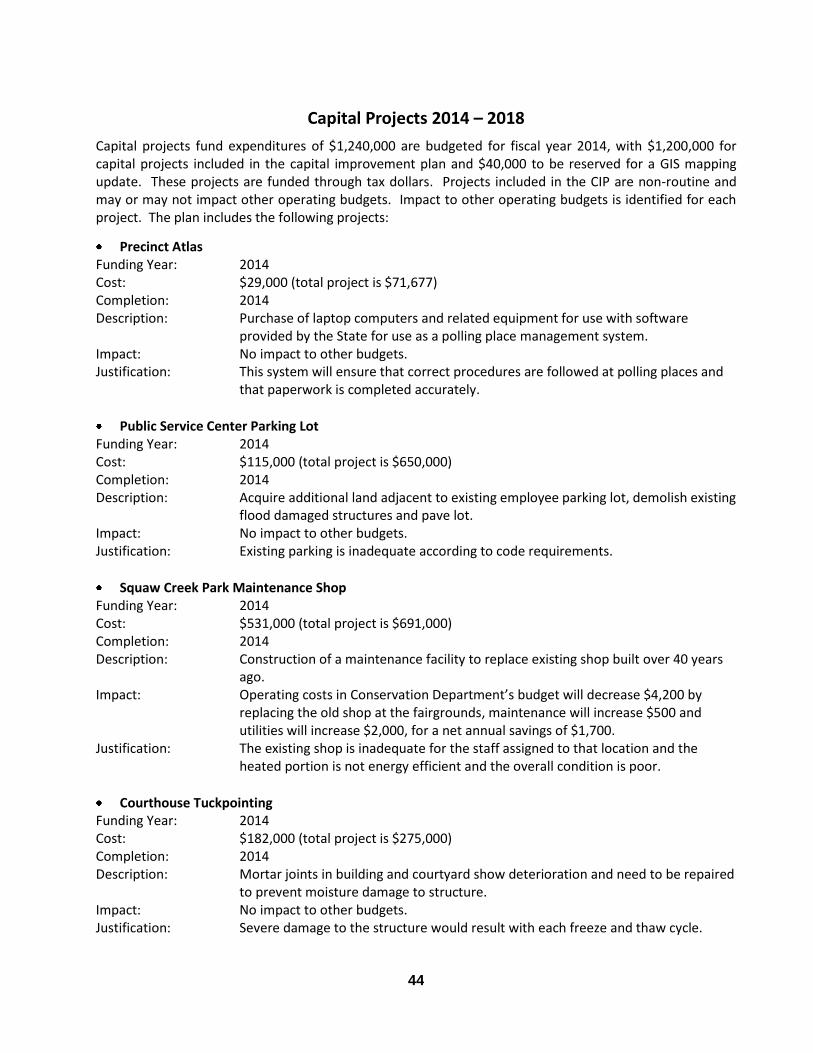

CAPITAL PROJECTS FUND

CAPITAL PROJECTS FUND NARRATIVE ................................................................................................................................... 40 CAPITAL PROJECTS FUND STATEMENT .................................................................................................................................. 42 CAPITAL PROJECTS FUND BALANCE ANALYSIS ......................................................................................................................... 43 CAPITAL PROJECTS 2014 - 2018 ....................................................................................................................................... 44 CAPITAL PROJECTS OPERATING IMPACT ................................................................................................................................ 50

DEBT SERVICE FUND

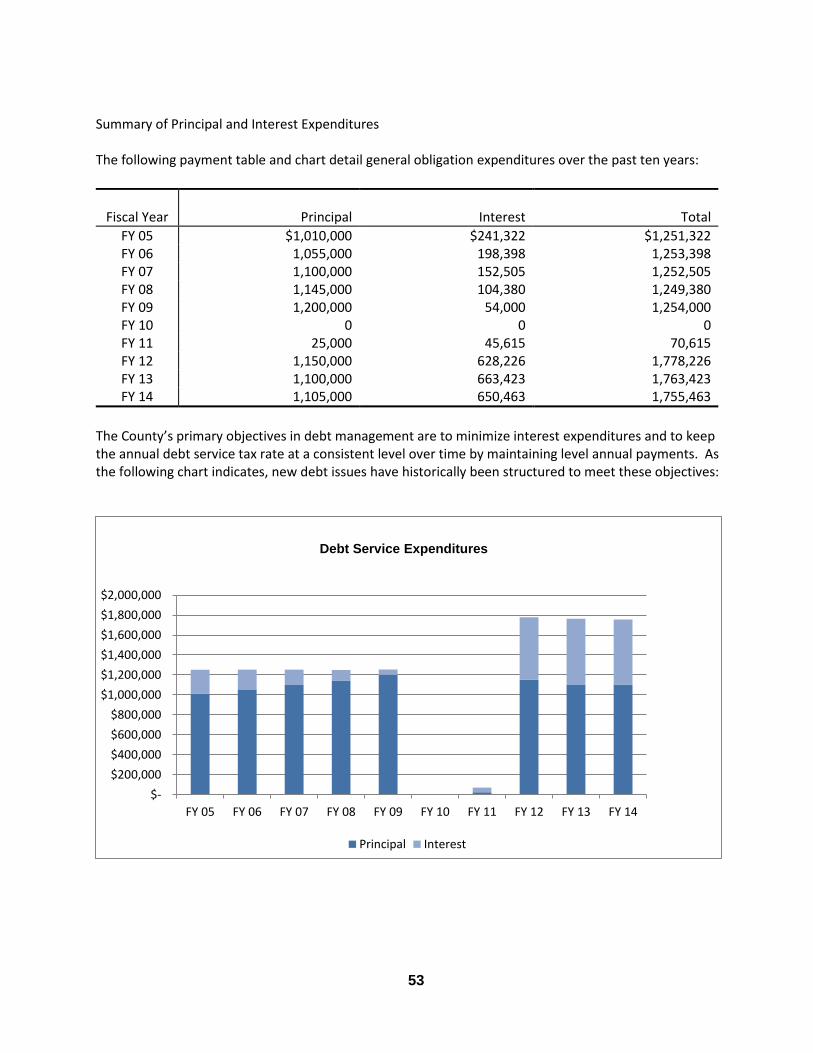

DEBT SERVICE FUND NARRATIVE ......................................................................................................................................... 51 DEBT SERVICE FUND STATEMENT ......................................................................................................................................... 54 DEBT SERVICE FUND BALANCE ANALYSIS ............................................................................................................................... 55

DEPARTMENTAL INFORMATION

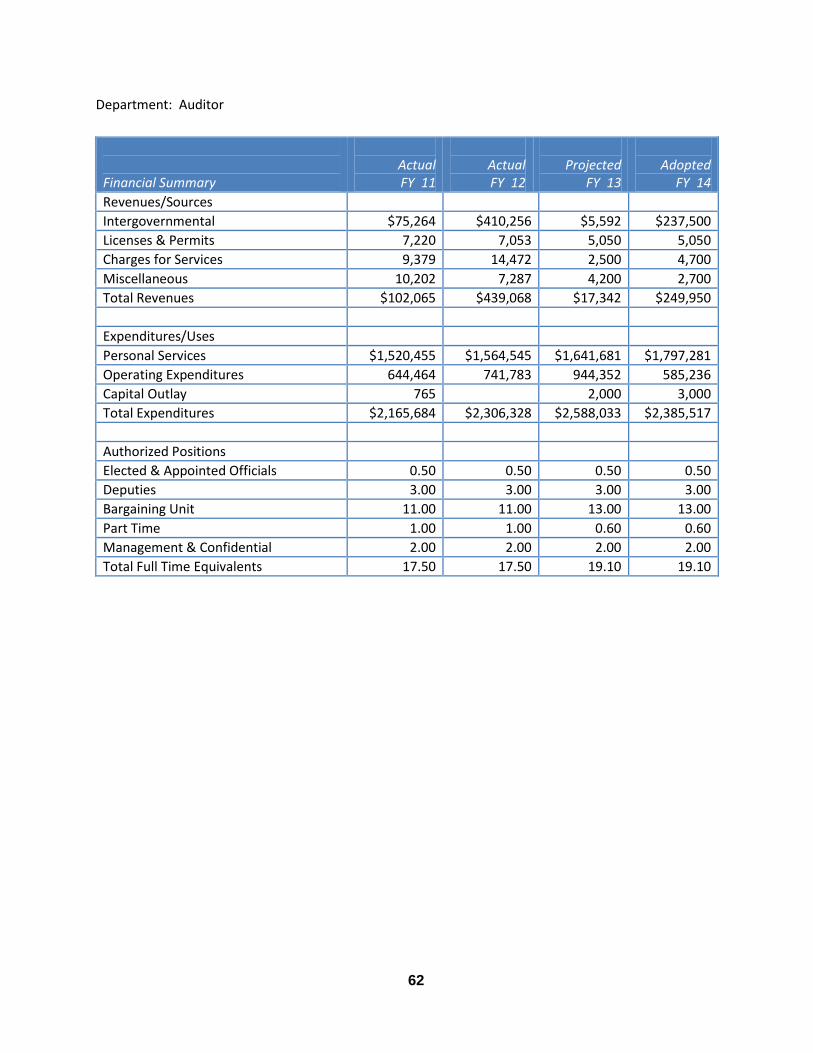

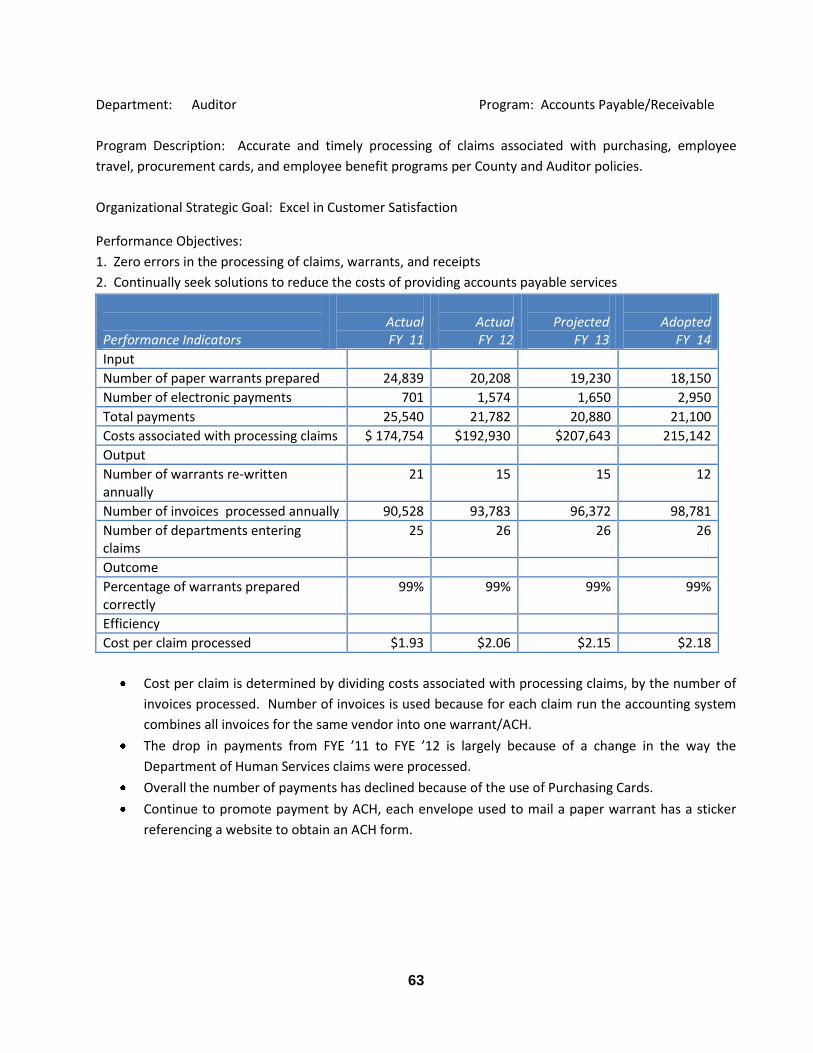

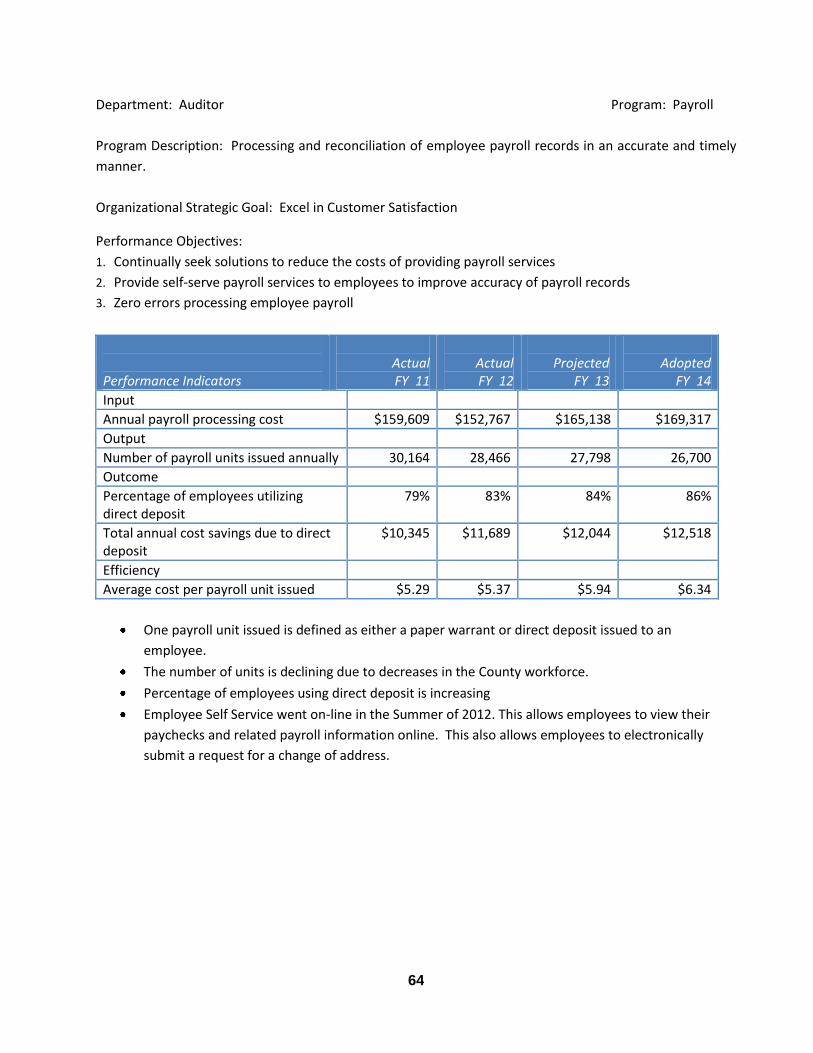

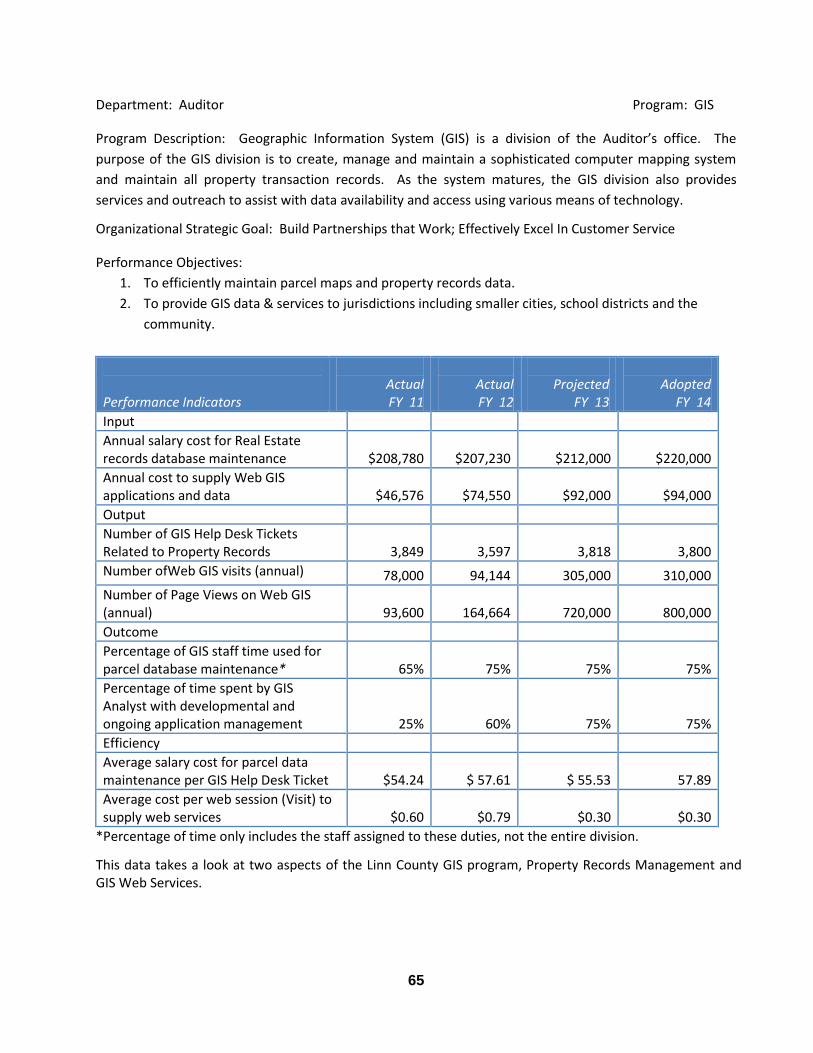

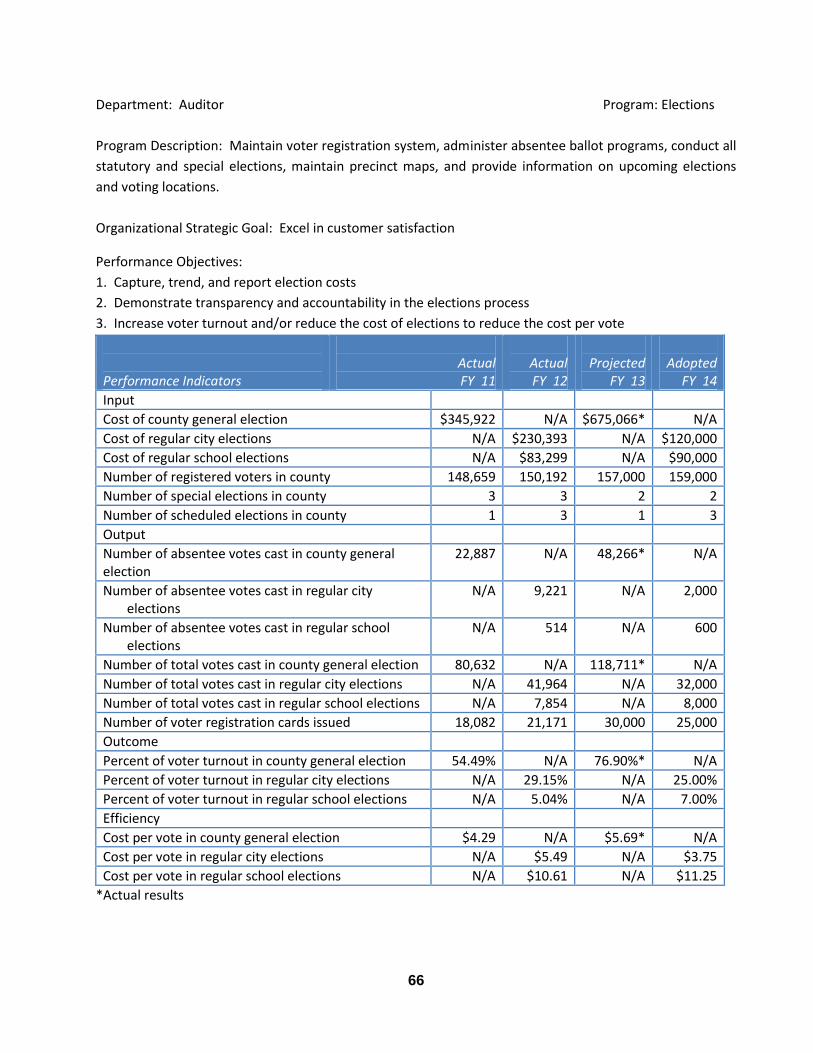

PERFORMANCE MEASUREMENT .......................................................................................................................................... 56 PERFORMANCE INDICATORS & FINANCIAL SUMMARIES: ATTORNEY ....................................................................................................................................................................... 57 AUDITOR ........................................................................................................................................................................ 62

(Continued)

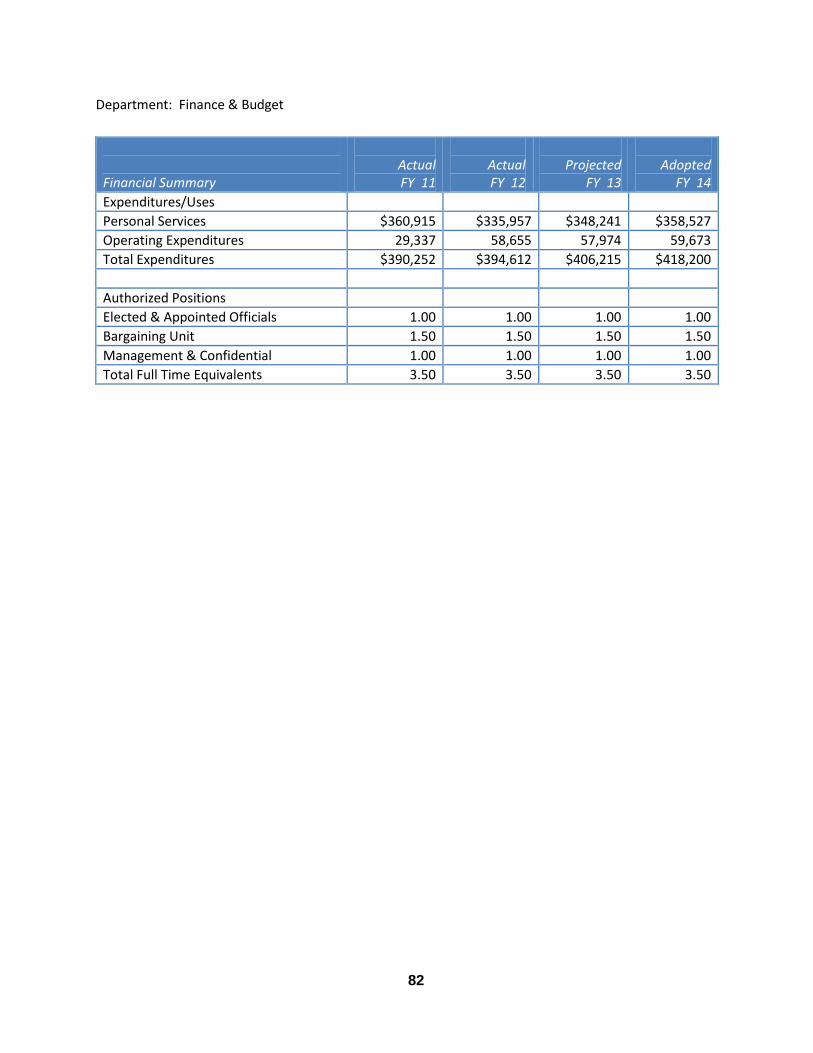

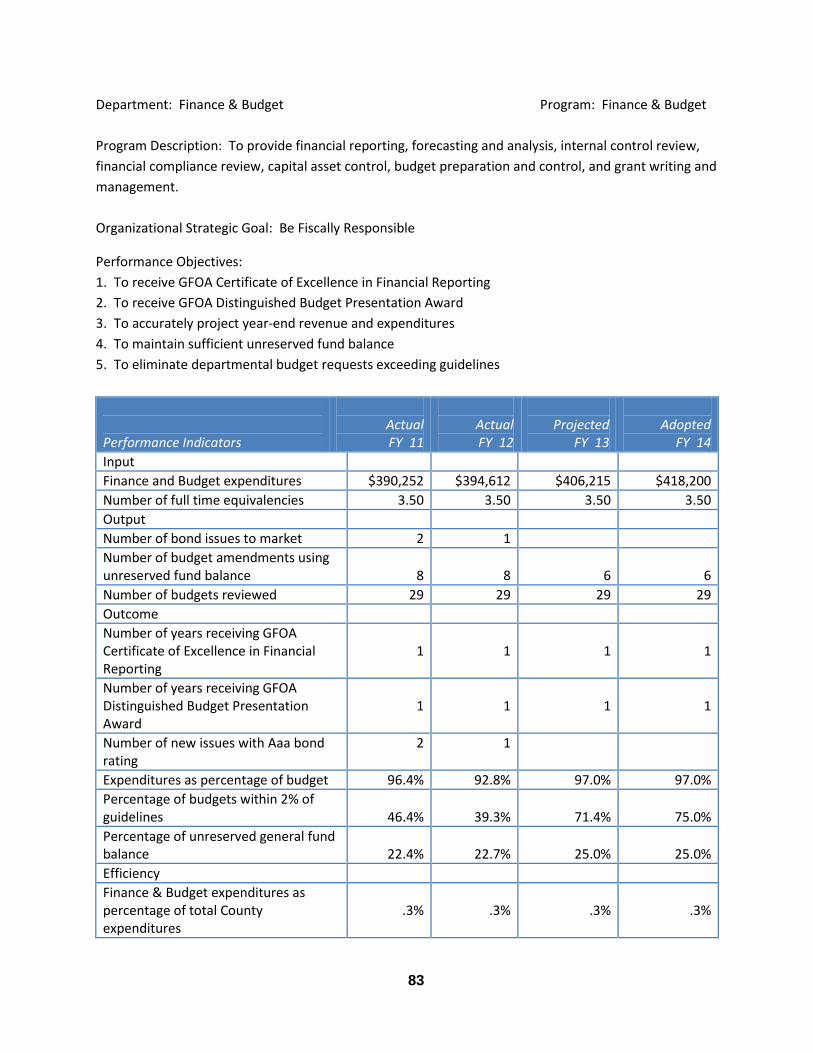

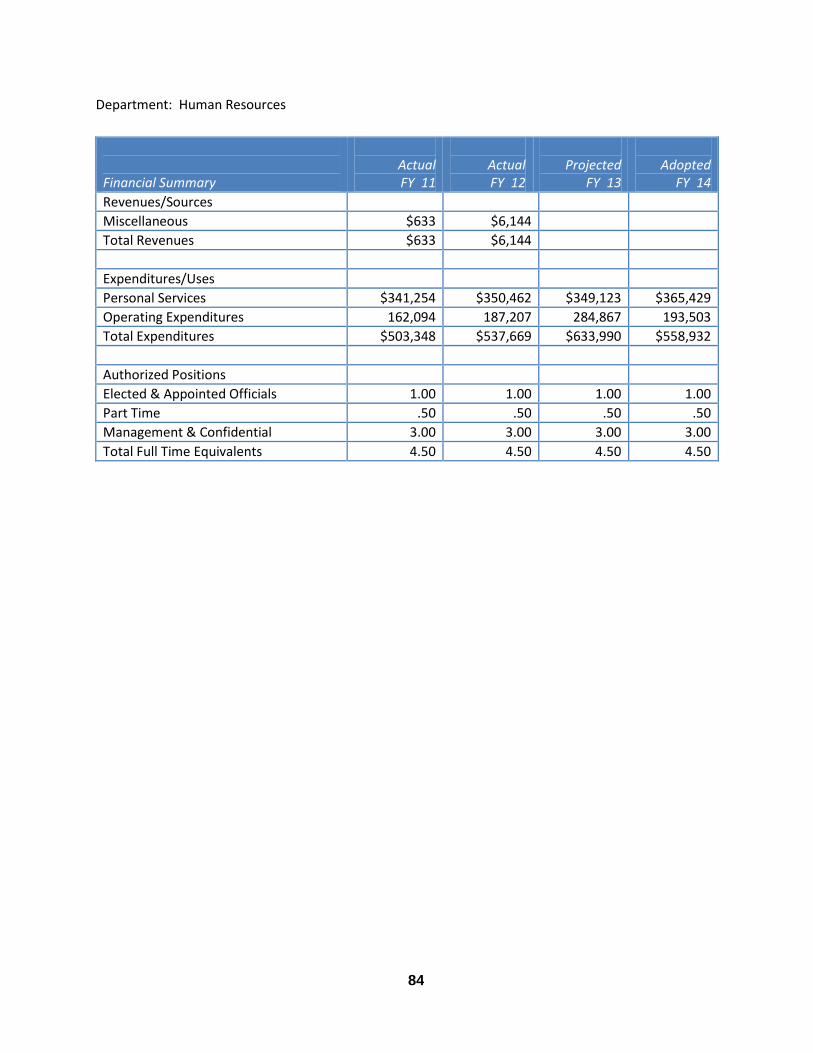

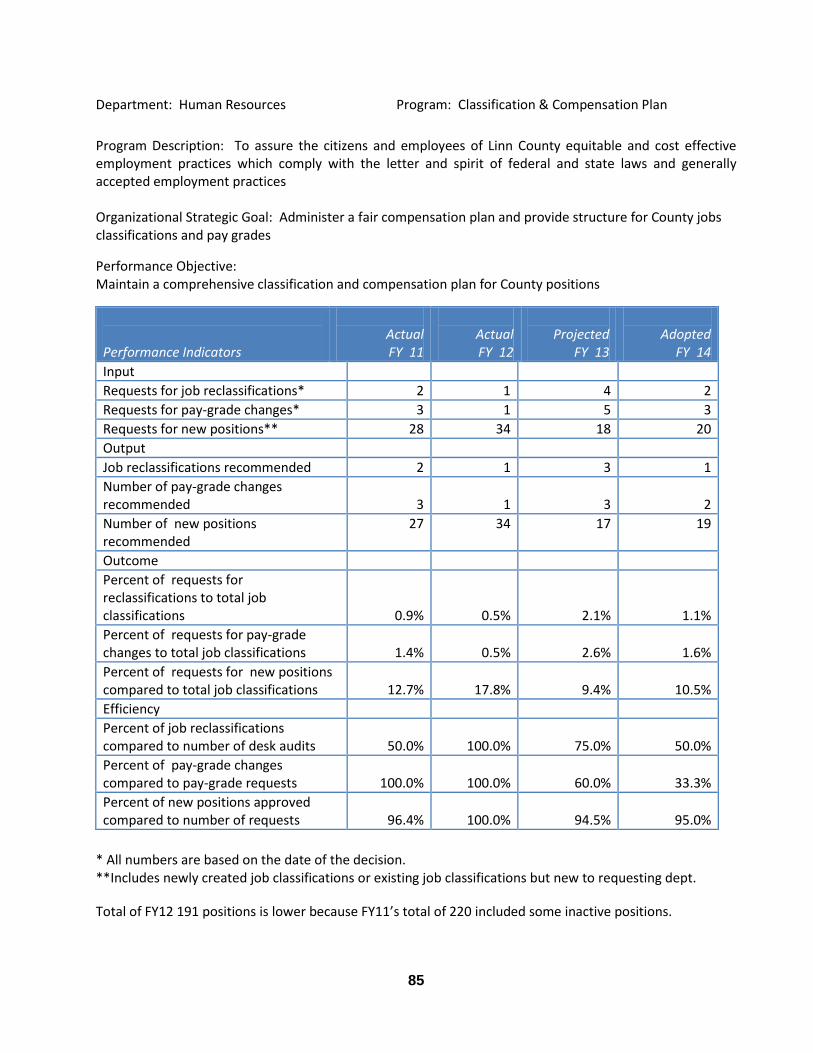

DEPARTMENTAL INFORMATION (CONTINUED)

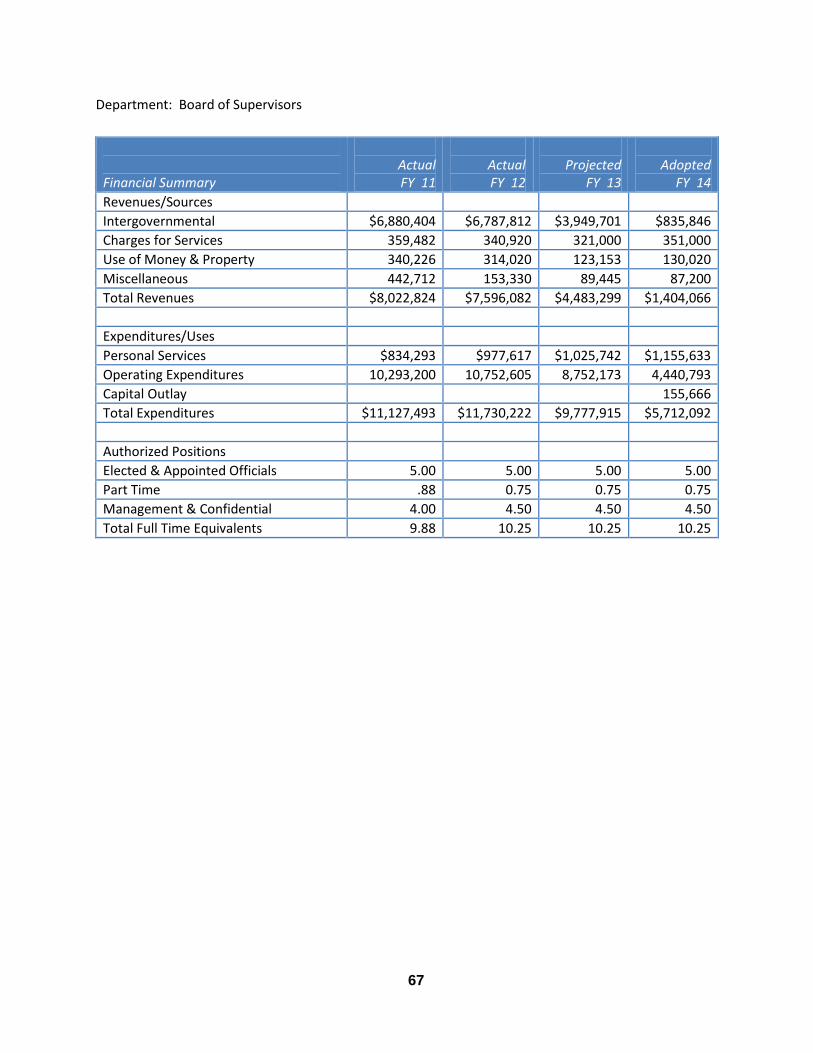

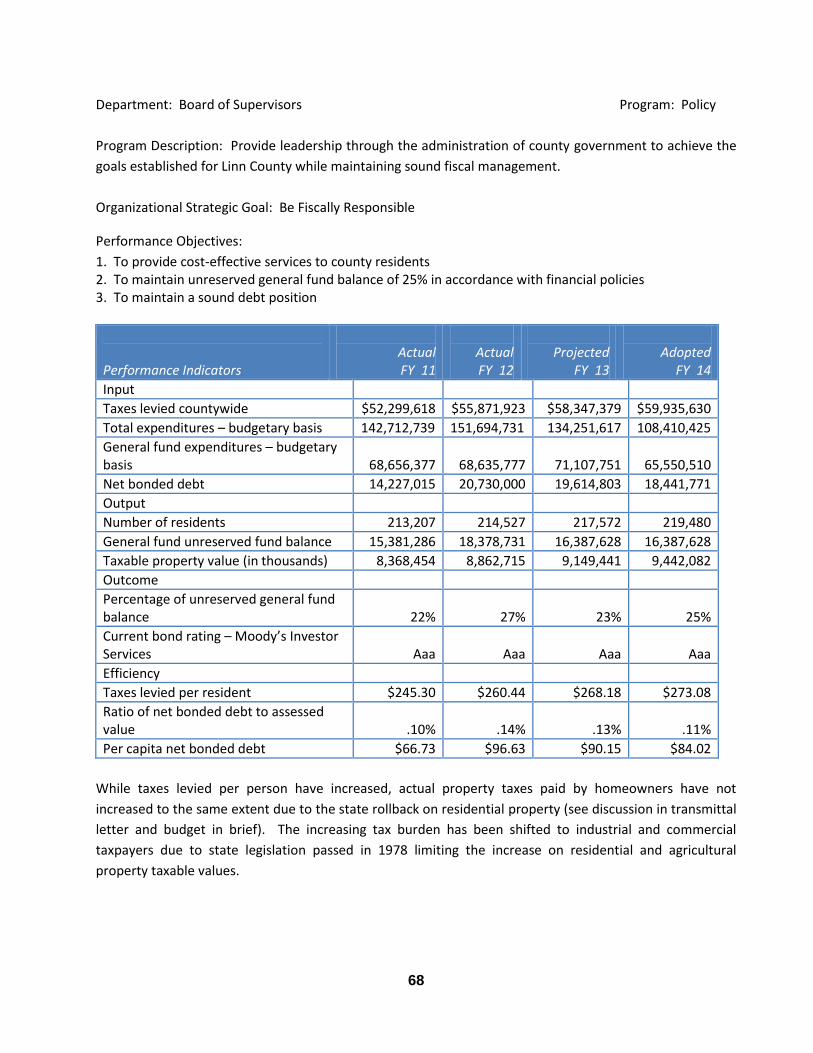

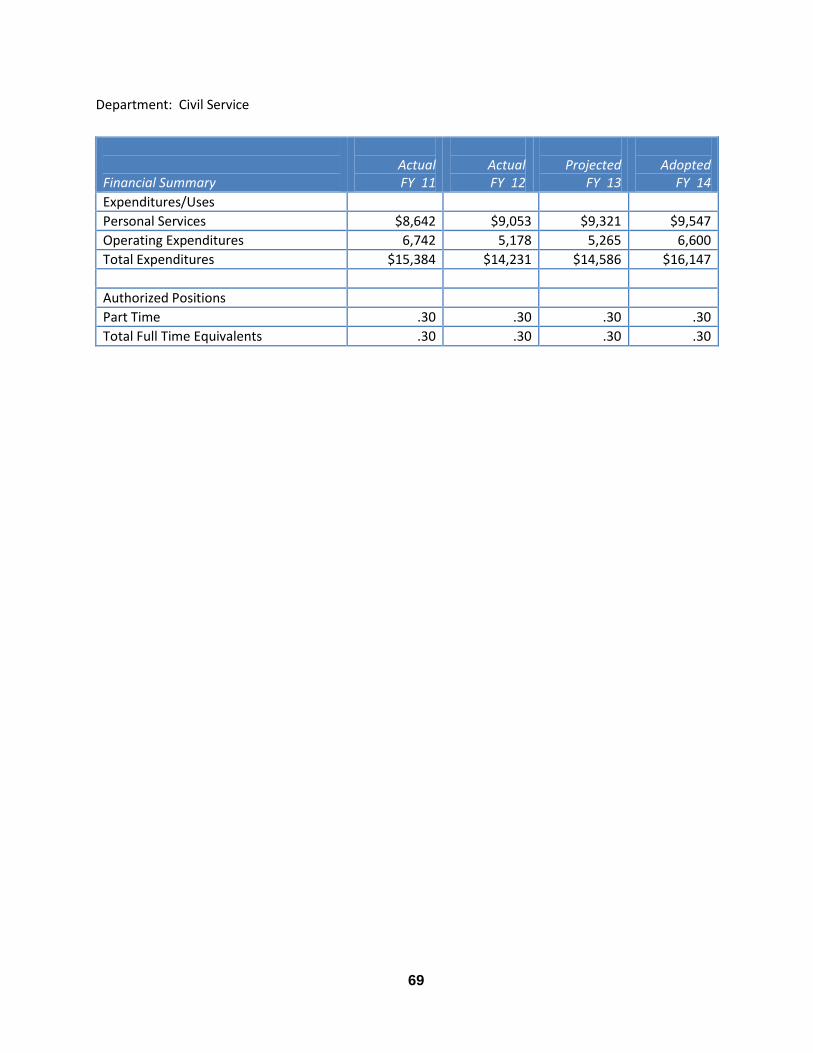

PERFORMANCE INDICATORS & FINANCIAL SUMMARIES (CONTINUED): BOARD OF SUPERVISORS .................................................................................................................................................... 67 CIVIL SERVICE .................................................................................................................................................................. 69 CONSERVATION ................................................................................................................................................................ 71 COURT EXPENSE ............................................................................................................................................................... 74 ENGINEER ....................................................................................................................................................................... 76 FACILITIES ....................................................................................................................................................................... 80 FINANCE & BUDGET .......................................................................................................................................................... 82 HUMAN RESOURCES ......................................................................................................................................................... 84 INFORMATION TECHNOLOGY ............................................................................................................................................... 91 JUVENILE JUSTICE ............................................................................................................................................................. 93 LCCS ............................................................................................................................................................................. 95 LIFTS ........................................................................................................................................................................... 117 MEDICAL EXAMINER ....................................................................................................................................................... 119 PLANNING & DEVELOPMENT ............................................................................................................................................ 121 PUBLIC HEALTH .............................................................................................................................................................. 123 PURCHASING ................................................................................................................................................................. 130 RECORDER..................................................................................................................................................................... 132 RISK MANAGEMENT ........................................................................................................................................................ 134 SHERIFF ........................................................................................................................................................................ 136 SOIL CONSERVATION ....................................................................................................................................................... 144 STATE WELFARE ............................................................................................................................................................. 146 TREASURER ................................................................................................................................................................... 148 VETERAN AFFAIRS ........................................................................................................................................................... 151

SUPPLEMENTAL INFORMATION GLOSSARY OF TERMINOLOGY ............................................................................................................................................ 153 ACRONYMS ................................................................................................................................................................... 168 FINANCIAL POLICIES ........................................................................................................................................................ 160 BUDGET PROCESS ........................................................................................................................................................... 164 BUDGET CALENDAR ......................................................................................................................................................... 165 STATISTICAL INFORMATION DEMOGRAPHIC STATISTICS ............................................................................................................................................... 167 PRINCIPLE EMPLOYERS ............................................................................................................................................................ 168 PRINCIPLE TAXPAYERS ...................................................................................................................................................... 169 ASSESSED VALUE AND ACTUAL VALUE OF TAXABLE PROPERTY ................................................................................................ 170

4

March 13, 2013 Board of Supervisors and Citizens County of Linn, Iowa: The fiscal year 2014 budget for the County of Linn is respectfully submitted. Resources have been allocated in accordance with the County’s mission statement, “to provide all residents the most efficient and responsive public services, while maintaining sound fiscal management in order to enhance the quality of life.” Development of the budget was in accordance with short-term policies that included a countywide levy rate of $6.11 and an ending general fund balance equal to 25% of budgeted expenditures. Budgeting for Outcomes (BFO) was used to allocate available funding of $1.0 million to fund offers submitted during the budget process. In June of 2008, record flooding damaged many county facilities including the Correctional Center, Courthouse, Administrative Office Building and several other county-operated facilities. Five years later, Linn County is nearing the completion of construction projects to repair or replace damaged buildings. The Sheriff’s Office was the first building to be reconstructed, followed by the completion of two new buildings, the Community Services Building and the Juvenile Justice Center, both completed in the fall of 2011. The reconstructed Administrative Office Building opened to the public as the new Public Service Center in June of 2012, and the Correctional Center and Courthouse are currently nearing completion with redesigned building layouts. The new and remodeled buildings were designed to be energy efficient and offer improved customer service by locating high traffic areas near public entrances. Countywide valuation growth of 3.2% allowed the County to maintain the property tax levy rate of $6.11. Although the countywide levy rate remains unchanged, some taxpayers will pay more, as a result of taxable value changes called rollbacks, as determined each year by the State of Iowa. Residential taxpayers and agricultural land owners will pay approximately 4.1% more than in fiscal year 2013. Commercial and industrial taxpayers will pay the same unless their actual assessed value increased because a commercial business is taxed at 100% of assessed value. Residential property is taxed at 53% and agricultural property is taxed at 60% of assessed value. The levy rate of $6.11 per thousand of taxable value is less than the countywide rate of $6.15 in fiscal 2009 prior to the flood. The rural services levy rate will remain at $3.71, resulting in a combined rural levy rate of $9.83 paid by residents in the unincorporated areas. Overall property taxes levied will increase by 3.5% from fiscal year 2013, due to the increase in countywide taxable value and 4.7% increase in the unincorporated areas that pay the additional rural services rate. Funding decisions as to the best allocation of financial resources were made with regard to the Linn County Strategic Plan for fiscal years 2011-2015. This plan was developed when representatives from various departments participated in a series of strategic planning sessions to update the previous plan. Changes or trends impacting Linn County were identified and related key elements or attributes defining the County’s future success were subsequently determined.

5

The plan includes a list of seven strategies and goals for each of the strategies as follows: Strategy 1: Excel in Customer Satisfaction Provide excellent service to customers with responsive and accurate information. Goals:

A. Solicit and consider feedback from customers when making decisions B. Select and retain qualified people and provide high quality training C. Establish measurable customer service standards D. Create a consistent service message that can be shared by all departments

Strategy 2: Develop a Communications Plan Utilize diverse channels to increase awareness of services and programs provided to customers and encourage shared communication. Goals:

A. Maintain regular communications with the public B. Share and discuss important information with employees C. Educate the public by providing information about who we are and what we do D. Create a County branding strategy E. Promote and share successes

Strategy 3: Improve Infrastructure Ensure infrastructure meets the needs of employees and the public. Goals:

A. Build, rebuild, and maintain county buildings, equipment, and facilities, including damage caused by the Flood of 2008

B. Update and maintain a disaster recovery plan C. Increase energy efficiency D. Maintain and enhance technology utilizing the employee technology committee

Strategy 4: Enhance Quality of Life Provide and promote opportunities to improve emotional, social, environmental, economic, and physical well-being. Goals:

A. Provide a properly maintained secondary roads system B. Promote public access to trails, waterways, parks, green space, bike paths, camping, and

other recreational activities C. Maintain a professional, responsive, and efficient public safety, public health, and social

welfare system

6

Strategy 5: Build Partnerships Participate in effective partnerships and new opportunities for joint participation in projects and delivery of services. Goals:

A. Collaborate to address problems, common issues, concerns, or needs B. Actively engage in open communications and build equitable relationships C. Collectively define roles and responsibilities in partnerships D. Provide opportunities for increased partner interactions E. Address emerging trends

Strategy 6: Create and Foster a Culture of Ownership Demonstrate a sense of pride in the organization along with shared responsibility for outcomes. Goals:

A. Develop and cultivate diverse and respectful employee relationships B. Promote positive results through employee empowerment C. Recognize and acknowledge employee achievements D. Offer effective and applicable employee training E. Create and support a safe, positive, fun, and engaging work place

Strategy 7: Be Fiscally Responsible Demonstrate sound fiscal practices. Goals:

A. Demonstrate use of financial analysis in county decisions B. Establish outcome based quality assurance C. Recognize employees for fiscally responsible decisions D. Proactively seek alternative resources for funding E. Identify potential liabilities and exposures to minimize risk F. Utilize an effective risk management policy and plan

7

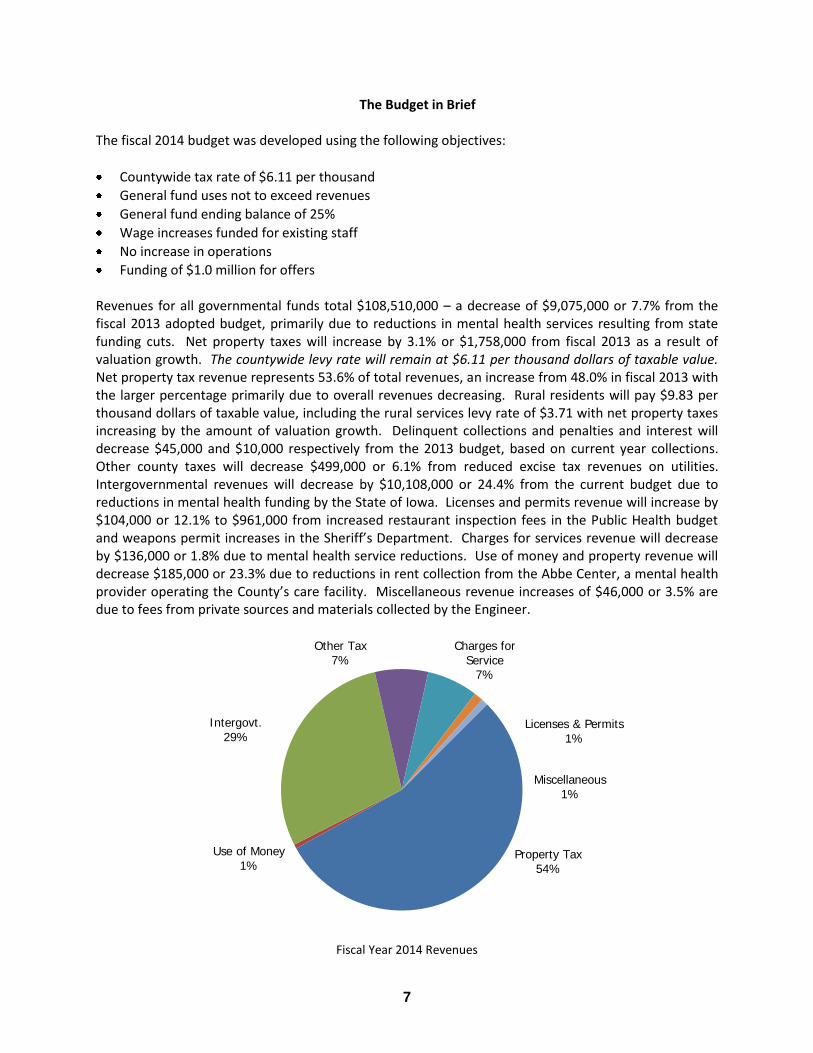

The Budget in Brief The fiscal 2014 budget was developed using the following objectives:

Countywide tax rate of $6.11 per thousand

General fund uses not to exceed revenues

General fund ending balance of 25%

Wage increases funded for existing staff

No increase in operations

Funding of $1.0 million for offers Revenues for all governmental funds total $108,510,000 – a decrease of $9,075,000 or 7.7% from the fiscal 2013 adopted budget, primarily due to reductions in mental health services resulting from state funding cuts. Net property taxes will increase by 3.1% or $1,758,000 from fiscal 2013 as a result of valuation growth. The countywide levy rate will remain at $6.11 per thousand dollars of taxable value. Net property tax revenue represents 53.6% of total revenues, an increase from 48.0% in fiscal 2013 with the larger percentage primarily due to overall revenues decreasing. Rural residents will pay $9.83 per thousand dollars of taxable value, including the rural services levy rate of $3.71 with net property taxes increasing by the amount of valuation growth. Delinquent collections and penalties and interest will decrease $45,000 and $10,000 respectively from the 2013 budget, based on current year collections. Other county taxes will decrease $499,000 or 6.1% from reduced excise tax revenues on utilities. Intergovernmental revenues will decrease by $10,108,000 or 24.4% from the current budget due to reductions in mental health funding by the State of Iowa. Licenses and permits revenue will increase by $104,000 or 12.1% to $961,000 from increased restaurant inspection fees in the Public Health budget and weapons permit increases in the Sheriff’s Department. Charges for services revenue will decrease by $136,000 or 1.8% due to mental health service reductions. Use of money and property revenue will decrease $185,000 or 23.3% due to reductions in rent collection from the Abbe Center, a mental health provider operating the County’s care facility. Miscellaneous revenue increases of $46,000 or 3.5% are due to fees from private sources and materials collected by the Engineer.

Fiscal Year 2014 Revenues

Property Tax 54%

Use of Money 1%

Intergovt. 29%

Other Tax 7%

Charges for Service

7%

Miscellaneous 1%

Licenses & Permits

1%

8

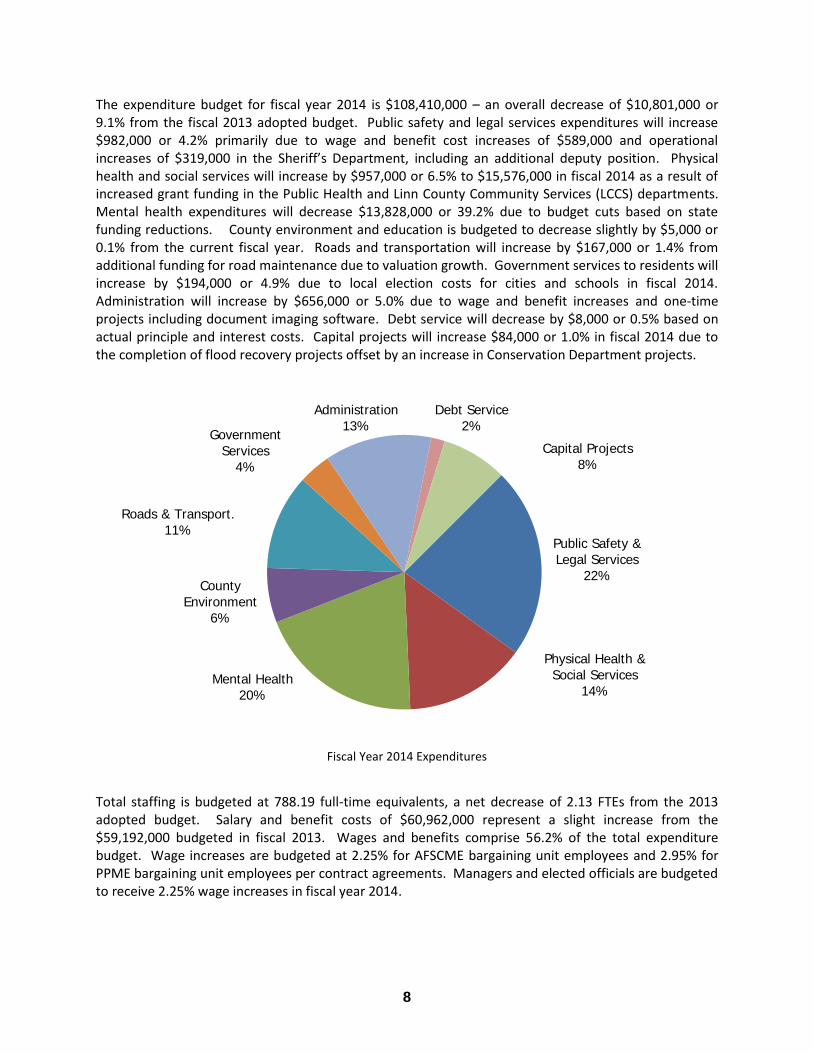

The expenditure budget for fiscal year 2014 is $108,410,000 – an overall decrease of $10,801,000 or 9.1% from the fiscal 2013 adopted budget. Public safety and legal services expenditures will increase $982,000 or 4.2% primarily due to wage and benefit cost increases of $589,000 and operational increases of $319,000 in the Sheriff’s Department, including an additional deputy position. Physical health and social services will increase by $957,000 or 6.5% to $15,576,000 in fiscal 2014 as a result of increased grant funding in the Public Health and Linn County Community Services (LCCS) departments. Mental health expenditures will decrease $13,828,000 or 39.2% due to budget cuts based on state funding reductions. County environment and education is budgeted to decrease slightly by $5,000 or 0.1% from the current fiscal year. Roads and transportation will increase by $167,000 or 1.4% from additional funding for road maintenance due to valuation growth. Government services to residents will increase by $194,000 or 4.9% due to local election costs for cities and schools in fiscal 2014. Administration will increase by $656,000 or 5.0% due to wage and benefit increases and one-time projects including document imaging software. Debt service will decrease by $8,000 or 0.5% based on actual principle and interest costs. Capital projects will increase $84,000 or 1.0% in fiscal 2014 due to the completion of flood recovery projects offset by an increase in Conservation Department projects.

Fiscal Year 2014 Expenditures

Total staffing is budgeted at 788.19 full-time equivalents, a net decrease of 2.13 FTEs from the 2013 adopted budget. Salary and benefit costs of $60,962,000 represent a slight increase from the $59,192,000 budgeted in fiscal 2013. Wages and benefits comprise 56.2% of the total expenditure budget. Wage increases are budgeted at 2.25% for AFSCME bargaining unit employees and 2.95% for PPME bargaining unit employees per contract agreements. Managers and elected officials are budgeted to receive 2.25% wage increases in fiscal year 2014.

Public Safety &

Legal Services

22%

Physical Health &

Social Services

14% Mental Health

20%

County

Environment

6%

Roads & Transport.

11%

Government

Services

4%

Administration

13%

Debt Service

2%

Capital Projects

8%

9

ACKNOWLEDGMENTS The Government Finance Officers Association of the United States and Canada (GFOA) presented the Distinguished Budget Presentation Award to the County for its fiscal year 2013 budget document. This was the 17th consecutive year that the County has received this prestigious award. Preparation of the annual budget document would not have been accomplished without the assistance of all department heads and elected officials, especially in the area of performance measurement reporting. The challenge of providing services to the residents of the County while maintaining public facilities and infrastructure continues. By working cooperatively with the public, we are confident that the County will continue to maximize the services provided to meet the needs of residents in the most effective and efficient manner. Respectfully submitted, _________________________ _________________________ Dawn Jindrich, Budget Director Steve Tucker, Finance Director

9

ACKNOWLEDGMENTS The Government Finance Officers Association of the United States and Canada (GFOA) presented the Distinguished Budget Presentation Award to the County for its fiscal year 2013 budget document. This was the 17th consecutive year that the County has received this prestigious award. Preparation of the annual budget document would not have been accomplished without the assistance of all department heads and elected officials, especially in the area of performance measurement reporting. The challenge of providing services to the residents of the County while maintaining public facilities and infrastructure continues. By working cooperatively with the public, we are confident that the County will continue to maximize the services provided to meet the needs of residents in the most effective and efficient manner. Respectfully submitted, _________________________ _________________________ Dawn Jindrich, Budget Director Steve Tucker, Finance Director

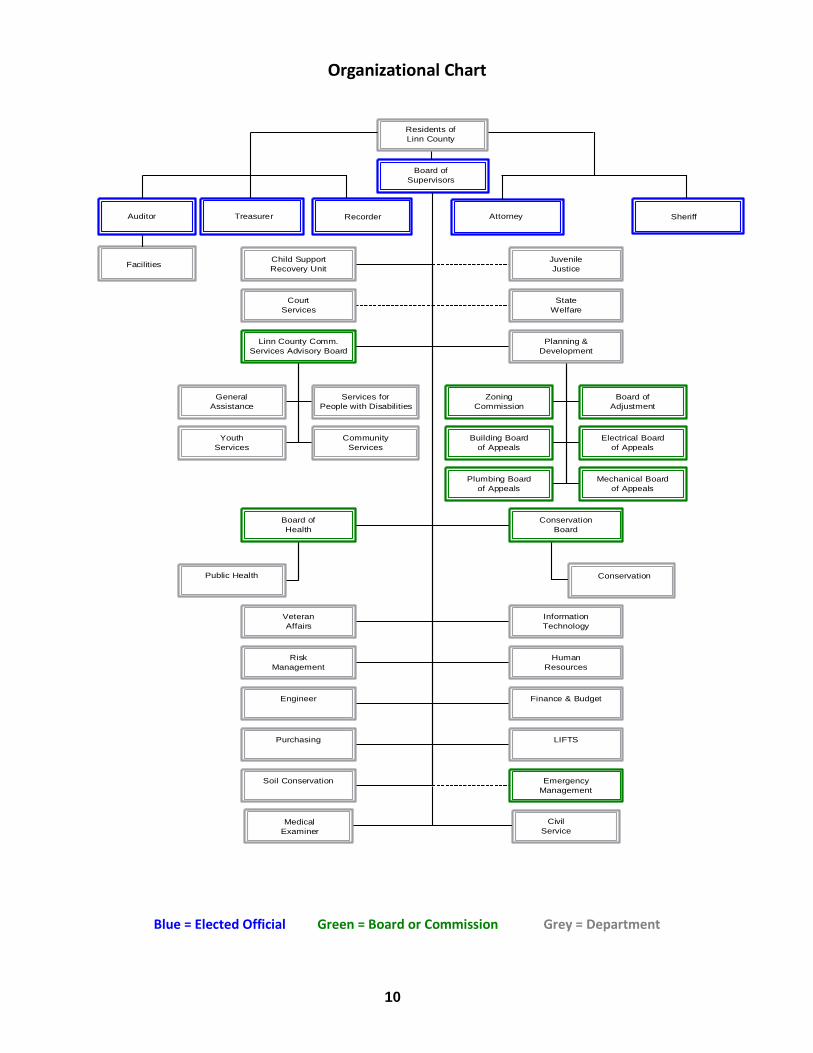

10

Residents of

Linn County

Board of

Supervisors

Auditor Treasurer Recorder Sheriff

Facilities

Conservation

Medical

Examiner

Civil

Service

Attorney

Child Support

Recovery Unit

Juvenile

Justice

Court

Services

State

Welfare

General

Assistance

Services for

People with Disabilities

Youth

Services

Community

Services

Linn County Comm.

Services Advisory Board

Zoning

Commission

Board of

Adjustment

Building Board

of Appeals

Electrical Board

of Appeals

Plumbing Board

of Appeals

Mechanical Board

of Appeals

Planning &

Development

Public Health

Board of

Health

Conservation

Board

Veteran

Affairs

Information

Technology

Risk

Management

Human

Resources

Engineer Finance & Budget

Purchasing LIFTS

Soil Conservation Emergency

Management

Blue = Elected Official Green = Board or Commission Grey = Department

11

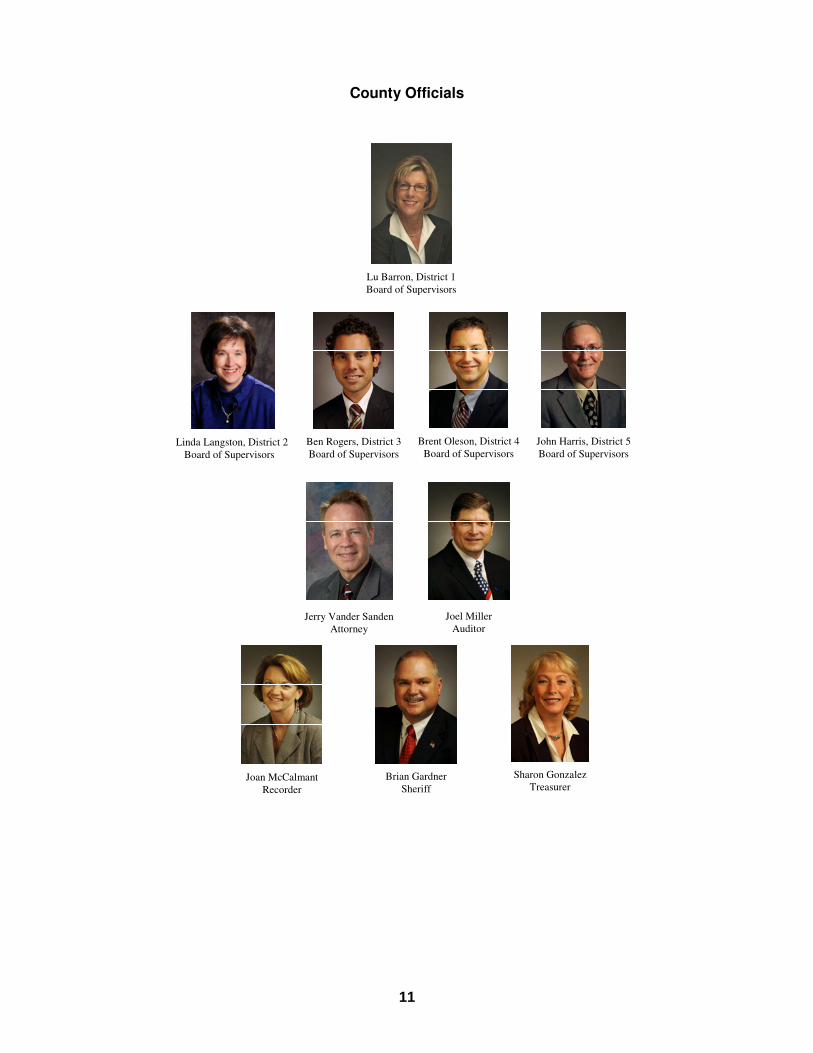

County Officials

Lu Barron, District I

Board of Supervisors

Oleson, District 4 John Harris, District 5

Board of Supervisors Board of Supervisors

Board of Supervisors Board of Supervisors

Joan McCalmant

Recorder

Brian Gardner

Sheriff

Sharon Gonzalez

Treasurer

Jerry Vander Sanden

Attorney

Joel Miller

Auditor

Linda Langston, District 2

Board of Supervisors

Ben Rogers, District 3

Board of Supervisors

Brent Oleson, District 4

Board of Supervisors

John Harris, District 5

Board of Supervisors

Lu Barron, District 1

Board of Supervisors

11

County Officials

Lu Barron, District I

Board of Supervisors

Oleson, District 4 John Harris, District 5

Board of Supervisors Board of Supervisors

Board of Supervisors Board of Supervisors

Joan McCalmant

Recorder

Brian Gardner

Sheriff

Sharon Gonzalez

Treasurer

Jerry Vander Sanden

Attorney

Joel Miller

Auditor

Linda Langston, District 2

Board of Supervisors

Ben Rogers, District 3

Board of Supervisors

Brent Oleson, District 4

Board of Supervisors

John Harris, District 5

Board of Supervisors

Lu Barron, District 1

Board of Supervisors

12

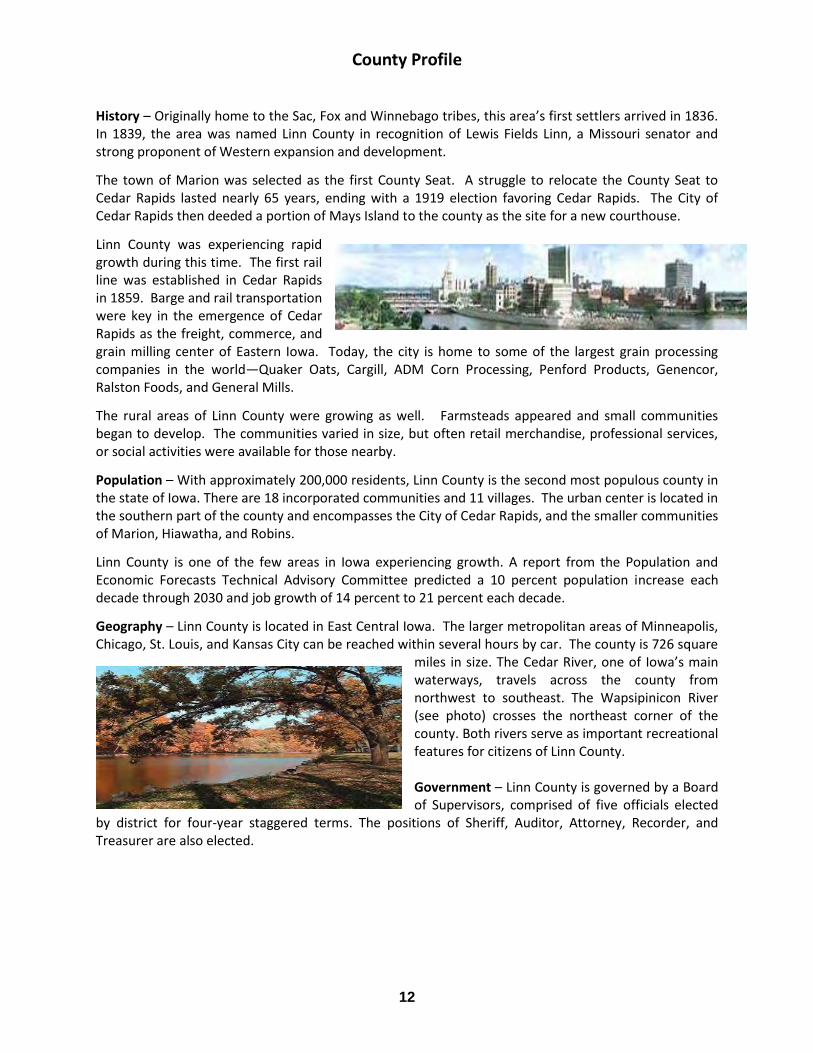

History – Originally home to the Sac, Fox and Winnebago tribes, this area’s first settlers arrived in 1836. In 1839, the area was named Linn County in recognition of Lewis Fields Linn, a Missouri senator and strong proponent of Western expansion and development.

The town of Marion was selected as the first County Seat. A struggle to relocate the County Seat to Cedar Rapids lasted nearly 65 years, ending with a 1919 election favoring Cedar Rapids. The City of Cedar Rapids then deeded a portion of Mays Island to the county as the site for a new courthouse.

Linn County was experiencing rapid growth during this time. The first rail line was established in Cedar Rapids in 1859. Barge and rail transportation were key in the emergence of Cedar Rapids as the freight, commerce, and grain milling center of Eastern Iowa. Today, the city is home to some of the largest grain processing companies in the world—Quaker Oats, Cargill, ADM Corn Processing, Penford Products, Genencor, Ralston Foods, and General Mills.

The rural areas of Linn County were growing as well. Farmsteads appeared and small communities began to develop. The communities varied in size, but often retail merchandise, professional services, or social activities were available for those nearby.

Population – With approximately 200,000 residents, Linn County is the second most populous county in the state of Iowa. There are 18 incorporated communities and 11 villages. The urban center is located in the southern part of the county and encompasses the City of Cedar Rapids, and the smaller communities of Marion, Hiawatha, and Robins.

Linn County is one of the few areas in Iowa experiencing growth. A report from the Population and Economic Forecasts Technical Advisory Committee predicted a 10 percent population increase each decade through 2030 and job growth of 14 percent to 21 percent each decade.

Geography – Linn County is located in East Central Iowa. The larger metropolitan areas of Minneapolis, Chicago, St. Louis, and Kansas City can be reached within several hours by car. The county is 726 square

miles in size. The Cedar River, one of Iowa’s main waterways, travels across the county from northwest to southeast. The Wapsipinicon River (see photo) crosses the northeast corner of the county. Both rivers serve as important recreational features for citizens of Linn County. Government – Linn County is governed by a Board of Supervisors, comprised of five officials elected

by district for four-year staggered terms. The positions of Sheriff, Auditor, Attorney, Recorder, and Treasurer are also elected.

13

Economy – Linn County continues to be Iowa’s largest manufacturing center with total goods producing employment of 22,900 or 19.7% of total non-farm employment. Service producing employment of 93,200 represents the balance of non-farm employment. The diverse agricultural, industrial and service based companies provide economic stability to the local economy. Modest growth in manufacturing will continue even though major employment gains continue to be in service industries with financial activities representing the largest growth area from the prior year. Only about 2% of Linn County employment population is directly employed in farming. Education – Three private four-year liberal arts colleges are located in Linn County, and the University of Iowa, University of Northern Iowa, and Iowa State University are all within easy driving distance. Iowa’s third-largest educational institution, Kirkwood Community College, provides two-year vocational and technical training degrees and ample continuing education opportunities.

Life – Residents of Linn County enjoy the excitement of a modern and bustling metro area and the beauty and solitude of the bucolic countryside. The Cedar and Wapsipinicon Rivers offer boating, fishing, and swimming opportunities. The Linn County Conservation Department also maintains many public parks, recreational, and natural areas for enjoyment. The award-winning Cedar Rapids Symphony offers regular performances and the Paramount Theatre, a picturesque 1920s downtown landmark, provides a variety of cultural events throughout the year.

14

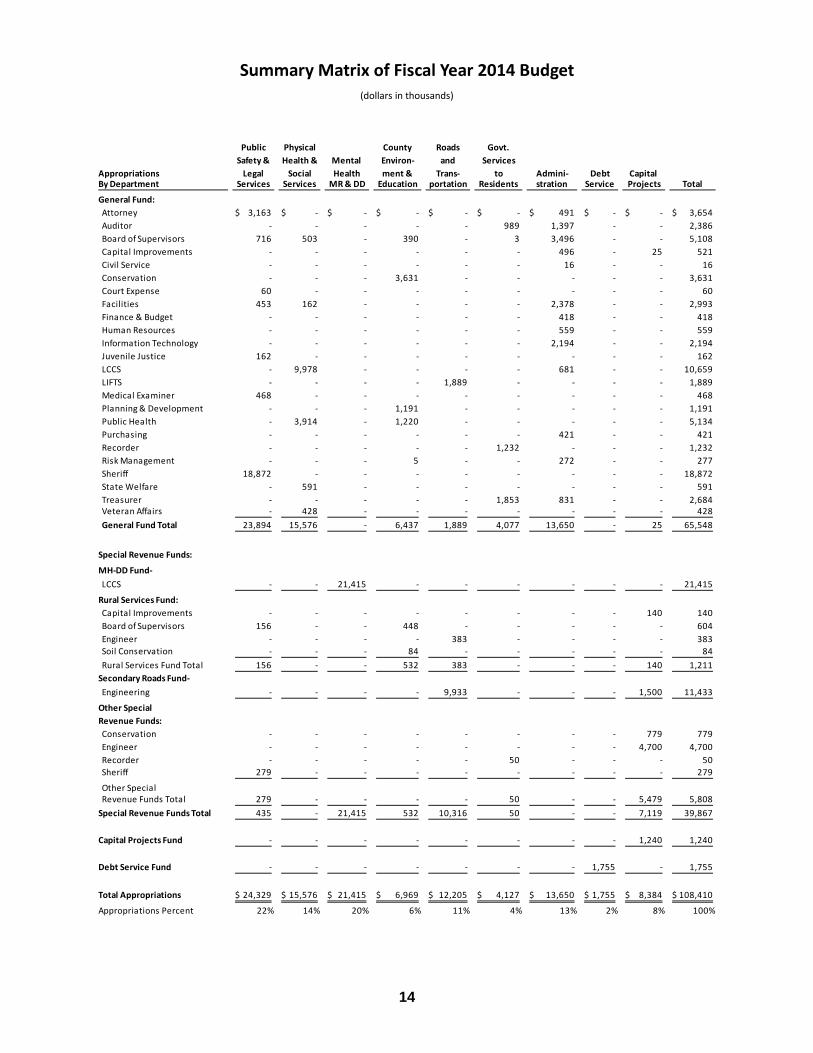

(dollars in thousands)

Public Physical County Roads Govt.

Safety & Health & Mental Environ- and Services

Appropriations Legal Social Health ment & Trans- to Admini- Debt Capital By Department Services Services MR & DD Education portation Residents stration Service Projects Total

General Fund:

Attorney 3,163$ -$ -$ -$ -$ -$ 491$ -$ -$ 3,654$

Auditor - - - - - 989 1,397 - - 2,386

Board of Supervisors 716 503 - 390 - 3 3,496 - - 5,108

Capital Improvements - - - - - - 496 - 25 521

Civil Service - - - - - - 16 - - 16

Conservation - - - 3,631 - - - - - 3,631

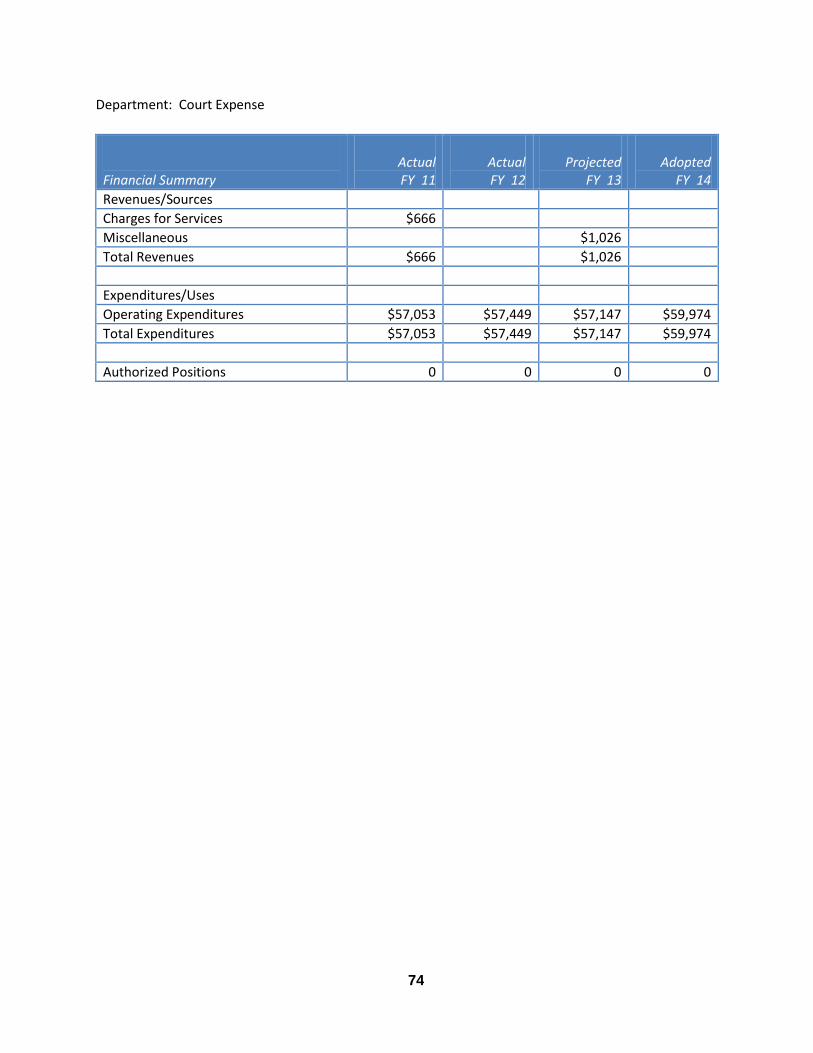

Court Expense 60 - - - - - - - - 60

Facilities 453 162 - - - - 2,378 - - 2,993

Finance & Budget - - - - - - 418 - - 418

Human Resources - - - - - - 559 - - 559

Information Technology - - - - - - 2,194 - - 2,194

Juvenile Justice 162 - - - - - - - - 162

LCCS - 9,978 - - - - 681 - - 10,659

LIFTS - - - - 1,889 - - - - 1,889

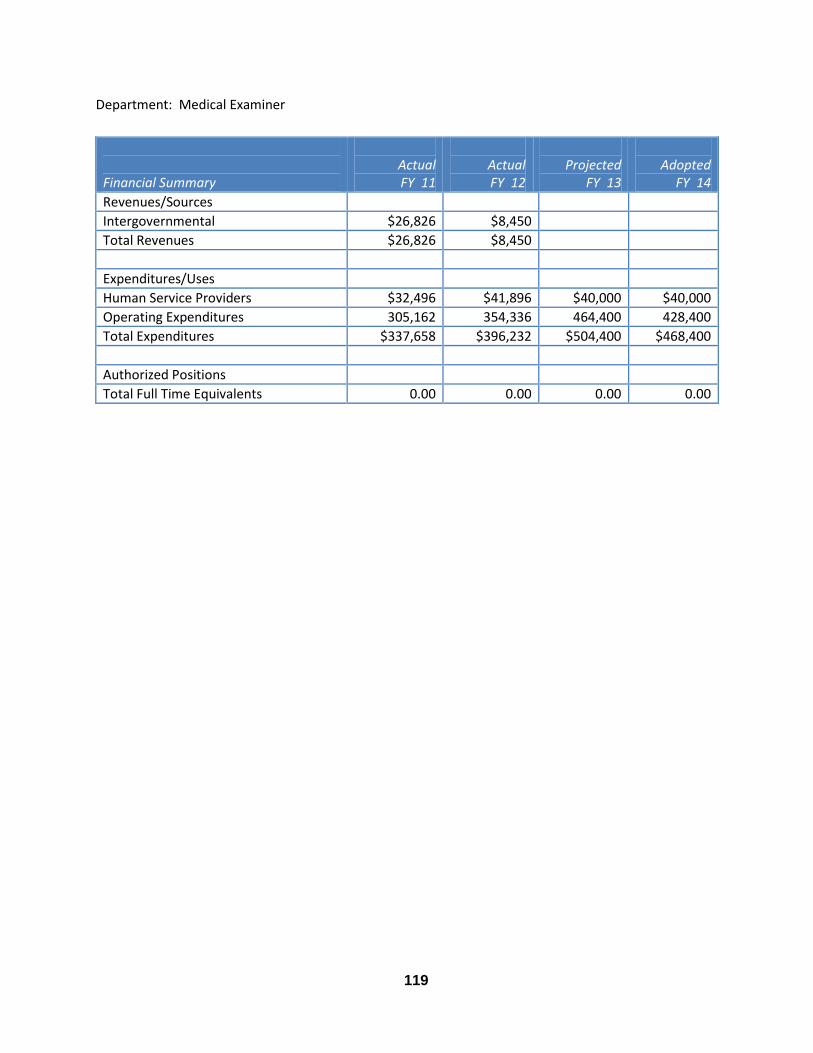

Medical Examiner 468 - - - - - - - - 468

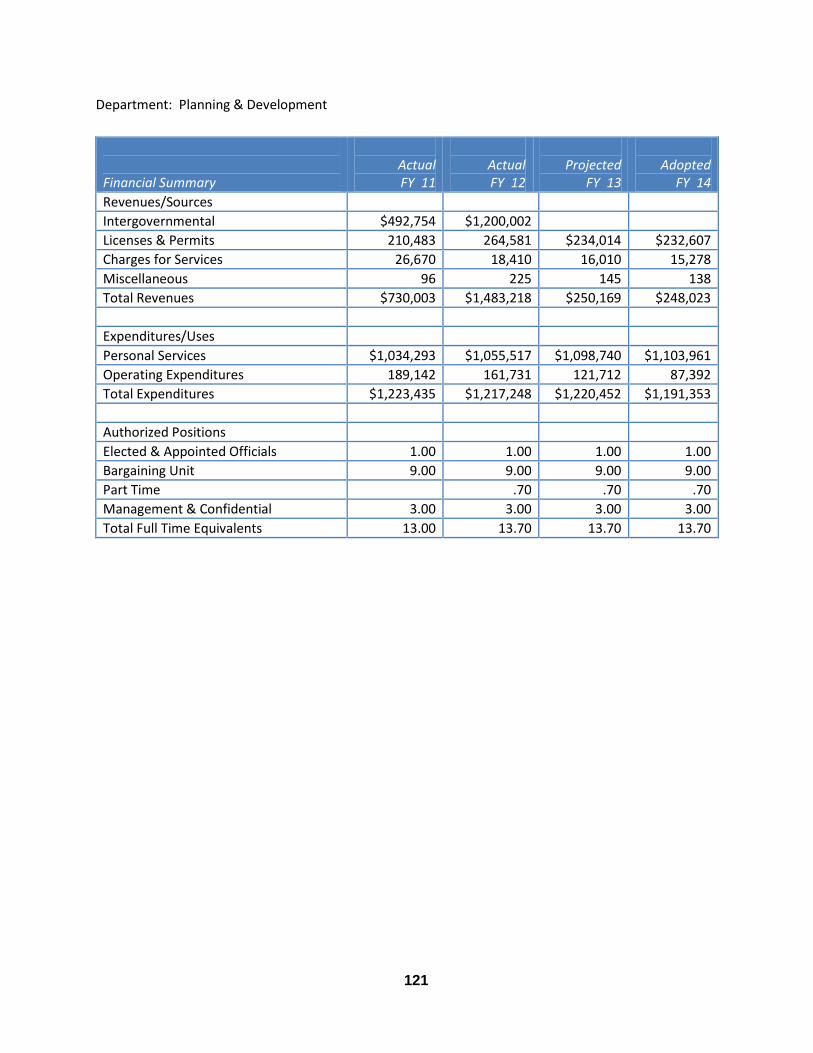

Planning & Development - - - 1,191 - - - - - 1,191

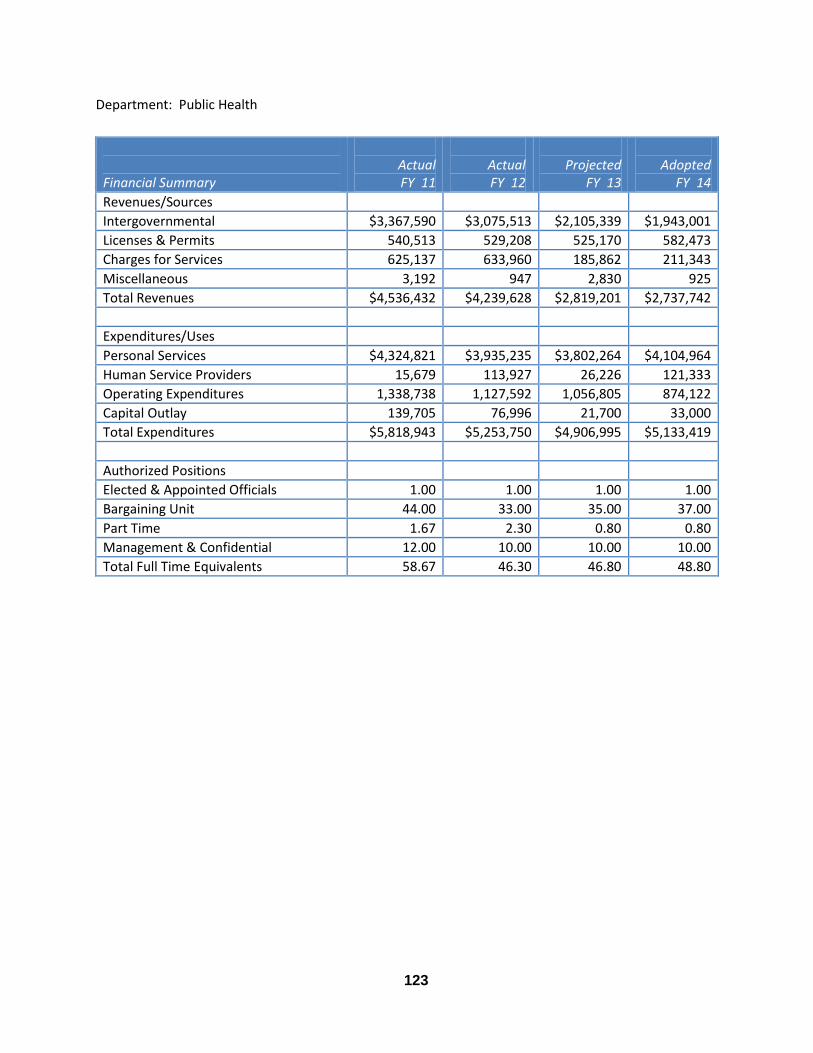

Public Health - 3,914 - 1,220 - - - - - 5,134

Purchasing - - - - - - 421 - - 421

Recorder - - - - - 1,232 - - - 1,232

Risk Management - - - 5 - - 272 - - 277

Sheriff 18,872 - - - - - - - - 18,872

State Welfare - 591 - - - - - - - 591

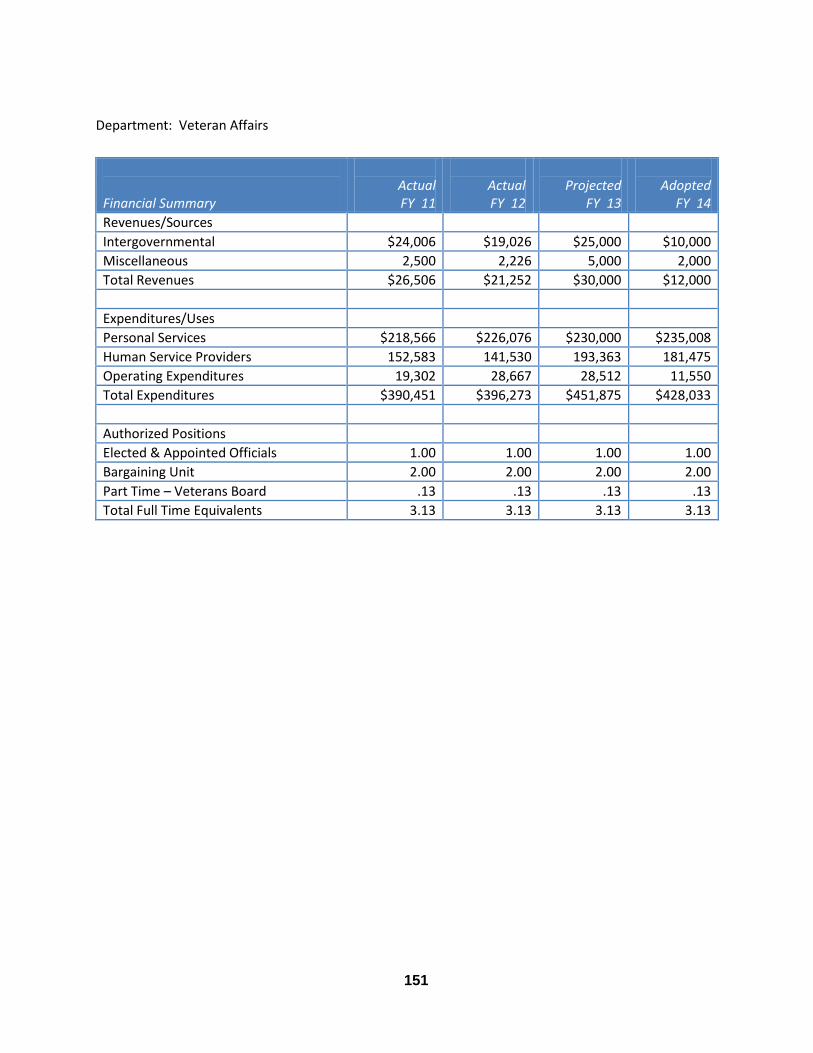

Treasurer - - - - - 1,853 831 - - 2,684 Veteran Affairs - 428 - - - - - - - 428

General Fund Total 23,894 15,576 - 6,437 1,889 4,077 13,650 - 25 65,548

Special Revenue Funds:

MH-DD Fund-

LCCS - - 21,415 - - - - - - 21,415

Rural Services Fund:

Capital Improvements - - - - - - - - 140 140

Board of Supervisors 156 - - 448 - - - - - 604

Engineer - - - - 383 - - - - 383

Soil Conservation - - - 84 - - - - - 84

Rural Services Fund Total 156 - - 532 383 - - - 140 1,211

Secondary Roads Fund-

Engineering - - - - 9,933 - - - 1,500 11,433

Other Special

Revenue Funds:

Conservation - - - - - - - - 779 779

Engineer - - - - - - - - 4,700 4,700

Recorder - - - - - 50 - - - 50

Sheriff 279 - - - - - - - - 279

Other Special Revenue Funds Total 279 - - - - 50 - - 5,479 5,808

Special Revenue Funds Total 435 - 21,415 532 10,316 50 - - 7,119 39,867

Capital Projects Fund - - - - - - - - 1,240 1,240

Debt Service Fund - - - - - - - 1,755 - 1,755

Total Appropriations 24,329$ 15,576$ 21,415$ 6,969$ 12,205$ 4,127$ 13,650$ 1,755$ 8,384$ 108,410$

Appropriations Percent 22% 14% 20% 6% 11% 4% 13% 2% 8% 100%

15

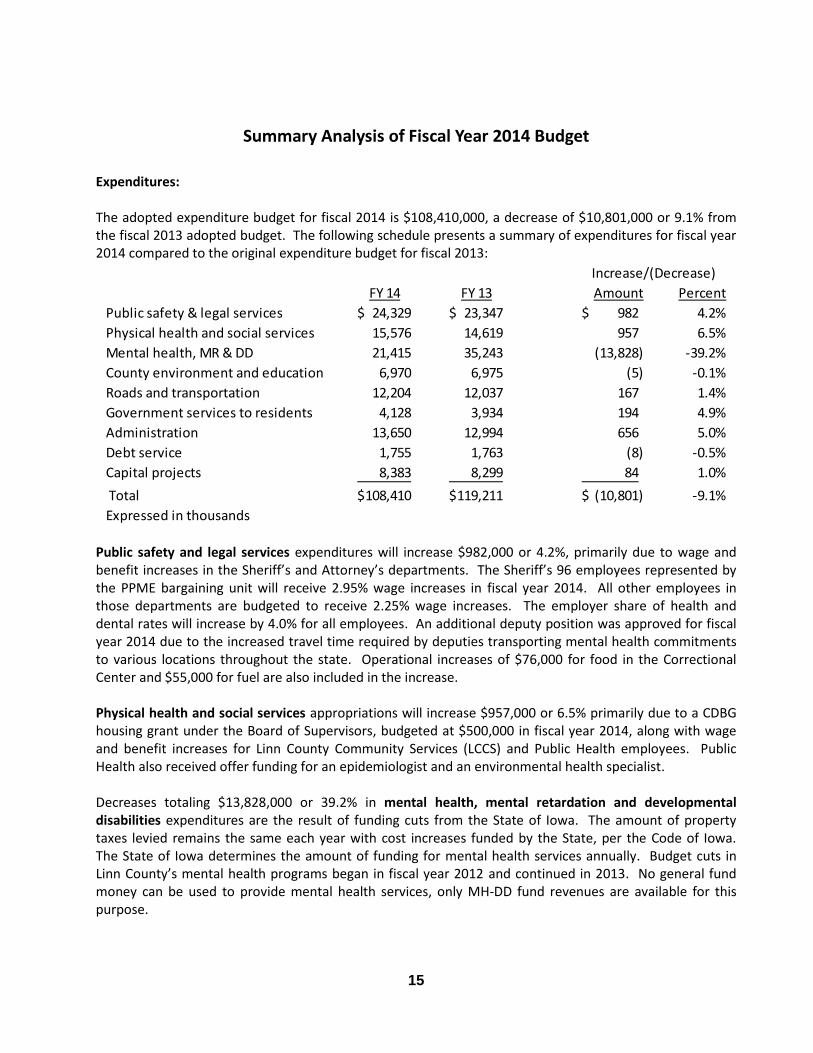

Expenditures: The adopted expenditure budget for fiscal 2014 is $108,410,000, a decrease of $10,801,000 or 9.1% from the fiscal 2013 adopted budget. The following schedule presents a summary of expenditures for fiscal year 2014 compared to the original expenditure budget for fiscal 2013:

Public safety and legal services expenditures will increase $982,000 or 4.2%, primarily due to wage and benefit increases in the Sheriff’s and Attorney’s departments. The Sheriff’s 96 employees represented by the PPME bargaining unit will receive 2.95% wage increases in fiscal year 2014. All other employees in those departments are budgeted to receive 2.25% wage increases. The employer share of health and dental rates will increase by 4.0% for all employees. An additional deputy position was approved for fiscal year 2014 due to the increased travel time required by deputies transporting mental health commitments to various locations throughout the state. Operational increases of $76,000 for food in the Correctional Center and $55,000 for fuel are also included in the increase. Physical health and social services appropriations will increase $957,000 or 6.5% primarily due to a CDBG housing grant under the Board of Supervisors, budgeted at $500,000 in fiscal year 2014, along with wage and benefit increases for Linn County Community Services (LCCS) and Public Health employees. Public Health also received offer funding for an epidemiologist and an environmental health specialist. Decreases totaling $13,828,000 or 39.2% in mental health, mental retardation and developmental disabilities expenditures are the result of funding cuts from the State of Iowa. The amount of property taxes levied remains the same each year with cost increases funded by the State, per the Code of Iowa. The State of Iowa determines the amount of funding for mental health services annually. Budget cuts in Linn County’s mental health programs began in fiscal year 2012 and continued in 2013. No general fund money can be used to provide mental health services, only MH-DD fund revenues are available for this purpose.

Increase/(Decrease)

FY 14 FY 13 Amount Percent

Public safety & legal services 24,329$ 23,347$ 982$ 4.2%

Physical health and social services 15,576 14,619 957 6.5%

Mental health, MR & DD 21,415 35,243 (13,828) -39.2%

County environment and education 6,970 6,975 (5) -0.1%

Roads and transportation 12,204 12,037 167 1.4%

Government services to residents 4,128 3,934 194 4.9%

Administration 13,650 12,994 656 5.0%

Debt service 1,755 1,763 (8) -0.5%

Capital projects 8,383 8,299 84 1.0%

Total 108,410$ 119,211$ (10,801)$ -9.1%

Expressed in thousands

16

County environment and education expenditures for fiscal 2014 will remain nearly the same with a $5,000 or 0.1% decrease from fiscal 2013. Expenditures for roads and transportation will increase $167,000 or 1.4% increase from the fiscal 2013 budget due to increases in the Engineer’s equipment operations and LIFTs department wages and benefits increases. Government services to residents will increase by $194,000 and administration expenditures will increase by $656,000 in fiscal 2014. The $194,000 or 4.9% increase is due to elections costs for city elections in the fall of fiscal year 2014. The $656,000 or 5.0% increase in administration is due to wage and benefit increases, in addition to $279,000 for funding of offers including the purchase of software to be used for document imaging and $120,000 for additional custodial staff to maintain additional space in the newly completed buildings. Debt service will decrease slightly by $8,000 from $1,763,000 to $1,755,000 or 0.5% based on decreased interest payments for the County’s outstanding bond issues. Capital projects funding was approved based on the five-year Capital Improvement Plan (CIP) plus flood recovery expenditures and construction projects for roads and parks. Capital projects expenditures will increase by $84,000 or 1.0% due to some small projects for the Engineer that will be funded from the rural fund in fiscal year 2014. Capital Projects included in the $8,383,000 capital projects service area are:

Road construction - $6,200,000 (secondary roads and LOST fund – routine expenditures)

Conservation projects - $778,000 (REAP, reserve and LOST funds – routine expenditures)

Capital improvements - $1,200,000 (capital projects fund – nonroutine expenditures)

Capital repairs - $140,000 (rural fund – routine expenditures)

Capital repairs - $25,000 (general fund – routine expenditures)

GIS mapping - $40,000 (capital projects fund – routine repair expenditures)

17

Salaries and benefits of $60,962,000 comprise 56.2% of the expenditure budget for fiscal 2014, an increase of $1,770,000 or 3.0% from fiscal 2013, including a 2.13 FTE net decrease in overall staffing. Bargaining unit employees represented by AFSCME are budgeted to receive 2.25% increases in fiscal 2014. Sheriff’s deputies represented by PPME will receive 2.95% wage increases. Management and elected officials and their deputies are budgeted to receive 2.25% increases, with the exception of the Board of Supervisors. The Board had reduced their pay to 80% of the approved amount in fiscal year 2009 but will return to 100% of their approved salaries in fiscal 2014. Equipment replacement for Sheriff’s patrol cars is budgeted at $218,000 for the replacement of ten vehicles, net of trade-in values. Annual replacement of 10 vehicles is targeted by the department. The Engineering department has been budgeting for equipment replacement of approximately $500,000 annually for several years, but that amount was increased to $700,000 in fiscal 2012 due to cost increases in the price of heavy equipment. In fiscal 2014, $740,000 is budgeted for equipment purchases. Conservation plans for $200,000 annually to replace vehicles and equipment. The fiscal 2014 budget includes $200,000 for annual equipment replacement. Revenues: A revenue budget of $108,510,000 was adopted for fiscal year 2014, a decrease of $9,075,000 or 7.7%. The following schedule presents a summary of revenue for fiscal 2014 in comparison to the original fiscal 2013 budget:

Increase/(Decrease)

FY 14 FY 13 Amount Percent

Property taxes levied 59,935$ 57,888$ 2,047$ 3.5%

Less delinquent taxes (188) (184) (4) 2.2%

Less credits to taxpayers (1,552) (1,267) (285) 22.5%

Net current property taxes 58,195 56,437 1,758 3.1%

Delinquent property taxes collected 48 93 (45) -48.4%

Penalties & interest on taxes 812 822 (10) -1.2%

Other county taxes 7,746 8,245 (499) -6.1%

Intergovernmental 31,383 41,491 (10,108) -24.4%

Licenses & permits 961 857 104 12.1%

Charges for service 7,412 7,548 (136) -1.8%

Use of money and property 609 794 (185) -23.3%

Miscellaneous 1,344 1,298 46 3.5%

Total 108,510$ 117,585$ (9,075)$ -7.7%

Expressed in thousands

18

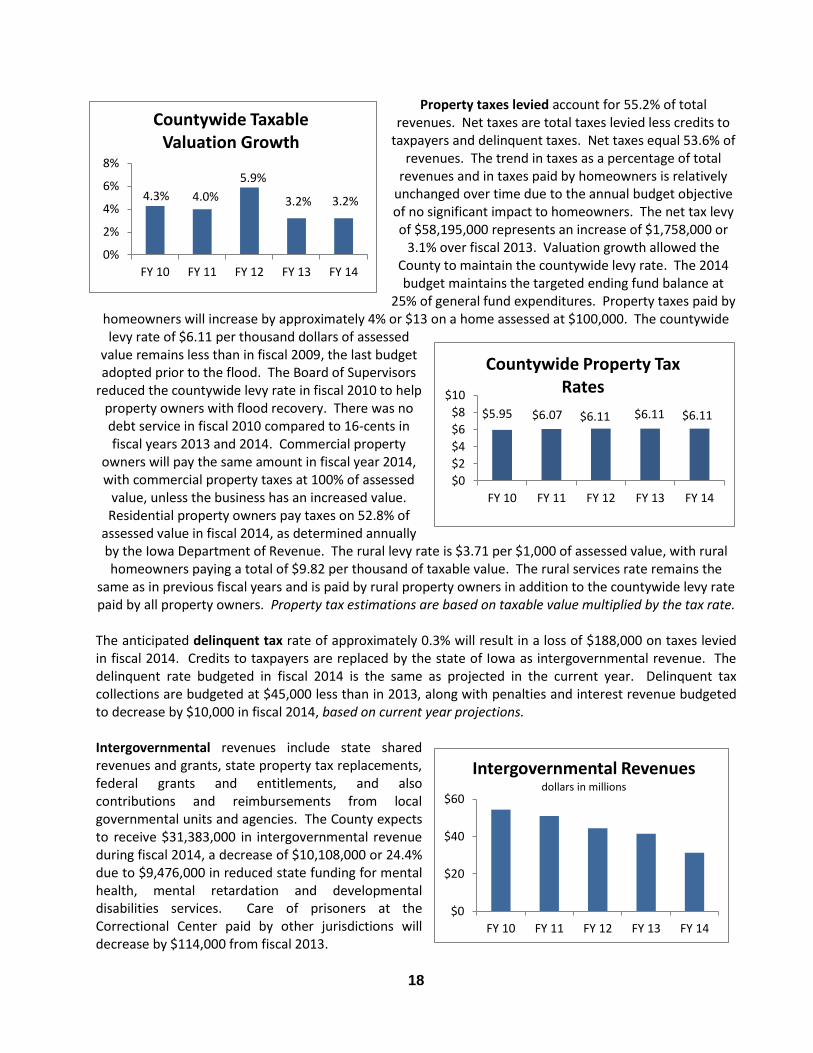

Property taxes levied account for 55.2% of total revenues. Net taxes are total taxes levied less credits to

taxpayers and delinquent taxes. Net taxes equal 53.6% of revenues. The trend in taxes as a percentage of total

revenues and in taxes paid by homeowners is relatively unchanged over time due to the annual budget objective of no significant impact to homeowners. The net tax levy of $58,195,000 represents an increase of $1,758,000 or

3.1% over fiscal 2013. Valuation growth allowed the County to maintain the countywide levy rate. The 2014 budget maintains the targeted ending fund balance at

25% of general fund expenditures. Property taxes paid by homeowners will increase by approximately 4% or $13 on a home assessed at $100,000. The countywide levy rate of $6.11 per thousand dollars of assessed

value remains less than in fiscal 2009, the last budget adopted prior to the flood. The Board of Supervisors

reduced the countywide levy rate in fiscal 2010 to help property owners with flood recovery. There was no debt service in fiscal 2010 compared to 16-cents in fiscal years 2013 and 2014. Commercial property

owners will pay the same amount in fiscal year 2014, with commercial property taxes at 100% of assessed

value, unless the business has an increased value. Residential property owners pay taxes on 52.8% of

assessed value in fiscal 2014, as determined annually by the Iowa Department of Revenue. The rural levy rate is $3.71 per $1,000 of assessed value, with rural homeowners paying a total of $9.82 per thousand of taxable value. The rural services rate remains the

same as in previous fiscal years and is paid by rural property owners in addition to the countywide levy rate paid by all property owners. Property tax estimations are based on taxable value multiplied by the tax rate.

The anticipated delinquent tax rate of approximately 0.3% will result in a loss of $188,000 on taxes levied in fiscal 2014. Credits to taxpayers are replaced by the state of Iowa as intergovernmental revenue. The delinquent rate budgeted in fiscal 2014 is the same as projected in the current year. Delinquent tax collections are budgeted at $45,000 less than in 2013, along with penalties and interest revenue budgeted to decrease by $10,000 in fiscal 2014, based on current year projections. Intergovernmental revenues include state shared revenues and grants, state property tax replacements, federal grants and entitlements, and also contributions and reimbursements from local governmental units and agencies. The County expects to receive $31,383,000 in intergovernmental revenue during fiscal 2014, a decrease of $10,108,000 or 24.4% due to $9,476,000 in reduced state funding for mental health, mental retardation and developmental disabilities services. Care of prisoners at the Correctional Center paid by other jurisdictions will decrease by $114,000 from fiscal 2013.

4.3% 4.0%

5.9%

3.2% 3.2%

0%

2%

4%

6%

8%

FY 10 FY 11 FY 12 FY 13 FY 14

Countywide Taxable Valuation Growth

$5.95 $6.07 $6.11 $6.11 $6.11

$0

$2

$4

$6

$8

$10

FY 10 FY 11 FY 12 FY 13 FY 14

Countywide Property Tax Rates

$0

$20

$40

$60

FY 10 FY 11 FY 12 FY 13 FY 14

Intergovernmental Revenues dollars in millions

19

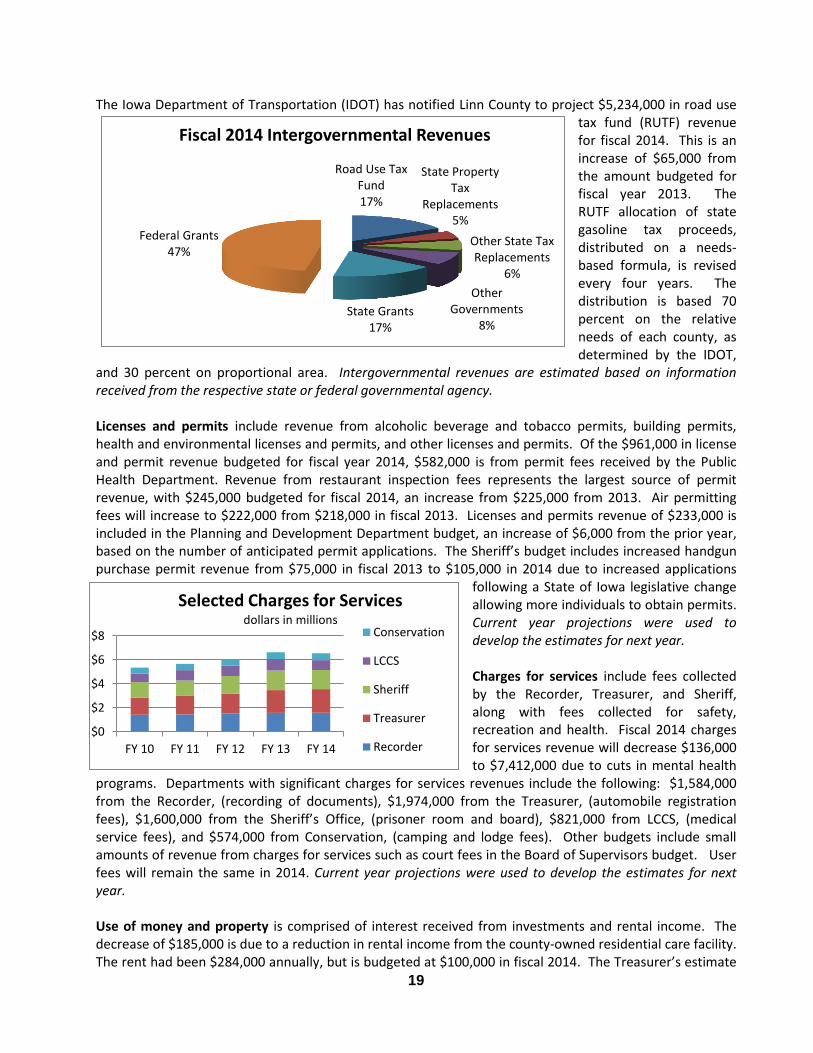

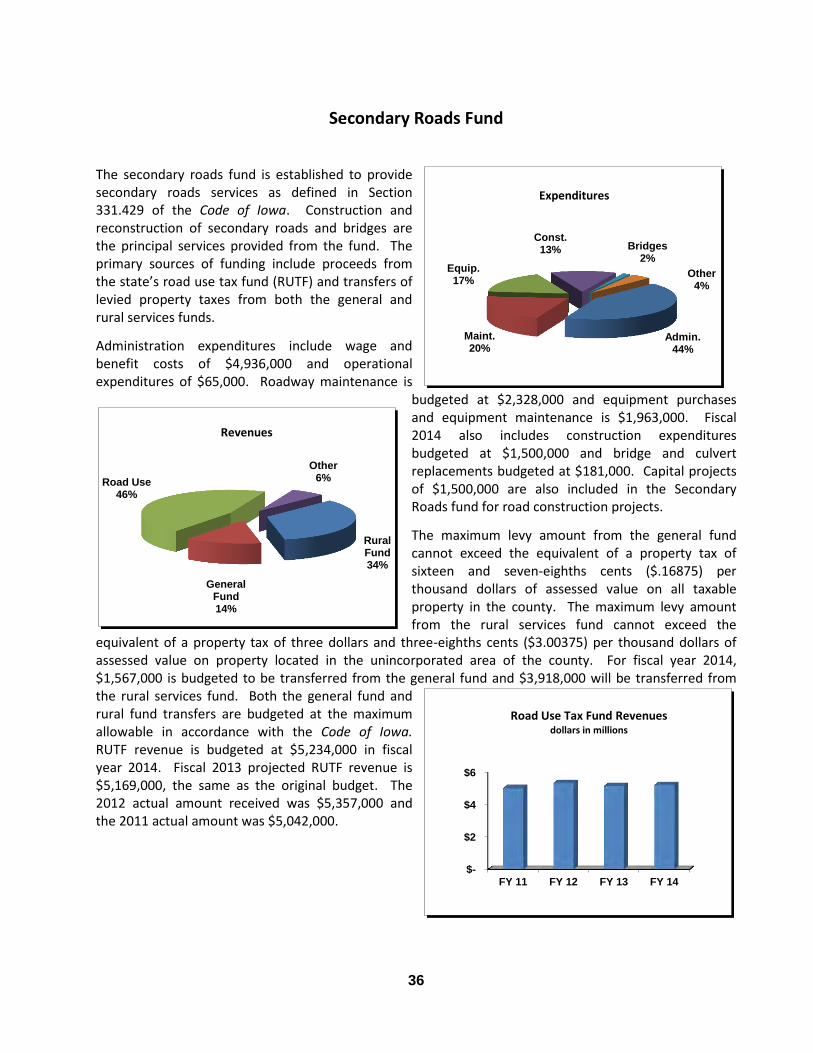

The Iowa Department of Transportation (IDOT) has notified Linn County to project $5,234,000 in road use tax fund (RUTF) revenue for fiscal 2014. This is an increase of $65,000 from the amount budgeted for fiscal year 2013. The RUTF allocation of state gasoline tax proceeds, distributed on a needs-based formula, is revised every four years. The distribution is based 70 percent on the relative needs of each county, as determined by the IDOT,

and 30 percent on proportional area. Intergovernmental revenues are estimated based on information received from the respective state or federal governmental agency. Licenses and permits include revenue from alcoholic beverage and tobacco permits, building permits, health and environmental licenses and permits, and other licenses and permits. Of the $961,000 in license and permit revenue budgeted for fiscal year 2014, $582,000 is from permit fees received by the Public Health Department. Revenue from restaurant inspection fees represents the largest source of permit revenue, with $245,000 budgeted for fiscal 2014, an increase from $225,000 from 2013. Air permitting fees will increase to $222,000 from $218,000 in fiscal 2013. Licenses and permits revenue of $233,000 is included in the Planning and Development Department budget, an increase of $6,000 from the prior year, based on the number of anticipated permit applications. The Sheriff’s budget includes increased handgun purchase permit revenue from $75,000 in fiscal 2013 to $105,000 in 2014 due to increased applications

following a State of Iowa legislative change allowing more individuals to obtain permits. Current year projections were used to develop the estimates for next year. Charges for services include fees collected by the Recorder, Treasurer, and Sheriff, along with fees collected for safety, recreation and health. Fiscal 2014 charges for services revenue will decrease $136,000 to $7,412,000 due to cuts in mental health

programs. Departments with significant charges for services revenues include the following: $1,584,000 from the Recorder, (recording of documents), $1,974,000 from the Treasurer, (automobile registration fees), $1,600,000 from the Sheriff’s Office, (prisoner room and board), $821,000 from LCCS, (medical service fees), and $574,000 from Conservation, (camping and lodge fees). Other budgets include small amounts of revenue from charges for services such as court fees in the Board of Supervisors budget. User fees will remain the same in 2014. Current year projections were used to develop the estimates for next year. Use of money and property is comprised of interest received from investments and rental income. The decrease of $185,000 is due to a reduction in rental income from the county-owned residential care facility. The rent had been $284,000 annually, but is budgeted at $100,000 in fiscal 2014. The Treasurer’s estimate

$0

$2

$4

$6

$8

FY 10 FY 11 FY 12 FY 13 FY 14

Selected Charges for Services dollars in millions

Conservation

LCCS

Sheriff

Treasurer

Recorder

Road Use Tax Fund 17%

State Property Tax

Replacements 5%

Other State Tax Replacements

6%

Other Governments

8% State Grants

17%

Federal Grants 47%

Fiscal 2014 Intergovernmental Revenues

20

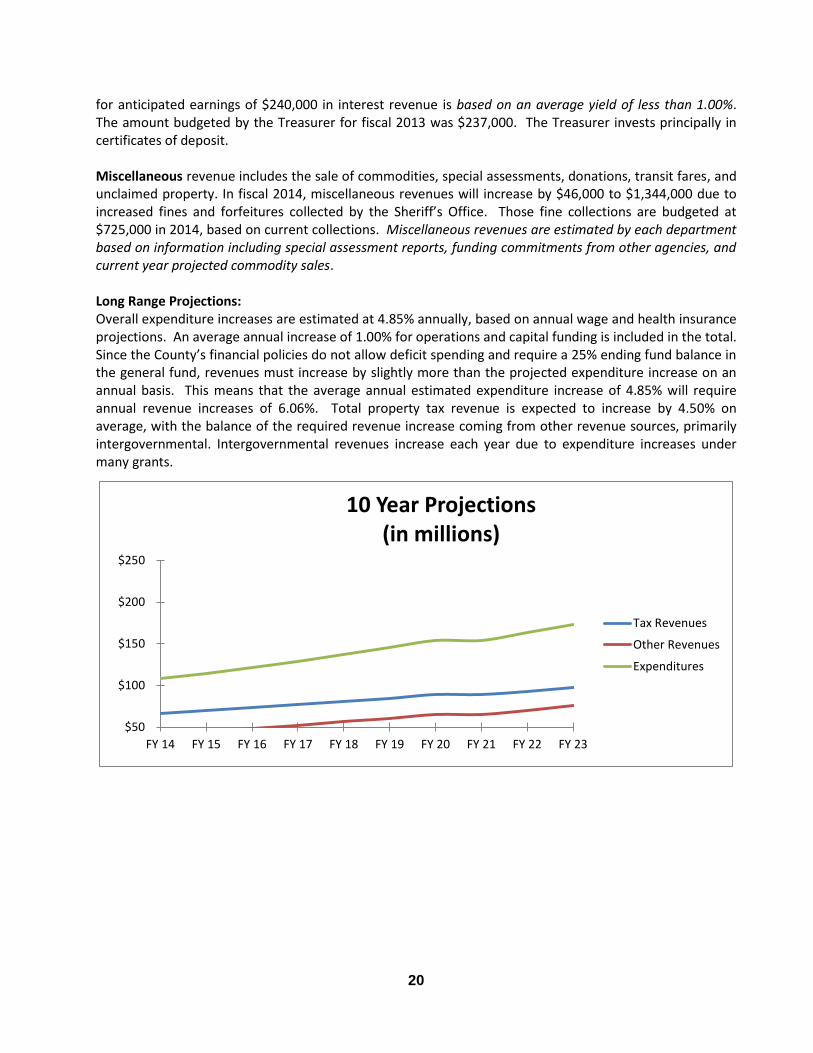

for anticipated earnings of $240,000 in interest revenue is based on an average yield of less than 1.00%. The amount budgeted by the Treasurer for fiscal 2013 was $237,000. The Treasurer invests principally in certificates of deposit. Miscellaneous revenue includes the sale of commodities, special assessments, donations, transit fares, and unclaimed property. In fiscal 2014, miscellaneous revenues will increase by $46,000 to $1,344,000 due to increased fines and forfeitures collected by the Sheriff’s Office. Those fine collections are budgeted at $725,000 in 2014, based on current collections. Miscellaneous revenues are estimated by each department based on information including special assessment reports, funding commitments from other agencies, and current year projected commodity sales. Long Range Projections: Overall expenditure increases are estimated at 4.85% annually, based on annual wage and health insurance projections. An average annual increase of 1.00% for operations and capital funding is included in the total. Since the County’s financial policies do not allow deficit spending and require a 25% ending fund balance in the general fund, revenues must increase by slightly more than the projected expenditure increase on an annual basis. This means that the average annual estimated expenditure increase of 4.85% will require annual revenue increases of 6.06%. Total property tax revenue is expected to increase by 4.50% on average, with the balance of the required revenue increase coming from other revenue sources, primarily intergovernmental. Intergovernmental revenues increase each year due to expenditure increases under many grants.

$50

$100

$150

$200

$250

FY 14 FY 15 FY 16 FY 17 FY 18 FY 19 FY 20 FY 21 FY 22 FY 23

10 Year Projections (in millions)

Tax Revenues

Other Revenues

Expenditures

21

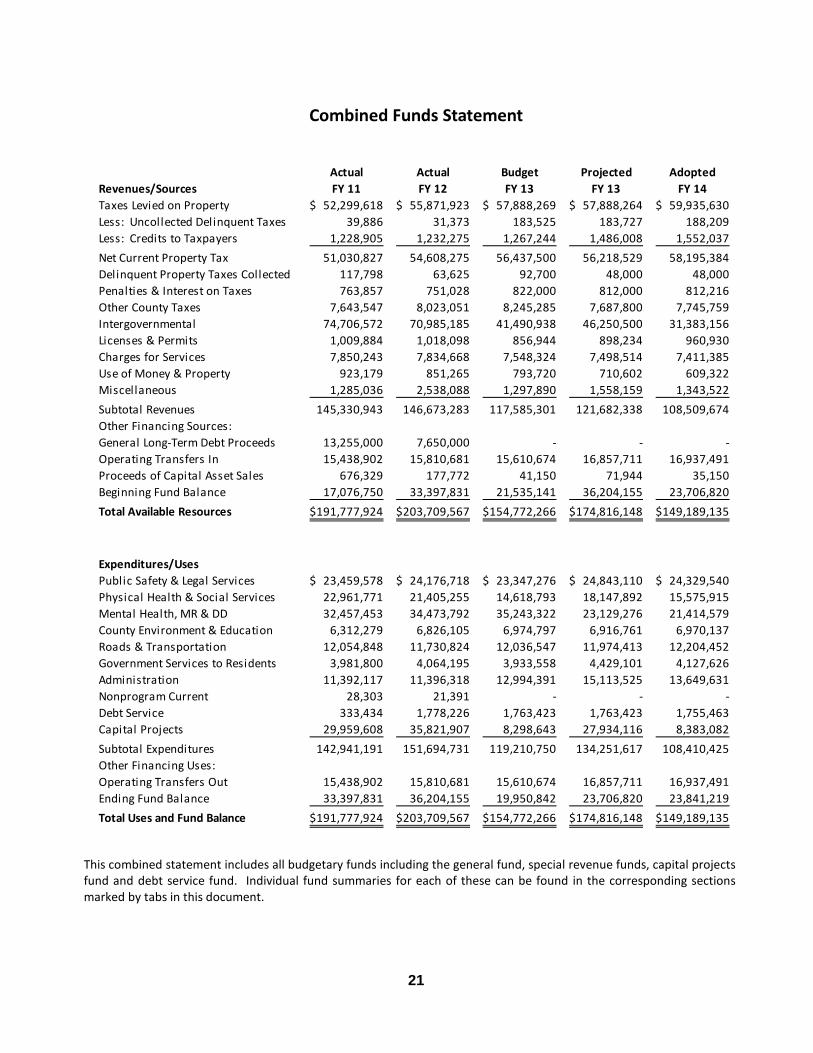

This combined statement includes all budgetary funds including the general fund, special revenue funds, capital projects fund and debt service fund. Individual fund summaries for each of these can be found in the corresponding sections marked by tabs in this document.

Actual Actual Budget Projected Adopted

Revenues/Sources FY 11 FY 12 FY 13 FY 13 FY 14

Taxes Levied on Property 52,299,618$ 55,871,923$ 57,888,269$ 57,888,264$ 59,935,630$

Less: Uncollected Delinquent Taxes 39,886 31,373 183,525 183,727 188,209

Less: Credits to Taxpayers 1,228,905 1,232,275 1,267,244 1,486,008 1,552,037

Net Current Property Tax 51,030,827 54,608,275 56,437,500 56,218,529 58,195,384

Delinquent Property Taxes Collected 117,798 63,625 92,700 48,000 48,000

Penalties & Interest on Taxes 763,857 751,028 822,000 812,000 812,216

Other County Taxes 7,643,547 8,023,051 8,245,285 7,687,800 7,745,759

Intergovernmental 74,706,572 70,985,185 41,490,938 46,250,500 31,383,156

Licenses & Permits 1,009,884 1,018,098 856,944 898,234 960,930

Charges for Services 7,850,243 7,834,668 7,548,324 7,498,514 7,411,385

Use of Money & Property 923,179 851,265 793,720 710,602 609,322

Miscellaneous 1,285,036 2,538,088 1,297,890 1,558,159 1,343,522

Subtotal Revenues 145,330,943 146,673,283 117,585,301 121,682,338 108,509,674

Other Financing Sources:

General Long-Term Debt Proceeds 13,255,000 7,650,000 - - -

Operating Transfers In 15,438,902 15,810,681 15,610,674 16,857,711 16,937,491

Proceeds of Capital Asset Sales 676,329 177,772 41,150 71,944 35,150

Beginning Fund Balance 17,076,750 33,397,831 21,535,141 36,204,155 23,706,820

Total Available Resources 191,777,924$ 203,709,567$ 154,772,266$ 174,816,148$ 149,189,135$

Expenditures/Uses

Public Safety & Legal Services 23,459,578$ 24,176,718$ 23,347,276$ 24,843,110$ 24,329,540$

Physical Health & Social Services 22,961,771 21,405,255 14,618,793 18,147,892 15,575,915

Mental Health, MR & DD 32,457,453 34,473,792 35,243,322 23,129,276 21,414,579

County Environment & Education 6,312,279 6,826,105 6,974,797 6,916,761 6,970,137

Roads & Transportation 12,054,848 11,730,824 12,036,547 11,974,413 12,204,452

Government Services to Residents 3,981,800 4,064,195 3,933,558 4,429,101 4,127,626

Administration 11,392,117 11,396,318 12,994,391 15,113,525 13,649,631

Nonprogram Current 28,303 21,391 - - -

Debt Service 333,434 1,778,226 1,763,423 1,763,423 1,755,463

Capital Projects 29,959,608 35,821,907 8,298,643 27,934,116 8,383,082

Subtotal Expenditures 142,941,191 151,694,731 119,210,750 134,251,617 108,410,425

Other Financing Uses:

Operating Transfers Out 15,438,902 15,810,681 15,610,674 16,857,711 16,937,491

Ending Fund Balance 33,397,831 36,204,155 19,950,842 23,706,820 23,841,219

Total Uses and Fund Balance 191,777,924$ 203,709,567$ 154,772,266$ 174,816,148$ 149,189,135$

22

Department

Actual FY 11

Actual FY 12

Budget FY 13

Proposed

FY 14

Change

Attorney 38.30 37.30 38.30 37.30 (1.00)

Auditor 17.50 17.50 18.60 19.10 0.50

Board of Supervisors 9.88 10.25 10.25 10.25 0.00

Child Support Recovery Unit 22.00 20.00 0.00 0.00 0.00

Civil Service 0.30 0.30 0.30 0.30 0.00

Conservation 39.01 41.01 41.74 41.74 0.00

Court Expense 0.00 0.00 0.00 0.00 0.00

Engineer 68.00 66.00 70.80 68.80 (2.00)

Facilities 31.50 30.90 29.50 31.25 1.75

Finance & Budget 3.50 3.50 3.50 3.50 0.00

Human Resources 4.50 4.50 4.50 4.50 0.00

Information Technology 17.00 16.00 18.00 18.00 0.00

Juvenile Justice 0.00 0.00 0.00 0.00 0.00

LCCS 231.39 216.47 228.20 224.12 (4.08)

LIFTS 22.40 22.40 22.40 22.40 0.00

Medical Examiner 0.00 0.00 0.00 0.00 0.00

Planning & Development 13.00 13.70 13.70 13.70 0.00

Public Health 58.67 46.30 46.80 48.80 2.00

Purchasing 3.70 3.70 3.70 3.70 0.00

Recorder 14.00 14.00 14.00 14.00 0.00

Risk Management 3.00 3.00 3.00 3.00 0.00

Sheriff 177.52 177.80 183.60 184.60 1.00

Soil Conservation 1.00 1.00 1.00 1.00 0.00

State Welfare 0.00 0.00 0.00 0.00 0.00

Treasurer 34.00 35.00 35.30 35.00 (0.30)

Veteran Affairs 3.13 3.13 3.13 3.13 0.00

Total Full -Time Equivalents 813.30 783.76 790.32 788.19 (2.13)

23

Staffing for fiscal year 2014 included a net decrease of 2.13 FTEs. Departmental changes included the following:

Attorney – eliminated 1.00 FTE attorney position

Auditor – reduced 0.50 FTE elected official position budgeted in Facilities department for FY 14. Added 1.00 FTE administrative secretary position budgeted in Facilities department for FY 13.

Engineer – eliminated 2.00 FTE equipment operators.

Facilities – added 0.50 FTE elected official position budgeted in the Auditor’s office for FY 13. Reduced 1.00 FTE administrative secretary position budgeted in the Auditor’s office for FY 14. Added 2.25 FTE part-time custodian positions.

LCCS – MHDD staffing decreased 0.87 FTEs including a 1.00 FTE reduction related to the SCL level of service and a 0.13 increase in clerical services. Core services decreased staffing by 4.68 FTEs. Included is a reduction of the General Assistance director from full-time to a 0.50 FTE position, a reduction of 2.00 FTE social workers in Home Health due to loss of Medicaid funding, a 0.25 FTE increase in Child and Youth Development substitute positions, a 1.43 FTE reduction in protective homemakers as a result of reorganization with the Family Visitation Center staff and the Protective Home Health program, and a reduction of two 0.50 FTE clerical staff positions in General Home Health and Aging and Disability Resource Center, the result of funding reductions. Juvenile Detention and Alternatives increased staffing by 1.47 FTEs. A loss in funding reduced Detention Education staff by 0.30 FTEs while increased grant funding for “trackers” increased LINK Tracker program by 1.77 FTEs.

Public Health – added a 1.00 FTE epidemiologist and a 1.00 FTE environmental health specialist.

Sheriff – added a 1.00 FTE from patrol deputy for mental health transportation.

24

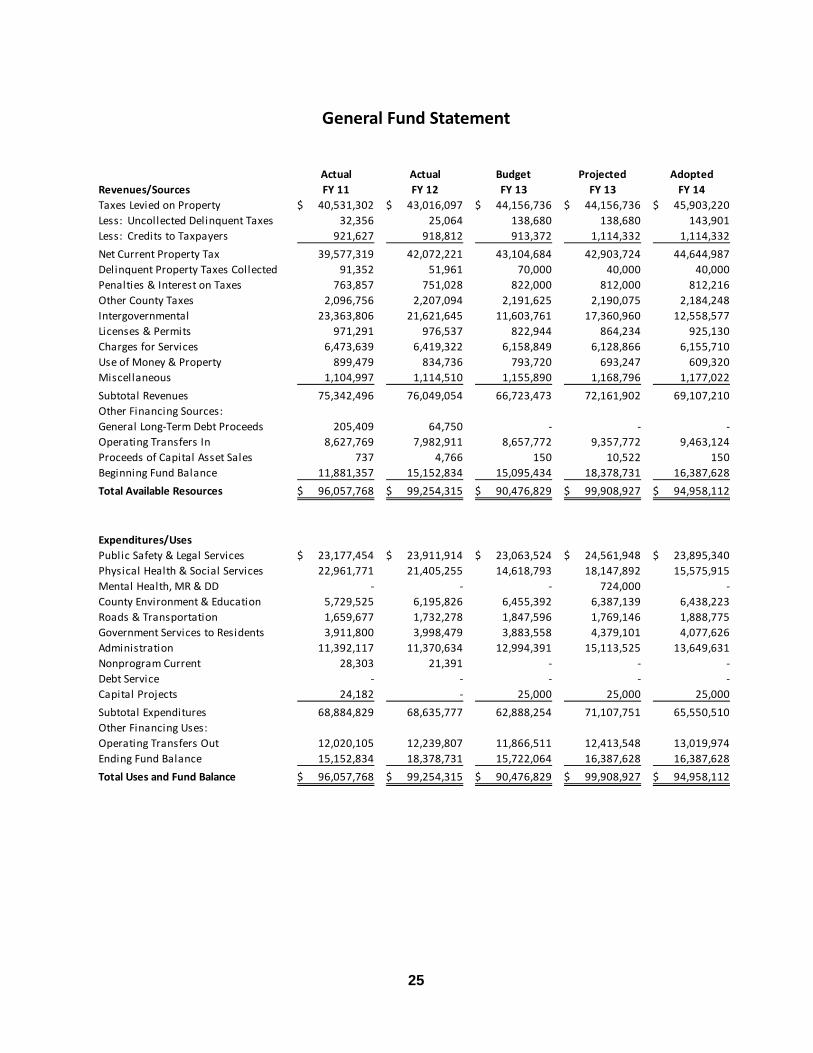

The general fund is the operating fund of Linn County. It is used to account for all financial resources except those required legally or by sound financial management to be accounted for in another fund. The general fund is comprised of two separate funds, the general basic and the general supplemental. The general basic has a maximum levy rate of $3.50 per $1,000 of taxable valuation. The general supplemental fund is for specific uses as defined in Section 331.424 of the Code of Iowa. These uses include substance abuse care and treatment, foster care for a child under jurisdiction of the juvenile court, elections and voter registration, employee benefits, tort liability and property insurance, operation of the courts, and local emergency management agency funding. The fiscal year 2014 general basic fund levy rate per thousand is $3.50 and the general supplemental levy rate per thousand is $1.58019. The general basic rate is the same as in fiscal 2013 and the general supplemental rate represents a 3-cent increase. General fund taxes levied on property total $45,903,220 in fiscal 2014.

25

Actual Actual Budget Projected Adopted

Revenues/Sources FY 11 FY 12 FY 13 FY 13 FY 14

Taxes Levied on Property 40,531,302$ 43,016,097$ 44,156,736$ 44,156,736$ 45,903,220$

Less: Uncollected Delinquent Taxes 32,356 25,064 138,680 138,680 143,901

Less: Credits to Taxpayers 921,627 918,812 913,372 1,114,332 1,114,332

Net Current Property Tax 39,577,319 42,072,221 43,104,684 42,903,724 44,644,987

Delinquent Property Taxes Collected 91,352 51,961 70,000 40,000 40,000

Penalties & Interest on Taxes 763,857 751,028 822,000 812,000 812,216

Other County Taxes 2,096,756 2,207,094 2,191,625 2,190,075 2,184,248

Intergovernmental 23,363,806 21,621,645 11,603,761 17,360,960 12,558,577

Licenses & Permits 971,291 976,537 822,944 864,234 925,130

Charges for Services 6,473,639 6,419,322 6,158,849 6,128,866 6,155,710

Use of Money & Property 899,479 834,736 793,720 693,247 609,320

Miscellaneous 1,104,997 1,114,510 1,155,890 1,168,796 1,177,022

Subtotal Revenues 75,342,496 76,049,054 66,723,473 72,161,902 69,107,210

Other Financing Sources:

General Long-Term Debt Proceeds 205,409 64,750 - - -

Operating Transfers In 8,627,769 7,982,911 8,657,772 9,357,772 9,463,124

Proceeds of Capital Asset Sales 737 4,766 150 10,522 150

Beginning Fund Balance 11,881,357 15,152,834 15,095,434 18,378,731 16,387,628

Total Available Resources 96,057,768$ 99,254,315$ 90,476,829$ 99,908,927$ 94,958,112$

Expenditures/Uses

Public Safety & Legal Services 23,177,454$ 23,911,914$ 23,063,524$ 24,561,948$ 23,895,340$

Physical Health & Social Services 22,961,771 21,405,255 14,618,793 18,147,892 15,575,915

Mental Health, MR & DD - - - 724,000 -

County Environment & Education 5,729,525 6,195,826 6,455,392 6,387,139 6,438,223

Roads & Transportation 1,659,677 1,732,278 1,847,596 1,769,146 1,888,775

Government Services to Residents 3,911,800 3,998,479 3,883,558 4,379,101 4,077,626

Administration 11,392,117 11,370,634 12,994,391 15,113,525 13,649,631

Nonprogram Current 28,303 21,391 - - -

Debt Service - - - - -

Capital Projects 24,182 - 25,000 25,000 25,000

Subtotal Expenditures 68,884,829 68,635,777 62,888,254 71,107,751 65,550,510

Other Financing Uses:

Operating Transfers Out 12,020,105 12,239,807 11,866,511 12,413,548 13,019,974

Ending Fund Balance 15,152,834 18,378,731 15,722,064 16,387,628 16,387,628

Total Uses and Fund Balance 96,057,768$ 99,254,315$ 90,476,829$ 99,908,927$ 94,958,112$

26

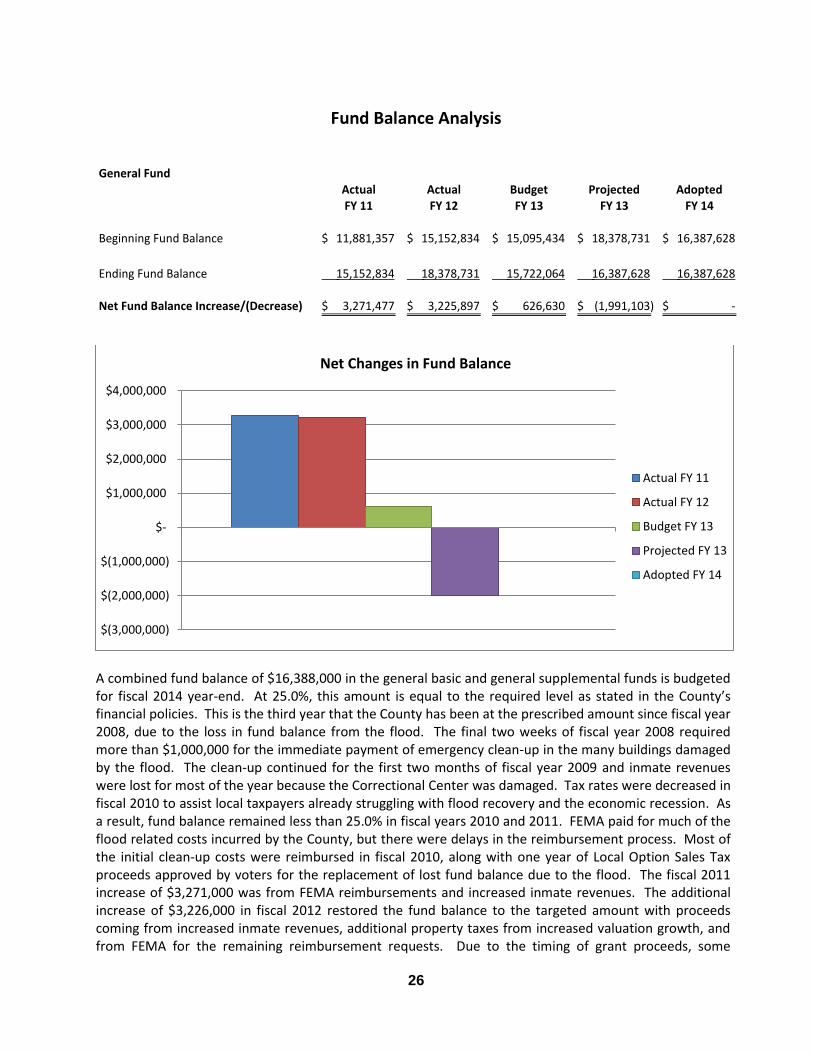

General FundActual Actual Budget Projected Adopted

FY 11 FY 12 FY 13 FY 13 FY 14

Beginning Fund Balance 11,881,357$ 15,152,834$ 15,095,434$ 18,378,731$ 16,387,628$

Ending Fund Balance 15,152,834 18,378,731 15,722,064 16,387,628 16,387,628

Net Fund Balance Increase/(Decrease) 3,271,477$ 3,225,897$ 626,630$ (1,991,103)$ -$

A combined fund balance of $16,388,000 in the general basic and general supplemental funds is budgeted for fiscal 2014 year-end. At 25.0%, this amount is equal to the required level as stated in the County’s financial policies. This is the third year that the County has been at the prescribed amount since fiscal year 2008, due to the loss in fund balance from the flood. The final two weeks of fiscal year 2008 required more than $1,000,000 for the immediate payment of emergency clean-up in the many buildings damaged by the flood. The clean-up continued for the first two months of fiscal year 2009 and inmate revenues were lost for most of the year because the Correctional Center was damaged. Tax rates were decreased in fiscal 2010 to assist local taxpayers already struggling with flood recovery and the economic recession. As a result, fund balance remained less than 25.0% in fiscal years 2010 and 2011. FEMA paid for much of the flood related costs incurred by the County, but there were delays in the reimbursement process. Most of the initial clean-up costs were reimbursed in fiscal 2010, along with one year of Local Option Sales Tax proceeds approved by voters for the replacement of lost fund balance due to the flood. The fiscal 2011 increase of $3,271,000 was from FEMA reimbursements and increased inmate revenues. The additional increase of $3,226,000 in fiscal 2012 restored the fund balance to the targeted amount with proceeds coming from increased inmate revenues, additional property taxes from increased valuation growth, and from FEMA for the remaining reimbursement requests. Due to the timing of grant proceeds, some

$(3,000,000)

$(2,000,000)

$(1,000,000)

$-

$1,000,000

$2,000,000

$3,000,000

$4,000,000

Net Changes in Fund Balance

Actual FY 11

Actual FY 12

Budget FY 13

Projected FY 13

Adopted FY 14

27

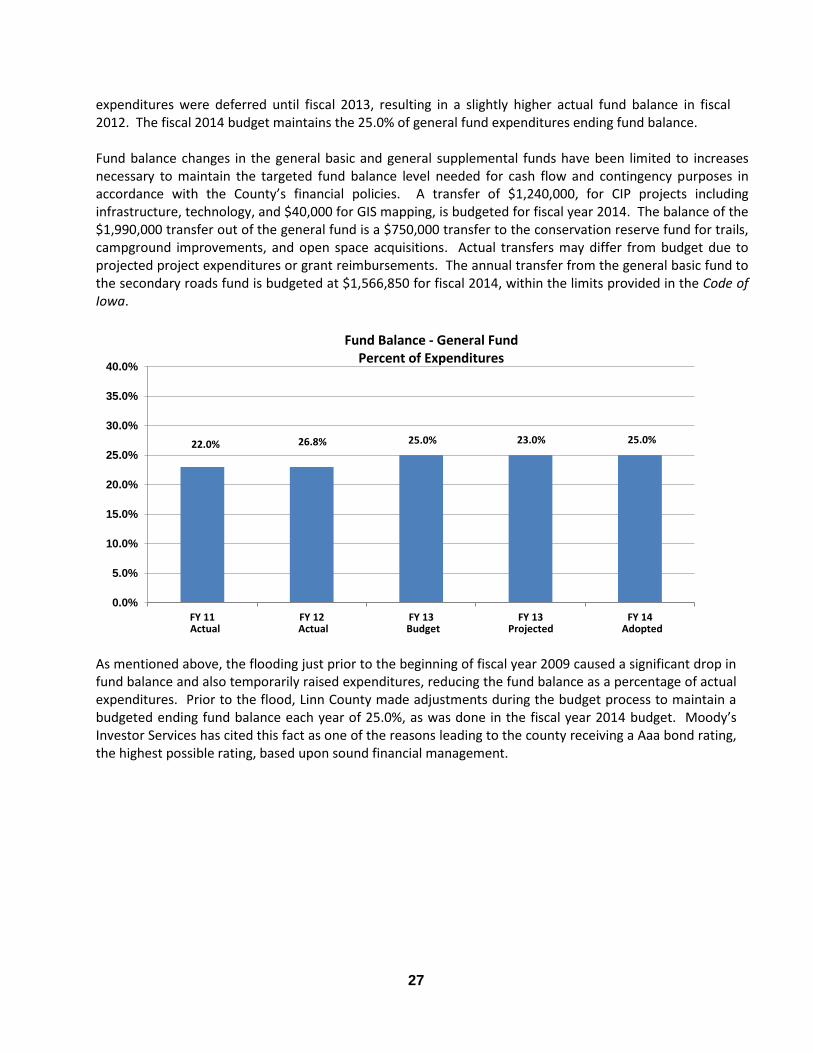

expenditures were deferred until fiscal 2013, resulting in a slightly higher actual fund balance in fiscal 2012. The fiscal 2014 budget maintains the 25.0% of general fund expenditures ending fund balance. Fund balance changes in the general basic and general supplemental funds have been limited to increases necessary to maintain the targeted fund balance level needed for cash flow and contingency purposes in accordance with the County’s financial policies. A transfer of $1,240,000, for CIP projects including infrastructure, technology, and $40,000 for GIS mapping, is budgeted for fiscal year 2014. The balance of the $1,990,000 transfer out of the general fund is a $750,000 transfer to the conservation reserve fund for trails, campground improvements, and open space acquisitions. Actual transfers may differ from budget due to projected project expenditures or grant reimbursements. The annual transfer from the general basic fund to the secondary roads fund is budgeted at $1,566,850 for fiscal 2014, within the limits provided in the Code of Iowa.

As mentioned above, the flooding just prior to the beginning of fiscal year 2009 caused a significant drop in fund balance and also temporarily raised expenditures, reducing the fund balance as a percentage of actual expenditures. Prior to the flood, Linn County made adjustments during the budget process to maintain a budgeted ending fund balance each year of 25.0%, as was done in the fiscal year 2014 budget. Moody’s Investor Services has cited this fact as one of the reasons leading to the county receiving a Aaa bond rating, the highest possible rating, based upon sound financial management.

22.0% 26.8% 25.0% 23.0% 25.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

FY 11 FY 12 FY 13 FY 13 FY 14Actual Actual Projected Adopted

Fund Balance - General Fund Percent of Expenditures

Budget

28

Special revenue funds are used to account for the proceeds of specific revenue sources (other than special assessments or major capital projects) that are legally restricted to expenditures for specified purposes. The funds included in this section and their purposes are as follows: MH - DD Fund – To account for taxes levied to provide mental health services to the mentally ill, the mentally

retarded, and the developmentally disabled.

Rural Services Fund – To account for taxes levied to benefit the rural residents of the County. The primary

use of this fund is for the transfer of funds to the secondary roads fund.

Inmate Commissary Fund – To account for the sale of personal and convenience items to prisoners in the

correctional center and revenues from inmate phone calls with profits used for purposes of prisoner welfare

and rehabilitation.

Gifts and Donations Fund – Gifts and donations received by the County are accounted for in this fund, with

the exception of Conservation gifts which are deposited in the Conservation Reserve fund.

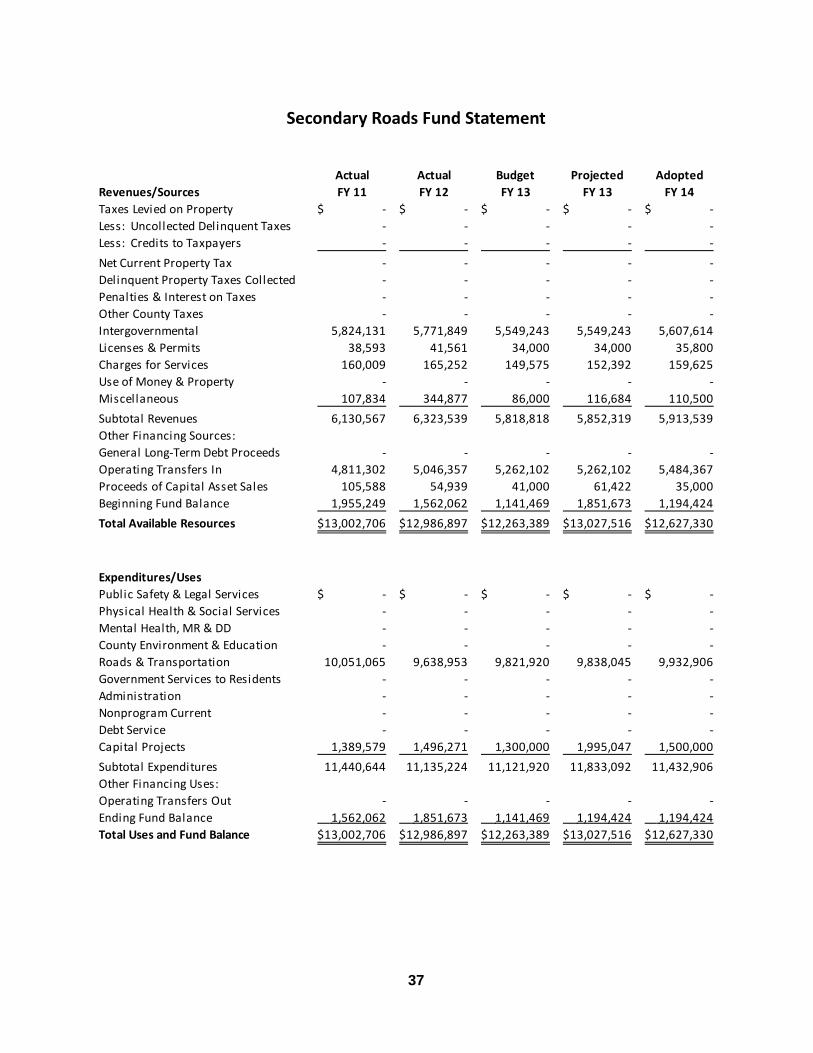

Secondary Roads Fund – To account for state revenues allocated to the County to be used to maintain and

improve the county's roads.

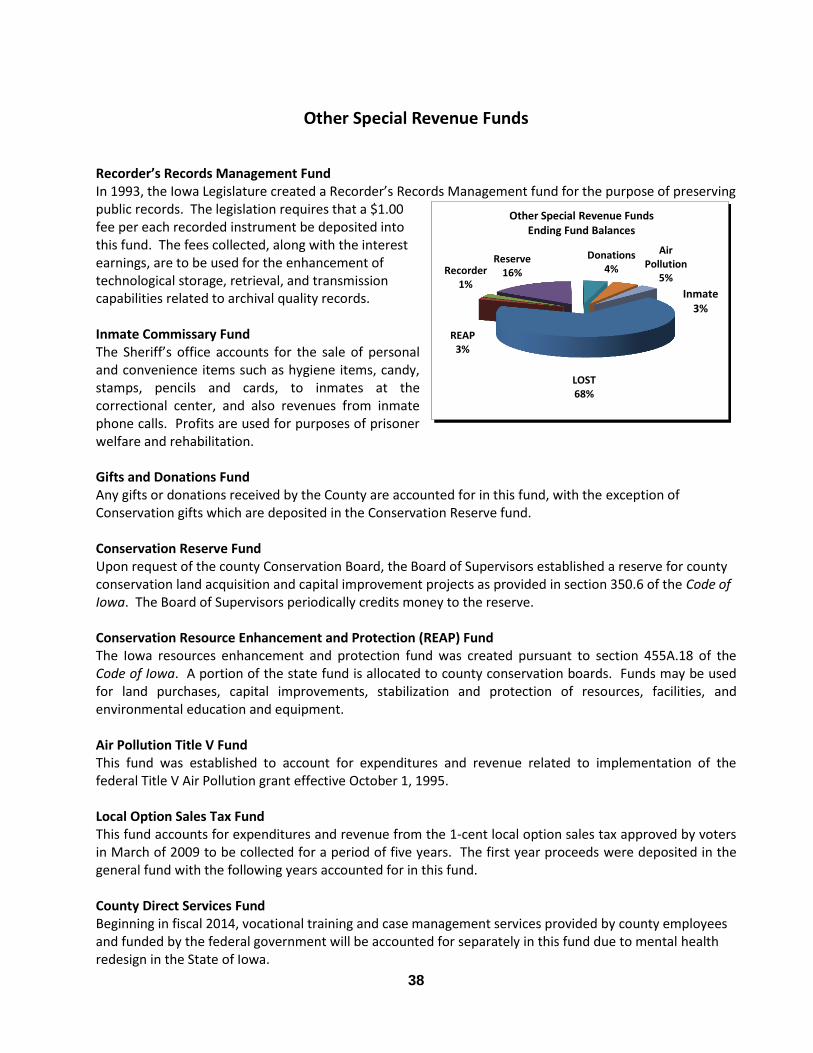

Recorder's Records Management Fund – To account for fees collected for each recorded transaction to be

used for the purpose of preserving and maintaining public records.

Conservation Reserve Fund – To account for funds deposited with the County to be used for conservation

purposes.

Conservation Resource Enhancement and Protection (REAP) Fund – To account for state funds received by

the County to be used for County conservation land acquisition and capital improvement projects.

Air Pollution Title V Fund – To account for permit fees collected from industry for all major sources of air

pollution emissions.

Local Option Sales Tax Funds – To account for the use of sales tax proceeds by the Engineer and

Conservation, a separate fund has been established for each of these departments.

County Direct Services Fund – To account for mental health fees that fund services provided directly by Linn

County staff and no longer included in the MH-DD fund.

29

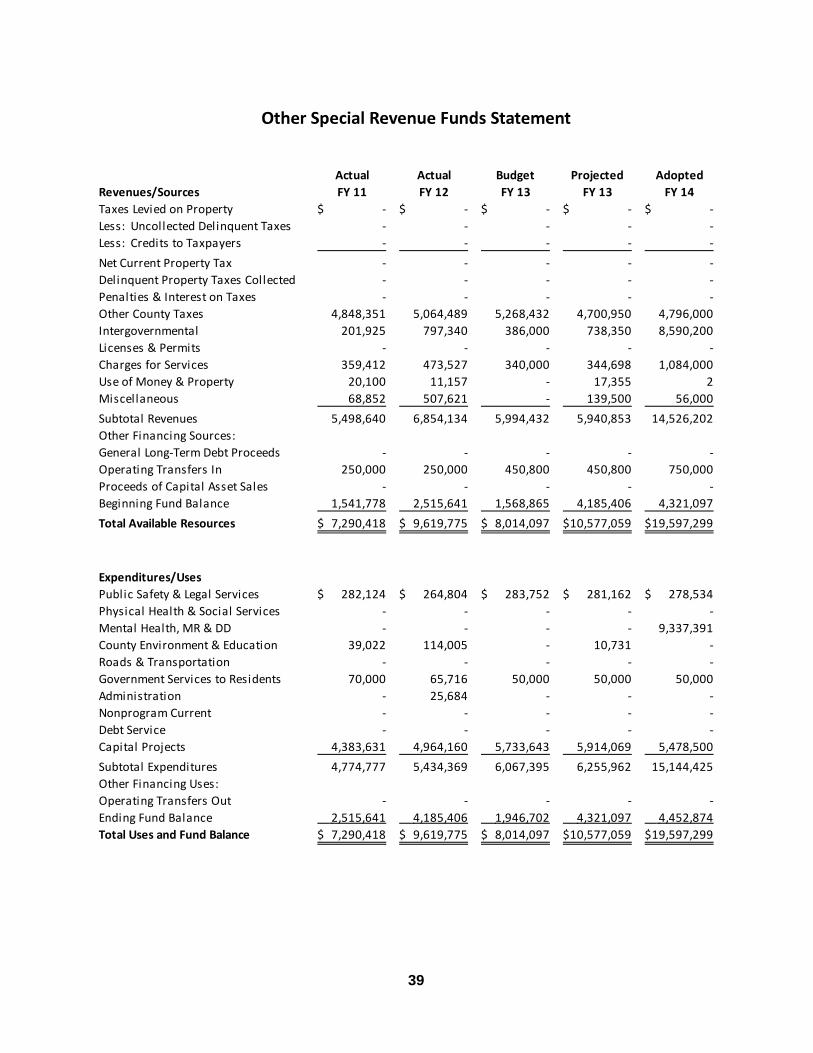

Actual Actual Budget Projected Adopted

Revenues/Sources FY 11 FY 12 FY 13 FY 13 FY 14

Taxes Levied on Property 11,700,964$ 11,918,975$ 12,220,795$ 12,220,790$ 12,460,706$

Less: Uncollected Delinquent Taxes 7,530 5,754 40,133 40,133 39,394

Less: Credits to Taxpayers 305,785 293,710 289,671 289,671 355,700

Net Current Property Tax 11,387,649 11,619,511 11,890,991 11,890,986 12,065,612

Delinquent Property Taxes Collected 26,293 10,524 18,500 5,500 5,500

Penalties & Interest on Taxes - - - - -

Other County Taxes 5,543,498 5,769,976 5,980,023 5,412,666 5,487,884

Intergovernmental 29,592,924 30,035,778 29,635,919 18,451,192 18,561,996

Licenses & Permits 38,593 41,561 34,000 34,000 35,800

Charges for Services 1,376,604 1,415,346 1,389,475 1,369,648 1,255,675

Use of Money & Property 23,700 14,607 - 17,355 2

Miscellaneous 180,039 852,498 142,000 256,184 166,500

Subtotal Revenues 48,169,300 49,759,801 49,090,908 37,437,531 37,578,969

Other Financing Sources:

General Long-Term Debt Proceeds - - - - -

Operating Transfers In 5,061,302 5,296,357 5,712,902 5,712,902 6,234,367

Proceeds of Capital Asset Sales 105,588 54,939 41,000 61,422 35,000

Beginning Fund Balance 8,637,588 8,994,269 6,321,073 8,615,240 6,702,489

Total Available Resources 61,973,778$ 64,105,366$ 61,165,883$ 51,827,095$ 50,550,825$

Expenditures/Uses

Public Safety & Legal Services 282,124$ 264,804$ 283,752$ 281,162$ 434,200$

Physical Health & Social Services - - - - -

Mental Health, MR & DD 32,457,453 34,473,792 35,243,322 22,405,276 21,414,579

County Environment & Education 582,754 630,279 519,405 529,622 531,914

Roads & Transportation 10,395,171 9,998,546 10,188,951 10,205,267 10,315,677

Government Services to Residents 70,000 65,716 50,000 50,000 50,000

Administration - 25,684 - - -

Nonprogram Current - - - - -

Debt Service - - - - -

Capital Projects 5,773,210 6,460,431 7,033,643 7,909,116 7,118,082

Subtotal Expenditures 49,560,712 51,919,252 53,319,073 41,380,443 39,864,452

Other Financing Uses:

Operating Transfers Out 3,418,797 3,570,874 3,744,163 3,744,163 3,917,517

Ending Fund Balance 8,994,269 8,615,240 4,102,647 6,702,489 6,768,856

Total Uses and Fund Balance 61,973,778$ 64,105,366$ 61,165,883$ 51,827,095$ 50,550,825$

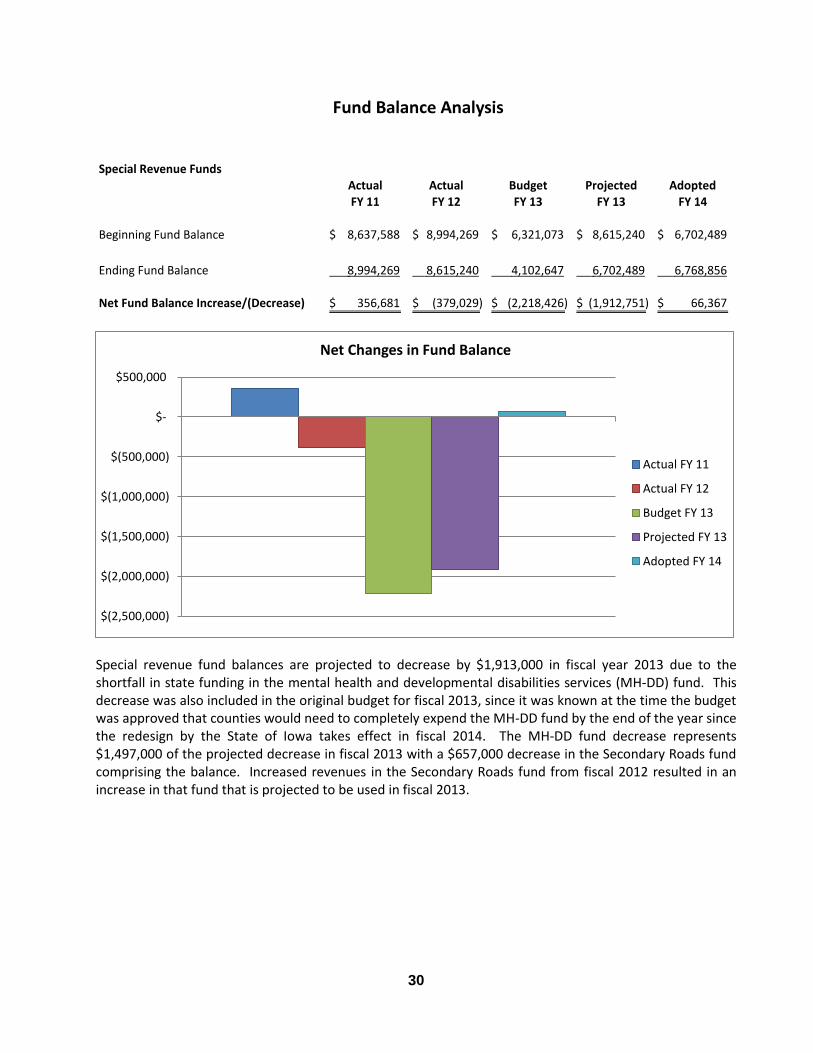

30

Special Revenue Funds

Actual Actual Budget Projected Adopted FY 11 FY 12 FY 13 FY 13 FY 14

Beginning Fund Balance 8,637,588$ 8,994,269$ 6,321,073$ 8,615,240$ 6,702,489$

Ending Fund Balance 8,994,269 8,615,240 4,102,647 6,702,489 6,768,856

Net Fund Balance Increase/(Decrease) 356,681$ (379,029)$ (2,218,426)$ (1,912,751)$ 66,367$

Special revenue fund balances are projected to decrease by $1,913,000 in fiscal year 2013 due to the shortfall in state funding in the mental health and developmental disabilities services (MH-DD) fund. This decrease was also included in the original budget for fiscal 2013, since it was known at the time the budget was approved that counties would need to completely expend the MH-DD fund by the end of the year since the redesign by the State of Iowa takes effect in fiscal 2014. The MH-DD fund decrease represents $1,497,000 of the projected decrease in fiscal 2013 with a $657,000 decrease in the Secondary Roads fund comprising the balance. Increased revenues in the Secondary Roads fund from fiscal 2012 resulted in an increase in that fund that is projected to be used in fiscal 2013.

$(2,500,000)

$(2,000,000)

$(1,500,000)

$(1,000,000)

$(500,000)

$-

$500,000

Net Changes in Fund Balance

Actual FY 11

Actual FY 12

Budget FY 13

Projected FY 13

Adopted FY 14

31

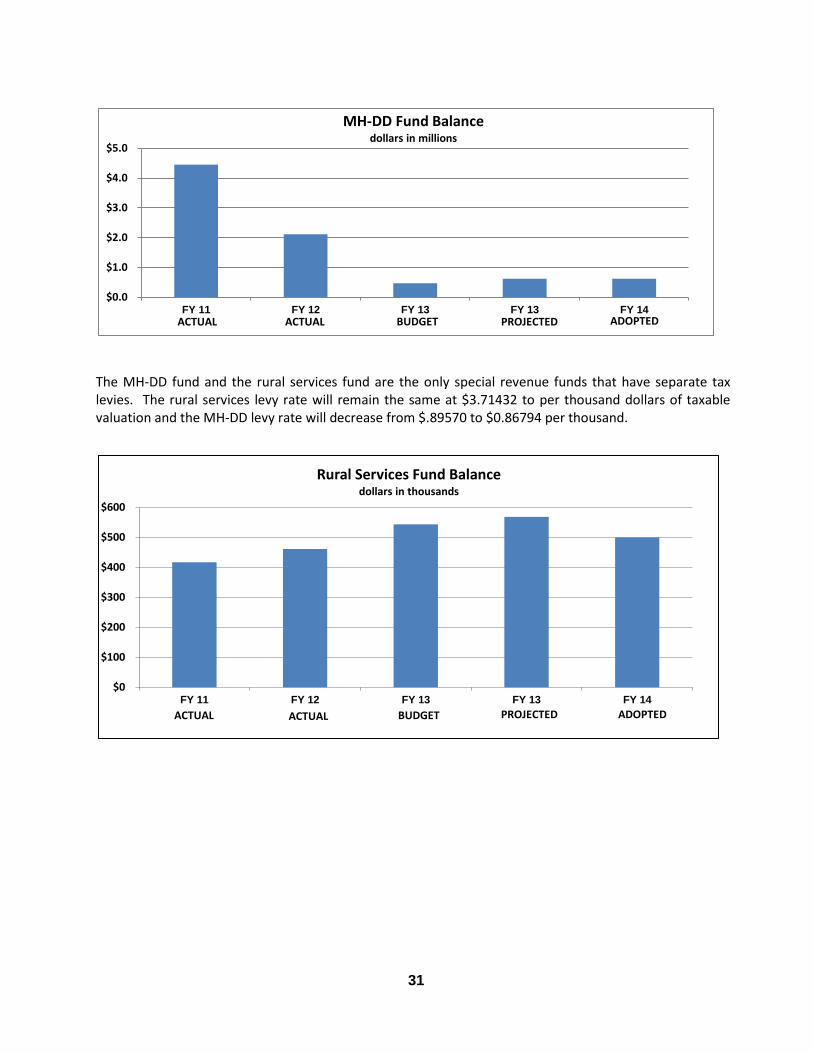

The MH-DD fund and the rural services fund are the only special revenue funds that have separate tax levies. The rural services levy rate will remain the same at $3.71432 to per thousand dollars of taxable valuation and the MH-DD levy rate will decrease from $.89570 to $0.86794 per thousand.

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

FY 11 FY 12 FY 13 FY 13 FY 14

MH-DD Fund Balance dollars in millions

ACTUAL ACTUAL BUDGET PROJECTED ADOPTED

$0

$100

$200

$300

$400

$500

$600

FY 11 FY 12 FY 13 FY 13 FY 14

Rural Services Fund Balance dollars in thousands

ACTUAL ACTUAL BUDGET PROJECTED ADOPTED

32

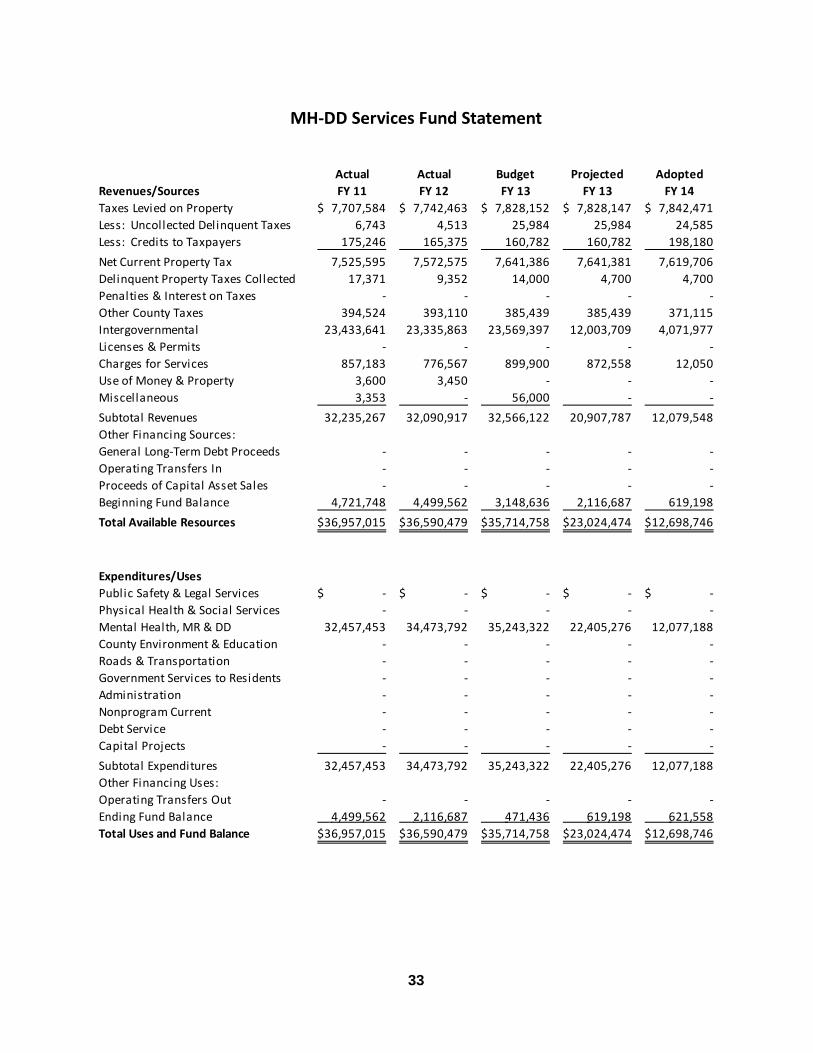

MH-DD Services Fund

The MH-DD services fund is used to provide mental health, mental retardation, and developmental disabilities services to county residents as defined in Section 331.424A of the Code of Iowa.

Linn County has budgeted $2.2 million in transition funding and $1.9 million in mental health equalization funding from the State of Iowa. These revenue sources replace allowable growth and property tax relief funding received from the State in previous fiscal years, at a much reduced level. The amounts included in the fiscal 2014 budget are preliminary estimates until the legislature determines funding for the fiscal year. Budget adjustments will be made when actual funding is determined. The new plan from the State of Iowa takes effect in fiscal year 2014 with regional funding, rather than funding to each county. The region that Linn County is a part of does not have the same programs and requested that vocational training and county provided case management programs be removed from the MH-DD fund. Since those programs are of great value to those receiving services and do not require county funding, a new special revenue fund, County Provided Services, was established to account for the revenues and expenditures. The County Provided Services fund includes expenditures of $5,595,000 for county provided services, primarily vocational training, and $3,742,000 for county provided case management, for a total of $9,337,000 in fiscal year 2014. The MH-DD property tax levy in Linn County is limited to $8,195,141 by the Code of Iowa. This results in a levy rate decrease each year that the county valuation increases, as Linn County levies the maximum amount allowed.

Developmental Disabilities

3% Mental Retardation

7%

Chronic Mental Illness 41% Mental Health

43%

Administration 6%

MH-DD Services Fund Expenditures Fiscal Year 2014

33

-

Actual Actual Budget Projected Adopted

Revenues/Sources FY 11 FY 12 FY 13 FY 13 FY 14

Taxes Levied on Property 7,707,584$ 7,742,463$ 7,828,152$ 7,828,147$ 7,842,471$

Less: Uncollected Delinquent Taxes 6,743 4,513 25,984 25,984 24,585

Less: Credits to Taxpayers 175,246 165,375 160,782 160,782 198,180

Net Current Property Tax 7,525,595 7,572,575 7,641,386 7,641,381 7,619,706

Delinquent Property Taxes Collected 17,371 9,352 14,000 4,700 4,700

Penalties & Interest on Taxes - - - - -

Other County Taxes 394,524 393,110 385,439 385,439 371,115

Intergovernmental 23,433,641 23,335,863 23,569,397 12,003,709 4,071,977

Licenses & Permits - - - - -

Charges for Services 857,183 776,567 899,900 872,558 12,050

Use of Money & Property 3,600 3,450 - - -

Miscellaneous 3,353 - 56,000 - -

Subtotal Revenues 32,235,267 32,090,917 32,566,122 20,907,787 12,079,548

Other Financing Sources:

General Long-Term Debt Proceeds - - - - -

Operating Transfers In - - - - -

Proceeds of Capital Asset Sales - - - - -

Beginning Fund Balance 4,721,748 4,499,562 3,148,636 2,116,687 619,198

Total Available Resources 36,957,015$ 36,590,479$ 35,714,758$ 23,024,474$ 12,698,746$

Expenditures/Uses

Public Safety & Legal Services -$ -$ -$ -$ -$

Physical Health & Social Services - - - - -

Mental Health, MR & DD 32,457,453 34,473,792 35,243,322 22,405,276 12,077,188

County Environment & Education - - - - -

Roads & Transportation - - - - -

Government Services to Residents - - - - -

Administration - - - - -

Nonprogram Current - - - - -

Debt Service - - - - -

Capital Projects - - - - -

Subtotal Expenditures 32,457,453 34,473,792 35,243,322 22,405,276 12,077,188

Other Financing Uses:

Operating Transfers Out - - - - -

Ending Fund Balance 4,499,562 2,116,687 471,436 619,198 621,558

Total Uses and Fund Balance 36,957,015$ 36,590,479$ 35,714,758$ 23,024,474$ 12,698,746$

34

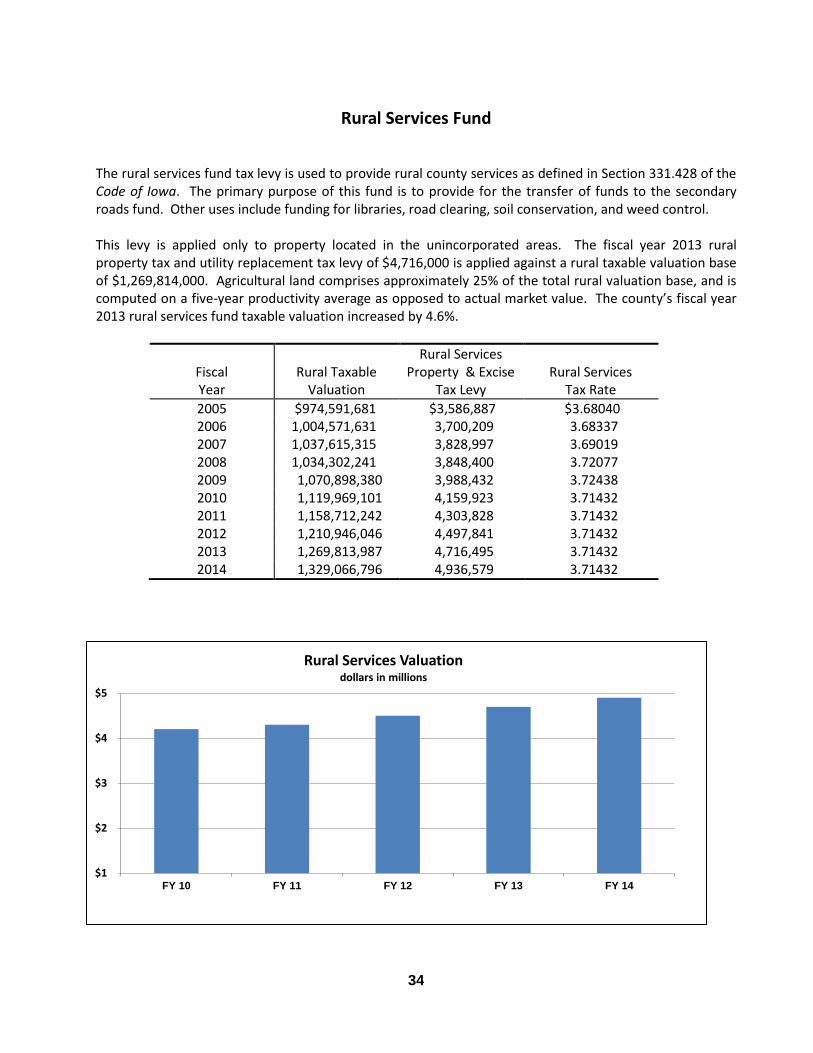

The rural services fund tax levy is used to provide rural county services as defined in Section 331.428 of the Code of Iowa. The primary purpose of this fund is to provide for the transfer of funds to the secondary roads fund. Other uses include funding for libraries, road clearing, soil conservation, and weed control. This levy is applied only to property located in the unincorporated areas. The fiscal year 2013 rural property tax and utility replacement tax levy of $4,716,000 is applied against a rural taxable valuation base of $1,269,814,000. Agricultural land comprises approximately 25% of the total rural valuation base, and is computed on a five-year productivity average as opposed to actual market value. The county’s fiscal year 2013 rural services fund taxable valuation increased by 4.6%.

Fiscal Year

Rural Taxable

Valuation

Rural Services Property & Excise

Tax Levy

Rural Services

Tax Rate

2005 $974,591,681 $3,586,887 $3.68040 2006 1,004,571,631 3,700,209 3.68337 2007 1,037,615,315 3,828,997 3.69019 2008 1,034,302,241 3,848,400 3.72077 2009 1,070,898,380 3,988,432 3.72438 2010 1,119,969,101 4,159,923 3.71432 2011 1,158,712,242 4,303,828 3.71432 2012 1,210,946,046 4,497,841 3.71432 2013 1,269,813,987 4,716,495 3.71432 2014 1,329,066,796 4,936,579 3.71432

$1

$2

$3

$4

$5

FY 10 FY 11 FY 12 FY 13 FY 14

Rural Services Valuation dollars in millions

35

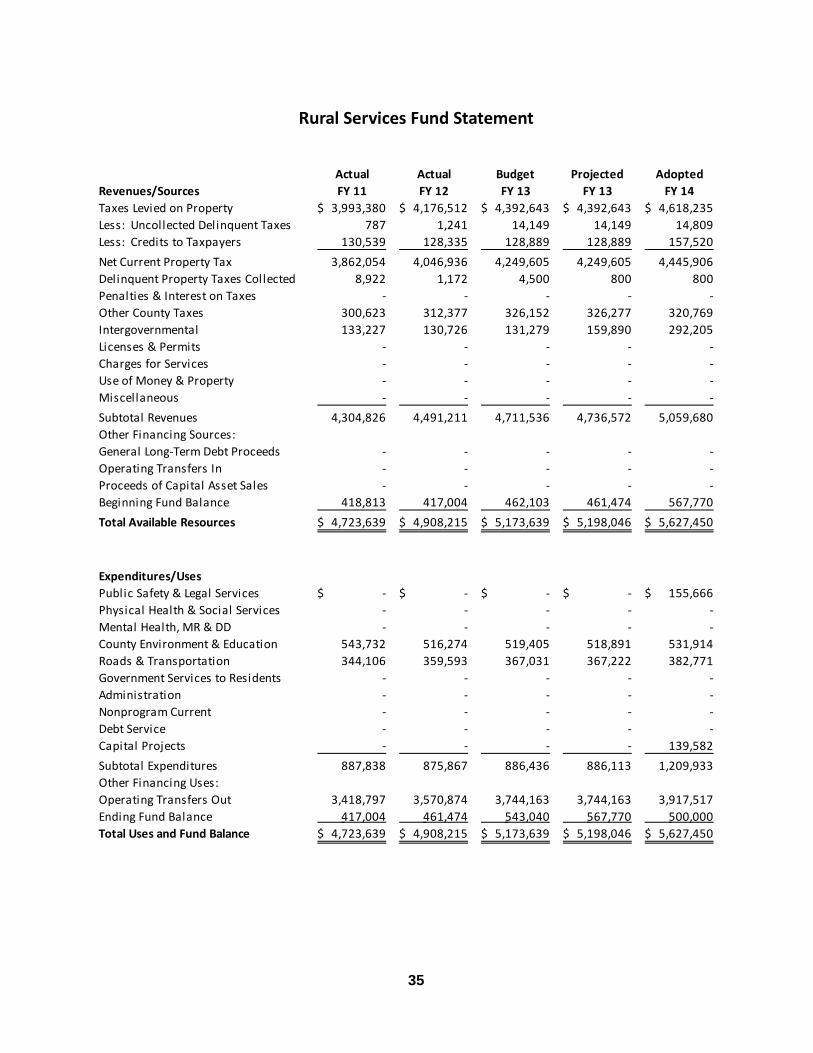

Actual Actual Budget Projected Adopted

Revenues/Sources FY 11 FY 12 FY 13 FY 13 FY 14

Taxes Levied on Property 3,993,380$ 4,176,512$ 4,392,643$ 4,392,643$ 4,618,235$

Less: Uncollected Delinquent Taxes 787 1,241 14,149 14,149 14,809

Less: Credits to Taxpayers 130,539 128,335 128,889 128,889 157,520

Net Current Property Tax 3,862,054 4,046,936 4,249,605 4,249,605 4,445,906

Delinquent Property Taxes Collected 8,922 1,172 4,500 800 800

Penalties & Interest on Taxes - - - - -

Other County Taxes 300,623 312,377 326,152 326,277 320,769

Intergovernmental 133,227 130,726 131,279 159,890 292,205

Licenses & Permits - - - - -

Charges for Services - - - - -

Use of Money & Property - - - - -

Miscellaneous - - - - -

Subtotal Revenues 4,304,826 4,491,211 4,711,536 4,736,572 5,059,680

Other Financing Sources:

General Long-Term Debt Proceeds - - - - -

Operating Transfers In - - - - -

Proceeds of Capital Asset Sales - - - - -

Beginning Fund Balance 418,813 417,004 462,103 461,474 567,770

Total Available Resources 4,723,639$ 4,908,215$ 5,173,639$ 5,198,046$ 5,627,450$

Expenditures/Uses

Public Safety & Legal Services -$ -$ -$ -$ 155,666$

Physical Health & Social Services - - - - -

Mental Health, MR & DD - - - - -

County Environment & Education 543,732 516,274 519,405 518,891 531,914