Executive summary for ministers and senior officials Toolkit

326

Executive summary for ministers and senior officials Toolkit: A guide for hiring and managing advisors for private participation in infrastructure Summary

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Executive summary for ministers and senior officials Toolkit

Executive summary for ministers andsenior officials

Toolkit:A guide for hiring and managing advisors for private participation in infrastructure

Summary

Frontier cover 9 25/4/01 4:14 pm Page 1

page 1 PPI advisory services – executive summary for ministers and senior officials

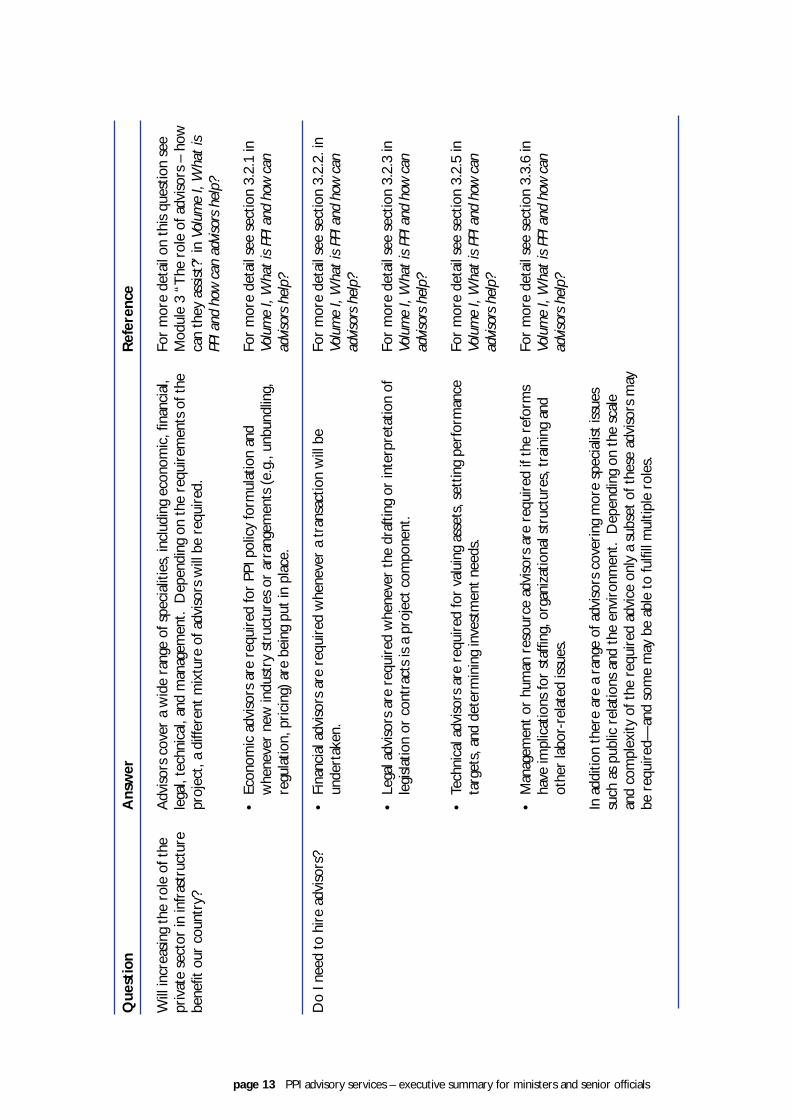

This summary sets out the key issues of interest for ministers and senior policymakers who are considering whether to hire advisors. It is one component of alarger Toolkit that defines the need for and the role of advisors at each stage ofa Private Participation in Infrastructure (PPI) program. The summary does notdiscuss the details of PPI, nor does it address all of the issues that need to beconsidered when appointing advisors. The officials involved in taking forwardreform or implementation should refer to the detailed manuals in the Toolkitfor further information. (See the relevant cross-references.) Summary answersto a number of frequently asked questions are provided at the end of thissummary.

Private sector provision of infrastructure

Over the period 1990 – 1999 the private sector has made massiveinvestment in infrastructure in developing countries. According to theWorld Bank’s PPI Database, the private sector invested $580 billion ininfrastructure in developing countries between 1990 and 1999. This trendis the result of increased recognition by national, state and localgovernments of the ability of the private sector to assume many of therisks involved in the construction and operation of infrastructure projects.The decrease in the funds available to national, state and localgovernments for infrastructure investment has also had an impact.

See Module 1 “Principles of selection of advisory services to support PPI”of Volume I, What is PPI and how can advisors help? for further information.

PPI has increaseddramatically over

the last decade.

PPI advisory services executive summary for ministersand senior officials

Need for advisors

Governments embarking on introducing PPI need not, and should not,tackle the reforms unaided. Infrastructure is a large and relatively complexpart of an economy. Affordable power, safe water supply, effectivetelecommunication services and reliable transport systems are vital to acountry’s economic growth and improved quality of life of its citizens. Specialist advisors can provide the requisite expertise and experience toensure the success of the reform process, and have the necessaryindependence to advise on the appropriate path.

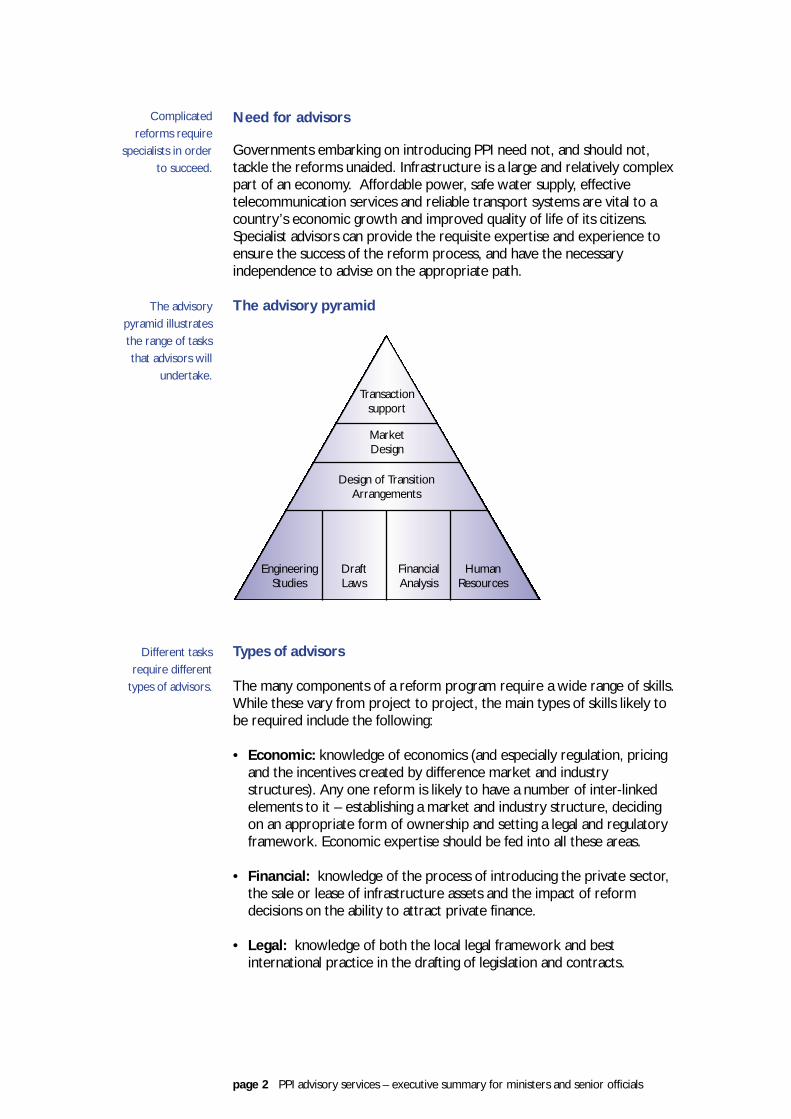

The advisory pyramid

Types of advisors

The many components of a reform program require a wide range of skills.While these vary from project to project, the main types of skills likely tobe required include the following:

• Economic: knowledge of economics (and especially regulation, pricingand the incentives created by difference market and industrystructures). Any one reform is likely to have a number of inter-linkedelements to it – establishing a market and industry structure, decidingon an appropriate form of ownership and setting a legal and regulatoryframework. Economic expertise should be fed into all these areas.

• Financial: knowledge of the process of introducing the private sector,the sale or lease of infrastructure assets and the impact of reformdecisions on the ability to attract private finance.

• Legal: knowledge of both the local legal framework and bestinternational practice in the drafting of legislation and contracts.

page 2 PPI advisory services – executive summary for ministers and senior officials

Complicatedreforms require

specialists in orderto succeed.

The advisorypyramid illustratesthe range of tasksthat advisors will

undertake.

Different tasksrequire different

types of advisors.

MarketDesign

Transactionsupport

Design of TransitionArrangements

FinancialAnalysis

HumanResources

DraftLaws

EngineeringStudies

• Technical: knowledge of the engineering, operational and othertechnical aspects of the infrastructure sector in question, including theability to divide assets both horizontally (e.g., creating many watercompanies where there was originally only one) and vertically (e.g.,separating water distribution from bulk water supply). Engineers willalso advise on the condition of existing assets, rehabilitation needs andnew investment requirements.

Other specialists’ services (e.g., public relations, pension funds and humanresources) may also be required.

See Module 3 “The role of advisors – how can they assist?” of Volume I,What is PPI and how can advisors help? for further information.

Advisory services and project success

Future private sector participation depends on investors’ confidence inboth the country and the government. The role of advisors will have animpact on whether potential investors decide to invest. Appropriateselection and use of advisors builds confidence in the reform process by:

(1)Demonstrating the existence of transparent and fair selectionprocesses from an early stage. Potential future investors will judgethe government by its past actions.

(2) Attracting advisors with a strong reputation. Their willingness tosee their names attached to a project or piece of advice acts as a signalthat they feel it is thorough and correct.

(3) Introduction of a well-designed reform program. Where the newindustry and market structures, contracts regulatory regime, and legalframework are comprehensive, potential investors will be re-assuredthat the government and its advisors understand the process withwhich they are dealing.

The reform process

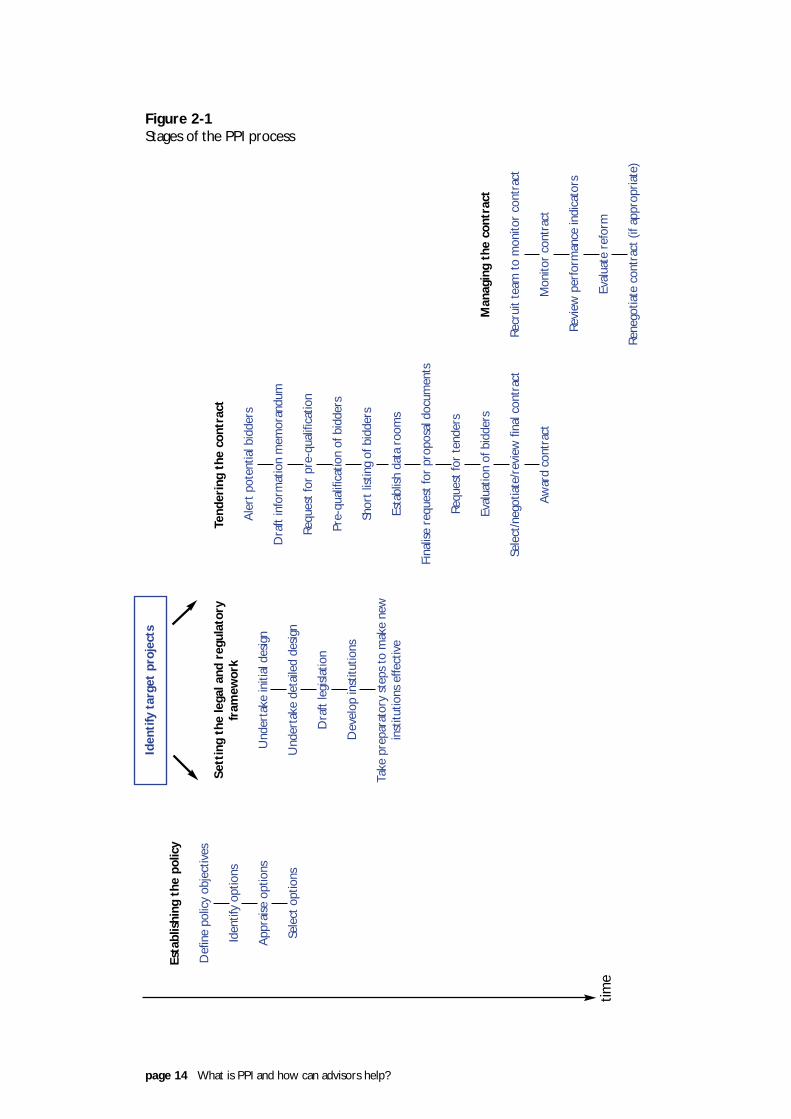

The precise process to be followed will depend on the project in question.However, four general stages can be set out:

(1) Establishing the policy(2) Setting the legal and regulatory framework(3) Tendering the contract(4) Managing the contract

The emphasis on a particular stage will vary with each reform program.The creation of a competitive markets will mean little or no on-goingmanagement of a contract. At the other extreme, purchasing of a loss-making utility under a long-term concession will make substantial demands

page 3 PPI advisory services – executive summary for ministers and senior officials

A strong advisoryteam substantially

improves thelikelihood of

success.

There are fourmain stages to thereform process…

on contract management. Part of the role of advisors is to develop areform program which is appropriate to the project in question.

Advisory input into stage one – formulating the policy

Setting the general framework (i.e. form of PPI, industry and marketstructure and regulatory framework) is mainly the responsibility ofeconomists – whether sourced from specialist economic consultancies, orfrom banking, accounting or management consultancy firms with economicskills. Technical advisors (i.e. engineers) may also be called upon tocontribute to the scoping of objectives of a PPI project or reform programsince they will be required to provide information on existinginfrastructure and on long-term investment needs.

See Module 3 “The role of advisors – how can they assist?” of Volume I,What is PPI and how can advisors help? for further information.

page 4 PPI advisory services – executive summary for ministers and senior officials

Economic advisorsoften take the lead

during the initialstages of the PPI

process.

Scope theproject

Economic

Technical

Identifythe options

Economic

FinancialLegal

Technical

Appraise theoptions

Economic

FinancialLegal

TechnicalEnvironmental

PRHR

Choosepreferred

option

Economic

N/a

Supporting

Lead

Advisory input into stage two – establishing the legal andregulatory framework

See Module 3 “The role of advisors – how can they assist?” of Volume I,What is PPI and how can advisors help? for further information.

Economic advisors will play a prominent role in the initial design ofcompetitive markets, regulatory systems and contract structures. As thework proceeds to detail design and preparation of legal instruments, therole of economists will decline and the role of other advisors – inparticular legal advisors – will increase.

During the second stage legal advisors will draft or amend any lawsrequired to put in place the agreed framework. Financial advisors will havea relatively small input into stage two of the PPI process. Their primaryrole will be to continue to advise on the impact of option changes oninvestor confidence. Financial advisors will additionally be involved inestimating asset values. Technical advisors will play a crucial role in theidentification and valuation of the assets.

Depending upon the form of PPI, human resource advisors, environmentaladvisors, and pension and insurance specialists may be involved inestablishing the legal and regulatory framework.

The role of advisors in the third stage – tendering the PPI contract

Financial advisors are generally best placed to ensure the success of thefinal transaction. Therefore, their main input comes during the third stagewhen the transaction is undertaken.

During the third phase, legal advisors will draft or amend any requiredcontracts, licences or other agreements required to implement thereform, often under the direction of the financial advisors. The roles ofeconomic and technical advisors will be limited to checking documentation

page 5 PPI advisory services – executive summary for ministers and senior officials

Legal advisors maytake the lead on

the drafting oflegislations and

regulations.

In the third stage ofthe process, the

transaction isundertaken.

Initial anddetaileddesign

Economic/Financial

FinancialLegal

Technical

Legislationand other

legalinstruments

Legal

EconomicFinancial

EnvironmentalPension

Institutionaldevelopment

Economic

FinancialLegal

TechnicalPension

HR

Preparatorysteps*

Economic/Financial

FinancialLegal

TechnicalEnvironmental

PensionHRPR

Supporting

Lead

* asset valuation, establish regulatory system, set initial tariff

sent out in the request for proposals (RFP) for its economic and technicalcontent. Their expertise might also be drawn on during the process oftender evaluation.

As the point of contract agreement draws closer, both legal and financialadvisors will become more involved. Their roles will be particularlyfocused on the negotiation of the final contract. During stage three, thefinancial advisors will be involved in the detailed evaluation of theproposed contract, advising the government during the negotiations. Thelegal advisor will have primary responsibility for ensuring that the finalcommercial agreement is properly reflected in the binding documents.The legal advisors will also be involved in arranging for the various PPIparties to enter into the PPI project agreements. They will be able toadvise on the various terms and conditions included in the main contractfor services, and where relevant, supplier, construction and maintenancecontracts.

There may also be an important role for legal advisors in reaching contractclose. Contracts will often involve a set of conditions that must be metbefore the contract is fully effective. These may relate to finalizing, forexample, the finance or concluding subsidiary contracts. The legal advisorwill ensure that these conditions are met.

Public relations advisors will be involved in the later stages of a PPItransaction when the government is in a position to alert potentialinvestors of a specific project.

See Module 3 “The role of advisors – how can they assist?” of Volume I,What is PPI and how can advisors help? for further information.

page 6 PPI advisory services – executive summary for ministers and senior officials

Financial advisorsoften lead the

selection,negotiation and

transactionfinalization.

Alertpotentialbidders

Financial/PR

Procurement

Draft IM*/establish data

room/issueRFP

Financial/Legal

TechnicalEnvironmental

HRPR

Prequal/shortlist/

finalise andissue RFP

Financial

LegalTechnical

EnvironmentalPRHR

Evaluate/negotiate/

awardcontract

Legal/Financial

EconomicTechnical

EnvironmentalPRHR

Procurement

Supporting

Lead

*IM: information memorandum

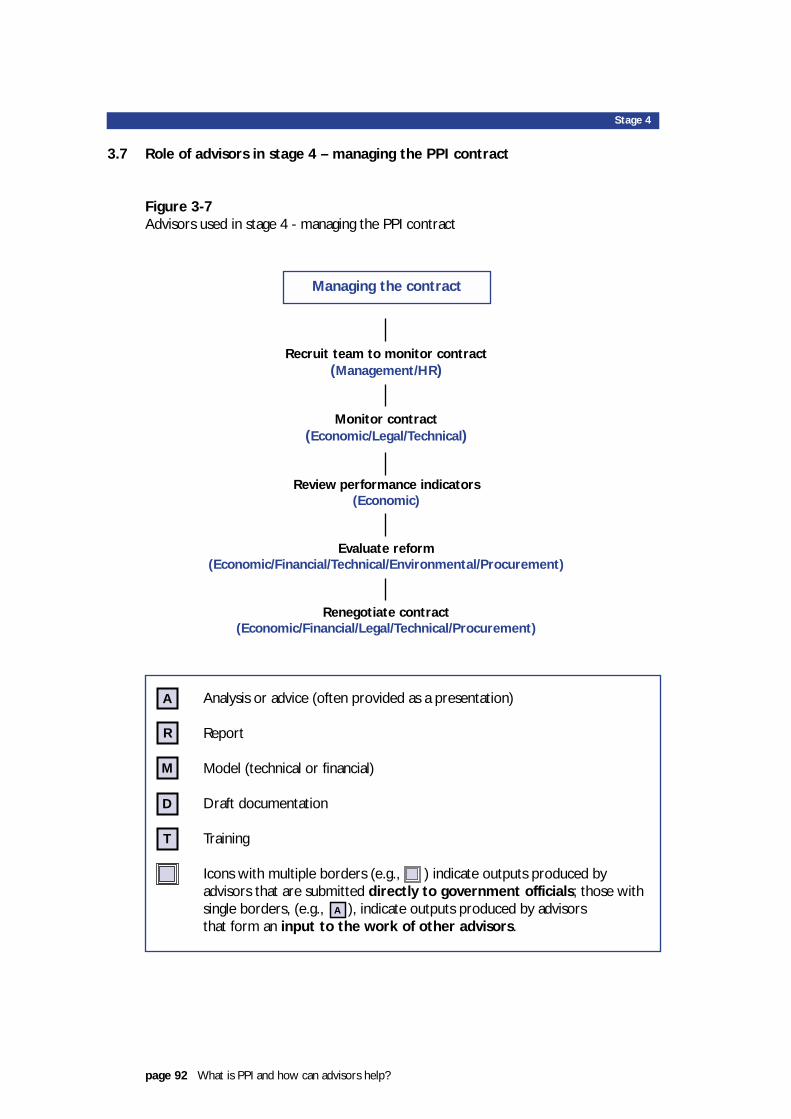

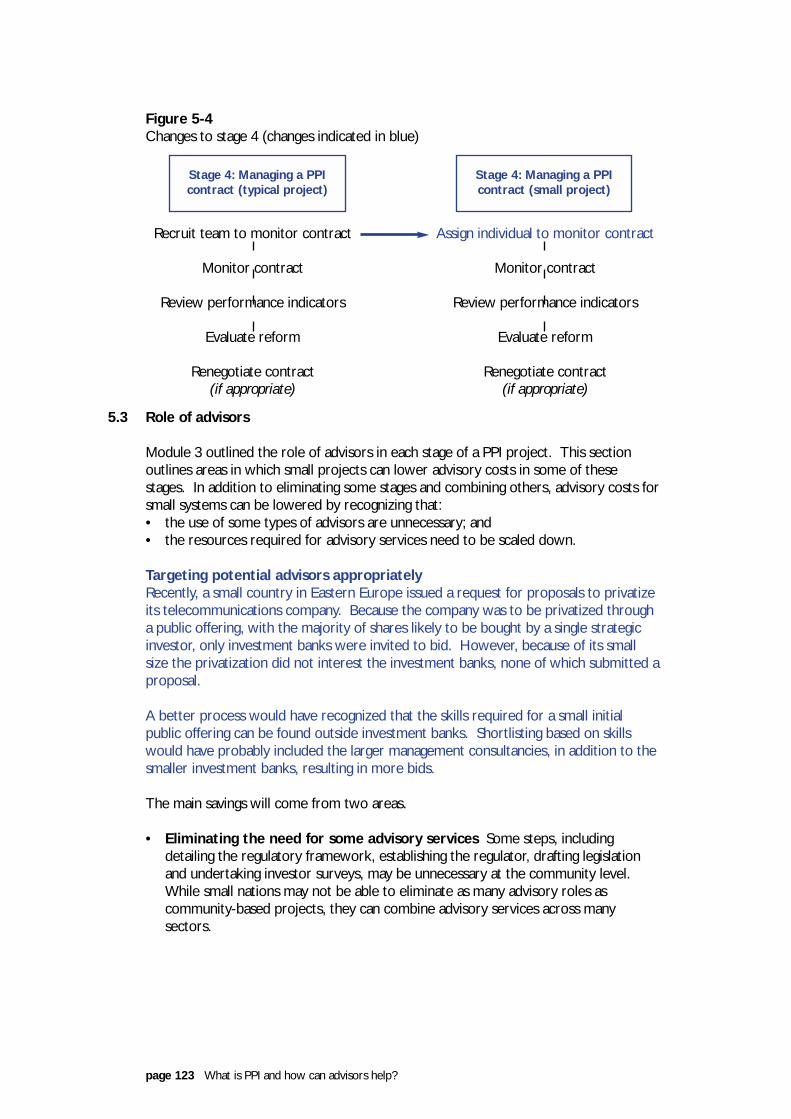

Advisory input into stage four – managing the PPI contract

Once the PPI contract has been agreed, advisors may still be needed toundertake certain tasks. Economic advisors may be required to reviewperformance indicators and evaluate the reform. Legal and financialadvisors will be involved in any contract re-negotiation that might occur.Technical advisors will be involved in monitoring the contract.

Government

The ultimate success of the project depends on the government. Itrequires the government to select advisors appropriately, manage thoseadvisors effectively, follow-up on the recommendations of advisors andmanage the final PPI contract, license or other agreements. The presenceof advisors with relevant skills and experience helps government meet itsobjectives, but does not remove its overall responsibility for success.

Setting realistic timetables

It is important that a realistic approach is taken to setting out the timetableover which tasks are to be undertaken by advisors. A consultancy projectundertaken over too short a time runs the risk of generating inappropriateadvice. Equally important, rushing to implement correct advice can causeproblems (e.g., potential investors are not sufficiently informed about theopportunity and thus do not bid; or stakeholders feel they were notconsulted and so resist the reform initiative).

Ideally a “bottom up” approach should be taken to setting a timetable. Itshould be based on the tasks that the project will comprise and anestimate of the time required for those tasks to be undertaken. Wherethe advisors will need to arrange meetings and discussions with a widenumber of individuals or organizations, this should be reflected in thetimetable. While political goals will inevitably influence the timescale forreform, they should not be the sole driver.

In addition, when setting the wider timetable for PPI reform (as opposed

page 7 PPI advisory services – executive summary for ministers and senior officials

Government playsa vital role in

contractmanagement.

The process oftimetable setting

begins with anappropriatedefinition of

requirements fromadvisors.

Recruitmonitoring

team

Government

HR

Monitorcontract

Government

EconomicLegal

Technical

ReviewPerformance

Indicators

Economic

Technical

Evaluate/renegotiate

Legal

EconomicLegal

TechnicalProcurement

Supporting

Lead

to the timetable which advisors will work to) it is important to bear inmind that the whole process of selecting and hiring advisors can takeseveral months. Time should to be built into the overall PPI timetable toallow for this process.

On occasion, political imperatives will require a transaction to be deliveredwithin a short period of time. However, the costs will be higher and theprospects of success lower when the timetable is too compressed.

Setting the budget

All too often, budgets for advisors are set during the public expenditureplanning rounds or at the start of the financial year, well before there is aclear idea of the range, type and scale of the advisory services required.This approach can lead to problems if the resources allocated to paying foradvisory services are insufficient.

Hence, just as a bottom-up approach should be taken to setting thetimetable, a similar approach should be adopted for establishing themaximum budget allocated to the payment of advisory services. Ideally,the budget for advisory services should reflect the time that thegovernment believes that it will take to complete all of the tasks to beundertaken. This means that the budget should be defined after the draftterms of reference have been drawn up. In addition, the budget shouldtake into account not just the time required, but also the type of advisorsthat are needed.

In some cases, at least part of the advisors’ costs can be financed withinthe transaction itself. For example, financial advisors may be paid a shareof the sale price. While this still creates a cost to government orconsumers, it also provides a stronger incentive for the advisors to delivera successful outcome. However, this approach cannot be used for alladvisors.

See Module 4 “Defining the project and the contract” of Volume I, What isPPI and how can advisors help?

Selection of advisors

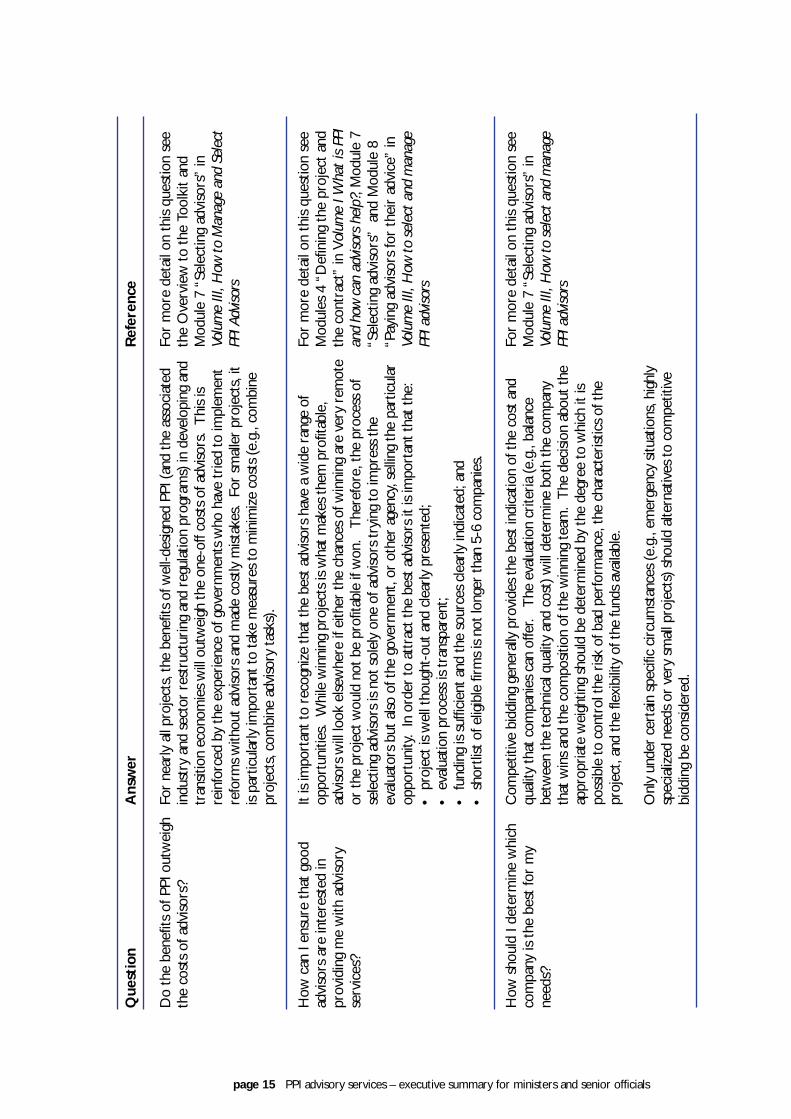

The selection of advisors will vary from project to project depending, inpart, on the country in which it is being undertaken, the type of projectand the source of financing. However, best practice selection shouldfollow four main rules.

• Transparency: as much information as possible should be madepublicly available. A transparent process eliminates doubt about thequality of the final winning team. Furthermore, it is a pre-requisite tothe participation of most top consultancies, who will not bother toparticipate in a process that is opaque and difficult to understand.

page 8 PPI advisory services – executive summary for ministers and senior officials

Advisors don’tcome free.

The selection ofadvisors varies

from project toproject but should

transparent, fair,cost-effective andfree of conflict of

interest.

• Fairness: all parties are treated equally. All parties receive the sameinformation at the same time, and are evaluated on the same criteria.

• Cost-effectiveness: costs should be minimized without sacrificingquality. Costs can be minimized and quality of service maintained bychoosing and employing the appropriate selection method (e.g., a formof competitive bidding and by understanding the likely cost componentsof the work while drafting the terms of reference).

• Freedom from conflicts of interest: the selection process shouldavoid both actual and perceived conflicts of interest. This requiresavoiding the participation of companies that may be involved asinvestors or consumers, the participation of government officials whohave current or recent connections to the companies involved and thelinking of rewards to anything other than performance.

Under most circumstances selecting advisors will follow a competitivetendering process.

See Modules 7 and 8, “Selecting advisors” and “Paying advisors for theirhelp” in Volume III, How to select and manage PPI advisors for a discussion ofother approaches to selecting advisors.

When is competitive tendering appropriate?

Note: The dollar amounts are indicative only

page 9 PPI advisory services – executive summary for ministers and senior officials

Is thecontract in

excess of e.g.,US $50,000?

Start

Is this a

new project?

Is it a discrete

piece of work?

Does each stage

require different expertise?

Was the previous project

done well

Is thecontract in

excess of e.g.,US $150,000?

Does it require different

skills to the previous project?

Sole source

CompetitiveBidding

CompetitiveBidding

CompetitiveBidding

Sole source

CompetitiveBidding

CompetitiveBidding

Indefinite quantity contracts

No

No

No

Yes

Yes

Yes

Yes

Yes

Yes

Yes

No

No

No

No

Help with paying for advisory services

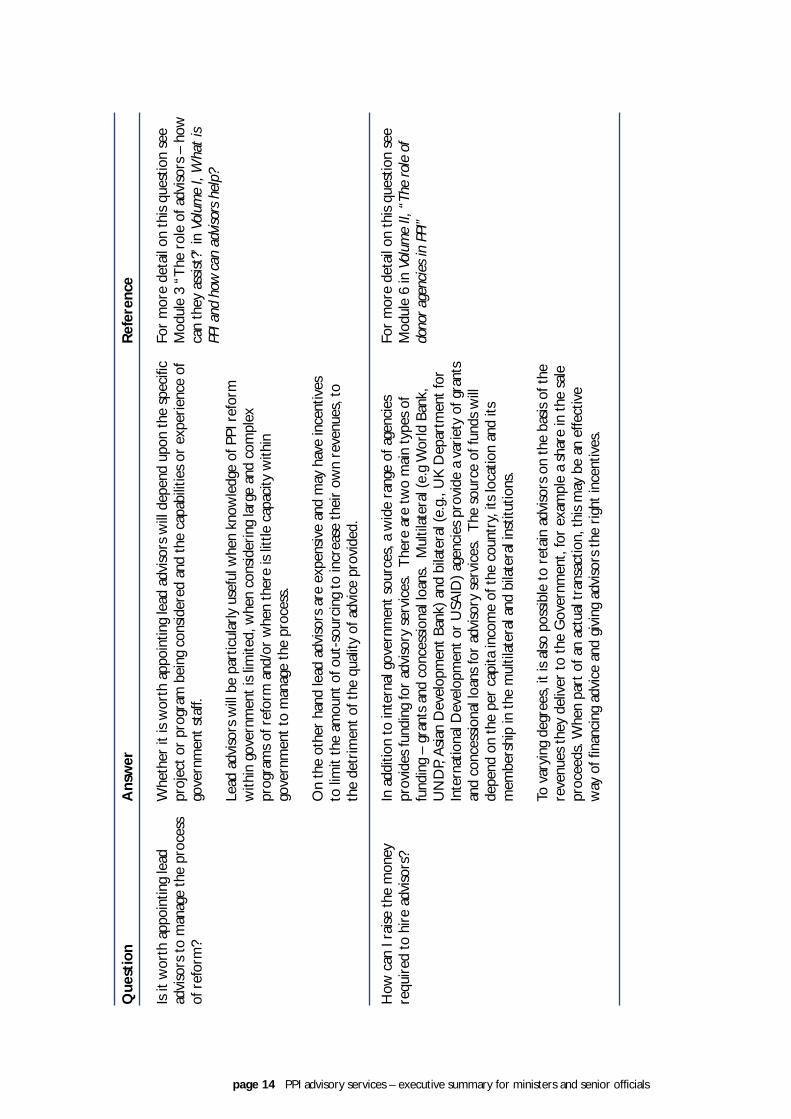

Paying for advisors can be costly. Many of the donor agencies provide anexternal source of funds for hiring advisors. Further, donors can provideexpertise in the hiring process that governments can use to ensure thatthey choose appropriate advisors. Donor agencies also have experience inproject management to ensure that the governments’ advisors performsatisfactorily. Donor agencies often place restrictions on the governmentrelated to the eligibility of potential advisors and require the use of theirown procurement rules which contain prescriptive guidelines for the hiringof advisors.

There are broadly two sorts of donor agencies from which governmentscan obtain funds for advisory services (often called “technical assistance”).Most developed countries have bilateral aid agencies and/or trust fundsthat provide funds on concessional or grant terms to other governmentsand foreign entities. In addition, many governments contribute funds tomultilateral donor agencies that then lend the funds, on both market andconcessional terms, to governments in developing countries. The mainmultilateral and bilateral agencies are outlined in Tables 1 and 2respectively.

See Module 6, which is Volume II, The role of donor agencies in PPI for moredetails about donor agencies and other sources of funds.

Table 1Main multilateral agencies

*: membership often includes states outside the area in which the organization provides funds.**: the EU also has a regular TA program run through the Commission. Funding from the program depends onbilateral agreements between the EU and the government in question.***: Technical Assistance lending refers to loans offered specifically to pay for the hiring of advisors. These figures donot include trust funds managed by the multilateral aid agencies or technical assistance funded out of sectoral loans.^: excludes trust funds managed by the World Bank which disbursed approximately US$1.3 billion in fiscal year1999.^^: based on Euro 1.15 = US$1. N/a – Not available.

page 10 PPI advisory services – executive summary for ministers and senior officials

Agency

World Bank: IDA/IBRD

Asian Development Bank (ADB)

Inter-American Development Bank (IADB)

African Development Bank (AfDB)

European Bank for Reconstruction and

Development (EBRD)

United Nations Development Program (UNDP)

European Union (PHARE, TACIS)**

Caribbean Development Bank (CDB)

Aid Coverage*

Global

Asia

Central and South America and the

Caribbean

Africa

Eastern Europe, Former and Current

Soviet States

Global

TACIS: former Soviet states, Russia

and Mongolia PHARE: Eastern

Europe,

Regional members cover the

Caribbean

Technical Assistance

lending***, US$ million

(year ending)

706 (1999)^

173 (1999)

106 (1998)

61 (1998)

597 (1998)^^

N/a

TACIS: <430 (1998)^^

PHARE: <900 (1998)^^

(est, TA not separated

from project lending)

< 50 (est, TA not

separated from project

lending)

Table 2

Main bilateral agencies

Early on in the process, a government intent on reform should considerthe institutional changes that will be required to implement the PPI orsectoral reform program. The reform process will need a structure forpolitical management and a structure for official control.

There are three approaches that can be taken to institutional reform.

• A centralized approach – the government establishes a unit tomanage the PPI process within a central department, such as the financeministry.

• A decentralized approach – the government establishes a dedicatedunit within the department or ministry that has responsibility for thesector that is being reformed.

• A hybrid approach – line ministries or agencies retain responsibilityfor the PPI implementation but a central unit provides best practice andadvice on PPU implementation to other ministries. Alternatively adedicated unit could be formed from one or more ministries.

There is no simple answer to the question of what is the best institutionaldesign for managing the PPI process. The solution will need to reflect thecircumstances of the individual sector, country and PPI reform in question.Irrespective of the approach chosen, however, it is of crucial importancethat those in charge of the PPI process have the authority, funding andother resources to undertake the set of necessary tasks. The set of skillsrequired and the time needed to manage advisors properly should not beunder-estimated. Poor management of good advisors will only wastevaluable public money. Consequently, governments may need to makespecial arrangements to recruit and retain the best individuals to managePPI advisors.

See Module 9, “Managing the PPI advisory services” in Volume III, How toselect and manage PPI advisors.

page 11 PPI advisory services – executive summary for ministers and senior officials

Institutional reformis an integral part of

the PPI process.

There are anumber of

institutional modelsthat can be

adopted.

Agency*

CIDA

DANIDA

AFD

GTZ

JBIC

NORAD

SIDA

SDC

DFID

USAID

Country

Canada

Denmark

France

Germany

Japan

Norway

Sweden

Switzerland

UK

USA

Contact details

Http://www.acdi-cida.gc.ca/index.htm

Http://www.um.dk/

Http://www.afd.fr/

Http://www.gtz.de/

Http://www.jbic.go.jp/

Http://odin.dep.no/ud/engelsk/index-b-n-a.html

Http://www.sida.org/Sida/jsp/Crosslink.jsp?d=10

7&a=4827&v=7

http://194.230.65.134/dezaweb2/home.asp

Http://www.dfid.gov.uk/

Http://www.usaid.gov/

Coverage

Global

Mainly sub-Saharan Africa

Mainly North and West Africa

Mainly Africa

Mainly Asia

Mainly Africa

Mainly sub-Saharan Africa and

South Asia

Gobal

Mainly Commonwealth

Global

page 12 PPI advisory services – executive summary for ministers and senior officials

Que

stio

n

Will

incr

easin

g th

e ro

le o

f the

priv

ate

sect

or in

infr

astr

uctu

rebe

nefit

our

cou

ntry

?

Do

I nee

d to

hire

adv

isors

?

Ref

eren

ce

For

mor

e de

tail

on t

his

ques

tion

see

Mod

ules

1 a

nd 2

, “Pr

inci

ples

of

sele

ctin

g ad

viso

ry s

ervi

ces

to s

uppo

rtPP

I” a

nd “

Iden

tifyi

ng t

he s

tage

s of

PPI

– w

hat

is PP

I?” in

Vol

ume

I, W

hat

is PP

Ian

d ho

w c

an a

dviso

rs h

elp?

For

mor

e de

tail

on t

his

ques

tion

see

Mod

ule

1 an

d 2

“Prin

cipl

es o

fse

lect

ing

advi

sory

ser

vice

s to

sup

port

PPI”

and

“Id

entif

ying

the

sta

ges

of P

PI–

wha

t is

PPI?”

inVo

lum

e I,

Wha

t is

PPI

and

how

can

adv

isors

hel

p?

Ans

wer

PPI h

as a

num

ber

of a

dvan

tage

s:•

It tr

ansf

ers

som

e of

the

risk

ass

ocia

ted

with

man

agin

g, o

pera

ting

and/

orin

vest

ing

in in

fras

truc

ture

from

the

gov

ernm

ent

to t

he p

rivat

e se

ctor

.•

It ca

n in

crea

se e

ffici

ency

of b

asic

ser

vice

s, a

nd s

o re

duce

cos

ts.

•It

free

s up

gov

ernm

ent

fund

s fo

r us

e el

sew

here

, e.g

., in

pov

erty

alle

viat

ion.

•It

brin

gs n

ew e

xper

tise

into

the

sec

tor.

How

ever

, the

PPI

pro

cess

is c

ompl

ex a

nd, i

n or

der

to c

reat

e th

ese

bene

fits,

req

uire

s ex

pert

ise t

hat

may

not

exi

st w

ithin

gov

ernm

ent.

Usin

g th

e pr

ivat

e se

ctor

to

prov

ide

advi

sory

ser

vice

s ha

s a

num

ber

ofad

vant

ages

.•

It al

low

s th

e pu

blic

sec

tor

to a

cces

s gl

obal

and

tec

hnic

al e

xper

tise

ofte

nno

t pr

esen

t in

the

gov

ernm

ent.

•It

can

prev

ent

the

gove

rnm

ent

from

mak

ing

cost

ly m

istak

es.

•It

faci

litat

es t

he t

rans

fer

of k

now

ledg

e fr

om t

he p

rivat

e to

the

pub

licse

ctor

.•

It br

ings

legi

timac

y to

the

PPI

pro

cess

– t

he u

se o

f ind

epen

dent

advi

sors

can

ofte

n pl

ace

an e

xter

nal s

tam

p of

end

orse

men

t on

the

gove

rnm

ent’s

pro

posa

ls, in

crea

sing

inve

stor

and

pub

lic c

onfid

ence

If th

e go

vern

men

t is

cont

empl

atin

g PP

I, th

en it

sho

uld

take

adv

anta

ge o

fth

e ex

pert

ise in

the

priv

ate

sect

or.

The

Dec

isio

n-M

aker

’s R

efer

ence

Gui

de t

o H

irin

g an

d M

anag

ing

PP

I A

dvis

ors

Out

line

Thi

s m

ini-g

uide

dra

ws

out

the

com

mon

pro

blem

s fa

ced

by t

hose

sel

ectin

g ad

viso

rs a

nd s

umm

ariz

es s

olut

ions

. It

prov

ides

a s

et o

f com

mon

que

stio

nsth

at a

rise

and

brie

f ans

wer

s to

the

m—

alon

g w

ith r

efer

ence

s to

the

mai

n gu

ides

for

mor

e de

taile

d in

form

atio

n.

page 13 PPI advisory services – executive summary for ministers and senior officials

Que

stio

n

Will

incr

easin

g th

e ro

le o

f the

priv

ate

sect

or in

infr

astr

uctu

rebe

nefit

our

cou

ntry

?

Do

I nee

d to

hire

adv

isors

?

Ref

eren

ce

For

mor

e de

tail

on t

his

ques

tion

see

Mod

ule

3 “T

he r

ole

of a

dviso

rs –

how

can

they

ass

ist?”

in V

olum

e I,

Wha

t is

PPI a

nd h

ow c

an a

dviso

rs h

elp?

For

mor

e de

tail

see

sect

ion

3.2.

1 in

Volu

me

I, W

hat

is PP

I and

how

can

advis

ors

help

?

For

mor

e de

tail

see

sect

ion

3.2.

2. in

Volu

me

I, W

hat

is PP

I and

how

can

advis

ors

help

?

For

mor

e de

tail

see

sect

ion

3.2.

3 in

Volu

me

I, W

hat

is PP

I and

how

can

advis

ors

help

?

For

mor

e de

tail

see

sect

ion

3.2.

5 in

Volu

me

I, W

hat

is PP

I and

how

can

advis

ors

help

?

For

mor

e de

tail

see

sect

ion

3.3.

6 in

Volu

me

I, W

hat

is PP

I and

how

can

advis

ors

help

?

Ans

wer

Adv

isors

cov

er a

wid

e ra

nge

of s

peci

aliti

es, i

nclu

ding

eco

nom

ic, f

inan

cial

,le

gal,

tech

nica

l, an

d m

anag

emen

t. D

epen

ding

on

the

requ

irem

ents

of t

hepr

ojec

t, a

diffe

rent

mix

ture

of a

dviso

rs w

ill b

e re

quire

d.

•Ec

onom

ic a

dviso

rs a

re r

equi

red

for

PPI p

olic

y fo

rmul

atio

n an

dw

hene

ver

new

indu

stry

str

uctu

res

or a

rran

gem

ents

(e.g

., un

bund

ling,

regu

latio

n, p

ricin

g) a

re b

eing

put

in p

lace

.

•Fi

nanc

ial a

dviso

rs a

re r

equi

red

whe

neve

r a

tran

sact

ion

will

be

unde

rtak

en.

•Le

gal a

dviso

rs a

re r

equi

red

whe

neve

r th

e dr

aftin

g or

inte

rpre

tatio

n of

legi

slatio

n or

con

trac

ts is

a p

roje

ct c

ompo

nent

.

•Te

chni

cal a

dviso

rs a

re r

equi

red

for

valu

ing

asse

ts, s

ettin

g pe

rfor

man

ceta

rget

s, a

nd d

eter

min

ing

inve

stm

ent

need

s.

•M

anag

emen

t or

hum

an r

esou

rce

advi

sors

are

req

uire

d if

the

refo

rms

have

impl

icat

ions

for

staf

fing,

org

aniz

atio

nal s

truc

ture

s, t

rain

ing

and

othe

r la

bor-

rela

ted

issue

s.

In a

dditi

on t

here

are

a r

ange

of a

dviso

rs c

over

ing

mor

e sp

ecia

list

issue

ssu

ch a

s pu

blic

rel

atio

ns a

nd t

he e

nviro

nmen

t. D

epen

ding

on

the

scal

ean

d co

mpl

exity

of t

he r

equi

red

advi

ce o

nly

a su

bset

of t

hese

adv

isors

may

be r

equi

red—

and

som

e m

ay b

e ab

le t

o fu

lfill

mul

tiple

rol

es.

page 14 PPI advisory services – executive summary for ministers and senior officials

Que

stio

n

Is it

wor

th a

ppoi

ntin

g le

adad

viso

rs t

o m

anag

e th

e pr

oces

sof

ref

orm

?

How

can

I ra

ise t

he m

oney

requ

ired

to h

ire a

dviso

rs?

Ref

eren

ce

For

mor

e de

tail

on t

his

ques

tion

see

Mod

ule

3 “T

he r

ole

of a

dviso

rs –

how

can

they

ass

ist?”

in V

olum

e I,

Wha

t is

PPI a

nd h

ow c

an a

dviso

rs h

elp?

For

mor

e de

tail

on t

his

ques

tion

see

Mod

ule

6 in

Vol

ume

II, “

The

role

of

dono

r age

ncie

s in

PPI

”

Ans

wer

Whe

ther

it is

wor

th a

ppoi

ntin

g le

ad a

dviso

rs w

ill d

epen

d up

on t

he s

peci

ficpr

ojec

t or

pro

gram

bei

ng c

onsid

ered

and

the

cap

abili

ties

or e

xper

ienc

e of

gove

rnm

ent

staf

f.

Lead

adv

isors

will

be

part

icul

arly

use

ful w

hen

know

ledg

e of

PPI

ref

orm

with

in g

over

nmen

t is

limite

d, w

hen

cons

ider

ing

larg

e an

d co

mpl

expr

ogra

ms

of r

efor

m a

nd/o

r w

hen

ther

e is

little

cap

acity

with

ingo

vern

men

t to

man

age

the

proc

ess.

On

the

othe

r ha

nd le

ad a

dviso

rs a

re e

xpen

sive

and

may

hav

e in

cent

ives

to li

mit

the

amou

nt o

f out

-sou

rcin

g to

incr

ease

the

ir ow

n re

venu

es, t

oth

e de

trim

ent

of t

he q

ualit

y of

adv

ice

prov

ided

.

In a

dditi

on t

o in

tern

al g

over

nmen

t so

urce

s, a

wid

e ra

nge

of a

genc

ies

prov

ides

fund

ing

for

advi

sory

ser

vice

s. T

here

are

tw

o m

ain

type

s of

fund

ing

– gr

ants

and

con

cess

iona

l loa

ns.

Mul

tilat

eral

(e.g

Wor

ld B

ank,

UN

DP,

Asia

n D

evel

opm

ent

Bank

) and

bila

tera

l (e.

g., U

K D

epar

tmen

t fo

rIn

tern

atio

nal D

evel

opm

ent

or U

SAID

) age

ncie

s pr

ovid

e a

varie

ty o

f gra

nts

and

conc

essio

nal l

oans

for

advi

sory

ser

vice

s. T

he s

ourc

e of

fund

s w

illde

pend

on

the

per

capi

ta in

com

e of

the

cou

ntry

, its

loca

tion

and

itsm

embe

rshi

p in

the

mul

tilat

eral

and

bila

tera

l ins

titut

ions

.

To v

aryi

ng d

egre

es, i

t is

also

pos

sible

to

reta

in a

dviso

rs o

n th

e ba

sis o

f the

reve

nues

the

y de

liver

to

the

Gov

ernm

ent,

for

exam

ple

a sh

are

in t

he s

ale

proc

eeds

. Whe

n pa

rt o

f an

actu

al t

rans

actio

n, t

his

may

be

an e

ffect

ive

way

of f

inan

cing

adv

ice

and

givi

ng a

dviso

rs t

he r

ight

ince

ntiv

es.

page 15 PPI advisory services – executive summary for ministers and senior officials

Que

stio

n

Do

the

bene

fits

of P

PI o

utw

eigh

the

cost

s of

adv

isors

?

How

can

I en

sure

tha

t go

odad

viso

rs a

re in

tere

sted

inpr

ovid

ing

me

with

adv

isory

serv

ices

?

How

sho

uld

I det

erm

ine

whi

chco

mpa

ny is

the

bes

t fo

r m

yne

eds?

Ref

eren

ce

For

mor

e de

tail

on t

his

ques

tion

see

the

Ove

rvie

w t

o th

e To

olki

t an

dM

odul

e 7

“Sel

ectin

g ad

viso

rs”

inVo

lum

e III

, How

to

Man

age

and

Sele

ctPP

I Adv

isors

For

mor

e de

tail

on t

his

ques

tion

see

Mod

ules

4 “

Def

inin

g th

e pr

ojec

t an

dth

e co

ntra

ct”

in V

olum

e I W

hat

is PP

Ian

d ho

w c

an a

dviso

rs h

elp?

, Mod

ule

7“S

elec

ting

advi

sors

” a

nd M

odul

e 8

“Pay

ing

advi

sors

for

thei

r ad

vice

” in

Volu

me

III, H

ow t

o se

lect

and

man

age

PPI a

dviso

rs

For

mor

e de

tail

on t

his

ques

tion

see

Mod

ule

7 “S

elec

ting

advi

sors

” in

Volu

me

III, H

ow t

o se

lect

and

man

age

PPI a

dviso

rs

Ans

wer

For

near

ly a

ll pr

ojec

ts, t

he b

enef

its o

f wel

l-des

igne

d PP

I (an

d th

e as

soci

ated

indu

stry

and

sec

tor

rest

ruct

urin

g an

d re

gula

tion

prog

ram

s) in

dev

elop

ing

and

tran

sitio

n ec

onom

ies

will

out

wei

gh th

e on

e-of

f cos

ts o

f adv

isors

. T

his

isre

info

rced

by

the

expe

rienc

e of

gov

ernm

ents

who

hav

e tr

ied

to im

plem

ent

refo

rms

with

out a

dviso

rs a

nd m

ade

cost

ly m

istak

es.

For

smal

ler

proj

ects

, it

is pa

rtic

ular

ly im

port

ant t

o ta

ke m

easu

res

to m

inim

ize

cost

s (e

.g.,

com

bine

proj

ects

, com

bine

adv

isory

task

s).

It is

impo

rtan

t to

reco

gniz

e th

at th

e be

st a

dviso

rs h

ave

a w

ide

rang

e of

oppo

rtun

ities

. W

hile

win

ning

pro

ject

s is

wha

t mak

es th

em p

rofit

able

,ad

viso

rs w

ill lo

ok e

lsew

here

if e

ither

the

chan

ces

of w

inni

ng a

re v

ery

rem

ote

or th

e pr

ojec

t wou

ld n

ot b

e pr

ofita

ble

if w

on.

The

refo

re, t

he p

roce

ss o

fse

lect

ing

advi

sors

is n

ot s

olel

y on

e of

adv

isors

tryi

ng to

impr

ess

the

eval

uato

rs b

ut a

lso o

f the

gov

ernm

ent,

or o

ther

age

ncy,

selli

ng th

e pa

rtic

ular

oppo

rtun

ity.

In o

rder

to a

ttra

ct th

e be

st a

dviso

rs it

is im

port

ant t

hat t

he:

•pr

ojec

t is

wel

l tho

ught

-out

and

cle

arly

pre

sent

ed;

•ev

alua

tion

proc

ess

is tr

ansp

aren

t;•

fund

ing

is su

ffici

ent a

nd th

e so

urce

s cl

early

indi

cate

d; a

nd•

shor

tlist

of e

ligib

le fi

rms

is no

t lon

ger

than

5-6

com

pani

es.

Com

petit

ive

bidd

ing

gene

rally

pro

vide

s th

e be

st in

dica

tion

of th

e co

st a

ndqu

ality

that

com

pani

es c

an o

ffer.

The

eva

luat

ion

crite

ria (e

.g.,

bala

nce

betw

een

the

tech

nica

l qua

lity

and

cost

) will

det

erm

ine

both

the

com

pany

that

win

s an

d th

e co

mpo

sitio

n of

the

win

ning

team

. T

he d

ecisi

on a

bout

the

appr

opria

te w

eigh

ting

shou

ld b

e de

term

ined

by

the

degr

ee to

whi

ch it

ispo

ssib

le to

con

trol

the

risk

of b

ad p

erfo

rman

ce, t

he c

hara

cter

istic

s of

the

proj

ect,

and

the

flexi

bilit

y of

the

fund

s av

aila

ble.

Onl

y un

der

cert

ain

spec

ific

circ

umst

ance

s (e

.g.,

emer

genc

y sit

uatio

ns, h

ighl

ysp

ecia

lized

nee

ds o

r ve

ry s

mal

l pro

ject

s) s

houl

d al

tern

ativ

es to

com

petit

ive

bidd

ing

be c

onsid

ered

.

page 16 PPI advisory services – executive summary for ministers and senior officials

Que

stio

n

How

sho

uld

I man

age

and

over

see

the

com

pany

tha

t I h

ire?

Ref

eren

ce

For

mor

e de

tail

on t

his

ques

tion

see

Mod

ules

8 “

Payi

ng a

dviso

rs fo

rth

eir

advi

ce”

and

Mod

ule

9“M

anag

ing

PPI a

dviso

ry s

ervi

ces”

inVo

lum

e III

, How

to

sele

ct a

ndm

anag

e PP

I adv

isors

Ans

wer

Proj

ect m

anag

emen

t enc

ompa

sses

a w

ide

rang

e of

issu

es. T

wo

main

que

stio

ns a

re th

efo

llow

ing.

(1) H

ow d

oes t

he g

over

nmen

t ens

ure

quali

ty o

ver s

omet

hing

abo

ut w

hich

it m

ay h

ave

relat

ively

little

kno

wle

dge

and

the

resu

lts o

f whi

ch m

ay n

ot b

e ev

iden

t unt

il af

ter t

hepr

ojec

t is c

ompl

eted

?(2

) How

doe

s the

gov

ernm

ent p

reve

nt th

e pr

ojec

t run

ning

ove

r tim

e or

ove

r bud

get,

or b

oth?

Qua

lity

assu

ranc

eTh

ere

are

a nu

mbe

r of p

ossib

le m

easu

res.

•

If th

e so

urce

of f

unds

is a

lend

ing

agen

cy th

en it

can

ass

ist w

ith q

ualit

y as

sura

nce,

draw

ing

on e

xper

ienc

e fro

m si

mila

r pro

ject

s else

whe

re.

•Th

e ad

visor

s may

be

prov

ided

with

ince

ntive

s to

perfo

rm su

ch a

s pay

men

tm

ilest

ones

tied

to sp

ecific

out

puts

, suc

cess

fees

, bon

us p

oint

s for

futu

re c

ompe

titive

tend

ers,

shar

es, p

ositi

ve e

valu

atio

ns a

nd p

erfo

rman

ce re

fere

nces

. •

A le

ad a

dviso

r hire

d on

a lo

nger

term

con

trac

t may

be

used

to a

sses

s the

qua

lity

ofth

e sh

orte

r ter

m w

ork.

Kee

ping

with

in b

udge

tTh

ere

may

be

legi

timat

e re

ason

s for

pro

ject

s ove

r-ru

nnin

g (e

.g.,

new

task

s app

eare

don

ce th

e pr

ojec

t was

star

ted)

. H

owev

er, i

t is v

ital t

hat t

he g

over

nmen

t can

dist

ingu

ishbe

twee

n th

e va

lid a

nd in

valid

reas

ons.

In a

dditi

on to

ens

urin

g th

ere

is a

man

ager

ingo

vern

men

t tha

t kee

ps tr

ack

of ti

me

and

budg

et, s

ever

al ot

her m

easu

res s

houl

d be

cons

ider

ed.

•Lu

mp

sum

con

trac

ts p

rovid

e m

axim

um in

cent

ives f

or c

ompa

nies

to fi

nish

on

budg

etan

d w

ithin

the

time

sugg

este

d. T

heir

disa

dvan

tage

is th

at c

ompa

nies

may

sacr

ifice

quali

ty to

do

so.

•Po

tent

ial fo

r fut

ure

wor

k pr

ovid

es a

n in

cent

ive to

com

plet

e cu

rren

t wor

k on

tim

ean

d bu

dget

as w

ell a

s to

the

quali

ty re

quire

d.

•Su

cces

s fee

s give

com

pani

es in

cent

ives t

o m

ake

thei

r ow

n de

cisio

ns a

bout

how

far i

tis

wor

th c

omm

ittin

g fu

rthe

r res

ourc

es in

an

atte

mpt

to im

prov

e th

e ou

tcom

e.

What is PPI and how can advisors help?

Toolkit:A guide for hiring and managing advisors for private participation in infrastructure

Volume I

Frontier cover 9 25/4/01 4:14 pm Page 2

Acknowledgements

This toolkit was funded by the Public-Private Infrastructure Advisory Facility (PPIAF), a multi-donor technical assistance facility aimed at helping eliminate poverty andachieve sustainable development through private involvement in infrastructure.

Jordan Schwartz, task manager, and Chiaki Yamamoto, project staff, of the WorldBank’s Private Provision of Public Services Group, led the project. Michael Webb,Najma Rajah and Matthew Bell of Frontier Economics prepared the toolkit incollaboration with WS Atkins Management Consultants and Denton Wilde Sapte.

The toolkit benefited from the inputs of an Advisory Group comprisingrepresentatives from international development institutions and the private sector.Members of the Advisory Group included Adrian Becher (Emerging MarketsPartnership Ltd); Tom Briggs (Enron Europe Ltd); Philip Curry (Bechtel EnterprisesInternational Ltd); Angelo Dell'atti and Eric Moreau (Lyonnaise des Eaux Ltd); SabineEngelhard (Inter-American Development Bank); Peter Fanning (4Ps); Peter Greiner(former Energy Secretary, Government of Brazil); Inder Mirchandani (CJ Associates);Emmanual Nyrinkindi (Utility Reform Unit, Government of Uganda); Terry Pike(Department for International Development, United Kingdom); Tim Wilson (WSAtkins Management Consultants); and Ian Alexander, Ghassan Alkhoja, Judy Bobb,Penelope Brook, Giovanni Casartelli, Benedictus Eijbergen, Jean-Louis Ginnsz, PhilipGray, Vincent Gouarne, Monika Kosior, Jose Luis Irigoyen, Subramaniam Vijay Iyer,Omer Karasapan, and Warrick Smith (The World Bank). PPIAF staff, led by RussellMuir, provided oversight.

What is PPI and how can advisors help?

What is PPI and how can advisors help?

Table of contents

Section . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page

Acknowledgements

1. Principles of selection for advisory services to support PPI . . . . . . . . . . . . . . .1

1.1 Private sector involvement can increase efficiency – and access new sources of finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

1.2 Governments still play a fundamental role . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

1.3 Governments can use the private sector to meet objectives more effectively . . . . . .6

1.4 Effective use of the private sector requires a strong advisory team . . . . . . . . . . . . . .7

1.5 Obtaining a strong advisory team is expensive and presents a challenge . . . . . . . . . .7

1.6 Governments need to purchase advisory services effectively . . . . . . . . . . . . . . . . .10

1.7 A strong government team will reduce the concerns of potential investors . . . . . . .12

2. Identifying the stages of PPI – what is PPI? . . . . . . . . . . . . . . . . . . . . . . . . . . .13

2.1 Stage 1: Formulating policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

2.2 Stage 2: Setting the legal and regulatory framework . . . . . . . . . . . . . . . . . . . . . . . .25

2.3 Stage 3: Tendering the contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

2.4 Stage 4: Managing a PPI contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38

2.5 Variations from the standard PPI process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40

3. The role of advisors – how can they assist? . . . . . . . . . . . . . . . . . . . . . . . . . . .47

3.1 When to appoint advisors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47

3.2 Lead advisors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .51

3.3 Differing types of expertise needed to guide officials through the PPI process . . . . .53

3.4 Role of advisors in stage 1 - policy formulation . . . . . . . . . . . . . . . . . . . . . . . . . . . .62

3.5 Role of advisors in stage 2 – establishing the legal and regulatory framework . . . . .67

3.6 Role of advisors in stage 3 – tendering the contract . . . . . . . . . . . . . . . . . . . . . . . .80

3.7 Role of advisors in stage 4 – managing the PPI contract . . . . . . . . . . . . . . . . . . . . .92

What is PPI and how can advisors help?

3.8 Use of local advisors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .97

3.9 Use of advisors by potential investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .98

Useful Reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .101

4. Defining the project and the contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .102

4.1 Scoping consultancy projects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .102

4.2 Resolving conflicts of interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .111

4.3 Designing appropriate payment methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .115

4.4 Packaging advisory services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .116

4.5 Meeting constraints . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .117

5. Use of advisors for small-scale projects . . . . . . . . . . . . . . . . . . . . . . . . . . . . .119

5.1 Definition of a small project . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .119

5.2 Project implementation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .121

5.3 Role of advisors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .123

5.4 Role of the competitive tendering process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .127

5.5 Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .129

Useful Reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .129

Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .130

What is PPI and how can advisors help?

page 1 What is PPI and how can advisors help?

1. Principles of selection for advisory services to support PPI

Outline of this Module

What this Module does:This Module describes the rationale for increasing private sector participation ininfrastructure, and the implications for selection of advisors. It outlines the basictenets of selection and the link between a successful Private Participation inInfrastructure (PPI) program and the proper use of advisors.

The Module provides an initial overview of PPI and the use of advisors. It does notenter into any detail about their selection or use, which is covered in later Modules.

Who should read this Module:The Module should be read by officials from central agencies within government whoare responsible for setting policy for private sector participation and the use ofadvisors; officials from ministries involved in the implementation of specific reforms;and the staff of financial or other agencies that handle procurement. Officials involved inimplementation should use it as an introduction to the process of procuring advisorsfor PPI.

1.1 Private sector involvement can increase efficiency – and access new sourcesof finance

Over the period 1990–1998 the private sector made massive investment ininfrastructure sectors in developing countries around the world. Figure 1-1 shows theinvestment expenditures in projects with private sector participation (PSP) by maininfrastructure sector (energy, telecommunications, transport, and water andsanitation) and year.

Defining the term PPI:PPI = Private Provision of InfrastructurePPI refers to the use of the private sector to manage, maintain, expand, operateand/or invest in infrastructure services. The areas of infrastructure covered by thistoolkit include: energy, telecommunications, transport and water and sanitation.

Figure 1-1Total investment in infrastructure in developing countries, by sector (1990–1999)

Source: World Bank, PPI DatabaseNote: Developing countries, defined as low and middle-income countries by the World Bank

page 2 What is PPI and how can advisors help?

Figure 1-2Total investment in infrastructure in developing countries, by region (1990–1999)

Key:EAP: East Asia and Pacific LAC: Latin America and Caribbean SA: South AsiaECA: Europe and Central Asia MENA: Middle East and North Africa SSA: Sub-Saharan African

Source: World Bank, PPI DatabaseNote: Developing countries, defined as low and middle-income countries by the World Bank

The figures show a steady rise in private participation in PPI1 until the financial crisisthat struck Southeast Asia and subsequently spread throughout the developing world.Available data indicate that investment interest is returning in response to the region’srecovery.

Despite the large inflow of funds, there is significant unmet demand for PPI. Asgovernments become increasingly comfortable with transferring risk to the privatesector, and as new financial instruments and contracts are created, demand for privateinvestment increases. There are two main reasons for the overall increase in, anddemand for, PPI:

(1) Increased recognition by national, state and local governments of the ability of theprivate sector to assume many of the risks involved in the construction and operationof infrastructure projects.

The transfer of additional risks to the private sector provides increased incentivesto manage these risks appropriately, leading to better investment decisions andmore efficient service provision. While these incentives are broadly similar tothose in the public sector aimed at ensuring a well-managed service, privatecompanies, driven by the needs of shareholders and financiers, face closer scrutiny,which strengthens these incentives. These groups tend to be more demanding –

1 PPI is a subset of private sector participation (PSP)—it is PSP in infrastructure.

page 3 What is PPI and how can advisors help?

and better informed – than taxpayers. Provided that PPI is well structured, thispressure should deliver the government’s objectives more effectively.

(2) Decreased funds available to national, state and local governments forinfrastructure investment, both when compared to total investment requirements andto many other possible uses for these funds.

Private participation does not change the need for consumers or taxpayers topay for major investments. The government’s financial position is notfundamentally changed if it pays for a service (e.g., water provision) rather thanfor assets (e.g., a storage dam and pipelines).

However, private participation can bring financial benefits. The costs may belower if efficiency is increased. Major discrete financing requirements will besmoothed over a number of years. The greater clarity required for PPI alsomeans that major investment, operational and management decisions and theirfinancial implications will be better managed.

Restructuring may also reduce or remove the need for government financing.For example, if investments in electricity generation can be secured againstfuture sales of electricity, the government does not need to be directly involvedin financing. In theory, this is not an issue of ownership: a government-ownedcompany could equally have secured finance against future revenue. In practice,the involvement of private companies often creates the impetus for thegovernment to withdraw.

In recent years, governments have transferred more significant risks to the privatesector for infrastructure provision. Increasingly, this has meant that private companiesare not only exposed to the risk of completion on time and within budget (as happenswhen contractors build a runway, a bridge, or a treatment plant for a publicauthority); they are increasingly exposed to risks of whether a project is needed at all,whether it meets quality requirements, and whether its costs of delivery arecompetitive in the long term, as well as many of the environmental risks associatedwith infrastructure projects.

There are several entities over which the risks associated with PPI may be spread:• government (i.e., tax payers); • consumers;• the project company that sponsors a project;• the construction company that builds it; • the financiers that back the project; and• the operations and maintenance company.

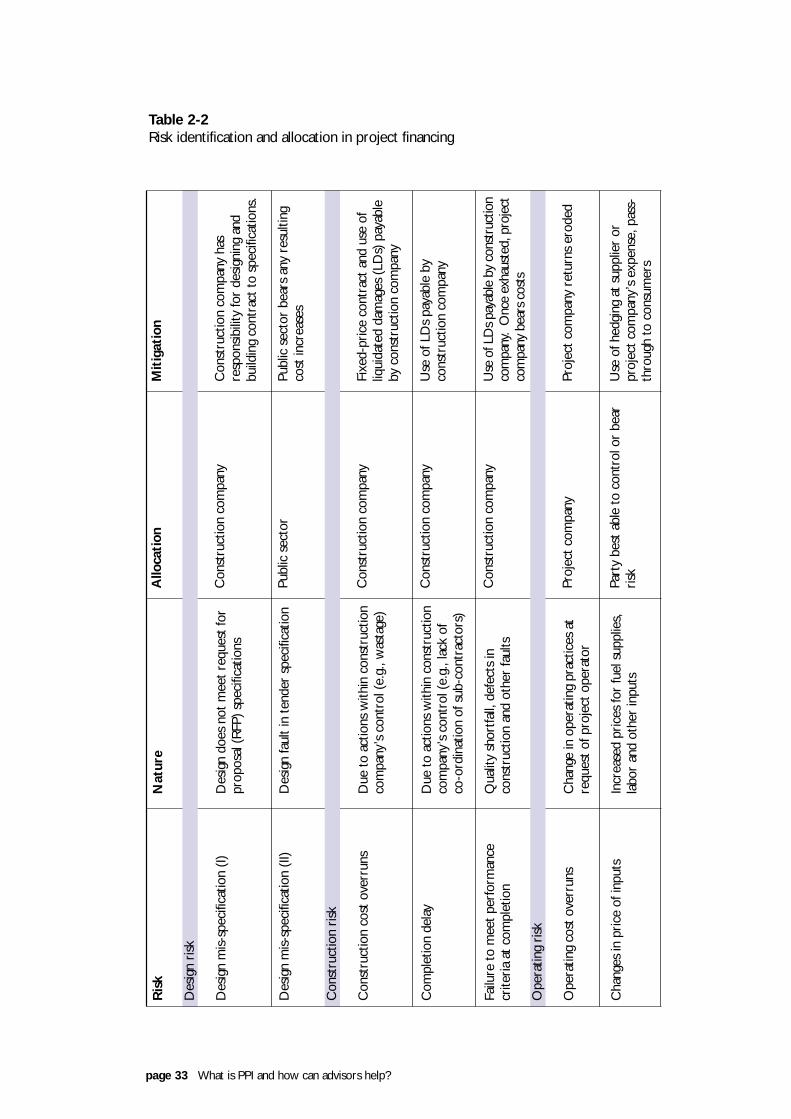

It is the assumption of significant risk by the private sector in the provision ofinfrastructure that is captured under the broad term PPI. The precise risk transferredto the private sector will depend on the form of PPI (e.g., service contract, concessionor equity sale) and the project in question. The link between risk and the differentforms of PPI is examined in detail in Module 2. Table 2-2 presents a more detailedoutline of the risks associated with PPI.

page 4 What is PPI and how can advisors help?

1.2 Governments still play a fundamental role

Increased PPI is often accompanied by structural changes in public sector industries.The reform model has implications for the successful structuring of PPI and alsoimplies a number of economic and political changes that encompass:• the current budgetary spending on infrastructure;• government policy;• the role of competition as the private sector is introduced;• the government’s responsibilities with the introduction of PPI; and• the appropriate internal organization of government to implement PPI.

BudgetIn most developed and developing countries, governments raise and spend directly30–50% of GDP, using these funds to provide the framework for civil society: law andorder, the justice system, defense, foreign affairs and other public goods. All too often,the definition of public goods is stretched to encompass services which could beprovided efficiently without tapping to government’s budget.

Defining public goodsA public good is one where the benefits of its provision cannot be limited only to thosewho pay for it, and where its use does not limit the quantity available to others. Streetlighting is an example of a public good. Anyone using the street benefits from the light andthe fact that one person uses it does not decrease the amount available for someone else.

In some countries, public goods are defined broadly and, as a result, significant sumsare spent on welfare payments. This is almost universally true of education and healthservices. To varying degrees, governments also provide a much broader range ofservices across areas that are not strictly public goods: water and sanitation, transport,power and telecommunications. In most cases, cost recovery for these services fromend users is possible and provision can be limited to those who pay for it.

PolicyGovernments around the world have increasingly recognized that their role should bein setting policy for service provision, and not in providing services. This separation ofpolicymaking from provision makes it possible to introduce the private sector, andcompetition, in the provision of assets and services. Along with the transfer of risk,competition is the most effective tool for increasing efficiency and reducing costs.

CompetitionIncreasingly, governments have also found that their policy objectives can be fully metwithin a competitive market. Their policy role may then be reduced to setting theframework for competitive markets (e.g., introducing competition laws to avoid abuseof market power). Over the last decade, many governments have reduced theirdirect involvement in many industries and have relied on the workings of thecompetitive market to protect consumer interests.

Recommendation 1.1: Effective PPI requires that responsibility for theprovision of a service be separated from government policy-making. Thestructure for PPI should ensure that these responsibilities are clearlyassigned and separated.

page 5 What is PPI and how can advisors help?

Target-settingIt is increasingly common for governments to set themselves and their representativesexplicit targets for withdrawing from direct oversight of infrastructure industries. In Poland, the energy regulator has a legal obligation to withdraw from the directoversight of the electricity generation market as soon as it is sufficiently competitive.Although this creates another set of challenges (i.e., deciding when the market issufficiently competitive to permit withdrawal), it recognizes the ability of acompetitive market to meet some of the government’s objectives.

1.3 Governments can use the private sector to meet objectives more effectively

While some services can be provided through interaction between consumers and themarket, there are important areas where there is less scope for governmentwithdrawal.

The presence of natural monopoliesThe first is where prices cannot be set through competition due to the existence of anatural monopoly.

This might be true of a rail line or a gas distribution system, where—it is moreefficient to have a single integrated network servicing a particular area, rather thanseveral competing networks.

What is a natural monopoly?A natural monopoly exists when costs decrease as the amount produced within asingle company increases. Ever-decreasing costs within the company mean that it ismore efficient for a single producer to meet demand than several smaller producers.

Governments may still favor private participation in these areas but want to avoid therisk to consumers from private monopolies. One way forward is to allow a privatecompany to own and operate the utility, but under the scrutiny of an independentgovernment agency—a regulator.

Provision of loss-making servicesA second area from which the government cannot withdraw is the provision of anecessary but loss-making service. There are many reasons why governments mightwant services to be provided, even at a loss. Public transport may be subsidizedbecause the cost to society of private transport in terms of environmental degradation(from pollution) and quality of life (from traffic congestion) cannot be fully recoveredfrom automobile drivers. Road systems are usually provided free, in part because ofthe difficulty of charging. Water and other services may be intentionally under-pricedfor reasons of public health. Postal services in rural communities are often cross-subsidized by urban populations for reasons of social equity.

It is important to note that a loss-making service does not have to be provided by agovernment. The private sector can be contracted to supply the service, for which itreceives an explicit payment from the government, or certain consumers may beprovided with a direct subsidy from the government to pay for the service. Thebenefits of competition can then still be realized through periodic competition for thecontract.

page 6 What is PPI and how can advisors help?

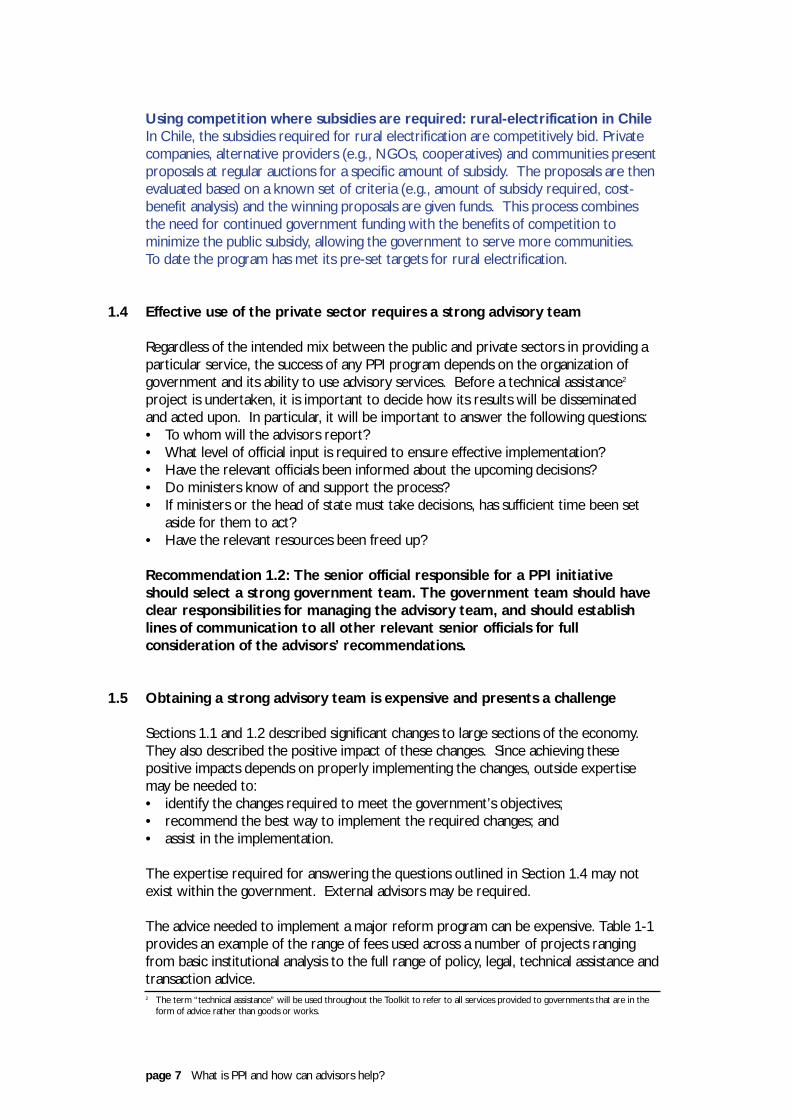

Using competition where subsidies are required: rural-electrification in ChileIn Chile, the subsidies required for rural electrification are competitively bid. Privatecompanies, alternative providers (e.g., NGOs, cooperatives) and communities presentproposals at regular auctions for a specific amount of subsidy. The proposals are thenevaluated based on a known set of criteria (e.g., amount of subsidy required, cost-benefit analysis) and the winning proposals are given funds. This process combinesthe need for continued government funding with the benefits of competition tominimize the public subsidy, allowing the government to serve more communities. To date the program has met its pre-set targets for rural electrification.

1.4 Effective use of the private sector requires a strong advisory team

Regardless of the intended mix between the public and private sectors in providing aparticular service, the success of any PPI program depends on the organization ofgovernment and its ability to use advisory services. Before a technical assistance2

project is undertaken, it is important to decide how its results will be disseminatedand acted upon. In particular, it will be important to answer the following questions:• To whom will the advisors report?• What level of official input is required to ensure effective implementation?• Have the relevant officials been informed about the upcoming decisions?• Do ministers know of and support the process?• If ministers or the head of state must take decisions, has sufficient time been set

aside for them to act? • Have the relevant resources been freed up?

Recommendation 1.2: The senior official responsible for a PPI initiativeshould select a strong government team. The government team should haveclear responsibilities for managing the advisory team, and should establishlines of communication to all other relevant senior officials for fullconsideration of the advisors’ recommendations.

1.5 Obtaining a strong advisory team is expensive and presents a challenge

Sections 1.1 and 1.2 described significant changes to large sections of the economy.They also described the positive impact of these changes. Since achieving thesepositive impacts depends on properly implementing the changes, outside expertisemay be needed to:• identify the changes required to meet the government’s objectives;• recommend the best way to implement the required changes; and• assist in the implementation.

The expertise required for answering the questions outlined in Section 1.4 may notexist within the government. External advisors may be required.

The advice needed to implement a major reform program can be expensive. Table 1-1provides an example of the range of fees used across a number of projects rangingfrom basic institutional analysis to the full range of policy, legal, technical assistance andtransaction advice. 2 The term “technical assistance” will be used throughout the Toolkit to refer to all services provided to governments that are in the

form of advice rather than goods or works.

page 7 What is PPI and how can advisors help?

Table 1-1Representative costs of hiring advisors

Country & year

Pakistan(1985-87)

Cambodia (1996-98)

Georgia(2000)

Philippines(1995)

Uganda (1998–99)

Brazil(1990s)

Source: Frontier Economics

Governments spend such large sums on advisors because of the benefits they obtainfrom them, including the avoidance of costly mistakes.

However, governments face a significant challenge in managing advisors in order toobtain the best service from them. Managing advisors involves a number of steps. • First, the government must identify the individuals or companies best placed to

undertake the project .• Second, the government must sign contracts that provide the advisors with