Brand and product integration in horizontal mergers and acquisitions

Journal of Financial Economics 11 (1983) 225-240. North-Holland Publishing Company

EXAMINING ANTITRUST POLICY TOWARDS HORIZONTAL MERGERS*

Robert STILLMAN

Lexecon Inc., Chicago, IL 60603, USA

Received June 1980, final version received March 1982

A horizontal merger must result in higher product prices to consumers to be anticompetitive or socially inefficient. Higher product prices, however, imply increased profits for rivals to the merging firms. Therefore, if a horizontal merger is to reduce consumer welfare, rival firms must rise in value at the time of events increasing the probability of the merger and fall in value when the probability of the merger declines. This paper uses daily stock return data from a sample of rivals to 11 horizontal mergers attempted between 1964 and 1972 that were challenged by the antitrust enforcement agencies. The paper tests the hypothesis that, but for the government’s action, these mergers would have resulted in higher product prices. On balance, the data favor the null hypothesis of no anticompetitive effect.

1. Introduction

Section 7 of the Clayton Act makes illegal any merger where the effect ‘may be substantially to lessen competition or to tend to create a monopoly’.’ The Celler-Kefauver amendment of 1950 significantly extended the reach of this statute and, since that time, the Federal Trade Commission (FTC) and the Department of Justice (DOJ) have brought several hundred Section 7 cases. In the past, many of these cases have been brought against vertical and conglomerate mergers. Now, however, with the release of the Justice Department’s new Merger Guidelines, the government’s enforcement of section 7 has been refocussed. Summarizing the Antitrust Division’s present policy, Assistant Attorney General William F. Baxter has stated: ‘Mergers are never troublesome except insofar as they give rise to horizontal problems’.2

An antimerger policy that focuses exclusively on horizontal mergers is consistent in principle with economic efficiency. Mergers between current

*This paper is derived from my dissertation research and I would like to thank the members of my U.C.L.A. committee for their assistance: Harold Demsetz (chairman), Benjamin Klein, Edward Learner. and Richard Roll. 1 would also like to thank Peter Dodd, Michael Jensen and Richard Ruback for thier comments. Finally. thanks are due to Laurence Levin for his timely computer assistance.

‘I5 U.S.C.A. 518. ‘Justice Department’s new merger guidelines may be ready by winter, Baxter indicates’,

Antitrust and Trade Regulations Report A-5, Aug. 13, 1981. The Merger Guidelines released on June 14, 1982.

0304-405x/83/$03.00 0 Elsevier Science Publishers

1027 were

226 R. Stillman, Antitrust horizontal merger policy

producers of close substitutes by definition increase industry concentration, and economists have long accepted as a theoretical proposition the link between concentration and collusion (tacit or explicit). The link is traced most articulately by Stigler (1968) in his theory of oligopoly. Other industrial organization models suggest a similar basis for concern with horizontal mergers. For example, in the dominant firm model, the demand facing the dominant firm becomes less elastic as the market share of the fringe firms diminishes.3 Thus, the acquisition of a rival by the dominant firm increases the dominant firm’s market power as measured by the Lerner index and, all

else equal, results in an increased gap between price and marginal cost. In Cournot-Nash models of firm interaction, the equilibrium price rises as the number of firms declines. Thus, in these models too horizontal mergers imply less efficient resource allocation, all else equal.

But while horizontal mergers have the clearest anticompetitive potential, there are also potential efficiency gains from such mergers that the new antimerger policy may sacrifice. In addition to the obvious possibility of complementarities in production and distribution, managers in the same industry may have a comparative advantage at identifying mismanaged firms. By foreclosing these managers from the market for corporate control, an anti-horizontal merger policy may impair efficient allocation of managerial talent and, perhaps more importantly, weaken significantly the incentive of incumbent managers to maximize the value of their firms. As Manne (1965)

and others have suggested, the threat of take-over disciplines management and helps reduce agency costs.

The research reported in this paper contributes to the analysis of whether there is a social efficiency basis for the antitrust policy against horizontal mergers. The paper asks: Is there any evidence that the horizontal mergers challenged in the past by the federal government would have resulted in higher product prices to consumers? Daily stock market data from a sample of 11 challenged horizontal mergers attempted between 1964 and 1972 are studied and the conclusion is that the data do not reject the null hypothesis of no anticompetitive effect.4

The most significant limitation on the study is that, unavoidably, the sample includes no horizontal mergers that would have occurred, but were deterred by antitrust enforcement policy. If antimerger policy succeeds in deterring firms from even attempting the most anticompetitive mergers, actual challenges could be almost exclusively against socially efficient mergers and yet the policy might still be consistent with efficiency. Of course, on the other hand, the less discerning the government is in its challenges, the more firms will be deterred from attempting cost-saving, socially efficient mergers - the deterrent effect cuts both ways.

%ee Landes and Posner (1981) for an exposition of the dominant firm model. 4This conclusion is consistent with the findings of Eckbo (1983), who uses a similar

methodology to test the hypothesis.

R. Stillman, Antitrust horizontal merger policy 221

The body of the paper is divided into three sections. The following section develops simple testable implications of the hypothesis that the challenged

horizontal mergers would have raised product prices and thereby reduced consumer welfare. Section 3 follows with a description of the sample of challenged horizontal mergers studied and how the sample was selected. Section 4 discusses the empirical technique used to test the inefficiency hypothesis and then reports the estimation results.

2. Testable implications of the inefficiency hypothesis

As mentioned in the introduction, the link between an antitrust policy directed against horizontal mergers and economic efficiency is derived from several models of industrial organization. Stigler’s oligopoly theory, the dominant firm model (when the merger involves the dominant firm), and Cournot-Nash interaction models all share the implication that, other things equal, horizontal mergers tend to result in higher product prices in equilibrium. If the industry produces a heterogeneous good, the basic implication is that quality-adjusted prices will tend to be higher post-merger.

Very few challenged horizontal mergers survive government litigation without the merging firms at least agreeing to a consent decree that in some way restricts their behavior. Therefore, it is not practicable to test the inefficiency hypothesis directly by studying the pattern of post-merger product prices. In the sample of mergers studied in this paper, only two of eleven mergers resulted in an unambiguous legal victory for the merging firms. In the remainder of the cases, there either was no post-merger period to observe (the merger was abandoned or divestiture was ordered) or behavior in the post-merger period has been constrained by a consent decree.

An alternative and empirically tractable approach to testing the inefficiency hypothesis builds on an indirect implication of the hypothesis. In

the industrial organization models discussed above, not only do product prices tend to be higher following a horizontal merger: in addition, a price- increasing horizontal merger benefits other firms in the industry affected by the merger. In the dominant firm model, the rivals are sheltered by a price umbrella. In the tacit collusion models - a label that adequately describes

both Stigler’s oligopoly model and Cournot-Nash models - the rival firms restrict output and share in the resulting increase in industry-wide profits.

Thus, an implication of the inefficiency hypothesis is that the value of rival firms should increase as the result of anticompetitive horizontal mergers. This capital value implication makes stock market data the natural vehicle for empirical testing. Maintaining a ‘rational expectations’ or ‘efficient markets’ assumption, today’s stock prices represent the capital market investors’ best estimate of the present discounted value of a share in firms expected future net income. If the announcement of a horizontal merger changes investors’ expectations about future product prices and hence firms income, the

228 R. Stillman, Antitrust horizontal merger policy

announcement will coincide with an abnormal rise or fall in stock values. The inefficiency hypothesis predicts that events that raise the probability of a merger occurring should coincide with abnormally high returns on the stock of rivals to the merging firms, while probability-decreasing events (such as judicial decisions against the merger) should coincide with abnormally low returns on rivals’ stock.

This set of predictions will be tested in section 4 on a sample of challenged horizontal mergers described in section 3. It is worth noting here, however, that the pattern of abnormal returns just described, although necessary for a horizontal merger to be socially inefficient, is not sufIicient.5 First, as Williamson (1968) demonstrates, higher product prices can be consistent with efficiency if accompanied by significant production cost savings. In terms of the dominant firm model, the merger may both reduce marginal costs and make the dominant firm’s demand curve less elastic. The equilibrium price may rise and yet total production costs may decline sufficiently to offset the deadweight loss from the price increase. Thus, one could observe a pattern of abnormal returns consistent with the inefftciency hypothesis, and yet the horizontal merger might be efficient on balance. Second, a merger event may signal more than a change in the probability of a merger occurring. For

example, a merger announcement may signal the existence of hitherto unappreciated economies of scale that can be realized by rivals as well as by the merging firms. Investors might speculate that the rivals themselves are likely to merge and realize the same scale economies and, thus, investors could react to news of a socially efficient merger that would actually lower product prices by bidding up the stock price of rival tirms.‘j

3. Constructing a sample of challenged horizontal mergers

3.1. Sample selection criteria

To test the hypothesis that horizontal mergers challenged by the government would have reduced consumer welfare had they gone

5More precisely, the pattern of abnormal returns described is a necessary condition of conventional industrial organization models. There are other models, such as Thompson and Faith (1979) that emphasize the threat to consumer welfare posed by predatory behavior. If a horizontal merger facilitates predatory behavior and in this way results in long-run higher product prices, rival firms obviously need not benefit from efficiency-reducing horizontal mergers. Firms outside the merger will be victims along with consumers. Whether predatory behavior is, in fact, ever observed is a long debated subject in industrial organization that is not addressed here.

6There are other signalling scenarios. For example, a judicial decision against a merger may establish a precedent and signal that future antitrust actions against firms in the industry are likely to be decided in favor of the government. This antitrust ‘overhang’ is equivalent in effect to regulation detrimental to the interests of all firms in the industry. Thus, the partial effect of blocking a horizontal merger could be to raise product prices (indicating the merger would have been efficient) and yet rivals’ value might fall with this merger event.

R. Stillman, Antitrust horizontal merger policy 229

unchallenged, a sample of mergers with the following characteristics is required. The sample must consist of horizontal mergers (a) challenged by either DOJ or the FTC; (b) in industries with identifiable rivals that are large enough to be traded on the New York or American stock exchanges; (c) for which it is possible to isolate events that unambiguously had an effect on the perceived likelihood of the merger.

The rationale for the first two criteria is obvious. The study concerns horizontal mergers, therefore challenged vertical, conglomerate and potential competition mergers are of no interest. Since the empirical tests will require stock market data, any merger in industries where firms are not traded on the two major exchanges, and hence are not on the stock return of the Center for Research in Security Prices (CRSP) at the University of Chicago, is also of little value to this study.

The rationale for the third criterion - that there be clearly identifiable events affecting the perceived likelihood of the merger - is also obvious in that little would be learned by examining stock price movements of rivals on dates when investors’ assessments of the probability of a merger were unchanged. This problem, of course, is encountered in any study using stock market data and typically the response is to study returns over some longer period extending before and possibly after the hypothesized ‘event date’ to

ensure that returns on the true event date have been recorded. The cost of this usually unavoidable empirical compromise is that the power of the ensuing tests is reduced from what it would be were the true event date

known. By measuring returns over a longer period, the variance about the predicted normal return expands and it becomes more difficult to reject the null hypothesis of no abnormal performance. As will be discussed below, one of the attractive features of this study is that this problem can be circumvented; it is possible to infer from data on the merging firms returns whether a hypothesized event actually occasioned investor reaction.

3.2. Identifying challenged horizontal mergers in industries j& which stock return data are available on identifiable rivals ~

The principal source of data on mergers challenged by the government under section 7 is the Merger Case Digest compiled by the American Bar Association (ABA). At the time research began on this study, data were available in the Digest on section 7 cases filed in 1970 or earlier. For the years 1971-1974, short summaries of merger cases reported in the Commerce Clearing House (CCH), Trade Regulation Reporter, were used to identify horizontal cases. Constructing the sample of 11 mergers reported in table 1 from the ABA and CCH lists was largely a process of excluding mergers for failing to meet one of the criteria described above. Since the CRSP daily return tape begins at July 1, 1962, the first reason for eliminating a section 7

230 R. Stillman, Antitrust horizontal merger policy

Table 1

Challenged horizontal mergers in the sample.

Acquiring (Acquired)

Chrysler (Mack Trucks)

Schenley (Buckingham)

Russell Stover (Fanny Farmer)

General Dynamics

(UEC)

Sterling Drug (Lehn and Fink)

Bendix (Fram)

Cooper Industries (Waukesha Motor)

Atlantic Richlield (Sinclair)

Gould National (Clevite)

Warner Lambert (Parke Davis)

Jim Walter (Panacon)

Merger year

1964

1964

1965

1966

1966

1967

1967

1968

1969

1970

1972

Industry

Heavy trucks

Liquor distilling

Candy

Coal

Health and beauty aids

Filters

Natural gas engines

Oil relining

Batteries

Ethical drugs

Roofing materials

Complaint year Agency Outcome

Merger 1964 DOJ abandoned

1966 DOJ Consent

Merger 1965 DOJ abandoned

Pro-def. 1967 DOJ decision

Pro-def. 1969 FTC decision

1967 FTC Consent

Merger 1967 DOJ abandoned

1969 DOJ Consent

1969 DOJ Consent

Pro-govt. 1971 FTC decision

Pro-govt. 1974 FTC decison

case from the sample was if the merger was announced prior to that date. This filter eliminated many cases, nevertheless it left 104 DOJ and 59 FTC cases from the Merger Case Digest as initial candidates for inclusion in the

study. Next, bank mergers and mergers in heavily regulated industries, such as

telecommunications, were exluded for the reason that the link, if one exists, between horizontal mergers and anticompetitive behavior does not seem likely to be as significant in a regulated environment.7 Then, mergers that according to the ABA or CCH description were not primarily horizontal or cases that complained of a series of mergers were excluded. The reason for excluding the multiple merger complaints was that in these the government was complaining of the cumulative effect of the mergers and did not claim

‘Actually, this is an empirical question that could be tested. As a practical matter, however, virtually all the mergers excluded for this reason were bank mergers involving local banks. It is unlikely that the rivals to such firms would be traded on major stock exchanges and therefore such mergers would drop from the sample for this reason.

R. Stillman, Antitrust horizontal merger policy 231

that any one merger had a significant effect on product prices. This theory cannot be tested using the methodology employed here.

These filters reduced the universe of Digest cases to 45 DOJ and 22 FTC challenged horizontal mergers. Next, mergers in which neither the acquired nor acquiring firm were traded on the New York or American stock exchanges were excluded on the grounds that it was unlikely that rivals to these firms would be on the CRSP tape either. This left 28 DOJ and 17 FTC cases from the Digest as possible candidates. At this point, an attempt was made to identify the other firms in the industries that the government alleged would have been adversely affected by the challenged mergers. The first source for this information was the published opinions in cases that were litigated. These decisions often contain a description of the industry and identify industry members. The other source of data was fact memoranda prepared by the enforcement agencies in preparation for filing complaints.

These memoranda were obtained by filing a request under the Freedom of Information Act. In some cases, the memoranda could not be located, while in others there was no description of other firms in the supposedly affected industries. After this penultimate filter, the universe of candidate mergers was reduced to 18.

3.3. Identifying unambiguous merger event dates

The next step in constructing the sample involved collecting dates of events likely to have affected the perceived probability that the 18 mergers would ultimately be consummated. The following events were hypothesized to be of this type: merger rumors and announcements; decisions by the courts on government motions for temporary restraining orders and preliminary injunctions; decisions by district courts (DOJ complaints) and administrative law judges (FTC complaints) on the merits of the merger

complaints; and decisions by appellate courts such as the commissioners of the FTC, the Court of Appeals, and the Supreme Court. The primary sources for these dates were the Wall Street Journal and docket sheets kept by the DOJ and FTC (showing the dates of the complaint and any subsequent litigation events).

The question then became whether these events were truly events - did they transmit any new information to the capital markets? The fortunate feature of this study is that there is an empirical means of answering this question. Several studies of mergers, most recently Dodd (1980), have found large, significantly positive abnormal returns accruing to acquired firms on the day of and day prior to merger announcements. From this, one can infer that if merger events of the type identified above truly conveyed new information, then on or about these dates there should have been discernible abnormal movements in the stock of the would-be acquired firm and, though

Tab

le

2

Des

crip

tion

of m

erge

r ev

ents

in

th

e sa

mpl

e of

11

mer

gers

in

th

e pe

riod

S/

644/

72

and

dem

onst

ratio

n th

at

inve

stor

s re

acte

d to

th

ese

even

ts.a

Mer

ger

Eve

nt

Chr

ysle

r M

ack

Sche

nley

B

ucki

ngha

m

Rus

sell

Stov

er

Fann

y Fa

rmer

Gen

eral

D

ynam

ics

Uni

ted

Ele

ctri

c C

oal

Ster

ling

Dru

g L

ehn

and

Fink

mer

ger

anno

unce

d af

ter

clos

e of

tra

ding

, W

SJ

5141

64

com

plai

nt

tiled

, 71

3016

4

prel

imin

ary

inju

nctio

n,

8117

164

mer

ger

agre

e-

men

t an

noun

ced,

W

SJ

8127

164

mer

ger

agre

e-

men

t an

noun

ced,

W

SJ

2191

65

maj

or

stoc

k pu

r-

chas

e by

G

ener

al

Dyn

amic

s,

WSJ

91

2916

6

Leh

n an

d Fi

nk

an-

noun

ced

rece

ivin

g se

vera

l ac

quis

ition

bi

ds,

incl

udin

g on

e,

from

St

erlin

g,

WSJ

l/

31/6

6

Leh

n an

d Fi

nk

appr

oved

bi

d fr

om

Ster

ling,

W

SJ

3128

166

Stoc

k Pr

edic

ted

obse

rved

ef

fect

Mac

k +

WI64

0.0634

0.0465

514164

0.0767

0.0424

Mac

k

Mac

k

Sche

nley

Fann

y Fa

rmer

UE

C

Leh

n an

d Fi

nk

+ 2/I/66

0.1475

0.0400

Dat

e A

ctua

l re

turn

Upp

er

or

low

er

boun

d of

95%

co

nfid

ence

in

terv

al

_ 7131164

- 8117164

+ 8126164

+ 214165

2/S/65

218165

+ 9130166

-0.1

070

-0.1

243

0.05

81

0.02

91b

0.02

82b

0.02

74b

0.16

67

-0.0354

-0.0364

0.0256

0.0365

0.0352

0.0346

0.0304

Leh

n an

d Fi

nk

+ 3128166

0.11

04

0.0402

Ben

dix

Fram

Coo

per

Wau

kesh

a

Atla

ntic

R

ichf

ield

Si

ncla

ir

Oil

Gou

ld

Nat

iona

l C

levi

te

War

ner

Lam

bert

Pa

rke

Dav

is

Jim

W

alte

r

Ster

ling

+

Fram

+

Coo

per

+

FTC

ju

dge

dism

isse

d co

mpl

aint

, S/

12/7

1

Fram

ag

reed

to

m

erge

r in

pr

inci

ple,

W

SJ

l/3/

61

Coo

per

plan

s to

ac

quir

e re

mai

nder

of

sh

ares

W

SJ

7/25

/61

com

plai

nt

file

d,

l/15/

69

Sinc

lair

tem

pora

ry

rest

rain

ing

orde

r, l/1

7/69

mer

ger

agre

e-

men

t an

noun

ced,

31

1016

9

Cle

vite

Park

e D

avis

ag

reed

to

m

erge

r in

pr

inci

ple,

W

SJ

7/31

/70

Park

e D

avis

Jim

W

alte

r ag

reed

to

bu

y 89

%

stoc

k in

tere

st,

WSJ

41

4172

Jim

W

alte

r

_ l/1

6/69

-0

.095

5 -

0.03

29

+

3/10

/69

0.10

93

0.04

45

5/12

/71

0.03

61

0.02

53

5113

171

0.02

22

0.02

18

12/2

8/M

0.

0751

0.

0373

t/3

/61

0.11

32

0.04

06

7125

161

0.10

51

0.04

70

+

7/31

/70

0.12

33

0.05

17

+

4141

72

0.06

08

0.04

09

“Sou

rces

: W

all

Stre

et

Jour

nal

(WSJ

);

dock

et

shee

ts

on

tile

at

the

FTC

an

d D

OJ;

an

d fa

ct

mem

oran

da

prep

ared

by

en

forc

emen

t ag

enci

es

prio

r to

til

ing

a co

mpl

aint

. ‘T

he

ratio

of

the

th

ree-

day

cum

ulat

ive

resi

dual

to

th

e th

ree-

day

stan

dard

er

ror

is 2

.73.

234 R. Stihan, Antitrust horizontal merger policy

less certainly, the would-be acquiring firm. (Surprisingly, Dodd also finds small, but significantly negative abnormal returns on the stock of acquiring

firms over the same announcement period.) To implement this test, the following market model was estimated by

ordinary least squares for each merging firm having daily stock return data available:

R[, = cli + BiRmt + &it,

where

Ri, =return on security i over period t, R,, =return on value weighted market portfolio over period t,

&it =disturbance term over period t.

The estimation period was the twelve month period ending one month

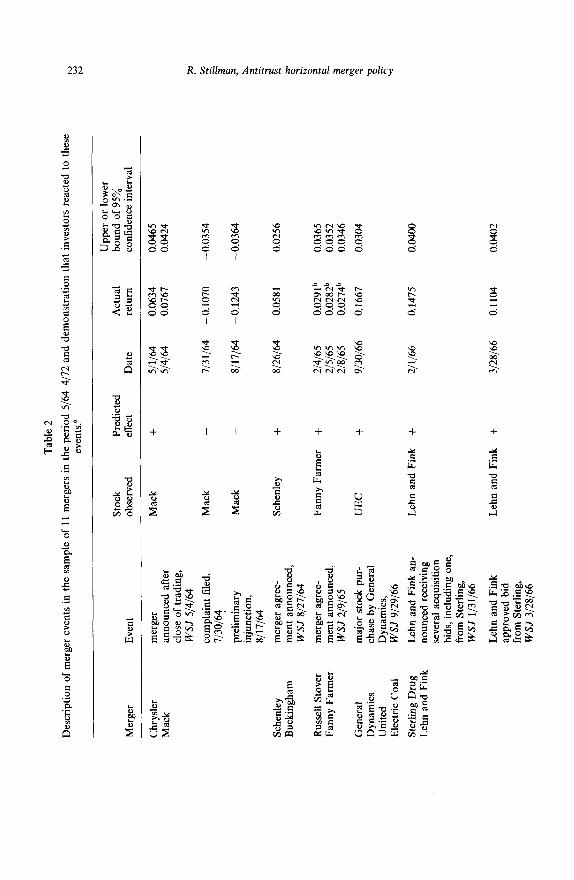

after the hypothesized event dates. Examining the residuals from these regressions, there was a striking correspondence between outliers and hypothesized event dates in 11 of the 18 mergers. The results from these 11

mergers are reported in table 2, which shows the merger; the nature and date of the merger event; the stock observed (which is always the stock of the acquired firm unless no returns were available for this firm); the predicted effect on the firm’s value given the nature of the hypothesized event; the date of the outlier; the actual return on that date; and the upper or lower bound of the 95 percent confidence interval about the predicted normal return for that date. In each instance reported, actual returns on days on or about the hypothesized event date were outside the 95 percent confidence interval and, in most cases, considerably so. In the empirical work reported in section 4, the dates of these outliers (and only these dates) are considered event dates - the dates on which new information concerning the mergers reached the capital markets.

4. Empirical results

4.1. Estimation technique

The inefficiency hypothesis - the hypothesis that challenged horizontal mergers would have, but for the government’s action, led to increased product prices - implies that rival firms in industries affected by challenged mergers should have risen in value when the mergers in the sample became more likely and depreciated when the probability of these mergers declined. To test this hypothesis, equally weighted portfolios of the stock of rivals were formed and, for each merger and significant merger event in the sample, the following modified market model was estimated by ordinary least squares:

R. Stillman, Antitrust horizontal merger policy 235

R,, = up + B,Rmt + Y,D, + ~ptt where

R,, =return on equally weighted portfolio of rivals over period t, R,, = return on value weighted market portfolio over period t, D, =dummy variable that has a value of one if period t is an event date

and zero otherwise,

&Pi =disturbance term on portfolio of rivals over period t.

The dummy variables in these regressions measure abnormal returns. In each regression, there is one dummy variable for each merger event date. For example, in the Chrysler-Mack merger, where the capital markets apparently reacted to news of the merger on May 1 and May 4, 1964, the regression would contain two dummy variables, the tirst taking a value of one on May 1 and the second taking a value of one only on May 4. As before, estimation was over a twelve-month period ending one month after the event date (the latest event date in cases such as Chrysler-Mack). Because the effects of the merger information have been purged by the dummy variables, the intercept and market return coefficients are not influenced by the merger events.

4.2. Estimation results

The underlying objective of this study is to determine whether the antitrust enforcement agencies have tended to challenge horizontal mergers that would have in fact resulted in higher product prices. To this end, abnormal returns on portfolios of the stock of rivals to firms engaged in challenged horizontal mergers have been estimated for days on which the perceived probability of the mergers evidently changed. The results are summarized in table 3. The table lists, for each merger in the sample, the firms in the portfolio of rival$ the merger event; the date of the event; the sign on the rivals’ abnormal return predicted by the inefficiency hypothesis; the abnormal return estimate;

and the t-statistic on this estimate. Where there are two days on which the capital markets appear to have reacted to a particular event (e.g., the May 1 and May 4, 1964 reactions to the news of the Chrysler-Mack merger), or where two merger events occurred in roughly the same time period (e.g., the complaint filed against the Chrysler-Mack merger on July 30 and the preliminary injunction against the merger on August 17, 1964) the magnitude and significance of the sum of the dummy variable coefficients is reported. These multiple day abnormal return estimates are enclosed in parentheses in the table. This manner of reporting multiple day results is similar to the

‘The number of rivals varies from merger to merger because the number of identifiable rivals with traded stock varies.

Tab

le

3

Abn

orm

al

retu

rns

on

port

folio

s of

riv

al

tirm

s on

da

ys

whe

n ch

alle

nged

ho

rizo

ntal

m

erge

rs

beca

me

mor

e or

le

ss

likel

y fo

r 11

sa

mpl

e m

erge

rs

in

the

peri

od

_5/6

44/7

2.”

Mer

ger

Firm

s in

po

rtfo

lio

of r

ival

s E

vent

D

ate

Pred

ictio

n of

ine

ffic

ienc

y hy

poth

esis

A

bnor

mal

re

turn

f-st

atis

tic

on

abno

rmal

re

turn

Chr

ysle

r M

ack

Inte

rnat

iona

l H

arve

ster

Gen

eral

M

otor

s

mer

ger

5/l/6

4 +

anno

unce

men

t

5141

64

(5/t/

64

(1)

+ S/

4/64

)

com

plai

nt

7130

164

_

file

d

prel

imin

ary

inju

nctio

n g/

17/6

4 _

(7/3

0/64

(-

) +

8/l

7/64

)

0.01

01

1.53

0.00

62

0.94

(0

.016

3)

(1.7

4)

- 0.

0040

-0

.60

0.00

05

0.07

(-0.

0035

) (-

0.37

)

Sche

nley

B

ucki

ngha

m

Nat

iona

l m

erge

r g/

26/6

4 +

0.00

09

0.14

D

istil

lers

an

noun

cem

ent

Heu

blei

n

Bro

wn

Fore

man

Am

eric

an

Dis

tille

rs

Rus

sell

Stov

er

Bar

tons

Fa

nny

Farm

er

Can

dy

mer

ger

2141

65

+ 0.

0216

0.

86

anno

unce

men

t 21

5165

+

o.oo

o2

0.01

2/

g/65

+

- 0.

0209

-0

.83

WW

5 t

2151

65

(+)

(0.0

010)

(0

.02)

t

2181

65)

Gen

eral

D

ynam

ics

Con

oco

Uni

ted

Stan

dard

O

il E

lect

ric

Coa

l of

Ohi

o

stoc

k pu

rcha

se

by

Gen

eral

D

ynam

ics

9130

166

+ 0.

0041

0.

50

Ster

ling

Dru

g L

ehn

and

Fink

W

arne

r L

ambe

rt

Leh

n an

d Fi

nk

2/l/6

6 +

0.00

57

Pfiz

er

rece

ived

m

erge

r bi

ds

Am

eric

an

Leh

n an

d Fi

nk

3128

166

+ 0.

0103

C

yana

mid

ap

prov

ed

bid

from

St

erlin

g

WI66

(+)

(0.0

160)

t

3128

166)

FTC

ju

dge

5112

171

+ -

0.00

09

dism

isse

d 5/

13/7

1 0.

0177

co

mpl

aint

(5

1121

71

(+)

(0.0

169)

+5

/13/

71)

Ben

dix

Fram

G

ener

al

Mot

ors

mer

ger

agre

emen

t 12

1281

66

+ -0

.001

3

l/3/6

7 ( 1

2128

166

(=)

0.04

54

(0.0

441)

+

l/3/6

7)

0.98

1.77

(1.9

4)

-0.1

2 2.30

(1.5

4)

-0.1

4 4.99

(3

.42)

Tab

le

3 (c

ontin

ued)

Mer

ger

Firm

s in

po

rtfo

lio

of r

ival

s E

vent

D

ate

Pred

ictio

n of

ine

flic

ienc

y hy

poth

esis

A

bnor

mal

re

turn

t-st

atis

tic

on

abno

rmal

re

turn

Coo

per

Wau

kesh

a W

orth

ingt

on

Cat

erpi

llar

Inge

rsol

l-R

and

Dre

sser

In

dust

ries

Coo

per

plan

s st

ock

purc

hase

7/25

/61

+ 0.

0020

0.

22

Atla

ntic

R

ichl

ield

C

onoc

o co

mpl

aint

l/1

6/69

_

0.00

61

1.21

Sinc

lair

O

il Sh

ell

file

d;

Stan

dard

O

il te

mpo

rary

of

Ind

iana

re

stra

inin

g E

xxon

or

der

Tex

aco

Gou

ld

Nat

iona

l C

levi

te

Uni

on

Car

bide

E

SB

PR

Mal

lory

mer

ger

agre

emen

t 31

1016

9 +

- 0.

0057

-0

.58

War

ner

Lam

bert

A

mer

ican

H

ome

mer

ger

l/3 l

/IO

+

0.00

08

0.09

Park

e D

avis

Pr

oduc

ts

agre

emen

t U

pjoh

n Sm

ithkl

ine

Am

eric

an

Cya

nam

id

Jim

W

alte

r Pa

naco

n C

erta

in-T

eed

John

s M

anvi

lle

Flin

tkot

e

mer

ger

agre

emen

t 41

4172

+

0.00

16

0.15

“The

da

ta

in

tabl

e 2

indi

cate

th

at,

for

som

e m

erge

rs,

inve

stor

s ap

pear

to

ha

ve

reac

ted

to

a si

ngle

ev

ent

on

mor

e th

an

one

day.

In

ot

her

case

s,

two

mer

ger

even

ts

occu

rred

ve

ry

clos

e in

tim

e.

In

such

in

stan

ces,

ta

ble

3 re

port

s ab

norm

al

retu

rns

and

t-st

atis

tics

for

the

indi

vidu

al

days

in

dica

ted

in

tabl

es

2 an

d fo

r th

e re

leva

nt

mul

tiple

-day

pe

riod

. T

hese

m

ultip

le-d

ay

stat

istic

s ar

e en

clos

ed

in

pare

nthe

ses.

R. Stillman, Antitrust horizontal merger policy 239

cumulative residual approach adopted in other stock market studies,’ except that it provides a more powerful test of the inefficiency hypothesis; abnormal returns on days where there is no evidence that the capital markets were reacting to merger information are excluded from the test statistic.

Of the 11 mergers in the sample and 18 merger event dates, in only two instances does the stock of rival firms exhibit an abnormal return that is consistent with the inefficiency hypothesis and significant at the live percent level. On January 3, 1967, the day that Fram. agreed in principle to merge with Bendix, the stock of General Motors had an abnormal positive return of 4.54 percentage points. This abnormal return, which is not obviously

explained by some other event specific to General Motors,” is almost live times the standard error of the disturbance term. However, General Motors stock exhibits no similar abnormally high return on December 28, 1966 when Fram stock rose by 7.51 percent apparently in anticipation of the merger. In fact, General Motors stock performed abnormally poorly on that day, although insignificantly so.

The other abnormal return significant in the direction predicted by the inefficiency hypothesis occurred on May 13, 1971, the day after an FTC judge dismissed the complaint against the merger between Sterling Drug and Lehn and Fink. The portfolio of Warner Lambert, Pfizer, and American Cyanamid had an abnormal positive return of 1.77 percentage points (t- statistic of 2.30). The significance of this result is somewhat surprising since, as reported in table 2, the return on Sterling Drug stock for that date was

only marginally abnormal. However, it is interesting to note that when Lehn and Fink announced approval of Sterling Drug’s bid on March 28, 1966, a day on which Lehn and Fink stock rose by 11.04 percent against a predicted normal return of 0.11 percent, the portfolio of rivals also experienced a marginally significant positive abnormal return. Thus, there seems at least weak evidence that the returns on the stock of rivals to this merger conform to the pattern predicted by the inefficiency hypothesis.

5. Conclusion

The Justice Department’s new Merger Guidelines make horizontal mergers

the principal target of merger antitrust policy. The topic of this paper is the record of past governmental efforts to block horizontal mergers. In particular, is there any evidence that horizontal mergers challenged in the past by the Department of Justice and Federal Trade Commission would

‘See, for example, Fama, Fisher, Jensen and Roll (1969), Mandelker (1974), and Ellert (1976). “On January 4 1967 the Wall Street Journal printed two stories concerning General Motors: 3 1

one reporting that 1966 production statistics were below the 1965 level; the other reporting plans to expand a Toledo, Ohio transmission plant.

240 R. Stillman, Antitrust horizontal merger policy

have resulted, but for the government’s action, in higher product prices to consumers?

Daily stock market data from a sample of 11 challenged horizontal mergers attempted between 1964 and 1972 are used to test this hypothesis. If a horizontal merger raises product prices, other firms in the industry affected by the merger benefit. Therefore, if the challenged mergers in the sample would have been socially inefficient, rivals to the merging firms should have risen in value on days of events that increased the probability of the mergers and depreciated on days of events that decreased the probability of the mergers.

The results reported in section 4 indicate that rivals in only one merger (Sterling Drug - Lehn and Fink) in the sample of 11 exhibited a pattern of abnormal returns generally consistent with the predictions of the inefficiency hypothesis. The rival in one other merger (Bendix-Fram) revealed a mixed pattern of abnormal returns: significant in the direction of the ineftIciency hypothesis at the time of one event, insignificant at the time of another event. The rivals in the other nine mergers exhibited no abnormal returns of any kind. If the sample studied here is representative of the universe of challenged horizontal mergers, these findings suggest that on balance the government has brought Section 7 cases against horizontal mergers that were not expected by investors to have any appreciable effect on product prices.

American Bar Association, 1970, Merger case digest (American Bar Association, Chicago, IL). Commerce Clearing House, Trade Regulation Reporter (Commerce Clearing House, New York). Demsetz, H., 1973, Industry structure, market rivalry, and public policy, Journal of Law and

Economics 16, l-10. Dodd, P., 1980, Merger proposals, management discretion and stock holder wealth, Journal of

Financial Economics 8, 105-137. Eckbo, B., 1983, Horizontal mergers, collusion, and stockholder wealth, Journal of Financial

Economics, this issue. Ellert, J., 1976, Mergers, antitrust law enforcement and stockholder returns, Journal of Finance

31, 715-732. Fama, E., L. Fisher, M. Jensen and R. Roll, 1969, The adjustment of stock prices to new

information, International Economic Review 10, 1-21. Landes, W. and R. Posner, 1981, Market power in antitrust cases, Harvard Law Review 94,

937-996. Mandelker, G., 1974, Risk and return: The case of merging firms, Journal of Financial

Economics 1, 303-336. Manne, H., 1965, Mergers and the market for corporate control, Journal of Political Economy

78, 11&120. Stigler, G., 1968, The organization of industry (Richard D. Irwin, Homewood, IL). Thompson, E. and R. Faith, 1979, A model of non-competitive interdependence and anti-

monopoly laws, Discussion paper no. 143 (University of California, Los Angeles, CA). Williamson, O., 1968, Economies as an antitrust defense: The welfare tradeoff, American

Economic Review 58, 18-36.

Copyright © 2022 FDOKUMEN